Bahasa

Halaman

Hukum

A COMPARATIVE ASSESSMENT OF THE FACTORS THAT

ATTRACT OIL SECTOR FDI IN NIGERIA AND ANGOLA.

J.W. EGGINK

20672330

Dissertation submitted in partial fulfilment of the requirements for the

degree Magister Commercii in International Trade at the Potchefstroom

Campus of the North-West University

Supervisor: Mr. R. Wait

Co-supervisor: Dr. H. Bezuidenhout

November 2013

i

Preface

This dissertation is submitted in partial fulfilment of the requirements for the degree

Magister Commercii in International Trade at the Potchefstroom Campus of the

North-West University. The purpose of this dissertation is to determine domestic and

global factors that influence FDI inflows in the Angolan and Nigerian oil industries.

The dissertation explores benefits and costs of FDI and its determinates, as well as

how FDI links to current trends in the oil industry on global, regional and national

levels. This dissertation should be of interest to decision makers at government and

industry level, especially in developing African countries.

Acknowledgements

I would like to thank all friends and family for their continued moral support and

motivation throughout the gruelling times. Without your support this study would not

have been possible.

Firstly, I would like to thank my study supervisor Mr. R. Wait and co-supervisor Dr. H.

Bezuidenhout for their time and effort.

Secondly, I would like to thank my family, not only for being the motivation to

undertake the task of furthering my studies, but also for supporting me financially

and morally during my studies.

Thirdly, I would like to single out my mother, Dr. M.E. Eggink, for being an inspiration

by completing her studies during this period.

Lastly, I would like to thank Elana Joynt and her family for their continued support

and motivation throughout the period of this study.

J.W. Eggink

Potchefstroom, March 2014

ii

Abstract

This dissertation focuses on Foreign Direct Investment (FDI) in the oil sector of

Africa, more specifically in Nigeria and Angola. A large problem faced by most

African countries is their low domestic investment. This is due to the low savings

rates in these countries. FDI serves as a supplement to domestic investment and

therefore allows for increased production and growth in the region that can ultimately

lead to better development. Further, FDI brings forth positive spill over effects that

can further increase levels of development in African countries. Therefore, it is

beneficial for African countries to achieve higher levels of FDI inflows. The African oil

sector has, in recent years, received much deserved attention as Africa supplied

approximately 11 percent of worldwide oil supply and the African untapped oil

reserves constitute approximately 10 percent of the total worldwide proven oil

reserves in 2010. There are currently 19 African countries known to have significant

oil reserves and further surveying may increase this number. This dissertation

focuses on Nigeria and Angola as these countries are the continent’s largest

producers of oil and their oil sectors are the sectors with the strongest FDI inflows.

Through economic and policy reforms and increased share in global oil supply, it is

believed that these countries can be the drivers of economic growth and

development in the region.

Greater FDI is needed to fully exploit the available oil resources. Although many

studies have been done on the factors that attract FDI, very few studies have

focussed on oil sector specific FDI. Therefore, the aim of this dissertation is to

determine and compare the factors that attract oil sector FDI in Nigeria and Angola.

This dissertation undertakes both a literature review and an empirical analysis. The

literature review provides an overview of FDI theory, the motives for investment, the

types and benefits thereof; an overview of the African and, more specifically, the

Nigerian and Angolan oil industry and the influence that FDI inflows have had on this

sector. The current FDI inflow trends and oil sector FDI in Nigeria and Angola are

reviewed. The dissertation examines and compares the current state of the Nigerian

and Angolan oil industries. The empirical analysis consists of a country comparison

through four least square regression models (domestic models for Nigeria and

iii

Angola and global models for both countries) using data between 1990 and 2011

obtained from the World Data Bank and the 2012 BP statistical review. The data

used will describe the traditional determinants of FDI inflows as set out in literature

review and other determinants derived from past studies of FDI inflows in transitional

economies and oil sector dependent countries. In Nigeria and Angola, the problems

of lack of accurate and sufficient data over a longer time period persist, as they do in

most African countries.

The main findings are that significant domestic influences of FDI inflows in Angola

include: lower public power to entice private gain; better policies that are effectively

enforced to improve civil and public services; and the proven oil reserves. This

entails that government policy, transparency and their oil reserves are held in high

regard by the foreign investors in Angola. In Nigeria, however, domestic influences of

FDI inflows include: better citizen ability to select a government; freedom of

expression; freedom of association and a free media; better ability of the government

to formulate and implement sound policies and regulations that permit and promote

private sector development; and oil production. This indicates that democracy,

government policy and oil production are highly regarded by foreign investors who

invest in Nigeria. Therefore, it can be argued that, even though results for factors

influencing FDI inflows differ, there are similarities as government policy and the oil

sector in general influence both countries even though the issues in both countries

are not necessarily the same. However, on a global level, investment in the two

countries is driven by completely different factors. According to the models, Angolan

FDI inflows are driven by global oil production (supply) in the previous year whereas

FDI inflows in Nigeria are correlated to the oil price in the previous year. Both of

these models, however, leave much to be desired as they have low R2 values which

indicate that they explain very little of what influences FDI inflows in the countries.

Key words: Foreign Direct Investment (FDI); oil sector; oil sector FDI; African FDI;

Nigeria; Angola.

iv

Opsomming

Hierdie verhandeling fokus op direkte buitelandse investering in die Afrika oliesektor

en meer spesifiek op Nigerië en Angola se oliesektore. 'n Groot probleem wat ervaar

word deur die meeste Afrika-lande is hul lae binnelandse investering. Dit is grootliks

as gevolg van die lae spaarkoers in hierdie lande. direkte buitelandse investering

dien as 'n aanvulling tot binnelandse investering en daarom kan verhoogde

produksie en groei bereik word wat uiteindelik kan lei tot beter ontwikkeling. Direkte

buitelandse investering kan ook lei tot positiewe oorspoel-effekte wat die vlak van

ontwikkeling in Afrika-lande kan verhoog. Daarom is dit voordelig vir Afrika-lande om

hoër vlakke van direkte buitelandse investeringsinvloei te bereik. Die Afrika

oliesektor het in afgelope jare baie aandag geniet, omdat Afrika verantwoordelik is

vir ongeveer 11 persent van die wêreldwye olieproduksie en Afrika se onontginde

oliereserwes maak ongeveer 10 persent van die totale wêreldwye bewese

oliereserwes in 2010 uit. Daar is tans 19 Afrika-lande wat noemenswaardige

oliereserwes het en daar word verwag dat hierdie getalle in die toekoms kan styg

met verdere eksplorasie. Hierdie studie fokus spesifiek op Nigerië en Angola, omdat

hierdie lande Afrika se grootste olieprodusente is en die oliesektor die sektor in

Afrika is wat tans die sterkste direkte buitelandse investeringsinvloei ontvang.

Volgens sekere ekonome kan hierdie lande die dryfkrag vir ekonomiese groei en

ontwikkeling in die streek wees as hulle die nodige ekonomiese en

beleidshervormings toepas en ‘n groter aandeel in die globale olie-aanbod bekom.

Groter direkte buitelandse investeringsinvloei word benodig om die beskikbare

oliehulpbronne te ontgin en in inkomste te omskep. Alhoewel daar al menigte studies

gedoen is oor die faktore wat direkte buitelandse investeringsinvloei aantrek, het

baie min studies spesifiek gefokus op oliesektor direkte buitelandse investering. Die

doel van hierdie studie is dus om vas te stel watter faktore direkte buitelandse

investering in Nigerië en Angola se oliesektore aantrek en om die faktore in die twee

lande te vergelyk.

Die studie bestaan uit 'n literatuurstudie en 'n empiriese analise. Die literatuurstudie

verskaf 'n oorsig oor direkte buitelandse investeringsteorie, die motiewe vir

investering, die tipes direkte buitelandse investering en voordele daarvan, sodat 'n

v

oorsig gegee kan word van die Afrika en, meer spesifiek, die Nigeriese en Angolese

olie-sektore en die invloed wat direkte buitelandse investeringsinvloei op hierdie

sektor het. Die huidige direkte buitelandse investeringsinvloei-tendense en oliesektor

direkte buitelandse investering in Nigerië en Angola word dan hersien. Die studie

ondersoek en vergelyk dan die huidige toestand van die Nigeriese en Angolese olie-

industrie. Die empiriese ontleding bestaan uit 'n vergelyking tussen die lande deur

vier regressiemodelle (plaaslike modelle vir Nigerië en Angola en globale modelle vir

beide lande), deur gebruik te maak van data tussen 1990 en 2011 verkry van die

World Data Bank en die BP statistical review 2012. Die data sal die tradisionele

determinante van direkte buitelandse investeringsinvloei, soos uiteengesit in

literatuuroorsig, beskryf en ander faktore wat afgelei word van vorige studies oor

direkte buitelandse investeringsinvloei in ontwikkelende ekonomieë asook oliesektor-

afhanklike lande. 'n Gebrek aan akkurate en voldoende data oor 'n langer tydperk is

egter ‘n probleem wat voorkom in Nigerië en Angola soos in die meeste Afrika-lande.

Die modelle was geïnterpreteer en vergelyk en die bevindinge was dat beduidende

plaaslike invloede van direkte buitelandse investeringsinvloei in Angola die volgende

insluit: laer openbare bevoegdheid het om private gewin te bewerkstellig; 'n beter

beleid wat effektief afgedwing word om burgerlike en openbare dienste te verbeter;

en die bewese olie reserwes te lok. Dit behels dat die regeringsbeleid, deursigtigheid

en hul olie-reserwes hooggeag word deur buitelandse beleggers wat belê in Angola.

Die beduidende Nigeriese plaaslike invloede van buitelandse investeringsvloei het

egter die volgende ingesluit: beter burgerlike vermoë om 'n regering te kies; vryheid

van uitdrukking; vryheid van assosiasie en vrye media; beter regeringsvermoë om

gesonde beleide te formuleer en te implementer; regulasies wat toelaat dat privaat-

sector ontwikkeling bevorder word; en olieproduksie. Dit dui daarop dat demokrasie,

regeringsbeleid en olieproduksie hooggeag word deur buitelandse beleggers wat

belê in Nigerië. 'n Mens kan dus argumenteer dat daar wel ooreenkomste bestaan

tussen die lande se plaaslike invloede op direkte buitelandse investering. Die

ooreenkomste dui dat beide lande beïnvloed word deur regeringbeleid en die

oliesektor in die algemeen, selfs al is die kwessies in beide lande nie noodwendig

dieselfde nie. Op ‘n globale vlak word investering in die twee lande egter deur

heeltemal ander faktore gedryf. Volgens die modelle in die bogenoemde afdelings

vi

word Angolese direkte buitelandse investeringsinvloei gedryf deur globale

olieproduksie (aanbod) in die vorige jaar, terwyl direkte buitelandse

investeringsinvloei in Nigerië gekorreleer is met die olieprys in die vorige jaar. Albei

hierdie modelle laat egter veel te wense oor, as gevolg van hul lae R-kwadraat wat

aandui dat die onafhanklike veranderilkes baie min verduidelik van wat direkte

buitelandse investeringsinvloei in die lande beïnvloed.

Sleutelwoorde: direkte buitelandse investering; oliesektor; oliesektor direkte

buitelandse investering; direkte buitelandse investering in Afrika; Nigerië; Angola.

vii

Table of contents

Preface ........................................................................................................................ i

Acknowledgements ..................................................................................................... i

Abstract ....................................................................................................................... ii

Opsomming ................................................................................................................ iv

List of tables ............................................................................................................... xi

List of figures ............................................................................................................. xii

List of abbreviations ................................................................................................. xiii

Chapter 1: Introduction and context of analysis ......................................................... 1

1.1. Introduction: Rationale and context ............................................................... 1

1.1.1. The oil sector ............................................................................................. 3

1.1.1.1. Nigeria ................................................................................................. 8

1.1.1.2. Angola ................................................................................................. 8

1.2. Problem statement ........................................................................................ 9

1.3. Motivation .................................................................................................... 10

1.4. Objectives ................................................................................................... 10

1.4.1. Sub-objectives ......................................................................................... 10

1.5. Research method ........................................................................................ 11

1.6. Outline of the dissertation ........................................................................... 11

Chapter 2: Literature review of FDI and the oil sector .............................................. 12

2.1. Introduction ................................................................................................. 12

2.2. FDI theory ................................................................................................... 12

2.2.1. FDI Definitions ......................................................................................... 12

viii

2.2.2. Categorising FDI ...................................................................................... 14

2.2.2.1. Categorising FDI according to the direction of flow ........................... 14

2.2.2.2. Categorising FDI according to investment type ................................. 14

2.2.2.3. Categorising FDI according to investors’ motivations ........................ 15

2.2.3. Benefits of FDI ......................................................................................... 15

2.2.3.1. Direct positive effects of FDI.............................................................. 15

2.2.3.2. Indirect positive effects of FDI ........................................................... 16

2.2.4. Costs of FDI .......................................................................................... 17

2.2.5. Determinants of FDI ................................................................................. 19

2.2.5.1. Macro determinants of FDI ................................................................ 19

2.2.5.2. Micro determinants of FDI ................................................................. 21

2.3. Oil sector theory .......................................................................................... 23

2.3.1. Types of oil reserves ............................................................................ 24

2.3.2. Upstream versus downstream investment ............................................ 25

2.3.3. Role players in the oil sector ................................................................. 26

2.3.3.1. Small independent oil companies .................................................. 26

2.3.3.3. Fully integrated multi-national oil companies (MNOCs) ................. 26

2.3.3.2. National oil companies (NOCs) ...................................................... 27

2.3.3.4. Other companies (Service companies) .......................................... 27

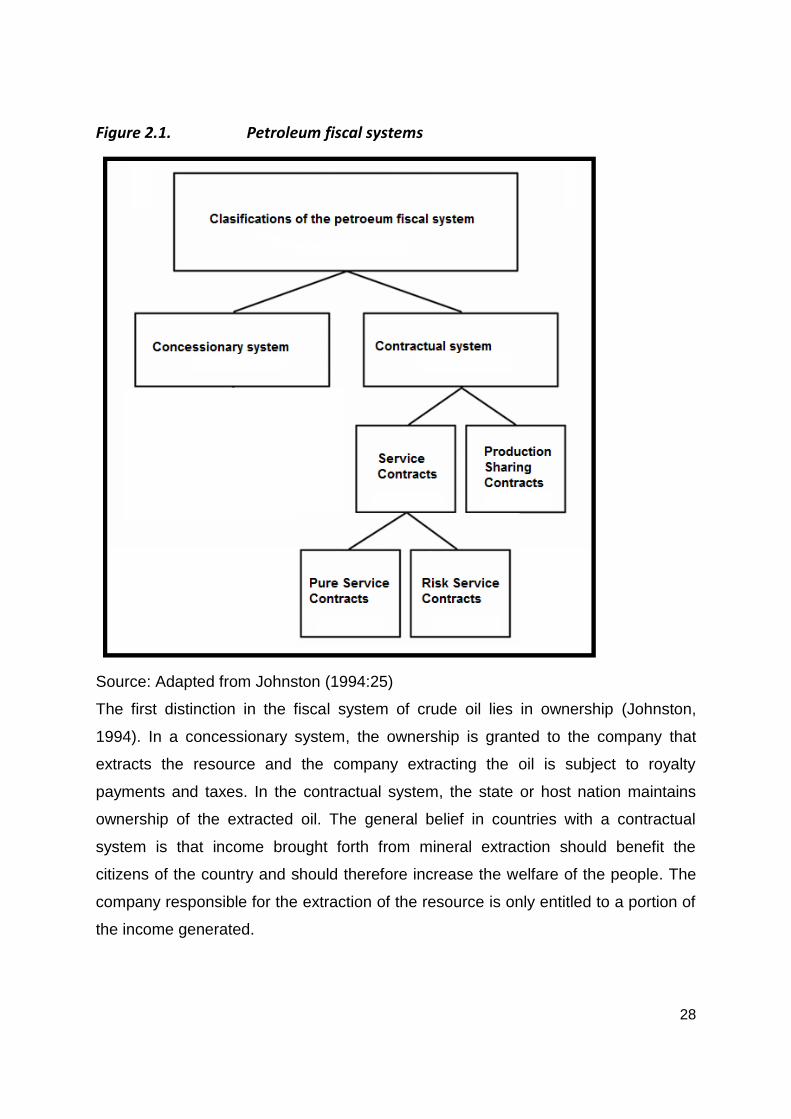

2.3.4. Classifications of Petroleum fiscal systems .......................................... 27

2.3.5. The natural resource curse ................................................................... 29

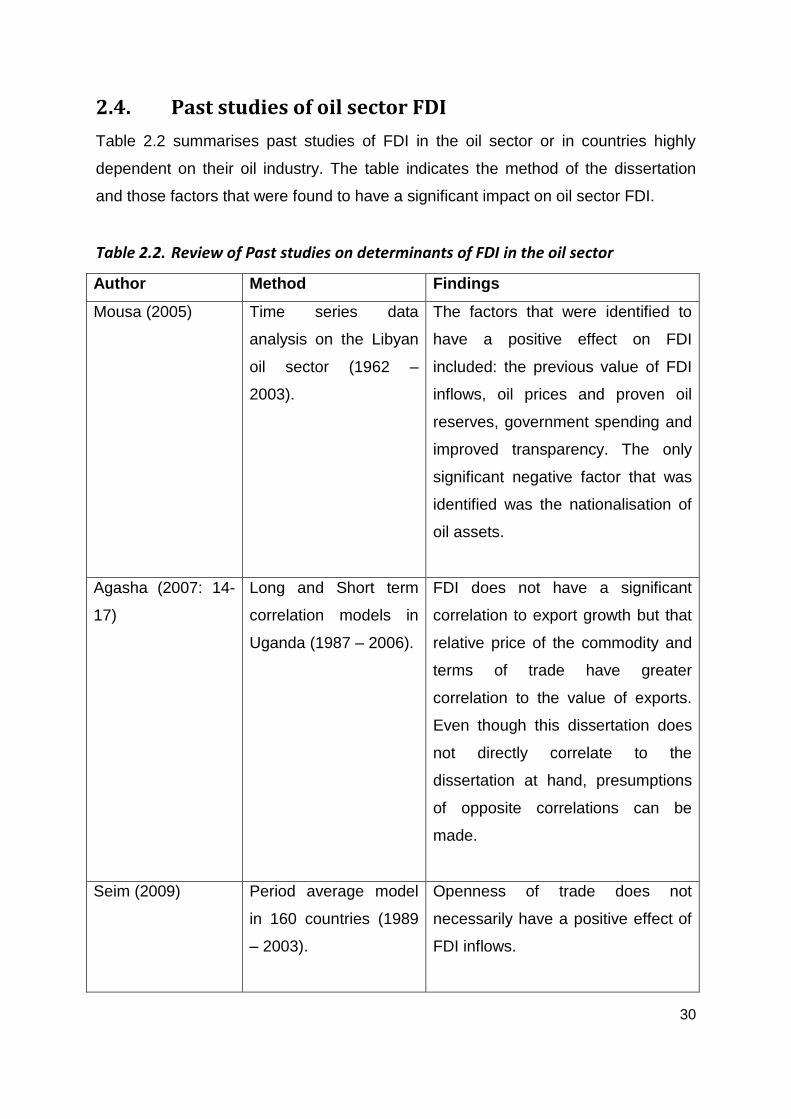

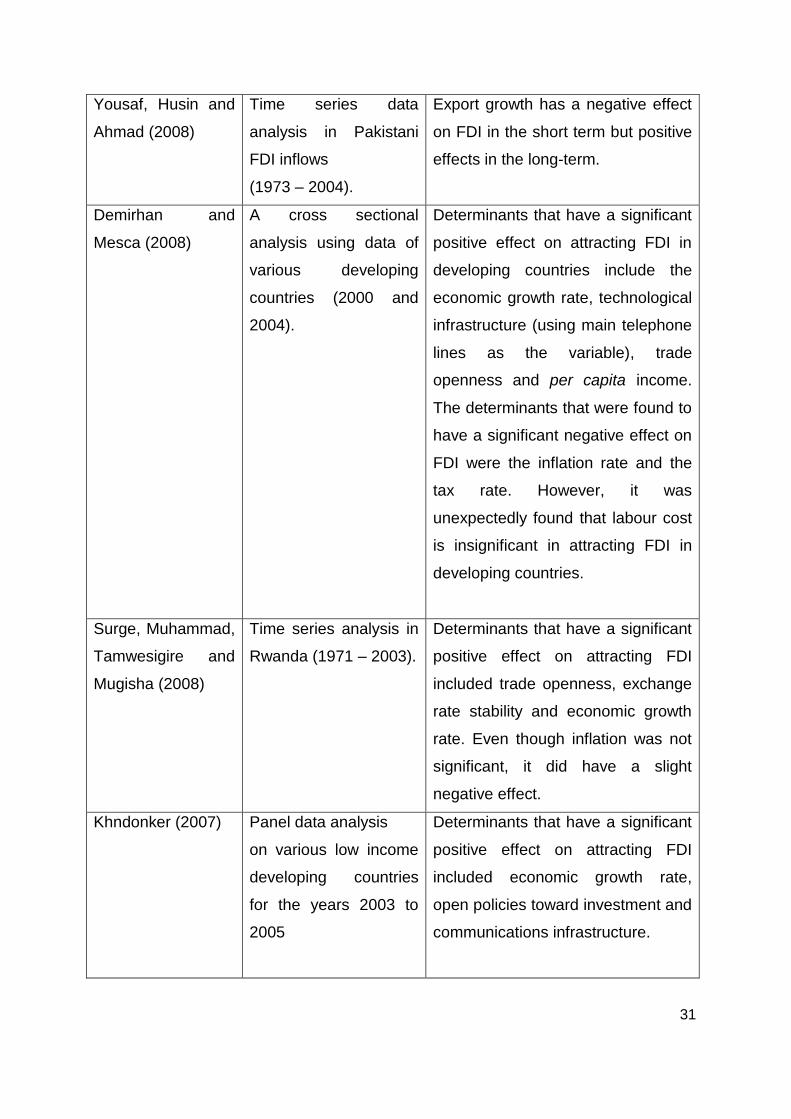

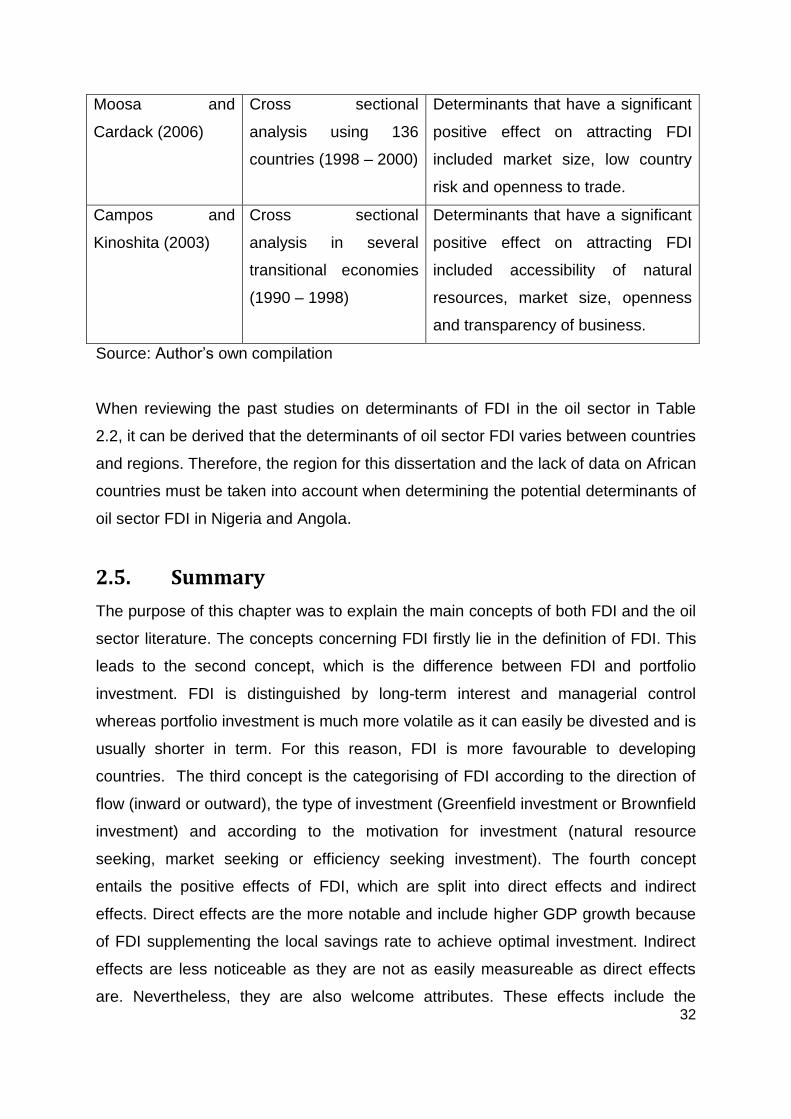

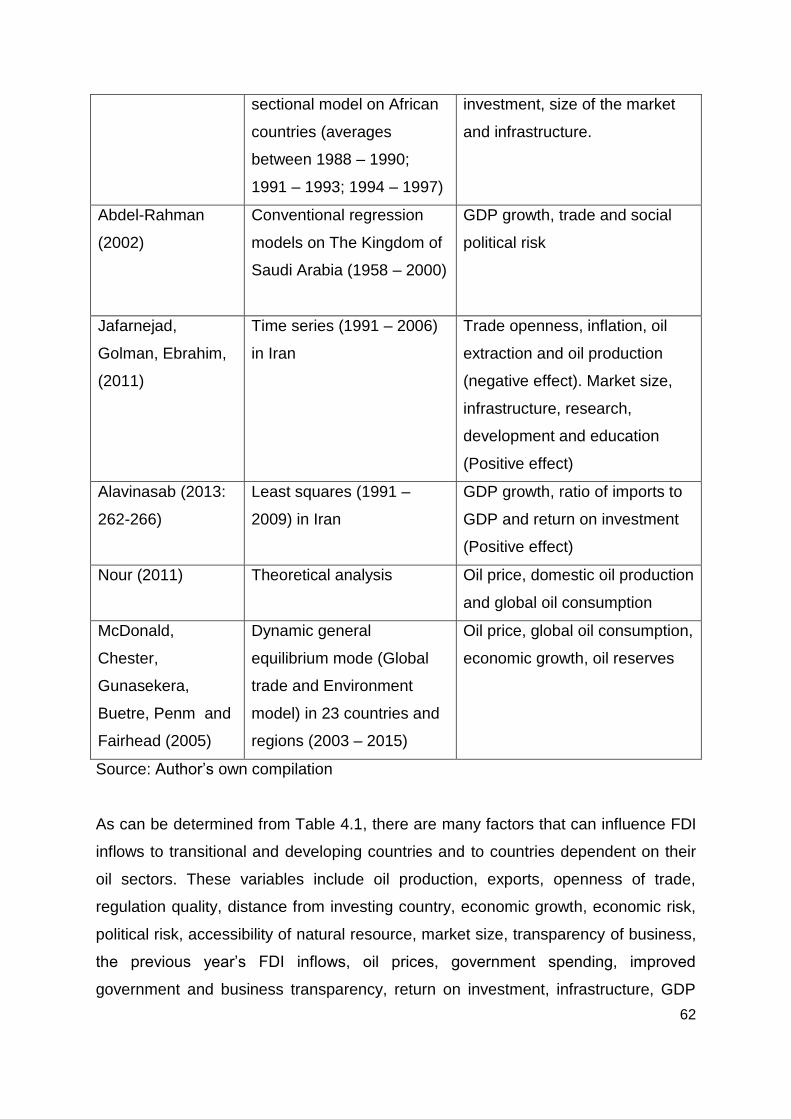

2.4. Past studies of oil sector FDI....................................................................... 30

2.5. Summary ..................................................................................................... 32

Chapter 3 – Current trends in FDI inflows and the Oil Sector ................................... 35

3.1. Introduction ................................................................................................. 35

ix

3.2. Global trends ............................................................................................... 36

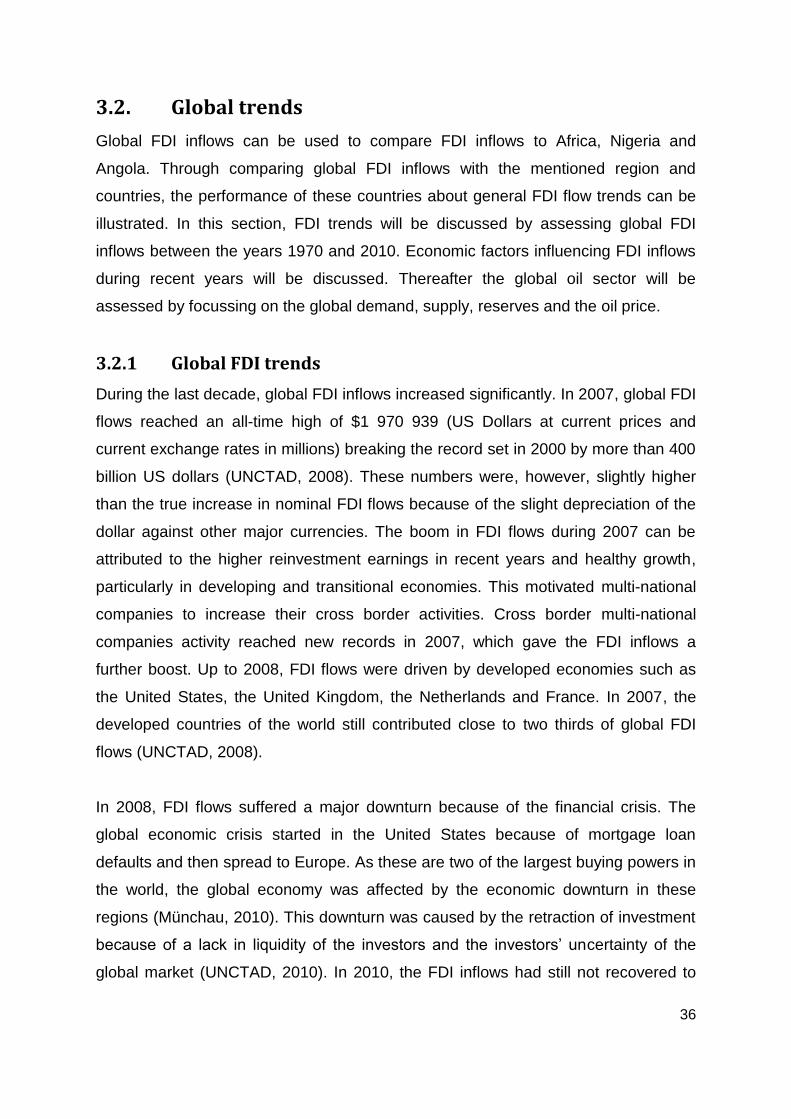

3.2.1 Global FDI trends ................................................................................. 36

3.2.2. Global oil sector and FDI trends ........................................................... 38

3.3. Africa ........................................................................................................... 42

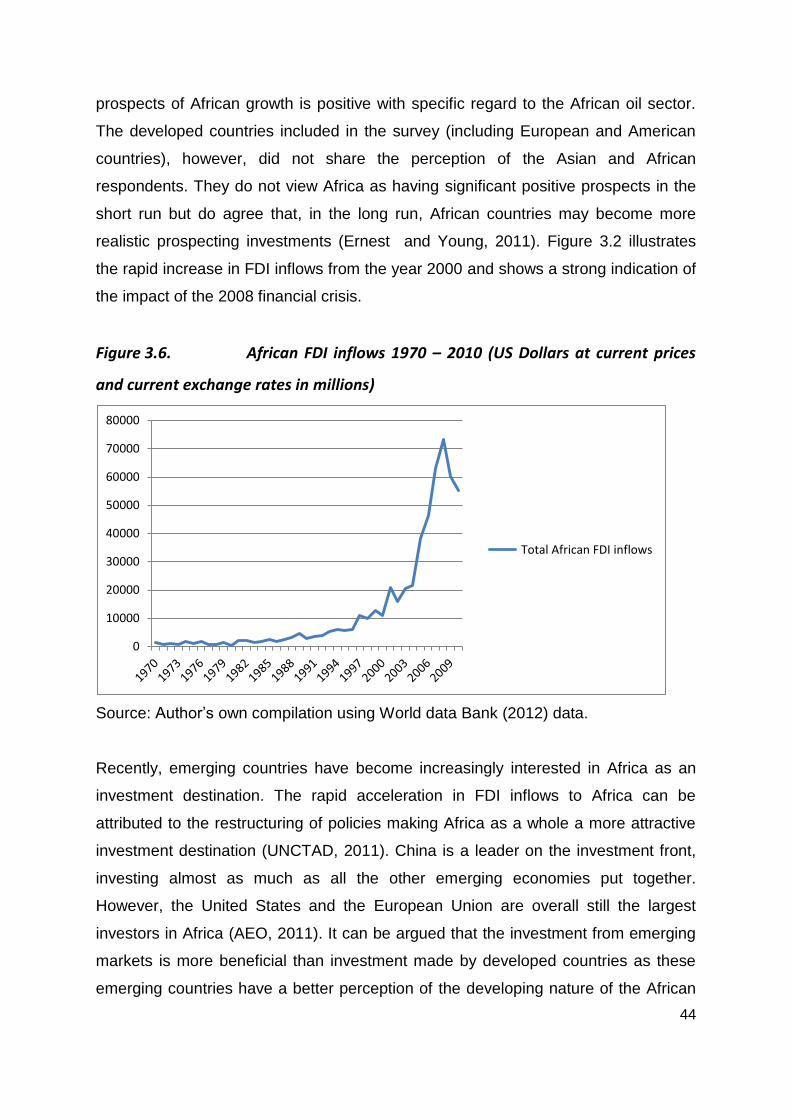

3.3.1. African FDI trends ................................................................................. 43

3.3.2 FDI inflows in the African oil sector ....................................................... 45

3.4. Nigeria and Angola .................................................................................. 50

3.4.1. Nigeria ..................................................................................................... 50

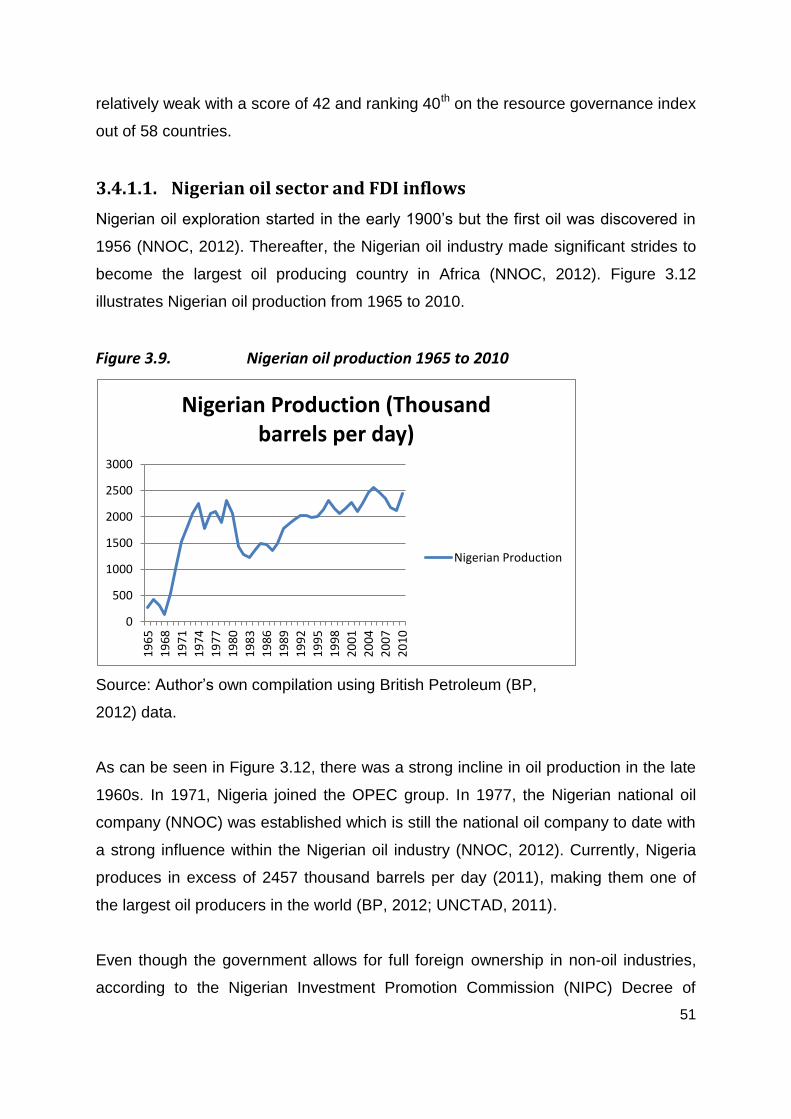

3.4.1.1. Nigerian oil sector and FDI inflows .................................................... 51

3.4.2. Angola ...................................................................................................... 54

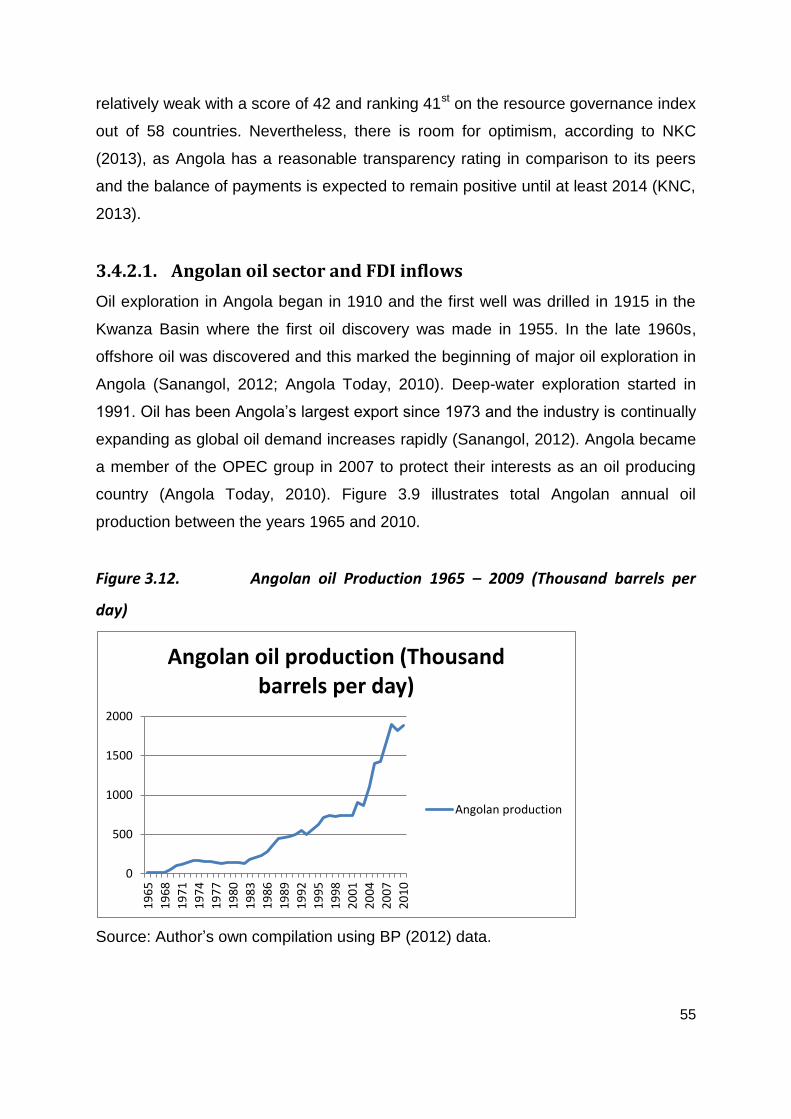

3.4.2.1. Angolan oil sector and FDI inflows .................................................... 55

3.5. Summary ..................................................................................................... 58

Chapter 4 –Empirical Analysis of oil sector FDI in Nigeria and Angola .................... 60

4.1. Introduction of oil sector FDI in Nigeria and Angola .................................... 60

4.2. Theoretical framework ................................................................................. 61

4.3. Empirical analysis ...................................................................................... 63

4.3.1. Factors expected to influence oil sector FDI ........................................ 63

4.3.2. Data description ................................................................................... 63

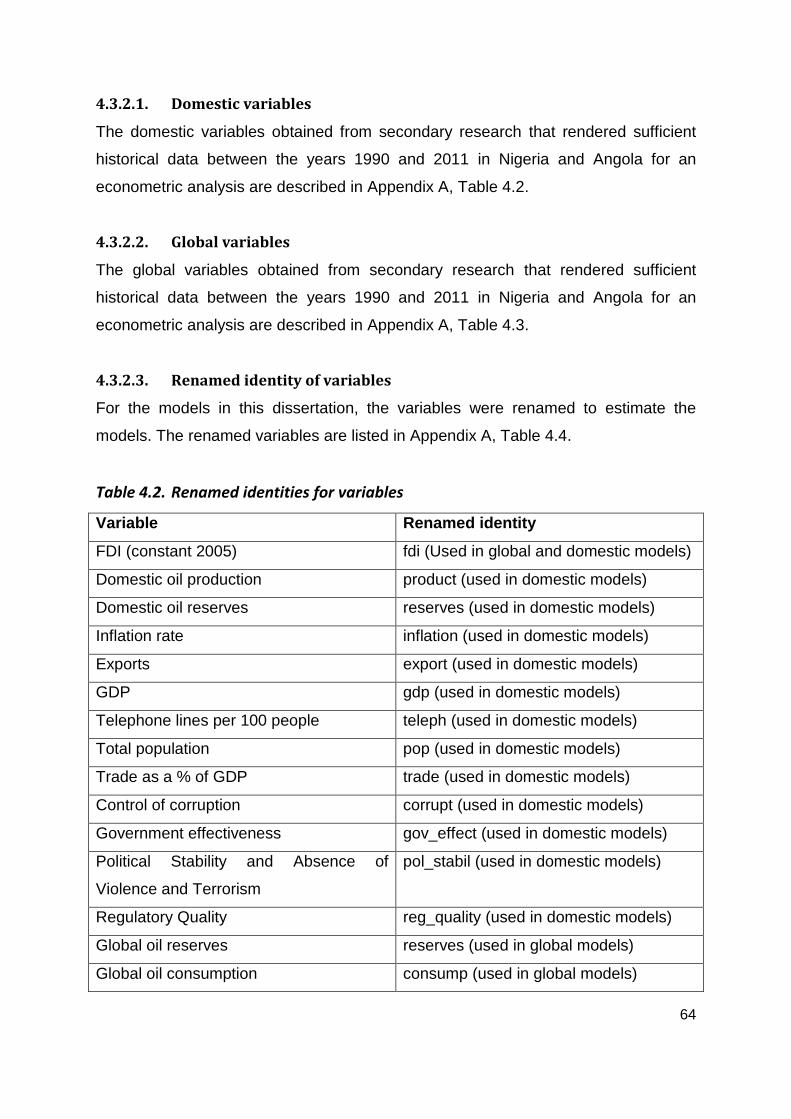

4.3.2.1. Domestic variables ......................................................................... 64

4.3.2.2. Global variables ............................................................................. 64

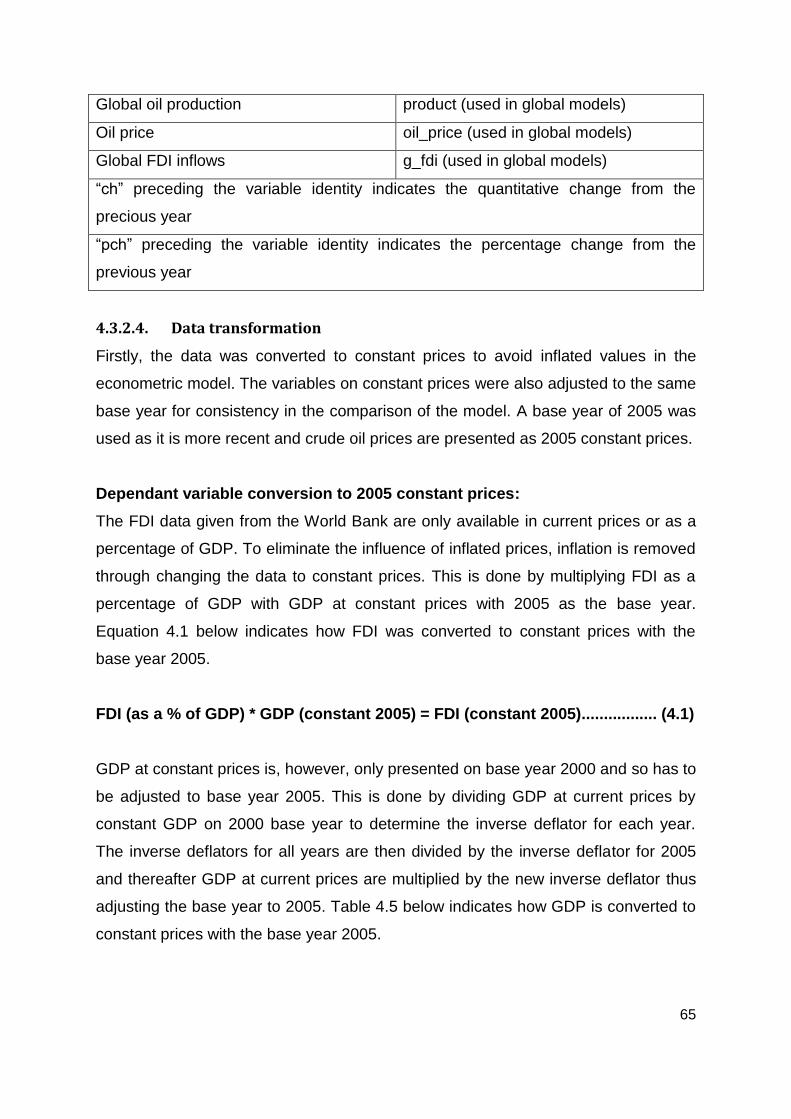

4.3.2.3. Renamed identity of variables ........................................................ 64

4.3.2.4. Data transformation ........................................................................ 65

4.3.3. The FDI functions ................................................................................. 66

4.3.3.1 Nigerian econometric analysis ....................................................... 67

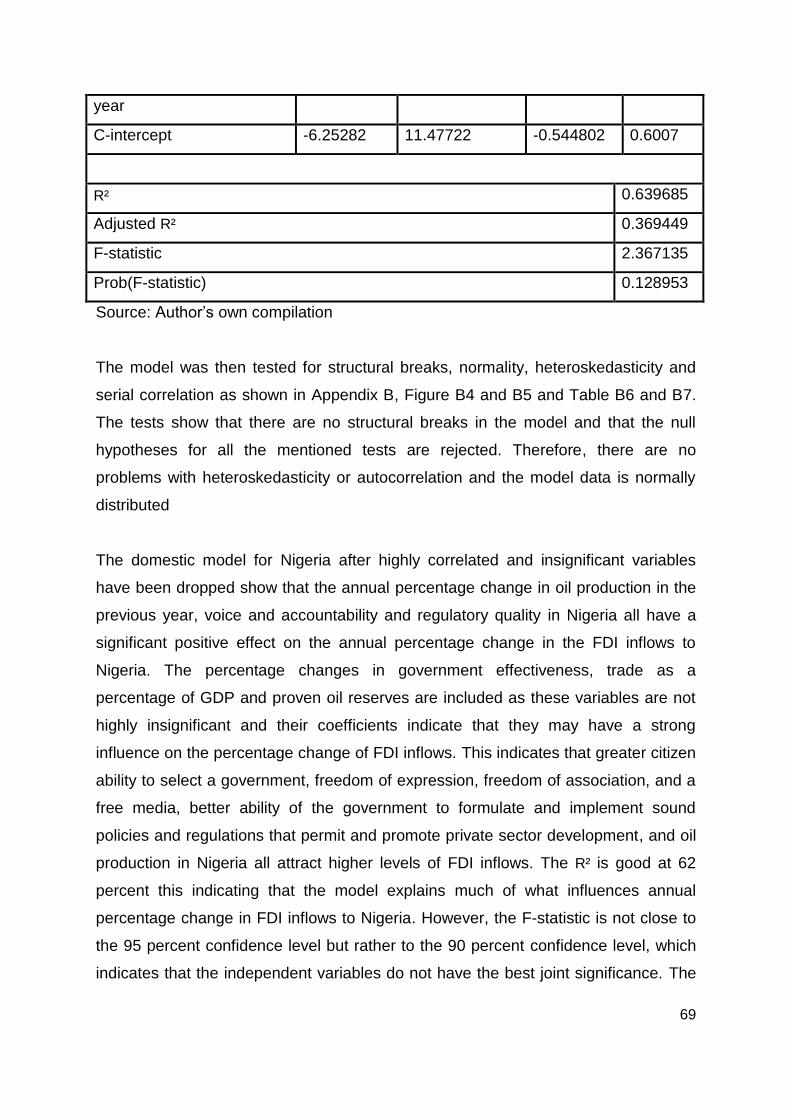

4.3.3.1.1 Nigerian domestic model............................................................ 67

x

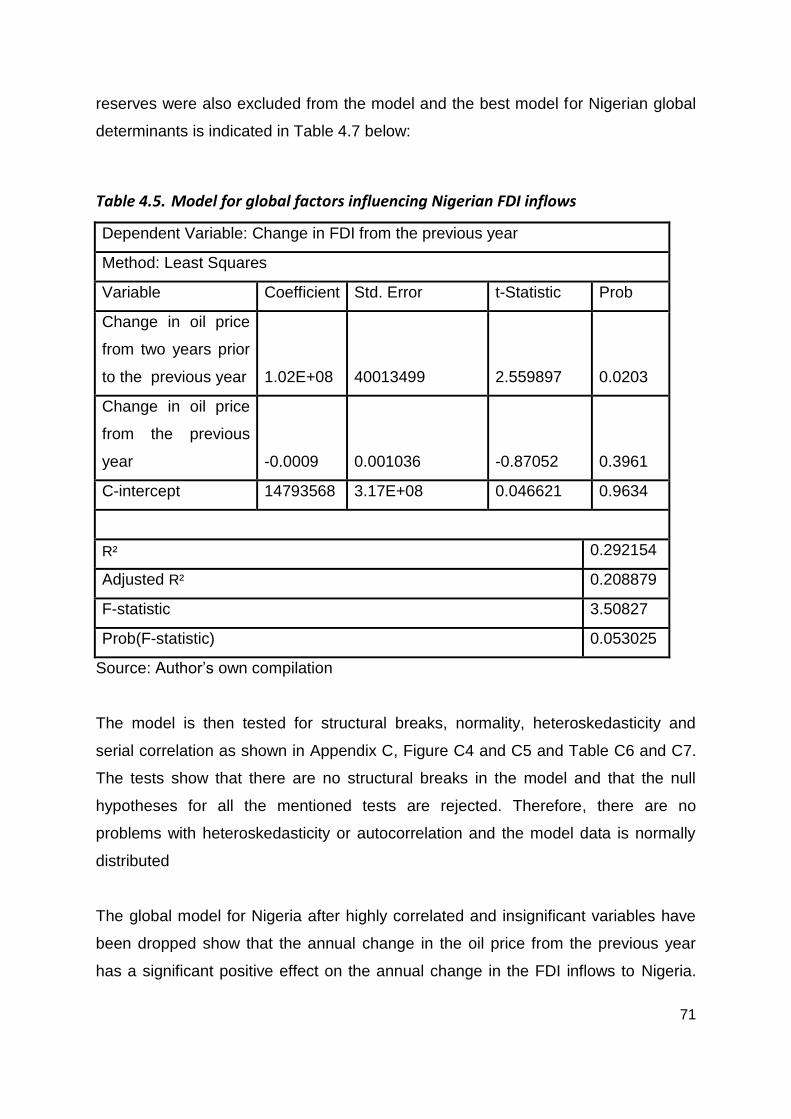

4.3.3.1.2. Nigerian global model ............................................................... 70

4.3.3.2 Angolan econometric analysis ....................................................... 72

4.3.3.2.1. Angolan domestic model ........................................................... 72

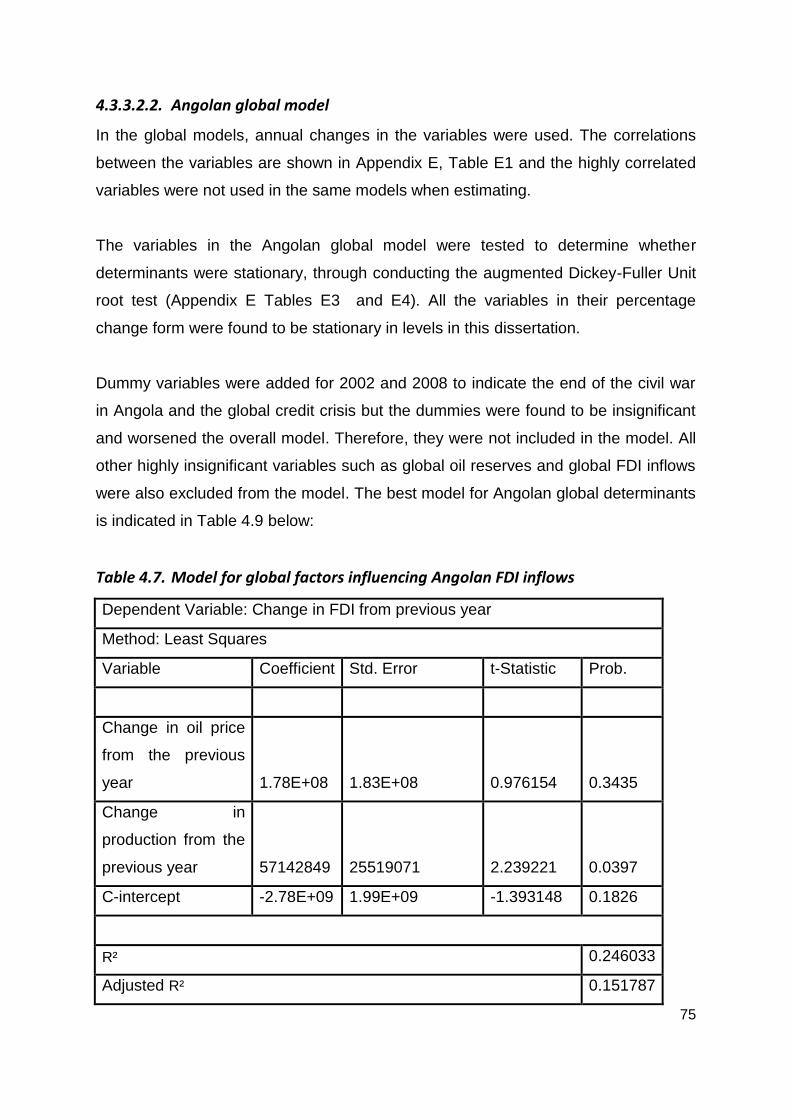

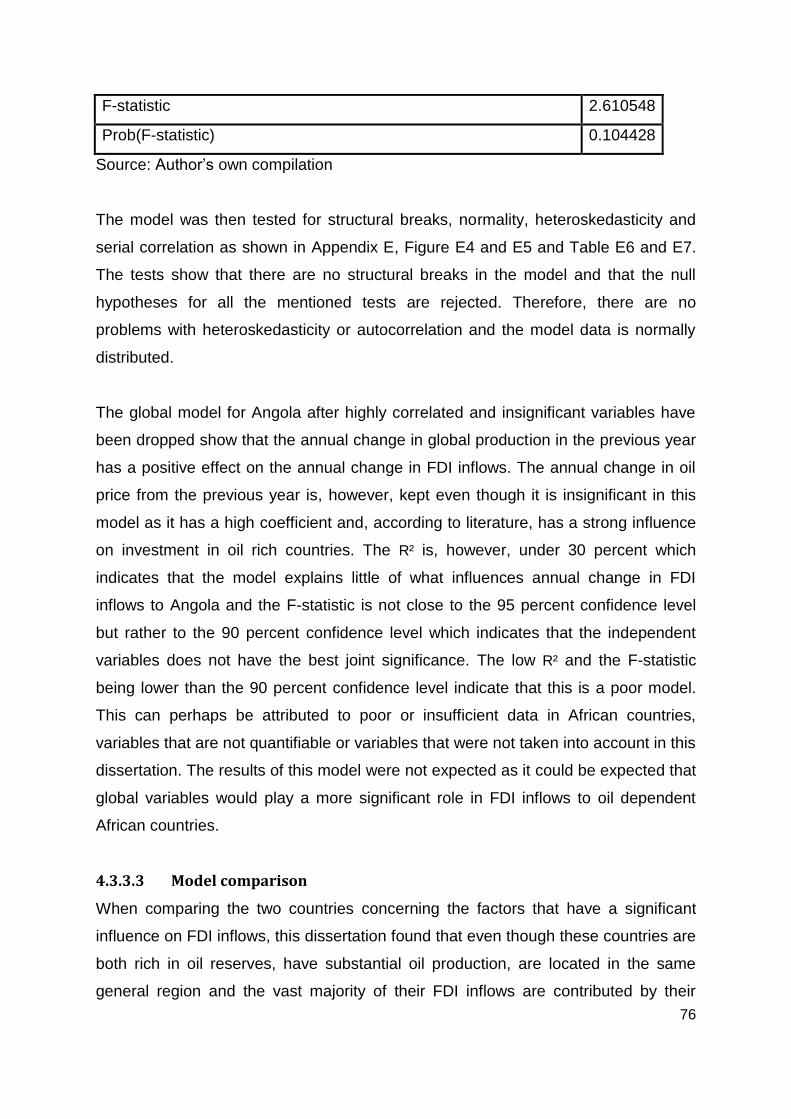

4.3.3.2.2. Angolan global model ............................................................... 75

4.3.3.3 Model comparison .......................................................................... 76

4.4. Conclusion .................................................................................................. 77

Chapter 5 – Summary, Conclusion and Recommendations .................................... 80

5.1. Summary ..................................................................................................... 80

5.2. Conclusion .................................................................................................. 85

Reference list ........................................................................................................... 86

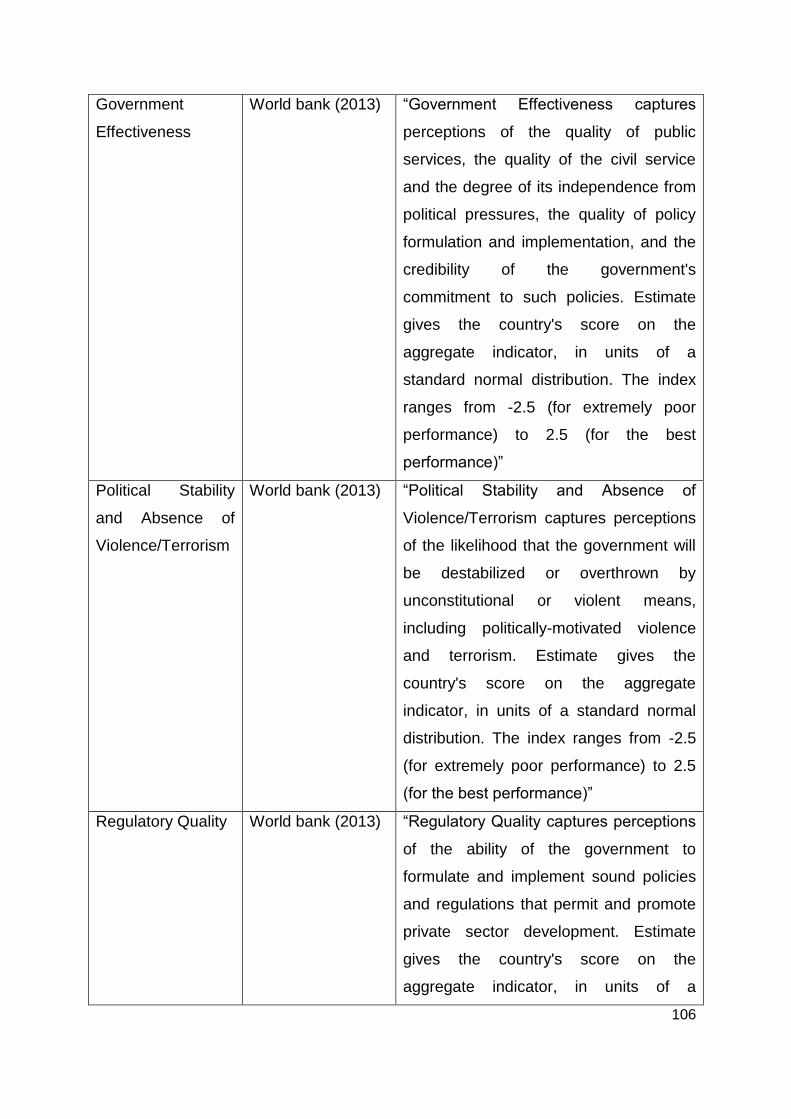

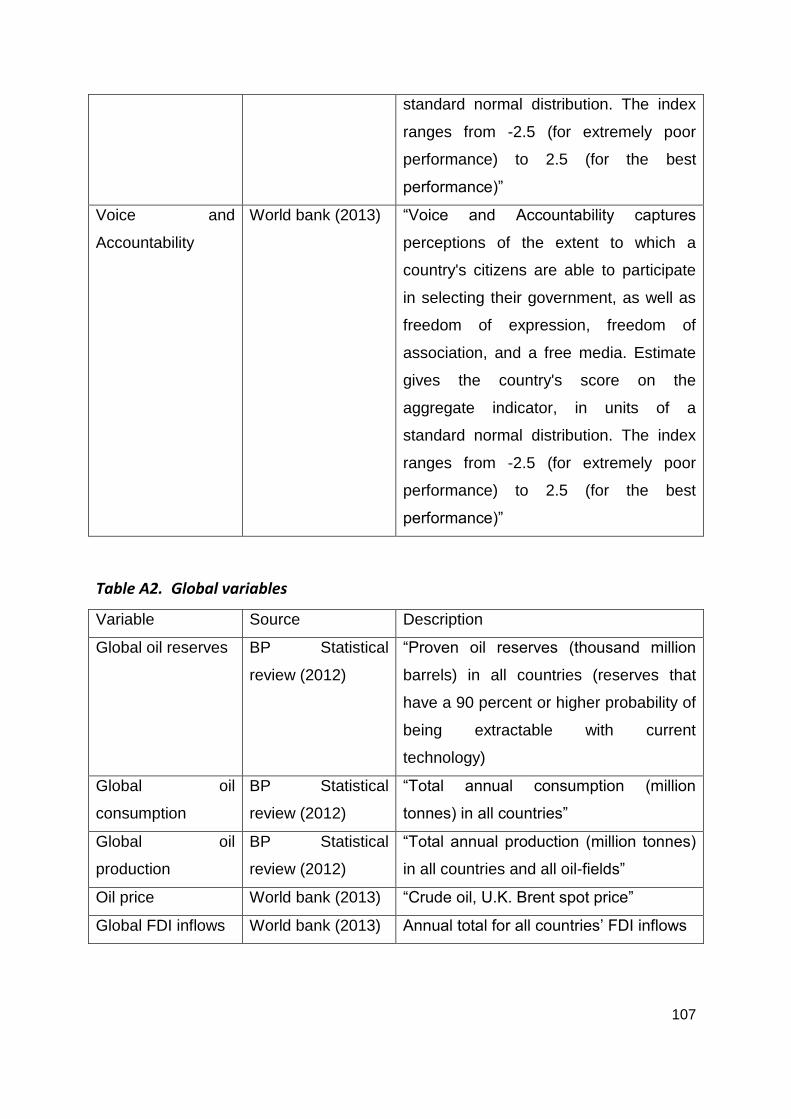

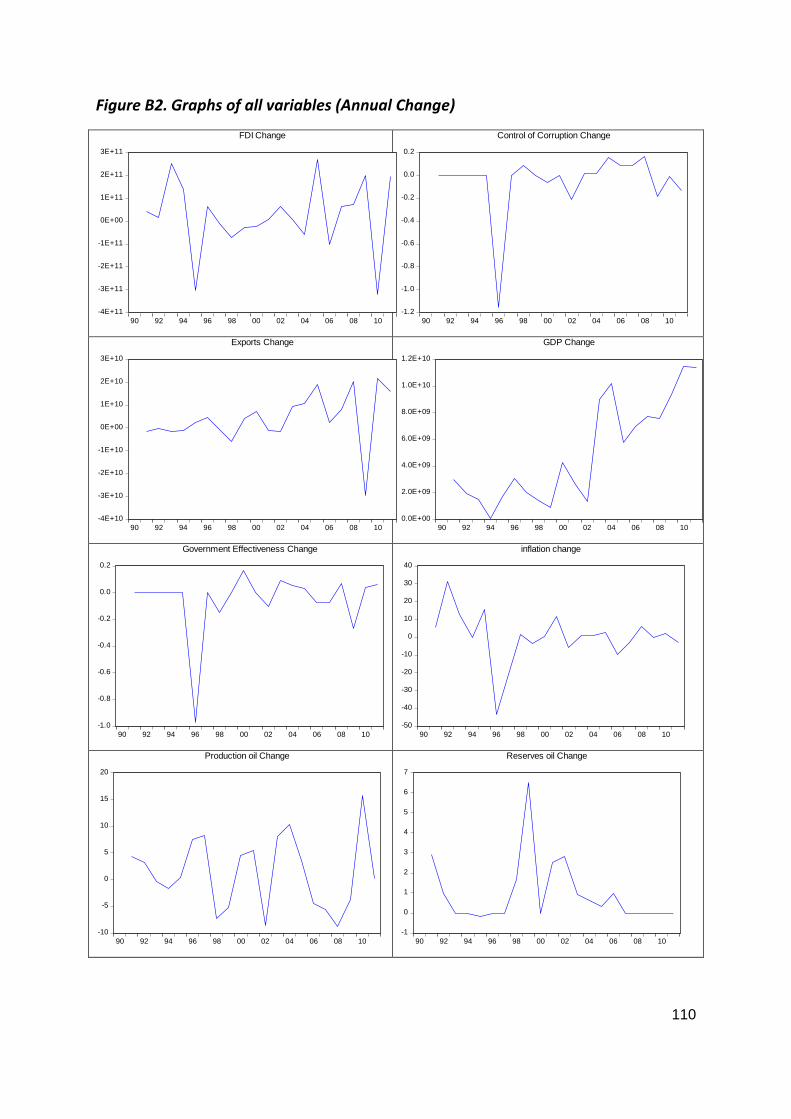

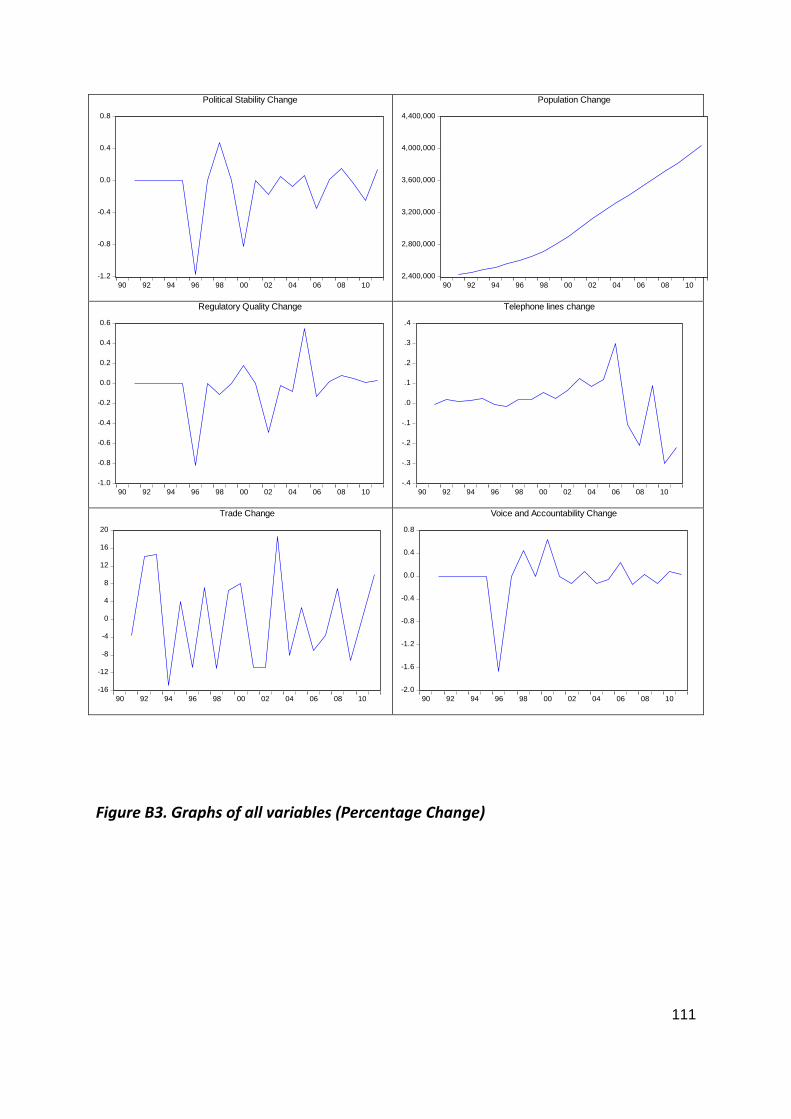

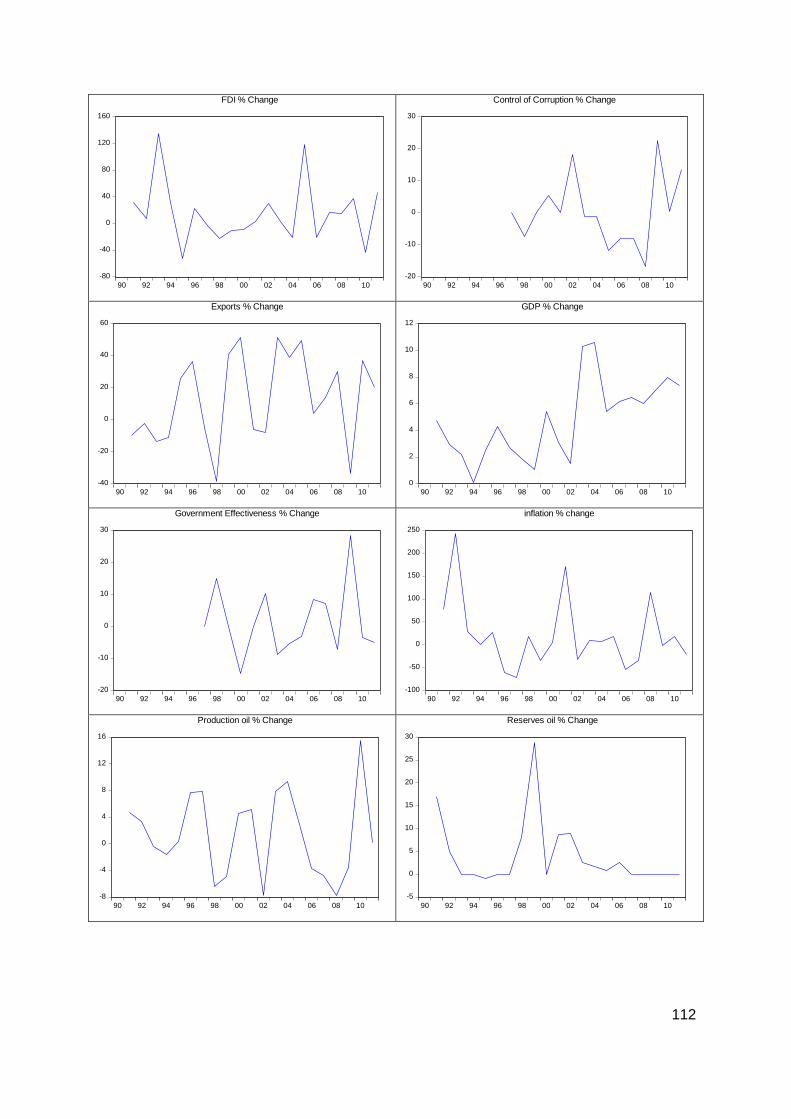

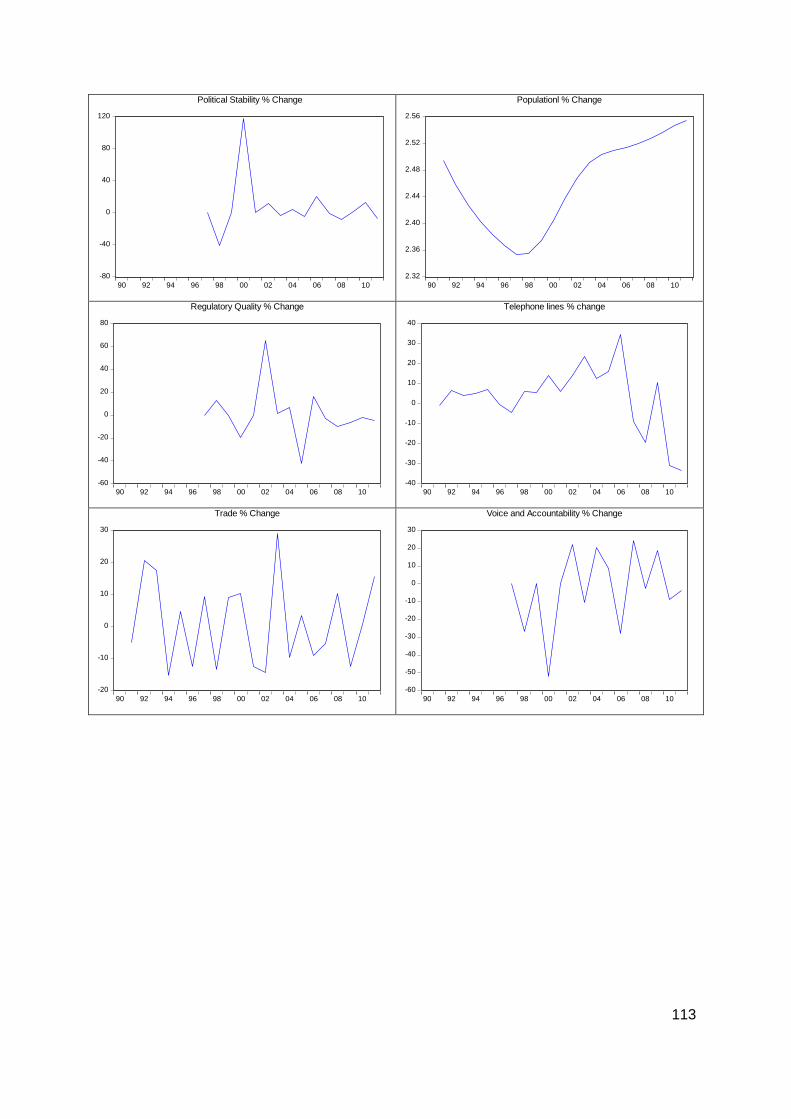

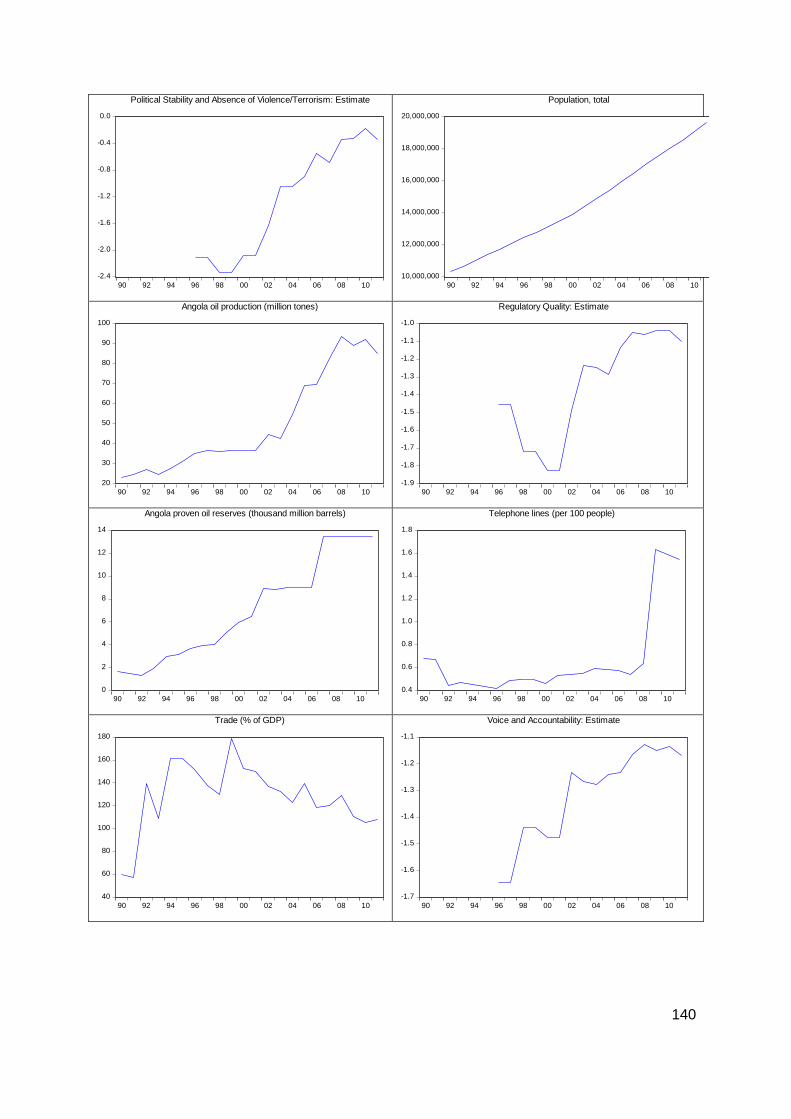

Appendix A Description of variables ................................................................... 103

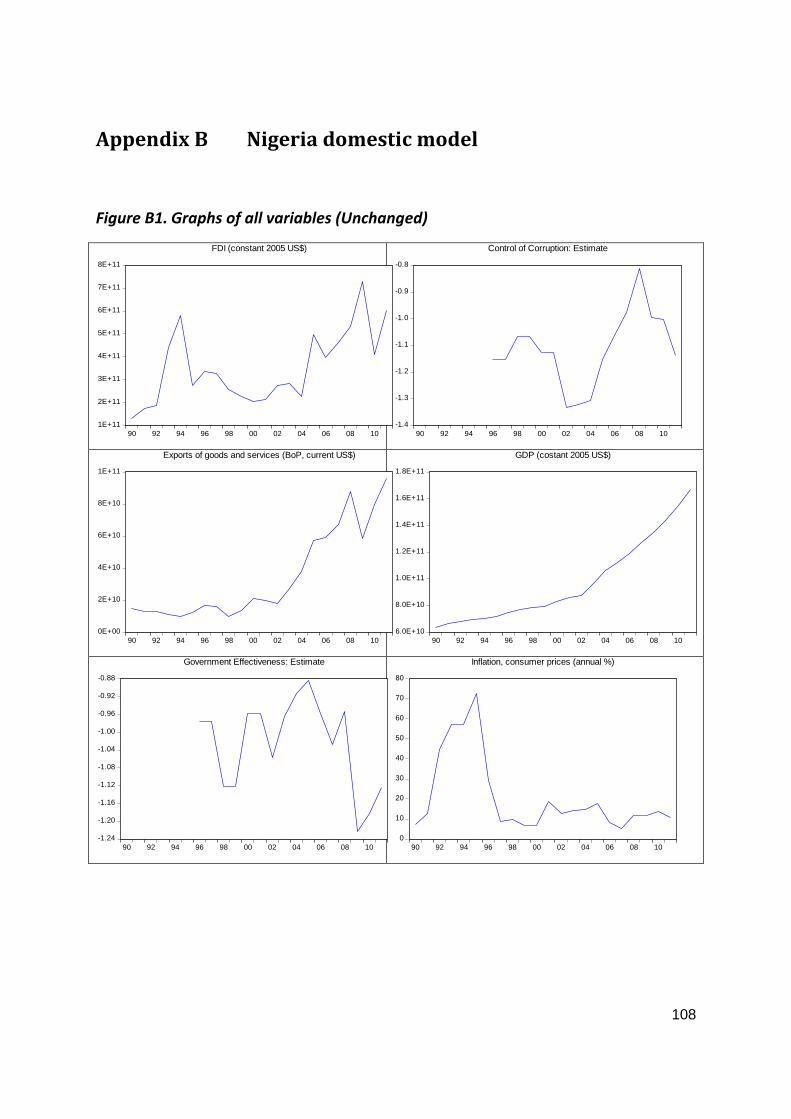

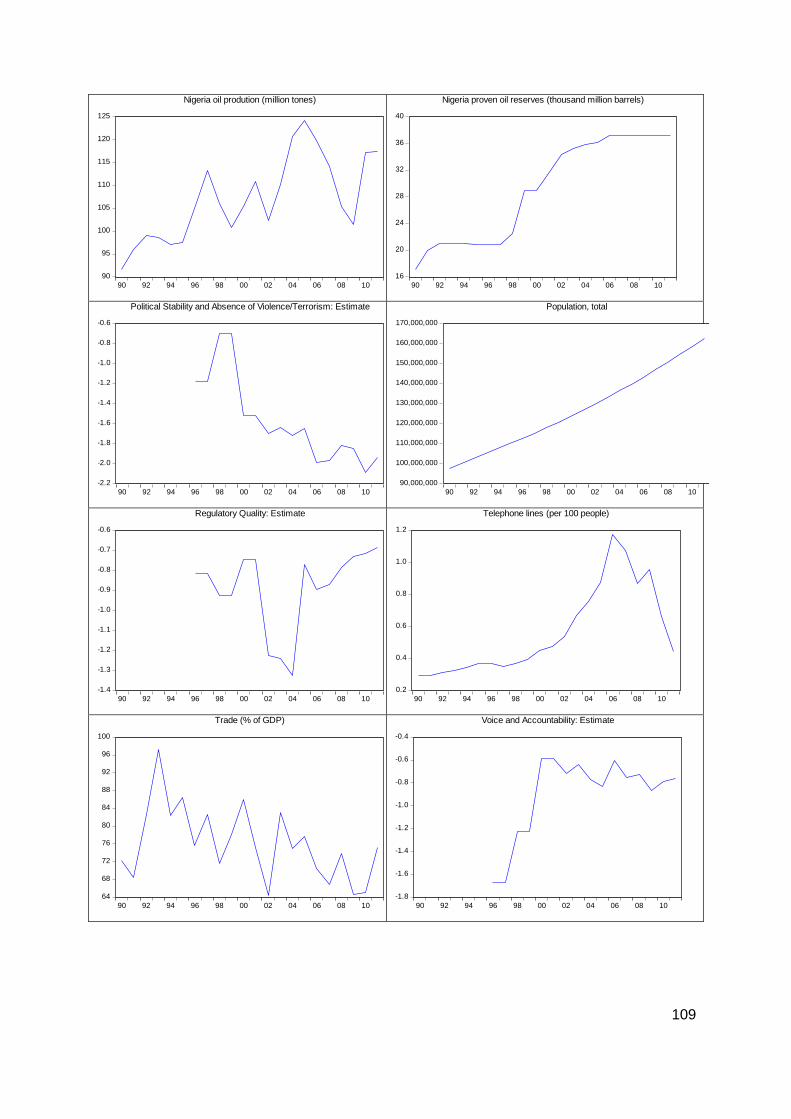

Appendix B Nigeria domestic model ................................................................... 108

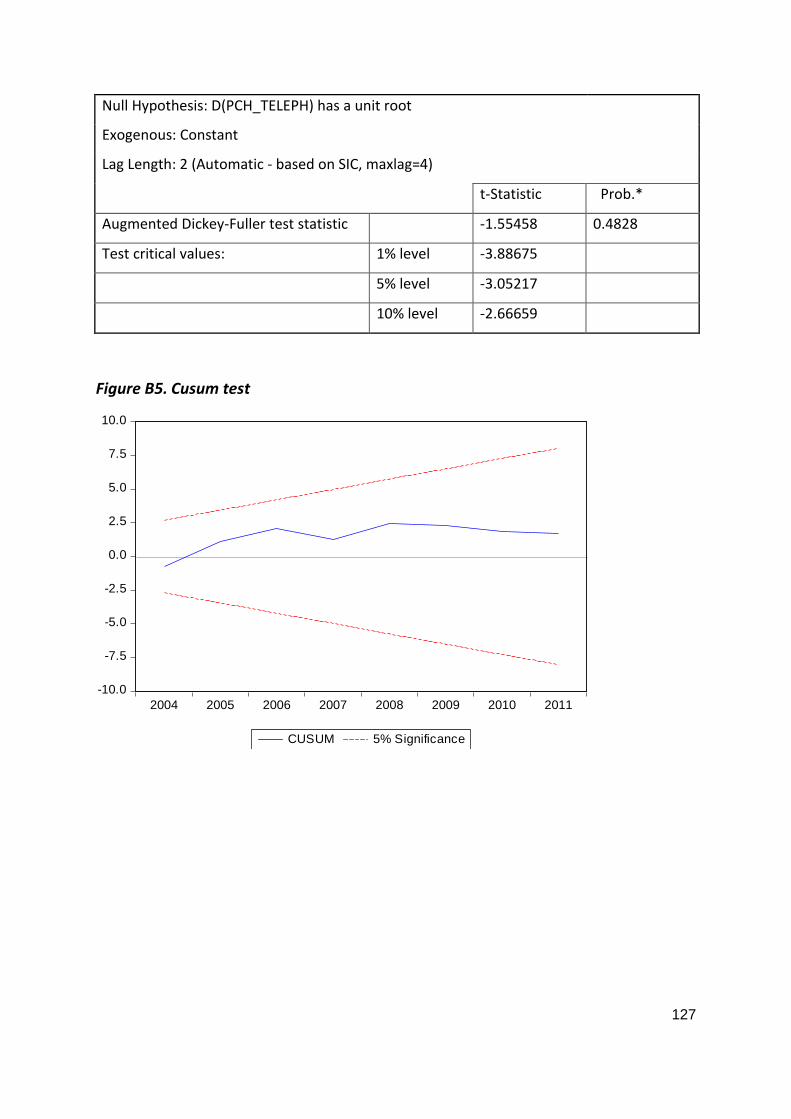

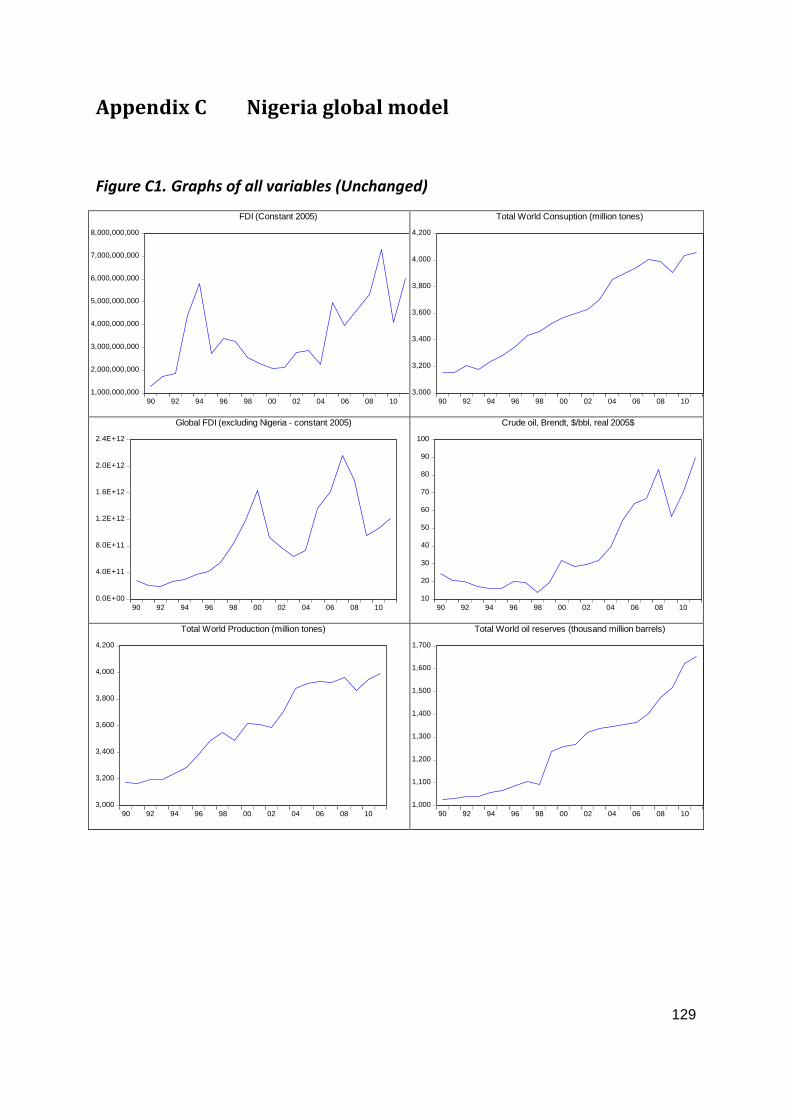

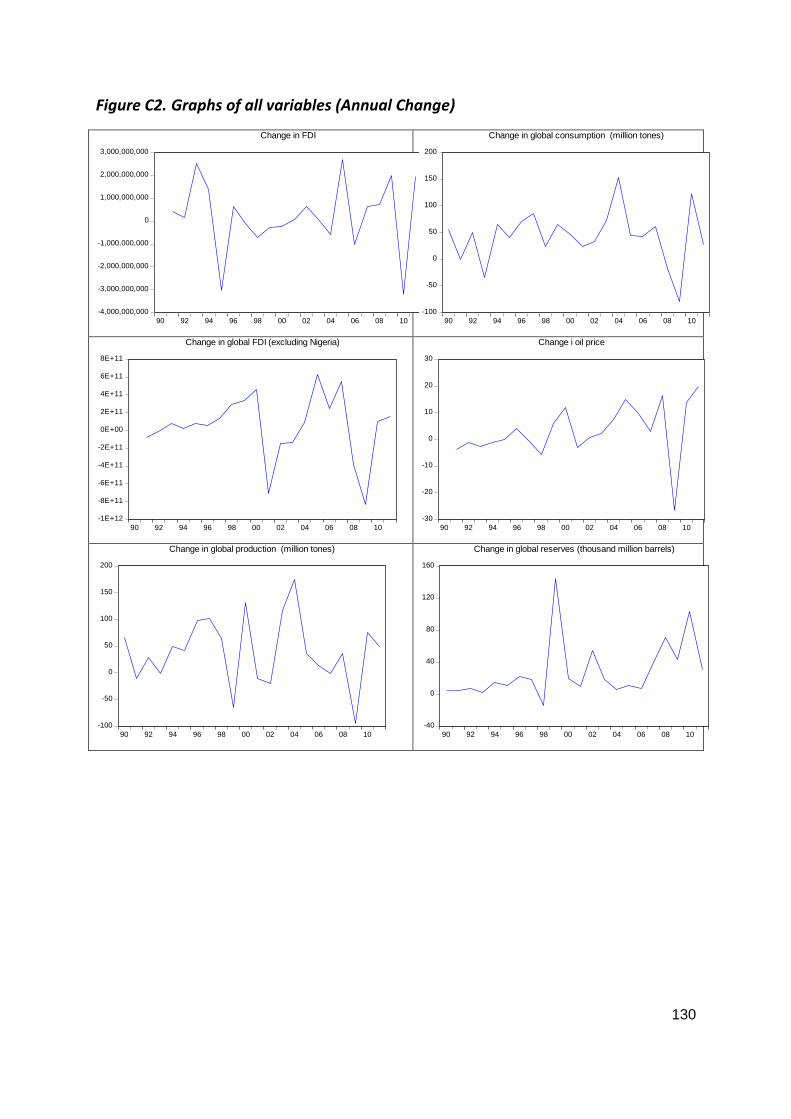

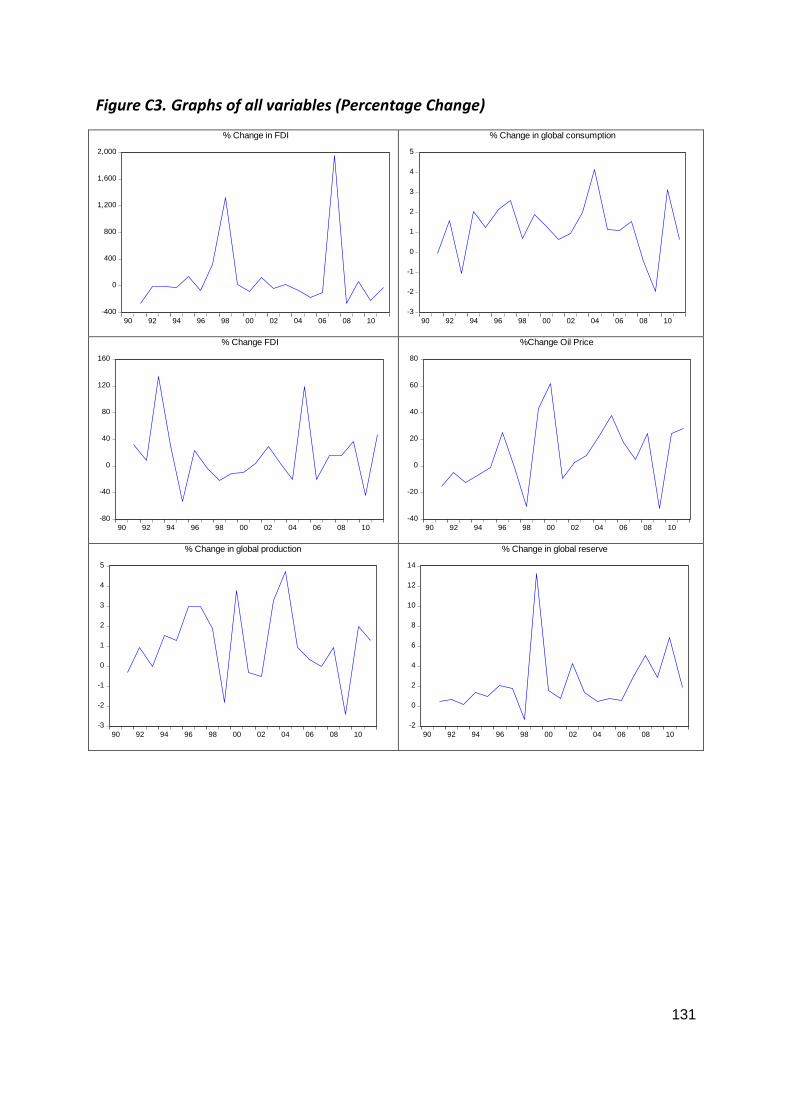

Appendix C Nigeria global model ........................................................................ 129

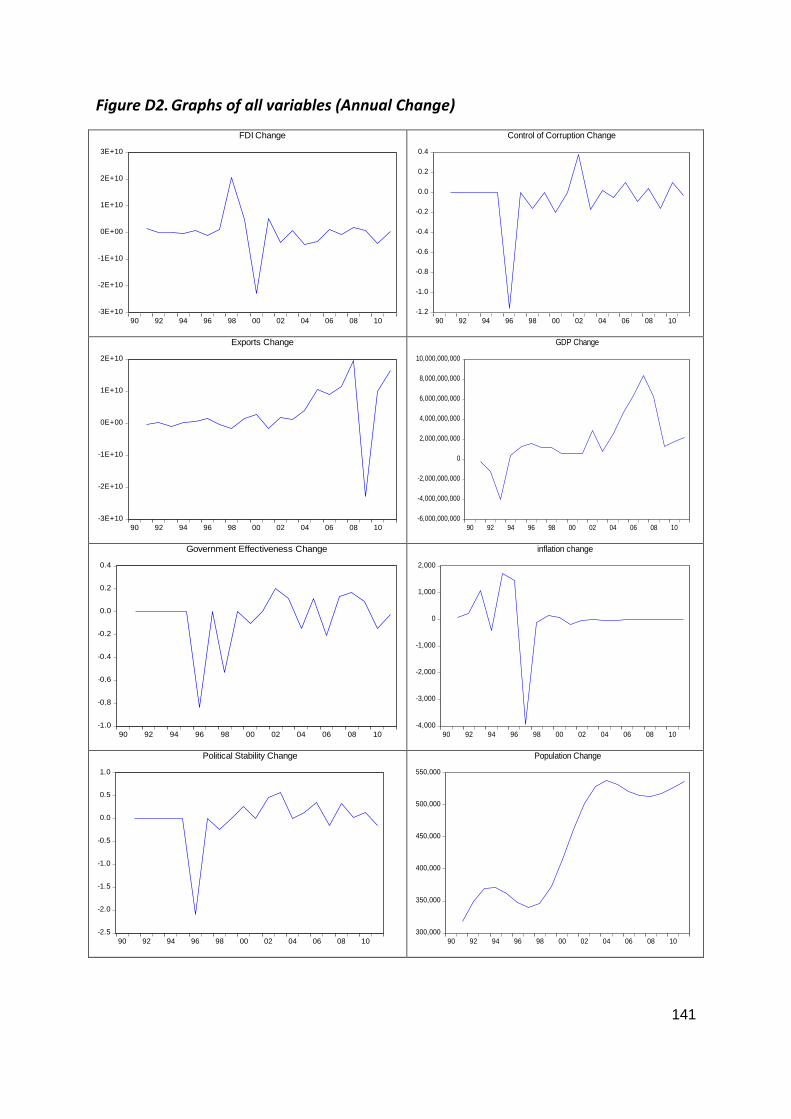

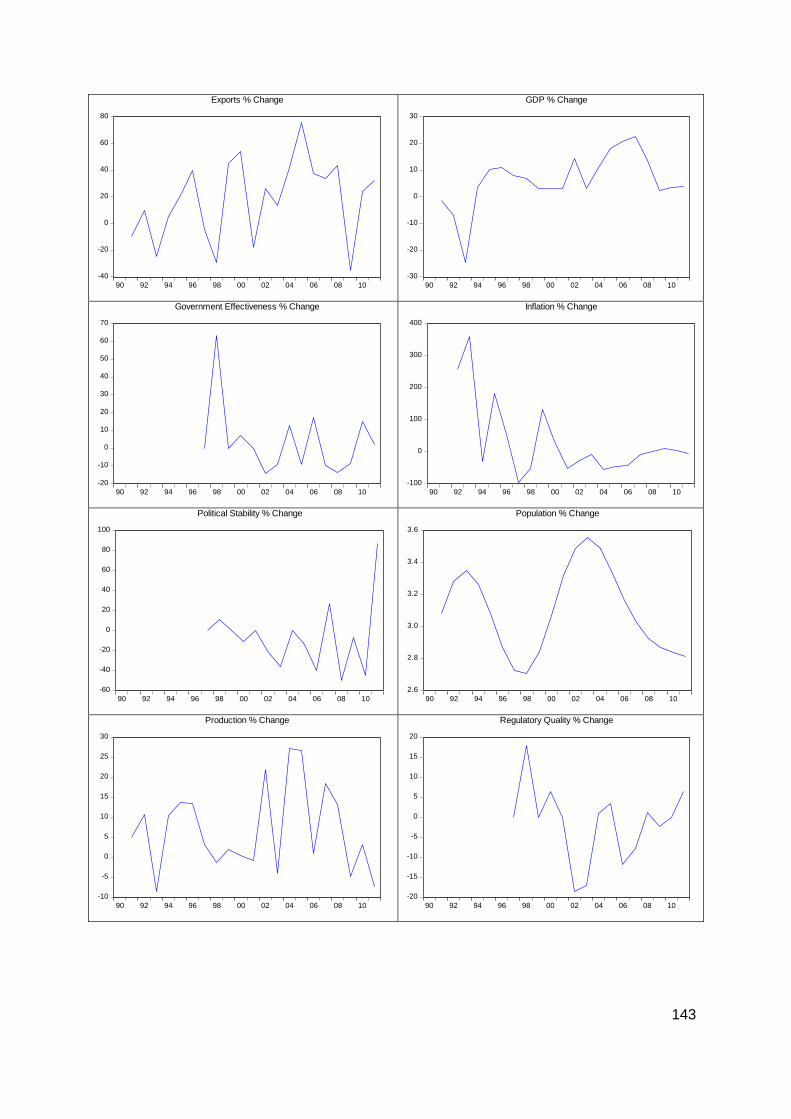

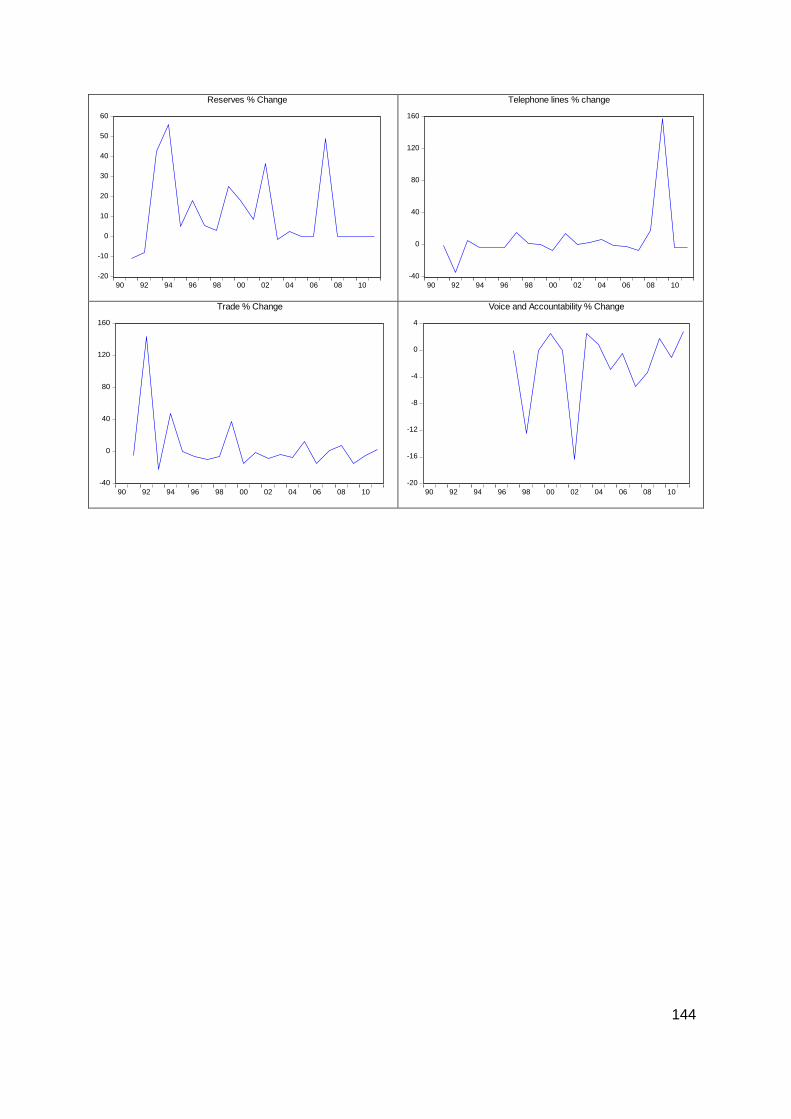

Appendix D Angola domestic model ................................................................... 139

Appendix E Angola Global model ....................................................................... 161

xi

List of tables

Table 1.1: Review of studies on African oil ......................................................... 7

Table 2.1. Production and reserves of top African oil producing countries (2012)

........................................................................................................ 24

Table 2.2. Review of Past studies on determinants of FDI in the oil sector ...... 30

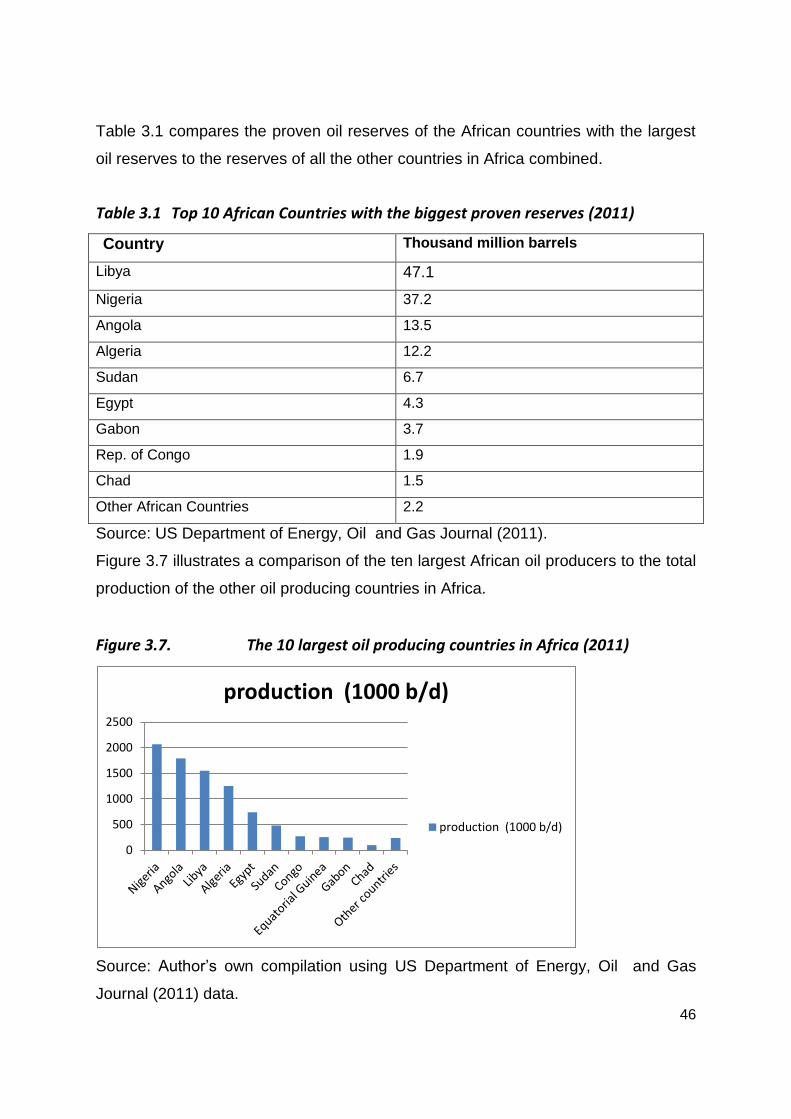

Table 3.1 Top 10 African Countries with the biggest proven reserves (2011) . 46

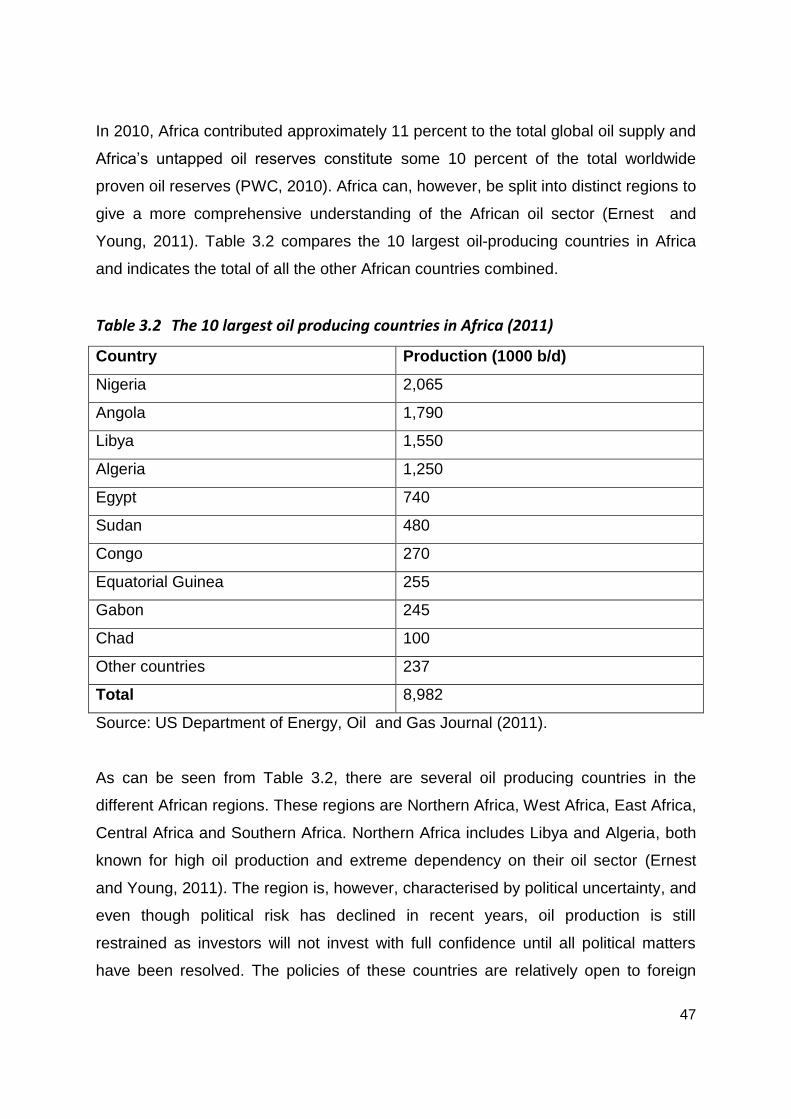

Table 3.2 The 10 largest oil producing countries in Africa (2011) ................... 47

Table 4.1 Factors found to have an influence on FDI inflows .......................... 61

Table 4.2. Renamed identities for variables ..................................................... 64

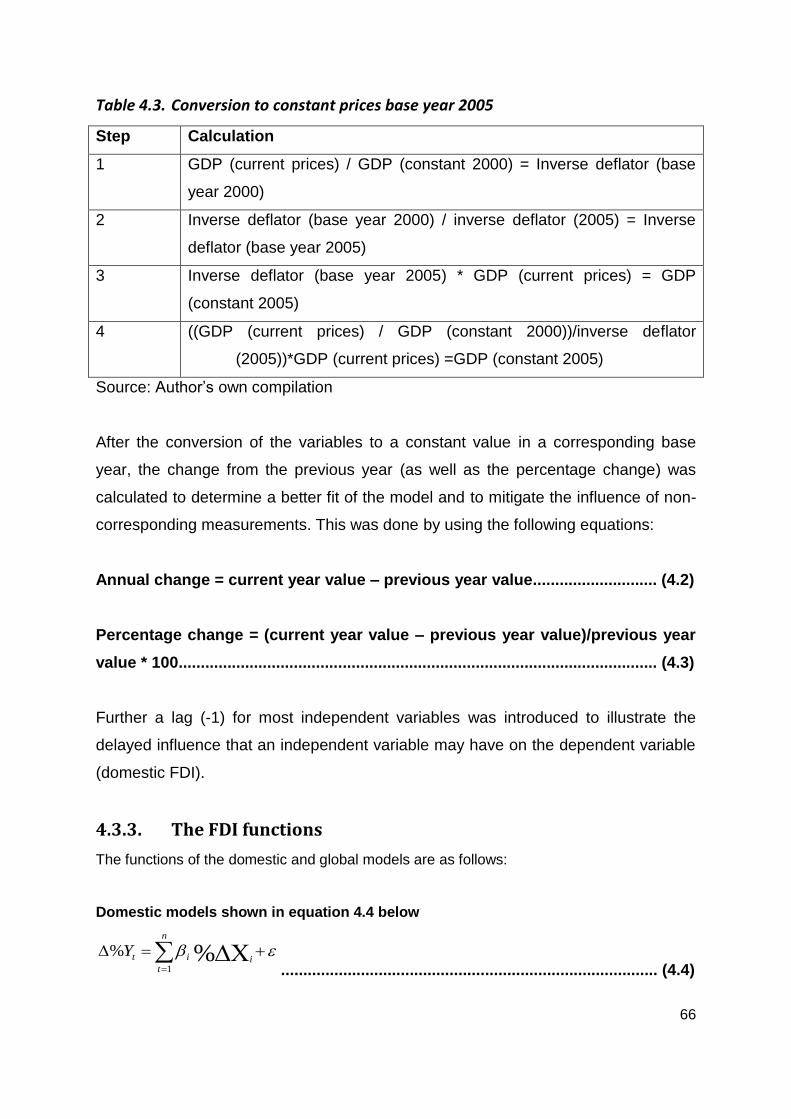

Table 4.3. Conversion to constant prices base year 2005................................ 66

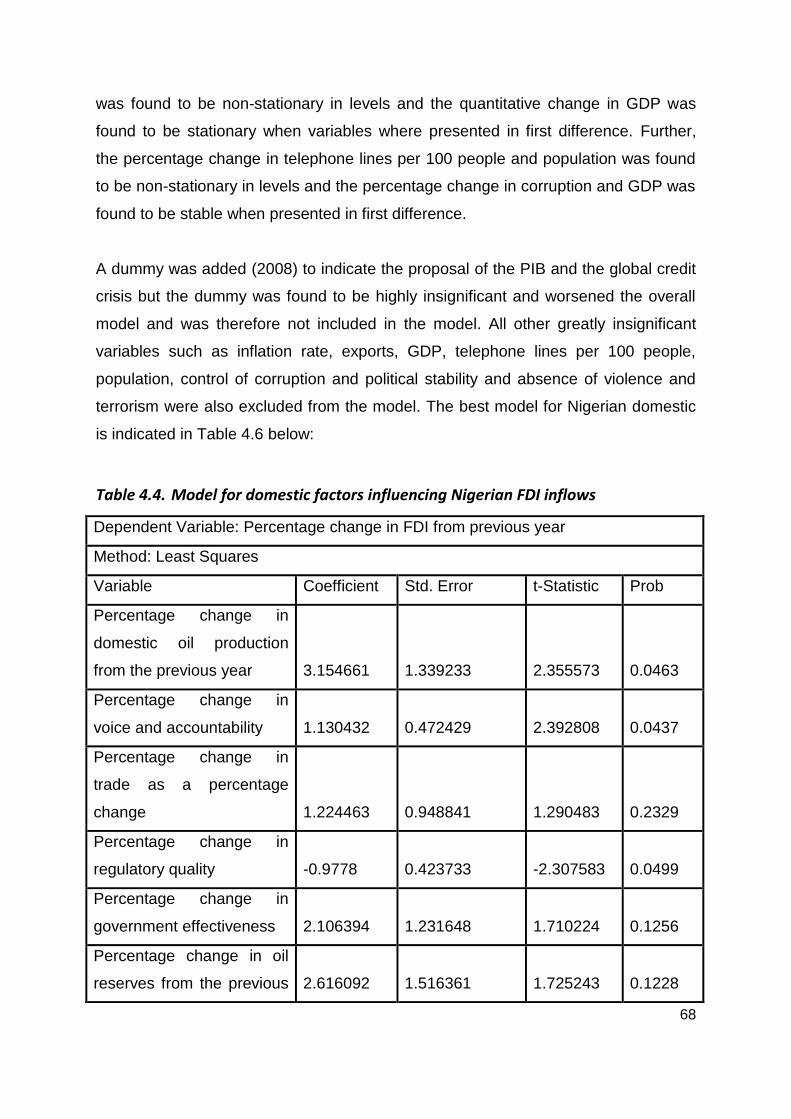

Table 4.4. Model for domestic factors influencing Nigerian FDI inflows ........... 68

Table 4.5. Model for global factors influencing Nigerian FDI inflows ................ 71

Table 4.6. Model for domestic factors influencing Angolan FDI inflows ........... 73

Table 4.7. Model for global factors influencing Angolan FDI inflows ................ 75

xii

List of figures

Figure 2.1. Petroleum fiscal systems ................................................................. 28

Figure 3.1. Global FDI inflows 1970 – 2010 (US Dollars at current prices and

current exchange rates in millions) .................................................. 37

Figure 3.2. Global consumption 1965 – 2010 (Thousand barrels per day) ........ 39

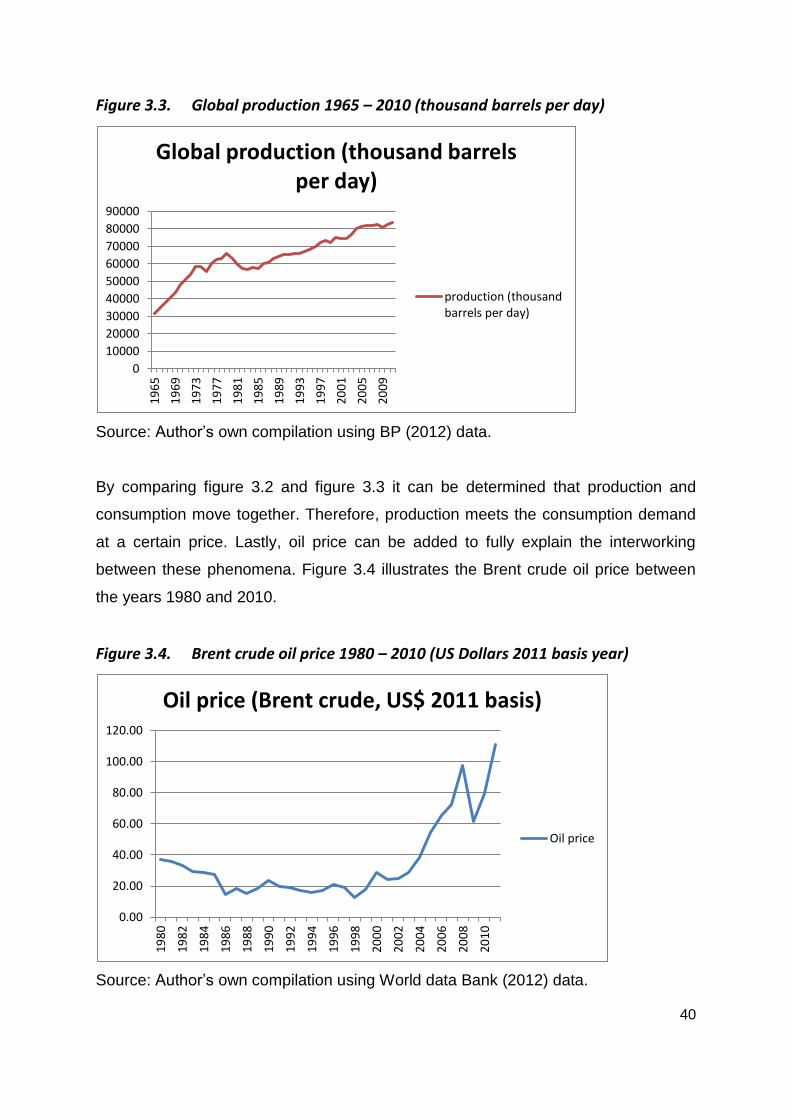

Figure 3.3. Global production 1965 – 2010 (thousand barrels per day) ............ 40

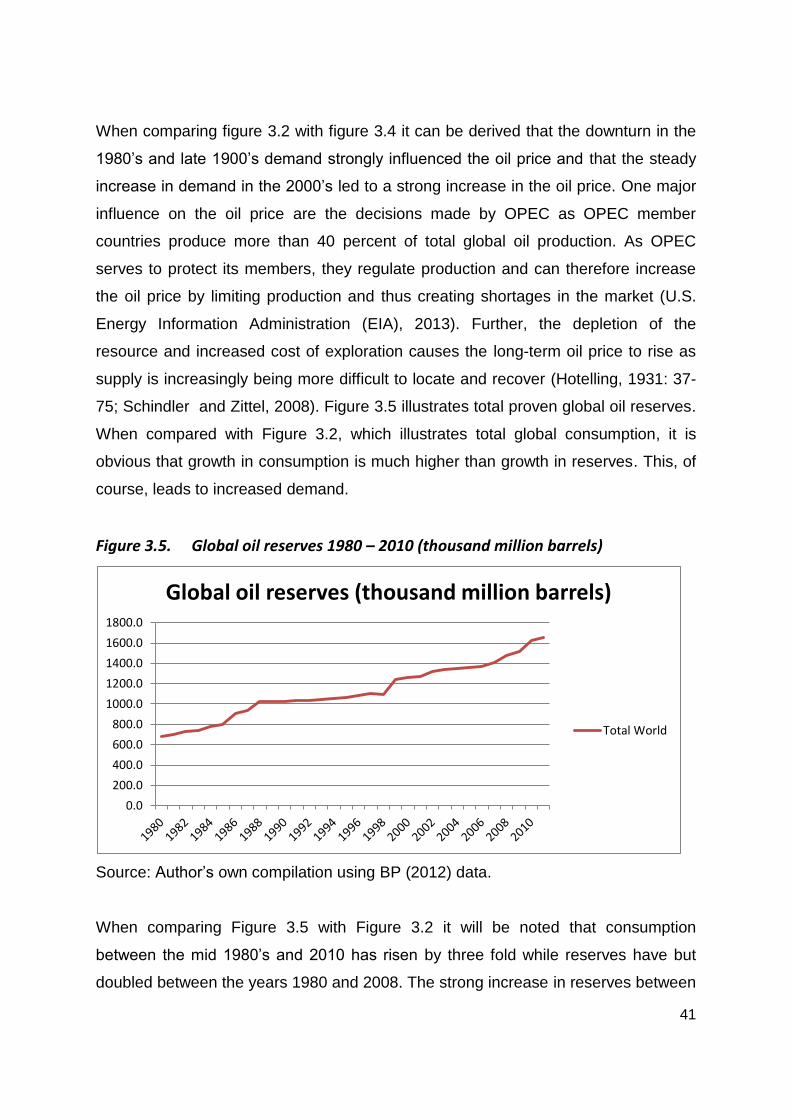

Figure 3.4. Brent crude oil price 1980 – 2010 (US Dollars 2011 basis year) ..... 40

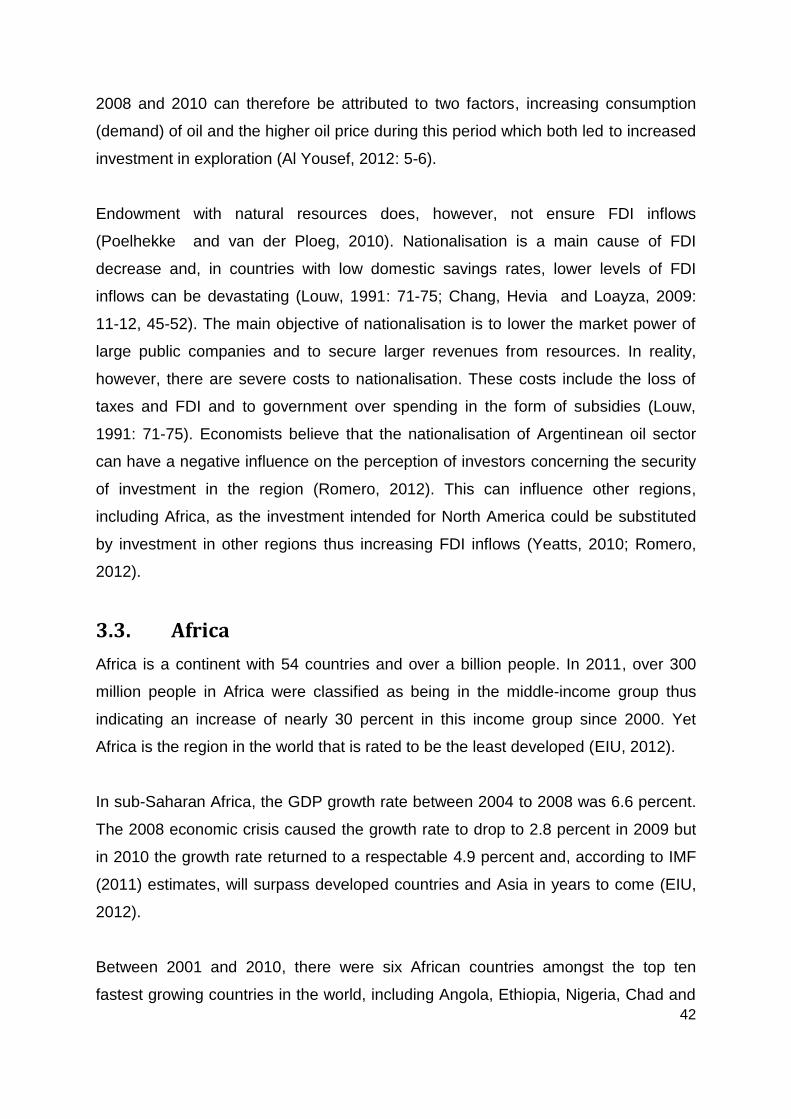

Figure 3.5. Global oil reserves 1980 – 2010 (thousand million barrels) ............. 41

Figure 3.6. African FDI inflows 1970 – 2010 (US Dollars at current prices and

current exchange rates in millions) .................................................. 44

Figure 3.7. The 10 largest oil producing countries in Africa (2011) ................... 46

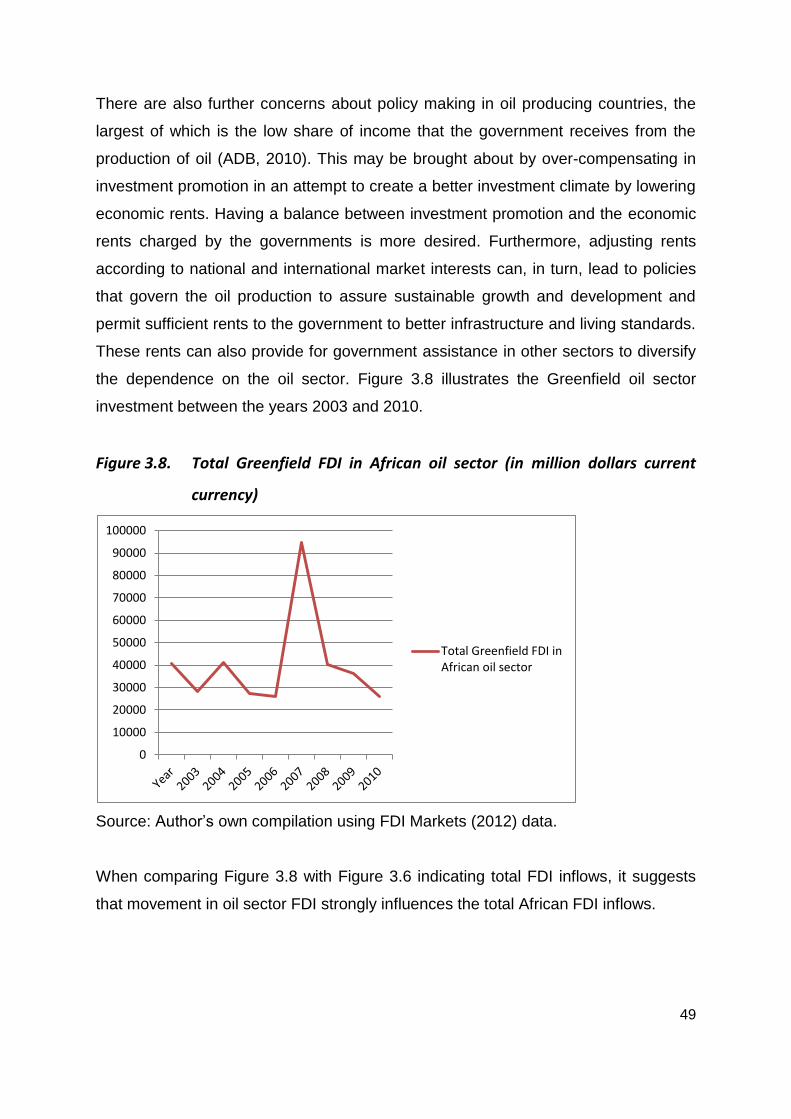

Figure 3.8. Total Greenfield FDI in African oil sector (in million dollars current

currency) ......................................................................................... 49

Figure 3.9. Nigerian oil production 1965 to 2010 ............................................... 51

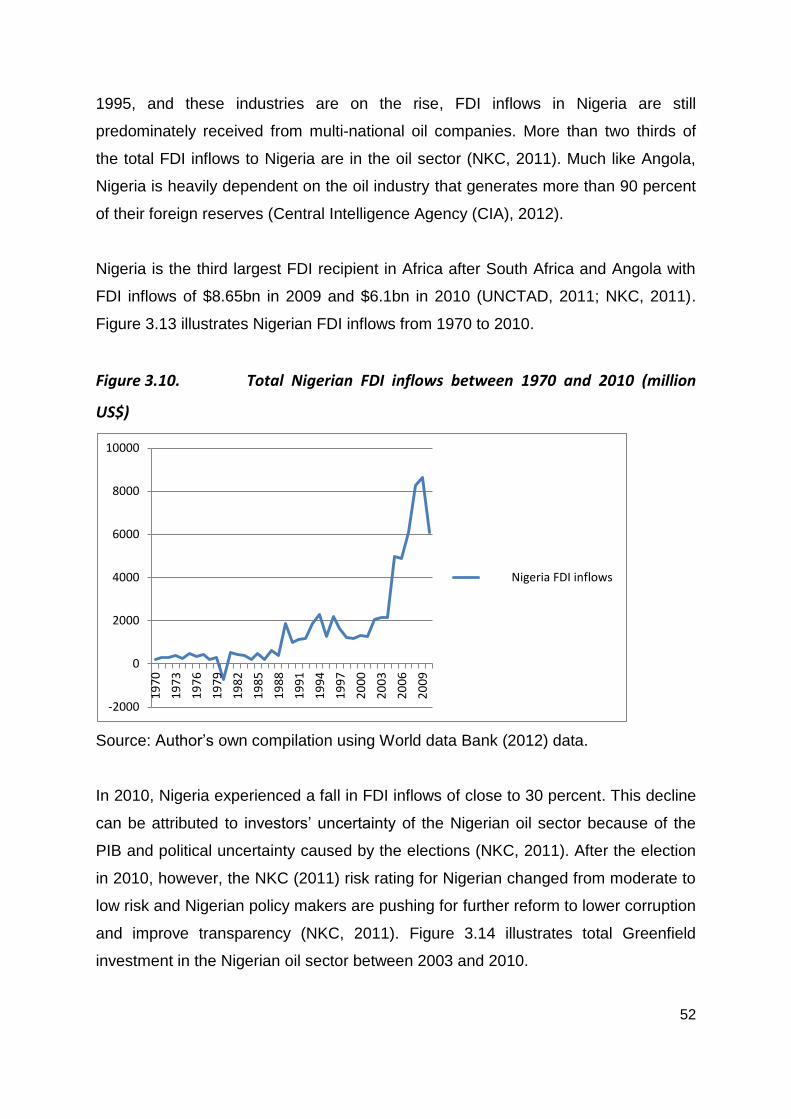

Figure 3.10. Total Nigerian FDI inflows between 1970 and 2010 (million US$)... 52

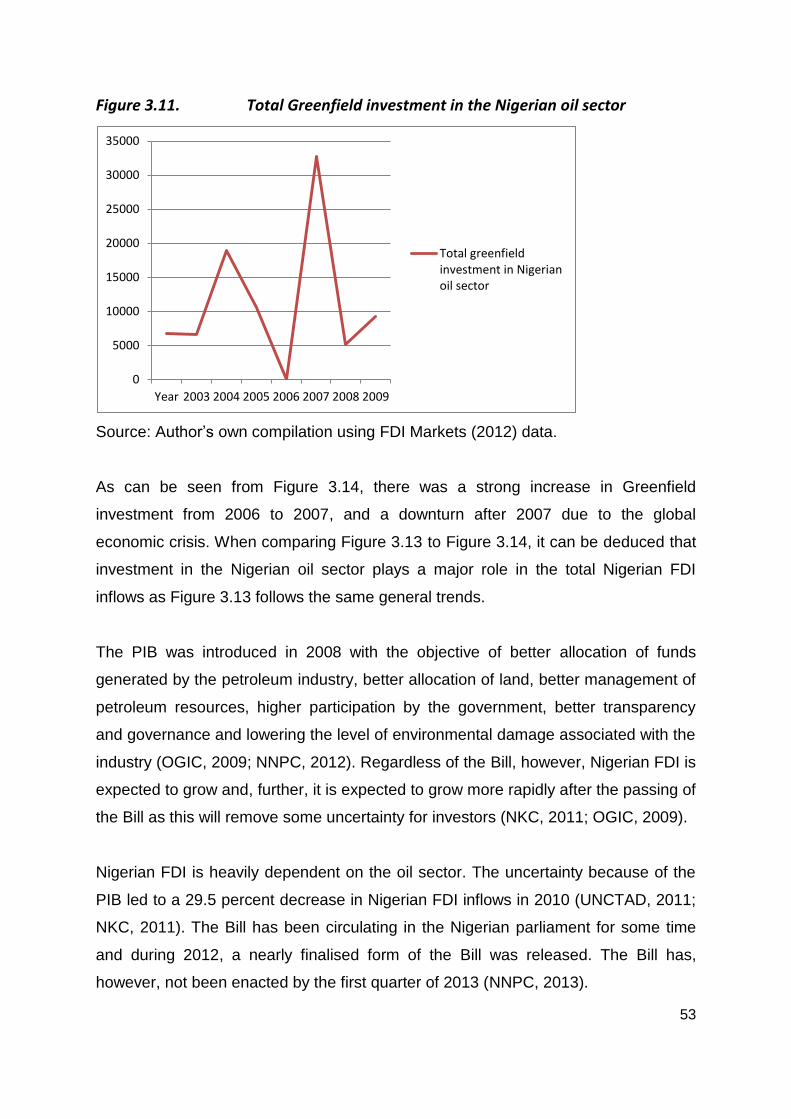

Figure 3.11. Total Greenfield investment in the Nigerian oil sector ..................... 53

Figure 3.12. Angolan oil Production 1965 – 2009 (Thousand barrels per day)... 55

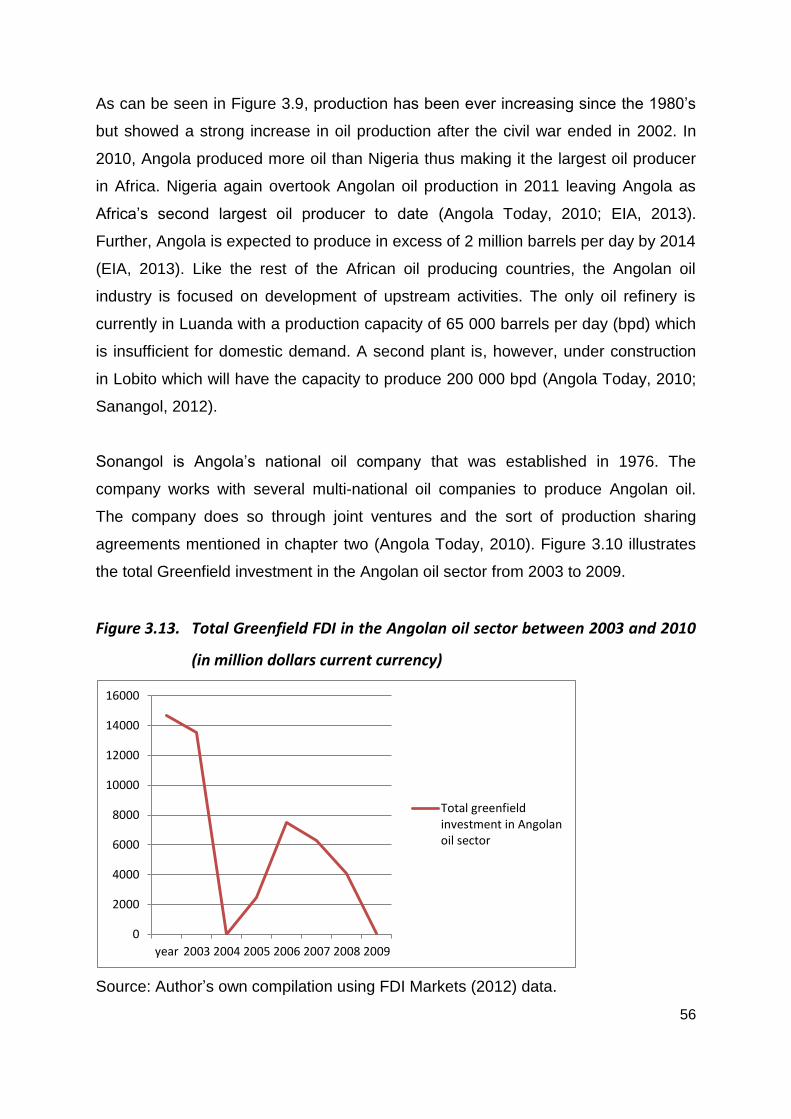

Figure 3.13. Total Greenfield FDI in the Angolan oil sector between 2003 and

2010 (in million dollars current currency) ......................................... 56

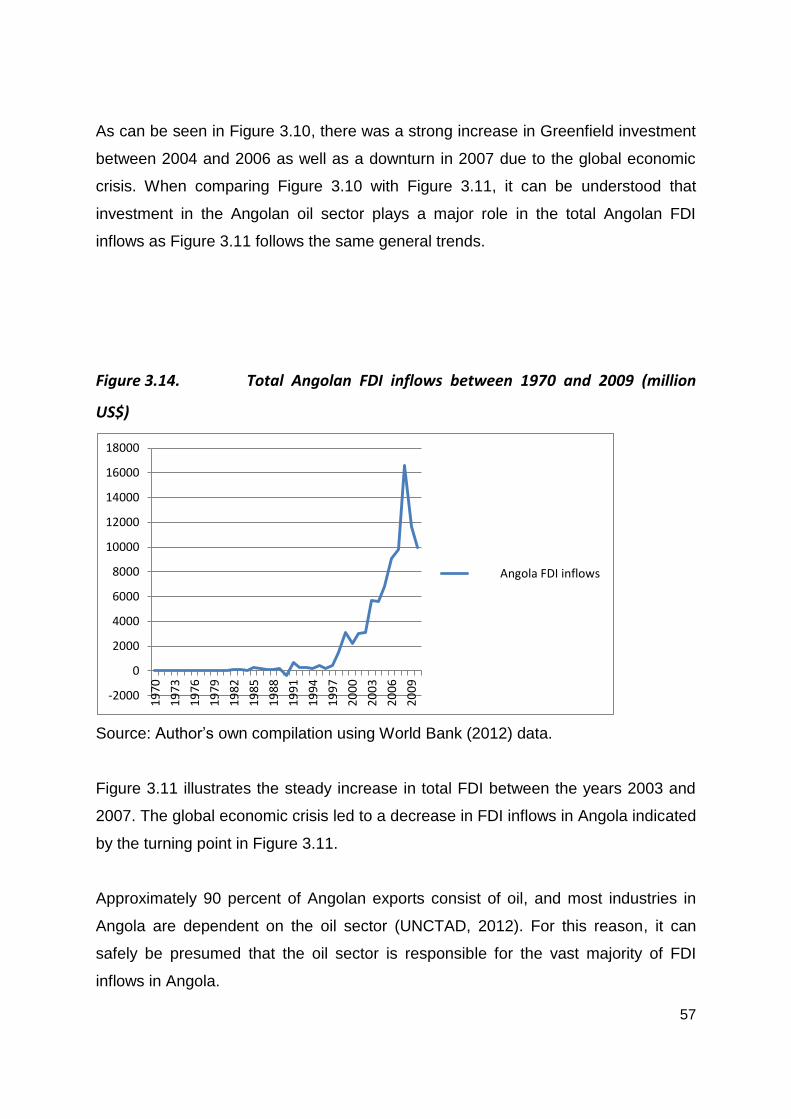

Figure 3.14. Total Angolan FDI inflows between 1970 and 2009 (million US$) ... 57

xiii

List of abbreviations

BP: British Petroleum

Bpd: Barrels per day

CIA: Central Intelligence Agency

COMESA: Common Market for Eastern and Southern Africa

CRF: Council on Foreign Relations

EAC: East African Community

EIA: U.S. Energy Information Administration

FAO: Food and Agriculture Organisation

FDI: Foreign Direct Investment

GDP: Gross Domestic Product

IMF: International Monetary Fund

IOCs: International oil companies

LDCs: Least developed countries

LNG: Liquefied Natural Gas

MNCs: Multi-national companies

MNOCs: Multi-national oil companies

NCEMA: National Centre for Economic Management and Administration

NIPC: Nigerian Investment Promotion Commission

NNPC: Nigerian National Petroleum Corporation

NOCs: National oil companies

OECD: Organisation for Economic Co-operation and Development

xiv

OGIC: Oil and Gas sector reform Implementation Committee

OPEC: Organization of the Petroleum Exporting Countries

PIB: Petroleum Industry Bill

PSA: Production Sharing Agreement

PSC: Production Sharing Contract

SADC: Southern African Development Community

SAP: Structural Adjustment Programme

SPE: Society of Petroleum Engineers

UNECA: United Nations Economic Commission for Africa

UNCTAD: United Nations Conference on Trade and Development

WPC: The World Petroleum Congress

1

Chapter 1: Introduction and context of analysis

1.1. Introduction: Rationale and context

Africa is a continent with vast natural resources. However, a major problem faced by

Africa is the lack of local investment because of the low domestic savings rates.

Nevertheless, Africa is a continent with potential, as much of Africa’s natural

resources have lain untapped for many years. Foreign direct investment (FDI) has

given African countries a way to supplement their lack in investment United Nations

Conference on Trade and Development (UNCTAD, 2011). In most oil rich African

countries, the oil sector receives the majority of FDI inflows and outweighs all the

other sectors combined (UNCTAD, 2011; Levitt, 2011).

Traditionally, FDI in Africa was primarily attracted by natural resources like gold and

coal but for some time now the oil industry has been showing an increased ability to

attract FDI (Levitt, 2011). The oil sector is currently the highest FDI recipient sector

in Africa and is, according to many economists, the continent’s way forward and a

doorway to a brighter future concerning sustainable economic growth and

development (Levitt, 2011).

Nigeria and Angola are the largest oil producing countries in Africa (UNCTAD, 2011;

US Department of Energy, 2011). Further, these countries also have the second and

third biggest oil reserves in Africa (BP, 2012; OPEC, 2011). Therefore, these two

countries were chosen as subjects as they not only have significant oil reserves and

production but are also both heavily dependent on FDI in their oil sectors (UNCTAD,

2011). Therefore, this dissertation will focus on oil sector FDI inflows to Nigeria and

Angola. The aim of this dissertation is to identify the factors that influence FDI inflows

to the oil sectors of Nigeria and Angola.

FDI is defined as long-term investment made by entities outside the borders of the

host country (UNCTAD, 2005). The aim of these investments is to gain a long-

standing interest in a sector with good prospects for growth. To qualify as FDI, the

investor must acquire at least ten per cent of the company’s voting stock (UNCTAD,

2

2005). Alternatively, a new business can be established or an existing business can

be acquired as a whole by the foreign investors (UNCTAD, 2005). There is,

therefore, a clear distinction between FDI and portfolio investment as portfolio

investment entails limited control of the company. It is generally shorter in term and

therefore more volatile (Goldstein and Razin, 2006: 32-33).

Within FDI, two main categories of investment can be distinguished, namely,

Greenfield investment and Brownfield investment (Paull, 2008: 9-15). Greenfield

investment is the direct investment through funding of new facilities in the host

country. This type of investment is optimal for the host country as it provides linkages

to the global market place, the transfer of knowledge and technology as well as

contributing to job creation (Qiu and Wang, 2011: 836-838). Brownfield investment

consists of mergers and acquisitions. Ownership of existing assets owned by local

firms is transferred to foreign companies (Paull, 2008: 9-15). This form of investment

does not necessarily lend itself to long-term benefits in the local economy unlike

Greenfield investment (Estrinet and Meyer, 2011: 3-5).

FDI is seen as a positive attribute for any economy but it is especially beneficial to

African countries (Lumibla, 2005). Most African countries have a low savings rate

that is insufficient to fund local investment (Kirk and Celemens, 1999). FDI has the

potential to have a positive effect on a number of economic factors within the host

country. These positive effects include higher foreign currency reserves, growth in

the countries’ gross domestic production (GDP) and job creation in the sector where

investment has been made. All of the aforementioned influences can ultimately lead

to higher living standards of the general population (Lumibla, 2005; Levitt, 2011).

Multi-national companies (MNCs) or multi-national oil companies (MNOCs) are the

main sources of FDI to developing countries and this creates a number of other

benefits. These benefits include new technology being obtained, easier access into

world markets, training of the workforce and new skills they obtain, as well as new

ideas and procedures (Kehl, 2009: 1-11). In comparison to other companies, MNCs

are more beneficial as these companies have the means for greater expenditure in

research and development (Kehl, 2009: 1-11). These benefits can improve the

3

shortcomings of the African labour and commodities markets. The commodities

market is supplemented by higher investment and the labour market by a rise in

technical knowledge (Perkins, Radelet and Lindauer, 2006:418 - p426). However,

there are costs associated with FDI. These costs include the crowding out of local

firms, higher strain on infrastructure, the fiscal burden on authorities in the host

country and the increased dependency of the economy in the investing country

(OECD, 2002).

It must be noted that investors have different motivations for investing abroad. The

main motivations include market seeking, efficiency seeking and resource seeking

(Kudina and Jakubiak, 2008). Market seeking entails that companies invest in

companies within countries with strong demand whereas efficiency seeking

motivates investors to invest in companies in certain countries because they can

produce goods more cost effectively than in others (Kudina and Jakubiak, 2008).

Finally, resource-seeking FDI is investment in a country that is richly endowed in

natural resources to realise financial gain from the extraction of these resources

(Makino, Lau and Yeh, 2002: 403-421). Even though Africa is a fast growing region,

the region does not possess a particularly enriched market as the per capita income

is relatively low and the lack of technical knowledge makes the region less efficient

than developing countries in other regions. Therefore, the main motivation for

investing in Africa is often resource seeking, as Africa is richly endowed with natural

resources (Makino and Lau andYeh, 2002: 403-421; Southall and Melber, 2010:

171-173; Kudina and Jakubiak, 2008).

1.1.1. The oil sector

Oil sector investment can take place in two divisions of the sector, that is, the

upstream and the downstream divisions. Upstream investment entails the funding of

exploration and production activities in the oil industry while downstream investment

entails funding of, amongst others, refinery and marketing activities (Fauli-Oller,

Sandoris and Santamaria, 2011: 884-898). This dissertation is focused on the

upstream sector.

4

A country’s oil endowment is measured through reserves in the country. Proven oil

reserves are the estimated quantities of oil that can, with reasonable certainty, be

extracted for commercial use under clear economic conditions, operating measures

and government regulation (National Centre for Economic Management and

Administration (NCEMA), 2003). In addition to proven reserves, oil reserves may

also be measured in terms of probable and possible reserves (BP, 2011). Probable

reserves indicating estimated oil reserves that have a 50 percent or higher chance of

being technically and economically extractable and possible reserves are estimated

reserves that can prove to be significant but have a lower than 50 percent chance of

being technically and economically extractable (Society of Petroleum Engineers

(SPE) and The World Petroleum Congress (WPC), 2004). Both probable and

potential reserves may become proven reserves with further exploration (BP, 2011;

SPE and WPC 1997).The level of proven, probable and possible reserves is the

most important factor for attracting oil sector FDI (UNCTAD, 2009).

Upstream exploration is conducted by many different types of companies. These

companies include small independent oil companies, national oil companies (NOCs)

and fully integrated oil companies (Petro Strategies, 2011). Firstly, small

independent oil companies focus on exploration. By utilising all their resources in the

field of exploration these companies are able to compete with larger integrated oil

companies (Petro Strategies, 2011; Akello, 2010). Secondly, integrated oil

companies are well known companies like Chevron and Shell as they usually supply

oil to consumers worldwide. These companies are multi-national and are listed on

the stock exchange. Their investment in African countries is much larger than that of

small independent companies (Petro Strategies, 2011; Kingdom Zephyr, 2011).

Thirdly, national oil companies are state owned oil entities that usually exist in oil rich

countries. Examples of these companies include Sanangol in Angola and the

Nigerian National Petroleum Corporation (NNPC) in Nigeria. These companies are

amongst the largest in the world but, unlike integrated oil companies, their objectives

are related to the economic wellbeing of the country rather than to an increase in

equity or shareholder value (Pirog, 2007). Nigeria and Angola are both part of the

Organisation of Petroleum Exporting Countries (OPEC), which is an

intergovernmental organisation with 12 member countries. The function of OPEC is

5

to unify and coordinate the policies of developing oil-exporting countries (OPEC,

2011). OPEC’s objective is to safeguard its members by stabilising oil prices and

assuring members of a steady, sustainable income through their oil sector. In

attempts to stabilise oil prices, OPEC formulates quotas for production for each

member country to counter over production or unfair competition (OPEC, 2011).

There are currently 19 African countries identified as significant producers of oil.

Most of these countries have shown strong economic growth partially because of

foreign direct investment in their oil sectors (Ernst and Young, 2011). According to

estimates, there is in excess of 7.3 trillion US dollars’ worth of oil in Eastern Africa

alone (Levitt, 2011). FDI inflows to the oil rich African countries have continued to

grow over recent years and other countries, including countries in Southern Africa,

have discovered oil fields within their borders (Ernst and Young, 2011). The rapid

growth of the economies of Asian countries is one of the more prominent reasons for

the higher investment in the African oil industry. In particular, the growth in China

triggered strong demand for African oil and China is now one of the biggest

contributors to the higher FDI received by the African oil sector. Chinese interest in

the African oil industry showed an increase during the 1990’s with Africa contributing

20 percent of their oil imports in 1999. This continued to rise to 31 percent in 2005 as

Africa now plays a large role in China’s new growth strategy (Zhao, 2007: 399-415).

Chinese oil imports from Africa remained nearly unchanged at 30 percent of their

total oil imports but this percentage is expected to change in the near future as

Reuters (2013) forecasts that Chinese oil demand will increase from 2.5 million bpd

in 2005 to 9.2 million bpd in 2020 (CFR , 2012). However, China is not the only

country interested in African oil. Because of the recent rise in oil prices, the

developed world has also shown interest in African oil (Ernst and Young, 2011;

Harding, 2012; UNCTAD, 2011).

The level of investment is, however, still highly dependent on the attitude of the host

governments towards foreign investors (UNCTAD, 2008). For example, FDI inflows

in the Nigerian oil industry dropped during 2011 because of their proposed

Petroleum Industry Bill (PIB). The Bill was introduced in 2008 with the objectives of

the vesting of petroleum, better allocation of land, better management of petroleum

6

resources, higher participation by the government, better transparency and

governance and lowering the level of environmental damage associated with the

industry (Oil and Gas sector reform Implementation Committee (OGIC), 2009). The

Bill has not yet been passed but is regarded as less favourable to transnational

companies as the government seeks to regulate the oil sector more closely by

introducing stricter criteria for the licensing rights of oil exploration in Nigeria

(UNCTAD, 2011). In contrast, less regulated countries such as Ghana attracted

higher FDI levels and have therefore thrived (UNCTAD, 2011). African governments

have for some time now worked on removing unnecessary regulations and

restrictions, controlling corruption and improving the ease of doing business. By

changing policies, these governments attempt to improve the investment climate to

attract more FDI (UNCTAD, 2008; UNCTAD, 2011; ADB, 2009).

There are contrasting views on the impact of abundant resources, and more

specifically, the oil abundance in Africa. This is widely known as the “resource curse”

(Clarke, 2010). The resource curse entails that the resource abundance of

developing countries has a negative effect in the forms of political instability, more

corruption, a hostile environment and a decline in growth in other sectors of the

economy. In many African countries, including Nigeria and Angola, this seemed to

be the case as these countries have been severely influenced by civil war and

terrorism (Southall and Melber, 2009: 171-173). Mismanagement of foreign funds

and outdated policies are viewed as the main cause of the negative impact of

abundant natural resources in developing countries (Ernst and Young. 2011). These

causes lead to a small percentage of the population realising financial gain while the

rest remain in severe poverty. Therefore, it is important for these countries to

implement the necessary economic reform and support structures to realise

sustainable economic growth and development (Clarke, 2010; Southall and Melber,

2009: 171-173; Ernst and Young. 2011). However, the management of oil revenue

and the so-called oil curse falls outside the scope of this dissertation.

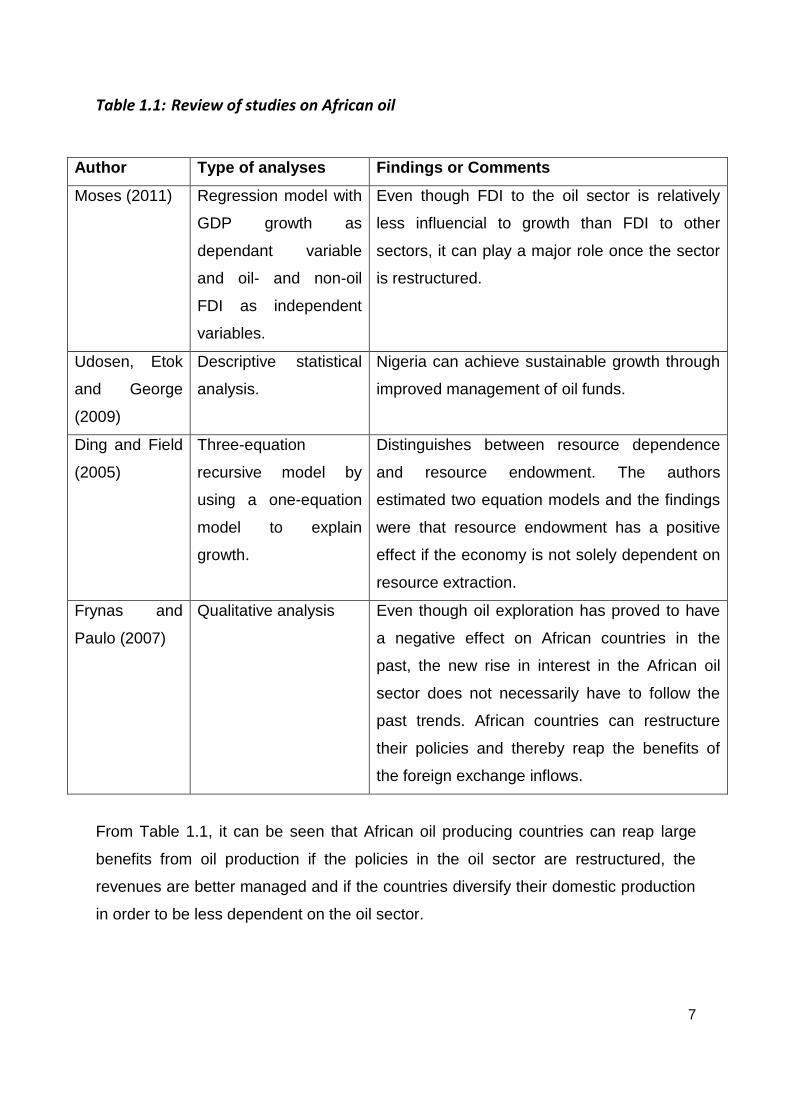

A review of the literature suggests that oil in Africa may in the future create

sustainable economic growth and development. Table 1.1 summarises the literature

on growth and oil sector FDI in Africa.

7

Table 1.1: Review of studies on African oil

Author Type of analyses Findings or Comments

Moses (2011) Regression model with

GDP growth as

dependant variable

and oil- and non-oil

FDI as independent

variables.

Even though FDI to the oil sector is relatively

less influencial to growth than FDI to other

sectors, it can play a major role once the sector

is restructured.

Udosen, Etok

and George

(2009)

Descriptive statistical

analysis.

Nigeria can achieve sustainable growth through

improved management of oil funds.

Ding and Field

(2005)

Three-equation

recursive model by

using a one-equation

model to explain

growth.

Distinguishes between resource dependence

and resource endowment. The authors

estimated two equation models and the findings

were that resource endowment has a positive

effect if the economy is not solely dependent on

resource extraction.

Frynas and

Paulo (2007)

Qualitative analysis Even though oil exploration has proved to have

a negative effect on African countries in the

past, the new rise in interest in the African oil

sector does not necessarily have to follow the

past trends. African countries can restructure

their policies and thereby reap the benefits of

the foreign exchange inflows.

From Table 1.1, it can be seen that African oil producing countries can reap large

benefits from oil production if the policies in the oil sector are restructured, the

revenues are better managed and if the countries diversify their domestic production

in order to be less dependent on the oil sector.

8

1.1.1.1. Nigeria

Nigeria is one of the most prosperous countries in sub-Saharan Africa and, even

though they have had problems with terrorism, corruption and violent uprisings in the

north of the country, it is still currently considered a low-to-moderate risk country for

foreign investment (NKC, 2011). Nigeria is currently rated as a lower middle income

country with a GDP of approximately 193 billion US$, the majority of which is earned

by the oil sector (World Bank, 2010).

The search for oil in Nigeria started in the early 1900s but had little success until the 1950s

when Shell first exported oil from Nigeria (Obasi, 2003). Since then the industry has

experienced steady growth and a resulting increase in FDI inflows. Nigeria joined OPEC in

1971 and thereafter the Nigerian oil sector experienced two major booms of FDI inflows. The

first was in 1986 when Nigeria adopted the Structural Adjustment Programme (SAP) that

entailed, amongst other things, that the fiscal policy was more stable, that the currency value

was more realistic and tariff levels were revised. The second can be attributed to the

Nigerian Investment Promotion Commission (NIPC) decree in 1995, which eradicated all

restrictions on foreign shareholding in the country (Moses, 2011: 333-343; NCEMA, 2003).

Currently, Nigeria is estimated as the African country with the second largest

untapped oil reserves. Even so, Nigeria only produces at 30 percent capacity (Levitt,

2011). In an attempt to improve transparency and control of the Nigerian oil sector,

the PIB was proposed and is in the process of being implemented. Even though the

bill has not yet been passed, the fact that the government would like to more closely

regulate the oil sector has discouraged many foreign investors. This led to a

downturn in total FDI inflows to Nigeria as the oil industry contributes some 60

percent of the Nigerian FDI inflows (Levitt, 2011; UNCTAD, 2011).

1.1.1.2. Angola

The 27 year Angolan civil war characterised the country as being politically unstable.

The war ended in 2002 but even before the end of the war, the country’s economic

state was improved by foreign interest in their offshore oil reserves (Food and

Agriculture Organisation (FAO), 2011). Even though the country is now seen as

being relatively politically stable, the war severely damaged the infrastructure and

9

reconstruction is still under way (USAID, 2011). Angola is currently rated as a lower

middle-income country with a GDP of approximately 75 billion USD, the majority of

which is earned by the oil sector (FAO, 2011).

Oil production in Angola started in the 1950’s and, ever since, the country has

become more dependent on the oil industry (OPEC, 2011). In 1998, Angola

experienced an upwards spike which boosted their FDI inflows from under 200

million US$ to over 1.4 billion US$. This increase was due to large offshore oil

exploration that attracted various foreign investors and in 2007, Angola joined the

OPEC group (OPEC, 2011). From that time, the FDI inflows have shown a strong

increase with the exception of periods of downturn due to perceptions of political

instability (FAO, 2011).

Angola is currently one of the region’s largest FDI recipients and the majority of FDI

inflows are attributed to the oil sector. The Angolan oil sector became the largest oil

exporter to China in 2005, contributing more than 50 percent of China’s oil imports

(Zhao, 2007: 399-415). One significant problem currently faced by Angola is that

their oil output exceeds their OPEC quota (UNCTAD, 2011).

1.2. Problem statement

A problem faced by Africa is the lack of local investment because of the low savings

rate. To explore and develop Africa’s oil resources, investment funding and

knowledge in the field is required. Africa lacks both of these assets. Nigeria and

Angola are two of the largest oil producers in Africa. By attracting FDI to this sector,

not only will the Nigerian and Angolan oil sectors gain the necessary funding for oil

extraction but they will also gain knowledge from transnational corporations. Greater

FDI is needed to fully exploit their available oil resources. Although many studies

have been undertaken on the factors that attract FDI, few studies have focussed on

oil sector specific FDI. Therefore, the aim of this dissertation is to determine and

compare the factors that attract oil sector FDI in Angola and Nigeria.

10

1.3. Motivation

Nigeria and Angola are both countries richly endowed with crude oil. The problem

faced by the vast majority of the African continent however is to develop and extract

these resources to better their poor development standing. To develop the upstream

sector, investment funding and knowledge in the field is required. Africa lacks in both

investment funding and technical knowledge. By attracting FDI to this sector, not

only will the Nigerian and Angolan oil sectors gain the necessary funding for oil

extraction but they will also gain knowledge from transnational corporations.

1.4. Objectives

The main objective of this dissertation is, primarily, to determine the external factors

and internal factors that influence FDI inflows to the Nigerian and Angolan oil sector.

Secondly, the dissertation will compare the main contributing factors to establish

which of the factors play a significant role in attracting FDI to oil sector in these

countries in order to identify similarities and differences.

1.4.1. Sub-objectives

The sub-objectives of this dissertation are to:

Provide a literature review of FDI and the oil industry.

Review the current trends, in FDI flows and in the oil sector from a global, an

African and a country specific perspective.

Analyse the literature and current trends in Nigeria and Angola in order to

determine the factors that may have an influence on attracting oil sector FDI.

Use FDI data and test the factors that may have a significant influence on

attracting FDI inflows to the oil sectors of Nigeria and Angola.

Compare the findings of both countries and draw conclusions from this

comparison and thereafter, to make recommendations.

11

1.5. Research method

This dissertation will undertake both a literature review and an empirical analysis.

The literature review will provide an overview of FDI theory, the motives for

investment, the types and benefits thereof; an overview of the African and, more

specifically, the Nigerian and Angolan oil industries and the influence that FDI inflows

have had on these sectors. The current FDI inflow trends in Nigeria and Angola will

be reviewed and oil sector FDI compared to the other FDI attracting industries. The

dissertation will then examine and compare the current state of the Nigerian and

Angolan oil industries.

The empirical analysis will consist of a country comparison through four least square

regression models (domestic models for Nigeria and Angola and the global models

for both countries) using data between 1990 and 2011 obtained from the World data

Bank and the BP statistical review 2012. The data used will describe the traditional

determinants of FDI inflows laid out in literature review and other determinants

derived from past studies of FDI inflows in transitional economies and oil sector

dependent countries. However, it must be noted that the lack of accurate and

sufficient time series data for Nigeria and Angola constrains the analysis.

1.6. Outline of the dissertation

The remainder of this dissertation is structured as follows: Chapter two provides a

literature review of FDI theory and oil sector theory. Chapter three provides an

overview of current trends in FDI inflow trends and the oil sector in a global, African

and country specific perspective, focusing on Nigeria and Angola. Chapter four then

provides a theoretical framework and detailed description of the data used before

presenting a domestic and global model for Nigeria and Angola and comparing the

influencing factors in each country. Finally, Chapter five summarises the dissertation

and provides recommendations for further studies.

12

Chapter 2: Literature review of FDI and the oil sector

2.1. Introduction

Through a theoretical explanation of FDI and the oil sector, a better understanding

can be reached of the necessity of FDI to developing countries in Africa and of the

role that the African oil industry plays in obtaining higher level of FDI. Thereafter, the

factors influencing the oil sector FDI can be investigated.

This chapter will consist of two sections, the first of which will discuss the literature

on FDI (Section 2.2). This will include the difference between FDI and portfolio

investment, different types of FDI, benefits and costs of FDI and the determinants of

FDI. The second section will discuss oil industry theory (Section 2.3) which will

include investment type, oil reserves, the different companies who invest in the

industry and the contrasting views of the so-called oil curse.

2.2. FDI theory

As discussed in chapter one, FDI can be highly beneficial to African countries by

supplementing their savings rates as well as having a positive influence on the

industry in which the investment is made. Therefore, the theoretical foundations of

FDI are explained in this section to facilitate a better understanding of the following

chapter on the current trends in FDI.

2.2.1. FDI Definitions

FDI can be defined as:

“the objective of obtaining a lasting interest by a resident entity in one

economy in an economy other than that of the investor. The lasting

interest implies the existence of a long-term relationship between the

direct investor and the enterprise and a significant degree of influence on

the management of the enterprise. Direct investment involves both the

initial transaction between the two entities and all subsequent capital

13

transactions between them and among other affiliated enterprises, both

incorporated and unincorporated” (OECD, 1996).

The standard definition for FDI according to UNCTAD (2005) is:

“A long-term relationship involving a significant degree of influence on the

management of the enterprise encompasses a heterogeneous group of

corporate actors, some with complex integrated production structures,

others with little more than a sales outlet in a single foreign market, a

problem that is hardly resolved by reducing the control threshold to a

minimum 10 per cent equity claim”.

According to the International Monetary Fund (IMF, 1993), FDI has three

components:

1. equity investment,

2. reinvested earnings, and short-

3. and long-term inter-company loans between parent firms and foreign

affiliates.

The main difference between FDI and other investments from abroad lie in the

lasting interest and control by foreign investors through management of the host

company.

Therefore, FDI and foreign Portfolio investment must not be confused. Portfolio

investment entails the purchase of securities on the stock market (Rutherford, 1995:

1299-1324). Portfolio investors do not necessarily intend to influence the

management or direction of the company, the investment is usually shorter in term

and funds can more easily be divested (UNCTAD, 1998). In contrast, FDI investors

have a much higher interest in the wellbeing of the company and therefore, the

investors seek to influence the management to better productivity (Itay and Razin,

2005). Further, FDI investment is usually long-term and therefore more stable when

considering the company’s growth prospects (Rutherford, 1995: 1299-1324;

UNCTAD, 1998; Itay and Razin, 2005). FDI is also less susceptible to the effect of

changing exchange rates than is portfolio investment because a lower valued

14

currency can lead to lower cost of production, which will have a positive effect on

direct investors (UNCTAD, 1999).

2.2.2. Categorising FDI

FDI can be categorised by its direction, the type of investment and the investors’

motivations. Firstly, the direction is dependent on whether FDI flows into the “home”

economy from abroad or if investment flows outward from the “home” country to a

foreign economy (IMF, 1993). Secondly, the investment type refers to whether

investment is made by obtaining a share of an existing company in the host country

or obtaining the existing company as a whole or investing to fund new facilities in the

host country (Estrinet and Meyer, 2011: 3-5). Lastly, FDI can also be categorised by

the reason for investors to choose a certain country to invest in. These reasons may

include the procurement of a certain natural resource, the penetration of a growing

market or better production efficiency in the foreign market than in the local market

(Basu and Srinivasan, 2002; UNCTAD, 1998).

2.2.2.1. Categorising FDI according to the direction of flow

The direction can be distinguished by either inflows or outflows. FDI inflows are the

investment capital received from investors abroad or non-resident investors into a

certain host country (IMF, 1993). FDI outflows on the other hand are local investors

or residents of the “home” country funding activities abroad (IMF, 1993).

2.2.2.2. Categorising FDI according to investment type

The type of investment can be divided into Greenfield or Brownfield investment

(Nocke and Yeaple, 2006: 1-4) as previously stated. Greenfield investment is direct

investment through the funding of new facilities in the host country. This type of

investment is optimal for the host country as it provides linkages to the global market

place, the transfer of knowledge and technology as well as job creation (Qiu and

Wang, 2011: 836-838). Brownfield investment, on the other hand, consists of

mergers and acquisitions. Ownership of existing assets owned by local firms is

transferred to foreign companies (Paull, 2008: 9-15). This form of investment does

15

not necessarily lend itself to long-term benefits to the local economy, as does

Greenfield investment (Estrinet and Meyer, 2011: 3-5).

2.2.2.3. Categorising FDI according to investors’ motivations

Investors seek certain benefits that the host country possesses that encourage the

investor to invest in the country. These motivations include natural resource seeking,

efficiency seeking and market seeking investment (Basu and Srinivasan, 2002;

UNCTAD, 1998). Natural resource seeking investment entails the search for specific

resources of which the host country is endowed with. Included in this classification is

investment from abroad in exploration of oil, gold and coal in African countries.

Secondly, market-seeking investment entails that investors would invest in the host

country because of the sheer size of the local market and the economic growth in the

host country. Lastly, efficiency seeking investment entails that investors are driven to

invest in the host country to reap the benefits of special features that the host

country possesses. These features may include low cost labour, a highly skilled work

force or technological and infrastructural superiority (Basu and Srinivasan, 2002;

UNCTAD, 1998).

2.2.3. Benefits of FDI

The benefits of FDI can be divided into direct and indirect effects of FDI. Direct

effects include supplementing local savings to achieve greater production within the

host country while indirect effects include several effects that better growth and

development in a country through the interest of foreign investors and the presence

of foreign firms (Lumblila, 2005).

2.2.3.1. Direct positive effects of FDI

The positive correlation between FDI and economic growth has been proven by a

number of empirical studies including studies by Braunstein and Epstein (2000) and

by Gallagher and Zarsky (2003: 19-44). Higher availability of capital in the host

country leads to higher production and therefore to an increase in GDP growth

(Dabla-Norris, Honda, Lahreche, Verdier, 2010: 4-17).

16

In developing countries, this is all the more evident as their low domestic savings

rate is the reason for lower domestic investment (Kirk and Celemens, 1999).

Through increased FDI inflows, the gap between the domestic savings rate and the

desired investment level can be filled. This can cause FDI to have a larger effect on

economic growth in developing countries than in developed countries (Dabla-Norris,

et al, 2010: 4-17).

2.2.3.2. Indirect positive effects of FDI

Most indirect effects of FDI arise from multi-national corporations (MNCs) who invest

in the host country. MNCs are usually large businesses that operate in a number of

countries. The expansion of these companies into countries abroad is usually a

result of strong growth in the company due to their superiority in technological

advances and better productivity when compared to other and smaller companies

(Aggarwal, Berrill, Hutson and Kearney, 2010: 557-577).

The first positive externality brought about by MNCs is the transfer of technology.

This can be attributed to research and development, as MNCs are known for their

expenditure in these areas. The transfer of technology arises as other businesses

observe the MNC and adopt some of their processes and, thereby, become more

efficient (Keller, 2009: 1-5, 59-61). Secondly, it is the probability of knowledge

transfers from MNCs. This entails the transfer of knowledge from one employee to

another or skills obtained through in house training by the MNC. These skills and

knowledge obtained from the MNC can be transferred by the employee leaving the

MNC and thereafter applying the newfound knowledge and skills in another local

company (Keller, 2009: 1-5, 59-61). Thirdly, the employment level in the country is

increased as jobs are created through expansion of the companies within which

investment takes place. Some studies, however, found employment not to be

proportional to the amount of FDI being invested. The findings were that FDI does

increase per capita income that promoted economic development (Waldkirch,

Nunnenkamp and Bremont, 2009). Finally, companies investing in a country or

region will ensure that infrastructure is in place for their operations and this will in

turn motivate the government concerning infrastructure development (ECOSOC,

2000; UNCTAD, 1999).

17

There are several other positive indirect influences of FDI. Three of these influences

include the promotion of international safety standards, better resource allocation

and stronger financial markets (Lumblila, 2005).

2.2.4. Costs of FDI

The majority of studies find that the effects of FDI on the economy are positive

(Blomstrom, Kokko and Zejan, 2000: 7-9; Sjohlomn, 1999). However, there are

contrasting views on the effects of FDI in developing countries. There are costs of

FDI to the host country including the cost of FDI to the host country through the

crowding out effect (Aitken and Harrison, 1999: 605-617) and constraints of

absorbing the positive effects of FDI (Alfaro Chanda, Kalemli-Ozcan and Sayek

2009: 242-256), as well as over dependency on FDI (Adams, 2009: 939-949;

Rhagavan, 2000).

The crowding out effect is also known as the market stealing effect (Aitken and

Harrison, 1999: 605-617). It entails that the domestic demand in the host country

moves away from domestic firms to multi-national firms, and that the domestic firms

suffer more because the lower demand outweighs the positive effects from spillovers

from the multi-national firms. As there may be large gap in technology when

comparing domestic firms to foreign firms in developing countries, the possibility of

the crowding out effect is larger than in developed countries. Therefore, policies in

the host country should be formulated to best suit the host economy as excessive

FDI inflows may not be in the host country’s best interest (Meyer, 2004: 259-277;

Blomstrom, et al. 2000: 7-9).

Constraints in developing countries may include technological constraints,

infrastructural constraints, educational and healthcare constraints, corruption and

political instability (Alfaro Chanda, Kalemli-Ozcan and Sayek 2009: 242-256).

According to the World Bank (2011), the constraints are caused by a lack of linkages

between the local firms, the local economy and the MNCs. Firstly, technological

constraints occur when the host country does not have the capacity to absorb the

spill-overs because of the technological gap between the host country and the multi-

18

national company (Alfaro, 2003: 13-16). Secondly, infrastructural constraints can be

classified as telecommunications or physical infrastructural constraints. These

constraints cause barriers in absorbing the FDI and therefore the effects of the FDI

might be less than desired (Alfaro, 2003: 13-16). Thirdly, a lack of education and

health care in developing countries play a large role in the deterioration of the

workforces’ productivity as less money is spent on education because of high

mortality rates. This is also why several African countries have a less productive

workforce and, with the high number of AIDS victims in this region, knowledge in the

workforce is lost (Simtowe and Kinkingninhoun-Medagbe, 2011: 2118-2131).

Fourthly, corruption is a cause of lower beneficial influences of FDI being absorbed

as the money being invested only makes the rich and powerful richer and more

powerful. It also leads to lower trust by investors and therefore lowers the country’s

FDI inflow as a whole (Kenisarin and Andrews-Speed, 2008: 301-316). Finally,

political instability is another constraint in obtaining and absorbing FDI as investors

observe countries with political instability as having higher risk for their investments

where government spending may be not be contributing to economic growth

(Neuhaus, 2006).

However, these constraints are not necessarily negative effects of FDI but are rather

a motivation for improvement in developing countries. An increase in FDI is usually

found to have a positive effect on the economy and the general standard of living in

the population even if these effects are not proportionate to the amount of FDI

inflows (Alfaro Chanda, Kalemli-Ozcan and Sayek 2009: 242-256).

Further, high dependence on FDI is also seen as a negative effect on growth and

development as it may cause monopolisation as only one or a few companies with

the means obtained through FDI can deliver the product or service with no

competition in the market. These companies can therefore dominate pricing in their

sector (Rhagavan, 2000). This in turn can negatively influence productivity, income

distribution and employment (Ajayi, 2006; Rhagavan, 2000). High dependence also

implies that the host country is subject to the performance of the investing countries

and investing companies (Adams, 2009: 939-949).

19

2.2.5. Determinants of FDI

FDI inflows are an important element for economic growth in developing countries,

as these countries need to supplement local investment to achieve optimal

investment levels (Kirk and Celemens, 1999). Further, the local economy can

benefit through indirect effects of FDI (Keller, 2009: 1-5, 59-61). To increase the

levels of FDI inflows, it is important to understand those factors that play a significant

role in attracting FDI inflows. These factors can be divided into macro and micro

determinants as explained below.

2.2.5.1. Macro determinants of FDI

Macro-economic determinates exist throughout the whole economy of the host

country and they include political risk, exchange rates, inflation rates, openness of

the market, domestic investment, value of exports and the budgetary deficit (Naude

and Krugell, 2003: 2-12).

Political risk includes social instability, internal and external conflicts and

expropriation within the host country (Musonera, 2008). It can influence a company

through production disruption, damage to property and even the confiscation of

goods (Lucas, 1993: 391-406). Political risk may be brought about by change in

government rule and the nature of the new government, the mind-set of the opposing

parties, the possibility of labour disruptions, the possibility of domestic terrorism,

corruption and the competence of the legal system (Naude and Krugell, 2003: 2-12).

Investors may be expected to invest in a country with sound political stability rather

than in a politically unstable country.

The influence of exchange rates varies between countries (Blonigen, 2005: 4-18). It

can be argued that a devaluation of the host countries currency leads to lower

production cost relative to the country of the investor that can give the company in

the host country an internationally competitive advantage if the business is export

orientated. If the business relies heavily on imports, the opposite may be true as the

production cost relative to other countries may in fact increase (Naude and Krugell,

2003: 2-12). The opposite can also be argued through the returns of investment

20

being larger as the host countries currency appreciates (Froot and Stein, 1991:

1215-1216). The motivation for investment plays a large role in the desired exchange

rate as market seeking investors would prefer a higher valued currency in the host

country whereas efficiency seeking and resource seeking investors would most

probably prefer a higher currency value in the host country (Blonigen, 2005: 4-18).

Volatile fluctuation in the currency is however expected to decrease FDI inflows to

the host country as it raises doubt concerning the economic stability of the host

country (Urata and Kawai, 2000: 79-103).

It can be argued that a higher inflation rate leads to higher returns on investment as

the higher price in the host country relative to the country of the investor may lead to

greater profitability (Botric and Skuflic, 2005: 2-7, 14-20). A contrasting argument

holds, however, that inflation is an indicator of economic stability in the host country

and therefore higher or volatile inflation rates have a negative effect on the

perception of investors that subsequently entails lower FDI inflows (Demirhan and

Masca, 2008: 357-363; Urata and Kawai, 2000: 79-103).

Similar to exchange rates, the effect of trade and investment openness is linked to

the motivation for investment. Openness in terms of trade leads to lower FDI through

market seeking investors as exporting goods to the host country may be more cost

efficient. Greater openness of trade may, however, increase FDI inflows to the host

country by efficiency seeking and resource-seeking investors as these investors

would like to export goods from the host country (Seim, 2009: 11-70). In general and

especially in developing countries, however, FDI will increase with more relaxed

investment and trade policies. The more restrictive the policies, the lower the FDI

inflows will be (Onyeiwu and Sherestha, 2004: 98-105).

Domestic savings contribute to the current growth and development in a country and

indicate whether there is sufficient infrastructure. In resource rich countries, however,

domestic savings is believed to have a less significant influence on FDI inflows

(Ndikumana and Verick, 2008: 2-5, 26-27). Domestic savings is strongly correlated

with the openness of the host country. The openness of the host country does,

however, not necessarily entail that the host country has a high quantitative value of

21

exports (Singh and Jun, 1995). Yousaf, Hussain and Ahmad (2008: 35-56) found

that export growth has a negative effect on FDI in the short term but a positive effect

in the long-term. This may be because the company is not restricted to their local

market and can display larger margins of growth and therefore higher revenue

(Naude and Krugell, 2003: 2-12).

A government budget deficit usually leads to an increase in taxation. Therefore, it

can have a direct influence on the company being invested in by the foreign

investors (Azam, Khan, Hunjra, Ahmad and Chani, 2010: 4306-4313). This means

that a large budgetary deficit can lead to tax uncertainty and the resulting lower FDI

inflows (Naude and Krugell, 2003: 2-12).

2.2.5.2. Micro determinants of FDI

Micro-economic determinants exist on an industry level that directly influences the

profitability and cost of FDI. These include growth within the market, the market size,

the cost of labour, the policies of the host countries government and trade barriers

(Naude and Krugell, 2003: 2-12).

Growth within the market is particularly imperative to market seeking investors as the

growth of the market indicates potential growth for the company that is being

invested in and therefore growth of investment and revenue for the investor (Botric

and Skuflic, 2005: 2-7, 14-20). This determinant is not as significant to resource or

efficiency seeking investors as their interest lies with factors other than that

concerning the local market, including cost, skill level and productivity of labour and

the cost and accessibility of resources.

There is a vast literature on market size as a determinant of FDI. The conclusion of

the majority of the studies shows that a country with a larger population is likely to

receive higher FDI as this indicates larger local demand for the host company

(Resmini, 2000: 65-89; Bevan and Eastrin, 2000: 7-9). Similar to growth in the

domestic market, however, market size is more significant to market seeking

investors and does not pertain to resource seeking and efficiency seeking investors

to the same degree (Botric and Skuflic, 2005: 2-7, 14-20).

22

Lower labour cost in the host country relative to the investors’ country can attract

higher levels of FDI as this may lead to lower production costs. This especially

pertains to efficiency seeking FDI but can also have an influence on both market

seeking and resource seeking investment (Nunes, Oscategui and Peschiera, 2006:

2-11)

Policies of the host country’s government will influence the decision to invest in a

foreign country, as investors will expect certain advantages from investing in the

location. The policies and structures put in place by the host government lay the

foundations for the investment climate in the country. These foundations include the

quality of infrastructure, the quality of public services and the skills level of the

general population (Te Velde, 2001). International companies tend to invest in

countries with more stable economic policies that are investment friendly as

government policies may influence the operations of the company that is invested in

(Musonera, 2008). The host government also initiates and enforces laws that may

influence the investor’s decisions. These laws include tax laws, liability laws, trade

restrictions and property rights (Musonera, 2008). According to Morgan (1998), the

more liberal the laws are, the more likely FDI inflows are to increase and the

management within such an investment climate will be more efficient and likely to

lead to improved spill over’s into the host economy.

Trade barriers can take the form of tariff or non-tariff barriers (Fliess and Busquets,

2006: 5-8). Tariffs include import and export taxes as well as any duties paid to the

governing body to transport goods across a countries border. Non-trade barriers

include a number of elements that hinder trade between countries. Amongst others,

these barriers include import and export tariffs and quotas, customs administration

and technical, health and safety restrictions (Fliess and Busquets, 2006: 5-8). The

impacts of trade barriers are uncertain as FDI inflows may increase because of

higher trade barriers as FDI may be the only way that companies can cost effectively

enter the market. On the other hand, companies that would like to export or have to

import goods for production reasons may be reluctant to invest in a country with high

trade barriers and this may deter FDI inflows (Lim, 2001: 4-9, 10-12).

23

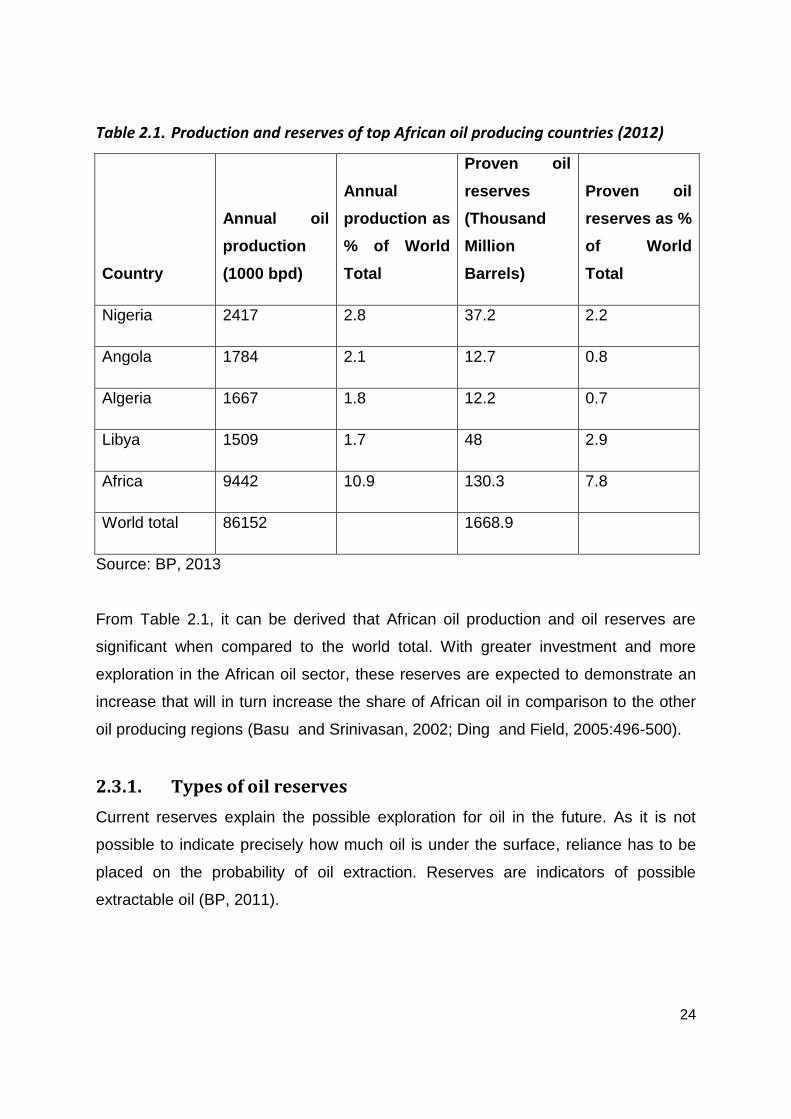

2.3. Oil sector theory

Traditionally FDI in Africa was mainly attracted by natural resources like gold and

coal but for some time now, the oil industry has been showing an increased ability to

attract FDI (Levitt, 2011). The oil sector is currently the highest FDI recipient sector

in Africa and, according to many economists, the oil industry is the continent’s way

forward and a doorway to a brighter future regarding sustainable economic growth

and development (Levitt, 2011).

Africa is a well-endowed continent when considering their crude oil reserves (ADB, 2010). In

2010, Africa supplied approximately 11 percent of worldwide oil supply and the African

untapped oil reserves constitutes of approximately 10 percent of the total worldwide proven