Time to revisit: upgrade to Buy - The page cannot be found

30

See important disclosures, including any required research certifications, beginning on page 28 ■ What's new Despite Bharat Heavy Electricals Ltd’s (BHEL) 20% share-price correction over the past month, we are encouraged by its 19% YoY order-backlog growth for 1Q FY16, the first double-digit growth for 4 years. We also see a good order pipeline (of at least 20GW annually) over FY16-18E, and now like its valuation. As a result, we upgrade our rating to Buy (1) from Sell (5). ■ What's the impact We see a V-shaped recovery for BHEL’s revenue, with FY16 marking the bottom for its order execution, as well as further earnings downgrades by the market. We forecast a strong pick-up in revenue from FY17E (+25% YoY) on a strong order backlog (up 19% YoY for 1Q FY16) with 9GW order wins. EBITDA margin recovery. For FY15-18E, we see a 6pp improvement on the end of its negative operating leverage, a pick- up in order execution, and favourable commodity prices. We lower FY16E earnings by 13%, but raise FY17-18E earnings by 4-8%, in line with the changes in our revenue and order-inflow forecasts. ■ What we recommend We now rate BHEL as a Buy (1), backed by a higher 12-month TP of INR243 (from INR225), based on an unchanged target PER of 18x on our revised FY17E EPS. We see near- term share-price catalysts in potential new-order wins, leading to order-inflow growth of over 40% YoY for FY16E and an FY16-18E earnings CAGR of 35%. The key risk: delays in the finalisation of power- sector orders, and the impact this would have on BHEL. It may seem ironic that the order outlook for the power sector (ie, BHEL) is recovering when India’s power deficit and utilisation levels are at historical lows (2% and 60%, respectively), but we believe that new-project orders being planned by the state and central utilities over FY16-18E are largely based on long- term demand expectations. ■ How we differ We believe the market is underestimating BHEL’s order- execution and EBITDA recovery. Industrials / India BHEL IN 15 September 2015 Bharat Heavy Electricals Time to revisit: upgrade to Buy • Recovery in order growth in FY15 (10% YoY) to continue over FY15-18E at a 17% CAGR, on annual order pipeline of 20GW • We expect 25% YoY revenue growth for FY17E, and EBITDA margin expansion of 6pp over FY15-18E • Upgrading to Buy (1); raising TP to INR243; we forecast a net profit CAGR of 35% over FY16-18E Source: Daiwa forecasts Source: FactSet, Daiwa forecasts Industrials / India Bharat Heavy Electricals BHEL IN Target (INR): 225.00 243.00 Upside: 14.8% 11 Sep price (INR): 211.75 Buy (from Sell) Outperform Hold Underperform Sell 1 2 3 4 5 Forecast revisions (%) Year to 31 Mar 16E 17E 18E Revenue change (6.2) 7.4 6.6 Net profit change (13.1) 8.0 4.8 Core EPS (FD) change (13.1) 8.0 4.8 90 100 110 120 130 180 210 240 270 300 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Share price performance Brt Heavy (LHS) Relative to SENSEX Index (RHS) (INR) (%) 12-month range 197.80-297.00 Market cap (USDbn) 7.80 3m avg daily turnover (USDm) 15.75 Shares outstanding (m) 2,448 Major shareholder President of India (63.1%) Financial summary (INR) Year to 31 Mar 16E 17E 18E Revenue (m) 293,587 365,811 396,131 Operating profit (m) 17,844 34,716 39,563 Net profit (m) 20,657 33,043 37,926 Core EPS (fully-diluted) 8.440 13.500 15.495 EPS change (%) 45.5 60.0 14.8 Daiwa vs Cons. EPS (%) 0.0 10.2 n.a. PER (x) 25.1 15.7 13.7 Dividend yield (%) 0.9 1.4 1.9 DPS 2.000 3.000 4.000 PBR (x) 1.5 1.4 1.3 EV/EBITDA (x) 12.1 7.4 5.1 ROE (%) 5.9 9.0 9.6 Saurabh Mehta (91) 22 6622 1009 [email protected] Ajay Devnani (91) 22 6622 1015 [email protected] How do we justify our view? How do we justify our view?

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Time to revisit: upgrade to Buy - The page cannot be found

See important disclosures, including any required research certifications, beginning on page 28

■ What's new Despite Bharat Heavy Electricals Ltd’s (BHEL) 20% share-price correction over the past month, we are encouraged by its 19% YoY order-backlog growth for 1Q FY16, the first double-digit growth for 4 years. We also see a good order pipeline (of at least 20GW annually) over FY16-18E, and now like its valuation. As a result, we upgrade our rating to Buy (1) from Sell (5). ■ What's the impact We see a V-shaped recovery for BHEL’s revenue, with FY16 marking the bottom for its order execution, as well as further earnings downgrades by the market. We forecast a strong pick-up in revenue from FY17E (+25% YoY) on a strong order backlog (up 19% YoY for 1Q FY16) with 9GW order wins.

EBITDA margin recovery. For FY15-18E, we see a 6pp improvement on the end of its negative operating leverage, a pick-up in order execution, and favourable commodity prices. We lower FY16E earnings by 13%, but raise FY17-18E earnings by 4-8%, in line with the changes in our revenue and order-inflow forecasts. ■ What we recommend We now rate BHEL as a Buy (1), backed by a higher 12-month TP of INR243 (from INR225), based on an unchanged target PER of 18x on our revised FY17E EPS. We see near-term share-price catalysts in potential new-order wins, leading to order-inflow growth of over 40% YoY for FY16E and an FY16-18E earnings CAGR of 35%. The key risk: delays in the finalisation of power-sector orders, and the impact this would have on BHEL. It may seem ironic that the order outlook for the power sector (ie, BHEL) is recovering when India’s power deficit and utilisation levels are at historical lows (2% and 60%, respectively), but we believe that new-project orders being planned by the state and central utilities over FY16-18E are largely based on long-term demand expectations.

■ How we differ We believe the market is underestimating BHEL’s order-execution and EBITDA recovery.

Industrials / IndiaBHEL IN

15 September 2015

Bharat Heavy Electricals

Time to revisit: upgrade to Buy

• Recovery in order growth in FY15 (10% YoY) to continue over FY15-18E at a 17% CAGR, on annual order pipeline of 20GW

• We expect 25% YoY revenue growth for FY17E, and EBITDA margin expansion of 6pp over FY15-18E

• Upgrading to Buy (1); raising TP to INR243; we forecast a net profit CAGR of 35% over FY16-18E

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Industrials / India

Bharat Heavy ElectricalsBHEL IN

Target (INR): 225.00 243.00

Upside: 14.8%

11 Sep price (INR): 211.75

Buy (from Sell)

OutperformHoldUnderperformSell

1

2

3

4

5

Forecast revisions (%)Year to 31 Mar 16E 17E 18ERevenue change (6.2) 7.4 6.6Net profit change (13.1) 8.0 4.8Core EPS (FD) change (13.1) 8.0 4.8

90

100

110

120

130

180

210

240

270

300

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15

Share price performance

Brt Heavy (LHS)Relative to SENSEX Index (RHS)

(INR) (%)

12-month range 197.80-297.00Market cap (USDbn) 7.803m avg daily turnover (USDm) 15.75Shares outstanding (m) 2,448Major shareholder President of India (63.1%)

Financial summary (INR)Year to 31 Mar 16E 17E 18ERevenue (m) 293,587 365,811 396,131Operating profit (m) 17,844 34,716 39,563Net profit (m) 20,657 33,043 37,926Core EPS (fully-diluted) 8.440 13.500 15.495EPS change (%) 45.5 60.0 14.8Daiwa vs Cons. EPS (%) 0.0 10.2 n.a.PER (x) 25.1 15.7 13.7Dividend yield (%) 0.9 1.4 1.9DPS 2.000 3.000 4.000PBR (x) 1.5 1.4 1.3EV/EBITDA (x) 12.1 7.4 5.1ROE (%) 5.9 9.0 9.6

Saurabh Mehta(91) 22 6622 1009

Ajay Devnani(91) 22 6622 [email protected]

How do we justify our view?How do we justify our view?

Industrials / India BHEL IN

15 September 2015

- 2 -

Time to revisit: upgrading to Buy .................................................................................................. 6

Investment summary .................................................................................................................. 6

Recovery in order inflows ........................................................................................................... 9

Other initiatives to help order recovery ..................................................................................... 11

Other opportunities ................................................................................................................... 12

Improving fuel security .............................................................................................................. 13

Execution recovery and slow-moving orders ............................................................................ 14

EBITDA margin recovery ........................................................................................................... 16

Valuation and recommendation ................................................................................................ 17

Risks ........................................................................................................................................... 18

Appendix 1: India’s power situation .......................................................................................... 19

Appendix 2: India power sector order pipeline for FY16-17 ..................................................... 21

Appendix 3: power plants still in operation that are older than 25 years of age ..................... 22

Appendix 4: recent order pricing trends .................................................................................. 24

Appendix 5: glossary of terms ................................................................................................... 25

Contents

Industrials / India BHEL IN

15 September 2015

- 3 -

Growth outlook BHEL: revenue growth and net profit

We expect order-inflow recovery to continue over FY15-18E at a CAGR of 17% (began to pick up in FY15, at 10% YoY). We also see a pick-up in order execution from 2H FY16, and believe that FY16 is likely to be the bottom in terms of order execution and profitability, with the full impact of strong order execution only coming in from FY17. Over FY16-18, we forecast revenue and earnings to increase at CAGRs of 16% and 35%, respectively.

Source: Company, Daiwa forecasts

Valuation BHEL: 1-year-forward PER (x)

We are upgrading BHEL to Buy (1) from Sell (5). We also increase our 12-month target price to INR243 (from INR225), based on an unchanged target FY17E PER of 18x, to reflect the increase in our earnings forecasts. After the 20% share-price correction over the past month, we find BHEL’s current valuation, at FY17E PER of 15.7x, reasonable – it is trading at an over 20% discount to its historical average. Its EPS are also in the early part of the recovery cycle.

Source: Bloomberg, Company, Daiwa forecasts

Earnings revisions BHEL: EPS-forecast revisions

The Bloomberg consensus has been cutting its earnings forecast for BHEL for the past 3 years. And similarly, its FY16-17E earnings have been cut by 20-38% over past 12 months. However, with the recent order wins and improved visibility of orders, we expect this earnings-cut cycle to end and for these factors to become key stock-price catalysts.

Source: Bloomberg

How do we justify our view?

Growth outlook

Valuation

Earnings revisions

4 7 10 17

24 29 31

43

60

70 66

35

14 21

33 38

(30)

(20)

(10)

0

10

20

30

40

0

10

20

30

40

50

60

70

80

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Net Profit (LHS) Revenue growth YoY (RHS)

(INRbn) (% )

05

101520253035404550

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

(PER)

28.4x Avg+1S.D.

20.5x Avg

12.6x Avg-1S.D.

8

9

10

11

12

13

14

15

16

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

May

-15

Jun-

15

Jul-1

5

Aug-

15

Sep-

15

FY16E FY17E

(INR)

12.9

8.8

12.6

10.1

15.8

11.7

13.112.5

14.2

Buy (from Sell)

OutperformHoldUnderperformSell

1

2

3

4

5

Industrials / India BHEL IN

15 September 2015

- 4 -

Key assumptions

Profit and loss (INRm)

Cash flow (INRm)

Source: FactSet, Daiwa forecasts

Year to 31 Mar 2011 2012 2013 2014 2015 2016E 2017E 2018EValue of new contracts added (%) 2.5 (63.5) 43.2 (11.5) 10.0 42.0 6.1 6.5Orderbook (INRbn) 1,556 1,282 1,097 973 972 1,108 1,195 1,280Book-to-Bill (x) 4.8 3.1 2.3 2.0 2.5 3.6 4.0 3.4

Year to 31 Mar 2011 2012 2013 2014 2015 2016E 2017E 2018EPower revenue 322,990 366,833 381,868 314,956 233,914 227,203 288,685 313,641Industry revenue 99,476 112,956 102,379 76,133 67,916 66,384 77,127 82,491Other Revenue 0 0 0 0 0 0 0 0Total Revenue 422,466 479,789 484,247 391,088 301,830 293,587 365,811 396,131Other income 0 0 0 0 0 0 0 0COGS (230,817) (280,845) (280,156) (231,565) (174,203) (169,459) (208,092) (223,814)SG&A (25,361) (32,228) (37,766) (33,085) (36,373) (29,359) (36,581) (35,652)Other op.expenses (85,874) (75,643) (81,961) (91,069) (81,041) (76,926) (86,422) (97,102)Operating profit 80,413 91,072 84,364 35,369 10,213 17,844 34,716 39,563Net-interest inc./(exp.) 5,721 7,626 4,797 4,984 7,195 8,999 10,834 12,975Assoc/forex/extraord./others 3,920 4,324 5,163 9,790 3,992 3,534 3,042 3,235Pre-tax profit 90,054 103,023 94,324 50,143 21,400 30,378 48,592 55,773Tax (29,942) (32,623) (28,177) (15,535) (7,207) (9,721) (15,550) (17,847)Min. int./pref. div./others 0 0 0 0 0 0 0 0Net profit (reported) 60,112 70,400 66,147 34,608 14,193 20,657 33,043 37,926Net profit (adjusted) 60,112 70,400 66,147 34,608 14,193 20,657 33,043 37,926EPS (reported)(INR) 122.798 28.763 27.025 14.139 5.799 8.440 13.500 15.495EPS (adjusted)(INR) 122.798 28.763 27.025 14.139 5.799 8.440 13.500 15.495EPS (adjusted fully-diluted)(INR) 24.560 28.763 27.025 14.139 5.799 8.440 13.500 15.495DPS (INR) 31.150 6.400 5.405 2.830 1.160 2.000 3.000 4.000EBIT 80,413 91,072 84,364 35,369 10,213 17,844 34,716 39,563EBITDA 85,854 99,072 93,898 45,198 20,986 28,945 46,252 51,597

Year to 31 Mar 2011 2012 2013 2014 2015 2016E 2017E 2018EProfit before tax 90,054 103,023 94,324 50,143 21,400 30,378 48,592 55,773Depreciation and amortisation 5,444 8,027 9,542 9,890 10,777 11,101 11,536 12,033Tax paid (29,328) (31,832) (32,375) (21,313) (10,299) (9,721) (15,550) (17,847)Change in working capital (40,247) (85,852) (55,523) (5,340) (18,457) 51,350 (20,805) 52,411Other operational CF items (5,606) (9,640) (3,369) 5,492 (3,777) (22,454) (25,632) (29,725)Cash flow from operations 20,318 (16,274) 12,598 38,871 (356) 60,653 (1,858) 72,644Capex (17,238) (12,979) (9,758) (6,697) (4,568) (7,000) (8,000) (8,000)Net (acquisitions)/disposals (3,585) (215) 650 100 35 10 10 10Other investing CF items 9 10 10 10 10 10 10 10Cash flow from investing (20,814) (13,184) (9,098) (6,587) (4,523) (6,980) (7,980) (7,980)Change in debt 351 286 13,044 12,330 (26,046) 0 0 (9)Net share issues/(repurchases) 0 0 0 0 0 0 0 0Dividends paid (14,563) (17,937) (16,486) (13,156) (5,940) (5,727) (8,591) (11,455)Other financing CF items 0 0 0 0 0 0 0 0Cash flow from financing (14,212) (17,651) (3,441) (825) (31,986) (5,727) (8,591) (11,464)Forex effect/others 0 0 0 0 0 0 0 0Change in cash (14,708) (47,110) 59 31,459 (36,866) 47,946 (18,429) 53,201Free cash flow 3,080 (29,254) 2,840 32,174 (4,924) 53,653 (9,858) 64,644

Financial summary

Industrials / India BHEL IN

15 September 2015

- 5 -

Balance sheet (INRm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

Company profile

BHEL is India's largest engineering company in the power-equipment and industrial-systems segments. The company has a total installed capacity of 20GW. It also provides services to the process and hydro-carbon industries, as well as the defence sector and Indian Railways.

As at 31 Mar 2011 2012 2013 2014 2015 2016E 2017E 2018ECash & short-term investment 96,302 66,720 77,321 118,729 98,127 168,507 175,689 258,595Inventory 109,630 135,487 117,638 97,976 101,017 90,133 99,972 104,408Accounts receivable 273,546 357,406 398,882 399,530 376,373 321,740 360,800 325,587Other current assets 35,467 31,407 30,739 34,075 35,836 26,568 27,625 29,796Total current assets 514,945 591,019 624,580 650,309 611,353 606,949 664,086 718,387Fixed assets 51,631 56,662 56,908 53,711 46,934 42,834 39,298 35,264Goodwill & intangibles 0 0 0 0 0 0 0 0Other non-current assets 26,027 20,079 19,799 23,891 26,384 26,384 26,384 26,384Total assets 592,603 667,760 701,287 727,912 684,671 676,166 729,768 780,035Short-term debt 1,633 1,930 14,999 27,387 1,243 1,243 1,243 1,234Accounts payable 84,366 107,781 103,562 94,084 94,565 79,177 87,777 92,608Other current liabilities 305,065 304,317 278,285 275,970 248,017 239,970 260,521 279,495Total current liabilities 391,065 414,028 396,846 397,441 343,825 320,390 349,540 373,337Long-term debt 0 0 0 0 0 0 0 0Other non-current liabilities 0 0 0 0 0 0 0 0Total liabilities 391,065 414,028 396,846 397,441 343,825 320,390 349,540 373,337Share capital 4,895 4,895 4,895 4,895 4,895 4,895 4,895 4,895Reserves/R.E./others 196,643 248,837 299,546 325,575 335,951 350,880 375,332 401,803Shareholders' equity 201,538 253,732 304,441 330,471 340,846 355,776 380,227 406,698Minority interests 0 0 0 0 0 0 0 0Total equity & liabilities 592,603 667,760 701,287 727,912 684,671 676,166 729,768 780,035EV 423,611 453,490 455,958 426,937 421,396 351,015 343,833 260,918Net debt/(cash) (94,668) (64,790) (62,322) (91,343) (96,884) (167,264) (174,446) (257,361)BVPS (INR) 411.706 103.666 124.383 135.018 139.257 145.357 155.347 166.162

Year to 31 Mar 2011 2012 2013 2014 2015 2016E 2017E 2018ESales (YoY) 26.7 13.6 0.9 (19.2) (22.8) (2.7) 24.6 8.3EBITDA (YoY) 45.0 15.4 (5.2) (51.9) (53.6) 37.9 59.8 11.6Operating profit (YoY) 47.2 13.3 (7.4) (58.1) (71.1) 74.7 94.6 14.0Net profit (YoY) 39.5 17.1 (6.0) (47.7) (59.0) 45.5 60.0 14.8Core EPS (fully-diluted) (YoY) 39.5 17.1 (6.0) (47.7) (59.0) 45.5 60.0 14.8Gross-profit margin 45.4 41.5 42.1 40.8 42.3 42.3 43.1 43.5EBITDA margin 20.3 20.6 19.4 11.6 7.0 9.9 12.6 13.0Operating-profit margin 19.0 19.0 17.4 9.0 3.4 6.1 9.5 10.0Net profit margin 14.2 14.7 13.7 8.8 4.7 7.0 9.0 9.6ROAE 33.3 30.9 23.7 10.9 4.2 5.9 9.0 9.6ROAA 11.2 11.2 9.7 4.8 2.0 3.0 4.7 5.0ROCE 44.2 39.7 29.3 10.4 2.9 5.1 9.4 10.0ROIC 63.4 42.1 27.4 10.1 2.8 5.6 12.0 15.2Net debt to equity n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Effective tax rate 33.2 31.7 29.9 31.0 33.7 32.0 32.0 32.0Accounts receivable (days) 207.5 240.0 285.0 372.6 469.1 434.0 340.5 316.2Current ratio (x) 1.3 1.4 1.6 1.6 1.8 1.9 1.9 1.9Net interest cover (x) n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Net dividend payout 25.4 22.3 20.0 20.0 20.0 23.7 22.2 25.8Free cash flow yield 0.6 n.a. 0.5 6.2 n.a. 10.4 n.a. 12.5

Financial summary continued …

Industrials / India BHEL IN

15 September 2015

- 6 -

Time to revisit: upgrading to Buy

Given the recovery in the order inflow in FY15, which should continue over FY16-18E, we see a V-shaped recovery for revenue, with FY16 marking the bottom for order execution and consensus earnings downgrades. We expect a strong pick-up in revenue from FY17 (25% YoY). Upgrading to a Buy (1) due to: 35% net profit CAGR over FY16-18E, improving order-backlog visibility, and likely order execution pick-up from FY17E.

Investment summary

We upgrade our rating on BHEL to Buy (1) from Sell (5), as: 1) we believe the recovery seen in order growth in FY15 (10% YoY) will continue over FY15-18E, at a 17% CAGR, as we see orders of 20GW annually, largely from state and central utilities, 2) we expect a strong order-execution pick-up from FY17, on an improving order backlog (up by 19% YoY as at end-1Q FY16), with the company winning 9GW in orders over the past 12 months (including a few orders with shorter timelines), steps by the central government to improve coal availability and the rising pace of approvals by the Ministry of Environment and Forests (MoEF), and 3) we expect its EBITDA margin to recover over FY15-18E by 6pp, on the back of the end of negative operating leverage, driven by a pick-up in order execution and favourable commodity prices. We believe near-term share-price catalysts could come from potential new-order wins, leading to order-inflow growth of over 40% YoY for FY16E and a net profit CAGR of 35% over FY16-18E. Recovery in order inflow We expect BHEL to win power-sector orders worth 9.3GW in FY16E. The company received 4.1GW in orders for 1Q FY16 (including 4GW in orders from TSGENCO, a state utility) and is the lowest bidder for

about 5GW worth of projects (includes 3GW orders from NTPC and 1GW from NHPC). We believe the recovery in order growth for FY15 (10% YoY) will continue over FY15-18E, at a 17% CAGR, as we see orders of 20GW annually, largely from state and central utilities (see pages 9 and 10 for the order pipeline for FY16-17E and FY18-19E, respectively). Based on the status of each order (environment and forest approval, land acquisition and coal source finalisation), we see that the order pipeline for FY16-17E is already in the advanced stages and do not expect further delays in these orders getting placed (see appendix 2 on page 21 for the status of each project in the pipeline for FY16-17E). It may seem ironic that the order outlook for the power sector (ie, BHEL) is recovering when India’s power deficit and utilisation levels are at historical lows (2% and 60%, respectively; please see Appendix 1 for India’s power situation on page 19), but we believe that the new-project orders being planned by the state and central utilities over FY16-18E are largely based on long-term demand expectations. BHEL: order inflow

Source: Company, Daiwa forecasts

BHEL: order book and growth YoY

Source: Company, Daiwa forecasts

112165 182 189

356

512

597 590 605

221

317280 308

438 465495

0

100

200

300

400

500

600

700

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

(INRbn)

320 376 550

852

1,170

1,443 1,641

1,353 1,151

1,015 1,010

1,108 1,195

1,280

(20)

(10)

-

10

20

30

40

50

60

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

0

300

600

900

1,200

1,500

1,800

Order book (LHS) Growth YoY (RHS)

(INRbn) (% )

Industrials / India BHEL IN

15 September 2015

- 7 -

Strong execution pick-up only from FY17 We expect a strong pick-up in BHEL’s order execution from FY17E on an improving order backlog over the past 12 months, as it has won 9GW worth of orders, approval issues have been resolved by the MoEF, and coal availability has risen on Coal India’s (CIL) ramped-up production and the auctioning and allocation of coal blocks. BHEL has received 6GW of orders from TSGENCO, of which 2GW worth are to be executed on shorter timelines (24-36 months), helping the order execution pick-up that we see for BHEL, in our view. Currently, about 23% of BHEL’s current order backlog (INR250bn) comprises stranded projects, and the worst-case scenario in terms of customer default is only INR33.4bn (current receivables from these projects, as per management). BHEL: order book growth YoY and revenue growth YoY

Source: Company, Daiwa forecasts

EBITDA margin recovery We expect BHEL’s EBITDA margin to recover by 6pp over FY15-18E, on the back of the end of negative operating leverage, with a pick-up in order execution as well as favourable commodity prices. We also believe that an improving working-capital cycle, with higher advance payments from customers (on more orders if the aforementioned ordering scenario takes place) and the timely repayment to vendors will aid in lowering interest costs attached to outsourced parts of its order, and help to boost the EBITDA margin.

BHEL: revenue growth YoY and EBITDA margin

Source: Company, Daiwa forecasts

Accordingly, we forecast revenue CAGR of 16%, leading to a net profit CAGR of 35% for FY16-18E. BHEL: revenue growth and net profit

Source: Company, Daiwa forecasts

Valuation We value BHEL at 18x FY17E PER and increase our 12-month target price to INR243 (from INR225), reflecting an increase in our FY17E earnings. As the shares have corrected by 20% over the past month, we find BHEL’s valuation reasonable, at FY17E PER of 15.7x, particularly as the stock is trading at a more than a 20% discount to its historical average, and because its EPS is still in the early stages of the recovery cycle. BHEL: 1-year-forward PER (x)

Source: Bloomberg, Company, Daiwa forecasts

(30)

(20)

(10)

0

10

20

30

40

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

(20)

(10)

0

10

20

30

40

50

60

Order book growth Y oY (LHS ) Revenue growth YoY (RHS)

(% ) (% )

5

7

9

11

13

15

17

19

21

(30)

(20)

(10)

0

10

20

30

40

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Revenue growth YoY (LHS) EBITDA margin (RHS)

(% ) (% )

4 7 10 17

24 29 31

43

60

70 66

35

14 21

33 38

(30)

(20)

(10)

0

10

20

30

40

0

10

20

30

40

50

60

70

80

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Net Profit (LHS) Revenue growth YoY (RHS)

(INRbn) (% )

05

101520253035404550

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

PER

28.4x Avg+1S.D.

20.5x Avg

12.6x Avg-1S.D.

PERPER

Industrials / India BHEL IN

15 September 2015

- 8 -

BHEL: book-to-bill ratio and PER

Source: Company, Bloomberg

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

10

20

30

40

50

Mar

-04

Sep-

04M

ar-0

5Se

p-05

Mar

-06

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Sep-

14M

ar-1

5Se

p-15

PER (LHS) Book to bill ratio (RHS)

(x) (x)

Industrials / India BHEL IN

15 September 2015

- 9 -

Recovery in order inflows

Order inflows We expect BHEL to win power-sector orders worth 9.3GW in FY16E. The company already received 4.1GW orders in 1Q FY16 and is L1 in about 5GW worth of projects. These projects include: Status of L1 orders Projects MW Status NTPC Barethi 2,640 Land is available. Awaiting EC. Captive coal is

available. Mahagenco Bhusawal 660 Land and EC are available. Coal linkage is

available. NTPC Rourkela 250 Both land and EC are not available. NHPC Pakal dul – hydro-electric project

1,000 Received EC. Land is not available.

SPIC Tuticorin 525 Land and EC are available. Fuel source is imported coal.

Pranahita 696 - 5,771

Source: MoEF, Media articles, Daiwa

In addition to these, BHEL expects order finalisation for another 15GW worth over the next year. BHEL received orders of INR308bn in the FY15, a jump of 10% YoY from INR280bn in FY14. Of the total orders, ~80% were from the power sector and the rest from the industry sector. Bottlenecks faced by the industry India’s power-generation equipment industry has been going through a dull phase since FY11 due to issues related to coal availability, fund constraints, land acquisition, clearances, competition from foreign players, etc. This has led to the continuous shrinking of order-inflow opportunities for BHEL. Its annual ordering opportunities decreased from ~20GW in FY11 to ~8GW in FY15. Current scenario With a new government at the centre (elected in May 2014), such issues have started to get resolved gradually. The new government has introduced an online platform for approvals for environmental and forest projects. Both these online systems are aimed at ensuring timely approvals for power projects and the coal blocks linked to them. To ease the coal shortage in India, the government has been pushing Coal India (COAL IN, INR333.8, Buy [1]) for ramped-up production growth (8.5% YoY since the new government has come to power; see Pump up the volume, 22 July 2015) and has engaged in the auction/allotment of coal blocks with 9.7bn tonnes of extractable reserves to the power sector. We expect this to reduce the uncertainty of coal and assure fuel supply

to power projects that are stuck due to the non-availability of coal. BHEL’s order inflow, which has been lacklustre over the past few years, is now showing signs of improvement. We expect the order recovery seen in FY15 to continue over FY16-17E, as we see orders worth 20GW annually over FY16-18E largely from state and central utilities (please refer to the tables on page 9-10 for a detailed breakup). This will likely be on the back of improved fuel security, faster environmental and forest approvals, the ‘plug and play model’ for UMPPs, the government’s initiatives such as ‘Make in India’ and ‘24x7 Power for all’, the replacement of some 25-year-old power plants, etc. Over the next couple of years, we expect orders to mainly come from central (NTPC [not rated]) and state utilities. Unless the problems relating to tariff disputes, coal-block de-allocation, the backing down by state utilities (they are not buying power due to unaffordability) and balance sheets can be solved, supply issues will not be resolved, and there will not be any capacity additions by private sector companies, in our view. BHEL: order inflow

Source: Company, Daiwa forecasts

BHEL: order book and growth YoY

Source: Company, Daiwa forecasts

112165 182 189

356

512

597 590 605

221

317280 308

438 465495

0

100

200

300

400

500

600

700

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

(INRbn)

320 376 550

852

1,170

1,443 1,641

1,353 1,151

1,015 1,010

1,108 1,195

1,280

(20)

(10)

-

10

20

30

40

50

60

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

0

300

600

900

1,200

1,500

1,800

Order book (LHS) Growth YoY (RHS)

(INRbn) (% )

Industrials / India BHEL IN

15 September 2015

- 10 -

Order pipeline for FY16 and FY17Project Client Configuration Size (MW) Coal source Cost (INRbn) Status Central Barethi NTPC 660x4 2,640 Captive coal 180 Bidding opened in July 2014. Awaiting environmental

clearance (EC). Katwa NTPC 660x2 1,320 - 100 Terms of reference (ToR) granted in December 2014 Pudimadaka NTPC 1000x4 4,000 Imported 240 Tenders invited in March 2015, Environmental Impact

Assessment (EIA) studies currently in progress Ramagundam (Telangana) NTPC 800x2 1,600 SCCL, MCL, SECL 110 Applied for ToR for revision of capacity in December 2014 Bilhaur NTPC 660x2 1,320 Existing coal blocks 66 Awaiting policy change requiring delinking EC/ FC (forest

clearance) Singareni 3rd unit NTPC 600x1 600 No coal linkage - Base data collection is in process for EC Rourkela NTPC-SAIL JV 250x1 250 - - Tender issued for EPC package in July 2014 Maitree Project (Bangladesh) BIFPCL (JV of NTPC and

BPDB) 660x2 1,320 - 90 Tender invited for EPC package in February 2015

Ghatampur TPP JV of NLC and UPRVUNL 660x3 1,980 Imported 144 Got EC based on imported coal Sundargarh MCL 800x2 1,600 - 90 800 acres of land was acquired in September 2014 Pakal dul hydro project NHPC 250x4 1,000 NA 106 Order almost finalised. Consortium with Patel Engineering State Nellore APGENCO 800x1 800 Imported 84 EC proposal submitted in April 2015 Kothagudem APGENCO 800x1 800 Imported 53 EC proposal submitted in July 2014 Panipat HPGENCO 800x1 800 Existing coal block 44 Got the existing coal linkage Patratu TPP JSEB 660x2 1,320 - 75 Banhardih coal block deallocated now, earlier allocated to it Bhusawal TPP unit 6 MSPGCL 660x1 660 Coal linkage 45 Land acquired for the project in July 2014 Nashik Expansion TPP MSPGCL 660x1 660 Coal linkage 38 EC proposal submitted in March 2015 Banswara TPP RRVUNL 660x2 1,320 - 79 REIA study could not start due to agitation by local people KaliSindh Phase-II RRVUNL 660x2 1,320 - 79 NOC for EC has been issued Udangudi TANGEDCO 660x2 1,320 Imported 87 Bids scrapped and new tenders will come up Harduaganj TPP Stage-2 UPRVUNL 660x1 660 Existing coal block 39 Bidding initiated in July 2014 Panki Expansion UPRVUNL 660x1 660 - 47 ToR granted in September 2014 Private Khandwa Dwarkesh Energy 660x2 1,320 Imported 74 Will use imported coal till coal linkage is made available Tuticorin SPIC Ltd 525x1 525 Imported 26 Waiting 6 months for approval from the regulatory

commission Others

Cheyyur UMPP Coastal Tamil Nadu Power 660x6 4,000 Imported 242 Awaiting the new bidding document to be finalised.

Bedabahal UMPP Odisha Integrated Power 800x5 4,000 Captive coal 252 Awaiting the new bidding document to be finalised.

Total 37,795

Source: Company, Daiwa

Note: For details of each project please see Appendix 2

Industrials / India BHEL IN

15 September 2015

- 11 -

Order pipeline for FY18 and FY19 Project Client MW Status Central Kajra TPP NTPC, BSPGCL and LBCPL 660x2 Feasibility report is in process Talcher TPS Expansion NTPC 660x2 Required land is available and all other statutory clearances are in place Singrauli TPP Stage 3 NTPC 500x1 Awaiting EC Trincomalee project (Sri Lanka) JV of NTPC and CEB 250x2 Feasibility report is in process State Vodarevu TPP stage-I APGENCO 800x2 Received approval from AP Government in July 2014. No clearance obtained yet. Srikakulam TPP JV of APGENCO and PTC 800x3 Not yet received any clearance Sattupally TPP APGENCO 600x1 Not yet received any clearance Vijayawada IGCC - BHEL JV of APGENCO and BHEL 182x1 Not yet received any clearance Pirpainti TPP Nalanda Power (CESC Ltd) 660x3 Awaiting FC and land acquisition Buxar TPP SJVNL 660x2 Awaiting EC and land acquisition Salka TPP ICPL 660x2 Awaiting fuel linkage and land acquisition Godhna TPP (KPCL) L&T and KPCL 800x2 Not yet received any clearance Wanakbori TPP Extension GSECL 800x1 No land acquisition yet Sinor TPP GSECL 800x2 Not yet received any clearance Jewargi TPP Power company of Karnataka Ltd 660x2 Awaiting FC Edlapur TPP KPCL (JV of KPCL and BHEL) 800x1 Awaiting final EC Gulbarga TPP Power Company of Karnataka Ltd 660x2 Land acquisition is in process Satpura TPP Extension MPPGCL 660x1 Awaiting fuel linkage Shahpura TPP NHDC(JV of NHPC & Govt of MP) 660x2 Not yet received any clearance Dondaicha TPP MSPGCL 550x6 Land acquisition is in process (516Ha land acquired) and awaiting final EC GHTP Lehra Mohabbat Ext Stage-III PSEB 250x2 Not yet received any clearance Sagardighi TPP Phase 3 WBPDCL 500x2 Not yet received any clearance Private Dahej TPP Adani power 660x4 Received only EC and could come up for bidding in 2 years UMPP Proposed UMPPs 12,000 Bihar, Jharkhand, Uttar Pradesh Total 41,902

Source: Company, Daiwa

Other initiatives to help order recovery

‘Plug and Play’ model for UMPPs In the Union budget 2015-16, the government proposed that 5 new Ultra Mega Power Projects (UMPPs) be set up in FY16 under the ‘Plug and Play model.’ To address the concerns investors and lenders had over the previous rules, the Ministry of Power (MoP) has come up with a new standard bidding document for case II bidding in August 2015 under which bidding for UMPPs will take place. This new bid document seems to have been positively received by stakeholders, and should kick-start the process of inviting tenders for the UMPPs. Under the ‘Plug and Play’ model, all regulatory clearances and fuel linkages must be in place before the projects go to auction. Under this model, implementation of the projects can be carried out more quickly, though implementation of the model will be challenging.

Replacement of 25-year-old power plants Power plants that have completed 25 years of operation start to face problems of frequent breakdowns, inefficiency and pollution, leading to lower utilisation. The government has therefore included in its guidelines requirements for all old and inefficient power plants to be gradually replaced with new generation energy-efficient super critical technology (sub critical is older, inefficient technology and the newer, more efficient one is known as super critical). The phasing in of newer-generation plants will enhance production capacity, as well as maximise power generation in India from lower usage of coal. Also, it will take less time to replace old technology with modern and environment-friendly technology as the fuel linkages, land are in place already, and other necessary approvals can be fast-tracked. About 25GW of the power plants in India, namely those of NTPC and other state utilities, are older than 25 years of age. The government plans to replace these inefficient units with new, bigger plants at the same locations with the assured coal supplies. The coal linkages granted to an old unit will be automatically

Industrials / India BHEL IN

15 September 2015

- 12 -

transferred to the new unit with similar super critical capacity. Most of India’s 25GW of capacity is sub critical, in the range of 110/220MW. Given the planned capacity of new super critical power plants is higher than that for the old plants, additional coal linkages may be provided by Coal India. The additional coal required by the new super critical plants will be provided on the basis of an annual MoU and not a long-term fuel supply agreement (FSA). Of the 25GW of capacity that has completed 25 years of operations (as shown in appendix 3), the government might decommission those plants first that had a plant load factor (PLF) of less than 40% during FY14. These projects totalling 6GW of capacity could present an order opportunity over the next couple of years. The government has already taken initiatives aimed at decommissioning plants with a PLF of 40%. In the first week of May 2015, the NTPC signed an MoU with Jharkhand State Electricity Board (JSEB) to build a 6400MW power plant in Patratu, in the Ramgarh district of Jharkhand. A power plant already exists in Patratu, totalling 840mw. The new plan includes scrapping this old plant and setting up 4 800MW units in the first phase, and another 4 units of 800mw in the second phase. The existing Patratu plant is operating at a PLF of 5%. New emission standards for coal-based thermal-power plants Based on the new norms, thermal power plants have to either invest in pollution control equipment, or older plants have to shut and plan replacements. To tighten the pollution norms, the Ministry of Environment, Forest and Climate Change (MoEF and CC) in May 2015 issued a draft notification for new emission limits and water consumption by the coal based thermal power plants. Now, power companies have to make investments in equipment like electrostatic precipitators (ESP) and fuel gas de-sulfurisation units, which help them keep their emissions in check and comply with the new proposed norms. Refurbishing and installing a new ESP, in order to comply with the proposed new norms, should present BHEL with order opportunities over the next few years, albeit not very meaningful in size since the value per MW is small.

Other opportunities

Nuclear In terms of nuclear power projects, BHEL is engaged in nuclear turbine generator sets, piping systems, surface condensers, feed water heaters, moisture separators and re-heaters, switchgears, automation and control systems, etc. Nuclear projects like Gorakhpur, Haryana (2x700MW), Kudankulam, Tamil Nadu (6x1050MW), Jaitapur, Maharashtra (6x1700MW), Mithi Virdi, Gujarat (6x1250MW) are some of the projects that are in the planning stage and could be put up for tender, and thus likely to create new order opportunities for BHEL over the next 4-5 years. Solar The new government has a strong focus on renewables with a target of 175GW capacity additions till 2022, comprising 100GW of solar, 60GW of wind, 10GW of biomass and 5GW of small hydro. These initiatives will also present order opportunities for BHEL. In the 1Q FY16 earnings call, the company highlighted the potential for scaling up its solar business (EPC target of 100MW for FY16, potentially doubling to 200MW in FY17). It has a presence in the entire chain, ie, solar photovoltaic (PV) systems, solar water heating systems, solar street light and grid interactive solar PV power plant. Its proposal for a solar PV manufacturing facility has been approved for solar PV facility (480MW) by the committee of secretaries and is waiting for the cabinet committee to take up at any time. The required capex for the facility is INR24bn and 40% of this requirement will be available from a National Clean Energy Fund (NCEF) as a capital subsidy. Defence and submarines BHEL is expecting an increase in naval orders from the Ministry of Defence Government of India (guns this year and submarines next year). It supplies super rapid gun mounts (SRGM), integrated platform management systems (IPMS) for naval ships, as well as thermos-pressed components and strategic equipment, etc. to the Indian defence forces. BHEL already manufactures 76mm naval guns and has been nominated by the Ministry of Defence to make 127mm and 30mm guns, which it is now bidding for.

Industrials / India BHEL IN

15 September 2015

- 13 -

The Ministry of Defence will announce the bid winners in FY16. The company has also formed a consortium with Mishra Dhatu Nigam Limited (Midhani) and Hindustan Shipyard Limited (HSL) to jointly bid to build P-75 (i) submarines for the Indian Navy. Railways The company provides alternating current (AC) and direct current (DC) traction motors, AC traction alternators, DC traction generators, traction systems, locomotives, coaches, etc, to Indian Railways (a state-owned enterprise. The company has submitted a tender to set up a diesel and electric locomotive factory in Bihar, which is currently being evaluated by Indian Railways. For the diesel factory, it has partnered with General Electric (GE), and for the electric factory, the selection of a partner is under way. It is also currently participating in a railway-locomotives tender for 15 high-speed trains in a partnership with Kawasaki and Toshiba, which is expected to be finalised by March 2016.

Improving fuel security

India has seen coal shortages for more than 5 years, which is a major concern for new projects as well as existing projects. The lack of coal availability has delayed the execution of existing orders as well as the finalisation of new orders for BHEL and the whole industry. Though, in the past 14 months, the new government has taken steps to improve coal availability in the short term, as well as medium and long term. The government has started with coal block auctions/ allotments, after the Supreme Court had cancelled all past allocations in August 2014; it has also pushed Coal India to ramp up production, resulting in an 8.5% YoY increase in coal production in the past 14 months. Coal block auctions/allocation The Supreme Court of India’s cancellation in August 2014 of 204 coal blocks, that had been allocated from 1993 to 2010, led to uncertainty relating to existing and new projects. However, since then the Ministry of Coal has put in place a framework to auction and allot 204 cancelled coal blocks. Until now, 46 mines have been auctioned/ allotted, with reserves of 9.7bn tonnes going to the power sector.

The NTPC has been allotted 5 coal mines in the allotment process with coal reserves of 2.3bn tonnes which had earlier belonged to the NTPC only. Under the new law, the NTPC can use the coal from any of its block for any of its power plants, given the prior approval of the central government. The NTPC has planned to come up with more than 13GW of thermal power capacity additions over FY16-17 and already issued Notices Inviting Tenders (NITs) for 8.5GW of projects. Given it has coal linkages/blocks in place for getting environmental and forest clearance, the NTPC should be able to come up with the above-mentioned order opportunity in the next 2 years without any delay. Increase in CIL production volume CIL’s volume production over the past 14 months (after new government came in to power) has been reasonably strong. In FY15, it produced 494m tonnes (up 6.9% YoY) and in first 5 months of FY16 it produced 192m tonnes (up 9.3% YoY). The growth is in line with the government’s ambitious target for CIL to meet 1bn tonnes of coal production by 2019-20. CIL meeting this target will lead to future coal supply certainty and will aid in converting BHEL and for the power-equipment industry’s order pipeline into an order inflow, which has been stuck due to the non-availability of coal. If CIL increases coal production and guarantees supply to future projects, these could be implemented. CIL: production and growth YoY

Source: Company

Environmental and forest approvals Many coal projects have gotten stuck over the past few years due to a delay in environmental and forest approvals. In order to speed up the process of approvals, the MoEF launched a system for online submission of applications for environmental and forest approvals in May and July 2014, respectively. This new system ensures that power projects which

33 35 35

40 44

47 47 48

57

42 41 39

35 36

11.5

9.0

5.2

14.8 13.3

5.7

(1.7)

12.7

7.2

10.7

12.9 12.4

5.5 4.8

(3)

0

3

6

9

12

15

20

25

30

35

40

45

50

55

60

Jul-1

4

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr-1

5

May

-15

Jun-

15

Jul-1

5

Aug-

15

Coal production (LHS) % Change (RHS )

(m tonnes) (% )

Industrials / India BHEL IN

15 September 2015

- 14 -

have been stuck due to delays in environmental approvals and non-availability of coal on account of delays in EC and FC, get clearance in a timely manner.

Execution recovery and slow-moving orders

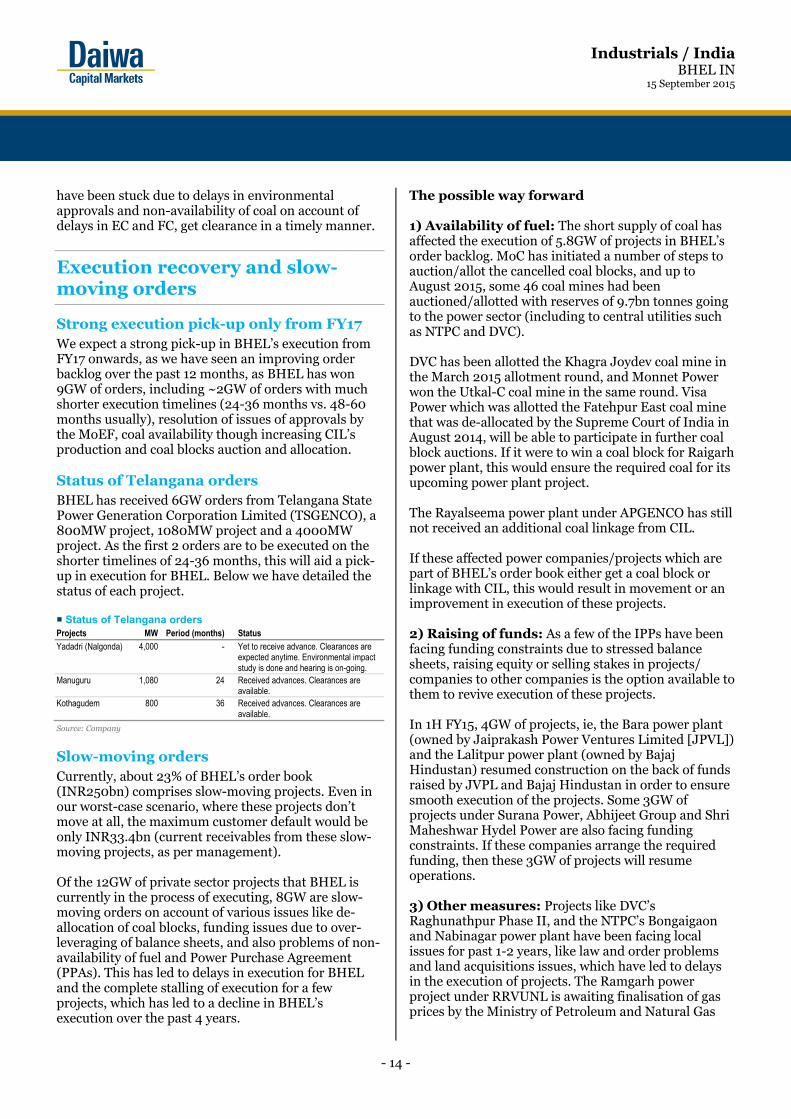

Strong execution pick-up only from FY17 We expect a strong pick-up in BHEL’s execution from FY17 onwards, as we have seen an improving order backlog over the past 12 months, as BHEL has won 9GW of orders, including ~2GW of orders with much shorter execution timelines (24-36 months vs. 48-60 months usually), resolution of issues of approvals by the MoEF, coal availability though increasing CIL’s production and coal blocks auction and allocation. Status of Telangana orders

BHEL has received 6GW orders from Telangana State Power Generation Corporation Limited (TSGENCO), a 800MW project, 1080MW project and a 4000MW project. As the first 2 orders are to be executed on the shorter timelines of 24-36 months, this will aid a pick-up in execution for BHEL. Below we have detailed the status of each project. Status of Telangana orders Projects MW Period (months) Status Yadadri (Nalgonda) 4,000 - Yet to receive advance. Clearances are

expected anytime. Environmental impact study is done and hearing is on-going.

Manuguru 1,080 24 Received advances. Clearances are available.

Kothagudem 800 36 Received advances. Clearances are available.

Source: Company

Slow-moving orders Currently, about 23% of BHEL’s order book (INR250bn) comprises slow-moving projects. Even in our worst-case scenario, where these projects don’t move at all, the maximum customer default would be only INR33.4bn (current receivables from these slow-moving projects, as per management). Of the 12GW of private sector projects that BHEL is currently in the process of executing, 8GW are slow-moving orders on account of various issues like de-allocation of coal blocks, funding issues due to over-leveraging of balance sheets, and also problems of non-availability of fuel and Power Purchase Agreement (PPAs). This has led to delays in execution for BHEL and the complete stalling of execution for a few projects, which has led to a decline in BHEL’s execution over the past 4 years.

The possible way forward 1) Availability of fuel: The short supply of coal has affected the execution of 5.8GW of projects in BHEL’s order backlog. MoC has initiated a number of steps to auction/allot the cancelled coal blocks, and up to August 2015, some 46 coal mines had been auctioned/allotted with reserves of 9.7bn tonnes going to the power sector (including to central utilities such as NTPC and DVC). DVC has been allotted the Khagra Joydev coal mine in the March 2015 allotment round, and Monnet Power won the Utkal-C coal mine in the same round. Visa Power which was allotted the Fatehpur East coal mine that was de-allocated by the Supreme Court of India in August 2014, will be able to participate in further coal block auctions. If it were to win a coal block for Raigarh power plant, this would ensure the required coal for its upcoming power plant project. The Rayalseema power plant under APGENCO has still not received an additional coal linkage from CIL. If these affected power companies/projects which are part of BHEL’s order book either get a coal block or linkage with CIL, this would result in movement or an improvement in execution of these projects. 2) Raising of funds: As a few of the IPPs have been facing funding constraints due to stressed balance sheets, raising equity or selling stakes in projects/ companies to other companies is the option available to them to revive execution of these projects. In 1H FY15, 4GW of projects, ie, the Bara power plant (owned by Jaiprakash Power Ventures Limited [JPVL]) and the Lalitpur power plant (owned by Bajaj Hindustan) resumed construction on the back of funds raised by JVPL and Bajaj Hindustan in order to ensure smooth execution of the projects. Some 3GW of projects under Surana Power, Abhijeet Group and Shri Maheshwar Hydel Power are also facing funding constraints. If these companies arrange the required funding, then these 3GW of projects will resume operations. 3) Other measures: Projects like DVC’s Raghunathpur Phase II, and the NTPC’s Bongaigaon and Nabinagar power plant have been facing local issues for past 1-2 years, like law and order problems and land acquisitions issues, which have led to delays in the execution of projects. The Ramgarh power project under RRVUNL is awaiting finalisation of gas prices by the Ministry of Petroleum and Natural Gas

Industrials / India BHEL IN

15 September 2015

- 15 -

(MoPNG), and the Government of India (GoI). Meanwhile, Ideal Energy’s Bela power project has not yet received environmental approval. These are some

of issues that cannot be resolved within a stipulated time frame, and as such these 3.5GW of projects will remain mired in uncertainty.

BHEL’s slow moving projects Project name Developer Capacity (MW) Status Slow moving orders Raghunathpur Phase ll DVC 1,320 A 10km water corridor pipeline for a plant has not materialised due to social unrest Bongaigaon TPP NTPC 750 Frequent bands, slow progress in civil work by contractors, etc, has been affecting

the project Nabinagar TPP NTPC 1,000 Land acquisition and security-related issues have led to delays in the overall project Rayalseema TPP APGENCO 600 Additional coal linkage is pending Ramgarh RRVUNL 160 Finalisation of its gas price is being considered by MoPNG, GoI Amravati Phase II Indiabulls Power 1,350 No FSA or PPA Nashik Phase II Indiabulls Power 1,350 No FSA or PPA Raichur Surana Power 420 Fund constraints Raigarh Visa Power 1,200 The Fatehpur East coal block was cancelled by SC Malibrahmani Monnet Power 1,050 Late approvals and land acquisitions have led to delays, leading to cost overruns Chandwa Phase I and II Abhijeet Group 1,080 Abhijeet Group has not received the approval of existing lenders for restructuring the

loan given for Chandwa Phase I and II power plant Bela Ideal Energy 270 EC has yet to be received Gorgi (Sidhi, Singrauli) DB Power 1,320 Signed FSA with M/s Dynamic Concepts PTE as an interim measure and is request

for an FSA for the long-term linkage of domestic fuel is at the advanced stages of consideration

Maheshwar HEP SMHPCL 400 No funds to complete the project or for R&R activities Total 12,270 Slow moving orders as a % of the total order book 23% Projects starting to move Lalitpur Bajaj Hindusthan 1,980 Project has started moving driven by fund raising Bara TPP Jaypee 1,980 Raised INR15bn via a QIP in July 2014 Total 3,960 BHEL’s total order book 53,397 Source: Company, Media articles, Daiwa

Industrials / India BHEL IN

15 September 2015

- 16 -

EBITDA margin recovery

We forecast the EBITDA margin to recover by a combined 6pp over FY15-18E, as we see its negative operating leverage ending soon on a pick-up in orders, as well as more favourable commodity prices. Also its improving working capital cycle, with higher advances from customers (on higher orders if the above ordering scenario occurs) and the timely repayment of vendors would aid in lowering the interest costs attached to outsourced parts of an order will also help the company improve its margin. BHEL: revenue growth YoY and EBITDA margin

Source: Company, Daiwa forecasts

BHEL: EBITDA margin

Source: Company, Daiwa forecasts

BHEL: raw material and as % of sales

Source: Company, Daiwa forecasts

BHEL: gross margin and EBITDA margin

Source: Company, Daiwa forecasts

Employee costs Management expects around 8,000 employees to retire over the next 4 years (about 2,200 people every year), which will help the company control its employee-related costs. However, on the back of the implementation of the 7th Pay Commission (salaries are revised every 10 years) from 1 January 2017, this will result in higher employee costs, and as such we are factoring into our model per employee cost CAGR of over 20% over FY16-18E. BHEL: number of employees

Source: Company, Daiwa forecasts

5

7

9

11

13

15

17

19

21

(30)

(20)

(10)

0

10

20

30

40

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Revenue growth YoY (LHS) EBITDA margin (RHS)

(% ) (% )

16.8

19.0 20.5

19.0

15.8

17.7

20.3 20.6 19.4

11.6

7.0

9.9

12.6 13.0

5

7

9

11

13

15

17

19

21

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

(% )

51 71

86 104

156 178

199

251 236

177

142 143 175 188

44

47

50

53

56

59

0

50

100

150

200

250

300

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Raw materials (LHS) % of sales (RHS)

(INRbn) (%)

4

8

12

16

20

24

20

22

24

26

28

30

32

34FY

05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Gross margin (LHS) EBITDA margin (RHS)

(% ) (% )

48 47

44 43 43 42 44

46 46 47

49 48

48

45

43 41

39

30

35

40

45

50

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

('000)

Industrials / India BHEL IN

15 September 2015

- 17 -

BHEL: employee expenses and employee expenses as a % of revenue

Source: Company, Daiwa forecasts

Valuation and recommendation

We upgrade our rating on BHEL to Buy (1) from Sell (5) as we believe: 1) the recovery in order growth for FY15 (10% YoY) to continue over FY15-18E, at a CAGR of 17%, on the back of orders of 20GW p.a, largely from the state and central utilities, 2) we expect strong order execution from FY17, as we see its order backlog improving (up 19% YoY as at the end of 1Q FY16) on the back of 9GW in orders being won over the past 12 months, including orders with shorter timelines, and backed by government measures to improve the availability of coal and a quicker pace of MoEF approval, and 3) that the EBITDA margin will recover over FY15-18E by a combined 6pp on the end of its negative operating leverage, the pick-up in order execution and favourable commodity prices.

Near-term share price catalysts would come from potential new order wins (it is the lowest bidder for 5GW orders worth about INR150-200bn), leading to order growth of over 40% YoY for FY16 and an FY16-18 earnings CAGR of 35%.

We value BHEL at a target PER of FY17E of 18x and are raising our 12-month target price to INR243, from INR225, reflecting increase in earnings that we see for FY17E. Given the 20% share price correction over past month, we find BHEL’s current valuation at 15.7x FY17E PER reasonable, as this is still more than a 20% discount to its past average, and because its EPS is still in the early part of the recovery cycle.

BHEL: 1-year forward PER (x)

Source: Bloomberg, Company, Daiwa forecasts

BHEL: book to bill ratio and PER

Source: Company, Bloomberg

BHEL: one-year-forward PER bands

Source: Bloomberg, Company, Daiwa forecasts

14 15 16 17 19 24 26

30

64

54 55 58 59 55 53

59

70

8

10

12

14

16

18

20

22

0

10

20

30

40

50

60

70

80

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

E

FY17

E

FY18

E

Employee expenses (LHS) Employee costs as a % of revenue (RHS)

(INRbn) (%)

05

101520253035404550

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

(PER)

28.4x Avg+1S.D.

20.5x Avg

12.6x Avg-1S.D.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

0

10

20

30

40

50

Mar

-04

Sep-

04M

ar-0

5Se

p-05

Mar

-06

Sep-

06M

ar-0

7Se

p-07

Mar

-08

Sep-

08M

ar-0

9Se

p-09

Mar

-10

Sep-

10M

ar-1

1Se

p-11

Mar

-12

Sep-

12M

ar-1

3Se

p-13

Mar

-14

Sep-

14M

ar-1

5Se

p-15

PER (LHS) Book to bill ratio (RHS)

(x) (x)

0100200300400500600700800900

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

16x22x 28x

10x

(INR)

Industrials / India BHEL IN

15 September 2015

- 18 -

BHEL: EV/EBITDA bands

Source: Bloomberg, Company, Daiwa forecasts

Risks

The main risk to our investment thesis would be any delays in finalising power orders in the sector. Secondary risks would be a greater-than-expected decline in revenue for FY16, due to unexpected delays in some orders from 2H FY16. Another risk would be if it has to be more aggressive in its pricing due to continued intense competition, and finally any plans by the government to sell stake in the company would also be a risk to our call.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Mar

-06

Sep-

06

Mar

-07

Sep-

07

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

Sep-

15

16x 12x 8x 4x

(INRbn)

Industrials / India BHEL IN

15 September 2015

- 19 -

Appendix 1: India’s power situation

Bringing electricity to villages and rural households The power shortage situation in India seems to have improved over the past 6 years, from an 11% power deficit in FY09 to 2% YTD for FY16. But, in reality the number of power shortages experienced each year is very high, in contrast to the data published by CEA. This is visible from the percentage of rural households with electricity as compared to the percentage of villages that have electricity. As per India’s Rural Electrification Policy, a village will be classified as having electricity based on a certificate issued by the Gram Panchayat (local government), certifying that:

1) Basic infrastructure, such as distribution transformers and distribution lines, are provided in inhabited localities, as well as a minimum of one dalit basti (hamlet) where it the infrastructure exists.

2) Electricity is provided to public places like schools, panchayat offices, health centres, dispensaries, community centres, etc.

3) The number of households with electricity is at least 10% of the total number of households in a village.

The third condition appears out of sync to us. From the third chart on this page, 97% of villages had electricity in India as at May 2015. But only 55% of rural households had electricity as per the Census of India 2011. According to the Census 2011, states like Bihar, Uttar Pradesh, Jharkhand, Odisha and West Bengal has had a rural household electrification rate of less than the all-India average of 55%. Also, in these states, the difference between the percentage of villages with electricity and the percentage of rural households with electricity was very high as shown in the chart below. To counter this issue, the Forum of Regulators has set up a sub-group that has come up with a ‘Mission Mode’ approach to solving the issue quickly.

The all-India energy requirements and availability of electricity

Source: CEA

Note: YTD FY16 = as at 31 July 2015

All-India peak demand and demand for power met

Source: CEA

Note: YTD FY16= as at 31 July 2015

Percentage of villages and rural households with electricity and power deficit

Source: Planning commission, CEA

Note: Power deficits are as at 31 July 2015, Villages with electricity data is as at 31 May 2015, the rural household electrification data is as per the Census 2011

Main source of lighting As per the Census 2011, households are split into 6 groups depending on their main source of lighting ie, electricity, kerosene, solar, other oil, any other source, and no lighting. Of these, most households either have electricity or use kerosene for lighting.

778 831 862 938 996 999

1,068

367

692 746 788 859 910 957 1,030

359

-11%

-10%-9%

-8% -9% -4% -4%

-2%

(50%)

(40%)

(30%)

(20%)

(10%)

0%

0

200

400

600

800

1,000

1,200

1,400

FY09 FY10 FY11 FY12 FY13 FY14 FY15 YTDFY16

Energy Requ irement Energy Ava ilable

(BU)

106 113 118 125 130 133 143 143

92 99 105 112 118 126 137 139 -14%

-13% -11%-11% -9%

-5% -4% -3%

(50%)

(40%)

(30%)

(20%)

(10%)

0%

0

20

40

60

80

100

120

140

160

180

FY09 FY10 FY11 FY12 FY13 FY14 FY15 YTDFY16

Peak Demand Demand met

(GW)

96 99

93 92 100

97

97 90

1024

32 36 40

55 58 58

-2

-12

-1 -1 0-2

0 0

(14)

(12)

(10)

(8)

(6)

(4)

(2)

0

0

20

40

60

80

100

Biha

r

UP

Jhar

khan

d

Odi

sha

WB

Indi

a

MP

Raja

stha

n

% of villages with electricity % of rural households with electricityPower Deficit (RHS)

(% ) (% )

Industrials / India BHEL IN

15 September 2015

- 20 -

According to the Census 2011, at the all-India level, 67.2% of households used electricity for lighting, while for kerosene, the all-India dependence was 31.4%. In Bihar, UP, Jharkhand and Odisha, more than 50% of total households use kerosene as the source of lighting, which is worse than the average of 31% for the whole of India. % of total households that use kerosene as the main source of lighting in India (Census 2011)

Source: Census 2011

Note: Period is 2011

In rural areas, the situation is even worse in terms of Kerosene use in states like Bihar, UP, Jharkhand and Odisha. Some 55.3% of households use electricity for lighting in rural India and 43.2% rely on Kerosene. % of rural households use kerosene as a main source of lighting in India (Census 2011)

Source: Census 2011

Note: Period is 2011

The dependence on kerosene as a source of lighting proves that the electricity is still a distant dream in states like Bihar, UP, Jharkhand and Odisha.

Penetration levels of home appliances and electricity per capacity consumption In India, 31% of the households own a refrigerator, 10% own a washing machine, 6.8% have an air conditioner and 5.3% own a microwave. The growing Indian middle class and rising income levels will lead to long-term demand growth for these products, which will translate into higher demand for these for power and eventually higher demand for power equipment. Penetration rate in India (FY14)

Source: Statista

The per capita consumption of electricity in India was 884Kwh for 2011-12, versus 3,045 Kwh for the rest of the world in 2011-12, according to the World Bank. Even among Brazil, Russia, India, China and South Africa (BRICS) nations, India’s per capita consumption of electricity is the lowest. Per capita electric power consumption of countries (kWh)

Source: World Bank, CEA

The government announced programmes in 2014, such as ‘Make in India’ and ‘Digital India’, in a bid to turn India into a manufacturing hub and an electronically empowered country, ie, using more technology. Both these programmes will lead to greater demand for electricity in the coming years.

82

6255 53

32 31 3123

15 11 80

102030405060708090

Biha

r

UP

Odi

sha

Jhar

khan

d

MP

Indi

a

Raja

stha

n

Chh

attis

garh

Mah

aras

htra

Utta

rakh

and

Guj

arat

(% )

88

7566 63

43 41 39

28 2415 13

0102030405060708090

Biha

r

UP

Jhar

khan

d

Odi

sha

Indi

a

MP

Raja

stha

n

Chh

attis

garh

Mah

aras

htra

Utta

rakh

and

Guj

arat

(% )

31.0

10.0 6.8 5.3

0

5

10

15

20

25

30

35

Refrige rator Washing mach ine Air conditioner Microwaves

(% )

13.4

8.4

6.4 5.7

4.6

2.9 3.0 2.4 0.8

13.2

7.8 6.5

5.5 4.6

3.3 3.0 2.4 0.9 0.0

2.0

4.0

6.0

8.0

10 .0

12 .0

14 .0

USA Japan Russia UK SouthAfrica

China World Brazil Ind ia

2010-11 2011-12

(kwh in '000)

Industrials / India BHEL IN

15 September 2015

- 21 -

Appendix 2: India power sector order pipeline for FY16-17

Order pipeline for FY16 and FY17Project Client Size (MW) EC Land availability Status Central Barethi NTPC 2,640 N Y ToR granted in October 2014. NIT issued Katwa NTPC 1,320 N Y ToR granted in December 2014 Pudimadaka NTPC 4,000 N Y Tender opened in March 2015, EIA studies are in progress and MoEF expects it to

be completed by May Ramagundam (Telangana) NTPC 1,600 N Y Applied for a ToR for revision of capacity in December 2014. NIT issued in

February 2015 Bilhaur NTPC 1,320 N N EC proposal submitted in July 2014, awaiting policy change requiring delinking

EC/FC Singareni 3rd unit NTPC 600 N N Base data collection is in process for EC

Rourkela NTPC-SAIL JV 250 - - Tender issued for EPC package in July 2014. At advanced stage of the bidding process

Maitree Project (Bangladesh) BIFPCL (JV between NTPC and BPDB)

1,320 - - Tenders invited for the EPC package in February 2015

Ghatampur TPP JV between NLC and UPRVUNL

1,980 Y Y Received EC based on imported coal

Sundargarh MCL 1,600 N Partial 800 acres of land acquired in September 2014 Pakal dul hydro project NHPC 1,000 Y N Set up consortium with Patel Engineering State Nellore (Krishnapatnam) APGENCO 800 N Y EC proposal submitted in April 2015 Kothagudem (Vijayawada) APGENCO 800 N Y EC proposal submitted in July 2014 Panipat HPGENCO 800 N Y Received existing coal linkage Patratu TPP JSEB 1,320 N Y Banhardih coal block now de-allocated Bhusawal TPP unit 6 MSPGCL 660 Y Y Land acquired for the project in July 2014 Nashik Expansion TPP MSPGCL 660 N Y EC proposal submitted in March 2015 Banswara TPP RRVUNL 1,320 N N REIA study did not start due to social unrest KaliSindh Phase-II RRVUNL 1,320 N - Public hearing conducted by RSPCB in July 2014 and the NOC for EC was issued Udangudi TANGEDCO 1,320 Y Y Bids scrapped and new tenders will come up Harduaganj TPP Stage-2 UPRVUNL 660 Y Y Bidding initiated in July 2014 Panki Expansion UPRVUNL 660 N Y ToR granted in September 2014 Private Khandwa Dwarkesh Energy 1,320 Y N Received EC in August 2014 and will use imported coal until coal linkage if

available Tuticorin SPIC Ltd 525 Y Y Has been waiting 6 months to getting approval from the regulatory commission Others Cheyyur UMPP Coastal Tamil Nadu Power 4,000 Y Partial Bids cancelled and new tenders will come up with new terms and conditions Bedabahal UMPP Odisha Integrated Power 4,000 Y Partial Bids cancelled and new tenders will come up with new terms and conditions Total 37,795

Source: Company, Daiwa

Note: Y= Yes, N= No, Partial= some land is still available

Industrials / India BHEL IN

15 September 2015

- 22 -

Appendix 3: power plants still in operation that are older than 25 years of age

India: coal-based power projects older than 25 years of age still in operation Name of Project Name of Utility/Company State Years of Commissioning Operational Capacity (MW) Years it has been in operation Central Ramagundam STPS NTPC Andhra Pradesh 1983, 1984 600 31 Korba STPS NTPC Chhattisgarh 1983 to 1987 1,100 31 Badarpur NTPC Delhi 1973 to 1981 705 41 Vindhyachal NTPC Madhya Pradesh 1987 420 27 Talcher TPS NTPC Odisha 1969 to 1983 460 45 Singrauli NTPC Uttar Pradesh 1982 to 1987 2,000 32 Farakka NTPC West Bengal 1986, 1987 600 28

Total 5,885 States Dr. NT TPS (Vijaywada) APGENCO Andhra Pradesh 1979 to 1980 420 35 Ramagundam B APGENCO Andhra Pradesh 1971 63 43 Barauni BSEB Bihar 1983 to 1985 220 31 Muzaffarpur KBUNL Bihar 1985, 1986 220 29 Korba West Hasdeo CSEB Chhattisgarh 1983 to 1986 840 31 Korba - East Bank CSEB Chhattisgarh 1968 to 1981 440 46 Wanakbori GSECL Gujarat 1982 to 1987 1,260 32 Ukai GSECL Gujarat 1976 to 1985 850 38 Gandhinagar GSECL Gujarat 1977 240 37 Panipat HPGCL Haryana 1979 to 1987 440 35 Bokaro B DVC Jharkhand 1986 210 28 Chandrapura DVC Jharkhand 1964, 1965 390 50 Patratu JSEB Jharkhand 1984 to 1986 220 30 Raichur KPCL Karnataka 1985 to 1986 420 29 Satpura MPPGCL Madhya Pradesh 1967 to 1984 893 47 Amarkantak Extension MPPGCL Madhya Pradesh 1977 240 37 Koradi MAHAGENCO Maharashtra 1974 to 1983 1,080 40 Nashik MAHAGENCO Maharashtra 1970 to 1981 880 44 Chandrapur MAHAGENCO Maharashtra 1983 to 1986 840 31 Parli MAHAGENCO Maharashtra 1980 to 1987 630 34 Bhusawal MAHAGENCO Maharashtra 1979 to 1982 420 35 Guru Nanik Dev - Bathinda PSEB Punjab 1974 to 1979 440 40 Ropar PSEB Punjab 1984, 1985 420 30 Kota RRVUNL Rajasthan 1983 220 31 Neyveli M\C NLC Tamil Nadu 1986 to 1988 630 28 Tuticorin TNEB Tamil Nadu 1979 to 1982 630 35 Ennore TNEB Tamil Nadu 1970 to 1975 450 44 Kothagudem TSGENCO Telangana 1966 to 1978 720 48 Obra UPRVUNL Uttar Pradesh 1967 to 1982 1,374 47 Anpara UPRVUNL Uttar Pradesh 1986 to 1988 630 28 Parichha UPRVUNL Uttar Pradesh 1984, 1985 220 30 Panki UPRVUNL Uttar Pradesh 1976, 1977 210 38 Harduaganj UPRVUNL Uttar Pradesh 1977, 1978 170 37 Durgapur DPL West Bengal 1985 110 29 Durgapur DVC West Bengal 1966 to 1982 350 48 Kolaghat WBPDCL West Bengal 1984, 1985 420 30 Bandel WBPDCL West Bengal 1982 210 32 Santaldih WBPDCL West Bengal 1974 to 1981 480 40

Total 18,900 Grand Total 24,785

Source: CEA, state utilities

Note: Years of operation – from the year of commissioning of power plant to 2014

Industrials / India BHEL IN

15 September 2015

- 23 -