Work Now, Pay Later: Young workers, precarious employment and pension contributions

12

Natasha Segal 992643421 1 Pension Contributions among Young Canadians in Precarious Employment INTRODUCTION Are some types of unavoidable conditions (such as being a woman, being an immigrant, being young and being precariously employed) more predictive of decreased pension contributions and increased old-age poverty? Cook et. Al, for example, contends that, holding all else constant, fundamental characteristics linked to mediocre employment include being a woman. My research investigates the effects of precarious employment on young people’s pension contributions. This work provides a greater understanding of the types of circumstances that may influence pension contributions, which could be used in future to target and evaluate pension savings incentivization policies. A 2012 Law Commission of Ontario (LCO) report estimates that 22% of Canadian jobs fit the precarious definition. Youth are among those most affected by precarious employment because they increasingly feel compelled to take on unpaid internships as their only opportunity to gain work experience. Although precarious employment affects members of both low and middle class income households, certain populations appear more likely to experience ongoing precarious, low paid employment that lacks benefits and other income safety net structures. A plethora of research dictates that youth appear on of the hardest-hit categories of greater risk of precarious employment entrenchment due to their lack of skills and newness to the employment world. Are some types of unavoidable conditions (such as being a woman or being precariously employed) more predictive of decreased pension contributions and thus greater gamble for old- age poverty? Cook et. Al, for example, contends that, holding all else constant, fundamental characteristics linked to mediocre employment include being a woman. (Gordon B. Cooke, 2009) My research investigates the effects of precarious employment on young people’s pension contributions. This work provides a greater understanding of the types of circumstances that may influence the likelihood of pension contributions, which could be used in future to target and evaluate pension savings incentivization policies. Through research into work and life effects on pension contribution practices by differently employed young people over time, differences in Canadian firms over time, My research expands on The Rich and the Rest of Us: The Changing Face of Canada’s Growing Gap (Yalnizyan, 2007) by way of pension contribution trends examination for young people in precarious employment today.

Transcript of Work Now, Pay Later: Young workers, precarious employment and pension contributions

Natasha Segal 992643421

1

Pension Contributions among Young

Canadians in Precarious Employment

INTRODUCTION

Are some types of unavoidable conditions (such as being a woman, being an immigrant, being

young and being precariously employed) more predictive of decreased pension contributions and

increased old-age poverty? Cook et. Al, for example, contends that, holding all else constant,

fundamental characteristics linked to mediocre employment include being a woman. My research

investigates the effects of precarious employment on young people’s pension contributions. This

work provides a greater understanding of the types of circumstances that may influence pension

contributions, which could be used in future to target and evaluate pension savings

incentivization policies.

A 2012 Law Commission of Ontario (LCO) report estimates that 22% of Canadian jobs fit the

precarious definition. Youth are among those most affected by precarious employment because

they increasingly feel compelled to take on unpaid internships as their only opportunity to gain

work experience. Although precarious employment affects members of both low and middle

class income households, certain populations appear more likely to experience ongoing

precarious, low paid employment that lacks benefits and other income safety net structures. A

plethora of research dictates that youth appear on of the hardest-hit categories of greater risk of

precarious employment entrenchment due to their lack of skills and newness to the employment

world.

Are some types of unavoidable conditions (such as being a woman or being precariously

employed) more predictive of decreased pension contributions and thus greater gamble for old-

age poverty? Cook et. Al, for example, contends that, holding all else constant, fundamental

characteristics linked to mediocre employment include being a woman. (Gordon B. Cooke,

2009) My research investigates the effects of precarious employment on young people’s pension

contributions. This work provides a greater understanding of the types of circumstances that may

influence the likelihood of pension contributions, which could be used in future to target and

evaluate pension savings incentivization policies.

Through research into work and life effects on pension contribution practices by differently

employed young people over time, differences in Canadian firms over time, My research

expands on The Rich and the Rest of Us: The Changing Face of Canada’s Growing Gap

(Yalnizyan, 2007) by way of pension contribution trends examination for young people in

precarious employment today.

Natasha Segal 992643421

2

In correspondence with the The Rich and

the Rest of Us: The Changing Face of

Canada’s Growing Gap (Yalnizyan, 2007),

I will use Statistics Canada Workplace and

Employee Survey (SLID).

My analysis is also inspired by the

innovative work of Paul Bernard et. Al.

CAPTURING THE LIFECOURSE The

contribution of a Panel Study of Lifecourse Dynamics (PSLD) to public policy analysis in

Canada (Paul Bernard, 2008). As a result of the proposed survey within the abovementioned

work, My research, hopes to capture the “lifecourse nature of the human experience” (Paul

Bernard, 2008, p. 3) as it pertains to pension contribution practices among young Canadians to

better allow policy makers to address and target future policy recommendations and routes.

To gain a clearer understanding of young people’s

pension contribution evolution, analyses based on

longitudinal data are vital. To that end, my research

makes use of the Longitudinal Survey of Labour and

Income Dynamics (SLID) (2004-2008) in order to

investigate the circumstances under which young people

are more likely to contribute to their personal pensions.

By utilizing longitudinal data with a specialized

methodology, my research provides insights into the

relationship between genders, low wages, income,

employment precarity, and pension contribution.

My research addresses the role of specific employment and lifespan characteristics, such as

gender and income as well as the number of jobs participants were employed in during the year,

and the contributions of these characteristics to a young person’s investment in her pension.

The links found for young people’s pension contributions will allow policy and decisions makers

to create and target better policies in order to ensure the elderly populations of tomorrow provide

well for themselves today.

BACKGROUND

As labour is characteristically the chief expense firms’ face, employers wish to minimize their

human resource costs. (Institute for Competitiveness & Prosperity and Martin Prosperity

HYPOTHESIS

1. As instances of precarious work increase

among young Canadians, pension contributions

decrease.

Dependent variables Pension contribution (Dichotomized

variable)

Independent variables Gender

Many jobs

Low pay

Earnings

Involuntary part time employment

Natasha Segal 992643421

3

Institute, October) Unpaid internships and precarious employment contracts decrease firms’

expenses. (Institute for Competitiveness & Prosperity and Martin Prosperity Institute, October)

The term precarious employment, is often used by economists to describe workers who are in an

unstable employment position, have limited control over working conditions and wages, and lack

union protection or clear regulations governing their workplace.

According to the “It is more than Poverty Report” published by United Way and McMaster

University, precarious employment has increased by nearly 50% in the last 20 years and, the

Canadian Center for Policy Alternatives, notes Canada ranks 17th out of 28 OECD countries for

workforce proportions of involuntary part-time workers. Around 67% of Canadian youth aged

16-24 are employed in involuntarily precarious. (United Way, 2013)

As youth are disproportionately represented in employment characterized by unstable work

conditions and lack of clear regulations and permanent opportunities, young workers face

disproportionately higher risks of future job losses if Canada’s economic recovery declines thus

possibly aggravating pre-crisis conditions. (Institute for Competitiveness & Prosperity and

Martin Prosperity Institute, October) Legislation created to protect workers during times of

steady employment has not caught up to Ontario’s current employment environment. Labour

policy should respond to new employment conditions in order to safeguard Ontario’s economic

success and ensure a more prosperous retirement for today’s young workers.

As Baby Boomers age and increase their dependence on healthcare and pension systems, losses

incurred from youth entrenchment in precarious forms of employment will compound. As these

youth age, Canada’s health care system will grow less capable of caring for their needs. One

way to mitigate this issue may be to produce targeted policy interventions toward increased

pension contributions. To help create maximum gains for young people’s pension outcomes,

intervention should begin as early as possible and target the most vulnerable young populations –

those entrenched in employment precarity that is characterized by low wages and irregular

schedules. As pension investment compounds over time, each year’s worth of lost savings also

compounds overall deadweight losses once pension is collected. That which today’s youth will

not be able to afford upon retirement will fall onto the countries shoulders thus creating a lag in

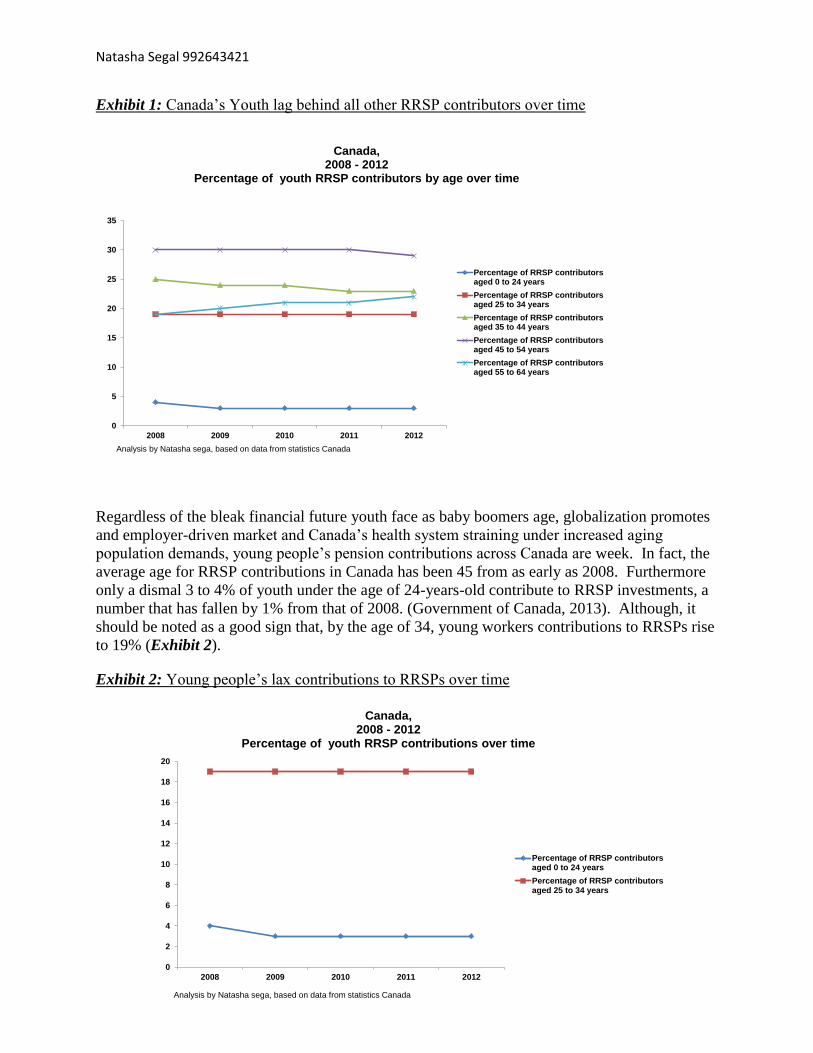

productivity and individual prosperity. Currently, Canadian young people are the smallest RRSP

contributing population. (Government of Canada, 2013) (Exhibit 1) Without proper pension

savings during their working lives, Canadian human capital will suffer; country affluence will

diminish.

Natasha Segal 992643421

4

Exhibit 1: Canada’s Youth lag behind all other RRSP contributors over time

Regardless of the bleak financial future youth face as baby boomers age, globalization promotes

and employer-driven market and Canada’s health system straining under increased aging

population demands, young people’s pension contributions across Canada are week. In fact, the

average age for RRSP contributions in Canada has been 45 from as early as 2008. Furthermore

only a dismal 3 to 4% of youth under the age of 24-years-old contribute to RRSP investments, a

number that has fallen by 1% from that of 2008. (Government of Canada, 2013). Although, it

should be noted as a good sign that, by the age of 34, young workers contributions to RRSPs rise

to 19% (Exhibit 2).

Exhibit 2: Young people’s lax contributions to RRSPs over time

0

2

4

6

8

10

12

14

16

18

20

2008 2009 2010 2011 2012

Percentage of RRSP contributorsaged 0 to 24 years

Percentage of RRSP contributorsaged 25 to 34 years

Canada,2008 - 2012

Percentage of youth RRSP contributions over time

Analysis by Natasha sega, based on data from statistics Canada

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2012

Percentage of RRSP contributorsaged 0 to 24 years

Percentage of RRSP contributorsaged 25 to 34 years

Percentage of RRSP contributorsaged 35 to 44 years

Percentage of RRSP contributorsaged 45 to 54 years

Percentage of RRSP contributorsaged 55 to 64 years

Analysis by Natasha sega, based on data from statistics Canada

Canada,2008 - 2012

Percentage of youth RRSP contributors by age over time

Natasha Segal 992643421

5

The time to mitigate future losses is now. Pension lags must be offset through present-day

government support for youth in precarious employment to move toward better health outcomes

and increased economic gains right now and for their future.

SCOPE

Because youth entrenchment in precarious employment is a growing area of concern, as is

Canada’s ageing population and declining birthrates, I will explore youth pension contribution

rates by gender, wage, amount of jobs in the current year of survey, and income.

METHODOLOGY

I chose a mixed model that incorporates both random and fixed interpretative output abilities as

the data explored is based on survey results that have provided this research with many time

variant variables. Time variant variables often require fixed effect models to account for the

changes that can take place over at the level two variance. The models chosen for further

investigation examine populations of young workers contribute to pensions based on their work

and life circumstances via the following questions:

1. Young workers in involuntary part time employment?

2. Young workers with low wages?

3. Young workers with multiple jobs?

4. Young women?

Variables were chosen from the person data of the SLID data sets for years 2004, 2006, and

2008. Hypotheses was tested first on 2004 data, without additional year variables in order to find

relationships that may add information to the hypotheses posed. Once the base year data was

tested against the hypotheses, data sets were appended by year and across time, in order to

inspect:

5. changes in young worker pension contributions by gender over time;

6. changes in young worker pension contributions by earning levels over time;

7. differences in types of employment and their correspondence to young worker pension

contribution over time

From these outcomes, an xtmixed multiple regression model was utilized to test slope of young

worker pension contributions over time in relation to gender, earnings, and types of employment

over time. The dependent variable, pension contribution, was dichotomized. As all the variables

in this research proved time variant, fixed effects (instead of random) were found of better fit for

more relevant output generation. That is, fixed effects were chosen to deal with the possibility

that independent variables (being time variant) is assumed to possibly bias the outcome due to its

possibility for change over time.

Dummy variables for low wage, multiple jobs, and gender were created as were interaction

variables between low wages and multiple jobs in order to test for particular trends in young

people’s pension contributions. To this end, age of respondents was dichotomized to produce a

“youth” variable outcome of all respondents over the age of 16 and bellow or at the age of 35.

Natasha Segal 992643421

6

Wages for youth were also dichotomized into a variable that splits wages between low wages

(cut off at $11.00 CAD) and the rest.

Job precarity variables were also created in accordance to the definition of precarity found under

the definitions section of this paper. These variables include low wages, involuntary part time

employment and multiple jobs.

Because variables were time variant, the following multilevel fixed-coefficient model was

created using the xtlogit random and fixed approaches with income embedded within each model

in order to remain clear that income is the best predictor of ability to financially contribute to

pension investments:

Fixed

Random

To test for precarious employment effects on young people’s pension contribution outcomes over

time:

Natasha Segal 992643421

7

To test for effects of gender on young people’s pension contributions over time:

To test for effects of low pay on young people’s pension contributions:

PREVIOUS RESEARCH

In her The Rich and the Rest of Us: The

Changing Face of Canada’s Growing Gap

research, Armine Yalnizyan inspects

Canadian inequality as reflected in

distributions of income over time, through

research that incorporates both the national

survey data from the Survey of Consumer

Finances (SCF) and Survey of Labour and

Income Dynamics (SLID). Published under

the Canadian Centre for Policy Alternatives,

‘Growing Gap’ project, this work exposes

income disparity over time for families with

young children -- just below half of the

Canadian population. (Yalnizyan, 2007)

The impacts of Canadian taxes and transfers

for progressive income redistribution were

also examined through reflection on the

‘after-tax’ earnings of Canadian families

with children. (Yalnizyan, 2007) It was

discovered that progressive taxation through

transfer plays a vital constructive role in

income redistribution and income inequality

reduction, remarking that “Canada’s tax and

transfer system helped to mitigate the

earnings gap”. (Yalnizyan, 2007, p. 27)

Nevertheless this research determines that

Data Sources and Definitions

The Survey of Labour and Income Dynamics (SLID) has

produced longitudinal data since 1993 with bi-annual

surveys -- alternating between labour and income

response requirements – for six consecutive waves of

years.

Each six-year epoch is termed a “panel”. Fresh panels

originate every three years. Each panel characterizes

Canadian population in the period of sample selection.

Thus, additional panel identifiers have been added to the

file to check for potential cohort effects. Bootstrap

weights from the final year of each panel were also

added to ensure accurate variance estimation.

Definitions For the purposes of this research, definitions are as

follows:

Youth

The portion of Canadian population that is between 16

and up to and including 35-years-old

Precarious Employment

Economists use the term “precarious” to describe

workers who are in an unstable employment position,

have limited control over working conditions and wages,

and lack union protection or clear regulations governing

their workplace.

Natasha Segal 992643421

8

“the tax and transfer system did not significantly reverse the trend in reduced shares of income

for the majority of families”. (Yalnizyan, 2007, p. 12)

Mapping Young people’s pension contributions

Lack of access to workplace delivered benefits and the inevitability of multiple simultaneous

employment contracts limits young workers’ abilities to access appropriate dental and extended

health care coverage and additionally restrains young workers’ disposable incomes, as they are

less able to mitigate the impacts of precarious employment on their overall health outcomes.

(Institute for Competitiveness & Prosperity and Martin Prosperity Institute, October)

Constrained occupation options force many young workers to pursue admission into low-skilled,

precarious jobs, for instance, the cyclically delicate, retail sector. (ILO, 2012) The United Way’s

It’s More Than Poverty report, states that over 80% of workers in precarious employment are

vulnerable to illness or injury without the health benefits and income safety net relied upon by

permanent employees. (United Way, 2013) Furthermore, workers in precarious employment

situations who do get benefits often don’t have family coverage. (United Way, 2013, p. 41) For

many employment-related benefits, such as vacation pay, health benefits and severance pay,

length of service determines eligibility. In today’s precarious employment environment, many

workers may (for example) never work at any given job for over twelve months and thus may

never qualify for two weeks of paid vacation (Vulnerable workers and precarious work final

report p.41). Thus, “employment protections that cover only standard forms of employment are

not responsive to the needs of increasing numbers of workers in non-standard working

relationships”( Vulnerable workers and precarious work final report p.41).

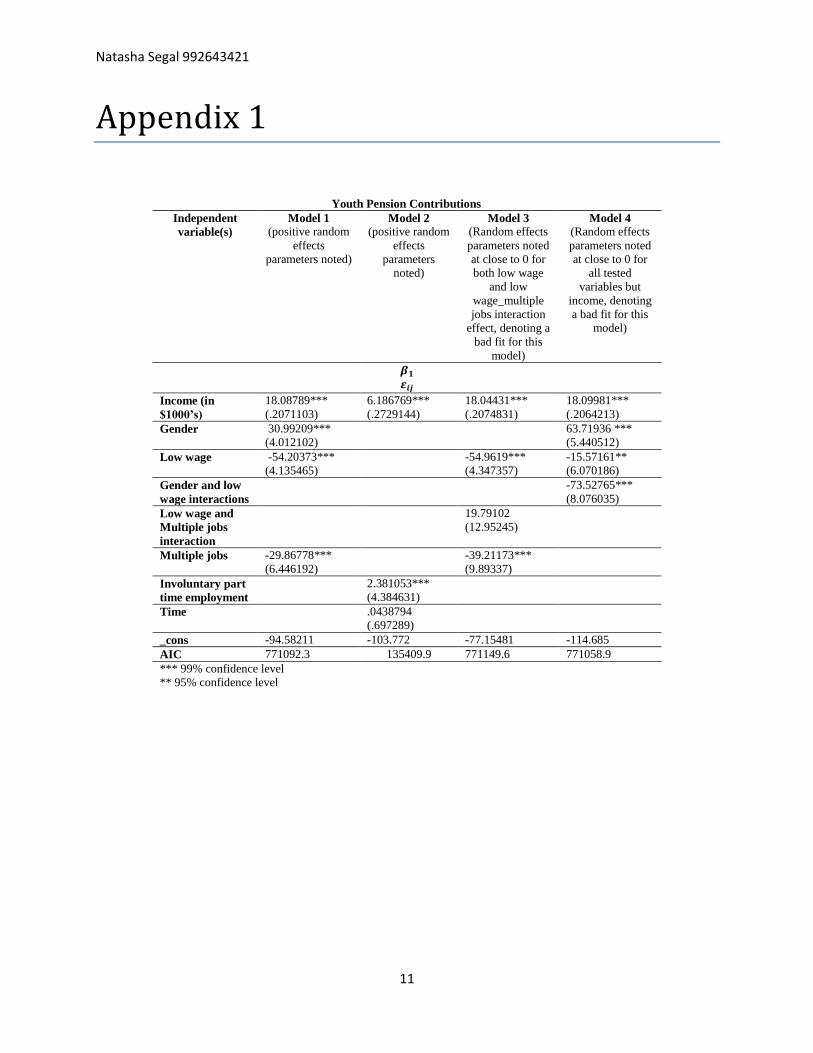

As I map young people’s pension contributions vis a vis various models, discussion of model

output (bellow) will be demonstrated by a model output chart found in Appendix one.

Model 1 examines the effect of low wages, gender and multiple jobs on youth pension

contributions. At the 99% significance rate, I found that:

1. Pension contributions rise by 18.1 with each additional thousand dollar growth in

income;

2. As gender moves from male for female, pension contributions rise by $40. That is,

women invest approximately $40 more into their pensions than men;

3. As a worker moves from one job into more than one job, pension contributions sink by

$30. This is to say that, at the 99% confidence level, multiple jobs in one year for one

worker appear to negatively correlate to pension contributions.

4. As wages move from non-low wage to low wage, pension contributions fall by $54.20

Model 2 examines the effect of income, involuntary part time employment, and time on youth

pension contributions. At the 99% significance rate, I found that:

Natasha Segal 992643421

9

1. This model suggested that pension contributions rise by $6.2 with each additional

thousand dollar growth in income. This produces confusion as the previous model

predicted almost twice that amount of growth. In order to ascertain which model

exhibited the “best fit”, or is better predictor or pension contributions, the AIC criterion

were consulted. At an AIC output of 135409.9, model 2 outperformed model 1 by a

difference of 635682.4 (Model 1 AIC: 771092.3), thus proving itself the better pension

contribution predictor of the two models.

2. As young workers move from non-involuntary to involuntary part time employment,

pension contributions rise by $2.38; however, this may be explained more as a matter of

income growth (if the young worker moved from non-pay to pay employment as opposed

to part time involuntary employment necessarily having a positive effect of pension

contributions.

Model 3 examines the effect of income, low wage, multiple jobs, and the interaction effects

between multiple jobs and low wages on youth pension contributions. At the 99% significance

rate, I found that:

1. This model suggested that pension contributions rise by $18 with each additional

thousand dollar growth in income. This produces confusion as the previous model

predicted almost half that amount of growth. In order to ascertain which model exhibited

the “best fit”, or is better predictor or pension contributions, the AIC criterion were

consulted. At an AIC output of 771149.6, model 2 outperformed model 3 by a difference

of 635739.7 (Model 2 AIC: 135409.9), thus model 2 again exhibited superior fit to model

3 (as well as model 1) as the better pension contribution predictor of the three models.

2. As wages move from non-low wage to low wage, pension contributions fall by $55. This

is a very close account of the model 1 output as well with only a slight difference of

approximately .70 cents. However, it should be noted that AIC for model three is slightly

higher than that of model 1 indicating model one as the better predictor in this case.

3. As a worker moves from one job into more than one job, pension contributions sink by

$39. This is to say that, at the 99% confidence level, multiple jobs in one year for one

worker appear to negatively correlate to pension contributions. This is about $9 higher

than the predicted outcome of model 1; however, it should be noted that AIC for model

three is slightly higher than that of model 1 indicating model one as the better predictor in

this case.

The interaction effects of low wages and multiple jobs show that the total effects on pension

contribution as the young worker moves to a low wage job decrease (as per above) but, if the

young worker is also working at more than one job, pension contributions amount to $19.8 -

$55. This means that the interaction effect can slightly mitigate pension contribution losses

but not to any significant level. Furthermore, the p-value of this output calculation was quite

high, denoting a lack of significance.

Model 4 examines the effect of income, gender, low wages, and the interaction effects between

gender and low wages on youth pension contributions. At the 99% and 95% (see Appendix 1 for

further detail) significance rate, I found that:

Natasha Segal 992643421

10

1. This model suggested that pension contributions rise by $18 with each additional

thousand dollar growth in income. In order to ascertain which model exhibited the “best

fit”, or is better predictor or pension contributions, the AIC criterion were consulted.

Once again, model 2 again exhibited superior fit to model 4 (as well as model 1 and 2) as

the better pension contribution predictor of the three models. (For full details please refer

to Appendix A)

2. This model suggested that pension contributions rise by $64 as the variable moves from

male to female; however, model one suggests a much lower rise of approximately $31.

In order to ascertain which model exhibited the “best fit”, or is better predictor or pension

contributions, the AIC criterion were consulted. Although the AIC criterion appears

minimally lower than that of model 1, model 4’s Random effects parameters were noted

at close to 0 for all tested variables but income, denoting a bad fit for this model, as

opposed to model one whose positive random effects parameters demonstrated a much

better fit. (For full details please refer to Appendix A)

3. As wages move from non-low wage to low wage, pension contributions fall by $15.

However, this is a very different reading from model 3. Thus, it should be noted that AIC

for model three is slightly higher than that of model 4 indicating model 4 as the better

predictor in this case. This said, we should note that random effects parameters for both

model 3 and 4 denote a close to 0 outcome for both of these variables in both models thus

neither model appears a good enough fit at this time.

4. The interaction effects of low wages and gender show that the total effects on pension

contribution as the young worker moves to a low wage job decrease by $15.60 if they are

male but, if the young worker is also a female, pension contributions increase by $57.4

($73.00 - $15.60). This means that although young women tend to participate more in

pension contributions, participation still plunges by approximately $15.60, when women

earn low wages.

As the interaction effect between multiple jobs and low wages appeared to lack significance in

both tested models, the interaction variable will not be used in models going forward. Also, in

all initially tested models, time appears to have no relevancy according to the P-value so, time

was not included in most of the models relied upon in this research output as it appears to have

no significance.

Conclusion

At a 99% confidence level, these models show that young people’s pension contribution choices

are negatively affected by the presence of precarious employment, as recognized through low

wages, multiple jobs and low income. The effects appear worse for males than for females;

however, females with children and young lone parent family heads were not taken into account

in these regressions. Thus, these outcomes are best suited to policies aimed at single young

people in the workforce. This is to say that, policies that specifically target young people

(especially young men) in precarious employment toward increased earnings, higher wages, and

improved employment outcomes – decreased amounts of jobs held per year, for example –

should positively correlate to improved pension contribution for young people.

Natasha Segal 992643421

11

Appendix 1

Youth Pension Contributions

Independent

variable(s)

Model 1

(positive random

effects

parameters noted)

Model 2

(positive random

effects

parameters

noted)

Model 3

(Random effects

parameters noted

at close to 0 for

both low wage

and low

wage_multiple

jobs interaction

effect, denoting a

bad fit for this

model)

Model 4

(Random effects

parameters noted

at close to 0 for

all tested

variables but

income, denoting

a bad fit for this

model)

Income (in

$1000’s)

18.08789***

(.2071103)

6.186769***

(.2729144)

18.04431***

(.2074831)

18.09981***

(.2064213)

Gender 30.99209***

(4.012102)

63.71936 ***

(5.440512)

Low wage -54.20373***

(4.135465)

-54.9619***

(4.347357)

-15.57161**

(6.070186)

Gender and low

wage interactions

-73.52765***

(8.076035)

Low wage and

Multiple jobs

interaction

19.79102

(12.95245)

Multiple jobs -29.86778***

(6.446192)

-39.21173***

(9.89337)

Involuntary part

time employment

2.381053***

(4.384631)

Time .0438794

(.697289)

_cons -94.58211 -103.772 -77.15481 -114.685

AIC 771092.3 135409.9 771149.6 771058.9

*** 99% confidence level

** 95% confidence level

Natasha Segal 992643421

12

Bibliography

Gordon B. Cooke, I. U. (2009). Barriers to training access. Perspectives Statistics Canada — Catalogue no.

75-001-X, 25.

Government of Canada. (2013, December 19). Registered pension plans (RPPs), contributions to

registered pension plans, by sector, type of plan and contributory status. Retrieved April 15,

2014, from Statistics Canada: http://www5.statcan.gc.ca/cansim/pick-

choisir?lang=eng&p2=33&id=2800026

ILO. (2012). Employment Sector Employment Working Paper No. . Retrieved April 4, 2014, from ILO:

http://www.ilo.org/wcmsp5/groups/public/---ed_emp/---

emp_policy/documents/publication/wcms_190864.pdf

ILO. (2012). Vulnerable Workers and Precarious Work. Toronto: Law Commission of Ontario.

Institute for Competitiveness & Prosperity and Martin Prosperity Institute. (October, October). The

Institute for Competitiveness & Prosperity. Retrieved April 4, 2014, from UntaPPed PotentIal:

Creating a better future for service workers:

http://www.competeprosper.ca/uploads/WP17_FINAL_V2.pdf

Ontario ministry of children and youth. (2012). Stepping Up: Jobs for Youth. Retrieved april 14, 2014,

from Employment and Entrepreneurship:

http://www.children.gov.on.ca/htdocs/English/topics/youthopportunities/steppingup/employm

ent.aspx

Paul Bernard, C. B. (2008). CAPTURING THE LIFECOURSE The contribution of a Panel Study of Lifecourse

Dynamics (PSLD) to public policy analysis in Canad. Longitudinal Social and Health Surveys in an

International Perspective, (p. 39).

United Way. (2013). It’s More than Poverty Employment Precarity and Household Well-being. Toronto:

United Way.

Yalnizyan, A. (2007). The Rich and the Rest of Us: The Changing Face of Canada’s Growing Gap. Canadian

Journal of Sociology Online, 6.