What matters now - Kearney

20

impact What matters now 23 October 2020 kearney.com 15 ISSUE

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of What matters now - Kearney

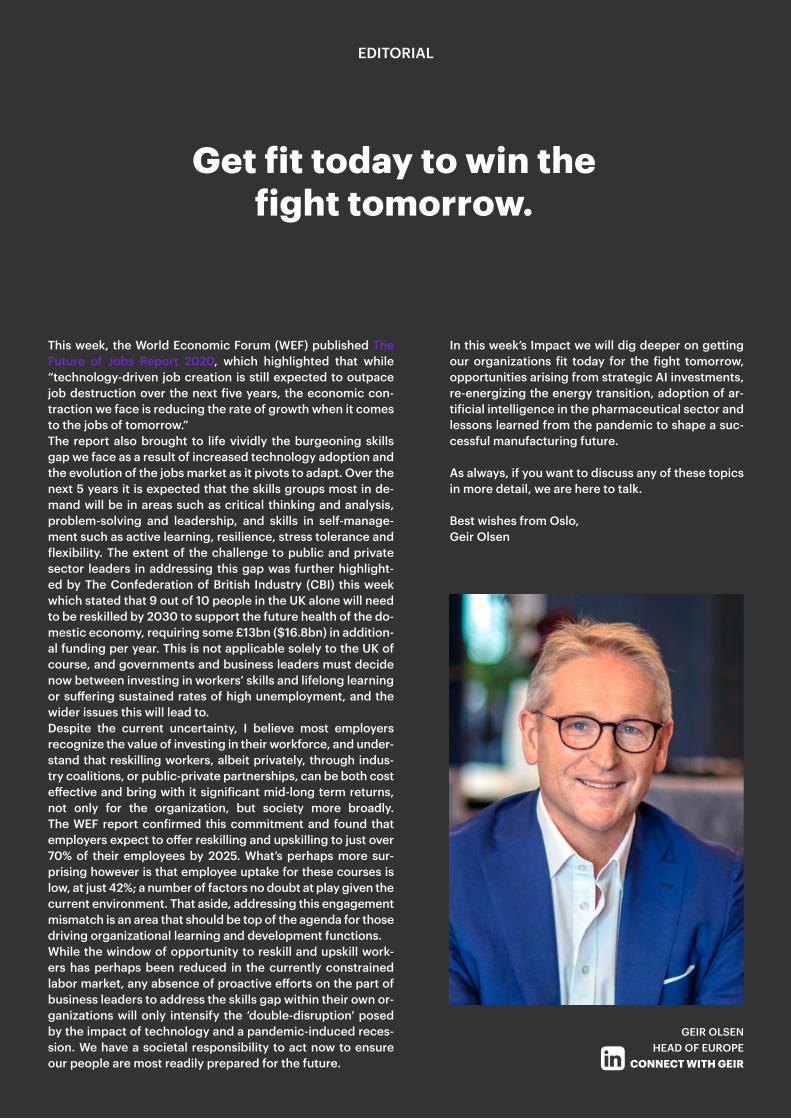

This week, the World Economic Forum (WEF) published The Future of Jobs Report 2020, which highlighted that while “technology-driven job creation is still expected to outpace job destruction over the next five years, the economic con-traction we face is reducing the rate of growth when it comes to the jobs of tomorrow.” The report also brought to life vividly the burgeoning skills gap we face as a result of increased technology adoption and the evolution of the jobs market as it pivots to adapt. Over the next 5 years it is expected that the skills groups most in de-mand will be in areas such as critical thinking and analysis, problem-solving and leadership, and skills in self-manage-ment such as active learning, resilience, stress tolerance and flexibility. The extent of the challenge to public and private sector leaders in addressing this gap was further highlight-ed by The Confederation of British Industry (CBI) this week which stated that 9 out of 10 people in the UK alone will need to be reskilled by 2030 to support the future health of the do-mestic economy, requiring some £13bn ($16.8bn) in addition-al funding per year. This is not applicable solely to the UK of course, and governments and business leaders must decide now between investing in workers’ skills and lifelong learning or suffering sustained rates of high unemployment, and the wider issues this will lead to.Despite the current uncertainty, I believe most employers recognize the value of investing in their workforce, and under-stand that reskilling workers, albeit privately, through indus-try coalitions, or public-private partnerships, can be both cost effective and bring with it significant mid-long term returns, not only for the organization, but society more broadly. The WEF report confirmed this commitment and found that employers expect to offer reskilling and upskilling to just over 70% of their employees by 2025. What’s perhaps more sur-prising however is that employee uptake for these courses is low, at just 42%; a number of factors no doubt at play given the current environment. That aside, addressing this engagement mismatch is an area that should be top of the agenda for those driving organizational learning and development functions. While the window of opportunity to reskill and upskill work-ers has perhaps been reduced in the currently constrained labor market, any absence of proactive efforts on the part of business leaders to address the skills gap within their own or-ganizations will only intensify the ‘double-disruption′ posed by the impact of technology and a pandemic-induced reces-sion. We have a societal responsibility to act now to ensure our people are most readily prepared for the future.

EDITORIAL

GEIR OLSENHEAD OF EUROPE

CONNECT WITH GEIR

In this week’s Impact we will dig deeper on getting our organizations fit today for the fight tomorrow, opportunities arising from strategic AI investments, re-energizing the energy transition, adoption of ar-tificial intelligence in the pharmaceutical sector and lessons learned from the pandemic to shape a suc-cessful manufacturing future.

As always, if you want to discuss any of these topics in more detail, we are here to talk.

Best wishes from Oslo,Geir Olsen

Get fit today to win the fight tomorrow.

On October 16, I spoke at the first ever Y20 summit, hosted virtual-ly in Saudi Arabia, on the Future of Work. Bringing together young leaders from all G20 countries, we were able to discuss the impact of technology on job displacement, new job creation and transfor-ming skillsets. At the heart of this shift, we talked about why real progress is defined by the humans at its core and why “being rea-dy” is as much about building a new culture as it is about adapting to a new structure.Our discussion spanned far and wide, so I’ll aim to get to heart of where things stand and what this means from a future preparedness perspective.

Technology changes the way we work. It has since the invention of the wheel. But as we enter the third decade of the 21st Century, technolo-gical innovation is accelerating a revolutionary shift in the fundamental structures of how, why and when we work. The question is: Are we ready for it?

Future Fit Starts Today

FUTURE OF WORK

TEXT BY ALEX LIU

Out of workJobs being replaced by machines is a fear rooted firmly in the collec-tive imagination. Dystopia in films and literature has played a signifi-cant part in creating anxieties and unease around this issue; AI out-wits or outpowers the Human and they are at war. And yet, we forget that in the previous industrial revolution, machines replaced just as many labor-intensive agricultural jobs as they will in the next.Today the threat to jobs is from robotics, AI, and other rapidly ad-vancing technologies. I believe that while the threat is real, and the shift will be challenging, there is no alternative but to embrace it, putting humans first. Easier said than done, yes, but automation is imminent and inevitable – 2013 analysis by Fray and Osborne found that as many as 47% of jobs in the US were subject to automation; in the seven years since this report, technology has developed ex-ponentially.1 Our most important focus, therefore, should be the im-mediate social cost if policymakers and citizens do not prepare and protect the most vulnerable. Who, then, is it that must be targeted?Ultimately, there will be few industries left unturned, however, low-skill and middle-skill jobs will take the greatest hit. Many low-skill manual tasks will be displaced by ro-bots, redefining the job entirely. At the same time, the middle is being “squeezed” and those in occu-pations in logistics & transportation through to of-fice clerks, will find themselves in most need of retraining. While it’s true that breakthroughs in ma-chine learning are putting high-skill jobs based on information-gathering and pattern-identification at risk too, many of these workers possess the soft skills that make them more adaptable to change.On a global scale, low-income populations will be impacted disproportionately without intervention. That’s exactly why harvesting the real value of auto-mation must be an international, collaborative effort.

Are we Future Fit?Automation is displacing and augmenting, not re-placing and eliminating. Tasks will be replaced, yes, but humans cannot be. Platform, demand, and in-novation driven growth will take the labor market to new platforms and new places, and it will create as much as it will take over. It is estimated, for exam-ple, that the move towards a green economy could create net growth of 18 million new jobs by 2030. In turn, we are likely to see positive changes to how we work including: extra time for part-time work and multiple occupations; a results and people-oriented focus rather than routine; growth of remote working capability; and pay based on output rather than time.The promise is flexible and fluid. However, right now, half of the world’s population are under 30, a quarter of who are under 14, and 90% live in developing countries. The initial economic implications are, as the OECD predicts, that youth employment will take a hit as automation takes over. Considering the people cost, I put to the pa-nel Kearney’s conclusion that human capital development must be front, back and center of the transition.It goes without saying that young people hold great potential, but the global digital divide, unequal and limited access to mentoring, skills mismatch, rapid technological developments, a growing city/ rural gap, all threaten to hamper getting Future Fit. I believe human capital should be the most important focus for a stable, sustained and prosperous future. So how do we get ready for this together?

Getting ready“Readiness” is two way: employees must prepare for the workplace of the future; and companies and cultures must work hard to ena-

“Platform, demand, and innovationdriven growth will take the labor

market to new platforms and newplaces, and it will create as much

as it will take over.”

1 . C

arl B

ened

ikt F

rey

and

Mic

hael

A. O

sbor

ne, “

The

Futu

re o

f Em

ploy

men

t: H

ow S

usce

ptib

le A

re J

obs

to C

ompu

teris

atio

n?”,

20

13

Connect with Alex

ble and unlock worker potential. Francesco Profumo, Italy’s Former Minister of Education, predicts that there will be a 40+% increase in the number of jobs held over the course of the working lives of millennials. This is positive. The idea of humans as production line capital is coming to an end as automation takes on the manual mo-notony. We should be excited, but aware of the mountain ahead.As I see it, getting to the top of the mountain comes down to de-veloping a breadth of skills that are most essentially human. The best future workers need skills that are both hard and people ba-sed, they need depth and a passion for lifelong learning, and final-ly, they need the confidence to follow their own path and run their own race. How will this be achieved? At a business level, companies need to instill a culture of joy, inclusion and justice, to attract, de-velop, retain and inspire the workers of future. For the future work-force, governments, policymakers, educators and citizens have a responsibility to leave no child left behind. The fourth industrial evolution is here, and every event like the Y20, that gives our youth a platform to voice their future concerns and solutions with the lea-ders of today, matters tremendously.

“The best future workers need skills that are both hard and people

based, they need depth and a passion for lifelong learning, and

finally, they need the confidence to follow their own path and run

their own race.”

Striking gold with your AI investments

ARTIFICIAL INTELLIGENCE

TEXT BY JOHN GOMES, SAHIL MEHRA, BRENDAN RATTER

Self-driving vehicles. Robotic surgeons. Ad-aptive networks. Without a doubt, the trans-formative possibilities of artificial intelligen-ce (AI) are being heavily hyped—and AI will be one of the defining technology trends of our century as it comes into widespread usa-ge. No one wants to miss out on such a po-tentially lucrative investment opportunity.But caution is warranted, as investing in AI requires finding niches that are likely to bring strong financial returns while also ensuring alignment with the investor’s strategy, visi-on, and capabilities. This challenge is com-pounded by the fierce competition among investors in this market, especially from hy-per-scale cloud computing companies such as Google and Amazon that are rapidly buy-ing up stakes in AI firms. Finding the sort of industry-defining “gold nuggets” that will live

up to the hype and earn a significant return requires extensive study of the market.So, how can investors strike gold? To start, they can approach potential AI investments from the perspective of ecosystems built around a defined value proposition for end customers. Such an approach prioritizes use cases with a clear path to monetizati-on, as opposed to the fundamental techno-logy stacks that—while valuable in their own right—don’t have as clear a route to market. Below, we present thoughts on some of the-se AI ecosystems, along with a framework for approaching AI investments and a tangible example of an investment scenario.

Ecosystem overviewEach use-case-driven ecosystem that a com-pany may consider investing in is at a diffe-

rent level of maturity. Investors looking to make multiple AI investments will look to do so across a wide time horizon. Those taking a more narrowly focused investment approach are more prone to invest in ecosystems that enhance their own technology or match their own strategic priorities.Ecosystems with higher maturity have a fair amount of certainty around their use cases, but commensurately higher barriers to en-try around premium acquisition or invest-ment targets. Less mature technologies tend to be more broadly platform based and heavily research oriented, with less certain-ty around their ultimate use cases. Figure 1 presents 14 AI ecosystems across three bro-ad levels of maturity.Many of the AI technologies in the high-matu-rity category are already present in the mar-

H I G H M AT U R I T Y M E D I U M M AT U R I T Y L O W M AT U R I T Y

Network controllers to transform static networks into dynamic ones running with limited intervention

Adaptive networks

Machines in factories or warehouses that have situation awareness and autonomous operation

Industrial automation

Hosted platforms allowing dev teams to use advanced AI features as a service

AIaaS

Chips and software designed to efficiently power complex and compute-intensive AI applications

AI hardware and firmware

Vehicles (cars, trucks, and so on that use sensing and localization technology to drive without human intervention

Smart bots or task automation

Hardware or software that provides an alternative digital reality for end users; includes AR, VR, MR

XR systems

Devices or algorithms which provide insights to improve health outcomes (for example, diagnostics, drug discovery)

Smart health technology

Machines which operate with auto- nomy; applications across industries (for example, medical robots for surgery, personal service robots)

Smart robots

Devices uses “quantum bits” (qubits) to solve high-complexity problems (for example, optimization)

Quantum computing

AI ecosystems have varied maturity levels

Source: Kearney analysis

Algorithms to identify, counteract sophisticated cyber-attacks with minimal human intervention

Security and surveillance

Analytics for businesses to discover deeper insights, make predictions, and enhance decision-making (for example, targeted promos, next best action)

BI and advanced analytics

External sensors or direct connection between the brain and external device

Brain–computer interfaces

Capability of a machine to emulate human-like general intelligence

Artificial general intelligence

Vehicles (cars, trucks, and so on) that use sensing and localization technology to drive without human intervention

Autonomous vehicles

“Investing in AIrequires finding

niches that are likely to bring strong finan-cial returns while also

ensuring alignment with the investor’s

strategy, vision, and capabilities.”

Figure 1

ket, with expectations that they could rapidly come to widespread adoption. For example, technologies associated with industrial auto-mation are already used in leading-edge fac-tories in which machines communicate with one another as well as humans.Conversely, the ecosystems in the low-matu-rity grouping are at least half a decade from fruition. To cite one example, brain–compu-ter interfaces will enable people to interact directly with computers through their brain activity, which could ultimately yield techno-logy with a market value in the tens or hun-dreds of billions of dollars.

A framework for AI investingIrrespective of the current maturity level of a given ecosystem, striking AI gold requi-res investing in ecosystems that combine financial attractiveness and alignment with the investor’s unique strategy, culture, and strengths. The financial attractiveness of a potential investment depends on three cri-teria that are largely agnostic to an inves-tor’s specific strategy: total addressable market (TAM), competitive intensity, and technological maturity. Strategic align-ment, on the other hand, depends more on the individual investor’s investment thesis and the role it ultimately wants to play in the ecosystem. Strategic alignment criteria include value capture potential, how well an investment plays to an investor’s strengths, and the portfolio approach. Figure 2 provi-des definitions of these criteria.We can portray financial attractiveness and strategic alignment on a two-by-two frame-

Investments in AI ecosystems should consider both financial attractiveness and strategic alignment

F I N A N C I A L AT T R A C T I V E N E S S S T R AT E G I C A L I G N M E N T

Source: Kearney analysis

Total addressable market (TAM) How big the market will get. The larger an ecosystem’s TAM,

the more room there is for companies of all sizes to carve out a sustainable niche.

Value capture potentialHow easily the AI-focused investor can capture available economic value in the ecosystem. Where a company is positioned in the ecosystem’s vertical, and how likely that slice is to capture available value for its shareholders, also matters.

Competitive intensity How competitive the market is for investments,

(which drives up entry multiples and price) and products (affecting future profitability and therefore exit multiples).

Play to strengths Alignment of the ecosystem with the investor’s competen-cies and strategic direction, and hence the ability to drive synergy from any deal.

Technological maturity The anticipated time to a technology’s return on investment with longer time horizons and greater uncertainty lowering

the prospects of immediate return on investment.

Portfolio approachAn investor’s financial appetite for AI “bets” varies in both scale and time horizon. By default, balancing investments across several ecosystems at varying maturity levels is appropriate, but other approaches are possible.

“The financial attractiveness of a potential invest-ment depends on total addressable market (TAM),

competitive intensity, and technological maturity.”

Figure 2

Connect with JohnConnect with SahilConnect with Brendan

work and then populate the four quadrants with the AI ecosystems within our purview. Figure 3 portrays one way a large hardware manufacturer might do so. Ideally, an in-vestor would look for opportunities in tho-se Gold rush ecosystems that are both large and attractive; however, substantial value can also be found in the more niche Dia-monds in the rough quadrant. Pure-play fi-nancial investors, or those playing a volume game, will find opportunities in the Copper mine quadrant, where there is still money to be made for those that lead with scale.

Putting the framework to useStrategic alignment depends on an investor’s unique circumstances. A company may try to identify financially attractive, strategically aligned AI firms within specific ecosystems where it can add value in order to help them grow. To do so it would have to target specific ecosystems, then develop a focused pipeline of investment candidates with true techni-cal or market differentiation. In this case, the ecosystems in the top and bottom right qua-drants provide fertile ground to explore.To exemplify how the framework is put to

use, consider how strategic alignment plays out for our hypothetical hardware manufac-turer in two ecosystems: industrial automati-on and brain–computer interfaces. Both sco-re highly on the strategic alignment axis for this potential investor even though the latter is a highly speculative technology with an uncertain TAM.Industrial automation meshes with this inves-ting company’s strategy because so many of its applications require onboard processing, giving hardware manufacturers a potential role to play. Several aspects of the robotics value chain also align with hardware manu-facturers’ strengths; onboard chipsets will be an important part of end solutions, as will system engineering and integration across a variety of specialized applications. In terms of portfolio fit, the well-defined applications with known value make industrial automati-on suitable in instances where a path to cash flow is more important.Brain–computer interfaces will require safe, secure hardware. A generic platform (for example, the “Intel Inside” of BCI) will likely win out over single-purpose applications be-cause no user will require multiple interfaces.

These factors position hardware players to capture significant value. BCI technology plays to hardware manufacturers’ strengths; already, some are investing in adjacent tech-nologies such as neuromorphic computing that may provide useful IP to augment BCI, and hardware makers understand the inter-faces required to make BCI a reality. But this is still a speculative ecosystem, so it may prove better suited to investors looking to round out their portfolios with longer-term bets.AI clearly offers some exciting investment potential, but it is not a market to enter casu-ally or with expectations of a rapid return on investment outside of the most mature offe-rings, which will be priced accordingly.

Segmentation of AI ecosystem attractiveness for a hypothetical hardware manufacturer

S T R AT E G I C A L I G N M E N T

Market opportunity, value capture potential, tech m

aturityF

INA

NC

IAL

AT

TR

AC

TIV

EN

ES

S

Copper mine

Fool’s gold

Goldrush

Diamonds in the rough

BI and advanced analytics

Low strategic alignment, high financial attractiveness; pure-play financial—large markets but no magic spark

High strategic alignment and financial attractiveness; solid nuggets with large markets and path to synergy

Low strategic alignment and financial attractiveness; may look flashy, but better left alone

High strategic alignment, low financial attractiveness; real value from searching the non-obvious

Complementarity, synergy opportunities, portfolio fit, competitive intensity

Smart bots/task automation

Smart robots

XR systems Autonomous vehicles

Industrial automation

Adaptive networks

Security and surveillance AI hard-/firmware

Brain–computer interfaces

Smart health

Quantum computingAIaaS

Artificial general intelligence

Source: Kearney analysis

Figure 3

MANUFACTURING AND PRODUCTION

TEXT BY AZAZ FARUKI, DR. BENEDIKT FRANK, BENOIT GOUGEON, SUMEET LADSAONGIKAR

It’s now clear that we are living and working in a world destined for continuous change: po-litical instability, economic turmoil, techno-logical disruption, environmental instability, and future pandemics. The recent crisis has challenged all aspects of the supply chain, leading to drastic shifts in demand, produc-tion facility closures, mass layoffs, and tight shipping capacity. As a result, companies are beginning to shift their focus—from creating the lowest-cost supply chains to building re-silience, contingency plans, and risk mitiga-tion into those supply chains.As the pandemic unfolded, manufacturers were faced with an unexpected mismatch between demand and resources, including workforce availability, demand peaks, and regulatory changes. This forced them to find new and creative ways of operating factories that would allow them to meet exceptional demand, mitigate the impacts of the slow-down, or simply continue running, while re-maining compliant with regulation and cor-porate social responsibility commitments.As companies adapted, traditional assump-tions about managing manufacturing and extended supply chains were challenged, opening up a number of new possibilities for organizing operations. As Bertrand Pic-card, the first man to fly around the world in a solar-powered airplane, said: “Innova-tion is often more about removing barriers to unlock existing ideas, than about gene-rating new ones.”While some of their approaches were clear-

Don’t Pay Twice for the Crisis: 8 Lessons for Manufacturing

ly temporary and unsustainable, others have the potential to be more long lasting. In fact, based on our conversations with global COOs and manufacturing executives, many of these solutions will prove useful beyond the imme-diate crisis and enable sustainable improve-ments and step changes in the future. These solutions primarily sit across three areas: peo-ple, process, and technology. See Figure 1.

Get prepared to pivot and adapt to the un-predictableThere is a small window of opportunity to capture the value of learnings from our ex-perience during the pandemic. It is crucial that companies use the momentum that has been created to build on these ideas. There is always a temptation to take the time to fur-ther refine learnings. Resist the urge—other-wise your operations will revert to the way they were. Learnings gleaned from this crisis are only the tip of the iceberg, however. Capturing their full value will require leaders to dig dee-per and expand new ways of working where applicable. This means focusing not only on where new approaches happened to work during the crisis, but on where they might work in other situations or areas. For exam-ple, labor flexibility proved to be possible between maintenance and production du-ring the crisis. Why not explore flexible staf-fing models between indirect and direct la-bor or between those in quality control and those in production?Translating these learnings into sustainable ways of working will likely not come from the current organization. In fact, if manufactu-

rers return to the status quo, barriers to new practices are likely to arise. Leaders should therefore create a special squad to over-see exceptional changes—a cross-functio-nal team that works in an agile manner, in-cluding sprints, proof of concepts, and other agile practices.Making the most of the current crisis compri-ses three steps. First, map out fundamental assumptions (sacred cows) that were challen-ged in manufacturing plants due to the crisis across people, process, and technology di-mensions. Second, understand what it would take to sustain and scale these changes be-yond this crisis. Third, embed these changes in new ways of working by making simulta-neous changes in organization structure, key performance indicators, and incentives.

None of this is easy, because these are deci-sions that can affect a company’s future ma-nufacturing processes and operating model. But we have learned—and are still learning—from the pandemic that manufacturers need to be prepared to pivot and adapt to the un-predictable. Those that find a way will come out ahead. Those that fail to do so will find that opportunity eludes them.

11 22 33 448 lessons for manufacturing

Build a multi-skilled,adaptable workforce

Share capabilitiesand team with other

companies

Pool resources and allocate them

dynamically

Challenge level of indirect employees

physically working in a plant

55 66 77 88Boost performance and customer experience

by refocusing portfolio on the core

Build optionality for greater resilience in

supply chains

Shoot for agility – reduce time to market

for new products

Avoid disruption – use technology to

ensure a safe working environment

Source: Kearney analysis

This is an extract from the White Paper “Don’t pay

twice for the crisis: 8 lessons for manufacturing”.

Discover the full version

“There is a small window of opportu-

nity to capture the value of

learnings from our experience during

the pandemic.”

Connect with BenoitConnect with BenediktConnect with AzazConnect with Sumeet

ENERGY

COVID-19 re-energizing the energy transition

TEXT BY ROMAIN DEBARRE, RICHARD FORREST, TOM HARPER, SAFIA LIMOUSIN

The pandemic is the first crisis of its kind with unusual implications for the energy industry. A sharp drop in car-bon emissions has revealed the size of the climate change challenge.

The combination of COVID-19 and an oil shock has disrupted the global transition to green energy. Businesses that had been racing to establish their position in a low-carbon world are now fixated on short-term safety and stability. As the industry looks forward, the ru-les of the game have changed. Agile players that understand how this new normal will impact their strategies will win the energy tran-sition race.

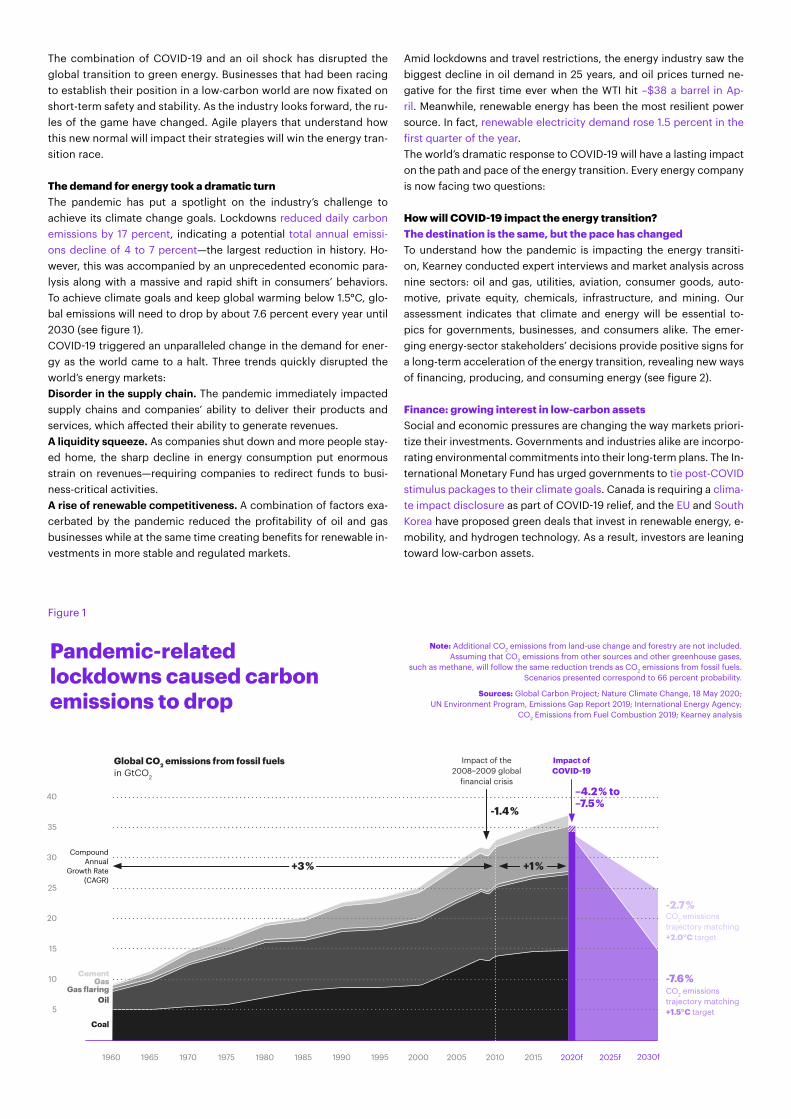

The demand for energy took a dramatic turn The pandemic has put a spotlight on the industry’s challenge to achieve its climate change goals. Lockdowns reduced daily carbon emissions by 17 percent, indicating a potential total annual emissi-ons decline of 4 to 7 percent—the largest reduction in history. Ho-wever, this was accompanied by an unprecedented economic para-lysis along with a massive and rapid shift in consumers’ behaviors. To achieve climate goals and keep global warming below 1.5°C, glo-bal emissions will need to drop by about 7.6 percent every year until 2030 (see figure 1). COVID-19 triggered an unparalleled change in the demand for ener-gy as the world came to a halt. Three trends quickly disrupted the world’s energy markets: Disorder in the supply chain. The pandemic immediately impacted supply chains and companies’ ability to deliver their products and services, which affected their ability to generate revenues. A liquidity squeeze. As companies shut down and more people stay-ed home, the sharp decline in energy consumption put enormous strain on revenues—requiring companies to redirect funds to busi-ness-critical activities. A rise of renewable competitiveness. A combination of factors exa-cerbated by the pandemic reduced the profitability of oil and gas businesses while at the same time creating benefits for renewable in-vestments in more stable and regulated markets.

Amid lockdowns and travel restrictions, the energy industry saw the biggest decline in oil demand in 25 years, and oil prices turned ne-gative for the first time ever when the WTI hit –$38 a barrel in Ap-ril. Meanwhile, renewable energy has been the most resilient power source. In fact, renewable electricity demand rose 1.5 percent in the first quarter of the year.The world’s dramatic response to COVID-19 will have a lasting impact on the path and pace of the energy transition. Every energy company is now facing two questions:

How will COVID-19 impact the energy transition? The destination is the same, but the pace has changedTo understand how the pandemic is impacting the energy transiti-on, Kearney conducted expert interviews and market analysis across nine sectors: oil and gas, utilities, aviation, consumer goods, auto-motive, private equity, chemicals, infrastructure, and mining. Our assessment indicates that climate and energy will be essential to-pics for governments, businesses, and consumers alike. The emer-ging energy-sector stakeholders’ decisions provide positive signs for a long-term acceleration of the energy transition, revealing new ways of financing, producing, and consuming energy (see figure 2).

Finance: growing interest in low-carbon assets Social and economic pressures are changing the way markets priori-tize their investments. Governments and industries alike are incorpo-rating environmental commitments into their long-term plans. The In-ternational Monetary Fund has urged governments to tie post-COVID stimulus packages to their climate goals. Canada is requiring a clima-te impact disclosure as part of COVID-19 relief, and the EU and South Korea have proposed green deals that invest in renewable energy, e-mobility, and hydrogen technology. As a result, investors are leaning toward low-carbon assets.

Pandemic-related lockdowns caused carbon emissions to drop

40

35

30

25

20

15

10

5

1960 1965 1970 1975 1980 1985 1990 1995 2000 20102005 2015 2020f 2025f 2030f

Global CO2 emissions from fossil fuelsin GtCO2

Note: Additional CO2 emissions from land-use change and forestry are not included. Assuming that CO2 emissions from other sources and other greenhouse gases,

such as methane, will follow the same reduction trends as CO2 emissions from fossil fuels. Scenarios presented correspond to 66 percent probability.

Sources: Global Carbon Project; Nature Climate Change, 18 May 2020; UN Environment Program, Emissions Gap Report 2019; International Energy Agency;

CO2 Emissions from Fuel Combustion 2019; Kearney analysis

Impact of the 2008–2009 global

financial crisis

-1.4 %

-2.7 %CO2 emissions trajectory matching +2.0°C target

-7.6 %CO2 emissions trajectory matching +1.5°C target

Coal

Oil

CementGas

Gas flaring

Impact of COVID-19

–4.2 % to –7.5 %

+3 %Annualincrease +1 %

Figure 1

Compound Annual

Growth Rate (CAGR)

Produce: a transformation of the power mix makes strategic sense for many COVID-19 has accelerated the transformation of the energy mix. For example, targets to reduce greenhouse gas emissions were part of many oil and gas strategies before the pandemic, but oil majors such as BP, Shell, and Total have strengthened their ambition by announ-cing a net-zero target by 2050. The lifetime carbon impact of pro-ducts and services is now coming to light, and if consumers or re-gulators start making decisions about what they buy based on the overall carbon impact, entire value chains will be impacted.

Consume: consumer behaviors are driving shifts in demand and decarbonization, but the pace and nature of these changes vary More than 85 percent of organizations have encouraged or man-dated that their employees work from home. As a result, road traf-fic plummeted by more than 40 percent, and digital collaboration tools have enjoyed a major surge. Many companies are saying these

remote ways of working will be the new normal, and some govern-ments are adapting their mobility regulations to become more effi-cient. These shifts reveal the power of consumers—both businesses and individuals—to create major shifts.

How should companies respond? For now, most businesses are focusing on survival. But as the number of COVID-19 cases decreases and work picks up, leaders will need to prepare for what comes next.

Technology is borderless; adoption is localThe pandemic has provided a catalyst to reshape the path for-ward. The right strategy will take into account at least four dimen-sions: regulation, technology economics, technology constraints, and consumers’ acceptance and demand. When making business decisions, take an end-to-end view on the investments, ecosystem partnerships, and potential moves from other companies to ensure sustainable business models.

“The right strategy will take into account at least four dimensions:

regulation, technology economics, technology constraints,

and consumers’ acceptance and demand.”

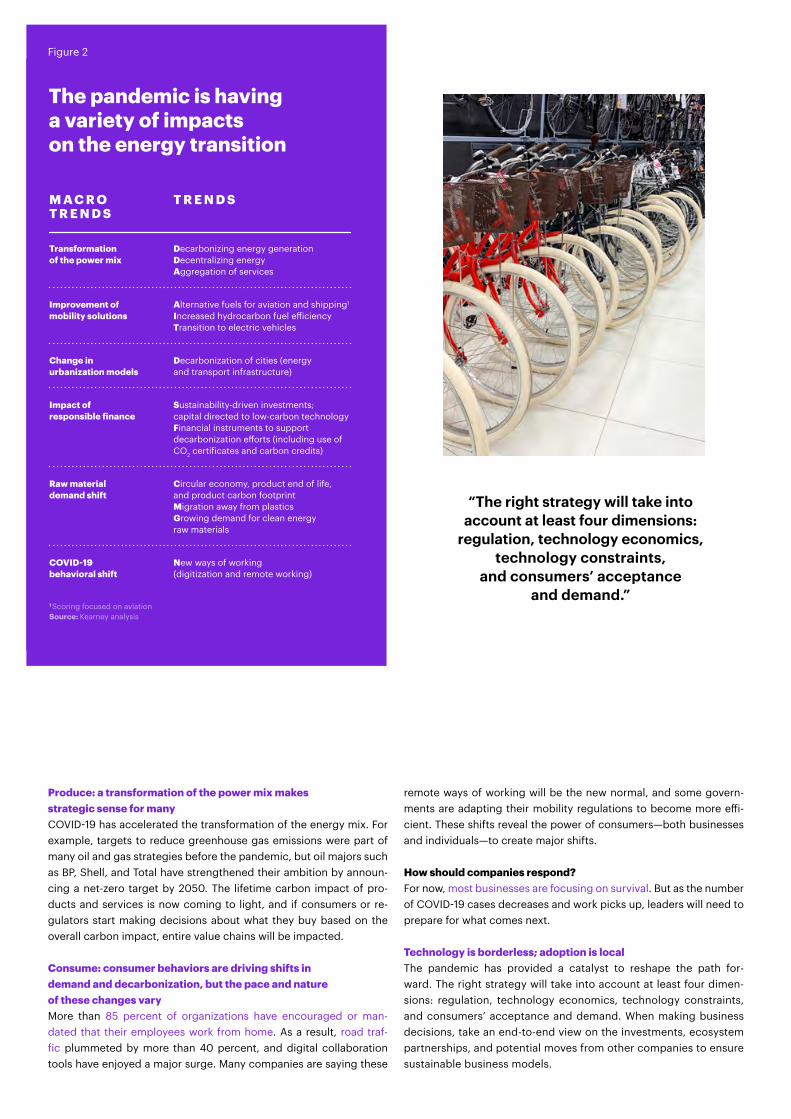

The pandemic is having a variety of impacts on the energy transition

M A C R O T R E N D S

T R E N D S

Decarbonizing energy generationDecentralizing energyAggregation of services

Transformation of the power mix

Alternative fuels for aviation and shipping1

Increased hydrocarbon fuel efficiencyTransition to electric vehicles

Improvement of mobility solutions

Decarbonization of cities (energy and transport infrastructure)

Change in urbanization models

Sustainability-driven investments; capital directed to low-carbon technologyFinancial instruments to support decarbonization efforts (including use of CO2 certificates and carbon credits)

Impact of responsible finance

Circular economy, product end of life, and product carbon footprintMigration away from plasticsGrowing demand for clean energy raw materials

Raw material demand shift

New ways of working (digitization and remote working)

COVID-19 behavioral shift

1 Scoring focused on aviationSource: Kearney analysis

Figure 2

Connect with Romain Connect with RichardConnect with Tom Connect with Safia

Don’t miss the “green recovery” funding Energy companies’ focus is switching from ad-dressing the immediate implications of CO-VID-19 to navigating the downturn that the pan-demic has triggered. Stimulus packages and financial support seem to be central to many go-vernment strategies. Bold moves and rapid ac-tion will be needed to get on board the “green recovery funds” when they appear.

Drive an agenda with M&A opportunities and strategic partnerships Small and large businesses are in a unique po-sition to explore radical moves that weren’t on the table before the pandemic. No one business has all of the capabilities to win, but a combina-tion of service, consumer platform, and geogra-phical footprint undoubtedly hold the key. With COVID-19 shifting balance sheets and altering priorities, now is the ideal time to reassess part-nering and M&A strategies.

Reset supply chains for post-pandemic de-mand while making a leap for decarbonization COVID-19 has forced a supply chain reset, and management tends to be laser-focused on busi-ness continuity in the short term—shedding light on opportunities to make big steps forward. “We have seen two years’ worth of digital transfor-mation in two months,” Microsoft CEO Satya Nadella said. These opportunities will be central to readjusting cost bases in the short term. It is not inconceivable that some form of end-to-end carbon pricing becomes embedded into the cost of producing and selling across the globe.

Watch out for sudden and seismic consumer shifts As consumer behaviors begin to force busines-ses to adapt, companies have had to respond quickly. With COVID-19 putting a spotlight on the amount of change needed to achieve the climate change targets, the leaders will find a credible way to track, understand, and respond. Although not straightforward, the geopolitical, pandemic, and social forces will li-kely trigger the next consumer-led shift in the near future.

Spurring the energy transition COVID-19 has revealed both the instability of hydrocarbon markets and the endorsement for comparatively stable revenues of low-carbon infrastructure investments. Amid the immediate economic shock, financial recovery plans are taking shape. At this time of mas-sive change, not taking the risks of an acquisition or a bold move to latch onto a regulation or stimulus change should be weighed against the consequences of inaction. The long-term winners of the energy transition will be shaped over the next few years, and early movers are likely to see the biggest rewards. Agility and bold leader-ship will be vital at this important crossroads.

To read the full report please visit Kearney.com

The authors wish to thank Anna Martynenko, Christian Tapolcai, Amy Reynolds, and Caitlin Bailey for their valuable contributions to this report.

“The long-term winners of theenergy transition will be shaped over the next

few years, and earlymovers are likely to see the biggest rewards. Agility and bold leadership will

be vital at this important crossroads.”

How coronavirus has accelerated the adoption of

Artificial Intelligence by pharmaceutical companies

HEALTHCARE

TEXT BY PAULA BELLOSTAS MUGUERZA

and treatment, and sophisticated technolo-gies will only help speed up the process of finding the most effective medicines.In January, Google DeepMind debuted AlphaFold which predicts the structure of several under-studied proteins, including those associated with COVID-19. Predicting protein structures would typically be a long drawn out process, but now scientists can use this technology to better understand the novel coronavirus, thus helping in the quest for a vaccine that triggers an optimum im-mune response. Scientists are also able to use AI to sift through all existing literature on a disea-se, study the disease’s structure and consi-der how effective certain drugs might be in treating it, which has helped them determine drugs currently available on the market that could be repurposed to treat the virus. AI can also track the spread of diseases and pick up anomalies that might be of concern. Intriguingly, Canadian artificial intelligence platform BlueDot was able to detect a cluster of unusual pneumonia cases in Wuhan befo-

Coronavirus has accelerated the shift to digi-tal across sectors, which have adapted their products, services and operating models to fit the current climate. Most companies were already digitising pre-pandemic, but corona-virus injected increased urgency to make the change. The pharmaceutical industry has of-ten been considered a laggard in terms of its digital maturity, but its pivotal role in the coro-navirus crisis has provided companies across the sector with the impetus to rapidly imple-

ment the most cutting-edge technologies. At the heart of the majority of these digital ad-vancements are AI and machine learning. AI in the fight against COVID-19AI often conjures up dystopian imagery, but there is no greater testament to the bene-fits of artificial intelligence and machine le-arning than if they can assist with the current crisis. With a collective sense of uncertainty, many are pinning their hopes on a vaccine

re the world even knew about coronavirus. In certain countries, such as China, AI is being used in collaboration with track and trace apps on phones to aggregate and analyse data about the virus and learn about how contagious it is and how it spreads. Companies have already started AI transformationsCoronavirus might have led to an uptick in companies using AI to clear the path for breakthroughs, but firms have already been adopting these sophisticated technologies in all areas of healthcare.A recent study by Kearney revealed 68% of global industry leaders in the pharmaceutical and healthcare sectors see AI and advanced analytics as major value drivers, so most firms are well aware of their combined potential. An example of a company leading the way is Novartis. With the combined efforts of CDO Bertrand Bodson and visionary Head of Drug Development John Tsai and key members of the team like Bruno Villetelle, the drug ma-nufacturer has amassed a database of a de-cade’s worth of clinical trials, which forms the core of an AI-powered central command centre. Scientists and technicians at Novartis have been able to analyse all its global clini-cal trials to predict trial schedules and quali-ty outcomes across the organisation. The firm has also employed AI to facilita-te its drug development process, compi-ling 20 years of data from 2 million patients and using this information to design pionee-ring new drugs. Critically, they are not do-ing it alone but reaching out into the eco-system through their innovation centre in Silicon Valley, which actively partners with AI and machine learning start-ups working in the biopharma field. The case of Novartis demonstrates how important it is that com-panies adapt their working methods and in-vest shrewdly to successfully implement an AI transformation.Similarly, the medical device company, Med-tronic, has created alliances with both tech giants and promising start-ups to develop in-novative AI-supported products. The firm ac-quired technology from Nutrino, a nutrition insights platform that had built a predictive glycemic response algorithm, and with this platform, partnered with IBM Watson to crea-te a glucose monitoring tool that predicts whether a diabetic patient will have low glu-cose within a one-to four-hour period. Disease management tools are likely to wit-ness a proliferation of valuable applications in the aftermath of the coronavirus pande-mic as the long-term impacts of the virus are, as yet, poorly understood. A further negati-ve side effect of the pandemic has been a wholesale delay and sometimes suspension of treatment for people with chronic condi-

tions. This will create a backlog requiring ur-gent attention as the pandemic recedes. AI tools will be critical to managing this backlog effectively, and companies will likely need to implement these technologies to rejuvenate their business methods. The barriers to adoption AI is incredibly useful, but it has its limitations. These drawbacks have caused resistance to its adoption by some companies and health-care providers. First and foremost, data is not infallible and bias within data sets can lead to biases being inherently built into algorithms. Privacy and cybersecurity risks are also top of mind for Chief Data Officers across the indus-try as well as the significant infrastructure in-vestment required to integrate data sets and create data lakes that the organisation can tap into for research and commercial insights. Despite these concerns, artificial intelligen-ce might be the productivity multiplier that the pharmaceutical company needs more than ever right now. What’s on the horizonThere are exciting developments on the ho-rizon for AI in healthcare – from discovery to diagnostics to care delivery and ongoing pa-tient monitoring. In areas like pain manage-ment, we are now on the brink of being able to blend artificial intelligence and virtual reali-ty to create simulations that cocoon patients from their pain or the pangs of withdrawal. This might help with the dependence that many patients have on powerful painkillers. Companies like Helpsy are developing chat-bots to help with patient care. These chat-bots can nurse and triage patients. In the future we may see virtual nursing assistants become commonplace, but there’s no deny-ing the value of in-person care.

“There are exciting developments on the horizon for AI in healthcare – from discovery to diagnostics to care delivery

and ongoing patient monitoring.”

Connect with Paula

We will also likely see surgeries conducted with robotic assistance. AI-assisted robotics can analyse previous surgical data to guide the surgeon’s hands. Research found an AI-assisted robotic technique created by Mazor Robotics demonstrated a five-fold decrease in surgical complications compared with sur-geons operating unaided.The pharmaceutical industry has been scru-tinised in recent years over R&D productivi-ty, pricing and obsolete engagement mo-dels, and AI and machine learning could be the game changer technologies that trans-form the sector. With coronavirus domina-ting people’s concerns, more sophisticated tech could lead us towards a vaccine or cure. What’s more, with delays in treatments and other illnesses being neglected whilst co-ronavirus cases fill hospitals, the medicines and treatments that we receive at the other end of this crisis will have to be capable at dealing with a backlog of sick patients. AI might just be the key to achieving a success-ful resolution.

Joy, really? In these challenging times, joy can frequently feel like a distant memory. That’s why now, more than ever, discussions need to be held on how to cultivate more joy@work—wherever and whenever “work” may be. On this podcast, we’ll interview leaders and thinkers about how to bring more joy into our everyday work lives. We’ll have conversations around creating solidarity, connection, and communi-ty on our teams as an enabler of a larger societal move toward higher purpose, equality, and justice in our No Normal world.

Download the latest episode:Managing a global team through empathic leadership, with Alicia TillmanSAP is literally at the center of global business; the company touch-es nearly 80 percent of the world’s transactions. Global CMO Alicia Tillman oversees thousands of employees across the world and her core values of transparency, empathy, and good corporate citizen-ship have helped her guide her team through this tumultuous time.What does it mean to lead with empathy now, and in the future? Alicia joined Kearney Chairman and Joy@Work Host Alex Liu to dis-cuss the importance of empathy in leadership, the structural steps she’s taken to address issues of diversity and inclusion, and how she’s balanced all of these responsibilities during the pandemic.

You can listen to this episode and subscribe to the fortnightly series on Apple podcast, Google Play, Stitcher, or Spotify. To listen to the season two trailer, hear our 3 other podcasts in this series released to date, or learn more about our upcoming guests, click here.

Joy@Work – season 2

KEARNEY PODCAST

HOST: ALEX LIU, MANAGING PARTNER, KEARNEY

Connect with Alex

C R E D I T S

Concept, editing, design

SZ Scala GmbH, Munich

Dominik Wüchner, Moritz Gaudlitz, Ellen Verick,

Iryna Baumbach

Photos and illustrations

All images by Kearney

As a global consulting partnership in more

than 40 countries, our people make us

who we are. We’re individuals who take as

much joy from those we work with as the

work itself. Driven to be the difference be-

tween a big idea and making it happen, we

help our clients break through.

kearney.com

This is a publication of A.T. Kearney, Inc.

For more information, permission to reprint or translate this work, and all other correspond-

ence, please email [email protected].

A.T. Kearney Korea LLC is a separate and independent legal entity operating under the Kearney

name in Korea. A.T. Kearney operates in India as A.T. Kearney Limited (Branch Office), a branch

office of A.T. Kearney Limited, a company organized under the laws of England and Wales.

© 2020, A.T. Kearney, Inc. All rights reserved.

A B O U T U S