1145 FIC Annual Report 2008.indd - Financial Intelligence ...

96

2008 annual report financial intelligence centre fic

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 1145 FIC Annual Report 2008.indd - Financial Intelligence ...

2008annual report

fi nancial intelligence centrefic

PUBLISHED BY FINANCIAL INTELLIGENCE CENTRE

Private Bag X115

Pretoria 0001

South Africa

Tel: +27 12 309 9200

Fax: +27 12 309 9491

Design and layout: Formeset Digital Pretoria

Printing and binding: Formeset Printers Cape (Pty)Ltd

ISBN: 978-0-621-37992-7

RP: 167/2008

fi nancial intelligence centrefic

Annual Report2007 – 2008

31 July 2008

Mr T A Manuel, MP

Minister of Finance

Report of the Director of the Financial Intelligence Centre for the

period 1 April 2007 to 31 March 2008

I have the honour to submit the Annual Report of the Financial

Intelligence Centre which gives an account of the Centre’s activities

and achievements for the period 1 April 2007 to 31 March 2008.

M Michell

Director

CONTENTS

Administrative Information 1

Accounting Authority’s Statement 2

Acronyms used 6

Director’s Report 7

Performance Report 41

Audit Committee Report 51

Report of the Auditor-General 53

Statement of Financial Position 60

Statement of Financial Performance 61

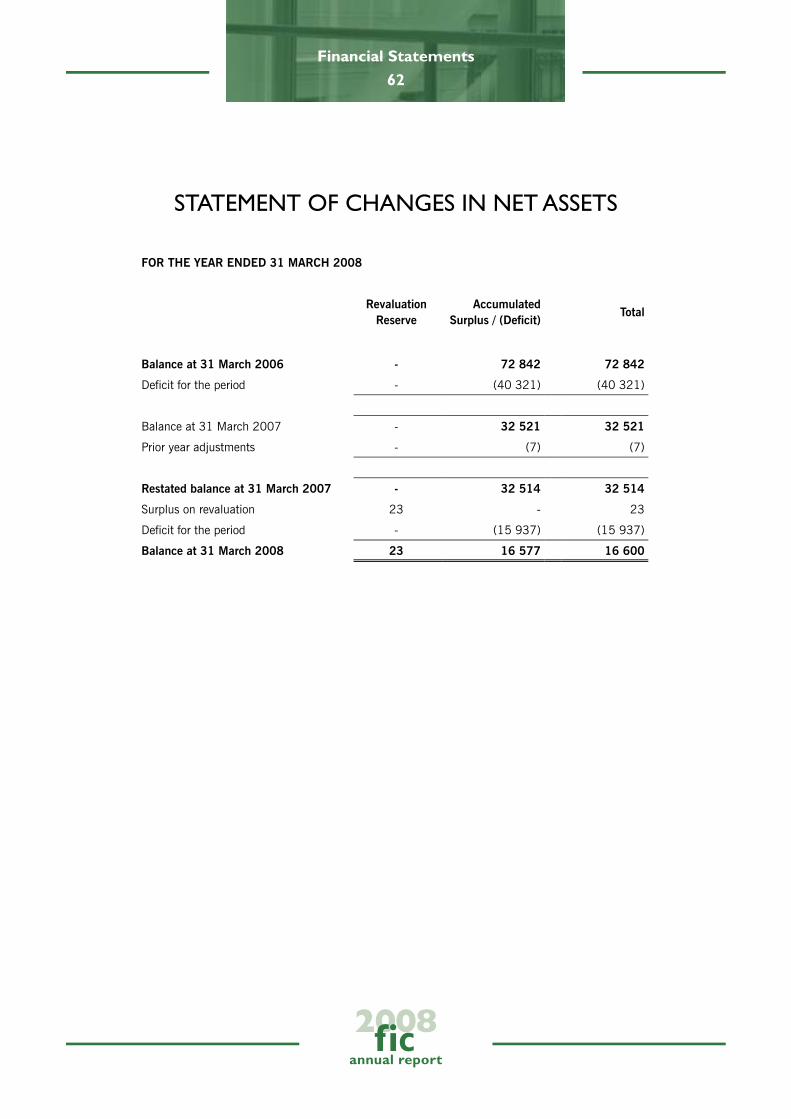

Statement of Changes in Net Assets 62

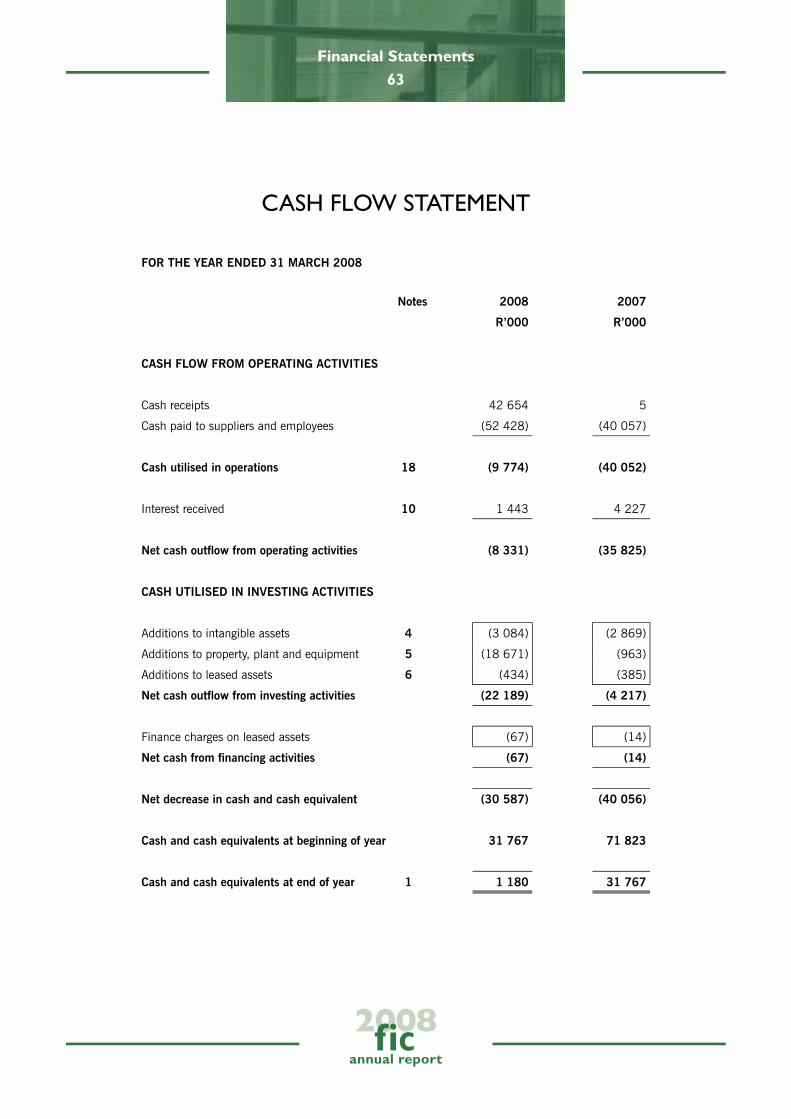

Cash Flow Statement 63

Accounting Policies 64

Notes to the Annual Financial Statements 72

Materiality and Significant Framework 85

1

ADMINISTRATIVE INFORMATION

Administrative Information

DIRECTOR

Mr M Michell

CHIEF FINANCIAL OFFICER

Ms A Puoane

POSTAL ADDRESS

Private Bag X115

Pretoria 0001

South Africa

PHYSICAL ADDRESS

240 Vermeulen Street

Pretoria 0002

South Africa

TELEPHONE

+27 12 309 9200

FAX

+27 12 309 9491

WEBSITE

www.fic.gov.za

BANKERS

Standard Bank

2

ACCOUNTING AUTHORITY’S STATEMENT

The Financial Intelligence Centre has been operating for five years. The process to build the Centre

started slowly, with the two years immediately after its establishment having consisted primarily

of developing a framework and procedures for its operations. Since then the pace has quickened

sharply.

The Centre has now received a total of 90,067 suspicious transaction reports, and the process of

referrals to the law enforcement authorities has become more efficient with an increasing number of

referrals made each year. There are also very positive signs of the extent to which the referrals are

being used in investigations to track the proceeds of crime.

The analysis of suspicious transaction reports and making referrals to the law enforcement authorities

for investigation remains only part of the Centre’s work. The Compliance and Prevention Department,

working closely with the various supervisory bodies, closely monitors compliance with the Financial

Intelligence Centre Act (FIC Act). During this past year it undertook a series of 212 joint audit reviews

of businesses and 27 independent audits of post office branches.

The Legal and Policy Department has the responsibility for the administration for the FIC Act,

consistently monitoring policy developments at home and abroad, interpreting the legislation and

liaising with a host of partners in this regard.

The activities of these departments are underpinned and supported by the Corporate Services

department, without which the Centre could not receive its results. Great strides have been made

in capacity-building, the development of the IT system, and oversight of the Centre. Management

is proud of the fact that the Centre has received an unqualified audit report from the Office of the

Auditor-General again this year.

Yet, these nevertheless remain early steps in the journey to create a sustainable and consolidated anti-

money laundering and combating of financing of terrorism (AML/ CFT) system within South Africa.

The Centre itself has the challenging mission which is –

“To establish and maintain an effective policy and compliance framework and operational capacity

to oversee compliance and to provide high quality, timeous financial intelligence for use in the fight

against crime, money laundering and terror financing in order for South Africa to protect the integrity

and stability of its financial system, develop economically and be a responsible global citizen.”

This mission still requires many years of effort to be accomplished.

The FIC Act, as one piece of legislation which interlinks with the Prevention of Organised Crime Act

(POC Act) and the Protection of Constitutional Democracy Against Terrorist and Related Acts Act

Accounting Authority’s Statement

3

(POCDATARA Act), aims to protect South Africa’s financial system, its institutions, the state and our

citizens from being abused by criminals and terrorists and their networks, while seeking to create

tools for law enforcement to more effectively prevent money laundering and financing of terrorism

activities.

The Centre has made great progress in fulfilling its mandate during the past year. This has only been

possible because of the relationships with the many different stakeholders which have grown and

deepened in the past year.

The Centre is happy to report that there has been a noticeable increase in the extent and quality of

the interaction with a growing range of diverse accountable and reporting institutions and businesses.

This has had a positive effect on the compliance environment, while accepting that this area shall

need long-term development before institutions will be fully compliant. There has been a significant

improvement of the relationship with the various supervisory bodies, which are now better able

and equipped to implement their responsibilities with respect to the FIC Act. The Centre and the

law enforcement authorities have continued to work well during the year which has resulted in

further consolidation of the respective relationships and has led to greater efficiency in the sharing of

information for investigative purposes.

Among the achievements for the past financial year and set out in detail in this report, the Centre:

Completed 85 joint inspections for FIC Act non-compliance together with the relevant

supervisory bodies for casinos and bookmakers, estate agents, authorised dealers in foreign

exchange, insurance companies, financial service providers, collective investment scheme

managers, members of the JSE and branches of the Post Office bank; Issued Guidance Note 4 providing clarification for accountable institutions on suspicious

transactions reporting; Continued to hold feedback sessions with accountable institutions, supervisory bodies and

law enforcement authorities; Received 24,580 suspicious transaction reports during the 2007/08 financial year and made

999 referrals to the law enforcement authorities for investigation worth in excess of R2 billion

as part of its responsibility to capture, analyse and refer reports; Secured the first convictions for non-compliance of the Financial Intelligence Centre Act in the

matter of the State vs Maddock; Initiated research to identify trends and reporting and to eventually enable the Centre to issue

regular typologies reports; Issued the draft FIC Act Amendment Bill and completed preparations for Parliament to consider

the Bill; Completed the detailed design and specification identification for the development of the

Centre’s new IT system in preparation for the process to build the new IT system;

Accounting Authority’s Statement

4Accounting Authority’s Statement

Completed the first step of the move away from the National Treasury buildings to the Centre’s

new premises; Continued to develop close working relationships with the various supervisory bodies enabling

the transference of knowledge to the different industry sectors and the skills determine

compliance in terms of the FIC Act; Strengthened working relations with the various law enforcement authorities and liaised

closely in order to ensure greater use of the Centre’s information for investigations; Finalised preparations to deploy an official from the Centre to work in the Secretariat of the

Eastern and Southern Africa Anti-Money Laundering Group; Prepared for the mutual evaluation of South Africa by the FATF and ESAAMLG; by interacting

with various counterparts across government and facilitating workshops; Completed preparations to re-locate the IT and Analysis sections of the Centre to new

premises; Continued to recruit staff to the positions created within the establishment as well as

introduced various talent management processes to ensure that the Centre is able to maximise

its potential to retain skilled and enthusiastic staff; and Received an unqualified audit from the Office of the Auditor-General for the 2007/2008

financial year.

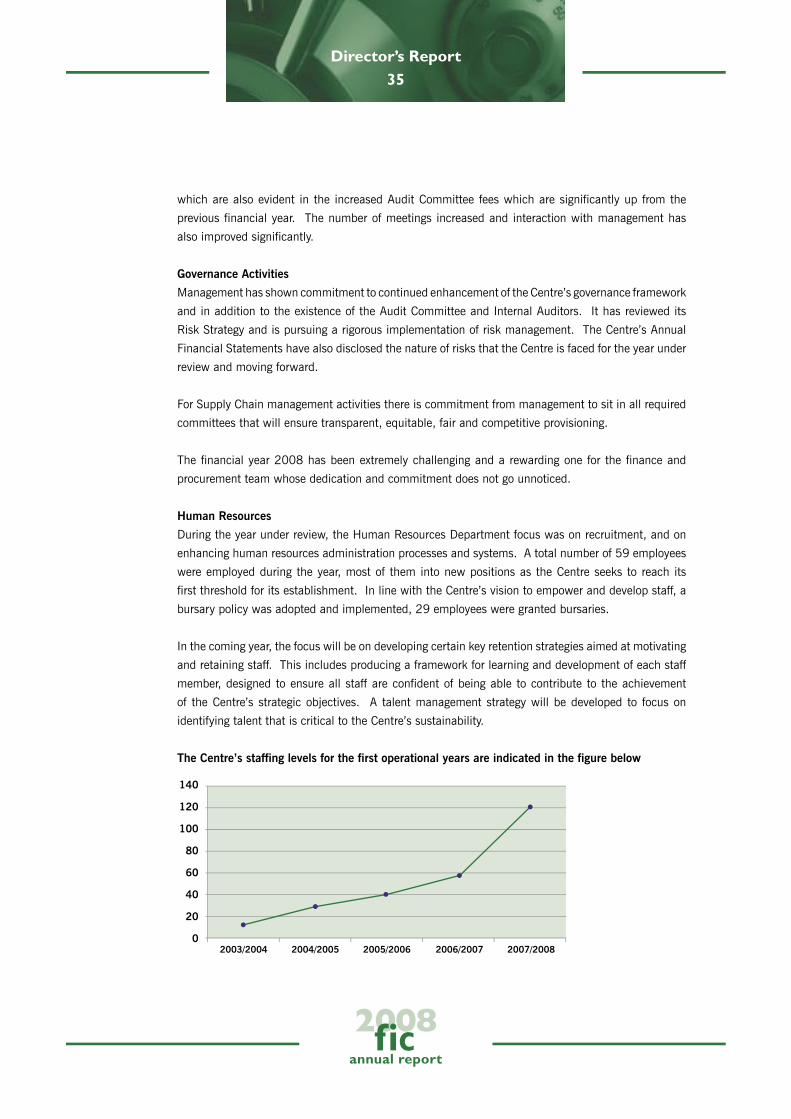

The Centre’s staff complement has grown during the year and will continue to do so until it reaches

the threshold of the first stage in its development. All of the Centre’s staff have demonstrated their

focus on the objectives and have done everything and more to achieve the targets set for it. I want

to recognise their contribution and the many hours of overtime worked and extra effort made and to

indicate my deep appreciation for their efforts and commitment.

I want to express my deep appreciation for the support and assistance provided to the Centre and

to me over the past five years by the Director-General, Lesetja Kganyago, and all officials from the

National Treasury. They have always gone out of their way to assist me and the Centre, thereby

ensuring that we have been able to carry out our work and that the Centre achieves its targets year

after year. In particular I wish to thank the members of the National Treasury’s Technical Assistance

Unit for their special efforts of assistance.

The members of the Centre’s Audit Committee under the stewardship of its Chairperson, Mr Clive

Kneale, have provided the Centre and management with oversight and guidance during the past year,

keeping us focused and on track. This has made a very big difference to our efforts and is warmly

appreciated by all the Centre’s management and staff.

I want also to thank the Deputy Minister of Finance, Mr Jabu Moleketi, MP for his support of the

Centre and its work previously and during the past year.

I wish to reserve a particular word of gratitude to the Minister of Finance, Mr Trevor Manuel, MP,

for the consistency of his guidance and encouragement since the inception of the Centre. He has

5

been a tough taskmaster who has always set the high of standards for me and everyone working in

the Centre. He has concerned himself with our work, raised concerns when necessary, and always

ensured we remain focused on our objectives.

Murray Michell

Director

8 August 2008

Accounting Authority’s Statement

6Acronyms Used

ACRONYMS USED

ADLA Authorised Dealer in Foreign Exchange with Limited Authority

AFU Asset Forfeiture Unit

AML/ CFT Anti-Money Laundering/ Combating of Financing of Terrorism

BSD Banking Supervision Department of the South African Reserve Bank

CENTRE Financial Intelligence Centre, as established under the FIC Act

CIPRO Companies and Intellectual Property Registration Office

DSO Directorate of Special Operations

EAAB Estate Agency Affairs Board

Egmont Group Organisation of financial intelligence units from 108 different countries

ESAAMLG Eastern and Southern Africa Anti-Money Laundering Group 1

FATF Financial Action Task Force 2

FIC Act Financial Intelligence Centre Act, Act No. 38 of 2001

FIC Financial Intelligence Centre, as established under the FIC Act

FIU Financial Intelligence Unit

FSB Financial Services Board

FSRB FATF-Style Regional Body

IRBA Independent Regulatory Board of Auditors

MOU Memorandum of Understanding

NGB National Gambling Board

PLA Provincial Licensing Authorities

POCA Prevention Of Organised Crime Act, Act No. 121 of 1998

POCDATARA Protection Of Constitutional Democracy Against Terrorist and Related Activities

Act, Act No. 33 of 2004

SAPS South African Police Service

SARS South African Revenue Service

SCCU Special Commercial Crimes Unit

STR Suspicious Transaction Report

1 ESAAMLG comprises of the following 14 Member States, namely: the Republics of Botswana; Kenya; Malawi; Mozambique; Mauritius; Namibia; South Africa; Seychelles; Tanzania; Uganda; Zambia and Zimbabwe; and the Kingdom’s of Lesotho and Swaziland.

2 The FATF comprises the following members: Argentina; Australia; Austria; Belgium; Brazil; Canada; China; Denmark; European Commission; Finland; France; Germany; Greece; Gulf Co-operation Council; Hong Kong, China; Iceland; Ireland; Italy; Japan; Kingdom of the Netherlands*; Luxembourg; Mexico; New Zealand; Norway; Portugal; Russian Federation; Singapore; South Africa;

Director’s Report

annual report

2008fic

7

Director’s Report8

DIRECTOR’S REPORT

BACKGROUNDIntroduction

The systems to combat money laundering and terror financing in South Africa remain relatively

young. The implementation of legislation against money laundering gained momentum with the

commencement in 2002 of the Financial Intelligence Centre Act, of 2001 and the development of the

Financial Intelligence Centre as an institution. The framework for the combating of terror financing is

even more recent with legislation in this regard commencing in May 2005.

South Africa has developed a comprehensive legal structure to combat money laundering and financing

of terrorism. The main statutes are the Prevention of Organised Crime Act, 1998 and the Financial

Intelligence Centre Act, 2001. The current provisions dealing with the manipulation of the proceeds

from unlawful activities are contained in the Prevention of Organised Crime Act. This Act contains

three offences which combine to criminalise a wide range of money laundering activities. These are

the offences of money laundering, assisting another to benefit from the proceeds of crime and of

acquisition, possession or use of such proceeds. These provisions came into force in January 1999.

The Financial Intelligence Centre Act, 2001 (the FIC Act) 3 has as its principle objective establishment

of the Financial Intelligence Centre for it to assist in the identification of the proceeds of unlawful

activities and the combating of money laundering activities and more recently, the financing of terrorist

and related activities. The FIC Act also introduces a regulatory framework of measures concerning

client identification, record-keeping, reporting of information and internal compliance structures which

apply to a broad range of financial and non-financial institutions as well as defines the anti-money

laundering responsibilities of supervisory bodies.

Terror financing is criminalised broadly in the Protection of Constitutional Democracy against Terrorist

And Related Activities Act of 2004. This Act criminalises acts of terrorism, as well as a range of

activities specified in Conventions of the United Nations on matters such as hostage taking, threatening

the safety of civil aviation and terrorist bombings, for example.

South Africa also has a structure for recovery of the proceeds of criminal activity that is close to the

height of the evolutionary scale of proceeds of crime models. The South African model comprises

of a conviction-based confiscation procedure as well as a so-called civil forfeiture procedure without

requiring a conviction.

3 All countries are required to set up a financial intelligence unit as set out in Recommendation 26 of the Financial Action Task Force: “Countries should establish an FIU that serves as a national centre for receiving (and if permitted, requesting), analysing, and disseminating disclosures of STR and other relevant information concerning suspected ML or FT activities. The FIU can be established either as an independent governmental authority or within an existing authority or authorities”.

Director’s Report9

In addition, South Africa has developed a regulatory framework of measures concerning client

identification, record-keeping, reporting of information and internal compliance structures which apply

to a broad range of financial and non-financial institutions through the provisions of the Financial

Intelligence Centre Act, 2001.

Over the past five years South Africa has been involved in a process of developing and bedding

down the structures to give effect to the measures referred to above, such as the development of the

Financial Intelligence Centre and the capacity to investigate and prosecute money laundering cases

as well as to oversee compliance with regulatory measures.

The Republic of South Africa held its first democratic, post-apartheid elections in April 1994. The

institutions of state, as well as within the private sector, have been undergoing a rigorous process of

transformation. This process introduced certain additional vulnerabilities, leaving them open to be

exploited by criminal elements. Thus it was important for Government that there should be a parallel

process to protect the institutions and the system as a whole from crime as government set policies to

reintegrate South Africa’s economy, and more specifically, its financial sector, into the global systems

of trade and finance after years of sanctions and marginalisation. The introduction of anti-money

laundering legislation was a vital component of this process at the time, to be bolstered by anti-terror

financing legislation a short while later.

However, while the process to protect the institutions was underway, a complementary, seemingly

contradictory process, was also at play.

Financial Sector Charter

According to a government-commissioned survey, in 2006 at least 49% of the total adult population

in South Africa was “unbanked”. These people were excluded from formal financial services and

without a bank account or formally excluded from credit. The survey indicated that of those without

access to banking services, 99% were black people, 49% lived in rural areas and 55% were women.

On the one hand there was a danger that the gains of the democratic transition could pass this large

grouping of people by completely, while on the other hand it was important to effect a shift from a

cash-based economy to an economy in which large sections of the population had deep roots in the

formal financial services sector.

The Financial Sector Charter was launched in November 2003, signaling a key milestone in the

transformation of the financial sector and embodies an agreement among the major financial institutions

(such as banks, insurance companies, brokers and exchanges) on a set of service provisions and

empowerment targets. The goal was for the Charter to seek by 2008 to include an additional 8 million

clients (or 80% of people in the Living Standard Measure (LSM) 1 - 5

4) to the existing base of clients

4 The poorest 60% of the population

Director’s Report10

in the financial sector, taking the total number to in excess of 21 million clients. The Charter seeks

to ensure the broad-based transformation of the sector, based on the following elements: human-

resource development (HRD), procurement and enterprise development, access to financial services,

empowerment financing, ownership, control and corporate social investment.

The importance of this policy objective led to the introduction of an exemption to the FIC Act, thereby

enabling banks to offer a set of services to people who had not previously been banked and whose

income and transaction capacity meant they could be regarded as low-risk clients to the bank.

Importantly, in order to open an account the customer only needed to produce a South African

identity document, without having also to show a utility bill. This provision required that the banks

closely monitor these accounts and ensure that the defined, low-level thresholds do not get exceeded.

If this were to happen then the account must be frozen until the account holder had represented

him-or herself to be identified to the usual requirements. With these controls in place, the new

banking product, called the Mzansi account, was introduced by the major South African banks and

the PostBank on 25th October 2004. By the end of the financial year, Mzansi had led to the creation

of nearly 4 million new bank account holders.

The Financial Intelligence Centre

The Financial Intelligence Centre (the Centre) was established in terms of Section 2 of the Financial

Intelligence Centre Act, 2001 (the FIC Act) 5. The principle objective of the Centre is to assist in the

identification of the proceeds of unlawful activities and the combating of money laundering activities

and the financing of terrorist and related activities. But it does this as an integrated part of a complex

system involving a wide range of different government and business partners.

Other objectives of the Centre include that it: Make information collected by it available to investigating authorities, the intelligence services

and the South African Revenue Service to facilitate the administration and enforcement of the

laws of the Republic; and Exchange information with similar bodies in other countries regarding money laundering

activities and similar offences.

In terms of section 4 of FIC Act the Centre must perform the following functions in order to

achieve its objectives: Process, analyse and interpret information disclosed to it; Inform, advise and co-operate with investigating authorities, supervisory bodies, the South

African Revenue Service and the intelligence services;

5 All countries are required to set up a financial intelligence unit as set out in Recommendation 26 of the Financial Action Task Force: “Countries should establish an FIU that serves as a national centre for receiving (and if permitted, requesting), analysing, and disseminating disclosures of STR and other relevant information concerning suspected ML or FT activities. The FIU can be established either as an independent governmental authority or within an existing authority or authorities”.

Director’s Report11

Monitor and give guidance to accountable institutions, supervisory bodies and other persons

regarding the performance by them of their duties and their compliance with the provisions of

the FIC Act; and Retain all information received pursuant to compliance with the provisions of the FIC Act.

If the Financial Intelligence Centre Act defined a number of specific objectives for the Centre, the long-

term outcome Government anticipated was that the Centre will contribute to the country’s efforts to

ensure that its financial system has integrity, has stability and that the economy is able to develop to

its full potential, freeing its people from poverty and the legacy of apartheid. Obviously a single piece

of legislation cannot do this, which is why the Anti-Money Laundering and Combating of Financing of

Terrorism (AML/ CFT) system requires that there should be the integration and alignment of several

other laws and processes for it to become successful.

For this to be realised, all those individuals and entities involved in money laundering or terror financing

would need to be successfully prosecuted and that the country could say with confidence that it is

free of these crimes. The role of the Centre is to ensure that the information it is able to provide to

law enforcement authorities is used in a non-partisan manner and for use in cases that can have

high-impact through their successful prosecution. This will require a high degree of compliance and

accountability from all those businesses which are required to implement the provisions of the anti-

money laundering laws as well as report to the Centre. This degree of compliance will be an indication

of the extent to which systemic prevention has been entrenched within the business community.

This requires that the Centre’s mandate and responsibilities are understood by all its partners and

stakeholders. Moreover, business and the general public should be aware of money laundering and

terror financing threats and understand why certain measures are needed to reduce the threats. An

important element of this, which is also a demonstration of compliance, will be for business to ensure that

generally it has systems and capacity to administer its compliance obligations while being able to report

to the Centre. On the other hand, the Centre will need to demonstrate to the law enforcement authorities

that its information is relevant and of high quality and can make a difference to their investigations.

Table 1: The anticipated outcomes from the introduction of South Africa’s AML/ CFT system

RSA financial system has integrity and is stable and the economy develops

Those involved in ML / TF are successfully prosecuted RSA is free of ML / TF

The Centre’s Intelligence is used in non-partisan enforcement in high profile and high impact AML/ CTF cases (Use of Centre outputs)

Responsible, accountable and reporting institutions and businesses comply with AML/ TF requirements (Provision of inputs to the Centre)

Business and the public avoid getting involved in ML/ TF and are not abused by criminals and their networks in this regard (Systematic prevention)

The Centre’s mandate is understood by all the relevant partners

The Law enforcement authorities regard the information from the Centre to be relevant and of high quality

Business and the public are aware of the AML/ CFT vulnerabilities and threats and the need for the prevention thereof

Businesses have the systems and capacity in place to deal with and report on ML/ TF

Director’s Report12

For South Africa’s anti-money laundering and combating of terror financing system to work, a “generic

value chain” is required, which involves the coordinated and integrated efforts from a wide range of

different partners. These roles are dependent on one another.

South Africa’s AML/ CFT Reporting Architecture

For example, the FIC Act requires that various businesses must comply with the relevant laws, and

therefore need to know their customers and report suspicious transactions to the Centre. The Centre

receives these reports and subjects them to scrutiny. If it deems that there is indeed suspicious

transaction activity, a referral is then made to the relevant authorities for investigation and eventual

prosecution. The steps in the process are dependent on one another. The system as a whole cannot

become fully functional or effective if the different component parts do not properly function as a unit

within this chain (refer to Illustration 1).

The Minister of Finance has mandated the Centre to facilitate and enable the development of a system

to comprehensively combat money laundering and the financing of terrorism.

The Centre has been given the responsibility to act as the pivot in the transfer of information, but also

in ensuring that the total, environment or system becomes and remains functional. This requires a

dynamic partnership approach which facilitates interaction between the private and public sectors. It

also requires that the Centre take responsibility, as the “glue”, for ensuring that the system as a whole

is held together. This is part of an all-of-government approach within South Africa.

International Standard - Financial Action Task Force 40+9 Rs

The Centre

Data StorageAnalysisReferralsInsurance

Casino

Bank

Reports

Supe

rvis

ory

Bod

ies

(FSB

, SA

RB

, et

c)M

onito

r C

ompl

ianc

e of

Acc

ount

able

Ins

t’s

Investigations & Prosecutions

Referrals

Accountable Institutions, eg.

SAPS

NPA- DSO- AFU

SARS

Intelligence Agencies

InvestigativeAuthorities &Intelligence

Agencies, eg.

The Centre

Policy &

Country E

val

Awareness

InternationalLinks fiu’s

Sharing

Illustration 1: AML/ CFT Reporting Architecture in South Africa

Director’s Report13

Illustration 2: Value chain for AML/ CFT

The “value chain can be illustrated as in illustration 2, where compliant businesses report to the

Centre before the information is used in eventual prosecutions.

The process draws together and coordinates the results of three critical pieces of legislation: the

Financial Intelligence Act, which creates the establishment of the Centre and imposes obligations

on business (in the form of accountable institutions) while providing investigative tools for law

enforcement authorities; the Prevention of Organised Crime Act (POCA), which criminalises the act

of money laundering and creates a penalty regime; and the Protection of Constitutional Democracy

Against Terrorism and Related Activities Acts (POCDATARA Act), which criminalises the financing of

terrorism and creates obligations on businesses to report such suspicions to the Centre.

This mandate requires that the Centre work across sections of business to facilitate partnership

arrangements with various government departments and agencies. The FIC Act requires that the

Centre has a regulatory oversight of the Supervisory Bodies listed in the schedule to the FIC Act to

ensure that they properly monitor the levels of compliance by accountable institutions.

Of particular importance is that an “all-of-government” system be developed to AML/ CFT, which

typically involves far more than only the law enforcement authorities. Within the AML/ CFT

framework various government departments play an important role in this system. For example, the

National Treasury (with responsibility for financial sector policy and remittance matters), Departments

of Home Affairs (identity issues and immigration), Foreign Affairs (United Nations interactions and

foreign policy matters), Social Development (for overseeing issues pertaining to the functioning of

non-government organisations), Trade and Industry (which has oversight for policy and monitoring

of industry sectors such as gambling and real estate as well as the registration of companies), public

entities (for example the PostBank) and others. This is an approach which is required of all countries

by the Financial Action Task Force (FATF) 6 which sets out a list of standards to be met. These

standards are expressed through a series of “Recommendations”, forty which deal with combating

money laundering and another nine for the financing of terrorism. The so-called “40+9” encourage a

range of partnership arrangements, especially within and between various government departments,

entities and agencies.

Prosecuting authorities take to court for

prosecution

Prosecuting authorities

court for prosecution

Law enforcement authorities conduct

investigations

Law enforcement

conduct investigations

The Centre analyses and refers info toinvestigating

authorities

The Centre analyses and

authorities

The Centre receives reports

The Centre

Business makes

SuspiciousTransaction

Reports to the Centre

Business makes

Reports to the Centre

Business is adequately

supervised and is

compliant with laws

6 South Africa became a member of the Financial Action Task Force in June 2003. It had become a member of the Eastern and Southern Africa Anti-Money Laundering Group (ESAAMLG) in August the previous year.

Director’s Report14

These are all important elements of the system which cannot work properly if they are not attended to.

The Centre has interpreted its legal mandate as a series of strategic objectives in which it seeks to: Assist the investigating authorities, intelligence services and the SARS in the identification of

the proceeds of unlawful activities and the combating of money laundering activities and the

financing of terrorist and related activities;

These objectives, responsibilities and obligations contained in South Africa’s anti-money

laundering and combating of financing of terrorism legislation derive from certain United

Nations Conventions and Security Council Resolutions. The Conventions have been translated by

the Financial Action Task Force (FATF) into a set of globally-accepted standards dealing with the

combating of money laundering and financing of terrorism (40 Recommendations against money

laundering and 9 Special Recommendations against financing of terrorism – the “40+9”). The

FATF is composed of 34 countries and of which South Africa became a member in 2003. Thus

far 176 countries have consented to implement and apply the AML/ CFT standards.

The standards require that all countries implement a range of core measures to give effect to the

standards. These include the need for countries to:

Criminalise, in legislation, money laundering and financing of terrorism; and

Implement administrative preventative measures to be taken by financial institutions and

non-financial businesses and professions. These include rigorous reporting requirements (eg

suspicious transactions; terror finance); customer due diligence (Know Your Customer); record

keeping; staff training; and the appointment of a compliance officer. Sanctions are required for

non-compliance.

Law enforcement authorities must have the legal capacity to investigate and prosecute and other

measures; availability of resources.

A financial intelligence unit (such as the Centre) should be established to act as an intermediary

between the private and public sectors facilitating and enabling various relationships. It should

also be enabled to receive data from the reporting businesses, analyse it and refer the results

of the process to law enforcement for investigation when necessary. The Centre is required to

function independently of interference and be fully resourced.

All countries must ensure that various forms of international cooperation are made possible,

including information sharing between financial intelligence units, mutual legal assistance,

extradition, and various forms of technical assistance, including training and support to other

countries and their AML/ CFT entities.

Box 1: FATF 40+9 Recommendations and Standards

Director’s Report15

Make information collected by it available to these departments and entities to facilitate the

administration and enforcement of the laws of the Republic; and to Exchange information with financial intelligence units in other countries regarding money

laundering activities and similar offences.

These objectives are premised on the Centre’s vision, mission and values.

Mission

To establish and maintain an effective policy and compliance framework and operational capacity

to oversee compliance and to provide high quality, timeous financial intelligence for use in the fight

against crime, money laundering and terror financing in order for South Africa to protect the integrity

and stability of its financial system, develop economically and be a responsible global citizen.

Vision

The Financial Intelligence Centre will strive to be the leading player in the aggressive combating of

money laundering and terror financing to reduce crime for the benefit of South African citizens today

and in the future.

The Centre will earn the trust, respect and support of our stakeholders for the quality of our information,

be recognised for the sustainability of our organisation with the loyalty and achievements of skilled

staff and the success of our efforts.

Values

The values of the Financial Intelligence Centre provide the platform for its future success. The Centre

seeks to ensure that all staff incorporate and utilise these values as a reference for all of their work

and activities. To this end, all of the Centre’s staff will: In the spirit of Ubuntu, demonstrate integrity in everything that we do (with amongst others,

respect, honesty, trust, discipline, humility and loyalty); Demonstrate pride and discipline in our work, accepting accountability and being prepared to

‘go the extra mile’; Strive for excellence and professionalism by effectively making a difference in executing our

mandate by offering solutions, while not presenting problems only; Value individuals and allow space for creativity and growth; Optimise our relationship with stakeholders and partners; and Ensure the security of organisational assets and information.

The Centre makes a serious effort to ensure that these values are continuously integrated into all

aspects of its work.

Director’s Report16

The Centre became operational on 3 February 2003 at which time banks and other reporting

institutions started reporting to the Centre via electronically. All suspicious transaction reports (STRs),

as per the legislation, is received by the Centre in Pretoria which is South Africa’s national centre for

the receiving, analysing and dissemination of information. Every disclosure received by the Centre

undergoes an initial evaluation process and is assessed against internal rules to identify cases which

have possible money laundering and/or terror financing indicators. Once such an instance has been

identified the matter is allocated to an analyst. Thereafter the intelligence cycle is followed to develop

a tactical / strategic intelligence product.

The Centre does not investigate crime. Rather, the information it produces is meant to support the

existing investigative bodies and other role players in the intelligence and criminal justice system.

During the past 2007/08 financial year, the Centre received 24,580 Suspicious Transactions Reports.

This denotes a 15% increase in comparison to the previous year, 2006/07.

The financial sector submitted 22,411 STR reports to the Centre, which comprises 91% of all reports

received, while the non financial sector filed 2 169 such reports, which is 9% of all reports received.

Compared year-on-year the reporting trend appears unchanged. Of the STR reports received from the

financial sector, 62% were received from money remitters while 27% received were from banks.

The Centre also monitors and gives guidance to relevant entities regarding their compliance with

the FIC Act, which it does in terms of section 4(c) of the FIC Act. The Centre issued guidance on

suspicious transaction reporting for accountable institutions and others (Guidance Note 4 of 13

March 2008) on the manner of reporting and the procedures that should be followed when reporting

(see Box 2 below).

The Centre has access to a variety of sources of financial, administrative and law enforcement

information through a number of mechanisms in order to effectively realise its objective of receiving,

analysing, and disseminating valuable financial intelligence. The primary source of financial

intelligence is STR information the Centre obtains from various accountable institutions, businesses

or people with statutory reporting obligations. In this regard section 28A and section 29 of the FIC

Act are applicable.

This guidance note issued by the Financial Intelligence Centre is divided into six parts and

provides guidance as follows:

Part 1 provides information to help persons determine whether they fall within the category of

persons for whom a reporting obligation under section 29 of FICA could arise.

Part 2 provides information to help persons determine when the obligation to report under

section 29 of the FIC Act arises.

Box 2: Guidance Note 4 on Suspicious Transaction Reporting

Director’s Report17

The Centre also has both direct and indirect access, by arrangement, to non-publicly available

databases maintained by certain other government departments or government agencies. In these

instances, the Centre depends on the relevant governmental agency maintaining the database to

extract the required information at the Centre’s request. Having the ability to access these sources of

information ultimately adds value to the analysis product of the Centre and can assist law enforcement

agencies to better focus of their investigations.

Part 3 provides information to help persons understand the nature of a suspicion.

Part 4 provides examples of indicators that may be taken into consideration to determine whether

a transaction should give rise to a suspicion.

Part 5 provides information on the implications of making a report under section 29 of the FIC

Act to the Centre.

Part 6 provides a step-by-step guideline to the use of the internet-based reporting mechanism.

Furthermore, the guidance note provides the following information on the manner in which an

STR should be submitted.

A report under section 29 of the FIC Act must be made by means of internet based reporting

provided by the Centre at: www.fic.gov.za. An STR may not be posted. Only in exceptional cases

may an STR be sent via fax or delivered by hand to the Centre. The reporting form is available

from the Centre or its website: Reporters also have the option of submitting STRs via batch reporting. This method

is utilised when high volumes of STRs are submitted to the Centre on a regular basis.

Reports are submitted in bulk to the following email address: [email protected]. In terms of Regulation 23 of the FIC Act there are certain prescribed particulars that

should be contained in an STR. The following basic information should be contained in

an STR: The person or entity making the report; The transaction that is reported; Any account/s involved in the transaction; The person conducting the transaction or the entity on whose behalf it is

conducted; The representative, if any who is conducting the transaction on behalf of

another; and General information concerning the transaction.

The electronic reporting form consists of eight parts numbered from Part A to Part H. It is

imperative to complete all fields in each part that are applicable to the situation which is reported

such as full names and surname of subject, identity number, passport number, addresses and

similar particulars. Reporters are encouraged to supply as much details as they have available

at all times.

Director’s Report18

The Centre has further direct access to commercial databases that would afford it a variety of

information which offers the Centre access to information pertaining to registered legal entities and

the composition of their governing structures, credit histories of individual and entities, as well as

ownership of property.

Other methods to access information include secondments, Memoranda of Understanding and

information shared with other financial intelligence units via the Egmont secure web. The Centre also

makes use of open sources of information such as internet and the media.

With the ability to access these different types of databases and sources of information, the Centre

is able to produce a balanced product that enables the Law Enforcement Agencies to better focus

on and investigate its targets. The combination of the information from various sources mentioned

above, together with the analysis of STRs and additional documents, enable the Centre to properly

undertake its mandate.

The Centre is therefore entitled to disseminate a broad category of information to domestic authorities

for investigation or action, when the Centre reasonably believes such information is required to

investigate suspected unlawful activity. The Centre is mandated in terms of its objectives under

section 3 of the FIC Act to make information collected by it available to investigating authorities, the

South African Revenue Service and the intelligence agencies.

The FIC Act (section 40) provides for information to be provided either upon the initiative of the Centre

or upon written authority of an authorised officer in these government entities.

The Centre performs analysis on selected STRs before dissemination. The Centre refers a package of

information, which will normally includes the demographical profile of the subject, banking exposure

and transacting pattern with specific reference to any unusual or suspicious transacting, corroborated

with specific examples to this effect. Information referred to domestic authorities therefore includes

the Centre’s analysis and interpretation of the reported information and where possible, substantiated

conclusions regarding possible involvement with certain predicate offences. This is done with the

understanding that information provided should be integrated into the intelligence bases of the

domestic authorities and investigated in line with their respective mandates.

An assumption is often made that every STR which is reported to the Centre automatically leads to

a referral from it to the investigating authorities. This is not the case. Typically, the Centre’s reports

may involve information from a number of STRs reported over time, where there is some underlying

link to the information reported. The possibility even exists that information from a particular STR

may be referred to law enforcement on more than one occasion.

In addition to disseminating self-initiated reports to domestic law enforcement authorities, the Centre

also supplies information drawn from STR’s to law enforcement upon request from a particular

Director’s Report19

agency. Normally this information is required to be used in a pending investigation. All requests

must be made by an appointed Authorised Officer so that the legal obligations are met and to ensure

integrity of the requesting process. The Centre is kept informed of the current Authorised Officers in

the domestic authorities and provides training to them to ensure that the integrity of information is

maintained even during the investigation stage.

The Centre is created as a statutory body with legal personality and operates outside the public

service but within the public administration, as envisaged in section 195 of the Constitution of the

Republic of South Africa, 1996 . It is registered as a section 3(a) entity in terms of the Public Finance

Management Act.

This status enables the Centre (as per section 5 of the FIC Act) to develop its own policies and

frameworks, such as remuneration and determine its staffing and skills requirements.

The Director, who is the accounting authority for the Centre, reports directly to the Minister of Finance

and to Parliament for the performance of the Centre. The Director of the Centre has the authority

to take all decisions of the Centre in the exercise of its powers and the performance of its functions.

The Director shall however perform these functions subject to any policy framework which may

be prescribed by the Minister. Consequently the Centre only provides strategic information to the

Minister and policy makers.

The sources of the Centre’s funds are restricted by law to money appropriated annually by Parliament

for the purposes of the Centre, any government grants made to it and any other money legally acquired

by it. The Centre may accept donations only with the prior written approval of the Minister.

The Centre is not an investigative agency and does not form part of any of the local law enforcement

agencies or the domestic intelligence community.

The Centre’s reputation depends on the integrity, accuracy and reliability of the information it receives

and that which it disseminates. It has therefore put in place a number of risk mitigating measures to

guard against violations of information integrity.

Dissemination of information is legislated in section 40 of the FIC Act. It provides for the dissemination

of information to investigating authorities, the South African Revenue Service and intelligence services.

It also provides for the dissemination of information to entities outside the Republic which performs

similar function as to those of the Centre.

It also clearly stipulates who is entitled to request information from the Centre and defines the

requirements to access information from the Centre.

To ensure that the Centre disseminates information in accordance with the relevant legal provisions,

referrals of information must be approved by the Director or a designated Senior Official of the Centre

Director’s Report20

and be collected by an authorised officer of the recipient agency. This is a controlled process where

the authorised officer has to formally acknowledge receipt of the product. Another mode of delivery is

the secure Egmont website which enables information exchange amongst the Egmont members.

The Centre releases information, including the Annual Report, which is published on the Centre’s

website at www.fic.gov.za. The Annual Reports contain information on the following: The number of requests received from local and international stakeholders; The number of STRs received from accountable institutions; and The number of referrals disseminated to various domestic authorities.

The Centre’s Annual Report is another valuable source of feedback to accountable institutions.

The Centre also conducts stakeholder feedback sessions with various stakeholders to discuss past

activities, challenges and successes, emerging trends and typologies, with a view to improving their

anti-money laundering efforts and future cooperation. In addition the Centre provides public feedback

by means of an electronic query facility. Members of the public can make enquiries relating to the

FIC Act and the Centre via the Centre’s website. A response is forwarded within five (5) days of the

initial query. During this financial year the Centre responded to 368 queries.

The Centre became a member of the Egmont Group of Financial Intelligence Units in 2003. In

doing so the Centre agreed to the adherence of the principles laid out in the Egmont Group Charter.

The Centre supports the widest possible co-operation and exchange of information amongst Egmont

members. This is done on the basis of reciprocity or mutual agreement and following the rules

established in the Egmont Principles of Information Exchange. To give effect the above, the Centre

promotes: free exchange of information for purposes of analysis at FIU level; no dissemination or use

of the information for any other purpose without prior consent of the providing FIU; and protection of

the confidentiality of the information. Furthermore the Centre’s decision to exchange information is

not affected by the status of other FIU’s.

The Centre is steadily increasing the number of Memoranda of Understanding that it has with its

FIU counterparts within Egmont. In addition to the sharing of information with Egmont Group

members, the Centre has also entered into agreements on the sharing of information with the financial

intelligence unit of Zimbabwe, which is not an Egmont member. As more FIUs are established in the

region, so the Centre is likely to develop the ability to cooperate with them and sign agreements for

the exchange of information.

Communication between the Centre and other countries takes place directly via the Egmont Secure

Web without the interference of any intermediary bodies. Requests from counterpart FIU’s are dealt

with in the same manner as a domestic disclosure, but as a matter of higher priority. All international

requests are submitted in compliance with the Principles for Information Exchange that have been set

out by the Egmont Group, considering provisions of information sharing arrangements as set out in

agreements amongst the Centre and other FIU’s.

Director’s Report21

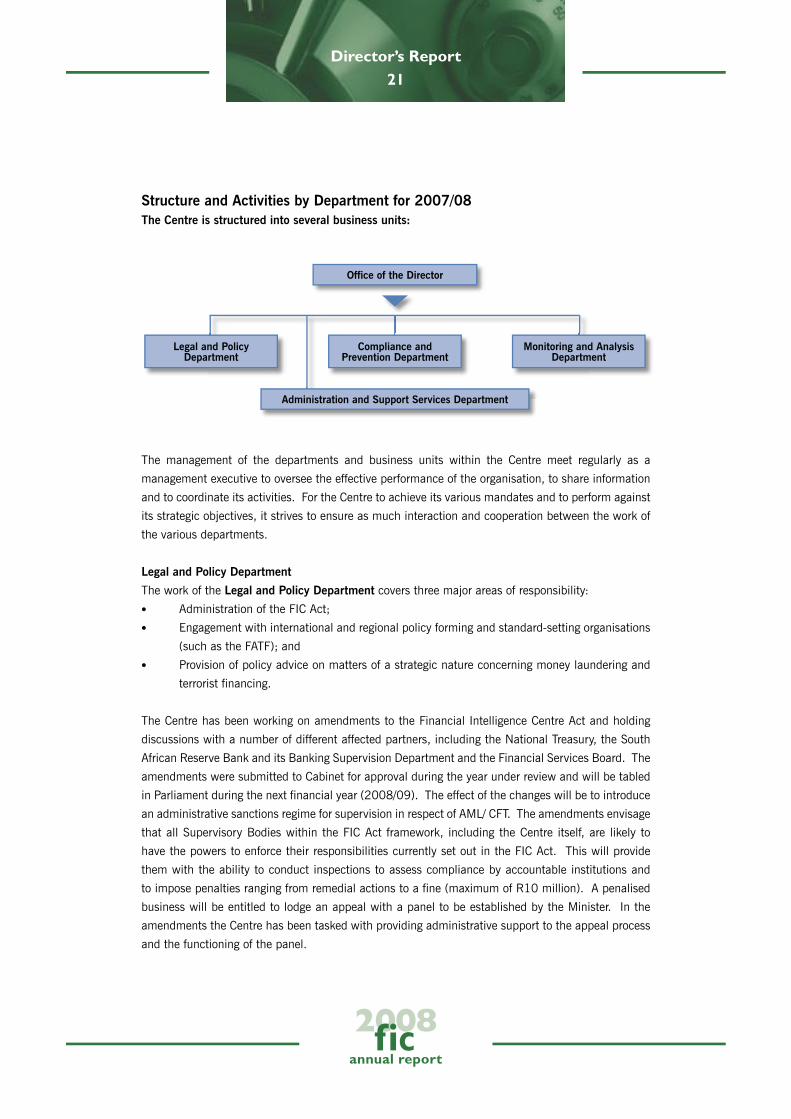

Structure and Activities by Department for 2007/08The Centre is structured into several business units:

The management of the departments and business units within the Centre meet regularly as a

management executive to oversee the effective performance of the organisation, to share information

and to coordinate its activities. For the Centre to achieve its various mandates and to perform against

its strategic objectives, it strives to ensure as much interaction and cooperation between the work of

the various departments.

Legal and Policy Department

The work of the Legal and Policy Department covers three major areas of responsibility: Administration of the FIC Act; Engagement with international and regional policy forming and standard-setting organisations

(such as the FATF); and Provision of policy advice on matters of a strategic nature concerning money laundering and

terrorist financing.

The Centre has been working on amendments to the Financial Intelligence Centre Act and holding

discussions with a number of different affected partners, including the National Treasury, the South

African Reserve Bank and its Banking Supervision Department and the Financial Services Board. The

amendments were submitted to Cabinet for approval during the year under review and will be tabled

in Parliament during the next financial year (2008/09). The effect of the changes will be to introduce

an administrative sanctions regime for supervision in respect of AML/ CFT. The amendments envisage

that all Supervisory Bodies within the FIC Act framework, including the Centre itself, are likely to

have the powers to enforce their responsibilities currently set out in the FIC Act. This will provide

them with the ability to conduct inspections to assess compliance by accountable institutions and

to impose penalties ranging from remedial actions to a fine (maximum of R10 million). A penalised

business will be entitled to lodge an appeal with a panel to be established by the Minister. In the

amendments the Centre has been tasked with providing administrative support to the appeal process

and the functioning of the panel.

Office of the Director

Legal and Policy Department

Compliance and Prevention Department

Monitoring and Analysis Department

Administration and Support Services Department

Director’s Report22

Consultations in respect of the amendment of the Schedules were held with six Provincial Licensing

Authorities: the Gambling Boards for the Free State, Western Cape, Mpumalanga, North West, Kwa-

Zulu/Natal and Limpopo provinces. Discussions were held with the South African Reserve Bank on

the way forward in respect of amending the reference to the SARB in Schedule 2 of the Act in order to

clarify and make more specific the responsibilities of the different departments within the SARB that

have a role within the national AML/ CFT framework. Meetings were also held between the Centre

and the following stakeholders in respect of the process to amend the Schedules: the Land Bank; the

Independent Regulatory Board of Auditors; and the Department of Trade and Industry (in respect of

the Estate Agency Affairs Board’s role as a supervisory body).

The Legal and Policy Department has continued to coordinate the Centre’s involvement with the FATF

and the ESAAMLG and has facilitated its involvement in various meetings. Officials from the Centre

attended the three FATF plenary meetings held annually (in June 2007, October 2007 and February

2008). In addition, an inter-sessional meeting of the FATF Working Group on Money Laundering and

Terror Financing was attended during May 2007.

The Centre also ensures that all South African delegates to these meetings are properly prepared for

the various discussions to be held at the FATF meetings. Thus it coordinated documented input for

the FATF Working Group on Terrorist Financing and Money Laundering on Special Recommendation

III and for Trade Based Money Laundering in preparation of the June 2008 Plenary meeting. Officials

from the Centre also attended a conference on developing a Risk Based Approach to AML/ CFT.

Members of the Centre participated in the FATF Mutual Evaluations of Canada, as well as the United

Kingdom, both of which required several follow-up meetings.

The Legal and Policy Department also initiated the preparations for the South African Mutual

Evaluation process, which will see an on-site assessment by the FATF and ESAAMLG assessors

in August 2008. South Africa will undergo an assessment (a mutual evaluation) of its system to

combat money laundering and terrorist financing. The objective of the mutual evaluation will be to

assess the adequacy of the South African legal framework to combat money laundering and terrorist

financing, as measured against the international standard of the FATF’s 40 Recommendations on

Money Laundering and 9 Special Recommendations on Terrorist Financing, as well as the effective

implementation of the South African legal framework by its competent authorities.

The Centre has been involved in raising awareness of the evaluation process and the applicable

standards among the South African authorities which will be assessed in the course of the mutual

evaluation process. This also entails assisting those authorities to prepare for their role in the

evaluation process.

A series of preparatory workshops were held during the year to initiate the processes to prepare for

the mutual evaluation and demonstrated a number of deficiencies, particularly the need for greater

Director’s Report23

awareness amongst the authorities of their responsibilities as well as pointed out the need for greater

coordination. In the course of the process reports are made to Cabinet to inform members of progress

being made.

The Legal and Policy Department has also coordinated South Africa’s involvement in the Eastern

and Southern Africa Anti-Money Laundering Group (ESAAMLG) activities. A senior official from the

Department participated in an ongoing process over the year to improve the efficiency of the ESAAMLG

Secretariat and assisted with the compilation of a typology questionnaire on a cash courier project.

Preparations have been made to deploy an official from the Centre to the ESAAMLG Secretariat during

the forthcoming year.

Officials from the Centre accompanied the Deputy Minister of Finance to the 7th ESAAMLG Council of

Ministers meeting held in Gaborone, Botswana in August 2007 and participated in the March 2008

ESAAMLG Task Force meetings of Senior Officials which were held in Dar-es-Salaam, Tanzania.

The Legal and Policy Department coordinated the Centre’s activities to provide technical assistance

to countries of the region during the year. This involved assistance to the Ministry of Finance in

Mozambique in the setting up of its Financial Intelligence Unit and included training workshops and

signing of a Memorandum of Understanding with the Mozambique Department of Finance.

Other technical assistance also took place during the year: a presentation was delivered on “Financial

Analysis and Dissemination of Information” for a financial intelligence unit capacity-building workshop

which took place in Botswana in February 2008. The Centre also hosted visits for delegations

from Mozambique, Lesotho, Malawi, Tanzania and Namibia at different times during the year, which

included workshops and training on various matters of establishing a financial intelligence unit as well

as on the roll-out of AML/ CFT legislation.

An official from the Centre presented a part of the IMF assessment report on Mauritius’s AML/ CFT

system to the ESAAMLG Plenary meeting in August last year, while another participated in conducting

the Mutual Evaluation of Seychelles.

Compliance and Prevention Department

The work of the Compliance and Prevention Department is to focus on compliance oversight of

the FIC Act. A core function is to inform, advise and collaborate with the supervisory bodies to

ensure their effective supervision of compliance. Another function is to liaise with accountable and

reporting institutions to assist them in applying and implementing the compliance provisions within

their respective institutions. The preventative focus includes a strong public awareness outlook for

the general public, the issuance of guidance notes for accountable institutions and the provision of

compliance training on FIC Act obligations to affected entities. The work of this department requires

a close liaison with our colleagues inside the Centre on compliance-related issues and externally with

the supervisory bodies and accountable institutions.

Director’s Report24

During the period the Compliance and Prevention Department formulated guidance in draft form in

several areas, which guidance will be finalised in the next financial year. The draft guidance under

preparation include guidance related to the casino industry, estate agents, and know-your-customer

requirements for non-banking financial institutions. The Guidance Note on suspicious transaction

reporting by accountable institutions was published in the government gazette on 13 March 2008.

The Compliance and Prevention Department has also been at the forefront of developing a framework

to implement a risk-sensitive approach to AML/ CFT compliance in the South African regulatory

environment. Such an approach is nearly complete and, after interaction with the FATF to ensure

that global standards and approaches are being complied with, there will be engagement with various

institutions to ensure industry is involved in the process. In this regard, the head of the department

was invited to attend and chair a sector working group at the FATF Private-Public sector industry on

the risk-based approach in Berne, Switzerland, on 11 December 2007.

The Department has also developed an implementation framework for the FIC Act amendments

which provides for the Centre’s capacity requirements and budget. It is also developing an approach

to ensure the inspectorate process is accompanied by rigorous procedures and manuals and that the

process can withstand rigorous legal scrutiny.

The relationship between the Centre and the various supervisory bodies has been steadily strengthened

and there is a growing cooperation and sharing of information between them. These include the

Estate Agency Affairs Board, the National Gambling Board, the Banking Supervision Department of

the Reserve Bank, Law Society of South Africa, the Companies and Intellectual Property Registration

Office, the Financial Services Board and the JSE Exchange.

In the process of these interactions this year, the Compliance and Prevention Department has

facilitated for the Centre to sign Memoranda of Understanding with the National Gambling Board,

Estate Agency Affairs Board, the Independent Regulatory Board of Auditors and the Companies and

Intellectual Property Registration Office. These MOU’s set out the basis for cooperation and the

shared responsibilities between the different parties.

The Compliance and Prevention Department has been involved in ongoing interactions with various

supervisory bodies, including the conduct of on-site joint compliance reviews over the past three

years, as reflected in the table and graph below. They show that the monitoring of compliance has

increased significantly in the year under review

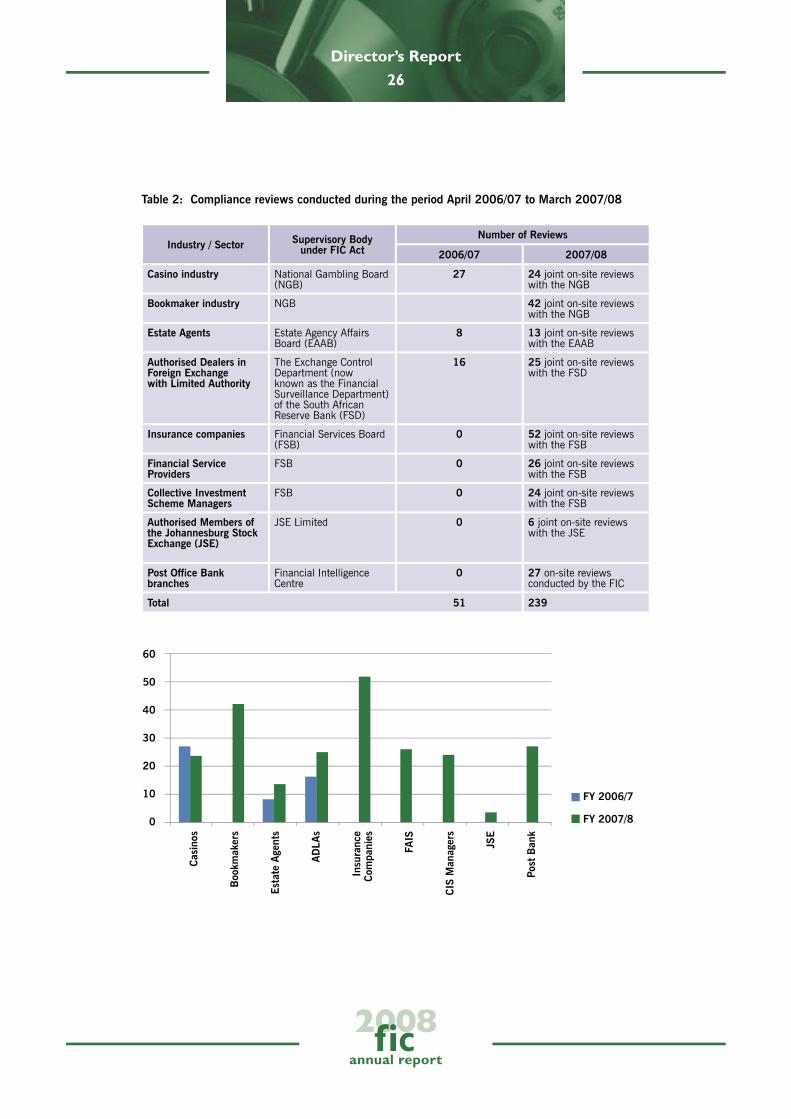

In the period under review, the Compliance and Prevention Department conducted a series of joint

audits for FIC Act non-compliance with several supervisory bodies, These include 24 on-site visits to

casinos together with the National Gambling Board and visits to 42 bookmakers. The department

conducted 13 reviews of estate agents together with the Estate Agency Affairs Board, while it

conducted 25 joint reviews with the Exchange Control Department of the South African Reserve Bank

of Authorised Dealers in foreign exchange with limited authority (ADLAs).

Director’s Report25

In addition, together with the Financial Services Board, the Compliance and Prevention Department

conducted joint on-site reviews for FIC Act non-compliance of 52 insurance companies, 26 financial

service providers, and 24 collective investment scheme managers, as well as 6 on-site visits of JSE

members.

With the consent of the Post Office bank, the Compliance and Prevention Department conducted

independent on-site audits of 27 Postbank branches across Gauteng province.

While these joint audits were being undertaken, the Banking Supervision Department of the South

African Reserve Bank had independently consolidated its process to monitor AML/ CFT compliance

matters amongst the country’s banks. This process has led to regular meetings between the Centre

and the BSD to report on progress and share information. The Centre uses these meetings as a

platform to provide the BSD with information regarding the reporting by banks to the Centre and an

assessment of the quality of such reports.

The general comment is that there is a broad measure of compliance across all sectors which has

resulted in “partially compliant findings”. The identified areas for remedial action by accountable

institutions will now be monitored by the lead supervisory bodies and supported on request by the

Compliance and Prevention Department.

As a result of many of the on-site visits, the Centre has conducted a series of compliance remedial

training sessions. For example, the Compliance and Prevention Department provided remedial

training to bookmakers in Mpumalanga, Free State and North West provinces; it conducted training

programmes at 10 imbizos held by the Estate Agency Affairs Board held around the country and a

national group of estate agents; training of collective insurance schemes managers; and a workshop

of attorneys in NorthWest Province. These sessions were accompanied by presentations made to

various workshops and conferences.

It was agreed by all supervisory bodies that the joint on-site review process of accountable institutions

by the relevant supervisory body and the Centre, as represented by its Compliance and Prevention

Department, will continue for the foreseeable future. The value derived is not only in the findings

themselves, but in the development of inspection expertise, the sharing of AML/ CFT knowledge and

the sharing of information by the individual assessors. The Centre believes the process of joint audits

or inspections continues to create a solid platform for the period after the FIC Act Amendment Bill

process has been completed and the new responsibilities take effect. At that stage the supervisory

bodies will be expected to have their own capacity to conduct compliance inspections.

Table 2 overleaf reflects the growing involvement of the joint on-site review process and the firming

of the partnership between a supervisory body and the Centre to together make South Africa a more

compliant nation in the area of AML/ CFT compliance.

Director’s Report26

Industry / Sector Supervisory Bodyunder FIC Act

Number of Reviews

2006/07 2007/08

Casino industry National Gambling Board (NGB)

27 24 joint on-site reviews with the NGB

Bookmaker industry NGB 42 joint on-site reviews with the NGB

Estate Agents Estate Agency Affairs Board (EAAB)

8 13 joint on-site reviews with the EAAB

Authorised Dealers in Foreign Exchangewith Limited Authority

The Exchange Control Department (now known as the Financial Surveillance Department) of the South African Reserve Bank (FSD)

16 25 joint on-site reviews with the FSD

Insurance companies Financial Services Board (FSB)

0 52 joint on-site reviews with the FSB

Financial Service Providers

FSB 0 26 joint on-site reviews with the FSB

Collective Investment Scheme Managers

FSB 0 24 joint on-site reviews with the FSB

Authorised Members of the Johannesburg Stock Exchange (JSE)

JSE Limited 0 6 joint on-site reviews with the JSE

Post Office Bank branches

Financial Intelligence Centre

0 27 on-site reviews conducted by the FIC

Total 51 239

Table 2: Compliance reviews conducted during the period April 2006/07 to March 2007/08

FY 2006/7

FY 2007/8

60

50

40

30

20

10

0

Cas

inos

Boo

kmak

ers

Est

ate

Age

nts

AD

LAs

Insu

ranc

e C

ompa

nies

FAIS

CIS

Man

ager

s

JSE

Post

Ban

k

Director’s Report27

The Compliance and Prevention Department has also met with the Pretoria Masters Office on matters

involving access to deeds registers. The Department has met with or interacted with thirty-eight of

the country’s banks.

The Centre commented on and advised the Minister of Finance on matters affecting AML/ CFT

policy and the implementation thereof and provided him with several briefing notes. It also advised

the National Treasury on the impact of the draft Cooperative Banks Bill on the FIC Act and the

Department of Trade and Industry on the National Gambling Act amendments and the interpretation

of the customer due diligence requirements in respect of suretyship arrangements, as well as the

Department of Foreign Affairs in its interactions with its country counterparts.

The Centre is pleased to report on the following successful prosecution involving an accountable

institution for non-compliance under the FICA.

State v Maddock Inc (accused 1) and Graham Allen Maddock (accused 2)

Accused 1 – Maddock Inc.

Count 105: Failure to identify persons in contravention of section 46(1) read with section 21

of the FIC Act.

Count 106: Failure to keep records in contravention of section 47(a) read with section 22 of

the FIC Act.

Count 107: Failure to formulate and implement internal rules in contravention of section 61

read with section 42(1), 42(2) and 42(3) of the FIC Act.

Count 108: Failure to provide training in contravention of section 62(a) read with section 43(a)

of the FIC Act.

Count 109: Failure to appoint a compliance officer in contravention of section 62(b) read with

section 43(b) of the FIC Act.

Penalty received in relation to Count 105 to 109: a fine of R10 Million wholly suspended for 5

years.

Accused 2 – Graham Allen Maddock

Count 54 to 103: failure to report suspicious and unusual transactions in contravention of

section 52 read with section 29 of the FIC Act

Penalty received in relation to Count 54 to 103: six years imprisonment of which three years’

imprisonment is suspended for five years.

Box 3: First successful prosecution: FIC Act non-compliance charges

Director’s Report28

The Centre was also involved in clarifying the relationship between it the investigating authorities and

the Special Commercial Crimes Courts which prosecutes various forms of commercial crime and the

Centre, attended a workshop with SCCU involving about 50 delegates. The department was part of

the workshop preparation and provided significant input.

The Director addressed the National Gambling Board and members attended a workshop to discuss

the compliance implications for the casino industry of the FIC Act.

The Centre also provided advice and input for the Financial Regulatory Symposium and the process to

develop a more coordinated approach to enforcement matters across the financial sector.

The Compliance and Prevention department also runs the public queries section for the Centre,

through which the Centre provides public feedback by means of an electronic query facility. These

have also formed the basis for the Centre’s Frequently Asked Questions (FAQs), which are posted on

our website. Members of the public can make enquiries relating to the FIC Act and the Centre via the

Centre’s website through the “Feedback” e-mail link. The Compliance and Prevention department

is working toward issuing a response within five (5) days of the initial query. During this financial

year the Centre responded to 368 queries, which is lower than the 404 queries raised last year by

members of the public. This may well be a sign that a better understanding of the FIC Act is being

embedded in our society.

Monitoring and Analysis Department

The Monitoring and Analysis Department receives information from reporting and accountable

institutions relating to alleged money laundering and terror financing activities. The department also

receives spontaneous disclosures from international counterparts and members of the public. The

information is then stored, analysed, contextualised and distributed to law enforcement authorities

and intelligence agencies where further investigation is deemed necessary. This department also

receives and responds to both international and domestic requests. In addition, the department also

maintains relationships with law enforcement authorities and conducts feedback sessions, as well as

training interventions, such as that for authorised officers or for financial investigators.

The Monitoring and Analysis Department has developed rigorous procedures for the receipt of

information and the authorised process of adding value to it before referring anything to the law

enforcement authorities for investigation. These procedures are being incorporated into the new IT

system which the Centre is busy developing.

The information received from STRs has proved to be invaluable to the Centre in constructing

comprehensive and detailed financial profiles of individuals and entities that are suspected of being

involved in organised crime, tax evasion, violent crime and suspected financing of terrorism. The

information received has allowed the Centre the ability to forward regular and comprehensive intelligence

pictures to the security and law enforcement agencies within the Republic. The Centre has also been

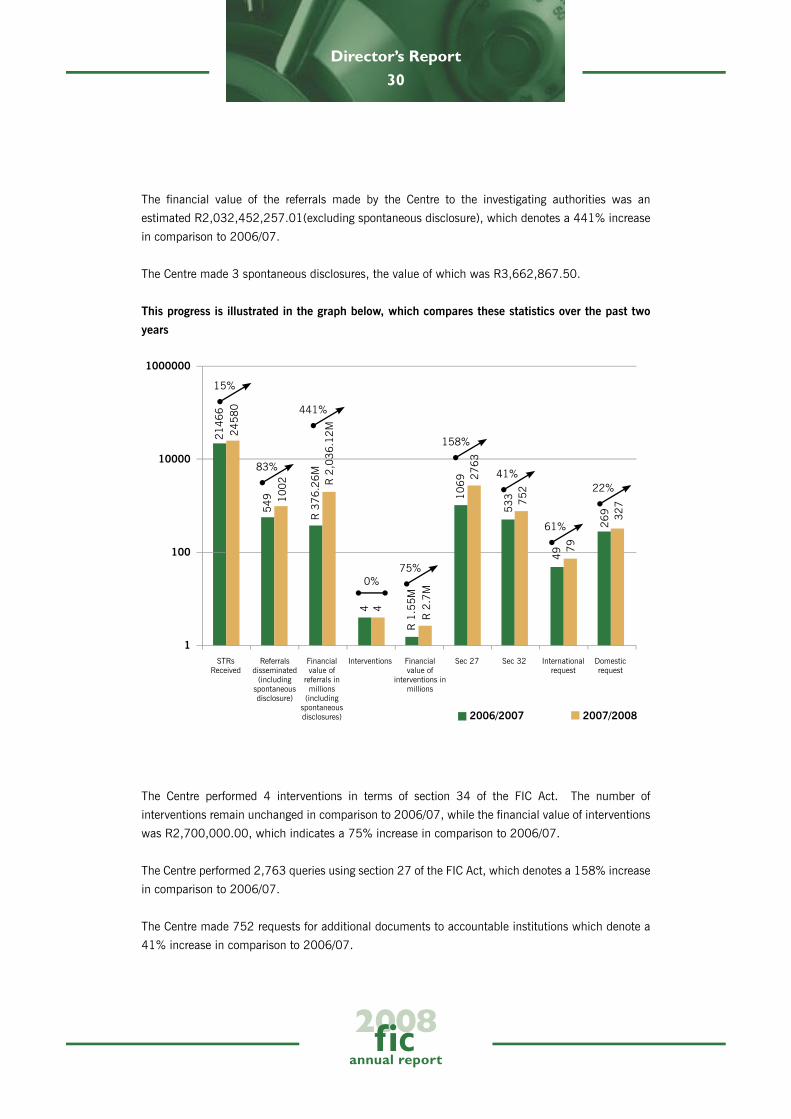

Director’s Report29

able to trace previously undetectable financial links between these individuals under investigation and

their associates. Feedback received from the recipients of these referrals has confirmed the vital role

of the Centre (and by implication the reporting institutions), in assisting the South African government

in fulfilling its obligations in terms of the global efforts to combat AML and CFT.

Analysis of Suspicious Transaction Reporting to the Centre

Suspicious Transaction Reports made to the Financial intelligence Centre

Financial Year No of STRs Accumulated Total

2002/ 2003 991

2003/ 2004 7 480 8 471

2004/ 2005 15 757 24 228

2005/ 2006 19 793 44 021

2006/ 2007 21 466 65 487

2007/ 2008 24 580 90 067

An analysis of these reports has shown the following information

The reporting institutions made 24,580 Suspicious Transactions Reports to the Centre between 1

April 2007 and 29 February 2008, which denotes a 15% increase in comparison to 2006/07.

Of these, 62% of the reports were received from money remitters, while 27% received were from

banks.

In the financial year 22,411 reports were received from the financial sector constituting 91% of all

reports received. The non-financial sector filed 2,169 reports, constituting just 9% of all reports

received.

The Centre created 999 referrals which were disseminated to investigating authorities, which denotes

an 83% increase in comparison to 2006/07.

Financial

Non-financial

91%

9%25000

20000

15000

10000

5000

0

2006/2007 2007/2008

2667 2169

12% 9%

91%88%

1879922411

Director’s Report30