Bursa Mekteb-i Sultanîsi (Bursa Erkek Lisesi) ve Şeref Defteri

Upload

khangminh22Category

view

1download

0

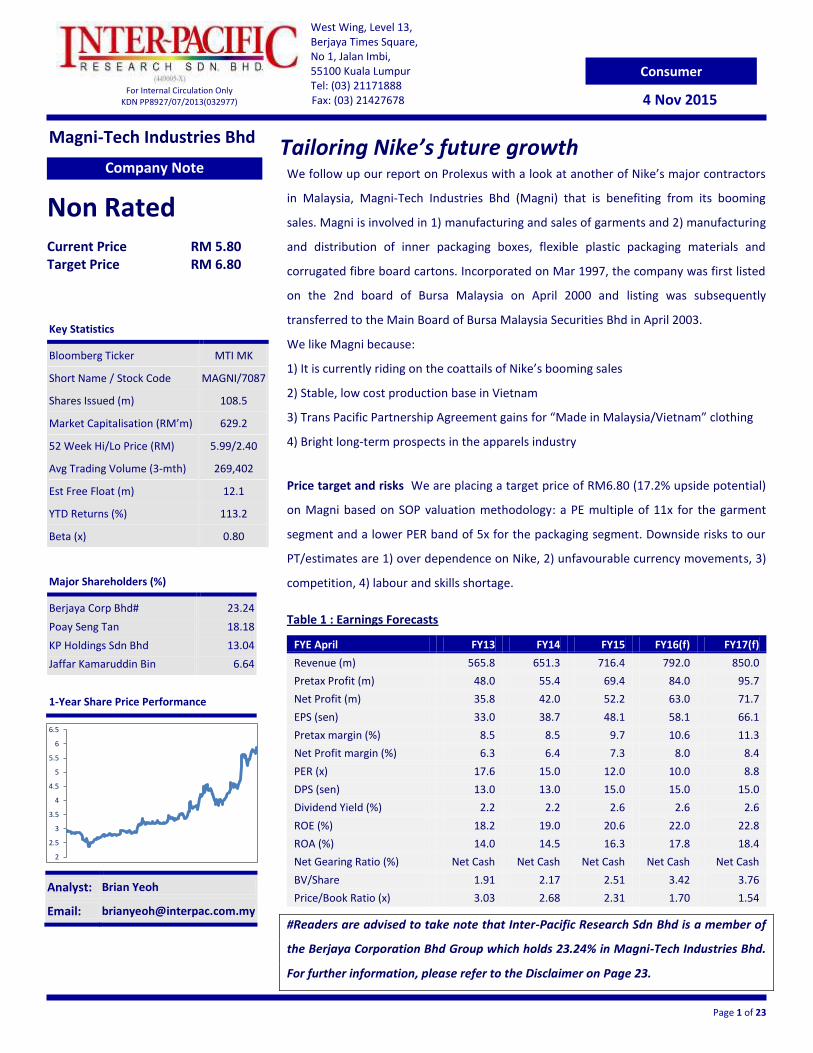

Key Statistics

Bloomberg Ticker MTI MK

Short Name / Stock Code MAGNI/7087

Shares Issued (m) 108.5

Market Capitalisation (RM’m) 629.2

52 Week Hi/Lo Price (RM) 5.99/2.40

Avg Trading Volume (3-mth) 269,402

Est Free Float (m) 12.1

YTD Returns (%) 113.2

Beta (x) 0.80

Major Shareholders (%)

Berjaya Corp Bhd#

Poay Seng Tan

KP Holdings Sdn Bhd

Jaffar Kamaruddin Bin

23.24

18.18

13.04

6.64

Page 1 of 23

West Wing, Level 13, Berjaya Times Square, No 1, Jalan Imbi, 55100 Kuala Lumpur Tel: (03) 21171888 Fax: (03) 21427678

For Internal Circulation Only KDN PP8927/07/2013(032977)

Consumer

4 Nov 2015

Company Note

Non Rated

Current Price RM 5.80 Target Price RM 6.80

Analyst: Brian Yeoh

Email: [email protected]

1-Year Share Price Performance

2

2.5

3

3.5

4

4.5

5

5.5

6

6.5

Magni-Tech Industries Bhd

We follow up our report on Prolexus with a look at another of Nike’s major contractors

in Malaysia, Magni-Tech Industries Bhd (Magni) that is benefiting from its booming

sales. Magni is involved in 1) manufacturing and sales of garments and 2) manufacturing

and distribution of inner packaging boxes, flexible plastic packaging materials and

corrugated fibre board cartons. Incorporated on Mar 1997, the company was first listed

on the 2nd board of Bursa Malaysia on April 2000 and listing was subsequently

transferred to the Main Board of Bursa Malaysia Securities Bhd in April 2003.

We like Magni because:

1) It is currently riding on the coattails of Nike’s booming sales

2) Stable, low cost production base in Vietnam

3) Trans Pacific Partnership Agreement gains for “Made in Malaysia/Vietnam” clothing

4) Bright long-term prospects in the apparels industry

Price target and risks We are placing a target price of RM6.80 (17.2% upside potential)

on Magni based on SOP valuation methodology: a PE multiple of 11x for the garment

segment and a lower PER band of 5x for the packaging segment. Downside risks to our

PT/estimates are 1) over dependence on Nike, 2) unfavourable currency movements, 3)

competition, 4) labour and skills shortage.

Table 1 : Earnings Forecasts

FYE April FY13 FY14 FY15 FY16(f) FY17(f)

Revenue (m) 565.8 651.3 716.4 792.0 850.0

Pretax Profit (m) 48.0 55.4 69.4 84.0 95.7

Net Profit (m) 35.8 42.0 52.2 63.0 71.7

EPS (sen) 33.0 38.7 48.1 58.1 66.1

Pretax margin (%) 8.5 8.5 9.7 10.6 11.3

Net Profit margin (%) 6.3 6.4 7.3 8.0 8.4

PER (x) 17.6 15.0 12.0 10.0 8.8

DPS (sen) 13.0 13.0 15.0 15.0 15.0

Dividend Yield (%) 2.2 2.2 2.6 2.6 2.6

ROE (%) 18.2 19.0 20.6 22.0 22.8

ROA (%) 14.0 14.5 16.3 17.8 18.4

Net Gearing Ratio (%) Net Cash Net Cash Net Cash Net Cash Net Cash

BV/Share 1.91 2.17 2.51 3.42 3.76

Price/Book Ratio (x) 3.03 2.68 2.31 1.70 1.54

#Readers are advised to take note that Inter-Pacific Research Sdn Bhd is a member of

the Berjaya Corporation Bhd Group which holds 23.24% in Magni-Tech Industries Bhd.

For further information, please refer to the Disclaimer on Page 23.

Tailoring Nike’s future growth

Page 2 of 23

Magni-Tech Industries Bhd

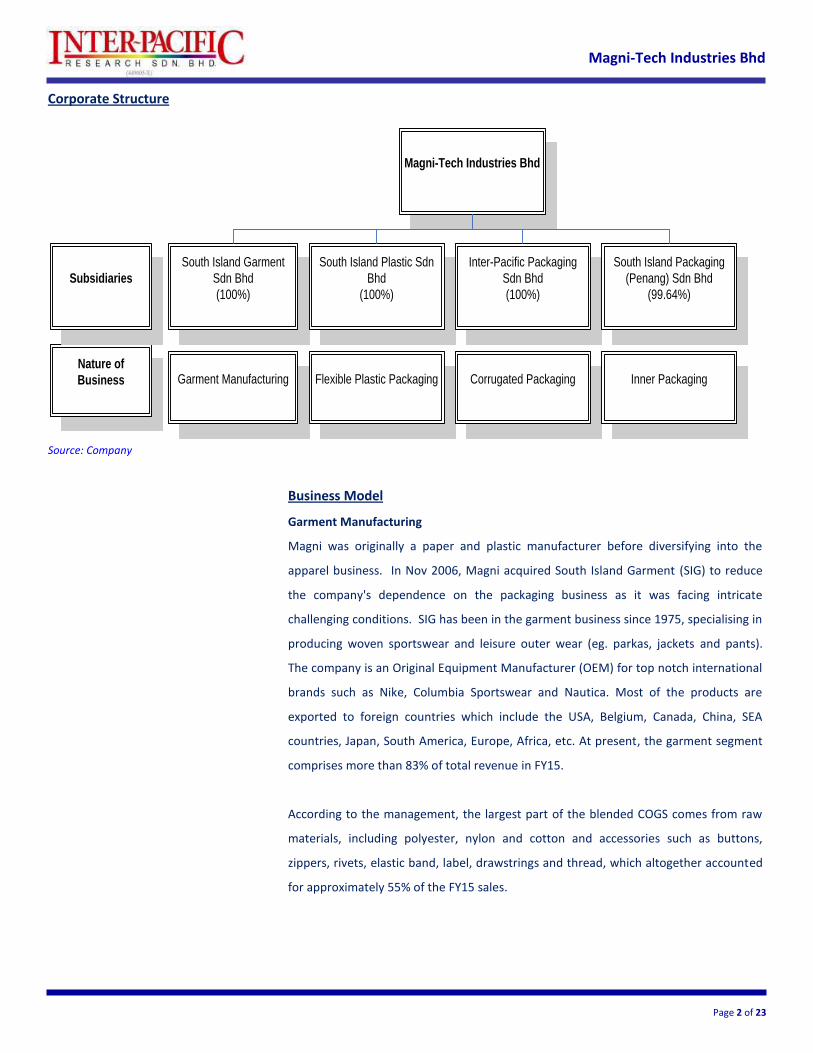

Corporate Structure

Magni-Tech Industries Bhd

South Island Garment

Sdn Bhd

(100%)

South Island Plastic Sdn

Bhd

(100%)

Inter-Pacific Packaging

Sdn Bhd

(100%)

South Island Packaging

(Penang) Sdn Bhd

(99.64%)

Garment Manufacturing

Flexible Plastic Packaging

Corrugated Packaging

Inner Packaging

Nature of

Business

Subsidiaries

Source: Company

Business Model

Garment Manufacturing

Magni was originally a paper and plastic manufacturer before diversifying into the

apparel business. In Nov 2006, Magni acquired South Island Garment (SIG) to reduce

the company's dependence on the packaging business as it was facing intricate

challenging conditions. SIG has been in the garment business since 1975, specialising in

producing woven sportswear and leisure outer wear (eg. parkas, jackets and pants).

The company is an Original Equipment Manufacturer (OEM) for top notch international

brands such as Nike, Columbia Sportswear and Nautica. Most of the products are

exported to foreign countries which include the USA, Belgium, Canada, China, SEA

countries, Japan, South America, Europe, Africa, etc. At present, the garment segment

comprises more than 83% of total revenue in FY15.

According to the management, the largest part of the blended COGS comes from raw

materials, including polyester, nylon and cotton and accessories such as buttons,

zippers, rivets, elastic band, label, drawstrings and thread, which altogether accounted

for approximately 55% of the FY15 sales.

Page 3 of 23

Magni-Tech Industries Bhd

Exhibit 1: Corrugated boxes

Source: Boxilimited

Table 2: Breakdown of corrugated packaging products purposes

Corrugated Packaging Product Purpose

Single faced corrugated sheets General-purpose wrapping and scratch prevention Single wall corrugated cartons Used as smaller or inner carton for protective cover

Double wall corrugated cartons Used as outer cartons for storage and distribution

Single wall corrugated fittings Used for nesting or as dividers

Double wall corrugated fittings Used as reinforcement of cartons Source: Company, Inter-Pacific

Packaging Business

The packaging segment's activities are undertaken by Magni-Tech’s 3 subsidiaries'

manufacturing facilities in Malaysia. Packaging products such as corrugated

boards/sheets, fittings and fibreboard cartons and boxes are typically used by the

manufacturing sector. The electronics, food, beverage, healthcare and tobacco sectors

are the company's end-customers. Packaging products manufactured by the group are

sold mainly locally but a sizeable percentage is used in the packaging of manufactured

products that are ultimately exported.

The market for corrugated packaging products can be roughly divided into local users

(65% by turnover) and Licensed Manufacturing Warehouses (35%) (which perform

some light value-added services for manufacturers such as break-bulk and

customisation of packaging for specific markets). The market can also be classified by

way of end-users. These include the Electronics industry, Plastics and Rubber-based

products, Toiletries, Food & Beverage Industry and the Textiles Industry. A final

category of end use customer is the Corrugated Packaging Converter.

The Flexible Plastic Packaging Products and the Inner Packaging Boxes business can

both be classified by the end-market served viz local businesses (72%), the Free Trade

Zones (1.4%), Licensed Manufacturing Warehouses (21.2%) and export destinations

(5.4%). They can also be classified by way of specifying the end users which are mainly

the manufacturing segments identified above.

Corrugated Carton Manufacturing

Corrugated packaging manufacturing involves upstream as well as downstream

processes. In the upstream portion of activities, industrial kraft, testliner and medium

paper is converted into corrugated boards through a process called corrugating. A

subsequent downstream process transforms corrugated boards into corrugated

products in a step called conversion into die cut trays, containers and cartons.

Integrated operations involves sourcing kraftliner, testliner and medium paper which

upon being corrugated, boards are manufactured which are then converted into other

products.

Page 4 of 23

Magni-Tech Industries Bhd

IPP manufactures corrugated boards which are then converted by SIPP into generic final

corrugated cartons and die cut trays customised for end customer needs. They are

mainly sold to customers in the northern Peninsular region due to the bulky nature and

high transport costs that will not justify their being transported over longer distances.

Raw materials used are largely kraftliner and testliners, which are more appropriately

labeled Kraft Paperboard and Recycled Paperboard. "Kraftliner" is defined as "paper or

paperboard whose fibre content has no less than 80% fibre obtained by the chemical

sulfate or soda processes". Semi chemical fluting (medium) paper is defined as

containing no less than 65% unbleached hardwood fibres obtained by a semi-chemical

pulping process. There is no formal definition of "testliner" but the term is used in the

Pacific Rim when referring to papers of different bursting strengths. But because some

grades of testliner have lower burst factors than experienced with Rule 41 of the US

National Railroad Freight Committee’s Uniform Freight Classification compliant boards

that meet edge crush tests, basis weight and combined board burst requirements due

to their containing high amounts of recycled fibres. Lower grades of testliner have

come to be associated with recycled fibres. Many Pacific Rim customers rely on a visual

inspection of any board sheet, and if contaminants are visible on the surface, the board

is judged to be testliner.

Kraftliners involving chemically sourced virgin fibres are always imported, from the US,

Canada and New Zealand. Testliners and corrugating medium paper are available

locally. Other raw materials such as printing ink and glue are also sourced locally.

Manufacturing of corrugated boards and cartons is carried out at Inter-Pacific Packaging

S/B's 27,797 m2 facility in Batu 13, Jalan Kelang Lama, in Puchong which has a built up

area of 15,362m2. Operating on 2 shifts with 167 employees, it has a capacity of 36,000

mt p.a. but currently production is running at 23,822 mt/month or at 66% of capacity.

Flexible Plastic Packaging Materials Manufacturing

The group manufactures a range of flexible plastic packaging materials such as

wrappers, paper bags, stationery and labels for industrial & commercial use e.g.:

Plastic bags for wrapping food products e.g. bread, frozen food, cereals, snacks,

noodles etc.

Plastic sheets used in the agriculture and the construction and building industry.

Laminated plastic products used in high end packaging of products.

Plastic packing used in automated packaging machinery.

Page 5 of 23

Magni-Tech Industries Bhd

Exhibit 2: Inner box

Source: diytrade

The raw materials include various types of polymer plastics resins such as

polypropylene, low density polyethylene, linear low density polyethylene, high

molecular polyethylene, and nylon film and polyester film or other materials that meet

customer requirements. They are mostly sourced locally.

Flexible laminated plastics packaging manufacturing uses a composite of base materials

that enhances the properties of the base materials used. While they involve higher

costs, they also offer better finish, aesthetic appeal, and project the image of quality

and offer convenience and flexibility and may also offer better insulation against air,

water and light and the leaching of harmful substances into food. Almost all the raw

materials are locally sourced.

Manufacturing and distribution mainly serving customers in the northern West

Malaysian region is undertaken from South Island Plastic S/B's factory and warehouse,

both in the Prai Industrial Estate on sites measuring 7,050 m2 and 3,979 m2 built upon

with corresponding gross built up areas of 5,990 m2 and 1,674 m2 respectively. It

employs 167 workers and operating on 3 shifts. The production run rate is currently

3,006mt/month or at 83.5% of the annual capacity of 3,600 mt p.a.

Another small factory in Kawasan MIEL in the Prai Industrial Estate owned by the group

is currently rented out for RM180,000 p.a.

Inner Packaging Boxes

Inner box printing and packaging raw materials such as printing ink and glue are mainly

imported from the US, Japan and Indonesia due to specifications imposed by licensed

manufacturing warehouses and free trade zone clients.

South Island Packaging (Penang) S/B's own 8,027 m2. production facilities undertaking

printing, die-cutting and finishing are located in the Prai Industrial Estate, covering an

area of 6,334 m2 currently operate on 3 shifts employing 168 employees. Production

run rate is 3,686 mt/month compared to a capacity of 4,200 mt p.a. , effectively

operating 88% of capacity.

Page 6 of 23

Magni-Tech Industries Bhd

Graph 1: Garment segment cost to sales (%) Graph 2: Packaging segment cost to sales (%)

#Others include Other factory overheads and GP ratio *Others include change in closing stocks and GP ratio

Source: Company, Inter-Pacific

Graph 3: Revenue Contribution by Product Group (RM mil)

Graph 4: FY14 Revenue Breakdown by Country (RM mil)

Source: Company, Inter-Pacific

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

06 07 08 09 10 11 12 13 14 15

Packaging materials

Garment

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

07 08 09 10 11 12 13 14 15

Others*

Africa

Australia

Canada

South America

Other Asian countries

China

European countries

United States of America

Malaysia

65%

18%

17% Material Costs

Labour andOverheads

Others*55% 25%

20% Material cost

Labour andsubcontract cost

Others#

Page 7 of 23

Magni-Tech Industries Bhd

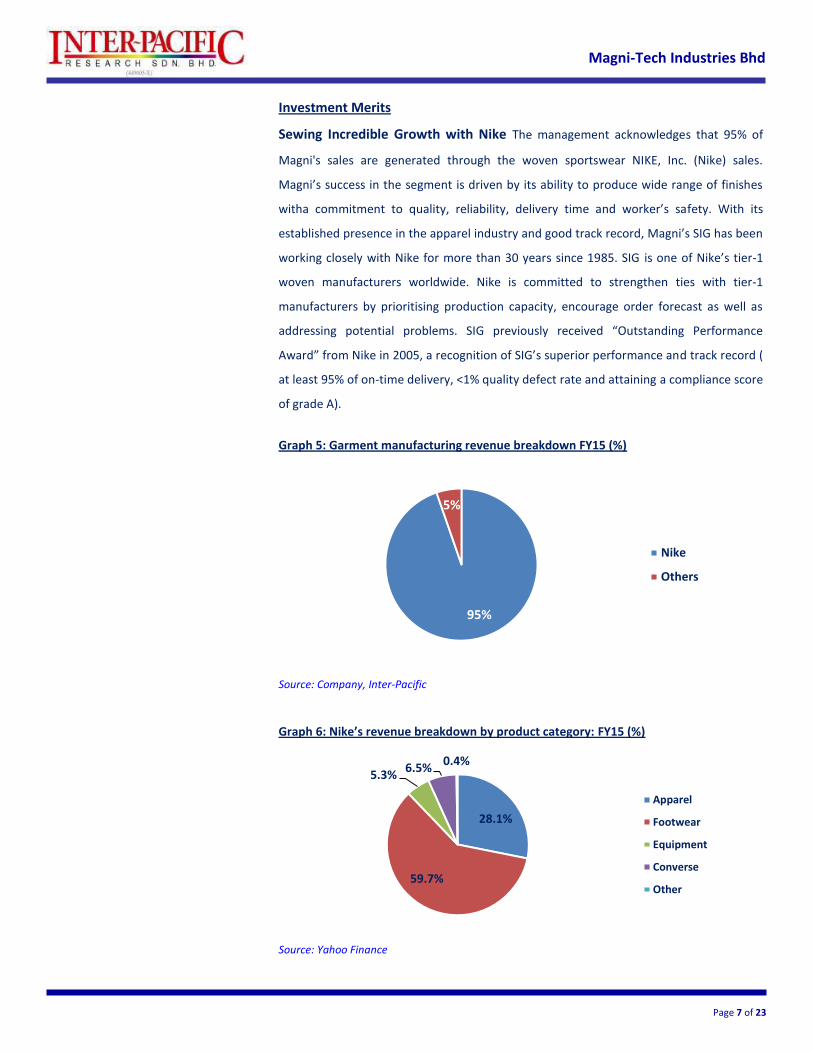

Investment Merits

Sewing Incredible Growth with Nike The management acknowledges that 95% of

Magni's sales are generated through the woven sportswear NIKE, Inc. (Nike) sales.

Magni’s success in the segment is driven by its ability to produce wide range of finishes

witha commitment to quality, reliability, delivery time and worker’s safety. With its

established presence in the apparel industry and good track record, Magni’s SIG has been

working closely with Nike for more than 30 years since 1985. SIG is one of Nike’s tier-1

woven manufacturers worldwide. Nike is committed to strengthen ties with tier-1

manufacturers by prioritising production capacity, encourage order forecast as well as

addressing potential problems. SIG previously received “Outstanding Performance

Award” from Nike in 2005, a recognition of SIG’s superior performance and track record (

at least 95% of on-time delivery, <1% quality defect rate and attaining a compliance score

of grade A).

Graph 5: Garment manufacturing revenue breakdown FY15 (%)

Source: Company, Inter-Pacific

Graph 6: Nike’s revenue breakdown by product category: FY15 (%)

Source: Yahoo Finance

95%

5%

Nike

Others

28.1%

59.7%

5.3% 6.5%

0.4%

Apparel

Footwear

Equipment

Converse

Other

Page 8 of 23

Magni-Tech Industries Bhd

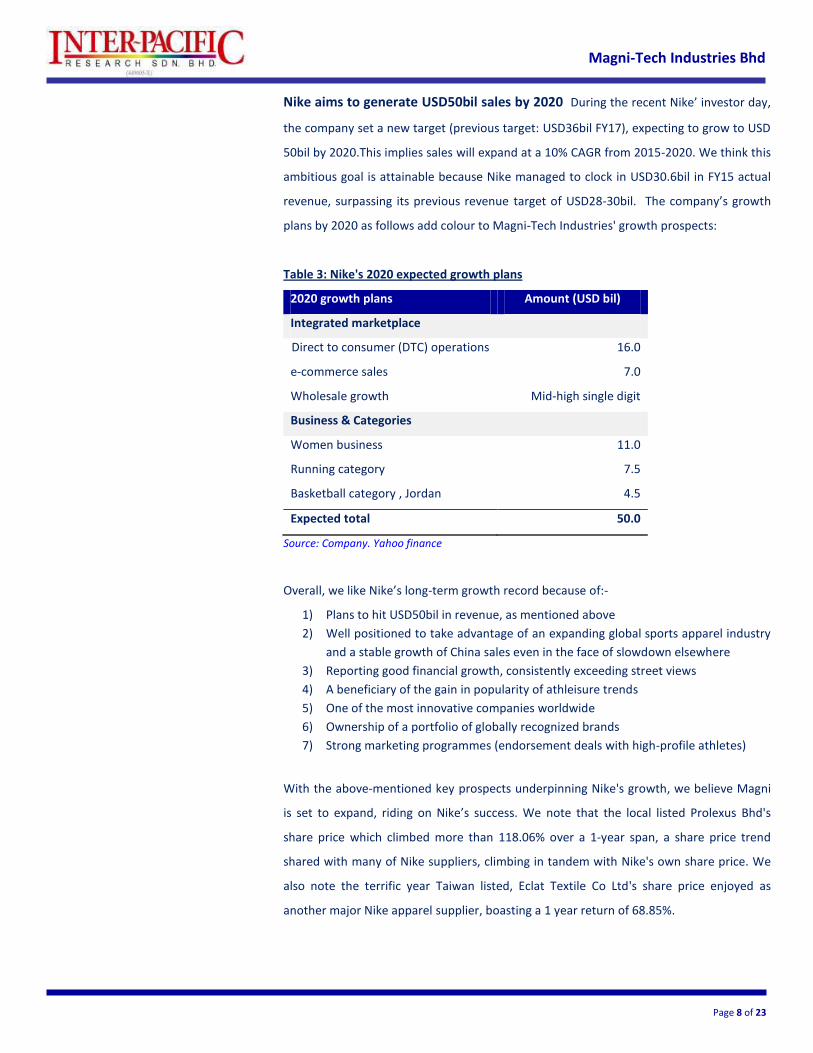

Nike aims to generate USD50bil sales by 2020 During the recent Nike’ investor day,

the company set a new target (previous target: USD36bil FY17), expecting to grow to USD

50bil by 2020.This implies sales will expand at a 10% CAGR from 2015-2020. We think this

ambitious goal is attainable because Nike managed to clock in USD30.6bil in FY15 actual

revenue, surpassing its previous revenue target of USD28-30bil. The company’s growth

plans by 2020 as follows add colour to Magni-Tech Industries' growth prospects:

Table 3: Nike's 2020 expected growth plans

2020 growth plans Amount (USD bil)

Integrated marketplace

Direct to consumer (DTC) operations 16.0

e-commerce sales 7.0

Wholesale growth Mid-high single digit

Business & Categories

Women business 11.0

Running category 7.5

Basketball category , Jordan 4.5

Expected total 50.0

Source: Company. Yahoo finance

Overall, we like Nike’s long-term growth record because of:-

1) Plans to hit USD50bil in revenue, as mentioned above

2) Well positioned to take advantage of an expanding global sports apparel industry

and a stable growth of China sales even in the face of slowdown elsewhere

3) Reporting good financial growth, consistently exceeding street views

4) A beneficiary of the gain in popularity of athleisure trends

5) One of the most innovative companies worldwide

6) Ownership of a portfolio of globally recognized brands

7) Strong marketing programmes (endorsement deals with high-profile athletes)

With the above-mentioned key prospects underpinning Nike's growth, we believe Magni

is set to expand, riding on Nike’s success. We note that the local listed Prolexus Bhd's

share price which climbed more than 118.06% over a 1-year span, a share price trend

shared with many of Nike suppliers, climbing in tandem with Nike's own share price. We

also note the terrific year Taiwan listed, Eclat Textile Co Ltd's share price enjoyed as

another major Nike apparel supplier, boasting a 1 year return of 68.85%.

Page 9 of 23

Magni-Tech Industries Bhd

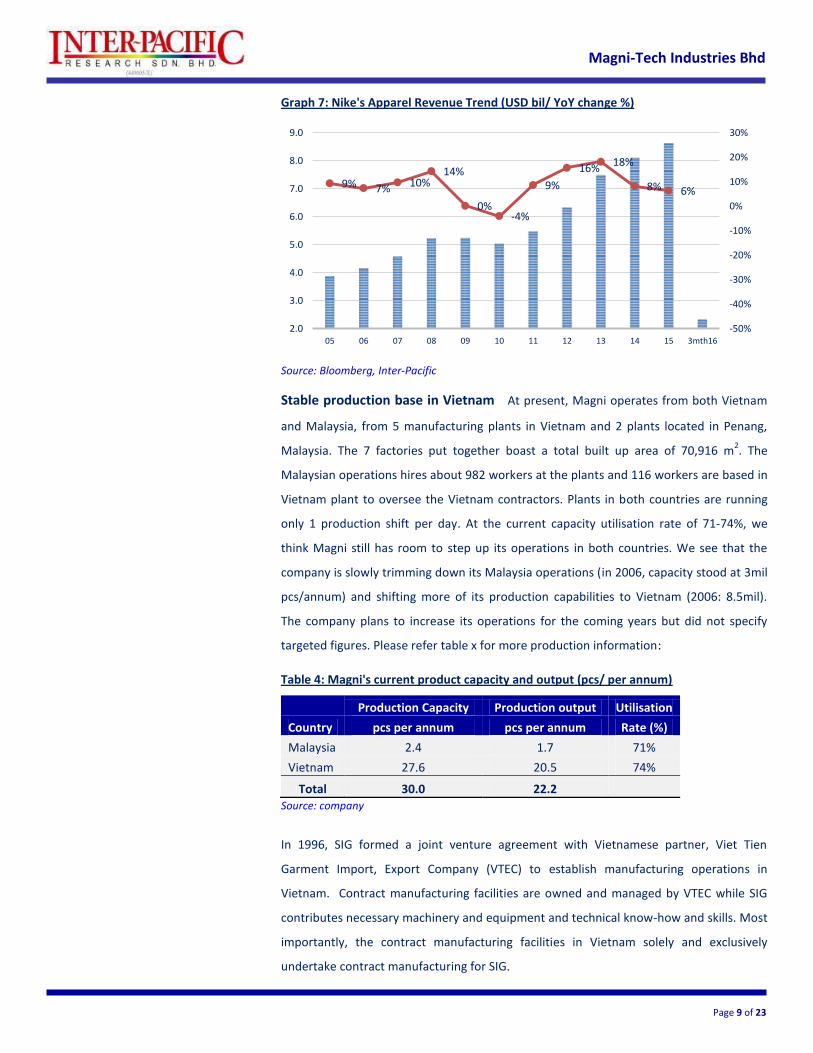

Graph 7: Nike's Apparel Revenue Trend (USD bil/ YoY change %)

Source: Bloomberg, Inter-Pacific

Stable production base in Vietnam At present, Magni operates from both Vietnam

and Malaysia, from 5 manufacturing plants in Vietnam and 2 plants located in Penang,

Malaysia. The 7 factories put together boast a total built up area of 70,916 m2. The

Malaysian operations hires about 982 workers at the plants and 116 workers are based in

Vietnam plant to oversee the Vietnam contractors. Plants in both countries are running

only 1 production shift per day. At the current capacity utilisation rate of 71-74%, we

think Magni still has room to step up its operations in both countries. We see that the

company is slowly trimming down its Malaysia operations (in 2006, capacity stood at 3mil

pcs/annum) and shifting more of its production capabilities to Vietnam (2006: 8.5mil).

The company plans to increase its operations for the coming years but did not specify

targeted figures. Please refer table x for more production information:

Table 4: Magni's current product capacity and output (pcs/ per annum)

Production Capacity Production output Utilisation

Country pcs per annum pcs per annum Rate (%)

Malaysia 2.4 1.7 71%

Vietnam 27.6 20.5 74%

Total 30.0 22.2 Source: company

In 1996, SIG formed a joint venture agreement with Vietnamese partner, Viet Tien

Garment Import, Export Company (VTEC) to establish manufacturing operations in

Vietnam. Contract manufacturing facilities are owned and managed by VTEC while SIG

contributes necessary machinery and equipment and technical know-how and skills. Most

importantly, the contract manufacturing facilities in Vietnam solely and exclusively

undertake contract manufacturing for SIG.

9% 7% 10% 14%

0% -4%

9%

16% 18%

8% 6%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

05 06 07 08 09 10 11 12 13 14 15 3mth16

Page 10 of 23

Magni-Tech Industries Bhd

Exhibit 3: Sewing workshop Exhibit 4: VTEC's quality control workers at work

Source: Company Source: Vietnam Pictorial

VTEC, a government controlled company (managed by the Ministry of Industry), is one of

Vietnam’s largest apparel manufacturing company. With a workforce of more than

20,000 workers, the company specialises in the manufacturing of garments and trading

of materials and accessories for the garment sector, equipment and components and

import-export services. Most of the products are tailored for export markets, such as the

US (Perry Ellis, Target, Nike, Adidas, Columbia, Dockers, Levi's, A&F.), Europe (Nike,

Adidas, Zara, Liz Claireborne), Japan (Uniqlo, Mitsui, Itochu Viettien) and other ASEAN

countries. On the company website, VTEC discloses multiple joint ventures with foreign

partners from Taiwan, Hong Kong and the United Kingdom). VTEC also diversified to non-

apparel business such as construction, warehouse, forwarding, finance and real estate.

A research paper by the World Bank credits VTEC for its strength in 1) deploying a pool of

productive and highly trained and skilled contingent workers compared with other

companies in the same industry 2) capable of executing large-size order contracts 3)

VTEC’s products have a reputation for quality 4) its being a Vietnam Textile and Garment

Corporation, receiving much support from the Corporation. We are comfortable that

Magni has partnered a reliable affiliate, and this sets the company's operations in the

right direction in Vietnam.

Page 11 of 23

Magni-Tech Industries Bhd

TPP: leading to more “Made in Malaysia/Vietnam” clothing labels The Trans-

Pacific Partnership (TPP) is an agreement that aims to liberalise trade and set common

guidelines within the 12 member pact, which includes the U.S., Canada, Mexico, Peru

Chile and in the Asia-Pacific (APAC) includes Australia, Brunei, Japan, Malaysia, New

Zealand, Singapore and Vietnam. While minimal details of the deal have been publicly

disclosed, we think the TPP agreement could involve eliminating/lowering duties on

apparel/footwear imports to the US from both Malaysia and Vietnam. Current tariff

rates range between 0 - 20% for Malaysia while in Vietnam, this ranges between 5-30%.

According to the Eurasia Group, a global political risk research and consulting firm, the

apparel sectors in Malaysia and Vietnam are expected to observe a 37% and 50%

growth exports by 2025. Vietnam enjoys a higher percentage growth because it exports

>60% of its apparel output to the U.S. (est. market share 9%) and Japan. The deal would

not only increase the share of Malaysian and Vietnamese apparels in the US market but

also deliver some indirect benefits to companies sourcing directly from affected

countries. (e.g. cuts in regulatory delays, accelerating time-to-market, cost effectiveness

and a leaner supply chain).

While we appreciate the potential benefits of the TPP agreement, we note that the

inclusion of the ‘yarn forward’ rule of origin will have unfavourable effect on the

Malaysia and Vietnam apparel industry. Basically, the rule requires that TPPA nation

fabric production uses member-produced yarn in textiles in order to qualify for the

duty-free access. Implementation of TPP agreement may cause a sudden shortage of

yarn supply amongst member, heightening the cost of production as participating

nations are not able to import from existing non-participating members. We think the

development is still vague and has a long way to go. Going forward, itis unlikely to be a

game changer for members’ economic prospect as some of the provisions to lower tariff

barriers will only take effect over many years. Nonetheless, Magni said it is finalizing the

agreements with its suppliers if TPP agreement materializes, as reported in The Edge

Financial Daily.

Page 12 of 23

Magni-Tech Industries Bhd

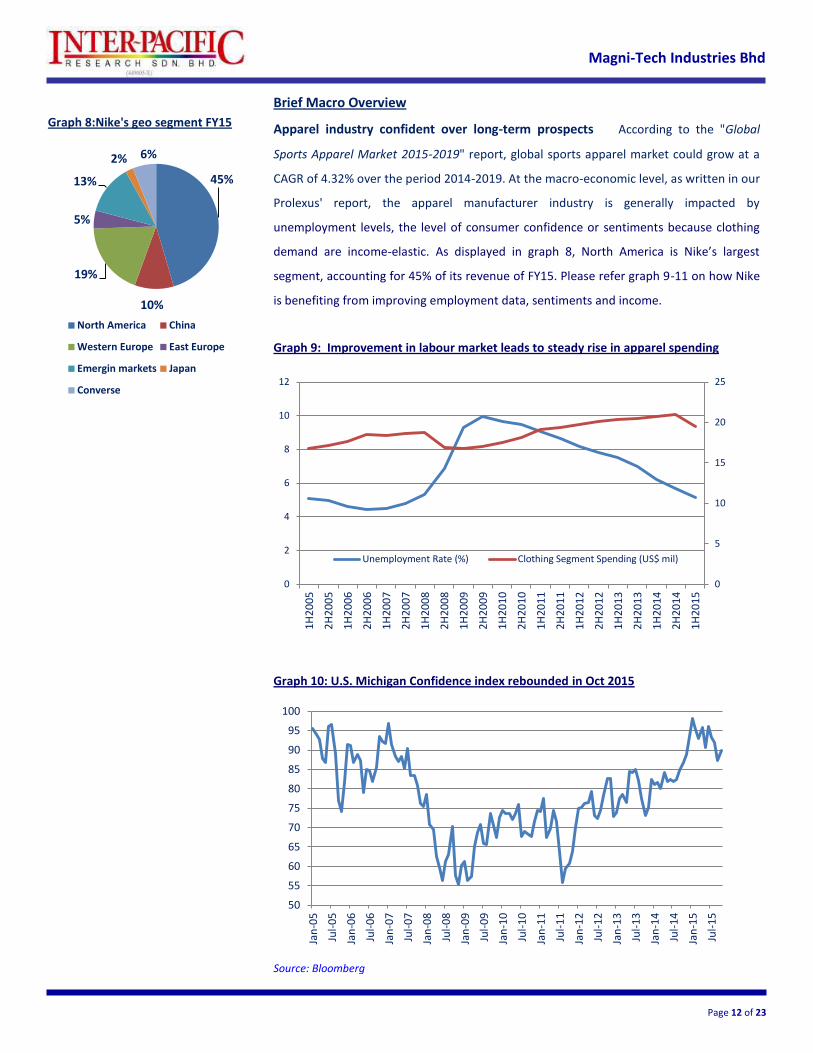

Graph 8:Nike's geo segment FY15

45%

10%

19%

5%

13%

2% 6%

North America China

Western Europe East Europe

Emergin markets Japan

Converse

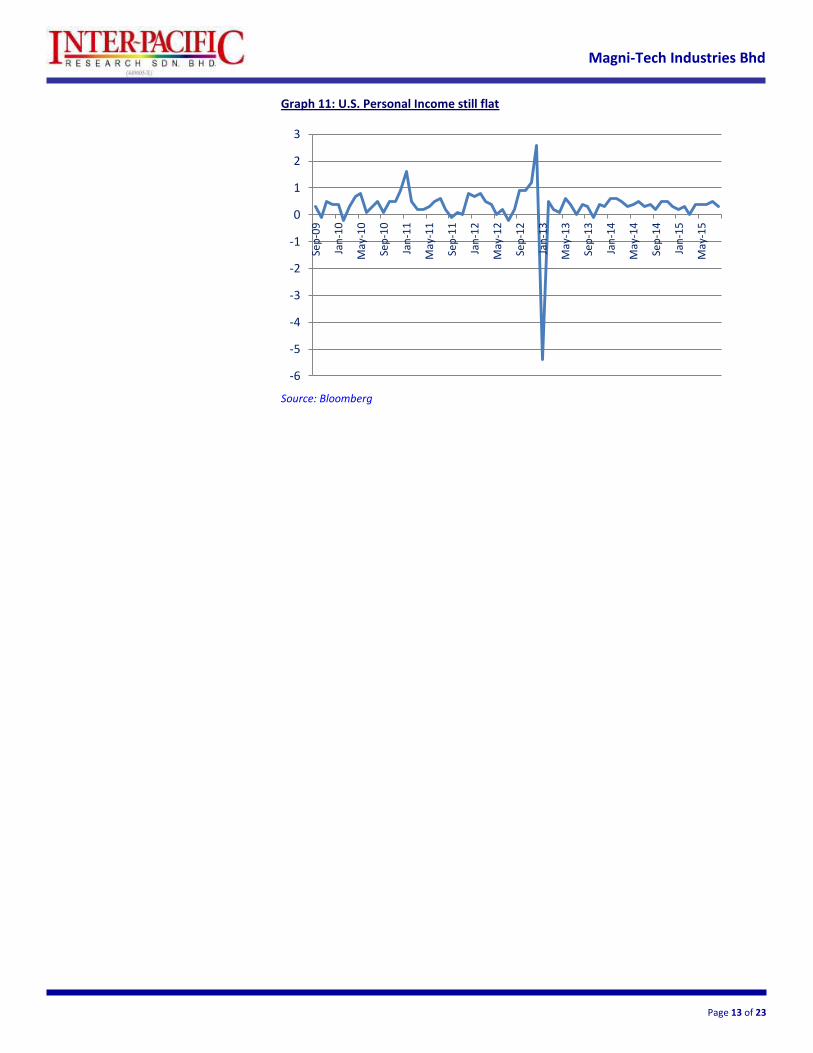

Brief Macro Overview

Apparel industry confident over long-term prospects According to the "Global

Sports Apparel Market 2015-2019" report, global sports apparel market could grow at a

CAGR of 4.32% over the period 2014-2019. At the macro-economic level, as written in our

Prolexus' report, the apparel manufacturer industry is generally impacted by

unemployment levels, the level of consumer confidence or sentiments because clothing

demand are income-elastic. As displayed in graph 8, North America is Nike’s largest

segment, accounting for 45% of its revenue of FY15. Please refer graph 9-11 on how Nike

is benefiting from improving employment data, sentiments and income.

Graph 9: Improvement in labour market leads to steady rise in apparel spending

Graph 10: U.S. Michigan Confidence index rebounded in Oct 2015

Source: Bloomberg

0

5

10

15

20

25

0

2

4

6

8

10

12

1H

20

05

2H

20

05

1H

20

06

2H

20

06

1H

20

07

2H

20

07

1H

20

08

2H

20

08

1H

20

09

2H

20

09

1H

20

10

2H

20

10

1H

20

11

2H

20

11

1H

20

12

2H

20

12

1H

20

13

2H

20

13

1H

20

14

2H

20

14

1H

20

15

Unemployment Rate (%) Clothing Segment Spending (US$ mil)

50

55

60

65

70

75

80

85

90

95

100

Jan

-05

Jul-

05

Jan

-06

Jul-

06

Jan

-07

Jul-

07

Jan

-08

Jul-

08

Jan

-09

Jul-

09

Jan

-10

Jul-

10

Jan

-11

Jul-

11

Jan

-12

Jul-

12

Jan

-13

Jul-

13

Jan

-14

Jul-

14

Jan

-15

Jul-

15

Page 13 of 23

Magni-Tech Industries Bhd

Graph 11: U.S. Personal Income still flat

Source: Bloomberg

-6

-5

-4

-3

-2

-1

0

1

2

3

Sep

-09

Jan

-10

May

-10

Sep

-10

Jan

-11

May

-11

Sep

-11

Jan

-12

May

-12

Sep

-12

Jan

-13

May

-13

Sep

-13

Jan

-14

May

-14

Sep

-14

Jan

-15

May

-15

Page 14 of 23

Magni-Tech Industries Bhd

Financials

Income Statement

Uptrending Revenues Magni has registered a track record of uninterrupted profits

since 2007, with its performance mainly tracking Nike’s sales performance. The company

delivered a 10-year revenue CAGR of 22.5% from 2005 to 2015, surviving many of the

crises that impacted the world economy. The figures starting 2009 in Chart 8 coincide

with the inclusion of full year contribution from the garment business rather than the

packaging business alone.

Graph 12: Revenue 8-year Actual & Forecast (2009-2017f RM' mil)

Source: Company, Inter-Pacific

Poised for stronger earnings growth Our forecasts are for Magni to achieve revenues

of RM792mil/RM850mil in FY16/FY17 respectively, climbing 10%/7.3% YoY, with net

income reaching RM63mil/RM71.7mil, up 20.7%/13.8% YoY respectively. This is based

on a 10% CAGR from 2010-2015 extrapolated into future years, as guided by

management’s minimum expectations moving forward. We assume a gradual ramp-up in

production capacity and expanding export sales in FY16. Revenues may continue to

increase post-2016, supported by the continued increase in orders from Nike, but we

have not imputed any pickup in the pace of increase in orders, to be conservative.

Balance Sheet

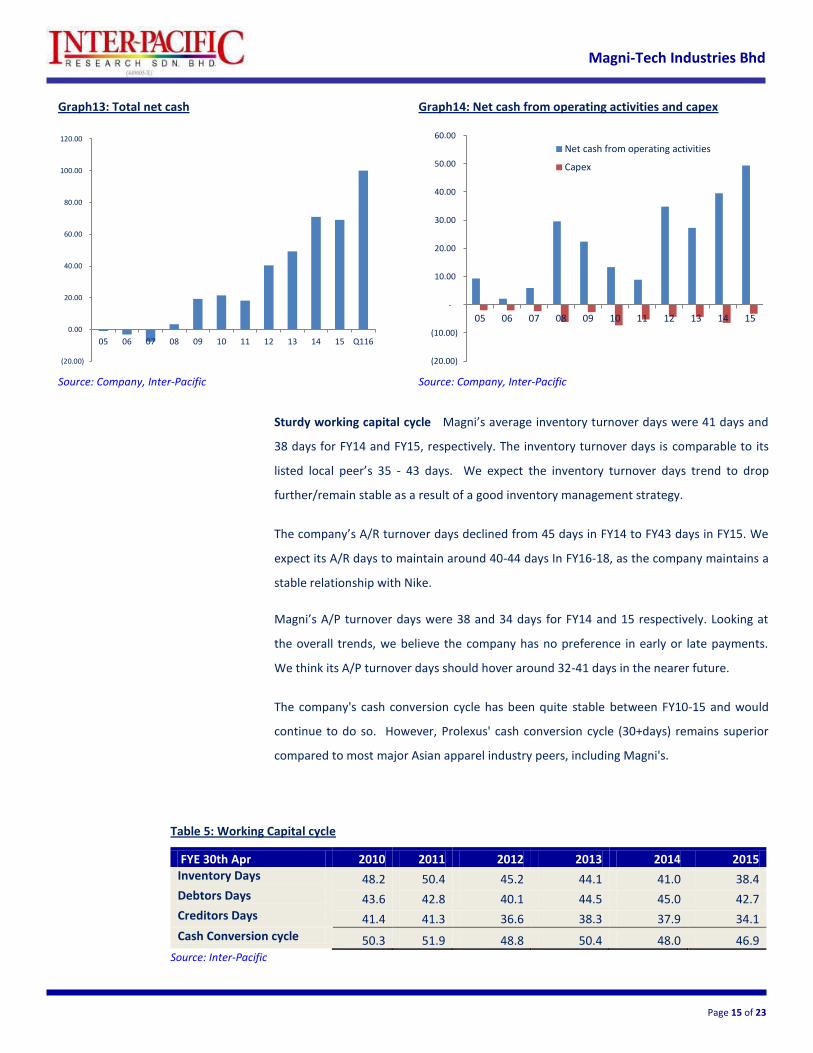

Cash-rich As at July 2015, Magni has a total net cash of RM100mil, a treasury cash pile

of RM0.92per share. The company has been generating healthy operating cash flows and

has been in a net cash position since 2008. With thislarge amount of cash in hand, Magni

has enough cash to fund capex for plant expansions or seek M&A opportunities.

-5

0

+5

+10

+15

+20

+25

300

400

500

600

700

800

900

09 10 11 12 13 14 15 16f 17f

Revenue % change YoY

Page 15 of 23

Magni-Tech Industries Bhd

Table 5: Working Capital cycle

FYE 30th Apr 2010 2011 2012 2013 2014 2015 Inventory Days 48.2 50.4 45.2 44.1 41.0 38.4 Debtors Days 43.6 42.8 40.1 44.5 45.0 42.7 Creditors Days 41.4 41.3 36.6 38.3 37.9 34.1

Cash Conversion cycle 50.3 51.9 48.8 50.4 48.0 46.9 Source: Inter-Pacific

Graph13: Total net cash

Source: Company, Inter-Pacific

(20.00)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

05 06 07 08 09 10 11 12 13 14 15 Q116

Graph14: Net cash from operating activities and capex

Source: Company, Inter-Pacific

(20.00)

(10.00)

-

10.00

20.00

30.00

40.00

50.00

60.00

05 06 07 08 09 10 11 12 13 14 15

Net cash from operating activities

Capex

Sturdy working capital cycle Magni’s average inventory turnover days were 41 days and

38 days for FY14 and FY15, respectively. The inventory turnover days is comparable to its

listed local peer’s 35 - 43 days. We expect the inventory turnover days trend to drop

further/remain stable as a result of a good inventory management strategy.

The company’s A/R turnover days declined from 45 days in FY14 to FY43 days in FY15. We

expect its A/R days to maintain around 40-44 days In FY16-18, as the company maintains a

stable relationship with Nike.

Magni’s A/P turnover days were 38 and 34 days for FY14 and 15 respectively. Looking at

the overall trends, we believe the company has no preference in early or late payments.

We think its A/P turnover days should hover around 32-41 days in the nearer future.

The company's cash conversion cycle has been quite stable between FY10-15 and would

continue to do so. However, Prolexus' cash conversion cycle (30+days) remains superior

compared to most major Asian apparel industry peers, including Magni's.

Page 16 of 23

Magni-Tech Industries Bhd

Table 6: Overall margins comparison with listed peer

GP margin 2009 2010 2011 2012 2013 2014 2015 2016f 2017f

Magni 11.4% 14.3% 14.8% 14.5% 16.0% 14.8% 15.9% 16.5% 16.9%

Prolexus 12.5% 15.0% 13.1% 15.4% 16.8% 17.5% 19.7% 23.1% 23.4%

EBIT margin 2009 2010 2011 2012 2013 2014 2015 2016f 2017f

Magni 4.1% 5.9% 5.4% 7.7% 8.6% 8.6% 9.8% 10.7% 11.3%

Prolexus 2.6% 4.9% 3.2% 5.9% 8.3% 8.3% 8.3% 9.0% 9.5%

PATMI margins 2009 2010 2011 2012 2013 2014 2015 2016f 2017f

Magni 3.0% 4.4% 3.9% 5.7% 6.3% 6.4% 7.3% 8.0% 8.4%

Prolexus 0.2% 2.5% 2.8% 5.4% 7.3% 7.1% 7.3% 7.8% 8.3% Source: Inter-Pacific

Graph15: Magni-Tech Margins breakdown 8-year Actual & Forecasts (2009-2017f) (%)

Source: Inter-Pacific

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

09 10 11 12 13 14 15 16f 17f

GP Margins EBIT Margins PATMI Margins

Profitability

Margins steadily rising We expect GP margins to improve to 16.5%/16.9% respectively

for FY16/FY17 on better economies of scale and cost control initiatives, bolstered by a

lean manufacturing system already in place. When comparing margins among direct

peers, we note that Magni’s GP margin trails behind Prolexus. This is because as a

strategy, Magni aims for higher volume, manufacturing garments of basic and simple

styles but higher volume. Although this helps to increase productivity and reduce

wastage, the margins are much lower than Prolexus’ more varied product offerings. On

the other hand, Magni’s EBIT margins and PATMI margins are better off than Prolexus’

due to its bigger size of operations. We think this scenario might change as we observe

Prolexus appears poised to be more aggressive in its expansion plans, moving forward.

Page 17 of 23

Magni-Tech Industries Bhd

Graph 16: ROE Trend Actual & Forecast (2005-2016f) (%)

Source: Inter-Pacific

Stable dividends Magni does not adopt an explicit dividend policy. The company has

been steadily increasing DPS since 2005, even though it does not have an explicit dividend

policy. Magni recently announced its final dividend of 3 per share ex-date to be set on 9th

Nov 2015. We note that its dividend payout ratio has been on a declining trend since

listing. With a higher earnings base going forward, we think there is still possibility the

company will declare stable/higher dividends. Assuming the company kept dividend

payouts above 25%, the expected dividend yield is about 2.5%.

Graph 17: Dividend Payout (RM sen) and Dividend Payout Ratio (%)

Source: Company, Inter-Pacific

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

05 06 07 08 09 10 11 12 13 14 15 (a/f) 16f

Magni Prolexus

9

8

9

13 13

15 15

20%

25%

30%

35%

40%

45%

50%

-

2

4

6

8

10

12

14

16

10 11 12 13 14 15 16f

DPS (Sen)

Payout Ratio (%)

Page 18 of 23

Magni-Tech Industries Bhd

Risk

Dependent on a single customer Magni is heavily dependent on the success of Nike

which accounts for 95% of apparel revenues, representing an outsized customer risk.

Losing Nike will negatively affect the company's future earnings. We think the risk is low

because SIG has a working relationship of at least 30 years with Nike. Any strain in the

company’s relationship with Nike could disrupt its entire apparel segment business

model. Besides, SIG previously bagged Nike's tier-1 status for woven manufacturers

worldwide. This history of long relationship and track record provides us some

consolation that an abrupt cessation is not probable anytime soon. In view of SIG’s

capability to develop and produce a wide range of product types ranging from basic to

highly technical seam sealed garments, Magni is confident that it would be able to

switch its operations to serve other customers such as Adidas, Fila, Puma and Reebok

whom they had working relationships with.

Unfavourable currency fluctuation The company's sales and purchases are mainly

quoted in USD. A 10% weakening in USD would affect bottom-line earnings (~5% to 7%

changes to PBT). The company uses forward foreign currency contracts to hedge USD

denominated sales.

Competitive risks With Nike continuing its strong growth performance, we believe

competition in the garments industry will intensify in 2016; apparel players will rush to

fill orders up their capacities, competing for the same orders/clients. They will therefore

have to defend their margins with higher production efficiencies (improving

output/hour). Magni also faces competition from new entrants to the industry,

particularly from other low-cost producers in China, India, Sri Lanka, Vietnam and

Bangladesh.

Page 19 of 23

Magni-Tech Industries Bhd

Management - Board of Directors

Executive Chairman Tan Sri Dato’ Seri Tan Kok Ping

Managing Director Tan Poay Seng

Executive Director Tan Kok Aun

Non-Independent Non-Executive Directors H’ng Cheok Seng

Tan Thiam Chai

Independent Non-Executive Directors Mawan Noor Aini Binti Md. Ismail

Tan Poh Heng

Alternate Director Chang Chuen Hwa

(Alternate Director to Tan Poay Seng)

Tan Sri Dato’ Seri Tan Kok Ping has more than 40 years of experience in various business

sectors which include property development, manufacturing of consumer electronics,

garment, corrugated and plastic packaging products. He also sits on the Board of a

subsidiary of Berjaya Land Bhd as well as in several private limited companies. He was

previously Managing Director and Deputy Chairman of Berjaya Sports Toto Bhd, Non-

Executive Chairman of Berjaya Retail Bhd, Chairman of Penang Joint Chambers of

Commerce and Deputy President of The Associated Chinese Chambers of Commerce and

Industry of Malaysia. He is the Executive Adviser and former President of Penang Chinese

Chamber of Commerce.

Mr Tan Poay Seng is the son of Tan Sri Dato’ Seri Tan Kok Ping and has been the Managing

Director of Magni-Tech Industries Bhd since 2000. He was Managing Director of Fila Sports

Malaysia S/B (which markets and retails sportswear in Malaysia) and also South Island

Garment S/B before that. He holds a Diploma in Hotel Management from Hotel Consult in

Switzerland.

Mr Tan Kok Aun, a mechanical engineering graduate of Trinity College, Ireland. He is

brother to Tan Sri Dato’ Seri Tan Kok Ping and pioneered South Island Packaging (Penang)

S/B after it was set up in 1973. He has 40 years of experience and knowledge in the printing

and packaging industry.

Mr H’ng Cheok Seng holds a professional membership of the Association of Chartered

Certified Accountants and held positions in multinational electronics & electrical and

garment companies prior to assuming a position with the Berjaya Group since 1997.

Page 20 of 23

Magni-Tech Industries Bhd

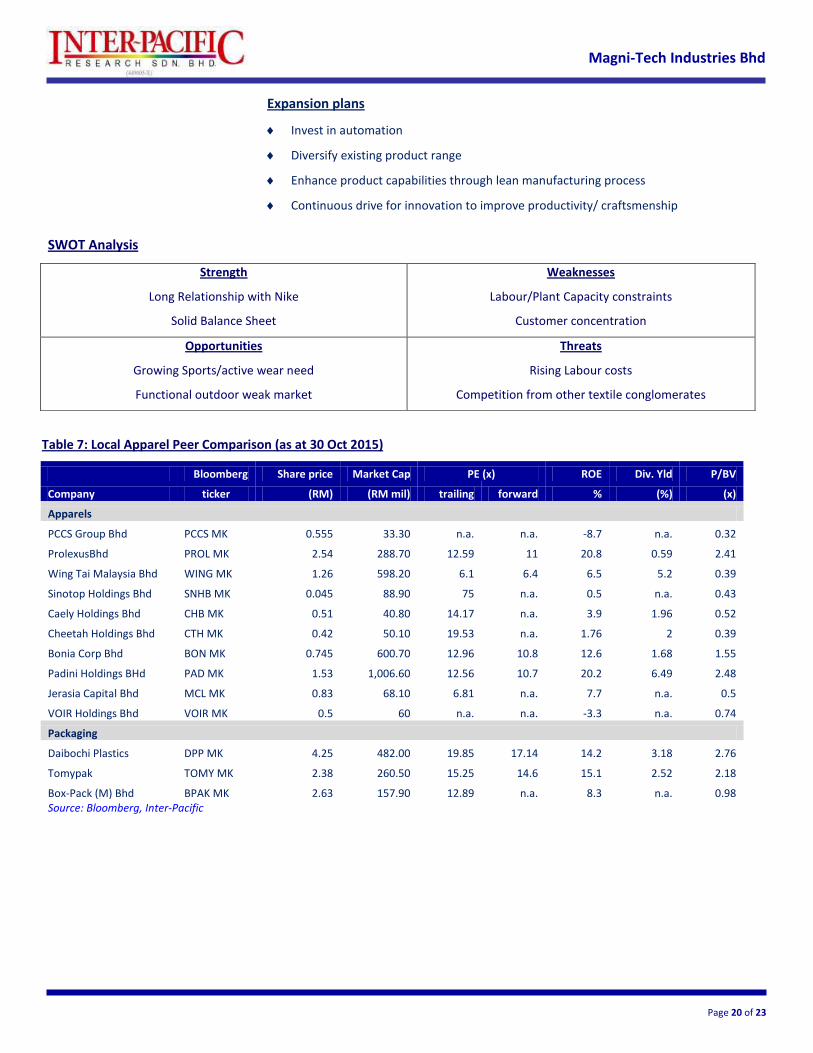

SWOT Analysis

Table 7: Local Apparel Peer Comparison (as at 30 Oct 2015)

Bloomberg Share price Market Cap PE (x) ROE Div. Yld P/BV

Company ticker (RM) (RM mil) trailing forward % (%) (x)

Apparels

PCCS Group Bhd PCCS MK 0.555 33.30 n.a. n.a. -8.7 n.a. 0.32

ProlexusBhd PROL MK 2.54 288.70 12.59 11 20.8 0.59 2.41

Wing Tai Malaysia Bhd WING MK 1.26 598.20 6.1 6.4 6.5 5.2 0.39

Sinotop Holdings Bhd SNHB MK 0.045 88.90 75 n.a. 0.5 n.a. 0.43

Caely Holdings Bhd CHB MK 0.51 40.80 14.17 n.a. 3.9 1.96 0.52

Cheetah Holdings Bhd CTH MK 0.42 50.10 19.53 n.a. 1.76 2 0.39

Bonia Corp Bhd BON MK 0.745 600.70 12.96 10.8 12.6 1.68 1.55

Padini Holdings BHd PAD MK 1.53 1,006.60 12.56 10.7 20.2 6.49 2.48

Jerasia Capital Bhd MCL MK 0.83 68.10 6.81 n.a. 7.7 n.a. 0.5

VOIR Holdings Bhd VOIR MK 0.5 60 n.a. n.a. -3.3 n.a. 0.74

Packaging

Daibochi Plastics DPP MK 4.25 482.00 19.85 17.14 14.2 3.18 2.76

Tomypak TOMY MK 2.38 260.50 15.25 14.6 15.1 2.52 2.18

Box-Pack (M) Bhd BPAK MK 2.63 157.90 12.89 n.a. 8.3 n.a. 0.98 Source: Bloomberg, Inter-Pacific

Strength

Long Relationship with Nike

Solid Balance Sheet

Weaknesses

Labour/Plant Capacity constraints

Customer concentration

Opportunities

Growing Sports/active wear need

Functional outdoor weak market

Threats

Rising Labour costs

Competition from other textile conglomerates

Expansion plans

Invest in automation

Diversify existing product range

Enhance product capabilities through lean manufacturing process

Continuous drive for innovation to improve productivity/ craftsmenship

Page 21 of 23

Magni-Tech Industries Bhd

Valuation

At fair valuation, Magni could be worth RM6.80 based on a sum-of-parts valuation.

Imputing 11x PE FY16 to its garments division which is similar to its our target multiples for

listed peer Prolexus' of 11x and pegging a 5x PE FY16 to its packaging division, which is

c.220% lower than the industry average of 16x due to its smaller contribution to Magni, a

fair value appears to be RM6.80 (ex-bonus price: RM4.53), we feel that current price level

will provide some 17.2% upside to the share price. In view of the strong CAGR and EBITDA

growth expectations, we believe that current valuations remain attractive despite the

recent price appreciation.

Graph 18: SOP waterfall graph (RM)

Source: Inter-Pacific

5.44 0.44

0.92 6.80

0

1

2

3

4

5

6

7

8

Garments Packaging Cash Per Share Target Price

Page 22 of 23

Magni-Tech Industries Bhd

Appendices Table 8: Nike apparel contract manufacturers in ASEAN region as at 30th Oct 2015

No. Country Company No. Country Company

1 THAILAND ADVANCED PRINTING (THAILAND) COMPANY LIMITED 53 MALAYSIA SONG LIN GARMENT SDN BHD

2 THAILAND ELTA COMPANY LIMITED 54 MALAYSIA SOUTH ISLAND GARMENT SDN. BHD. (MAGNI)

3 THAILAND FUTURE GARMENT CO., LTD 56 MALAYSIA TAI WAH GARMENTS INDUSTRY SDN BHD

8 THAILAND HI-TECH APPAREL CO. LTD.(SOI91) 56 MALAYSIA UNITED SWEETHEARTS GARMENT SDN BHD

11 THAILAND HONG SENG KNITTING COMPANY LIMITED. 57 VIETNAM ASIA GARMENT MANUFACTURER (VN)

13 THAILAND NAN YANG GARMENT CO., LTD. 58 VIETNAM MAXPORT GARMENT JOINT STOCK COMPANY

17 THAILAND NICE APPAREL CO., LTD. 62 VIETNAM CCH TOP (VN) CO., LTD.

19 THAILAND OPTECH CO., LTD. 63 VIETNAM CONG TIEN GARMENT JOINT STOCK COMPANY

20 THAILAND PILOTKNIT SPORT WEAR CO.,LTD. 64 VIETNAM E-TOP (VIETNAM) CO.,LTD

21 THAILAND RAJA UCHINO CO.,LTD. 65 VIETNAM ECLAT TEXTILE CO., LTD

22 THAILAND SHEICO (THAILAND) CO., LTD. 66 VIETNAM ESQUEL GARMENT MANUFACTURING (VIETNAM) CO., LTD

23 THAILAND VERTEX APPAREL CO., LTD. 67 VIETNAM FAR EASTERN APPAREL (VIETNAM) LIMITED

24 CAMBODIA SABRINA (CAMBODIA) GARMENT MANUFACTURING 68 VIETNAM FASHION GARMENTS LTD.

25 CAMBODIA SHEN ZHOU (CAMBODIA) CO., LTD 70 VIETNAM GREEN VINA

26 CAMBODIA TOP SUMMIT GARMENT INC. 71 VIETNAM HANSAE TG CO LTD

27 INDONESIA PRIMA SEJATI SEJAHTERA, PT 72 VIETNAM HANSAE VIET NAM CO., LTD.

28 INDONESIA PT DONG A DECAL 73 VIETNAM HONG SENG THAI-VINA CO., LTD.

29 INDONESIA PT EAGLE NICE INDONESIA 75 VIETNAM HUNG LONG GARMENT AND SERVICE JOINT STOCK COMPANY

30 INDONESIA PT GREENTEX INDONESIA UTAMA 76 VIETNAM I.S VIETNAM CO., LTD

31 INDONESIA PT KAHOINDAH CITRAGARMENT 77 VIETNAM LONG AN EXPORT GARMENT JOINT STOCK COMPANY (LASGE)

32 INDONESIA PT KUKDONG INTERNATIONAL 78 VIETNAM MAXPORT J.S.C

33 INDONESIA PT MITRA GARINDO PERKASA 79 VIETNAM NAM HA GARMENT JOINT STOCK COMPANY

34 INDONESIA PT MORICH INDO FASHION 80 VIETNAM NAM THIEN COMPANY LIMITED

35 INDONESIA PT PANCAPRIMA EKABROTHERS 81 VIETNAM ORIENTAL GARMENT AN GIANG CO LTD

36 INDONESIA PT PANTJATUNGGAL KNITTING MILL 83 VIETNAM QUANG VIET ENTERPRISE CO., LTD

37 INDONESIA PT R PRIMA JAYA 84 VIETNAM S.J VINA CORPORATION

38 INDONESIA PT SANDANG MUTIARA CEMERLANG 85 VIETNAM SAITEX INTERNATIONAL VIETNAM L.TD

39 INDONESIA PT SEMARANG GARMENT 87 VIETNAM SON KHA SCREEN PRINTING CO. LTD

40 INDONESIA PT TRIGOLDENSTAR WISESA 88 VIETNAM SPRING PRINTING CO LTD

41 INDONESIA PT TUNTEX GARMENT INDONESIA-CKP 89 VIETNAM TAGTIME VIET TIEN CO., LTD

42 INDONESIA PT TUNTEX GARMENT INDONESIA-TGR 90 VIETNAM THUAN PHUONG EMBROIDERIES & GARMENTS CO., LTD

43 INDONESIA PT YONGJIN JAVASUKA 91 VIETNAM TTG CO. LTD.

44 INDONESIA PT. CCH INDONESIA 92 VIETNAM UNIPAX CO., LTD

45 INDONESIA PT. GRAND BEST INDONESIA 93 VIETNAM UNITED SWEETHEARTS GARMENT (VIETNAM) CO., LTD.

46 INDONESIA PT. PILAR PUTERA SEJATI 94 VIETNAM VIET HONG GARMENT EXPORT CO., LTD.

47 MALAYSIA CHIT GUAN (BP) SDN BHD 95 VIETNAM VIET TIEN GARMENT CORPORATION

48 MALAYSIA GOLDEN VERTEX SDN BHD 96 VIETNAM VINH HUNG - JOINT VENTURE CO., LTD (TMI VIETNAM)

49 MALAYSIA HONSIN APPAREL SDN. BHD. ( PROLEXUS) 97 VIETNAM VINH TIEN GARMENT FACTORY

51 MALAYSIA LIKA SILKSCREEN 98 VIETNAM YUPOONG VIET NAM

52 MALAYSIA PLAS INDUSTRIES SDN BHD

Source: Nike

Page 23 of 23

Magni-Tech Industries Bhd

IMPORTANT: This report has been prepared from sources that are believed to be reliable but we do not hold ourselves responsible for its completeness and accuracy. All opinions and estimates in this report are subject to change without notice. We do not accept any liability that may arise from the use of information in this report. Inter-Pacific Research SdnBhd and or its associates may from time to time have interest and/or underwriting commitments in the company being reported. This report is for internal circulation only and the contents or any part thereof cannot be reproduced in any manner whatsoever except with the prior written consent of Inter-Pacific Research Sdn Bhd.

Published and Printed by:

Inter-Pacific Research Sdn Bhd (449005-X)

West Wing, Level 13,

Berjaya Times Square,

No.1, Jalan Imbi,

55100 Kuala Lumpur

General Line : 03-2117 1888 Fax : 03-2142 7678

Ratings System

Ratings: Description:

BUY Total return is expected to exceed 15% in the next 12 months NEUTRAL Total return is expected to be between above –15% to 15% in the next 12 months SELL Total return is expected to be below -15% in the next 12 months

Abbreviation

Abbreviation Definition Abbreviation Definition

PER Price Earnings Ratio CAGR Compounded Annual Growth Rate PEG PER to Growth CAPEX Capital Expenditure EPS Earnings per Share DPS Dividend per Share FYE Financial Year End ROA Return on Asset FY Financial Year ROE Return on Equity CY Calendar Year PBT Profit Before Tax MoM Month-on-Month PAT Profit After Tax QoQ Quarter-on-Quarter EV Enterprise Value YoY Year-on-Year EBIT Earnings Before Interest And Tax YTD Year-to-Date EBITDA EBIT Depreciation &Amortisation p.a. Per Annum WACC Weighted Average Cost of Capital DCF Discounted Cash Flow NTA Net Tangible Asset FCF Free Cash Flow BV Book Value NAV Net Asset Value

Ratings System

Ratings: Description:

BUY Total return is expected to exceed 15% in the next 12 months NEUTRAL Total return is expected to be between above –15% to 15% in the next 12 months SELL Total return is expected to be below -15% in the next 12 months

Abbreviation

Abbreviation Definition Abbreviation Definition

PER Price Earnings Ratio CAGR Compounded Annual Growth Rate PEG PER to Growth CAPEX Capital Expenditure EPS Earnings per Share DPS Dividend per Share FYE Financial Year End ROA Return on Asset FY Financial Year ROE Return on Equity CY Calendar Year PBT Profit Before Tax MoM Month-on-Month PAT Profit After Tax QoQ Quarter-on-Quarter EV Enterprise Value YoY Year-on-Year EBIT Earnings Before Interest And Tax YTD Year-to-Date EBITDA EBIT Depreciation &Amortisation p.a. Per Annum WACC Weighted Average Cost of Capital DCF Discounted Cash Flow NTA Net Tangible Asset FCF Free Cash Flow BV Book Value NAV Net Asset Value

Copyright © 2022 FDOKUMEN