1452494044ECO_P3_M31_E-Text.pdf - BSc Chemistry

14

____________________________________________________________________________________________________ ECONOMICS PAPER No. 3: Fundamentals of Microeconomic Theory MODULE No. 31: Williamson’s Model of Managerial Discretion Subject ECONOMICS Paper No and Title 3: Fundamentals of Microeconomic Theory Module No and Title 31: Williamson’s Model of Managerial Discretion Module Tag ECO_P3_M31

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of 1452494044ECO_P3_M31_E-Text.pdf - BSc Chemistry

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Subject ECONOMICS

Paper No and Title 3: Fundamentals of Microeconomic Theory

Module No and Title 31: Williamson’s Model of Managerial Discretion

Module Tag ECO_P3_M31

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

TABLE OF CONTENTS

1. Learning Outcomes

2. Introduction

3. Williamson’s Theory of Managerial Discretion

4. Utility Function of Managers

5. The Simplified Model of Managerial Discretion

6. Summary

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

1. Learning Outcomes

After studying this module, you shall be able to

Know the concept of managerial theory of firm

Why Williamson model is different from other managerial theories?

Williamson’s Utility Function

Understand why utility maximization is the goal of the managers rather than profit

maximization?

Know the four different categorization of profits

Know the preferences of managers and profit curve

2. Introduction

In recent years, new theories of the firm have been developed under oligopoly which lay

stress on the role of the managers and their behavioral patterns on the price and output

decisions of the firm. It pointed out that profit maximization is not the only goal of the

managers as they are trying to pursue other goals as well. Besides, behavioral theory, the

other theories that developed was managerial theory of the firm. The three theories of the

firm which have been developed in the recent years are managerial theories of

Williamson, Marris and Baumol.

Baumol propounded a model of sales maximization in his book “Business behavior,

value and growth”. The sales maximization model says that managers of the firms seek to

maximize their sales revenue subject to a profit constraint. Under this, the objective of the

managers is to maximize sales. When the profits of firm reaches a level which is

considered satisfactory by the shareholders then managers are free to maximize their

revenue by promoting sales instead of maximizing profit. According to Marris, the

manager of the firm tries to maximize the rate of growth of the firms, that is, the

maximization of the rate of growth of demand for the products of the firm, and of the

growth of its capital supply rather than maximization of profits. In pursuing this

objective, the firm has two constraints. First, the constraints set by the available

'managerial team and its skills, and second, the financial constraint set by the desire of

managers to achieve maximum job security. The managers by jointly maximizing the rate

of growth of demand and capital maximizes their own utility as well as utility of the

shareholders. The conflicting interests of owners and management coincide with the

objective of balanced growth of the firm as it ensures fair return on owner's capital and

faith in managers who achieve this goal.

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

3. Williamson’s Theory of Managerial Discretion

Williamson’s model of managerial discretion was developed by Oliver E. Williamson in

1964. Williamson like other managerial theory of the firm assumes that utility

maximization is the sole objective of the managers of a joint stock organization. It is also

known as “Managerial discretion Theory”. Williamson emphasize that managers are

motivated by their own self interest and they tries to maximize their own utility function.

Alike Baumol sales maximization model, the utility maximization objective of the

managers are subject to the constraint that after tax profits are large enough to pay

dividends to the shareholders. However, it is pointed out that utility maximization by the

self interest seeking managers is possible only in corporate form of the business

organization as there exists separation of ownership and control. This is basically the

principal agent problem. It explains the relationship between the principal (owner) and

the agent (who performs owner’s works). The principal agent shows that whenever the

difference between ownership and control exist, then the self interest of agent makes

profits lower than in a situation where principals act as their own agents.

Profit works as a limit to the manager’s utility maximization as the shareholders require a

minimum profit to be paid out in the form of dividends. If this minimum profits is not

covered, then job security of the managers is put in danger. But, the managers are able to

hold a powerful position if (i) firm is showing a reasonable rate of growth, (ii) minimum

dividends are paid to the shareholders and (iii) profits at any time are at acceptable level.

Here the manager’s decision on price and output differs from the manager’s decision on

price and output of profit maximization firm.

Assumptions: The Williamson’s model is based on some assumptions. These are:

(i) Imperfect Competition

(ii) Separation of Ownership and management.

(iii) A minimum profit to be able to pay to the shareholders.

The factors that affect the interest of the self seeking managers are:

a. Salary and Other form of Monetary Compensation

b. Management Slack or Non-essential Management Perquisites

c. Number of Staff under the Control of a Manager

d. Magnitude of Discretionary Investment expenditure by the Manager.

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Let us study them in detail.

a. Salary and other form of Monetary Compensation: The salary and other form of

monetary compensation is one of the most important factor in determining the

utility of the managers. Higher the income the managers receive, the better is the

standard of living and status. So, higher the salary and other monetary

compensation and perks, higher is the utility of the managers.

b. Management Slack or Non-essential Management Perquisites: The second factor

that is determining the utility of the managers is the amount of management slack.

The management slack consists of non-essential management perquisites such as

well-furnished office, luxurious cars, entertainment expenses etc. These perks are

giving the incentive to the managers to enhance their status and prestige in the

organization which in turn contributing to the efficiency of the firm’s operation.

These non-essential perquisites are also the part of the cost of production of the

firm.

c. Number of Staff under the Control of a Manager: The third factor that is

determining the utility of the managers is the number of staff under the control of

a manager. The greater the number of staff under the control of a manager, the

more powerful is the manager. More staff under manager enhances his status and

prestige. According to Williamson, there exist positive relationship between the

number of staff and salary of the managers. In the utility maximization model of

Williamson, he used a single variable for the number of staff and salary of the

managers as “monetary expenditure on the staff”.

d. Magnitude of Discretionary Investment expenditure by the Manager: The fourth

important factor that is determining the utility of the managers is the magnitude of

discretionary investment expenditure by the manager. The discretionary

investment refers to the amount of resources left at a manager’s disposal to be

able to spend at his own discretion. This enhances his status and prestige in

organization. Here, the discretionary investment by the managers does not include

those investment expenditures that are necessary for the survival of the firm. The

discretionary investment by the manager includes spending on furniture, latest

equipment, decoration material etc.

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

4. Williamson’s Utility Function

The managerial utility function includes variables such as salary, status, prestige, job

security and other monetary compensation. Out of these, salary is the only quantitative

variable which is measurable. On the other hand, all other variables except salary are

non- quantifiable i.e. not measurable. In the utility maximization model of Williamson,

he used a single variable for the number of staff and salary of the managers as “monetary

expenditure on the staff”. The utility function of managers is a function of salary,

monetary expenditure on the staff and the discretionary investment.

𝑈 = 𝑓1(𝑆, 𝑀, 𝐼𝐷)

Where U is utility

S is monetary expenditure on the staff

M is the management slack.

𝐼𝐷 is discretionary investment.

Here, the variables expenditure on staff salary, management slack and disc retionary

investment is used the unquantifiable concepts like power, status, job security, dominance

etc. The variable expenditure on staff, management slack and disinvestment can be

assigned some nominal values.

There exists a positive relationship between decision variables (S, M and 𝐼𝐷 ) and utility.

Any increase in the decision variables increase the utility of the managers. But the firm

always choose their values subject to the constraint, S ≥0 and D≥0. Williamson also

assumes that the law of diminishing marginal utility applies so that when additions are

made to each of the decision variable S, M and 𝐼𝐷, they yield smaller increments to the

utility to the manager.

Demand curve faced by the firm is downward sloping: Under Williamson’s model the

demand curve faced by the firm is downward sloping. The demand function can be

written as:

Q = 𝑓2(P, S, Ɛ)

P = 𝑓3 (Q, S, Ɛ)

Where Q is output

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

P is price

S is staff expenditure

Ɛ the demand-shift parameter reflecting autonomous changes in demand

Demand curve is negatively sloped implies a negative relationship between price and

quantity i.e., 𝜕𝑃

𝜕𝑄< 0.

As price increases quantity decreases and as prices decreases then quantity increases. It

is also assumed that the demand is positively related to staff expenditure and to the

demand shift parameter ε. Thus,

𝜕𝑃

𝜕𝑆> 0 𝑎𝑛𝑑

𝜕𝑃

𝜕Ɛ> 0

Any increase in staff expenditure causes an upward shift in the demand curve and thus

allow the charging of a higher price. The same holds for any other change in the demand

shift parameter which shifts the demand curve upward. It may be an increase in income,

change in taste in favour of a good etc.

Cost of Production: The total cost of production is assumed to be an increasing function

of output. This can be expressed as

C = 𝑓4 (Q)

Where C is cost

Q is output

The total cost increases with the increase in the level of output i.e. 𝜕𝐶

𝜕𝑄> 0.

Concept of profit in the model: The various concepts of profit used in the Williamson

model needs to be understood clearly before moving to the main model. Williamson has

put forth four main concepts of profits. These are actual profit, discretionary profit,

reported profit and minimum profit.

(i)Actual profit II: The actual profit is defined as the revenue from sales less the

production costs and the staff expenditure.

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Π = R – C – S where R is revenue, C is the cost of production and S is the staff

expenditure.

(ii) Reported Profit πR: This is the profit reported to the tax authorities. Reported profit

(πR) is the difference between actual profits and supplementary or nonessential

managerial emoluments as represented by the management slack. It is the actual profit

minus the managerial emoluments (M) which are tax deductible. So,

πR = π – M = R – C - S – M

(iii)Minimum Profit (π0): Minimum profit (π0) is the amount of profits (after tax) which

is required to be paid as acceptable dividend to the shareholders of the firm. If the

shareholders do not get reasonable dividends they may sell their share and thereby expose

the firm to the risk of being taken over by others, or alternatively they will vote for the

change of the top management. Both of these actions by the shareholders will reduce the

job security of the top managerial team. Hence, some minimum profits should be earned

by the manager for the shareholders in the form of dividends to keep them satisfied.

Through this he can ensure his job safety. To meet this objective, the reported profits

must be at least as high as minimum profit (π0) plus the tax (T) that must be paid to the

government. This is mathematically expressed as:

πR ≥ π0 + T

The tax function is of the form T = Ť + t. πR

Where t is marginal tax rate or unit profit tax and Ť is the lump sum tax.

iv) Discretionary profit (πD): Discretionary profit is the amount of profit left after

subtracting from the actual profit (π) the minimum profit requirement (π0) and the tax

(T). It can be expressed as:

πD = π – π0 – T

Discretionary Investment (ID): Discretionary investment is the amount left from the

reported profit after subtracting the minimum profit (π0) and the tax (T). It can be

expressed as:

ID = πR - π0 – T

Discretionary profit is different from discretionary investment. Discretionary profits are

the amount left after minimum profit (π0) and tax (T) are deducted from actual profits

(πD = π – π0 – T) but discretionary investment equals the amount left from the reported

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

profit after subtracting the minimum profit (π0) and the tax (T). Thus, we have

discretionary investment

ID = πR – π0 – T

Since difference between reported profits (πR) and actual profits (π) arises due to

management slack, discretionary profits. It can be written as πD = ID + Amount of

management slack. Thus, if management slack is zero then

πR = π and πD = ID

5. The Simplified Model of Managerial Discretion

Under Willaimson’s model, the objective is the maximisation of the utility function

subject to the minimum profit constraint. The minimum profit should be such that it is

sufficient to pay satisfactory profit to shareholders and pay for necessary investment.

Here we are taking a simple case where there is no management slack i.e. M=0.

Objective Max U=f(S,𝐼𝐷)

Subject to π ≥ π0 + T

As there is no management slack, the discretionary investment absorbs all the

discretionary profit. Thus the managerial utility function can be written as

U=f[S,( π - π0 + T)]

Here, we are also assuming that there is no lumpsum tax i.e. Ť=0 so that T=t π. Thus,

U=f[S,( 1-t)π - π0 ]

Where ( 1-t)π - π0 is the discretionary profit πD.

Graphical Representation of the Williamson’s model: The graphical representation of

the equilibrium of the firm requires the construction of the indifference curves map of

managers and the profit curve. An indifference map is the family of indifference curves.

An indifference curve is a curve which shows different combination of two goods

yielding the same level of satisfaction to the consumer. In other words, it identifies the

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

various combinations of goods among which the consumer is indifferent. Here, the

indifference curve under Williamson model shows the relationship between monetary

expenditure on the staff and the discretionary investment. These are the two variable that

are determining the utility function of the managers. The indifference curve is shown in

the figure where staff expenditure (S) is measured on x-axis and discretionary profit (ΠD)

on y-axis. Each indifference curve shows various combinations of staff expenditure (S)

and discretionary profit (ΠD) which give the same level of satisfaction to the managers.

Consider the figure 1 below:

Figure 1: Indifference Map

It is assumed that the indifference curves of managers are of well behaved:

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Indifference curves are downward sloping

They are convex to the origin implying diminishing marginal rate of substitution

of staff expenditure and discretionary profit.

Two indifference family of indifference curves can never intersect each other

Higher the indifference curve higher is the level of satisfaction.

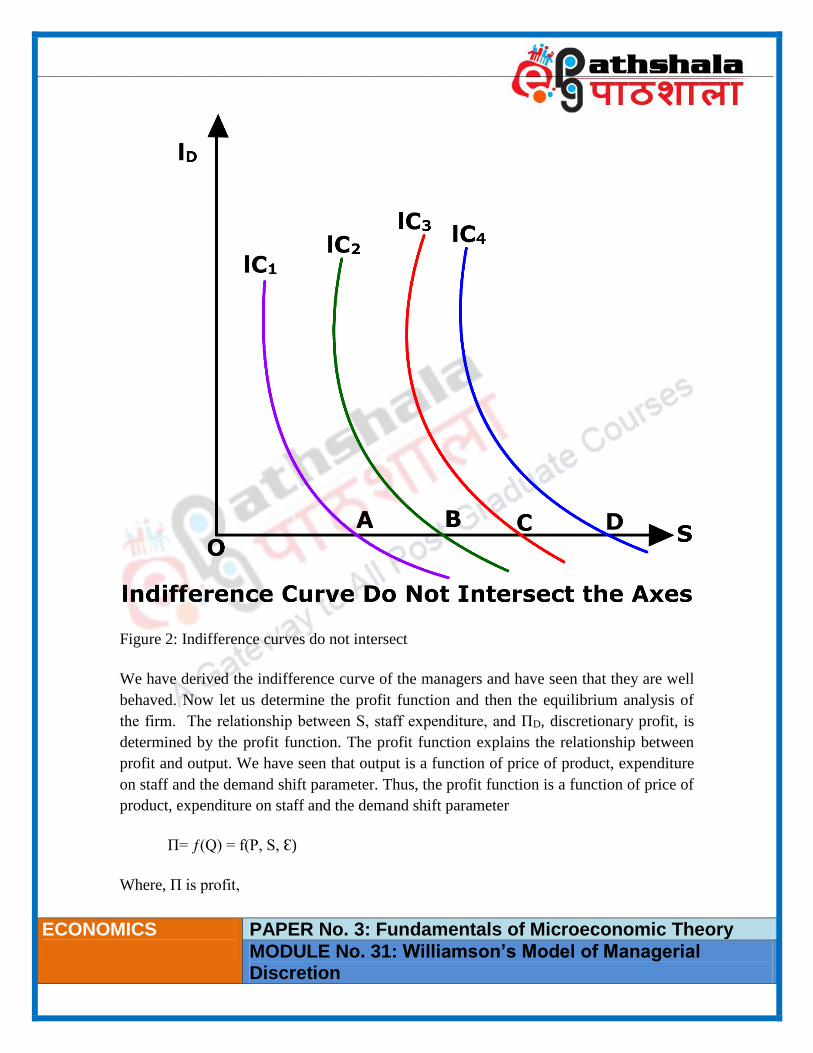

The indifference curves do not intersect the axes. The indifference curves do not

intersect the axes. This is very important property and need to be explained

properly. We have seen that expenditure on staff and discretionary profit are

positively related to utility function of the managers. Any increase in expenditure

on staff or discretionary profit or in both results in an increase in the satisfaction

of the managers by increasing the utility. This assumption restricts the choice of

managers to positive levels of both staff expenditures and discretionary profits,

implying that the firm will choose values of ΠD and S ‘that will yield positive

utility. It is shown in the figure. If the indifference curve do not intersect the axes

then the model excludes the corner solutions, such as points A, B, C, D etc.,

where discretionary profit (ΠD) would be zero in the final equilibrium of the firm.

Consider figure 2:

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Figure 2: Indifference curves do not intersect

We have derived the indifference curve of the managers and have seen that they are well

behaved. Now let us determine the profit function and then the equilibrium analysis of

the firm. The relationship between S, staff expenditure, and ΠD, discretionary profit, is

determined by the profit function. The profit function explains the relationship between

profit and output. We have seen that output is a function of price of product, expenditure

on staff and the demand shift parameter. Thus, the profit function is a function of price of

product, expenditure on staff and the demand shift parameter

Π= ƒ(Q) = f(P, S, Ɛ)

Where, Π is profit,

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

Q is output

P is price

S is expenditure on staff

Ɛ demand-shift parameter reflecting autonomous changes in demand

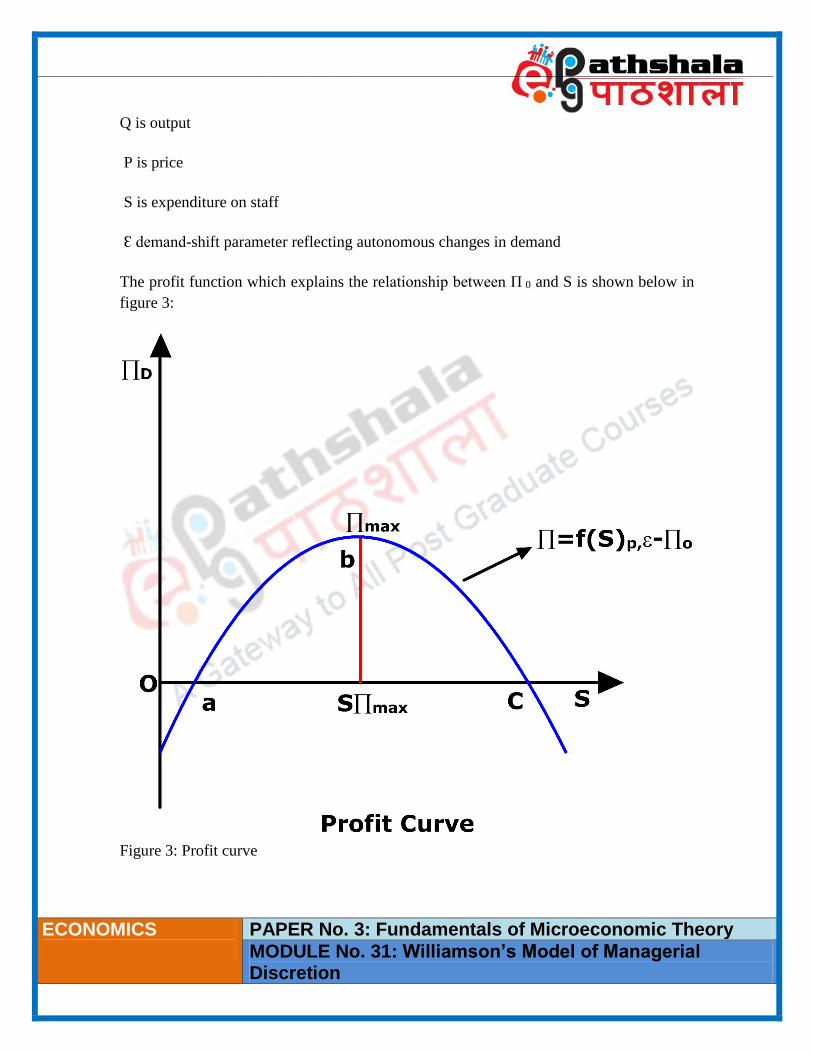

The profit function which explains the relationship between Π 0 and S is shown below in

figure 3:

Figure 3: Profit curve

____________________________________________________________________________________________________

ECONOMICS

PAPER No. 3: Fundamentals of Microeconomic Theory

MODULE No. 31: Williamson’s Model of Managerial Discretion

We can see from the figure that profit curve initially rises, reaches a maximum and then

falls thereafter as the level of production increases. It starts increasing from point a,

reaches maximum at point b and then starts falling and becomes negative after reaching

point c. So, initially both discretionary profits and staff expenditures increases with the

level of production. This increase continues till the maximum point on the profit curve.

Beyond point b where with the increase in production profit curve starts falling, staff

expenditures continue to increase. If these expenditures continue to increase and exceed

point ‘c’, then the minimum profit constraint is not satisfied. So the region before point

‘a’ and to the right of ‘c’ are not feasible solutions. It should be clear from the above

discussion that the drawn profit curve does not include the minimum profit requirement

Π0. Williamson’s model implies higher output, lower price and lower level of profit than

the profit- maximization model.

6. Summary

Williamson’s model of managerial discretion was developed by Oliver E. Williamson in

1964. Williamson like other managerial theory of the firm assumes that utility

maximization is the sole objective of the managers of a joint stock organization. It is also

known as “Managerial discretion Theory”. Williamson emphasize that managers are

motivated by their own self-interest and they tries to maximize their own utility function.

Alike Baumol sales maximization model, the utility maximization objective of the

managers are subject to the constraint that after tax profits are large enough to pay

dividends to the shareholders. However, it is pointed out that utility maximization by the

self-interest seeking managers is possible only in corporate form of the business

organization as there exists separation of ownership and control.