Warrants - ASX Online

39

Understanding trading and investment warrants Warrants

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Warrants - ASX Online

Understanding trading and investment warrants

Warrants

ASX DerivativesA division of Australian Stock Exchange Limited (ABN 48 001 314 503)

Disclaimer of liabilityThe information contained in the Warrants Explanatory Booklet(which includes any insert/s and is hereafter referred to as ‘theBooklet’) is provided by Australian Stock Exchange Limited (ASX),and its subsidiaries in good faith. Although ASX has made everyeffort to provide accurate information at the date of publication,it does not give any representations or warranties as to theaccuracy, reliability or completeness of the information in theBooklet. Accordingly ASX, its subsidiaries and their employees,officers and contractors shall not, to the extent permitted by law,be liable for any loss or damage arising in any way (including byway of negligence) from or in connection with anything providedin or omitted from the Booklet or from any action taken, orinaction, in reliance on the Booklet.

General information only The Booklet contains general information only. The information isnot intended as, and must not be construed as, investment adviceand does not contain recommendations, reports, analysis or otheradvisory information relating to securities or issuers of securities.Nor does the Booklet contain an invitation or offer to invest insecurities or other financial products or any investment agreementnor to exercise any rights conferred by an investment, to acquire,dispose of, to underwrite or convert an investment or containinformation calculated to lead directly or indirectly to personsdoing so. You should not take any action or fail to do so in relianceon anything contained in, or omitted from, the Booklet. It isrecommended that you consult a licensed adviser (and an ASXaccredited derivatives adviser for warrants or other derivatives) forinformation and advice tailored to your specific objectives,circumstances and needs.

Nothing in the Booklet is to be taken as ASX endorsing, promotingor expressing any opinion on any securities, warrant issuers orwarrant series. Nor do ASX, its subsidiaries or their employees orofficers endorse, promote or express any opinion about, or assumeany responsibility for, any material (in whole or in part) in theBooklet which is acknowledged as someone else’s contribution.

CopyrightThe Booklet is the copyright of ASX 2001. No part of the Bookletmay be copied, reproduced, published, stored in a retrieval systemor transmitted, in any form or by any means in whole or in part(except where such use constitutes fair dealing under theCopyright Act), without the prior written permission of ASX orits subsidiaries.

TrademarksAll Ordinaries and SEATS are registered trademarks of ASXOperations Pty Limited (ABN 42 004 523 782). CHESS is aregistered trademark of ASX Settlement and Transfer CorporationPty Limited (ABN 49 008 504 532).

is a trademark of ASX Operations Pty Ltd.

S&P™ is a trade mark of Standard & Poor’s, a division of TheMcGraw-Hill Companies Inc.

Copyright ASX 2001.All rights reserved.Edition 7, printed April 2001.ABN 98 008 624 691

Introduction 2

Before you begin 3What are warrants? 3About this booklet 3Warrants and ETOs 4

The ASX warrant market 5

Warrant characteristics 7Call or put warrants 7Deliverable or cash settled 7Expiry date 7Underlying instrument 7Exercise style 8Exercise price (or strike price) 8Issue size 8‘Warrants per share’ or conversion ratio 8Covered warrants 9Index multiplier 9Barrier levels 9Cap levels 9

Types of warrants 10Equity warrants 11

International equity warrants 11Equity barrier warrants 12

Index warrants 12Barrier index warrants 13Foreign index warrants 13

Instalment warrants 14Endowment warrants 15Capital Plus warrants 15Low Exercise Price warrants 16Capped warrants 17

Premium Income (PIE) warrants 18Currency warrants 18

Advantages of warrants 19Leverage or gearing 19Speculation 20Investment 20Portfolio protection – hedging 20Limitation of loss 20Market exposure 20Tailored to meet specific requirements 20

Risks with warrants 22Issuer risk – ASX is not a guarantor 22Liquidity risk 22Currency risk 23Leverage (or gearing) risk 23

Suspension from trading 23Limited life 23Early termination or expiry – Extraordinary Events 23National Guarantee Fund not a guarantor in all cases 23General market risks 23

Warrant issuers and the Offering Circular 25Who issues warrants? 25Offering Circulars 25

Trading and settlement 26Secondary trading of warrants 26Warrant codes 26Market making 26Trading information 26Short selling 27Suspension from trading 27Warrant settlement – secondary trading 27Warrant settlement – exercise or expiry 27

When no exercise has occurred 27Issuer fails to meet its obligations 27

Adjustments 27

Warrant pricing 28Price or level of the underlying instrument 28

Delta 28Exercise price and expiry date 29Volatility of the underlying instrument 29Interest rates 30Dividends 30Exchange rates 30Other influences on price 30Time value and intrinsic value 32

How to start trading warrants 33Accredited derivatives advisers 33Warrant client agreement form 33Incentive payments 34Subscribing for warrants 34

Glossary of terms 35

Further information 36The ASX website 36Booklets 36Courses 36Contact details 36

DerivativesDivision

1800 028 585

1

Contents

DerivativesDivision1800 028 585

2

Introduction

Warrants – A new investing alternativeThe 1990s saw a dynamic financial marketbecome established in Australia offeringconcepts that were innovative for privateinvestors. In the past decade characterisedby its innovation, the rapidly growingwarrants market was at the cutting edge.This was achieved by an increased variety ofinvesting choices and opportunities foractive traders and medium and long terminvestors. The growth in the use of warrantsand the development of warrant conceptscontinue to create a new investingalternative for personal investors alongsidetraditional choices like shares, interestpaying securities and investment trusts.

Warrants:• are financial products traded on ASX;• include a no-obligation entitlement to

either acquire or relinquish an interest inanother investment asset, like shares orunits in a trust;

• have a set life during which they exist – a time period – that must always be considered;

• serve a particular purpose thatconcentrates on important aspects ofinvesting in the related assets over aperiod of time: for example, to pursue ashort term trading opportunity, tomaximise the income potential or tomaximise the capital gain that can be earned.

Because different warrants serve differentpurposes, this makes it important todistinguish between them and appreciateexactly what they offer and how they can beused. Before you consider becoming involvedin warrants you need to know the differencesbetween call and put warrants, betweendifferent warrant types such as endowmentand instalment warrants, what indexwarrants do and how currency, portfolio andenhanced income warrants work.

You need to understand the risks of tradingor investing in warrants and the marketgenerally, and what makes warrantsdifferent from the related investments onwhich they are based. All forms of investinghave risks and within investment categories,like the warrant family, the different risks ofparticipation should be appreciated in orderto invest in an informed manner.

This booklet will provide you with a basicintroduction to warrants that you can thenwork from.

John Wasiliev

DerivativesDivision

1800 028 585

3

Before you begin

What are warrants?Warrants are financial instruments issued bybanks and other institutions and are tradedon the Australian Stock Exchange (ASX)equities market. They are very broadly splitinto products with investment purposes andproducts with trading purposes.

Warrants are a form of derivative – that is,they derive their value from another ‘thing’(underlying instrument). Some are contractswhich give holders the right to call fordelivery of, or to put the underlyinginstrument (eg. a share) to the warrantissuer for a particular price according to theterms of issue. Alternatively, others entitleholders to receive a cash payment relatingto the value of the underlying instrument ata particular time (eg. index warrants).

Warrants may be issued over securities (suchas shares or debentures), a portfolio ofdifferent securities, a share price index,currencies, or commodities.

The range of financial instruments traded as warrants has evolved over time so that it is now difficult to define particularcharacteristics of all warrants. Warrantscover a wide spectrum of risk profiles,investment objectives and likely returns.

Some warrants have higher risk/returnprofiles than others that offer lower riskfeatures such as capital guarantees.

About this bookletThis booklet contains an outline of commonfeatures and a general description of mosttypes of warrants. It is not an exhaustive or complete analysis of all warrant typesand features.

The main objective is to provide you withgeneral information about warrants andabout some of the risks of trading orinvesting in warrants.

Before buying warrants, you shouldunderstand the terms and risks associatedwith the particular warrant series. Youshould read the disclosure document (calledthe offering circular) prepared by the issuerof the warrants and seek specific advicefrom your accredited derivatives adviser.

Warrants are often a form of option and so (to varying degrees), the basic principlesof options generally apply to warrants. Thisbooklet assumes you have a reasonableunderstanding of the basic principles of options. Page 36 contains details of where you can obtain further informationabout options.

Risk/Return Spectrum

Lower Risk Higher Risk

Lower Return Higher Return

Capital Guaranteed Medium or Shorter Short Term SophisticatedProducts Term Investments Trading Products

eg Capital plus eg Instalments eg Barrier index warrants

Longer Term Investment Short Term TradingStyle Products Productseg Endowments eg Equity and Instalments and Index Warrants

▲

The booklet also contains various commentsby John Wasiliev, a financial reporter. Johnhas many years experience reporting onfinancial markets. In particular, Johncurrently has a weekly warrant column in“The Australian Financial Review” whichreports on the latest trends and productswhich are brought to the marketplace.

ImportantIt is important that you understand:

• ASX grants permission for warrants tobe traded on its market (called‘admission to trading status’) on theapplication of warrant issuers. ASXdoes not guarantee the performance ofwarrant issuers nor does it vouch forthe accuracy of the offering circular.

• You must make your own creditassessment of the warrant issuer of aparticular warrant series.

• Warrants have a limited life and cannotbe traded after the relevant expirydate. The terms of a warrant series maybe subject to adjustments or thewarrants may expire early in particularcircumstances. Depending upon thecircumstances the price of mostwarrants will fall rapidly as theyapproach expiry.

• Warrants do not have standardisedterms. The terms may vary considerablybetween different series (even betweenwarrants of the same type) anddifferent warrant issuers. You shouldseek information regarding the specificterms of issue for a series of warrantsbefore you trade in a series.

• There are different risk and returnprofiles for different warrant series.Some warrants have features that makethem more risky than others. You shouldseek specific advice about the risks andfeatures of a warrant series from youraccredited derivatives adviser.

• Some advisers may be paid commissionsor other benefits by warrant issuers inrelation to the sale of particularwarrants. Your adviser is obliged todisclose to you any commissions orother benefits which may influencehis/her recommendation.

Warrants and ETOsASX also operates a derivatives market forexchange traded options (ETOs). To varyingdegrees (depending on the type), warrantshave similarities to ETOs which distinguishthem from shares.

Warrants and options are primarily financialproducts that allow you to gain exposure to the underlying instrument withoutnecessarily owning that instrument.

Warrants and ETOs do not give directcontrol over the underlying instrument untilexercise and unlike shares, will expire aftera certain period of time. There are howeversome key differences between warrants andETOs such as:

• Warrants are traded on the ASX equitiestrading system – SEATS – whereas ETOsare traded on the ASX options tradingsystem – DTF (Derivatives Trading Facility).

• Settlement of warrant trades occurs onCHESS in the same manner as sharetransactions are processed. The OptionsClearing House Pty Ltd (OCH), whichcontrols the clearing of ETOs has noinvolvement in settling warrant trades.

• Unlike ETOs, you cannot write warrantsand there are no margin paymentsassociated with warrants to cover the risk of financial loss due to adversemarket movements.

• The terms of ETOs are standardised andare set by ASX, whereas the terms ofdifferent warrant series are set by theissuer and can be quite diverse.

• There are more types of warrants thanETOs. Some of these types of warrantshave little in common with ETOs.

DerivativesDivision1800 028 585

4

DerivativesDivision

1800 028 585

5

The ASX warrant market

Warrants are traded in many key financialmarkets of the world. ASX has operated awarrant market since 1991.

Trading in warrants in Australia has becomeincreasingly popular in recent years. Thefirst chart shows the increase in the numberof warrants traded. The second chart showstrading volume and value in recent years.

The market began by trading equity callwarrants only. Others types have beenintroduced over time. There are now anumber of different warrants available for trading or investment including equity warrants, instalment warrants, index warrants, currency warrants andendowment warrants. These (and others) are discussed later in this booklet.

As at 6 April 2001 there were 13 activewarrant issuers and over 930 warrant seriesavailable for trading or investment.

Monthly period

0

50

100

150

200

250

300

350

Mar-01

Dec-00

Sep-

00

Jun-0

0

Mar-00

Dec-99

Sep-

99

Jun-9

9

Mar-99

Dec-98

Sep-

98

Jun-9

8

Mar-98

Dec-97

Sep-

97

Jun-9

7

Mar-97

Dec-96

Sep-

96

Jun-9

6

Mar-96

Dec-95

0

100

200

300

400

500

600

700

800

900

1000

Warrants – New Listings and Month-end Totals

Total warrants at m

onth-end

Warrants quoted during month

Total warrants at month-end

War

rant

s qu

oted

dur

ing

mon

th

Appreciate the relationshipsWarrants are offered on a range oftraditional and non traditional investmentassets. Examples of traditional assets areshares in companies and units in investmenttrusts. There are also warrants on somefascinating non-traditional investmentassets. They include specially constructedportfolios of shares, warrants on currenciesand on local and international marketindices, like the S&P™/ASX 200 Share PriceIndex, the U.S. Standard & Poors (S&P 500)Index and the Japanese Nikkei 225 Index.

Because you’re not buying or selling theactual investments, but rather buyingwarrants that give you the choice ofwhether to buy or sell – which you may nottake advantage of – warrants can allow aninvesting position to be established for afraction of the cost of a transactioninvolving the actual assets.

In some instances, warrants prices canrepresent a small proportion of the value ofthe related investment: as little as 1–to–2per cent or less for ‘highly geared’ or‘leveraged’ warrants. In other cases, theremay be only a small price differentialbetween the warrant and the investment.Yet in both circumstances and all situationsin between, warrants can offer a differentinvestment result than a commitment to therelated investments.

John Wasiliev

DerivativesDivision1800 028 585

6

Quarterly period

0

500

1000

1500

2000

2500

3000

Mar-01

Sep-

00

Mar-00

Sep-

99

Mar-99

Sep-

98

Mar-98

Sep-

97

Mar-97

Sep-

96

Mar-96

Sep-

95

Mar-95

Sep-

94

Mar-94

$0

$200

$400

$600

$800

$1000

$1200

$1400

Warrant Market Activity (per quarter)

Value ($ millions)

Quarterly volume

Quarterly value

Volu

me

(mill

ions

)

Some features or characteristics form partof many warrants. Some of these aredescribed below – some appear in allwarrant types and some do not. As we statemany times, warrants do not necessarilyhave standardised terms. The terms arespecified by the warrant issuer within theconstraints of the ASX Business Rules andthe law. This means the terms may varysignificantly between different warranttypes, between different series of the sametype of warrant and between differentwarrant issuers.

The terms and conditions of a particularwarrant series are set out in a documentprepared by the warrant issuer called anoffering circular. To obtain a copy of anoffering circular, you should speak to youradviser or the warrant issuer. Some warrantissuers put their offering circulars on theirweb sites. A number of offering circulars arealso available on the ASX website.

When reading the offering circular, youshould be aware that some issuers usedifferent terminology for different types ofwarrants. Where this occurs, the offeringcircular will generally contain a table tocross-reference the terms to generallyknown concepts.

Call or put warrantsWarrants can be either call warrants or putwarrants. Call warrants benefit from anupwards price movement in the underlyinginstrument whereas put warrants benefitfrom a downward trend.

A deliverable call warrant generally givesyou the right to buy the underlyinginstrument (eg a share) from the warrantissuer at a particular price on, or before, aparticular date. A deliverable put warrantgenerally gives you the right to sell theunderlying instrument to the warrant issuerat a particular price on, or before, aparticular date. For cash settled calls andputs, the value of the warrant is paid to you in cash.

Deliverable or cash settledDeliverable warrants are settled in the firstinstance by a transfer of the underlyinginstrument, eg. equity warrants. Cashsettled warrants are settled by a cashpayment by the warrant issuer to you, eg.index warrants. Some deliverable warrantsmay also provide for cash settlement incertain circumstances.

In some cases a large number of warrantsmay need to be exercised to give rise to adelivery obligation, eg. international equitywarrants. The terms of issue will identify anyexercise conditions.

Expiry dateThe expiry date is the last date on which thewarrant can be exercised. Trading in awarrant generally ceases on the expiry date.Under some circumstances warrants may beexpired early if the warrant has been validlyexercised the issuer will be obliged to deliveror take delivery of the underlyinginstrument or make a cash paymentaccording to the terms of the warrant series.

Underlying instrumentA warrant derives its value from some other ‘thing’ or instrument. It is generallythe instrument which you have the right to buy or sell or against which a cashpayment is made. The underlyinginstrument may be a security (such as ashare in a company), a share price index, acommodity or a currency. Some warrantsare over a ‘basket’ or ‘portfolio’ of securities. The basket may consist of securities inentities with similar activities, for examplemining or manufacturing. Warrants over abasket of securities give exposure to theperformance of a group of securities or aparticular industry. In some circumstances,the underlying instrument may be adjustedduring the life of the warrant. The offeringcircular should explain when this may occur.

DerivativesDivision

1800 028 585

7

Warrant characteristics

A warrant derives its value from someother instrument.

Exercise styleWarrants are usually American style orEuropean style exercise. American stylemeans you can exercise the warrant at anytime on or before the expiry date. Europeanstyle means you can only exercise thewarrant on the expiry date of the warrant.Occasionally warrants are a mixture ofAmerican and European, eg. they may beEuropean up to a point and then Americanthereafter. The terms of the warrant serieswill set out how you may exercise thewarrant. You should be familiar with theterms relating to exercise. A failure to followthe terms may mean the exercise of thewarrant is not effective. Warrants may betraded on ASX up to and including theexpiry date.

Exercise price (or strike price)This is the amount of money which must bepaid by you (in the case of a call warrant) orby the warrant issuer to you (in the case ofa put warrant) for the transfer of each ofthe underlying instrument(s) (not includingany brokerage or stamp duty charges).

In the case of cash settled warrants, thedifference between the exercise price(generally called the exercise level) and thevalue of the underlying instrument at expiryis paid on settlement.

The exercise price is generally fixed whenthe warrants are issued. However, theexercise price could be variable. Forexample, the exercise price of endowmentwarrants and some instalment warrants is not fixed. Further, the exercise price ofsome warrants may be in a foreign currency– eg. currency warrants and internationalequity warrants.

Some issuers charge for costs associatedwith the exercise of the warrant (eg. stampduty or brokerage costs), and so the amountpayable on exercise may be more than thestated exercise price.

The exercise price or the basis forcalculating the exercise price will bespecified in the offering circular preparedby the warrant issuer.

Like the underlying instrument, the exerciseprice may be adjusted in certaincircumstances. Again, the offering circularshould explain when this may occur.

Issue sizeThis is the number of warrants that may beissued in a particular warrant series. Thewarrant issuer may reserve the right toapply to ASX to have more warrants issuedin the same series without notice to holders.

Conversion ratio or ‘Warrants per share’The conversion ratio is the number ofwarrants that must be exercised to requirethe transfer of the underlying instrument.The terms of issue may require one warrantto be exercised to trigger settlement.Alternatively, a number of warrants mayneed to be exercised. These are sometimesknown as ‘fractional warrants’.

ExampleA 4:1 call warrant over BHP ordinary sharesrequires you to exercise 4 warrants to buy1 BHP share. Sometimes the ratio worksthe other way, for example, 1 warrantcould be over 2 shares. This may be shownas 0.5:1, but of course, you must alwaysexercise whole numbers of warrants.

Don’t forget that the conversion ratio is notthe only term that must be satisfied totrigger a settlement obligation – refer to theoffer circular for other conditions relatingto a valid exercise.

The conversion ratio will affect the price of the warrants (but not the leverage). Ahigher conversion ratio means a lowerwarrant price. While trading prices arequoted on a per warrant basis the exerciseprice is quoted on a per share (or underlyinginstrument) basis. It is therefore importantto know the conversion ratio of a warrantseries before investing.

The conversion ratio of a warrant may beaffected following a corporate action by the underlying company, eg. as a result of anew issue or a capital reconstruction.

DerivativesDivision1800 028 585

8

DerivativesDivision

1800 028 585

9

Covered warrantsA warrant is said to be covered if thewarrant issuer places the underlyinginstrument in a trust or similar custodialarrangement on behalf of the holder. To becalled ‘fully-covered’, the warrant seriesmust meet particular criteria of the ASXBusiness Rules. Most instalment warrantsare covered.

Index multiplierThis is only relevant to index warrants. It isthe figure used to determine the amountpayable to you on exercise or expiry.

As a formula,

The intrinsic value of a call index warrant on exercise or expiry

= the index multiplier

x (closing level of the index – the exercise level of the warrant).

ExampleIf the closing level of the index is 3,000points and the exercise level of a call indexwarrant is 2,800 points then the warranthas an intrinsic value of 200 points. If theindex multiplier is 1 cent then you areentitled to receive $2.00 per warrant(being $0.01 x (3,000-2,800)).

Barrier levelsSome warrants have barrier features. A barrier level is a defined level that causessome event to occur. Some barriers causethe warrant to terminate before the originalexpiry date. Others may cause anadjustment to the exercise price and barrierlevel (and the warrant continues untilexpiry) but may require you to make anadditional payment to the issuer. Otherbarriers simply cause the exercise price (or level) and barrier to be reset. Theconsequences of triggering a barrier levelwill be specified in the offering circular

for the warrant series. Barrier levels arenominated by the issuer before warrants areissued. The barrier can be above or belowthe exercise price (or level) of the warrant.Warrants may expire worthless if they areout-of-the-money when the barrier istriggered. If however, the warrants are in-the-money, then the issuer may be obligedto pay a cash amount to holders. Thedescriptions of index warrants and equitywarrants in the Types of Warrants sectionof this booklet include examples of warrantswith barrier levels.

Cap levelsSome warrants have their upside potentialcapped at a certain level. This is sometimescalled the cap level.

Cap levels are different to barriers. Caplevels generally do not cause the warrant toterminate but will limit the upside profitpotential of the warrant. A cap level is fixedby the issuer when the warrant is issued. If,on exercise or expiry, the value of theunderlying instrument is above the caplevel, settlement of the warrant is based ona return equal to the cap level (and not thevalue of the underlying instrument). Youcould be entitled to a cash payment or to atransfer of the underlying instrument atvalue equal to the cap level. Cap levels areused in a number of different warrant types.In some warrants the cap level is anessential feature. In these warrants, theposition of the cap relative to the currentshare price has a significant economicimpact on how the warrant works. Thedescription of capped warrants in the Typesof Warrants section of this booklet hasexamples of these warrants.

Calls 407

As at April, 2001

25International 16Cap Plus

Index 32

Puts 116 Endowments 80

Instalments 221

PIE’s 26

Currency 7

DerivativesDivision1800 028 585

10

Types of warrants

There has been strong growth and muchproduct innovation in the warrant market inrecent years. This is likely to continue. Inbroad terms, warrants can be viewed astrading products or investment products.Some may fall into both categories. Tradingproducts are generally frequently tradedand relatively short dated. They have ahigher risk/return profile to the investmentstyle products. Index warrants, currencywarrants and equity warrants usually fallwithin this category. Investment styleproducts have other features to attractinvestors. These warrants tend to be longerdated and are less frequently traded. Theyhave a lower risk/return profile and oftenhave a higher initial outlay compared totrading warrants. Endowment warrants,capital plus warrants and PIE warrants areinvestment style products. Instalmentwarrants bridge the trading-investmentgap, ie. some investors hold shares fortrading purposes and some hold them for

longer term investment purposes and thesame could be said for instalment warrants.

Before buying warrants, you shouldunderstand the risks and features of thewarrant series you are considering. Werecommend you read the offering circularprepared by the warrant issuer and seekadvice from your accredited derivativesadviser. Offering circulars are available onthe ASX web site (www.asx.com.au).

Set out below is a general overview of somedifferent types of warrants. It does notdescribe all warrants on the market. Further,some warrants may have different featuresor a combination of the features described.Therefore, you should not assume that thesedescriptions will reflect particular warrantsyou may consider buying. From time to timewe may add further information about newwarrant types or features to the ASX website at www.asx.com.au.

Types of warrants on ASX

Equity warrantsEquity call and put warrants are issued oversecurities (in some cases securities quotedon an Exchange other than ASX). Theexercise price is usually set reasonably closeto the value of the security at the time ofissue. The expiry date is usually anythingfrom about three months to three yearsfrom the date of issue (average 9 months).Equity warrants can be American orEuropean exercise style and, if exercised, aresettled in the first instance by delivery ofthe underlying security. Equity warrants aregenerally highly traded, particularly whenthey are short dated.

ExampleWarrant code QANWDA Underlying Ordinary shares Instrument Qantas Airways Ltd Warrant type Equity call warrant Expiry date 23 November 2000 Exercise price $3.75 Exercise style American Conversion ratio 1 warrant : 1 share Settlement Physical delivery

This is a call warrant over the ordinaryshares in Qantas Airways Limited (QAN). It isan American style warrant with an expirydate of 23 November 2000 and an exerciseprice of $3.75. The holder of a QANWDAwarrant has the right to buy one QAN sharefor $3.75 on or before 23 November 2000.

International equity warrantsInternational equity warrants are equity calland put warrants over securities quoted onan overseas exchange. This raises otherissues that you should consider. You shouldspeak to your accredited adviser about theadditional complexities of these warrants.For example:

• Time zone differences between ASX’smarket and the overseas market – ie. thehome market for the underlyingsecurities may not be open for trading atthe same time as ASX’s market is open fortrading in the warrants. Note howeverthe securities may be quoted on morethan one exchange and there could betrading hours overlapping with ASX (suchas in Hong Kong).

• Delivery of the underlying securities –the settlement, ownership and custodialarrangements in the overseas jurisdictionwill differ from arrangements in relationto ASX quoted securities. You may needto make arrangements to hold thesecurities overseas.

• ASX supervision – ASX does not superviseor regulate trading in relation to theunderlying securities. This is primarily theresponsibility of regulatory bodies withinthe jurisdiction of the underlyingsecurities. As a result companyannouncements and historical tradingdata will not be available from ASX,although offering circulars will identifyother places where this information canbe accessed.

• Restrictions on exercise – additionalconditions may be placed on exercise, forexample, requiring a minimum (large)number of securities to be delivered beforethe warrants can be validly exercised.

ExampleWarrant code ZMSWGA Underlying Microsoft Corporation Instrument Common stock Home (Principal) NASDAQ ExchangeWarrant type International equity

call warrantExpiry date 23 May 2001 Exercise price US$110 Exercise style AmericanConversion ratio 10 warrants: 1 share Minimum 10,000 warrantsExercise QuantitySettlement Physical delivery

DerivativesDivision

1800 028 585

11

This is an international equity call warrantover the common stock of MicrosoftCorporation. It is an American style warrantwith an expiry date of 23 May 2001 and anexercise price of US$110. The amount paidto exercise the warrants is the Australiandollar equivalent of the exercise price basedon the exchange rate at the time of exercise(calculated in accordance with the terms ofissue). In this example, you must exercise aminimum of 10,000 warrants (with anequivalent exercise value of US$110,000) tocall for delivery of the stock (1000 shares).You could take a smaller position (ie. holdless than 10,000 warrants) and profit frommovements in Microsoft shares by sellingthe warrants in the market rather thanexercising and taking delivery of the stock.

Equity barrier warrantsEquity barrier warrants are equity warrantswith a barrier feature that generally causesthe warrant to terminate before the originalexpiry date. In some cases the triggering ofa barrier level may cause the exercise priceand barrier to be reset.

ExampleWarrant code ECPWNAUnderlying Ecorp LimitedInstrument Ordinary sharesWarrant type Equity barrier

call warrantExpiry date 29 September 2000Exercise price $1.00 Barrier Level $1.70Exercise style European Conversion ratio 2 warrants : 1 shareSettlement Physical delivery

This is a barrier call warrant over the ordinaryshares in Ecorp Limited (ECP). It is a Europeanstyle warrant with an expiry date of 29September 2000 and an exercise price of$1.00. The holder of two ECPWNA warrantshas the right to buy one ECP share for $1.00on 29 September 2000. If prior to expiry themarket price (as defined in the terms of issue)closes at or below $1.70 the warrant willterminate before the original expiry date. Inthe event that the barrier is hit the warrantholder may receive a payment equal to thedifference between the exercise price and theaverage market price over the periodimmediately following the barrier beingtriggered (as calculated in accordance withthe terms of issue).

Index warrants arebased on a share priceindex and may be settledin cash.

Index warrantsIndex warrants are linked to theperformance of a share price index such asthe S&P™/ASX 200 Share Price Index or aforeign index. The exercise level (rather thanexercise price) is expressed in index points.These warrants are cash settled on exerciseor expiry. Generally speaking, indexwarrants are highly traded and short dated(average 3 months).

Example 1 – Call index warrantWarrant code XPIWSA Underlying Share Price IndexinstrumentWarrant type Index call warrant Expiry date 29 November 2000Exercise level 3,100 pointsIndex multiplier $0.005 (1 index point

= half a cent)Exercise style EuropeanSettlement Cash Payment

If the closing level of the Share Price Indexis at 3,300 points on the expiry date, thenyou will be entitled to receive a cashpayment equal to $1.00 per warrant. This iscalculated as the (closing level of the index– exercise level) x index multiplier ie.(3,300–3,100) x $0.005 = $1.00 per warrant.

DerivativesDivision1800 028 585

12

Barrier index warrantsSome index warrants contain barrier levels(see the Warrant Characteristics section ofthis booklet about barrier levels). Theconsequences of triggering the barrier willbe defined in the terms of issue of theparticular warrant series.

Example 2 – Barrier index warrantWarrant code XJOWMAUnderlying S&P™/ASX 200 instrument Share Price IndexWarrant type Resetting barrier

index call warrant Expiry date 28 November 2000Exercise level 3,075 pointsReset Exercise 3,275levelBarrier levels At or below 2,775

points on any business day then the Exercise Level will change to 3,275 points.

Index multiplier $0.005Exercise style European Settlement Cash payment

If the closing level of the S&P™/ASX 200Share Price Index is at or below 2,775 pointson any business day before 28 November2000, then the Exercise Level of the warrantwill change to 3,275 points. As discussed inthe section on barriers, some barriers havedifferent consequences which you will findin the terms of issue.

Foreign index warrantsIndex warrants may also be issued overforeign indices which represent movementson overseas exchanges. These warrants canhave index multipliers in either Australiandollars or the foreign currency (with theforeign amount converted back toAustralian dollars at the time of settlement).You should speak to your accreditedderivatives adviser about the uniquefeatures of foreign index warrants.

Example 3 – Foreign index warrantsWarrant Code XSPWMEUnderlying S&P 500 Composite instrument Stock Price IndexWarrant type Index Call warrantExpiry date 15 December 2000Exercise level 1,525 pointsIndex multiplier US$0.005Exercise style EuropeanSettlement Cash payment

If the closing level of the S&P500 CompositeShare Price Index is 1,675 points on theexpiry date, then you will be entitled toreceive a cash payment equal to US$0.75per warrant. This is calculated as the (closinglevel of the index – exercise level) x indexmultiplier ie. (1,675-1,525) x US$0.005 =US$0.75 per warrant.

InnovationIndex warrants were successful newinnovations for the warrants market in1998. In late 1998 and early 1999 thisconcept was extended to warrants on the US S&P 500 Composite Stock PriceIndex and the Japanese Nikkei 225 Index and to barrier and dual barrier indexwarrants. Currency warrants and cappedwarrants continued the trend towardinnovative products.

John Wasiliev

DerivativesDivision

1800 028 585

13

There tends to be a close relationshipbetween movements in instalment warrantprices and movementsin the underlying shareor other instrument.

Instalment warrantsInstalment warrants give holders the rightto buy the underlying shares or instrumentby payment of several instalments (usuallytwo or three) during the life of the warrant.Instalment warrants are often coveredwarrants with the underlying instrumentbeing held in trust/custody for the benefitof the holder.

A common feature of instalment warrants is that you are entitled to any dividends ordistributions and possibly franking creditspaid by the underlying instrument during thelife of the warrant. Some instalments alsopass on voting entitlements of the underlyinginstrument. An interest component is usuallypart of the payments due.

By their nature, instalment warrants are callwarrants that can be either European orAmerican exercise style and they usuallyhave a life of between 12 months and 10 years. On valid exercise and payment ofthe final instalment, the holder will beentitled to receive the underlyinginstrument. Some also give you an option toput the underlying instrument back to theissuer and receive a cash payment. Not allinstalment warrants have the samestructure or features and you should talk toyour accredited derivatives adviser aboutthe taxation consequences of investing ininstalment warrants.

At the time of issue, the gearing level ofinstalments is usually about 50%, i.e. youpay 50% up front and the issuer lends youthe remaining 50% (plus interest). Someinstalments have higher gearing levels (50%to 100%) when issued. These havesometimes been called ‘HOTS’.

ExampleWarrant code AMPIXAUnderlying Ordinary shares ofinstrument AMP LimitedWarrant type Instalment warrantExpiry date 26 July 2001 Exercise price $10.00 Exercise style EuropeanSettlement Physical delivery

If AMP’s share price was around $20 at thetime of issue of the warrants then youwould have paid about $11 for the warrant(about half the share price at the time plus an element of prepaid interest). You can then pay $10 to exercise thewarrant any time on or before 26 July 2001to receive one AMP share per warrant.

Because you only pay about half of theunderlying share price when buying theinstalment, the issuer lends you the otherhalf of the purchase price. This is why there is a prepaid interest component in thefirst instalment.

There tends to be a close relationshipbetween movements in instalment warrantprices and movements in the underlyingshare or other instrument.

Rolling instalment warrants are a newvariation on existing instalments. They havea much longer life – up to 10 years. Eachyear the exercise price may be reset by theissuer. At the end of each year, you maychoose to take delivery of the underlyingsecurity, cash out the warrant or roll intothe following year. If you do nothing youwill automatically be rolled into thefollowing year. Rolling into the followingyear means that you accept the newexercise price. This may mean that you willneed to pay an additional amount to theissuer. If you don’t pay this amount, theissuer may terminate some of your warrantsand use the proceeds to meet the amountdue. Conceptually, these warrants can beseen as a series of consecutive one yearinstalment warrants with the exercise pricebeing reset each year.

Some instalment warrants may be acceptedas collateral by OCH.

DerivativesDivision1800 028 585

14

Endowment warrantsEndowment warrants are long termwarrants typically with a 10 year life. Theyare generally over an ASX quoted security orbasket of securities and have a Europeanexercise style. Endowment warrants arepromoted as investment products to bebought by investors and held until expiry.

The structure of an endowment warrantprovides for you to pay between 30 and 65percent of the market value of theunderlying security at the time of issue. Theexercise price (called the outstandingamount) is initially the remaining sum plusother costs and is specified when thewarrant is issued. The outstanding amountvaries over the life of the warrant. In thisrespect endowment warrants differ frommost warrants as they do not have a fixedexercise price.

The outstanding amount is reduced by anydividends that are paid in relation to theunderlying security. In some instancesfranking credits and other payments mayalso reduce the outstanding amount.However, an interest rate is also applied andthe outstanding amount is increased bythese interest amounts.

At expiry, if you exercise the warrant and pay the balance of the outstandingamount (if any) the issuer will transfer the underlying securities to you. If thereductions applied against the outstandingamount exceed the interest incurred overthe life of the warrant, the outstandingamount will have decreased. It could reduceto zero prior to or at expiry. If this occursyou may only have to pay a nominalexercise price such as one cent.

An investor in endowment warrants istaking a long term view on the underlyingcompany’s dividend policy versus interestrates with the hope that the dividends willoutweigh the interest payments and theoutstanding amount will reduce over time.

The issuers of endowment warrants canprovide you with details of the outstandingamount and the expiry dates of particularendowment warrant series.

ExampleWarrant code CBAECE Underlying Ordinary shares ininstrument Commonwealth Bank

of Australia Warrant type Endowment warrantExpiry date 18 August 2006Outstanding 9.95 amount when first issued –14 February 1996 Outstanding 7.502amount as at 30 June 2000 Applicable 6.203interest rate* (as at 30 June 2000)

Market price Bid $27.53,of CBA shares offer $27.68 (as at 30 June 2000)

Conversion ratio 1:1 Exercise style European *The interest rate used for this warrant is the 180 day Bank Bill Swap Rate.

Capital Plus warrantsCapital Plus warrants cover a basket ofsecurities specified by the issuer. They areissued for around $1,000 and at least thisamount will be returned to you at expirywhich is usually about 5 years from theissue date. They are generally Europeanstyle warrants and you can elect to eitherreceive the underlying securities or a cash payment (following the sale of theunderlying securities).

Around the issue date, the warrant issuerwill assign a gearing rate, generally between10% and 30%, to the warrants. On expirythe issuer applies this rate to any increase in the value of the portfolio.

DerivativesDivision

1800 028 585

15

ExampleYou buy Capital Plus warrants on 30March 2000 over a basket of securities inthe following companies: AMC, AMQHA,BLD, CBA, CSR, GIO, LLC, NAB, ORG SRP,BHP, and WOW. The cost of each warrantis $1,000. The number of shares of eachcompany in the basket is determined bythe issuer so that the total value is$1,000. The gearing rate for thesewarrants is 15%.

Assume the value of the basket has risento $2,000 on the expiry date. You couldexercise the warrant and call for deliveryof the basket or alternatively, you couldinstruct the issuer to sell the securities inthe basket. If you decided to receive thecash payment, you would be entitled toreceive your initial $1,000 investmentplus an amount equal to the increase in the value of the basket plus an extra15% of this increase.

SummaryValue of the basket on expiry $2,000Initial value of basket $1,000Increase in value $1,000

Payment to holderInitial investment $1,000Increase in value $1,000Gearing (15% of profit) $150

Total payment to holder $2,150

If the value of the portfolio had fallen tosay $500 at the expiry date then theinitial investment of $1,000 would bepaid to the warrant holder.

Low Exercise Price warrantsA low exercise price warrant is usually anequity call warrant with an exercise pricethat is very low relative to the market priceof the underlying instrument at the time of issue (eg. 1 cent). The buyer of a lowexercise price warrant effectively pays the full value of the underlying instrumentat the outset.

DerivativesDivision1800 028 585

16

Sorting out investment warrantsInstalment and endowment warrants areboth more investment style than tradingwarrants. With endowment warrants, the time period is long term – about 10 years. Endowment warrants arestructured in such a way that dividendsare applied toward the outstandingamount and at expiry a payment as smallas 1 cent may be all that is necessary toexercise the warrant, although it couldbe more if the dividends don’t cover thebalance owed and interest obligations.The time involved in instalment warrantsis shorter: from 12 months to 3 years (butup to 10 years in some cases). The initialdeposit is also substantial, generallyaround 50 per cent of the agreedpurchase price. But the agreement thistime is that any dividends andimputation credits that flow throughfrom the shares are received by thewarrant holder.

John Wasiliev

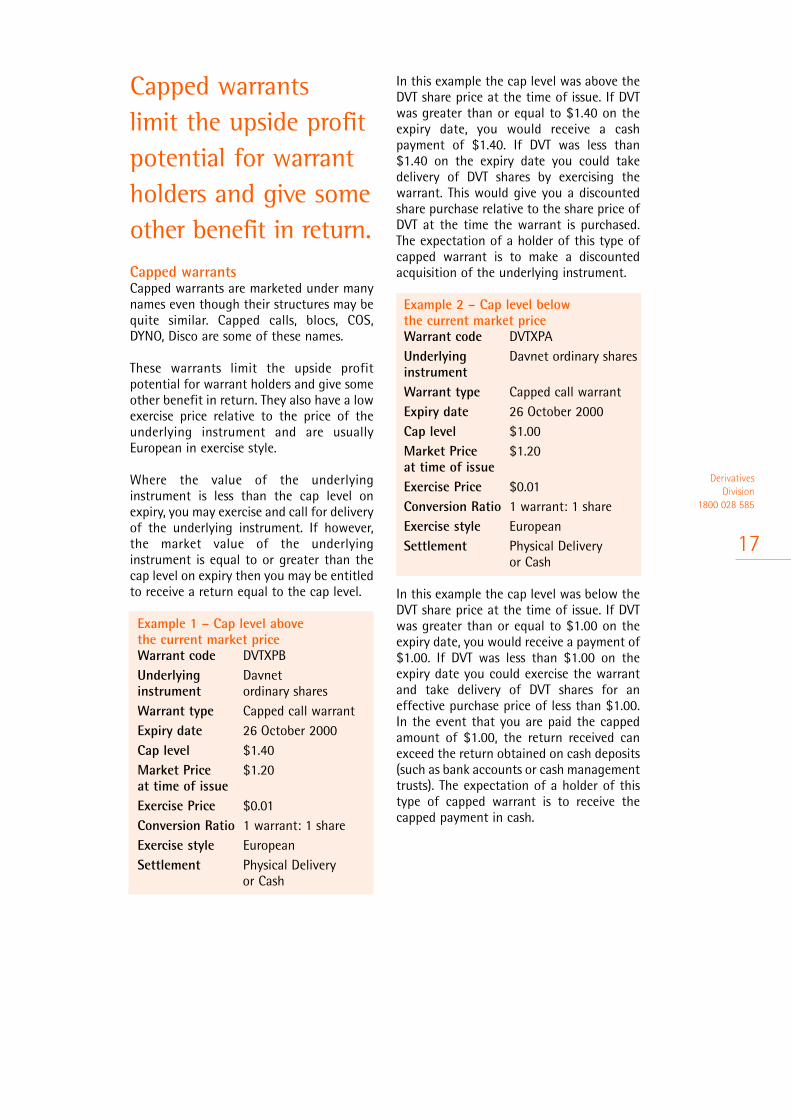

Capped warrants limit the upside profitpotential for warrantholders and give someother benefit in return.Capped warrantsCapped warrants are marketed under manynames even though their structures may bequite similar. Capped calls, blocs, COS,DYNO, Disco are some of these names.

These warrants limit the upside profitpotential for warrant holders and give someother benefit in return. They also have a lowexercise price relative to the price of theunderlying instrument and are usuallyEuropean in exercise style.

Where the value of the underlyinginstrument is less than the cap level onexpiry, you may exercise and call for deliveryof the underlying instrument. If however,the market value of the underlyinginstrument is equal to or greater than thecap level on expiry then you may be entitledto receive a return equal to the cap level.

Example 1 – Cap level above the current market priceWarrant code DVTXPBUnderlying Davnet instrument ordinary sharesWarrant type Capped call warrantExpiry date 26 October 2000Cap level $1.40Market Price $1.20at time of issueExercise Price $0.01Conversion Ratio 1 warrant: 1 shareExercise style EuropeanSettlement Physical Delivery

or Cash

In this example the cap level was above theDVT share price at the time of issue. If DVTwas greater than or equal to $1.40 on theexpiry date, you would receive a cashpayment of $1.40. If DVT was less than$1.40 on the expiry date you could takedelivery of DVT shares by exercising thewarrant. This would give you a discountedshare purchase relative to the share price ofDVT at the time the warrant is purchased.The expectation of a holder of this type ofcapped warrant is to make a discountedacquisition of the underlying instrument.

Example 2 – Cap level below the current market priceWarrant code DVTXPAUnderlying Davnet ordinary sharesinstrumentWarrant type Capped call warrant Expiry date 26 October 2000Cap level $1.00Market Price $1.20at time of issueExercise Price $0.01Conversion Ratio 1 warrant: 1 shareExercise style European Settlement Physical Delivery

or Cash

In this example the cap level was below theDVT share price at the time of issue. If DVTwas greater than or equal to $1.00 on theexpiry date, you would receive a payment of$1.00. If DVT was less than $1.00 on theexpiry date you could exercise the warrantand take delivery of DVT shares for aneffective purchase price of less than $1.00.In the event that you are paid the cappedamount of $1.00, the return received canexceed the return obtained on cash deposits(such as bank accounts or cash managementtrusts). The expectation of a holder of thistype of capped warrant is to receive thecapped payment in cash.

DerivativesDivision

1800 028 585

17

Premium Income (PIE) warrantsAnother type of capped warrant offers“premium income” as the benefit in returnfor giving up some profit potential. Thesewarrants contain some of the cappedwarrant features mentioned above as wellas some features of instalment warrants.They are issued over a parcel of shares so thewarrants have a high face value. Warrantholders pay most of the value of the parcelup-front and have a right to purchase theparcel for a low exercise price relative to theface value. The parcel of shares is held ontrust for the warrant holders and theyreceive any dividends and franking credits.In addition, holders will receive a furtherdistribution called premium income which is payable by the issuer twice a year andranges from 2% to over 6%.

Like other capped warrants, the upsideprofit potential is capped. For the exampleshown below the cap level is 1.25 times theinitial share price. If on exercise, the shareprice is equal to or less than the cap level,you are entitled to receive the parcel ofshares. However, if the share price is greaterthan the cap level then, on exercise, you areentitled to receive a reducing number ofshares equal to the capped value of thebasket. You may also exercise a put optionand require the issuer to purchase the parceland pay you cash.

ExampleWarrant code NCPXXY Underlying Basket of 428 instrument News Corporation

Limited ordinary sharesWarrant type Premium Income

Equity Warrant Expiry date 20 April 2001Cap level $14.406 Exercise price $1.00 Conversion ratio 1 warrant: 1 basketExercise style European Settlement Delivery/cash

Currency warrants give holders exposure to movements in theexchange rate betweentwo different currencies.

Currency warrantsHolders of currency warrants may exchangean amount of foreign currency forAustralian dollars on or before the expirydate. The value of the warrant rises and fallsin line with movements in the exchangerate. For example, holders of AUD/USD callwarrants benefit from an increase in theAUD/USD exchange rate and holders ofAUD/USD put warrants benefit from adecrease in the AUD/USD exchange rate.

ExampleWarrant code AXUWMB Underlying AUDinstrument Warrant type Call warrant Expiry date 30 November 2000Exercise Level $US6.20 Exercise style European Settlement Physical Delivery

or Cash

In this example, you pay $US6.20 andreceive $A10.00.

“Trigger” currency warrants are essentially‘binary’ or ‘digital’ currency options (alsoknown as ‘all or nothing’ options). In thisparticular type of warrant, if a trigger eventoccurs prior to expiry you receive a fixedcash payment. If a trigger event doesn’toccur the pay out is zero.

The trigger level is normally set ‘out of the money’.

DerivativesDivision1800 028 585

18

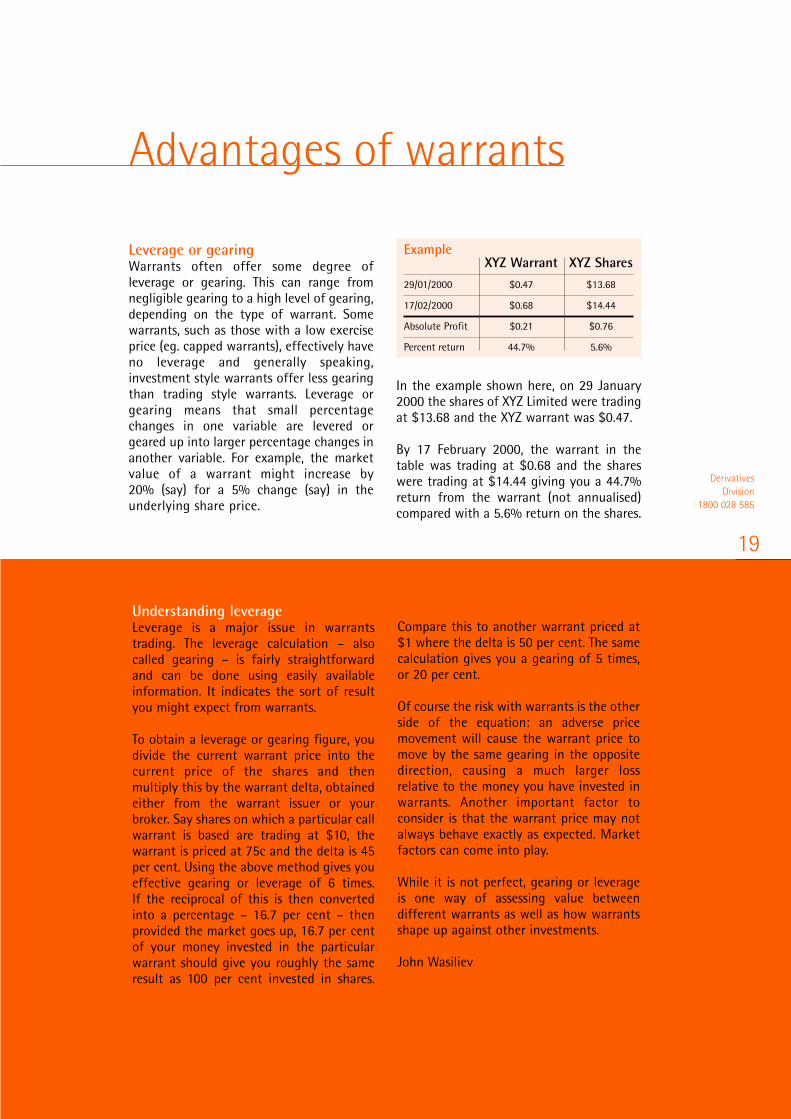

Leverage or gearingWarrants often offer some degree ofleverage or gearing. This can range fromnegligible gearing to a high level of gearing,depending on the type of warrant. Somewarrants, such as those with a low exerciseprice (eg. capped warrants), effectively haveno leverage and generally speaking,investment style warrants offer less gearingthan trading style warrants. Leverage orgearing means that small percentagechanges in one variable are levered orgeared up into larger percentage changes inanother variable. For example, the marketvalue of a warrant might increase by 20% (say) for a 5% change (say) in theunderlying share price.

ExampleXYZ Warrant XYZ Shares

29/01/2000 $0.47 $13.68

17/02/2000 $0.68 $14.44

Absolute Profit $0.21 $0.76

Percent return 44.7% 5.6%

In the example shown here, on 29 January2000 the shares of XYZ Limited were tradingat $13.68 and the XYZ warrant was $0.47.

By 17 February 2000, the warrant in thetable was trading at $0.68 and the shareswere trading at $14.44 giving you a 44.7%return from the warrant (not annualised)compared with a 5.6% return on the shares.

DerivativesDivision

1800 028 585

19

Advantages of warrants

Understanding leverageLeverage is a major issue in warrantstrading. The leverage calculation – alsocalled gearing – is fairly straightforwardand can be done using easily availableinformation. It indicates the sort of resultyou might expect from warrants.

To obtain a leverage or gearing figure, youdivide the current warrant price into thecurrent price of the shares and thenmultiply this by the warrant delta, obtainedeither from the warrant issuer or yourbroker. Say shares on which a particular callwarrant is based are trading at $10, thewarrant is priced at 75c and the delta is 45per cent. Using the above method gives youeffective gearing or leverage of 6 times. If the reciprocal of this is then converted into a percentage – 16.7 per cent – thenprovided the market goes up, 16.7 per centof your money invested in the particularwarrant should give you roughly the same result as 100 per cent invested in shares.

Compare this to another warrant priced at$1 where the delta is 50 per cent. The samecalculation gives you a gearing of 5 times,or 20 per cent.

Of course the risk with warrants is the otherside of the equation: an adverse pricemovement will cause the warrant price tomove by the same gearing in the oppositedirection, causing a much larger lossrelative to the money you have invested inwarrants. Another important factor toconsider is that the warrant price may notalways behave exactly as expected. Marketfactors can come into play.

While it is not perfect, gearing or leverageis one way of assessing value betweendifferent warrants as well as how warrantsshape up against other investments.

John Wasiliev

DerivativesDivision1800 028 585

20

This higher gearing effect associated withthe warrant is also known as leverage.However a decrease in the value of theunderlying instrument will also result in greater percentage decreases in the value of the warrant, ie. leverage works in both ways.

SpeculationA speculator is a trader who is prepared tobear more risk in return for an expectedhigher return. If a speculator believes thatthe value of a particular asset will rise inthe future they could purchase the assetnow in anticipation. An alternative wouldbe to buy a deliverable call warrant over the same asset. The difference betweenthese and other alternatives is the cost of investment.

Purchasing a leveraged warrant costs lessthan purchasing the underlying asset. Thereis however the risk that the warrant will beworthless at the expiry date.

InvestmentSome warrants are structured as longerterm investment style products. Theadvantages of investing in these types of products might be capital growth,income, capital protection or a combinationdepending on the nature of the product.

Portfolio protection – hedgingEquity and index put warrants allow you toprotect the value of your portfolio againstfalls in the market or in particular shares.Put warrants allow you to lock in a sellingprice for the underlying instrument.Protecting your position in this way iscalled hedging. A hedge is a transactionwhich reduces or offsets the risk of acurrent holding.

Limitation of lossIf the value of the underlying instrument isless than the exercise price of the warrantat expiry then a call warrant will expireworthless. Your maximum loss* is theamount paid for the warrant. While youcan lose your entire investment in thewarrants, you have to compare that loss tothe size of the exposure the warrantholding gave you, and what an equivalentexposure in the underlying instrumentwould have cost.

ExampleIf you buy 1000 ANZ call warrants whichhave a current market price of $0.50 perwarrant, then the maximum amount youcan lose is $500 (ie. $0.50 x 1000)*.

However, these warrants may give youexposure to $10,000 (say) of ANZ shares, soa similar exposure in the shares would costyou $10,000. If the share price droppedsignificantly you could lose far more thanthe $500 you invested in the warrants.

(*excluding transaction costs when youpurchase the warrant)

Market exposureSome warrants, such as index and basketwarrants, offer you the opportunity toprofit from movements in the market or ina sector without necessarily owning a largeportfolio which effectively tracks themarket or sector. Foreign index warrants,international equity warrants and currencywarrants allow you to gain exposure tooverseas and other markets.

Tailored to meet specific requirementsWarrant issuers have flexibility instructuring warrants which allows a warrantseries to be tailored to the investment needsof a particular kind of investor. For example,index warrants may appeal to investorslooking to profit from moves in a particularindex over a short period of time, whileendowment warrants may appeal toinvestors looking for long term exposure.

An opportunity to pursue a viewWhen you buy investments like shares, youdo so with the over-riding expectation theprice will go up. There are investment-stylewarrants – instalment, endowment, andcapital plus portfolio warrants – where thesame strong positive price-relatedexpectation is the main reason for buying.

On the other hand, your expectation whenyou buy a warrant for trading purposes canbe the same or you may think the price ismore likely to retreat. And depending onhow strongly you think the price movementmight be – in whatever direction and overwhat time period you expect your view tobe proved correct – a particular warrant canbe chosen from the range on offer that willbest suit your opinion.

This is one of the most importantcharacteristics of warrants: their specificpurpose of allowing a personal view aboutcertain investments over a specified time to be pursued. The time may be very short,a day, a few days, weeks or months in thecase of warrants that serve a tradingpurpose. Or there are warrants that aredesigned as investments as they can bebought with a time horizon measured inyears. Yet because warrants are traded onthe market, it is possible to change a vieweither after it has delivered a desired result;or if for some reason, a strategy no longerseems appropriate.

John Wasiliev

There are certain risks involved in investingand trading warrants. This section outlinessome of the general risks associated withmost warrants, but it does not deal with allaspects of risks associated with warrants.Different warrant series will have specificrisks and different risk profiles. You shouldonly invest in warrants if you understandthe nature of the products (specifically yourrights and obligations) and the extent ofyour exposure to risk. Before you invest youshould carefully assess your experience,investment objectives, financial resourcesand other relevant considerations anddiscuss these with your accreditedderivatives adviser. You should not rely onthe booklet as a complete explanation of therisks of investing in warrants.

Issuer risk – ASX is not a guarantorWhile ASX provides the platform forwarrants to be traded, neither ASX nor itssubsidiaries in any way guarantee theperformance of the warrant issuer or thewarrants issued.

Each warrant is a contract between thewarrant issuer and you. You are thereforeexposed to the risk that the issuer (or itsguarantor, where relevant) will not performits obligations under the warrant. You must make your own assessment of thecredit risk associated with dealing with thewarrant issuer.

Warrant issuers are not covered by marginsor other forms of security lodged with ASX,OCH, or any other party. The risks associatedwith issuing warrants are managed entirelyby the warrant issuer. Covered warrantsallow the issuer to reduce this risk by placingthe underlying instrument in a coverarrangement to meet its obligations underthe warrant.

To help you evaluate the ability of an issuerto meet its obligations, the offering circularcontains information on the financialsituation of the issuer and guarantor (ifapplicable). Some issuers are listed on ASXand therefore provide this information tothe market on a regular basis.

...there are no spread or quantityobligations applied tothe market makingrequirements.

Liquidity riskThis is the risk that you will not be able tosell your warrants for a reasonable price inthe market. This could be because there areinsufficient orders to buy your warrants, orthe price at which others are prepared tobuy them is very low. Warrant issuersundertake to ASX to make markets bymaintaining buy and sell orders in themarket for the life of the warrant. This is toensure there is sufficient liquidity in awarrant series so that you can readily buyand sell warrants. However, there are nospread or quantity obligations applied to themarket making requirements. The quality ofmarket making will depend on competitivepressures. In times of extreme volatility thereliability of market makers to maintain amarket will be put under stress. You shouldbe aware that in these situations, thepresence of suitable quotes in the marketcannot always be assured.

DerivativesDivision1800 028 585

22

Risks with warrants

DerivativesDivision

1800 028 585

23

Currency riskInternational equity warrants and indexwarrants may give rise to foreign currencyrisk. In the case of index warrants thiscurrency exposure may arise where theindex multiplier is denominated in foreigncurrency. Likewise, international equitywarrants may give rise to currency risk.

Leverage (or gearing) riskAs well as being a benefit, leverage orgearing is also a risk of trading warrants.This concept is discussed in the Advantagesof warrants section.

Suspension from tradingASX may suspend or remove a warrantseries from trading, for example, if thewarrant issuer is unwilling, unable or failsto comply with the ASX Business Rules.ASX may also suspend trading in warrantsin the interests of maintaining a fair andorderly market and to protect investors. A relevant consideration would be thesuspension of the underlying security of anequity warrant.

Limited lifeWarrants have an expiry date and thereforea limited life. On expiry warrants ceasetrading and can no longer be exercised. It ispossible a warrant will expire without yourexpectations being realised. You shouldmake an assessment whether the warrantsyou have selected have sufficient time toexpiry for your market views to be realised.Also, a warrant’s value erodes over its life.This is called time decay. Time decayaccelerates as warrants near expiry.

Early termination or expiry –Extraordinary EventsIn certain circumstances a warrant mayterminate or lapse before the expiry date. An example would be where anextraordinary event occurs or some barrierlevels are triggered. Barrier levels arediscussed in the warrant characteristicssection of the booklet.

Issuers generally reserve the right tonominate extraordinary events which mayresult in the early expiry of the warrantseries. These events may vary depending onthe type of warrant. Examples of thepossible extraordinary events include:

• the suspension of trading in the warrant(except if it is caused by the issuer);

• the suspension of trading in theunderlying securities;

• the de-listing of the underlying company;• compulsory acquisition of the underlying

securities following a successful take-over bid.

What actually happens when an extraor-dinary event occurs depends on the type ofwarrant in question and the terms of issuefor that series. The expiry date may bebrought forward or the warrants may simplylapse with a payment in certain circumstances.

Extraordinary events should be taken intoconsideration when assessing the merits ofa warrant.

National Guarantee Fund not a guarantor in all casesThe National Guarantee Fund (NGF) is a poolof assets that is available to meet valid claimsarising from dealings with brokers in certaincircumstances. Under certain circumstancesyou may be able to claim against the NGF inrelation to secondary trading in warrants onthe stock market conducted by ASX. Claimscan in no way relate to the primary issue ofthe warrants or the settlement obligations ofthe issuer arising from the exercise or lapseof the warrant.

General market risksThe market price of warrants is affected bythe same risks that affect all stock marketinvestments such as movements in domesticand international markets, the present andanticipated economic environment, investorsentiment, interest rates, exchange ratesand volatility (see the later discussion forthe impact of volatility on warrant prices).

Disciplines and strategiesThe trading nature of many warrants makesit essential to develop disciplines andstrategies in order to capitalise onopportunities and manage the risks ofinvesting. Given the most importantfundamental is what happens to the price ofthe investment on which the warrant isbased, a logical strategy is trying to predictwhich direction this will go and howpowerfully the price move is likely to beover a period of time.

Establishing a system to predict relatedinvestment price movement must be part ofany serious medium term warrant strategy.A system may be fundamentally driven orbased on technical analysis, or acombination of both. The bottom line is thatit will help determine which warrants tobuy. In warrant-speak, this trading approachis described as a directional strategy. It is astraightforward strategy for new entrantsand the aim is trying for a maximum profitbased on a directional view. But thedirectional view must also include a view ontime. You will buy a different warrant if youexpect investment action to take place nextweek as distinct from some time over thenext three to six months. You might beprepared to take more premium decay riskin a more immediate transaction. Decay isalways greater the closer a warrant movestowards expiry. Warrant premiums decay

slower the more time there is before thewarrant expires.

An alternative strategy is to trade on viewsof whether warrants are cheap or expensive.This is a short term “quick profits” strategyfor the dedicated, informed and wellresourced market participant.

The strategy is generally described asvolatility trading as it focuses not so muchon broad directional trends but on thevolatile price vibrations that warrants candisplay. When the price of a relatedinvestment (like shares) becomes volatile,rising sharply or falling dramatically, a gapcan develop in the relationship between theinvestment and the warrant. The warrantscan trade in a more volatile or a less volatilefashion than the shares, by displayingextreme or unexpected price behaviour.

If a warrant price becomes more volatile, saya call warrant rises more sharply on arelative basis when a share price rallies orremains strong and independent of anyprice retreat, it becomes more expensive.Warrants become cheap if the price doesn’tmove in line with the related investment or even moves in the opposite direction than expected.

John Wasiliev

Who issues warrants?Warrants may only be issued by institutionsthat meet the eligibility criteria set out inthe ASX Business Rules. In general terms,institutions eligible to issue warrants must:

• be subject to the Banking Act; or• be a government; or• have a securities dealers licence (or

overseas equivalent), an investment gradecredit rating, and sufficient net tangibleassets;

• have a guarantor that meets any of theabove categories, or

• issue fully covered warrants.

In addition, other institutions which are notobjected to by ASX and the AustralianSecurities and Investments Commission(ASIC) may also issue warrants.

A list of all warrants and warrant issuers isavailable on the ASX internet site. Go towww.asx.com.au and look in the Warrantsection under Trading Information.

Offering CircularsWarrant issuers are required to produce anOffering Circular for warrant series. AnOffering Circular sets out information forinvestors to assess the risks, rights andobligations associated with the warrant andthe warrant issuer’s capacity to fulfill itsobligations. An offering circular must begiven to all persons offered or invited tosubscribe for the warrants.

A list of all warrants andwarrant issuers is availableon the ASX internet site.Go to www.asx.com.au andlook in the warrant sectionunder Trading Information.

The Offering Circular will generally containthe terms of issue of a warrant series. Theterms of issue are the contractual rights andobligations of both the issuer and warrantholder. In addition to the terms, the issuermay have other obligations, for example,under the ASX Business Rules.

You are encouraged to read the relevantoffering circular and terms of issuedocument before investing in a particularwarrant series. Offering circulars areavailable on the ASX web site (asx.com.au).

ImportantWhile ASX considers a proposed warrantseries as part of an application foradmission to trading status, ASX does notwarrant the accuracy or truth of thecontents of the offering circular.Admission to trading status should not betaken in any way as an indication of themerits of the particular warrants or issuer.

Neither ASX, its subsidiaries, and theNational Guarantee Fund in no wayguarantee the performance of thewarrant issuer. You must independentlyassess the credit worthiness of thewarrant issuer.

DerivativesDivision

1800 028 585

25

Warrant issuers and the Offering Circular

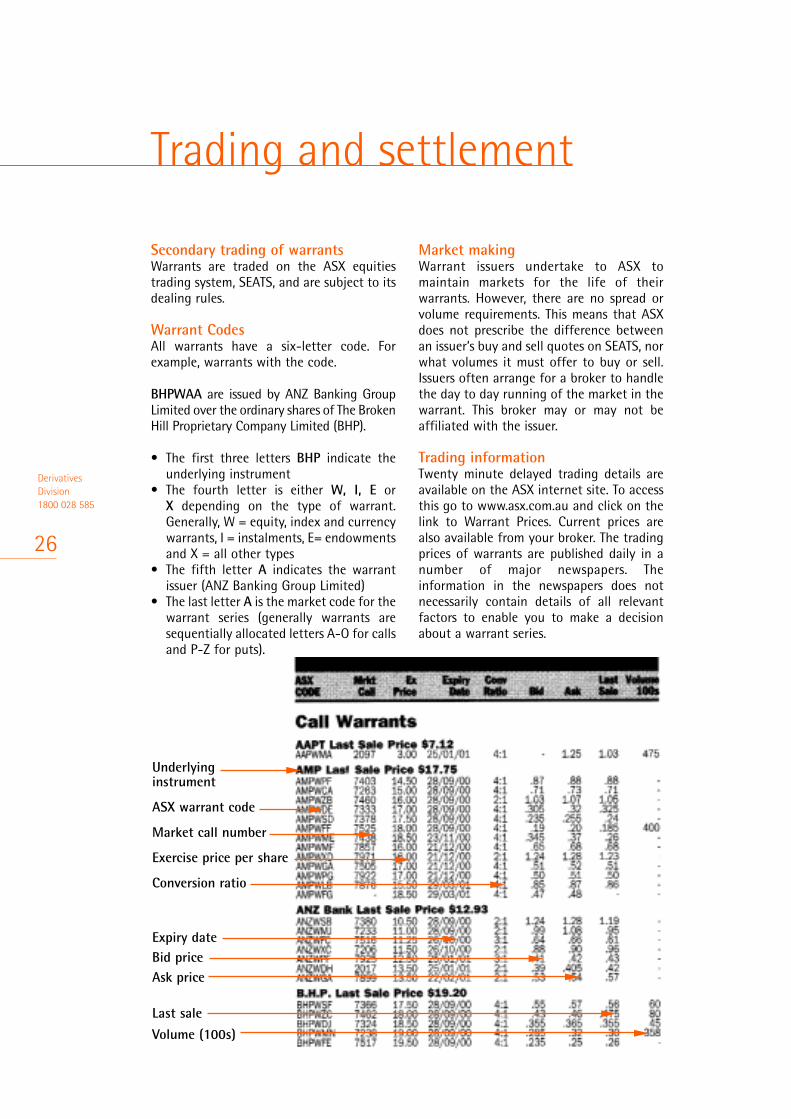

Secondary trading of warrantsWarrants are traded on the ASX equitiestrading system, SEATS, and are subject to itsdealing rules.

Warrant CodesAll warrants have a six-letter code. Forexample, warrants with the code.

BHPWAA are issued by ANZ Banking GroupLimited over the ordinary shares of The BrokenHill Proprietary Company Limited (BHP).

• The first three letters BHP indicate theunderlying instrument

• The fourth letter is either W, I, E or X depending on the type of warrant.Generally, W = equity, index and currencywarrants, I = instalments, E= endowmentsand X = all other types

• The fifth letter A indicates the warrantissuer (ANZ Banking Group Limited)

• The last letter A is the market code for thewarrant series (generally warrants aresequentially allocated letters A-O for callsand P-Z for puts).

Market makingWarrant issuers undertake to ASX tomaintain markets for the life of theirwarrants. However, there are no spread orvolume requirements. This means that ASXdoes not prescribe the difference betweenan issuer’s buy and sell quotes on SEATS, norwhat volumes it must offer to buy or sell.Issuers often arrange for a broker to handlethe day to day running of the market in thewarrant. This broker may or may not beaffiliated with the issuer.

Trading informationTwenty minute delayed trading details areavailable on the ASX internet site. To accessthis go to www.asx.com.au and click on thelink to Warrant Prices. Current prices arealso available from your broker. The tradingprices of warrants are published daily in anumber of major newspapers. Theinformation in the newspapers does notnecessarily contain details of all relevantfactors to enable you to make a decisionabout a warrant series.

DerivativesDivision1800 028 585

26

Trading and settlement

Underlying instrument

ASX warrant code

Market call number

Exercise price per share

Conversion ratio

Expiry dateBid priceAsk price

Last sale

Volume (100s)

▲▲

▲

▲

▲

▲

▲

▲

▲

▲

Short sellingShort selling occurs where a person sellssecurities which he or she does not own atthe time of the transaction. As a generalrule, warrants are not permitted to be shortsold in the market. This means that youmust generally own a warrant before youmay sell it.

Suspension from tradingRefer to discussion in the section Risks with warrants.

Warrant settlement – secondary tradingFor secondary trading warrants are settledin the same manner as other securitiestraded on SEATS. This is through the equitiessettlement system, CHESS. OCH, whichclears ETO transactions, is not involved inwarrant transactions.

Details of warrant trades are sent to CHESSto effect settlement. For this to occur, youmust be either issuer-sponsored or broker-sponsored. Your broker can help you withsponsorship arrangements.

You are required to settle your warranttransaction within the normal settlementperiod for a share transaction and you willreceive regular statements of your warrantholdings in the same manner as shareholdings. You will receive a HolderIdentification Number (HIN) if you arebroker-sponsored or a Shareholder ReferenceNumber (SRN) if you are issuer-sponsored.

If the warrant has anintrinsic value on expiry,warrant issuers aregenerally required topay you a cash paymentof at least 90% of theintrinsic value if youdon’t exercise.

Warrant settlement – exercise or expiryA warrant offering circular will explain therequirements for a valid or effective exerciseof the warrant. Generally, you will berequired to lodge an exercise notice on orbefore a certain time. You must ensure therequirements for exercise are met to ensurethe warrants are validly exercised. A failureto validly exercise (or an ineffectiveexercise) may mean that you are not able toinsist on transfer of the underlyinginstrument. It should be noted that in thecase of international equity warrants,transfer of the underlying instrument islikely to occur in an overseas jurisdiction.For further information, see the Types ofWarrants section of the booklet aboutinternational equity warrants.

When no exercise has occurredIf you hold deliverable warrants but do notexercise them before expiry you may beentitled to a cash payment, often called an“assessed value payment” (or AVP). If thewarrant has an intrinsic value on expiry,warrant issuers are generally required to payyou a cash payment of at least 90% of theintrinsic value. Again the offering circularwill explain the circumstances in which thispayment will be made and how the paymentwill be calculated.

Issuer fails to meet its obligations When a deliverable warrant is exercised theterms of issue will provide for delivery ofthe underlying instrument and payment ofthe exercise price. If a warrant issuer doesnot meet its settlement obligations within20 business days following valid (oreffective) exercise, you may ask for aliquidated damages payment. Alternatively,you could pursue other legal remediesagainst the issuer.

AdjustmentsThe offering circular may contain termsproviding for adjustment to the exerciserights of warrants where there is a changeto the underlying instrument. Where theunderlying instrument is an equity security,adjustments generally occur where there isa corporate action such as a reduction incapital, a new issue or reconstruction in theunderlying security. In the case of indexwarrants, adjustments often relate to themodification or discontinuance of theindex. When an adjustment occurs, theunderlying instrument, the exercise priceand other variables could be changed.

DerivativesDivision

1800 028 585

27

It is important to have some understandingof how the market prices of warrants aredetermined. There is no simple answer tothis question and a complete explanation isfar beyond the scope of this booklet.

Warrant pricing is a subset of general optionor derivative pricing and involves the use ofcomplex mathematical techniques to buildpricing models. These pricing models havebeen developed over the past 30 years. Thepioneering work was published by FischerBlack, a mathematician, and Myron Scholes,an economist, in 1973.

Warrants prices are influenced by:

• the price or level of the underlyinginstrument

• the exercise price of the warrant• the expiry date or the time left to expiry• the volatility of the underlying instrument• interest rates• dividends

The table below shows how the variablefactors affect warrant prices.

Price or level of the underlying instrumentThis is perhaps the most obvious of thepricing determinants and it is also the mostimportant. However, a common misunder-standing is to assume that the price of theunderlying is the only determinant ofwarrant value. It is quite possible in somesituations for a share price to go up and yetthe price of a corresponding equity callwarrant to remain steady (or even fall invalue). This could occur if one or more of theother factors had changed and outweighedthe effect of the increasing share price. Inpractice, it is often changes in volatility oran impending dividend payment whichcauses this effect.

DeltaThe rate of change of a warrant price withrespect to a change in the price of theunderlying instrument is called the delta ofa warrant. Theoretical values for call warrantdeltas range from 0 to 1 and put warrantdeltas from 0 to -1.

DerivativesDivision1800 028 585

28

Warrant pricing

▲

▲

▲

▲

Factors in Pricing Change in Change in Call Change in Put Variable Warrant price Warrant price

Exercise Price Increase

Underlying Share Price Increase

Time to Expiry Decrease

Volatility Increase

Interest Rates Increase

Dividend Expectations Increase

▲

▲

▲

▲

▲

▲

▲

▲