Value Partners Management Consulting Limited

40

report FEBRUARY 2014 ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of Value Partners Management Consulting Limited

report FEBRUARY 2014

ATM BENCHMARKINGSTUDY 2014 AND INDUSTRY REPORT

ATM Benchmarking Study 2014 and Industry Report

A report based on the ATMIA Benchmarking Study 2014

Published by Value Partners Management Consulting LtdKings Buildings, 7th Floor,16 Smith Square, London SW1P 3HQ, UK

February 2014

Written by Francesco Burelli, Andrey Gorelikov, Marco Labianca

If you would like an electronic copy please write to: [email protected]

For more information on the issues raised in the report please contact:[email protected]@valuepartners.com

valuepartners.com atmia.com

Copyright © Value Partners Management Consulting LimitedAll rights reserved

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

1 EXECUTIVE SUMMARY 5

2 INTRODUCTION 9

3 THE GLOBAL ATM MARKET 13

4 SCOPE OF THE ATMIA BENCHMARKING STUDY 2014 17

5 KEY FINDINGS OF THE ATMIA BENCHMARKING STUDY 2014 19

5.1. COST METRICS AND PERFORMANCE MONITORING 19

5.1.1. TRANSACTION PROCESSING 21

5.1.2. CASH MANAGEMENT 21

5.1.3. COST OF HARDWARE 24

5.1.4. PERFORMANCE MONITORING 24

5.2. FRAUD AND DISPUTE MANAGEMENT 27

5.3. REVENUE AND PROFITABILITY 28

5.4. COMPLAINT MANAGEMENT 29

5.5. VALUE ADDED SERVICES AND MULTIFUNCTIONALITY 31

6 CONCLUSIONS 39

CONTENTS

Disclaimer: This report illustrates some of the key general findings of the ATMIA Benchmarking Study 2014 developed jointly by ATMIA and Value Partners, with the addition of industry trends, analysis and commentary from Value Partners.

Participation in the ATM Benchmarking study is strictly confidential and selected examples mentioned in the Value Partners commentary section on industry trends do not necessarily imply participation to the ATM Benchmarking study.

4—5

What is remarkable is the degree to which benchmarking has become associated with organisational improvement in the post-modern era”Dr. J.P. Moriarty, Lincoln University, “A theory of benchmarking” 2008

“

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

WELCOME TO THIS SECOND REPORT OF ATMIA’S GLOBAL ATM BENCHMARKING STUDY. LAUNCHED IN 2012, THIS BENCHMARKING STUDY’S ARRIVAL WAS ESPECIALLY RELEVANT FOR THE 21ST CENTURY GIVEN THE CONTINUED GLOBALISATION OF THE ATM INDUSTRY AND ITS ENTRY INTO A DYNAMIC NEW PHASE OF REPOSITIONING. THE ATM TERMINAL IS BECOMING THE DOMINANT TOUCH-POINT SELF-SERVICE DEVICE FOR CARDHOLDERS AND MORE RECENTLY, FOR MOBILE PHONE ACCOUNT-HOLDERS.

ATM BENCHMARKING PROVIDES A BANK OR INDEPENDENT ATM DEPLOYER WITH A SCORECARD OF ITS ORGANISATIONAL PERFORMANCE, MEASURED AGAINST ITS COMPETITORS NATIONALLY, REGIONALLY AND GLOBALLY. BENCHMARKING METRICS HIGHLIGHT AREAS REQUIRING IMPROVEMENT AS WELL AS CURRENT ORGANISATIONAL STRENGTHS, GIVEN THE INCREASED STRATEGIC INTEREST IN ATMS WITHIN THE BANKING SECTOR AGAINST A BACKGROUND OF ROBUST GLOBAL CASH DEMAND AND GROWTH IN ATM SHIPMENTS. THIS REPORT BY VALUE PARTNERS FOR ATMIA IS AN IMPORTANT REMINDER THAT BENCHMARKING IS A VITAL CORPORATE TOOL FOR IMPROVING EFFICIENCIES AND STEPPING UP THE LEVEL OF TECHNOLOGICAL AND SYSTEMS INNOVATION.

AS DR. J.P. MORIARTY OF LINCOLN UNIVERSITY CORRECTLY STATED IN THE 2008 STUDY, A THEORY OF BENCHMARKING: “WHAT IS REMARKABLE IS THE DEGREE TO WHICH BENCHMARKING HAS BECOME ASSOCIATED WITH ORGANISATIONAL IMPROVEMENT IN THE POST-MODERN ERA.”

IT WAS XEROX CORPORATION WHO PIONEERED INTERNAL AND EXTERNAL BENCHMARKING IN THE 1980S TO DRIVE FORWARD THEIR SUCCESS AFTER THEY STARTED TO LOSE “FIRST MOVER” ADVANTAGE AND MARKET DOMINANCE AS HIGH-QUALITY RIVAL JAPANESE PRODUCTS SNATCHED SIGNIFICANT MARKET SHARE. DAVID T. KEARNES, XEROX’S CEO FROM 1982–1990, ONCE DESCRIBED BENCHMARKING AS “THE CONTINUOUS PROCESS OF MEASURING PRODUCTS, SERVICES AND SUCCESSFUL IN-HOUSE QUALITY IMPROVEMENT PROCESS AGAINST THE TOUGHEST COMPETITORS OR THOSE COMPANIES RECOGNISED AS INDUSTRY LEADERS.”

FOREWORD

6—7

ATMIA BELIEVES THAT THERE HAS NEVER BEEN A BETTER TIME FOR ANNUAL GLOBAL ATM BENCHMARKING TO ENSURE THAT ATM OWNERS STAY AHEAD OF THE CURVE AS THEIR TERMINAL EVOLVES INTO THE DOMINANT SELF-SERVICE PAYMENT DEVICE IN THE WORLD.

THE ATM IS EVOLVING RAPIDLY AS WE SPEAK. IT HAS MOVED FROM A TELLER-REPLACEMENT TECHNOLOGY INTO GREATER VALUE ADDING FUNCTIONALITY, ENABLING MOBILE PHONE CREDIT, LOANS, COUPONS, BILL PAYMENTS AND EVEN INTERNATIONAL MONEY TRANSFERS. THERE IS STILL MUCH TO LEARN IN THIS TIME OF GLOBAL TECHNOLOGICAL AND STRATEGIC CHANGE; MORE IMPORTANTLY, THERE IS STILL MUCH TO IMPROVE.

BENCHMARKING REMAINS ONE OF THE MOST VALUABLE TOOLS IN THE COMPETITIVE ARSENALS OF ATM DEPLOYERS TO MEASURE THEMSELVES AGAINST THE BEST. THE PURPOSE REMAINS THE SAME AS IT WAS FOR XEROX BACK IN THE 1980S, NAMELY, TO IMPROVE COMPETITIVE EFFICIENCY AS A SOURCE OF PRODUCTIVITY GROWTH AND TO TURN AROUND SUB-OPTIMAL ASPECTS BY EMULATING A SUPERIOR PERFORMING MODEL.

MAY THE 2014 GLOBAL ATM BENCHMARKING STUDY, THE SECOND IN OUR SERIES, CONTINUE THE GOOD WORK IN IMPROVING ATM PERFORMANCE AS OPERATORS RACE TO BECOME TOP PERFORMERS.

MICHAEL LEECEO ATMIA

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Cash re-circulation assumed a key role in the reduction of the cost of cash, benefiting not only the financial servic-es institutions that adopt them, but the economy and society at large by reduc-ing the amount of cash in circulation.

The general findings of the previous study have been confirmed during the course of the Benchmarking Study 2014, with significant cost disparities being outlined across a number of cost metrics regardless that overall cost efficiencies appear, in general, to be improving. Amongst the most impor-tant findings of the study has been the highly diverse cost of cash, hardware and transaction processing for partici-pants in the survey, despite the broadly similar nature of ATM operations globally. Once again, little correlation between the size, location, or type of ATM operator and their costs was found in the analysis.

ATMs continue to be one of the main touch-points for the customers of financial institutions. Growth rates of the number of ATMs, transacted volumes and values are different among the regions of the world, but mostly exceed-ing the GDP growth rates, underling the importance and potential of the ATM channel. Following the success of its first ATM Benchmarking Study of 2012, ATMIA has once again, undertaken a global ATM benchmarking exercise in collaboration with Value Partners. A total of 42 survey respondents have participated. Once again uptake has seen the participation of some of the largest ATM operators globally, in-cluding banks and Independent ATM deployers, some of which took part at group level with multiple subsidiaries submitting their data so benefiting from intra-group benchmarks and a view of in-house best-practices. The value and the interest for such an exercise was once again confirmed by the fact that two thirds of the participants of 2012 have joined again this important ATMIA’s initiative.

ATMs have changed their historical role of a mere cash dispenser and are expanding their potential to offer a wider range of services to banked, underbanked and unbanked popula-tions. Available added functionality vary significantly to a wide range of services and ATM operators are starting to implement Value Added Services strate-gies in a more selective manner than what was previously outlined during the course of the previous study.

EXECUTIVE SUMMARY1

8—9

The 2014 study was built upon the areas in scope of the previous study and expanded to include areas such as ATM revenues. This is a highly sensitive and confidential part of the study but it is fair to say that not all participants may have a strategy whereby profits are generated from the ATM channel. IADs have the ATM as a main line of business but for banks, in particular, the ATM is a channel that is complementary to other services and often leverages purely as on a cost-substitution basis. Profitable or less profitable organisa-tions are evenly distributed across the various regions with the imbalance between costs and revenue appearing to cause losses that are not necessary affecting close competitors, likely on the basis of different management strategies for ATMs estates between organisations. Nonetheless, this rein-forces the working hypothesis deriving from the analysis of the costs sections that overall there are potential areas of improvement that are waiting to be investigated and realised by a number of ATM operators.

Despite the high focus on availability and on performance management, it was outlined that few ATM operators monitor and manage cardholder satis-faction measures such as those related to complaint management. This latter finding potentially points to opportunity for diversification and com-petitive advantage that has yet to be fully explored by the industry at large.For more detailed conclusions of the findings of the ATM Benchmarking Study 2014 please see section 5 of the report.

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Automatic Teller Machines (ATMs) remain one of the main channels for the provision of retail banking services. Their importance is proved by the con-tinuous growth of the channel in terms of the number of ATM units installed and the volume and value of transac-tions. Different regions show different rates of growth, with a common growth trend for rates of growth that exceed GDP growth. This points to the fact that financial institutions are continuing to invest in this self-service channel, but also that retail and SME consumers continue to use this important banking touch-point to access their funds. Over-all, industry research estimates that the number of installed ATMs units was over 2.75m in 2013, and is forecasted to grow to over 3.22m by 2016, a 17% increase over a 3-year period.

The overall value of cash dispensed in 2013 is estimated to $10.47tn,1 with an increase of 26% over the same time-frame to over $13.19tn. This cash dis-pensed through ATMs remains critical to future cash accessibility and wider glo-bal economic development, despite the crucial and growing role that electronic payment methods will play, and the increasing penetration and rapid pace of innovation in the non-cash payments landscape that will be complementary to the functions enabled by ATMs.

As outlined in the previous ATM Bench-marking and Industry Report,2 ATMs increasingly serve more functions than the simple provision of cash and as a key touch-point between people and financial institutions. They realise and expand their potential to offer a wider range of services to banked, under-banked and unbanked populations.

INTRODUCTION2

Despite this rapid growth, penetration and access to ATMs remain unevenly distributed, as reported by the World-Bank,3 with South Asia and Sub-Saha-ran Africa being the regions with the highest growth, albeit from a very low baseline.

The ATM industry’s offering has evolved significantly since its inception in the early 1960s, becoming a key enabler of branch innovation, and now evolving in parallel to internet banking and newly developing mobile banking channel, developing its role from a pure teller substitution / cash dispensing service to being one of, if not in many cases, the most important touch-point between a financial services organisation and its retail and SME customers. ATMs keep providing a low-cost-to-serve channel to financial institutions for an increasing number of services ranging from access to current account funds and informa-tion, enabling cash and cheque deposits and now enabling access to a wider range of services. Within this context, ATMs keep playing a key role for the reduction of the cost of cash through re-circulation, benefitting not only the financial services institutions that adopt them, but the economy and society at large by reducing the amount of cash in circulation.

1 Source: Timetric 20142 ATMIA and Value Partners, ATM Benchmarking Study 2012 and Industry Report3 Source: Global Partnership for Financial Inclusion, financial inclusions indicators 2014

0

500

1,000

1,500

2,000

2,500

3,000

3,500

20072006 2008 2009 2010 2011 2012 2013 2014 2015 2016

+8%

+6%

06-16CAGR

3%

4%

12%

6%

12%

0

20,000

10,000

30,000

40,000

50,000

60,000

70,000

80,000

20072006 2008 2009 2010 2011 2012 2013 2014 2015 2016

4%

06-16CAGR

6%

21%

4%

13%

+12%

+6%

NUMBER OF ATMS, 2006-16 (‘000)

NUMBER OF ATM TRANSACTIONS, 2006-16 (MLN)

Source: Timetric 2014

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Following the success of its first ATM Benchmarking Study 2012, and on the feedback received from the organisa-tions that took part to the former exer-cise, ATMIA has once again, undertaken a global ATM Benchmarking exercise in collaboration with Value Partners. Approximately 65% of the banks and independent ATM deployers (IAD) that took part to the 2012 study participated again to this second round, and were joined by others to a total 42 survey respondents, some of which participat-ed through subsidiaries from multiple countries.

Of these, around 65% are based in mature economies and 35% in emerging or transitioning economies. Similar to the previous round of ATM Benchmark-ing, the vast majority of responses to the general invitation to participate came from some of the largest ATM operators globally, including banks and IADs.

Although some of the insights from the survey and its general conclusions have been included in this report, the full findings of the benchmarking study are exclusively available to respondents.

NorthAmerica South&CentralAmerica MiddleEast&Africa Europe AsiaPacific

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

20072006 2008 2009 2010 2011 2012 2013 2014 2015 2016

2%

06-16CAGR

12%

21%

7%

16%

+13%

+9%

VALUE OF ATM TRANSACTIONS, 2006-16 ($BN)

NorthAmerica

Europe

EastAsia&Pacific

LatinAmerica&Caribbean

MiddleEast&Africa

SouthAsia

Sub-SaharanAfrica

2%

04-12CAGR

27%

63%

17%

5%

4%

7%

0

10

20

30

40

50

180

190

200

210

220

200720062004 2005 2008 2009 2010 2011 2012

GLOBAL ATM NUMBERS (PER 100,000 ADULTS)

Source: World Bank, ECB, Value Partners analysis

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

THE GLOBAL ATM MARKET

3

4 ATM Benchmarking Study 2012 and Industry Report

The number of ATMs installed globally has grown rapidly at a rate of 8% CAGR of the installed base between 2006 and 2012. The growth rate is expected to remain high at a CAGR of 6% between 2012 and 2016. While this may be wrongly seen a slow-down in a pace of growth that is outstripping that of GDP, it is an indicator that some markets might have reached saturation. While this may be a credible working hypothesis for some countries, there is still significant disparity in the availability and access to this channel, as highlighted by World Bank statistics.

Overall, the African and Asia-Pacific regions are driving growth, with North America growing at a slower pace of 2% CAGR between 2004 and 2012. Africa and Asia-Pacific contribute the largest part of overall ATM unit growth, driven by a combination of population growth, economic development and a rollout of financial services which is pushing demand for non-branch ac-cess to cash, financial information and other services. As highlighted in the ATM Benchmarking Report 2012, the role of the ATM channel has changed from that of a mere cash dispenser to being in many cases, the primary channel for retail financial services.

Compared to the findings of two years ago, there are earlier signs of a refine-ment of the services offered through the channel. Mobile penetration, together with the increasing access to financial services and financial education, are not only changing the role of the ATM but also expanding the role of cards (and mobile handsets). ATM functionalities are evolving from being a simple instru-ment providing access to cash outside of bank working hours to a means for customers to access a much wider range of services offered by banks, and in few cases in partnerships with governments.

It was reported in the previous edi-tion of the ATMIA ATM Benchmarking Study and Industry Report that in 2009 the number of ATMs exceeded the number of bank branches in low-income countries.4 Over the last two years, the installation of ATM units has increased in all countries across all regions, includ-ing North America, which has shown an increase of 3% CAGR between 2006 and 2012. In comparison, Europe’s installed base grew by 6% CAGR in the same period, both the Middle East and Africa and Asia Pacific by 12% and South and Central America by 4%.

All rates are higher than GDP growth for the same period in each respective region. Similarly, in all regions, the growth value of cash withdrawals has been in line with or in excess of inflation rates, suggesting that consum-ers are increasing the use of the ATM channel to access funds.

AUSTRALIA CHINA

200

8

200

9

2010

2011

2012

200

8

200

9

2010

2011

2012

1,000 12,000

0

0% 0%

1% 1%

2% 2%

3% 3%

4% 4%

5% 5%

0

800 10,000

50 5,000

6008,000

100 10,000

4006,000

150 15,000

200

4,000

2,000

0 0

200 20,000

+22%

+30%

2008 2009 2010 2011 2012

5,175

5,269

6,358

6,722

8,359

9,187

10,313

12,352

11,453

15,264

-1%

0%

2008 2009 2010 2011 2012

870

154

563

156

851

155

844

154

827

152

MIL

LIO

NS

MIL

LIO

NS

CN

Y B

N

AU

D B

N

GDPgrowth(annual%)

Inflation,consumerprices (annual%)

Householdfinalconsumption expenditure(annual%growth)

TRANSACTIONS PER TYPE OF TERMINAL: ATM VS. POSDYNAMICS OF CASH WITHDRAWALS AT ATM VS SELECTED ECONOMIC TRENDS

Source: WorldBank, BIS, Value Partners analysis

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

While general terms are valid pointers, it is to be noted that different countries may see different ATM channel dynam-ics, regardless of broadly similar positive economic conditions. Ultimately, the unique characteristics of the infra-structure in each country, the country’s consumer payment habits and the dynamics of its domestic retail bank-ing industry drive very different type of mutations in the development of the channel and its leverage by consumers and bank alike. For example, looking at two large economies in the Asia Pacific region, China and Australia, the trends of the number of cash withdrawals at ATMs are very different, despite both countries experiencing positive GDP growth, low inflation and growth in household final consumption expenditure.

This ATM growth in developing econo-mies, especially in the Asia-Pacific region, means that those countries often lead the way in terms of the value added offerings available at ATMs, but as time goes by and ATM acquirers in other parts of the world continue to extend the functionality of their ATM portfo-lio, this is less likely to be the case. In general, Asia remains the global leader in terms of cash recycling, for example, while countries in which ATMs are an established and widespread channel are facing a country-wide wave of upgrades due to the transition to EMV compliant technology. The practice of extending the working life of older units beyond their depreciation period remains, de-spite ongoing innovation in the channel.

The ATM market continues to grow globally, in terms of the quantity of ATMs proportional to the population, in the volume and value of transactions captured through the channel and in the quantity and quality of services on offer. Mobile and online channels, along with POS terminals, are evolving to complement rather than displace the role of ATMs as a key financial services channel. Ensuring the availability, reli-ability and quality of services remains a key driver for the success of the retail banking industry: “the second most common means of access in the past 12 months was via an ATM or online bank-ing, both at 74%” of respondents to the Federal Reserve Board’s survey.5 This is in line with a number of similar findings and statements from other sources confirming the importance of ATMs for the retail banking industry, even in an online banking context, with 53% of online banking customers identifying ATM access as a key choice criteria in choosing a bank, more than double the next most important criteria.6

5 Board of Governors of the Federal Reserve System, Consumers and Mobile Financial Services 2013, March 20136 Compete.com

Source: EMVco, MasterCard, Visa, American Express, Value Partners analysis

81%

15%

94%

68%81%

16%

95%

73%

2011 20112011 20112012 20122012 2012

+20%

+36% +4%

+2% +1%

+2%

41%

77%

49%

79%

2011 20112012 2012

21%

76%

29%

77%

2011 20112012 2012

26%

50%

27%

51%

2011 20112012 2012

0%

+3%

0%

+7%

EMVCards

EMVTerminals

Canada,LatinAmerica &theCarribbean

UnitedStates (datanotavailable)

Africa&theMiddleEast

AsiaPacific

EuropeZone1 (Western&CentralEurope)

EuropeZone2 (EasternEurope)

GLOBAL EMV COMPLETION OF CARDS AND TERMINALS (INCLUDING ATMS AND POS TERMINALS)

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

SCOPE OF THE ATMIA BENCHMARKING STUDY 2014

4

During 2013, Value Partners, in partner-ship with ATMIA, collected statistics from 42 ATM operators, in order to expand, update and build upon the insightful uti-lisation and cost benchmarking baseline developed previously. Sixteen of these responses were from Europe, ten from Asia, five from Middle East and Africa and eleven from the Americas.

In addition to these detailed responses, a purely qualitative questionnaire was completed by a further four ATM operators. The second round of Bench-marking built on the categories and metrics of the first round with expanded detail for the Value Added Services and Fraud sections and with the addition of Revenue and Quality of services sections.

Anonymous data was gathered in the following areas of ATM management:

• General Estate Statistics (e.g. the size and offering of the respondents’ ATM estate)

• Cash Management (e.g. replenish-ment and reliability information)

• Transaction Management (e.g. transaction costs and data transmission figures)

• ATM performance monitoring (e.g. costs of performance monitor-ing)

• Estate Management (e.g. hardware statistics and malfunctioning figures)

• Fraud, Crime & Dispute (e.g. frequen-cy and cost of ATM crime)

• Revenues (e.g. fees and commis-sions)

• Quality of services (e.g. customer complaint management policies and statistics)

Statistics collected from 42 ATM operators, in order to expand, update and build upon the insightful utilisation and cost benchmarking baseline developed previously in 2012

18—19

The purpose of this survey was to pro-vide participants with renewed insights into the performance and cost structure of their ATM estates with the additional detail on revenue and profitability indi-cators and with more comprehensive insights into the Value Added Services and Fraud management and prevention.

The value of such insights is especially important as ATMs are proving to be a much needed channel for Financial Institutions as well as representing a profitable business line. With cost controls being kept high on the agendas of all financial institutions in particular in times of more accurate capital allocation due to tighter compliance requirements, such a capital intensive channel that is also central to customer interaction, will benefit from an objective view of per-formance and a way to compare against industry best-practices.

YES NO

Of the newly participating organisa-tion less than half were already making industry comparisons prior to joining the ATMIA ATM Benchmarking study, proving, once again, the interest and the value of such type of exercise for ATM Operators.

Some of the statistics gathered are included in the report below on a “base 100 normalised index” basis. Some graphs and statistics include most of the sample, but not all of the 42 respond-ents, since some submissions were not fully completed. Others, meanwhile, reflect findings from the full sample.

The underlying philosophy of the exer-cise is that through such cooperation the ATM industry, together with ATMIA and domestic banking communities will be able to provide pointers that lead to improved efficiency and performance. By leveraging the data and information shared, service quality can be improved whilst reducing operating expenses, all the while ensuring the protection of sensitive information and competitive advantages.

Source: ATMIA Benchmarking Study 2014, Value Partners analysis

DO YOU MAKE REGIONAL OR NATIONAL COMPARISONS WITH ANY COMPETITOR OR SIMILAR OPERATOR?

0% 100%

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

KEY FINDINGS OF THE ATMIA BENCHMARKING STUDY 2014

5

7 Source: KL Guide, ATM Software Trends and Analysis, 6th Edition, 20138 Asian Banker Research, 2011, ‘Understanding the cost of handling cash in Asia Pacific Building an integrated cash supply chain to improve cash handling efficiency’

5.1. Cost metrics and performance monitoring While ATM operators were especially keen to bring down expenditure in a pe-riod of economic crisis, despite the signs of economic recovery in many markets, financial institutions are now facing the challenge of tighter capital regulatory requirements. Cost control has always been an important area of focus for all parts of the banking industry and this keeps being of particular importance in the capital intensive ATM industry. Cost efficiency is a key requisite to profitably operate a business within a channel that absorbs a relatively higher liquidity compared to other business lines of the financial services industry.

Cutting operational costs is by far the most critical change as highlighted by the 2013 ATM Software Trends and Analysis report7. Improving functional-ity for the customer was the second, followed by integration with other self-service channels. In light of this, the comparison of cost indicators across the 2012 and 2014 benchmarking study is pointing to an indicative, general cost reduction of about 7-8% on average. After investigating such cost perform-ance improvements, participants appear to have benefitted by technology up-grades, modernisation of ATM portfolios and an overall refinement of manage-ment practices.

One of the key findings of the previous ATMIA ATM Benchmarking Study 2012 consisted in outlining the lack of cost advantage provided by economies of scale in this channel.

This counterintuitive conclusion sug-gested that ATM Operators were not able to fully leverage scale to drive cost efficiency and that there was a significant potential for optimising ATM operations. The instances in which the lack of correlation was outlined during the course of the previous study match the findings of this second benchmark-ing exercise.

5.1.1. Transaction processingAlthough management theory assumes that the size of operations is one of the most critical drivers for variable unit cost, such as processing, as a result of economies of scale, this was – once again - not found to be the case amongst the respondents to the ATMIA Benchmarking Study 2014.

This is also in line with Value Partners’ experiences in the card issuing and POS acceptance industries, again, proving to be the case in the ATM industry. Once again, there are a number of potential explanations for this, ranging from contract management to a lack of price transparency from vendors and, in some markets, competitiveness with regards to alternative processing, platform providers and outsourcers.

Labour also remains a prominent cost for ATM operators, especially in mature markets where technology outsourc-ing and process streamlining have already reduced costs such as machine downtime8. Automated fault-detection systems, integrated servicing and re-plenishment schedules and centralised ATM software environments continue to be potential ways in which ATM opera-tors may control their costs.

CO

ST

PE

R T

RA

NSA

CT

ION

Note: average of transaction = 100

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

NUMBER OF TRANSACTIONS

COST PER TRANSACTION VS. NUMBER OF TRANSACTIONS

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

5.1.2. Cash managementCash, together with the cost of hard-ware, and increasingly the cost of security and fraud prevention, remains one of the major cost components of an ATM business. A key opportunity to reducing costs lies in enhanced cash re-circulation functionalities while accurate forecasting of cash demand, ensuring that ATMs are provisioned with the right amount of cash needed, remain key drivers of cost efficiency as well as ensuring ATM availability and avoidance of out-of-cash downtime.

Differently from the findings of the previous Benchmarking study, this time participants appear to adopt increas-ingly in-house intelligence for cash forecasting purposes with the use of forecasting software remaining widely used. This difference compared to the previous study is driven not only by new participating organisations but also by changes within cash forecasting practic-es of few ATM operators that took part in both rounds of the ATM Benchmark-ing study. Some companies surveyed do not perform cash demand forecasting at all, implying that significant improve-ments could be made in the manage-ment of cash in the ATM system.

Source: ATMIA Benchmarking Study 2014

Similarly to the findings of the ATMIA Benchmarking Study 2012, this study found that ATM operators continue to have different approaches to cash replenishment, with the frequency of replenishment being inversely propor-tional to the amount reloaded and the float stored within the ATM. In analysing the frequency of cash replenishment, after normalising the data to take into account the economic characteristics of each participant’s economy, ATM locations and geographical dispersion across each participant’s country, a number of common trends emerged:

• ATMs located within bank branches are typically loaded more often

• Different ATM locations tend to be replenished to different levels of float

• Countries with lower incidence of attacks to ATMs and ATM theft tend to have high amounts of float

• Replenishment value and frequency can vary significantly according to the geographical dispersion of ATM locations

For this latter point the survey recorded a variety of behaviours, whilst showing similarities amongst participants from the same country, region or size and type of operator, are far from homoge-nous globally. More generally, the survey found cases of very different cash refill-ing approaches even amongst directly competing ATM operators. In particular, during the course of this study and differently from the previous find-ings, these differences appeared to be predominantly driven by the approach towards reducing potential losses in case of ATM theft. This is once again based on the assumption that less cash stored at the ATM leads to lower losses in the case of a criminal attack.

0% 100%

FORECASTING SOFTWARE

IN-HOUSE INTELLIGENCE

DO NOT PERFORMCASH DEMAND FORECASTING

HOW DO YOU PERFORM CASH DEMAND FORECASTING?

AVERAGE NUMBER OF REPLENISHMENT EVENTS PER YEAR PER ATM

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

COST OF REPLENISHMENT EVENT VS. AVERAGE NUMBER OF REPLENISHMENT EVENTS PER YEAR PER ATM

CO

ST

OF

RE

PLE

NIS

HM

EN

T E

VE

NT

VA

VE

RA

GE

VA

LUE

OF

CA

SH

HE

LD IN

AN

AT

M

AVERAGE NUMBER OF REPLENISHMENT EVENTS PER YEAR PER ATM

AVERAGE VALUE OF CASH HELD IN AN ATM VS NUMBER OF REPLENISHMENTS PER ATM PER ANNUM

Note: Base 100 normalised index

(-)R2 = 0,55

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Once again few instances of cash replenishment behaviour were investi-gated with the conclusion that, some-times the cost of the more frequent reloads exceeded the cost of total losses incurred.

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

It is to be noted that while this observa-tion is analytically relevant, it is also im-portant to note that crime against ATMs appear to be perpetrated sometimes in a consistent but near-random manner, incentivising ATM Operators to focus on preventing and minimising losses rather than adopting risk-weighted approaches.

Cash recirculation is far from being the norm and ATM replenishment remains a key area in which effective management can keep costs to a minimum and main-tain maximum reliability. Differently from the participants to the previous round of benchmarking when cash recircula-tion was a feature resulting hardly in use by ATM operators, this study has found that over 17% of the participating sample benefits from cash recirculation. Overall cost of cash must take in account the opportunity cost of cash that is de-pendent upon the amount of cash locked in cassettes and vaults and upon the cost of the liquidity. This is sometimes calculated as a weighted cost of capital but more often consists of an internal transfer rate from the central treasury unit or from a third party lender. In the case of the previous study the findings outlined that cash provided by a third party can be cheaper than that provided by treasury. However, in this case the variance, netted from interest base line differences, is less wide than that found during the previous study.

The previous graph shows that, in line with the findings of 2012, that the more replenishments the lower the cost of each individual replenishment, with a group of high frequency replenished ATMs representing in-branch estates. As in the previous case more remote locations with an higher cost of cash re-plenishment because of travel distanc-es, however, may potentially providing a case for considering the deployment of ATM recirculating units.

DO THE ATMS IN YOUR NETWORK TAKE DEPOSITS? IF YES, WHAT PROPORTION?

<20%

20%-40%

40%-60%

>60%

ARE YOU CONDUCTING PILOTS REGARDING THE IMPLEMEN-TATION OF FULL CASH RECY-CLING CAPABILITY IN YOUR ATM NETWORK?

COMPARATIVE OPPORTUNITY COST OF CASH (CENTRAL BANK INTEREST RATE = 100, MAXIMUM AND MINIMUM RANGES SHOWN)

100%

+83.7.3%

-81.6%

INTERNALTRANSFER RATE

3RD PARTY LENDER

100%

+105.3%

-47.3%

YES

NO

YES

NO0% 0%

100% 100%

24—25

5.1.3. Cost of hardwareHardware is the major cost compo-nent for ATM operators. Similarly to the previous study, the benchmarking study recorded significantly different approaches to depreciation, the exten-sion of the useful life of ATM hardware and vendor management. The majority of operators are opting for a multiven-dor policy. Hence, one would assume that this would lead to a high level of competitiveness in the ATM market and a narrow range of ATM unit costs. Once again, this was not the case as the cost of ATM units varies greatly between participants.

From the benchmarking sample the cost of hardware was found to have little correlation with the type, size and location of the organisation.

5.1.4. Performance monitoringPerformance monitoring is composed of a number of activities that are critical to the ATM business and in some cases concern nearly all aspects of ATM oper-ations, from activity monitoring to cash management and fraud prevention. Er-ror monitoring largely takes place in real time but performance monitoring is an activity that is deployed through varied approaches to monitoring the ATM estate with the aim to maximise uptime and performance.

Once again the majority of surveyed ATM operators produce internal per-formance monitoring reports on a daily basis, although some appear to opt for monthly updates on the performance of the ATM estate.

COST OF HARDWARE (AVERAGE = 100)

ATM HARDWARECOST

100

+131.8%

-17.5%

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

WHAT IS YOUR VENDOR POLICY? IF YOU HAVE A MULTI VENDOR POLICY, HOW MANY VENDORS DO YOU USE?

0%

100%

SINGLEVENDOR

MULTI VENDOR

0% 100%

FREQUENCY OF PERFORMANCE MONITORING REPORTS PRODUCED

Hourly Daily Weekly Monthly

OUTCOURCED

AUDITS

REAL TIMEMONITORING

0% 80%

WHAT METHODS DO YOU USE TO IDENTIFY ERRORS AT ATMS?

2

3

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

YES

NO

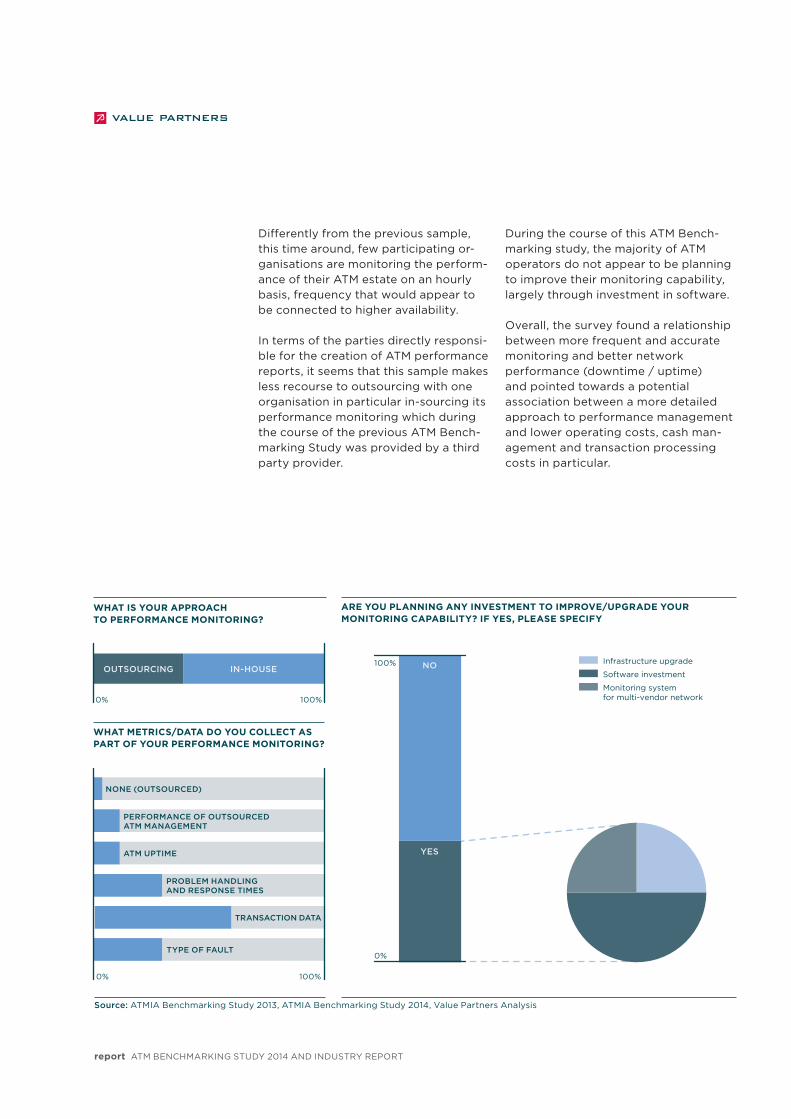

Differently from the previous sample, this time around, few participating or-ganisations are monitoring the perform-ance of their ATM estate on an hourly basis, frequency that would appear to be connected to higher availability.

In terms of the parties directly responsi-ble for the creation of ATM performance reports, it seems that this sample makes less recourse to outsourcing with one organisation in particular in-sourcing its performance monitoring which during the course of the previous ATM Bench-marking Study was provided by a third party provider.

ARE YOU PLANNING ANY INVESTMENT TO IMPROVE/UPGRADE YOUR MONITORING CAPABILITY? IF YES, PLEASE SPECIFY

During the course of this ATM Bench-marking study, the majority of ATM operators do not appear to be planning to improve their monitoring capability, largely through investment in software.

Overall, the survey found a relationship between more frequent and accurate monitoring and better network performance (downtime / uptime) and pointed towards a potential association between a more detailed approach to performance management and lower operating costs, cash man-agement and transaction processing costs in particular.

Source: ATMIA Benchmarking Study 2013, ATMIA Benchmarking Study 2014, Value Partners Analysis

0% 100%

NONE (OUTSOURCED)

PERFORMANCE OF OUTSOURCED ATM MANAGEMENT

ATM UPTIME

PROBLEM HANDLINGAND RESPONSE TIMES

TRANSACTION DATA

TYPE OF FAULT

Infrastructureupgrade

Softwareinvestment

Monitoringsystem formulti-vendornetwork

WHAT METRICS/DATA DO YOU COLLECT ASPART OF YOUR PERFORMANCE MONITORING?

0% 100%

OUTSOURCING IN-HOUSE

WHAT IS YOUR APPROACH TO PERFORMANCE MONITORING?

0%

100%

FRAUD, CRIME AND DISPUTE – SECURITY MEASURES

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

0%

100%

100%

0%

% OF FLEET COVERED BY SECURITY MEASURE

% OF PARTICIPANTS HAVING SECURITY MEASURES IN PLACE

BU

ILD

ING

AL

AR

MS

CC

TV

CO

VE

RA

GE

TR

AN

SA

CT

ION

EN

CR

YP

TIO

N M

EA

SU

RE

S/M

AC

IN

AN

TI-

RA

M R

AID

BO

LLA

RD

S

AN

TI-

SK

IMM

ING

JA

MM

ING

ME

AS

UR

ES

EN

HA

NC

ED

AT

M L

OC

KIN

G S

YS

TE

MS

FO

R T

HE

CA

BIN

ET

AN

TI-

RA

M R

AID

AN

CH

OR

AG

E P

LIN

TH

S/A

NT

I-T

HE

FT

DE

VIC

ES

TR

AN

SA

CT

ION

RE

VE

RS

AL

FR

AU

D/D

ISP

EN

SE

R M

AN

IPU

LA

TIO

N D

ET

EC

TIO

N

AL

AR

MS

IN A

TM

SE

CU

RIT

Y E

NC

LOS

UR

ES

EN

HA

NC

ED

AT

M L

OC

KIN

G S

YS

TE

MS

FO

R T

HE

SE

CU

RIT

Y E

NC

LOS

UR

E

AT

M F

AS

CIA

AN

D C

AB

INE

T A

LA

RM

S

AN

TI-

CA

SH

TR

AP

PIN

G P

HY

SIC

AL

PR

EV

EN

TIO

N M

EA

SU

RE

S

AN

TI-

SK

IMM

ING

DE

TE

CT

ION

ME

AS

UR

ES

RE

MO

TE

MO

NIT

OR

ING

FO

R U

NU

SU

AL

TR

AN

SA

CT

ION

PA

TT

ER

NS

AN

TI-

CA

RD

TR

AP

PIN

G D

ET

EC

TIO

N S

EN

SO

RS/

ME

AS

UR

ES

EN

HA

NC

ED

BU

ILD

ING

AN

D P

ER

IME

TE

R S

EC

UR

ITY

A M

IRR

OR

TO

DE

TE

CT

SH

OU

LDE

R S

UR

FIN

G

PIN

PA

D S

HIE

LDS/

GU

AR

D

RE

MO

TE

MO

NIT

OR

ING

FO

R U

NU

SU

AL

AT

M D

EV

ICE

BE

HA

VIO

UR

EN

HA

NC

ED

PH

YS

ICA

L S

EC

UR

ITY

FO

R C

AS

H S

HU

TT

ER

S

HIG

HE

R S

PE

CIF

ICA

TIO

N S

EC

UR

ITY

EN

CLO

SU

RE

S

CA

SH

PR

OT

EC

TIO

N S

YS

TE

MS

SU

CH

AS

IBN

S/D

YE

STA

ININ

G

INT

ER

NA

L C

AG

ES/

LOC

KIN

G B

AR

S TO

PR

OT

EC

T C

AS

SE

TT

ES

SE

CU

RIT

Y G

UA

RD

S A

T A

TM

LO

BB

IES

AT

M R

OO

M S

MO

KE

PR

OT

EC

TIO

N S

YS

TE

MS

AN

TI-

CA

SH

TR

AP

PIN

G D

ET

EC

TIO

N S

EN

SO

RS

AN

TI-

DE

PO

SIT

TR

AP

PIN

G D

ET

EC

TIO

N S

EN

SO

RS

AN

TI-

SO

LID

EX

PLO

SIV

E A

TTA

CK

ME

AS

UR

ES

DE

FE

NS

IBLE

SPA

CE

S (P

AIN

TE

D L

INE

S)

AT

AT

MS

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

5.2. Fraud and dispute managementFraud is and will remain a serious chal-lenge to the industry and is an area in which all participants appear to be investing significantly. The amount of investment is not yet at the same level as those absorbed by the estate invest-ment or by cash float, but is increasing rapidly versus other operational costs. Once again, the survey found a high level of variability between the levels of fraud experienced by respondents with most organisations participating to both rounds of benchmarking, reporting higher fraud losses.

DISPUTE AND FRAUD STATISTICS(AVERAGE = 100, MAXIMUM AND MINIMUM RANGES SHOWN)

COSTPER DISPUTE

NUMBEROF DISPUTECASES PER

TRANSACTION

While disputes can originate from causes other than fraud (e.g. card-holder errors, processing errors, etc.), the analysis has outlined a correlation between the number of fraud cases and the number of disputes and their respective unit cost. Once again, on the basis of the data analysed during the course of this round of benchmarking, fraud is – to-gether with malfuctionings - appearing to be a key driver of dispute cases and their associated costs.

100 100

+46.9%

+166.4%

-85.6%

-95.9%

DO YOU HAVE OTHER SECURITY MEASURES IN YOUR REAL ESTATE?IF YES, HOW MANY?

YES 1-3

+10

0%

100% NO

NUMBER OF FRAUD CASES PER ATM

0%

100%

AT

MIA

BE

NC

HM

AR

KIN

G

ST

UD

Y 2

012

AT

MIA

BE

NC

HM

AR

KIN

G

ST

UD

Y 2

014

28—29

5.3. Revenue and profitabilityThe ATMIA ATM Benchmarking study 2014 expanded from the pure cost focus of 2012 to include revenues. This is a highly sensitive and confiden-tial part of the study but it is fair to say that not all participants may have a strategy whereby profits are generated from the ATM channel. IADs have the ATM as a main line of business but for banks, in particular, the ATM is a channel that is complementary to other services and often leverages purely as on a cost-substitution basis. While the vast majority of participants have not provided a breakdown of revenues by services (e.g. withdrawal, mobile top-up, etc.) the vast majority supplied revenue figures for transac-tion and cardholder fees that have been used to calculate the pro-forma profit-ability of the ATM estates.

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

AVERAGETRANSACTION

MARGIN

100

+424.6%

-192.4%

TOTALMARGIN

100

+438%

-44.5%

Profitable or less profitable organisa-tions are evenly distributed across the various regions with the imbalance between costs and revenue appearing to cause losses that are not necessary affecting close competitors, likely on the basis of different management strat-egies for ATMs estates between organi-sations. Nonetheless, this reinforces the working hypothesis deriving from the analysis of the costs sections that on the whole, potential areas of improve-ment are waiting to be investigated and realised by a number of ATM Operators.

Where losses have been seen, in gener-al, overall cash withdrawal transaction margins continue to result in a slightly wider range than the total marking of the ATM product line. In many cases, the losses of cash withdrawals are balanced by margin origination from value added services that are seen to be dragging the overall economic performance of a couple of estates back into positive from a distinct loss making position.

The majority of ATM Operators, do not account for on-us transactions with an internal transfer price, de-facto penalis-ing the economic performance of their ATM estate while providing a nominal cost advantage to their ATM portfo-lio. While it appears to be a common practice, it distorts the actual financial results of the ATM and debit card busi-ness units.

AVERAGE TRANSACTION PROFITABILITY STATISTICS (AVERAGE = 100, MAXIMUM AND MINIMUM RANGES SHOWN)

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

5.4. Complaint managementATM Operators are investing considera-bly in performance monitoring activities, mostly with the aim to maximise ATM availability and avoid downtime. While most participants monitor and manage the performance of their ATMs through a variety of ATM reports, only few - about a quarter of the total number of participants - collect data on complaints from card-holders. Of these, the vast majority has implemented a formal complaint handling policy. This latter include the option of a formal compensation for the lack of service to disgruntled cardholders.

PARTICIPANTS COLLECT DATA ON COMPLAINTS

DO YOU HAVE A COMPLAINT POLICY?

IS COMPENSATION OFFERED?

0% 0%

100% 100%

YES

YES

NO

YES

NO

NO

Over half of recorded complaints appear to be originating from card captured due to an ATM malfunction and just over a quarter is due to cash not dispensed despite the account being debited due to a malfunction. As a channel there is great effort be-ing invested to ensure availability and avoiding poor service but, data appears to indicate that very few ATM opera-tors are taking in account factors like customer satisfaction.

The analysis did not venture into inves-tigating the rationale for such a choice but the findings have outlined that there may be an untapped opportunity to leverage customer satisfaction as a source of competitive advantage. This would need to be investigated and validated based on the competitive landscape and characteristics of each estate.

COMPLAINTS MANAGEMENT

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

CARD CAPTUREDATM MALFUNCTION

CASH NOT DISPENSEDA/C DEBITED

ATM MALFUNCTION

CARD CAPTUREDISSUER REQUEST

ATM OUT OF ORDER

OTHER

TRANSACTION SLOW OR INCOMPLETECOMMUNICATIONS MALFUNCTION

PRICING COMPLAINT

CASH RETRACTED

PROPORTION OF COMPLAINTS RECEIVED PER YEAR

CASH NOT DISPENSEDA/C NOT DEBITEDATM MALFUNCTION

CASH NOT DISPENSEDCUSTOMER ERROR

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

5.5. Value added services and multi-functionalityThe role of the ATM channel continues to change. That was one of the five general conclusions from the previous ATM Benchmarking Study and it is a trend that emerged even strongly dur-ing second exercise. The role and the range of functionalities that are being offered through the ATM are fundamen-tally changing the nature of the chan-nel. This is because as many customers interact with their financial institution increasingly via the ATM as well as other self-service touch-points, the user experience of ATMs itself is keeping being re-designed around a self-service concept.

Increasing consumer familiarity with digital interfaces driven by the growing uses of smart phones and tablets is one of the key enablers that are accelerat-ing the potential changing role of ATM estates.

Compared to the previous study, the current analysis outlined two key trends in regards to multi-functionality:

I. Multi-functionality is – in most cases – becoming the norm

II. ATM operators are starting to select the services they wish to offer through their estates

ATM advertising functionality continues to be common throughout all geogra-phies. Message personalisation is now a growing feature that is offered in over 50% of the cases, about twice as much compared to the findings of the previ-ous ATM Benchmarking study.

Advertising initiatives on ATM are grow-ing by as much as 13% year-on-year, being perceived by bank institutions and advertisers “as a more effective and efficient way of advertising than direct mail/email and any other standard form of advertising”. Indeed, according to NCR Inc., ATM adverts are 65% less expensive and 200% more effective than direct mail.

Cash withdrawals and mini-statements are thus no longer the only services that an ATM operator can offer to customers but, based upon the findings from the analysis, they remain the predominant service demanded by ATM users.

Source: Press, Company websites

TYPES OF ATM ADVERTISING

DIRECT MARKETING

3RD PARTY ADVERTISING

COUPONING

% OF PARTICIPANTS, OFFERING A SERVICE

Withinthenextyear Withinthenext5years Notplanningtoaddservice Servicesdeclaredplannedtobe dismissedbysomeparticipants

VALUE ADDED SERVICES

0%

100%

100%

0%

% OF FLEET COVERED BY SECURITY MEASURE

BA

LA

NC

E E

NQ

UIR

IES

PR

INT

ED

RE

CE

IPT

S

PIN

SE

RV

ICE

S

MIN

I STA

TE

ME

NT

S

MO

BIL

E T

OP

-UP

S

AC

CO

UN

T T

RA

NS

FE

RS

BIL

L P

AY

ME

NT

S

INT

EL

LIG

EN

T D

EP

OS

IT

DY

NA

MIC

CU

RR

EN

CY

CO

NV

ER

SIO

N F

OR

TO

UR

IST

S

CH

AR

ITY

DO

NA

TIO

NS

OT

HE

R

CO

UP

ON

ING

CA

RD

LE

SS

WIT

HD

RA

WA

L

PE

RS

ON

TO

PE

RS

ON

RE

MIT

TAN

CE

S (I

NIT

IAT

ED

)

PE

RS

ON

TO

PE

RS

ON

RE

MIT

TAN

CE

S (C

OL

LE

CT

ED

)

PA

YM

EN

T O

F T

AX

ES

/FIN

ES

LOY

ALT

Y R

EW

AR

DS

FX

RE

MIT

TAN

CE

S

PA

SS

BO

OK

PR

INT

ING

TR

AV

EL

TIC

KE

TS

EN

TE

RTA

INM

EN

T E

VE

NT

TIC

KE

TS

E-W

AL

LE

T T

OP

UP

RO

AD

TO

LL

S

LIC

EN

CE

S

LOT

TE

RY

TIC

KE

TS

SP

OR

TS

EV

EN

T T

ICK

ET

S

STA

MP

S S

AL

ES

EV

EN

T T

ICK

ET

S

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

Source: ATMIA Benchmarking Study 2014, Value Partners Analysis

DO PARTICIPANTS ADVERTISE ON BEHALF OF 3RD PARTIES?IF NO, WHY?

YES

NO

YES

NO

Generic

Cardholder-specific

Splitbetween‘onus’and ‘notonus’customers

Incompatibletechnology

CompanyPolicy

Other

This trend toward multifunctionality is not limited to mature ATM markets, but is common throughout geographies. As this trend continues, the two potential challenges highlights in the previous ATM Benchmarking Study 2012 are starting to be addressed by ATM opera-tors. The first is related to cost man-agement, with the increase in available services requiring a constant review of how to best optimise ATM expenditure.

The second is complexity, with mul-tifunctionality necessarily involving connections with 3rd party telecom-munication networks, with all the interoperability and reliability issues this implies.

The current study analysed a shift in multi-functionality trends compared to two years ago; after that most par-ticipating organisations having imple-mented functionalities that were on their wish lists during the course of the previous study.

Nowadays attention and plans are be-ing paid to fewer value added services and with ATM Operators starting to selectively dismiss a few services, in a drive to optimise queues at ATM or that are not profitable or not taken up by consumers as expected.

CASH WITHDRAWAL WITHBALANCE ENQUIRY

CASH WITHDRAWAL ONLY

BALANCE ENQUIRY ONLY

OTHER

DO PARTICIPANTS UNDERTAKE SALES OR MARKETING?IF YES, WHAT TYPE?

WHAT ARE THE MOST POPULAR OR FREQUENTLY TRANSACTED SERVICES?

VALUE ADDED SERVICES – ADVERTISING

0%

0%

100%

100%

0% 80%

34—35

CONCLUSIONS6

Similarly to the previous study, the ATM Benchmarking Study 2014 has provided participants with an insight into key performance metrics of their respective ATM estates. While the findings specific to each participants are confidential to participating organisations, there are a number of general conclusions that have been developed during the course of the analysis. These do not contradict but, on the contrary build upon the findings of the previous Benchmarking Study.

The conclusions are:

• Economies of scale are (still) not a source of competitive advantage Once again it was found that a larger scale does not necessarily result in lower unit costs. While, in general terms costs have been decreasing relatively to the previous ATM Benchmarking study, there is still no correlation between scale and cost efficiency. Once again no single operator has emerged as an obvious best performer amongst all partici-pants.

• Fraud is a growing challenge Fraud is a growing challenge to the industry and ATM Operators are increasing their efforts to prevent and combat it. Investment in fraud prevention measures is increasing as, in general, fraud losses continues to increase.

• ATMs can be a profitable business line but with exceptions While the majority of participants are showing profitable ATM businesses, a minority is apparently running loss-making estates. It is to be noted that not all ATM Operators have a strategy whereby profits are generated from the ATM channel, this conclusion

is reinforcing the working hypothesis that the cost imbalances outlined in the first conclusion may provide opportunities to improve overall ATM economic performance

• Cardholder satisfaction is not a typical driver to ATM management Very few participants appear to be tracking cardholder complaints (or other types of customer satisfac-tion measures) in parallel to ATM performance monitoring. While availability and uptime are important drivers for ATM performance, could customer satisfaction be a source of competitive advantage too?

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

• Selective multifunctionality is the ATM business model of the future In line with what the conclusions and findings of the 2012 Study, multifunctionality is now an estab-lished, dominant business model for ATMs. ATM operators appear to be developing selective approach-es to multi-functionality with some Value Added Services being phased out in parallel to a more selective approach to Value Added Services being implanted in evolving the role of the ATM.

Value Partners believes that the ATM channel is, and will continue to be, for the foreseeable future, one of the most important channels of the banking industry and, with very few exceptions, the main touch-point between retail fi-nancial institutions and their customers.

The development of other channels such as internet and mobile banking is currently proving complementary to ATM industry and it is far from being a threat to ATMs. Within this context, ATM business management and the result-ing fundamental economics should not be overlooked, since current business practices appear to offer potential for improvement.

As referred to previously, the content of this report refers to the general results of the ATMIA ATM Benchmark-ing Study 2014 and are general in nature. Survey participants have exclusive access to the full findings and are provided with a customised report detailing their performance relative to a number of benchmarks.

If you would like to participate in the survey in future years, please contact your ATMIA regional director or write to [email protected].

The development of other channels such as internet and mobile banking is currently proving complementary to ATM industry and it is far from being a threat to ATMs

36—37

ABOUT VALUE PARTNERS MANAGEMENT CONSULTING

Value Partners has an established financial institutions practice with a track record in cards, payments and transaction banking. Over a quarter of our projects are now on behalf of financial institu-tions. We have completed projects with top banks, issuers, acquirers, proc-essors and payments schemes.

The firm also works across all sectors of the telecom-munications and digital marketplace, as one of the largest TMT practices worldwide. This, together with our thought leader-ship position in the finan-cial services industry, has enabled Value Partners to excel within the context of industry convergence.

Over the last 21 years we have delivered real ben-efits for our clients, 60% of whom have been with us for over 10 years, build-ing on our deep industry insights into key issues for these sectors. Value Part-ners has played a primary role in the development of innovative solutions, espe-cially those at the cross-roads between industries. We have assisted 3 of the world’s top 5 banks, the leading European financial institutions and the main telecoms operators in Europe, Asia, Middle East and Latin America.

We serve the largest private equity firms with an interest in financial services, telco and media industry. Value Partners helps its clients adapt their business models in an increasingly complex business environment, to maximise impact and returns in the financial services, payments, telco, technology and digital media spaces.

Founded in Milan in 1993, Value Partners’ rapid growth testifies to the val-ue it has created for clients over time. Today, it draws on 20 partners and over 250 professionals from 23 nations, working out of offices in Milan, London, Istanbul, Dubai, São Paulo, Buenos Aires, Beijing, Hong Kong and Singapore. Value Partners has built a portfolio of more than 350 international clients – from the original 10 in 1993 – with a worldwide revenue mix.

valuepartners.com

report ATM BENCHMARKING STUDY 2014 AND INDUSTRY REPORT

ABOUT ATMIA

The ATM Industry Associa-tion, founded in 1997, is a global non-profit trade as-sociation with over 4,000 members in 60 countries. The membership base covers the full range of this worldwide industry comprising over 2.3million installed ATMs.

ATMIA has chapters around the world in the United States, Canada, Eu-rope, India, Latin America, Asia-Pacific, Asia, Africa and the Middle East. ATMIA has just launched a new international certified eTraining programme for ATM Operators (for both banks and independent ATM deployers. In addi-tion, the association runs an ATMIA Consulting and Training practice as well as a range of industry committees to deal with Government Relations and regulatory monitoring, ATM security, best prac-tices and ATM deployer issues.

ATMIA’s provides a one-stop online resource for member information with security best practices, industry white papers, articles, research findings, ATM business efficiency best practices, compliance material, Corporate Gov-ernance best practices, Glossary of ATM Terms, a Gallery of Technology, on-line ATM Risk Assessment system, industry calendar and more.

atmia.com

For more information on the issues raised in the report please contact:[email protected]@valuepartners.com

ATM business management and the resulting fundamental economics should not be overlooked, since current business practices appear to offer potential for improvement

Co

pyr

igh

t ©

Val

ue

Par

tner

s M

anag

emen

t C

on

sult

ing

Lim

ited

. All

rig

hts

res

erve

d