Bahasa

Halaman

Hukum

SURVEY OF INNOVATION,INTELLECTUAL PROPERTY

CREATION & USAGE AMONG SINGAPORE FIRMS

PREPARED BY A/PROF WONG POH KAM

HO YUEN PING

ANNETTE SINGH

NUS ENTREPRENEURSHIP CENTRE

FOR IP ACADEMY (SINGAPORE)

FEBRUARY 2006

p_ii

CONTENT PAGE

CONTENTS

2 INTRODUCTION

3 SURVEY OBJECTIVES

3 SURVEY OVERVIEW

4 SAMPLE DEMOGRAPHICS

9 STATISTICAL ERROR BOUNDS

10 INNOVATION

10 INNOVATIVENESS OF FIRMS

13 INNOVATION ACTIVITIES AND EXPENDITURE

16 INNOVATION CO-OPERATION

19 PROBLEMS AND OBSTACLES IN INNOVATION

21 IP CREATION

22 PATENTS

26 NON-PATENT IP

28 USAGE OF OWN IP

28 USAGE OF PATENTS

34 USAGE OF NON-PATENT IP

36 USAGE OF EXTERNAL IP

36 LICENSING-IN OF PATENTS

39 LICENSING-IN OF NON-PATENT IP

43 INTERNAL ENVIRONMENT FOR IP CREATION AND IP STRATEGY

43 INTERNAL ENVIRONMENT FOR IP CREATION

45 IP STRATEGY

49 EXTERNAL ENVIRONMENT FOR IP CREATION AND USAGE

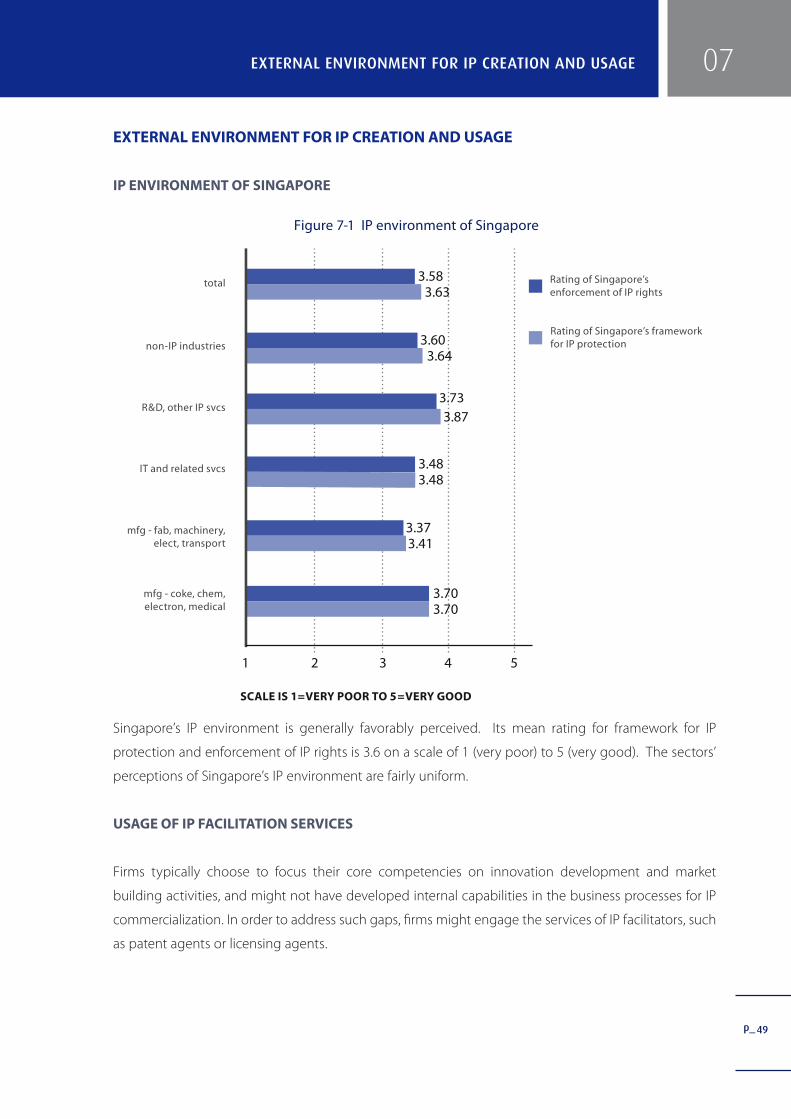

49 IP ENVIRONMENT OF SINGAPORE

49 USAGE OF IP FACILITATION SERVICES

52 IP ENFORCEMENT AND INFRINGEMENT

p_ iii

CONTENT PAGE

55 SUMMARY AND CONCLUSIONS

55 INNOVATION

55 IP CREATION AND USAGE

57 SINGAPORE’S IP ENVIRONMENT

57 POLICY IMPLICATIONS

59 REFERENCES

61 ANNEX A - SELECTED INNOVATION AND IP INDICATORS FOR SPECIFIC INDUSTRIES

66 ANNEX B - COMPARISON BETWEEN WEIGHTED AND UNWEIGHTED DATA

68 ANNEX C - ERROR BOUNDS

71 ANNEX D - CORRELATION MATRICES

73 ANNEX E - TESTS OF DIFFERENCES

74 ANNEX F - REGRESSION ANALYSIS

LIST OF FIGURES

10 Figure 2-1 Innovating firms (Firms that have introduced new product or process

innovation to the market in last 3 years)

11 Figure 2-2 Product and process innovators

12 Figure 2-3a Turnover (volume/output) from new/significantly improved products

(processes) introduced during the last three years (by sector)

12 Figure 2-3b Turnover (volume/output) from new/significantly improved products

(processes) introduced during the last three years (by employee size of firm)

15 Figure 2-4a Innovation intensity (% of sales spent on innovation activities) and R&D

intensity (% of sales spent on R&D activities) (by sector)

15 Figure 2-4b Innovation intensity (% of sales spent on innovation activities) and R&D

intensity (% of sales spent on R&D activities) (by employee size of firm)

16 Figure 2-5 Collaboration on innovation activities in the last three years

16 Figure 2-6 Parties involved in developing product innovations introduced within the

last three fiscal years

p_

CONTENT PAGE

iv

17 Figure 2-7 Parties involved in developing process innovations introduced within the

last three fiscal years

19 Figure 2-8 Government assistance/support for innovation activities in the last three

years

20 Figure 2-9 Types of government innovation assistance/support schemes received in

the last three years

22 Figure 3-1a Firms which have applied for patents (by sector)

22 Figure 3-1b Firms which have applied for patents(by innovativeness of firm)

23 Figure 3-2a Location of patent applications (by sector)

23 Figure 3-2b Location of patent applications (by innovativeness of firm)

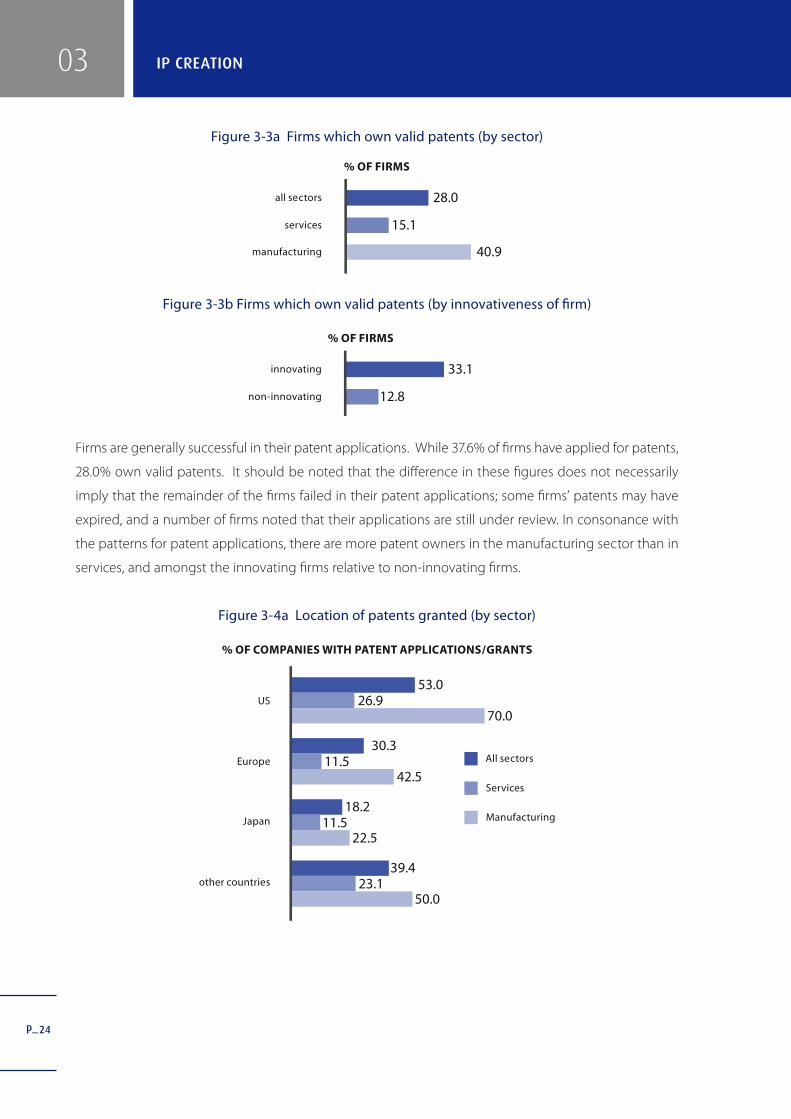

24 Figure 3-3a Firms which own valid patents (by sector)

24 Figure 3-3b Firms which own valid patents (by innovativeness of firm)

24 Figure 3-4a Location of patents granted (by sector)

25 Figure 3-4b Location of patents granted (by innovativeness of firm)

25 Figure 3-5a Mean number of patents applied for and granted (by sector)

26 Figure 3-5b Mean number of patents applied for and granted (by innovativeness of

firm)

26 Figure 3-6a Ownership of non-patent IP (by sector)

26 Figure 3-6b Ownership of non-patent IP (by innovativeness of firm)

26 Figure 3-7a Types of non-patent IP owned (by sector)

27 Figure 3-7b Types of non-patent IP owned (by innovativeness of firm)

28 Figure 4-1a Usage of patents (by sector)

29 Figure 4-1b Usage of patents (by innovativeness of firm)

29 Figure 4-2a Revenue from using patents in-house (% of turnover) (by sector)

30 Figure 4-2b Revenue from using patents in-house (% of turnover) (by innovativeness

of firm)

30 Figure 4-3 Revenue from licensing patents to third parties (% of turnover)

34 Figure 4-4a Revenue from licensing out non-patent IP (% of turnover) (by sector)

34 Figure 4-4b Revenue from licensing-out non-patent IP (% of turnover) (by

innovativeness of firm)

36 Figure 5-1a Licensing-in of patents from third parties (by sector)

36 Figure 5-1b Licensing-in of patents from third parties (by innovativeness of firm)

37 Figure 5-2 Revenue from licensed-in patents1 (% of turnover)

38 Figure 5-3 Cost of licensing-in patents1 (% of revenue)

39 Figure 5-4a Licensing-in of non-patent IP (by sector)

40 Figure 5-4b Licensing-in of non-patent IP (by innovativeness of firm)

40 Figure 5-5a Types of non-patent IP licensed-in (by sector)

p_

CONTENT PAGE

v

40 Figure 5-5b Types of non-patent IP licensed-in (by innovativeness of firm)

41 Figure 5-6 Revenue from licensed-in non-patent IP1 (% of turnover)

43 Figure 6-1a Firms which give incentives for generation of patentable inventions

(sector)

43 Figure 6-1b Firms which give incentives for generation of patentable inventions (by

innovativeness of firm)

44 Figure 6-2a Have inventors of patents left firm? (% yes, by sector)

44 Figure 6-2b Have inventors of patents left firm? (% yes, by innovativeness of firm)

44 Figure 6-3 Parties in charge of IP matters

46 Figure 6-4a Relative importance of forms of IP protection in Singapore to enterprise

strategy for capturing commercial value from innovation (Mean score)

47 Figure 6-4b Relative importance of forms of IP protection abroad to enterprise

strategy for capturing commercial value from innovation (Mean score)

48 Figure 6-5 Effectiveness of IP strategies used as mechanisms to protect the

competitive advantage of enterprise’s innovation (% of firms rating IP strategy as

effective)

49 Figure 7-1 IP environment of Singapore

50 Figure 7-2 Use of IP facilitation services

50 Figure 7-3 Type of Singapore-based IP service providers used

51 Figure 7-4 Type of foreign-based IP service providers used

51 Figure 7-5 Usage of Singapore-based IP service providers

52 Figure 7-6 Satisfaction with Singapore-based IP services providers (Mean score by

users of service)

54 Figure 7-7 Action taken in IP disputes in the last three years

54 Figure 7-8 Ease of resolution of IP disputes in the last three years(Mean score by

those who have taken action)

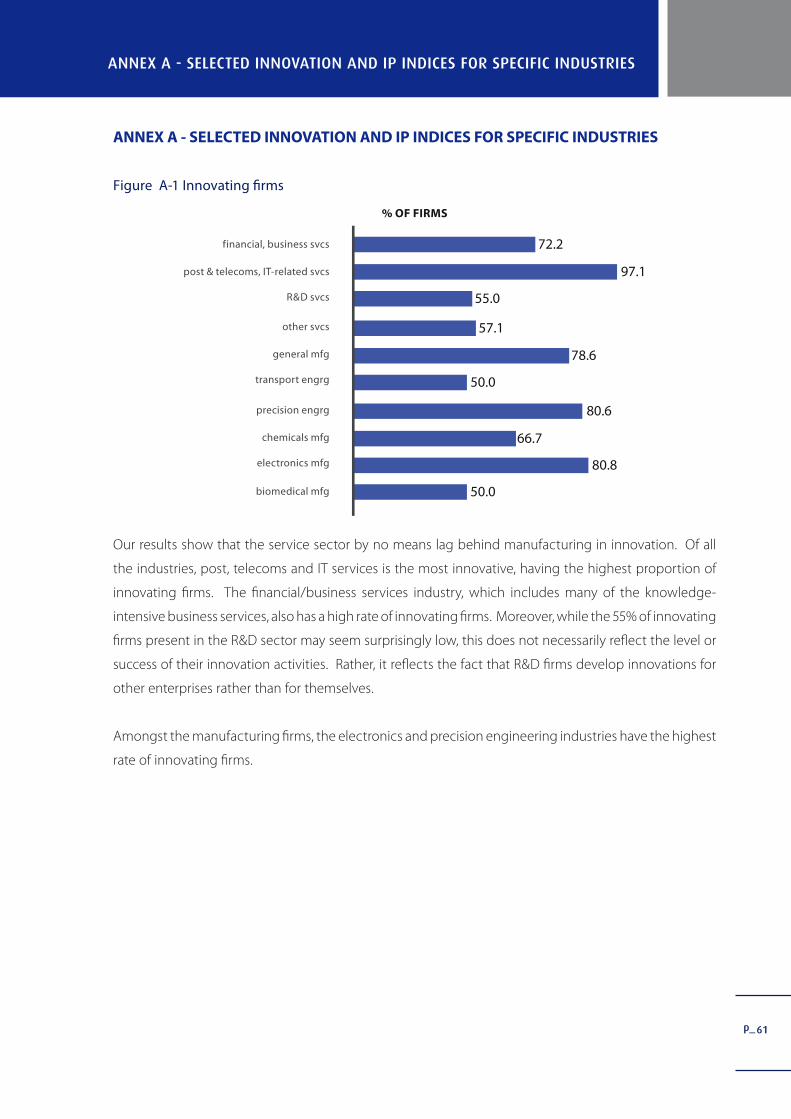

61 Figure A-1 Innovating firms

62 Figure A-2 Product innovators

62 Figure A-3 Process innovators

63 Figure A-4 Firms which have applied for patents

63 Figure A-5 Firms which own valid patents

64 Figure A-6 Ownership of non-patent IP

64 Figure A-7 Licensing-in of patents from third parties

65 Figure A-8 Licensing-in of non-patent IP

p_

CONTENT PAGE

vi

LIST OF TABLES

4 Table 1-1 Profile of Returns

6 Table 1-2 Number of Employees in Respondent Firms

6 Table 1-3 Total Revenue in Respondent Firms

7 Table 1-4 Proportion of Total Revenues from Exports in Respondent Firms

7 Table 1-5a Respondent Firms by Ownership Status

8 Table 1-5b Ownership Status of Firms: Comparison between IP Survey Respondents

and A*STAR Survey Respondents

8 Table 1-6 Respondent Firms by Age

10 Table 2-1 Summary table of indicators of innovativeness

11 Table 2-2 Innovating firms: Singapore vs selected European countries

13 Table 2-3a Innovation activities undertaken in Singapore (by sector)

14 Table 2-3b Innovation activities undertaken overseas (by sector)

14 Table 2-4a Innovation activities undertaken in Singapore (by nationality of firm)

14 Table 2-4b Innovation activities undertaken overseas (by nationality of firm)

17 Table 2-5a Innovation collaboration partners in Singapore

18 Table 2-5b Innovation collaboration partners overseas

19 Table 2-6 Problems encountered in innovation

21 Table 3-1 Summary table of indicators of IP creation and usage

31 Table 4-1a Economic importance of patents (by sector)

31 Table 4-1b Economic importance of patents (by innovativeness of firm)

32 Table 4-2 Parties to whom patents are licensed-out

33 Table 4-3a Reasons for not utilizing patents (by sector)

33 Table 4-3b Reasons for not utilizing patents (by innovativeness of firm)

35 Table 4-4a Economic importance of non-patent IP (by sector)

35 Table 4-4b Economic importance of non-patent IP (by innovativeness of firm)

36 Table 5-1 Parties from whom firms license-in patents

38 Table 5-2a Economic importance of licensed-in patents (by sector)

39 Table 5-2b Economic importance of licensed-in patents (by innovativeness of firm)

41 Table 5-3a Economic importance of licensed-in non-patent IP (by sector)

41 Table 5-3b Economic Importance of non-Patent IP (by innovativeness of firm)

45 Table 6-1 Stage of IP strategy adoption

53 Table 7-1a Frequency with which firms have experienced IP infringement by external

parties in Singapore the last 3 years

53 Table 7-1b Frequency with which firms have experienced IP infringement by external

parties overseas the last 3 years

p_

CONTENT PAGE

vii

66 Table B-1 Comparison of sectoral distribution of sample and population

67 Table B-2 Comparison of weighted and unweighted data for selected indicators

68 Table C-1 Standard Error Bound Estimates of the Percentage of Innovating Firms

69 Table C-2 Standard Error Bound Estimates of the Percentage of Firms who Own

Patents

70 Table C-3 Standard Error Bound Estimates of the Mean Cumulative No. of Patents

Granted (In effect, not expired)

71 Table D-1 Indicators of Innovation and Patent Ownership

72 Table D-2 Indicators of Innovation, Patent Ownership and Stage of IP Strategy

73 Table E-1 Indicators of IP creation and usage in innovating vs non innovating firms

74 Table F-1 Regression with Dependent : Share of Revenue from new products/

services introduced in last 3 years

75 Table F-2 Regression with Dependent : Average growth in sales in last 3 fiscal years

p_2

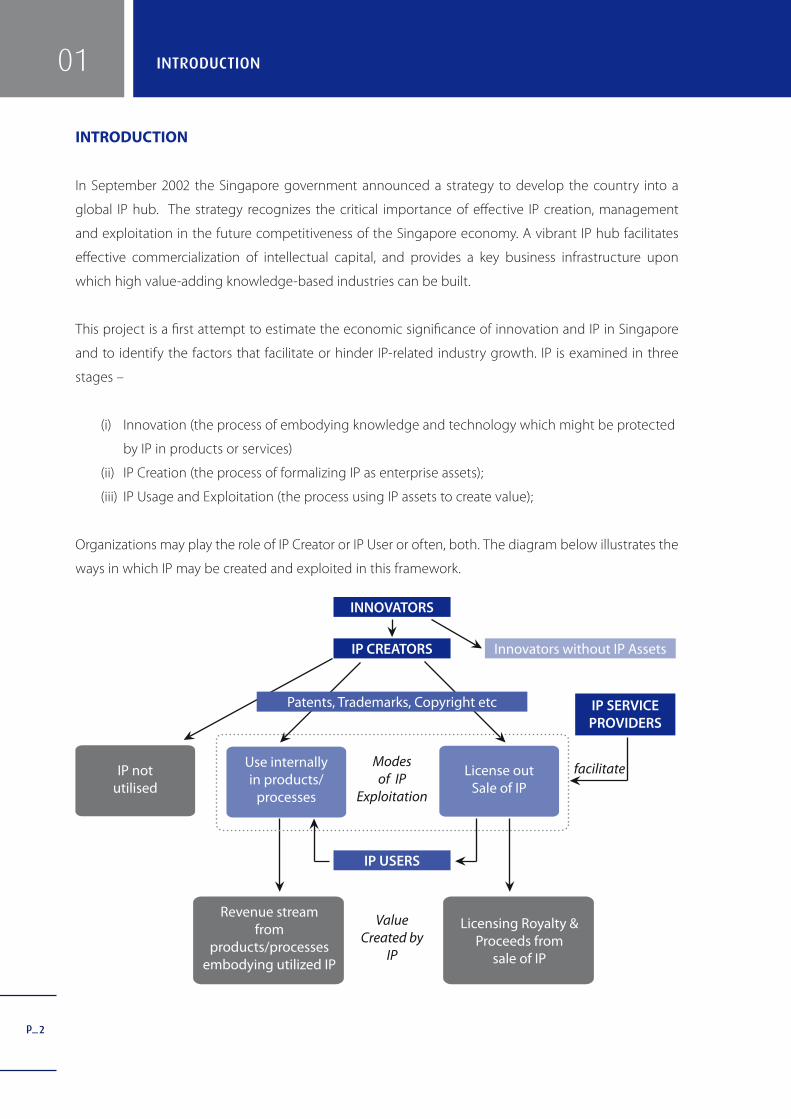

INTRODUCTION

In September 2002 the Singapore government announced a strategy to develop the country into a

global IP hub. The strategy recognizes the critical importance of effective IP creation, management

and exploitation in the future competitiveness of the Singapore economy. A vibrant IP hub facilitates

effective commercialization of intellectual capital, and provides a key business infrastructure upon

which high value-adding knowledge-based industries can be built.

This project is a first attempt to estimate the economic significance of innovation and IP in Singapore

and to identify the factors that facilitate or hinder IP-related industry growth. IP is examined in three

stages –

(i) Innovation (the process of embodying knowledge and technology which might be protected

by IP in products or services)

(ii) IP Creation (the process of formalizing IP as enterprise assets);

(iii) IP Usage and Exploitation (the process using IP assets to create value);

Organizations may play the role of IP Creator or IP User or often, both. The diagram below illustrates the

ways in which IP may be created and exploited in this framework.

����������

�����������

��������

����������������������������

�����������������������������������

���������������

����������������������

�����������

������������

���������������

��

�������������������

���������������������������������������

���������������������������������

����������

��������������������

����������������������������������

����������

01 INTRODUCTION

p_3

SURVEY OBJECTIVES

The IP Academy (IPA) commissioned the project team from the NUS Entrepreneurship Centre to conduct

a survey of innovation and IP creation and usage among the high-tech manufacturing and service

sectors in Singapore.

The objectives of the survey include:

• Identify the emerging structure, performance and development constraints of several key IP-

based industries in Singapore.

• Develop relevant indicators and baseline estimates on IP creation and usage for Singapore to

facilitate benchmarking in leading advanced countries in the world.

SURVEY OVERVIEW

Sampling Frame

The research framework for this study positions innovation activities as the basis for IP creation, as

presented in the framework diagram. Given the focus of the study on IP creation and usage, the base

for our survey should be firms with innovating activities, rather than all firms in Singapore. As such,

the most appropriate sampling frame should comprise firms involved in any form of innovation effort,

including firms that have successfully innovated new products/ services as well as those that might still

be in the early stages of innovation efforts.

One such existing database is the register of firms maintained by the Agency for Science, Technology and

Research (A*STAR) for the annual National Survey of R&D in Singapore. The A*STAR register comprises

organizations in Singapore that are known to perform R&D. The register is updated annually, using

information from the previous year R&D Survey as well as through a Preliminary Survey of organizations

that are potentially performing R&D but are not on the register. The list of organizations included in the

Preliminary Survey is compiled annually from various sources and includes all firms that are in receipt of

government R&D grants.

The sampling frame used in this study predominantly comprised firms in the A*STAR register for 2004,

augmented with other known knowledge-intensive firms and firms from knowledge-intensive industries,

including several university spin-offs1 . Following the A*STAR register, the full spectrum of manufacturing

and professional services were included, regardless of whether they fall within the classification of

1 We are grateful to A*STAR for their assistance in making the registry of organisations performing R&D available to us.

01INTRODUCTION

p_4

knowledge-based industries as defined by Toh et al (2002)2. This provides a better picture of IP creation

and usage in Singapore, given that such activities occur in all sectors of the economy, not merely those

typically considered to be IP-intensive.

Due to this focus on firms with innovation efforts, the sampling frame corresponds largely to knowledge

intensive sectors such as high-tech manufacturing and knowledge-based services such as ICT services.

Thus, the results in this report are not meant to be generalized to all firms in Singapore. However, the

results do give a reasonable depiction of the IP creation and usage amongst firms which are already

involved in some form of innovation efforts.

Survey Methodology

The survey instrument used is a structured self-administered questionnaire (see Annex G) designed

by the NEC research team. Data was collected by postal survey, with questionnaires being sent out

to approximately 2,500 firms. Telephone follow up was conducted to clarify doubtful or missing

information. Fieldwork was launched in April 2005 and closed in end July 2005 with a total of 188

responses achieved.

SAMPLE DEMOGRAPHICS

Table 1-1 Profile of Returns

SSIC 200 CLASSIFICATION OF INDUSTRIES (IN ACCORDANCE WITH A*STAR’S NATIONAL R&D SURVEY) INDUSTRY

SAMPLE POPULATION

NO. OF RETURNS

% DISTRIBUTION

% DISTRIBUTION

Manufacturing 94 50.0 49.3

242, 3211 Biomedical 4 2.1 2.6

31 Electronics 26 13.8 13.0

21092, 23, 24 (excluding 242), 25213, 261, 2699

Chemicals 6 3.2 7.6

25191-93, 25199, 25211, 25214-16, 25218-19, 2522, 28113, 2813, 2891-94, 28951, 28959, 28993, 28995, 28997-99, 29 (excluding 29231-32, 293-294), 301-303, 32 (excluding 32202)

Precision Engineering

36 19.1 15.4

(continued on next page)

2 See Toh, M.H., Tang H.C. and Choo, A. (2002). “Mapping Singapore’s knowledge-based economy”, Economic Survey of Singapore – Third Quarter 2002, Singapore: Ministry of Trade

and Industry. Toh et al provided a classification of knowledge-based and non-knowledge-based industries which itself was based on that used by the OECD.

01 INTRODUCTION

p_5

(continued from previous page)

25121, 29231-32, 2926, 331-334, 339

Transport Engineering

8 4.3 3.6

15-16, 17-20, 22, 21 (excluding 21092), 2511, 25122, 25194, 25212, 25217, 2691-95, 26991-95, 27, 28111-12, 28114, 28119, 2812, 28952, 28991-92, 28994, 28996, 293-4, 304-5, 309, 32202, 34-35

GeneralManufacturing

14 7.4 7.1

Services 94 50.0 50.7

731 R&D 20 10.6 7.1

64, 72 Post & Telecoms, IT

related34 18.1 17.0

65-66, 74 Financial and business

services18 9.6 8.6

45, 50-51, 55, 60-63, 70-71, 732, 75, 80, 85, 90-93, 95, 99 Other services 22 11.7 18.0

Total 188 100.0 100.0

Table 1-1 shows the distribution of returns and population distribution (where the population distribution

is assumed to follow the distribution of firms in the respondents to the A*STAR survey). A total of

188 returns were obtained: 94 from the manufacturing sector; and 94 were from the service sector.

In comparison with the population, the precision engineering industry and R&D services have been

slightly oversampled, and the chemicals industry and other services have been undersampled.

In order to ensure representativeness of the sample, weights are derived from a comparison of the

sample sectoral distribution with the sectoral distribution of the population of respondents to the

A*STAR survey. However, given the very close correspondence between the sample and population

distribution, there is little difference between weighted and unweighted results (see Annex B for a

comparison of weighted and unweighted results). As such, the unweighted results have been given in

this report unless otherwise stated.

01INTRODUCTION

p_6

Table 1-2 Number of Employees in Respondent Firms

NUMBER OF EMPLOYEESMANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

Small firm 36.6 82.8 59.7

<10 8.6 39.8 24.2

10-49 28.0 43.0 35.5

Medium-sized firm 33.4 14.0 23.7

50-99 18.3 11.8 15.1

100-199 15.1 2.2 8.6

Large firm 30.2 3.2 16.7

200-499 15.1 2.2 8.6

500-999 9.7 0.0 4.8

1000+ 5.4 1.1 3.2

Total 100.0 100.0 100.0

Note: Numbers may not sum to exactly 100% due to rounding errors

More than half of responding firms have fewer than 50 employees (i.e. are small firms). Almost one-

quarter of firms are medium-sized, having between 50 to 199 employees, and 16.7% of firms are large

firms, having 200 or more employees.

Our sample has a high proportion of small firms within the service sector, whereas the manufacturing

sector has a more even distribution between small, medium and large firms

Table 1-3 Total Revenue in Respondent Firms

TOTAL REVENUE FOR LATEST FISCAL YEAR

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

<$5 million 23.3 75.0 48.9

$5-$9.9 million 14.4 11.4 12.9

$10-$49.9 million 25.6 9.1 17.4

$50-$99.9 million 8.9 1.1 5.1

$100-$499 million 17.8 0.0 9.0

$500-$999 million 3.3 1.1 2.2

$1-$4.9 billion 4.4 1.1 2.8

$5 billion and above 2.2 1.1 1.7

Total 100.0 100.0 100.0

01 INTRODUCTION

p_7

Almost half of the responding firms have less than S$5 million in total revenue for their latest fiscal year.

The majority of these are service firms. Conversely, most of the 6.7% of responding firms with sales

revenues of at least $500 million are manufacturing firms.

Table 1-4 Proportion of Total Revenues from Exports in Respondent Firms

% OF TOTAL REVENUE FROM EXPORTS

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

0% 12.4 27.5 19.5

>0-10% 11.2 18.8 14.8

>10-40% 12.4 13.8 13.0

>40-70% 20.2 17.5 18.9

>70% 43.8 22.5 33.7

Total 100.0 100.0 100.0

Almost one-fifth of the responding firms do not export at all, most of which are service firms. One-third

of responding firms have extensive export operations, with exports contributing more than 70% of their

total revenue.

Table 1-5a Respondent Firms by Ownership Status

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

Foreign firm 30.9 32.2 31.5

Wholly foreign-owned firm 27.7 16.1 21.9

50% or less locally owned firm 3.2 16.1 9.6

Local firm 69.2 67.7 68.4

More than 50% locally owned firm 16.0 16.1 16.0

Wholly locally-owned firm 53.2 51.6 52.4

of which subsidiary or affiliate of a larger enterprise group

20.0 16.7 18.4

Total 100.0 100.0 100.0

Just over half of the responding firms are wholly locally-owned firms, of which 18.4% are subsidiaries

or affiliates of a larger enterprise group. About one-third are foreign-owned firms (i.e. are 50% or less

locally-owned, including those that are wholly foreign-owned). Both the manufacturing and service

sectors have equivalent proportions of foreign vs local ownership.

01INTRODUCTION

p_8

Of the foreign-owned firms, over one-quarter are US-owned, about one-third are Japanese-owned,

about one-fifth each are European-owned and almost one-fifth are owned by other Asian countries.

Table 1-5b Ownership Status of Firms: Comparison between IP Survey Respondents and A*STAR

Survey Respondents

FOREIGN FIRM LOCAL FIRM TOTAL

% OF FIRMS

IP Survey Respondents

Manufacturing 30.9 69.2 100

Services 32.2 67.7 100

All sectors 31.5 68.4 100

A*STAR Survey Respondents

Manufacturing 46.4 53.6 100

Services 29.1 70.9 100

All sectors 37.7 62.3 100

A comparison between the respondents to our survey and that of the A*STAR National R&D survey

reveals that for our survey, local firms are over-represented in the manufacturing sector, whereas they

are under-represented in the services sector. Overall, local firms are over-represented in our sample. It

should be noted however, that our definition of local and foreign firms differs slightly from that used

by A*STAR. A*STAR classifies firms as local if they are at least 30% locally owned, whereas we have only

classified firms as local if they are at least 50% locally owned.

Table 1-6 Respondent Firms by Age

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

5 years or less 17.0 47.8 32.3

6-10 years 14.9 26.1 20.4

11-20 years 31.9 19.6 25.8

21-30 years 22.3 5.4 14.0

>30 years 13.8 1.1 7.5

Total 100.0 100.0 100.0

The service firms in our sample tend to be quite young. About one-third of the responding firms have

been established five years ago or less, and most of these are from the services sector. By contrast, the

01 INTRODUCTION

p_9

01INTRODUCTION

bulk of manufacturing respondents have been in operation for more than ten years.

STATISTICAL ERROR BOUNDS

Statistical estimates from survey data are subject to sampling error. This report shows the actual sample

statistics based on the collected data. As an indicator of the reliability of these sample estimates,

Annex C reports the 95% population and strata sampling error bounds for both proportion and mean

estimates.

p_10

INNOVATION

In this section, we present the summary findings on the innovation activities of firms, through which IP

assets may be created. We follow the convention of the European Community’s Community Innovation

Survey by defining “innovating firms” as those that have introduced a new product or service

onto the market for their own enterprise within the last 3 fiscal years. This measure of innovation

regards the innovation process as one that adds value to organizations through deployment and

commercialization.

Table 2-1 Summary table of indicators of innovativeness

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

% of innovating firms 75.5 74.2 74.9

% of product innovators 67.0 66.7 66.8

%of process innovators 47.3 35.5 41.4

MANUFACTURING SERVICES ALL SECTORS

%

% of turnover from new/significantly improved products introduced duing last 3 years*

45.0 20.4 38.9

% of volume/output from new/significantly improved processes introduced during last 3 years*

8.0 24.2 12.0

Spending on innovation activities as % of sales*

6.3 1.2 4.8

In-house R&D spending as % of sales* 4.7 0.7 3.7

*Data has been weighted by sales size

INNOVATIVENESS OF FIRMS

Figure 2-1 Innovating firms (Firms that have introduced new product or process innovation to the

market in last 3 years)

all sectors

services

manufacturing

% OF FIRMS

74.9

74.2

75.5

02 INNOVATION

p_11

The survey reveals that three-quarters of firms are innovating firms, that is, they have introduced a

product or process innovation onto the market for their own enterprise within the last three years. The

remaining quarter of the firms may have engaged in innovating activities but have not yet launched

actual products/processes in the marketplace at the time of the survey3. Alternatively, they may be

developing innovations for other enterprises. Manufacturing and services are equally innovative as

measured by the proportion of innovating firms in each sector.

Figure 2-2 Product and process innovators

In general, product innovation in firms is more common than process innovation. 66.8% of firms have

introduced product innovations for their own enterprise in the last three years, whilst only 41.4% have

introduced process innovations in this period.

Although product innovation is equally common in the manufacturing and service sectors, process

innovation is more common in the manufacturing sector, due to the precision engineering industries.

Table 2-2 Innovating firms: Singapore vs selected European countries

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS

Singapore 75.5 74.2 74.9

Denmark 95.3 93.3 94.0

Finland 88.6 93.5 90.3

Netherlands 93.7 92.9 93.3

Norway 91.5 88.9 89.5

Sweden 84.0 85.5 84.7

Note: Data for Europe is for 2001, and only includes firms with innovation activity Source for European data: Calculated from Innovation in Europe: Results for the EU, Iceland and Norway, 2004 edition. Downloaded from ftp://ftp.cordis.lu/pub/innovation-smes/docs/results_from_cis3_for_eu_iceland_norway.pdf

all sectors

% OF FIRMS

41.466.8

services35.5

66.7

manufacturing47.3

67.0

ProcessInnovator

Product Innovator

3 This is indicated by the fact that a number of firms who have not introduced product or process innovations within the last three years reported that they nevertheless do engage

in innovation activities

02INNOVATION

p_12

In order to provide an international benchmark of Singapore firms’ innovation efforts, the proportion of

innovating firms in Singapore is compared with those of Denmark, Finland, Netherlands, Norway and

Sweden. Being small advanced countries, they provide a more realistic comparison for Singapore, itself

a small economy, than larger countries such as the United States and Japan. Furthermore, data is readily

available for these countries from the results of the Third Community Innovation Survey (CIS3), conducted

by the European Union in 2001.

The results show that the proportion of innovators in Singapore is relatively low. While 74.9% of firms

surveyed in Singapore have introduced a product/process innovation within the last three years, the

equivalent proportion ranged from 94.0% in Denmark to 84.7% in Sweden in 2001. This in fact may

be an overestimate of Singapore’s international standing, given that CIS3 covers all manufacturing and

service sectors, including low-tech, medium-tech and high-tech industries, while the Singapore survey

mainly covered the high-tech, knowledge-intensive sectors. Thus the innovation figures for Singapore

may be higher in comparison to Europe than they would otherwise be.

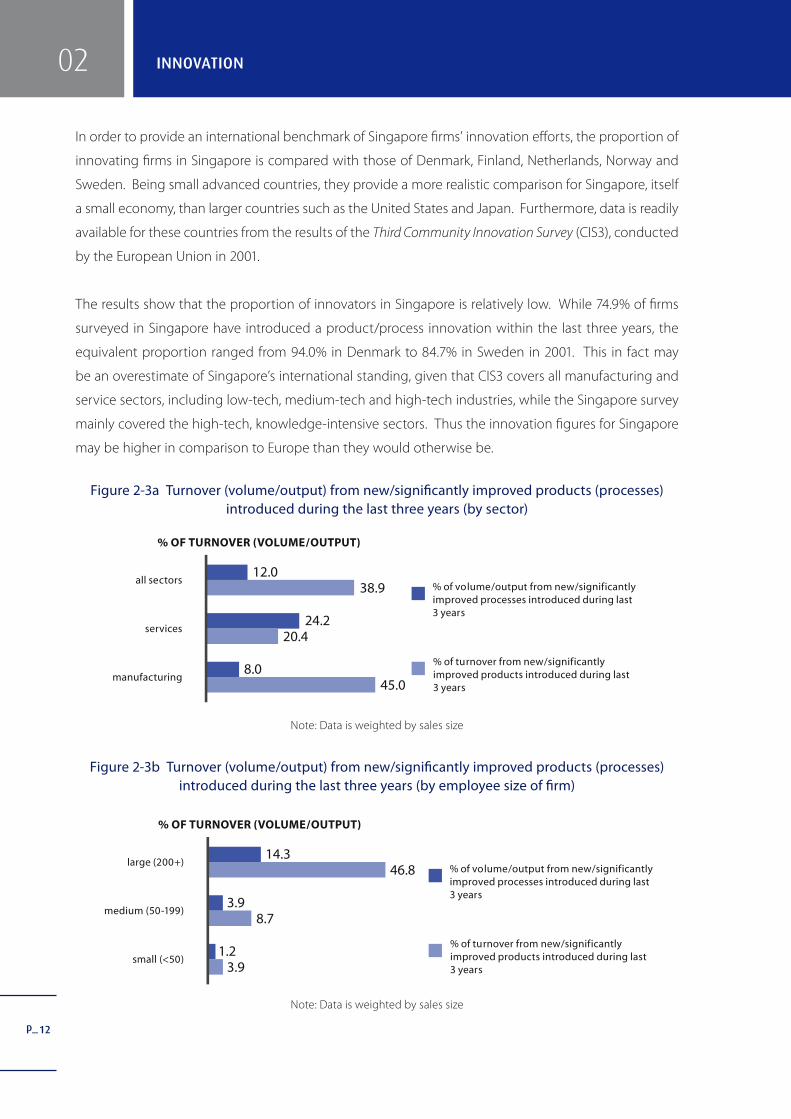

Figure 2-3a Turnover (volume/output) from new/significantly improved products (processes) introduced during the last three years (by sector)

Note: Data is weighted by sales size

Figure 2-3b Turnover (volume/output) from new/significantly improved products (processes) introduced during the last three years (by employee size of firm)

Note: Data is weighted by sales size

% OF TURNOVER (VOLUME/OUTPUT)

% of volume/output from new/significantlyimproved processes introduced during last 3 years

% of turnover from new/significantlyimproved products introduced during last 3 years

large (200+)14.3

46.8

medium (50-199)3.9

8.7

small (<50)1.2

3.9

02 INNOVATION

% OF TURNOVER (VOLUME/OUTPUT)

% of volume/output from new/significantlyimproved processes introduced during last 3 years

% of turnover from new/significantlyimproved products introduced during last 3 years

all sectors12.0

38.9

services24.2

20.4

manufacturing8.0

45.0

p_

03

13

Successful innovation does not end with the creation of a new product or process; it must also be

deployed. Commercialization is one means of deploying a product innovation. One measure, then, of

the success of an innovating firm is the proportion of turnover that comes from innovative products.

The survey revealed that on average, 38.9% of firms’ turnover comes from product innovations that

have been introduced in the last three years. Manufacturing firms and large firms have the highest

share of their turnover coming from product innovations.

Another means of deploying innovation is to incorporate process innovations into firms’ manufacturing

or service processes. This can be measured by the proportion of production volume/service output

that uses new/improved processes. On average, 12.0% of firms’ volume/output is generated from new/

improved processes introduced over the last three years. Service firms have a higher share of output

generated by process innovations than do manufacturing firms.

Regression analysis shows that commercialization of innovations is positively influenced by having

knowledge workers in the firm (proxied by the percentage of employees who are university graduates),

ownership of patents, and firms’ R&D intensity (See Annex F, Table F-1). Thus, undertaking innovation

activities such as R&D does boost implementing of innovations into the market. This in turn spurs

company growth, as average sales growth is found to be positively influenced by the share of turnover

contributed by new products/services introduced by firms (see Annex F, Table F-2)

INNOVATION ACTIVITIES AND EXPENDITURE

Table 2-3a Innovation activities undertaken in Singapore (by sector)

MANUFACTURING SERVICES ALL SECTORS

% OF INNOVATING FIRMS

Intramural R & D 66.7 66.7 66.7

Extramural R & D 21.7 14.9 18.4

Acquisition of machinery & equipment 68.1 36.4 52.6

Acquisition of other external knowledge 38.2 27.7 33.1

Training 72.1 63.6 67.9

Market introduction of innovations 53.6 56.7 55.1

Design, other preparations for production/deliveries

75.4 56.1 65.9

02INNOVATION

p_14

Table 2-3b Innovation activities undertaken overseas (by sector)

MANUFACTURING SERVICES ALL SECTORS

% OF INNOVATING FIRMS

Intramural R & D 11.6 15.2 13.3

Extramural R & D 10.1 6.0 8.1

Acquisition of machinery & equipment 23.2 12.1 17.8

Acquisition of other external knowledge 22.1 9.2 15.8

Training 22.1 18.2 20.1

Market introduction of innovations 20.3 31.3 25.7

Design, other preparations for production/deliveries

21.7 13.6 17.8

Table 2-4a Innovation activities undertaken in Singapore (by nationality of firm)

FOREIGN LOCAL

% OF INNOVATING FIRMS

Intramural R & D 54.5 72.5

Extramural R & D 13.3 20.9

Acquisition of machinery & equipment 56.8 50.5

Acquisition of other external knowledge 25.0 37.1

Training 75.0 64.4

Market introduction of innovations 48.9 58.2

Design, other preparations for production/deliveries

65.9 65.9

Table 2-4b Innovation activities undertaken overseas (by nationality of firm)

FOREIGN LOCAL

% OF INNOVATING FIRMS

Intramural R & D 20.5 9.9

Extramural R & D 13.3 5.5

Acquisition of machinery & equipment 18.2 17.6

Acquisition of other external knowledge 20.5 13.5

Training 29.5 15.6

Market introduction of innovations 24.4 26.4

Design, other preparations for production/deliveries

22.7 15.4

02 INNOVATION

p_15

0302INNOVATION

Training, in-house R&D and other preparations for implementing innovations are the most commonly

conducted innovation activities in Singapore, each undertaken by about two-thirds of innovating

firms. Firms still largely favor conducting their own R&D; outsourcing of R&D is relatively uncommon.

Innovation through the acquisition of existing machinery, equipment and knowledge is more common

amongst the manufacturing sector than the service sector.

The importance of proximity for innovation activities is reflected in the fact that a much lower proportion

of firms conduct their innovation overseas. Not surprisingly however, foreign-owned firms more

commonly conduct their innovation activities overseas than local firms. The most common innovation

activities conducted outside Singapore are market introduction of innovations and training.

Figure 2-4a Innovation intensity (% of sales spent on innovation activities) and R&D intensity (% of sales spent on R&D activities) (by sector)

Note: Data is weighted by sales size

Figure 2-4b Innovation intensity (% of sales spent on innovation activities) and R&D intensity

(% of sales spent on R&D activities) (by employee size of firm)

Note: Data is weighted by sales size

One measure of the intensity of firms’ innovation efforts is the percentage of their sales revenue that they

spend on such activities. On average, firms spend 4.8% of their sales revenue on innovation activities.

Most of this (3.7% of sales revenue) is spent on in-house R&D. Manufacturing firms and large firms are

the most innovation- and R&D-intensive, spending a larger proportion of their turnover on innovation

activities, including R&D, as compared to services firms and small and medium sized firms.

% OF SALES

In-house R&D spending as % of sales

Spending on innnovationactivities as % of sales

all sectors3.7

4.8

services0.7

1.2

manufacturing4.7

6.3

% OF SALES

In-house R&D spending as % of sales

Spending on innnovationactivities as % of sales

4.25.7

1.81.9

1.61.3

large (200+)

medium (50-199)

small (<50)

p_16

INNOVATION CO-OPERATION

Figure 2-5 Collaboration on innovation activities in the last three years

Interactions between actors in an innovation system are key determinants of its performance, for only

when these linkages are adequately developed will innovations be effectively developed and deployed

(Wong 2003). The firms have some way to go in this respect, with less than half of the innovating firms

having co-operation arrangements on innovation activities with other enterprises/institutions during

the last three fiscal years.

Figure 2-6 Parties involved in developing product innovations introduced within the last three fiscal years

02 INNOVATION

% OF INNOVATING FIRMS

all sectors

services

manufacturing

42.6

41.4

43.7

% OF PRODUCT INNOVATORS

All sectors

Services

Manufacturing

5.34.9

mainly other enterprisesor institutions

own enterprise in co-operationwith other enterprises/institutions

mainly own enterpriseor enterprise group

5.6

16.725.4

8.1

78.069.7

86.3

p_

Figure 2-7 Parties involved in developing process innovations introduced within the last three fiscal years

The limited degree of collaboration between firms is further reflected by the fact that most firms report

that the innovations introduced within the last three years have been developed on their own, or

within their enterprise group. More than three quarters of product and process innovators are in this

category. For product innovators however, the service sector appears to be more interdependent in

this respect, with one-quarter of its firms having introduced innovations which were jointly developed

in co-operation with other parties.

Table 2-5a Innovation collaboration partners in Singapore

MANUFACTURING SERVICES ALL SECTORS

% OF INNOVATING FIRMS WITH INNOVATING COLLABORATION

Universities or other HEIs 58.1 46.4 52.5

Government/public research institutes 51.6 50.0 50.8

Suppliers of equipment, materials, components or software

41.9 21.4 32.2

Clients or customers 22.6 32.1 27.1

Other enterprises within enterprise group 29.0 3.6 16.9

Commercial laboratories/R&D enterprises 25.8 7.1 16.9

Consultants 12.9 17.9 15.3

Competitors and other firms from same industry

9.7 3.6 6.8

Where innovation collaboration does take place, our survey shows that linkages between innovating firms

and the public sector are relatively well-developed. The most common co-operation arrangements for

firms are with local HEIs (higher education institutions) and the government/public research institutes/

centers (PRICs). This is encouraging, because the public R&D and tertiary education sectors are a main 17

0302INNOVATION

% OF PROCESS INNOVATORS

All sectors

Services

Manufacturing

5.29.1

mainly other enterprisesor institutions

own enterprise in co-operationwith other enterprises/institutions

mainly own enterpriseor enterprise group

2.3

18.818.2

19.3

76.072.7

78.4

p_18

source of basic research, and adequate linkages ensure that firms in the private sector have access to the

research conducted in universities/PRICs so they can apply it in developing their own innovations. It

also reflects that the measures implemented by A*STAR (Agency for Science, Technology and Research)

to increase collaborations between the sectors have had some success.

Amongst the private sector collaboration partners, the most commonly cited are suppliers and

customers. Collaboration with suppliers is relatively more common with manufacturing firms, while

collaboration with clients or customers is more common with service firms. These results are to be

expected, given the strong relationship that has developed in the manufacturing sector between MNC

buyers and local suppliers. In contrast, the service firms largely incorporate the knowledge-intensive

business services which support innovation in their clients and therefore require a higher level of co-

operation with them.

Table 2-5b Innovation collaboration partners overseas

MANUFACTURING SERVICES ALL SECTORS

% OF INNOVATING FIRMS WITH INNOVATION COLLABORATION

Suppliers of equipment, materials, components or software

35.5 17.9 27.1

Clients or customers 25.8 14.3 20.3

Other enterprises within enterprise group 22.6 7.1 15.3

Consultants 16.1 14.3 15.3

Commercial laboratories/R&D enterprises 6.5 14.3 10.2

Universities or other HEIs 12.9 7.1 10.2

Competitors and other firms from same industry

9.7 0.0 5.1

Government/public research institutes 6.5 3.6 5.1

Firms’ innovation activities are quite highly internationalized, with more than one-quarter of innovating

firms reporting innovation collaboration with parties overseas. Overseas partners are predominantly

business partners, both suppliers and customers/clients. On average, manufacturing firms appear to

have a higher level of internationalization in their innovation activities, usually having a higher incidence

of collaboration with overseas partners than service firms.

02 INNOVATION

p_19

0302INNOVATION

PROBLEMS AND OBSTACLES IN INNOVATION

Table 2-6 Problems encountered in innovation

MANUFACTURING SERVICES ALL SECTORS

MEAN SCORE

Economic Factors

Lack of appropriate sources of finance 3.39 3.68 3.54

Innovation costs too high 3.35 3.54 3.44

Excessive perceived economic risks 3.11 2.84 2.98

Internal Factors

Lack of qualified personnel 3.13 2.95 3.04

Lack of information on markets 2.87 2.97 2.92

Lack of information on technology 2.86 2.40 2.63

Organization rigidities within the enterprise

2.01 1.86 1.93

Other Factors

Lack of customer responsiveness to new goods or services

3.02 3.00 3.01

Insufficient flexibility of regulations or standards

2.48 2.27 2.38

Note: Scale from 0 = not relevant to 5 = extremely important

The main problems faced by firms in undertaking innovation are financial; a lack of adequate financing

and the high cost of innovation are considered to be the most important problems, both in the

manufacturing and the service sector. A lack of qualified personnel and lack of customer responsiveness

to new goods or services are also perceived to be important problems.

Figure 2-8 Government assistance/support for innovation activities in the last three years

% OF INNOVATING FIRMS

all sectors

services

manufacturing

44.3

47.8

40.8

p_20

Given that obtaining adequate financing is the biggest hurdle for firms’ innovation activities, government

support for innovation is particularly important. Less than half the innovating firms have received

government assistance/support for their innovation activities within the last three years. The sectors

are fairly even matched in this respect, although the service sector has a slight advantage, with 47.8%

of its innovating firms having received some kind government assistance compared to 40.8% in the

manufacturing sector.

Figure 2-9 Types of government innovation assistance/support schemes received in the last three years

By far the most commonly used innovation assistance scheme is the Innovation Development Scheme

(IDS), utilized by almost half the innovating firms who received government assistance/support in

their innovation activities. There are sectoral differences in the government support schemes used by

innovating firms. Those in the manufacturing sector more commonly use IDS and GET-UP than the

service sector, while the converse is true for PAF-Plus and LETAS

Other innovation support schemes not specifically mentioned in our survey but also used by firms

include EDB’s Research Incentive Scheme for Firms (RISC), The Enterprise Challenge (TEC), and the

Innovation for Environmental Sustainability Fund (IES).

% OF INNOVATING FIRMS RECEIVING GOVT SUPPORT/ASSISTANCE

All sectors

Services

Manufacturing

14.3LETAS

IDS

other

GET-UP

PAF-Plus

T-up

6.9

10.911.4

10.9

10.3

48.445.7

51.7

34.431.4

37.9

3.15.7

1.60

0

3.4

02 INNOVATION

p_21

IP CREATION

In this section, the creation of IP assets is analyzed, focusing on patents. A patent is a property right in

the commercial use of a device and grants its holder legal ownership of a novel, nontrivial and useful

invention. This study emphasizes patent IP as patents represent innovations with high commercialization

value. An invention must demonstrate potential commercial value before a patent is granted. The table

below summarizes the findings on the indicators of IP creation and usage that will be discussed in

greater detail in this section and in section 4.

Table 3-1 Summary table of indicators of IP creation and usage

NON-INNOVATING

INNOVATING ALL FIRMS

% OF FIRMS

Firms which own IP 46.8 64.3 59.9

Firms which have applied for patents 21.3 43.2 37.6

Firms which own valid patents 12.8 33.1 28.0

Firms which own non-patent IP 40.4 51.4 48.7

Firms which license-in patent 10.6 20.1 17.7

Firms which license-in non-patent IP 12.8 16.5 15.6

NON-INNOVATING

INNOVATING ALL FIRMS

%

Contribution of patents utilized in-house (% of turnover in latest fiscal year covered by patent applications or patents granted)*

0.00 2.77 1.87

Contribution of patents licensed out (% of revenue in latest fiscal year contributed by royalties generated by licensing out to 3rd parties)*

0.00 0.02 0.01

Contribution of licensing non-patent IP to 3rd parties (% of revenue contributed by royalties)*

0.01 1.39 1.05

Contribution of products/services that use licensed-in patents (% of turnover in latest fiscal year)*

0.00 0.63 0.51

Contribution of products/services that use licensed-in non-patent IP (% of turnover in latest fiscal year)*

0.09 0.20 0.18

*Data is weighted by sales size Note 1: Innovating firms are those that have introduced a new product or service for their own enterprise within the last

03IP CREATION

p_22

three fiscal years. Thus it should not be assumed that non-innovating firms do not engage in innovation. On the contrary, they may also be actively undertaking in innovation activities and creating IP. Note 2: This report does not comprehensively test for statistical difference between estimates for non-innovating versus innovating firms. As an illustrative example, tests for difference in proportions reported in this table are presented in Annex E Table E-1.

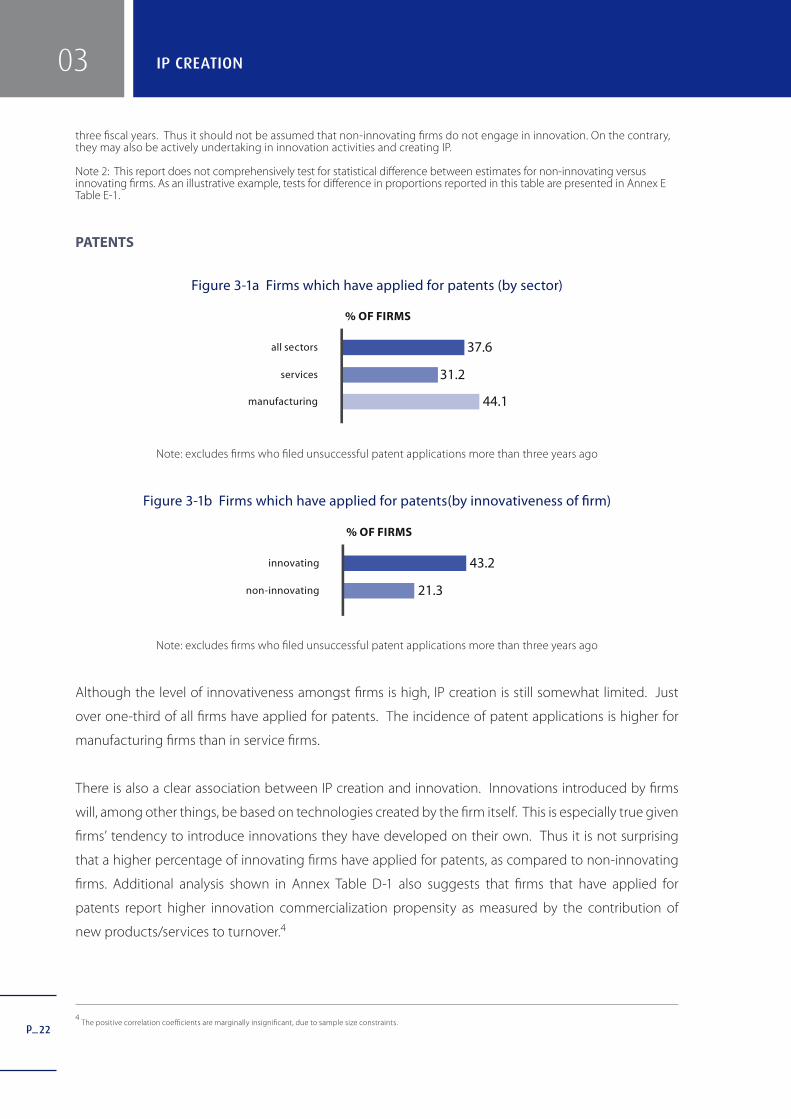

PATENTS

Figure 3-1a Firms which have applied for patents (by sector)

Note: excludes firms who filed unsuccessful patent applications more than three years ago

Figure 3-1b Firms which have applied for patents(by innovativeness of firm)

Note: excludes firms who filed unsuccessful patent applications more than three years ago

Although the level of innovativeness amongst firms is high, IP creation is still somewhat limited. Just

over one-third of all firms have applied for patents. The incidence of patent applications is higher for

manufacturing firms than in service firms.

There is also a clear association between IP creation and innovation. Innovations introduced by firms

will, among other things, be based on technologies created by the firm itself. This is especially true given

firms’ tendency to introduce innovations they have developed on their own. Thus it is not surprising

that a higher percentage of innovating firms have applied for patents, as compared to non-innovating

firms. Additional analysis shown in Annex Table D-1 also suggests that firms that have applied for

patents report higher innovation commercialization propensity as measured by the contribution of

new products/services to turnover.4

% OF FIRMS

all sectors

services

manufacturing

37.6

31.2

44.1

% OF FIRMS

innovating

non-innovating

43.2

21.3

4 The positive correlation coefficients are marginally insignificant, due to sample size constraints.

03 IP CREATION

p_23

Figure 3-2a Location of patent applications (by sector)

Figure 3-2b Location of patent applications (by innovativeness of firm)

Patent applications by the firms have a broad international scope. Although the US as the world’s largest

technology market is naturally the most frequently cited location, firms also commonly file patent

applications in Europe, Japan and other countries, with the ‘other’ countries including regional countries

such as Singapore, Hong Kong, Taiwan, China and Korea.

While a greater proportion of non-innovating firms have applied for patents in the US than innovating

firms, the reverse is true for all the other regions. However, it should be noted that the patents held by

non-innovating firms, who have not introduced a new product/service in the last three years, are on

average likely to be older than innovating firms. As such, their patent applications would on average

also have been filed earlier, and so this geographical pattern could be the result of the differing age of

patents rather than a reflection of innovating firms having a more global outlook in protecting their IP

through patenting.

% OF FIRMS WITH PATENT APPLICATIONS/GRANTS

Innovating

Non-innovating

61.050.0

54.240.0

45.830.0

81.490.0

other countries

Europe

Japan

US

03IP CREATION

����������������������������������������������

�����������

��������

�������������

�����������������������

������

�����

��

����

��������

����

��������

����

��������

����

p_24

Figure 3-3a Firms which own valid patents (by sector)

Figure 3-3b Firms which own valid patents (by innovativeness of firm)

Firms are generally successful in their patent applications. While 37.6% of firms have applied for patents,

28.0% own valid patents. It should be noted that the difference in these figures does not necessarily

imply that the remainder of the firms failed in their patent applications; some firms’ patents may have

expired, and a number of firms noted that their applications are still under review. In consonance with

the patterns for patent applications, there are more patent owners in the manufacturing sector than in

services, and amongst the innovating firms relative to non-innovating firms.

Figure 3-4a Location of patents granted (by sector)

% OF FIRMS

all sectors

services

manufacturing

28.0

15.1

40.9

% OF FIRMS

innovating

non-innovating

33.1

12.8

% OF COMPANIES WITH PATENT APPLICATIONS/GRANTS

All sectors

Services

Manufacturing

53.026.9

other countries

Europe

Japan

US

70.0

30.311.5

42.5

18.211.5

22.5

39.423.1

50.0

03 IP CREATION

p_25

Figure 3-4b Location of patents granted (by innovativeness of firm)

The locations of patents held by the firms are fairly well distributed around the world. Innovating

firms are more likely to own patents in countries outside the US than are non-innovating firms. Other

countries where firms own patents include Singapore, China, Hong Kong, Korea, Taiwan.

Figure 3-5a Mean number of patents applied for and granted (by sector)

Note: Excludes two firms with very high patenting activity. Including them would raise the mean number of patent applications to 23.7 for manufacturing and 16.3 for all sectors. Similarly, the mean number of patents granted over the last 3 years would increase to 16.9 for manufacturing and 11.0 for all sectors, and the mean cumulative number of patents granted (still in effect, not expired) would increase to 154.9 for manufacturing and 92.3 for all sectors. There would be no change to the means for the service sector.

% OF FIRMS WITH PATENT APPLICATIONS/GRANTS

Innovating

Non-innovating

53.650.0

33.910.0

19.610.0

41.130.0

other countries

Europe

Japan

US

NO. OF PATENTS

All sectors

Services

Manufacturing

11.23.8

total no. of patentsgranted over

last 3 years

total no. of patentapplications over

last 3 years

total cumulative no.of patents granted

(in effect, not expired) 16.7

5.82.5

8.3

9.45.9

12.1

03IP CREATION

p_26

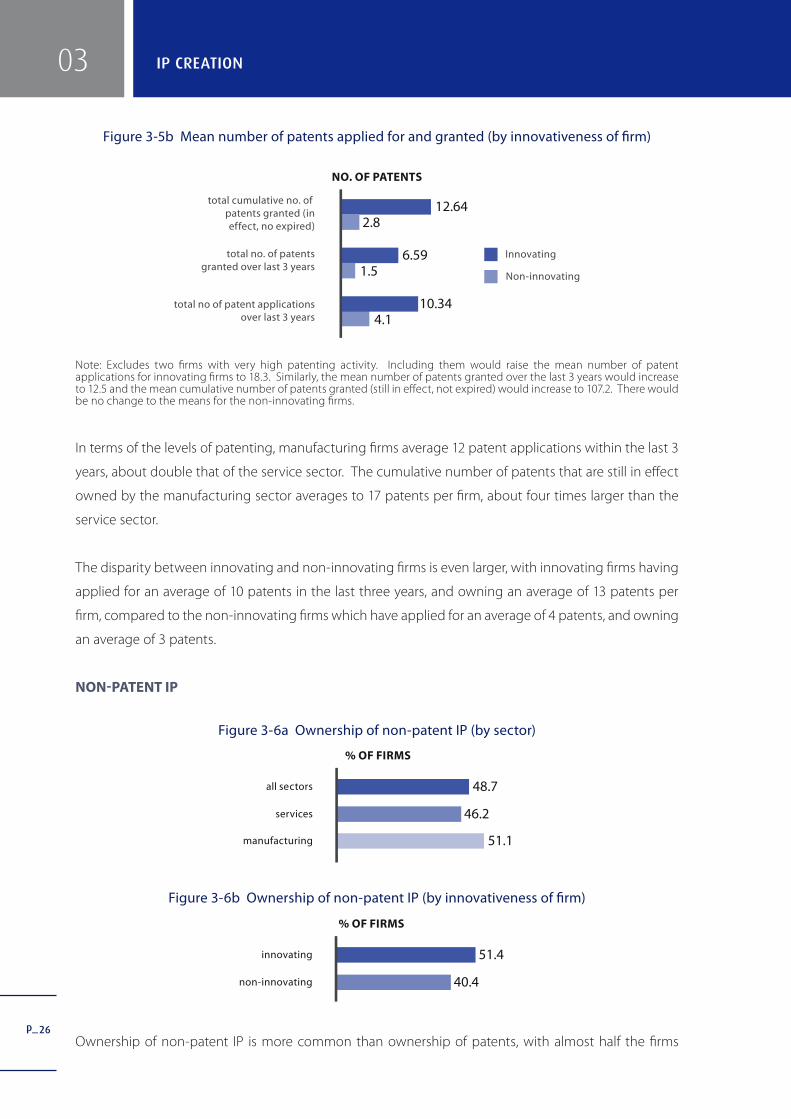

Figure 3-5b Mean number of patents applied for and granted (by innovativeness of firm)

Note: Excludes two firms with very high patenting activity. Including them would raise the mean number of patent applications for innovating firms to 18.3. Similarly, the mean number of patents granted over the last 3 years would increase to 12.5 and the mean cumulative number of patents granted (still in effect, not expired) would increase to 107.2. There would be no change to the means for the non-innovating firms.

In terms of the levels of patenting, manufacturing firms average 12 patent applications within the last 3

years, about double that of the service sector. The cumulative number of patents that are still in effect

owned by the manufacturing sector averages to 17 patents per firm, about four times larger than the

service sector.

The disparity between innovating and non-innovating firms is even larger, with innovating firms having

applied for an average of 10 patents in the last three years, and owning an average of 13 patents per

firm, compared to the non-innovating firms which have applied for an average of 4 patents, and owning

an average of 3 patents.

NON-PATENT IP

Figure 3-6a Ownership of non-patent IP (by sector)

Figure 3-6b Ownership of non-patent IP (by innovativeness of firm)

Ownership of non-patent IP is more common than ownership of patents, with almost half the firms

% OF FIRMS

all sectors

services

manufacturing

48.7

46.2

51.1

% OF FIRMS

innovating

non-innovating

51.4

40.4

03 IP CREATION

��������������

����������

��������������

��������

�������

��������

��������������������������������������������������������������

���������������������������������������������

������������������������������������������������

p_27

owning some form of non-patent IP. The sectors are fairly evenly matched in their incidence of non-

patent IP ownership, although the manufacturing sector does have a slight advantage over services.

Innovating firms are more likely to own non-patent IP than non-innovating firms, but the difference is

not as great as with patent ownership.

Figure 3-7a Types of non-patent IP owned (by sector)

Figure 3-7b Types of non-patent IP owned (by innovativeness of firm)

Trademarks are the most commonly owned form of non-patent IP, followed by copyright and trade

secrets. Sectoral differences are evident in the types of non-patent IP held by firms. Manufacturing

firms more commonly own trademarks and registered design, whereas service firms – largely due to the

IT services industry – more commonly owns copyright (including software).

% OF FIRMS

Innovating

Non-innovating

20.717.0

4.30

23.610.6

104.3

trade secrets

database rights

copyright(including software)

registered design

trademarks35.7

23.4

03IP CREATION

% OF FIRMS

All sectors

Services

Manufacturing

19.819.4trade secrets

database rights

copyright(including software)

registered design

trademarks

20.2

3.24.3

2.1

20.325.8

14.9

8.62.2

14.9

32.626.9

38.3

p_

04 USAGE OF OWN IP

USAGE OF OWN IP

In this section, we examine the extent to which IP assets, focusing on patents, are being commercialized

by firms. Broadly, IP may be commercialized in two ways: used internally to produce products or

services, or licensed out to other organizations for royalty income. Alternatively, IP assets may remain

uncommercialized by the firm if they are not utilized in any form.

USAGE OF PATENTS

In this section, we restrict our discussion to firms’ usage of patents that are still in effect (i.e. they have

not expired).

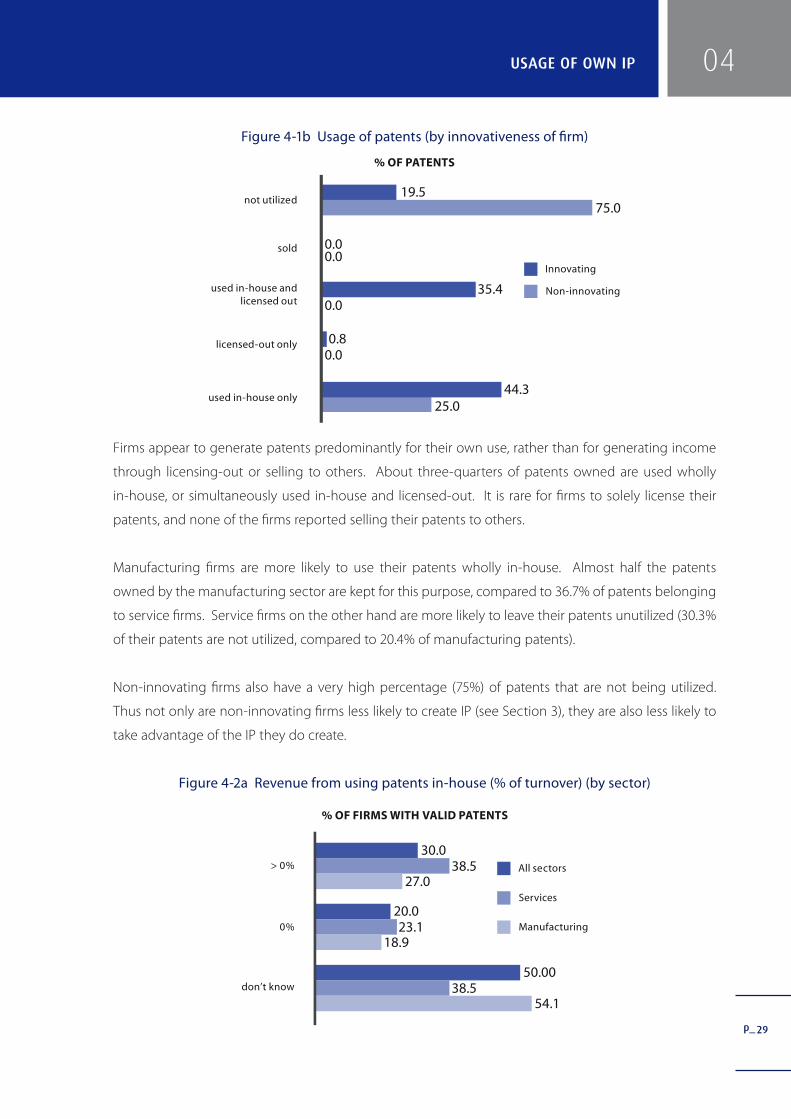

Figure 4-1a Usage of patents (by sector)

% OF PATENTS

All sectors

Services

Manufacturing

22.430.3not utilized

sold

used in-house andlicensed out

licensed-out only

used in-house only

20.4

0.000.0

33.533.0

33.6

0.70.0

0.9

43.336.7

45.0

0.0

28

p_29

04USAGE OF OWN IP

Figure 4-1b Usage of patents (by innovativeness of firm)

Firms appear to generate patents predominantly for their own use, rather than for generating income

through licensing-out or selling to others. About three-quarters of patents owned are used wholly

in-house, or simultaneously used in-house and licensed-out. It is rare for firms to solely license their

patents, and none of the firms reported selling their patents to others.

Manufacturing firms are more likely to use their patents wholly in-house. Almost half the patents

owned by the manufacturing sector are kept for this purpose, compared to 36.7% of patents belonging

to service firms. Service firms on the other hand are more likely to leave their patents unutilized (30.3%

of their patents are not utilized, compared to 20.4% of manufacturing patents).

Non-innovating firms also have a very high percentage (75%) of patents that are not being utilized.

Thus not only are non-innovating firms less likely to create IP (see Section 3), they are also less likely to

take advantage of the IP they do create.

Figure 4-2a Revenue from using patents in-house (% of turnover) (by sector)

% OF PATENTS

Innovating

Non-innovating

19.575.0

0.0

0.0

0.0

0.0

35.4

0.8

44.325.0

not utilized

sold

used in-house andlicensed out

licensed-out only

used in-house only

% OF FIRMS WITH VALID PATENTS

All sectors

Services

Manufacturing

30.038.5> 0%

0%

don’t know

27.0

20.023.1

18.9

50.0038.5

54.1

p_30

Figure 4-2b Revenue from using patents in-house (% of turnover) (by innovativeness of firm)

Figure 4-3 Revenue from licensing patents to third parties (% of turnover)

Note: No data is available for non-innovating firms, as none of the non-innovating firms in our sample reported

licensing-out their patents

It appears from our survey that firms have limited systems for tracking the results of their patent usage.

Half of the firms who own patents do not know how much of their revenue is generated by using

them in-house, and one-fifth do not know how much is generated by licensing them out. This is more

apparent with the manufacturing firms, although this could also be due to the fact that manufacturing

MNCs operating in Singapore sometimes have their IP managed by their head offices overseas. As

such, the data on the commercial results of their patent usage is not available to the Singapore office.

The lack of tracking is also more evident amongst non-innovating firms, two-thirds of whom reported

not knowing how much revenue is generated by the use of products/processes developed from their

patents.

% OF FIRMS WITH VALID PATENTS

All sectors

Services

Manufacturing

7.914.2> 0%

0%

don’t know

5.4

70.671.4

70.3

21.614.3

24.3

% OF FIRMS WITH VALID PATENTS

Innovating

Non-innovating

32.60.0

33.321.7

45.766.7

> 0%

0%

don’t know

04 USAGE OF OWN IP

p_31

Table 4-1a Economic importance of patents (by sector)

MANUFACTURING SERVICES ALL SECTORS

All firms

Contribution of patents utilized in-house (% of turnover in latest fiscal year covered by patent applications or patents granted)

4.13 0.20 1.87

Contribution of patents licensed out (% of revenue in latest fiscal year contributed by royalties generated by licensing out to 3rd parties)

0.01 0.02 0.01

Patent-owning firms only

Contribution of patents utilized in-house (% of turnover in latest fiscal year covered by patent applications or patents granted)

12.37 41.35 12.94

Contribution of patents licensed out (% of revenue in latest fiscal year contributed by royalties generated by licensing out to 3rd parties)

0.01 1.98 0.04

Note: Data is weighted by sales size

Table 4-1b Economic importance of patents (by innovativeness of firm)

NON -INNOVATING

INNOVATING

All firms

Contribution of patents utilized in-house (% of turnover in latest fiscal year covered by patent applications or patents granted)

0.00 2.77

Contribution of patents licensed out (% of revenue in latest fiscal year contributed by royalties generated by licensing out to 3rd parties)

0.00 0.02

Patent-owning firms only

Contribution of patents utilized in-house (% of turnover in latest fiscal year covered by patent applications or patents granted)

0.00 12.98

Contribution of patents licensed out (% of revenue in latest fiscal year contributed by royalties generated by licensing out to 3rd parties)

0.00 0.04

Note: Data is weighted by sales size

On average, technologies from patents used in firm products/processes contribute 1.9% of firms’

turnover (12.9% for firms which own valid patents). Thus in-house use of patents is a much greater

source of revenue contribution than licensing-out of patents, which only contributes 0.01% of firm’s

04USAGE OF OWN IP

p_32

turnover (or 0.04% for firms which own valid patents). Although patent ownership is more common in

the manufacturing sector than the service sector, patent-owning service firms are much more successful

in commercializing their patents than those in manufacturing, earning a higher average percentage of

revenue from using their patents in-house (41.4% for services vs 12.4% for manufacturing) and from

licensing them to third parties (2.0% for services vs 0.01% for manufacturing).

Additionally, it was found revenues generated by using patents in-house correlates with the degree

of innovation commercialization. None of the non-innovating firms reported earning revenue from

utilizing their patents. Furthermore, Annex Table D-1 shows that firms with higher rates of innovation

commercialization earn larger shares of turnover from patent applications or patents granted.5

Table 4-2 Parties to whom patents are licensed-out

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS WITH PATENTS LICENSED-OUT

Foreign-based firms in the same line of business 75.0 50.0 68.8

Foreign-based firms not in the same line of business

33.3 50.0 37.5

Parent firm or affiliated firm within the enterprise group

33.3 25.0 31.3

Sg-based firms not in the same line of business 8.3 25.0 12.5

Sg-based firms in the same line of business as the enterprises

0.0 0.0 0.0

Other firms 0.0 0.0 0.0

When firms do license-out their patents, they most commonly do so to foreign-based firms operating

in the same line of business. The manufacturing sector focuses its licensing-out operations heavily

on these firms, whereas those in the service sector tend to license-out to foreign firms regardless of

whether they are in the same line of business or not. It thus appears that manufacturing sector patents

are more specialized, whereas service sectors patents are more general and able to be applied to other

industries.

5 The positive correlation coefficients are marginally insignificant, due to sample size constraints.

04 USAGE OF OWN IP

p_33

Table 4-3a Reasons for not utilizing patents (by sector)

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS WITH NON-UTILIZING PATENTS

Technology no longer aligned with firm strategy 42.1 16.7 36.0

Other reason 36.8 33.3 36.0

Technology considered too risky to be successfully commercialized

26.3 0.0 20.0

Technology not prioritized internally 10.5 33.3 16.0

Firm lacks resources to utilize the patent(s) 10.5 33.3 16.0

Cannot find suitable partner or recipient to utilize patent

10.5 16.7 12.0

Market for technology does not meet firm’s financial criteria

5.3 0.0 4.0

Table 4-3b Reasons for not utilizing patents (by innovativeness of firm)

NON -INNOVATING

INNOVATING

% OF FIRMS WITH NON-UTILIZING PATENTS

Technology no longer aligned with firm strategy 0.0 40.9

Other reason 66.7 31.8

Technology not prioritized internally 0.0 18.2

Firm lacks resources to utilize the patent(s) 0.0 18.2

Technology considered too risky to be successfully commercialized

33.3 18.2

Cannot find suitable partner or recipient to utilize patent 33.3 9.1

Market for technology does not meet firm’s financial criteria 0.0 4.5

A number of firms reported that they own patents that are in effect but are not being commercialized.

Because the development of novel innovations carries risks and uncertainties, firms might, at some

point, strategically decide to define certain technologies as being non-significant for their current

competitive position. Such non-core technologies are not directly linked to the firm’s core business or

are not utilized in current or future products. Another possible reason for non-utilization is defensive

patenting, in which a firm files for a technology that it has no intention of using merely to prevent a

competitor from filing.

04USAGE OF OWN IP

p_34

In our survey, the most common reason for not utilizing patents is a mismatch between the technology

based on the patent and firm strategy. This appears to be a bigger problem for manufacturing than

for service firms, who most commonly cite resource constraints and a lack of priority placed on the

technology.

For non-innovating firms, non-utilization of patents is often the technology being perceived as too risky

for successful commercialization, or an inability to find suitable partners to use the patent.

Quite a number of firms cited other reasons for not utilizing their patents, including the immaturity of

the technology, the product from the technology being under design/development, and defensive

patenting.

USAGE OF NON-PATENT IP

Figure 4-4a Revenue from licensing out non-patent IP (% of turnover) (by sector)

Figure 4-4b Revenue from licensing-out non-patent IP (% of turnover) (by innovativeness of firm)

% OF FIRMS WHICH OWN NON-PATENT IP

All sectors

Services

Manufacturing

25.935.6> 0%

none

unable to tell

16.4

61.254.8

67.4

12.99.5

16.3

% OF FIRMS WHICH OWN NON-PATENT IP

Innovating

Non-innovating

30.0

72.2

11.2

58.2

11.916.7

> 0%

0%

don’t know

04 USAGE OF OWN IP

p_35

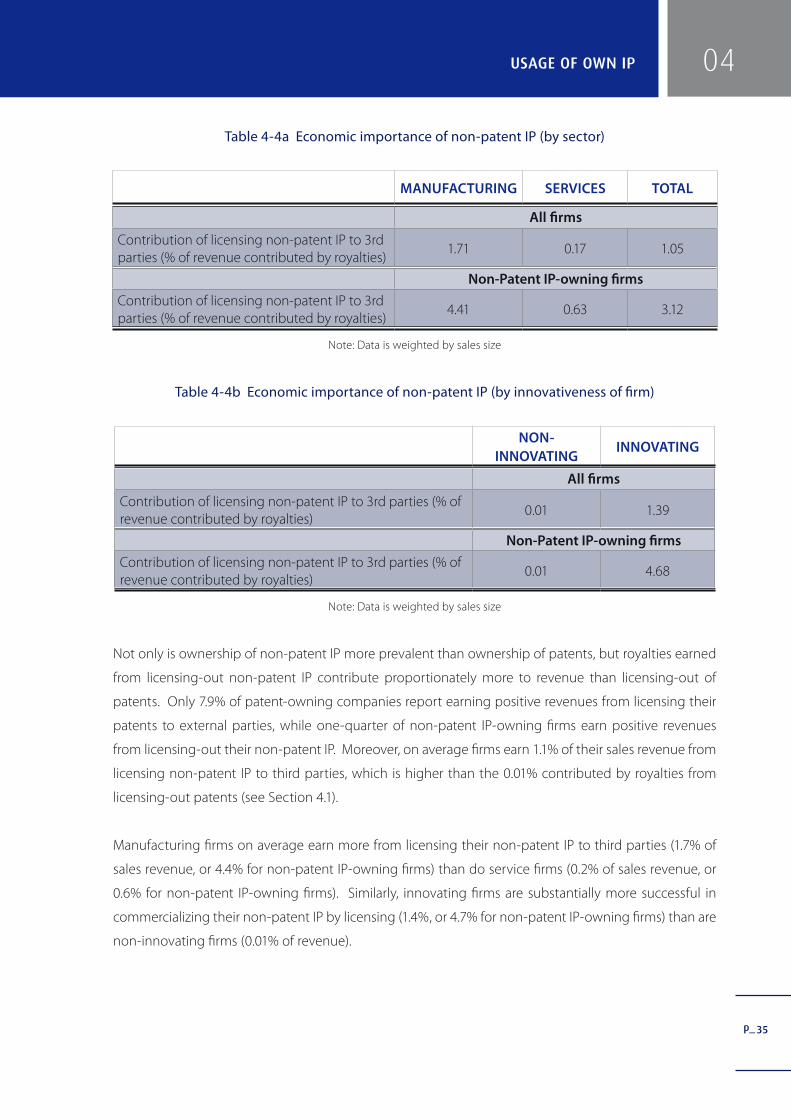

Table 4-4a Economic importance of non-patent IP (by sector)

MANUFACTURING SERVICES TOTAL

All firms

Contribution of licensing non-patent IP to 3rd parties (% of revenue contributed by royalties)

1.71 0.17 1.05

Non-Patent IP-owning firms

Contribution of licensing non-patent IP to 3rd parties (% of revenue contributed by royalties)

4.41 0.63 3.12

Note: Data is weighted by sales size

Table 4-4b Economic importance of non-patent IP (by innovativeness of firm)

NON-INNOVATING

INNOVATING

All firms

Contribution of licensing non-patent IP to 3rd parties (% of revenue contributed by royalties)

0.01 1.39

Non-Patent IP-owning firms

Contribution of licensing non-patent IP to 3rd parties (% of revenue contributed by royalties)

0.01 4.68

Note: Data is weighted by sales size

Not only is ownership of non-patent IP more prevalent than ownership of patents, but royalties earned

from licensing-out non-patent IP contribute proportionately more to revenue than licensing-out of

patents. Only 7.9% of patent-owning companies report earning positive revenues from licensing their

patents to external parties, while one-quarter of non-patent IP-owning firms earn positive revenues

from licensing-out their non-patent IP. Moreover, on average firms earn 1.1% of their sales revenue from

licensing non-patent IP to third parties, which is higher than the 0.01% contributed by royalties from

licensing-out patents (see Section 4.1).

Manufacturing firms on average earn more from licensing their non-patent IP to third parties (1.7% of

sales revenue, or 4.4% for non-patent IP-owning firms) than do service firms (0.2% of sales revenue, or

0.6% for non-patent IP-owning firms). Similarly, innovating firms are substantially more successful in

commercializing their non-patent IP by licensing (1.4%, or 4.7% for non-patent IP-owning firms) than are

non-innovating firms (0.01% of revenue).

04USAGE OF OWN IP

p_36

05 USAGE OF EXTERNAL IP

USAGE OF EXTERNAL IP

Firms might also choose to license-in technologies from other organizations. Technology licensing

activities facilitate technology transfer and knowledge sharing between licensees and licensors, and are

particularly effective for commercializing inventions originating from universities and public research

institutes. Licensing-in of external IP is also an effective method of technology acquisition for firms that

lack resources for in-house research and development functions.

LICENSING-IN OF PATENTS

Figure 5-1a Licensing-in of patents from third parties (by sector)

Figure 5-1b Licensing-in of patents from third parties (by innovativeness of firm)

Only a minority of firms (17.7%) license-in patents from third parties. Licensing-in is more common in

the manufacturing sector than in the services sector. Innovating firms are also more likely to license-

in patents than non-innovating firms, highlighting the importance of diffusion of technology and

knowledge in the innovation process.

Table 5-1 Parties from whom firms license-in patents

MANUFACTURING SERVICES ALL SECTORS

% OF FIRMS WHO LICENSE-IN PATENTS

Foreign-based firms in the same line of business as enterprise

47.4 35.7 42.4

Foreign-based firms not in the same line of business as enterprise

36.8 35.7 36.4

(continued on next page)

% OF FIRMS

all sectors

services

manufacturing

17.7

15.1

20.4

% OF FIRMS

innovating

non-innovating

20.1

10.6

p_37

05USAGE OF EXTERNAL IP

(continued from previous page)

Technology rights granted by external buyers for contract manufacturing or services

15.8 28.6 21.2

Parent firm or affiliated firm within the enterprise group

21.1 14.3 18.2

Foreign universities or public research institutes 10.5 21.4 15.2

Local universities or public research institutes 21.1 7.1 15.2

Singapore-based firms not in the same line of business

5.3 14.3 9.1

Singapore-based firms in the same line of business as the enterprises

0.0 14.3 6.1

Knowledge flows through licensing of patents appears to be stronger between Singapore-based and

foreign-based firms than amongst Singapore-based firms. Just as firms most commonly license-out

their patents to foreign-based firms (see Section 4.1), they also most commonly license-in patents from

foreign-based firms. Technology transfer from universities and PRICs via licensing is relatively rare,

although where it does occur, manufacturing firms are more likely to license-in from local universities/

PRICs, whereas service firms more commonly do so from foreign institutions.

Figure 5-2 Revenue from licensed-in patents1 (% of turnover)

1 Excludes patents licensed-in from parent firm and other affiliates, and technology rights granted by external buyers for

contract manufacturing or services

Firms are more careful to track the revenue generated from using licensed-in patents than they are with

patents they have created themselves. Only about 15% of firms who license in patents report that they

do not know how much this contributes to their revenue (compared to about two-thirds of firms who

license-out their patents, see Section 4.1).

���������������������������������

�����������

��������

�������������

������������

����

�����������

����

��������

����

�������

����

p_38

Figure 5-3 Cost of licensing-in patents1 (% of revenue)

1Excludes patents licensed-in from parent firm and other affiliates, and technology rights granted by

external buyers for contract manufacturing or services

Table 5-2a Economic importance of licensed-in patents (by sector)

MANUFACTURING SERVICES TOTAL

All firms

Contribution of products/services that use licensed-in patents (% of turnover in latest fiscal year)

0.73 0.10 0.51

Cost of licensing-in of patents (% of revenue in latest fiscal year)

1.36 0.08 0.95

Firms who license-in patents only

Contribution of products/services that use licensed-in patents (% of turnover in latest fiscal year)

1.67 11.86 1.78

Cost of licensing-in of patents (% of revenue in latest fiscal year)

2.65 10.20 2.71

Note: Data is weighted by sales size

% OF FIRMS WHO LICENSE-IN PATENTS

All sectors

Services

Manufacturing

55.849.9> 0%

none

do not know

60.0

26.542.9

7.1

15.0

17.6

25.0

05 USAGE OF EXTERNAL IP

p_39

Table 5-2b Economic importance of licensed-in patents (by innovativeness of firm)

NON -INNOVATING

INNOVATING

All firms

Contribution of products/services that use licensed-in patents (% of turnover in latest fiscal year)

0.00 0.63

Cost of licensing-in of patents (% of revenue in latest fiscal year) 0.04 1.15

Firms who license-in patents only

Contribution of products/services that use licensed-in patents (% of turnover in latest fiscal year)

0.00 1.78

Cost of licensing-in of patents (% of revenue in latest fiscal year) 0.89 2.75

Note: Data is weighted by sales size

On average, revenue generated by licensed-in patents contributes a very small proportion of firms’

turnover. Although almost half the firms who license-in patents report earning positive revenues from

them, overall they only contribute 0.5% of turnover (or 1.8% for firms who license-in patents).

Amongst firms which do license patents from third parties, service firms are more heavily dependent on

such external technology. A much greater percentage of their revenue (10.2%) goes to paying royalties

for licensed-in patents, and utilizing the patents contributes a greater share of their revenue (11.9%) than

for the manufacturing sector (2.7% and 1.7% respectively).

Overall, firms are not recovering the cost of their licensed-in patents, spending more on the royalties

(1.2% of turnover, or 2.8% for firms who license-in patents) than these technologies contribute (0.6% of

turnover, or 1.8% for firms who license-in patents). This is particularly evident for non-innovating firms,

none of which reported earning revenue from utilizing their licensed-in patents.

LICENSING-IN OF NON-PATENT IP

Figure 5-4a Licensing-in of non-patent IP (by sector)

% OF FIRMS

all sectors

services

manufacturing

15.6

20.4

10.8

05USAGE OF EXTERNAL IP

p_40

Figure 5-4b Licensing-in of non-patent IP (by innovativeness of firm)

As with licensing-in of patents, licensing-in non-patent IP is only practised by a minority of firms.

However, licensing-in of non-patent IP is more common in the services sector than in manufacturing,

and among innovating firms as compared to non-innovating firms.

Figure 5-5a Types of non-patent IP licensed-in (by sector)

Figure 5-5b Types of non-patent IP licensed-in (by innovativeness of firm)

% OF FIRMS

innovating

non-innovating

16.5

12.8

database rights

copyright(including software)

registered design

trademarks

% OF FIRMS

Innovating

Non-innovating

0.0

8.5

0.0

12.9

2.22.1

2.92.1

05 USAGE OF EXTERNAL IP

����������

�����������

��������

�������������

���������������������

�����������������������������