Bahasa

Halaman

Hukum

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

51

Fiscal deficit and its impact on inflation, Causality and Co-integration: The

Experience of Pakistan (1960-2010)

Ammama (Corresponding Author)

Department of Economics, Preston University Islamabad, Pakistan

E-mail: [email protected]

Dr. Khalid Mughal

Assistant Professor, Preston University Islamabad, Pakistan

E-mail: [email protected]

Dr. Muhammad Aslam Khan

Professor, Preston University Islamabad, Pakistan

E-mail: [email protected]

ABSTRACT

The main objective of this paper is to examine the impact of fiscal deficit on inflation. The fiscal

deficit in Pakistan continues to deteriorate and pose risks for sustainability of growth in the

longer time horizon. This paper reexamines the issue in the light of broader data and such

modeling approach which incorporates the key features of the theory. The paper establishes that

within sample, inflation in Pakistan is mainly attributed to unsustainable fiscal deficit. The

question whether fiscal deficit generates inflation in long term prespective or otherwise,

Cointegration and Granger-causality test are employed. Secondary data from 1960 to 2010 show

a strong relationship between fiscal deficit and inflation. Growth in deficits, whether measured

by amounts or by deficit-output ratios, positively Granger causes inflation. So this study

concluded that fiscal deficit displayed a powerful effect on inflation in Pakistan and there is need

of coordination between monetary and fiscal policy to curb the inflation. From Engel-Granger

cointegration test there exist a long run relationship between BD [budget deficit] and CPI

[consumer price index].

Key Words: Fiscal deficit, inflation, GDP (gross domestic product) growth, BDGDP (budget

deficit ratio to GDP growth), Pakistan

Paper Type: Research Paper

INTRODUCTION

The fiscal deficit is the difference between the government's total expenditure and its total

receipts (excluding borrowing). The elements of the fiscal deficit include (a) the revenue deficit,

which is the difference between the government’s current (or revenue) expenditure and total

current receipts (that is, excluding borrowing) and (b) capital expenditure. The fiscal deficit can

be financed by borrowing from the Central bank of Pakistan. (Which is also called deficit

financing or money creation) and market borrowing (from the money market, that is mainly from

banks). Two arguments are generally given in order to link a high fiscal deficit to inflation. The

first argument is based on the fact that the part of the fiscal deficit which is financed by

borrowing from the central bank of Pakistan leads to an increase in the money stock. Some

Far East Research Centre www.fareastjournals.com

52

people believe that higher money stock automatically leads to inflation. The second argument

linking fiscal deficits and inflation is that in an economy in which the output of some essential

commodities cannot be increased, the increase in demand caused by a larger fiscal deficit will

raise prices. (Bhattacharya, 2009).

Fiscal based theories of inflation have been especially prominent in the developing countries

literature, where it has long been recognized that less efficient tax collection, political instability,

and more limited excess to external borrowing tend to lower the relative cost of seignorage in

these countries. (Alesina and Drazen, 1991; Cukierman, Edwards, & Tabellini, 1992; Calvo and

vegh.1999). Several institutional and structural factors are believed to cause the expenditure-

adjustment coefficient to exceed the revenue-adjustment coefficient. Even if governments fully

recognize the need to restrain expenditures during periods of inflation, they find it difficult to

reduce their commitments in real terms. (Aghevli & Khan, 1978).

Catao and Terrones (2005), using panel of 23 emerging market countries for the period 1970-

2000 to investigate determinants of inflation. They found that a one percentage point

reduction in the ratio of fiscal deficit to GDP lowered long-run inflation by 1.5 to 6 percentage

points. Researchers had checked the impact of fiscal deficit on inflation and how fiscal deficit

always leads towards inflation in Pakistan. And how large budget deficits lower the GDP growth

and budget deficit ratio to GDP growth. Researchers had checked that fiscal deficit is efficient

determinant of inflation. And verify the gap of GDP growth and budget deficit ratio to GDP

growth in Pakistan. Methods of Unit Root Test, Granger Causality Test and co-integration are

used to verify the empirical results.

The objective of this study is to find out the direct or indirect impact of fiscal deficit on inflation

and finds out how non-planned expenditures cause huge fiscal deficit inflation in Pakistan. To

throw light upon these perspectives, the relationship between budget deficit and inflation is to be

examined. Secondly it investigates for long run relationship between these variables with current

data.

LITERATURE REVIEW

An economy going through a recession the government is not allowed to play any role in

boosting demand. Domestic inflation in Pakistan is related with volatility in government

borrowing from central bank in the long run. But in the short run, inflation is also affected by

volatility in GBCB [Government borrowing from Central Bank]. (Haider & Safdar, 2007).

There are several theories to explain the relationship between inflation and deficits transmission

mechanism, mainly including the following which Present evidence empirical literature relevant

to this concept.

An immense literature available on fiscal vis-a -vis monetary determinants of inflation.

Therefore, many economist intend to categorize the literature for Pakistan into two sets

including studies which used government borrowing as a determinant of inflation and those

which have not incorporated this determinant in their model setup. (Haider & Safdar, 2007).

Budget deficit (BD) weekly causes inflationary pressures, but rather impacts strongly on

general price level through the impact on money aggregates (say, M1 and M2) and public

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

53

expectations, which in turn trigger volatility in prices. Since, government borrows from

different sources to finance budget deficits (Sachs & Larrain, 1993).

The central government of any developing country finances their budget deficit through

monetizing process (borrowing from central bank). High monetization leads to higher

inflationary pressure to the economy. Thus borrowing from the central bank is considered as a

leading indicator of domestic inflation. In line with the above phenomenon, the main

motivation of this paper is to assess whether volatility in government borrowing the main

reason of fiscal deficit has an impact of domestic inflation in Pakistan. (Haider & Safdar, 2007).

Ache, Asif Idrees and Khan Muhammad Salem (2006) used empirical approach of Jhansen

cointegration analysis and VCEM model take CPI as the dependent variables and regressors are

consolidated fiscal deficit and total bank borrowing take sample period of 1973-2003 Findings

are “The empirical results suggest that in the long run inflation is not only related to fiscal

imbalances but also to the sources of financing fiscal deficit”.

S K Hyder and Ahmed, Q Masood (2006) used empirical approach OLS (ordinary least square)

method and verifying results through Breusch Godfrey Serial Correlation LM and augmented

Dickey fuller tests CPI as the dependent Variable, Regressor government sector borrowing (Plus

NFA and other items) as the ratio to real GNP, real demand relative to real supply, on-

government sector borrowing (plus borrowing of autonomous bodies) as ratio of real GNP, price

index of imports and exchange rate, government taxes as the ratio of manufacturing sector value

added, lagged CPI and support price of wheat take sample period of 1972-2005 Findings “The

most important determinants of inflation are adaptive expectations, private sector credit and

rising imports prices whereas fiscal policy contribution to inflation was minimal. Specifically if

government sector borrowing as the ratio to GNP changed by 10% then the resulting change in

CPI will be around 1%”.

Aslam and Anjum, S Waseem (1996) used empirical approach of sustainable deficit econometric

model for Pakistan is estimated, Dependent variables growth rate of GNP, inflation rate, interest

rate of foreign debt etc, Regressors a number of assumptions regarding growth rate of GNP,

inflation and interest rate on foreign debt. Taken three time periods 1980’s, 1985-95 and 1993-

98, Findings “throughout the period under analysis, fiscal deficit was not sustainable”.

Aslam and Ahmed Naveed (1995) used empirical approach of simultaneous model and OLS i.e.

regressions of money supply equation, real cash balance equation, price equation and output

equation and export supply equation. Dependent variables CPI,money supply, demand for real

cash balances, exports.Regressors (1) money supply equation-international reserves, domestic

financing of budget deficit including banking and non-banking system, commercial banks credit

to private sector(2) demand for real cash balances-income, proxy for cost of holding real

balances(3) price-equation income, money supply, import price. Taken three time periods 1973-

92, 1973-82 and 1982-92, Findings “Domestic financing of budget deficit; particularly from the

banking system is inflationary in long run. Money supply is not exogenous, rather it depends on

the position of international reserves and fiscal deficit and it has emerged as an endogenous

variable”.

Far East Research Centre www.fareastjournals.com

54

Zulfiqar and Sardar (2004) used empirical approach of VAR and regressors CPI inflation, WPI

inflation, PR/USD, M2, LSM index, oil prices. Sample periods 1988:1 to 2003:9. Findings

“Little exchange rate pass through to domestic CPI inflation”. Ehsan U and Mohsin S. khan

(2002) used empirical approach of single equation and VAR in first differences OLS. A

dependent variable CPI and WPI.Regressor US dollar exchange rate, foreign price index. Sample

period was 1982-2001 and Findings “there is no exchange rate pass- through to domestic prices”.

Ahmed, Eatzaz and M Munir (2000) used empirical approach of Cointegration analysis.

Dependent variables are M1 and M2.Regressors index of industrial production, interbank call

money rate, CPI inflation. Sample period 1972:1 to 1996:1.Findings “Inflation is the better

measures of opportunity cost than interest rate, money demand adjust sluggish, and there was a

structural break in the early 1990’s”.

Ahmed, Eitzaz and Saima Ahmed Ali (1999a) empirical approach used single equation use Engle

Granger cointegration test, 2- equation with 2SLS. Dependent variable CPI and exchange

rate.Regressors Exchange rate, import prices, world prices, money supply, GDP, forex

researves.Sample period (1982: ii: 1996: iv).Findings “CPI reacts to change in import prices (due

to change in world prices or exchange rate) and money supply. Exchange rate responds to

domestic and world prices”. Hussain, Akhter (1994) used empirical approach Engel/Granger 2-

stage, Johenson.Dependent variables M1 and M2.Regressors GDP, yield on government bonds,

market call rate, and CPI inflation. Time period 1951-1991.Findings “Meaningful cointegration

relationship (money demand function) for the post -1972 period”.

Khan Ashfaque H (1994) used empirical approach Engel/Granger 2-stage.Dependent variable

M1 and M2.Regressors real income, real interest rate(short term and medium term),nominal

interest rate(short term and medium term),Inflation. Time period (1971: iii to 1993: iii).Findings

“Cointegration relationship between M2 (and M1) and real income and real interest rate,

inflation”. Ahmed, Eitzaz, and Harim Ram (1991) used empirical approach OLS.Dependent

variables WPI, CPI, GNP deflator and absorption deflator inflation.Regressors real GNP growth,

growth rate of unit value of imports, growth rate of M1/M2, lagged inflation. Time period 1960-

1988 Findings “Inflation is determined by real GNP growth, unit value of import growth,

nominal money growth and lagged inflation”.

Chaudry, M Slam, and Naveed Ahmed (1996) used empirical approach OLS. Dependent variable

CPI inflation. Regressors broad money, GDP growth, share of service sector, public debt and

import prices. Time period 1972-1992.Findings “Inflation results from money growth and

structural factors such as growth, share of service sector, imports and public debt”.

ECONOMETRICS METHODOLOGY

The long run relationship between the inflation and budget deficit is examined using

Cointegration technique and the short-run adjustment between the budget deficit and inflation to

account for the long run relationship is examined using Error correction model. Engle and

Granger (1987) proposed a straightforward test whether two I (1) variables are cointegrated of

order CI (1, 1). By definition, of cointegration necessitates that the variables be integrated of the

same order. Thus, the first step in the analysis is to pretest each variable to determine its order of

integration. The Augmented Dickey Fuller test is used to infer the number of unit roots (if any)

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

55

in each of the variables. If both the variables {Yt} and {Xt} are I (1), then the long run

relationship is estimated in the form of

In order to determine whether the variables are actually cointegrated, the residual sequence from

this equation is tested for unit roots using Augmented Dickey Fuller test. The rejection of null

hypothesis implies that the residual sequence is stationary and thus the series is cointegrated of

order (1, 1). If the variables are cointegrated, the residuals from the equilibrium regression can be

used to estimate the error correction model given by the optimal lag length to be used in the error

correction model has been determined using SBC criterion.

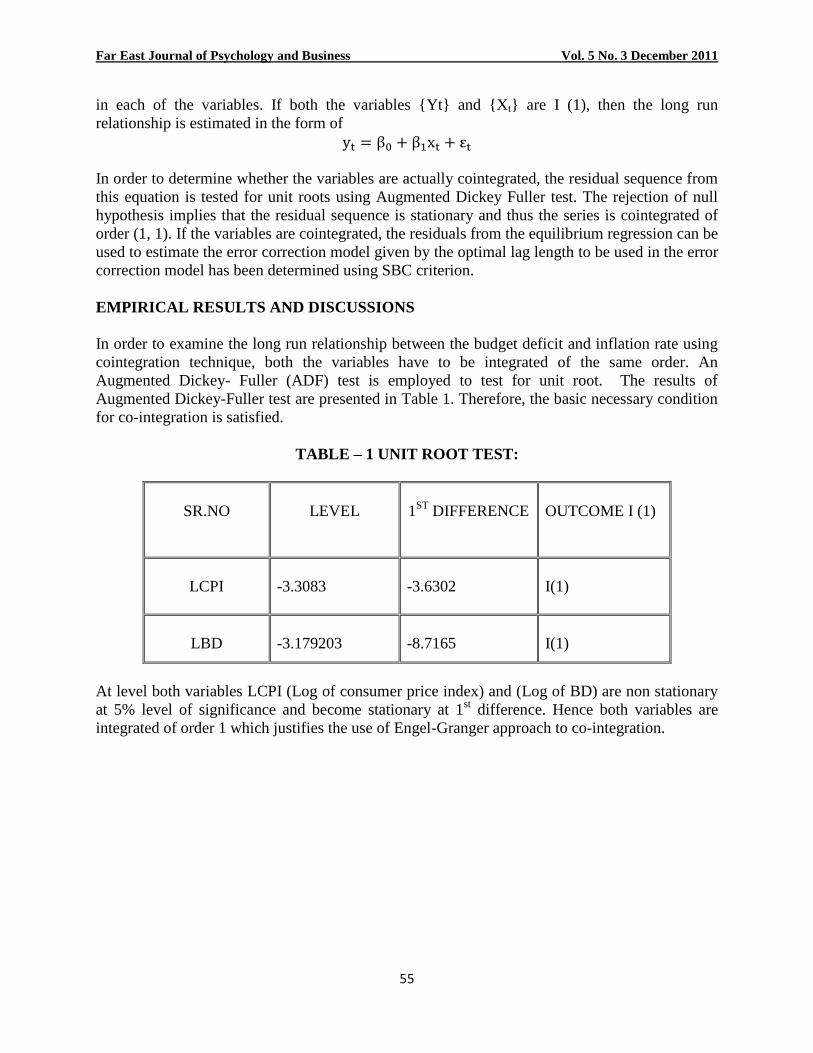

EMPIRICAL RESULTS AND DISCUSSIONS

In order to examine the long run relationship between the budget deficit and inflation rate using

cointegration technique, both the variables have to be integrated of the same order. An

Augmented Dickey- Fuller (ADF) test is employed to test for unit root. The results of

Augmented Dickey-Fuller test are presented in Table 1. Therefore, the basic necessary condition

for co-integration is satisfied.

TABLE – 1 UNIT ROOT TEST:

SR.NO

LEVEL

1ST

DIFFERENCE

OUTCOME I (1)

LCPI

-3.3083

-3.6302

I(1)

LBD

-3.179203

-8.7165

I(1)

At level both variables LCPI (Log of consumer price index) and (Log of BD) are non stationary

at 5% level of significance and become stationary at 1st difference. Hence both variables are

integrated of order 1 which justifies the use of Engel-Granger approach to co-integration.

Far East Research Centre www.fareastjournals.com

56

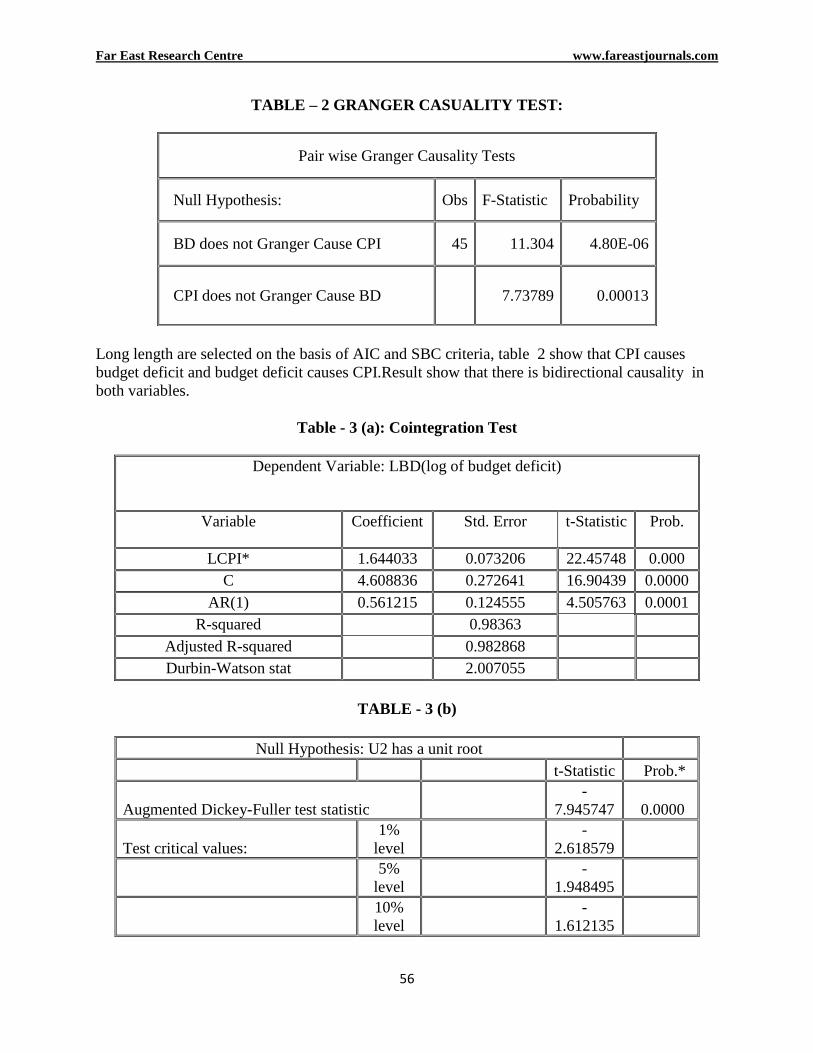

TABLE – 2 GRANGER CASUALITY TEST:

Long length are selected on the basis of AIC and SBC criteria, table 2 show that CPI causes

budget deficit and budget deficit causes CPI.Result show that there is bidirectional causality in

both variables.

Table - 3 (a): Cointegration Test

Dependent Variable: LBD(log of budget deficit)

Variable Coefficient Std. Error t-Statistic Prob.

LCPI* 1.644033 0.073206 22.45748 0.000

C 4.608836 0.272641 16.90439 0.0000

AR(1) 0.561215 0.124555 4.505763 0.0001

R-squared 0.98363

Adjusted R-squared 0.982868

Durbin-Watson stat 2.007055

TABLE - 3 (b)

Null Hypothesis: U2 has a unit root

t-Statistic Prob.*

Augmented Dickey-Fuller test statistic

-

7.945747 0.0000

Test critical values:

1%

level

-

2.618579

5%

level

-

1.948495

10%

level

-

1.612135

Pair wise Granger Causality Tests

Null Hypothesis: Obs F-Statistic Probability

BD does not Granger Cause CPI 45 11.304 4.80E-06

CPI does not Granger Cause BD 7.73789 0.00013

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

57

*LCPI: log of consumer price index

Regress CPI on BD, the coefficient of BD is positive and highly significant. Which show that

BD. positively affect the prices in Pakistan over the period reviewed and error term obtained

from the above regression is stationary at that level, implies that there does long run relationship

Between BD and CPI.Cointegration exist between CPI and BD.

Inflation, GDP growth, and Budget deficit ratio to GDP growth:

YEARS

INFLATION GDP GROWTH BDGDP

1960’*

1970's*

3.30

11.76

6.44

5.08

4.08

5.19

1980's* 7.27 6.42 4.99

1990,* 9.72 4.98 5.28

2000 4.37 3.90 5.28

2001 3.15 2.00 4.09

2002 3.29 3.10 3.62

2003 2.91 4.70 3.62

2004 7.44 7.50 2.34

2005 9.06 9.00 3.34

2006 7.92 5.80 4.28

2007 7.80 6.80 4.34

2008 20.30 7.20 7.42

2009 20.77 3.60 5.20

2010 11.49 4.40 4.90

*Shows the average of ten years

Source: World Development Indicator (2009-10)

This table shows the average trend of inflation, GDP (gross domestic product) growth and

BDGDP (budget deficit ratio to GDP) in the years of 1960’s, 70’s, 80’s and 90’s and the trend

between the years 2000-10.

Far East Research Centre www.fareastjournals.com

58

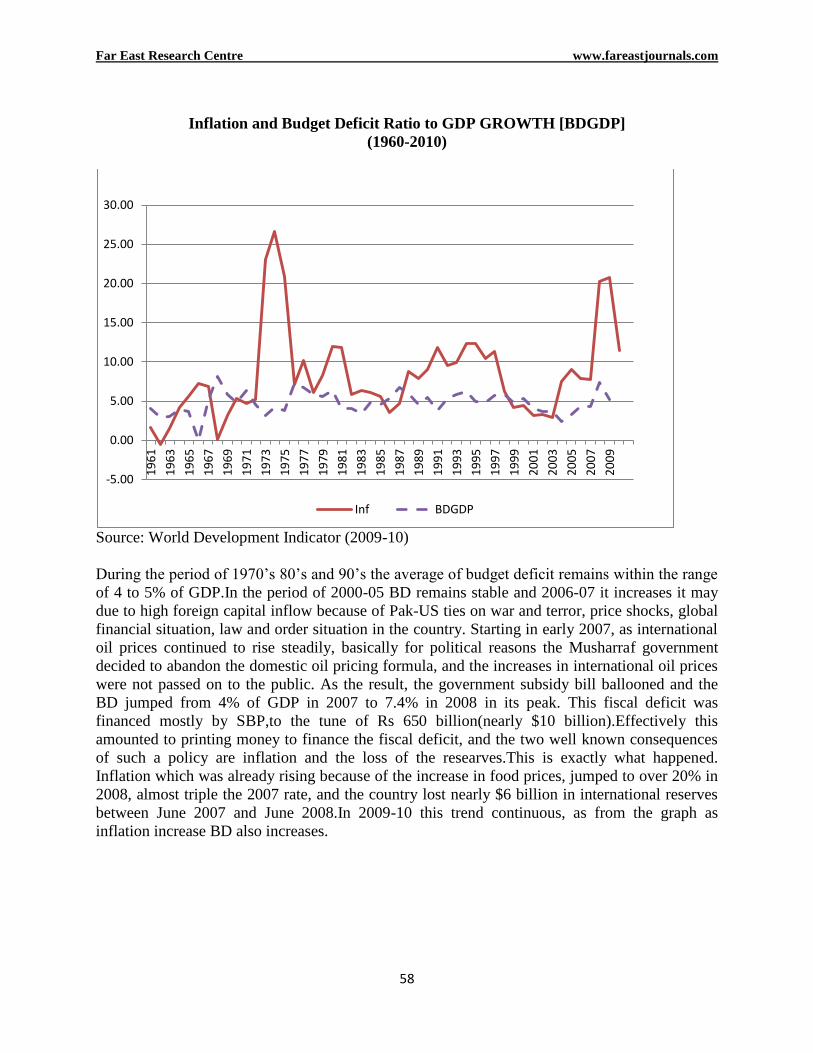

Inflation and Budget Deficit Ratio to GDP GROWTH [BDGDP]

(1960-2010)

Source: World Development Indicator (2009-10)

During the period of 1970’s 80’s and 90’s the average of budget deficit remains within the range

of 4 to 5% of GDP.In the period of 2000-05 BD remains stable and 2006-07 it increases it may

due to high foreign capital inflow because of Pak-US ties on war and terror, price shocks, global

financial situation, law and order situation in the country. Starting in early 2007, as international

oil prices continued to rise steadily, basically for political reasons the Musharraf government

decided to abandon the domestic oil pricing formula, and the increases in international oil prices

were not passed on to the public. As the result, the government subsidy bill ballooned and the

BD jumped from 4% of GDP in 2007 to 7.4% in 2008 in its peak. This fiscal deficit was

financed mostly by SBP,to the tune of Rs 650 billion(nearly $10 billion).Effectively this

amounted to printing money to finance the fiscal deficit, and the two well known consequences

of such a policy are inflation and the loss of the researves.This is exactly what happened.

Inflation which was already rising because of the increase in food prices, jumped to over 20% in

2008, almost triple the 2007 rate, and the country lost nearly $6 billion in international reserves

between June 2007 and June 2008.In 2009-10 this trend continuous, as from the graph as

inflation increase BD also increases.

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00

19

61

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

Inf BDGDP

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

59

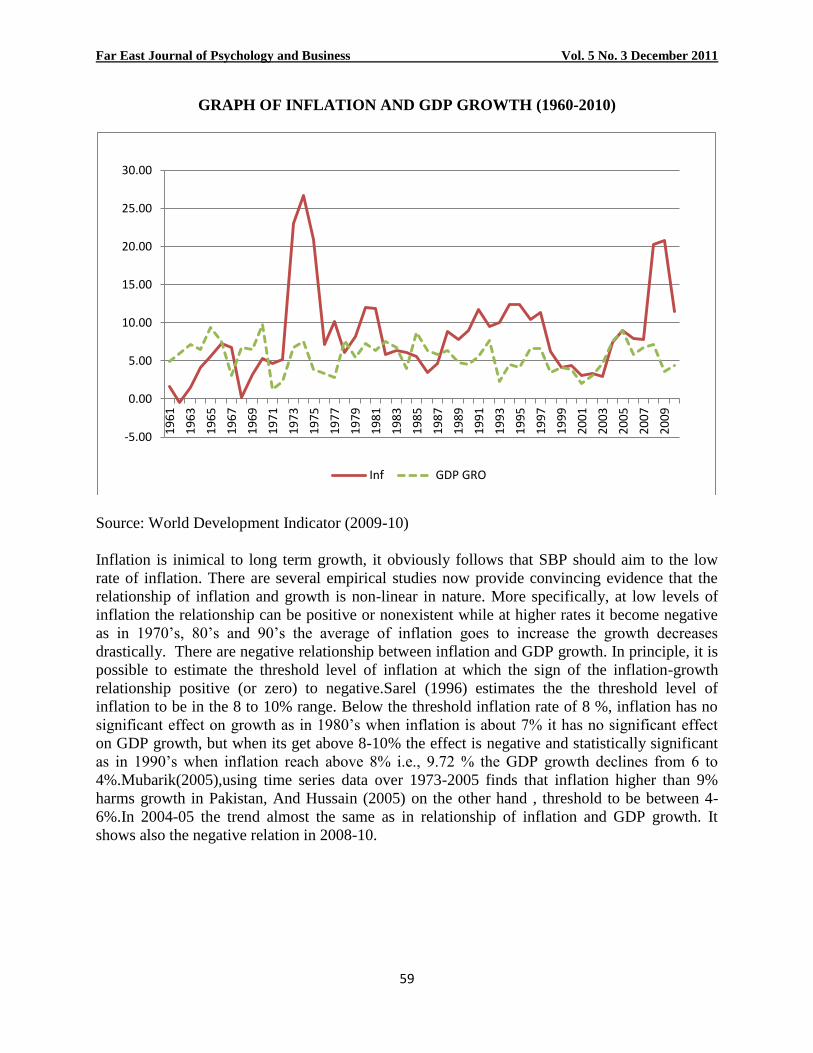

GRAPH OF INFLATION AND GDP GROWTH (1960-2010)

Source: World Development Indicator (2009-10)

Inflation is inimical to long term growth, it obviously follows that SBP should aim to the low

rate of inflation. There are several empirical studies now provide convincing evidence that the

relationship of inflation and growth is non-linear in nature. More specifically, at low levels of

inflation the relationship can be positive or nonexistent while at higher rates it become negative

as in 1970’s, 80’s and 90’s the average of inflation goes to increase the growth decreases

drastically. There are negative relationship between inflation and GDP growth. In principle, it is

possible to estimate the threshold level of inflation at which the sign of the inflation-growth

relationship positive (or zero) to negative.Sarel (1996) estimates the the threshold level of

inflation to be in the 8 to 10% range. Below the threshold inflation rate of 8 %, inflation has no

significant effect on growth as in 1980’s when inflation is about 7% it has no significant effect

on GDP growth, but when its get above 8-10% the effect is negative and statistically significant

as in 1990’s when inflation reach above 8% i.e., 9.72 % the GDP growth declines from 6 to

4%.Mubarik(2005),using time series data over 1973-2005 finds that inflation higher than 9%

harms growth in Pakistan, And Hussain (2005) on the other hand , threshold to be between 4-

6%.In 2004-05 the trend almost the same as in relationship of inflation and GDP growth. It

shows also the negative relation in 2008-10.

-5.00

0.00

5.00

10.00

15.00

20.00

25.00

30.00 1

96

1

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

Inf GDP GRO

Far East Research Centre www.fareastjournals.com

60

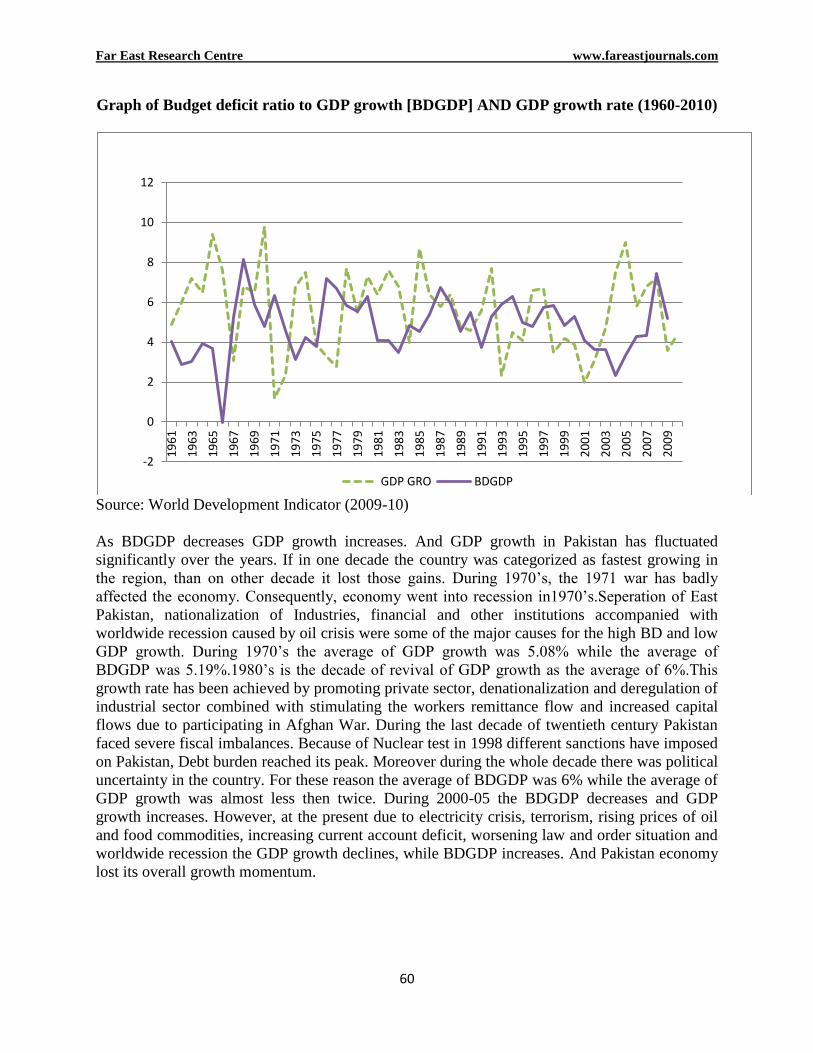

Graph of Budget deficit ratio to GDP growth [BDGDP] AND GDP growth rate (1960-2010)

Source: World Development Indicator (2009-10)

As BDGDP decreases GDP growth increases. And GDP growth in Pakistan has fluctuated

significantly over the years. If in one decade the country was categorized as fastest growing in

the region, than on other decade it lost those gains. During 1970’s, the 1971 war has badly

affected the economy. Consequently, economy went into recession in1970’s.Seperation of East

Pakistan, nationalization of Industries, financial and other institutions accompanied with

worldwide recession caused by oil crisis were some of the major causes for the high BD and low

GDP growth. During 1970’s the average of GDP growth was 5.08% while the average of

BDGDP was 5.19%.1980’s is the decade of revival of GDP growth as the average of 6%.This

growth rate has been achieved by promoting private sector, denationalization and deregulation of

industrial sector combined with stimulating the workers remittance flow and increased capital

flows due to participating in Afghan War. During the last decade of twentieth century Pakistan

faced severe fiscal imbalances. Because of Nuclear test in 1998 different sanctions have imposed

on Pakistan, Debt burden reached its peak. Moreover during the whole decade there was political

uncertainty in the country. For these reason the average of BDGDP was 6% while the average of

GDP growth was almost less then twice. During 2000-05 the BDGDP decreases and GDP

growth increases. However, at the present due to electricity crisis, terrorism, rising prices of oil

and food commodities, increasing current account deficit, worsening law and order situation and

worldwide recession the GDP growth declines, while BDGDP increases. And Pakistan economy

lost its overall growth momentum.

-2

0

2

4

6

8

10

12 1

96

1

19

63

19

65

19

67

19

69

19

71

19

73

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

GDP GRO BDGDP

Far East Journal of Psychology and Business Vol. 5 No. 3 December 2011

61

FINDINGS

History of Pakistan has often witnessed that government’s resorts to seignorage at time of fiscal

distress. It should therefore come as no surprise that much of the contemporary macroeconomics

literature has focused on fiscal behavior when trying to explain why inflation has varied so

widely, both across countries and over time, in recent decades in Pakistan. Fiscal deficit is

considered one of the major determinants of inflation, in the inflation literature of Pakistan.

Increasing fiscal deficits is a persistent problem faced by Pakistan. This research finds that fiscal

dominance hypothesis in determining inflation in the case of Pakistan economy. In connection

with this hypothesis, the results depict important information that the impact of government

borrowing which is the main reason of fiscal deficit from central bank on domestic inflation is

economically and statistically significant. Further, the empirical evidence suggests that there is a

strong long run relationship between domestic inflation and volatility in government

borrowing from central bank. In particular, it suggests incorporating the trend effects of

government borrowing from monetary authorities in inflation modeling. Finally these findings

may help in understanding inflation experience in Pakistan.

CONCLUSIONS

Our empirical results show that there is positive long run relationship LBD (Log of budget

deficit) and LCPI (Log of consumer price index).BD (budget deficit) causes Inflation i.e. BD is

the important determinant of Inflation. This paper sought to address the issue of fiscal deficit and

its impact on inflation. On the other hand there is much more favorable to fiscal based theories of

inflation than previous research had found. The deficit-inflation relationship comes out as

surprisingly strong in Pakistan, also in contrast with the earlier literature. From Engel-Granger

cointegration test there exist a long run relationship between BD and CPI.There is cointegration

between BD and CPI.

If the government of Pakistan is allowed to continue the size of deficits and debt to expand, then

the resulting rise in interest rates will force the central bank buying government bonds through

open market operations to maintain the level of interest rates, while the end result of this

approach will enable the currency increasing supply and eventually lead to inflation from

happening. In addition, when the size of fiscal deficit and national debt accumulated to a certain

extent, the Government's sustainable conditions for the credit will be broken, once the

Government, through the bonds can not be expected to achieve results, then it can only rely on

seigniorage to make up for all of the budget deficit, then the same will eventually lead to the

occurrence of inflation in Pakistan.

Recommendations

Therefore, the future, our government should follow the following two aspects at least do a good

job on the budget deficit inflation risk, prevention work: first, to strengthen the independence of

the central bank, clear the central bank's monetary policy objectives. Right to give a legal

guarantee for the independence of the central bank will help cut the budget deficit and the money

supply of the internal relations, thereby limiting the Government directly through the central

bank the possibility of an overdraft to cover the deficit. Therefore, our government should

present the implementation of prudent fiscal policy as an opportunity, through the establishment

Far East Research Centre www.fareastjournals.com

62

of a sound modern tax collection system, optimize the Structure of government spending and

speed up the reform of budget management system and other means to create conditions for the

gradual reduction of fiscal deficit.

Future Gap

The empirical results suggested that fiscal imbalances and weak forecaster for future

inflation in economies under study. More specifically, they found that the predicted rise in fiscal

deficit scenario in future could possibly impact in an insignificant manner towards

increasing inflation in the economy. The authors further observed that their results should be

used with much caution as econometrically evaluating the inter-temporal budget constraint is

vulnerable to non-stationary and time dependence problems.

References

Akhter (1987), Impact of inflation on fiscal deficits in the Bangladesh economy. Pakistan

Development Review.

Bhattacharya J (2009, Aug 21), “The Fiscal Deficit”.

Blanchard, Oliver and Fisher, Stanley, 1989, Lectures on Macroeconomics, Cambridge,

Massachusetts: The M IT Press.

Budina, N. and Sweder van Wijnbergen, Fiscal Deficits, Monetary Refom & inflation In

Transition Economies: The case of Romania, East Eurpeon Series No.37

September, 1996

Catao, L., Terrones, M.E. (2003),”Fiscal Deficits and inflation” .Washington,IMF,WP/03/65

Haider, Danna & Khan, Sandbar Ullah, (2007). "Does Volatility in Government, Borrowing

Leads to Higher Inflation”? Evidence from Pakistan," MPRA Paper 17008,

Izák V Prague Economic Papers, 2005, vol. 2005, issue 1, pp. 3-16.

Pakistan Economic Survey, (2009-2010), Ministry of Finance, Government of Pakistan.

Rother, P. (2004), “Fiscal Policy and Inflation Volatility“. Frankfurt/M, European Central Bank,

WP No.317.

Sargent, T., Wallace, N. (1981), “Some Unpleasant Monetarist Arithmetic“. Federal Reserve

Bank of Minneapolis Quarterly Review, 5 (3), fall, pp. 1-17.Statistical Annex of

European Economy (2004). Brussels, European Commission, ECFIN/174/2004.

Sergent, Thomas, 1982, “The Ends of Four Big Inflations, “In Robert Hall, ed., Inflation, Causes

and Effects, Vol.108, pp.997-1032.

State Bank Pakistan Research Bulletin Volume 6, No. 1, May, 2010 Response of Long-term

Interest Rate to Fiscal Imbalance: Evidence from Pakistan.

Tanzi, Vito, Blazer, Mario, 1993, “Effects of Inflation on Measurement of Fiscal Deficits:

Conventional versus Operational Measures, “In Mario Blejer and Adrienne

Cheasty, eds., How to Measure the Fiscal Deficit, Washington D.C.: International

Monetary Fund.

Copyright © 2022 FDOKUMEN