Title Covers Options-5 - ICMA

373

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Title Covers Options-5 - ICMA

History of

Management AccountingProfession in Pakistan

Institute of Cost and ManagementAccountants of Pakistan

Estd. 1951

This book depicts milestones achieved, and progress made, by the Institute during the initial fifty-five years of its

establishment i.e., from 1951 to 2006.

© ALL RIGHTS RESERVED

No part of this work covered by the copyright hereon may be reproduced or used in anyform or by any means-graphic, electronic or mechanical, including photocopying,

recording, taping, web distribution or information storage and retrieval systems – withoutthe written permission of the publisher.

For permission to use material from this text or product, contact us on:Tel.: (92-21) 99243900, Fax: (92-21) 99243342

e-mail: [email protected]

Printed atMAS Printers, Karachi, Pakistan.

Published by:Research Department

Institute of Cost and Management Accountants of Pakistan

Dedication

This book is dedicated toMr. Mohammad Shoaib, the founder

President and the moving force behind theestablishment of the Institute. Hispioneering contributions for the

development of Cost and ManagementAccounting profession in the Sub-continent

will always be remembered.

Foreword

Institutional histories are important for their intrinsic academic worth;but their real value lies in the opportunity they afford to understand andappreciate the past in which is deeply rooted the present which, in turn,decides the contours and colours of the future. Institutional histories canthus be likened to a crystal-ball simultaneously mirroring an institution’syesterday, today and tomorrow- all as parts of an inherently inter-connected episode. This was exactly the object that inspired andmotivated the Institute of Cost and Management Accountants of Pakistan

to publish the History of Management Accounting Profession in Pakistan now in your hands.

The Institute was founded in 1951 and the profession of management accounting has been inexistence as a statutorily regulated profession since 1966. More than half a century haselapsed and no serious attempt seems to have been made - at least not in documentedmemory - to trace the genesis of the profession in Pakistan and its upbringing over the years.Now that the profession has reached its prime youth and is destined to grow further, theInstitute has proudly recapitulated and narrated the story of its birth and gradualdevelopment. This the Institute has done in the hope that knowing where we have come from and realising where we stand today will help us reach where we aspire and deserve to be as acherished, honourable, respected and self-respecting profession actively serving the society.Hence this book.

I am indeed pleased and honoured to present this book to the readers with some sense ofaccomplishment but in all humility. I would like to assure them that all possible efforts havebeen made to present an authentic, objective and comprehensive account; but the chances ofunintended mistakes and unintentional omissions cannot be ruled out. My only request tothe readers is to magnanimously overlook them.

Hasan A. Bilgrami, FCMAPresident

July 2009

Preface

The Institute deserves my deepest appreciation for publishing this book,to pay lasting homage and glowing tributes to its founders. This historical document takes us through time, depicting the evolution of theManagement Accounting Profession, with special reference to thedevelopment made by the Institute.

By the time I had assumed the office of Chairman, Research Committee,this publication was already scheduled to go to press. I can onlyappreciate here the tremendous efforts made by all the concerned, particularly mypredecessors and members of Research, Quality Assurance & Ethics Committee. I especiallyacknowledge with gratitude the valuable contribution made by Mr. M. H. Asif, FCMA whohad been instrumental in bringing out this valuable publication.

This publication attempts to further strengthen the roots of management accountingprofession in our country. At the same time, it also highlights the pivotal role played by theInstitute in developing and strengthening the profession. I hope that the readers, particularly the Management Accountants, would find this book a useful addition to their library andreinforce their sense of belonging to this Institute.

Masud Muzaffar, FCMAChairman, Research, Quality

Assurance & Ethics Committee

July 2009

About the Book

It takes a tremendous amount of deep thinking, meticulous planning andpainstaking efforts to create new institutions. But when institutions socreated attain a certain level of maturity and earn recognition and respect,not many bother to remember how they were born and brought up. Theinspiring saga of courage and determination underlying their existingstature is buried deep in the sands of time. The long and arduous distancetraversed is forgotten and the memory of those who toiled tirelessly tobuild them brick by brick recedes into oblivion. Only some yellowedpapers remain in dusty archives to tell the story. But the institutions do

stand as living realities, immortalising the memory of, and paying lasting homage to, theirfounders and builders.

Our Institute and, in fact, the profession of Management Accounting itself were founded inPakistan by a few men of vision and determination in difficult and inhospitable conditions.To repay the debt, though only partly, the Institute could not have possibly found a betterway than to tell the story of how a new profession was created in a new country; what it hadto go through to establish and get recognized; and to progress and reach where it standstoday. This is a story of courage and dedication, of trials and tribulations, of failings andaccomplishments. In the end, it is a success story worth telling.

The institutional history covered in the book essentially spans over 55 years – from 1951 to2006. Historical account of the profession of accounting, however, goes back to its genesis inancient times. Even if that period was set aside, there still remained more than half a centuryto cover – heaps of material to dig out, sift, collate and piece together to form a compact story.As it normally happens in developing countries like ours, information available was neithercomplete nor coherent. Moreover, the aspects to cover were too many in number and toovaried in nature. Arranging the disjointed pieces into an intelligible and coherent narrationwas not an easy task. Equally difficult was to ensure accuracy and objectivity. How far havewe been able to surmount these obstacles is best left to the readers to decide.

The book is divided into 13 chapters, each describing a different facet of the Institute, not inisolation from each other but one logically leading to the other in naturally flowingprogression. Together they unfold the story of the Institute which, in essence, is the history ofthe profession of management accounting in Pakistan.

The First Chapter attempts to trace the roots of the profession from the ancient times throughthe medieval ages to the modern age. It also highlights the contribution the Muslims made to

the knowledge of mathematics, which is often ignored by historians. The birth of modernaccounting has also been discussed with special reference to the emergence of costaccountancy and to the various legislations enacted by the British for India, in which aredeeply rooted our professional procedures and practices.

Chapter Two specifically and exclusively narrates the story of the founding of the Institute in1951. How and why was it conceived? Who founded it? What were its objects and purposes?What problems and difficulties it had to face in its initial years? What role did assistance from Canada under the Colombo Plan play in its development? What efforts were made toestablish links with foreign professional bodies? How was the Institute housed in its ownbuilding? These are the main questions addressed in this chapter.

Chapter Three describes the creation of the Institute as a statutory body and the regulation ofthe profession by an act of the Parliament. It also tells the story of why and how was the nameof the Institute changed from Pakistan Institute of Industrial Accountants to its present name.

Described at length in the Fourth Chapter is the Council of the Institute – its composition,functions, committees, branches and meetings. Brief life sketches of all those who have so farserved the Council as President have also been included as a mark of respect and with a sense of indebtedness.

Among the main purposes of the Institute’s creation are education and examinations. Howand to what effect are these purposes served is the subject matter of the next two chapters.Education through coaching classes and correspondence courses, periodic syllabusrevisions, entrance requirements, other educational and training initiatives, matters relatingto books and libraries, students’ enrolment over the years and the Institute’s fees structureform part of the Fifth Chapter. And the Sixth Chapter discusses examination policy andsystem, the criteria of granting exemptions, awards and prizes. It also analyses statistics ofcandidates taking and passing examinations in all the past years.

Then comes Chapter Seven to take a close look at the members, both Fellows and Associates.How are their names entered in the Institute’s Register? Where are they located? What arethey doing and where? What opportunities are available to them? These are some of thequestions attempted in this chapter.

The next Chapter surveys the various programmes aimed at the members’ continuingprofessional education and their professional development. The numerous seminars andconferences arranged, computer courses run and the journal published by the Institute havebeen discussed in this chapter.

Research and publications represent two other very important areas of activity, not onlyfrom the professional point of view but also as means of furthering the objects of CPE andprofessional development. The Institute’s performance in these areas is reviewed at length in

About the Book

Chapter Nine. Also included for ready reference are abridged resumes of important researchstudies conducted.

The Tenth Chapter is devoted to the description and discussion of professional ethics. Itcontains the professional do’s and dont’s prescribed by the Institute for its members,discusses the efforts made to frame a formal code in the light of IFAC’s guidelines andreviews the development of SAFA’s Code of Ethics, which has recently been adopted by theInstitute’s Council for its members in Pakistan.

ICMAP is an active member of various international professional organizations. ChapterEleven describes the aims, objects and activities of these bodies with a view both tounderscoring the obligations devolving on members of the profession in Pakistan andhighlighting the benefits and opportunities flowing from their membership. Other aspects ofthe Institute’s international relations have also been discussed in this Chapter.

The Twelfth Chapter contains a description of ICMA’s Secretariat – of its administrative set-up, its executive heads, its financial position and the many services it renders for themembers’ benefit and welfare.

The concluding chapter of the book makes an attempt to explain the demanding challengesconfronting the Institute in the wake of the transition through which the profession globallyis passing; highlights the many constraints under which the profession has to survive in aninhospitable local environment; and frankly and honestly brings to fore the challenges theInstitute is facing. Most purposefully, the chapter elucidates what future strategy is beingadopted to manage the change and to enhance the Institute’s and the profession’seffectiveness, utility, reputation, standing and status.

The book also contains a large number of tables to illustrate or substantiate variousstatements made. These list facts or figures which could not have been included in the mainbody of the book either because of their length or for fear of interrupting the flow. However,where immediate reference is necessary for analysis, tables have been made part of thenarrative notwithstanding their length and the threatened break in continuity.

Many historical accounts contain frequent references to documents to which the readers donot have easy access. Care has been taken to ensure that this book does not suffer from suchan inadequacy. With this object in view, important documents, to which references havebeen made in the book, have been added at the end as appendices. We do not want ourreaders to have to make rounds of the libraries in order to fully understand the context andpoint of reference of what the book talks about. Hence this arrangement.

I will be failing in my duty if I do not place on record the Institute’s, and of course my own,deep sense of gratitude and unreserved appreciation for the encouragement and support wereceived from many people in the present venture. Their number being too large to cover, Ican only thank them all collectively. I must, however, specifically mention a few friends

About the Book

without whose helpful involvement, this book could not have seen the light of day. The firstamong them is a highly respected past President of ICMAP, Mr. Khurshid Ahmad, who infact fathered the idea to compile the history of the profession in Pakistan. He was sold on theidea so emotionally and pursued it so vehemently that there was no way the project wouldnot have been initiated. And when it did finally get underway after protracted delay,Mr.Khurshid, despite old age and ill health, was always there to offer guidance andmotivation. Also deserving a special mention is Mr. Qaisar Mufti, my worthy predecessor,who undertook the actual initiation of work on the project which had been lingering on forquite some time. It was he who got all the relevant material retrieved from old dusty files,had it thoroughly checked for accuracy and, most importantly, went on a hunt for acompetent professional, who could provide technical guidance and support. What a strokeof luck it was that Mr. Ismail Patel, a very experienced senior officer of the InformationService of Pakistan, now retired, agreed to assist. I have worked with him closely and have no hesitation in saying that his intense involvement, beyond the call of duty on many occasions,ensured a high quality narration and compilation. He helped not only in writing and editingbut also in proof reading, page layout and final production. I am personally indebted to him.

I sought comments on the draft, from many senior members who have, over the years,contributed to the growth of Management Accounting Profession in Pakistan, and speciallyacknowledge the detailed input from Mian Mumtaz Abdullah and Mr. Muhammad Rafi, our two former Presidents.

I should also gratefully acknowledge the hard work done by Mr.Kamaluddin, AdvisorResearch, Mr. Shahid Anwar, Deputy Director Research and their team for digging out andcollecting the heaps of information on which this book is based and for the arduouscompilation of data included in it.

Finally, I must profoundly thank the successive National Councils for their continuedsupport and valuable guidance which served as enduring sources of inspiration andencouragement in the entire process of conceiving, initiating and completing this venture.

Our most sincere effort has been to make the History of Management Accounting Professionin Pakistan as authentic and as easily readable and intelligible as an institutional historyshould be. Who but you can be an honest judge of our success or otherwise?

M. H. Asif, FCMAChairman

Research, Quality Assurance & Ethics Committee

June 2008

About the Book

Contents

Foreword

Preface

About the Book

Chapter One: Forget Not Thy Roots ......................................................................................17

– In Ancient Times ................................................................................17

– Forgotten Muslim Brilliance .............................................................19

– Birth of Modern Accounting.............................................................23

– In British India ....................................................................................25

– Emergence of Cost Accounting........................................................26

Chapter Two: A Sapling Planted............................................................................................33

– Background .........................................................................................34

– The Idea ...............................................................................................35

– Founding Fathers ...............................................................................37

– Objects..................................................................................................38

– Teething Problems .............................................................................40

– Assistance Under Colombo Plan .....................................................47

– Reaching Out ......................................................................................49

– A Place Called Home ........................................................................50

Chapter Three: On The Statute Book.......................................................................................53

– The Act.................................................................................................53

– Rose by Another Name .....................................................................56

Chapter Four: At the Helm: The Council .............................................................................59

– Composition........................................................................................59

– Functions .............................................................................................62

– Committees .........................................................................................66

– Branch Councils..................................................................................67

– Meetings ..............................................................................................68

– Presidents ............................................................................................70

Chapter Five: Fulfilling Raison d’ etre (A): Education ......................................................79

– Syllabus................................................................................................79

– Entrance Requirements .....................................................................92

– Coaching..............................................................................................95

– Correspondence Courses ..................................................................97

– Canadian Help....................................................................................99

– Other Initiatives................................................................................100

– Books and Libraries .........................................................................102

– Enrolment ..........................................................................................104

– Fees .....................................................................................................106

Chapter Six: Fulfilling Raison d’ etre (B): Examinations ..............................................107

– Policy..................................................................................................107

– System................................................................................................109

– Exemptions........................................................................................110

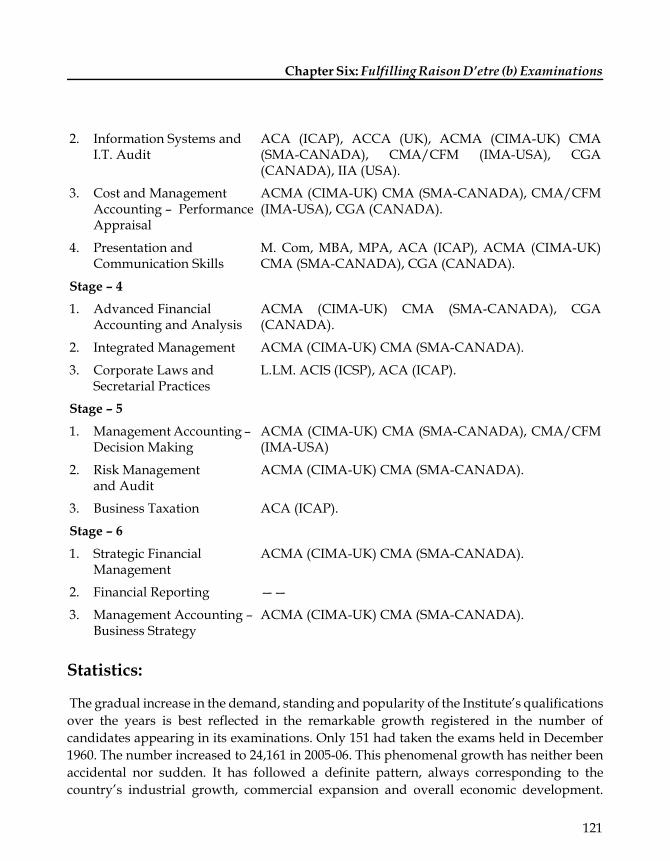

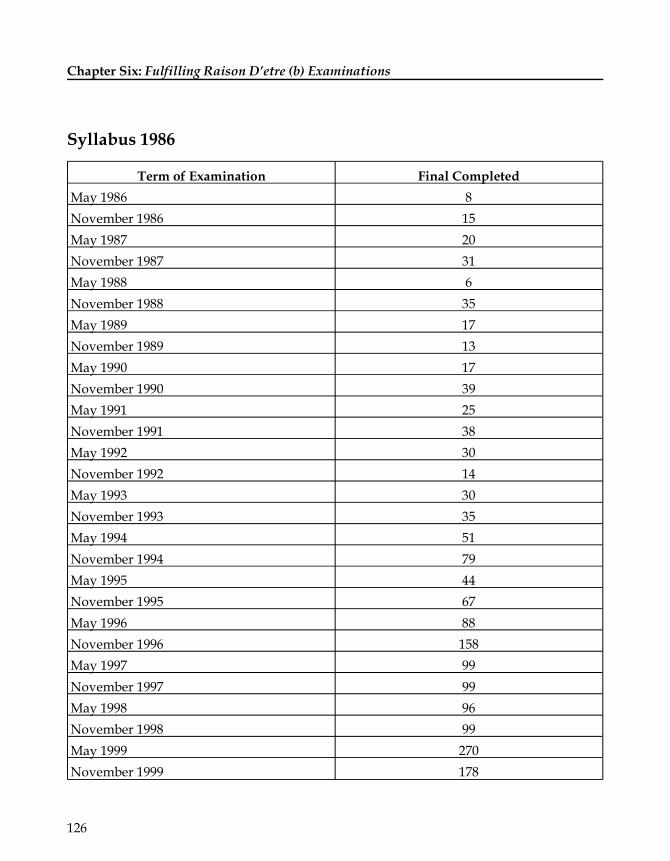

– Statistics .............................................................................................121

– Awards and Prizes ...........................................................................128

Contents

Chapter Seven: Proud Products: The Members....................................................................131

– Categories..........................................................................................131

– The Register.......................................................................................133

– Membership Profile .........................................................................137

Chapter Eight: Keeping Up-to-Date ......................................................................................149

– IFAC Guidelines ...............................................................................150

– CPD Programme ..............................................................................156

– Seminars and Conferences..............................................................159

– Computer Courses ...........................................................................174

– Journal of the Institute.....................................................................176

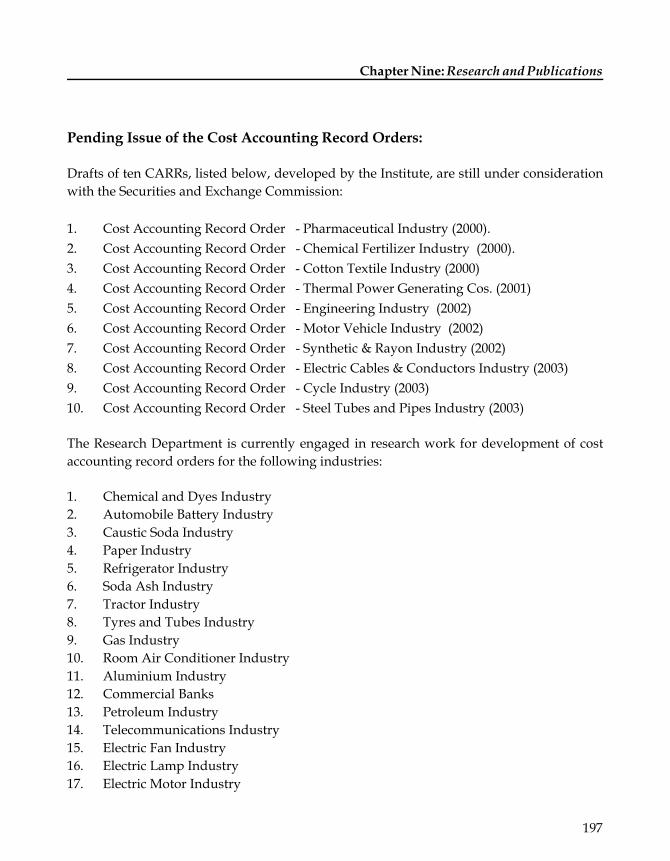

Chapter Nine: Research and Publications ...........................................................................179

– Research Department ......................................................................179

– Research Studies...............................................................................183

– Cost Accounting Records Rules .....................................................195

– Publications.......................................................................................202

Chapter Ten: Professional Ethics ........................................................................................203

– Legal Provisions ...............................................................................203

– IFAC Code of Ethics.........................................................................207

– SAFA Code........................................................................................208

– Salient Features.................................................................................211

Contents

Chapter Eleven: In Global Fraternity ........................................................................213

– Coming Out of Shell ........................................................................213

– International Accounting Standards Board (IASB).....................215

– International Federation of Accountants (IFAC).........................216

– Confederation of Asian and Pacific Accountants (CAPA).........221

– South Asian Federation of Accountants (SAFA) .........................221

– Visitors from Abroad.......................................................................223

– Exposure Drafts ................................................................................225

Chapter Twelve: The Secretariat .............................................................................................227

– Administrative Set-Up.....................................................................227

– Executive Directors ..........................................................................230

– Finances .............................................................................................232

– A Friend Indeed................................................................................234

Chapter Thirteen: The Road Ahead ..............................................................................237

– Global Challenge ..............................................................................237

– Environmental Constraints.............................................................238

– Institutional Problems .....................................................................241

– Change Management.......................................................................243

– Future Strategy .................................................................................244

– The Strategic Action Plan................................................................247

Contents

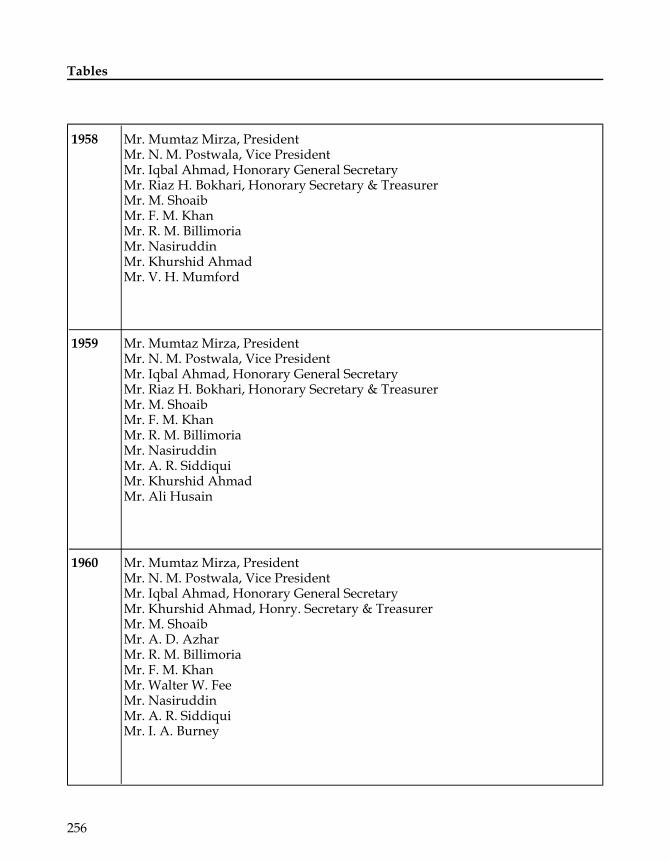

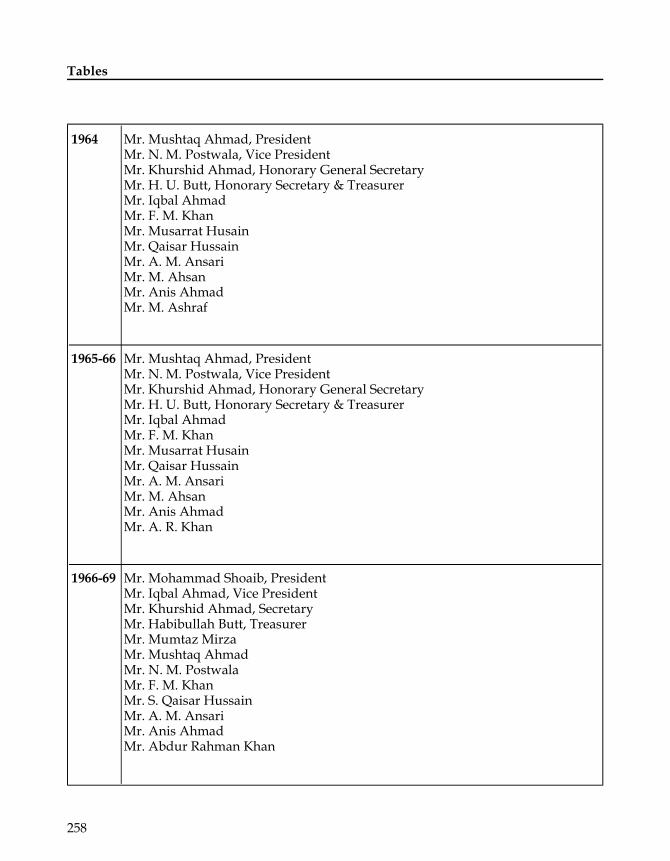

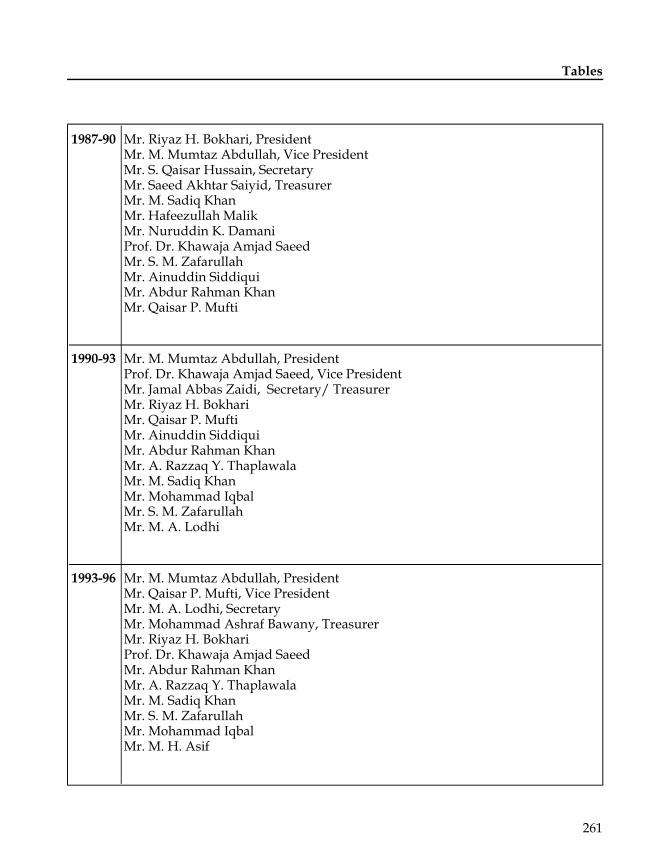

Tables .............................................................................................................255

I Composition of National Council (1951-2006) .............................255

II Chairmen of Standing Committees (1966-2006) ..........................265

III Branch Councils (1966-2006)...........................................................268

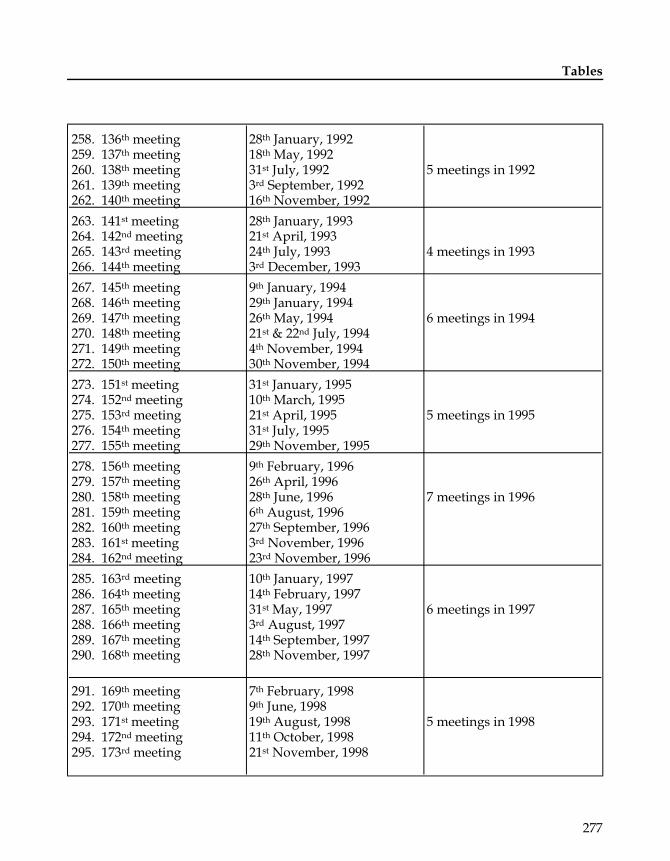

IV Council Meetings (1951-2006).........................................................270

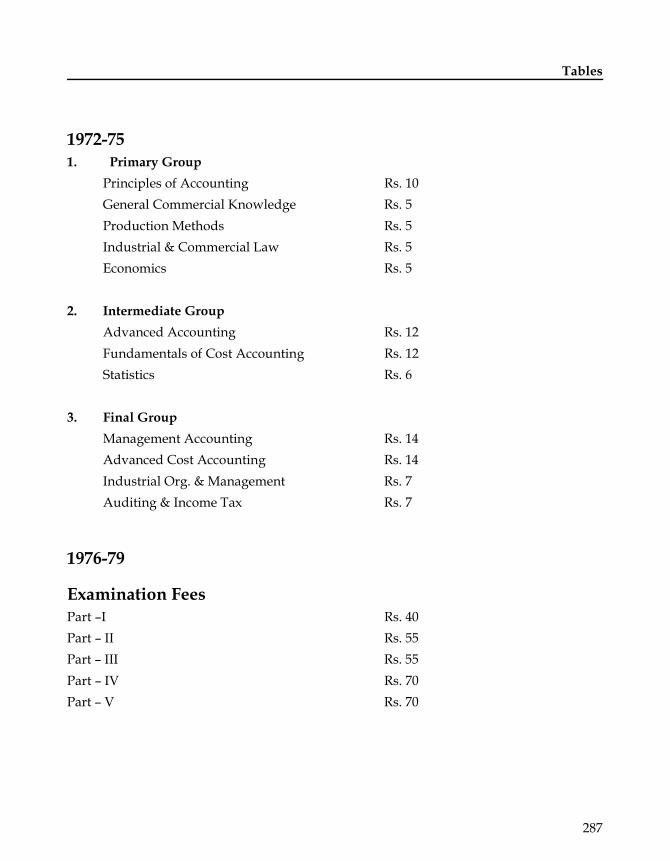

V Students Fees (1951-2006) ...............................................................280

VI (A) Tuition Fees (1968-1973) ..................................................................282

VI (B) Tuition Fees (1973-1985) ..................................................................283

VI (C) Tuition Fees (1986-1995)....................................................................284

VI (D) Tuition Fees (1995-2005) ..................................................................285

VI (E) Tuition Fees (2006-2007) ..................................................................285

VII Examination / Exemption Fees (1951-2006).................................286

VIII Yearwise Membership Growth (1951-2006) .................................294

IX Membership Fees (1951-2006) ........................................................296

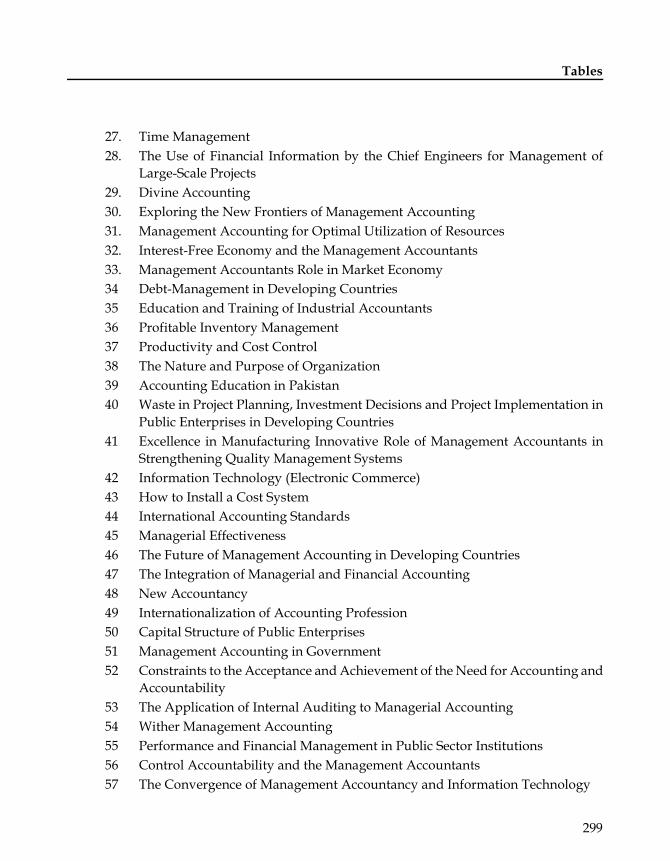

X Publications.......................................................................................298

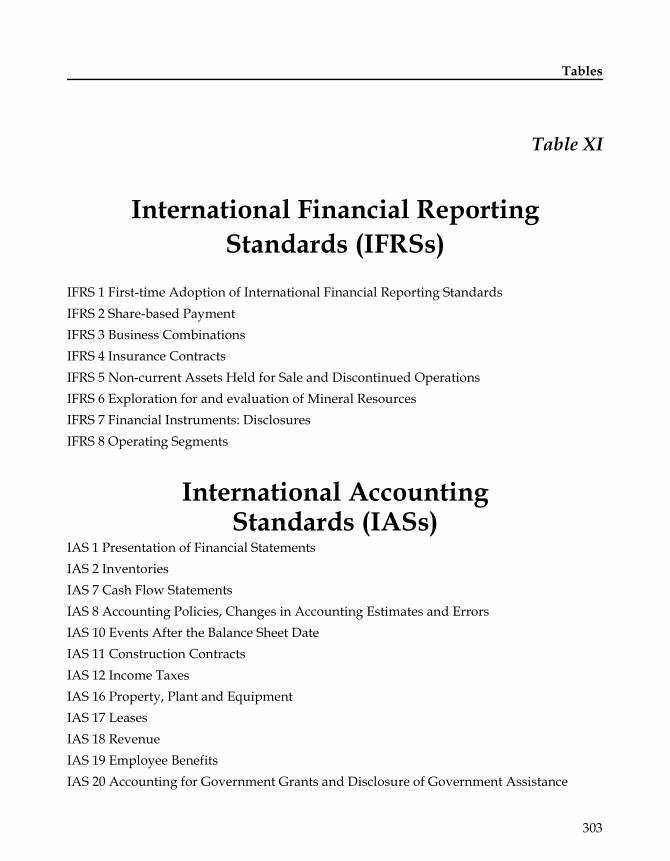

XI International Financial Reporting/Accounting Standards........303

XII SAFA Projects assigned to ICMAP................................................305

XIII Organizational Structure.................................................................306

Appendices .....................................................................................................307

A Memorandum of Association.........................................................307

B Articles of Association.....................................................................312

C Cost and Management Accountants Act, 1966 ............................335

Down the Memory Lane (Pictorial View)..............................................................................361

Contents

Chapter One

Forget Not Thy Roots

Barring a few exceptions emerging particularly during the last century of the lastmillennium, all branches of knowledge can, with little stretching, be traced to the ancienttimes or at least to the medieval. Accounting is no exception. Museums of the world are fullof archeological evidence to indicate that past civilizations dating back to about 3000 B.C.resorted to record keeping of events and economic transactions, which are really the basis ofall accounting.

In Ancient Times:

The Chaldacan-Babylonian civilization, which gave the world the first organizedgovernment, was the producer of the oldest surviving business record. The sixth king of thefirst dynasty of Babylonian, Hammurabi, ordered his scribes to record his Code of nearly 300rules and regulations covering business and social conditions. The Code of Hammurabi isrecorded on a seven feet tall black column. The finest example of Akkadian languagecuneiform and scripts are preserved on this shaft. The original is in the Louver in Paris andone copy is on exhibit in the Oriental Museum, University of Chicago. And it is to the times of Babylonian empire that authors have generally traced the origin of accounting. It is said thatnumerous storehouses existed throughout Babylonia to receive taxes and dues paid in kind.Records of these taxes were kept by scribes, using slabs of fine clay on which they wrote withsharp pointed styli. They can be considered to be the earliest accountants.

After the destruction of the Babylonian empire, Egypt emerged as the commercial andcultural centre of the world. Here too scribes formed the pivots on which the wholemachinery of the treasury and other departments turned. They recorded taxes and tributes to the Pharaohs on papyrus scrolls in ink the ageless durability of which even today intriguesthe scientists. Bookkeeping is said to have been taught in Egyptian schools as early as 1700B.C. and the University of Alexandria is said to have later had a chair of Accounting.

But it is to ancient Greece that mathematics owes its greatest debt. The many treatises writtenby master mathematicians of Greece are classics from which the world learned the basics.

17

Ancient Greece is also credited with developing banking far beyond anything previouslyknown. Originating in the temples, banking gradually moved into private hands and it wasthere that the cheque system is believed to have had first come into use. The Greeks were alsothe first people who minted gold coins and issued them about 600 B.C.

The Alexandrian period of Greek civilization ended with Rome’s conquest of Egypt, the lastof Alexander’s kingdoms. Roman orator Cicero boasted that the Romans were not dreamerslike the Greeks, but applied their study of mathematics to the useful. Nothingmathematically significant was, however, accomplished by the Romans. They did give theworld the Roman numericals but those were cumbersome for calculation. Despite thisdrawback, the use of Roman numericals continued in some European schools, until about1600 and in book-keeping for another century. The Romans’ most significant contribution toaccounting was that they introduced the practice of preparing statements of financialposition for payment of tax.

After the decline of Greece and Rome, mathematics flourished for hundreds of years in Indiawhere it was largely used as a tool for astronomy. So far as the art and practice of accountingis concerned, Hindu historians and some Western researchers insist that a fairly developedsystem was in vogue in ancient India even in the times of the Vedas and Upanisads. Informing this opinion, they rely heavily on the discussion in the Vedas of matters like thesystem of land revenue, currency, trade, various occupations as well as the general social and economic conditions obtaining in those times. The fabulous riches of India and its trade withforeign lands are well recorded in history. It can be safely argued that commercialtransactions and the extensive scale of trading operations could not have been carried outwithout systematic record keeping.

Profuse references are quoted by Indian writers from ancient treatises to substantiate theirclaim that accountancy had its origin in India, and not in Babylonia. A later treatise writtensometime between the 4th and 5th century A.D., Naradiya Dharmasastra discusses subjectslike money lending on interest, and matters like sureties, pledges, witnesses, oaths, etc.However, the culminating point with regard to the setting up of economic and financial basecan be had from Arthashastra written by Kautilya, King Chundragupta’s minister. Itcontains a separate chapter dealing with “The business of keeping accounts in the office ofaccountants”. This is cited by Indian authors to prove beyond doubt that not only did acomplete system of book keeping and accounting but also the vocation of accountants existed in ancient India.

Hindus of the Vedic times are also credited with the invention of zero, which gave the worldten basic digits and paved the way for the decimal system. Some scholars have written that

18

Chapter One: Forget Not Thy Roots

before the creation of the symbol zero, each digit was written in different symbol. When aHindu wanted to record 10, he wrote it down as “1.”; just a dot in the right hand row. Whenhe reached 100, complications set in because he recorded it as “1..” and he soon found that hefrequently miss-read his dots. As a remedy, the dot was changed to “ 0 “ and with that wasgone forever the risk of mistaking 10 or 100 and even 1000 with 1. With the development ofbetter numeric symbols, mathematics became an exact workable science.

For long, many believed that the decimal system of numerals was invented by the Arab. Even today, the numerals we use are known as “Arabic numerals”. No doubt these numerals wereinfluenced by India’s mathematics, which was leant by the Muslim world either throughmerchants trading with the west coast of India or through Muslim armies who conqueredSind in 612 A.D. But equally true is the fact that the Muslim mathematicians re-wrote thenumerals and with that made it possible to work out simple fractions and decimal fractionswhich they described during the Middle Ages. That brings us to the contributions theMuslims made to mathematics.

Forgotten Muslim Brilliance:

Recent research paints a new picture of the debt the modern world owes to Arabic/Islamicmathematics. Certainly many of the ideas which were previously thought to have beenbrilliant new conceptions due to European mathematicians of the sixteenth, seventeenth andeighteenth centuries are now known to have been developed by Arabic/Islamicmathematicians around four centuries earlier. In many respects the mathematics studiedtoday is far closer in style to that of the Arabic/Islamic contribution than to that of the Greeks.

There is a widely held view that, after a brilliant period for mathematics when the Greeks laid the foundations for modern mathematics, there was a period of stagnation before theEuropeans took over where the Greeks left off at the beginning of the sixteenth century. Thecommon perception of the period of 1000 years or so between the ancient Greeks and theEuropean Renaissance is that little happened in the world of mathematics except that someArabic translations of Greek texts were made which preserved the Greek learning so that itwas available to the Europeans at the beginning of the sixteenth century.

The Muslims learned from the Greeks who loved mathematics and geometry. Theyborrowed from India a number system that had a zero and rewrote it as their own. Theyborrowed from the Babylonians whose number system was based on 60 and from the ancientEgyptians who had the maths and geometry skills to build incredible pyramids. So from thebeginning, “Arabic maths” was a mixing of international knowledge. But the Muslims made

19

Chapter One: Forget Not Thy Roots

additional contributions of their own, and through their study and written work preservedthe knowledge of mathematics that otherwise might have been lost to the world.

This period began under the Caliph Harun ar-Rasheed, the fifth Caliph of the Abbasiddynasty, whose reign began in 786. He encouraged scholarship and the first translations ofGreek texts into Arabic were made during ar-Rasheed's reign. The next Caliph, al-Ma'mun,encouraged learning even more strongly than his father ar-Rasheed. He set up the House ofWisdom in Baghdad which became the centre for both the work of translating and of ofresearch. Al-Kindi (born 801) and the three Banu Musa brothers worked there, as did thefamous translator Hunayn ibn Ishaq. It should be emphasized here that the translations intoArabic at this time were made by scientists and mathematicians and not by language expertsignorant of mathematics, and the need for the translations was stimulated by the mostadvanced research of the time. It is important to realize that the translating was not done forits own sake, but was done as part of the current research effort.

Perhaps one of the most significant advances made by Muslim mathematicians began at thistime with the work of al-Khwarizmi, namely the beginnings of algebra. It is important tounderstand just how significant this new idea was. It was a revolutionary move away fromthe Greek concept of mathematics, which was essentially geometry. Algebra was a unifyingtheory which allowed rational numbers, irrational numbers, geometrical magnitudes, etc., toall be treated as “algebraic objects”. It gave mathematics a whole new development path somuch broader in concept to that which had existed before, and provided a vehicle for futuredevelopment of the subject. Another important aspect of the introduction of algebraic ideaswas that it allowed mathematics to be applied to itself in a way which had not happenedbefore.

Al-Khwarizmi also helped to bring “Arabic numerals” into use in the Islamic empire as wellas later in Europe. The introduction of Arabic numerals was one of the greatest advances inthe history of mathematics. These numerals were influenced by Indian numerals, whichwere reworked by Al-Khwarizmi. Much later, the Europeans changed the Arabic numeralsinto the numerals in use today. It was a system based on place values and a decimal system of tens. This system had a zero to hold a place. These numbers were much easier to use forcalculation than the Roman system. Addition, subtraction, multiplication and division thenbecame easy.

Around the tenth century, three systems of counting were in use in the Arab world. The firstof the three systems was the finger-reckoning arithmetic which derived from counting on the fingers with the numerals written entirely in words. This system was used by the businesscommunity. Mathematicians such as Abu'l-Wafa (born 940) wrote several treatises using this

20

Chapter One: Forget Not Thy Roots

system. Abu'l-Wafa himself was an expert in the use of Indian numerals but these, in his ownwords “did not find application in business circles and among the population of the EasternCaliphate for a long time”. Hence he wrote his text using finger-reckoning arithmetic sincethis was the system used by the business community. The second of the three systems wasthe sexagesimal system, with numerals denoted by letters of the Arabic alphabet. It cameoriginally from the Babylonians and was most frequently used by the Arabic mathematicians in astronomical work. The third system was the arithmetic of the Indian numerals andfractions with the decimal place-value system. But there was not a standard set of symbols.Different parts of the Arabic world used slightly different forms of the numerals. At first, theIndian methods were used by the Arabs with a dust board. A dust board was needed because the method required the moving of numbers around in the calculation and rubbing some outas the calculation proceeded. The dust board allowed this to be done in the same sort of waythat one can use a blackboard, chalk and a blackboard eraser. However, al-Uqlidisi (born 920) showed how to modify the methods for pen and paper use. Al-Baghdadi also contributed toimprovements in the decimal system.

It was this third system of calculating which allowed most of the advances in numericalmethods by the Arabs. It allowed the extraction of roots by mathematicians such as Abu'l-Wafa and Omar Khayyam (born 1048). Omar Khayyam also showed how to express roots ofcubic equations by line segments obtained by intersecting conic sections. The discovery ofthe binomial theorem for integer exponents by al-Karaji (born 953) was a major factor in thedevelopment of numerical analysis based on the decimal system. Al-Kashi (born1380)contributed to the development of decimal fractions not only for approximating algebraicnumbers, but also for real numbers. His contribution to decimal fractions is so major that formany years he was considered as their inventor.

Abu Kamil (born 850) worked on integer solutions of equations. Thabit ibn Qurracontributed impressively to amicable numbers while al-Haytham (born 965) was the first toattempt to classify all even perfect numbers. In addition to very valuable work on algebra,number theory and number systems, the Arab mathematicians made considerablecontributions to geometry, trigonometry and mathematical astronomy. The last notableMuslim mathematician of that age was Al-Khashi (born 1390) who calculated 1 (pi) to 16decimal places, which was the best until about 1700. After him, Arabic / Muslimmathematics closed as did the whole Muslim civilization while scholarship in Europe was on the up- swing.

The virtual halt of mathematics in the Muslim world represents an intriguing paradox ofhistory. It had had an impressive start. By the year 900, the acquisition of past mathematicswas complete. After that Muslim scholars began to build on what they had acquired and in

21

Chapter One: Forget Not Thy Roots

that they made good progress in the right direction with speed. But then they suddenlystopped. The momentum they had gained over two hundred years should have taken theminto the Age of Renaissance but that was not to be. Why? An answer can better be attemptedby researchers in the rise and fall of civilizations.

While tracing the origins of record-keeping and numerals and the development ofmathematics, we have skipped over the genesis of some other important developmentsdirectly related to accounting, such as the medium of exchange and the institution ofbanking. How did they happen to be? A brief historical account seems in order to understand the background of the birth of accounting.

One of man’s first coins was minted in ancient Greece during the days of King Croesus ofLydia around 560 B.C. His subjects mined vast amounts of gold and coined “Gold Stater”.After him, when Alexander the Great ruled the Greek empire around the Mediterraneanfrom 336 to 343 B.C., he decreed that the likeness of his own helmeted head be used on theGold Stater and Silver Tetradrachm as the official coins of trade.

The Romans were probably the first to make coins of various monetary values. Several typeswere minted, each displaying the head of a god or goddess. The Uncia was the unit of value.The Sextans was worth 2 Uncias; the Quadrans 3 Uncias; the Trien 4 Uncias etc. These coinscirculated in the trade during the time of Caesar and the Roman Republic (225-27 B.C.).Under Augustus, Rome’s first Emperor (27 B.C. to 14 A.D.), the Romans went one stepfurther. The bronze Sestertius, the Silver Denarius, and the Gold Aurius gave the Romans aflexible coinage system much like we have today.

Gradually, as governments established their monetary system, a very important accountingtool was born. Now records could be maintained in understandable values - the value of themedium of exchange being the common denominator in all records and financial reports ofthe tradesman’s world.

It was in Greece again that banking took the form of an institutionalized practice. Thewealthy merchant could not afford to leave his gold and silver at home or in his place ofbusiness. Thieves thrived on such tangible treasure, so the prudent rich man deposited histreasury with the priest of local temple. This was good insurance because no thief would dare to taunt the wrath of gods by stealing from the temple. Receipt for these treasures was givenby the custodian priest to the owner depositor. These receipts were than used to transactmore business or repay debts and served as currency as they passed from one merchant toanother. The final holder in due course could claim the treasure described in the receipt fromthe temple custodian when he desired. Gradually, this service moved from the temple to

22

Chapter One: Forget Not Thy Roots

private hands, assuming in the process more mundane and commercial character. Athensbecame a great commercial center and it was there that the cheque system is believed to havehad first come into use.

History rolled on and human civilization reached what is known as the Middle Ages. By thethirteenth century, many goldsmiths and silversmiths had come on the scene all overEurope, Italy being in the forefront. The Italian money merchant, called a camsore, displayedhis coins in neatly arranged piles on a bench known as a banco; thus our word “bank”.

The original bank of Venice was founded in 1171 A.D. A few years later (1178), merchants ofGenoa founded the bank of San Giorgio. One of its famous customers was none other thanChristopher Columbus. The Gold Genovina (ducat) was issued and used in marts of trade,around Genoa in 1252. The bankers’ guild was organized in Florence the same year. One ofthe great banking families, the de Medicis, controlled this banking system for 300 years (1434-1737). Other noble banking houses, the Fuggers and the Rothschilds, performed importantbanking services in Germany and other European countries. Thus banking was born to servebusinessmen, and later on, the public in all financial matters. No wonder then thatprofessional accountants (as distinct from scribes and officials concerned with the collectionand accounting of taxes) are also said to have first appeared in Italy.

Birth of Modern Accounting:

Although the term “rationator” meaning accountant had been introduced as early as 831A.D., it was not until 1495 that the concepts of modern accountants were clearly defined byan Italian mathematician, Luca di Borgo Pacioli who was destined to be given the title “Thefather of Modern Accounting”. Pacioli was born in 1445 A.D. in the province of Tuscany.After receiving a liberal education, he became a foremost mathematician and taught in manyItalian universities, including those in Florence, Venice, Padua, Naples and Rome. Hisabilities were recognized by a contemporary mathematician, the famous Leonardo di Vinci,later to become one of the world’s most great artists. Their common interest in mathematicsproduced a mutual and beneficial friendship.

Pacioli is credited with the authorship of the first written work on algebra, geometry andbook-keeping, entitled “Summa de Arithmetica Geometria Proportiomoni &Proportionalita” (Everything about Arithmetic, Geometry and Proportions) written in 1494.The next year, 1495, Pacioli wrote “De Computiset Scripturis” which clearly defined doubleentry bookkeeping principles, thus crediting this Franciscan Monk as “father of modernaccounting”. Another treatise on bookkeeping, the first written in English, was prepared by

23

Chapter One: Forget Not Thy Roots

John Gough of London, in 1543. The first formal course in accounting was presented tostudents at the collegio dei Raonati in Venice in 1581.

The Italian method of bookkeeping was further developed in Europe from the sixteenthcentury. It was in the sixteenth century that specific journals were introduced for recording of different types of transactions and the practice of financial statements was evolved. The useof separate inventory accounts for different types of merchandise was introduced in theseventeenth century. Three methods of treating fixed assets were evolved by the eighteenthcentury. Accounting as a science was recognized in 1742 in Milan, Italy, when a scale of legalaccountants’ fees was established officially.

But it was not until the nineteenth century that the profession of accountancy emerged in theform familiar to us today. The development of commerce, trade and industry accentuated the need for competent persons with knowledge and ability to practice accountancy and help the development of the corporate structure of business, which had led to a division betweenownership of funds and their management. This need of the time was undoubtedly one of the strongest influences on the evolution of both accounting and auditing and was in the mainresponsible for their present day refinement. In response to this need, several developmentsoccurred in accounting in the nineteenth century, such as: development in accountingtechniques for prepayments and accruals, development of funds statements, developmentfor complex issues like the computation of earnings per share, accounting for businesscomputations, accounting for inflation, long-term leases, and accounting for the newproducts of financial engineering.

As the profession of accountancy gained recognition and importance, professional bodies ofaccountants started to be formed.

The first Society of Accountants was organized in Edinburgh, Scotland in 1854. This wasfollowed by similar organizations in Glasgow in 1855 and London in 1870. In 1880, a RoyalCharter was granted to the Institute of Chartered Accountants in England and Wales as thefirst national body of professional accountants. Other national organizations wereconstituted as follows: In 1896, the American Association of Public Accountants which laterbecame the American Institute of Certified Public Accountants. In 1902, the CanadianInstitute of Chartered Accountants. In 1928, the Institute of Chartered Accountants inAustralia, which had its beginnings in the Adelaide Society of Accountants of 1885 and theAustralasian Corporation of Public Accountants established in 1907.

24

Chapter One: Forget Not Thy Roots

In British India:

When companies started to mushroom in India during the days of the British Raj,accountancy gradually gained a better standing in commercial concerns. Accountantsbecame important because of the need for keeping accounts of the flourishing and expanding trading operations, due to the need for auditing and in response to the importance of relianceon the growing concepts of continuity, periodicity and accruals. On its part, the Governmentalso realized the need to regulate the functioning of companies and enacted the followinglegislations:

(i) Joint Companies Act (XLIII of 1850)(ii) Joint Companies Act (XIX of 1857)(iii) Joint Companies Act (VII of 1860)(iv) Indian Companies Act 1866(v) Joint Stock Companies Arrangement Act 1870 and Indian Companies Act 1882.

The first three were all modelled on the English Joint Stock Companies Acts, whereas thefourth one was nothing but a transcript of the English Companies Act of 1862 with necessarymodifications to suit the Indian conditions. The first three pieces of legislation did notcontain any elaborate provisions directly dealing with accounts, but the 1866 Act did, for thefirst time, make substantial provisions regarding maintenance of books of accounts and theirannual audit. When the English law, on which the 1866 Act was modelled, underwentvarious amendments through different subsequent legislations, all the alterations wereadopted in the Indian law in what is known as the Indian Companies Act, 1882. This Act toodid not contain any detailed provisions regarding books, making of accounts and auditthough a table in the Act did contain some important provisions, but the adoption of thoseprovisions was optional. Even so, several companies started to include in their Articlesprovisions on those lines. Neither was the audit of accounts made compulsory by the Act norwere qualifications of auditors prescribed with the result that it remained open to anyone tostyle himself as an “auditor” and act as an independent auditor whenever a company choseto have its accounts audited.

In subsequent years, conditions of companies changed substantially. Industrial andcommercial activities flourished and public interest in them also increased. Shareholders ofcompanies now wanted their interests to be properly protected. Showing a goodappreciation of the changing situation and with a view to safeguarding public interest, theBritish Government enacted the Indian Companies Act, 1913. The new Act, which replacedthe Act of 1882 and all the subsequent amending Acts, was intended to regulate

25

Chapter One: Forget Not Thy Roots

comprehensively the working of companies and also contained specific provisions relatingto accounts and audit. Finding specific mention in the Act were matters like requirement tokeep proper books of accounts, Annual Balance Sheet, contents of the Balance Sheet, itsauthentication and Auditor’s Report, rights of members to their copies, qualifications andappointment of auditors and their powers and duties. One of the sections of the Act provided that no person could be appointed as auditor unless he held certificate from competentauthority entitling him to act as such.

The Companies Act, 1913 thus gave a real fillip to the organized development of theprofession of accounting and audit in India. But it must be added with some sense ofrepentance that the promising occupation did not attract many Indian Muslims. For quitesome time, the field of audit and accountancy remained almost an exclusive domain of theHindus and, to some extent, of Paris in addition to the imported foreigners. And this issurprising, considering that the concept of accounting is intrinsically built into Islam’ssystem of reward and punishment for all man’s actions from cradle to grave. What is Islam’sconcept of the Day of Judgment? It is the day when all human beings shall be resurrected andthe balance sheet of all that each of them did in life, prepared by two guardians appointed toconstantly make entries of each and every of his actions in his book of accounts, shall bepresented to him and, on the basis of that, a final judgment shall be made of his perpetualabode – either Hell or Heaven.

Says Allah in the Holy Quran : Nay, but ye deny the judgment. Lo! There are above youguardians. Generous and recording. Who know (all) that ye do. (Surah 82 : 9-12)

At another place, He exhorts thus:

And every man’s augury have We fastened to his own neck, and We shall bring forth for himon the Day of Resurrection a book which he will find wide open. (And it will be said untohim): Read thy book. Thy soul sifficeth as reckoner against thee this day (Surah 17 : 13-14)

Such direct references in the Holy Book to record keeping by guardians above man and hisfinal accountability on the basis of the recorded account should have been enoughmotivation for the Muslims to enthusiastically turn to accounting profession. Somehow thatdoes not seem to have happened to the extent it should have.

Emergence of Cost Accounting:

While various all important developments were taking place in the accounting profession inthe beginning of the twentieth century, a new subject was sprouting to branch off from the

26

Chapter One: Forget Not Thy Roots

main discipline of accountancy: Cost accounting. When was it in history that merchants didnot calculate the cost of their merchandise before deciding at what price to sell them? Butwhen modern manufacturing began, involving a number of tangible and some intangibleinputs, determination of cost gradually became a complex matter.

The Industrial Revolution depended on inventors and entrepreneurs, not accountants.However, it was the survival of their firms that required innovative accounting and, later, the development of a profession. Big business, particularly the railroads, required capitalmarkets that depended on accurate and useful information. This was supplied by theexpanding accounting profession. Turn of the century America saw the rise of really bigbusiness, governable because of improvement in cost accounting. But the Crash of 1929 andthe subsequent Great Depression demonstrated problems with capital markets, businesspractices, and considerable deficiencies in cost and management accounting practices.

Considerable progress in manufacturing was made in Britain during the early part of theIndustrial Revolution. Many of those early firms went bankrupt. Little credit went tomanufacturing operations and continuing operations and expansion was funded primarilyfrom retained earnings. During depressions, declining demand led to liquidity crises thatmost firms could not deal with. Adequate cost accounting was useful in any circumstances,but essential in bad times. Surviving firms developed cost and management accountingsystems to determine, manage and bifurcate costs for all phases of their operations, including primitive analysis of overhead costs. Costs could be related to specific products and pricescould be set differentially, based on product costs and potential demand for specificproducts. Costs could be altered to increase efficiency, based on factors such as materialprices, differential wage rates, transportation costs. Policies could be modified whendepressions hit to reduce costs and attempt to maintain product demand.

Cost accounting records are found from the early 19th century for New England textile mills.At Lyman Mills, materials costing included freight and insurance, calculated on a first-infirst-out basis. Payroll records were kept daily by employee hours for each process.Overhead was spread to mill accounts based on multiple criteria, such as floor space ornumber of materials and usually treated as a period cost. Unit costs were calculated todetermine prices, initially with prime costs (direct materials and labour) and later includingoverhead.

Many of the basic approaches to cost accounting were developed after 1880. The ScientificManagement analysis of mass production was a major factor. Engineers using job analysis aswell as time and motion studies determined “scientific” standards of material and labour toproduce each unit of output. Complex machines required complex engineering and efficient

27

Chapter One: Forget Not Thy Roots

use of workers to perform specialized and repetitive tasks. Standard costs became asignificant efficiency measure. Frederick Taylor analyzed the best ways to use labour andmachines and standards were determined to minimize waste. The focus was on cost cuttingrather than product quality. Actual costs could be compared to standard costs to measureperformance and the variances between actual and standard analyzed to determine potential corrective action. Measuring and allocating overhead costs also were major concerns ofScientific Management.

Big business would be organized around a centralized headquarters, with dozens of plantsaround the region and often across the nation or around the world. Standard products weremass-produced for a large domestic market. Many firms were multi-national. How werethese operations controlled a half century before the first primitive computers? Organizationcontrol was based on simplification, specialization of jobs, and a management hierarchy.Second, costs and performance were coordinated using timely cost accounting reportsdeveloped over decades with the assistance of Scientific Management engineers.

The Du Pont Powder Company was a leader in using a centralized accounting system tocontrol decentralized and geographically disbursed manufacturing operations. Sales,finance, and purchasing were separated from manufacturing and each departmentdeveloped specialized strategies to maximize performance. Senior management focused oncoordinating activities and long-term strategy. Performance measurement was a key factorand Du Pont accountants developed return on investment (ROI) as an efficiency tool andstandard of performance. An asset accounting system, based on a complete inventory ofplant and equipment, made the use of ROI possible. Thus, individual departments could beevaluated by local profit measurement. Daily time sheets and materials usage logs were used to prepare monthly mill production records to measure production operating efficiency. Netearnings were forecast based on product sales estimates and projected earnings per unit.Cash projections were based on net earnings forecasts, which were used to determine newproject financing.

Cost considerations assumed greater importance as industrialists and other businesscommunities were faced with new competitions and challenges in the wake of the first World War. Executives and engineers of industrial units, particularly in the United Kingdom, intheir anxiety to control costs and protect their units from heavy losses, began to feelincreasingly concerned about cost accounting records. An enduring answer to their concernscame on 8th March, 1919, when the Institute of Cost and Works Accountants was formed inLondon, as a limited company with the following first objects:

28

Chapter One: Forget Not Thy Roots

(i) To provide an organization for cost accountants, works accountants, estimating and costclerks, and others engaged in occupations requiring a mathematical and technicalknowledge of industry in all its branches, embracing in such knowledge the costs ofproduction, manufacture or sale of all articles produced, manufactured, or sold, in orderto secure for them a definite professional status by means of a system of examination andthe issue of Certificate of Competency.

(ii) To promote and protect the mutual interests of members of the Institute and, as far aspossible, to assist them to obtain adequate remuneration for their services.”

The National Association of Cost Accountants was formed in the United States in 1919. In thefollowing year, the Society of Industrial and Cost Accountants of Canada began itsoperations. About 1930, Australia and New Zealand inaugurated their cost accountantsorganizations. But in the beginning, hardly any attempts were made to assess theprofitability of application of different factors of production in varying doses. Systematic cost accounting till then had no application and product or process-wise cost analysis was rareoccurrence.

The Second World War changed the way cost accounting was looked at as well as the manner in which it was practiced. During the War, cost accountancy earned real importance andbegan to be applied in industry as an essential requirement. As it grew in stature, its scopewas enlarged and its concepts and methods were improved and it began to attain therefinement that characterizes it today. But that was a later development. In the periodbetween the two World Wars, costing was still passing through its formative phase as a newbranch of accountancy. It got a real boost when British educational institutions wereawakened to its significance. One such attempt was made in October 1926 when a lecture on“The Place of Accountancy in Commerce”, delivered at the London School of Economics, had the following to say about the importance of cost accounting and what needed to be done toturn it into a useful practice:

“In recent years the importance of costing has been realized, but there is room for considerable improvement in the methods as generally adopted in this country. A costing system whichdoes not give accurate results is worse than useless; in fact, it may prove to be a great danger.In these days of severe competition, both at home and abroad, a reliable costing system is avital necessity to a manufacturing business. Costing is a highly technical and involvedmatter in many cases and the organization of the system requires considerable skill andthought. It is not purely an accountancy problem. To be successful, the cooperation of thetechnical officers of the concern is absolutely necessary. Further, it is not only essential thatthe system shall be complete and efficient, but it must be carried out rigidly in practice.

29

Chapter One: Forget Not Thy Roots

“Often, in practice, the systems adopted are basically unsound and incomplete. Of necessity,therefore, the results are inaccurate. In such circumstances commonly the manufacturerbecomes most dissatisfied with the results and comes to the conclusion that costing is of novalue. It is the particular system which is at fault and if the results are not accurate itcertainly is of no value and all the time and labour expended have been wasted.

“Costing systems can be made too elaborate and great skill and experience is necessary in theorganization of a system which will give accurate results in a clear and simple manner. Thereis no question, however, that in all cases a reliable system can be evolved and that accuratecosting is of the greatest value to management.

“Speaking generally, costing in this country in my view is not satisfactory and considerabledevelopment is necessary in order to place it upon a satisfactory footing. There is a great needfor scientific education and if the manufacturers of this country are to maintain their place inthe markets of the world, far greater attention must be paid to this subject than has been thecase in the past.

“In practice, it is not uncommon to find the costing system separated completely from theaccounts department, but they should be interlinked and, therefore, the costing departmentshould be under the direction of the chief accountant.”

Now we turn to India where, during the War, the Government became the largest buyer of anumber of imported and indigenously produced goods for meeting the war needs. This,coupled with the curtailment of supplies of goods to India from foreign countries due toblockade, risks involved in transshipments and the diversion of productive facilities inexporting countries to the production of war supplies, created a scarcity in the country. Thisscarcity began to show its effect on prices and production costs in Ordnance Factories, whichrose higher.

In spite of the Government factories working at their full capacity, many contracts had to beplaced with private contractors for non-conventional items which were specially required for War on top priority basis. As there was no time to follow normal procurement procedure ofobtaining quotations, the British War Cabinet decided to place orders for such items on costplus basis on well known and competent suppliers. The fixation of plus, say 5% to 20%,depended on the nature and volume of order. After completing the supplies, the supplierfurnished his bill along with cost statement for payment after checking. The disputes on thequestion of actual cost of goods supplied to the Government necessitated properinvestigation into the cost structure of supplies, which could not be carried by untrainedpersons. Thus the need for qualified cost accountants began to be felt not only for

30

Chapter One: Forget Not Thy Roots

investigation into cost structure of supplies by the contractors but also for ascertaining cost of production in government factories. Initially, the services of a few foreign experts wererequisitioned, who with the help of locally available cost accountants, introduced elaboratesystem of costing in Ordinance Factories. Since the total demand could not be met bybringing foreign experts on loan, the training of cost accountants within the country becameessential. An attempt to open a branch of British Institute of Cost and Works Accountants inIndia did not materialize.

The War boom had given ground to the growth of many mushroom businesses. Someprominent accountants noticed with concern that the application of wasteful methods inindustries, uneconomic production of goods and services and unplanned investments in alldirections would have to be heavily paid for in the long run. Some sort of control measuresappeared to them to be essential. According to them, the remedy lay in the wide applicationof Cost Accounting Techniques in industry. The necessity of an organization to not onlyteach cost accounting but also to provide proper training facilities was felt.

Some of these accountants met Government officials who were thinking on the same lines.After several meetings between them, an Institute under the name of “Indian Institute of Cost and Works Accountants” was formally registered on 14.6.1944 under the Companies Act (Itwas replaced by the Institute of Cost and Works Accountants of India established by an Actin May, 1959). In the early stages of the Institute’s existence, the progress was very slow.Except in Government establishments catering to War needs, there was virtually no costaccounting in the country. The Defense Ministry realized the important role of costaccountants in industrial activities and this led the Ministry to encourage people in itsemployment to pass the Institute’s examinations. The Ministry also deputed candidates toreceive training in the Institute’s training center at Calcutta. With the cessation of the War, alarge number of Government employees became surplus hands. Some cost accountants were drawn to private industry, which soon began to feel advantage of employing them. Costaccountancy started to gain ground in industry.

The sub-continent achieved independence in 1947 after a historic, long and heroic struggle.India was partitioned and Pakistan was carved out as a new independent state on 14th

August 1947. The new state continued with the same accounting practices, rules andregulations that were in force when the British authorities departed. In the same way, theGovernment of Pakistan adopted the Auditors’ Certificate Rules 1932 for regulating theprofession of accounting in Pakistan. These rules provided the conditions relating toeducation and training that made a person eligible for registration as a professionalaccountant.

31

Chapter One: Forget Not Thy Roots

The profession of accountancy started to grow slowly under these rules. Some of theRegistered Accountants established their practicing business and some of them preferred towork in the accounts and finance departments of private firms. However, the practicingRegistered Accountants were mainly involved in the work of accounting. They had to carryout auditing jobs in compliance with legislations such as the Companies Act, 1913, Civil andCommercial Codes and Auditors’ Certificate Rules 1932 (subsequently 1950). But there wereserious problems of education and training of professional accountants. The PakistanCouncil of Accountancy, which was established under the Auditors’ Certificate Rules 1950,could not adequately fulfil its responsibilities. In view of this, the Pakistan Institute ofAccountants was formed in 1950 as an independent body to safeguard and promote theinterests of Registered Accountants. Its membership was restricted to RegisteredAccountants and to them only.

Cost accountancy, on the other hand, found itself in the wilderness in the new country. It hadvirtually no separate existence, no teaching arrangements, no professional recognition, noinstitutional framework and only a few practitioners. But the need for it was unmistakablythere and it was becoming pressing and urgent as Pakistan was starting to break ground inthe virgin field of industrialization. The upcoming industries and expanding commercerequired qualified cost and industrial accountants. The London Institute was there to serveas a model and there was the Calcutta precedent to follow. There were also at least a fewdedicated men of relevant experience. The stage was all set for a new initiative and it didcome in 1951 – within less than four years of Pakistan’s coming into being.

32

Chapter One: Forget Not Thy Roots

Chapter Two

A Sapling Planted

The date: 23rd May 1951. The place: Karachi, the capital of the newly born state of Pakistan. Inthe scorching sun of a hot and humid summer afternoon, a young man came out of theVictorian-style splendid red-stone building of Chief Court, now the Sindh High Court.Holding tight in his hand a folder, he hurried towards the nearby office of his boss, his gaitexhibiting excitement and his face radiating with joy. He wanted to be with his boss in a winkto break to him the good news – the news that his and his friends’ dream had at long lastcome true. In the folder in the young man’s hand was an official certificate to that effect.

The young man’s boss was Mr. M. Shoaib, Financial Advisor on Communications to theGovernment of Pakistan and the certificate was the Certificate of Incorporation of thePakistan Institute of Industrial Accountants under the Indian Companies Act VII of 1913 (asapplicable to Pakistan). The Certificate, bearing No. SIND 856 of 1951-1952, was signed byRegistrar of Joint Stock Companies for Sind. It read:

“I hereby certify that The Pakistan Institute of Industrial Accountants is this dayincorporated under the Indian companies Act, VII of 1913 (as applicable to Pakistan) and that the Company is Limited.

Given under my hand at Karachi this twenty-third day of May, one thousand nine hundredand fifty-one.”

SignedRegistrar of Joint Stock Companies for Sind,

Karachi.

These few lines heralded the turning into reality of the vision of a group of seven friendspropelled into action by a keen desire to provide sustainable institutionalized assistance forthe development of industries in a country which had just been born. The point calls for some elaboration to bring home the real value and significance of what those seven visionaries hadset out to create and why.

33

Background:

When Pakistan came into existence in 1947, the economy the new state inherited wasbasically agricultural. More than 80% of its population living in the rural areas earned itslivelihood from agriculture. The country’s major crops were rice, jute, cotton, wheat andsugarcane. But the country had negligible industrial base. There were only a handful ofindustries to manufacture goods from the raw material the fertile lands produced or to usethe natural resources the country was bestowed with. The contribution of industry towardsGDP in 1949-50 was only 7.7 percent.

The nascent Government was struggling to establish itself in almost a vacuum. Even suchbasic equipment as chairs, desks, typsewriters and so on was so meagre and scattered as to be virtually non-existent. There were no buildings suitable to house government offices; only afew vehicles and a weak, limited and unreliable communication network. To top the list ofthe teething problems of the new state struggling in the virtual absence of resources intrained men and material was the Herculean task of providing food and shelter to themillions of immigrants from India. Without going into the details of what problems theGovernment and people of Pakistan had to face in the initial years – which is now well-known history – suffice it to say that, on achieving independence, few countries in moderntimes must have confronted hardships and difficulties of the order and magnitude as didPakistan.

In those testing times of empty coffers but high expectations, it was of utmost importance tourgently encourage and promote business and commerce and to initiate a process ofindustrialization and utilization of the natural resources that were available. If the economyof the country was to be put on a sustainable sound footing, industrialization was the key.

The Government was quick to realize this and, within months after independence, organized an Industrial conference. The main aim of the conference was to encourage the investors toset up industries based on locally produced raw materials like jute, cotton, sugarcane, hidesand skins. The Government also established some institutions in the public sector to providedirect help and assistance for the rapid development of industries. Such institutions, set up as early as 1948, included the Development Bank, Industrial Finance Corporation andIndustrial Investment and Credit Corporation. Besides the Government’s keenness andsense of urgency to see new industries come up, the market also demanded and dictated thesetting up of particularly consumer goods industries. It was a huge, demanding open marketoffering unlimited virgin field. What else could the potential industrial investors ask for?

34

Chapter Two: A Sapling Planted

A process of building and developing industries on an intensive scale soon began and wasfurther intensified with each passing year. Many large and modern plants were establishedand were expanding with the latest in equipment and technical processes. Banks and bigcommercial concerns also began to spring up across the country. And that was just thebeginning – the beginning of what promised to be a fast, un-ending and vibrant process ofindustrial growth.

The Idea:

It was against this background of Pakistan’s struggle for economic survival in its formativeyears that a group of seven friends, all accountants, met in Karachi in the winter of 1951,hardly four years after partition, to think of ways to provide sustainable professional support to the country’s just initiated industrial advance. They had several brain-storming sessions to analyze the needs, define possible solutions and fine-tune their ideas. The unmistakableconclusion they finally reached was that Pakistan’s rapid advance in commerce and industrywas in dire need of large numbers of qualified persons having wide knowledge of businessaffairs and a particular knowledge of the firm with which they were to be engaged, includingits organization, its product and its methods of production, its handling of materials, labourand overheads, its compilation of costs, its income tax matters, and the interpretation of itsaccounting data to management.

They were convinced that no industrial concern of any size would be able to succeed in itsendeavours without the data and advice which flows from a well-organized accountingdepartment. Not only is its value in the historical accounting data, which is normallydeveloped from the records, but equally in the inherent control of the costs of production and the facility with which it makes possible sound forecasting and planning for the future. Andin meaningfully planning for the future, the cost data usually collected for product- pricingand the preparation of financial statements has to be combined with industry-specifictechnical knowledge to improve operating practices, that is, to create greater efficiency bychanging established technical, organizational and administrative methods with new ideasgenerated through cost awareness.

The group could foresee that the expanding industrial sector would soon be faced with newchallenges and problems. Some industries were still fortunate enough to continue to enjoysomewhat of a protected market and to maintain an enviable profit position. However,others were already beginning to feel the effects of competition from both at home andabroad, with the added complications of big business and, in many cases, a reduction in theprofit margin. Many businesses were already finding a much greater necessity for efficientorganization and operations, and the necessity of more closely matching costs of production

35

Chapter Two: A Sapling Planted