Ph.D. Admission List - Neville Wadia Institute of Management ...

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|1

TRaNsiT ORiENTED DEvElOPmENT

aT NEvillE aND CENTERREal EsTaTE DEsiGN aND DEvElOPmENT 48-452

Olaitan awomoloBo Jun

alexandre KinneyTing Wang

Hau-Wen WuYifan Xu

5 Dec 2013

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|2

1 | PROJECT DEsCRiPTiON

Concept & Proposed Uses:

a $112.2 million dollar transit-oriented development at Centre and Neville will invigorate the neighborhood by attracting young, socially-minded professionals to the best in modern urban living: 84,629 sf of diverse food and shopping options, active night life, and convenient access to extensive public transit options, all within a quick walk of 247,840 sf feet of new, contemporary-style apartments (149 studios, 134 one-bedrooms, and 74 two-bedrooms ).

Center and Neville is already a busy area, drawing consumers from around the city, commuters, local residents and students to its convenience stores, fast food, and middle Eastern food specialties. The entry to the East Busway intersects with several major bus lines including the 54 and the 71a and 71c, making it a natural hub for improved transit. The site also forms the gateway to the northern half of the Urban lab proposal to create a transit corridor and park space connecting the allegheny and monongahela Rivers via the lawrenceville elevated rail, the East Busway valley, Neville street, and Junction Hollow.

Bike and pedestrian paths will offer access into newly developed public park space along the slopes of the East Busway. With these new public park spaces and variety of transit options, the site will become an attractive area for residents looking for a quick commute to any neighborhood where the workplace is already well established and/or growing, including the south side, Oakland, shadyside, East Liberty, Bloomfield, Laurenceville, the strip, and Downtown.

Transit-oriented development offers the opportunity for higher-density housing than currently exists at the site. at the same time, services and amenities that young professionals and student want, like convenient grocery shopping, places to hang out and study, restaurants and bars, are almost completely lacking in the area.

What the area does have is a rare0 concentration of middle Eastern food, and a customer base that ranges all ages and cultures.

Our proposal is to develop retail and food opportunities that will make this an attractive area for young professionals seeking the convenience of improved public transit, while also serving the existing customer base of local families, students, and commuters passing through. We want to develop a variety of retail opportunities, attracting customers of a range of ages, cultural backgrounds, and income levels. in addition, we want to create a small outdoor park that becomes the gateway for the newly developed green space of the East Busway.

lastly, we want to improve the area without destroying what is already good about it! in order to preserve the strong local business that are already on Centre ave, we will leave those buildings intact, building instead on vacant lots, and only demolishing small row houses to accommodate increased street-level retail and multistory housing.

Of course, sustainable strategies will be employed in construction.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|3

2 | siTE lOCaTiON maP

Bounded by Centre ave, Baum Blvd, Melwood Ave and Enfield St, our site is largely unoccupied green space encompassing the entry to the East Busway and the outlet of a train tunnel, making it an ideal location for transit oriented development. We can improve upon the existing commercial and residential stock, improve transit options, and create a public green space at the same time!

OaklandNeighborhood

Downtown Pittsburgh

Allegheny River

Monongahela River

Figure 1: Context of Oakland neighborhood in relation to

Figure 2: Context of site in relation to Oakland Neighborhood

source: Base map generated from Gis map.

aREa OF sElECTiON

CENTRE avE.

BaUm BlvD.

NEvillE sT. POTENTial EXPaNsiON

NEiGHBORHOOD aREa

WalliNGFORD sT.

BaYaRD sT.

CRaiG sT.

DEvONsHiRE sT.

ENFiElD

sT.

GlENN WaY

maRiPOE sT.

maRCH WaY

mOEWOOD avE.

millvalE avE.

BROUGHTON

sT.

maRTiN lUTHER KiNG JR. BUsWaY

mElW

OOD avE.

GOlD WaYBiGElOW

BlvD.

DiTHRiDGE sT.

DOllaR sT.

CHEsNEY WaYBEllEFiElD avE.

lEONaRD sT.

EllsWORTH avE.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|4

OPR-B

RM-M

UNC

LNC

RM-M

R1D-VL

UI

26-S-169

52-A-43

52-A-38

52-A-35

52-A-32

52-A-30

52-A-28

52-A-26

52-A-24

52-A-22

27-D-258

27-D-255

27-D-286

27-D-289

27-D-292

27-D-295

27-D-298

27-D-308

27-D-241

27-D-244

27-D-250

27-D-252

27-D-253

27-D-254

26-S-300

26-S-282

26-S-280

26-S-225

26-S236

26-S-23B

26-S-170

26-S-17126-S-172

26-S-17326-S-174

26-S-17626-S-17726-S-178

26-S-17926-S-18026-S-18126-S-184

26-S-186

26-S-185

26-S-189~198

Centre Avenue

Melw

ood Avenue

Melw

ood Avenue

N Craig St.

N N

eville St.

E Busway Ram

p

N N

eville St.Baum Blvd

En�eld St.

WallingFord St.

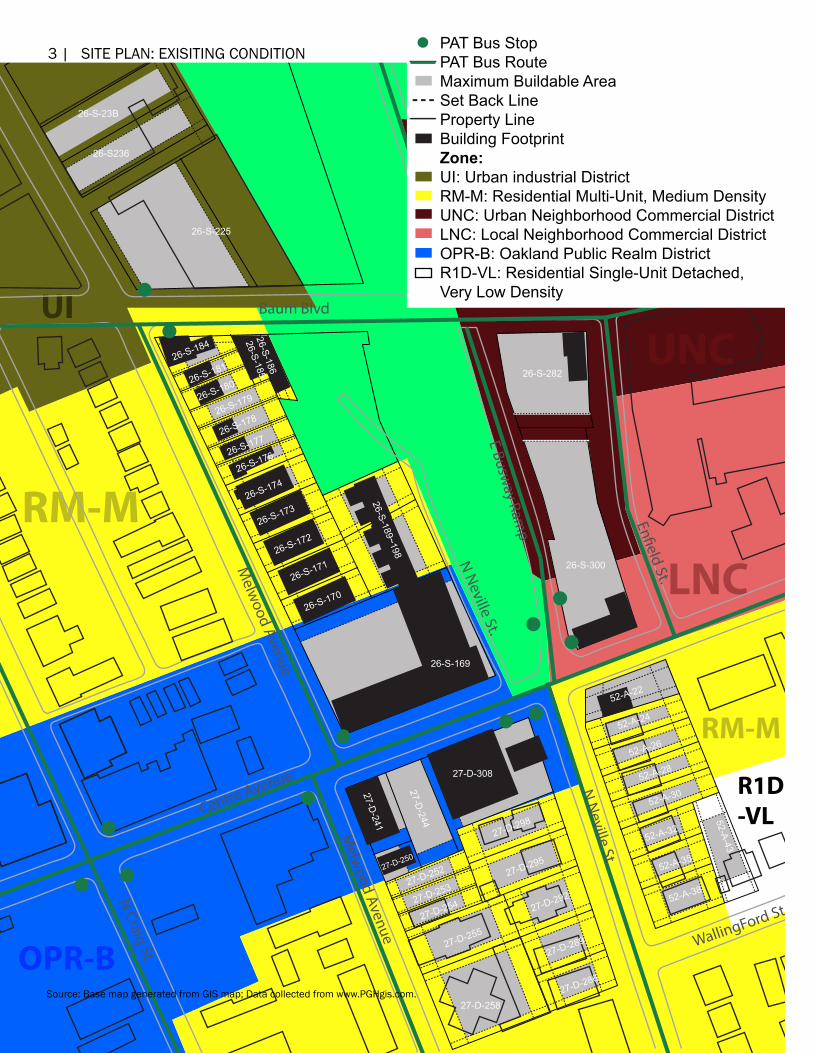

PAT Bus StopPAT Bus RouteMaximum Buildable AreaSet Back LineProperty LineBuilding Footprint Zone:UI: Urban industrial DistrictRM-M: Residential Multi-Unit, Medium DensityUNC: Urban Neighborhood Commercial DistrictLNC: Local Neighborhood Commercial DistrictOPR-B: Oakland Public Realm DistrictR1D-VL: Residential Single-Unit Detached, Very Low Density

source: Base map generated from Gis map; Data collected from www.PGHgis.com.

3 | siTE PlaN: EXisiTiNG CONDiTiON

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|5

3 | siTE PlaN: PROPOsED_GROUND FlOOR

OPR-B

RM-M

UNC

LNC

RM-M

R1D-VL

UI

Centre Avenue

Melw

ood Avenue

Melw

ood Avenue

N Craig St.

N N

eville St.

E Busway Ram

p

N N

eville St.

Baum Blvd

En�eld St.

WallingFord St.

restaurant

park

new OPR-B zoning boundary

restaurants/stores

demolished buildings

pedestrian bridge

existing restau-rants

boutiques

bakery

co�eeshop

tram/bus station

Asian market

existing commercial

underground parking perimeter

parking entry

reading room

source: Base map generated from Gis map.

EXisTiNG BUilDiNG

vEHiClE PaRKiNG: 603 BiKE PaRKiNG: 178

PROPOsED BUilDiNG

PROPsED UNDERGROUND PaRKiNG

DEmOlisED BUilDiNG

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|6

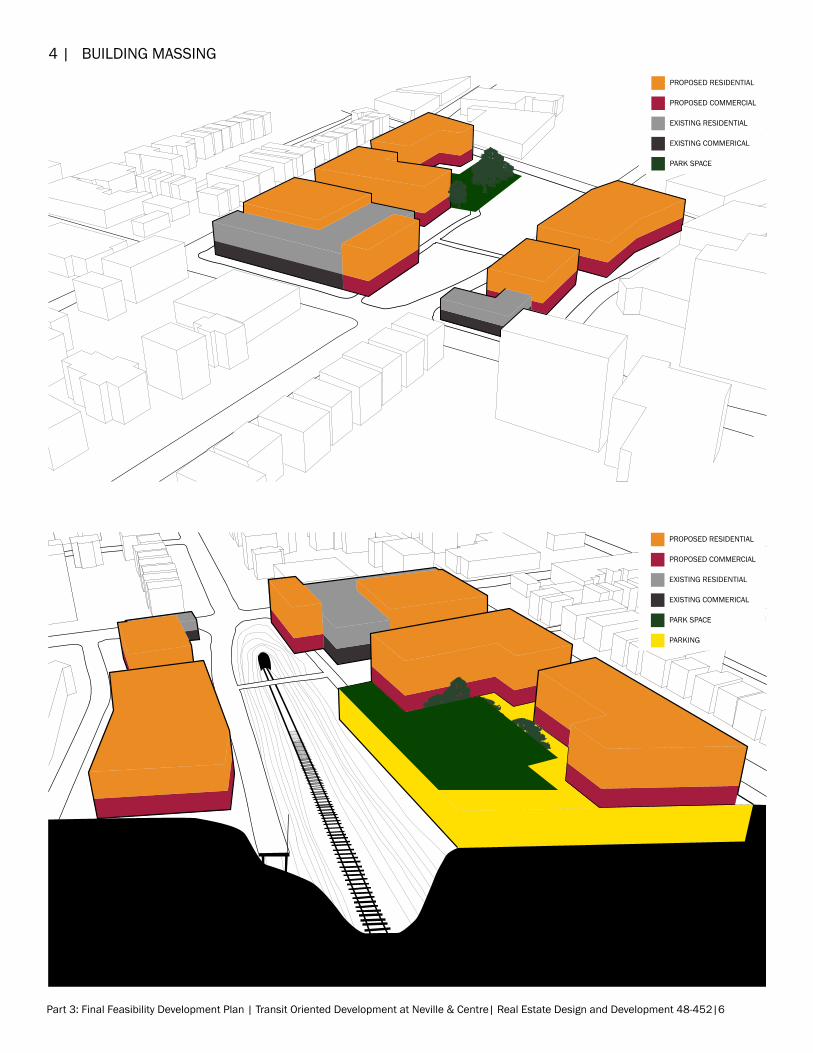

PROPOsED REsiDENTial

PROPOsED COmmERCial

EXisTiNG REsiDENTial

EXisTiNG COmmERiCal

PaRK sPaCE

PaRKiNG

PROPOsED REsiDENTial

PROPOsED COmmERCial

EXisTiNG REsiDENTial

EXisTiNG COmmERiCal

PaRK sPaCE

4 | BUilDiNG massiNG

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|7

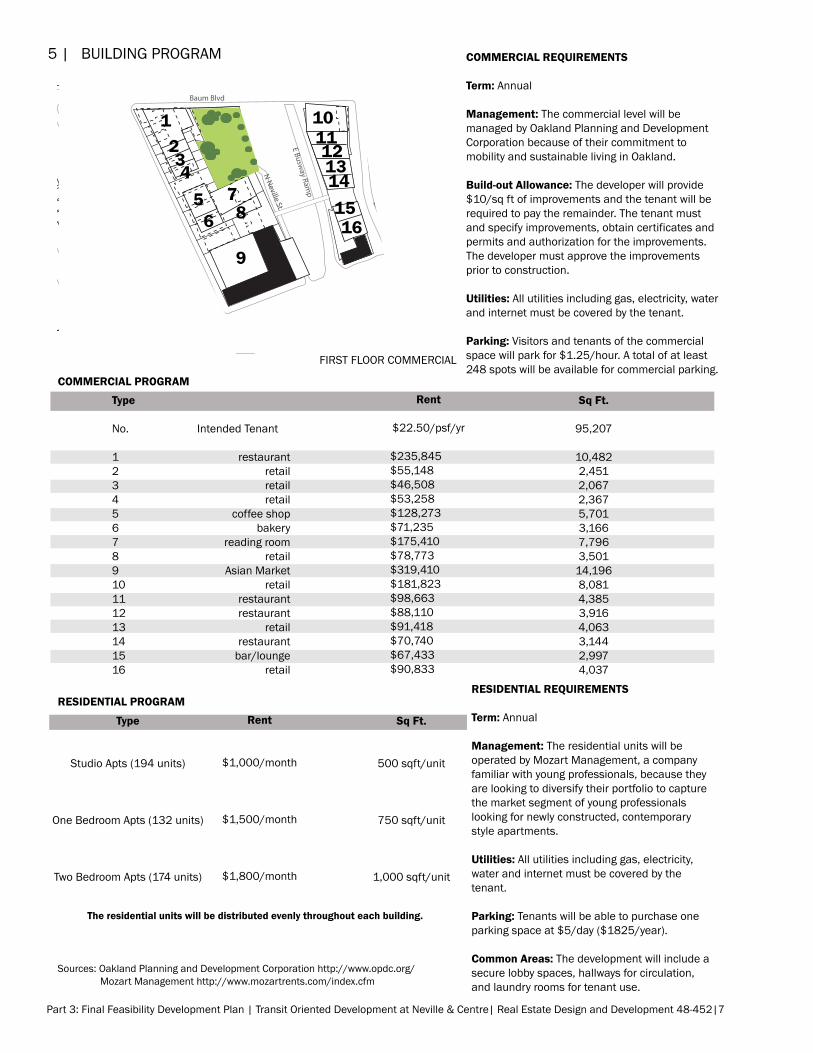

5 | BUilDiNG PROGRam

Centre Avenue

Melw

ood Avenue

N N

eville St.

E Busway Ram

p

N N

eville St.

Baum Blvd

En�eld St.

Type

No. Intended Tenant

12345678910111213141516

Rent

$22.50/psf/yr

$235,845 $55,148 $46,508 $53,258 $128,273 $71,235 $175,410 $78,773 $319,410 $181,823 $98,663 $88,110 $91,418 $70,740 $67,433 $90,833

restaurantretailretailretail

coffee shopbakery

reading roomretail

Asian Marketretail

restaurantrestaurant

retailrestaurant

bar/loungeretail

FIRST FLOOR COMMERCIAL

COMMERCIAL PROGRAM

RESIDENTIAL PROGRAM

Sq Ft.

95,207

10,4822,4512,0672,3675,7013,1667,7963,501

14,1968,0814,3853,9164,0633,1442,9974,037

COMMERCIAL REQUIREMENTS

Term: Annual

Management: The commercial level will be managed by Oakland Planning and Development Corporation because of their commitment to mobility and sustainable living in Oakland.

Build-out Allowance: The developer will provide $10/sq ft of improvements and the tenant will be required to pay the remainder. The tenant must and specify improvements, obtain certificates and permits and authorization for the improvements. The developer must approve the improvements prior to construction.

Utilities: All utilities including gas, electricity, water and internet must be covered by the tenant.

Parking: Visitors and tenants of the commercial space will park for $1.25/hour. A total of at least 248 spots will be available for commercial parking.

RESIDENTIAL REQUIREMENTS

Term: Annual

Management: The residential units will be operated by Mozart Management, a company familiar with young professionals, because they are looking to diversify their portfolio to capture the market segment of young professionals looking for newly constructed, contemporary style apartments.

Utilities: All utilities including gas, electricity, water and internet must be covered by the tenant.

Parking: Tenants will be able to purchase one parking space at $5/day ($1825/year).

Common Areas: The development will include a secure lobby spaces, hallways for circulation, and laundry rooms for tenant use.

Sources: Oakland Planning and Development Corporation http://www.opdc.org/ Mozart Management http://www.mozartrents.com/index.cfm

The residential units will be distributed evenly throughout each building.

1234

5 78

9

101112131415166

Type

Studio Apts (194 units)

One Bedroom Apts (132 units)

Two Bedroom Apts (174 units)

Rent

$1,000/month

$1,500/month

$1,800/month

Sq Ft.

500 sqft/unit

750 sqft/unit

1,000 sqft/unit

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|8

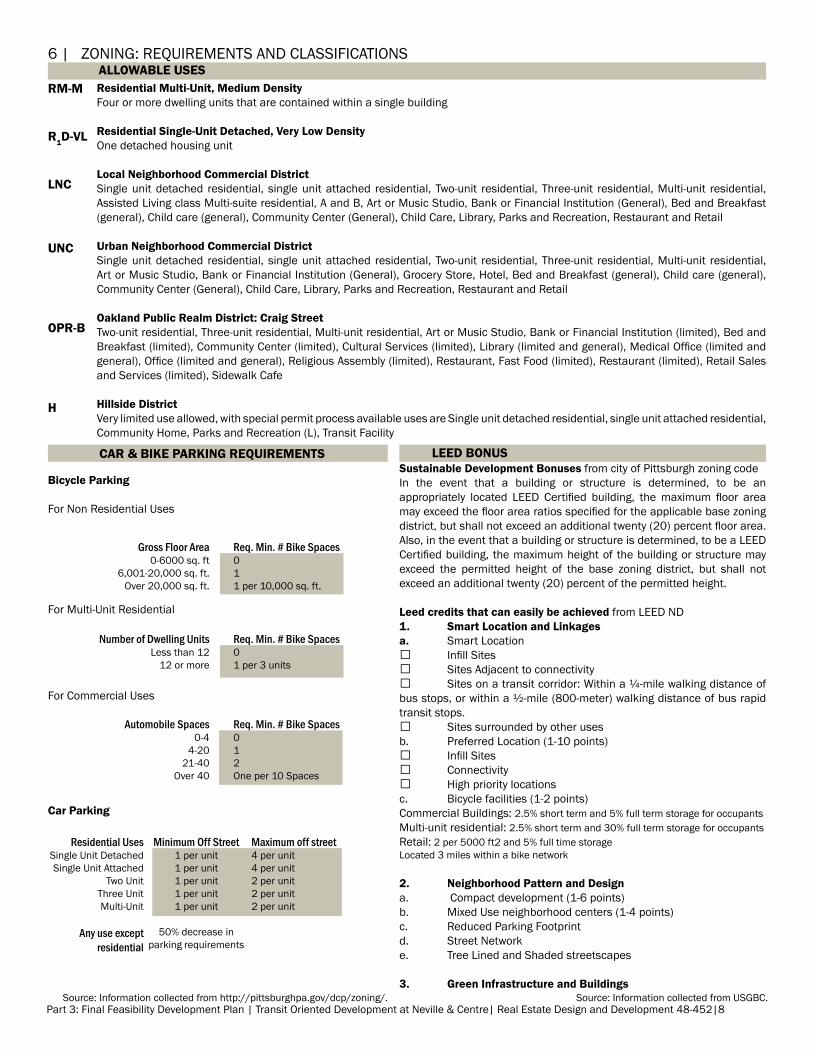

6 | ZONiNG: REQUiREmENTs aND ClassiFiCaTiONsALLOWABLE USES

CAR & BIKE PARKING REQUIREMENTS LEED BONUS

RM-M

R1D-VL

LNC

UNC

OPR-B

H

Residential Multi-Unit, Medium DensityFour or more dwelling units that are contained within a single building

Residential Single-Unit Detached, Very Low DensityOne detached housing unit

Local Neighborhood Commercial Districtsingle unit detached residential, single unit attached residential, Two-unit residential, Three-unit residential, multi-unit residential, assisted living class multi-suite residential, a and B, art or music studio, Bank or Financial institution (General), Bed and Breakfast (general), Child care (general), Community Center (General), Child Care, library, Parks and Recreation, Restaurant and Retail

Urban Neighborhood Commercial Districtsingle unit detached residential, single unit attached residential, Two-unit residential, Three-unit residential, multi-unit residential, art or music studio, Bank or Financial institution (General), Grocery store, Hotel, Bed and Breakfast (general), Child care (general), Community Center (General), Child Care, library, Parks and Recreation, Restaurant and Retail

Oakland Public Realm District: Craig StreetTwo-unit residential, Three-unit residential, multi-unit residential, art or music studio, Bank or Financial institution (limited), Bed and Breakfast (limited), Community Center (limited), Cultural Services (limited), Library (limited and general), Medical Office (limited and general), Office (limited and general), Religious Assembly (limited), Restaurant, Fast Food (limited), Restaurant (limited), Retail Sales and services (limited), sidewalk Cafe

Hillside Districtvery limited use allowed, with special permit process available uses are single unit detached residential, single unit attached residential, Community Home, Parks and Recreation (l), Transit Facility

Bicycle Parking

For Non Residential Uses

For multi-Unit Residential

For Commercial Uses

Car Parking

Gross Floor Area 0-6000 sq. ft

6,001-20,000 sq. ft.Over 20,000 sq. ft.

Number of Dwelling Units less than 12

12 or more

Automobile Spaces0-4

4-2021-40

Over 40

Residential Uses single Unit Detachedsingle Unit attached

Two UnitThree Unitmulti-Unit

Any use except residential

Minimum Off Street1 per unit1 per unit1 per unit1 per unit1 per unit

50% decrease in parking requirements

Req. Min. # Bike Spaces 011 per 10,000 sq. ft.

Req. Min. # Bike Spaces 01 per 3 units

Req. Min. # Bike Spaces 012One per 10 spaces

Maximum off street 4 per unit4 per unit2 per unit2 per unit2 per unit

Sustainable Development Bonuses from city of Pittsburgh zoning codein the event that a building or structure is determined, to be an appropriately located LEED Certified building, the maximum floor area may exceed the floor area ratios specified for the applicable base zoning district, but shall not exceed an additional twenty (20) percent floor area. also, in the event that a building or structure is determined, to be a lEED Certified building, the maximum height of the building or structure may exceed the permitted height of the base zoning district, but shall not exceed an additional twenty (20) percent of the permitted height.

Leed credits that can easily be achieved from lEED ND1. Smart Location and Linkagesa. smart location Infill Sites Sites Adjacent to connectivity Sites on a transit corridor: Within a ¼-mile walking distance of bus stops, or within a ½-mile (800-meter) walking distance of bus rapid transit stops. Sites surrounded by other usesb. Preferred location (1-10 points) Infill Sites Connectivity High priority locations c. Bicycle facilities (1-2 points)Commercial Buildings: 2.5% short term and 5% full term storage for occupantsmulti-unit residential: 2.5% short term and 30% full term storage for occupantsRetail: 2 per 5000 ft2 and 5% full time storagelocated 3 miles within a bike network

2. Neighborhood Pattern and Designa. Compact development (1-6 points)b. mixed Use neighborhood centers (1-4 points)c. Reduced Parking Footprintd. street Networke. Tree lined and shaded streetscapes

3. Green Infrastructure and Buildings source: information collected from UsGBC.source: information collected from http://pittsburghpa.gov/dcp/zoning/.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|9

6 | ZONiNG: REQUiREmENTs aND ClassiFiCaTiONs

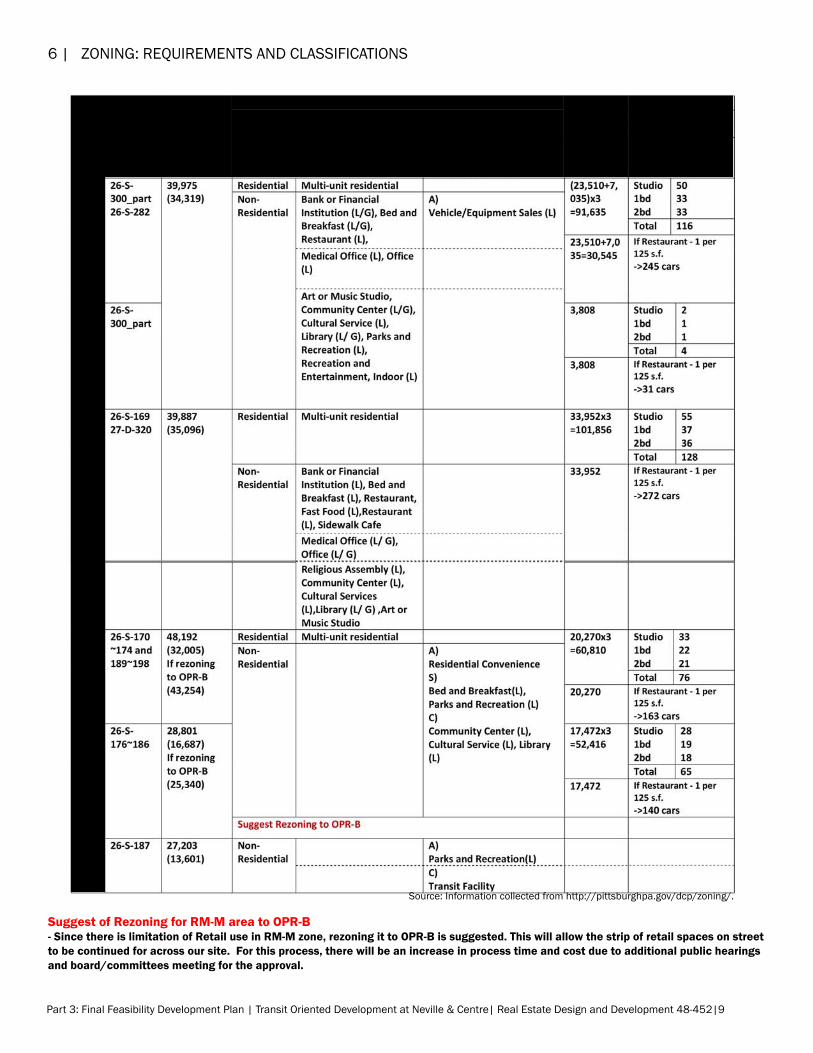

Suggest of Rezoning for RM-M area to OPR-B- Since there is limitation of Retail use in RM-M zone, rezoning it to OPR-B is suggested. This will allow the strip of retail spaces on street to be continued for across our site. For this process, there will be an increase in process time and cost due to additional public hearings and board/committees meeting for the approval.

source: information collected from http://pittsburghpa.gov/dcp/zoning/.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|10

Address Lot Area

Existing Building Footprint

Maximum Buildable area State Code Use Code Owner Land Value

Building Value

Total Value

LNCLocal Neighborhood Commercial

26-S-300 4703 CENTRE AVE 22,320 3,437 20,088 Commercial

SMALL DETACHED RET(UNDER 10,000)

CRESCENT REALTY & INVESTMENT CO (ETAL) and 2 co-owners 174,200 116,300 290,500

UNC

Urban Neighborhood Commercial

26-S-282 4712 BAUM BLVD 17,655 1,994 14,231 Commercial

FAST FOOD/DRIVE THRU WINDOW ABRAMS FAMILY ASSOCIATES 462,900 97,300 560,200

OPR-BOakland Public Realm

26-S-169 4635 CENTRE AVE 38,387 19,909 35,096 CommercialRETL/APT'S OVER

4631 MELWOOD AVENUE ASSOCIATES LLC 400,500 1,199,500 1,600,000

27-D-320 4653 CENTRE AVE 1,500 combine Commercial

SMALL DETACHED RET(UNDER 10000 TRACY JAMES E 52,000 61,500 113,500

H Hillside District

26-S-187 4654 BAUM BLVD 27,203 0 13,601 CommercialCOMM AUX BUILDING MARTIN MEDIA 300 0 300

RM-M

Residential Multi-Unit, Moderate Density (3-4 Stories)

26-S-170 316 MELWOOD AVE 5,603 3,117 1,971 CommercialAPART: 5-19 UNITS

MELWOOD NEVILLE ASSOCIATES LLC PA LIMITED LIABILITIES COMPANY 55,000 307,300 362,300

26-S-171 322 MELWOOD AVE 5,507 3,103 1,762 CommercialAPART: 5-19 UNITS MELWOOD NEVILLE ASSOCIATES LLC 60,000 332,500 392,500

26-S-172 326 MELWOOD AVE 5,621 3,032 1,805 CommercialAPART: 5-19 UNITS MELWOOD NEVILLE ASSOCIATES LLC 30,000 269,300 299,300

26-S-173 330 MELWOOD AVE 5,666 2,899 1,781 CommercialAPART: 5-19 UNITS MELWOOD NEVILLE ASSOCIATES LLC 40,000 282,100 322,100

26-S-174 334 MELWOOD AVE 6,100 2,846 1,959 CommercialAPART: 5-19 UNITS MELWOOD NEVILLE ASSOCIATES LLC 50,000 300,100 350,100

26-S-176 340 MELWOOD AVE 3,750 1,240 1,191 CommercialAPART: 5-19 UNITS TUCKFELT GARY L 70,000 236,600 306,600

26-S-177 342 MELWOOD AVE 3,750 811 1,654 ResidentialSINGLE FAMILY

NATIONAL BUILDERS AND ACCEPTANCE CORPORATION 17,500 75,100 92,600

26-S-178 344 MELWOOD AVE 3,750 719 1,916 Residential TWO FAMILY RUB-A-DUB-DUBINC 17,500 61,200 78,700

26-S-179 346 MELWOOD AVE 3,750 0 1,703 CommercialCOMM AUX BUILDING KARMIC PROPERTIES LLC 16,500 3,500 20,000

26-S-180 348 MELWOOD AVE 2,800 913 1,236 ResidentialSINGLE FAMILY AKBAR MOHAMMAD SHAHARIAR 15,600 82,100 97,700

26-S-181 350 MELWOOD AVE 2,800 972 1,008 ResidentialSINGLE FAMILY YAM DAVID & EVA WAI MAN (W) 15,600 54,700 70,300

26-S-184 352 MELWOOD AVE 3,983 2,306 1,437 CommercialAPART: 5-19 UNITS TUCKFELT GARY L 35,000 210,000 245,000

26-S-185 4650 BAUM BLVD 1,651 3,603 1,297 CommercialOFFICE - 1-2 STORIES KARMIC PROPERTIES LLC 15,000 50,000 65,000

26-S-186 4652 BAUM BLVD 2,567 combine CommercialOFFICE - 1-2 STORIES KARMIC PROPERTIES LLC 20,000 55,000 75,000

26-S-189 217 N NEVILLE ST 2,006 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 9,000 17,000 26,00026-S-190 219 N NEVILLE ST 1,898 2,782 3,104 Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-191 221 N NEVILLE ST 1,899 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-192 223 N NEVILLE ST 2,131 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 9,300 17,000 26,30026-S-193 225 N NEVILLE ST 2,035 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 9,100 17,000 26,10026-S-194 227 N NEVILLE ST 1,883 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-195 229 N NEVILLE ST 1,884 4,113 5,466 Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-196 231 N NEVILLE ST 1,885 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-197 233 N NEVILLE ST 1,885 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 8,800 17,000 25,80026-S-198 235 N NEVILLE ST 2,189 combine Residential ROWHOUSE MELWOOD NEVILLE ASSOCIATES LLC 9,400 17,000 26,400

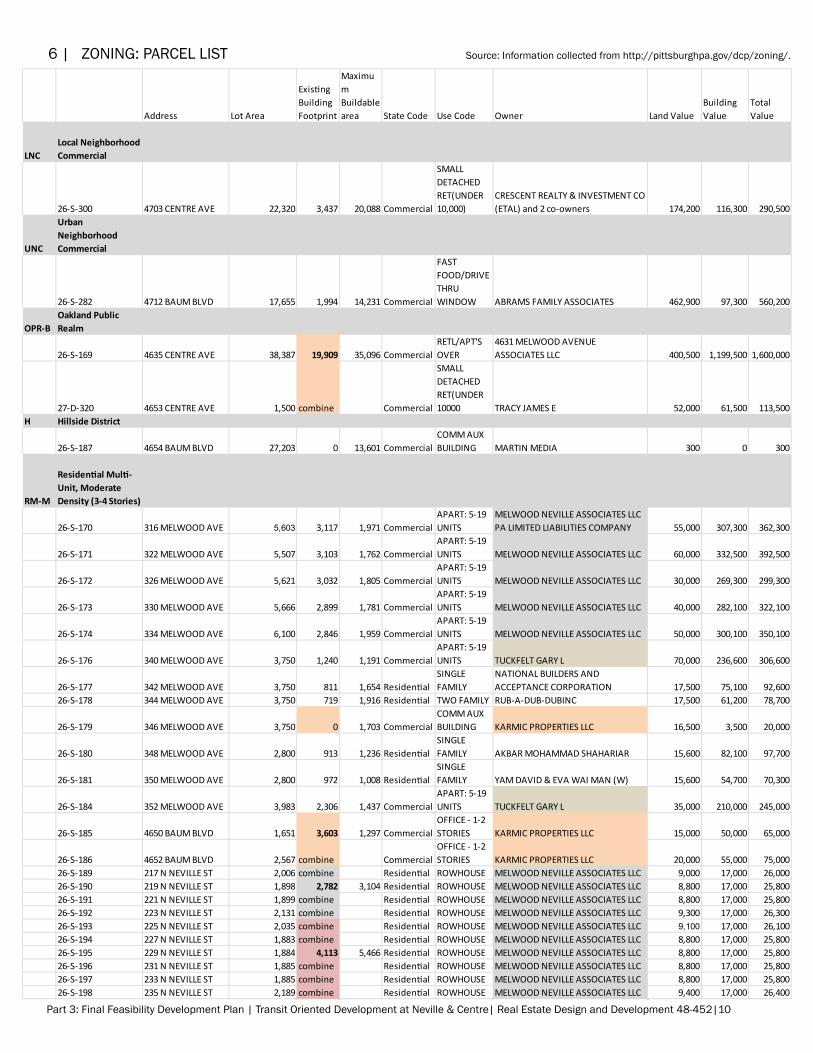

6 | ZONiNG: PaRCEl lisT source: information collected from http://pittsburghpa.gov/dcp/zoning/.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|11

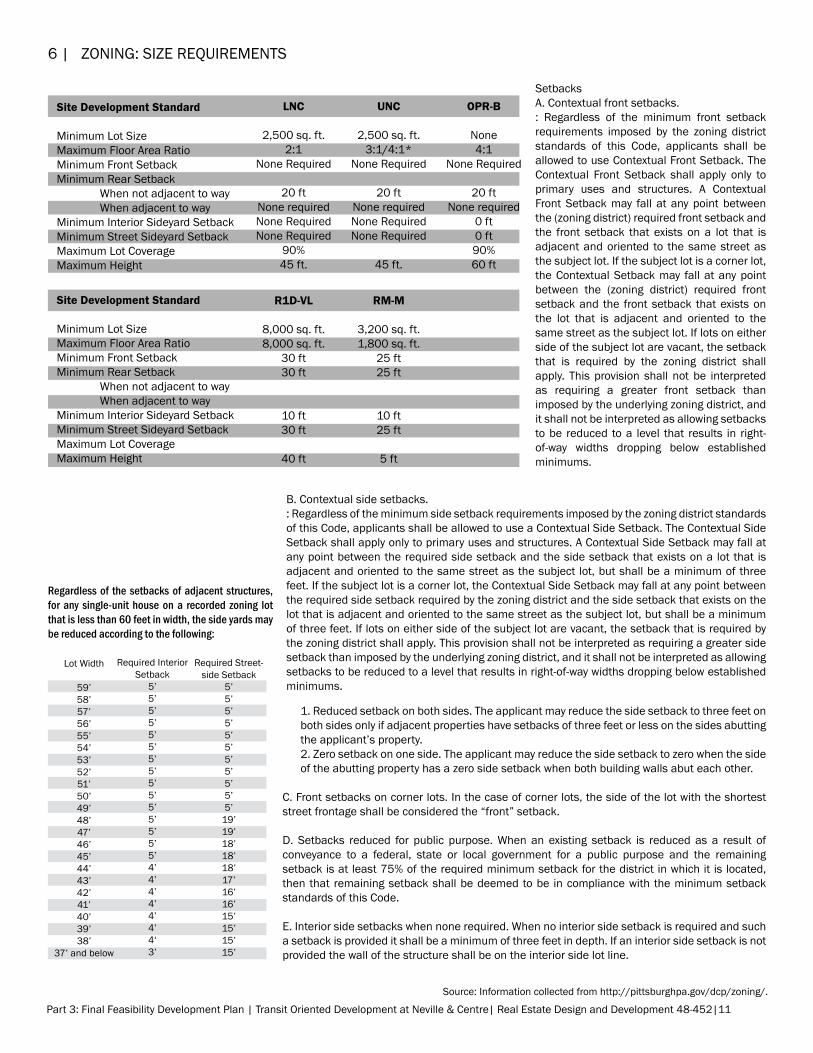

6 | ZONiNG: siZE REQUiREmENTs

1. Reduced setback on both sides. The applicant may reduce the side setback to three feet on both sides only if adjacent properties have setbacks of three feet or less on the sides abutting the applicant’s property.2. Zero setback on one side. The applicant may reduce the side setback to zero when the side of the abutting property has a zero side setback when both building walls abut each other.

C. Front setbacks on corner lots. in the case of corner lots, the side of the lot with the shortest street frontage shall be considered the “front” setback.

D. setbacks reduced for public purpose. When an existing setback is reduced as a result of conveyance to a federal, state or local government for a public purpose and the remaining setback is at least 75% of the required minimum setback for the district in which it is located, then that remaining setback shall be deemed to be in compliance with the minimum setback standards of this Code.

E. interior side setbacks when none required. When no interior side setback is required and such a setback is provided it shall be a minimum of three feet in depth. if an interior side setback is not provided the wall of the structure shall be on the interior side lot line.

Regardless of the setbacks of adjacent structures, for any single-unit house on a recorded zoning lot that is less than 60 feet in width, the side yards may be reduced according to the following:

setbacksa. Contextual front setbacks. : Regardless of the minimum front setback requirements imposed by the zoning district standards of this Code, applicants shall be allowed to use Contextual Front setback. The Contextual Front setback shall apply only to primary uses and structures. a Contextual Front setback may fall at any point between the (zoning district) required front setback and the front setback that exists on a lot that is adjacent and oriented to the same street as the subject lot. if the subject lot is a corner lot, the Contextual setback may fall at any point between the (zoning district) required front setback and the front setback that exists on the lot that is adjacent and oriented to the same street as the subject lot. if lots on either side of the subject lot are vacant, the setback that is required by the zoning district shall apply. This provision shall not be interpreted as requiring a greater front setback than imposed by the underlying zoning district, and it shall not be interpreted as allowing setbacks to be reduced to a level that results in right-of-way widths dropping below established minimums.

Lot Width

59’58’57’56’55’54’53’52’51’50’49’48’47’46’45’44’43’42’41’40’39’38’

37’ and below

Required Interior Setback

5’5’5’5’5’5’5’5’5’5’5’5’5’5’5’4’4’4’4’4’4’4‘3’

Required Street-side Setback

5’5’5’5’5’5’5’5’5’5’5’

19’19’18’18’18’17’16’16’15’15’15’15’

Site Development Standard

Minimum Lot Size Maximum Floor Area RatioMinimum Front SetbackMinimum Rear Setback When not adjacent to way When adjacent to wayMinimum Interior Sideyard SetbackMinimum Street Sideyard SetbackMaximum Lot CoverageMaximum Height

Site Development Standard

Minimum Lot Size Maximum Floor Area RatioMinimum Front SetbackMinimum Rear Setback When not adjacent to way When adjacent to wayMinimum Interior Sideyard SetbackMinimum Street Sideyard SetbackMaximum Lot CoverageMaximum Height

LNC

2,500 sq. ft.2:1

None Required

20 ftNone requiredNone RequiredNone Required

90%45 ft.

UNC

2,500 sq. ft.3:1/4:1*

None Required

20 ftNone requiredNone RequiredNone Required

45 ft.

OPR-B

None4:1

None Required

20 ftNone required

0 ft0 ft90%60 ft

R1D-VL

8,000 sq. ft.8,000 sq. ft.

30 ft30 ft

10 ft30 ft

40 ft

RM-M

3,200 sq. ft.1,800 sq. ft.

25 ft25 ft

10 ft25 ft

5 ft

B. Contextual side setbacks. : Regardless of the minimum side setback requirements imposed by the zoning district standards of this Code, applicants shall be allowed to use a Contextual side setback. The Contextual side setback shall apply only to primary uses and structures. a Contextual side setback may fall at any point between the required side setback and the side setback that exists on a lot that is adjacent and oriented to the same street as the subject lot, but shall be a minimum of three feet. if the subject lot is a corner lot, the Contextual side setback may fall at any point between the required side setback required by the zoning district and the side setback that exists on the lot that is adjacent and oriented to the same street as the subject lot, but shall be a minimum of three feet. if lots on either side of the subject lot are vacant, the setback that is required by the zoning district shall apply. This provision shall not be interpreted as requiring a greater side setback than imposed by the underlying zoning district, and it shall not be interpreted as allowing setbacks to be reduced to a level that results in right-of-way widths dropping below established minimums.

source: information collected from http://pittsburghpa.gov/dcp/zoning/.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|12

7 | maRKET aNalYsis: siTE PlaN

CENTRE AVE.

TRURO PL.

WALLINGFORD ST.

NEVILLE ST.ENFIELD ST.

S. MILLVALE AVE.

E BUSWAY RAM

P

MELW

OOD AVE.

GOLD WAY

N. CRAIG ST.

BAUM BLVD.

BUILDING USESFoodRetail/ServicesCar dealership/maintenanceOffice/WarehouseVacant lotsVacant BuildingsCommunity ServicesApartments 40 unitsApartments 5-19 unitsResidential Single Family/townhomesPort Authority Transit StopParkingP

P

P

P

P

P

P

P

P

P

P

P

P

P

P

P

P

source: Base map generated from Gis map; Data collected through site visit observation.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|13

CENTRE AVE.

TRURO PL.

WALLINGFORD ST.

NEVILLE ST.ENFIELD ST.

S. MILLVALE AVE.

E BUSWAY RAM

P

MELW

OOD AVE.

GOLD WAY

N. CRAIG ST.

BAUM BLVD.

Community servicesApartments 40 unitsApartments 5-19 unitsResidential Single Family/townhomes

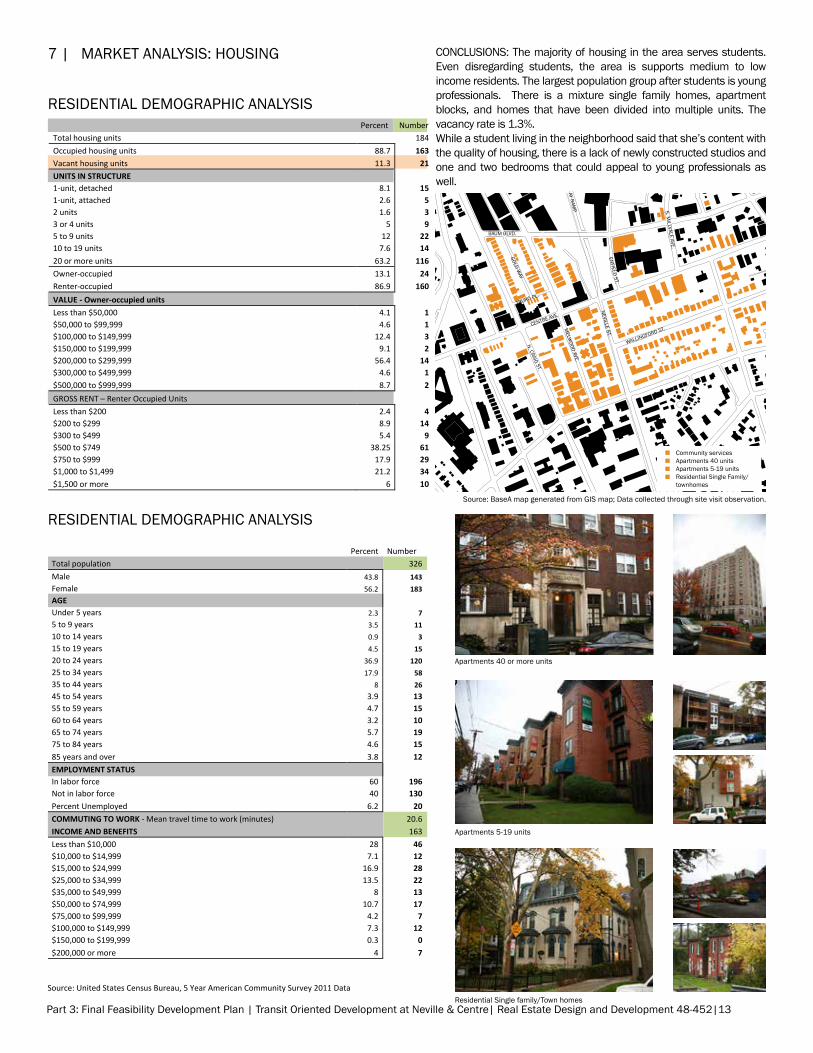

Percent Number

Total housing units

184 Occupied housing units 88.7 163 Vacant housing units 11.3 21 UNITS IN STRUCTURE 1-unit, detached 8.1 15 1-unit, attached 2.6 5 2 units 1.6 3 3 or 4 units 5 9 5 to 9 units 12 22 10 to 19 units 7.6 14 20 or more units 63.2 116 Owner-occupied 13.1 24 Renter-occupied 86.9 160 VALUE - Owner-occupied units

Less than $50,000 4.1 1 $50,000 to $99,999 4.6 1 $100,000 to $149,999 12.4 3 $150,000 to $199,999 9.1 2 $200,000 to $299,999 56.4 14 $300,000 to $499,999 4.6 1 $500,000 to $999,999 8.7 2 GROSS RENT – Renter Occupied Units

Less than $200 2.4 4 $200 to $299 8.9 14 $300 to $499 5.4 9 $500 to $749 38.25 61 $750 to $999 17.9 29 $1,000 to $1,499 21.2 34 $1,500 or more 6 10

CONClUsiONs: The majority of housing in the area serves students. Even disregarding students, the area is supports medium to low income residents. The largest population group after students is young professionals. There is a mixture single family homes, apartment blocks, and homes that have been divided into multiple units. The vacancy rate is 1.3%.While a student living in the neighborhood said that she’s content with the quality of housing, there is a lack of newly constructed studios and one and two bedrooms that could appeal to young professionals as well.

7 | maRKET aNalYsis: HOUsiNG

Source: United States Census Bureau, 5 Year American Community Survey 2011 Data

REsiDENTial DEmOGRaPHiC aNalYsis

REsiDENTial DEmOGRaPHiC aNalYsis

apartments 40 or more units

apartments 5-19 units

Residential single family/Town homes

source: Basea map generated from Gis map; Data collected through site visit observation.

Percent Number

Total population

326 Male 43.8 143 Female 56.2 183 AGE Under 5 years 2.3 7 5 to 9 years 3.5 11 10 to 14 years 0.9 3 15 to 19 years 4.5 15 20 to 24 years 36.9 120 25 to 34 years 17.9 58 35 to 44 years 8 26 45 to 54 years 3.9 13 55 to 59 years 4.7 15 60 to 64 years 3.2 10 65 to 74 years 5.7 19 75 to 84 years 4.6 15 85 years and over 3.8 12 EMPLOYMENT STATUS In labor force 60 196 Not in labor force 40 130 Percent Unemployed 6.2 20 COMMUTING TO WORK - Mean travel time to work (minutes)

20.6

INCOME AND BENEFITS 163 Less than $10,000 28 46 $10,000 to $14,999 7.1 12 $15,000 to $24,999 16.9 28 $25,000 to $34,999 13.5 22 $35,000 to $49,999 8 13 $50,000 to $74,999 10.7 17 $75,000 to $99,999 4.2 7 $100,000 to $149,999 7.3 12 $150,000 to $199,999 0.3 0 $200,000 or more 4 7

Source: United States Census Bureau, 5 Year American Community Survey 2011 Data (the other table as well)

Percent Number

Total housing units

184 Occupied housing units 88.7 163 Vacant housing units 11.3 21 UNITS IN STRUCTURE 1-unit, detached 8.1 15 1-unit, attached 2.6 5 2 units 1.6 3 3 or 4 units 5 9 5 to 9 units 12 22 10 to 19 units 7.6 14 20 or more units 63.2 116 Owner-occupied 13.1 24 Renter-occupied 86.9 160 VALUE - Owner-occupied units

Less than $50,000 4.1 1 $50,000 to $99,999 4.6 1 $100,000 to $149,999 12.4 3 $150,000 to $199,999 9.1 2 $200,000 to $299,999 56.4 14 $300,000 to $499,999 4.6 1 $500,000 to $999,999 8.7 2 GROSS RENT – Renter Occupied Units

Less than $200 2.4 4 $200 to $299 8.9 14 $300 to $499 5.4 9 $500 to $749 38.25 61 $750 to $999 17.9 29 $1,000 to $1,499 21.2 34 $1,500 or more 6 10

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|14

CENTRE AVE.

TRURO PL.

WALLINGFORD ST.

NEVILLE ST.ENFIELD ST.

S. MILLVALE AVE.

E BUSWAY RAM

P

MELW

OOD AVE.

GOLD WAY

N. CRAIG ST.

BAUM BLVD.

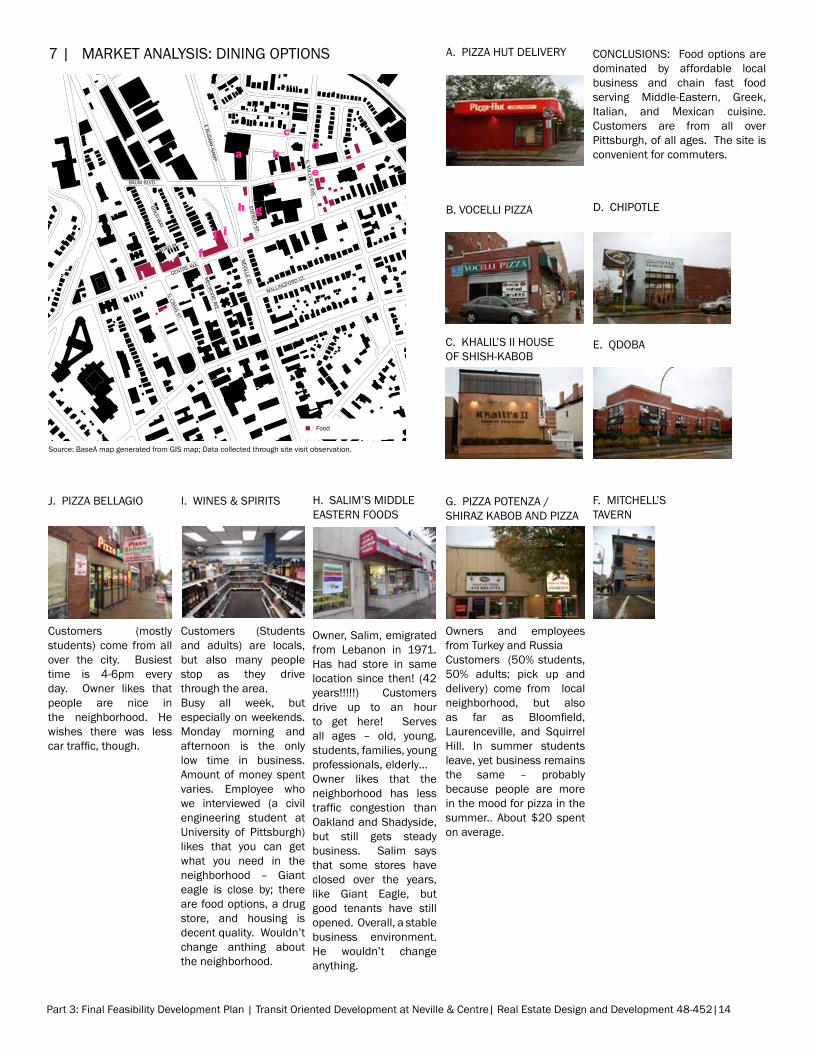

Food

Customers (mostly students) come from all over the city. Busiest time is 4-6pm every day. Owner likes that people are nice in the neighborhood. He wishes there was less car traffic, though.

Customers (students and adults) are locals, but also many people stop as they drive through the area.Busy all week, but especially on weekends. monday morning and afternoon is the only low time in business. amount of money spent varies. Employee who we interviewed (a civil engineering student at University of Pittsburgh) likes that you can get what you need in the neighborhood – Giant eagle is close by; there are food options, a drug store, and housing is decent quality. Wouldn’t change anthing about the neighborhood.

Owner, salim, emigrated from lebanon in 1971. Has had store in same location since then! (42 years!!!!!) Customers drive up to an hour to get here! serves all ages – old, young, students, families, young professionals, elderly…Owner likes that the neighborhood has less traffic congestion than Oakland and shadyside, but still gets steady business. salim says that some stores have closed over the years, like Giant Eagle, but good tenants have still opened. Overall, a stable business environment. He wouldn’t change anything.

G. PiZZa POTENZa / sHiRaZ KaBOB aND PiZZa

H. salim’s miDDlE EasTERN FOODs

i. WiNEs & sPiRiTsJ. PiZZa BEllaGiO

E. QDOBa

F. miTCHEll’sTavERN

Owners and employees from Turkey and RussiaCustomers (50% students, 50% adults; pick up and delivery) come from local neighborhood, but also as far as Bloomfield, laurenceville, and squirrel Hill. in summer students leave, yet business remains the same – probably because people are more in the mood for pizza in the summer.. about $20 spent on average.

CONClUsiONs: Food options are dominated by affordable local business and chain fast food serving middle-Eastern, Greek, italian, and mexican cuisine. Customers are from all over Pittsburgh, of all ages. The site is convenient for commuters.

a. PiZZa HUT DElivERY

B. vOCElli PiZZa D. CHiPOTlE

C. KHalil’s ii HOUsE OF sHisH-KaBOB

a

c

be

d

f

gh

ij

7 | maRKET aNalYsis: DiNiNG OPTiONs

source: Basea map generated from Gis map; Data collected through site visit observation.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|15

CENTRE AVE.

TRURO PL.

WALLINGFORD ST.

NEVILLE ST.ENFIELD ST.

S. MILLVALE AVE.

E BUSWAY RAM

P

MELW

OOD AVE.

GOLD WAY

N. CRAIG ST.

BAUM BLVD.

Retail/ServicesCar dealership/maintenanceOffice/WarehouseVacant lotsVacant Buildings

Car63%

Walking37%

Bus0%

CVS Customer Statistics (Weekdays)

Car Walking Bus

Car67%

Walking33%

Bus0%

CVS Customer Statistics (Weekends)

Car Walking Bus

There is a high density of car dealers in luxury cars on Baum Blvd. This might be due to the high density of car maintenance services in the area. The average rental rate in the area is $6-$10 psf/yrfor automotive property.

There are some vacant warehouses and shops in the area.

The services in the area include supermarket (Cvs), Bank (PNC), and gas station (aTGO). Cvs has a higher customer rate in the weekdays, with a high rate of customers coming by vehicles (63%). The customers in Cvs are mainly 30 to 50, sometimes customers carrying children with them to Cvs. There are 2 customers per minute in the rush hours during weekdays. The rental rate for the retail store is $25-$34 psf/year.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1

0.4

0.2

0Cust

omer

rate

(per

min

ute)

CVS Customer Rate (Weekends)

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1

1.3

0.775

0Cust

omer

rate

(per

min

ute)

CVS Customer Rate (Weekdays)

Customers are locals as well as many commuters who stop as they drive through. Customers are all ages, old and young.Friday nights are the busiest time. The employee we spoke with likes that the neighborhood is so culturally diverse.she does wish that police patrolled the streets at night, so that people would feel more comfortable. she doesn’t actually feel that there is much crime in the area, but with the boarded-up stores people think that the neighborhood is dangerous.

iNTERviEW: mONEY maRT

There are several car maintenance services near Baum Blvd. The high density of car dealers and car maintenance services suggests that a major customer type is commuters by car.

The vacancy rate in Pittsburgh has decreased to 4.1% comparing to 4.5% in the second quarter. The rate is also lower than the U.s. National Retail vacancy rate, 6.7%.

CONClUsiONs:We noticed that there are not many people getting off the bus in the area. Hence, according to the major customer type and the retail type in the area, we suggest that the customers in the area are mostly car-based. Developing improved public transit, we have the opportunity to relieve traffic congestion, while offering new services and retail opportunities to both existing and new public transit commuters.

7 | maRKET aNalYsis: sERviCE iNDUsTRY

CaR DEalERsHiP sERviCE

vaCaNCY

CaR maiNTaNENCE

source: Basea map generated from Gis map; Data collected through site visit observation.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|16

7 | maRKET aNalYsis: OPPORTUNiTiEs FOR DEvElOPmENT

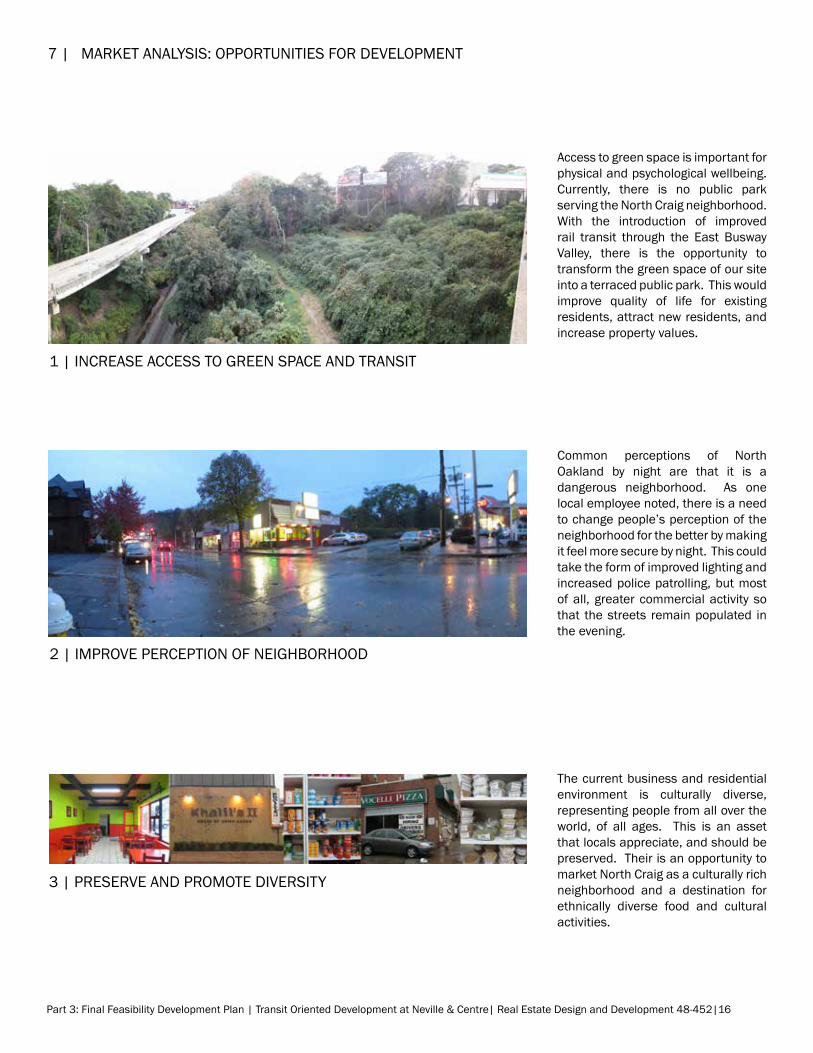

access to green space is important for physical and psychological wellbeing. Currently, there is no public park serving the North Craig neighborhood. With the introduction of improved rail transit through the East Busway valley, there is the opportunity to transform the green space of our site into a terraced public park. This would improve quality of life for existing residents, attract new residents, and increase property values.

1 | iNCREasE aCCEss TO GREEN sPaCE aND TRaNsiT

2 | imPROvE PERCEPTiON OF NEiGHBORHOOD

3 | PREsERvE aND PROmOTE DivERsiTY

Common perceptions of North Oakland by night are that it is a dangerous neighborhood. as one local employee noted, there is a need to change people’s perception of the neighborhood for the better by making it feel more secure by night. This could take the form of improved lighting and increased police patrolling, but most of all, greater commercial activity so that the streets remain populated in the evening.

The current business and residential environment is culturally diverse, representing people from all over the world, of all ages. This is an asset that locals appreciate, and should be preserved. Their is an opportunity to market North Craig as a culturally rich neighborhood and a destination for ethnically diverse food and cultural activities.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|17

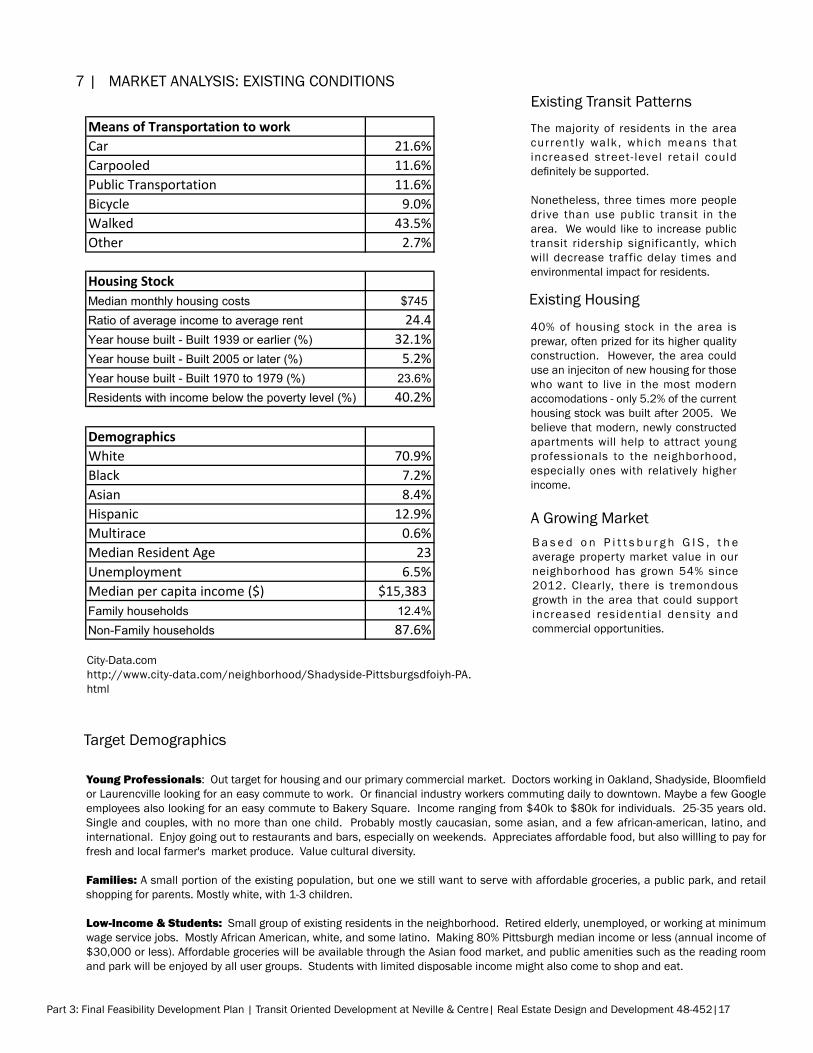

Means of Transportation to workCar 21.6%Carpooled 11.6%Public Transportation 11.6%Bicycle 9.0%Walked 43.5%Other 2.7%

Housing StockMedian monthly housing costs $745Ratio of average income to average rent 24.4Year house built - Built 1939 or earlier (%) 32.1%Year house built - Built 2005 or later (%) 5.2%Year house built - Built 1970 to 1979 (%) 23.6%Residents with income below the poverty level (%) 40.2%

DemographicsWhite 70.9%Black 7.2%Asian 8.4%Hispanic 12.9%Multirace 0.6%Median Resident Age 23Unemployment 6.5%Median per capita income ($) $15,383Family households 12.4%Non-Family households 87.6%

Existing Transit PatternsThe majority of residents in the area current ly walk, which means that increased street- level retai l could definitely be supported.

Nonetheless, three times more people drive than use public transit in the area. We would like to increase public transit ridership significantly, which will decrease traffic delay times and environmental impact for residents.

Existing Housing

Target Demographics

40% of housing stock in the area is prewar, often prized for its higher quality construction. However, the area could use an injeciton of new housing for those who want to live in the most modern accomodations - only 5.2% of the current housing stock was built after 2005. We believe that modern, newly constructed apartments will help to attract young professionals to the neighborhood, especially ones with relatively higher income.

Young Professionals: Out target for housing and our primary commercial market. Doctors working in Oakland, Shadyside, Bloomfield or Laurencville looking for an easy commute to work. Or financial industry workers commuting daily to downtown. Maybe a few Google employees also looking for an easy commute to Bakery square. income ranging from $40k to $80k for individuals. 25-35 years old. single and couples, with no more than one child. Probably mostly caucasian, some asian, and a few african-american, latino, and international. Enjoy going out to restaurants and bars, especially on weekends. appreciates affordable food, but also willling to pay for fresh and local farmer's market produce. value cultural diversity.

Families: a small portion of the existing population, but one we still want to serve with affordable groceries, a public park, and retail shopping for parents. mostly white, with 1-3 children.

Low-Income & Students: small group of existing residents in the neighborhood. Retired elderly, unemployed, or working at minimum wage service jobs. mostly african american, white, and some latino. making 80% Pittsburgh median income or less (annual income of $30,000 or less). affordable groceries will be available through the asian food market, and public amenities such as the reading room and park will be enjoyed by all user groups. students with limited disposable income might also come to shop and eat.

a Growing marketB a s e d o n P i t t s b u r g h G i s , t h e average property market value in our neighborhood has grown 54% since 2012. Clearly, there is tremondous growth in the area that could support increased residential density and commercial opportunities.

City-Data.comhttp://www.city-data.com/neighborhood/shadyside-Pittsburgsdfoiyh-Pa.html

7 | maRKET aNalYsis: EXisTiNG CONDiTiONs

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|18

7 | maRKET aNalYsis: PROPOsED NEW UsEs

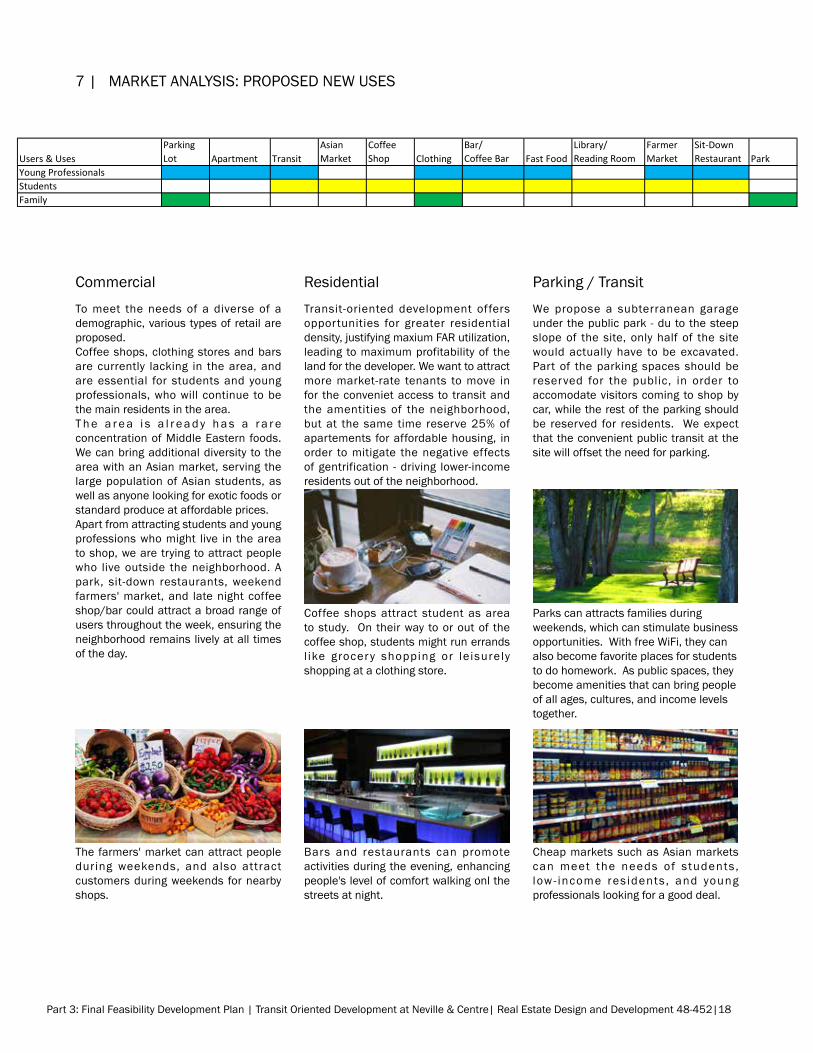

Users & UsesParking Lot Apartment Transit

Asian Market

Coffee Shop Clothing

Bar/Coffee Bar Fast Food

Library/Reading Room

Farmer Market

Sit-DownRestaurant Park

Young ProfessionalsStudentsFamily

CommercialTo meet the needs of a diverse of a demographic, various types of retail are proposed. Coffee shops, clothing stores and bars are currently lacking in the area, and are essential for students and young professionals, who will continue to be the main residents in the area.T h e a r e a i s a l r e a d y h a s a r a r e concentration of middle Eastern foods. We can bring additional diversity to the area with an asian market, serving the large population of asian students, as well as anyone looking for exotic foods or standard produce at affordable prices.apart from attracting students and young professions who might live in the area to shop, we are trying to attract people who live outside the neighborhood. a park, sit-down restaurants, weekend farmers' market, and late night coffee shop/bar could attract a broad range of users throughout the week, ensuring the neighborhood remains lively at all times of the day.

ResidentialTransit-oriented development offers opportunities for greater residential density, justifying maxium FaR utilization, leading to maximum profitability of the land for the developer. We want to attract more market-rate tenants to move in for the conveniet access to transit and the amentities of the neighborhood, but at the same time reserve 25% of apartements for affordable housing, in order to mitigate the negative effects of gentrification - driving lower-income residents out of the neighborhood.

Parking / TransitWe propose a subterranean garage under the public park - du to the steep slope of the site, only half of the site would actually have to be excavated. Part of the parking spaces should be reserved for the public, in order to accomodate visitors coming to shop by car, while the rest of the parking should be reserved for residents. We expect that the convenient public transit at the site will offset the need for parking.

The farmers' market can attract people during weekends, and also attract customers during weekends for nearby shops.

Coffee shops attract student as area to study. On their way to or out of the coffee shop, students might run errands l ike grocer y shopping or le isurely shopping at a clothing store.

Bars and restaurants can promote activities during the evening, enhancing people's level of comfort walking onl the streets at night.

Parks can attracts families during weekends, which can stimulate business opportunities. With free WiFi, they can also become favorite places for students to do homework. as public spaces, they become amenities that can bring people of all ages, cultures, and income levels together.

Cheap markets such as asian markets can meet the needs of students , low - income res idents , and young professionals looking for a good deal.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|19

after development, the apartment rent on our site will increase to over $1,000 per month, so our target customers for housing is relative high income young professionals ($60,000 in average), specially UPmC employees. Our site is only two blocks away from their workplace, and they will be more willing to spend more money on housing for better place and on leisure activities such as bars and sit-down restaurants.

most of the parking lots are for the tenants in the apartments, and others are preserved for customers coming with cars (families).

The target customers for the asian market are international (asian) students, since they are the group who tend to save money by cooking theirselves during their time in school. an asian market provides relatively cheap food ingredients, and exclusive ingredients for making asian dishes. it will also serve any other students or young professionals looking for a deal.

The main group of customers we expect in coffee shop is students or single young professionals in leisure. a lot of students in Pittsburgh live in Oakland and shadyside, so a coffee shop or reading room provides a quality alternatives work environment. also, the coffee shop is targeting american students, who are more willing than international students to spend money on espresso drinks.

We expect to have two types of target customers in fast food restaurant, in two time periods. The means of transportation to work in the area are mainly by walking, so we suggest that it is possible for professionals working near the site to come to the fast food restaurants during lunch time. On the other hand, students who lives in Oakland or shadyside will be the target customers during dinner time, since the restaurants are located on their way back home.

The library or reading room is public access and provides free Wi-Fi. The target customers will be students living in the neighborhood, and probably low-income coming for the free Wi-Fi. The library, asian market and fast food tend to have the same target customers, so the interaction between the three area will lead to more customers than we expected.

The public transit is mainly for young professionals, students and existing residents who do not have a car.

american students coming from high income families and single young professionals with medium or high income are the main potential customers in bars and coffee bars, and the convenient public transit makes this a perfect late-night hang out.

Bars / Coffee Bars

apartments

Parking lots

asian market

Coffee shop

Fast Food

Transit

library / Reading Room

7 | maRKET aNalYsis: UsER GROUPs

Farmers' market

a farmers' market in the park will to local families and young professionals on the weekend.

sit-Down Restaurants

sit-down restaurants will be visited occasionally by families, but the main market will be young professionals and students from higher-income families.

ParkGreen space wi l l be valued by ever yone in the neihgborhood - currently their is no park serving the North Oakland area. We expect in particular that families will like coming here on weekends with their kids, and that students and young professionals might also enjoy reading or studying outside, perhaps with a picnic. in the summer, we image Pittsburgh Film makers showing films on an outdoor screen.

Clothing storeslocally-owned boutiques and perhaps one or two national chains will serve neighborhood locals, including mothers, young professional women living in the development, and occasionally students. There may be one speciality men's clothing store, although the market demand is probably not be great enough for this. a mixture of stores focusing on accesories, everyday clothes, and maybe one higher-end boutiqu with modern style dresses and semi-formal clothing.

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|20

6 | maRKET aNalYsis: COmPaRaBlEs

DivERsiTY:White: 79.4%Black: 2.6%asian: 16.5%Hispanic: 0.1%multi-race: 1.3%

COMPARISON

DisTaNCE FROm siTE:1.8 miles

at $65 million for 252,000 sq ft of retail and 360 apartments, East side iii yields more leasable space for the cost than our project ($112.2 million for 84,629 sq ft of retail and 357 apartments).

The median age for our area is younger than in the East End: 23 vs 35. This indicates the higher density of students, who our development should serve. at the same time, the proximity to transit to downtown and to UPmC shadyside and Oakland could make our rentals attractive to more young professionals in their late 20s to mid 30s.

additionally, there is more racial diversity in our neighborhood than in East liberty, particularly a higher asian population, supporting our decision to target retail to more diverse cultural groups.

Our site is one of the gateways to the East Busway, so we can expect high commuter levels comparable to what is experienced at the site of the East liberty Transit Center.

EasT siDE iii + EasT liBERTY TRaNsiT CENTERPROJECT CHARACTERISTICS

CONsTRUCTiON:New

BUs sTaTiON:1,000 daily bus departures and arrivals

RETail: 252,700 sf

Retail alower level: 39,000 sfUpper level: 39,000 sf

Retail B14,305 sf

Retail Clower level: 6,300 sfUpper level: 7,400 sf

Retail Danchor Tenant: 145,000 sfGround level: 16,000 sf

Residential:360 apartments

COsT:$65 million$15 million Tiger iv federal grant for transit stop

maRKET

locals and Commuter(33,000 Port authority commuters/day)

mixed income(average Household income = $81,774 for over 100,000 families in trade area - highest average in Pittsburgh)

mixed Education (52% collage educated and above in 1-mile radius of site)

students (41,500) and Workers (38,000) from 2 of Pittsburgh top 10 employers, within 2 miles of site

$170 million in annual sales for 4 major food stores in 3-block radius.

source: moore, andew “East side iii and $52 million East liberty Transit Center moving forward together.” POP City. 2/20/13, accessed 11/17/2013 h t t p : / / w w w . p o p c i t y m e d i a . c o m / d e v n e w s /eastsideiii022013.aspx

source: Brill, Christine and Jonathan Kline. “East liberty Transit Center.” Studio for Spatial Practice. 2/20/13, accessed 11/17/2013 http://studiofsp.com/urbanism/east-liberty-station/

“Eastside iii, iv, and v.” The Mosites Company. accessed 11/17/2013 http://www.mosites.net/portfolio_3.html

Retail A Lower Level: 39,000 sf Upper Level: 39,000 sf Retail B 14,305 sf Retail C Lower Level: 6,300 sf Upper Level: 7,400 sf

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|21

6 | maRKET aNalYsis: COmPaRaBlEsTotal Employees:1 mile: 12,4043 miles: 94,6535 miles: 270,714

Over $131,700,000.00 spent on dining out & over $138,059,381.00 spent on apparel service purchases in the neighboring communities in 2010

DivERsiTY:similar to East End iii

sUsTaiNaBiliTYLEED-Platimum certifiedsolar Pvlow-Flow FixturesGreen RoofNatural DaylightingRecycled & local materials

COMPARISONDisTaNCE FROm siTE:2.1 miles

Our project costs $112 million for 332, 469 sf ($336psf), compared to Bakery square at $135 million for 250,000 sf ($540psf), so our project might yield more leasable area for less money. However, as we are unable to determine the square footage of spring Hill suites and the parking at Bakery square, this comparison is likely flawed. The fact that Bakery square was adaptive reuse probably indicates a higher cost of construction than our project, however.The median household income in our neighborhood is about half of what it is surrounding Bakery square: about $40,000 for areas immediately adjacent to our site, supporting our decision to have retail offerings for middle to upper-middle-class young professionals, students, and low-income residents.We are adopting some of the same sustainable strategies including green roof and natural daylighting. in addition, we are striving for passive house energy efficiency standards with high insulation and energy recovery ventilators.

BaKERY sQUaREPROJECT CHARACTERISTICS

CONsTRUCTiON:adaptive Reuse & New

COmmERCial: 250,000 sf21 Tenants, including:Retail ClothingFast Food & CoffeeHi TechmedicalFitness/HealthBankHotel

Ground Floor Retail121,060 sq. ft.

Fitness Center41,550 sq. ft.

Office216,080 sq. ft.

Hotel – marriott springHill suites110 rooms

Parking932 garage | 99 surface

COsT:$135 million(including $1 million environmental remediation)$10 million TiF

maRKET

Residential Population:1 mile: 27,6903 miles: 181,7195 miles: 337,765

median age: 35.5 yrs

mixed incomeaverage Household income for neighboring communities: $81,663.0014.2% of Households have net worth of over $500,000.00

mixed Education (51% collage educated and above in surrounding area)

students (41,500) and Workers (38,000) from 2 of Pittsburgh top 10 employers, within 2 miles of site (University of Pittsburgh and Carnegie mellon University)

source: “Bakery square Development (Former Nabisco Factory.” Western Pennsylvania Brownfields Center. accessed 11/17/2013http://www.cmu.edu/steinbrenner/brownfields/

Retail A Lower Level: 39,000 sf Upper Level: 39,000 sf Retail B 14,305 sf Retail C Lower Level: 6,300 sf Upper Level: 7,400 sf

source: “leasing information.” Bakery Square. accessed 11/17/2013 http://bakery-square.com/lease/

“Google’s decision to lease more space at Bakery square expected to attract new businesses.” POP City. 1/12/13, accessed 11/17/2013 http://www.popcitymedia.com/devnews/googleexpansion011211.aspx

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|22

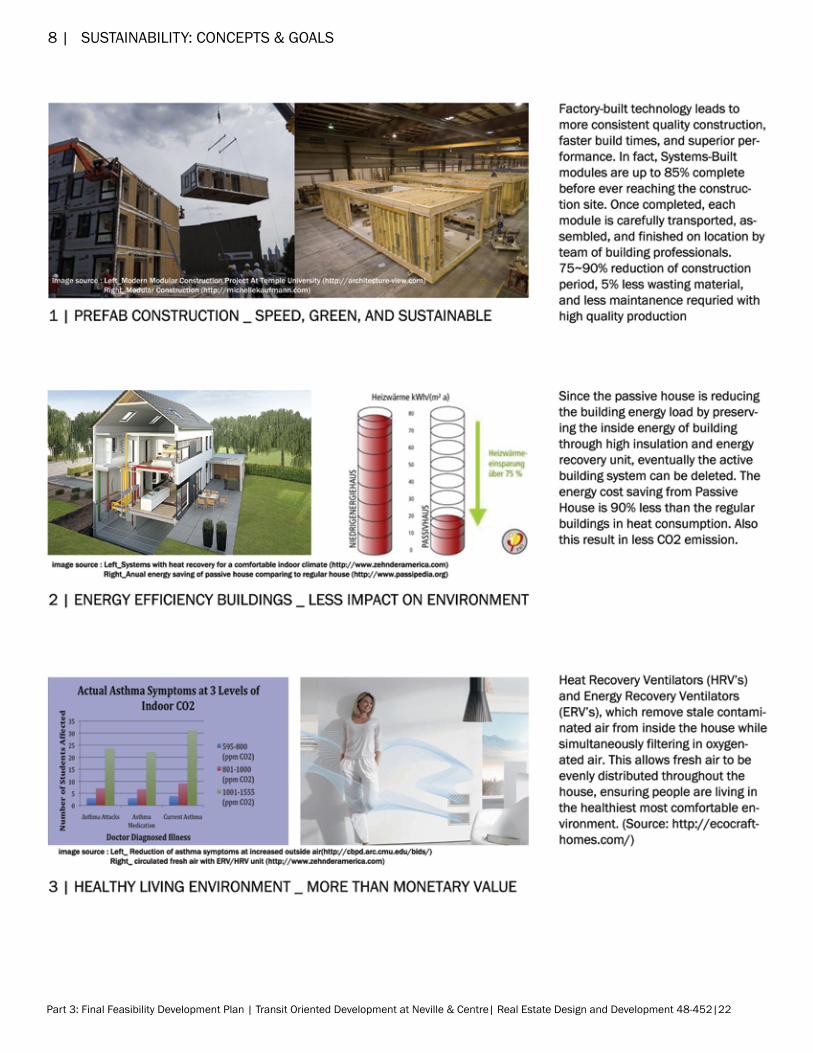

8 | sUsTaiNaBiliTY: CONCEPTs & GOals

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|23

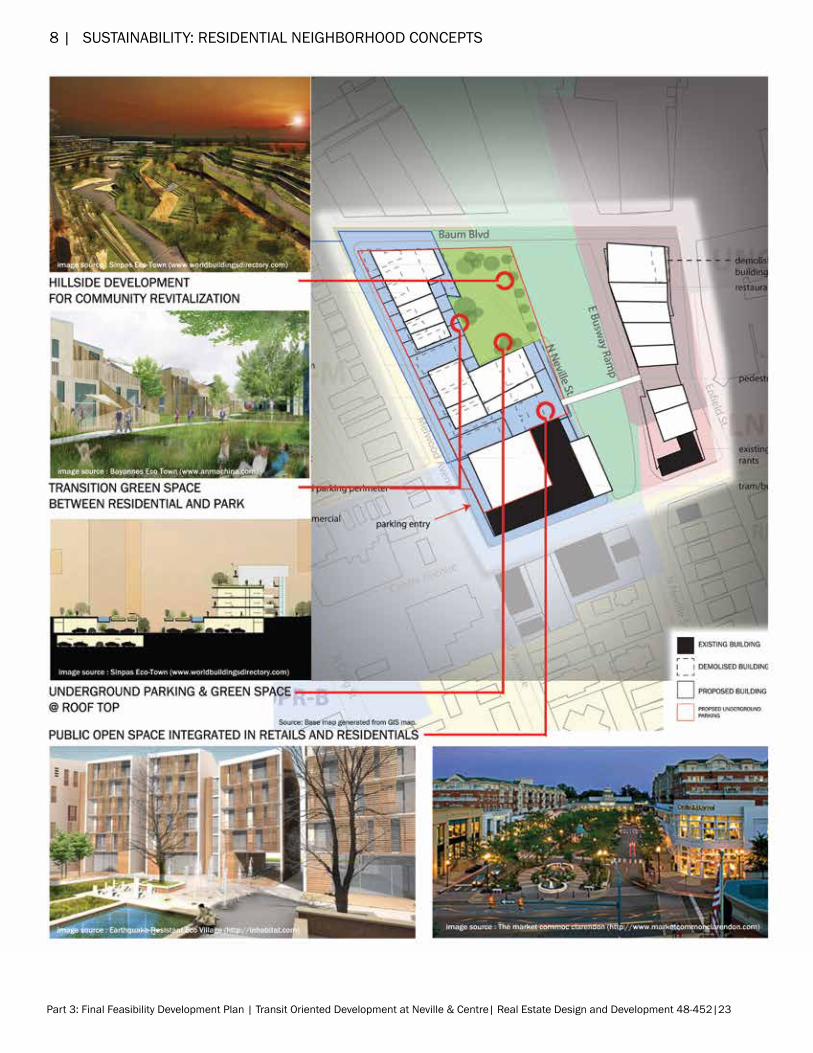

8 | sUsTaiNaBiliTY: REsiDENTial NEiGHBORHOOD CONCEPTs

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|24

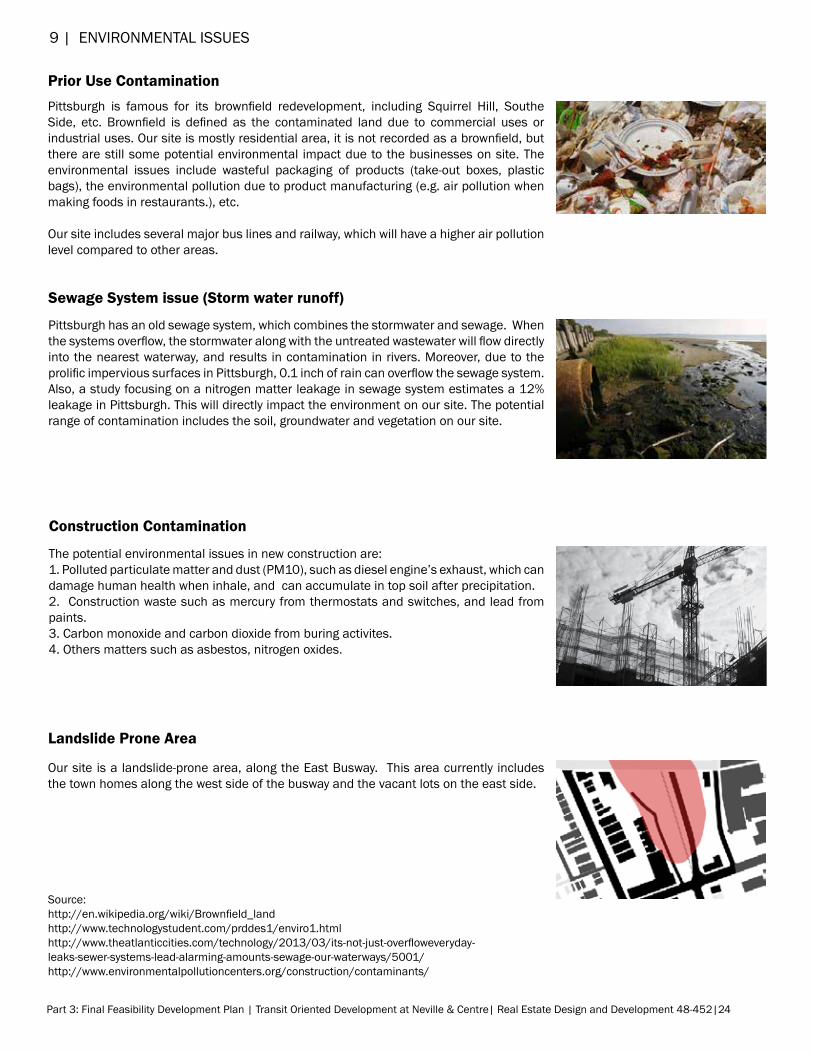

Landslide Prone Area

Our site is a landslide-prone area, along the East Busway. This area currently includes the town homes along the west side of the busway and the vacant lots on the east side.

Construction Contamination

The potential environmental issues in new construction are:1. Polluted particulate matter and dust (Pm10), such as diesel engine’s exhaust, which can damage human health when inhale, and can accumulate in top soil after precipitation.2. Construction waste such as mercury from thermostats and switches, and lead from paints.3. Carbon monoxide and carbon dioxide from buring activites.4. Others matters such as asbestos, nitrogen oxides.

Prior Use ContaminationPittsburgh is famous for its brownfield redevelopment, including Squirrel Hill, Southe Side, etc. Brownfield is defined as the contaminated land due to commercial uses or industrial uses. Our site is mostly residential area, it is not recorded as a brownfield, but there are still some potential environmental impact due to the businesses on site. The environmental issues include wasteful packaging of products (take-out boxes, plastic bags), the environmental pollution due to product manufacturing (e.g. air pollution when making foods in restaurants.), etc.

Our site includes several major bus lines and railway, which will have a higher air pollution level compared to other areas.

Sewage System issue (Storm water runoff)

Pittsburgh has an old sewage system, which combines the stormwater and sewage. When the systems overflow, the stormwater along with the untreated wastewater will flow directly into the nearest waterway, and results in contamination in rivers. moreover, due to the prolific impervious surfaces in Pittsburgh, 0.1 inch of rain can overflow the sewage system. also, a study focusing on a nitrogen matter leakage in sewage system estimates a 12% leakage in Pittsburgh. This will directly impact the environment on our site. The potential range of contamination includes the soil, groundwater and vegetation on our site.

source: http://en.wikipedia.org/wiki/Brownfield_landhttp://www.technologystudent.com/prddes1/enviro1.htmlhttp://www.theatlanticcities.com/technology/2013/03/its-not-just-overfloweveryday-leaks-sewer-systems-lead-alarming-amounts-sewage-our-waterways/5001/http://www.environmentalpollutioncenters.org/construction/contaminants/

9 | ENviRONmENTal issUEs

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|25

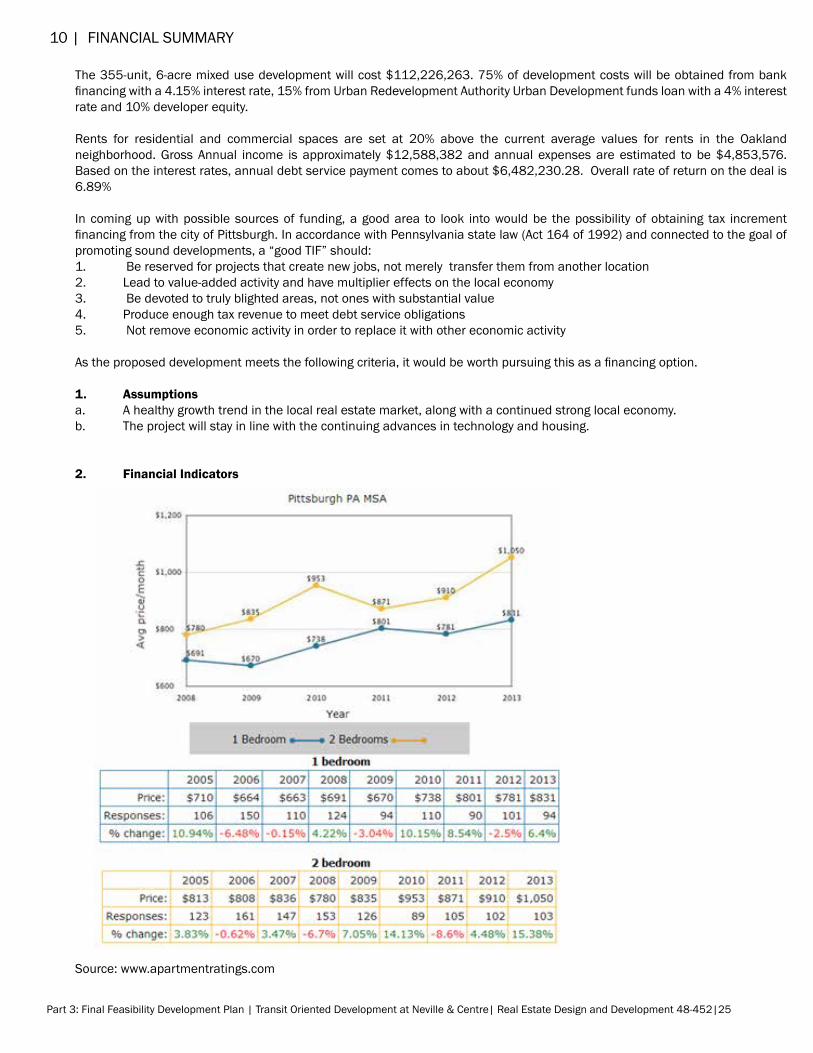

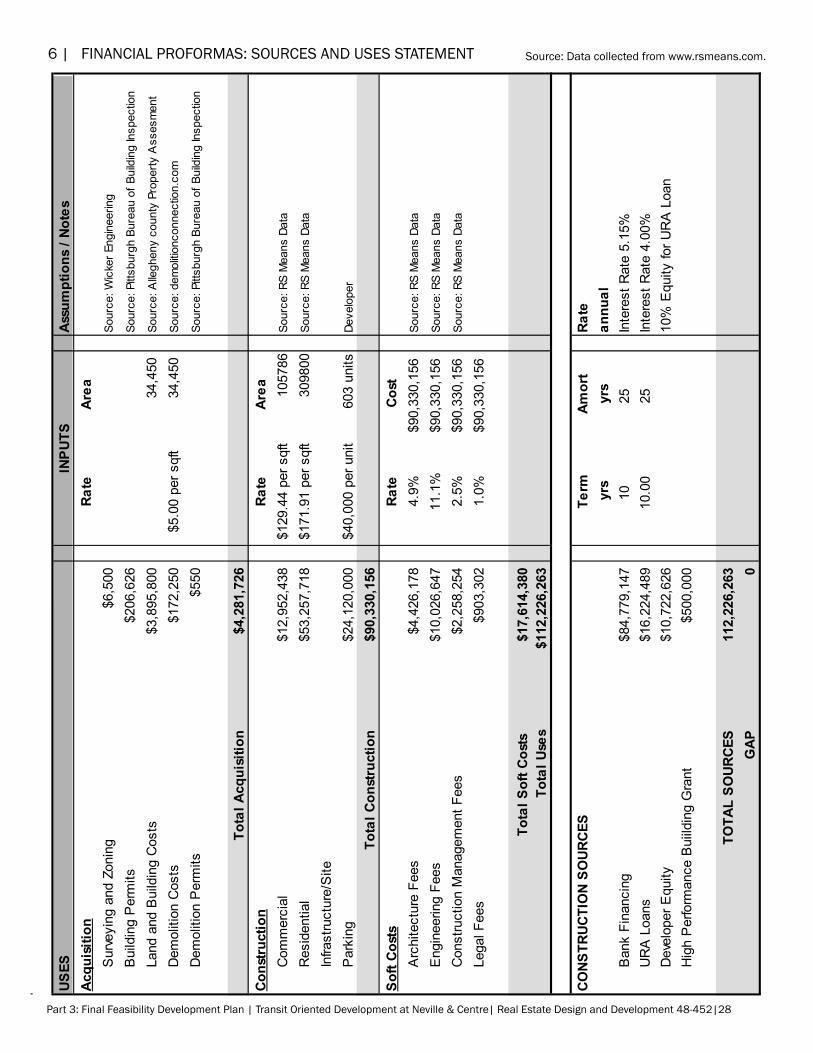

The 355-unit, 6-acre mixed use development will cost $112,226,263. 75% of development costs will be obtained from bank financing with a 4.15% interest rate, 15% from Urban Redevelopment Authority Urban Development funds loan with a 4% interest rate and 10% developer equity.

Rents for residential and commercial spaces are set at 20% above the current average values for rents in the Oakland neighborhood. Gross annual income is approximately $12,588,382 and annual expenses are estimated to be $4,853,576. Based on the interest rates, annual debt service payment comes to about $6,482,230.28. Overall rate of return on the deal is 6.89%

in coming up with possible sources of funding, a good area to look into would be the possibility of obtaining tax increment financing from the city of Pittsburgh. In accordance with Pennsylvania state law (Act 164 of 1992) and connected to the goal of promoting sound developments, a “good TiF” should:1. Be reserved for projects that create new jobs, not merely transfer them from another location2. lead to value-added activity and have multiplier effects on the local economy3. Be devoted to truly blighted areas, not ones with substantial value4. Produce enough tax revenue to meet debt service obligations5. Not remove economic activity in order to replace it with other economic activity

As the proposed development meets the following criteria, it would be worth pursuing this as a financing option.

1. Assumptionsa. a healthy growth trend in the local real estate market, along with a continued strong local economy. b. The project will stay in line with the continuing advances in technology and housing.

2. Financial Indicators

source: www.apartmentratings.com

10 | FiNaNCial sUmmaRY

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|26

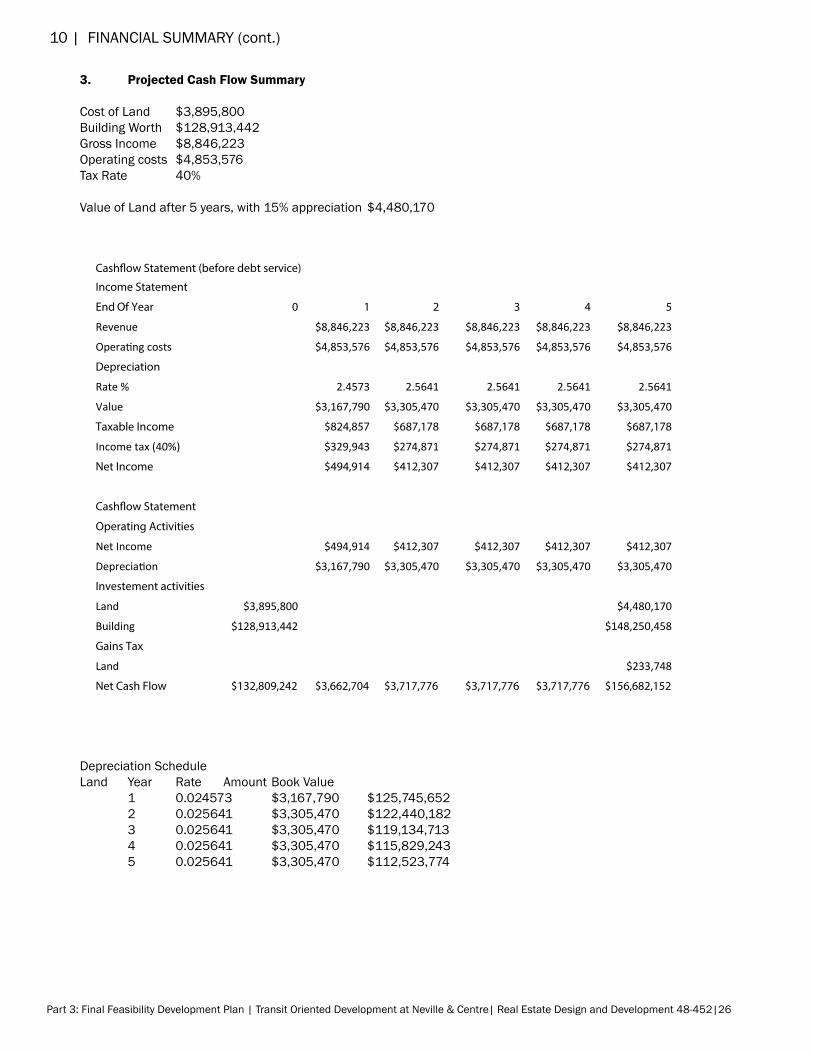

3. Projected Cash Flow Summary

Cost of land $3,895,800 Building Worth $128,913,442 Gross income $8,846,223 Operating costs $4,853,576 Tax Rate 40% value of land after 5 years, with 15% appreciation $4,480,170

Depreciation schedule land Year Rate amount Book value 1 0.024573 $3,167,790 $125,745,652 2 0.025641 $3,305,470 $122,440,182 3 0.025641 $3,305,470 $119,134,713 4 0.025641 $3,305,470 $115,829,243 5 0.025641 $3,305,470 $112,523,774

Cash�ow Statement (before debt service) Income Statement

End Of Year 0 1 2 3 4 5

Revenue

$8,846,223 $8,846,223 $8,846,223 $8,846,223 $8,846,223

Operating costs

$4,853,576 $4,853,576 $4,853,576 $4,853,576 $4,853,576

Depreciation Rate %

2.4573 2.5641 2.5641 2.5641 2.5641

Value

$3,167,790 $3,305,470 $3,305,470 $3,305,470 $3,305,470

Taxable Income

$824,857 $687,178 $687,178 $687,178 $687,178

Income tax (40%)

$329,943 $274,871 $274,871 $274,871 $274,871

Net Income

$494,914 $412,307 $412,307 $412,307 $412,307

Cash�ow Statement Operating Activities Net Income

$494,914 $412,307 $412,307 $412,307 $412,307

Depreciation

$3,167,790 $3,305,470 $3,305,470 $3,305,470 $3,305,470

Investement activities Land $3,895,800

$4,480,170

Building $128,913,442

$148,250,458

Gains Tax Land

$233,748

Net Cash Flow $132,809,242 $3,662,704 $3,717,776 $3,717,776 $3,717,776 $156,682,152

Depreciation Schedule Land Year Rate Amount Book Value

1 0.024573 $3,167,790 $125,745,652

2 0.025641 $3,305,470 $122,440,182

3 0.025641 $3,305,470 $119,134,713

4 0.025641 $3,305,470 $115,829,243

5 0.025641 $3,305,470 $112,523,774

10 | FiNaNCial sUmmaRY (cont.)

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|27

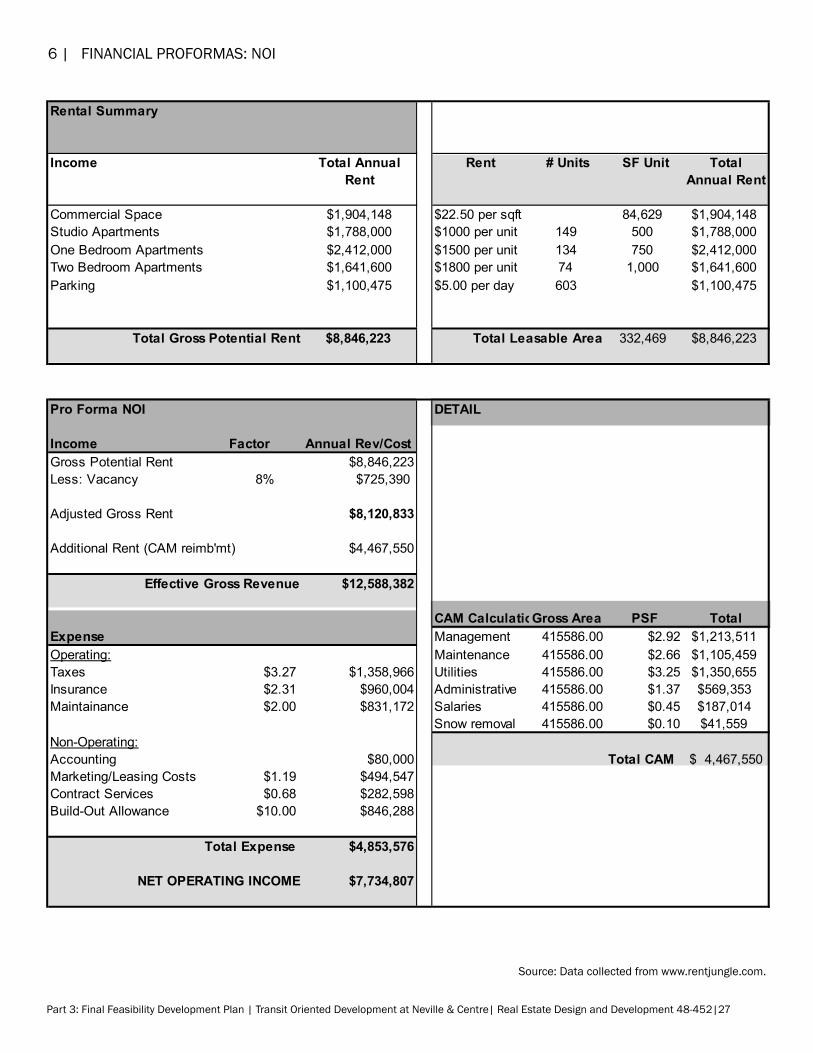

6 | FiNaNCial PROFORmas: NOi

source: Data collected from www.rentjungle.com.

Rental Summary

Income Total Annual Rent

Rent # Units SF Unit Total Annual Rent

Commercial Space $1,904,148 $22.50 per sqft 84,629 $1,904,148Studio Apartments $1,788,000 $1000 per unit 149 500 $1,788,000One Bedroom Apartments $2,412,000 $1500 per unit 134 750 $2,412,000Two Bedroom Apartments $1,641,600 $1800 per unit 74 1,000 $1,641,600Parking $1,100,475 $5.00 per day 603 $1,100,475

Total Gross Potential Rent $8,846,223 Total Leasable Area 332,469 $8,846,223

Pro Forma NOI DETAIL

Income Factor Annual Rev/CostGross Potential Rent $8,846,223Less: Vacancy 8% $725,390

Adjusted Gross Rent $8,120,833

Additional Rent (CAM reimb'mt) $4,467,550

Effective Gross Revenue $12,588,382

CAM CalculationGross Area PSF TotalExpense Management 415586.00 $2.92 $1,213,511Operating: Maintenance 415586.00 $2.66 $1,105,459Taxes $3.27 $1,358,966 Utilities 415586.00 $3.25 $1,350,655Insurance $2.31 $960,004 Administrative 415586.00 $1.37 $569,353Maintainance $2.00 $831,172 Salaries 415586.00 $0.45 $187,014

Snow removal 415586.00 $0.10 $41,559Non-Operating:Accounting $80,000 Total CAM 4,467,550$ Marketing/Leasing Costs $1.19 $494,547Contract Services $0.68 $282,598Build-Out Allowance $10.00 $846,288

Total Expense $4,853,576

NET OPERATING INCOME $7,734,807

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|28

6 | FiNaNCial PROFORmas: sOURCEs aND UsEs sTaTEmENT source: Data collected from www.rsmeans.com.US

ESIN

PUTS

Assu

mpt

ions

/ No

tes

Acqu

isiti

onRa

teAr

eaS

urve

ying

and

Zon

ing

$6,5

00So

urce

: Wic

ker E

ngin

eerin

g

Bui

ldin

g P

erm

its$2

06,6

26So

urce

: Pitt

sbur

gh B

urea

u of

Bui

ldin

g In

spec

tion

Land

and

Bui

ldin

g C

osts

$3,8

95,8

0034

,450

Sour

ce: A

llegh

eny

coun

ty P

rope

rty A

sses

men

t

Dem

oliti

on C

osts

$172

,250

$5.0

0 pe

r sqf

t34

,450

Sour

ce: d

emol

itionc

onne

ctio

n.co

m

Dem

oliti

on P

erm

its$5

50So

urce

: Pitt

sbur

gh B

urea

u of

Bui

ldin

g In

spec

tion

Tota

l Acq

uisi

tion

$4,2

81,7

26Co

nstru

ctio

nRa

teAr

eaC

omm

erci

al$1

2,95

2,43

8$1

29.4

4 pe

r sqf

t10

5786

Sour

ce: R

S M

eans

Dat

a

Res

iden

tial

$53,

257,

718

$171

.91

per s

qft

3098

00So

urce

: RS

Mea

ns D

ata

Infra

stru

ctur

e/S

iteP

arki

ng$2

4,12

0,00

0$4

0,00

0 pe

r uni

t60

3 un

itsDe

velo

per

Tota

l Con

stru

ctio

n$9

0,33

0,15

6So

ft Co

sts

Rate

Cost

Arc

hite

ctur

e Fe

es$4

,426

,178

4.9%

$90,

330,

156

Sour

ce: R

S M

eans

Dat

a

Eng

inee

ring

Fees

$10,

026,

647

11.1

%$9

0,33

0,15

6So

urce

: RS

Mea

ns D

ata

Con

stru

ctio

n M

anag

emen

t Fee

s$2

,258

,254

2.5%

$90,

330,

156

Sour

ce: R

S M

eans

Dat

a

Lega

l Fee

s$9

03,3

021.

0%$9

0,33

0,15

6

Tota

l Sof

t Cos

ts$1

7,61

4,38

0To

tal U

ses

$112

,226

,263

CONS

TRUC

TIO

N SO

URCE

STe

rmAm

ort

Rate

yrs

yrs

annu

alB

ank

Fina

ncin

g$8

4,77

9,14

710

25In

tere

st R

ate

5.15

%U

RA

Loa

ns$1

6,22

4,48

910

.00

25In

tere

st R

ate

4.00

%D

evel

oper

Equ

ity$1

0,72

2,62

610

% E

quity

for U

RA

Loa

nH

igh

Per

form

ance

Bui

ildin

g G

rant

$500

,000

TOTA

L SO

URCE

S11

2,22

6,26

3G

AP0

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|29

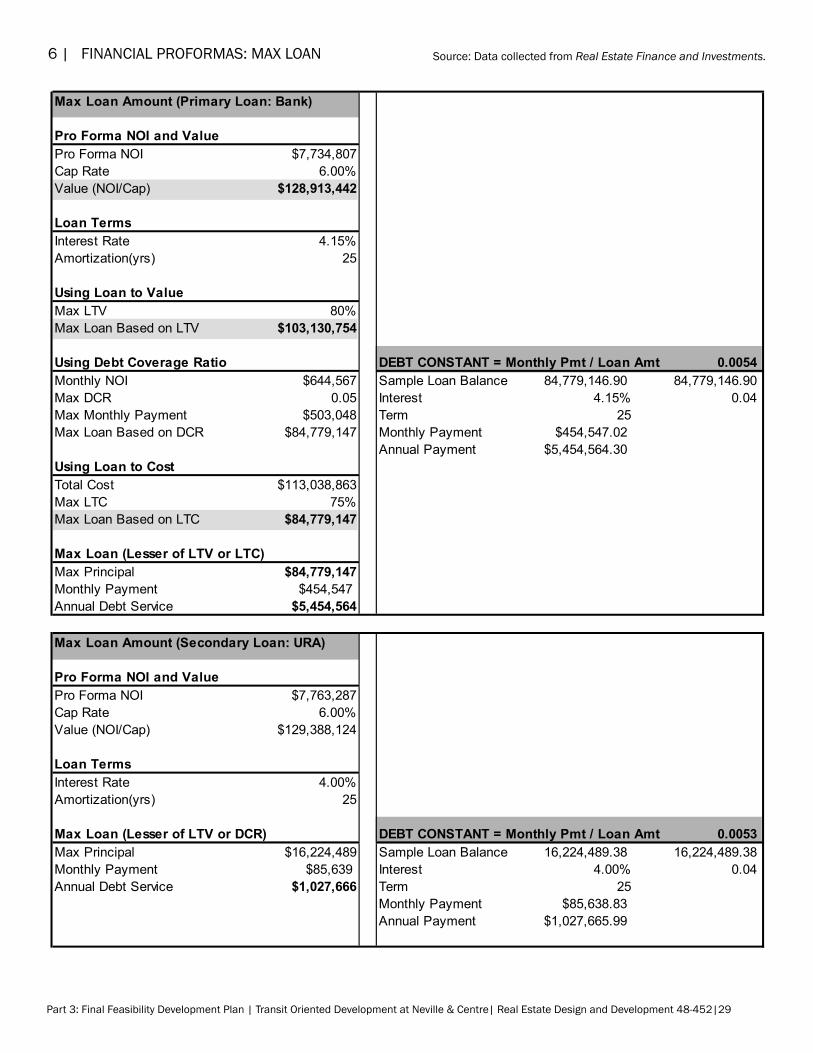

6 | FiNaNCial PROFORmas: maX lOaN source: Data collected from Real Estate Finance and Investments.

Max Loan Amount (Primary Loan: Bank)

Pro Forma NOI and ValuePro Forma NOI $7,734,807Cap Rate 6.00%Value (NOI/Cap) $128,913,442

Loan TermsInterest Rate 4.15%Amortization(yrs) 25

Using Loan to ValueMax LTV 80%Max Loan Based on LTV $103,130,754

Using Debt Coverage Ratio DEBT CONSTANT = Monthly Pmt / Loan Amt 0.0054Monthly NOI $644,567 Sample Loan Balance 84,779,146.90 84,779,146.90Max DCR 0.05 Interest 4.15% 0.04Max Monthly Payment $503,048 Term 25Max Loan Based on DCR $84,779,147 Monthly Payment $454,547.02

Annual Payment $5,454,564.30Using Loan to CostTotal Cost $113,038,863Max LTC 75%Max Loan Based on LTC $84,779,147

Max Loan (Lesser of LTV or LTC)Max Principal $84,779,147Monthly Payment $454,547Annual Debt Service $5,454,564

Max Loan Amount (Secondary Loan: URA)

Pro Forma NOI and ValuePro Forma NOI $7,763,287Cap Rate 6.00%Value (NOI/Cap) $129,388,124

Loan TermsInterest Rate 4.00%Amortization(yrs) 25

Max Loan (Lesser of LTV or DCR) DEBT CONSTANT = Monthly Pmt / Loan Amt 0.0053Max Principal $16,224,489 Sample Loan Balance 16,224,489.38 16,224,489.38Monthly Payment $85,639 Interest 4.00% 0.04Annual Debt Service $1,027,666 Term 25

Monthly Payment $85,638.83Annual Payment $1,027,665.99

Part 3: Final Feasibility Development Plan | Transit Oriented Development at Neville & Centre| Real Estate Design and Development 48-452|30

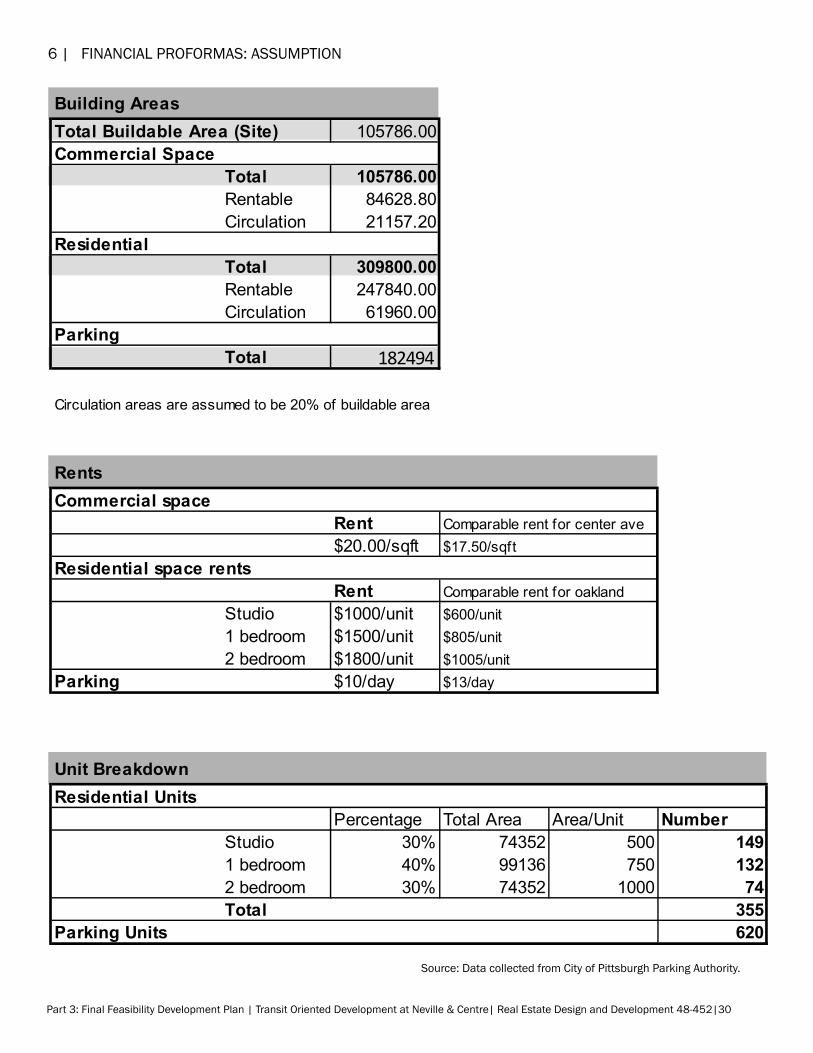

6 | FiNaNCial PROFORmas: assUmPTiON

source: Data collected from City of Pittsburgh Parking authority.

Building AreasTotal Buildable Area (Site) 105786.00Commercial Space

Total 105786.00Rentable 84628.80Circulation 21157.20

ResidentialTotal 309800.00Rentable 247840.00Circulation 61960.00

ParkingTotal

Circulation areas are assumed to be 20% of buildable area

RentsCommercial space

Rent Comparable rent for center ave$20.00/sqft $17.50/sqft

Residential space rentsRent Comparable rent for oakland

Studio $1000/unit $600/unit1 bedroom $1500/unit $805/unit2 bedroom $1800/unit $1005/unit

Parking $10/day $13/day

Unit BreakdownResidential Units

Percentage Total Area Area/Unit NumberStudio 30% 74352 500 1491 bedroom 40% 99136 750 1322 bedroom 30% 74352 1000 74Total 355

Parking Units 620

182494

Copyright © 2022 FDOKUMEN