The Role of Performance-Related Pay in Renegotiating the "Effort Bargain": The Case of the British...

23

ILRReview Volume 57 | Number 3 Article 2 April 2004 e Role of Performance-Related Pay in Renegotiating the "Effort Bargain": e Case of the British Public Service David Marsden London School of Economics Follow this and additional works at: hp://digitalcommons.ilr.cornell.edu/ilrreview

-

Upload

independent -

Category

Documents

-

view

1 -

download

0

Transcript of The Role of Performance-Related Pay in Renegotiating the "Effort Bargain": The Case of the British...

ILRReview

Volume 57 | Number 3 Article 2

April 2004

The Role of Performance-Related Pay inRenegotiating the "Effort Bargain": The Case of theBritish Public ServiceDavid MarsdenLondon School of Economics

Follow this and additional works at: http://digitalcommons.ilr.cornell.edu/ilrreview

The Role of Performance-Related Pay in Renegotiating the "EffortBargain": The Case of the British Public Service

AbstractMuch of the academic and policy literature on performance-related pay (PRP) focuses on its role as anincentive system. Its role as a means for renegotiating performance norms has been largely neglected. Thisstudy examines the introduction of performance-related pay, based mostly on appraisals by line managers, inBritain’s public services during the 1990s. Previous research indicates that PRP failed to motivate many of thestaff and that its operation was divisive. Nevertheless, other information suggests that productivity rose. Thisarticle seeks to resolve the paradox using contract theory to show that performance pay was the instrument ofa major renegotiation of performance norms, and that this rather than motivation was the principal dynamic.Goal-setting and appraisal by line managers played a key role in this process.

Cover Page FootnoteFor helpful advice and comments, the author thanks workshop participants at the Centre for EconomicPerformance, the Society for the Advancement of Socio-Economics, and the University of Grenoble. He alsothanks the numerous managers, union officials, and staff of the various public organizations for their time andhelp with the study. He also thanks Stephen French and Ray Richardson for their agreeing to let him use theresults of the surveys he conducted jointly with them.

This article is available in ILRReview: http://digitalcommons.ilr.cornell.edu/ilrreview/vol57/iss3/2

350

Industrial and Labor Relations Review, Vol. 57, No. 3 (April 2004). © by Cornell University.0019-7939/00/5703 $01.00

T

THE ROLE OF PERFORMANCE-RELATED

PAY IN RENEGOTIATING THE “EFFORT BARGAIN”:

THE CASE OF THE BRITISH PUBLIC SERVICE

DAVID MARSDEN*

Much of the academic and policy literature on performance-related pay(PRP) focuses on its role as an incentive system. Its role as a means forrenegotiating performance norms has been largely neglected. This study exam-ines the introduction of performance-related pay, based mostly on appraisals byline managers, in Britain’s public services during the 1990s. Previous researchindicates that PRP failed to motivate many of the staff and that its operation wasdivisive. Nevertheless, other information suggests that productivity rose. Thisarticle seeks to resolve the paradox using contract theory to show that perfor-mance pay was the instrument of a major renegotiation of performance norms,and that this rather than motivation was the principal dynamic. Goal-setting andappraisal by line managers played a key role in this process.

*The author is Professor of Industrial Relations,London School of Economics, and a member of theCentre for Economic Performance. For helpful ad-vice and comments, he thanks workshop participantsat the Centre for Economic Performance, the Societyfor the Advancement of Socio-Economics, and theUniversity of Grenoble. He also thanks the numerousmanagers, union officials, and staff of the variouspublic organizations for their time and help with thestudy. He also thanks Stephen French and RayRichardson for their agreeing to let him use theresults of the surveys he conducted jointly with them.

A data appendix with additional results, and com-puter programs used to generate the results pre-sented in the paper, are available from author atLondon School of Economics, Industrial Relations,Houghton St, London WC2A 2AE; e-mail ,[email protected]. Copies of the questionnairesand summaries of the survey results may be found inMarsden and Richardson (1992) and Marsden andFrench (1998), both available online fromwww.cep.lse.ac.uk.

here is a paradox to be explained con-cerning the spread of performance-

related pay (PRP) in the British publicservices. In the public policy debate it hasbeen common to associate the introduc-tion of PRP with the aim of improvingincentives and motivation among publicemployees (Brown and Heywood 2002).

This has been a key element in governmentand top management thinking in the Brit-ish public services, echoed in two recentgovernment reports (Bichard 1999;Makinson 2000), and it has been of long-standing interest in the work of the OECD’spublic management reform program(Maguire 1993; OECD 2002). It is also arecurrent theme in much of the PersonnelEconomics and Human Resource Manage-

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 351

ment literature (for example, Lazear 1998;Milkovich and Wigdor 1991; Mitchell et al.1990; Armstrong and Murlis 1994). Start-ing in the late 1980s, the British publicservices embarked on the most systematicand sustained policy of extending and de-veloping performance-related pay of anyOECD country, mostly replacing annualseniority-related pay increments with per-formance-related ones based on goal-set-ting and appraisals by line managers, some-times called “appraisal-related pay” (ACAS1990). Nevertheless, surveying both aca-demic research findings and inside man-agement information, the government’sMakinson report concluded that perfor-mance pay had not motivated public em-ployees in Britain, and its operation hadbeen divisive (Makinson 2000). Given thatthe policy has been sustained by three suc-cessive prime ministers of quite differentpolitical persuasion, two Conservative andone Labor, as well as successive top manag-ers, its continued use cannot plausibly beexplained by political dogma. Likewise, inthe face of such evidence, the perseveranceof top public management and of succes-sive governments is hard to understand ifemployee motivation is the main story. Weneed to look elsewhere for an explanation.

In this article, I argue that the alternativeexplanation can be found in the use ofperformance pay, and of performance man-agement more widely, to provide a frame-work for renegotiating performance stan-dards—the “effort bargain”—with publicemployees. This is consistent both withrising organizational performance, whichwould explain top management’s persever-ance, and with the repeated evidence thatPRP has failed to motivate many publicemployees.

Two examples from the fieldwork thataccompanied the survey data, which areanalyzed later, illustrate the kinds ofchanges management has sought to intro-duce with the aid of PRP. In one of thehospitals, management wanted to moveaway from the practice of covering extendedworking after normal hours and on week-ends by means of overtime and weekendpremium payments. It wanted a more flex-

ible system that would provide cover in amore patient-centered way on which man-agement could draw as extra time wasneeded. In exchange, it would reward co-operative behavior with a higher basic sal-ary and performance pay. In the tax ser-vice, management wanted employees tochange from a focus on working to prede-termined standards dictated by their jobclassifications to a focus on individual per-formance. This, it believed, would be moreresponsive to the demands from individualtaxpayers, and would better reflect the dif-ferences in ability between individual em-ployees in similar jobs.

In both examples, there is a degree ofworking “smarter,” but also a significantelement of working more intensively whenthat is necessary to meet the patient’s ortaxpayer’s needs. In conforming to thischanged work model, public employees alsobecome more exposed to the uncertaintiming of citizens’ demands, and have lesscontrol over their pace and manner of work.Even where management obtains unions’agreement to such changes, it has still tomake the deal stick on the shop and officefloor. Line managers are the strategic linkin the chain translating the abstract objec-tives of change into the everyday tasks thatindividual public servants undertake; hencethe importance of goal-setting and ap-praisal. But they are also potentially a weaklink, as they come under pressure fromtheir staff to be lenient with work assign-ments and over-generous with performancerewards. The widely observed upward “drift”in performance appraisal and pay awardsstems from just such pressures (see, forexample, Milkovich and Wigdor 1991).

In both examples, one can see that in-centive and goal-setting features of perfor-mance pay still play a key part in the story,but motivation is only their secondary func-tion. Their primary function, through ap-praisal and goal-setting, I argue, has beento enable management to redefine the es-tablished performance norms in their or-ganization, and then to obtain effectivecompliance with those norms, with the ex-plicit or tacit agreement of as many employ-ees as possible.

352 INDUSTRIAL AND LABOR RELATIONS REVIEW

Performance Management as a Meansof Renegotiation: Main Theories

It has been common to analyze the work-ings of PRP in recent years through thelenses of three main theories: agency, ex-pectancy, and goal-setting theory. Thesetheories shed much light on the static in-centive and appraisal processes present inPRP. They have focused mainly on howmanagement can influence employees’choice between different levels of effort orcare in their work for a given set of perfor-mance norms. To understand the changesoccurring in the British public services,however, one needs to complement theperspective provided by these theories witha more dynamic analysis of inducementsfor employees to agree to, and work within,a new set of performance norms.

The idea of renegotiation is most simplyexplained in terms of contract theory. Aworker and a firm agree to the terms oftheir exchange when the worker is hired. Akey feature of the employment contract isthat it should be open-ended in terms ofboth its duration and its content. Workersagree to give the employer’s agent, man-agement, some flexibility to adapt that con-tent to changing demands, but only withincertain limits (Coase 1937). From time totime, these limits require revision. Such ajuncture becomes an occasion for renego-tiation. This time, however, each party hasmade investments in the relationship and isvulnerable to pressure tactics from theother. Much of the contract literatureemphasizes pay because of changes in themarket valuation of employee output(Malcomson 1997). Less visible, but just asimportant for management, is its ability torevise job boundaries, and redefine thenature and standards of performance thatit requires from employees. These stan-dards, which may include qualitative as-pects of performance, are usually the sub-ject of a tacit understanding between staffand management, sometimes called the“effort bargain.”

By what processes does renegotiationcome about? Many recent studies (for ex-ample, Teulings and Hartog 1998) have

focused on the role of collective bargain-ing. Their main interest, however, hasbeen in pay adjustments. Pay rules aregenerally codified by virtue of their inclu-sion in collective agreements and individualcontracts of employment. In contrast, manyof the rules relating to workers’ job bound-aries and performance standards contain alarge uncodified element. It is common forjobs to deviate considerably from their for-mal job descriptions, and for their contentsto be highly “idiosyncratic,” to useWilliamson’s (1975) term. The features ofa given job are therefore accessible to highermanagement only through the eyes of first-line managers. To renegotiate perfor-mance, management needs to get rightdown to the level of individual jobs, and tothe relationship between individual em-ployees and their line managers. Collectiveagreements often set the overall framework,but ultimately this kind of negotiation hasto occur between line managers and indi-viduals or small groups of employees in thesame office or hospital ward.

At the time of hiring, workers who do notlike the supervisory practices and incentivesystems the employer offers can just walkaway, so there is a process of self-selectionthat matches these job features to workers’preferences.1 However, when the timecomes for changing work practices and in-centive systems in an established organiza-tion, the employer faces an incumbent workforce whose preferences for or against thenew system may vary considerably. In thechange, some will expect to be winners,and others, losers. To get everyone toengage positively in the new system, man-agement would have to offer a very attrac-tive, and costly, deal. It might thereforeprefer to make the new deal attractive to asufficient proportion of its staff so that thescheme functions tolerably well, and to

1Lazear (1998) attributed a good deal of the in-creased productivity associated with output-based payto such self-selection processes, as more productiveemployees are attracted by the higher earnings op-portunities offered by incentive pay.

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 353

forego the support of the remaining staff inorder to keep within some budgetary limit.Indeed, the two hospitals in the data setused in this article took just that path. Theygave incumbent employees a choice, and sodid not have to buy out those who weremost strongly attached to the old system.Thus, one may consider management asoperating with a kind of “median voter”model (albeit probably based on a higherthreshold than 50%) whereby it designs theincentives so as to attract enough of itsemployees to make the new scheme effec-tive, subject to an overall budget constraint.

Thus, the renegotiation perspective leadsus to expect any net performance improve-ments in this study to depend on the effectsof both the move to new work norms andthe attractiveness of the incentives providedby the new pay system, PRP. However,neither effect is uniform across all employ-ees. Some will be positively attracted to thenew deal, which comprises both new normsand new incentives. They are likely to bewell motivated and to deliver higher per-formance. Others may resent the new ar-rangements and not find the pay schememotivating. Nevertheless, their lack ofmotivation may not necessarily translateinto a decline in their performance. Suchemployees must weigh the benefits of ac-cepting the new scheme against the costs offinding an alternative. They may not likethe new system, but they may still choose towork within it because changing jobs is notworth their while, and they do not wish tobe dismissed. The greater managementattention to goal setting and performanceappraisal that accompanies PRP is likely toincrease the effectiveness with which thenew work norms are monitored and dis-courage reduced performance. Providedperformance of the discontented does notfall too much, the organization may stillbenefit from the increased performance ofthose who engage positively, assuming theydo so in sufficient numbers.

In this reading, renegotiation and incen-tive can be complementary functions ofPRP, and one can say that the incentivemechanisms and, particularly, the goal-set-ting mechanisms have to be working prop-

erly for PRP to be an effective means ofchanging work norms. Agency theory alsoprovides a picture of the static functions ofPRP. It explains how performance andoutput incentives encourage employees towork hard (and not to “shirk”) when man-agement finds it costly to monitor theireffort closely. It proposes that manage-ment can respond by tying pay to output soas to induce employees to choose a higherlevel of effort (Lazear 1995, Chap. 2), andalso by investing in better systems of workdesign and performance evaluation to im-prove the correlation between performancemeasures and effort, thus strengtheningincentive effects (Milgrom and Roberts1992:226). It also warns against the dys-functions of inappropriate incentives, suchas individual incentives that discouragecooperation among colleagues (Drago andGarvey 1998).2

Expectancy theory, associated for ex-ample with Vroom (1964), Porter andLawler (1968), Lawler (1971, Chap. 6),and Furnham (1997), like agency theory,treats employees as having a degree ofchoice and places a strong emphasis onthe motivational effects of incentives, andthe problems posed by poorly definedtargets. Simplifying somewhat, it identi-fies a potentially virtuous circle. Employ-ees will respond to the incentive or re-ward on offer if they value it (its valence),if they believe good performance will beinstrumental in bringing the desired re-ward (instrumentality), and if they expecttheir efforts will achieve the desired per-formance (expectancy). The circle of Va-lence-Instrumentality-Expectancy can bebroken at a number of points. Employ-ees may feel they lack scope to increasetheir effort, or that their effort will makelittle difference to their performance,such as might arise if they are given inap-propriate work targets by management.This undermines expectancy. They may

2Strictly speaking, their evidence relates to promo-tion.

354 INDUSTRIAL AND LABOR RELATIONS REVIEW

believe that management lacks the com-petence or the good faith to evaluate andreward their performance fairly, a view thatundermines instrumentality and may causeemployees to see the schemes as unfair anddivisive. Applying these considerations torenegotiation, one can see that employeesare more likely to buy into a new incentivescheme when they perceive it as operatingfairly and able to deliver the promised re-wards.

Goal-setting theory places less empha-sis on rewards and stresses the motivatingpower of defining appropriate work goalsand engaging employee commitment tothem (Locke and Latham 1990; Lathamand Lee 1986; Brown and Latham 2000).Of special relevance in the current con-text is the emphasis on dialogue betweenline managers and employees to exchangeinformation about realistic goals, and onagreeing to goals so that employees adoptthem as their own. This framework al-ready contains the germs of a negotia-tion process between employees and theirmanagers, and so it is easy to see how thebasic idea can be applied in the contextof renegotiating performance norms.Goal-setting may be especially importantfor the employees who do not like thenew system, but still prefer not to changejobs. In such cases, it provides manage-ment with a channel to clarify the newstandards and establish agreed levels ofcompliance.

Thus, although the last three ap-proaches, agency, expectancy and goalsetting, differ in emphasis, they point tothe same key processes and variables forthe analysis of performance pay systems:reward and motivation on the one hand,and goal definition and evaluation onthe other. Mostly, this literature has fo-cused on questions of motivation andincentive for given sets of performancenorms. However, it is clear that a certainlevel of motivational effectiveness is re-quired from PRP if it is to serve as a basisfor the renegotiation of performancenorms. Thus, in terms of empirical ob-servation, there is a great deal of overlapbetween the renegotiation perspective

and the motivational perspective in thevariables to be tracked. The main differ-ence in terms of outcomes is that therenegotiation perspective predicts im-proved performance from PRP even insome cases where large numbers of em-ployees claim not to be motivated by it,whereas the motivational perspective pre-dicts that widespread “disenchantment”of the kind Makinson (2000) noted willlead to disappointing performance.

These considerations can be expressedinformally in a simple model. The incen-tive that employees perceive from a PRPscheme (perceived incentive) will be afunction of the additional financial re-ward associated with good performance,the quality and effectiveness of the goal-setting and appraisal process, and thescope for employees to improve theirperformance. This is summarized inequation (1). Conversely, when theseprocesses function badly, one can expectemployees to experience PRP as divisiveand demotivating (equation 2). Finally,if the goal-setting process is enablingmanagement to communicate new per-formance standards and make them stick,then it should have a direct effect onemployee performance. That is, to theextent that renegotiation contributes toimproved performance, the direct per-formance effects of the goal-setting andappraisal process should gain in impor-tance relative to the indirect performanceeffects that hinge on motivat ionalchanges (equation 3).

(1) Perceived incentive = f(extra fi-nancial reward, appraisal quality,clear targets, scope for employ-ees to boost performance, con-trol variables)

(2) Perceived divisiveness = f(extrafinancial reward, appraisal qual-ity, clear targets, scope for em-ployees to boost performance,control variables)

(3) Performance level = f(perceivedincentive, perceived divisiveness,appraisal quality, interactions,control variables)

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 355

Data and DescriptiveEvidence on Motivation and

Divisiveness of Performance Pay

The analysis in this article reworks thedata collected by LSE’s Center for Eco-nomic Performance in a series of attitudesurveys across a range of public services onemployee and line manager judgments asto the effects of performance pay (seeMarsden and Richardson 1992, 1994;Marsden and French 1998).

Summary evidence on employees’ re-sponses to PRP and their disenchantmentwith it is summarized in Table 1, based onthe employee replies to the CEP attitudesurveys. These relate to six areas of publicservice work: the Inland Revenue in 1991and 1996 (tax service); the EmploymentService (job placement and benefit pay-ments); two National Health Service trusthospitals; and head teachers in primaryand secondary schools. These were chosento represent a cross-section of public orga-nizations using performance pay at the time.Methodological details are summarized inthe appendix. In brief, mailed question-naires asked employees and line managersabout their personal experiences with theoperation of their performance pay andappraisal scheme in their service—theirviews as to whether the scheme providedthem with an incentive to perform in spe-cific ways, whether their jobs gave themscope to do so, and how management oper-ated their scheme—and also solicited somebiographical data. Many of the motiva-tional questions were modeled on expect-ancy theory. In some cases, managers gavetheir support to the research, and it waspossible to survey a sample of all employeescovered by the scheme in their organiza-tion. In other cases, managers refusedaccess for the survey work, although theydid provide other information, and theunions provided a sample frame based ontheir membership lists. All the services hadhigh union membership rates.3 In the or-

ganizations where management cooper-ated, both union members and non-mem-bers were included in the sample, and itappeared that membership had no greatinfluence on replies. Line managers werealso included in the sample, and their re-plies could be linked to those of otheremployees by their place of work.

The CEP evidence of employee disen-chantment with PRP shown in Table 1 isbroadly consistent with the results of otherattitudinal surveys that applied the samemethodology as was used by Marsden andRichardson (1992), notably, Thompson(1993), Kessler and Purcell (1993), Heery(1998), IRS (1999), and, in the privatesector, Carroll (1993). Despite broad sup-port for the principle of linking pay toperformance, only a small percentage ofemployees thought their existing perfor-mance pay schemes provided them with anincentive to work beyond job requirementsor to take more initiative. Of even moreconcern to top public management was theevidence that the performance pay schemesin place were seen by staff to be divisive andto undermine cooperation among staff, anda worrying percentage of line managersreported that the schemes had made staffless willing to cooperate with management.Note, however, the substantial minority ofline managers who reported that PRP hadcaused many of the staff to work harder.

These negative staff reactions cannot beexplained as the result of naïve design ele-ments in the schemes. (The schemes aresummarized in the methods appendix,Table A1.) With the possible exception ofthe scheme in force in the tax service in1991, which was one of the first in opera-tion, all of the schemes obeyed the existingcanons of good HR practice (as set out, forexample, by ACAS 1990, and Armstrongand Murlis 1994) and had been developedwith substantial inputs from private sectorexpertise. They were seriously thought-outschemes. Cognizant that ratings often driftupward, and that the schemes’ applicationcan be discriminatory, planners incorpo-rated substantial review mechanisms in allthe schemes, and information was sharedwith the relevant unions on the distribu-

3It was 90% in the Inland Revenue, 60% in theEmployment Service middle management grades stud-ied, and around 90% among head teachers. Publichospitals are also highly unionized.

356 INDUSTRIAL AND LABOR RELATIONS REVIEW

tion of ratings across different categories ofstaff and workplaces. Reflecting the degreeof task complexity in many public servicejobs, all the individual schemes involvedperformance appraisals by line managersbased on a mixture of judgment and re-corded data. Written records were kept ofappraisals. Nor was the financial incentivenegligible. Up to the top of the pay scalefor a person’s grade, PRP replaced annualsalary increments and was consolidated intobasic pay, and several years of good perfor-mance could lead to substantially faster payprogression. For those who would previ-ously have “topped out” at the maximumfor their grade, PRP brought the opportu-nity of non-consolidated annual bonuses insome organizations, and of further pro-gression in others.

Measurement of Key Variables

The analysis uses three outcome vari-ables: two motivational variables built upfrom subjective responses to questionsshown in Table 1, and a third based onobjective information, appraisal scores, thatcould be checked against archival data.The survey questions relating to “perceivedincentive” in Table 1 were chosen to repre-sent aspects of the three incentive theories.The first two questions capture the per-ceived disutility or cost to the employee ofeffort required to gain the reward: willing-ness to work beyond job requirements, andwillingness to take more initiative in orderto get PRP. The one entails more effort; theother, more risk of failure. The third ques-tion captures the element of perceived re-ward for good work as opposed to “shirk-ing.” This measure of perceived incentiveis close to that of valence of rewards inexpectancy theory: are the rewards suffi-ciently valued to warrant the extra effort?

The downside, “perceived divisiveness,”is explored by three questions chosen tocapture the disutility of poorer work rela-tions and of diminished cooperation, ei-ther of which may jeopardize the achieve-ment of work targets. If staff are less willingto help their colleagues, the risk of failureto achieve targets is individualized, and the

safety net of helping hands is removed.Likewise, the pay system could cause jeal-ousies among staff. Reduced willingness tocooperate with management captures thevertical as opposed to the horizontal as-pects of cooperation among work col-leagues. The indices of perceived incentiveand divisiveness were computed simulta-neously using factor analysis based on thesequestions.

For the third outcome variable, employ-ees reported their latest appraisal scorebefore the survey date. It is likely that thesescores were accurately recalled, since theydirectly affected employees’ pay. The dis-tributions of appraisal scores by occupa-tional and demographic variables in thesample surveys were compared with archi-val data obtained from the organizations.These comparisons indicate that, by andlarge, respondents reported the appraisalscores accurately, and there were no obvi-ous response biases by appraisal scores.Because performance was graded differ-ently across the organizations, outcomeswere classified into a binary scale of “supe-rior” and “acceptable,” the latter includingboth satisfactory ratings and the very smallnumber of unsatisfactory ratings.

The key independent variable, the qual-ity of the appraisal process (“appraisal qual-ity”), plays a central part in both agencyand expectancy theory. This is built upfrom three survey items, asking employeeswhether they know what they need to do toget a good appraisal; whether they are ableto do it; and whether they understand theirlast appraisal rating. These questions werevalidated against a larger and more con-crete set of descriptive questions about theappraisal process used in one of the study’shospitals, and which were very unlikely tobe colored by whether or not the employeegot a good rating.4 For clarity of target-setting in PRP, just one question could bematched across the organizations: did PRPlead managers to set targets more clearly?

4A detailed analysis of these checks can be foundin Marsden (2003).

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 357

This was supplemented by a question toline managers in the same office on thescope employees have to raise their per-formance.

The strength of financial incentivescould not be measured directly, becausegood appraisals trigger performance pay,and this study uses appraisal scores as ameasure of employee performance. How-ever, its presence can be assessed indi-

rectly in two ways. On the one hand,those on the top of the pay scale for theirgrade get one-time bonuses instead of anincrease in their basic salary. One wouldexpect such employees to feel less incen-tive than the others. On the other, thosewho were both of long service and ontheir grade maximum would rememberthe former pay system of about 3–4 yearsbefore, with its ceilings on pay, whereas

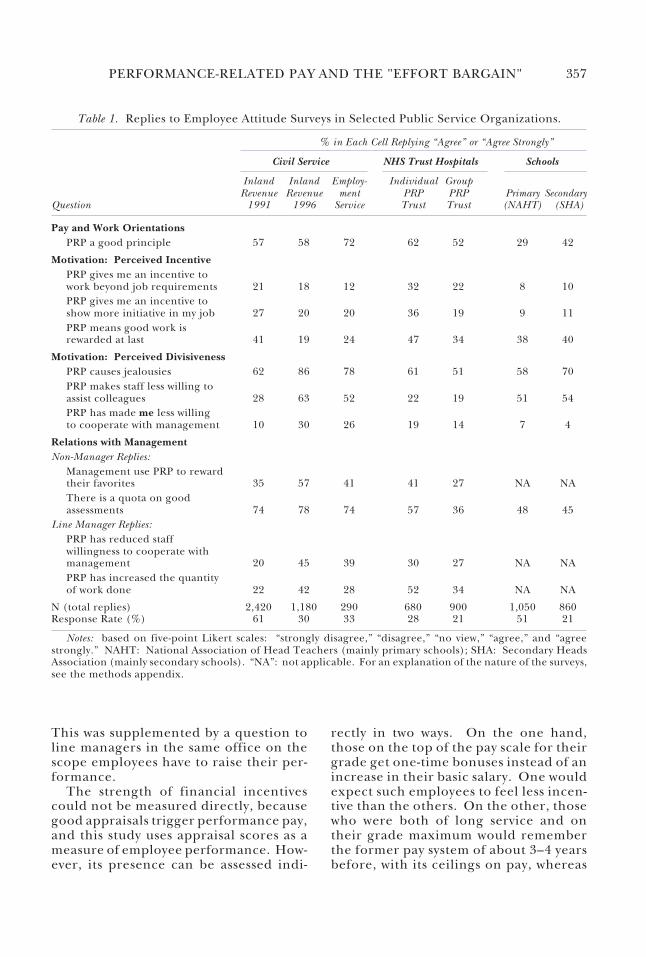

Table 1. Replies to Employee Attitude Surveys in Selected Public Service Organizations.

% in Each Cell Replying “Agree” or “Agree Strongly”

Civil Service NHS Trust Hospitals Schools

Inland Inland Employ- Individual GroupRevenue Revenue ment PRP PRP Primary Secondary

Question 1991 1996 Service Trust Trust (NAHT) (SHA)

Pay and Work OrientationsPRP a good principle 57 58 72 62 52 29 42

Motivation: Perceived IncentivePRP gives me an incentive towork beyond job requirements 21 18 12 32 22 8 10PRP gives me an incentive toshow more initiative in my job 27 20 20 36 19 9 11PRP means good work isrewarded at last 41 19 24 47 34 38 40

Motivation: Perceived DivisivenessPRP causes jealousies 62 86 78 61 51 58 70PRP makes staff less willing toassist colleagues 28 63 52 22 19 51 54PRP has made me less willingto cooperate with management 10 30 26 19 14 7 4

Relations with ManagementNon-Manager Replies:

Management use PRP to rewardtheir favorites 35 57 41 41 27 NA NAThere is a quota on goodassessments 74 78 74 57 36 48 45

Line Manager Replies:PRP has reduced staffwillingness to cooperate withmanagement 20 45 39 30 27 NA NAPRP has increased the quantityof work done 22 42 28 52 34 NA NA

N (total replies) 2,420 1,180 290 680 900 1,050 860Response Rate (%) 61 30 33 28 21 51 21

Notes: based on five-point Likert scales: “strongly disagree,” “disagree,” “no view,” “agree,” and “agreestrongly.” NAHT: National Association of Head Teachers (mainly primary schools); SHA: Secondary HeadsAssociation (mainly secondary schools). “NA”: not applicable. For an explanation of the nature of the surveys,see the methods appendix.

358 INDUSTRIAL AND LABOR RELATIONS REVIEW

those more recently recruited would not.Thus, an additional measure of the pres-ence of financial incentive from PRP canbe found by interacting employees’ be-ing on their grade maximum with theirlength of service.

Affective commitment, as measured byMeyer and Allen (1997), provides an in-direct proxy for “shirking” behavior,which is otherwise difficult to explore ina questionnaire survey administered tothe individuals concerned. Individualshirking is bad for the employer and usu-ally bad also for one’s work colleagues, asit usually disrupts their work and adds totheir workload. In contrast, commitment,and especially affective commitment,implies a degree of emotional identifica-tion with one’s workplace and one’s workcolleagues. I included this variable inthe analysis on the supposition that com-mitment might be strong among publicemployees, many of whom have quite longservice. In the regression, commitmentenhanced the perceived incentive of PRPand reduced its perceived divisiveness.

A number of organizational and de-mographic controls are used. Organiza-tion dummies are included to control forfixed effects arising from differences be-tween the schemes operating in each or-ganization, most notably variations in theshare of employees getting “superior”ratings owing to differences in the designof their schemes. Occupational controlsare used, comparing each occupationalgroup to managers, the one occupationthat can be clearly identified across allthe organizations. Among the many pos-sible effects captured by “occupation,”one of special interest is the degree ofcontrol employees have over their work.The clerical and service occupations gen-erally have less control over the detail oftheir work than do managers and profes-sionals, and hence less scope to respondto performance pay incentives. On theother hand, the simpler nature of theirtasks may make their performance easierto evaluate. Length of service and gen-der are also included as independentvariables.

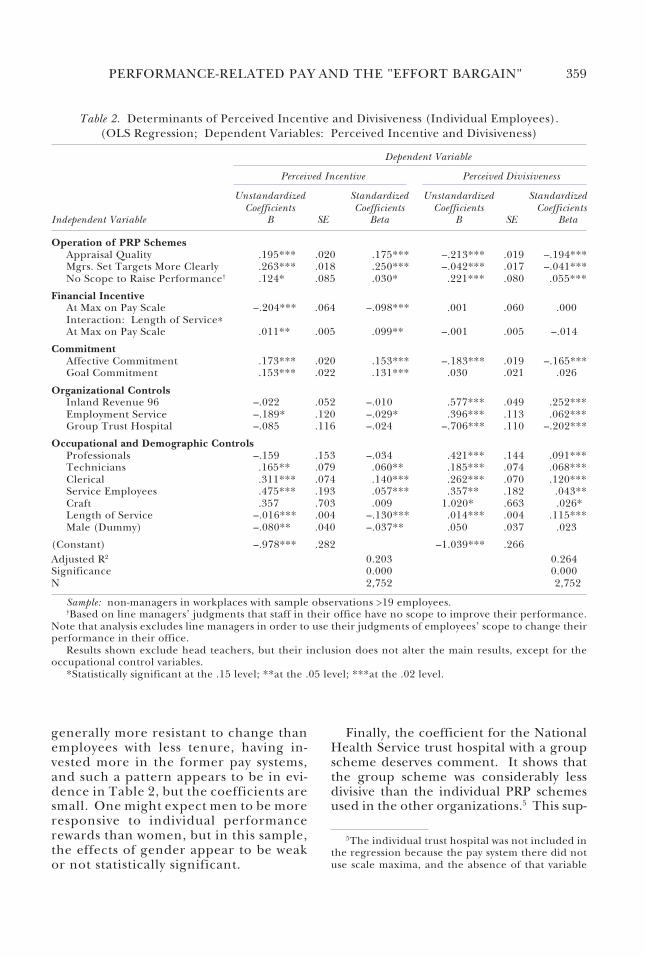

Regression Results 1: PerceivedIncentive and Divisiveness

The regression results shown in Table 2,from equations (1) and (2) above, showthat having an effective appraisal increasedemployees’ perceived incentive and re-duced perceptions of divisiveness. Themeasures of perceived incentive and divi-siveness, as well as that of appraisal quality,were all based on factor analysis, and sohave a mean of zero and a standard devia-tion of unity. The standardized coefficientsimply, therefore, that a unit increase in themeasure of appraisal quality will lead tochanges of +.17 and –.19, respectively, inmeasures of perceived incentive and per-ceived divisiveness. Likewise, the judgmentby employees that PRP has led line manag-ers to set clearer targets boosts perceivedincentive and reduces perceived divisive-ness, although the way the variable wasmeasured makes the coefficients hard tocompare with those on appraisal quality.Consistent with the theories reviewed ear-lier, when line managers judge that em-ployees lack scope to improve their perfor-mance, perceived divisiveness increases,although the effect on incentive is barelystatistically significant.

The results also show that the lesser re-wards from PRP associated with being on thetop of one’s pay scale diminish perceivedincentive. In contrast, the positive interac-tion with length of service suggests that longer-serving employees are conscious of the im-provement in opportunities over the age-incremental pay system of earlier years, whichprovided no scope for extra pay.

The control variables deserve comment.The perceived incentive of PRP rises atlower levels of the organizational hierar-chy, but so does perceived divisiveness. Theexception is professionals, who appear tofind PRP particularly divisive, possibly be-cause they have long been accustomed toexercise considerable discretion in theirwork and so resent the extra managementcontrol that comes with performance man-agement. Length of service and genderwere introduced as additional demographiccontrols. Long-service employees may be

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 359

generally more resistant to change thanemployees with less tenure, having in-vested more in the former pay systems,and such a pattern appears to be in evi-dence in Table 2, but the coefficients aresmall. One might expect men to be moreresponsive to individual performancerewards than women, but in this sample,the effects of gender appear to be weakor not statistically significant.

Finally, the coefficient for the NationalHealth Service trust hospital with a groupscheme deserves comment. It shows thatthe group scheme was considerably lessdivisive than the individual PRP schemesused in the other organizations.5 This sup-

Table 2. Determinants of Perceived Incentive and Divisiveness (Individual Employees).(OLS Regression; Dependent Variables: Perceived Incentive and Divisiveness)

Dependent Variable

Perceived Incentive Perceived Divisiveness

Unstandardized Standardized Unstandardized StandardizedCoefficients Coefficients Coefficients Coefficients

Independent Variable B SE Beta B SE Beta

Operation of PRP SchemesAppraisal Quality .195*** .020 .175*** –.213*** .019 –.194***Mgrs. Set Targets More Clearly .263*** .018 .250*** –.042*** .017 –.041***No Scope to Raise Performance† .124* .085 .030* .221*** .080 .055***

Financial IncentiveAt Max on Pay Scale –.204*** .064 –.098*** .001 .060 .000Interaction: Length of Service∗At Max on Pay Scale .011** .005 .099** –.001 .005 –.014

CommitmentAffective Commitment .173*** .020 .153*** –.183*** .019 –.165***Goal Commitment .153*** .022 .131*** .030 .021 .026

Organizational ControlsInland Revenue 96 –.022 .052 –.010 .577*** .049 .252***Employment Service –.189* .120 –.029* .396*** .113 .062***Group Trust Hospital –.085 .116 –.024 –.706*** .110 –.202***

Occupational and Demographic ControlsProfessionals –.159 .153 –.034 .421*** .144 .091***Technicians .165** .079 .060** .185*** .074 .068***Clerical .311*** .074 .140*** .262*** .070 .120***Service Employees .475*** .193 .057*** .357** .182 .043**Craft .357 .703 .009 1.020* .663 .026*Length of Service –.016*** .004 –.130*** .014*** .004 .115***Male (Dummy) –.080** .040 –.037** .050 .037 .023

(Constant) –.978*** .282 –1.039*** .266Adjusted R2 0.203 0.264Significance 0.000 0.000N 2,752 2,752

Sample: non-managers in workplaces with sample observations >19 employees.†Based on line managers’ judgments that staff in their office have no scope to improve their performance.

Note that analysis excludes line managers in order to use their judgments of employees’ scope to change theirperformance in their office.

Results shown exclude head teachers, but their inclusion does not alter the main results, except for theoccupational control variables.

*Statistically significant at the .15 level; **at the .05 level; ***at the .02 level.

5The individual trust hospital was not included inthe regression because the pay system there did notuse scale maxima, and the absence of that variable

360 INDUSTRIAL AND LABOR RELATIONS REVIEW

ports the evidence of Drago and Garvey(1998) that strong individual incentives maydiminish helping behavior among col-leagues if they get in the way of individualtargets.

Thus, a first conclusion is that the per-formance pay and appraisal schemes wereactively influencing employee motivation,and that they did so in the manner pre-dicted by the mainstream theories.

Regression Results 2: Impact onAppraised Performance

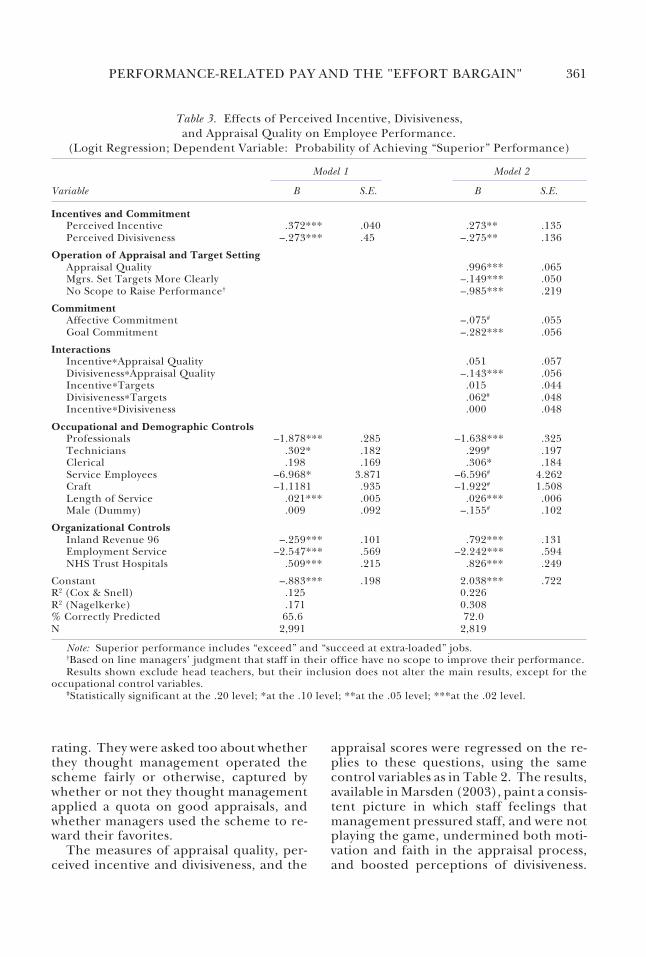

The second set of regression results, re-ported in Table 3, is based on equation (3)above. The left-hand column shows theeffect of perceived incentive and divisive-ness on employee performance as mea-sured by the latest appraisal score, and theright-hand column includes also appraisalquality and reports the interactions amongthese variables. To facilitate comparisonacross schemes, the performance variablehad to be simplified into a binary one—whether or not the employee’s performancehad been graded as “superior”—so a logis-tic regression was used.

The results show quite clearly that incen-tive and divisiveness affect individual per-formance. The effect of the first is positiveand the effect of the second negative, andboth effects are strongly statistically signifi-cant. As a guide, which can only be ap-proximate given the crude nature of theLikert scales, one can say that a one stan-dard deviation increase in perceived incen-tive would raise the probability of “superiorperformance” by about 0.6 and a similarincrease in perceived divisiveness wouldreduce it by about 0.4.6 The strong coeffi-

cient for appraisal quality warrants com-ment: it implies that a standard deviationincrease in appraisal effectiveness wouldlead to roughly a 0.7 increase in the prob-ability of superior performance. The ro-bustness of this coefficient, despite the in-clusion of interaction terms, indicates thatthere is also a strong direct effect of ap-praisal on performance, in line with therenegotiation perspective.

Appraisal and theRe-Negotiation of Performance

Because management has to renegotiateperformance norms within a budget con-straint, it is likely that the terms offered willbe accepted voluntarily by some employ-ees, but will find only involuntary compli-ance from others who do not feel adequatelycompensated. This suggests there will be“two faces” to appraisal. It can provideincentives by clarifying work goals and giv-ing recognition, but it can also be a vehiclefor management to pressure employees intogiving higher levels, or different kinds, ofperformance, for fear of losing pay or evenlosing their jobs.

The CEP survey data for the tax serviceprovide some evidence supporting that pre-diction. In line with concerns raised by thedepartment’s Review Team (Inland Rev-enue 1994b), respondents were askedwhether, despite the express philosophy ofvoluntarism enunciated by the service’sperformance management scheme (InlandRevenue 1995), the staff felt pressured toaccept management’s choice of objectives.To address a second concern of the ReviewTeam, they were also asked whether theythought everyone was in effect given thesame targets, despite the philosophy thattargets should be adapted to the capabili-ties of individual employees. They werealso asked about the negotiation of objec-tives: whether they thought those who wereawarded superior appraisals did so becausethey were cleverer at negotiating their ob-jectives, and whether, when agreeing to theobjectives, they were more concerned withavoiding the risk of a bad appraisal thanwith aiming for a superior performance

excluded a category of data essential to the regres-sion.

6The standard deviation of both perceived incen-tive and perceived divisiveness is 1.0. The logisticregression estimates the change in the log of the oddsof achieving superior performance associated with aunit change in a given independent variable, that is,log(p/(1 – p)), where p is the probability of the event,that is, achieving superior performance. With a stan-dard deviation of 1 for both motivation variables, p =e exp(b)/(1 + e exp(b)), where b is the regressioncoefficient.

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 361

rating. They were asked too about whetherthey thought management operated thescheme fairly or otherwise, captured bywhether or not they thought managementapplied a quota on good appraisals, andwhether managers used the scheme to re-ward their favorites.

The measures of appraisal quality, per-ceived incentive and divisiveness, and the

appraisal scores were regressed on the re-plies to these questions, using the samecontrol variables as in Table 2. The results,available in Marsden (2003), paint a consis-tent picture in which staff feelings thatmanagement pressured staff, and were notplaying the game, undermined both moti-vation and faith in the appraisal process,and boosted perceptions of divisiveness.

Table 3. Effects of Perceived Incentive, Divisiveness,and Appraisal Quality on Employee Performance.

(Logit Regression; Dependent Variable: Probability of Achieving “Superior” Performance)

Model 1 Model 2

Variable B S.E. B S.E.

Incentives and CommitmentPerceived Incentive .372*** .040 .273** .135Perceived Divisiveness –.273*** .45 –.275** .136

Operation of Appraisal and Target SettingAppraisal Quality .996*** .065Mgrs. Set Targets More Clearly –.149*** .050No Scope to Raise Performance† –.985*** .219

CommitmentAffective Commitment –.075# .055Goal Commitment –.282*** .056

InteractionsIncentive∗Appraisal Quality .051 .057Divisiveness∗Appraisal Quality –.143*** .056Incentive∗Targets .015 .044Divisiveness∗Targets .062# .048Incentive∗Divisiveness .000 .048

Occupational and Demographic ControlsProfessionals –1.878*** .285 –1.638*** .325Technicians .302* .182 .299# .197Clerical .198 .169 .306* .184Service Employees –6.968* 3.871 –6.596# 4.262Craft –1.1181 .935 –1.922# 1.508Length of Service .021*** .005 .026*** .006Male (Dummy) .009 .092 –.155# .102

Organizational ControlsInland Revenue 96 –.259*** .101 .792*** .131Employment Service –2.547*** .569 –2.242*** .594NHS Trust Hospitals .509*** .215 .826*** .249

Constant –.883*** .198 2.038*** .722R2 (Cox & Snell) .125 0.226R2 (Nagelkerke) .171 0.308% Correctly Predicted 65.6 72.0N 2,991 2,819

Note: Superior performance includes “exceed” and “succeed at extra-loaded” jobs.†Based on line managers’ judgment that staff in their office have no scope to improve their performance.Results shown exclude head teachers, but their inclusion does not alter the main results, except for the

occupational control variables.#Statistically significant at the .20 level; *at the .10 level; **at the .05 level; ***at the .02 level.

362 INDUSTRIAL AND LABOR RELATIONS REVIEW

Staff feelings of pressure and managementbad faith did not bear a statistically signifi-cant relationship with appraisal scores, soone can rule out the “sour grapes” factor.7

One group of employees was especiallylikely to report feelings of duress: part-timers, who are particularly numerous inthe public sector. Being an objective char-acteristic, part-time status will not be influ-enced by the employees’ experience withtheir PRP scheme. Given that many staffbecome part-time in order to reconcile workand domestic responsibilities, they are par-ticularly likely to be unhappy about the newtrade-off between new work norms and re-ward and hence to renegotiate reluctantly.The replies show that they were twice aslikely as full-time staff to report staff beingpressured to agree to targets, and they werealso more likely to express cynical viewsabout the operation of appraisal.

A final question is whether feelings ofduress arise because some line managersare just bad at appraisal and goal-setting,and so do it in a threatening way, in whichcase, better design and more training mightbe the answer. This was suggested in someof the internal management reviews in thetax service (for example, Inland Revenue1997). Alternatively, the malaise amongemployees might be caused by employerpressure to raise performance, as part of arenegotiation of performance levels. Toexplore the causes of the perception ofduress more fully, it is helpful to considerthe respective roles of individual and col-lective bargaining (Table 4).

One indication of the intensity of rene-gotiation at the individual level is the de-gree to which the new scheme is madecompulsory for all employees. At the In-land Revenue and the Employment Ser-vice, the schemes were universal and com-pulsory, and all employees had to agree towork objectives and accept monitoring oftheir progress. In contrast, at the two hos-

pitals, incumbent employees were offereda choice between the new scheme withhigher basic pay and PRP, and the oldnationally negotiated time-based pay scaleswithout PRP. By offering this choice, man-agement avoided conflict with some groupsof employees, who either were hostile orstood to lose accumulated premium pay-ments they had under the old pay system.School head teachers were in an intermedi-ate position, because the implementationof performance pay at their schools de-pended on the initiative of school gover-nors, whom they could often influence.Finally, the scheme in force at the InlandRevenue in 1991 was very much a hybridbetween the old seniority-incremental sys-tem and the new performance manage-ment system. In the words of the unionnegotiators, it was “bolted on” to the oldpay and appraisal system. Performance paymeant accelerated movement up the oldincremental scale: there were carrots butno sticks. Thus, ranking the organizationson this measure of individual negotiationindicates that greater intensity is broadlyassociated with stronger perceptions of di-visiveness.

Collective bargaining has played a some-what smaller role, because it cannot domuch more than set up a framework andestablish incentives. The levering up ofperformance levels and the detailed reori-entation of performance has to be done atthe individual level between line managersand their staff. Nevertheless, the two col-lective agreements that ushered in perfor-mance pay at the Inland Revenue wereconflictual. The 1988 agreement was ob-tained with a management threat that ifPRP were not included, there would be nonational agreement, and the 1993 agree-ment was preceded by a bitter strike despiteearly joint management-union workingparties on pay reform. The hospitals hadthe least conflictual introduction of perfor-mance pay, as it came with new provisionsfor local bargaining. Thus, prima facie, itwould seem that the pressure from man-agement as expressed through the extentand intensity of individual negotiation par-tially accounts for the different levels of

7The one exception was seeking objectives to avoida bad appraisal, which was negatively related to theperson’s appraisal score.

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 363

perceived divisiveness in the various orga-nizations in this study (Table 4).

Discussion of Possible Objections

Before moving to conclusions, six pos-sible objections to the renegotiation hy-pothesis need to be considered: (a) Didappraisal scores influence reporting of ap-praisal quality, thus undermining the valid-ity of a key statistical relationship support-ing the renegotiation thesis? (b) Did ap-praised performance represent actual per-formance, or just management leniency?(c) Did performance improvements repre-sent “working smarter rather than harder,”and hence require no renegotiation? (d)Would not the elimination of widespread“shirking” also explain resentment coupledwith higher productivity? (e) Could newrecruits attracted by higher performancepay account for the rise in productivity,with incumbent employees remaining dis-

contented? (f) Was PRP a “lightning rod”for general discontent about work reorga-nization?

(a) It is possible that employees’ perfor-mance appraisal scores color their report-ing of the quality of their appraisal processand the measures of perceived incentiveand divisiveness. Although a recent studyfound that appraisal scores had little influ-ence on perceptions of the appraisal pro-cess, this may depend on how the process isoperated in different organizations (Boswelland Boudreau 2000). I investigated thisissue further in two ways. The first test,using the richer descriptive data collectedon the appraisal process in the CEP study’stwo hospitals, shows that those data alsocorrelated well with the measures of ap-praisal quality. The second test was a two-stage least squares regression aimed at pre-dicting (1) perceived incentive and per-ceived divisiveness from the appraisal qual-ity variable shown in Table 2, and then,

Table 4. Intensity of Re-Negotiation and Perceived Divisiveness.

Divisiveness: Role ofStandardized Standard Individual

Mean Error Agreement on PRP Role of Collective Agreement

Inland Revenue 1996 0.472 .035 Compulsory for all 1993 pay agreement afterstrike

Employment Service 0.252 .061 Compulsory for all Series of agreements fordifferent staff grades1994–95

Schools: Head Teachers 0.142 .060 Compulsory if adopted Implemented by govern-by school governors ment after pay review as

one criterion for pay awardsby school governors

Hospital with Individual –0.041 .066 Voluntary for current Implemented by localPRP staff management;

subsequent agreement withunions

Inland Revenue 1991 –0.158 .067 Compulsory but no losers 1988 pay agreement

Hospital with Trust- –0.486 .067 Voluntary for current Implemented by localWide Bonus staff management; subsequent

agreement with unions

Note: mean perceived divisiveness for all organizations combined is 0, with a standard deviation of 1, and amean for each organization of between 0.9 and 1.

The standardized means were computed using the same regression as in Table 2, but excluding the questionson scope to raise performance, and on the maximum pay for the grade so that results could also be calculatedfor head teachers and staff in the individual PRP hospital. This makes no difference to the rank order ofdivisiveness by organization, nor does using the raw mean calculated directly from the sample.

364 INDUSTRIAL AND LABOR RELATIONS REVIEW

using those predicted values, (2) perfor-mance appraisal scores. The coefficientson the predicted levels of incentive anddivisiveness had the correct signs and werehighly statistically significant, and so con-firm that even though there may be someperceptual bias caused by the employee’sappraisal score, it was not such as to under-mine the model proposed here.8

(b) A second potential objection is thatappraisal scores do not represent actualperformance or productivity so much asthe leniency of line managers. There isconsiderable evidence from other studies(for example, Milkovich and Wigdor 1991)that appraisal scores are prone to inflationas lenient managers use them to buy peaceand sort out other organizational prob-lems. It is therefore necessary to checkwhether the measure of appraised perfor-mance in this study was sufficiently robust.Three checks were made and are analyzedin detail in Marsden (2003).

First, top management had the neces-sary procedures to monitor appraisals byline managers. All but one of the schemesin this study involved mechanisms for thenext higher level of management to “grand-parent” appraisals by the line managers forwhom they were responsible (the one ex-ception being head teachers, for whomsuch a procedure was not feasible). Thedistribution of appraisal scores was alsomonitored to ensure compliance with anti-discrimination legislation, and in severalcases, such as the Inland Revenue, informa-tion on the distribution of scores was sharedwith the main trade unions. In several casesthere were also appeal procedures. Finally,in the conduct of appraisals, considerableemphasis was placed on agreeing to writtenobjectives, and appraising against these.Thus, although appraisal is necessarily judg-mental, there were a number of checks onhow that judgment was exercised.

As a second check, I analyzed the distri-bution of appraisal scores across adminis-

trative units in the Inland Revenue for whicha good ten-year time series could be ob-tained, and compared their evolution overtime with that of the units’ operationalperformance targets published in its an-nual report and accounts. These includedsuch indicators as the percentage of taxcases processed within a fixed deadline,and quality targets such as response timeand, latterly, percentage of work correctfirst time. What emerges is that top man-agement used the targets it set for the ad-ministrative units in order to control thebehavior of local line managers, and theymanaged to continue meeting quality andoutput targets at a time when staff numberswere falling. This pattern, coupled with theincreasing sophistication of targets and in-creasing use of probability sampling proce-dures for their measurement, indicates agood degree of control by top manage-ment.

The third check consists of an evaluationof productivity. Productivity was increas-ing steadily through much of the period,measured by real tax revenue per employeeand by the ratio of tax yield to cost ofcollection. Rising economic activity bringsrising tax revenue per taxpayer, but it alsoincreases the number of tax transactions asmore enter employment, and more variedsources of income and saving make tax filesmore complex. Part of the increased loadmay have been eased by new technologyand by “Self-Assessment,” which shiftedsome obligations from the tax service ontotaxpayers, but even these required consid-erable changes to staff work routines andmethods, and throughout, the unions weredrawing attention to the workload implica-tions.

(c) Even though organizational perfor-mance improved, a number of other ques-tions remain. One might ask whether theimprovement was simply the result of staffworking “smarter” rather than “harder,”with no need for renegotiation. To someextent, this is a misleading dichotomy, be-cause working “smarter” may also requiregreater mental effort at one’s job. Thatreservation aside, however, a substantialminority of line managers, who have to

8The results are reported in Marsden (2003) andare available from the author.

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 365

appraise their colleagues’ performance,replied that PRP had caused many of thestaff to worker harder (Table 1 above).This view was also echoed in an interviewwith one senior HR manager at the InlandRevenue, who, indeed, turned the expres-sion “smarter, not harder” on its head:people were working, he said, “harder butnot smarter.” This was so largely because,especially at junior levels, staff lacked theexpertise and resources to design new workmethods themselves.9 Increased work loadis also reflected in the growth in the per-centage of posts in the tax service classed as“extra loaded,” that is, with “objectives sig-nificantly more stretching than the aver-age” (Inland Revenue 1994a). Standing atabout 8% of staff in 1993, it grew for threeyears, leveling off at about 17–18% by 1996.Thus, in the organization with the bestdata, the evidence points strongly to in-creased work load and mental effort ac-companying PRP.

(d) If PRP eliminated widespread “shirk-ing” among public servants, might that notaccount for the rise in both productivityand employee resentment? This construc-tion is not consistent with the levels oforganizational commitment found: thegreat majority of respondents (67%) felt astrong sense of commitment to their placeof work.10 There may have been a smallminority of “shirkers,” but their numbersseem insufficient to explain the widespreaddisenchantment noted in this study andothers.

(e) Lazear’s (1998) finding that improv-ing incentives attracted more productiverecruits suggests the possibility that pro-ductivity rose as a result of the new recruits,while incumbent staff felt alienated. This isruled out by the low levels of recruitment inthe public services during the 1990s, and bythe lack of influence of length of service inthe regression analysis.

(f) Might PRP have acted simply as a“lightning rod” for the resulting discontentcaused by other organizational changes?This might seem plausible had PRP shownno motivational effects, and had there beenno link between appraisal quality and indi-vidual performance, but the statistical analy-sis showed that PRP was a central instru-ment in the renegotiation.

Thus, all of these possible objections canbe set aside. The solution to the paradoxnoted at the start is that PRP was as much avehicle for renegotiating the effort bargainas it was for motivating employees to per-form better.

Conclusion

I have argued in this article that the mainimpact of the introduction of PRP acrosslarge sections of the British public servicesduring the 1990s was to facilitate the rene-gotiation of performance norms. Whenintroducing a new incentive scheme to anestablished work force, management is al-most certain to encounter a wide spread ofemployee preferences and the problem ofwinners and losers. Thus even when ascheme is well designed and managers arewell prepared to operate it, there will veryfrequently be not only employees who re-spond favorably, and agree to the newnorms, but also others who resent the normsand consider themselves worse off. Whereasthe former are positively motivated to im-prove or adapt their performance, the lat-ter are not, and managers hold them to thenew performance norms by means of goal-setting and appraisal. In this way, one canexplain why successive governments andtop managers have believed in the merits ofPRP for the public services despite the evi-dence—of which they were certainly

9To make his point, he gave an interesting ex-ample. Under the new system, staff telephone workplayed an important part in keeping close to the“customer,” yet many staff saw this as “queue jump-ing” and as slowing down their work. In one case, thestaff set up a team to answer the phone and bank upinquiries, but this then distanced them from the“customer” and slowed down response times. Thusthe local staff’s attempts to work smarter to meet theiroutput targets undermined their management’s goalof a more customer-centered service.

10The correlation between responses to this ques-tion and the constructed measure of commitmentused in Table 2 was 0.736, statistically significant atthe 1% level.

366 INDUSTRIAL AND LABOR RELATIONS REVIEW

aware—that many employees saw little in-centive and much divisiveness.

To some extent, renegotiation hasemerged as a latent rather than an explic-itly stated goal of PRP in the British publicservices. When senior managers at theInland Revenue were asked in 1991 aboutthe goals of the PRP scheme they operatedthen, they responded in terms of motiva-tion (Marsden and Richardson 1991). Like-wise, officials of the union representingInland Revenue staff had encouraged thestaff to complete the questionnaires be-cause they expected the survey to demon-strate publicly what they knew from discus-sions with their members: that the schemewas not motivating staff. The second In-land Revenue scheme, introduced in 1993,did not speak of renegotiation, but it diduse the language of agreeing to objectivesand establishing a “contract” with individualemployees, and of relating these to thedepartment’s operating plans. Neverthe-less, the prevailing language of public policydebate, as noted in the introduction, re-mains that of motivation and incentive,even while the success of the schemes inhelping public management to reshapepublic service performance lies in a differ-ent domain, that of negotiation.

This is where contract theory, and someof the older industrial relations literature,may prove helpful in understanding what isgoing on. Both stress that the rules andpractices we observe in organizations areoutcomes of a negotiated order. Unionsand their workplace representatives may beweaker now than in years past, but the labormarket continues to confer sometimes con-siderable individual bargaining power onworkers. Of course, a large organizationcan always face down an individual worker,no matter how skilled or talented, but feworganizations can afford a gradual bleed-ing away of their skilled personnel. Thusone has to consider the initial position thatmanagement seeks to change by means ofPRP as one that is the result of a negotia-tion, albeit an implicit one. This is not amedium onto which management can justimpose an optimal design. Rather, it has tonegotiate its way to an approximation of

that design, and in so doing respect thevarious budgetary and efficiency constraintsit must satisfy to meet its own objectives.

In his Journal of Economic Literature reviewof work on incentives, Prendergast (1999)commented on the need to extend thestudy of incentives beyond CEOs, sales, andsports personnel. Such personnel oftenhave short job tenures, and the high rate oflabor turnover means that self-selectionoften brings about a match between em-ployee preferences and the type of incen-tive offered by the organization. The Brit-ish public service has highlighted the oppo-site problem whereby high labor stability,especially during the early to mid-1990s,meant that employers had to obtain resultsfrom new incentive schemes when imple-menting them for a large incumbent workforce. Many of these people may be critical,if not of the principle behind such schemes,then of the new management practices andmethods of work associated with them. Adifficult decision for management is where todraw the line between those who support andthose who oppose a new incentive scheme,and whether to go for administrative simplic-ity by applying the same scheme to all em-ployees, or to allow a degree of choice.

Finally, the public service experience ofrenegotiation has highlighted the key roleof line managers. They are essential to therenegotiation process because they are thelink between top management’s goals andthe way ordinary staff carry out their jobs.This introduces another layer in the princi-pal-agent analysis of incentives. Line man-agers’ abilities and interests are not identi-cal to those of top management, and theyhave no protective gatekeepers controllingstaff access to them. When agreeing toperformance objectives with individual staff,the pressures on them to be lenient aregreat. What seems to have kept these pres-sures mostly at bay has been the articula-tion between performance objectives at dif-ferent levels within the public organiza-tions. This has provided support to linemanagers, and given them the means tokeep a focus on broader organizationalperformance when establishing individualobjectives. It has not always worked. At the

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 367

Employment Service, shortly after the CEPsurvey, the controls did break down, andmanagers and staff appeared to collude inover-reporting of job placements by somelocal offices (Marsden and French 1998).In contrast, the internal auditing controlsin the tax service, which I followed overseveral years from the published accounts,show use of increasingly sophisticated pro-cedures.11 Indeed, after the misreporting

incident, the Employment Service changedits methods of internal auditing, an indica-tion that it took its internal performanceindicators seriously. The importance ofthis intervening level of performance man-agement should not be underestimated. Ina famous case in the British automobileindustry, lack of attention to this level trans-formed top management’s much heralded“Measured Daywork” scheme into what itswork force nicknamed “Leisure Daywork,”and productivity collapsed. The Britishpublic services appear by and large to haveavoided such an outcome by attending tothe agents of renegotiation, line managers.

11For an analysis of these, see Marsden (2003).The Inland Revenue annual report and accounts arepublished as Parliamentary Papers by the StationeryOffice, London.

368 INDUSTRIAL AND LABOR RELATIONS REVIEW

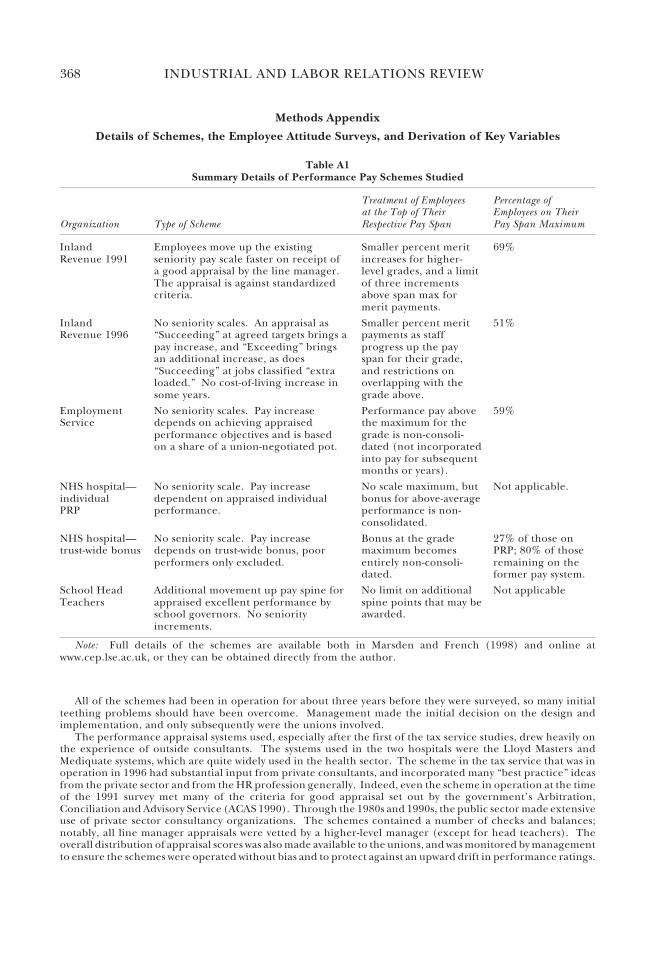

Methods Appendix

Details of Schemes, the Employee Attitude Surveys, and Derivation of Key Variables

Table A1Summary Details of Performance Pay Schemes Studied

Treatment of Employees Percentage ofat the Top of Their Employees on Their

Organization Type of Scheme Respective Pay Span Pay Span Maximum

Inland Employees move up the existing Smaller percent merit 69%Revenue 1991 seniority pay scale faster on receipt of increases for higher-

a good appraisal by the line manager. level grades, and a limitThe appraisal is against standardized of three incrementscriteria. above span max for

merit payments.

Inland No seniority scales. An appraisal as Smaller percent merit 51%Revenue 1996 “Succeeding” at agreed targets brings a payments as staff

pay increase, and “Exceeding” brings progress up the payan additional increase, as does span for their grade,“Succeeding” at jobs classified “extra and restrictions onloaded.” No cost-of-living increase in overlapping with thesome years. grade above.

Employment No seniority scales. Pay increase Performance pay above 59%Service depends on achieving appraised the maximum for the

performance objectives and is based grade is non-consoli-on a share of a union-negotiated pot. dated (not incorporated

into pay for subsequentmonths or years).

NHS hospital— No seniority scale. Pay increase No scale maximum, but Not applicable.individual dependent on appraised individual bonus for above-averagePRP performance. performance is non-

consolidated.

NHS hospital— No seniority scale. Pay increase Bonus at the grade 27% of those ontrust-wide bonus depends on trust-wide bonus, poor maximum becomes PRP; 80% of those

performers only excluded. entirely non-consoli- remaining on thedated. former pay system.

School Head Additional movement up pay spine for No limit on additional Not applicableTeachers appraised excellent performance by spine points that may be

school governors. No seniority awarded.increments.

Note: Full details of the schemes are available both in Marsden and French (1998) and online atwww.cep.lse.ac.uk, or they can be obtained directly from the author.

All of the schemes had been in operation for about three years before they were surveyed, so many initialteething problems should have been overcome. Management made the initial decision on the design andimplementation, and only subsequently were the unions involved.

The performance appraisal systems used, especially after the first of the tax service studies, drew heavily onthe experience of outside consultants. The systems used in the two hospitals were the Lloyd Masters andMediquate systems, which are quite widely used in the health sector. The scheme in the tax service that was inoperation in 1996 had substantial input from private consultants, and incorporated many “best practice” ideasfrom the private sector and from the HR profession generally. Indeed, even the scheme in operation at the timeof the 1991 survey met many of the criteria for good appraisal set out by the government’s Arbitration,Conciliation and Advisory Service (ACAS 1990). Through the 1980s and 1990s, the public sector made extensiveuse of private sector consultancy organizations. The schemes contained a number of checks and balances;notably, all line manager appraisals were vetted by a higher-level manager (except for head teachers). Theoverall distribution of appraisal scores was also made available to the unions, and was monitored by managementto ensure the schemes were operated without bias and to protect against an upward drift in performance ratings.

PERFORMANCE-RELATED PAY AND THE "EFFORT BARGAIN" 369

Measures of internal performance were also checked by the Audit Office, which has overall responsibility formonitoring the quality of public spending. All of these features of the schemes help ensure the reliability ofindividual performance ratings.

The attitudinal data were collected by means of questionnaires mailed to individual employees in eachorganization. Most of these questionnaires were completed on the employee’s own time. In three organiza-tions, management cooperated with the study, providing complete lists of employees from which the samplecould be drawn and allowing use of the organization’s internal mail for distribution and return of thequestionnaires. Lacking management support for the 1996–97 surveys of the civil service departments and forschools, I used union membership lists in those cases, but the potential harm to the sample’s representativenessis limited because membership density is very high—about 90% in the Inland Revenue grades covered, 60% forthe relevant grades in the Employment Service, and 90% among head teachers. In the hospitals, all staff wereincluded except medical doctors, who were outside the PRP scheme.

The staff grades covered were the following. In the Inland Revenue all grades were included except highermanagement and most clerical grades, which were represented by other unions and covered by different PRPschemes. In the Employment Service, those covered were mostly in middle management grades. In schools,head teachers were covered, there being no PRP for classroom teachers at the time.

Most of the attitudinal questions used 5-point Likert scales, ranging from “disagree strongly” to “agreestrongly.” Questions were piloted with groups of employees or, where management cooperation was lacking,with groups of union members. Preliminary results were presented to the organizations and interpretationsdiscussed with management and unions in feedback seminars.

The questionnaires were divided into sections, each dealing with a specific theme: general attitudes towardpay and performance; employee judgments of whether or not it gave them an incentive; their personalexperience with their most recent performance appraisal; and line managers’ views of the effects of the schemeon staff. The full text of the questionnaires can be found in Marsden and Richardson (1992) and Marsden andFrench (1998).

The survey response rate was 43% overall, but the questionnaire was long, with over 100 questions. Detailsby organization are given in the main text and in Table 1. Response patterns were compared with suchdemographic and other breakdowns as were available. Response rates were higher among the more managerialoccupations, but all occupational levels were well represented in the sample. The distribution of respondentsby gender, age or length of service, and (where asked) ethnic background and full- and part-time status did notgreatly diverge from the corresponding distribution across the relevant organization’s work force, according toemployment figures the organization provided. There was also a good response from across the regional officesof the tax and the employment services. Response patterns were compared with appraisal markings and foundto be very similar across performance ratings.

REFERENCES

ACAS. 1990. Appraisal Related Pay. ACAS AdvisoryBooklet No. 14. London: HMSO.

Armstrong, Michael, and Helen Murlis. 1994. RewardManagement: A Handbook of Remuneration Strategyand Practice. 3rd ed. London: Kogan Page.

Bichard, Michael (Chair). 1999. “Performance Man-agement: Civil Service Reform—A Report to theMeeting of Permanent Heads of Departments.”Sunningdale, 30 Sept.–1 Oct. 1999. Cabinet Office,London. Ref: CABI–5195/9912/D4.

Boswell, Wendy, and John W. Boudreau. 2000. “Em-ployee Satisfaction with Performance Appraisals andAppraisers: The Role of Perceived Appraisal Use.”Human Resource Development Quarterly, Vol. 11, No. 3(Fall), pp. 283–99.

Brown, Michelle, and John S. Heywood, eds. 2002.Paying for Performance: An International Comparison.Armonk, N.Y.: M. E. Sharpe.

Brown, Trevor C., and Gary P. Latham. 2000. “TheEffects of Goal Setting and Self-Instruction Train-ing on the Performance of Unionized Employees.”Relations Industrielles, Vol. 55, No. 1 (Winter), pp.80–95.

Carroll, Marylin. 1993. “Performance-Related Pay: A

Comparative Study of the Inland Revenue and aHigh Street Bank.” MSc diss., Faculty of Technol-ogy, UMIST, Manchester, October.

Coase, Ronald H. 1937. “The Nature of the Firm.”Economica, Vol. 4 (November), pp. 386–405.

Drago, Robert, and Gerald T. Garvey. 1998. “Incen-tives for Helping on the Job: Theory and Evidence.”Journal of Labor Economics, Vol. 16, No. 1 (January),pp. 1–25.

Furnham, Adrian. 1997. The Psychology of Behavior atWork: The Individual in the Organization. Hove andNew York: Psychology Press.

Heery, Edmund. 1998. “A Return to Contract? Per-formance-Related Pay in a Public Service.” Work,Employment & Society, Vol. 12, No. 1 (March), pp. 73–95.

Industrial Relations Services (IRS). 1999. IRS Studyfor PCS on Performance-Related Pay. London: Publicand Commercial Services Union (PCS).

Inland Revenue. 1994a. “Second Quality Review ofPerformance Management.” Chairman’s Newsletter,10.04. London.

___. 1994b. “Chairman’s Second Quality Review ofPerformance Management.” Summaries of the Reports

370 INDUSTRIAL AND LABOR RELATIONS REVIEW

of the Review Team and the Advisory Panel. London.____. 1995. The Guide (Management’s Guide for

Employees to Performance Management). Lon-don.

____. 1997. The Chairman’s Third Quality Review ofPerformance Management. London, February.

Kessler, Ian, and John Purcell. 1993. “DiscussionPaper on Staff Pay Survey at Amersham Interna-tional.” Mimeo, Templeton College, Oxford.

Latham, Gary P., and Thomas W. Lee. 1986. “GoalSetting.” Chap. 6 in Edwin A. Locke, ed., Generaliz-ing from Laboratory to Field Settings. Lexington, Mass.:Lexington Books, D. C. Heath.

Lawler, Edward E., III. 1971. Pay and OrganizationalEffectiveness: A Psychological View. New York: McGraw-Hill.

Lazear, Edward P. 1995. Personnel Economics. Cam-bridge, Mass.: MIT Press.

____. 1998. Personnel Economics for Managers. NewYork: Wiley.

Locke, Edwin A., and Gary P. Latham. 1990. A Theoryof Goal Setting and Task Performance. EnglewoodCliffs, N.J.: Prentice-Hall.

Maguire Maria, ed. 1993. Pay Flexibility in the PublicSector. Paris: OECD.

Makinson, John (Chair). 2000. Incentives for Change:Rewarding Performance in National Government Net-works. London: Public Services Productivity Panel,HM Treasury.

Malcomson, James M. 1997. “Contracts, Hold-Up,and Labor Markets.” Journal of Economic Literature,Vol. 35, No. 4 (December), pp. 1916–57.

Marsden, David W. 2003. “Renegotiating Perfor-mance: The Role of Performance Pay in Renegoti-ating the Effort Bargain.” Discussion Paper No.578, Center for Economic Performance, LondonSchool of Economics. Available online from http://cep.lse.ac.uk.

Marsden, David W., and Ray Richardson. 1992. “Mo-tivation and Performance-Related Pay in the PublicSector: A Case Study of the Inland Revenue.” Dis-cussion Paper No. 75, Centre for Economic Perfor-mance, London School of Economics. Available(under Publications, Discussion Papers) online fromhttp://cep.lse.ac.uk.

____. 1994. “Performing for Pay? The Effects of‘Merit Pay’ on Motivation in a Public Service.” Brit-

ish Journal of Industrial Relations, Vol. 32, No. 2(June), pp. 243–62.

Marsden, David W., and Stephen French. 1998. “Whata Performance: Performance-Related Pay in thePublic Services.” Centre for Economic PerformanceSpecial Report, London School of Economics. Avail-able under Publications, Special Reports onlinefrom http://cep.lse.ac.uk.

Meyer, John P., and Natalie J. Allen. 1997. Commit-ment in the Workplace: Theory, Research, and Applica-tion. Thousand Oaks, Calif.: Sage.