Network Working Group G. Chen Internet-Draft China Mobile ...

Upload

khangminh22Category

view

4download

0

Volkswagen Group ChinaDr. Jörg Mull, Executive Vice President, Finance

Morgan Stanley Investor VisitBeijing, January 22nd, 2013

Our Momentum in China

Outlook Market Development

Investments Volkswagen Group China

Driven by Design, Technology and Brand Image

Financial results, challenges and opportunities

2

Content

Introduction of Volkswagen Group China (VGC)

Volkswagen production facilities in China History1985: Founding of Shanghai Volkswagen Automotive Co. (SVW) as joint venture with Shanghai Automotive Industrial Corporation (SAIC). 8 million vehicles produced as of June 2012.

1991: Founding of FAW-Volkswagen Automotive Co. Ltd. (FAW-VW) as second joint venture with First Automotive Work (FAW). 6 million vehicles produced as of June 2012.

2004: Founding of Volkswagen Group China for coordination and management of activities of Volkswagen Group within China.

Today: 17 Volkswagen companies and subsidiaries respectively (including finance and sales companies).

Total investments 1985-2012Planned Investments 2013-2015Employees 2011

€ 15.7 Billion€ 9.8 Billion

48,058

Volkswagen Transmission

Shanghai VolkswagenPowertrain

FAW-Volkswagen(Volkswagen, Audi)

Volkswagen FAW Engine

Volkswagen FAW Platform

Shanghai Volkswagen

Shanghai Volkswagen(Volkswagen, ŠKODA)

Volkswagen AutomaticTransmission

Volkswagen China Investment Company

Beijing

Shanghai

DalianChangchun

Chengdu Nanjing

FAW-Volkswagen

Car production plants

Component plants

Headquarter Volkswagen Group China

3

Yizheng

Volkswagen as a pioneer in China

1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2012

1985 2011

1985 2011

4

Successful partnership with FAW and SAIC

1991

FAW 60%, VW AG 30%, AUDI AG 10%

1,319,000 units

1985

SAIC Motor 50%, VW AG 50%

1,304,000 units

Foundation

Share

Deliveries 2012

Foundation

Share

Deliveries 2012

5

Volkswagen

Jetta Sagitar Magotan

New Bora CC Golf

Audi

Audi A4L Audi A6L Audi Q3 Audi Q5

Volkswagen

Lavida Santana Passat

Polo Touran Tiguan

Škoda

Fabia Rapid Octavia Superb

VW, VWN

Other Brands

Audi

Locally Produced(‘000 Units)

Import FBU1)

(‘000 Units)

FAW-VW

SVW

Deliveries of Volkswagen in China January to December 2012

Ʃ 189.7 Ʃ 2,622.8

88.4

83.1

18.2

Total Deliveries Region China 2,813

6

995.9 322.7

235.71.068.5

1) incl. Hongkong; Source: Volkswagen Group China

Our Momentum in China

Outlook Market Development

Investments Volkswagen Group China

Driven by Design, Technology and Brand Image

Financial results, challenges and opportunities

7

Content

Q3 2012 GDP reached 7.4% growth year on year, and the economy is now on a path of stable growth

8Source: Deutsche Bank, last update December 2012.

7.4%

Q4/12EQ1/12

7.7%

Q3/12

9.1%

Q2/12

7.6%8.1%

Q4/11

8.9%

Q3/11Q2/11

9.5%

Q1/11

9.7%

Q4/10

9.8%

Q3/10

9.6%

Q2/10

10.3%

Q1/10

11.9%

Q1/13E Q2/13E Q3/13E Q4/13E

7.9%8.2% 8.4% 8.5%

2010 2011 2012 2013(forecast)

CAGR10.3%

CAGR9.2%

CAGR7.7%

CAGR8.2%

After a strong boom in the past years, passenger car market growth in China is stabilizing and will develop further in the future

9

>20.000

+35%+8%

+9%

CAGR >7%*

+54%

CAGR +19%

2020E2013E2012

13.537

2011

12.388

2010

11.457

2009

8.482

2008

5.503

2003

2.266

Total Passenger Car Market –China (incl. HK)(‘000 Units)

* EstimateData Source: Volkswagen Group China / IHS Global Insight

Current 5-year-plan: New growth model with focus on domestic market

11th 5-year-plan 2006-2010

12th 5-year-plan 2011-2015

Multi-National-Companies and infrastructure projects as growth generatorBig growth in manufacturing tradeJobs in cities to keep unemployment lowInternationally comparable price stability and well-adjusted foreign trade balance

Domestic consumption as growth acceleratorMegacities as growth generator Focus on environmental protection and energy efficiencyEncouragement of Chinese innovationsSocial stability due to balanced allocation of prosperity Selective policies for foreign investment as well as globalization of Chinese companies

To date:Focus on export and quantitative growth

Now:Focus on domestic market and qualitative growth

10

Mega and small cities will be the engine of GDP growth

Remark: 6 mega cities in 2010 (Shanghai, Beijing, Chongqing, Shenzhen, Tianjin, Guangzhou)Source: McKinsey Insights China – Macroeconomic model updated April 2012

Distribution by city size2005819 cities

2020865 cities

% of GDP2005 2020

City Level (Urban Population)

Big town (<0.5M)

Small (0.5-1.5M)

Mid-sized (1.5-5.0M)

Big (5-10M)

Mega (10M+)

New cities

3

7

5

6

52

33

169

166

378

46544

202

58

12

3

424

335

85

11

10 1313 2727

2222

2727

1515

1212

2626

1010

2323 2626

11

Zhejiang

Heilongjiang

Jilin Liaoning

Hebei Tianjin

Shandong

Henan

Anhui Jiangsu

Jiangxi

Fujian

Guangdong

Hunan

Hubei

Hainan

Beijing

Shanghai

Inner Mongolia

Shanxi

Guangxi

Yunnan Guizhou

Sichuan

Shaanxi

Ningxia Gansu

Qinghai Tibet

Xinjiang

Chongqing

GDP Growth development is expected to differentiate more strongly between the various Chinese regions

Source: Provincial Government Report

Estimate of Chinese GDP 2012 per Province

Province ExpectedGrowth 2012

Total GDP 2011 (trillion RMB)

Inner Mongolia 15.0% 1.40Guizhou 14.0% 0.56

Chongqing 13.5% 1.00Shaanxi 13.0% 1.20Hainan 13.0% 0.25Anhui 12.6% 1.50

Sichuan 12.0% 2.00Heilongjiang 12.0% 1.10

Tianjin 12.0% 1.10Shanxi 12.0% 1.10

Jilin 12.0% 1.04Gansu 12.0% 0.52Ningxia 12.0% 0.21Qinghai 12.0% 0.16Yunnan 12.0% 0.88Liaoning 11.0% 2.20Hunan 11.0% 1.96Fujian 11.0% 1.75Guanxi 11.0% 1.20Xinjiang 11.0% 0.66

Tibet 11.0% 0.06Henan 10.0% 2.70Hubei 10.0% 1.80Jiangxi 10.0% 1.20

Shangdong 9.5% 4.54Hebei 9.0% 2.40

Guangdong 8.5% 5.30Zhejiang 8.5% 3.18Jiangsu 8%-10% 4.80

Shanghai 8.0% 1.92Beijing 8.0% 1.60

Expected GDP Growth 2012

12-15%

10-12%

8-10%

12

Content

Our Momentum in China

Outlook Market Development

Investments Volkswagen Group China

Driven by Design, Technology and Brand Image

Financial results, challenges and opportunities

13

Go West and Go South Strategy for further growth

Existing production site

New production site

Urumqi

Chengdu

Changchun

NanjingYizheng

Shanghai

NingboFoshan

Beijing

“Go South Strategy”

“Go West Strategy”

14

Further strengthening of partnerships with SAIC and FAW

SAIC FAW

Signing ceremony April 23rd, 2012 in WolfsburgAgreement about Urumqi plant

Signing ceremony April 23rd, 2012 in WolfsburgIntention to extend JV contract with FAW

15

Volkswagen Group China: Planned product portfolio in 2015 with 94 models

Note: number of product models

Commercial Vehicles

CKD 34 FBU 60 94

16

Content

Our Momentum in China

Outlook Market Development

Investments Volkswagen Group China

Driven by Design, Technology and Brand Image

Financial results, challenges and opportunities

17

Volkswagen Passat – Special design elements for Chinese customers

Radiator grill Tail lamps Speaker covering Wheel program

18

Passat USA

Passat China

Latest TSI- and DSG-technologies of Volkswagen Group for China

2010

RecuperationStart-stop

Low rolling friction

Fleet emissions

Future‘s technology

Optimized gearsNew enginegeneration

New TSI generation

Prototypes with innovative Technologies

e-Traction

[CO2/km] [Volume]

19

Content

Our Momentum in China

Outlook Market Development

Investments Volkswagen Group China

Driven by Design, Technology and Brand Image

Financial results, challenges and opportunities

20

Volkswagen Group China reported another strong operating result for the first three quarters of 2012

Source: Volkswagen Group China

1) SVW Group/FAW-VW Group

Deliveries to Customers

Production (100%)1)

Operating profit (quotal)

(’000 Units)

(’000 Units)

(€ m)

1,024

975

395

2008

1,400

1,387

831

2009 2010

1,923

1,914

1,907

2011

2,259

2,202

2,616

Q1-Q32012

2,005

1,953

2,806

21

Challenges in a regulatory environment

Risk of restrictive policies for new car sales in developed Eastern Megacities

Additional megacities like Hangzhou, Shenzhen, Xi'An et al.are expected to introduce similar restriction measures

22

Shanghai

Beijing

Guangzhou

Quota

120k cars/year

240k cars/year

< 120k cars/year(not fixed)

Demanding requirements for fleet consumption

Details for Phase IV still under review

Volkswagen Group China has relevant strategies in place

23

Future growth prospects also coming from less developed regions and Tier 2-3 cities

Production and Dealer network extension will support

Growth in Western and Southern provinces

Different measures in place to realize the ambitious fleet consumption targets

New technologies and products will help to achieve targets

“Go South Strategy”

“Go West Strategy”

Engine andtransmissiontechnology

E-Traction

Vehiclemeasures

TSI

Downsizing

Dual clutch transmission

Recuperation

Start-Stop

Optimal ATM

Weight reduction

Aerodynamic optimization

Reduction of electricconsumption

Hybrid EVs

BEVs

Plug-in hybrid EVs

Additional business opportunities

24

Growing Chinese used car market Financial Services expects increase in retail finance share2)

Volkswagen Financial Services also aims to establish- Mobility packages- Long Term Rental & Fleet Business- Insurance Related & After Sales Services

2010

2.4

2016E2014E2012

+30% p.a.

2018E

20.0

million units

Total Used Car Market forecast1)

Roll out and Implementation of the successful Volkswagen Group used car brand “Das WeltAuto” in the Chinese dealer network

stronger finance demand expected

cash buyer dominance

1) Source: China Automotive Dealer Association 2) Based on the total passenger car sales in the market China

2012 2018

Volkswagen Group China

25

Volkswagen Group China is well positioned to maintain its number one position in the market and seize additional opportunities in the future

Delivered vehicles in million units

0

0,5

1

1,5

2

2,5

3

3,5

Disclaimer

This presentation contains forward-looking statements and information on the business development of the Volkswagen Group. These statements may be spoken or written and can be recognized by terms such as “expects”, “anticipates”, “intends”, “plans”, “believes”, “seeks”, “estimates”, “will” or words with similar meaning. These statements are based on assumptions relating to the development of the economies of individual countries, and in particular of the automotive industry, which we have made on the basis of the information available to us and which we consider to be realistic at the time of going to press. The estimates given involve a degree of risk, and the actual developments may differ from those forecast.

Consequently, any unexpected fall in demand or economic stagnation in our key sales markets, such as in Western Europe (and especially Germany) or in the USA, Brazil or China, will have a corresponding impact on the development of our business. The same applies in the event of a significant shift in current exchange rates relative to the US dollar, sterling, yen, Brazilian real, Chinese renminbi and Czech koruna.

If any of these or other risks occur, or if the assumptions underlying any of these statements prove incorrect, the actual results may significantly differ from those expressed or implied by such statements.

We do not update forward-looking statements retrospectively. Such statements are valid on the date of publication and can be superceded.

This information does not constitute an offer to exchange or sell or an offer to exchange or buy any securities.

26

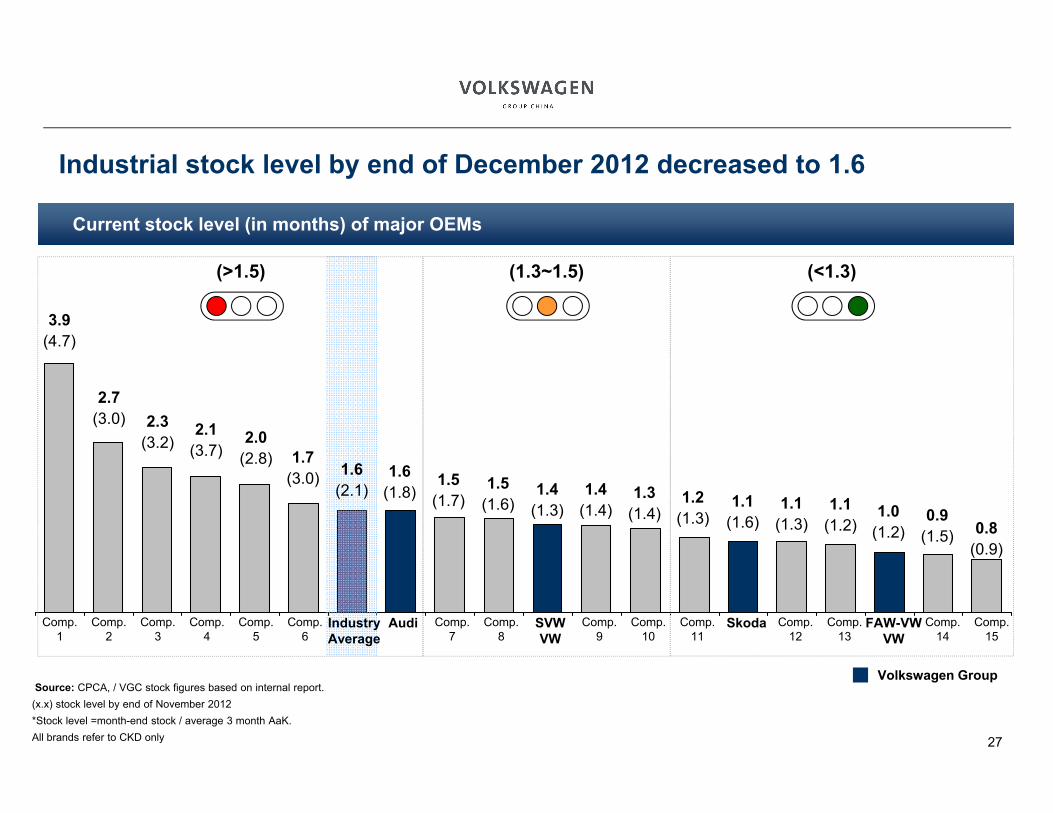

Source: CPCA, / VGC stock figures based on internal report.(x.x) stock level by end of November 2012*Stock level =month-end stock / average 3 month AaK. All brands refer to CKD only

(>1.5) (1.3~1.5)

Volkswagen Group

3.9(4.7)

2.7(3.0) 2.3

(3.2)2.1

(3.7)1.6

(2.1)

2.0(2.8) 1.7

(3.0) 1.6(1.8)

1.5(1.7)

1.5(1.6)

1.4(1.3)

1.4(1.4)

1.3(1.4)

1.2(1.3)

1.1(1.6)

1.1(1.3)

1.0(1.2)

0.9(1.5) 0.8

(0.9)

Audi SkodaComp.6

Comp.5

Comp.15

Comp.9

Comp.12

Comp.3

Comp.10

Comp.8

Comp.1

Comp.14

Comp.4

IndustryAverage

Comp.11

Comp.2

Comp.7

SVW VW

FAW-VW VW

Comp.13

1.1(1.2)

(<1.3)

27

Industrial stock level by end of December 2012 decreased to 1.6

Current stock level (in months) of major OEMs

Copyright © 2022 FDOKUMEN