THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM TO SYRIA – A...

18

Jebel Bishri in Context Introduction to the Archaeological Studies and the Neighbourhood of Jebel Bishri in Central Syria Proceedings of a Nordic Research Training Seminar in Syria, May 2004 Edited by Minna Lönnqvist BAR International Series 1817 2008

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM TO SYRIA – A...

Jebel Bishri in Context

Introduction to the Archaeological Studies and the Neighbourhood of Jebel Bishri in Central Syria

Proceedings of a Nordic Research Training Seminar in Syria, May 2004

Edited by

Minna Lönnqvist

BAR International Series 1817 2008

This title published by Archaeopress Publishers of British Archaeological Reports Gordon House 276 Banbury Road Oxford OX2 7ED England [email protected] www.archaeopress.com BAR S1817 Jebel Bishri in Context: Introduction to the Archaeological Studies and the Neighbourhood of Jebel Bishri in Central Syria. Proceedings of a Nordic Research Training Seminar in Syria, May 2004 © the individual authors 2008 ISBN 978 1 4073 0303 1 Printed in England by Alden HenDi, Oxfordshire All BAR titles are available from: Hadrian Books Ltd 122 Banbury Road Oxford OX2 7BP England [email protected] The current BAR catalogue with details of all titles in print, prices and means of payment is available free from Hadrian Books or may be downloaded from www.archaeopress.com

73

THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN

MONETARY SYSTEM TO SYRIA – A RE-EVALUATION

Kenneth Lönnqvist Department of Archaeology, Department of History,

University of Helsinki, Finland

Fig. 1. The Tax Law of Palmyra. The State Hermitage Museum Collections, St. Petersburg. Courtesy the Hermitage. Photo: Kenneth Lönnqvist 2007.

1. Introduction In the second settlement of Asia of Rome in 67-66/63 BC - which some scholars describe as a political rather than a military one - the Roman general Pompey created several new provinces and enlarged those already in existence in the East, which in practical terms meant that the Roman influence expanded towards the Euphrates. The Seleucid monarchy was abolished in the region, and a new province under the name of Syria was created in 64 BC (Plut. Pomp., 39) out of the former Seleucid territory. The provincialisation of Judaea began in AD 6 when the former Herodian kingdom was demoted to the status of a Roman procuratorial province.

The main goal of this study is to briefly trace – through epigraphic and numismatic data – the introduction and circulation of Roman coinage in Syria, an event that

reflects the actual beginning of the Roman economic and thus political supremacy in the region. The timeframe of this study covers the period from the establishment of the province of Syria in the Late Republican period to the Early Imperial period. Some of the new numismatic material presented will extend the discussion to the second and third centuries AD, although the primary intention is to cover the period from the first century BC to the first century AD, which also represents the assumed introduction date of the Roman denarii coinage to the region. However, it should be remembered that the provincial boundaries did change significantly over time, as did apparently the circulation of many coinages, too. Compared to the modern Arab Republic of Syria, Roman Syria included a narrow stretch of land between the Mediterranean Sea and Palmyra (whether included or not from the beginning). During the reign of Diocletian (AD 284-305) the eastern border was

JEBEL BISHRI IN CONTEXT

74

reinstated so that a chain of small towns, fortresses and fortified garrisons formed the eastern frontier of the Roman empire, or what has been called The Strata Diocletiana largely understood as the Eastern Limes. The Strata Diocletiana as it has been reconstructed (Southern and Dixon 2000: 28) from documentary, textual and archaeological evidence started northeast of Bostra in the south and continued north through Palmyra, Oriza (Taibeh) to Resapha and further to Sura on the Euphrates (Poidebard 1934). It additionally was conjoined to a triangular area of the Euphrates Limes eastwards through the fortress of Zenobia (Halabiya) and further towards Dura Europos the latter of which had, however, been left in ruins after the Sassanian conquest and remained in ruins in the time of Diocletian. (See more on Zenobia in this volume in Hanna-Riitta Toivanen’s article and on Dura Europos in Charlotte Børlit’s article). The triangular space left between Shukhne, Oriza, Resafa, Sura, Zenobia and Dura Europos is occupied by the mountain of Jebel Bishri in the Palmyrene fringe, the context of which this study belongs to. In-depth discussions regarding surveys of all ancient coinages in the region, provincial and military arrangements on the Eastern Limes and the general political history of the Roman period are in general left outside the scope of the present study. It should also be emphasized that several concrete research problems in the realm of numismatics, history and archaeology as presented in this study are clearly linked with the fact that the existing source material at our disposal is unevenly preserved. Having said this, it must also be noted that no wholly satisfactory answers can be put forward to all the questions raised in this short study, meaning some questions may in the end prove unanswerable. The present state of the discourse regarding various models for the circulation, use and purpose of coins in the Roman world in general has been put forth by others and there is no need to reproduce these theories here. Instead, the problem of dating the introduction of the Roman monetary system to Syria is illustrated by discussing the Tax Law of Palmyra and the recently published silver coin hoards from Khirbet Qumran (Lönnqvist 2007a). The epigraphical evidence dealt with concentrates on the Tax Law, whereas additional evidence is sought from relevant Greek, Aramaic and Latin inscriptions that have been published. Like the coin hoards, also the early Imperial inscriptions can broadly speaking be defined as sporadic and selective.1

1 The used main publications concerning the epigraphical data consist of the North Semitic Inscriptions (NSI), Corpus Inscriptionum Semiticarum (CIS), Palmyrene Aramaic Texts (PAT), the Orientis

The numismatic focus of the study will be on the published coinages of Roman Syria as presented especially in K. Butcher’s Coinage in Roman Syria, Northern Syria, 64 BC – AD 253 (2004). Background for the study is sought in the coinages of Judaea (see Meshorer 1982, hereafter referred to as AJC, and Meshorer 2001, hereafter called TJC). Sources for the Syrian mints are available, e.g., in the Roman Imperial Coinage (RIC I, 1923 -), G. Bruck (1961), Late Roman Bronze Coinage (LRBC 1972) and V. Failmezger (2002), the latter covering the Late Roman periods VI-VIII of RIC or the transitional period from paganism to Christianity in AD 294-364. Syrian provincial coin hoards are listed in An Inventory of Greek Coin Hoards (IGCH 1973 by Thompson et al.) and the Coin Hoards (CH 1975-) published by the Royal Numismatic Society in London. However, a relevant inventory of coin hoards that have been found in Syria and Israel is also found in K. Butcher’s already referred work (2004: 270 ff., see Appendix 1). I am certain that in the future answers will be both sought and found particularly in the field of archaeometallurgy and the chemical and metallurgical composition of Roman coinage and metalwork, technology and traditions. As these issues that are relevant for this summarising study have previously been dealt with (Lönnqvist 2007b: 1-246), the presentation here is brief. For instance, the development of the base coin metals, alloys and the fineness of the Roman coinage is still one of the most unfamiliar chapters in Roman numismatics and history. As previously pointed out, the complexity of the subject is illustrated in the standard work on the Roman provincial coins Roman Provincial Coinage by Burnett – Amandry – Ripollès (1992-), which even in the up-dated volumes includes very little information about the archaeometallurgical investigations of the Roman coinage, in spite of its other major credits. Another small critical note could be that coins that would normally appear in connection with, e.g., archaeological excavations, coin hoards or stray-finds

Graeci Inscriptiones Selectae (OGIS), Inscriptiones Graecae (IG) and the Corpus Inscriptionum Latinarum (CIL). A short catalogue version of some of the Palmyrene inscriptions in the Museum of Palmyra is found also in K. Al As’ad and M. Gawlikowski (1997) and K. Al As’ad and J.-B. Yon (2001). However, my impression is that the publications that deal, for instance, with the Palmyra Museum material would likely not have circulated much outside Syria, largely explaining why the views expressed in these publications as a rule are absent from western publications. As far as the epigraphical evidence is concerned, an avenue that has been covered here is the important customs tariff of Palmyra or the Palmyrene tax law from the first century A.D. Local Syrian epigraphical data mentioned above with some new precisions are used to illustrate the importance of this inscription in specific to this case study.

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

75

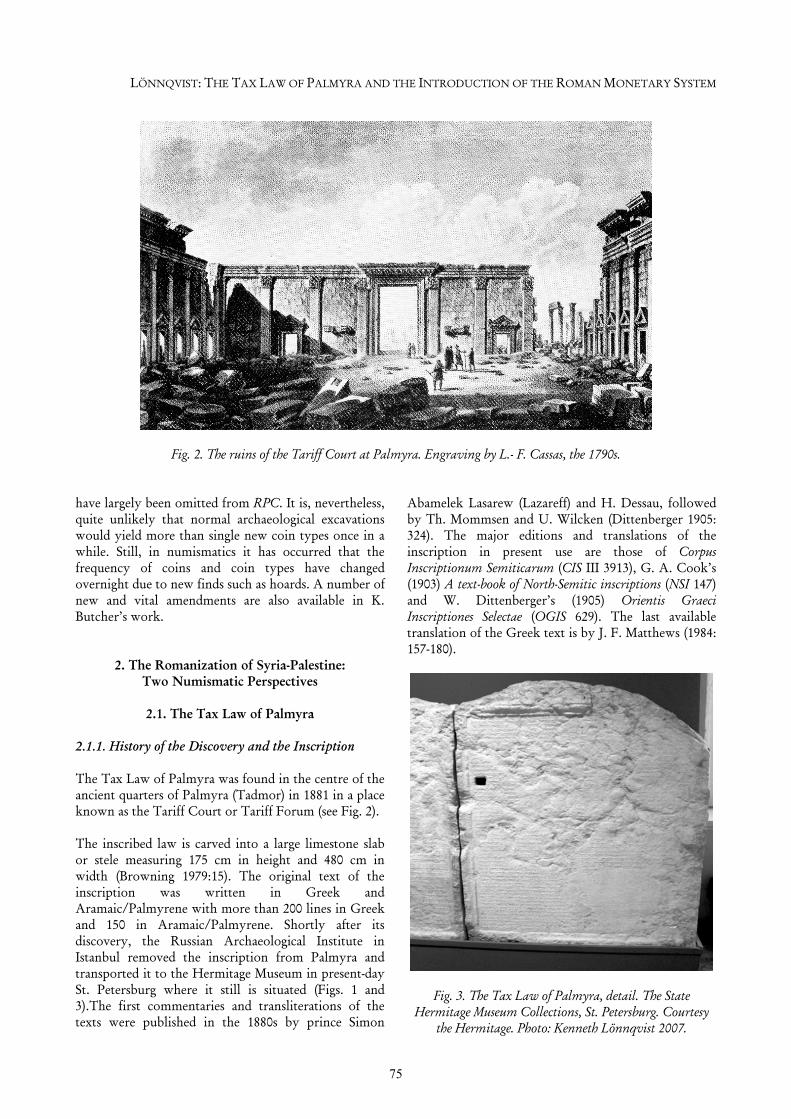

Fig. 2. The ruins of the Tariff Court at Palmyra. Engraving by L.- F. Cassas, the 1790s. have largely been omitted from RPC. It is, nevertheless, quite unlikely that normal archaeological excavations would yield more than single new coin types once in a while. Still, in numismatics it has occurred that the frequency of coins and coin types have changed overnight due to new finds such as hoards. A number of new and vital amendments are also available in K. Butcher’s work.

2. The Romanization of Syria-Palestine: Two Numismatic Perspectives

2.1. The Tax Law of Palmyra

2.1.1. History of the Discovery and the Inscription

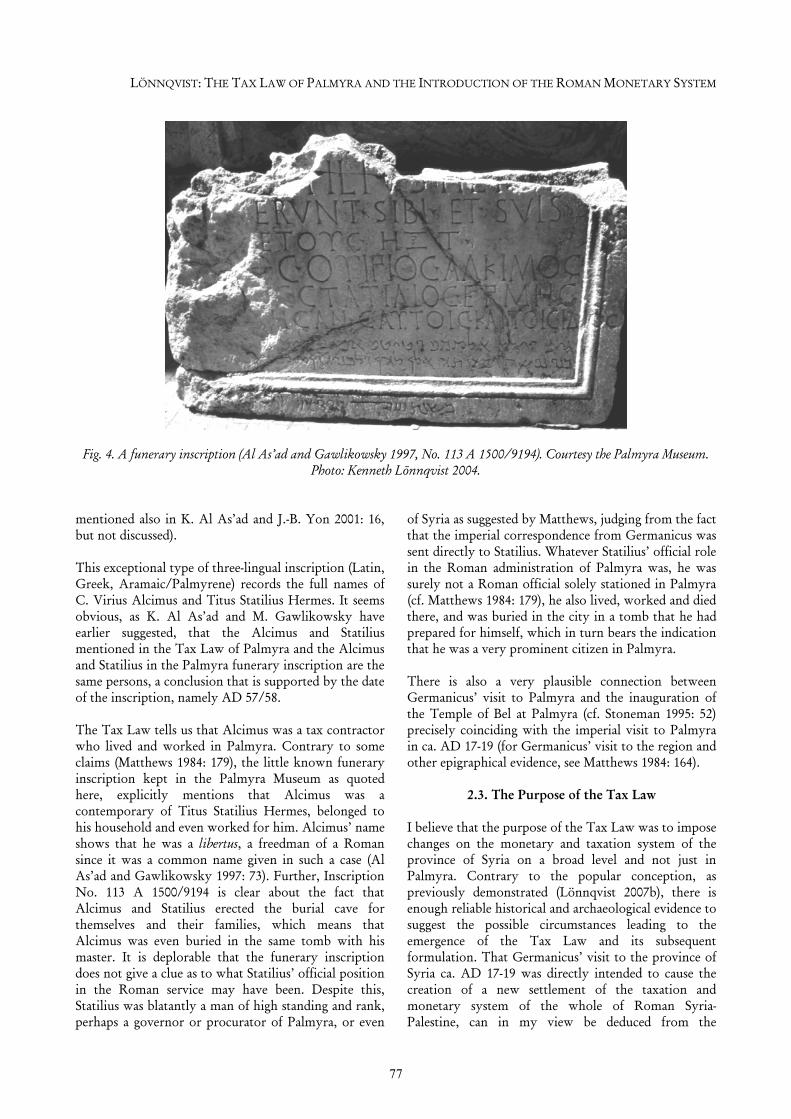

The Tax Law of Palmyra was found in the centre of the ancient quarters of Palmyra (Tadmor) in 1881 in a place known as the Tariff Court or Tariff Forum (see Fig. 2). The inscribed law is carved into a large limestone slab or stele measuring 175 cm in height and 480 cm in width (Browning 1979:15). The original text of the inscription was written in Greek and Aramaic/Palmyrene with more than 200 lines in Greek and 150 in Aramaic/Palmyrene. Shortly after its discovery, the Russian Archaeological Institute in Istanbul removed the inscription from Palmyra and transported it to the Hermitage Museum in present-day St. Petersburg where it still is situated (Figs. 1 and 3).The first commentaries and transliterations of the texts were published in the 1880s by prince Simon

Abamelek Lasarew (Lazareff) and H. Dessau, followed by Th. Mommsen and U. Wilcken (Dittenberger 1905: 324). The major editions and translations of the inscription in present use are those of Corpus Inscriptionum Semiticarum (CIS III 3913), G. A. Cook’s (1903) A text-book of North-Semitic inscriptions (NSI 147) and W. Dittenberger’s (1905) Orientis Graeci Inscriptiones Selectae (OGIS 629). The last available translation of the Greek text is by J. F. Matthews (1984: 157-180).

Fig. 3. The Tax Law of Palmyra, detail. The State Hermitage Museum Collections, St. Petersburg. Courtesy

the Hermitage. Photo: Kenneth Lönnqvist 2007.

JEBEL BISHRI IN CONTEXT

76

2.1.2. The nature and importance of the Tax Law The inscription has been characterized as an edict, a customs law or decree concerning the taxation of the city of Palmyra in the early Roman imperial period (abbreviated Trf). But, as I have previously attempted to show (Lönnqvist 2007b), the Tax Law has implications which go beyond the city borders of Palmyra and even the provincial borders of Syria. The importance of the inscription may thus be discerned in several different fields of administration and history of the entire Roman East, not just with regard into the local economy of the city of Palmyra or Syria at large. Its significance can hardly be overestimated since there are so few primary sources from this period. For instance, J. F. Matthews (1984: 157) called the Palmyra inscription “one of the most important single items of evidence for the economic life of any part of the Roman empire”. Matthews (1984: 172) also defined the Tax Law of Palmyra as a lex portus, in the way that it defined transit taxes or in the way that tolls (portoria) passed on goods that were transported into the Roman Empire mainly by caravan trade (and which were a source of great wealth to the city of Palmyra) through Palmyra, although the city was not a harbour by water in a physical sense (see also the discussion of the ports of trade following K. Polanyi’s model in Eivind Seland’s article in this volume). However, the nature of this short study restricts me from discussing the importance of the Tax Law of Palmyra as a possible source of revenue or wealth for the Palmyrene people (cf. Stoneman 1995: 58-59). One may, however, venture to inquire whether the variety and number of commodities such as slaves, perfumes, ointments or Italian wool listed in the Tax Law of Palmyra represent the entirety of trade in luxury goods. Especially the importance of trading slaves in the East has apparently been largely underestimated as there was a substantial demand for slave labour in the Roman Empire, and nearly all of the physical work depended on a constant flow of cheap manpower. I will therefore limit myself here to merely commenting on the inscription from the perspective of the introduction and possible use of the Roman monetary system in Syria in the Roman period, and demonstrating how I believe Palmyra and the inscription relate to Syria-Palestine on a broader provincial, administrative and numismatic level.

2.2. Prosopography and Dating of the Tax Law

The Tax Law has been dated to the penultimate year of Emperor Hadrian’s reign or AD 137, albeit, there is a general agreement that the original form of the text

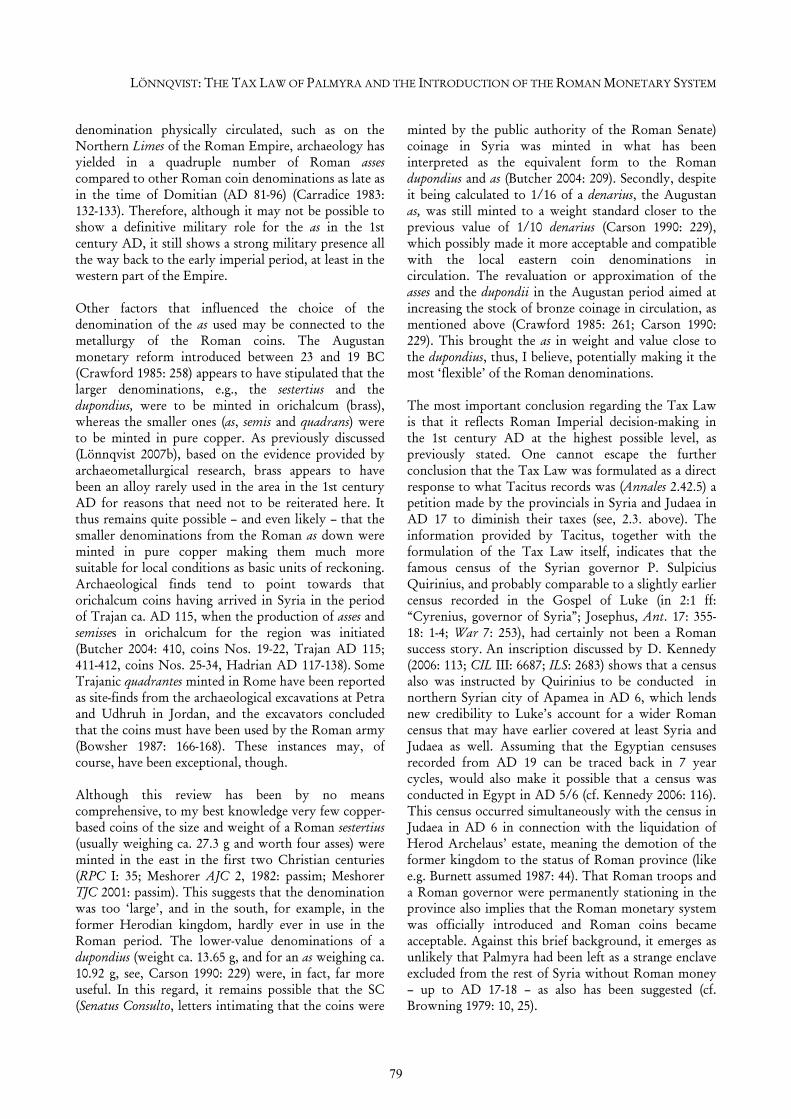

goes back to the early first century AD. The reading of the Tax Law furthermore implies that a new second century AD tax tariff was to be exhibited in Palmyra, not only in the same spot as the predecessor, but on the very same stone. Unfortunately, the fragmentary state of preservation common to both texts does not always allow one determine where the new text begins and the old ends (NSI 147: 334, line 10). However, more recent numismatic and archaeological data does enable some important amendments to be made, for example, to J.F. Matthew’s translation and explanation of the Greek text. At first glance, the Seleucid dating system found on the inscription appears to have occasioned some surprises (NSI 147: 320, cf. Matthew 1984: 161), but this is not necessarily the case. For instance, many of the principal silver coins that were minted and circulated in the region in the Roman period continued to use Seleucid or other “non-Roman” dating systems well into the first century AD or beyond. In the same way the coin weights and coin denomination systems may have kept their Hellenistic traditions throughout the entire period of Roman provincial coinage in Syria until the mid 3rd century AD, as recently argued by Butcher (2004: 50, 268). As far as the dating of the Tax Law to the 1st century AD is concerned, there is some new evidence that needs to be briefly assessed. Several high-ranking Roman officials are mentioned in the Greek and Aramaic text (NSI 147: 319, lines 42, 56; 326, line 15; 330, line 22; 339, L.4; OGIS 629: 336, line 154; 338, line 168) of the inscription, which confirms a 1st century date. The first one mentioned is Germanicus Caesar, the nephew and adopted heir of Emperor Tiberius (AD 14-37). Germanicus was sent on an imperial mission to Syria in AD 17-19 with command over all provinces beyond the Hellespont, but it appears that he was assassinated en route and died in AD 19. Other persons mentioned are Gnaeus Domitius Corbulo, the governor of Syria (AD 60-63), Mucianus (possibly C. Licinius Mucianus, legatus of Syria AD 67-69. (For Mucianus and his coins, see, e.g. Butcher 2004: 194, 240, 351), and a certain Barbarus or Marinus, the governor, the latter names not being attested to in other sources. Moreover, there is a mentioning of a Roman called Statilius in the inscription. NSI (147, 339, line 4) states that he may have been a Roman procurator in Syria, while OGIS (629: 336) refers to him as “Homo ceteroqui ignotus”. Matthews (1984: 179) says of Statilius that he was “perhaps a Roman procurator of Syria”. As to the identity of this enigmatic Statilius in the Tax Law, there is a funerary inscription kept in the garden of the Palmyra Museum which mentions two persons called Alcimus/Alkimos and Statilius (see Fig. 4 and Al As’ad and Gawlikowsky 1997, No. 113 A 1500/9194;

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

77

Fig. 4. A funerary inscription (Al As’ad and Gawlikowsky 1997, No. 113 A 1500/9194). Courtesy the Palmyra Museum. Photo: Kenneth Lönnqvist 2004.

mentioned also in K. Al As’ad and J.-B. Yon 2001: 16, but not discussed). This exceptional type of three-lingual inscription (Latin, Greek, Aramaic/Palmyrene) records the full names of C. Virius Alcimus and Titus Statilius Hermes. It seems obvious, as K. Al As’ad and M. Gawlikowsky have earlier suggested, that the Alcimus and Statilius mentioned in the Tax Law of Palmyra and the Alcimus and Statilius in the Palmyra funerary inscription are the same persons, a conclusion that is supported by the date of the inscription, namely AD 57/58. The Tax Law tells us that Alcimus was a tax contractor who lived and worked in Palmyra. Contrary to some claims (Matthews 1984: 179), the little known funerary inscription kept in the Palmyra Museum as quoted here, explicitly mentions that Alcimus was a contemporary of Titus Statilius Hermes, belonged to his household and even worked for him. Alcimus’ name shows that he was a libertus, a freedman of a Roman since it was a common name given in such a case (Al As’ad and Gawlikowsky 1997: 73). Further, Inscription No. 113 A 1500/9194 is clear about the fact that Alcimus and Statilius erected the burial cave for themselves and their families, which means that Alcimus was even buried in the same tomb with his master. It is deplorable that the funerary inscription does not give a clue as to what Statilius’ official position in the Roman service may have been. Despite this, Statilius was blatantly a man of high standing and rank, perhaps a governor or procurator of Palmyra, or even

of Syria as suggested by Matthews, judging from the fact that the imperial correspondence from Germanicus was sent directly to Statilius. Whatever Statilius’ official role in the Roman administration of Palmyra was, he was surely not a Roman official solely stationed in Palmyra (cf. Matthews 1984: 179), he also lived, worked and died there, and was buried in the city in a tomb that he had prepared for himself, which in turn bears the indication that he was a very prominent citizen in Palmyra. There is also a very plausible connection between Germanicus’ visit to Palmyra and the inauguration of the Temple of Bel at Palmyra (cf. Stoneman 1995: 52) precisely coinciding with the imperial visit to Palmyra in ca. AD 17-19 (for Germanicus’ visit to the region and other epigraphical evidence, see Matthews 1984: 164).

2.3. The Purpose of the Tax Law I believe that the purpose of the Tax Law was to impose changes on the monetary and taxation system of the province of Syria on a broad level and not just in Palmyra. Contrary to the popular conception, as previously demonstrated (Lönnqvist 2007b), there is enough reliable historical and archaeological evidence to suggest the possible circumstances leading to the emergence of the Tax Law and its subsequent formulation. That Germanicus’ visit to the province of Syria ca. AD 17-19 was directly intended to cause the creation of a new settlement of the taxation and monetary system of the whole of Roman Syria-Palestine, can in my view be deduced from the

JEBEL BISHRI IN CONTEXT

78

explanation given by the Roman historian Tacitus in Annales (2.42.5). Tacitus informs us that in the year AD 17 (i.e. the year Germanicus was sent to the east) the Syrians and Jews ‘petitioned’ to diminish their taxes which they felt were too heavy: “provinciae Suria atque Iudaea, fessae oneribus, deminutionem tributi orabant”. The text in fact refers to both the provinces of Syria and Judaea participating in this petition which may have concerned the tributum soli, a land tax, and the tributum capitis, the ‘head-tax’ (Millar 1994: 110). But, as F. Millar (1994: 48) states Tacitus does not make it clear by whom or to whom the petition was presented. However, the formulation of some of the answers presented below implies clearly that the petition was made to the Roman Emperor. Given the four facts that are being emphasised here, which according to my best knowledge have not all been directly associated before, namely that there was a Roman census conducted in Judaea (and in Syria) in AD 6, as will be discussed later, an apparently official petition for reducing the taxes made in AD 17 by Syrians and Jews, a most high-ranking imperial representative or the adopted heir of Emperor Tiberius (Germanicus) sent on an imperial mission to Syria in AD 17-19 with the commands over all the provinces in the region, and then finally a new imperial record of taxation and use of Roman coin denominations being stipulated in Palmyra in AD 17-19, we can rather safely infer that these events were not random but seem to have formed a sequence of consequences. This clearly suggests that what occurred at Palmyra in AD 17-19 was probably a response to a petition made directly to the Emperor by the provincials in Syria and Judaea.

2.4. Preliminary Numismatic Implications Firstly, it may be concluded that there are likely to have been large similarities in the readings of the two Tax Laws, but that the 2nd century version must have brought new details and precision to the prototype of the 1st century law. It is, of course, also plausible that many changes had taken place in the provincial money market in the time that had elapsed between the two versions of the law. A significant difference between the old and the new versions was that the new law clarified in writing the exact amount of taxes that were to be exacted as revenue, listing further the individual goods that could and would be taxed, which in turn suggests that these may have been missing from the 1st century law (see Matthews 1984: 174 and Butcher 2004: 194). Still, the two most important numismatic implications of the Tax Law are: 1) the Greek reckoning system in Syria had been officially abolished by Emperor Tiberius’ rule in ca. AD 17-18, and 2) thenceforth the

tariffing of goods and paying of taxes in Palmyra took place in Roman coins or ‘Italian asses’ (one ass or assarion is normally counted as 1/16 of a Roman denarius). The collection of taxes or taxes charged are in the Greek text of the Tax Law consistently known as prassein, paraprassein or derivates thereof, meaning ‘to exact payment’ (PAT 1996: 352). NSI 147, 2 c) reads: “The tax on slaughtered animals by the denarius must be reckoned, as also Germanicus Caesar, in the letter which he wrote to Statilius, explained that it was indeed right that .. the taxes (should be) levied by the Italian assarius...”; in Aramaic “dy h’ksř dy [yh]n mksy’ ’py ’sr ’ytlq [’]”, or that it is right for the taxes to be according to the Italian assarius. In the same passage (NSI 147: 327, line 19, modius; 328, line 46, says Italian modius) we also have a reference to the Roman dry measure of ‘modius’ (in Aramaic md’), i.e., that beside Roman coin units Roman weights had additionally been introduced. It may be good to recapitulate here briefly that although Roman coin denominations were widely used in the Late Republican - Early Imperial period, it does not automatically follow that also Roman weight standards were used (Knapp 1987: 19, RPC I 1992: 31. See, Browning 1979: 17, for the modius). In the case of the 1st century AD Palmyra, it is known that both Italian coins and weights had been introduced into Syria and were effective (de iure) during Emperor Tiberius’ rule. However, having said this, we may immediately note that the same epigraphical evidence shows that the Roman denarii system and coin denominations were by no means the only ones in use, a circumstance that needs to be defined more closely. In effect, the Tax Law stipulated that “any tax of less than a denarius the tax collector will exact according to custom in small coin called κέρμα, i.e. local civic bronze or copper-based coins” (OGIS 629, p. 336, line 157, note 121). The text of 2c reads in Aramaic (Trf: 107): “wmdy gw mn dnr hyb mks’ hyk ‘dt’”. In particular what is meant by “local” will be further discussed in due course. Equally problematic is the question, why the taxes in the Tax Law were reckoned in ‘Italian asses’ and not, for instance, directly in Roman denarii (Trf: 56). Pursuing this line of argument for the counting in ‘Italian asses’, one may suggest that the asses had always been closely connected to the Roman army and army payments. The legionary pay in the Roman Republican period was to the 2nd century BC retariffed or computed in asses, albeit the payments were executed in denarii (Crawford 1985: 145). Later the as was replaced by the sestertius (Crawford 1985: 147) as the unit of accounting. Whatever the ‘military significance’ of the as later on in the 1st century AD, though, it is worth noting that in the predominantly military areas where the coin

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

79

denomination physically circulated, such as on the Northern Limes of the Roman Empire, archaeology has yielded in a quadruple number of Roman asses compared to other Roman coin denominations as late as in the time of Domitian (AD 81-96) (Carradice 1983: 132-133). Therefore, although it may not be possible to show a definitive military role for the as in the 1st century AD, it still shows a strong military presence all the way back to the early imperial period, at least in the western part of the Empire. Other factors that influenced the choice of the denomination of the as used may be connected to the metallurgy of the Roman coins. The Augustan monetary reform introduced between 23 and 19 BC (Crawford 1985: 258) appears to have stipulated that the larger denominations, e.g., the sestertius and the dupondius, were to be minted in orichalcum (brass), whereas the smaller ones (as, semis and quadrans) were to be minted in pure copper. As previously discussed (Lönnqvist 2007b), based on the evidence provided by archaeometallurgical research, brass appears to have been an alloy rarely used in the area in the 1st century AD for reasons that need not to be reiterated here. It thus remains quite possible – and even likely – that the smaller denominations from the Roman as down were minted in pure copper making them much more suitable for local conditions as basic units of reckoning. Archaeological finds tend to point towards that orichalcum coins having arrived in Syria in the period of Trajan ca. AD 115, when the production of asses and semisses in orichalcum for the region was initiated (Butcher 2004: 410, coins Nos. 19-22, Trajan AD 115; 411-412, coins Nos. 25-34, Hadrian AD 117-138). Some Trajanic quadrantes minted in Rome have been reported as site-finds from the archaeological excavations at Petra and Udhruh in Jordan, and the excavators concluded that the coins must have been used by the Roman army (Bowsher 1987: 166-168). These instances may, of course, have been exceptional, though. Although this review has been by no means comprehensive, to my best knowledge very few copper-based coins of the size and weight of a Roman sestertius (usually weighing ca. 27.3 g and worth four asses) were minted in the east in the first two Christian centuries (RPC I: 35; Meshorer AJC 2, 1982: passim; Meshorer TJC 2001: passim). This suggests that the denomination was too ‘large’, and in the south, for example, in the former Herodian kingdom, hardly ever in use in the Roman period. The lower-value denominations of a dupondius (weight ca. 13.65 g, and for an as weighing ca. 10.92 g, see, Carson 1990: 229) were, in fact, far more useful. In this regard, it remains possible that the SC (Senatus Consulto, letters intimating that the coins were

minted by the public authority of the Roman Senate) coinage in Syria was minted in what has been interpreted as the equivalent form to the Roman dupondius and as (Butcher 2004: 209). Secondly, despite it being calculated to 1/16 of a denarius, the Augustan as, was still minted to a weight standard closer to the previous value of 1/10 denarius (Carson 1990: 229), which possibly made it more acceptable and compatible with the local eastern coin denominations in circulation. The revaluation or approximation of the asses and the dupondii in the Augustan period aimed at increasing the stock of bronze coinage in circulation, as mentioned above (Crawford 1985: 261; Carson 1990: 229). This brought the as in weight and value close to the dupondius, thus, I believe, potentially making it the most ‘flexible’ of the Roman denominations. The most important conclusion regarding the Tax Law is that it reflects Roman Imperial decision-making in the 1st century AD at the highest possible level, as previously stated. One cannot escape the further conclusion that the Tax Law was formulated as a direct response to what Tacitus records was (Annales 2.42.5) a petition made by the provincials in Syria and Judaea in AD 17 to diminish their taxes (see, 2.3. above). The information provided by Tacitus, together with the formulation of the Tax Law itself, indicates that the famous census of the Syrian governor P. Sulpicius Quirinius, and probably comparable to a slightly earlier census recorded in the Gospel of Luke (in 2:1 ff: “Cyrenius, governor of Syria”; Josephus, Ant. 17: 355-18: 1-4; War 7: 253), had certainly not been a Roman success story. An inscription discussed by D. Kennedy (2006: 113; CIL III: 6687; ILS: 2683) shows that a census also was instructed by Quirinius to be conducted in northern Syrian city of Apamea in AD 6, which lends new credibility to Luke’s account for a wider Roman census that may have earlier covered at least Syria and Judaea as well. Assuming that the Egyptian censuses recorded from AD 19 can be traced back in 7 year cycles, would also make it possible that a census was conducted in Egypt in AD 5/6 (cf. Kennedy 2006: 116). This census occurred simultaneously with the census in Judaea in AD 6 in connection with the liquidation of Herod Archelaus’ estate, meaning the demotion of the former kingdom to the status of Roman province (like e.g. Burnett assumed 1987: 44). That Roman troops and a Roman governor were permanently stationing in the province also implies that the Roman monetary system was officially introduced and Roman coins became acceptable. Against this brief background, it emerges as unlikely that Palmyra had been left as a strange enclave excluded from the rest of Syria without Roman money – up to AD 17-18 – as also has been suggested (cf. Browning 1979: 10, 25).

JEBEL BISHRI IN CONTEXT

80

In the new 2nd century AD Tax Law the Romans wanted to tackle a fiscal difficulty which had obviously developed in the course of the early first century AD, since there appears not to have been any previously fixed scheme of taxation allowing the levying of taxes ‘precisely’. NSI 147, p. 333, line 6, calls this taxation ‘by custom’ or loose taxation. The new tariff (Trf. I: 11) stipulated that ‘the tax collector was not allowed to collect anything in excess from anyone’. This formulation of the inscription and decree makes it clear that, for instance, bankers, merchants, money-changers (collectarii, see, the New Testament and the Talmud: Baba Qama 113 a, NSI 147, p. 333; line 6) and especially the tax collectors or the publicani (Aramaic ‘gwr. Trf I: 11) featured as dishonest in several local sources. A 2nd century inscription from Pergamum (OGIS 484) quoted, e.g., by Burnett (1987: 102), also from the time of Hadrian (AD 117-138) alike Palmyra’s later second Tax Law, explains how the system was abused: ”For although they [the bankers] were bound to accept 16 asses per denarius from the tradesmen, small stallholders and fishmongers, all of whom normally deal in small bronze, and to pay out 17 asses to those who wished to exchange a denarius, they were not satisfied with the exchange of asses, but even in cases where someone bought a fish for silver denarii they exacted an as for each denarius”. Consequently, a customer may have been charged 17 or perhaps even 18 asses instead of 16, depending on whether he was selling or buying Roman denarii, what the exchange rate (collybus, agio or the commission) of the day was, and by which metal one was paying in. An agio or a banker’s commission of 1/60 was also extracted from the taxpayers in connection with the payment of taxes such as the dichoenicion and the prosdiagraphomenon, as the taxes were computed in copper-alloy but levied in silver coins (Duncan-Jones 1994: 48), reminiscent of the situation described in the Pergamum inscription. Two further numismatic implications of the Tax Law are: firstly that the city was allowed to levy its own taxes in the 1st and 2nd centuries AD and reap the profits thereof, and secondly that the formulation of the law reveals that economic and monetary conditions in Palmyra were unsatisfactory and needed to be mended by issuing new decrees. It is permissible to question here what the actual situation was that the Romans wanted to improve in Syria or Palmyra. Further, how was their response eventually formulated, and moreover, did the Roman response lead to something? I have recently suggested (Lönnqvist 2007b) that the absence of fixed taxation rates in Palmyra in the 1st AD is likely to have been a fruitful source of local disputes (as, e.g., Cooke NIS: 333 stated). The Aramaic/

Palmyrene inscriptions from Palmyra also specify with clarity that there were many disputes between the merchants and the tax-collectors in Palmyra (Trf. I:7 vs. CIS 3915: 3), although it still remains rather unlikely that local disputes of this kind alone would have been enough to activate the administration in Rome or elsewhere to introduce new imperial laws or edicts to improve the situation. This suggestion rests on the frequent finds in Egyptian papyri which demonstrate that the level of provincial taxation remained uniformly high in the east even throughout the Late Roman period, and that the sums extracted from taxpayers consistently and significantly exceeded the permitted and fixes amounts without any noticeable Roman intervention, at least not in the case of Egypt (Millar 1994: 50-51, for the papyri and taxes see Duncan-Jones 1994: 63). Similar cases are also recorded in Roman Judaea (see Isaac 1991: 458-461). It must therefore be suggested, at least preliminarily, where the Roman motives for the intervention into the Palmyrene conflict stemmed from. This may be taken as evidence for the locals having ‘back-slided’ from the Roman monetary system, which the Roman administration wanted to reconfirm by issuing an official decree. This is far more realistic, which better explains than that the decree had merely been an attempt to heal the relationship between the local merchants and tax-collectors.

3. The Romanization of Syria: A Final Monetary Perspective

The extent of integration into the Roman realm, or what is usually defined as ‘Romanization’ of the province of Syria would have to be dealt with in the areas where some traces can be discerned. These would largely be the coinage and the fiscal aspects, as suggested above. The Tax Law of Palmyra brings about two fundamental questions concerning the Roman coinage in the east: firstly, the date of the introduction of the Roman monetary system to Syria and secondly, what kind of effects the Law had on the existing provincial monetary system.

3.1. The Arrival of the Roman denarii in Syria Fortunately, the numismatic evidence is by any means clear with regards to one crucial point. The territorial expansion of Rome and the installation of the Roman province of Syria in the Late Republican period in 64/63 BC did not automatically entail that the Roman denarii were introduced or imported to the region (Baldus 1987: 121-151; Butcher 2004: passim). There is no numismatic or archaeological evidence from Syria or

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

81

Judaea for the support of the claim that the Romans had even effectively tried to introduce the Roman denarii system to the region in the Late Roman Republican period. An explanation would be, as some scholars have suggested, that the Romans may instead have directly ‘taken over the traditional coinages’ (e.g. by Baldus 1987: 146) in the areas under their rule. In fact, one can now conclude with the final two previously unpublished lots of silver of the Khirbet Qumran hoards published in 2007 (Lönnqvist 2007a), that the first major injection of Roman denarii to Syria-Palestine took place in the Neronian period at the earliest, not in the Augustan period, as previously thought. Therefore, there is a firm foundation to the claim made that Syria was one of the last provinces to transfer in practice to the Roman denarii system (e.g. Butcher 2004: 192-195). This seems to have happened, as explained above, some 120 years after the establishment of the province of Syria. An obvious sign of the local conservatism of previously mentioned is furthermore that the dating system of the Tax Law is in accordance with the old Seleucid system, not according to the era of the Roman Emperor, in spite of the inscription explicitly demanding the use of Roman coin denominations and Roman weights. When the territory controlled by Rome expanded in the 1st and 2nd centuries AD, we know that the acceptance of the denarii must have increased considerably, at least in geographical terms. But, at the same time we have no clear information as to how the volume or circulation of the denarii coinage developed in response to the enlarged territory, as pointed out for instance in Roman Provincial Coinage. In the end, the presence of Roman denarii in the eastern Mediterranean world should be seen as an equation of the numismatic principle, that, on the one hand, hoards preserve the frequency of coins in the monetary pool better than site-finds, which represent random losses of coin (Casey 1986: 60). Again on the other hand, coins would enter the archaeological record only if they were minted from dies that lasted long enough, circulated in large enough quantities and existed in a plentiful supply in the specified area, and lastly, perhaps also if the population had the willingness to both accept and use the coinage. This is, of course, a simplified model for the recovery of coins to research through natural and scientific processes. Notwithstanding there are other important conditions that influence the survival rate and recovery of ancient coins in the Near East that should at least given some mention here. It is throughout recognized, for instance, that there are major differences in archaeological research, both in terms of chronology, spatiality, accuracy and excavation techniques, which directly

affect the amount of coins brought ‘back’ to scientific study. In short, as previously pointed out (Lönnqvist 2007b), the archaeological field work that, e.g., the Finnish Archaeological Project in Syria (SYGIS) has done in 2000-2006 in the desert area northeast of Palmyra and along the Euphrates River, has established that the Roman infrastructure in this area of Syria is only gradually being revealed. A considerable amount of objects, including noble coins and coin hoards, are also apparently lost due to looting. Therefore, it seems that the present archaeological picture of Roman Syria is probably somewhat biased as less research has been carried out along the border zone where most of the Roman military troops were stationed and where much currency circulated, as demonstrated by comparable finds in military contexts in the west. The strongest – and in fact the hitherto only argument – that the denarius may have circulated in the very early Julio-Claudian period in Syria-Palestine (Butcher 2004: 195) is based on the material from Khirbet Qumran at the Dead Sea. I have made a new revision of the chronology and composition of the Khirbet Qumran silver hoards (Lönnqvist 2007: 1-72). Now it is, however, conclusive that the former chronology of the site and the burial date of the silver coin hoards have not only been controversial but mostly inaccurate. Consequently, thinking about the possible date of introduction of the denarius to Syria, it is possible to say now that the burial date of at least two, if not all the three of the Qumran silver coin hoards are not Augustan as originally suggested by the excavator of Qumran, Father R. de Vaux (1956: 568-569; Sharabani 1980: 274). This is because the earliest possible closing date of the hoards seems to be Neronian ca. AD 60-70, and the latest one associates the two hoards to the Severan period with a closing coin minted AD 206-210. The uncertainties are due to the fact that the original composition of the three silver hoards is not precisely known, and the original list of the contents of the hoards prepared in 1955 by the French numismatist H. Seyrig was never published. Nevertheless, the existing and published numismatic evidence with countermarked and closing coins in the report of the two Amman lots of the Qumran silver (Lönnqvist 2007a) provides a terminus post quem date of AD 52/53-66 for the burial of the hoards. Again as has previously been mentioned (Lönnqvist 2007a: 32), this conforms very well to the burial date of all the other major coin hoards recorded thus far in Syria-Palestine, including that of Mt. Carmel (CH I, No. 118; CH II, No. 134) also containing Roman denarii. The rule of Emperor Nero signified the turning-point for the minting of silver from Tyre, but the process came to an abrupt end at the latest during the First Jewish War

JEBEL BISHRI IN CONTEXT

82

(AD 66-70). At the same time a new but debased tetradrachm coinage (‘eagle coinage’) imitating the Tyrian eagle type was initiated at Antioch, the importance of which has already been discussed by several scholars. According to my knowledge the earliest references of gold aurei circulating widely in the region are from Josephus accounts of the First Jewish War (A.D. 66-70). The aurei were said to have circulated in large numbers in Jerusalem following the sack of the city in the country during the First Jewish War to the extent that “throughout Syria the standard of gold was depreciated to half its former value” (War 5: 421, 550; 6: 317). The archaeological stray or excavation finds recorded in Jerusalem among other places support the presence of some Late Republican and Early Imperial denarii and aurei from various minting periods, but none of the coins are – according to the given information – stratified or from clearly datable contexts (Ariel 1982: 312-315; 2007, correspondence). Furthermore, we have three aurei among the finds of valuable Roman coins in Jerusalem that were minted by Tiberius and Nero, those may actually have been injected and circulated later, e.g. during the First Jewish War rather than earlier, since once again, the coins are not from datable archaeological deposits. The absence of Roman coin hoards in Jerusalem prior to AD 70 has previously been pointed out by D.T. Ariel (1982: 285). The well-known quotations from the New Testament (Matt. 22:19, Mark. 12: 15, Luke 20: 24-25 etc.) referred to as the story of the ‘tribute penny’ indicate the presence of Roman Imperial denarii in some quantity in the area in the Julio-Claudian era. Still these references are not very helpful in determining the size of Roman coinage in circulation. A. Burnett (1987: 43) has therefore emphasised that “denarii clearly played an important role by the reign of Tiberius, but they never supplanted or even dominated the locally produced silver coinage”, which picture also emerges from the archaeological sources previously mentioned. Thus as far as the archaeological surveys are concerned, Roman denarii do not appear as common archaeological site finds or hoards in Roman Syria or Judaea before the early second century AD, despite decades of intensive research, for instance, in Jerusalem. From this period we have, e.g., the 2nd century AD Aramaic inscriptions and funerary texts in Palmyra (CIS 3948:3, with a payment of 300 denarii of gold or ‘old gold denarii’, in Greek chrysa palaia de denaria). We have also records of transactions of aurei, showing that the Aramaic speaking population of Palmyra used the same monetary terminology as the Jewish Rabbis in their commentaries to describe Roman noble coins. The term dinar zahav, זהב or זהוב, or the ‘gold dinar’ is a standard

monetary term for the Roman aureus of gold and later the solidus in the Rabbinic literature (see Sperber 1991: 31). This reinstates the overall conclusion that Roman Imperial denarii would not have played a major role in the local monetary economy before AD 60-70. Hence, although we have Roman Imperial coins cited in the Tax Law of Palmyra in AD 17/18, archaeology does not corroborate the conception of Roman imperial coins nevertheless having been physically present in notable quantities in the district during the that period.

3.2. Local vis à vis Roman Coins in the Monetary System of Syria

The described numismatic circumstances raise therefore further question concerning, how far-reaching conclusions can be made regarding the presence or absence of Roman coins and regarding the Roman monetary system in Syria in the Julio-Claudian period, if we use the Tax Law of Palmyra as our only source? The first question to be asked is: what may have been the motivation behind officially establishing that the taxes should be tariffed according to the Roman monetary system, and in Roman coin denominations that simultaneously were not even physically available? It thus appears that the Tax Law of Palmyra cannot be directly used as evidence for the case that the coinage was in circulation in Palmyra in the 1st century AD or that the coins necessarily would have consisted of the denominations that the decree actually recorded. A reminiscent Hellenistic inscription (IG II/III2 1534B, Athenian Asclepieion, Inventory V) previously discussed by the present author (Lönnqvist 1997: 122-126) is a mid-third century BC record of foreign coin dedications to the city of Athens. The Athenian inscription clearly states that Macedonian silver coins did circulate in the city of Athens during its oppression, and that these silver coins were dedicated to the local sanctuary. However, archaeological research within the city or even the whole peninsula of Attica has not yielded any of these Macedonian silver coins. Therefore, it was concluded that the coins recorded in the Athenian Asclepieion inscription were primarily references to coin weights (weights of silver) according to the Attic standard, not so much to the exact denominations or the ethnicity of the foreign coins (Lönnqvist 1997:125). In further support of the argument from classical Athens is a coinage law dating to 375/374 BC (Buttrey 1979: 33-46), and its later Hellenistic counterpart (IG II/III2, 1013), dated to the end of the 2nd century BC, that legislation was used to legally enforce, e.g., a city’s

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

83

coinage. The point was not necessarily to exclude the circulation of foreign coinage (although in some occasions such as Ptolemaic Egypt, this may have been the case) or make it unacceptable. Instead, by legally enforcing a coinage the city or the state would make profit by charging a premium through the exchange, either when exchanging foreign silver (peregrinus nummus) to Roman coins, silver to bronze coins, or vice versa. In classical Athens the premium charged was 5%, meaning a 5% overvaluation between the actual face value and the bullion or metallic value of the coin was charged. Whether this is incidental or not for Roman Syria, as well as our case study specified in this paper is difficult to say. But, as already suggested the premiums recorded in the 1st and 2nd century AD inscriptions were normally as high as 10-15%. From the coin weights and fineness of the 2nd century Trajanic denarii, in relation to the Syrian tetradrachm (counted 4 denarii to one tetradrachm) that Butcher (2004: 204) presents, we can also calculate that one Syrian tetradrachm contained precisely 5% less silver than 4 denarii, bearing the implication that the Syrian tetradrachm may have been overvalued 5% in comparison to the Roman denarius. With this in mind there might in addition be a case for Butcher’s suggestion (2004: 205) that is that Syrian provincial tetradrachms were accepted for tax payments because the Romans were circulating the coins in huge numbers and apparently at a premium, on top of which it may even have been enhanced with an additional surcharge when the conversion from local or provincial currency to Roman denarii took place. If a remote parallel to the ancient Roman monetary system in the same region is permitted, we may think of the Near East and the role the US dollar has there today. Prices and commodities in the Near East are regularly tariffed in US dollars, often in the small local economies that have weak currencies and a high inflation, although their use might even be prohibited in official contexts. In this “system” the foreign currency remains a “ghost currency” as defined by K. Butcher (2004: 257) when dealing with ancient currencies, a currency not physically present. Instead its function is to be used as a unit of reckoning and commuting only the dollar prices artificially into local units of reckoning with a higher total price. The obvious long-term benefits are a better economy, stability and higher incomes for the local “system”. In this “system” even the local governments tolerate the accounting in the “ghost” currency because of direct tax benefits and revenues, even if it might be politically or ideologically controversial. We can conclude, however, that the knowledge, existence and supremacy of the Roman tariffing system

in the 1st century AD would undoubtedly have promoted in due course as scholars have pointed out, a practical shift towards the use of Roman coins and denominations, the more they became available. The fact that taxes and prices were tariffed in Roman denominations should be taken as evidence for the locals having been familiar with the Roman monetary system and coin denominations. But, again, sources are silent on what the relationship between Roman and local coinages was, which exchange rates may have been reckoned and what the ways of reconciling the coinages with each other were. This conclusion would make it clear that Roman denominations were not in a reasonably wide use or abundant in Syria-Palestine in the 1st century AD, whereas ‘local’ denominations should in principle have been predominant and in general use. Unfortunately here too the evidence of the local denominations is very fragmentary and the question, about the κέρμα, i.e., the local civic bronze, will probably remain unanswerable, as illustrated above. If one finally reverts to consider the role of this local small change, the bronze or copper-alloy coins that are called by various names such as κέρμα, λεπτÄσ, χαλκÄς in the Tax Law of Palmyra and other sources, one encounters a perplexing and confusing archaeological situation. With regard to Palmyra, for instance, one immediately assumes that the city must have struck its own coinage in the Imperial period forming the base for its economy and used by the people for the flourishing trade and for paying the taxes. However, this appears only to have been the case during Queen Zenobia’s revolt against Rome and building the short-lived “Palmyrene empire” (see more in Stoneman). The excavations in the city of Palmyra conducted since the 1950s have resulted in virtually no coin finds from the Early Roman period (Krzyżanowska 1960: 217-221, 226-236; Krzyżanowska 1963: 184-189, 192-194; Krzyżanowska 1979: 44-52), as most of the identifiable bronze coins are Roman Imperial coins dating to the 2nd-4th centuries AD. Instead the excavations have yielded a seemingly huge number of tesserae in various materials and forms, the function of which is unclear (du Mesnil du Buisson 1944) although some may have been used as theatre tickets. The local population has informed us that long ago it was still possible to find hundreds of coins in the sand dunes outside the city, but the identification and whereabouts of all these coins are not available. The coins that have survived and are presently displayed in the Palmyra Museum (ca. 300 specimens) exhibition consist of the ordinary Hellenistic, Roman and Byzantine Imperial silver and bronze coins as well as a small hoard of gold coins from the early Byzantine period from the Camp of

JEBEL BISHRI IN CONTEXT

84

Diocletian (verbal information, Director W. Asa’ad, the Palmyra Museum). Three identifiable minute coin types that were minted either by or for Palmyra meet the following description in The Catalogue of the Greek Coins in the British Museum, Catalogue of the Greek Coins of Galatia, Cappadocia, and Syria 1964, 149-150, Nos. 1-7): ΠΑΛΜVΡΑ, Female (Atergatis), rev. Nike. Obv.: ΠΑΛΜ[VΡΑ?], Tyche of Palmyra, rev. lion. Obv.: Bearded male (Malakbel?), rev. Atergatis? The male is thought to be Malakbel, one of the most important gods of Palmyra (Al As’ad and Gawlikowski 1997, No. 7 = CIS 3927). The female is thought to be Atargatis (Venus), the Syrian Goddess. The Palmyrene coins in the catalogue do not have the name of the Emperor or the Imperial portrait, although obverses of civic coinage in Syria usually featured the Emperor’s portrait. The reverses, on the other hand, of civic coinage were rarely used for Imperial propaganda and would normally reflect things such as the local life, economy or religion (Butcher 2004: 218-238). The Palmyrene small bronze coinage is typical, with an emphasis on deities, ‘foundation types’ such as Tyche or palm trees which may have a connection to with the city of Palmyra. The lion is also common on Syrian coin types (Hierapolis, Heliopolis, Samosata, Aradus) representing goddess Atargatis, or in combination with minor types or symbols such as astral attributes (stars, crescents etc.). In this respect, the few coin types from Palmyra in existence, their increasingly small denominational value and the effectively small number of coins that has been recovered over what was become a period of centuries, makes it difficult to estimate what role these may have played in the local economy of Palmyra, if any. Whether these coins recovered as archaeological site-finds would have been part of this particular local small change (κέρμα) mentioned in the Tax Law, remains to be proven. A. Krzyżanowska suggested that these specifically Palmyrene coins would have been inaugurated in Emperor Hadrian’s reign, a theory which may well be true (Krzyżanowska 1979: 52). This follows the dating of the coins given by W. Wroth in the BMC catalogue (p. 149): “first and second centuries AD, period of Septimius Severus and family”. A. Krzyżanowska recorded that from the local and regional coinage recovered in the excavations of Palmyra, ca. 20% was Palmyrene, 35% was from the mint of Antioch and 7% from Damascus, whereas the rest of the mints are represented on an average with 0.5-3.0%. Of the ca. 50% of the identified Roman Imperial coinage, 26% came from Antioch while the rest of the ca. 24% identified percentage originated from eight different Imperial mints (Krzyżanowska 1979: 47, Table

I, 48 Table II, 50 Table III). As anticipated and later explained (Butcher 2004: 163, 179), only a tiny fraction of the identified coins are chronologically from the Early Imperial period. Therefore, we may perhaps be led back to A. Krzyżanowska’s previous suggestion that Antioch was by far the largest supplier of coins to this region in the 1st-2nd centuries AD. A similar case has been demonstrated with Dura Europos that did not mint at all in the Roman period. The total of coins found at Dura is 14017 coins, but none were minted in the city (Butcher 2004: 162-163, 179; see also coins found in context of the deceased soldiers at Dura Europos in Charlotte Stuhr-Børlit’s article in this volume).

3.3. Aspects of the Syrian Monetary Economy Because large numbers of Roman coins appear not have circulated in Syria (Palmyra) or Roman Judaea by the time the Tax Law of Palmyra was first codified in the 1st century AD, it follows that the Roman coin denominations were mere units of reckoning or units of account. As mentioned above, Butcher calls this a “ghost currency”. Since Roman coins were not available in quantities large enough for taxation purposes by locals in the 1st century AD, taxes must have been collected in either local civic or provincial Imperial silver coins (such as those minted at Antioch). However, although the taxes could be collected in local or provincial bronze or silver denominations, we cannot assume that these coins were sent as taxes to the Imperial treasury in Rome. It implies (as assumed, e.g., Butcher 2004: 258) the existence of a system where taxes and other dues were somehow either calculated into or physically converted into Roman Imperial coins (denarii - aurei) before being either sent to Rome or integrated into the taxation records on a provincial level as incomes (whether required a physical transportation of the coins as shipments to Rome, or the shipping of the actual tax surpluses only when the deductions for the provincial administration and the upkeep of the army had been made, need not to concern us here). It was worthwhile encouraging a system in which bronze had to be commuted into silver or vice versa because it was extremely profitable, albeit it was a continuous source of complaints, at least from the customer’s point of view, throughout the Imperial period. In the case of bronze coinages, the profit did not come from the people’s use of a city’s coins in that particular city, since coinage in Syria did not operate in a closed monetary system. Profit was generated through the general fact that silver and bronze needed to be exchanged, and these fluctuating exchange rates, commissions and surcharges have on good grounds also been called “taxes” either directly charged, stipulated or

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

85

encouraged to be collected with various leases by Rome. The formulation of the inscriptions and decrees that have been shortly cited here leaves little doubt about the fact that the system was effective and economically viable. To illustrate this point Palmyra had, according to an inscription dated to “Year 425” or AD 114 (Emperor Trajan, see CIS 3994), a public treasury (thesaurus publicus), ענושת called in Aramaic or a ‘fiscus’ that generated “large sums of money”, כסף ענושתא (est pecunia e mulctis collecta). The office holders of the in Aramaic or ענושותא bore the title of ענושתאÐργυροταμι´ν in Greek (office of a Ðργυροταμίας or the treasurer of a city, cf. CIG 2787, 2817, IG 22, 11000), which may be translatable into ‘quaestores’. Also, funerary inscriptions of local publicani recovered, display that all these elements were present in Palmyra too (the Neronian funerary inscription in CIS 4235, also from Palmyra, mentions Lucius Spedius Chrysanthus, the publican (publicanus), who died in the “Year 369” or AD 58. These Roman offices are direct equivalents with the publicani mentioned in NIS 147 = CIS 3913, that were responsible for the collecting of taxes in the Tax Law of Palmyra (I, line 6). L. Spedius was ‘conductor vectigalium apud Palmyrenos’, as mentioned in CIS 4235, p. 336. This latter inscription is, as previously mentioned, contemporary to the inscription of C. Virius Alcimus and Titus Statilius, which was raised amazingly also in AD 57/58. It seems therefore possible to concur with previous suggestions that the reforming of the coinages in the province of Syria and the nearby areas in the 60s AD under Nero, the re-organization of the provincial mints and the initial establishment of mints in the East for the production of denarii (assumed in RPC 1992: 53), are connected. The general pattern from the Julio-Claudian period is thus one of gradual replacement of the local and Roman silver with the Roman denarii. Something of this development is further recorded by the Roman historian Tacitus (Histories II, 82), who states that the branch mints were established for the production of tetradrachms and Roman denarii.

4. Conclusions and Summary

The importance, role and impact of the military expenditure on initiating, circulating and using coinages will remain under discussion for many years to come and perhaps no conclusive answers will be forthcoming, unless new sources are recovered accidentally. This road of explanation is littered with historians and even numismatists trying to explain that there is a fixed relationship between the need for the state expenditure

or wages paid to the Roman soldiers and the issue pattern of new coin. In my view the Tax Law emphasizes without any ambiguity that Palmyra was economically and monetarily integrated with the rest of the province and the Empire from the Julio-Claudian period onwards. Hence, this paper makes the arguably somewhat bold assumption that the new taxation laws introduced in Palmyra in the Tiberian period must have reflected the Roman attitude to the Roman coinage and taxation in the province of Syria on a provincial level, rather than being something characteristic of Palmyra alone. This assertion is supported by the literary sources quoted and discussed. It is also quite possible that one indirect goal of the decree was to make the local coinage systems and denominations more compatible and translatable into Roman denominations. It is also possible that the Tax Law was intended to bring the Palmyrene people ‘back’ more closely to the Roman monetary system in addition to that the official reckoning in Roman denominations became compulsory in AD 17/18, although archaeology does not support the concept that Roman coins would have dominated the money market in any way. The motives for introducing an official way of tariffing prices and taxes in Roman denominations must be sought from the Roman fiscal policy.

The installation of the Roman province of Syria in 64/63 BC did therefore not result in the direct introduction of Roman denarii to the region. The documentary and archaeological evidence suggests that the introduction of the Roman denarii and reckoning system took place de iure following the AD 6 census in Roman Judaea, and in Syria ca. AD 17-18 at the latest. In this period new taxation laws were passed in the city of Palmyra by the imperial legate Germanicus Caesar, who created a new monetary and taxation settlement for Syria. However, the first larger injections of Roman denarii did de facto take place only about half a century later in the 60s AD, when the large regional silver coinages had been either reformed and discontinued, and the local Roman denarii mint system established. This would probably have resulted in a local minting of denarii as well.

Sources and Bibliography Al As’ad, K. & Gawlikowsky, M. (1997) The Inscriptions in the Museum of Palmyra. Warsaw. Al As’ad, K. & Yon, J.-B. (2001) Inscriptions de Palmyre. Promenades épigraphiques dans la ville antique de Palmyre. Guides archéologiques de l’Institut française d’archéologie du Proche-Orient, No 3. Beyrouth-Damas-Amman.

JEBEL BISHRI IN CONTEXT

86

Aleshire, S.B. (1989) The Athenian Asclepieion. The People, their Dedications, and the Inventories. Amsterdam. Ariel, D.T. (1982) A survey of coin finds in Jerusalem, in Liber Annuus 32, pp. 273-326. Baldus, H.R. (1987) Syria, in The Coinage of the Roman World in the Late Republic. Proceedings of a Colloquium Held at the British Museum in September 1985 (Eds. Burnett, A.M. – Crawford, M. H. British Archaeological Reports (BAR), International Series No. 326. London, pp. 121-151. Ball, W. (2000) Rome in the East. The Transformation of an Empire. Glasgow. Berger, A. (1973) Encyclopedic Dictionary of Roman Law. Transactions of the American Philosophical Society. New Series. Vol. 43. Part 2. Philadelphia. BMC= A Catalogue of the Greek Coins in the British Museum (1964) Catalogue of the Greek coins of Galatia, Cappadocia, and Syria. Ed. by W. Wroth. Reprint, Bologna. Bowsher, J.M.C. (1987) Trajanic quadrantes from Arabia, in The Numismatic Chronicle 147, pp. 166-168. Browning, Iain (1979) Palmyra. Fakenham, Norfolk. Bruck, G. (1961) Die spätrömische Kupferprägung. Graz. Burnett, A.M. & Crawford, M.H. (eds.) (1987) The Coinage of the Roman World in the Late Republic. Proceedings of a colloquium held at the British Museum in September 1985. British Archaeological Reports (BAR), International Series No. 326. London. Burnett, A. (1987) Coinage in the Roman World. London. Burns, R.. (1994) Monuments of Syria. An Historical Guide. Bridgend. Mid Glamorgan. Buttrey, T. V. (1979) The Athenian Currency Law of 375/4 B.C., in Greek Numismatics and Archaeology, Essays in honour of Margaret Thompson, Wetteren, pp. 33-46. Cambridge Ancient History (1984) Vol. VII. Part I. The Hellenistic World. Especially Chapter 8: Cultural, social and economic features of the Hellenistic world. Davies, J. K. Cambridge.

Caley, E.R. (1939) The Composition of Ancient Greek Bronze Coins. The American Philosophical Society. Philadelphia. Caley, E.R. (1964) Analysis of Ancient Metals. Pergamon Press. Oxford. Carradice, I. (1983) Coinage and Finances in the Reign of Domitian A.D. 81-96. British Archaeological Reports. BAR International Series 178. Oxford. Carson, R.A.G. (1990) Coins of the Roman Empire. Cambridge Carter, G.F. (1983) Chemical analysis of copper-based Roman coins, in Israel Numismatic Journal 6-7, pp. 22-38. Cary, M. & Scullard, H. H. (1984) A History of Rome down to the Reign of Constantine. Reprint, Hong Kong. Casey P. J. (1986) Understanding Ancient Coins. London. CCAM or Touratsoglou 1993 = see Touratsoglou 1993, below. CH = Coin Hoards see below. Christiansen, E. (1988) The Roman Coins of Alexandria. Quantitative studies. Vol. 1. History Departament at Aarhus University (PhD-thesis). Aarhus. Coin Hoards I- (1975-) The Royal Numismatic Society. London. Cook, G.A. (1903) A Text-book of North-Semitic Inscriptions, Moabite, Hebrew, Phoenician, Aramaic, Nabataean, Palmyrene, Jewish. Oxford. Cope, L.H. (1972) The metallurgical analysis of Roman Imperial silver and aes coinage, in Methods of Chemical and Metallurgical Investigation of Ancient Coinage, ed. by Hall, E.T. – Metcalf, D.M., Royal Numismatic Society, Oxford, pp. 3-47. Craddock, P.T. (1995) Early Mining and Production. Edinburgh. Crawford, M. (1970) Money and Exchange in the Roman World, in The Journal of Roman Studies, Vol. 60, pp. 40-48. Crawford, M.H. (1974) Roman Republican Coinage I-II. I Introduction and Catalogue, II Studies, Plates and Indexes. Cambridge.

LÖNNQVIST: THE TAX LAW OF PALMYRA AND THE INTRODUCTION OF THE ROMAN MONETARY SYSTEM

87

Crawford, M.H. (1985) Coinage and Money under the Roman Republic. Italy and the Mediterranean Economy. Cambridge. CRWLR or Touratsoglou (1987) = see Burnett, A.M. – Crawford, M. H. 1987, above. Dittenberger, Wilhelmus 1905 (1970) Orientis Graeci Inscriptiones Selectae. Supplementum Sylloges Inscriptionum Graecarum. Leipzig/Hildesheim. Donceel, R. (1992) Reprise des travaux de publication des Fouilles au Khirbet Qumran, in Revue Biblique, Vol. 99, pp. 557-573. Donceel, R., Donceel-Voûte, P. (1994) The Archaeology of Khirbet Qumran, in Methods of Investigation of the Dead Sea Scrolls and the Khirbet Qumran Site, Present Realities and Future Prospects, Annals of the New York Academy of Sciences, Vol. 722, June 20th, 1994, ed. by Wise, M.O., Golb, N., Collins, J. J. and Pardee, D.G. New York, pp. 557-573. Duncan-Jones, R. (1994) Money and Government in the Roman Empire. Cambridge. Failmezger, V. (2002) Roman Bronze Coins: From Paganism to Christianity 294-364 A.D. Washington D.C. Hill, P.V., Kent, J.P.C. & Carson, R.A.G. (1972) Late Roman Bronze Coinage A.D. 324-498. Part I, The Bronze Coinage of the House of Constantine A.D. 324-346, Part II, Bronze Roman Imperial coinage of the later empire A.D. 346-498. London. Hillers, D. R. & Cussini, E. (eds.) (1996). See Palmyrene Aramaic Texts below. Hopkins, K. (1980) Taxes and Trade in the Roman Empire (200BC – AD 400), in The Journal of Roman Studies, Vol. 70, pp. 101-125. Howgego, C. J. (1985) Greek Imperial Countermarks. Studies in the Provincial Coinage of the Roman Empire. Royal numismatic society special publication no. 17. London. Howgego, C. J. (1992) The Supply and Use of Money in the Roman World, in The Journal of Roman Studies 82, pp. 1-31. IG = Inscriptiones Graecae. Isaac, B. (1991) The Roman army in Judaea: police duties and taxation, in Roman Frontier Studies, Proceedings of the XVth international congress of

Roman frontier studies, ed. by Maxfield, V.A. and Dobson, M. J. Exeter, pp. 458-461. Kennedy, D. (2006) Demography, the Population of Syria and the Census of Q. Aemilius Secundus, in the Levant 38, pp. 109-124. Knapp, Robert C. (1987) Spain, in The Coinage of the Roman World in the Late Republic. Proceedings of a Colloquium Held at the British Museum in September 1985 (Eds. Burnett, A.M. – Crawford, M.H. British Archaeological Reports (BAR), International Series No. 326. London, pp. 19-41. Krzyżanowska, A. in Michałowski, K. (1960) Palmyre, Fouilles Polonaises 1960, Université de Varsovie, Centre d’Archéologie Mediterranéenne dans la République arabe unie au Caire. Warszawa.

Krzyżanowska, A. in Michałowski, K. (1963) Palmyre, Fouilles Polonaises 1961, Université de Varsovie, Centre d’Archéologie Mediterranéenne dans la République Arabe Unie au Caire. Warszawa. Krzyżanowska, A. (1979) La circulation monétaire à Palmyre d’après le materiel provenant des fouilles, in Polish Numismatic News 3, pp. 44-52. LRBC = see Hill – Kent – Carson above. Lönnqvist, K. (1997) Studies on the Hellenistic Coinage of Athens: The Impact of Macedonia on the Athenian Money Market in the 3rd century B.C., in Early Hellenistic Athens, Symptoms of a Change, ed. by J. Frösén, Papers and Monographs of the Finnish Institute at Athens, Vol. VI, Vammala, pp. 119-145. Lönnqvist, K. & Lönnqvist, M. (2006) The Numismatic Chronology of Qumran: Fact and Fiction, in The Numismatic Chronicle 166, pp. 121-165. Lönnqvist, K. (2007a) The Report of the Amman lots of the Qumran Silver Coin Hoards. New Chronological Aspects of the Silver Coin Hoard Evidence from Khirbet Qumran at the Dead Sea. Amman. Lönnqvist, K. (2007b) New Perspectives on the Roman Coinage on the Eastern Limes in the Late Republican and Early Roman period. Helsinki 2008. Matthews, J.F. (1984) The Tax Law of Palmyra: Evidence for Economical History in a City of the Roman East, in The Journal of Roman Studies 74, pp. 157-180.

JEBEL BISHRI IN CONTEXT

88

Meshorer, Y. (1975) Nabataean Coins. Qedem 3. Monographs of the Institute of Archaeology. The Hebrew University of Jerusalem. Jerusalem. Meshorer, Y. (1982) Ancient Jewish Coinage. Volume II: Herod the Great through Bar Cochba. New York. Du Mesnil du Buisson, R. (1944) Les tessères et les monnaies de Palmyra un art, une culture et une philosophie grecs dans les moules d’une cite et d’une religion sémitiques. Paris. Meshorer, Y. (2001) A Treasury of Jewish Coins. Jerusalem. Mommsen, T. (1887) 1952 Römisches Staatsrecht 2:1. Graz. Mommsen, T. (1860) 1956 Geschichte des Römischen Münzvesen. Graz. Oddy, A. & Cowell, M. (1998) Metallurgy in Numismatics. Vol. 4 (with various others and articles). Royal Numismatic Society Special Publication No. 30. London. Ørstedt, P. (1985) Roman Imperial Economy and Romanization. A study in Roman Imperial administration and the public lease system in the Danubian provinces from the first to the third century A.D. Copenhagen. Poidebard, A. (1934) La Trace de Rome dans le Désert de Syrie. Le Limes de Trajan a la conquète arabe, recherches aériennes (1925-1932). Texte. Atlas. Bibliothèque Archéologique et Historique. Tome XVIII. The Palmyra Museum, Coin Collections. Palmyrene Aramaic Texts (1996) Ed. by Hillers, D.R.. and Cussin, E. Baltimore, Maryland. Pflaum, H.-G. (1950) Les Procurateurs Equestres sous le Haut-Empire Romain. Paris. RIC = Roman Imperial Coinage, see below Richardson, J. (1976) Roman Provincial Administration 227 B.C.-117 A.D. Inside the Roman World. London. Roman Imperial Coinage (RIC) I- (1923-) London. Roman Provincial Coinage (RPC) Vol. I. (1992) From the death of Caesar to the death of Vitellius (44 BC-AD 69). Part I: Introduction and Catalogue. Part II: Indexes

and Plates. Ed. by Burnett, A. Amandry, M. & Ripolles, P.P.. Cambridge. Roman Provincial Coinage (RPC) Supplement I. (1998) Ed. by. Burnett, A., Amandry, M. & Ripolles, P.P. Cambridge. Roman Provincial Coinage (RPC) Vol. II. (1999) From Vespasian to Domitian (AD 69-96). Part I: Introduction and Catalogue. Ed. by Burnett, A., Amandry, M. & Carradice, I. London/Paris. RPC = Roman Provincial Coinage, see above Sperber, D. (1991) Roman Palestine 200-400 Money and Prices. Bar Ilan Studies in Near Eastern Languages and Culture. Second Edition with Supplement. Jerusalem. Stevenson, G.H. (1951) The Provinces and their Government, Ch. 10, in Cambridge Ancient History, Vol. IX, The Roman Republic 133-44 BC. Cambridge. Stoneman, R. (1995) Palmyra and Its Empire. Zenobia’s Revolt against Rome. Ann Arbor, Michigan. Symmachus = Q. Aureli Symmachi. Relationes (1963). Ed. by M. Adams. London. Thompson, M., Mørkholm, O. & Kraay, C. M. (eds.) (1973) An Inventory of Greek Coin Hoards. New York. Touratsoglou, Y. (1993) The Coin Circulation in Ancient Macedonia (ca. 200 B.C.-268-286 A.D.) The Hoard Evidence. Bibliotheca of the Hellenic Numismatic Society 1. Athens. Walker, D. (1976-1978) The Metrology of the Roman Silver Coinage. British Archaeological Reports (BAR), Supplementary Series. 5, 1976; 22, 1977 and 40, 1978. Oxford.