TOWN COUNCIL MEETING Agenda - Los Gatos

300

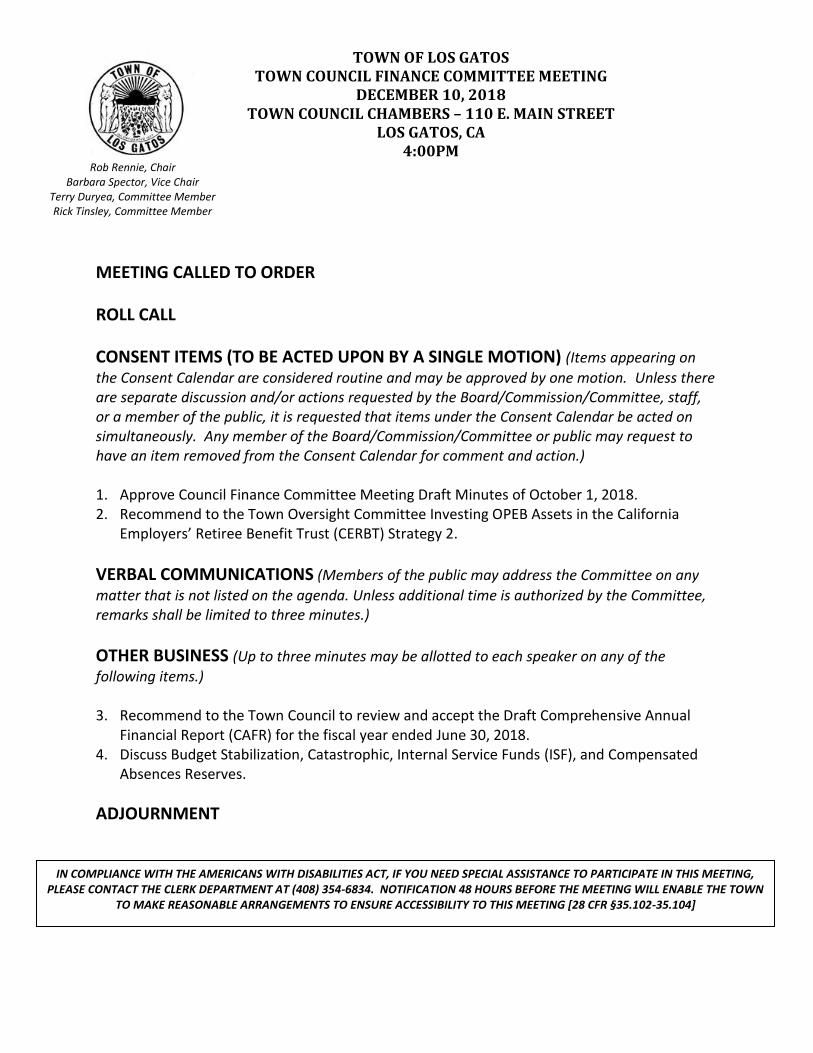

TOWN OF LOS GATOS TOWN COUNCIL FINANCE COMMITTEE MEETING DECEMBER 10, 2018 TOWN COUNCIL CHAMBERS – 110 E. MAIN STREET LOS GATOS, CA 4:00PM MEETING CALLED TO ORDER ROLL CALL CONSENT ITEMS (TO BE ACTED UPON BY A SINGLE MOTION) (Items appearing on the Consent Calendar are considered routine and may be approved by one motion. Unless there are separate discussion and/or actions requested by the Board/Commission/Committee, staff, or a member of the public, it is requested that items under the Consent Calendar be acted on simultaneously. Any member of the Board/Commission/Committee or public may request to have an item removed from the Consent Calendar for comment and action.) 1. Approve Council Finance Committee Meeting Draft Minutes of October 1, 2018. 2. Recommend to the Town Oversight Committee Investing OPEB Assets in the California Employers’ Retiree Benefit Trust (CERBT) Strategy 2. VERBAL COMMUNICATIONS (Members of the public may address the Committee on any matter that is not listed on the agenda. Unless additional time is authorized by the Committee, remarks shall be limited to three minutes.) OTHER BUSINESS (Up to three minutes may be allotted to each speaker on any of the following items.) 3. Recommend to the Town Council to review and accept the Draft Comprehensive Annual Financial Report (CAFR) for the fiscal year ended June 30, 2018. 4. Discuss Budget Stabilization, Catastrophic, Internal Service Funds (ISF), and Compensated Absences Reserves. ADJOURNMENT Rob Rennie, Chair Barbara Spector, Vice Chair Terry Duryea, Committee Member Rick Tinsley, Committee Member IN COMPLIANCE WITH THE AMERICANS WITH DISABILITIES ACT, IF YOU NEED SPECIAL ASSISTANCE TO PARTICIPATE IN THIS MEETING, PLEASE CONTACT THE CLERK DEPARTMENT AT (408) 354-6834. NOTIFICATION 48 HOURS BEFORE THE MEETING WILL ENABLE THE TOWN TO MAKE REASONABLE ARRANGEMENTS TO ENSURE ACCESSIBILITY TO THIS MEETING [28 CFR §35.102-35.104]

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of TOWN COUNCIL MEETING Agenda - Los Gatos

TOWN OF LOS GATOS TOWN COUNCIL FINANCE COMMITTEE MEETING

DECEMBER 10, 2018 TOWN COUNCIL CHAMBERS – 110 E. MAIN STREET

LOS GATOS, CA 4:00PM

MEETING CALLED TO ORDER

ROLL CALL

CONSENT ITEMS (TO BE ACTED UPON BY A SINGLE MOTION) (Items appearing on

the Consent Calendar are considered routine and may be approved by one motion. Unless there are separate discussion and/or actions requested by the Board/Commission/Committee, staff, or a member of the public, it is requested that items under the Consent Calendar be acted on simultaneously. Any member of the Board/Commission/Committee or public may request to have an item removed from the Consent Calendar for comment and action.) 1. Approve Council Finance Committee Meeting Draft Minutes of October 1, 2018. 2. Recommend to the Town Oversight Committee Investing OPEB Assets in the California

Employers’ Retiree Benefit Trust (CERBT) Strategy 2.

VERBAL COMMUNICATIONS (Members of the public may address the Committee on any

matter that is not listed on the agenda. Unless additional time is authorized by the Committee, remarks shall be limited to three minutes.)

OTHER BUSINESS (Up to three minutes may be allotted to each speaker on any of the

following items.) 3. Recommend to the Town Council to review and accept the Draft Comprehensive Annual

Financial Report (CAFR) for the fiscal year ended June 30, 2018. 4. Discuss Budget Stabilization, Catastrophic, Internal Service Funds (ISF), and Compensated

Absences Reserves.

ADJOURNMENT

Rob Rennie, Chair Barbara Spector, Vice Chair

Terry Duryea, Committee Member Rick Tinsley, Committee Member

IN COMPLIANCE WITH THE AMERICANS WITH DISABILITIES ACT, IF YOU NEED SPECIAL ASSISTANCE TO PARTICIPATE IN THIS MEETING, PLEASE CONTACT THE CLERK DEPARTMENT AT (408) 354-6834. NOTIFICATION 48 HOURS BEFORE THE MEETING WILL ENABLE THE TOWN

TO MAKE REASONABLE ARRANGEMENTS TO ENSURE ACCESSIBILITY TO THIS MEETING [28 CFR §35.102-35.104]

110 E. Main Street Los Gatos, CA 95030 ● 408-354-6832 www.losgatosca.gov

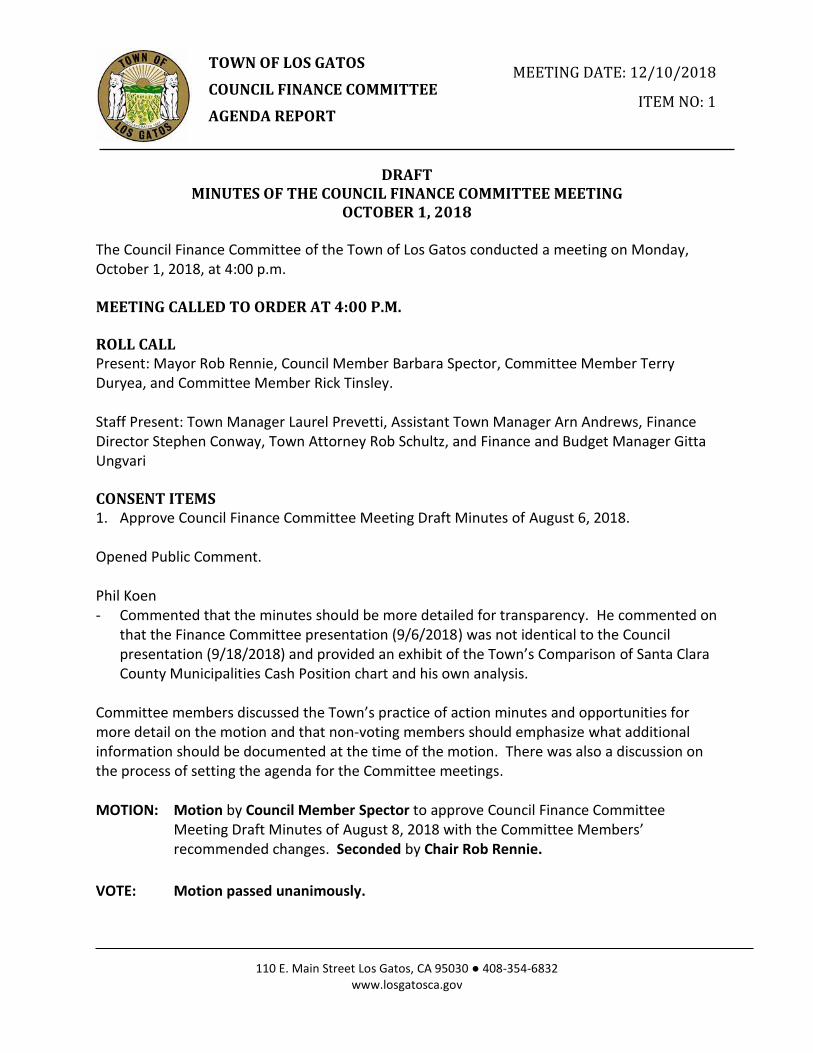

TOWN OF LOS GATOS

COUNCIL FINANCE COMMITTEE

AGENDA REPORT

MEETING DATE: 12/10/2018

ITEM NO: 1

DRAFT MINUTES OF THE COUNCIL FINANCE COMMITTEE MEETING

OCTOBER 1, 2018 The Council Finance Committee of the Town of Los Gatos conducted a meeting on Monday, October 1, 2018, at 4:00 p.m. MEETING CALLED TO ORDER AT 4:00 P.M. ROLL CALL Present: Mayor Rob Rennie, Council Member Barbara Spector, Committee Member Terry Duryea, and Committee Member Rick Tinsley. Staff Present: Town Manager Laurel Prevetti, Assistant Town Manager Arn Andrews, Finance Director Stephen Conway, Town Attorney Rob Schultz, and Finance and Budget Manager Gitta Ungvari CONSENT ITEMS 1. Approve Council Finance Committee Meeting Draft Minutes of August 6, 2018. Opened Public Comment. Phil Koen - Commented that the minutes should be more detailed for transparency. He commented on

that the Finance Committee presentation (9/6/2018) was not identical to the Council presentation (9/18/2018) and provided an exhibit of the Town’s Comparison of Santa Clara County Municipalities Cash Position chart and his own analysis.

Committee members discussed the Town’s practice of action minutes and opportunities for more detail on the motion and that non-voting members should emphasize what additional information should be documented at the time of the motion. There was also a discussion on the process of setting the agenda for the Committee meetings. MOTION: Motion by Council Member Spector to approve Council Finance Committee

Meeting Draft Minutes of August 8, 2018 with the Committee Members’ recommended changes. Seconded by Chair Rob Rennie.

VOTE: Motion passed unanimously.

PAGE 2 OF 4 SUBJECT: DRAFT MINUTES OF THE COUNCIL FINANCE COMMITTEE MEETING OF

OCTOBER 1, 2018 OCTOBER 16, 2018

C:\Users\lseastrom\Desktop\New folder\01 Item 1 - Minutes for 10-1-2018 Finance Committee Meeting Draft.docx 12/5/2018 11:07:27 AM

VERBAL COMMUNICATIONS Phil Koen - Referenced the September 21st, 2018 Bartel Presentation to the Council Oversight

Committee and provided excerpt material from the presentation and CALPERS actuarial evaluations. He recommended that excess cash balances should be used to pay an additional lump-sum payment to CalPERS.

OTHER BUSINESS 2. Review the quarterly performance report for the Town of Los Gatos IRS Section 115 Pension

Trust for the period ending June 30, 2018. Mr. Andrew Brown (PARS) presented via teleconference the IRS Section 115 Pension Trust fund quarterly performance. Opened Public Comment. Phil Koen - Distributed a CalPERS performance report and recommended to distribute it with the

quarterly performance report and to benchmark the IRS 115 Trust performance to CalPERS performance.

Closed Public Comment. Staff and Mr. Brown addressed the Committee’s and the public questions. Based on the Committee’s discussion, staff agreed that the quarterly process of the fund performance relative to the benchmark will be part of the standard review process for both the Council Finance Committee and for the Council Oversight Board. The Council Finance Committee and the Council Oversight Board will also annually review the asset allocation and determine if this is still the appropriate asset allocation under management at that time. 3 Review the performance report for the California Employers’ Retiree Benefit Trust (CERBT)

for the period ending June 30, 2018. Stephen Conway, Finance Director, presented the staff report. Opened Public Comment. None

Closed Public Comment.

PAGE 3 OF 4 SUBJECT: DRAFT MINUTES OF THE COUNCIL FINANCE COMMITTEE MEETING OF

OCTOBER 1, 2018 OCTOBER 16, 2018

C:\Users\lseastrom\Desktop\New folder\01 Item 1 - Minutes for 10-1-2018 Finance Committee Meeting Draft.docx 12/5/2018 11:07:27 AM

The Committee reviewed the report and asked questions of staff. 4 Discuss and recommend to the Town Council proposed revisions to the Town of Los Gatos

IRS Section 115 Pension Trust and California Employers’ Retiree Benefit Trust (CERBT) Investment Policy.

Arn Andrews, Assistant Town Manager, presented the staff report. Opened Public Comment. Phil Koen - Distributed excerpts from the staff report and September 21st, 2018 Bartel Presentation and

commented on his concerns regarding the staff report and the IRS 115 Trust. He commented that the IRS 115 was designed for budget stabilization and the policy language does not reflect that. Mr. Koen noted that the only way to fund pension unfunded liability is to pay CalPERS directly.

Closed Public Comment. Staff addressed the Committee’s questions. After discussion with different point of views explored, the Committee recommended that the new language in the Policy clarify the potential multiple purposes for the use of the 115 funds. In addition, the Committee requested to review the reserve levels in various Town funds at a future meeting. MOTION: Motion by Council Member Spector recommend to the Town Council proposed

revisions to the Town of Los Gatos IRS Section 115 Pension Trust and California Employers’ Retiree Benefit Trust (CERBT) Investment Policy by clarifying that: “Funds in the 115 Pension Trust may be used for long-term capital accumulation and appreciation, additional discretionally payments (ADPs), and pension contribution management strategies.” Seconded by Chair Rob Rennie.

VOTE: Motion passed unanimously.

PAGE 4 OF 4 SUBJECT: DRAFT MINUTES OF THE COUNCIL FINANCE COMMITTEE MEETING OF

OCTOBER 1, 2018 OCTOBER 16, 2018

C:\Users\lseastrom\Desktop\New folder\01 Item 1 - Minutes for 10-1-2018 Finance Committee Meeting Draft.docx 12/5/2018 11:07:27 AM

ADJOURNMENT: The meeting adjourned at 6:09 p.m.

This is to certify that the foregoing is a true

and correct copy of the minutes of the

September 1, 2018 meeting as approved by the

Council Finance Committee. Gitta Ungvari, Finance and Budget Manager

PREPARED BY: ARN ANDREWS ASSISTANT TOWN MANAGER Reviewed by: Town Manager, Finance Director, and Town Attorney

110 E. Main Street Los Gatos, CA 95030 ● 408-354-6832

www.losgatosca.gov

TOWN OF LOS GATOS

FINANCE COMMITTEE REPORT

MEETING DATE: 12/10/2018

ITEM NO: 2

ITEM NO: 11

DATE: NOVEMBER 30, 2018

TO: COUNCIL FINANCE COMMITTEE

FROM: LAUREL PREVETTI, TOWN MANAGER

SUBJECT: RECOMMEND TO THE TOWN OVERSIGHT COMMITTEE INVESTING OPEB ASSETS IN THE CALIFORNIA EMPLOYERS’ RETIREE BENEFIT TRUST (CERBT) STRATEGY 2

RECOMMENDATION:

Recommend to the Town Oversight Committee investing OPEB assets in the California Employers’ Retiree Benefit Trust (CERBT) Strategy 2.

BACKGROUND: The Town provides a healthcare benefit for all eligible employees. The healthcare plan pays all, or a portion of, health insurance premiums for qualified retirees and their survivors and dependents. Healthcare benefits are also referred to as Other Post-Employment Benefits or OPEB. The Town’s healthcare plan is managed as an Internal Revenue Code Section 115 Trust which is administered by the Town Pension and OPEB Trusts Oversight Committee. The Oversight Committee (composed of the Town Council) is responsible for the management and control of the healthcare assets. The healthcare assets are maintained at CalPERS and currently invested in the CalPERS managed California Employers’ Retiree Benefit Trust (CERBT) Strategy 1. In 2009, the Town Council approved a Finance Department recommendation to initiate a ten-year phase in of pre-funding future OPEB obligations. Prior to 2009, the Town like most other cities, followed the generally accepted government accounting principle of paying OPEB benefits on a “pay as you go” basis. This method recognized only the current cost of payments to actual retirees but didn’t recognize the future cost of benefits related to active employees. The Finance Department recommendation also included participating in the CERBT Fund. As

PAGE 2 OF 4 SUBJECT: RECOMMEND TO THE TOWN OVERSIGHT COMMITTEE INVESTING OPEB ASSETS

IN CERBT STRATEGY 2 DATE: NOVEMBER 30, 2018

C:\Users\lseastrom\Desktop\New folder\Item 2 -OPEB Trust Asset Allocation Final.docx 12/5/2018 11:08 AM SLL

BACKGROUND (continued): the table below illustrates, the Town has pre-funded $12,360,000 since the Trust Fund was established. In addition, the Town’s investment in CERBT Strategy 1 has earned approximately $4.2 million in investment earnings with an average annualized rate of return of 8.33%.

Account summary as of July 31, 2018 (Source: CalPERS Annual Review)

Initial contribution (6/29/2009) $400,000

Additional contributions $11,960,000

Disbursements ($0)

CERBT expenses ($53,431)

Investment earnings $4,212,256

Total assets $16,518,825

Average annualized internal rate of return (6/29/2009-7/31/2018) 8.33%

Since the initial $400,000 prefunding in 2009 the OPEB funded status has grown steadily due to the additional contributions and investment earnings. Based on the June 30, 2017 Retiree Healthcare Plan Actuarial Valuation performed by Bartel Associates, the funded status of the plan has grown to 55%.

Valuation Date Total OPEB Liability Actuarial Value of

Assets Funded Status

6/30/2013 $19,211,000 $4,866,000 25%

6/30/2015 $20,977,000 $8,238,000 39%

6/30/2017 $24,773,000 $13,605,000 55%

Projected 6/30/2018 $26,390,000 $16,148,000 61.2%

Source: Bartel Associates Actuarial Valuations

PAGE 3 OF 4 SUBJECT: RECOMMEND TO THE TOWN OVERSIGHT COMMITTEE INVESTING OPEB ASSETS

IN CERBT STRATEGY 2 DATE: NOVEMBER 30, 2018

C:\Users\lseastrom\Desktop\New folder\Item 2 -OPEB Trust Asset Allocation Final.docx 12/5/2018 11:08 AM SLL

BACKGROUND (continued): It is important to note that during the development of the 2017 actuarial valuation the Oversight Committee elected to lower the discount rate from 7.25% to 6.75%. Since the development of the 2017 actuarial valuation, the Town’s bargaining groups and Management and Confidential employees agreed to eliminate the current retiree healthcare benefit prospectively for new employees. In addition, CalPERS released the 2018 investment return data for the CERBT strategies. Based on the significance of the aforementioned changes, staff asked Bartel Associates to update the 2017 valuation. With the lowering of the discount rate by 50 basis points (bps), the elimination of the healthcare benefit prospectively, and the updated 2018 investment returns, it is appropriate to revisit the asset allocation options provided by CalPERS. DISCUSSION: CalPERS CERBT Asset Allocation Strategies The California Employers’ Retiree Benefit Trust (CERBT) provides multiple options for investment of the Town’s healthcare assets. The CalPERS managed CERBT provides three distinct asset allocations. Each asset allocation has varying degrees of exposure to equity, fixed income, Treasury Inflation Protected Securities (TIPS), Real Estate Investment Trusts (REITs), and commodities. Following are the three asset allocations:

2018 Asset Allocation Targets

Strategy 1 Strategy 2 Strategy 3

2018 2018 2018

Global Equity 59%

40%

22%

Fixed Income 25%

43%

50%

Global Real Estate (REITs) 8%

8%

8%

Treasury Inflation Protected Securities

(TIPS)

5%

5%

16%

Commodities 3%

4%

5%

PAGE 4 OF 4 SUBJECT: RECOMMEND TO THE TOWN OVERSIGHT COMMITTEE INVESTING OPEB ASSETS

IN CERBT STRATEGY 2 DATE: NOVEMBER 30, 2018

C:\Users\lseastrom\Desktop\New folder\Item 2 -OPEB Trust Asset Allocation Final.docx 12/5/2018 11:08 AM SLL

DISCUSSION (continued): The differing investment options provided by CalPERS represent varying degrees of investment risk/return profiles. As the table below illustrates a reduction in equity exposure correlates to a reduction in long-term expected returns and a reduction in the variability of those returns as expressed by standard deviation. It is generally accepted practice that the expected return of an asset allocation should track the discount rate used for actuarial valuations. Given the expected return profiles of the three CERBT strategies, Strategy 2 most closely aligns (7.01%) with the current discount rate of 6.75%.

2018 Asset Allocation Strategies

Strategy 1 Strategy 2 Strategy 3

2018 2018 2018

Expected Long Term Annualized Rate

of Investment Return 7.59% 7.01% 6.22%

Discount Rate

Determined by

Actuary

(Currently 6.75%)

Determined by

Actuary

(Currently 6.75%)

Determined by

Actuary

(Currently 6.75%)

Standard Deviation of Expected

Investment Returns 11.83% 9.24% 7.28%

CONCLUSION: Staff recommends that the Council Finance Committee recommend to the Town Oversight Committee approval of staff recommended asset allocation California Employers’ Retiree Benefit Trust (CERBT) Strategy 2. Approval of this recommendation will align the current discount rate (6.75%) used for the Healthcare Actuarial Valuations with the appropriate CalPERS long-term expected return (7.01%) associated with CERBT Strategy 2. In addition the lower volatility associated with the asset allocation of CERBT Strategy 2 will reduce the relative risk of the assets under management.

PREPARED BY: STEPHEN CONWAY Finance Director Reviewed by: Town Manager, Assistant Town Manager, and Town Attorney

110 E. Main Street Los Gatos, CA 95030 ● 408-354-6832 www.losgatosca.gov

TOWN OF LOS GATOS

COUNCIL FINANCE COMMITTEE REPORT

MEETING DATE: 12/10/2018 ITEM NO: 3 DESK ITEM

DATE: DECEMBER 10, 2018

TO: COUNCIL FINANCE COMMITTEE

FROM: LAUREL PREVETTI, TOWN MANAGER

SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

REMARKS: Attachment 2 contains public comments received after the distribution of the Council Finance Committee packet between 11 a.m. on Friday December 7, 2018 and before 11:00 a.m. on Monday December 10, 2018. Below are responses to a Council Finance Committee’s member inquiries (in bold type) regarding the Draft Comprehensive Annual Financial Report (CAFR). The inquiries

1) An inquiry about increased expenses reported on the Statement of Activities calculated by the Committee member at 25% from in total expenses since 2016. Generally, the primary reason for the large percentage increases are the result of capital project expenditures that are reflected in the Parks and Public Works category, with substantial expenditures in the Almond Grove for fiscal year end 2018 and 2017 as compared to 2016. The Town Council put a hold on capital project activity in 2016 which is reflected in much lower Parks and Public Works expenditures. After adjusting for capital projects, the increases are attributable as explained in the Management’s Discussion and Analysis (MD&A).

2) An inquiry on the nature of the increase to Non-Major Governmental Funds of $814K for the year. The primary reason for the increase can be found on pages 102 and 103 of the Draft 2018 CAFR wherein substantial revenues $807K were received in the Storm Drains fund from development projects.

PAGE 2 OF 2 SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT

COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

DATE: DECEMBER 10, 2018

N:\MGR\AdminWorkFiles\Council Committee - FINANCE\2018\12-10-2018\Item 3 - Desk Item.docx 12/10/2018 1:21 PM

REMARKS (continued):

3) A general question on workers compensation claims and practices. Staff has not analyzed other cities annual costs, yet the Town is very proactive in providing employee safety training, holding regular safety committee meetings, offering wellness programs, and taking other steps to manage this cost.

4) An inquiry of the budget variances on page 42 of the Draft 2018 CAFR at a more detailed level than provided on the MD&A on page 26. Staff verified with its auditor that the primary purpose of the MD&A is to discuss the major reasons for variances as opposed to line-by-line detail. More detailed analysis is a separate scope of work that is outside of the CAFR presentation.

5) A general question/comment about the nature of the Town’s OPEB liability as to the legal obligation imposed on the Town. The Town’s independent actuaries and auditors recognize an obligation exists.

6) An inquiry similar that expressed interest in the details regarding the transfers to the Internal Service Funds. All transfers in or out of Internal Service Funds are Council approved as per the schedules attached to Item 4 Desk Item.

7) A suggestion to add OPEB along with Pension on deferred inflows/outflows. Staff agrees and will make that change on the final CAFR.

8) A suggestion to check for a typo on capital asset additions. Staff agrees, and will change the amount to $9.984 million in the final draft CAFR to agree to the footnote totals on page 67.

Attachment previously distributed with the Staff Report: 1. Draft Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018. Attachment received with Desk Item: 2. Public comments received after the distribution of the Council Finance Committee packet

between 11 a.m. on Friday December 7, 2018 and before 11:00 a.m. on Monday December 10, 2018.

GUNGVARI

Typewritten Text

ATTACHMENT 2

PREPARED BY: STEPHEN CONWAY Finance Director Reviewed by: Town Manager, Assistant Town Manager, and Town Attorney

110 E. Main Street Los Gatos, CA 95030 ● 408-354-6832 www.losgatosca.gov

TOWN OF LOS GATOS

COUNCIL FINANCE COMMITTEE REPORT

MEETING DATE: 12/10/2018 ITEM NO: 3

ADDENDUM

DATE: DECEMBER 5, 2018

TO: COUNCIL FINANCE COMMITTEE

FROM: LAUREL PREVETTI, TOWN MANAGER

SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

REMARKS: After the distribution of the Finance Committee Packet, staff discovered a typographical error on page 4 of the Staff Report. The correct sentence referring to the excess revenue is:

“Presented in this statement is a $4.4 million excess of revenues over expenditures for the fiscal year.“

Attachment (previously distributed with the Staff Report): 1. Draft Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018.

PREPARED BY: STEPHEN CONWAY Finance Director Reviewed by: Town Manager, Assistant Town Manager, and Town Attorney

110 E. Main Street Los Gatos, CA 95030 ● 408-354-6832 www.losgatosca.gov

TOWN OF LOS GATOS

COUNCIL FINANCE COMMITTEE REPORT

MEETING DATE: 12/10/2018

ITEM NO: 3

DATE: DECEMBER 4, 2018

TO: COUNCIL FINANCE COMMITTEE

FROM: STEPHEN CONWAY, FINANCE DIRECTOR

SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2017

RECOMMENDATION: Recommend to the Town Council to review and accept the Draft Comprehensive Annual Financial Report (CAFR) for the fiscal year ended June 30, 2018.

BACKGROUND: The Town contracts with an independent certified public accountant to examine the books, records, inventories, and reports of all officers and employees who receive, handle, or disburse public funds each fiscal year. The FY 2017/18 audit was performed by Badawi & Associates CPA’s, an experienced firm specializing in audit services for California public agencies. The firm also prepared the Draft CAFR for the Town of Los Gatos (see Attachment 1).

The information contained in the CAFR provides detailed financial information which the Los Gatos community and others can use to better understand the fiscal standing of the Town. In addition, the financial information contained in the document is reviewed by the credit rating agencies annually and used to affix a credit rating for the Towns outstanding debt obligations. In 2018, Moody’s rating service affirmed the Town’s general credit rating of Aaa. The Aaa rating is well above the median rating of Aa3 for similar sized cities nationwide. DISCUSSION: At the meeting, Finance staff will present to the Town Council Finance Committee the draft audited Comprehensive Annual Financial Report (CAFR) dated June 30, 2018. Town’s independent auditor will be available for the Committee’s discussion.

PAGE 2 OF 4 SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT

COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

DATE: DECEMBER 4, 2018

C:\Users\lseastrom\Desktop\New folder\Item 3 - FY 2017-18 CAFR Finance Committee Staff Report.docx 12/5/2018 11:08 AM

DISCUSSION (Cont’d): Highlights of the draft audited financial results include: Financial Section. The auditor has given the Town’s financial statements a “clean” audit opinion for the year ended June 30, 2018 (see the fourth paragraph of the auditor’s opinion on Page 13 of the Financial Section of the report) giving reasonable assurance that the financial statements are “free of material misstatement.”

Statement of Net Position. The Statement of Net Position (page 34) serves as a useful indicator of a government’s financial position. The Town had net assets of $109.2 million at fiscal year end as compared to $117 million the prior year, an overall decrease of 6.6% for the fiscal year.

The Town’s net position decreased by $7.8 million during the fiscal year largely as a result of the beginning FY 2017/18 net position being restated and reduced by approximately $8.5 million as required by the implementation of GASB 75 regarding the financial reporting of other post-employment benefits (OPEB). Prior to the implementation of GASB 75, the Town was only required to report its Net OPEB Obligation (NOO) in the notes section of its CAFR. With this latest GASB pronouncement, all of the Town’s pension and OPEB obligations are reflected fully in the financial statements.

The largest portion of the net assets, $102.1 million, represents the Town’s investment in its capital assets and infrastructure. Restricted assets of $7.0 million are resources that are subject to external restrictions on how they may be used. The remaining $0.2 million in net assets are unrestricted legally, but have been designated as to use in various reserve accounts or held in Internal Service Funds. Again, this is an overall financial position indicator and is not the amount of current resources available for budgetary purposes.

Management’s Discussion and Analysis (MD&A) (pages 18 through 29)

Page 18 of the CAFR begins the MD&A section of the report wherein summaries are presented for the Town on an entity-wide basis and fund type basis. Information is provided in this section with a year-to-year view, explaining how fund balances have changed between fiscal years ending June 30, 2017 and June 30, 2018. Information is also presented on the adopted General Fund budget and any significant budget adjustments made during FY 2017/18 (page 25). Basic Financial Statements (pages 31 through 89, including footnotes)

Located within this section are basic financial statements, including the “entity-wide” Statement of Net Position and Statement of Activities, financial statements for the fund types

PAGE 3 OF 4 SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT

COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

DATE: DECEMBER 4, 2018

C:\Users\lseastrom\Desktop\New folder\Item 3 - FY 2017-18 CAFR Finance Committee Staff Report.docx 12/5/2018 11:08 AM

DISCUSSION (Cont’d):

including Governmental Funds (such as the General Fund), Proprietary Funds, and the Private Purpose Trust Funds (Redevelopment Successor Agency). An important item for consideration is the General Fund Budget and Actual presented on page 42. Presented in this statement is a $4.2 million excess of revenues over expenditures for the fiscal year. This result for the fiscal year provided a source to fund the Budget Stabilization and Catastrophic Reserves at 25% of operating expenditures, provide an additional $690,000 of funding to the Pension/OPEB Reserve, and allocate $3.7 million to the Capital Projects Reserve per the Town’s adopted General Fund Reserve Policy.

The footnotes section provides details on significant items such as the Town’s cash and investments (Note 2 beginning on page 63), its long term obligations (Certificates of Participation) related to bonded debt (Note 6 page 69), the net pension liability for both the Town’s miscellaneous and safety pension plans (Note 9 page 73), and a discussion of the Town’s other post-employment benefit plan (Note 10 page 79).

Required Supplementary Information (pages 92 through 96)

The Schedules of Pension Plan Contributions are provided in this section.

Supplementary Information (pages 98 through 113)

This section provides budget to actual information for “non-major” funds which represent less than 10% of the Town’s total assets/liabilities/revenues or expenditures.

Statistical Section (pages 117 through 133)

This section presents demographic statistics and ten-year historical financial data for the Town, including information on assessed valuations, fund balances, debt, property tax rates, personnel (full-time equivalent) history, principle employers, and other financial and demographic disclosures.

CONCLUSION: Mr. Ahmed Badawi, C.P.A., managing partner of Badawi & Associates, will be participating in the Committee meeting. If you have questions prior to the meeting, please contact Director Conway and staff will share responses to the questions to the full Committee. Upon review and recommendation of the draft CAFR by the Council Finance Committee, staff is bringing the final CAFR forward to the Town Council for its consideration on Tuesday, December 18, 2018.

PAGE 4 OF 4 SUBJECT: RECOMMEND TO THE TOWN COUNCIL TO REVIEW AND ACCEPT THE DRAFT

COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2018

DATE: DECEMBER 4, 2018

C:\Users\lseastrom\Desktop\New folder\Item 3 - FY 2017-18 CAFR Finance Committee Staff Report.docx 12/5/2018 11:08 AM

FISCAL IMPACT: There is no fiscal impact to provide recommendation to the Town Council for this report.

Attachment: 1. Draft Comprehensive Annual Financial Report for the Fiscal Year Ended June 30, 2018.

C A L I F O R N I A

T L G

Comprehensive Annual Financial ReportFiscal Year ending June 30, 2018

lseastrom

Typewritten Text

ATTACHMENT 1

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

Dra

ft 12

/04/

2018

Cover Photos: Ravon

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

lseastrom

Typewritten Text

Dra

ft 12

/04/

2018

TOWN OF LOS GATOS

CALIFORNIA

Dra

ft 12

/04/

2018

Dra

ft 12

/04/

2018

TOWN HISTORY

The name Los Gatos comes from “El Rancho de Los Gatos.” A ranch established in 1839 by aMexican land grant and so named because of the large number of mountain lions in the area. In1854, James Alexander Forbes purchased some of this land and built a flour mill. In 1860, thefirst hotel was opened to provide a stage stop on the toll road which had been built between SanJose and Santa Cruz.

Wheat production gave way to orchards, and rapid growth ensued when the railroad reachedLos Gatos in 1878. The residential subdivisions of Broadway, Bayview, Fairview, and AlmondGrove were built in the 1880’s. By 1887, the population had grown to 1,500 and Los Gatans votedto incorporate.

Fruit industries faded slowly during the Depression and World War II, but the postwar periodbrought an influx of people and associated residential and commercial development. Highway17 was constructed through the center of Town. Growth levelled off in the early 1970’s, leavingLos Gatos with its small town atmosphere and pedestrian oriented downtown.

Because of its distance from other centers of population, Los Gatos developed as a completecommunity including residential, business and industrial elements. Preserving Los Gatos as acomplete and well balanced community has been and remains a prominent goal of thecommunity. From the first 100 acre Town site in 1890 with a population of 1,652, Los Gatos grewslowly so that by 1963 the area was 6.3 square miles, with a population of 11,750. Today LosGatos covers between 14 and 15 square miles and has a population of 30,601. This growth overthe last 80 years resulted in a community with vibrant business districts, well maintainedneighborhoods, and lovely parks and open spaces.

As it exists now, the Town’s boundaries encompass a wide variety of terrain, ranging from levelland to steep and densely wooded hillsides. The sharp visual contrasts among these features andcharming architecture create a picturesque setting of the Town. In the midst of the growth ofSilicon Valley, Los Gatos attracts people with a preference for the Town’s distinctive, high qualitynatural and urban environment.

Dra

ft 12

/04/

2018

Dra

ft 12

/04/

2018

TOWN OF LOS GATOS, CALIFORNIA

COMPREHENSIVE ANNUAL FINANCIAL REPORTFOR THE FISCAL YEAR ENDED JUNE 30, 2018

TABLE OF CONTENTS

INTRODUCTORY SECTION:

Letter of Transmittal........................................................................................................................... 1Organization Chart.............................................................................................................................. 7Principal Officers............................................................................................................................... .. 8GFOA Award ............................................................................................................................... ........ 9

FINANCIAL SECTION:

Independent Auditor’s Report .......................................................................................................... 13

Management’s Discussion and Analysis............................................................................................ 18

Basic Financial Statements:

Government Wide Financial Statements:Statement of Net Position ....................................................................................................... 34Statement of Activities............................................................................................................. 35

Fund Financial Statements:Governmental Funds:Balance Sheet ....................................................................................................................... 38Reconciliation of the Governmental Funds Balance Sheet to theStatement of Net Position ................................................................................................ 39

Statement of Revenues, Expenditures and Changes in Fund Balances................................ 40Reconciliation of Governmental Funds Statement of Revenues, Expenditures,and Changes in Fund Balances to the Statement of Activities ......................................... 41

Statement of Revenue, Expenditures and Changes in Fund Balances –Budget and Actual (GAAP) General Fund ......................................................................... 42

Proprietary Funds – Internal Service Funds:Statement of Net Position.................................................................................................... 44Statement of Revenue, Expenses and Changes in Net Position........................................... 45Statement of Cash Flows...................................................................................................... 46

Fiduciary Funds:Statement of Fiduciary Net Position .................................................................................... 48Statement of Changes in Fiduciary Net Position .................................................................. 49

Notes to the Basic Financial Statements......................................................................................... 51

Required Supplementary Information:

Schedule of Proportionate Share of Net Pension Liability:CalPERS Misc. Agent Multiple Employer Plan ............................................................................. 92CalPERS Safety Cost Sharing Plan................................................................................................ 93

Schedule of Pension Plans ContributionsMiscellaneous Agent Multiple Employer Plan ............................................................................ 94Safety Cost Sharing Plan.............................................................................................................. 94

Actuarial Methods and Assumptions used for Pension ActuariallyDetermined Contributions........................................................................................................... 94

Schedule of Changes in Net OPEB Liability and Related Ratios ...................................................... 95Schedule of Employer Contributions .............................................................................................. 95Actuarial Methods and Assumptions used for 2017/18 OPEB ActuariallyDetermined Contribution ............................................................................................................ 96

Dra

ft 12

/04/

2018

TOWN OF LOS GATOS, CALIFORNIA

COMPREHENSIVE ANNUAL FINANCIAL REPORTFOR THE FISCAL YEAR ENDED JUNE 30, 2018

TABLE OF CONTENTS

SUPPLEMENTARY INFORMATION:

Major Governmental Fund Schedules (other than the General Fund):Schedule of Revenue, Expenditures and Changes in Fund Balance –Budget and Actual (GAAP) Appropriated Reserves Fund ............................................................ 99

Nonmajor Governmental Funds:Combining Balance Sheets.............................................................................................................. 100Combining Schedule of Revenues, Expenditures and Changes inFund Balances.............................................................................................................................. 102

Budgeted Nonmajor Funds Combining Schedule of Revenues, Expenditures andChanges in Fund Balances – Budget and Actual (GAAP).............................................................. 104

Internal Service Funds:Combining Statement of Net Position ............................................................................................ 108Combining Statement of Revenue, Expenses and Changes in Net Position ................................... 109Combining Statement of Cash Flows .............................................................................................. 110

Private Purpose Trust Funds:Combining Statement of Fiduciary Net Position............................................................................. 112Combining Statement of Changes in Fiduciary Net Position........................................................... 113

STATISTICAL SECTION:Net Position by Component............................................................................................................ 118Changes in Net Position .................................................................................................................. 119Fund Balances, Governmental Funds.............................................................................................. 120Changes in Fund Balances, Governmental Funds ........................................................................... 121Assessed Value and Estimated Actual Value of Taxable Property .................................................. 122Direct and Overlapping Property Tax Rates.................................................................................... 123Principal Property Tax Payers ......................................................................................................... 124Property Tax Levies and Collections................................................................................................ 125Ratios of Outstanding Debt by Type ............................................................................................... 126Direct and Overlapping Governmental Activities Debt................................................................... 127Legal Debt Margin........................................................................................................................... 128Demographic and Economic Statistics ............................................................................................ 129Principal Employers......................................................................................................................... 130Full time Equivalent Town Government Employees by Function/Program ................................... 131Operating Indicators by Function/Program .................................................................................... 132Capital Assets Statistics by Function/Program................................................................................ 133

OTHER INDEPENDENT AUDITOR’S REPORTS:

Independent Auditor’s Report on Internal Control over Financial Reporting and on Complianceand Other Matters Based on an Audit of Financial Statements Performed in Accordance withGovernment Auditing Standards................................................................................................. 137

Dra

ft 12

/04/

2018

INTRODUCTORY SECTION

Dra

ft 12

/04/

2018

This page intentionally left blank

Dra

ft 12

/04/

2018

TOWNOFLOSGATOS

OFFICE OF THE TOWNMANAGER

December 4, 2018

Honorable Mayor and Town Council,

I am pleased to submit the Town’s Comprehensive Annual Financial Report (CAFR) forthe fiscal year ending June 30, 2018. This report was prepared by the FinanceDepartment in conjunction with the Town Manager’s Office, which assumesresponsibility for the accuracy of the data and the completeness and fairness of thepresentation and all disclosures. The information in this report is intended to presentthe reader with a comprehensive view of the Town’s financial position and the results ofits operations for the fiscal year ending June 30, 2018, along with additional disclosuresand financial information designed to enable the reader to gain an understanding of theTown’s financial activities.

This report was prepared as prescribed in Governmental Accounting Standards Board(GASB) Statement No. 34, Basic Financial Statements and Management’s Discussion andAnalysis for State and Local Governments (GASB 34). This GASB Statement requiresmanagement to provide a narrative introduction, overview, and analysis to accompanythe basic financial statements in the form of a Management’s Discussion and Analysis(MD&A). This letter of transmittal is designed to complement the MD&A and should beread in conjunction with it. The MD&A can be found immediately following theIndependent Auditor’s Report.

This Comprehensive Annual Financial Report is organized into three sections:

I. The Introductory Section includes the table of contents, letter of transmittal,listing of elected officials, Town administrative personnel, and an organizationchart delineating organizational structure.

II. The Financial Section includes the independent auditors’ opinion, the MD&A, thebasic financial statements, notes to the financial statements, combiningstatements of non major funds, and required supplemental information.

III. The Statistical Section includes both financial and non financial data about theTown.

1

Dra

ft 12

/04/

2018

Mayor and Town CouncilDecember 4, 2018

The Comprehensive Annual Financial Report is prepared in accordance with GenerallyAccepted Accounting Principles (GAAP) promulgated by the Governmental AccountingStandards Board (GASB) and includes the audit report of Badawi & Associates, theTown’s independent certified public accountants.

This Comprehensive Annual Financial Report will be submitted to the GovernmentFinance Officers Association for consideration of its Achievement of Excellence Award infinancial reporting certification. This award is granted only to entities whose reportsmeet the highest standards of municipal financial reporting.

THE REPORTING ENTITY AND ITS SERVICES

Los Gatos is a general law Town, incorporated under the laws of California in 1887. TheTown is located in the foothills and level terrain of the Santa Clara Valley, in an areareferred to internationally as “Silicon Valley.” From the first 100 acre Town site and an1890 population of 1,652, Los Gatos grew slowly so that by 1963 the area was 6.3square miles, with a population of 11,750. Today Los Gatos covers approximately 15square miles with a population of 30,601. This growth over the last 80 years resulted ina community with vibrant business districts, well maintained neighborhoods, and lovelyparks and open spaces. Preserving Los Gatos as a complete and well balancedcommunity has been, and remains a prominent goal for the community.

Five council members are elected at large for staggered four year terms to govern theTown. The Mayor and Vice Mayor are appointed by the Council from its own ranks andserve for one year terms. The Town Manager and Town Attorney are appointed andsupervised directly by the Council. The Town Manager oversees traditional municipalservices such as Public Safety, Parks and Public Works, Community Development, aPublic Library, and Town Administration including Human Resources and Finance.

This report includes all funds of the Town of Los Gatos. As of February 1, 2012, inaccordance with Assembly Bill 1X26, the Redevelopment Agency (RDA) for the Town ofLos Gatos was dissolved. Until its dissolution, the Town of Los Gatos RedevelopmentAgency was governed by a board that was the same as the Town’s governing body.Therefore, the financial activities of the Redevelopment Agency through January 31,2012 had been blended into the Town’s basic financial statements. As a result of thedissolution, the RDA Successor Agency private purpose trust fund was created while theCertificates of Participation (COP) RDA Debt Service Fund and Redevelopment AgencyLow & Moderate Housing Capital Projects Fund were closed out as of June 30, 2012 andare now being held in the Successor Agency Trust Fund.

2

Dra

ft 12

/04/

2018

Mayor and Town CouncilDecember 4, 2018

ECONOMIC CONDITIONS AND OUTLOOK

Consistent with other Silicon Valley communities, the economy is strong andeconomically sensitive revenues, such as Property Tax, Transient Occupancy Tax,Business License Tax and License and Permit revenues have increased as projected. TheTown is seeing early indications of softening in the housing market with homes for salestaying on the market longer than the previous year. However, the value of the homesales remains high. A recent report listed the San Jose Sunnyvale Santa ClaraMetropolitan Statistical Area (MSA) as one of the markets with home prices the furthestabove pre recession peaks nationally at 57 percent.

General Fund revenues (including transfer ins) increased 8.1% from the prior year.Property tax revenues are a significant source of support for General Fund operations,comprising approximately 39% of General Fund revenues in FY 2017/18. For FY 2017/18property tax receipts of $16.0 million were $1.2 million higher than the prior year’scollection, reflecting the continued desirability of the Town, its environment, cultureand educational opportunities. Based on valuation projections by the Santa ClaraCounty Assessor’s Office, Los Gatos property values are anticipated to continue withmoderate growth rates for the near term. Property taxes also increased moderatelydue to a change in property tax distribution methodology due to the dissolution of theCalifornia redevelopment agencies. It should be noted that this increase represents asmall portion of the total loss of redevelopment tax increment previously collected priorto the aforementioned redevelopment dissolution which occurred in February 2012.

The Town relies heavily on sales tax revenues to support General Fund operations,comprising approximately 18.7% of General Fund revenues in FY 2017/18. For FY2017/18 sales tax receipts of $7.6 million were $1.2 million lower than the prior year’scollection. Sales tax revenues continue to trend lower due to the negative impactassociated with increased online sales versus brick and mortar shopping, decreasedgasoline prices during much of the fiscal year and the continued impact of the 2011business model change of Netflix.

Effective February 1, 2012, redevelopment agencies were dissolved and suspended allactivities, with the exception of the implementation of existing contracts and paymentof enforceable obligations entered into prior to February 1, 2012. While the SuccessorAgency will continue to receive tax increment revenue to pay enforceable obligations,like debt service, funding for administrative services and various programreimbursements has been eliminated.

The Town is also preparing for an increase in pension employer rates due to changes toeconomic and demographic actuarial assumptions adopted by CalPERS. Town Council isproactively managing and working to control the anticipated cost escalation in itspension and other post employment benefits (OPEB). To date the Council has adopted

3

Dra

ft 12

/04/

2018

Mayor and Town CouncilDecember 4, 2018

additional discretionary pension strategies in excess of $16.0 million and prefunded$12.0 million towards OPEB obligations.

Despite the reductions to various sources of local government revenue and increasingcosts due to unfunded federal and state mandates, the Town has maintained highservice levels due to the General Fund’s strong fiscal health through FY 2017/18. Towncontinues its outreach to the community, the League of California Cities, and locallegislators to prevent and limit any future revenue losses and mandated cost increases.

MAJOR INITIATIVES

Major initiatives addressing the critical capital asset and infrastructure needs of theTown were a priority for the fiscal year. Approximately $9.2 million in Towninfrastructure and other capital asset improvements were made in FY 2017/18,including $3.9 million in street improvement projects including improvements to majorarterials and neighborhood collector streets to enhance pedestrian and traffic safetyTown wide, $0.1 million in vehicle and equipment, and approximately $0.1 million onretaining walls and park improvements. In addition, the Town invested $5.1 million invarious projects that are currently in progress, including approximately $4.8 million onthe Almond Grove Street project, and other facility, park, and infrastructureimprovement projects.

Additional infrastructure improvements are scheduled in accordance with the Town’sapproved Capital Improvement Plan, and will continue into future years. All of theseimprovements are funded either through grants, or via revenues accumulated fromprior year budget savings and/or excess revenues per Town Council policy.

ACCOUNTING SYSTEM AND BUDGETARY CONTROL

The effectiveness of internal control is considered in the development and evaluation ofthe Town’s accounting system. Internal accounting controls are designed to providereasonable but not absolute assurance regarding:

1) safeguarding of assets against loss from unauthorized loss or disposition,

2) accuracy and reliability of accounting data, and

3) adherence to managerial policy.

The concept of reasonable assurance recognizes that the cost of internal control shouldnot outweigh the benefits, and that management must make estimates and judgmentsin evaluating these costs and benefits.

4

Dra

ft 12

/04/

2018

Mayor and Town CouncilDecember 4, 2018

All governmental fund types use the modified accrual basis of accounting. This meansthat revenues are recorded when measurable and available rather then when received.Measurable means the amount can be determined and available means the cash isreceived within sixty days after the end of the fiscal year. Expenditures are recordedwhen the liability is incurred, rather than when paid. An exception to this rule isprincipal and interest on general long term debt, which is not recognized by debt servicefunds until it is due.

Proprietary (internal service) funds are accounted for using the accrual basis ofaccounting, similar to that used by corporations. Proprietary fund revenues arerecognized when they are earned rather than when the cash is received, even if the cashis not available and proprietary fund expenses are recognized when they are incurred.

With the implementation of GASB 34, the Town now prepares its Basic FinancialStatements on the accrual basis.

Internal accounting procedures have been developed to provide reasonable assuranceregarding the safeguarding of assets and the reliability of financial records for preparingfinancial statements and maintaining asset accountability.

An annual operating budget and five year capital improvement plan is adopted by theTown Council on a basis consistent with generally accepted accounting principles. Allbudget adjustments and transfers between funds must be approved by the TownCouncil during the fiscal year. The Town Manager is authorized to transferunencumbered appropriations within a budget category, within a fund. Appropriationsare valid for each fiscal year and lapse at year end.

AWARDS

The Town’s Comprehensive Annual Financial Report for the fiscal year ended June 30,2017 was awarded a Certificate of Achievement for Excellence in Financial Reporting bythe national Government Finance Officers Association. This prestigious awardrecognizes the report’s conformance with strict accounting and reporting standardsestablished by the Government Accounting Standards Board and government financeorganizations. This award is annual in nature and valid for one year only. This year’sreport will be submitted for award consideration by this organization, as we believe itcontinues to meet these standards.

INDEPENDENT AUDIT

State law requires an annual audit of the Town’s accounts by independent certifiedpublic accountants. The accounting firm of Badawi & Associates performs this functionfor the Town of Los Gatos, and their report is included in the financial section of theCAFR.

5

Dra

ft 12

/04/

2018

Mayor and Town CouncilDecember 4, 2018

ACKNOWLEDGEMENTS

The preparation of this Comprehensive Annual Financial Report, as presented herein, isthe result of the combined efforts and dedicated services of the excellent staff of theDepartment of Finance. Special thanks to Gitta Ungvari, Finance and Budget Manager,Mark Gaeta, Accountant; Melissa Ynegas, Finance Analyst; Diane Howard, PayrollSpecialist; and Kenneth Stiles, Administrative Technician for their efforts in preparingthis report.

Respectfully submitted,

____________________________ ___________________________________Laurel Prevetti Stephen D. ConwayTown Manager Director of Finance

6

Dra

ft 12

/04/

2018

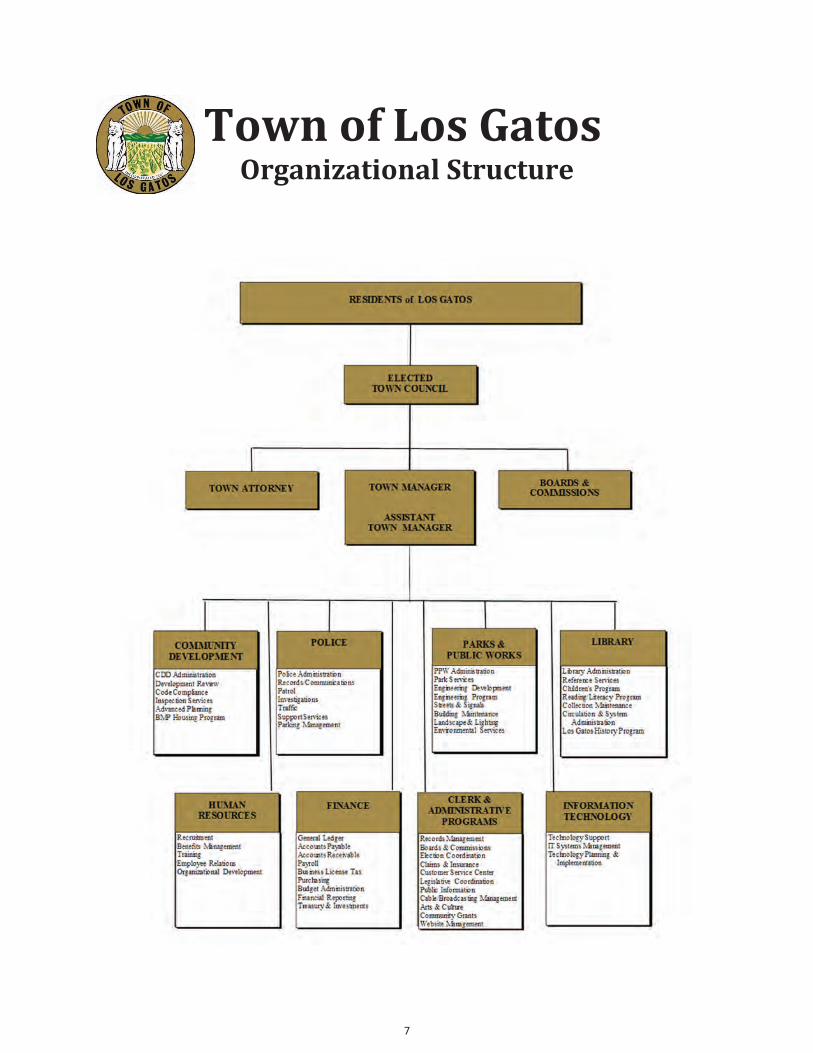

Town of Los GatosOrganizational Structure

7

Dra

ft 12

/04/

2018

TOWN OF LOS GATOSPRINCIPAL OFFICERS

JUNE 30, 2018

TOWN COUNCIL

Mayor Rob RennieVice Mayor Steven LeonardisCouncil Member Marcia JensenCouncil Member Marico SayocCouncil Member Barbara Spector

COUNCIL APPOINTEES

Town Manager Laurel PrevettiTown Attorney Robert Schultz

APPOINTED OFFICIALSAssistant Town Manager Arn AndrewsChief of Police Peter DecenaCommunity Development Director Joel PaulsonParks and Public Works Director Matt MorleyLibrary Director Ryan BakerFinance Director Stephen ConwayHuman Resources Director Lisa Velasco

8

Dra

ft 12

/04/

2018

9

Dra

ft 12

/04/

2018

This page intentionally left blank

10

Dra

ft 12

/04/

2018

FINANCIAL SECTION

11

Dra

ft 12

/04/

2018

This page intentionally left blank

12

Dra

ft 12

/04/

2018

INDEPENDENT AUDITOR’S REPORT

To the Honorable Mayor and Members of the Town Council of theTown of Los Gatos

Los Gatos, California

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, each major fund, and theaggregate remaining fund information of the Town of Los Gatos, California, as of and for the year ended June 30,2018, and the related notes to the financial statements, which collectively comprise the Town’s basic financialstatements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordancewith accounting principles generally accepted in the United States of America; this includes the design,implementation, and maintenance of internal control relevant to the preparation and fair presentation offinancial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our auditin accordance with auditing standards generally accepted in the United States of America and the standardsapplicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of theUnited States. Those standards require that we plan and perform the audit to obtain reasonable assurance aboutwhether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in thefinancial statements. The procedures selected depend on the auditor’s judgment, including the assessment of therisks of material misstatement of the financial statements, whether due to fraud or error. In making those riskassessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of thefinancial statements in order to design audit procedures that are appropriate in the circumstances, but not for thepurpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express nosuch opinion. An audit also includes evaluating the appropriateness of accounting policies used and thereasonableness of significant accounting estimates made by management, as well as evaluating the overallpresentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our auditopinions.

13

Dra

ft 12

/04/

2018

To the Honorable Mayor and Members of the Town Council of the Town of Los Gatos

Los Gatos, California Page 2

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respectivefinancial position of the governmental activities, each major fund, and the aggregate remaining fund informationof the Town as of June 30, 2018, and the respective changes in financial position and, where applicable, cash flowsthereof for the year then ended in accordance with accounting principles generally accepted in the United States ofAmerica.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussionand analysis, budgetary comparison information pension related schedules and OPEB related schedules on pages18 29 and 92 96 be presented to supplement the basic financial statements. Such information, although not a partof the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it tobe an essential part of financial reporting for placing the basic financial statements in an appropriate operational,economic, or historical context. We have applied certain limited procedures to the required supplementaryinformation in accordance with auditing standards generally accepted in the United States of America, whichconsisted of inquiries of management about the methods of preparing the information and comparing theinformation for consistency with management’s responses to our inquiries, the basic financial statements, and otherknowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provideany assurance on the information because the limited procedures do not provide us with sufficient evidence toexpress an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprisethe Town of Los Gatos, California’s basic financial statements. The introductory section, major funds (other thanGeneral fund and Special revenue funds) budgetary schedules, combining and individual nonmajor fund financialstatements, and statistical section are presented for purposes of additional analysis and are not a required part ofthe basic financial statements.

The major funds (other than General fund and Special revenue funds) budgetary schedules, combining andindividual nonmajor fund financial statements are the responsibility of management and were derived from andrelate directly to the underlying accounting and other records used to prepare the basic financial statements. Suchinformation has been subjected to the auditing procedures applied in the audit of the basic financial statementsand certain additional procedures, including comparing and reconciling such information directly to the underlyingaccounting and other records used to prepare the basic financial statements or to the basic financial statementsthemselves, and other additional procedures in accordance with auditing standards generally accepted in theUnited States of America. In our opinion, the combining and individual nonmajor fund financial statements are fairlystated, in all material respects, in relation to the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit ofthe basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

14

Dra

ft 12

/04/

2018

To the Honorable Mayor and Members of the Town Council of the Town of Los Gatos

Los Gatos, California Page 3

Other Reporting Required by Government Auditing Standards

In accordance with Government Auditing Standards, we have also issued our report dated [DATE] on ourconsideration of the Town’s internal control over financial reporting and on our tests of its compliance with certainprovisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is todescribe the scope of our testing of internal control over financial reporting and compliance and the results of thattesting, and not to provide an opinion on internal control over financial reporting or on compliance. That report isan integral part of an audit performed in accordance with Government Auditing Standards in considering the Town’sinternal control over financial reporting and compliance.

Badawi and AssociatesCertified Public AccountantsOakland, California[DATE]

15

Dra

ft 12

/04/

2018

This page intentionally left blank

16

Dra

ft 12

/04/

2018

Management’s Discussion and Analysis

17

Dra

ft 12

/04/

2018

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following discussion and analysis of the Town of Los Gatos financial performanceprovides an overview of the Town’s financial activities for the fiscal year ending June 30,2018. This information is presented in conjunction with the audited financialstatements that follow this section.

FINANCIAL HIGHLIGHTS

Town assets exceeded its liabilities at the close of FY 2017/18 by $109,262,066 (netposition). Of this amount, $170,590 (unrestricted net position) may be used to meetthe Town’s ongoing obligations to its community and creditors.

The Town’s net position decreased by $7.8 million during the fiscal year largely as aresult of the beginning FY 2017/18 net position being restated and reduced byapproximately $8.5 million as required by the implementation of GASB 75 regardingthe financial reporting of other post employment benefits (OPEB). Prior to theimplementation of GASB 75 the Town was only required to report its Net OPEBObligation (NOO) in the notes section of its CAFR. With this latest GASBpronouncement all of the Town’s pension and OPEB obligations will now bereflected fully in the financial statements.

Total fund balances for governmental funds at year end were $49,353,921, adecrease of $3,797,817 (7%) from the prior year. Fund balances decreased primarilyfor increased expenditures, capital spending, and the $1.2 million transfer to theTown IRS 115 Pension Trust.

At the end of FY 2017/18, fund balance for the General Fund was $30,428,684,approximately 82% of General Fund expenditures for the current fiscal year.

The Town’s total capital assets increased by $5,833,077 to $102,098,729 net ofdepreciation.

OVERVIEW OF THE FINANCIAL STATEMENTS

The financial statements presented herein include all of the activities of the Town andits component units using the integrated approach as prescribed by GASB Statement No.34.

Government Wide Financial Statements

The government wide financial statements present the financial picture of the Townfrom an economic resources measurement focus using the accrual basis of accounting.

18

Dra

ft 12

/04/

2018

The statement of net position presents information on all of the Town’s assets andliabilities, with the difference between the two reported as net position. Over time,increases or decreases in net position may serve as a useful indicator of whether thefinancial position of the Town is improving or deteriorating.

The statement of activities presents information showing how the Town’s net positionchanged during the most recent fiscal year. All changes in net position are reported assoon as the underlying event giving rise to the change occurs, regardless of the timing ofrelated cash flows. Thus, revenues and expenses are reported in this statement forsome items that will only result in cash flows in future fiscal periods (e.g., uncollectedtaxes and earned but unused vacation leave).

Both of the government wide financial statements distinguish functions of the Townthat are principally supported by taxes and intergovernmental revenues (governmentalactivities) from other functions that are intended to recover all or a significant portion oftheir costs through user fees and charges (business–type activity). The governmentalactivities of the Town include public safety, parks and public works, communitydevelopment, library, community services, debt service, and general government. TheTown has no business type activities.

The government wide financial statements include not only the Town itself (known asthe primary government), but also a legally separate Town of Los Gatos RedevelopmentAgency (the Agency) for which the Town was financially accountable. In accordancewith Assembly Bill (AB) 1X26 which provides for the dissolution of all redevelopmentagencies in the State of California, the Town of Los Gatos agreed to serve as thesuccessor agency and thereby to hold the assets until they were distributed to otherunits of state and local government. In accordance with AB 1X26, the Town of Los GatosRedevelopment Agency dissolved and ceased to operate as a legal entity on February 1,2012.

Prior to February 1, 2012, the final seven months of activity of the redevelopmentagency continued to be reported in the governmental funds of the Town. AfterFebruary 1, 2012, the assets and activities of the dissolved redevelopment agency arereported in a fiduciary fund (RDA Successor Agency private purpose trust fund) in thefinancial statements of the Town. Additional information on the dissolution of the RDAand this fiduciary fund can be found in Note 12 in the notes to basic financialstatements.

Fund Financial Statements

A fund is a grouping of related accounts that is used to maintain control over resourcesthat have been segregated for specific activities or objectives. The Town, like other localgovernments, uses fund accounting to ensure and demonstrate compliance with

19

Dra

ft 12

/04/

2018

finance related legal requirements. The funds of the Town are segregated into threecategories: governmental funds, proprietary funds, and fiduciary funds.

Governmental funds – The Town’s basic services are reported in governmental funds,which focus on how money flows into and out of those funds and the balances left atyear end that are available for spending. These funds are reported using the modifiedaccrual basis of accounting, which measures cash and other financial assets that canreadily be converted to cash. The governmental fund statements provide a detailedshort term view of the Town’s general government operations and the basic services itprovides. Governmental fund information helps determine whether there are more orfewer financial resources that can be spent in the near future to finance the Town’soperations. Both the governmental fund balance sheet and the governmental fundstatement of revenues, expenditures, and changes in fund balances provide areconciliation to facilitate this comparison between governmental funds andgovernmental activities.

Proprietary funds – The Town maintains one type of proprietary fund: internal servicefunds. Proprietary funds are reported using the accrual basis of accounting. Internalservice funds are an accounting tool used to accumulate and allocate costs internallyamong the Town’s various functions. The Town uses internal service funds to accountfor its fleet of vehicles, computer equipment, risk management activities, and otheritems. The Internal Service funds are included within governmental activities in thegovernment wide financial statements.

Fiduciary funds – Fiduciary funds are used to account for resources held for the benefitof parties outside the Town. Fiduciary funds are not reflected in the government widefinancial statements because the resources of those funds are not available to supportthe Town’s own programs.

Included in fiduciary funds is the RDA Successor Agency private purpose Trust Fundcreated upon the dissolution of the former Redevelopment Agency. The Trust Fund wascreated to hold the assets of the former Redevelopment Agency until they aretransferred for governmental purposes to other entities, or distributed to the underlyingtaxing jurisdictions in Santa Clara County after the payment of enforceable obligations.

Notes to basic financial statements

The notes provide additional information essential to a full understanding of the dataprovided in the government wide and fund financial statements. The notes to basicfinancial statements can be found on pages 51 89 of this report.

20

Dra

ft 12

/04/

2018

Government wide Financial Analysis

Net position may serve over time as a useful indicator of a government’s financialposition. In the case of the Town, assets exceeded liabilities by $109 million at the endof the current fiscal year.

2018 2017Current and other Assets 77,527,309$ 76,851,804$Capital Assets 102,098,729 96,265,652Total Assets 179,626,038$ 173,117,456$

Deferred Outflows Pension 19,177,172 15,666,410Current Liabilities 19,125,206 15,368,467Long Term Liabilities Outstanding 66,492,020 50,630,426Total Liabilities 85,617,226$ 65,998,893$

Deferred Inflows Pension 3,923,918 5,778,114Net PositionNet Investment in Capital Assets 102,098,729 96,265,652Restricted 6,992,747 5,627,707Unrestricted 170,590 15,134,420Total Net Position 109,262,066$ 117,027,779$

Town of Los GatosNet Position

Governmental ActivitesFor the Year Ended June 30, 2018

Capital assets represent approximately 57% of the Town’s total assets consisting ofinvestments made by the Town in permanent or long lived assets (e.g., land, buildings,infrastructure, machinery and equipment), less any related debt used to acquire thoseassets still outstanding. The Town uses these capital assets to provide services toresidents and customers; consequently, these assets are not available for futurespending. Although the Town’s investment in its capital assets is reported net of relateddebt, it should be noted that the resources needed to repay this debt must be providedfrom other sources since the capital assets themselves cannot be used to liquidate theseliabilities.

For the current year, Net Investment in Capital Assets increased by $5,833,077 as aresult of approximately $10 million in capital improvements made during the fiscal year,offset by $4.2 million in capital assets depreciation and retirements.

An additional portion of the Town’s net position (6.4%) represents resources that aresubject to external restrictions on how they may be used. The balance of unrestrictednet position may be used to meet the Town’s ongoing obligations to citizens, customers,and creditors. The Town’s unrestricted net position represents approximately 0.2% ofthe Town’s net position at year end.

21

Dra

ft 12

/04/

2018

Governmental activities

2018 2017Revenues:Program revenues:

Charges for Services 11,982,107$ 10,162,547$Operating Grants and Contributions 1,906,224 1,503,108Capital Grants and Contributions 348,437 779,880

General Revenues:Property Taxes 15,958,406 14,756,214Sales Taxes 7,466,253 8,925,276Franchise Taxes 2,474,814 2,366,908Other Taxes 2,667,840 2,351,223Motor Vehicle in Lieu 16,483 14,056Investment Earnings 333,120 192,260Miscellaneous 622,105 528,946

Total Revenues 43,775,789 41,580,418

Expenses:Police Department 15,545,521 14,587,597Parks and Public Works 10,047,003 9,502,707General Government 9,155,819 6,771,628Community Development 4,667,609 5,093,459Library Services 3,087,684 2,868,748Sanitation 536,296 466,762

Total Expenses 43,039,932 39,290,901

Change in Net Position 735,857 2,289,517

Net Position, beginning 117,027,779 112,514,506Prior Period Adjustments GASB 75 (8,501,570) 2,223,756Net Position, as restated GASB 75 108,526,209 114,738,262

Net Position, Ending 109,262,066$ 117,027,779$

Town of Los GatosStatement of Activities

For the Year Ended June 30, 2018

As shown in the schedule above, governmental activities for the year decreased theTown’s net position by $7,765,713. Key elements of the decrease in net position are asfollows:

Property tax revenues collected for the Town accounted for 37% of total Townrevenues. Property tax revenues for Town activities increased by $1.2 million or8.1%, from FY 2016/17 due primarily to the continued strong economy, the

22

Dra

ft 12

/04/

2018

continued strong demand for housing in Los Gatos, and several newdevelopments being added to the tax roll.

Sales tax revenue of $7.5 million accounted for approximately 17% of the Town’stotal revenues for the year. The 16% decrease of approximately $1.5 millionfrom the prior year collections is largely due to the timing of the final “triple flip”payment and the reclassification of other sales tax revenue to the prior period.

Other taxes and miscellaneous revenues of $3.3 million accounted for 7.5% oftotal revenues, increasing by 14% from the prior year. This increase wasprimarily the result of the higher amount of Transient Occupancy Tax collected inFY 2017/18 as compared to the prior year.

Investment earnings of $602,420 net of amortized premiums increased by$140,680 from the prior year. This increase is due primarily to the increasinginterest rate environment in anticipation of stronger economic growth.

Total expenditures increased by approximately $3.7 million from the prior year.This increase was largely due to increased pension expenses and the $1.2 millioncontributed to the Town’s IRS 115 Pension Trust during FY 2017/18.

Unrestricted fund balance of $170,590 as of June 30, 2018 reflecting a $15million decrease resulting primarily from the net impacts of the implementationof GASB 75 and net additions to infrastructure in the current fiscal year. Foradditional information, please refer to Note 1 and Note 10.

FINANCIAL ANALYSIS OF THE TOWN’S FUNDS

The Town uses fund accounting to ensure and demonstrate compliance with financerelated legal requirements.

Governmental funds

The focus of the Town’s governmental funds is to provide information on near terminflows, outflows, and balances of spendable resources. As of the end of FY 2017/18,the Town’s governmental funds reported combined ending fund balances of$49,353,921, a decrease of $3,797,817 in comparison with the prior year. Fund balancesdecrease primarily due to capital expenditures and additional $1.2 million transfer tothe Town IRS 115 Pension Trust Fund.

Approximately 86% or $42,361,174 of the total amount of governmental fund balancesof $49,353,921 is committed, assigned or unassigned fund balance, which is availablefor spending subject to Town direction and approval. The remainder of fund balance isrestricted therefore not available for new spending but limited as to use for (1)

23

Dra

ft 12

/04/

2018