Banc of America Securities LLC - CA.gov

136

OFFICIAL STATEMENT NEW ISSUE-BOOK ENTRY ONLY RATING: STANDARD & POOR'S: SP-1+ (See "RATING" herein.) In the opinion of Orrick, Herrington & Sutcliffe LL Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other things, the accuracy of certain representation and compliance with certain covenants, interest on the Notes is excluded from gross income for federal income tax purposes under section 103 of the Inteal Revenue Code of 1986 and is exempt from State of Califoia personal income taxes. In the rther opinion of Bond Counsel, interest on the Notes is not a specc preference item for purposes of the federal individual or corporate alteative minimum taxes, although Bond Counsel observes that such interest is included in adjusted current eaings in calculating federal corporate alteative minimum taxable income. Bond Counsel ex- presses no opinion regarding other tax consequences related to the ownership or disposition o or the accrual or receipt of interest on, the Notes. See "TAX EXEMPTION' herein. $55,000,000 COUNTY OF SANTA BARBARA, CALIFORNIA 2004-2005 TAX AND REVENUE ANTICIPATION NOTES SERIES A Dated: July 1, 2004 Due: July 26, 2005 The County of Santa Barbara, California (the "County") 2004-2005 Tax and Revenue Anticipation Notes, Series A (the "Notes") will be issued as fully registered Notes and, when issued, will be registered in the name of and held by Cede & Co., as nominee for The Depository Trust Company ("DTC"). Ownership interest in the Notes may be purchased in book-entry form only in denominations of $5,000 or any integral multiple thereof. So long as DTC or its nominee, Cede & Co. , is the registered owner of the Notes, payments of principal of and interest on the Notes will be made directly to DTC or its nominee, Cede & Co., which will remit such payments to the DTC Participants, which will in turn remit such payments to the beneficial owners of the Notes. See "THE NOTES-Book-Entry-Only System" herein. The Notes are not subject to redemption prior to maturity. The Notes will be issued in an aggregate principal amount of $55,000,000 on July 1, 2004 and will mature on July 26, 2005. The rate of interest and offering price or yield for the Notes are shown below. Interest on the Notes will be payable on July 1, 2005 and at maturity. Principal Amount $55,000,000 Interest Rate 3.00% Yield 1.56% Under certain circumstances, as described further herein, the County may issue in fiscal year 2004-2005 an additional series of 2004-2005 Tax and Revenue Anticipation Notes (the "Notes of Series B") in an amount not to exceed $15,000,000 (collectively, the Notes and the Notes of Series B are the "2004 Notes" or the "2004-2005 Notes"). See "THE NOTES-General Provisions" herein. The purpose of the note program is to finance, in part, the County's general fund cash flow requirements during the 2004-2005 fiscal year. In accordance with California law, the Notes are general obligations of the County, solely payable as to both principal and interest om taxes, income, revenue, cash receipts and other moneys of the County attributable solely to the fiscal year 2004-2005 and legally available for payment thereof. The principal of and interest on the Notes constitutes a first lien on the amounts pledged, and to the extent not paid om such pledged monies, are payable from any other lawfully available monies of the County. This cover page is r reference only. Investors must read the entire Official Statement in order to obtain information essential to the making of an informed investment decision. The Notes will be offered when, as and if issued and received by the Underi ter, subject to the approval of validity by Orrick, Herrington & Sutcliffe LLP, Bond Counsel. Certain other legal matters will be passed upon for the County by County Counsel and for the Underwriter by Fulbright & Jaworski L.L.P., Los Angeles, California. The Notes, in definitive form, will be available for delivery through the facilities of DTC on or about July 1, 2004 in New York, New York. Banc of America Securities LLC Dated: June 24, 2004

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Banc of America Securities LLC - CA.gov

OFFICIAL STATEMENT NEW ISSUE-BOOK ENTRY ONLY RATING:

STANDARD & POOR'S: SP-1+ (See "RATING" herein.)

In the opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming, among other things, the accuracy of certain representation and compliance with certain covenants, interest on the Notes is excluded from gross income for federal income tax purposes under section 103 of the Internal Revenue Code of 1986 and is exempt from State of California personal income taxes. In the further opinion of Bond Counsel, interest on the Notes is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, although Bond Counsel observes that such interest is included in adjusted current earnings in calculating federal corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Notes. See "TAX EXEMPTION' herein.

$55,000,000 COUNTY OF SANTA BARBARA, CALIFORNIA

2004-2005 TAX AND REVENUE ANTICIPATION NOTES SERIES A

Dated: July 1, 2004 Due: July 26, 2005 The County of Santa Barbara, California (the "County") 2004-2005 Tax and Revenue Anticipation Notes, Series A (the "Notes") will be issued as fully registered Notes and, when issued, will be registered in the name of and held by Cede & Co., as nominee for The Depository Trust Company ("DTC"). Ownership interest in the Notes may be purchased in book-entry form only in denominations of $5,000 or any integral multiple thereof. So long as DTC or its nominee, Cede & Co., is the registered owner of the Notes, payments of principal of and interest on the Notes will be made directly to DTC or its nominee, Cede & Co., which will remit such payments to the DTC Participants, which will in turn remit such payments to the beneficial owners of the Notes. See "THE NOTES-Book-Entry-Only System" herein. The Notes are not subject to redemption prior to maturity.

The Notes will be issued in an aggregate principal amount of $55,000,000 on July 1, 2004 and will mature on July 26, 2005. The rate of interest and offering price or yield for the Notes are shown below. Interest on the Notes will be payable on July 1, 2005 and at maturity.

Principal Amount $55,000,000

Interest Rate 3.00%

Yield 1.56%

Under certain circumstances, as described further herein, the County may issue in fiscal year 2004-2005 an additional series of 2004-2005 Tax and Revenue Anticipation Notes (the "Notes of Series B") in an amount not to exceed $15,000,000 (collectively, the Notes and the Notes of Series B are the "2004 Notes" or the "2004-2005 Notes"). See "THE NOTES-General Provisions" herein. The purpose of the note program is to finance, in part, the County's general fund cash flow requirements during the 2004-2005 fiscal year. In accordance with California law, the Notes are general obligations of the County, solely payable as to both principal and interest from taxes, income, revenue, cash receipts and other moneys of the County attributable solely to the fiscal year 2004-2005 and legally available for payment thereof. The principal of and interest on the Notes constitutes a first lien on the amounts pledged, and to the extent not paid from such pledged monies, are payable from any other lawfully available monies of the County. This cover page is for reference only. Investors must read the entire Official Statement in order to obtain information essential to the making of an informed investment decision. The Notes will be offered when, as and if issued and received by the Underwriter, subject to the approval of validity by Orrick, Herrington & Sutcliffe LLP, Bond Counsel. Certain other legal matters will be passed upon for the County by County Counsel and for the Underwriter by Fulbright & Jaworski L.L.P., Los Angeles, California. The Notes, in definitive form, will be available for delivery through the facilities of DTC on or about July 1, 2004 in New

York, New York. Banc of America Securities LLC

Dated: June 24, 2004

No dealer, broker, salesperson or other person has been authorized by the County or the Underwriter to give any information or to make any representations other than those contained herein and, if given or made, such other information or representation must not be relied upon as having been authorized by the County or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Notes by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale.

This Official Statement is not to be construed as a contract with the purchasers of the Notes. Statements contained in this Official Statement which involve estimates, forecasts or matters of opinion, whether or not expressly so described herein, are intended solely as such and are not to be construed as a representation of facts.

The information set forth herein has been obtained from official sources which are believed to be reliable but it is not guaranteed as to accuracy or completeness, and is not to be construed as a representation by the Underwriter. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the County since the date hereof. This Official Statement is submitted in connection with the sale of the Notes referred to herein and may not be reproduced or used, in whole or in part, for any other purpose, unless authorized in writing by the County.

The Underwriter has provided the following sentence for inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information.

The Notes have not been registered under the Securities Act of 1933, in reliance upon an exemption contained in such Act. The Notes have not been registered under the securities laws of any state.

IN CONNECTION WITH THIS INITIAL OFFERING, THE UNDERWRITER MAY OVERALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF THE NOTES AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME. THE UNDERWRITER MAY OFFER AND SELL THE NOTES TO CERTAIN DEALERS AND BANKS AT PRICES LOWER THAN THE PUBLIC OFFERING PRICE STATED ON THE COVER PAGE HEREOF AND SAID PUBLIC OFFERING PRICE MAY BE CHANGED FROM TIME TO TIME BY THE UNDERWRITER.

z

r- d".3

Lf') !--V) er� t. •. n C)

U.l-

Ci :I:

..a: �: �: ... -·�1.....,.J

t �. .. ��u

0,l

�� ') >-. . . I

. \• .. or: __ , :::::i(:: -_;,

-) �1'� ....:r o> CJ ri

COUNTY OF SANTA BARBARA

Joseph Centeno, Chair Susan Rose, Vice Chair Naomi Schwartz Gail Marshall Joni L. Gray

Michael F. Brown Bernice James Harry Hagen Stacey Matson Robert W. Geis Theo Fallati Stephen Shane Stark Jennifer Christensen

BOARD OF SUPERVISORS

Fifth District Second District

First District Third District

Fourth District

COUNTY OFFICIALS County Administrator

Treasurer-Tax Collector Assistant Treasurer-Tax Collector

UNDERWRITER Banc of America Securities LLC

Los Angeles, California

BOND COUNSEL

Treasury Finance Chief Auditor-Controller

Chief Deputy Controller County Counsel

Deputy County Counsel

./

Orrick, Herrington & Sutcliffe LLP / San Francisco, California

This page intentionally left blank

TABLE OF CONTENTS

Section

INTRODUCTION ....................................................................................................................................... 1 Continuing Disclosure .............................................................................................................................. 1

COUNTY OF SANTA BARBARA 2004-2005 SHORT-TERM FINANCING PROGRAM .......•....... 2

THE NOTES ................................................................................................................................................ 2 General Provisions ......................................................... . ......................................................................... 2 Book-Entry-Only Systeni ........................................................................................................................... 2 Authority for Issuance . . . ... . ... .. .. . .. . .. ...... . . . . . .. .......... . .. . . .. . ... ... . ........ . .. ... ... .. . . . . . .... .... . . . ... .. . .... .. . . .. . . . . . .... ... . .... . 2 Purpose of Issue .... . ... . . . .... . . . . . ... ..... ..... .. . .. . . . . . ... . . . . ... .. ... ........ ..... .. ...... ..... .... ..... . . .. .. . .. . .... .. . ... ......... ... .. .... .. .. . 2 Security for the 2004-2005 Notes . .... . ............. .. . .. ........ .. . . ... .... .. .. . .. . . ... .. . ........ .. .. ... . . . .. .... .. .... . .... . . .. .... . . . ...... 3 Investment of Note Proceeds and Repayment Account .......... . . . . . . . . .... .. . . ...... . ..... .. . ...... .. .. . .. . . . . ... .. . ... . ... ... . .. 4

AVAILABLE SOURCES OF PAYMENT ............................................................................................... 4 Intrafitnd Borrowing and Cash Flow ........................................................................................................ 5

TAX MATTERS ......................................................................................................................................... 8

LEGAL MATTERS .................................................................................................................................... 9

RISK FACTORS ....................................................................................................................................... 10 State Funding of Counties . . ....... . . ... . .. ....... .. .. .......... . . .. .. . .. . ...... .... ... . . . . . . ........ . . . ...... . . . .... .... .. ..... . . . . ... ...... . .. . JO

LEGALITY FOR INVESTMENT IN CALIFORNIA .......................................................................... 10

RATING ..................................................................................................................................................... 10

LITIGATION ............................................................................................................................................ 10

UNDERWRITING .................................................................................................................................... 10

ADDITIONAL INFORMATION ............................................................................................................ 11

OFFICIAL STATEMENT CERTIFICATION ...................................................................................... 11

Appendix

COUNTY FINANCIAL AND DEMOGRAPHIC INFORMATION ................................................. A-1

FORM OF LEGAL OPINION .............................................................................................................. B-1

COUNTY AUDITED FINANCIAL STATEMENTS FOR FISCAL YEAR 2002-2003 ................... C-1

STATEMENT OF INVESTMENT POLICY ....................................................................................... D-1

FORM OF CONTINUING DISCLOSURE CERTIFICATE ............................................................. E-1

BOOK-ENTRY ONLY SYSTEM ......................................................................................................... F-1

This page intentionally left blank

OFFICIAL STATEMENT $55,000,000

COUNTY OF SANTA BARBARA, CALIFORNIA 2004-2005 TAX AND REVENUE ANTICIPATION NOTES

SERIES A

INTRODUCTION

This Official Statement, including the cover page and Appendices, provides certain information concerning the sale and delivery of the 2004-2005 Tax and Revenue Anticipation Notes, Series A (the "Notes") of the County of Santa Barbara, California (the "County"). The Notes are general obligations of the County, but are payable only out of taxes, income, revenue, cash receipts and other moneys of the County received for the general fund of the County during or attributable to fiscal year 2004-2005 (July 1, 2004 through June 30, 2005) and which are generally available for the payment of current expenses and other obligations of the County. The County's 2004-2005 short-term financing program provides for the issuance of $55,000,000 of the Notes on July 1, 2004, and for the issuance of an additional series of 2004-2005 Tax and Revenue Anticipation Notes (the "Notes of Series B") on or before December 15, 2004 in an amount not to exceed $15,000,000 (collectively, the Notes and the Notes of Series B are referred to herein as the "2004 Notes" or "2004-2005 Notes").

The Notes are being issued to finance, in part, the County's general fund cash flow requirements during the 2004-2005 fiscal year. The proceeds received from the sale of the Notes will allow the County to cover periods of deficits resulting from an uneven flow of revenues. County general fund expenditures tend to occur in relatively level amounts throughout the year, while receipts follow an uneven pattern. Cash receipts from secured property tax installment payments primarily occur in December and April, while payments from other government agencies occur at irregular intervals. As a result, the general fund's cash balance shows a deficit during parts of the fiscal year. The Notes are intended to finance such cashflow deficits.

Brief descriptions of the Notes, the security and sources of payment for the Notes, the County and its financial status follow. Such descriptions do not purport to be comprehensive or definitive. All references herein to various documents, including the Resolution (as defined below), are qualified in their entirety by reference to the forms thereof, all of which are available for inspection at the offices of the County.

Continuing Disclosure

The County will provide notice, during the time the Notes are outstanding, of the occurrence of certain enumerated events, if material. The specific nature of the information to be contained in the notices of material events and certain other terms of the continuing disclosure obligation are included herein under the caption "APPENDIX E - FORM OF CONTINUING DISCLOSURE CERTIFICATE." These covenants have been made in order to assist the Underwriter in complying with S.E.C. Rule 15c2-l 2(b )( 5). The County has never failed to comply in all material respects with any previous undertaking with regard to said Rule to provide annual reports or notices of material events.

1

COUNTY OF SANTA BARBARA 2004-2005 SHORT-TERM FINANCING PROGRAM

, A) The Notes will be secured by a pledge of certain taxes, income, revenue, cash receipts and other /; Y moneys of the County received for the general :fiwd.o.f the County during or attributable to the 2004-2005 � fiscal year and which are generallyavailable for the payment of current expenses and other obligations of

f

the County. See "THE NOTES-Security for the 2004-2005 Notes" herein. The Resolution of the Board of Supervisors of the County of Santa Barbara (the "Board") captioned "In the M atter of Providing for the Borrowing of Funds for Fiscal Year 2004-2005 and the Issuance and Sale of County of Santa Barbara, California, 2004-2005 Tax and Revenue Anticipation Notes therefor," which was adopted on M ay 25, 2004, (the "Resolution"), provides for the borrowing of funds for fiscal year 2004-2005 through the issuance and sale of the 2004 Notes.

THE NOTES

General Provisions

The Notes will be executed and delivered in fully registered form (without coupons) in denominations of $5, 000 or integral multiples thereof. Principal of and interest on the Notes are payable in lawful money of the United States of America. Principal and interest are payable by the County to the registered owner of the Notes, Cede & Co., as nominee of the Depository Trust Company ("DTC") in New York, New York (see "Book-Entry-Only System" below). The Notes will mature on July 26, 2005. Interest on the Notes will be payable on July 1, 2005 and at maturity, computed on the basis of a 360-day year comprising twelve 30-day months.

The Resolution authorizes the County to issue in fiscal year 2004-2005 the Notes of Series B in an amount not to exceed $15,000,000. The Notes of Series B, if issued, will be issued on or before December 15, 2004, and shall mature (without option of prior redemption) on a date within thirteen months after the date of original issuance of the Notes of Series B and will be secured ratably with the Notes. See "THE NOTES-Security for the 2004-2005 Notes" herein.

Book-Entry-Only System

The Certificates will be initially registered in the name of Cede & Co., as nominee of The Depository Trust Company, New York, New York ("DTC"). DTC will act as securities depository for the Certificates. Owners will not receive physical certificates representing their ownership interests in the Certificates, except in the event that use of the book-entry system for the Certificates is discontinued. See "THE CERTIFICATES-General Provisions" and "APPENDIX F-BOOK-ENTRY ONLY SYSTEM." In the event that the book-entry only system described in APPENDIX F is no longer used with respect to the Certificates, the Certificates will be registered in accordance with the Trust Agreement described herein. See "APPENDIX F - BOOK - ENTRY ONLY SYSTEM - Discontinuation of Book-Entry Only System; Payment to Beneficial Owners."

Authority for Issuance

The Notes are issued under the authority of Article 7.6, Chapter 4, Part 1, Division 2, Title 5 (commencing with Section 53850) of the California Government Code (the "Act") and pursuant to the Resolution.

Purpose of Issue

�

Issuance of the Notes will provide moneys for fiscal year 2004-2005 County general fund ' expenditures, including current expenses, capital expenditures and to discharge other obligations or tdebtedness of the County.

.}

,;JG'<--'

2

Security for the 2004-2005 Notes

The principal amount of the 2004-2005 Notes, together with the interest thereon, shall be payable from taxes, income, revenue, cash receipts and other moneys that are received by the County for the general fund of the County during or attributable to fiscal year 2004-2005 and that are generally available for the payment of current expenses and other obligations of the County (the "Unrestricted Revenues").

As security for the payment of the principal of and interest on the 2004-2005 Notes, the County pledges to deposit in trust in a restricted cash account within the general fund of the County designated as the "2004-2005 Tax and Revenue Anticipation Note Repayment Account" (the "Repayment Account"): (i) from the first Unrestricted Revenues received by the County during the period commencing on December 20, 2004, and ending on January 31, 2005 (a "Pledge Period") an amount equal to fifty percent (50%) of the principal amount of the 2004-2005 Notes issued and (ii) from the first Unrestricted Revenues received by the County during the period commencing on April 21, 2005, and ending on May 31, 2005, (also a "Pledge Period") an amount that, together with the amount on deposit in the Repayment Account (net of earnings on moneys thereon), will be sufficient to pay the principal of and interest on the 2004-2005 Notes at maturity. The amounts pledged by the County for deposit into the Repayment Account from the Unrestricted Revenues received during each indicated Pledge Period are herein called the "Pledged Revenues."

In the event that there have been insufficient Unrestricted Revenues received by the County by the third business day prior to the end of any such Pledge Period to permit the deposit into the Repayment Account of the full amount of the Pledged Revenues required to be deposited with respect to such Pledge Period, then the amount of any deficiency in the Repayment Account shall be satisfied and made up from any other moneys of the County lawfully available for the payment of the principal of the 2004-2005 Notes and the interest thereon (all as provided in the Act) (the "Other Pledged Moneys") on such date or thereafter on a daily basis, when and as such Pledged Revenues and Other Pledged Moneys are received by the County.

The Pledged Revenues with respect to the Pledge Period in which received shall be deposited by the Treasurer-Tax Collector of the County in the Repayment Account commencing the third business day of each respective Pledge Period, and thereafter at intervals of no more than every five business days, and applied as directed in the Resolution; and the Other Pledged Moneys, if any, shall be deposited by the Treasurer in the Repayment Account on the third business day prior to the end of such Pledge Period, and on each business day thereafter, until the full amount of the moneys required for repayment has been so deposited in the Repayment Account; provided that, if on the date that is six months from the date of issuance of the Notes, amounts deposited in the County general fund attributed to the sale of the Notes and, if issued, the Notes of Series B have not been withdrawn previously as required by the requirements of the Resolution, the amounts to be deposited in the Repayment Account during the Pledge Period in which received shall be deposited as soon as received. The principal of and interest on the 2004-2005 Notes shall constitute a first lien and charge on, and shall be payable from, moneys in the Repayment Account.

The Treasurer shall use the moneys in the Repayment Account on the interest payment date and maturity date of the 2004-2005 Notes to pay the principal of and interest on the 2004-2005 Notes. If on the maturity date of the Notes there are insufficient moneys in the Repayment Account to pay the principal of and interest on all the 2004-2005 Notes, the moneys in the Repayment Account shall be allocated on a pro rata basis to the principal of and interest on the Notes and the Notes of Series B, respectively. Any moneys remaining in the Repayment Account after such payment, or after provision for such payment has been made, shall be transferred to the general fund of the County.

The United States Court of Appeals for the Ninth Circuit has not decided whether a County that has filed for bankruptcy would be required to set aside revenues pledged under the note resolution following bankruptcy. Because the Treasurer is in possession of the taxes and other revenues that will be

3

set aside to pay the Notes and may invest these funds in the pooled investment fund, should the County go into bankruptcy, a court might hold that the owners of the Notes do not have a valid lien on the Pledged Revenues, the Other Pledged Money or amounts on deposit in the Repayment Account. In that case, unless the Note owners could "trace" the funds, the Note owners would be merely unsecured creditors of the County. There can be no assurance that the holders could successfully so "trace" the pledged taxes and other revenues. Investment of Note Proceeds and Repayment Account

Proceeds of the Notes deposited in the County general fund and moneys in the Repayment Account may be invested as permitted by Section 53601 of the California Government Code and according to the Treasurer and Tax-Collector's Investment Policy, except that no moneys shall be invested in reverse repurchase agreements, and no such investments shall have a maturity date later than the maturity date of the 2004 Notes to be paid from such investments. Alternatively, proceeds of the Notes may be deposited in an account entitled the "Note Proceeds Account" within the County general fund. Moneys in the Note Proceeds Account and the Repayment Account may also be invested in the following additional permitted investments: investment agreements with or the obligations of which are guaranteed by (a) a domestic bank, financial institution or insurance company with the financial capacity to honor its senior obligations of which is rated at least "AA" by Standard & Poor's; or (b) a foreign bank, the longterm debt of which is rated at least "AA" by Standard & Poor's (a "Qualified Provider"); provided, that the investment agreement shall provide that if during its term the provider's (or, if guaranteed, the guarantor's) rating by Standard & Poor's falls below "AA-", the provider must within 10 days assign the investment agreement to a Qualified Provider reasonably acceptable to the County or collateralize the investment agreement by delivering or transferring in accordance with applicable state and federal laws (other than by means of entries on the provider's books) to the County or a third party acting solely as agent therefor, United States Treasury Obligations that are free and clear of any third-party liens or claims at sufficient collateral levels to maintain the highest short-term rating on the Notes.

The proceeds of any such investments from moneys in the Repayment Account shall be retained in the Repayment Account until payment of principal and interest ( or provision therefor) has been made in full, at which time any excess amount shall be transferred to the general fund of the County. See "AVAILABLE SOURCES OF PAYMENT", "APPENDIX A-COUNTY FINANCIAL AND DEMOGRAPHIC INFORMATION-County Treasurer's Investment Pool" and "APPENDIX DSTATEMENT OF INVESTMENT POLICY."

AVAILABLE SOURCES OF PAYMENT

The Notes, in accordance with California law, are general obligations of the County, but are payable only out of the taxes, income, revenue, cash receipts and other moneys of the County received for the general fun<;!2f the County during or attributable to the fiscal year 2004-2005 and legally available for payment thereof. The County may, under existing law, issue securities, such as the Notes, only if the principal thereof and interest thereon will not exceed 85 percent of the estimated uncollected moneys available for the payment of such securities.

A 1978 change in the Constitution of the State of California substantially limited the County's ability to levy ad valorem taxes. However, California counties now are permitted by State law under SB 2557 to impose certain fees to raise general revenue. The estimated amount needed to repay the Notes and the interest thereon is approximately $56.79 million. The County estimates that the moneys available for payment of the Notes will be in excess of $314.46 million as indicated in the following table.

4

ESTIMATED REVENUE AVAILABLE FOR PAYMENT OF 2004-2005

TAX AND REVENUE ANTICIPATION NOTES Estimated-Unrestricted Available Fund Balance at June 30, 2004 Taxes Licenses, permits and franchises F ines, forfeitures and penalties Use of money and property Intergovernmental Revenues Charges for current services Miscellaneous Other F inancing Sources

Total

Source: County Auditor-Controller

Intrafund Borrowing and Cash Flow

$ 3,437 ,000 1 05 ,087, 000 1 4, 1 28,000 3,994,000 3,223,000

75 ,746 ,000 62, 848,000

872,000 45,1 24,000

31 4.459 000

County general fund expenditures tend to occur in relatively level amounts throughout the fiscal year. Conversely, receipts have followed an uneven pattern primarily as a result of secured property tax installment payment dates in December and April and as a result of delays and uneven payments from other government agencies, the two largest sources of County revenues.

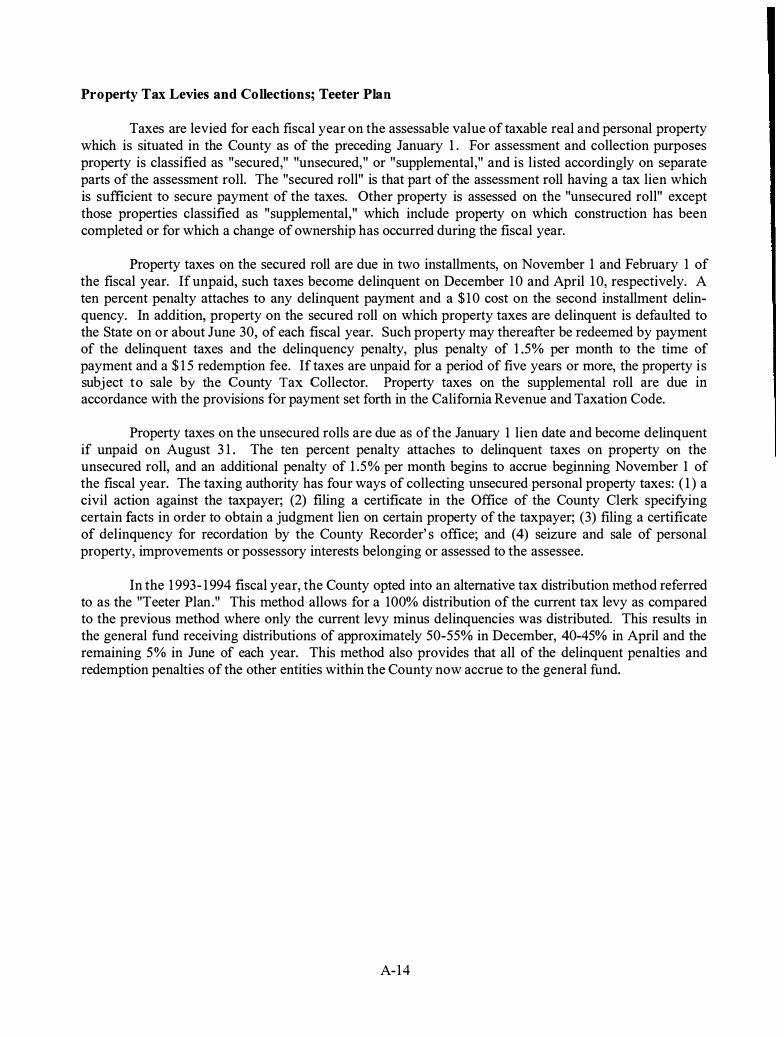

In addition to issuing short-term notes, the County has occasionally used, when necessary, legally permitted "intrafund" borrowing (borrowing against certain of the County's own funds) to cover temporary cash needs. In fiscal year 2003-2004, the County will use such intrafund borrowing to fund the financing of an estimated $7. 4 million of net property tax advances made by the County to local agencies pursuant to the Teeter Plan. See "APPENDIX A-COU NTY FINANCIAL AND DEMOGRAPHIC INF ORMATION-Property Tax Levies and Collections; Teeter Plan" herein.

In fiscal year 2004-2005 , the County will again use intrafund borrowing and the Notes to comprise a funding cycle for the financing of an estimated $7 .0 million of net property tax advances made by the County to local agencies pursuant to the Teeter Plan. Initially, the County will use proceeds of the Notes and intrafund borrowing to finance the estimated $6.0 million of net Teeter Plan advances relating to 1995-1 996 through 2003-2004 delinquencies, while subsequently the County will use intrafund borrowing to cover any temporary cash shortfalls subsequent to when repayment accounts for the Notes are set aside in April 2005 . The intrafund borrowing will be repaid, in part, when the County issues its 2005-2006 Tax and Revenue Anticipation Notes in early July 2005 . The County expects to repeat the funding cycle in subsequent fiscal years until sufficient tax delinquencies and fines have been collected to finance future Teeter Plan advances or until an alternative funding mechanism is implemented.

The Auditor-Controller has prepared the accompanying General Fund Cash Flow Analysis for the fiscal year 2003-2004 and a proj ected cash flow for fiscal year 2004-2005 . The projected cash flow for 2004-2005 was prepared based on the current infonnation available. In the cash flows, in order to reflect the County's participation in the Teeter Plan, the Auditor-Controller has listed the proceeds and distributions pertaining to the Teeter Plan as line items under the Apportioned Tax Resources Fund (the "ATRF") subheading in the respective "Receipts" and "Disbursements" headings. In June of each fiscal year, the County advances funds to complete the 1 00% distribution of that fiscal year's tax levy. Subsequently, the County collects the delinquent taxes and their attributable penalties and interest over a period of several fiscal years. As the County collects these payments, it makes payments on the associated borrowed funds. Although ATRF proceeds are detailed in these cash flows, the pledged funds for the repayment of the Notes will come solely from unrestricted monies of the general fund.

5

Accounting Period Ending

BEGINNING BALANCE

RECEIPTS: GENERAL FUND:

Taxes Licenses, Permits, Franchises Fines, Forfeitures & Penalties Use of Money and Property Intergovernmental - State Intergovernmental - Federal I ntergovernmental - Other Charges for Services Miscellaneous Revenue Operating Transfers In Loan/Advance Collections TRAN Proceeds

GENERAL FUND TOTAL ATRF:

Loan 93/4 & Subsequent Collections 92/3 & Prior Collections 93/4 & Subsequen

TEETER PLAN TOT AL COMBINED TOTAL

DISBURSEMENTS: GENERAL FUND:

Salaries and Benefits

1(

Retirement Contribution Health & Gen Liability lnsuran Workers' Compensation Services and Supplies Other Charges Operating Transfers Out Fixed Assets TRAN Principal TRAN Interest Loans and Advances

GENERAL FUND TOTAL ATRF:

Loan Repay 92/3 & Prior Loan Repay 93/4 & Subseque Distributions to Locals

TEETER PLAN TOTAL COMBINED TOTAL

ENDING BALANCE

COUNTY OF SANTA BARBARA, CALIFORNIA GENERAL, APPORTIONED TAX RESOURCE (ATRF) AND TOBACCO SETTLEMENT FUNDS CASH FLOW IN FISCAL YEAR 2003-04

ACTUAL THRU APRIL

Julv Auqust September

32,293,326 23,387,807 1 8,549,337

2,227,770 1 ,080 ,154 1 ,534,971 1 ,060,0 1 6 1 ,023,278 903,060

1 36,735 36,590 76,298 1 ,333,350 91 ,680 328,959 4,801 ,594 4,367,084 3,430,344 1 ,418 ,926 1 ,748,496 1 , 1 73 ,995

1 60,080 9,2 19 1 1 ,3 13 1 ,669,5 1 9 5,361 ,529 6,986,359

29,388 53,938 41 8,869 1 ,487,750 1 ,488, 1 62 1 ,766,278 5,374,441 3,058,487 2,771 ,353

45,000,000 0 0

64,699,569 1 8 ,31 8,617 1 9,40 1 ,799

2,035,630 3,437,836 2,035,630 0 3,437,836

66,735, 1 99 1 8,3 18,617 22,839,635

1 9,747,303 1 1 ,932,660 1 1 ,982,441 22,000,000 0 0

9,000,000 0 0 7,500,000 0 0

3,094,384 2,929,861 3,712,573 975,707 1 ,603,607 887,863

3,643,235 3 ,946,501 3,796,771 23,994 31 ,786 77,722

0 0 0 0 0 0

2,593,268 2,712,672 4,284,836 68,577,891 23,1 57,087 24,742,206

7,062,827 3,437,836

7,062,827 0 3,437,836 75,640,718 23, 157,087 28,180,042

23,387,807 1 8,549,337 1 3,208,930

October

13,208,930

1 0,305,291 1 ,0 1 9,661

352,620 540,269

2,992,738 1 , 1 10,426

893 4 , 191 ,3 17

1 60 , 139 1 ,609,61 8 4,440,338

0 26,723,31 0

0 26,723 ,310

1 1 ,840,61 1 0 0 0

2,933,479 925,666

4,299,946 46,890

0 0

6,767,028 26,813,620

0 26,813 ,620

1 3, 1 18,620

November

13, 1 1 8,620

9,994,364 801 ,21 3 257,107

96,664 4,446,281

52,606 6,461

2,639,844 1 27, 135

1 ,488,274 6,41 3,397

0 26,323,346

0 26,323,346

12,357,574 0 0 0

3 ,144,898 1 ,670,971 4,801 ,383

33,074 0 0

7,486,403 29,494,303

0 29,494,303

9,947,663

December

9,947,663

31 ,498,252 1 ,256,948 1 ,053,021

351 , 168 3,933,663 1 ,308,059

6 1 2 7,122,739

225,669 2,589, 155 7,450,91 1

0 56,790 , 197

0 56,790,197

18 , 132,049 0 0 0

3,882,235 785,340

4,680,456 21 ,628

0 0

9,922,906 37,424,6 14

0 37,424,61 4

29,3 1 3,246

6

January February March April Mav

29,31 3,246 8,739 , 130 3,560,459 1 ,062,034 1 3 ,803,003

2,897,775 1 ,466,797 1 ,694,546 32,453,831 1 ,840,000 915,41 8 932,520 1 ,297,424 2,146,799 1 ,279,000 309, 1 1 7 9,592 289,81 1 1 , 1 97,655 221 ,000 438,717 46,684 228,283 761 ,581 31 ,000

5,443,851 7,050 ,140 4,374,461 6,973,041 5,404,000 686,482 94,676 216,371 1 ,789,657 730,000

74, 183 1 ,387 1 ,951 1 3,619 13,000 3,892,470 2,629,290 8,350, 1 34 6 ,397,375 6,268,000

1 19,572 67,282 1 94,846 4,384,992 98,000 9,504,066 1 ,487,524 1 ,835,203 1 ,5 10,774 1 1 ,713,000

1 0, 1 70,145 8,926,876 7,464,950 8,731 ,846 8,000,000 0 0 0 0 0

34,451 ,796 22,71 2,768 25,947,980 66,361 , 1 70 35,597,000

1 , 1 22,765 955,369 1 , 1 22,765 0 0 955,369 0

35,574,561 22,71 2,768 25,947,980 67,316,539 35,597,000

1 1 ,999,065 1 1 ,873,398 1 1 ,860,71 9 1 2,099,894 1 2,000,000 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0

2,724,093 2,909, 196 3,1 68,852 3,320,254 3,785,000 1 ,51 0,792 1 ,765,767 962,005 1 ,385,422 1 ,659,000 6,472,602 3,773,783 4,470,680 5,438,690 3,523,000

1 37,795 95,019 74 ,361 22 ,618 84,000 22,500,000 0 0 22,500,000 0

478,356 0 0 478,356 0 9,203,209 7,474,276 7,909,788 8,374,967 7,758,000

55,025,91 2 27,891 ,439 28,446,405 53,620,201 28,809,000

1 , 1 22,765 955,369

1 , 1 22,765 0 0 955,369 0 56,148,677 27,891 ,439 28,446,405 54,575,570 28,809,000

8,739,130 3,560,459 1 ,062,034 13,803,003 20,591 ,003

June

Total 20,591 ,003

2,982,000 99,975,751 1 ,665,000 14,300,337

351 ,000 4,290,546 17,000 4,265,355

6,309,000 59,526, 1 97 1 , 1 1 8,000 1 1 ,447,694

14,000 306,71 8 6,460,000 61 ,968,576

1 08,000 5,987,830 1 ,948,000 38,427,804 8,500,000 8 1 ,302,744

0 45,000,000 29,472,000 426,799,552

1 3,384,000 13 ,384,000 0

7,551 ,600 1 3,384,000 20,935,600 42,856,000 447,735, 1 52

12,000,000 1 57,825,714 0 22,000,000 0 9,000,000 0 7,500,000

4,034,000 39,638,825 1 ,660,000 1 5,792, 140 4,392,000 53,239,047

1 84,000 832,887 0 45,000,000 0 956,712

7,975,000 82,462,353 30,245,000 434,247,678

0 12,578,797

7,400,000 7,400,000 7,400,000 1 9,978,797

37,645,000 454,226,475

25,802,003

Accounting Period Ending

BEGINNING BALANCE

RECEIPTS:

GENERAL FUND: Taxes Licenses, Permits, Franchises Fines, Forfeitures & Penalties Use of Money and Property

Intergovernmental - State

Intergovernmental - Federal Intergovernmental - Other

Charges for Services

Miscellaneous Revenue Operating Transfers In

Loan/Advance Collections TRAN Proceeds

GENERAL FUND TOTAL

ATRF:

Loan 93/4 & Subsequent Collections 92/3 & Prior

Collections 93/4 & Subsequen TEETER PLAN TOTAL

COMBINED TOTAL

DISBURSEMENTS:

GENERAL FUND:

Salaries and Benefits Retirement Contribution Health & Gen Liability lnsuran Workers' Compensation

Services and Supplies Other Charges

Operating Transfers Out

Fixed Assets TRAN Principal

TRAN Interest Loans and Advances

GENERAL FUND TOTAL ATRF:

(

Loan Repay 92/3 & Prior

Loan Repay 93/4 & Subseque Distributions to Locals

,r

TEETER PLAN TOT AL

COMBINED TOTAL

ENDING BALANCE

, - 1 ,v...,1--v I L-LJ """-' "'"-• ,r-l�, , II I - · ' I , _ 1 ,_'"" I I u, 1 ,- - - - · , ...... _ \' �· • " J • �· .. ....... • - -· ·- .,,.. """ - - • , --· · · -· � • • -· · - - -· - - · , . -- • • ·

July August September October November December January February March

25,802,000 1 9,957,307 1 3,987,307 6,281 ,307 6,630,307 4,1 15,307 30,495,307 1 1 ,81 3,307 5,471 ,307

2 , 153,000 947,000 1 ,425,000 1 1 ,636,000 1 1 ,3 1 0,000 34,894,000 3,165,000 1 ,541 ,000 1 ,780,000

1 ,045,000 1 ,009,000 890,000 1 ,005,000 790,000 1 ,239,000 903,000 91 9,000 1 ,279,000 1 27,000 34,000 7 1 ,000 329,000 240,000 981 ,000 288,000 9,000 270,000

1 ,577,000 72,000 264,000 463,000 76,000 272,000 386,000 37,000 1 14,000

4,428,000 3,937,000 2,878,000 2,383,000 4,027,000 3,447,000 12 , 154,000 6,970,000 3,945,000

1 , 172,000 1 ,444,000 969,000 91 7,000 43,000 1 ,080,000 567,000 78,000 1 79,000

67,000 4,000 5,000 0 3,000 0 31 ,000 1 ,000 1 ,000

1 ,693,000 5,438,000 7,086,000 4,251 ,000 2,677,000 7,224,000 3,948,000 2,667,000 8,469,000

15 ,000 27,000 21 1 ,000 59,000 64,000 1 14 ,000 60,000 34,000 98,000

1 ,895,000 1 ,895,000 2,250,000 2,050,000 1 ,896,000 3,298,000 10,1 05,000 1 ,895,000 2,337,000

5,394,000 3,070,000 2,782,000 5,457,000 7,437,000 9,479,000 1 0,208,000 8,960,000 7,993,000

55 ,000,000 0 0 0 0 0 0 0 0

74,566,000 1 7,877,000 18 ,831 ,000 28,550,000 28,563,000 62,028,000 41 ,81 5,000 23, 1 1 1 ,000 26,465,000

4,000 3,000 2,000 2,000,000 1 ,888,000 1 ,466,000 1 , 144,000

2,000,000 0 1 ,892,000 0 0 1 ,469,000 0 1 , 146,000 0

76,566,000 1 7,877,000 20,723,000 28,550,000 28,563,000 63,497,000 4 1 ,81 5,000 24,257,000 26,465,000

1 9,979,000 1 2,677,000 12 ,730,000 12,579,000 13 , 128,000 1 9,263,000 1 2,747,000 12,614,000 1 2,600,000

25,000,000 0 0 0 0 0 0 0 0

9,600,000 0 0 0 0 0 0 0 0

9,000,000 0 0 0 0 0 0 0 0

3,095,000 2,931 ,000 3,722,000 2,995,000 3 , 122,000 3,892,000 2,784,000 2,885,000 3 ,166,000

857,000 1 ,409,000 780,000 813,000 1 ,441 ,000 690,000 1 ,294,000 1 ,581 ,000 845,000

3,767,000 4,081 ,000 3,926,000 4,999,000 4,872,000 3,872,000 6,912 ,000 3,789,000 4,609,000

32,000 42,000 103,000 62,000 44,000 29,000 1 82,000 1 25,000 98,000

0 0 0 0 0 0 27,500,000 0 0

0 0 0 0 0 0 894,000 0 0

2,588,000 2,707,000 5,276,000 6,753,000 8,471 ,000 7,902,000 8 , 184,000 8,459,000 7,393,000

73,91 8,000 23,847,000 26,537,000 28,201 ,000 31 ,078,000 35,648,000 60,497,000 29,453,000 28,71 1 ,000

4,000 3,000 2,000

8,492,693 1 ,888,000 1 ,466,000 1 , 144 ,000

8,492,693 0 1 ,892,000 0 0 1 ,469,000 0 1 ,1 46,000 0

82,410,693 23,847,000 28,429,000 28,201 ,000 31 ,078,000 37,1 1 7,000 60,497,000 30,599,000 28,71 1 ,000

1 9,957,307 1 3,987,307 6,281 ,307 6,630,307 4,1 1 5,307 30,495,307 1 1 ,81 3,307 5,471 ,307 3,225,307

7

April May June

Total

3,225,307 9,368,307 20,049,307

32,085,000 1 ,932,000 2,1 32,000 105,000,000

2, 1 1 7,000 1 ,261 ,000 1 ,643,000 14, 100,000 1 , 1 1 6,000 206,000 328,000 3,999,000

644,000 24,000 1 3,000 3,942,000 7,883,000 1 1 , 109,000 5,004,000 68,165,000

1 ,478,000 603,000 923,000 9,453,000

6,000 5,000 5,000 1 28,000

6,488,000 6,357,000 6,551 ,000 62,849,000

4,381 ,000 49,000 54,000 5,1 66,000

1 ,924,000 10,098,000 2,481 ,000 42, 124,000

7,764,000 7,528,000 7,528 ,000 83,600,000

0 0 0 55,000,000

65,886,000 39,172,000 26,662,000 453,526,000

12,777,000 12,777,000

1 ,000 1 0,000

722,000 7,220,000 723,000 0 1 2,777,000 20,007,000

66,609,000 39, 1 72,000 39,439,000 473,533,000

12,854,000 12,748,000 1 2,748,000 1 66,667,000

0 0 0 25,000,000

0 0 0 9,600,000

0 0 0 9,000,000

3,386,000 3 ,786,000 4, 121 ,000 39,885,000

1 ,204,000 1 ,457,000 1 ,459,000 13 ,830,000

5,517 ,000 3,643,000 5,375,000 55,362,000

30,000 1 1 1 ,000 242,000 1 , 100,000

27,500,000 0 0 55,000,000

894,000 0 0 1 ,788,000 8,358,000 6,746,000 6,963,000 79,800,000

59,743,000 28,491 ,000 30,908,000 457,032,000

1 ,000 10 ,000

722,000 1 3 ,712 ,693

7 ,000,000 7,000,000

723,000 0 7,000,000 20,722,693

60,466,000 28,491 ,000 37,908,000 477,754,693

9,368,307 20,049,307 21 ,580,307

TAX MATTERS

In the opinion of Orrick, Herrington & Sutcl iffe LLP ("Bond Counsel"), based upon an analysis of existing laws, regulations, rul ings and court decisions, and assuming, among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Notes is

,excluded from gross income for federal-income tax purposes under Section 1 03 of the Internal Revenue Code of 1986 (the "Code") and is exempt from State of California personal income taxes, Bond Counsel is of the further opinion that interest on the Notes is not a specific preference item for purposes of the federal individual or corporate al ternative minimu�taxes, al though Bond Counsel observes that such interest is included in adj usted current earnings when calculating corporate al ternative minimum taxable income. A complete copy of the proposed form of opinion of Bond Counsel is set forth in "APPENDIX B - FORM OF LEGAL OPINION" hereto.

Notes purchased, whether at original issuance or otherwise, for an amount higher than their principal amount payable at maturi ty ( or, in some cases, at their earl ier call date) ("Premium Notes") will be treated as having amortizable bond premium. No deduction is allowable for the amortizable bond premium in the case of Notes, l ike the Premium Notes, the interest on which is excluded from gross income for federal income tax purposes. However, the amount of tax-exempt interest received, and a Beneficial Owner' s basis in a Premium Note, will be reduced by the amount of amortizable bond premium properly allocable to such Beneficial Owner. Beneficial Owners of Premium Notes should consult their own tax advisors with respect to the proper treatment of amortizable bond premium in their particular circumstances.

The Code imposes various restrictions, conditions and requirements relating to the exclusion from gross income for federal income tax purposes of interest on obligations such as the Notes. The County has made certain representations and covenanted to comply with certain restrictions, conditions and requirements designed to ensure that interest on the Notes will not be included in federal gross income. Inaccuracy of these representations or failure to comply with these covenants may result in interest on the Notes being included in gross income for federal income tax purposes, possibly from the date of original issuance of the Notes. The opinion of Bond Counsel assumes the accuracy of these representations and compliance with these covenants. Bond Counsel has not undertaken to determine ( or to inform any person) whether any actions taken (or not taken), or events occurring (or not occurring), or any other matters coming to Bond Counsel's attention after the date of issuance of the Notes may adversely affect the value of, or the tax status of interest on, the Notes.

One of the covenants of the County referred to above requires the County to reasonably and prudently calculate the amount, if any, of excess investment earnings on the proceeds of the Notes which must be rebated to the United States, to set aside from lawfully available sources sufficient moneys to pay such amounts and to otherwise do all things necessary and within its power and authority to assure that interest on the Notes is excluded from gross income for federal income tax purposes. Under the Code, if the County spends 100% of the proceeds of the Notes within six months after issuance, there is no requirement that there be a rebate of investment profi ts in order for interest on the Notes to be excluded from gross income for federal income tax purposes. The Code also provides that such proceeds are not deemed spent until all other available moneys (less a reasonable working capital reserve) are spent. The County expects to satisfy this expenditure test or, if it fails to do so, to make any required rebate payments from moneys received or accrued during to the 2004-2005 fiscal year. To the extent that any rebate cannot be paid from such moneys, the law of California is unclear as to whether such covenant would require the County to pay any such rebate. This would be an issue only if it were determined that the County' s calculations of expenditures of Note proceeds or of rebatable arbitrage profits, if any, were incorrect.

Certain requirements and procedures contained or referred to in the Resolution, the Tax Certificate, and other relevant documents may be changed and certain actions (including, without l imitation, defeasance of the Notes) may be taken or omitted under the circumstances and subject to the

8

terms and conditions set forth in such documents. Bond Counsel expresses no opinion as to any Note or the interest thereon if any such change occurs or action is taken or omitted upon the advice or approval of bond counsel other than Orrick, Herrington & Sutcliffe LLP.

Although Bond Counsel is of the opinion that interest on the Notes is excluded from gross income for federal income tax purposes and is exempt from State of California personal income taxes, the ownership or disposition of, or the accrual or receipt of interest on, the Notes may otherwise affect a Beneficial Owner's federal, state or local tax liability. The nature and extent of these other tax consequences depends upon the particular tax status of the Beneficial Owner or the Beneficial Owner's other items of income or deduction. Bond Counsel expresses no opinion regarding any such other tax consequences.

Future legislation, if enacted into law, or clarification of the Code may cause interest on the Notes to be subject, directly or indirectly, to federal income taxation, or otherwise prevent Beneficial Owners from realizing the full current benefit of the tax status of such interest. The introduction or enactment of any such future legislation or clarification of the Code may also affect the market price for, or marketability of, the Notes. Prospective purchasers of the Notes should consult their own tax advisers regarding any pending or proposed federal tax legislation, as to which Bond Counsel expresses no opinion.

The opinion of Bond Counsel is based on current legal authority, covers certain matters not directly addressed by such authorities, and represents Bond Counsel's judgment as to the proper treatment of the Notes for federal income tax purposes. It is not binding on the Internal Revenue Service ("IRS") or the courts. Furthermore, Bond Counsel cannot give and has not given any opinion or assurance about the future activities of the County, or about the effect of future changes in the Code, the applicable regulations, the interpretation thereof or the enforcement thereof by the IRS . The County has covenanted, however, to comply with the requirements of the Code.

Bond Counsel' s engagement with respect to the Notes ends with the issuance of the Notes, and, unless separately engaged, Bond Counsel is not obligated to defend the County or the Beneficial Owners regarding the tax-exempt status of the Notes in the event of an audit examination by the IRS. Under current procedures, parties other than the County and its appointed counsel, including the Beneficial Owners, would have little, if any, right to participate in the audit examination process. Moreover, because achieving judicial review in connection with an audit examination of tax-exempt Notes is difficult, obtaining an independent review of IRS positions with which the County legitimately disagrees, may not be practicable. Any action of the IRS, including but not limited to selection of the Notes for audit, or the course or result of such audit, or an audit of Notes presenting similar tax issues may affect the market price for, or the marketability of, the Notes, and may cause the County or the Beneficial Owners to incur significant expense.

LEGAL MATTERS

The validity of the Notes and certain other legal matters are subject to the approving opinion of Orrick, Herrington & Sutcliffe LLP, Bond Counsel. A complete copy of the proposed form of Bond Counsel opinion is contained in "APPENDIX B -FORM OF LEGAL OPINION" hereto. Bond Counsel undertakes no responsibility for the accuracy, completeness or fairness of this Official Statement. Underwriters' Counsel takes no responsibility for the accuracy, completeness or fairness of this Official Statement.

9

RISK FACTORS

State Funding of Counties

The County receives a significant portion of its funding from subventions by the State. As a result, decreases in the revenues received by the State can affect subventions made by the State to the County and other counties in the State. The potential impact of State budget actions on the County in particular, and other counties in the State generally, in future fiscal years is uncertain at th is time. For a discussion of the potential impact of State budget actions for fiscal year 2003 -2004 on the County in particular, and other counties in the State generally, see APPENDIX A - COUNTY FINANCIAL AND DEMOGRAPHIC INFORMATION "County F inancial Information - State Budget Acts."

LEGALITY FOR INVESTMENT IN CALIFORNIA

Under provisions of the California Financial Code, the Notes are legal investments for commercial banks in the State to the extent that the Notes, in the informed opinion of the investor bank, are prudent for the investment of funds of its depositors and under provisions of the California Government Code, are eligible to secure deposits of public moneys in the State.

RATING

The County has obtained a rating of "SP-1 +" on the Notes from Standard & Poor's, a division of The McGraw-Hill Companies, Inc. ("Standard & Poor's"). Certain information was supplied by the County to the rating agency to be considered in evaluating the Notes. The rating issued reflects only the views of the rating agency, and any explanation of the significance of such rating should be obtained from the rating agency at Standard & Poor's, 55 Water Street, New York, NY 10041. There is no assurance that any rating will be retained for any given period of time or that the same will not be revised downward or withdrawn entirely by the rating agency if, in its j udgment, circumstances so warrant. The County undertakes no responsibility either to bring to the attention of the owners of any Notes any downward revision or withdrawal of any rating obtained or to oppose any such revision or withdrawal. Any such downward revision or withdrawal of the rating obtained may have an adverse effect on the market price of the Notes.

LITIGATION

No litigation is pending or threatened concerning the validity of the Notes, and a certificate of the County Counsel to that effect will be furnished to the purchaser at the time of the original delivery of the Notes. The County is not aware of any litigation pending or threatened questioning the political existence of the County or contesting the County's ability to issue and retire the Notes.

There are a number of lawsuits and claims pending against the County. The aggregate amount of the uninsured liabilities of the County and the timing of any anticipated payments that may result from judgments and claims will not, in the opinion of the County Auditor-Controller after consultation with County Counsel, impair the County's ability to repay the Notes.

UNDERWRITING

The Notes are being purchased for public offering by Banc of America Securities LLC (the "Underwriter"). The Underwriter has agreed to purchase the Notes for an aggregate price of the principal amount of $55,000,000 plus a premium of $83 2,700 and less an underwriter's discount of $74,770 for a total of $55,757,93 0. The Underwriter will purchase all of the Notes if any are purchased. The obligation to make such purchase is subj ect to certain terms and conditions as set forth in the Contract of Purchase.

10

ADDITIONAL INFORMATION

The purpose of this Official Statement is to supply information to prospective buyers of the Notes. Summaries and explanations of the Notes, the Resolution and of statutes and documents contained herein do not purport to be complete, and reference is made to said documents and statutes for full and complete statement of their provisions.

The County regularly prepares a variety of reports, including audits, budgets and related documents, as well as certain monthly activity reports. Any owner of a Note may obtain a copy of any such report, as available, from the County Auditor/Controller's office at 105 East Anapamu Street, Room 1 09, Santa Barbara, CA 93 10 1 .

All data contained herein have been taken or constructed from County records and other sources. Appropriate County officials, acting in their official capacity, have reviewed this Official Statement and have determined that as of the date hereof the information contained herein is, to the best of their knowledge and belief, true and correct in all material respects and does not contain an untrue statement of a material fact or omit to state a material fact necessary in order to make the statements made herein, in light of the circumstances under which they are made, not misleading. An appropriate County official will execute a certificate to this effect upon delivery of the Notes. This Official Statement and its distribution have been duly authorized and approved by the Board of Supervisors.

OFFICIAL STATEMENT CERTIFICATION

As of its date this Official Statement is true to the best knowledge of the County, is complete and correct in all material respects, and does not include any untrue statement of a material fact or omit to state a material fact necessary in order to make the statements in this Official Statement, in light of the circumstances under which they are made, not misleading.

The execution and delivery of this Official Statement by the Treasurer-Tax Collector of the County of Santa Barbara has been duly authorized by the County.

SANTA BARBARA COUNTY, CALIFORNIA

By: Isl Bernice James Treasurer-Tax Collector

11

This page intentionally left blank

APPENDIX A

County Financial and Demographic Information

This page intentionally left blank

APPENDIX A

COUNTY FINANCIAL AND DEMOGRAPHIC INFORMATION

TABLE OF CONTENTS

GENERAL INFORMATION .................................................................................................................... 1 County Powers . . . . . . . . . . . . . . . . . . . . . . ..... . . . . . . . . . . . . . . . .. . . . . . . . . . .. . .. . .. . . . . ... . . . . . . ...... . . . . . .. . . . .. . . . ... .. . .. . . . . . . . . .. . . . . . . .. . .. . . . . . . . . . . . .. . 1 Petition to Split the County and Form a New County .......... . . . . .............. . . . ... ......... . . ........ . ......... . . .. . . ....... . . . I Administration and Management . . . . ... .... . . . . ........ . . . ............. . . . . . . . . .... . .... . ................. . . . . . . . ......... . . . . . . .. . ....... . . .. 2 County Employees and Labor Relations . .. ....... . .. .. . . . ...... . . .. . . . . .............. . . . . . ......... . . . .. . . ............. . . . . . ... .... .... . . . 3

COUNTY FINANCIAL INFORMATION ............................................................................................... 3 State Budget Acts . . .... . . . . ... . . . . . . . . . . . . . . . . . . . . . .... ....... . . . . . . . ....... . . . . ... ....... ... . . . . . . . . ...... . ... . . . . . . . . . ...... . .. . ... . . . . . . . . . . . . . . . . . . 3 County Budget Process .. . . .. . . . .. . . . .. . . . . . . . . .... . .. .. . .. . . . . . . . . .. . . . . . . ... . . ... . . . . . . . . . .. . . . .. . . . . ... . . . . . . .. . . . . . . . . . . . . . . . . . . . . ... . ... . . . .. .. 8 Financial Statements . . . . . .......... . . . . . . . ........... ...... . . . ...... . . .... . .... . ..... . . . . . . . . . . . . ... .... . .. . .. . ............ . . . . . . ............ . . . . . . 11 Source: County of Santa Barbara General Purpose Financial Statements, ending June 30, 1999, 2000, 2001, 2002, and 2003 . . . . . 12 Property Valuation .................. . . . . . ................. . . . ........... . . . ..... ........ . . . .. . . .. . . ......... . . ..... . . . ..... . . . . . . . . . .... . .... ....... 13 Property Tax Levies and Collections; Teeter Plan .. .. . ............. . . . . . . . ............ . . . .. . . . . . ...... . . . . . . . . . ... ........... . . ... 14 Historical Tax Inj'ormation .. . . . . . . . ............. .... . . . .. . ... . . ....... ......... . . . . . . . . . . .... . .... . .... . . . . . . . . . . . . . . . . . . ... . . . . . . . ... . . . . . .. . . 15 Largest Property Taxpayers ..... . ........ . .. . ........ ....... . . .. . . . . .. . .............. . ............ . . . ... . . ....... . . . . . ..... . . .......... . . . . .... 15 Other Taxes and Revenues .. . . ..... .................. . . . ........ .................... ................ . ... ............. ..... . . . ...... . . . .. . . . . . ... 16 Revenues and Expenditure Trends ............. . . . . ...... . . . . . ............. . . . . . . . . .......... . . . . .. . . . ........... . ... . . .......... . . . . . . ..... 1 7 County Employee Retirement Plan and Deferred Compensation Plan .... . ... . . .......... . . . . . .... . . . . .. . .. . ... . . . . . . . . 1 7

DEBT AND OTHER FINANCIAL OBLIGATIONS OF THE COUNTY .......................................... 19 Debt Authorization . ...... ... ... . . . ... ................ .. . . . . ....... . . . . ... ............. . . .............. . . . . . . . . . . ..... . . . . . . . . . ........ . . . . . . ........ 19 Long-Term Obligations of the County . . . . ......... ..... . . . . . . . . ..... .... .. . .. . .. . . .. ...... . . . . . ... ....... . . ... .. . . .. . ........ . . . . . . . .... . 19 Payment Schedule for Certain Long-Term Obligations of the County ... . . . . . . . .. . ..... . . . .. . . . . .............. . . . . . ... . . 19 Future Financings . . .......... . . . . . . . . ........... . . . . .... . ...... . . ........ ..... . . . . . . .......... . ... ..... . ... .......... ... . ........ .. . . . . . . . . . . . . ..... 20 Direct and Overlapping Bonded Debt ...... . . . . . .... . . . ...... . . .......................... . . . ........... . . ... . . . . . ..... . . . . . . . . . . . . ... . . . . 20

COUNTY TREASURER'S INVESTMENT POOL .............................................................................. 21

CONSTITUTIONAL AND STATUTORY LIMITS ON TAXES AND APPROPRIATIONS .......... 23 Article XIIIA of the State Constitution ..... ....... . ... . . . . . . ...... . . . . . . ............ . . . . . . . . . ... ........... . . . ......... . . . . . .. . . . . ....... . 2 3 Article XIIIB of the State Constitution ..... . .... ... . .. . . . . . ...... . . . . . . . . ...... . .......... . . . ........... . . . . . . . ..... . . . . . . . . . . . ........... 24 Articles XIIIC and XIIID of the State Constitution ....... ............. . . . . ..... . . . . . . ......... . . . . . ... ......... . . ........ ...... . . .. 25 Future Initiatives .. . . ..... . . . . . ......... . .... . . . . ..... . . ......... . . .......... . . .. . . .. . ....... . . ................... . . . . . ..... ...... . . . . . . .......... .... 26

COUNTY DEMOGRAPHIC INFORMATION .................................................................................... 26 Population ..... . . ............... . . . . ........... . . . ... ...... . . ..... . . . ............ . . . . . . . ........ . ... . . . . . ........... . ... . . ....... . . . . ............... . . . . . 26 Industry and Employment . ...... . . . . . . . . ............ . . .. . .. ........... . .......... ... . . . .................... . . . .... .......... . . . . . .... ........ ... 26 Commercial Activity ......... ..... . . . . . ............. . ...................... . . ........... . . . . . . . .. ........... . . . . ..... . ....... . . . . . . . .... . .... . . . . ... 28 Constn1ction Activity ............... . . . . . ........... ..... ... . . ............. ... .......... . . . .. . . . . . ......... . . ............. . . ..... .... .. . . . .... . . .... 2 9 Personal Income .... . . . ..... ........... . . . . ......... . . ..... .... ........... .. .. . . ....... .. . . ...... ........... . . . ... . ... ............. ....... . . ..... . . . . 30

This page intentionally left blank

APPENDIX A

COUNTY FINANCIAL AND DEMOGRAPHIC INFORMATION

GENERAL INFORMATION

Santa Barbara County, located approximately 100 miles north of Los Angeles and 300 miles south of San Francisco, was established by an act of the State legislature on February 1 8, 1 850. The County occupies an area of 2, 774 square miles, of which one-third is located in the Los Padres National Forest. There are eight incorporated cities located wholly or partially within the County: Santa Barbara, Santa Maria, Lompoc, Carpinteria, Guadalupe, Solvang, Buellton, and Goleta.

On November 6, 200 1 , residents of a portion of the Goleta Valley voted to incorporate into the new City of Goleta which was incorporated on February 1 , 2002. The County has entered into a revenueneutrality agreement with the new City and does not expect the incorporation to have a material impact on the finances or service obligations of the County.

The largest employment categories in the County include government, services, wholesale and retail trade, and manufacturing. The mild climate, picturesque coastline, scenic mountains and numerous state parks and beaches have made the County a popular recreational area.

County Powers

The County is a general law county and political subdivision of the State of California and its rights, powers, privileges, authority, functions and duties are established by the constitution and laws of the State. The County is divided into five districts on the basis of registered voters and population, as required by State statute. Supervisors are elected from each district by the voters of the district to serve staggered four-year terms. The Chairman is elected by and from members of the Board. The Board exercises the powers of the County.

Petition to Split the County and Form a New County

Supporters of the movement to split the County of Santa Barbara and form Mission County circulated a petition to place the issue on the ballot for voter approval. Between April 2003 and September 30, 2003, county split advocates were required to gather enough signatures from qualified voter on the petition to form a new county in order to proceed with the proposed county formation. Pursuant to Government Code Section 23321 (b), petitioners must equal in number not less than 25 percent of the number of electors within the territory of the proposed new county as of the date of the last preceding election for governor.

The petition was turned in to Clerk on November 12, 2003 , within the requisite 60-day period. The County Clerk had 30 days, or until December 1 2, 2003, to complete a review of the petition. The County Clerk completed the review of the petition on December 12, 2003, and determined that the petition contained the requisite number of signatures and met the additional requirements for qualification. Thus the petition was deemed sufficient.

A-1

Since the county split supporters have obtained the requisite signatures, a County Formation Review Commission will be established according to the provisions of Government Code Section 23331. The Governor has appointed five commissioners - two from the proposed new county, two from the territory that will remain as the County of Santa Barbara, and one appointee from outside of both areas. The Mission County Formation Commission members are: former Santa Barbara Mayor Harriet Miller; Montecito resident and retired airline executive Ted Tedesco; Santa Maria resident and 5th District Planning Commissioner Jack Boysen; former Solvang City Councilwoman June Christensen; and former an Luis Obispo County Assessor Dick Frank. The Commission will determine the terms and conditions of county formation, including the allocation of debt between the newly formed county and Santa Barbara County. The formation election will occur at a general election according to statutory timing requirements, most likely in the year 2006. A majority of voters in the proposed new county and in the whole County must approve the county split.

The last county formation petition registered in Santa Barbara County occurred in 1977. On July 24, 1977, a petition to split the County of Santa Barbara and form a new county (Los Padres County) was filed with the Clerk of the Board. The resulting 1978 County Formation Review Commission produced a detailed Final Report, dated June 26, 1978, analyzing the probable effects of creating the new county. The county split proposal was placed on the November 1978 ballot but failed to receive sufficient voter support to trigger formation of Los Padres County.

Administration and Management

County officials oversee the County' s daily operations. County administration includes 17 officials appointed by the Board of Supervisors (the "Board") and six officials elected by county-wide vote, including the Treasurer/Tax Collector/Public Administrator, the Auditor-Controller, the Assessor/County Clerk-Recorder, the District Attorney, the Superintendent of Schools, and the Sheriff. Many boards, commissions and committees assist the Board and County officials.

The background and experience of selected administrative personnel and elected officials most directly involved with the issuance of the Certificates are summarized below.

County Treasurer-Tax Collector - The County Treasurer - Tax Collector -Public Guardian -Public Administrator is elected by voters of the County to a four-year term. Bernice James was elected by the voters in 2002 and assumed office in January 2003 . Ms. James received a bachelor' s degree in business administration from the University of Arizona. She has served in County government for more than 24 years, including almost eight years as Assistant County Treasurer-Tax Collector-Pub lic Administrator.

Auditor-Controller -The County Auditor-Controller is elected by the voters of the County to a four-year term. Robert W. Geis was elected Auditor-Controller in 1990 and assumed his office in January 1991. Mr. Geis, a certified public accountant and certified public finance officer, received a bachelor' s degree in business administration from Ohio State University. Mr. Geis has served in County government for more than 21 years, including five years as Assistant County Treasurer. Prior to such time, Mr. Geis was a corporate internal auditor.

County Administrator - The County Administrator, Michael F. Brown, is appointed by the Board and exercises overall responsibility for sound and effective management of County Government pursuant to Board policy. Mr. Brown holds a bachelor' s degree in Government and Regional Economics from the California State University at Northridge and a master's degree in Public Administration with an emphasis on Municipal Finance from the University of Texas at

A-2

Austin. Mr. Brown' s more than 31 years of local government experience includes service as City Manager of Tucson, Arizona, City Manager of Berkeley, Cal ifornia, Deputy City Manager and Budget Director of Hartford, Connecticut, and First Deputy Commissioner of the Connecticut Department of Housing. Mr. Brown has received numerous awards including the Carolyn Kean Memorial Award of the International City Management Association, the Publ ic Technology, Inc. Achievement Award for Geobased Data Systems and an honorary doctorate in Public Administration from Tucson University.

County Counsel - The County Counsel is appointed by the Board for a four-year term. Stephen Shane Stark was fi rst appointed County Counsel in April 1994. Mr. Stark graduated from the George Washington University Law School in 19 68. He came to Santa Barbara County in 1987, serving as Chief Deputy County Counsel before his current appointment. His prior positions include Assistant Corporate Counsel for the District of Columbia and Assistant City Attorney for the City of Santa Monica.

County Employees and Labor Relations

As of April 1, 2004, the County employed 4,193 full-time equivalent employees. The County provides certain health insurance, life insurance, disability and retirement benefits to its employees. For additional infonnation regarding the retirement pl an, see "COUNTY FINANCIAL INFORMATIONCounty Employee Retirement Plan and Deferred Compensation Plan."

There are currently nine operating labor organizations that represent County employees. The County currently has signed Memoranda of Understanding with all nine of those groups that are effective, in each case, through at least October 10, 2004.

COUNTY FINANCIAL INFORMATION

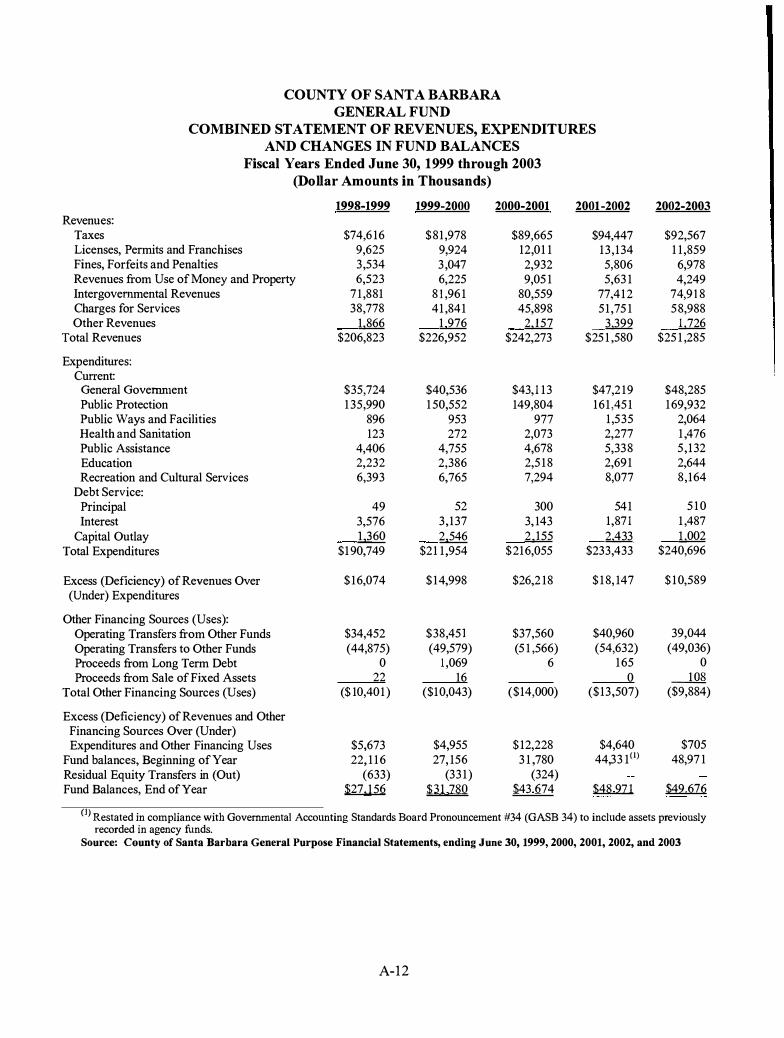

Following is a description of the County' s financial information, including State budget acts that affect the County' s finances, funding for County services, the County' s General Fund Balance Sheet, the County's Combined Statement of Revenues and Expenditures, the County' s budget process and adopted budget, the County's major revenues and expenditures, and certain other financial infonnation.

State Budget Acts

The following information concerning the State' s 2003-2004 fiscal year budget and 2004-2005 fiscal year budget has been obtained from publicly available infonnation which the County believes to be reliable; however, the County takes no responsibil ity as to the accuracy or completeness thereof and has not independently verified such information.

State budget decisions have a profound impact on the County because the County is the provider of many State-mandated services. Cal ifornia counties are political subdivisions of the State and have a much closer economic tie to the State than that of other governmental entities.

The Governor and the Legislature have repeatedly demonstrated their will ingness to involve local government funding in solving state-level budget problems. The property tax shifts of 1992 and 1993, resul ting in the creation of the Educational Revenue Augmentation Fund ("ERAF") is the best example, but the "real ignment" of human service programs in the early 1990s also involved cost and risk shifts from the State to counties and had a significant negative fiscal impact on counties for several years after inception.

A-3

State Budget for Fiscal Year 2003-2004.

The final 2003-2004 State Budget (the "2003-2004 Budget") was signed into law by Governor Davis on August 2, 2003. According to the Legislative Analyst' s Office, the 2003-2004 Budget assumed fi scal year 2003-2004 revenues of $72.8 bill ion, expenditures of $70.8 billion, and a year-end reserve of $2 bill ion and also provided for the issuance of a deficit-financing bond to offset the $10.7 billion 2002-2003 fiscal year-end deficit. The 2003-2004 Budget provided for repayment of the bond financing from existing resources and through a multi-stage shift of sales and property tax revenues. Other prescribed borrowings included pension obligation bonds and tobacco securitization bonds. The 2003-2004 Budget also addressed the budget shortfall through a combination of program savings, borrowing, new revenues, funding shifts and deferrals. Program savings were to be achieved through reductions in education, suspensions of social services cost-of-living adj ustments, selected Medi-Cal provider rate reductions and employee compensation savings. Some reductions in higher education, trial courts and resources were offset by higher fees. The 2003-2004 Budget also rel ied on an increase in vehicle license fees and the issuance of deficit bonds secured by a sales tax increase and a tax swap between local governments and the State, among other things, to close the proj ected $38 bill ion deficit. The 2003-2004 Budget also relied on $2.2 billion in new federal funds to cover State costs during the 2002-2003 and 2003-2004 fiscal years.

Proposed Governor's Budget for Fiscal Year 2004-2005.

Governor Schwarzenegger announced his proposed 2004-2005 State Budget (the "Proposed 2004-2005 Budget") on January 9, 2004, addressing an accumulated State debt of $22.1 bill ion and projecting a State Budget shortfall totaling approximately $14 billion in fiscal year 2004-2005. The Governor' s proposed economic recovery plan includes the California Economic Recovery Bond Act which was approved by California voters at the March 2, 2004 statewide election, and authorizes the issuance of up to $15 bill ion in State bonds to finance the negative General Fund reserve balance and other General Fund obl igations undertaken prior to June 30, 2004.

Sign ificant features of the Proposed 2004-2005 Budget relating to local governments include the following: