Bahasa

Halaman

Hukum

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

4

A Study of Computer Hardware and Software Services

Exports of India

G. V. Vijayasri, Research Scholar, Department of Economics, Andhra University, Visakhapatnam, Andhra Pradesh,

India

ABSTRACT

The Computer Hardware and Computer Software Services

exports have been widely studied and also examine the

production, Changes in the direction of Computer

Hardware and Computer Software Services Exports and

also study the major items and companies wise Exports of

Computer Hardware and Computer Software Services. To

assess the status of the Exports, relevant data and

information have been collected from secondary sources. .

It is shown that the software and service sector not only

contributes significantly to export earnings and GDP but

also emerges as a major source of employment generation

in the country. Besides, the information technology (IT)

sector has served as a fertile ground for the growth of a

new entrepreneurial class with innovative corporate

practices and has been instrumental in reversing the brain

drain, raising India’s brand equity and attracting foreign

direct investment (FDI) leading to other associated

benefits. . Middle East countries remain the top

destination of export for Computer Hardware during the

year 2011-12. Personal Computer has emerged to be the

top item of export during the year 2011-12. . While the

Computer Hardware sector in India is currently small,

there are several advantages that India offers that can be

effectively leveraged to achieve higher growth.

Keywords: Information Technology, Exports, Computer Hardware

and Software Services, Production

INTRODUCTION:

Information Technology (IT) is the industry, which

through the use of computers and other supporting,

equipment helps in the spread of knowledge. The term

information technology includes computers and

communication Technology along with associated

software. Information Technology (IT) is the acquisition,

processing, storage and dissemination of vocal, pictorial,

textual and numerical information by a micro-electronics-

based combination of computing and telecommunications.

IT is the technology (hardware & Software) requires for

the processing of data and other information. IT is a term

that encompasses all forms of used to store, exchange and

use information in its various forms (business data, voice

conversations, still images, motion pictures, multimedia

presentations, and other forms including those not yet

conceived). It is a convenient term for including both

telephony and computer technology in the same word. It is

the technology that is driving what has often been called

“the information Revolution”.

Information Technology for some time was synonyms to

computers. The term is commonly used as a synonym for

computers and computer networks, but it also

encompasses other information distribution technologies

such as television and telephones. Several industries are

associated with information technology, such as computer

hardware, software, electronics, semiconductors, internet,

telecom equipment, e-commerce and computer services.

The basic distinction in IT is between hardware and

software. The Computer Hardware and Computer

Software/ Services industry, a comparatively new entrant

in India‟s export horizon, has emerged as a fore-runner

among all industries and has been consistently trading on

a high growth path in recent years.

Every computer consists of hardware and software. Both

the hardware and the software are very important for the

way in which the computer operates. Any problem that

might occur within the function of computer hardware or

software influences the way in which the computer

functions. This is why it is very important for all of us to

become aware of what our computer consists of and how

its components operate so as to be able to overcome

certain problems that might occur within our PC. The

hardware is considered the most important part within a

computer because even the software is influenced by it.

This is way it is very useful to know about the importance

of computer hardware so as to become aware of the

necessity of buying good quality components for our PC

so that it might function properly.

OBJECTIVES:

1. To analyse the performance of India‟s Software

and Hardware Industry.

2. To analyse the changes in the direction of India‟s

computer Software and Computer Hardware

exports

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

5

3. To examine the trends in Computer Software and

Computer Hardware production and exports of

India

A multi-pronged approach has been adopted for the study

on Computer Hardware and Computer Software Services

Exports of India. To assess the status of the Exports,

relevant data and information have been collected from

secondary sources. This secondary data was collected

from Electronics and Computer Software Export

Promotion Council of India (ESC). This paper makes an

attempt to delineate various dimensions of Computer

Hardware and Software services exports from India.

SERVICES AND SOFTWARE VS.

HARDWARE

The services and software segment of IT industry in India

is more robust than its hardware counterpart. India has

become one of the most favoured destinations for sourcing

software and ITES. The revenue of IT services & software

and ITES-BPO taken together reached US $ 22.2 billion

during 2004-05 out of which US $ 17.3 billion was earned

through export. India ranks high in comparison to its

competitors such as China, Philippines, Ireland, Australia,

Canada, etc., in various parameters such as quality of the

labour pool, cost advantage, linguistic capabilities, project

management skills, and overall quality control. In

addition, India is able to offer a 24x7 services and

reduction in turnaround times by leveraging time zone

differences. India's unique geographic positioning makes

this possible. Emerging as one of the key investment

markets in the country, the ITES-BPO segment of the

industry is on a rapid growth path. This segment generated

revenue of US $ 5.7 billion in 2004-05, representing a

growth of 46% over the previous year. Although 90% of

the revenue is generated through export, there has been

tremendous growth in domestic market as well. The size

of domestic market in the ITES-BPO segment increased

from US $ 300 million in 2003-04 to US $ 600 million in

2004-05. Hardware segment of the IT industry in India

has not shown the same level of progress as experienced

by ITES and software (It is also true that hardware

segment of the IT industry has not received the kind of

government support received by its other counterparts.

Complications in the local indirect tax structure and high

rates of excise and sales taxes have only added to the

industry's woes. It is also evident from the fact that while

pharmaceutical and automobile companies are encouraged

to do R&D through a 150% write- off on expenditure, no

such facility has ever been extended to hardware. Again,

while labour laws have been amended for IT services &

software and ITES-BPO segment, no such initiative has

been taken for the hardware segment). Profitably

manufacturing semiconductors and other sophisticated

hardware components typically requires infrastructure,

large scale investments in capacity, and accumulated

experience that India does not possess, and is not in a

position to acquire easily (Singh, 2002). However, India

does perform numerous hardware assembly tasks

internally, almost entirely for the domestic market.

Hardware components are typically imported from the

Southeast or East Asian countries. As was the case with

several East Asian countries, it is also possible for India to

transform its capability from assemblers of sophisticated

components produced elsewhere to producer of hardware

through learning by doing. The design of hardware

typically involves the development and use of appropriate

software codes, therefore, hardware design could be a

promising area for the Indian IT sector. It is imperative

that India should focus on the areas where software

expertise matters more than the manufacturing

infrastructure. Obviously, it will still require significant

improvement in infrastructure, broader labour law reform,

and careful assessment of market demand. As Desai

(2000) pointed out, there is a need for flexible labour laws

not only to boost hardware segment of the industry but

also to realize full benefits of growth in India's IT sector.

In fact, a flexible and transparent regime of labour laws

would contribute to increased employment and

productivity and, therefore, appropriate legislation would

be in the interest of both workers and manufacturers

(Rigidity in labour laws is one of the main reasons of

sluggish growth in employment in India. It is amazing to

know that India's employment elasticity of output growth

is declining dramatically, e.g., from 0.52 during 1983-

1994 to 0.16 during 1993-2000.Therefore, the growth rate

of employment declined from 2.7% per annum during

1983-94 to 1.1% during 1993-2000 when the growth of

output, i.e., GDP, accelerated from 5.2% to 6.7% per

annum).

Production of computer hardware increased from Rs.

14970 crore (US$ 3286 million) estimated in the year

2010-11 to Rs. 16500 crore (US$ 3438 million) in the

year 2011-12. Production of computer hardware registered

a growth of 10 percent (5 percent in US$ terms) in the

year 2011-12. Production of Computer Hardware has been

growing at an annual average growth rate of 5.21 percent

(3 percent in US$ terms) during the past five years. The

production of Computer Software Services increased from

Rs. 308150crore (US$ 64956 million) estimated in the

year 2009-10 to Rs. 341200 crore (US$ 74890 million) in

the year 2010-11. Export of Computer Hardware

registered a steep decline of 31.58 percent (28.76 percent

in US$ terms) during the year 2010-11 over the year

2009-10. In value terms export of Computer Hardware is

estimated to be Rs. 1300 crore (US$ 285 million) during

2010-11 down from Rs. 1900 crore (US$ 401 million) in

2009-10.The Export of Computer Software Services

increased from Rs. 241950 crore (US$ 51001 million)

estimated in the year 2009-10 to Rs. 262500 crore (US$

57616 million) in the year 2010-11.

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

6

COMPUTER SOFTWARE INDUSTRY IN

INDIA

„The rapid growth of ITES-BPO and the IT industry as a

whole has made a deep impact on the socio-economic

dynamics of the country. The total IT Software and

Services employment has grown from 284,000 in 1999-

2000 to 1.63 million in 2006-07 and expected to reach 2.0

million marks in 2007- 08 (excluding employment in

Hardware sector). The indirect employment attributed by

the sector is estimated to about 8.0 million in the year

2007-08. Hence, Indian Software industry can continue to

have manpower led growth creating large scale

employment.

It is a well known fact that export oriented software and

service sector is indeed the driving force of Indian IT

industry and it is widely held as the engine of growth and

earner of foreign exchange. Its share in total software

industry has increased from 34.69 per cent in 1985-86 to

77.51 per cent in 2007- 08. „At an annual growth rate of

50 per cent over the last decade (1990-00), the Indian

software and service sector has expanded faster than in

any other Countries of the world of comparable size‟

(Raghavan and Nair, 2001).

Software is a knowledge driven industry. It requires a

team of highly skilled professionals for its success. Today,

the Indian IT Services and ITES sector employs over 25

lakh knowledge professionals during the past five years.

Almost all major IT players in the world have set up

subsidiaries or collaborations in India. The major

attraction being an "abundance of technically qualified

and cheap software manpower". This may have been the

case before the start of the growth phase, but now there is,

in fact, an acute shortage of qualified and trained

manpower. This is getting reflected in the spiralling

salaries (one of the highest average starting salary today),

and more importantly, a frequent job-hopping culture.

India, today have 7 Indian Institute of Technologies (IITs)

and over 300 other Regional Engineering colleges /

private colleges imparting IT education. As per a study

approximately 5, 00,000 people are needed every year to

meet the growth targets of the software industry.

However, the total production from education and training

institutions today is only about a third of this.

Thus, India has established a definite superiority in

software services production. Recognizing the enormous

significance of the Indian IT sector especially software

export.

COMPUTER HARDWARE INDUSTRY IN

INDIA:

The computer hardware& peripheral industry showed

lacklustre performance during 2008-09. SMEs, retail,

BPO/IT-enabled services and corporate sectors

demonstrated restraint in IT purchases due to concerns of

liquidity and general economic performance. The demand

for Personal Computers (PCs) has remained sluggish.

Deteriorating overall business condition has made a dent

on demand in 2008-09, which is reflected in the

decelerated growth rate in production of computer

hardware. Most hardware companies import almost 70

percent of their raw material requirement. Depreciation in

the Indian rupee adversely affected the raw material cost

and continued to impact the industry margins and arrested

the price drops in IT products. The overall PC sale for

2008-09 is expected to drop to 6.78 million as against 7.34

million during 2007-08. The production figure for this

segment for the year 2008-09 is estimated to be Rs.

13,490 crore with growth plummetingby15percent.

A total of 5.27 million desktops and 1.5 million notebooks

estimated to be consumer in 2008-09. Desktop sales

estimated to decline by 4% while that of notebooks 21%.

The slowdown in consumption can be attributed to the

dampening of consumer sentiment in India due to the

global economic crises, especially in the second-half of

2008-09.

The total PC sales during the first half of 2009-10 (April -

September 2009), with desktop computers, notebooks and

net books taken together, were 3.71 million units,

registering a growth of about one percent over the

corresponding period in the last fiscal year. Out of this

total PC sale, the total sale of desktops is estimated at 2.61

million and that of notebooks & net books at 1.1 million.

While desktop sales have declined by 11%, that of

notebooks & notebooks have grown by 43% over the

same period of last year. In the enterprises, the overall

consumption in the PC market was led by telecom,

banking and financial service sectors, and education and

households segments. Verticals such as BPO/IT-enabled

services, retail and the Government, which traditionally

account for significant proportion of the IT market, were

very conservative in their IT spends in First half (April-

September) of 2009-10.

India is one of the fastest-growing IT systems adoption of

non traditional businesses like and hardware market in the

Asia-Pacific education, retail, healthcare & hospitality,

etc. region. Most of the prominent global vendors and

some locals have strong presence in the Indian market.

Most MNCs have their assembly units in India.

PC sales are expected to record a growth of 12 from Rs.

14430 crore (US$ 3042 million) per cent in 2010-11 to

touch 9.7 million. The estimated in the year 2009-10 to

Rs. 14970 Notebook sales are estimated to be 3.5 million

crore (US$ 3286 million) in the year 2010-11. in 2010-11

against 2.5 million in 2009-10, a growth of 40 per cent.

This shows that Notebooks have caught the fancy of the

consumers. Desktop sales are expected to reach 6.2

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

7

million in 2010-11 against 5.5 million in 2009-10, a

growth of 12.7 per cent. As regards servers, sales posted a

growth of 41 per cent during second quarter 2010-11 on

account of the easing of the Economic slowdown.

Establishments which had been postponing their major IT

purchases in last few quarters are now ready to invest in

IT, which could be the major reason for the growth in the

server sales. The Server market is expected to register

positive growth in the future as the Server market expands

to smaller cities and Small and Medium Businesses

(SMBs). The small city growth is largely fuelled by the

larger organizations strengthening their base in smaller

cities on account of cost advantages. The SMB growth is

largely fuelled by the India is one of the fastest-growing

IT systems adoption of non traditional businesses like and

hardware market in the Asia-Pacific education, retail,

healthcare & hospitality, etc.

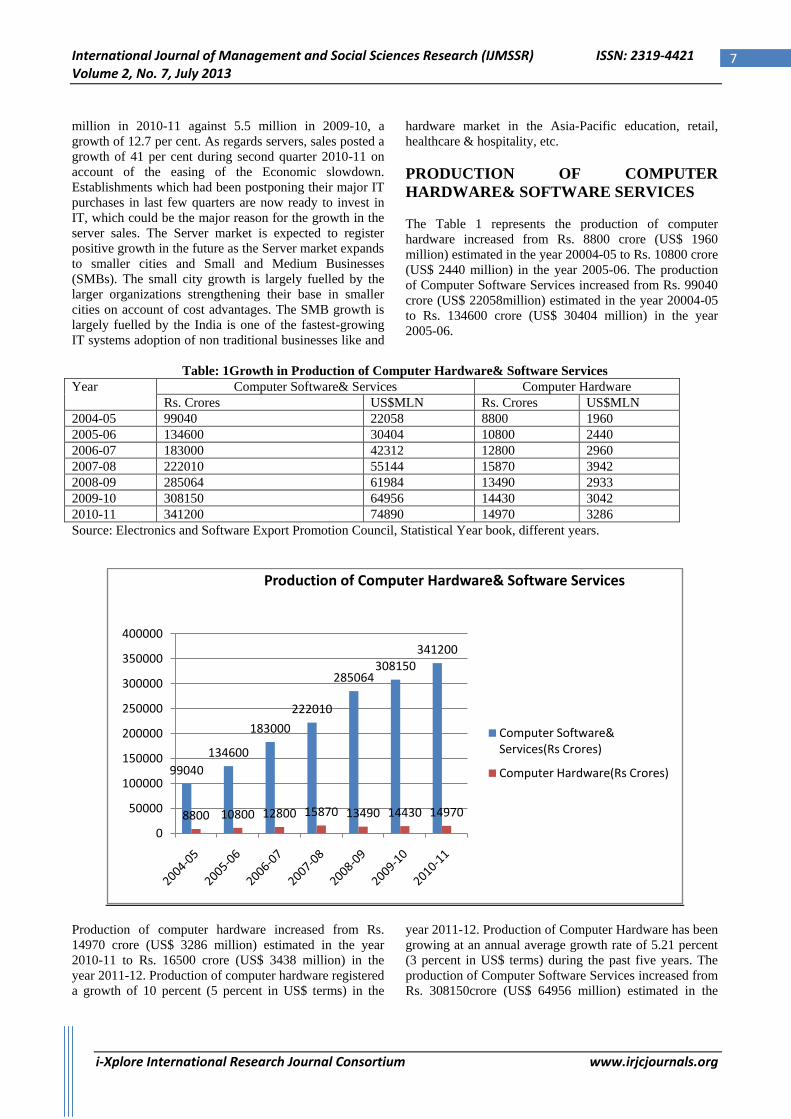

PRODUCTION OF COMPUTER

HARDWARE& SOFTWARE SERVICES

The Table 1 represents the production of computer

hardware increased from Rs. 8800 crore (US$ 1960

million) estimated in the year 20004-05 to Rs. 10800 crore

(US$ 2440 million) in the year 2005-06. The production

of Computer Software Services increased from Rs. 99040

crore (US$ 22058million) estimated in the year 20004-05

to Rs. 134600 crore (US$ 30404 million) in the year

2005-06.

Table: 1Growth in Production of Computer Hardware& Software Services

Year Computer Software& Services Computer Hardware

Rs. Crores US$MLN Rs. Crores US$MLN

2004-05 99040 22058 8800 1960

2005-06 134600 30404 10800 2440

2006-07 183000 42312 12800 2960

2007-08 222010 55144 15870 3942

2008-09 285064 61984 13490 2933

2009-10 308150 64956 14430 3042

2010-11 341200 74890 14970 3286

Source: Electronics and Software Export Promotion Council, Statistical Year book, different years.

Production of computer hardware increased from Rs.

14970 crore (US$ 3286 million) estimated in the year

2010-11 to Rs. 16500 crore (US$ 3438 million) in the

year 2011-12. Production of computer hardware registered

a growth of 10 percent (5 percent in US$ terms) in the

year 2011-12. Production of Computer Hardware has been

growing at an annual average growth rate of 5.21 percent

(3 percent in US$ terms) during the past five years. The

production of Computer Software Services increased from

Rs. 308150crore (US$ 64956 million) estimated in the

99040

134600

183000

222010

285064308150

341200

8800 10800 12800 15870 13490 14430 14970

0

50000

100000

150000

200000

250000

300000

350000

400000

Production of Computer Hardware& Software Services

Computer Software& Services(Rs Crores)

Computer Hardware(Rs Crores)

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

8

year 2009-10 to Rs. 341200 crore (US$ 74890 million) in

the year 2010-11.

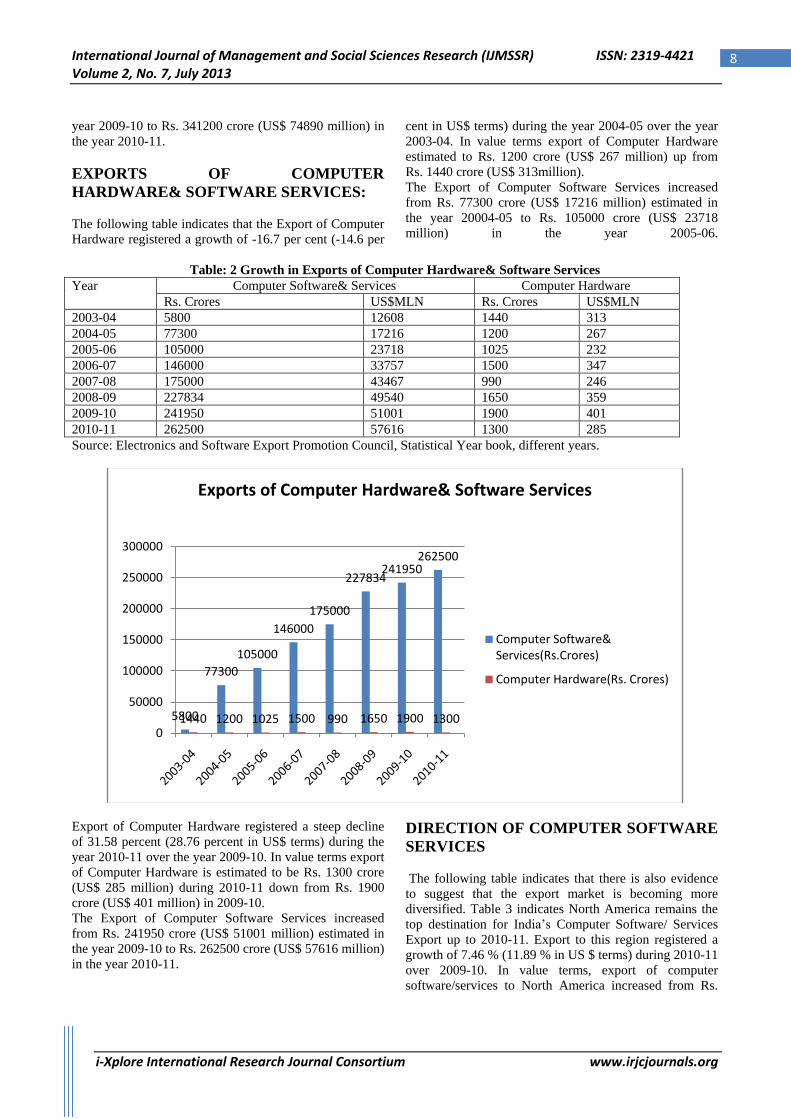

EXPORTS OF COMPUTER

HARDWARE& SOFTWARE SERVICES:

The following table indicates that the Export of Computer

Hardware registered a growth of -16.7 per cent (-14.6 per

cent in US$ terms) during the year 2004-05 over the year

2003-04. In value terms export of Computer Hardware

estimated to Rs. 1200 crore (US$ 267 million) up from

Rs. 1440 crore (US$ 313million).

The Export of Computer Software Services increased

from Rs. 77300 crore (US$ 17216 million) estimated in

the year 20004-05 to Rs. 105000 crore (US$ 23718

million) in the year 2005-06.

Table: 2 Growth in Exports of Computer Hardware& Software Services

Year Computer Software& Services Computer Hardware

Rs. Crores US$MLN Rs. Crores US$MLN

2003-04 5800 12608 1440 313

2004-05 77300 17216 1200 267

2005-06 105000 23718 1025 232

2006-07 146000 33757 1500 347

2007-08 175000 43467 990 246

2008-09 227834 49540 1650 359

2009-10 241950 51001 1900 401

2010-11 262500 57616 1300 285

Source: Electronics and Software Export Promotion Council, Statistical Year book, different years.

Export of Computer Hardware registered a steep decline

of 31.58 percent (28.76 percent in US$ terms) during the

year 2010-11 over the year 2009-10. In value terms export

of Computer Hardware is estimated to be Rs. 1300 crore

(US$ 285 million) during 2010-11 down from Rs. 1900

crore (US$ 401 million) in 2009-10.

The Export of Computer Software Services increased

from Rs. 241950 crore (US$ 51001 million) estimated in

the year 2009-10 to Rs. 262500 crore (US$ 57616 million)

in the year 2010-11.

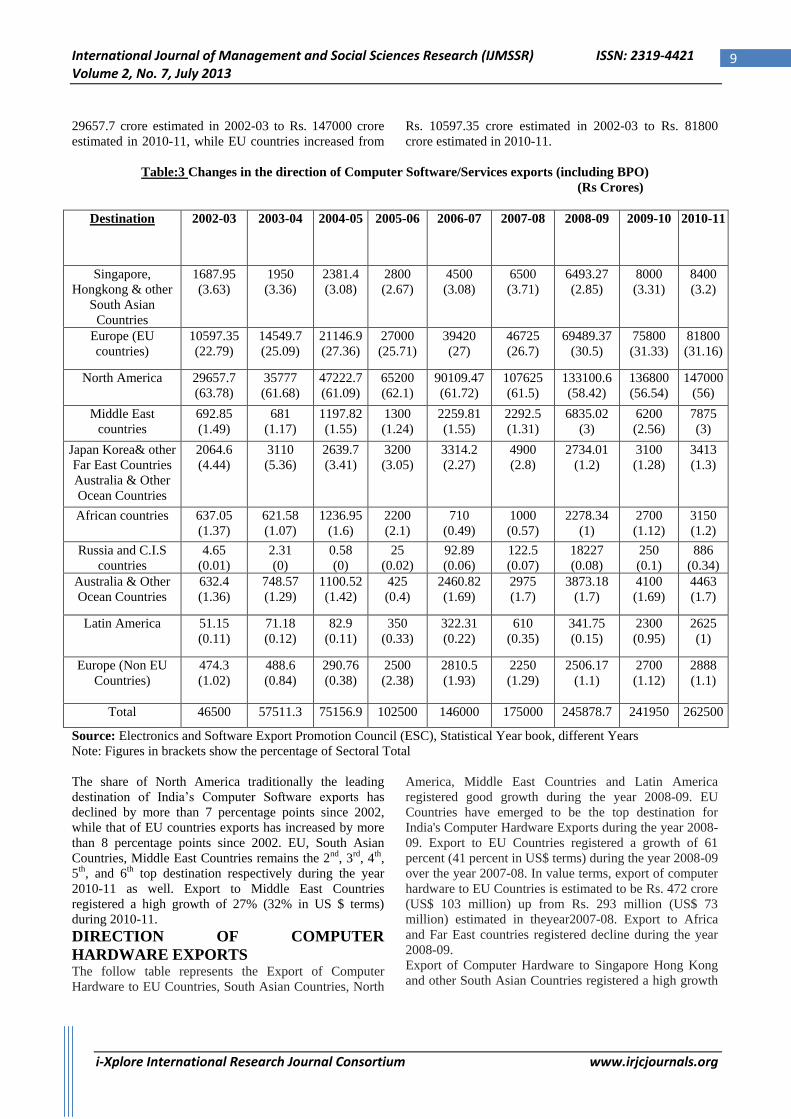

DIRECTION OF COMPUTER SOFTWARE

SERVICES

The following table indicates that there is also evidence

to suggest that the export market is becoming more

diversified. Table 3 indicates North America remains the

top destination for India‟s Computer Software/ Services

Export up to 2010-11. Export to this region registered a

growth of 7.46 % (11.89 % in US $ terms) during 2010-11

over 2009-10. In value terms, export of computer

software/services to North America increased from Rs.

5800

77300

105000

146000

175000

227834241950

262500

1440 1200 1025 1500 990 1650 1900 13000

50000

100000

150000

200000

250000

300000

Exports of Computer Hardware& Software Services

Computer Software& Services(Rs.Crores)

Computer Hardware(Rs. Crores)

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

9

29657.7 crore estimated in 2002-03 to Rs. 147000 crore

estimated in 2010-11, while EU countries increased from

Rs. 10597.35 crore estimated in 2002-03 to Rs. 81800

crore estimated in 2010-11.

Table:3 Changes in the direction of Computer Software/Services exports (including BPO)

(Rs Crores)

Destination 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11

Singapore,

Hongkong & other

South Asian

Countries

1687.95

(3.63)

1950

(3.36)

2381.4

(3.08)

2800

(2.67)

4500

(3.08)

6500

(3.71)

6493.27

(2.85)

8000

(3.31)

8400

(3.2)

Europe (EU

countries)

10597.35

(22.79)

14549.7

(25.09)

21146.9

(27.36)

27000

(25.71)

39420

(27)

46725

(26.7)

69489.37

(30.5)

75800

(31.33)

81800

(31.16)

North America 29657.7

(63.78)

35777

(61.68)

47222.7

(61.09)

65200

(62.1)

90109.47

(61.72)

107625

(61.5)

133100.6

(58.42)

136800

(56.54)

147000

(56)

Middle East

countries

692.85

(1.49)

681

(1.17)

1197.82

(1.55)

1300

(1.24)

2259.81

(1.55)

2292.5

(1.31)

6835.02

(3)

6200

(2.56)

7875

(3)

Japan Korea& other

Far East Countries

Australia & Other

Ocean Countries

2064.6

(4.44)

3110

(5.36)

2639.7

(3.41)

3200

(3.05)

3314.2

(2.27)

4900

(2.8)

2734.01

(1.2)

3100

(1.28)

3413

(1.3)

African countries 637.05

(1.37)

621.58

(1.07)

1236.95

(1.6)

2200

(2.1)

710

(0.49)

1000

(0.57)

2278.34

(1)

2700

(1.12)

3150

(1.2)

Russia and C.I.S

countries

4.65

(0.01)

2.31

(0)

0.58

(0)

25

(0.02)

92.89

(0.06)

122.5

(0.07)

18227

(0.08)

250

(0.1)

886

(0.34)

Australia & Other

Ocean Countries

632.4

(1.36)

748.57

(1.29)

1100.52

(1.42)

425

(0.4)

2460.82

(1.69)

2975

(1.7)

3873.18

(1.7)

4100

(1.69)

4463

(1.7)

Latin America

51.15

(0.11)

71.18

(0.12)

82.9

(0.11)

350

(0.33)

322.31

(0.22)

610

(0.35)

341.75

(0.15)

2300

(0.95)

2625

(1)

Europe (Non EU

Countries)

474.3

(1.02)

488.6

(0.84)

290.76

(0.38)

2500

(2.38)

2810.5

(1.93)

2250

(1.29)

2506.17

(1.1)

2700

(1.12)

2888

(1.1)

Total 46500 57511.3 75156.9 102500 146000 175000 245878.7 241950 262500

Source: Electronics and Software Export Promotion Council (ESC), Statistical Year book, different Years

Note: Figures in brackets show the percentage of Sectoral Total

The share of North America traditionally the leading

destination of India‟s Computer Software exports has

declined by more than 7 percentage points since 2002,

while that of EU countries exports has increased by more

than 8 percentage points since 2002. EU, South Asian

Countries, Middle East Countries remains the 2nd, 3rd, 4th,

5th, and 6th top destination respectively during the year

2010-11 as well. Export to Middle East Countries

registered a high growth of 27% (32% in US $ terms)

during 2010-11.

DIRECTION OF COMPUTER

HARDWARE EXPORTS The follow table represents the Export of Computer

Hardware to EU Countries, South Asian Countries, North

America, Middle East Countries and Latin America

registered good growth during the year 2008-09. EU

Countries have emerged to be the top destination for

India's Computer Hardware Exports during the year 2008-

09. Export to EU Countries registered a growth of 61

percent (41 percent in US$ terms) during the year 2008-09

over the year 2007-08. In value terms, export of computer

hardware to EU Countries is estimated to be Rs. 472 crore

(US$ 103 million) up from Rs. 293 million (US$ 73

million) estimated in theyear2007-08. Export to Africa

and Far East countries registered decline during the year

2008-09.

Export of Computer Hardware to Singapore Hong Kong

and other South Asian Countries registered a high growth

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

10

of 51 percent (47 percent in US$ terms) during the year

2009-10 making this region the top destination for India‟s

export of Computer Hardware. In value terms, export of

computer hardware to this region is estimated to be Rs.

569 crore (US$ 120 million) up from Rs. 376 crore (US$

82 million) estimated in the year 2008-09. Export to

Middle East countries, Africa and Far East countries

registered growth during the year 2009-10. Export to

North America, LAC and Oceanic countries registered

decline during 2009-10.

Table: 4 Changes in the direction of Computer Hardware Exports (Rs Crores)

Destination 2002-03 2003-04 2005-06 2006-07 2007-08 2008-09 2009-10 2010-11 2011-12

Singapore,

Hongkong & other

South Asian

Countries

208

(37.82)

647.18

(44.94)

220

(21.46)

83.5

(5.57)

147

(14.85)

375.92

(22.78)

569

(38.38)

499

(29.95)

400

(19.05)

Europe (EU

countries)

82

(14.91)

130.28

(9.05)

67

(6.54)

165

(11)

293

(29.6)

472.01

(28.61)

500

(26.32)

260

(20)

240

(11.43)

North America 127

(23.09)

453.6

(34.5)

511.5

(49.9)

1070

(71.33)

31

(3.13)

356.05

(21.58)

274

(14.42)

190

(14.62)

400

(19.05)

Middle East

countries

122

(22.18)

118.43

(8.22)

44

(4.29)

48

(3.2)

81

(8.18)

195.14

(11.83)

266

(14)

150

(11.54)

770

(36.67)

Japan Korea other

Far East Countries

Australia & Other

Ocean Countries

7

(1.27)

25.7

(3.87)

165

(16.1)

100

(6.67)

324

(32.73)

53.9

(3.27)

125

(6.58)

79

(6.08)

125

(5.95)

African countries 2.56

(0.47)

28.72

(1.99)

12

(1.17)

30

(2)

80

(8.08)

55.71

(3.38)

75

(3.95)

38

(2.92)

65

(3.10)

Russia and C.I.S

countries

0.3

(0.05)

1.1

(0.08)

0.5

(0.05)

1.6

(0.11)

2

(0.2)

6.6

(0.4)

12

(0.63)

12

(0.92)

4

(0.19)

Australia & Other

Ocean Countries

1

(0.18)

1.8

(0.13)

3

(0.29)

0.5

(0.03)

2

(0.2)

16.41

(0.99)

15

(0.79)

4

(0.31)

10

(0.48)

Latin America

0

(0)

0

(0)

1

(0.1)

1

(0.07)

29

(2.93)

114.69

(6.95)

60

(3.16)

65

(5)

80

(3.81)

Europe (Non EU

Countries)

0.14

(0.03)

3.02

(0.21)

1

(0.1)

0.4

(0.03)

1

(0.1)

3.58

(0.22)

4

(0.21)

3

(0.23)

6

(0.29)

Total 550 1440 1025 1500 900 1650 1900 1300 2100

Source: Electronics and Software Export Promotion Council (ESC), Statistical Year book, different Years

Note: Figures in brackets show the Percentage of Sectoral Total

Singapore, Hong Kong and other South Asian Countries

remain the top destination for export of computer

hardware from India. Export to all the regions except

Latin America registered a declined in export during the

year 2010-11.Middle East countries remains the top

destination for export of Computer hardware from India in

the year 2011-12. Singapore, Hong Kong and other South

Asian Countries are second top exporters of computer

hardware. But all the destinations of the percentage of

sectoral total are declined compare with 2010-11.

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

11

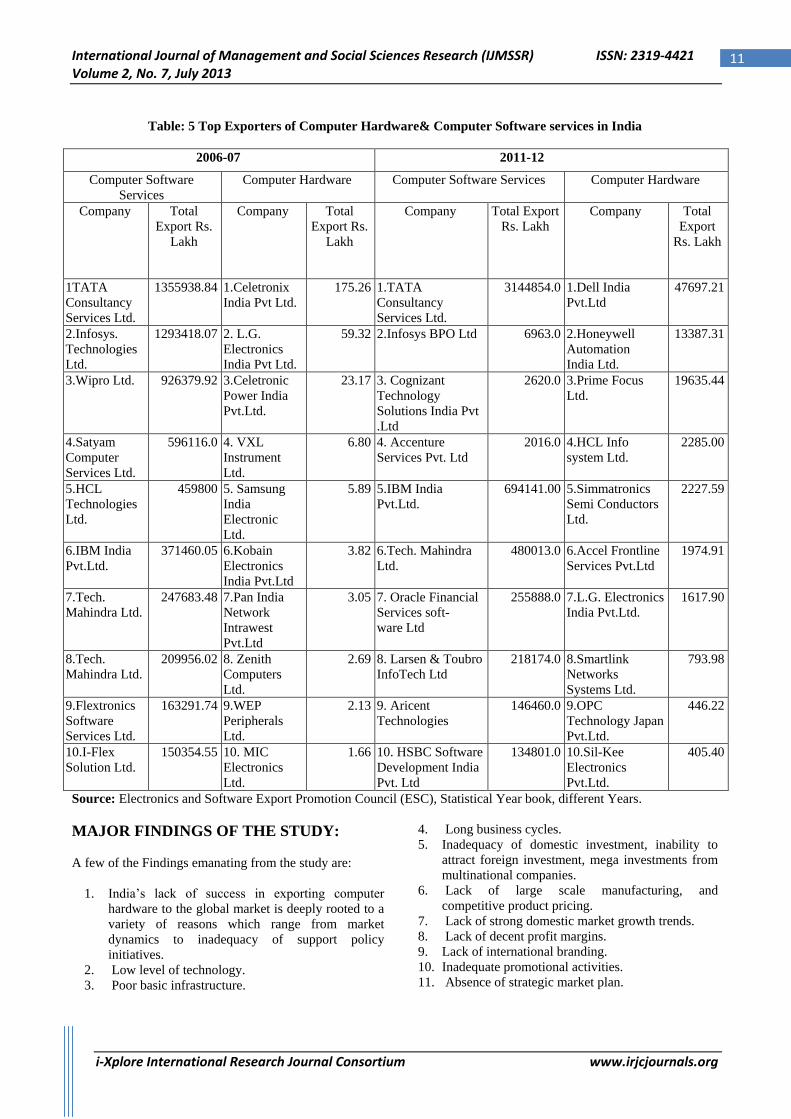

Table: 5 Top Exporters of Computer Hardware& Computer Software services in India

2006-07 2011-12

Computer Software

Services

Computer Hardware Computer Software Services Computer Hardware

Company Total

Export Rs.

Lakh

Company Total

Export Rs.

Lakh

Company Total Export

Rs. Lakh

Company Total

Export

Rs. Lakh

1TATA

Consultancy

Services Ltd.

1355938.84 1.Celetronix

India Pvt Ltd.

175.26 1.TATA

Consultancy

Services Ltd.

3144854.0 1.Dell India

Pvt.Ltd

47697.21

2.Infosys.

Technologies

Ltd.

1293418.07 2. L.G.

Electronics

India Pvt Ltd.

59.32 2.Infosys BPO Ltd 6963.0 2.Honeywell

Automation

India Ltd.

13387.31

3.Wipro Ltd. 926379.92 3.Celetronic

Power India

Pvt.Ltd.

23.17 3. Cognizant

Technology

Solutions India Pvt

.Ltd

2620.0 3.Prime Focus

Ltd.

19635.44

4.Satyam

Computer

Services Ltd.

596116.0 4. VXL

Instrument

Ltd.

6.80 4. Accenture

Services Pvt. Ltd

2016.0 4.HCL Info

system Ltd.

2285.00

5.HCL

Technologies

Ltd.

459800 5. Samsung

India

Electronic

Ltd.

5.89 5.IBM India

Pvt.Ltd.

694141.00 5.Simmatronics

Semi Conductors

Ltd.

2227.59

6.IBM India

Pvt.Ltd.

371460.05 6.Kobain

Electronics

India Pvt.Ltd

3.82 6.Tech. Mahindra

Ltd.

480013.0 6.Accel Frontline

Services Pvt.Ltd

1974.91

7.Tech.

Mahindra Ltd.

247683.48 7.Pan India

Network

Intrawest

Pvt.Ltd

3.05 7. Oracle Financial

Services soft-

ware Ltd

255888.0 7.L.G. Electronics

India Pvt.Ltd.

1617.90

8.Tech.

Mahindra Ltd.

209956.02 8. Zenith

Computers

Ltd.

2.69 8. Larsen & Toubro

InfoTech Ltd

218174.0 8.Smartlink

Networks

Systems Ltd.

793.98

9.Flextronics

Software

Services Ltd.

163291.74 9.WEP

Peripherals

Ltd.

2.13 9. Aricent

Technologies

146460.0 9.OPC

Technology Japan

Pvt.Ltd.

446.22

10.I-Flex

Solution Ltd.

150354.55 10. MIC

Electronics

Ltd.

1.66 10. HSBC Software

Development India

Pvt. Ltd

134801.0 10.Sil-Kee

Electronics

Pvt.Ltd.

405.40

Source: Electronics and Software Export Promotion Council (ESC), Statistical Year book, different Years.

MAJOR FINDINGS OF THE STUDY:

A few of the Findings emanating from the study are:

1. India‟s lack of success in exporting computer

hardware to the global market is deeply rooted to a

variety of reasons which range from market

dynamics to inadequacy of support policy

initiatives.

2. Low level of technology.

3. Poor basic infrastructure.

4. Long business cycles.

5. Inadequacy of domestic investment, inability to

attract foreign investment, mega investments from

multinational companies.

6. Lack of large scale manufacturing, and

competitive product pricing.

7. Lack of strong domestic market growth trends.

8. Lack of decent profit margins.

9. Lack of international branding.

10. Inadequate promotional activities.

11. Absence of strategic market plan.

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

12

12. Lack of initiatives for new product development.

13. Inadequate investment in research and

development.

14. Lack of global strategic partnerships.

15. Lack of Indian grey market and lack of Indian

brand recognition.

SUGGESTIONS:

A few of the Suggestions emanating from the study are:

We need effective Govt. policy, managerial attitudes and

cyber-savvy leaders to encourage high risk, long term

investment. Comprehensive curricula must be put in place

to cater to the demands of the emerging technologies and

changing needs of the industry. Industry-Academia

collaboration has to be strengthened. Specific IT

graduation focusing on Industry needs can be introduced

after 10+2. Software education centers like NIIT,

APTECH, SSI, etc. must launch up -to –date courses

keeping pace with the present demands at home and

abroad. Easy access to educational loan to the students of

IT courses should be provided. A national level test just

like All India Engineering and Medical Entrance

Examination can be conducted to tap the young talents to

the IT industry after 10+2. Special attention must be paid

to the marketing and brand building. Overcoming

infrastructural bottlenecks like uninterrupted power

supply, communication facilities are the need of the hour.

Broader basening of our overseas software market,

concentration on high end software products, more

regional diversification of software industry, diffusion of

the information technology to the domestic market etc. are

the need of the hour. More private participation, both

domestic and foreign, is crucial for providing high quality

power supply and communication facilities like high band

width. Efforts must be paid to tap the best talents of Indian

software experts for promoting the original software like

Windows by investing more on Research and

Development (R&D), providing facilities of international

standards and by paying attractive salary. There is also a

need to attract substantial amounts of Foreign Investment

and Technology to rejuvenate Indian IT Industry and

make it more competitive globally. An influx of foreign

capital and Technology would expose Indians to the latest

technologies. Last but not least, making available cheap

hardware by reducing excise duty, sales tax can go a long

way to provide a growth spurt to the Industry.

Government of India and the Indian Computer Hardware

manufacturers have to work in tandem, and take some

proactive initiatives. The initiatives to be taken by the

Government of India include: (i) Identification of a vision

and strategic growth plan.(ii) Reducing operational costs

of manufacturing and improving business attractiveness.

(iii) Promoting single manufacturing clusters. (iv)

Promoting R&D activities and human resource

development. (v) Promoting India as an ideal destination

for Computer Hardware manufacturing.(vi) Promoting

anchor investment in Indian Computer Hardware industry.

(vii) Relaxation of Labour Laws. (viii) Identification of

thrust areas and development of incubators. (ix) Skill

development.(ix) Pro-active policies for development of

entrepreneurship in hardware sector like software.

CONCLUSION:

From the foregoing analysis, it is clear that software and

hardware an area which will work as a catalyst to make

India a „Global IT Super Power‟. Over the years Software

has been growing at high rate of over 45 per cent. The

share of software export in total export as well as its

contribution to GDP has steadily increased over the years.

That software sector has emerged as a foreign exchange

earner and generator of large scale employment

opportunities. India is one of the fastest-growing IT

systems and hardware market in the Asia-Pacific region.

Most of the prominent global vendors and some locals

have strong presence in the Indian market. Most MNCs

have their assembly units in India. So the Computer

Hardware and Computer Software Sectors are very

important for development of Indian Economy.

REFERENCES:

[1] A Brief Report on “Electronics Industry in India”,

Corporate Catalyst India, August 2012.

[2] Electronics and Software Export Promotion

Council (ESC), Statistical Year book, different

Years.

[3] Arora, A. and S. Athreya (2002) „The Software

Industry and India‟s Economic Development‟,

Information Economics and Policy, 14(2): 252-273.

[4] Arora, A., V. S Arunachalam, J. Asundi and F.

Ronald (2001) „The Indian Software Services

Industry‟, Research Policy, 30 (8): 1267-87.

[5] Asheref Illiyan “Performance, Challenges and

Opportunities of Indian Software Export”, Journal

fo Theoretical and Applied Information

Technology, pp: 1088-1103.

[6] Athreye, S. (2005), The Indian Software industry

and its evolving service capability, Industrial and

Corporate Change, Vol. 14(3), 2005: 393-418.

[7] Electronics and Software Export Promotion

Council (ESC), Statistical Year book, different

Years

[8] Economic Survey (2006-07), Government of India.

[9] Eleventh Five Year Plan (2002-07), Information

Technology Sector.

[10] Government of India (2012), Economic Survey,

Ministry of Finance, New Delhi

[11] Heeks R., (1996) India‟s software industry, state

policy, liberalization and industrial Development.

New Delhi: Sage Publications

International Journal of Management and Social Sciences Research (IJMSSR) ISSN: 2319-4421 Volume 2, No. 7, July 2013

i-Xplore International Research Journal Consortium www.irjcjournals.org

13

[12] Joseph, K.J. (2005), “Strategic Approach to

Strengthening the International Competitiveness in

Knowledge Based Industries: Electronics Industry”

RIS-P#88/2005 RIS, New Delhi.

[13] Kumar (2006), “World Electronic Component

Production Scenario: An Indian Perspective”

Electronics Information and Planning, Vol 33, 3 –4,

Dec2005-Jan-2006, Dept.of IT, Government of

India.

[14] K J Joseph “India‟s Software Industry in

Transition”, May 2012, A Background Paper

Prepared for the Information Economy Report

2012.

[15] Ministry of Communications & Information

Technology, Information Technology –Annual

Report 2007-08 & 2008-09, Department of

Information Technology.

[16] “Productivity & Competitiveness of Indian

Manufacturing – IT Hardware & Electronics

Sector”. National Productivity Council, New Delhi.

[17] Sanjay K Singh. Information Technology in India:

Present Status and Future Prospects for Economic

Development.

Copyright © 2022 FDOKUMEN