THE ULTIMATE GUIDE TO BOOTSTRAPPING STARTUP ...

19

THE ULTIMATE GUIDE TO BOOTSTRAPPING STARTUP VENTURES AND SIDE HUSTLES ABDO RIANI Bootstrapping is three things: A Strategy A Mindset An Option This guide will, ✓ Expose you to different bootstrapping strategies. ✓ Help you adopt the bootstrapping mindset, and ✓ Show you why bootstrapping, although usually is the only option, can be the best option.

-

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of THE ULTIMATE GUIDE TO BOOTSTRAPPING STARTUP ...

THE ULTIMATE GUIDE TO BOOTSTRAPPING STARTUP VENTURES AND SIDE

HUSTLES

ABDO RIANI

Bootstrapping is three things:

A Strategy A Mindset An Option

This guide will,

✓ Expose you to different bootstrapping strategies.

✓ Help you adopt the bootstrapping mindset, and

✓ Show you why bootstrapping, although usually is the only option, can be the best

option.

BOOTSTRAPPING AS AN OPTION

----------------------------

Bootstrapping is about using existing and self-generated funds to start and grow a

business without referring to outside capital like investors and banks.

Are you familiar with Basecamp, Mailchimp, Slack, Qualtrics, Apple, Microsoft, GitHub,

Braintree Payments, and Shopify?

All of those companies bootstrapped the first phases of their businesses. In fact,

companies like Basecamp, Mailchimp and Slack have never received a single round of

funding.

According to Fundable, less than 1% of startups are funded and even those that receive

funding, don’t attract investors’ attention until they’ve proven that they have built a

fundable startup.

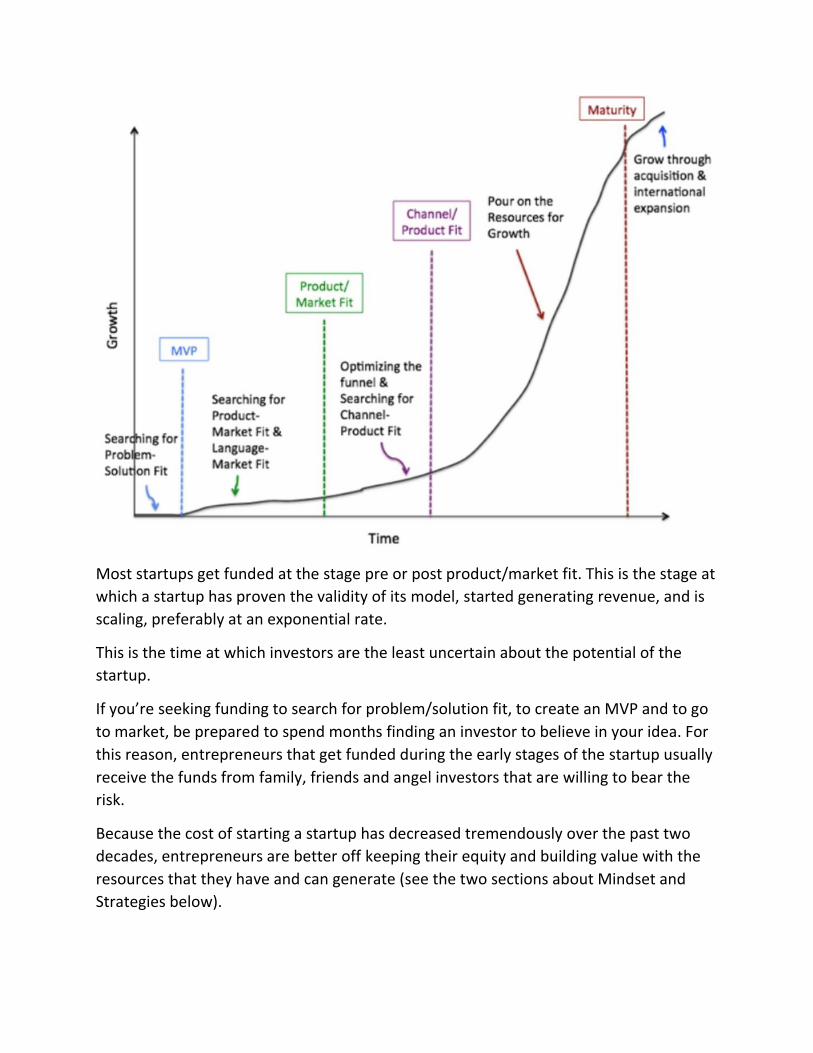

To help you understand when you’re most likely to get funded, take a look at the graph

below that depicts startup growth stages according to Morgan Brown.

Most startups get funded at the stage pre or post product/market fit. This is the stage at

which a startup has proven the validity of its model, started generating revenue, and is

scaling, preferably at an exponential rate.

This is the time at which investors are the least uncertain about the potential of the

startup.

If you’re seeking funding to search for problem/solution fit, to create an MVP and to go

to market, be prepared to spend months finding an investor to believe in your idea. For

this reason, entrepreneurs that get funded during the early stages of the startup usually

receive the funds from family, friends and angel investors that are willing to bear the

risk.

Because the cost of starting a startup has decreased tremendously over the past two

decades, entrepreneurs are better off keeping their equity and building value with the

resources that they have and can generate (see the two sections about Mindset and

Strategies below).

Jeff Epstein, an operating partner at the firm Bessemer Venture Partners and an

entrepreneurship lecturer at Stanford University, has developed a checklist with key

milestones that entrepreneurs have to meet to minimize investment risk. Here it is:

Seed stage: Trying to prove product-market fit and raise approximately $2.5 million.

What entrepreneurs need to show investors:

• A credible story that someone on the team will build the product.

• A prototype that demonstrates the product’s key features.

• Data from customers who have used your “minimum viable product” and given

feedback

• Actual usage metrics from customers who are using your product

• Proof of product-market fit:

o For business-to-business (B2B) startups, at least 10 paying customers who can

serve as references

o For consumer-facing startups with paying customers, at least 100 paying

customers who can serve as references

o For consumer-facing startups offering a free service, at least 100,000 monthly

active users

A fair question I hear most aspiring and starting entrepreneurs ask is,

But how am I going to afford reaching advanced stages like this without

funding?

That’s when bootstrapping comes into play. It should now be clear that at the

beginning, you’re on your own. If you have some savings, if your parent and friends can

help, consider yourself a bit ahead of the curve, and if you’re not, you will need to figure

it out.

The next sections are about how to figure it out.

BOOTSTRAPPING AS A MINDSET

----------------------------

Bootstrapping is a highly creative process. There are many standard approaches that

entrepreneurs can follow to generate money for reinvestment into their ventures

without referring to banks, family, friends or investors but to become a true

bootstrapper, you should understand how unlimited the options can be to fund a

venture under limited to no budget.

Expert bootstrappers are the real deal business people. They understand the parties

that will benefit from a transaction conditioned on the availability of resources and use

their business sense to find ways to combine efforts to accomplish a goal.

Take the example of a retailer who’s looking to acquire a competitor at price X. This

retailer doesn’t have the funds to buy the competition. The straight forward answer

would be to get a loan or an investor on board. A true business man would ask: who’s

going to benefit from this acquisition? In this case, the manufacturer and distributor

could double their volume if the retailer acquired the competitor. How likely are those

partners (manufacturer and distributor) to help the retailer fund the acquisition?

Chances are they will listen and consider covering a portion of the acquisition if the

retailer signed an exclusivity deal with them.

This was a random example that shows how the bootstrapping strategies that a founder

can use to move the needle are a function of their business sense and openness to find

and create win-win scenarios.

In a couple of paragraphs, that’s the bootstrapping mindset. It doesn’t take a high level

of bootstrapping or business expertise to adopt the mindset and use to start and grow

your ventures under limited to no budget.

An expert would probably find a solution, direction or a plan faster but if you

understand the power of the bootstrapping mindset, your research will involve around

finding ways to achieve your goals around your available resources.

The third and last section of this guide will get into the core of our question:

bootstrapping startups ventures and side hustles.

BOOTSTRAPPING AS A STRATEGY

----------------------------

What is the difference between a side hustle (small business) and a

startup?

In two sentences,

When you are a building a new stream of income like consulting, freelance

programming, design, a mechanic shop, etc. your main goal is to execute on an existing

(valid) business model.

When you are building a startup, your main goal is to validate a business model.

Assume that you’re a skilled cook and you’ve always wanted to start a restaurant.

The restaurant business model has existed for centuries and as long as your food is

good, the steps that you need to follow are clear: find a good location, cook good food,

customer walks in, make a sale and the transaction is closed. (example of a small

business)

Now assume that you are looking to tweak this business model by asking your

customers to stay at home and just call or use an app when they want to buy food and

you’ll deliver it to where they are.

This is a new model that isn’t necessarily going to make sense to every buyer.

Some people will like it, others will try to get used to it and others will completely reject

the idea because their goal may not necessarily be to just order food, they may want to

get out of the house, see different restaurant options, buy other things from other

stores.

The bootstrapping mindset is the same for both but the approach can change.

Let us first cover the most important strategies and ideas for bootstrapping a side hustle

and a startup and then use examples for both.

THE CUSTOMER IS THE MOST IMPORTANT FUNDING SOURCE.

There are many non-equity funding sources that founders can use to fund their

businesses but if I (and probably every business owner in the world) had to pick one

channel, it would be the customer.

Funding the business with customers’ money is not always feasible but when it is, it

serves as both a validation and an investment. In other words,

1. The mere fact that your customers are paying for your upcoming product is a

very strong validation sign that you’re onto something.

2. Through the customer, you will also generate the funds to build the product or go

to market soon.

This can be accomplished through a pre-sale strategy. So, let’s start with that.

While there are many approaches to pre-selling products and services, the two essential

ingredients to a successful pre-sale are:

The audience.

You may say, well, an audience is important for any type of sale.

The truth is, the pre-selling audience is not like any other audience. People that will

commit to a product that has not yet been created will almost never be strangers that

found you from a Facebook post or tweet.

The people that are most likely to commit to your product are those who know you,

have spoken with you and are confident that you will meet their expectations as you

promise.

Building relationships is thus the first and most important part of any successful pre-

sale. One of the approaches that helped me raise a few thousands of dollars multiple

times goes as follows:

1. Build a list of 100 potential buyers through content marketing (writing quality

posts), social media groups, Meetups and other social events, personal reach

outs, etc. It shouldn’t take you longer than a month to put this list together.

2. Meet with every person on the list and interview them to better understand their

needs, pain points and expectations.

3. Ask 10 people from the group to join you as part of a customer advisory board.

4. With those 10, prototype and design the functionality of your application.

5. With the designs, go back and meet the other 90, tell them you’re currently

making good progress to create this product and you are pre-selling access to the

first 100.

6. If only 10 out of the 100 purchased and you need 100 buyers to fund your first

version, scale your interviews by 10. So, meet with 1,000. To reach this many

people, social media ads, podcasts and partnerships with influencers will help

you speed the process.

The offer (the product).

Although most entrepreneurs pre-sell their products before building it to validate the

idea and generate sales to fund product development, a pre-sales campaign is a good

strategy to boost sales even if the product is built and ready to launch.

For the sake of this guide, let’s assume that you have not built the product yet.

In this case, what you need is a clear vision and even better a visual presentation of how

the product will look when it’s ready. By following the 6 steps above, you should have

everything you need to convey the benefits of the product through an email, webinar or

video like Dropbox did to build traction for its product.

Your offer and the product can be a sum of 5 slides showing the most important

features or benefits of the solution, how it’s different from existing products and how it

will benefit the user. This presentation ends with a payment link that people can use to

pre-order your product. For this, you can use Celery’s landing pages to accept payment.

This pre-sales approach works for selling digital products like courses and trainings,

hardware products or software startup solutions. Let’s use two examples to make things

clearer.

---------------

Idea: food on demand

Strategy 1: getting hands dirty

Your hypothesis is that your target buyers (exp. busy households) are willing to pay a

premium if their favorite food is delivered to where they are.

Without any website or application of any kind, begin by offering ordering and delivery

services by going from door to door and through social media. Use Canva to create a

banner then print for distribution and/or share online starting with family, friends and

acquaintances. Give them a number to call for ordering and when they do, go and

deliver the food yourself. You can use Square to accept payment.

When the founders of DoorDash started, they put a landing page together in an

afternoon, emailed everyone on their and got the first order the same day. They didn’t

necessarily need a website but one can help for credibility and reach.

Strategy 1.1: leverage your network

If you are not starting with a group of friends (co-founders), don’t hesitate to seek help

from family and friends as a favor. For instance, if you get more orders than you can

possibly handle by your own, get your brother, sister, parents and friends to help you

deliver the food or do simpler tasks like picking up the phone and assigning orders.

If you have a full-time job, specify in the brochures that your services are open from say

6-11 pm. It’s the execution that matters even if it’s for a few hours a day.

Strategy 1.2: leverage the power of content

Either through a Medium blog or by purchasing and customizing a theme from

marketplaces like Themeforest, start creating content that educates your target buyers

about the topic that your product falls under. In this case, it’s food. Things like, the best

restaurants in town, how to save time and money from food delivery services, etc. And

do the same thing on social media. This will help you build awareness and trust.

Strategy 2: learn from strategy 1 and reinvest the gains

The time you will spend getting your hands dirty will help you learn what your

customers need and expect. It’ll help you define what exactly needs to be built to create

a more efficient way of ordering and delivering the product (food in this case). You’ll

know what functionality your web or mobile app needs to include.

With the money you generate from the first strategy, you will now have enough funds

to invest in a scalable version of your service: an application.

Strategy 3: pre-sell

Before we get into the product development stage, we need another layer of validation

and an approach to secure more funds. In this scenario, go back to those who used your

services and offer them an incentive (discount) for pre-buying say 50 future deliveries. If

you charge $2 per delivery, then offer them, for the sake of the example, 50% off for

pre-paying 50 future deliveries. They would pay you $50 instead of one hundred. Do this

with 50 customers and you’ll have $2,500.

Strategy 4: outsource

Use marketplaces like Upwork and Freelancer to find talent from all over the world to

help you build, market and refine your product.

With the amount you generated so far, you should have enough funds to build the initial

version of the product. At this stage, you may still keep the funds until further validation

stages by using app development platforms like Bubble. These platforms enable you to

build applications even if you don’t code and more importantly, they don’t cost much.

In either case, start by building the core of the product: the feature(s) that contributes

directly to the purpose of the application: in this case, it’s ordering food.

Strategy 4.1: ask for discounts

Every time you decide to use a tool (analytics, project management, accounting, etc.)

find the email of the company and don’t be afraid to ask for a discount. Most of the

time, these companies understand the struggles faced by startup founders especially at

the beginning of their ventures and wouldn’t mind extending a free trial or giving you

20-50% off.

Strategy 5: Delay payments

Assuming you have successfully built a product that helped you scale the venture and

your startup now needs more features to improve user experience, boost sales,

minimize churn rate, etc. For the sake of the example, assume the product needs

$10,000 of working hours. Do not hesitate to negotiate with the person/team to pay the

amount over 3-6 months or even longer depending on your growth rate, sales and

expected demand. Most freelancers, I found, are OK extending payments and

supporting you until you generate enough funds. Be sure to reward them with a bonus

later on.

All the while, spend 20% of your weekly time on starting and building relationships with

potential investors and co-founders.

Comment on a potential co-founder’s medium post, email them directly, appreciate

their portfolio, discuss future projects, keep them in the loop.

Email investors congratulating them for their recent portfolio company exit and

investment. Comment on their blog posts, request to interview them, tell them what

you’re doing and follow up frequently with updates.

---------------

Idea: Gym

Kale Panoho sold $202,500 worth of subscriptions to his gym within 14 days before he

had a facility, a team or any asset to show. He did it through pre-sales. In 3 steps:

1. Build the audience. Find people on campus, on the street, in parks, on social

media and through recommendations.

2. Then ask all of your interviewees to give you a 25% investment right now (make

an estimate on price) and you will look into creating your product or give you

some of that service while you figure out the gears of how it is going to work. If it

isn’t going to work out I’ll refund the money.

3. Begin research, create your product, start serving and launch your business

---------------

You saw two examples of how pre-sales can help you validate your idea, go to market

quickly and generate revenue before even building the product.

Here are 30 bootstrapping strategies that you should be familiar with so that when

faced with an investment decision, you can better evaluate your options.

1. Initially, sell big quantities of the product at a discount to secure enough funds

to proceed.

This is an excellent approach especially if you use it to reward your beta users and those

who gave you some time to discuss their needs and expectations. Like I said in the

presentations, the more people you meet with at the beginning, the better are your

chances of building the right product. That’s not all. Those interviewees and beta users

can fund you big time. I raised over $2,000 from early sales for my first venture and tens

of thousands of dollars on many more products over the years.

2. Impose an advance payment.

If you’re building a startup, think about advance payments as a presale. Like you saw

above, if you’re building an on-demand startup, you can presell 20, 30 or 50 deliveries.

Although some enterprise products require a one-time set up fee, “Imposing” a down

payment is more common if you’re selling a product or a service in the traditional sense

like freelancing. In this case, always with almost no exceptions, request an advance

payment. This will protect your downside while giving you some revenue to fund the

initial stages of the project.

3. Presell the product.

Much like 1 and 2, consider pre-selling your product or service not necessarily for a

discount but also by enticing the buyer with other relevant and related services. For one

of my startups, I added consulting as part of the presales package. Put your buyer in

front of you and design the best pre-sales package for them. If you’re building an

innovative solution, you can simply limit use to a certain number of buyers to create

urgency.

4. Share office space.

If you are building software, in my opinion, there is no need for an office at all. As long

as you have a computer and internet connection in your home, make that your office. If

you need some sort of equipment, check the nearest college.

5. Share equipment with other businesses.

Besides checking your local university, if you need any sort of expensive equipment, put

a list of companies and people that have it and then reach out to ask for permission to

use it after hours. If no one agrees, offer to pay them a small rent for using it. One of

these three options will solve the problem. If you’re at school, I found a lot of success

when mentioning that I am a student. People usually want to help students.

6. Co pay employees with other businesses to minimize overhead.

I once asked one of my friends to help me design a few slides. When I kept coming back

to him, he said, “do you have $200? why don’t you help me pay my designer and I’ll give

you his contact information so you too can work together.” When I looked at the cost of

hiring a designer for a few hours a week, I found my friend’s proposal a lot cheaper.

Keep this in mind.

7. Customize contracts with suppliers, manufacturers, distributors and customers.

Some companies spend tens of thousands of dollars to create a few common

agreements for clients and partners. What I found is that, big or small, every

person/company will make an exception at any time if there is a benefit from the

relationship. Just keep this fact in mind when negotiating terms with your key

stakeholders.

8. Borrow equipment, tools and skills.

Just ask. Pick up the phone or go in person and ask if you can borrow what you need.

Believe me, people will lend you very valuable assets if you seem trustworthy.

I think it’s time for another reminder. These strategies are a proof that no matter how

limited your resources are, you can get your hands dirty to start and build a lot of value.

Although they may not be an option later when you’re scaling, they’re how anyone can

overcome lack of funding to turn an idea into a valuable and profitable company.

9. Find volunteers.

Some people just want to learn, others want to add an experience to their resume,

others just want to help you. Find those people and get them involved. There’s a

common debate about whether a startup should get the involvement of volunteers and

interns. The argument against is that it takes a lot of time to get the person (people)

trained and supervised. Keep this in mind and make your decision accordingly.

10. Exchange products and services.

You may not have a thousand dollars for an explainer video for your startup but you

may have design, programming, marketing, or other skills to offer in exchange.

Exchanging products and services works best if 1) you and the other party are in a

relatively similar stage, such as both at the initial stages and have similar needs, and/or

2) you can help the other party accomplish an expensive or hard goal like acquiring big

clients or closing a partnership with a key supplier, etc.

11. Delay payments.

When there’s a fit, everyone will find a way to make something happen. If you can’t

commit a big amount today, ask if you could split or delay the payment whether it’s with

contractors, suppliers, manufacturers, employees, or any key stakeholder.

12. Use income from outside sources like a job.

Antonio, founder of Viamente, relied on his wife’s support and salary to cover living

expenses until his venture turns into profitability. He preferred to focus 100% on his

startup and used his wife’s income to survive the initial stages. It didn’t take long until

he proved the validity and viability of his startup to get a small investment that helped

him take the company to another level fairly quickly until he sold it 12 months later for

$45 million. An income from a current job is a big plus especially if you can make time

for your startup.

13. Use savings.

Some people prefer to use their savings instead of doing many things at the same time.

From experience, the best time to use savings is when you pass the first “vague” stages

of the business and have built traction to justify further investments in time and money.

In other words, start part-time while working full or part time at your existing job and

when you start gaining traction and some early sales, focus more on your startup while

using your savings to compensate for the lower salary.

14. Carefully use credit cards if cash is needed urgently.

Marc Cuban once said, “only morons use loans to start their businesses.” This statement

is in my opinion even more significant if you’re building a startup (not small business)

given the extra layer of uncertainty. Using credit cards is worse, however, if you know

you’re getting a check some time in the next 2-3 weeks, you can use your credit card if

you need to make a payment and then pay it back as soon as you get paid. I used this

approach to fund the first two AspireIT projects when I had a client but not the money

to hire the team. I used my credit card to pay the team and as soon as I received the

first payment from the client, I paid my card back.

15. Get friends and family’s help.

The estimate for recording and editing the lectures of the Bootstrap a Startup Program

is a little over $7,000. Luckily before investing in a video editor, I remembered that a

family member is passionate about videography and likes to record and edit videos on

the side. She was more than happy to do everything for free. I followed the same

approach for my first startup. I went to the school library and met a guy who helped me

design the whole web app. Your network is extremely valuable. Never hesitate to ask.

16. Focus on one thing (product/service) at a time.

This year, you’ll have over 100 ideas and at least 10 “great” ones. I know it’s not easy

but it’s extremely important that you focus on one idea at a time. To be clear, you

should have one single vision and strategy but feel free to brainstorm to come up with

many ideas to help you accomplish the 1 goal (vision) that you have.

To use an example, if you’re building a food on demand startup, research, ask and think

about ways to get the food delivered on time or get more drivers, etc. But if you’re

brainstorming ways to maybe also drive people (same business model but different

ideas), you will be distracted from the first and either end up missing both goals or do

OK at both and not exceptionally well at any. This is even more important if you are

bootstrapped.

17. Focus on what sells.

Soon you will know what sticks. Focus on that. If you try to make everything (every

feature, product, etc.) works, you’ll miss the big opening. The big opening is the clearly

open door to user needs from which you can learn, understand and expand into other

areas (features) quickly. Find what works and focus entirely on it. Save time by looking

at what’s working for your competitors.

18. Work from home.

Nowadays, many multi million dollar startups are managed 100% remotely. Working

from home saves me close to $10,000/year. An amount I could invest in marketing,

product development, hiring, entertainment or anything else. If you can, do everything

from home for as long as possible and regardless of whether you’re building hardware

or software.

19. Hire interns.

Some interns will save you time and add a lot of value others will eat up resources. From

experience, I found the best formula to be 80% repetitive task and 20% learning,

creative and contributions. In other words, assigning interns repetitive and time-

consuming tasks will not require a lot of training time and will save you a lot of time

doing the tasks yourself. In the meanwhile, interns are usually hungry to learn and

contribute more. Spend a couple of hours a week training them to learn and do more

challenging work over time. Here too, you can hire interns and work with them

remotely.

20. Speed up invoicing.

It’s easy to put this on paper but the ideal scenario is to get paid as soon as possible,

maybe even before you deliver the product (preselling and/or advance payment). Just

like some people will make exceptions to help at the beginning, you are not in a position

where you can extend or delay payment for the customer yet. Collect cash soon and be

transparent about payment deadlines.

21. Charge interest on overdue accounts.

This applies more to hardware or any other tangible products, however, at the

beginning and in order to overcome the newcomer challenge, you may not have the

leverage to impose interest on overdue accounts. Keep the late payment penalty in your

terms but focus more on attracting the best clients (see below).

22. Use Factoring.

Factoring is when you sell the invoices to a commercial finance company at a discount,

get most of the money upfront and use it to fund production. For instance, assume you

start accepting orders for your upcoming product and got 100 orders that you need to

deliver within 30 days but you don’t have the cash to manufacture and distribute it fast

because you’ll only get paid when you deliver. Factoring can help in this situation. You

can also use the same idea directly with your buyers: pay upfront and get X discount.

23. Choose customers who pay quickly.

Especially if you sell business to business products, you can research to learn a little

more about the company you’re about to sell to. If you see red flags, you may be better

off passing than dealing with the headaches.

24. Cease relationships with those who don’t pay on time.

In other words, cut your losses soon. Add contract cancelation to your terms and make

sure you warn (nicely) the client at different occasions about the consequence.

Exceptions can also be made but you should know if the client truly needs a little more

time or is just wasting your time.

25. Build win-win partnerships.

Not just for exchanging products and services or customizing contracts with key

stakeholders, look for value adding partnership opportunities that can strengthen your

product, expose you to different markets, help you gain credibility and awareness in the

marketplace.

26. Use city, state and nation wide grants.

There are many grants that don’t take more than 1-2 hours of work to apply to. For

instance, one of the chambers of commerce in my region grants $10,000 to the best 5

business plans. All you need is to submit a 4-page double spaced business plan. The

same type of grant is usually offered at school. So start by checking chambers, economic

development centers, universities, business organizations, etc. Those are easy to apply

to and the competition is usually low. You also have national grants that give $50,000+

to the winners. Those are a little more challenging and time consuming but if you see a

great opportunity, I highly recommend that you apply.

27. Start a side hustle to fund initial stages.

The best side hustles are the ones that solve problems similar to what you are working

on solving with a scalable product. For instance, Mailchmip used to be an email

marketing/design agency, Balsamiq used to be a design agency, Kissmetrics used to be a

marketing agency, etc. This is ideal but not essential. In any case, a side hustle especially

if you are a student and don’t have a job, the best way to fund the initial stages of your

startup is through a side hustle.

28. Outsource.

Outsource as much as possible but first exhaust your own human capital. In other

words, outsource everything you can’t do. As I mentioned earlier, many multi million-

dollar startups started and are growing remotely so building and managing a team

overseas doesn’t necessarily have to be a temporary solution. It can be a great way to

grow too.

29. Experiment before you invest significant amounts.

In other words, before building a product (web/mobile app or hardware), find ways to

serve users manually or by leveraging existing tools. If you’re looking to build an Uber

like application, start by creating a Facebook ride sharing group and encourage riders to

post their requests on the group. You’ll quickly build enough traction so that by the time

you launch your app, people will be eagerly waiting for it. If things don’t work out, at

least you’ll know that’s not an idea worth pursuing very soon and before making major

investments.

30. Align your skills with product core so you can do most of the work before

seeking help.

If you can directly contribute or completely build at least the first versions of the

product, you are off to a great start because you will be able to control you next move

cheaply and quickly. Many first-time startup founders believe that as long as the

product is good, all they have to do is get it in front of the right people. When they

quickly realize they need imminent changes, they get stuck and feel upset no matter

how good the first version is. If you can choose, start ventures with products you can

build.

NEXT STEPS

----------------------------

The goal of this guide is to help you build a bootstrapping foundation that’ll enable you

to start and grow a business of any kind whether you’re funded or not.

But as with any guide or book, you can only go so deep on a given subject, and you may

have questions about the why, what, and how of some of these strategies and their

application.

For this, I have gotten into so much detail to discuss the execution (application) part of

bootstrapping startup ventures and side hustles in the Bootstrap a Startup Program.

I invite you to learn more and reserve your spot so that when the program is live you get

priority access.

Here is where to learn more: Bootstrap a Startup program.

And if you have any questions, don’t hesitate to reach out to me at

Respectfully,

-Abdo