THE ROLE OF ACCOUNTING RATIO ANALYSIS IN ...

46

THE ROLE OF ACCOUNTING RATIO ANALYSIS IN MEASURING FINANCIAL PERFORMANCE OF A FIRM A CASE OF MUKWANO GROUP OF COMPANIES BY ALIGANYIRA JOHNSON REG NO: 1164—05014-09566 A DISSERTATION SUBMITTED TO THE COLLEGE OF ECONOMICS AN1~ MANAGEMENT IN PARTIAL FULFILLMENT OF THE REQUIREMENT FOR THE AWAR]~ OF A BACHELOR’S DEGREE OF BUSINESS ADMINISTRATION OF KAMPALA INTERNATIONAL UNIVERSITY FEBRUARY, 2019

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of THE ROLE OF ACCOUNTING RATIO ANALYSIS IN ...

THE ROLE OF ACCOUNTING RATIO ANALYSIS IN MEASURING FINANCIAL

PERFORMANCE OF A FIRM A CASE OF MUKWANO

GROUP OF COMPANIES

BY

ALIGANYIRA JOHNSON

REG NO: 1164—05014-09566

A DISSERTATION SUBMITTED TO THE COLLEGE OF ECONOMICS

AN1~ MANAGEMENT IN PARTIAL FULFILLMENT OF THE

REQUIREMENT FOR THE AWAR]~ OF A BACHELOR’S

DEGREE OF BUSINESS ADMINISTRATION OF

KAMPALA INTERNATIONAL

UNIVERSITY

FEBRUARY, 2019

DECLARATION

I ALIGANYIRA JOHNSON declare that this is my origina work and to the best of my

knowledge, it has never been submitted to any University or institution for a degree award.

Signed ~ Date..~J ?~L.2°ALIGANYIRA JOHNSON

1164—05014-09566

APPROVAL

This research report has been submitted for examination with my approval as a university

examination supervisor.

Sign Date...~~J~J~° 7’MS. TURAItIIRWt~,LOVENCE

(Supervisor)

DEDICATION

I have dedicated this work to my beloved parents Mr. Nyarubona Collins and Mrs.

Barnanyisa Eve, elder brothers Rugenyi Jean, Babyenda Timothy, Sunday Godfrey, Ruweza

Torn and Nyurnbayabo Bernard plus my sister Byaruhwenda Mary for their endless support,

up bring and care since childhood. Love you and may the almighty God reward you

abundantly.

III

ACKNOWLEDGEMENT

I acknowledge that my success is due to the Almighty God who has enabled me to produce

this work for His mercy and good will.

Sincere thanks go to my supervisor Mrs. Turabiirwe Lovence for the great support and

guidance she has given me in compiling the five chapters inside this research dissertation,

thank you very much.

Special appreciation goes to my relatives and all my friends for the moral and psychological

support they rendered to me during my stay at Kampala international university.

Lastly appreciation goes to all Business Administration students and the head of department

for the good knowledge they imparted on to me for accomplishment of this course.

iv

TABLE OF CONTENTS

DECLARATION

APPROVAL ii

DEDICATION iii

ACKNOWLEDGEMENT iv

TABLE OF CONTENTS v

LIST OF ACRONYMS viii

LIST OF FIGURES ix

LIST OF TABLES x

ABSTRACT xi

CHAPTER ONE

INTRODUCTION OF THE STUDY

1.0 Introduction I

1.1 Background of the study

1.2 Statement of the Problem 2

1.3 Purpose of the study 3

1.4 Objectives of the Study 3

1.4.1 General Objective 3

1.4.2 Specific objectives 3

1.5 Research questions 3

1.6 Scope of the study 4

1.6.1 Geographical scope 4

1.6.2 Time scope 4

1.6.3 Content scope 4

1.7 Significance of the Study 4

1.8 Conceptual framework 5

CHAPTER TWO 6

LITERATURE REVIEW 6

2.Olntroduction 6

2.1 Review of the key concepts 6

2.1.1 Financial ratio 6

2.1.2 Financial Performance 6

2.2 Forms of ratio used by organizations 6

v

2.2.1 Cash flow ratios .6

2.2.2 Leverage (debit) Financial Ratios 7

2.2.3 Liquidity (solvency) Financial Ratios 7

2.2.4 Financial Operation Ratios (Asset Efficiency) ratios 7

2.2.5 Profitability Financial Ratios 8

2.2.6 Valuation ratios (market value ratios) 8

2.3 Role of accounting ratio analysis in measuring financial performance of organizations 8

2.4 Limitations of ratio analysis in measuring performance of organizations 10

2.5 Conclusion 12

CHAPTER THREE 13

METHODOLOGY 13

3.1 Introduction 13

3.2Research design 13

3.3Study population 13

3.4Sample size 13

3.5Sampling Techniques and Procedures 14

3.5.1 Simple Random Sampling 14

3.5.2Purposive Sampling 14

3.6 Data collection methods 14

3.6.1 Primary data 15

3.6.2Secondary Data 15

3.7Data collection instruments 15

3.7.1 Self-Administered Questionnaires 15

3.8Validity and Reliability 15

3.8.1 Validity 15

3.8.2 Reliability 15

3.9 Data Collection Procedures 16

3.loDataAnalysis 16

3.11 Ethical Considerations 16

CHAPTER FOUR 17

PRESENTATION OF RESULTS! FINIMNGS 17

4.1 Introduction 17

4.2 General Findings 17

4.3 Questionnaires Distributed and Returned 17

vi

4.4 Presentation of the findings according to the objectives 20

4.5 To find out the role of accounting ratio analysis in measuring financial performance of

Mukwano Group of Companies 23

4.6 To find out whether there are limitations of ratio analysis in measuring Performance of

Mukwano Group of Companies Limited 24

CHAPTER FIVE 25

CONCLUSIONS AND RECOMMENDATIONS 25

5.1 Introduction 25

5.2 Conclusion 25

5.3 Recommendations 26

5.3.1 Forms of ratio used by Mukwano to measure performance 26

5.3.2 Role of accounting ratio analysis in measuring financial performance 26

5.3.3 Limitations of ratio analysis in measuring performance 26

5.4 Areas for further research 27

REFERENCES 28

APPEN]MXI 31

QUESTIONNAIRE SCHEDULE 31

APPENDIX II 34

Sample Size for the Given Population Sizes 34

vii

LIST OF ACRONYMS

CPA Certified Public Accountants

SAQs Self-Administered Questionnaire

UK United Kingdom

USA United States of America

VIII

LIST OF FIGURES

Figure 1.1 shows the Conceptual framework 5

Figure 4.1 shows Age of the respondents 18

ix

LIST OF TABLES

Table 3.1 shows the Sample size 14

Table 4.1 shows the Questionnaires distributed and retur ned 17

Table 4.2 shows Gender of the respondents 18

Table 4.3 shows Marital status of the respondents 19

Table 4.4 shows Education level of the respondents 20

Table 4.5 shows whether profitability ratios are among the forms of ratio used 20

Table 4.6 shows whether liquidity ratios also compose accounting ratio analysis forms used

by Mukwano group of industries 21

Table 4.7 shows whether debt ratios are amongst the Forms of Ratio used by the Company 21

Table 4.8 shows whether performance ratios are also used by Mukwano group of industries to

measure financial performance 22

Table 4.9 shows whether investment evaluation ratios are used by Mukwano group of

companies 22

Table 4.10: The role of accounting ratio analysis in measuring financial performance of

Mukwano group of companies 23

Table 4.11: Limitations of Ratio Analysis in Measuring Performance of Mukwano Group of

Companies Limited 24

x

ABSTRACT

The purpose of this study was to investigate the role of Accounting Ratio analysis in

measuring financial performance of Mukwano Group of Companies. The study was guided

by three research objectives specifically to identify the different forms of ratio used by

Mukwano group of companies, determine the role of accounting ratio analysis in measuring

financial performance and identi1~’ the limitations of ratio analysis in measuring performance.

The study was covered using a cross sectional and a case study research designs which

seemed applicable for the research based on Accounting Ratio Analysis. The study was based

on a Self-Administered Questionnaire (SAQs) which were used because they are the most

suitable in a survey that involves a large number of respondents. A total of 108 employees

were randomly selected, although at last only 74 were retrieved. Data was analyzed using

frequency tables and percentages and the study concluded that despite the achievements, gaps

between this accounting ratio and performance still exist for example false accounting,

comparison is not possible if different firms adopt different accounting policies, Ratio

analysis becomes less effective due to price level changes and Lack of proper standards

affects the appropriateness of ratio analysis. The study recommends the organization to

provide a good proper working condition for accomplishment of the assigned tasks which

should be backed by eenhancement of employee involvement programs and provision of

employee training and refresher programs.

xi

CHAPTER ONE

INTRODUCTION OF THE STUDY

1.0 Introduction

This chapter presents the background to the study, statement of the problem, objectives of the

study, research questions, scope and significance of the study.

1.1 Background of the study

To Altman (2008), in countries where financial instability is rife and financial intuitions are

becoming popular, when it comes to investing, the sound analysis of financial statements is

one of the most important elements in the fundamental analysis process. At the same time,

the massive amount of numbers in a company’s financial statement can be bewildering and

intimidating to many investors, creditors and those who are concern with the financial

statement.

Beaver, W. (2017), asserts that financial ratios serve a similar purpose, but you must know

what is being measured to construct a ratio and to understand the significances of the

resulting number” (Stanly 1994).The statement used for accounting ratio analysis is the

annual financial report of a firm which consists of three financial statements; the balance

sheet, income statement and cash flow statement. The analysis conducted in each of this

statement provides the vital information required regarding the financial performance of the

firm for making sound investment decisions. Analysts therefore depend on the use of the

financial statements to provide the data needed to update accounting ratios. According to

Igben (1999), “Accounting {or financial} ratio consist of the fraction, proportion or

percentage which compare the relationship between one variable item in a set financial

statements with another item in the financial statements. Consequently Accounting ratios are

vital for the analysis and interpretation of financial statements”.

Block (2009) defines accounting as the process of systematically recording, measuring, and

communicating information about financial transactions. At the heart of accounting is the

double-entry bookkeeping method. This involves making at least two recording entries for

every transaction: a debit in one account and a credit in another account. The method helps

prevent errors because the sum of the debits should equal the sum of the credits. The three

major financial statements produced by accounting are the income statement, the balance

sheet and the cash flow statement.

Bondoc M, 2013 defines accounting as the systematic and comprehensive recording of

financial transactions pertaining to a business. Accounting also refers to the process of

summarizing, analyzing and reporting these transactions to oversight agencies, regulators and

tax collection entities. The financial statements that summarize a large company’s operations,

financial position and cash flows over a particular period are a concise summary of hundreds

of thousands of financial transactions it may have entered into over this period.

To Brigham, 2008, accounting ratios are indicators of a commercial entity’s performance and

financial situation. We calculate the majority of ratios from data that the firm’s financial

statements provide. Accounting ratios, also known as financial ratios, are used to measure the

efficiency and profitability of a company based on its financial reports. They provide a way

of expressing the relationship between one accounting data point to another, and are the basis

of ratio analysis.

This was attributed to the fact that an accounting ratio compares two line items in a

company’s financial statements, namely made up of its income statement, balance sheet and

cash flow statement. These ratios can be used to evaluate a company’s fundamentals and

provide information about the performance of the company over the last quarter or fiscal

year. Examples of financial ratios include gross margin, operating margin, the debt-to-equity

ratio, the quick ratio and the payout ratio

Financial performance as argued by Brealey , 2013 is a subjective measure of how well a

firm can use assets from its primary mode of business and generate revenues. This term is

also used as a general measure of a firm’s overall financial health over a given period of time,

and can be used to compare similar firms across the same industry or to compare industries or

sectors in aggregation. There are many different ways to measure financial performance, but

all measures should be taken in aggregation. Line items such as revenue from operations,

operating income or cash flow from operations can be used as well as total unit sales.

Furthermore, the analyst or investor may wish to look deeper into financial statements and

seek out margin growth rates or any declining debt.

1.2 Statement of the Problem

Many firms, institutions and businesses have knowledge about accounting ratios, analysis and

its interpretation. Some businesses make use of these ratios but apply them wrongly, others

also use the right method but give wrong interpretations to it and most firms do not apply at

2

all. The need to determine the financial performance of the firm is crucial for making

informed decisions concerning the further deployment of resources and investment decisions.

This can only be done through accounting ratio analysis. Eventually this is not often an easy

task to unddrtake as many investors and business owners lack the understanding and skill to

perform accounting ratio analysis’ Accounting ratios facilitates the determination of the

efficiency and profitability of a firm which is fundamental for investment decisions based on

the firms financial reports. Accounting ratio facilitate the comparison of two aspects of a

financial statement .Some examples of accounting ratios include the dividend ratio, gross

margin ratio, debt-to-equity ratio and operating margin ratio. It is because of the above

problems that prompted the researcher of this study to write about the use of accounting ratio

and its interpretation, Brigham (2015).

1.3 Purpose of the study

To examine the role of accounting ratio analysis in measuring financial performance of

Mukwano group of companies.

1.4 Objectives of the Study

1.4.1 General Objective

To examine the role of accounting ratio analysis in measuring financial performance of

Mukwano group of companies.

1.4.2 Specific objectives of this study were;

i. To identi~’ the different forms of ratio used by Mukwano group of companies.

ii. To determine the role of accounting ratio analysis in measuring financial performance

of Mukwano group of companies.

iii. To identify the limitations of ratio analysis in measuring performance of Mukwano

group of industries.

1.5 Research questions

i. What are the different forms of ratio used by Mukwano group of companies?

ii. What is the role of accounting ratio analysis in measuring financial performance of

Mukwano group of companies?

iii. What are the limitations of ratio analysis in measuring performance of Mukwano

group of industries?

3

1.6 Scope of the study

1.6.1 Geographical scope

The study was conducted in Mukwano group of companies a manufacturing industry located

in Kampala city along Jinja road near industrial area. It was established in 1980 and deals in

the production of a variety of beauty products for example smearing jelly, soaps, body lotions

and creams.

1.6.2 Time scope

The study was cross sectional and covered a period of five months, from October 2018 to

early February 2019. The period was enough for the researcher to acquire necessary

information required for the study.

1.6.3 Content scope

The study was limited to the roles of accounting ratio analysis in measuring financial

performance of a firm.

1.7 Significance of the Study

The research shall proffer a structural appraisal of accounting ratio analysis for the

determination of the firm’s financial performance and investment decision.

The finding of the study may benefit academicians to enrich their knowledge and research

work; this is because the study may act as a secondary source of data to them

The study may help the policy makers in different firms to identify the loopholes in their

system and therefore lay strategies of strengthening ratio analysis in their firms.

4

1.8 Figure 1 Conceptual framework

A conceptual framework showing the relationship accounting ratio analysis and financial

performance of Mukwano group of companies

INDEPENDENT VARIABLE DEPEN1~ENT VARIABLEFinancial PerformanceAccounting financial ratios

o Profitability Ratios Profitability

o Liquidity Ratios a Sales growth

o Debt Ratios I e Efficiency

o Performance Ratios

o Investment Evaluation Ratios

EXTRANEOUS VARIABLESo False accounting data gives false ratios

o Comparison not possible

o Limited use of a Single Ratio

o Window Dressing

o Lack of proper standards

Source: (Mugaga 2006; Schubeler, 1996; Thomas, 1998; Rand & Marxen, 2000) and

modified by the researcher

From the conceptual framework above, there are many accounting ratios used in measuring

financial performance of firms and these are; profitability ratio, liquidity ratios, debt ratios,

performance ratios and investment evaluation ratios. Hence in the long run these lead to more

profits, increase in sales and efficiency when it comes to service delivery and quality

produce. However, accounting ratio towards financial performance has always come with

challenges like false accounting data which gives false ratios, at times comparisons for the

ratios becomes impossible, use of a single ratio, window dressing on addition to lack of

proper standards from accountants themselves.

5

CHAPTER TWO

LITERATURE REVIEW

2.Olntroduction

This chapter was based on documentary reviews of literature related to the study variables

aimed at enlightening the readers about the currents, gaps and how to close the gaps. The

section was organized as introduction, literature and the summary of the literature.

2.1 Review of the key concepts

2.1.1 Financial ratio

Martikainen, (2013),defines financial ratios as the numerical value created from two or more

values taken from a company’s financial statements i.e. its balance sheet, income statement or

statement of cash flow. Typically, financial ratios are presented as a quantified metric in the

form of a percentage, multiple or a ratio which aims to evaluate the financial, operational

performance and competitiveness of a company.

The financial Ratio Analysis has been developed over many years and it has become more

than a tool of evaluation. It helps tax department’s credit analysis in banks, financial market

councils and CPA Accountants to determine some critical points in theirjobs.

2.1.2 Financial Performance

In a study conducted by Collis and Jarvis (2016) on financial performance of small private

companies in the U.K., the most useful sources of information are the periodic management

account (i.e. the balance sheet and income statement), cash flow information and bank

statements (of course bank statement are another form of cash flow information but generated

externally) (Collis, 2012) suggest is critical to the success and survival ofa small business.

2.2 Forms of ratio used by organizations

2.2.1 Cash flow ratios

These can be used to answer questions on a company’s performance since debt obligations

are met with cash. Such an analysis will result in adequate lines of credit, unrestricted cash

6

availability, debt maturity schedules with respect to financing requirements and the

willingness to issue common equity. It will allow an analyst to examine a company’s

financial health and how the company is managing its operating, investment and financing

cash flows (Palepu Penman, 2010). A lack of cash flow data has caused problems for

investors and analysts in assessing a company’s performance, liquidity, financial flexibility

and operating capability (Gombola and Ketz 2013).

2.2.2 Leverage (debit) Financial Ratios

According to Helfert, 2011, this group of financial ratios show the percentage of a

company’s capital structure that is made up on debt or liabilities owed to external parties, also

it focuses on a company’s ability to meet its long-term debt obligations. Focusing on the

long-term solvency in general, the more leveraged and higher amount of debt financing

relative to equity financing, the owner faces then greater is the risk.

2.2.3 Liquidity (solvency) Financial Ratios

Hermanson et al (2012) explains that the liquidity or solvency ratios group focuses on a

firm’s ability (current assets and current liabilities) to meet its short-term debt obligations. In

other words, it lets you know the resources available for a firm to use in order to pay its

current obligation and expenses. If a company cannot maintain a short-term debt-paying

ability, it will not be able to maintain a long-term debt-paying ability, nor will it be able to

satisfy its stockholders.

2.2.4 Financial Operation Ratios (Asset Efficiency) ratios

To Horrigan, (2013), the Financial Operation Ratios group which is sometimes called asset

management ratios, measure the efficiency with which a firm manages and controls its assets

(utilizing its capital) in generating sales and earnings. Investors can use these in order to

analyze a company’s or management’s ability to efficiently use resources and how effective it

converts its purchases and inventory to sales and then its sales to cash.

7

2.2.5 Profitability Financial Ratios

Horrigan, J.O. (2015), explains that the profitability ratios group, also known as performance

ratios, assesses the company ability to earn profits on sales, assets and equity, it measures the

return earned on a company’s capital and the financial cushion relative to each dollar of sales,

These are critical to determining the attractiveness of investing in company shares and

investors in using these ratios widely, much like the operational performance ratios, these

ratios give users a good understanding of how well the company utilized its resources(assets)

in generating profit and shareholder value.

2.2.6 Valuation ratios (market value ratios)

James, 2008, the valuation ratios group indicates to the market value of a stock in terms of

some measure of a company’s fundamentals such as EP, book value, BPS, ROE and

dividends. These ratios are the ones that investors tend to look at on a daily basis and they

change whenever the price of the stock changes. These ratios allow you to compare your

company to others in your industry.

2.3 Role of accounting ratio analysis in measuring financial performance of

organizations

Analyzing Financial Statements

To Jooste L (2016), Ratio analysis is an important technique of financial statement analysis.

Accounting ratios are useful for understanding the financial position of the company.

Different users such as investors, management, bankers and creditors use the ratios to analyze

the financial situation of the company for their decision making purpose.

Judging Efficiency

Wessels D. (2010), explains that accounting ratios are important for judging the company’s

efficiency in terms of its operations and management. They help judging how well the

company has been able to utilize its assets &earn profits using Accounting, Financial

Statements, Selection and Accountancy.

8

Locating Weakness

According to Lasher, (2017), accounting ratios can also be used in locating weakness of the

company’s operations even though its overall performance may be quite good. Management

can then pay attention to the weakness and take remedial measures to overcome them.

Formulating Plans

To Lewellen (2014), although accounting ratios are used to analyze the company’s past

financial performance, they can also be used to establish future trends of its financial

performance. As a result, they helps in formulating the company’s future plans for knowing

efficiencies, Financial position and for reaching companies goals and objectives.

Comparing Performance

For Murphy, (2009), it is essential for a company to know how well it is performing over the

years and as compared to the other firms of the similar nature. Besides, it is also important to

know how well its different divisions are performing among themselves in different years.

Ratio analysis facilitates such comparison.

Further Ohlson, (2010), explains that ratio analysis helps to reveal, compare and interpret

salient features of financial statements. When applied to a set of financial statements,

financial ratios highlight significant aspects of the financial position and operational results of

a business requiring further investigation. They help to identify the strengths and weaknesses

of a business. In fact, ratio analysis helps to evaluate the past performance, the present

condition, and the future prospects of a business.

Horrigan (2015) says ratios analysis has come into existence since early ages and the main

reason of the development of ratio analysis was its use in the analysis of the properties of

ratios in 300 B.C. in recent time it is used as a standard tool for the analysis of financial

statement. In nineteenth century main reasons of using ratio analysis are power of financial

institutions and shifting of management to professional managers.

Bird and McHugh (2017) adopt an efficient Shapiro-Wilk small-sample test for the normality

of financial ratios for an Australian sample of five ratios over six years. Like Deakin they

find in their independent study that normality is transient across financial ratios and time.

9

Richardson and Davidson (2014) used eleven ratios to examine that the successful firms has

higher ratios than unsuccessful firms. Although this study was immature but immaturity was

ignored by considering the vital contribution this study has in the evaluation of usefulness of

ratios. Security and exchange commission of America was formed in 1934. This also expands

the flow and number of financial statements and with the help of this peripheral factor

importance of ratio analysis further enhanced and realized.

2.4 Limitations of ratio analysis in measuring performance of organizations

Ratio analysis is a very important tool of financial analysis but despite it’s being

indispensable, the ratio analysis suffers from a number of limitations. These limitations

should be kept in mind while making use of the ratio analysis;

False accounting data gives false ratios

According to Ross (2009), Accounting ratios are calculated on the basis of given data given

in profit and loss account and balance sheet. Therefore, they will be only as correct as the

accounting data on which they arc based for example, if the closing stock is over-valued, not

only the profitability will be overstated but also the financial position will appear to be better.

Therefore, unless the profit and loss account and balance sheet are reliable, the ratios based

on them will not be reliable.

Comparison not possible if different firms adopt different accounting policies

Further Schrirnpf (2010), explains that there may be different accounting policies adopted by

different firms with regard to providing depreciation, creation of provision for doubtfbl debts,

method of valuation of closing stock for instance, one finn may adopt the policy of charging

depreciation on straight-Line basis, while other may charge on written-down value method.

Such differences make the accounting ratios incomparable.

Limited use of a Single Ratio

To Stanly, 2014, the analyst should not merely rely on a single ratio. He should study several

connected ratios before reaching a conclusion. For example, the Current Ratio of a firm may

be quite satisfactory, whereas the Quick Ratio may be unsatisfactory.

10

Window Dressing

Some companies in order to cover up their bad financial position resort to window dressing

i.e., showing a better position than the one, which really exists. They change their balance

sheet in such away that the important facts and truth may be concealed.

Lack of proper standards

Circumstances differ from firm to firm hence no single standard ratio can be fixed for all the

firms against which the actual ratio may be compared. Ratios alone are not adequate for

proper conclusions; ratios derived from analysis of statements are not sure indicators of good

or bad financial position and profitability of a firm. They merely indicate the probability of

favorable or unfavorable position.

Lack of Standard of Comparison

No fixed standards can be laid down for ideal ratios for example, current ratio is said to be

ideal if current assets are twice the current liabilities but this conclusion may not be

justifiable in case of those concerns which have adequate arrangements with their bankers for

providing funds when they require, it may be perfectly ideal if current assets are equal to or

slightly more than current liabilities.

Quantitative Analysis

Ratios are tools of quantitative analysis only and qualitative factors are ignored while

computing the ratios for example, a high current ratio may not necessarily mean sound liquid

position when current assets include a large inventory consisting of mostly obsolete items.

Ratios Account for one Variable

Since ratios account for only one variable, they cannot always give correct picture since

several other variables such Government policy, economic conditions, availability of

resources, should be kept in mind while interpreting ratios. Ratio analysis can be used to

compare information taken from the financial statements to gain a general understanding of

the results, financial position, and cash flows of a business. This analysis is a useful tool,

especially for an outsider such as a credit analyst, lender or stock analyst.

11

Operational changes

A company may change its underlying operational structure to such an extent that a ratio

calculated several years ago and compared to the same ratio today would yield a misleading

conclusion. For example, if you implemented a constraint analysis system, this might lead to

a reduced investment in fixed assets, whereas a ratio analysis might conclude that the

company is letting its fixed asset base become too old.

Accounting policies

Different companies may have different policies for recording the same accounting

transaction. This means that comparing the ratio results of different companies may be like

comparing apples and oranges for example, one company might use accelerated depreciation

while another company uses straight-line depreciation or one company records a sale at gross

while the other company does so at net.

Inflationary effects

Financial statements are released periodically and therefore, there are time differences

between each release. If inflation has occurred in between periods, then real prices are not

reflected in the financial statements. Thus, the numbers across different periods are not

comparable until they are adjusted for inflation.

2.5 Conclusion

Financial performance of any firm or bank can be calculated with the help of financial ratios.

Financial ratio plays an important role to check the condition of any bank or company either

is in profit or loss. By using ratios companies can determine financial strength or weaknesses

as well as opportunities in the market or industry. Ratios can provide the actual picture of the

firm’s financial position. Financial ratios assist analysts to acquired insight knowledge of

firm’s financial situation. Data from different financial statements has used to calculate the

ratios. Financial ratios can tell the investors future performance of firms by looking past

trends.

12

CHAPTER THREE

METHODOLOGY

3.1 Introduction

This chapter presents the research design, the study population, sample size, sample

techniques and procedures, data collection methods and instruments, validity and reliability,

data analysis, measurement of variables and ethical considerations.

3.2 Research design

The study adopted a cross sectional and a case study research designs. According to Amin

(2005), studies of this nature may be more productively undertaken because data can be

collected from a cross section of a population in a short time from a large number of cases for

purposes of drawing valid conclusions to represent the entire population of the study. Hence

for a research study related to accounting and measurement of financial performance, this

worked better in especially investigating performance at Mukwano group of companies.

3.3 Study population

Due to the fact that Mukwano group of companies employs more than 8000 people, a study

was based on analysis of the internal employees especially those working as human resources

and from the accounting department and if agreed the managing director hence making a total

of 150 representatives. The selection process was as follows; the managing director in charge

of performance of the company (1), workers from the accounting department (20), managers

from various department of the organization (6), employees from various departments at

Mukwano group of industries (100), company stakeholders (23) and 10 from the human

resource department of the organization (Primary data, 2018).

3.4 Sample size

Hence in accordance to the target groups of people chosen above, the sample size was

estimated through use of Morgan and Krejcie’s table (1970) of sample size determination

which estimates that if the target population is 150 the sample size becomes 108 as seen on

Appendix ii. Basing on the sample above, this study used simple random sampling for those

in the Top Management, Managers since it is good for in-depth analysis and it enables high

representation of the population, less bias, and simplifies data interpretation and analysis of

13

results (Black, 1999). While purposive sampling was used for, other key selected informants

because it allowed for probing more on examining applicability of accounting ratio analysis

and financial performance.

Table 3.1 Sample size

Category Population Sample Sampling technique

Top management 1 1 Purposive sampling

Accounts Department 20 15 Purposive sampling

Managers from different 6 6 Purposive sampling

departments

Stakeholders 23 20 Simple Random sampling

Other Employees 100 60 Simple Random sampling

Human resource department 10 6 Purposive sampling

Total 150 108

Source: Primary Data

3.5 Sampling Techniques and Procedures

3.5.1 Simple Random Sampling

The participants in the study was selected through simple random sampling method for

respondents among them administrators and Senior Accountant to have an equal chance of

being selected to be part of the study. Simple random sampling is best because it is easy to

collect data when the population members are similar to one another on important variable

(Gay, 1996).

3.5.2 Purposive Sampling

Purposive sampling was used for selecting the particular groups of people in the population

especially Managers and accounts officers. This sampling procedure was used for its cost

efficiency and effectiveness to collect specific information and allowed for probing for clarity

(Kothari, 2004).

3.6 Data collection methods

The study used both primary and secondary data collection methods as complementary.

14

3.6.1 Primary data

This is data collected from respondents in the field and for this time it was got from

Mukwano group of companies’ selected respondents.

3.6.2 Secondary Data

This is the data that was gotten from various resource centres like internet sources, libraries,

news papers and journals.

3.7 Data collection instruments

3.7.1 Self-Administered Questionnaires

The research instrument included the Self-Administered Questionnaire (SAQs). SAQs were

used because they are the most suitable in a survey that involves a large number of

respondents (Amin, 2005). In addition, (SAQs) was very suitable for the target respondents

given their high levels of English literacy. Finally, SAQs consumed less time and money

compared to other methods (Alston & Bowels, 1998)

3.8 Validity and Reliability

3.8.1 Validity

Validity is the ability of the research instrument to measure what it aims or is supposed to

measure. According to Amin (2005), the research instrument must be appropriate for the

study objectives to be achieved. The researcher will consult and discuss validity instrument

with colleagues and supervisors to limit errors as much as possible (these were judges who

were having more experience in relation to field results).

3.8.2 Reliability

Reliability of an instrument is the dependability or the trustworthiness of an instrument.

According to Amin (2005), it is the degree to which the instrument consistently measures

what it is supposed to measure. This method was picked on a single pre-test group and

showed the degree to which the items in the questionnaire are inter-correlated. To get the

reliability, the data was entered in the computer and analyzed using frequency tables and

percentages.

15

3.9 Data Collection Procedures

The researcher discussed with supervisors about the procedures of conducting research and

after he sought for approval on validity and reliability of the instruments. Then an

introductory letter was obtained from College of Economics and management for the

researcher to present in the field at Mukwano group of companies so as to create rapport with

the respondents.

3.10 Data Analysis

This is the process of bringing understanding and meaning to data collected for validity and

reliability (Sekaran, 2003). Data collected from the field was first sorted, edited, coded and

entered into in the computer using frequency tables and percentages. Qualitative data was

analyzed and presented in form of texts and interviews, impressions, words, photos; symbols

are examined and presented using descriptive or narrative method where the researcher

presented detailed literature description of the respondents’ views for the reader to make their

opinions (Bell, 1993).

3.11 Ethical Considerations

Ethically the researcher focused on infringement on the privacy and confidentiality of the

respondents, informed consent, avoiding duplication of other studies, honesty and

dissemination of the report findings to respondents. The study was not based on application

of force but sticked to reconciliation and humbleness to gather data. The different

respondents had the opportunity to respond freely with no salient intimidation or force or

promise of reward.

16

CHAPTER FOUR

PRESENTATION OF RESULTS! FINDINGS

4.1 Introduction

This chapter deals with the presentation, analysis and interpretation of the findings in relation

to the objectives of the study and the research questions. The data is presented using Tables

and figures for easy interpretation and understanding.

4.2 General Findings

The research considered a sample a sample size of 108 respondents of which one (1) was a

top manager (0,9%), fifteen (15) were from accounts department (13.8%), six (6) were

managers from different departments (5.5%), twenty (20) were stakeholders (18.5%), sixty

(60) were from other employees (55.5%), while six (6) were coming from the human

resource department (5.5%).

4.3 Questionnaires Distributed and Returned

One hundred eight (108) questionnaires were distributed to the respondents, seventy four (74)

of which were returned while thirty four (34) were not returned. This was because of the

commitments the respondents had at their places of work. This was illustrated in the Table

below:

Table 4.1: Questionnaires distributed and returned

Response Frequency Percentage (%)

Returned 74 68.5

Not Returned 34 31.5

Total 108 100

Source: Primary Data 2019

The Table illustrates that eighty (108) questionnaires were issued for the research study,

(68.5%) of which were returned and (31.5%) were not returned. This portrayed maximum

cooperation of the respondents.

17

Table 4.2: Gender of the respondents

Gender Frequency Percentage (%)

Male 48 64.9

Female 26 35.1

Total 74 100

Source: Primary Data 2019

Gender of the respondents was found necessary for consideration by the researcher so as to

ensure gender sensitivity and equality. However, of the returned seventy four (74)

questionnaires, it was discovered that forty eight (48) respondents were male while twenty six

(26) respondents were female an implication that the research also took into consideration

gender sensitivity.

Figure 4.1: Age of the respondents

Age of the Respondents

40 25.7%

2~ ~~36-45 Age of the Respondents ~ Age of the Respondents

46-55S6andabove

Source: Primary Data

This was deemed necessary for the study by the researcher so as to ensure the age limit of the

respondents to be considered for the research since the minors (respondents below the age of

l8years) were not considered liable for the study since their ideas were still believed to be

premature as opposed to the great level of mature reasoning that the research required. This

was observed in objective three of the research questionnaire which required the respondents

to fully examine the limitations of ratio analysis in measuring performance of Mukwano

group of industries. However, responses to this showed that 25.7% were at the age of 21-35,

35.1% were at the age of 36-45, while 24.3% were at the age of 46-55 and 14.9% were at the

18

age of 56 and above. Taking the age limit of 36-45, which is a simple majority figure, the

results portrayed that the company had energetic, potential, well skilled and qualified staff

which helped it enhance its smooth running and enabled the researcher to make conclusions

and recommendations for the study easily.

Marital status of the respondents

This was also put into consideration by the researcher so as to identify the responsibilities

possessed by the various respondents responses to this were however acquired using question

3 of the research questionnaire where the responses found out that 19 of the respondents were

single for both male and female with a percentage of (47.5%) while the married respondents

were 15 (37.5%), 4 of them were widowed (10%) and 2 of the respondent were divorced

(5%).

Table 4.3: Marital status of the respondents

Single 17 23.0

Divorced 10 13.5

Widowed 11 14.9

Separated 9 12.2

Total 74 100

Source: Primary Data

Considering the responses above, it was established that 36.5% of the respondents were

married, 23.0% were single, 13.5% were divorced while 14.9% were widowed and 12.2%

were separated. Taking 36.5% as a simple majority figure, this concludes that Mukwano

group of companies limited had responsible staff capable of boosting its performance.

19

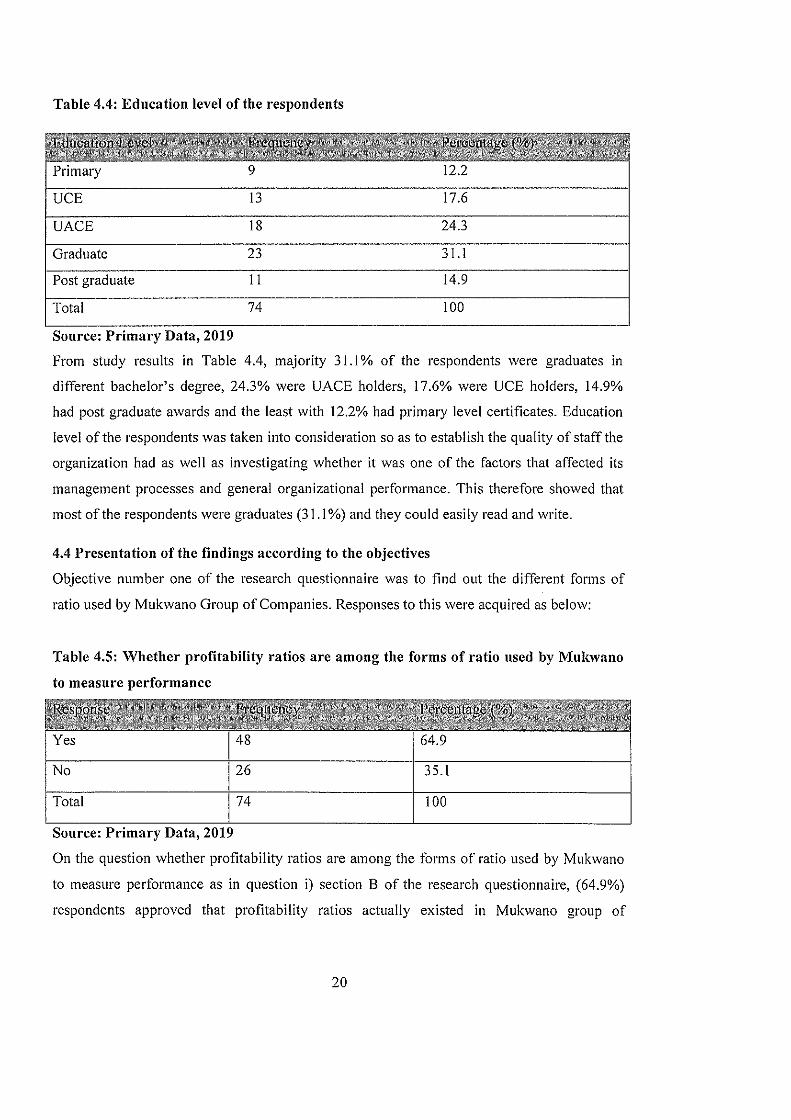

Table 4.4: Education level of the respondents

UCE 13 17.6

UACE 18 24.3

Graduate 23 31.1

Post graduate 11 14.9

Total 74 100

Source: Primary Data, 2019

From study results in Table 4.4, majority 3 1.1% of the respondents were graduates in

different bachelor’s degree, 24.3% were UACE holders, 17.6% were UCE holders, 14.9%

had post graduate awards and the least with 12.2% had primary level certificates. Education

level of the respondents was taken into consideration so as to establish the quality of staff the

organization had as well as investigating whether it was one of the factors that affected its

management processes and general organizational performance. This therefore showed that

most of the respondents were graduates (31 .1%) and they could easily read and write.

4.4 Presentation of the findings according to the objectives

Objective number one of the research questionnaire was to find out the different forms of

ratio used by Mukwano Group of Companies. Responses to this were acquired as below:

Table 4.5: Whether profitability ratios are among the forms of ratio used by Mukwano

No 26 35.1

Total 74 100

Source: Primary Data, 2019

On the question whether profitability ratios are among the forms of ratio used by Mukwano

to measure performance as in question i) section B of the research questionnaire, (64.9%)

respondents approved that profitability ratios actually existed in Mukwano group of

Primary 9 12.2

to measure performance

Yes 48 64.9

20

companies limited while 35.1% disapproved that the organization does not use profitability

ratio in its operations.

This response therefore portrayed that the organization actually uses profitability ratio in

measuring financial performance something that has facilitated its production and general

performance improvements taking 64.9% as a simple majority response figure.

Table 4.6 shows whether liquidity ratios also compose accounting ratio analysis forms

used by Mukwano group of industries

Agree 27 36.5

Disagree 16 21.6

Strongly Disagree 8 10.8

Total 74 100

Source: Primary Data 2019

From study findings in Table 4.6, 31.1%

company uses liquidity ratio to improve its

liquidly ratio is used, while 21.6% disagreed

they use accounting ratio at some issues they

broad view that accounting ratio are used

performance of its employees.

Table 4.7 shows whether debt ratios are amongst the Forms of Ratio used by the

Company

Srongly Agree

Agree 12 16.2

Disagree 24 32.4

Strongly Disagree 16 21.6

Total 74 100

Source: Primary Data 2019

Srongly Agree 23 31.1

of the respondents strongly agreed that the

performance, 36.5% agreed to the view that

to the view and 10.8% strongly disagreed that

did not disclose to the researcher. This gives a

by Mukwano group of industries to improve

21

Results in table 4.7 above indicated that Debt ratios are also applied by Mukwano group of

companies to improve its performance. This was so due to the fact that majority respondents

with 32.4% disagreed to the view that debt ratio is used by the company, 21.6% strongly

disagreed while 29.7% strongly agreed to the view and 16.2% had an agreement. This

therefore implied that debt ratio is not highly applied in the organization.

Table 4.8 shows whether performance ratios are also used by Mukwano group of

industries to measure financial performance

Agree 30 40.5

Disagree 10 13.5

Strongly Disagree 14 18.9

Total 74 100

Source: Primary Data, 2019

Table 4.8 results depicted that majority 40.5% agreed to the view that performance ratio are

also applied by Mulcwano to improve financial performance of the organization, 27.02%

strongly agreed to the view and 18.9% strongly disagreed while 13.5% had a disagreement an

indication that the organization uses performance ratio to find out whether the organization is

getting more profits out of the good performance of its employees.

Table 4.9 shows whether investment evaluation ratios

companies

are used by Mukwano group of

Srongly Agree 34 45.9

Agree 10 13.6

Disagree 18 24.3

Strongly Disagree 12 16.2

Total 74 100

Source: Primary Data 2019

22

Results from Table 4.9 depicted that majority 45.9% strongly agreed to the view that

Mukwano group of industries uses investment ratios, 13.6% agreed to the view while 24.3%

disagreed and 16.2% strongly disagreed. This therefore implied that the organization invests

in different procedures and after makes evaluations to find out which product is performing

better or worse.

4.5 To find out the role of accounting ratio analysis in measuring financial performance

of Mukwano Group of Companies

Objective number two of the research was to find out the role of accounting ratio analysis in

measuring financial performance of Mukwano Group of Companies and responses to this

were given as below:

Table 4.10: The role of accounting ratio analysis in measuring financial performance of

Mukwano group of companies

67.5

It is used by Mukwano especially when judging efficiency 3 4.05

It helps in locating weakness 11 14.8

It is used in formulating plans 7 9.4

It is used to make a comparison of performance of different 3 4.05

employees at Mukwano

Total 74 100

Source: Primary Data 2019

Results from Table 4.10 above indicated that majority 67.5% of the respondents

acknowledged that the ratio analysis is used by Mukwano to analyze its financial

performance followed by 14.8% who accepted that It helps in locating weakness, 9.4%

argued that it is used in formulating plans and the least with 4.05% had a similar argument

that it is used when judging for efficiency as well as making a comparison of performance of

different employees. This therefore implied that Mukwano mostly uses accounting ratio to

analyze financial performance.

It is used by the organization to analyze Financial

Statements

50

23

4.6 To find out whether there are limitations of ratio analysis in measuring Performance

of Mukwano Group of Companies Limited

Objective number three of the research was aimed at finding out whether there are

Limitations of ratio analysis in measuring Performance of Mukwano Group of Companies

and responses to this were therefore given as seen below:

Table 4.11: Limitations of Ratio Analysis in Measuring Performance of Mukwano

Group of Companies Limited

False accounting data which gives false ratios

At times the comparison is not possible if different firms 14 18.9

adopt different accounting policies

Ratio analysis becomes less effective due to price level 12 16.2

changes

It may be misleading in the absence of absolute data for 17 23.0

Mulcwano

Lack of proper standards affects the appropriateness of 11 14.9

ratio analysis

Total 74 100Source: Primary Data, 2019

Results further depicted that majority 27.2% stated that false accounting data which gives

false ratios, 23.0% stated that ration analysis can at times be misleading in the absence of

absolute data for Mukwano while 18.9% stressed that at times the comparison is not possible

if different firms adopt different accounting policies though 16.2% stated that ratio analysis

becomes less effective due to price level changes and 14.9% argued that lack of proper

standards affects the appropriateness of ratio analysis.

24

CHAPTER FIVE

CONCLUSIONS AND RECOMMENDATIONS

5.1 Introduction

This chapter gives a succinct summary of the major findings of the research, conclusion with

also recommendations as well as areas for further research. The recommendations are based

on the researchers’ analysis and interpretations of the findings. The summary of the research

findings outline briefly the objectives of the research.

5.2 Conclusion

In a wrap-up, the researchers observed that there are different forms of ratio used by

Mukwano group of companies. This was concluded basing on the following responses as

summarized in chapter four, 64.9% of the respondents stated that profitability ratio are among

the forms of ratio used by the organization to measure financial performance, 67.6% stated

that the organization uses liquidity ratio while 55.9% stressed that debt ratios are used by the

organization to measure for financial performance though 67.5% stated that performance

ratios are also used by the organization and 59.5% gave other options that they use

investment evaluation ratios. The results indicated that at Mukwano Group of Companies,

majority respondents agreed to the view that liquidity ratio is the mostly used ratio used.

The study also found out that accounting ratio analysis in measuring financial performance

plays roles like analysis of financial statements (67.5%) and others argued that it has helped

the organization when judging for efficiency (4.05%), others with a response rate of 14.8%

argued that it helps in locating weakness, 9.4% stated that it is used in formulating plans

while 4.05% sighted out that it is used to make a comparison of performance of different

employees at Mukwano group of companies.

Furthermore, it was discovered that there are limitations of ratio analysis in measuring

Performance of Mukwano Group of Companies Limited since 27.2% of the respondents

stated that false accounting data which gives false ratios, 18.9% stated that at times the

comparison is not possible if different firms adopt different accounting policies while 16.2%

stressed that ratio analysis becomes less effective due to price level Changes though 23.0%

stated that ratio analysis may be misleading in the absence of absolute data for Mukwano and

14.9% argued that the lack of proper standards affects the appropriateness of ratio analysis.

25

This therefore implied that majority respondents accepted that 27.2% of the respondent’s

false accounting information affects accounting ratio.

5.3 Recommendations

The research therefore provided the following recommendations for the study, chapter four of

the study:

5.3.1 Forms of ratio used by Mukwano to measure performance

From the findings of the study results depicted that profitability, liquidity, debt ratio among

others are the forms of ratio used by the company, however it is recommendable that the

organization improves on the debt ratio used by the organization to manage the budgets.

5.3.2 Role of accounting ratio analysis in measuring financial performance of Mukwano

Group of Companies

From findings in chapter four it was analyzed that ratio analysis plays roles like analysis of

finacial performnace, judging efficiency, helps in locating weakness, used in formulating

plans and it is used to make a comparison of performance of different employees at

Mukwano. It is however recommended that the organization provides good proper working

conditions for accomplishment of the assigned tasks. This should be backed by enhancement

of employee involvement programs and provision of employee training and refresher

programs.

5.3.3 Limitations of ratio analysis in measuring performance of Mukwano Group of

Companies Limited

From study results, it was indicated that ratio analysis is limited by a varierty of factors

ranging from false accounting data, comparison is not possible, ratio naalysis is ineffective

and lack of proper standards. Hence it is recommneded that Mukwano group of comapnires

enhances good recruitment procedures to eanble analysis of ratios and as well overcome

challenges related to incidents like false accounting data which gives false ratios.

26

5.4 Areas for further research

The researcher feels that due to the limited time and resources available to them during the

period of this study, enough research has not been exhausted in this study and therefore

recommends other upcoming and intending researchers to carry out a further research on the

role of employee involvement on ratio analysis of the organization and as well provide fro

mitigation measures to proper application of ratio analysis in organizations.

27

REFERENCES

Altman E.I. (2008), Financial Ratios, Discriminant Analysis and the Prediction of Corporate

Bankruptcy, “The Journal of Finance” vol. 23, no. 4.

Baruch Lev, Financial Statement Analysis: A New Approach (Englewood Cliffs, New Jersey:

Prentice-Hall, Inc., 2014).

Beaver, W. (2017), “Financial Statement Analysis”, Handbook of Modern Accounting, eds

Davidson, S. and Well, R., 2nd ed. McGraw-Hill.

Bird, R.G., and McHugh A.J. (2017), “Financial ratios - an empirical study”, Journal of

Business Finance and Accounting 4/1, 29-45.

Block S.B. (2009), A study of financial analysis: practice and theory, “Financial Analysts

Journal” vol. 55, no. 4.

Bondoc M. D., Taicu M, 2013, Expenses analysis based on information provided by the

profit and loss account company performance diagnosis stage, Annals of the University of

Petroani, Economics, 13(1), p.5-p.l4

Brealey R., Myers 8.20 13, Principles of corporate finance, The McGraw-Hill Companies.

Brigham E., Houston J.,2008, Fundamentals of financial management, South-Western

College Pub, 2008

Brigham E.F., Ehrhardt MC. (2015), Financial Management, 11 edition, USA.

Collis and Jarvis (2016) financial information and the management of small private

companies.

Collis J, Jarvis R (2012), Financial Information and the Management of Small Private

Companies, Journal of small business and Enterprise Development, vol. 9, no.2, pp 100-110.

Gombola, M.J., and Ketz, J.E. (2013), “A note on cash flow and classification patterns of

financial ratios”, Accounting Review 63/1, 105-114.

Helfert E. 2011, Financial analysis tools and techniques a guide for managers, The McGraw

Hill Companies

28

Hermanson, Roger H. James Don Edwards, & Michael W. Maher. (2012). Accounting

Principles 5th ed. Boston, MA Richard D. Irwin, Inc.

Horrigan, J.O. (2013), “Methodological implications of non-normally distributed financial

ratios: acomment”, Journal of Business Finance and Accounting 10/4, 683-689.

Horrigan, J.O. (2015), Some empirical bases of financial ratio analysis”, Accounting

Review, July 1965, 558-568.

James 0. Horrigan, 2008,”A Short History of Financial Ratio Analysis,” Accounting Review,

XLII , 284-94.

Jooste L (2016), Cash Flow ratios as a yardstick for evaluating financial performance in

Koller

T, Goedhart M, Wessels D. (2010), Valuation: Measuring and Managing the Value of

Companies, 5th ed, John Wiley & Sons, Hoboken.

Lasher, William R. (2017). Practical Financial Management St. Paul MN: West Publishing

Company.

Lewellen J. (2014), Predicting Returns with Financial Ratios, “Journal of Financial

Economics” vol. 74.

Martikainen, T. (2013), “Stock returns and classification pattern of firm-specific financial

variables: empirical evidence with Finnish data”, Journal of Business Finance and

Accounting 20/4, 537-557.

Murphy J.J. (2009), Technical Analysis of the Financial Markets: A Comprehensive Guide to

Trading Methods and Applications (New York Institute of Finance).

Ohlson J.A., (2010), Financial Ratios and the Probabilistic Prediction of Bankruptcy,

“Journal of Accounting Research” vol. 18, no. 1.

Penman S.H, (2010), Financial Statement Analysis and Security Valuation, 4th ed, McGraw

Hill, New York.

Richardson, F.M., and Davidson, L.F. (2014), “On linear discrimination with accounting

ratios”, Journal of Business Finance and Accounting 11/4, 511-525.

29

Schrirnpf A., (2010), International stock return predictability under model uncertainty,

“Journal of International Money and Finance” vol. 29.

Stanly B. Block and Geoffrey A. Hirt 2014 Financial Management, seventh edition Page

51 Stroe R., Armeanu D., Finances, ABS Publishing House

30

APPENDIX I

QUESTIONNAIRE SCHEDULE

THE ROLE OF ACCOUNTING RATION ANALYSIS IN MEASURING FINANCIAL

PERFORMANCE OF A FIRM. A CASE STUDY OF MUKWANO GROUP OF

COMPANIES

Questionnaires for key informants

Dear Respondent

I am Aliganyira Johnson a student from Kampala International University pursuing a

bachelor’s degree of business administration (finance and accounting) year three, semester

two. The questionnaire has been designed for sole purpose of collecting data on the Role of

Accounting Ratio Analysis in Measuring Financial Performance of a Firm a Case of

Mukwano Group of Companies. Thus the questionnaire below will help me gather the data

required for my topic of research, therefore you are requested to respond to the following

questions appropriately for the purposes of my academic research and I declare that the

information given shall be treated with Maximum confidentiality it deserves for academic

purpose. Tick one or write the relevant information in the space provided.

PART A: GENERAL INFORMATION

Please tick the appropriate box that suits your agreement.

1. Gender

Male EElFemale

2. Age bracket of respondents

21-35 years

36-45 years

46-Ssyears

56 and above

3. Education Background of respondents

Primary

Secondary (UCE & UACE) ~

Graduate

Post Graduate

31

4. Marital Status of respondents

Single

Married

Widowed

Divorced

Separated

PART B: The Role of Accounting Ratio Analysis in Measuring Financial Performance

of a Firm

Kindly indicate the extent to which you agree with the following statements concerning

different forms of ratio used by Mukwano group of companies

Use the scale of;

Code 1 2 3 4 5

Status Strongly Agree Strongly disagree Disagree Not sure

agree

1~2~3~4~5

Different forms of ratio used by Mukwano group of companies

Profitability Ratios are among the forms of ratio used by Mukwano to measure

performance

Liquidity Ratios also compose accounting ration analysis forms used by — — —

Mukwano group of industries

Debt Ratios are amongst the forms of ratio used by the company — — —

Performance Ratios are also used by Mukwano group of industries to measure — — —

financial performance

Investment Evaluation Ratios are among the forms of ratio used by Mukwano

to measure performance

Role of accounting ratio analysis in measuring financial performance of Mukwano group

of companies

it is used by the organization to analyze Financial Statements

it is used by Mukwano especially when judging efficiency

it helps in locating Weakness

it is used in formulating Plans

It is used to make a comparison of performance of different employees at

Mukwano

32

Ratio analysis helps to reveal, compare and interpret salient features of

financial statements

Limitations of ratio analysis in measuring performance of Mukwano group of industries

The application of ratio analysis creates false accounting data which gives

false ratios

At times the comparison is not possible if different firms adopt different — —

accounting policies

Ratio analysis becomes less effective due to price level changes

Ratios may be misleading in the absence of absolute data for organizations

like Mukwano

Limited use of a Single Ratio is a challenge for Mukwano when it uses ration

analysis in especially determining performance of distributors

Lack of proper standards affects the appropriateness of ratio analysis

33

APPENDIX II

Sample Size for the Given Population Sizes (N)

N S N S N S N S N S

10 10 100 80 280 162 800 260 2800 338

15 14 110 86 290 165 850 266 3000 341

20 19 120 92 300 169 900 269 3500 346

25 24 130 97 320 175 950 274 4000 351

30 28 140 103 340 181 1000 278 4500 354

35 32 150 108 360 186 1100 285 5000 357

40 36 160 113 380 191 1200 291 6000 361

45 40 170 118 400 196 1300 297 7000 364

50 44 180 123 420 201 1400 302 8000 367

55 48 190 127 440 205 1500 306 9000 368

60 52 200 132 460 210 1600 310 10000 370

65 56 210 136 480 214 1700 313 15000 375

70 59 220 140 500 217 1800 317 20000 377

75 63 230 144 550 226 1900 320 30000 379

80 66 240 148 600 234 2000 322 40000 380

85 70 250 152 650 242 2200 327 50000 381

90 73 260 155 700 248 2400 331 75000 382

95 76 270 159 750 254 2600 335 10000 384

SOURCE: Krejcie and Morgan (1970), determining sample size for research activities

34