Bahasa

Halaman

Hukum

0

FY 2005 Business ResultsFY 2005 Business ResultsFebruary 10, 2006

1

Disclaimer

The figures for the 2005 fiscal year herein, which were prepared in accordance with Korea GAAP, are based on the pre-audited financial statements of Hana Financial Group Inc. (“the Company”), therefore, are subject to any possible changes in the due course. Therefore, certain subsequent events or circumstances, which may occur between the time of reading this presentation and the audit report date, could have a material impact on the accompanying financial statements and notes thereto.

The Company was incorporated, by stock swap transactions among its subsidiaries, Hana Bank, DI&S, Hana I&S, and Hana Institutes of Finance, on December 1, 2005.

The Company’s net income for the 2005 fiscal year was drawn using equity method for subsidiaries’operation results from October 1, 2005 (Deemed acquisition date) to December 31, 2005. However, its consolidated income was prepared using subsidiaries’ operating results for the full year ended December 31, 2005 to enhance comparability with those of previous years.

The operating results of Daehan Investment & Securities Co. Ltd. (“DI&S”) for the year ended December 31, 2005 contains extra-ordinary losses, incurred before Hana Bank’s acquisition, resulted from business restructuring process, which was led by Korean Deposit Insurance Co. (ex-shareholder of DI&S, “KDIC”). Accordingly, normalized operating results of DI&S were used for estimation of the Company’s normal operating results.

Reflecting such grounds mentioned above, the information contained in these slides does not require independent verification. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of any information contained herein, must be presented by the management of the Company, and can not be used for any other purposes other than for the activities related to IR of the Company.

2

Contents

• The Group Overview

• Profitability

• Business Volume

• Asset Quality

• Vision and Strategy

3

The Group Overview

• Financial Statements

• Business Highlights

• Milestone

• Structure and Roles

• Snapshot

4

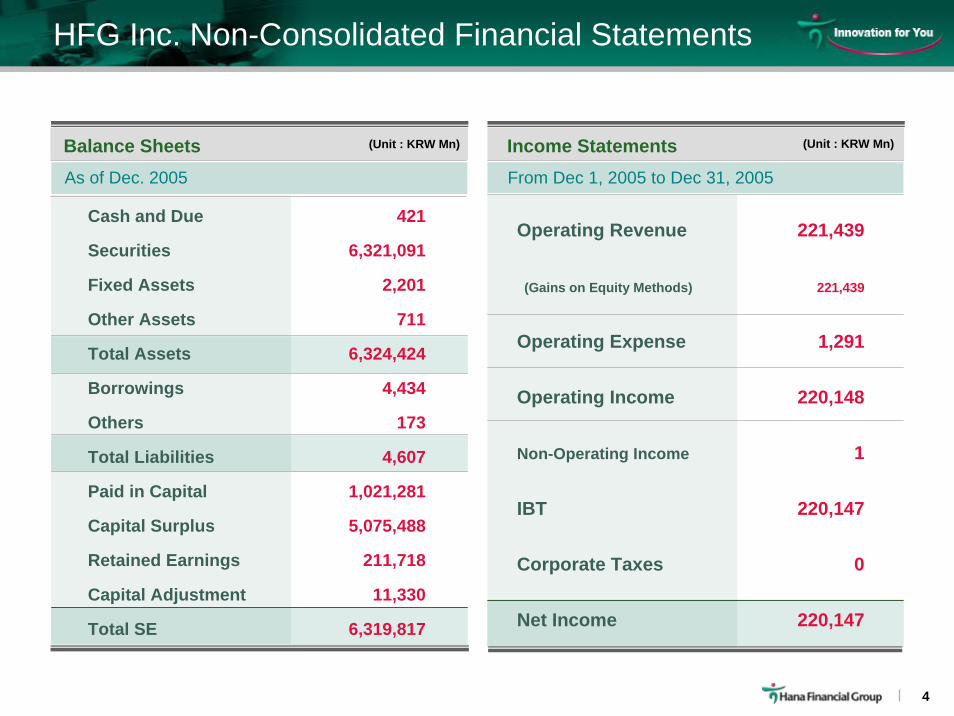

HFG Inc. Non-Consolidated Financial Statements

From Dec 1, 2005 to Dec 31, 2005As of Dec. 2005

Balance Sheets (Unit : KRW Mn)

Cash and Due 421

Securities 6,321,091

Fixed Assets 2,201

Other Assets 711

Total Assets 6,324,424

Borrowings 4,434

Others 173

Total Liabilities 4,607

Paid in Capital 1,021,281

Capital Surplus 5,075,488

Retained Earnings 211,718

Capital Adjustment 11,330

Total SE 6,319,817

Income Statements (Unit : KRW Mn)

Operating Revenue 221,439

(Gains on Equity Methods) 221,439

Operating Expense 1,291

Operating Income 220,148

Non-Operating Income 1

IBT 220,147

Corporate Taxes 0

Net Income 220,147

5

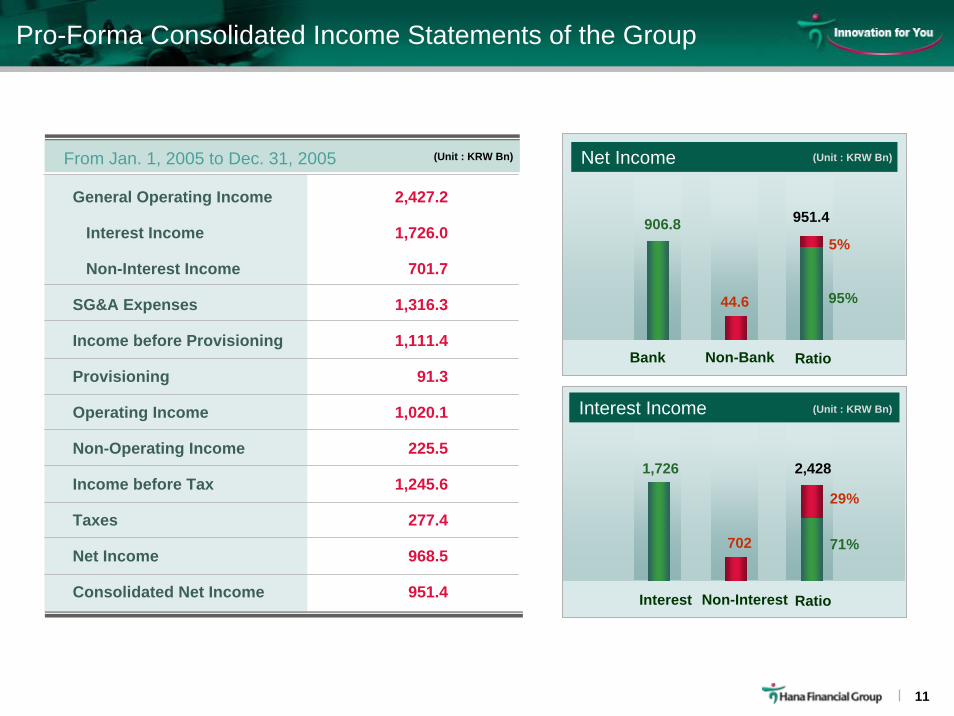

From Jan. 1, 2005 to Dec. 31, 2005

General Operating Income 2,427.2

Interest Income 1,726.0

Non-Interest Income 701.7

SG&A 1,316.3

Income before Provisioning 1,111.4

Provisioning 91.3

Operating Income 1,020.1

Non-Operating Income 225.5

Income before Taxes 1,245.6

Taxes 277.4

Net Income 951.4

As the end of Dec. 2005

* Pro-Forma Income Statements was prepared using subsidiaries’ operating results for the full year ended Dec 31, 2005 to enhance comparability with those of previous years.

Pro-Forma Consolidated Financial Statements of the Group

Balance Sheets (Unit: KRW Bn)

Loans 62,666.4

Securities 15,632

Dues from Banks 1,682.6

Other Revenue Earning Assets 18,211.5

Non Revenue Earning Assets 8,115.3

Total Assets 106,308.5

Deposits 62,024.6

Borrowings/Debentures 20,422.3

Other Liabilities 17,232.5

Total Liabilities 99,679.4

Shareholders’ Equity 6,629.1

Total Liab. & SE 106,308.5

(Unit: KRW Bn)Income Statements

6

2005 Business Highlights of the Group

Net Income 951.4 KRW Bn

ROE 16.28%

EPS 4,658 KRW

ROA 1.07%

7

Milestone of the Group

80%

100%

120%

140%

160%

180%

MarketCAP

4.9 KRW Tn

+76%

22%p outperformed relative to the market

Promotion Committee for the Establishment of HFG. May 16, 2005

Acquisition of DI&SMay 2, 2005

Establishment of HFG Dec. 1, 2005

Obtained Approval for the Establishment of HFG. Oct. 18, 2005

Moody’s Baa1

S&P A-

Fitch A-

MarketCAP

9.5 KRW Tn

Jan.1,2005 Dec.31,2005

HanaBank and HFG

Kospi index

8

Structure and Roles of the Group

Credit Card

Products CombiningFinance & Distribution

Hana Securities

Pipeline for Derivatives& Capital Market Product Supply

ITMC

World ClassAsset Mgmt. Company

Hana Life Insurance

Optimized Insurance Portfolio for Customer Needs

Hana CapitalProduct Development in Consumer Finance

Hana Bank

Main Distribution Channelof Financial Group

DI&S

Open ArchitectureFund Store

Hana I&S

IT Support for Financial Group

Hana Institute of Finance

Think Tank of Financial GroupShared Knowledge Center

HFG

Group Planning & Strategy,Financial Management

Strategy &Shared Services

Product Development Engine

Distribution Channel

9

The Snapshot of the Group

Net Income

Asset

144

3616

Capital

1991 1995 2000 2005 1991 1995 2000 2005

Branch & Employees

1995 2000 2005

951

106.3

51.2

16.02.4

1991

0.3 0.81.8

6.3

1991 1995 2000 2005 1991 1995 2000 2005

Branch Employees

1156

267

682

522 1,456

3,276

7,120

(unit : KRW Tn) (unit : KRW Tn)

(unit : KRW Bn)

Hana Bank HFG

10

Profitability• Pro-Forma Consolidated I/S (Group)

• Operating Income Breakdown

• NIS & NIM Trends (Bank)

• Non- Interest Income (Bank)

• Fees and Commissions (Group)

• Credit Card (Bank)

• C/I Ratio (Group)

11

Net Income

Interest Non-Interest Ratio

1,726

702 71%

29%

Pro-Forma Consolidated Income Statements of the Group

906.8

44.6

Bank Non-Bank Ratio

General Operating Income 2,427.2

Interest Income 1,726.0

Non-Interest Income 701.7

SG&A Expenses 1,316.3

Income before Provisioning 1,111.4

Provisioning 91.3

Operating Income 1,020.1

Non-Operating Income 225.5

Income before Tax 1,245.6

Taxes 277.4

Net Income 968.5

Consolidated Net Income 951.4

95%

5%

Interest Income

2,428

From Jan. 1, 2005 to Dec. 31, 2005

951.4

(Unit : KRW Bn)

(Unit : KRW Bn)

(Unit : KRW Bn)

12

Operating Income Breakdown

Interest 76

Commissions 72

Disposition &

Valuation- 100

Others- 83

Interest38

Securities115

Brokerage102

Others109

2004

Bank

2005

Bank

2005

HFG

(unit : KRW Bn)Bank->HFG

2,4272,099 2,064

363363

13

Interest Revenue & Interest Expense

NISNIS 2.18 2.19 2.09 2.18 2.19 2.09 2.22 2.13 2.42*

Average Lending Rate 5.81 5.76 5.55 5.63 5.53 5.94

Average Funding Rate 3.63 3.57 3.46 3.41 3.40 3.52

NIMNIM 2.14 2.14 2.06 2.14 2.14 2.06 2.19 2.15 2.50*

NIM & NIS Trends (Bank)

2004 3Q 4Q 2005 1Q 2Q 3Q 4Q

(Unit : KRW Bn)

Int. RevenueInt. Expense

4,070 4,1484,362

2,0472,606 2,573

2,8982,690

2002 2003 2004 2005

(Unit : %, Quarterly Cumulative Basis)

* New FSS Standard. Previous FSS Standard: NIM 2.22%, NIS 2.21% [Quarterly Cumulative Base]

** New FSS Standard. Previous FSS Standard: NIM 2.16%, NIS 2.16% [Yearly Cumulative Base]

NIS & NIM (Unit : %)

1.96

2.21

2.38**

2.35**

2.372.14

2.032.10

2002 2003 2004 2005

NIMNIS

14

Fee IncomeFee Income 835.4

Credit Card 245.5

Beneficiary Certi. 142.0

Others in KRW 119.1

Others in FC 56.3

Trust 63.5

Brokerage 102.1

Bancassurance 49.4

Other Fee Income 57.5

OthersOthers -133.7

NonNon--Interest IncomeInterest Income 701.7

2005

566

269 68%

32%

BANK Non-Bank Ratio

(Unit : KRW Bn)

Non-Interest Income (Group)

HFG

Fee Generation

Fee Composition Breakdown

Credit Card 29%

Bene. Cert. 17%KRW.14%

Trust 8%

Other Fee Income7%

FC 7%

Brokerage 12%

Bancassurance 6%

(Unit : KRW Bn)

835

15

Fee and Commissions (Group)

2003 2004 20052003 2004 2005

Commission

2003 2004 20052003 2004 2005

Initial Premium Total

Beneficiary Certificates (Funds)

Bancassurance*

16.8 16.7114 113

10274.0

5.7

91.4

(unit : KRW Bn)Sales Commission

243197

315

11

2949

(unit : KRW Bn)

(unit : KRW Tn)

DI&S

Hana Bank

14.4

142

* Hana Bank only

(unit : KRW Bn)

16

Credit Card (Bank)

Credit Card Asset

Lump Sum

Installment

Cash Advance

Sales

Lump Sum

Installment

Cash Advance

Fee Income*

Holders (thousands)

2003 2004 2005

* Corporate purchase card included

974 9201,031

651618796

2003 2004 2005

2.42.0

2.5

2005 2004 YoY %YoY

1,031

464

332

215

8,917

5,396

1,466

2,054

246

2,536

920

365

286

233

7,747

4,168

1,213

2,365

235

2,035

111

99

46

-17

1,170

1,228

254

-311

11

501

12%

27%

16%

-7%

15%

29%

21%

-13%

5%

25%

(Unit: KRW Bn)

4.6%2.1%

1.8%

45%58% 63%

250235

246 Fee Income(KRW Bn)Members (Mn)Usage Ratio

Delinquency

Card Asset

Card Sales Asset

Credit Card Asset Trends (unit : KRW Bn)

Client Growth Trends

17

Salaries & Wages 598.7

Office Expenses 462.0

Taxes and Dues 52.9

Provisions for Severance 66.9

Depreciation 135.8

Total 1,316.3

C/I Ratio (Group)C/I Ratio (Group)

C/I Ratio (Group)

Salaries

44.0% 42.3% 42.1%

Office Expense

☞ C/I Ratio based on cost excluding amortization of Goodwill

2002 2003 2004 2005

48.4%

202

379

219

882527

Hana Bank C/I Ratio (Unit : KRW Bn)

355

457

228

1,041

327

379

219

925

306

348

228

Others

2005

(Unit: KRW Bn)

54.2%

18

Business Volume • Total Assets and Total Sales (Group)

• Loan (Bank)

• Deposit in KRW (Bank)

19

Loans 62.7

Securities 15.6

Dues From Banks 1.7

Credit Card 2.0

Stocks 2.8

Trust 10.9

Others 2.5

Non Revenue Earning 8.1

Total 106.3

(Unit: KRW Tn)

Total Assets

Total Assets & Total Sales (Group)

Total Sales

Total Sales 72.9

B / A 61.6

LCF 20.6

Others 41.0

T / A 11.3

Sales of Indirect Products 24.2

Beneficiary Cert. 23.9

Bancassurance 0.3

Total 97.2

(Unit: KRW Tn)

2005 2005

20

Loan Portfolio

Loan (Bank)

Household

Unsecured

Secured

SME

SOHO

Large Corp

TotalTotal

53.8 56.9

2003 2004 2005

21.1

18.8

Household (Unsecured) Household (Secured)SME Large Corp.

9.1

22.7

19.5

9.3

23.7

20.9

9.7

60.8

4.7 5.36.5

(Unit: KRW Tn)

2005 2004

28.0

5.3

22.7

19.5

5.9

9.39.3

56.956.9

30.2

6.5

23.8

20.9

5.7

9.79.7

60.860.8

2.2

1.1

1.0

1.4

-0.1

0.30.3

3.93.9

7.7%

21.5%

4.5%

7.2%

-2.0%

3.6%3.6%

6.9%6.9%

%YoYYoY (Unit: KRW Tn)

21

Deposit in KRW (Bank)

(Unit: KRW Bn)

Low Cost Funding 16,360 14,844 1,517 10.2%

Core Deposit 9,570 9,030 539 6.0%

Demand Deposit 2,490 2,606 -115 -4.4%

Passbook 7,080 6,425 655 10.2%

MMDA 6,791 5,813 977 16.8%

Time Deposit 28,943 31,737 -2,794 -8.8%

Installment Deposit 6,664 5,783 882 15.2%

Marketable Deposit 5,464 3,691 1,773 48.0%

TotalTotal 57,43157,431 56,05456,054 1,3771,377 2.5%2.5%

28.5%

25.9%26.5%

16.4% 16.1%16.7%

LCF / Total Core Deposit / Total

2003 2004 2005

14.816.4

13.9

8.89.6

9.0

LCF Trend (Unit : KRW Tn)2005 2004 %YoYYoY

22

Asset Quality• Asset Classification (Bank)

• Delinquency (Bank)

• Provisioning (Bank)

23

Total Credit NPL Precautionary

2005 2004 YoY %YoY

(Unit: KRW Bn)

Normal

Precautionary

Substandard

Doubtful

Estimated Loss

Total Credits

Precautionary & Below

Substandard & Below

Allowance

Cov. (Precau. & Below)

Cov. Against Sub.& Below

2002 2003 2004 2005

Asset Classification (Bank)

Precautionary & NPL

1,047

980

1,435 1,350

1,134

863636

1,060

56.357.2

60.165.0

63,258

1,060

473

83

79

64,954

2.61%

0.98%

811

47.9%

127.6%

57,861

1,350

606

133

124

60,074

3.68%

1.44%

966

43.6%

111.9%

5,397

-290

-133

-50

-45

4,879

-1.07%

- 0.46%

-155

4.2%

15.7%

9%

-22%

-22%

-37%

-36%

8%

-16.0%

(Unit: KRW Tn)

24

1.090.991.13 0.92

1.471.35

1.66

0.92

4.67

2.10 2.39 2.09

1.06

1.94

0.92

2004 3Q 4Q 2005 1Q 2Q 3Q

Total Credit CardCorporate Household

1.49

1.20 1.32

0.95 1.02

4Q

0.88

1.80

0.83

0.89

Delinquency (Bank)

Delinquency Trend (Unit : %)2005 2004 YoY %YoY

(Unit: KRW Bn)

Delinquency Ratio (%)

Delinquency Amount

Total Loans

Corporate

Large Corp.

SME

Household

Unsecured

Mortgage

Credit Card

0.89%

564.9

63,810

277.8

4.2

273.5

251.2

31.1

220.1

35.9

1.20%

708.2

58,995

391.4

1.8

389.6

276.8

30.6

246.2

40.0

-0.31%

-143.3

4,815

-113.6

2.4

-116.1

-25.3

0.5

-26.1

-4.1

-

-20.2%

8.2%

-29.0%

135.1%

-29.8%

-9.1%

1.6%

-10.5%

-10.3%

25

Provisioning (Bank)

Transfer to Reserve for PLL (Unit : KRW Bn)

829322

154

2002 2003 2004 2005

96

1.74%1.98%

1.44%

0.98%

Sub & Below

Amount

Coverage Ratio

2002 2003 2004 2005

95.1%98.3%

111.9%127.6%

46.0%43.4% 43.6%

47.9%

Sub & Below

Precau. & Below

(Unit : KRW Bn)

Quarterly YoY%

1Q 2Q 3Q 4Q

Corporate 195.3 35.3 0.5 17.8 19.9 73.5 - 62.4%

Household 78.5 24.1 -0.4 5.3 -3.4 25.5 - 67.5%

Credit Card 47.7 3.7 3.4 5.5 -16.2 -3.5 - 107.3%

Total 321.5 63.1 3.5 28.6 0.3 95.5 -70.3%

Transfer to reserve for possible loan loss

2004 2005

26

Strategy• Vision 2009

• Vision Roadmap

• Management Strategies

• Synergy Strategies

27

Vision 2009

Premier Financial Service Network

World’s Top 100Financial Group Quality Excellence

Asset Tier 1 MarketCap

EnhanceNon-Banking

Sector

EnhanceRegionalNetworkin Asia

RiskManagement by GlobalStandard

Maximize Group SynergyBanking + Non-Banking + Collaborated Product + Brand Value + Human Resources

Leading Financial Group in East Asia

28

Vision Roadmap

1991 1998 2002 2004 2005 2006 2009

Asset 1.3

4488

92130 (E)

2003

StreamlineOrganization

Build aDistinctivePlatform

LeveragePlatform for AcceleratedGrowth

PremierFinancial ServicesNetwork

•Transformed to Bank

Hana Bank• P&A with

ChungchongBank

• M&A with Boram Bank

Hana Bank

• M&A withSeoul Bank

NewHana Bank

Hana FinancialNetwork

Hana Financial

Group Inc.

Top 3 by Total Asset

In Korea

Top 1by Productivity

& Asset Quality

In Korea

World Top 100

by Tier 1 Capital & Total Asset

World Top 100by Market

Capitalization

(Unit : KRW Tn)

29

Management Strategies

Banking Sector

Achieving

Vision

• Sharing of Customer & Cross Selling

• Integrated Sales Strategy Promotion

• Collaborated Product Development

• Specialized Human Resource

• Efficiency in Cost & Management

• Expansion of Managerial Strategic Flexibility

Non-BankingSector

• Securities• Insurance• Asset Mgmt.• Credit Card• Capital

Maximizing Group Synergy2006 2009

Hana I&S

IT Support for Financial Group

Hana Institute of Finance

Think Tank of Financial GroupShared Knowledge Center

HFG

Group Planning & Strategy,Financial Management

Strategy &Shared Services

30

Synergy Strategies

• Restructure group branch strategy• Pursue BIB, BWB

• Review HWA and upgrade product portfolio• Release group package products (inc. credit cards)

• Increased customer information sharing (target marketing)• Utilize customer information at call center

• Integrated group marketing • Establish cross-selling index

• Integrated procurement system

Establish one-stop financial service station based business model

Development of competitive group products

Establish and pilot test integrated CRM

Increase cross-selling customers

Realize cost synergies

Launch integrated service channel to pursue growth through a comprehensive financial business model

31

Appendix • Major Shareholders

• HFG Domestic Operation Network

• Organizational Structure of HFG

32

Major Shareholders

Capital Structure

5,597

(499.6)

-

5,075

1,021

1st Dec. 2005 2005

211.7Retained Earnings

6,320Total ShareholdersEquity

11.3Capital Adjustment

5,075Capital Surplus

1,021Paid- In Capital

Source: Company, As the end of 2005

Temasek Templeton Allianz NationalPension

Fund

9.06%

8.13%

4.84%3.41%

9.34%

GoldmanSachs

Major Shareholders (unit : KRW Bn)

33Source: Company

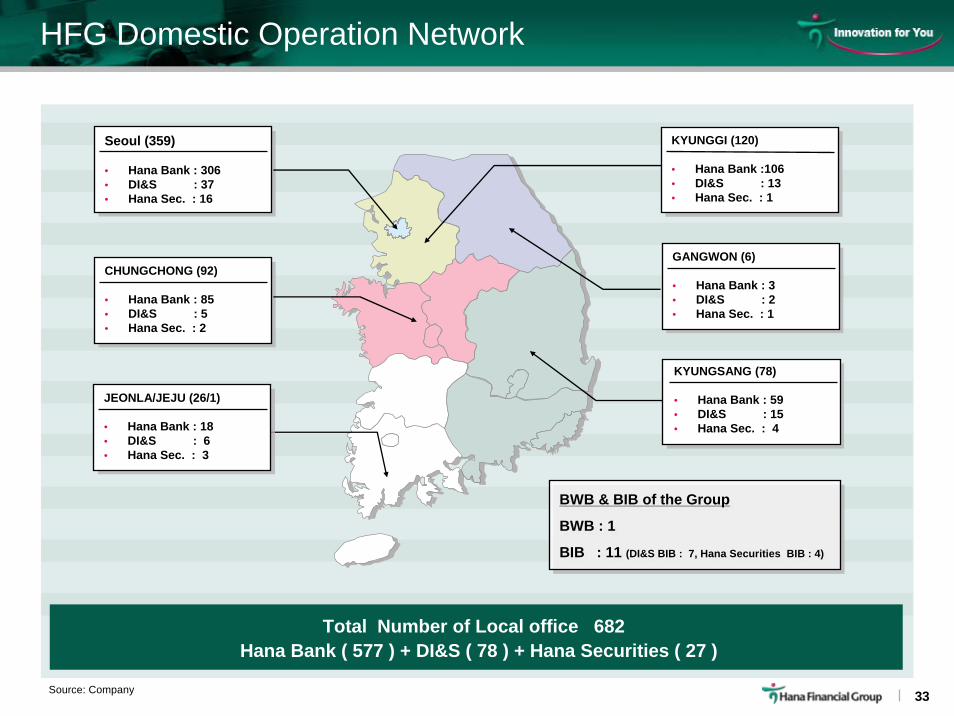

HFG Domestic Operation Network

Total Number of Local office 682 Hana Bank ( 577 ) + DI&S ( 78 ) + Hana Securities ( 27 )

CHUNGCHONG (92)

• Hana Bank : 85• DI&S : 5• Hana Sec. : 2

Seoul (359)

• Hana Bank : 306• DI&S : 37• Hana Sec. : 16

JEONLA/JEJU (26/1)

• Hana Bank : 18• DI&S : 6• Hana Sec. : 3

KYUNGGI (120)

• Hana Bank :106• DI&S : 13• Hana Sec. : 1

GANGWON (6)

• Hana Bank : 3• DI&S : 2• Hana Sec. : 1

KYUNGSANG (78)

• Hana Bank : 59• DI&S : 15• Hana Sec. : 4

BWB & BIB of the Group

BWB : 1

BIB : 11 (DI&S BIB : 7, Hana Securities BIB : 4)

BWB & BIB of the Group

BWB : 1

BIB : 11 (DI&S BIB : 7, Hana Securities BIB : 4)

34

Organizational Structure of HFG

BOD

GSM

Financial Planning Team

Chairman & CEO

CEO & President

Steering Committee for BOD

Audit Committee

Outside DirectorNomination Committee

Risk Management Committee

Management Compensation Committee

Management Strategy Committee

General Service Team Synergy Integration Team Audit & Compliance Team

Public Relations Team Risk Management TeamSubsidiary

Management TeamStrategy

Development Team

Source: Company

Top Related

Copyright © 2022 FDOKUMEN