Bahasa

Halaman

Hukum

Bank Activities in Gas, Power and CoalIn collaboration with Utility Trading

Lionel GreeneDerivatives & Options Trading

Jun 2010

2

Bank activities in Gas, Power and CoalIn collaboration with Utility Trading

3Nature of the Commodities

Natural Gas

Power

Coal

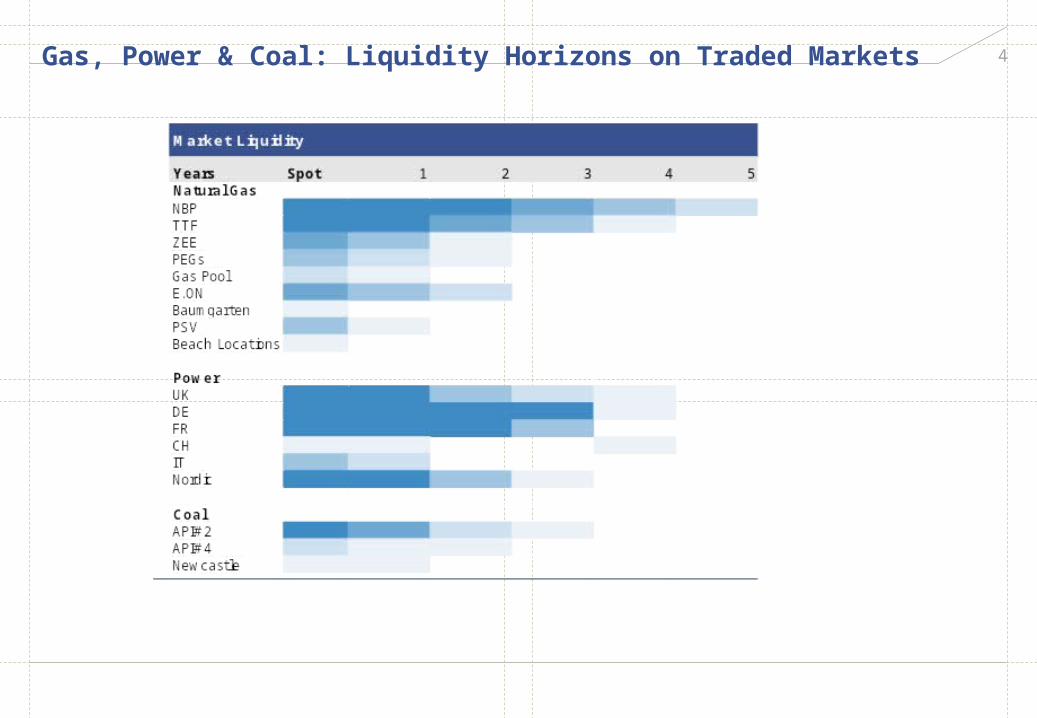

4Gas, Power & Coal: Liquidity Horizons on Traded Markets

5Physical Commodities

As with any physical commodity that has independent value apart from its investment value, the markets involve three sets of activities: Production, distribution, and consumption. Those activities give rise to several types of services. E.g., distribution in gas markets involves moving physical gas from the wellhead, through the gathering system, to a processing facility, and then on through the main line to receipt points-with possible stops along the way at storage facilities for balancing purposes. Before deregulation, this complex activity was often managed by one entity that had control over a significant portion of the local distribution system. Naturally, this arrangement led to concerns about monopoly power and resulted in heavy regulation that both controlled and sustained the problem. Concerns about the enormous inefficiency of this situation led to the onset of deregulation. The process has entailed two things. An often forced unbundling of the services and the creation of markets to mediate the provision of the services

The extent of deregulation varies with commodities and locations. The degree to which the interaction among the components of the value chain is handled through markets or by public utilities also varies considerably

The organisation details of the physical markets have a substantial impact on the workings of the corresponding forward and derivative markets. Given the complexity of some of those markets, a perfect example is the electricity market that trades several cash products, understanding the interaction of optionality, risk, and expectations within and between different markets presents a challenge that should not be underestimated

6Energy Derivatives

A number of energy derivative products cannot be found in any other markets. For example, various volumetric options, such as swing, recalls and nominational which have been developed to manage risks associated with meeting the demand in natural gas or power have no parallel in financial markets. Similarly exceptional are all kinds of load serving structures There are standard products-futures, forwards, swaps options. But even they have unique features due to their predominantly physical nature. They settle differently and are defined differently. Even the commodities underlying these products are different Electricity seems like a perfect commodity, since all electrons are naturally identical, but the impression is deceptive. Power delivered at any particular hour, block of hours, day, week, month and so on, represents a different commodity because electricity cannot be stored and thus must be studied independently Non-storability of power is also a reason why most of the well known financial theories may not be applicable to electricity derivatives. Finally, energy derivatives include structures whose complexity may surpass anything that one encounters elsewhere, namely, energy assets, such as power plants and gas storage. These assets are equivalent to a complex portfolio of options whose definition requires understanding of a great variety of economic, operational, regulatory and other issuesThe complex features of energy derivatives are neither artificial nor avoidable but a natural consequence of the needs and challenges of the energy markets

7The Traded Market and Instruments

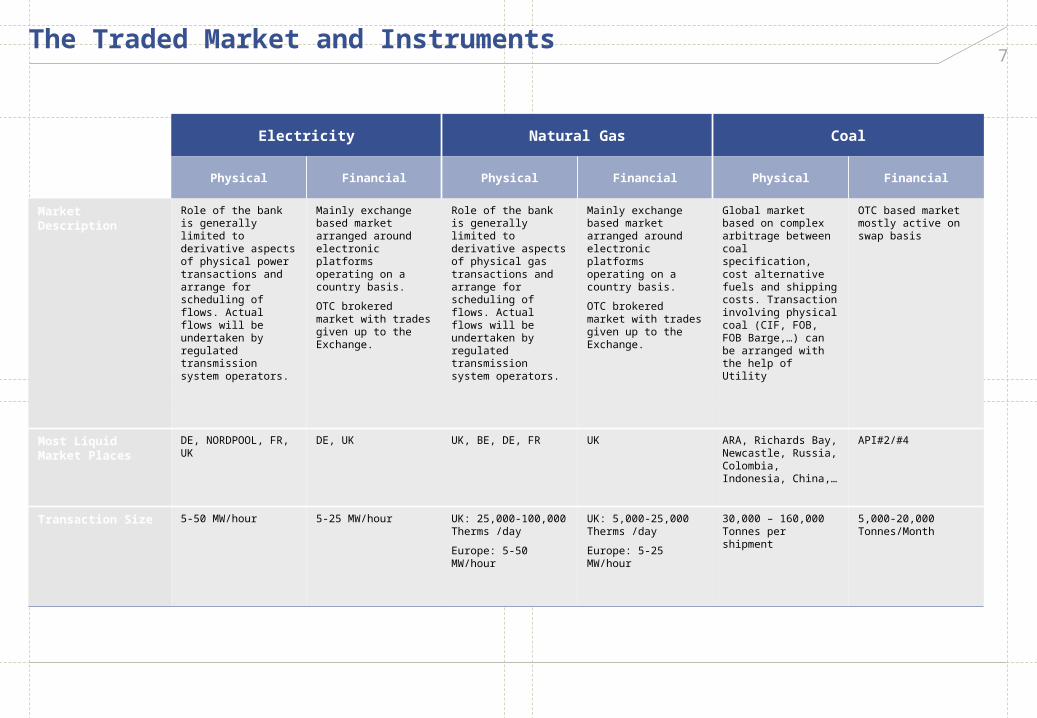

Electricity Natural Gas Coal

Physical Financial Physical Financial Physical Financial

Market Description

Role of the bank is generally limited to derivative aspects of physical power transactions and arrange for scheduling of flows. Actual flows will be undertaken by regulated transmission system operators.

Mainly exchange based market arranged around electronic platforms operating on a country basis.OTC brokered market with trades given up to the Exchange.

Role of the bank is generally limited to derivative aspects of physical gas transactions and arrange for scheduling of flows. Actual flows will be undertaken by regulated transmission system operators.

Mainly exchange based market arranged around electronic platforms operating on a country basis.OTC brokered market with trades given up to the Exchange.

Global market based on complex arbitrage between coal specification, cost alternative fuels and shipping costs. Transaction involving physical coal (CIF, FOB, FOB Barge,…) can be arranged with the help of Utility

OTC based market mostly active on swap basis

Most Liquid Market Places

DE, NORDPOOL, FR, UK

DE, UK UK, BE, DE, FR UK ARA, Richards Bay, Newcastle, Russia, Colombia, Indonesia, China,…

API#2/#4

Transaction Size 5-50 MW/hour 5-25 MW/hour UK: 25,000-100,000 Therms /dayEurope: 5-50 MW/hour

UK: 5,000-25,000 Therms /dayEurope: 5-25 MW/hour

30,000 – 160,000 Tonnes per shipment

5,000-20,000 Tonnes/Month

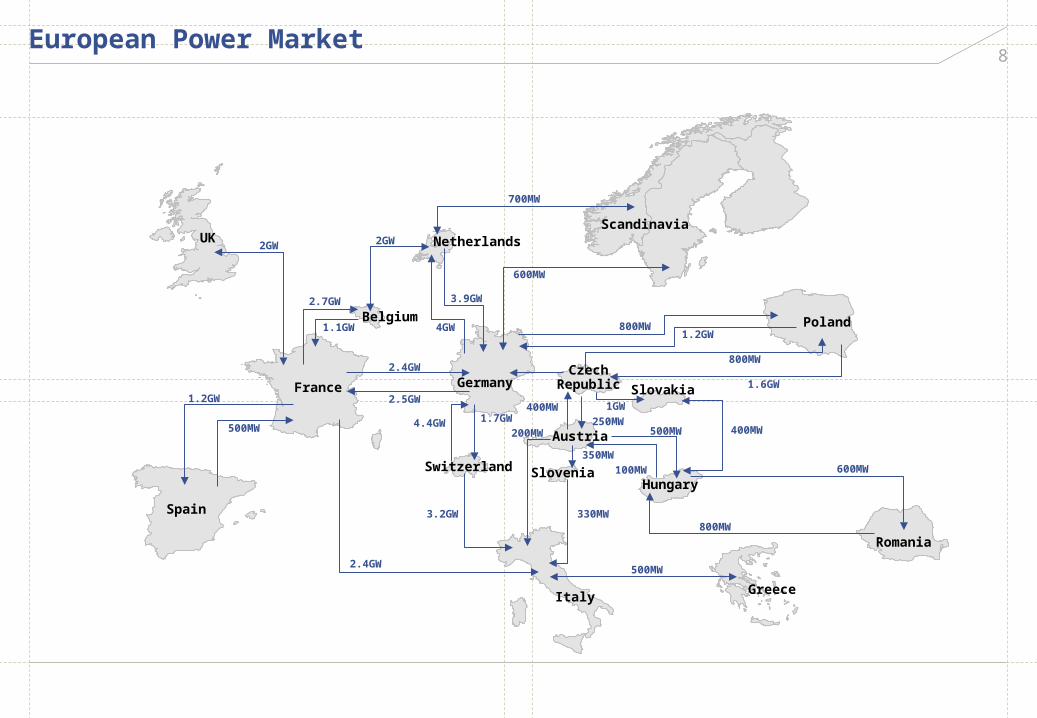

8European Power Market

2GWUK

Spain

France Germany

Switzerland

Italy

Slovenia

Austria

Hungary

SlovakiaCzech

Republic

Poland

Greece

Romania

ScandinaviaNetherlands

Belgium

1.2GW

500MW

2.4GW

2.5GW

2.4GW

2.7GW

1.1GW

2GW

700MW

3.9GW

4GW

600MW

800MW 1.2GW

800MW

1.6GW

1GW250MW

400MW

350MW

200MW

330MW3.2GW

4.4GW 1.7GW

600MW

800MW

500MW

400MW500MW

100MW

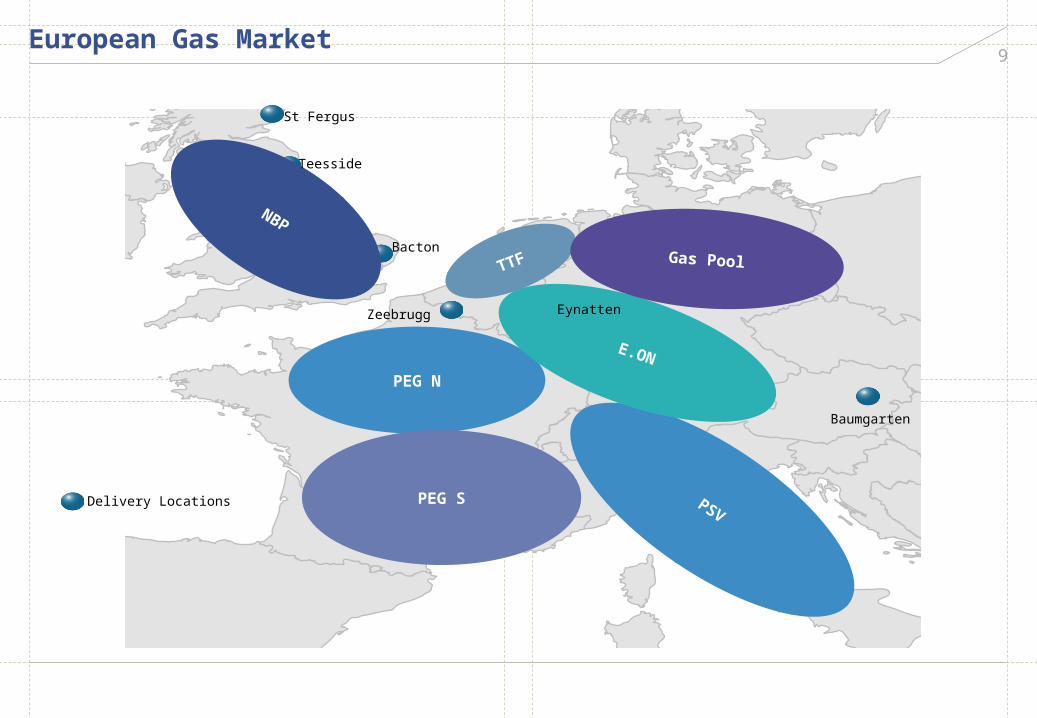

9European Gas Market

NBP

PEG N

PEG S PSV

E.ON

TTF

St Fergus

Teesside

Bacton Oude / Bunde

EynattenZeebrugg

Baumgarten

Delivery Locations

Gas Pool

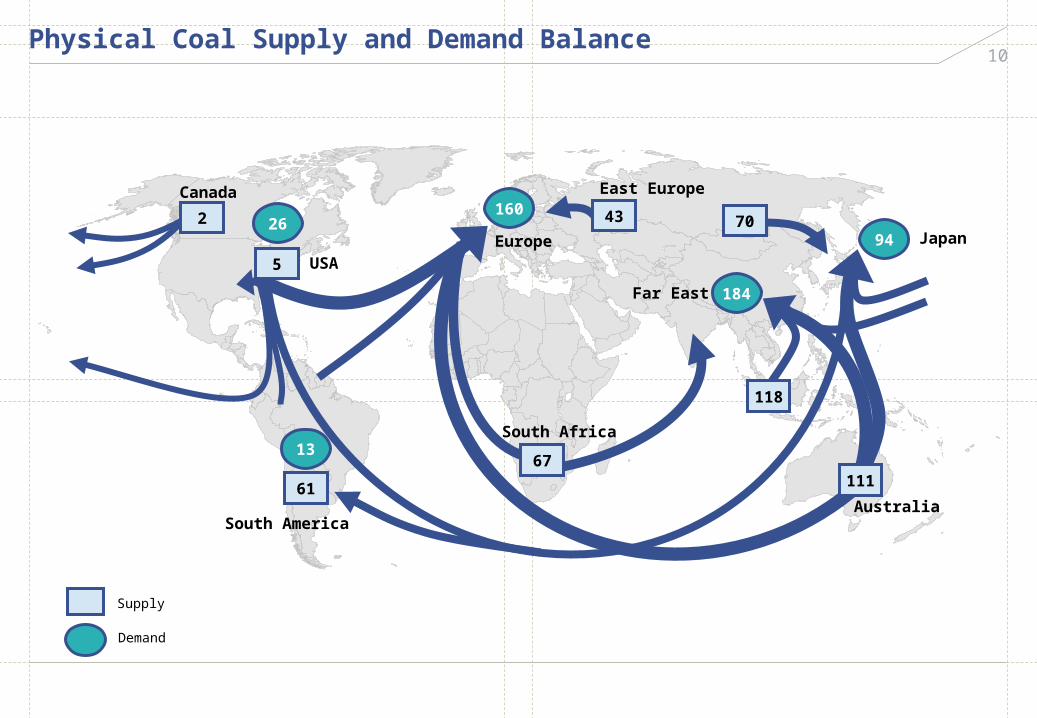

10Physical Coal Supply and Demand Balance

2

5

43 70

67111

118

160

13

61

26

184

94

Australia

Japan

Far East

South Africa

South America

USA

Canada

Europe

East Europe

Demand

Supply

11Natural Gas

The main factors affecting demand for natural gas are the Industrial customers, residential and commercial customers and electricity generation. The heaviest residential consumption is during the winter months for home heating, reflected in the relatively high winter prices and low summer prices. It’s worth noting that the relative consumption of natural gas in summer and winter might be affected in the future by the growing stock of gas-powered electrical generation

There are five categories of market participants:Gas producersPipeline companiesLocal delivery companiesConsumersMarketers

The first four market players have well defined roles along the value chain of the industry. Marketers serve as intermediaries, managing the interactions of the other parties.

12Natural Gas Market

The natural gas market is a collection of locations at which the delivery and receipt of the commodity takes place. The participating parties contract for two services.

Delivery and receipt of natural gas at a given locationTransportation of natural gas between two different locations

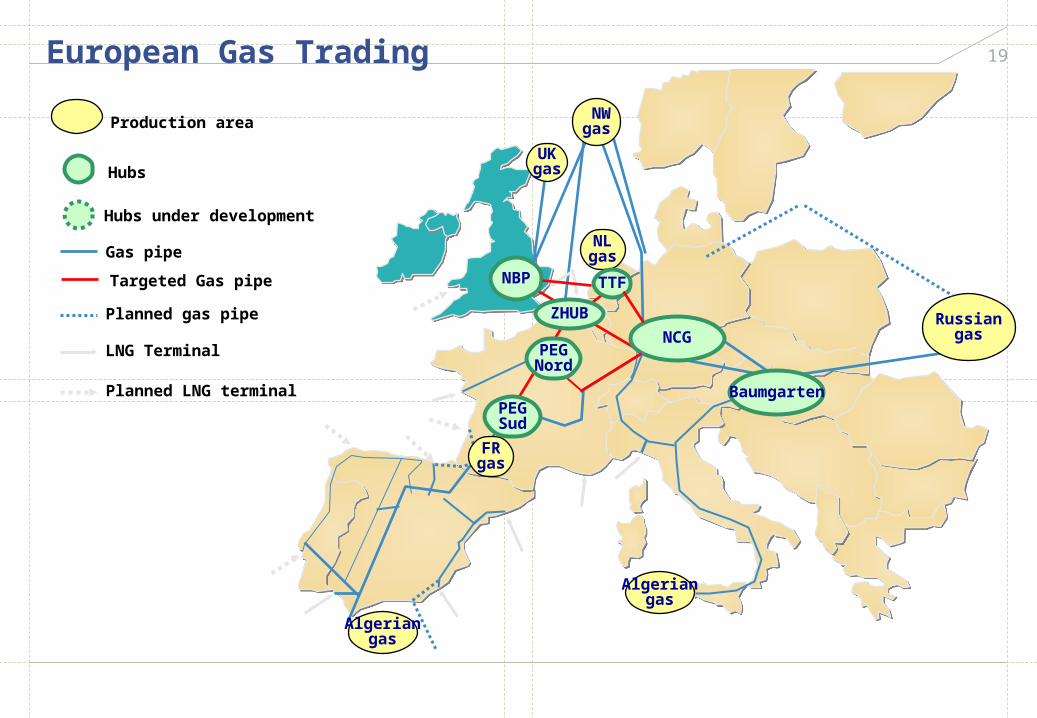

Depending on their position in the pipeline system, these locations experience different volumes of transactions. Some locations have developed into significant trading hubs. The main European trading hubs are UK NBP, Zeebrugge, Netherlands TTF

13Natural Gas UK NBP

The National Balancing Point, commonly referred to as the NBP, is a virtual trading location for the sale and purchase and exchange of UK natural gas. It is the pricing and delivery point for the ICE (IntercontinentalExchange) natural gas futures contract

It is the most liquid gas trading point in Europe and is a major influence on the price that domestic consumers pay for their gas at home. Gas at the NBP trades in pence per therm

It is similar in concept to the Henry Hub in the United States - but differs in that it is not an actual physical location

Unlike continental European trading hubs such as Zeebrugge and TTF, trades made at the NBP are not required to be balanced, and there is no fixed penalty for being out of balance. Instead, shippers out of balance at the end of the day are automatically balanced through the 'cash-out' procedure whereby the shipper is automatically made to buy or sell the required quantity of gas to balance their position at the marginal system buy or sell price for that day. This cash out process is not considered to be a penalty in the same way as those imposed on shippers in continental markets, because the cash-out prices are often very close to the spot price. As a result of this daily market liquidity, the UK's NBP is frequently used to balance a shipper's position on the continent by way of the Bacton - Zeebrugge interconnector

14Natural Gas UK NBP 1

National Grid plc is the network operator in Great Britain. They are responsible for the physical transportation of gas, as shippers are required only to nominate quantities entering and/or exiting the network, and not the transport route which the gas should physically follow. The National Grid has the power to bring the system into balance, if shippers as a whole are out of balance. This is achieved by trading on the OCM (see below) and passing the cost onto gas shippers through the cash-out system. When the system is short of gas it tends to force prices at the NBP up. When the system is long gas, the price is forced down. This can provide an advantageous trading environment to a shipper which has flexible flow contracts

Trades at the NBP are made via the OCM trading system, an anonymous trading service managed by APX-ENDEX to which offers or requests for gas at a nominated price can be posted. The minimum amount of gas that may be traded on the OCM is 4,000 therms, so if a shipper's position is long or short by a volume less than 4,000 therms they may be forced simply to leave their balance to cash out

15Natural Gas Zeebrugge Hub

The Zeebrugge Hub is the natural gas trading point in Belgium. It is connected to the National Balancing Point (UK) via the InterconnectorThe Zeebrugge Hub is a so-called physical hub, with natural gas made available from delivery borders in the Zeebrugge area, the nearby LNG terminal or the Belgian marketOptimum flexibility is the key strength of the Zeebrugge Hub: any gas traded at the hub can either be re-traded or shipped through the network of Belgian TSO Fluxys. Through the Fluxys system gas can be delivered into the Belgian market or at one of the borders for onward transmission in any direction throughout EuropeThe Zeebrugge area is considered to be the most important natural gas landing point in the EU27. Connecting to a variety of pipe gas and LNG sources, the Zeebrugge area has an overall throughput capacity of about 48 bcm/y. This corresponds with roughly 10% of the border capacity needed to supply the EU27As for pipe gas flows, the Zeebrugge area gives access to natural gas from Norwegian and British offshore production fields in the North Sea as well as from Germany and RussiaWorldwide LNG supply is available through the Zeebrugge LNG terminal. The terminal has three primary shippers and standard provisions are in place to facilitate spot LNG deliveries

16Natural Gas Netherlands TTF

The Title Transfer Facility, more commonly known as TTF, is a virtual trading point for natural gas in the Netherlands. Set up by Gasunie in 2003, it is almost identical to the National Balancing Point (NBP) in the United Kingdom and allows gas to be traded within the Dutch network. The TTF is operated by an independent subsidiary of Gasunie, Gas Transport Services B.V. Physical short-term gas trading is handled by APX Gas NL B.V. and gas futures contracts are traded through Endex N.V.

Gas at TTF usually trades in euros per megawatt hour.

17Natural Gas Delivery

Three are three types of transactions commonly govern delivery of natural gas, namely Baseload Firm, Baseload Interruptible, Swing

Baseload FirmIn this transaction the delivering party is expected to perform according to the contract under any conditions (with the exception of force majeure). Liquidated damages and financial penalties are imposed for non-performance.

Baseload InterruptibleDelivery can be interrupted; interruptibility conditions may or may not be specified in the contract.

SwingThe volume of gas is adjusted daily at the buyer’s discretion. Swing contracts are typically used for daily pipeline volume balancing requirements

18Natural Gas Transportation

Natural gas transportation transactions have similar contractual provisions. There are two categories of the transportation services

Firm Transportation Service (FTS). The highest priority service

Interruptible Transportation Contract. Under this contract a pipeline has an option to interrupt the service on short notice without a penalty. The interruption generally occurs in peak-load seasons as a result of demands from firm service customers. Although most of the firm capacity is subscribed, there is an active “secondary market” trading this capacity. When the holder of the firm space on a pipeline sells some of the capacity, the transaction is referred to as capacity release.

19

Hubs under development

Gas pipe

Hubs

European Gas Trading

Planned gas pipe

LNG Terminal

Planned LNG terminal

UKgas

NBP

NLgas

Algeriangas

Algeriangas

RussiangasNCG

Baumgarten

TTF

NWgas

ZHUB

PEGNord

Production area

FRgas

PEGSud

Targeted Gas pipe

20Power Markets

The design of efficiently functioning electricity markets has proven to be a challenging undertaking. The physical characteristics of the commodity are quite unlike those in the fuel markets. On of the crucial features of electricity markets-and one that differentiates it from other commodity markets-is the need for real time balancing of locational supply and demand. This requirement flows from the technological characteristics of supply and distribution. Since electricity cannot be stored, instantaneous supply and demand must always be in balance; otherwise the integrity of the whole system might be compromised. This peculiar feature of the electricity markets introduces the need for an additional set of services beyond production and distribution: balancing and reserve resources. Therefore, the supply of electricity involves three types of activities:

Generation TransmissionAncillary services (balancing)

Around the world, there are considerable differences in the extent to which these activities are mediated through markets and/or public utilities

The common feature of virtually all solutions is the presence of an independent system operator (ISO), which maintains the system. The services can be managed by either a highly centralised market under the control of the ISO or through a sequence of bilateral markets, with the ISO only playing a limited role as a sole buyer of some of the services

The solutions includes a system where the ISO manages provision, contracting and infrastructure for all the activities of the electricity markets-generation transmission and balancing. In other markets, the ISO is mainly involved in the procurement of generation while transmission is left to bilateral markets with only a rudimentary presence of the ISO as the buyer of the final product. Finally, some markets are purely bilateral, with only a symbolic presence of the system operator

21Power Ancillary Services

In electricity markets, instantaneous supply and demand must always be in balance; otherwise the integrity of the whole system might be compromised. This creates the need to hold reserves to balance instantaneous variations in load. The way this need is handled depends on the market design. In some regions the need is satisfied by requiring generators to withhold part of their generation capacity of committed units for the so called spinning reserve. In practice this means that a generation unit does not ramp up to full capacity unless called upon by the market administrators (ISOs) to help balance the system in a contingency

Another solution is to create a market that supplies those services. A number of pool markets use this method. In the market-based scheme, the generators have a choice of committing their available capacity either to the energy market or to one of the ancillary services markets

In some regions, ancillary services markets are composed or as many as seven products. A typical list includes:

Spinning reserves: Resources synchronised to the system that are available immediately and that can be brought to full capacity within 10minsNon-spinning reserves: Resources not synchronised to the system that are available immediately and can be brought to full capacity within 30minsEnergy balance: Resources needed for correcting supply/demand imbalancesRegulation: Reactive energy to maintain the phase angle of the systemReactive power supply: Services to maintain voltage of the transmission line, as such it is locationally specific

22Power Primary Market Structures

The cash markets takes on two contracting structures: Pools and bilateral marketsPools

The main characteristics of the pool market is the formal establishment of the market (system) clearing price at which all cash (energy) transactions clear. Examples include the Nordic Power Exchange (Nord Pool), European Energy Exchange (EEX), POWER NEXT

Bilateral MarketsAll transactions are entered into by two parties and are independent on any other transactions in the market. Examples include the UK power market

The products offered by pool markets vary widely from market to market. Several markets trade the main energy cash products as well as the ancillary services

The different energy cash markets areDay-ahead. This market transacts for generation of energy the next day. Every hour is transacted separately. In some markets, the structure of the bid is very simple; in other markets start-up and no-load bids can also be transactedWithin-day. This market transacts for generation of energy within the day. Every hour is transacted separately

23Power Forward Markets

Forward markets are markets in which the parties contract for the delivery of energy in the future. The future in question can be near (e.g. balance-of-week and balance-of-month) or quite far (e.g. monthly forward contracts that cover periods months or even years into the future). The forward markets take on three basic forms:

Bilateral or Broker-based (Over-the-Counter). The trading involves either direct contact between two parties or contact mediated by a broker (possible an electronic broker like InterContinental Exchange, voice brokers or hybrid voice/electronic platform brokers)Market Maker based. The trading is centered around a market maker who posts two-sided (for buying and selling) quotes, stands behind every transaction, and can carry inventory (examples include Essent Xpress)Exchange-based. The trading centres around a central exchange that matches up buyers and sellers and guarantees the performance of the transactions without taking an outright position and carrying inventory (EEX, ICE)Frequently encountered power products includeBaseload : Power delivered 24/7 every dayPeak: Power delivered 08:00-20:00 week daysOff peak: Power delivered 20:00-08:00 week days and 24/7 weekendsShaped blocks: Power delivered to a profile specified by the customer

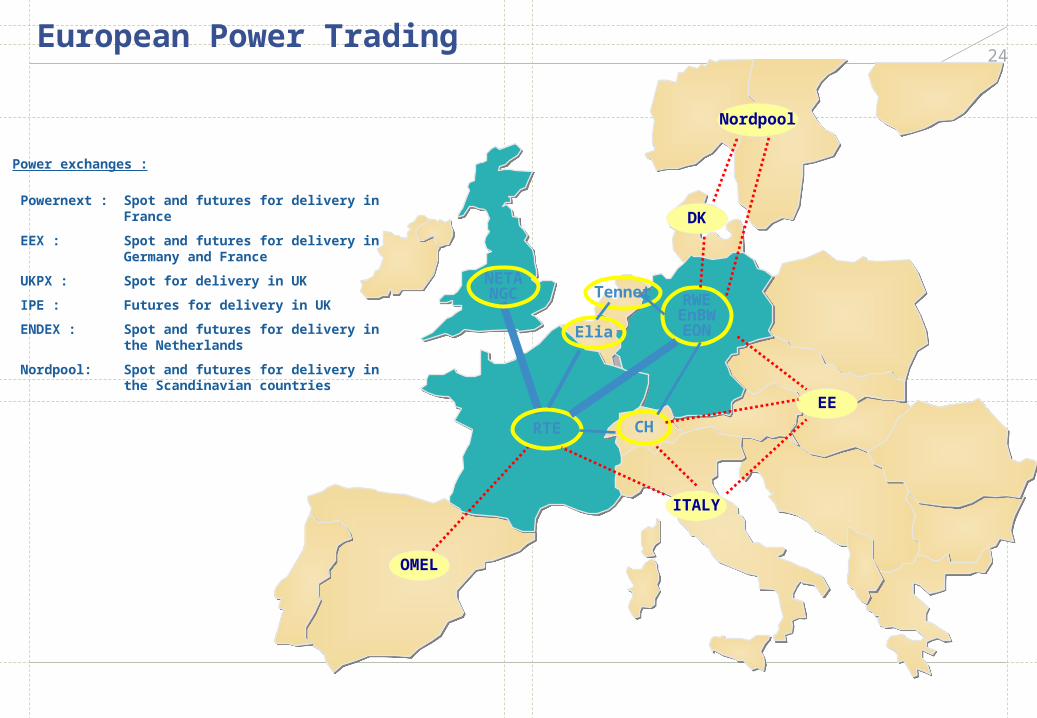

24European Power Trading

RTE

OMEL

NETANGC RWE

EnBWEON

ITALY

EECH

Tennet

Nordpool

DK

Elia

Power exchanges :

Powernext : Spot and futures for delivery in France

EEX : Spot and futures for delivery in Germany and France

UKPX : Spot for delivery in UKIPE : Futures for delivery in UKENDEX : Spot and futures for delivery in

the NetherlandsNordpool: Spot and futures for delivery in

the Scandinavian countries

25Coal

Coal is a global industry, with cola mined commercially in over 50 countries and used in over 70. Cola is readily available from a wide variety of sources in a well-supplied market. Coal can be transported to demand centres quickly, safely and easily by ship and rail. A large number of suppliers are active in the international coal market, ensuring a competitive and efficient market

The way that coal is transported to where it will be used depends on the distance to be covered. Coal is generally transported by conveyor or truck over short distances. Trains and barges are used for longer distances within domestic markets, or alternatively coal can be mixed with water to form a coal slurry and transported through a pipeline

Ships are commonly used for international transportation, in sizes ranging from:Handysize vessel of about 40-60,000 DWTPanamax vessel of about 60-80,000 DWT (Technically the maximum size vessel that can transit the Panama Canal)Capesize 80,000 DWT (A ship which is too large to transit the Panama Canal and thus has to sail via Cape of Good Hope from Pacific to Atlantic and vice versa)DWT - Deadweight Tonnes – deadweight capacity of vessel comprising cargo, bunker fuel, fresh water, stores, etc

Coal is traded all over the world, with coal shipped huge distances by sea to reach markets.Over the last twenty years

seaborne trade in steam coal has increased on average by about 7% each year seaborne coking coal trade has increased by 1.6% a year

26Coal trade

Overall international trade in coal reached 937Mt in 2008; while this is a significant amount of coal it still only accounts for about 16% of total coal consumed. Most coal is used in the country in which it is producedTransportation costs account for a large share of the total delivered price of coal, therefore international trade in steam coal is effectively divided into two regional marketsthe Atlantic market, made up of importing countries in Western Europe, notably the UK, Germany and Spain. the Pacific market, which consists of developing and OECD Asian importers, notably Japan, Korea and Chinese Taipei. The Pacific market currently accounts for about 57% of world seaborne steam coal tradeAustralia is the world’s largest coal exporter. It exported over 252Mt of hard coal in 2008, out of its total production of 325Mt. International coking coal trade is limited. Australia is also the largest supplier of coking coal, accounting for 53% of world exports. The USA and Canada are significant exporters and China is emerging as an important supplierCoal has many important uses worldwide. The most significant uses are in electricity generation, steel production, cement manufacturing and as a liquid fuel. Around 5.8 billion tonnes of hard coal were used worldwide last year and 953 million tonnes of brown coal. Since 2000, global coal consumption has grown faster than any other fuel. The five largest coal users - China, USA, India, Japan and Russia - account for 72% of total global coal useDifferent types of coal have different uses. Steam coal - also known as thermal coal - is mainly used in power generation. Coking coal - also known as metallurgical coal - is mainly used in steel production

27Basic Products and Structures

Futures, forwards, swaps and options are the most frequently used risk management tools. The popularity of these contracts stems form the facts that they are standardised, well understood and are, without exception, the most liquid instruments available to a risk manager

The main exchanges for futures trading are ICE, EEX, Nordpool

Specs for Phelix Baseload Cal-2011 futures contract on EEXContract: Future on the average of all prices in the hourly auction on the Power Spot Market price (Phelix)Contract size: 8760 MWhPrice quote: Eur/MWhDelivery: Cash Settlement

Specs for UK natural gas futures on ICEContract: Natural gas supplied to the British Gas Tran Co, the pipeline operator, to the National Balancing Point (NBP), the central locationContract size: 1000 therms per calendar dayPrice quote: pence/thermDelivery: Physical, made each day during the contract period

28Swaps/Forwards

Swaps in energy similar to swaps in financial markets and are natural generalisations of forward contracts (which themselves can be viewed as a one-period swap). The most frequently encountered is a fixed-price swap in which for a specified period one counterparty pays another a fixed payment and in exchange receives a payment linked to a certain floating index. He fixed period can be the same every period or vary according to a specified schedule. The floating period is typically connected to a commodity spot price or price index. The floating price is typically averaged

Typical examples of indices are:ICEEEXPlattsHerenArgus

29Options

There is not much difference between calls and puts in energy markets and calls and puts in other markets. What sets them apart is an unusual diversity of traded energy options, a natural consequence of the diversity in the underlying commodity, especially power. Option can be physical delivery or financial dependent on the same indices as used for the Swaps. Typically energy options include

LocationExercise timeDelivery conditionsStrikeVolume

Options can be:Hourly exercise, day-ahead notificationDay-ahead exerciseWeekly exerciseMonthly, Quarterly, Seasonal or Yearly exercise.

30Swing Options

A swing option grants the option holder the right to take/give . . .A volume of some specified productWith a volume ‘swing’ between some minimum and maximum volumeWithin some defined time periodAt some pre-agreed price

This option structure was developed in response to hedging and operation needs for volumetric exposure

The technology involved in the pricing swing options is very useful for the valuation and risk management of such corporate assets as ‘Take-or-Pay’ contracts, Hydro plants, Storage facilities, constrained(CO2/NO2) thermal power plants, etc

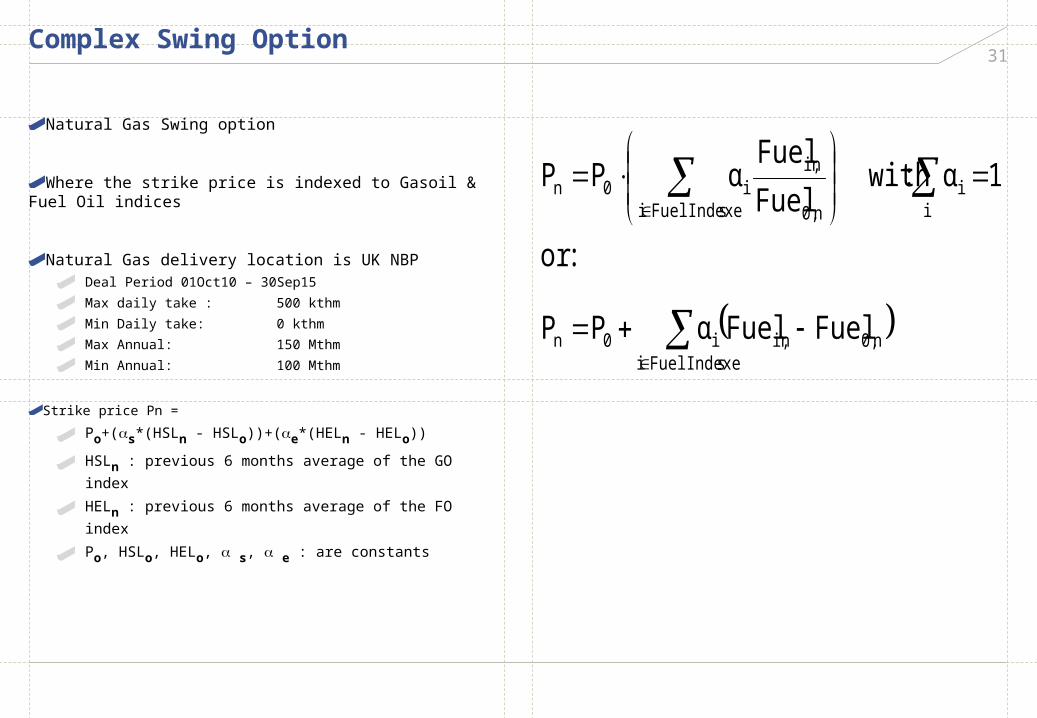

31Complex Swing Option

Natural Gas Swing option

Where the strike price is indexed to Gasoil & Fuel Oil indices

Natural Gas delivery location is UK NBPDeal Period 01Oct10 – 30Sep15Max daily take : 500 kthmMin Daily take: 0 kthmMax Annual: 150 MthmMin Annual: 100 Mthm

Strike price Pn =Po+(s*(HSLn - HSLo))+(e*(HELn - HELo))HSLn : previous 6 months average of the GO indexHELn : previous 6 months average of the FO indexPo, HSLo, HELo, s, e : are constants

FuelFuelαPP

:or

1α : withFuelFuelαPP

sFuelIndexein0,ni,i0n

ii

sFuelIndexei n0,

ni,i0n

32‘ark Spread

Differential between the price of electricity (output) and the price of it’s primary fuels (inputs)

Primary fuels are natural gas, coal, oil and uranium.

The dark spread between electricity coal and the spark spread between electricity and natural gas are the most common

‘ark spreads and options on ‘ark spreads are traded OTC

The ‘ark spread can be used to financially replicate the physical reality of a power plant. Merchant plants can use the ‘ark spread to lock into their production margin

33Spread Options

It is impossible to underestimate the significance of spread options in the energy markets, Practically every energy asset and every structured deal has a spread option embedded in it

By definition, a spread option is an option on a spread, that is an option holder has the right but not the obligation to enter into a forward or spot spread contract

Spread options are in turn a subset of basket options and the technology for pricing and risk managing these products are essentially the same

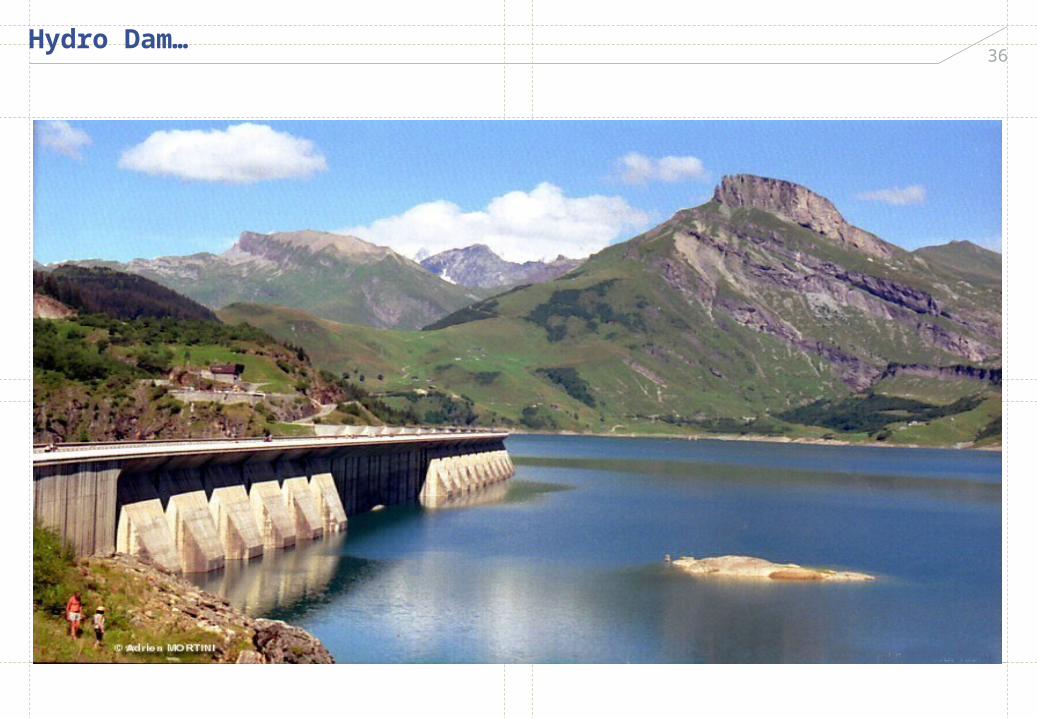

34Hydro Plant Pricing

A generic Hydro plan is defined byStart/End water levelRate of inflow/outflowMin/max dam capacityCoefficient of efficiencyVariable costsMin/max generation level

Hydro plants are priced in our theoretical framework using the American monte-carlo technique due to the early exercise feature and the high dimensionality of the problem

35Hydro Dam

36Hydro Dam…

37Power Plants

It is not difficult to see that in principle a merchant power plant is a spread option

That is an option between on the spread between the power and fuel prices

If P is the spot price of power, G is the price of fuel, HR is the heat rate and V is the variable cost of running the plant (ex-fuel), then the decision to run or not to run the plant is straightforward

Consider two cases1. If P –HR*G – V > 0, run the plant2. If P – HR*G –V <= 0, do not run the plant

38Thermal Plant Pricing

A generic Thermal plan is defined byInput fuel priceHeat rate/EfficiencyStart-up/shut-down costsRamp rateVariable costsFX rate if fuel price is in a different currency from power priceMin/max generation levelMin/max runtime, min/max offline time

Thermal plants are priced in our theoretical framework using the American monte-carlo technique due to the early exercise feature and the high dimensionality of the problem

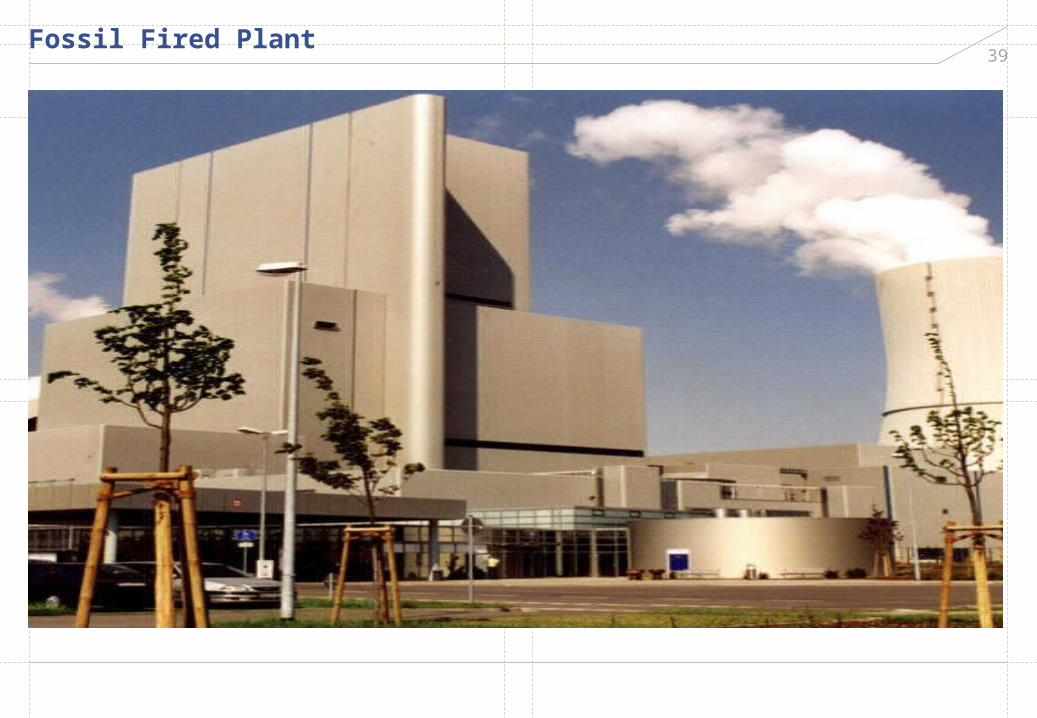

39Fossil Fired Plant

40Combined Cycle Plant

41Tolling agreements

One of the most popular power products, the tolling agreement, comes in different shapes and forms. The simplest way to represent this agreement is to view it as a call option on power with a floating strike linked to fuel prices. In real life applications the tolling contracts can be interpreted as leasing contracts on a plant wherein the “toller”, the buyer of the call option, has the right to the plant output at his or her discretion

A typical tolling agreement has the following characteristics:The length of the contract is typically short–to-medium (years)The toller has the right but not the obligation to use the plant and to call for the firm delivery of energy on a specified time frameWhenever the toller decides to exercise this right they should pay for the energy according to the contractual arrangmentsHeat_rate x Fuel_price + VOMThe Heat_rate is a measure of how efficiently the generating unit converts the energy content of the primary fuel into power. It is important to note that when the Heat_rate is presented as a constant, it is done to simplify matters and is merely an approximation. In reality it varies with a number of parameters, including the ambient temperature and generation levelThe toller has to pay regular (monthly, quarterly, etc) premium to the plant owner for having the right to the plant output. This option premium is frequently called a capacity payment

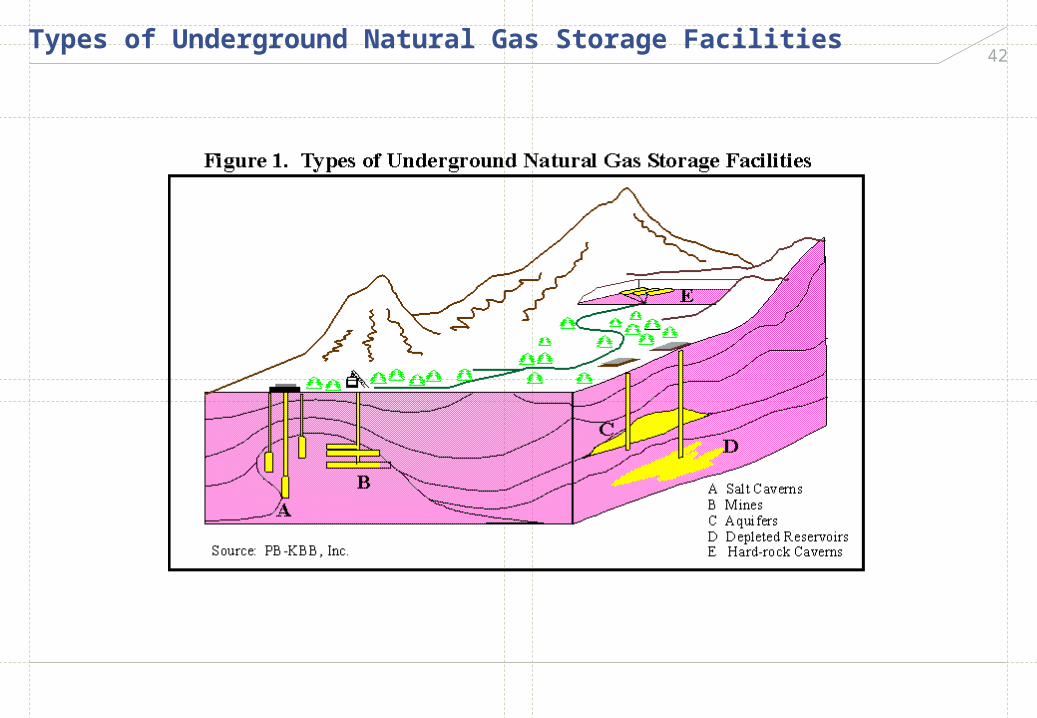

42Types of Underground Natural Gas Storage Facilities

43Gas Storage Pricing

Gas storage is defined by Maximum capacityInjection rate and withdrawal rate. The injection and withdrawal rate can depend on the inventory levelAdditional characteristics are unit injection and withdrawal costs (pumping and transportation)Fuel injection and withdrawal lossesThe capacity is in general, a hole in the ground from a depleted field, salt domes/caverns or aquiferYou can start with the storage full and return it full or start empty and return it empty or some other such combination.

Gas storage units are priced in our theoretical framework using the American monte-carlo technique due to the early exercise feature and the high dimensionality of the problem

44In the beginning…

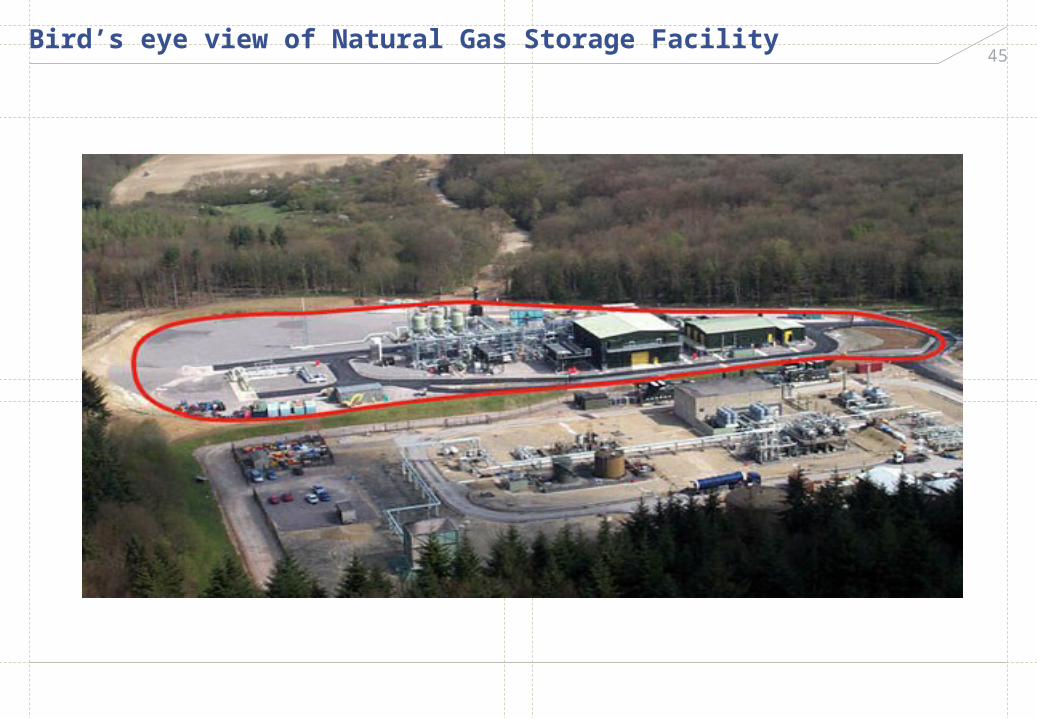

45Bird’s eye view of Natural Gas Storage Facility

46Purpose of Natural Gas Storage

Allows the holder to capitalise on cash-and-carry arbitrage opportunities in the markets.These opportunities exist because the volume of

storage available to the market is not sufficient to neutralise transient fluctuations in demand.

Types of storage contracts:1. Physical : these range from very-short-cycle

(filled and emptied in a few days) to seasonal products. Widely used across Europe.

2. Virtual : these contracts provide “storage” of PHYSICAL gas. Value is extracted by CALLing previously “stored” gas for sale into the spot market or from PUTting gas into storage for forward delivery.

Storage would, in theory, provide market stability Take advantage of seasonal arbitrage

opportunities

47Transmission

Interconnector/transportation capacity contracts grant you the right but not the obligation to flow gas/power between two points in the system

They have the following characteristicsSource pointDelivery pointMaximum capacityTransmission lossesCommodity chargeTransmission period

Transmission units are priced in our theoretical framework using the finite difference technique due to low dimensionality of the problem

48Transmission

Consider a frequently encountered transmission contract: a right to move power or gas from a liquid point A to a liquid point B

The value of this contract is simply the value of the option on the spread between the endpoint prices

Therefore, the decision on using a transmission line or pipeline is made on a monthly, daily or hourly basis then the total value of the transmission contract is the evaluation of a series of options on the spread between the endpoint prices with the strike being a transmission line tariff

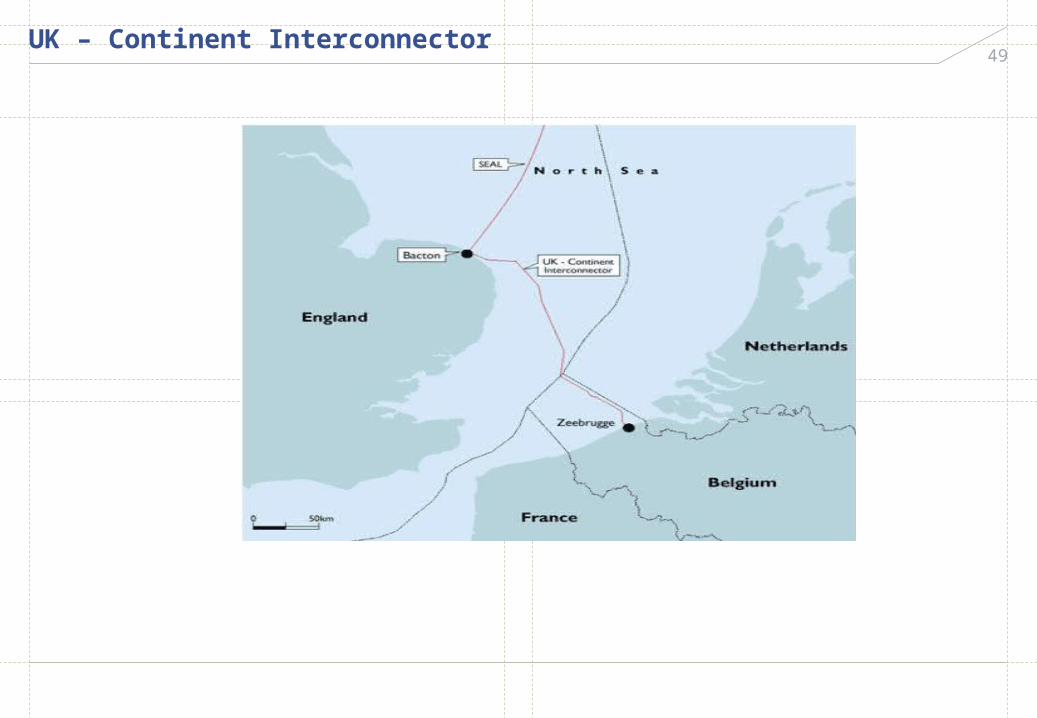

49UK – Continent Interconnector

50Zeebrugge

51Other Spread Products

Aluminium producer would like to buy electricity delivered on the national grid in Holland on a price formula indexed to the price of the LME 3-month aluminium contract for a period of 10 years

Oil producer would like to sell natural gas delivered at UK NBP index to the price of barges FOB Rotterdam gas oil 0.2%S, barges FOB Rotterdam 1%S fuel oil, and IPE Brent first nearby crude oil futures contract

Customer has indexed linked power purchases and wishes to reduce its risk to the index “I”I = P * Average( Brent * FX) + (1-P)*Average (Power)Where: P = percentage of Brent in basketBrent = Price of first nearby Brent futures contract traded on the IPEFX = EUR/USD exchange rate published daily by the European Central BankPower = Mid-market quotation reported by Platts for base-load power delivered on the French high voltage gridAverage = daily arithmetic average Product = I – Call (Ic) + Put (Ip)

52Pricing Analytics

Deal pricing for all products is consistent with the hedged portfolio approach for contingent claims pricing as developed by Black-Scholes(1971)/Merton(1973)

53Pricing Analytics …

The theoretical valuation is based on:

The application of the expectation hypothesis in a risk-neutral universe

Availability of traded assets (such as Swaps, Swaptions, etc.) with sufficient liquidity and depth

Frictionless markets

The imposition of arbitrage-free valuation constraints on a diffusion process with spikes

Deterministic discount functions

Ito++ s calculus which is a mathematical tool box for doing tricky calculations with random processes

For each class of products a partial differential equation (PDE) will be developed that determines its temporal behaviour

Using this PDE and the appropriate boundary conditions, solutions will be obtained for specific products

54Numerical Methods

The numerical techniques are not models in and of themselves

They are merely methods for solving a partial differential equation

The partial differential equation and it’s associated boundary conditions are derived from the theoretical frame-work describing the behaviour of prices

The theoretical frame-work is the model universe that we operate in

The numerical techniques available are Monte-Carlo simulation, Numerical Integration (via application of Green’s Function techniques with Gaussian Quadrature) or Finite-Difference techniques (explicit, semi-implicit or implicit)

The integral equation technique is the optimal method for generalized, accurate and fast solutions for “mathematically defined” path independent products

In the general case of path dependent products the Finite Difference and Monte Carlo (least squares) simulation are best at present

55Risk Decomposition

Dynamically hedged risksForward prices and higher momentsCorrelation between different markets

Other market related risksSpikes, Basis, Model and Replication

56Residual Market Risks

Spike risk arises when the expectation of the size-and-frequency of large price-moves over the term of the product is significantly different from that observed in practice. This risk cannot be dynamically hedge.

Basis risk arises when the when the instrument used for hedging is different from the instrument that requires hedging

Replication risk arises when the portfolio of hedging instruments does not over time track or replicate the behaviour of the more exotic instrument exactly

Model risk arises when the behaviour of the market assumed by the model is significantly different from that observed in practice

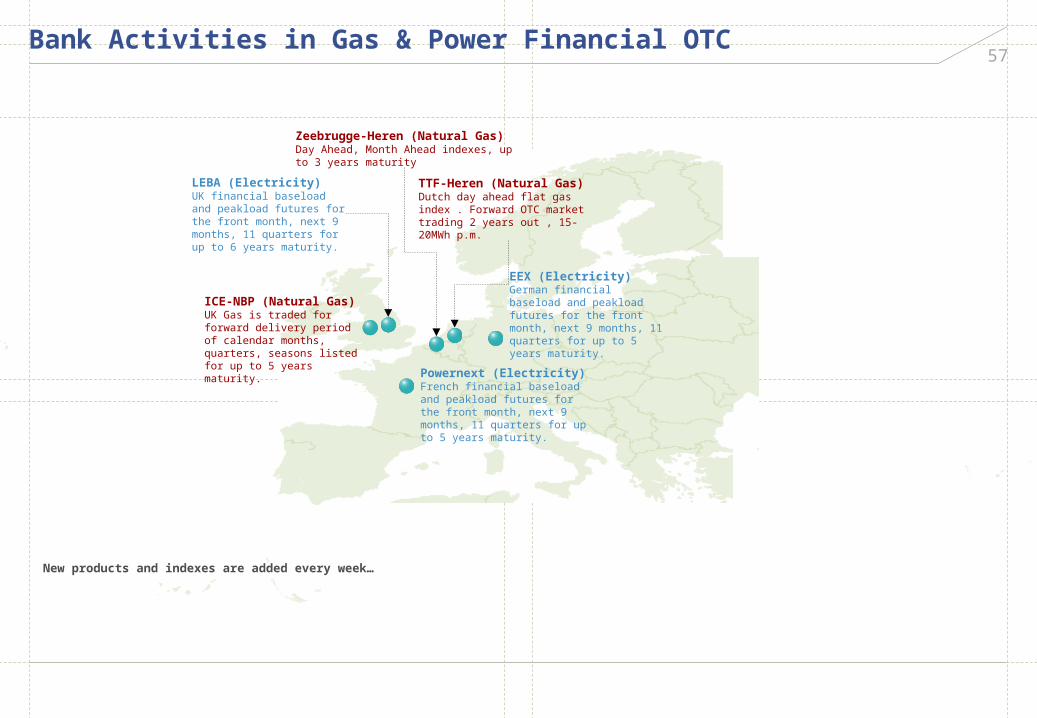

57Bank Activities in Gas & Power Financial OTC

ICE-NBP (Natural Gas)UK Gas is traded for forward delivery period of calendar months, quarters, seasons listed for up to 5 years maturity.

EEX (Electricity)German financial baseload and peakload futures for the front month, next 9 months, 11 quarters for up to 5 years maturity.

New products and indexes are added every week…

Powernext (Electricity)French financial baseload and peakload futures for the front month, next 9 months, 11 quarters for up to 5 years maturity.

LEBA (Electricity)UK financial baseload and peakload futures for the front month, next 9 months, 11 quarters for up to 6 years maturity.

TTF-Heren (Natural Gas)Dutch day ahead flat gas index . Forward OTC market trading 2 years out , 15-20MWh p.m.

Zeebrugge-Heren (Natural Gas)Day Ahead, Month Ahead indexes, up to 3 years maturity

58Other Markets

Nord PoolThis is the single financial energy market for Norway, Denmark, Sweden and Finland. Nord Pool market was created in 1996 as a result of the establishment of common electricity market of Norway and Sweden. Finland joined in 1998, Western Denmark in 1999 and Eastern Denmark in 2000. Nord pool ASA provides a marketplace for financial trading in electrical power, emission allowances and emission credits. Market membership includes energy producers, energy intensive industries, large consumers, distributors, funds, investment companies, banks, brokers, utilities, and financial institutions. It has more than 420 members in total, including exchange members, clearing clients, members and representatives in 20 countries. Nord Pool ASA provides a market place for the trade on derivative contracts in the financial market. Financial electricity contracts are used to guarantee prices and manage risk when trading power. It offers contracts of up to six years duration, with contracts for days, weeks, months, quarters and years. It is one of the largest and most liquid power derivatives exchange

Eastern EuropeThese are pool markets similar to Germany with liquidity in the underlying of up to 1 year with relatively low trading volumes at presentThe most liquid markets are Poland, Czech republic, Hungary

Spain, ItalyThese are pool markets similar to Germany with liquidity in the underlying of up to 2 years with relatively low trading volumes at present

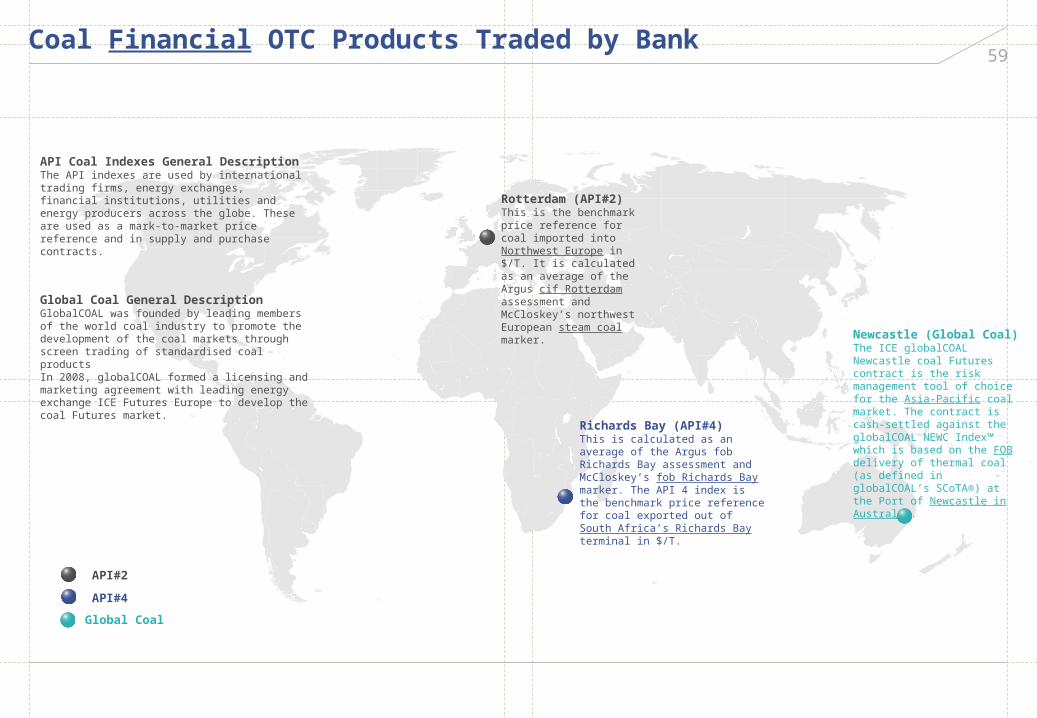

59Coal Financial OTC Products Traded by Bank

Richards Bay (API#4)This is calculated as an average of the Argus fob Richards Bay assessment and McCloskey’s fob Richards Bay marker. The API 4 index is the benchmark price reference for coal exported out of South Africa’s Richards Bay terminal in $/T.

Newcastle (Global Coal)The ICE globalCOAL Newcastle coal Futures contract is the risk management tool of choice for the Asia-Pacific coal market. The contract is cash-settled against the globalCOAL NEWC Index™ which is based on the FOB delivery of thermal coal (as defined in globalCOAL’s SCoTA®) at the Port of Newcastle in Australia.

Global CoalAPI#4API#2

Rotterdam (API#2)This is the benchmark price reference for coal imported into Northwest Europe in $/T. It is calculated as an average of the Argus cif Rotterdam assessment and McCloskey’s northwest European steam coal marker.

API Coal Indexes General DescriptionThe API indexes are used by international trading firms, energy exchanges, financial institutions, utilities and energy producers across the globe. These are used as a mark-to-market price reference and in supply and purchase contracts.

Global Coal General DescriptionGlobalCOAL was founded by leading members of the world coal industry to promote the development of the coal markets through screen trading of standardised coal productsIn 2008, globalCOAL formed a licensing and marketing agreement with leading energy exchange ICE Futures Europe to develop the coal Futures market.

60JV Options Activities

German Power PhysicalEuropean MonthsEuropean QuartersEuropean Years

NordpoolEuropean MonthsEuropean QuartersEuropean Years

UK NBP Gas PhysicalEuropean Months European QuartersEuropean Seasons

TTF Gas PhysicalEuropean Months European QuartersEuropean Seasons

Coal API2 SwapsFinancial Weekly Average Months European QuartersEuropean Years

Top Related

Copyright © 2022 FDOKUMEN