Wall Street's Farm Team

26

April 14, 2008 IBERIABANK CORPORATION IBKC/NASDAQ Continuing Coverage: The Little Bank that Could! Investment Rating: Market Outperform PRICE: $ 44.18 S&P 500: 1,328.32 DJIA: 21.34 RUSSELL 2000: 686.07 IBERIABANK is well positioned for the changes in interest rates and oil and gas prices. Hurricane devastation creates opportunities in the Gulf Coast region. Acquisitions in 2007 create challenges and opportunities for 2008. IBERIABANK is sheltered from sub-prime default threats. Experienced management provides strategic direction and consistent returns. Earnings are expected to rise in 2008. Our 12-month target price is $56.67. Valuation 2007 A 2008 E 2009 E EPS $ 3.27 $ 3.99 $ 4.40 P/E 13.5x 11.1x 10.1x CFPS $ 5.82 $ 5.65 $ 6.44 P/CFPS 7.6x 7.8x 6.9x Market Capitalization Stock Data Equity Market Cap (MM): $ 568.64 52-Week Range: $37.44 - $55.97 Enterprise Value (MM): $ 593.92 12-Month Stock Performance: -8.72% Shares Outstanding (MM): 12.87 Dividend Yield: 3.03% Estimated Float (MM): 10.80 Book Value Per Share: $ 38.70 6-Mo. Avg. Daily Volume: 42,883 Beta: 1.06 Company Quick View: Location: Lafayette, Louisiana Industry: Regional Banking Description: IBERIABANK is the second-largest bank holding company based out of Louisiana. Key Products & Services: Consumer and commercial loans and deposits Company Web site: www.iberiabank.com Analysts: Investment Research Manager: Daniela Fernandez de Cordova Lindsay Bofman Elizabeth Heinen Will Petter Kaitlin Snider Wall Street's Farm Team The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's A.B. Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. BURKENROAD REPORTS

-

Upload

independent -

Category

Documents

-

view

3 -

download

0

Transcript of Wall Street's Farm Team

April 14, 2008

IBERIABANK

CORPORATION IBKC/NASDAQ

Continuing Coverage: The Little Bank

that Could!

Investment Rating: Market Outperform PRICE: $ 44.18 S&P 500: 1,328.32 DJIA: 21.34 RUSSELL 2000: 686.07

IBERIABANK is well positioned for the changes in interest rates and

oil and gas prices.

Hurricane devastation creates opportunities in the Gulf Coast region.

Acquisitions in 2007 create challenges and opportunities for 2008.

IBERIABANK is sheltered from sub-prime default threats.

Experienced management provides strategic direction and consistent

returns.

Earnings are expected to rise in 2008.

Our 12-month target price is $56.67.

Valuation 2007 A 2008 E 2009 E

EPS $ 3.27 $ 3.99 $ 4.40

P/E 13.5x 11.1x 10.1x

CFPS $ 5.82 $ 5.65 $ 6.44

P/CFPS 7.6x 7.8x 6.9x

Market Capitalization Stock Data

Equity Market Cap (MM): $ 568.64 52-Week Range: $37.44 - $55.97

Enterprise Value (MM): $ 593.92 12-Month Stock Performance: -8.72%

Shares Outstanding (MM): 12.87 Dividend Yield: 3.03%

Estimated Float (MM): 10.80 Book Value Per Share: $ 38.70

6-Mo. Avg. Daily Volume: 42,883 Beta: 1.06

Company Quick View: Location: Lafayette, Louisiana

Industry: Regional Banking

Description: IBERIABANK is the second-largest bank holding company based out of

Louisiana.

Key Products & Services: Consumer and commercial loans and deposits

Company Web site: www.iberiabank.com

Analysts: Investment Research Manager:

Daniela Fernandez de Cordova Lindsay Bofman

Elizabeth Heinen

Will Petter

Kaitlin Snider

Wall Street's Farm Team

The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's A.B. Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment.

BU

RK

EN

RO

AD

RE

POR

TS

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

2

STOCK PRICE

PERFORMANCE

Figure 1:

5-year Stock Price

Performance

Source: http://finance.yahoo.com. All figures as of April 14, 2008

INVESTMENT

SUMMARY

We give IBERIABANK a rating of Market Outperform. Our 12-month

target price is $56.67 per share, an increase of 28%, from April 14, 2008 at

a price of $44.18. We based our estimates on three different valuation

models: relative price to earnings ratio, price to book value ratio, and the

dividend discount model.

In forecasting the 12-month target price, we considered multiple economic

indicators and the firm’s corporate strategies and goals. Although the

banking industry is severely affected by current economic conditions,

IBERIABANK is better positioned in comparison to the industry average.

IBERIABANK is currently slightly liability sensitive and with falling

interest rates it enjoys increased profits from the spread on its fixed rate

loans. Additionally, IBERIABANK Corp. is not substantially invested in

construction loans, which have been a downfall for a large portion of

banks. IBERIABANK’s strict lending policy in other areas has shown

constant growth and profitability.

Ben Graham

Analysis

Ben Graham is considered the father of fundamental equity analysis. He

developed eight hurdles that can be used to assess the value and growth

potential of stocks. Based on the Ben Graham analysis the Company’s

stock is undervalued because it passes three of the first five hurdles. The

stock is not considered a growth stock because it does not pass any of the

last three hurdles. See Table 8 at the end of this report for a complete

analysis.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

3

PREVIOUS

BURKENROAD

RATINGS AND

PRICES

Table 1: Historical Ratings & Prices

Date Rating Price

04/05/07 Market Perform $60.03

04/20/06 Market Outperform $55.72

10/29/04 Market Perform $46.65

11/18/03 Market Perform $40.33

12/31/02 Market Perform $29.73

11/12/01 Buy $19.59

01/09/01 Buy $15.37

INVESTMENT

THESIS

Based on a 12-month target price of $56.67 per share, we assign

IBERIABANK a rating of Market Outperform. We base this rating on

the following information:

IBERIABANK is

well positioned for

the changes in

interest rates and

oil and gas prices.

Currently, as the nationwide economy heads towards a projected

recession, the Federal Reserve Board is expected to continue lowering

interest rates to stimulate the economy. The Fed Rate is likely to fall as

low as 2.25% by the end of 2008 but is expected to increase in 2009. This

change in the interest rate affects short-term rates more dramatically than

long term rates, which are market driven. IBERIABANK’s liability-

sensitive position is advantageous during this falling interest rate period;

however, it is shifting towards a neutral position in preparation for the

expected rate increase in 2009. This move will benefit IBERIABANK in

the future and the upward sloping yield curve will be advantageous to

IBERIABANK’s spread in 2008. Additionally, as oil and gas prices

continue to rise, IBERIABANK will indirectly benefit through further

deposit growth.

Hurricane

devastation creates

opportunities in the

Gulf Coast region.

While the economic conditions around the country are deteriorating,

IBERIABANK’s locations in southern Louisiana are more isolated from

these effects than other regions in the country because of opportunities that

arose after Hurricanes Katrina and Rita. Currently, the unemployment

rates for Louisiana are low compared to the national average. We expect

this trend to continue as businesses return to the area. Furthermore, with

estimated total rebuilding costs of $127 billion and as families in hurricane

affected regions rebuild, IBERIABANK’s loan and deposit accounts will

continue to grow.

Acquisitions in

2007 create

challenges and

opportunities for

2008.

IBERIABANK’s acquisition of Pulaski Investment Corporation

(“Pulaski”) and Pocahontas Bancorp Inc. (“Pocahontas”) created both

opportunities and challenges for the Company. These acquisitions

transferred some troubled construction loans and nonperforming assets to

IBERIABANK. Pulaski had 4.93% of its loans past due in 4Q07, thereby,

bringing IBERIABANK’s total consolidated past due loans to 1.66%.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

4

This acquisition also exposed IBERIABANK to the unsteady housing and

construction environment in Arkansas. Yet, relative to its peers, the

percentage of construction and development loans within IBERIABANK’s

total loan portfolio remains significantly lower. Despite these difficulties,

IBERIABANK continues to take aggressive action to remedy the situation

for 2008. The effects of this effort to resolve bad loans will result in an

overall growth in IBERIABANK’s earnings. Furthermore, the Pulaski

acquisition created an increase in non-interest income, shielding more of

IBERIABANK’s revenue from the deteriorating economic environment.

IBERIABANK is

sheltered from sub-

prime default

threats.

Prior to the Pulaski and Pocahontas acquisitions, IBERIABANK had no

exposure to sub-prime loans because of the Company’s strict lending

policy. However, with these acquisitions, IBERIABANK assumed a

higher level of marginal construction loans that it has worked diligently to

remove from the Company’s portfolio. Therefore, the Company is well

guarded from the threat of default on sub-prime loans during the poor

economic conditions in 2008.

Experienced

management

provides strategic

direction and

consistent returns.

An experienced management team continues to provide IBERIABANK

with strategic direction and consistent shareholder returns. IBERIABANK

avoids entering saturated markets. Management seeks expansion areas

with minimal banking presence and exploits opportunities in those regions.

In this way, IBERIABANK delivers personalized service and develops

relationships with its customers. This aspect coupled with

IBERIABANK’s ability to diversify product-wise and geographically,

contributes to IBERIABANK’s success and higher shareholder returns.

Earnings are

expected to rise in

2008.

IBERIABANK’s earnings are up 13% from 4Q06 to 4Q07. Deposits also

increased 1% and loans rose 4% in 4Q07 relative to the 3Q07 quarter.

Additionally, IBERIABANK’s shareholders have continued to receive an

annual increase in EPS of 9% over the past seven years. We expect these

increasing trends to continue. IBERIABANK’s stock price has gone up by

16% since 2003; however, its stock price fell by 20% between 4Q06 and

4Q07. This decrease in price can partly be attributed to the economic

slowdown and a bearish market. Yet IBERIABANK is well positioned for

2008. This outlook, accompanied with an expected rise in earnings, will be

reflected in the future stock price.

VALUATION Our twelve month target price of $56.67 was determined via three

different valuation methods: relative price to earnings ratio, price to book

value ratio, and DDM (see Table 2 below for further details).

Relative P/E The price/earnings per share method averages the current price/earnings

ratio for the Company’s peers and multiplies it by forecasted earnings per

share to project future stock prices. This relative valuation model relates

IBERIABANK to its peers and forecasts earnings. Therefore, we gave it a

weight of 50% for a target price of $50.60.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

5

Relative Price/BV The price/book value method uses IBERIABANK’s forecasted book value

per share and relates it to the Company’s peers’ P/BV ratio. We found this

to be another tool that relates IBERIABANK’s future value to that of its

competitors. We gave it a weight of 30% for a target price of $60.60.

Dividend Discount

Model

The dividend discount model uses forecasted dividends and discounts

them to the present period. We found that IBERIABANK’s price per share

was most accurately projected through the dividend discount model.

Therefore, we gave it a weight of 20% for a target price of $65.94.

Table 2: Valuation

Valuation Model Target

Price Weight

Weighted

Valuation

Relative PE $50.60 50% $25.30

Relative BV $60.60 30% $18.18

DDM $65.94 20% $13.19

Target Price 100% $56.67

INDUSTRY

ANALYSIS

IBERIABANK Corporation operates in a competitive environment with

approximately 50 other banks positioned in the southeast area of the

United States. IBERIABANK primarily operates as a holding company

and has a thrift, also known as a savings and loan institution, as one of its

subsidiaries. The three main advantages of using a holding company

structure are an improvement in economies of scale, greater access to

capital, and the ability to spread gains—as well as losses—across each of

the holding company’s subsidiaries. Furthermore, through holding

companies, banks are able to enter and compete in different industry

segments through mergers and acquisitions. In addition to its status as a

holding company, IBERIABANK functions as a commercial bank with its

primary sources of revenues coming from the ability to grow deposits and

issue loans.

Most Influential

Macroeconomic

Factors

Among the most influential economic factors affecting the banking

industry is the Federal Funds Rate, the rate banks charge one another to

borrow funds overnight. The difference between this rate and the rate

banks charge customers is known as the spread and is where a bank can

make profits. The banking industry as a whole started slowing down in

August 2007 when the Federal Reserve began lowering interest rates.

However, the consequences of rate fluctuations on individual banks

depend upon whether the bank is asset or liability sensitive. Liability-

sensitive banks typically hold long-term assets and short-term liabilities.

When interest rates fall, liabilities cost less and asset values do not

decrease drastically. Therefore, liability-sensitive banks, like

IBERIABANK, benefit from falling interest rates.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

6

Credit risk is also among the top economic factors influencing the banking

industry and can pose the most significant risk to a bank’s overall

performance. During an economic boom, banks tend to make loans to less

desirable candidates, known as sub-prime loans. The majority of sub-

prime loans are mortgage loans. When the economy slows down,

borrowers are more likely to default on the sub-prime loans, and

consequently, will increase a bank’s loan losses. IBERIABANK is well

positioned for the ensuing recession because it has no exposure to the sub-

prime loan division.

Currently, there is a dramatic excess of houses on the market. As a result

of the housing market downturn, commercial developers have difficulty

making payments to banks on their construction loans. Hence, banks with

a large percentage of their portfolio consisting of commercial construction

loans experience significant losses. IBERIABANK has relatively low

construction exposure within its portfolio.

The receding market also impacts consumer spending, which results in

fewer consumer loans. Economic forecasts predict that unemployment will

increase in 2008. The prolonged housing slump, rising gas prices, and

consumer sentiment about the slowing economy also greatly impact

consumer spending. As a result, bank revenues across the industry will

experience declines.

Competitive

Environment

The banking industry is an extremely competitive environment with many

barriers to entry. In addition to the strict regulatory environment imposed

by the Federal Reserve, a large amount of capital and a large customer

base are required to create a bank. In Louisiana, no bank holds more than

25% of the market share, and smaller regional banks compete with some

of the larger national banks. Furthermore, the industry is entering a period

of consolidation in which many banks are expanding through the

acquisition of smaller regional banks.

Within the industry, a bank’s customers function as the buyers and the

depositors; the credit market and the central bank, constitute the suppliers.

The buyers have little bargaining power, which is limited to their ability to

use another bank for similar products. The depositors as suppliers have no

bargaining power and must accept the interest rate or price the bank is

willing to pay. Similarly, the credit market and the central bank have

limited bargaining power because the product supplied, money, is

unlimited.

Banks find it difficult to compete based on prices. A bank loses customers

to competition by increasing interest rates as a means of improving profit

margins and because there is wide availability of comparable products.

Therefore, banks create a competitive advantage through diversification of

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

7

their product lines, innovative technology, and improved customer service.

Through its acquisitions over the past several years, IBERIABANK has

expanded the products and services it offers to customers.

Hurricane Katrina

and Hurricane Rita

Two and a half years after the storms, the banking industry in the Gulf

Coast region is still feeling the effects of the 2005 hurricane season.

Building loans for customers in the affected region continue to provide a

significant source of revenues. The Gulf Coast is also experiencing a

steady increase in population as people return to the area. This population

increase, accompanied by lower unemployment and a higher per capita

income, provides an advantage to banks along the Gulf Coast.

COMPANY

DESCRIPTION

IBERIABANK Corporation’s relationship-based approach to banking

began 121 years ago and gives the Company a strong foundation for

tomorrow.

History, Locations,

and Facilities

IBERIABANK Corporation (IBKC/NASDAQ) began its 121 year

history with the formation of Iberia Building Association, the first lending

institution in New Iberia, Louisiana, in 1887. At that time, Iberia Building

Association aimed at helping the working class purchase homes.

The Company remained relatively quiet until the 1980s when it entered a

period of acquisition and expansion that continues today. As the

Company’s operations began to evolve, so did its name. The renamed

Iberia Savings Bank acquired Acadia Savings & Loan in 1989 to build

deposit accounts, diversify product lines, and widen its customer base.

With this acquisition and the many that followed, Iberia Savings Bank was

able to open more branches throughout Acadia and Lafayette Parishes.

When Iberia Savings Bank demutualized and began issuing public stock in

1995, ISB Financial was created as its holding company. Its current

moniker, IBERIABANK, was adopted in 1997. From the Company’s

headquarters in Lafayette, IBERIABANK operates fifty branches in the

Acadiana region, Baton Rouge, New Orleans, and northern Louisiana.

Additionally, the recent acquisitions of Pulaski Investment Corporation,

the holding company for Pulaski Mortgage Company and Lenders Trust,

Pulaski Bank and Trust, and Pocahontas Bancorp., the holding company

for First Community Bank, expanded the bank’s presence into Arkansas,

Oklahoma, Mississippi, Missouri, and Texas and allowed IBERIABANK

to enter title insurance and trust management sectors. IBERIABANK

Corporation currently has approximately 150 combined offices with over

1400 employees.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

8

Figure 2: Branch Locations

Source: SNL Financial

Products IBERIABANK transformed from a small company providing mortgages to

farming communities into a fully inclusive commercial bank for private

and commercial clients. IBERIABANK offers a wide array of deposit and

lending products and services. These include checking and savings

accounts, commercial, consumer, and mortgage loans, brokerage and

insurance services, credit cards, online banking, and a variety of

investment vehicles. Many of these investment products are available

through Iberia Financial Services, a subsidiary of IBERIABANK.

Figures 3 and 4 indicate the composition of IBERIABANK’s deposits and

loan portfolios. According to these charts, certificates of deposit make up

the majority of the Company’s deposits. Additonally, the commericial loan

segment is the largest in IBERIABANK’s loan portfolio.

Figure 3: Deposit Composition

Source: www.sec.gov

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

9

Figure 4: Loan Portfolio Composition

Source: www.sec.gov

Strategy Over three decades of acquisition and expansion, IBERIABANK has

broadened its presence throughout much of Louisiana and the surrounding

area. This steady expansion helps IBERIABANK accomplish its mission

to provide exceptional value-based client service. More convenient

locations allow the Company to better serve its client base—the backbone

of its corporate strategy.

This corporate strategy hinges on exceptional customer service and the

ability to exceed clients’ expectations. The relationship-based approach

relies on local decision making and proximity to the client. IBERIABANK

delivers fast results, allowing the client more time for the things that

matter most in life. In addition to a comprehensive financial product line,

IBERIABANK offers customized products and services that are tailored to

fit individual client needs. More importantly, IBERIABANK’s long-term

strategy is to improve profitability and reduce risk. The ultimate goal of

this strategy is to increase the stock price by showing consistently

increasing earnings.

Finally, IBERIABANK also focuses its strategy towards gaining market

share in Louisiana and entering new markets. It continually strives for

growth that is consistent with high performance. The Company plans to

accomplish its goal through continued expansion via acquisitions and the

development of its new branches while still maintaining its focus on the

importance of building and maintaining client relationships. This strategy

keeps shareholders’ interests in mind.

Competitors IBERIABANK is ranked fifth in market share among 160 institutions in

Louisiana. The bank holds the number one market share in the Acadiana

region, specifically in Lafayette and Iberia. IBERIABANK also has the

second largest market share in the northeastern region of Louisiana. As a

member of the banking, lending, and insurance industries,

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

10

IBERIABANK's top competitors are JPMorgan Chase & Company and

MidSouth Bancorp Inc. Other regional competitors include Capital One

Financial Corporation, GS Financial Corp., Hancock Holding Company,

Teche Holding Company, and Whitney Holding Corp.

Latest

Developments

Although the end of 2007 witnessed an uncooperative interest rate

environment, IBERIABANK was able to continue its project of expansion

through acquisitions and new branch development.

In February 2007, IBERIABANK completed the acquisitions of Pulaski

Investments Corp., the holding company for Pulaski Mortgage Company

and Lenders Trust, for $130.8 million and Pocahontas Bancorp Inc., the

holding company for First Community Bank, for $75.4 million. In April

2007, Pulaski Bank merged with First Community Bank to become

“Pulaski Bank and Trust Company,” a federal stock savings bank

headquartered in Little Rock, Arkansas.

These acquisitions give IBERIABANK exceptional opportunities for

growth. IBERIABANK has diversified its operations by acquiring high-

quality credit card operations and the largest independent title insurance in

Arkansas and Louisiana. Moreover, the acquisitions allow IBERIABANK

to cater to a broad customer base because different industries drive each

state’s economy: Louisiana’s economy is based on oil, natural gas, and

fishing, while Arkansas’ economy excels in manufacturing, food products,

and electrical equipment. A positive impact of these acquisitions is

reflected in IBERIABANK’s rise in quarterly earnings, which can be

attributed in great part to solid loan and deposit growth in the new

branches.

Additionally, IBERIABANK is following up on its largest branch

expansion, which began in 2005. In a 15-month period, the Company

opened 14 new branches in Baton Rouge, Houma, Elmwood, LaPlace,

Prairieville, Slidell, Covington, Broussard, Monroe, and New Orleans,

Louisiana. The main goal is to continue to help clients rebuild their homes

and businesses after hurricanes Katrina and Rita. The Louisiana population

is increasing as people return after the hurricanes; in 2007, the state gained

50,000 new residents. The population rebound will help the bank

accomplish its growth strategy through geographic expansion and client

growth.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

11

Figure 5: Number of Branches

Source: www.fdic.gov.

PEER

ANALYSIS

IBERIABANK’s primary peers were selected based on comparable

business drivers, products and services rendered, target customers, and

location. The following information and data indicates IBERIABANK’s

position among its peers: MidSouth Bankcorp Incorporated, Teche

Holding Corporation, and Whitney Holding Corporation. According to the

data below, IBERIABANK’s higher P/E ratio and lower Dividend Yield

places it as a growth company among its peers.

Table 3: Peer Ratio Comparison

Company Ticker

Symbol

Stock

Price

Market

Cap. P/E

Div.

Yield ROA P/B

Whitney Holding Corp. WTNY 22.03 1,460M 10.05 5.4% 1.42% 1.18

MidSouth Bancorp Inc. MSL 21.50 142.82M 16.37 1.3% 1.06% 2.06

Teche Holding Corp. TSH 34.50 76.31M 11.53 3.9% 0.95% 1.11

IBERIABANK Corp. IBKC 44.18 578.47M 13.75 3.0% 1.02% 1.13

Source: http://finance.yahoo.com. All figures as of April, 14, 2008

MidSouth Bancorp

Incorporated

(MSL/AMEX)

MidSouth targets local individuals and small-to mid-cap businesses

through its 33 locations throughout Louisiana, eastern Texas, and along

the I-10 corridor. MidSouth Bancorp Inc. is the holding company for

MidSouth Bank. In addition to providing standard retail services,

MidSouth Bank also provides real estate mortgages and commercial,

consumer, construction, and short-term business loans. Real estate

mortgages comprise 40% of its loan portfolio and commercial loans

account for an additional 30%.

Teche Holding

Corporation

(TSH/AMEX)

Teche, the fourth-largest publicly traded bank in Louisiana, operates 20

locations throughout southern Louisiana. Teche Holding Corp. serves as

the holding company for Teche Federal Bank, which offers conventional

retail services and an array of loan options to its individual and

commercial clientele. Over 50% of Teche’s loan portfolio consists of

residential mortgages.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

12

Whitney Holding

Corporation

(WTNY/NASDAQ)

Whitney Holding Corp. is the holding company for Whitney National

Bank, with over 140 locations in Alabama, Florida, Louisiana, Mississippi,

and Texas. Whitney meets the needs of its individual and small business

clients through a variety of banking and financial products and services

including, but not limited to, commercial and retail services, mortgages,

and loans. Whitney has expanded from its commercial base to include

international banking, investment, trust, and consumer services. Real

estate and construction loans account for 44% of Whitney’s loan portfolio.

MANAGEMENT

PERFORMANCE

AND

BACKGROUND

IBERIABANK completed a significant overhaul of its senior management

team in the late 1990s. The new team is characterized by noteworthy

banking understanding that persisted through the challenges of the

Louisiana energy crisis in the 1980s. As IBERIABANK continues its rapid

expansion, management's experience is expected to lead the bank in a

promising way.

Return on average equity is a measure of how well management is

performing. The average peer ROE is an average of the Company’s three

main competitors, Whitney Bank, Teche Holdings, and MidSouth

Bancorp. In comparison to its peers, IBERIABANK has performed below

its peers.

Table 4: ROE Comparison

IBERIABANK ROE Average Peer ROE

2007 10.11% 12.25%

2006 12.86% 13.35%

2005 8.41% 11.26%

2004 12.98% 13.05%

Source: http://finance.yahoo.com. All figures as of April 14, 2008

Daryl G. Byrd President and Chief Executive Officer (52)

Mr. Byrd joined IBERIABANK in 1999 as president, and was appointed

chief executive officer in 2000. Mr. Byrd has 33 years of banking

experience, including 30 years in the Louisiana market. Previous positions

include president and chief executive officer for Bank One New Orleans

for one year and executive vice president of First Commerce Corporation

from 1992 to 1998.

Anthony J. Restel Senior Executive Vice President, Chief Financial Officer, and Chief

Credit Officer (38)

Mr. Restel was hired by IBERIABANK in 2001 as vice president and

treasurer. In 2005, he was appointed chief financial officer and senior

executive vice president. Finally, in 2006 he was appointed chief credit

officer. Mr. Restel began his career with First National Bank of Commerce

in New Orleans. He then served as vice president of Bank One’s Energy

Group for four years, before joining the IBERIABANK’s executive

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

13

management team. At IBERIABANK, he implemented the bank's asset

liability management system, established critical processes to provide

short-term and long-term forecasting, and launched a derivative financing

program for the Company’s clients.

Michael J. Brown Senior Executive Vice President (43)

Mr. Brown has worked with IBERIABANK since 1999. He worked for

seven years as senior executive vice president and chief credit officer. He

gave up the latter position in 2006 when he was chosen to manage all of

the Company’s markets, which include Louisiana, Arkansas, Tennessee,

and Oklahoma. Mr. Brown is also responsible for the Company’s wealth

management. Prior to joining IBERIABANK, he served as chief credit

officer for Bank One’s Louisiana commercial operations.

John R. Davis Senior Executive Vice President (46)

Mr. Davis has been responsible for mergers and acquisitions/finance and

investor relations since 2001. He is also the director of financial strategy,

mortgage and title insurance companies. He has served IBERIABANK

since 1999 when he entered as chief strategic planning officer. Before

joining IBERIABANK’s team, he held a similar position in Crestar

Financial in Richmond, Virginia. He also worked from 1993 to 1997 as

senior vice president of First Commerce Corporation in New Orleans.

Michael A. Naquin Senior Executive Vice President (46)

Mr. Naquin has served IBERIABANK since 2004. He serves as senior

executive vice president for each of the banks and is the director of retail,

facilities, and treasury management. Prior to joining IBERIABANK, he

held different senior roles at Bank One, including commercial banking

manager for Arizona and California from 2002 to 2004.

Management

Incentives

IBERIABANK maintains a performance-based compensation program for

its senior executive officers. This is to ensure that the financial interests of

the management and shareholders are aligned. The performance is

measured by an independent consultant and management is rewarded

accordingly. For the quarter ending December 31, 2007, management did

not receive an annual bonus, primarily as a result of the overall poor

performance in the banking industry and management’s not reaching all of

its set goals for the period.

Board of Directors IBERIABANK’s board of directors comprises a well rounded group of

individuals, most of whom are independent of the Company. The chairman

of the board is William H. Fenstermaker, who is also the chairman and

chief executive officer of F. H. Fenstermaker and Associates Incorporated.

Additionally, the board includes a lawyer, a CPA, multiple other company

presidents, vice presidents, and CEOs. Daryl G. Byrd, president and CEO

of IBERIABANK Corporation and IBERIABANK, and Pulaski Bank sits

on the board as well.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

14

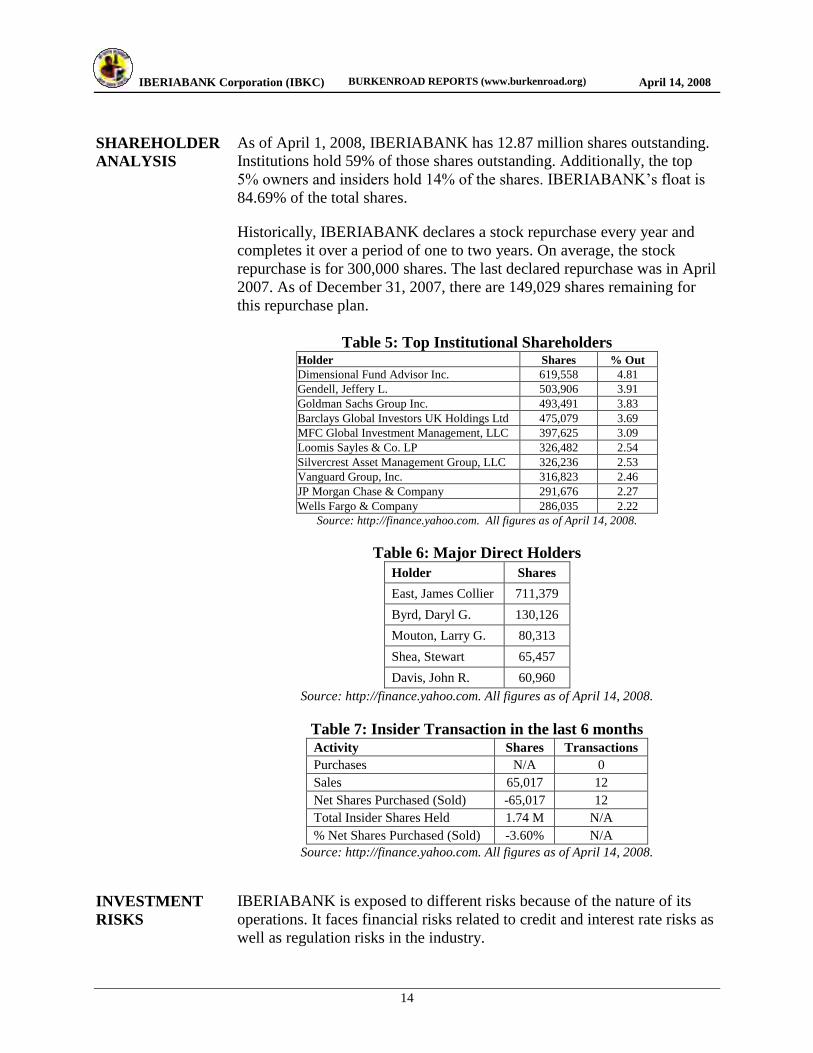

SHAREHOLDER

ANALYSIS

As of April 1, 2008, IBERIABANK has 12.87 million shares outstanding.

Institutions hold 59% of those shares outstanding. Additionally, the top

5% owners and insiders hold 14% of the shares. IBERIABANK’s float is

84.69% of the total shares.

Historically, IBERIABANK declares a stock repurchase every year and

completes it over a period of one to two years. On average, the stock

repurchase is for 300,000 shares. The last declared repurchase was in April

2007. As of December 31, 2007, there are 149,029 shares remaining for

this repurchase plan.

Table 5: Top Institutional Shareholders Holder Shares % Out

Dimensional Fund Advisor Inc. 619,558 4.81

Gendell, Jeffery L. 503,906 3.91

Goldman Sachs Group Inc. 493,491 3.83

Barclays Global Investors UK Holdings Ltd 475,079 3.69

MFC Global Investment Management, LLC 397,625 3.09

Loomis Sayles & Co. LP 326,482 2.54

Silvercrest Asset Management Group, LLC 326,236 2.53

Vanguard Group, Inc. 316,823 2.46

JP Morgan Chase & Company 291,676 2.27

Wells Fargo & Company 286,035 2.22

Source: http://finance.yahoo.com. All figures as of April 14, 2008.

Table 6: Major Direct Holders

Holder Shares

East, James Collier 711,379

Byrd, Daryl G. 130,126

Mouton, Larry G. 80,313

Shea, Stewart 65,457

Davis, John R. 60,960

Source: http://finance.yahoo.com. All figures as of April 14, 2008.

Table 7: Insider Transaction in the last 6 months Activity Shares Transactions

Purchases N/A 0

Sales 65,017 12

Net Shares Purchased (Sold) -65,017 12

Total Insider Shares Held 1.74 M N/A

% Net Shares Purchased (Sold) -3.60% N/A

Source: http://finance.yahoo.com. All figures as of April 14, 2008.

INVESTMENT

RISKS

IBERIABANK is exposed to different risks because of the nature of its

operations. It faces financial risks related to credit and interest rate risks as

well as regulation risks in the industry.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

15

Operational Risks Asset Quality and Loan Losses: IBERIABANK has conservative loan

charge-off and nonaccrual guidelines that have protected the Company

from large loan losses and from increases in nonperforming assets. The

Company also adjusts its allowance for loan losses quarterly to account for

credit losses and changes in the mix of performing loans. These

procedures look at two factors. First, they look at troubled credit loans

within the portfolio. Secondly, they compare the mix of risky and risk-

averse performing loans. Management then uses these procedures to

calculate the net allowance change needed. Current market conditions

have forced IBERIABANK to increase its allowance for loan losses as the

housing slump extends to northwest Arkansas, Memphis, and north

Mississippi.

Fraud Risk: IBERIABANK is exposed to fraud risk by both employees

and people outside the Company. Management regularly reviews and

updates internal controls, disclosure controls and procedures, and

corporate governance policies and procedures.

Environmental Risk: IBERIABANK operates in an area prone to

environmental disasters such as hurricanes, tornadoes, and tropical storms.

These events may positively or negatively affect the operations of the

Company, considering it is highly sensitive to local economies and such

events may cause changes in demographics.

Acquisition Risk: IBERIABANK is constantly seeking opportunities to

expand through the acquisition of companies that match its interests. To do

so, the Company must obtain regulatory approval, which may require it to

close branches to meet requirements. Additionally, IBERIABANK may

not always realize the expected revenue increases, cost savings, increases

in geographic or product presence, or other projected benefits from an

acquisition because of difficulties integrating the acquired company.

Financial Risks Credit Risk: IBERIABANK has a predetermined set of requirements for

comparing risk and reward when lending money. This thorough evaluation

has lead to a significant decrease in nonperforming loans over the past five

years. Additionally, IBERIABANK takes advantage of its relatively

smaller size by monitoring its loan progress carefully.

Interest Rate Risk: The continued decrease in the Federal Funds rate

from 5.25% on January 30, 2007 to 3.00% on January 30, 2008 has not

posed a significant problem for IBERIABANK. The Company’s liability-

sensitive balance sheet aided its performance in recent quarters.

Additionally, an adaptive plan using interest rate swap contracts is used to

hedge risk in the event of fluctuations in interest rates.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

16

Regulations The Federal Deposit Insurance Corporation and the Federal Reserve

regulate the banking industry, and the Office of Thrift Supervision

regulates the thrift industry. New regulations are common in the banking

industry and include such regulations as the Sarbanes-Oxley Act of 2002.

This act specifies that top executives are personally responsible for the

accuracy and timeliness of their company’s financial data. Furthermore, it

adds an increased stress on upper management and additional accounting

and information technology costs. These regulations are mandated by the

government with the possibility of an investigation, hefty fines, or even

being shut down if banks do not comply.

FINANCIAL

PERFORMANCE

AND

PROJECTIONS

When preparing our valuation, we made several assumptions about the

industry and the future economic environment. Additional assumptions

were made based on relevant historical trends that we believe provide a

more accurate forecast.

Interest rates to

decrease in 2008,

banks benefit.

The Federal Reserve is expected to continue lowering interest rates

throughout 2008. Based on this information, IBERIABANK will continue

to benefit from the decreasing interest rate because of its liability-sensitive

position. The falling interest rates also caused the yield curve to shift to a

more favorable position for the banking industry. This change allows for

an increase in IBERIABANK’s spread.

The

macroeconomic

outlook is

favorable.

While the majority of the United States experienced a decline in market

stability in the beginning of 2008, the Gulf Coast region prospered and

continued with remarkable growth. We expect this trend to carry on

throughout 2008 and into future years. Another trend we anticipate to

continue is the increase in crude oil prices. Both trends will benefit

IBERIABANK’s earnings.

Interest rates and

the economic

environment are

key revenue

drivers.

Several key revenue drivers for IBERIABANK include interest rates, the

yield curve, and the overall economic environment of the Gulf Coast

region. To develop forecasts for the economic environment, we used

historical data on population, per capita income, unemployment, and the

consumer price index from the FDIC website.

SITE VISIT Our team had the opportunity to visit IBERIABANK’s downtown New

Orleans location in February 2008. At this visit, we spoke with Anthony

Restel, the senior executive vice president, chief credit officer, and CFO.

We discussed the current economic situations and how IBERIABANK is

positioning itself for the future. Specifically, Mr. Restel spoke of how

IBERIABANK is beginning to shift from a liability-sensitive to a neutral

position in order to prepare for the future rate changes. He also mentioned

that IBERIABANK will benefit from the rising oil and natural gas prices

because the Company is an indirect beneficiary of that industry.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

17

Additionally, when questioned about his opinion on the Pocahontas and

Pulaski acquisitions, Mr. Restel recognized that although there are current

difficulties in the transition period, the acquisitions will prove to be

beneficial to the shareholders in the long run. The Company is taking

aggressive action to remedy the problems caused by the construction loans

obtained through the Pulaski acquisition.

We found the meeting informative, and it was a great opportunity to get an

inside perspective of IBERIABANK’s strategy and operations.

SOURCES OF

INFORMATION

We based our research on several different sources. The foundation of our

report is based on IBERIABANK’s financial reports and press releases. In

addition, we obtained valuable information from Mr. Anthony Restel,

IBERIABANK’s CFO, during our site visit, and from Mr. John Davis,

investor relations, during three conference calls we arranged.

We also spoke with the CEO of a similar regional bank. He talked about

the current situation in the banking industry and provided guidance on

how to analyze a bank’s financial statements. Based on this information,

we looked at different government and state databases, particularly at the

Federal Reserve Bank of Atlanta, to prepare our forecasts. Finally, we

reinforced our research by consulting Yahoo! Finance, InvestextPlus,

Hoovers, and Bloomberg.

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

18

BEN GRAHAM

ANALYSIS

Earnings per share (ttm) 3.27$ Price: $44.18

Earnings to Price Yield 7.40%

10 Year Treasury (2X) 7.10%

P/E ratio as of 12/31/03 21.6

P/E ratio as of 12/31/04 22.0

P/E ratio as of 12/31/05 22.8

P/E ratio as of 12/31/06 16.5

P/E ratio as of 12/31/07 14.3

Current P/E Ratio 13.5

Dividends per share (ttm) 1.32$ Price: 44.18$

Dividend Yield 2.99%

1/2 Yield on 10 Year Treasury 1.78%

Stock Price 44.18$

Book Value per share as of 12/31/07 38.99$

150% of book Value per share as of 12/31/07 58.48$

Interest-bearing debt as of 12/31/07 893,770$

Book value as of 12/31/07 498,059$

Current assets as of 12/31/07 868,488$

Current liabilities as of 12/31/07 436,146$

Current ratio as of 12/31/07 2.0

EPS for year ended 12/31/07 3.27$

EPS for year ended 12/31/06 3.57$

EPS for year ended 12/31/05 2.24$

EPS for year ended 12/31/04 3.01$

EPS for year ended 12/31/03 2.74$

EPS for year ended 12/31/07 3.27$ -8%

EPS for year ended 12/31/06 3.57$ 59%

EPS for year ended 12/31/05 2.24$ -26%

EPS for year ended 12/31/04 3.01$ 10%

Stock price data as of April 14, 2008

IBERIABANK (IBKC)

Table 8Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury

YES

Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs

NO

Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury

YES

Hurdle # 4: A Stock Price less than 1.5 BV

YES

Hurdle # 5: Total Debt less than Book Value

NO

Hurdle # 6: Current Ratio of Two or More

NO

Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years

NO

Hurdle # 8: Stability in Growth of Earnings

NO

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

19

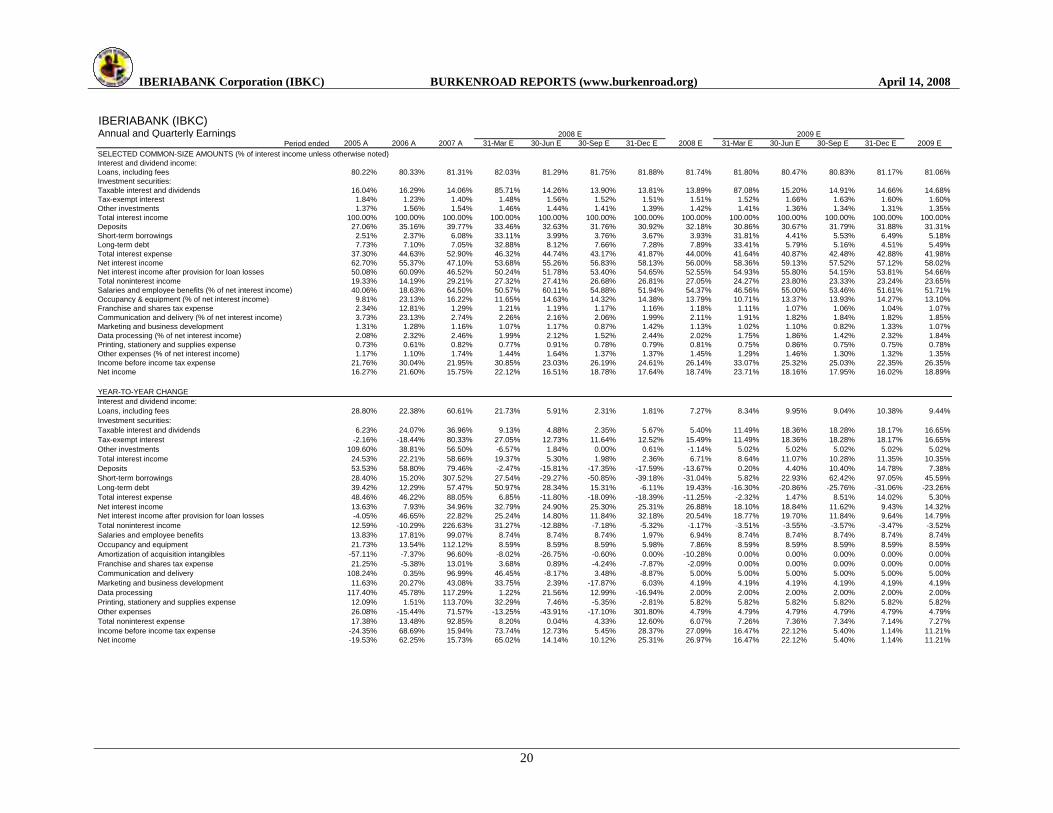

IBERIABANK (IBKC)Annual and Quarterly EarningsIn thousands

Period ended 2005 A 2006 A 2007 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2008 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2009 E

Interest and dividend income:

Loans, including fees 108,492$ 132,771$ 213,239$ 56,031$ 56,337$ 57,815$ 58,549$ 228,731$ 60,704$ 61,943$ 63,041$ 64,628$ 250,316$

Mortgage loans held for sale, including fees 709 992 4,440 1,006 1,006 1,006 1,006 4,025 1,006 1,006 1,006 1,006 4,025

Investment securities:

Taxable interest and dividends 21,698 26,920 36,869 9,265 9,886 9,831 9,878 38,860 10,330 11,701 11,628 11,672 45,331

Tax-exempt interest 2,494 2,034 3,668 1,010 1,078 1,072 1,077 4,236 1,126 1,276 1,268 1,272 4,942

Other investments 1,855 2,575 4,030 996 996 996 996 3,984 1,046 1,046 1,046 1,046 4,184

Total interest income 135,248 165,292 262,246 68,308 69,303 70,720 71,506 279,836 74,213 76,972 77,989 79,625 308,798

Interest expense: 0.0312

Deposits 36,597 58,116 104,297 22,855 22,614 22,459 22,112 90,040 22,901 23,608 24,796 25,381 96,686

Short-term borrowings 3,395 3,911 15,938 2,946 2,764 2,657 2,624 10,991 3,118 3,398 4,315 5,171 16,002

Long-term debt 10,458 11,743 18,492 5,837 5,626 5,416 5,206 22,085 4,885 4,453 4,021 3,589 16,948

Total interest expense 50,450 73,770 138,726 31,638 31,005 30,532 29,942 123,117 30,904 31,459 33,132 34,141 129,636

Net interest income 84,798 91,522 123,520 36,670 38,298 40,188 41,564 156,720 43,309 45,513 44,857 45,484 179,162

Provision for loan losses 17,069 (7,803) 1,525 2,349 2,412 2,423 2,484 9,668 2,546 2,559 2,623 2,637 10,365

Net interest income after provision for loan losses 67,729 99,325 121,995 34,321 35,886 37,764 39,080 147,051 40,762 42,954 42,234 42,847 168,797

Noninterest income: 1.35 1.27 1.44 1.26 1.31 0.84 0.98 1.07 1.07 1.07 1.07 1.07 1.07

Service charges on deposit accounts 13,427 13,167 19,964 5,172 5,212 5,212 5,217 20,813 5,631 5,621 5,616 5,596 22,463

ATM fee income 2,709 3,429 4,934 1,209 1,419 1,209 1,419 5,255 1,287 1,511 1,287 1,511 5,596

Gain on sale of loans, net 2,497 745 16,744 4,186 4,186 4,186 4,186 16,744 2,500 2,500 2,500 2,500 10,000

Title income 17,293 4,323 4,323 4,323 4,323 17,293 4,421 4,421 4,421 4,421 17,682

Broker commissions 4,054 5,487 1,618 1,699 1,784 1,873 6,974 1,967 2,065 2,168 2,277 8,477

Gain on sale of property 826 99 132 Gains (losses) on sale of investments, net (39) (4,083) 1,113 Income from bank owned life insurance 1,979 2,085 3,530 913 913 913 913 3,652 933 933 933 933 3,733 Trading gains and settlements on swaps 1,330 (136)

Other income 4,742 2,624 7,533 1,242 1,242 1,242 1,242 4,966 1,269 1,269 1,269 1,269 5,077

Total noninterest income 26,141 23,450 76,594 18,663 18,993 18,868 19,173 75,697 18,008 18,320 18,194 18,507 73,029

Noninterest expense:

Salaries and employee benefits 33,973 40,023 79,672 18,544 23,020 22,054 21,587 85,204 20,165 25,032 23,982 23,474 92,654

Occupancy and equipment 8,319 9,445 20,035 4,273 5,603 5,756 5,977 21,609 4,640 6,085 6,250 6,491 23,466

Amortization of acquisition intangibles 1,207 1,118 2,198 493 493 493 493 1,972 493 493 493 493 1,972

Franchise and shares tax expense 3,161 2,991 3,380 827 827 827 827 3,309 827 827 827 827 3,309

Communication and delivery 3,107 3,118 6,142 1,675 1,500 1,739 1,535 6,449 1,759 1,575 1,826 1,611 6,772

Marketing and business development 1,766 2,124 3,039 729 811 613 1,014 3,166 759 845 638 1,056 3,299

Data processing 1,837 2,678 5,819 1,192 1,505 1,554 1,684 5,935 1,216 1,535 1,585 1,718 6,054

Professional services 2,103 3,973 925 1,252 1,058 1,118 4,353 953 1,290 1,090 1,151 4,484

Printing, stationery and supplies expense 992 1,007 2,152 529 629 552 568 2,277 560 665 584 601 2,410

Other expenses 10,076 8,520 14,618 2,724 3,278 3,463 5,854 15,319 2,855 3,435 3,629 6,135 16,053

Total noninterest expense 64,438 73,127 141,028 31,913 38,918 38,108 40,656 149,595 34,228 41,782 40,905 43,557 160,473 Income before income tax expense 29,432 49,648 57,561 21,071 15,962 18,524 17,596 73,153 24,542 19,492 19,524 17,796 81,353

Income tax expense 7,432 13,953 16,250 5,963 4,517 5,242 4,980 20,702 6,945 5,516 5,525 5,036 23,023

Net income 22,000$ 35,695$ 41,311$ 15,108$ 11,445$ 13,282$ 12,616$ 52,451$ 17,596$ 13,976$ 13,999$ 12,760$ 58,330$

Earnings per share - basic 2.40$ 3.80$ 3.39$ 1.18$ 0.90$ 1.05$ 0.99$ 4.12$ 1.39$ 1.10$ 1.10$ 1.00$ 4.59$

Earnings per share - diluted 2.24$ 3.57$ 3.27$ 1.15$ 0.87$ 1.01$ 0.96$ 3.99$ 1.33$ 1.05$ 1.05$ 0.96$ 4.40$

Basic shares 9,155 9,401 12,203 12,762 12,725 12,695 12,683 12,716 12,690 12,695 12,705 12,715 12,701

Diluted shares for calculating EPS and CFPS 9,813 9,993 12,641 13,119 13,135 13,153 13,184 13,148 13,233 13,257 13,285 13,312 13,270

2008 E 2009 E

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

20

IBERIABANK (IBKC)Annual and Quarterly Earnings

Period ended 2005 A 2006 A 2007 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2008 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2009 E

SELECTED COMMON-SIZE AMOUNTS (% of interest income unless otherwise noted)

Interest and dividend income:

Loans, including fees 80.22% 80.33% 81.31% 82.03% 81.29% 81.75% 81.88% 81.74% 81.80% 80.47% 80.83% 81.17% 81.06%

Investment securities:

Taxable interest and dividends 16.04% 16.29% 14.06% 85.71% 14.26% 13.90% 13.81% 13.89% 87.08% 15.20% 14.91% 14.66% 14.68%

Tax-exempt interest 1.84% 1.23% 1.40% 1.48% 1.56% 1.52% 1.51% 1.51% 1.52% 1.66% 1.63% 1.60% 1.60%

Other investments 1.37% 1.56% 1.54% 1.46% 1.44% 1.41% 1.39% 1.42% 1.41% 1.36% 1.34% 1.31% 1.35%

Total interest income 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00% 100.00%

Deposits 27.06% 35.16% 39.77% 33.46% 32.63% 31.76% 30.92% 32.18% 30.86% 30.67% 31.79% 31.88% 31.31%

Short-term borrowings 2.51% 2.37% 6.08% 33.11% 3.99% 3.76% 3.67% 3.93% 31.81% 4.41% 5.53% 6.49% 5.18%

Long-term debt 7.73% 7.10% 7.05% 32.88% 8.12% 7.66% 7.28% 7.89% 33.41% 5.79% 5.16% 4.51% 5.49%

Total interest expense 37.30% 44.63% 52.90% 46.32% 44.74% 43.17% 41.87% 44.00% 41.64% 40.87% 42.48% 42.88% 41.98%

Net interest income 62.70% 55.37% 47.10% 53.68% 55.26% 56.83% 58.13% 56.00% 58.36% 59.13% 57.52% 57.12% 58.02%

Net interest income after provision for loan losses 50.08% 60.09% 46.52% 50.24% 51.78% 53.40% 54.65% 52.55% 54.93% 55.80% 54.15% 53.81% 54.66%

Total noninterest income 19.33% 14.19% 29.21% 27.32% 27.41% 26.68% 26.81% 27.05% 24.27% 23.80% 23.33% 23.24% 23.65%

Salaries and employee benefits (% of net interest income) 40.06% 18.63% 64.50% 50.57% 60.11% 54.88% 51.94% 54.37% 46.56% 55.00% 53.46% 51.61% 51.71%

Occupancy & equipment (% of net interest income) 9.81% 23.13% 16.22% 11.65% 14.63% 14.32% 14.38% 13.79% 10.71% 13.37% 13.93% 14.27% 13.10%

Franchise and shares tax expense 2.34% 12.81% 1.29% 1.21% 1.19% 1.17% 1.16% 1.18% 1.11% 1.07% 1.06% 1.04% 1.07%

Communication and delivery (% of net interest income) 3.73% 23.13% 2.74% 2.26% 2.16% 2.06% 1.99% 2.11% 1.91% 1.82% 1.84% 1.82% 1.85%

Marketing and business development 1.31% 1.28% 1.16% 1.07% 1.17% 0.87% 1.42% 1.13% 1.02% 1.10% 0.82% 1.33% 1.07%

Data processing (% of net interest income) 2.08% 2.32% 2.46% 1.99% 2.12% 1.52% 2.44% 2.02% 1.75% 1.86% 1.42% 2.32% 1.84%

Printing, stationery and supplies expense 0.73% 0.61% 0.82% 0.77% 0.91% 0.78% 0.79% 0.81% 0.75% 0.86% 0.75% 0.75% 0.78%

Other expenses (% of net interest income) 1.17% 1.10% 1.74% 1.44% 1.64% 1.37% 1.37% 1.45% 1.29% 1.46% 1.30% 1.32% 1.35%

Income before income tax expense 21.76% 30.04% 21.95% 30.85% 23.03% 26.19% 24.61% 26.14% 33.07% 25.32% 25.03% 22.35% 26.35%

Net income 16.27% 21.60% 15.75% 22.12% 16.51% 18.78% 17.64% 18.74% 23.71% 18.16% 17.95% 16.02% 18.89%

YEAR-TO-YEAR CHANGE

Interest and dividend income:

Loans, including fees 28.80% 22.38% 60.61% 21.73% 5.91% 2.31% 1.81% 7.27% 8.34% 9.95% 9.04% 10.38% 9.44%

Investment securities:

Taxable interest and dividends 6.23% 24.07% 36.96% 9.13% 4.88% 2.35% 5.67% 5.40% 11.49% 18.36% 18.28% 18.17% 16.65%

Tax-exempt interest -2.16% -18.44% 80.33% 27.05% 12.73% 11.64% 12.52% 15.49% 11.49% 18.36% 18.28% 18.17% 16.65%

Other investments 109.60% 38.81% 56.50% -6.57% 1.84% 0.00% 0.61% -1.14% 5.02% 5.02% 5.02% 5.02% 5.02%

Total interest income 24.53% 22.21% 58.66% 19.37% 5.30% 1.98% 2.36% 6.71% 8.64% 11.07% 10.28% 11.35% 10.35%

Deposits 53.53% 58.80% 79.46% -2.47% -15.81% -17.35% -17.59% -13.67% 0.20% 4.40% 10.40% 14.78% 7.38%

Short-term borrowings 28.40% 15.20% 307.52% 27.54% -29.27% -50.85% -39.18% -31.04% 5.82% 22.93% 62.42% 97.05% 45.59%

Long-term debt 39.42% 12.29% 57.47% 50.97% 28.34% 15.31% -6.11% 19.43% -16.30% -20.86% -25.76% -31.06% -23.26%

Total interest expense 48.46% 46.22% 88.05% 6.85% -11.80% -18.09% -18.39% -11.25% -2.32% 1.47% 8.51% 14.02% 5.30%

Net interest income 13.63% 7.93% 34.96% 32.79% 24.90% 25.30% 25.31% 26.88% 18.10% 18.84% 11.62% 9.43% 14.32%

Net interest income after provision for loan losses -4.05% 46.65% 22.82% 25.24% 14.80% 11.84% 32.18% 20.54% 18.77% 19.70% 11.84% 9.64% 14.79%

Total noninterest income 12.59% -10.29% 226.63% 31.27% -12.88% -7.18% -5.32% -1.17% -3.51% -3.55% -3.57% -3.47% -3.52%

Salaries and employee benefits 13.83% 17.81% 99.07% 8.74% 8.74% 8.74% 1.97% 6.94% 8.74% 8.74% 8.74% 8.74% 8.74%

Occupancy and equipment 21.73% 13.54% 112.12% 8.59% 8.59% 8.59% 5.98% 7.86% 8.59% 8.59% 8.59% 8.59% 8.59%

Amortization of acquisition intangibles -57.11% -7.37% 96.60% -8.02% -26.75% -0.60% 0.00% -10.28% 0.00% 0.00% 0.00% 0.00% 0.00%

Franchise and shares tax expense 21.25% -5.38% 13.01% 3.68% 0.89% -4.24% -7.87% -2.09% 0.00% 0.00% 0.00% 0.00% 0.00%

Communication and delivery 108.24% 0.35% 96.99% 46.45% -8.17% 3.48% -8.87% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00%

Marketing and business development 11.63% 20.27% 43.08% 33.75% 2.39% -17.87% 6.03% 4.19% 4.19% 4.19% 4.19% 4.19% 4.19%

Data processing 117.40% 45.78% 117.29% 1.22% 21.56% 12.99% -16.94% 2.00% 2.00% 2.00% 2.00% 2.00% 2.00%

Printing, stationery and supplies expense 12.09% 1.51% 113.70% 32.29% 7.46% -5.35% -2.81% 5.82% 5.82% 5.82% 5.82% 5.82% 5.82%

Other expenses 26.08% -15.44% 71.57% -13.25% -43.91% -17.10% 301.80% 4.79% 4.79% 4.79% 4.79% 4.79% 4.79%

Total noninterest expense 17.38% 13.48% 92.85% 8.20% 0.04% 4.33% 12.60% 6.07% 7.26% 7.36% 7.34% 7.14% 7.27%

Income before income tax expense -24.35% 68.69% 15.94% 73.74% 12.73% 5.45% 28.37% 27.09% 16.47% 22.12% 5.40% 1.14% 11.21%

Net income -19.53% 62.25% 15.73% 65.02% 14.14% 10.12% 25.31% 26.97% 16.47% 22.12% 5.40% 1.14% 11.21%

2008 E 2009 E

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

21

IBERIABANK (IBKC)Annual and Quarterly Balance SheetsIn thousands

Period ended 31-Dec-05 A 31-Dec-06 A 31-Dec-07 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 31-Dec-08 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 31-Dec-09 E

Assets

Cash and cash equivalents:

Cash and due from banks 66,697$ 51,078$ 93,263$ 90,240$ 92,119$ 90,575$ 89,259$ 89,259$ 92,975$ 92,646$ 90,011$ 80,757$ 80,757$

Interest-bearing deposits in banks 60,103 33,827 29,842 35,024 35,753 35,154 34,643 34,643 36,085 35,958 34,935 31,343 31,343

Total cash and cash equivalents 126,800 84,905 123,105 125,264 127,871 125,729 123,902 123,902 129,061 128,604 124,946 112,100 112,100

Investment securities:

Available for sale, at fair value 543,495 558,832 745,383 794,706 788,809 792,558 797,636 797,636 873,101 834,288 806,804 815,411 815,411

Held to maturity 29,087 22,520 59,494 64,111 65,235 65,533 65,938 65,938 69,560 69,655 69,855 69,744 69,744

Mortgage loans held for sale 10,515 54,273 57,695 57,695 57,695 57,695 57,695 57,695 57,695 57,695 57,695 57,695 57,695

Loans, net of unearned income, less allowance 1,880,434 2,204,080 3,391,754 3,506,386 3,599,887 3,617,018 3,707,226 3,707,226 3,800,637 3,819,429 3,914,276 3,936,215 3,936,215

Premises and equipment, net 55,010 71,007 122,452 123,839 125,208 126,585 127,968 127,968 129,358 130,756 132,161 133,573 133,573

Goodwill and acquisition intangibles 93,167 92,779 231,177 230,684 230,191 229,698 229,205 229,205 228,712 228,219 227,726 227,233 227,233

Other assets 114,084 114,640 185,898 188,364 189,128 189,534 189,927 189,927 190,601 191,013 191,430 191,858 191,858

Total assets 2,852,592$ 3,203,036$ 4,916,958$ 5,091,050$ 5,184,024$ 5,204,349$ 5,299,497$ 5,299,497$ 5,478,725$ 5,459,658$ 5,524,893$ 5,543,829$ 5,543,829$

Liabilities and stockholders' equity

Liabilities:

Deposits:

Noninterest-bearing 350,065$ 354,961$ 468,001$ 487,933$ 491,684$ 491,684$ 492,157$ 492,157$ 531,214$ 530,267$ 529,793$ 527,899$ 527,899$

Interest-bearing 1,892,891 2,067,621 3,016,827 3,196,618 3,257,442 3,274,606 3,297,383 3,297,383 3,466,499 3,472,882 3,484,879 3,480,394 3,480,394

Total deposits 2,242,956 2,422,582 3,484,828 3,684,551 3,749,126 3,766,290 3,789,540 3,789,540 3,997,713 4,003,149 4,014,672 4,008,293 4,008,293

Short-term borrowings 745 202,605 436,146 416,146 456,146 466,146 546,146 546,146 536,146 536,146 616,146 666,146 666,146

Long-term debt 250,212 236,997 457,624 441,437 425,250 409,063 392,876 392,876 359,602 326,328 293,053 259,779 259,779

Other liabilities 95,110 21,301 40,301 40,836 41,001 41,089 41,175 41,175 41,321 41,410 41,500 41,593 41,593

Total Liabilities 2,589,023 2,883,485 4,418,899 4,582,970 4,671,523 4,682,588 4,769,737 4,769,737 4,934,781 4,907,032 4,965,372 4,975,811 4,975,811

Stockholders' equity:

Common stock of $1 par Value 11,802 12,379 14,800 14,800 14,800 14,800 14,800 14,800 14,800 14,800 14,800 14,800 14,800

Additional paid-in-capital 190,655 214,483 361,746 362,868 363,998 365,137 366,285 366,285 367,441 368,605 369,779 370,961 370,961

Retained earnings 150,107 173,794 197,911 208,593 215,536 224,236 232,185 232,185 245,017 254,131 263,168 270,861 270,861

Unearned Compensation (9,594)

Accumulated other comprehensive income (5,629) (3,306) 5,725 5,725 5,725 5,725 5,725 5,725 5,725 5,725 5,725 5,725 5,725

Treasury stock (73,772) (77,799) (82,123) (83,906) (87,558) (88,137) (89,235) (89,235) (89,040) (90,636) (93,951) (94,329) (94,329)

Total stockholders' equity 263,569 319,551 498,059 508,080 512,501 521,761 529,760 529,760 543,943 552,626 559,521 568,018 568,018

Total liabilities and stockholders' equity 2,852,592$ 3,203,036$ 4,916,958$ 5,091,050$ 5,184,024$ 5,204,349$ 5,299,497$ 5,299,497$ 5,478,725$ 5,459,658$ 5,524,893$ 5,543,829$ 5,543,829$

2008 E 2009 E

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

22

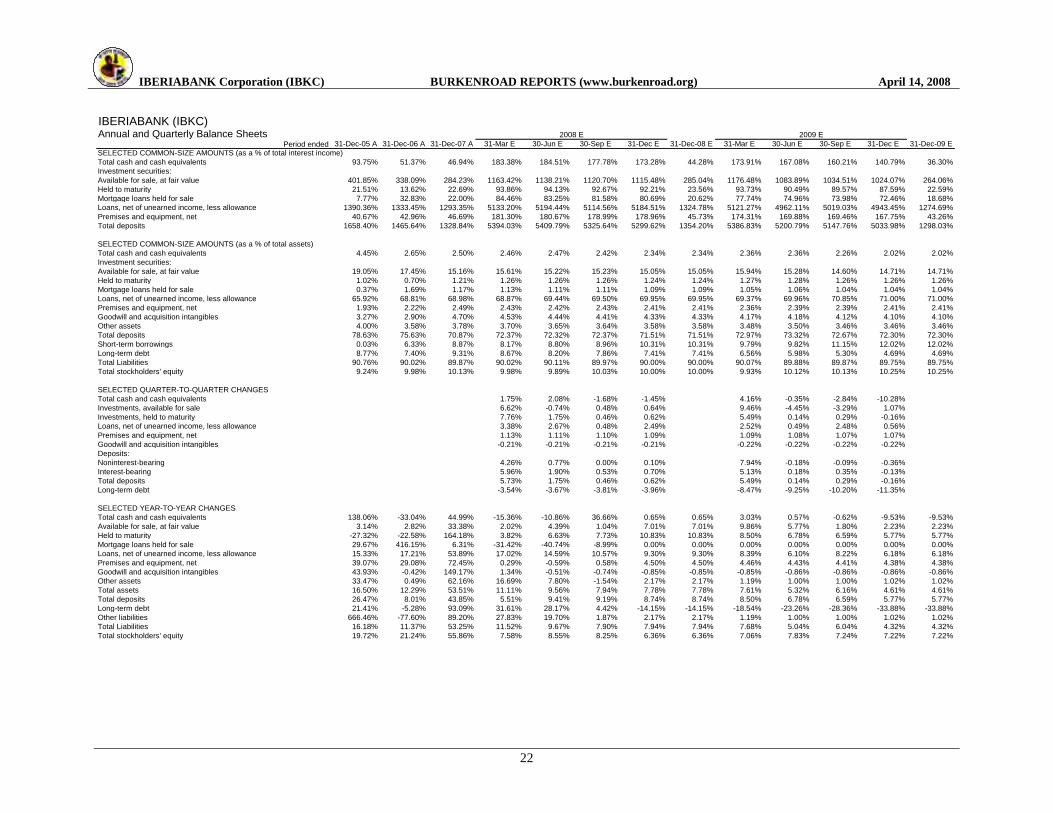

IBERIABANK (IBKC)Annual and Quarterly Balance Sheets

Period ended 31-Dec-05 A 31-Dec-06 A 31-Dec-07 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 31-Dec-08 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 31-Dec-09 E

SELECTED COMMON-SIZE AMOUNTS (as a % of total interest income)

Total cash and cash equivalents 93.75% 51.37% 46.94% 183.38% 184.51% 177.78% 173.28% 44.28% 173.91% 167.08% 160.21% 140.79% 36.30%

Investment securities:

Available for sale, at fair value 401.85% 338.09% 284.23% 1163.42% 1138.21% 1120.70% 1115.48% 285.04% 1176.48% 1083.89% 1034.51% 1024.07% 264.06%

Held to maturity 21.51% 13.62% 22.69% 93.86% 94.13% 92.67% 92.21% 23.56% 93.73% 90.49% 89.57% 87.59% 22.59%

Mortgage loans held for sale 7.77% 32.83% 22.00% 84.46% 83.25% 81.58% 80.69% 20.62% 77.74% 74.96% 73.98% 72.46% 18.68%

Loans, net of unearned income, less allowance 1390.36% 1333.45% 1293.35% 5133.20% 5194.44% 5114.56% 5184.51% 1324.78% 5121.27% 4962.11% 5019.03% 4943.45% 1274.69%

Premises and equipment, net 40.67% 42.96% 46.69% 181.30% 180.67% 178.99% 178.96% 45.73% 174.31% 169.88% 169.46% 167.75% 43.26%

Total deposits 1658.40% 1465.64% 1328.84% 5394.03% 5409.79% 5325.64% 5299.62% 1354.20% 5386.83% 5200.79% 5147.76% 5033.98% 1298.03%

SELECTED COMMON-SIZE AMOUNTS (as a % of total assets)

Total cash and cash equivalents 4.45% 2.65% 2.50% 2.46% 2.47% 2.42% 2.34% 2.34% 2.36% 2.36% 2.26% 2.02% 2.02%

Investment securities:

Available for sale, at fair value 19.05% 17.45% 15.16% 15.61% 15.22% 15.23% 15.05% 15.05% 15.94% 15.28% 14.60% 14.71% 14.71%

Held to maturity 1.02% 0.70% 1.21% 1.26% 1.26% 1.26% 1.24% 1.24% 1.27% 1.28% 1.26% 1.26% 1.26%

Mortgage loans held for sale 0.37% 1.69% 1.17% 1.13% 1.11% 1.11% 1.09% 1.09% 1.05% 1.06% 1.04% 1.04% 1.04%

Loans, net of unearned income, less allowance 65.92% 68.81% 68.98% 68.87% 69.44% 69.50% 69.95% 69.95% 69.37% 69.96% 70.85% 71.00% 71.00%

Premises and equipment, net 1.93% 2.22% 2.49% 2.43% 2.42% 2.43% 2.41% 2.41% 2.36% 2.39% 2.39% 2.41% 2.41%

Goodwill and acquisition intangibles 3.27% 2.90% 4.70% 4.53% 4.44% 4.41% 4.33% 4.33% 4.17% 4.18% 4.12% 4.10% 4.10%

Other assets 4.00% 3.58% 3.78% 3.70% 3.65% 3.64% 3.58% 3.58% 3.48% 3.50% 3.46% 3.46% 3.46%

Total deposits 78.63% 75.63% 70.87% 72.37% 72.32% 72.37% 71.51% 71.51% 72.97% 73.32% 72.67% 72.30% 72.30%

Short-term borrowings 0.03% 6.33% 8.87% 8.17% 8.80% 8.96% 10.31% 10.31% 9.79% 9.82% 11.15% 12.02% 12.02%

Long-term debt 8.77% 7.40% 9.31% 8.67% 8.20% 7.86% 7.41% 7.41% 6.56% 5.98% 5.30% 4.69% 4.69%

Total Liabilities 90.76% 90.02% 89.87% 90.02% 90.11% 89.97% 90.00% 90.00% 90.07% 89.88% 89.87% 89.75% 89.75%

Total stockholders' equity 9.24% 9.98% 10.13% 9.98% 9.89% 10.03% 10.00% 10.00% 9.93% 10.12% 10.13% 10.25% 10.25%

SELECTED QUARTER-TO-QUARTER CHANGES

Total cash and cash equivalents 1.75% 2.08% -1.68% -1.45% 4.16% -0.35% -2.84% -10.28%

Investments, available for sale 6.62% -0.74% 0.48% 0.64% 9.46% -4.45% -3.29% 1.07%

Investments, held to maturity 7.76% 1.75% 0.46% 0.62% 5.49% 0.14% 0.29% -0.16%

Loans, net of unearned income, less allowance 3.38% 2.67% 0.48% 2.49% 2.52% 0.49% 2.48% 0.56%

Premises and equipment, net 1.13% 1.11% 1.10% 1.09% 1.09% 1.08% 1.07% 1.07%

Goodwill and acquisition intangibles -0.21% -0.21% -0.21% -0.21% -0.22% -0.22% -0.22% -0.22%

Deposits:

Noninterest-bearing 4.26% 0.77% 0.00% 0.10% 7.94% -0.18% -0.09% -0.36%

Interest-bearing 5.96% 1.90% 0.53% 0.70% 5.13% 0.18% 0.35% -0.13%

Total deposits 5.73% 1.75% 0.46% 0.62% 5.49% 0.14% 0.29% -0.16%

Long-term debt -3.54% -3.67% -3.81% -3.96% -8.47% -9.25% -10.20% -11.35%

SELECTED YEAR-TO-YEAR CHANGES

Total cash and cash equivalents 138.06% -33.04% 44.99% -15.36% -10.86% 36.66% 0.65% 0.65% 3.03% 0.57% -0.62% -9.53% -9.53%

Available for sale, at fair value 3.14% 2.82% 33.38% 2.02% 4.39% 1.04% 7.01% 7.01% 9.86% 5.77% 1.80% 2.23% 2.23%

Held to maturity -27.32% -22.58% 164.18% 3.82% 6.63% 7.73% 10.83% 10.83% 8.50% 6.78% 6.59% 5.77% 5.77%

Mortgage loans held for sale 29.67% 416.15% 6.31% -31.42% -40.74% -8.99% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Loans, net of unearned income, less allowance 15.33% 17.21% 53.89% 17.02% 14.59% 10.57% 9.30% 9.30% 8.39% 6.10% 8.22% 6.18% 6.18%

Premises and equipment, net 39.07% 29.08% 72.45% 0.29% -0.59% 0.58% 4.50% 4.50% 4.46% 4.43% 4.41% 4.38% 4.38%

Goodwill and acquisition intangibles 43.93% -0.42% 149.17% 1.34% -0.51% -0.74% -0.85% -0.85% -0.85% -0.86% -0.86% -0.86% -0.86%

Other assets 33.47% 0.49% 62.16% 16.69% 7.80% -1.54% 2.17% 2.17% 1.19% 1.00% 1.00% 1.02% 1.02%

Total assets 16.50% 12.29% 53.51% 11.11% 9.56% 7.94% 7.78% 7.78% 7.61% 5.32% 6.16% 4.61% 4.61%

Total deposits 26.47% 8.01% 43.85% 5.51% 9.41% 9.19% 8.74% 8.74% 8.50% 6.78% 6.59% 5.77% 5.77%

Long-term debt 21.41% -5.28% 93.09% 31.61% 28.17% 4.42% -14.15% -14.15% -18.54% -23.26% -28.36% -33.88% -33.88%

Other liabilities 666.46% -77.60% 89.20% 27.83% 19.70% 1.87% 2.17% 2.17% 1.19% 1.00% 1.00% 1.02% 1.02%

Total Liabilities 16.18% 11.37% 53.25% 11.52% 9.67% 7.90% 7.94% 7.94% 7.68% 5.04% 6.04% 4.32% 4.32%

Total stockholders' equity 19.72% 21.24% 55.86% 7.58% 8.55% 8.25% 6.36% 6.36% 7.06% 7.83% 7.24% 7.22% 7.22%

2008 E 2009 E

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

23

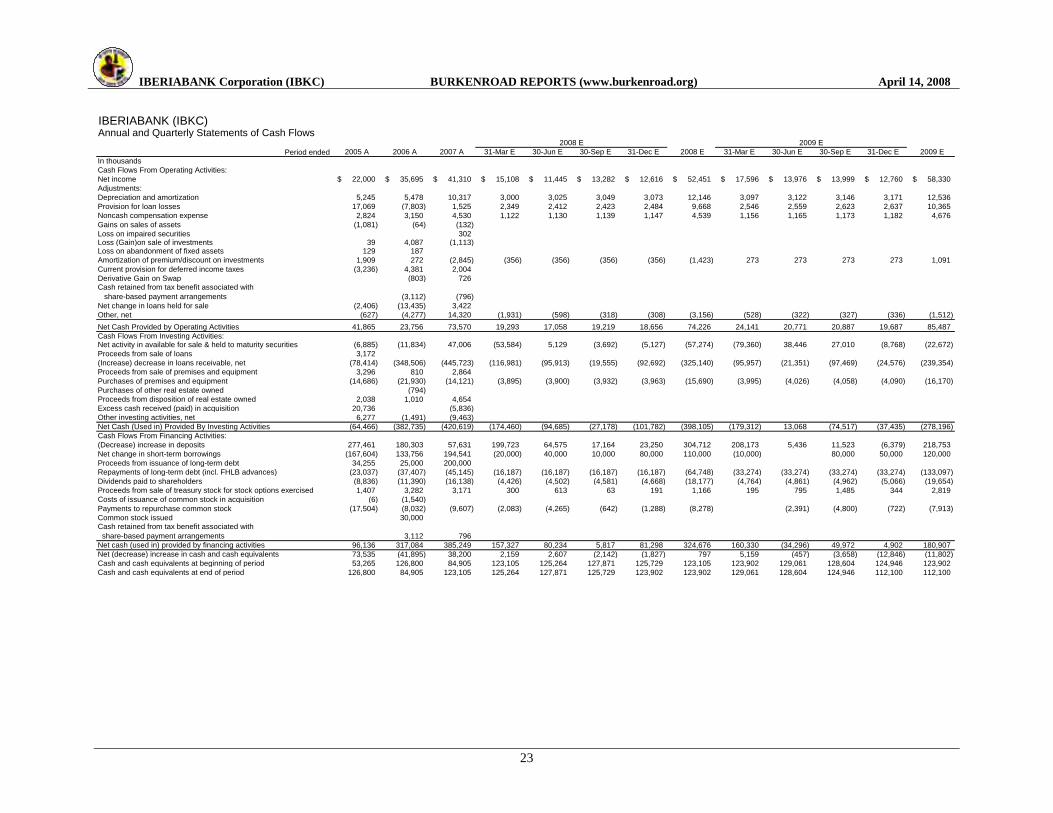

IBERIABANK (IBKC)Annual and Quarterly Statements of Cash Flows

Period ended 2005 A 2006 A 2007 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2008 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2009 E

In thousands

Cash Flows From Operating Activities:

Net income 22,000$ 35,695$ 41,310$ 15,108$ 11,445$ 13,282$ 12,616$ 52,451$ 17,596$ 13,976$ 13,999$ 12,760$ 58,330$

Adjustments:

Depreciation and amortization 5,245 5,478 10,317 3,000 3,025 3,049 3,073 12,146 3,097 3,122 3,146 3,171 12,536

Provision for loan losses 17,069 (7,803) 1,525 2,349 2,412 2,423 2,484 9,668 2,546 2,559 2,623 2,637 10,365

Noncash compensation expense 2,824 3,150 4,530 1,122 1,130 1,139 1,147 4,539 1,156 1,165 1,173 1,182 4,676

Gains on sales of assets (1,081) (64) (132)

Loss on impaired securities 302 Loss (Gain)on sale of investments 39 4,087 (1,113) Loss on abandonment of fixed assets 129 187

Amortization of premium/discount on investments 1,909 272 (2,845) (356) (356) (356) (356) (1,423) 273 273 273 273 1,091

Current provision for deferred income taxes (3,236) 4,381 2,004

Derivative Gain on Swap (803) 726 Cash retained from tax benefit associated with

share-based payment arrangements (3,112) (796)

Net change in loans held for sale (2,406) (13,435) 3,422

Other, net (627) (4,277) 14,320 (1,931) (598) (318) (308) (3,156) (528) (322) (327) (336) (1,512)

Net Cash Provided by Operating Activities 41,865 23,756 73,570 19,293 17,058 19,219 18,656 74,226 24,141 20,771 20,887 19,687 85,487

Cash Flows From Investing Activities:Net activity in available for sale & held to maturity securities (6,885) (11,834) 47,006 (53,584) 5,129 (3,692) (5,127) (57,274) (79,360) 38,446 27,010 (8,768) (22,672)

Proceeds from sale of loans 3,172

(Increase) decrease in loans receivable, net (78,414) (348,506) (445,723) (116,981) (95,913) (19,555) (92,692) (325,140) (95,957) (21,351) (97,469) (24,576) (239,354)

Proceeds from sale of premises and equipment 3,296 810 2,864

Purchases of premises and equipment (14,686) (21,930) (14,121) (3,895) (3,900) (3,932) (3,963) (15,690) (3,995) (4,026) (4,058) (4,090) (16,170)

Purchases of other real estate owned (794)

Proceeds from disposition of real estate owned 2,038 1,010 4,654

Excess cash received (paid) in acquisition 20,736 (5,836)

Other investing activities, net 6,277 (1,491) (9,463)

Net Cash (Used in) Provided By Investing Activities (64,466) (382,735) (420,619) (174,460) (94,685) (27,178) (101,782) (398,105) (179,312) 13,068 (74,517) (37,435) (278,196)

Cash Flows From Financing Activities:

(Decrease) increase in deposits 277,461 180,303 57,631 199,723 64,575 17,164 23,250 304,712 208,173 5,436 11,523 (6,379) 218,753

Net change in short-term borrowings (167,604) 133,756 194,541 (20,000) 40,000 10,000 80,000 110,000 (10,000) 80,000 50,000 120,000

Proceeds from issuance of long-term debt 34,255 25,000 200,000

Repayments of long-term debt (incl. FHLB advances) (23,037) (37,407) (45,145) (16,187) (16,187) (16,187) (16,187) (64,748) (33,274) (33,274) (33,274) (33,274) (133,097)

Dividends paid to shareholders (8,836) (11,390) (16,138) (4,426) (4,502) (4,581) (4,668) (18,177) (4,764) (4,861) (4,962) (5,066) (19,654)

Proceeds from sale of treasury stock for stock options exercised 1,407 3,282 3,171 300 613 63 191 1,166 195 795 1,485 344 2,819

Costs of issuance of common stock in acquisition (6) (1,540)

Payments to repurchase common stock (17,504) (8,032) (9,607) (2,083) (4,265) (642) (1,288) (8,278) (2,391) (4,800) (722) (7,913)

Common stock issued 30,000 Cash retained from tax benefit associated with

share-based payment arrangements 3,112 796

Net cash (used in) provided by financing activities 96,136 317,084 385,249 157,327 80,234 5,817 81,298 324,676 160,330 (34,296) 49,972 4,902 180,907

Net (decrease) increase in cash and cash equivalents 73,535 (41,895) 38,200 2,159 2,607 (2,142) (1,827) 797 5,159 (457) (3,658) (12,846) (11,802)

Cash and cash equivalents at beginning of period 53,265 126,800 84,905 123,105 125,264 127,871 125,729 123,105 123,902 129,061 128,604 124,946 123,902

Cash and cash equivalents at end of period 126,800 84,905 123,105 125,264 127,871 125,729 123,902 123,902 129,061 128,604 124,946 112,100 112,100

2008 E 2009 E

IBERIABANK Corporation (IBKC) BURKENROAD REPORTS (www.burkenroad.org) April 14, 2008

24

IBERIABANK CORP.Ratios

2005 A 2006 A 2007 A 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2008 E 31-Mar E 30-Jun E 30-Sep E 31-Dec E 2009 E

Performance Measurements

Gross interest margin 5.88% 6.36% 7.63% 1.63% 1.60% 1.61% 1.60% 6.44% 1.60% 1.64% 1.65% 1.66% 6.56%

Net interest margin 3.68% 3.52% 3.60% 0.87% 0.88% 0.92% 0.93% 3.61% 0.93% 0.97% 0.95% 0.95% 3.80%

Loan interest margin 6.02% 6.47% 6.75% 1.60% 1.56% 1.58% 1.57% 6.31% 1.59% 1.60% 1.61% 1.62% 6.42%

Other interest and dividends margin 4.21% 4.70% 5.07% 1.24% 1.28% 1.27% 1.27% 5.06% 1.27% 1.41% 1.45% 1.47% 5.59%

2.08% 2.89% 3.57% 0.74% 0.70% 0.69% 0.67% 2.80% 0.68% 0.68% 0.71% 0.73% 2.80%

Interest expense on short-term borrowings 2.17% 3.70% 4.27% 0.69% 0.63% 0.58% 0.52% 2.40% 0.58% 0.63% 0.75% 0.81% 2.79%

Interest expense on long-term debt 4.31% 4.87% 5.26% 1.30% 1.30% 1.30% 1.30% 5.19% 1.30% 1.30% 1.30% 1.30% 5.19%

Gain on sale of loans/Average loans available for sale 19.10% 3.77% 22.26% 7.26% 7.26% 7.26% 7.26% 29.02% 4.33% 4.33% 4.33% 4.33% 17.33%

Efficiency Ratio 58.1% 63.6% 70.5% 57.7% 67.9% 64.5% 66.9% 64.4% 55.8% 65.5% 64.9% 68.1% 63.6%

Provision for loan losses ratio 1.01% -0.40% 0.06% 0.07% 0.07% 0.07% 0.07% 0.28% 0.07% 0.07% 0.07% 0.07% 0.28%

Loans to Deposits ratio 83.8% 91.0% 97.3% 95.2% 96.0% 96.0% 97.8% 97.8% 95.1% 95.4% 97.5% 98.2% 98.2%

Earning assets to interest-bearing liabilities 117.72% 114.61% 109.55% 109.96% 109.87% 110.08% 110.07% 110.07% 110.89% 111.11% 111.14% 111.44% 112.25%

Non-interest expense to average assets 2.55% 2.54% 3.66% 0.67% 0.80% 0.77% 0.81% 3.04% 0.66% 0.79% 0.77% 0.81% 3.04%

Non-interest revenue to total revenue 23.6% 20.4% 38.3% 33.7% 33.2% 31.9% 31.6% 32.6% 29.4% 28.7% 28.9% 28.9% 29.0%

Equity to Assets Ratio 9.3% 9.4% 9.8% 10.1% 9.9% 10.0% 10.1% 10.0% 10.0% 10.0% 10.1% 10.1% 10.0%

Financial Risk (Leverage) Ratios

Total debt/equity ratio 9.82 9.02 8.87 9.02 9.12 8.97 9.00 9.00 9.07 8.88 8.87 8.76 8.76

Total LT debt/equity ratio 0.95 0.74 0.92 0.87 0.83 0.78 0.74 0.74 0.66 0.59 0.52 0.46 0.46

Tier 1 Leverage Ratio 3.38% 2.97% 2.22% 1.79% 1.75% 1.73% 1.70% 1.74% 1.64% 1.63% 1.62% 1.60% 1.62%

Total debt ratio 0.91 0.90 0.90 0.90 0.90 0.90 0.90 0.90 0.90 0.90 0.90 0.90 0.90

Profitability/Valuation Measures

Gross profit margin 70.21% 68.07% 70.37% 68.71% 65.33% 63.43% 60.96% 70.73% 62.70% 59.81% 57.04% 54.82% 65.33%

Book value per share 43.93$ 53.26$ 83.01$ 84.68$ 85.42$ 86.96$ 88.29$ 88.29$ 90.66$ 92.10$ 93.25$ 94.67$ 94.67$

Return on assets 0.86% 1.22% 1.06% 0.31% 0.23% 0.26% 0.25% 1.05% 0.33% 0.26% 0.26% 0.24% 1.09%

Return on equity 9.23% 13.06% 10.80% 3.08% 2.32% 2.65% 2.45% 10.50% 3.35% 2.62% 2.59% 2.32% 10.86%

Dividend payout ratio 40.16% 31.91% 39.06% 29.30% 39.33% 34.49% 37.00% 34.66% 27.07% 34.78% 35.45% 39.70% 33.69%

2009 E2008 E

Interest expense on deposits as a % of deposits

BURKENROAD REPORTS RATING SYSTEM Market Outperform: This rating indicates that we believe forces are in place that would enable this

company's stock to produce returns in excess of the stock market averages over the next 12 months.

Market Perform: This rating indicates that we believe the investment returns from this company’s

stock will be in line with those produced by the stock market averages over the next 12 months.

Market Underperform: This rating indicates that while this investment may have positive

attributes, we believe an investment in this company will produce subpar returns over the next 12

months.

BURKENROAD REPORTS RATING SYSTEM

CPFS is calculated using operating cash flows excluding working capital changes.

All amounts are as of the date of the report as reported by Bloomberg or Yahoo Finance

unless otherwise noted. Betas are collected from Bloomberg.

Enterprise value is based on the equity market cap as of the report date, adjusted for long-

term debt, cash, and short-term investments reported on the most recent quarterly report date.

12-month Stock Performance is calculated using an ending price as of the report date.

The stock performance includes the 12-month dividend yield.

2007-2008 COVERAGE UNIVERSE AFC Enterprises Inc. (AFCE) McMoRan Exploration Co. (MMR)

Amerisafe Inc. (AMSF) MidSouth Bancorp Inc. (MSL)

Callon Petroleum Company (CPE) NATCO Group Inc. (NTG)

Cal-Maine Foods Inc. (CALM) Parkway Properties Inc. (PKY)

Carbo Ceramics Inc. (CRR) PetroQuest Energy Inc. (PQ)

CLECO Corporation (CNL) Pool Corporation (POOL)

Conn’s Inc. (CONN) Powell Industries Inc. (POWL)

Craftmade International Inc. (CRFT) Rollins Incorporated (ROL)

Crown Crafts Inc. (CRWS) RPC Incorporated (RES)

EastGroup Properties Inc. (EGP) Sally Beauty Holdings (SBH)

Energy Partners Ltd. (EPL) Sanderson Farms Inc. (SAFM)

EnergySouth Inc. (ENSI) SEACOR Holdings Inc. (CKH)

First M&F Corporation (FMFC) Shaw Group Inc. (SGR)

Frozen Food Express (FFEX) Stone Energy Corp. (SGY)

Gulf Island Fabrication Inc. (GIFI) Superior Energy Services Inc. (SPN)

Hibbett Sports Inc. (HIBB) Team Incorporated (TMI)

Hornbeck Offshore Services Inc. (HOS) Teche Holding Company (TSH)

IBERIABANK Corp. (IBKC) Tuesday Morning Corp. (TUES)

ION Geophysical Corp. (IO) W&T Offshore (WTI)

Marine Products Corp. (MPX) Willbros Group Inc. (WG)

Peter Ricchiuti Pamela Shaw Karla Timmons

Director of Research Senior Director of Accounting Abe Topham

BURKENROAD REPORTS BURKENROAD REPORTS Associate Directors of Research

Tulane University Tulane University BURKENROAD REPORTS

New Orleans, LA 70118-5669 New Orleans, LA 70118-5669 Tulane University

(504) 862-8489

(504) 865-5430 Fax

(504) 865-5033

(504) 865-5430 Fax

New Orleans, LA 70118-5669

(504) 862-8489

[email protected] [email protected] (504) 865-5430 Fax

Wall Street's Farm Team

The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's A.B. Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment.

Named in honor of William B. Burkenroad Jr., an alumnus and a longtime supporter ofTulane’s business school, and funded through contributions from his family and friends,BURKENROAD REPORTS is a nationally recognized program, publishing objective, high quality investment research reports on public companies in our region. Students at Tulane University’s A. B. Freeman School of Business prepare these reports.