Bahasa

Halaman

Hukum

Mathematics 2022, 10, 860. https://doi.org/10.3390/math10060860 www.mdpi.com/journal/mathematics

Article

Econophysics Techniques and Their Applications

on the Stock Market

Florin Turcaș 1, Florin Cornel Dumiter 2,* and Marius Boiță 2

1 ANEVAR, 011158 Bucharest, Romania; [email protected] 2 Economics and Technical Department, “Vasile Goldiș” Western University of Arad, 310025 Arad, Romania;

[email protected]; [email protected]

* Correspondence: [email protected]

Abstract: Exact sciences have achieved many results, validated in practice. Although their

application in economics is difficult due to the human factor involved, the lack of conservation laws,

and experimental difficulties, it must be highlighted that the consistent bibliography gathered in

recent years in this field encourages the econophysics approach. The objective of this article is to

validate and/or define a few stock strategies, based on known results from mathematics, physics,

and chemistry. The scope of this research demonstrates that statistics (in portfolio theory), geometry

(in technical analysis), or financial mathematics can be used in the capital market. Many of the exact

science results corresponded to strategies applicable to investors. Unlike the material world,

financial markets have additional components that must be considered: human psychology,

sociology at the firm level, and behavioral unpredictability. The findings obtained in this research

enable the enormous vastness of the exact science results that can be a fertile source for new

investment strategies. This article concludes that in order for mathematical theories to be applied to

the stock market, it is essential that the start-up conditions (initial assumptions) are validated in the

market.

Keywords: econophysics; interdisciplinarity; technological strategies; sustainable development;

technical analysis

MSC: 91B80; 46N10; 62P20; 97M40

1. Introduction

“Econophysics represents the ultimate connection between mathematics, physics,

engineering, and economics [1]”.

There are three fundamental differences between natural sciences and economic ones

(with this research mostly analyzing the stock differences).

The first difference is that natural sciences are objective, while economic laws must

consider the subjective side, namely, the human factor. The laws of physics, chemistry, or

mathematics apply universally, regardless of the will of the observer. In quantum

mechanics, it is recognized that some observations influence the results, but not by our

will. In economics, and particularly stock markets, participants’ attitudes are decisive for

the evolution of quotations. Herd behavior, exuberance, panic, confidence,—or the lack

thereof—are drivers, especially in key moments of the stock market development.

Moreover, if scientific observations are quantifiable phenomena, social, behavioral, and

psychological effects are more difficult to express in equations.

The second difference concerns the experimental aspect. In the natural sciences, it is

customary to formulate a hypothesis, which practical experiments then confirm, improve,

or reject. There are also exact science situations where experiments cannot be performed

as the theoreticians would like, e.g., cosmology, anthropology, and geology. However,

the primary theories on which they are based are experimentally verifiable. Science cannot

Citation: Turcas, F.; Dumiter, F.C.;

Boita, M. Econophysics Techniques

and Their Applications on the Stock

Market. Mathematics 2022, 10, 860.

https://doi.org/10.3390/math

10060860

Academic Editors: Gheorghe Săvoiu

and Zhiping Chen

Received: 31 January 2022

Accepted: 4 March 2022

Published: 8 March 2022

Publisher’s Note: MDPI stays

neutral with regard to jurisdictional

claims in published maps and

institutional affiliations.

Copyright: © 2022 by the authors.

Licensee MDPI, Basel, Switzerland.

This article is an open access article

distributed under the terms and

conditions of the Creative Commons

Attribution (CC BY) license

(https://creativecommons.org/license

s/by/4.0/).

Mathematics 2022, 10, 860 2 of 25

experiment on the stock markets. Namely, it cannot separate the facts to demonstrate

precisely that a certain theory is valid. Reverse head and shoulders have no scientific

explanation, with the most plausible being that it is self-confirming: when analysts call it,

most investors become cautious, which automatically leads to a trend shift. We do not

know how to define the expression “there is a 70% chance for the market to grow”. We do

not have 100 cases to count the 70 favorable. The psychological approach “up to what

odds do you bet on growth?” cannot be applied, because it depends essentially on the

amount invested and the attitude of the investor towards risk, much more than on the

opinion of market evolution. It cannot be checked whether the positive growth of a

portfolio is due to the theory applied in the selection of securities or due to the evolution

of the securities (market) itself.

The third difference relates to the basic laws of the theories. In physics, the basics are

the conservation laws: energy, impulse, kinetic momentum, electrical charge, symmetry,

etc. There is also an exception: the second law of thermodynamics, which states that

entropy always increases. In the economy, nothing is constant. In addition to the

continuous growth trend in the overall markets (due to technological development,

expansion into new geographic areas, etc.), no monetary amount is constant, regardless

of the economic area considered. Portfolio values are not constant, and this is the main

reason stocks are bought and sold. The only null result is on the futures market, where

the loss of a part is wholly found in the win of its counterpart. A lack of conservation laws

makes it difficult to formulate theories, including extreme (minimum, maximum) and

optimal trajectory issues.

However, the results of the exact sciences are to be found in economics. Statistics are

the basic method of modeling economic phenomena. On the stock market, it is noted that

many theoretical results start from Gaussian statistics, although statistical data does not

confirm this distribution.

The Black–Scholes–Merton (BSM) model for evaluating options is another example

of mathematical theory (derived from fluid flow physics) applied in the economy.

It is appreciated that the results obtained by exact sciences such as mathematics,

physics, and chemistry can be adapted and applied in the economy, and especially in the

stock market.

The main objective of this paper is to tackle the application of econophysics in the

stock market area, both on the international level and at the Romanian level. In this study,

the most important features that influence the impact of econophysics upon the stock

market are the following: the weather phenomenon; the magnitude of earthquakes; the

complexity of the poker game; the structure, implication, and application of the Le

Chatelier principle; and important features such as random walks and dynamic

phenomena.

In this paper, we have explored a wide range of known theories that started from the

natural sciences, we have resolved their basic rationale, and verified their application in

the stock market. In contrast to the immutable laws of nature, in cases where it is analyzed,

social phenomena (especially the financial ones) appear as events related to the human

participant’s subjectivity. The article did not explore the psychological aspect but only the

application of the objective laws to economic activities. The general conclusion is that

although derived from different knowledge areas and using different methods and

approaches, natural and stock market phenomena share the same common basis:

precision areas and different time correlation, a general legitimacy right in seemingly

chaotic environments, and periodicities. The data analyzed in this article refers, in general,

to stock quotes. The quotes and their history have been accessed from several public

websites. The technical analysis has been conducted by several specialized software that

are freely available, especially Windows Excel.

Regarding the methodology, it can be emphasized that each of the exposed

phenomena had been presented in correlation to their stock market interpretation. The

testing process was an immediate one: at any point, the conditions draw near to those of

Mathematics 2022, 10, 860 3 of 25

the examples enriched in this paper in order to determine whether the suggested theory

can be verified or not. The investment strategies must be subject to other study materials

of a larger scale.

The structure of this paper is as follows: Section 2 highlights the current state of the

art, presenting the theoretical and empirical background for using econophysics related to

stock markets. Section 3 represents the core of the paper, which tackles some important

features related to econophysics applied to the stock market, namely, the weather,

earthquakes, poker, Le Chatelier principle, random walks, dynamic phenomena, and

financial betting. Section 4 presents the conclusions and remarks regarding the main

findings of the empirical research related to the application of econophysics to stock

markets.

2. Literature Review

Fractal theory was the first technique related to the application of econophysics on

the stock market. The pioneering work (Peters, 1994) [2] was continued by Mandelbrot

with the development of an approach capable of explaining market deviations from

Gaussian statistics and accrediting the fractal character of the markets through Hurst’s

exponent. The results are not universally appreciated, although fractal structures can be

identified on the charts of titles’ evolution as the results show in Figure 1. Another highly

important work focuses on the application of thermodynamics in the economy (Sergeev,

2008) [3]. However, the principles of thermodynamics start from the conservation of

energy, but the amount of money in the economy (with which energy is assimilated) is

not preserved.

Figure 1. Fractal structures empirically found on the DJIA course. Source: Authors’ processing is

based on data available on Incredible Charts Pro.

McCauley investigated the lack of a real balance in financial markets in 2004 [4]. It

was intended to explain the real market movement, in contradiction of current theories,

which starts from the premise of how the market should evolve in order to fill certain

mathematical theories. Richmond, Mimkes, and Hutzler (2013) applied more complex

mathematical theories in the economy [5]. A Romanian group of authors made a

Mathematics 2022, 10, 860 4 of 25

compendium on econophysics, edited in 2013 under the direction of Gheorghe Săvoiu [6].

It synthesizes results from various economic and mathematical domains.

Other interesting works in this field include Chakrabarti et al. (2006) [7], Cockshott

et al. (2009) [8], and Roehner (2002) [9]. Preiss (2011) [10] tackles the econophysics

phenomenon throughout the analyses between time series and their correlation of a time

series. The author concludes that time series over a short time scale are influenced by

typical behavioral patterns of the financial market’s participants. Liang et al. (2013) [11]

analyze the Chinese stock markets by the impact of their physical properties and conclude

that econophysics has a direct impact upon the Chinese stock market based on a large

amount of economic data over a long-run time horizon.

Chakrabarti et al. (2011) [12] highlight the econophysics domain within the agent-

based models, concluding that there are three important models which must be taken into

account: an agent-based model of order-driven markets, kinetic theory models, and game

theory models. Other interesting studies developed by Vasconcelos (2004) [13], Choi

(2014) [14], Forte (2017) [15], and Swingler (2017) [16] analyze the application of agent-

based models within the econophysics framework, suggesting the importance of the

impact of this phenomenon upon stock markets.

Bali (2011) [17], Schafer (2012) [18], and Kakarot-Handtke (2013) [19] developed

various studies about the importance of econophysics applied to stock markets within

several features and characteristics in terms of criticisms and opportunities.

Aamir and Ali Shah (2018) [20] analyze the period between 2001 and 2005 in relation

to the Pakistan and Asian emerging economies co-movements through Phillips–Perron

and Dickey–Fuller tests. The authors conclude that there are several important forces of

integration between the Asian emerging stock market and Pakistan. Other authors test the

sustainability of the stock market using the VIX Index and reveal that the market volatility

influence has a great impact among different stock markets through an important feature

such as diversification (Ruan, 2018) [21].

Nasr et al. (2018) [22] provide a qualitative overview regarding the linkages between

BRICS countries and highlight the heterogeneity in stock market returns based on several

underlying criteria. Their main conclusion is that BRICS countries react differently

regarding the rating changes, depending upon their connections with the global market

variables. The usage of mining techniques in measuring the connections between the

impact of social media and stock market modeling suggests that features such as public

opinions, news articles, and technical analyses can result in significant success (Kollintza-

Kyriakoulia et al., 2018) [23].

Li and Wu (2017) [24] link the stock market performance in relation to firm

manufacturing and the wholesale and retail industry in China, revealing that empirical

results are significant in cases where it used the Fama–French factor model. Drezewski et

al. (2018) [25] establish correlations between sustainable development strategies and bio-

inspired trading strategies and conclude that using the Forex market optimization

algorithms can obtain some important future development strategies. The linkage

between forecasting stock prices and neural approaches can be explained by a hybrid

modeling approach combining analytical and computing models (Paluch and Jackowska-

Strumillo, 2018) [26].

Nguyen and Yuun (2019) [27] suggest a different type of approach using transfer

learning in order to determine the market prediction based upon short-term stock price

and conclude that stock relationship information can be a panacea regarding the

improvement of prediction accuracy. Herzog and Osamah (2019) [28] use a reverse

engineering approach in order to determine option pricing and suggest that their

approach is highly significant in establishing important future research directions. The

impact of portfolio diversification has an effect on domestic and foreign stocks, suggesting

that there is a significant impact of correlation volatilities and risks associated with a

diversified portfolio (Nayan, 2019) [29].

Mathematics 2022, 10, 860 5 of 25

The usage of calendar anomalies upon 11 CEE stock markets reveals that the turn-of-

the-month effect affects only market returns. especially in the short periods established at

the end of one month and the start of a new month (Arendas and Kotlebova, 2019) [30].

The significant positive results of stock market analysis by using a Markov chain to

improve future air quality suggest that this can be an important tool to help governments

insert prevention actions during a difficult weather period (Zakaria et al., 2019) [31]. The

market volatility in the conditions of premiums for sustainable and non-sustainable

components highlights that a hedging strategy is needed in order to provide an important

shield against future uncertainty (Thu Truong and Kim, 2019) [32].

Blackledge et al. (2019) [33] provide interesting and important analyses regarding

important features such as econophysics, fractional calculus, fractal market, and future

price predictions. In this study, the authors conclude that econophysics can be applied to

the stock market by using Einstein’s evolution equation, the fractal market hypothesis,

and the fractional Poisson equation. Other authors used a minimum spanning tree and

cross-correlation coefficient in order to determine the statistical properties of the foreign

exchange market and concluded that the results are not stable in the Asia and Latin

America cluster but are stable in the Middle East cluster (Wang et al., 2013) [34].

The applications of econophysics and bio-medical entropy were revealed by using

permutation entropy to understand biomedical systems and the analysis of economic

markets (Zanin et al., 2012) [35]. Fry and Brint (2017) [36] developed a model to investigate

if there are any linkages between bubbles in opinion polls and betting markets before the

23 June 2016 UK vote to remain or not remain in the EU. The authors concluded that their

research had a significant impact in explaining the reasons for the UK voting to leave the

EU.

Ahmad et al. (2016) [37] used graphical representation to examine stock behavior in

relation to several time series. The authors concluded that a certain causal relationship

between stock returns and volatility can be identified in several important Asian stock

markets. Moreover, Rudzkis and Valkaviciene (2014) [38] developed several underlying

regression models to help identify the global and key macroeconomic indicators and their

impact on stock prices indices. The main findings of this study highlight that in the case

of small open economies, the price indices of individual sectors vary upon several

macroeconomic regressors. Vveinhardt et al. (2016) [39] analyze the Mean Reversion

Phenomenon and reveal several investment opportunities and stock prices returns, but

the results have inconsistencies due to the market’s reactions based on different periods.

Ruxanda and Badea (2014) [40] predict stock market conditions by using artificial

neural networks; this study offers a quid pro quo upon the configuring structure of these

networks upon the Romanian BET index. The aftermath of the neural networks reveals

that the direction of the DAX-30 stock market index can be predicted by using hybrid

fuzzy neural networks (Garcia et al., 2018) [41]. Ahmed et al. (2018) [42] examine the

relationship between stock returns and volatilities and suggest that the evolution of a

developed market differs significantly from emerging markets due to the higher returns

of the emerging stock markets. Janda et al. (2014) [43] enables the construction of a

sustainable financial portfolio throughout a microfinance investment funds scheme and

conclude that investors can be socially responsible by using financial indicators in

microfinance.

Ulusoy et al. (2012) [44] tackled the problem of hierarchical tree and minimal

spanning tree approaches in the period 2006–2010 for top 40 UK companies based on the

London Stock Exchange Index. They concluded that financial market dynamics can be

successfully predicted by using information theory and statistical physics. In the

aftermath, Ulusoy (2017) [45] reveals the importance of using econophysics in the financial

market domain due to the complex natural network function of the stock market.

Garcia and Requena (2019) reviewed some of the newest studies in the economic

literature regarding the fractal market hypothesis and proposed an FD4 exponent model

that can lead to the improvement of empirical results [46].

Mathematics 2022, 10, 860 6 of 25

Summarizing, all of this research, as well as numerous articles (especially those

published on Cornell’s arxiv.org platform, but not limited to them), outline the intense

interest of mathematicians and physicists in applying results in the economy. This paper

contributes to applying the theories of exact science when selecting stock market

strategies.

3. Methodology and Empirical Results

In the empirical study methodology, some examples of theories in the exact sciences

and attempts to translate them into stock market strategies are considered. The results are

listed below. Although not spectacular, practical results urge us to continue our

econophysics approach.

3.1. Weather

The connection between meteorology and the capital market is direct: on the Chicago

Mercantile Exchange, betting can be made on climatic derivatives. Climatological values

that are involved include temperature, rainfall, and snowfall, with the most important,

according to the cmegroup.com official site, being Heating Degree Day (HDD) and

Cooling Degree Day (CDD) contracts. Various strategies have been analyzed (Jewson and

Brix, 2005 [47]; Alexandridis and Zapranis, 2013 [48]).

Arbitrage on this market has direct positive effects for hotel managers, tourism

companies, agricultural producers, and insurers; in return, speculators can make

substantial profits. Figure 2 presents an example of how to apply arbitrage on weather

derivatives. A summer hotel owner (or tourist agency) would like summer to be as sunny

as possible. However, if the weather is cool, the hotel owner (or tourist agency) will lose

customers and profit will be reduced. Therefore, speculators can be bet that high

precipitation will occur, the average temperature will be low, or there will be many windy

days, etc. Conversely, a climatologist (or an environmentalist or a meteorologist) who

knows the effects of global warming will bet exactly the opposite: drought, heat, or

scorching heat. Thus, a situation that does not suit anyone can become a solution where

everyone benefits (a win-win situation): the hotelier secures a normal level of earnings (if

not from customers, then from financial derivatives) and environmentalists take

advantage of their studies on climate change (at least financially, if proposed measures to

limit the effects of the greenhouse effect are still to be seen).

Figure 2. Precision of meteorological predictions. Source: Authors’ processing is based on data

available on http://www.weatheronline.co.uk (accessed on 12 July 2016).

Another feature, namely the precision of the results, was pursued in this paper. The

next graph is the forecast for a week, i.e., the exact situation of surface pressure, according

Mathematics 2022, 10, 860 7 of 25

to http://www.weatheronline.co.uk (accessed on 12 July 2016). Weather predictions are

typically valid for a week. Depression has been established in northern Europe, and its

evolution is predicted with acceptable accuracy. However, in surrounding areas, precision

is lacking; for example, Iceland is at the limit, and there predictions become inaccurate.

The link to the capital market is direct and the resulting conclusion is simple: when

the indicators or the technical oscillators are at a limit, their precision is desirable and the

confidence we show must be limited (increased caution). Figure 3 shows that the RSI

oscillator for the BET index of the Bucharest Stock Exchange is generally an excellent

signal to confirm the trend, where the arrow represents the upward trend. However, in

the maximum area, as it can be seen in the circle part of the figure, it indicates many false

sales signals because it is at the upper limit of its relevance. Therefore, just as weather’s

predictions are good overall but not plausible at the extremes, the oscillators of the

technical analysis work well only in the median range of their variation range. The

conclusion is similar to the engineering results valid for any mechanical measuring device:

the precision is higher in the middle of the measuring scale and lower towards the

extremities.

Figure 3. The precision of technical oscillators. Source: Authors’ processing is based on data

available on https://www.ifbfinwest.ro/complexcharts/index.php?id_lista=1786 (accessed on 12

September 2014).

3.2. Earthquakes

Although they cannot be accurately predicted, earthquakes, especially those in active

seismic areas, have a repeatability that allows an estimation of the likelihood of their

occurrence as it is highlighted in Figure 4. Practically, the accumulated tensions tend to

unravel even more violently as more time passes between two successive earthquakes.

Thus, a good indicator of seismic risk is the period between earthquakes and their

frequency. On the stock exchange, this is focused upon the application of the conclusion

regarding concerning crises (downward periods highlighted with blue line). Visually, it

seems natural to define a crisis, being the portion of the graph on which a more

pronounced decrease occurs (some such drops are outlined empirically with black line in

Figure 5).

Mathematically, the loss period is defined in Excel as the area of the chart where

downgrading happens marked with the blue line, and the crises where the minima have

exceeded a certain threshold set a priori established by the red line. To work directly with

Mathematics 2022, 10, 860 8 of 25

relative variations, we considered the logarithmic values in the 10th quote. By plotting the

logarithmical quotient of the day i, the condition that the area of the graph is one of the

losses is 𝑦𝑖+1 < 𝑦𝑖𝑦𝑖 + 1 < 𝑦𝑖 , and one of the crises is 𝑦𝑚𝑎𝑥 − 𝑦𝑘< p, where 𝑦𝑚𝑎𝑥 is the

maximum value previously reached (historical maximum until k) and p is the discomfort

threshold imposed by the investor. Thus, one can check the buy-and-hold stratagem,

which for an ascending market (such as the American one) should bring reasonable

returns. The results are represented in Figure 6, with the discomfort threshold set at 0.065

(about 16%).

Figure 4. Earthquake magnitude worldwide. Source: Authors’ processing is based on data available

on http://earthquake.usgs.gov/earthquakes/eqarchives/year/info_1990s.php (accessed on 20 July

2017).

Figure 5. Periodically, the stock exchange suffers a significant correction. Source: Authors’

processing in Microsoft Excel is based on data available on http://stooq.com/q/?s=%5Edji (accessed

on 20 July 2017).

Figure 6. The crisis periods are analyzed on the DJIA chart. Source: Authors’ processing is based on

data downloaded from http://stooq.com/site (accessed on 20 July 2017).

Mathematics 2022, 10, 860 9 of 25

For an index that experienced a steady growth throughout the analyzed period, the

results are not encouraging as most of the time the market has not risen, with quotes below

the previous historical highs (the red chart). Moreover, for periods marked with green

rectangles, the decrease from the previous maximum exceeded the discomfort threshold

predefined by the investor. It means that if the investor bought the maximum, the investor

would have to wait for a period equal to the width of the rectangle (quite high, in some

cases) for the investment to go into profit. It has been verified for the entire period between

1900 and June 2016 that the definition of the periods of crisis has a more drastic effect on

the buy-and-hold strategy (Figure 7).

Figure 7. Periods of DJIA decline. Source: Authors’ processing is based on data available

http://stooq.com/ (accessed on 20 July 2017).

One can object that the definition of the crisis is not a standardized one. Some

investors buy on a declining market, so those periods of decline and crisis are not defined

between the same values for all investors. Nor does the Rolling Windows method, applied

in the Matlab program according to Tsinaslanidis and Zapranis, produce better results

(2016) [49] (Figure 8).

Mathematics 2022, 10, 860 10 of 25

Figure 8. Maximum and minimum determined by the Rolling Windows method. Source: Authors’

processing is based on graphics generated in Matlab for 200-, 500-, and 1000-day windows using

data available on http://stooq.com/ (accessed on 20 July 2017).

3.3. Poker

Any Texas Hold’em player knows he usually does not play more than 10–15% of his

hands. The main reason is not having wrong hands, but the patience to know opponents

and to wait for a favorable situation (Purdy, 2005) [50]. The players (speculators) on the

stock exchange seem to forget that although the market has a general trend of growth, not

every moment is conducive to investment. A good measure of the reward/risk ratio is

RAROC (Risk Adjusted Return on Capital), defined as the ratio between the estimated

profit (affected by the associated risk) and the invested capital (Prokopczuk, 2004) [51].

The strategy adopted to the capital market could be synthesized as follows: a

variation limit is set and changes the position only when this limit is reached. Profit is

calculated only when the contract is closed because only then is the result (profit or loss)

marked. In practice, this would mean that the investor retains his position as long as the

opposite variation does not exceed the limit he has a priori imposed. When this limit is

reached, the investor closes his position and immediately opens a contrary one. This

ensures that the investor will not remain in the wrong position relative to the market more

than he initially imposed himself (potential losses are limited).

Applied to DJIA, the strategy would lead to the following results, for a required 9%

variation limit (see Figure 9). Where the DJIA (blue) chart is above the “Entry” (red) chart,

the investor’s position is long. Otherwise, it is short. The results are not spectacular at all,

but they depend on the required limit, so the correlation between the predefined variation

and the realized profit was analyzed. The results presented in Figure 10 and Table 1 do

not encourage the application of the strategy, being very sensitive to small variations of

the arbitrarily imposed limit. The brutal variation of profit, based on relatively minor

variations in the stop-loss safety, confirms the nonlinear character of the linkage, similar

to chaos theory (Mandelbrot, 2004) [52].

The key point is that the strategy does NOT yield good returns, even if an investor is

cautious and decides that in a contrary variation on the market (reasonable, around 10%)

to leave the position and take the opposite position. Therefore, the stop-loss technique is

not unbeatable, having previously shown that neither buy-and-hold strategy was. A

poker player would conclude that it is not the luck of having good cards but the style of

play that is decisive. A stockbroker will conclude that gains cannot be achieved simply by

taking a position and expecting it to materialize in a lasting trend. It is recommended that

the position be taken (abandoned) whenever the market demands it, without waiting for

the opposite movement to reach an arbitrarily imposed limit.

Mathematics 2022, 10, 860 11 of 25

Figure 9. Default Output Limit Exit Strategy. Source: Authors’ processing is based on data available

on http://stooq.com/ (accessed on 20 July 2017).

Figure 10. Profit dependency on the predefined stop-loss limit. Source: Authors’ processing is based

on the results obtained in Figure 9.

Table 1. Nonlinear variation of total profit is based on the pre-imposed stop-loss limit.

Per cent stop-loss 7.0% 8.0% 8.5% 9.0% 9.2% 9.5% 9.7% 10.0% 10.5%

Profit −5941.8 794.1 7476.0 7683.3 8595.2 7370.5 5393.1 3787.7 4440.0

Source: Authors’ processing is based on the results obtained in Figure 9.

3.4. Le Chatelier Principle

The principle of Le Chatelier is thus: “If a dynamic equilibrium is disturbed by changing

the conditions, the position of equilibrium moves to counteract the change.” In the economy,

Samuelson first applied this principle in 1947 to explain the dynamic balance between

supply and demand. In the stock market, the best example of this is the placement of large

volume orders as is presented in Figure 11. In the first instance, the market acts to

counteract the disturbance, i.e., attempts to absorb the large volume of bid/ask shares. If

the investor succeeds, the balance is restored. However, if the perturbation is too strong,

the balance can no longer be maintained at the same level of quotations and the market

shifts to another price level.

Mathematics 2022, 10, 860 12 of 25

Figure 11. Volume divergence. Source: Authors’ processing is based on data available on Incredible

Charts Pro.

This approach contradicts an essential assertion of the technical analysis, according

to which volume confirms the trend (Murphy, 1999) [53]; that is, the volume should be

rising when the trend is bull and descending when the trend is bear. The DJIA graph,

drawn with the Incredible Charts Pro program, shows that volume does not oscillate as

Murphy predicted. Volume has grown steadily in the 2000s, then increased dramatically

with the 2007–2009 crisis, so that with the rebound of markets its fall will be even more

pronounced. This evolution can be explained by both the Le Chatelier principle and the

herd spirit, which manifests itself mainly in times of crisis and exuberance.

3.5. Random Walk

A photon that leaves the center of the sun reaches us 100,000–1,000,000 years after it

hits a lot of nuclei in space. We considered the series of DJIA quotations from 2 January

1900 to 24 June 2016. We logged the series and considered daily variations (returns).

Statistically, the mean of the logarithmic differences is 0.00007958 and the standard

deviation of the entire population is 0.00483597. With these parameters, we generated a

similar number (30,248) of random numbers, using the normal probability distribution,

with the same defining parameters (the previously calculated average and dispersion) in

Windows Excel (Random Number Generation). These were considered daily variations

of hypothetical logarithmic series, called Random, which were then reconstituted and

represented on the same graph as the initial DJIA series as is highlithened in Figure 12.

In Figure 12, the results highlight that randomly generated series behave similarly to

actual quotes, showing more or less steep trends, rises, and decreases. Each generation

produces different results, but all have the same characteristics. For securities with a

higher volatility history (SIF1) as it is shown in Figure 13, the situation is different: the

randomly generated series exhibits reasonable deviations from the trend, as opposed to

the actual quote whose fluctuations are far beyond the limits required by the Gaussian

distribution.

Mathematics 2022, 10, 860 13 of 25

Figure 12. DJIA compared to randomly generated series. Source: Authors’ processing is based on

data available on http://stooq.com/ (accessed on 20 July 2017).

Figure 13. SIF1 chart, compared with randomly generated titles. Source: Authors’ processing is

based on data available on www.bvb.ro (accessed on 10 December 2018).

3.6. Dynamic Phenomena

The foundations of catastrophe theory were discovered when it was found that the

evolution of dynamic (nonlinear) systems mainly depends on the initial conditions: a

small deviation could produce results that differ exponentially.

Many areas of physics recognize chaos theory:

• The gravity problem with three bodies;

• The double pendulum;

• The strange attractors;

• Jerk circuit in electronics, etc.

The capital market is a dynamic system, so we expect the Butterfly effect (The flap of

a butterfly’s wings in Brazil set off a tornado in Texas) to apply in practice. Indeed, the initial

conditions accepted for the selection of securities in a portfolio may influence the

investment decision.

Suppose an investor decided on the composition of a portfolio formed from three

titles: SIF1, BRD, and SNP. Based on an analysis of the period 2001–2017, it is evident that

starting from the same point, SIF1 keeps on top of all the other titles, being the most

attractive. If the analyzed period is restricted to 2005–2017, BRD is the best title, and if we

started in 2008, SNP has the best evolution. In the analysis based on the latest period (since

2013), SNP should have been avoided altogether.

Mathematics 2022, 10, 860 14 of 25

The contradiction reached is a paradox, not an error of reasoning. In all analyses

presented in Figure 14, namely (a–d), the graphs started from the same starting point, but

the result and the evolution were different. Thus, the conclusions, all of which are correct,

of four analysts can differ radically, only because the analyzed period is different. No one

is wrong, but no one has the absolute truth either. Nevertheless, this is also the charm of

technical analysis, which is the combination of exact mathematical results and the art of

interpreting them, the analyst’s reasoning, and experience.

(a)

(b)

(c)

(d)

Mathematics 2022, 10, 860 15 of 25

Figure 14. (a–d): Importance of selection of the initial point. Source: Authors’ processing is based on

data available on www.bvb.ro (accessed on 12 February 2018).

3.7. Size Matters

Different behavior produces a physical reality within different scales. Thereby, at the

minimum scale dimensions (on a subatomic scale), strong forces are prevailing (the

connection between quarks). At the atomic level, electromagnetic forces are occurring

which govern the connection of atoms. At the cosmic level, the gravitational force becomes

the most crucial feature, determining the galaxies and solar systems’ evolutions. A similar

conclusion is observed throughout the analysis of the different types of graphical

correlation. In the next example, the Dow Jones index and the gold quotation on the

American market were analyzed according to the Intermarket theory (Murphy). Thus,

these two features must be inversely correlated.

The conclusions differ according to the analyzed period. In Figure 15a, it can be

observed that the two titles are uncorrelated. Beyond a relative increase of both titles, there

are periods in which both graphs have similar variation and other periods in which the

titles vary in opposition, but also other sections in which one is on bearing and the other

has a trend. In this case, the conclusion is that the two titles are uncorrelated. In Figure

15b (drawn on different periods), the graphics are inversely correlated: when one is

decreasing, the other is increasing and vice versa. Finally, in Figure 15c, the graphics are

positively correlated, with both titles simultaneously having the same evolution variation.

In this situation, the results represent a shortcoming of the technical analysis.

Depending on the historical period selection, a technical analyst can graphically

demonstrate the direct correlation, the inverse correlation, or the absence nexus for the

two selected titles. The explanations have both economic and behavioral foundations.

Gold is a limited natural resource. The DJIA stocks are conventional entities theoretically

unlimited, as much as the global production has an increasing trend. Gold cannot

infinitely increase; the stocks are not unlimited, either as number or value. Therefore, in

the long run, the two titles cannot be correlated.

In the short run, if the stock market keeps good time, investors will prefer stocks. In

a case where there are crises signals, investors will flee from gold (which is a defensive

action). According to this view, it can be explained by the inverse correlation. In the

medium run, if the economy registers a soundtrack and there are no danger signs,

investors can diversify their portfolio and will invest in both stock and in gold, especially

if government securities cannot offer an attractive interest rate. Thereby, in periods of

moderate economic growth and economic calm, the two titles can register a direct

correlation.

Mathematics 2022, 10, 860 16 of 25

(a)

(b)

(c)

Mathematics 2022, 10, 860 17 of 25

Figure 15. (a–c): Graphical comparison between titles evolution of different periods. Source:

Authors’ processing is based on data available on Incredible Charts Pro.

3.8. Financial Betting

Even if it seems attractive, there are no financial bets similar to the ones mentioned.

At most, there is financial betting which proposes odds below 50%, if the quotation will

increase or decrease in the next period as is presented in Figure 16.

Figure 16. Explanatory screen binary bet. Source: Authors’ processing is based on data available on

binary.com (accessed on 17 September 2020).

Hedging (arbitrage) is the main barrier to revealing realistic forecasts regarding the

evolution of prices. Hedging supposes the sale (at a higher price) and the purchase (at a

lower price), simultaneously, on two markets, of one and the same title (or a derivative,

directly connected with the basic one). Because the two courses will be mathematically

equal at maturity, the speculator wins the difference regardless of the closing price.

Therefore, whatever the experts’ forecasts regarding the market evolution, the spot course

and futures course may not differ too much (at most with the risk-free interest and the

costs of the operations, or due to the current variations as a consequence of the inertia of

the markets).

Mathematics 2022, 10, 860 18 of 25

The advantage of the financial bets is that the opportunity of hedging does not exist,

therefore, the quotations can be as realistic as possible.

However, the following problem arises: what happens if the real probability, p’i,

known by the gamblers is different to the one calculated by the bookmaker, pi? In a simple

case in which we have two betting options (1 and 2) presented in Figure 16, an elementary

algebraic calculation shows that the maximum potential gain is reached if the available

amount is played in full on the bet that has a higher chance of realization than those listed

(p’i-pi = max).

However, according to Table 2, it can be noted that the potential loss of the gambler

also increases (if the bet does not succeed, the entire invested amount will be lost), but the

probability of failure is smaller.

Table 2. Spot-bet hedging does not bring profit to speculators.

Current price 10.00 Ron/share

Initial investment 200.00 Ron

Number of shares 20.00 Shares

Expected price 9.50 10.00 11.00 Ron/share

Chance 70% 10% 20% 100%

Bet odds 1.43 10.00 5.00

Weighted result without hedging −10.00 0.00 20.00 Ron

−3.00 Ron

Hedging investment 200.00 Ron

Weighted result with hedging 75.71 −200.00 −180.00 Ron

−3.00 Ron

Source: Authors’ own processing.

A little more complicated is the situation in which more variants of betting exist and

the gamblers appreciate quotations differently than the brokers as is revealed by Table 3

and Table 4. As in the case with two betting variants, the entire investment must be

allocated where the actual probabilities are greater than the reversed quotations. An

algebraic calculation reveals, in the case of two increases in the gambler’s probabilities

compared to those of the broker, p’1 > p1 and p’2 > p2, that the entire amount should be

invested when the ratio between growth and the broker’s quotation, p′i−pi

pi, is a maximum.

Table 3. The gain of the gambler appreciates the chances more accurately than the broker.

Variant Betting House Gambler Gain

Probability Odds Probability Bet Absolut Revised

1 40% 2.50 30% 0.00 −1.00 −0.30

2 60% 1.67 70% 1.00 0.67 0.47

TOTAL 100% 1.00 100% 1.00 0.17

Source: Authors’ own processing.

Table 4. How to invest if the broker’s quotation is considered wrong.

Variants Betting House Gambler Gain

Probability Odds Probability Bet Absolut Revised

1 25% 4.00 30% 1.00 3.00 0.90

2 35% 2.86 40% 0.00 −1.00 −0.40

3 40% 2.50 30% 0.00 −1.00 −0.30

TOTAL 100% 1.00 100% 1.00 0.20

Source: Authors’ own processing.

Mathematics 2022, 10, 860 19 of 25

The result may be easily verified/established numerically using the Solver utility in

Windows Excel.

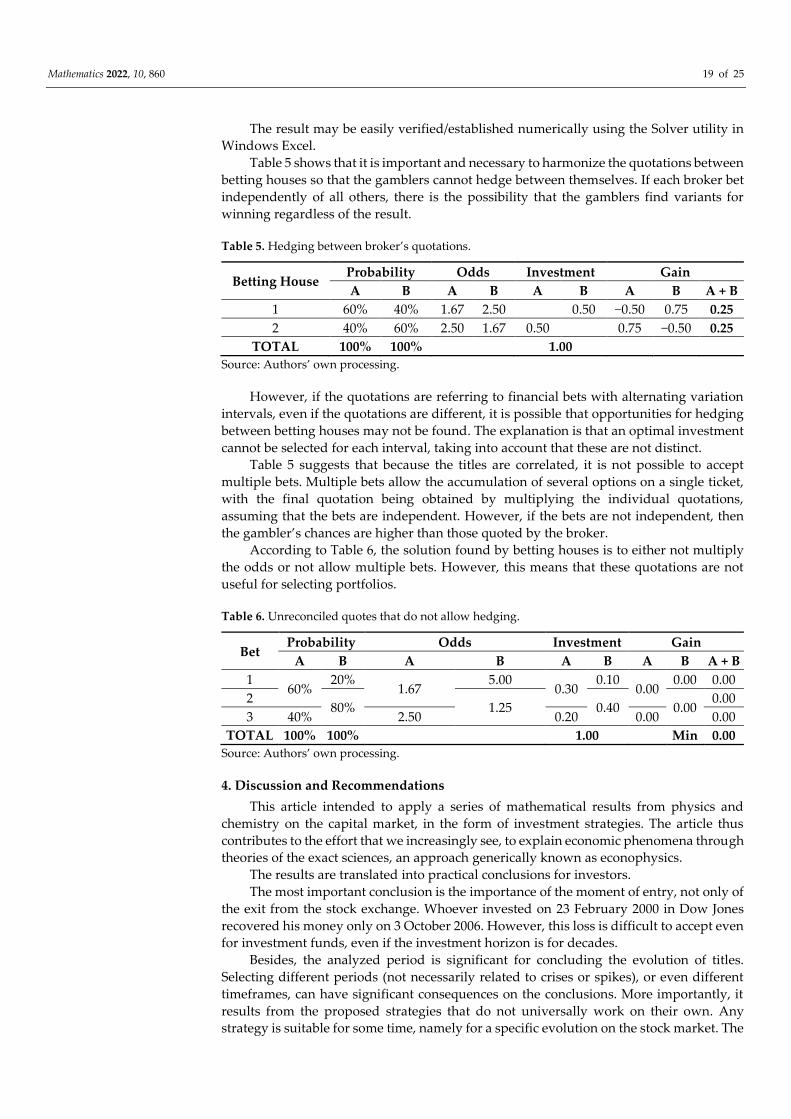

Table 5 shows that it is important and necessary to harmonize the quotations between

betting houses so that the gamblers cannot hedge between themselves. If each broker bet

independently of all others, there is the possibility that the gamblers find variants for

winning regardless of the result.

Table 5. Hedging between broker’s quotations.

Betting House Probability Odds Investment Gain

A B A B A B A B A + B

1 60% 40% 1.67 2.50 0.50 −0.50 0.75 0.25

2 40% 60% 2.50 1.67 0.50 0.75 −0.50 0.25

TOTAL 100% 100% 1.00

Source: Authors’ own processing.

However, if the quotations are referring to financial bets with alternating variation

intervals, even if the quotations are different, it is possible that opportunities for hedging

between betting houses may not be found. The explanation is that an optimal investment

cannot be selected for each interval, taking into account that these are not distinct.

Table 5 suggests that because the titles are correlated, it is not possible to accept

multiple bets. Multiple bets allow the accumulation of several options on a single ticket,

with the final quotation being obtained by multiplying the individual quotations,

assuming that the bets are independent. However, if the bets are not independent, then

the gambler’s chances are higher than those quoted by the broker.

According to Table 6, the solution found by betting houses is to either not multiply

the odds or not allow multiple bets. However, this means that these quotations are not

useful for selecting portfolios.

Table 6. Unreconciled quotes that do not allow hedging.

Bet Probability Odds Investment Gain

A B A B A B A B A + B

1 60%

20% 1.67

5.00 0.30

0.10 0.00

0.00 0.00

2 80% 1.25 0.40 0.00

0.00

3 40% 2.50 0.20 0.00 0.00

TOTAL 100% 100% 1.00 Min 0.00

Source: Authors’ own processing.

4. Discussion and Recommendations

This article intended to apply a series of mathematical results from physics and

chemistry on the capital market, in the form of investment strategies. The article thus

contributes to the effort that we increasingly see, to explain economic phenomena through

theories of the exact sciences, an approach generically known as econophysics.

The results are translated into practical conclusions for investors.

The most important conclusion is the importance of the moment of entry, not only of

the exit from the stock exchange. Whoever invested on 23 February 2000 in Dow Jones

recovered his money only on 3 October 2006. However, this loss is difficult to accept even

for investment funds, even if the investment horizon is for decades.

Besides, the analyzed period is significant for concluding the evolution of titles.

Selecting different periods (not necessarily related to crises or spikes), or even different

timeframes, can have significant consequences on the conclusions. More importantly, it

results from the proposed strategies that do not universally work on their own. Any

strategy is suitable for some time, namely for a specific evolution on the stock market. The

Mathematics 2022, 10, 860 20 of 25

investor should continually analyze the applicability of the theory and the market trend,

to decide when to apply a specific strategy and when to leave the market.

From a theoretical point of view, in this study, it has been worthwhile trying to apply

mathematical (physical) theories, with a large number of participants, diversity of

concepts, and multitude of factors of influence often causing the market to behave as a

complex physical system. The main issues are the adequacy of theory to market reality

(for example, Gaussian statistics are not appropriate, so most statistical conclusions—

including VaR—do not apply in practice), the absence of conservation laws (as a basis for

mathematical physics), and the difficulty of quantifying the influence of the human factor.

The study directions opened by econophysics are broad; practically, any theory in the

exact sciences can have a correspondent in the economy, with the art being in adapting

them to reflect the realities of the market. This article also proposes a practical side: the

establishment of strategies based on mathematical theories. Although the conclusion is

that the application is not direct and purely objective, the subjective side of the investment

process can be greatly reduced and improved.

Regarding recommendations for future research, the following suggestions should

be emphasized. In the first place, on what should be focused the forecast of future

quotations and related probabilities? On technical analysis, of course. The fact that the

market is moving in (Murphy, 1999) [53] is a truth that has been repeatedly demonstrated.

Nor should the fundamental analysis be omitted, given that the issuers tend to have

quotations that bring indicators to the values close to those of the market (Rossi and Forte,

2016) [54]. For those who use automated trading or a computerized selection of titles,

statistical analysis and game theory are essential. Taking into account that there are

millions of sites and even books (Pesavento, 2015) [55] that recommend esoteric methods,

behavioral analysis should not be neglected.

However, the approaches using different reasoning can lead to different results. An

eloquent example presented in Figure 17 is represented by a series of bets which, although

they refer to the same final result (0–0), because they start from different premises, lead to

unequal probabilities.

The question is whether it is a big mistake if it is determined that the probabilities for

investment decisions do not strictly respect the principles of No Dutch Book. Does it seem

to be wrong to quote 50% long chances and 51% short chances (probabilities coming from

different reasoning)? However, these probabilities are not meant for betting, but only for

your own investment decision. In addition, these situations are not totally wrong: after

all, the mathematical probability is defined as limN→∞

n

N, where n is the number of favorable

cases divided by the total number of cases N. Mathematically, the condition of

complementarity must be respected only at infinity. It is as equally likely that the next roll

of a coin will be Heads or Tails. However, it is very likely that after six rolls, consecutive

series of similar results appear. To what probability should it be given priority?

Figure 17. Different odds for the same bet. Source: Authors’ processing is based on data available

on unibet.ro (accessed on 20 February 2020).

Mathematics 2022, 10, 860 21 of 25

It can be noticed that even more interesting is the fact that the stock exchange is being

manipulated. It runs large investors, large arbitrators, speculators, brokerage houses,

high-speed automated trading systems, ordinary citizens persuaded by telephone to

“invest”, etc. Consciously or not, hostile or not, every transaction is a manipulation of the

price. The buyer wants to acquire a price as low as possible, to the detriment of the seller.

In addition, the buyer does this to then sell more expensively when he thinks the price

will decrease. It is not illegal, immoral, or unfair. Simply, the market is made up of actors

who try to use randomness in their favor.

This observation could change the basic perspective of probabilities. The ideal toss of

a coin or the perfect throw of a dice has been scientifically studied. However, what if the

producer confessed to cheating the coin? Unfortunately, the person died before specifying

in which way and how large the asymmetry is. Specific devices that make a non-

destructive analysis and lead us to a deterministic result cannot be identified. However,

if the records of the last 100 throws exist, can the probability of the 101st throw be

estimated? In theory, it is 50–50%, although it is known that this is not right, but it is not

known how wrong it is. Or 52–48% in favor of the first throws, although it is known that

100 throws are not statistically relevant (they do not meet the Law of Large Numbers or

the central limit theorem)?

Applied on the stock exchange, the observation gives rise to further reasoning. It

cannot be precisely determined if the coin is ideal or fake. It can be identified that there

are 55–45 H–T cases after 100 throws. In what hypothesis can be established the

probability of 101 attempts? If one number is drawn more frequently than another in the

lottery, is it reasonable to assume that the balls were not manufactured perfectly equal?

Returning to the subject of the problem: if it is noticed that a certain phenomenon related

to an issuer, can it be believed (is there an associated logic?) or not? Do fractals have a say

here?

Another problem would be the adjustment, via the application of Bayesian models

to re-evaluate the probabilities based on events that have already occurred (Grover, 2013)

[56]. Here, however, a problem can already be identified (Tijms, 2019) [57]: an initial

intuited probability of 20% (prior probability) leads to a deduced probability (posterior

probability) of 52.2%, while an initial probability of 50% leads to a final one of 81.4%, with

a chance factor (likelihood factor) of 35/8. In this example, the psychological (subjective)

effect of mistrust is amplified if a practical result is negative, which is neither logical nor

beneficial.

5. Conclusions

The main conclusion of the article is that all possible knowledge from other areas

(mathematics, physics, chemistry, sociology, and psychology) should be used to shape the

capital market. Current economic assumptions are:

• Investors act rationally;

• Profit must be maximized (the worst strategy is to try and sell at the highest and buy

at the lowest price);

• Rational report between economy and consumption;

• Static equilibrium theories;

They are not applicable to financial markets.

It is likely that financial markets are the most complex scientific phenomenon

possible, because of acts that are objective, natural laws (statistical laws, economic and

financial realities, and automated trading programs), and random opinions and impulsive

actions from a multitude of investors and speculators, with the most diverse professional

qualifications, perceptions, styles, and possible conceptions.

Comments were received during the presentation of the paper at different

conferences that neural networks and cyberlearning systems are the solution to market

success. Undeniably, they have practical applicability, as long as automated systems make

Mathematics 2022, 10, 860 22 of 25

most of the transactions, with the majority of them working in the feedback loop

(learning). Their deficiency is that they use past situations to make decisions; this is where

the tsunami example came in.

Another example is added to this study. The creators of the AlphaGo (Netflix Reportage:

AlphaGo) program succeeded in defeating the Go world champion, Lee Sodol, 4–1. Go is

a game that is suitable for modern cyber systems because the analysis of 50 moves forward

gives a clear advantage to the computer. Furthermore, the algorithm is the learning one:

thousands of games were introduced into the memory of the computer and it was

programmed to conclude its preparatory games. In this sense, it is not a thought process

but a data processing one. In the only game he won, Lee Sedol made an unexpected move.

It is not known whether it was a good or bad one, but the computer was confused and lost

lamentably, making incredible mistakes. Is it still necessary to compare the crisis when

people simply lose their heads?

The conclusions of this study reveal that the best evidence that the stock market

mechanism had been understood would come if a bookmaker would open quotas for an

average period: not one day, because it would be a lottery; not one year, because it has to

react to market movements. Do not let speculators bet these odds because it would only

be another venue for derivatives. Odds should be established by the professional house,

which has sufficient interest to be fair: without excessive regulations and supervision,

with only the usual precautions in the industry, and with slight chances of arbitrage.

Based on what will the bookmaker act?

• On probabilities, of course. Nevertheless, they are limited: they operate on a

subatomic level (quantum mechanics) or molecular (gas theory), where an

astronomical number of physical events need to be processed statistically. On the

capital market, the best evidence of non-adaptation is that VaR did not work in crisis:

simply, the decreases exceeded the statistical threshold.

• On the technical analysis, obviously. Strong trends beat everything, so they cannot

be overlooked. However, this is again limited. When trying to obtain results only

from the study of graphs, my colleagues received an unpleasant surprise.

• Financial (fundamental) analyses are mandatory. Quotations shall take account of

the results of issuers, but in a manner that is neither linear nor immediate and

sometimes irrelevant.

• On other considerations, yes. Market sentiment (measured by established indices:

SWFX, Sentix, SSI, ISE), macroeconomic trends, and the behavioral study of the

relevant market can all provide valuable information, even if they are very hard to

quantify numerically.

• Would corrections be necessary? Of course: feedback loops, machine learning, and

Bayes.

• Besides, it is considered that the market stage can be determinant (it cannot be

accepted that periods of soars, stagnation, or collapse can be integrated into a single

strategy).

Fractal principles also apply to the capital market. Elliott’s waves are an elegant

example: each wave consists of subwaves, in the same structure. There are five

movements in the direction of the trend and three in the opposite direction.

As with the technique (the accuracy of the measuring devices is superior in the

middle of the scale), on the major part of strong trends, the results of the technical analysis

are applied much better than at the ends (at the beginning or finish of the trend).

Although the market is on an upward secular trend, crises, declines, or even periods

of marasmus (trading) exist and are unpredictable in duration and intensity. Like

earthquakes, it is known for sure that they will happen, but not when and with what

strength.

Mathematics 2022, 10, 860 23 of 25

The comparison with poker is almost trivial. There are also people in the markets

who have different strategies, who try to manipulate the market, and who enter or exit

the investments in an unpredictable way compared to other participants.

Obviously, each individual transaction is part of a random walk of the fight between

bid and ask. However, just as obvious is that, overall, the market is moving in waves,

according to the Dow theory. The physical laws of the Brownian movement are known;

those of the capital markets remain to be determined.

There are no good or bad stocks; there are only appropriate entry/exit times in/from

the market. At different times, different stocks perform well or poorly; investors turn their

eyes from those that have already performed excellently to those that are lagging behind.

Over different periods, things happen similarly: some stocks rise thanks to speculators;

others grow more slowly, thanks to investors who capitalize them.

Financial bets are prohibited or restricted and cannot be “marketed” similarly to

sports betting. However, similar mathematical reasoning may be beneficial in estimating

future developments, provided that a system is found for assigning probabilities for

future quotations and performances. Moreover, the system is compatible with evaluation

theories, which recommend mediating the results of scenarios weighted with their

probability.

The extension of the approach for studying the applicability of the laws of physics,

chemistry, biology, etc. (not only mathematics) on the capital market is limited only by

the knowledge in the field and by interdisciplinary collaboration, which is increasingly

used in the contemporary sciences.

The methodology enriched in this paper deals with several themes and subjects

which had been treated into general shape, without entering into the minor details. It can

be noted that technical analyses also treat hundreds of graphical formations, indicators,

and oscillators, each with its own mentality and, in most cases, without any

interconnection between them. These features have not solely any yield but are correlated

and can lead to investment strategies and tactics of real success.

The article methodology proposes to review, evaluate, and assess a wide range of

ideas regarding the econophysics phenomenon which have not been explored in similar

academic papers. Any of these ideas can be extended and investigated in detail and/or

adapted. The presentation is general in nature in order to convey to the reader the basic

ideas for possible stock market theories that they may be interested in investigating in

detail. Some of these ideas, plus similar ones, will be developed further by the authors in

future papers. The scope of this paper is to encourage researchers to bend down upon

mathematical, physical, and engineering dedicated theories that can also be applied in

economics, especially on the stock market.

In conclusion, econophysics is the first step towards diversifying research directions.

The way we see the possibility of adopting new theories is the collaboration between

specialists from various fields of science and capital market practitioners. Take any

scientific field and you will find similarities with the stock exchange; you may even find

appropriate strategies.

Author Contributions: Conceptualization, F.T. and F.C.D.: design, F.T. and F.C.D.; data collection,

F.T. and F.C.D.; data analysis—development, F.T. and F.C.D.; data analysis—interpretation, F.T.

and F.C.D.; literature review, M.B. All authors have read and agreed to the published version of the

manuscript.

Funding: This research received no external funding.

Institutional Review Board Statement: Not applicable.

Informed Consent Statement: Not applicable.

Data Availability Statement: Not applicable.

Acknowledgments: The authors thank the anonymous reviewers and editor for their valuable

contribution.

Mathematics 2022, 10, 860 24 of 25

Conflicts of Interest: The authors do have not any competing financial, professional, or personal

interests from other parties.

References

1. Slanina, F. Essentials of Econophysics Modelling; Oxford University Press: Oxford, UK, 2014.

2. Peters, E.E. Fractal Market Analysis; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 1994.

3. Sergeev, V. The Thermodynamic Approach to Market; 2008. Available online: arXiv:0803.3432v1[physics.soc-ph] (accessed on 7

October 2017).

4. McCauley, J.L. Dynamics of Markets. Econophysics and Finance; Cambridge University Press: Cambriege, UK, 2004.

5. Richmond, P.J.; Mimkes, J.; Hutzler, S. Econophysics and Physical Economics; Oxford University Press: Oxford, UK, 2013.

6. Săvoiu, G. Econophysics. Background and Applications in Economics, Finance, and Sociophysics; Academic Press, Elsevier: Cambridge,

MA, USA, 2013.

7. Chakrabarti, B.K.A.; Chakrabortiand, A.C. Econophysics and Sociophysics. Trends and Perspectives; Wiley-VCH Verlag GmbH & Co.

KGaA: Weinheim, Germany, 2006.

8. Cockshott, W.P.; Cottrell, A.F.; Michaelson, G.J.; Wright, I.P.; Yakovenko, V.M. Classical Econophysics; Taylor & Francis Group,

Oxfordshire, UK, 2009.

9. Roehner, B.M. Patterns of Speculation. A Study in Observational Econophysics; Cambridge University Press: Cambriege, UK, 2002.

10. Preiss, T. Econophysics-complex correlations and trend switchings in financial time series. Eur. Phys. J.-Spec. Top. 2011, 194, 5–86,

doi:10.1140/epjst/e2011-01397-y.

11. Liang, Y.; Yang, G.; Huang, J.P. Progress in physical properties of Chinese stock market. Front. Phys. 2013, 8, 438–450,

doi:10.1007/s11467-013-0366-0.

12. Chakrabarti, A.; Toke, I.M.; Patriarca, M.; Aberger, F. Econophysics review: II. Agent-based models. Quant. Financ. Taylor Fr. 2011,

11, 1013–1041. https://doi.org/10.1080/14697688.2010.539249

13. Vasconcelos, G.L. A Guided Walk Down Wall Street: An Introduction to Econophysics. Braz. J. Phys. 2004, 34, 1039–1065.

14. Choi, J. Application of Physics and Geometry to Finance; 2014. Available online:

https://pdfs.semanticscholar.org/5784/6ba194cc0f664d0e547b85d8f1d3542ea256.pdf (accessed on 7.10.2017).

15. Forte, U. Econophysics: The Emergence of Complexity Patterns in a Stock Market Using Agent Based Models; 2017. Available online:

http://terna.to.it/tesineEconofisica/The%20emergence%20of%20complexity%20patterns%20in%20a%20stock%20market%20using

%20agent%20based%20models.pdf (accessed on 7.10.2017).

16. Swingler, A.J. An Econophysics Approach to Short Time-Scale Dynamics of the Equities Markets; 2017. Available online:

https://dukespace.lib.duke.edu/dspace/bitstream/.../Swingler_duke_0066D_14101.pdf? (accessed on 7.10.2017).

17. Bali, S. Econophysics, Thermoeconomics and Phynance. J. Int. Soc. Res. 2011, 4, 379–388.

18. Schafer, R. Econophysics: Quantitative Studies of Equity and Credit Markets; 2012. Available online: https://duepublico.uni-duisburg-

essen.de/servlets/DerivateServlet/Derivate-34569/Schaefer_Rudi_Habil.pdf (accessed on 7.10.2017).

19. Kakarot-Handtke, E. Toolism! A Critique of Econophysics; MPRA Paper No. 46630; 2013. Available online: http://mpra.ub.uni-

muenchen.de/46630/ (accessed on 7.10.2017).

20. Aamir, M.; Ali Shah, S.Z. Determinants of Stock Market Co-Movements between Pakistan and Asian Emerging Economies. J. Risk

Financ. Manag. 2018, 11, 1–14.

21. Ruan, L. Research on Sustainable Development of the Stock Market Based on VIX Index. Sustainability 2018, 10, 4113.

22. Nasr, A.B.; Cunado, J.; Demirer, R.; Gupta, R. Country Risk Ratings and Stock Market Returns in Brazil, Russia, India, and China

(BRICS) Countries: A Nonlinear Dynamic Approach. Risks 2018, 6, 1–22.

23. Kollintza-Kyriakoulia, F.; Maragoudakis, M.; Krithara, A. Measuring the Impact of Financial News and Social Media on Stock

Market Modeling Using Time Series Mining Techniques. Algorithms 2018, 11, 1–24.

24. Li., B.; Wu, K. The Price of Environmental Sustainability: Empirical Evidence from Stock Market Performance in China.

Sustainability 2017 9, 1452.

25. Drezewski, R.; Dziuban, G.; Pajak, K. The Bio-Inspired Optimization of Trading Strategies and its Impact on the Efficient Market

Hypothesis and Sustainable Development Strategies. Sustainability 2018, 10, 1460.

26. Paluch, M.; Jackowska-Strumillo, L. Hybrid Models Combining Technical and Fractal Analysis with ANN for Short-Term

Prediction of Close Values on the Warsaw Stock Exchange. Appl. Sci. 2018, 8, 2473.

27. Nguyen, T.T.; Yoon, S. A Novel Approach to Short-Term Stock Price Movement Prediction using Transfer Learning. Appl. Sci. 2019,

9, 4745.

28. Herzog, B.; Osamah, S. Reverse Engineering of Option Pricing: An AI Application. Int. J. Financ. Stud. 2019, 7, 1–12.

29. Nayan, S. The Influence of Domestic and Foreign Shocks on Portfolio Diversification Gains and the Associated Risks. J. Risks Financ.

Manag. 2019, 12, 1–26.

30. Arendas, P.; Kotlebova, J. The Turn of the Month Effect on CEE Stock Markets. Int. J. Financ. Stud. 2019, 7, 1–19.

31. Zakaria, N.N.; Othman, M.; Sokkalingam, R.; Daud, H.; Abdullah, L.; Kadir, E.A. Markov Chain Model Development for

Forecasting Air Pollution Index of Miri, Sarawak. Sustainability 2019, 11, 5190.

32. Thu Truong, T.T.; Kim, J. Premium for Non-Sustainable and Sustainable Components of Market Volatility: Evidence from the

Korean Stock Market. Sustainability 2019, 11, 5123.

Mathematics 2022, 10, 860 25 of 25

33. Blackledge, J.; Kearney, D.; Lamphiere, M.; Rani, R.; Walsh, P. Econophysics and Fractional Calculus: Einstein’s Evolution

Equation, the Fractal Market Hypothesis, Trend Analysis and Future Price Prediction. Mathematics 2019, 7, 1057.

34. Wang, G.J.; Xie, C.; Chen, Y.J.; Chen, S. Statistical Properties of the Foreign Exchange Network at Different Time Scales: Evidence

from Detrended Cross-Correlation Coefficient and Minimum Spanning Tree. Entrophy 2013, 15, 1643–1662.

35. Zanin, M.; Zunino, L.; Rosso, O.A.; Papo, D. Permutation Entropy and Its Main Biomedical and Econophysics Application: A

Review. Entropy 2012, 14, 1553–1577.

36. Fry, J.; Brint, A. Bubbles, Blind-Spots and Brexit. Risks 2017, 5, 1–15.

37. Ahmad, N.; Raheem Ahmed, R.; Streimikiene, D. Empirical Analysis of Stock Returns and Volatility: Evidence from Asian Stock

Markets. Technol. Econ. Dev. Econ. 2016, 22, 808–829, doi:10.3846/20294913.2016.1213204.

38. Rudzikis, R.; Valkaviciene, R. Econometric Models for the Impact of Macroeconomic Processes on the Stock Market in Baltic

Countries. Technol. Econ. Dev. Econ. 2014, 20, 783–800, doi:10.3846/20294913.2014.949901.

39. Vveinhardt, J.; Streimikiene, D.; Rizwan, A.R.; Nawaz, A.; Rehman, A. Mean Reversion: An Investigation from Karachi Stock

Exchange Sectors. Technol. Econ. Dev. Econ. 2016, 22, 493–511, doi:10.3846/20294913.2016.1181685.

40. Ruxanda, G.; Badea, L.M. Configuring Artificial Neural Networks for Stock Market Predictions. Technol. Econ. Dev. Econ. 2014,

20, 116–132, doi:10.3846/20294913.2014.889051.

41. Garcia, F.; Guijarro, F.; Oliver, J.; Tamosiuniene, R. Hybrid Fuzzy Neural Network to Predict Price Direction in the German

DAX-30 Index. Technol. Econ. Dev. Econ. 2018, 24, 2161–2178. https://doi.org/10.3846/tede.2018.6394.

42. Ahmed, R.R.; Vveinhardt, J.; Streimikiene, D.; Ghauri, S.P.; Ashraf, M. Stock Returns, Volatility and Mean Reversion in

Emerging and Developed Financial Markets. Technol. Econ. Dev. Econ. 2018, 24, 1149–1177.

https://doi.org/10.3846/20294913.2017.1323317.

43. Janda, K.; Rausser, G.; Svarovska, B. Can Investment in Microfinance Funds Improve Risk-Return Characteristics of a

Portfolio?” Technol. Econ. Dev. Econ. 2014, 20, 673–695, doi:10.3846/20294913.2013.869514.

44. Ulusoy, T.; Kekin, M.; Shirvani, A.; Deviren, B.; Kantar, E.; Donmez, C.C. Complexity of Major UK Companies between 2006

and 2010: Hierarchical Structure Method Approach. Phys. Stat. Mech. Appl. 2012, 391, 5212–5131.

45. Ulusoy, T. Price Fluctuations in Econophysics. In Global Financial Crises and its Ramifications on Capital Markets; Hacioglu, U.,

Dincer, H., Eds. Springer Cham: Cham, Switzerland, 2017; pp. 459–474.

46. Garcia, M.D.L.N.L.; Requena, J.P.R. Different Methodologies and uses of the Hurst Exponent in Econophysics. Stud. Appl. Econ.

2019, 37, 96–108.

47. Jewson, S.; Brix, A. Weather Derivative Valuation. The Meteorological, Statistical, Financial and Mathematical Foundations; Cambridge

University Press: Cambriege, UK, 2005.

48. Alexandridis, A.K.; Zapranis, A.D. Weather Derivatives. Modeling and Pricing Weather-Related Risk; Springer Science & Business

Media: New York, NY, USA, 2013.

49. Tsinaslanidis, P.E.; Zapranis, A.D. Technical Analysis for Algorithmic Pattern Recognition; Springer International Publishing:

Switzerland, doi:10.1007/978-3-319-23636-0.

50. Purdy, D. The Illustrated Guide to Texas Hold’em; Sourcebooks, Inc.: Naperville, IL, USA, 2005.

51. Prokopczuk, M.; Rachev, S.; Trück, S. Quantifying Risk in the Electricity Business: A RAROC-Based Approach; 2004. Available online:

http://www.pstat.ucsb.edu/about/research/papers/report10_2004%5b1%5d.pdf (accessed on 7.10.2017).

52. Mandelbrot, B.B.; Hudson, R.L. The (mis)Behavior of Markets; Basic Books: New York, NY, USA, 2004.

53. Murphy, J.J. Technical Analysis of the Financial Markets; New York Institute of Finance: New York, NY, USA, 1999.

54. Rossi, E.; Forte, G. Assessing Relative Valuation in Equity Markets; Palgrave Macmillan: London, UK, 2016.

55. Pesavento, L. A Trader’s Guide to Financial Astrology. Forecasting Market Cycles Using Planetary and Lunar Moments; John Wiley &

Sons, Inc.: Hoboken, NJ, USA, 2015.

56. Grover, J. Strategic Economic Decision-Making; New York Springer Science and Business Media: New York, NY, USA, 2013.

57. Tijms, H. Surprises in Probability. Seventeen Short Stories; CRC Press Taylor & Francis Group: Boca Raton, FL, USA, 2019.

Top Related

Copyright © 2022 FDOKUMEN