training manual for chemical cluster

111

TRAINING MANUAL FOR CHEMICAL CLUSTER Guidelines for Energy Professionals for preparing bankable DPRs Devki Energy Consultancy Pvt. Ltd. Vadodara, Gujarat, India www.devkienergy.com [email protected]

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of training manual for chemical cluster

TRAINING MANUAL FOR CHEMICAL CLUSTER

Guidelines for Energy Professionals for preparing bankable DPRs

Devki Energy Consultancy Pvt. Ltd. Vadodara, Gujarat, India

www.devkienergy.com

2

CONTENTS

1. INTRODUCTION ............................................................................................................................................. 6

1.1 PROJECT BACKGROUND .............................................................................................................................. 6

1.2 PROJECT ACTIVITIES .................................................................................................................................... 7

2. OVERVIEW OF ANKLESHWAR CLUSTER ............................................................................................... 8

2.1 ANKLESHWAR INDUSTRY PROFILE .............................................................................................................. 8

2.2 MSME PROFILE – ANKLESHWAR ................................................................................................................ 9

3. BARRIERS TO FINANCING ENERGY EFFICIENCY ............................................................................ 10

3.1 PERSPECTIVES OF STAKEHOLDERS ............................................................................................................ 10

3.2 POLICY & REGULATORY PERSPECTIVE ...................................................................................................... 10

3.3 EQUIPMENT/SERVICE PROVIDERS’ PERSPECTIVE ...................................................................................... 11

3.4 END USER PERSPECTIVE ............................................................................................................................ 12

3.5 FINANCIERS/LENDER PERSPECTIVE .......................................................................................................... 13

4. UNDERSTANDING FINANCIALS OF MSME UNITS ......................................................................... 15

4.1 CLASSIFICATION ........................................................................................................................................ 15

4.2 OWNERSHIP OF UNITS ............................................................................................................................... 15

4.3 BALANCE SHEET ........................................................................................................................................ 18

4.4 ASSETS........................................................................................................................................................ 18

4.5 INTANGIBLE ASSETS .................................................................................................................................. 19

4.6 CURRENT ASSETS ....................................................................................................................................... 19

4.7 LIABILITIES- CAPITAL ACCOUNT .............................................................................................................. 20

4.8 PROFIT & LOSS ACCOUNT ......................................................................................................................... 20

4.9 LOANS ........................................................................................................................................................ 20

4.10 CURRENT LIABILITIES ................................................................................................................................ 20

4.11 FINANCIAL RATIOS .................................................................................................................................... 21

4.12 CREDIT MONITORING ANALYSIS (CMA) ................................................................................................. 23

5. PREPARATION OF BANKABLE DPRS .................................................................................................... 25

5.1 INTRODUCTION .......................................................................................................................................... 25

5.2 WORKING CAPITAL ................................................................................................................................... 25

5.3 FUND BASED FACILITIES............................................................................................................................ 26

5.4 NON FUND BASED FACILITIES .................................................................................................................. 27

5.5 PREPARATION OF DPRS ............................................................................................................................ 27

5.6 BANKER’S PERSPECTIVE............................................................................................................................. 29

5.7 PREPARATION OF IGDPR .......................................................................................................................... 31

6. FUNDING SCHEMES FROM GOVERNMENT & FINANCIAL INSTITUTIONS .......................... 34

6.1 INTRODUCTION .......................................................................................................................................... 34

3

6.2 CREDIT GUARANTEE FUND TRUST FOR MICRO AND SMALL ENTERPRISES (CGTMSE) ......................... 35

6.3 CREDIT LINKED CAPITAL SUBSIDY SCHEME (CLCSS) ............................................................................. 38

6.4 SIDBI SCHEME FOR FUNDING PROJECTS THROUGH INDO JAPAN COLLABORATION ON ENERGY

SAVING IN MSME SECTORS ................................................................................................................................... 41

6.5 KFW-SIDBI SCHEME FOR FINANCING ENERGY EFFICIENCY PROJECTS IN THE MSME SECTOR............. 43

7. ENERGY AUDIT ............................................................................................................................................. 47

7.1 ENERGY MANAGEMENT ............................................................................................................................ 47

7.2 ENERGY AUDIT .......................................................................................................................................... 47

7.3 ENERGY AUDIT INSTRUMENTS .................................................................................................................. 49

7.4 ANALYTICAL TECHNIQUES ........................................................................................................................ 50

7.5 HEAT TRANSFER CALCULATIONS .............................................................................................................. 51

7.6 ESTIMATING COST OF IMPLEMENTATION .................................................................................................. 53

7.7 THE PLANT ENERGY STUDY REPORT .......................................................................................................... 53

7.8 BARRIERS TO SUCCESSFUL IMPLEMENTATION .......................................................................................... 55

8. IDENTIFYING ENERGY SAVING PROJECTS ....................................................................................... 58

8.1 INTRODUCTION .......................................................................................................................................... 58

8.2 BOILERS ...................................................................................................................................................... 58

8.2 THERMIC FLUID HEATERS .......................................................................................................................... 65

8.3 DRYERS ...................................................................................................................................................... 66

8.4 DISTILLATION PROCESS ............................................................................................................................. 77

8.5 HOT/COLD RECOVERY .............................................................................................................................. 79

8.6 ELECTRIC MOTORS .................................................................................................................................... 84

8.7 BELTS & GEARS ............................................................................................................................................ 0

8.8 PUMPS & FANS ............................................................................................................................................ 1

8.9 COOLING TOWERS ....................................................................................................................................... 8

8.10 COMPRESSED AIR ........................................................................................................................................ 8

8.11 REFRIGERATION & AIR CONDITIONING SYSTEM ...................................................................................... 13

9. ANNEXURE-1 .................................................................................................................................................. 19

9.1 BANKS IN ANKLESHWAR ........................................................................................................................... 19

10. ANNEXURE-2: SME FINANCE SCHEMES .......................................................................................... 20

List of Figures

FIGURE 1-1: PROGRAM OVERVIEW ................................................................................................................................ 7

FIGURE 2-1: ANKLESHWAR MAP ................................................................................................................................... 8

FIGURE 2-2: MSME CHEMICAL CLUSTER .................................................................................................................... 9

FIGURE 3-1: BARRIERS TO FINANCING- SUMMARY ..................................................................................................... 14

FIGURE 6-1: MSME ADVANCES- BREAK UP ................................................................................................................ 34

4

FIGURE 8-1: FLASH STEAM .......................................................................................................................................... 63

FIGURE 8-2: FLOW CONTROL OPTIONS ....................................................................................................................... 64

FIGURE 8-3: ECONOMISER ........................................................................................................................................... 65

FIGURE 8-4: DRYING CURVE........................................................................................................................................ 66

FIGURE 8-5: SPIN FLASH DRYER ................................................................................................................................. 69

FIGURE 8-6: SPRAY DRYER ........................................................................................................................................... 70

FIGURE 8-7: FLUIDISED BED DRYER ............................................................................................................................. 70

FIGURE 8-8: TRAY DRYER ............................................................................................................................................ 71

FIGURE 8-9: RECIRCULATION OF EXHAUST IN DRYING .............................................................................................. 73

FIGURE 8-10: HEAT PUMP DRYING.............................................................................................................................. 74

FIGURE 8-11: DISTILLATION COLUMN ........................................................................................................................ 77

FIGURE 8-12: MOTOR EFFICIENCY .............................................................................................................................. 84

FIGURE 8-13: MOTOR LOADING, EFFICIENCY & PF ..................................................................................................... 84

FIGURE 8-14: MOTOR LOSSES ...................................................................................................................................... 85

FIGURE 8-15: PUMP CURVES .......................................................................................................................................... 1

FIGURE 8-16: PUMP CURVES ......................................................................................................................................... 2

FIGURE 8-17: SAVING BY VFDS .................................................................................................................................... 5

FIGURE 8-18: PART LOAD OPERATION OF SCREW COMPRESSOR ................................................................................ 10

List of Tables:

TABLE 4-1: MSME UNITS - CLASSIFICATION ............................................................................................................. 15

TABLE 4-2: CAPITAL ACCOUNT- SOLE PROPRIETORSHIP ............................................................................................ 16

TABLE 4-3: CAPITAL - PARTNERSHIP FIRMS ............................................................................................................... 16

TABLE 4-4: PRIVATE LIMITED COMPANY-EXTRACT OF BALANCE SHEET ................................................................... 17

TABLE 4-5: NET PROFIT MARGIN ............................................................................................................................... 22

TABLE 5-1: WORKING CAPITAL LIMITS ....................................................................................................................... 25

TABLE 6-1: MSME ADVANCES GROWTH IN GUJARAT ............................................................................................... 34

TABLE 6-2: LIST OF BANKS .......................................................................................................................................... 38

TABLE 6-3: EQUIPMENTS/TECHNOLOGIES ELIGIBLE ................................................................................................... 40

TABLE 6-4: FINANCIAL PARAMETERS ......................................................................................................................... 43

TABLE 8-1: FUELS AND CALORIFIC VALUES ............................................................................................................... 58

TABLE 8-2: EXCESS AIR ................................................................................................................................................ 59

TABLE 8-3: BOILER CONVERSION ............................................................................................................................ 60

TABLE 8-4: HEAT LOSSES FROM PIPE SURFACES .......................................................................................................... 60

TABLE 8-5: SUMMARY OF LOSSES ................................................................................................................................ 61

TABLE 8-6: SELECTION OF TRAPS ................................................................................................................................ 62

TABLE 9-3: DRYER EFFICIENCY ................................................................................................................................... 68

TABLE 9-4: ADVANTAGES OF HEAT PUMP DRYING .................................................................................................... 74

TABLE 8-9: EXISTING CONDITION ............................................................................................................................... 76

TABLE 8-10: AFTER MODIFICATION ............................................................................................................................ 76

5

TABLE 8-11: SAVING POTENTIAL ................................................................................................................................ 76

TABLE 9-8: HEAT PUMP ASSISTED CHLORINE EVAPORATION .................................................................................... 83

TABLE 8-13: MOTOR SIZING ........................................................................................................................................ 85

TABLE 8-14: COMPARISON OF REWINDING & REPLACEMENT.................................................................................... 86

TABLE 8-15: HIGH EFFICIENCY MOTORS ..................................................................................................................... 86

TABLE 8-16: MOTOR REPLACEMENT ............................................................................................................................. 0

TABLE 8-17: EFFICIENCY OF GEAR & BELT DRIVES........................................................................................................ 1

TABLE 8-18: SAVING BY IMPELLER TRIMMING .............................................................................................................. 6

TABLE 9-15: PNEUMATIC VS ELECTRICAL PUMPS ....................................................................................................... 11

TABLE 9-16: COMPRESSED AIR LEAKAGE .................................................................................................................... 11

TABLE 9-17: EFFECT OF HIGHER TEMPERATURE ON EFFICIENCY ............................................................................... 14

TABLE 9-18: INCREASE IN COP .................................................................................................................................. 14

TABLE 9-19: REPLACEMENT OF EVAPORATORS .......................................................................................................... 16

6

1. Introduction

1.1 Project Background

1.1.1 The Micro, Small and Medium Enterprises Sector (MSME) is a critical segment of the Indian

economy. It has a large share in employment generation and contributes significantly to

manufacturing output as well as exports of the country.

1.1.2 The potential for growth and stability of this sector is however being hampered by factors

like obsolete technology, information deficiencies, lack of financing avenues for

technological up gradation and conservative management practices. These factors are also

likely to create energy inefficiencies.

1.1.3 The Bureau of Energy Efficiency (BEE), a statutory body under the Ministry of Power, and Small Industries Development Bank of India (SIDBI) are jointly executing a Project

“Financing Energy Efficiency at MSMEs”. This project forms a part of the Global

Environment Facility (GEF) Programmatic Framework (2010-14) for promoting Energy

Efficiency in India with an objective to increase demand for energy efficiency investments in

targeted MSME clusters and to build their capacity to access commercial finance.

1.1.4 The GEF implementation agency for this project is World Bank. The project aspires to

address the current gap in the understanding between energy auditors and bank loan officers

and demonstrate a viable mechanism of synergic tie-up between MSMEs, energy auditors,

financial consultants/chartered accountants, local industrial or MSME associations and local

bankers.

1.1.5 The project has been launched at the following five MSME clusters from different industrial

sectors, namely, Ankleshwar (Chemical), Faridabad (Mixed), Kolhapur (Foundry), Pune

(Forging) and Tirunelveli (Lime kiln).

1.1.6 Devki Energy Consultancy Pvt. Ltd. is providing technical assistance to energy professionals at the

Ankleshwar Cluster, which involves capacity building of energy professionals in techno-

economic feasibility studies and development of bankable Detailed Project Reports.

1.1.7 The primary objective of the assignment is to develop a constituency of trained energy

auditors and energy professionals for the MSME Chemical clusters with specific knowledge

in:

� Production processes in various types of industries in the cluster, viz., Chemicals,

Pesticides, Dye & Dyestuffs, Petroleum Products, Rubber, Bulk Drugs, Pharmaceuticals,

Packaging, etc.

7

� Identifying potential for energy savings in equipments and processes in these industries

� Developing implementable energy saving schemes in these industries

� Preparing bankable DPRs

� Schemes available with banks/FIs for financing energy saving schemes

1.2 Project Activities

1.2.1 A brief activity chart followed by us for implementing this project is given below.

Figure 1-1: Program overview

Review of cluster information

•Identify chemical MSME units in Ankleshwar by discussions with BEE, Industry Associations & End Users

•Review & compile information on EE in the Ankleshwar cluster such as energy norms, current technologies, penetration of EE technologies, barriers, etc.

Walk through audits to validate review findings

•Identify plants for conducting walkthough audits considering scale of production, production process and technology. About 25 audits to be done in the Ankleshwar chemical cluster.

•Develop a Cluster specific template for data collection, monitoring & measurements, energy saving calculations. The Walk Through Audit Report will include process flow charts, energy & material balance, energy use information and practices, energy production norms, information gaps, case studies, etc.

Developing training modules

•Discussions with FIs to understand existing schemes and documentation requirements to prepare guidelines for training energy professionals to prepare bankable DPRs

•Modules will be developed by discussions with Associations, FIs & BEE to highlight govt /FI initiatives, technological interventions to save energy cost, M&V techniques, financial evaluation methods, etc.

Imparting Training to

Energy Professionals

•Three training programs will be conducted with number of participants 25-30 in each program.

•Candidates for training will be selected in consultation with BEE regarding qualifications and experience

•A half-day industry visit will be organised after each program to familiarise participants with the processes, practices and barriers in MSME in the cluster.

•Design, collect & disseminate feed back from programs to BEE

8

2. Overview of Ankleshwar Cluster

2.1 Ankleshwar Industry profile

2.1.1 Ankleshwar is one of the historical cities of Gujarat in Bharuch district. The city is also well

connected with the metro cities of Mumbai and Delhi by road (NH 8), rail and air

(approximately 90 kms from Vadodara and Surat airports). One of the notable attractions of

Ankleshwar is the 132 year old Golden Bridge over the river Narmada, that connects it with

Bharuch city.

2.1.2 The city is also primarily identified with the presence of Ankleshwar Industrial Estate, one of

the largest industrial townships of Asia. This estate was set up by GIDC in the mid 70s and

today there are more than 1200 Micro, Small and Medium industrial units engaged in

manufacturing, trading and providing various services. Most of the industries being from the

chemical sector, Ankleshwar is also recognised as a major chemical zone of the State.

2.1.3 Ankleshwar also provides industrial and social infrastructure to other nearby estates like

Panoli and Jhagadia as indicated in the map below.

Figure 2-1: Ankleshwar map

2.1.4 35% of the total exports of the State are from this area. Ankleshwar is contributing significantly to the growth of Gujarat State as well as the nation.

9

2.1.5 Many MNC companies and large corporates also have manufacturing facilities at GIDC

Ankleshwar; some of the well known names are Aventis Pharma, Asian Paints, Bayer

Cropscience, Cadila Healthcare, Lupin, UPL etc.

2.2 MSME profile – Ankleshwar

2.2.1 Of the 1200 units in Ankleshwar GIDC, around 450 units can be classified as chemical units

in MSME. These units can be further classified under the following industrial sector

� Chemicals

� Dyes, Pigments & Colours

� Pesticides & Fertilisers

� Packaging

� Petroleum Products

� Pharma & Bulk Drugs

� Plastics & Rubber

2.2.2 The following figure illustrates the number of units coming under various categories.

Figure 2-2: MSME Chemical Cluster

2.2.3 The majority of industries fall into Dyes & Pigments sector. General chemicals & pharma-

bulk drugs also contribute significantly in terms of numbers in this cluster.

450 MSME Chemical Units

Chemicals84

Petroleum products

10

Dyes, Pigments, Paints &

Colour 179

Plastics & Rubber 72

Pesticides & Fertilizers 4

Packaging 22

Pharma & Bulk

Drugs 79

10

3. Perspectives on Financing Energy Efficiency

3.1 Perspectives of Stakeholders

3.1.1 Big ticket Energy Efficiency projects in the MSME sector have often suffered due to non-

availability of finance. Financing Barriers are broadly segregated to understand the

perspectives of the stakeholders:

• Policy & Regulatory Perspective

• Equipment/Service providers’ Perspective

• End Users’ Perspective

• Financiers’/Lenders’ Perspective

3.2 Policy & Regulatory Perspective

3.2.1 Energy pricing structures often do not send the right signals to end users to improve their

energy efficiency.

3.2.2 One of the important financial barriers being faced by MSMEs today is the difficulty in

providing technical and financial information to banks and companies to routinely negotiate

loans for implementing energy efficiency interventions.

3.2.3 Reserve Bank of India has issued guidelines & directives to banks regarding priority sector

lending, including MSMEs. Bank lending to the Micro and Small Enterprises is reckoned as

priority sector advances; lending to Medium enterprises is not eligible to be included for the

purpose of computation of priority sector lending. The domestic commercial banks are

expected to enlarge credit to the priority sector and ensure that priority sector advances

(which include the micro and small enterprises sector) constitute 40% of Adjusted Net Bank

Credit (ANBC) or credit equivalent amount of Off-Balance Sheet Exposure, whichever is

higher. However, the priority sector also includes agriculture, housing etc. and hence there

are no separate targets for loans to MSEs alone.

3.2.4 Banks have been advised to achieve a 20 per cent year-on-year growth in credit to Micro and

Small enterprises and a 10 per cent annual growth in the number of Micro enterprise

accounts.

11

3.2.5 Serious market failures exist in most jurisdictions. The perception is that governments are

not providing a clear and compelling set of targeted policies and incentives to pursue energy

efficiency interventions across the economy at a meaningful scale. Most of the government

subsidies/incentives are generally targeting renewable energy investments like wind energy,

solar thermal and solar photovoltaic, micro hydro etc. The rapid, policy-led growth in

renewable energy investment in many countries is highlighted as a positive example that

should be emulated.

3.2.6 Market driven mechanisms such as Clean Development Mechanism (CDM) have not

penetrated the MSME sector because of high transaction costs as compared to the benefits.

The Perform, Achieve, Trade mechanism, initiated by BEE, which is targeting only

designated consumers under the Energy Conservation Act, is not available as an incentive

for MSMEs.

3.2.7 Most financial institutions lack awareness about the impact of energy efficient

equipment/processes on the bottom line and resultant environmental benefits; for example,

a loan may be granted more easily for pollution control equipment than energy efficient

equipment.

3.3 Equipment/Service Providers’ Perspective

3.3.1 Absence of sufficient information from the customers and lack of customer awareness are

often major impediments in implementation of energy efficiency projects. Company

purchase policies often encourage purchases at the lowest cost, disregarding the issue of

energy efficiency and potential energy cost savings.

3.3.2 Techno-economic feasibility analyses of any energy saving projects are typically done by

energy auditor or the vendor of the energy efficient equipment; often insufficient knowledge

of financial analyses results in a report that does not provide all information required by a

banker or financier. For example, a typical feasibility study makes assumptions for various

factors for estimating energy savings, such as energy cost, operating hours, production levels,

discount rates, inflation in costs and other factors beyond the control of unit owner.

Sensitivity analysis is required to understand the base case, best case and worst case scenarios

and build the confidence level of the industry owner and the financier; often this is not done.

For large investments, the bankers may be interested in understand the impact on CMA

data, which may require the skills of a chartered accountant; lack of access to qualified

professionals to do this type of analyses often limits further development of energy saving

interventions. The scope of such analyses is often limited by the professional charges that

the unit owner is willing to spend on such activity.

12

3.3.3 The process for loan approval for project financing also often tends to be a tedious process;

the efforts are often disproportionately high and not worth especially if the loan amount is

small. High risk projects, that can be implemented on an ESCO basis, also do not take off

at times as establishing water-tight Monitoring & Verification protocols is also difficult in

some cases. It may also be difficult to secure the rights over the Energy Efficient equipment

and/or collect payment installments in the event of dispute over performance.

3.3.4 Poor documentation and inability of the industry owner to communicate issues to the

banker may also result in non-availability of funding for potentially lucrative energy saving

projects.

3.4 End Users’ Perspective

3.4.1 Very high perceived risks of some energy efficiency projects, mistrust in unduly optimistic

projections in project reports of auditors/vendors etc. can often derail the implementation

of energy efficiency projects.

3.4.2 Lack of money , lack of time, absence of experts for designing & project planning or lack of

internal expertise for implementation are genuine problems faced by MSMEs. Many unit

owners may have good conceptual knowledge but are unable to take these forward due to

the mentioned reasons.

3.4.3 Cash flows from saving energy are not conventional revenues, so it discourages commercial

financial institutions (CFI)s' entry into this market. Energy cost savings are often not

considered as positive cash flows into the plant boundary like money from sales of products.

3.4.4 Even in cases wherein the payback periods are short and huge savings are expected, energy

efficiency projects are often not implemented because of high startup cost, especially due to

production shutdown requirements for implementation. Often high investment projects are

filtered based on simple payback periods, which considers only the savings in the first year;

use of IRR or other methods, which provide a more holistic understanding of economics

over the life time of the equipment, are often not used.

3.4.5 Additional project costs for engineering analyses & design, additional utility requirements,

disruptions to production during implementation, additional staffing & training and other

overheads are often ignored in calculation resulting overly optimistic scenarios and

misleading economics. Due to small size of projects, due diligence requirements from a

project financing perspective create relatively high transaction costs, resulting in

managements giving low priority to such projects.

13

3.5 Financiers’/Lenders’ Perspective

3.5.1 The contributions of energy savings to cash flow often cannot be differentiated from main

cash flow which may increase or decrease due to a variety of factors. Often the

contributions of energy saving projects get masked due to variations in cash flow due to

other reasons, which lead to finance persons doubting the real contribution of energy saving

projects.

3.5.2 Low collateral asset value of energy efficient equipment results in difficulties in creating

creditworthy financing structures. Collateral value is low because for most energy efficiency

projects equipment represents a small share of total project cost but may have high

engineering development and installation costs.

3.5.3 Energy efficiency projects often represent a relatively small position of business for major

banks and may be perceived as high credit risk. Unfavorable financial position indicated in

balance sheet may also demand more collateral to fund the project.

3.5.4 Energy professionals should make an attempt to transgress their limitations in understanding

of finance to ensure the Investment Grade Detailed Project Reports (IGDPR) prepared by

them

3.5.5 The following diagram shows the broad category of barriers to implementing energy

efficiency schemes.

14

Energy pricing High Project development costs

Lack of awareness of EE New technologies and contractual mechanisms

Procurement policies favor lowest cost

Limited demand for EE goods

Higher project development and upfront costs

Small sizes widely high transaction costs

Import duties on EE equipment

Diffuse/diverse markets Ability/willingness to pay incremental cost

High perceived risk as these are traditional asset based

Unclear or underdeveloped institutional framework for EE

New contractual mechanisms(ESCOs)

Low EE benefits relative to other costs

Other higher return, low risk projects are more attractive

Lack of testing facilities, poor enforcement of standards

Limited technical, business, risk management skills, Limited financing/equity

Perceived risk of new tech/systems, mixed incentives, lack of credible data

Behavioral biases

Figure 3-1: Barriers to financing- summary

Barriers to investment in energy efficiency

Policy /

Regulatory

Equipment vendors /

Service providers

End Users Banks /FIs

15

4. Understanding Financials of MSME Units

4.1 Classification

4.1.1 A unit is classified as MSME (Micro, Small or Medium Enterprise) based on the investment in Plant and Machinery.

Table 4-1: MSME Units - Classification

Manufacturing Sector Investment in plant & machinery

Does not exceed twenty five lakh rupees Micro Enterprises Small Enterprises More than twenty five lakh rupees but does not

exceed five crore rupees Medium Enterprises More than five crore rupees but does not exceed

ten crore rupees Service Sector Investment in plant & machinery

Does not exceed ten lakh rupees: Micro Enterprises Small Enterprises More than ten lakh rupees but does not exceed

two crore rupees Medium Enterprises More than two crore rupees but does not exceed

five core rupees

4.2 Ownership of Units

Sole Proprietorship Firms

4.2.1 Sole proprietorship is the oldest and most common form of business in India. It is a

business enterprise exclusively owned, managed and controlled by a single person with all

authority, responsibility and risk.

4.2.2 A distinct disadvantage, however, is that the owner of a sole proprietorship remains

personally liable for all the business's debts. So, if a sole proprietor business runs into

financial trouble, creditors can bring lawsuits against the business owner. If such suits are

successful, the owner will have to pay the business debts with his or her own money.

4.2.3 The amount in the Proprietor’s capital account is reflected in the liabilities section of the

balance sheet under sources of funds.

16

Table 4-2: Capital account- Sole proprietorship

Particular Current Year (Amount in Rs)

Previous Year (Amount in Rs)

Capital Account Opening Balance xxx xxx Add – Addition to Capital xxx xxx Interest on Capital xxx xxx Net Profit earned during the year xxx xxx Less - Withdrawals xxx xxx Closing Balance of Capital Account xxxx xxxx

Partnership Firms

4.2.4 Partnership concerns are formed when more than one person owns the business and they

have jointly signed a Partnership Deed.

4.2.5 At least two members are required to start a partnership business. But the number of

members should not exceed 10 in case of “banking business” and 20 in case of “other

business”. If the number of members exceeds this maximum limit, then that business is not

called as a partnership business legally.

4.2.6 The Partnership Firm’s capital account is reflected in the liabilities section of the balance

sheet under sources of funds as shown in table 4.3. This is the net worth of the Partnership

Firm

Table 4-3: Capital - Partnership firms

Partner Capital Account ( Mr. B)

Opening Balance xxx xxx

Add – Addition to Capital xxx xxx

Interest on Capital xxx xxx

Net Profit ( as per Profit Sharing Ratio) xxx Xxx

Remuneration

Less - Withdrawals xxx Xxx

Closing Balance of Capital Account xxxx Xxxx

Particular Current Year (Amount in Rs)

Previous Year (Amount in Rs)

Partner Capital Account ( Mr. A) Opening Balance xxx xxx Add – Addition to Capital xxx xxx Interest on Capital xxx xxx Net Profit ( as per Profit Sharing Ratio) xxx xxx

Remuneration Less - Withdrawals xxx xxx Closing Balance of Capital Account xxxx xxxx

17

Private Limited Company

4.2.7 A private limited company is a voluntary association that offers limited liability or legal

protection for its shareholders but that places certain restrictions on its ownership. These

restrictions are defined in the company's bye laws or regulations and are meant to prevent

any hostile takeover attempt.

4.2.8 The major ownership restrictions are:

� Shareholders cannot sell or transfer their shares without offering them first to other

shareholders for purchase,

� Shareholders cannot offer their shares to the general public over a stock exchange ,

� The number of shareholders should not be less than two and not more than fifty.

4.2.9 Private Limited company is a fully owned by a group of promoters. All shares of the

company are held with promoters and their relatives. Details of shareholder’s funds are

found in the liabilities section of the balance sheet of the private limited company as detailed

in table 4.4 below.

Table 4-4: Private Limited company-extract of balance sheet

Particular Current Year (Amount in Rs)

Previous Year (Amount in Rs)

Shareholder’s Funds A) Share Capital Account ( Note No -1) xxxx xxxx B) Reserve & Surplus Account ( Note No -2) xxxx xxxx

Particular Current Year (Amount in Rs)

Previous Year (Amount in Rs)

Share Capital Account Authorized Equity shares of Rs 10 each with voting rights (No Share xxx )

xxx xxx

Issued ,Subscribed & fully paid up Equity shares of Rs 10 each with voting rights (No. Share xxx)

xxx xxx

Particular Current Year (Amount in Rs)

Previous Year (Amount in Rs)

Reserve & Surplus Account

Surplus /Deficit in the statement of Profit and Loss Account

xxx xxx

18

4.3 Balance Sheet

4.3.1 A financial statement summarizes a company's assets, liabilities and Shareholders' Fund at a

specific point in time. These three balance sheet segments give investors an idea as to what

the company owns and owes, as well as the amount invested by the shareholders.

4.3.2 An audited balance sheet generally comprises of the following:

• Directors’ Report.

• Auditor’s Report

• Balance Sheet

• Profit and Loss Account

4.3.3 The first page of the balance sheet contains a summary of all the balances in the various

asset and liability accounts of the company. The total of all the assets must equal the total of

all the liabilities.

4.4 Assets

4.4.1 The Assets part of the balance sheet generally comprise of the following.

4.4.2 This section of the balance sheet contains the book value of all the fixed assets of the

firm/company i.e. summary of the cost of asset less depreciation for the year.

4.4.3 Fixed Assets are assets used within the business and not acquired for the purposes of resale.

4.4.4 Examples include:

• Land and buildings

• Plant and machinery (Eg. boilers, chillers, Reactors etc.)

• Fixtures and fittings, such as light fittings and shelves

• Motor vehicles like vans and cars.

4.4.5 Fixed assets are shown at original cost (purchase price) or valuation (including all expenses

that are incurred before it is ready for use. Depreciation* is charged on the asset at a rate

prescribed under the Income Tax Act 1961 and Companies Act 1956.

*Depreciation is the measure of wearing out of a fixed asset. Fixed assets are expected to wear

out and become less efficient. Depreciation is calculated as the estimate of this measure of

wearing out and is a charge in the Profit and loss Account.

19

No Depreciation should be charged on land while depreciation is to be charged on all other

assets.

4.5 Intangible Assets

4.5.1 An intangible asset is an identifiable non-monetary asset, without physical

substance, held for use in the production or supply of goods or services, for

rental to others, or for administrative purposes. Eg. Copyright, Patents etc

4.6 Current Assets

4.6.1 Current assets are assets which can be easily liquidated within a period of 12 months or as

per operating cycle of business concern. The following can be classified under current assets:

• Cash and Bank Balances

• Government and other deposits

• Fixed Deposits with banks

• Sundry Debtors or Receivables (domestic & export, outstanding for less than six months)

• Inventory (Stock of Raw materials)

• Stocks in process

• Finished goods

• Other consumable spares and packing

• Advances and prepaid expenses

• Advance Tax

• Others – Deposits etc

20

4.7 Liabilities- Capital Account

4.7.1 Proprietor’s capital account or Partnership Firm’s capital account or Share Capital account in

the case of Private Limited companies wherein the Paid up Capital will actually give an idea

regarding the amount of money the promoters of the company have brought into the

business.

4.7.2 The credit/ (Debit) balance in the profit and loss account is called a surplus/(Deficit) and, at

the end of an accounting period, the company may decide to transfer part of the profits to

“Reserve” head in the balance sheet; the reserve created out of profits transferred from

Profit and Loss account is called General Reserve.

4.7.3 The company can use the general reserve for various purposes including issue of bonus

shares to shareholders and payment of dividend when profits are insufficient.

4.8 Profit & Loss Account

4.8.1 Profit & loss Account is a Financial Statement summarizes the revenues, costs and expenses

incurred during a specific period of time, usually a fiscal quarter or year. These records

provide information that shows the ability of a company to generate profit by increasing

revenue and reducing costs. The P&L statement is also known as a "statement of profit and

loss", an "income statement" or an "income and expense statement".

4.9 Loans

Working Capital Loan- Current outstanding of working capital loans are mention .Example Cash Credit

Unsecured Loans- Outstanding loans from promoters, their friends and relatives, which are

not secured by any collateral.

4.10 Current Liabilities

A. From Banks

Short term borrowings from banks (including bills purchased & discounted and the excess borrowings placed on repayment basis)

B. Other Current Liabilities

• Short term borrowings (others)

• Sundry Creditors (trade)

• Advance Payments from customers/deposits from dealers, agents etc.

• Provision for taxation

21

• Dividend payable

• Other statutory liabilities

• Installments of term loans/ deferred payment credits / etc. due within one year

• Other current liabilities and provisions due within one year

4.11 Financial Ratios

Current Ratio

4.11.1 This is the most fundamental ratio in Financial Analysis. It is also known as Liquidity Ratio

and is calculated as under:

���������� = (�������������)/(�������������)

Having a current ratio of 1.33 is ideal.

4.11.2 The current ratio is a liquidity ratio which estimates the ability of a company to pay back

short-term obligations. This ratio is also known as cash asset ratio, cash ratio, and liquidity

ratio. A higher current ratio indicates the higher capability of a company to pay back its

debts.

Quick Ratio

4.11.3 The quick ratio also referred as the “acid test ratio” or the “quick assets ratio”, this ratio is a

gauge of the short term liquidity of a firm. The quick ratio is helpful in measuring a

company’s short term debts with its most liquid assets.

The formula used for computing quick ratio is:

(������������� − ���������)/(�������������)

A higher quick ratio indicates the better position of a company.

Debt Equity Ratio

4.11.4 This ratio gives an idea regarding the total debt or borrowings of the entity against the

capital or the tangible net worth of the entity.

������������ = ���/���

TOL stands for Total outside Liabilities.

22

TNW stands for Tangible Net Worth.

��� = �������ℎ − ����!���������

Debt Service Coverage Ratio (DSCR)

4.11.5 The Debt Service Coverage ratio (DSCR), also known as "debt coverage ratio" (DCR), is

the ratio of cash available for debt servicing to interest, principal and lease payments. It is a

popular benchmark used in the measurement of an entity's (person or corporation) ability to

produce enough cash to cover its debt (including lease) payments. The higher this ratio, the

easier it is to obtain a loan. This terminology is also used in commercial banking and may be

expressed as a minimum ratio that is acceptable to a lender; it may be a loan condition or

covenant.

�"�� = (#�� + ��%��&��� + ��������)/(��%�'������!���)

Net Profit Margin

The Net Profit margin is a number which indicates the efficiency of a company in cost

control. A higher net profit margin shows more efficiency of the company at converting its

revenue into actual profit. This ratio is a good way of making comparisons between

companies in the same industry, for such companies are often subject to similar business

conditions.

The formula for computing the Net Profit Margin is:(NetProfit)/(NetSales)

Table 4-5: Net Profit Margin

Acceptable Values

A ) Ratios

Current Ratio 1.33 Debt: Equity 1.5 to 2:1(preferred)

TOL/TNW Not More than 3:1

Gross Average DSCR 1.75 – 2.00 PBDIT/Interest More than 2.5

B) Promoters’ Contribution as % age to Total Cost of Project

25% to 30%

23

4.12 Credit Monitoring Analysis (CMA)

4.12.1 The financials of a company are classified in a spreadsheet in a particular format. This forms

the CMA data of the entity.

4.12.2 CMA Data means credit monitoring arrangement data. This data is provided by a company

to a bank for getting a loan from the bank. Banks analyse this data and decide whether the

loan should be sanctioned as well as set the drawing power/limits.

4.12.3 The CMA generally consists of 5 years data including 2 years Audited balance sheets and 1

year’s estimated/provisional (i.e. current year) balance sheet and the future projected balance

sheets for the remaining years. In the case of a Term Loan, CMA includes data till the

repayment of a loan and, in case of a WC, current year ‘s and following year’s projections.

4.12.4 The Fund flow statement, changes in working capital report, ratio analysis and maximum

permissible bank finance (MPBF) report.

4.12.5 Banks want to decrease risk of default of loan. Over a period of time, if any company is not

in position to repay the loan, it becomes bad debt. The reason for the default may be due to

the fact that the bank did not analyze the financial and solvency position of company. By

getting CMA data, bankers will be in the position to understand the financial position of the

company. So, every bank should demand CMA Data and analyze it in depth. CAs generally

provide the service of preparing and analyzing the CMA data on the behalf of the company

and bank.

4.12.6 With studying the balance sheet, the bank will know as to whether the financial position of

the entity is sound or not, and whether the assets are debt free or mortgaged.

4.12.7 With the fund flow statement, banks get an idea regarding the inflows and outflows of

funds. It also gives the exact picture as to whether the company is wasting their funds or

using the funds for growing the business.

4.12.8 The profit and loss account gives details of the appropriation of profits etc. to the banker. It

also helps in understanding the earning cycle which gives a further understanding of how

expenses are being met.

4.12.9 With changes in working capital report, the banker will know the changes in current assets

and current liabilities. It also gives a picture of short term solvency of the entity i.e. if the

entity has enough money to pay the current liabilities, it will be difficult to misuse its long

term resources.

24

4.12.10 With ratio analysis, banks can understand the financial position of the entity quickly.

4.12.11 Maximum permissible bank finance (MPBF) generally should not be more than 75% of the

working capital of the entity, which helps set loan limits.

4.12.12 RBI has introduced clause for inclusion of the CMA data with the aim of protecting the

customers’ deposits in bank.

25

5. Preparation of Bankable DPRs

5.1 Introduction

5.1.1 A company can be endowed with assets and profitability but requires liquidity or cash for

Expansion / Diversification / Technology up-gradation / Face competition and also meet

with its day to day operating requirements like procurement of raw materials, routine

expenses like local conveyance, salaries, rent etc. The firm/company is said to be short of

liquidity if its assets cannot readily be converted into cash.

5.2 Working Capital

5.2.1 Working capital, also known as net working capital or NWC, is a financial metric which

represents operating liquidity available to a business. Along with fixed assets such as plant

and equipment, working capital is considered a part of operating capital. If current assets are

less than current liabilities, an entity has a working capital deficiency or working capital

deficit.

���4�!�%�� = (�������������) − (�������������)

5.2.2 Positive working capital is required to ensure that a firm is able to continue its operations

and that it has sufficient funds to satisfy both maturing short term debt and upcoming

operational expenses. The management of working capital involves managing inventories,

accounts receivable & payable and cash.

5.2.3 There are two types of limits which are generally set by banks:

Table 5-1: Working capital limits

Type Fund Based Non-fund Based Meaning With Fund Based Limit, the

Company actually gets money (Cash)

With Non-fund based limit, the bank makes payment on behalf of company

Examples of fund based limits are: 1. Cash Credit 2. Term Loans 3. Demand Loan 4. Bank Overdraft etc.

Examples of Non fund based limits are: 1. Bank Guarantee 2. Letter of Credit etc.

26

5.2.4 Working capital loans are provided by banks or financial institutions and are tailored to

suit the precise requirements of the client through any of the various instruments available or

are structured as a combination of cash credit, demand loan, bill financing and non-funded

facilities.

5.3 Fund Based Facilities

Cash Credit

5.3.1 Cash Credit (CC) is a facility that has the features of a loan as well as bank account. When a

person opens a CC account with the bank, he is being provided specified CC limit for the

purpose of carrying on his business. For this purpose he is required to submit Stock

Statements each month to the bank. The bank charges interest each month for operating

the CC account. Once the CC account is opened, the person can start issuing cheques. The

bank will then debit the account holder’s account & the account holder will credit the bank

account in his books. This is exactly the opposite of the normal current account. They need

not maintain any balance, but have to pay cheques subject to the CC limit granted by the

bank.

Term Loan

5.3.2 Term loans are given to purchase fixed assets like plant and machinery, which are long term

assets. It is a loan from a bank of a specific amount with a specified repayment schedule

and a floating interest rate. Term loans usually mature between one to ten years.

Demand Loan

5.3.4 Is a loan (such as an overdraft) with or without a fixed maturity date, but which can be

recalled anytime (often on a 24-hour notice) by the lender and must be paid in full on the

date of demand. Also, the borrower can pay off a demand loan at any time without incurring

early-payment penalties. Demand loans often require collateral and are also called “call

loans”.

Overdraft Facilities

5.3.5 A loan arrangement under which a bank extends credit up to a maximum amount (called

overdraft limit) against which a current account customer can write cheques or make

withdrawals. It is one of the most common forms of business borrowing. Overdraft facility

is against a security like Bank Deposits / NSC / mortgage etc. pledged to the Bank.

27

5.4 Non Fund Based Facilities

Bank Guarantee

5.4.5 A guarantee from a lending institution ensuring that the liabilities of a debtor will be met i.e.

if the debtor fails to settle a debt, the bank will cover it. A bank guarantee enables the

customer (debtor) to acquire goods, buy equipment, or draw down loans, and thereby

expand business activity.

Letter of Credit

5.4.6 A letter from a bank guaranteeing that a buyer's payment to a seller will be received on time

and for the correct amount. In the event that the buyer is unable to make payment on the

purchase, the bank will be required to cover the full or remaining amount of the purchase.

5.4.7 Letters of credit are often used in international transactions to ensure that payment is

received. Due to the nature of international dealings including factors such as distance,

differing laws in each country and difficulty in knowing each party personally, the use of

letters of credit has become a very important aspect of international trade. The bank also

acts on behalf of the buyer (holder of letter of credit) by ensuring that the supplier will not

be paid until the bank receives a confirmation that the goods have been shipped.

5.5 Preparation of DPRs

5.5.5 In the normal course of an Energy Audit, the Energy Auditor submits his findings and

recommends retrofits or replacement of existing equipment with more energy efficient

equipment. The investment figure is given in the form of cost of equipment plus additional

costs for infrastructure adjustments. To justify the investment, usually Payback Period is

calculated, which is quite simplistic and is generally suitable only for small investments with

very fast payback periods of only few months (less than a year). Simple Payback Period

calculation does not consider the time value of money. When the investments are large, usually

Detailed Project Reports (DPRs) are made, wherein Internal Rate of Return (IRR) is

calculated, Which considers all cash inflows and out flows, including interest, depreciation

etc. while IRR is a good parameters to evaluate the project with large investment, as far as

the clients are concerned, bankers need more information than Payback Period and/or IRR

to fund the project; they insist on evaluating the financials of the company, both historical

and future projections, to satisfy themselves about the company’s ability to repay the loan

through positive cash flows.

28

5.5.6 After a brief mention of Payback Period and IRR, the bankers’ perspective is elaborated in

this section. If the DPR provides unambiguous information on the impact of the project on

the financials of the company, the chances of getting bank funds for the project improves.

Payback Period

5.5.7 The payback period i.e. the length of time required to recover the cost of an investment, is

computed based on the monetary value of expected savings divided by cost of investment.

Please note that this calculation does not consider the interest cost, annual maintenance cost

etc.

#��&4%���5 = �����"��!�/������'���

Internal Rate of Return

5.5.8 Since payback period ignores the “time value of money”, we also compute the Internal Rate

of Return (IRR) and/or Net Present Value (NPV) of the proposed investment; these are the

two most-used measures for evaluating an investment.

5.5.9 NPV is the difference between the present value of cash inflows and the present value of

cash outflows. NPV is used in capital budgeting to analyze the profitability of an investment

or project. NPV analysis is sensitive to the reliability of future cash inflows that an

investment or project will yield.

5.5.10 IRR is the rate of return on investment at which the cash inflows equal the cash out flows

i.e. NPV = 0.

NPV = 0; or

PV of future cash flows − Initial Investment = 0; or

CF1

+ CF2

+ CF3

+ ... − Initial Investment = 0 ( 1 + r )1 ( 1 + r )2 ( 1 + r )3

Where, r is the internal rate of return; CF1 is the period one net cash inflow; CF2 is the period two net cash inflow, CF3 is the period three net cash inflow, and so on ...

29

5.5.11 The following graph explains that IRR is the discount rate when NPV is zero.

Example

5.5.12 Find the IRR of an investment having initial cash outflow (investment) of Rs 213,000. The

cash inflows (cost reduction) during the first, second, third and fourth years are expected to

be Rs 65,200, Rs 96,000, Rs 73,100 and Rs 55,400 respectively.

Solution

Assume that r is 10%.

NPV at 10% discount rate = Rs18,372

Since NPV is greater than zero we have to increase discount rate, thus

NPV at 13% discount rate = Rs 4,521

But it is still greater than zero we have to further increase the discount rate, thus

NPV at 14% discount rate = Rs 204

NPV at 15% discount rate = (Rs 3,975)

Since NPV is fairly close to zero at 14% value of r, therefore

IRR ≈ 14%

5.6 Banker’s Perspective

5.6.5 A bank generally sanctions a Term Loan for such an investment; the banker conducts a

holistic evaluation of the investment which involves evaluation the existing financial position

of the company/firm for the last three years, estimating and projecting the financials for the

coming years, after factoring in the proposed loan etc.

5.6.6 The projected balance sheet can be prepared by taking into account the need of the business

to expand its activities in the future. In such cases, it has to project the required assets it

intends to purchase, the corresponding cash resources it would be able to generate and the

external sources of finance it would require after considering its internal cash resources.

30

5.6.7 Documents required by a bank/financial institution for appraising a Term Loan Proposal:

Sr. No.

Annexure

Verification

A Company

1 MOA & AOA Basic Document for Company Formation

2 PAN KYC

3 Address Proof of a Regd. Office KYC

4 Last 3 years ITRs and Audited BS Financial position

5 Bank Statements of last 6 months To see the flow of funds

B Licenses / Approvals To ensure that the proper permission and approvals. 1 Excise Registration

2 GST/CST/VAT Registration

3 Service Tax Registration

4 Industrial License – SSI Registration

C Factory Land & Building Documents

1 Ownership documents if owned and Lease Deed if leased

To ensure the ownership

2 Title Clearance Report To ensure the encumbrance of property

3 Valuation Report To ascertain the market value of the property.

D Promoters/Guarantors

1 PAN KYC

2 Address Proof KYC

3 Last 3 years Income Tax Returns Financial Position 4 Net Worth Details along with Proofs Credit facilities

5 Names & Activities of all Associate Concerns, Last 3 years Audited BS

To know the business activities

6 Saving Account Bank Statements of last 6 months To see the flow of funds. 7 If existing accounts and loans are with another

bank/FI

• Copy of sanction letter of borrowings with other banks including working capital loans

• Repayment schedules and repayment track records of above loans

• Bank statements of CC/CA/OD accounts with other banks

To know other liabilities of Business

8 Detailed project report including SWOT analysis, market trends, growth prospects.

To know industrial scenario of Business

31

� Copy of CA certified Audited Financials of the Firm/Company for last three financial years

or CA certified balance sheet and P&L account (if the financials of the firm are not audited)

� CMA data with last three audited financial data, estimates for current/following financial

years and projections for next three financial years (or more, this varies from bank to bank).

� CA certified Net Worth statements of the promoters

� Specifications of the equipment being financed including cost and other overheads

� Detailed profile of the client

� Detailed Project Report (DPR) including SWOT analysis, market trends, growth prospects,

prevailing industry scenario.

5.7 Preparation of IGDPR

5.7.5 The Investment Grade Detailed Project Report (IGDPR) should include the following:

1. Introduction of the company

• Mention company founding year and briefly describe company history, including qualifications and experience of promoters and key persons.

• Describe briefly the product types and growth in production volumes over the years.

2. Products

• Mention all products and byproducts produced by the company presently, along with annual production volumes.

3. Brief Overview of the Industry

• Describe the product and product sub-categories

• Mention typical users of the product

• Briefly describe market scenario in India & world and potential for growth in the foreseeable future

• Regulatory scenario for product quality and export & import

4. Strengths, Weakness, Opportunities & Threats (SWOT) Analysis

• Present results of SWOT analysis of the Company; Typical issues to be considered are:

� Ability to exploit market potential and increase market share � Advantages in terms of product range, quality & volumes to capture higher market

share

32

� Likely obsolescence of products or processes, especially if processes are causing environmental pollution.

� Marketing network, both national and global reach. � Financial strength for technology upgrades and expansion of production � Profit margins & ability to beat the competition in the market � Regulatory issues enforced by governments and/or local bodies; for example, in

Ankleshwar, strictures of the Gujarat Pollution Control Board often results in increased lead time for project implementation.

5. Manufacturing process in brief

• Mention and briefly describe the important steps in the manufacturing process.

• Mention the energy source and/or utilities consumed in each process step. 6. Review of Energy Consumption

• Provide quantitative information on all energy sources used on a monthly basis for at least one year.

• Provide information on monthly energy costs for all energy sources independently.

• Correlate energy consumption with production and calculate Specific Energy Consumption, if possible

7. Energy Cost Saving Measures with Analyses

• Technical basis for recommendation

• Quantifications of savings

• Specifications of new equipment, retrofits and additional infrastructure required i.e. additional utilities, civil work etc.

• Investments required for the project, including equipment, instrumentation and other associated infrastructure

• Additional maintenance requirements

• Additional manpower man power requirements

8. Detailed Financial Calculations

• Quantification of investment required

• Assumed lifetime of the project (usually 10 or 15 years)

• Quantification of annual maintenance costs over the assumed life time of the recommended equipment

• Assumption of energy costs during the life time of the project

• Calculation of IRR and DSCR

• Sensitivity analysis considering changes in assumptions related to energy and other costs

• Impact on CMA data (required only when the project investment and/or impact are large)

33

9. Plan for Capacity Building

• Training requirements to ensure correct operation of recommended equipment to maximize energy cost savings

10. Plan for Project Management

• Special expertise for project design, installation and commissioning

• Production shutdown required for implementing the project

• Time line for the project 11. Sources for Project Funding

• Contacts on prospective lending agencies

• Information of specific funding schemes for MSMEs

12. Monitoring and Verification Protocol

• Instrumentation required for monitoring energy savings.

• Unambiguous calculation methodology for measuring the energy consumption and specific energy consumption before and after implementation of the project

• Methodology for calculating net cost savings on a monthly basis.

34

6. Funding Schemes from Government & Financial Institutions

6.1 Introduction

6.1.1 The following break up of loans to MSMEs in Gujarat gives a clear picture of the major

lenders in Gujarat. The major players are State Bank of India, Bank of Baroda & Bank of

India together contributing to about 50% of the advances. A private sector bank also has

significant presence in Gujarat MSME financing. The Growth rate in lending to MSMEs in

Gujarat has exceeded the targets set by RBI & Ministry of Finance.

Figure 6-1: MSME advances- break up

Table 6-1: MSME advances growth in Gujarat

35

6.1.2 Most of the public sector banks and private sector banks have a presence in Ankleshwar city

with either with branches/extension counters in the GIDC. Some co-operative banks and

credit societies are also operating in Ankleshwar.

6.1.3 A detailed list of banks in the public sector, private sector & cooperative sector is given in

Annexure-1. Typical lending rates of these public sector banks vary from 12.5% to 16%

depending on the amount sanctioned, credit rating etc. Lending rates of private banks are

generally 2%-5% higher than PSU banks. Cooperative banks have higher interest rates than

PSU & Private sector banks.

6.2 Credit Guarantee Fund Trust for Micro and Small Enterprises

(CGTMSE)

Objective

6.2.1 Government of India launched Credit Guarantee Scheme (CGS) so as to strengthen credit

delivery system and facilitate flow of credit to the MSE sector. Ministry of Micro, Small &

Medium Enterprises (MSME, Government of India) and SIDBI have set up CGTMSE to

ensure availability of bank credit without the hassles of collaterals / third party guarantees

for setting up a Micro and Small Enterprises (MSE).

6.2.2 The lender gives importance to project viability and secure the credit facility purely on the

primary security of the assets financed. The lender, availing guarantee facility, endeavors to

give composite credit to the borrowers so that the borrowers obtain both term loan and

working capital facilities from a single agency. The CGS seeks to reassure the lender that, in

the event of a MSE unit, which availed collateral free credit facilities, fails to discharge its

liabilities to the lender, the Guarantee Trust would make good the loss incurred by the

lender up to 75 / 80/ 85 per cent of the credit facility.

Credit Guarantee

6.2.3 Any collateral / third party guarantee free credit facility (both fund as well as non- fund

based) extended by eligible institutions, to new as well as existing Micro and Small

Enterprise, including Service Enterprises, with a maximum credit cap of Rs. 100 lakh are

eligible to be covered.

6.2.4 The guarantee cover available under the scheme is to the extent of 75% / 80% of the

sanctioned amount of the credit facility, with a maximum guarantee cap of Rs.62.50 lakh /

Rs. 65 lakh. The extent of guarantee cover is 85% for micro enterprises for credit up to Rs.5

lakh.

36

6.2.5 The extent of guarantee cover is 80% (i) Micro and Small Enterprises operated and/or

owned by women; and (ii) all credits/loans in the North East Region (NER). In case of

default, the Trust settles the claim up to 75% (or 80%) of the amount in default of the credit

facility extended by the lending institution.

6.2.6 The lender should cover the eligible credit facilities as soon as they are sanctioned. In any

case, the lender should apply for guarantee cover in respect of eligible credits, sanctioned in

one calendar quarter, latest by end of subsequent calendar quarter. Guarantee will

commence from the date of payment of guarantee fee and shall run through the agreed

tenure of the term credit in case of term loans / composite loans and for a period of 5 years

where working capital facilities alone are extended to borrowers, or for such period as may

be specified by the Guarantee Trust in this behalf.

Eligible Lending Institutions

6.2.7 All scheduled commercial banks and specified Regional Rural Banks, NSIC, NEDFI,

SIDBI, which have entered into an agreement with the Trust for the purpose, are Member

Lending Institutions (MLIs) of CGTMSE.

Eligible Borrowers New as well as existing Micro and Small Enterprises.

Maximum Risk Cover

6.2.8 Of the credit facilities extended by MLIs, the Trust guarantees, in case of default by the

borrower, up to 75 per cent (85% for select category of borrowers), of the defaulted the

principal amount in respect of term credit, including interest on principal for one quarter and

/ or outstanding working capital advances (inclusive of interest), as on the date of account

becoming NPA, or as on the date of filing the suit. Other charges such as penal interest,

commitment charge, service charge, or any other levies/ expenses shall not qualify for the

guarantee cover.

Rehabilitation Assistance

6.2.9 Units, covered under CGTMSE, becoming sick due to factors beyond the control of

management, assistance for rehabilitation extended by the lender could also be covered

under the scheme provided the overall assistance is within the credit cap of Rs.100 lakh.

Non-Eligibility

6.2.10 Any facility given on the basis of collateral security or third party guarantee shall be

disqualified for coverage under the scheme. The Trust also reserves the right to reject any

application for the guarantee cover, if it deems necessary.

37

Guarantee Fee

6.2.11 For credit facility up to Rs.5 lakh, an upfront Guarantee Fee (GF) of 1% of the amount

sanctioned will have to be paid to the Trust by the MLI. For amounts sanctioned beyond

Rs.5 lakh and up to Rs.100 lakh, the GF is 1.5%; while for credit facility up to Rs. 50 lakh

for units in the North Eastern Region including Sikkim, the GF is 0.75%. The GF will have

to be paid within 30 days from the date of first disbursement of credit facility by the MLI to

a borrower.

Annual Service Fee

6.2.12 Guarantee cover extended by CGTMSE in respect of any specific borrower shall be valid,

provided the MLI concerned pays an Annual Service Fee (ASF) of 0.50% on the amount

guaranteed for credit facilities up to Rs. 5 lakh and 0.75% on the amount guaranteed for

credit facilities beyond Rs. 5 lakh and up to Rs. 100 lakh. Such ASF is to be paid by the MLI

on or before 31st May of that year. The Trust reserves the right to revise the guarantee fee /

annual service fee from time to time.

Cost To the Borrower

6.2.13 The Credit Guarantee Scheme leaves it to the discretion of the MLIs to decide about

passing on the incidence of Guarantee Fee and Annual Service Fee to the borrower or

alternatively they may decide to bear it themselves.

Interest Rate Payable by Borrower

6.2.14 The MLI shall follow the guidelines issued by RBI. However, interest rate shall not exceed 3

per cent over and above the Prime Lending Rate of the MLI, excluding the annual service

fee.

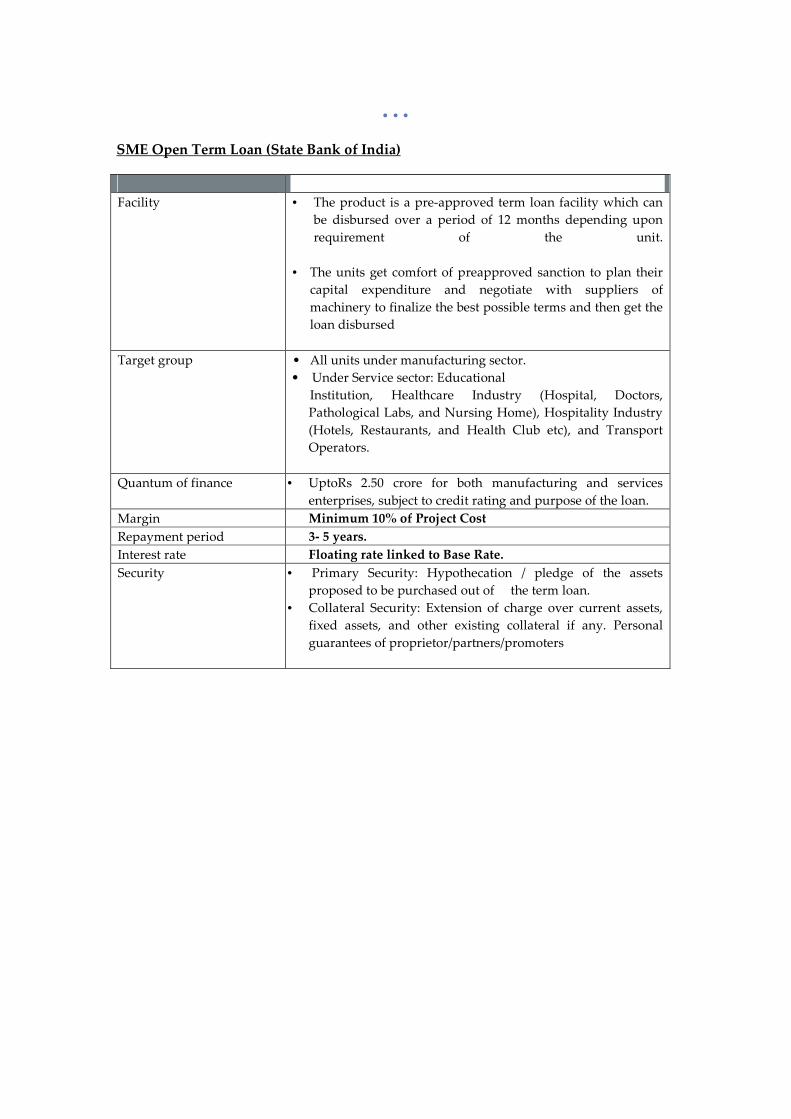

6.2.15 Details of some the schemes offered by public sector banks are given in Annexure-2 similar

such loans are being offered by private sector banks like Axis Bank, ICICI Bank etc.

38

6.3 Credit Linked Capital Subsidy Scheme (CLCSS)

6.3.1 For Technology up-gradation of the Small Scale Industries, the Ministry of Small Scale

Industries is operating a scheme for Small Scale Industries (SSI) called the Credit Linked

Capital Subsidy Scheme (CLCSS). The Scheme aims at facilitating technology up-gradation

by providing upfront capital subsidy to SSI units, including tiny, khadi, village and coir

industrial units, on institutional finance (credit) availed of by them for modernization of their

production equipment (plant and machinery) and techniques.

6.3.2 The Scheme (pre-revised) provided for 12 per cent capital subsidy to SSI units, including tiny

units, on institutional finance availed of by them for induction of well established and

improved technology in selected sub-sectors/products approved under the Scheme. The

eligible amount of subsidy calculated under the pre-revised scheme was based on the actual

loan amount not exceeding Rs. 40 lakh.

• The ceiling on loans under the Scheme has been raised from Rs. 40 lakh to Rs. 1 crore

• The admissible capital subsidy is to be calculated with reference to the purchase price of

plant and machinery, instead of the term loan disbursed to the beneficiary unit

• The practice of categorization of SSI units in different slabs on the basis of their present

investment for determining the eligible subsidy is followed .

6.3.3 The Small Industries Development Bank of India (SIDBI) and the National Bank for

Agriculture and Rural Development (NABARD) will continue to act as the Nodal Agencies

for the implementation of this scheme.

6.3.4 The following nine Public Sector Banks/ Government Agencies have also been inducted as

nodal banks/agencies for implementation and release of capital subsidy under the CLCSS:

Table 6-2: List of Banks