Transaction Processing Rules | Mastercard

368

Transaction Processing Rules 13 August 2020 TPR

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of Transaction Processing Rules | Mastercard

Transaction ProcessingRules

13 August 2020

TPR

Summary of Changes, 13 August 2020

The following are changes with the most recent publication of this document.

Chapter Number Rule NameSource or Explanation ofRevisions

Chapter 2 Authorization andClearing Requirements

Europe Region2.21 Co-badged Cards—Acceptance Brand Identifier

AN 2457—Revised Standards—Exit of the United Kingdomfrom the European UnionAN 3492—Revised Rates andStandards—Interchange FeeRegulation in Liechtenstein

Chapter 3 AcceptanceProcedures

3.1.1 Mastercard CardAcceptance Procedures

AN 2696 Revised Standards—Introducing the MastercardDigital First Card Programand Related Card DesignStandards

3.4 Mastercard CardholderVerification RequirementsLatin America and theCaribbean Region > 3.4Mastercard CardholderVerification Requirements

AN 3478—Revised Standards—PIN Processing Exceptionfor Domestic PeruTransactions

3.5 Maestro CardholderVerification Requirements

AN 3466—Revised Standards—Contactless Single-Tap PINRequest Support in WesternEurope and the Nordics andthe Baltics

Chapter 4 Card-PresentTransactions

Europe Region > 4.10Purchase with Cash BackTransactions

AN 3488—Purchase withCash Back in Belarus,Georgia, and Kazakhstan—Service Fees and RevisedStandards

United States Region > 4.10Purchase with Cash BackTransactions

AN 3887—Revised Standards—Purchase With Cash BackTransactions for the U.S.

Chapter 5 Card-Not-PresentTransactions

5.1.1 E-commerceTransactions—Acquirer andMerchant Requirements

AN 3472—Revised Standards—Directory ServerSubmission of Identity CheckTransactions

Summary of Changes, 13 August 2020

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 2

Chapter Number Rule NameSource or Explanation ofRevisions

Middle East/Africa Region >5.1.1 E-commerceTransactions—Acquirer andMerchant Requirements

5.1.2 E-commerceTransactions—IssuerRequirements

AN 3325—Revised Standards—Regulatory Status Updateand Smart AuthenticationEnrollment for South AfricaAN 3353—Revised Standards—Regulatory Status andEMV 3-D Secure IdentityCheck Mandate Update forQatar

Europe Region > 5.8.1Acquirer Requirements

AN 2457—Revised Standards—Exit of the United Kingdomfrom the European Union

Chapter 7 TerminalRequirements

Europe Region > 7.6.2 HybridATM Terminal and BankBranch TerminalRequirements

AN 2978—Revised Standards—Contactless to BecomeStandard in ATMs in CzechRepublic and Poland

7.3 Contactless PaymentFunctionality7.3.1 Contactless ReaderRequirements

Asia/Pacific Region > 7.3Contactless PaymentFunctionality

Canada Region > 7.3Contactless PaymentFunctionality

Europe Region > 7.3Contactless PaymentFunctionality

Latin America and theCaribbean Region > 7.3Contactless PaymentFunctionality

Middle East/Africa Region >7.3 Contactless PaymentFunctionality

AN 3340—Revised Standards—Retiring ContactlessMagnetic Stripe ModeTechnology

Europe Region >7.4.1 Contactless–enabledPOS Terminals

AN 3466—Revised Standards—Contactless Single-Tap PINRequest Support in WesternEurope and the Nordics andthe Baltics

Summary of Changes, 13 August 2020

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 3

Chapter Number Rule NameSource or Explanation ofRevisions

Appendix A GeographicRegions

Middle East/Africa Region AN 3763 Revised Standardsfor Recognition of the WestAfrican Economic andMonetary Union in theLicensing Standards

Appendix C TransactionIdentification Requirements

Payment Transactions AN 1853—Revised Standards—Push PaymentTransactions Mandate andMoneySend MCC Expansion

Summary of Changes, 13 August 2020

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 4

Applicability of Rules in this Manual

This manual contains Rules for Activities.

The Rules in this manual pertain to the processing of Transactions and PaymentTransactions. As used herein, a Transaction means a transaction resulting from theuse of a Mastercard®, Maestro®, or Cirrus® Card, Access Device, or Account, as thecase may be. As used herein, a Payment Transaction means a Payment TransferActivity (PTA) Transaction that transfers funds to an Account. A PaymentTransaction is not a credit that reverses a previous purchase (includes MoneySendPayment Transactions).

For the purposes of Standards applicable to Payment Transactions, Issuer meansthe Receiving Institution (RI), and Acquirer means the Originating Institution (OI).

The below table describes the applicability of the Rules for particular types ofTransactions or Payment Transactions. Please note that the term “POSTransaction” refers to a Transaction that occurs at a Merchant location, whether ina Card-present environment at an attended or unattended POS Terminal, or in aCard-not-present environment. In a Card-not-present environment, this mayinclude electronic commerce (“e-commerce”), mail order, phone order, or recurringpayment Transactions.

Rules relating to… Apply to…

Mastercard POSTransactions

A POS Transaction conducted with a Mastercard Card.

Maestro POS Transactions A POS Transaction conducted with:• A Maestro Card, or• A Mastercard Card issued using a BIN identified by the

Corporation as “Debit Mastercard” and routed to theMastercard® Single Message System.

ATM Transactions A Transaction conducted with a Mastercard, Maestro, orCirrus Card at an ATM Terminal and routed to theInterchange System.

Manual Cash DisbursementTransactions

A cash withdrawal Transaction conducted at:• A Customer financial institution teller or Bank Branch

Terminal with a Mastercard Card, or• A Bank Branch Terminal with a Maestro or Cirrus Card

and routed to the Interchange System.

1 If a particular brand or brands is not mentioned in a Rule that applies to Transactions, then the Ruleapplies to Mastercard, Maestro, and Cirrus.

Applicability of Rules in this Manual

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 5

Rules relating to… Apply to…

Mastercard Mobile RemotePayment (MMRP)Transactions

A POS Transaction performed by an enrolled consumerusing a mobile device registered by the Issuer or its ServiceManager and having Mastercard Mobile Remote Paymentfunctionality. The consumer, as a Mastercard or MaestroCardholder, initiates and authenticates payments byentering a PIN or mobile-specific credentials on the mobiledevice.

Payment Transactions A PTA Transaction that transfers funds to an Account. APayment Transaction is not a credit that reverses a previouspurchase. Includes MoneySend Payment Transactions.

Modifying Words and Acronyms

From time to time, the meanings of the above terms are modified by the additionof another word or acronym. For example, a Debit Mastercard POS Transactionmeans a Transaction resulting from the use of a Debit Mastercard Card at thepoint of sale (POS). However, for ease of use, not every modifying term is defined.While Mastercard alone interprets and enforces its Rules and other Standards,these Transaction Processing Rules endeavor to use defined terms and other termsand terminology in a plain manner that will be generally understood in thepayments industry.

Variations and Additions to the Rules for a Geographic Area

Variations and/or additions (“modifications”) to the Rules are applicable ingeographic areas, whether a country, a number of countries, a region, or otherarea. In the event of a conflict between a Rule and a variation of that Rule, themodification is afforded precedence and is applicable. The Rules set forth in thismanual are Standards and Mastercard has the sole right to interpret and enforcethe Rules and other Standards.

1 If a particular brand or brands is not mentioned in a Rule that applies to Transactions, then the Ruleapplies to Mastercard, Maestro, and Cirrus.

Applicability of Rules in this Manual

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 6

Contents

Summary of Changes, 13 August 2020.......................................................................2

Applicability of Rules in this Manual.............................................................................5

Chapter 1: Connecting to the Interchange System and AuthorizationRouting..................................................................................................................................... 21

1.1 Connecting to the Interchange System......................................................................................231.2 Authorization Routing—Mastercard POS Transactions........................................................... 231.3 Authorization Routing—Maestro, Cirrus, and ATM Transactions............................................24

1.3.1 Routing Instructions and System Maintenance................................................................241.3.2 Chip Transaction Routing......................................................................................................251.3.3 Domestic Transaction Routing.............................................................................................25

1.4 ATM Terminal Connection to the Interchange System.............................................................251.5 Gateway Processing.......................................................................................................................261.6 POS Terminal Connection to the Interchange System.............................................................26Variations and Additions by Region....................................................................................................26Asia/Pacific Region................................................................................................................................26

1.4 ATM Terminal Connection to the Interchange System....................................................... 271.6 POS Terminal Connection to the Interchange System....................................................... 27

Canada Region.......................................................................................................................................271.3 Authorization Routing—Maestro, Cirrus, and ATM Transactions...................................... 27

1.3.3 Domestic Transaction Routing....................................................................................... 271.4 ATM Terminal Connection to the Interchange System....................................................... 27

Europe Region.........................................................................................................................................281.1 Connecting to the Interchange System.................................................................................281.2 Authorization Routing—Mastercard POS Transactions......................................................281.3 Authorization Routing—Maestro, Cirrus, and ATM Transactions...................................... 28

1.3.2 Chip Transaction Routing................................................................................................281.3.3 Domestic Transaction Routing....................................................................................... 28

1.4 ATM Terminal Connection to the Interchange System—SEPA Only................................. 29Latin America and the Caribbean Region......................................................................................... 29

1.4 ATM Terminal Connection to the Interchange System....................................................... 291.6 POS Terminal Connection to the Interchange System....................................................... 29

United States Region............................................................................................................................291.1 Connecting to the Interchange System.................................................................................291.3 Authorization Routing—Maestro, Cirrus, and ATM Transactions...................................... 30

1.3.1 Routing Instructions and System Maintenance.......................................................... 301.3.3 Domestic Transaction Routing....................................................................................... 30

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 7

1.4 ATM Terminal Connection to the Interchange System....................................................... 30Additional U.S. Region and U.S. Territory Rules................................................................................31

1.3 Authorization Routing—Maestro, Cirrus, and ATM Transactions...................................... 31

Chapter 2: Authorization and Clearing Requirements....................................... 322.1 Acquirer Authorization Requirements......................................................................................... 35

2.1.1 Acquirer Host System Requirements—U.S. Region Only................................................. 362.2 Issuer Authorization Requirements..............................................................................................36

2.2.1 Issuer Host System Requirements...................................................................................... 362.2.2 Stand-In Processing Service.................................................................................................37

Accumulative Transaction Limits.............................................................................................38Chip Cryptogram Validation in Stand-In................................................................................38

2.2.3 ATM Transaction Requirements for Mastercard Credit Card Issuers............................382.3 Authorization Responses............................................................................................................... 392.4 Performance Standards................................................................................................................ 39

2.4.1 Performance Standards—Acquirer Requirements............................................................402.4.2 Performance Standards—Issuer Requirements................................................................40

Issuer Failure Rate (Substandard Level 1)............................................................................. 40Issuer Failure Rate (Substandard Level 2)............................................................................. 40Calculation of the Issuer Failure Rate..................................................................................... 40

2.5 Preauthorizations............................................................................................................................402.5.1 Preauthorizations—Mastercard POS Transactions..........................................................412.5.2 Preauthorizations—Maestro POS Transactions................................................................412.5.3 Preauthorizations—ATM and Manual Cash Disbursement Transactions..................... 42

2.6 Undefined Authorizations..............................................................................................................422.7 Final Authorizations........................................................................................................................422.8 Message Reason Code 4808 Chargeback Protection Period..................................................432.9 Multiple Authorizations..................................................................................................................442.10 Multiple Clearing Messages........................................................................................................442.11 Full and Partial Reversals............................................................................................................ 45

2.11.1 Full and Partial Reversals—Acquirer Requirements........................................................462.11.2 Full and Partial Reversals—Issuer Requirements............................................................ 472.11.3 Reversal for Conversion of Approval to Decline..............................................................472.11.4 Reversal to Cancel Transaction......................................................................................... 48

2.12 Full and Partial Approvals .......................................................................................................... 482.13 Refund Transactions and Corrections.......................................................................................49

2.13.1 Refund Transactions—Acquirer Requirements................................................................502.13.2 Refund Transactions—Issuer Requirements.................................................................... 50

2.14 Balance Inquiries...........................................................................................................................512.15 CVC 2 Verification for POS Transactions.................................................................................522.16 CVC 3 Verification for Maestro Magnetic Stripe Mode Contactless Transactions—Brazil Only...............................................................................................................................................52

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 8

2.17 Euro Conversion—Europe Region Only...................................................................................... 522.18 Transaction Queries and Disputes.............................................................................................52

2.18.1 Retrieval Requests and Fulfillments................................................................................. 522.18.2 Compliance with Dispute Procedures.............................................................................. 53

2.19 Chargebacks for Reissued Cards............................................................................................... 532.20 Correction of Errors......................................................................................................................532.21 Co-badged Cards—Acceptance Brand Identifier.................................................................... 53Variations and Additions by Region....................................................................................................54Asia/Pacific Region................................................................................................................................54

2.1 Acquirer Authorization Requirements....................................................................................542.2 Issuer Authorization Requirements........................................................................................ 54

2.2.1 Issuer Host System Requirements.................................................................................542.5 Preauthorizations......................................................................................................................54

2.5.2 Preauthorizations—Maestro POS Transactions.......................................................... 54Canada Region.......................................................................................................................................54

2.2 Issuer Authorization Requirements........................................................................................ 552.12 Full and Partial Approvals......................................................................................................55

Europe Region.........................................................................................................................................562.1 Acquirer Authorization Requirements....................................................................................562.2 Issuer Authorization Requirements........................................................................................ 58

2.2.2 Stand-In Processing Service........................................................................................... 582.2.3 ATM Transaction Requirements for Mastercard Credit Card Issuers...................... 59

2.3 Authorization Responses..........................................................................................................592.4 Performance Standards...........................................................................................................59

2.4.2 Performance Standards—Issuer Requirements...........................................................592.5 Preauthorizations......................................................................................................................60

2.5.2 Preauthorizations—Maestro POS Transactions.......................................................... 602.5.3 Preauthorizations—ATM and Manual Cash Disbursement Transactions................61

2.7 Final Authorizations..................................................................................................................612.8 Message Reason Code 4808 Chargeback Protection Period............................................ 612.9 Multiple Authorizations............................................................................................................ 622.11 Full and Partial Reversals.......................................................................................................63

2.11.1 Full and Partial Reversals—Acquirer Requirements.................................................. 632.11.2 Full and Partial Reversals—Issuer Requirements.......................................................64

2.12 Full and Partial Approvals......................................................................................................642.13 Refund Transactions and Corrections................................................................................. 65

2.13.1 Refund Transactions—Acquirer Requirements.......................................................... 652.13.2 Refund Transactions—Issuer Requirements...............................................................65

2.14 Balance Inquiries......................................................................................................................652.15 CVC 2 Verification for POS Transactions............................................................................652.17 Euro Conversion.......................................................................................................................662.21 Co-badged Cards—Acceptance Brand Identifier...............................................................66

Latin America and the Caribbean Region......................................................................................... 68

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 9

2.16 CVC 3 Verification for Maestro Magnetic Stripe Mode Contactless—Brazil Only.......68United States Region............................................................................................................................68

2.1 Acquirer Authorization Requirements....................................................................................682.1.1 Acquirer Host System Requirements............................................................................ 68

2.2 Issuer Authorization Requirements........................................................................................ 692.2.1 Issuer Host System Requirements.................................................................................692.2.2 Stand-In Processing Service........................................................................................... 69

2.4 Performance Standards...........................................................................................................722.4.2 Performance Standards—Issuer Requirements...........................................................72

2.5 Preauthorizations......................................................................................................................722.5.2 Preauthorizations—Maestro POS Transactions.......................................................... 72

2.11 Full and Partial Reversals.......................................................................................................722.11.1 Full and Partial Reversals—Acquirer Requirements.................................................. 722.11.2 Full and Partial Reversals—Issuer Requirements.......................................................74

2.12 Full and Partial Approvals......................................................................................................742.14 Balance Inquiries......................................................................................................................74

Chapter 3: Acceptance Procedures............................................................................. 763.1 Card-Present Transactions............................................................................................................79

3.1.1 Mastercard Card Acceptance Procedures......................................................................... 79Suspicious Cards.........................................................................................................................80

3.1.2 Maestro Card Acceptance Procedures...............................................................................803.2 Card-Not-Present Transactions................................................................................................... 803.3 Obtaining an Authorization...........................................................................................................80

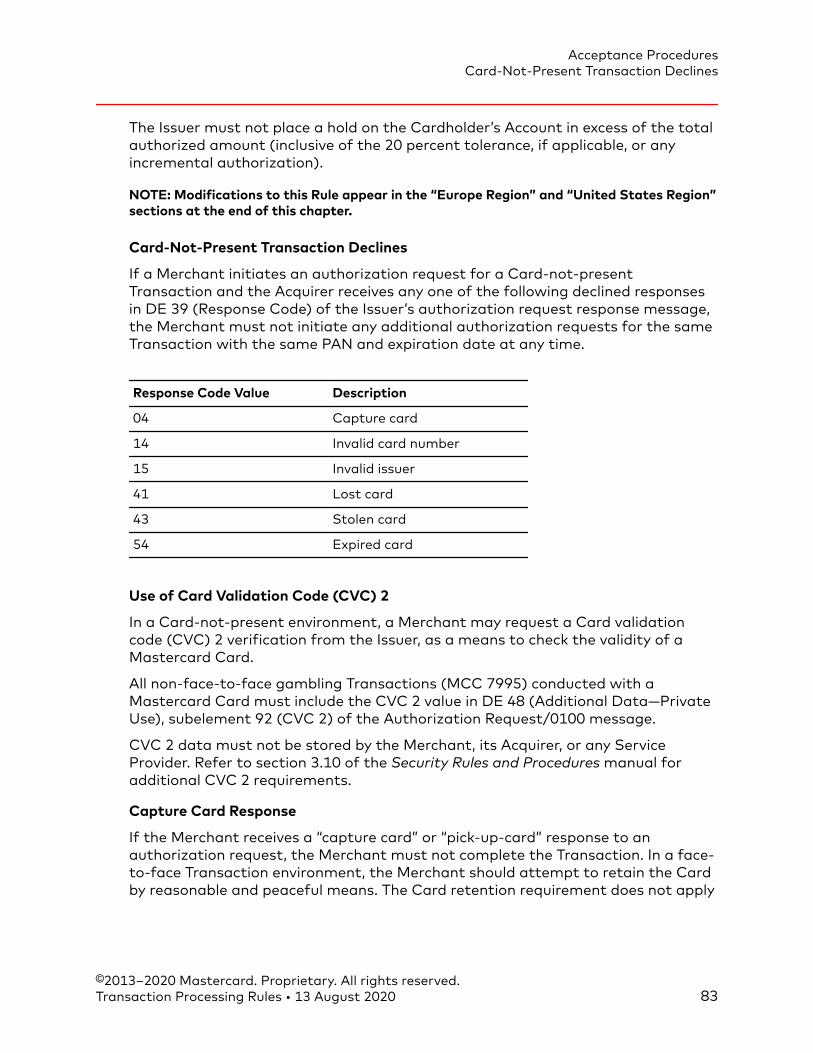

3.3.1 Mastercard POS Transaction Authorization Procedures................................................ 81Authorization of Lodging, Cruise Line, and Vehicle Rental Transactions.......................... 82Authorization When the Cardholder Adds a Gratuity..........................................................82Card-Not-Present Transaction Declines.................................................................................83Use of Card Validation Code (CVC) 2..................................................................................... 83Capture Card Response.............................................................................................................83

3.3.2 Maestro POS Transaction Authorization Procedures......................................................843.4 Mastercard Cardholder Verification Requirements.................................................................. 84

CVM Not Required for Refund Transactions................................................................................85Use of PIN for Mastercard Magnetic Stripe Transactions........................................................ 85

3.5 Maestro Cardholder Verification Requirements........................................................................863.6 Use of a PIN for Transactions at ATM Terminals and Bank Branch Terminals..................... 873.7 Use of a Consumer Device CVM...................................................................................................883.8 POI Currency Conversion...............................................................................................................88

3.8.1 Cardholder Disclosure—Attended POS Terminal..............................................................893.8.2 Cardholder Disclosure—Unattended POS Terminal......................................................... 893.8.3 Cardholder Disclosure—ATM Terminal................................................................................903.8.4 Cardholder Disclosure—Transaction Receipt Information...............................................90

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 10

3.8.5 Transaction Processing Requirements................................................................................913.9 Multiple Transactions—Mastercard POS Transactions Only....................................................913.10 Partial Payment—Mastercard POS Transactions Only.......................................................... 913.11 Specific Terms of a Transaction.................................................................................................92

3.11.1 Specific Terms of an E-commerce Transaction.............................................................. 923.12 Charges for Loss, Theft, or Damage—Mastercard POS Transactions Only....................... 933.13 Providing a Transaction Receipt.................................................................................................93

3.13.1 POS and Mastercard Manual Cash Disbursement Transaction ReceiptRequirements....................................................................................................................................953.13.2 ATM and Bank Branch Terminal Transaction Receipt Requirements..........................963.13.3 Primary Account Number (PAN) Truncation and Expiration Date Omission............ 963.13.4 Prohibited Information........................................................................................................973.13.5 Standard Wording for Formsets.......................................................................................97

3.14 Returned Products and Canceled Services.............................................................................. 973.14.1 Refund Transactions............................................................................................................98

3.15 Transaction Records.....................................................................................................................993.15.1 Retention of Transaction Records...................................................................................100

Variations and Additions by Region..................................................................................................100Asia/Pacific Region............................................................................................................................. 100

3.14 Returned Products and Canceled Services.......................................................................1003.14.1 Refund Transactions....................................................................................................100

Canada Region.....................................................................................................................................101Europe Region......................................................................................................................................101

3.1 Card-Present Transactions....................................................................................................1013.1.1 Mastercard Card Acceptance Procedures..................................................................101

3.2 Card-Not-Present Transactions........................................................................................... 1013.3 Obtaining an Authorization...................................................................................................102

3.3.1 Mastercard POS Transaction Authorization Procedures.........................................102Authorization of Lodging, Cruise Line, and Vehicle Rental Transactions.................. 102Authorization When the Cardholder Adds a Gratuity..................................................102

3.3.2 Maestro POS Transaction Authorization Procedures.............................................. 1023.5 Maestro Cardholder Verification Requirements................................................................ 1033.8 POI Currency Conversion....................................................................................................... 1033.13 Providing a Transaction Receipt.........................................................................................103

3.13.1 POS and Mastercard Manual Cash Disbursement Transaction ReceiptRequirements............................................................................................................................1033.13.3 Primary Account Number (PAN) Truncation and Expiration Date Omission.... 104

3.14 Returned Products and Canceled Services.......................................................................1043.14.1 Refund Transactions....................................................................................................104

Latin America and the Caribbean Region.......................................................................................1053.4 Mastercard Cardholder Verification Requirements.......................................................... 1053.5 Maestro Cardholder Verification Requirements................................................................ 105

Middle East/Africa Region................................................................................................................. 105

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 11

3.14 Returned Products and Canceled Services.......................................................................1053.14.1 Refund Transactions....................................................................................................105

United States Region..........................................................................................................................1063.3 Obtaining an Authorization...................................................................................................106

3.3.1 Mastercard POS Transaction Authorization Procedures.........................................106Authorization When the Cardholder Adds a Gratuity..................................................106

3.5 Maestro Cardholder Verification Requirements................................................................ 107Additional U.S. Region and U.S. Territory Rules............................................................................. 107

3.14 Returned Products and Canceled Services.......................................................................1073.14.1 Refund Transactions....................................................................................................107

Chapter 4: Card-Present Transactions....................................................................1084.1 Chip Transactions at Hybrid Terminals..................................................................................... 1114.2 Offline Transactions Performed on Board Planes, Trains, and Ships.................................. 1124.3 No-CVM Magnetic Stripe and Contact Chip Maestro POS Transactions—EuropeRegion Only...........................................................................................................................................1124.4 Contactless Transactions at POS Terminals............................................................................1134.5 Contactless Transit Aggregated Transactions........................................................................ 113

4.5.1 Mastercard Contactless Transit Aggregated Transactions..........................................1134.5.2 Maestro Contactless Transit Aggregated Transactions............................................... 114

4.6 Contactless Transactions at ATM Terminals............................................................................1154.7 Contactless-only Acceptance.....................................................................................................1154.8 Mastercard Consumer-Presented QR Transactions at POS Terminals...............................1164.9 Quick Payment Service (QPS) Program—Mastercard POS Transactions Only................. 1174.10 Purchase with Cash Back Transactions..................................................................................1174.11 Transactions at Unattended POS Terminals.........................................................................119

4.11.1 Automated Fuel Dispenser Transactions...................................................................... 1194.12 PIN-based Debit Transactions—United States Region Only...............................................1194.13 PIN-less Single Message Transactions—United States Region Only................................. 1204.14 Merchant-approved Maestro POS Transactions.................................................................. 1204.15 Mastercard Manual Cash Disbursement Transactions........................................................121

4.15.1 Non-discrimination Regarding Cash Disbursement Services.................................... 1214.15.2 Maximum Cash Disbursement Amounts...................................................................... 1214.15.3 Discount or Service Charges............................................................................................1224.15.4 Mastercard Acceptance Mark Must Be Displayed.......................................................122

4.16 Encashment of Mastercard Travelers Cheques.................................................................... 1224.17 ATM Transactions.......................................................................................................................122

4.17.1 “Chained” Transactions.................................................................................................... 1234.17.2 ATM Transaction Branding...............................................................................................123

4.18 ATM Access Fees.........................................................................................................................1234.18.1 ATM Access Fees—Domestic Transactions....................................................................1234.18.2 ATM Access Fees—Cross-border Transactions............................................................. 123

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 12

4.18.3 ATM Access Fee Requirements........................................................................................124Transaction Field Specifications for ATM Access Fees.......................................................124Non-discrimination Regarding ATM Access Fees................................................................124Notification of ATM Access Fee............................................................................................. 124Cancellation of Transaction....................................................................................................124Sponsor Approval of Proposed Signage, Screen Display, and Receipt............................124ATM Terminal Signage.............................................................................................................125ATM Terminal Screen Display................................................................................................. 125ATM Transaction Receipts.......................................................................................................126

4.19 Merchandise Transactions at ATM Terminals........................................................................1264.19.1 Approved Merchandise Categories................................................................................ 1264.19.2 Screen Display Requirement for Merchandise Categories.........................................127

4.20 Shared Deposits—United States Region Only.......................................................................127Variations and Additions by Region..................................................................................................128Asia/Pacific Region............................................................................................................................. 128

4.10 Purchase with Cash Back Transactions............................................................................ 1284.11 Transactions at Unattended POS Terminals....................................................................128

4.11.1 Automated Fuel Dispenser Transactions.................................................................1284.18 ATM Access Fees...................................................................................................................128

4.18.1 ATM Access Fees—Domestic Transactions.............................................................. 128Canada Region.....................................................................................................................................129

4.10 Purchase with Cash Back Transactions............................................................................ 1294.11 Transactions at Unattended POS Terminals....................................................................129

4.11.1 Automated Fuel Dispenser Transactions.................................................................1294.18 ATM Access Fees...................................................................................................................130

4.18.1 ATM Access Fees—Domestic Transactions.............................................................. 130Europe Region......................................................................................................................................130

4.1 Chip Transactions at Hybrid Terminals................................................................................1304.2 Offline Transactions Performed on Board Planes, Trains, and Ships.............................1304.3 No-CVM Magnetic Stripe and Contact Chip Maestro POS Transactions.....................1304.4 Contactless Transactions at POS Terminals...................................................................... 1314.5 Contactless Transit Aggregated Transactions...................................................................132

4.5.1 Mastercard Contactless Transit Aggregated Transactions.................................... 1324.5.2 Maestro Contactless Transit Aggregated Transactions..........................................132

4.10 Purchase with Cash Back Transactions............................................................................ 1334.11 Transactions at Unattended POS Terminals....................................................................136

4.11.1 Automated Fuel Dispenser Transactions.................................................................1364.14 Merchant-approved Maestro POS Transactions.............................................................1374.15 Mastercard Manual Cash Disbursement Transactions.................................................. 137

4.15.2 Maximum Cash Disbursement Amounts.................................................................1374.18 ATM Access Fees...................................................................................................................138

4.18.1 ATM Access Fees—Domestic Transactions.............................................................. 1384.19 Merchandise Transactions at ATM Terminals...................................................................138

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 13

4.19.1 Approved Merchandise Categories...........................................................................138Latin America and the Caribbean Region.......................................................................................139

4.4 Contactless Transactions at POS Terminals...................................................................... 1394.5 Contactless Transit Aggregated Transactions...................................................................139

4.5.2 Maestro Contactless Transit Aggregated Transactions..........................................1394.10 Purchase with Cash Back Transactions............................................................................ 1394.18 ATM Access Fees...................................................................................................................141

4.18.1 ATM Access Fees—Domestic Transactions.............................................................. 141Middle East/Africa Region................................................................................................................. 142

4.10 Purchase with Cash Back Transactions............................................................................ 142United States Region..........................................................................................................................143

4.1 Chip Transactions at Hybrid Terminals................................................................................1434.10 Purchase with Cash Back Transactions............................................................................ 1434.11 Transactions at Unattended POS Terminals....................................................................145

4.11.1 Automated Fuel Dispenser Transactions.................................................................1454.12 PIN-based Debit Transactions............................................................................................1454.13 PIN-less Single Message Transactions.............................................................................. 1454.15 Mastercard Manual Cash Disbursement Transactions.................................................. 146

4.15.2 Maximum Cash Disbursement Amounts.................................................................1464.15.3 Discount or Service Charges......................................................................................146

4.18 ATM Access Fees...................................................................................................................1474.18.1 ATM Access Fees—Domestic Transactions.............................................................. 147

4.19 Merchandise Transactions at ATM Terminals...................................................................1474.19.1 Approved Merchandise Categories...........................................................................147

4.20 Shared Deposits....................................................................................................................1474.20.1 Non-discrimination Regarding Shared Deposits.................................................... 1474.20.2 Terminal Signs and Notices........................................................................................ 1484.20.3 Maximum Shared Deposit Amount.......................................................................... 1484.20.4 Deposit Verification.....................................................................................................1484.20.5 ATM Terminal Clearing and Deposit Processing..................................................... 1494.20.6 Shared Deposits in Excess of USD 10,000.............................................................. 1494.20.7 Notice of Return...........................................................................................................1494.20.8 Liability for Shared Deposits......................................................................................150

Chapter 5: Card-Not-Present Transactions..........................................................1515.1 Electronic Commerce Transactions...........................................................................................153

5.1.1 E-commerce Transactions—Acquirer and Merchant Requirements............................1535.1.2 E-commerce Transactions—Issuer Requirements.......................................................... 1555.1.3 Use of Static AAV for Card-not-present Transactions..................................................156

5.2 Mail Order and Telephone Order (MO/TO) Transactions...................................................... 1575.3 Credential-on-File Transactions.................................................................................................1575.4 Recurring Payment Transactions...............................................................................................158

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 14

5.4.1 Recurring Payment Transactions for High-Risk Negative Option BillingMerchants....................................................................................................................................... 160

5.5 Installment Billing for Domestic Transactions—Participating Countries Only...................1615.5.1 Applicability of Rules........................................................................................................... 1615.5.2 Definitions.............................................................................................................................1625.5.3 Transaction Processing Procedures.................................................................................. 162

5.6 Transit Transactions Performed for Debt Recovery............................................................... 1635.7 Use of Automatic Billing Updater..............................................................................................1645.8 Authentication Requirements—Europe Region Only.............................................................. 1655.9 Merchant-initiated Transactions—EEA Only............................................................................165Variations and Additions by Region..................................................................................................165Asia/Pacific Region............................................................................................................................. 165

5.1 Electronic Commerce Transactions......................................................................................1655.1.1 E-commerce Transactions—Acquirer and Merchant Requirements...................... 1665.1.2 E-commerce Transactions—Issuer Requirements.....................................................166

5.2 Mail Order and Telephone Order (MO/TO) Transactions.................................................1675.3 Credential-on-File Transactions........................................................................................... 1685.7 Use of Automatic Billing Updater.........................................................................................168

Canada Region.....................................................................................................................................1685.7 Use of Automatic Billing Updater.........................................................................................168

Europe Region......................................................................................................................................1685.1 Electronic Commerce Transactions......................................................................................169

5.1.1 E-commerce Transactions—Acquirer and Merchant Requirements...................... 1695.1.2 E-commerce Transactions—Issuer Requirements.....................................................1705.1.3 Use of Static AAV for Card-not-present Transactions............................................ 171

5.2 Mail Order and Telephone Order (MO/TO) Maestro Transactions.................................1715.2.1 Definitions....................................................................................................................... 1715.2.2 Intracountry Maestro MO/TO Transactions—Cardholder Authority.....................1725.2.3 Intracountry Maestro MO/TO Transactions—Transactions Per CardholderAuthority....................................................................................................................................1725.2.4 Intracountry Maestro MO/TO Transactions—CVC 2/AVS Checks.........................173

5.3 Credential-on-File Transactions........................................................................................... 1735.4 Recurring Payment Transactions..........................................................................................1735.5 Installment Billing for Domestic Transactions—Participating Countries Only............. 175

5.5.3 Transaction Processing Procedures.............................................................................1875.6 Transit Transactions Performed for Debt Recovery..........................................................1875.7 Use of Automatic Billing Updater.........................................................................................187

5.7.1 Issuer Requirements.......................................................................................................1875.7.2 Acquirer Requirements.................................................................................................. 190

5.8 Authentication Requirements...............................................................................................1915.8.1 Acquirer Requirements.................................................................................................. 1915.8.2 Issuer Requirements.......................................................................................................191

5.9 Merchant-initiated Transactions – EEA, United Kingdom and Gibraltar Only.............191

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 15

Latin America and the Caribbean Region.......................................................................................1935.1 Electronic Commerce Transactions......................................................................................193

5.1.1 E-commerce Transactions—Acquirer and Merchant Requirements...................... 1935.1.2 E-commerce Transactions—Issuer Requirements.....................................................193

5.7 Use of Automatic Billing Updater.........................................................................................193Middle East/Africa Region................................................................................................................. 193

5.1 Electronic Commerce Transactions......................................................................................1935.1.1 E-commerce Transactions—Acquirer and Merchant Requirements...................... 1935.1.2 E-commerce Transactions—Issuer Requirements.....................................................194

5.7 Use of Automatic Billing Updater.........................................................................................194United States Region..........................................................................................................................194

5.7 Use of Automatic Billing Updater.........................................................................................194

Chapter 6: Payment Transactions.............................................................................1956.1 Payment Transactions................................................................................................................. 196

6.1.1 Payment Transactions—Acquirer and Merchant Requirements.................................. 1966.1.2 Payment Transactions—Issuer Requirements.................................................................197

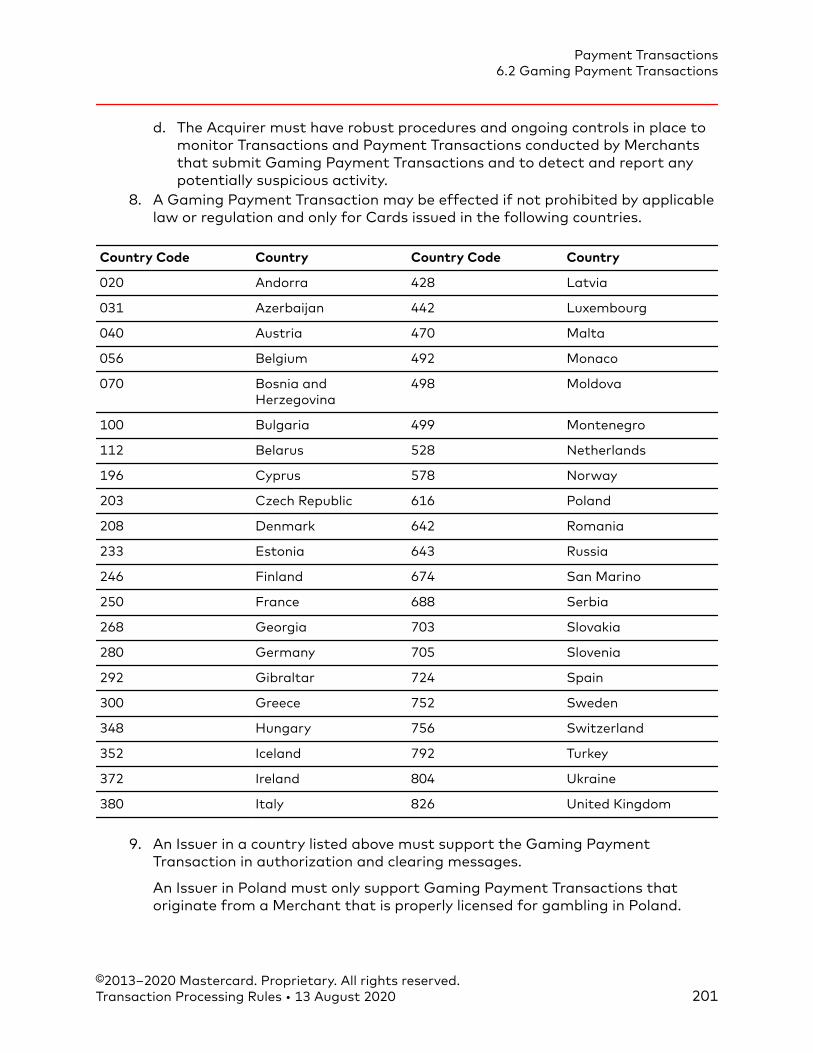

6.2 Gaming Payment Transactions..................................................................................................1986.3 MoneySend Payment Transactions........................................................................................... 198Variations and Additions by Region..................................................................................................199Europe Region......................................................................................................................................199

6.1 Payment Transactions............................................................................................................1996.1.1 Payment Transactions—Acquirer and Merchant Requirements.............................1996.1.2 Payment Transactions—Issuer Requirements........................................................... 200

6.2 Gaming Payment Transactions............................................................................................ 2006.3 MoneySend Payment Transactions......................................................................................202

Middle East/Africa Region................................................................................................................. 2026.2 Gaming Payment Transactions............................................................................................ 202

United States Region..........................................................................................................................2046.2 Gaming Payment Transactions............................................................................................ 204

Chapter 7: Terminal Requirements............................................................................2067.1 Terminal Eligibility.........................................................................................................................2097.2 Terminal Requirements................................................................................................................209

7.2.1 Terminal Function Keys for PIN Entry...............................................................................2107.2.2 Terminal Responses............................................................................................................. 2117.2.3 Terminal Transaction Log................................................................................................... 211

7.3 Contactless Payment Functionality.......................................................................................... 2117.3.1 Contactless Reader Requirements................................................................................... 212

7.4 POS Terminal Requirements.......................................................................................................2127.4.1 Contactless–enabled POS Terminals............................................................................... 213

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 16

7.4.2 Contactless-only POS Terminals.......................................................................................2157.4.3 Mobile POS (MPOS) Terminals..........................................................................................2157.4.4 Mastercard Consumer-Presented QR-enabled POS Terminals...................................2177.4.5 Signature-based Maestro POS Terminals.......................................................................2177.4.6 POS Terminals Using Electronic Signature Capture Technology (ESCT)...................217

7.5 ATM Terminal and Bank Branch Terminal Requirements.......................................................2187.5.1 ATM Terminals......................................................................................................................2197.5.2 Bank Branch Terminals....................................................................................................... 2197.5.3 Contactless Payment Functionality................................................................................. 219

7.6 Hybrid Terminal Requirements...................................................................................................2207.6.1 Hybrid POS Terminal Requirements................................................................................. 220

Hybrid POS Terminal and Chip-only MPOS Terminal Displays.........................................2217.6.2 Hybrid ATM Terminal and Bank Branch Terminal Requirements................................. 222

7.7 Mastercard Consumer-Presented QR Functionality.............................................................. 222Variations and Additions by Region..................................................................................................223Asia/Pacific Region............................................................................................................................. 223

7.3 Contactless Payment Functionality.....................................................................................2237.4 POS Terminal Requirements................................................................................................. 224

7.4.3 Mobile POS (MPOS) Terminals.................................................................................... 2257.5 ATM Terminal and Bank Branch Terminal Requirements................................................. 2257.6 Hybrid Terminal Requirements..............................................................................................225

Canada Region.....................................................................................................................................2267.3 Contactless Payment Functionality.....................................................................................2267.4 POS Terminal Requirements................................................................................................. 226

7.4.1 Contactless–enabled POS Terminals..........................................................................2267.4.3 Mobile POS (MPOS) Terminals.................................................................................... 226

7.4.4 Mastercard Consumer-Presented QR-enabled POS Terminals...................................2277.5 ATM Terminal and Bank Branch Terminal Requirements................................................. 227

Europe Region......................................................................................................................................2277.1 Terminal Eligibility................................................................................................................... 2277.2 Terminal Requirements...........................................................................................................2287.3 Contactless Payment Functionality.....................................................................................228

7.3.1 Contactless Reader Requirements..............................................................................2287.4 POS Terminal Requirements................................................................................................. 228

7.4.1 Contactless–enabled POS Terminals..........................................................................2297.4.3 Mobile POS (MPOS) Terminals.................................................................................... 2327.4.5 Signature-based Maestro POS Terminals..................................................................232

7.5 ATM Terminal and Bank Branch Terminal Requirements................................................. 2337.5.2 Bank Branch Terminals..................................................................................................233

7.6 Hybrid Terminal Requirements..............................................................................................2337.6.1 Hybrid POS Terminal Requirements............................................................................2347.6.2 Hybrid ATM Terminal and Bank Branch Terminal Requirements............................234

Latin America and the Caribbean Region.......................................................................................234

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 17

7.3 Contactless Payment Functionality.....................................................................................2357.4 POS Terminal Requirements................................................................................................. 235

7.4.1 Contactless–enabled POS Terminals..........................................................................2367.6 Hybrid Terminal Requirements........................................................................................ 236

Middle East/Africa Region................................................................................................................. 2367.3 Contactless Payment Functionality.....................................................................................2367.6 Hybrid Terminal Requirements..............................................................................................237

7.6.1 Hybrid POS Terminal Requirements............................................................................237United States Region..........................................................................................................................237

7.3 Contactless Payment Functionality.....................................................................................2377.4 POS Terminal Requirements................................................................................................. 237

7.4.1 Contactless–enabled POS Terminals..........................................................................2377.4.3 Mobile POS (MPOS) Terminals.................................................................................... 2387.4.4 Mastercard Consumer-Presented QR-enabled POS Terminals............................. 238

7.5 ATM Terminal and Bank Branch Terminal Requirements................................................. 2387.6 Hybrid Terminal Requirements..............................................................................................239

Additional U.S. Region and U.S. Territory Rules............................................................................. 2397.6 Hybrid Terminal Requirements..............................................................................................239

7.6.1 Hybrid POS Terminal Requirements............................................................................239Hybrid POS Terminal and Chip-only MPOS Terminal Displays....................................239

Appendix A: Geographic Regions............................................................................... 241Asia/Pacific Region............................................................................................................................. 242Canada Region.....................................................................................................................................243Europe Region......................................................................................................................................243

Single European Payments Area (SEPA)...................................................................................244Latin America and the Caribbean Region.......................................................................................245Middle East/Africa Region................................................................................................................. 245United States Region..........................................................................................................................247

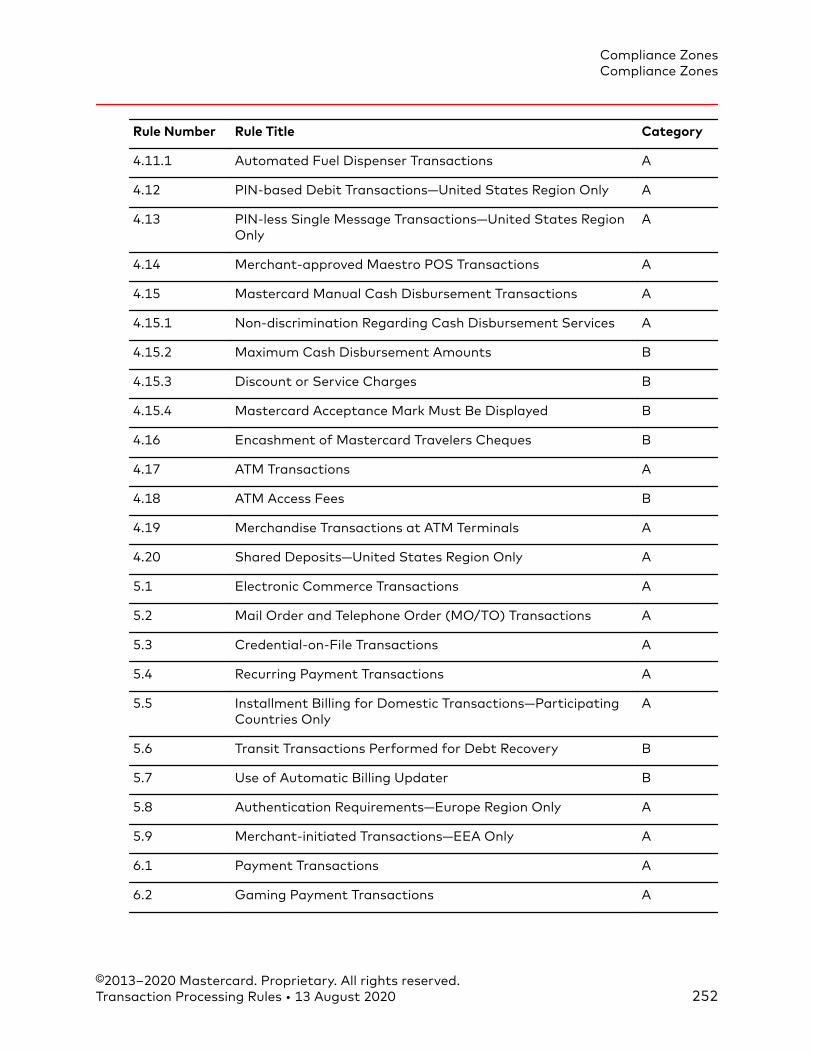

Appendix B: Compliance Zones................................................................................... 248Compliance Zones...............................................................................................................................249

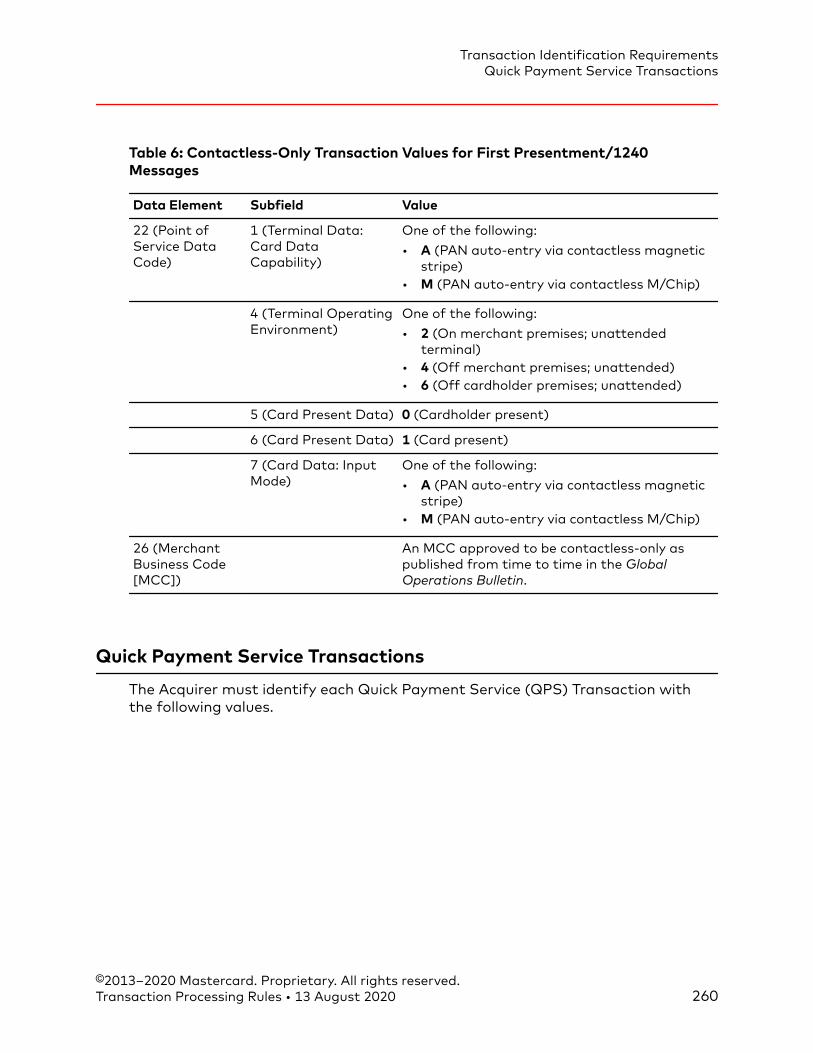

Appendix C: Transaction Identification Requirements.................................... 254Transaction Date.................................................................................................................................255Contactless Transactions...................................................................................................................255

Contactless Transit Aggregated Transactions......................................................................... 256Contactless-only Transactions.................................................................................................... 259

Quick Payment Service Transactions...............................................................................................260Payment Transactions........................................................................................................................261Electronic Commerce Transactions..................................................................................................263

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 18

Electronic Commerce Transactions at Automated Fuel Dispensers .........................................264Digital Secure Remote Payment Transactions...............................................................................268

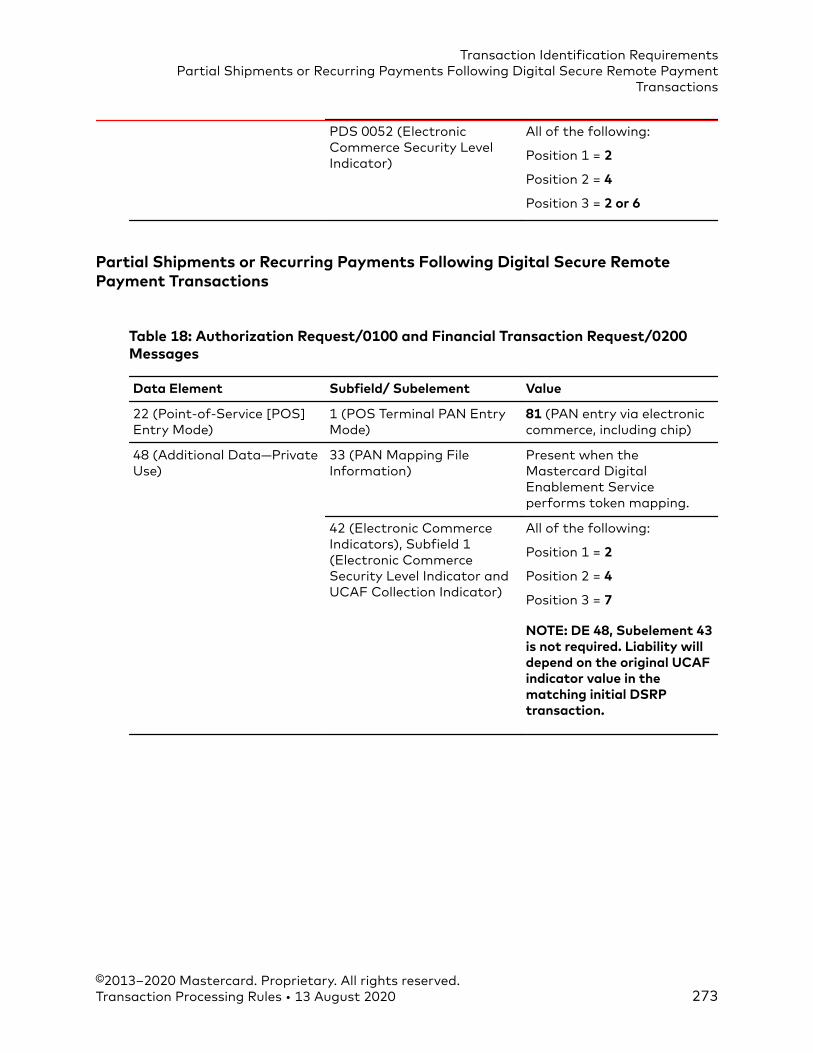

Digital Secure Remote Payment Transactions Containing Chip Data.................................268Digital Secure Remote Payment Transactions Containing UCAF Data...............................271Partial Shipments or Recurring Payments Following Digital Secure Remote PaymentTransactions....................................................................................................................................273

Mastercard Mobile Remote Payment Transactions...................................................................... 275Mastercard Biometric Card Program Transactions.......................................................................275

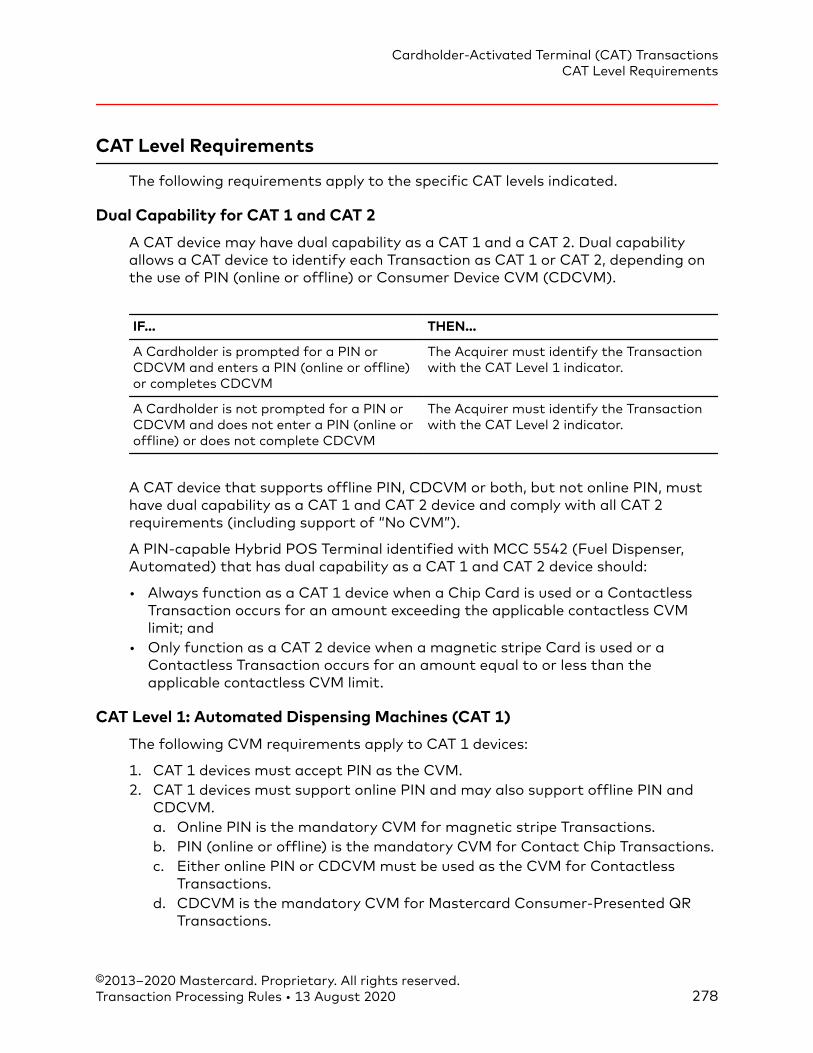

Appendix D: Cardholder-Activated Terminal (CAT) Transactions.............. 276CAT Transactions.................................................................................................................................277CAT Level Requirements.....................................................................................................................278

Dual Capability for CAT 1 and CAT 2......................................................................................... 278CAT Level 1: Automated Dispensing Machines (CAT 1)..........................................................278CAT Level 2: Self-Service Terminal (CAT 2)...............................................................................279CAT Level 3: Limited Amount Terminals (CAT 3)......................................................................281CAT Level 4: In-Flight Commerce (IFC) Terminals (CAT 4).....................................................282CAT Level 6: Electronic Commerce Transactions (CAT 6).......................................................285CAT Level 7: Transponder Transactions (CAT 7).......................................................................285CAT Level 9: Mobile POS (MPOS) Acceptance Device Transactions (CAT 9)......................285

Appendix E: CVM Limit Amounts...............................................................................287Overview...............................................................................................................................................288CVM Limit Amounts............................................................................................................................288

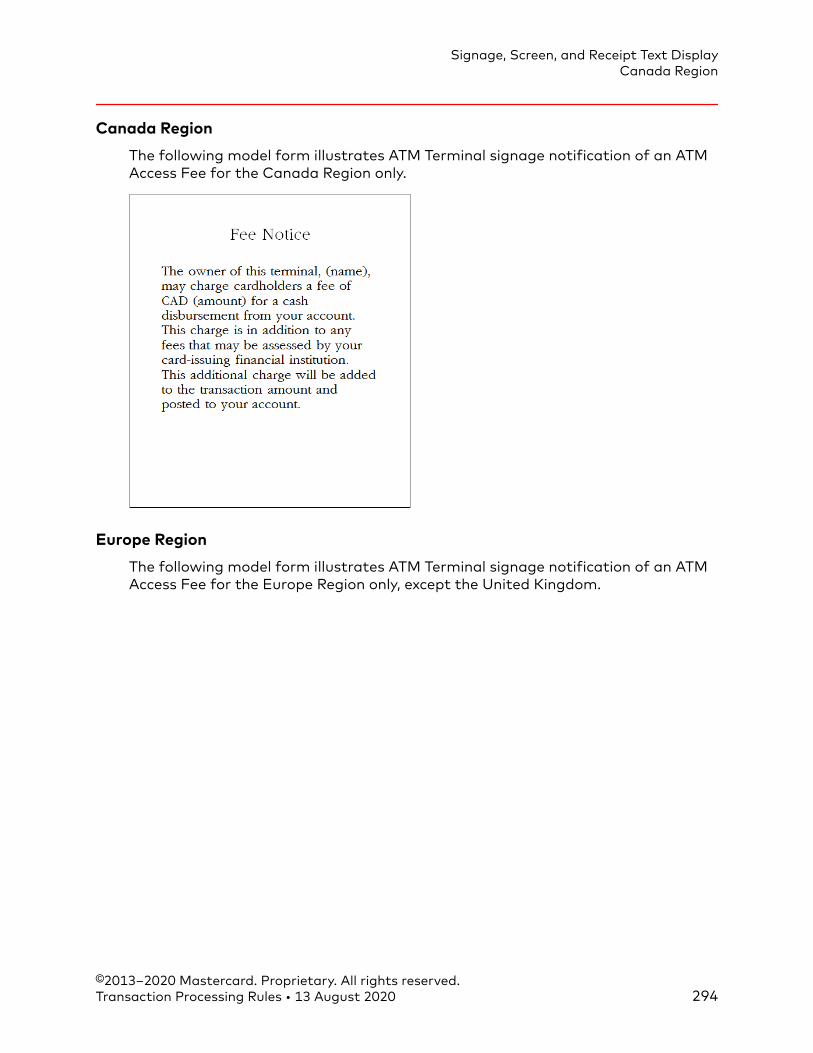

Appendix F: Signage, Screen, and Receipt Text Display.................................. 289Screen and Receipt Text Standards.................................................................................................291Models for ATM Access Fee Notification at ATM Terminals.........................................................292Models for Standard Signage Notification of an ATM Access Fee.............................................292

Asia/Pacific Region........................................................................................................................292Australia.....................................................................................................................................293

Canada Region...............................................................................................................................294Europe Region.................................................................................................................................294

United Kingdom........................................................................................................................295Latin America and the Caribbean Region..................................................................................296

Argentina, Brazil, Chile, Colombia, Ecuador, Mexico, Panama, Peru, Puerto Rico,and Venezuela...........................................................................................................................296

Middle East/Africa Region............................................................................................................297United States Region.................................................................................................................... 298

Models for Generic Terminal Signage Notification of an ATM Access Fee................................298Asia/Pacific Region........................................................................................................................298

Contents

©2013–2020 Mastercard. Proprietary. All rights reserved.Transaction Processing Rules • 13 August 2020 19

Australia.....................................................................................................................................299Canada Region...............................................................................................................................300Europe Region.................................................................................................................................300

United Kingdom........................................................................................................................301Latin America and the Caribbean Region..................................................................................302

Argentina, Brazil, Chile, Colombia, Ecuador, Mexico, Panama, Peru, Puerto Rico,and Venezuela...........................................................................................................................302

Middle East/Africa Region............................................................................................................303United States Region.................................................................................................................... 304

Models for Screen Display Notification of an ATM Access Fee................................................... 304Asia/Pacific Region........................................................................................................................304

Australia.....................................................................................................................................305Canada Region...............................................................................................................................306Europe Region.................................................................................................................................306

United Kingdom........................................................................................................................307Latin America and the Caribbean Region..................................................................................308

Argentina, Brazil, Chile, Colombia, Ecuador, Mexico, Panama, Peru, Puerto Rico,and Venezuela...........................................................................................................................308

Middle East/Africa Region............................................................................................................309United States Region.................................................................................................................... 310

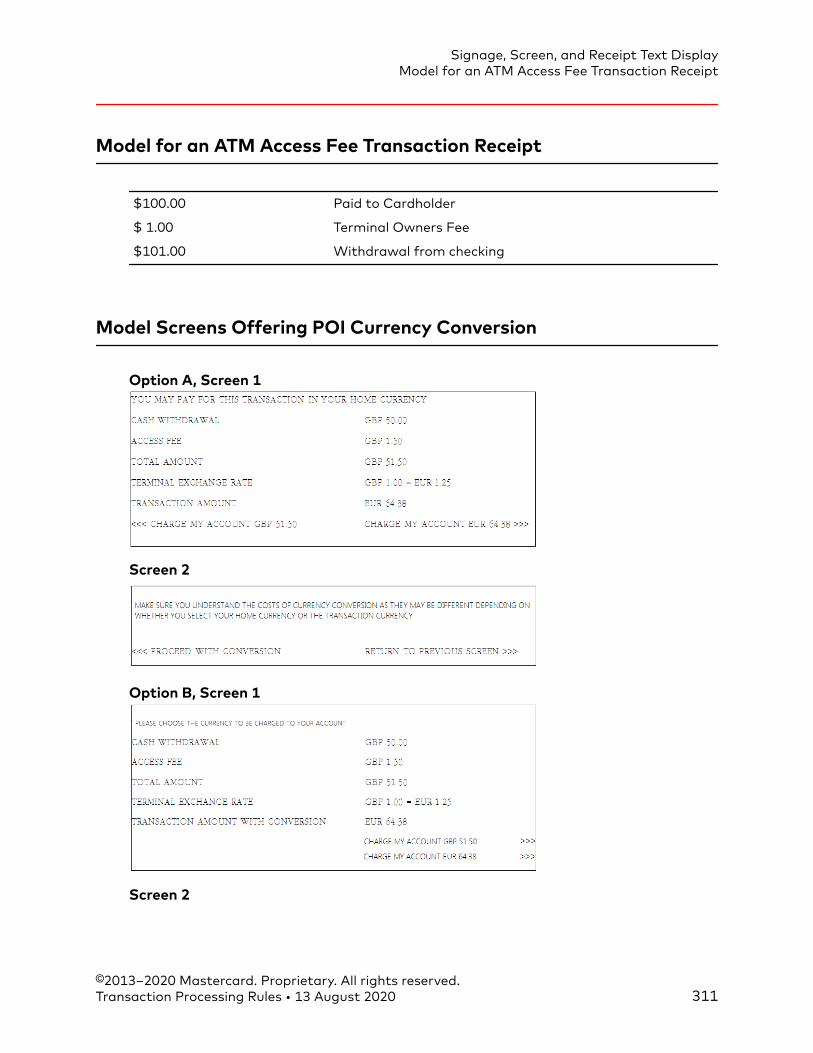

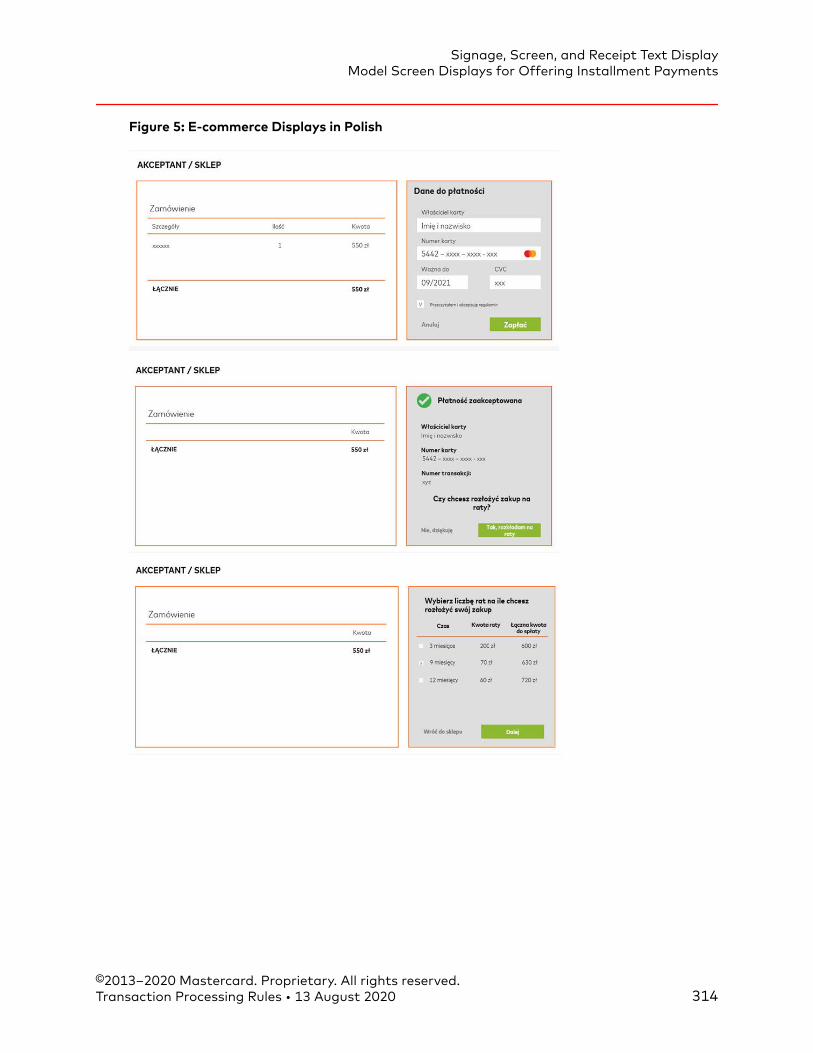

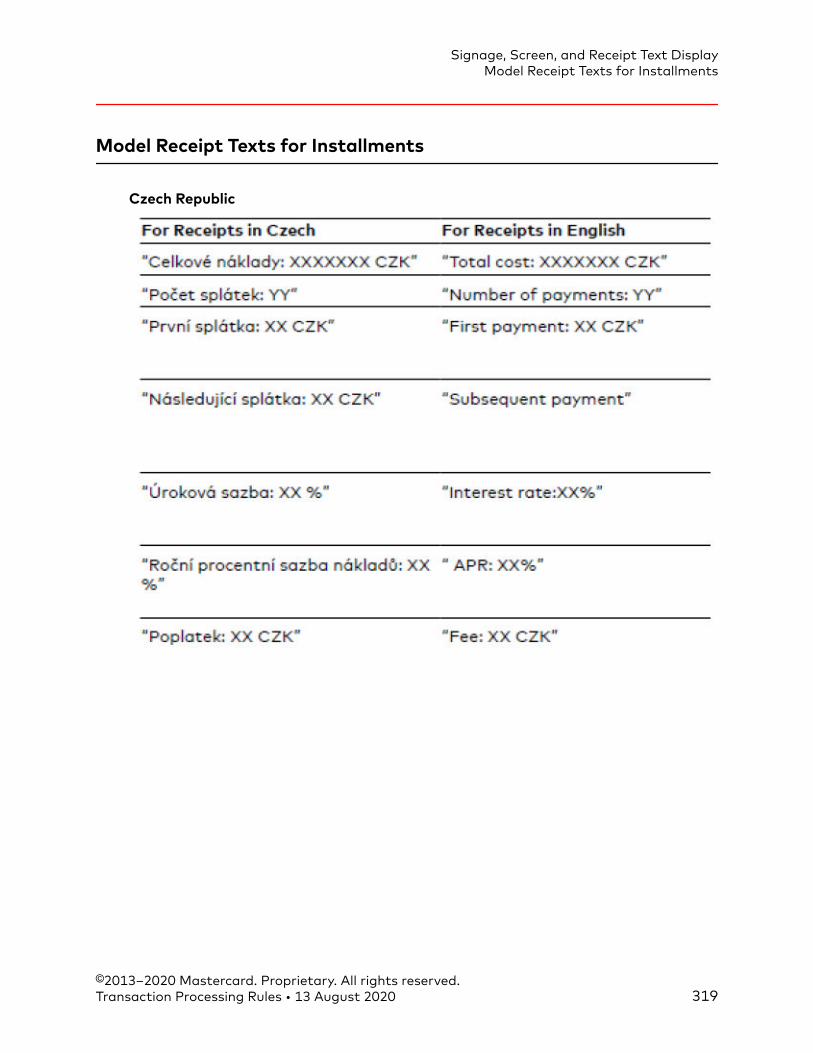

Model for an ATM Access Fee Transaction Receipt....................................................................... 311Model Screens Offering POI Currency Conversion........................................................................ 311Model Receipt for Withdrawal Completed with POI Currency Conversion.............................. 312Model Screen Displays for Offering Installment Payments.........................................................312Model Receipt Texts for Installments...............................................................................................319

Appendix G: Best Practices...........................................................................................322Digital Goods Purchases.................................................................................................................... 323

Appendix H: Definitions..................................................................................................325