Time-Series Properties and Predictability of Greek Exchange Rates

13

Time-Series Properties and Predictability of Greek Exchange Rates Gregory Koutmos; Panayiotis Theodossiou Managerial and Decision Economics, Vol. 15, No. 2. (Mar. - Apr., 1994), pp. 159-167. Stable URL: http://links.jstor.org/sici?sici=0143-6570%28199403%2F04%2915%3A2%3C159%3ATPAPOG%3E2.0.CO%3B2-4 Managerial and Decision Economics is currently published by John Wiley & Sons. Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available at http://www.jstor.org/about/terms.html. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtained prior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content in the JSTOR archive only for your personal, non-commercial use. Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained at http://www.jstor.org/journals/jwiley.html. Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printed page of such transmission. The JSTOR Archive is a trusted digital repository providing for long-term preservation and access to leading academic journals and scholarly literature from around the world. The Archive is supported by libraries, scholarly societies, publishers, and foundations. It is an initiative of JSTOR, a not-for-profit organization with a mission to help the scholarly community take advantage of advances in technology. For more information regarding JSTOR, please contact [email protected]. http://www.jstor.org Thu Jan 24 13:55:00 2008

Transcript of Time-Series Properties and Predictability of Greek Exchange Rates

Time-Series Properties and Predictability of Greek Exchange Rates

Gregory Koutmos; Panayiotis Theodossiou

Managerial and Decision Economics, Vol. 15, No. 2. (Mar. - Apr., 1994), pp. 159-167.

Stable URL:

http://links.jstor.org/sici?sici=0143-6570%28199403%2F04%2915%3A2%3C159%3ATPAPOG%3E2.0.CO%3B2-4

Managerial and Decision Economics is currently published by John Wiley & Sons.

Your use of the JSTOR archive indicates your acceptance of JSTOR's Terms and Conditions of Use, available athttp://www.jstor.org/about/terms.html. JSTOR's Terms and Conditions of Use provides, in part, that unless you have obtainedprior permission, you may not download an entire issue of a journal or multiple copies of articles, and you may use content inthe JSTOR archive only for your personal, non-commercial use.

Please contact the publisher regarding any further use of this work. Publisher contact information may be obtained athttp://www.jstor.org/journals/jwiley.html.

Each copy of any part of a JSTOR transmission must contain the same copyright notice that appears on the screen or printedpage of such transmission.

The JSTOR Archive is a trusted digital repository providing for long-term preservation and access to leading academicjournals and scholarly literature from around the world. The Archive is supported by libraries, scholarly societies, publishers,and foundations. It is an initiative of JSTOR, a not-for-profit organization with a mission to help the scholarly community takeadvantage of advances in technology. For more information regarding JSTOR, please contact [email protected].

http://www.jstor.orgThu Jan 24 13:55:00 2008

Time-series Properties and Predictability of Greek

Exchange Rates Gregory Koutmos

Fair$eld Uniuersity, Fairfield, C T , U S A

and Panayiotis Theodossiou Rzitgers Uniuersity, Camden, h rJ , U S A

This paper explores the time-series properties and predictability of weekly percentage changes in the Greek drachma exchange rates with respect to the currencies of major trading-partner countries, such as the USA, Germany, the UK, France, Italy and Japan. The analysis is carried out using the EGARCH-M model along with the power exponential distribution. Percentage changes in the Greek drachma with respect to the German mark, the French franc, the Italian lira and Japanese yen are predictable using past information. The volatility of Greek exchange rates is best represented by an EGARCH process and as such is predictable using past volatility measures. Moreover, volatility of the Greek drachma with respect to the German mark and Italian lira positively influences future movements in these exchange rates. The hypothesis that volatility is an asymmetric function of past innovations is rejected in all cases. Following the inclusion of the Greek drachma in the ECU currency basket, its value has been depreciating at a higher rate with respect to the German mark and Italian lira and at a lower rate with respect to the US dollar. Also, its volatility with respect to the German mark, the French franc, and the Italian lira has decreased, whereas its volatility with respect to the US dollar has increased.

INTRODUCTION cies behave as Martingale processes with leptokur- tic distributions and conditionally heteroskedastic

Early research on the stochastic behavior of price (GARCH) errors. Bollerslev (1987), Hsieh (1988) changes (returns) of financial assets is based on the and Akgiray and Booth (1990), among others, re- assumptions of normality and constant conditional port similar findings for other major currencies. In variance (homoskedasticity). Mandelbrot (1963) all cases, a low-order GARCH process provides a and Fama (1965) find that the empirical distribu- reasonable characterization of the time-series be- tion of price changes of financial assets is leptokur- havior of these currencies1 tic when compared to the normal distribution, thus A European currency that has not received any rejecting the assumption of normality. Mandelbrot attention in the finance literature is the Greek (1967) and Fielitz (1971) provide evidence rejecting drachma. Greece is a full member of the European the assumptions of homoskedasticity and inde- Community (EC) and its currency was added to the pendence over time. To avoid these problems, European Currency Unit (ECU) on 17 September recent papers use the generalized autoregressive 1984. The Greek drachma is still outside the Ex- conditional heteroskedasticity (GARCH) model al- change Rate Mechanism QERM) which requires ong with a variety of parametric specifications to currencies to remain within a pre-set parity band explore the stochastic behavior of price changes of (range). When bilateral exchange rates move out- financial assets (see Bollerslev et al., 1992, for an side the parity band, participating countries inter- extensive literature review). vene to realign their currencies. Greece is expected

Exchange rates behave like other financial assets. to fully participate in the ERM; therefore, a thor- Baillie and Bollerslev (1989) find that short-run ough understanding of the stochastic properties of exchange rate changes of major European curren- its currency will enable the EC countries to better

CCC 0143-6570/94/020159-09 01994 by John Wiley & Sons, Ltd.

-- -

160 G. KOUTMOS AND P. THEODOSSIOU

manage the ECU basket. In addition, the Greek currency can be used as a surrogate to study the stochastic behavior of new currencies to be included in the ECU basket, such as that of Portugal or future EC members with similar economic attri- butes to Greece.

Exchange rate movements are perhaps the most important factors affecting sales and profit fore- casts, capital budgeting plans and the value of international investments. In this respect, changes in exchange rates have a significant impact on the world's political and economic stability and the welfare of individual countries. Predicting changes in bilateral Greek exchange rates is an important task for EC and other trading-partner countries. This permits multinational firms, financial institu- tions and importing and exporting firms operating in Greece or abroad more successfully to hedge exchange rate risk exposure.

This paper investigates the time-series properties and predictability of the Greek drachma with re- spect to the currencies of major trading-partner countries such as the USA, Germany, the UK, France, Italy and Japan. In addition, it examines the behavior of the conditional mean and volatility of these exchange rates following the inclusion of the drachma in the ECU basket and addresses the issue of asymmetric volatility, i.e. whether unexpec- ted appreciations and depreciations of the Greek currency have a different impact on its future volatility. The investigation of these issues is carried out using the exponential GARCH-in-mean (EGARCH-M) approach along with the power exponential distribution.

The paper is organized as follows. In the. next section we discuss the data and present some pre- liminary findings. The third section outlines the EGARCH-M model. The fourth section elaborates on the major empirical findings. The paper ends with a summary and conclusions.

DATA AND PRELIMINARY RESULTS

The data include weekly exchange rates for the Greek drachma relative to the US dollar, the Ger- man mark, the British pound, the French franc, the Italian lira and the Japanese yen. The data cover the period 15 January 1982 to 31 August 1990 (451 observations). The exchange rates, denoted by St, are Friday's closing spot rates as reported in The Wall Street J o ~ r n a l . ~ The quotations are selling

rates for interbank transactions in denominations of at least one million US dollars. In all cases St gives the exchange rate between the drachma per unit of each currency. The six Greek exchange rates under investigation are for major trading partner countries. Table 1 shows that Greece supplies about 57.8% of its exports and receives about 55.7% of its imports from these countries. The largest trading partner country is Germany, followed by Italy, France, the UK, the USA and Japan.

Several papers have documented the existence of unit roots in the logarithm of foreign exchange rates. For example, Doukas and Rahman (1987) find that many foreign currency futures have single unit roots (i.e. the generating process can be ap- proximated by random walks). Meese and Single- ton (1982) report similar results for the natural logarithm of spot and forward exchange rates. To investigate the issue of unit roots for Greek ex-change rates, we use the augmented Dickey-Fuller and the Phillips-Perron tests (see Dickey and Ful- ler, 1979, 1981, and Phillips and Perron, 1988, for theoretical details). The Dickey-Fuller method in- volves estimating the model

and testing the null hypothesis H,: a, = O versus HI: a,<O, where st-log(St), y:-st-s ,-,, and t is a time trend. The Phillips-Perron test involves esti- mating the model

and testing the null hypothesis H,: b, =1 versus HI : b, <1, where T is the sample size. For each model, acceptance of the null hypothesis implies that a unit root is present in st. The ordinary-least-squares method is used to obtain estimates and standard

Table 1. Exports-imports to Major Trading-part- ner Countries

Country Exports (%) Imports (%)

Unlted States Germany United Kingdom France Italy Japan All six countries

6.33 24.88

7.31 8.62

15.96 1.03

57.79

3.53 20.00

5.00 7.60

13.58 5.95

55.65

Note: Data are expressed in percentages calculated using averages for the period 1982 to 1990. Source: Directions of Trade Statistics Yearbook, International Monetary Fund, 1990.

161 GREEK EXCHANGE RATES

errors for the parameters of both models. The kurtosis (K), the Kolmogorov-Smirnov D-statistic standard errors for the Phillips-Perron model are for normality, the Ljung-Box (LB) statistics for 6 adjusted for serial correlation using the and 12 lags, and the Lagrange Multiplier (LM) test Newey-West method with four lags (Newey and statistic for conditional heteroskedasticity. West, 1987). Table 2 reports the results for the The means for the y, series are statistically signi- logarithms of Greek exchange rates (s,) and their ficant (5% level) and indicate that the Greek drac- first differences (y:). The hypothesis of a unit root is hma has been depreciating at an average weekly accepted in all cases for the logarithms of exchange rate of 0.2182% with respect to the US dollar, rates and rejected for the first differences. In this 0.2991% with respect to the German mark, respect, first differencing is necessary to further 0.2185% with respect to the British pound, investigate the stochastic properties of the six Greek 0.2383% with respect to the French franc, 0.2274% exchange rates. with respect to the Italian lira and 0.3143% with

Table 3 reports several preliminary statistics for respect to the Japanese yen. The compounded weekly percentage changes in Greek exchange ra- annual depreciation rates are 12%, 16.8%, 12%, tes, calculated using the formula y,= 100 * 13.2%, 12.5% and 17.7%, respectively. The depre- (st-st- ,). The statistics reported are the mean and ciation of the Greek currency should not be surpris- the variance, the measures for skewness (S) and ing in light of the fact that Greece has had a trade

Table 2. Testing for Unit Roots in Greek Exchange Rates Greek Greek Greek Greek Greek Greek

drachma/ drachma/ drachma/ drachma/ drachma/ drachma/ US dollar German mark British pound French franc Italian lira Japanese yen

Logarithm o f exchange rates, st ADF - 1.79 - 1.25 -2.32 - 1.83 - 1.90 -0.15 PP - 1.97 - 1.30 -2.51 - 1.84 -2.04 0.02

First difference, yT =st - s , , ADF -10.32" -8.33" -9.19" -8.11" -8.49" -8.39" PP -18.94" -23.02" -22.40" -22.35" -22.49" -21.28"

Notes: Data cover the period 15 January 1982 t o 31 August 1990 (451 weeks). ADF: Augmented Dickey-Fuller test statistic. PP: Phillips-Perron test statistic. "Significant at the 5% level. Significance implies that the hypothesis o f a unit root is rejected.

Table 3. Preliminary Statistics for Percentage Changes in Greek Exchange Rates Greek Greek Greek Greek Greek Greek

drachmai drachma/ drachma/ drachma/ drachma/ drachma/ US dollar German mark British pound French franc Italian lira Japanese yen

Mean Variance S K D-statistic LM LB(6) LB(12) LB2(6) LB2(12)

Notes: Percentage changes in exchange rates are calculated using the formula y,= 100*(st -st- ,) where st =log (St) is the natural logarithm o f exchange rates. S is skewness; K is Kurtosis; D-statistic is the Kolmogorov-Smyrnov statistic; LM is the Lagrange Multiplier test statistic for conditional heteroskedasticity; LB(N) and LB2(N) are the Ljung-Box test statistics for serial correlation in the y, and y,2 series, respectively. "Statistically significant at the 5% level.

162 G. KOUTMOS AND P. THEODOSSIOU

deficit with all six countries over the sampling E, =yt-pt represents a market innovation or shock, period. The skewness and kurtosis measures indi- t,= &,lo, is a standardized innovation, and g(5,) is an cate that all series are positively skewed and highly asymmetric function of A positive (negative) 5, leptokurtic relative to the normal di~tr ibut ion.~ implies an unexpected drachma depreciation (ap- Similarly, the D-statistics reject the assumption of normality4. Rejection of normality can be partially attributed to intertemporal dependencies in the moments of the series.

The Ljung-Box (LB) test statistics are used to test for first- and second-moment dependencies in the distribution of the y, series.' The LB statistics indicate that (percentage) changes in the Greek drachma with respect to the US dollar, the German mark, the Italian lira and the Japanese yen are serially correlated. The LB2 statistics for the squared series (y;) are all statistically significant, providing evidence of strong second-moment de- pendencies (conditional heteroskedasticity) in the distribution of Greek exchange rate change^.^ Moreover, the Lagrange Multiplier test statistics for conditional heteroskedasticity suggest that the y, series can be modeled as GARCH processes.

EGARCH-M MODELS FOR GREEK EXCHANGE RATES

This paper employs the EGARCH-M model, de- veloped by Nelson (1991), to study the time-series behavior of the Greek exchange rates. The model is described by the following equations:

+ z=,4j log (0:- j) + dDJ

where y, denotes weekly percentage changes in Greek exchange rates, f ( . ) , p,, and 0: denote the conditional probability density function, the condi- tional mean, and the conditional variance of y, based on the information set I ,_ , , v is a scale parameter for f ( . ), D, is a dummy variable that takes the value of one for the post-inclusion period of the drachma in the ECU basket (17 September 1984) and the value of zero for the pre-inclusion period,

preciation). The conditional mean p, is linearly related to past

innovations (moving-average process), the condi- tional standard deviation, o,, and the dummy vari- able D,. The moving-average component captures serial correlation in the y, series. The inclusion of the standard deviation is intended to test for pos- sible linkages between the first and second moments of the distribution of y,. The dummy-variable com- ponent tests for structural changes in the condi- tional mean equation following the inclusion of the Greek drachma in the ECU basket.

The conditional variance 0; is specified as an exponential function of past standardized inno- vations and past conditional variances. Normally, larger values for innovations or past conditional variances will result in larger values for o: (i.e. larger volatility). The parameter 6 of g(t,) relates unexpected changes in exchange rates (t,) to volatil- ity in an asymmetric fashion. Provided that ai>0, a positive value for 6 implies that unexpected drac- hma depreciations (positive t,)have a larger impact on future volatility than unexpected drachma ap- preciations (negative t,). A negative value for 6 implies the opposite. Similarly, the dummy-variable component tests for structural changes in the condi- tional variance following the inclusion of the drac- hma in the ECU basket. Stationarity of 0; requires

that xJq= 1 (Nelson, 1991). l + j <

The most commonly used parametric specifica- tion for f ( . ) is that of the standard normal distribu- tion (e.g. Engle, 1982; Akgiray, 1989). Other popular parametric specifications include the Student's t-distribution (Bollerslev, 1987; Baillie and Bollerslev, 1989; Akgiray and Booth, 1990) and the power exponential distribution (Nelson, 1991; Akgiray et al., 1991; Booth et al., 1992). In this paper we employ the power exponential distribution which includes the normal distribution as a special case. The power exponential density function is:

where r ( . ) is the gamma function and v is a scale parameter, to be estimated, controlling the shape of the power exponential distribution. For v =2, the

163 GREEK EXCHANGE RATES

power exponential density function reduces to

which is the density for the normal distribution. Because the normal distribution is nested within the power exponential distribution, likelihood ratio tests can be used to determine which of the two distributions provides the best fit to the data. Other densities nested within the power exponential are the double exponential or Laplace distribution (for v = 1) and the uniform or rectangular distribution (for v + a).

Estimates for the parameter vector (@-(Po, . . . ,d) are obtained by maximizing the sample log- likelihood function

which is highly non-linear in the parameters. The maximization of L ( . )is based on the Berndt et al. (1974) algorithm. The specification of the lag order of the conditional mean and the conditional vari- ance equations (i.e. k, p, and q) is accomplished by means of the log-likelihood ratio test. Also, re- sidual-based diagnostic tests are performed to as- sess the robustness of the models.

EMPIRICAL FINDINGS

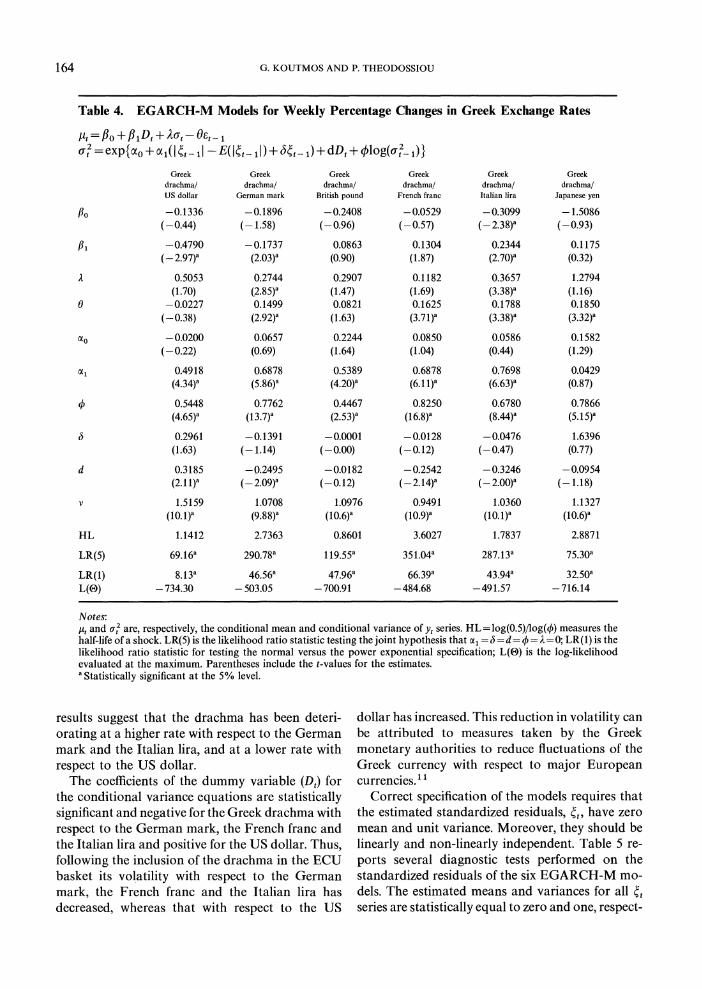

The maximum likelihood estimates for the EGARCH-M models are reported in Table 4. A single-lag specification for the moving-average component of the conditional mean equations and an EGARCH (1,l) specification for the conditional variance equations provide an adequate representa- tion of the time-series behavior of weekly percent- age changes in Greek exchange rates. Diagnostic tests on the standardized residuals indicate that the models are r o b u ~ t . ~

The log-likelihood ratio statistics for testing the normal against the power exponential distribution EGARCH-M models, LR(l), range from 8.12 (US dollar) to 66.38 (French franc). These statistics follow the X 2 distribution with one degree of fre- edom which is due to the restriction imposed for the normal distribution, i.e. v =2. All log-likelihood ratio test statistics are statistically significant, indic- ating that the power exponential distribution pro- vides a better representation of the stochastic be- havior of the Greek exchange rates series than the

normal distribution. The superiority of the power exponential distribution is attributed to its ability to better account for the leptokurtosis present in the series.

The estimated values of the scale parameter v range from 0.9491 (French franc) to 1.5159 (US dollar). Specifically, the empirical probability dis- tributions of changes in the Greek drachma relative to the German mark, British pound, French franc, Italian lira and Japanese yen are very close to a Laplace distribution while that of the US dollar falls between the Laplace and the normal distribution.

The moving-average coefficients 0 of the condi- tional mean equations for the German mark, Fre- nch franc, Italian lira and Japanese yen are statist- ically significant, suggesting that percentage changes in these exchange rates are predictable using past innovations. Also, the EGARCH-M coefficient A. is statistically significant and positive for the German mark and the Italian lira, indicating that the conditional standard deviation (volatility) has a positive impact on the conditional mean of the series. That is, higher volatility in these exchange rates is associated with devaluations of the drachma.

The results for the conditional variance equa- tions indicate the presence of conditional heteroske- dasticity in the series. the coefficients for past in- novations (a,) and past conditional variances ($) are statistically significant for all six exchange rates, indicating that future volatility is predictable using past in f~rmat ion .~ The coefficient $ is less than one in all cases, implying that the conditional variance is stationary and mean reverting.'' The persistence of past shocks on volatility for each series is measured using the half-life (HL) of a shock, calculated as HL =log(0,5)/log($). The half-life of a shock on volatil- ity ranges from approximately one week (British pound) to almost four weeks (French franc).

The asymmetry coefficient 6 is statistically insig- nificant in all cases, rejecting the hypothesis of asymmetric volatility for Greek exchange rates. It appears that the two-sided nature of foreign ex-change rates makes volatility asymmetries unlikely. Thus, unexpected appreciations and depreciations of the drachma have a similar impact on future volatility.

Following the inclusion of the drachma in the ECU basket the conditional means of percentage changes in the Greek drachma with respect to the German mark and the Italian lira have increased, whereas that for the US dollar has decreased. These

--- - - - --

164 G. KOUTMOS AND P. THEODOSSIOU

Table 4. EGARCH-M Models for Weekly Percentage Changes in Greek Exchange Rates

Greek Greek Greek Greek Greek Greek drachma/ drachma/ drachma/ drachma/ drachma/ drachma/ US dollar German mark Brlt~sh pound French franc Italian lira Japanese yen

Notes: p, and CT,? are, respectively, the conditional mean and conditional variance of y, series. HL=log(0.5)/log(4) measures the half-life of a shock. LR(5) is the likelihood ratio statistic testing the joint hypothesis that cr, = 6 = d = 4 =I-=0;LR(1) is the likelihood ratio statistic for testing the normal versus the power exponential specification; L(O) is the log-likelihood evaluated at the maximum. Parentheses include the t-values for the estimates. "Statistically significant at the 5% level.

results suggest that the drachma has been deteri- dollar has increased. This reduction in volatility can orating at a higher rate with respect to the German be attributed to measures taken by the Greek mark and the Italian lira, and at a lower rate with monetary authorities to reduce fluctuations of the respect to the US dollar. Greek currency with respect to major European

The coefficients of the dummy variable (Dl )for currencies.' the conditional variance equations are statistically Correct specification of the models requires that significant and negative for the Greek drachma with the estimated standardized residuals, r,, have zero respect to the German mark, the French franc and mean and unit variance. Moreover, they should be the Italian lira and positive for the US dollar. Thus, linearly and non-linearly independent. Table 5 re-following the inclusion of the drachma in the ECU ports several diagnostic tests performed on the basket its volatility with respect to the German standardized residuals of the six EGARCH-M mo- mark, the French franc and the Italian lira has dels. The estimated means and variances for all t, decreased, whereas that with respect to the US series are statistically equal to zero and one, respect-

165 GREEK EXCHANGE RATES

Table 5. Diagnostics Tests for the EGARCH-M Models Greek Greek Greek Greek Greek Greek

drachmai drachma/ drachma/ drachma/ drachmaj drachmaj US dollar (Zerman mark British pound French franc Italian l ~ r a Japanese yen

-0.0075 -0.0029 1.0161 0.9926 0.1231 -0.1434 3.7259 5.7122 3.9697 5.0146 0.0382 0.0404 8.03 5.43

13.35 11.48 2.15 4.35 5.63 14.11

Notes: Kaand K are, respectively, the theoretical and empirical kurtosis for the distribution of the standardized residuals. For the power exponential distribution, Ka=r(5/v) T(l/v) T(3/v)-'. S is the skewness; D-statistic is the Kolmogorov-Smyrnov statistic testing the hypothesis that the standardized residuals follow the power exponential distribution; LB(n) and LB2(n) are the Ljung-Box statistics. Parentheses include the t-values for the estimates. astatistically significant at the 5% level.

ively. The Ljung-Box test statistics on 5, and 5; are statistically insignificant, providing support for cor- rect specification of the conditional mean and conditional variance equations. The skewness, kur- tosis and Kolmogorov-Smyrnov D-statistics indi- cate that the empirical distributions of Greek ex- change rates are closer to the power exponential than the normal distribution.

SUMMARY AND CONCLUSIONS

This paper explores the time-series behavior and predictability of weekly percentage changes in the Greek drachma exchange rates with respect to the US dollar, the German mark, the British pound, the French franc, the Italian lira and the Japanese yen. In addition, it examines the behavior of the condi- tional mean and conditional variance (volatility) of percentage changes in these exchange rates follow- ing the inclusion of the drachma in the ECU basket and addresses the issue of asymmetric volatility, i.e. whether unexpected appreciations and deprecia- tions of the Greek currency have a different impact on its future volatility. The investigation of these issues is carried out using the EGARCH-M approach along with the power exponential dis- tribution.

The conditional mean of percentage changes in the Greek drachma exchange rates with respect to the German mark, the French franc, the Italian lira and the Japanese yen are best represented by a

moving-average process of order one and as such they are predictable using past innovations. In addition, percentage changes in the Greek drachma exchange rates with respect to the German mark and the Italian lira are positively influenced by their conditional standard deviations. The latter implies that, other things being equal, higher volatility leads to a depreciation of the drachma with respect to these currencies. These findings are in direct viola- tion of the Martingale model, a hypothesis used often in economic equilibrium models for exchange rates. Volatility in all Greek exchange rates is best represented by an EGARCH (1,l) process, thus current volatility is predictable using past innova- tions and past volatility measures. The hypothesis of asymmetric volatility is rejected for all Greek exchange rates. In this respect, unexpected appreci- ations and depreciations of the Greek currency have a similar impact on its volatility over time. The conditional variance for each series is stationary and mean-reverting.

Following the inclusion of the Greek currency in the ECU (European Currency Unit) basket, its value has been depreciating at a higher rate with respect to the German mark and the Italian lira and at a lower rate with respect to the US dollar. Also, its volatility with respect to the German mark, the French franc and the Italian lira has decreased, whereas its volatility with respect to the US dollar has increased.

Log-likelihood ratio tests, as well as several model diagnostic tests indicate that the power

166 G. KOUTMOS AND P. THEODOSSIOU

exponential distribution provides a better charac- terization of the stochastic behavior of Greek ex- change rates changes than the normal distribution. This is attributed to the flexibility of the power expone~ltial to 'accommodate' the leptokurtosis present in the data.

The above findings are useful in many respects. Greece is expected to fully participate in the Ex- change Rate Mechanism (ERM) system, therefore a thorough understanding of the time-series proper- ties of its currency enables EC countries to better manage the ECU basket, In addition, the Greek currency can be used as a surrogate to study the stochastic behavior of currencies to be included in the ECU basket, such as that of Portugal, or future EC members with similar economic attributes to Greece.

Exchange rate movements are important factors affecting sales and profit forecasts, capital budge- ting plans and the value of international invest- ments. The models presented in this paper can be used to predict future movements and volatility patterns in Greek exchange rates. This is an import- ant task because it permits multinational firms, financial institutions and importing and exporting firms operating in Greece, the EC and other tradin- g-partner countries more successfully to hedge ex- change rate risk exposure. Also, forecasts of volatil- ity can be used directly as inputs in valuation models for foreign currency options. In particular, the variance of percentage changes in exchange rates is an important determinant in the Black and Scholes currency option pricing formula (Solnik, 1991, pp. 299-301).

Moreover, the time-series properties of exchange rates have important implications for currency mar- ket equilibrium models and the pricing of currency options, futures and forward contracts. Many of these models are based on the assumptions that exchange rates follow the random walk or the Martingale model and that exchange rate changes are normally distributed. These assumptions are violated for Greece. Therefore a need exists to adjust the models so that they provide better ap- proximations of reality.

Acknowledgements

The authors would like to thank John Doukas, Ira Horowitz, George Philippatos and two anonymous referees for valuable comments and suggestions.

NOTES

1. See Bailie and McMahon (1989, Chapter 4) for a comprehensive review of studies on the time-series properties of exchange rates.

2. In cases where Friday's values were not available, Thursday's values were used to ensure continuity in the data series.

3. It is possible that the conditional distribution is normal even though the unconditional distribution is leptokurtic.

4. The Kolmogorov-Smyrnov statistic is calculated as D,,=max I F,,(y)-F,(y) 1 where F,, is the empirical cumulative distribution of y, and Fo(y) is the postu- lated theoretical distribution.

5. The Ljung-Box statistic for N lags is calculated as

LB(N)= T(T+ 2)zlN=, (r?/T-j), where r j is the

sample autocorrelation for j lags and T is the sample size.

6. If a process {y,) is a white noise, then {y:} will also be a white noise. Time dependence in {y:} indicates non- linear time dependence in {y,}.

7. If z is a standardized power exponential random variable, then E lzl =T(~/v)/[~(~/v)T(~/v)]'/~and K* = r ( 5 / ~ ) r ( l / ~ ) / r ( 3 / ~ ) ~ .

8. Several related stud~es find that a low-order GARCH specification appears to adequately represent many financial series (c.g. Bollerslev et al., 1992).

9. Using Eqn (5)it can be shown that the s-period-ahead forecast of the log of the conditional variance is given by E,Clog (a?+,)] =a0 (1 -42)/(1 -4)+ d o g (a:).

10. The log of the unconditional variance is glven by log(a2)=a,/(l - (b). The conditional variance can be written in terms of the unconditional variance as

where the dummy variable is omitted. This formula- tion of the conditional variance shows that in the absence of shocks the conditional variance ap-proaches its unconditional mean with speed equal to 4.

11. Full participation of Greece in the ERM system requires some minimum stability of the drachma with respect to the ECU basket.

REFERENCES

V. Akgiray (1989). Conditional heteroskedasticity in time series of stock returns: evidence and forecasts. Journal qf Business 62, January, 55-80.

V. Akgiray and G. C. Booth (1990). Modeling the stochas- tic behavior of Canadian foreign exchange rates. Jour- nal of Mu[tiilatioizul Financial Management 1, 43-71.

V. Akgiray, G. G. Booth, J . J. Hatem and C. Mustafa (1991). Conditional dependence in precious metal pri- ces. The Financial Review 26, August, 367-86.

167 GREEK EXCHANGE RATES

R. T. Baillie and T. Bollerslev (1989). The message in daily exchange rates: a conditional variance tale. Journal of Business and Economic Statistics 7, July, 297-305.

R. T. Baillie and P. C. McMahon (1989). The Foreign Exchange Market: Theory and Econometric Evidence, Cambridge, MA: Cambridge University Press.

E. K. Berndt, H. B. Hall, R. E. Hall and J. A. Hausman (1974). Estimation and inference in nonlinear structural models. Annals of Econornic and Social Measurement 4, October, 653-66.

T. Bollerslev (1987). A conditional heteroskedastic time series model for speculative prices and rates of return. Review of Economics and Statistics 69, August, 542-7.

T. Bollerslev, R. Y. Chou and K. F. Kroner (1992). ARCH modeling in finance: a review of the theory and empir- ical evidence. Journal of Econometrics 52, AprilIMay, 5-59.

G. G. Booth, J. J. Hatem, I. Virtanen and P. Yli-Olli (1992). Stochastic modeling of security returns: evid- ence from the Helsinki Stock Exchange. European Journal of Operational Research 56, 98-106.

D. A. Dickey and W. A. Fuller (1979). Distribution of the estimates for autoregressive time series with unit root. Journal of the American Statistical Association 74, June, 427-32.

D. A. Dickey and W. A. Fuller (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econornetrica 49, July, 1057-72.

J. Doukas and A. Rahman (1987). Unit roots tests. Journal of Financial and Quantitative Analysis 22, March, 101-8.

R. F. Engle (1982). Autoregressive conditional heteroske- dasticity with estimates of the variance of U.K. infl- ation. Econornetrica 50, July, 987-1008.

E. F. Fama (1965). The behavior of stock market prices. Journal of Business 38, January, 34-105.

B. D. Fielitz (1971). Stationary of random data: Some implications for the distribution of stock price changes. Journal of Financial and Quantitative Analysis 6, June, 1025-34.

D. Hsieh (1988). The statistical properties of daily foreign exchange rates: 1974-1983. Journal of International Economics 24, February, 129-45.

B. Mandelbrot (1963). The variation of certain specula- tive prices. Journal of Business 36, October, 394-419.

B. Mandelbrot (1967). The variation of some other spe- culative prices. Journal of Business 40, October, 393-413.

R. A. Meese and K. J. Singleton (1982). O n unit roots and the empirical modeling of exchange rates. Journal of Finance 37, September, 1029-35.

D. Nelson (1991). Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59, March, 347-70.

W. K. Newey and K. D. West (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econotnetrica 55, May, 703-8.

P. C. B. Phillips and P. Perron (1988). Testing for a unit root in time series regression. Biornetrika 75, 335-46.

B. Solnik (1991). International Investments, Reading, MA: Addison-Wesley.

You have printed the following article:

Time-Series Properties and Predictability of Greek Exchange RatesGregory Koutmos; Panayiotis TheodossiouManagerial and Decision Economics, Vol. 15, No. 2. (Mar. - Apr., 1994), pp. 159-167.Stable URL:

http://links.jstor.org/sici?sici=0143-6570%28199403%2F04%2915%3A2%3C159%3ATPAPOG%3E2.0.CO%3B2-4

This article references the following linked citations. If you are trying to access articles from anoff-campus location, you may be required to first logon via your library web site to access JSTOR. Pleasevisit your library's website or contact a librarian to learn about options for remote access to JSTOR.

References

Conditional Heteroscedasticity in Time Series of Stock Returns: Evidence and ForecastsVedat AkgirayThe Journal of Business, Vol. 62, No. 1. (Jan., 1989), pp. 55-80.Stable URL:

http://links.jstor.org/sici?sici=0021-9398%28198901%2962%3A1%3C55%3ACHITSO%3E2.0.CO%3B2-R

The Message in Daily Exchange Rates: A Conditional-Variance TaleRichard T. Baillie; Tim BollerslevJournal of Business & Economic Statistics, Vol. 7, No. 3. (Jul., 1989), pp. 297-305.Stable URL:

http://links.jstor.org/sici?sici=0735-0015%28198907%297%3A3%3C297%3ATMIDER%3E2.0.CO%3B2-J

A Conditionally Heteroskedastic Time Series Model for Speculative Prices and Rates ofReturnTim BollerslevThe Review of Economics and Statistics, Vol. 69, No. 3. (Aug., 1987), pp. 542-547.Stable URL:

http://links.jstor.org/sici?sici=0034-6535%28198708%2969%3A3%3C542%3AACHTSM%3E2.0.CO%3B2-A

Distribution of the Estimators for Autoregressive Time Series With a Unit RootDavid A. Dickey; Wayne A. FullerJournal of the American Statistical Association, Vol. 74, No. 366. (Jun., 1979), pp. 427-431.Stable URL:

http://links.jstor.org/sici?sici=0162-1459%28197906%2974%3A366%3C427%3ADOTEFA%3E2.0.CO%3B2-3

http://www.jstor.org

LINKED CITATIONS- Page 1 of 3 -

Likelihood Ratio Statistics for Autoregressive Time Series with a Unit RootDavid A. Dickey; Wayne A. FullerEconometrica, Vol. 49, No. 4. (Jul., 1981), pp. 1057-1072.Stable URL:

http://links.jstor.org/sici?sici=0012-9682%28198107%2949%3A4%3C1057%3ALRSFAT%3E2.0.CO%3B2-4

Unit Roots Tests: Evidence from the Foreign Exchange Futures MarketJohn Doukas; Abdul RahmanThe Journal of Financial and Quantitative Analysis, Vol. 22, No. 1. (Mar., 1987), pp. 101-108.Stable URL:

http://links.jstor.org/sici?sici=0022-1090%28198703%2922%3A1%3C101%3AURTEFT%3E2.0.CO%3B2-0

Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of UnitedKingdom InflationRobert F. EngleEconometrica, Vol. 50, No. 4. (Jul., 1982), pp. 987-1007.Stable URL:

http://links.jstor.org/sici?sici=0012-9682%28198207%2950%3A4%3C987%3AACHWEO%3E2.0.CO%3B2-3

The Behavior of Stock-Market PricesEugene F. FamaThe Journal of Business, Vol. 38, No. 1. (Jan., 1965), pp. 34-105.Stable URL:

http://links.jstor.org/sici?sici=0021-9398%28196501%2938%3A1%3C34%3ATBOSP%3E2.0.CO%3B2-6

Stationarity of Random Data: Some Implications for the Distribution of Stock Price ChangesBruce D. FielitzThe Journal of Financial and Quantitative Analysis, Vol. 6, No. 3. (Jun., 1971), pp. 1025-1034.Stable URL:

http://links.jstor.org/sici?sici=0022-1090%28197106%296%3A3%3C1025%3ASORDSI%3E2.0.CO%3B2-C

The Variation of Certain Speculative PricesBenoit MandelbrotThe Journal of Business, Vol. 36, No. 4. (Oct., 1963), pp. 394-419.Stable URL:

http://links.jstor.org/sici?sici=0021-9398%28196310%2936%3A4%3C394%3ATVOCSP%3E2.0.CO%3B2-L

http://www.jstor.org

LINKED CITATIONS- Page 2 of 3 -

The Variation of Some Other Speculative PricesBenoit MandelbrotThe Journal of Business, Vol. 40, No. 4. (Oct., 1967), pp. 393-413.Stable URL:

http://links.jstor.org/sici?sici=0021-9398%28196710%2940%3A4%3C393%3ATVOSOS%3E2.0.CO%3B2-Y

On Unit Roots and the Empirical Modeling of Exchange RatesRichard A. Meese; Kenneth J. SingletonThe Journal of Finance, Vol. 37, No. 4. (Sep., 1982), pp. 1029-1035.Stable URL:

http://links.jstor.org/sici?sici=0022-1082%28198209%2937%3A4%3C1029%3AOURATE%3E2.0.CO%3B2-V

Conditional Heteroskedasticity in Asset Returns: A New ApproachDaniel B. NelsonEconometrica, Vol. 59, No. 2. (Mar., 1991), pp. 347-370.Stable URL:

http://links.jstor.org/sici?sici=0012-9682%28199103%2959%3A2%3C347%3ACHIARA%3E2.0.CO%3B2-V

A Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation ConsistentCovariance MatrixWhitney K. Newey; Kenneth D. WestEconometrica, Vol. 55, No. 3. (May, 1987), pp. 703-708.Stable URL:

http://links.jstor.org/sici?sici=0012-9682%28198705%2955%3A3%3C703%3AASPSHA%3E2.0.CO%3B2-F

Testing for a Unit Root in Time Series RegressionPeter C. B. Phillips; Pierre PerronBiometrika, Vol. 75, No. 2. (Jun., 1988), pp. 335-346.Stable URL:

http://links.jstor.org/sici?sici=0006-3444%28198806%2975%3A2%3C335%3ATFAURI%3E2.0.CO%3B2-B

http://www.jstor.org

LINKED CITATIONS- Page 3 of 3 -