Untitled - Virtual Campus Sign In

409

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Untitled - Virtual Campus Sign In

AGRICULTURALECONOMICS

THIRD EDITION

H. Evan DrummondUniversity of Florida

John W. GoodwinOklahoma Panhandle State University

Prentice Hall

Boston Columbus Indianapolis New York San Francisco Upper Saddle River

Amsterdam Cape Town Dubai London Madrid Milan Munich Paris Montreal Toronto

Delhi Mexico City São Paulo Sydney Hong Kong Seoul Singapore Taipei Tokyo

Editor in Chief: Vernon AnthonyAcquisitions Editor: Bill LawrensenEditorial Assistant: Lara DimmickDirector of Marketing: David GesellCampaign Marketing Manager: Leigh Ann SimsCurriculum Marketing Manager: Thomas HaywardSenior Marketing Coordinator: Alicia WozniakMarketing Assistant: Les RobertsProduction Editor: Holly ShufeldtCover Art Director: Jayne ConteCover Designer: Bruce KenselaarCover and chapter opener art: IstockLead Media Project Manager: Karen BretzFull-Service Project Management: Saraswathi Muralidhar, GGS Higher Education ResourcesComposition: GGS Higher Education Resources, A Division of PreMedia Global Inc.Printer/Binder: Edwards BrothersCover Printer: Lehigh-Phoenix Color Corp.

Credits and acknowledgments borrowed from other sources and reproduced, with permission, in this textbookappear on appropriate page within text.

Copyright © 2011, 2004 Pearson Education, Inc., publishing as Prentice Hall, One Lake Street, Upper SaddleRiver, NJ 07458. All rights reserved. Manufactured in the United States of America. This publication is protected byCopyright, and permission should be obtained from the publisher prior to any prohibited reproduction, storage in aretrieval system, or transmission in any form or by any means, electronic, mechanical, photocopying, recording, orlikewise. To obtain permission(s) to use material from this work, please submit a written request to PearsonEducation, Inc., Permissions Department, Prentice Hall, One Lake Street, Upper Saddle River, NJ 07458.

Many of the designations by manufacturers and seller to distinguish their products are claimed as trademarks.Where those designations appear in this book, and the publisher was aware of a trademark claim, the designationshave been printed in initial caps or all caps.

10 9 8 7 6 5 4 3 2 1

Library of Congress Cataloging-in-Publication DataDrummond, H. Evan (Harold Evan)

Agricultural economics / H. Evan Drummond, John W. Goodwin.—3rd ed.p. cm.

Includes bibliographical references and index.ISBN-13: 978-0-13-607192-1ISBN-10: 0-13-607192-9

1. Agriculture—Economic aspects. 2. Agriculture—Economic aspects—United States.I. Goodwin, John W. II. Title.

HD1433.D78 2011338.1—dc22

2009052979

Paper bound ISBN-13: 978-0-13-607192-1ISBN-10: 0-13-607192-9

Loose leaf ISBN-13: 978-0-13-506990-4ISBN-10: 0-13-506990-5

Preface ixNew to This Edition xiiAcknowledgments xiii

part oneFoundations

1The Food Industry 2Major Sectors—An Overview 2

Farm Service Sector 2Producers 3Processors 3Marketers 4

Contemporary Issues in the Food Industry 4Farm Structure 4Concentration 6Globalization 6Coordination 7Alternative Energy Sources 8

Summary 10

Key Terms 10

Problems and Discussion Questions 11

Sources 11

2Introduction to AgriculturalEconomics 13Agricultural Economics 13

Basis for Economics 14

Basic Economic Decisions 14

Economic Systems 14

Levels of Economic Activity 15Microeconomics 16Market Economics 16Macroeconomics 17

Basic Skills of the Agricultural Economist 18Economic Models 18Ceteris Paribus 19Opportunity Cost 19Diminishing Returns 20Marginality 21Logical Fallacies 22

Facts, Beliefs, and Values 24

Words 24

Summary 25

Key Terms 25

Problems and Discussion Questions 26

Sources 26

Appendix: Expressing Relationships 27

Relationships 27

Reading Graphs 29

Slope of a Line 31

Slope of a Curve 33

Special Cases 34

Key Terms 34

3Introduction to Market PriceDetermination 35Markets 35

Demand and Supply 36Demand 36Supply 38

Price Determination 39

Changes in Supply and Demand 41Demand Shifters 44Supply Shifters 45Supply or Demand 45

Summary 46

Key Terms 46

Problems and Discussion Questions 46

contents

iii

part twoMicroeconomics

4The Firm as a Production Unit 50Perfectly Competitive Markets 50

The Perfectly Competitive Firm 51Objective of the Perfectly Competitive Firm 51Conditions of Perfect Competition 52Behavior of the Perfectly Competitive Firm 53

Production 53Fixed and Variable Inputs 54Length of Run 54Returns to Scale 54

The Production Function 55The Total Product 56Diminishing Marginal Product 57

Summary 58

Key Terms 59

Problems and Discussion Questions 59

5Costs and Optimal Output Levels 60Environment of the Firm 60

Optimal Output Level 61Costs of the Firm 61Revenue of the Firm 66Profit Maximization 67Behavior of the Loss-Minimizing Firm 70

Summary 72

Key Terms 72

Problems and Discussion Questions 73

Appendix I: Factor-Factor Model 74

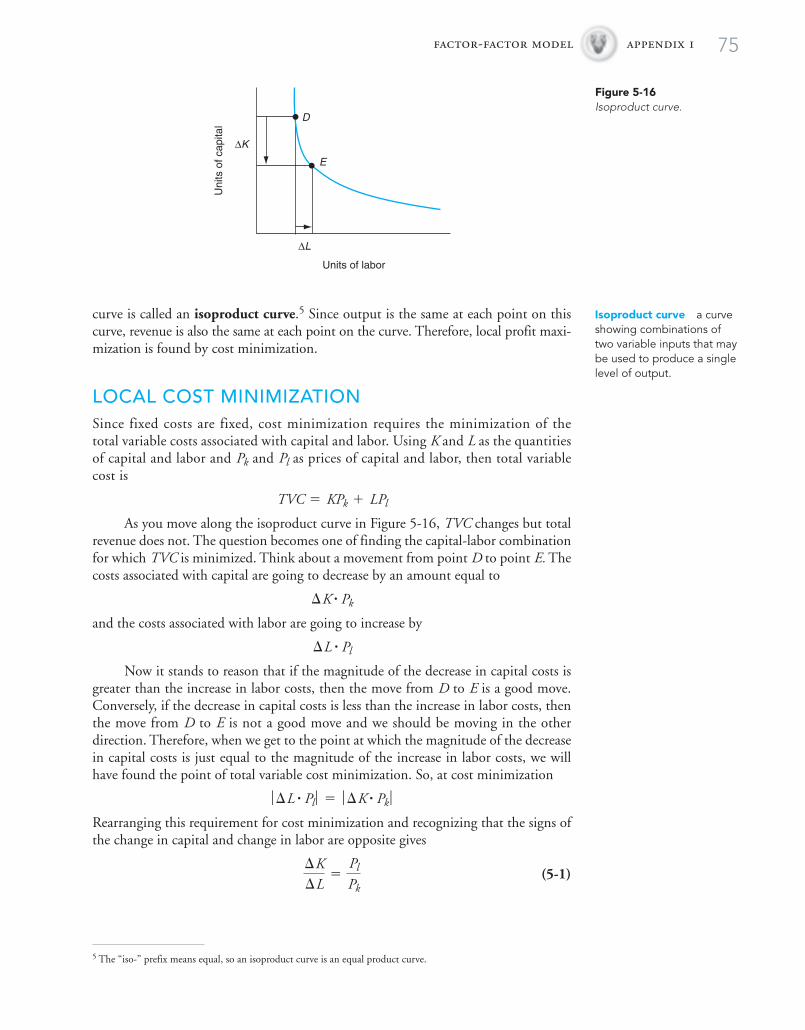

Local Cost Minimization 75

Constant Output 76

Local Profit Maximization 76

Graphical Solution 76

Expansion Path 78

Key Terms 79

Appendix II: Product-Product Model 80

Local Revenue Maximization 80

Graphical Solution 81

Generalization 83

Key Terms 83

iv contents

6Supply, Market Adjustments, and Input Demand 84Supply Curve of the Firm 84

Market Supply 85

Market Adjustments 86Dynamic Relationship Between the Firm

and the Market 86Cost Structure and Price Variability 88

Profit-Maximizing Input Use 89Value of the Marginal Product 90Profit Maximization 90Input Demand of the Firm 92Input Demand Shifters 92

Summary 92

Key Terms 93

Problems and Discussion Questions 93

7Imperfect Competition and GovernmentRegulation 94Market Structure 94

Perfect Competition 95Structure 95Conduct 95

Pure Monopoly 96Structure 96Barriers to Entry 97Conduct of the Monopoly Firm 98Unprofitable Monopolies 99Performance 100

Monopolistic Competition 101Structure 101Conduct of the Monopolistically

Competitive Firm 102Performance 104

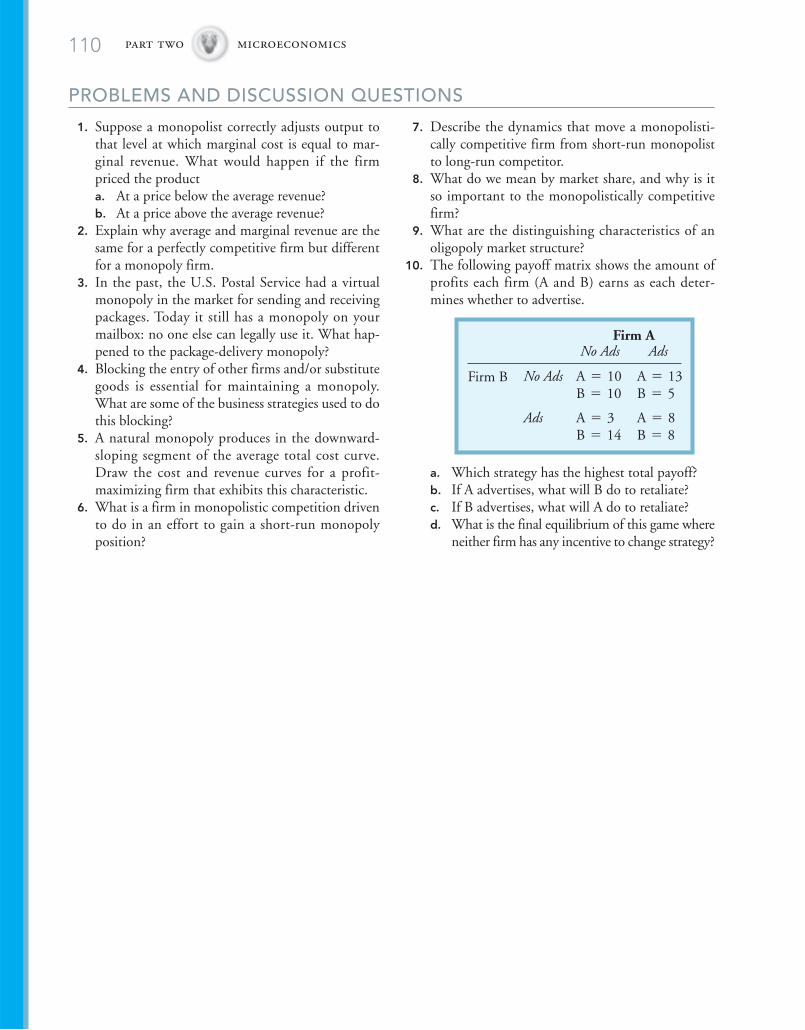

Oligopoly 104Structure 104Conduct 105Game Theory 105

Government Regulation 106Railroads 106Standard Oil 107Antitrust 107Natural Monopolies 107Marketing Orders in Agriculture 108

contents v

Summary 108

Key Terms 109

Problems and Discussion Questions 110

8The Theory of Consumer Behavior 111The Law of Demand 111

Real Income and Substitution Effects 111Substitution Effect 112Real Income Effect 112

Market Demand and Individual Demand 112

Utility Analysis 113Assumptions about the Utility Model 113Deriving the Demand Curve 117

The Market Demand Function 118

Summary 118

Key Terms 119

Problems and Discussion Questions 119

Appendix: Indifference Curve Analysis 120

Utility Maximization 122

The Impact of Changes in Ceteris ParibusConditions 124

Substitutes and Complements 126

Derivation of the Individual Demand Curve 128

Summary 130

Key Terms 130

Problems and Discussion Questions 130

9The Concept of Elasticity 131Elasticity of Demand 132

Elasticity of Demand Related to Total Revenue 135

Factors Affecting Demand Elasticity 136

Cross-Price Elasticity 138

Income Elasticity 139

Elasticity of Supply 140

Price Discrimination 141

Summary 142

Key Terms 143

Problems and Discussion Questions 143

part threeMacroeconomics

10Money and Financial Intermediaries 146What Is Money? 146

Money as a Medium of Exchange 146Money as a Store of Wealth 148Money as a Basis for Keeping Records 148

What Backs Money? 148Legal Tender 149Money and Prices 149

The Money “Supply” 149M1 150Near-Monies 150Credit and Debit Cards 151

Financial Markets 151The Commercial Banking System 151Financial Failures 154Banks in the New Millennium 159

Summary 160

Key Terms 160

Problems and Discussion Questions 161

Sources 161

11The Circular Flow of Income 162Final Goods 163

Production 163Consumption 164

The Circular Flow 165The Physical Flow 165The Economic Flow 166The Basic Principle 167

Gross Domestic Product and National Income 169The Gross Domestic Product 169National Income 170Measurement Difficulties 170The Price Level and GDP 171

The Circular Flow by Economic Sector 175Households 175Business Firms 175Governments 176The Foreign Sector 176The Total System 177

vi contents

The Role of Financial Intermediaries 178

Summary 180

Key Terms 180

Problems and Discussion Questions 181

Sources 181

12Monetary Policy 182The Money Supply and Economic Activity 183

Objectives of Macroeconomic Policy 183How Monetary Policy May Affect These

Objectives 184

Implementing Monetary Policy 188Federal Reserve System 188Money Creation 189Instruments of Monetary Policy 190

Summary of Monetary Policy 194

Summary 194

Key Terms 195

Problems and Discussion Questions 195

Sources 195

13Fiscal Policy 196Debt and Deficits 197

The Classical School 198Say’s Law 198Classical Macroeconomic Policy 199

The Keynesian Revolution 200The Great Depression 200The Keynesian Contribution 201Fiscal Policy in the 1930s 204

Summary 206

Key Terms 206

Problems and Discussion Questions 207

Sources 207

14International Trade 208Changing U.S. Trade Patterns 208

Role of Trade in the U.S. Economy 208From Creditor to Debtor 209

The Importance of World Trade to U.S.Agriculture 210

Exports 210Imports 211

Why Do Nations Trade? 212The Basis for Trade 213Excess Supply/Demand 214A Simple Trade Model 215

Gains from Trade 216

Restraints to Trade 218Tariffs 218Quotas 220Restrict Domestic Demand 221

Foreign Exchange Markets 222

Trade Agreements 226General Agreement on Tariffs and Trade 226North American Free Trade Agreement 226

Summary 227

Key Terms 227

Problems and Discussion Questions 228

Sources 229

15Agricultural Policy 230The Perfect Food System 231

The Economic Environment of Agricultural PolicyIssues 231Agricultural Price Support Policies 232Agricultural Income Support Policies 236Current Price/Income Support Policies 236Average Crop Revenue Election—A New

Alternative 239

Conservation Reserve Program 240

U.S. Farm Policy in a Global Context 240

Summary 241

Key Terms 242

Problems and Discussion Questions 242

Sources 242

part fourAdvanced Topics

16Food Marketing: From Stable to Table 244Food Marketing Defined 245

Food Marketing Creates Utility 245The Four Utilities of Food Marketing 245

contents vii

Why Do Food Marketing Firms Produce Utility? 246Choices 246

The Food Bill 247Away from Home Share 247

The Food Marketing Bill 248Size and Composition 248

By Commodity 249Farm Service Marketing Bill 251

Food Market Levels 252Assemblers 252Commodity Processors 252Food Processors 253Distributors 253Retailers 253Vertical Integration 254Industrialization 254

Market Functions 255Primary Functions 255Facilitating Functions 255

Marketing Margins 256Derived Demand 256Derived Supply 257Market Equilibrium 258Dynamic Adjustment 258Gains from Marketing Efficiency 259Elasticity by Market Level 261

Food Market Regulations 262

Summary 263

Key Terms 264

Problems and Discussion Questions 264

Sources 264

17Futures Markets 266Risk Management 266

Futures Markets 267Exchanges 268Futures Contracts 269Futures Contract Prices 272Basis of Futures Contracts 273Speculators 274Hedgers 275

Options 280

A Final Word 283

Summary 284

Key Terms 285

Problems and Discussion Questions 285

Sources 287

18Financial Markets 288How Firms Obtain Funds 288

Stock 289Newly Issued Stock 289Previously Issued Stock 292Stock Price Determinants 293Reading Stock Reports 294Stock Splits 296Classes of Stock 297Types of Stocks 297Market Indicators 298Investors and Speculators 299Summary—What Makes Stock Prices Go Up

and Down? 300

Bonds 301Characteristics of Bonds 301Trading of Bonds 304Bond Prices 305Bond Price Quotations 306Other Bond Features 308

Mutual Funds 309How a Mutual Fund Works 310Managers and Advisors 311Types of Funds 312How to Read Mutual Fund Quotations 313Closed-End Funds 314

Summary 315

Key Terms 315

Problems and Discussion Questions 316

Sources 317

19Investment Analysis 318Typical Life of an Investment 319

Economic Profitability of an Investment 319Present Value 319Net Present Value 322Internal Rate of Return 323

Evaluating Alternatives 324

Summary 324

Key Terms 325

viii contents

Problems and Discussion Questions 325

Sources 325

20Farm Service Sector 326Purchased Inputs 326

Direct Sales 326Franchise Agents 326General Store 327Cooperatives 327

Insurance 331Crop Insurance 331Revenue Insurance 331

Credit 332Types of Credit 332Sources of Credit 332

Farm Labor 334Tenant Labor 334Labor Contractors 335Custom Hire 335Consultants 335

Summary 336

Key Terms 336

Problems and Discussion Questions 337

Sources 337

21The Economics of Market Failure 338Advantages of Markets 338

Coordination 338Prices Driven to Minimum Cost 339Disequilibria Are Self-Correcting 339No Coercion 339

Types of Market Failure 339Poorly Defined Property Rights 340Public Goods 342Common Property Goods 343

Externalities Cause Market Failure 345Externalities Defined 346Private and Social Costs/Benefits 346Pesticide Use—An Example of Externalities 346Higher Education—Another Example of

Externalities 347Optimal Level of Pollution 349Benefit-Cost Analyses 351Policy Alternatives 352

Information Asymmetries 355Used Cars 355Baseball’s Free Agents 356

Problems in Dealing with Market Failure 356Information Failure 357Economic Efficiency Considerations 357Equity Considerations 357

Summary 358

Key Terms 359

Problems and Discussion Questions 359

Sources 360

22The Malthusian Dilemma 361The Neo-Malthusians 362

The Non-Malthusians 363

The Demographic Transition 365Traditional 365Developing 366Developed 367

Land 368

Summary 369

Key Terms 369

Problems and Discussion Questions 369

Sources 369

23Economic Development and Food 370Quantity of Food 371

For Want of Food 371Who Is Hungry? 372Why Hunger? 374

Food Demand During Development 375Quantity 375Quality 375Processing and Marketing 376

Summary 376

Key Terms 376

Problems and Discussion Questions 377

Sources 377

Glossary 378

Index 390

ix

PrefaceThis text is designed for a one-semester (or two-quarter sequence) introductorycourse in agricultural and environmental economics. Many texts view agriculturaleconomics in a rather narrow context of the profit-maximizing farm business. We pre-fer a broad view of the food system that emphasizes linkages between and amongfinancial institutions, the macroeconomy, world markets, government programs,farms, agribusinesses, food marketing, and the environment. The objective of this textis to cover many topics lightly rather than any one or two topics in depth. The text isdesigned to allow for and encourage a maximum of “skipping around” rather thanrequiring a strict sequential ordering of the chapters.

Economics is about decision making. It deals with how decisions are madeunder varied conditions and situations. It also deals with the evaluation or implica-tions of alternative decisions for a given situation. Since decisions are a fact of every-day life, economics is with us in most of what we do. Even monastic monks who sellfruitcakes to support their spiritual endeavors make economic decisions when theydecide which ingredients to buy and what price to ask for their product.

You, the college student, are surrounded by economic decisions as you pursueacademic success at the institution of your choice. Several of the economic decisionsyou must make will be discussed to briefly introduce you to six economic conceptsthat will recur throughout this book. These concepts form the foundation of howeconomists approach decision making.

SUPPLY AND DEMANDThere is probably no better-known (and more poorly understood) concept in eco-nomics than supply and demand. Supply and demand are the central nervous systemof the economic system—they are the key to price determination. One decision thateach college or university student must make is “What am I going to major in?” Thespecific answer to that question depends upon the criterion used by the individualstudent to make a choice.

A student who bases his or her choice of a major on potential income is certainlyinto the use of supply and demand. In today’s market, we all know that computerengineers, on average, earn more than high school teachers. Why is that? It is a simplematter of supply and demand in the determination of the price (i.e., wage) for com-puter engineers and for high school teachers. In Chapter 3, the basic foundations ofsupply and demand will be examined in detail.

OPPORTUNITY COSTA second fundamental concept of economics is the concept of opportunity cost.Whenever a resource is employed in one activity, that means it can’t be used inanother. Something must be given up to do something else. That is, if you are attend-ing class, you can’t be earning money by flipping hamburgers at the same time. Thevalue of what is foregone is the opportunity cost of doing something else.

A relevant economic question that each college student should ask is “Whatdoes it cost for me to attend the university?” Most students will think of “costs” astuition, residence hall fees, meals, and so on. From the economist’s point of view,probably the single biggest cost (if you are in a public university) is the opportunity

x preface

cost of the student’s own time. By attending college, you are foregoing the incomeyou would earn by flipping burgers at the Burger Barn. Full-time pay at minimumwage (which is probably what you would make as a high school graduate) is about$14,500. Therefore, $14,500 is a minimum estimate of your annual opportunity costof attending the university.1

DIMINISHING RETURNSA basic concept in economics is that as you add more of something while holdingeverything else constant, the additional benefit from each additional unit eventuallybegins to decline. That is, the benefits increase at a decreasing rate. This we calldiminishing returns.

In the context of the university student, this is illustrated by asking a familiarquestion: “How much should I study for the next test?” Initially, you might think theanswer is “as much as possible,” but closer examination will show that, after somepoint, the additional benefit associated with each additional hour of study will beginto decline and eventually fall so low that you are probably better off to get some sleeprather than pulling an all-nighter.

Diminishing returns are something we find in all kinds of economic activity.Eating, sleeping, fertilizing house plants (ouch!), and exercising all exhibit diminish-ing returns—eventually.

As with most things in economics, you can look at one coin with two sides. Itmatters not which side you look at, the other is always the mirror image. In the caseof decreasing returns, the other side of the coin is increasing costs. That is, as returnsincrease at a constant rate, the cost of earning those returns will increase at an increas-ing rate. Same coin—two sides.

MARGINALITYThe discussion of diminishing returns unwittingly introduced you to the concept ofmarginality. The margin in economic terms refers to the “next additional” unit. So inthe previous example, when we spoke of “an additional hour of study,” we equallycould have said “a marginal hour of study.” In most economic analyses, it is what hap-pens on the margin that dictates decision making.

A question many postsecondary students ask is “Should I get a 2-year associate’sdegree or a 4-year bachelor’s degree?” The economist would evaluate this question byasking what the marginal costs and marginal returns are for the extra 2 years. That is,assume you have the 2-year associate’s, and then base your decision on the costs andreturns of the additional or marginal 2 years to earn the bachelor’s degree.

The economic theory of the firm is based on marginal revenues and marginalcosts. The economic theory of the consumer is based on marginal utility and mar-ginal cost. The investment decision of 2 more years of higher education is based onthe marginal returns and marginal costs (including opportunity costs) of that invest-ment. On a daily basis, the manager of a supermarket must decide whether to add anew product to the shelves that will force the elimination of some other productfrom the shelves. What are the marginal (additional) benefits of adding the new

1 One reason so few students pursue a Ph.D. is that the opportunity cost of doing so is very high. Ph.D. candidatesalready have a master’s degree and could easily be earning $40,000 to $60,000 (their opportunity cost) per year for the3 or 4 years spent studying for the Ph.D. So typically, the opportunity cost of seeking a Ph.D. easily exceeds$200,000. That’s quite an investment.

preface xi

product versus the marginal (additional) costs or removing the old product? In pol-lution control, the decision about more abatement depends on marginal benefits andmarginal costs. In other words, it is safe to say that in economics, all of the action ison the margin. So, economists are (to mix a metaphor) marginal characters.

COSTS AND RETURNSAs illustrated earlier, most of economics deals with the trade-off between costs andreturns. Measuring the costs and returns associated with some economic activities canbe a little tricky. Identifying the costs associated with most economic activities is usu-ally fairly straightforward once the concept of opportunity cost has been mastered.

The nature of economic returns to an economic activity is a little less cut anddried. We use different terms to refer to returns in different situations, but nonethe-less they are all returns. In the theory of the firm, we call returns revenue. In the the-ory of the consumer, we call returns utility. In investment analysis, we call returnsreturns. And, finally, in resource and environmental economics, we call returnsbenefits. Estimating returns often involves making a number of assumptions about thetiming of the returns, the duration of the returns, and the value of the returns.

For example, what is the return on a bachelor’s degree? The main return is thata B.S. graduate typically earns more than a high school graduate. The salary differencebetween the two at the present time is easy to measure. But will those salary differ-ences still be the same 5 or 10 years from now? If we assume that they will remain thesame, then we can easily calculate the lifetime earnings difference attributed to theB.S. degree. But there are probably other important returns to education that can’t bemeasured as easily, such as the pleasure one receives from being a college student andthe returns to networking initiated during the college experience.

What is critical is that we evaluate alternatives by comparing the costs andreturns of a marginal decision. That is what economics is all about. That is the scienceof decision making.

EXTERNALITIESFinally, economists talk about economic activities in terms of transactions. A typicaltransaction involves a seller and a buyer making a trade. A college student attendingthe university to increase his or her earning power is an economic transaction.

Frequently, the parties to a transaction do not bear all of the economic costs ofthat transaction and/or do not receive all of the economic returns of that transaction.When that happens, we call the costs not borne or the returns not captured externalitiesof the transaction. The economics of attending college is full of externalities. On thecost side, much of the cost of attending is not borne by the student but instead by stategovernment and/or the university foundation through gifts and grants. On the returnsside, society captures some returns because a college graduate will presumably be a bet-ter citizen and will be less likely to become a burden on society as a prison inmate (a very expensive proposition). These are benefits society receives from your educationthat you do not capture directly. Hence they are externalities.

A FINAL WORDEconomics is frequently called “the dismal science.” It is our fervent hope that yourstudy of economics and the reading of this book will not be a dismal experience. Infact, we hope it will be an enlightening and enjoyable one. In an effort to keep a

xii preface

potentially ponderous text somewhat light, we occasionally poke fun at one target oranother. Rest assured, our intention is to amuse and not to offend. If you feeloffended by anything in this text or have any other comments about the text, pleasedrop us an e-mail at [email protected] with your comments. Thanks.

H. Evan DrummondJohn W. Goodwin

NEW TO THIS EDITIONChanges made to this edition are in response to suggestions by several externalreviewers and observations of student response as the authors use the text in theirown teaching:

• Chapters have been substantially reorganized into four sections:Foundations, Microeconomics, Macroeconomics, and Advanced Topics.

• Micro now precedes macro—a change that many reviewers suggested.• Material has been added to several chapters dealing with the 2008/09 finan-

cial crises in the United States.• A section of futures options has been added, showing how options can be

used as a risk management tool.• The chapter on agricultural policy has been completely revamped to cover

the 2007 farm bill.• Numerous chapters have been shortened with the elimination of material

that students have found boring.• Economic data, most of which was for 2000 or 2001 in the second edition,

has been updated as much as possible to 2007 or 2008.• For many chapters, a new end-of-chapter feature called “Sources” has been

added with website addresses relevant to the material of the chapter.• The test bank in the Instructor’s Manual has been substantially edited to

remove redundant questions.

xiii

AcknowledgmentsThe authors and the publisher would like to thank the following reviewers for theirtime and valuable feedback:

Bert Greenwalt, ProfessorAgricultural EconomicsArkansas State UniversityJonesboro, AR

Laura Gow, Assistant ProfessorAgricultural and Resources EconomicsOSU Agricultural Program at EOULa Grande, OR

Barrett E. Kirwan, Assistant ProfessorAgricultural and Resource EconomicsUniversity of MarylandCollege Park, MD

Joey Mehlhorn, Associate ProfessorAgribusinessUniversity of Tennessee at MartinMartin, TN

Kerry W. Tudor, ProfessorAgricultural EconomicsIllinois State UniversityNormal, IL

This page intentionally left blank

part oneFoundations

1The Food IndustryIN AN EARLIER TIME, FARMER BROWN ENTERED HIS PIG PEN AND HOLLERED “SOO-E”to call his pigs to dinner. On college campuses today a similar call of “pizza” can usu-ally attract an immediate crowd of students. Food is one of the great universals inour lives and one of the things that brings us together. The industrial complex thatproduces, processes, and distributes that food is one of the largest industries in theworld. It is estimated that approximately one-fifth of all jobs in the United Statesare related to some aspect of the food industry, even though farmers representonly 1.6 percent of the population. In many developing countries, more than halfof the labor force is engaged in agriculture. There can be little doubt that on aglobal basis the food industry is the largest industry in terms of people employedand value of product. In a later chapter we will talk about that industry in the devel-oping world. For now, we will talk about the food industry in the United States andthe rest of the developed world.

MAJOR SECTORS—AN OVERVIEWThere is a universal myth that Mom (or Grandma) prepares the Thanksgivingfeast. And, like many myths, it is sure to endure even if it is at variance to reality.In this case, the reality is that someone other than Mom produced the feed thatwas fed to the turkey in Minnesota or North Carolina, and that someone else con-verted that turkey on the hoof to the Butterball® that Mom bought at the store,and that someone else delivered that turkey to Mom’s favorite supermarket in far-away Deming, New Mexico. Each “someone” is part of the food industry that pre-

pared the Thanksgiving feast—Mom (or Grandma)was little more than the final actor on the stage

when the curtain came down.The food industry (other than Mom

or Grandma) can be divided into fourmajor sectors: farm service, producers,

processors, and marketers. For every$100 spent at the supermarket, the farmservice sector accounts for about $12while the production sector (i.e., farm-ers) accounts for about $7. The remain-

ing $81 goes to processors of agriculturalcommodities and the marketing system

that brings food to your table.

Farm Service SectorAs shown in Figure 1-1, the farm servicesector provides the producer with theinputs he or she buys, such as feed, fertil-izer, fuel, equipment, and chemicals.Many of the firms in the farm service

Farm service sectorthose firms that produceand distribute the goodsand services that farmers(producers) buy as a part oftheir business activities.

Food industry all firms,large and small, engaged inthe production, processing,and/or distribution of food,fiber, and other agriculturalproducts.

the food industry chapter one 3

Farm service sector(implement dealers, chemical

sales, etc.)

Producers(Farmers,

ranchers, etc.)

Processors(Manufacturers,

bottlers, etc.)

Marketers(Distributors,retailers, etc.)

Figure 1-1The food industry.

sector are household names such as John Deere, DuPont, and Monsanto. These arelarge, multinational corporations with networks of local sales representatives. There isalso a variety of small, local service companies in any rural community that serves thediverse needs of local farmers for irrigation equipment, farm structures, and so on.

The farm service sector is not limited to the sellers of goods. There are alsonumerous firms that provide farmers with services such as banking, accounting,insurance, legal advice, and agronomic consulting. As farming becomes increasinglycomplex, farmers are pressed to rely heavily on providers of farm services. It is a fast-growing and highly localized sector of the food industry.

ProducersThe producers sector includes all of those firms engaged in the biological processesassociated with the production of food and fiber. Farmers, ranchers, grove owners,and nursery owners are examples of producers. As shown in Figure 1-1, producers buyfrom the farm service sector and sell to the processor sector. The unique thing aboutproducers is the link, often a nostalgic link, to the biological processes of producingraw food products. While the link to Mother Nature is appealing, we will see shortlythat most producers are rapidly becoming little more than food factories.

ProcessorsThe processors sector creates value by converting raw agricultural commodities intothose products that consumers want. Processors change the form of food and createvalue in the process. As shown in Figure 1-2, processors can be divided into twogroups: commodities processors (such as flour milling which turns wheat into flour)and food products processors (such as the bread baker who turns flour into bread).Frequently, one company will engage in both activities, such as Hershey, whichprocesses cocoa beans and manufactures chocolate bars, or ConAgra Foods, whichprocesses soybeans into soybean oil, which is used to produce margarine under theBlue Bonnet®, Fleischmann’s®, and Parkay® brands. Incidentally, ConAgra Foodsalso sells soybean oil directly under the Wesson® and Pam® brands.

Food product processors can be further divided into those that produce for theretail food consumer and those that produce for food service distributors. Todayroughly one-half of all spending on food is for food eaten away from home—it is thismarket that the food product processors serve.

Producers sector thosefirms engaged in theproduction of raw food,fiber, and other agriculturalproducts.

Processors sector thosefirms that convert rawagricultural products intofood products in the formthat the consumereventually buys.

Commodities processorsbuy raw agriculturalproducts that have not beenprocessed and convertthem into food ingredients.A flour miller who buyswheat and sells flour is anexample.

Food product processorsbuy food ingredients andprocess them into the formwhere they are ready forsale to the consumer. Forexample, Hunt’s buystomatoes and vinegar andmakes them into ketchup.

Food service distributorsthose firms that distributefood products from foodproduct processors to awayfrom home dining facilities.

4 part one foundations

Commodity processors

Food product processorsAt-home Food service

Wholesalers Distributors

RetailersRestaurants,

institutions, etc.

Final food consumer

Figure 1-2Detail of the processors andmarketers sectors.

A good example of a food product processor is the Coca-Cola Company. It buyshigh-fructose corn sweetener from a commodity processor such as ADM or Cargilland combines it with other ingredients using their secret formula to produce Coke®

in cans and bottles for the retail market and in bulk for the food service industry.Following the diagram in Figure 1-2, we can understand that Coca-Cola also playsthe role of wholesaler and distributor in the marketing sector. So, Coca-Cola spansboth the last half of the processing sector and the first half of the marketing sector.

MarketersThe marketers sector also creates value in the food industry by changing the timeand place of food. Wheat is harvested in Kansas in June. The consumer wants a ham-burger bun in Rhode Island in December. The distribution system that ties the pro-ducer and consumer together is the marketing system. It brings the consumer whatshe wants, where she wants it, and when she wants it. The absolutely incredible thingabout the marketing system is that you can almost always get what you want, whenand where you want it. The food marketing system is so effective and efficient thatmost of us take it for granted. Only when the system is disrupted by a hurricane or amassive snow storm do we recognize how flawlessly and easily the food distributionsystem usually operates.

CONTEMPORARY ISSUES IN THE FOOD INDUSTRYThe food industry, like any other major industry, is in a continuous dynamic ofchange and adjustment. In the remainder of this chapter we will highlight some of thetrends and issues in American agriculture. The issues discussed are by no meansexhaustive of the many issues facing American agriculture, but they should serve tosuggest some of the matters that agricultural economists deal with and some of thechallenges that face potential leaders in the food industry.

Farm StructureIn a Jeffersonian view of the nation, farmers were the bedrock of democracy. Many areconcerned today that this bedrock is crumbling and that the family farm is giving wayto large, impersonal, factory farms. Today farmers constitute about 1.6 percent of thepopulation of the United States. Characterizing the attributes of the American farmsand farmers is known as the study of farm structure. That is, what do farms andfarmers in the United States look like today? Is this an endangered species?

If there is one lesson to be learned from the study of farm structure in theUnited States, it is that there is no such thing as an “average” farm. As is the case inmany situations, averages cover up more than they reveal.

Marketers sector the setof firms that distributes foodproducts from processors tothe final consumer whenand where the consumerwants it. That consumer maybe a retail shopper orsomeone eating at an awayfrom home dining facility.

Farm structure the study and analysis of farmcharacteristics such as thephysical and economic sizeof farms, ownership offarms, and characteristics ofthe farm manager and his or her family.

the food industry chapter one 5

Number of Farms There are roughly 2 million farms in the United States today. In1915, there were 6.5 million farms, so in slightly less than a century, we have “lost”about 4.5 million farms. The United States Department of Agriculture (USDA)defines a farm as any establishment that produces (or should produce) at least $1,000of farm products each year.1 Thus, an individual who sells a couple of fattened cattleis considered to be a farmer.

Since there are roughly 305 million Americans, the average American farmerfeeds himself and 152 other Americans. Agricultural exports account for an additional50 or so mouths to feed, so the average American farmer actually feeds approximately200 people. Thus, our food chain, viewed as an inverted pyramid from producer toconsumer, has a very narrow base.

Ownership There is a myth, frequently propagated by the popular press, that farm-ing is being taken over by large, corporate farms. The other side of this coin is that thefamily farmer—owner and operator—is disappearing. To some extent, in limitedcases, the myth has some validity, but in the broad scheme of things it is little morethan a myth.

Of the 2 million farms in the United States, 98 percent are family farms that pro-duce about 85 percent of the total value of agricultural production.2 About 90 percentof these family farms are owned by sole proprietors, and the remainder is owned bypartnerships or multifamily corporations. Nonfamily farms, mostly owned by nonfam-ily corporations or cooperatives, currently are only 2.2 percent of all farm units, butthey produce 15.2 percent of total farm output. The bottom line is that at the currenttime, the self-employed family farmer is very much a part of our social fabric.

Farm Types Recently the USDA has started classifying farms into a typology basedon the characteristics of the farm operator and the value of farm sales. In creating thistypology, one of the critical questions asked of farm operators is “What is your pri-mary occupation?” About 14 percent, or nearly 300,000 farmers, responded “retired.”An astounding 40 percent of farm operators listed their primary occupation as a non-farm occupation. That is, they are just hobby farmers who primarily work off thefarm and maintain the farm as part of their lifestyle. As a group, these hobby farmsoperated at an economic loss. Retirement and hobby farms sure aren’t producing whatthe rest of us eat, but they represent a majority of total farm units.

Another 38 percent of farm operators listed their primary occupation as farmingbut had gross sales of less than $250,000. Assuming a profit rate of 3 percent of sales,a farm with sales of $250,000 would only generate $7,500 of profit—hardly enoughto support a farm family. In addition, most of these farms had sales of less than$100,000. These economically nonviable farmers aren’t the folks who are producingmuch of what the rest of us eat, either.

That leaves 8 percent, or about 160,000, of farms that are large, economicallyviable enterprises that produce most of the food and fiber in the food industry. In fact,these few farms produce about two-thirds of the sales of all farms.

So, what is the typical American farm like? In terms of numbers, most farms areeither retirement homes or hobby farms. The trend among these “farms” is increasingnumbers and smaller farm size—it is a way of life rather than an economic unit. Interms of food production, there are about 160,000 farms that produce most of what

Farm defined by the U.S.Department of Agricultureas any establishment thathas (or should have had) atleast $1,000 of sales ofagricultural products duringthe year.

Typology a systemdeveloped by the USDAthat classifies farms basedon economic size andcharacteristics of the farmoperator.

1 Farm products include food, fiber, turfgrass, ornamentals, flowers, and a variety of other specialty crops. Excludedare seafood and forestry.2 Data for this and the next section are drawn from Structure and Finances of U.S. Farms: Family Farm Report, 2007edition, Robert A. Hoppe, Penni Korb, Erik J. O’Donoghue, and David E. Banker, Economic Research Service,USDA, Economic Information Bulletin #24, June 2007.

6 part one foundations

we eat. Almost all of these farms are family farms, with only about 20,000 large, non-family farms. And the clear trend among these food producers is toward fewer, largerfarm units. Also, these large farms are becoming increasingly specialized in what theyproduce, legitimizing the term food factories.

ConcentrationA current concern, and one that has generated several legislative proposals at thenational level, is the degree of industrial concentration in some of the food process-ing sectors. Concentration is an economic concept that refers to the degree to which asmall number of firms control a large share of the market. The most common methodfor measuring concentration is the percentage of the total market accounted for bythe four (or any other number) largest producers. For instance, in the United States,87 percent of breakfast cereal is produced by the four largest producers, and virtuallyall baby food is produced by the three largest processors.

By far the greatest concern about concentration is in the meat packing business.About 85 percent of all beef is processed (i.e., slaughtered) by four companies thathave been rapidly buying out smaller competitors as the industry consolidates. Worseyet (in the eyes of many), one of these four firms is foreign owned. Moreover, a largepoultry producer, Tyson Foods, recently bought the second-largest beef processor. Inother words, concentration and consolidation are crossing species lines that had pre-viously separated processors. Some beef cattle producers have called for federal legisla-tion that would prevent any further consolidation.

Is concentration bad? Processors say that by consolidating into fewer, largerfirms they are able to cut costs, which benefits consumers. Opponents argue that con-centration provides the processors with unusual market power that allows them tobuy from farmers who have little market power at prices that border on exploitation.For example, it is becoming common for meat packers (i.e., processors) to force pro-ducers to sign secret contracts such that no one knows what price other beef cattleproducers are receiving or what price other packers are paying. This has been com-mon practice in the broiler (i.e., chicken) business for years. Another example of thealleged use of market power is the practice of offering a potential new farmer a veryattractive price. The farmer does the arithmetic and decides that this will be a profitablebusiness venture. The farmer makes the investment in new facilities and produces thefirst batch at the agreed-upon, attractive prices. When the processor comes back with acontract for a second batch, the farmer finds that the offered price is substantiallybelow the price in the first contract. What is the farmer to do? He has no marketpower, he has no alternatives to the one local processor, and he has a large investmentthat he has to pay off.

GlobalizationIn most instances, commodity processors tend to be on the forefront of globalizationbecause the demand for processing technologies is truly global. We all need food tosurvive. Among the commodity processors, most of the successful processors are veryinternationalized with processing facilities all over the globe. To fail to behave globallyin the commodity processing business is a recipe for corporate failure.

In food products processing, the drive to globalization has not been as strong, asconsumers in each country have different tastes and preferences. While a soybean is asoybean in every country, the final food product may be soy protein meal in one coun-try, tofu in another, and a nice steak in a third. There are three truly global food productprocessing companies: Coca-Cola, Unilever, and Nestlé, with Nestlé being the largestprocessor of food products in the world. While most Americans only associate Nestléwith chocolate bars and hot cocoa mix, Nestlé also appears in this country under brand

Concentration thedominance of an industry bya few firms, usuallymeasured by thepercentage of the totalmarket owned by thelargest four (or any othernumber) firms.

Market power the abilityof a firm or group of firms to control price and/orquantity traded in a marketbecause of the dominanceof the firm(s) in the market.

Globalization theexpansion of firms acrossnational boundaries.

the food industry chapter one 7

names such as Nescafé®, Taster’s Choice®, Perrier®, Friskies®, Alpo®, Mighty Dog®,Baby Ruth®, Butterfinger®, PowerBar®, and Carnation®. On a global basis, Nestlé’sstrong suit is in the infant formula market. Many food product processing companiesare making a big push to globalize, realizing that growth of the processed food market inthe United States is basically stagnant, while the growth of the processed food market inmany developing countries is exploding. This is an emerging challenge for domesticstand-outs like the Campbell Soup Company, H. J. Heinz, and Hershey Co.

Critics of globalization have three strong arguments. First is the issue of foodsecurity. Every country wants to be certain that its nutritional needs will be met. Asthe food industry is becoming globalized, individual countries are losing control tomultinational companies that may have objectives different from those of the individ-ual countries. Second is the issue of global concentration, which is similar to the issueof industrial concentration mentioned previously. An example is the acquisition of one ofthe largest beef processors in the United States by a Brazilian firm that has become theworld’s largest beef processor. Finally, many individuals are concerned about the loss ofnational identity associated with globalization. Skeptics see the future of a homogenizedworld in which French and Swiss cheeses all turn into cheddar.

CoordinationMarketers are the companies that tie the final food consumer to the processor. Theirjob is to make certain that whatever the consumer wants is there when and where theconsumer wants it. As shown in Figure 1-2, the traditional retail marketing system isquite distinct from the food service distribution system. The communication systemthat conveys consumer wants to the producer is called coordination. Traditionally,coordination has been accomplished by prices sending messages from one link in themarketing chain to the next. This system is rapidly changing with management andstrategic alliances replacing markets and the price system of allocation. Thanks totechnology, consumers can also send signals to producers using toll-free hotlines, web-sites, and product blogs.

As noted earlier, about one-half of expenditures on food is for food to be pre-pared at home. Notwithstanding the bucolic appeal of farmers’ markets and roadsidevendors, most food purchased for home consumption is purchased at a retail super-market. Traditionally, most retail stores purchased food from wholesalers, who pur-chased food in bulk from processors and sold it in smaller batches to retailers. Manyretailers, particularly the smaller ones, still use this system. However, many of thelarger chains combine the wholesale and retail functions into a single firm, therebyreducing transaction costs. Those reduced costs can be passed on to the consumer inthe form of lower prices or captured by the producer in the form of higher profits.

For many years, the largest food retailer in the United States in terms of salesvolume was Kroger.3 It sold about $66 billion of food and other items per yearthrough nearly 2,500 retail outlets, many of which carry the Kroger name.4 Wal-Martis at about one out of five retail food dollars. Kroger is not only into wholesaling butalso into food product processing, with 42 manufacturing plants producing some3,000 products that are sold through the Kroger chain.

This illustrates one of the dominant trends in the food system—verticalintegration. This refers to combining several steps in the food system chain into a single

Coordination thecommunication system thatconveys consumer wants toproducers. Traditionally,prices were the primarymeans of communication.More recently managementinformation systems havereplaced prices.

3 Today Wal-Mart is the largest food retailer. One of the causes of Wal-Mart’s rapid expansion in the food retailingbusiness has been their embrace of nonmarket coordination.4 Total food expenditures in the United States are about $1,000 billion. About half of that, or $500 billion, is throughretail outlets, so Kroger commands about one out of eight retail food dollars. Wal-Mart is at about one out of fiveretail food dollors.

Vertical integration thecombination of differentbusinesses at differentstages of theproduction/marketingsequence under a singlemanagement.

8 part one foundations

management system. Vertical integration allows the firm to coordinate different stagesin the food system through management, whereas without integration that coordina-tion is accomplished through the ebb and flow of markets and market prices. So, withvertical integration as a dominant trend, we are seeing a rise in the role of manage-ment and a decline in the role of markets in the coordination of the food system.

What are the pros and cons of nonmarket coordination? Markets and prices arehighly visible. Consequently, the consumer has many choices. On the other hand,nonmarket coordination can be more efficient (particularly in large volumes) thanmarket price coordination, resulting in lower prices to the consumer. What does theconsumer want? More choice or lower prices? The answer is clear when one comparesthe success of Sears (“Good, better, and best”) and Wal-Mart (“Always low prices”)over the past 20 years.

Alternative Energy SourcesHigh chicken prices cause consumers to think about the “other white meat.” Likewise,high gasoline prices cause consumers to consider alternatives to petroleum-basedenergy sources. The alternatives range from tar sands to hydrogen, but the alternativethat is of most interest is biofuels. In recent years, there has been a lot of renewedinterest in biofuels—particularly ethanol. But, this interest is not all that new. Thevery first diesel engines of the 19th century ran on soy oil. During World War II,Hitler used soy oil to propel the German war machine. So biofuels have been with usfor as long as the internal combustion engine has been around. The science of pro-ducing biofuels hasn’t changed much during the past century, but the politics andeconomics have changed substantially, leading to a renewed interest in biofuels.

Today, most of the interest is in ethanol as an alternative to gasoline, althoughsome truckers are using soy-based fuel as an alternative to diesel. Let’s begin with afew facts about ethanol. What is ethanol? It is a form of alcohol. Can it be burned?Sure—remember the alcohol lamp you had in your chemistry lab. How do you makeit? Here humankind has lots of experience. Humans have been making alcohol formillennia, but because our ancient ancestors lacked automobiles, they drank the stuffinstead. Whether it is in the tank or in the tummy, it is essentially the same stuff thatis made in the same way.

In the United States, at the present time, virtually all ethanol is produced fromcorn; however, other plant sources can be used to produce ethanol. For instance, inBrazil, ethanol is produced from sugar cane.5 Many have suggested that a better sourcematerial for ethanol in the United States would be switchgrass or even wood pulp as nei-ther of these competes with food for human consumption. Unfortunately, neither ofthese alternative energy sources has sufficient production to support a viable industry,nor do they have the technology to economically support industrial-scale production.

The ultimate objective of using corn-based ethanol is to reduce our consump-tion of imported petroleum. An unintended consequence is an added stimulus to themarket for corn. If you are a corn producer, this is good. If you are a corn consumer(such as a dairy farmer), then this is bad. While some people think we can grow ourway out of the energy crisis, there are a variety of issues associated with this alternativefuel that may mitigate this rosy projection:

• Because of its corrosive characteristics, ethanol is more difficult to transport thangasoline. Existing petroleum pipelines can’t handle ethanol. As a consequence,

Biofuels alternatives topetroleum-based fuelsproduced from biological orplant-based feedstocks.

Ethanol A biofuel form ofalcohol that can be mixedwith gasoline for use inautomobiles.

5 Other biofuel feedstocks used in other countries include palm oil, wheat, cassava, sorghum, and, even, wine (a sur-plus commodity in Europe). See Coyle, William, “The Future of Biofuels: A Global Perspective,” Amber Waves,Vol. 5, Issue 5, Economic Research Service, USDA, 2008.

the food industry chapter one 9

most ethanol is found in the midwestern part of the United States where mostof our corn and ethanol are produced.

• Ethanol does not have as many BTUs (British Thermal Units) per gallon asgasoline. Therefore, burning ethanol reduces the number of miles per gallon,meaning that you need more gallons to go a given distance.

• Using ethanol as a fuel reduces carbon emissions from automobiles.Nonetheless, most studies show that the carbon emissions generated by pro-ducing corn and then ethanol are greater than the carbon emissions saved.

• If every bushel of corn currently produced in the United States were con-verted into ethanol, we would still need imported oil to sustain our currentlevel of consumption. Corn ethanol alone is not going to solve our petroleumaddiction completely.

• The “fuel-versus-food” argument suggests that by converting corn to fuel, weare reducing the amount of food that is available, thus driving the price of foodupward. Most studies suggest that the impact of ethanol production on foodprices is very small. In 1992/93, the United States produced about 9.5 billionbushels of corn and no ethanol. In 2008/09, the United States produced 12.1 billion bushels and used 3.6 billion bushels for ethanol. As shown inFigure 1-3, what was available for nonfuel use in 2008/09 was just a little lessthan what had been available in past years.

• Most of the consumption of ethanol is not driven by market forces butinstead by government mandates and a $0.54 per gallon subsidy for produc-ing the stuff.

• Some observers point out that substituting ethanol for gasoline causes theprice of crude oil to fall. This is true, but note that the Chinese consumer bene-fits just as much as the U.S. consumer because we are all part of a global marketfor crude oil.

So, what is the bottom line on biofuels? So long as we continue to be lockedinto corn-based ethanol as the only viable alternative to gasoline, the economics andthe environmental impacts seem to be a wash—neither is a clear winner. In addition,it is safe to say that agriculture is not going to solve the “energy crisis” facing theUnited States.

0

2000

4000

6000

8000

10000

12000

14000

Mill

ions

of b

ushe

ls

2002

/3

2003

/4

2004

/5

2005

/6

2006

/7

2007

/8*

2008

/9**

Non-ethanol Ethanol

*estimate**projection

Figure 1-3Total corn production inthe United States, andproportion used toproduce ethanol.

10 part one foundations

Another alternative energy source that has become widely used in Spain andGermany is wind power. Both countries have massive “farms” of turbines that pro-duce electricity with virtually no adverse environmental impact (there is some noisepollution associated with wind power). The prospect for wind power in the UnitedStates is not bright. While the technology for wind power is well developed, peopleand wind are spatially separated in much of the United States. That is, we have lots ofwind in Kansas and lots of people in New York. But the transmission cost of electric-ity from Kansas to New York is prohibitive. So while some local wind farms maydevelop to serve the needs of the remaining folks in Kansas and Iowa, wind is notgoing to be a significant factor in the total energy market in the United States.

SUMMARY

The food industry consists of literally millions of firmsworking in one or more of four distinct sectors: thefarm service sector, the producers sector, the processorssector, and the marketers sector. While the activitiesperformed in each of the four sectors are distinct, manyfirms in the food industry have vertically integratedacross sector boundaries.

In the farm service sector, we find firms that pro-duce inputs and/or services that are purchased by pro-ducers. These include feed manufacturers, implementdealers, chemical companies, lawyers, bankers, andfarm consultants. The common thread of all firms inthe farm service sector is that their primary consumer isthe producer (farmer, rancher, and so on).

Producers refer to all who produce and harvest ourfood, fiber, and other agricultural commodities. Farmers,ranchers, nursery operators, vineyard and orchard oper-ators, grove owners, and others are included in the pro-ducers sector.

Processors buy raw agricultural commodities fromproducers and sell finished food products to the mar-keters sector. Some processors are commodity processors.These firms buy, store, and transport raw agriculturalcommodities and then convert those commodities intofood ingredients. Food product processors buy theseingredients and use them to produce the food products

we eat. Some firms are commodity processors only,others are food product processors only, and still othersdo both.

Marketer firms buy food products from processorsin bulk, store them, transport them, and distributethem to consumers in small, convenient lots. One mar-keter chain serves the needs of the retail food customerwhile another serves the needs of the food servicesector.

Five contemporary issues illustrate some of the eco-nomic currents in American agriculture:

1. Farm structure: Is the family farm being replacedby large corporate farms?

2. Concentration: Are processors becoming so largeand so few in number that they exert excessivemarket power over the producer?

3. Globalization: Does globalization serve the needsof consumers?

4. Coordination: What is the impact of nonmarketcoordination and vertical integration on consumerprices and consumer choices?

5. Alternative energy sources: What are the advan-tages and disadvantages of corn-based ethanol andother biofuels?

KEY TERMS

BiofuelsCommodities processorsConcentrationCoordinationEthanolFarm

Farm service sectorFarm structureFood industryFood product processorsFood service distributorsGlobalization

Market powerMarketers sectorProcessors sectorProducers sectorTypologyVertical integration

the food industry chapter one 11

PROBLEMS AND DISCUSSION QUESTIONS

1. Identify the four sectors in the food industry. Forfirms in each of the four sectors, identify what theybuy and what they sell. From what firms do theybuy inputs, and to what firms do they sell theiroutputs?

2. An important part of the farm service sector is theCooperative Extension Service, which has an office invirtually every county of the United States. Contactthe local office of your Cooperative Extension Serviceor visit the website of your state office of CooperativeExtension Service to determine what this publiclyfunded agency does. Who are the clientele, and whatare the services provided?

3. What proportion of all farm units in the UnitedStates is economically viable with sales of at least$250,000 per year?

4. Discuss the following proposition and its implica-tions: Most farm owners are more interested in arural way of life than in food production.

5. What is vertical integration? What are the advan-tages of vertical integration? What are the concernsabout vertical integration?

6. What is concentration in the processor sector andwhy is it considered to be a threat to producers?

7. Identify the major beef packers (i.e., commodityprocessors) in the United States and the share ofthe market held by each.

8. What is globalization?9. Marketers engaged in food retailing tend to be

regional phenomena. What are the leading food

retailers in your region? Are these retailers part of alarger chain such as Kroger or SUPERVALU?

10. During the 1990s Wal-Mart went from no foodretailing to being the largest food retailer in theUnited States. Has Wal-Mart, with its superstores,arrived in your community as a food retailer? Meetwith the store manager of a local supermarketand ask what the impact of Wal-Mart will be, orhas been, for traditional food retailing in yourcommunity.

11. Which food service distributor serves your studentunion? Get on the Internet or visit with a sales rep-resentative to learn more about this food servicedistributor. The director of your student union canhelp you with this task.

12. What portion of our total corn crop is currentlybeing used for biofuel? (Hint: See Sources #6)

13. What are the alternatives to petroleum beyondbiofuels?

14. What are the biofuel alternatives to corn ethanol?15. What are the pros and cons of using gasoline com-

bined with corn ethanol?16. What are the pros and cons of using pure ethanol

to completely replace petroleum-based fuels? For areal-world example of this, study the experience ofBrazil 20 or 30 years ago as they used their abun-dant sugarcane crop to produce cane ethanol,which replaced gasoline in many automobiles.

SOURCES

1. Archer Daniels Midland is not only the largestcommodity processor in the United States, but it isalso unique in that it has virtually no vertical inte-gration in either direction. Get a profile of thisinteresting company by visiting them at www.admworld.com.

2. ConAgra Foods is an example of a large commodityprocessor that has a high level of vertical integra-tion. It is a food processor as well as a commodityprocessor and produces for both the consumermarket and the food service market. Visit www.conagra.com to profile this major agriculturalprocessor.

3. Kraft Foods is the largest food processor in theUnited States. While the name Kraft is usually

associated with cheese, it produces a variety of foodproducts under a large number of well-knownbrand names. List the domestic brands used byKraft. You can prepare your list from their websiteat www.kraft.com.

4. Traditional food retailers in the United States tendto be both vertically and horizontally (manysimilar firms under a single management) inte-grated. Examples are Kroger (www.kroger.com)and SUPERVALU (www.supervalu.com). In bothwebsites, check out the “about the company” links.

5. At almost any highly visible international meeting,there are groups of protesters who are against glob-alization. One of the largest, most visible protestgroups is Greenpeace. Visit their U.S. website at

12 part one foundations

www.greenpeaceusa.org to learn why they opposeglobalization. What are their arguments againstglobalization?

6. For the best, most recent information about cropproduction and use in the United States and ona global basis, go to a monthly publication ofthe USDA called World Agricultural Supply andDemand Estimates (WASDE). This publicationprovides actual data for the past two crop years andestimates for the current or next crop year. The

monthly publication is available at www.usda.gov/oce/commodity/wasde.

7. The USDA is conducting a long-range researchproject dealing with the changing structure ofAmerican agriculture. The project is known asthe Agricultural Resources Management Survey(ARMS). An entry link to the publications result-ing from this project can be found at www.ers.usda.gov/Briefing/ARMS.

2Introduction to AgriculturalEconomicsAS THE NAME RIGHTLY IMPLIES, AGRICULTURAL ECONOMICS IS THAT PART OF

economics that surveys agriculture and the food industry in its many facets andforms. The agricultural economist is concerned with the entire food and fiber sys-tem, from the inputs used in production all the way through the production, pro-cessing, distribution, and consumption chain.

The food and fiber system is related to almost every facet of our economyand our environment. As a result, the study of agricultural economics necessarilyencompasses a great deal more than just the activities of the farmer or rancher.Since the food and fiber system is an important part of our natural environment,some agricultural economists deal with issues of resource conservation, pollutioncontrol, and water management. Others study the agribusiness sector as pur-chasers, processors, and distributors of food and fiber products.

As these examples illustrate, the scope of agricultural economics is verybroad and quite diverse. The common thread is that each deals with one of themany facets of the food system described in Chapter 1.

AGRICULTURAL ECONOMICSEconomics is a social science. The objective of any scientific inquiry is to observeand describe a particular range of phenomena, to organize those observationsinto recognizable patterns, and, where sufficient regularity warrants, to for-mulate “laws.” It is these laws that give the scientist a basis on which tomake predictions. The social scientist must deal with the laws of humannature, and since humans are not consistent in their behavior, the laws ofthe social scientist are necessarily less reliable and more open to excep-tion than those of the physical or biological scientist.Nevertheless, the economic behavior of most per-sons is generally consistent and, therefore, to somedegree predictable.

Economics is that particular social sciencethat deals with the allocation of scarce resourcesamong an unlimited number of competing alterna-tive uses. Economists use the word “resources” todescribe anything tangible: wheat, barbedwire, hamburgers, water, labor, clean air, andrecreation facilities. Every resource is rela-tively scarce, meaning that the availabilityof every resource is insufficient to satisfyall of its potential users. Scarcity createsthe need for a system to allocate theavailable resource among some of thosepotential users. Agricultural economics

Economics the socialscience that deals with theallocation of scarce resourcesamong an unlimited numberof competing alternativeuses.

Agricultural economicsthe social science that dealswith the allocation of scarceresources among thosecompeting alternative usesfound in the production,processing, distribution, and consumption of foodand fiber.

14 part one foundations

is the social science that deals with the allocation of scarce resources among thosecompeting alternative uses found in the production, processing, distribution, andconsumption of food and fiber.

BASIS FOR ECONOMICSThe study of economics rests on three foundations: self-interest, scarcity, and choice.Without scarcity, there would be no need for an allocation system. Before the indus-trial revolution there was no scarcity of clean air. It was consumed in unlimited quan-tities at a zero price with no choices to be made about who was to get it and howmuch of it they should get. Such is not the case today. Clean air is now quite costly.We pay for it with each dollar we spend on pollution control. We also pay an evendearer price—the damage to our health that pollution causes. Both of these costs areevidence of the scarcity of air, and both indicate the need for an allocation system.

Choice is important because without choices there is no decision to be made. Aspreviously stated, economics is about decision making and allocation. Without choicesthere would be no need for economics. A supermarket is the epitome of choice. Withapproximately 30,000 different bar codes in one store the consumer is given choicesof goods, brands, sizes, and flavors. Because of these choices our lives are enriched.

In addition to scarcity and choice, there is a third equally important driving forceof economics: self-interest. Self-interest is what drives the consumer to seek more “stuff”at a lower price. It is self-interest that drives the producer to produce as efficiently aspossible. It is what encourages the trucker to ship produce from one region to another.All economic activity is driven by self-interest. It is the fuel that drives the engine.

BASIC ECONOMIC DECISIONSEvery economic system must resolve five basic issues:

1. What to produce. Should we use our abundant corn crop to produce meator alcohol fuel?

2. How to produce it. Should tomatoes be grown in greenhouses inMinneapolis for the central Minnesota market, or should they be producedin the fields of south Florida and shipped to Minnesota? Should thosetomatoes be produced using chemical insecticides, or should they be grownwithout chemicals?

3. How much to produce. As contrary as it may sound, you will learn in alater chapter that one of the biggest problems in agriculture in the UnitedStates is a tendency to overproduce. How much is enough?

4. When to produce. Should a stand of timber be cut today and used forpulp, or should it be left growing for several more years until it reaches adiameter sufficient to serve as saw timber?

5. For whom to produce. Should this year’s production of sirloin steaks beequally distributed among everyone in the society, or should some potentialconsumers be excluded from the market because of financial limitations?

ECONOMIC SYSTEMSThe basic questions of what, how, how much, when, and for whom must be answeredin each society: they simply cannot be avoided. The institutional and political systemsof each society determine the manner in which these decisions will be made. At one

introduction to agricultural economics chapter two 15

extreme of possible allocation mechanisms lies the free market or price system. Inthis system, each individual producer and consumer, restricted only by financialresources, is free to choose what, how, how much, and when to produce or consume.The financial resources of each consumer resolves the “for whom” question. At theother extreme is the command system in which all decisions with respect to what,how, how much, when, and for whom are made by a central planning agency or otheradministrative individual such as an absolute dictator or tribal chief.

An advantage of the price system is that it provides the consumer with sovereigntyand freedom in making economic decisions. In addition, the price system is a veryefficient mechanism for making most of the “what,” “how,” “how much,” and “when”decisions. But, the price system has shortcomings even its most ardent supporters rec-ognize. First, when it comes to making the “for whom” decision, the price system isfar from egalitarian. In a price system, the old adage that the rich get richer and thepoor get poorer has some validity. Second, there are a number of resources that a pricesystem cannot efficiently allocate. These goods, frequently called public goods or non-market goods, include education, national defense, and fire protection.

The advantages of a command system are that it is very effective in allocatingpublic goods and it can be quite egalitarian in making the “for whom” decision. Thedisadvantages of a pure command allocation system are the loss of individual free-dom to make economic decisions and the inherent inefficiencies of central planningagencies.

The political institutions of the United States fully embrace a price system forallocating resources but with some adjustments to correct for the difficulties noted ear-lier. To address the “for whom” question for goods that are considered to be necessaryfor all citizens, we have a number of programs designed to transfer economic powerfrom the relatively rich to the relatively poor. Examples include the progressive incometax system, Medicare, public education, food stamps, and the Social Security system.The institutional fabric of the United States includes a pure command allocation systemfor some public goods such as national defense, and a mixed price/command system forother goods such as higher education.

LEVELS OF ECONOMIC ACTIVITYThere is a great deal of similarity between a wood screw and a common nail: bothmay be used to fasten two pieces of wood together, and both are longer than they arewide. While both a hammer and a screwdriver can be used to insert either into a pieceof wood, only one tool is best suited for each of the wood fastening devices.Economics is not unlike wood fastening devices: just as a hammer should be chosento drive a nail, the appropriate economic tool must be chosen to fit the particular eco-nomic problem being analyzed. Much of the economic misinformation that appearsdaily in the press, and with alarming frequency on the tongues of aspirants to publicoffice, is a consequence of using an inappropriate economic tool for the particulareconomic problem being discussed.

Economics can be divided into three parts: microeconomics, market economics,and macroeconomics. The important distinction among the three is the level of aggre-gation of the analysis. As will be demonstrated later, what is valid logic when dealingwith the economics of the individual may not necessarily be valid when dealing withthe economics of a group or an entire society. Thus, as the level of aggregationchanges, the economic tools must also be changed. An ordinary screwdriver may servethe needs of the home owner well, but it would be totally inappropriate for the pro-duction worker on an assembly line who is expected to drive thousands of screws aday. Again, the level of aggregation is critical.

Price system an allocativesystem in which economicchoices are based on prices.

Command system anallocative system in whicheconomic choices are madeby some centraladministrative unit.

Efficient a generaleconomic concept used in avariety of situationsmeasuring output per unitof input. The higher theratio, the more efficient theprocess.

16 part one foundations

MicroeconomicsMicroeconomics deals with the economics of individual producers and consumers.The microeconomics of production examines the economics of the individual pro-ducer or firm as that firm acquires resources and combines them in the productionprocess to earn as much profit as possible. The production management decisions thataffect the profit of the firm include which inputs to purchase, what production tech-nique to use, which product to produce, how much of each product to produce, andwhen to produce them. Obviously, the firm manager, whether farmer or rancher orowner of a donut shop, is deeply involved in the “what,” “how,” “how much,” and“when” allocation decisions. In the study of production microeconomics, we willdevelop a set of management rules detailing how the rational firm manager shouldresolve production management decisions to maximize the profit that the firm is ableto earn from a given set of productive resources.

The other branch of microeconomics deals with the behavior of the individualconsumer—hence, the microeconomics of consumption. The consumer is facedwith the economic problem of deciding what to purchase given the limited resources(i.e., money and time) available. The role of scarcity, choice, and self-interest in mak-ing consumption decisions is clearly and poignantly expressed by the face of a youngchild clutching a few precious coins in a store full of candy. The individual consumermust make a number of consumption decisions on a daily basis. Many of these deci-sions are not the products of conscious deliberation; instead, they tend to be habitualor impulsive. The consumer must decide what to buy and what not to buy. Should Ibuy pork or beef for supper tomorrow? Or should I buy neither so that I will haveenough money to buy a hot new CD? An examination of the economics of these deci-sions will enable us to develop some general rules of behavior suggesting how con-sumers will react to changes in relative prices or incomes. The consumer must alsodecide when to consume. Should I go into debt today to buy a new SUV, or shouldI continue to save so that I can buy the SUV later without going into debt? After all,the old Honda will do almost everything a new SUV will do.

Each consumer faces the inevitability of scarcity in the form of a limited budget.Given this scarcity, each consumer in a price allocation system uses his or her sover-eignty to resolve the “for whom” allocative decision. The “for whom” consumptiondecisions that a price system entails may be modified by subsidized school breakfastand lunch programs, food stamps, and other government programs.

Market EconomicsMarkets are the primary price determination mechanism found in the institutionalframework of most countries. To the economist, a market is established wheneverpotential buyers and potential sellers interact to establish prices and exchange goods.A market should be distinguished from a marketplace. The latter refers to a physicallocation, while the former refers to the interaction of buyers and sellers irrespective oftheir physical location. Auctions on the Internet provide a vivid example of the differ-ence between a market and a marketplace.