Why Malaysian Second Board Companies Switch Auditors: Evidence of Bursa Malaysia

8

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 13 (2008) © EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm Why Malaysian Second Board Companies Switch Auditors: Evidence of Bursa Malaysia Shahnaz Ismail Department of Accounting and Finance University College of Science and Technology Malaysia (KUSTEM) 21030 Mengabang Telipot, Kuala Terengganu, Terengganu E-mail: [email protected] Tel: (609)-668-3166; Fax (609)-669-7191 Huson Joher Aliahmed Department of Accounting and Finance Universiti Putra Malaysia (UPM), 43400 UPM Serdang, Selangor E-mail: [email protected] Tel: (603)-8948-7599; Fax (613)-8948-6188 Annuar Md. Nassir Department of Accounting and Finance Universiti Putra Malaysia (UPM), 43400 UPM Serdang, Selangor E-mail: [email protected] Tel: (603)-8948-7599; Fax (613)-8948-6188 Mohamad Ali Abdul Hamid Department of Accounting and Finance, Universiti Putra Malaysia (UPM) 43400 UPM Serdang, Selangor E-mail: [email protected] Tel: (603)-8948-7599; Fax (613)-8948-6188 Abstract The auditor switching phenomenon was found to have implications to the value credibility of financial reporting and the cost of monitoring management activities Therefore, it has been widely and extensively studied in developed countries by academicians, accounting professionals and industry experts due to the great number of switches in the early 1970s. Despite the growing concerns of this issue, few studies appear to have been made in Malaysia to examine the significant reasons of auditor switching. Thus, this study was conducted with the objective of identifying major determinants of auditor switch among companies listed on Second Board of Bursa Malaysia, formerly known as Kuala Lumpur Stock Exchange (KLSE), especially during the period from 1997 to 1999, which coincide with the Asian financial crisis. In order to examine the determinants of auditor switch among second board companies, this study uses logistic regression model, in particular, the stepwise method. From the results, this study indicates that leverage, growth turnover, financing activities, longevity of audit engagement and audit fee were the significant determinants of auditor switch during the period of financial

-

Upload

terengganu -

Category

Documents

-

view

4 -

download

0

Transcript of Why Malaysian Second Board Companies Switch Auditors: Evidence of Bursa Malaysia

International Research Journal of Finance and Economics ISSN 1450-2887 Issue 13 (2008) © EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm

Why Malaysian Second Board Companies Switch Auditors: Evidence of Bursa Malaysia

Shahnaz Ismail Department of Accounting and Finance

University College of Science and Technology Malaysia (KUSTEM) 21030 Mengabang Telipot, Kuala Terengganu, Terengganu

E-mail: [email protected] Tel: (609)-668-3166; Fax (609)-669-7191

Huson Joher Aliahmed Department of Accounting and Finance

Universiti Putra Malaysia (UPM), 43400 UPM Serdang, Selangor E-mail: [email protected]

Tel: (603)-8948-7599; Fax (613)-8948-6188

Annuar Md. Nassir Department of Accounting and Finance

Universiti Putra Malaysia (UPM), 43400 UPM Serdang, Selangor E-mail: [email protected]

Tel: (603)-8948-7599; Fax (613)-8948-6188

Mohamad Ali Abdul Hamid Department of Accounting and Finance, Universiti Putra Malaysia (UPM)

43400 UPM Serdang, Selangor E-mail: [email protected]

Tel: (603)-8948-7599; Fax (613)-8948-6188

Abstract

The auditor switching phenomenon was found to have implications to the value credibility of financial reporting and the cost of monitoring management activities Therefore, it has been widely and extensively studied in developed countries by academicians, accounting professionals and industry experts due to the great number of switches in the early 1970�s. Despite the growing concerns of this issue, few studies appear to have been made in Malaysia to examine the significant reasons of auditor switching. Thus, this study was conducted with the objective of identifying major determinants of auditor switch among companies listed on Second Board of Bursa Malaysia, formerly known as Kuala Lumpur Stock Exchange (KLSE), especially during the period from 1997 to 1999, which coincide with the Asian financial crisis. In order to examine the determinants of auditor switch among second board companies, this study uses logistic regression model, in particular, the stepwise method. From the results, this study indicates that leverage, growth turnover, financing activities, longevity of audit engagement and audit fee were the significant determinants of auditor switch during the period of financial

International Research Journal of Finance and Economics - Issue 13 (2008) 124

crisis. However, receiving qualified audit report was not found to be the factor of auditor switch among the Second Board companies in Malaysia during this period.

Keywords: auditor switch, auditor change, second board companies, KLSE, Bursa Malaysia, crisis period

1. Introduction Issues concerning auditor switch phenomenon has been well studied and documented in literatures by researchers, academicians and practitioners in developed countries. The phenomenon has been vastly studied since large number of switches were reported in the United States in early 1970�s1. Since then, the American Institute of Certified Public Accountants (AICPA) agreed that switching of auditor was the major problem faced by the CPA (Fried and Shiff, 1981).

Decision to switch auditors by client firm was due to the principle-agent problem in separation of ownership and control of a firm (Jensen and Meckling, 1972) and the separation of risk bearing, decision-making and control function in firms (Fama and Jensen, 1983). The conflict of interest in the presence of information asymmetry appears to arise in the growth of modern companies today due to absentee owners that has led to the use of professional managers to manage the daily business. The manager who is the actual person running a firm, generally, has more information about the �true� financial position and results of operations of the firm rather than the shareholders. The reporting of this financial information to the owner (shareholder), generally, follows the accounting principles. In order to avoid manipulation of financial reporting by the manager, the need for auditor arises.

Auditors play a vital role in reducing information risk, which is the prime economic reason behind the demand for audit and auditing services. In performing their duty, auditors were said to face a substantial role conflict because they tried to maintain the professional norms and at the same time have to consider the managers (client) wishes (Chi M.K. and Ho S.S., 1999). Therefore, if the auditors appear to have different opinion with the manager, it will lead to conflict of interest between them. As the result, the manager will decide to expunge the incumbent auditors and replaced it with a new one.

Auditor switch decision involves change of incumbent auditor resulting in the choice of quality differentiated audit firms to realign the characteristics of the audit firm, with the growing need of clients under changing circumstances. Changes in management, disagreement between client and auditor, dissatisfaction over audit fees, need of expert auditors and client with financial health problems have been found to be associated with the auditor switch decisions.

The differences among audit firms discussed in most literatures explain the specialization in audit technology and emphasizes on audit quality and reputation. Although differ in several important respects, both perspectives however share a common view of audit engagement decisions that is clients purchase audit services from the least cost supplier and switch auditors in response to changes in the amount or type of services required. Cost structure variations occurred because of the differences in auditor�s �brand name� resulting from investments in expertise and quality control mechanism.

Market competition, furthermore, induces clients and audit firms to align themselves to achieve efficient utilization of specialized resources and �brand name� investments. So, auditors of comparable size with the client and clientele mix have similar cost structures. Changes in the client�s operations and activities over time can erode the incumbent auditor�s competitive advantage. Rapid growth by client firms entails substantial increases in transaction volume and accounting complexity. These factors interrupt the economies available to the incumbent auditors, enabling the client to obtain fee reductions (or increase service for the same fee) through replacement of auditors. Conversely, when the level and scope of activities undergo significant contraction, client firm can achieve audit fee reductions by changing audit firms with relatively few specialised resources. So, client firms that replace their incumbent auditor with a substantially larger (smaller) firm are predicted to exhibit

1 Fortune 500 reported that 250 companies in the United States switched auditors between 1971 to 1974 (Bedingfield and Loeb, 1974).

125 International Research Journal of Finance and Economics - Issue 13 (2008)

systematic growth (contraction) in their activities around the time of replacement (Johnson and Lys, 1990).

In the emerging economies like Malaysia, only a few studies have been documented on the issues of auditor switches, choice of auditors and the wealth effect to investors, if any. This gives an avenue to conduct further research. Hence, the objective of this study is to determine the characteristics of auditor switch and examines auditor switch behaviour during the financial crisis of 1997 using the Second Board data.

The rest of the paper is organized as follows; section 2 reviews prior literature on auditor switches while section 3 describe the data and methodology. The findings of the study are highlighted in section 4. Finally, section 5 concludes the study.

2. Prior Studies The phenomenon of auditor switch was found to have implications to the value credibility of financial reporting and the cost of monitoring management activities. Therefore, this issue has been extensively researched in developed countries and recently it has also been studied by researchers in Asian countries such as Hong Kong, Singapore, Malaysia and Korea. The findings of the studies appear to be consistent between these countries and comply with the agency theory literature.

Client firm that foresee a reduction in their business activities were predicted to benefit from a replacement of less prestigious audit firms with comparatively higher prestige auditors. Such a replacement is considered upgrading of auditors. Therefore, client firms that foresee a reduction in their business activities were predicted to benefit from replacing higher prestige auditors with comparatively lower prestige auditors. Such replacement is considered a downgrading.

Findings from previous researchers shown that companies determine to switch their incumbent auditors due to factors such as management changes, disagreement between client and auditor and dissatisfactions over audit fees (Burton and Roberts, 1967; Bedingfield and Loeb, 1974; Woo and Koh, 2001), dissatisfaction with service by the auditors, disagreement over accounting issues, change of engagement partner, resignation, initial public offerings, rapid growth and search for credible auditors (Krishnan, 1994; Johnson and Lys, 1990). Other significant reasons include leverage, income manipulation (Woo and Koh, 2001; Lee, 2002), audit fees, qualified audit report and audit quality (Chow and Rice, 1982; Craswell, 1988; Francis and Wilson, 1988; Simon and Francis, 1988; Pong and Whittington, 1994; Butterworth and Houghton, 1995; Deis and Giroux, 1996; Gregory and Collier, 1996; Hartwell, Lightle and Moreland, 2001), need for auditor expertise and relationship between auditor and management (Addam and Allred (2000; Williams, 1988).

In Malaysia, 135 auditor switches were reported among Main Board listed companies during a 10-year period from 1986 to 1996 (Huson, Ali, Annuar, Ariff and Shamsher, 2000). It implies that auditor switching is an important phenomenon not only to the developed countries but also to the emerging new economies like Malaysia. However, studies on auditor switching is a new scope in Malaysia with few documentation.

A primary study by Takiah and Ghazali (1993) examined the association between qualified audit opinions and the effects on auditor switching. Unfortunately, they failed to ascertain significant association between qualified reports and auditor switching. This might probably due to the short study period of three years from 1986 to 1989 coupled with a small sample size. In the study, they also found that reporting of losses or profits was not the primary reason of auditor switch.

In a similar study on qualified audit report and auditor switching, Hasnah and Ali (1997), found a different sets of results. Their results suggest that client firm receiving qualified opinion is more likely to switch auditors than one who receives a clean report (unqualified report). Thus, the findings failed to support the previous findings by Takiah and Ghazali (1993). In the same study, they also found that client firms tend to switch auditors following seriousness of audit qualification but there were no tendency of switching to Big-6 (now Big-5) audit firms or non Big-6 (now non Big-5) auditors in order to get unqualified opinion. This suggests that opinion shopping is not popular in Malaysia.

International Research Journal of Finance and Economics - Issue 13 (2008) 126

Recently, a wider aspect of auditor switch phenomenon was studied by Huson et al. (2000). The study examines the economic rationale for auditor switch by Malaysian listed firms examining auditor switch effect on share prices. The study concentrates on the Malaysian auditing environment focusing on Main Board companies listed in Kuala Lumpur Stock Exchange (KLSE). This study covers the period from 1986 to 1996. Throughout the 10-year period, there were 135 switches, but only 108 switches were analysed. Huson et al. (2000) divided the switches into two groups, namely, Tier 1 (Big-4 auditors) and Tier 2 (Non Big-42 auditors). This study reported that management change and turnover growth have potential effects on auditor change but audit fees and auditor report have no effect to the phenomenon. Furthermore, changes to a higher prestigious (Big-4) or less prestigious (Non Big-4) auditors were determined by asset growth, purchase of fixed asset to total asset, leverage and changes in financing activities. The study also reported that investors react positively to changes to higher prestige (Big-4) auditors and reacted negatively to changes to a lower prestige (Non Big-4) auditors. However, there is no evidence of significant wealth effect on auditor switch announcement.

3. Data and Research Methodology (i). Data

This study employs secondary data as the main source of information analysis. The names of switched companies, the date of auditor switch and the financial data that proxies for determinants of auditor switch were extracted from the minutes of the annual general meeting, companies' annual reports and annual companies handbooks. The financial information was then converted into selected financial ratios.

Thirty one Second Board companies were reported to switch auditors from 1997 until 1999. Only twenty three companies with 26 switches were usable for subsequent analysis. The switched companies were analysed together with 26 control companies (firms that did not switch audit firm), that met the stated criteria for this research.

(ii). Research Methodology

Parametric test This study used simple parametric test of mean differences of the characteristics of sample firms (client firm switching audit firms) and control firms (client firm that did not switch audit firms). Mean differences of the important characteristics in auditor switch that were tested include turnover of sale, turnover of assets, return on asset, change in financing, earnings per share, leverage and liquidity position of firms.

Auditor Switch Model The stepwise logistic regression technique was used to ascertain the decision of auditor switch during the period of financial crisis in Malaysia. The functional forms of logistic regression model adopted in this study was as follows:

Y = 0 + b1X1+ 2 X2 + 3 X3+ 4 X4 + ��+ 16 X16 LONG + (1) Explanation for the equation 1 above are as follows: Y = Switch with Y = 1 or 0 indicating that a client did (1) or did not switch auditors (0). X= the variables identified for the model. The variables are management change (MGT),

change in chairman of audit committee (AUDCOM), change of company name (NAME), qualified audit report (REPO), bumiputra ownership (OWNER), change in audit fee (FEE), liquidity (LIQ), firms leverage (LEV), sale growth of firm prior and after auditor switch (GRO), asset growth prior and after auditor switch (GRAS), firms financing (FIN), return

2 Big-4 auditors are KPMG Peat Marwick, Ernst and Young, Price Waterhouse Coopers and Deloitte Touche Tohmatsu.

127 International Research Journal of Finance and Economics - Issue 13 (2008)

on asset prior to auditor switch (ROA), firm size prior to auditor switch (SIZE) and longevity of audit engagement (LONG).

The results from the logit analysis were evaluated based on the positive and negative sign of beta ( ).

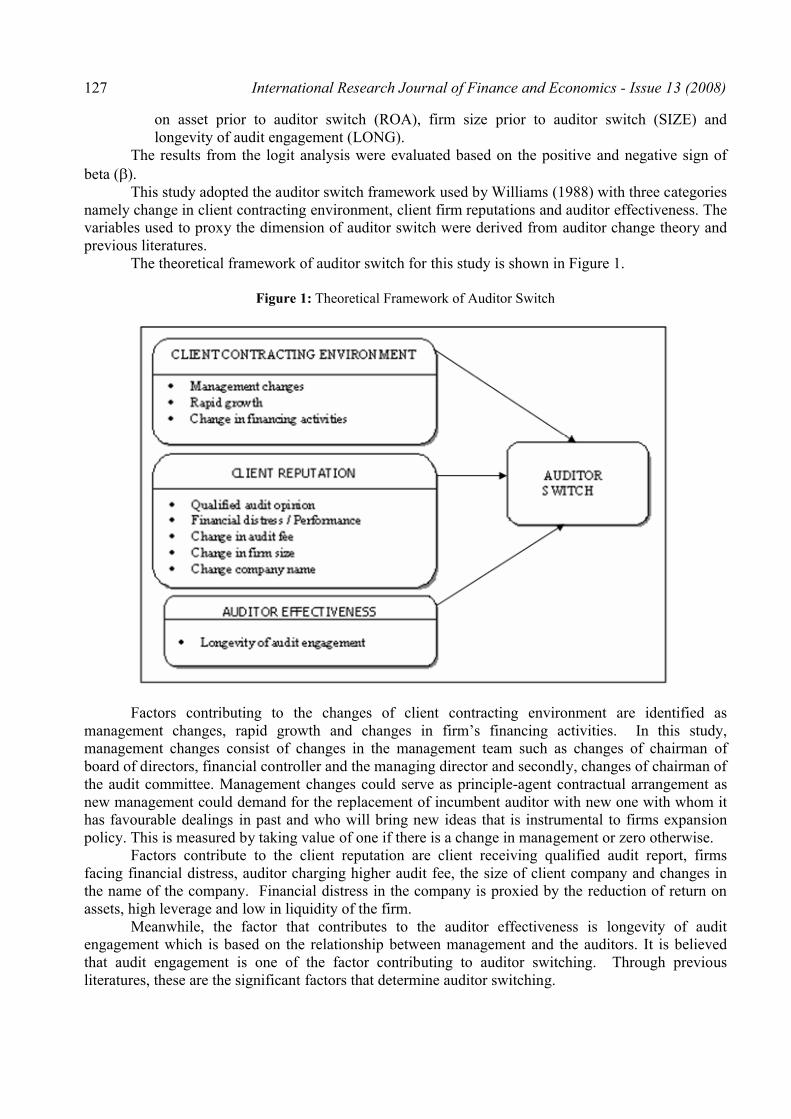

This study adopted the auditor switch framework used by Williams (1988) with three categories namely change in client contracting environment, client firm reputations and auditor effectiveness. The variables used to proxy the dimension of auditor switch were derived from auditor change theory and previous literatures.

The theoretical framework of auditor switch for this study is shown in Figure 1.

Figure 1: Theoretical Framework of Auditor Switch

Factors contributing to the changes of client contracting environment are identified as management changes, rapid growth and changes in firm�s financing activities. In this study, management changes consist of changes in the management team such as changes of chairman of board of directors, financial controller and the managing director and secondly, changes of chairman of the audit committee. Management changes could serve as principle-agent contractual arrangement as new management could demand for the replacement of incumbent auditor with new one with whom it has favourable dealings in past and who will bring new ideas that is instrumental to firms expansion policy. This is measured by taking value of one if there is a change in management or zero otherwise.

Factors contribute to the client reputation are client receiving qualified audit report, firms facing financial distress, auditor charging higher audit fee, the size of client company and changes in the name of the company. Financial distress in the company is proxied by the reduction of return on assets, high leverage and low in liquidity of the firm.

Meanwhile, the factor that contributes to the auditor effectiveness is longevity of audit engagement which is based on the relationship between management and the auditors. It is believed that audit engagement is one of the factor contributing to auditor switching. Through previous literatures, these are the significant factors that determine auditor switching.

International Research Journal of Finance and Economics - Issue 13 (2008) 128

Statistical Test Individual Coefficient Estimates This study used the maximum likelihood estimators (MLE) based on the likelihood of the function in measuring the relationship between the exogenous independent variables and the dependent variable.

MLE is also used to measure the coefficient estimates which in turn, measures the changes in the ratio of the probabilities, termed as the odd ratio. The test statistics used to test the null hypothesis that a coefficient bk is zero is as follows:

kt =k

k

s

b (3)

Where the kb is the coefficient of the predictor variable and ks = standard error of the

coefficient of the individual variable in the auditor switch model. When kb is zero, the variable kX has

no effect on Y .

Goodness of Fit Test A goodness of fit measure is a summary statistic indicating the accuracy with which the model approximates the observed data as the measure of R2 in the linear regression model. The F statistics is used in the normal regression analysis. This F statistics can be used to test the jointly hypothesis that all coefficient except, intercept, are zero. However likelihood ratio principle is used in the logistic regression model. This principle suits exactly the same purpose as of the F statistics. The functional form of Likelihood Ratio Test is as below:

LR = -2 [ln ( � ) - ln ( �*)] (4)

Where ln ( � ) = the value of the likelihood function of full (unrestricted) model and ln ( � *)= the maximum value of the likelihood function if all coefficient except the intercept (restricted) are zero.

Instead of maximizing the squared deviations (least squares), logit analysis maximizes the 'likelihood' that an event will occur. The likelihood ratio produces a statistic that follows approximately a chi-square distribution with k-1 (k being the number of independent variables) degree of freedom if the joint null hypothesis is true. The computed chi-square value used to test the hypothesis that all coefficients except the intercept, are zero (0). It is the same hypothesis that is tested in standard regression using overall F-statistics.

4. Findings Differences in characteristics of switch and non-switch companies

Table 1 presents the test results on the characteristics of client firms that switched their auditors and those control firms. The mean difference on the characteristics of liquidity and leverage were based on 5 years average period whereas turnover growth of sales, total asset growth, financing activities, return on asset and total asset size of the switch and non-switch companies were based on period of pre switch 3 years and post switch of 2 years. The purpose of the mean test is to observe the difference in the groups of switched and non-switch auditors.

The results suggest that both switched and non-switched groups are distinctly different from one another in a number of dimensions. For example, leverage of switched groups are higher than the non-switched group with mean value of 86.94% and 65.66% respectively (statistically significant at t-value=1.787). Liquidity, financing and return on asset for switched group was 116%, 44.07% and -2.97% respectively lower than the non-switched group. However, average sale growth and average asset growth were reported to be higher for switched group compared to non-switched group. Mean for average sale growth was 32.66% for switched group while only 20.11% for non switched group. Average mean for asset growth of switched group was 41.9% and 35.6% for the non switched group.

129 International Research Journal of Finance and Economics - Issue 13 (2008)

The differences on liquidity, sale growth, asset growth, financing, return on asset and average asset size of the two groups were not significant at the conventional level.

Table 1 : Simple Parametric Test for mean Difference Between Switch and Non Switch Group

Characteristics Switch Companies Mean Non-Switch Companies Mean t-value Liquidity 1.1657 1.6269 -1.444 Leverage 0.8694 0.6566 1.787** Sale growth 0.3266 0.2011 0.892 Asset growth 0.419 0.356 0.477 Financing 0.4407 0.4860 -0.735 ROA -0.0297 -0.03717 -1.488 Asset size 11.5471 11.5990 -0.347

**Significant at 10% level

Determinants of auditor switch

Table 2 presents the results of the logistic regression model explaining the determinants of auditor switch companies. Initially, 16 variables were analysed using maximum likelihood estimation procedure in stepwise logistic regression based on centred data. In the initial step, stepwise regression identified LEV, GROA, FINB and LONG as significant variables. However, in the final step, the procedure selected five variables, namely, FEE, LEV, GROA, FINB and LONG as the significant variables. These variables met the 0.10 and 0.05 levels of significance for inclusion in the final model. The chi-square value for the overall model was 26.47 percent with 6 degree of freedom (significant at 0.05 level).

The results support the notion that that auditor switch decisions of companies listed on second board of Bursa Malaysia (formerly known as KLSE) is mainly determined by leverage, sales growth, financing, longevity of audit engagement and audit fee. The findings from this study supports the earlier studies documented in developed countries . In the Malaysian context, the findings are consistent with Huson et. al (2000) and Takiah et. al (1993) that there is no significant relationship between qualified audit report and subsequent auditor switch.

Table 2: Logistic Regression Result of Auditor Switch

Variables p-value Model specification Percent FEE 0.091** Chi-Square 26.476* LEV 0.018* Overall percentage 78.8 GROA 0.047* Prediction rate FINB 0.046* Switch group 73.1 LONG 0.105** Non-Switch Group 84.6

*Significant at 5% level **Significant at 10% level

Conclusion This study documents that initially there were 28 companies (with 31 switches) among Second Board listed companies occurred during the period of Asian financial crisis period. However only 23 companies (with 26 switches) were usable for subsequent analysis. Using stepwise regression analysis, the findings shown that auditor switch in Malaysia during the crisis period is determined by leverage, sales growth, financing, longevity of audit engagement and audit fee. The findings are consistent with previous findings in the earlier studies in developed countries. Furthermore, consistent with studies by Huson et.al (2000) and Takiah et.al (1993), this study provides non-corroborating evidence that client intends to switch auditors after receiving qualified audit report from their incumbent auditors. Also, this study postulates that client firm tends to exercise cost cutting during financial crisis period by switching to less-expensive audit services.

International Research Journal of Finance and Economics - Issue 13 (2008) 130

References [1] Adams, H. Lon and Allred A. (2002). Why the Fastest-Growing Companies Hire and Fire Their

Auditors. http://www.nysscpa.org/cpajournal. Accessed on 17 July 2002. [2] Bedingfield J.P and Loeb S.E. (1974). Auditor Change : An Examination. Journal of

Accountancy, March: 66-69. [3] Burton, J.C. and Roberts, W. (1967). A Study of Auditor Changes. Journal of Accountancy,

April, 31-36. [4] Butterworth, S. and Houghton, K.A. (1995). Auditor Switching : The Pricing of Audit Services.

Journal of Business Finance and Accounting, 22(3),323-344. [5] Chow, C. and Rice, S. (1982). Qualified Audit Opinion and Auditor Changes. The Accounting

Review, 2(April), 326-335. [6] Craswell, A.T. (1988) The Association Between Qualified Opinions and Auditor Switches.

Accounting and Business Research. 19(73) : 23-31. [7] Deis, D.R. and Giroux, G. (1996). The Effect of Auditor Changes on Audit Fees, Audit Hours

and Audit Quality. Journal of Accounting and Public Policy, 15, 55-76. [8] Fama, E.F and Jensen, M.C. (1983a). Separation of Ownership and Control. Journal of Law

and Economics, XXVI (June), 301-324. [9] Francis J.R and Wilson, E.R. (1988). Auditor Change: A Joint Test of Theories Relating to

Agency Cost and Auditor Differentiation. Accounting Review, October, 663-683. [10] Fried, D. and Schiff, A. (1981). Audit Switches and Associated Market Reaction. The

Accounting Review, 2 (October), 324-341. [11] Gregory, A. and Collier, P. (1996). Audit Fees and Auditor Change:An Investigation of the

Persistence of Fee Reduction by Type of Change. Journal of Business Finance and Accounting, 23(1), 13-29.

[12] Hartwell C., Lightle S. and Moreland K. (2001). The Client Acceptance Decision : Is the Third Time the Charm of Is It Three Strikes and You�re Out? Ohio CPA Journal, 60(4), 31-35.

[13] Hasnah, H., Ali, M.A.H, and Goh Y.P. (April 1997). Qualified Audit Reports and Auditor Switching : A Malaysian Experience. Paper presented at the Accounting Conference, Pulau Pinang.

[14] Huson, A.J., Ali, M., Annuar, M.N, Ariff, M and Shamsheer M. (2000). Audit Switch Decisions of Malaysian Listed Firms : Test of Determinants of Wealth Effect. Capital Market Review, 8 (1 & 2), 1-24.

[15] Jensen, M.C. and Meckling, W.H. (1976). Theory of the Firm : Managerial Behaviour, Agency Costs and Ownership Structure. Journal of Financial Economics, 3, 305-360.

[16] Johnson, W. and Lys, T. (1990). The Market for Audit Services : Evidence From Voluntary Auditor Changes. Journal of Accounting and Economics, 12, 281-308.

[17] Krishnan, J. (1994). Auditor Switching and Conservatism. Accounting Review, 69(1), 200-216. [18] Lee H.Y (2002). An Empirical Study of Auditor Switch. Working Paper. University of Oregon,

United States. [19] Pong, C.K.M and Whittington, G. (1994). The Determinants of Audit Fees: Some Empirical

Models. Journal of Business, Finance and Accounting, 21, 1071-1095. [20] Simon, D.T and Francis, J.R. (1988). The Effects of Auditor Change on Audit Fees: Tests of

Price Cutting and Price Recovery. The Accounting Review, XIII (2), 255-269. [21] Takiah, M.I and Ghazali, S.M. (1993). Incidence of Qualified Opinions and the Effects on

Auditor Switching : An Empirical Study in Malaysia. Jurnal Pengurusan, December, 53-63. [22] Williams, D.D. (1988). The Potential Determinants of Auditor Change. Journal of Business

Finance and Accounting, XV, 243-261. [23] Woo E-Sah and Koh H.C (2001). Factors Associated With Auditor Changes : A Singapore

Study. Accounting and Business Research, 31(2), 133-144.