Visibility and Logistic Control Tower - the Accenture case -

111

1 School of Industrial and Information Engineering Master of Science in Management Engineering Visibility and Logistic Control Tower - the Accenture case - Supervisor: Prof. Marco Melacini Master Graduation Thesis by: Gianmarco Tenti [894336] Academic year 2019-2020

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Visibility and Logistic Control Tower - the Accenture case -

1

School of Industrial and Information Engineering

Master of Science in Management Engineering

Visibility and Logistic Control Tower

- the Accenture case -

Supervisor:

Prof. Marco Melacini

Master Graduation Thesis by:

Gianmarco Tenti [894336]

Academic year 2019-2020

2

TABLE OF CONTENTS

TABLE OF CONTENTS .................................................................................................................................2

TABLES INDEX ..............................................................................................................................................4

FIGURES INDEX ............................................................................................................................................5

ABSTRACT ......................................................................................................................................................7

EXECUTIVE SUMMARY ..............................................................................................................................8

THE PROBLEM ......................................................................................................................................... 8

THE ACCENTURE CASE ......................................................................................................................... 8

METHODOLOGY AND OBJECTIVES .................................................................................................. 9

LIMITATIONS OF THE ANALYSIS .................................................................................................... 10

THE CONSULTING INDUSTRY ................................................................................................................11

THE SERVICE .......................................................................................................................................... 11

THE HISTORICAL BACKGROUND .................................................................................................... 22

THE PLAYERS ......................................................................................................................................... 24

PESTLE ANALYSIS ................................................................................................................................. 27

PORTER’S FIVE FORCES ..................................................................................................................... 33

FUTURE TRENDS ................................................................................................................................... 36

ACCENTURE .................................................................................................................................................38

HISTORY ................................................................................................................................................... 38

INTERNAL ORGANIZATION ............................................................................................................... 40

THE CONTINUOUS GROWTH ............................................................................................................. 43

SWOT ANALYSIS .................................................................................................................................... 44

THE SUPPLY CHAIN MANAGEMENT ....................................................................................................47

THE DEFINITION ................................................................................................................................... 47

SUPPLY CHAIN’S HISTORY ................................................................................................................ 48

TODAY’S SUPPLY CHAIN .................................................................................................................... 51

FUTURE SUPPLY CHAIN ...................................................................................................................... 52

THE VISIBILITY ..........................................................................................................................................56

THE CONTEXT ........................................................................................................................................ 56

THE DEFINITION ................................................................................................................................... 57

THE BENEFITS OF VISIBILITY .......................................................................................................... 57

DYNAMIC CAPABILITIES .................................................................................................................... 59

3

TECHNOLOGIES .................................................................................................................................... 61

THE LOGISTIC CONTROL TOWER .......................................................................................................64

THE DIGITAL SUPPLY CHAIN............................................................................................................ 64

THE DEFINITIONS ................................................................................................................................. 65

THE LCT IMPLEMENTATION ............................................................................................................ 71

LCT TECHNOLOGIES ........................................................................................................................... 73

THE PROJECT IN ACCENTURE ..............................................................................................................76

THE CLIENT ............................................................................................................................................ 76

THE BUSINESS CASE ............................................................................................................................. 76

THE SCOPE .............................................................................................................................................. 76

THE INITIAL FORECAST ..................................................................................................................... 78

ACCENTURE’S PROPOSAL.................................................................................................................. 79

LCT IMPLEMENTATION ...................................................................................................................... 81

JDA SOFTWARE ..................................................................................................................................... 82

CONTINUOUS IMPROVEMENT INITIATIVES ................................................................................ 84

KPIs MONITORING ................................................................................................................................ 91

SHIPPEO PARTNERSHIP .................................................................................................................... 102

ACTUAL BENEFITS OF THE PROJECT .......................................................................................... 105

CONCLUSIONS AND FOLLOW UPS ................................................................................................. 107

REFERENCES .............................................................................................................................................109

4

TABLES INDEX

Table 1 – National management consulting markets (sample of 15 countries) .............................................. 28

Table 2 – MC employment growth rate (2013-2017) ...................................................................................... 29

Table 3 – MC Turnover and MC Employment trend for the European panel (2013-2017) ............................ 30

Table 4 – Accenture’s revenues split by operating group ............................................................................... 42

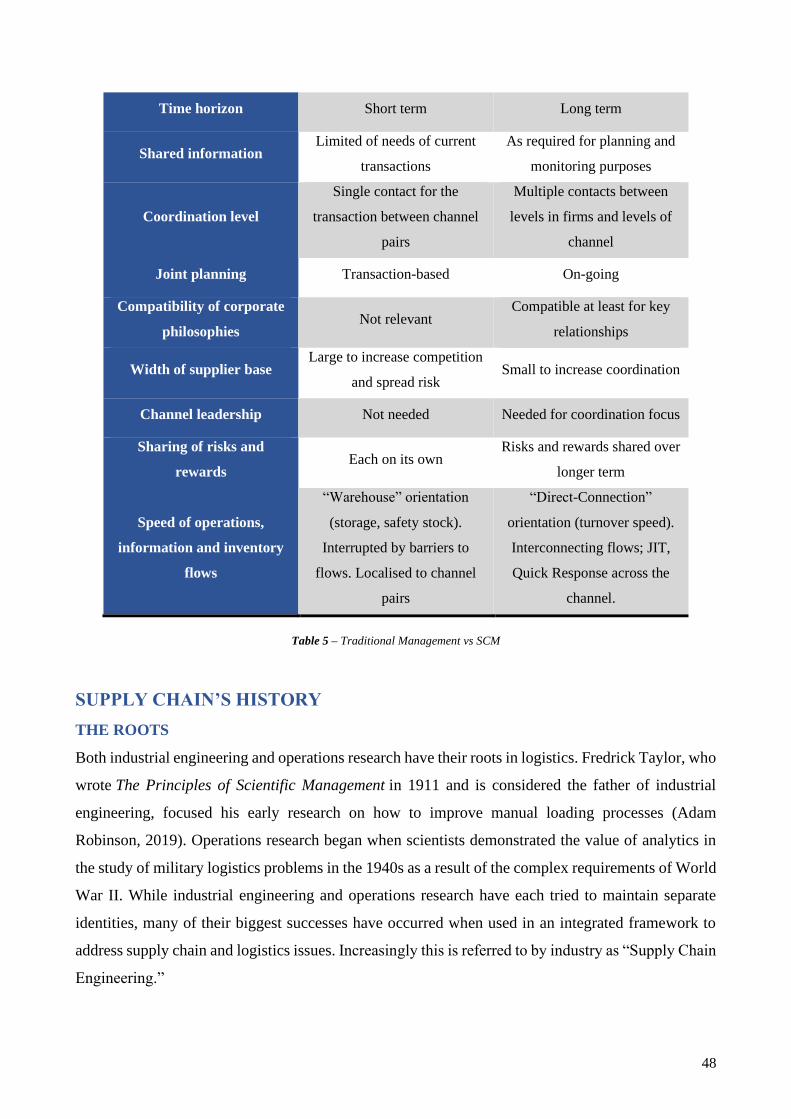

Table 5 – Traditional Management vs SCM ................................................................................................... 48

Table 6 – Performance affected by visibility ................................................................................................... 59

Table 7 – 3PL vs 4PL ...................................................................................................................................... 67

Table 8 – LCT’s benefits ................................................................................................................................. 71

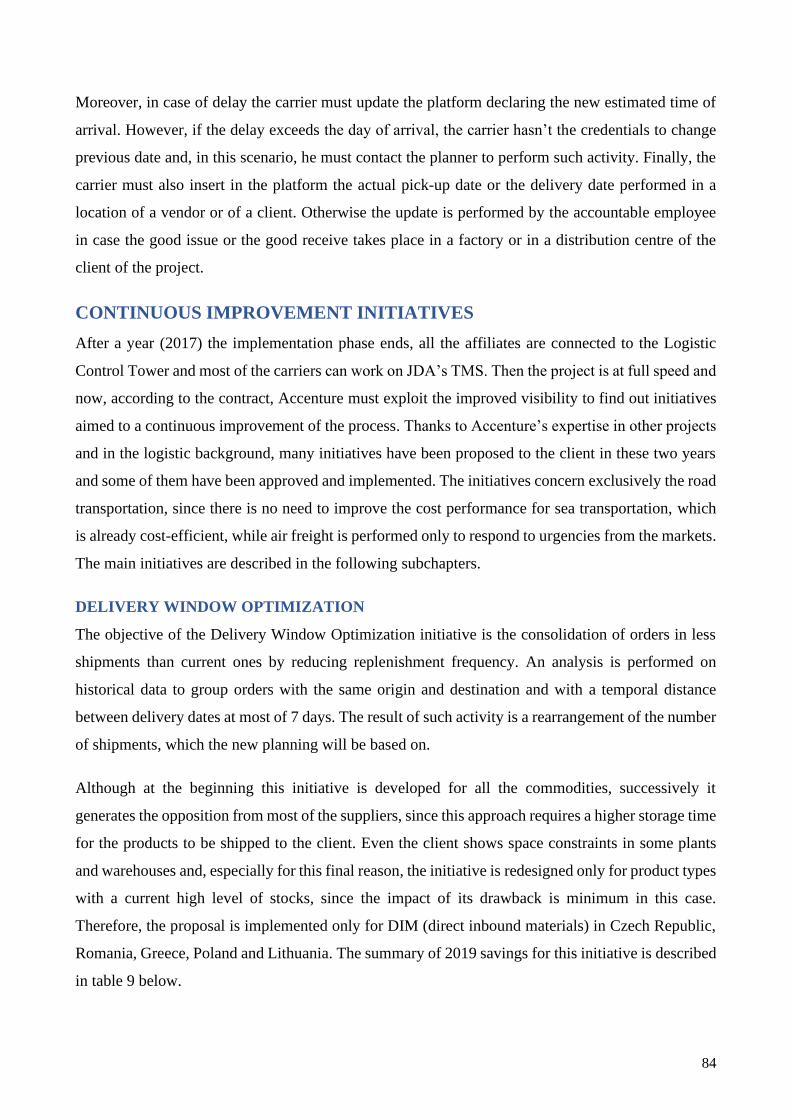

Table 9 – Delivery Window Optimization 2019 savings ................................................................................. 85

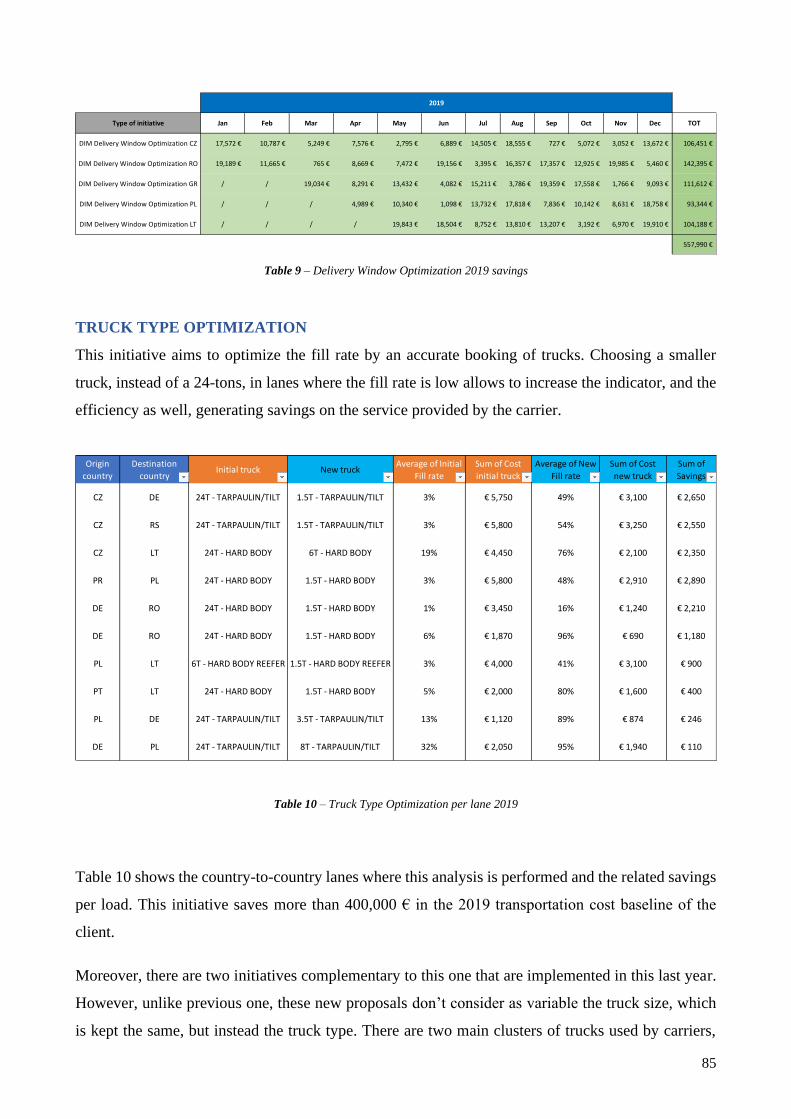

Table 10 – Truck Type Optimization per lane 2019 ........................................................................................ 85

Table 11 – Roundtrips 2019 analysis and forecast per lane ........................................................................... 86

Table 12 – Multipick 2019 analysis and forecast ............................................................................................ 87

Table 13 – Multipick 2019 savings.................................................................................................................. 88

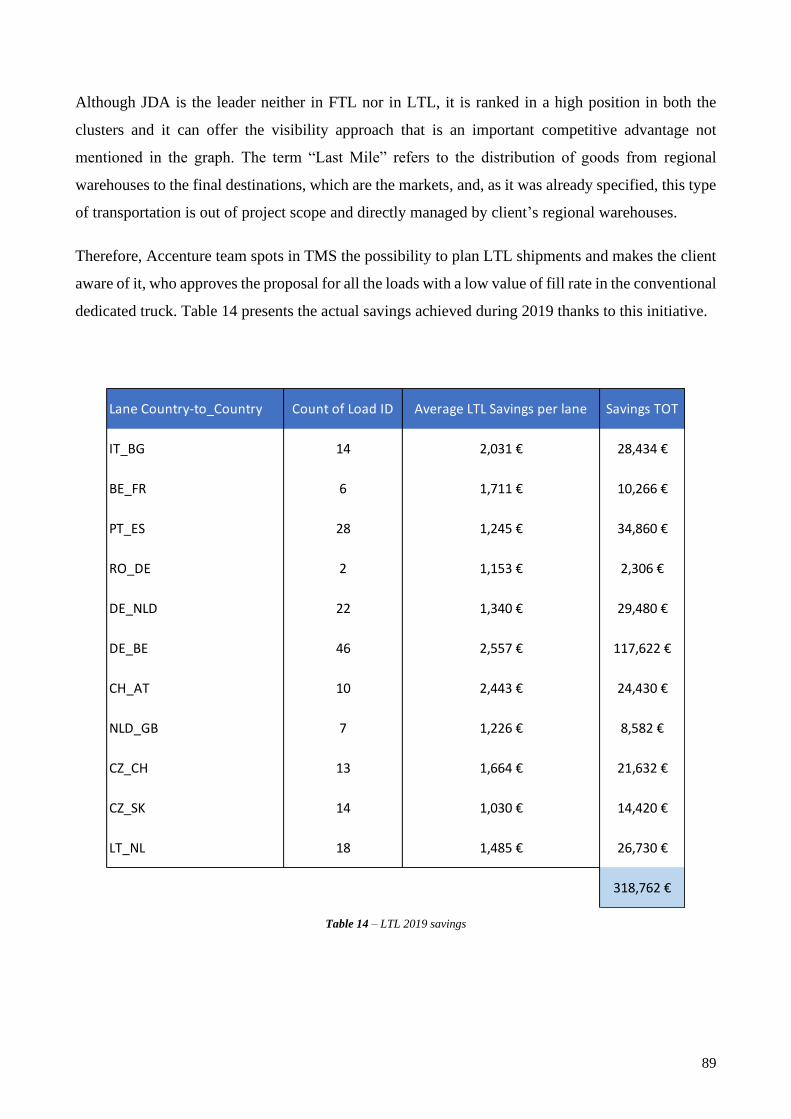

Table 14 – LTL 2019 savings .......................................................................................................................... 89

Table 15 – Procurement Contribution 2019 savings ...................................................................................... 90

Table 16 – Trucks Volume Conversion table .................................................................................................. 95

5

FIGURES INDEX

Figure 1 – Methodology’s flow ......................................................................................................................... 9

Figure 2 – Strategy consulting services .......................................................................................................... 12

Figure 3 – Operations consulting services ..................................................................................................... 14

Figure 4 – Financial advisory services ........................................................................................................... 17

Figure 5 – Human resources consulting services ........................................................................................... 19

Figure 6 – Technology and IT consulting services ......................................................................................... 21

Figure 7 – Foundation age and location of major Brand Consultancies ...................................................... 23

Figure 8 – 2018 revenues split by locations of the Top 5 Consulting Service Providers ............................... 25

Figure 9 – Accenture IPO on the New York Stock Exchange ......................................................................... 39

Figure 10 – Accenture’s global presence ....................................................................................................... 41

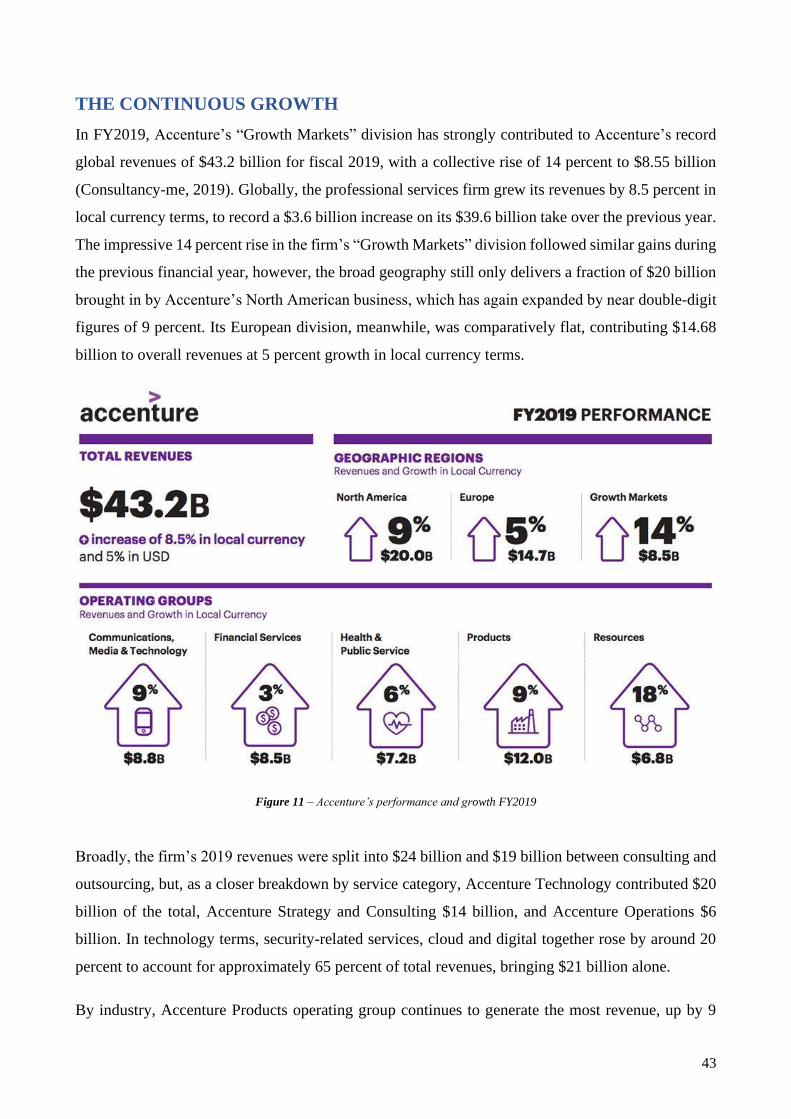

Figure 11 – Accenture’s performance and growth FY2019 ........................................................................... 43

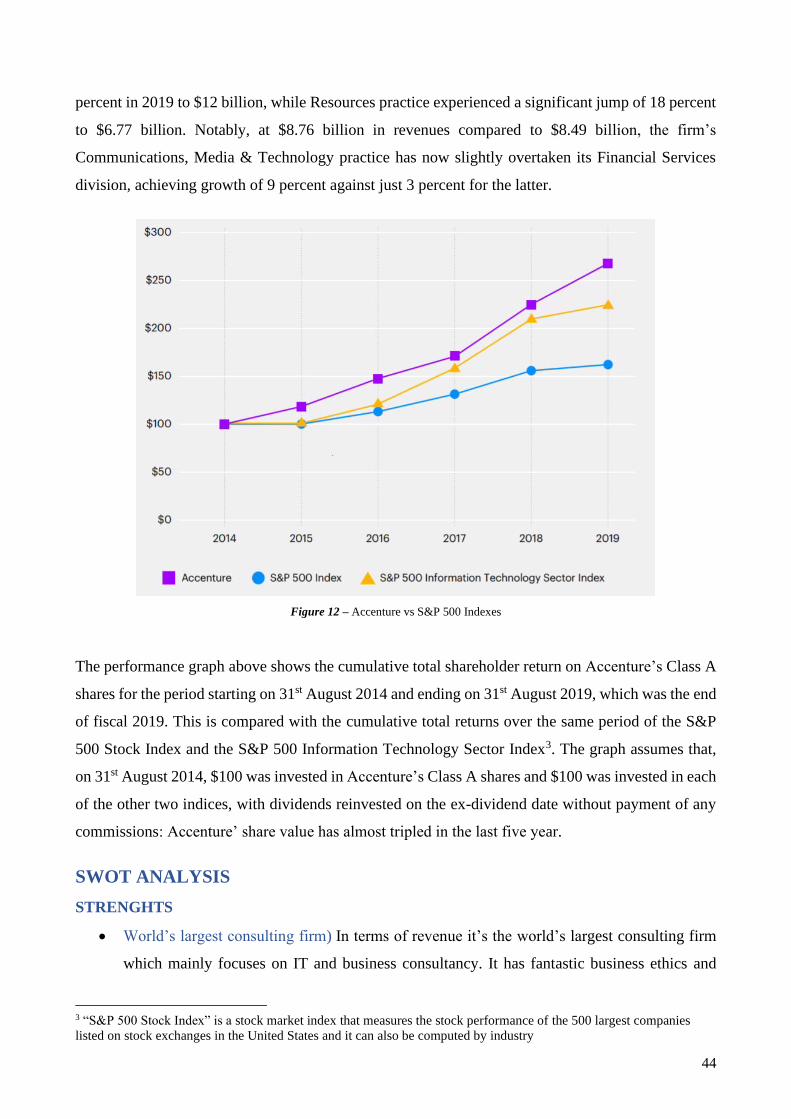

Figure 12 – Accenture vs S&P 500 Indexes .................................................................................................... 44

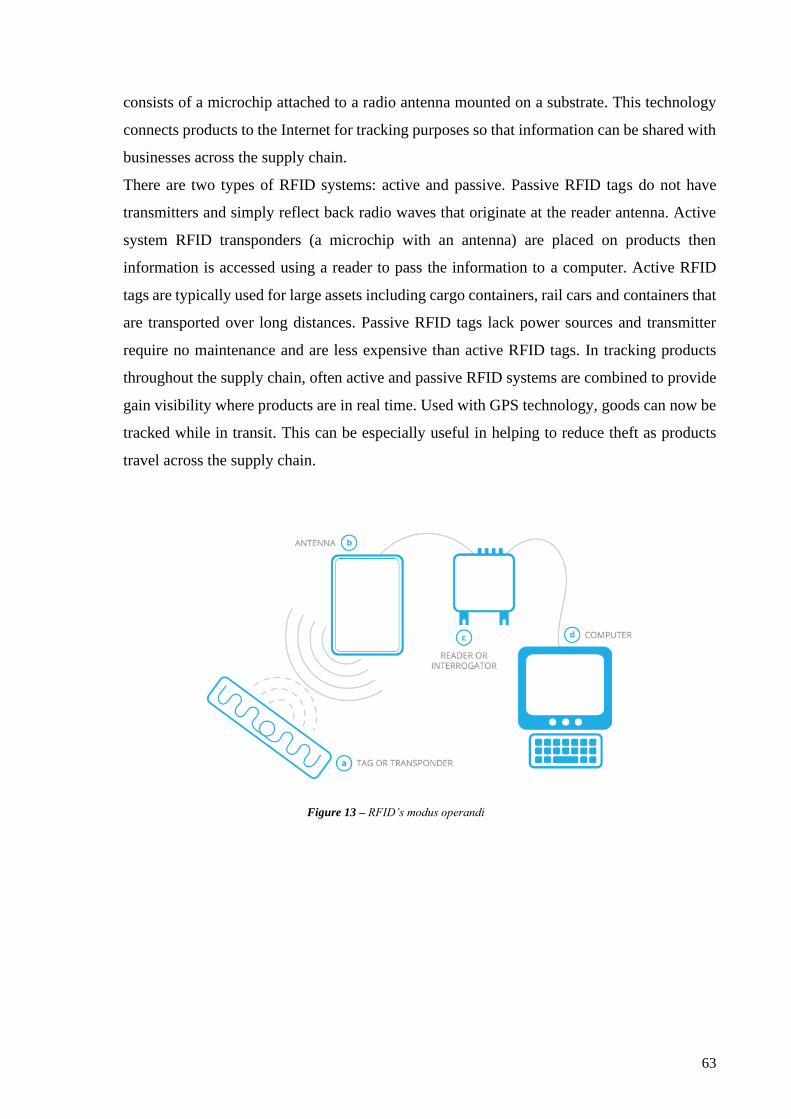

Figure 13 – RFID’s modus operandi .............................................................................................................. 63

Figure 14 – xPL approaches ........................................................................................................................... 65

Figure 15 – LCT’s framework......................................................................................................................... 69

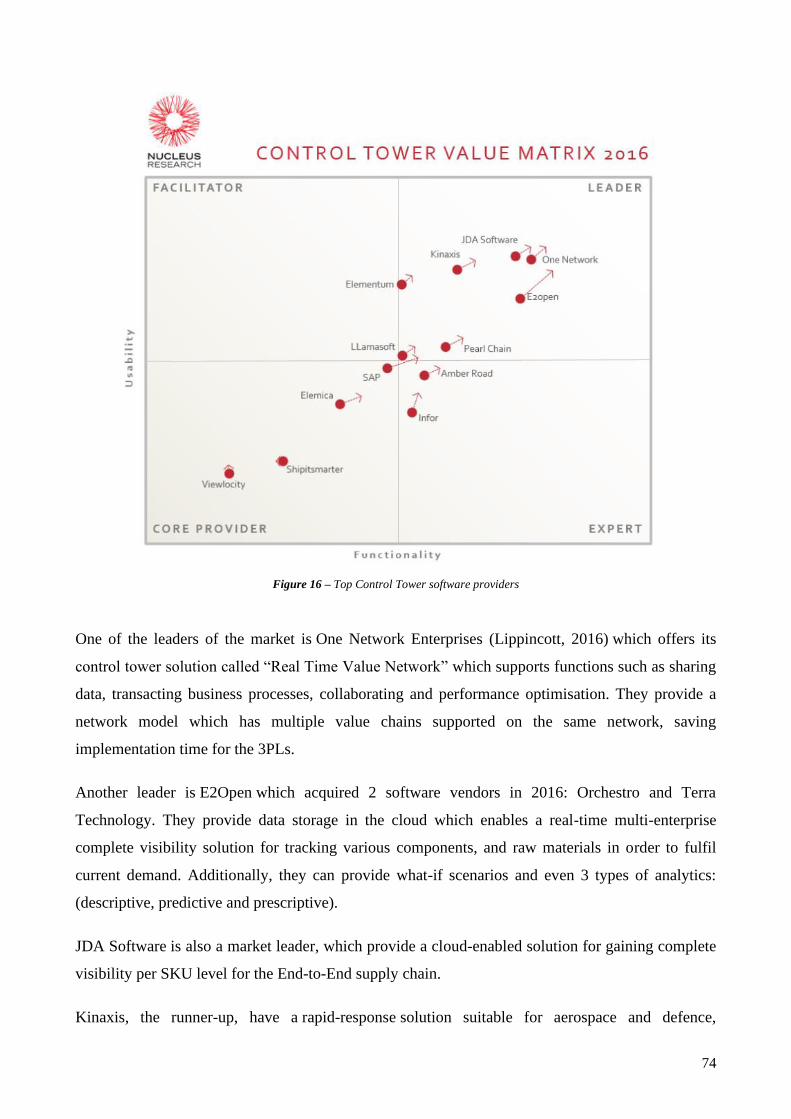

Figure 16 – Top Control Tower software providers ....................................................................................... 74

Figure 17 – Geographic transport flow allocation ......................................................................................... 77

Figure 18 – First round savings forecast ........................................................................................................ 78

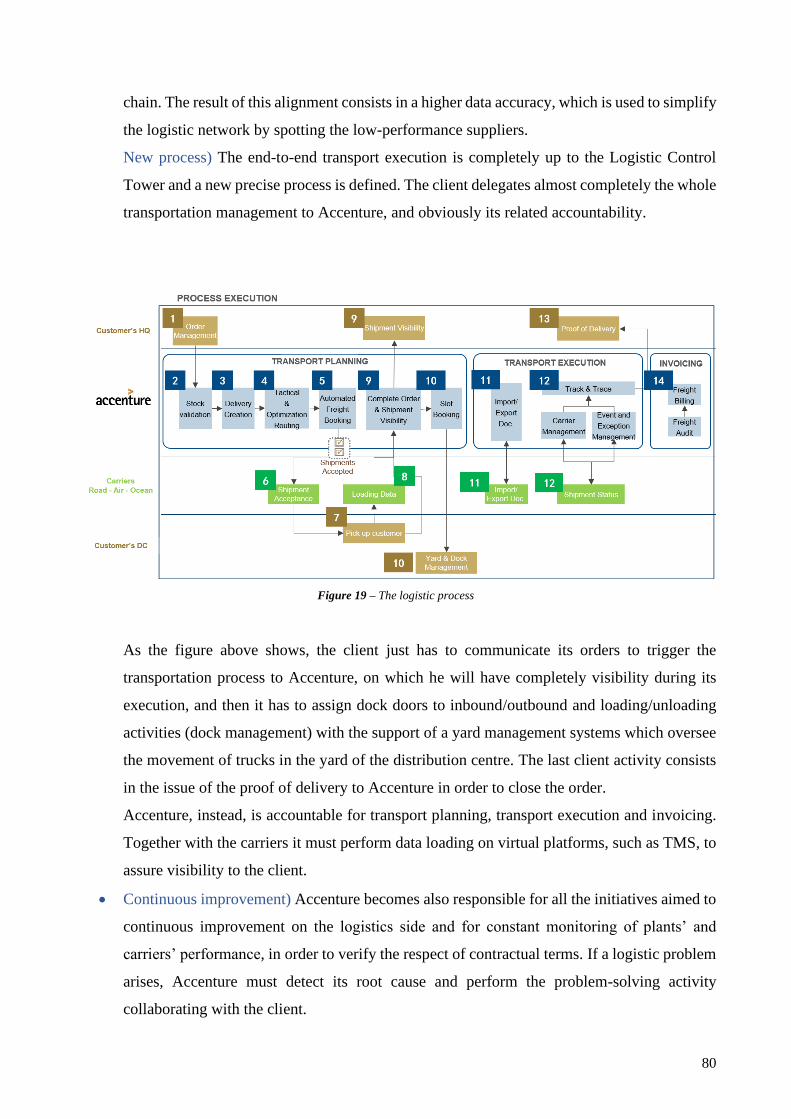

Figure 19 – The logistic process ..................................................................................................................... 80

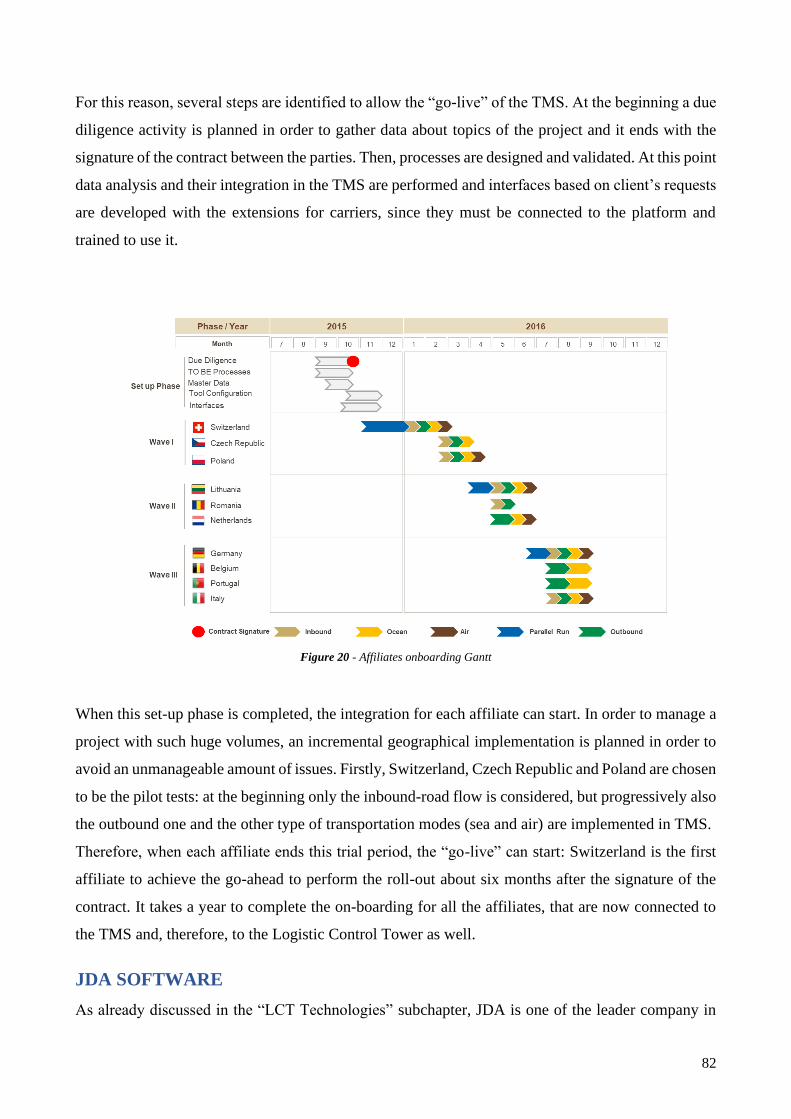

Figure 20 - Affiliates onboarding Gantt ......................................................................................................... 82

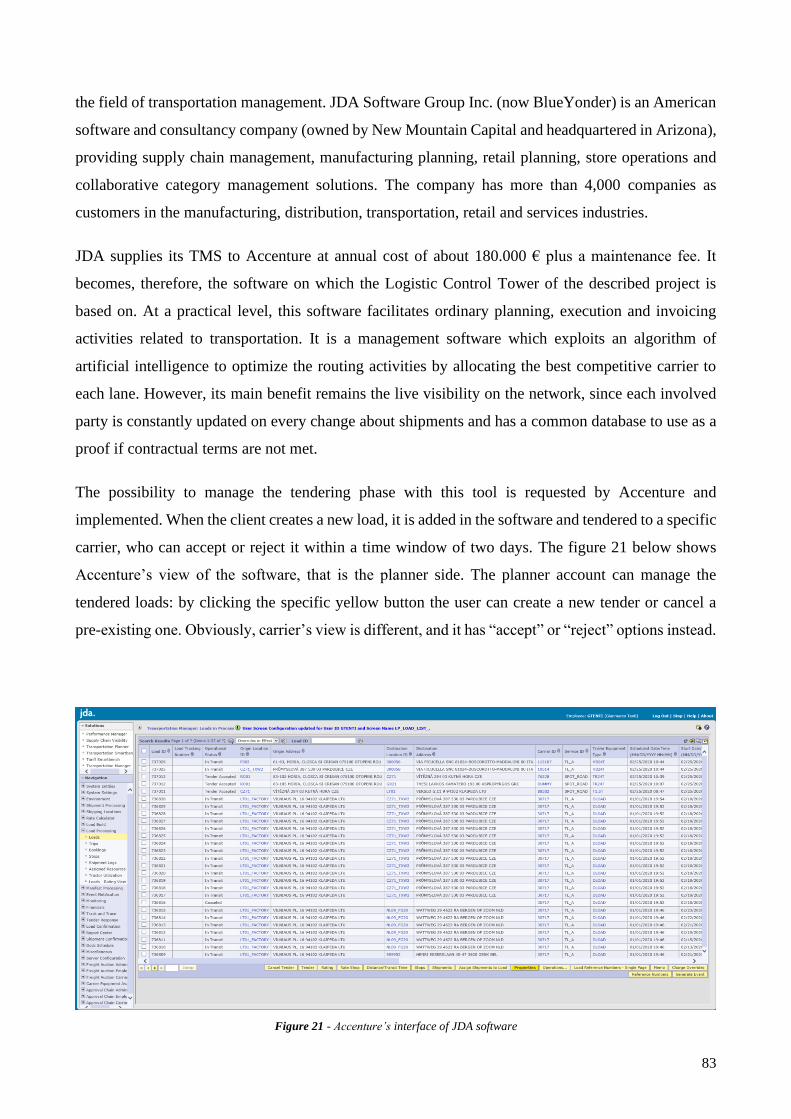

Figure 21 - Accenture’s interface of JDA software ........................................................................................ 83

Figure 22 – Logistic platforms split by transportation type ........................................................................... 88

Figure 23 – Example of KPIs identification decision tree .............................................................................. 91

Figure 24 – Contractual Fill rate by Affiliate ................................................................................................. 95

Figure 25 – Contractual Fill Rate vs Physical Fill Rate ................................................................................ 96

Figure 26 – Shipment and Delivery Note volumes .......................................................................................... 97

Figure 27 – On Time Shipments by Affiliate ................................................................................................... 97

6

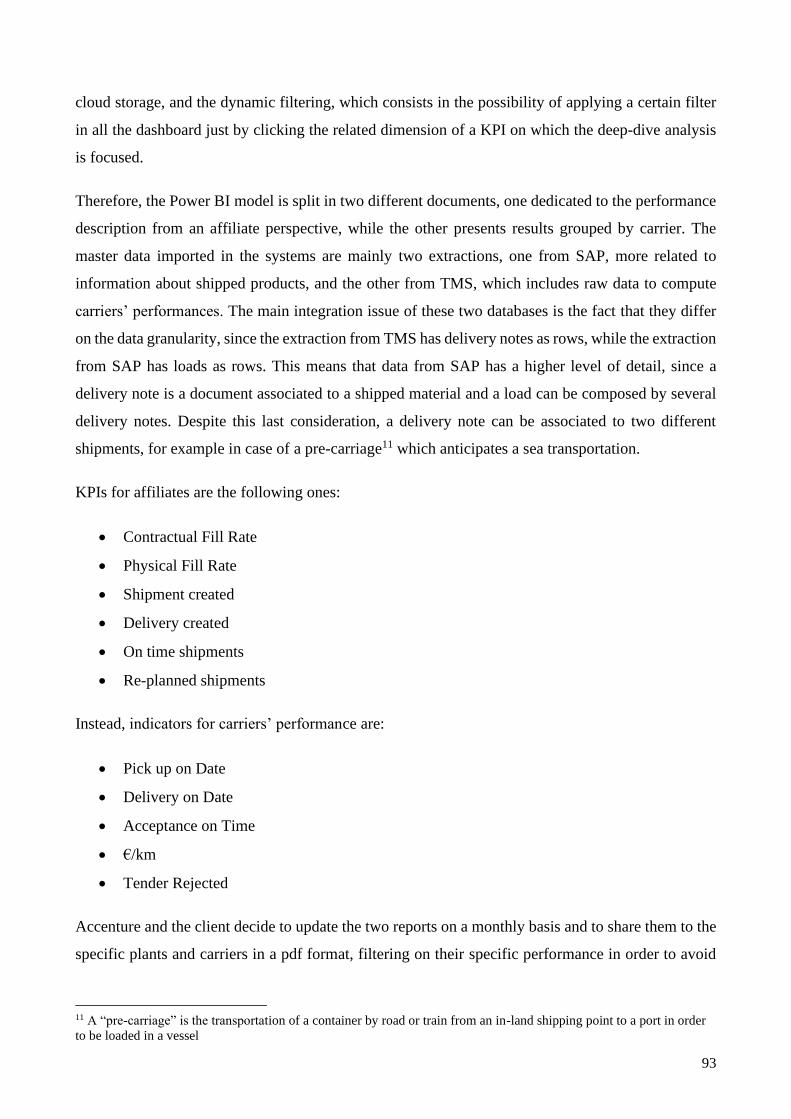

Figure 28 – Re-planned Shipments ................................................................................................................. 98

Figure 29 – Transportation planning process ................................................................................................ 99

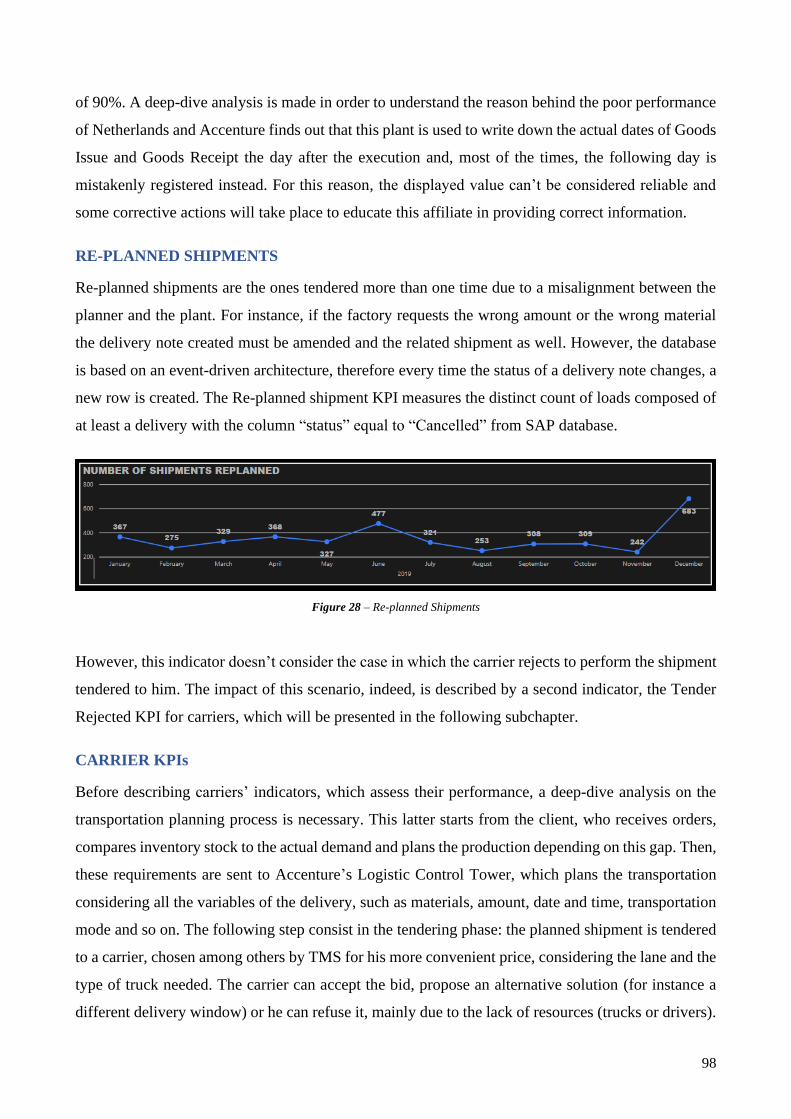

Figure 30 – Carriers’ operational KPIs ....................................................................................................... 100

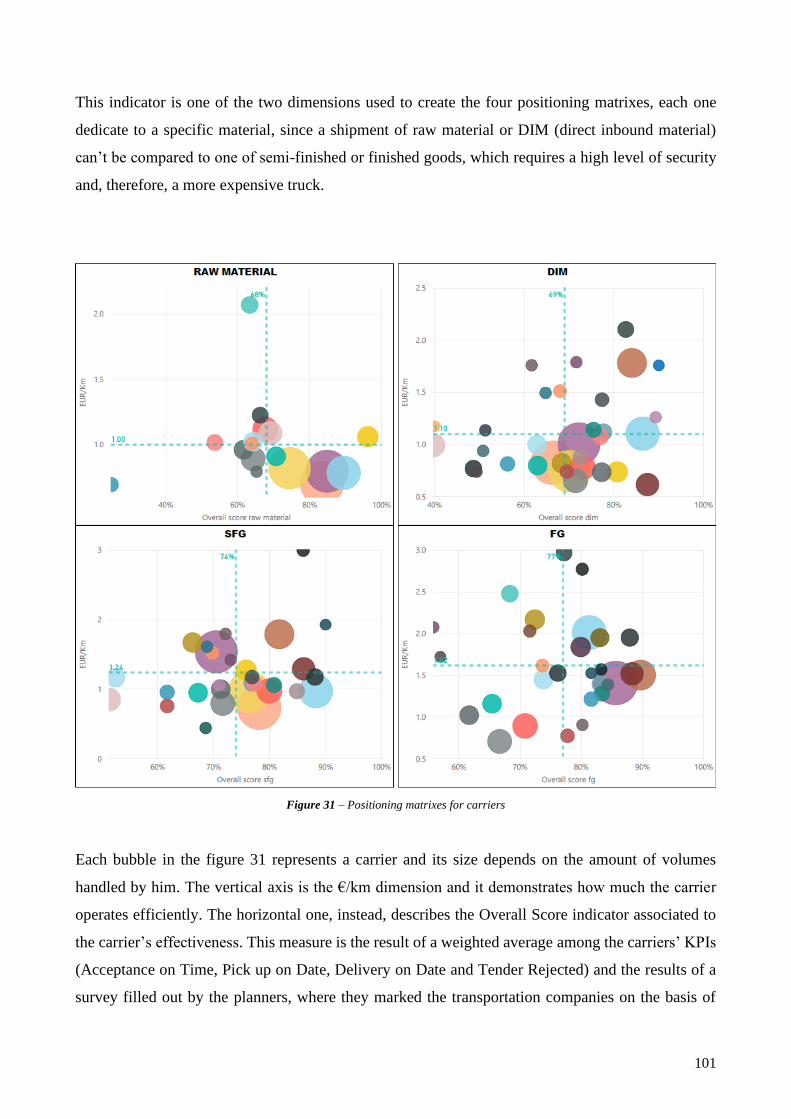

Figure 31 – Positioning matrixes for carriers .............................................................................................. 101

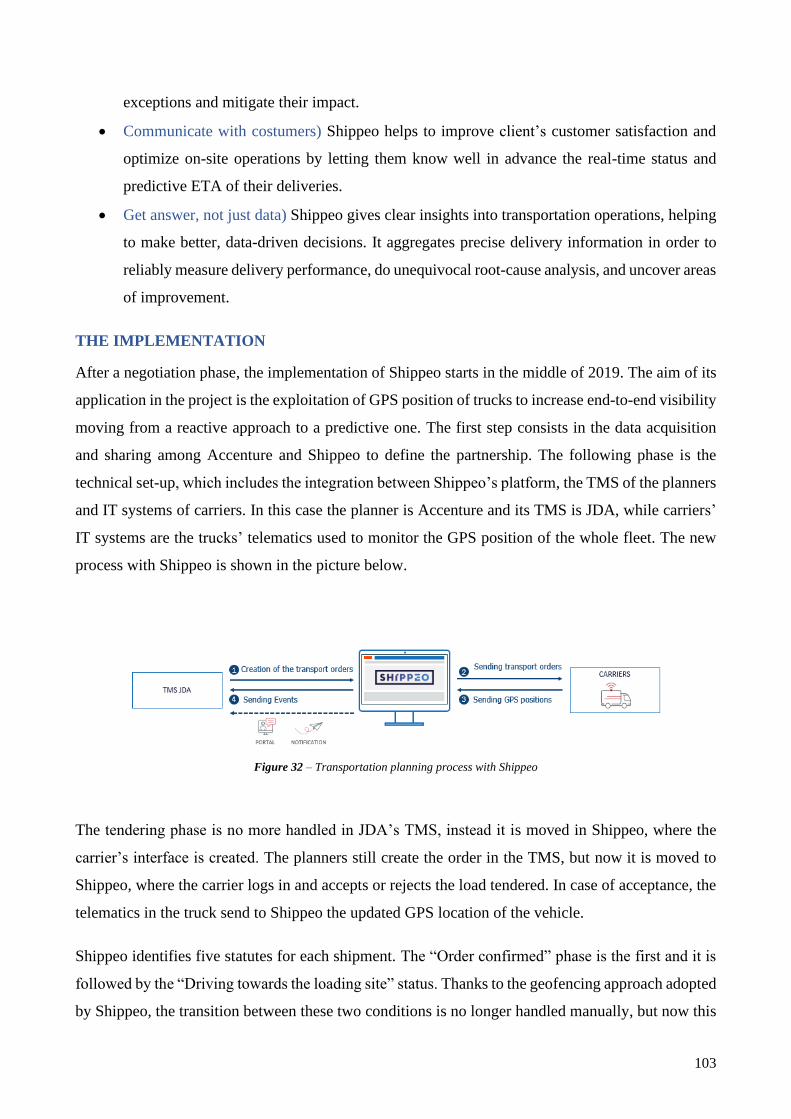

Figure 32 – Transportation planning process with Shippeo ......................................................................... 103

Figure 33 – Transport statutes and geofencing in Shippeo .......................................................................... 104

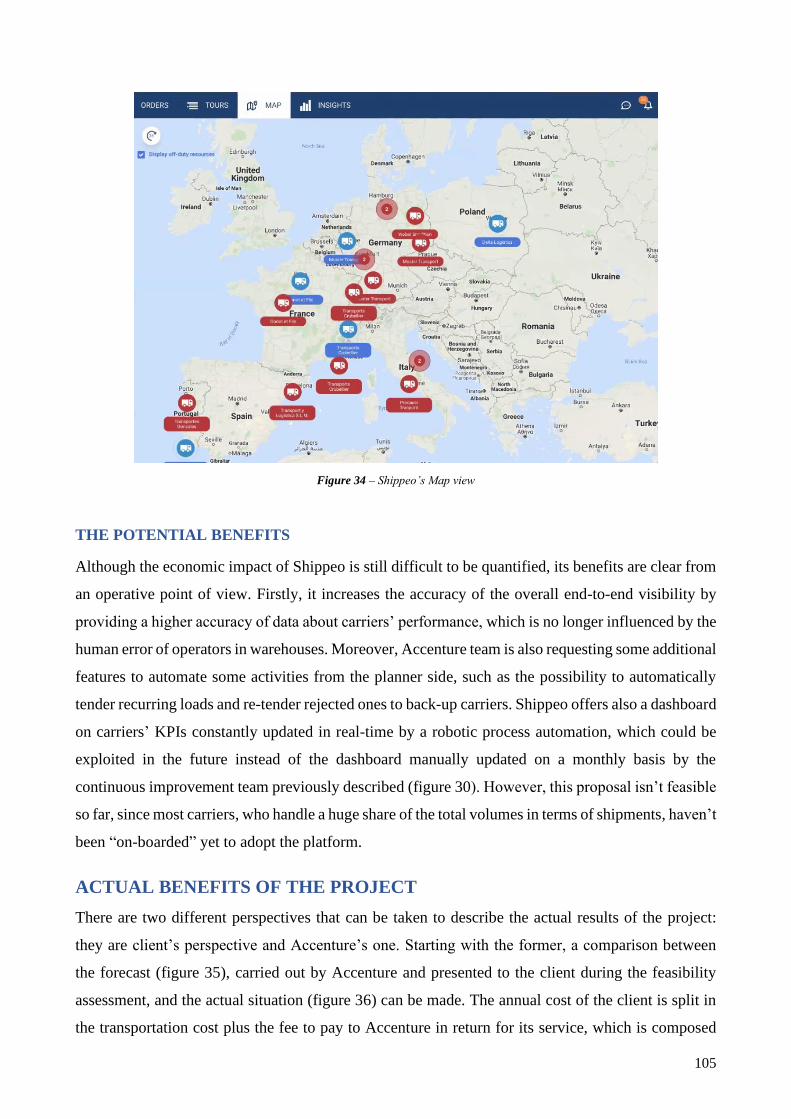

Figure 34 – Shippeo’s Map view .................................................................................................................. 105

Figure 35 - Planned total transportation cost .............................................................................................. 106

Figure 36 – Actual total transportation cost ................................................................................................. 106

Figure 37 – Accenture’s profit from the project ........................................................................................... 107

7

ABSTRACT

The purpose of this thesis is to clarify the “visibility” concept in a logistic perspective and to identify

the main approaches to increase it, as the Logistic Control Tower (LCT).

The thesis starts with a brief introduction about the history of the consulting sector, in order to make

the reader aware of the environment in which Accenture operates, and to provide a comprehensive

view of the firm.

Successively, a literature review about the history and trends of the supply chain management is

submitted. Therefore, the focus is moved to the clarification of the “visibility” concept and to the

explanation on the theory of the Logistic Control Tower. Initially, the advantages of this configuration

are presented in a qualitative way from the evidence of the literature, but successively also a

quantitative approach is made possible thanks to the direct experience of the candidate, who, during

the internship, has been in touch with a project in which Accenture plays the role of the Logistic

Control Tower for an important firm of consumer goods.

This document can be considered as an attempt to show what are the possible savings achievable with

the external LCT implementation, and as a guideline for those firms with a low logistic capability,

which should consider the idea of outsource it, and for others already relying on 4PLs, without having

visibility on what they are paying for, which should review their logistic strategy.

8

EXECUTIVE SUMMARY

THE PROBLEM

The aim of this document is to respond to the difficult question on how a firm can reach the

operational excellence in such complicated and wide field as the logistic one. In the past the logistic

capability wasn’t considered as a competitive advantage by most of the industries, but nowadays the

situation has changed. Thanks to trends such as the globalization and the digitalization, the

transportation and the inventory management have started to assume a strategical value for firms’

business in the last years. However, not all the companies are able to exploit these new advantages

for many reasons, including their tendency of not dedicating time and effort to activities whom they

are used to consider non-core. For this reason, firms tend to outsource such activities to logistic

service provider operators. Two different cases are distinguished by the literature: if only the logistic

execution is outsourced, the carrier who performs the service is called a third party logistic service

provider (3PL), while if both the execution and the management of logistic flows are externalized,

the entity which provides the service is defined a fourth party logistic service provider (4PL). This

document focuses on this last scenario and on how the creation of a central hub (the Logistic Control

Tower), where all the logistic data are visible, improves overall supply chain’s performances.

THE ACCENTURE CASE

Accenture plc, stylised as Accenture, is an Irish-domiciled multinational professional services

company that provides services in strategy, consulting, digital, technology and operations to a B2B

market. The candidate exploits his experience from the internship in the firm to describe an

Accenture’s project where the firm plays the 4PL role for its client. One of the main objectives of the

thesis is to show to the reader how a consulting firm can be a perfect provider of this type of service,

highlighting the value added whom it can bring, while a carrier company can’t.

The project started in 2016 and a five-year duration is defined (until 2020 included). In this timeframe,

Accenture is accountable for the redesign of the transport management for the client starting from the

Logistic Control Tower set-up, the renegotiation of contracts with carriers on behalf of the client and

TMS integration. Moreover, Accenture will be committed in some operative activities, such as order

management, planning, and execution, auditing and billing. Since 2017 Accenture offers an Analytics

service, which allows the issue of standards reports and dashboard to monitor cost per lane and carrier,

as well as their performance with a continuous improvement perspective. The scope of the project

consists in the transportation management of inbound and outbound flows for 4 types of commodities

(raw materials, direct inbound materials, semi-finished goods and finished goods) from or to all the

9

European factories of the clients. The project mainly focuses on managing overland truck

transportation and ocean; despite of that, and due to punctual urgent order requirement, airfreight

orders are also managed.

METHODOLOGY AND OBJECTIVES

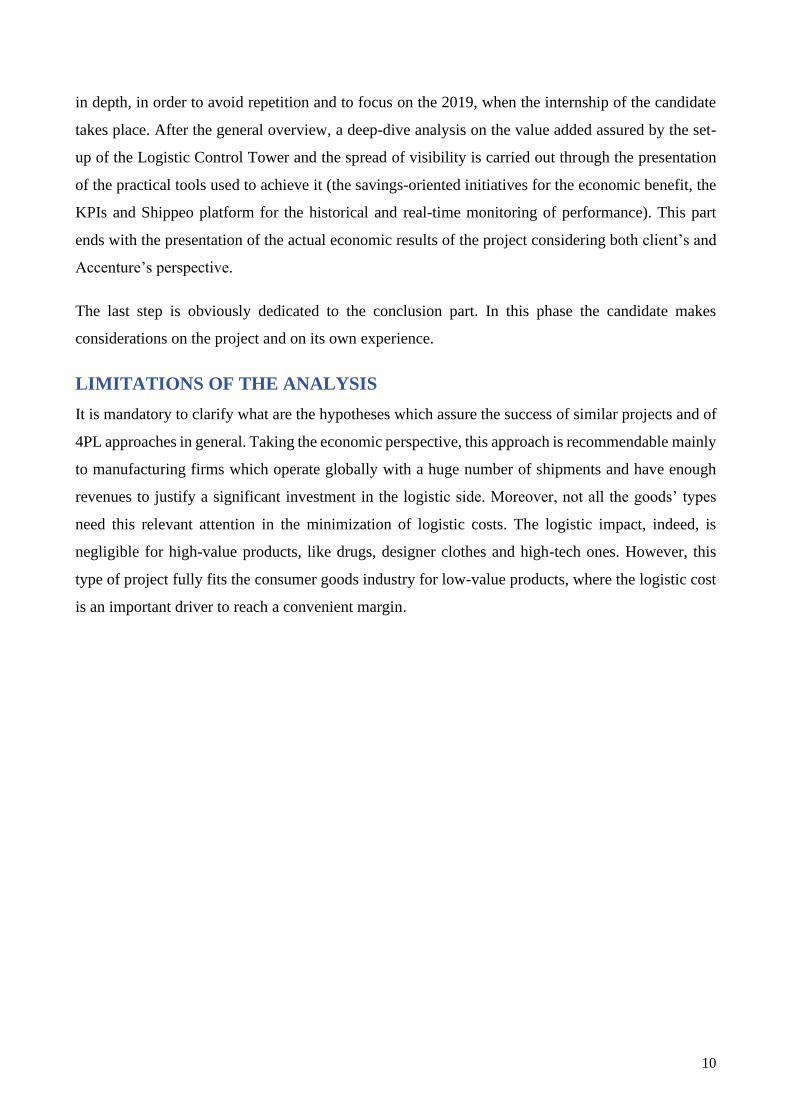

The main objectives whom the candidate wants to achieve are:

• Introduce the reader to the theory behind the concepts of visibility and Logistic Control

Tower;

• Prove the advantages of their deployment through Accenture’s practical case.

Figure 1 shows the flow describing the steps in which the candidate has arranged the draft of the

document.

Figure 1 – Methodology’s flow

The first macro-phase is the setting of the introduction. The candidate decided to fill this part with

the description of the background in which the project takes place. A top-down approach is adopted

in this case: before the industry is introduced and successively the firm. The information on the sector

come from internet researches performed by the candidate, while he also exploited firm’s database to

get articles about Accenture.

The second step consists in the literature review. Firstly, a general introduction on the concept of

Supply Chain management is made in order to show its history and evolution through the years. Its

main trends are described, and then the focus is moved to the pillars which the project is based on.

This part is the result of a re-elaboration of articles found by the candidate about discussed topics.

After the presentation of previous information, according to the candidate, the reader has enough

knowledge to be introduced to the project in the third macro-phase. Therefore, the collaboration

between Accenture and the client is described from the origin, which consists in the initial request, to

the current time, covering a 4-year timeframe. However, not all the years of the project are discussed

10

in depth, in order to avoid repetition and to focus on the 2019, when the internship of the candidate

takes place. After the general overview, a deep-dive analysis on the value added assured by the set-

up of the Logistic Control Tower and the spread of visibility is carried out through the presentation

of the practical tools used to achieve it (the savings-oriented initiatives for the economic benefit, the

KPIs and Shippeo platform for the historical and real-time monitoring of performance). This part

ends with the presentation of the actual economic results of the project considering both client’s and

Accenture’s perspective.

The last step is obviously dedicated to the conclusion part. In this phase the candidate makes

considerations on the project and on its own experience.

LIMITATIONS OF THE ANALYSIS

It is mandatory to clarify what are the hypotheses which assure the success of similar projects and of

4PL approaches in general. Taking the economic perspective, this approach is recommendable mainly

to manufacturing firms which operate globally with a huge number of shipments and have enough

revenues to justify a significant investment in the logistic side. Moreover, not all the goods’ types

need this relevant attention in the minimization of logistic costs. The logistic impact, indeed, is

negligible for high-value products, like drugs, designer clothes and high-tech ones. However, this

type of project fully fits the consumer goods industry for low-value products, where the logistic cost

is an important driver to reach a convenient margin.

11

THE CONSULTING INDUSTRY

“Management consulting is an independent professional advisory service assisting managers and

organizations to achieve organizational purposes and objectives by solving management and

business problem, identifying and seizing new opportunities, enhancing learning and implementing

changes.”

(Sabath & Kubr, 1977)

The global consulting market grew 9% reaching $188 billion in 2018 (Blackmore, Dean; Short, 2017).

Consulting services represented 19% of the overall IT services market in 2018, and the second-fastest-

growing segment, behind infrastructure as a service (IaaS) and infrastructure utility services. This

growth is driven by several factors, among them the merging of other markets into consulting.

Specifically, consultancies have enhanced their expertise by acquiring digital agencies, bringing with

them human-centred methods and a focus on user experience (digital design and innovation). They

have gained added revenue through innovation workshops leading to downstream work, advising on

new technologies and agile approaches.

THE SERVICE

What are the types of services provided by consulting firms? At the heart of the industry stand six

main domains: Strategy Consulting, Operations Consulting, Financial Advisory, HR Consulting and

Technology Consulting (Consultancy.Uk, 2018).

STRATEGIC CONSULTING

Strategy consulting, often referred to as strategy consultancy, strategic advisory or boardroom

consulting, is considered by the majority as the most high-end and prestigious segment within this

professional services industry. Strategy means “a plan with the aim of achieving long term goals" and

organisations regularly engage with consultants of this stream to seek support in developing or

implementing business strategies. The strategy consulting domain develops corporate, organisational

or functional strategies to private sector clients and helps public sector organisations and institutions

with economic policy. Strategy consulting services consists of eight disciplines: Corporate Strategy,

Business Model Transformation, Economic Policy, Mergers and Acquisitions, Organisational

Strategy, Functional Strategy, Strategy and Operations and Digital Strategy.

12

Figure 2 – Strategy consulting services

Corporate strategy, also referred to as strategic management, encompasses the formulation of

enterprise-wide and business unit strategies and goals. Strategy consultants are regularly assigned to

support the design of vision and mission statements, the development of strategic plans and the setup

of implementation roadmaps (which outline activities and resources needed to implement the

plans). Some examples of strategic advisory projects are the assessment of strategic options, the

support of business planning processes and the development of market entry strategies (when

companies want to enter new markets or launch new products).

Like corporate strategy, Business Model Transformation (BMI) also focuses on the design and

development of future-proof strategies, with the key difference that it includes fundamental changes

in how business is conducted, often triggered by major modifications in the external environment.

Business Model Transformation in addition has a wider scope than strategy, looking at a set of

organisational and operational elements and how they interact to achieve a common goal, such as

value propositions, customer segments, cost structures and organisational structures. Due to the

disruptive nature of technology in recent years, consultants of this stream in many cases work close

to Digital strategy.

The Economic Policy service area includes a range of economic advisory facilities that aid

governments and international institutions with policy setting. Most offerings cover fiscal policy,

which deals with government actions regarding taxation, budgets and spending and monetary policy,

that is related to central banking actions regarding the money supply and interest rates, or government

interventions across areas such as the labour market, national ownership, housing and so on. Further

offerings within this segment are impact assessments (such as a socio-economic benefits study),

financial valuation analysis in cases of disputes (economic litigation), economic studies for antitrust

cases, competition investigations and merger proceedings, conducted both for corporates or

governments authorities.

Strategy consultants are, together with corporate finance advisors, M&A lawyers and investment

bankers, also active in the M&A sector, with attention on strategic and commercial activities in the

13

pre-deal phase, although consultancies in many cases are too engaged to manage the initial period of

the post-merger integration phase. Strategy consulting firms serve companies and investors, for

instance, with building business cases to understand the economic drivers of M&A, and moreover

provide due diligence work on potential targets to clients. Other services that strategy consultants can

offer in this environment include the facilitation of the establishment of alliances and joint ventures,

managing divestitures/carve-outs and facilitating Initial Public Offerings (IPOs).

Organisational Strategy analyses the levers which an organisation needs to improve in order to, over

time, deliver the strategy of the enterprise. Main propositions include designing organisational

structures and corporate governance, assessing organisational competitiveness, developing human

capital strategies and supporting change management programmes.

Functional Strategy involves the development of strategic plans and roadmaps for organisational

functions, which can range from sales and marketing to finance, HR, supply chain, R&D or

procurement.

Over the past decade, strategic management and operational management have increasingly

converged, as topics such as process management, operations and technology have become

increasingly important elements of strategy execution. Consequently, several offerings which

historically were centred around strategic advisory have been expanded to include operational

considerations, and as a result the Strategy & Operations domain has gained significant importance.

The domain is not only served by strategy consulting firms that have moved towards operations, but

also operations specialist that have ramped up their strategic skills and large technology firms that

leverage their tech expertise to create an edge. Going forward, the lines between strategy, operations

and technology are forecasted to blur further, with an increasing number of consultancies set to play

a role in the field, adding competition to the landscape.

In line with the rise of technology, digital strategies have surfaced to the forefront of strategic work,

not just enabling business ambitions, but more than ever representing the crux between success and

failed strategies, and as a result, the market for Digital Strategy has shown unprecedented late growth.

The service area brings together elements from strategy and IT Organisation, and spans offerings

such as developing a strategy for digital operations, the design of a corporate IT or online strategy,

drafting approaches for analytics or cloud transitions, as well as high-level work for technology areas

such as architecture, governance and application management.

14

OPERATIONS CONSULTING

Operations consulting, also referred to as operations management, is described as advisory and/or

implementation services that improve a company's internal operations and performance in the value

chain. Operations management consulting projects create more effective client operations by advising

on and supporting with the implementation of changes to target operating model, functional business

processes, management systems, culture and so on. The market for operations consulting and

management services contains eight disciplines: Organisational Operations, Sales & Marketing,

Supply Chain, Sourcing & Procurement, Finance, Business Process Management, Research &

Development and Outsourcing.

Figure 3 – Operations consulting services

Organisational Operations is based on improving the performance of all aspects that support the

organisation’s structure; including organisation design, governance (across functions and

departments), roles and responsibilities, and employee performance. Typical activities concern either

the implementation of organisational strategies, such as workforce optimisation or the redesign of

employee roles, or are stimulated by an event or a crisis, such as a merger or a transition as part of a

broader corporate restructuring effort.

From a functional perspective, operations consulting aims at improving the processes, ways of

working and underlying systems across a broad range of areas, of which Sales & Marketing, Supply

Chain, Sourcing & Procurement, Finance and Research & Development are the largest areas in terms

of size. Sales & Marketing investigates how sales operations can be improved, including boosting

channel management, professionalising the level of customer support (i.e. from call centres to

specialised helpdesks) and advancing engagement with clients, commonly defined as customer

relationship management (CRM). Other areas under Sales & Marketing embrace the optimisation of

account and promotion management, Sales and Operations Planning (S&OP) and the improvement

of workforce effectiveness. Sales & Marketing include, among others, the fields of customer and

market research, marketing intelligence, product design and engineering, category management and,

lastly, customer experience and loyalty.

15

Supply Chain Management (SCM) consultants aim at streamlining the supply-side activities across

the full value chain, spanning from production to logistics (inbound/outbound) and warehousing

to customer delivery. Key offerings can be the supply side optimization of Sales and Operations

Planning, the enhancement of planning accuracy (i.d. demand planning, forecasting), manufacturing

operations improvement, logistics optimisation (i.d. network design, transport modes), inventory

management and managing operations risk. The latter area embraces all non-compliance-driven

efforts (which sit within Financial Advisory) aimed at minimising the risk of supply chain failures to

normal business operations. Key activities consist in the assessment of gross operating risk, the

development of operations risk mitigation plans, scenario modelling, and the development of

frameworks to automate responses to operations disruptions. One of the major growth areas in Supply

Chain Management consulting is sustainability: considering the growing value attached to corporate

social responsibility, companies are investing significantly in improving the ecological footprint of

their operations. Supply chain consultants typically work downstream of research and development

(i.d. product development, marketing) and upstream of sales and post-sale activities (i.d. sales,

customer service).

The Sourcing & Procurement segment of operations management concerns all procurement activities

aimed at finding, evaluating and engaging suppliers for acquiring goods and services. Consultants

can, for instance, support by decreasing the sourcing cost of raw materials or product/service

components, enhancing contracting terms and conditions with manufacturers/suppliers and managing

interaction with suppliers (including outsourced contracts, also known as supplier relationship

management). Key offerings consist in conducting a spend analysis in order to find synergies,

improving both the direct as well as indirect procurement operations and supporting clients with

transitioning to a greener procurement portfolio.

Services related to the Finance department, also known as CFO services, focus on a range of financial

activities. More strategic offerings can be mergers and acquisitions, capital budgeting and asset

management, although these services are commonly also part of the Financial Advisory service

portfolio of consulting firms, as well as financial planning and target operating model development,

which belong to the field of operations consulting. Implementation services aim to improve the

performance of one or a group of financial processes, such as order to cash, procure to pay, cash

management, working capital and the financial closing and reporting process. Finance operations

consists in supporting decision-making and consultants are frequently engaged to improve the flow

of relevant information to the appropriate stakeholders (management reporting) through, for instance,

data management, business intelligence and financial dashboards. Engagements that seek to raise the

16

maturity of the entire finance organisation, known as finance transformations, represent the largest

directive consultants can be given in the domain.

Business Process Management (BPM) focuses on improving operational performance by optimising

a company's business processes and it is, therefore, also defined as process management and/or

process improvement. The BPM landscape embraces several streams, such as business process

design, which sets out to define the ‘to-be’ situation and model process flow and activities to support

the blueprint, and business process re-engineering (BPR), which re-designs the entire process cycle,

commonly performed to reduce inefficiencies or complexity. Continuous improvement techniques

seeking to systematically remove waste from processes, such as Lean, Six Sigma or Lean Six Sigma,

form another major part of BPM projects, and although they come from and for long flourished in

industrial sectors, such as automotive and manufacturing, lean principles nowadays are applied across

industries, and expert consultants (or certified advisors) are frequently hired to facilitate such

transitions.

The Research & Development (R&D) service area represents the business side of innovation.

Consultants are engaged to develop and improve the bottom-line of innovation spend, which spans

from optimising new product development (NPD) processes, to boosting portfolio complexity

management and improving the efficiency of the R&D organisation, both from a “hard” (i.d.

structure/process/system) as well as a “soft” (i.d. human capital) point of view. Product lifecycle

management (PLM) is another source of productivity enhancement in the area of innovation.

Decisions involving how long to keep a product in a portfolio and when to take a product out of

service can be particularly difficult to make internally, therefore, consultants are frequently brought

in to advise around the elimination of no-longer-profitable products and to extend the profitable life

of products currently in the market.

Outsourcing advisors deal with client’s uncertainty related to the outsourcing of responsibilities and

activities to third parties. While outsourcing in its early years consisted mainly in the offshoring of

labour-intensive activities to low wage countries, the domain has over the past decades grown into

one of the largest services markets, and today it has become a mainstream line of operating models.

Consultants typically help clients with the design and build of outsourcing blueprints (mainly for

back-office processes such as finance and accounting, HR and recruitment, legal, IT infrastructure

and applications) and subsequently support the transitions. Recently, there has been a trend towards

bringing certain activities back to home base geographies (“reshoring”), and advisors also are

intensively involved with such projects. Establishing Shared Services is by the literature also

17

considered as part of the Outsourcing domain, because it is based on similar skills and expertise

(moving processes towards a new owner) and typically may include an outsourcing component if

organisations choose for an external party. Prior to establishing a Financial (FSSC) or HR (HRSSC)

Shared Service, consultants help with, among others, the harmonisation and standardisation of

processes, as well the shift towards a common template.

FINANCIAL ADVISORY

The Financial Advisory (or financial consulting) segment delivers consulting services based on a

strong financial analytical fundament. Service offerings include a wide variety of topics, such

as transaction services, risk management, tax advisory, real estate advisory, compliance and litigation

services to name a few. However, financial and accounting skills are always core competences of the

services delivered. The market for financial advisory consists of eight main disciplines: Transaction

Services, Corporate Finance, Crisis & Recovery, Risk Management, Accounting Advisory, Tax

Advisory, Real Estate Advisory and Forensics & Litigation.

Figure 4 – Financial advisory services

Corporate finance is the area of consulting dealing with funding and capital structure matters. Key

propositions are financing (including alternative investments) restructuring, working capital

management (also closely tied to the finance consulting segment within operations consulting), IPO’s

and capital markets.

Transaction services provides to the client a range of services related to the acquisition, merger or

divestiture of an organisation. Services vary from setting a M&A strategy, target screening, valuations

and due diligence in the pre-deal process to post-merger integration support and other operational

transaction services after a deal has been unveiled.

When companies are in financial difficulties, they commonly turn to crisis & recovery advisors.

Experts support them funding the root-causes (short term) and subsequently ensuring

countermeasures are in place for the longer term. Key services include insolvency (or bankruptcy)

18

management (consultants are often called in as administrators), restructuring, turnaround advisory

and debt management.

Risk management consultants support organisations with ensuring that uncertainty in the enterprise

and market does not impact (or minimally) business goals. Main offerings consist in, among others,

risk management (analysing risks and ensuring a process and governance are in place to mitigate

risks), risk control (setting up the right warning systems that can detect risks), internal audit

(assessments aimed at mapping risk profiles and compliance) and IT risk, which covers the growing

risks in the information technology area, such as cybersecurity, digital governance and enterprise data

management.

The tax advisory segment centres around supporting enterprises’ adherence to tax law, which includes

propositions such as corporate tax strategy, location advisory, transfer pricing and tax aligned supply

chains.

Accounting advisory focuses on helping clients with optimising the accounting and financial

reporting challenges facing their businesses and the finance function. Projects typically concern

boosting the efficiency of the accounting function, improving financial reporting quality and flows,

and ensuring compliance to regulatory requirements at all levels, such as International Financial

Reporting Standards (IFRS), globally and local legislation.

The real estate advisory segment supports clients with financial matters in the area of real estate and

property management. Key offerings can be location advisory, real estate valuations, transaction

support on property deals, and optimising real estate asset portfolios (often in combination with

financial asset management). Clients typically include four stakeholders’ types: governments and

local municipalities (i.e. area development), housing corporations (i.e. strategic supply management,

risk management), companies (i.e. portfolio management, location support) and real estate investors

(i.e. due diligence, portfolio analyses).

The forensics & litigation segment helps clients with a range of services that follow from actual or

anticipated disputes or litigation cases. Propositions include dispute advisory, forensic accounting

services (which combines accounting, auditing and investigative skills), litigation support and

electronic discovery (or e-discovery). Work can span across industries and topics – a forensic

consultant (also known as an auditor or investigative auditor) can bring economic damages

calculations for governments, antitrust bodies or companies, support tax fraud or money laundering

investigations or examine digital crimes such as cyber-attacks or data theft.

19

HR CONSULTING

Human resource (HR) consulting, also referred to as human capital advisory or HRM consulting,

embraces advisory and implementation activities related to the management of an organisation’s

human capital and the HR function. The scope of services ranges from overall work on human capital

strategy to the design and deployment of a compensation and benefits framework for the

transformation of the HR function. The market for human resource consulting services include

eight main disciplines: Human Capital Strategy, Compensation & Benefits, Organisational Change,

HR Function, Talent Management, HR Analytics, Learning & Development and HR Technology.

Figure 5 – Human resources consulting services

Human capital strategy involves a variety of strategic work in the HR domain, such as defining a

corporate culture, organisation design, setting up a people strategy that supports key pillars in the

business, as well as the design of HR-related strategies in the area of among others diversity,

recruitment and talent management.

Compensation & benefits, a segment also known as total rewards, concerns all aspects of employee

compensation and benefits, from base and variable pay to bonus schemes and other secondary benefits

across the entire organisation (from board level to employees on the work-floor). The discipline also

includes pensions/retirement consulting, and advisory services related to health and welfare.

Organisational change covers the people side of change, aimed to successfully lead and integrate

changes in organisational structure, ways of working or cultural changes within an enterprise. Change

management is the heart of the service area, spanning advisory expertise to tools and actions and its

main offerings are leadership alignment, stakeholder management, change interventions and cultural

management. Organisational change services can be sold as standalone offerings by consultancies,

however, typically they are grouped into larger functional transformations to safeguard the people

side of change.

The HR function area embraces all activities related to improving the functioning of the human

resource department. Offerings span from developing and implementing a HR target operating or HR

20

delivery model, to the implementation of HR systems and technologies, or other HR transformations

that boost processes and organisational efficiency.

Talent management concerns all activities required to recruit, retain and develop talent, as well as

having the right structure and processes in place to ensure professionals can perform optimally. Key

propositions encompass strategic workforce planning (the science to anticipate on present and future

human capital needs by matching business goals with HR data) recruitment and retention, workforce

effectiveness and performance management.

Through the rise of data and new technologies, HR analytics has grown into a fully developed service

area within HR consulting. HR analytics applies analytic processes to the human capital with the key

objective of adding insights and value to HR activities.

The learning & development service line, also referred to as training & development, is composed by

activities aimed to improve the performance of individuals and groups. The scope span from

organisational and competency development across leadership, departments and functions to support

the training and education needs of individuals. Learning & Development also embraces the soft side

of development, such as coaching and mentoring, as well as the technological side of training, such

as the development and implementation of learning management systems.

Lastly, HR technology is the field specialised in all systems and tools used in the HR department,

including large ERP modules by SAP, Oracle or Microsoft, and more niche solutions per functional

domain.

IT CONSULTING

IT consulting, also referred to as technology consulting, concerns services aimed to help clients on

how they can utilise information technology (IT) and digital to optimally achieve their business goals.

The IT consulting segment includes advisory and implementation services but excludes transactional

IT activities. The broad market for IT consulting services contains eight main disciplines: IT Strategy,

IT Architecture, IT Implementation, ERP services, Systems Integration, Data Analytics, IT Security

and Software Management.

21

Figure 6 – Technology and IT consulting services

IT strategy refers to strategic IT propositions and IT advisory, offerings which commonly represent

the first phase of any IT undertaking. Engagements typically last between six weeks to six months

depending on the complexity, with an average of two to three months. Examples of projects consists

in defining a corporate IT strategy, setting up a business case for an ERP system or designing a

cybersecurity vision (engagements that set the stage for further IT work).

IT architecture concerns the IT processes and systems and defines the technological blueprint that

enables business processes. Projects typically last between 6 to 12 months and architecture services

precede any IT implementation or systems integration efforts. Examples of consulting offerings are,

among others, defining an enterprise landscape, implementing a service-oriented architecture (SOA),

or guiding the outsourcing of architecture processes to an external vendor.

Enterprise Resource Planning (ERP) services supports clients with designing, implementing and/or

maintaining ERP systems and modules. Key propositions consist in ERP package selections, business

process redesigns based on an ERP template, and implementations of, for instance, SAP or Oracle

products.

The systems integration domain refers to how different computing systems and software applications

can link together in order to ensure systems acts as a coordinated whole. It requires ERP

systems/modules which can interact with other and more tailored applications in the IT landscape.

IT security encompasses risk, security and compliance responsibilities in the IT landscape, while the

IT implementation line of business includes all services related to the design and implementation of

technology-driven projects.

Software management refers to the practice that consists in managing and optimising the purchase,

deployment, maintenance, utilisation, and disposal of software applications within an organisation.

Lastly, data analytics, an upcoming domain, includes all the techniques and tools that can turn large

amounts of data into valuable information in order to support decision making. Typical propositions

22

in this segment are business intelligence, workforce analytics, customer intelligence, data

warehousing (big data) and predictive modelling.

THE HISTORICAL BACKGROUND

One of the first consulting firms of the kind known today was established in Chicago in 1914 by

Edwin Booz under the name “Business Research Services” (Sabath & Kubr, 1977). In the 1920s,

Elton Mayo, with his Hawthorne experiment, triggered research and consulting in human relations.

Another important consulting work in human resource management and motivation was started by

Mary Parker Follett. Interest in more effective selling and marketing was promoted by people such

as Harold Whitehead, the author of Principles of salesmanship, written in 1917. Several consulting

firms were established during the 1920s. These were increasingly able to analyse business

organizations in their whole, treating manufacturing and productivity problems in a wider perspective

of sales and opportunities of business expansion.

Consulting in finance, including financing the enterprise and financial control of operations, also

started developing rapidly. Several new management consultants had a background in accountancy

and experience drawn from working with firms of public accountants. This is the case of James O.

McKinsey, a protagonist of the general management and comprehensive diagnostic approach to a

business enterprise, who established his own consulting firm in 1925, and today is regarded as one of

the founders of the consulting profession.

In the 1920s and 1930s, management consulting developed, not only in the United States and in Great

Britain, but also in France, Germany, and other industrialized countries. However, its volume and

scope remained limited. There were only few firms, prestigious but rather small, and their services

were exploited mainly by the larger business corporations. The consultant remained unknown to most

small and medium-sized firms. Meanwhile, assignment requests began coming from governments:

this was the start of consulting for the public sector.

Consulting for governments, and for the army as well, played an important role during the Second

World War. The United States realized that the war was a major management challenge and that

gathering the country’s best management expertise was essential to win on the battlefield. In addition,

operations research and other analytical techniques, applied first for military purposes, rapidly found

their way into business and public management, adding a new dimension to the facilities offered by

consultants.

23

Figure 7 – Foundation age and location of major Brand Consultancies

Post-war reconstruction, the rapid expansion of business coupled with the acceleration of

technological change, the emergence of new developing economies and the growing

internationalization of the world’s industry, commerce and finance, created particularly favourable

opportunities and growing demands for management consulting. This was the period in which most

consulting firms that exist today were established and in which the consulting business achieved the

power and the technical reputation it enjoys at present. For example, PA, the largest consulting firm

in the United Kingdom, had only six consultants in 1943, but 370 in 1963, and over 1,300 based in

22 countries in 1984. The total number of full-time management consultants in the United States was

assessed at 100,000 at the end of the 1980s, six times the number that existed in the mid-1960s (Sabath

& Kubr, 1977).

Since the 1940s, the spread of management consulting has been impressive by any standard.

Significant qualitative changes have also occurred. To meet their clients’ needs and to attract clients

from new sectors of economic and social activity, management consultants developed several

strategies, creating and offering new special facilities, specializing sectors or, on the contrary,

providing broad comprehensive packages of services.

Most management consultants were able to be associated with the latest developments in management

and related fields that can interest their clients, and to offer new sophisticated services before anyone

else. The computer business, the use of information technologies in all aspects of management and

accounting, and new communication technologies are examples of such areas. Consultants do not

hesitate to step out of the traditional domain of the management field and deal with plant automation,

communication systems, quality control, equipment design, software development, economic studies,

environmental protection and other clients’ interests.

24

Competition in management consulting has greatly increased since 1950. In addition to improving

service quality and offering new sorts of facilities, management consultants have become more

dynamic and even aggressive in searching for new clients and trying to convince potential ones that

they can offer a higher value than others. This has led many developments in the advertising and

marketing of consulting services.

By the 1950s a distinct hierarchy of management consulting firms had emerged, led by three

companies: McKinsey & Company; Booz, Allen & Hamilton; and Cresap, McCormick & Page

(McKenna, 2001). These leading firms had grown rapidly during the post-war growth, and in the

early 1960s they expanded into Western Europe. The American consulting firms encountered little

competition and extraordinary demand as they moved into foreign markets; by the mid-1960s

American entrepreneurs dominated the world market for organizational advice. More similar than

different, the three leading firms all had their roots in Chicago, they hired their future partners almost

exclusively from the top Harvard Business School graduates, and at one point during the 1960s they

were all headquartered in a single building in New York City.

In the late 1960s, however, this comfortable oligopolistic structure started to deteriorate. Accounting

firms like Arthur Andersen & Company and “strategy” consulting firms, like the Boston Consulting

Group, began to move into the market for consulting services. The strategy firms stole business from

the top, while the accounting firms won routine assignments from the bottom. By the 1970s, although

McKinsey & Company, Booz, Allen & Hamilton, and Cresap, McCormick & Paget no longer

dominated the market for management consulting services, the model of the professional firm with

its related system of rewards remained the central organizational form among management consulting

firms. Only recently large, publicly owned, technology-based corporations like EDS, IBM, and

AT&T have built consulting divisions that rival the older consulting firms if not in size, at least in

their profitability per consultant.

THE PLAYERS

The 9.0% CC1 growth in consulting services in 2018 confirms the continuing demand for

organizations seeking help with the ambition and design of their technology strategies (Blackmore,

Dean; Short, 2017). Collectively, the top 10 consultancies grew 9.8% in CC in 2018 consulting

revenue.

1 “CC” means “Constant Currencies”. they are exchange rates used to eliminate the effect of fluctuations when

calculating financial performance numbers for publication in financial statements

25

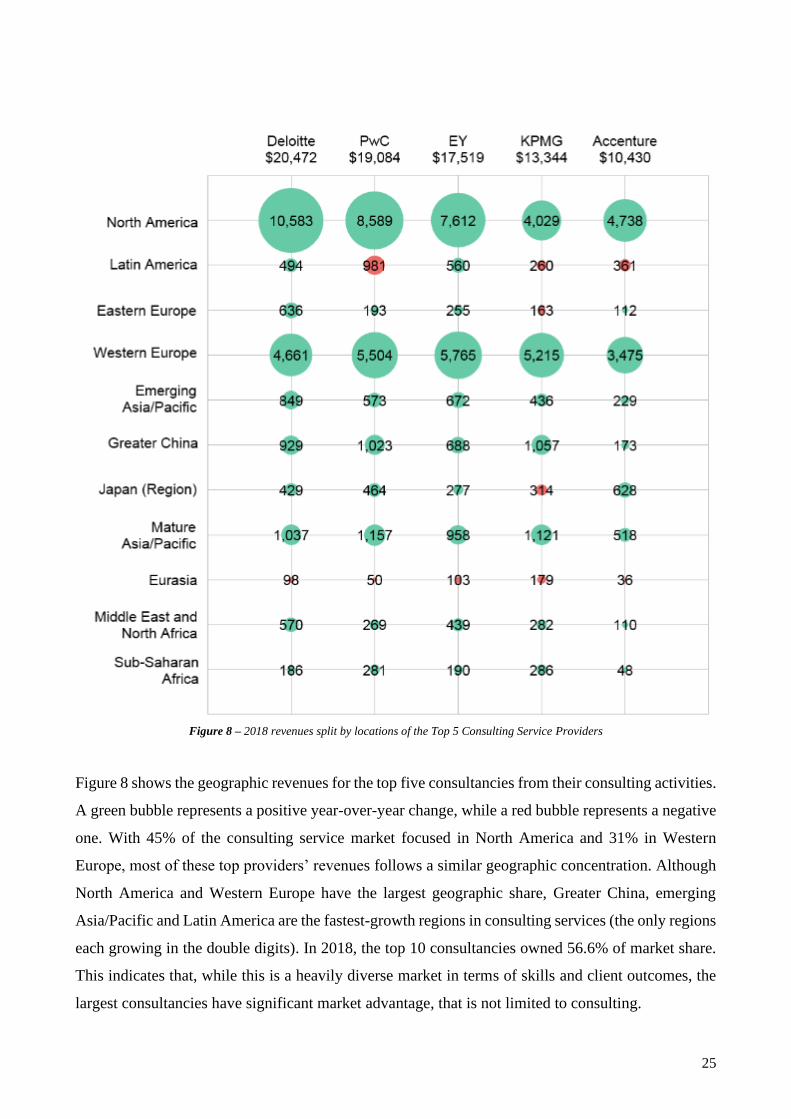

Figure 8 – 2018 revenues split by locations of the Top 5 Consulting Service Providers

Figure 8 shows the geographic revenues for the top five consultancies from their consulting activities.

A green bubble represents a positive year-over-year change, while a red bubble represents a negative

one. With 45% of the consulting service market focused in North America and 31% in Western

Europe, most of these top providers’ revenues follows a similar geographic concentration. Although

North America and Western Europe have the largest geographic share, Greater China, emerging

Asia/Pacific and Latin America are the fastest-growth regions in consulting services (the only regions

each growing in the double digits). In 2018, the top 10 consultancies owned 56.6% of market share.

This indicates that, while this is a heavily diverse market in terms of skills and client outcomes, the

largest consultancies have significant market advantage, that is not limited to consulting.

26

DELOITTE

Deloitte Touche Tohmatsu Limited, commonly referred to as Deloitte, is a multinational professional

services network. Deloitte is one of the "Big Four" accounting organizations and the largest

professional services network in the world by revenue and number of professionals with headquarters

in London. Deloitte provides audit, tax, consulting, enterprise risk and financial advisory services

with approximately 312,000 professionals globally. In FY2 2019, the network earned a record $46.2

billion in aggregate revenues. As of 2017, Deloitte is the 4th largest privately-owned company in the

United States. Deloitte has been ranked number one by market share in consulting by Gartner, and

for the fourth consecutive year, Kennedy Consulting Research and Advisory ranks Deloitte number

one in both global consulting and management consulting based on aggregate revenue.

PWC

PricewaterhouseCoopers International Limited is a multinational professional services network with

headquarters in London. PwC ranks as the second largest professional services firm in the world and

is considered one of the Big Four accounting firms, along with Deloitte, EY and KPMG. PwC is a

network of firms in 158 countries, 721 locations, with 250,930 people. As of 2018, 28% of the

workforce worked in Asia, 28% in North America and the Caribbean and 30% in Western Europe.

The company's global revenues were $41.3 billion in FY 2018 and it provides services to 420 out of

500 Fortune 500 companies. The firm in its present form was created in 1998 by a merger between

two accounting firms: Coopers & Lybrand, and Price Waterhouse. Both firms had histories dating

back to the 19th century. The trading name was shortened to PwC in September 2010 as part of a

rebranding effort. As of 2019, PwC is the 5th-largest privately-owned company in the United States.

EY

Ernst & Young Global Limited, commonly known as Ernst & Young or simply EY, is a multinational

professional services firm headquartered in London. EY is one of the largest professional services

firms in the world. Along with Deloitte, KPMG and PricewaterhouseCoopers, it is considered one of

the Big Four accounting firms. It primarily provides assurance (which includes financial audit), tax,

consulting and advisory services to its clients. Like many of the larger accounting firms in recent

years, EY has expanded into markets adjacent to accounting, including strategy, operations, HR,

technology, and financial services consulting. EY operates as a network of member firms which are

structured as separate legal entities in a partnership, which has over 270,000 employees in over 700

offices in 150 countries around the world. The firm's current partnership was formed in 1989 by a

merger of two accounting firms: Ernst & Whinney and Arthur Young & Co.. It was pertinently named

2 “FY” means “Fiscal Year”

27

Ernst & Young until a rebranding campaign officially changed its name to EY in 2013, although this

initialism was already used informally prior to its authorising adoption. In 2019, EY was the seventh

largest privately-owned organization in the United States. EY has continuously been ranked on

Fortune magazine's list of the “100 Best Companies to Work For” for the past 21 years, longer than

any other accounting firm.

KPMG

KPMG International Cooperative, or simply KPMG, is a multinational professional services network,

and one of the Big Four accounting organizations, along with Deloitte, Ernst & Young (EY), and

PricewaterhouseCoopers (PwC). Seated in Amstelveen, in Netherlands, KPMG is a network of firms

in 154 countries, with 207,050 people and has three lines of services: financial audit, tax, and

advisory. Its tax and advisory services are further divided into various service groups. The name

"KPMG" stands for "Klynveld Peat Marwick Goerdeler". It was chosen when KMG (Klynveld Main

Goerdeler) merged with Peat Marwick in 1987.

ACCENTURE

An entire chapter will be dedicated to Accenture, since it is the host of the project described in this

thesis.

PESTLE ANALYSIS

POLITICAL

The increase in protectionism politics has impacted the global free trade (S&P, 2017). A major portion

of consultancy business’s revenue comes from United Kingdom and Brexit will severely impact it.

Immediate consequence is the low business visibility and economic uncertainty in the environment.

The new policies in the region will significantly affect the revenues and cost of operation. Moreover,

3 out of the Big Four are financial based in London. The Brexit has raised the economic volatility and

has led to decrease in revenue of UK operations due to sharp depreciation in GBP post the referendum.

ECONOMIC

Since 2004, the Consulting industry has recovered significantly: all firms are now aggressively

recruiting again. Most firms were surprisingly resilient to the Great Recession of 2008 and 2009.

Currently, most consulting offices are working at full capacity and the prospect for the sector is very

positive. Top consulting firms continue to compete with investment banks and each other for the top

candidates from universities and business school programs across the country, offering highly

attractive compensation packages and career opportunities. At many top business schools, as much

as 1/3 of the graduating class will sign with consulting firms upon graduation (Street of Walls, 2013).

28

Table 1 – National management consulting markets (sample of 15 countries)

Table 1 shows the size of the management consulting markets in M$ for the fifteen countries in the

sample and its strength in terms of the proportion of the country’s GDP and of the number of the

population (Haslam, Bodenstein, & Abdel-jaber, 2018).

SOCIAL

The European Management Consulting employment in 2017 has grown by 5.2%, continuing its

positive trend. In 2017 all the countries included in the report have achieved a significant growth, the

only exceptions being Greece and Slovenia where employment registered just a slight increase.

Austria, France and Switzerland are showing very high growth in the employment levels, a clear

indicator that MC companies in these countries believe that the industry growth is going to last. While

data are fragmented, it appears that employment growth is concentrated mainly in the large and very

large consulting companies (i.e. those with more than 50 employees).

Country

Size of management

consulting market (2017

data, M$)

Strength of management

consulting sector to GDP

(M$ MC/BN$ GDP)

Strength of management

consulting sector per

capita – M$/pop (M)

USA 63,185 32,6% 194.7

UK 10,006 38.2% 151.1

Germany 9,141 25.9% 116.2

France 5,111 19.8% 78.6

Australia 5,003 37.8% 205

China 4.992 4.1% 3.5

Canada 3,912 23.7% 106.9

Spain 1,662 12.7% 35.8

Italy 1,412 7.3% 23.8

Netherlands 1,402 15.4% 82.5

Japan 1,408 2.9% 11

Switzerland 1,241 18.3% 146

Brazil 1,183 5.8% 5.7

Russia 493 3.1% 3.4

Austria 321 7.7% 36.9

29

Table 2 – MC employment growth rate (2013-2017)

Management Consulting is traditionally a “people” business. An increase in turnover, unless driven

by a variation in price levels, is related to an increase in billed hours and therefore in employment.

However, in the short term, the employment trend does not always match turnover growth. Given the

time required for the development of a consultant, many consulting firms, when a recovery is

forecasted, may hire in anticipation or, during a recession period, may retain their consultants.

Moreover, during a period of turnover growth, MC companies often partially balance the increased

workload by asking their consultants to stay overtime. A comparative analysis of the past six years’

trend in MC turnover vs. MC employment highlights that the MC employment level has grown

slightly less than the MC turnover: 5.6% per year vs. 6.6% per year (Cerruti, Borra, Appolloni,

Benedetto, & Elisabetta, 2018). In 2013 MC employment grew more than MC turnover and since

then the turnover has increased at a faster pace.

30

Table 3 – MC Turnover and MC Employment trend for the European panel (2013-2017)

TECHNOLOGICAL

Management consulting firms work across a wide variety of industries and are always looking for

ways to offer new services and improve the business (Geneca, 2019). In order to serve

today’s technology-expert customers and employees, it is more important than ever for companies to

adapt their processes to quickly changing markets. As businesses are keeping getting more and more

competitive, firms need to ensure they are in aligned with the latest technology trends in order to

maintain a competitive advantage.

• Automation and AI) When looking to improve efficiencies, the first step in management

consulting should be automating and streamlining any possible process. Why wouldn’t

businesses have a machine do the same job as a human employee if it can be done at a quicker

pace, cheaper rate, and more accurate level? This does not replace the need for human

workers, but elevates the roles allowing the employees to either focus on complex tasks that

require more brainpower or the human touch. An example of this would be incorporating

chatbots in customer service. It would allow actual representatives to spend time dealing with

more complex issues which could ultimately add value to the user experience. Automating

repetitive processes in your management consulting can free up the valuable time allowing to

reach more clients. Many management consulting firms have seized the opportunity to use AI

to their advantage, and a few big-name firms have launched entire programs and divisions

dedicated to AI and analytic solutions. More and more management consulting companies are

increasing use of automation and AI, which is providing firms the ability to help more clients

to improve productivity, lower spending costs and design new growth opportunities.

• Blockchain) Blockchain is a secured, public database that can be likened to an accounting

ledger: it is a place where transactions occur and can be recorded. Any industry that is

dependent on large amounts of records needing to be accessed and exchanged will see

disruption from blockchain making banking, real estate, healthcare, and the government at the

31

head of the line. Just as all companies look for ways to grow and expand their audiences,

management consulting firms need to provide strategic offerings and to be aligned with new

technologies. Blockchain offers new advantages for management consulting firms to examine.

According to Forbes, “The security is built into a blockchain system through the distributed

timestamping server and peer-to-peer network, and the result is a database that is managed

autonomously in a decentralized way.” Faster, more secure financial transactions, the ability

to establish an identity, and a more efficient way to establish contracts are just a few of the

advantages management consulting firms can offer through blockchain. As blockchain

eliminates the need of intermediaries in a process, transactions can be recorded and completed

much faster. Accenture recently advertised the future of this technology as “Blockchain will

supercharge artificial intelligence and IoT to make everything from supply chains to digital

identity management smarter and more secure.”

• Data Analytics) Many companies in today’s world use data analytics to draw conclusions and

make informed business decisions in order to increase revenue, improve efficiencies, and gain

a competitive advantage. While there are various data analytic applications that can be tested,

the process also has multiple parts, in addition to analysing the actual data. There are many

steps involved in collecting, organizing, testing and revising the data to ensure accurate

information has been obtained. As the data analytics process can be intimidating, management

consulting firms are able to step in and help companies organize the process from the very

beginning. Management consultants set the strategy and design the full data action plan. They

are also able to interpret technologies based on their business value and help companies to

change market conditions. When data has been analysed and new initiatives need to be

implemented, management consulting firms will be there to help ensure things run smoothly.

As clients continue to make more and more data-driven business decisions, management

consulting firms will keep improving the data analytics process.

• Digitalization) Digitalization has many different meanings and can be interpreted in several

ways, but for those in the management consulting industry, the idea is straight-forward.

Digitalization can be summed up as shifting business processes into digital formats in order

to increase revenue, improve efficiencies and provide more valuable opportunities. Clients

will expect digital products to remain, after the management consulting firm concludes

business, to ensure an effective business transformation for the future. Consultants without

digital tools will need to build some to attract and maintain their clients, as well as stand out

from competitors. To define the digital transformation, Boston Consulting Group says

“Leveraging digital technologies is more than just good business, it’s crucial to stay relevant

32

and profitable. Companies lacking in this area risk losing ground to newer entrants and

business models that are going to disrupt markets with innovative products and

services.” Digitalization presents a massive opportunity for management consulting firms, but

they must first rethink their own business models and update their own processes before it

will take them anywhere.

LEGAL

All the Big Four accounting firms have come under fire over their client relationships in recent years

(Financial Times, 2018). One prominent example of accountants getting too close to clients

is KPMG’s relationship with South Africa’s billionaire Gupta family, which has been at the centre of

a huge government corruption scandal over a 15-year period that ended in 2016.

EY, meanwhile, was fined $9.3m by the SEC two years ago for failing to take appropriate action

when it emerged that two audit partners had formed improperly close relationships with clients. One

of the partners had become involved romantically with the chief accounting officer at a company she

audited, while the other partner spent more than $100,000 on corporate entertainment for the chief

financial officer of a listed company he audited.

More recently, PwC has been criticised in the UK for its work for collapsed retailer BHS. The UK

regulator raised concerns about PwC’s failure to adequately monitor conflicts of interest after it

emerged the firm earned eight times more from consulting work for BHS than it did from auditing.

The firm’s lead partner on the audit, Steve Denison, agreed to a 15-year ban from the industry after

the regulator found he recorded just two hours of work on the audit.

Meanwhile, Deloitte is under investigation over its work for Frankfurt and Johannesburg-listed

retailer Steinhoff, which last year revealed a black hole of more than 5bn€ in its accounts.

Shareholders have criticised Deloitte, which audited Steinhoff for at least 18 years, for “seriously

failing in its statutory task as auditor” by giving the retailer an unqualified audit shortly before the

accounting irregularities were uncovered.

ENVIRONMENTAL

Efforts towards renewable energy and technologies producing low emissions are obtaining more and

more government funding. Organizations that invest in research and development within these areas

are also growing and are one of the places where environmental consultants can be found. They have

extensive knowledge on environmental regulations and can advise clients in private industry or public

government institutions on how to handle possible fines, legal action or misguided transactions. An

33

environmental consultant addresses issue such as (CareerExplorer, 2019):

• land and water contamination;

• waste management policies;

• environmental management systems;