2015-0054 CHFFA OS.xps - CA.gov

182

REFUNDING ISSUE—Book-Entry Only RATING: S&P “A+” See “RATING” herein. In the opinion of Quint & Thimmig LLP, Larkspur, California, Bond Counsel, subject to compliance by the Authority and the Corporation with certain covenants, under present law, interest on the Bonds is excludable from gross income of the owners thereof for federal income tax purposes and is not included as an item of tax preference in computing the federal alternative minimum tax for individuals and corporations, but such interest is taken into account in computing an adjustment used in determining the federal alternative minimum tax for certain corporations. In addition, in the opinion of Bond Counsel, interest on the Bonds is exempt from personal income taxation imposed by the State of California. See “TAX MATTERS” herein. $11,965,000 CALIFORNIA HEALTH FACILITIES FINANCING AUTHORITY Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens) Series 2015 Dated: Date of delivery Due: April 1, as shown below The $11,965,000 California Health Facilities Financing Authority Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2015 (the “Bonds”), will constitute limited obligations of the California Health Facilities Financing Authority (the “Authority”) secured under the provisions of the Indenture and the Loan Agreement described herein, and will be equally and ratably payable from loan payments made by Lincoln Glen Manor for Senior Citizens (the “Corporation”) to the Authority under the Loan Agreement and from certain funds held under the Indenture. The proceeds of the Bonds will be used to (a) provide for the advance refunding of a portion of the outstanding California Municipal Finance Authority Insured Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2011 (the “Refunded 2011 Bonds”), the proceeds of which were used to (i) refund, on a current basis, all outstanding ABAG Finance Corporation for Nonprofit Corporations Insured Certificates of Participation (Lincoln Glen Manor for Senior Citizens), Series 2000, executed and delivered to (A) refinance certain existing indebtedness of the Corporation, (B) finance the renovation of existing buildings, and (C) finance the costs of construction of a 31 unit assisted living facility; (ii) finance the conversion of 8 independent living units (from a 20 unit building) into 11 memory care beds for patients suffering from Alzheimer’s disease and dementia; and (iii) finance the expansion, remodeling and updating of the Corporation’s Central Manor, all located at the Corporation’s multi-level facility for the elderly at 2671 Plummer Avenue in the City of San Jose, California, owned or to be owned and operated by the Corporation; (b) fund a reserve fund for the Bonds; and (c) pay a portion of the costs of issuance of the Bonds (collectively, the “Refinancing Plan”). See “THE REFINANCING PLAN” herein. Bonds will not be secured by any property of the Authority other than the pledge of Revenues, as and to the extent specified in the Indenture. Revenues will primarily consist of loan payments made by the Corporation. No form of taxation will be pledged or levied to provide for payment with respect to the Bonds. The Authority will assign to U.S. Bank National Association, San Francisco, California, as trustee (the “Trustee”), its interests under the Loan Agreement and will grant to the Trustee a lien on and pledge of Revenues, monies and investments held in the funds and accounts created under the Indenture. The Loan Agreement shall contain terms and conditions that are on parity with those terms and conditions of the loan agreement relating to the Refunded 2011 Bonds. Pursuant to the Loan Agreement, the Corporation will be required to make payments to the Authority sufficient to pay all principal of and interest on the Bonds. See “SECURITY FOR THE BONDS” herein. The Bonds will be issued as fully registered bonds and, when delivered, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). DTC will act as securities depository for the Bonds. Individual purchases of interests in the Bonds will be made in book-entry form only. Purchasers of such interests will not receive physical certificates. Interest on the Bonds is payable semiannually on each April 1 and October 1, commencing October 1, 2015. Principal of and interest on the Bonds is payable directly to DTC by the Trustee. Upon receipt of payments of principal of, premium, if any, and interest on the Bonds, DTC will in turn remit such payments to the DTC Participants for subsequent disbursement to the beneficial owners of the Bonds, as described herein. See “The BONDS—Description of the Bonds” and “—Book-Entry Only System” herein and APPENDIX F — “BOOK-ENTRY ONLY SYSTEM.” The Bonds will be subject to redemption prior to maturity as described herein. Pursuant to the California Constitution Article XVI, Section 4, and California Health and Safety Code, Division 107, Part 6, Chapter 1, payment of the principal of and interest on the Bonds will be insured by the Office of Statewide Health Planning and Development of the State of California (the “Office”), and all debentures issued in payment of any claims under such insurance will be fully and unconditionally guaranteed by the State of California, all as more fully described herein. The following firm served as registered municipal advisor to the Corporation on this financing: HG WILSON MUNICIPAL FINANCE INC. THE BONDS ARE NOT A DEBT OR LIABILITY OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF OR A PLEDGE OF THE FAITH AND CREDIT OF THE STATE OF CALIFORNIA OR ANY SUCH POLITICAL SUBDIVISION BUT SHALL BE PAYABLE SOLELY FROM THE FUNDS PROVIDED THEREFOR. NEITHER THE STATE OF CALIFORNIA NOR THE AUTHORITY SHALL BE OBLIGATED TO PAY THE PRINCIPAL OF THE BONDS, OR THE PREMIUM, IF ANY, OR INTEREST THEREON, EXCEPT FROM THE FUNDS PROVIDED UNDER THE LOAN AGREEMENT AND THE INDENTURE, AND NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF, INCLUDING THE AUTHORITY, IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE PREMIUM, IF ANY, OR INTEREST ON THE BONDS, EXCEPT TO THE EXTENT EXPRESSLY PROVIDED THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE ISSUANCE OF THE BONDS SHALL NOT DIRECTLY OR INDIRECTLY OR CONTINGENTLY OBLIGATE THE STATE OF CALIFORNIA OR ANY POLITICAL SUBDIVISION THEREOF TO LEVY OR TO PLEDGE ANY FORM OF TAXATION OR TO MAKE ANY APPROPRIATION FOR THEIR PAYMENT, EXCEPT TO THE EXTENT EXPRESSLY PROVIDED THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE AUTHORITY HAS NO TAXING POWER. SEE THE INSIDE FRONT COVER FOR THE MATURITY SCHEDULES FOR THE BONDS For a discussion of some of the risks associated with the purchase of the Bonds, see “BONDHOLDERS’ RISKS” herein. This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision. The Bonds will be offered when, as and if issued and received by the Underwriters, subject to an approving legal opinion of Quint & Thimmig LLP, Larkspur, California, Bond Counsel, and certain other conditions. Certain legal matters will be passed upon for the Authority by its counsel, the Attorney General of the State of California. Certain matters will be passed upon for the Underwriters by their counsel, Jennings, Strouss & Salmon, PLC, Phoenix, Arizona. Certain matters will be passed upon for the Corporation by Wilson Law Group, PC, San Diego, California, as Counsel to the Corporation and as Disclosure Counsel. It is expected that the Bonds, in definitive form, will be available for delivery through the facilities of DTC, on or about February 11, 2015. HONORABLE JOHN CHIANG Treasurer of the State of California As Agent for Sale Southwest Securities Dated: January 30, 2015

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2015-0054 CHFFA OS.xps - CA.gov

REFUNDING ISSUE—Book-Entry Only RATING: S&P “A+”See “RATING” herein.

In the opinion of Quint & Thimmig LLP, Larkspur, California, Bond Counsel, subject to compliance by the Authority and the Corporation with certain covenants, under present law, interest on the Bonds is excludable from gross income of the owners thereof for federal income tax purposes and is not included as an item of tax preference in computing the federal alternative minimum tax for individuals and corporations, but such interest is taken into account in computing an adjustment used in determining the federal alternative minimum tax for certain corporations. In addition, in the opinion of Bond Counsel, interest on the Bonds is exempt from personal income taxation imposed by the State of California. See “TAX MATTERS” herein.

$11,965,000CALIFORNIA HEALTH FACILITIES

FINANCING AUTHORITY Insured Refunding Revenue Bonds

(Lincoln Glen Manor for Senior Citizens) Series 2015

Dated: Date of delivery Due: April 1, as shown below

The $11,965,000 California Health Facilities Financing Authority Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2015 (the “Bonds”), will constitute limited obligations of the California Health Facilities Financing Authority (the “Authority”) secured under the provisions of the Indenture and the Loan Agreement described herein, and will be equally and ratably payable from loan payments made by Lincoln Glen Manor for Senior Citizens (the “Corporation”) to the Authority under the Loan Agreement and from certain funds held under the Indenture.

The proceeds of the Bonds will be used to (a) provide for the advance refunding of a portion of the outstanding California Municipal Finance Authority Insured Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2011 (the “Refunded 2011 Bonds”), the proceeds of which were used to (i) refund, on a current basis, all outstanding ABAG Finance Corporation for Nonprofit Corporations Insured Certificates of Participation (Lincoln Glen Manor for Senior Citizens), Series 2000, executed and delivered to (A) refinance certain existing indebtedness of the Corporation, (B) finance the renovation of existing buildings, and (C) finance the costs of construction of a 31 unit assisted living facility; (ii) finance the conversion of 8 independent living units (from a 20 unit building) into 11 memory care beds for patients suffering from Alzheimer’s disease and dementia; and (iii) finance the expansion, remodeling and updating of the Corporation’s Central Manor, all located at the Corporation’s multi-level facility for the elderly at 2671 Plummer Avenue in the City of San Jose, California, owned or to be owned and operated by the Corporation; (b) fund a reserve fund for the Bonds; and (c) pay a portion of the costs of issuance of the Bonds (collectively, the “Refinancing Plan”). See “THE REFINANCING PLAN” herein.

Bonds will not be secured by any property of the Authority other than the pledge of Revenues, as and to the extent specified in the Indenture. Revenues will primarily consist of loan payments made by the Corporation. No form of taxation will be pledged or levied to provide for payment with respect to the Bonds. The Authority will assign to U.S. Bank National Association, San Francisco, California, as trustee (the “Trustee”), its interests under the Loan Agreement and will grant to the Trustee a lien on and pledge of Revenues, monies and investments held in the funds and accounts created under the Indenture. The Loan Agreement shall contain terms and conditions that are on parity with those terms and conditions of the loan agreement relating to the Refunded 2011 Bonds. Pursuant to the Loan Agreement, the Corporation will be required to make payments to the Authority sufficient to pay all principal of and interest on the Bonds. See “SECURITY FOR THE BONDS” herein.

The Bonds will be issued as fully registered bonds and, when delivered, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York (“DTC”). DTC will act as securities depository for the Bonds. Individual purchases of interests in the Bonds will be made in book-entry form only. Purchasers of such interests will not receive physical certificates. Interest on the Bonds is payable semiannually on each April 1 and October 1, commencing October 1, 2015. Principal of and interest on the Bonds is payable directly to DTC by the Trustee. Upon receipt of payments of principal of, premium, if any, and interest on the Bonds, DTC will in turn remit such payments to the DTC Participants for subsequent disbursement to the beneficial owners of the Bonds, as described herein. See “The BONDS—Description of the Bonds” and “—Book-Entry Only System” herein and APPENDIX F — “BOOK-ENTRY ONLY SYSTEM.”

The Bonds will be subject to redemption prior to maturity as described herein.

Pursuant to the California Constitution Article XVI, Section 4, and California Health and Safety Code, Division 107, Part 6, Chapter 1, payment of the principal of and interest on the Bonds will be insured by the Office of Statewide Health Planning and Development of the State of California (the “Office”), and all debentures issued in payment of any claims under such insurance will be fully and unconditionally guaranteed by the State of California, all as more fully described herein.

The following firm served as registered municipal advisor to the Corporation on this financing: HG WILSON MUNICIPAL FINANCE INC.

THE BONDS ARE NOT A DEBT OR LIABILITY OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF OR A PLEDGE OF THE FAITH AND CREDIT OF THE STATE OF CALIFORNIA OR ANY SUCH POLITICAL SUBDIVISION BUT SHALL BE PAYABLE SOLELY FROM THE FUNDS PROVIDED THEREFOR. NEITHER THE STATE OF CALIFORNIA NOR THE AUTHORITY SHALL BE OBLIGATED TO PAY THE PRINCIPAL OF THE BONDS, OR THE PREMIUM, IF ANY, OR INTEREST THEREON, EXCEPT FROM THE FUNDS PROVIDED UNDER THE LOAN AGREEMENT AND THE INDENTURE, AND NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF, INCLUDING THE AUTHORITY, IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE PREMIUM, IF ANY, OR INTEREST ON THE BONDS, EXCEPT TO THE EXTENT EXPRESSLY PROVIDED THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE ISSUANCE OF THE BONDS SHALL NOT DIRECTLY OR INDIRECTLY OR CONTINGENTLY OBLIGATE THE STATE OF CALIFORNIA OR ANY POLITICAL SUBDIVISION THEREOF TO LEVY OR TO PLEDGE ANY FORM OF TAXATION OR TO MAKE ANY APPROPRIATION FOR THEIR PAYMENT, EXCEPT TO THE EXTENT EXPRESSLY PROVIDED THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE AUTHORITY HAS NO TAXING POWER.

SEE THE INSIDE FRONT COVER FOR THE MATURITY SCHEDULES FOR THE BONDS

For a discussion of some of the risks associated with the purchase of the Bonds, see “BONDHOLDERS’ RISKS” herein.

This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors must read the entire Official Statement to obtain information essential to the making of an informed investment decision.

The Bonds will be offered when, as and if issued and received by the Underwriters, subject to an approving legal opinion of Quint & Thimmig LLP, Larkspur, California, Bond Counsel, and certain other conditions. Certain legal matters will be passed upon for the Authority by its counsel, the Attorney General of the State of California. Certain matters will be passed upon for the Underwriters by their counsel, Jennings, Strouss & Salmon, PLC, Phoenix, Arizona. Certain matters will be passed upon for the Corporation by Wilson Law Group, PC, San Diego, California, as Counsel to the Corporation and as Disclosure Counsel. It is expected that the Bonds, in definitive form, will be available for delivery through the facilities of DTC, on or about February 11, 2015.

HONORABLE JOHN CHIANG Treasurer of the State of California

As Agent for Sale

Southwest Securities Dated: January 30, 2015

$11,965,000CALIFORNIA HEALTH FACILITIES FINANCING AUTHORITY

Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens)

Series 2015

MATURITY SCHEDULE CUSIP† Prefix: 13033L

Maturity (April 1)

Principal Amount

InterestRate Yield Price

CUSIP†

Suffix2018 $95,000 2.000% 0.980% 103.144% 5F0 2019 95,000 3.000 1.210 107.204 5G8 2020 100,000 3.000 1.450 107.647 5H6 2021 105,000 3.000 1.670 107.728 5J2 2022 560,000 5.000 1.880 120.750 5K9 2023 585,000 5.000 2.050 122.007 5L7 2024 615,000 5.000 2.200 123.063 5M5 2025 650,000 5.000 2.340 123.882 5N3 2026 680,000 5.000 2.490 122.365c 5P8 2027 715,000 5.000 2.610 121.167c 5Q6 2028 750,000 5.000 2.700 120.277c 5R4 2029 785,000 3.000 3.120 98.634 5S2 2030 810,000 3.000 3.200 97.612 5T0 2031 835,000 3.125 3.270 98.190 5U7 2032 860,000 3.125 3.320 97.464 5V5 2033 890,000 3.125 3.360 96.824 5W3 2034 915,000 3.250 3.380 98.176 5X1 2035 945,000 3.250 3.420 97.537 5Y9 2036 975,000 3.250 3.440 97.159 5Z6

† – Copyright 2014, American Bankers Association. CUSIP data in this Official Statement are provided by CUSIP Global Service operated by CUSIP Service Bureau, which is managed on behalf of the American Bankers Association by Standard & Poor's. Standard & Poor's is a unit of The McGraw-Hill Companies, Inc. The data are not intended to create a database and do not serve in any way as a substitute for the CUSIP Global Services. CUSIP numbers are provided for convenience of reference only. None of the Authority, the Office, the Corporation, and the Underwriters assume any responsibility for the accuracy of the CUSIP data. The CUSIP number for a specific maturity is subject to being changed after delivery of the Bonds as a result of various subsequent actions, including a refunding in whole or in part or as the result of the procurement of a secondary market portfolio insurance or other similar enhancement by investors that is applicable to all or a portion of certain maturities of the Bonds.

c – Priced to the April 1, 2025 par call date.

i

GENERAL INFORMATION ABOUT THIS OFFICIAL STATEMENT

Use of Official Statement. This Official Statement is submitted in connection with the sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds.

Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the Corporation, in any press release and in any oral statement made with the approval of an authorized officer of the Corporation, the words or phrases “will likely result,” “are expected to”, “will continue”, “is anticipated”, “estimate”, “project,” “forecast”, “expect”, “intend” and similar expressions identify “forward looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results, and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the Corporation since the date hereof.

Limit of Offering. No dealer, broker, salesperson or other person has been authorized by the Authority to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the Authority or the underwriting firms designated on the front cover hereof and set forth herein under the caption “UNDERWRITING” (the “Underwriters”). This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

Involvement of Underwriters. The Underwriters have reviewed the information in this Official Statement in accordance with, and as a part of, their responsibilities to investors under the Federal Securities Laws as applied to the facts and circumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness of such information.

Involvement of Authority. The information relating to the Authority set forth herein under the captions “THE AUTHORITY” and “ABSENCE OF MATERIAL LITIGATION—The Authority” has been furnished by the Authority. The Authority does not warrant the accuracy of the statements contained herein relating to the Corporation nor does it directly or indirectly guarantee, endorse or warrant (1) the creditworthiness or credit standing of the Corporation, (2) the sufficiency of the security for the Bonds or (3) the value or investment quality of the Bonds. The Authority makes no representations or warranties whatsoever with respect to any information contained therein except for the information under the sections entitled “THE AUTHORITY” and “ABSENCE OF MATERIAL LITIGATION—The Authority.”

ii

Information Subject to Change. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Authority or the Corporation since the date hereof. All summaries of the documents referred to in this Official Statement, are made subject to the provisions of such documents, respectively, and do not purport to be complete statements of any or all of such provisions.

Offer and Sale of Bonds. The Underwriters may offer and sell the Bonds to certain dealers and others at prices lower than the public offering prices set forth on the cover page hereof and said public offering prices may be changed from time to time by the Underwriters.

THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXCEPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE. THESE SECURITIES HAVE NOT BEEN RECOMMENDED BY A FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY. FURTHERMORE, THE FOREGOING AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY OR DETERMINED THE ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

iii

TABLE OF CONTENTS Page Page

INTRODUCTORY STATEMENT............................1 THE AUTHORITY ....................................................3 THE CORPORATION ...............................................4 ESTIMATED SOURCES AND USES OF FUNDS.5 THE BONDS ..............................................................6

General...............................................................6 Redemption........................................................7 Debt Service Requirements...............................9 Book-Entry Only System................................10

SECURITY FOR THE BONDS ..............................10 Pledge Under the Indenture; Gross Revenues 10 Debt Service Reserve Account .......................11 Insurance..........................................................12 The Office’s Control of Remedies..................12 Deed of Trust...................................................13 Rate Covenant and Other Financial

Covenants ..............................................13 Parity Debt and Other Indebtedness ...............14

CALIFORNIA HEALTH FACILITY CONSTRUCTION LOAN INSURANCE PROGRAM .....................................................14 Description of the Insurance Policy................14 The Office, the Program and the Insurance

Fund .......................................................16 CERTAIN FINANCIAL INFORMATION

REGARDING THE STATE...........................21 BONDHOLDERS’ RISKS.......................................22

General.............................................................22 State Bond Insurance.......................................22 The Office’s Control of Remedies..................23 Maintenance of Credit Rating .........................23 Present and Prospective Federal and State

Regulation..............................................25 Health Care Regulation ...................................26 Impact of Disruptions in the Credit Markets

and General Economic Factors .............30 General Risks of Long Term Care Facilities ..30 Residential and Service Revenues and

Sources...................................................30 Licensing and Enforcement Matters ...............34

Regulatory and Enforcement Matters .............35 Risks Related to Tax Exempt-Status of Bonds

and Corporation.....................................39 Business Relationships and Other Business

Matters ...................................................42 Amendments to the Documents......................43 Additional Indebtedness..................................43 Bankruptcy ......................................................43 Certain Matters Relating to Enforceability.....44 Certain Risks Associated with the Deed of

Trust.......................................................45 Office’s Exclusive Rights under Deed of

Trust.......................................................47 Trustee’s Conditional Obligation to Foreclose47 Rights of Residents..........................................47 Limited Use Facility........................................47 Environmental Matters....................................48 Seismic Risk ....................................................48 Marketability of the Bonds .............................49 Other Possible Risk Factors ............................49

ABSENCE OF MATERIAL LITIGATION............50 The Authority ..................................................50 The Corporation ..............................................50

CONTINUING DISCLOSURE ...............................51 TAX MATTERS.......................................................53 APPROVAL OF LEGALITY ..................................56 RATING....................................................................56 UNDERWRITING ...................................................56 VERIFICATION OF MATHEMATICAL

COMPUTATIONS .........................................57 THE TRUSTEE ........................................................57 MUNICIPAL ADVISOR .........................................58 INDEPENDENT AUDITORS; FINANCIAL

STATEMENTS...............................................58 CERTAIN RELATIONSHIPS AMONG THE

PARTIES.........................................................58 MISCELLANEOUS .................................................59

APPENDIX A - INFORMATION CONCERNING THE CORPORATION APPENDIX B - AUDITED FINANCIAL STATEMENTS OF THE CORPORATION APPENDIX C - SUMMARY OF PRINCIPAL LEGAL DOCUMENTS APPENDIX D - FORM OF FINAL OPINION OF BOND COUNSEL APPENDIX E – FORM OF CONTINUING DISCLOSURE CERTIFICATE APPENDIX F – BOOK ENTRY SYSTEM APPENDIX G – FORM OF CONTRACT OF INSURANCE

OFFICIAL STATEMENT

$11,965,000CALIFORNIA HEALTH FACILITIES FINANCING AUTHORITY

Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens)

Series 2015

INTRODUCTORY STATEMENT

This Introduction is not a summary of this Official Statement. It is only a brief description of and guide to, and is qualified by, more complete and detailed information contained in the entire Official Statement, including the cover page and appendices hereto, and the documents summarized or described herein. A full review should be made of the entire Official Statement. The offering of the Bonds to potential investors is made only by means of the entire Official Statement.

This Official Statement is furnished in connection with the offering of $11,965,000 aggregate principal amount of Insured Refunding Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2015 (the “Bonds”), issued by the California Health Facilities Financing Authority (the “Authority”). All capitalized terms used in this Official Statement and not otherwise defined herein have the same meanings as in that certain Indenture, dated as of February 1, 2015 (the “Indenture”), by and between the Authority and U.S. Bank National Association, San Francisco, California, as trustee (the “Trustee”). See APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—Definitions.”

The Bonds will be issued under Articles 1 through 4 (commencing with section 6500) of Chapter 5 of Division 7 of Title 1 of the California Government Code (the “Act”), and the Indenture. The proceeds of the sale of the Bonds will be loaned to Lincoln Glen Manor for Senior Citizens, a California nonprofit public benefit corporation (the “Corporation”), pursuant to a Loan Agreement, dated as of February 1, 2015, between the Authority and the Corporation (the “Loan Agreement”) and, together with certain funds provided by the Corporation, will be used to (a) provide for the advance refunding of a portion of the outstanding California Municipal Finance Authority Insured Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2011 (the “Refunded 2011 Bonds”), the proceeds of which were used to (i) refund, on a current basis, all outstanding ABAG Finance Corporation for Nonprofit Corporations Insured Certificates of Participation (Lincoln Glen Manor for Senior Citizens), Series 2000, executed and delivered to (A) refinance certain existing indebtedness of the Corporation, (B) finance the renovation of existing buildings, and (C) finance the costs of construction of a 31 unit assisted living facility; (ii) finance the conversion of 8 independent living units (from a 20 unit building) into 11 memory care beds for patients suffering from Alzheimer’s disease and dementia; and (iii) finance the expansion, remodeling and updating of the Corporation’s Central Manor, all located at the Corporation’s multi-level facility for the elderly at 2671 Plummer Avenue in the City of San Jose, California, owned or to be owned and operated by the Corporation; (b) fund a reserve fund for the Bonds; and (c) pay a portion of the costs of issuance of the Bonds, all as more

2

particularly described herein. See “ESTIMATED SOURCES AND USES OF FUNDS” and “THE REFINANCING PLAN” herein.

The Loan Agreement shall contain terms and conditions that are on parity with those terms and conditions of the loan agreement relating to the Refunded 2011 Bonds. Pursuant to the Loan Agreement, the Corporation will be required to make payments to the Authority sufficient to pay all principal of, interest and premium, if any, on the Bonds. Such payments constitute revenues of the Authority (the “Revenues” as defined herein) pledged for payment of the Bonds.

In accordance with the California Health Facility Construction Loan Insurance Law, Chapter 1 of Part 6 of Division 107 of the California Health and Safety Code (the “Insurance Law”), the Authority and the Office of Statewide Health Planning and Development of the State of California (the “Office”) will enter into a Contract of Insurance, dated as of February 1, 2015, with the Corporation (the “Contract of Insurance”) pursuant to which the Office will insure the payment of principal of and interest on the Bonds in the event that amounts received by the Trustee pursuant to the Loan Agreement are not sufficient to pay in full, when due, principal of and interest on the Bonds. If monies are not available to pay principal of and interest on the Bonds, the Office will be obligated to continue to make payments on the Bonds or will instruct the Trustee to declare the principal of all Bonds then outstanding and interest accrued thereon to be due and payable immediately and make payment of such principal and interests and, upon the occurrence of certain events, shall notify the Treasurer of the State of California (the “State”) and the Treasurer will issue debentures to the holders of the Bonds, fully and unconditionally guaranteed by the State, in an amount equal to the principal of and the accrued interest on the Bonds. In connection with the Contract of Insurance, the Corporation will enter into a Regulatory Agreement, dated as of February 1, 2015 (the “Regulatory Agreement”), with the Authority and the Office. For a more detailed description of the obligation of the Office to insure the payment of the principal of and interest on the Bonds, the procedures with respect to an insurance default, the obligations of the Corporation pursuant to the Regulatory Agreement and the financial condition of the Office and the State of California, see “CALIFORNIA HEALTH FACILITY CONSTRUCTION LOAN INSURANCE PROGRAM,” “CERTAIN FINANCIAL INFORMATION REGARDING THE STATE,” “BONDHOLDER’S RISKS – State Bond Insurance,” “RATING,” APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – REGULATORY AGREEMENT,” and APPENDIX G—“FORM OF CONTRACT OF INSURANCE.”

THE BONDS DO NOT CONSTITUTE A DEBT OR LIABILITY OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF OR A PLEDGE OF THE FAITH AND CREDIT OF THE STATE OF CALIFORNIA OR ANY POLITICAL SUBDIVISION THEREOF, OTHER THAN THE AUTHORITY, BUT SHALL BE PAYABLE SOLELY FROM THE FUNDS PROVIDED THEREFOR. NEITHER THE STATE OF CALIFORNIA NOR THE AUTHORITY SHALL BE OBLIGATED TO PAY THE PRINCIPAL OF THE BONDS, OR THE REDEMPTION PREMIUM OR INTEREST THEREON, EXCEPT FROM THE FUNDS PROVIDED THEREFOR UNDER THE LOAN AGREEMENT, AND THE INDENTURE AND THE CONTRACT OF INSURANCE (EACH DESCRIBED HEREIN) OR TO THE EXTENT EXPRESSLY PROVIDED THROUGH THE INSURANCE PROGRAM DESCRIBED

3

HEREIN, AND NEITHER THE FAITH AND CREDIT NOR THE TAXING POWER OF THE STATE OF CALIFORNIA OR OF ANY POLITICAL SUBDIVISION THEREOF, INCLUDING THE AUTHORITY, IS PLEDGED TO THE PAYMENT OF THE PRINCIPAL OF OR THE REDEMPTION PREMIUM OR INTEREST ON THE BONDS, EXCEPT WITH RESPECT TO THE STATE OF CALIFORNIA, TO THE EXTENT EXPRESSLY PROVIDED IN THE CONTRACT OF INSURANCE OR THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE ISSUANCE OF THE BONDS SHALL NOT DIRECTLY OR INDIRECTLY OR CONTINGENTLY OBLIGATE THE STATE OF CALIFORNIA OR ANY POLITICAL SUBDIVISION THEREOF TO LEVY OR TO PLEDGE ANY FORM OF TAXATION OR TO MAKE ANY APPROPRIATION FOR THEIR PAYMENT EXCEPT, WITH RESPECT TO THE STATE OF CALIFORNIA, TO THE EXTENT EXPRESSLY PROVIDED IN THE CONTRACT OF INSURANCE OR THROUGH THE INSURANCE PROGRAM DESCRIBED HEREIN. THE AUTHORITY HAS NO TAXING POWER.

See the section of this Official Statement entitled “BONDHOLDERS’ RISKS” for a discussion of special factors that should be considered, in addition to the other matters set forth herein, in considering the investment quality of the Bonds.

All capitalized terms used in this Official Statement and not otherwise defined herein have the same meanings as in the Indenture, the Loan Agreement and the Regulatory Agreement. See APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—DEFINITIONS OF CERTAIN TERMS.”

Brief descriptions of the Bonds, the sources of payment for the Bonds, the Authority, the Corporation, special risk factors, the Indenture and other information are included in this Official Statement. Such descriptions and information do not purport to be comprehensive or definitive. The descriptions herein of the Bonds, the Indenture and other documents are qualified in their entirety by reference to each such document and the information with respect thereto included in the Bonds, such Indenture and other documents. Any statements made in this Official Statement involving matters of opinion or of estimates, whether or not so expressly stated, are set forth as such and not as representations of fact, and no representation is made that any of the estimates will be realized.

THE AUTHORITY

The Authority is a public instrumentality of the State of California organized and existing under and by virtue of the California Health Facilities Financing Authority Act, constituting Part 7.2 of Division 3of Title 2 of the California Government Code (the “Act”). The intent of the California Legislature in enacting the Act was to provide financing to health facilities and to pass along to the consuming public all or part of any savings realized by a participating health institution (as defined in the Act) as a result of tax-exempt financing. Pursuant to the Act, the Authority is authorized to issue its revenue bonds for the purpose of financing (including reimbursing expenditures made or refinancing indebtedness incurred for such purpose) the construction, expansion, remodeling, renovation, furnishing, equipping or acquisition of health

4

facilities operated by participating health institutions. The State Treasurer is authorized under the Act to sell such revenue bonds on behalf of the Authority.

The Authority may sell and deliver obligations other than the Bonds. These obligations will be secured by instruments separate and apart from the Indenture and the holders of such other obligations of the Authority will have no claim on the security for the Bonds. Likewise, the Owners of the Bonds will have no claim on the security for such other obligations that may be issued by the Authority.

Neither the Authority nor its independent contractors have furnished, reviewed, investigated or verified the information contained in this Official Statement other than the information contained in this section and the section entitled “ABSENCE OF MATERIAL LITIGATION—The Authority.” The Authority does not and will not in the future monitor the financial condition of the Corporation or otherwise monitor payment of the Bonds or compliance with the documents relating thereto. Any commitment or obligation for continuing disclosure with respect to the Bonds or the Corporation has been undertaken solely by the Corporation. See “CONTINUING DISCLOSURE” herein.

Organization and Membership

The Act provides that the Authority shall consist of nine members, including the State Treasurer, who shall serve as Chairman, the State Controller, the Director of Finance and two members appointed by each of the Senate Rules Committee, the Speaker of the State Assembly and the Governor of the State of California. The Chairman of the Authority appoints the Executive Director.

Outstanding Indebtedness of the Authority

As of September 30, 2014, the Authority had issued obligations aggregating $31,466,537,017 in an original principal amount and had outstanding obligations in the aggregate principal amount of $13,077,498,998.

THE CORPORATION

The Corporation is a California nonprofit public benefit corporation as described in section 501(c)(3) of the Code and is exempt from income taxation pursuant to section 501(a) of the Code. For more detailed information concerning the history, governance, organization, facilities, operations, and financial performance of the Corporation, see APPENDIX A—“INFORMATION CONCERNING THE CORPORATION” and APPENDIX B—“AUDITED FINANCIAL STATEMENTS OF THE CORPORATION.”

5

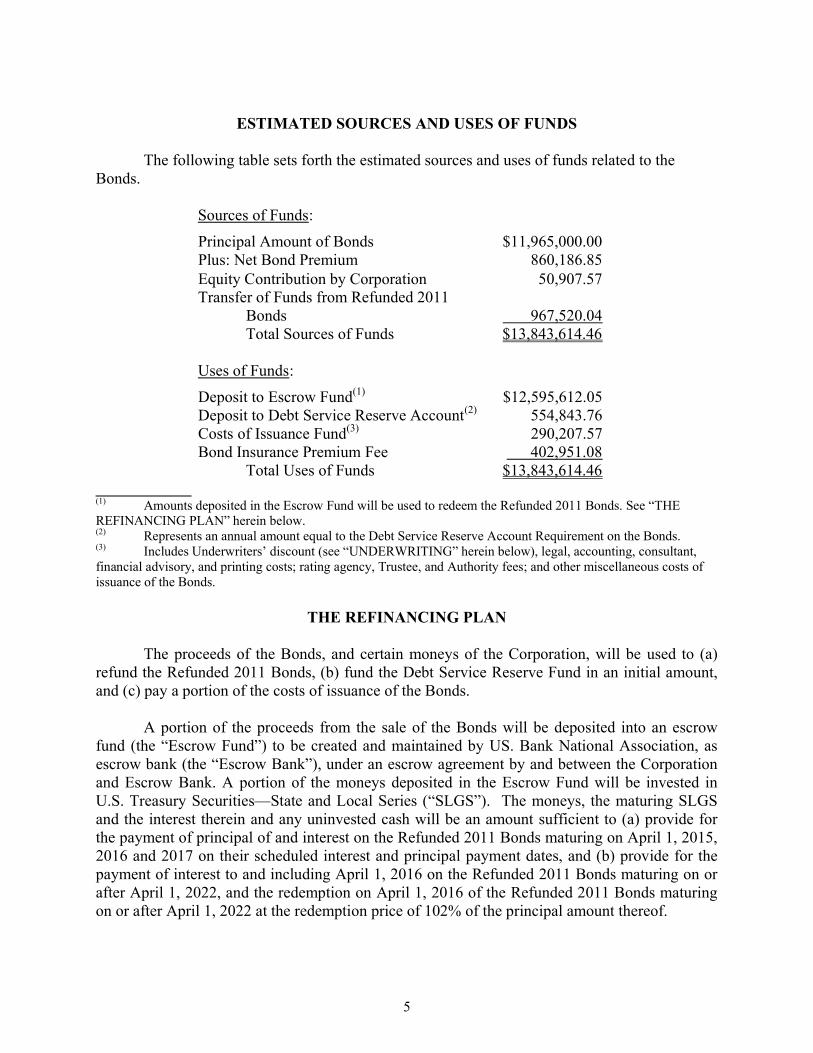

ESTIMATED SOURCES AND USES OF FUNDS

The following table sets forth the estimated sources and uses of funds related to the Bonds.

Sources of Funds:

Principal Amount of Bonds $11,965,000.00 Plus: Net Bond Premium 860,186.85 Equity Contribution by Corporation 50,907.57 Transfer of Funds from Refunded 2011 Bonds 967,520.04 Total Sources of Funds $13,843,614.46

Uses of Funds:

Deposit to Escrow Fund(1) $12,595,612.05 Deposit to Debt Service Reserve Account(2) 554,843.76 Costs of Issuance Fund(3) 290,207.57 Bond Insurance Premium Fee 402,951.08 Total Uses of Funds $13,843,614.46

(1) Amounts deposited in the Escrow Fund will be used to redeem the Refunded 2011 Bonds. See “THE REFINANCING PLAN” herein below. (2) Represents an annual amount equal to the Debt Service Reserve Account Requirement on the Bonds. (3) Includes Underwriters’ discount (see “UNDERWRITING” herein below), legal, accounting, consultant, financial advisory, and printing costs; rating agency, Trustee, and Authority fees; and other miscellaneous costs of issuance of the Bonds.

THE REFINANCING PLAN

The proceeds of the Bonds, and certain moneys of the Corporation, will be used to (a) refund the Refunded 2011 Bonds, (b) fund the Debt Service Reserve Fund in an initial amount, and (c) pay a portion of the costs of issuance of the Bonds.

A portion of the proceeds from the sale of the Bonds will be deposited into an escrow fund (the “Escrow Fund”) to be created and maintained by US. Bank National Association, as escrow bank (the “Escrow Bank”), under an escrow agreement by and between the Corporation and Escrow Bank. A portion of the moneys deposited in the Escrow Fund will be invested in U.S. Treasury Securities—State and Local Series (“SLGS”). The moneys, the maturing SLGS and the interest therein and any uninvested cash will be an amount sufficient to (a) provide for the payment of principal of and interest on the Refunded 2011 Bonds maturing on April 1, 2015, 2016 and 2017 on their scheduled interest and principal payment dates, and (b) provide for the payment of interest to and including April 1, 2016 on the Refunded 2011 Bonds maturing on or after April 1, 2022, and the redemption on April 1, 2016 of the Refunded 2011 Bonds maturing on or after April 1, 2022 at the redemption price of 102% of the principal amount thereof.

6

Following the foregoing redemption of the Refunded 2011 Bonds, the California Municipal Finance Authority Insured Revenue Bonds (Lincoln Glen Manor for Senior Citizens), Series 2011 (the “2011 Bonds”) with maturity dates of April 1, 2018 through April 1, 2021 shall remain outstanding. See “THE BONDS—Debt Service Reserve Account” herein below.

Sufficiency of the deposits in the Escrow Fund, the maturing principal of the SLGS therein, the investment earnings on such SLGS and the uninvested cash will be verified by Public Finance Grant Thornton LLP (the “Verification Agent”). See “VERIFICATION OF MATHEMATICAL ACCURACY” herein below. Assuming the accuracy of the Verification Agent’s computations, the Corporation’s obligations with respect to the Refunded 2011 Bonds will be discharged.

Upon the delivery of the Bonds and the deposit in the Escrow Fund of moneys sufficient to provide for the refunding of the Refunded 2011 Bonds, the Refunded 2011 Bonds will be deemed defeased and no longer outstanding. The holders of the Refunded 2011 Bonds will be entitled to payment solely out of the moneys or securities deposited in the Escrow Fund.

THE BONDS

General

The Bonds will be dated as of their date of delivery, and will bear interest at the rates set forth on the cover page of this Official Statement, payable semi-annually on each April 1 and October 1, commencing October 1, 2015. Subject to the redemption provisions set forth below, the Bonds will be payable at the principal corporate trust office of the Trustee, in San Francisco, California. Interest on the Bonds will be payable by check mailed by the Trustee on each interest payment date to the registered owners thereof as of the 15th day of the calendar month preceding the interest payment date (a “Record Date”) at the address shown on the registration books maintained by the Trustee.

The Bonds will be issued in denominations of $5,000 or any amounts in excess thereof in even $5,000 increments. The Bonds will be issuable in fully registered form only and, when issued and delivered, will be registered in the name of Cede & Co., as nominee of the Depository Trust Company, New York, New York (“DTC”). DTC will act as the depository of the Bonds and all payments due on the Bonds will be made to DTC or its nominee. Ownership interests in the Bonds may be purchased in book-entry form only. Purchasers will not receive certificates representing their interest in the Bonds purchased. So long as Cede & Co., as nominee of DTC, is the registered owner of the Bonds, references herein to the Owner or registered owner will mean Cede & Co. and will not mean the Beneficial Owners of the Bonds. So long as Cede & Co. is the registered owner of the Bonds, principal, premium, if any, and interest on the Bonds are payable by wire transfer by the Trustee to Cede & Co., as nominee of DTC, which is required in turn, to remit such amount to the Direct Participants for subsequent disbursement by the Direct Participants and the Indirect Participants (as defined herein) to the Beneficial Owners. See APPENDIX F—“BOOK-ENTRY SYSTEM.”

7

Redemption

General. The Bonds are subject to optional redemption, mandatory redemption and extraordinary redemption as described below.

Optional Redemption. The Bonds maturing before April 1, 2025, are not subject to optional redemption prior to maturity.

The Bonds maturing on or after April 1, 2026, are subject to redemption prior to their stated maturity, at the option of the Authority (which option shall be exercised as directed by the Corporation), in whole or in part by lot (in such maturities as are designated by the Corporation, or if the Corporation fails to so designate, in inverse order of maturity, and by lot within a maturity) on any date, upon at least forty-five (45) days prior written notice to the Trustee from the Corporation, from any source of available moneys, on or after April 1, 2025 at a redemption price equal to the principal amount of the Bonds called for redemption, together with accrued interest to the date fixed for redemption, without premium.

Redemption from Net Proceeds of Insurance or Condemnation. The Bonds are also subject to redemption prior to their respective stated maturities at the option of the Authority (which option shall be exercised as directed by the Corporation) in whole on any date, or in any part (in such amounts and of such maturities as may be specified by the Corporation, or if the Corporation fails to designate such maturities, in inverse order of maturity and by lot) on any interest payment date, upon forty-five (45) days prior written notice to the Trustee from the Corporation. Such redemption will be effected with moneys required to be deposited in the Special Redemption Account, which the Corporation has received from insurance or condemnation proceeds, in an amount equal to the principal amount of the Bonds redeemed plus accrued interest to the date fixed for redemption, without premium.

Notice of Redemption. Unless waived by any Owner of Bonds to be redeemed, official notice of any such redemption shall be given by the Trustee by mailing a copy of an official redemption notice by first class mail at least 30 days and not more than 60 days prior to the date fixed for redemption to the respective Owner of the Bond or Bonds to be redeemed at the address shown on the Bond Register.

Each notice of redemption shall state the redemption date, the place or places of redemption, the maturities, the date of issuance of the Bonds, the CUSIP number (if any) of the maturity or maturities and, if less than all of any such maturity, the distinctive numbers (or inclusive ranges of distinctive numbers) of the Bonds of such maturity, to be redeemed and, in the case of Bonds to be redeemed in part only, the respective portions of the principal amount thereof to be redeemed. Each such notice shall also state that on said date there will become due and payable on each of said Bonds the Redemption Price thereof or of said specified portion of the principal amount thereof in the case of a fully registered Bond to be redeemed in part only, together with interest accrued thereon to the redemption date, and that from and after such redemption date interest thereon shall cease to accrue, and shall require that such Bonds be then surrendered. Neither the Authority nor the Trustee shall have any responsibility for any defect in

8

the CUSIP number that appears on any Bond or in any redemption notice with respect thereto, and any such redemption notice may contain a statement to the effect that CUSIP numbers have been assigned by an independent service for convenience of reference and that neither the Authority nor the Trustee shall be liable for any inaccuracy in such numbers.

In the case of optional redemption of the Bonds, the notice of redemption shall state that the redemption is conditioned upon receipt by the Trustee of sufficient moneys to redeem the Bonds on the anticipated redemption date, and that the optional redemption shall not occur if, by no later than the scheduled redemption date, sufficient moneys to redeem the Bonds have not been deposited with the Trustee. In the event that the Trustee does not receive sufficient funds by the scheduled optional redemption date to so redeem the Bonds to be optionally redeemed, the Trustee shall provide written notice that the redemption did not occur as anticipated, and the Bonds for which notice of optional redemption was given shall remain Outstanding as if no optional redemption had been sought.

Official notice of redemption having been given as aforesaid and upon receipt by the Trustee of sufficient moneys to effect any such redemption, the Bonds or portions of Bonds to be redeemed shall, on the redemption date, become due and payable at the redemption price therein specified, and from and after such date interest with respect to such Bonds or portions of Bonds shall cease to be payable. All Bonds which have been redeemed shall be canceled and destroyed by the Trustee and shall not be reissued.

In addition to the foregoing notice, further notice shall be given by the Trustee to the Authority and to all Securities Depositories and to the Information Services, as set forth in the Indenture, but no defect in said further notice nor any failure to give all or any portion of such further notice shall in any manner defeat the effectiveness of a call for redemption if notice thereof is given as prescribed above.

Payment on Redemption of Bonds. Notice having been given as aforesaid, and the moneys for the redemption, including interest accrued from the preceding Payment Date to the date of redemption and premium, if any, having been set aside in the Redemption Fund, the Bonds to be redeemed shall become due and payable on said date of redemption, and, upon presentation and surrender thereof at the office or offices specified in said notice, said Bonds shall be paid at the unpaid principal amount with respect thereto, plus any such unpaid and accrued interest to said date of redemption.

If, on said date of redemption, moneys for the redemption of all the Bonds to be redeemed and premium, if any, together with interest to said date of redemption, shall be held by the Trustee so as to be available therefor on such Payment Date, and, if notice of redemption thereof shall have been given as aforesaid, then, from and after said Payment Date, interest with respect to the Bonds to be redeemed shall cease to accrue and become payable. If said moneys shall not be so available on said Payment Date, interest with respect to such Bonds shall continue to be payable until paid at the same rates as it would have been payable had the Bonds not been called for redemption.

9

Partial Redemption of Bonds. Upon surrender of any Bond redeemed in part only, the Trustee shall execute, and deliver to the Owner thereof, at the expense of the Corporation, a new Bond or Bonds of authorized denomination equal in aggregate principal amount to the unredeemed portion of the Bond surrendered and of the same maturity. Such partial redemption shall be valid upon payment of the amount thereby required to be paid to such Owner, and the Authority, the Corporation and the Trustee shall be released and discharged from all liability to the extent of such payment.

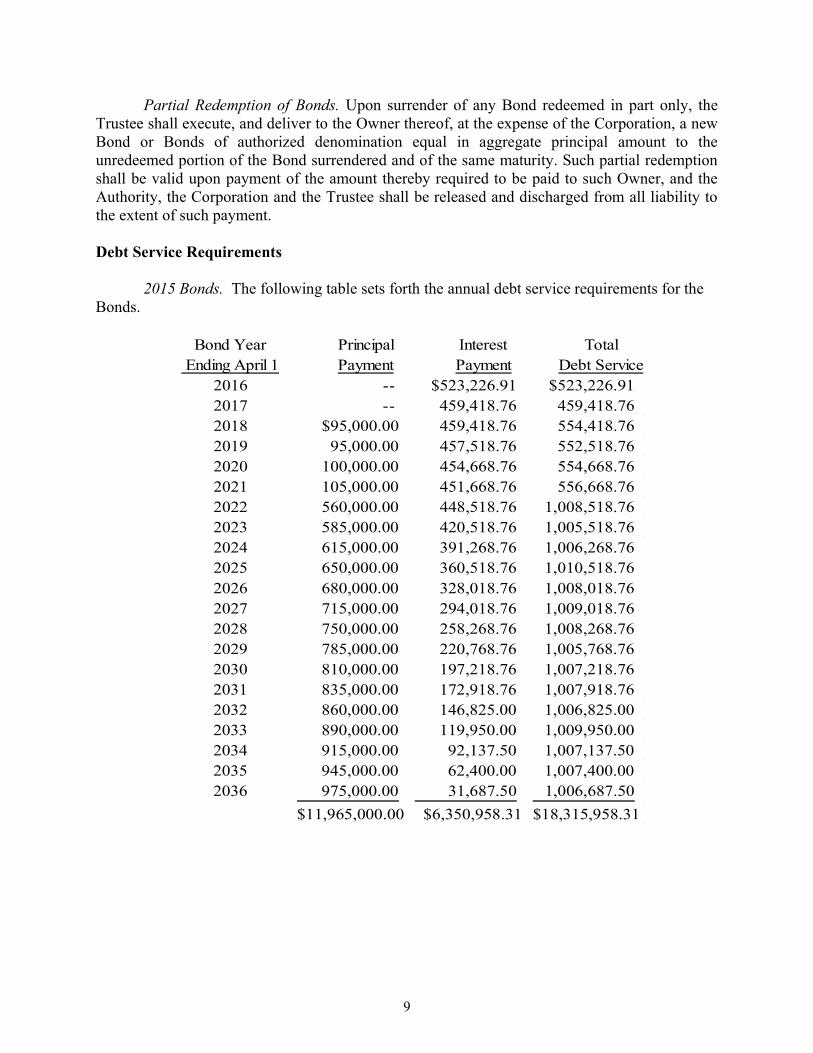

Debt Service Requirements

2015 Bonds. The following table sets forth the annual debt service requirements for the Bonds.

Bond Year Principal Interest Total Ending April 1 Payment Payment Debt Service

2016 -- $523,226.91 $523,226.912017 -- 459,418.76 459,418.762018 $95,000.00 459,418.76 554,418.762019 95,000.00 457,518.76 552,518.762020 100,000.00 454,668.76 554,668.762021 105,000.00 451,668.76 556,668.762022 560,000.00 448,518.76 1,008,518.762023 585,000.00 420,518.76 1,005,518.762024 615,000.00 391,268.76 1,006,268.762025 650,000.00 360,518.76 1,010,518.762026 680,000.00 328,018.76 1,008,018.762027 715,000.00 294,018.76 1,009,018.762028 750,000.00 258,268.76 1,008,268.762029 785,000.00 220,768.76 1,005,768.762030 810,000.00 197,218.76 1,007,218.762031 835,000.00 172,918.76 1,007,918.762032 860,000.00 146,825.00 1,006,825.002033 890,000.00 119,950.00 1,009,950.002034 915,000.00 92,137.50 1,007,137.502035 945,000.00 62,400.00 1,007,400.002036 975,000.00 31,687.50 1,006,687.50

$11,965,000.00 $6,350,958.31 $18,315,958.31

10

2011 Bonds. The following table sets forth the annual debt service requirements for the unrefunded 2011 Bonds not defeased pursuant to the Plan of Financing.

Bond Year Principal Interest Total Ending April 1 Payment Payment Debt Service

2015 -- $74,600.00 $74,600.00 2016 -- 74,600.00 74,600.00 2017 -- 74,600.00 74,600.00 2018 $380,000.00 74,600.00 454,600.00 2019 395,000.00 58,450.00 453,450.002020 415,000.00 40,675.00 455,675.002021 430,000.00 20,962.50 450,962.50

$1,620,000.00 $418,487.50 $2,038,487.50

Book-Entry Only System

The Bonds will be issuable in fully registered form only and, when issued and delivered, will be registered in the name of Cede & Co., as nominee of the Depository Trust Company, New York, New York (“DTC”). DTC will act as the depository of the Bonds and all payments due on the Bonds will be made to DTC or its nominee. Ownership interests in the Bonds may be purchased in book-entry form only. See APPENDIX F—“BOOK-ENTRY SYSTEM.”

SECURITY FOR THE BONDS

Pledge Under the Indenture; Gross Revenues

Subject to and for the purposes and on the terms and conditions set forth in the Indenture, there are pledged to secure the payment of the principal of, and interest on, the Bonds, all of the Revenues and any other amounts (including proceeds of the sale of the Bonds) held in any fund or account established pursuant to the Indenture (except the Rebate Fund). Subject to the terms of the Loan Agreement, the Gross Revenues of the Corporation are pledged to the payment of Loan Repayments and to secure the payments of the principal of, and interest on the Bonds and Parity Debt. “Gross Revenues” means, in general, all revenues, income, receipts and money received in any period by or on behalf of the Corporation related to the Facilities (other than donor-restricted gifts, grants, bequests, donations and contributions). See APPENDIX A—“INFORMATION CONCERNING THE CORPORATION—Sources of Revenues” and APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS— Definitions.” The pledge constitutes a lien on, and security interest in, such assets. The Authority assigns to the Trustee, for the benefit of the Owners, all of the rights, title and interest of the Authority in the Loan Agreement. The Trustee shall be entitled to and shall be required to take all steps, actions and proceedings reasonably necessary in its judgment to enforce, either jointly with the Authority or separately, all of the rights of the Authority under the Loan Agreement.

11

The Corporation agrees that, so long as any Bonds remain outstanding under the Indenture, all of the Gross Revenues shall be deposited as soon as practicable upon receipt in a fund designated as the “Gross Revenue Fund” which the Corporation shall establish and maintain at such banking or financial institution or institutions located in the State of California as the Corporation shall designate for such purpose (the “Depository Bank(s)”). Subject only to the provisions of the Loan Agreement permitting the application thereof for the purposes and on the terms and conditions set forth therein, the Corporation pledges and, to the extent permitted by law, grants a security interest to the Trustee in the Gross Revenue Fund to secure the payment of the principal of and interest on the Bonds and Parity Debt of the Corporation.

The pledge of Gross Revenues will be perfected to the extent that such security interest may be perfected by filing under the Uniform Commercial Code of the State of California and by entering into a deposit account control agreement, and the pledge may be subordinated to the interest and claims of others. Some examples of cases of subordination or prior claims are (i) statutory liens, (ii) rights arising in favor of the United States of America or any agency thereof, (iii) present or future prohibitions against assignment in any federal statutes or regulations, (iv) constructive trusts, equitable liens or other rights impressed or conferred by any State or federal court in the exercise of its equitable jurisdiction, (v) federal or State of California bankruptcy laws that may affect the enforceability of the Indenture or pledge of Gross Revenues, (vi) rights of third parties in Gross Revenues converted to cash and not in the possession of the Trustee or the Depository Bank(s), (vii) provisions prohibiting the direct payment of amounts due to providers from Medicare and Medi-Cal and other governmental programs to persons other than such providers; (viii) certain judicial decisions that cast doubt upon the right of the Trustee, in the event of the bankruptcy of the Corporation, to collect and retain accounts receivable from Medicare and Medi-Cal and other governmental programs; (ix) commingling of proceeds of Gross Revenues with other moneys of the Corporation not subject to the security interest in the Gross Revenues; (x) claims that might arise if appropriate financing or continuation statements are not filed in accordance with the California Uniform Commercial Code, as from time to time in effect; and (xi) claims that might arise if a deposit account control agreement is not in effect as to the bank deposits holding Gross Revenues. In addition, it may not be possible to perfect a security interest in any manner whatsoever in certain types of Gross Revenues (e.g., gifts, donations, certain insurance proceeds and grants) prior to actual receipt by the Corporation for deposit in the Gross Revenue Fund. Further, it is uncertain whether a security interest may be granted in Medicare and Medi-Cal and other governmental payments. While providers are currently prohibited from assigning such receivables, it is unclear whether this prohibition will be interpreted so as to preclude the granting of security interests. See “Parity Debt and Other Indebtedness” and “BONDHOLDERS’ RISKS—Certain Matters Relating to Enforceability” herein below. See also APPENDIX A—“INFORMATION CONCERNING THE CORPORATION—-Financial Information—Outstanding Indebtedness.”

Debt Service Reserve Account

On the date of delivery of the Bonds, the Debt Service Reserve Account will be funded in the amount of $554,843.76 from Bond proceeds. Upon the final maturity of the unrefunded 2011 Bonds on April 1, 2021, the remaining amount on deposit in the debt service reserve account for the 2011 Bonds ($455,675.00) will be transferred to the Trustee for deposit in the Debt Service

12

Reserve Account, bringing the total therein to $1,010,518.76, being equal to the Debt Service Reserve Account Requirement on such date. The Debt Service Reserve Account Requirement is, as of any date of calculation on and after April 1, 2021, an amount equal to the Maximum Annual Bond Service. “Maximum Annual Bond Service” is defined in the Indenture as, as of any date of calculation on and after April 1, 2021, the sum of (a) the interest falling due on the Outstanding Bonds (assuming that all then Outstanding Serial Bonds are retired on their respective maturity dates and that all then Outstanding Term Bonds are retired at the times and in the amounts provided for by Mandatory Sinking Account Payments), (b) the principal amount of then Outstanding Serial Bonds falling due by their terms, and (c) the aggregate amount of all Mandatory Sinking Account Payments required; all as computed for the Bond Year in which sum shall be largest. The Debt Service Reserve Account is required to be maintained in Investment Securities having a value equal to the Debt Service Reserve Account Requirement as such value is determined by the Trustee on or before each April 1 and October 1. The Corporation is required to make up any deficiencies resulting therein. See APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—INDENTURE” and “—LOAN AGREEMENT.”

Loan Agreement on Parity with That of Refunded 2011 Bonds

In connection with the issuance of the Bonds, the Corporation will execute the Loan Agreement pursuant to which the Corporation shall agree to abide by, adhere to and perform terms, conditions and covenants that shall be on parity with those terms, conditions and covenants of the loan agreement entered into by the Corporation in connection with the issuance of the Refunded 2011 Bonds. See APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—LOAN AGREEMENT.”

Insurance

The principal of and interest on the Bonds will be insured by the Office. If moneys are not available to pay the principal of or interest on the Bonds, the Office will be obligated to continue to make payments on the Bonds or shall instruct the Trustee to declare the principal of all Bonds then Outstanding and interest accrued thereon to be due and payable immediately and make payment of such principal and interest. Upon the occurrence of certain events, the Office shall notify the Treasurer, and the Treasurer shall issue debentures to the Holders of the Bonds fully and unconditionally guaranteed by the State in an amount equal to the principal of and accrued interest on the Bonds. See “CALIFORNIA HEALTH FACILITY CONSTRUCTION LOAN INSURANCE PROGRAM” herein.

The Office’s Control of Remedies

For as long as the Office is obligated and in compliance under the Contract of Insurance, all remedies of the Trustee (as assignee of the Authority) and Bondholders under the Indenture, the Loan Agreement, the Regulatory Agreement and the Deed of Trust shall be exercised solely by the Office.

13

Deed of Trust

In connection with the execution of the Loan Agreement and the issuance of the Bonds, the Corporation will execute a deed of trust (the “Deed of Trust”) pursuant to which the Corporation will grant to the trustee thereunder, for the benefit of the Office, holders of Parity Debt and the Authority, a first lien on, and security interest in, the certain property owned by the Corporation and located in Santa Clara County, California and described in the Deed of Trust, subject to Permitted Encumbrances, and subject to the right of the Corporation (with the prior consent of the Office) to remove certain property from the lien on and security interest in the Deed of Trust, as security for the performance of the Corporation’s obligations under the Loan Agreement, the Regulatory Agreement and the Contract of Insurance.

For so long as the Office is obligated under the Contract of Insurance, all rights under the Deed of Trust shall be exercised solely by the Office. With the consent of the Office, the Deed of Trust may be amended, subordinated or terminated at any time without the necessity of obtaining the consent of the Trustee, the Authority or the holders of the Bonds or Parity Debt. Accordingly, the Owners of the Bonds should not consider the Deed of Trust as security for payment of the Bonds. An ALTA title insurance policies on the Corporation’s property in an aggregate amount not less than the principal amount of the Bonds will be delivered at the time of issuance of the Bonds. See APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—DEED OF TRUST.”

Rate Covenant and Other Financial Covenants

The Corporation has agreed in the Loan Agreement to use its best efforts to maintain for each Fiscal Year a ratio (referred to as a “Rate Covenant”) of Aggregate Income Available for Debt Service to Maximum Aggregate Annual Debt Service of at least 1.25; provided, however, in computing Maximum Aggregate Annual Debt Service in any Fiscal Year there will not be included any Long-Term Indebtedness debt service on any Long-Term Indebtedness issued in such Fiscal Year unless the Corporation is required to make principal or interest payments on such Long-Term Indebtedness in the year in which such Long-Term Indebtedness is issued and, provided further, that in computing Maximum Aggregate Annual Debt Service in any Fiscal Year there will not be included debt service on any Long-Term Indebtedness if all principal of and interest due on such Long-Term Indebtedness in such Fiscal Year is paid from the proceeds of such Long-Term Indebtedness or from certain monies or certain Investment Securities held by a trustee or escrow agent for that purpose.

If this ratio, as calculated at the end of any Fiscal Year, is below the required level, the Corporation has covenanted to retain a Management Consultant of national recognition, within sixty (60) days after the receipt of all audits for such Fiscal Year, to make recommendations to increase such ratio for subsequent Fiscal Years of the Corporation at least to the level required or, if in the opinion of the Management Consultant the attainment of such level is impracticable, to the highest practicable level. The Corporation agrees, to the extent permitted by law, to follow the recommendations of the Management Consultant. So long as the Corporation (i) retains a Management Consultant of national recognition, (ii) follows such Consultant’s recommendations

14

to the extent permitted by law, and (iii) realizes Net Income Available for Debt Service equal to 1.0 times its Aggregate Debt Service, the Corporation will be deemed to have complied with the above requirement even if such ratio for the subsequent Fiscal Year of the Corporation is below the required level.

The Corporation is also required to maintain a current ratio of 1.50 to 1 and a minimum of 30 days cash on hand.

For information relating to the rate covenant, the current ratio and the days cash on hand requirement see APPENDIX C—“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—LOAN AGREEMENT—Rates and Charges; Debt Coverage; Current Ratio; Days Cash on Hand” and “—INDENTURE–Events of Default; Remedies Upon Default” and “—REGULATORY AGREEMENT—Rates and Charges; Current Ratio; Debt Coverage; Days Cash on Hand” and “—Remedies on Default.” The Bonds will continue to be insured by the Office in the manner described above even if an Event of Default were to occur.

Parity Debt and Other Indebtedness

The Corporation may incur other obligations or indebtedness, in some cases on a parity basis with the Bonds. Under certain circumstances provided in the Loan Agreement the Corporation may issue Short-Term Indebtedness and secure the lender of such Short-Term Indebtedness with a first priority security interest in the Corporation’s General Revenues pledged in security of the Bonds. In such event, the lien of the Trustee with respect to Gross Revenues comprised of accounts receivable will be junior to such lender’s security interest. See APPENDIX C-“SUMMARY OF PRINCIPAL LEGAL DOCUMENTS-Limitation on Indebtedness.”

CALIFORNIA HEALTH FACILITY CONSTRUCTION LOAN INSURANCE PROGRAM

Description of the Insurance Policy

General. The Corporation has received a conditional commitment from the Office for insurance of the Corporation’s payment of the principal and interest with respect to the Bonds. Insurance of the full amount of the principal and interest with respect to the Bonds (but not any premium) is evidenced by the Contract of Insurance and the Regulatory Agreement, both of which will be entered into by the Office, the Authority and the Corporation, concurrently with the execution and delivery of the Bonds. See APPENDIX G — “FORM OF CONTRACT OF INSURANCE” for the form and terms of the insurance provided by the Office. The Regulatory Agreement set out many of the financial covenants of the Corporation relating to, among other things, the maintenance of specified debt service coverage levels and the limitations on incurrence of additional indebtedness or disposition of assets by the Corporation. Prospective holders of the Bonds should note that the provisions of the Regulatory Agreement may be amended with the consent of the Office without the necessity of obtaining the consent of the holders of the Bonds or the holders of Parity Debt. See “CALIFORNIA HEALTH FACILITY CONSTRUCTION LOAN INSURANCE PROGRAM – Rights of the Office Under the

15

Regulatory Agreement” herein, and APPENDIX C — “SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—REGULATORY AGREEMENT.”

Insurance Law section 129050, subsection (a) requires that a loan must be secured by a first mortgage, first deed of trust or first priority lien on an interest of the borrower in real property and any other security agreement as the Office may require. For this purpose, the Corporation will grant a security interest in the Gross Revenue Fund and all of the Gross Revenues under the Loan Agreement and the Corporation will enter into the Deeds of Trust. Prospective holders of the Bonds should note that the provisions of the Deeds of Trust may be amended, subordinated or terminated at any time with the consent of the Office without the necessity of obtaining the consent of the holders of the Bonds or the holders of Parity Debt.

Incontestability and Non-Cancellability. Under Insurance Law section 129110, the Contract of Insurance is incontestable from the date of execution thereof, except in case of fraud or misrepresentation on the part of the lender. The Insurance Law and the Contract of Insurance impose certain continuing obligations on the Corporation as a condition of insuring the Bonds but specify that the remedies for breach of these obligations shall not include withdrawal or cancellation of the insurance. The insurance provided by the Contract of Insurance will terminate under certain circumstances, including payment in full by the Office of the insurance with respect to the Bonds or defeasance of the Bonds pursuant to the Indenture, as more fully described in APPENDIX G — “FORM OF CONTRACT OF INSURANCE.” See also APPENDIX C — “SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—CONTRACT OF INSURANCE.”

Procedures upon Default. If there is an event of default as specified under the Indenture (an “Event of Default”), the Trustee must notify the Office. The Trustee also must notify the Office if 30 days prior to an interest or principal payment date there are not sufficient available moneys held by the Trustee in the Revenue Fund (other than in the Debt Service Reserve Account) to make the next payment of principal or interest on the Bonds.

Pursuant to the Regulatory Agreement, if there is an Event of Default and the Trustee has notified the Office that available moneys in the Principal and Interest Accounts will be insufficient to pay in full the next succeeding payment of interest and/or principal when due, the Office shall cause a sufficient amount to be deposited in the Principal Account and/or Interest Account at least three Business Days prior to the date on which such payment is due. The money will come from the Debt Service Reserve Account held under the Indenture or from the Health Facility Construction Loan Insurance Fund (the “HFCLIF”) that is established by the Insurance Law (sections 129010, subsection (g) and 129200). The obligation of the Corporation to repay any money advanced from the HFCLIF is secured by the Deeds of Trust.

Following an Event of Default, the Office may either (i) continue to approve such transfers or make such payments described in the preceding paragraph as are necessary to provide for the timely payment of the principal of and interest with respect to the Bonds, (ii) accept title to the Facilities from the Trustee upon foreclosure pursuant to the Deeds of Trust or otherwise, (iii) accept an assignment of the security interest created under the Deeds of Trust and of all claims under the Indenture, or (iv) instruct the Trustee to declare the principal of the Bonds

16

then Outstanding and the interest with respect thereto to be immediately due and payable and make such payment from the HFCLIF. If funds in the HFCLIF are not sufficient to make the required payments described above, the Office shall notify the Treasurer who is required to issue debentures in place of such Bonds. See “The Office, the Program and the Insurance Fund—State Debentures” below.

Rights of the Office under the Regulatory Agreement. The Regulatory Agreement grants the Office extensive rights, including the right to attend and participate in all meetings of the Corporation’s Board of Directors. Additionally, the Regulatory Agreement prohibits the Corporation from taking certain actions without first obtaining the consent of the Office or meeting certain requirements in the Regulatory Agreement, including affiliating with, merging into, or consolidating with any entity; transferring cash or cash equivalents to any entity, including but not limited to a subsidiary or an affiliate of the Corporation; disposing or acquiring property; and incurring indebtedness. Additionally, upon the occurrence of an event of default under the Regulatory Agreement, Deeds of Trust or Indenture, the Office shall have the remedies provided in Insurance Law Section 129173. See APPENDIX C — “SUMMARY OF PRINCIPAL LEGAL DOCUMENTS—REGULATORY AGREEMENT.”

Rate Covenant and Other Financial Covenants. Under the Regulatory Agreement, the Corporation is required to fix, charge and collect rates, fees and charges which are reasonably projected to be sufficient in each Fiscal Year to produce Net Income Available for Debt Service of at least 1.25 times Maximum Aggregate Annual Debt Service for such Fiscal Year. The Regulatory Agreement also requires the Corporation to maintain, as of the end of each Fiscal Year, a ratio of current assets to current liabilities of at least 1.5 to 1, and at least thirty (30) Days Cash on Hand beginning with the Corporation’s Fiscal Year ending September 30, 2015. The measurement of Days Cash on Hand is taken at the end of each particular Fiscal Year. For more specific information relating to these covenants, see APPENDIX C – “SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – Regulatory Agreement.”

Covenants contained in the Regulatory Agreement may be waived or amended by the Office without the necessity of obtaining the consent of the owners of the Bonds, the Authority or any other party. For a further description of the rate covenant, the current ratio covenant and the Days Cash on Hand covenant, see APPENDIX C – “SUMMARY OF PRINCIPAL LEGAL DOCUMENTS – Regulatory Agreement – Rates and Charges; Debt Coverage; Current Ratio; Days Cash on Hand.” The Bonds will continue to be insured by the Office in the manner described above even if an Event of Default were to occur under financial or other covenants made by the Corporation.

The Office, the Program and the Insurance Fund

General. The California Health Facility Construction Loan Insurance Program (the “Program”) is authorized by Article XVI, Section 4 of the California Constitution and is provided for in the Insurance Law. The Program is operated by the Office, which has adopted regulations implementing the Program. Under the Insurance Law, the Office is currently authorized to insure health facility construction, improvement and expansion loans, as specified in the Insurance Law. Entities which may obtain insurance for their facilities include both public

17

agencies and nonprofit corporations, and authorized health facilities include a wide range from acute care facilities to local clinics, dependency centers and community mental health centers. The Insurance Law authorizes the Program to insure not more than $3,000,000,000 principal amount of loans at any time. As of October 31, 2014, the principal amount of loans insured under the Program was approximately $1,771,161,977, comprised of 110 loans.

Finances of the Program; Financial Reports. The Program is financed by an application fee of 0.5% of the loan applied for, but not to exceed $500 (Insurance Law section 129090), an inspection fee not in excess of 0.4% of the loan that is insured (Insurance Law section 129035), and an insurance premium due in full at closing not in excess of 3.0% of the total amount of principal and interest payable over the term of the loan (Insurance Law section 129040). The fees and premiums charged are deposited in the HFCLIF and are used to defray administrative expenses of the Program, to cure defaults on loans and to pay principal of and interest on insured bonds and certificates of participation prior to issuance of debentures by the Treasurer.

Under the Insurance Law, payments of principal and interest with respect to the Bonds or payments on the debentures would be made by the Office from the HFCLIF. As of October 31, 2014, the cash balance of the HFCLIF was approximately $169,680,900. The moneys in the HFCLIF are continuously appropriated to pay obligations insured by the Office under the Insurance Law. Insurance Law section 129215 states: “The Health Facility Construction Loan Insurance Fund, established pursuant to Section 129200, shall be a trust fund and neither the fund nor the interest or other earnings generated by the fund shall be used for any purpose other than those purposes authorized by this chapter.” The moneys in the HFCLIF are invested in the State’s Pooled Money Investment Account.

The Office is required by law to submit certain reports to the Legislature, consisting of two Annual Reports, and a State Plan. The State Plan is prepared every two years, as of January 1 of each odd- numbered year. The 2013 State Plan has not yet been released but is expected to be available in the Spring of 2015. The 2011 State Plan is available at the website of the Office. The Annual Reports to the Legislature for the year ended June 30, 2013 (the “2013 Annual Reports”), are available at the website of the Office. The Office also prepares monthly reports containing limited financial data. The most recent monthly report available from the Office is for the period ended October 31, 2014.