UK and Eurozone´s Labour Markets Reaction to the Financial Crisis in the perspective of the British...

17

1 UK and Eurozone´s Labour Markets Reaction to the Financial Crisis in the perspective of the British EU Membership – Application of the Phillips Curve Mgr. Ing. Barbora Fialová University of Economics in Prague Náměstí Winstona Churchilla 4,130 67, Praha 3 Phone: +420 732 238 375, e-mail: [email protected] Ing. Šimon Buryan University of Economics in Prague Náměstí Winstona Churchilla 4,130 67, Praha 3 Phone: +420 732 716 030, e-mail: [email protected] Abstract Aim of this paper is to access differences of labour market in the UK and selected Eurozone member states that are considered as a core of the EU. A model of the Phillips curve was proposed in this paper in order to study differences in labour market with regards to elasticity of unemployment rate to inflation rate and with regards to labour market-to-price level time lags. The article is also discussing reactions of selected countries to the financial crisis and primarily prospects of further integration of the UK to the EU/Eurozone. Accessing the differences of selected countries` labour markets is one of the vital findings for the future decision of the UK, whether it should deepen its economic ties with the EU/Eurozone or do the right opposite. JEL classification codes: E24 Keywords: UK, Eurozone, Phillips Curve, Labor markets, Differentiation Acknowledgements This paper has been supported by the project VŠE – IGA 7/2014.

Transcript of UK and Eurozone´s Labour Markets Reaction to the Financial Crisis in the perspective of the British...

1

UK and Eurozone´s Labour Markets Reaction to the

Financial Crisis in the perspective of the British EU

Membership – Application of the Phillips Curve

Mgr. Ing. Barbora Fialová

University of Economics in Prague

Náměstí Winstona Churchilla 4,130 67, Praha 3

Phone: +420 732 238 375, e-mail: [email protected]

Ing. Šimon Buryan

University of Economics in Prague

Náměstí Winstona Churchilla 4,130 67, Praha 3

Phone: +420 732 716 030, e-mail: [email protected]

Abstract

Aim of this paper is to access differences of labour market in the UK and selected Eurozone

member states that are considered as a core of the EU. A model of the Phillips curve was

proposed in this paper in order to study differences in labour market with regards to elasticity

of unemployment rate to inflation rate and with regards to labour market-to-price level time

lags. The article is also discussing reactions of selected countries to the financial crisis and

primarily prospects of further integration of the UK to the EU/Eurozone. Accessing the

differences of selected countries` labour markets is one of the vital findings for the future

decision of the UK, whether it should deepen its economic ties with the EU/Eurozone or do

the right opposite.

JEL classification codes: E24

Keywords: UK, Eurozone, Phillips Curve, Labor markets, Differentiation

Acknowledgements

This paper has been supported by the project VŠE – IGA 7/2014.

2

1. Introduction

The United Kingdom (UK) is well known as the "awkward" member of the European Union

(EU). The country had been a part of the ever-first enlargement of the European integration in

1973. Since then, the UK challenges constantly the ongoing integrational processes within the

European Community (EC) and lately EU. However tough is the British support for

strengthening the Single Market, a large number of British opt-outs has been negotiated and

performed on the other hand. Especially when seen from the Eurozone perspective, it is rather

possible that the UK would never accept the single currency (Allen, 2013).

When discussing the process of differentiated integration within the EU, the UK is

always the most obvious representative. This notion has been even invigorated after the

General Election in the UK in May 2015, when a quite surprising victory has been achieved

by the David Cameron´s Conservative party. In the perspective of the EU future, this is a

vital point, because of the previous Cameron´s pledge to arrange a referendum that would

decide whether the UK will keep on being an EU member or not any more. This commitment

should have been fulfilled under condition that the Conservatives manage to form a majority

Government in spring 2015. Even few days before the General Election this possibility

seemed to be rather improbable. Nevertheless, it is more than clear after the election that the

Conservatives would be able to govern the country on their own for the next five years. This

has strong implications for the future British approach to the European integration, because

the Conservatives will not be limited in conceptualising their new European policy unlike in

the previous coalition government, where they had partners in rather euro-positive Liberal

Democrats (The Economist, 2015).

This is supposed to result in a full implementation of the Cameron´s European policy

programme summed up in January 2013 as “reform, renegotiation, referendum”. In that time,

David Cameron delivered a so called Bloomberg speech, in which he made, apart from

complex reassessment of the EU-British relationship and its future prospects, an

announcement about planned renegotiation of the British EU membership and consequent

in/out referendum that would take place by the end of 20171 (Gov.uk, 2014a). However this

announcement has been more a reaction to domestic policy development2, the proposed

process of reviewing the balance of European competences in the UK would have be of an

essential importance for the future EU-UK relationship (Gov.uk, 2014b).

Aim of this paper is to contribute to the debate about EU competences in the UK

through accessing differences of British labour market on one side and selected Eurozone

member states representing the core of the European integration on the other side, as well as

we will discuss labour markets of the USA and the Eurozone as a group. Accessing the

differences of selected countries` labour markets could be one of the vital findings for the

future decision of the UK electorate, whether their country should deepen its economic ties

with the Eurozone or do the right opposite.

1 Justification for this announcement contained three main points (Policy Network 2013, 25): 1) the potential

discrimination of non-Euro countries by the Eurozone; 2) the over-reach of EU regulation onto national policy-

making; 3) the lack of legitimacy of EU processes and the need for a greater role of national parliaments. 2 The announcement has provoked a large number of negative reactions, most of all because the new European

policy programme has been highly influenced by rising British euro-scepticism resulting in increased strength of

the United Kingdom Independence Party (UKIP). Roger Liddle (2014, 220), for example, wrote about the

Bloomberg speech with respect to its general pro-European tone the following: “For all Cameron´s fine words, it

was a bad day for Britain.” Emerson and Blockmans (2013, 1) suggest that the process after the speech has been

“full of political and economics hazards”. On the other hand, according to the Policy Network Report for the

City of London Corporation, “beyond the initially negative reaction, David Cameron´s speech seems to are

opened up a debate on EU reform which most UK partners welcome” (Policy Network 2013, 37).

3

A model of the Phillips curve was proposed in this paper in order to study differences

in labour market with regards to elasticity of unemployment rate to inflation rate and with

regards to labour market-to-price level time lags in the selected countries. The article is also

discussing primarily prospects of further integration of the UK to the Eurozone and EU

markets.

1.1. Methodology and data

In order to be able to make qualified British labour markets differences analysis, we have

selected following reference countries:

- Germany

- France

- Italy

- The Netherlands

- USA

- plus the Eurozone as a group.

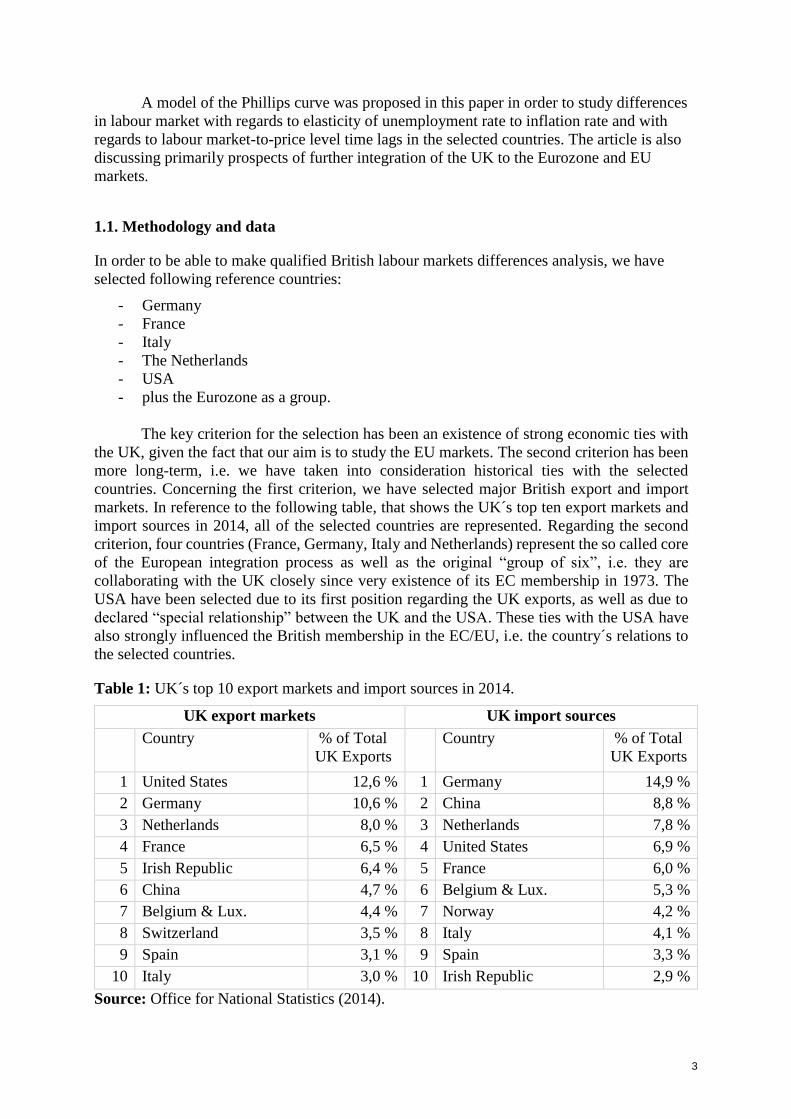

The key criterion for the selection has been an existence of strong economic ties with

the UK, given the fact that our aim is to study the EU markets. The second criterion has been

more long-term, i.e. we have taken into consideration historical ties with the selected

countries. Concerning the first criterion, we have selected major British export and import

markets. In reference to the following table, that shows the UK´s top ten export markets and

import sources in 2014, all of the selected countries are represented. Regarding the second

criterion, four countries (France, Germany, Italy and Netherlands) represent the so called core

of the European integration process as well as the original “group of six”, i.e. they are

collaborating with the UK closely since very existence of its EC membership in 1973. The

USA have been selected due to its first position regarding the UK exports, as well as due to

declared “special relationship” between the UK and the USA. These ties with the USA have

also strongly influenced the British membership in the EC/EU, i.e. the country´s relations to

the selected countries.

Table 1: UK´s top 10 export markets and import sources in 2014.

UK export markets UK import sources

Country % of Total

UK Exports

Country % of Total

UK Exports

1 United States 12,6 % 1 Germany 14,9 %

2 Germany 10,6 % 2 China 8,8 %

3 Netherlands 8,0 % 3 Netherlands 7,8 %

4 France 6,5 % 4 United States 6,9 %

5 Irish Republic 6,4 % 5 France 6,0 %

6 China 4,7 % 6 Belgium & Lux. 5,3 %

7 Belgium & Lux. 4,4 % 7 Norway 4,2 %

8 Switzerland 3,5 % 8 Italy 4,1 %

9 Spain 3,1 % 9 Spain 3,3 %

10 Italy 3,0 % 10 Irish Republic 2,9 %

Source: Office for National Statistics (2014).

4

The paper is analysing two basic data sets of the selected countries as well as of the

Eurozone as a group. The analysed period includes years 1998 – 2014. The first data set

which we have used has been the time series of unemployment rate evidenced by Eurostat.

The second data set, the time series of consumer price index, has been gained from the OECD

statistics.

Based on the above introduced data sets, we have constructed the OLS model for each

of the selected country´s labour market. We have used the Cochrane-Orcutt method to be able

to study the short term relation between inflation and unemployment. The created models of

individual countries´ labour markets enabled us to access country differences in different time

lags and different elasticities of unemployment rate to inflation.

Using methods of the time series statistical analysis, a model of the Phillips curve has

been developed for each of the countries (and Eurozone as a group). The models have been

created through using an autoregressive model, as well as using the method of Cochrane-

Orcutt, in order to filter out the possible autocorrelation effects. As already indicated above,

the models are working with short term (annual) data and are covering, as already indicated, a

period of the years 1998 – 2014.

2. Theory

This paper analyses a modelled Phillips curve of the British economy compared to selected

Eurozone member states, the USA and the Eurozone as a whole. A. W. Phillips originally

examined annual wage inflation and unemployment rates in the UK for rather longer period of

the years 1860–1957 (Phillips 1958). His concept has been later extended by Paul A.

Samuelson and Robert M. Solow by substituting price inflation for wage inflation, under

several conditions. The inverse relation has been valid for a short-term period, i.e. the so

called “short-term Phillips curve” was created (Samuelson and Solow, 1960). Later on, other

economists undertook similar research for other countries and concluded the same

relationship observations as Phillips and Samuelson with Solow.

Even before Phillips (already in 1926), Irving Fisher had described the relation

between inflation and the unemployment rate in an article in International Labour Review.

Based on data gained exclusively from the USA, covering the period of 1915–1925, he had

first found an extraordinarily high correlation between the rate of price changes and the

volume of trade. Continuing in analysing the given data set, he later discovered a strong

correlation between the rate of unemployment changes and the inflation. According to the

author, this could have had important implications for the then economic policy of the USA

given the fact that this relation had not been realised before. He also anticipates that the then

governments could be able to substantially prevent unemployment due to unemployment rate

and inflation correlation (Fisher, 1973).

However, the article of Irving Fisher had not been known to A. W. Phillips. The data

analysed by Phillips, published in his article called The Relation between Unemployment and

the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957 (published in

1958 in Economica), appeared to demonstrate an inverse as well as stable relationship

between unemployment and rising wages. The final curve designed from the data analysis

suggested, that “the rate of change of money wage rates can be explained by the level of

unemployment and the rate of change of unemployment, except in or immediately after those

years in which there is a sufficiently rapid rise in import prices to offset the tendency for

increasing productivity to reduce the cost of living” (Phillips, 1958: 299).

Samuelson and Solow (1960) have developed Phillips´ idea as follows. According to

their analysis, changes in the level of unemployment have a direct effect on the actual level of

5

price inflation. The accepted explanation during the 1960’s based on their work had been that

a fiscal stimulus, and increase in aggregate demand, would trigger the following sequence of

reactions. First, a fiscal policy stimulus to the economy increases demand for labour. Based

on this, the unemployment rate naturally falls down. However, firms now compete for smaller

labour force available, and they have to raise nominal wages in order to attract the workers.

That increases workers´ bargaining power which they logically use to get even higher nominal

wages. This of course has further effect on wage costs rise. Finally, given the fact that wage

costs are a substantial part of overall production costs, this results in an increased price of

final production, i.e. inflation rises.

During the 1960s and 1970s, the Phillips Curve became a policy guide within a

common governmental practice for many states. This policy, meanwhile becoming known as

stop-go, relied strongly on possibilities of fiscal policy.

Nevertheless, due to structural crises in the 1970´s, the stable relationship between

unemployment rate and inflation did not seemed to work in the same way as before. The

Phillips curve functioning in the economy became badly discredited because of the

unexpected experience of stagflation. However, later on, during the so called Keynesian

resurgence, the Phillips curve has been again used to justify expansionary monetary and fiscal

policy (Mulligan 2002).

Already before the crises, Edmund Phelps (1967) and Milton Friedman (1968)

challenged theoretical foundations of Phillips´ article. Both of these economists have argued

that nominal wages, which had been analysed by Phillips, were irrelevantly based on expected

workers´ behaviour. According to them, worker behaviour was dependent only on real wages,

i.e. inflation-adjusted-wages. Real wages would adjust in order to balance supply and demand

of labour. Natural rate of unemployment, also called the non-accelerating inflation rate of

unemployment (NAIRU), would then be established (Mulligan 2002).

To conclude this part, according to Phelps and Friedman, there is not just one Phillips

curve applicable for a given economy, but rather a series of short run Phillips Curves. In a

long term, the Phillips Curve has a shape of vertical line which shows the NAIRU. According

to the authors´ conclusions, the trade-off between unemployment rate and inflation is not

applicable in the long term.

Discussion on Phillips Curve is still divided in the economic theory. According to Ma

(2012), the modern Phillips curve still aims at identifying and searching for the trade-off

between the rate of inflation and the rate of unemployment as in the 1960´s. However, a fierce

debate about functionality of the curve has been led in economics already for more than fifty

years now. Especially questions regarding economic recession and dealing with it are opened

and probably will remain in that manner.

To sum up, The Phillips curve was primarily well-accepted by Keynesians, because

the curve provided a useful tool to conceptualise economic policies in order to set nominal

wages and unemployment in the best possible way. Later, neoclassical economists and

monetarist took part, when Milton Friedman and Edmund Phelps proposed a new version of

Phillips curve which focuses on the role of expectations on inflation and that is effective only

in the short term (Ma 2012).

3. British labour market as a key point for future arrangement with the EU

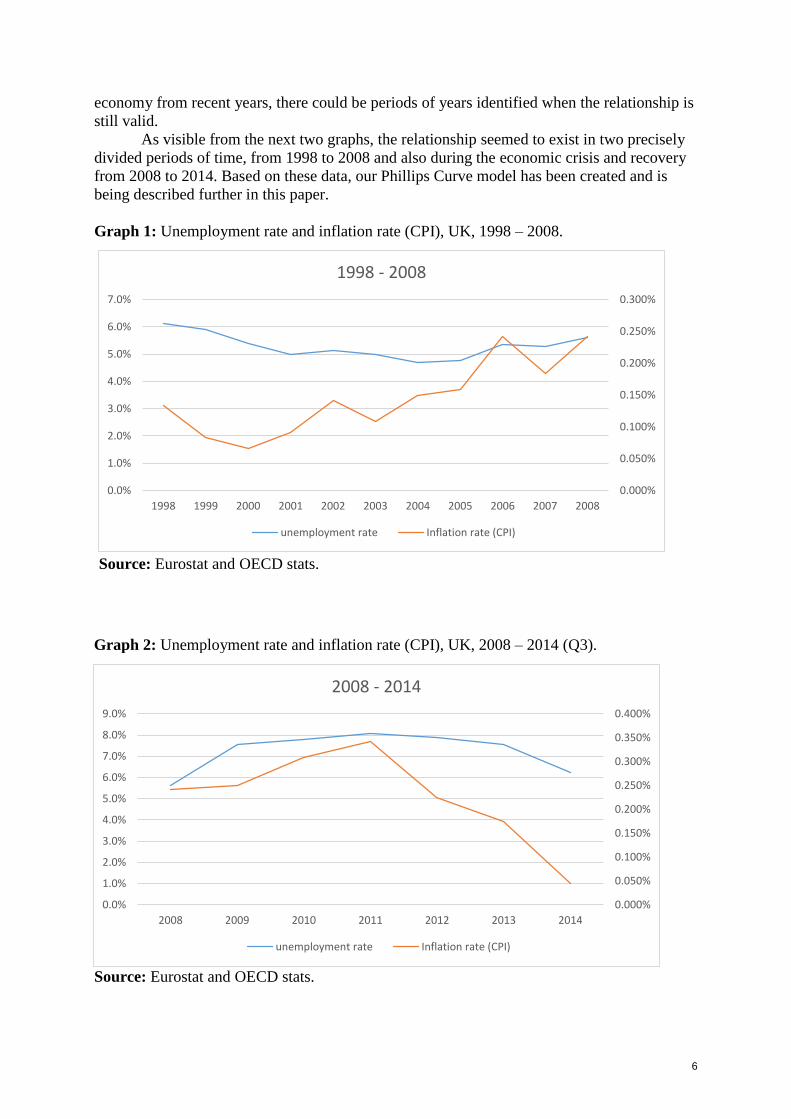

As suggested above, recent statistics support the view that the extreme trade-off between

unemployment and inflation rates that occurred according to Phillips in the past, are no longer

regarded as existing in the full original scale. However, based on our data set from the British

6

economy from recent years, there could be periods of years identified when the relationship is

still valid.

As visible from the next two graphs, the relationship seemed to exist in two precisely

divided periods of time, from 1998 to 2008 and also during the economic crisis and recovery

from 2008 to 2014. Based on these data, our Phillips Curve model has been created and is

being described further in this paper.

Graph 1: Unemployment rate and inflation rate (CPI), UK, 1998 – 2008.

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

1998 - 2008

unemployment rate Inflation rate (CPI)

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2008 2009 2010 2011 2012 2013 2014

2008 - 2014

unemployment rate Inflation rate (CPI)

Graph 2: Unemployment rate and inflation rate (CPI), UK, 2008 – 2014 (Q3).

Source: Eurostat and OECD stats.

Source: Eurostat and OECD stats.

7

When considering slighter longer term than in above described graphs, formerly,

supply side reforms3 have enabled the UK to implement expansive fiscal and monetary

policies in order to lower unemployment rate without experiencing rise of inflation rate. The

strengthened independence of the Bank and England has also played a role through

weakening the link between current and future inflation using the method of inflation

targeting. Last but not least, improvements in labour market flexibility have contributed to the

above stated, along with increased labour immigration. This point stays strongly in connection

with the British EU membership, because it is one of the sticking points when considering EU

competences in the UK.

The EU competences in the UK have been under thorough review in the past two years

(2012 – 2014). It has been an essential part of David Cameron´s plan summed up in the

slogan "reform, renegotiation, referendum" within the above mentioned Bloomberg speech in

January 2013. Anyway, while it has been not entirely clear how the government wanted to

influence the reform of the EU, which moreover is being already introduced4, the redefinition

of Britain's relationship with the EU, as a basis for future possible future referendum and

subsequent renegotiation, is already prepared5 (Parliament.uk 2014).

As already suggested above, labour market has been one of the disputable points based

not only on the Review findings. According to Emerson, Avery et al. (2014), prevailing

portion of the 32 analyses give (maybe unexpectedly) a very positive impression about the

European policies and their functioning in the UK. However, there is a very vital exception

regarding the studies on fundamental rights, and most importantly the exception concerning

the studies on free movement of persons and on social and employment policies. The latter

two are strongly connected to the labour markets.

The free movement of persons report suggests that there are significant differences in

opinion on this topic among the report contributors. Some of them considered free movement

of persons as both an essential part of the European Single Market and definitively positive

for the UK economy. Others however concentrated rather on negative effects of the free

movement of persons, such as possible increase of competition for jobs in the UK as well as

pressure on public services or housing. A discussion had been also led on the potential of

immigration from the new member states. This has been expected by several contributors to

create greater social inequality. (Gov.uk 2014c, 6).

As visible from the next table, immigration that is strongly connected to the issue of

the free movement of persons is a very important issue not only for the British politicians and

the Report stakeholders, but primarily for the British public that face problems arising from 3 During 1980s and 1990s various supply side policies have been introduced in the UK. During Margaret

Thatcher´s governments, privatisation has been carried out in order to slim down the state and to introduce

market functioning into the privatised industries. In some of them, the privatisation has led to strengthened

competition, lower prices and improved quality. In the same period, income taxes have been cut as well. The

most effective measure for labour market flexibility has been a reduction of Trade Unions´ power (Jenkins

2007). 4 The five principles defined in the Bloomberg speech by David Cameron, including above all competitiveness

and related Single Market importance, as well as the subsidiarity principle, flexibility, democratic accountability

and fairness, are highly in compliance with Jean-Claude Juncker’s reform program which aims at Single Market

importance and its support by the investment plan (Cameron 2013), (European Commission 2015). 5 The review has been finished in the end of 2014. The Review of the Balance of Competences is “an audit of

what the EU does and how it affects the UK” (Gov.uk 2012, 6). Government departments are supposed to

consult the Parliament and its committees, business, the devolved administrations, civil society, as well as

European partners and the EU institutions to look thoroughly at how the EU’s competences work in practice in

the UK. The main aim of the process is according to the governmental introduction (Gov.uk 2012, 6) to “inform

the public debate on the EU in the UK and Europe”. The review is not supposed to produce specific

recommendations for British European policy or to suggest future scenarios. The Review structure copies

broadly speaking the EU- accession chapters. The complete set comprises of 32 complex studies (Gov.uk 2012,

12).

8

the issue on a day-to-day basis. The public voice will be of an essential importance regarding

the future referendum on the British EU membership and that is why the free movement of

persons and its impact on British labour market needs to be watched.

Table 2: important issues for the EU and UK citizens.

EU Ranking UK Ranking

1 Unemployment (45%) Immigration (38%)

2

Economic situation

(24%) Unemployment (22%)

3 Immigration (18%)

Health & social security

(22%)

Source: Standard Eurobarometer 82 / autumn 2014

Even more disputable issue among the 32 reports of The Review of the Balance of

Competences is social and employment policy. Many analysis respondents were pragmatic

about the likelihood of continued EU competence in the UK in this area. Many of the

respondents who argued against the existing EU competence over social and employment

matters suggested that these policies were of a vital importance for the British future.

According to the report contributors, the social and employment policy needs to reflect

domestic culture and traditions, rather than integrate itself deeper into European structures

(Gov.uk 2014d, 6).

Functioning of the British labour market will be one of the key issues in discussions

about the future of the British EU membership. Especially problems arising from increasing

immigration flows from the newer EU member states could influence British public´s

decision in the referendum.

4. Findings

4.1. The model for the United Kingdom

In order to model Phillips Curve models for selected economies based on the above described

data, we have used the econometrical software Gretl. As mentioned above in the data and

methodology section, annual data for the time period of 1998 – 2014 have been used. In this

section, we discuss the model created for the British economy´s data.

In the following tables, the model parameters are introduced, as well as the results of

the tests of heteroscedasticity, autocorrelation and normality of residuals. Finally, the model

has enabled us to create a British Phillips Curve equation, which will be discussed in the

further sections.

9

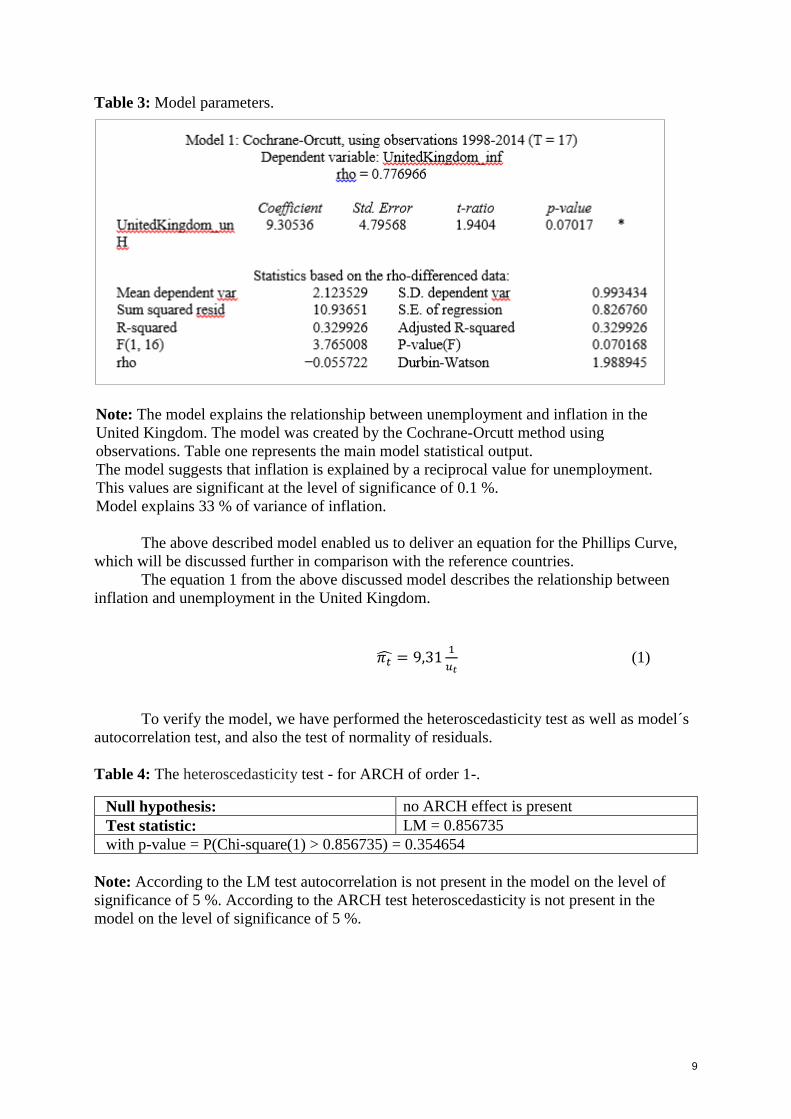

Table 3: Model parameters.

The above described model enabled us to deliver an equation for the Phillips Curve,

which will be discussed further in comparison with the reference countries.

The equation 1 from the above discussed model describes the relationship between

inflation and unemployment in the United Kingdom.

𝜋�̂� = 9,311

𝑢𝑡 (1)

To verify the model, we have performed the heteroscedasticity test as well as model´s

autocorrelation test, and also the test of normality of residuals.

Table 4: The heteroscedasticity test - for ARCH of order 1-.

Null hypothesis: no ARCH effect is present

Test statistic: LM = 0.856735

with p-value = P(Chi-square(1) > 0.856735) = 0.354654

Note: According to the LM test autocorrelation is not present in the model on the level of

significance of 5 %. According to the ARCH test heteroscedasticity is not present in the

model on the level of significance of 5 %.

Note: The model explains the relationship between unemployment and inflation in the

United Kingdom. The model was created by the Cochrane-Orcutt method using

observations. Table one represents the main model statistical output.

The model suggests that inflation is explained by a reciprocal value for unemployment.

This values are significant at the level of significance of 0.1 %.

Model explains 33 % of variance of inflation.

10

Table 5: Test for normality of residuals –

Null hypothesis: error is normally distributed

Test statistic: Chi-square(2) = 1.94689

with p-value = 0.37778

Note: The residuals of the model don´t have a normal distribution on the level of significance

of 5 %.

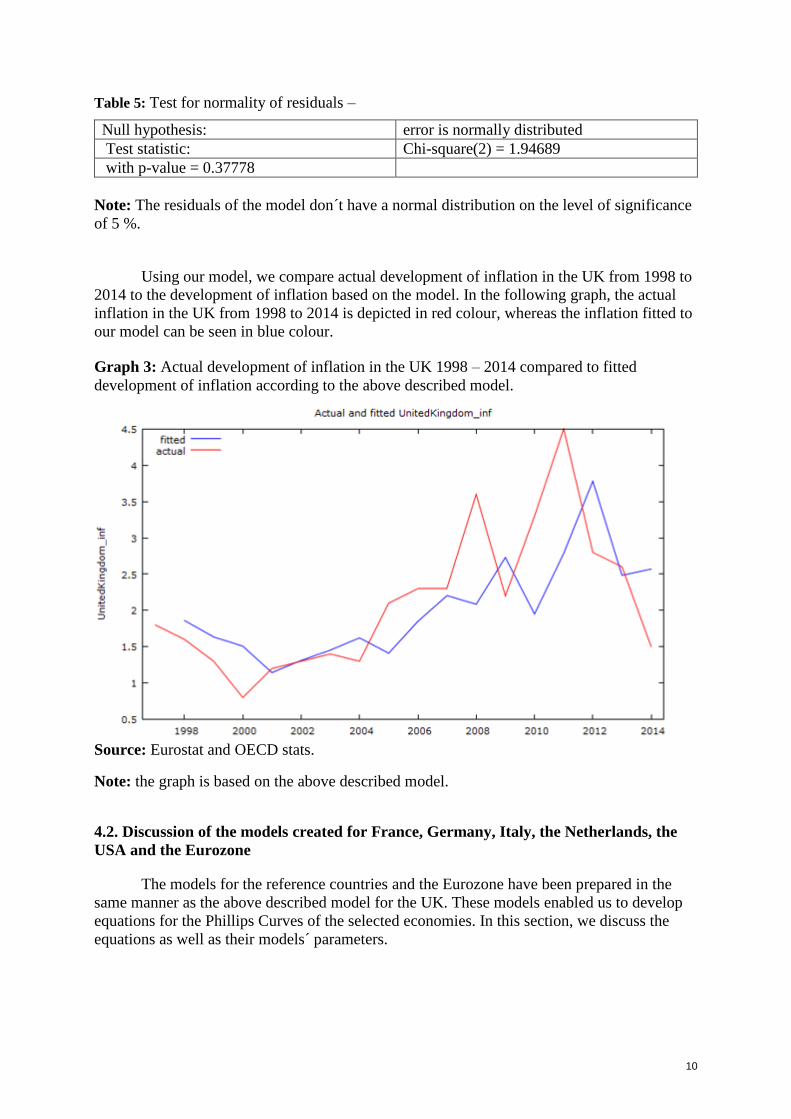

Using our model, we compare actual development of inflation in the UK from 1998 to

2014 to the development of inflation based on the model. In the following graph, the actual

inflation in the UK from 1998 to 2014 is depicted in red colour, whereas the inflation fitted to

our model can be seen in blue colour.

Graph 3: Actual development of inflation in the UK 1998 – 2014 compared to fitted

development of inflation according to the above described model.

Source: Eurostat and OECD stats.

Note: the graph is based on the above described model.

4.2. Discussion of the models created for France, Germany, Italy, the Netherlands, the

USA and the Eurozone

The models for the reference countries and the Eurozone have been prepared in the

same manner as the above described model for the UK. These models enabled us to develop

equations for the Phillips Curves of the selected economies. In this section, we discuss the

equations as well as their models´ parameters.

11

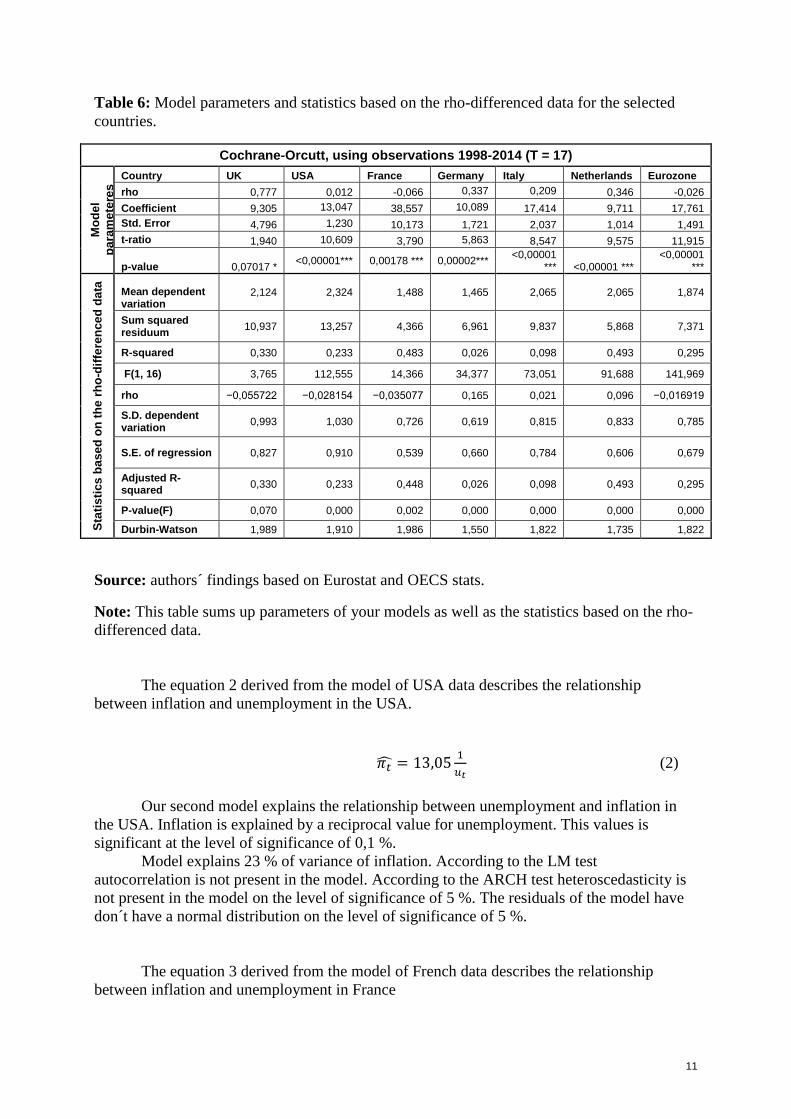

Table 6: Model parameters and statistics based on the rho-differenced data for the selected

countries.

Cochrane-Orcutt, using observations 1998-2014 (T = 17)

Mo

de

l

pa

ram

ete

res Country UK USA France Germany Italy Netherlands Eurozone

rho 0,777 0,012 -0,066 0,337 0,209 0,346 -0,026

Coefficient 9,305 13,047 38,557 10,089 17,414 9,711 17,761

Std. Error 4,796 1,230 10,173 1,721 2,037 1,014 1,491

t-ratio 1,940 10,609 3,790 5,863 8,547 9,575 11,915

p-value 0,07017 * <0,00001*** 0,00178 *** 0,00002***

<0,00001 *** <0,00001 ***

<0,00001 ***

Sta

tis

tics

ba

se

d o

n t

he

rh

o-d

iffe

ren

ce

d d

ata

Mean dependent variation

2,124 2,324 1,488 1,465 2,065 2,065 1,874

Sum squared residuum

10,937 13,257 4,366 6,961 9,837 5,868 7,371

R-squared 0,330 0,233 0,483 0,026 0,098 0,493 0,295

F(1, 16) 3,765 112,555 14,366 34,377 73,051 91,688 141,969

rho −0,055722 −0,028154 −0,035077 0,165 0,021 0,096 −0,016919

S.D. dependent variation

0,993 1,030 0,726 0,619 0,815 0,833 0,785

S.E. of regression 0,827 0,910 0,539 0,660 0,784 0,606 0,679

Adjusted R-squared

0,330 0,233 0,448 0,026 0,098 0,493 0,295

P-value(F) 0,070 0,000 0,002 0,000 0,000 0,000 0,000

Durbin-Watson 1,989 1,910 1,986 1,550 1,822 1,735 1,822

Source: authors´ findings based on Eurostat and OECS stats.

Note: This table sums up parameters of your models as well as the statistics based on the rho-

differenced data.

The equation 2 derived from the model of USA data describes the relationship

between inflation and unemployment in the USA.

𝜋�̂� = 13,051

𝑢𝑡 (2)

Our second model explains the relationship between unemployment and inflation in

the USA. Inflation is explained by a reciprocal value for unemployment. This values is

significant at the level of significance of 0,1 %.

Model explains 23 % of variance of inflation. According to the LM test

autocorrelation is not present in the model. According to the ARCH test heteroscedasticity is

not present in the model on the level of significance of 5 %. The residuals of the model have

don´t have a normal distribution on the level of significance of 5 %.

The equation 3 derived from the model of French data describes the relationship

between inflation and unemployment in France

12

𝜋�̂� = 38,571

𝑢𝑡− 2,68 (3)

The third model explains the relationship between unemployment and inflation in

France. Inflation is explained by a constant and a reciprocal value for unemployment. Both

values are significant at the level of significance 5 %.

Model explains 48 % of variance of inflation. The model as he a whole is according to

the F-test significant at the level of significance 5 %. According to the LM test,

autocorrelation is not present in the model at the level of significance 5 %. According to the

ARCH test, heteroscedasticity is not present in the model on the level of significance of 5 %.

The equation 4 derived from the model of German data describes the relationship

between inflation and unemployment in Germany

𝜋�̂� = 10,091

𝑢𝑡 (4)

The fourth model explains the relationship between unemployment and inflation in

Germany. Inflation is explained by a reciprocal value for unemployment. This value is

significant at the level of significance 5 %.

However, the model explains just 2,5 % of variance of inflation. The model as a

whole is according to the F-test significant at the level of significance 5 %. According to the

LM test, autocorrelation is not present in the model at the level of significance 5 %.

According to the ARCH test, heteroscedasticity is not present in the model on the level of

significance of 5 %.

The equation 5 derived from the model of Italian data describes the relationship

between inflation and unemployment in Italy.

𝜋�̂� = 17,411

𝑢𝑡 (5)

The fifth model explains the relationship between unemployment and inflation in Italy.

Inflation is explained by a reciprocal value for unemployment. The value is significant at the

level of significance 5 %.

Model explains 9,8 % of variance of inflation. According to the LM test,

autocorrelation is not present in the model at the level of significance 5 %. According to the

ARCH test, heteroscedasticity is not present in the model on the level of significance of 5 %.

The residuals of the model have don´t have a normal distribution on the level of significance

of 5 %.

The equation 6 derived from the model of Dutch data describes the relationship

between inflation and unemployment in the Netherlands.

𝜋�̂� = 9,711

𝑢𝑡 (6)

13

The next model explains the relationship between unemployment and inflation in

Netherlands. Inflation is explained by a reciprocal value for unemployment. This value is

significant at the level of significance 5 %.

Model explains 49 % of variance of inflation. According to the LM test,

autocorrelation is not present in the model at the level of significance 5 %. According to the

ARCH test, heteroscedasticity is not present on the level of significance of 5 %.

The equation 7 derived from the model of Eurozone data describes the relationship

between inflation and unemployment in the Eurozone.

𝜋�̂� = 17,761

𝑢𝑡 (7)

This model explains the relationship between unemployment and inflation in the

Eurozone. Inflation is explained by a reciprocal value for unemployment. This values is

significant at the level of significance of 0,1 %.

Model explains 30 % of variance of inflation. According to the LM test,

autocorrelation is not present in the model. According to the ARCH test, heteroscedasticity is

not present in the model on the level of significance of 5 %. The residuals of the model don´t

have a normal distribution on the level of significance of 5 %.

4.3. Results comparison

In this section, we discuss actual Phillips Curves developed based on our models.

14

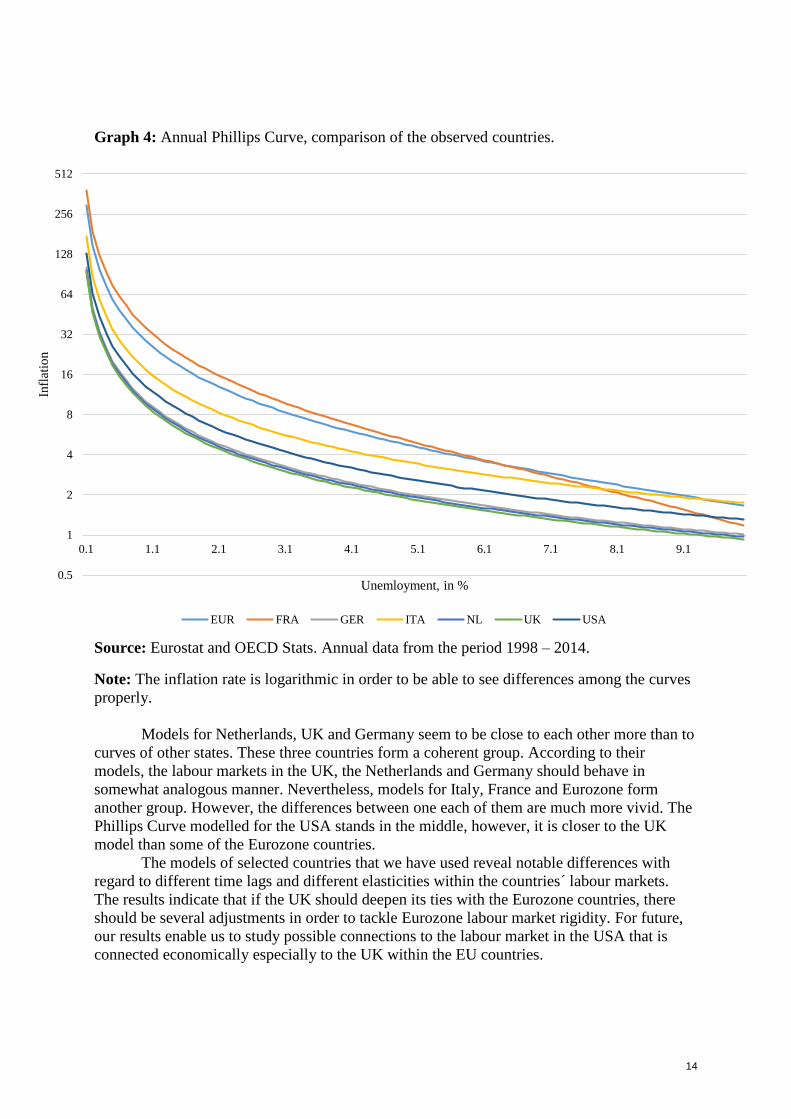

Graph 4: Annual Phillips Curve, comparison of the observed countries.

Source: Eurostat and OECD Stats. Annual data from the period 1998 – 2014.

Note: The inflation rate is logarithmic in order to be able to see differences among the curves

properly.

Models for Netherlands, UK and Germany seem to be close to each other more than to

curves of other states. These three countries form a coherent group. According to their

models, the labour markets in the UK, the Netherlands and Germany should behave in

somewhat analogous manner. Nevertheless, models for Italy, France and Eurozone form

another group. However, the differences between one each of them are much more vivid. The

Phillips Curve modelled for the USA stands in the middle, however, it is closer to the UK

model than some of the Eurozone countries.

The models of selected countries that we have used reveal notable differences with

regard to different time lags and different elasticities within the countries´ labour markets.

The results indicate that if the UK should deepen its ties with the Eurozone countries, there

should be several adjustments in order to tackle Eurozone labour market rigidity. For future,

our results enable us to study possible connections to the labour market in the USA that is

connected economically especially to the UK within the EU countries.

0.5

1

2

4

8

16

32

64

128

256

512

0.1 1.1 2.1 3.1 4.1 5.1 6.1 7.1 8.1 9.1

Infl

atio

n

Unemloyment, in %

EUR FRA GER ITA NL UK USA

15

5. Conclusion

In this paper, our aim was to develop Phillips Curves based on data from the last

seventeen years, in order to cover the crisis and consequent recovery period as well as the

growth period before. We have used annual data from Eurostat for the unemployment and

from the OECD stats for the annual inflation rates. We have developed models using the

software Gretl in order to set up relevant equations for the Phillips Curves. The results

enabled us to see major differences in labour markets´ behaviour in the UK, compared to the

Netherlands, Germany, the USA, Italy, France, and also the Eurozone as a whole.

The basic motivation for the above stated has been the UK´s awkward relationship to

the EU and the possible option that the referendum on staying in the UK will take place in

2017. In our opinion, the UK´s secession from the European integration would have

disastrous consequences both for the UK economy and the EU countries, especially those

from the Eurozone. Based on that, we think that developing arguments about British

economic ties and similarities to the Eurozone markets could somewhat enrich the debates

about the British membership and its meaning for the future.

As we can tell from our models, British labour markets behave almost in the same

manner as the labour markets of the Netherlands and Germany, which we consider as

important Eurozone members. However, there can be similarities observed also compared to

the USA´s labour market, which also represent the main UK exports market. On the other

hand, these ties does not have to be an argument for escaping the EU in the light of the

actually negotiated Transatlantic Trade and Investment Partnership (TTIP). This agreement

could even help the UK economy to ease its exports through the EU trade partnership frame.

16

References

[1] Allen, D., 2013. The United Kingdom: Towards Isolation and a Parting of the Ways? In:

Bulmer, S., Lequesne, Ch., 2013: The Member States of the European Union. Second

Edition. Oxford: Oxford University Press. Pp. 108–131. ISBN 978-0-19-954483-7.

[2] Cameron, D., 2013. EU Speech at Bloomberg [online]. Gov.uk, 23.1.2013. [2015-5-10].

Retrieved from: <https://www.gov.uk/government/speeches/eu-speech-at-bloomberg>.

[3] Emerson, M.; Blockmans, S., 2013. British Balance of Competence Reviews, Part I:

Competences about right, so far. EPIN Working Paper No. 35, October 2013. ISBN 978-94-

6138-362-4.

[4] Emerson, M; Avery. G. et al., 2014. British Balance of Competence Reviews, Part III:

More reform than renegotiation or repatriation. EPIN Working Paper No. 45, December

2014. ISBN 978-94-6138-431-7.

[5] European Commission, 2014. Standard Eurobarometer 82, Public opinion on the European

Union, autumn 2014. National Report – United Kingdom. [2015-5-15]. Retrieved from:

<http://ec.europa.eu/public_opinion/archives/eb/eb82/eb82_uk_uk_nat.pdfhttp://ec.europa.e

u/public_opinion/archives/eb/eb82/eb82_uk_uk_nat.pdf>.

[6] European Commission, 2015. The Commission and its priorities [online]. Europa.eu,

25.2.2015. [2015-4-17]. Retrieved from: <http://ec.europa.eu/index_en.htm>.

[7] Fisher, I., 1973. I Discovered the Phillips Curve: “A Statistical Relation between

Unemployment and Price Changes”. Journal of Political Economy, Vol. 81, No. 2, Part 1

(Mar. – Apr., 1973), pp. 496-502. [2015-5-8]. Retrieved from:

<http://www.jstor.org/stable/1830534>.

[8] Friedman, 1968. The Role of Monetary Policy. The American Economic Review, Vol. 58,

No. 1 (Mar., 1968), pp. 1-17. [2015-5-9]. Retrieved from:

<http://www.jstor.org/stable/1831652>.

[9] Gov.uk, 2012. Review of the Balance of Competences between the United Kingdom and the

European Union, Presented to Parliament by the Secretary of State for Foreign and

Commonwealth Affairs by Command of Her Majesty [online]. Foreign & Commonwealth

Office, © Crown copyright [2014-10-23]. ISBN 9780101841528. Retrieved from:

<https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/35458/eu-

balance-of-competences-review.pdf>.

[10] Gov.uk, 2014a. Guidance: Review of the balance of competences. Foreign &

Commonwealth Office, © Crown copyright [2015-5-8]. Retrieved from:

<https://www.gov.uk/review-of-the-balance-of-competences>.

[11] Gov.uk, 2014b. EU speech at Bloomberg. Cabinet Office, Prime Minister's Office, 10

Downing Street and The Rt Hon David Cameron MP, 23.1.2013, © Crown copyright [2015-

5-8]. Retrieved from: <https://www.gov.uk/government/speeches/eu-speech-at-bloomberg>.

[12] Gov.uk, 2014c. Review of the Balance of Competences between the United Kingdom and

the European Union. The Single Market: Free Movement of Persons. Home

Office and Department for Work and Pensions, 22.7.2014 [online]. © Crown copyright

[2015-5-10]. Retrieved from: <https://www.gov.uk/government/consultations/free-

movement-of-persons-review-of-the-balance-of-competences>.

[13] Gov.uk, 2014d. Review of the Balance of Competences between the United Kingdom and

the European Union. Social and Employment Policy. Department for Business, Innovation

& Skills, Department for Culture, Media & Sport, Department for Work and

Pensions, Foreign & Commonwealth Office , 22.7.2014 [online]. © Crown copyright [2015-

5-10]. Retrieved from: < https://www.gov.uk/government/consultations/review-of-uk-and-

eu-balance-of-competences-call-for-evidence-on-social-and-employment-policy>.

17

[14] Jenkins, 2007. Thatcher and Sons. A Revolution in Three Acts. London: Penguin Books.

ISBN 978-0-141-00624-6.

[15] Liddle, R., 2014. The Europe Dilemma: Britain and the drama of EU integration. London:

I.B. Tauris. ISBN 978-1-78076-223-4.

[16] Ma, J., 2012. Mystery of modern Phillips curve. Modern Economy, 3(8), 907-914. Retrieved

from <http://search.proquest.com/docview/1321120006?accountid=17203>.

[17] Mulligan, R. F., 2011. AN AUSTRIAN REHABILITATION OF THE PHILLIPS

CURVE. Cato Journal, 31(1), 87-98. [2015-5-13]. Retrieved from:

<http://search.proquest.com/docview/858458596?accountid=17203>.

[18] Office for National Statistics, 2014. UK Trade, December 2014. [2015-5-9]. Retrieved

from: <http://www.ons.gov.uk/ons/dcp171778_391926.pdf>.

[19] Parliament.uk, 2014. The future of the European Union: UK Government policy - Foreign

Affairs Committee [online]. © Parliamentary copyright 2013, 11. 6. 2013. [2015-5-10].

Retrieved from:

<http://www.publications.parliament.uk/pa/cm201314/cmselect/cmfaff/87/8708.htm>.

[20] Phelps, E., 1967. Phillips Curves, Expectations of Inflation and Optimal Unemployment

over Time. Economica, New Series, Vol. 34, No. 135, (Aug., 1967), pp. 254-281. [2015-5-

8]. Retrieved from: <http://www.jstor.org/stable/2552025>.

[21] Phillips, A. W., 1958. The Relation between Unemployment and the Rate of Change of

Money Wage Rates in the United Kingdom, 1861–1957. Economica, New Series, Vol. 25,

No. 100 (Nov., 1958), pp. 283-299. [2015-5-8]. Retrieved from:

<http://www.jstor.org/stable/2550759>.

[22] Policy Network, 2013. Britain´s Financial Services Industry in a Changing Europe. A

Policy Network Report for the City of London Corporation. Policy Network, December 12th

2013 [2015-5-8]. Retrieved from: <http://www.policy-

network.net/publications/4542/Britains-financial-services-industry-in-a-changing-Europe>.

[23] Samuelson, P. A.; Solow, R. M., 1960. Problem of Achieving and maintaining a Stable

Price Level. Analytical Aspects of Anti-Inflation Policy. The American Economic Review,

Vol. 50, No. 2, Papers and Proceedings of the Seventy-second Annual Meeting of the

American Economic Association (May, 1960), pp. 177-194. [2015-5-8]. Retrieved from:

<http.jstor.otg/stable/1815021>.

[24] The Economist, 2015. Cam again. 9th May 2015, from the print edition. [2015-5-9].

Retrieved from: <http://www.economist.com/news/leaders/21650722-conservatives-have-

triumphed-polls-governing-will-be-much-harder-cam-again>.