World Bank Group

227

FILE CmPY DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use Report No. 168a-BA THE CURRENT SITUATION AND PROSPECTS OF THE UNION OF BURMA July 25, 1973 South Asia Department This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without Bank Group authorization. The Bank Group does not accept responsibility for the aecuracy or cnmpletene-ss of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

Upload

khangminh22 -

Category

Documents

-

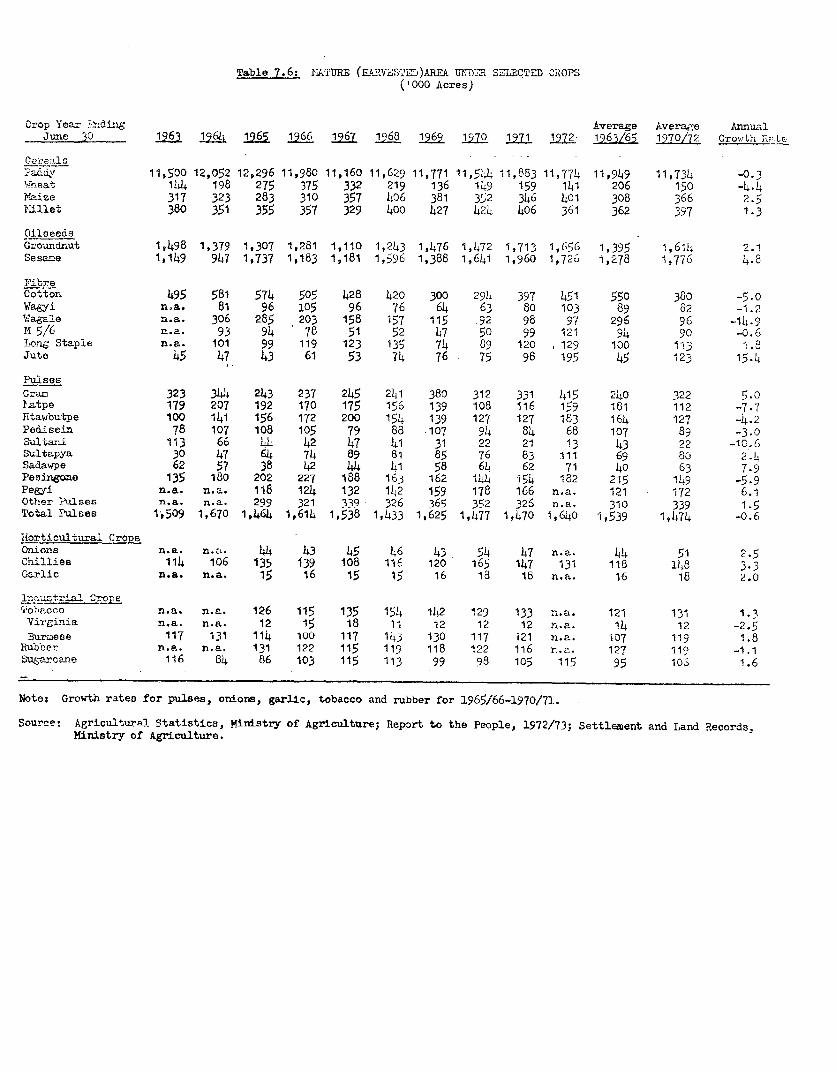

view

0 -

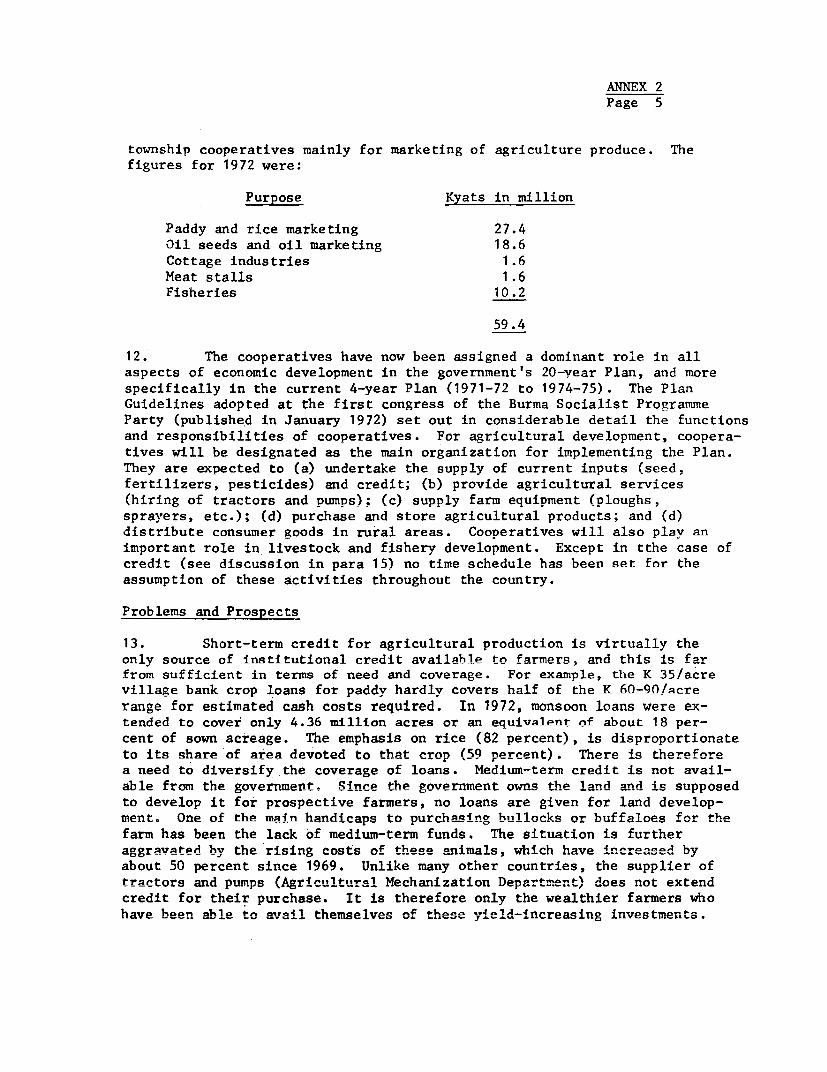

download

0

Transcript of World Bank Group

FILE CmPY

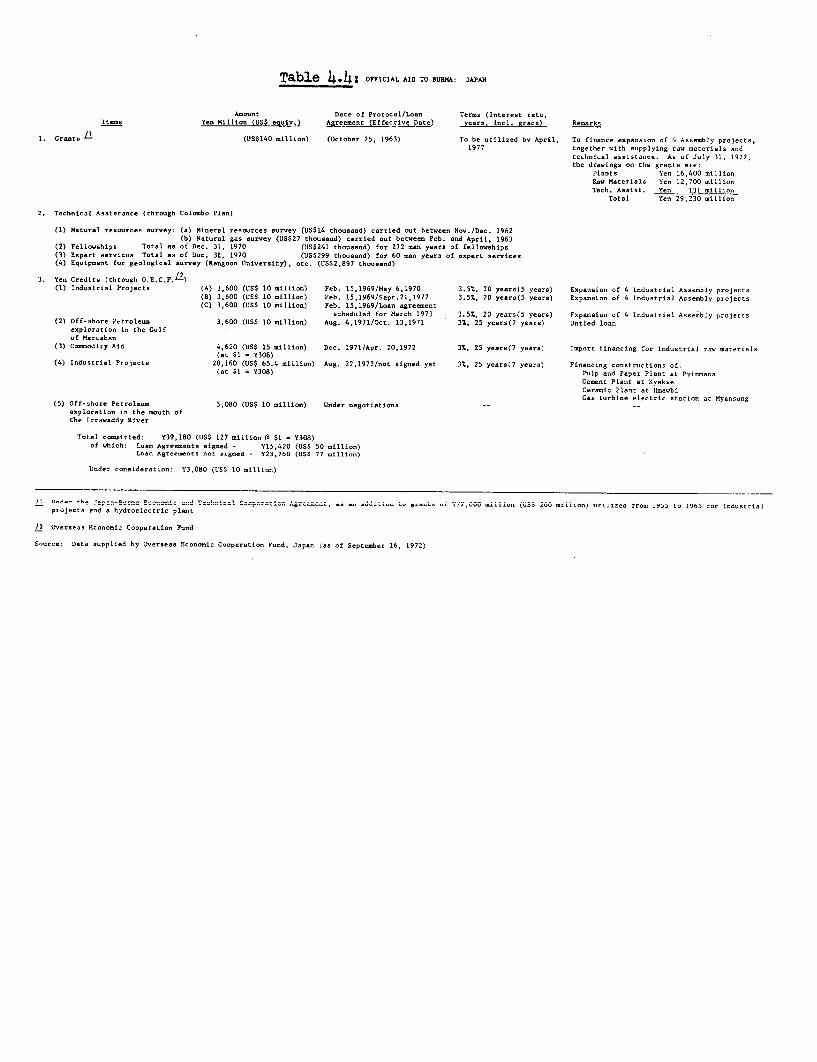

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No. 168a-BA

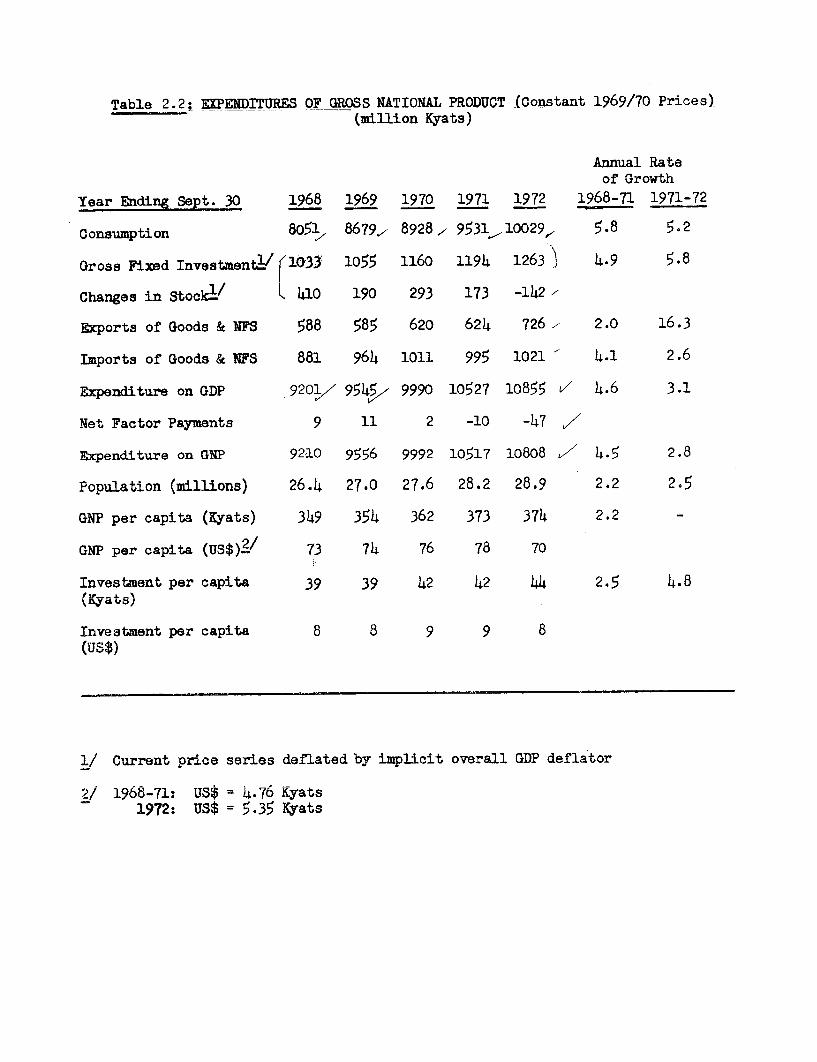

THE CURRENT SITUATION AND PROSPECTS

OF

THE UNION OF BURMA

July 25, 1973

South Asia Department

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaecuracy or cnmpletene-ss of the report.

Pub

lic D

iscl

osur

e A

utho

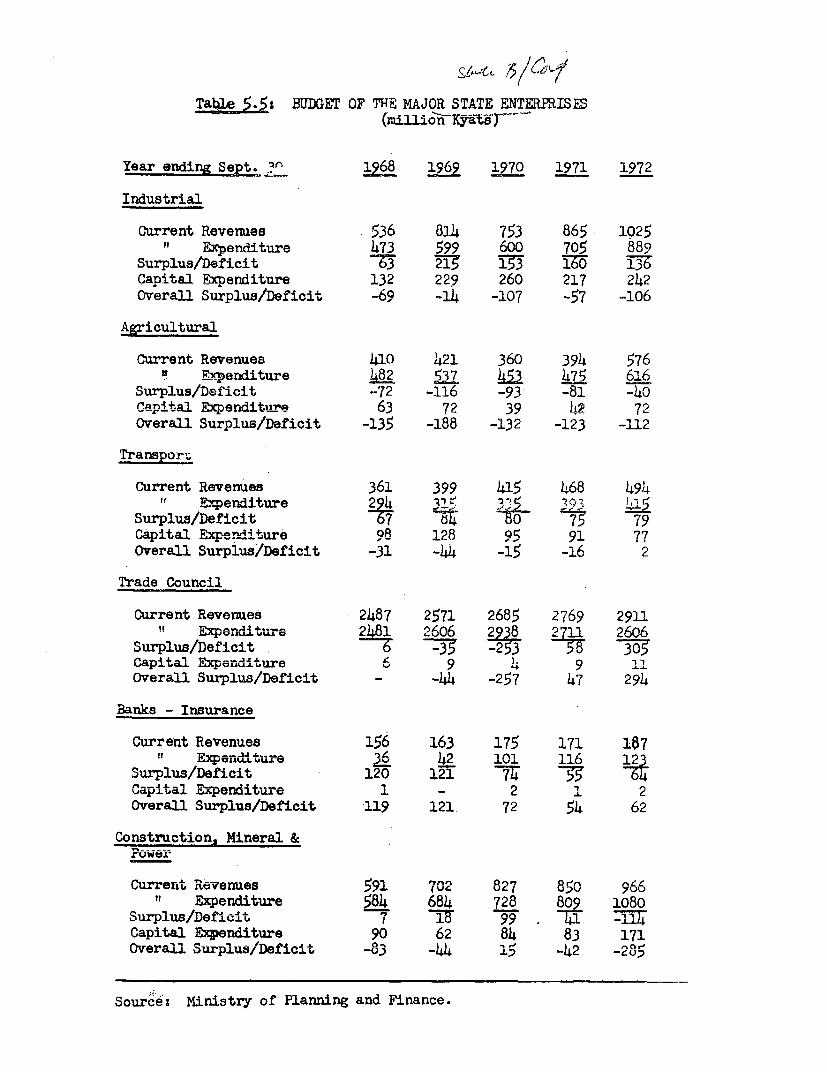

rized

Pub

lic D

iscl

osur

e A

utho

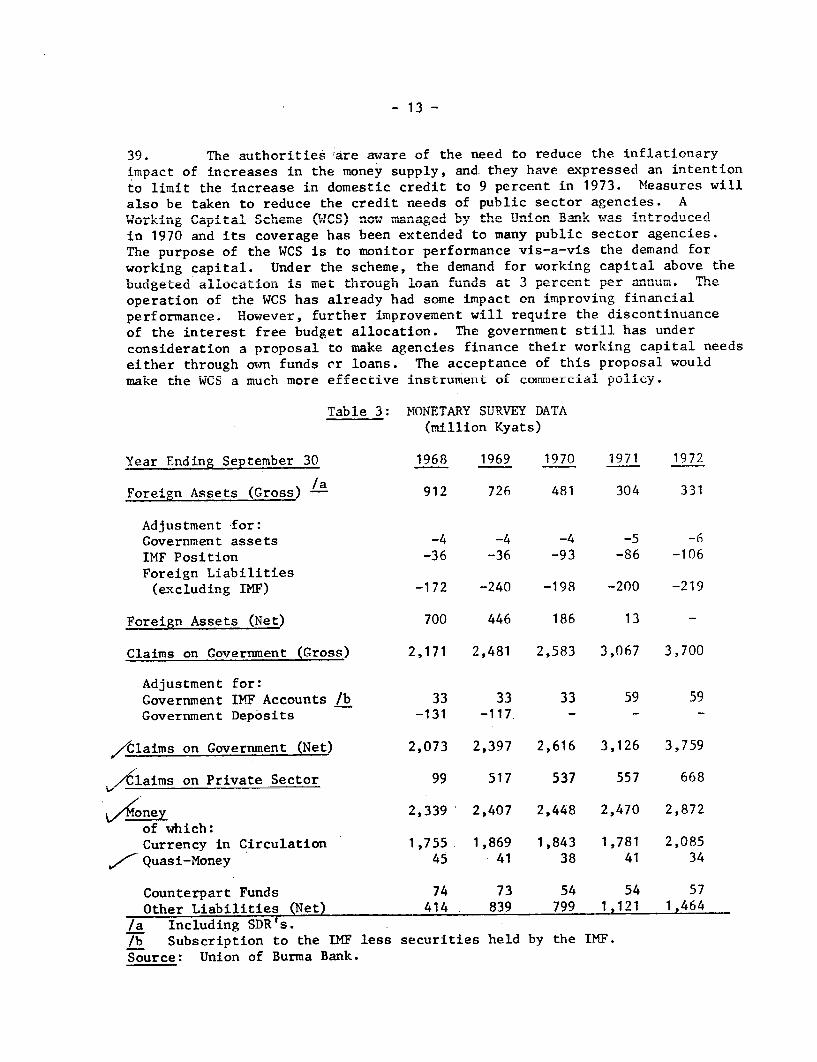

rized

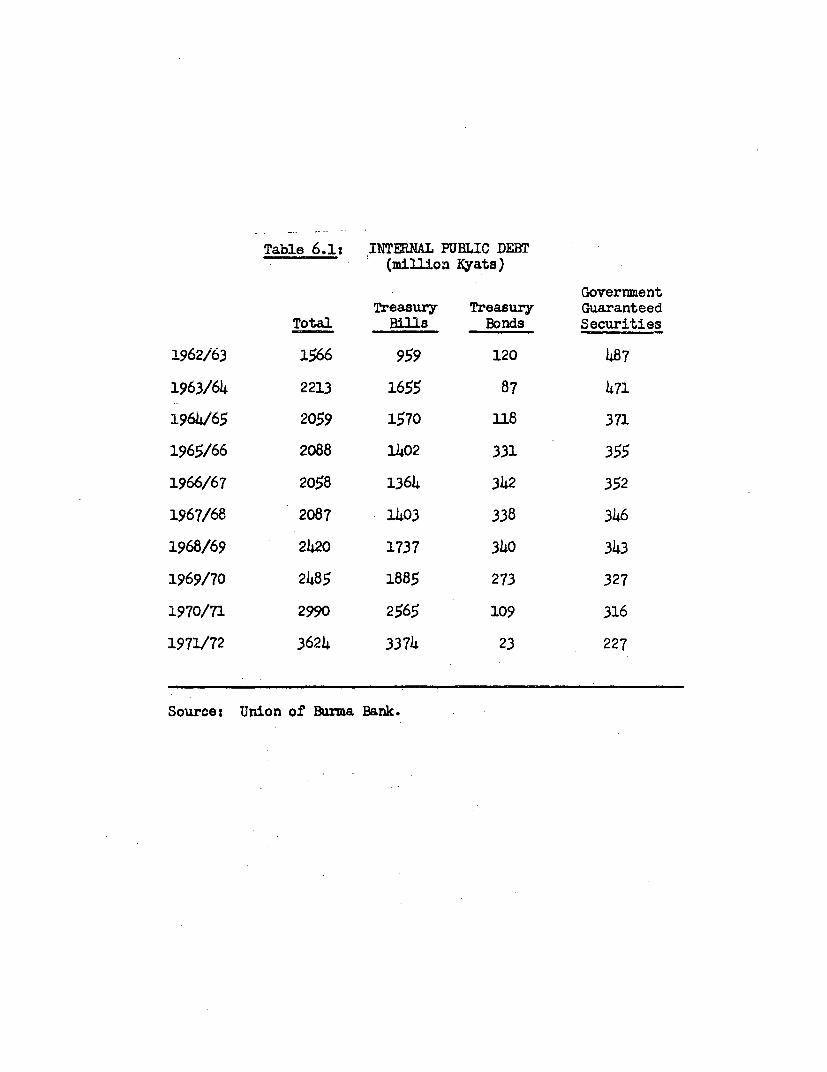

Pub

lic D

iscl

osur

e A

utho

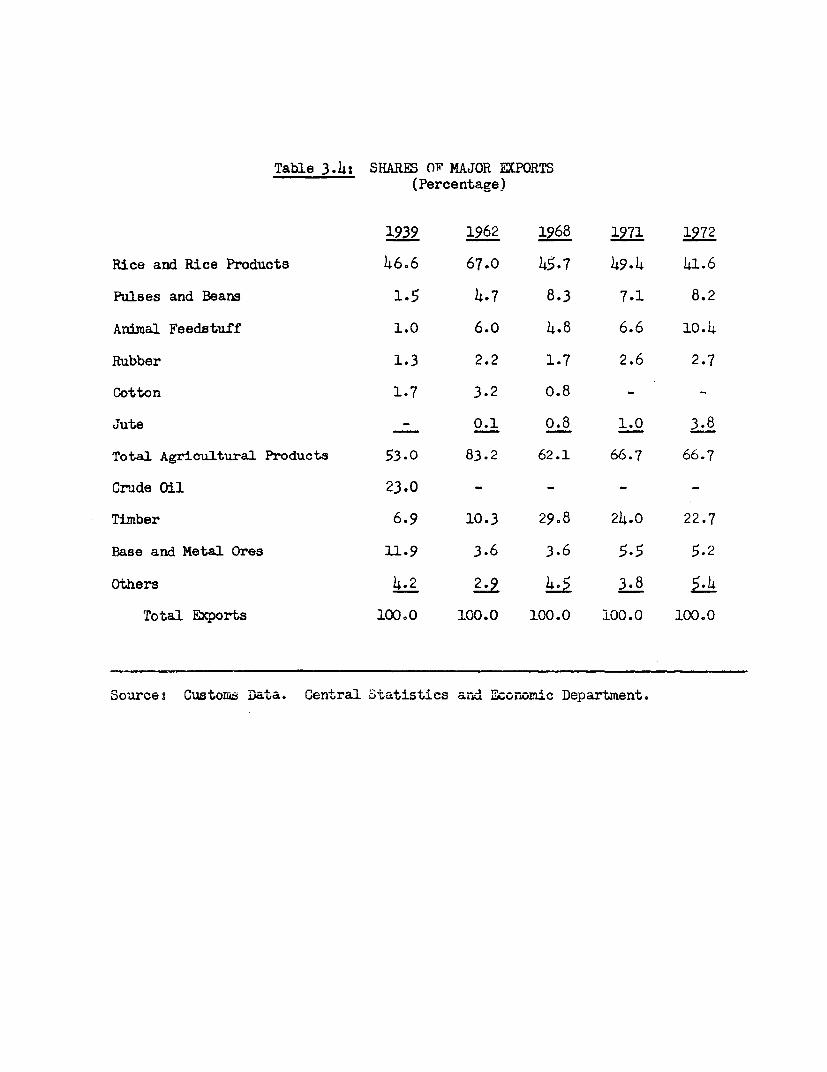

rized

Pub

lic D

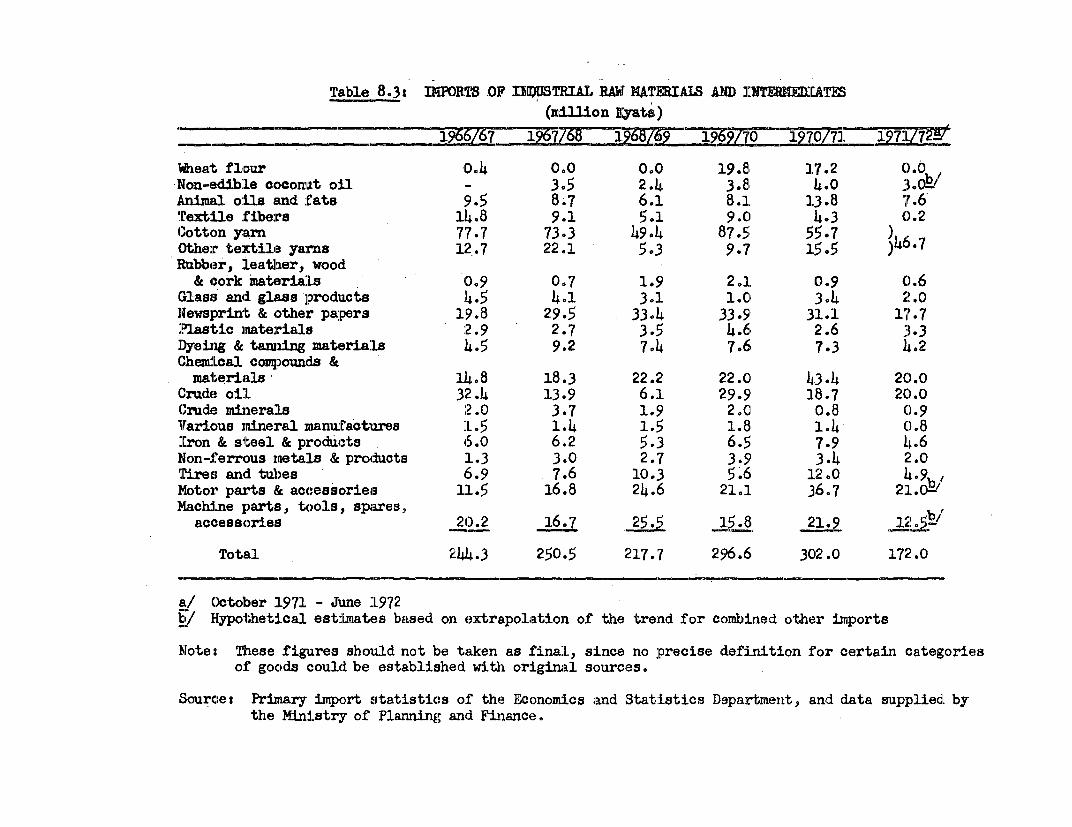

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Currency Unit - rKyat (KAY)

Through December 1971 - US$1 Ky 4.7619Ay 1 U$0U.21

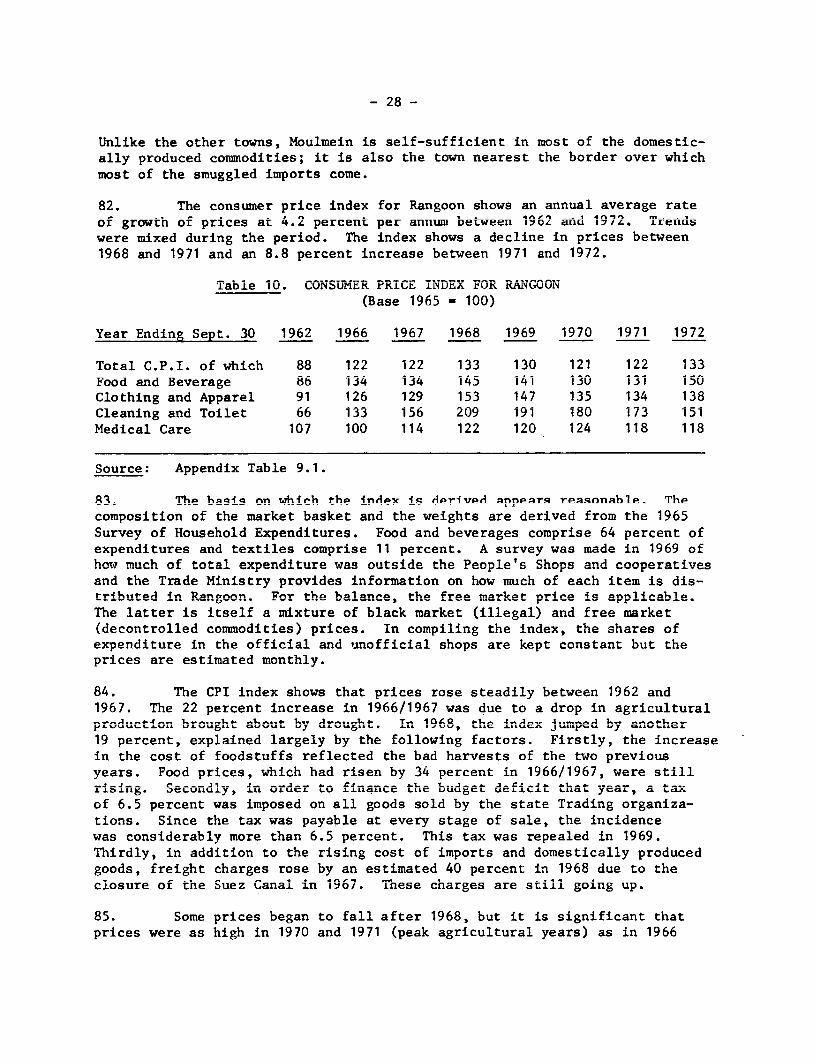

Ky 1,000 = US$210.00,,. l,OOO,OOO - 'uS$210,000.21 nftL V3 IJ,UUV Up±,UA.e

From December 1971 toFebruary 1973 US$1 = Ky 5.3h87

Kgy i US$0.19Ky 1,000 = US$186.96Ky 1,OOO,O0 = US1-86,961.32

From February 19, 1973 - uS = 4.818Ky 1 = US$0.21Ky 1,000 - US$07.74Ky l,OOO,OOO = US$207,736

Fiscal Year - October 1 - September 30

This Report is ba4ed upon the findings of.a missionwhich visited Burma in February 1973. The missionconsisted of:

Mrs. Chandra Hardy (Chief)Mr. James Hendry (Agricultural Economist)Mr. Choeng Chung (Agricultural Economist)Mr. V. Dragomanovic (Industrial Economist)Mr. David Turnham (Economist)Miss Meera Shah (General Economist)

TABLE OF CONTENTS

Page No.

COUNTRY DATA

SUffARY AND CONCLUSIONS ..... ..................... i-vi

INTRODUCTION .1

A. RECENT ECONOMIC DEVELOPMENTS .2

I. NATIONAL PRODUCT AND ITS USE .2

II. DISTRIBUTION AND TILE COOPERATIVES.

III. PUBLIC FINTANCE .

IV. MONEY AND CREDIT ....... .......................... 12

V. THE EXTERNAL SECTOR ...... ........................ 15

B. SOCIAL W4ELFARE INDICATORS ..... ................... 21

VI. MTANPOWER AND EMPLOYMENT ..... ..................... 21

VII. PRICES ANTD WAGES ....... .......................... 26

C. SOME MAJOR CONSTRAINTS TO GROWTH .... ............. 34

VIII. AGRICULTURE...................................... 34

LX. INDUSTRY...................................... 51

X. MOBILIZING RESOURCES FOR INVESTMCENT. ......... 62

D. TIlE ECONOMY IN PERSPECTIVE. ....................... 66

,U4L ,t,,,Mv, , nL r*LrN'¶7 I - wTfI

ZX 2 - A T'ICTT'IU AR CREDIT ATD COOPERATWVES

STATISTICAL APPENDIX

MAPS

ANNEX I

Page 1 of 2 pages

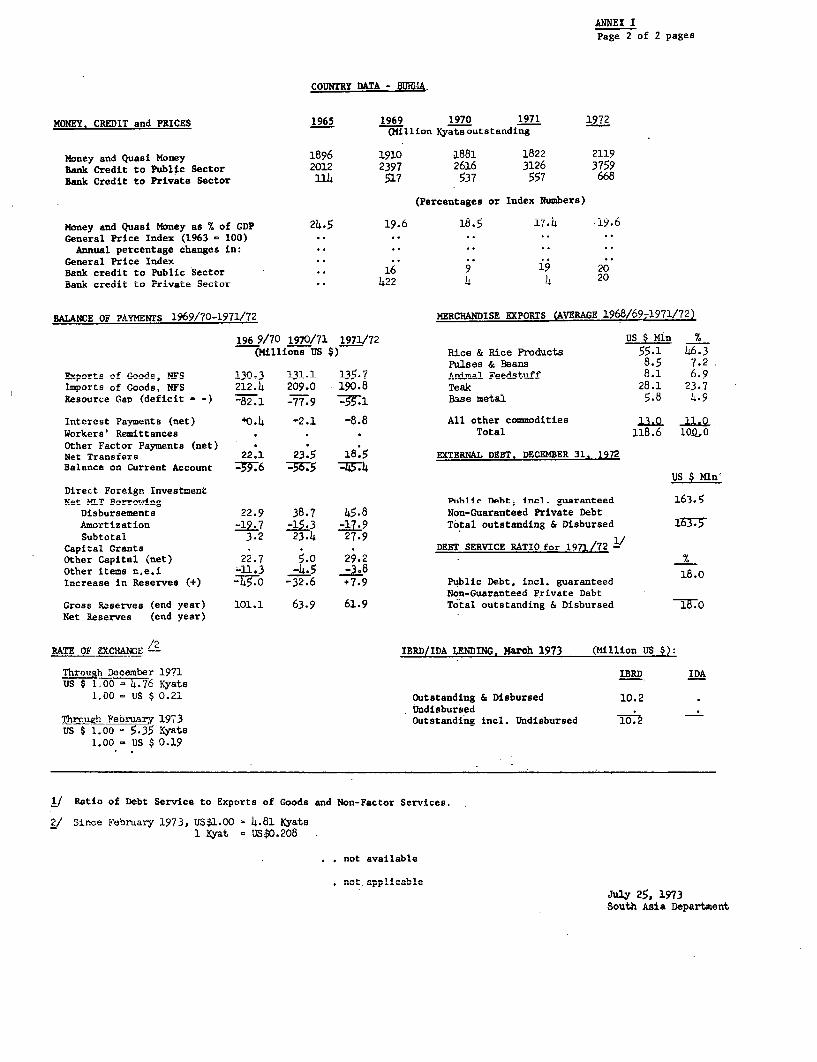

COUNTRY DATA - BURNA

AREA POiULATION DENSITY

678.528 km 2 28.9 million (19731/72). 42 per km"Ri'e of Growth: 2.3% (from 1965/66 to 1971/72) 1km of arable land

POPULATION CHARACTERISTICS 1970/71 (Selected Urban Areas) ALTH1970/71Crude Birth Rate (per 1,000) 38.B Population per physician 9,177Crude Death Rate (per 1,000) 11.1 Population per hospital bed 1,370Infant Mortality (per l,OOO live births) 59.8

INCOME DISTRIBUTION DISTRIBUTION OF LAND OWNERSHIP7. of national income, lowest quintile .% owned by top 10% of owners

highest quintile . . % owned by smallest 10% of owners

ACCESS TO PIPED WATER ACCESS TO ELECTRICITY% of population - urban ,% of population - urban

- rural - rural

NUTRITION 1969/70 EDUCATION 197O/7lCalorie intake as 7. of requirements 124 Adult literacy rate 7M6Per capita protein intake 60 Primary school enrollment 88%

GNP PER CAPITA in 197? US $ 85

GROSS NATIONAl PRODUCn T I?N 1071/72 ANNTUAL RATE OF GROWTH (7. constant prices)

US $ HMln. % 1962-66 1966-71 1971-72

GNP at Market Prices 2011 100'0 2.6 4.1 2.8Gross wixed Investment 241 12.0 5.2 3.9 5.8Gross National Saving - 172 8.6 .. -4.1 13.3Current Account Balance -45 -2.2Exports of Goods, NFrS 136 6.,7 -9M0 -10 6 16.3

Imports of Goods, NFS 191 9.5 -8.o -0.7 2.6

OUTPUT, LABOR FORCE ANDPRODUCTIVITY IN 19701/71

Value Added Labor Force V. A. Per WorkerUS S Mln. 7 Ml. 7. US$ _%

Agriculture 829.8 37.7 7.6 69.7 109.2 54.0Industry 275.2 12-5 0.8 7.3 344.0 170.0Services 1094.4 49.8 2.5 23.0 437.8 217.0Unal.-ocated . -

Total/Average 2199.4 100.0 10.9 100.0 201.8 10O.0

GOVERNMENT FINANCE 1971/72'netEral Govurnmnent TTniorin rovernment

Kya~ts Min. % of % of GDP average Kyats Man. % of % of average GDPGDP last three years 9LX last three Years

Current Receipts 8372 / 77.5 82.4 1959 18.1 18.7Current Expenditure 8336 V 77.1 82.1 2429 22,5 23.2Current Surplus 3' 36 ' 0.3 0.4 -470 -- T4- 3&45Capital Expenditures 852 7-9 8.4 228 2.1 2.2Exterl Assistance (net' 222 2.0 - 2.2

1/ The per capita GNP estimate is at 1972 market prices, calculated by the same conversiontechnique as the 1972 Wiorld Atlas. All other co-nversions to dollars in this table areat the &varage exchange rate prevailing 'du'ring the period covered.

not availablenot applicable

ANNEX IPage 2 of 2 pages

COUNTRY DATA - BUiUA.

MfWnv CREDVnIT and PRT-ES 1965 1969 1970 1971 1972(Million Kyatsoutstanding

Money and Quasi Money 1896 1910 1881 1822 2119Bank Credit to Public Sector 2012 2397 2616 3126 3759Bank Credit to Private Sector 114 517 537 557 668

(Percentages or Index Numbers)

Money and Quasi Money as 7 of GDP 24.5 19.6 18.5 17.4 -19.6General Price Index (1963 - 100) .. ..

Ann--,-! percentage chan"ges in: -* -v*

General Price IndexBank credit to Public Sector .. 16 9 19 20Bank credit to Private Sector - 22 4 h 20

BALANCE OF PAYMENTS i969/7U-iY97/ ( ERCHANDI;SbE AAEVPO (ArDVZAGA , , /6, 7 /7

196 9/70 1970/71 1971/72 US $ Min %(Millions US $) Rice & Rice Products 55.1 46.3

Putlses & Beans 8.5 7.27, or ts o f _-ood _, NF......S 130J 3 _3 135 .7 Ar o FedAtlfi3r 8.1 6.9Imports of Goods, NFS 212.4 209.0 190.8 Teak 28.1 23.7Resource Gap (deficit e -) - -77.9 - Base metal 5.8 4.9

Interest Payments (net) '0.4 -2.1 -8.8 All other commodities 1J3* 11.0Workers' Remittances . Total 118.6 lOQ,OOther Factor Payments (net)Net Transfers 22.1 23.5 18.5 EXTERNAL DEBT. DECEMBER 31. 1972Balance on Current Account .76 -56.5 j34

US $ MlnDirect Foreign InvestmentNet M-T Borroing Public Debt incl. guaranteed 163.5

Disbursements 22.9 38.7 45.8 Non-Guaranteed Private Debt

Amortization -19.7 -15.3 -17-9 Total outstanding & Disbursed 1

Subtotal 3.2 23. 27.9Capital Grants . . . DEBT SERVICE RATIO for 1971/72Other Capital (net) 22.7 5.0 29.2 %Other items n.e.i J -LL.± .8o 18.0Increase in Reserves (+) -15o -32.6 +7.9 Public Debt, incl. guaranteed

Non-Guaranteed Private DebtGross R3serves (end year) 101.1 63.9 61.9 Total outstanding & Disbursed lo.0Net Reserves (end year)

RATE OF EXCHANGE ZA IBRD/IDA LENDING. March 1973 (Million US $):

Through December 1971 IBRD IDAUS $ 1.00 = .76 Kyats

1.00 = US $ 0.21 Outstanding & Disbursed 10.2

UndisbursedThrough Febnaxy 1973 Outstandiniz incl. Undisbursed 10.2

US 1.00 35 Kyats1.00 - US $ 0.19

1/ Ratio of Debt Service to Exports of Goods and Non-Factor Services.

2/ Since February 1973, US4.00 = 4.81 Ityats1 Kyat = US$0.208

not available

not applicable

July 25, 1973South Asia Department

SUMMARY AND CONCLUSIONS

i. In 'the course of the past year, the Government of Burma madecontinuing efforts to widen its contacts with foreign countries and inter-national institutions. The most recent of these developments is Burma'sadmission to the Asian Development Bank in April 1973. On the economic front,considerable attention is being given to implementing the current Four YearPlan (1971/72-1974/75) and to devising measures to increase the rate ofeconomic growth.

ii. Last year was the first year of the current Four Year Plan (1971/72-1974/75). GDP in constant prices increased by 3.1 percent over the previousyear. This was lower than the average annual rate of growth of about 5.0percent experienced over the period 1968/69-1970/71 and it was also lowerthan the plan target of 4 percent per annum. The main reason for the slowgrowth of production was the continuing stagnation in agricultural output.Paddy production remained at around 8 million tons, while the output of someother important crops (groundnut and sesamum) declined. There was also amarked slowdown in livestock and fishery production.

iii Industrial output increased by 3.1 percent over the previous year.In view of the fact that most of what little investment there has been, overthe decade; has gone into the industrial sector and several new factoriescame into operation in recent years, this was not a good performance. Thegrowth of the manufacturing sector is partly constrained by the slow growthof agricultural production and the continued decline in imported raw materials,spare nprts- and comnponents. However, it is also a consequence of the very cleardisinvestment process which has been going on for some time. Industrialcapacity is rapidly being worn out due to noor reconstruction, replacement,depreciation and maintenance policies.

iv. The expansion of output during the year would have been evensmal'le b.u for tha increoaps in the ountput of the mining and services

sectors. Mineral output increased.by 12.0 percent in 1971/72, due primarilyto the 19 percent rise ln the production of criide oil The oaitnut of the

services sectors increased altogether by nearly 4 percent but there was no

increase ir. Acor.structior. activity.

v. -DurTig the year consumptior. ar.d oss fixed investment grFA faster

than GNP, by 5.2 percent and 5.8 percent respectively (in constant prices)...i.J.. er.tail.ed a subst.an,tial decrease i. stocks and increased use of forei gn

borrowing. The ratio of investment to GNP remained low at around 12 percent.National savi..gs remain at arounA 0 percer.t-of C-P. Pner capit income in

constant prices was K 374, showing no increase over the previous year. Thedecline JAX the dolilar vc-lue of estim.ated per. -apit ir.come from. $880 in1971 to $70 in 1972 was due to the devaluation of the Kyat in 1972.

vi. The functioning of the nationalized distribution sector continuesto be an important obstacle to development. It -aplifies scarcities andcreates price distortions which enhance the profitability of black-marketoperations. mne Government's respoLse to Udistribution problerms seemscentered on a drive to expand the cooperatives on a large scale at a rapid

rate. While there is clearly scope for improvement of consumer goods

distribution to which the cooperatives can contribute significantly, the

expansion of the role of the cooperatives to the extent now being planned

could prove an expensive venture with little immediate benefit to the economy.

vii. The continued worsening of the economic situation is also reflected

in widening budget and balance of payments deficits. The overall budget

deficit in 1972 was K 815 million, or 32 percent higher than in the previous

year. According to the revised estimates, K 488 million were to be financed

by gross foreign capital inflows and K 327 million by bank credit. This

level of deficit financing was not imuch higher than the average for the past

three years but its inflationary impact could no longer be cushioned by a

drawdown in foreign exchange reserves. Net reserves were negative at the

end of 1971/72, including liabilities to the IMF.

viii. No neT revenue measures were undertaken in 1971/72 and tax revenues

continued the decline which has been evident since 1964/65. Total receipts

were equal to 13. ercent of GDP in 1972, compared to 25 percent in 1965.

At the same time, there was an unprecedented jump in expenditures by 10

percent last -ear, corresponding to a 16 nercent increase in expenditures

on social and economic services and a 12 percent increase in the cost of

adm,iistration. Another important contributory factor to the rise in

current expenditures was the considerable increase in service payments on

internal and external public debt. The current revenues of the state

enterprises increased by 12 percent but this was wholly offset by increases

in current and capital. expenditures. The overall deficit of the state

enterprises was the same last year (K 121 million) as in the previous year.

ix. Control of the money supply has been an important instrument formaintaining prie stability and for most of the past decade, the growth of

the money supply was contained at less than 2 percent per annum. Last year,

hG.wever, the monetary picture changed drasticallv. During 1972, the money

supply and total liquidity increased by 16 percent, bringing the ratio of

money to GNF to 20 percent.

x. In 1971/72, the balance of paxj.ents showed an overall surplus of

nearly $8 million, compared to an overall deficit of $37 million in the

previous year but this, unforturately, did not result from a ny real irinrove-

ment in the external sector. The value of merchandise exports increased by

4 percent. Tne volum..e of rice exports was around 670,000 ton-s, dwn from

the previous year's '750,000 tons. The increase was mainly due to increases

in the exports of pulses, animal feedstuff, rubber and 4ute. It was also

due to higher expor.t prices for some of these commodities. The slight

improvement in the balarce of trade resulted from a 10 percen't de14ne in

the level of imports over the previous year. The major cut-back was in

imports of textiles and producer goods.

xi. Tne deterioration of Burma's terms of trade has been particularly

severe since 1968. The 36 percent deterioration in the terms of trade

between 1968 and 1971, was almost solely due to the 47 perceb.t drop in the

export price of rice over this period. The resulting decline in export

- iii -

earnings imposes a severe limitation on the country's import capacity andhence its economic development. This fall in the export price has beencompounded by a rise in the price of imports. In addition, the volume ofexports also fell. Over the past decade, the purchasing power of Burma'sexports have declined by 55 percent and it is currently less than 20 percentof its pre-war value.

xii. The 1972 current account deficit of $53 million was financed by asubstantial increase in foreign loan disbursements and an even more substantialincrease in miscellaneous capital inflows resulting from the repayment by SriLanka of rice export credits extended in 1971. the sale of gold and therevaluation of gross reserves.

xiii. Burma contracted several new loans during the past year, includingtwn largp loans frnm Jaan;n, -nd one from the Peonle's Renublic of China. Thesethree loans together amounted to $50 million. As of September 30, 1972, thetotal external debt was $308 mIllon, including an *ndishbrsed balanre of $144million. The average terns and conditions of these loans are very favorable.The gran t element on all the loans taken together is about 53 percent. Evenso, repayment obligations have been rising very rapidly and they accounted for52 percent of disbursements in 1972. The undisbursed balance of $144L ,i lioinis expected to be fully drawn down over the next five years and the debtservice ratio which is currently 18 percent i p to rise to ahout 21

percent by 1975.

xiv. The prospects for 1973, do not offer hope for much improvement inthe economic situation. B...a did not escape the effects of the bad weatherwhich has resulted in the present Asian grain crisis. Rice production is

do yar. esti,uated '=5percent. Th ln, h ugtestimates areUI.)LL )' 01 ~L .LUaLu I J IJ J1 'ff la. LII F_ ~ - - -

based on an export target of 800,000 tons of rice this year but the governmentUoes rLot now eApect export s a le s I.o bUe ..or e thl an 3000 00 tJons, at s. I- T.heoriginal budget estimates for 1973 show an even greater deficit than last year'sIL ut -L` vLew of thLe str'Igen.cy o,L the foreign exchar.ge cor.straint, t he govern-

ment is already in the process of cutting back imports and capital expenditures.1LIese cut-backlls will hiavle a severe i.mpact on t6-hae growtCh of output -nless thereis an offsetting increase in loan disbursements greater than is currentlyantLcLipate'U.

X-V. As notea in 'Last year's econoriic report, tle assessment ofperformance cannot be limited to the criterion of economic growth but musttake into account all of the country's objectives. It was also noted thatwhile economic performance has been poor, Burma's major success over thepast decade has been the provision of advanced social services 'or a populationof about 30 million with a per capita income of well below $100. Theseachievements are still there and these goals are still being pursued, but bynow, the possibility of further social progress is being endangered by thelack of job opportunities for the growing population and the stagnation, ifnot decline, in living standards.

xvi. The mission estimates that the labor force is about 12.8 million.No data are available for rural employment but it is believed that under-employment is fairly widespread in the rural areas. Preliminary results of

- iv -

the Urban Social Survey for 1972, show an unemployment rate of 6.5 percentfor the 10 major towns taken together. Another estimate (derived from laborexchange data) suggests an urban unemployment rate of 9.4 percent. By Asianstandards these are moderately high rates of unemployment, especially sincethe overall rate of unemployment generally corresponds to a rate among youngpeople two or three times as high.

xvii. The emergence of high and increasing levels of open unemploymentamong voung peonle is the beginnings of a different, and in some respects

more urgent, type of employment problem. The government's success in ex-panding the education system during the 1960's has resulted in an annual

outflow of high school and graduate students far in excess of available jobonportunities. Failure to provide enough obs, or iobs that match expecta-

tions can have serious consequences. The curtailment of expenditures onhi-her education and tho Rhift in expenditure to more vocational and technical

education which is required will, however, not provide the medium-termsolution to the -roblem of increasing unemployment. This can only be achievedthrough higher rates of economic growth.

xviii. Price stability has been an important component of the government's

economic objectives A fr. ceim s etent this has been achieved= The cost of

living index for Rangoon shows an average annual rate of growth of 4 percentper annum between 1962 and 1972. However, the ir.dex show.s severa1 disturbing

trends in recent years. For example, prices were as high in 1970 and 1971

(peakj agricultural years) as in a 1097 (.o years of drought). Th.e

slow growth and high costs of domestic production together with rising import

pr'ces ar,d increasir.g re.lance on deficit fina.-cing are the main factors

responsible for the pressure on prices. Last year, the Consumer Price IndexLor R-aLgooUL iLncreasedU uy 8 percent over the previous year. It should be

added that trends in Rangoon represent a floor of price trends for the

country as a wihole.

xix. Available data on wages and earnings indicate that earnings werevirtually static throughout much of the 1960's and 1970's, at least up to

the October 1972 revision of the wage structure. T.he mmajor chaanges in thenew wage and salary system (the first revision since 1947) are the consolida-tion of categories, the increase in the low level salary scale minima fromK 82 to K 100 per month and the reduction of the maxima at the other end of

the scale from K 2,100 to K 1,500 per month for riew entra..ts to LLese Jobs.

A general increase averaging roughly 11 percent was built into the new scales.

Tfhese increases are probably above the increases experienced by pr'Lvate sector

workers over the 1965-1972 period. Nevertheless, the increase in prices overthe last eighteen months has more than eliminated the partial restoration of

purchasing power implicit in the wage increases. With prices rising and

shortages of consumer goods becoming more acute, it seems that on balanceabsolute levels of living standards may have declined, albeit with varyingeffects on different segments of the population and parts of the country.

xx. The major economic problems continue to be the slow growth of

agricultural and industrial production, the acute shortage of foreignexchange and the inefficiency of the state enterprises. The main factors

cnsraining ithe grnwth nf agriculture are the disproportionately low level

of investment in agriculture and the unwillingness of the government (until

this year) to use pricing poliry to stimulate increases in production. The

low level of investment has left the rice sub-sector with little technical

capab.ility for further expansion i,n the short run and the emphasis on price

stability has been a factor depressing the production of several crops.

xxi. The government's policy towards the agricultural, sector is

currently in a transitional stage. Further rhanges will be reauired to

develop the country's agricultural resources to full advantage. The moreimportar.t st.eps inc.lu.de (i) the dApt3t-4rio of lenon' high vielding varieties

and the development of new ones; (ii) increased input use, particularlyof fertilizers; (iii) ir.creased inese t 4nirrigatin Pmhankment- drainage

and flood protection works; and (iv) improvements in price and marketing

policies.

xxii. It is recogni.zed that dIversification of the overall structure of

production has to be achieved through an expansion of the share of industry

in GDP and it is also recognized that Burma's potential for expanding the

industrial sector is basically good. So far, however, Burma hasinot beenvery successful in pursuing industr'al growth. TIs has been due in a.n

important degree to such factors as the lack of capital, the slow growthot agricuitural production and the shortage of foreign excha.nge but it hasalso been due to the neglect of the small-scale (largely private) sector whichstill accounts for more than hair of value-added In raLLufacturing; inadequate

pricing policies; insufficient replacement of existing capacity; the lackof incentives; the lack of correspondence witn market forces adll Inadequat

attention to putting the state enterprises on a self-sustaining, economicallyviable basis.

xxiii. The shortage of financial resources has been the dominant Lactor

in determining the low level of investment. However, current levels ofinvestment cannot lead to dynamic growth; indeed they will barely be enoughfor the task of rehabilitating existing productive capacity. The problem for

Burma is how to mobilize sufficient resources to carry out such ani expandleu

investment program. The government is, as yet, unwilling to consider taxincreases but this unpalatable decision will have to be maue soon. Efforts

will also have to be made to curtail the growth of expenditures, particularlyon administration and improve the management of public sector enterprises.

Given Burma's fundamental option for a socialist system, the main potential

source of domestic savings is the surplus of the public sector enterprise-.

The task of improving the management of'public sector enterprises is one which

cannot be further postponed.

xxiv. The need for foreign exchange is perhaps even greater than the

local currency constraint and another avenue for mobilizing resotrces for

investment is a dynamic export policy. The world market prospects for nearly

all of Burma's traditional exports are very good. This is even true for rice,

though probably not at today's extremely high prices. Burma supplies less

than one percent of the demand of the USA and Western Europe for'teak and

other hardwoods and less than one percent of world trade in minerals. Yet

-vi-

export promotion is not being given the priority it warrants. Poor export

performance is a direct corollary of the slow growth of production, but this

is not the only problem. The responsibility for exports is diffuse; coordina-

tion between producers and exporting agencies is inadequate, and there is a

lack of corresnondence between the domestic-and international price of export-

ables. Considerable increases in investment in agriculture, forestry andmining are required to increase and diversify production for export. At the

same time, an increased flow of exportables will require correspondinginprnuements in export marketing and pricing policies.

xxv= The government is aware of these problems and the determination

to come to grips with the economic problems endangering social progress,

has been gathering momentum over .the last year. Thus, the government has

substantially increased the'prices of paddy and other major crops; the

structure and level of wages have been revised and there is greater

flexibility in the use of piece rates, bonus schemes and other productivityincentrives. Tntprest rates on savings deposits have been increased and the

government hopes that this measure together with the expansion of the bankingnetwork will induce more private savin.s. The cooneratives are taking overretail distribution and it is hoped that this will bring about improvementsthrough the reductinn in stocks and wastages. The uniform selling price

of rice has been abolished. In the industrial and mining sectors several

schemes have been introduced, and others are under consideration for improving

efficiency. Though these measures may not be enough to reverse present trends,most of them represent steps in the right .irertin. They also represent

radical departures from previous policies and, as such, they warrant credit

andU support.

xxvi. The picture whIch emerges is therefore not unrelievedly discouraging.

All the macro-indicators point to a worsening economic situation. This is,however, partly due to the ,glect of the economy over the past decade, and

to the steady drop in the purchasing power of Burma's exports. For these

reasons, it would be unrealistic to expect a major reversal of these trends

in the immediate future. Moreover, the analysis of this report indicates

that the major economic probleems are deep=seated and it will require substantial

increases in investment over time to set the economy on the path of dynamic

growth. Tne basic causes for optimism are, however, the country's enor.mousresource potential and the evidence that -the authorities are making a seriouseffort to harness some of this potential. To develop these resources, even

at the modest rate of 4 percent per annum increase in GDP will require

substantial inflows of foreign assistance. In vjew of the under=investmentof the past decade and Burma's rich resource base, there is no dearth of

sound development projects and no question of the country's ability to absorb

foreign aid in some sectors effectively.

INTRODUCTION

1. In the course of the past year, the GuVveriment of Burma continued

its efforts to widen its contacts with foreign countries and international

institutions, and greater consideration is being given to encouragirng tour-

ism. The most recent of these developments is Burma's admission to the Asian

Development Bank in April 1973, and the pending extension of the seven-day

tourist visa to one month. On the economic front, considerable attention

was given to trying to implement the targets of the current Four Year Plan

(1971/72-1974/75), and to devising measures to increase the rate of economic

growth.

2. The government, in the course of the past year, has taken strong

measures, most notably a complete overhaul of the wage structure, an upward

adjustment of both wages and the procurement price of major crops (including

paddy, pulses and.cotton) and an unprecedented increase in interest rates

on savings deposits from 2 percent to 3-1/2 percent, tax-exempt. These and

other policy measures currently under consideration represent radical departures

from the types of policies which characterized the management of the economy

over the past decade. As noted in last year's Economic Report, over most of

the past decade the government devoted much of its energies and limi ted

resources to two overriding objectives -- unifying the country and creating a

social welfare state. By and large, the authorities have made notable progress

in the attainment of these political and social objectives, and it is a source

of pride to them that this has been accomplished witbout outside help.

3. At the same time, the neglect of the economy has resulted in a

lack of economic growth which is endangering the social progress which has

been made. lioreover, the measures now required to reverse the declining

trend in real per capita incomes and investment will have to be severe.

The economy of Burma is approaching that vicious constellation of circum-

stances which is all too familiar. As the economic situation worsens, the

measures which must be adopted to reverse the process become increasingly

more riskv and harsh, and thus tend to be not taken. Nor does postponement

make the solutions any easier.

4. Part A of this report (Chapters I-V) contains a review of recent

economic develonments, an evaluation of some of the more important policy

measures recently adopted and under consideration and a discussion of the

prospects for 1973.

5. Part B (chapters VT and VII) continues the discussion in the

previous economic report on the social progress which has been made but it

draws attention to two nroblems; namely, increasing rates of unemployment

and declining trends in real incomes which illustrate the limits to further

soc^il actio wrth the nresent economic constraints. Part C of the report

(Chapters VIII-X) contains an analysis of some of the major constraints to

BurmaIs economic development. The report discusses the problem of rice --

the dominant crop -- and its relation to other crops, and the prospects for

increasing the rate of agricultural growth-. The discussion of the industrial

sector focuses on three main problems -- the neglect of the small-scale

sector, prices and costs and the shortage of imported raw materials and

components. A third problem is the shortage of resources for investment,

which is discussed in Chapter X. The concludine ch2nter tries to place these

recent developments in perspective and relate them to the broader question of

how to achieve higher rates of econromic growth.

-2-

A. RECENT ECONOMIC DEVELOPMENTS

I. NATIONAL PRODUCT AND ITS USE

6. Last year was the first year of the current Four Year Plan (1971/72

- 1974/75). It is the first plan to reach the stage of Cabinet approval since

the early sixties and it is intended to be the first of a series of five Four

Year Plans for the long run development of the economy. The current plan

targets an overall increase in GDP at 4 percent per annum. The plan defines

sectoral targets for the agricultural, forestry, fishery, livestock, industry

and mining sub-sectors and it delineates what needs to be done to improve

the efficiency of the other sectors. The plan is a statement of the priority

given by the government to economic development but it is not a program for

specific action. It contains no analysis of financing, of economic inter-

relationships, nor of projects, and there is little indication as to how the

targets are to be achieved. Both the amount and the distribution of invest-

ment over the Plan neriod are to be maintained at the 1970/71 level. There

is, however, no means of determining whether this is a level of investment

which is consistent with the attainment of the sectoral targets. The

performance of the economy last year suggests that it is not.

7. In 1972, GDP in constant prices increased by 3.1 percent over the

previous year; which was lower than the average annual rate of growth of

4.7 percent experienced over the period 1968-1971, and was also lower than

the plan target of 4 percent per annum. The main reasons for the slow growth

of production were the near stagnation in agricultural output and the slow

grOwth of industrial production (Table 1).

Table 1: SECTORAL CO-TnOSITION OF GDP (constant 1969/70 Prices)

(millions Kyats)

Year Ending Sept. 30 1968 1969 1970 1971 1972

griculture (including-ivestock, fishe.;L

and forestry) 3,550 3,589 3,707 3,983 4,051

Industry 992 1,017 1,071 1,114 1j155

tining 94 91 111 117 131

Wholesale and Retai' Trade 2,397 1,452 2,535 2A,6R 2 751

Others 2,164 2,397 2,567 2,657 2,767

TOTAL GDP 9197 9,546 9,991 10,529 100855

GDP Annual Increase (%) - 3.8 4.7 5.4 3.1

Source: Ministry of Planning and Finance.

8. Agriculture. Taking account of variations in production due to

weather fluctuations, the growth of agricultural output over the past decade

was slightly over 2 percent per annum. Last year's performance represented

no significant departure from this trend. The value of crop production

increased by 1.3 percent, which was more than the planners had expected

because 1971 had been a bumper crop year. Forestry output also increased

more than had been planned, but livestock and fishery production were well

below the unrealistic target growth rate of 14 percent. Altogether, the

output value of the sector increased by 1.7 percent over the previous year

(Appendix Table 7.1).

9. The causes of this near stagnation of the agricultural sector

can be identified by examining the factors affecting the area, yield and

production of the major crops -- paddy, groundnut and sesamum, pulses, cotton,

jute, tobacco, sugarcane, onions and chillies (Appendix Table 7.2). Jute,

sugarcane, groundnut and sesamum, onions and chillies are the only crops

which increased by more than 2 percent per annum but, with the possible

exception of groundnuts, onions and sugarcane, the increase was solely due

to area expansion. The data show no real evidence of a breakthrough in

increasine agricultural productivity. Yields have either declined or remained

stagnant. Among the other crops, export pulses, maize and cotton production

have declined the most.

10 Rice-, the dominant crop and the country's largest export, has also

registered a poor record over the past decade. Once the largest rice

exporter in the world, Burma suffered severely from the devastation wrought

in World War II and from recurrent social disturbances. As a result of

extensave embankment and reclamation work carried out from 1958-1963, sown

acreage under paddy regained its pre-war level of 12.4 million acres in

1964. Since that time there has been no significant increase in area under

cultivation or in yields, and production has fluctuated around its pre-war

level of about 8 million tons. The drop in the exportable surplus from

1.5 million tons in 1963 to 650,000 tons in 1972, can therefore be explained

very simply hy the increases in population and per capita consumption of

2.2 percent and 1 percent per annum, respectively.

11. The details of the performance in 1972 and the prospects for 1973

are given in the Appendix Table 7.3. In 1972, paddy production was about

8 million tons. Compared to the previous year, there was a slight increase

in yields, but no increase in sown acreage. The acreage under cotton con-

tinued to expand in-1972,.probably at the expense of chillies and edible oil

crops. Cottonr. yleda were neP-third the level expected, however, and there

was no major increase in output. The decline in the retail price of edible

oils in 1970 and 1971 was a factor influencing the acreage under cultivation

and the production of oilseeds in 1972. The production of chillies was also

dow.n (by 32 percent) in 1972. Simi1ar,iv the wheat area continued the

decline which had been taking place since 1966 when prices were reduced from

K 19 to K 12 per basket. Harvested sugarcane production was less than half

of the plan target, but this was due to the failure to coordinate harvesting

and deliveries to the mills rather than a shortfall in production. Tobacco

and jute were the only two crops which did as well, or better, than expected.

12. The prospects for 1973 do not call for any major increase in

output. The first half of the crop year was beset by inadequate rains

-4-

in sone areas, as a result of which paddy production is estimated to fall

by around 0u percent. Th e government raised the nrocurement price of paddy

by 19 percent in January 1973, but it is too early to tell what effect this

is likely to have on pruction and procurement. The production of edible

oil crops is likely to be down by 20-30 percent, since these crops are

grown primarily in the drought areas. Th-.e production of cotton, wheat and

jute are not expected to be adversely affected by weather, but taken alto-

gether it seems unlikely that the plan target of a 2.8 percent increase in

total crop production will be achieved. There is also no reason to believe

that the increase in the output of the livestock and fishery sub-sectors

will be as high as 11 percent. Only for the forestry sub-sector is there a

likelihood production might achieve the target increase of 3.4 percent.

13. Industry. Industrial output increased by 3.1 percent over the

previous year. This was a poor performance, however, even if judged by

the past decadets standards, since most of what little investment there

has been has gone into the industrial sector. Public sector enterprises

receive the lion's share of the investment resources, and in recent years

several new factories (including two fertilizer plants, three textile mills,

and one each for paper and cement) came on stream. Gross output from the

public sector enterprises increased last year by 5 percent, bringing their

share of total industrial output to 44 percent; in conitrast, gross output

in the private sector declined by 3 percent.

14. The depressed growth rates of the manufacturing sector reflect

mainly the slow growth of agricultural production and the continual decline

in the availability of imported raw materials, spare parts and components.

But it is also partly a consequence of the very steady disinvestment process

which has been going on for some time. The level of public sector investment

in manufacturing over the past decade corresponded to about 2 percent of GDP

annually and most of it went into the establishment of new industries. As

a result, industrial capacity is rapidly being worn out (mainly in the

private sector, but also in the public sector) due to poor maintenance,

depreciation, repairs and replacement policies.

15. Minerals. The expansion of GDP during the year would have been

even smaller but for the increase in the output of the mining sector. For

the first time in the post-war period, output in the mining sector regis-

tered a remarkable 12 percent increase in 1972. This was due mainly to an

increase in the output of crude oil by 19 percent, in natural gas by 67

percent and in zinc by 16 percent. In all other items, mineral production

either stagnated or declined, so Burma remains far below pre-war production

levels in metallic minerals. Most of the increase in crude oil production

comes from new: oil wells, brought into operation during the last two years,

probably as a result of onshore exploration programs financed in part by a

$5.6 million loan from the Exim Bank and Manufacturers Hanover Trust, and

by a DM 22 million loan from the Federal Republic of Germany. These in-

creases in crude oil output all came from one field; the average daily

outntit of all other fields is' declining. Hence the necessity to intensify

exploration works,both onshore and offshore, which is reflected in the fact

that 48 nercent of the mining sector investment program has been earmarked

for oil exploration and field development works during the plan period.

16. The minerals sector as it stands today, with worn-out and out-dated equipment, well depleted higher-grade ore deposi--s an a slortage ofskilled labor, requires enormous investment and concerted efforts to re-store its ro; ir. Axot end U dutr4al deeo,lrt hs task is ,-<even more difficult by the insecurity which prevails in some of the most

importan m.4ing areas. It+ i9 r.ot possible o assess Ir quantLitat.ve term,sthe damage being caused by insurgent activities, but the effect on miningpr^uction, transportatior, L L the cosL oL new projects imist be sizeable.The problem of.labor shortages seems.to have eased somewhat during the pastyear, at least fUor unsIkilled wor'Kers. ±LLe goverILfi,enLt's attitude towardsincentive schemes is now more flexible, and the supply of consumer goodsto minir.L ares ILas been JLmprovedL. 1AccordLnLg to official statistics, thenumber of mine workers increased in 1972 by 11,500, or 46 percent, and thiswas tLhe f'rst time t'at the labor -eCLUitent service succeeded in attractinga large number of new mine workers.

17. Services. The output of the services sector -- which includesall non-commodity producing sectors -- increased by nearly 4 percent from1971 to 1972. Within the sector, however, there were significant variations.Output of the construction and telecommunications sub-sectors continued tostagnate and there was a further slowing down in the performance of thetransportation and power sub-sectors. Inadequate transportation and tele-communications, together with frequent breakdowns in the supply of power,constitute increasingly constraining bottlenecks to the growth of outputwhich point up the need for substantial increases in infrastructure invest-ment.

National Income

18. During the year, consumption and gross fixed investment grewfaster than the increase in GNP, by 5.2 percent and 5.8 percent, respectively(Appendix Table 2.2). This entailed a substantial decrease in stocks andincreased use of foreign borrowing. No data are available on the relativeshares of public and private consumption. According to the information whichis available, gross capital formation, in current prices, remained low ataround 12.percent of GNP, and a further decline in private sector investmentbrought its share of total investment to less than 30 percent. This comparesto a private sector share of slightly more than 50 percent in 1962. Inreal terms, pe.r capita gross fixed investment has been stagnant at $8since 1965.

19. Available data indicate that total national savings increased inboth absolute terms and as a proportion of GNP last year. Public savingsare negligible, and most of the increase is accounted for by a 20 percentincrease in private savings. The behavior of-private savings seemsparticularly unrealistic in view of the fact that per capita income inconstant prices was K 374, showing no increase over the previous year.The only-plausible explanation is that the figures refer to trends innominal savings, for such an increase would be consistent with the rapidexpansion in liquidity and savings held in deposits relative to the previLusyear. Even so, the share of national savings in GNP is still only around8 percent, and net external borrowing accounts for 3.5 percent of GNP.

-6-

II. DISTRIBUTION AND THE COOPERATIVES

20. hle huaJor cliaLge In economic organization last year fwas the con-siderable expansion in the role of cooperatives. Since 1970, membershipin the cooperatives has '-Lcreased by nearly one m4llion, bringIng the t^tal

to 5.7 million. The number of cooperatives is now 15,650, compared to

13,000 in 1970. Mxembership is voluntary and thLe cooperatives ae -ected to

appoint their own staffs. However, the Cooperative Ministry undertakes to

train managetial personnel, Or even tLU provide it, to eI..odsof

operation, extend credit, fix prices and appoint 6one-third- of th"e members

of each cooperative committee.

21. A large expansion has taken place in the num..ber o'f consumer co=

operatives, which have replaced most of the People's Shops dealing withfoodstuffs, textiles, household goods and gener'al stores. The mi3sion visitedseveral of these cooperatives and found them generally well-run and better

stocked than the People's Shops, which sold only the g6oa- ofL or.e particularTrading Corporation. Another imp'ortant development is the recent removal of

the subsidy elements in the domestic sales of rice. -ice was sold previouslythroughout the countfy at 20 Kyats per bag (2 cents per pound). The co-

operatives have now been instructed- to charge prices wh,ich co'ver cSt5s.

This-does not mean that the cooperatives will be free toj let prices adjust

to supply and demand forces, because the Government will st'ill set price

ceilings. The retail price of rice in Rangoon, for example, is not supposed

to exceed 2.5-3.5 cents per pound, depending on the quality. Nev'ertneless,the potential importance of the new policy can be gauged from the fact

that the budgetary losses on previously subsidized domestic rice sales were

estimated at K 70 million in 1971.

22. At the wholesale level, the current plarn is for each of the Trade

Corporations to establish depots in each of the 14 major divisions of the

country for distribution to the cooperatives. Government also hopes that

most of the now redundant employees of the Trade Ministry will be absorbed by

the Trade Corporation division depots and the cooperatives. Even with all

of these teething troubles, the consumer cooperatives may bring about improve-

ments in distribution if some of the more general problems'such as inadequate

transportation, storage and credit can be solved.

23. Meanwhile, the position of the priva'te retail traders remains

anomalous. The emphasis on cooperatives tends.to obscure the fact that the

private sector accounts for more than half of value added in the trade sector.Because private traders, operating with uncertain'legality, are subject toarbitrary seizure of their goods, the prices consumers pay presumably coversome of the risks of- private sector trade operations. Early this year, theGovernment issued a notification requiring the-registration of all privatedoctors and clinics. This action was taken with a view to 'supervisingstandards of operation. Similar action with regard to the7'regularization of

private retail trade could serve to improve the efficiency of distributionand thus be in the public's interest. Taking steps to legalize private

retail trade would perhaps not be so necessary if the cooperatives concentrated

their efforts on improving retail distribution, but, unfortunately, the

emphasis seems to be more on simply expanding the role of the cooperatives

in all aspects of the economy.

24. As a result, in addition to their wholesale and retail functions,

the cooperatives have replaced Trade Corporation No. I in the procurement,

processing and most of the distribution of rice. Trade Corporation No. I

will be responsible only for the processing of paddy for export and for dis-

tribution to the remote areas. The cooperatives have also replaced the

Ministry of Trade in the purchasing, processing and marketing of marine

products, textiles and industrial goods, both at the wholesale and retail

levels. Beginning this year the cooperatives are also to replace the Union

Bank in the provision of short-term credit to the farmers. This change has

many serious implications, not the least of which is the abolition of the

only existing institution for credit (the Village Banks) and its replacement

by something xwholly untried.

25. The change in the provision of credit also has important effects

on the pricing of agricultural commodities. Since the cooperatives have to

borrow funds from the Union Bank at 4-1/2 percent per annum to finance their

interest-free advanced Dayment scheme to farmers, they intend to cover this

by generating a surplus through their profit margins at various levels beyond

procurPment. The effect of this scheme is, therefore, to subsidize credit

to the farmers by the consumers. Furthermore, since the advanced payments to

farmers can be used for non-productive purposes, this scheme may be less

effective in improving production, than, say, increasing the procurement

prices. Further detais on credit and the cooperatives are provided in

Annex II.

26. The expansion of the cooperatives is creating considerableeconomic upheaval. The budget is feeling the impact of the loss of the

surplus from the Trade Council, increased administrative costs and interest-

free credit to the cooperatives. At the same time; there is as yet no sign

of significant improvements in the entire distribution network. On the

contrary, in the last quarter of 1972, the cooperatives were quite unableto handle efficiently the distribution of edible oils and these commodities

were again handed over to the private sector after three months. To put

it simply, expansion of the cooperative movement appears to be proceeding

too rapidly and on too mmany fronts, with little attention apparently being

given to the costs of this latest drive relative to the probable benefits.

Since, as noteu previously, t.he consumer cooperatives m,nv bring about some

improvement in retail distribution, it is not the principle of expansion ofthe role of the cooperatives in the economy which i hbeing nuestioned. Rather,

the doubts concern the timing of the expansion, the mode of operation and the

effects on cost and efficiency of the rapid expansion in a large number of

areas which is currently in progress.

- 8 -

III. PUBLIC FINANCE

27. The continued worsening of the economic situation is also reflectedin the widening budget deficit. In 1972, the overall budget deficit wasK 815 million, or 32 percent higher than in the previous year. (Table 2).

28. Current Revenues and Expenditures. Details of the Union Governmentcurrent receipts and expenditures (excluding interest payments) are shown inAppendix Tables 5.1 and 5.2. About 36 percent of government revenues comefrom income taxes; another 40 percent comes from indirect taxes, mainlycustoms duties, sales taxes and excise duties. Virtually all taxes (on income,production and expenditure) are collected by the Union Government from theBoards and Corporations. No new revenue measures were taken last year andtotal receipts registered a two percent decrease over the previous year.This continued a trend which has been steadily declining since 1965 and ismainly due to the slow rate of economic growth, the decline in exports andimports and the failure of the Boards and Corporations to show a taxablesurplus. Total receipts were equal to 13 percent of GDP in 1972 compared to25 percent of GDP in 1965.

29. At the same time, current expenditures continue to increase. Theunprecedented iump in expenditures by 10 percent last year was considerablyhigher than the 4 percent annual rate of increase registered over the pastdecade, and was due largely to a 10 percent increase in expenditures onthe social and economic services and a 12 percent increase in the cost ofadministration. The increase in expenditure on economic services resultedfrom the more than doubling of expenditure on the cooperatives. The increasein expenditure on social services was due to a 10 percent increase in theexpenditure on health and education and a 28 percent increase in pensions.For mnot of the nast decade- the growth of current expenditures was kept inline with the growth in revenue, although this was increasingly difficult tonronmplish over the npat four years. Even so; un to 1970. the current surnlus

of the Union Government was sufficient to finance its capital expenditurenrogam= T-act yper t-hp etst-ormnrv siirnpli on rctrrent acrount tuirne.d into a

deficit, however, while capital expenditures remained at the same level as in1971 (Asppen.dix Table 5.3).

-9

Table 2: CONSOLIDATED PUBLICECTOR BUDGET(million Kyats)

Est. BudgetYearx Ending Sept. 30 1968 1969 1970 1971 1972 1973

C urrent Revenues 6,524__ 7,036 ,-7,389 / 7,599 /V8,372 8,700

Union Government /a 1,826 1,810 1,953 1,855 1,959 1,674Local Bodies 69 70 71 79 82 79Boards & Corporations 4,629- 5,156- 5,365, 5,665. 6,331 6,947

urrent Expenditures 6,248,-'6,852_--7,399-- 7,517 /,336 8,694

Union Government /a 1,731 1,882 2,062 2,155 2,429 2,359Local Bodies 49 52 53 55 64 66Boards & Corporations 4,468 4,918 5,284 5,306 5,843 6,259

Current Surplus/Deficit 276 184 -10 82 35 16

Capital Expenditure 613 726 778 712 852 988

Union Government /a 202 209 278 222 228 264Local Bodies 10 13 12 10 17 17Boards & Corporations 4n1 504 488 480 607 707

Capital Revenues _b 1 61 117 13 1 1

Deficit to be Financed -336 -536 -671 -617 -815 -971of whichDomestic Borrowing /c 113 326 345 300 327 451Gross Foreign Borrowing 223 210 326 317 488 520

/a Including Special Accounts and the States.

/b Derived from the liquidation and sale of state assets.

/c Mostly bank financing.

Source: Ministry of Planning and Finance.

30. State Enterprises. The major source of government revenue is thecurrent surplus of the State Boards and Corporations, in particular Industry,Transport, Banks and Insurance. State enterprises are required to transferall receipts to the Union Government Consolidated Cash Fund, from which fundsare returned to the enterprises according-to their budget allocations. Lastyear, the current revenues of the state enterprises increased by 12 percent,but this was wholly offset by increases in current and capital expnditures.As a result the overall deficit of the state enterprises was the same lastyear (K 120 million) as in the previous year (Appendix Table 5.4). TheAgricultural Corporation has consistently shown a deficit. This is due tothe losses on the operation of the tractor and pump stations, the non-recoveryof loans and the non-payment for services. The current surplus of the state

-10-

manufacturing sector has been declining since 1969, while capital expend-

itures have been rising. The same is true of the transport agencies. Thegovernment's difficulties in handling wholesale and retail trade is reflected

in the performance of the Trade Council. As stated previously, producer

organizations are required to hand over goods at cost and only the Trade

Organizations are allowed profit margins. These profits are then to be

transferred to the government in the form of income taxes. However, since

the nationalization of trade in 1963, the Trade Council has shown a surplus

only in 1965, 1966 and again last year. The transference of responsibility

for internal distribution to the cooperatives is likely to have a negative

impact on the budget, but government officials hope that the huge losses on

the distribution operations can be reduced. The nationalized financial

institut'ons used to be a steady net contributor to government revenues, but

in recent years the surplus has been declining due to rising expenditures

associated with widening the network of branch banks and taking over the

numerous subtreasuries '(over 100) of the Government. Taken together, the

state enterprises have shown an overall deficit every year since 1965. The

main reasons for these continuing deficits were given in last year's report.

In brief, they reflect essentially the inadequate management of the state

enterprise sector.

31. Capital Expenditure. Public sector investment increased last

year by nearly 20 percent. Most of the increase took place in the State

Boards and Corporations, which accounted for 71 percent of the total. There

was no malor change in the distribution of investment. Industry continues

to take the major share, accounting for 40 percent of the total, but there

were substantial increases in investment in agriculture and mining. Invest-

ment in agriculture increased from K 42 million to K 72 million, increasing

its share from 9 percent to 12 percent. Investment in mining increased

from K 83 million to K 171 million, reflecting largely the disbursementson the Japanese loans for oil exploration.

32- Consolidated BudRet. The deficit of the Union Government accounted

for 86 percent of the public sector overall deficit of K 815 million for 1972.

In addition to what was said earlier,-another important contributory factor

to the rise in current expenditures was the considerable increase in service

payments on nublic debt. Interest charges on internal public debt increased

from K 75 million in 1971 to K 169 million in 1972, and interest charges

on external debt rose from K 133 million to K 176 million over the same

period. These increases were the direct outcome of the government's increas-lng reliance on Treasury Bill horrowing and short-term foreign credits to

finance the deficit. About 40 percent of last year's budget deficit was

financed by bank borrowing and the rest by disbursements on foreign loans

and grants. Although the government is increasing its reliance on foreign

borrowing to finance the deficit, and despite a leve1 of bank ffnancing in

1972 which was not much higher than the average for the past three years, the

inflationary impact could no lorer be cushioned by a drawdown in foreign

exchange reserves. Net reserves were negative at the end of 1972, including

the I'rnr stardLUy credit.

The 1973 Budget

33. The budget for 1973 does not indicate the likelihood of anyimprovement in the basic situation. According to the original estimates,Union Government current expenditures are slated to go up by a further 23percent, and revenLues are again expected to decline. The anticipated declinein revenues is largely due to the expected decrease in corporate income taxwhich would result from handing over the responsibility for distribution tothe cooperatives. It is not that the cooperatives are exempt from taxes,but no procedure has been established as yet for assessing and collectingtaxes from them. It is also very likely that the cooperatives will not show-much of a taxable surplus for some time. The decentralization of distributionwill also reduce profits to the non-taxable level. The budget also envisagesa substantial increase in capital outlays, and the resultant deficit may beup to 20 percent higher than last year's. Since disbursements on foreignloans and grants are not expected to increase by much, the budget anticipatessubstantial 'reliance on bank borrowing, which would raise the level ofdeficit financing to K 450 million.

34. Since the announcement of the 1973 Budget in September 1972,several events have occurred which will require major revisions in thebudget estimates. First, the original estimates did not include the costof providing salary increases, estimated to be K 190 million. Second, thebudget did not allow for a K 500 million increase in lending to the cooper-atives during 1973. Most of these loans are for advance purchases of paddyand are repayable at 4 percent interest, but at least K 150 million are tobe given interest free to the farmers as the cooperatives replace the VillageBanks. The implications of this change are discussed elsewhere, but sufficeit to say in this context that it will probably add another K 150 millionto the deficit.

35. On the other hand, the government is already engaged in the taskof cutting back certain other proposed increases in expenditures. Measureshave been initiated to reduce and/or postpone non-urgent expenditures. Forexample, the government no longer provides cars and drivers for seniorofficials. These employees are now allowed to purchase the cars and operatethem at their own expense. Also, a high level committee has been establishedto vet proposed expenditure increases, although it is not clear that thecommittee has much room for maneuver. Much of the increased cost of govern-ment administration goes toward the establishment of new institutions (suchas the People's Courts) and widening the functions of the Burma Socia istProgram Party, wich are funded almost entirely out of the budget. Partof this year's huge increase in expenditure reflects the cost of carryingout the long overdue population census. But in all candour, for most of therequired cutbacks in current expenditures. the critical decisions can onlybe taken at the highest levels of government where choices dictated byoverall considerations must be reconsidered in the light of a rapidlyworsening economic- situation.

36. On the capital expenditure side, the original budget estimateswere based upon the assimnption that rice exports would be as high as

- 12 -

300,000 tons this y'ear. The government now does not expect exkorts to bemore than 300,000 tons, and this entails substantial cutbacks in the tree

forein exchanrge allocation to the Boards and Corporationiis. Since theforeign exchange conitent of public sector investment is arou*d;50 percent,capital formation next year in the public sector is, at bes't, likely to hecontained at this year's level. Thfe careful management of m-onetary andfiscal w li-ciets over the past decade is the basis for th1e belief that effortswill b'e made to-redu'ce- reliance on deficit financing to,a muchi more manageablelevel than is indicated in the original budget estimates. No increase in

short-term inter-biank borrow'ing is expected but eff6qtts are being made toincrease the rate of disbursement on toreign loans and to cut-bacK current

and capital exp'endituies. Unfortuna'te-ly, any red'uction in capital expenditurewill hnve an advre imoinact on th'e outDut tarRets for 1973' and for this reason,

it would be preferable if the n'ec'essary reductions fell iore heavily on

current expennditu'es.

IV. MONEY AND. CREDIT

37. 1!onetary De-v"lnments. For m6st of the' D daecade.-contr6l of

the money supply'wAs- an impOrtant in'trtitent for mifTtain`ing price stability.Dm-teStic credit 6.sexpanid+h r4in1dlvj hlt- it wiAA noassible to contain thegrowth of the money supp"ly' ait less than 2 percent per annum right up to 1971

by sharply redti&ing ektetnal reservPs - st yeari nowever ; the To'nA,tqrvpicture changed drastically. Doimstic cre'dit (maiffnly to' the public sect-r)n.reased by ,a ii, inf1a'fioin v impart eas immediate because

there were no external reserves- whfich cou-ld be' drawn down. ,At the end of

1971 net forei, a-sets -- r- K 13' i,Wii Iton - hi.t- hv th:e end of 1972, thev werenil - actually negative by' about $30' mi'llion', if liabiliti-e"s to the IMF are

in.luded-. Duri.g.- 1797,. the mjg,,o9 a,,npl~ nn tnt21- linai{dftv iner'ased by

16 percent, bringing the ratio of money to GNP to 20 p'ercent.1/

38. According to' the reeulTations eovernini the- dpDerations of the UnionBank (thne only athorized fibat41iDl in.'tituitirn) e ninuel adivanre to th

Government should. not exceed 15 pe'rceit of e§timated' budget revenues. The

Govern.,ent has byjpassed this re -lafiorsiiiIp'lZby s1lling seruritie to the

Bank and almost all of the internal public debt is lield b'y the Union Bank

in the forL of r y i. .latte are, t-h.ro.e m.ot1i i nMiat-4nno beanyr4,

interest of one pe'rcent per annum.i Government sales' of Trea'sury Bills in-

creaseu by 22percen pet r ann-.. betweeer.1968 a 1971. L -- .oun

of Treasury Bills outstanding was'K 809 million, or 31 percent over the

previous year. '(Appe,idix Table 6.1).

1/ All this is'not immediately evide'nt from Table 3. Burimas monetary

statistics present some difficulties- oL ±1t.LepLULaLion,.

- 13 -

39. ..e author-e are aware -f the need to reduce thp infl ltionnrvimpact of increases in the money supply, and. they have expressed an intentionto limt- the increase in doumestic credit to 0 per-cnt in 1973. Meaclsrpes willLU L.LMLU.L L.16C LuLL. LLt- ' *~-~ ---

also be taken to reduce the credit needs of public sector agencies. A

Working Capital Scheme (UCS) now .-anaged by the Union Brnk wa introducdin 1970 and its coverage has been extended to many public sector agencies.

The purpose of the WC is to monitor performnance vis-a-vis the demand for

working capital. Under the scheme, the demand for working capital above the

budgeted allocation is ueL .uguh loa.n funds at 3 percent per -nnum. The

operation of the WCS has already had some impact on improving financial

performance. However, further lmprovemuent will require the discontinuanceof the interest free budget allocation. The government still has underconsideration a proposal to make agencies finance theiLr working capital needseither through own funds cr loans. The acceptance of this proposal wouldmake the WCS a much more effective instrument of commercial policy.

Table 3: MfNETARY S'uR.vEY DATA(million Kyats)

Year Ending September 30 1968 1969 1970 1971 1972

Foreign Assets (Gross) 912 726 481 304 331

Adjustment for:Government assets -4 -4 -4 -5 -6

IMF Position -36 -36 -93 -86 -106Foreign Liabilities(excluding IMF) -172 -240 -198 -200 -219

Foreign Assets (Net) 700 446 186 13 -

Claims on Government (Gross) 2,171 2,481 2,583 3,067 3,700

Adjustment for:Government IMF Accounts /b 33 33 33 59 59Government Deposits -131 -117. - - -

./Claims on Government (Net) 2,073 2,397 2,616 3,126 3,759

/Claims on Private Sector 99 517 537 557 668

,<oney 2,339 2,407 2,448 2,470 2,872

of which:Currency in Circulation 1,755 1,869 1,843 1,781 2,085

7- Quasi-Money 45 41 38 41 34

Counterpart Funds 74 73 54 54 57

Other Liabilities (Net) 414 839 799 1,121 1,464

/a Including SDR's./b Subscription to the IMF less securities held by the IMF.

Source: Union of Burma Bank.

- 14 -

40. Interest Rate, Savings and Credit. Since 1964, the interest onsavings deposits had been kept constant at a tax-exempt rate of 2 percentper annum. and ceilings were applied to the amount of the deposits whichcould earn interest. In January 1973, the government took the unprecedentedstep of raising the rate to 3.5 percent tax free, and abolished the limitson the size of deposits. The government hopes that this measure, togetherwith the exnansion of branch banks and credit societies. will increase themobilization of private savings.

41. Between 1968 and 1971, total savings held in the Union Bank in-creased mersrtelu by arounid npercent- per annum. Last yepr, tntal savings

(mostly in the form of deposits) increased by 11 percent (Appendix Table 6.2).Th.e reasons fnr thia aiiieln i-ncreas ar not quite clear. Owing to therapid increase in the money supply in recent years, total liquidity in thehr.oAas of tho -ubli4c hFa inreaosedA and there has hoben consoidoeahle hoari4ngn

During last year, there were rumors about another demonetization measureof K 20 notes and th4s may have prompted some flow of funds into the Bank.Another possible explanation is that the expansion of branch banks hasinduced peoplke to .h.old. .more of their savings in the fo-- of depositJs.

A) C-redit7 -tho nt4eori-. r ortnesetr 1 roislarel- limiste to short--term og-r4--_ r ~~~~~0_ __ -0_

cultural loans. Over the last three years, K 150 million were advancedannually to the farmers through the Village Bnks. These loans are -ade

available to the Village Banks at 3 percent per annum, and are relent tothIe farm.ers at a per L - .-- 6 pecet diAAfferetial, A4 ir. diAtion to a

compulsory saving of one percent of the loan, are held as savings deposits.T.f*LV are 11,000 Villlage B.ks i..th a -toa- --- t.iiL of- near tw. o mil-

lion. In recent years, the annual repayment on their loans averaged 90percent a an'" uiuele vallue of theIr .deosts gr--L--A L4 percenkt of thle loansadvanced in 1972. The Agricultural Corporation is the only other source of'nistitutional credit t0 thLe farmer>L .LL tL CorpULorLat.LioLL gives credit in the

form of inputs (fertilizer, seed, etc.) amounting to about K 15-18 million.Recovery rates are extremely low - about 35 prLcenLt of the anLual ad-vances -

and with defaults being generally written off, the Corporation has beenloosing at least K 11 million per year.

43. Beginning this year, the Cooperatives will initiate a system ofadvance payments to provide short term credit to farmers without interestrate charges. Participation in this scheme, applicable to all crops willbe voluntary. The Village Bank system will be discontinued, however, andthe Cooperatives will now have to establish units to take over the provisionof credit to at least the two million farmers who have been members ofthe Village Banks. It is not clear exactly how this proposal will be carriedout. Although a broad outline of the scheme has been described, no concreteprogram for implementation has been developed. The government hopes thatthe Cooperatives will succeed in procuring greater quantities of paddy, butit is doubtful whether this will materialize. It is not clear why it hasbeen decided to totally replace an efficient credit institution by one whichhas yet to be created and is totally untried, at the same time continuinganother system (input loans in kind) which has proven much less successfulon the criteria of repayment.

VU TT.h RYTRPMAT SVECTOR

Merchandise Trade

44. For most of the past decade, merchandise exports have declined,at .first slowly ar.d ten rapidly to aoLULLU $ IIJ LLU..L.L.Ult 110 L '19UO. D L.M.Ac

that time a slight reversal in the trend has been noticeable. Between1968 and 1971, the value of merchandise eports increased by 2 percent perannum. Last year, they went up by nearly 4 percent. However, the dollarvalue of exports ($125 million in 1972) is still below tne pre-war ievei($189 million) and less than half the 1962 level ($267 million).

45. The increase last year was mainly due to increases in the exportsof pu'lses, animal feedsturff, rubber and jute. it was also due to higherexport prices for some of these commodities. Exports of some non-agriculturalcommodities (minerals and gems) also increased last year, but not significant-ly. Rice exports, which currently account for 42 percent of the total, fellfrom $60 million (750,000 tons) in 1971 to $50 million (670,000 tons) in 1972.At the beginning of 1972 the world market price for Burma's rice was aboutthe same as in IY97 ($80 per ton) and the government anticipated a substantialincrease in paddy procurement. The target for rice exports in 1972 wasset accordingly at 920,000 tons'and, in an effort to recover-markets lostin 1968 and 1969, the Ministry of Trade concluded contracts for 850,000tons during the tirst halt ot 1972. However, the domestic procurement ofrice was 500,000 tons less than anticipated, and even by drawing down heavilyon stocks the government could only ship 670,000 tons by the end of theyear. Even more unfortunately, Burma was unable to take advantage of thenear doubling of export prices since May 1972, and nearly 200,000 tons outof this year's crop has already been sold at the 1971 prices. Rice sodominates the Burmese economy that the subject is discussed in greaterdetail in Chapter VIII.

46. Exports of timber products, which account for nearly 25 percentof total exports registered a'five percent decline in dollar values in 1972.The major obstacles to increased production continue to be insurgency in someforest areas and chronic production problems due to the shortage of felling,logging, extraction and processing equipment. Mineral exports increased by16 percent last year, but mineral production stagnates at a fraction of itspre-war level for much the same reasons as in forestry.

47. Merchandise imports also declined over the past decade, althoughthe decline was less pronounced thad in exports. The value of imports was$160 million in 1972 (compared to $220 million in 1962) but this representeda 10 percent decline over the previous year. Consumer good imports (milkproducts, wheat and textiles) account for about 15 percent of the total;imports of raw material, spare parts and component account for 37 percent,and capital goods imports for the rest. The data available for 9 monthsof 1972 suggest that the major cut-back was in imports of textiles, and thatproducer good imports were slightly below the 1971 level.

- 16 -

Pattern and Terms of Trade

48. There was no particular change in the pattern of Burma's tradein 1972. Asia (mainly India and Japan) continues to be the major tradingpartner accounting for more than 50 percent of imports and exports. WesternEurope accounts for around 30 percent. Over 70 percent of rice exports areto Asian countries - Sri Lanka. India. Philippines. SinRapore. Indonesia andBangladesh. The remaining 30 percent go to Western Europe, Eastern Europeand Africa in almost equal amounts. About 56 percent of the timber exportsare to Western Europe, 20 pecent to Japan and the remainder to Asia.

49. About 40 percent of Burma's imports from Asia come from Japan andthey consist lnrgely nf nnital gnond imnortq. Western Etironpe' sharp oftotal imports has remained the same over the last three years (around 30percent), although the crmposntion has chnngpd as the share of capital equip-ment has fallen and the share of raw materials has increase-d proportionately.There -as, however , ! a noticeable increoncan i m portf from. Rasteorn Europe

This probably reflects the fact that seven out of Burma's eleven generaltrade a-reemennts are w ith E? - etfe Euorean coun trie4 Sm qn f urther shif4tfs

in the pattern of trade may result from the recent currency realignments.It could be expected that exports to Japan and Western Europe nrd imports

from the US will increase, but for the most part, trade with other Asiancountr4 es is not ex-ected to chaon.e significantly.

50. ~Thk.e deterioration ir. Burr.,.a's t-sof tr_ade_ has been particularly1

severe since 1968 (Table 4). Taking the decade (1961-971) as a whole, thedecl.ine i4n the t*ermns of trade WaS 20n percent, largely duet to a 28 percentincrease in import prices, while export prices in 1971 were at about thesame level as i. 1961. T.-wevet a closer look at the data .reals r6 ha

export prices did fluctuate between those dates - they increased by about 44percent between 1961 and 1068 then A ropped sharply by 3percent between 19aand 1971. On the other hand, import prices rose steadily between 1961 and 1968and Lhave siLnce bUeen stable . T . contrast, Ath d A.erioration in thle O tus of

trade since 1968 has been 36 percent, almost solely due to the 47 percenta I tX 1-Q -C t v 4 K MU A14_ 4- -

Uiop LL Lllt. export pi UCe uL rIC 2 ,,uu. iLLA. reOsu.LgLL6 Uc.. L anLexpL

earnings imposes a severe limitation on the country's import capacity andhence its economic developmenLt. LLLis absoluteL limitatiLtLo n is comLpounded by

the deterioration in the terms of trade and the consequent decline in thepurchasing power of exports. Over the decade, the purchasiLng power of Burnma'sexports have declined by 55 percent, and it is currently less than 20 percentof its pre-war value.

- 17 -

Table 4: UNIT VALUE, QUANTUM INDICES AND TERMS OF TRADE1964 = 100

Pre-WarYear Ending September 30 1939-41 1961 1967 1968 1969 1970 1971

Export

Value Index 49 89 59 46 49 47 51Unit value 22 89 116 128 123 91 90

Quantum /a 222 100 51 36 39 52 56

Import

Value Index 28 99 75 70 69 72 77

unit -value 20 94 121 119 116 120 120

Quantum /a 142 106 62 58 60 60 64

Terms of Tradef 110 95 96 107 106 76 75

ICPurchasing Power of Exports 244 94 49 38 42 39 42

/a Quantum Indices: Ratio of value index to unit value index.

/b Terms of Trade: Ratio of export to import unit value index.

/c Purchasing Power of Exports: Value index of exports deflated by import

unit value index.

Source: Statistical Yearbook 1971, CSED and Mission Estimates.

Balance of Payments

51. In 1972, the balance of payments showed an overall surplus of