White Knights or Machiavellians? Understanding the ...

25

1 White Knights or Machiavellians? Understanding the motivation for reverse takeovers in Singapore and Thailand Pantisa Pavabutr 1 Thammasat University This draft: October 2017 Abstract We analyze the characteristics, return, and financial performance of 47 RTO sample firms in Singapore and Thailand between 2007‐2015. Given the existing regulatory screens imposed by Singapore and Thai exchanges, we cannot find evidence that firms choosing to list via RTOs signals a separating equilibrium of low type firms seeking a listing short‐cut. We argue that RTOs should not be evaluated as a choice of listing per se, but as part of the parcel of long‐term corporate strategy. Analysis in this paper yields important in sights on reverse takeovers from both investor and regulator perspectives. JEL Classification: G14, G34. Keywords: Reverse takeovers, Back‐door listings, Emerging markets. 1. Introduction Equity markets have both an allocation and monitoring role. The challenge for regulators is striking a delicate balance between overseeing transparency and fair rules governing listings for efficient allocation of resources and investor protection without delineating potential firms from entering organized exchanges. The dual paths to listing can be direct through an initial public offering (IPO) or indirect through a reversed takeover (RTO). An IPO is traditionally seen as a young company with full listing qualification coming of age and offering shares to the public. A reversed takeover is the process whereby a private company acquires a controlling stake in a public company in order to obtain listing status. In doing so, RTOs allows private firms to list and seek out growth opportunities by merging with public firms and to seek listing without too much dilution and vulnerability to market conditions. However, anecdotal and some selected empirical evidence suggests a dark side to RTOs as they are often referred to as “back‐door listings” with transactions associated with opaque firms wanting to bypass stringent listing rules or a method in which is a holding company of the shell firm tries to get rid of non‐performing assets by passing it along to the next uninformed investor. Under this setting, there are two issues where reversed takeovers are subject to debate. First, should reverse takeovers be allowed or should regulations be tightened? The second issue, is why should firms choose RTOs instead of IPOs? The drawbacks of RTOs is that their speed and cost saving benefits are often overestimated in particular with on‐going trends towards more regulatory scrutiny 1 Associate Professor of Finance, Thammasat Business School, [email protected]. The author wishes to thank the National Research Council, and Thailand Research Fund for grant support. The author appreciates research assistance from Sippapon Ithiprachayaboon, Prasit Sutthikamolsakul, and Nina Taphunwong. Comments welcomed.

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of White Knights or Machiavellians? Understanding the ...

1

White Knights or Machiavellians? Understanding the

motivation for reverse takeovers in Singapore and Thailand

Pantisa Pavabutr1

Thammasat University

This draft: October 2017

Abstract

We analyze the characteristics, return, and financial performance of 47 RTO sample firms in Singapore

and Thailand between 2007‐2015. Given the existing regulatory screens imposed by Singapore and Thai

exchanges, we cannot find evidence that firms choosing to list via RTOs signals a separating equilibrium

of low type firms seeking a listing short‐cut. We argue that RTOs should not be evaluated as a choice of

listing per se, but as part of the parcel of long‐term corporate strategy. Analysis in this paper yields

important in sights on reverse takeovers from both investor and regulator perspectives.

JEL Classification: G14, G34.

Keywords: Reverse takeovers, Back‐door listings, Emerging markets.

1. Introduction

Equity markets have both an allocation and monitoring role. The challenge for regulators is

striking a delicate balance between overseeing transparency and fair rules governing listings for efficient

allocation of resources and investor protection without delineating potential firms from entering

organized exchanges. The dual paths to listing can be direct through an initial public offering (IPO) or

indirect through a reversed takeover (RTO). An IPO is traditionally seen as a young company with full

listing qualification coming of age and offering shares to the public. A reversed takeover is the process

whereby a private company acquires a controlling stake in a public company in order to obtain listing

status. In doing so, RTOs allows private firms to list and seek out growth opportunities by merging with

public firms and to seek listing without too much dilution and vulnerability to market conditions.

However, anecdotal and some selected empirical evidence suggests a dark side to RTOs as they are

often referred to as “back‐door listings” with transactions associated with opaque firms wanting to

bypass stringent listing rules or a method in which is a holding company of the shell firm tries to get rid

of non‐performing assets by passing it along to the next uninformed investor.

Under this setting, there are two issues where reversed takeovers are subject to debate. First,

should reverse takeovers be allowed or should regulations be tightened? The second issue, is why

should firms choose RTOs instead of IPOs? The drawbacks of RTOs is that their speed and cost saving

benefits are often overestimated in particular with on‐going trends towards more regulatory scrutiny

1 Associate Professor of Finance, Thammasat Business School, [email protected]. The author wishes to thank the National Research Council, and Thailand Research Fund for grant support. The author appreciates research assistance from Sippapon Ithiprachayaboon, Prasit Sutthikamolsakul, and Nina Taphunwong. Comments welcomed.

2

pertaining RTOs in equity markets around the world (Sjostrom, 2008; Vermeulen , 2014). Pavkov (2006)

suggests that a complete analysis of benefits and costs of RTOs should include all stakeholders involved.

Our study contributes to the almost non‐existing research on RTOs in ASEAN. Using 47 RTO

sample firms in Singapore and Thailand between 2007‐2015, this paper addresses the above questions

through discussion of existing listing regulations on RTOs and empirical analysis return and financial

accounting performance. More specifically, it first briefly reviews existing regulations in Singapore and

Thailand whether they are conducive for firms to list by RTOs rather than by IPOs. Second, it empirically

analyzes the RTO samples by posing these questions 1), What are the characteristics of RTOs

transactions? 2) What is the investors’ experience in RTO transactions over short and long‐term periods,

and 3) What is the financial accounting performance of merged entity.

The paper finds that given the existing regulatory screens imposed by Singapore and Thai

exchanges, we cannot find evidence that firms choosing to list via RTOs signals a separating equilibrium

of low type firms seeking a short‐cut to listing. This is because both exchanges require the newly merged

entity to file a reapplication and comply with the same minimum standards as IPO listings. From

company circulars and financial advisors report of sample firms, the number of days to completing the

RTO transaction can be up to one year. In fact, about half of the RTO samples involve listing on the main

boards of Singapore Stock Exchange (SGX) and Stock Exchange of Thailand (SET); the other half on the

second boards of Catalist (CAT), and Market for Alternative Investment (MAI). If a RTO is a venue for

easy listing, then surely more transactions would have occurred on secondary boards where listing

requirement is more flexible, in particular on CAT. Second, after examining the characteristics of sample

RTO deals, we find 32 firms or 68% of the sample firms are classified by the auditor as financially

distressed, and approximately half of the transactions occur across firms with different industries. This

implies that outsider firms intend to takeover a “shell” or non‐performing firm in an unrelated industry.

Next, we examine the investor’s experience by measuring short‐term abnormal returns around RTO

announcements and long‐term 12 months return post‐announcement. The cumulative abnormal return

(CAR) of distressed firm RTOs during event window [‐10,10] around RTO announcement (MOU date), is

28.8% significantly higher than 8.4% of non‐distressed firms. Over a holding period of 12 months in

which the buy‐and‐hold abnormal return (BHAR) is evaluated, much of the original short‐term gain

reverted primarily because of continuing capital increases. Even so, the mean BHAR of RTO samples are

higher than the mean BHAR of control firm sample. Looking at financial performance, distressed firms’

net profit margins and return on assets improved after RTO completion, but non‐distressed firm

performance remains relatively superior to distressed ones.

In sum, in our analysis of short‐term and long term return performance we do not find evidence

that our sample RTOs transactions are causing market instability through fraud and pump‐and‐dump

schemes. If the ease of listing is not a reason for choosing RTO, then why do firms engage in these

transactions? From our analysis, we view that RTOs should not be perceived as a listing tool alone but

part of the parcel of long‐term corporate strategies where (i) the private firm can become a public

company without immediate large dilution in ownership and still have an option to raise more funds

later (many RTO transactions have warrant issue plans contingent on successful restructuring plans

post‐transaction); (ii) the private firm wishes to takeover a distressed or non‐distressed target public

firm by obtaining a bargain price since the target is substantially smaller and trading at a value weighted

average price (VWAP) in the bottom decile trading range of the exchanges; (iii) the public firm

controlling shareholders wishes to exit and is offered an attractive price to the private firm. RTO

3

transactions do provide a more liquid trading environment which facilitates exit, and iv), the motivation

could be unique to the firms themselves. 2

There are altogether five sections in this paper. Section 2 provides background discussions on

RTOs including deal structure, regulations, and related literature. Section 3 describes the sample data

and describes key features of RTO transactions. In section 4, both descriptive and empirical methods

are used to analyze the motivation for RTOs. Finally, section 5 concludes and discuss policy

implications for capital market development.

2. Background on RTOs

2.1 Deal structure

In a typical RTO the private company acquires a controlling stake in a public company in order

to obtain listing status by allowing the listed firm to acquire its assets or equity and in return receive

issued shares of the listed company.

Figure 1: Illustration of reverse takeover

Before transaction

After transaction

2 We also expect that by acquiring a loss‐making public firm, the private firm gains from tax shield.

However, we do not have unconsolidated financial statements of private firms to evaluate this conjecture. In Singapore’s case, some foreign outsider firms are already listed overseas, but explain that they prefer to list on

the Singapore exchanges to increase their international profile in Asian markets. With RTOs they do not need to

pay underwriting fees. Other outsider firms conduct RTOs as a short‐cut to international diversification (Perrenial

China Retail Trust transaction with St. James Holding) or a short‐cut to business diversification (Singha Estate

transaction with Rasa Property on SET).

Shareholders of

listed firm

Listed firm

Shareholders of

private firm

Private firm

Transfer assets

Cash transfer, private

placement or share swap

Shareholders of

listed firm

Merged firm

Shareholders of

private firm

(with more than

50% control)

4

Figure 1 illustrates the reverse takeover process. In exchange for assets transfer of private firm,

the listed firm may choose from one or combination of payment in cash, new shares issue through

private placement, borrow, or issue new shares to swap with private firm. In a RTO, the listed firm is

often referred to as a shell firm if it has the following properties: (a) no or nominal operations; and (b)

either: (1) no or nominal assets; (2) assets consisting solely of cash and cash equivalents; or (3) assets

consisting of any amount of cash and cash equivalents and nominal other assets.

Not all firms in our Singapore and Thai samples start out as “shell” firms; however, in the reverse

takeover process they can become one by liquidating their businesses or by agreeing to spin off its

current assets and liabilities at the time of the reverse merger. Some listed firms are profitable but are

struggling with poor business growth opportunities and seek reverse merger partners to strengthen

their industry positions through diversification and synergy.

Figure 2: Controlling structure in reverse take‐overs

Figure 2 shows a reverse take‐over between a public shell firm valued at $600,000 with share

priced at $0.1 and 6 million old shares outstanding and a private firm valued at $10 mn with 50 mn

shares outstanding at $0.2 per share. The financial advisor expects the merged entity to require $2mn

addition funds for restructuring process and issues 10 mn shares at $0.2 as private placement. Assume

for simplicity the combined firm value is estimated to remain at $0.2 per share (post‐consolidation issue

price). The public shell shareholders are offered pre‐consolidation issue price of $0.1 per share and then

Merged firm

Combined value $12.6 mn (63 mn

shares x $0.2

Private firm

value $ 10 mn

(50 mn shares

x $0.2)

Public firm

value $ 0.6

mn (3 mn new

shares x $0.2)

Private

placement $

2 mn (10 mn

shares x $0.2)

Value $

mn

No of

shares % Own

Private firm

shareholders 10 50 79%

Private

placement 2 10 16%

Public firm

shareholders 0.6 3 5%

12.6 63 100%

1:1 2:1

5

given share swap at a rate of 2 to 1 such deriving a post‐consolidated issue price3 of $0.2 per share and

that their original ownership value is set at $600,000. As a result, the new combined value of the firm

is $12.6 mn with private firm owners accounting for 79% (50/63) of merged firm control whereas private

investors account for 16% (10/63) and public shell shareholders account for 5% (3/63).

2.2 Reverse takeover regulations and process

An RTO is perceived as a “short‐cut” for a private (outsider) firm to achieve listing status and

bypass the lengthy process of an IPO and hence often referred to as “backdoor listing.” We discuss the

legal of definition of RTO and compare and contrast the IPO and RTO process next.

Both Singapore and Thai Exchanges apply bright line tests for two specific types of RTOs which

are transactions involving a change in control of a listed issuer and a very substantial acquisition (VSA).4

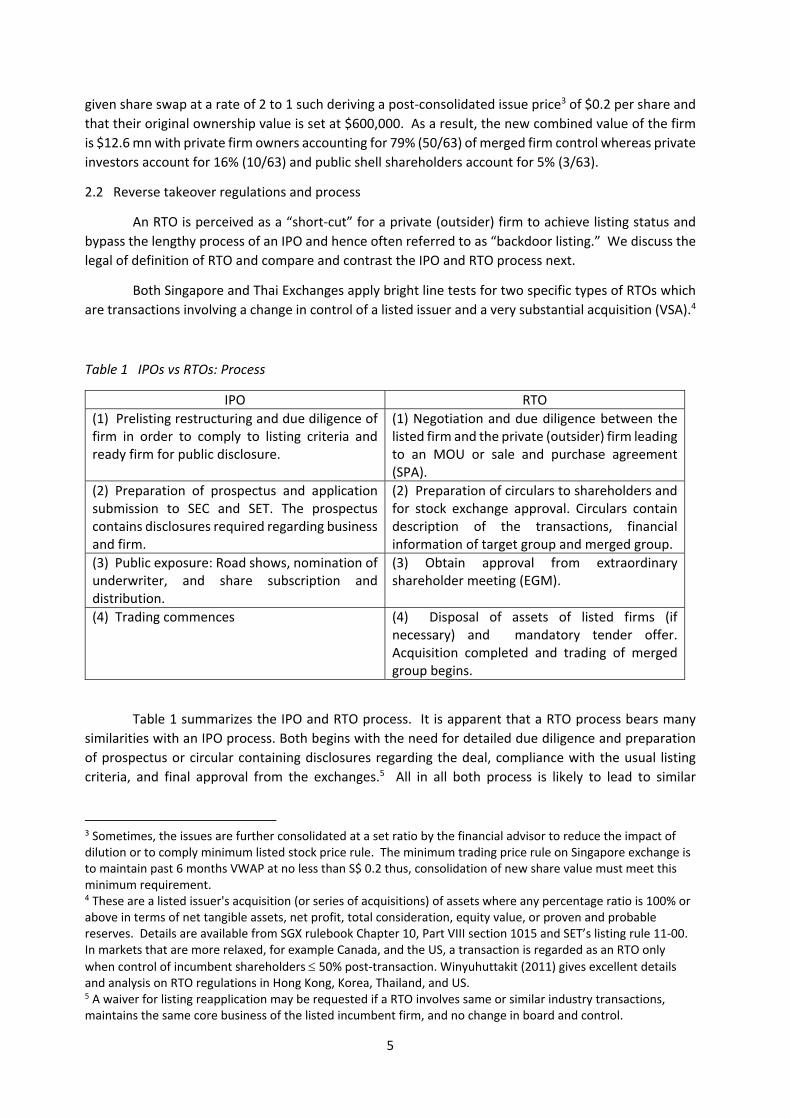

Table 1 IPOs vs RTOs: Process

IPO RTO

(1) Prelisting restructuring and due diligence of firm in order to comply to listing criteria and ready firm for public disclosure.

(1) Negotiation and due diligence between the listed firm and the private (outsider) firm leading to an MOU or sale and purchase agreement (SPA).

(2) Preparation of prospectus and application submission to SEC and SET. The prospectus contains disclosures required regarding business and firm.

(2) Preparation of circulars to shareholders and for stock exchange approval. Circulars contain description of the transactions, financial information of target group and merged group.

(3) Public exposure: Road shows, nomination of underwriter, and share subscription and distribution.

(3) Obtain approval from extraordinary shareholder meeting (EGM).

(4) Trading commences (4) Disposal of assets of listed firms (if necessary) and mandatory tender offer. Acquisition completed and trading of merged group begins.

Table 1 summarizes the IPO and RTO process. It is apparent that a RTO process bears many

similarities with an IPO process. Both begins with the need for detailed due diligence and preparation

of prospectus or circular containing disclosures regarding the deal, compliance with the usual listing

criteria, and final approval from the exchanges.5 All in all both process is likely to lead to similar

3 Sometimes, the issues are further consolidated at a set ratio by the financial advisor to reduce the impact of dilution or to comply minimum listed stock price rule. The minimum trading price rule on Singapore exchange is to maintain past 6 months VWAP at no less than S$ 0.2 thus, consolidation of new share value must meet this minimum requirement. 4 These are a listed issuer's acquisition (or series of acquisitions) of assets where any percentage ratio is 100% or above in terms of net tangible assets, net profit, total consideration, equity value, or proven and probable reserves. Details are available from SGX rulebook Chapter 10, Part VIII section 1015 and SET’s listing rule 11‐00. In markets that are more relaxed, for example Canada, and the US, a transaction is regarded as an RTO only

when control of incumbent shareholders 50% post‐transaction. Winyuhuttakit (2011) gives excellent details and analysis on RTO regulations in Hong Kong, Korea, Thailand, and US. 5 A waiver for listing reapplication may be requested if a RTO involves same or similar industry transactions, maintains the same core business of the listed incumbent firm, and no change in board and control.

6

timeframe to completion. However, dating the length of time required for the RTO process is not

straightforward as Table 1 may suggest.

A RTO transaction can be complicated further with more parties involved. As a matter of fact, it

begins with negotiation and due diligence process both public and private firms potentially adding time

and cost to the transaction and represents and “double‐lemons” problem. Once the terms and price are

agreed, upon board approval, a memorandum of understanding (MOU) is signed. The terms in the MOU

are disclosed to the exchange for reapplication of the merged entity for listing. Then after the parties

received the go ahead from the exchange, an extraordinary shareholder meeting (EGM) is called

requiring a super majority support. The merger can then legally begin as consolidated trading of shares

can start and hence the shares of the new entity can take on new value from that point.

With the process described above, we can say that there are two important event dates in the

process, the MOU date, which contains most information impact, and the EGM date that marks the

beginning of consolidated trading of shares of the merged entity. However, the true completion of the

acquisition can be lengthened as the merged firm may continue to carry separate share placement

exercise to meet capital needs or listing requirements on free float.

2.3 Related literature

RTOs have been used as an alternative means to list on an exchange for decades. Historically,

no significant regulatory review was required resulting in a shorter timeframe for listing completion and

substantial costs saved in terms of underwriting fees as the process requires neither a prospectus nor

an underwriter. In addition, timing of RTOs are not subject to market conditions as in IPOs. New

controlling owners of the firm generally suffer less share dilution, obtain the public firm at a relatively

economic price as opposed to regular mergers as well as an option to raise funds in the future.

Incumbent shareholders of the public firm benefit from a clearly defined exit strategy through the public

market.

Given a history of flexible regulatory environment, early research on RTOs tend to suggest a

separating equilibrium where high quality firms choose listing via IPOs and low quality firms choose

listing via RTOs. In Arellano‐Ostoa and Brusco (2002), a high type firm, distinguished by greater

probability of obtaining positive NPV projects, choose to signal with IPO whereas low quality firm with

low probability of positive NPV projects choose RTOs. The necessary conditions for a separating

equilibrium in the model is that the expected NPV of the high type firm is greater than that of the low

type firm and that the cost of completing IPO is higher than completing RTOs. A number of empirical

papers mainly based on US evidence support a separating equilibrium in listing choice as they find firms

choosing to list via RTOs instead of regular IPOs tend to be smaller firms with relatively higher level of

information asymmetry. Gleason et al. (2005) studies 121 RTO cases between 1987‐2001 AMEX, NYSE,

NASDAQ and find that they tend to be speculative in nature and fail to generate long‐term wealth gains.

In their sample, 46% RTO firms survived after first two years of listing. Using a slightly different period

on US market between 1990‐2002, Adjei, Cyree, and Walker (2005) document 42% of their sample firms

become delisted in first three years. Floros and Shastri (2009) find that firms choosing to list via RTOs

instead of regular IPOs tend to be smaller firms with relatively higher level of information asymmetry.

Thus, the authors view that RTOs cannot be compared to regular IPOs but rather to penny stocks IPOs.

Floros and Sapp (2011) focuses on valuation of shell firms traded on OTC or pink‐sheets that go through

RTOs. They find up to 48% in abnormal return in RTO announcements, but the long term performance

erases the gains as surviving firms earn post‐even annual return of ‐91%. The Canadian experience

7

with RTOs is similar as Carpentier, Cumming, and Suret (2009) documented lower quality firms opt for

the less regulated RTOs to obtain public listing . Wan‐Hussin (2002) documents the case of high profile

reverse take‐over completed in 1995 in Malaysia that resulted in a backdoor listing of a private

company, Jaya Tiasa Plywood, via listed Berjaya Textiles. The author finds increase wealth effects of

both minority shareholders and the former controlling shareholders. However, the work is limited to

one particular case and only short‐term wealth effects were documented.

Absence of early regulatory oversight has led to abuses and fraudulent conduct leading to

tightened RTO regulations. In US, increased reports of fraudulent activities in late 2000s has prompted

SEC to apply more stringent listing rules to list publicly. These additional requirements include minimum

share price maintenance, complying to filing requirements of financial reports, and a seasoning rule that

requires the merged entity to trade on OTC prior to official listing. Following fraudulent cases of Chinese

firms backdoor listing, the Hong Kong Exchange introduce the Main Board RTO Rules in March 2004

which virtually eliminated the practice of injecting non‐listed assets without a suitable track record for

listing into a listed shell in conjunction with a change of control. 6

Is the verdict out on RTOs? A look at RTO critique from legal and regulatory point of view offer

other perspectives. Pavkov (2006) encourages more empirical analysis of RTOs to help settle the policy

debate whether more regulatory intervention is necessary. Vermeulen (2014), notes that in recent

years, there is a dramatic increase in RTOs on ASEAN exchanges. Existing work on RTOs are primarily

limited to the US experience and cannot be comparable to the ASEAN experience where demand‐supply

and regulatory environments are very different. For example, the Canada and the US applied a laissez‐

faire approach towards RTOs in the past in order to support small and micro‐cap companies who were

unlikely to be able to afford the underwriter necessary for an IPO.

Singapore and Thailand on the other hand adopt a more conservative approach towards

regulating such that firms that undergo RTOs must undergo reapplication process to list on the exchange

and must meet the same minimum listing requirement as IPO firms. This means that the cost of

conducting RTOs in Singapore and Thailand is likely to be quite high. Although the direct costs of

underwriting fees present in regular IPOs is absent in RTOs, private firms engaging in such transactions

face numerous indirect costs. For example, the risk of overpaying for the shell firm if the financial

advisors’ place the value of the shell firm too high. There is also cost of restructuring the shell firm and

the risk that synergy value of the merged entity in a vertical or horizontal merger within firms of the

same industry does not materialize. Sjotrom (2008) argues that the costs of RTOs is underestimated,

after factoring in indirect costs, he finds that actual costs of IPOs and RTOs are in fact not that much

different. In the case of Singapore and Thailand, the reapplication requirement and disclosure effort

means that the speed advantage is unlikely to be that great. Thus, if the regulatory costs and indirect

costs are high, then why do firms still choose to go public with RTOs? Hsieh, Lyandres, and Zhdanov

(2009) propose a model that link’s a firm’s decision to go public with subsequent takeover strategy.

Completing an IPO reduces valuation uncertainty leading to a more efficient acquisition strategy.

6 See Rules on Backdoor Listings: a Global Survey, OECD, December 2014 and Charltons Solicitors, www.chartonslaw.com.

8

3. Sample Data Analysis

Between 2007‐2015, we identify RTO cases from stock exchange and SEC websites. A list of

Singapore RTO cases can be found of SGX website under the “Catalodge” page where important firm

disclosure information is publicized. Thai RTO cases can be tracked from SEC’s website where tender

offers, material asset acquisitions and disposals of listed firms are reported. 7 Details of individual RTO

deals are gathered from a combination of financial advisor reports and minutes of shareholders

meeting. We collect a total of 42 RTO cases in Singapore and 17 cases in Thailand. We find that ten

RTO transactions of the 42 in Singapore were aborted whereas two transactions of 17 were unsuccessful

in Thailand. The search is biased towards successful cases as information is more readily accessible.

Data is collected from various sources. We obtain market trading data from Datastream and

listed company accounting information from Worldscope. Our sample includes firms listed on both the

main and secondary boards in which case it is the Singapore Exchange (SGX) and Catalist (CAT) for the

Singapore sample and Stock Exchange of Thailand (SET) and Market for Alternative Investment (MAI)

for the Thai sample.

Table 2 Distribution of RTO activities 2007‐2015

The RTO sample reports the distribution of RTO activities announced by Singapore and Thailand

exchanges. This table report the RTO activities and the proportion of transactions along side with SGX

and SET year end index level and annual return. The sample includes firms on the main boards (SGX and

SET) and secondary boards (CAT and MAI).

Year No of firms

% of

sample Market index

Market return

All Singapore Thailand All Singapore Thailand Singapore Thailand

2007 1 0 1 2%

3,466

858 19% 26%

2008 1 1 0 2%

1,762

450 ‐49% ‐48%

2009 3 1 2 5%

2,898

735 64% 63%

2010 10 8 2 17%

3,190

1,033 10% 41%

2011 6 5 1 10%

2,646

1,025 ‐17% ‐1%

2012 10 8 2 17%

3,167

1,392 20% 36%

2013 16 13 3 27%

3,167

1,299 0% ‐7%

2014 10 4 6 17%

3,365

1,498 6% 15%

2015 2 2 0 3%

2,883

1,288 ‐14% ‐14%

Total 59 42 17 100%

7 http://infopub.sgx.com and https://www.set.or.th/set publishes Singaporean and Thai listed firms’ important announcements and circulars. Day of MOU of VSA appears here, where MOU date is unavailable we use date when first circular is publicly available from firms’ website or news sources.

9

Table 2 presents descriptive statistics for the sample RTO transactions in Singapore and Thailand

by sample year. The number of RTO activities for Singapore is highest in 2013 with 13 transactions

whereas for Thailand it is highest in 2014 with six transactions. The last four columns of Table 2 provide

end of year market index level and annual market return. There seems to be no apparent association

between market performance and intensity of RTO activities in Singapore. For example, in 2009 when

the annual market return on SGX surged by 64% only one RTO transactions came through. In the

following years 2010‐2011 when the market rose 10% and dropped 17% the number of transactions

was eight and five respectively. In Thailand’s case, RTO transactions appear to pick up when market

performance improves. As shown in 2014, the SET gained 15% following a 7% loss in 2013. The number

of reported transactions increased from three to six between 2013‐2014.8

Table 3 reports successful deal firm statistics which are segmented by country of listing and

then by distress or non‐distress status. Where relevant we report both average values and median

values in parentheses below. There are a total of 47 successful cases of which 32 are listings on

Singapore exchange and 15 on the Thai exchange. Approximately half of the entire sample firms (51%)

are declared financially distressed by the listed firm’s auditors. Data of the two markets combined

shows that RTO transactions are quite evenly split between main and secondary boards and between

transactions that occur within the same industry and across industries. Singapore sample firms are

slightly in favor of secondary board transactions (56% of all Singapore RTOs) and cross industry

transactions (also 56% of all Singapore RTOs). However, looking closely at the sample, only 10 out of

18 transactions on CAT are between cross industry firms.

8 Rank correlation between number of RTO transactions and market performance for Singapore and Thailand is 0.02 and 0.58, respectively.

10

Table 3 Characteristics of RTOs

The sample consists of 59 sample RTOs firms of which only 47 are successful cases and used in further

empirical analysis. The statistics reported in Table 3 are for success RTOs only. Deal value is in millions

of local currency (LCY). Relative deal size is computed from deal size divided by listed firms’ assets in

pre‐MOU year. Premium is pre‐consolidation issue price relative to 3‐month pre‐MOU value weighted

average closing price (VWAP) of listed firm. A foreign counter party is defined as a counter party firm

outside the listing sample that is incorporated or listed overseas. The table reports both mean and

median values. Median values where applicable are shown in parentheses. A firm is categorized as

financially distressed if the listed firms’ auditors report says so.

Singapore Thailand

Characteristics: All Distress Non‐

distress P‐value diff All Distress

Non‐distress

P‐value diff

Main board 14 9 5 8 6 2

% Main Board 44% 28% 16% 53% 40% 13%

Secondary 18 13 5 7 4 3

% Secondary 56% 41% 16% 47% 27% 20%

Same industry 14 7 7 8 3 5

Different industry 18 15 3 7 5 2

% Different industry 56% 47% 9% 47% 33% 13%

Deal value (LCY mn) 279 324 151 0.124 2,701 1,185 4,349 0.063

(141) (150) (35.6) 0.086 (1,725) (763) (3,187) 0.032

Relative size 12.17 14.6 5.61 0.213 7.36 7.98 5.48 0.390

(1.96) (2.49) (0.58) 0.079 (6.15) (8.55) (2.97) 0.224

Premium* 42% 35.7% 9.3% 0.517 149% 13.8% ‐15.5% 0.325

(‐6.9%) (11.2%) (‐14.1%) 0.432 (‐7.1%) (‐2.1%) (‐12.7%) 0.245

VWAP (LCY) 0.12 0.08 0.19 0.017 7.86 3.69 9.66 0.396

(0.09) (0.05) (0.15) 0.0008 (1.87) (1.75) (2.00) 0.648Days from MOU to EGM 260 222 79 65 Day from MOU to completion 321 371 217 88

Stock swap 22 15 7 5 4 1

%Stock swap 69% 47% 22% 33% 27% 7% Stock swap with cash/warrants 10 7 3 10 4 6 %Stock swap with cash/warrants 31% 22% 9% 67% 27% 40% Foreign counter‐party 18 15 3 None None None

% Foreign 56% 47% 9% %EPS growth 3 year pre‐MOU 111% ‐153.1% ‐83.6% 0.542 ‐176% ‐237.3% ‐154.3% 0.463

(‐79.7%) (‐86.1%) (‐52.4%) 0.075 (‐92%) (‐

232.5%) (‐91.7%) 0.648%Rev growth 3 year pre‐MOU ‐7.4% ‐11.6% 1.2% 0.433 ‐33.1% ‐46.5% ‐16.2% 0.171

(‐14.19%) (‐31.5%) (0.03%) 0.086 (‐30.5%) (‐

30.5%) (‐17.4%) 0.196

11

Note: Two outliers are removed from Singapore and Thai sample; namely Kyodo Allied Industries which was offered a tender

price four times its VWAP; and E for L which was offered a tender price of THB 25 compared to VWAP of only THB 1.54.

There are some notable commonalities between the characteristics of Singaporean and Thai

RTOs. First, the relative deal size computed from deal size divided by listed firms’ assets in pre‐MOU

year is larger for distressed samples both Singapore and Thai where the ratios are 14.6 and 7.98 times,

respectively. Relative deal size ratios for non‐distressed Singapore and Thai samples are 5.61 and 5.48.

We note that deal value in local currency terms of distressed firms are higher than non‐distressed in

Singapore transactions, but the reverse is true in Thai samples. In any case, we view that the relative

deal size is more important in understanding the bargaining power that outsider firms is likely to have

over distressed firms. Second, we note that distressed firm’s premiums are relatively higher than non‐

distressed firms. We define premium as the percentage difference between pre‐consolidation issue

price and 3‐month pre‐MOU value weighted average closing price (VWAP) of listed firm. In Singapore

RTOs, premiums of distressed firms are 35.7% compared to 9.3% of non‐distressed firms. In Thai RTOs,

non‐distressed firms are offered an average of 15% discount their historical VWAP.9 Third, we find that

distressed firms have substantially lower average 3‐year pre‐MOU EPS growth rates as well as

considerably lower average 3‐year pre‐MOU revenue growth. However, in general neither groups in

RTOs samples are doing well in both profitability and revenue generation prospects. For example, in

the Singapore distressed and non‐distressed groups, the %EPS growth is ‐153% and ‐84%; whereas the

% revenue growth is ‐11.6% and 1.2%. Fourth, we report two date intervals; time in days from MOU

date to EGM, and time in days from MOU to completion of capital raising. We focus on days from MOU

to EGM which usually marks the consolidated trading of shares of the merged entity. Usually, this takes

on average a little over six months or over 200 days for Singapore samples but around two to three

months for Thai samples. For some transactions that requires sizable capital raising, the entire process

takes up to six months to about one year. Thus, it is clear that RTOs are not exactly a short‐cut in terms

of time requirement to list and raise the necessary capital compared to IPOs.

There are also some differences between Singapore and Thai RTO samples in terms of outsider

firms of foreign origin and method of payment. From Table 3, more than half of RTO counter parties

on the Singapore exchange have foreign origin (incorporated outside Singapore). Some of these foreign

firms are located in off‐shore tax havens like British Virgin Islands, however, some are established and

even already listed overseas firms.

Based on the characteristics of the data observed, we offer a few analytical points about RTOs.

First, unlike what the popular press may suggest, it appears that RTOs are not short‐cuts to getting listed

given the length of time to completion. Neither are outsider firms small and of poor quality otherwise

the transaction would not have passed the re‐listing requirements of the exchange and the bulk of the

transactions would have occurred on secondary boards in particular given Singapore’s listing flexibility

on CAT which does not require a minimum market capitalization or profit history as long as there is

listing sponsor supporting the firm. Second, some foreign outsider firms prefer to list on the Singapore

exchange to increase its international footprint in Asian markets. For example, the Chaswood Group is

a large Food & Beverage holding company listed on Bursa Malaysia before signing RTO deal with Asia

Silk Group to list on CAT. Another example is India’s leading architectural services firm, RSP Architects

9 It is important not to overly interpret these premiums as being solely in favor for the incumbent listed firms. For example, St. James Holdings for example was offered a tender price approximately the same value as current trading price by outsider firm Perrenial China Trust. However, based on value of property appraisal, the value of the offer is worth 52% discount to appraised NAV of St. James.

12

Planners transaction with Rowsley which is an SGX listed firm engage in renewable energy. Third unlike

regular takeovers where the listed target firm have bargaining power enforcing acquirers to submit

higher bids (Stulz, 1988; Chiarella and Gatii, 2013), listed firms in reverse takeovers are substantially

smaller than the counter party outsiders if we consider the relative deal value of asset size of listed firm

is around 11 times and 7 times for Singapore and Thai samples. In any case, distressed firms are offered

fairly generous premiums above their VWAPs ensuring that incumbent shareholders can benefit from

the share swap.

Finally, we cannot assume that RTO transactions are in general a one‐sided gain in which the

outsider firm with stronger prospects and substantially larger size determines the terms limited

downside risk for outsider firms otherwise we would probably see transactions predominantly based on

share exchange. The use of solely share exchange makes the terms of the exchange contingent on the

target and potential synergy value and both incumbent and incoming shareholders both shares gains

and losses from the deal (Hansen, 1987). We observe that up to 31% and 67% of the RTO firms in

Singapore and Thailand use mixed mode of payment which involves combination of share swap with

cash and/or warrants. The use of mixed payment suggests that the outsider firm is unsure of merged

value. From our sample, more than half of RTO transactions in Singapore are based on share exchange

only. In the Thai sample more firms use combination of share exchange with cash and warrants. Listed

firms normally use additional cash raised from new private shareholders to pay for outsider firms’

assets. Thus, we expect the cash component indicates the incoming firm needs to retain immediate

value. The warrant issue component helps alleviate the impact of immediate dilution and provide a

delayed option to raise capital in the future if things go well.

4. Methods and results

4.1 Announcement reactions and short‐term performance

In this section we measure short‐term reactions to MOU announcements. The short‐term

reaction captures the short‐term wealth impact for incumbent shareholders. We also explore how RTO

transaction characteristics will have different wealth impact for investors. The standard event study

method (Mackinlay, 1997) is used to calculate abnormal return (AR), cumulative abnormal return (CAR)

from the market model, and relevant statistics

tititit RERAR | (1)

where itAR , itR , and titRE | are the abnormal, actual, and normal returns respectively. The

conditioning information, t is the market return.

13

Figure 1 Plot of cumulative market model abnormal return for RTO announcements (MOU date)

This figure plots the cumulative market model abnormal return for RTO announcements (MOU date).

Define abnormal return as tititit RERAR | where itAR , itR , and titRE | are the

abnormal, actual, and normal returns respectively. The conditioning information, t is the market

return.

Figure 1 a All sample and by market Figure 1 b Distressed vs non‐distressed

Figure 1 c Low vs high premium Figure 1 d Low vs high relative deal size

Figure 1a plots CARs for all firms, Singapore firms, and Thai firms combined 20 days before and after

the MOU date centered at day zero. The plot shows that the market gradually learns about the

forthcoming MOU and CAR drifts up to 28.5% by day 20 after MOU date. The plot also reveals the

announcement is quite unexpected in Singapore, unlike the Thai market where CARs has already drifted

up to almost 19% in days ‐20 to 0. Figures 1b), 1c), and 1d) illustrate CARs of firms separated by distress

status, premium level, and relative deal size level. By day 20, we can see that CAR differences is largest

with distress status where CAR of firms in distress rises to 43% compared to firms that are non‐distress

which sees CAR edging up only to around 10% The CAR of low premiums firms is 21% about half of CAR

of high premium firms which is 43%. When firms are separated by relative deal size, the differences in

CARs are quite small.

14

Table 4 Cumulative market model abnormal return around event windows

The sample consists of 47 firms on Singapore and Thai exchanges. The table reports cumulative market

model abnormal return for RTO announcements (MOU date). Define abnormal return as tititit RERAR | where itAR , itR , and titRE | are the abnormal, actual, and normal

returns respectively. The conditioning information, t is the market return. Cumulative abnormal return

between days 1 and 2 is derived from

kT

kTtitit ARCAR . The standard cumulative abnormal return

is 21

2121 ,

,,

i

ii

CARSCAR . T‐test statistics are tests for the null that CAR and SCAR are equal to

zero. P‐values relating tests of group mean and median differences are in italics.

Event window CAR t‐CAR SCAR t‐SCAR

All [‐10, 10] 0.204 3.31*** 1.402 2.46**

[‐20, 20] 0.218 2.82*** 1.119 2.63**

[‐10, 0] 0.095 2.37** 0.731 2.59**

[‐20, 0] 0.085 1.55 0.589 2.44**

[0, 10] 0.132 2.22** 1.328 2.15**

[0, 20] 0.156 2.74** 1.063 2.44**

Distress [‐10, 10] 0.288 2.99*** 1.796 1.98*

Non distress [‐10, 10] 0.084 1.81* 0.796 2.11*

Distress‐Non‐distress [‐10, 10] 0.204 1.00

Diff p‐value 0.0673 0.3194

Diff p‐value Wilcoxon 0.0990 0.3370

Low relative deal size [‐10, 10] 0.207 2.40** 1.731 1.68*

High relative deal size [‐10, 10] 0.201 2.22** 1.092 1.94*

High‐Low ‐0.006 ‐0.64

Diff p‐value 0.5604 0.5918

Diff value Wilcoxon 0.5677 0.5522

Low Premium [‐10, 10] 0.135 1.75* 0.769 2.31**

High Premium [‐10, 10] 0.306 3.00*** 2.19 1.97**

High‐Low 0.171 1.42

Diff p‐value 0.1798 0.2369

Diff value Wilcoxon 0.2311 0.3391

Table 4 formally tests the significance of CAR and the standardized cumulative abnormal return

(SCAR). Since SCAR is derived from CAR divided by the variance of CAR over the event window, extreme

observations are given less weight. We first report overall sample averages CAR and SCAR over different

windows and provide relevant test statistics (MacKinlay, 1997). The averages reaffirms that the market

15

gradually learns about the news and in general RTO are perceived as good news since both CARs and

SCARs are positive and significant at 1% level at windows [‐10, 10] and [‐20, 20]. Over both these

intervals, RTO firms’ CAR is slightly above 20%. We also find that the responses are stronger post‐MOU

since CAR and SCAR over [0, 10], and [0, 20] intervals are about twice as high (13% and 16%) as those

around windows [‐10, 0], and [‐20, 0].

The remainder of Table 4 tests differences in CAR and SCAR when firms are divided by RTO

characteristics as identified in Figure 1. Since the interval [‐10, 10] displays strongest reactions, the tests

are carried out and reported for this interval only. We find distress firms’ CAR is significantly higher than

those non distress. Average CAR and SCAR of distress firms over the event window is 28.8% and 1.79

compared to 8.4% and 0.79 of distressed firms. High RTO premiums firms also exhibit higher CAR and

SCAR though the statistical significance is weak. Firms with high or low relative deal size have very similar

abnormal return responses confirming Figure 1 d plot.

Overall the short‐term announcement results indicates that the market responds positively to

MOU announcements of RTO transactions. Distress firms cumulative returns are substantially higher

than non‐distress firms. This could be because they are trading at pre‐MOU VWAP that are very low or

because distress firms in general receive higher RTO offer premiums and thus investors look at size of

premium as positive signal for the newly merged firm.

4.2 Long term performances of RTO firms

4.2.1 Buy‐and‐hold abnormal returns (BHAR)

Buy‐and‐hold abnormal returns have come the standard of measuring long‐term abnormal

performances of corporate announcements (Barber and Lyon, 1997; Khotari and Warner, (2006). BHARs

measure the average multi‐period return from a strategy of investing in firms that are affected by an

event compared to investment in benchmark portfolios which can be the market or a controlled group

of similar non‐event firms. We calculate a one year BHAR for RTO firms in our sample compared to the

BHAR of an equal weighted averages buy and hold return of firms in the controlled group. The choice

of one‐year is to avoid increasing skewness and upward bias in measuring BHAR that is increasing the

holding period. Too long a holding period can cause the result to be confounded by other corporate

announcements or market events. We calculate a one‐year BHAR (from day T1 to T2 or 240 trading

days) for each RTO firm compared to a benchmark BHAR of non‐RTO firms. Define,

ititT

TtitT

TtTTi RERBHAR |11 2

1

2

121 ), , (2)

where the mean BHAR is the equal weighted average of individual firm BHARs and the conditioning

information, t is again the market return. The benchmark portfolio is selected by first excluding RTO

firms, then we eliminate firms in the top third market capitalization of the Singapore and Thai

exchanges. In an independent sort, we allocate firms into decile groups based on annual trading price

range. The top decile (most expensive) trading price range are eliminated. Our choice of control group

is preferred over a benchmark based on the entire market return which is influenced by performance

of large firms. The size of RTO targets are below the median market capitalization of each exchange and

they are typically “penny” stocks or are trading the a price range below the median trading price range

of the exchange (Pavabutr et. al, 2014). Small trading price range and small caps typically exhibits larger

16

price movements. The screening results in a control firm sample of 501 from the Singapore exchange

and 398 from the Thai exchange.

We can assume further that event‐firm abnormal returns are independent as occurrence is

quite random and spread out, there is little risk of threat that abnormal returns will be overly‐stated

as Mitchell and Stafford (2000) and Brav (2000) point out given a sample size of 47 firms spread out

over nine years.

Table 5 Mean BHARs for RTO firms

Panel A of the table reports 12 months BHARs of RTO and controlled portfolio group. BHARs for each

group are calculated as the difference between the equal weighted BHARs of event firms and controlled

portfolio group. The controlled portfolio group is selected by first separating firms on each stock

exchange then eliminated the top third market capitalization firms on both exchanges, Singapore and

Thailand. In a separate sort of decile trading price rankings, trading prices in the top decile (most

expensive stocks) are deleted. The column two‐sided p‐values report the parametric p‐value and non‐

parametric Wilcoxon p‐values (in parentheses) for differences between RTO sample BHAR and control

sample BHAR. The bootstrap p‐value is based on an empirical distribution created by simulating 1,000

pseudo samples. The p‐value is the fraction of mean BHARs from the pseudo samples in larger

magnitude than the original RTO sample mean. Panel B reports 12 month buy‐and‐hold returns (BHRs),

112

121 ), itT

TtTTi RBHR and BHAR of firms classified by distressed and non‐distressed status.

Similar p‐values described in Panel A test for differences between distressed and non‐distressed with

control sample BHARs.

Panel A

RTO sample Control Sample Two‐sided Bootstrap

BHAR BHAR p‐values p‐value

Mean 0.006 ‐0.008 0.1992 < 0.0001

Median ‐0.176 ‐0.189 (0.2516)

SD 0.816 0.758

Skewness 7.380 9.580

Panel B

Two‐sided Bootstrap

Distressed BHR BHAR p‐value p‐value

Mean 0.0127 ‐0.0601 0.6228 0.366152

Median ‐0.1269 ‐0.242 (0.7245)

SD 0.9900 1.025

Skewness 2.157 2.895

Non‐distressed

BHR BHAR

Mean 0.1878 0.0840 0.0538 < 0.0001

Median ‐0.0596 ‐0.0521 (0.0731)

SD 0.6929 0.4849

Skewness 1.643 2.2335

17

Panel A of Table 5 reports 12 months BHARs of RTO and controlled portfolio group. We can see

that both the RTO and controlled sample distributions have high positive skewness as usually

documented with long‐term abnormal returns. Figure 2a plots the empirical distribution of BHAR of

RTO firms illustrating the skewness. The mean BHAR of RTO firms are 0.6% compared to ‐0.8% of

controlled firms. The median BHAR of both groups shows overall underperformance relative to the

market at large. For the control samples, this is probably due to dominance of smaller firms as they

tend to underperform large caps in emerging markets. A two‐tailed test of difference between BHAR

of RTO and control sample firm groups using both parametric p‐values and non‐parametric p‐values

show that we cannot reject the null that RTO sample firms perform differently from the control sample.

The result points that while median RTO firms do not perform differently from controlled non‐RTO firms

relative to the entire market, there seems to be a general decline in price impact over the long‐term

relative to short‐term accumulated over 20 days post‐MOU.

Figure 2 Empirical and bootstrap distributions of BHARs

Figure 2a plots the empirical distribution of BHARs from sample RTO firms as described in equation 2.

Figure 2b plots the bootstrap distribution 1,000 from pseudo samples created by random selection of

control firms’ BHAR over the same event period as RTO firms. The vertical lines in Figure 2b are the

upper and lower confidence intervals at 5% based on the bootstrap estimates.

18

Given the skewness of the distribution and high return volatility, we also provide statistical

inference for the mean BHAR based on a simulated distribution. In a similar framework as in Ikenberry,

Lakonishok, and Vermaelen (1995) and Mitchell and Stafford (2000), we assign the evaluation date to a

randomly selected control group firms as described in the screening process earlier, we then compute

the mean BHAR for this pseudo sample in the same way as the original RTO sample group. This results

in one pseudo sample mean. We repeat this step to generate 1,000 BHAR mean and a bootstrap

distribution under the null. A bootstrap p‐value in the last column of Table 5 is calculated as a fraction

of the mean of the BHAR from the pseudo samples that are larger than the original RTO mean. Figure

2 b provides the distribution plot of the simulated sample mean BHAR. The one‐sided boot‐strap p‐

value indicates that the RTO sample mean of 0.06 is significantly different from the pseudo sample

mean.

Panel B of Table 5 reports BHR and BHAR of RTO firms classified by distressed and non‐

distressed status. We find that the average BHR and BHAR of non‐distressed firms are notably larger

than distressed firms. BHR of distressed firms are 0.0127 compared to 0.1878 of non‐distressed. This

points to the fact that distressed firm stock prices must be declining over 12 month period compared to

the short‐run response. In contrast, the BHR of non‐distressed firms remains close to CAR of

approximately 20% after the MOU announcement. Once again we report to test if distressed and non‐

distressed group average BHARs are different from controlled group average BHAR as well as the boot‐

strap p‐values. We find significant difference in the non‐distressed group.

4.2.2 What explains differences in BHARs?

The result in 4.2.2 is intriguing. Does the poor average BHAR performance of distressed firms

imply that distressed firm RTO are unsuccessful and losing value over time? To answer this question,

we run a linear model using the sample of 47 RTO firms. In each OLS model the dependent variable is

12 month BHAR post‐MOU. Explanatory variables in model 1 are those associated with RTO

characteristics; namely, relative deal size and premium both of which have shown important in

explaining differences in CAR. In model 2, we include on top of RTO characteristics, accounting variables

which are one year post‐MOU percentage changes in book value of equity, return on assets (ROA), and

net profit margins (NPM). The change in book value of equity controls for possible share offerings post‐

MOU. Since many RTO deals involved capital increases and new share offerings, which will ultimately

19

affect the book value of equity. In fact, on average RTO sample firms sees the number of shares doubled

and book value of equity on average increased over 10 folds due to merging with a bigger entity over

the course of 12 months post‐MOU. In model 3, we include natural log of turnover (number of shares

traded/total number of shares outstanding) and a distress status dummy. We find that three variables

which are relative deal size, change in book value of equity, and turnover are most important in

explaining differences in BHARs. BHAR is declining in relative deal size and percent change in book value

of equity. This is not surprising as large deals relative to listed firm pre‐transaction asset values requires

larger capital increase. The correlation between relative deal size ratio and book value of equity

increase is 0.86. We do not find premiums having a significant impact on BHAR even though they

generate very strong CAR response over the first 20 days of announcements. However, we do find that

firms that received high premiums do not experience as much large a change in book value of equity

and number of shares. The correlation between premium levels and change in book value is actually

negative (‐0.15). The distress dummy does not help explain the differences in BHAR well as this is

already reflected in relative deal size and change in equity book value. We believe there is no need to

add a country dummy to the model since RTO characters of Singapore and Thai firms are similar as

discussed in section 3.

Table 6 Determinants of BHARs

This table reports the coefficients from three OLS models with white corrected t‐statistics. The

dependent variable is BHARs of 47 RTO sample firms from Singapore and Thai exchanges. Relative deal

size is computed from deal size divided by listed firms’ assets in pre‐MOU year. Premium is pre‐

consolidation issue price relative to 3‐month pre‐MOU value weighted average unadjusted closing price

(VWAP) of listed firm. Percentage changes in return on assets (ROA) and net profit margin (NPM) is iss

change over one year from MOU. Turnover is computed from average annual turnover (number of

shares traded/total number of shares outstanding).

Model 1 Model 2 Model 3

Estimate t‐value Estimate t‐value Estimate t‐value

Relative deal size ‐0.0239 ‐2.63** ‐0.0203 ‐2.65*** ‐0.0209 ‐2.94***

Premium ‐0.0387 ‐0.64 ‐0.0352 ‐0.52 0.0159 0.22

%Chg. Book Equity ‐0.0049 ‐6.03*** ‐0.0048 ‐3.47*** ‐0.0037 ‐2.49**

%Chg. ROA ‐0.0242 ‐0.27 ‐0.1001 ‐0.91

%Chg. NPM ‐0.0326 ‐0.29 0.0928 0.51

lnTurnover 0.1283 2.06**

Distress 0.0706 0.31

AdjRsq 0.1892 0.1429 0.2452

Pr > F 0.0376 0.1203 0.0598

Note: **, and *** denotes statistical significance at 5% and 1% confidence.

4.2.3 Post‐RTO earnings performance

Long term evaluation of corporate announcements using returns is not a straight forward tasks

given that we are unable to control other changing information environment as well as the upward bias

documented in longer term computations of BHAR. Furthermore, using BHAR to evaluate the success

of RTO transactions alone are further complicated the fact that the an RTO event does not really have a

definitive completion date because of continuing recapitalization plan via private offerings, and warrant

20

exercise, and thus the length of holding periods of 6 months, 1 year or more can be deemed arbitrary.

Thus, as an alternative to merely examining BHAR, we evaluate long term financial performance of RTO

firms 3‐years post‐MOU. As we are still interested in the varying performance between the distressed

and non‐distressed group, Table 7 produce a two‐way mean comparison (within groups over different

time and between groups over the same time period) between distressed and non‐distressed firms over

before MOU and 3 years post‐MOU. The ratios selected measures general liquidity (cash ratio),

leverage (debt to assets, and debt to equity ratios), revenue generation and cost control (EPS and NPM),

and returns to investments (ROA, and ROE). 10

We find that all firms have lower cash holdings, but distressed firms must have taken more debt

as debt to assets has risen even though debt to equity has dropped given large positive change in equity.

Despite the book value of equity that has increased, the ROE of distressed firms has increased compared

to pre‐MOU periods. We find that distressed firms have significantly inferior NPM and ROA pre‐MOU

compared to non‐distressed firms. However, this gap has closed in 3 years after.

10 Only the cash ratio is chose to measure general liquidity since the our RTO samples are spread out over across varying industries 26% in finance and property, 11% in mining, 30% in technology, and the remainder spread out other industries such as consumer, retail, and manufacturing goods.

21

Table 7 Key financial ratios of distressed and non‐distressed firms

This table reports the key financial ratios of RTO sample firms classified by distressed and non‐

distressed status at end of MOU signing calendar year (referred to as before) and 3‐years after MOU

signing. ***,**,* denotes significance at 1%, 5%, and 10%, respectively.

Distressed Non‐ distressed Difference t‐stat p‐value

Cash ratio

Before 0.296 0.204 0.092 1.20 0.238

3 years after 0.113 0.114 0.001 0.00 0.996

Paired mean diff ‐0.169 ‐0.126

t‐stat (p‐value) ‐2.67 (0.018)*** ‐1.95 (0.087)*

Debt to assets

Before 0.173 0.237 ‐0.064 ‐0.98 0.332

3 years after 0.251 0.301 ‐0.050 ‐0.96 0.3467

Paired mean diff 0.159 0.107

t‐stat (p‐value) 2.73 (0.016)*** 1.52 (0.166)

Debt to equity

Before 1.449 0.698 0.751 1.18 0.2488

3 years after 0.683 0.981 ‐0.298 ‐0.86 0.407

Paired mean diff ‐0.6883 0.5097

t‐stat (p‐value) ‐0.53 (0.609) 1.89 (0.095)*

EPS

Before 0.017 0.202 ‐0.186 0.83 0.4193

3 years after 0.067 0.193 ‐0.125 ‐0.81 0.4398

Paired mean diff 0.018 ‐0.251

t‐stat (p‐value) 0.75 (0.473) ‐0.9 (0.399)

Net profit margin

Before ‐0.196 ‐0.026 ‐0.170 ‐1.96 0.061

3 years after 0.001 ‐0.007 0.008 0.12 0.9031

Paired difference 0.204 0.054

t‐stat (p‐value) 1.55 (0.181) 0.69 (0.519)

Return on assets

Before ‐0.152 0.055 ‐0.207 ‐2.61 0.0129

3 years after ‐0.004 0.061 ‐0.066 ‐1.94 0.0068

Paired difference 0.234 0.005

t‐stat 2.52 (0.026) 0.16 (0.881)

Return on equity

Before ‐0.128 0.138 ‐0.266 ‐3.37 0.0022

3 years after 0.014 0.154 ‐0.139 ‐1.86 0.0784

Paired difference 0.207 0.006

t‐stat (p‐value) 1.94 (0.094) 0.09 (0.934)

22

4.3 Liquidity of RTO firms

So far in this paper, we have examined how RTO deals have made an impact on short‐term and

long‐term return as well as financial performance. Returns measure the overall impact of investors’

wealth whereas financial performance measures how the transaction has altered the newly merged

entity. We finally explore liquidity of RTO firms before and after the transaction marked by the MOU

date as before. Liquidity has an important role in reducing the cost of capital for the firm as Acharya

and Pederson (2005) has shown theoretically and empirically in Liu (2006). Liquidity also plays an

important part in improving information efficiency as numerous papers in market microstructure argue

(see Stoll, 2000; O’Hara, 2003; and Chordia, Roll, and Subrahmanyam, 2008) and thus they are variables

that are monitored closely by regulators. Since there are numerous ways to measure liquidity, we select

the ubiquitous percentage bid‐ask spreads, and turnover. Bid‐ask spreads are typically strongly

associated with price impact or how a change in a unit trading volume can move price. Larger spreads

are also associated with asymmetric information. Table 8 report percentage bid‐ask spreads and

turnover, 12 months before and 12 months after MOU. The averages are derived from daily data

frequency. Both percentage spreads and turnover are significantly reduced. The largest reduction is

the Singaporean spread going down to 8.68% from a high of 13.99% pre‐MOU. Turnover has doubled

in the Singapore RTO firms increasing from 0.4% to 0.8% whereas turnover rise around 64% for Thai

RTO firms. Despite these increases, the post‐MOU liquidity improvement still place RTO stocks in the

bottom decile turnover compared to the rest of the Singapore and Thai exchanges (Pavabutr et al. 2014)

Table 8 Liquidity of RTO firms by exchange

This table reports liquidity measures of RTO sample firms. Percentage day‐ end bid‐ask spreads

computed from (ask‐bid)/closing price 12 months worth of daily averages and median (in parentheses)

before MOU and 12 months after MOU. Turnover is defined as percentage daily average number of

shares traded divided by total number of shares outstanding. Daily outlier observations at 1% and

99% are removed. Parametric p‐values and non‐parametric p‐values (in parentheses) are provided.

All Singapore Thailand

Measure Liquidity p‐value Liquidity p‐value Liquidity p‐value

% Bid‐ask spread

12 months before 10.67% 13.99% 1.39%

(5.00%) (8.33%) (1.09%)

12 months after 9.84% 0.0378 8.68% (0.0937) 0.95% < .0001

(2.94%) (< .0001) (5.47%) (< .0001) (0.75%) (< .0001)

% Turnover

12 months before 0.82% 0.40% 1.58%

(0.08%) (0.03%) (0.38%)

12 months after 1.10% (< .0001) 0.85% < .0001 2.59% 0.0002

(0.10%) (< .0001) (0.03%) (< .0001) (0.65%) (< .0001)

23

Conclusion and policy discussion

Using a sample of 47 firms on Singapore and Thai stock exchanges between 2007‐2015, we seek

to understand the motivation to list using reverse takeovers by comparing the RTO to IPO listing process,

analyzing the characteristics of RTO listed participants, evaluating the post‐transaction short‐term and

long‐term return performance, and examining post‐transaction financial performance. While the

popular press often treat these transactions with suspicion as they associate reverse takeovers as a

“back‐door” listing process where opportunistic private or outsider firms seek a short‐cut to listing and

create speculative hype on small caps, we find no evidence that such parable in our sample RTOs.

Can we regard outsider firms as White Knights? Perhaps so for shareholders of listed firms as

we find that RTO transactions provide an exit opportunity for incumbent listed shareholders as they can

gain from short‐term returns and improved liquidity of an otherwise forgotten illiquid stock. But do

these private investors succeed in rescuing troubled firms and turning the businesses around. Analyzing

the post‐transaction financial performance suggests some improvement in distressed firm performance,

but not without costs of tremendous dilution from continuous recapitalization. What is not so definitive

is why outside firms would want to list this way, if they are already of caliber to list via IPO with their

own profile? Our analysis suggests that we should not view outsider firm decisions to conduct RTO as a

means to list per se but as a corporate transaction strategy to achieve other ends such as becoming a

public company without immediate large dilution in ownership and still have an option to raise more

funds later, obtaining a distressed or non‐distressed target public firm at a bargain price especially those

with valuable property (see Circular of Perrenial Holdings transactions with St. James holdings in

Singapore), and finally, the motivation could be unique to the firms themselves. For example, the

Chaswood Group, already listed on Bursa Malaysia decides to reverse takeover Asia Silk Group to list on

CAT and explain that the choice of listing on the Singapore exchanges is to increase their international

profile in Asian markets. On the Thai exchange, Singha Estate choose to complete a RTO with Rasa

property as a short‐cut process to diversify the group’s business from food and beverage into real estate.

Going forward, the benefits are costs of RTOs should be studied on a case‐by‐case basis since they are

very unique transactions.

Should the regulators loosen requirements on RTOs? Indeed, reverse mergers can be predicted

to cause huge percentage‐wise increases in the stock price of a public firm upon the release of news as

we might find in any merger news. However, for small cap stocks with very low trading price, even if its

stock price rose from virtually zero to only a few cents, the gain could be enormous. Without investor

savvy and adequate enforcement, the combination of potentially huge gains and relatively

unsophisticated players is a recipe for market abuse. In the end, a totally unobtrusive approach towards

RTOs is likely to attract opportunistic Machiavellian behavior.

Fortunately, current rules in place impose the same minimum listing requirement on listings via

RTOS as on IPOs. So either way, we expect firms listing directly or indirectly are at par in terms of firm

quality. However, if RTOs are to be used as a means to attract potentially strong private firms to help

provide rehabilitation, and exit for incumbent public firms then perhaps some concessions should be

made on selected listing rules. This observation is probably more applicable in the Thai case as MAI is

subject to relatively tighter listing rules with both size and profit requirement unlike CAT listing where

neither requirement is present. In addition, it is important to provide investors and media education

that RTOs are well regulated transactions and that SEC and Stock Exchange approved deals are not

pump‐and‐dump schemes to avoid investor misunderstanding.

24

References

Adjei, F., K. Cyree, and M. Walker, 2008, The determinants and survival of reverse mergers vs. IPOs,

Journal of Economics and Finance 32: 176‐194.

Archarya, VV., and Pedersen OH., 2005. Asset pricing with liquidity risk, Journal of Financial Economics,

77(2), 375‐410.

Arellano‐Ostoa, A. and Brusco, S., 2002. Understanding reverse mergers: A first approach, Working

paper, Universidad Carlos III de Madrid.

Barber BM., and Lyon JD., 1997. Detecting long‐run abnormal stock returns: The empirical power and

specification statistics, Journal of Financial Economics, 43(3), 341‐372.

Berger, A.; Demsetz, R.; and Strahan, P. 1999. The consolidation of the financial services industry:

Causes, consequences, and implications for the future. Journal of Banking and Finance, 23 (February):

135–94.

Brav, A., 2000. Inference in long‐horizon event studies: A Bayesian approach with application to initial

public offerings, Journal of Finance, 55(5), 1979‐2016.

Carpentier, C., Cumming, D ., and Suret, JM., 2009. The value of capital market regulation: IPO versus

reverse mergers, Working Paper, CIRANO.

Chiarella C., and Gatti, S., 2013. How much to pay, and how, for opacity? Negotiating premiums and

method of payment in M&A, Working Paper, University of Bocconi.

Chordia, T., Roll, R., and Subrahmanyam, A., 2008. Liquidity and market efficiency, Journal of Financial

Economics, 87(2), 249‐268.

Floros, IV., and Sapp, TRA., 2011. Shell games: On the value of shell companies, Journal of Corporate

Finance, 17, 850‐867.

Floros, IV., and Shastri, K., 2009. A comparison of penny stock initial public offerings and reverse

mergers as alternative mechanisms for going public, SSRN.

Gleason, KC., Rosenthal, L., and Wiggins, RA., 2005. Backing into being public: an exploratory analysis

of reverse takeovers, Journal of Corporate Finance, 12, 54‐79.

Hansen, R., 1987. A theory of medium of exchange in mergers and acquisitions, Journal of Business,

60, 75‐96.

Hseih, J., Lyandres, E., and Zhdanov, A., 2009. A theory of merger‐driven IPOs, Working paper.

Khotari, S.P., and Warner, J.B., 2006. Econometrics of Event Studies, Handbook of Corporate Finance:

Empirical Corporate Finance. Vol A (Handbooks in Finance Series, Elsevier/North‐Holland) Ch. 1.

Ikenberry, D., Lakonishok J., and Vermaelen, T., 1995. Market underreaction to open market share

repurchases, Journal of Financial Economics, 39(2), 181‐208.

Liu, W., 2006. A liquidity‐augmented capital asset pricing model, Journal of Financial Econonomics,

82(3), 631‐671.

25

MacKinlay, AG., 1997. Event studies in economics and finance, Journal of Economic Literature, 34, 13‐

39.

Mitchell, L., and Stafford, E., 2000. Managerial decisions and long‐term stock price performance 73(3),

287‐329.

O’Hara, M., 2003, Liquidity and price discovery, Journal of Finance, 58(4), 1335‐1354.

Pakov, AR., 2006. Ghouls and Godsends? A critique of reverse merger policy, Berkeley Business Law

Journal, 3(2). 474‐513.

Pavabutr, P., Ghon, R., Sirodom, K., and Tian, G., 2014. Asian pennies are not like US pennies,

Development Bank of Japan, Discussion paper series, 1402.

Sjostrom, W., 2008. The truth about reverse mergers, Entrepreneurial Business Law Journal, 2(2) , 744‐

759.

Stoll, HR., 2000. Friction, Journal of Finance, 55(4), 1479‐1514.

Stulz, RM, 1988. Managerial control of voting rights: Financing policies and the market for corporate

control, Journal of Financial Economics, 20(1) 25‐54.

Vermeulen, EPM., 2014. Rules on backdoor listings: A global survey, Indonesia‐OECD Corporate

Governance Policy Dialogue.

Wan‐Hussin, WN., 2002. The reverse takeover of Berjaya Textiles and back‐door listing of Jaya Tiasa: A

Malaysian case.

Winyuhuttakit, P., 2011. Asset acquisition from unlisted company regarded as backdoor listing, Master

of Law Thesis, Chulalongkorn University.