Bahasa

Halaman

Hukum

The Companyst1 Half 2010

bb.com.br

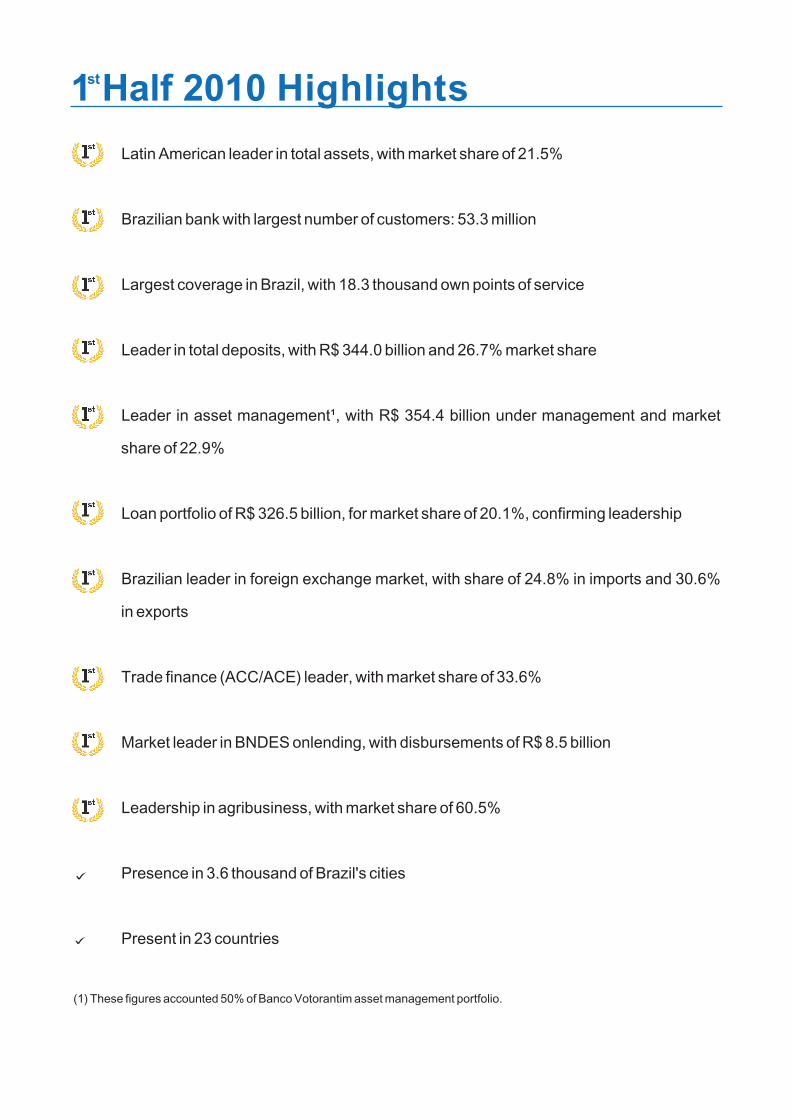

1 Half 2010 Highlights

Latin American leader in total assets, with market share of 21.5%

Brazilian bank with largest number of customers: 53.3 million

Largest coverage in Brazil, with 18.3 thousand own points of service

Leader in total deposits, with R$ 344.0 billion and 26.7% market share

Leader in asset management¹, with R$ 354.4 billion under management and market

share of 22.9%

Loan portfolio of R$ 326.5 billion, for market share of 20.1%, confirming leadership

Brazilian leader in foreign exchange market, with share of 24.8% in imports and 30.6%

in exports

Trade finance (ACC/ACE) leader, with market share of 33.6%

Market leader in BNDES onlending, with disbursements of R$ 8.5 billion

Leadership in agribusiness, with market share of 60.5%

Presence in 3.6 thousand of Brazil's cities

Present in 23 countries

(1) These figures accounted 50% of Banco Votorantim asset management portfolio.

st

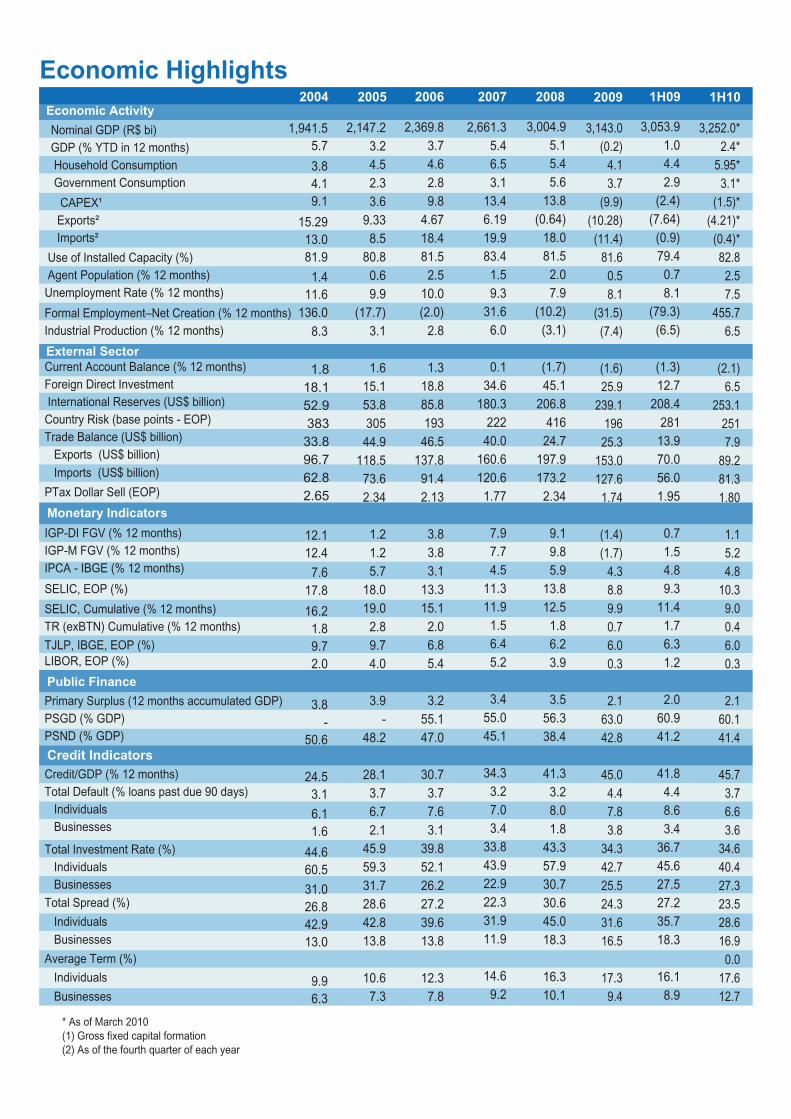

Economic Highlights

Economic Activity

* As of March 2010(1) Gross fixed capital formation(2) As of the fourth quarter of each year

2004 2005 2006 2007 2008 2009 1H09 1H10

External Sector

Monetary Indicators

Public Finance

Credit Indicators

Nominal GDP (R$ bi)

GDP (% YTD in 12 months)

Household Consumption

Government Consumption

CAPEX¹

Exports²

Imports²

Use of Installed Capacity (%)

Agent Population (% 12 months)

Unemployment Rate (% 12 months)

Formal Employment–Net Creation (% 12 months)

Industrial Production (% 12 months)

Current Account Balance (% 12 months)

Foreign Direct Investment

International Reserves (US$ billion)

Country Risk (base points - EOP)

Trade Balance (US$ billion)

Exports (US$ billion)

Imports (US$ billion)

PTax Dollar Sell (EOP)

IGP-DI FGV (% 12 months)

IGP-M FGV (% 12 months)

IPCA - IBGE (% 12 months)

SELIC, EOP (%)

SELIC, Cumulative (% 12 months)

TR (exBTN) Cumulative (% 12 months)

TJLP, IBGE, EOP (%)

LIBOR, EOP (%)

Primary Surplus (12 months accumulated GDP)

PSGD (% GDP)

PSND (% GDP)

Credit/GDP (% 12 months)

Total Default (% loans past due 90 days)

Individuals

Businesses

Total Investment Rate (%)

Individuals

Businesses

Total Spread (%)

Individuals

Businesses

Average Term (%)

Individuals

Businesses

2,147.2

3.2

4.5

2.3

3.6

9.33

8.5

80.8

0.6

9.9

(17.7)

3.1

1.6

15.1

53.8

305

44.9

118.5

73.6

2.34

1.2

1.2

5.7

18.0

19.0

2.8

9.7

4.0

3.9

-

48.2

28.1

3.7

6.7

2.1

45.9

59.3

31.7

28.6

42.8

13.8

10.6

7.3

2,369.8

3.7

4.6

2.8

9.8

4.67

18.4

81.5

2.5

10.0

(2.0)

2.8

1.3

18.8

85.8

193

46.5

137.8

91.4

2.13

3.8

3.8

3.1

13.3

15.1

2.0

6.8

5.4

3.2

55.1

47.0

30.7

3.7

7.6

3.1

39.8

52.1

26.2

27.2

39.6

13.8

12.3

7.8

2,661.3

5.4

6.5

3.1

13.4

6.19

19.9

83.4

1.5

9.3

31.6

6.0

0.1

34.6

180.3

222

40.0

160.6

120.6

1.77

7.9

7.7

4.5

11.3

11.9

1.5

6.4

5.2

3.4

55.0

45.1

34.3

3.2

7.0

3.4

33.8

43.9

22.9

22.3

31.9

11.9

14.6

9.2

3,004.9

5.1

5.4

5.6

13.8

(0.64)

18.0

81.5

2.0

7.9

(10.2)

(3.1)

(1.7)

45.1

206.8

416

24.7

197.9

173.2

2.34

9.1

9.8

5.9

13.8

12.5

1.8

6.2

3.9

3.5

56.3

38.4

41.3

3.2

8.0

1.8

43.3

57.9

30.7

30.6

45.0

18.3

16.3

10.1

3,143.0

(0.2)

4.1

3.7

(9.9)

(10.28)

(11.4)

81.6

0.5

8.1

(31.5)

(7.4)

(1.6)

25.9

239.1

196

25.3

153.0

127.6

1.74

(1.4)

(1.7)

4.3

8.8

9.9

0.7

6.0

0.3

2.1

63.0

42.8

45.0

4.4

7.8

3.8

34.3

42.7

25.5

24.3

31.6

16.5

17.3

9.4

3,053.9

1.0

4.4

2.9

(2.4)

(7.64)

(0.9)

79.4

0.7

8.1

(79.3)

(6.5)

(1.3)

12.7

208.4

281

13.9

70.0

56.0

1.95

0.7

1.5

4.8

9.3

11.4

1.7

6.3

1.2

2.0

60.9

41.2

41.8

4.4

8.6

3.4

36.7

45.6

27.5

27.2

35.7

18.3

16.1

8.9

3,252.0*

2.4*

5.95*

3.1*

(1.5)*

(4.21)*

(0.4)*

82.8

2.5

7.5

455.7

6.5

(2.1)

6.5

253.1

251

7.9

89.2

81.3

1.80

1.1

5.2

4.8

10.3

9.0

0.4

6.0

0.3

2.1

60.1

41.4

45.7

3.7

6.6

3.6

34.6

40.4

27.3

23.5

28.6

16.9

0.0

17.6

12.7

1,941.5

5.7

3.8

4.1

9.1

15.29

13.0

81.9

1.4

11.6

136.0

8.3

12.1

12.4

7.6

17.8

16.2

1.8

9.7

2.0

3.8

-

50.6

24.5

3.1

6.1

1.6

44.6

60.5

31.0

26.8

42.9

13.0

9.9

6.3

1.8

18.1

52.9

383

33.8

96.7

62.8

2.65

1.8

18.1

52.9

383

33.8

96.7

62.8

2.65

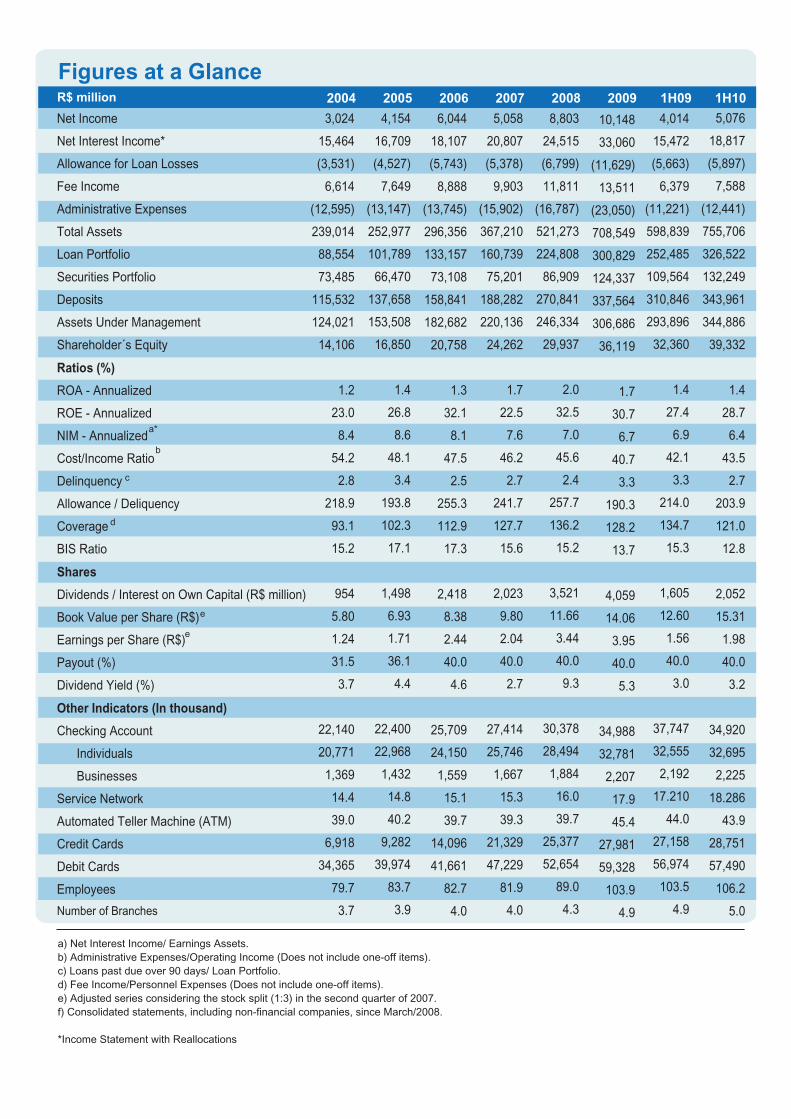

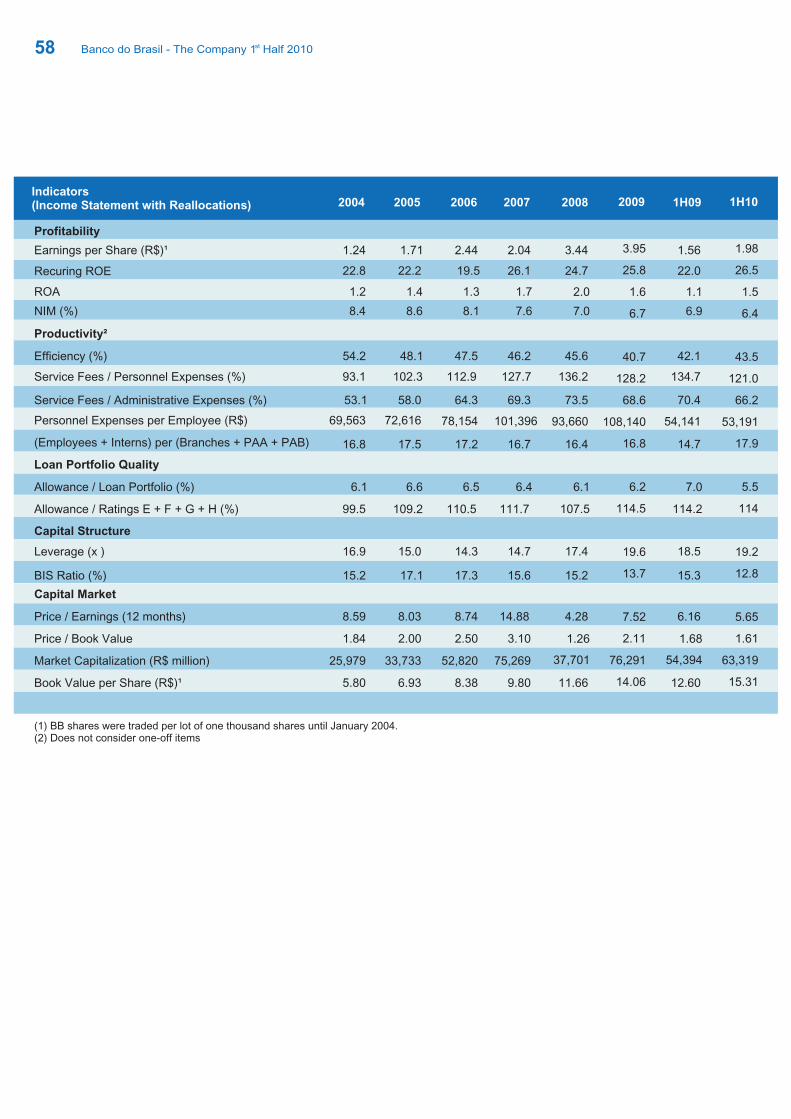

Figures at a GlanceR$ million 2004 2005 2006 2007 2008 2009

3,024

15,464

(3,531)

6,614

(12,595)

239,014

88,554

73,485

115,532

124,021

14,106

1.2

23.0

8.4

54.2

2.8

218.9

93.1

15.2

954

5.80

1.24

31.5

3.7

22,140

20,771

1,369

14.4

39.0

6,918

34,365

79.7

3.7

4,154

16,709

(4,527)

7,649

(13,147)

252,977

101,789

66,470

137,658

153,508

16,850

1.4

26.8

8.6

48.1

3.4

193.8

102.3

17.1

1,498

6.93

1.71

36.1

4.4

22,400

22,968

1,432

14.8

40.2

9,282

39,974

83.7

3.9

6,044

18,107

(5,743)

8,888

(13,745)

296,356

133,157

73,108

158,841

182,682

20,758

1.3

32.1

8.1

47.5

2.5

255.3

112.9

17.3

2,418

8.38

2.44

40.0

4.6

25,709

24,150

1,559

15.1

39.7

14,096

41,661

82.7

4.0

5,058

20,807

(5,378)

9,903

(15,902)

367,210

160,739

75,201

188,282

220,136

24,262

1.7

22.5

7.6

46.2

2.7

241.7

127.7

15.6

2,023

9.80

2.04

40.0

2.7

27,414

25,746

1,667

15.3

39.3

21,329

47,229

81.9

4.0

8,803

24,515

(6,799)

11,811

(16,787)

521,273

224,808

86,909

270,841

246,334

29,937

2.0

32.5

7.0

45.6

2.4

257.7

136.2

15.2

3,521

11.66

3.44

40.0

9.3

30,378

28,494

1,884

16.0

39.7

25,377

52,654

89.0

4.3

10,148

33,060

(11,629)

13,511

(23,050)

708,549

300,829

124,337

337,564

306,686

36,119

1.7

30.7

6.7

40.7

3.3

190.3

128.2

13.7

4,059

14.06

3.95

40.0

5.3

34,988

32,781

2,207

17.9

45.4

27,981

59,328

103.9

4.9

1H09 1H10

4,014

15,472

(5,663)

6,379

(11,221)

598,839

252,485

109,564

310,846

293,896

32,360

1.4

27.4

6.9

42.1

3.3

214.0

134.7

15.3

1,605

12.60

1.56

40.0

3.0

37,747

32,555

2,192

17.210

44.0

27,158

56,974

103.5

4.9

5,076

18,817

(5,897)

7,588

(12,441)

755,706

326,522

132,249

343,961

344,886

39,332

1.4

28.7

6.4

43.5

2.7

203.9

121.0

12.8

2,052

15.31

1.98

40.0

3.2

34,920

32,695

2,225

18.286

43.9

28,751

57,490

106.2

5.0

Net Income

Net Interest Income*

Allowance for Loan Losses

Fee Income

Administrative Expenses

Total Assets

Loan Portfolio

Securities Portfolio

Deposits

Assets Under Management

Shareholder´s Equity

Ratios (%)

ROA - Annualized

ROE - Annualized

NIM - Annualized

Cost/Income Ratio

Delinquency

Allowance / Deliquency

Coverage

BIS Ratio

Shares

Dividends / Interest on Own Capital (R$ million)

Book Value per Share (R$)

Earnings per Share (R$)

Payout (%)

Dividend Yield (%)

Other Indicators (In thousand)

Checking Account

Individuals

Businesses

Service Network

Automated Teller Machine (ATM)

Credit Cards

Debit Cards

Employees

Number of Branches

a) Net Interest Income/ Earnings Assets.

b) Administrative Expenses/Operating Income (Does not include one-off items).

c) Loans past due over 90 days/ Loan Portfolio.

d) Fee Income/Personnel Expenses

e) Adjusted series considering the stock split (1:3) in the second quarter of 2007.

f) Consolidated statements, including non-financial companies, since March/2008.

*Income Statement with Reallocations

(Does not include one-off items).

a*

b

c

d

e

e

Table of Contents

01. Economic Environment

02. Industry Outlook

03. Banco do Brasil Positioning

04. Financial Performance

05. Banco do Brasil Stock

06. Corporate Governance

6.1 Organizational Structure

6.2 Risk Management

6.3 Regulatory Capital

07. Human Resources

08. Social and Environmental Responsibility

09. Products and Services

9.1 Credit

9.1.1 Individuals

9.1.2 Businesses

9.1.3 Agribusiness

9.1.4 Foreign Trade

9.2 Securities

9.3 Funding

9.4 Asset Management

9.5 Capital Markets

9.6 Insurance, Pension Plans and Savings Bonds

9.7 Cards

10. Banco do Brasil Presence

10.1 Client Base

10.1.1 Retail

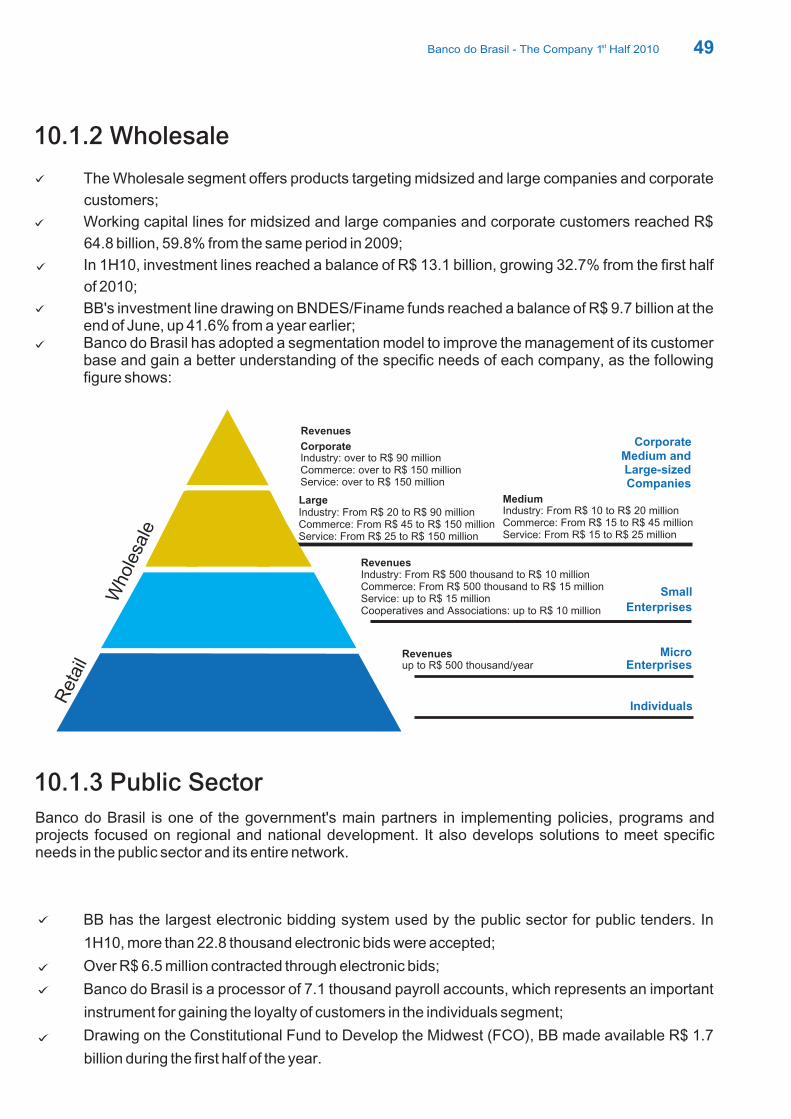

10.1.2 Wholesale

10.1.3 Public Sector

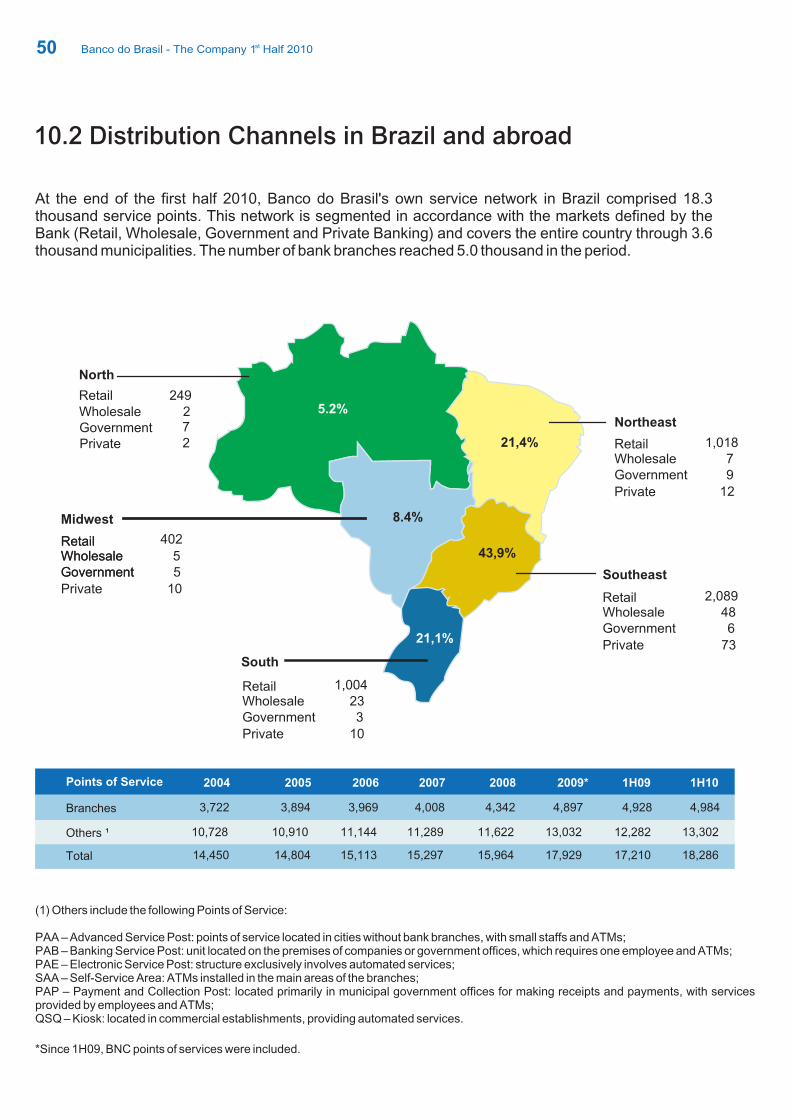

10.2 Distribution Channels in Brazil and Abroad

10.3 Technology Structure

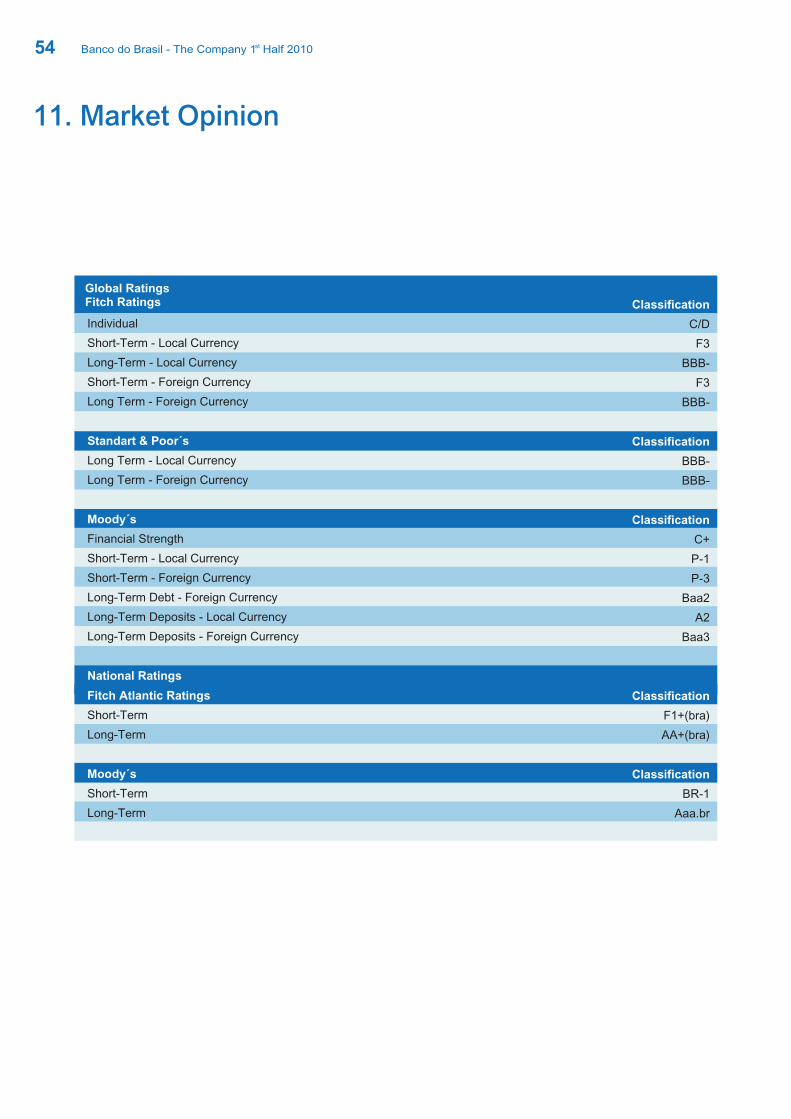

11. Market Opinion

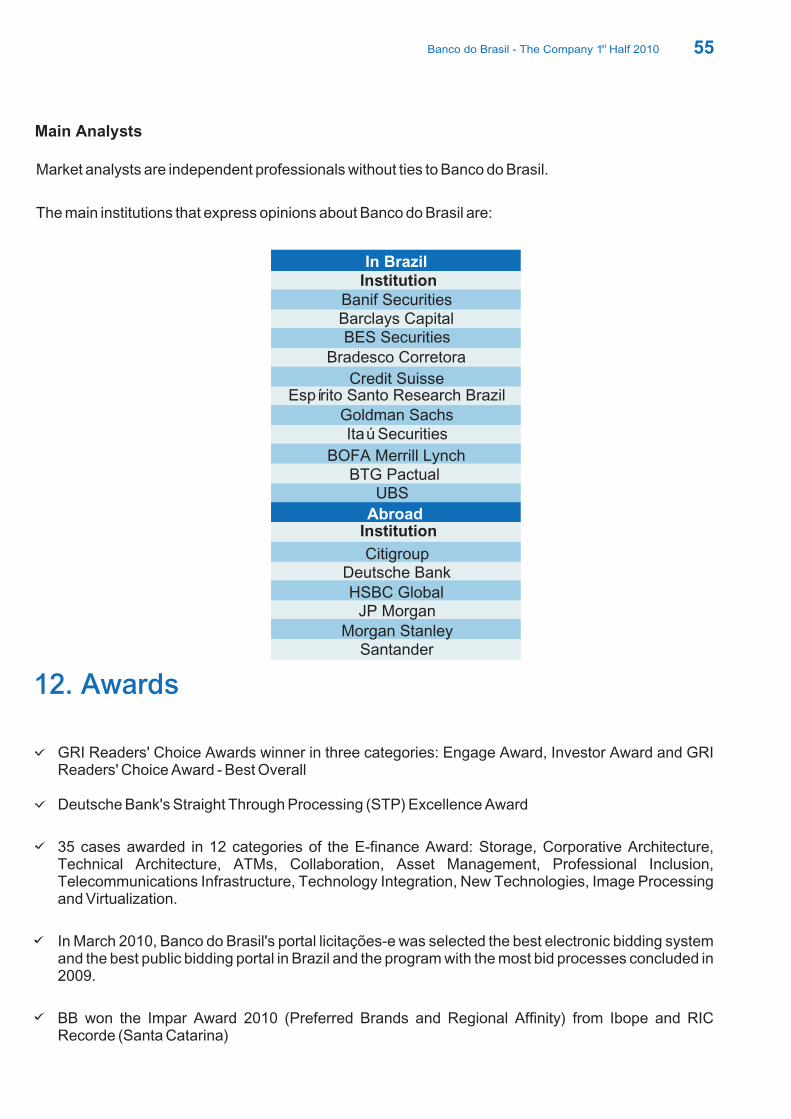

12. Awards

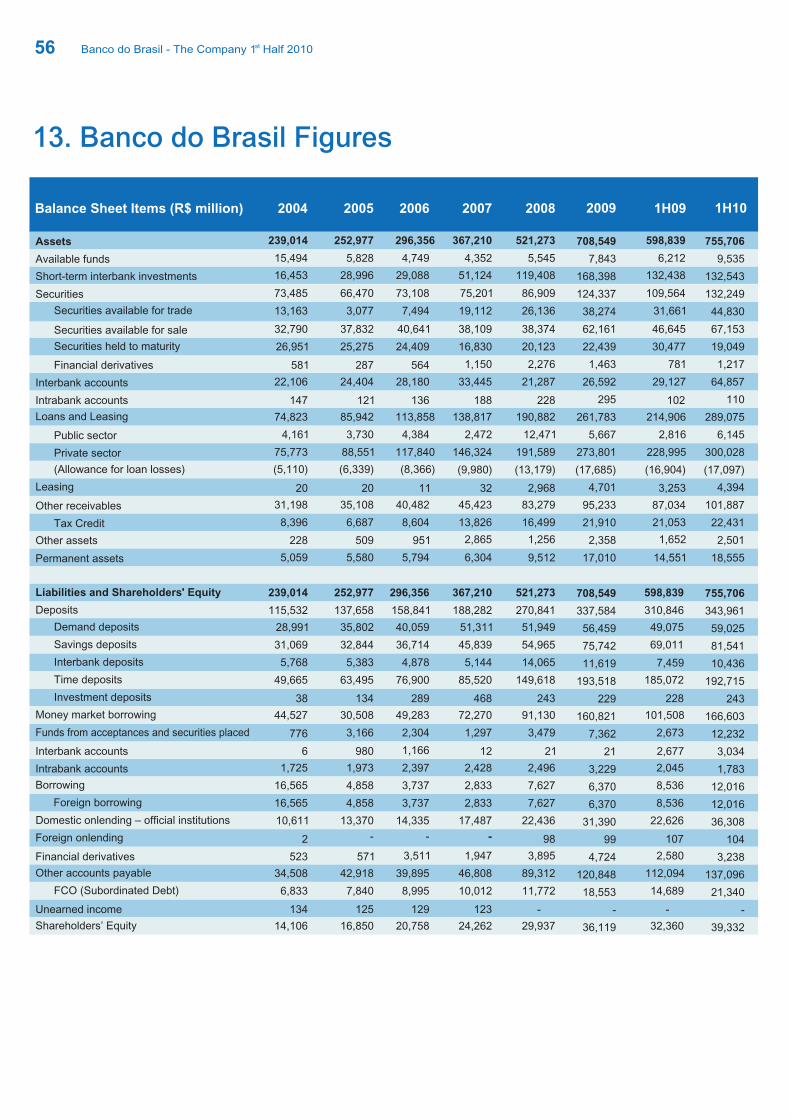

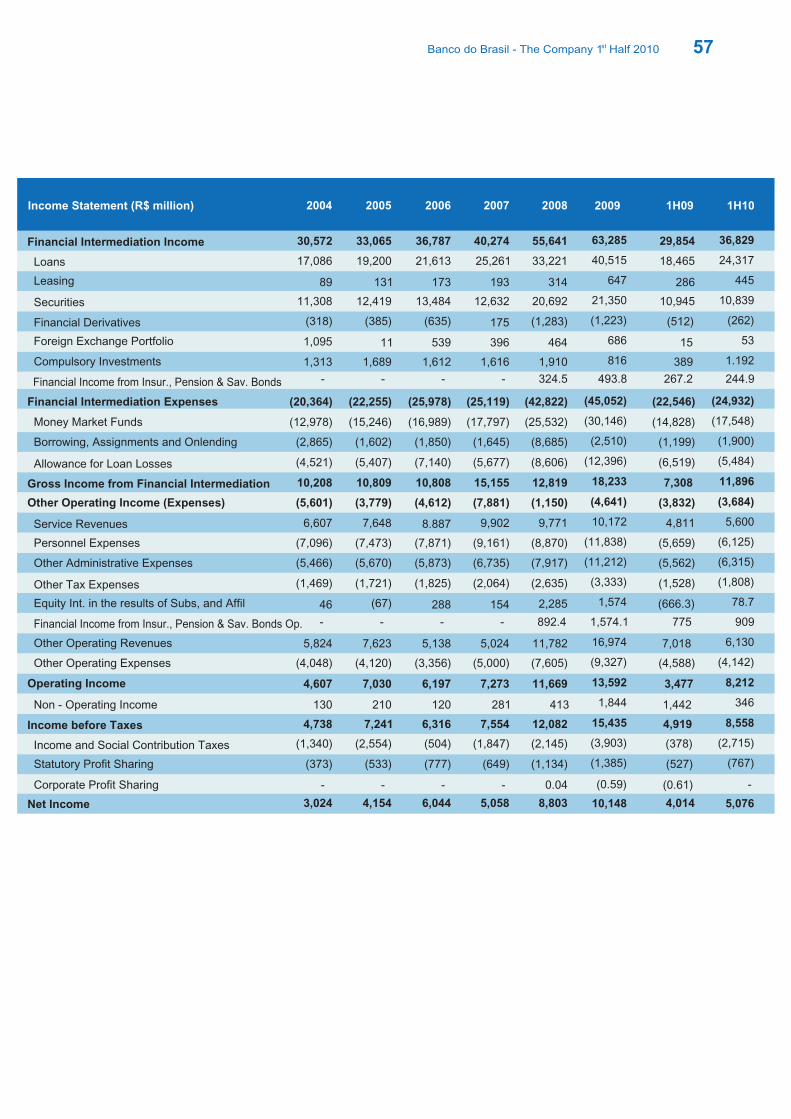

13. Banco do Brasil Figures

Distribution Network Abroad

Contact List

03

09

12

16

19

21

22

25

25

26

27

29

29

30

32

34

37

39

40

41

42

43

47

48

48

48

49

49

50

52

54

55

56

59

63

1Banco do Brasil - The Company 1 Half 2010st

3

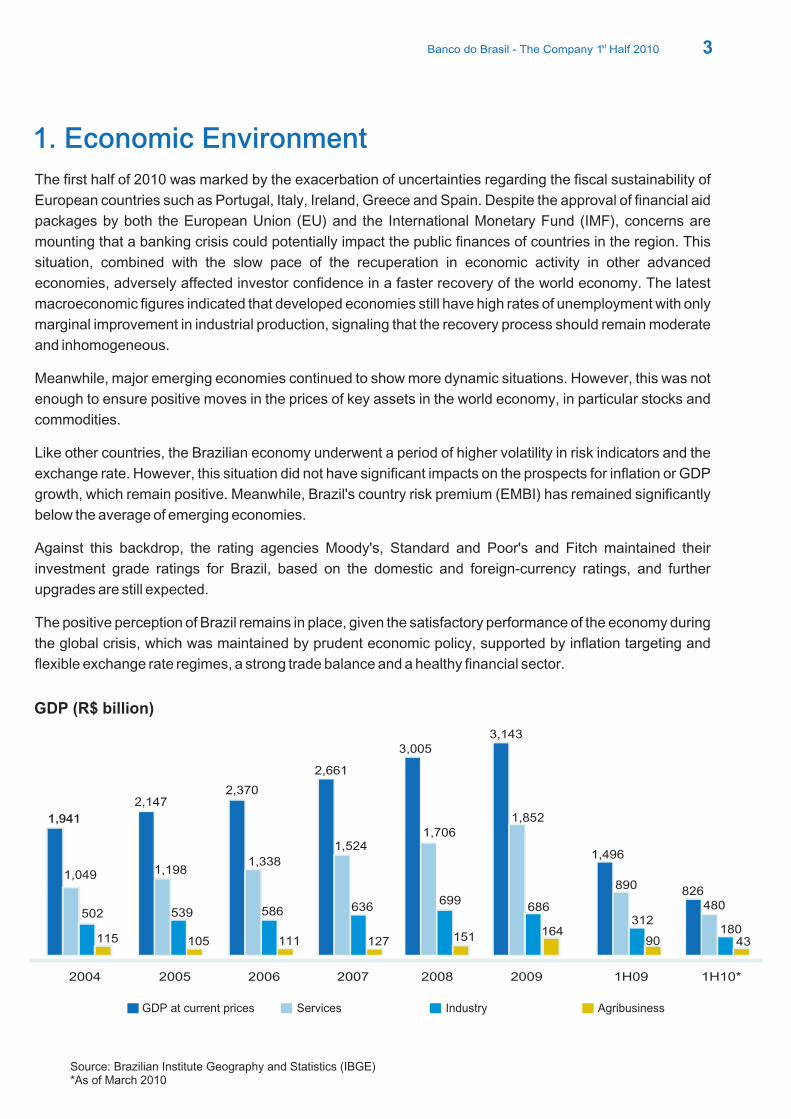

1. Economic Environment

The first half of 2010 was marked by the exacerbation of uncertainties regarding the fiscal sustainability of

European countries such as Portugal, Italy, Ireland, Greece and Spain. Despite the approval of financial aid

packages by both the European Union (EU) and the International Monetary Fund (IMF), concerns are

mounting that a banking crisis could potentially impact the public finances of countries in the region. This

situation, combined with the slow pace of the recuperation in economic activity in other advanced

economies, adversely affected investor confidence in a faster recovery of the world economy. The latest

macroeconomic figures indicated that developed economies still have high rates of unemployment with only

marginal improvement in industrial production, signaling that the recovery process should remain moderate

and inhomogeneous.

Meanwhile, major emerging economies continued to show more dynamic situations. However, this was not

enough to ensure positive moves in the prices of key assets in the world economy, in particular stocks and

commodities.

Like other countries, the Brazilian economy underwent a period of higher volatility in risk indicators and the

exchange rate. However, this situation did not have significant impacts on the prospects for inflation or GDP

growth, which remain positive. Meanwhile, Brazil's country risk premium (EMBI) has remained significantly

below the average of emerging economies.

Against this backdrop, the rating agencies Moody's, Standard and Poor's and Fitch maintained their

investment grade ratings for Brazil, based on the domestic and foreign-currency ratings, and further

upgrades are still expected.

The positive perception of Brazil remains in place, given the satisfactory performance of the economy during

the global crisis, which was maintained by prudent economic policy, supported by inflation targeting and

flexible exchange rate regimes, a strong trade balance and a healthy financial sector.

Source: Brazilian Institute Geography and Statistics (IBGE)*As of March 2010

GDP at current prices Services Industry Agribusiness

GDP (R$ billion)

2004

1,941

1,049

502

115

3,005

2,147

1,198

539

105

2005

2,370

1,338

586

111

2006

2,661

1,524

636

127

2007

1,706

699

151

2008

3,143

1,852

686

164

2009

1,496

890

312

90

826480

1H09 1H10*

18043

Banco do Brasil - The Company 1 Half 2010st

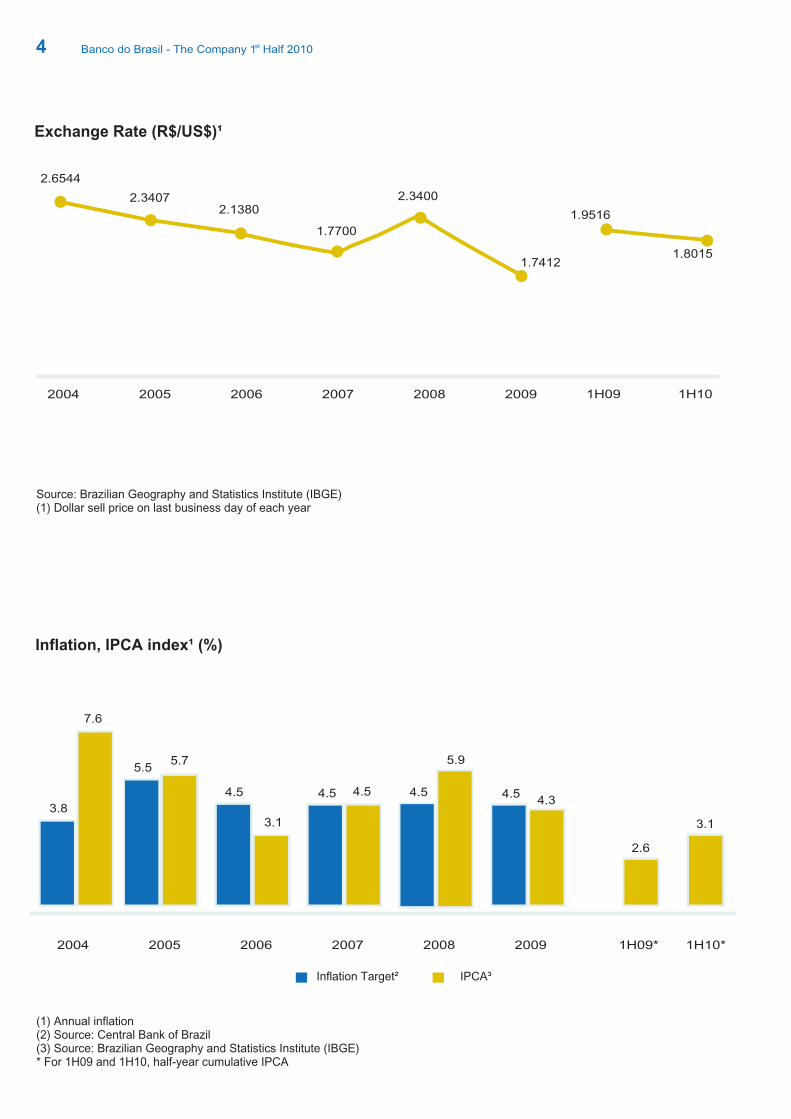

Exchange Rate (R$/US$)¹

Inflation, IPCA index¹ (%)

Source: Brazilian Geography and Statistics Institute (IBGE)(1) Dollar sell price on last business day of each year

(1) Annual inflation(2) Source: Central Bank of Brazil(3) Source: Brazilian Geography and Statistics Institute (IBGE)* For 1H09 and 1H10, half-year cumulative IPCA

Inflation Target² IPCA³

4

2004 2005 2006 2007 2008 2009

2.6544

2.34072.1380

1.7700

2.3400

1.7412

1.9516

1.8015

1H09 1H10

2004 2005 2006 2007 2008 2009

3.8

7.6

62,8

118,5

73,8

5.75.5

3.1

4.5 4.5 4.5 4.5

5.9

4.54.3

2.6

3.1

1H09* 1H10*

Banco do Brasil - The Company 1 Half 2010st

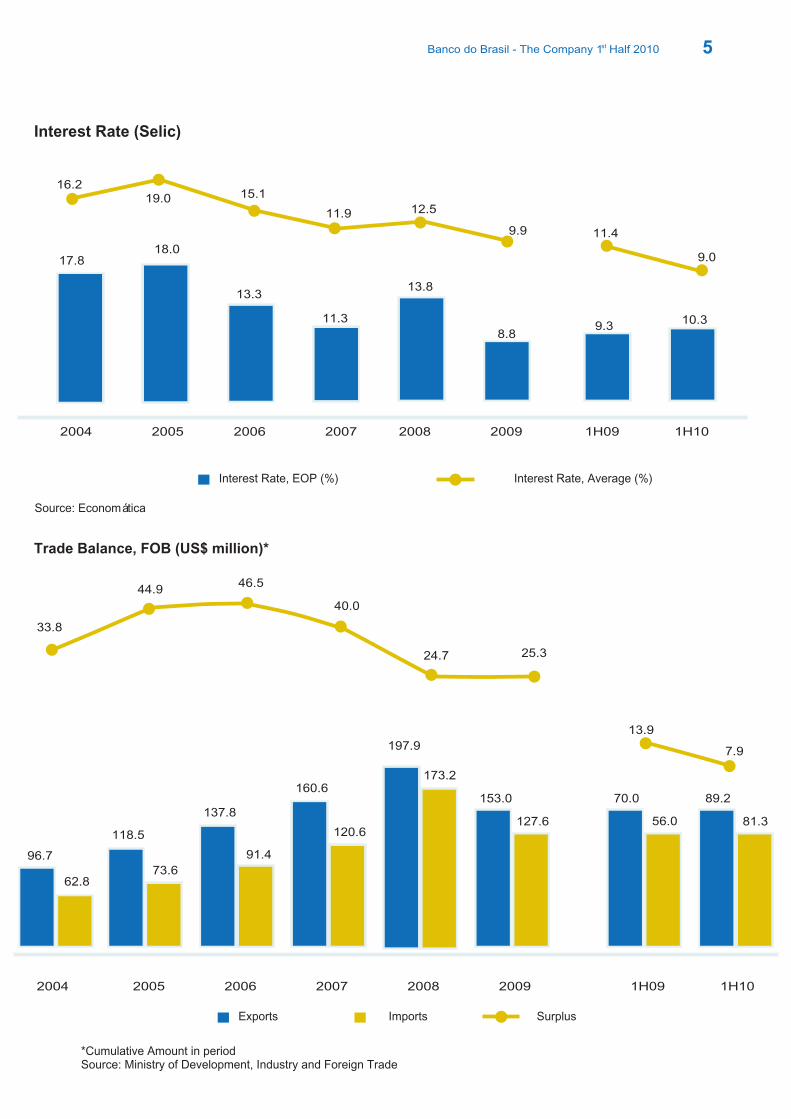

Interest Rate (Selic)

Trade Balance, FOB (US$ million)*

Source: Economática

*Cumulative Amount in periodSource: Ministry of Development, Industry and Foreign Trade

9.9

19.016.2

15.1

11.9 12.5

Interest Rate, EOP (%) Interest Rate, Average (%)

33.8

44.946.5

40.0

24.7 25.3

5

Exports Imports

11.4

9.017.818.0

13.3

11.3

13.8

2004 2005 2006 2007 2008 2009

8.89.3

10.3

1H09 1H10

13.9

7.9197.9

2004 2005 2006 2007 2008 2009

96.7

62.8

118.5

73.6

137.8

91.4

160.6

120.6

173.2

153.0

127.6

70.0

56.0

89.2

81.3

1H09 1H10

Surplus

Banco do Brasil - The Company 1 Half 2010st

Brazil Sovereign Risk¹

Internacional Reserves (US$ billion)

(1) End of periodSource: Bloomberg

Source: Central Bank of Brazil

6

383

305

193222

416

196

281

251

2004 2005 2006 2007 2008 2009 1H09 1H10

2004 2005 2006 2007 2008 2009

52.9 53.8

85.8

180.3

206.8

239.1253.1

208.4

1H09 1H10

Banco do Brasil - The Company 1 Half 2010st

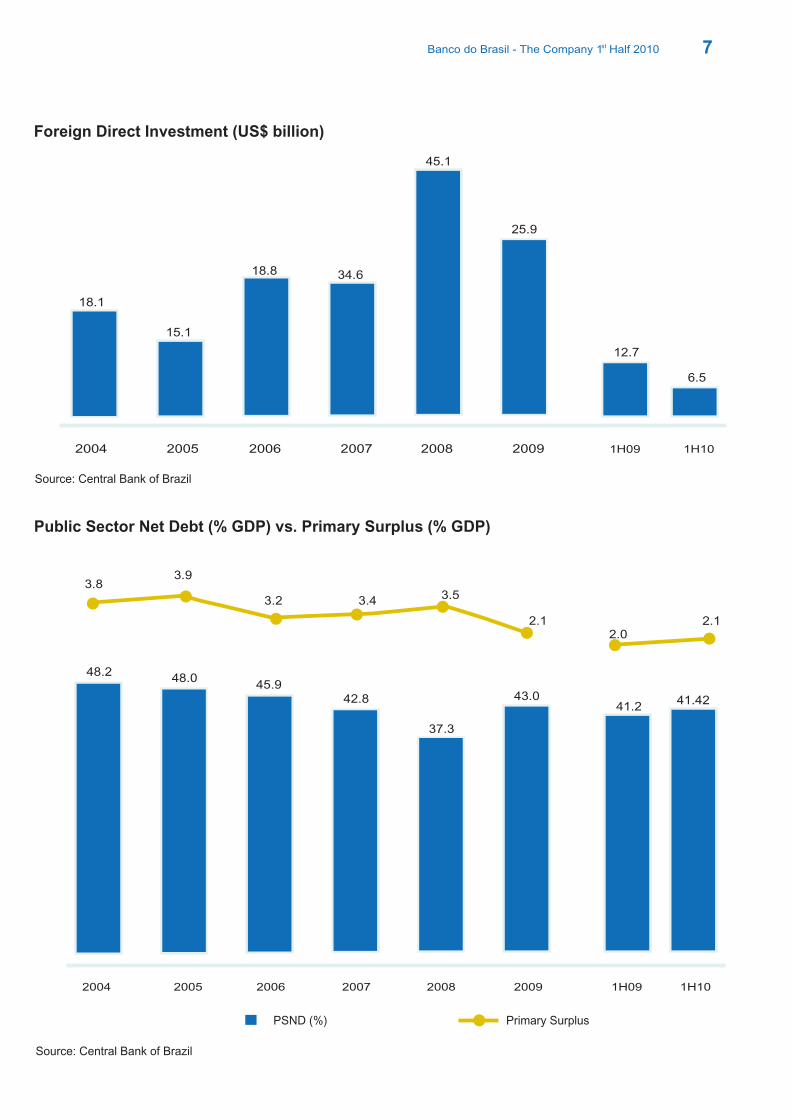

Foreign Direct Investment (US$ billion)

Public Sector Net Debt (% GDP) vs. Primary Surplus (% GDP)

Source: Central Bank of Brazil

Source: Central Bank of Brazil

PSND (%) Primary Surplus

18.1

15.1

18.8 34.6

45.1

25.9

2004 2005 2006 2007 2008 2009

12.7

6.5

1H09 1H10

3.83.9

3.2 3.4 3.5

2.12.0

2.1

48.248.0

45.942.8

37.3

43.0

2004 2005 2006 2007 2008 2009

41.241.42

1H09 1H10

7Banco do Brasil - The Company 1 Half 2010st

8

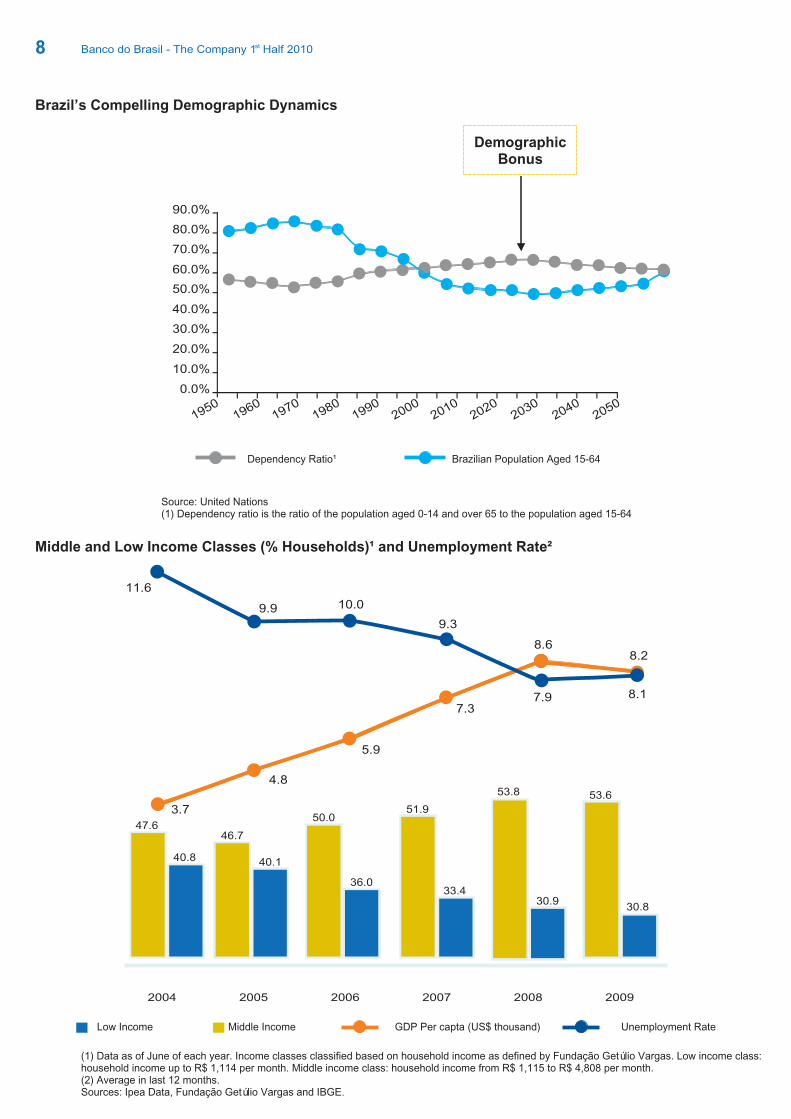

Brazil’s Compelling Demographic Dynamics

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

19501960

19701980

19902000

20102020

20302040

2050

Dependency Ratio¹ Brazilian Population Aged 15-64

Source: United Nations(1) Dependency ratio is the ratio of the population aged 0-14 and over 65 to the population aged 15-64

Middle and Low Income Classes (% Households)¹ and Unemployment Rate²

2004 2005 2006 2007 2008 2009

47.6

40.8

46.7

40.1

50.0

36.0

51.9

33.4

53.8

30.9

53.6

30.8

(1) Data as of June of each year. Income classes classified based on household income as defined by Fundação Getúlio Vargas. Low income class:household income up to R$ 1,114 per month. Middle income class: household income from R$ 1,115 to R$ 4,808 per month.(2) Average in last 12 months.Sources: Ipea Data, Fundação Getúlio Vargas and IBGE.

Low Income Middle Income GDP Per capta (US$ thousand) Unemployment Rate

11.6

9.9 10.0

9.3

8.68.2

8.17.97.3

5.9

4.8

3.7

DemographicBonus

Banco do Brasil - The Company 1 Half 2010st

9

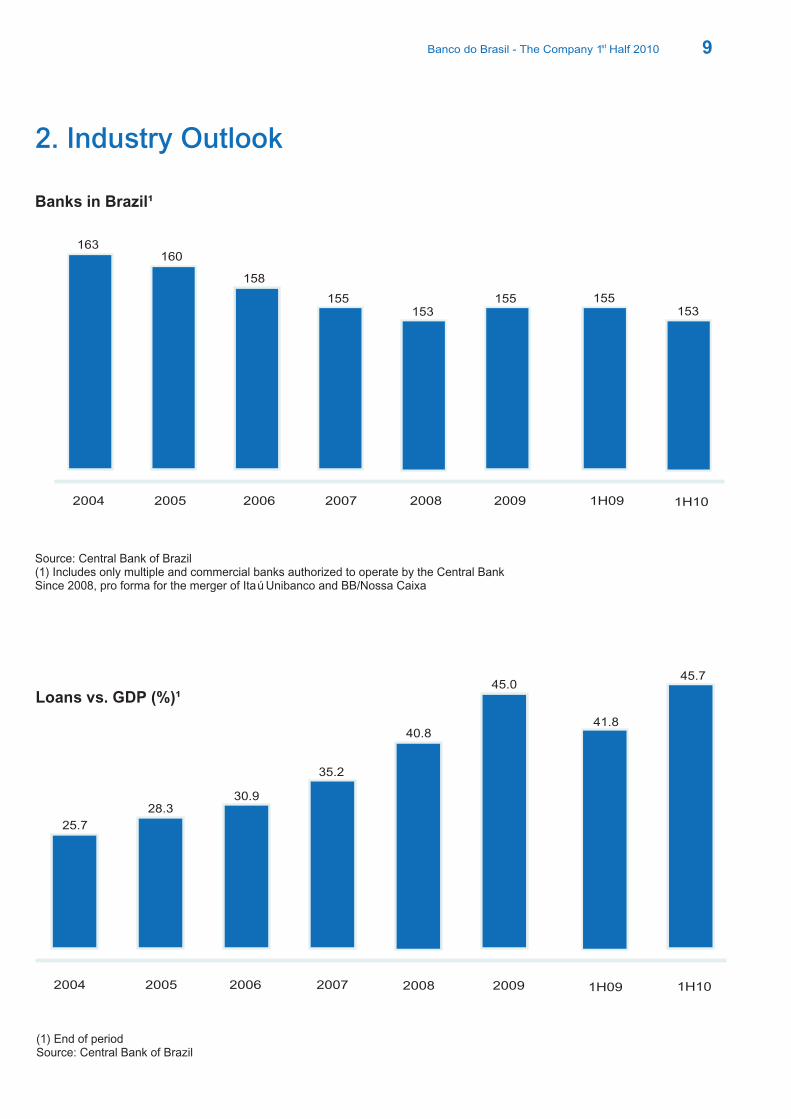

Banks in Brazil¹

(1) End of periodSource: Central Bank of Brazil

2. Industry Outlook

Loans vs. GDP (%)¹

Source: Central Bank of Brazil(1) Includes only multiple and commercial banks authorized to operate by the Central BankSince 2008, pro forma for the merger of Itaú Unibanco and BB/Nossa Caixa

2004 2005 2006 2007 2008 2009

163160

158

155153

1H09 1H10

155 155153

2004 2005 2006 2007 2008 2009

25.7

28.330.9

35.2

40.8

45.0

1H09 1H10

41.8

45.7

Banco do Brasil - The Company 1 Half 2010st

10

Loans by Segment, Free Resources (%)

Source: Central Bank of Brazil

Individuals Businesses

Main Individual Loan Operations

Source: Central Bank of Brazil

2004 2005 2006 2007 2008 2009

56.4

43.6

52.8 52.2 51.9 54.7 50.8

47.2 47.8 48.1 45.3 49.2

1H09 1H10

51.7 50.3

48.3 49.7

(R$ million) 2004 2005 2006 2007 2008 200949,356

17,151

38,065

8,027

9,800

105,428

70,739

31,704

50,685

11,260

10,974

143,658

88,710

48,149

63,475

13,418

11,760

177,363

100,928

64,686

81,481

17,150

12,985

317,561

133,025

78,890

139,145

22,088

16,040

394,287

164,323

107,883

157,950

25,699

15,790

469,863

Direct Consumer Credit

Payroll Loan

Vehicles

Credit Cards

Overdraft Account

Total (Free Resources)

1H09 1H10149,429

91,826

147,460

25,386

17,877

434,331

186,133

123,438

157,950

28,558

17,939

505,733

Banco do Brasil - The Company 1 Half 2010st

11

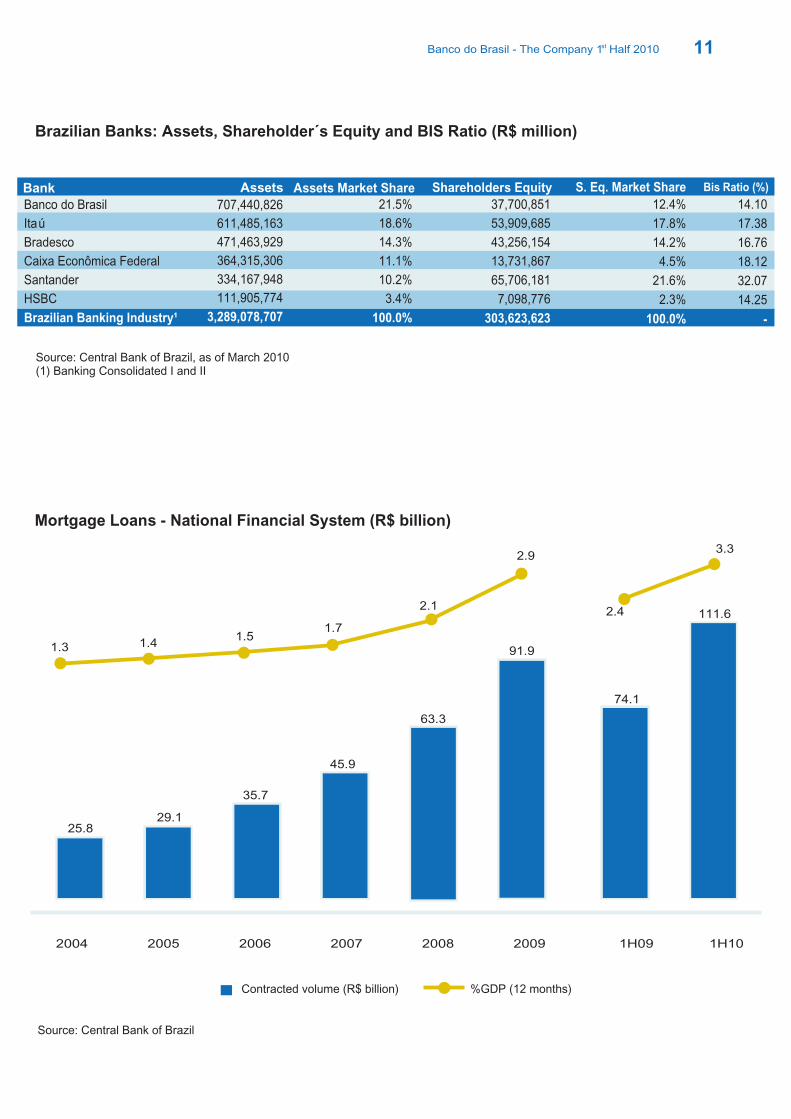

Brazilian Banks: Assets, Shareholder´s Equity and BIS Ratio (R$ million)

Source: Central Bank of Brazil, a(1) Banking Consolidated I and II

s of March 2010

Bank Assets Assets Market Share Shareholders Equity

707,440,826

611,485,163

471,463,929

364,315,306

334,167,948

111,905,774

3,289,078,707

21.5%

18.6%

14.3%

11.1%

10.2%

3.4%

100.0%

37,700,851

53,909,685

43,256,154

13,731,867

65,706,181

7,098,776

303,623,623

S. Eq. Market Share

12.4%

17.8%

14.2%

4.5%

21.6%

2.3%

100.0%

Bis Ratio (%)

14.10

17.38

16.76

18.12

32.07

14.25

-

Banco do Brasil

Itaú

Bradesco

Caixa Econômica Federal

Santander

HSBC

Brazilian Banking Industry¹

Mortgage Loans - National Financial System (R$ billion)

Source: Central Bank of Brazil

1.3 1.41.5

1.7

2.1

2.9

Contracted volume (R$ billion) %GDP (12 months)

2.4

3.3

2004 2005 2006 2007 2008 2009

25.829.1

91.9

35.7

45.9

63.3

1H09 1H10

74.1

111.6

Banco do Brasil - The Company 1 Half 2010st

12

3. Banco do Brasil positioning

Profile

Banco do Brasil is the largest bank in Latin America in terms of total assets as of June 30, 2010. It is a multiple-service bank with headquarters in Brasília and has a significant presence throughout Brazil, while also conducting operations in key global economic and financial centers. To expand its operations abroad, BB announced an agreement to acquire a controlling interest in Banco Patagonia in Argentina. BB was also authorized by the U.S. Federal Reserve to perform banking activities in U.S. territory.

The Bank focuses on sustainable results and performance that are compatible with its market leadership. BB acts as an agent of Brazil's federal government to implement its policies and programs involving agribusiness, small and micro businesses and foreign trade, as well as for the development of solutions that simplify the operations and services that cater to these economic sectors.

With over 200 years of operations, BB's principal strength is in Brazil's retail banking market, and its business can be grouped generally into seven general areas: banking services, investments, asset management, insurance, pension and financing, payment services and other businesses. The main activities of each segment are as follows:

Banking services: offering banking services to all customer segments;

Investments: investments in insurers and companies operating in the pension sector;

Asset management: administration and management of third-party assets, organization and administration of investment and other funds, management of portfolios and custody of marketable securities;

Insurance: health, life, financial, vehicle and agricultural;

Pension plans and financing: sale of private pension products and administration of pension plans;

Payment services: commercial payment services under corporate benefit plans, including meal, transportation and fuel plans; and

Other businesses, including:

· Acquisitions and management of bank real estate credit and leasing operations; · Investments in electric power;· Leasing of properties and other assets;· Management of consortium groups; and· Sales, installations and maintenance of computers and other electronic devices.

Mission: To be the solution in financial services and intermediation, to meet the expectations of customersand shareholders, to strengthen the commitment between employees and the Bank, and to

contribute to Brazil's development

Banco do Brasil - The Company 1 Half 2010st

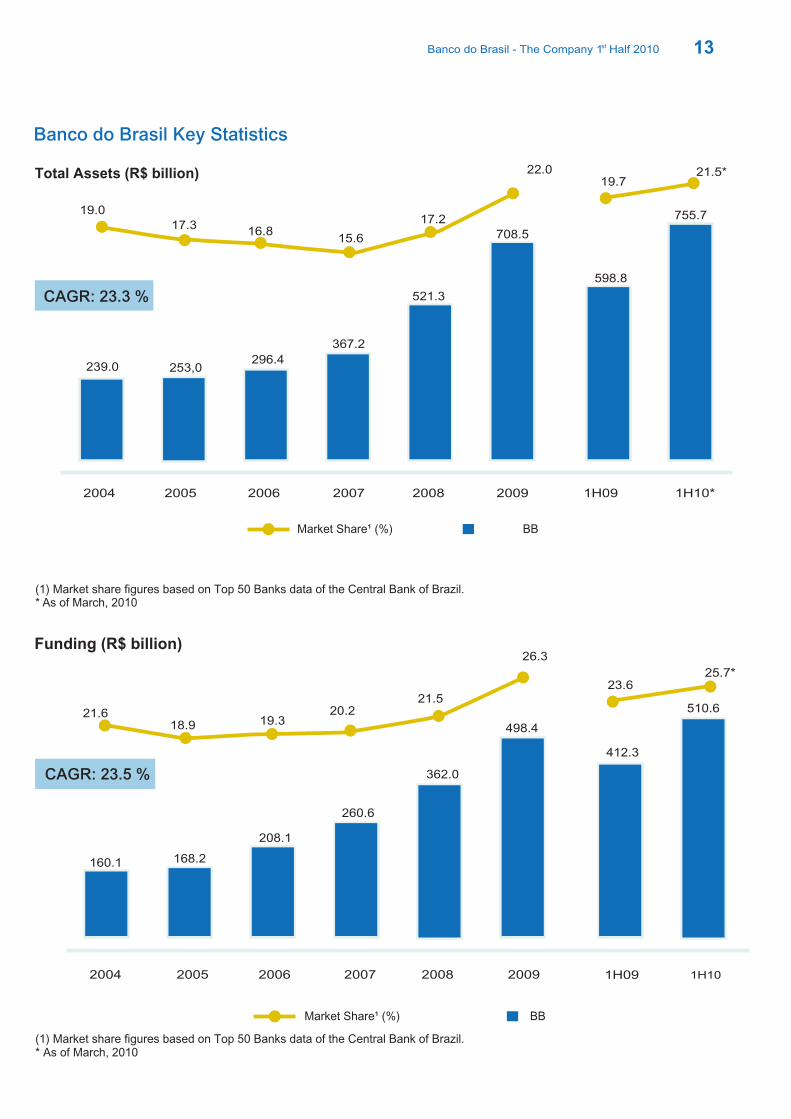

Total Assets (R$ billion)

Funding (R$ billion)

(1) Market share figures based on Top 50 Banks data of the Central Bank of Brazil. * As of March, 2010

(1) Market share figures based on Top 50 Banks data of the Central Bank of Brazil.* As of March, 2010

2004 2005 2006 2007 2008 2009

Banco do Brasil Key Statistics

13

19.0

17.316.8

15.6

17.2

22.0

21.618.9 19.3

20.221.5

26.3

Market Share¹ (%) BB

Market Share¹ (%) BB

19.721.5*

CAGR: 23.3 %

2004 2005 2006 2007 2008 2009

521.3

708.5

367.2

296.4253,0239.0

1H09 1H10*

598.8

755.7

1H09 1H10

160.1 168.2

208.1

260.6

362.0

498.4

CAGR: 23.5 %

412.3

510.6

23.625.7*

Banco do Brasil - The Company 1 Half 2010st

14

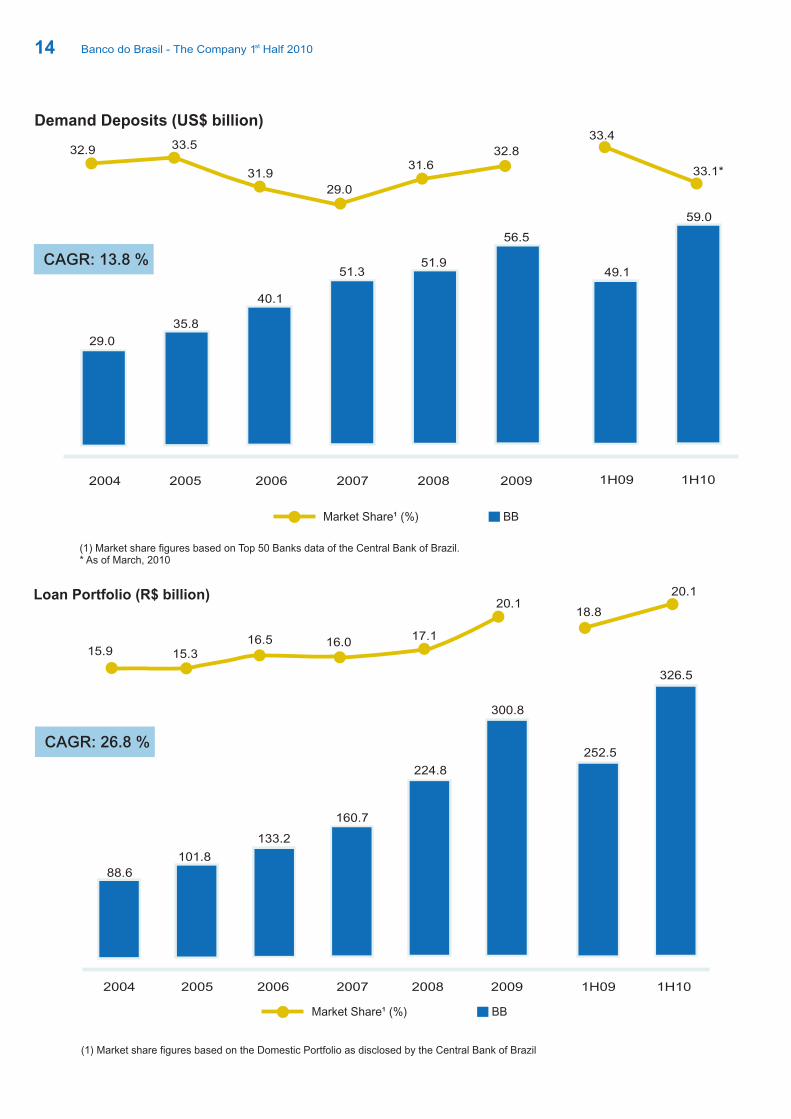

Demand Deposits (US$ billion)

Loan Portfolio (R$ billion)

(1) Market share figures based on the Domestic Portfolio as disclosed by the Central Bank of Brazil

(1) Market share figures based on Top 50 Banks data of the Central Bank of Brazil.* As of March, 2010

CAGR: 26.8 %

Market Share¹ (%) BB

CAGR: 13.8 %

32.9 33.5

31.9

29.0

31.632.8

29.0

35.8

40.1

51.351.9

56.5

2004 2005 2006 2007 2008 2009

49.1

59.0

1H09 1H10

33.4

33.1*

15.9 15.316.5 16.0

17.1

20.1

Market Share¹ (%) BB

88.6

101.8

133.2

160.7

224.8

300.8

2004 2005 2006 2007 2008 2009

252.5

326.5

1H09 1H10

18.8

20.1

Banco do Brasil - The Company 1 Half 2010st

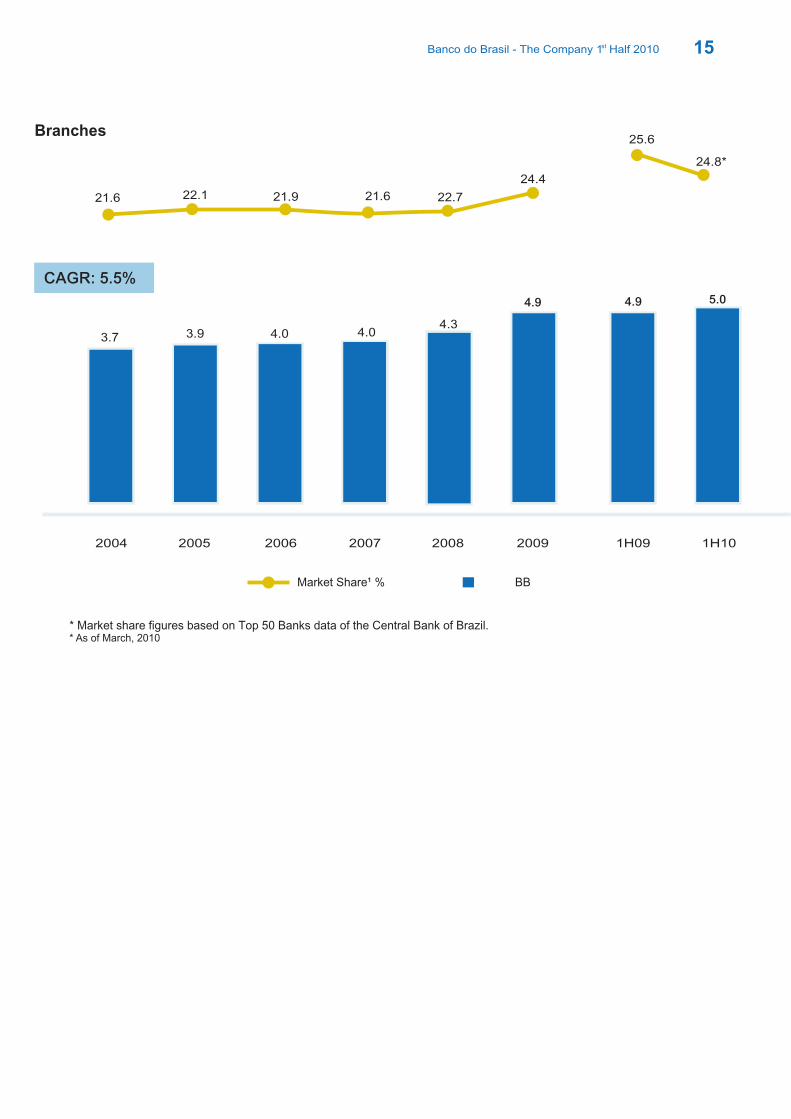

Branches

* Market share figures based on Top 50 Banks data of the Central Bank of Brazil.* As of March, 2010

21.6 22.1 21.9 21.6 22.7

24.4

15

Market Share¹ % BB

CAGR: 5.5%

2004 2005 2006 2007 2008 2009

3.7 3.9 4.0 4.04.3

4.9

1H09 1H10

5.04.9

25.6

24.8*

Banco do Brasil - The Company 1 Half 2010st

16

4. Financial Performance

In 1H10, Banco do Brasil recorded net income of R$ 5.1 billion and return on equity of 28.7%, which corresponds to earnings per share of R$ 1.98. Shareholders' equity increased 21.5% from the same period in 2009 to R$ 39.3 billion.

Net Income vs. ROE

Net Interest Income (NII) vs. Net Interest Margin (NIM)

15,48416,709

18,107

20,807

24,515

33,060

8.48.6

8.17.6

7.06.7

ROE % Net Income (R$ million)

NIM¹ (%) Net Interest Income¹ (R$ million)

23.026.8

32.1

22.5

32.530.7

2004 2005 2006 2007 2008 2009

3,024

4,154

6,0445,058

8,803

10,148

2004 2005 2006 2007 2008 2009

4,014

5,076

1H09 1H10

27.4 28.7

15,472

18,817

1H09 1H10

6.9

6.4

(1) Income statement with reallocations

Banco do Brasil - The Company 1 Half 2010st

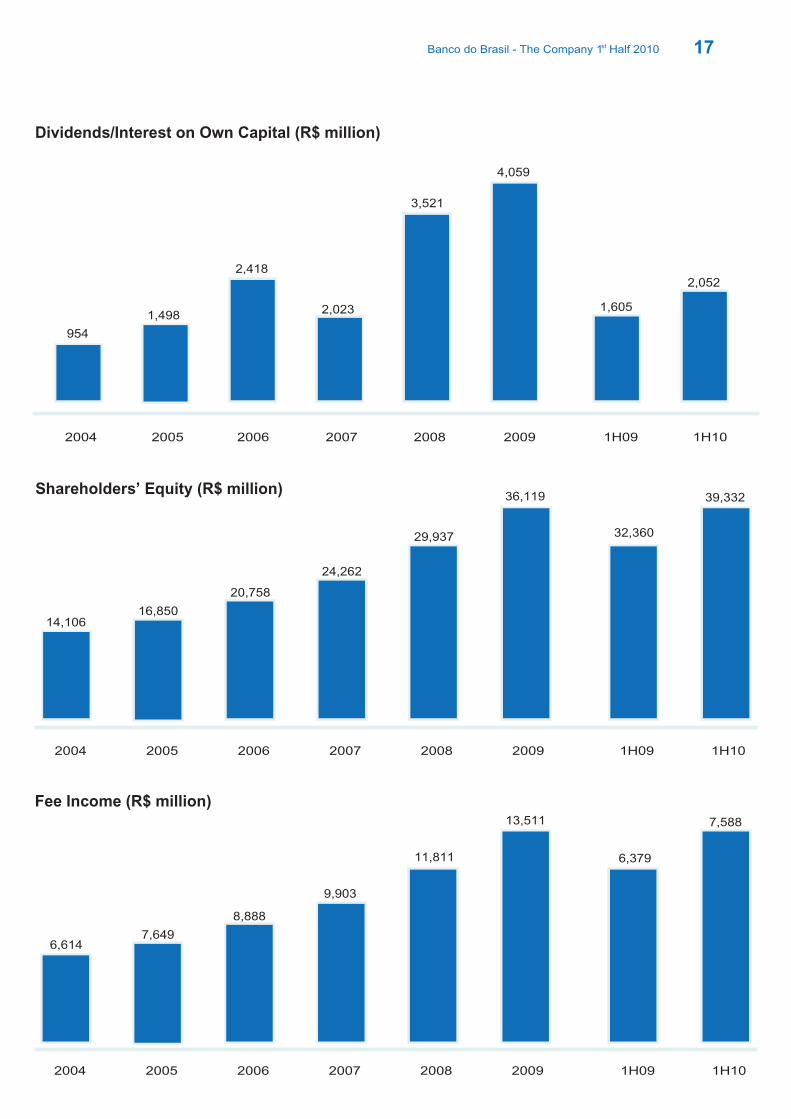

Dividends/Interest on Own Capital (R$ million)

Shareholders’ Equity (R$ million)

Fee Income (R$ million)

17

2004 2005 2006 2007 2008 2009

3,521

4,059

2,023

2,418

1,498

954

1H09 1H10

1,605

2,052

2004 2005 2006 2007 2008 2009

29,937

36,119

24,262

20,758

16,85014,106

1H09 1H10

32,360

39,332

2004 2005 2006 2007 2008 2009

11,811

13,511

9,903

8,888

7,6496,614

1H09 1H10

6,379

7,588

Banco do Brasil - The Company 1 Half 2010st

18

Administrative Expenses (R$ million)

Cost / Income Ratio (%)¹

Coverage Ratio (%)¹ ²,

2004 2005 2006 2007 2008 2009

136.2

128.2127.7

112.9

102.393.1

2004 2005 2006 2007 2008 2009

16,787

23,050

15,902

13,74513,14712,595

1H09 1H10

11,221

12,441

2004 2005 2006 2007 2008 2009

45.6

40.7

46.247.5

48.1

54.2

1H09 1H10

42.143.5

1H09 1H10

134.7121.0

(1) Does not include one-off items(2) Fee Income/Personnel Expenses

,

Banco do Brasil - The Company 1 Half 2010st

19

5. Banco do Brasil Stock

Banco do Brasil stock ended the first half of the year quoted at R$ 24.65, for gains of 23.7% in the last 12 months and devaluation of 16.2% in the quarter. Most of the price depreciation is explained by external factors, such as the slowing of the Chinese economy, weak consumer sentiment in the United States and concern with the fiscal sustainability of certain countries in the Euro Zone. Under this scenario, not even the positive projections for the Brazilian economy were sufficient to boost the local stock market.

In June 2010, Banco do Brasil carried out a public share offering. On June 30, after the bookbuilding process, Banco do Brasil stock was priced at R$ 24.65, which was in line with the closing price on that date. A total of 396 million shares were traded in the deal, with 286 million in the primary offer and 110 million in the secondary offer.

The offer amounted to R$ 9.8 billion, including the secondary offer. In the primary offer, the sale of new shares totaled R$ 7.0 billion, which will strength the institution's capital base and support its future growth. The offer also helped BB reach a free float of 30.4%.

In December 2009, Banco do Brasil launched its first American Depositary Receipts (ADR) Level 1 program in New York. On August 2, 2010, BB had 7.5 million outstanding ADRs, quoted at US$ 17.70.

In Brazil, BB stock was traded in all sessions on the São Paulo Stock Exchange (Bovespa) in 2010, with average daily trading volume of R$ 95.7 billion in the period. The stock remained a component of various stock indexes: Ibovespa, IBrX50, IBrX, Special Corporate Governance Index (IGC), Corporate Sustainability Index (ISE) and Special Tag-Along Index (ITAG). In the portfolio for the Ibovespa valid from May to August 2010, Banco do Brasil had the 13 highest weighting.th

Ownership Structure

National Treasury

Previ

Free Float

BNDESPar

National Treasury

Previ

Free Float

BNDESPar

21.8%

2.5%

10.2%65.5% 65.3%

21.9%

2.4%

10.4%

June 30, 2009 June 30, 2010 July 31, 2010¹

National Treasury

Previ

Free Float

BNDESPar

(1) Based on post-offering figures

59.2%

30.4%

0.01%

10.4%

rd

Banco do Brasil - The Company 1 Half 2010st

20

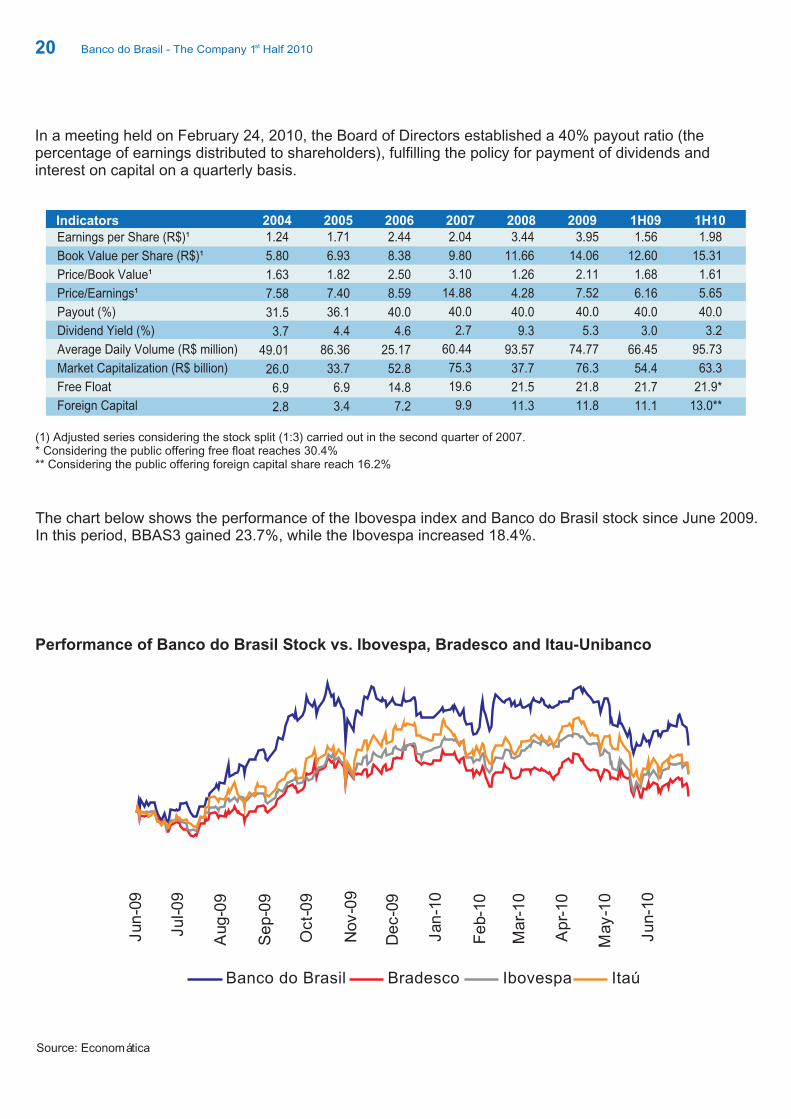

In a meeting held on February 24, 2010, the Board of Directors established a 40% payout ratio (the percentage of earnings distributed to shareholders), fulfilling the policy for payment of dividends and interest on capital on a quarterly basis.

The chart below shows the performance of the Ibovespa index and Banco do Brasil stock since June 2009. In this period, BBAS3 gained 23.7%, while the Ibovespa increased 18.4%.

Performance of Banco do Brasil Stock vs. Ibovespa, Bradesco and Itau-Unibanco

Source: Economática

(1) Adjusted series considering the stock split (1:3) carried out in the second quarter of 2007.* Considering the public offering free float reaches 30.4%** Considering the public offering foreign capital share reach 16.2%

Indicators 2004 2005 2006 2007 2008 20091.24

5.80

1.63

7.58

31.5

3.7

49.01

26.0

6.9

2.8

1.71

6.93

1.82

7.40

36.1

4.4

86.36

33.7

6.9

3.4

2.44

8.38

2.50

8.59

40.0

4.6

25.17

52.8

14.8

7.2

2.04

9.80

3.10

14.88

40.0

2.7

60.44

75.3

19.6

9.9

3.44

11.66

1.26

4.28

40.0

9.3

93.57

37.7

21.5

11.3

3.95

14.06

2.11

7.52

40.0

5.3

74.77

76.3

21.8

11.8

Earnings per Share (R$)¹

Book Value per Share (R$)¹

Price/Book Value¹

Price/Earnings¹

Payout (%)

Dividend Yield (%)

Average Daily Volume (R$ million)

Market Capitalization (R$ billion)

Free Float

Foreign Capital

1H09 1H101.56

12.60

1.68

6.16

40.0

3.0

66.45

54.4

21.7

11.1

1.98

15.31

1.61

5.65

40.0

3.2

95.73

63.3

21.9*

13.0**

Jun

-09

Ju

l-0

9

Aug

-09

Se

p-0

9

Oct-

09

Nov

-09

De

c-0

9

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-10

May

-10

Ju

n-1

0

Banco do Brasil Bradesco Ibovespa Itaú

Banco do Brasil - The Company 1 Half 2010st

21

6. Corporate GovernanceBanco do Brasil, which joined the Novo Mercado special corporate governance listing segment of the São Paulo Stock Exchange (Bovespa) in 2006, is committed to transparency, accountability, equitable treatment and social and environmental responsibility, aligning the organization's management with the interests of shareholders and society. BB has also adopted stricter corporate governance practices, and since the public offering in June, BB stock has reached a free float of 30.4%, above the 25.0% required by Novo Mercado regulations.

BB stock is also a component of the Special Tag-Along Stock Index (ITAG) and Special Corporate Governance Stock Index (IGC), which track the performance of companies with differentiated tag-along rights and corporate governance best practices, respectively.

Banco do Brasil's decisions are taken collectively at all company levels. To involve executives in the

definition and approval of strategies for the company's different businesses, Management draws on

committees, subcommittees and commissions at a strategic level, which imparts greater agility and security

to the decision-making process.

Market relations

Committees, Subcommittees and Commissions - Strategic Level

In the first half of 2010, BB participated in 34 meetings with domestic investors and analysts, five conferences and organized 16 conference calls with analysts and investors. In addition, due to the public offering, the IR Team intensified its participation in national and international roadshows, marking a presence in 14 countries and eight Brazilian cities. BB's Investor Relations program was recognized as one of the best among large companies. BB also provides up-to-date information to shareholders and analysts through its Investor Relations website (bb.com.br/ri).

Liquidy & Risk

Market

Global Risk

Business andCommunication

Superior Inquiry

AuditorsCommitee

Board Of Directors

Credit Limit

Resources

Committee

Subcommittee

Comission

Prevetion ofFinancial and

Exchange FraudOperations

Operations EmployeeAssignment

Operational Administrative

Credit Risk

OperationalRisk

Channels

WorkAgreement

Management Board Management of Assets& Liabilities

and Liquidity

Management of Assets& Liabilities

and Liquidity

InformationSecurity

InformationTechnology

Ethics Superior

States for Ethics

Cost Managementand Operational

Efficiency

Banco do Brasil - The Company 1 Half 2010st

22

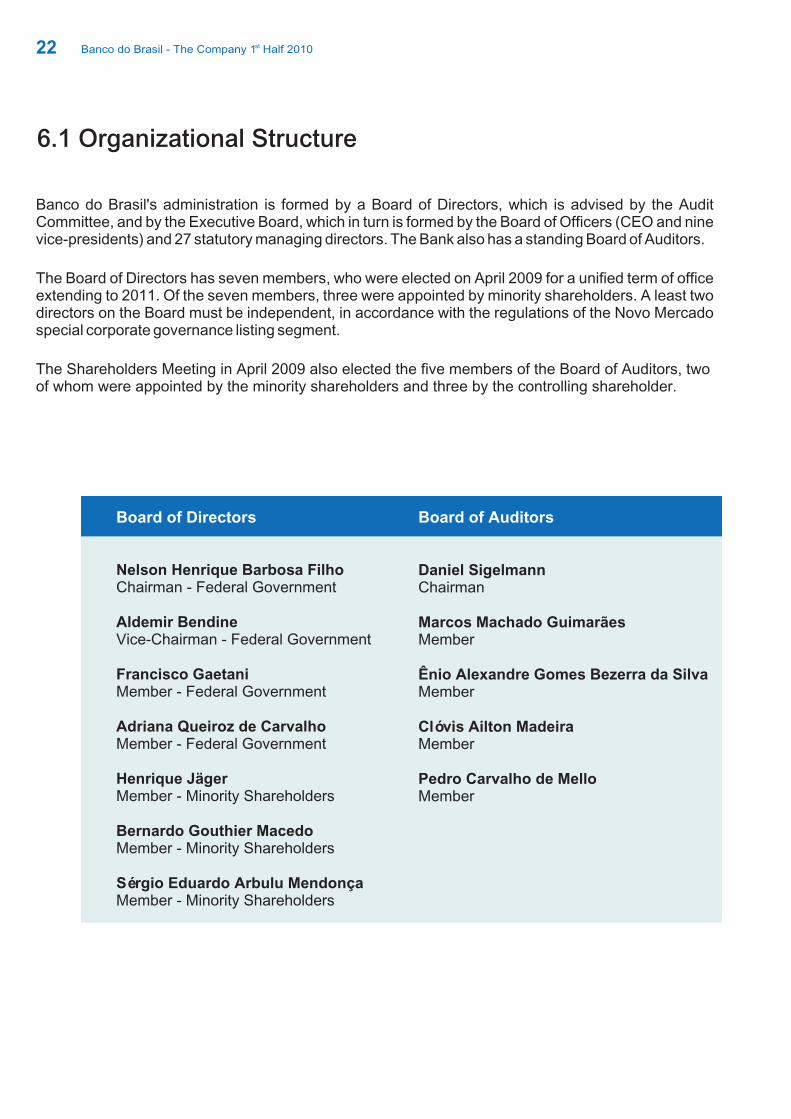

Banco do Brasil's administration is formed by a Board of Directors, which is advised by the Audit Committee, and by the Executive Board, which in turn is formed by the Board of Officers (CEO and nine vice-presidents) and 27 statutory managing directors. The Bank also has a standing Board of Auditors.

The Board of Directors has seven members, who were elected on April 2009 for a unified term of office extending to 2011. Of the seven members, three were appointed by minority shareholders. A least two directors on the Board must be independent, in accordance with the regulations of the Novo Mercado special corporate governance listing segment.

The Shareholders Meeting in April 2009 also elected the five members of the Board of Auditors, two of whom were appointed by the minority shareholders and three by the controlling shareholder.

6.1 Organizational Structure

Nelson Henrique Barbosa FilhoChairman - Federal Government

Aldemir BendineVice-Chairman - Federal Government

Francisco GaetaniMember - Federal Government

Adriana Queiroz de CarvalhoMember - Federal Government

Henrique JägerMember - Minority Shareholders

Bernardo Gouthier MacedoMember - Minority Shareholders

Sérgio Eduardo Arbulu MendonçaMember - Minority Shareholders

Daniel SigelmannChairman

Marcos Machado GuimarãesMember

Ênio Alexandre Gomes Bezerra da SilvaMember

Clóvis Ailton MadeiraMember

Pedro Carvalho de MelloMember

Board of Directors Board of Auditors

Banco do Brasil - The Company 1 Half 2010st

23

Bo

ard

of

Off

icers

Ban

co

do

Bra

sil S

.A.

Org

an

izati

on

al S

tru

ctu

re o

f th

e C

om

merc

ial B

an

k

Inte

rna

l A

ud

it

Dir

ecto

rsh

ips

CE

O

Un

its

Po

sit

ion

: J

un

e 3

0,

20

10

CE

O

of

Inte

rna

tio

na

lB

us

ine

ss

Wh

ole

sa

le

VP

of

Re

tail

Bu

sin

es

s

VP

of

Re

tail

an

dD

istr

ibu

tio

n

VP

of

Ag

rib

us

ine

ss

VP

of

Go

ve

rnm

en

t

VP

of

Fin

an

ce,

Ca

pit

al

Ma

rke

tsa

nd

IR

VP

of

Te

ch

no

log

ya

nd

Lo

gis

tic

s

VP

of

Pe

op

le M

an

ag

em

en

ta

nd

Su

sta

ina

ble

De

ve

lop

me

nt

VP

of

Cre

dit

,C

on

tro

lle

rsh

ipa

nd

Glo

ba

l R

isk

Co

mm

erc

ial

Inte

rna

tio

na

l

Lo

an

s a

nd

Fin

an

cin

g

Ins

ura

nc

e,

Pe

ns

ion

Pla

ns

an

dC

ap

ita

liza

tio

n

Hig

h I

nc

om

e

Ag

rib

us

ine

ss

Go

ve

rnm

en

t

Pe

ns

ion

Fu

nd

Ma

na

ge

me

nt

Fin

an

ce

Ca

pit

al

Ma

rke

ts

an

d I

nv

es

tme

nt

Inv

es

tor

Re

lati

on

s

Lo

gis

tic

s

Te

ch

no

log

y

So

ftw

are

De

ve

lop

me

nt

IT

Infr

ae

str

uc

ture

Op

era

tio

na

l

Su

pp

ort

Pe

op

le

Ma

na

ge

me

nt

Re

lati

on

s w

ith

Em

plo

ye

es

an

d

Sp

on

so

red

En

titi

es

Co

ntr

oll

ers

hip

Cre

dit

Ris

k

Ma

na

ge

me

nt

Re

es

tru

ctu

rin

g

of

Op

era

tio

na

l

As

se

ts

Ac

co

un

tin

g

Inte

rna

l

Co

ntr

ols

Str

ate

gy

Org

an

iza

tio

n

Se

cu

rity

Ma

na

ge

me

nt

Ma

rke

tin

g a

nd

Co

mm

un

ica

tio

n

Ex

ec

uti

ve

Se

cre

tari

at

Mic

ro

an

d S

ma

ll

En

terp

ris

es

Re

tail

Dis

trib

uti

on

Ne

two

rkM

an

ag

em

en

t

Su

sta

ina

ble

De

ve

lop

me

nt

Sã

o P

au

lo

Dis

trib

uti

on

Bo

ard

of

Au

dit

ors

Au

dit

Co

mm

itte

e

Bo

ard

of

Dir

ec

tors

Sh

are

ho

lde

rs G

en

era

l M

ee

tin

g

Dis

trib

uti

on

Ca

rds

Fo

reig

n

Tra

de

VP

an

d

an

d

Le

ga

l

Banco do Brasil - The Company 1 Half 2010st

24

RE

LA

TE

D C

OM

PA

NIE

S /

SH

AR

ES

CO

NT

RO

LL

ED

MA

NA

GE

DF

OU

ND

AT

ION

Po

sitio

n o

n J

une 3

0, 2010

CO

BR

AB

B-9

9.8

8%

ON

99.9

4%

Tota

lB

I-0

.007%

ON

0

.003%

T

ota

l

BB

LE

AS

ING

BB

- 1

00%

ON

100%

Tota

l

BB

CA

RT

ÕE

SB

B -

100%

ON

100%

Tota

l

BB

LE

AS

ING

Co

. L

TD

BB

- 1

00%

ON

1

00%

Tota

l

BB

D

TV

M

B

B -

100%

ON

100%

Tota

l

BB

SE

CU

RIT

IES

BA

MB

-100%

ON

1

00%

Tota

l

BB

TU

RIS

MO

B

AM

B -

99%

ON

BB

Leasi

ng -

1%

ON

100%

Tota

l

AT

IVO

S S

.A.

BB

BI -

49%

ON

74.5

0 %

Tota

lB

AM

B -

51%

ON

25.5

0%

Tota

l

B

AN

CO

DO

BR

AS

IL

BB

PR

EV

IDÊ

NC

IA

Priva

te P

ensi

on E

ntit

y

CA

SS

IP

RE

VI

FB

B

BB

CO

NS

ÓR

CIO

S

BB

-100%

ON

100%

Tota

l 1

00%

Tota

l

BR

AS

ILP

RE

V

49.9

9%

Tota

l

BR

AS

ILS

AÚ

DE

BB

Seguro

s 49.9

2%

ON

4

9.9

2%

Tota

l

BR

AS

ILC

AP

BB

Seguro

s 49.9

9%

ON

BR

AS

ILV

EÍC

UL

OS

BB

Seguro

s 40%

ON

7

0%

Tota

l

S

trate

gic

In

tere

st

Insu

ran

ce G

rou

p

B

B S

EG

UR

OS

CIB

RA

SE

CC

IEL

OC

BS

ST

EC

BA

N

Oth

er

Inte

rest

BB

BI

BB

AL

IAN

ÇA

PA

RT

ICIP

AÇ

ÕE

S

CA

DA

M

No

n-s

tra

teg

ic In

tere

st

S

tra

teg

ic In

tere

st

BA

NC

O

BV

PA

RT

ICIP

AÇ

ÕE

SV

OT

OR

AN

TIM

MA

PF

RE

NO

SS

AC

AIX

A

EB

P

ITA

PE

BI

KE

PL

ER

WE

BE

R

PR

ON

OR

NE

OE

NE

RG

IA

No

n-s

tra

teg

ic In

tere

st

S

trate

gic

In

tere

st

SB

CE

B

B-B

I 9.0

9%

ON

9.0

9%

Tota

lB

B

3.0

3%

ON

3

.03 %

Tota

l

B

B B

I

23.5

4%

O

N

2

3.5

4%

Tota

l

BB

BI

35

.00

%

ON

40

.35

%

To

tal

BB

BI

13

.53

%

ON

13

.53

%%

To

tal

BB

56

.19

% P

N

2

1.6

4%

To

tal

BB

49

.99

% O

N

5

0%

To

tal

B

NC

49

% O

N

49

% T

ota

l

B

B B

I

11.1

1%

O

N

11.1

1 T

ota

l

BB

-BI

19

% O

N

19

% T

ota

l

BB

-BI

1

7.5

7%

ON

17

.55

% T

ota

lB

BD

TV

M

0.0

2%

ON

0

.02

% T

ota

l

BB

1.7

7%

PN

1

.05

% T

ota

lB

B-B

I

5.5

1%

PN

3.2

7%

To

tal

BB

DT

VM

29

.51

% O

N

1

2.0

2%

To

tal

BB

-BI

8.8

1%

ON

8.8

1%

To

tal

BB

-BI

12.0

9%

ON

12.0

9%

Tota

l’’

BB

- C

onglo

mera

te -

Corp

ora

te C

onfig

ura

tion

SP

ON

SO

RE

D

BB

CO

RR

ET

OR

AB

B -

100%

ON

100%

Tota

l

BA

NC

O D

O B

RA

SIL

SE

CU

RIT

IES

L

LC

BB

- 1

00%

ON

100%

Tota

l

BE

SC

AV

AL

BB

– 1

00%

O

N

1

00%

Tota

l

NO

SS

A C

AIX

A A

DM

. D

E C

AR

TÕ

ES

B

B –

100%

ON

1

00%

Tota

l

NO

SS

A C

AIX

A C

AP

ITA

LIZ

AÇ

ÃO

B

B –

100%

ON

100%

Tota

l

BB

AL

IAN

ÇA

Alian

ça d

oB

rasil

BB

BI

BB

- 1

00%

ON

BA

NC

O D

OB

RA

SIL

AG

VIE

NA

BB

-100%

ON

100%

Tota

l

BB

US

A H

OL

DIN

GC

OM

PA

NY

, IN

C.

BB

AG

Vie

na -

100%

ON

100%

Tota

l

BB

MO

NE

Y

TR

AN

SF

ER

S,

INC

.B

B U

SA

Ho

ldC

o-1

00

% O

N

1

00

% T

ota

l

BA

MB

BB

-100%

ON

100%

Tota

l 100%

Tota

l

B

an

co

do

Bra

sil

Natio

nal T

reasu

ry

57.7

358 %

Pre

vi

BN

DE

SP

ar

Indiv

iduals

0.2

918 %

Inve

stim

ents

Guara

nte

e F

und

1.7

511 %

F

ore

ign C

apita

l

Caix

a F

I G

ara

ntia

Const

. N

ava

l

Exp

ort

Guara

nte

e F

und

5.4

244 %

10.3

720 %

2.4

285 %

Caix

a F

GH

AB

Inve

stim

ent

Fund

Com

panie

s

0.0

652 %

5.0

110 %

3.9

003 %

12.9

748 %

Sh

are

s in

Tre

asu

ry0

.04

51

%

BB

AL

IAN

ÇA

PA

RT

ICIP

AÇ

ÕE

SB

B -

100%

ON

100%

Tota

l

PA

RT

ICIP

AÇ

ÕE

S

BB

– 1

00%

O

N

100%

Tota

l

BB

Alia

nça

100%

O

N 1

00%

Tota

l

BB

Seguro

s 4

9.9

9%

ON

100%

PN

74.9

9%

Tota

l

FU

SE

SC

SIM

PR

EB

VE

PE

CO

NO

MU

S

Banco do Brasil - The Company 1 Half 2010st

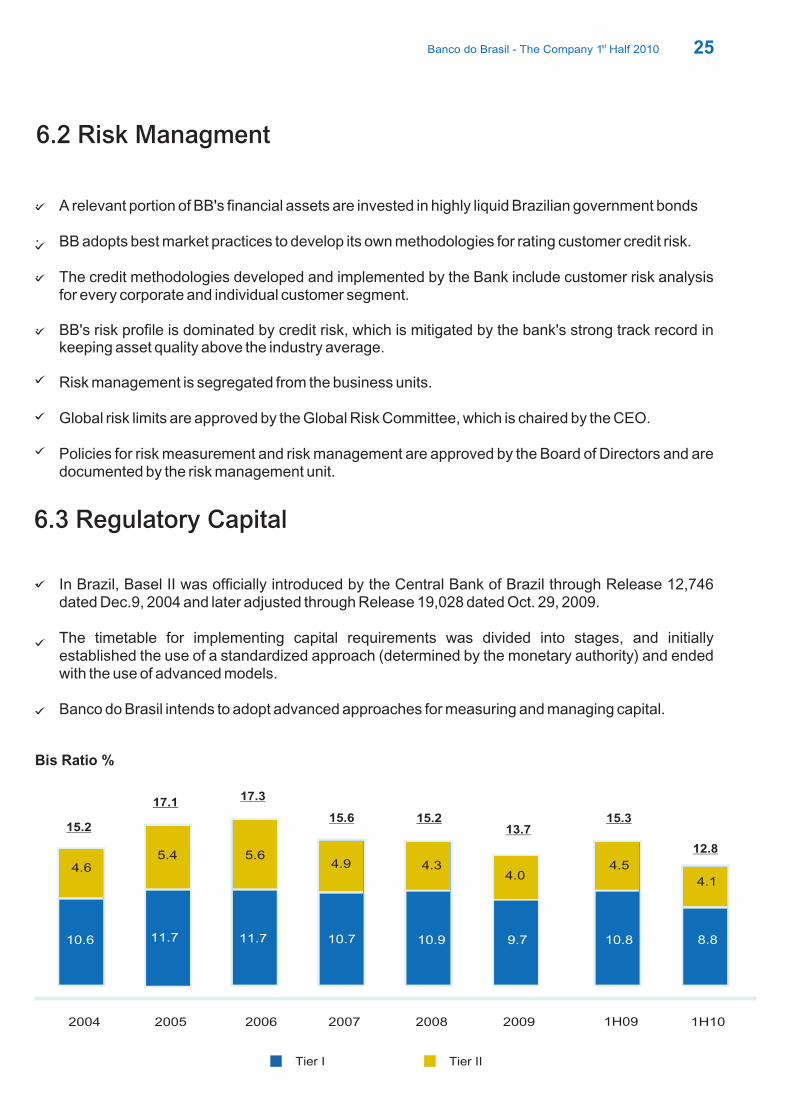

· A relevant portion of BB's financial assets are invested in highly liquid Brazilian government bonds · BB adopts best market practices to develop its own methodologies for rating customer credit risk.

· The credit methodologies developed and implemented by the Bank include customer risk analysis for every corporate and individual customer segment.

· BB's risk profile is dominated by credit risk, which is mitigated by the bank's strong track record in keeping asset quality above the industry average.

· Risk management is segregated from the business units.

· Global risk limits are approved by the Global Risk Committee, which is chaired by the CEO.

Policies for risk measurement and risk management are approved by the Board of Directors and are documented by the risk management unit.

25

6.2 Risk Managment

6.3 Regulatory Capital

· In Brazil, Basel II was officially introduced by the Central Bank of Brazil through Release 12,746 dated Dec.9, 2004 and later adjusted through Release 19,028 dated Oct. 29, 2009.

The timetable for implementing capital requirements was divided into stages, and initially established the use of a standardized approach (determined by the monetary authority) and ended with the use of advanced models.

Banco do Brasil intends to adopt advanced approaches for measuring and managing capital.

Bis Ratio %

Tier I Tier II

17.117.3

15.6 15.215.2

2004 2005 2006 2007 2008 2009

10.6 11.7 11.7 10.7 10.9

4.3

13.7

9.7

4.04.9

5.65.44.6

15.3

1H09 1H10

10.8

4.5

12.8

8.8

4.1

Banco do Brasil - The Company 1 Half 2010st

26

At the end of the first half, Banco do Brasil had 106.2 thousand employees, of which 59.0% were male

and 41.0% female. This workforce presented the following profile:

BB provided 113.6 hours of training per staff member during the year as part of its training program. In

addition, 3,759 employees were granted academic scholarships for undergraduate degrees, 5,307 for

graduate degrees, MBAs and master's degrees and 197 for language studies.

Age (%) Tenure (%) Education (%)

7. Human Resources

BB Stand -alone BNC BESC / BEP

35.7

29.2 25.4

27.5

Up to 5 years

From 6 to 10 years

From 11 to 20 years

Above 20 years

Up to 25 years

From 26 to 35 years

From 36 to 45 years

Above 45 years

46.5

21.9

6.2

21.8

0.629.3

48.3

7.6

Specialization, Master’s or Doctorate

High School

Elementary School

Bachelor’s Degree

Worksforce

79,725

83,751 82,672 81,855

86,059

103,971

14,150

2004 2005 2006 2007 2008 2009

2,818

14,027

87,126 14,150

1H09

3,148

86,316

1H10

106,241

14,150

2,752

12,797

89,194

2,878

106,241

Banco do Brasil - The Company 1 Half 2010st

BB offers a range of products and services that foster businesses which

directly support the country's sustainable development.

The bank provides credit lines and investment funds with environmental

attributes, such as the money market fund BB Referenciado DI Social 50.

BB is a component of the Corporate Sustainability Index (ISE) of the

BM&FBovespa.

27

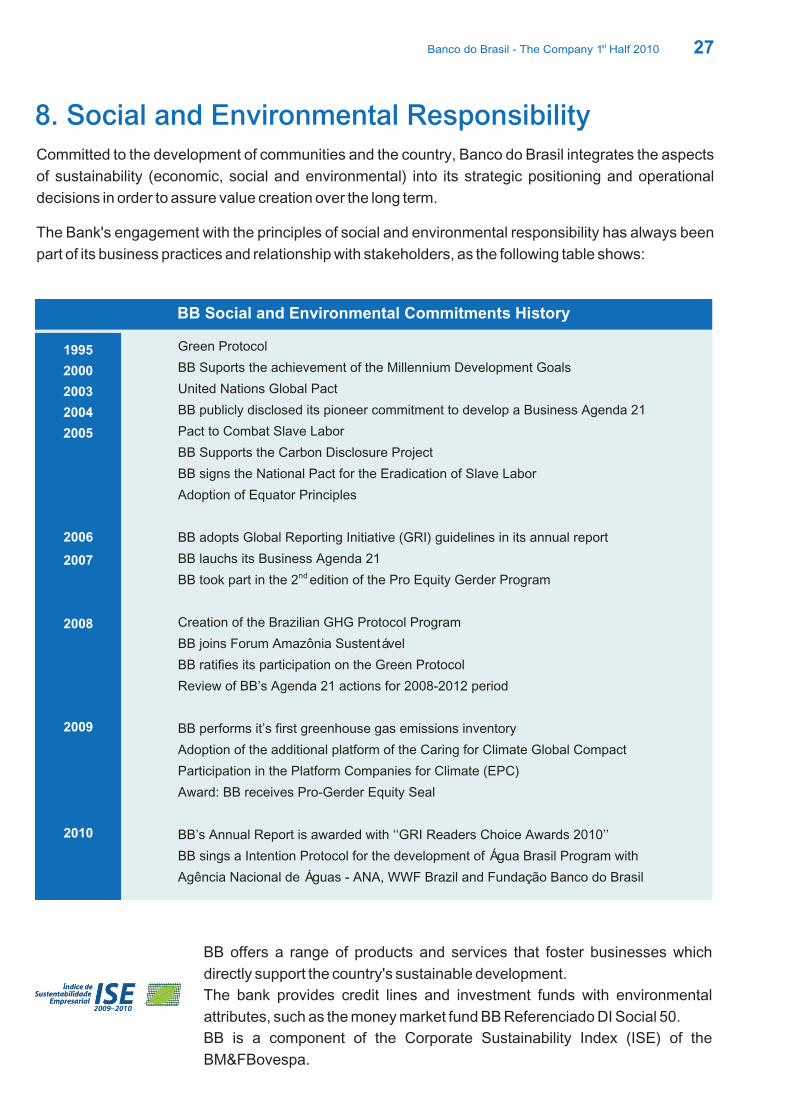

8. Social and Environmental ResponsibilityCommitted to the development of communities and the country, Banco do Brasil integrates the aspects

of sustainability (economic, social and environmental) into its strategic positioning and operational

decisions in order to assure value creation over the long term.

The Bank's engagement with the principles of social and environmental responsibility has always been

part of its business practices and relationship with stakeholders, as the following table shows:

Green Protocol

BB Suports the achievement of the Millennium Development Goals

United Nations Global Pact

BB publicly disclosed its pioneer commitment to develop a Business Agenda 21

Pact to Combat Slave Labor

BB Supports the Carbon Disclosure Project

BB signs the National Pact for the Eradication of Slave Labor

Adoption of Equator Principles

BB adopts Global Reporting Initiative (GRI) guidelines in its annual report

BB lauchs its Business Agenda 21

BB took part in the 2 edition of the Pro Equity Gerder Program

Creation of the Brazilian GHG Protocol Program

BB joins Forum Amazônia Sustentável

BB ratifies its participation on the Green Protocol

Review of BB’s Agenda 21 actions for 2008-2012 period

BB performs it’s first greenhouse gas emissions inventory

Adoption of the additional platform of the Caring for Climate Global Compact

Participation in the Platform Companies for Climate (EPC)

Award: BB receives Pro-Gerder Equity Seal

BB’s Annual Report is awarded with ‘‘GRI Readers Choice Awards 2010’’

BB sings a Intention Protocol for the development of Água Brasil Program with

Agência Nacional de Águas - ANA, WWF Brazil and Fundação Banco do Brasil

1995

2000

2003

2004

2005

BB Social and Environmental Commitments History

nd

2010

2009

2008

2006

2007

Banco do Brasil - The Company 1 Half 2010st

28

Banco do Brasil also innovated by disclosing on a quarterly basis the highlights of its Social and

Environmental Performance, presenting historical data and analyses that give the reader a better

understanding of how sustainability permeates the company's strategy and management. For more

information go to and read Chapter 9 of the MD&A.

An important approach in the area of sustainability is the BB Sustainable Regional Development (SRD)

strategy, which fosters sustainable development in various regions of Brazil, considering their potential,

vocation and characteristics. With the SRD strategy, BB acts not only as a financial institution, but also as a

catalyst to action, encouraging economic and social players to structure urban and rural activities that

generate income for local populations, in partnership with the federal government.

www.bb.com.br/ri

(1) Due to improvements in the SRD methodology, as of 1Q10, the concepts “Beneficiaries - SRD" and “Municipalities Served”were reviewed, which led to the refinement of the strategy basis and qualification of figures.

When granting loans, BB's responsible credit policy does not permit extending credit to companies that submit their

employees to degrading tasks or companies that have any kind of involvement with the sexual exploitation of children

or the use of child labor. In project finance, credit assessment is performed based on the Equator Principles.

In 2007, Banco do Brasil became Brazil's first bank to launch “Agenda 21

Empresarial”, an agenda of commitments that guides the sustainable

performance of companies. The launch was aligned with the commitment of

nations worldwide to put into practice a plan for sustainability in this century.

BB's Agenda 21 is structured around three dimensions: administrative

practices aimed at social and environmental performance, businesses focused

on sustainable development and private social investment. The commitment to

the development of initiatives in each dimension involves several strategic

business units. For more information on BB's Agenda 21 Empresarial, go to

www.bb.com.br.

On July 2010, BB was approved to be included in the F&C Global Emerging Markets Fund.

The fund is formed by shares in companies that contribute to sustainable development in

emerging markets and demonstrate the adoption of recognized standards of corporate

governance and management of the social and environmental impacts generated by its

operations.

1H09

1H10

4,045

4,087

16,483

17,531 3,827

4,739

957,388

1,188,749

727

841

3,664

4,612

4,904

5,355

8,388

5,858

2004

2005

2006

2007

2008

2009

428

1,482

2,502

3,998

4,028

4,073

1,370

4,062

6,052

13,507

14,974

16,886

642

1,503

2,788

4,553

4,787

4,696

327

1,020

1,324

2,466

1,212

711

120

375

1,020

2,829

4,679

4,480

48

169

866

3,099

5,466

5,232

14

105

314

714

4,676

7,803

PeriodAccredited

Branches SRD

Trainings

Municipalities

Served¹SRD

Beneficiaries¹Business Plans in

implementationBB ’s Planned

Funds-R$ million

Funds invested -

R$ million

SRD

under

development

projects

16,820

70,577

230,939

725,450

1,211,368

1,094,086

Banco do Brasil - The Company 1 Half 2010st

29

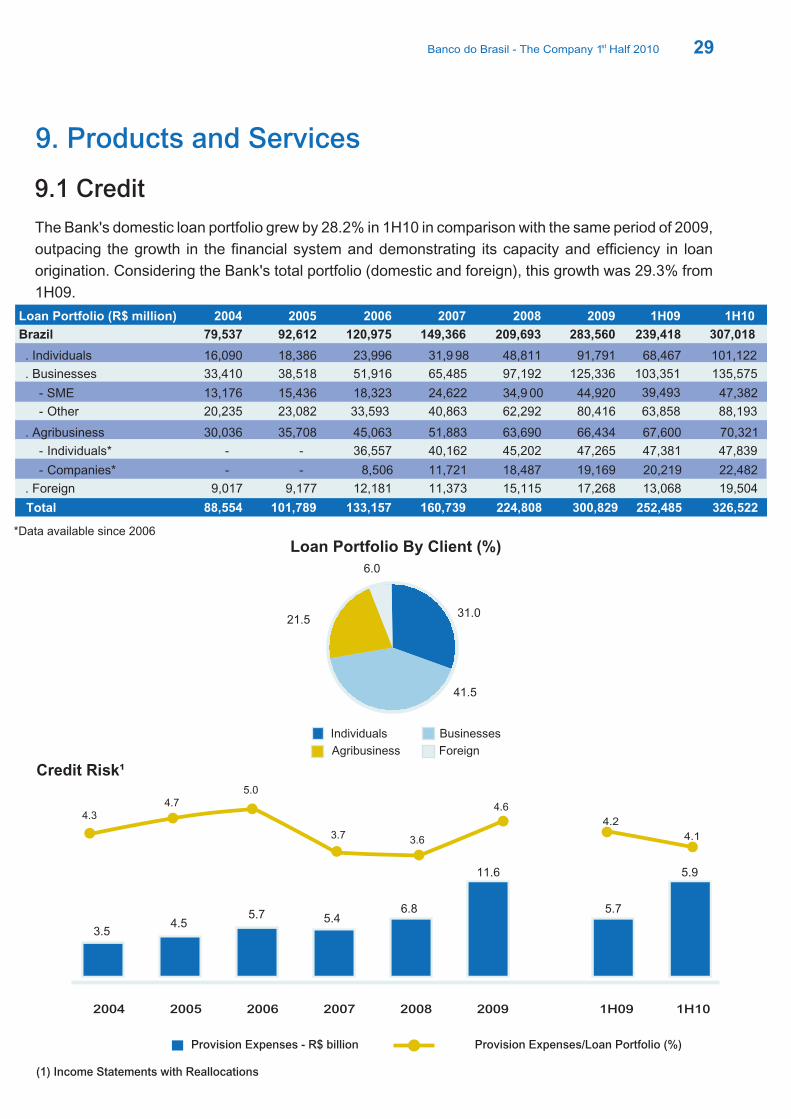

9. Products and Services

The Bank's domestic loan portfolio grew by 28.2% in 1H10 in comparison with the same period of 2009,

outpacing the growth in the financial system and demonstrating its capacity and efficiency in loan

origination. Considering the Bank's total portfolio (domestic and foreign), this growth was 29.3% from

1H09.

9.1 Credit

Loan Portfolio By Client (%)

Individuals Businesses

Agribusiness Foreign

31.0

6.0

21.5

41.5

Credit Risk¹

4.6

3.63.7

5.04.7

4.3

Provision Expenses - R$ billion Provision Expenses/Loan Portfolio (%)

*Data available since 2006

Loan Portfolio (R$ million) 2004 2005 2006 2007 2008 2009

Brazil 79,537 92,612 120,975 149,366 209,693 283,560

. Individuals 16,090 18,386 23,996 31,9 98 48,811 91,791

. Businesses 33,410 38,518 51,916 65,485 97,192 125,336

- SME 13,176 15,436 18,323 24,622 34,9 00 44,920

- Other 20,235 23,082 33,593 40,863 62,292 80,416

. Agribusiness 30,036 35,708 45,063 51,883 63,690 66,434

- Individuals* - - 36,557 40,162 45,202 47,265

- Companies* - - 8,506 11,721 18,487 19,169

. Foreign 9,017 9,177 12,181 11,373 15,115 17,268

Total 88,554 101,789 133,157 160,739 224,808 300,829

1H09 1H10

239,418 307,018

68,467 101,122

103,351 135,575

39,493 47,382

63,858 88,193

67,600 70,321

47,381 47,839

20,219 22,482 13,068 19,504

252,485 326,522

2004 2005 2006 2007 2008 2009

1.7

11.6

3.5 4.5

5.7 5.4 6.8

1H09 1H10

1.7

5.9

5.7

4.2

4.1

(1) Income Statements with Reallocations

Banco do Brasil - The Company 1 Half 2010st

30

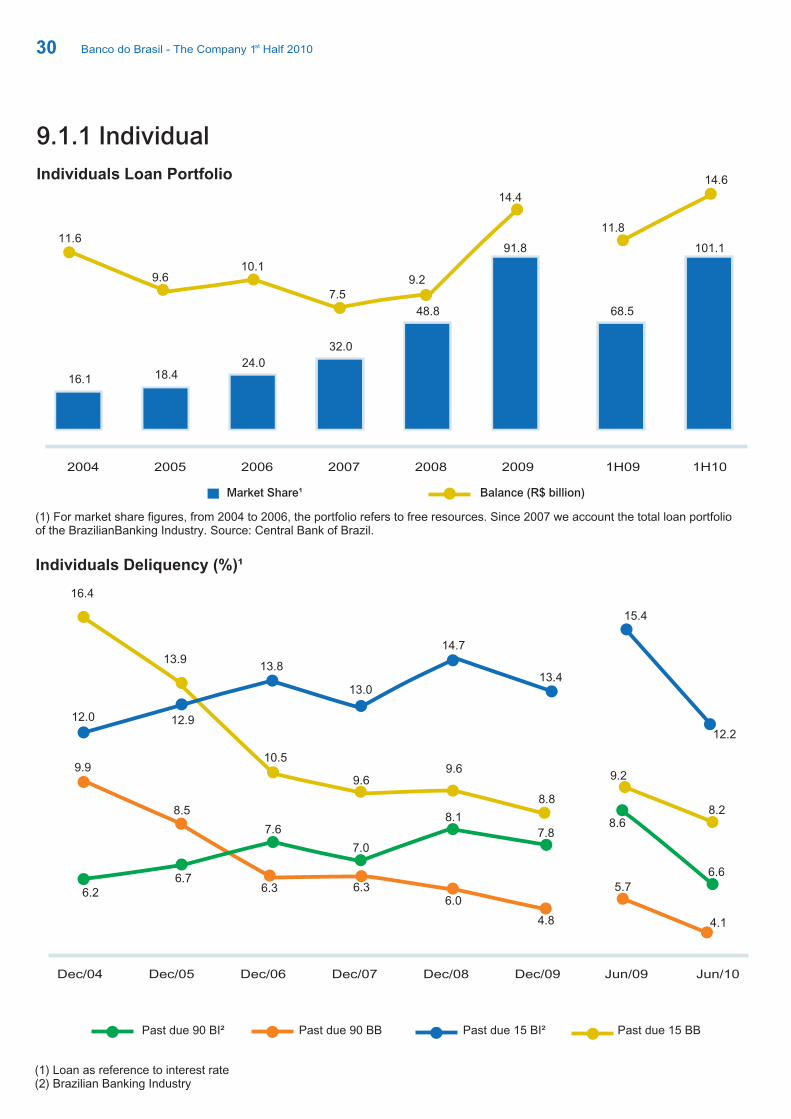

9.1.1 Individual

Individuals Loan Portfolio

Individuals Deliquency (%)¹

(1) Loan as reference to interest rate(2) Brazilian Banking Industry

Past due 90 BI² Past due 90 BB Past due 15 BI² Past due 15 BB

2004 2005 2006 2007 2008 2009

16.1 18.4 24.0

32.0

48.8

91.8

1H09 1H10

68.5

101.1

(1) For market share figures, from 2004 to 2006, the portfolio refers to free resources. Since 2007 we account the total loan portfolioof the BrazilianBanking Industry. Source: Central Bank of Brazil.

7.6

7.0

8.1

6.3

6.3

6.0

4.8

12.0

13.8

13.0

14.7

13.4

16.4

13.9

10.5

9.6

9.6

8.8

7.8

6.7

6.2

9.9

8.5

12.9

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Dec/09 Jun/09 Jun/10

15.4

12.2

9.2

8.28.6

6.6

5.7

4.1

11.6

9.610.1

7.59.2

14.4

11.8

14.6

Market Share¹ Balance (R$ billion)

Banco do Brasil - The Company 1 Half 2010st

31

Payroll Loans (R$ Billion)¹

Vehicle Loans

Market Share (%) Balance (R$ billion)

1.2

2.7

4.8

13.2

(1) Includes results from BV since 2H09.

The strategic partnership with Banco Votorantim started on 2009 allowed BB to continue expanding its

vehicle loan portfolio.

2005 2006 2007 2008 2009¹

0.2 0.9

3.0

6.7

20.7

1H09 1H10

8.2

22.85.5

13.6

(1) Includes results from BV and BNC

2004 2005 2006 2007 2008 2009¹

1.5

3.8

8.3

11.9

17.6

36.5

1H09 1H10

29.5

40.5

8.7

12.0

17.2

18.4

22.3

33.8

32.2

32.8

Market Share² (%) Balance (R$ billion)

Banco do Brasil - The Company 1 Half 2010st

(2) For market share figures, from 2004 to 2006, the portfolio refers to free resources.Since 2007 we account the total loan portfolio of the BrazilianBanking Industry. Source: Central Bank of Brazil.

32

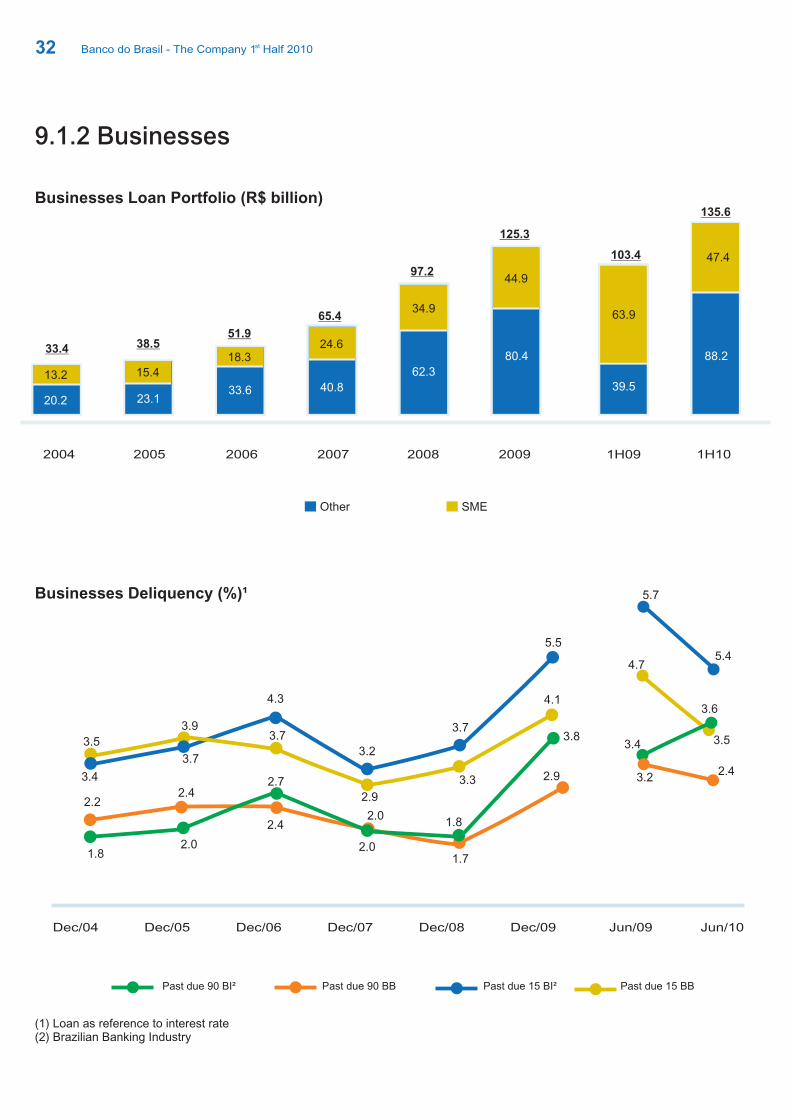

9.1.2 Businesses

Businesses Loan Portfolio (R$ billion)

Businesses Deliquency (%)¹

Other SME

Past due 90 BI² Past due 90 BB Past due 15 BI² Past due 15 BB

2004 2005 2006 2007 2008 2009

33.6 40.8

62.3

80.4

13.2

33.4 38.551.9

65.4

97.2

125.3

15.4

18.324.6

34.9

44.9

23.120.2

1H09 1H10

39.5

88.2

103.4

135.6

47.4

3.8

2.4

2.01.7

2.93.4

3.5

4.3

3.2

3.7

5.5

2.01.8

2.7

2.01.8

2.42.2

3.7

3.9

2.9

3.7

3.3

4.1

5.7

5.44.7

3.53.4

3.6

3.22.4

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Dec/09 Jun/09 Jun/10

(1) Loan as reference to interest rate(2) Brazilian Banking Industry

63.9

Banco do Brasil - The Company 1 Half 2010st

33

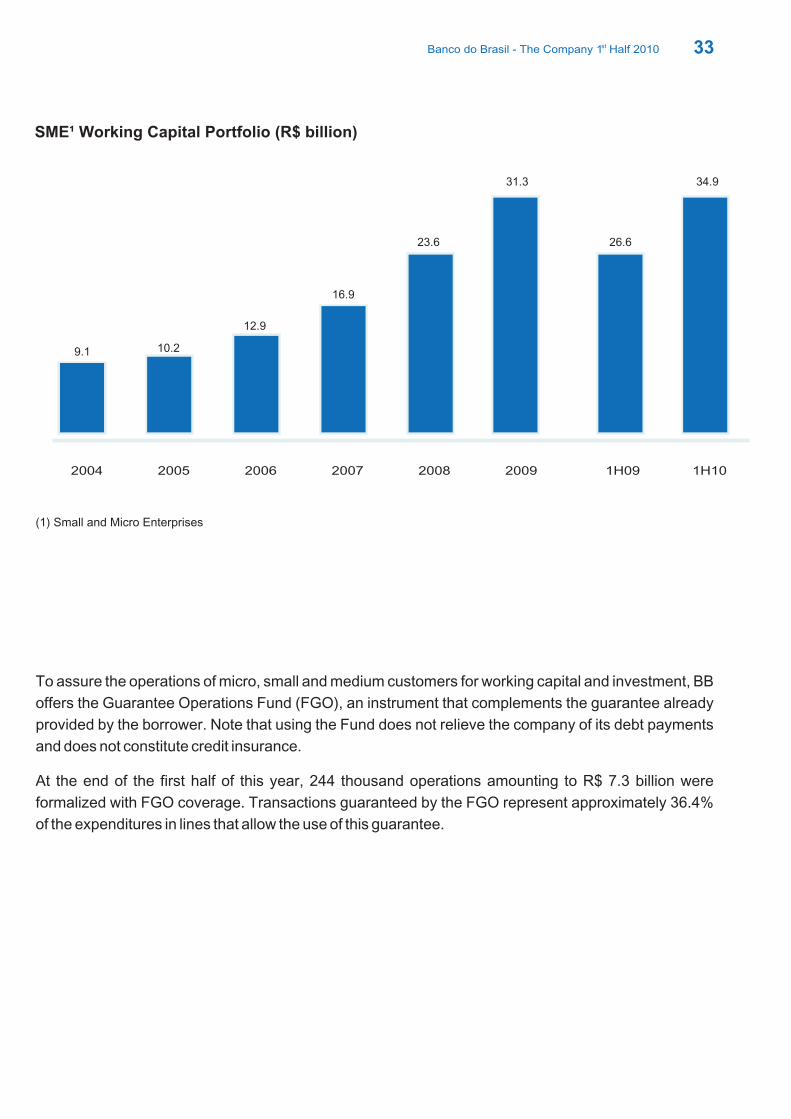

SME¹ Working Capital Portfolio (R$ billion)

(1) Small and Micro Enterprises

2004 2005 2006 2007 2008 2009

9.1 10.2

12.9

16.9

23.6

31.3

1H09 1H10

26.6

34.9

To assure the operations of micro, small and medium customers for working capital and investment, BB

offers the Guarantee Operations Fund (FGO), an instrument that complements the guarantee already

provided by the borrower. Note that using the Fund does not relieve the company of its debt payments

and does not constitute credit insurance.

At the end of the first half of this year, 244 thousand operations amounting to R$ 7.3 billion were

formalized with FGO coverage. Transactions guaranteed by the FGO represent approximately 36.4%

of the expenditures in lines that allow the use of this guarantee.

Banco do Brasil - The Company 1 Half 2010st

34

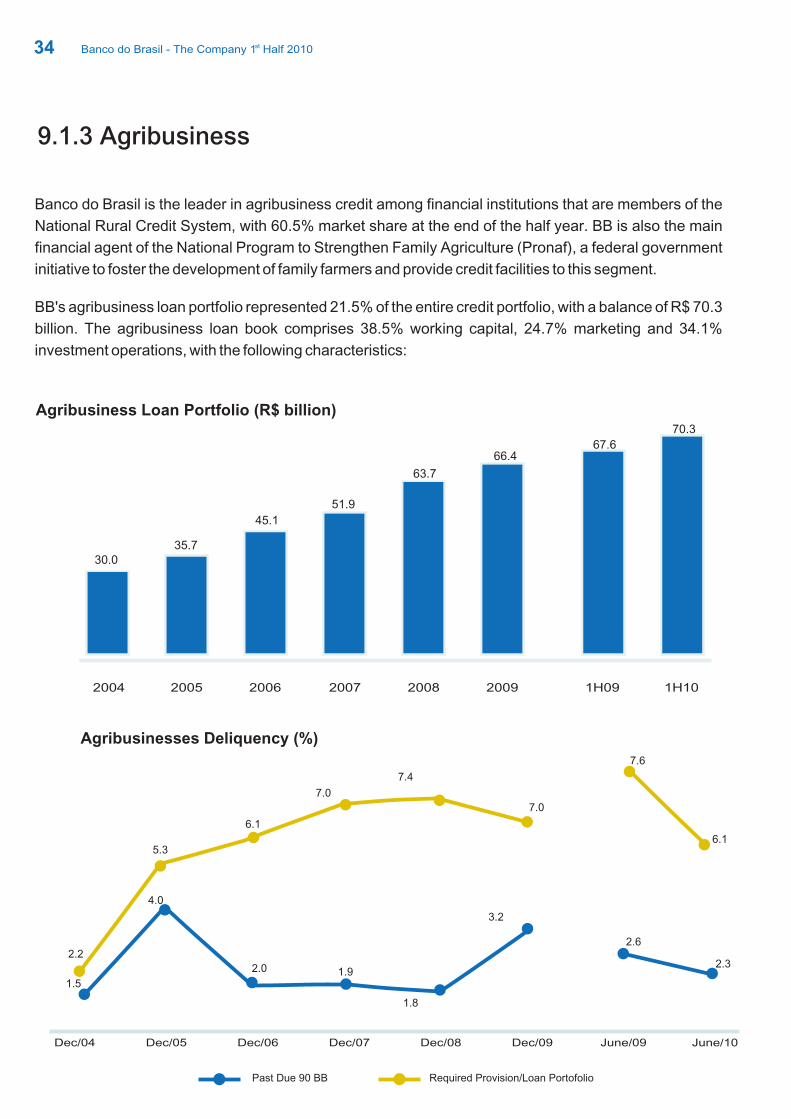

9.1.3 Agribusiness

Banco do Brasil is the leader in agribusiness credit among financial institutions that are members of the

National Rural Credit System, with 60.5% market share at the end of the half year. BB is also the main

financial agent of the National Program to Strengthen Family Agriculture (Pronaf), a federal government

initiative to foster the development of family farmers and provide credit facilities to this segment.

BB's agribusiness loan portfolio represented 21.5% of the entire credit portfolio, with a balance of R$ 70.3

billion. The agribusiness loan book comprises 38.5% working capital, 24.7% marketing and 34.1%

investment operations, with the following characteristics:

Agribusiness Loan Portfolio (R$ billion)

Agribusinesses Deliquency (%)

1.5

4.0

1.9

1.8

3.2

2.2

6.1

7.0

7.0

2.0

5.3

7.4

Past Due 90 BB Required Provision/Loan Portofolio

2004 2005 2006 2007 2008 2009

30.035.7

45.1

51.9

63.7

66.4

1H09 1H10

67.6

70.3

Dec/04 Dec/05 Dec/06 Dec/07 Dec/08 Dec/09 June/09 June/10

7.6

6.1

2.6

2.3

Banco do Brasil - The Company 1 Half 2010st

35

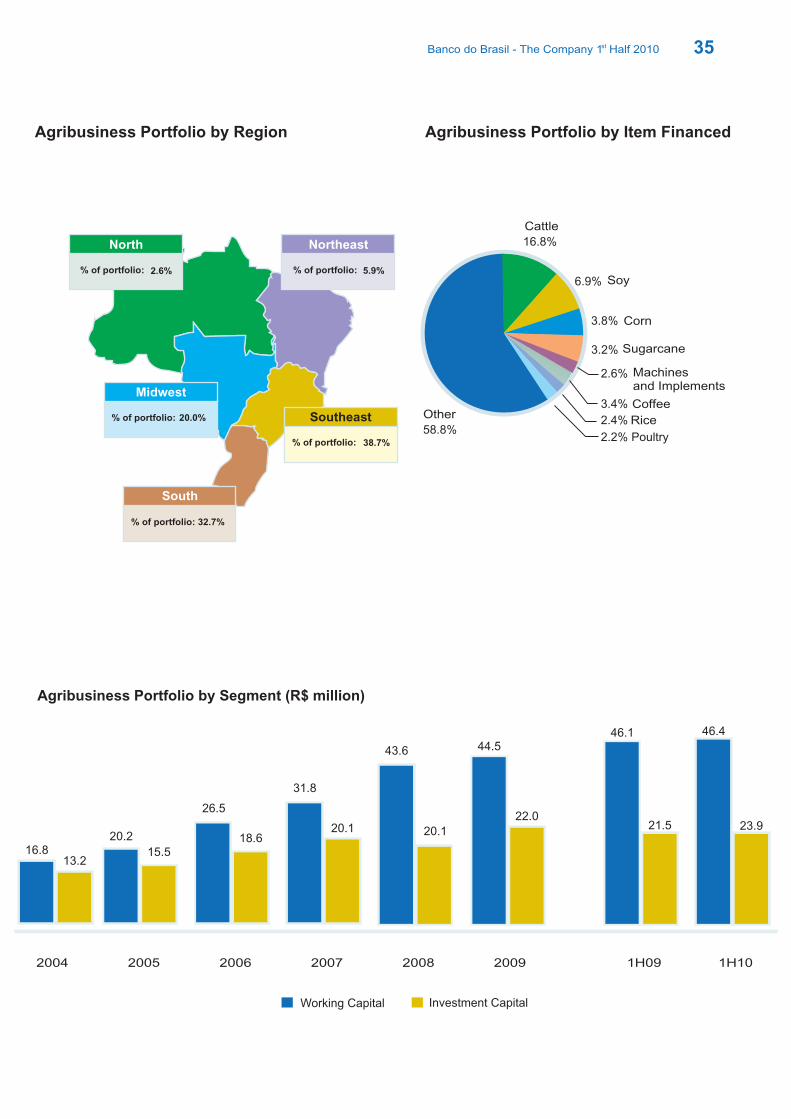

Agribusiness Portfolio by Region Agribusiness Portfolio by Financed Item

Agribusiness Portfolio by Segment (R$ million)

Southeast

% of portfolio: 38.7%

% of portfolio: 32.7%

South

6.9%

3.8%

3.2%

Other

58.8%

16.8%

2.6%

3.4%

2.4%

2.2% Poultry

Cattle

Soy

Corn

Sugarcane

Machines and Implements

Coffee

Rice

North

% of portfolio: 2.6%

Northeast

% of portfolio: 5.9%

Midwest

% of portfolio: 20.0%

16.820.2

26.5

31.8

43.6

20.1

22.0

44.5

20.118.6

15.513.2

2004 2005 2006 2007 2008 2009

Investment CapitalWorking Capital

21.5

46.1

1H09

23.9

46.4

1H10

Banco do Brasil - The Company 1 Half 2010st

36

The Bank has mechanisms to mitigate risk in the agribusiness loan portfolio. In the 2009/2010 marketing year, as of

June 2010, 61% of loan transactions were carried out with Agricultural Insurance or Proagro (government

insurance), amounting to R$ 9.0 billion.

MarketingAgricultural Costs Agroindustrial CreditInvestment Livestock Costs

National Program to Strengthen Family Agriculture (Pronaf)

Number of Contracts (thousand) Contracted Volume (R$ billion)

894

1,1481,034 1,037

887 915

15.5%

13.6%

26.1% 31.8%

39%

61%

Insured

Not Insured

Contracted Crop 2009/2010 Agri Insurance

13.0%

2004 2005 2006 2007 2008 2009

3.6

4.95.4

5.9

6.6

8.1

1H09

3.0

1H10

3.4

The National Program to Strengthen Family Agriculture (PRONAF) is a federal government program that helps

micro and small farmers who operate by directly employing labor and their families to become part of the

agribusiness chain, providing income improvements and adding value to products and properties by modernizing

the production system and enhancing the professionalism of these farmers.

249245

Family Agriculture

Banco do Brasil - The Company 1 Half 2010st

37

Foreign Exchange for Imports

In the first half of 2010, BB consolidated its leadership in the export and import market, with market

shares of 30.6% and 24.8% and contracted volumes of US$ 14.2 billion and US$ 10.4 billion,

respectively

Foreign Exchange for Exports

9.1.4 Foreign Trade

Market Share (%)

Market Share (%) Contracted Volume (US$ billion)

Contracted Volume (US$ billion)

23.922.3

23.8 24.2 24.7 25.4

27.2 27.0 26.5 26.628.0

31.1

2004 2005 2006 2007 2008 2009

25.9

34.239.4

51.2 54.247.1

1H09 1H10

23.225.6

31.330.6

2004 2005 2006 2007 2008 2009

13.5 15.920.7

26.1

34.534.1

1H09 1H10

14.319.5

24.524.9

Banco do Brasil - The Company 1 Half 2010st

BB is the exclusive financial agent of Proex, the federal government's Export Finance Program, with

balances of US$ 166 million under the Financing type and US$ 37 million under the Equalization type,

supporting the export market with a total of US$ 203.0 million. BB is also an important player in the Exim

program of the Brazilian Development Bank (BNDES), with volume reaching US$ 219.8 million in the half

year.

38

ACC/ACE

PROEX

Supported Companies Contracted Volume - Financing (US$ million)

30,37032,116

29,21127,185

20,557

16,560

409452

337358 359

400

Number of Contracts Contracted Volume (US$ billion)

2004 2005 2006 2007 2008 2009

9.0

11.9 12.1

15.1

13.0

10.9

1H09 1H10

5.56.2

7,785

8,936

2004 2005 2006 2007 2008 2009

286.0

428.9

382.9

331.6297.0

278.3

1H09 1H10

130.5

166.0

251263

Banco do Brasil - The Company 1 Half 2010st

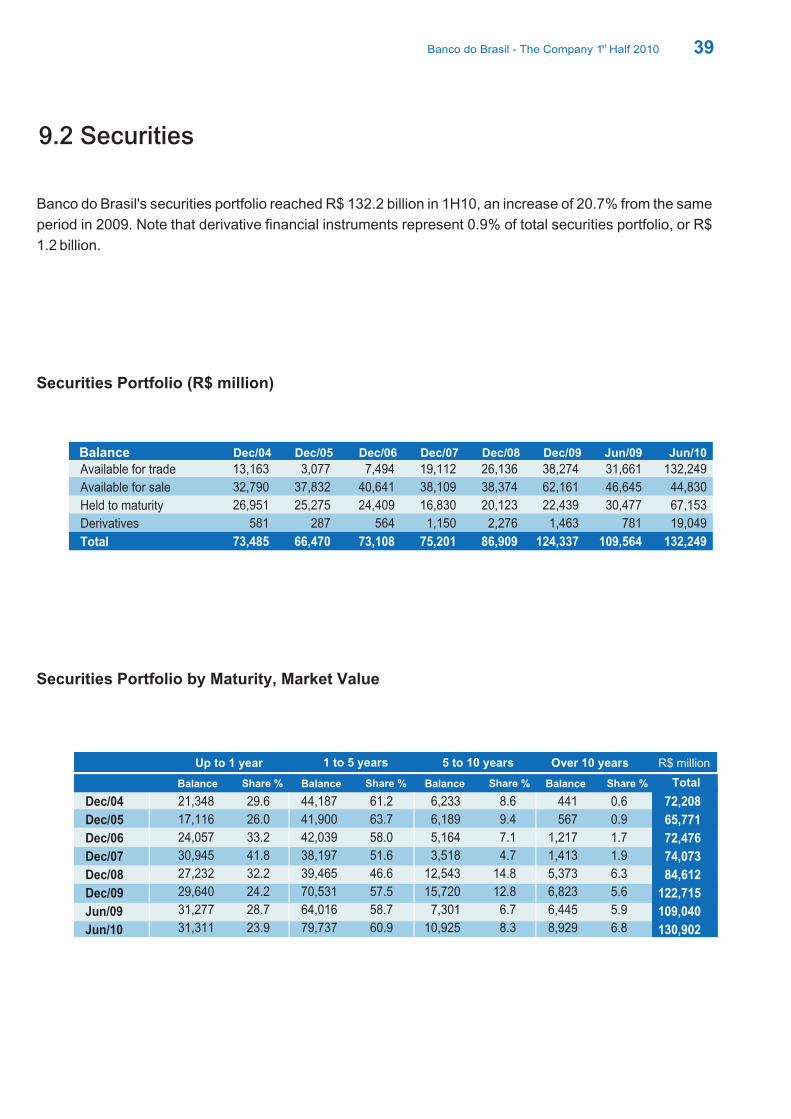

Banco do Brasil's securities portfolio reached R$ 132.2 billion in 1H10, an increase of 20.7% from the same

period in 2009. Note that derivative financial instruments represent 0.9% of total securities portfolio, or R$

1.2 billion.

39

9.2 Securities

Balance Dec/06 Dec/07 Dec/08 Dec/09 Jun/09 Jun/10

40,641

24,409

564

7,494

73,108

38,109

16,830

1,150

19,112

75,201

38,374

20,123

2,276

26,136

86,909

62,161

22,439

1,463

38,274

124,337

31,661

46,645

30,477

781

109,564

132,249

44,830

67,153

19,049

132,249

Available for trade

Available for sale

Held to maturity

Derivatives

Total

Securities Portfolio (R$ million)

Securities Portfolio by Maturity, Market Value

Dec/04 Dec/05

13,163

32,790

26,951

581

73,485

3,077

37,832

25,275

287

66,470

Balance Balance Balance BalanceShare %

Up to 1 year 1 to 5 years 5 to 10 years Over 10 years R$ million

Share % Share % Share % Total

Dec/04

Dec/05

Dec/06

Dec/07

Dec/08

Dec/09

Jun/09

Jun/10

72,208

65,771

72,476

74,073

84,612

122,715

109,040

130,902

21,348

17,116

24,057

30,945

27,232

29,640

31,277

31,311

29.6

26.0

33.2

41.8

32.2

24.2

28.7

23.9

44,187

41,900

42,039

38,197

39,465

70,531

64,016

79,737

61.2

63.7

58.0

51.6

46.6

57.5

58.7

60.9

6,233

6,189

5,164

3,518

12,543

15,720

7,301

10,925

8.6

9.4

7.1

4.7

14.8

12.8

6.7

8.3

441

567

1,217

1,413

5,373

6,823

6,445

8,929

0.6

0.9

1.7

1.9

6.3

5.6

5.9

6.8

Banco do Brasil - The Company 1 Half 2010st

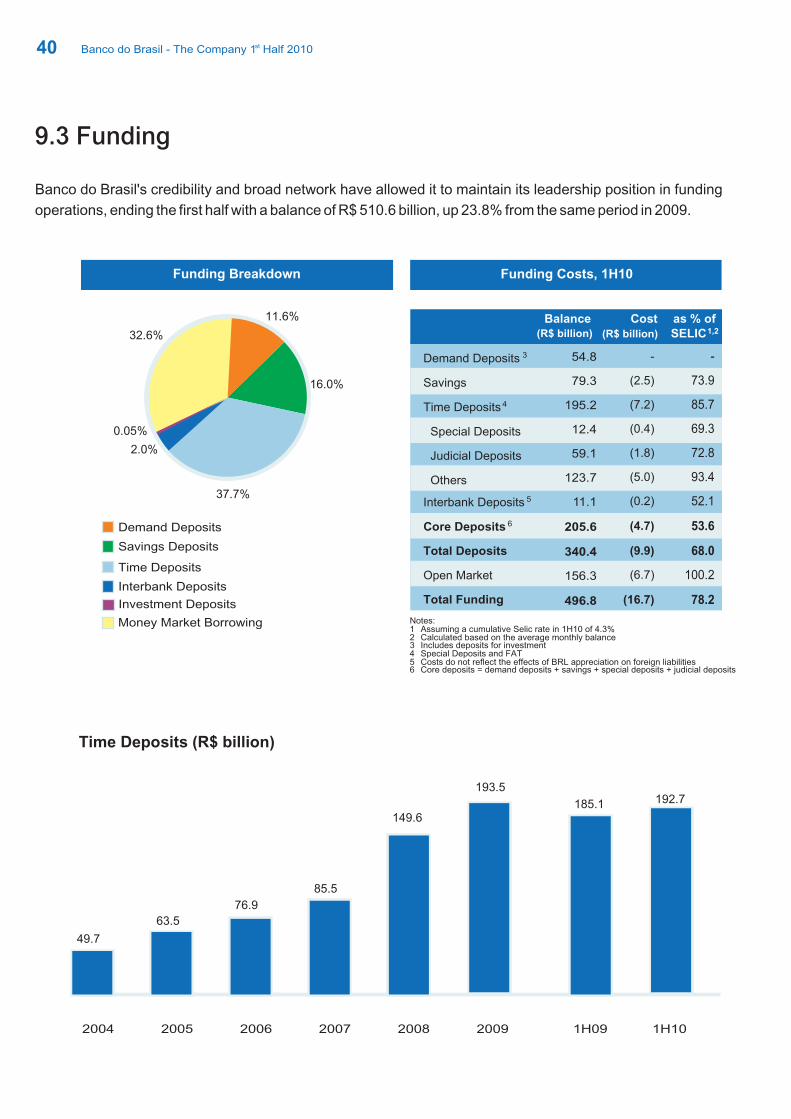

Banco do Brasil's credibility and broad network have allowed it to maintain its leadership position in funding

operations, ending the first half with a balance of R$ 510.6 billion, up 23.8% from the same period in 2009.

40

9.3 Funding

Time Deposits (R$ billion)

11.6%

2.0%

0.05%

16.0%

37.7%

Funding Breakdown Funding Costs, 1H10

Demand Deposits

Time Deposits

Savings Deposits

Interbank Deposits

32.6%

Money Market Borrowing Notes: 1 Assuming a cumulative Selic rate in 1H10 of 4.3%2 Calculated based on the average monthly balance3 Includes deposits for investment4 Special Deposits and FAT 5 Costs do not reflect the effects of BRL appreciation on foreign liabilities 6 Core deposits = demand deposits + savings + special deposits + judicial deposits

2004 2005 2006 2007 2008 2009

49.7

63.5

76.9

85.5

149.6

193.5

1H09 1H10

185.1 192.7

Investment Deposits

Banco do Brasil - The Company 1 Half 2010st

0

Cost (R$ billion)

as % ofSELIC1,2

Core Deposits

Balance (R$ billion)

Time Deposits 4

Savings

Interbank Deposits 5

Demand Deposits 3

Total Deposits

Special Deposits

Judicial Deposits

Others

Total Funding

6

54.8

79.3

195.2

12.4

59.1

123.7

11.1

205.6

340.4

156.3

496.8

-

(2.5)

(7.2)

(0.4)

(1.8)

(5.0)

(0.2)

(4.7)

(9.9)

(6.7)

(16.7)

-

73.9

85.7

69.3

72.8

93.4

52.1

53.6

68.0

100.2

78.2

Open Market

BB Administração de Ativos - Distribuidora de Títulos e Valores Mobiliários (BB DTVM), a wholly owned

subsidiary of Banco do Brasil, increased its market share at the end of the first half of 2010 to 22.3 %, from

20.3% in the same period of 2009, according to the Brazilian Financial and Capital Markets Association

(Anbima). Meanwhile, the balance of assets under management increased to R$ 344.9 billion, up 17.4%

from 1H09, composed of R$ 332.4 billion in investment funds and R$ 15.0 billion in managed portfolios.

41

9.4 Asset Management

Asset Management¹

(1) Excludes BV

Investment Funds and Managed Portfolios by Investment Profile / (%)Client

14.6

14.6

12.4

54.1

Fixed Income

Others

Multi-strategy

Equities

25.9

22.3

37.4

4.8

9.6

Institutional

Wholesale

Foreign Investor

Government

Retail

21.119.7

20.219.1

18.3

20.7

Market Share (%) Total Assets (R$ billion)

2004 2005 2006 2007 2008 2009

124.0

153.6182.7

220.1246.3

306.7

1H09 1H10

239.9344.9

20.3

22.3

Banco do Brasil - The Company 1 Half 2010st

42

9.5 Capital Markets

Banco do Brasil operates in local capital markets through BB Banco de Investimento S.A. (BB-BI). In the first half of 2010:

stBB-BI arranged 20 fixed-income issues totaling R$5.5 billion, placing 1 in the Anbima ranking,

with market share of 20.8%.

Securities: issue of two receivables-backed investment funds (FIDC) and mortgage-backed

securities (MBS) funds and one real estate fund, amounting to R$ 397 million.