THE UNIVERSITY OF HULL Factors affecting customer loyalty ...

418

THE UNIVERSITY OF HULL Factors affecting customer loyalty of different strategic groups in the Vietnamese supermarket sector being a Thesis submitted for the Degree of Doctor of Philosophy in the University of Hull by THI DIEM EM NGUYEN BA, Business Administration, University of Economics Ho Chi Minh city (Vietnam), 2006 MSc, International Business and Management, University of East London (United Kingdom), 2012 January 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of THE UNIVERSITY OF HULL Factors affecting customer loyalty ...

THE UNIVERSITY OF HULL

Factors affecting customer loyalty of different strategic groups in the

Vietnamese supermarket sector

being a Thesis submitted for the Degree of Doctor of Philosophy

in the University of Hull

by

THI DIEM EM NGUYEN

BA, Business Administration, University of Economics Ho Chi Minh city (Vietnam), 2006

MSc, International Business and Management, University of East London (United Kingdom),

2012

January 2019

i

ABSTRACT

The main objective of this research is to investigate factors affecting customer loyalty of

different supermarket strategic groups, as the term of strategic groups in the grocery sector

appears to have been ignored by most researchers and the topic of comprehensive factors

affecting customer loyalty are is under-researched. There were two main phases of emperical

research, including expert and supermarket-consumer interviews (Phase One) and

questionnaire survey (Phase Two). In particular, there were 3055 questionnaires collected

from 17 March 2018 to 27 July 2018 in the Vietnamese supermarkets through many

channels, including email, postal and face-to-face contact. After data screening, 2913

questionnaires remained in the dataset. The three main quantitative techniques used were

exploratory factor analysis (EFA), confirmatory factor analysis (CFA) and structural equation

modelling (SEM). The research used both SPSS and AMOS 24. The results revealed there are

seven main direct indicators for customer loyalty: retail brand experience, service quality

related to in-store employees’ knowledge and attitudes toward consumers, customer

satisfaction, promotion effects, switching costs, e-service quality related to a core e-service

quality scale, and alternative attractiveness. In that, customer satisfaction can explain only

17.8 percent variation in customer loyalty. In addition, price, habit and income also have a

slight positive impact on customer loyalty. This research also revealed seven main factors

directly and positively affecting customer satisfaction: customer perceived value, in-store

logistics, service quality related to service employees’ knowledge and attitudes toward

consumers, store image, customer experience, product quality, and alternative attractiveness

negatively relating to customer satisfaction. Besides that, switching costs and price also have

a slight direct impact on customer satisfaction. Furthermore, this research also found factors

directly and positively affecting customer perceived value, including price, in-store logistics,

trust, promotion effects, e-service quality related to a core e-service quality scale, service

quality and customer service, and that switching costs are negatively associated with

customer perceived value. The research also investigated differences across groups, including

strategic groups, age ranges, location, gender, income, education level and occupation. The

results showed that there were differences between groups regarding factors affecting

customer loyalty, customer satisfaction and customer perceived value. It is believed that the

research will prove meaningful for both academia and practitioners in understanding issues

relating to factors affecting customer loyalty, especially since multigroup analysis was

conducted to examine different relationships between constructs in the researched model; the

research also revealed that the term ‘strategic groups’ in the grocery sector should not be

ignored. The revised research framework generated in this research can be applied in any

industry or market. There are some limitations to this research which are presented in section

8.3 and recommendations for future research.

ii

ACKNOWLEDGEMENT

My PhD has been one of the most incredible milestones in my life and especially my

academic career. Spending more than 2 years full-time research with ceaseless self-learning

motivation, I have become more knowledgeable which I hope will enable me to contribute

more to the quality of education in my country, Vietnam. This thesis would have been

impossible to complete without support and encouragement from my family, supervisors and

friends.

First of all, I would like to express my deepest gratitude to my family who have

always been there to support me during my research journey, especially my mother and father

who always encourage me and give me their unconditional love. In addition, two other people

that have always been there to encourage me are my cutest baby girl, Nguyen Xuan Huyen

Anh and my partner, Charles Buchanan-Price, without whom I might not have been able to

achieve the necessary application to complete my PhD journey. Again, thank you and I love

you all, my lovely family.

Secondly, I would like to express my grateful appreciation to my first supervisor,

Professor David Bruce Grant and my second supervisor, Professor Christopher Bovis of the

University of Hull who have always shown their support and dedication while advising and

guiding my PhD work. Their valuable direction from the start of my PhD facilitated and

enhanced my whole research journey. Thanks to my supervisors’ encouragement and

guidance, I undertook self-study on quantitative research which I consider a significant

achievement in my PhD journey, and the acquisition of knowledge has been beneficial and

supportive throughout my PhD work and will remain so for the remainder of my future

academic career. Besides that, any problems related to my academic work have been guided

and quickly solved by my two incredible supervisors. I learned many things from them, have

received valuable detailed feedback at our frequent meetings, and have continually been

made aware of the importance of the quality and consistency of my work. Without my

supervisors’ dedicated and patient support, I may not have been able to complete my PhD

work. Again, Professor Grant and Professor Bovis, I feel honoured to have been one of your

PhD students.

Thirdly, I would like to thank all of my friends, colleagues and previous students who

have supported me during the data collection process; without your support, I would not have

been able to collect sufficient data to support my work. Especially, I would like to express my

appreciation to Associate Professor Xuan Lan Pham, University of Economics Ho Chi Minh

City, who is an expert in strategy and retailing in Vietnam, whose comments on the

Vietnamese retailing strategic groups facilitated my research. Thanks for your networking

introductions which enabled me to connect with other experts and participants.

Last but not least, I would like to thank John Balcombe, retired Strategy Advisor to

the BBC Trust, who has supported me immensily with his unquestionably professional

proofreading.

iii

ABSTRACT ............................................................................................................................................ i

ACKNOWLEDGEMENT .................................................................................................................... ii

LIST OF FIGURES ........................................................................................................................... viii

LIST OF TABLES ................................................................................................................................ x

LIST OF APPENDICES .................................................................................................................... xii

LIST OF ABBREVIATIONS ........................................................................................................... xiii

Chapter 1: Introduction ....................................................................................................................... 1

1.1 INTRODUCTION .............................................................................................................................. 1

1.2. RESEARCH BACKGROUND ............................................................................................................ 1

1.3. CONTEXT OF STUDY ..................................................................................................................... 3

1.4. RESEARCH OBJECTIVES ................................................................................................................ 4

1.5. RESEARCH QUESTIONS ................................................................................................................. 4

1.6. RESEARCH METHODOLOGY .......................................................................................................... 5

1.7. POTENTIAL CONTRIBUTIONS OF THIS RESEARCH ......................................................................... 5

1.8. THESIS OUTLINE ........................................................................................................................... 6

Chapter 2: Literature review ............................................................................................................... 9

2.1. AN APPROACH USED FOR SEARCHING LITERATURE REVIEW ........................................................ 9

2.2. LITERATURE REVIEW- STRATEGIC GROUPS ............................................................................... 12

2.2.1. Introduction ......................................................................................................................... 12

2.2.2. Business strategy and its performance ................................................................................ 12

2.2.3. Strategic groups................................................................................................................... 15

2.2.3.1. The origins of strategic group theory ........................................................................... 15

2.2.3.2. Strategic group theory .................................................................................................. 18

2.2.4. Competitive positioning and competitive analysis ............................................................. 24

2.2.5. Summary ............................................................................................................................. 25

2.3. RETAIL INDUSTRY ...................................................................................................................... 26

2.3.1. Introduction ......................................................................................................................... 26

2.3.2. Retail ................................................................................................................................... 26

2.3.2.1. Definition of retail and brief report on current global retail industry .......................... 26

2.3.2.2. Trends in the retailing industry .................................................................................... 30

2.3.2.3. Types of Retailers ........................................................................................................ 32

2.3.2.4. Issues related to customer buying behavior ................................................................. 32

2.3.3. Summary ............................................................................................................................. 34

2.4. THE VIETNAMESE RETAIL INDUSTRY INSIGHTS ......................................................................... 34

2.4.1. Introduction ......................................................................................................................... 34

2.4.2. Overview about the Vietnamese retail industry .................................................................. 34

2.4.2.1. Traditional retail channels: Wet markets, “Mon and Pop” small independent grocery

stores ......................................................................................................................................... 41

2.4.2.2 E-commerce .................................................................................................................. 42

2.4.3. PESTEL analysis- Industry life cycle and the five forces model ........................................ 43

2.4.4. Drivers of change in the retail industry in Vietnam ............................................................ 52

2.4.4.1. The government’s control ............................................................................................ 52

2.4.4.2. Consumer behaviour patterns ....................................................................................... 52

2.4.4.3. E-commerce ................................................................................................................. 53

2.4.5. Summary ............................................................................................................................. 53

iv

2.5. CUSTOMER LOYALTY ................................................................................................................. 53

2.5.1. Introduction ......................................................................................................................... 53

2.5.2. Consumer tastes, consumer habits, consumer preferences and consumer behaviour ......... 54

2.5.3. Customer experience and customer perceived value .......................................................... 56

2.5.4. Consumer satisfaction ......................................................................................................... 64

2.5.5. Perceived switching barriers ............................................................................................... 68

2.5.6. Brand experience................................................................................................................. 73

2.5.7. Service quality .................................................................................................................... 76

2.5.8. Corporate factors ................................................................................................................. 81

2.5.8.1. In-store logistics and store image ................................................................................. 81

2.5.8.2. Store accessibility and loyalty ...................................................................................... 87

2.5.8.3. Customer service .......................................................................................................... 89

2.5.8.4. E-service quality .......................................................................................................... 92

2.5.8.5. Loyalty programmes and promotion effects ................................................................ 94

2.5.8.6. Product quality and price ............................................................................................. 96

2.5.9. Corporate social responsibility, corporate image and customer loyalty ............................. 97

2.5.10. Trust ................................................................................................................................ 100

2.5.11. Habit ................................................................................................................................ 100

2.5.12. Customer loyalty ............................................................................................................. 101

2.5.13. Research gaps, proposed research framework and hypotheses ....................................... 103

2.5.13.1. Research gaps ........................................................................................................... 103

2.5.13.2. The proposed conceptual research framework and hypotheses ............................... 105

2.5.14. Summary ......................................................................................................................... 109

Chapter 3: Research Methodology .................................................................................................. 111

3.1. INTRODUCTION ......................................................................................................................... 111

3.2. RESEARCH OBJECTIVES AND RESEARCH QUESTIONS RESTATED .............................................. 111

3.3. RESEARCH PHILOSOPHY AND RESEARCH PARADIGMS ............................................................. 112

3.3.1. Research philosophy and research paradigms ................................................................... 112

3.3.2. Apply paradigms to the thesis research ............................................................................. 116

3.4. ETHICAL THEORIES ................................................................................................................... 118

3.4.1. Philosophy and normative ethical theories ....................................................................... 118

3.4.2. Ethical paradigm and its implication................................................................................. 120

3.5. RESEARCH PROCESS ................................................................................................................. 121

3.6. THE CHOICE OF RESEARCH METHODOLOGY ............................................................................. 123

3.7. RESEARCH METHOD: PHASE ONE_ STEP ONE_EXPERT INTERVIEWING .................................. 126

3.7.1. Chosen research strategies: semi-structured interview ..................................................... 126

3.7.2. Sample and contacting the experts .................................................................................... 127

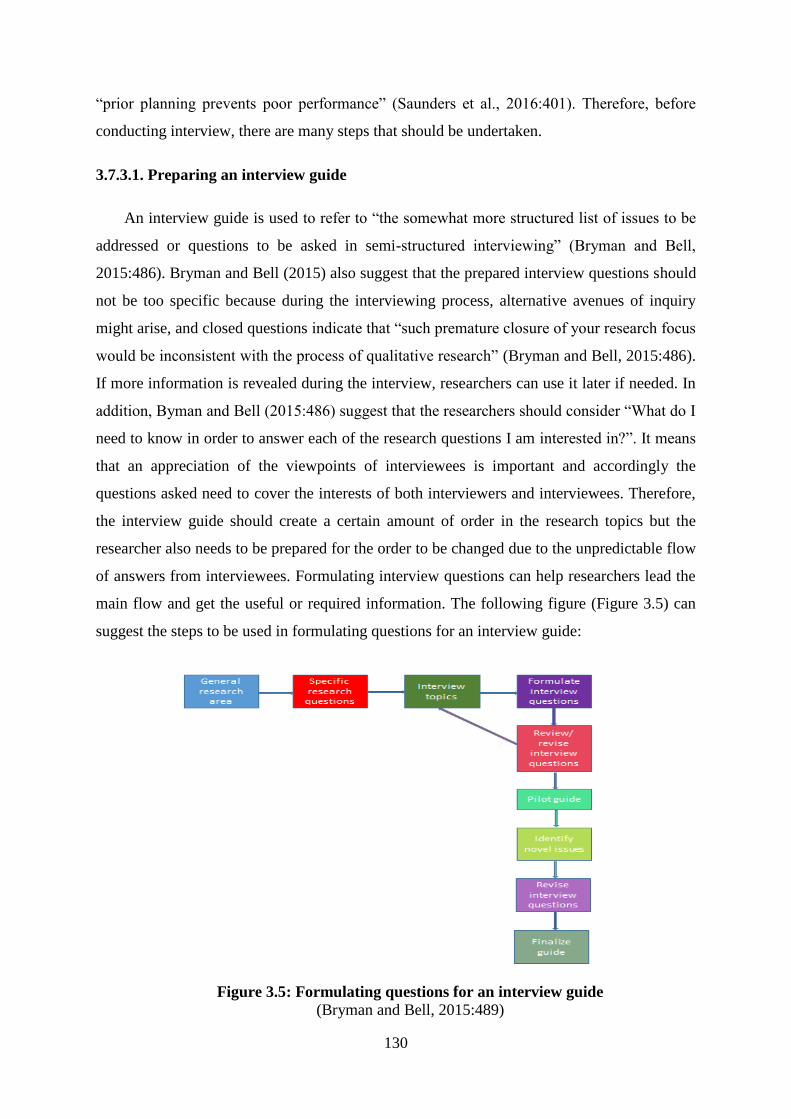

3.7.3. Interviewing guide development ....................................................................................... 129

3.7.3.1. Preparing an interview guide ..................................................................................... 130

3.7.3.2. Core questions ............................................................................................................ 132

3.7.3.3. Translation and back translation ................................................................................ 134

3.7.3.4. Conclusion ................................................................................................................. 136

3.7.4. Data collection .................................................................................................................. 136

3.7.5. Data analysis ..................................................................................................................... 137

3.8. RESEARCH METHOD: PHASE ONE _STEP TWO_SUPERMARKET CONSUMER INTERVIEWING ... 138

3.8.1. Sample size and contact .................................................................................................... 138

3.8.2. Interviewing contents ........................................................................................................ 139

v

3.8.3. Telephone and Internet-mediated interviews .................................................................... 139

3.8.4. Data analysis ..................................................................................................................... 140

3.9. RESEARCH METHOD: PHASE TWO_ QUESTIONNAIRE SURVEY................................................. 140

3.9.1. Survey Questionnaire ........................................................................................................ 140

3.9.2. Initial design and planning ................................................................................................ 141

3.9.2.1. Sampling frame identification .................................................................................... 142

3.9.2.2. Sample size ................................................................................................................ 142

3.9.2.3. Sampling design/sampling selection .......................................................................... 143

3.9.2.4. Locations selected for the study ................................................................................. 144

3.9.3. Scale Development, Reliability, Validity and replication ................................................. 144

3.9.3.1. Scale development ..................................................................................................... 145

3.9.3.2. Reliablility - Replication - Validity............................................................................ 146

3.9.4. Triangulation ..................................................................................................................... 150

3.9.5. Questionnaire Design and questionnaire construction ...................................................... 151

3.9.6. Data collection .................................................................................................................. 154

3.9.7. Data analysis ..................................................................................................................... 157

3.9.7.1. Exploratory factor analysis ........................................................................................ 158

3.9.7.2. Confirmatory factor analysis ...................................................................................... 159

3.9.7.3. Structural Equation Modeling_Goodness of fit ......................................................... 159

3.10. CONCLUSION .......................................................................................................................... 162

Chapter 4: Phase One - Qualitative data analysis.......................................................................... 164

4.1. STEP ONE - ANALYSIS FOR EXPERT INTERVIEWING: STRATEGIC GROUP MAPPING ................. 164

4.1.1. Introduction ....................................................................................................................... 164

4.1.3. Data analysis and discussion ............................................................................................. 165

4.1.4. Conclusion ........................................................................................................................ 170

4.1.5. Summary ........................................................................................................................... 170

4.2. STEP TWO - ANALYSIS FOR CONSUMER INTERVIEWING: CUSTOMER LOYALTY PERCEPTION .. 170

4.2.1. Introduction ....................................................................................................................... 170

4.2.3. Data analysis and discussion ............................................................................................. 173

4.2.4. Conclusion ........................................................................................................................ 190

Chapter 5: Phase Two - Quantitative data analysis ....................................................................... 193

Survey Descriptive Statistics and Exploratory Factor Analysis ................................................... 193

5.1. INTRODUCTION ......................................................................................................................... 193

5.2. DATA PREPARATION AND DATA SCREENING ............................................................................ 193

5.2.1. Data preparation ................................................................................................................ 193

5.2.2. Data screening ................................................................................................................... 193

5.2.2.1. Missing data ............................................................................................................... 193

5.2.2.2. Identification of outliers ............................................................................................. 194

5.2.2.3. Normality test - statistics ............................................................................................ 195

5.2.3. Response rate and Non-response bias ............................................................................... 196

5.3. DESCRIPTIVE STATISTICS ......................................................................................................... 197

5.3.1. Respondent demographic data .......................................................................................... 197

5.3.2. Shopping behaviour - Respondents’ choices .................................................................... 199

5.3.3. Mean and standard deviation values for all constructs ..................................................... 199

5.4. INTERNAL CONSISTENCY .......................................................................................................... 201

5.5. EXPLORATORY FACTOR ANALYSIS ........................................................................................... 203

5.5.1. The results from Exploratory factor analysis .................................................................... 203

vi

5.5.2. Conclusion ........................................................................................................................ 206

5.6. THE REVISED MODEL ................................................................................................................ 206

Chapter 6: Confirmatory factor analysis and structural equation modelling ............................ 208

(Construct validation and hypothesis testing) ................................................................................ 208

6.1. INTRODUCTION ......................................................................................................................... 208

6.2. UNIDIMENSIONALITY - INITIAL MODEL FIT .............................................................................. 208

6.3. CONSTRUCT VALIDITY ............................................................................................................. 211

6.3.1. Convergent and discriminant validity ............................................................................... 211

6.3.1.1. Convergent validity .................................................................................................... 211

6.3.1.2. Discriminant validity .................................................................................................. 211

6.3.1.3. Criteria summarizing.................................................................................................. 212

6.3.2. Results from construct validity ......................................................................................... 212

6.3.2.1. Convergent validity .................................................................................................... 212

6.3.2.2. Discriminant validity .................................................................................................. 216

6.3.2.3. Conclusion ................................................................................................................. 220

6.4. COMMON METHOD BIAS ........................................................................................................... 220

6.5. FINAL MEASUREMENT MODEL FIT ............................................................................................ 220

6.6. STRUCTURAL MODELS .............................................................................................................. 221

6.6.1. Multivariate assumptions .................................................................................................. 221

6.6.1.1. Outliers and influentials ............................................................................................. 221

6.6.1.2. Multicollinearity analysis ........................................................................................... 222

6.6.2. Structural model validity ................................................................................................... 224

6.6.3. Results from hypothesis testing ........................................................................................ 225

6.6.3.1. Direct effects .............................................................................................................. 225

6.6.3.4. Multigroup analysis.................................................................................................... 231

6.6.3.4.1. Comparison between retail strategic groups ....................................................... 231

6.6.3.4.2. Comparison between gender ............................................................................... 236

6.6.3.4.3. Comparison between income groups .................................................................. 237

6.6.3.4.4. Comparison between location ............................................................................. 240

6.6.3.4.5. Comparison between age groups ........................................................................ 242

6.6.3.4.6. Comparison between occupation ........................................................................ 246

6.6.3.4.7. Comparison between education levels ................................................................ 249

6.6.3.5. Conclusion ................................................................................................................. 251

Chapter 7: Discussion of the findings .............................................................................................. 252

7.1. INTRODUCTION ......................................................................................................................... 252

7.2. DIRECT EFFECTS’ DISCUSSION .................................................................................................. 252

7.2.1. Results from all hypotheses related to customer perceived value (CPV) ......................... 252

7.2.2. Results from all hypotheses related to customer satisfaction (CS) ................................... 257

7.2.3. Results from all hypotheses related to customer loyalty (CL) .......................................... 263

7.3. MULTI-GROUP COMPARISONS’ DISCUSSION (COMPARISONS ACROSS GROUPS FOR FACTORS

RELATED TO CUSTOMER LOYALTY) ................................................................................................ 272

Chapter 8: Conclusion ...................................................................................................................... 279

8.1. INTRODUCTION ......................................................................................................................... 279

8.2. SUMMARY OF MAIN FINDINGS .................................................................................................. 279

8.2.1. Conclusions regarding the research questions .................................................................. 279

8.2.2. Other conclusions .............................................................................................................. 284

vii

8.2.3. Contributions to theory, methodology and practice .......................................................... 285

8.2.3.1 Contribution to theory ................................................................................................. 285

8.2.3.2. Contribution to methodological level......................................................................... 286

8.2.3.3. Contribution to practice ............................................................................................. 288

8.3. THESIS LIMITATIONS AND RECOMMENDATIONS FOR FUTURE RESEARCH ............................... 290

REFERENCES .................................................................................................................................. 293

APPENDICES ................................................................................................................................... 329

viii

LIST OF FIGURES

Figure 1.1: A structure of thesis .............................................................................................................. 8

Figure 1.2: The process of selecting articles reviewed for this study ................................................... 11

Figure 2.2.1: The basic SCP model....................................................................................................... 18

Figure 2.2.2: Ilustrative map of the US chain saw industry .................................................................. 22

Figure 2.2.3: Average net profit before tax for market specialisation and company ownership .......... 22

Figure 2.2.4: Average net profit before tax for company’s pricing strategy and most important

customer type ........................................................................................................................................ 23

Figure 2.2.5: Strategic groups scheme .................................................................................................. 23

Figure 2.2.6: BCG matrix ..................................................................................................................... 25

Figure 2.2.7: Porter’s Five Forces Model – Fundamental determinants of industry competition ........ 25

Figure 2.3.1: Distribution Channel ....................................................................................................... 27

Figure 2.3.2: Top 250 quick statistics, FY2015 .................................................................................... 27

Figure 2.3.3: The top 20 global retailers, FY 2014 ............................................................................... 28

Figure 2.3.4: The top 20 global retailers, FY 2015 ............................................................................... 29

Figure 2.3.5: Global retail geographic analysis .................................................................................... 30

Figure 2.3.6: Stages in the Buying Process ........................................................................................... 33

Figure 2.4.1: The population pyramid of Vietnam ............................................................................... 35

Figure 2.4.2: Vietnam’s urban population ............................................................................................ 43

Figure 2.4.3: PESTLE analysis ............................................................................................................. 44

Figure 2.4.4: Vietnam inflation rate ...................................................................................................... 46

Figure 2.4.5: Vietnam GDP per capita .................................................................................................. 48

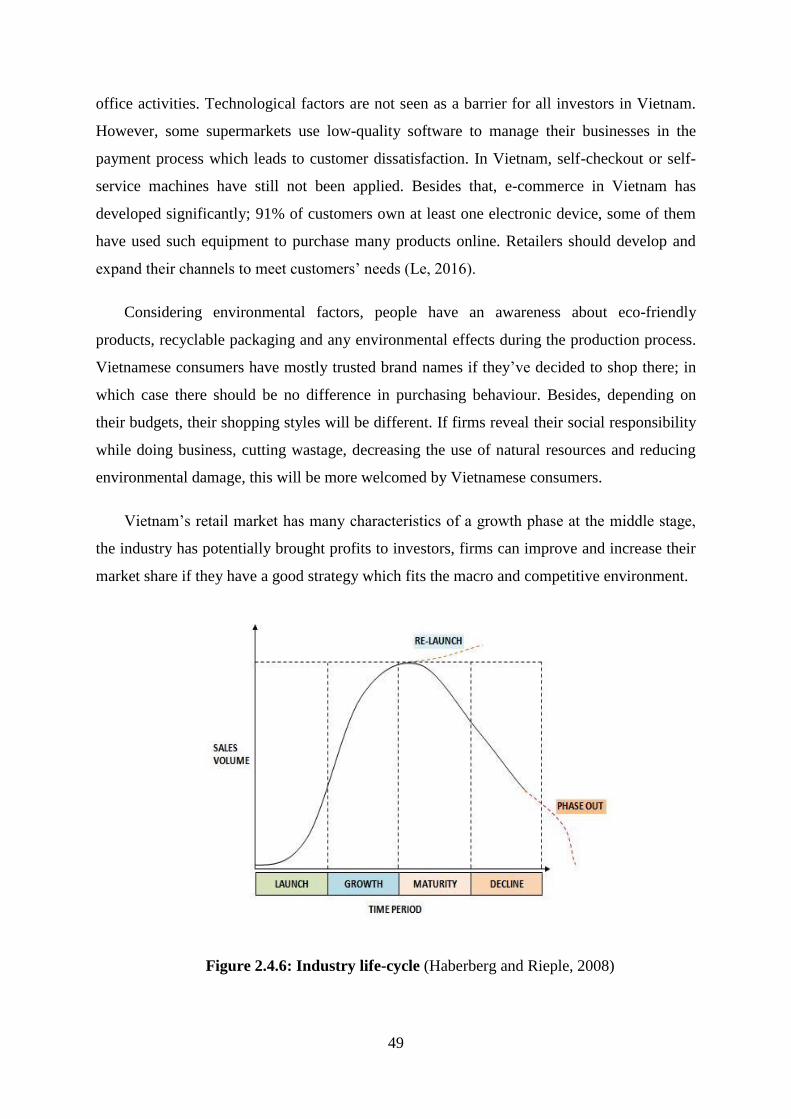

Figure 2.4.6: Industry life-cycle ............................................................................................................ 49

Figure 2.4.7: The Five Forces model .................................................................................................... 50

Figure 2.5.1: Factors affecting customer behaviour.............................................................................. 54

Figure 2.5.2: Application of the sequential incident technique to touch point research ....................... 58

Figure 2.5.3: Some ways in which customers measure their satisfaction ............................................. 66

Figure 2.5.4: Elements of customer service .......................................................................................... 66

Figure 2.5.5: The conceptual framework .............................................................................................. 71

Figure 2.5.6: Determinants of Perceived Service Quality..................................................................... 79

Figure 2.5.7: Service Quality Model ..................................................................................................... 79

Figure 2.5.8: Five dimensions of SERVQUAL model ......................................................................... 80

Figure 2.5.9: Entities in retail store operation ....................................................................................... 83

Figure 2.5.10: In-store logistics process ............................................................................................... 84

Figure 2.5.11: The relationship between in-store logistic, customer satisfaction and customer loyalty

.............................................................................................................................................................. 86

ix

Figure 2.5.12: The customer service factors ......................................................................................... 91

Figure 2.5.13: Historical development of service quality scale in online retail .................................... 93

Figure 2.5.14: The conceptual framework of e-service quality ............................................................ 93

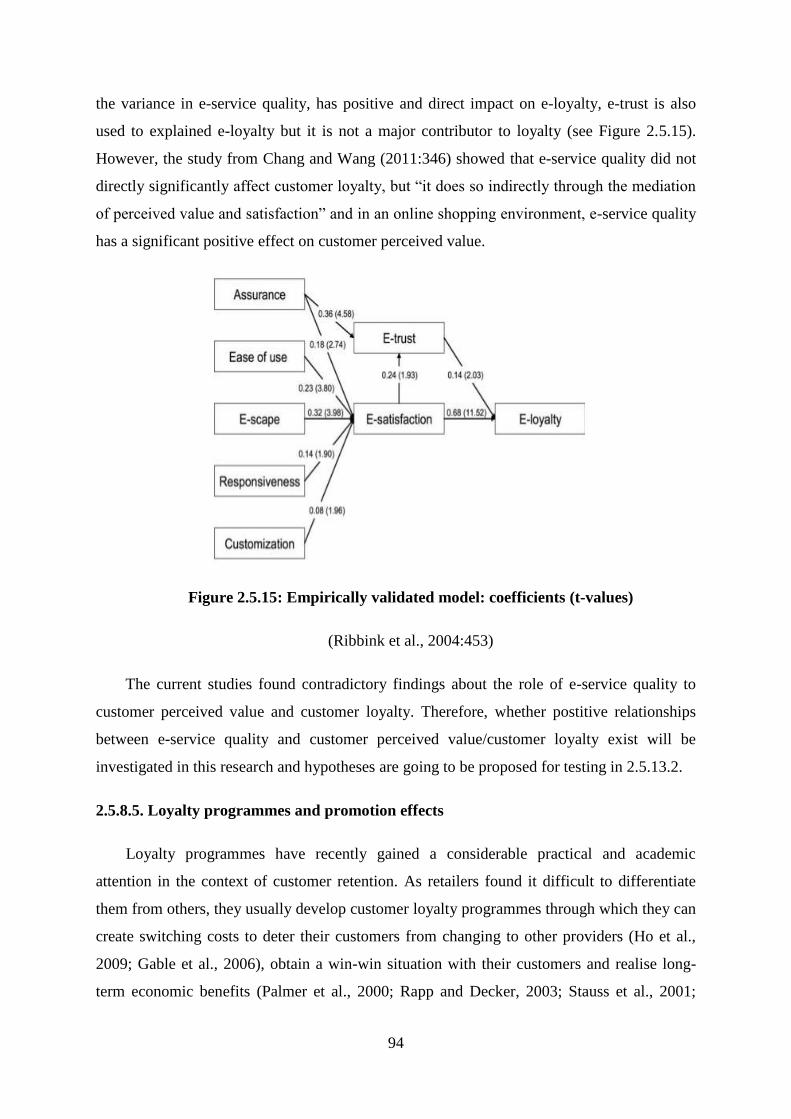

Figure 2.5.15: Empirically validated model: coefficients ..................................................................... 94

Figure 2.5.16: General frustration model .............................................................................................. 96

Figure 2.5.17: Final causal relationships for virtual mobile service ..................................................... 98

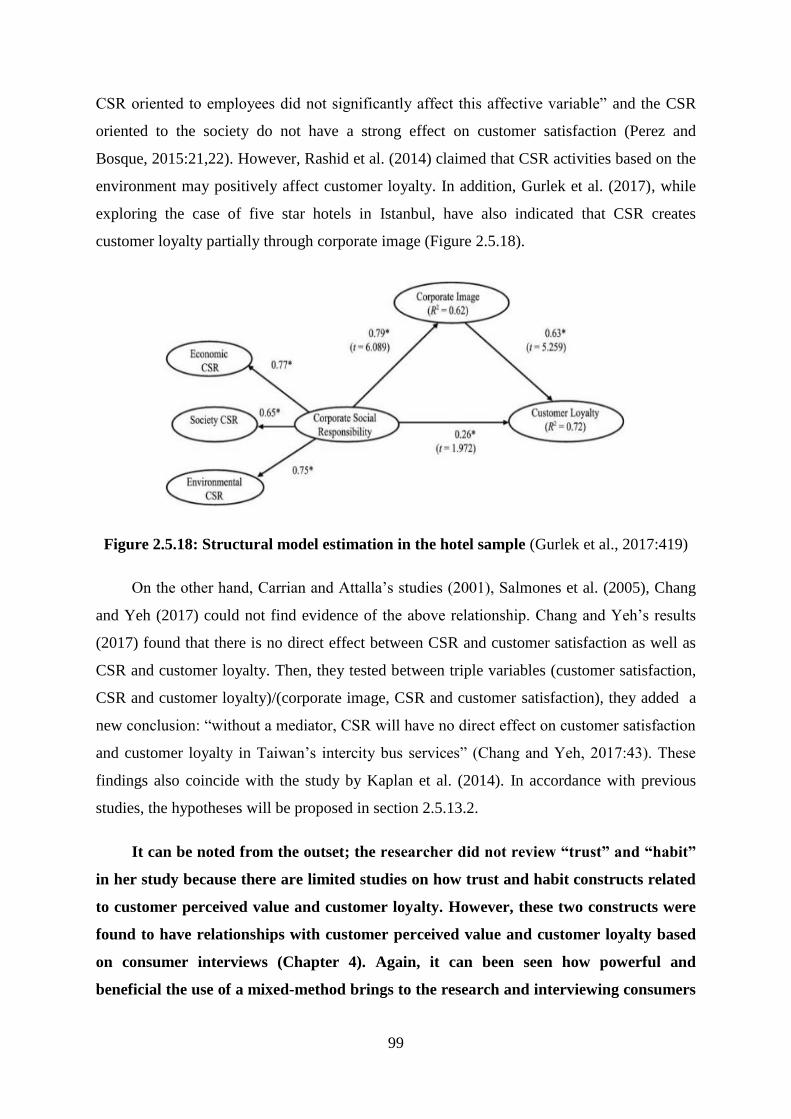

Figure 2.5.18: Structural model estimation in the hotel sample ........................................................... 99

Figure 2.5.19: The proposed conceptual model of this research ......................................................... 107

Figure 3.1: Different logics used in quantitative and qualitative studies ............................................ 115

Figure 3.2: The research process......................................................................................................... 122

Figure 3.3: The research process onion .............................................................................................. 123

Figure 3.4: Steps in the process of conducting a mixed methods study.............................................. 124

Figure 3.P: Procedure of two phases conducted in this research ........................................................ 125

Figure 3.5: Formulating questions for an interview guide .................................................................. 130

Figure 3.6: Some main questions that should be covered in all qualitative interviews ..................... 132

Figure 3.7: Data collection processes in Phase One ........................................................................... 137

Figure 3.8: Planning a survey ............................................................................................................. 141

Figure 3.9: Stage in the development of the loyalty scale .................................................................. 145

Figure 3.10: Testing goodness of measures-forms of reliability and validity ..................................... 146

Figure 3.11: Data collection process applied in Phase Three ............................................................. 156

Figure 3.12: Types of questionnaire ................................................................................................... 157

Figure 3.R: Main results from two phases .......................................................................................... 163

Figure 4.1: Contents of Chapter 5 and Chapter 6................................................................................ 192

Figure 5.1: Normal Probability Plot .................................................................................................... 196

Figure 5.2: The revised model for main study .................................................................................... 207

Figure 6.1: Results from CFA_1strun .................................................................................................. 209

Figure 6.2: Results from outlier testing_Cook’s distance analysis ..................................................... 222

Figure 6.3: The second SEM (SEM_2nd

run) ....................................................................................... 225

Figure 6.4: The results of revised model of this research ................................................................... 230

x

LIST OF TABLES

Table LR (Literature review) 1-2: Literature review approach .............................................................. 9

Table 2.3.1: Types of Retailers ............................................................................................................. 32

Table 2.4.1: Main supermarkets in Vietnam ......................................................................................... 40

Table 2.4.2: Vietnam’s Grocery Retail Sales by Channel, trillion VND .............................................. 41

Table 2.5.1: Summary of experience antecedent researches ................................................................. 58

Table 2.5.2: Experience Measurement Method .................................................................................... 59

Table 2.5.3: Items for scale development ............................................................................................. 60

Table 2.5.4: Variables used for the retail brand experience (RBE) model ........................................... 76

Table 2.5.5: Differences between products and services ...................................................................... 78

Table 2.5.6: Retail site store location selection main criteria comparison martrix ............................... 88

Table 2.5.7: Comparison matrix of sub criteria for store location main criteria ................................... 88

Table 3.1: Comparison of positivism and interpretivism paradigms .................................................. 114

Table 3.2: Comparison of quantitative and qualitative methodologies ............................................... 115

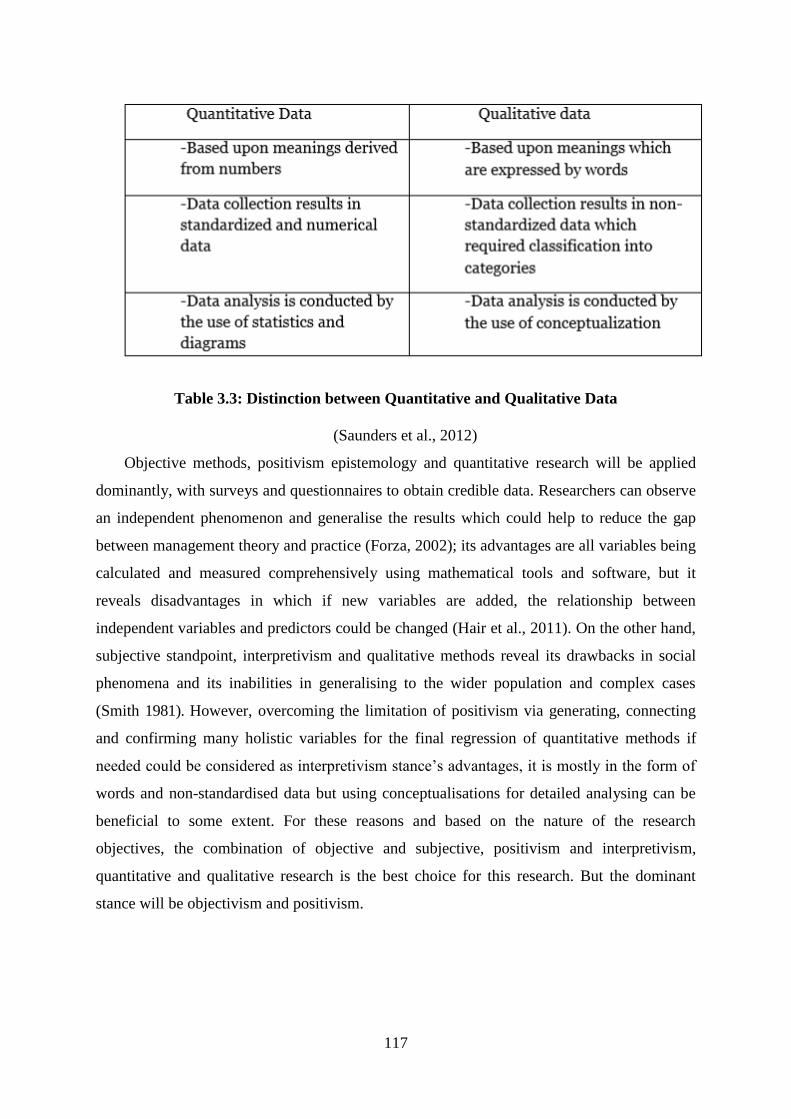

Table 3.3: Distinction between Quantitative and Qualitative Data ..................................................... 117

Table 3.4: Comparisions between purposive and probability sampling techniques ........................... 128

Table 3.5: Advantages of non-probability sampling techniques ......................................................... 129

Table 3.6: Structural of semi-structured interview protocol in Phase One (Step One) ....................... 134

Table 3.7: Translation techniques for questionnaires ......................................................................... 135

Table 3.8: The process of data analysis .............................................................................................. 138

Table 3.9: Advantages of Probability Sampling Techniques .............................................................. 144

Table 4.1: Details of interviewees from Phase One (supermarket consumers) .................................. 172

Table 4.2: Interviewees’ descriptive information ............................................................................... 173

Table 5.2: The descriptive statistics for all items in the dataset .......................................................... 201

Table 5.3: All remained variables after EFA ...................................................................................... 205

Table 6.1: Model fit of CFA_1strun .................................................................................................... 210

Table 6.3: Results from CFA_2thrun_Discriminant validity checking ............................................... 216

Table 6.4: Results from CFA_2nd

run, the correlation between RBEX and other constructs .............. 217

Table 6.5: Model fit from CFA_3rd

run ............................................................................................... 217

Table 6.6: Results from CFA_3thrun_ Discriminant validity checking .............................................. 217

Table 6.7: Results from data analysis (CFA_3rd

run) .......................................................................... 218

Table 6.8: Model fit of CFA_4thrun .................................................................................................... 218

Table 6.9: Results from CFA_4thrun_ Discriminant validity checking .............................................. 219

Table 6.11: Summarising results of CFA model fit ............................................................................ 220

Table 6.12: Results from zero constraints test .................................................................................... 220

Table 6.13: Multicollinearity analysis ................................................................................................ 224

xi

Table 6.14: Summarising results from SEM running (SEM_1strun, SEM_2

ndrun) ............................ 226

Table 6.M.1: Multigroup analysis for COOP or BIGC ad LOTTE MART ........................................ 232

Table 6.M.2: Multigroup analysis for COOP or BIGC and VINMART ............................................ 234

Table 6.M.3: Multigroup analysis for Lotte Mart and Vinmart .......................................................... 235

Table 6.M.4: Multigroup analysis for COOP or BIGC and AEON .................................................... 236

Table 6.M.5: Multigroup analysis for gender ..................................................................................... 237

Table 6.M.6: Multigroup analysis for “under 5 million VND (GB£170)” and “from 5 to 10 million

VND (GB£170-340)” income groups ................................................................................................. 238

Table 6.M.7: Multigroup analysis for “under 5 million VND (GB£170)” and “from 10 to 20 million

VND (GB£340-680)” income groups ................................................................................................. 239

Table 6.M.8: Multigroup analysis for Ho Chi Minh and Hanoi ......................................................... 240

Table 6.M.9: Multigroup analysis for Ho Chi Minh and Da Nang ..................................................... 241

Table 6.M.10: Multigroup analysis for Can Tho and Binh Duong ..................................................... 242

Table 6.M.11: Multigroup analysis for “18-22 and 22-30” age groups .............................................. 243

Table 6.M.12: Multigroup analysis for “22-30 and above 55” age groups ......................................... 244

Table 6.M.13: Multigroup analysis for “18-22 and 41-55” age groups .............................................. 245

Table 6.M.14: Multigroup analysis for “23-30 and 41-40” age groups .............................................. 246

Table 6.M.15: Multigroup analysis for “housewife and office staffs” occupation groups ................. 247

Table 6.M.16: Multigroup analysis for “students and self employment” occupation groups ............. 248

Table 6.M.17: Multigroup analysis for “self employment and office staffs” occupation groups ....... 249

Table 6.M.18: Multigroup analysis for “A levels and college, university” groups ............................ 250

Table 6.M.19: Multigroup analysis for “GCSE’s and college, university” groups ............................ 250

Table 7.1: Factors directly affecting customer perceived value.......................................................... 253

Table 7.2: Factors directly affecting customer satisfaction ................................................................ 258

Table 7.3: Factors directly affecting customer loyalty ........................................................................ 264

xii

LIST OF APPENDICES

Appendix 2.1 - All hypotheses proposed in this research ................................................................... 329

Appendix 2.2 - Linkage between hypotheses and research questions ............................................... 331

Appendix 2.3 - Latent factors and manifest varibles used in this research ......................................... 332

Appendix 3.1 – Research Ethics approval letter ................................................................................. 334

Appendix 3.2 - Guide used for expert’s semi-structured interviews................................................... 335

Appendix 3.3 – Questionnaire used in supermarkets’ consumer interviewing ................................... 337

Appendix 3.4 – Questionnaire survey ................................................................................................. 340

Appendix 3.5 - Measurement variables used from Section 2 to Section 6 in the questionnaire (Phase

Two) and code book for other questions used in questionnaire .......................................................... 349

Appendix 4.1 – Some more direct quote of supermarket’s consumer interviewing in Phase One ..... 354

Appendix 5.1 – Results from Tests of normality ................................................................................ 365

Appendix 5.2 - Normal probability plots ............................................................................................ 368

Appendix 5.3 – Independent samples test (Non-bias response).......................................................... 370

Appendix 5.4- Full pie-charts summarises all respondents’ demographic information...................... 374

Appendix 5.5 – The shopping behaviours of Vietnamese supermarket consumers ............................ 375

Appendix 5.6 – Internal consistency of all researched constructed before EFA ................................ 378

Appendix 5.7- KMO and Barlett’s Test- Communalities (EFA) ........................................................ 384

Appendix 5.8 - Total Variance Explained (EFA) ............................................................................... 385

Appendix 5.9 - Pattern matrix (EFA) .................................................................................................. 387

Appendix 5.10 – All measurement variables remained after EFA ..................................................... 390

Appendix 6.1 - Results from CFA_2ndrun ........................................................................................ 393

Appendix 6.2- The final CFAmodel_Results from CFA_4thrun_after construct validity checking ... 394

Appendix 6.3- Common method bias testing ...................................................................................... 395

Appendix 6.4 - The initial SEM (SEM_1strun) and its results ........................................................... 396

Appendix 6.5 - SEM_2rdrun_Final .................................................................................................... 397

Appendix 6.6 - Summarising all hypothesis testing results ................................................................ 399

Appendix 7.1- Comparison across groups for factors related to customer loyalty ............................. 400

Appendix 7.2- Comparison across groups for factors related to customer satisfaction ...................... 401

Appendix 7.3- Comparison across groups for factors related to customer perceived value ............... 403

xiii

LIST OF ABBREVIATIONS

CPV Customer perceived value

CS Customer satisfaction

CL Customer loyalty

ISL In-store logistics

SQ Service quality

ESQ E-service quality

ESQX1 E-service quality related to a website quality scale

ESQX2 E-service quality related a core quality scale

PROQ Product quality

CUSER Customer service

CUEXP Customer experience

STIMA Store image

COIMA Corporate image

CSR Corporate social responsibility

STAC Store accessibility

ALA Alternative attractiveness

SWC Switching costs

LPRO Loyalty programs

PROE Promotion effect

EFA Exploratory factor analysis

CFA Confirmatory factor analysis

SEM Structural equation modelling

CR Composite reliability, construct reliability

AVE Average variance extracted

MSV Maximum shared variance

RBV Resource-based view

1

Chapter 1: Introduction

1.1 Introduction

This introductory chapter presents some general background to the research conducted

by the researcher before explaining the context in which the empirical work will be explored.

Then, research problems will be indicated, followed by the approach used to investigate the

topics and will conclude with the structure of this thesis and its conclusions.

1.2. Research background

There are continuously debated theories related to customer loyalty and how firms can

achieve sustainable development. These issues are apparently proved to have a strong impact

on firms’ survival associated with their profits. The initial idea for this research in my area of

expertise, with five years experience researching the strategic management angle in business,

parallel with the question of how to keep customers loyal to a business. For this reason, the

researcher was skeptical about the term of strategic-groups in marketing, particularly when

looking at the relationships between factors affecting customer loyalty, which had been

largely under-researched. For example, whether satisaction is a main indicator of customer

loyalty as well as whether differences between factors affecting customer loyalty in a specific

industry exist in regarding to income, gender, location, age group, occupation and education

levels. The following contents will pave the way for the whole research by demonstrating

some basic information related to this research project.

The trends of globalisation and integration have made the world come closer and

customers around the world tend to move to the same consumption style. However, in many

cases, there are still different consumer behaviours in specific industries. The meaningful

considered question by most researchers and business practitioners is which factors affect

customer loyalty (El-Andt and Eid, 2016; Perez and Bosque, 2015; Gurlek et al., 2017;

Chang and Yeh, 2017; Chen and Hu, 2013) in specific business sectors. Customer loyalty is

defined as “a deeply held commitment to re-buy, re-patronise a preferred product or service

consistently in the future, thereby causing repetitive same-brand or same brand-set

purchasing, despite situational influences and marketing efforts having the potential to cause

switching behaviour” (Oliver, 1997:392). Many firms compete fiercely to attract more

2

customers. Customer loyalty is an ultimate goal and dream of all retailers; it could help firms

increase from 25-85 percent profit (Reichheld et al., 1990). According to Mutum et al.,

(2014), Stan et al. (2013), Qui et al. (2015), customers tend to be loyal to firms that offer

superior value compared to their rivals, and these customers are willing to have an intensive

relationship with firms over time that can help firms save much money for their marketing

campaigns as they launch new products or offer new services.

Based on strategic theories used in specific industries, different strategic groups might

have different factors affecting customer loyalty. Leask and Parker (2006) define a strategic

group as a group of corporations that employ the same or similar strategies in a specific

industry. The term strategic group seeks to identify configurations based on observing

firms’ behaviour and then explain differential performance. Similar characteristics of such

group will likely relate to cost structure, formal organisation, control systems, management

rewards and punishment. Such groups are important for retail logistics and supply chain

management (SCM) as different strategic positions of grocery retailers will shape their retail

supply chains and replenishment and fulfillment activities. However, previous research has

appeared not to investigate factors affecting customer loyalty in different strategic groups,

rather it examined specific industries and extrapolated results to the whole industry. This

means that the differences between strategic groups in the same industry have been ignored.

In addition, the relationship between customer satisfaction and customer loyalty as well as

which factors may affect customer loyalty has been unceasingly debated between scholars.

Kursunluoglu (2014:538) found “customer service had effects on customer satisfaction” and

“customer service could explain 13.9 percent of total variance in customer satisfaction and

12.5 percent of total variance in customer loyalty”. Kumar et al. (2013:258) demonstrated

that although there is a positive relationship between customer satisfaction and customer

loyalty, the variance that could be explained by just a satisfaction is very small (around 8

percent). Therefore, they proposed scholars should investigate customer loyalty with many

other variables such as customer perceived value, switching barriers and relational variables

such as trust, commitment, relationship age, and loyalty programme membership. In

contrast, Lou and Bhattacharya (2006) and Oliver (1997), Kim et al. (2004), Shankar et al.

(2003), Chadha and Kapoor (2009) found that customer satisfaction is a major driver of

customer loyalty and it is well-known and confirmed by many other researchers. Besides

that, factors constitute customer perceived value and customer satisfaction have also been

debated among scholars. Most studies, which relate to customer loyalty in the retailing

3

industry, have separately explored customer loyalty and specific factors such as brand

image, social responsibility, and switching cost. There is no research examining many such

factors simultaneously affecting customer loyalty.

Vietnam’s retail market is characterised as being one of the most dynamic markets in the

region with high annual growth rates. Hanoi and Ho Chi Minh City have been ranked

amongst the top 10 Asian cities for retail expansion in 2014. With a population of more than

93 million people, about 70 percent of them aged from 16 to 64 which is a factor in the

potential growth of the retail industry; this figure is also known as the “Golden retail index”

(Oxford Business Group, 2017) and Vietnam was placed sixth in the 2017 Global Retail

Development Index (GRDI) (Vietnamnet, 2017). In addition, from 2015 to 2020, Vietnam’s

urban population is forecast to grow by 2.6%, one of the highest growth rates in the region

(Retail in Asia, 2016; Le, 2016). With the population’s high propensity to absorb new things

and readily change consumption habits, the Vietnamese retail market can promise a huge

potential for both domestic as well as foreign investors. However, to the best of my

knowledge, there is no comprehensive published paper investigating customer loyalty in the

supermarket sector in Vietnam as well as Vietnamese consumption style. Therefore, in this

research, factors affecting customer loyalty of different strategic groups in the Vietnamese

food and consumer-goods industry will be explored. The findings will be of potential benefit

to all business and academic researchers, and strategic decision makers when they look at

customer loyalty of a specific industry in Vietnam, especially in applied business strategies

for sustainable success.

1.3. Context of study

Therefore, the aim of this thesis is to investigate factors affecting customer loyalty of

different strategic groups in Vietnamese supermarkets, as the term strategic groups in the

grocery sector has been ignored by most researchers and the topic of comprehensive factors

affecting customer loyalty is under-researched. The Vietnamese supermarkets have been

selected for four main reasons. Firstly, Vietnam’s retail industry is one of the most dynamic

markets in the region with high annual growth rates; there is a huge potential platform with

“Golden retail index” and profits as well as market share that investors can invest their

money to (Oxford Business Group, 2017). Secondly, supermarkets in Vietnam have been

generating a large amount of revenue compared to other modern retail formats (Vo, 2017).

Thirdly, it might be interesting to investigate customer loyalty in the Vietnamese retail

4

market due to a huge different culture across the country which could generate informative

findings. Finally, scholars understand the Vietnamese retail market via news posted in social

media and online newspapers in Vietnam, there are a limited number of official papers

published about the Vietnamese retail industry. Via this research, scholars and practitioners

can fully understand the whole picture of the Vietnamese retail industry, which will be

presented in Chapter 2.

1.4. Research objectives

Based on the background information the research objectives are as follows:

Provide insights into the Vietnamese retailing industry; classify all current

supermarket firms in Vietnam to their proper strategic groups.

Investigate factors directly affecting customer loyalty, customer satisfaction and

customer perceived value in Vietnamese supermarkets by simultaneously researching

and comparing different strategic groups.

Examine whether there are differences between factors affecting customer loyalty

based on age groups, location, income, gender, occupation and education level.

1.5. Research questions

There are five research questions proposed in this study based on the foregoing

background and research objectives:

RQ1: What factors directly affect customer loyalty in the Vietnamese supermarket sector and

at which level?

RQ2: Is customer satisfaction a major indicator for customer loyalty or not?

RQ3: What factors directly affect customer perceived value, customer satisfaction in the

Vietnamese supermarket sector and at what level?

RQ4: Are there any differences in terms of factors affect customer loyalty between strategic

groups in the Vietnamese retail industry?

RQ5: Are there differences between the factors affecting customer loyalty in the retail

industry based on income, gender, location, age groups, occupation and education levels?

5

1.6. Research methodology

Based on research objectives and research questions presented above, both primary data

and secondary data should be collected in order to answer the questions of which factors

affect customer loyalty and at what level. Therefore, this research is going to use a mixed

method involving both qualitative and quantitative research. Full explanation as to why this

methology should be used in this research will be presented in Chapter 3. The main

ontological and epistemological stances in this research are objectivism and positivism

respectively. The empirical study follows Cannon (2004) who suggested steps in the process

of conducting a mixed method which is believed to be the best way to investigate the gaps

presented later and answer all research questions, and it is comprised of two phases: Phase

One (Step One) is a strategic group mapping that all current supermarkets in Vietnam will be

grouped into different strategic groups based on interviewing experts in the Vietnamese retail

industry. Phase One (Step Two) is an inductive phase that will involve conducting semi-

structured interviews with about 21 consumers who currently shop at supermarkets across the

country, five main markets investigated will be Ho Chi Minh, Hanoi, Can Tho, Da Nang and

Binh Duong. Lastly, Phase Two will be a deductive phase that will consist of an edited

questionnaire survey related to factors affecting customer loyalty in Vietnam to test and

validate the variables and constructs which would be built based on background literature, the

conceptual model proposed in 2.5.13.2 and the results from Phase One (Step Two). In Phase

Two, descriptive statistics, including data frequencies, means, standard deviations and cross-

tabulation will be demonstrated. Exploratory factor analysis (EFA) will be used to examine

the data sets from the questionnaire and explore any latent constructs, remove duplicated

variables, determine underlying dimensions or factors which are not known a priori in a set of

correlated variables (Hair et at., 2011). Confirmatory factor analysis (CFA) and structural

equation modelling (SEM) will be used in this research to determine the validity, reliability

and relationships between many remaining variables after EFA. An analysis of SEM will also

be used in this research in order to demonstrate the relationships between constructs (Hair et

at., 2011).

1.7. Potential contributions of this research

Firsly, this research is going to generate a comprehensive research framework of factors

influencing customer loyalty, customer satisfaction and customer perceived value which can

be used by other researchers in the future to investigate other markets and industries. Based

6

on would-be-collected data in the Vietnamese grocery sector, the researcher will confirm the

relationship between constructs involved, which are benificial for practitioners, as well as

answer the question of whether satisfaction is a main indicator of customer loyalty. In

addition, the researcher expects to prove that the term strategic groups in any industry should

not be ignored when conducting multigroup analysis. The next potential contributions would

be mediation and moderation effects if possible. Finally, differences between the factors

affecting customer loyalty in the retail industry based on income, gender, location, age

groups, occupation and education levels will be revealed.

1.8. Thesis outline

The thesis is divided into 8 chapters. After this introductory chapter, the contents are as

follow:

Chapter 2: The objective of this chapter is presenting literature related to a research topic.

Section 2.1 will indicate the approach used for searching literature review.

Section 2.2 named “Literature review - strategic groups” has three main parts.

First, it provides knowledge around strategic groups, including emphasising the

importance of business strategy, review about some origins of strategic group

theories (resource based view and industrial theory), brief insight about strategic

group theory as well as how to shape firms into their specific groups. Then,

some literature related to competitive positioning and analysis will also be

mentioned. This section aims to demonstrate the meaning of strategic groups.

Then, Section 2.3 named “Retail industry”, will present a brief report on current

global retail industry, followed by trends in the retailing industry, which are

growing diversity of retail formats and globalisation, social media-driven

economy, changes in customers’ preferences. Then, the section will summarise

types of retailers and indicate many issues related to customer buying

behaviour.

Section 2.4 named “The Vietnamese retail industry – insights”, will demonstrate

the Vietnamese retail industry insight. In that, it focuses on the supermarket

format for food and consumer goods as well as current traditional retail channels

in Vietnam (wet or flea market, “Mom and Pop” small independent grocery

stores). Firstly, an overview of the Vietnamese retail industry, customer

7

preference will be explored, followed by PESTLE analysis, industry life cycle

and the five forces model applied in the Vietnamese retail industry. Finally,

drivers of change in the Vietnamese retail industry, which include the impact of

government control, consumer behaviour patterns, and e-commerce will be

presented.

Finally, Section 2.5 named “Literature review - Customer loyalty”, provides a

review of many aspects of customer loyalty such as customer taste and

preferences, customer experience and customer perceived value, customer

satisfaction, perceived switching cost and switching barriers, brand experience,

service quality and further dimensions related to corporate factors such as in-

store logistics and store image, store accessibility and store loyalty, customer

service, e-service quality and product quality. Finally, the debate around factors

affecting customer loyalty will be discussed and the research framework and

hypotheses will be proposed.

Chapter 3 : This chapter defines the research approaches and methodologies undertaken in

this thesis; it also indicates some issues relating to research quality, data

collection and analysis methods used during research (there are two phases of

empirical research conducted in this area).

Chapter 4: This chapter provides qualitative data analysis (results from Phase One - Step

One and Step Two).

Chapter 5: This chapter refers to the main study of this research, named “Survey descriptive

statistics and exploratory factor analysis” (Phase Two - Questionnaire survey).

Chapter 6: This chapter presents results from confirmatory factor analysis and structural

equation modelling (Phase Two - Questionnaire survey).

Chapter 7: This chapter aims to provide the interpretation of the findings and discussion.

Chapter 8: Conclusion of the research and the many implications that can be made. The

limitations of this research are also presented, followed by suggestions for future

research around the investigated topic.

Figure 1 will present the above information in a chart form:

8

Chapter 1: Introduction

Chapter 5: Phase Two – Survey

Descriptive Statistics and

Exploratory Factor Analysis

Chapter 6: Confirmatory factor

analysis and structural equation

modelling (Construct validation and

hypothesis testing)

Chapter 7: Discussion the findings

Chapter 2: Literature review

Chapter 3: Research methodology

Chapter 4: Qualitative data analysis

(Phase One)

Chapter 8: Conclusion

Figure 1.1: A structure of thesis

Based on these foundations, the next chapter will explore literature related to the research

topic.

9

Chapter 2: Literature review

2.1. An approach used for searching literature review

This aim of this section is to present an approach used for exploring the literature review.

Literature review plays a vital role in the development of any research area. It summarises

and establishes connections between previous works, demonstrates different streams and

results which can help researchers identify research gaps and provides opportunities for

proposing research directions (Martins and Pato, 2019). According to Webster and Watson

(2002:xv-xvi), “a high quality review is complete and focuses on concepts. A complete

review covers relevent literature on the topic and is not confined to one research

methodology, one set of journals, or one geographic region). Therefore, they suggested a

structured approach to determine source materials for literature review, including three main

steps: step one “the major contributions are likely to be in the leading journals”, focusing on

well-established journals of specific areas can be considered; step two of the process is “go

backward” by review citations for the articles identified in step 1 to decide which prior

articles should be examined; step three is “go forward” by using online database for that

specific field to identify articles citing the key articles identified in the previous steps, highly

related papers should be included in the review. Also, Webster and Watson (2002) also

suggested how to structure the review and they introduced both a concept-centric approach

and an author-centric approach which can be brieftly presented as follows:

Table LR (Literature review) 1-2: Literature review approach

Adapted from Salipante et al. (1982)

10

The above process can synthesise all highly-related papers which will be used to review.

As mentioned previously, the main objective of this research is to investigate factors affecting

customer loyalty of different strategic groups in the Vietnamese supermarket sector.

Therefore, it will relate to four themes/concepts: Strategic Groups, Retail Industry, the

Vietnamese Retail Context and Customer Loyalty. While exploring the literature reviewing

process, the research is going to focus on these themes in Chapter 2.

In order to engage deeply with the literature, all reading materials being used in this

research will be from online databases and books offered by University of Hull. In that,

reading some major books related to the retailing industry such as Levy and Weitz (2004),

Dawson and Lee (2004), Dawson et al. (2008) will enable the researcher to develop an

insight into the retailing industry, although it should be noted that the books noted above

were written by the UK’s retailing experts. In addition, following and adapting the guidance

of Webster and Watson (2002) on how to write a literature review, online database is now the

main resource for literature exploring. In these online databases, there are a huge number of

journals offered. The basic technique for searching is using key words relating to the four

themes mentioned above and some further key words attaching to those themes. Firstly, the

researcher is going to search the main keyword, and read many papers around that topic. And

then, if that reading highlights some new themes, the researcher will use the newly

highlighted keywords to explore the theme in greater depth. From the outset, the four main

themes mentioned above, revealed 2567 papers from 2007 to present. After eliminating

duplication, and loosely-related papers (2279), and based on specific research objectives and

concentrating on abstracts of papers found, there remained 288 papers which were used for

this thesis. The above filtering process was applied thoroughly for searching each core theme.

In references, the majority of listed papers were used for sourcing literature reviewed in this

thesis and articles selected for reviewing in this study should have been published in well-

established journals. For example, in order to explore the theories relating to strategic groups,

the researcher is going to employ an advanced search for “STRATEGIC GROUPS” with

updated papers (ie. an ideal paper can be after 2007), and then discover new keywords such

as “the origins of strategic groups” or “business strategy”. In respect of customer loyalty, the

keywords “CUSTOMER LOYALTY” will be searched first, only to discover a number of

new keywords based on this theme, such as “customer satisfaction”, “customer perceived

value”, “service quality”, “in-store logistics”, “customer behaviour” and so forth. This

technique will be applied to all four key themes. However, there are not many official

11

published reviews about the Vietnamese retailing industry on the two databases above, the

researcher will search the keywords “THE VIETNAMESE RETAIL INDUSTRY” via

Google and select high quality and reliable online magazines or news items to review in

respect of this theme. The above process explains how the literature review should be

structured and created. It guarantees that the following review (Chapter 2) matches with the

research’s objectives. The following figure (Figure 1.2) will briefly illustrate the process by