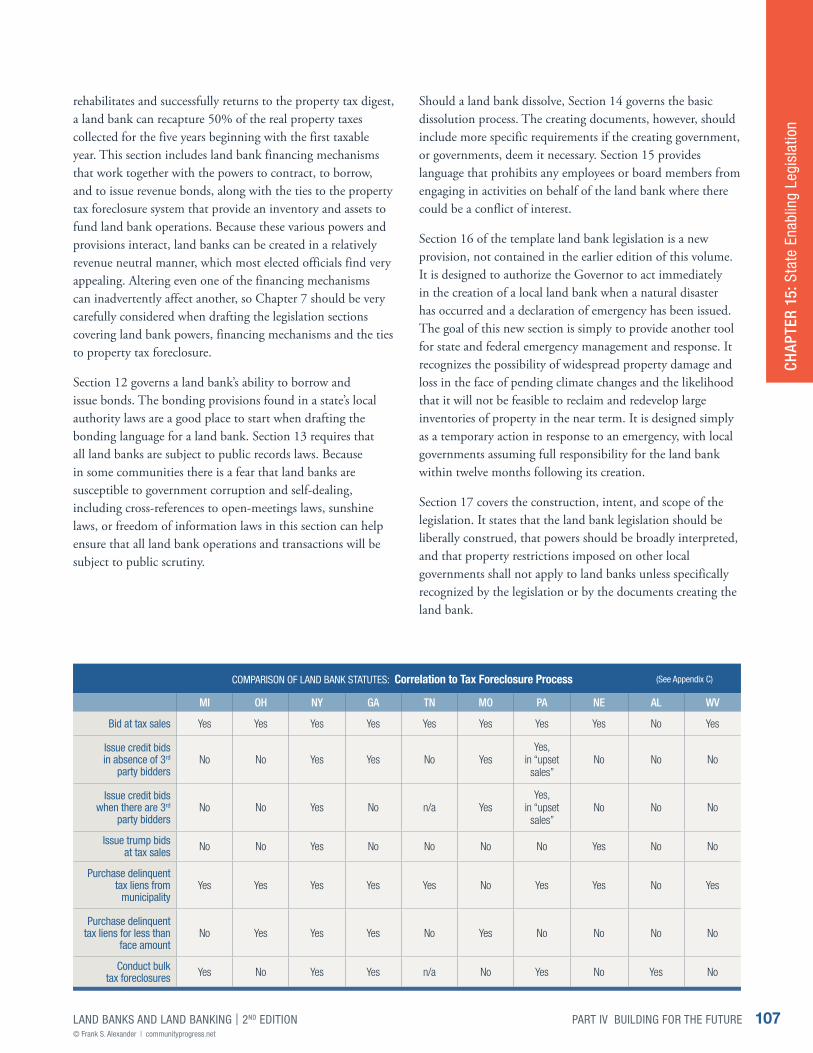

Bahasa

Halaman

Hukum

Land Banks andLand Banking

2ND EDITION | 2015

Frank S. AlexanderSam Nunn Professor of Law

Emory Law School

Co-founder & Senior AdvisorCenter for Community Progress

This volume is published and distributed by the: Center for Community Progress

111 E. Court Street, Suite 2C-1, Flint, MI 48502 tel: (877) 542-4842

The publication is available in electronic and print formats via www.communityprogress.net.

Copyright, 2015, 2011, Frank S. Alexander. All rights reserved.

ISBN-10: 0692405127 ISBN-13: 978-0-692-40512-3

2© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

Table of Contents

2ND EDITION | 2015

Land Banks andLand Banking

TABLE OF CONTENTS 3LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

FOREWORD by Tamar Shapiro, President and CEO, Center for Community Progress 8

INTRODUCTION 10

Part I. Understanding Abandonment CHAPTER 1: UNDERSTANDING THE INVENTORY 14

Vacant, Abandoned, Tax-Delinquent, and Foreclosed PropertiesUnderstanding the Costs of Neglect

CHAPTER 2: THE EVOLUTION OF LAND BANKS 18The First Generation: St. Louis, Cleveland, Louisville, AtlantaThe Second Generation: Genesee County & Michigan; OhioThe Third Generation of State Land Bank StatutesLand Banking Under Local Home Rule AuthorityLand Banks and Land Banking – Variations on the ThemeThe Federal Role and Neighborhood Stabilization in the Great RecessionA Comparative International Approach to Land Banking: China

CHAPTER 3: THE RANGE OF CHALLENGES 28Barrier: Lack of Awareness of the ProblemBarrier: Tax-Delinquent PropertiesBarrier: Title ProblemsBarrier: Property Disposition RequirementsBarrier: Inadequacy of Code EnforcementBarrier: Unknown OwnersBarrier: Lack of Control

CHAPTER 4: POTENTIAL SOLUTIONS 34Understanding and Evaluating the InventoryReforming Tax Foreclosure StatutesJudicial Tax ForeclosuresClarity and Flexibility in Disposition Criteria

Table of Contents

TABLE OF CONTENTS 4© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

Enhancing Code Enforcement ProceduresIdentifying Responsible PartiesJudicial Receiverships

CHAPTER 5: ADDITIONAL TOOLS AND ALTERNATIVES 42Land Banks as Regional Approaches Land Banks as DepositoriesLand Banks as Development PartnersLand Banking and Community Land TrustsLand Banks as Natural Disaster Responses

Part II. Creating and Operating a Land BankCHAPTER 6: CREATING ESSENTIAL POWERS FOR LAND BANKS 50

Property AcquisitionProperty ManagementProperty Disposition

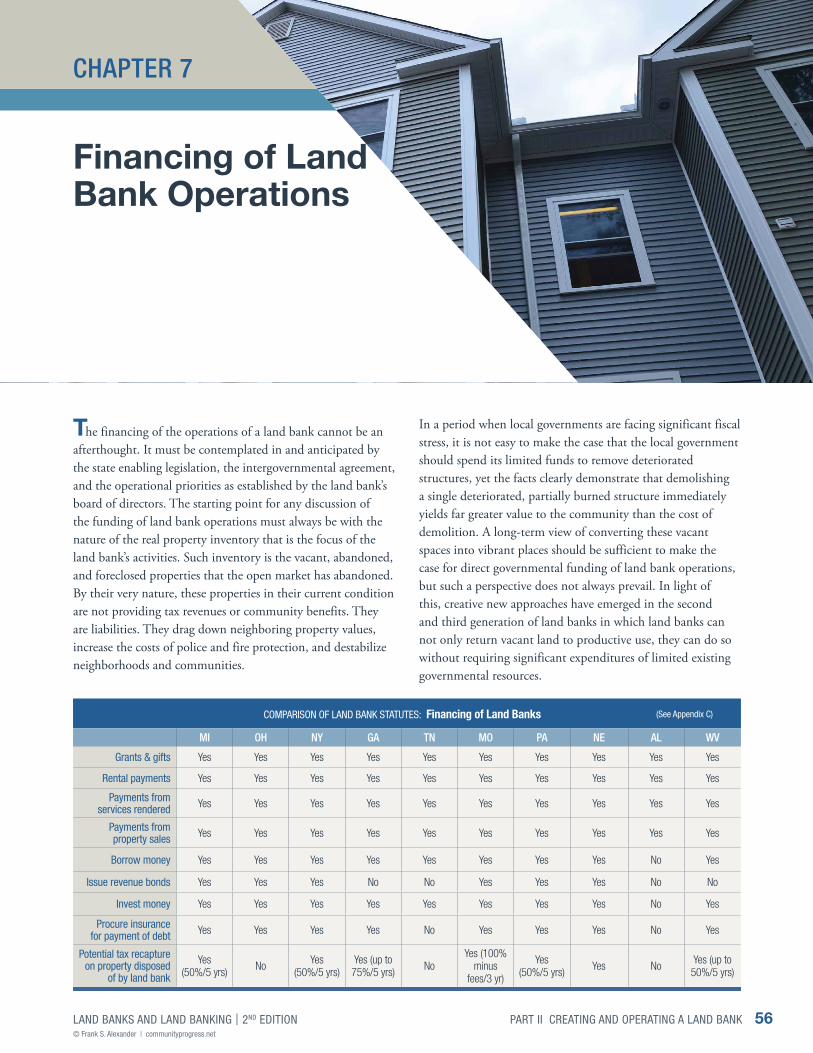

CHAPTER 7: FINANCING OF LAND BANK OPERATIONS 56General Revenue FundingInventory Cross-SubsidiesTax RecaptureDelinquent Tax Revolving FundsDedicated Funding from Delinquent Tax ChargesBorrowing and Bond Financing

CHAPTER 8: FORMING THE GOVERNANCE OF LAND BANKS 62Factors that Influence Land Bank GovernanceLegal Structures of Land BanksBoard of Directors of Land BanksStaffing Possibilities and Opportunities Selecting Public and Private RolesCommunity and Resident Engagement

CHAPTER 9: IDENTIFYING CORE PUBLIC POLICIES FOR LAND BANKS 68Identifying Critical Policy GoalsBuilding Upon Key Public PoliciesStrategic Banking of PropertiesThe Unintended Consequences of Success

CHAPTER 10: DETERMINING ADMINISTRATIVE POLICIES FOR DISPOSITION 74Establishing Property EligibilityIdentifying Eligible Property OwnersSetting Pricing PoliciesEnforcing Commitments

Table of Contents

TABLE OF CONTENTS 5LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

Part III. Three Land Bank ExamplesCHAPTER 11: ATLANTA LAND BANK 82

CHAPTER 12: GENESEE LAND BANK 88

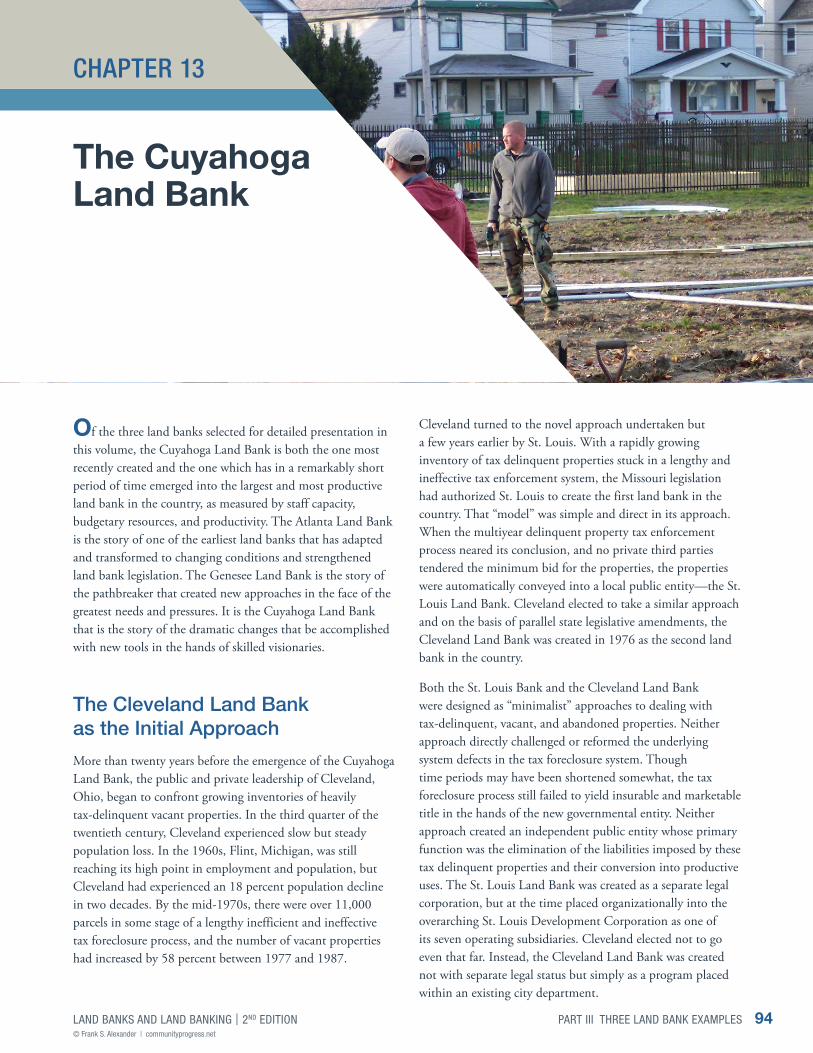

CHAPTER 13: CUYAHOGA LAND BANK 94

Part IV. Building for the FutureCHAPTER 14: THE CASE FOR LAND BANKING IN YOUR COMMUNITY 100

Building ConstituenciesAnticipating ObjectionsManaging ExpectationsDefining SuccessState Land Bank Associations

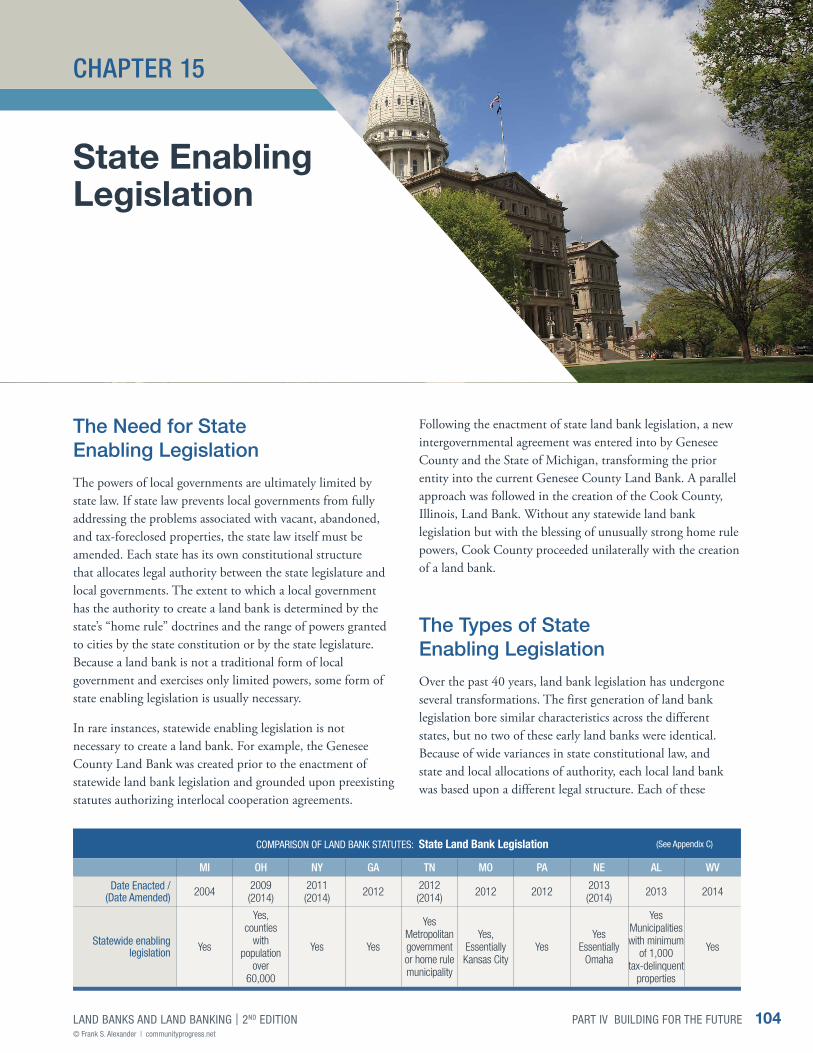

CHAPTER 15: STATE ENABLING LEGISLATION 104The Need for State Enabling LegislationThe Types of State Enabling LegislationDrafting State Enabling Legislation

CHAPTER 16: INTERGOVERNMENTAL AGREEMENTS 110Maximizing Intergovernmental CooperationDeveloping and Drafting Intergovernmental Agreements

CHAPTER 17: THE FUTURE OF LAND BANKING 112

Part V. Bibliography & AppendicesBIBLIOGRAPHY 116

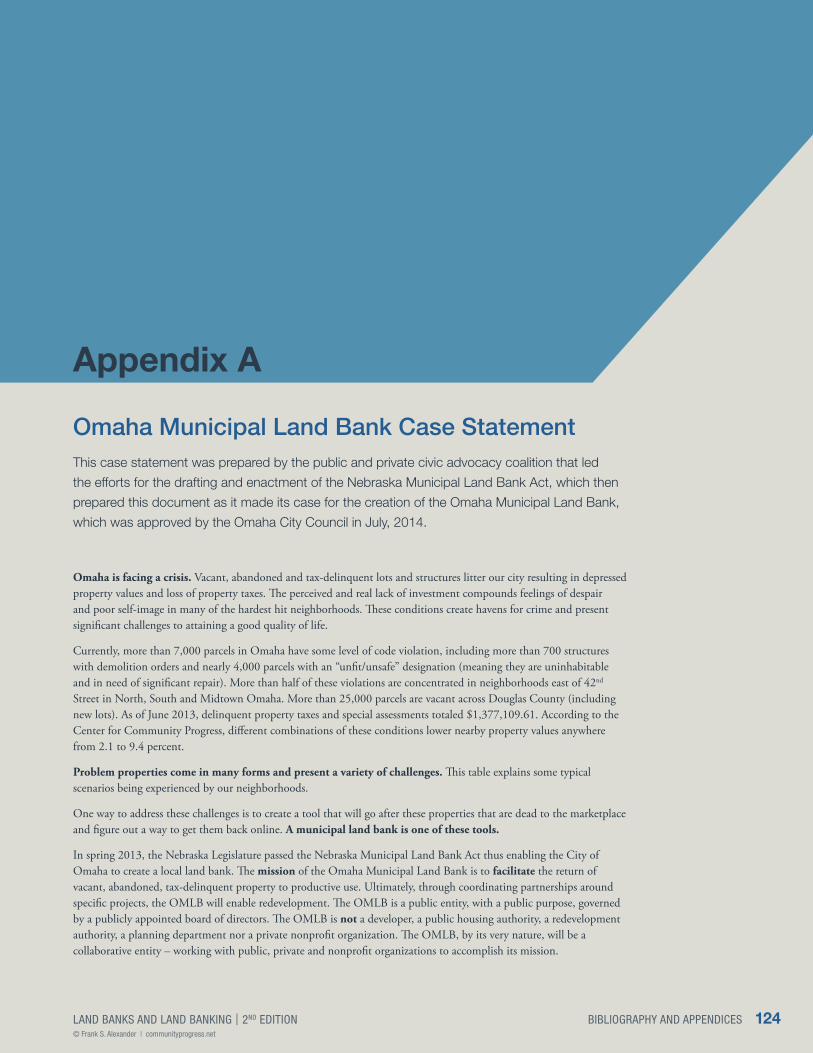

APPENDIX A: OMAHA MUNICIPAL LAND BANK CASE STATEMENT 124

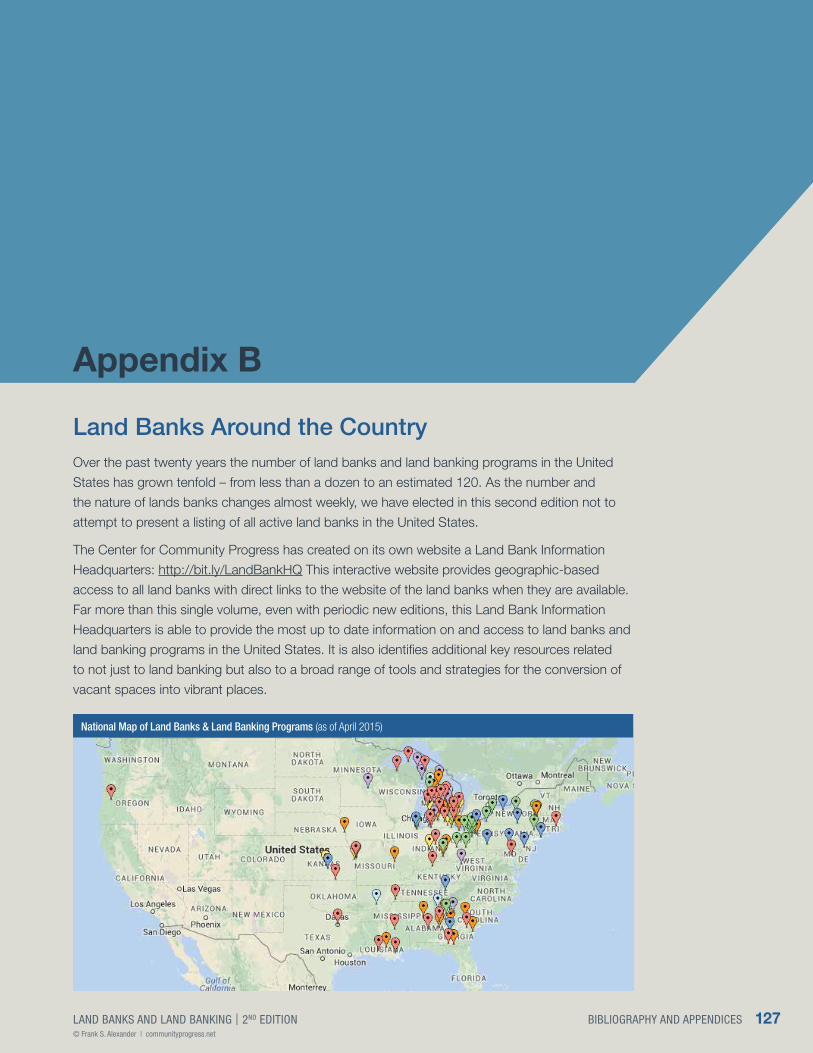

APPENDIX B: LAND BANKS AROUND THE COUNTRY 127

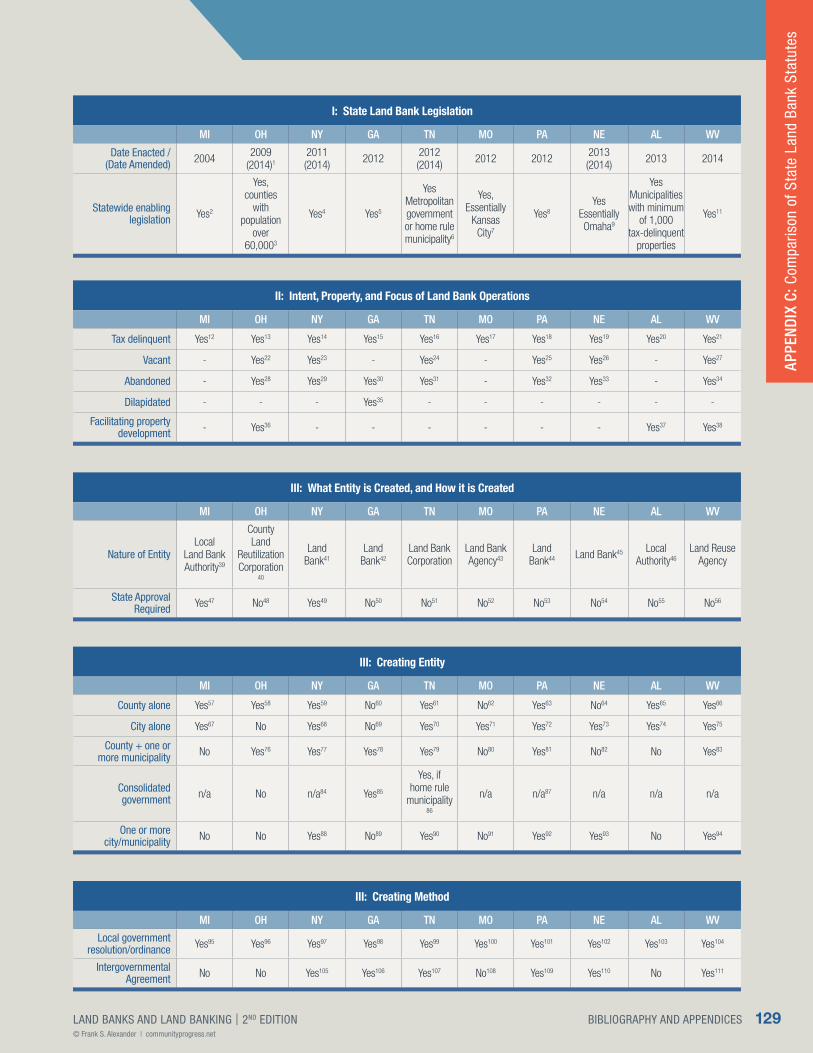

APPENDIX C: COMPARISON OF STATE LAND BANK STATUTES 128

APPENDIX D: TEMPLATE FOR LAND BANK LEGISLATION 142

APPENDIX E: SAMPLE ADMINISTRATIVE POLICIES 151

APPENDIX F: LAND BANK DEPOSITORY AGREEMENTS 160

About the Center for Community Progress

Founded in 2010, the Center for Community Progress is the only national nonprofit organization solely dedicated to building a future in which entrenched, systemic blight no longer exists in American communities. The mission of Community Progress is to ensure that communities have the vision, knowledge, and systems to transform blighted, vacant, and other problem properties into assets supporting neighborhood vitality. Community Progress serves as the leading resource for local, state, and federal policies and best practices that address the full cycle of property revitalization, from blight prevention, through the acquisition and maintenance of problem properties, to their productive reuse. Major support for Community Progress is provided by the Charles Stewart Mott Foundation and the Ford Foundation. More information is available at www.communityprogress.net.

6© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

About the Author

Frank S. Alexander is the Sam Nunn Professor of Law at Emory University School of Law and is Co-founder and Senior Advisor of the Center for Community Progress. He is the author or editor of eleven books and more than fifty articles in real estate finance, community development, and law and theology, including Georgia Real Estate Finance and Foreclosure Law 2014-2015 (10th ed., 2014). Professor Alexander’s work has focused on homelessness, affordable housing, and community development, serving as a Fellow of the Carter Center of Emory University (1993-96), and as a Commissioner of the State Housing Trust Fund for the Homeless (1994-98). He has served as Interim Dean of Emory University School of Law (2005-06), as Visiting Fellow at the Joint Center for Housing Studies, Harvard University (Fall Semester, 2007), and has testified before U.S. Congress concerning the mortgage foreclosure crisis. Professor Alexander received his JD from Harvard Law School, a Masters in Theological Studies from Harvard Divinity School, and his BA from the University of North Carolina.

7LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

Land banks have existed in the U.S.

for more than four decades, but

as recently as 2010, they were still

a relatively unexplored community

development tool. That was the year

the Center for Community Progress

opened its doors with the purpose

of advising communities on land

banks and other critical tools to

address vacancy, abandonment,

and tax delinquency.

At that time, a handful of states, most notably Michigan and Ohio, already had land bank enabling legislation on the books, and a small number of well-established land banks had emerged as examples from which to learn. A national community of practice related to land banking, however, had not yet formed, leaving many questions about best practices unanswered.

This landscape began to change in the wake of the 2008 housing market collapse and subsequent foreclosure crisis, as an increasing number of community development practitioners around the country came to view land banks as a potential game changer in their efforts to combat problem properties.

In this context, Frank Alexander released the first edition of Land Banks and Land Banking in 2011. It was the most comprehensive publication on land banking developed to date, and it helped to usher in a new era of sophistication in land banking.

In the four years since, eight additional states have passed some form of land bank legislation—a number of them modelling their statutes on template language included in Land Banks and Land Banking. Thousands of copies of the book have been distributed nationally and it has been recognized internationally, as well, with a Mandarin edition authorized for publication in China.

Land Banks and Land Banking has provided the foundation for countless training workshops for would-be and current land banking practitioners and it is safe to say that the book has affected the work of most, if not all, of today’s land bank practitioners.

In Land Banks and Land Banking, Frank not only coined the “generational” framework for land banks, identifying the characteristics of “first generation” and “second generation” land banks—his insight and recommendations in turn actually gave rise to the newest, third generation of land banks, which is described herein.

The first edition of Land Banks and Land Banking has remained unsurpassed as the authoritative resource on land banking until now, with the 2015 publication of this second edition.

Foreword

FOREWORD 8LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

This newest edition provides clear historic context about the development of land banking and elucidates the rapid evolution of land banking over the last four years. Practitioners will also find an expanded trove of practical resources, including extensive guidance on creating and operating a land bank in Part II and a detailed look at ensuring a strong future for land banks in Part IV.

Land banking is one of many tools that can be used to address vacant and abandoned properties. As its title suggests, this publication is focused squarely on land banks. But it also highlights the many important links between this tool and other systems that govern the use and reuse of land, including, perhaps most critically, property tax enforcement. In addition, it explores in what context a land bank is likely to be most impactful and when a community might be better served looking to other tools, entities, or strategies. Indeed, one of the most valuable lessons contained in this edition is the recognition that each community’s challenge is a little different and that the first step in any community’s fight against vacancy and blight must be to understand and diagnose the problem. Only then will it become clear which tools or strategies, including land banking, need to be part of the solution.

Communities that are considering the creation of a land bank and communities that are looking to improve the operations of an existing land bank would both do well to spend time studying these pages.

It is a privilege to work with, and learn from, Frank Alexander. His knowledge of community development, real estate finance, and land use law runs deep, surpassed only by his compassion and commitment to neighborhoods that have been, and continue to be, unfairly burdened by the impacts of problem properties and ineffective policy-making.

It is my hope, and expectation, that the second edition of Land Banks and Land Banking will reach even farther than the first, and that communities around the country will benefit from its guidance.

Tamar Shapiro President and CEO Center for Community Progress May 2015

FOREWORD 9LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

Introduction

Both people and land lie at the heart

of community. It is the people who

create the relationships, the dreams,

the spirit, and the culture. It is the land

that creates the place and the space.

As human relationships are constantly

evolving through times of nurture

and growth and times of conflict and

discord, so too are our uses of land.

We are dependent on other people,

yet we are also dependent on land.

We are stewards of land, and it

supports and protects us; we neglect

and abuse land, and it soon mirrors

our fractured community.

The story of land banks and land banking is essentially a parable of human frailty and hubris. Vacant, abandoned, and foreclosed properties that dot our neighborhoods and decimate our cities also define our core values. They are a reflection of the view that land is to be used and consumed, and then simply discarded, but they are also a refraction of the view that within each piece of property lies the possibility of renewal and renaissance. Vacant, abandoned, and foreclosed

properties are the discarded litter of a consumption society, but they are also the potential assets for building new relationships, new neighborhoods, and new communities.

Land banks are governmental entities that specialize in the conversion of vacant, abandoned, and foreclosed properties into productive use. The primary thrust of all land banks and land banking initiatives is to acquire and maintain properties that have been rejected by the open market and left as growing liabilities for neighborhoods and communities. The first task is the acquisition of title to such properties; the second task is the elimination of the liabilities; the third task is the transfer of the properties to new owners in a manner most supportive of local needs and priorities.

Land banks are relatively new additions to the toolbox of urban planning and community development. The first generation of land banks emerged as local government entities in the last quarter of the twentieth century in St. Louis, Cleveland, Louisville, and Atlanta. In each of these localities, the land banks were created in response to the growing inventories of properties stuck in the maze of nineteenth century property tax foreclosure laws. Out of sync with evolving federal constitutional due process requirements, these state foreclosure laws often created incentives for owners to simply walk away from the payment of taxes, and from the property itself. When accumulated taxes exceeded fair market value, no one could or would touch the property.

By the close of the twentieth century, public officials and urban planners realized that far more was at stake than simply the enforcement of delinquent property taxes. Each and every tract of vacant and abandoned property imposes costs on the

INTRODUCTION 10LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

adjoining properties, on the fabric of the neighborhood, and on the vitality of the community. Bolder and more creative approaches were required, and these emerged in the second generation of land banks led by Michigan and then by Ohio in the time frame of 2002-2009.

At the beginning of the emergence of this second generation of approaches, I prepared what was at the time the seminal text on land banks and land banking, Land Bank Authorities: A Guide for the Creation and Operation of Local Land Banks (2005). That publication was prompted by the insight and determination of Lisa Levy at the Local Initiatives Support Corporation (LISC) and Stephanie Jennings at the Fannie Mae Foundation. Both Lisa and Stephanie saw far more clearly than I did that vacant, abandoned, and foreclosed properties were at the heart of building and rebuilding our communities. LISC and the Fannie Mae Foundation made that first text possible, and made it accessible throughout the country.

The emergence of the second generation of land banks in Michigan is the story of the intentional restructuring of Michigan’s public policies to redirect control of tax-foreclosed properties from out-of-state investors back to local government entities, and land banks provided the viable structure. The Michigan statutes are about land banks and land banking, but they are also about providing new sources of revenues to acquire, remediate, and maintain the properties. They are about creating catalytic opportunities for new development when the private market says it isn’t possible. They are about creating hope in the face of despair. The second generation of land banks was next seen in Ohio, where the challenges faced by Cleveland and Cuyahoga County paralleled in many ways those of Flint and of Detroit. The Ohio land bank legislation was quite complex in its form and scope, and initially received a skeptical response in the state legislature, which limited its scope to Cuyahoga County. Within just one year, the legislature reversed course and expanded its scope to much of the state.

No one anticipated the mortgage crisis at the end of the first decade of the twenty-first century, but everyone felt its consequences. With the highest rates of mortgage foreclosures on record, the inventories of vacant and abandoned properties also reached levels never seen before. As specialists in these distressed assets, land banks quickly emerged as a key tool in the toolbox of urban planners in responding to this crisis. Land banks and land banking were recognized in federal law for the first time in 2008 as a targeted use for the Neighborhood Stabilization Program funding.

The prior edition of this volume was published in 2011 and marked the emergence of the third generation of land bank legislation. That edition included a template for state legislation together with a detailed analysis of key issues and powers. We were certainly hopeful it would make a difference, but we never dreamed that within less than three years eight new states would join Michigan and Ohio in enacting comprehensive land bank legislation – in many instances based largely on the template in the prior edition.

This new edition continues the thrust of the prior edition and once again includes a template for future state legislation. This new edition is far richer and deeper simply because it can now describe the experiences of these ten states, and over 125 separate land banks. Each and every land bank statute, local land bank entity, land banking policy, and procedure provides an opportunity to learn from successes and failures and constantly improve on this work. This edition, as with the prior one, is designed to provide context, to describe the wide range of approaches being taken, and to present the possibilities of dreams to be realized.

A work of this nature is never a solitary endeavor, though I bear full responsibility for all of the errors and omissions it may contain. My student research assistants at Emory Law School, my graduates who have dared to join me in this work, and most importantly my colleagues at the Center for Community Progress, have all been the true engines of these endeavors. Nothing would have been accomplished without them.

Frank S. Alexander May 2015

INTRODUCTION 11LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

12© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

PART I

Understanding Abandonment

Chapter 1UNDERSTANDING THE INVENTORY 14

Chapter 2THE EVOLUTION OF LAND BANKS 18

Chapter 3THE RANGE OF CHALLENGES 28

Chapter 4POTENTIAL SOLUTIONS 34

Chapter 5ADDITIONAL TOOLS AND ALTERNATIVES 42

PART I UNDERSTANDING ABANDONMENT 13LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

PART I UNDERSTANDING ABANDONMENT 14© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

CHAPTER 1

Understanding the Inventory

Vacant, Abandoned, Tax-Delinquent, and Foreclosed Properties

Over the past 40 years, a combination of conditions in many cities around the country has resulted in a growing incidence of vacant, abandoned, tax-delinquent, and foreclosed properties. There is extensive debate on what drives the “life cycle” of neighborhoods,1 from periods of decline and deterioration to their renaissance and rejuvenation.2 A much greater consensus exists as to the harms vacant and abandoned properties inflict on communities.3 As potential fire hazards and sites for drug trafficking,4 vacant and abandoned properties signal to the larger community that a neighborhood is on the decline, undermining the sense of community and discouraging any further investments.5 These disinvestments often spread across neighborhoods and affect the overall health of a city.

While both pose significant problems, vacancy and abandonment are not synonymous. Vacancy can be defined as property that is unoccupied. It is more common in commercial areas, and oftentimes a property is vacant simply because a property owner is holding onto it as a long-term investment. Abandonment, on the other hand, is a far stronger concept. An abandoned property suggests that the owner has ceased to invest any resources in the property, is foregoing all routine maintenance, and is making no further payments on related financial obligations such as mortgages or property taxes. Though abandoned by the owner, tenants may still occupy the property, or squatters may live there without permission.

Properties that are vacant and abandoned are often tax-delinquent as well. In fact, property tax delinquency is the most significant common denominator among vacant and abandoned properties. Tax-delinquent properties are problematic for local governments not only because of the likelihood that they are vacant and abandoned, but also because of their negative impact on tax revenues. While some property owners may fail to pay property taxes due to a lack of financial resources, others choose to “milk” the equity from the property and then abandon it. The lengthy periods of time required by antiquated property tax foreclosure systems only encourage a property owner’s decision to neglect further investments.6 In the vast majority of cases, the failure to pay property taxes signals the eventual fate of the property because it has long been recognized as a signal of eventual abandonment. However, tax delinquency is only an overlapping characteristic. Even occupied properties in excellent condition may be tax-delinquent, usually by inadvertence though occasionally by design.

The dramatic rise in the number of mortgage foreclosures from 2007-2013 as a result of the Great Recession presented yet another challenge in the increasing inventories of properties that are vacant, substandard, and possibly abandoned. In some jurisdictions, the mortgage foreclosure process is hampered by the lack of clarity on the identity of the mortgage lender and standing of the lender to conduct a foreclosure. In other jurisdictions, the very attempt to modify mortgage loans is constrained by conflicting incentives between loan servicers and the investors in the loans. In all jurisdictions, loan servicers and lenders are extremely reluctant to invest additional funds in vacant residential properties,

PART I UNDERSTANDING ABANDONMENT 15LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

preferring to minimize holding costs in the face of declining markets. These ambiguities, tensions, and uncertainties have given rise to a new phenomenon plaguing our neighborhoods and communities—that of “zombie mortgages”. Though the term “zombie mortgages” has different meanings in different contexts, the common elements are the existence of a mortgage on real property which is in default but for which the mortgagee elects not to proceed with enforcement through the final stages of foreclosure and transfer to a new owner. The owner, or former owner, believes that he or she no longer has any interest in the property and the mortgagee has either elected to “walk away” from the security or is reluctant to proceed with a foreclosure sale in fear of its own potential liability, should it become the foreclosure sale purchaser. Title to the property remains encumbered and fractured, the property remains vacant and continues to deteriorate, and the community bears all of the costs and losses.

The prevalence of vacant and abandoned properties never occurs in a vacuum. It always occurs in a particular set of social and economic conditions heavily influenced by federal, state, and local policies and by social and cultural biases. Public policies may create stable neighborhoods but they also may create conditions which lock the poor into urban slums replete with deteriorating properties. Class and race are reflected in, if not embodied by, land use plans, and the neighborhoods in decline tragically receive the fewest resources. No attempt to confront growing inventories of vacancy and abandonment can succeed without acknowledging the social and cultural biases that shape our policies.

The housing and economic crises of the Great Recession have had deep and far-reaching consequences for America’s communities. Throughout most of the United States, residential mortgage foreclosures rose to levels not experienced in 75 years, while some communities simultaneously experienced declines in property values of 25% or more. With an overwhelming concentration of foreclosures in particular neighborhoods, the number of vacant properties reached record levels.

Together, the ongoing national mortgage crisis and the steady economic decline of older industrial areas have created increasing numbers of vacant and abandoned properties that are placing ever greater stress on communities across the country. The sudden collapse of the mortgage markets and the drastic increase in foreclosure rates may be most intense in Southern and Southwestern regions, while gradual economic decline and industrial property abandonment may be more characteristic of cities in the Northeastern and Midwestern parts of the country. Unfortunately, some communities—

most notably Cleveland, Ohio, and Detroit, Michigan—are burdened by both pressures. Despite differences in metropolitan areas, the neighborhoods, schools, and local governments in every metropolitan community must bear the costs these large inventories of foreclosed, vacant, and abandoned properties induce. When demand for housing and new development disappears, what may have once been a strong and vibrant neighborhood or community can become a declining wasteland. Further complicating recovery, most local governments lack efficient and effective tools for halting and reversing such a serious consequence.

Understanding the Costs of Neglect

The ripple effect that vacancy or foreclosure can have on the surrounding neighborhood is well-documented. These external costs are far reaching and occur across a number of categories:

• Decreased property values of adjacent properties

• Decreased property tax revenues from nonpayment of taxes

• Decreased property tax revenues from declining property values of adjacent properties

• Increased costs of police and public safety for surveillance and response

• Increased incidence of arson resulting in higher costs of fire prevention

• Increased costs of local government code enforcement activities

• Increased costs of judicial actions

Mortgage foreclosures alone, independent of subsequent abandonment, have been found to reduce property values within one-eighth of a mile of the foreclosure by 0.9% in value.7 Multiple foreclosures had even greater cumulative adverse effects. The Center for Responsible Lending estimates that foreclosures of subprime home loans originated in 2005 and 2006 decrease the value of nearby properties by an average of $5,000.8 In aggregate, foreclosures on subprime loans are expected to cause a $202 billion decline in home values and the corresponding tax base.

Abandonment further amplifies the problems brought on by foreclosure. For example, a detailed study of Chicago in 2005 revealed that each property abandoned prior to foreclosure imposes average costs of almost $20,000 on the city, and

CHAP

TER

1: U

nder

stan

ding

the

Inve

ntor

y

Chapter 1 Endnotes1 See, e.g., Anthony Downs, Opening Up the Suburbs: An Urban

Strategy for America (1973).

2 See, e.g., John T. Metzger, Planned Abandonment: The Neighborhood Life-Cycle Theory and National Urban Policy, 11 HOUSING POLICY DEBATE 7 (2000); Anthony Downs, Comment on John T. Metzger’s “Planned Abandonment: The Neighborhood Life-Cycle Theory and National Urban Policy,” 11 HOUSING POLICY DEBATE 41 (2000).

3 John Accordino & Gary T. Johnson, Addressing the Vacant and Abandoned Property Problem, 22 J. URB. AFF. 301 (2000); William Spelman, Abandoned Buildings: Magnets for Crime?, 21 J. CRIM. JUST. 481–95 (1993).

4 John A. Jakle & David Wilson, Derelict Landscapes: The Wasting of America’s Built Environment 144-75 (1992); James R. Cohen, Abandoned Housing: Exploring Lessons from Baltimore, 12 Housing Policy Debate 415, 416 (2001).

5 EDWARD G. GOETZ, KRISTIN COOPER, BRET THIELE, & HIN KIN LAM, CENTER FOR URBAN AND REGIONAL AFFAIRS, Pay Now or Pay More Later: St. Paul’s Experience in Rehabilitating Vacant Housing 12 (1998); James Goldstein et al., Urban Vacant Land Redevelopment: Challenges and Progress (Lincoln Inst. of Land Policy, Working Paper, 2001).

6 See Frank S. Alexander, Tax Liens, Tax Sales and Due Process, 75 IND. L. J. 747 (2000).

7 Dan Immergluck & Geoff Smith, The External Costs of Foreclosure: The Impact of Single-Family Mortgage Foreclosures on Property Values, 17 HOUSING POLICY DEBATE 57 (2006).

8 Center for Responsible Lending, Subprime Spillover: Foreclosures Cost Neighbors $202 Billion; 40.6 Million Homes Lose $5,000 on Average 1 (2008).

9 Id.; William C. Apgar & Mark Duda, Minneapolis Homeownership Preservation Foundation, Collateral Damage: The Municipal Impact of Today’s Mortgage Foreclosure Boom (2005).

10 Patricia E. Norris & Nigel G. Griswold, Michigan State University Land Policy Institute, Economic Impacts of Residential Property Abandonment, Report #2007-05.

11 Catherine Lucey, Abandoned Properties Have Reduced City Home Values by an Average of $8,000, Study Finds, PHILA. DAILY NEWS, Nov. 11, 2010.

12 Community Research Partners & ReBuild Ohio, $60 Million and Counting: The Cost of Vacant and Abandoned Properties to Eight Ohio Cities (2008).

13 Matthew J. Samsa, Note, Reclaiming Abandoned Properties: Using Public Nuisance Suits and Land Banks to Pursue Economic Redevelopment, 56 CLEV. ST. LAW REVIEW 189, 196 (2008). See generally GEORGE L. KELLING & CATHERINE M. COLES, FIXING BROKEN WINDOWS: RESTORING ORDER AND REDUCING CRIME IN OUR COMMUNITIES (1996).

14 Dan Immergluck & Geoff Smith, The Impact of Single Family Mortgage Foreclosures on Crime, 21(6) Housing Studies 851 (2006).

15 Nat’l Vacant Properties Campaign, Vacant Properties: The True Costs to Communities 1 (2005).

16 Maghelal, Praveen, Simon A. Andrew, Sudha Arlikatti, Hee Soun Jang, FROM BLIGHT TO LIGHT: ASSESSING BLIGHT IN THE CITY OF DALLAS (2013).

17 Tri-COG Collaborative, Fiscal Impact of Blight on the Tri-COG Communities (September, 2013).

when that property includes a building damaged by arson, the costs reach an average of $34,000.9 In Flint, Michigan, an analysis revealed that property within 500 feet of a vacant and abandoned structure lost an average of 2.26% of its value.10 A study commissioned by Philadelphia in 2010 revealed that vacant and abandoned properties reduced the value of the city’s homes by an average of $8,000, incurred $20 million in annual maintenance costs, and deprived the city of $2 million a year in tax revenues.11 Further, a study of eight cities in Ohio found that 25,000 vacant and abandoned properties imposed approximately $15 million in direct annual costs to the cities and more than $49 million in cumulative lost property tax revenues.12

The “broken windows” theory asserts that “the mere existence of abandoned housing detrimentally affects a neighborhood because it demonstrates to outsiders and residents that the neighborhood is of the type that supports crime and poverty, creating a vicious cycle that encourages additional abandonment.”13 While this cycle may not carry a price tag in dollars, its impact on communities is established. For example, one study found that a one-percentage point increase in single-family residential mortgage foreclosures correlated with an increase in the number of non-property related violent crimes by 2.33%.14 In Austin, Texas, “blocks with unsecured [vacant] buildings had 3.2 times as many drug calls to police, 1.8 times as many theft calls and twice the number of violent calls as blocks without vacant buildings.”15 A comprehensive study of all forms of blight, and blight related costs, in Dallas, Texas, identified 16% of the geographic area of the City as “high blight” areas, containing 41% of all tax delinquent properties, and 47% of all public expenditures for demolitions.16 A study of these costs by the Council of Governments in Southwestern Pennsylvania revealed 20,077 vacant lots and 7.158 lots with blighted structures leading to direct costs to municipal services of $10,720,302, lost tax revenues of $8,637,875, and indirect costs associated with declining property values between $218 million and $247 million.17

In response to the rise of vacant and abandoned properties, the fall of property tax revenues, and mortgage foreclosures forcing families out of their homes, some localities have created land banks. A land bank is a governmental entity that focuses on the conversion of vacant, abandoned, and foreclosed properties into productive use. As entities intended to help a local government achieve legal, institutional, and systemic changes facilitating the reuse of a community’s problem properties, land banks take many forms. The next chapter details the origins and evolution of land banks across the country over the past 35 years and sets the course for what land banks can achieve in the future.

PART I UNDERSTANDING ABANDONMENT 16LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

In response to the rise of vacant and

abandoned properties, the fall of

property tax revenues, and mortgage

foreclosures forcing families out of

their homes, some localities have

created land banks. A land bank is a

governmental entity that focuses on the

conversion of vacant, abandoned, and

foreclosed properties into productive

use. As entities intended to help a local

government achieve legal, institutional,

and systemic changes facilitating

the reuse of a community’s problem

properties, land banks take many forms.

The next chapter details the origins

and evolution of land banks across the

country over the past 35 years and sets

the course for what land banks can

achieve in the future.

PART I UNDERSTANDING ABANDONMENT 17LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

PART I UNDERSTANDING ABANDONMENT 18LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

CHAPTER 2

The Evolution of Land Banks

The concepts of “land banks” and “land banking” first emerged in the 1960s as proposals for new urban planning tools. Metropolitan areas throughout the United States were experiencing two directly related trends in planning and development. The first was urban sprawl—the unconstrained and unrestrained shift of new development to ever-expanding rings of first tier and second tier suburbs. The second was the decline and abandonment of inner-city neighborhoods, which became the focus of massive public initiatives in the various programs of the Great Society—urban renewal and model cities.1 The urban renewal and model cities programs of the 1950s and 1960s were simply inadequate to deal with the social preferences for leaving behind the inner cities in favor of the promises of the suburbs.

It was in these dual trends of unregulated urban sprawl and inner-city abandonment that the idea of a land bank began to emerge. To militate against the largely unanticipated external costs of suburban and exurban development and its core value of exclusionary zoning, land banks were proposed as a form of a “land reserve” through which a public entity would engage in early acquisition of land to be held in reserve for future public uses.2 To militate against the growing inventory of abandoned, tax-delinquent inner-city properties, land banks were proposed as a governmental entity to acquire and manage the properties no longer accessible to or desired by the market. The conceptual roots of land banks and land banking thus lie at both ends of the market spectrum. In a heated private market consuming all available real estate, a land bank could preserve public spaces for future public needs and priorities. In

a collapsed market, leaving abandoned real estate as the litter of a consumption society, a land bank could serve to convert the liabilities into assets.

Over the past 50 years, the nature and function of land banks and land banking have developed far more in response to the contagion of abandonment than as a proactive reserve of land for future uses. The dominant focus in land banking has been on delinquent property taxes, both as a symbol of abandonment and as a leverage point to gain control of the property. In selected communities where market abandonment is neighborhood- or site-specific, land banks have been utilized as proactive land reserves. The dramatic increase in abandoned properties as a result of the record-high foreclosure rates of the Great Recession has pushed this acquisition and retention function to the forefront of many land banking programs.

The story of land banks and land banking can be viewed in three relatively distinct phases. The first phase, or first generation, was characterized by the creation of land bank as entities designed to deal with properties “stuck” in complex property tax enforcement systems. The second generation learned from the first and focused on a series of legislative amendments that broadened land bank powers and created explicit ties to property tax enforcement systems and reforms. The third generation, again learning from its predecessors, was built upon a relatively standard template for land bank legislation and enhanced programs designed to respond to the consequences of the Great Recession. No two state or local programs are identical, and no existing state statute or local land bank should be viewed as a model to be implemented in other jurisdictions. The success of land banks, and land

PART I UNDERSTANDING ABANDONMENT 19LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

banking, lies both in their targeted approach to complex issues of abandonment as well as their flexibility to be adapted to local conditions.

The First Generation: St. Louis, Cleveland, Louisville, Atlanta

The first generation of land bank programs is that of the last quarter of the twentieth century, and is exemplified by the land banks of St. Louis, Cleveland, Louisville, and Atlanta. The “lineage” of these four land bank authorities is relatively clear and direct. Following the formation and implementation of the St. Louis Land Bank between 1971 and 1973, state enabling legislation was approved in Ohio in 1976 that permitted the creation of the Cleveland Land Bank. A little more than a decade later, both Louisville (1989) and Atlanta (1991) created parallel land bank authorities with the approval of intergovernmental agreements.3 In each succeeding instance, the local governments examined the programs, priorities, structures, and policies of the preceding land bank authorities and then proceeded to adopt and to adapt a land banking program designed to fit the particular needs of each community.

This first generation of land banks had a common focus on addressing abandoned, tax-delinquent properties, and each served primarily to foster the conversion of tax-delinquent properties to productive use. No two of these early land banks were identical, however. Because of wide variances in state constitutional law, and state and local allocations of authority, each local land bank was based upon a differing legal structure. Each jurisdiction followed a different property tax foreclosure procedure, and each land bank adopted its own set of operating policies and priorities. While there was substantial overlap among the first generation of land banks, there were also substantial differences.

A common catalyst among the first generation of land banks was the lack of market access to tax-delinquent properties. Most property tax enforcement systems were designed in the late nineteenth century and have not been modified to reflect evolving federal constitutional due process requirements. Further, these systems did not anticipate the emergence of out-of-state investors in low-value speculative properties. In all four of the major first-generation land bank communities, there was a growing inventory of properties because (i) properties were never sold at tax sales, because tax liens exceeded fair market value and state law set minimum auction bids at the amount of delinquent taxes, (ii) property

tax foreclosures resulted in sales to investors, but these investors elected neither to invest in improvements to the property nor to pay subsequent years’ taxes, leaving the tax-delinquent inventory to be in a constant state of repetitive tax foreclosures, or (iii) by virtue of state law, the properties not sold to private investors automatically defaulted to the ownership of the local government, leaving the governmental departments with the most costly properties to maintain and the least resources and capacity to do so.

The state statutory authority that authorized this first generation of land banks bore similar characteristics across the four different states. In each instance, the primary inventory of the land bank was the residual inventory of the inefficient tax foreclosure process. In each instance, the creation and operation of a land bank was at the discretion of a local government, though some degree of intergovernmental collaboration was encouraged if not required by statute. Each local land bank was given express authority to transfer and dispose of its inventory in accordance with locally determined priorities, with an exemption from the classic requirement of sales at public auction to the highest bidder.

Each of the four major first-generation land banks was successful, but only when measured against the very limited range of powers and authority they were given and the very difficult nature of the real property inventory they were confronting. Each of these land banks did indeed facilitate the conversion of some of the inventory of vacant, abandoned, and tax-delinquent properties back into productive use. Throughout the 1980s and 1990s, these land banks were operating at maximum capacity if they managed and transferred up to 500 parcels of property each year (in the cases of St. Louis and Cleveland), or just 100 parcels per year (in the cases of Louisville and Atlanta). When this volume is measured against the annual volume of available inventory

St. Louis 1971

Cleveland 1976

Louisville 1989

Atlanta 1991

THE 1ST GENERATION OF LAND BANKS

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

PART I UNDERSTANDING ABANDONMENT 20© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

for land banking, which commonly was in the range of 1,000 to 2,000 parcels each year, the efficiency and effectiveness of these land bank initiatives fell short of reaching their potential.

In hindsight, the lack of capacity for the efficient and effective acquisition, management, and disposition of vacant, abandoned, and tax-delinquent properties can be attributed to several core features that were missing in each of these first-generation land banks. First, none of the land banks had any dedicated or internally generated source of funding for operations. Each of the four land banks had to rely upon direct or indirect general operating support from its local governments. Second, the property tax foreclosure laws themselves were rarely amended to any significant degree, leaving the properties targeted by the land banks tangled in a lengthy maze of archaic procedures and statutorily required waiting and redemption periods before the land bank could begin to control ownership of the property. Third, the lack of amendment of tax foreclosure laws meant that the inventory of tax-foreclosed properties, whether privately owned by investors or held by the land bank, lacked marketable and insurable title. This functionally prevented reuse by anyone in the absence of further legal proceedings. Fourth, a land bank’s exercise of powers and authority was not adequately grounded in intergovernmental collaboration, whether mandatory or permissive. In two instances, the land banking operations functioned simply as another program of the city (as in the case of Cleveland), or as an embedded program of another public authority (as in the case of St. Louis), with the consequence of vulnerability to other political and institutional priorities.

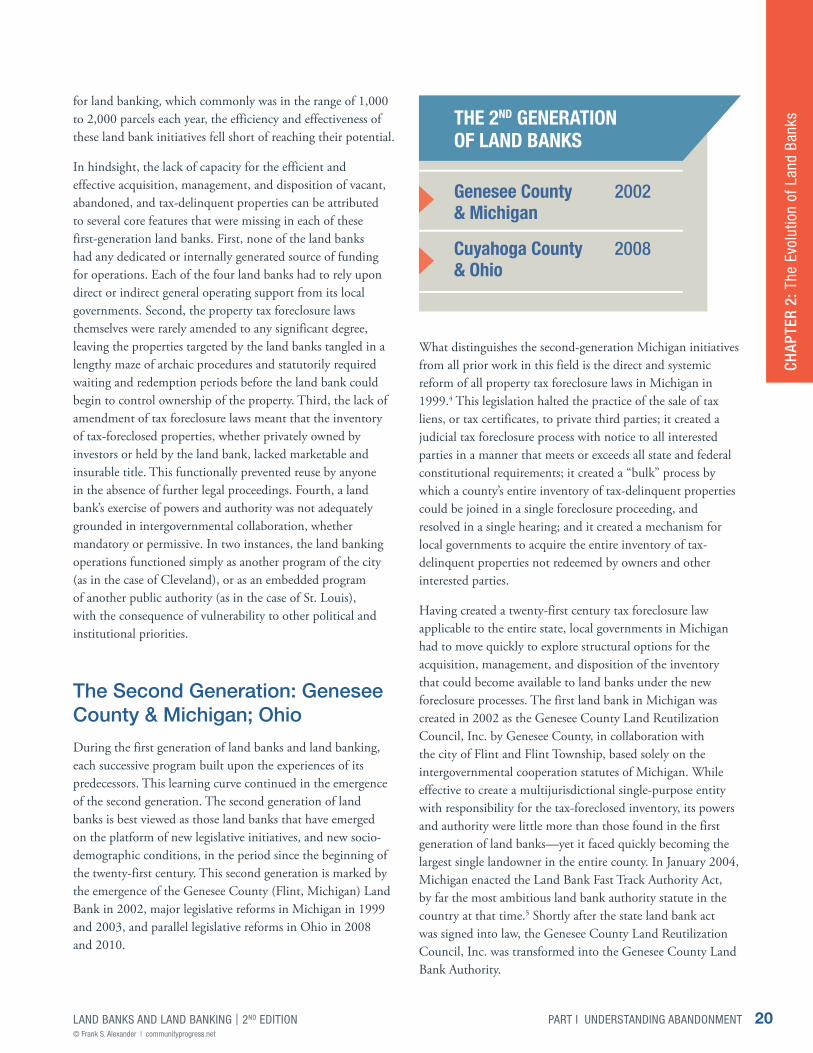

The Second Generation: Genesee County & Michigan; Ohio

During the first generation of land banks and land banking, each successive program built upon the experiences of its predecessors. This learning curve continued in the emergence of the second generation. The second generation of land banks is best viewed as those land banks that have emerged on the platform of new legislative initiatives, and new socio-demographic conditions, in the period since the beginning of the twenty-first century. This second generation is marked by the emergence of the Genesee County (Flint, Michigan) Land Bank in 2002, major legislative reforms in Michigan in 1999 and 2003, and parallel legislative reforms in Ohio in 2008 and 2010.

What distinguishes the second-generation Michigan initiatives from all prior work in this field is the direct and systemic reform of all property tax foreclosure laws in Michigan in 1999.4 This legislation halted the practice of the sale of tax liens, or tax certificates, to private third parties; it created a judicial tax foreclosure process with notice to all interested parties in a manner that meets or exceeds all state and federal constitutional requirements; it created a “bulk” process by which a county’s entire inventory of tax-delinquent properties could be joined in a single foreclosure proceeding, and resolved in a single hearing; and it created a mechanism for local governments to acquire the entire inventory of tax-delinquent properties not redeemed by owners and other interested parties.

Having created a twenty-first century tax foreclosure law applicable to the entire state, local governments in Michigan had to move quickly to explore structural options for the acquisition, management, and disposition of the inventory that could become available to land banks under the new foreclosure processes. The first land bank in Michigan was created in 2002 as the Genesee County Land Reutilization Council, Inc. by Genesee County, in collaboration with the city of Flint and Flint Township, based solely on the intergovernmental cooperation statutes of Michigan. While effective to create a multijurisdictional single-purpose entity with responsibility for the tax-foreclosed inventory, its powers and authority were little more than those found in the first generation of land banks—yet it faced quickly becoming the largest single landowner in the entire county. In January 2004, Michigan enacted the Land Bank Fast Track Authority Act, by far the most ambitious land bank authority statute in the country at that time.5 Shortly after the state land bank act was signed into law, the Genesee County Land Reutilization Council, Inc. was transformed into the Genesee County Land Bank Authority.

Genesee County 2002 & Michigan

Cuyahoga County 2008 & Ohio

THE 2ND GENERATION OF LAND BANKS

PART I UNDERSTANDING ABANDONMENT 21LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

The 2003 Michigan legislation ushered in the second generation of land banks. Land banks that are created under this model possess a dramatically different range of powers and possibilities than are found in the first generation of land banks, with the new statutes expressly addressing each of the four systemic limitations found in the first generation of land banks. These second-generation land banks have multiple sources of financing for their operations, freeing them from dependency on local government general revenue funding. The second-generation land bank programs reflect much more extensive intervention in the property tax foreclosure process, and in the case of Michigan, the ability to acquire all tax-foreclosed properties, not just the ones for which there is no third-party investor ready to purchase it. The properties land banks acquire in Michigan have insurable and marketable title, and are ready for reuse and redevelopment as determined by local market conditions. Finally, land banks in Michigan must be created by intergovernmental collaboration between a county (which is the unit with legal authority for tax foreclosures) and the Michigan Land Bank Fast Track Authority, the state land bank also created by the 2004 enabling legislation. In a structure not found in most other jurisdictions, the Michigan statute created a state authority both to deal with tax-foreclosed properties the state owned as well as to exercise a limited degree of supervisory oversight of all locally created land banks.

The advantages of the second generation of land banks and land banking became the basis for major legislative reforms in Ohio in 2008. With some of the highest vacancy and foreclosure rates in the country, the city of Cleveland and Cuyahoga County pressed for a new range of structural reforms that would permit the transformation of its first-generation Cleveland Land Bank into a far more efficient and effective entity. In 2008, the Ohio General Assembly built upon the lessons learned from strengths and weaknesses of the Cleveland land reutilization program, and from the statutes and programs of more than 25 other land banks across the country. As in the case of Michigan, this Ohio legislation is closely tied to reforms in the tax foreclosure system that were enacted two years earlier.6 As passed, the legislation was limited in its application to Cuyahoga County, but it was sufficient to permit the creation of the new Cuyahoga County Land Reutilization Corporation as the successor to the first-generation Cleveland Land Bank. The success of the new Cuyahoga Land Bank led the Ohio General Assembly to expand the geographic scope of the land bank enabling statute statewide in early 2010.7

Parallel to the Michigan model of empowering land banks to deal more effectively with vacant, abandoned, and tax-foreclosed properties, the Ohio statute focuses on key systemic changes. It creates significant new points of intervention in the existing tax foreclosure laws, though unlike Michigan it does so through specific and limited ties between land banks and the tax foreclosure process rather than basing its work on a wholesale reform of Ohio’s tax foreclosure laws. It permits the possibility of financing the operation of land banks by internalizing the significant interest and penalties on delinquent taxes rather than “exporting” these revenues to private tax lien investors. It authorizes land banks not merely to be the custodians of properties that the open market rejects, but to be proactive partners in the management, development, and overall transformation of liabilities into public assets.

The Third Generation of State Land Bank Statutes

A third generation of land banks has emerged over the past five years. It differs from the second-generation models found in Michigan and Ohio more in terms of form than in terms of substance.

The legislative reforms in both Michigan and in Ohio were extremely intricate in nature, very difficult to draft, and nearly impossible for a casual observer to decipher. The Michigan Land Bank Act was tied in its enactment to four separate acts, amending different provisions of Michigan law, all of which pertain in some manner to the operations of a land bank.8 The Ohio legislation was able to combine in a single act all of the various changes and amendments, but it necessitated amending over fifteen different sections of the Ohio Code. Without tracing and mastering the substance of these separate code sections, it is not easy to ascertain how the legislative surgery knits all of the pieces together.

The legislation of this third generation of land banks built upon the knowledge and experiences of the first two generations, seeking to present the possibilities of land bank creation in the clearest and most direct form possible. In the amazingly short period of time of less than three years, comprehensive landing banking legislation was introduced and enacted in eight states: New York (2011), Georgia (2012), Missouri (2012), Pennsylvania (2012), Tennessee (2012), Nebraska (2013), Alabama (2013), and West Virginia (2014). When considered together, along with Michigan (2003) and Ohio (2008), these ten states would have few common historical or socioeconomic characteristics. What is clear is

PART I UNDERSTANDING ABANDONMENT 22© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

that each of these jurisdictions shared a common commitment to the adoption of land banking as a new tool to be used to untangle the growing inventories of vacant, abandoned, and foreclosed properties.

The form of these third generation land bank statutes in large measure has been based on a legislative approach that is simpler to interpret and to apply. Instead of creating a legislative package of bills amending multiple different sections of existing state laws, the “template” legislation was often based on a single land bank bill set forth as an appendix to the prior edition of this volume. In each instance, however, the template legislation was modified to reflect the unique structures and characteristics of applicable state and local law, and to address the differing concerns of local constituencies. For some of these third generation land bank statutes, passage of the legislation was possible only by limiting its applicability to a small set of major metropolitan areas (such as the limit of Nebraska’s legislation to metropolitan Omaha, the limit of Missouri’s legislation to Kansas City, and the initial limit of Tennessee’s legislation to Oak Ridge). Such an approach can certainly still be very positive, at least for the jurisdictions affected; it can also end up being an interim step before the legislation is given wider geographic scope in subsequent years (as in the cases of Ohio and Tennessee). In rare instances, a land bank statute may be enacted in form, with little substantive impact on any locality, only to be

amended in a subsequent year to create the necessary and appropriate range of local government powers. An example of this is Alabama, which passed its original land bank act in 2009 and amended it in 2013 in a manner which made it possible for Birmingham to move forward with the creation of its land bank.

Land Banking under Local Home Rule Authority

Land banking initiatives normally require state legislative attention not simply because of the multiple jurisdictions within a state that are experiencing significant inventories of vacant and abandoned properties. Most commonly, action at the state legislative level is necessary because legal and policy systems and structures created at the state level create the incentives for property abandonment. Local governments usually lack adequate legal authority to implement land banking programs. In rare instances, however, a local government will possess a strong range of home rule authority by virtue of state constitutional home rule provisions, or legislative home rule applicable to narrow bands of large population areas or historically dominant communities. Though the original Genesee County Land Reutilization Corporation was created solely upon existing general powers and specific intergovernmental cooperation agreement powers, it lacked the range of powers to be truly effective and this prompted the enactment of the Michigan Land Bank Fast Track Authority Act shortly thereafter.

Perhaps the best example of the creation of a local land bank with a broad range of powers, and yet the absence of any general state land bank enabling legislation, is the Cook County Land Bank Authority. Created in January 2013, the legal authority of the Cook County Board of Commissioners derives primarily from a specific grant of home rule authority found in the Illinois constitution and applicable to Cook County. It is then supplemented by general Illinois statutes applicable to local governments and by express authorization for a wide range of intergovernmental agreements. This relatively unique set of powers allows the Cook County Board of Commissioners, and the Cook County Land Bank, both to address many of the issues related to vacant and abandoned properties and to collaborate with the small municipalities located within the county that lack both the legal authority and the capacity to address these issues by themselves.

New York 2011

Georgia 2012

Missouri 2012

Pennsylvania 2012

Tennessee 2012

Nebraska 2013

Alabama 2013

West Virginia 2014

THE 3RD GENERATION OF LAND BANKS

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

PART I UNDERSTANDING ABANDONMENT 23LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

Land Banks and Land Banking – Variations on the Theme

Land banking is the process or policy by which local governments acquire surplus properties and convert them to productive use or hold them for long-term strategic public purposes. Land banks are governmental entities that specialize in land banking activities. Other public agencies can undertake land banking, and not all communities need to create a separate land bank. In some communities, redevelopment authorities can and should serve a modified land banking function, and in others, a housing and community development department could manage a land banking function. In recent decades, redevelopment authorities have tended to be narrowly focused in a specific geographic area or on a specific redevelopment project, and often lack the flexibility to acquire surplus properties wherever they may exist, or to convert individual properties into productive use as new single-family residences. Similarly, housing and community development departments commonly lack capacity for property management, and are constrained by state and local laws in the terms for disposition of property.

It is certainly possible for a redevelopment authority to “house” a land bank or a land bank program. This was done in the very first land bank in the country, in St. Louis, and more recently in the state enabling legislation for the creation of the East Baton Rouge Redevelopment Authority. Though there may be advantages to such combined operations in the form of shared staff and infrastructure, the clear disadvantage lies in the possibility of confusion about the distinctive missions of redevelopment authorities and land banking initiatives. If

there is a consolidated legal or programmatic structure, careful attention must be placed on the importance of maintaining separate and autonomous operational responsibility for redevelopment goals and for land banking goals.

There is a dangerous tendency for local governments to look at land banks as the complete solution to the challenges they face. Such a dream, however, is often neither accurate with respect to the underlying facts nor realistic with respect to the necessary solutions. If a local government lacks the internal capacity to manage substandard properties, then creating a land bank whose staff will consist of the existing city agencies or departments will not change the outcome. Similarly, if a given local government is dominated by elected officials who insist on micromanaging each and every decision related to the real property of the government, then creating a land bank will accomplish little in terms of efficient operations unless the day-to-day governance authority of the land bank is separated from the elected public officials.

The Federal Role and Neighborhood Stabilization in the Great Recession

While land banking as a tool for converting vacant spaces into vibrant places is overwhelmingly a matter of state and local government policies, the advent of the Great Recession made it a national issue, as well. In July 2008, Congress passed the Housing and Economic Recovery Act of 2008 (HERA), marking the first time that land banking was expressly recognized in federal legislation.9 Congress’ statutory recognition of the severe costs borne by neighborhoods and local governments when properties are vacant or abandoned was significant. Section 2301 of HERA was titled “Emergency Assistance for the Redevelopment of Abandoned and Foreclosed Homes,” and it appropriated $4 billion “for the redevelopment of abandoned and foreclosed upon homes and residential properties.”10 This was the first federal legislation to recognize the economic toll that the increase in vacant and abandoned properties takes on local governments, and the first time that the federal government specifically allocated funding to address that problem.

HERA included parameters governing how its $4 billion appropriation, which came to be known as the Neighborhood Stabilization Program (NSP), could be distributed. Specifically, Congress targeted low- and moderate-income persons by requiring that all of the funds be used “with respect to individuals and families whose income does not exceed

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

PART I UNDERSTANDING ABANDONMENT 24© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

120% of area median income,” with at least 25% of the funds to be used to provide housing for “individuals or families whose incomes do not exceed 50% of area median income.”11 The permitted uses that Congress prescribed were still broad enough to accommodate the diverse needs of communities across the country. Apart from authorizing amounts made available to be used to “establish land banks for homes that have been foreclosed upon,” funds could also be used to (i) establish financing mechanisms, such as soft-seconds, loan loss reserves, and shared-equity loans; (ii) purchase and rehabilitate abandoned and foreclosed-upon properties to then sell, rent, or redevelop them; (iii) demolish blighted structures; and (iv) redevelop demolished or vacant properties.

In 2009, Congress enacted the American Recovery and Reinvestment Act (ARRA),12 which allocated an additional $2 billion for a second round of NSP funding (NSP2). NSP2 funds were allocated in response to competitive applications. NSP2 grantees were in areas with the greatest number and percentage of foreclosures, with capacity to execute projects and leverage potential financing, and with a concentration of investment to achieve neighborhood stabilization.

The ARRA also made a subtle change to the HERA provision authorizing funds for land banking. HERA permitted the allocation of funds to “establish land banks for homes that have been foreclosed upon,”13 while ARRA amended that language to read “establish and operate land banks for homes and residential properties that have been foreclosed upon.”14 This expanded statutory language allowed land banks to use NSP funds for operating costs associated with the land bank, as well as allowed land banks to use NSP funds to purchase and maintain residential properties.

In the depths of the Great Recession, additional federal funding initiatives supplemented NSP and NSP2. These included the “Hardest Hit Fund,” which provided resources for eighteen states directed primarily toward the avoidance of residential mortgage foreclosures through principal reductions and other loan modifications. The federal “Strong Cities: Strong Communities” (SC2) initiative was launched in July 2011, and by July 2014 had provided targeted federal financial assistance and technical assistance to twenty communities most devastated by the Great Recession.

Subprime residential mortgage lending practices, and their correlation with the mortgage foreclosure crisis that played a central role in the Great Recession, have resulted in an unanticipated source of revenues—at least in some jurisdictions. In those states that were direct plaintiffs against major lending institutions in various lawsuits related to predatory lending practices or foreclosures, or both, negotiated settlements provided funds directly to the plaintiffs. These funds could be used and were used in some jurisdictions to address the growing inventory of vacant and abandoned properties. In New York, the Attorney General issued $33 million in grants to land banks across the state for demolition or rehabilitation of blighted properties. In Michigan, the Attorney General designated $25 million for a statewide blight elimination program. Ohio allocated $75 million for the demolition of blighted structures and Illinois awarded $70 million for community revitalization and housing counseling.

A Comparative International Approach to Land Banking: China

It is far beyond the focus and scope of this volume to undertake a comparative international law and social policy perspective on land banking. There are certainly historical and contemporary parallels in Europe, in Africa, and in Asia, and much work remains to be done to take advantage of lessons learned from different countries with differing legal systems at different stages of social and economic development. One key parallel stands out, however, for both its differences and its similarities.

In the last quarter of the twentieth century, the People’s Republic of China (PRC) began its transformation to market economies, and possession of land use rights became a critical component. By some estimations, over 2,000 “land reserve centers” were created in the PRC within the last twenty years—as compared to less than 200 in the United States. These land reserve centers are rough parallels to the land

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

PART I UNDERSTANDING ABANDONMENT 25LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

banks in the United States. They are based on fundamentally different principles, yet they are faced with adopting parallel operating policies and procedures. They are subject to a fundamentally different legal system, yet they are faced with parallel inconsistent local government goals and objectives.

One of the first land reserve centers in the PRC—and in many ways today the strongest and largest—is the Shanghai Land Reserve Center, which was created in 1996. The national Ministry of Land and Resources of the PRC (MLR) issued a formal “Notice of the State Council on the Strengthening of the Administration of State-owned Land Resources” in 2001, and by the end of 2003 over 1,400 local land reserve centers had been created. The centerpiece of land administration, particularly insofar as pertains to the transition of land into new uses, was the issuance in 2007 by the MLR of a new regulation entitled “Measures on Land Reserve Administration”. These two policy declarations of the PRC are the foundations for the land reserve centers in China.

There are three fundamental differences in the cultures by which land banking has arisen in the United States and land reserve centers in China. These are (i) the nature of land ownership, (ii) the applicable stage of the life cycle of markets, and (iii) the nature of legal and political authority.

In the PRC, at least as of the last quarter of the twentieth century, private ownership of real property was rare, with virtually all land, waterways, and natural resources under the ownership and control of the national government. The lead national entity with responsibility for these resources became the MLR. Private development or development in cooperation with other state-owned enterprises was possible only through the creation of negotiated land use rights. In the United States, by stark contrast, the starting premise is the private ownership of real property, subject to varying degrees of land use regulation.

Because of this fundamentally different starting point of real property ownership, the role of land reserve centers in China stands at the opposite end of a market economy from that of land banks in the United States. In the PRC, the primary function of a land reserve center is to manage the transformation of government-owned real property into a market economy. The land is used to stimulate new construction and development, with the private transferee receiving a set of land use rights that are contractually negotiated. By contrast, land banking in the United States focuses on properties that have largely been abandoned by the private market, or are inaccessible to the private market due to a variety of legal and economic barriers.

The profound differences in the legal and political cultures between China and the United States by themselves present a challenge to any attempt at Western interpretation of the authorities, powers, and purposes of land reserve centers in China. While the United States system of a tripartite separation of powers into legislative, executive, and judicial function, grounded in a constitution, yet with a complex overlay of state and local powers, is certainly less than self-evident to foreign observers, the Chinese legal system is equally opaque. Grounded solely and almost exclusively in a centralized administrative state, laws take primarily the form of announcements, measures, decrees, and regulations. These are issued, in their most public form, by the national Ministries to their subordinate departments, units, and agencies. With twenty-two provinces, four municipalities, five autonomous regions, and two special administrative regions, the parallel with the hierarchy of state and local governments in the United States is a distant parallel at best.

Despite these significant differences, there are close and major points of similarities between the China land reserve centers and the United States land banks. One of the first of the common experiences is that both land reserve centers and land banks are created and operate not at the national level but at the “local” level. This is most evident in the creation of over 2,000 distinct land reserve centers within just a few years, each with some measure of authority and responsibility for land transactions. As is true in the United States, these local land reserve centers in China are given relatively broad discretion to direct the reuse, or new uses, of land in a manner that meets local socioeconomic conditions and goals. Emphasis is placed on local government adaptation and experimentation. The Shanghai Land Reserve Center functions as a pivotal market participant, using its land resources to generate and direct its priority new development and construction while at the same time retaining economic interests in the success of the development. By contrast, the Nanjing Land Reserve Center functions far more as a market regulator, emphasizing the permissible range of new uses of the land with minimal direct involvement and control.

The advantage of being adaptable and flexible to meet local conditions creates a set of tensions and challenges that are shared by both land reserve centers and land banks. Both entities are caught in the pressure to be financially self-sufficient, or to provide direct revenues to the local government, and at the same time to meet public goals of providing affordable housing with direct and indirect subsidy. Both land reserve centers and land banks are charged with moving land into an open market, yet at the same time have

CHAP

TER

2: T

he E

volu

tion

of L

and

Bank

s

Chapter 2 Endnotes1 U.S. President’s Comm. on Urban Housing (1968); U.S. Nat’l

Comm’n on Urban Problems (1969).

2 The most succinct proposal for the use of land banks as public land reserves was made by Professor Charles Harr, Professor of Law at Harvard Law School and formerly Assistant Secretary for Housing and Community Development. See CHARLES M. HAAR, U.S. CONG., HOUSE COMM. ON BANKING AND CURRENCY: PAPERS SUBMITTED TO SUBCOMM. ON HOUSING; PANELS ON HOUSING PRODUCTION, HOUSING DEMAND, AND DEVELOPING A SUITABLE LIVING ENVIRONMENT, WANTED: TWO FEDERAL LEVERS FOR URBAN LAND USE—LAND BANKS AND URBANK, 927-40 (June 1971).

3 For purposes of simplicity and clarity, the references to the cities that created the first generation of land banks are simply shorthand references. The formal identities of the programs are (i) the St. Louis Land Reutilization Authority (the “St. Louis Land Bank”); (ii) the Cleveland Land Reutilization Program (the “Cleveland Land Bank”), (iii) the Louisville and Jefferson County Landbank Authority, Inc. (the “Louisville Land Bank”), and (iv) the Fulton County/City of Atlanta Land Bank Authority, Inc (the “Atlanta Land Bank”). Of vital importance to note is that several of these first-generation models of land banks have undergone significant transformation in recent years. For example, the Louisville Land Bank was structurally reorganized following the merger of the city of Louisville and Jefferson County, and the Cleveland Land Bank largely replaced as to function by the Cuyahoga County Land Reutilization Corporation pursuant to the second-generation land bank statute enacted in 2008.

4 See 1893 Mich. Pub. Act 206, as amended by 1999 Mich. Pub. Act 123; MICH. COMP. LAWS §§ 211.1 et seq.

5 See 2003 Mich. Pub Act 258; MICH. COMP. LAWS § 124.751.

6 H.B. 294, 126th Leg. Gen. Assem., (Ohio June 28, 2006).

7 H.B. 313, 128th Leg. Gen. Assem., (approved by Governor, Ohio April 7, 2010).

8 The relationship between land bank authority activities and brownfield redevelopment is found in 2003 Mich. Pub. Act 259, MICH. COMP. LAWS §§ 125.2652 and 125.2663. The application of a five-year 50% tax recapture to properties conveyed by a land bank is found in 2003 Mich. Pub. Act 260 and 2003 Mich. Pub. Act 261, MICH. COMP. LAWS §§ 211.1021 and 211.7gg. The ability of the state to invest in loans to land bank authorities is found in 2003 Mich. Pub. Act 262, MICH. COMP. LAWS § 21.144(2)(f).

9 Housing and Economic Recovery Act of 2008, Pub. L. No. 110-289, 122 Stat. 2654 (2008).

10 Division B--Foreclosure Prevention, Title III, Pub. L. No. 110-289, §§ 2301-2305, 122 Stat. 2654 (2008) (hereinafter “Emergency Assistance Act”).

11 Housing and Economic Recovery Act of 2008, § 2301(f)(3)(A).

12 American Recovery and Reinvestment Act, Pub. L. No. 111-5, § 1201, 123 Stat. 115 (2009).

13 Housing and Economic Recovery Act of 2008, § 2301(c)(3)(C).

14 American Recovery and Reinvestment Act, Pub. L. No. 111-5, § 1201, 123 Stat. 218 (2009).

responsibility for creating or participating in comprehensive land use planning. Both forms of entities are challenged to move quickly and rapidly to use or reuse their inventories, but held responsible for the consequences of new use or reuse over the long term.

The division of the MLR with direct responsibility for land reserve centers in China is the Land Consolidation and Rehabilitation Center (LCRC). Beginning the fall of 2014, the LCRC initiated opportunities for international dialogue and education on the roles of its land reserve centers in comparison with land banks in the United States.

Land banks and land banking programs, as they have developed in the United States over the past twenty-five years, have their predominant focus on the elimination of the external costs of abandoned properties and the conversion of vacant spaces into vibrant places. Throughout the developed and the developing, world property abandonment is a shared concern. The underlying legal systems and the socioeconomic contexts vary greatly but common ground is to be found in the strategies and tools that are used to address abandonment. The opportunity for land banks in the United States to learn from the experiences of land reserves centers in China, and parallel entities in other countries, is invaluable and timely.

PART I UNDERSTANDING ABANDONMENT 26© Frank S. Alexander | communityprogress.net

LAND BANKS AND LAND BANKING | 2ND EDITION

Over the past 50 years, the nature and

function of land banks and land banking

have developed far more in response to

the contagion of abandonment than as a

proactive reserve of land for future uses.

The dominant focus in land banking has

been on delinquent property taxes, both

as a symbol of abandonment and as

a leverage point to gain control of the

property. In selected communities where

market abandonment is neighborhood-

or site-specific, land banks have been

utilized as proactive land reserves.

The dramatic increase in abandoned

properties as a result of the record-high

foreclosure rates of the Great Recession

has pushed this acquisition and retention

function to the forefront of many land

banking programs.

PART I UNDERSTANDING ABANDONMENT 27LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

PART I UNDERSTANDING ABANDONMENT 28LAND BANKS AND LAND BANKING | 2ND EDITION© Frank S. Alexander | communityprogress.net

CHAPTER 3

Range of Challenges