2006 Annual Results - PCCW

41

0 March 28, 2007 - Hong Kong For the year ended December 31, 2006 2006 Annual Results

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 2006 Annual Results - PCCW

0

March 28, 2007 - Hong Kong

For the year ended December 31, 2006

2006 Annual Results

1

This presentation contains "forward-looking statements" that are not

historical in nature. These forward-looking statements, which include,

without limitation, statements regarding PCCW's future results of

operations, financial condition or business prospects, are based on the

current beliefs, assumptions, expectations, estimates, and projections of

the directors and management of PCCW about the business and the

industry and markets in which PCCW operates. These statements are

not guarantees of future performance and are subject to risks,

uncertainties and other factors, some of which are beyond PCCW's

control and are difficult to predict. Actual results could differ materially

from those expressed, implied or forecast in these forward-looking

statements for a variety of factors. These factors are set out in PCCW’s

reports furnished to or filed with the United States Securities and

Exchange Commission (the “SEC”) including, but not limited to, PCCW’s

2005 Annual Report on Form 20-F filed with the SEC on May 11, 2006.

ForwardForward--Looking StatementsLooking Statements

2

概覽概覽概覽概覽

3

20062006年年(百萬美元) 20052005年年收益

董事會建議派發末期股息每股港幣12分,但仍須待股東通過後方可作實

20062006年財務表現年財務表現年財務表現年財務表現年財務表現年財務表現年財務表現年財務表現

股權持有人應佔溢利投資及其他收益EBITDA

收益股權持有人應佔溢利

2005年年年年 2006年年年年

204

2,885

161

3,287

EBITDA本年度溢利 853

80

875

5

239 209

(百萬美元)投資及其他收益

4

業務進展業務進展業務進展業務進展業務進展業務進展業務進展業務進展

完成「四網合一」平台-陸續推出新產品及服務固網業務更形鞏固- ARPU明顯趨於穩定寬頻-寬頻線路超過100萬條,Wi-Fi香港熱點增至逾3,000個收購SUNDAY全部資產,著手全面整合至本集團推出3G服務,提升網絡,並推出創新服務跨平台服務- 、 、「流動戲票」、 、「視察易」萃鋒、客戶聯絡中心及PCCW Global - 外間業務收益增長電訊盈科企業方案-贏得新合約,提高效率盈大地產-重建電話機樓取得進展

電視及內容電視及內容電視及內容電視及內容流動通訊流動通訊流動通訊流動通訊核心業務核心業務核心業務核心業務

已安裝 的用戶達758,000名,ARPU上升,頻道現已超過130條首選的體育節目平台-擁有英超聯、歐洲聯賽冠軍盃等獨家播放權增設廣告及互動業務,開拓新收益來源其他業務其他業務其他業務其他業務

5

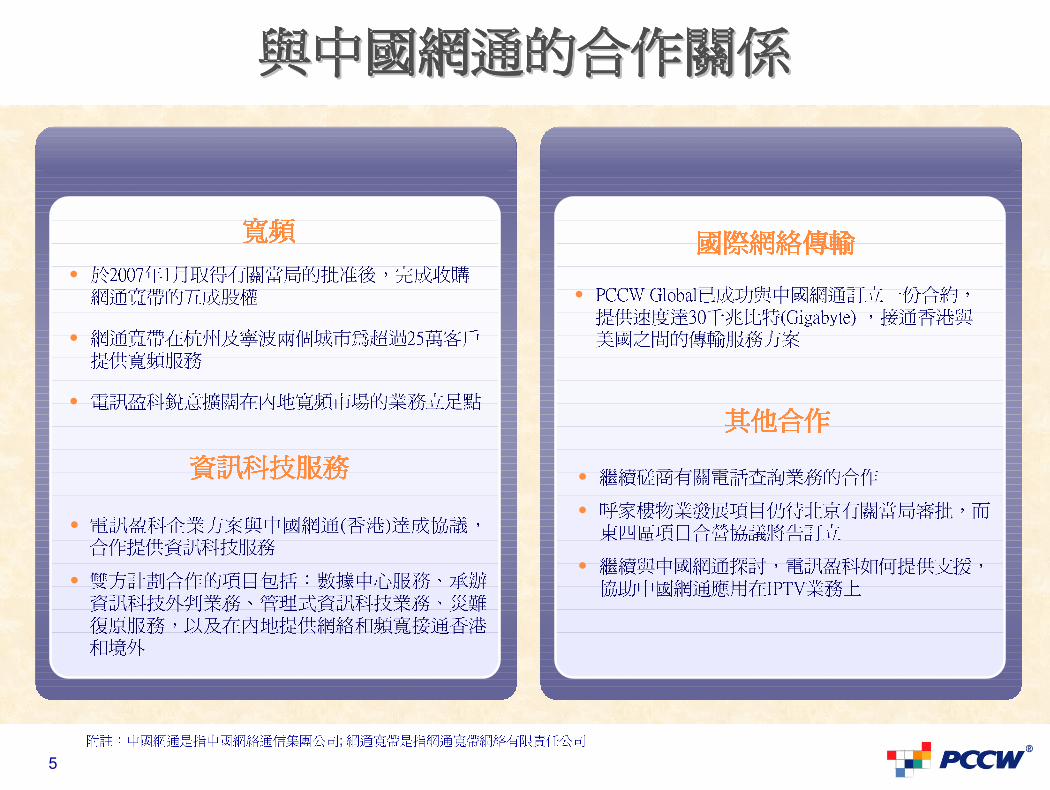

與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係與中國網通的合作關係

� 於2007年1月取得有關當局的批准後,完成收購網通寬帶的五成股權� 網通寬帶在杭州及寧波兩個城市為超過25萬客戶提供寬頻服務� 電訊盈科銳意擴闊在內地寬頻市場的業務立足點

寬頻寬頻寬頻寬頻

附註:中國網通是指中國網絡通信集團公司; 網通寬帶是指網通寬帶網絡有限責任公司資訊科技服務資訊科技服務資訊科技服務資訊科技服務

� 電訊盈科企業方案與中國網通(香港)達成協議,合作提供資訊科技服務� 雙方計劃合作的項目包括:數據中心服務、承辦資訊科技外判業務、管理式資訊科技業務、災難復原服務,以及在內地提供網絡和頻寬接通香港和境外

� 繼續磋商有關電話查詢業務的合作� 呼家樓物業發展項目仍待北京有關當局審批,而東四區項目合營協議將告訂立� 繼續與中國網通探討,電訊盈科如何提供支援,協助中國網通應用在IPTV業務上

其他合作其他合作其他合作其他合作� PCCW Global已成功與中國網通訂立一份合約,提供速度達30千兆比特(Gigabyte) ,接通香港與美國之間的傳輸服務方案國際網絡傳輸國際網絡傳輸國際網絡傳輸國際網絡傳輸

6

展望展望展望展望展望展望展望展望

透過跨平台傳送獨特內容,取得互利優勢,如 、 、、「視察易」等,日後陸續推出更多創新服務發揮「四網合一」在內容及應用服務方面的潛力加強固網服務的優勢,新增高速數據及視象服務保持市場佔有率,著重增加收益增加萃鋒、電訊盈科企業方案及客戶聯絡中心的外間業務收益新增來自廣告及交易的收益來源英超聯現場獨家播放權,令 增長持續強勁於2007年推出高清電視服務推出創新的跨平台服務,令 優於同業更加緊密融入「四網合一」,令市場推廣更為有效「高速下載分組接入」(HSDPA)及電訊盈科的Wi-Fi服務,應有助提升無線數據使用量

核心業務核心業務核心業務核心業務「「「「四網合一四網合一四網合一四網合一」」」」電視及內容電視及內容電視及內容電視及內容流動通訊流動通訊流動通訊流動通訊

7

Overview

8

The Board Has Recommended a Final Dividend of 12 HK Cents Per Share, Subject to Approval of Shareholders

2006 Financial Performance2006 Financial Performance

20062006年年20052005年年收益股權持有人應佔溢利投資及其他收益EBITDA

Revenue

2005 2006

204

2,885

161

3,287

853

80

875

5

239 209

(US$ million)

Investment & Other Gains

Profit Attributableto Equity Holders

Profit for the Year

EBITDA

9

758,000 installed, higher ARPU, and over 130 channels today

Premier platform for sports programming – exclusive EPL, UEFA, etc.

Advertising & Interactive Services established for new revenue streams

Achievements Achievements

Quad Play platform completed - new products & services coming

Solid fixed-line - ARPU showed clear signs of stabilization

Broadband - over 1m lines, increasing Wi-Fi hotspots to 3,000+ in HK

Acquired 100% SUNDAY assets, began full integration into the Group

Launched 3G, upgraded networks & introduced innovative services

Cross-platform services - , , ,MobileTix, , EasyWatch

CASCADE, Contact Centers and PCCW Global – external revenue growth

PCCW Solutions - major new contracts and efficiency gains

PCPD - made progress to redevelop telephone exchange buildings

TV & Content

Mobile

Core Business

Other

Businesses

10

CoCo--operation with China Netcomoperation with China Netcom

� Completed acquisition of 50% CNCBB stake after approvals from relevant authorities in Jan 2007

� CNCBB provides broadband services to 250,000+ customers in Hangzhou and Ningbo

� PCCW will strive to broaden its presence in broadband market in China

Broadband

Note: China Netcom refers to China Network Communications Group Corporation CNCBB refers to China Netcom Broadband Corporation Limited

IT Services

� PCCW Solutions and China Netcom (HK) signed agreement to cooperate in providing IT services

� Will cooperate in data center services, IT outsourcing, managed IT operations, disaster recovery services, and network & bandwidth provisioning in China connecting to Hong Kong and beyond

� Continued discussion on cooperation in directories business

� Hujialou property development project awaiting approval from Beijing authorities, and JV agreement for Dongsi project will be established

� Continue to explore ways that PCCW could support China Netcom’s IPTV deployment

Other Cooperation

� PCCW Global secured contract with China Netcom to provide 30 Gigabyte connectivity solution between HK and U.S.

International Connectivity

11

OutlookOutlook

Mutual benefit from cross-platform delivery of unique content like, EasyWatch, more to come

Mobile Innovative cross-platform services differentiate

Closer integration into Quad Play - more effective marketing

Unleashing Quad Play potential with content and applications

HSDPA and PCCW Wi-Fi should encourage wireless data usage

Quad Play

Core Business Enrich fixed-line offering with high speed data & video services

Maintain market share and focus on increasing revenue

More external revenue from CASCADE, PCCW Solutions & Contact Centers

New sources of revenue from advertising and transactions

Exclusive EPL live broadcast rights should sustain strong growth

Launch of HDTV service in 2007

Quad Play

TV & Content

12

Financial & Business Review

13

(US$ million)

Summary P&LSummary P&L2005 2006

Revenue 2,885 3,287

Cost of Sales (1,342) (1,627)

General and administrative expenses (1,033) (1,178)

Operating profit 510 482

Other gains, net 80 5

Losses on property, plant and equipment (7) (1)

Finance costs, net (217) (164)

Impairment losses on interests in jointly controlled companies and associates (1) 0

Share of results of associates & jointly controlled companies 16 5

Profit before taxation 381 327Profit before taxation (excluding other gains, net)

Taxation (142) (118)

Profit for the year 239 209

Attributable to:

Equity holders of the Company 204 161

Minority interests 35 48

301 322

up 14%

down 25%

up 7%

down 17%

% change

14

RevenueRevenue

(US$ million)

2004 2005 2006

3,287 2,949 2,885

PCCW Solutions

TSS

Mobile

+ 2% y-o-y

Up 14% y-o-y

Up 14% y-o-y

PCPD

Elimination

TV & Content+ 71% y-o-y

(115)

1,964

24

748

239

(114)

1,929

5577202

657

79(156)

1,971

95158212

931

76

+ 42% y-o-y

Other Businesses

89

(1) Restated for new segments

(2) Included post-acquisition results of SUNDAY in H2’05 and 2006

(1)( 2) (2)

+ 5% y-o-y

(1)

(2)

TV & Content

15

• Booked against

higher revenues

Cost of SalesCost of Sales

736 803 848

614 539

779

2004 2005 2006

1,627

1,3421,350 PCPD

Group Total

ex- PCPD

• In line with ex-PCPD revenue growth

(US$ million)

(1) (1)

(1) Included post-acquisition results of SUNDAY in H2’05 and 2006

16

ExpensesExpenses

757 690 785

325345

389

251218

163

128142

118

2004 2005 2006

1,4551,3951,461

Depreciation & amortization

Tax

Net finance costs

Operating costs

(US$ million)

(1)(1)

(1) Included post-acquisition results of SUNDAY in H2’05 and 2006

17

912 897 898

122

4 6 203

(24)(34) (36)(43)(137) (104) (98)

8797

EBITDAEBITDA

(US$ million)

2004 2005 2006

875

Up 3% y-o-yUp 3% y-o-y

TSS

Mobile

PCPD

Other Businesses

TV & Content

PCCW Solutions

842 853

Mobile

(2)

(1)( 2) (2)(1)

(1) Restated for new segments

(2) Included post-acquisition results of SUNDAY in H2’05 and 2006

PCCW SolutionsPCCW Solutions

18

Profit for the YearProfit for the Year

48

199 161

204

353

2004 2005 2006

209

239

202

Profit Attributable to Equity Holders

Minority Interests

(US$ million)

(1) (1)

(1) Included post-acquisition results of SUNDAY in H2’05 and 2006

80

Other Gains, Net

5

*

*

*

19

Debt ProfileDebt Profile

� US$450m convertible bonds due 2007 and US$456m guaranteed notes due 2013 redeemed in January 2007

� Average debt maturity at approximately 5 years

� Average cost of debt approximately 6.5% p.a. in 2006 Current cost of debt approximately 6% p.a.

� Raised revolving credit facilities of US$827m at PCCW in July 2006 and US$1,301m at HKTC in October 2006

� Total medium term revolving credit lines added up to US$2.1bn available for liquidity and debt retirement

(US$ million)

As of December 31, 2006

Gross debt: US$3,715m

2007 2008 2009 2010 2011 2014

$1,000

$500

2012 2013

$808$450

$956

$500

$456

2015

Revolving Credit Facilities

Guaranteed Notes

Convertible Bonds

US$ Bonds

Update

(1)

(1)

(1)

20

Credit FundamentalsCredit Fundamentals

(1) Based on gross debt/ net debt as at year end divided by EBITDA for the last year

(2) Based on EBITDA for the year divided by gross interest plus finance fees

(3) Net debt refers to the principal amount of short-term and long-term borrowings, minus cash and cash equivalent and certain restricted cash

(3)

Net Debt/EBITDA (1) as of Dec 31, 2006 is 2.9

Gross Debt/EBITDA (1)

4.24.7

2.1

4.5

3.0

’03 ’04 ’05 ’06

4.4 4.3

PCCW consolidated

HKTC

EBITDA/Interest (2)

3.3

8.2

3.2

8.5

3.2 2.9

6.6

2,529

2006

3,735

2003

(US$ million)

2004

3,368

2005

Net Debt

2,498

Gross Debt down 1 % y-o-y to US$ 3,715m

Net Debt up 1 % y-o-y to US$ 2,529m

’03 ’04 ’05 ’06

’03 ’04 ’05 ’06

’03 ’04 ’05 ’06

3.2

5.0

21

Operational &

Strategic Review

22

2006 2006 -- Invested in Quad Play PlatformsInvested in Quad Play Platforms

Solid Performance in Each of the Four Service Lines

23

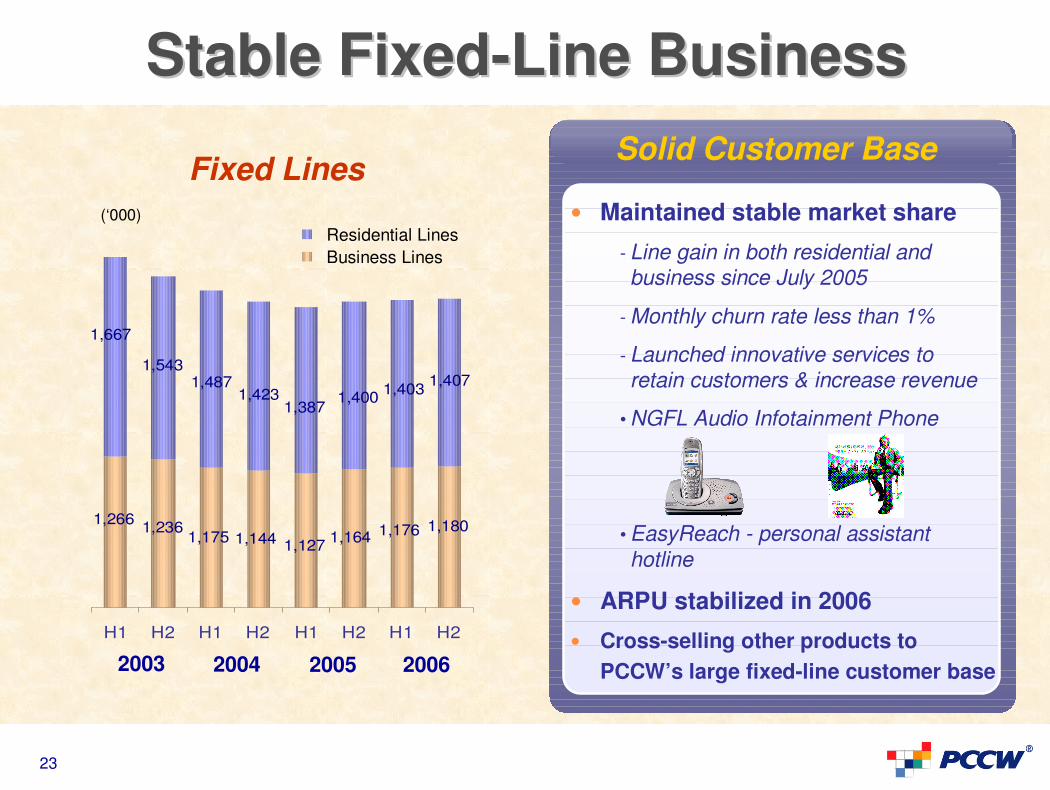

Stable FixedStable Fixed--Line Business Line Business

1,175 1,144 1,164

1,407

1,180

1,1271,1761,236

1,266

1,667

1,5431,487 1,403

1,4001,387

1,423

H1 H2 H1 H2 H1 H2 H1 H2

(‘000)

2003 2004 2005 2006

Residential Lines

Business Lines

Fixed Lines

� Maintained stable market share

- Line gain in both residential and business since July 2005

- Monthly churn rate less than 1%

- Launched innovative services to retain customers & increase revenue

• NGFL Audio Infotainment Phone

• EasyReach - personal assistant hotline

� ARPU stabilized in 2006

� Cross-selling other products to

PCCW’s large fixed-line customer base

Solid Customer Base

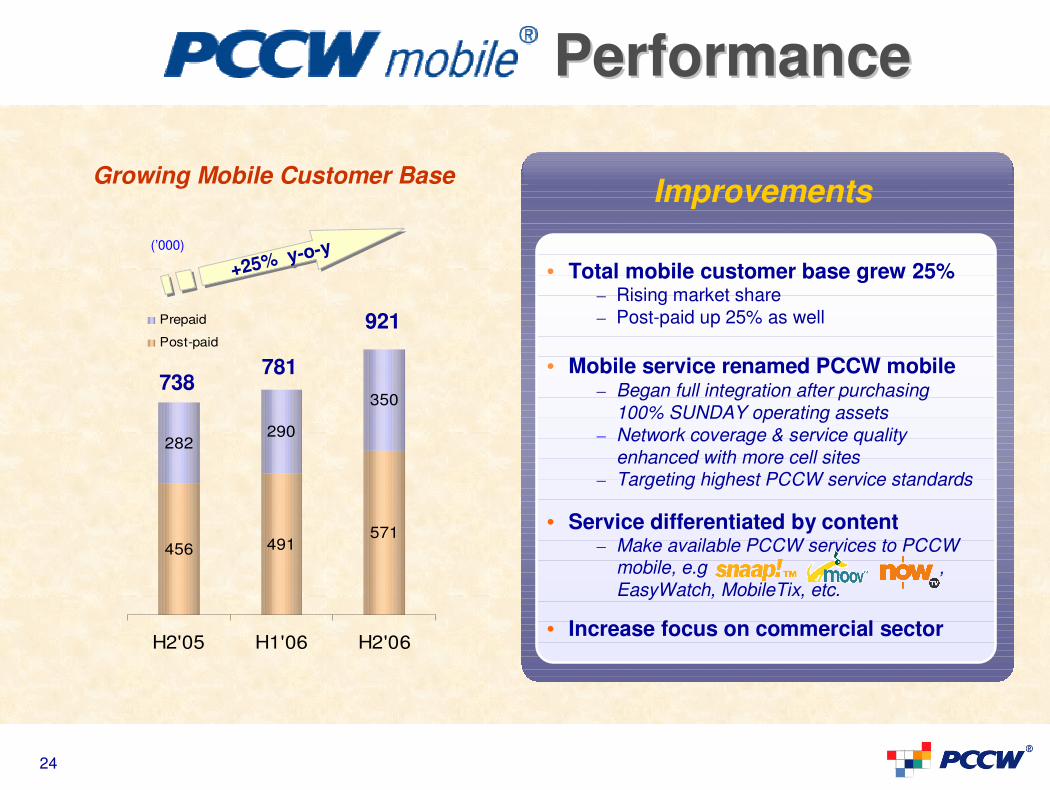

24

PerformancePerformance

456 491571

282290

350

H2'05 H1'06 H2'06

Prepaid

Post-paid

Growing Mobile Customer Base

(’000)

+25% y-o-y+25% y-o-y

738781

921

• Total mobile customer base grew 25%– Rising market share– Post-paid up 25% as well

• Mobile service renamed PCCW mobile– Began full integration after purchasing

100% SUNDAY operating assets– Network coverage & service quality

enhanced with more cell sites – Targeting highest PCCW service standards

• Service differentiated by content– Make available PCCW services to PCCW

mobile, e.g , EasyWatch, MobileTix, etc.

• Increase focus on commercial sector

Improvements

25

� Hong Kong’s first mobile

ticketing service

� Purchase cinema tickets on

handset, on-line and on

� Present MobileTix MMS

received on handset at cinema

scanner for admission

� Exclusive content

� First mobile TV utilizing multicast technology

� 6 initial channels of local & international news, finance & sports debuted in Jun ’06

� on-line and mobile

� 60,000+ songs & music videos in library

� Local and international top hit selections

� Playlist user experience

� Monthly fee plan, unlimited streaming

• 7 new entertainment and infotainment channels recently launched

TVB pleasureTVB entertainment news

MobileTixMobileTix

MobileTix MMS

2D bar code

InnovationsInnovations

on mobile on mobile

ChineseEnglish

26

Market Leader in BroadbandMarket Leader in Broadband

Broadband Lines Continue to Grow

460

5863

68

8894

99

952840

517558

660715

798

8074

H1 H2 H1 H2 H1 H2 H1 H2

629703

753796

2003 2004 2005

857

Wholesale

Business

Consumer 953

+17% y-o-y

+17% y-o-y(’000)

998

2006

� Achieved 17% growth y-o-y with low churn rate (remaining below 1%)

� Innovative services driving growth

− driving broadband demand

− largest digital music library in HK with over 20 international & local labels

− now.com.hk - most popular multimedia youth portal creating a mass user community

� Rapidly deploying dedicated 18Mb/s ADSL2+ for HDTV service

Achievements

1,117

27

Momentum ContinuesMomentum Continues

Strong Demand for

Paying base

2003 2004 2005

(’000)

+38% y

-o-y

+38% y

-o-y

2006

H2 H1 H2 H1 H2 H1

29

106147

269

361

192

441

271

549

391

608

444

758

501

H2

Installed base

Drivers

� Over 130 local & international channels- as of March 2007

� The strongest sports content line-up:- English Premier League, UEFA Euro 2008TM, Italian Serie A, J-League, UEFA Champions League, Brazilian League, and others

- On

� More than 50 exclusive world-class sports, movies, news and other entertainment channels:

- now Sports, ESPN, STAR Sports, HBO, STAR

Movies, Mei Ah, BNC and more

� Advanced Interactivity: now Select

including HBO On-demand, NGC, Golf, BNC

On-Demand services, snaap!, Dial-a-Dinner

� HDTV – Launching in H2 2007

28

Healthy Growth in ARPUHealthy Growth in ARPU

Strong Paying Base & ARPU

Growth

2003 2004 2005 2006

29

106

192

271

391444

501

57

70

105110 114 118

140

H2 H1 H2 H1 H2 H1 H2

(HK$/ month)

Mini Packs launched

Value packs further enhanced ARPU

Paying base ARPU

Paying base (’000)

ARPU Drivers

Premium content offering with English Premier League & other leading sports

Highly popular mini-packs & value plans with up-selling potential

� Mega Sports Packages from $178� Mini-packs from $184 � $368 and $488 Super Value Packs

Suite of innovative interactive services

� Dial-a-Dinner, snaap!, now Select, on-line merchandising with expanded catalogs, real time stock quotes etc.

29

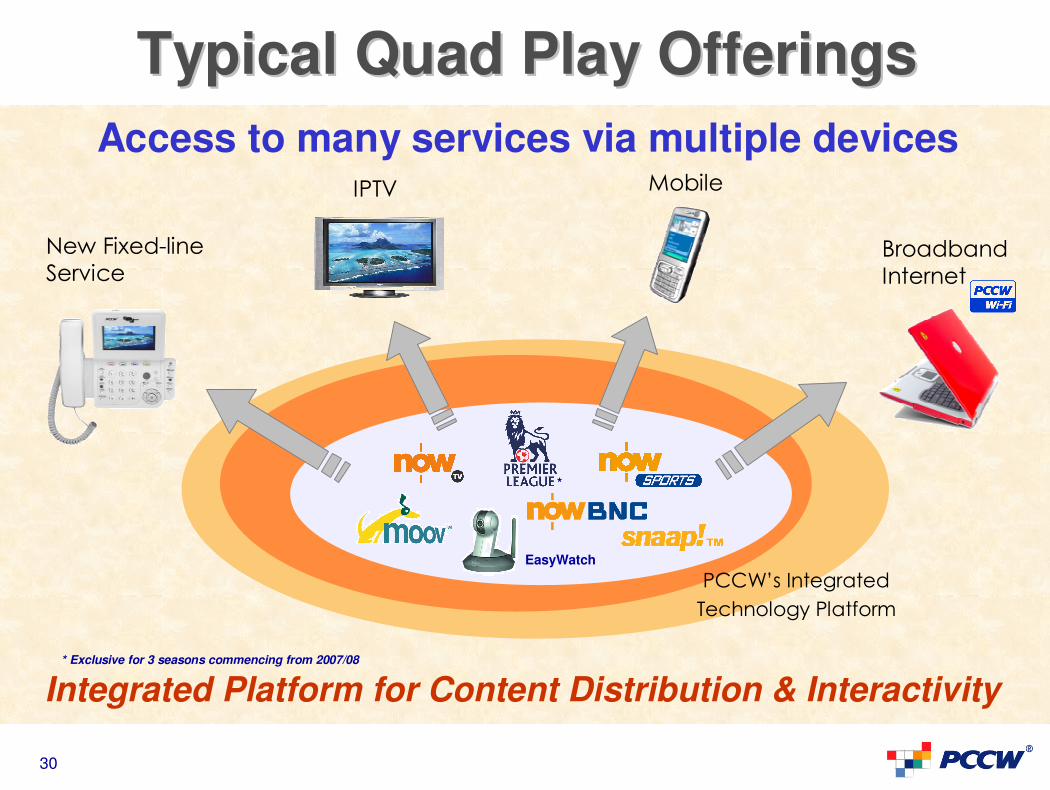

2007- Unleashing the Quad Play

Strategy to provide common content, applications and

transactions across all four platforms

To Give Customers Better Functionality, More Flexibility,

and to Increase Expenditure

30

Content Applications & Transactional Services

EasyWatch

PCCW’s Integrated

Technology Platform

*

Most Comprehensive

Sports & Football Content on Multiple Platforms

Broadband Internet

Mobile

New Fixed-line Service

IPTV

Access to many services via multiple devices

Typical Quad Play OfferingsTypical Quad Play Offerings

Integrated Platform for Content Distribution & Interactivity* Exclusive for 3 seasons commencing from 2007/08

31

PCCW Quad Play Example

Encouraging Consumers to Buy More Than One of Our Services

Share & view both photos & video, real time uploading and processing

� View & share photos & video on PC, mobile, New Fixed-line Service, and

(on channel 508)

� Free of charge sharing images within 3G network

- Enjoy basic plan free if subscribe to two or more PCCW services

� Online photo printing and deliver directly to your home

� Launched in March 2007

Unique Quad Play Service

32

Another PCCW Quad Play Example Another PCCW Quad Play Example -- EasyWatchEasyWatch

New Fixed-line

ServiceIPTV

� Simple and convenient one-stop-shop home/ business security and monitoring solution

� Viewed anytime anywhere even overseas

� Platform recording available

– Image stored at PCCW server

� Remote-controlled functions

– Pan-tilt and zoom, video recording, privacy protection, night mode and more

Unique Remote Monitoring Service

Wireless

camera

33

Third PCCW Quad Play Example Third PCCW Quad Play Example -- EPLEPL

*

* Exclusive for 3 seasons commencing from 2007/08

� 100% EPL games live rights

� EPL anytime anywhere over PCCW’s four delivery platforms

� Professional Cantonese commentators

� Innovative Network Personal Video Recording service (NPVR)

� now Select replay service to watch

already-played matches any time

English Premier League

Bringing Sports to Local Community Like It’s Never

Been Seen Before

34

Tremendous Quad Play OpportunitiesTremendous Quad Play Opportunities

* Exclusive for 3 seasons commencing from 2007/08

Unlocking Advertising & Transactional Capabilities of Unique Interactive Platform

Leveraging PCCW’s Unique Content Across All Platforms

*

35

Providing New Revenue Streams

Advertising and Interactive ServicesAdvertising and Interactive Services

Further Opportunities On PCCW Quad Play

Merchandising

Interactive Advertising

Broadcast Ads & Sponsorship

Transaction Services

Real Time stock QuotesDial a Dinner

Buy your Cinema ticket Order your meal

36

Complementing Complementing PCCWPCCW’’ss Quad Play Quad Play

Massive expansion of PCCW Wi-Fito 3,000+ Wi-Fi hotspots in HK For convenient high-speed

outdoor wireless broadband access to laptops, PDAs, mobile phones, and any

wireless-enabled devices

Wi-Fi at MTR stations in pipeline

37

2007- PCCW Has Unleashed the Quad Play

38

Appendix

PCCW Consolidated Debt Maturity ProfilePCCW Consolidated Debt Maturity Profile(US$ million)

$450$1,000

$250

2005 2006 2007 2008 2009 2010 2011 20312012 2013

$481$385

$1,154

$1,100

$96

$54 $956

$500

$456

Debt1

to EBITDA = (4,424 / 948) = 4.67XDec 2003

Dec 2005

Net Debt = 3,735

$1,000$500

$500

$456

$956

Net Debt = 2,529Dec 2006

$450

HK$750m Term Loan Facility

Revolving Credit Facilities 7.88% Guaranteed Note

Mandatory Convertible Note

Convertible Bonds

HK$3,003m Term Loan Facility US$ Bond

Japanese Yen Bond

$769 $1,000$500

$64 $500

$456

$956

Net Debt = 2,498

$450

$1,000

$250

$1,154$54

$1,100 $500

$456

$956

3

Dec 2004Net Debt = 3,368

$450

2005 2006 2007 2008 2009 2010 2011 20312012 2013

2007 2008 2009 2010 2011 20152012 2013

2006 2007 2008 2009 2010 2011 20152012 2013

1Includes Beijing property RMB loan

$808

Debt to EBITDA = (3,816 / 842) = 4.53x

Debt to EBITDA = (3,739 / 853) = 4.38x

Debt to EBITDA = (3,715 / 875) = 4.25x

2004

HKTC Debt Maturity ProfileHKTC Debt Maturity Profile(US$ million)

7.88% Guaranteed Note

Convertible Bonds

US$ Bond

Japanese Yen Bond

Dec 2006

2006 2007 2008 2009 2010 2011 2014

$1,000$500

2012 2013

$769$450

$64

$956

2015

Net Debt = 3,709Dec 2005

$500

$456

2007 2008 2009 2010 2011 2014

$1,000$500

2012 2013

$450$956

2015

$500

$456

2006 2007 2008 2009 2010 2011 2031

$1,000

$250

2012 2013

$956$450

Net Debt = 2,621Dec 2004

$500

$456

2006 2007 2008 2009 2010 2011 2031

$450

$1,000

$250

2012 2013

$500

HKTC Debt to EBITDA = (2,200 / 1,047) = 2.10XNet Debt =2,074Dec 2003

Revolving Credit Facilities

HKTC Debt to EBITDA = (2,656 / 889) = 2.99X

HKTC Debt to EBITDA = (3,739 / 876) = 4.27X

Net Debt = 2,888 HKTC Debt to EBITDA = (2,906 /911) = 3.19X

2005

2005

2004