The Philippines - Selected Issues for the 1983-87 Plan Period

177

Report No.3861-PH The Philippines Selected Issues for the 1983-87 Plan Period | .t J ''' -4'.. CF O )une 1, 1982 East Asia and Pacific Regional Office E}___£_____________-_ FOROFFICIALUSE ONLY Document of the WorldBank This document has a restricteddistribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bankauthorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

-

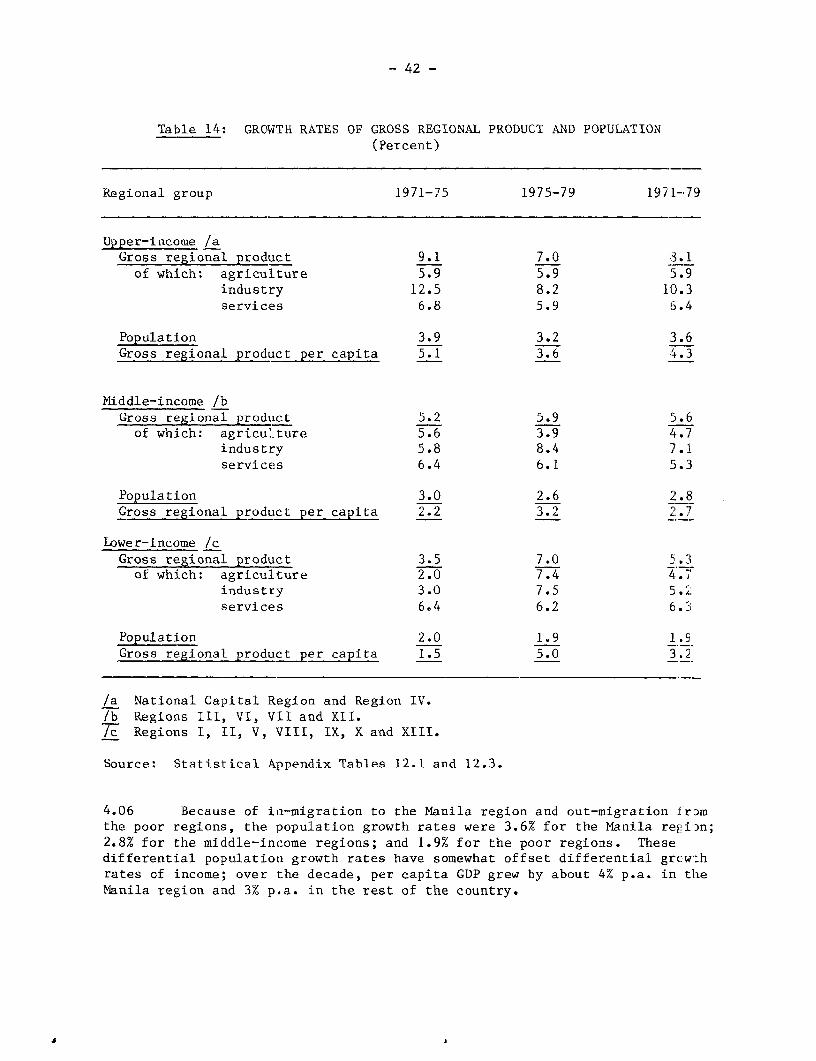

Upload

khangminh22 -

Category

Documents

-

view

2 -

download

0

Transcript of The Philippines - Selected Issues for the 1983-87 Plan Period

Report No. 3861-PH

The PhilippinesSelected Issues for the 1983-87 Plan Period

| .t J ''' -4'.. CF O

)une 1, 1982

East Asia and Pacific Regional Office E}___£_____________-_

FOR OFFICIAL USE ONLY

Document of the World Bank

This document has a restricted distribution and may be used by recipientsonly in the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

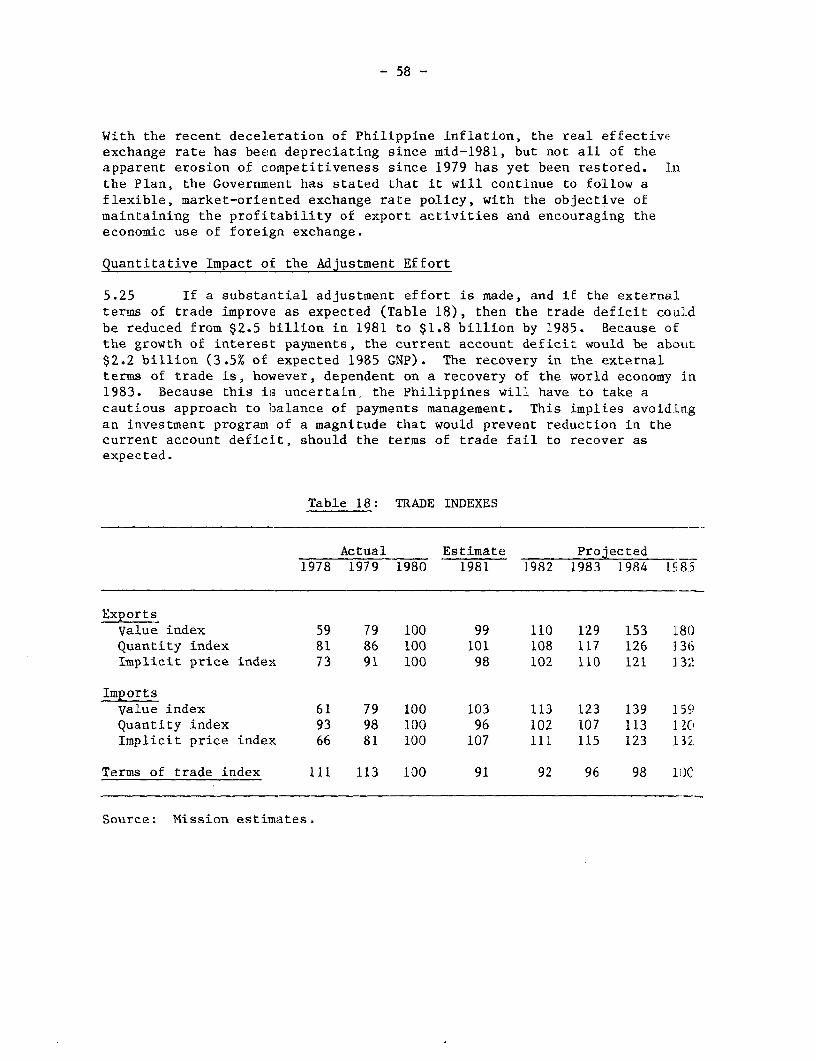

osur

e A

utho

rized

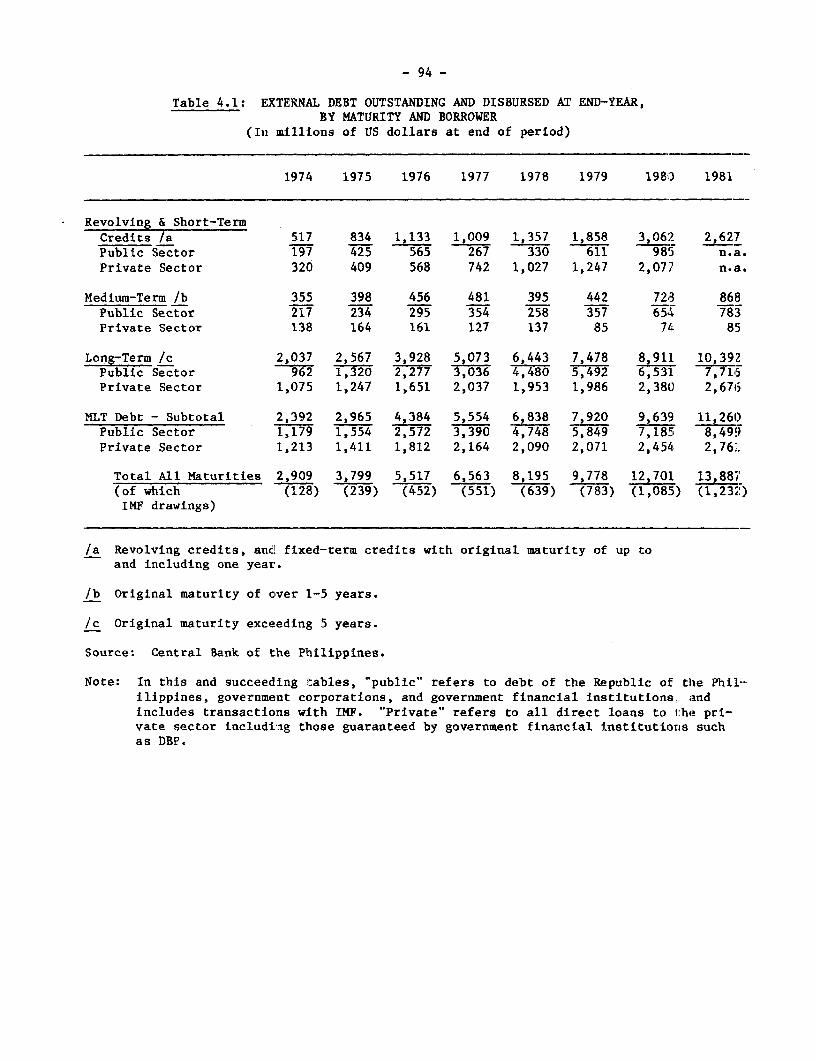

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

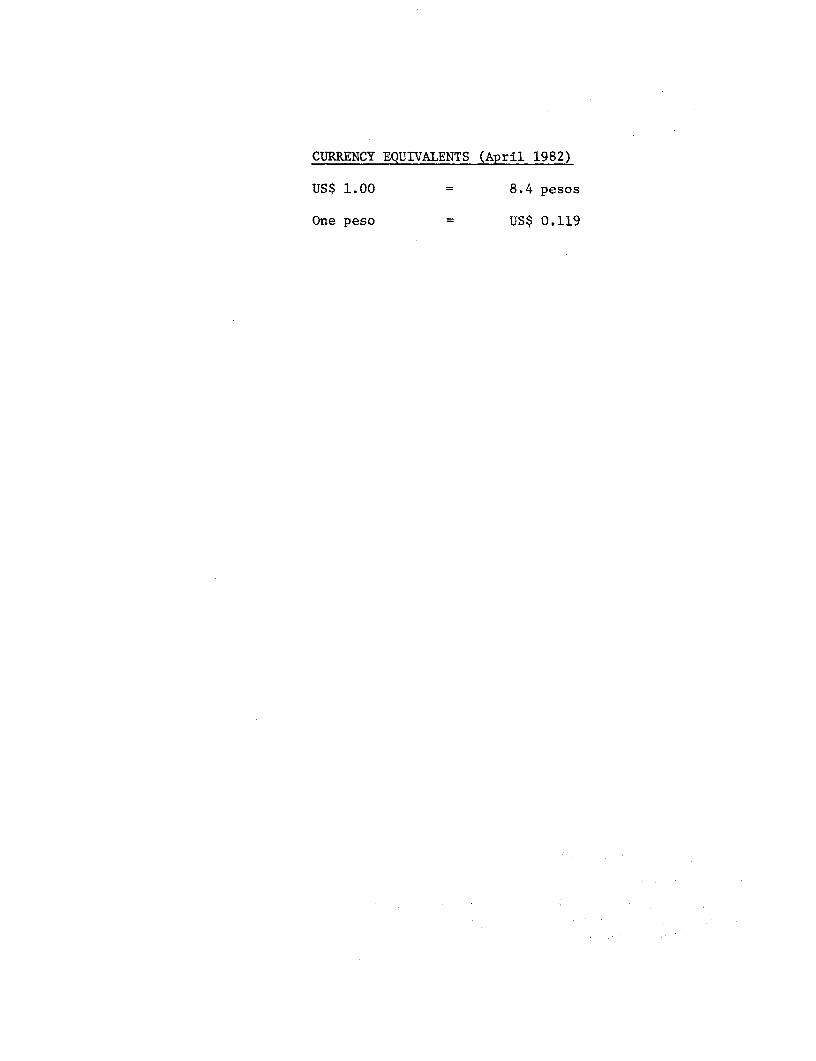

CURRENCY EQUIVALENTS (April 1982)

US$ 1.00 = 8.4 pesos

One peso = US$ 0.119

FOR OFFICIAL USE ONLY

THE PHILIPPINES

SELECTED ISSUES FOR THE 1983-87 PLAN PERIOD

Table of Contents

Page No.

WORLD BANK REPORTS ON THE PHILIPPINES, 1980-81

SUMMARY AND CONCLUSIONS . . . . . . . . . . . . . . . . . . . . . i

1. RECENT DEVELOPMENTS AND PROSPECTS FOR THE 1983-87 PLAN PERIOD 1

A. Recent Economic Developments . . . 1B. Strategy and.Prospects for the 1983-87 Plan Period . . . 3

2. RESOURCE MANAGEMENT

A. Overview of Savings and Investment . . . . . . . . . . . 15B. Mobilization and Allocation of Resources for Private

Investment: The Role of the Financial Sector . . . 18C. Public Sector Resource Mobilization . . . . . . . . . . 22

3. THE PUBLIC EXPENDITURE PROGRAM

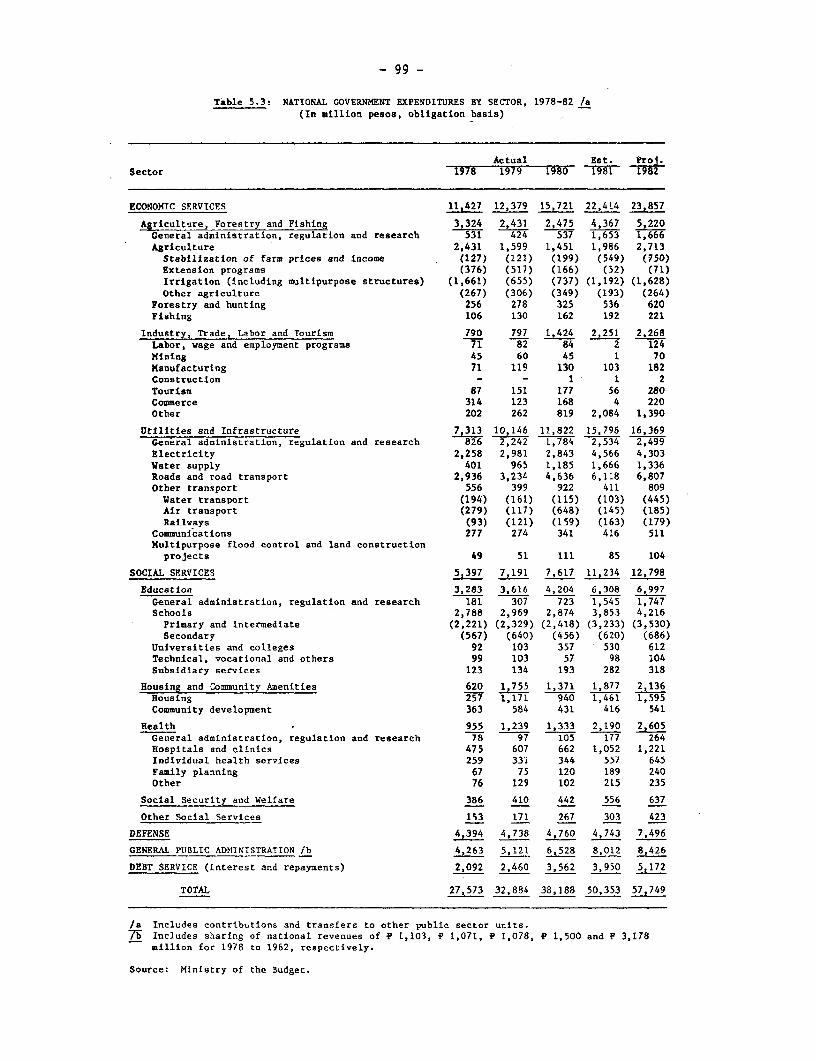

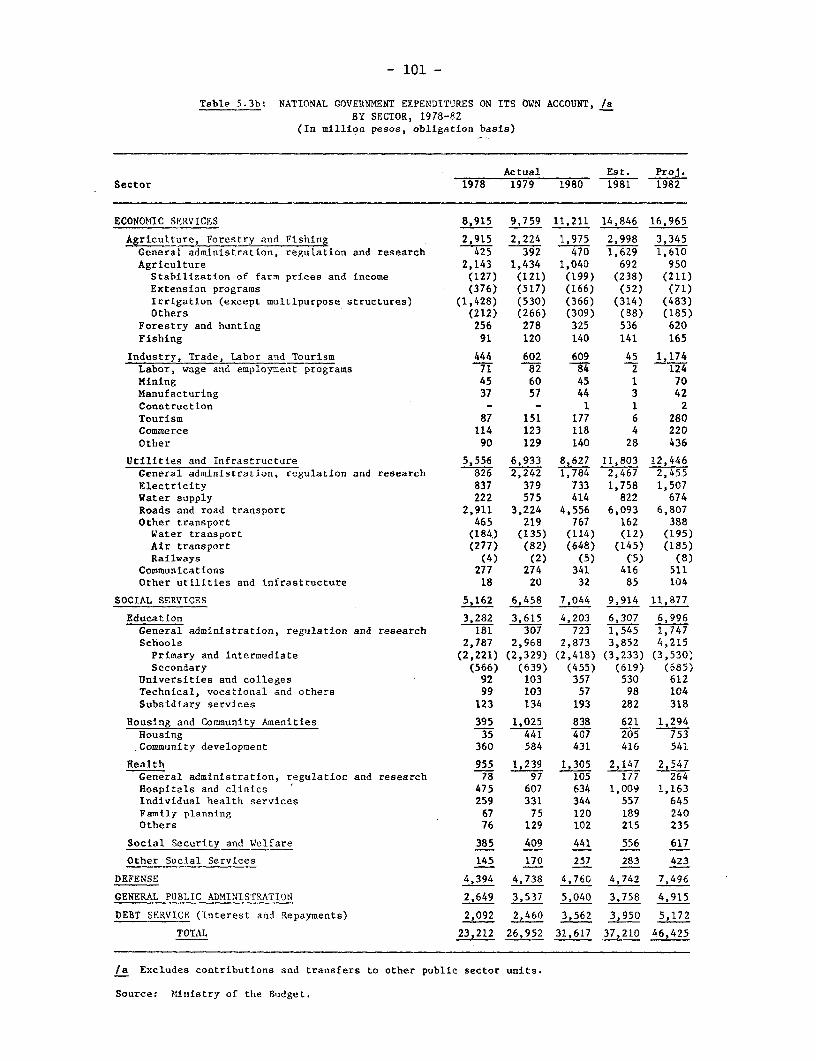

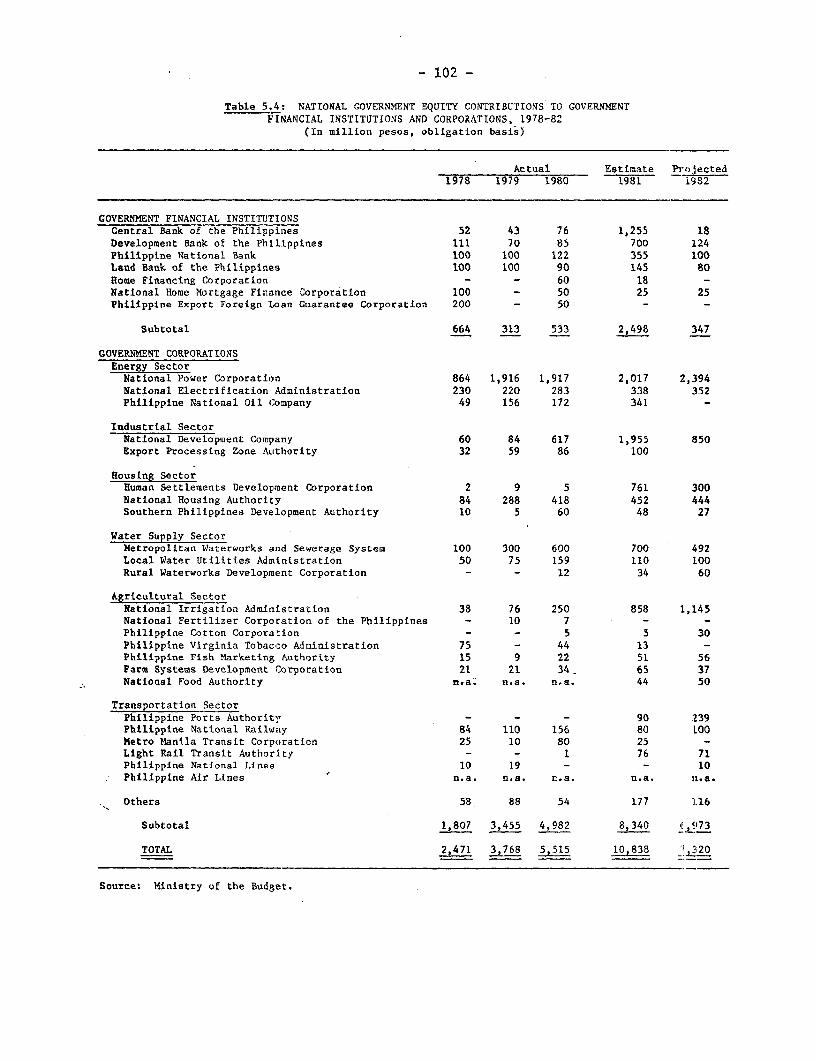

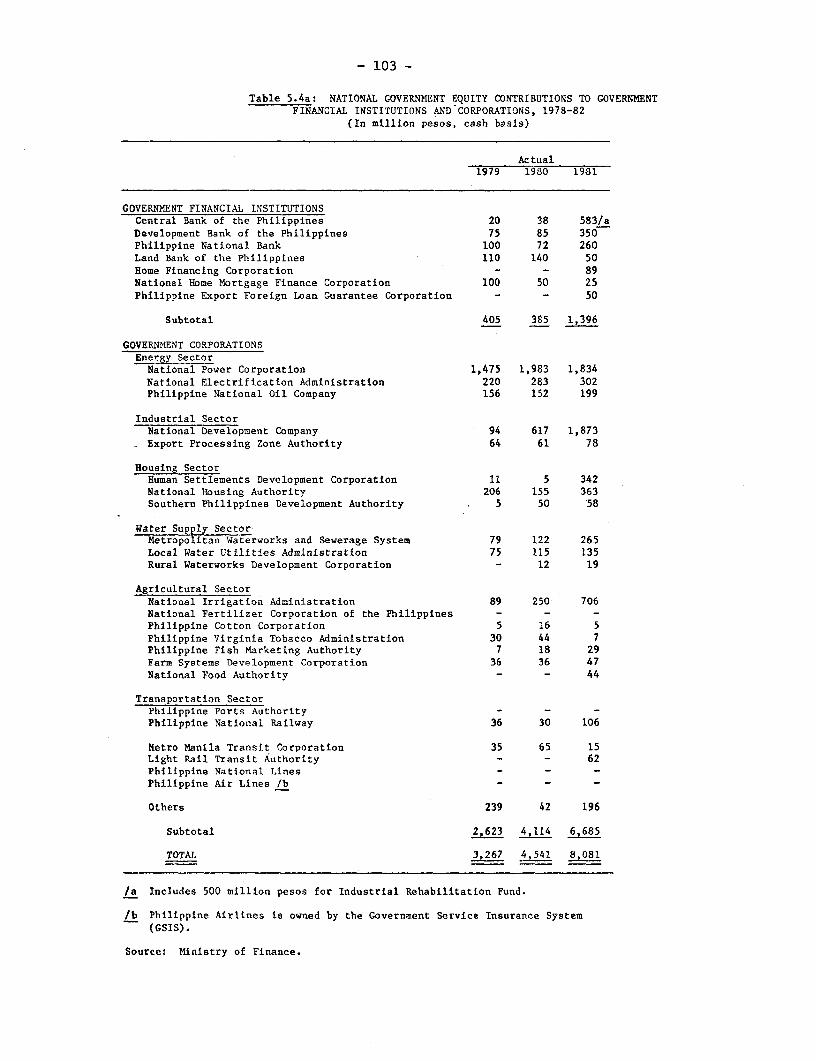

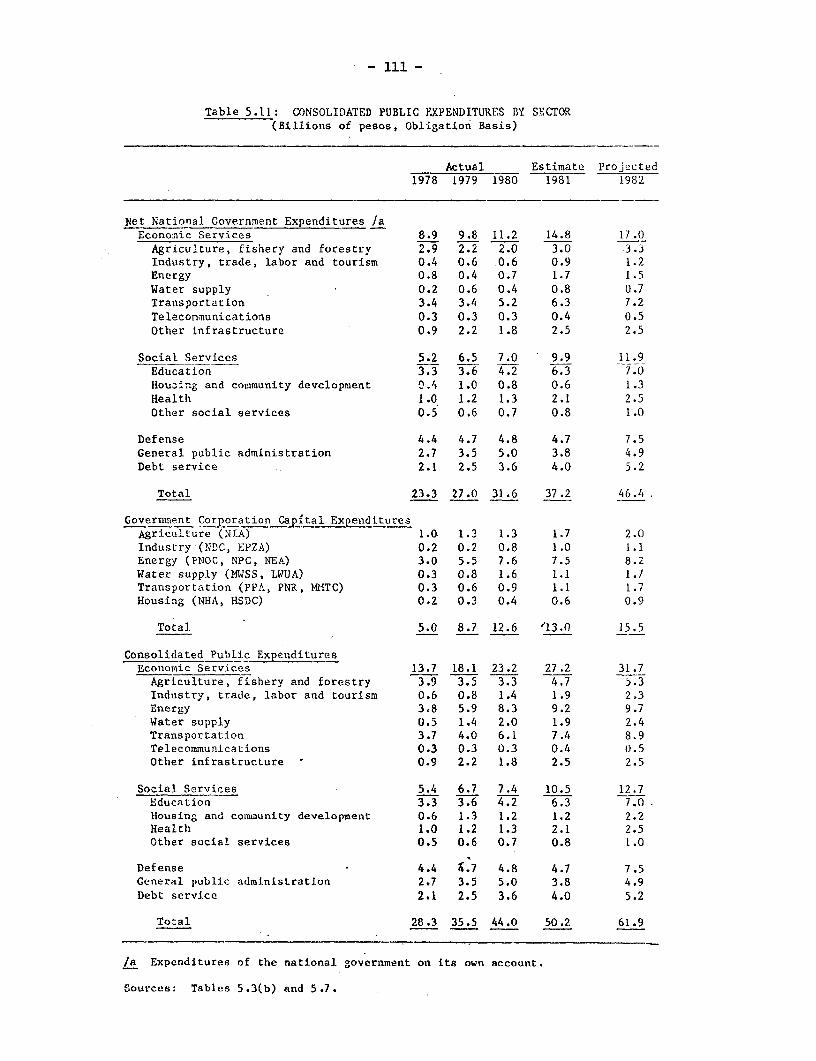

A. Level and Structure of Public Expenditures . . . . . . . 29B. Priorities Among and Within Sectors . . . . . . . . . . 32C. Planning and Execution of Public Expenditures .40D. The Role of the Public Sector . . . . . . . . . . . . . 40

4. REGIONAL ASPECTS OF DEVELOPMENT

A. Regional Disparities and Regional Growth . . . . . . . . 40B. Government Programs and Policies for Regional

Development . . . . . . . . . . . . . . . . . . . . . 43

5. THE BALANCE OF PAYMENTS

A. Recent Balance of Payments Developments. . . . . . . . . 49B. Adjustment in the Current Account. . . . . . . . . . . . 50C. External Capital Requirements . . . . . . . . . . . . .

STATISTICAL APPENDIX ... . . . . . . . . . . . . . . . . . . . . 63

MAP

This report was prepared by an economic mission which visited the Philippinesin September 1981. The mission consisted of Bruce Jones (Chief),Guenter Reif, Carroll Long, Chukwuma Obidegwu, Christian Moulin andVeronique Bandon. Sarshar Khan also contributed to the report in the areaof the energy sector and advised the mission in certain other areas. Adraft report was discussed with Government officials in Manila duringApril/May 1982.

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

TABLES IN TEXT

Page No.

1. Selected Growth Rates 22. Selected Economic and Social Indicators:

the Philippines and some other Asian Countries 53. Targeted Plan Growth Rates 74. Employment, Area, and Yields in Irrigated and Rainfed

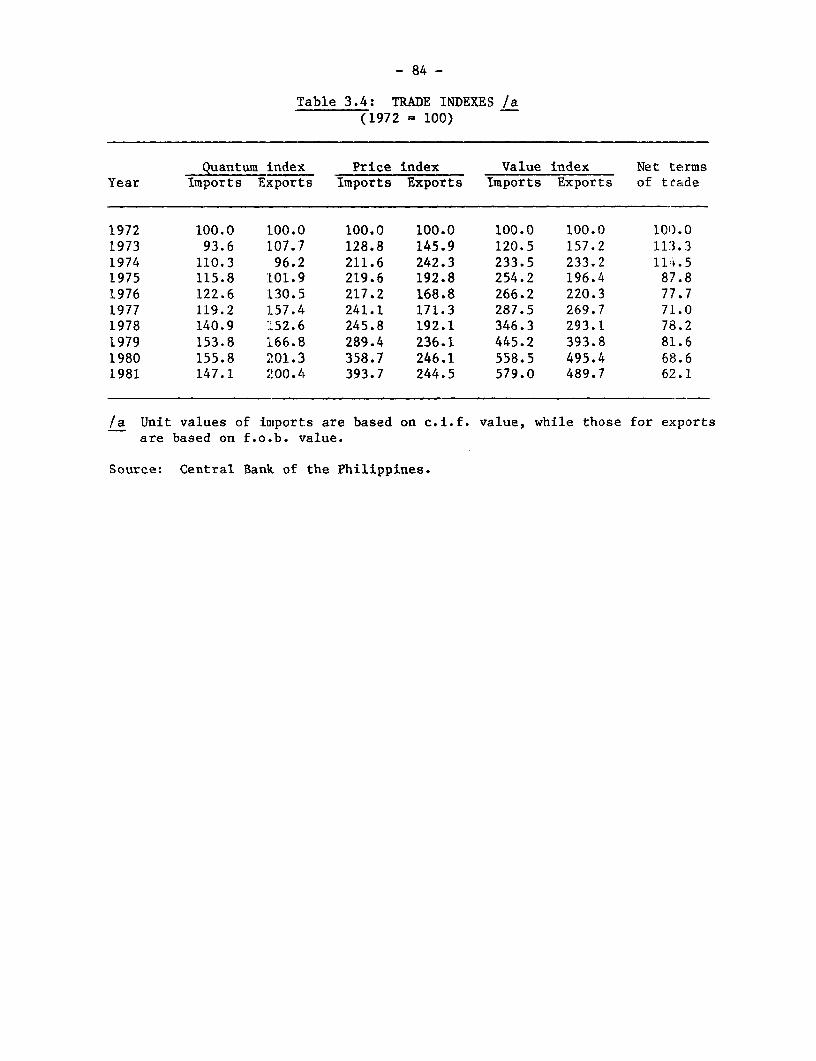

Agriculture 85. Labor Force and Employment 146. Investment aLnd Savings Ratios "167. Nominal and Real. Interest Rates 198. Public Sector Resource Mobilization 249. Major Tax Legislation in the 1978-82 Plan Period 2610. Financing of Government Corporation Investment '711. Structure of Public Expenditures 3012. Consolidated Public Expenditures by Sector 3313. Comparative Regional Data, 1975 4114. Growth Rates of Gross Regional Product and Population 4215. Regional Distribution of Infrastructure Investment 4416. Actual and Projected Current Account 5117. Actual and Projected Current Account (Percent of GNP) 5218. Trade Indexes 5319. Balance of Payments Summary 6020. External Debt and Debt Service 61

WORLD BANK REPORTS ON THE PHILIPPINES, 1980/81 /a

A. Sector Reports and Special Economic Studies

Aspects of Poverty: A Review and Assessment, No. 2984-PH, December 1980

Energy Sector Survey, No. 3199-PH, February 1982Irrigation Program Review, No. 3545-PH, June 1982Transportation Sector Report, forthcoming, 1982

B. Appraisal Reports

Agriculture and Rural Development

Medium-Scale Irrigation Project, No. 2811-PH, January 1980Rainfed Agricultural Development (Iloilo), No. 2695-PH, February 1980Third Livestock and Fisheries Credit Project, No. 2828-PH, June 1980Watershed Management and Erosion Control Project, No. 2920-PH, June 1980National Fisheries Development Project, No. 3387-PH, March 1981Agricultural Support Services Project, No. 3378-PH, June 1981Communal Irrigation Project, No. 3850-PH, May 1982

Structural Adjustment

Structural Adjustment Loan, No. P-3150-PH, August 1980

Industry

Industrial Finance Project, No. 3331-PH, April 1981Third Small and Medium Industries Project, No. 3838-PH, May 1982Textile Sector Project, No. P-3700-PH, March 1982

Energy

Coal Engineering Project, No. P-3343-PH May 1982

Transportation

Third Ports Project, No. 2830-PH, April 1980Rural Roads Improvement Project, No. 2896-PH, April 1980

/a Includes some reports available, or expected to be available, in early1982. A listing of World Bank reports on the Philippines distributed in1978 and 1979 is contained in the previous economic report, ThePhilippines: Domestic and External Resources for Development, No. 2674-PH,November 1979.

WORLD BANK REPORTS ON THE PHILIPPINES, 1980-81

Urban Development

Third Urban Development Project, No. 2703-PH, February 1980Manila Sewerage and Sanitation Project, No. 2792-PH, March 1980Urban Engineering Project, No. P-3150-PH, November 1981

Education

Sector Program for Elementary Education Project, No. 3423-PH, June 1981Vocational Training Project, No. 3750a-PH, March 1982

SUMMARY AND CONCLUSIONS

Recent Economic Developments

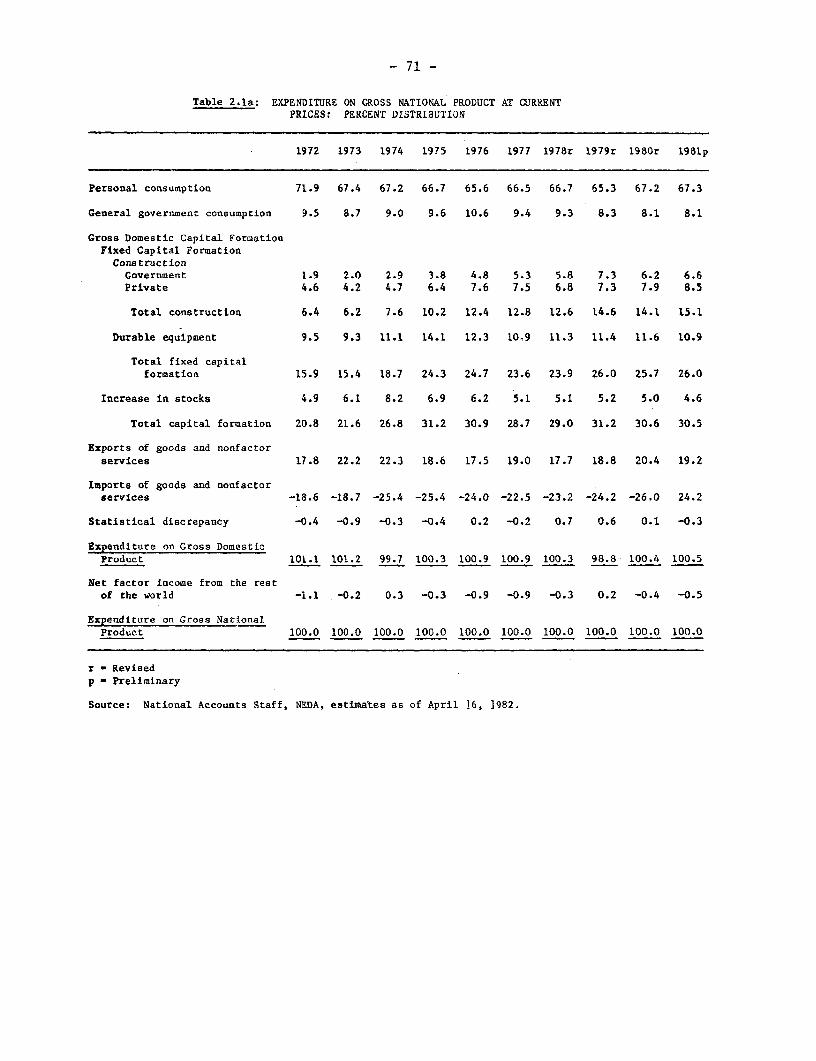

1. Recent economic developments have been dominated by a sharpdeterioration in the external terms of trade. The "second oil crisis" of1979 not only increased the price of a major import, but also brought aboutrecessionary conditions in the OECD countries and thereby falling prices andlittle quantitative growth for Philippine exports. From 1979 to 1981 theterms of trade deteriorated by 29%. Given the openness of the economy, thisresulted in deflation of domestic incomes and a slowdown in real domesticexpenditure. The growth rate of real GNP decelerated from 6.8% in 1978 to4.4% in 1980 and 3.8% in 1981. Recessionary conditions have persisted inthe early part of 1982, and it is expected that real GNP growth in 1982would be about 4%. Because of the deterioration in the external terms oftrade, the growth rate of real gross national income decelerated even moresharply, from 6.9% in 1978 to 2.3% in 1980 and 2.2% in 1981.

2. A number of private firms had financed long-term assets withshort-term liabilities, and were therefore in a vulnerable financialcondition when the economy decelerated and real interest rates shifted fromnegative to positive. Corporate financial difficulties led to a temporarycrisis of confidence in nonbank financial intermediaries in early 1981,which reinforced the effect of the terms of trade deterioration on businessconfidence and the level of private investment.

3. The Government took a number of measures, including expansion ofpublic investment, and Central Bank support to the financial institutions torestore and maintain confidence in the financial system, to counter theshort-term situation. At the same time, the Government has sustained itsongoing program of longer-term structural measures and investments designedto address the fundamental problems underlying the recent difficulties:considerable dependence of export earnings on a few commodities; heavydependence of the energy sector on imported petroleum; relativelyinefficient use of capital in the industrial sector, and excessivedependence of firms on short-term finance. The Government has also prepareda new Development Plan setting out its strategy for addressing these andother long-term challenges during the 1983-87 period.

Development Plan Strategy

4. The Development Plan strategy flows logically from its assessmentof the development challenges. The principal elements of the growthstrategy are the following:

(a) efficient exploitation of agricultural potentials for food,agro-energy, and export crops;

- ii -

(b) industrial development along the lines of comparative advantage,which would imply primarily labor-intensive industries, togetherwith selected capital-intensive industries based on domestic rawmaterials;

(c) expansion of necessary infrastructure to support the agriculturaland industrial growth;

(d) import-substituting investments and effective demand management inthe energy sector; and

(e) increased (lomestic resource mobilization, and more efficientresource ut:ilization.

It is expected that real GNP growth would be 6.5% p.a. during the Planperiod, and that the absorption of foreign savings would be reduced froan6.0% of GNP in 1981 to 2.6% of GNP in 1987. Equity aspects of developmentwould be pursued thrcough emphasis on employment generation; a more balancesdpattern of development among the regions; and increased public expendituresin sectors such as education, health, housing, and rural infrastructure.

5. The Plan is broadly appropriate to the Philippines' presentsituation and underlying development constraints. However, the Plan islargely strategic rather than quantitative in nature. The most criticalissues for the achievement of Plan targets are improvement in the efficiencyof resource use, and increased public sector resource mobilization.

6. Agricultural Strategy. The challenges and opportunities aresomewhat different in the irrigated and rainfed areas. Although the hig-lerproductivity of the irrigated lands is somewhat offset by a higherpopulation density, it appears that the average income per worker is higwErin the irrigated than in the rainfed areas. Furthermore, there are goodprospects for further income increases in the irrigated areas during thePlan period, since yields are presently considerably below the technologicalpotential.

7. The prospects for income growth in the rainfed areas are lesscertain. The strategy for the rainfed lowlands should consist of thepromotion of mixed farming systems comprising a range of crops and liveslocksuited to particular soils and rainfall patterns. The Government intend:!, tomake a major effort in corn during the Plan period, including disseminationof high-yielding disease-resistant varieties, and promotion of switching ofsome land from rainfed rice to corn. In some lowland areas there are alt:opotentials for commercial crops such as rubber, coffee, cotton, and cacao.The more steeply sloping uplands present a more difficult developmentproblem. The need is to combat soil erosion while simultaneously provid:nga livelihood for the people living in these areas. This can be accompli<;hedby switching land away from corn toward agro-forestry and foddercrop4

- iii -

livestock systems. However, such switching from annual subsistence cropsto longer-term cash crops requires credit, a substantial extension effort,land titling, and a reasonably good rural road network, all of which aresomewhat problematic in the upland areas.

8. Industrial Strategy. Just as the agricultural strategy is centeredaround the more productive utilization of land, the industrial strategy iscentered around the more productive utilization of capital. The principalelements of the Government's industrial strategy are:

(a) reform of trade policy and fiscal incentives for investment toencourage a more efficient and competitive industrial sector, withmore rapid growth of exports and employment;

(b) sector development programs to restructure specific industries toenable them to adjust to the policy reforms, and to promoteneglected industries with potential comparative advantages;

(c) a phased program of carefully selected major industrial projectsdesigned to deepen the industrial structure through thedevelopment of capital goods and intermediate goods industries;

(d) promotion of labor-intensive small and medium-scale industriesthrough technical, marketing and financial assistance; and

(e) regional dispersal of industry.

9. Population and Employment in the Plan Period. Two of the majorchallenges facing the Philippines in the Plan period are the highest levelof fertility and most rapidly growing labor force in East and SoutheastAsia. In the Plan it is projected that the crude birth rate will decline by16% from 1980 to 1987, leading to a decline in the population growth rateform 2.5% in 1980 to 2.2% in 1987. However, such a fertility decline couldbe achieved only with an intensified and more effective family planningeffort than indicated by the results of recent surveys.

10. The labor force is projected to increase by 3.7% annually duringthe Plan period, because the working-age population (reflecting the veryhigh fertility rates of the 1960s) is growing more rapidly than the totalpopulation, and because there is expected to be an increase in the laborforce participation rate. Between 1980 and 1987, the economy will have tofind jobs for 5 million persons, or 700,000 persons annually, if an increasein unemployment is to be prevented. The industrial policy reforms areexpected to promote more rapid growth of employment in the organized manu-facturing sector. However, the organized manufacturing sector presentlyaccounts for only a small share of total employment, and the labor forcewill grow so rapidly that most of the increment will have to be absorbed inthe already overcrowded agricultural and services sectors. The labor market

- iv -

situation therefore has a potential for stagnation or decline of real wagesand deterioration of income distribution. It will therefore be important inthe Plan period for the Government to utilize the fiscal system, both taxingand spending, for equity objectives.

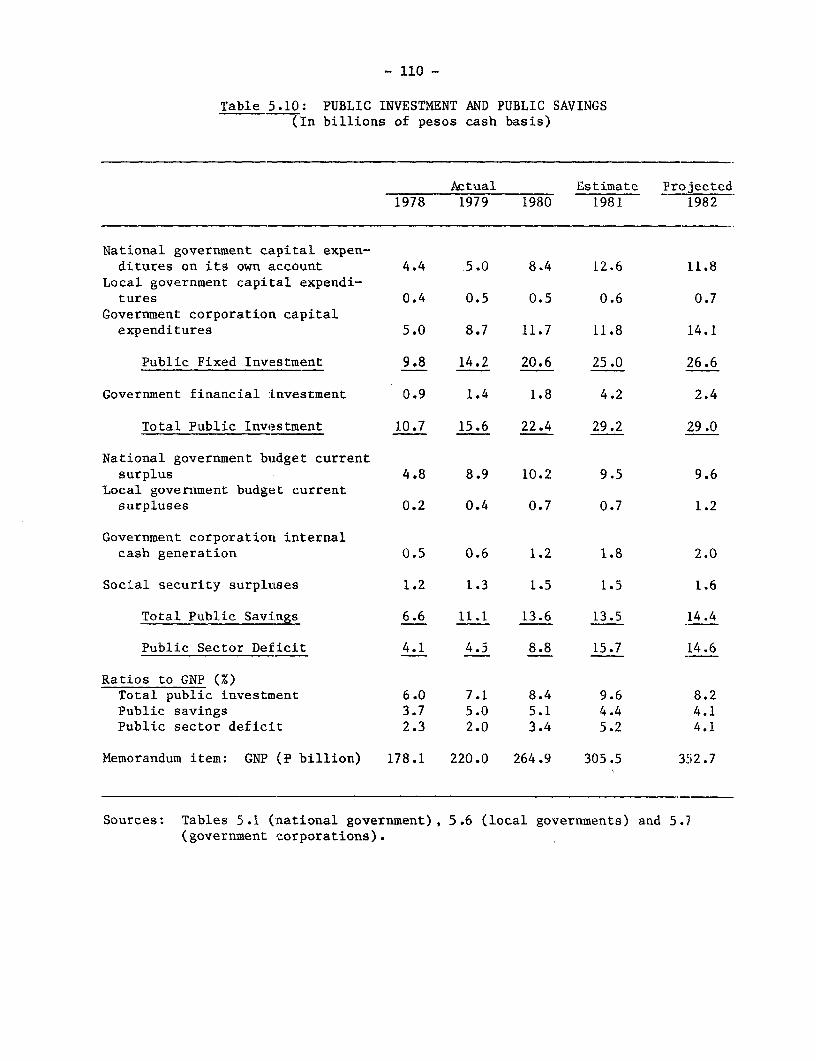

Resource Management

11. Reducing the present unsustainable level of foreign savingsabsorption will require some combination of increased domestic savings and areduced level of investment. The high level of investment in the 1970s hasnot been accompanied by a corresponding growth performance, indicating thatsome of the investment has been inefficient. The Government has recentlyimplemented industrial and financial policy reforms designed to improve theefficiency of private investment; steps are also needed to improve theefficiency of public investment. The financial sector reforms are alsoexpected to increase private sector resource mobilization. Substantialsteps will be necessary in the Plan period to increase public sectorresource mobilization.

12. Private Sav4ings and the Financial Sector. The objectives of t:heGovernment's financia.l sector policy are to promote savings, to increase! theshare of financial savings in total savings, and to increase theavailability of financial savings on a longer-term basis (long-term loans orequity). In keeping with these objectives, the Government implemented acomprehensive set of regulatory reforms and related measures in 1980-81:all interest rates, except for lending rates of up to two years' maturitVwere deregulated; legislated specialization of financial institutions ha3been substantially reduced; and monetary and fiscal incentives forlonger-term lending and equity investment have been provided.

13. Government banks - principally the Philippine National Bank (Plil),the Development Bank of the Philippines (DBP), and the Land Bank of thePhilippines (LBP) - account for 36% of the assets of the banking system.Their behavior is therefore a significant influence on the financial sysl:emas a whole. Because of widespread defaults as well as relatively lowinterest rates, the resource mobilization performance of these institutioinshas been poor, and these institutions have therefore been heavilydependent on government contributions and government-guaranteed foreignborrowings. The Government has recently raised the lending rates of theseinstitutions as part of the overall rationalization of interest rates in tQeeconomy, and new management has been brought to DBP. Sustained anddetermined efforts will be needed to improve the loan evaluation capabil:ltyand loan recovery performance of these institutions.

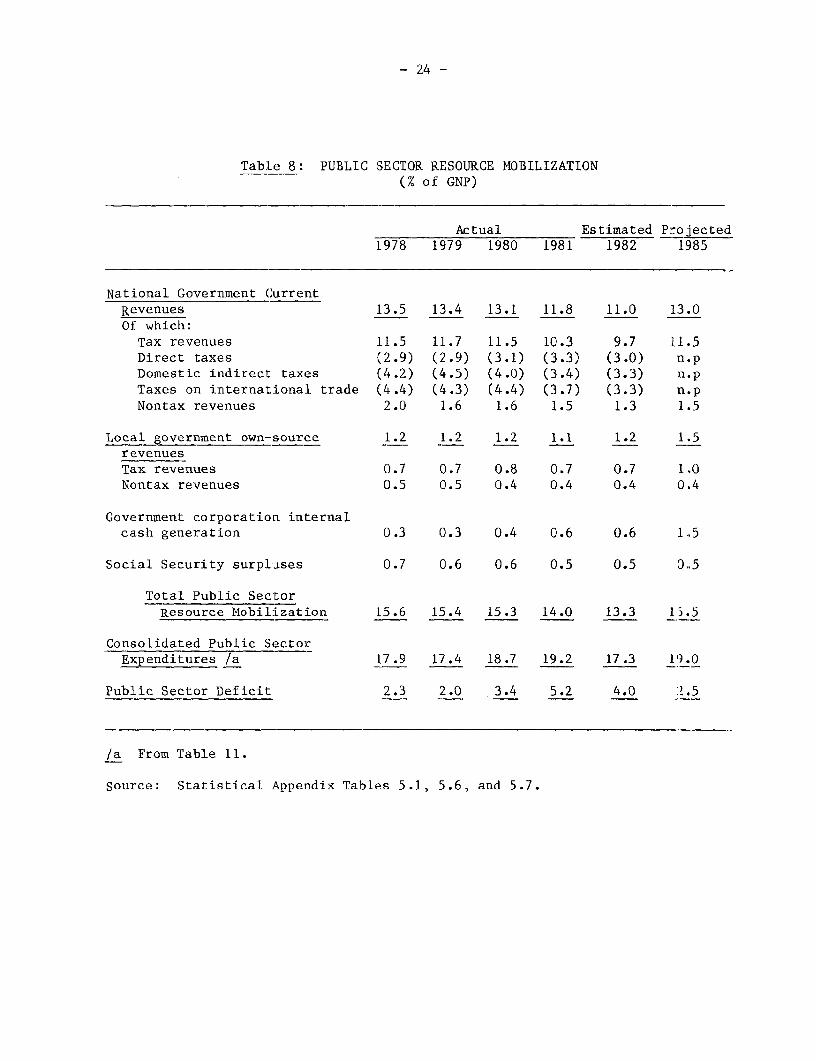

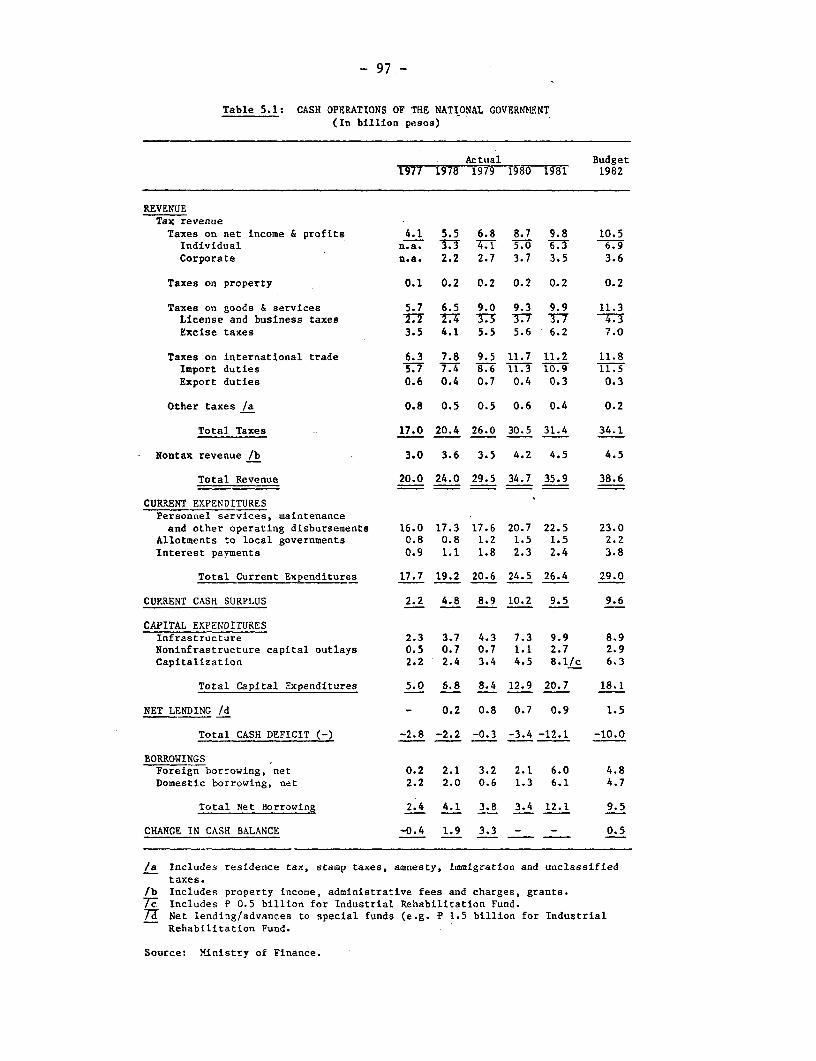

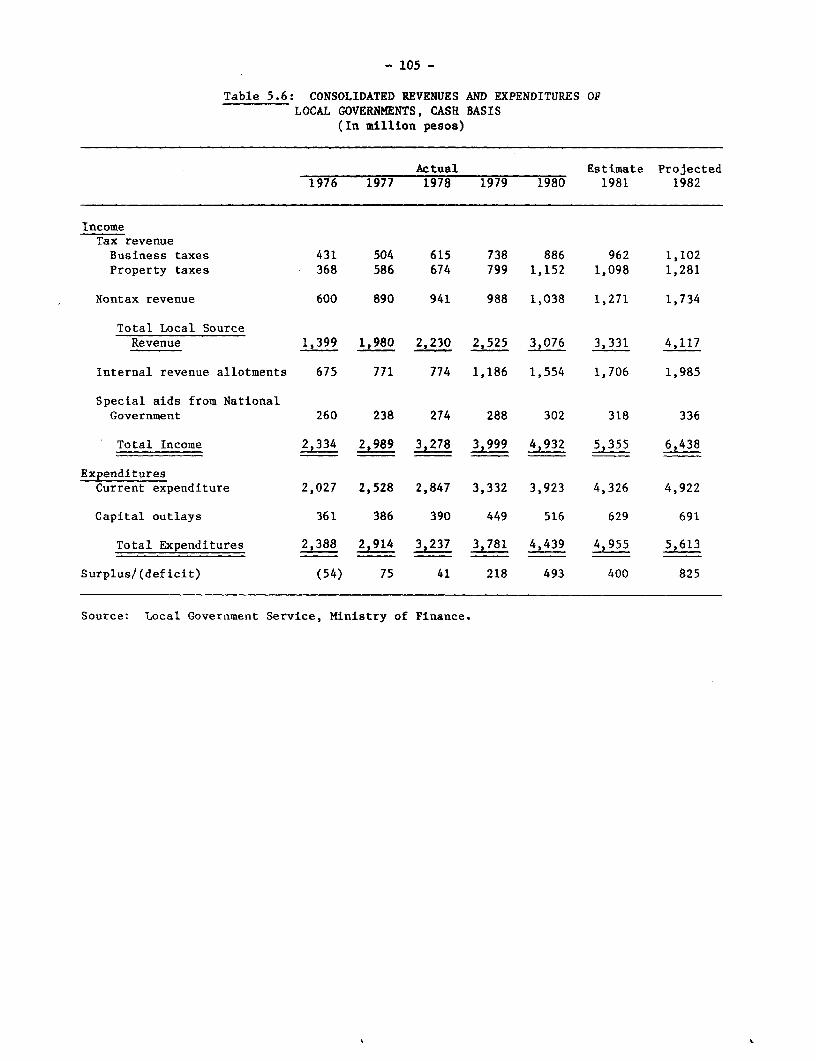

14. Public Sector Resource Mobilization. Because of the low level ofpublic sector resource mobilization, government current expenditures are toolow, project implementation has been deteriorating, and recently the publicsector deficit has become too high. During the 1983-87 Plan period, it

- v -

will be necessary to reduce the public sector deficit in relative terms, aspart of the overall effort to reduce the current account deficit in thebalance of payments in relative terms. Every aspect of public sectorresource mobilization - tax effort, cost recovery by government corporations,and loan recovery by government financial institutions - needs to besubstantially strengthened.

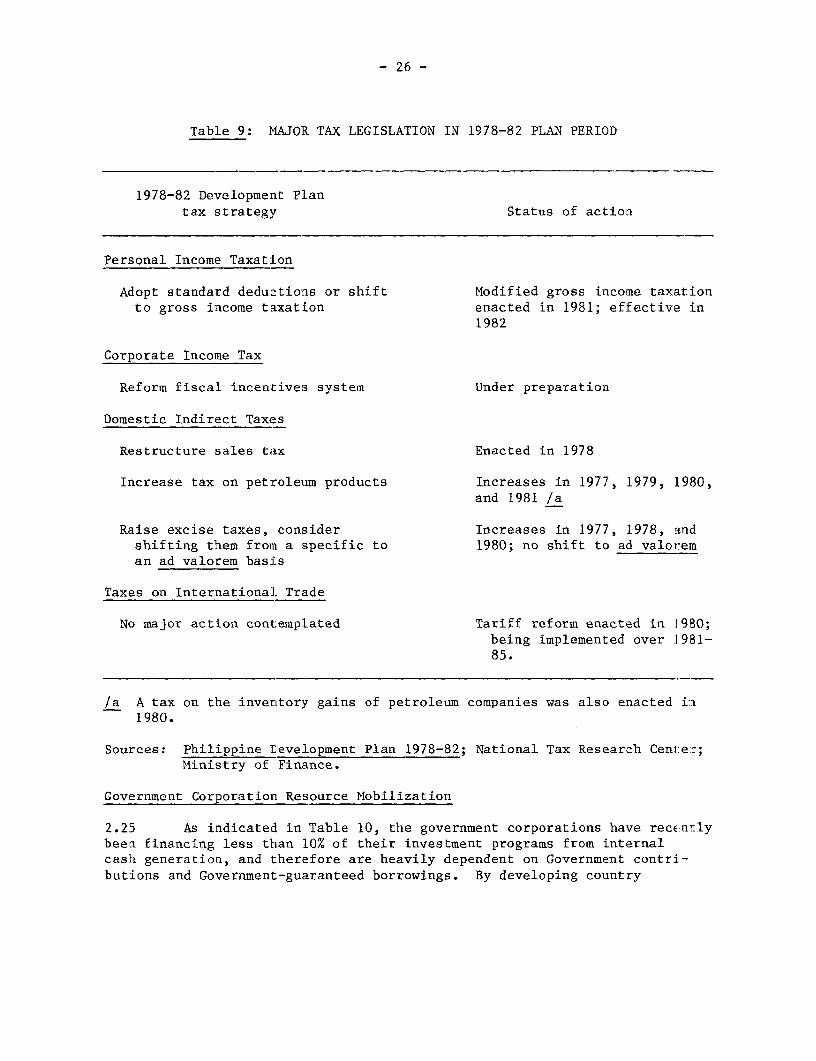

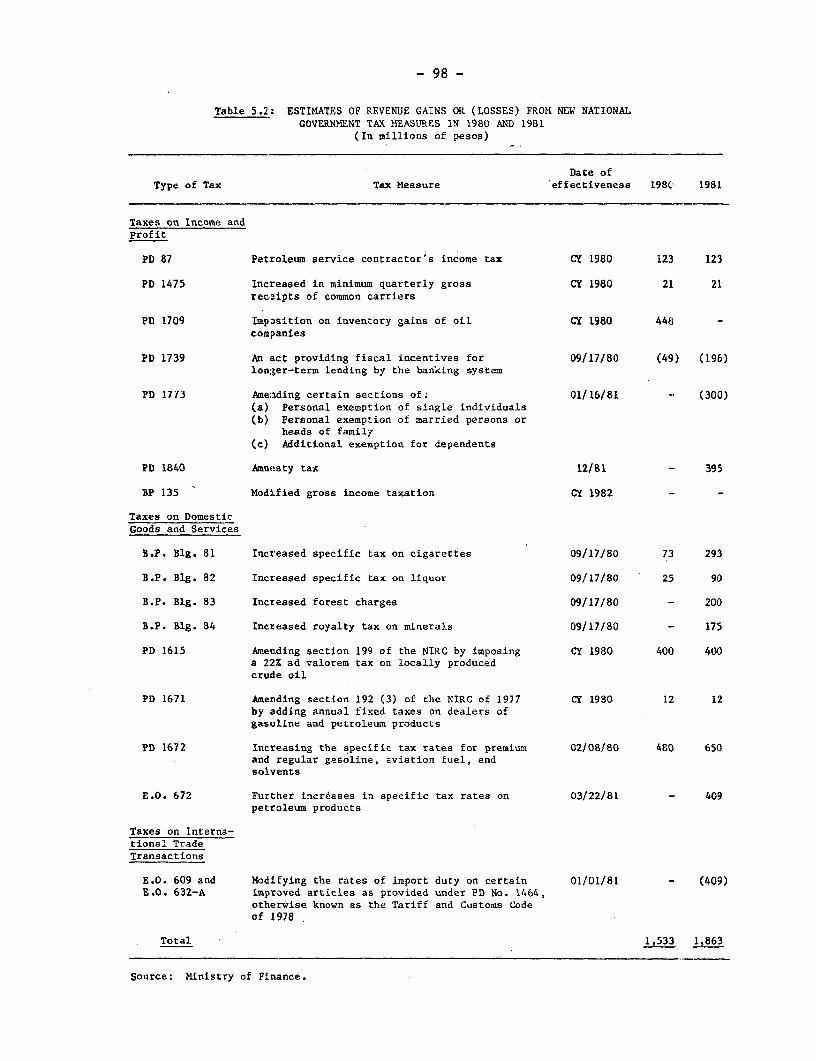

15. It was expected that the tax strategy described in the DevelopmentPlan for 1978-82 would increase national government and local government taxrevenues to an average of 14.6% of GNP during 1978-82, which would have beena broadly appropriate level. However, the tax ratio was only 12.3% in1978-80 and then fell back to 11.0% in 1981 under the impact of recessionaryconditions. The shortfall from Plan projections has been primarily in thearea of domestic taxation, although taxes on international trade alsoslipped sharply in 1981. The shortfall appears to reflect the followingfactors: the Plan underestimated the need for new tax measures, some of thecontemplated Plan tax reforms are either taking effect fairly late in thePlan period or otherwise have not been enacted; and the revenue performanceimplies that tax administration has not improved very much. A substantialimprovement in the tax effort will be needed if there is to be a reasonablechance of achieving the objectives of the 1983-87 Development Plan.

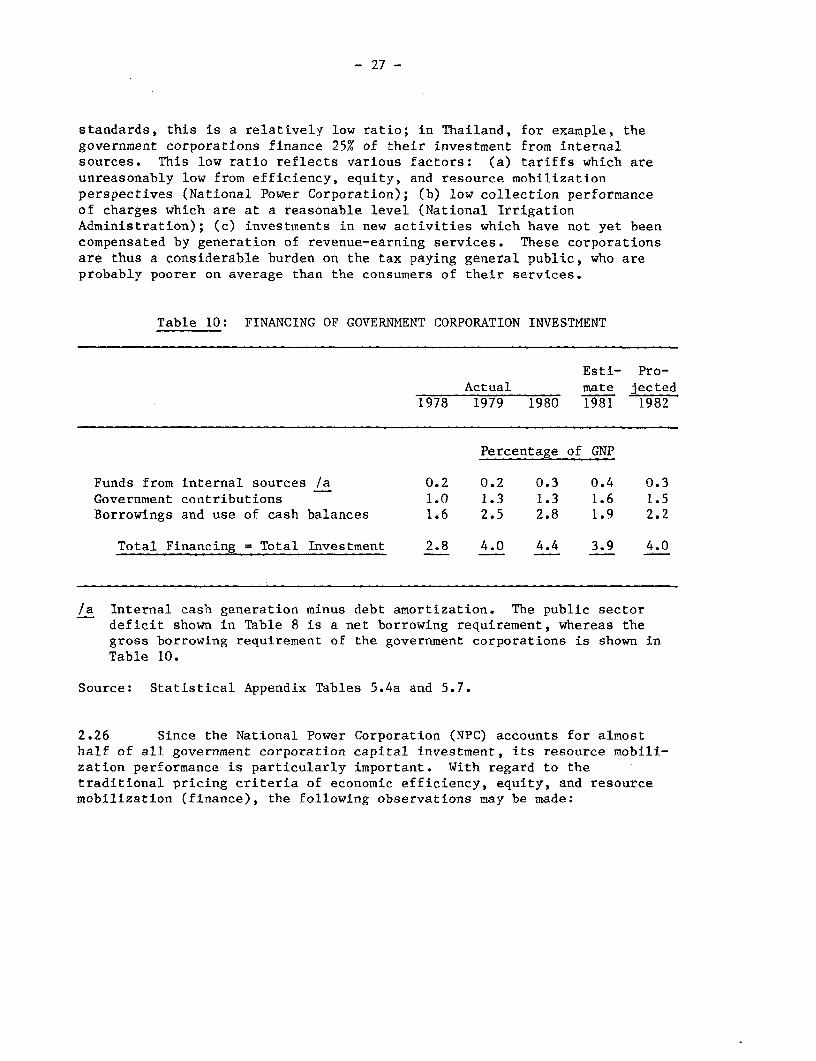

16. The government corporations have recently been financing less than10% of their investment programs from internal cash generation. Because ofthis low self-financing ratio, these investment programs have been heavilydependent on government contributions and government-guaranteed foreignborrowings. This reflects various factors. (a) tariffs which are unreason-ably low from efficiency, equity, and resource mobilization perspectives;(b) low collection performance of charges which are at a reasonable level,(c) investments in new activities which have not yet been compensated bygeneration of revenue-earning services. In the Plan, the Government hasstated that the charges of government corporations will be regularlyrevised, to reduce the dependence of these corporations on the budget andgenerate savings to finance expansion. A reasonable target would be toincrease government corporation internal cash generation to 1.5% of GNP in1985.

The Public Expenditure Program

17. The public expenditure program is one of the most importantinstruments available to the Government for promoting development. Becausepublic sector resource mobilization performance has been less than projectedin the Development Plan for 1978-82, public expenditures have also beenless, leading to a relatively low level of current expenditures and adeceleration, in the face of a much larger number of projects, in the paceof implementation of individual projects. During the next Plan period1983-87, it would be appropriate to emphasize not only increased publicsector resource mobilization but also better allocation of publicexpenditures, both substantively and procedurally.

- vi -

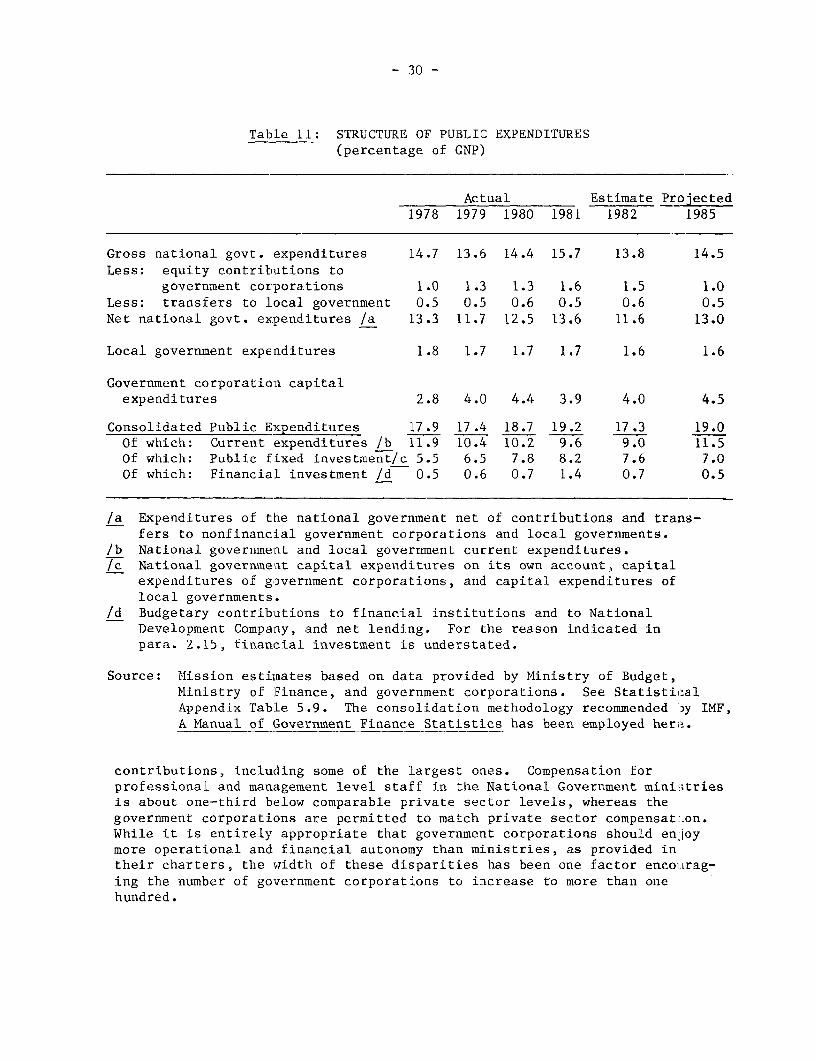

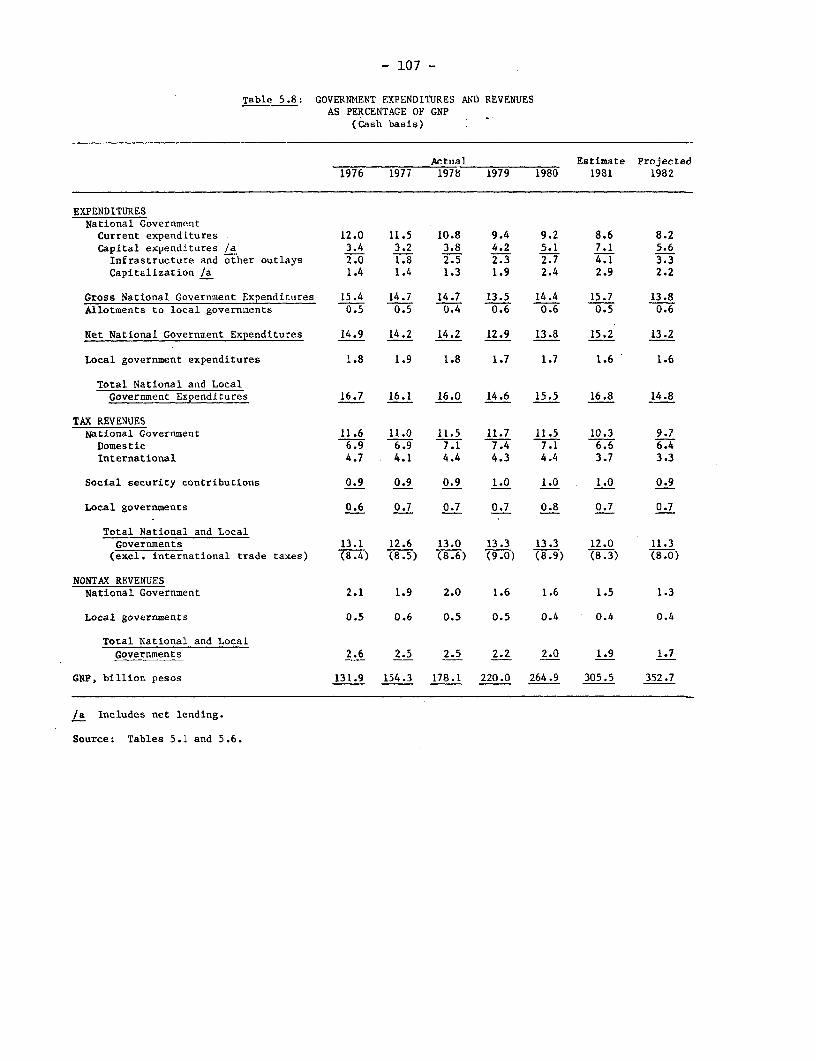

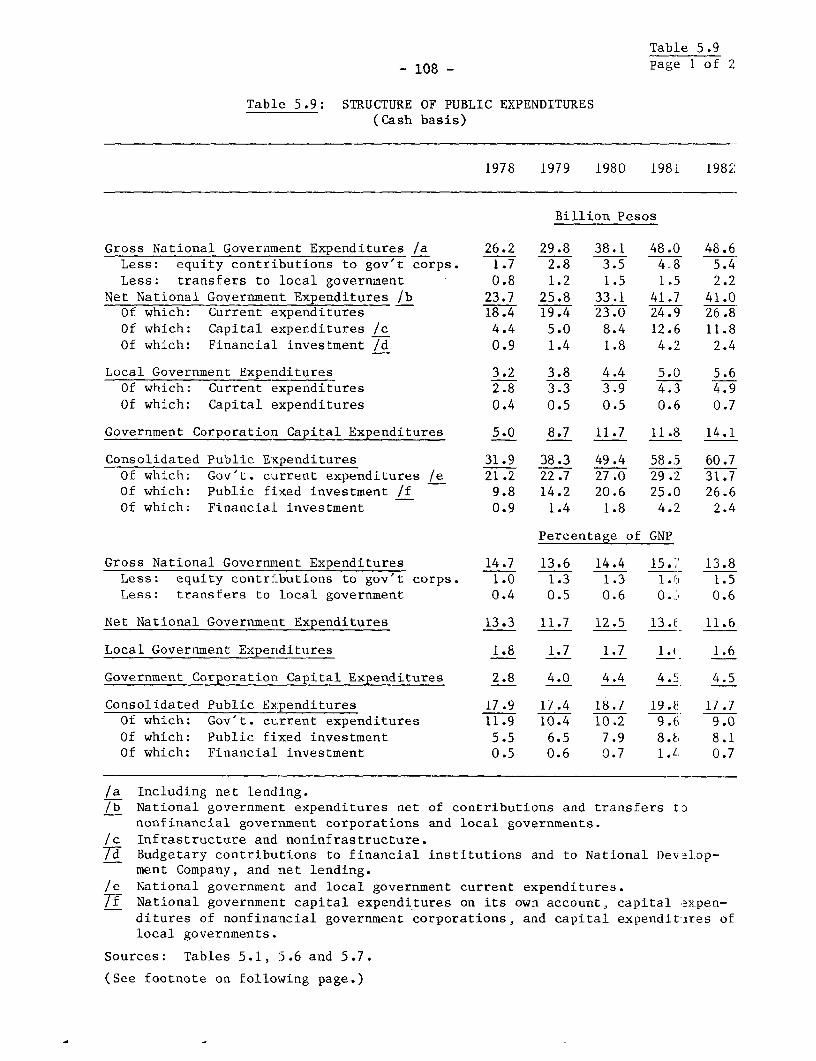

18. Level and Structure of Public Expenditures. A striking trend hasbeen the shift in the distribution of public expenditures between currentand investment expenditures. National government and local governmentcurrent expenditures have decreased from 13% of GNP in 1976 to an estimated9% of GNP in 1982. The reduction in current expenditures has resulted .ininadequate maintenance of roads and irrigation systems; insufficientoperating supplies in the health and education sectors; and civil servicecompensation levels which generate problems in retaining sufficient numbersof capable professional and managerial staff.

19. Public fixed investment, on the other hand, has increased from5.5% of GNP in 1978 to 8% of GNP in 1980-82. This principally reflects thegrowth of government corporation investment, due to an increase ininfrastructure investment in sectors dominated by revenue-earning entities,particularly the energy sector; and an increasing public sector role innon-infrastructure activities such as industrial projects, real estatedevelopment, and agricultural marketing, which traditionally have areas ofprimary private sect:or responsibility. There has also been an expansion ofGovernment financial investment; this reflects the need to support theliquidity of government financial institutions in the face of poor loaiarecovery, the Indust:rial Rescue Fund, and the KKK program. Over the mediumterm, the primary need t:o bring about a better balance by raising governmentcurrent expenditures to a more reasonable level while cutting back oninvestment expenditures.

20. Priorities Among Sectors. At the present time, the largestsectors accounting for the largest share of public expenditure are: energy3.4% of GNP; transportation, 2.5% of GNP; education, 2.1% of GNP; andagriculture, 1.8% of GNP. The sectors which have displayed the most rapidgrowth during the 1978-82 Plan period are energy, industry (because of theMIP program) and housing. The sectoral distribution prevailing at thepresent time appears to be broadly appropriate. Any further shift in favorof energy, industry, or housing, would unreasonably compress agriculture,non-energy infrastructure, eduction and health.

21. Planning and Execution of Public Expenditures. In order toenhance the Government-s capability to efficiently make choices amongcompeting sectoral priorities, strengthening the system for the financialand operational planning of the public sector is a high priority task.Appropriate concepts have been set out in the Budget Reform Decree:(a) strengthening of planning-programming-budgeting linkages; (b) shiftLngsome of the weight oE resource allocation decision-taking from an annuaLbasis to a medium-term basis ("long-term budgeting"); and (c) integrattigthe government corporations more effectively into the public sector invlest-ment program and financial strategy ("total resource budgeting"). In ol-derto implement these concepts, the Government intends to adopt a medium-termfinancial planning systerm, covering the government corporations as well asthe National Government proper, during the 1983-87 Plan period. This w:ould

- vii -

provide a more stable environment for programming by implementing agenciesand facilitate simplification of budget execution procedures.

22. The Role of the Public Sector. The public sector has recentlybecome increasingly directly involved in activities which traditionally inthe Philippines have been areas of primarily private sector responsibility.There are well-justified rationales for some but not all of these involve-ments. These involvements have come at a time when the Government has notyet completed the task of providing basic public services, such as ruralroads and bridges or sanitary water supply, to all segments of the popu-lation, and when public sector project implementation has been deterioratingbecause of lack of funds. They have also given rise to some concern in thePhilippine private sector as to the relative roles of the public and privatesectors. In the new Plan the Government has, however, reaffirmed that theprivate sector will be the leading partner in development, and that the roleof public sector is to provide direction and basic support. This shouldprovide the basis for a more sharply focussed but more effective publicsector development effort.

Regional Aspects of Development

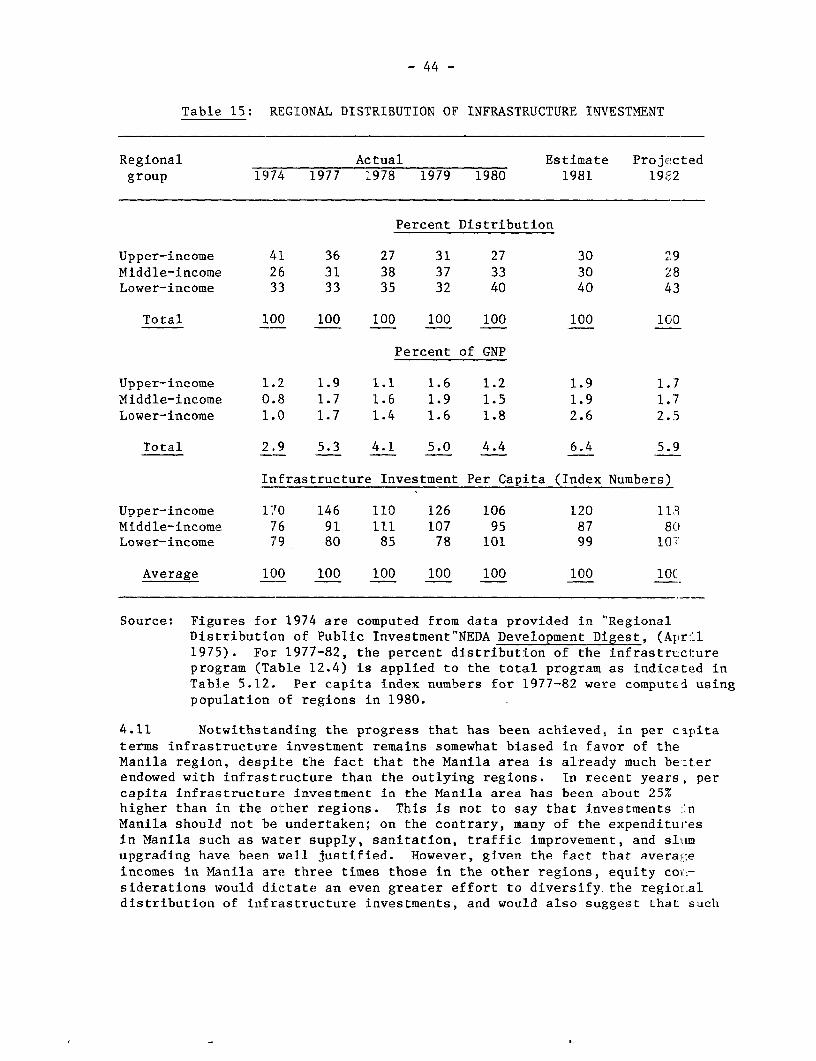

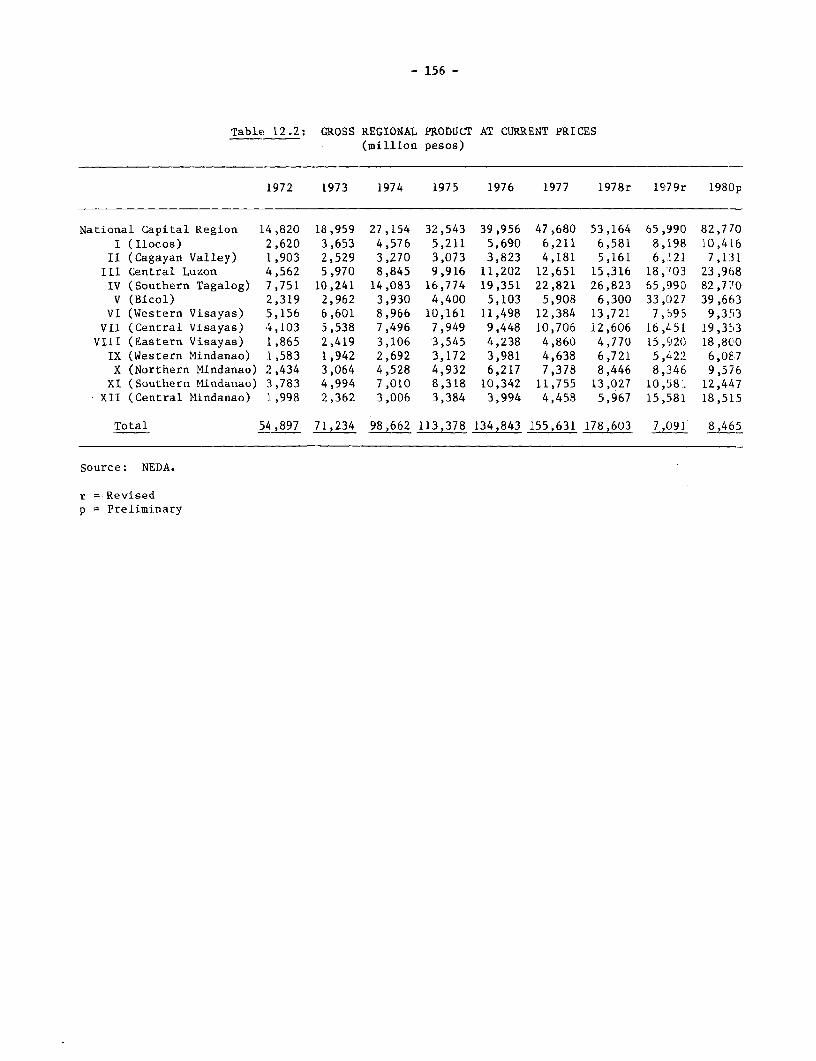

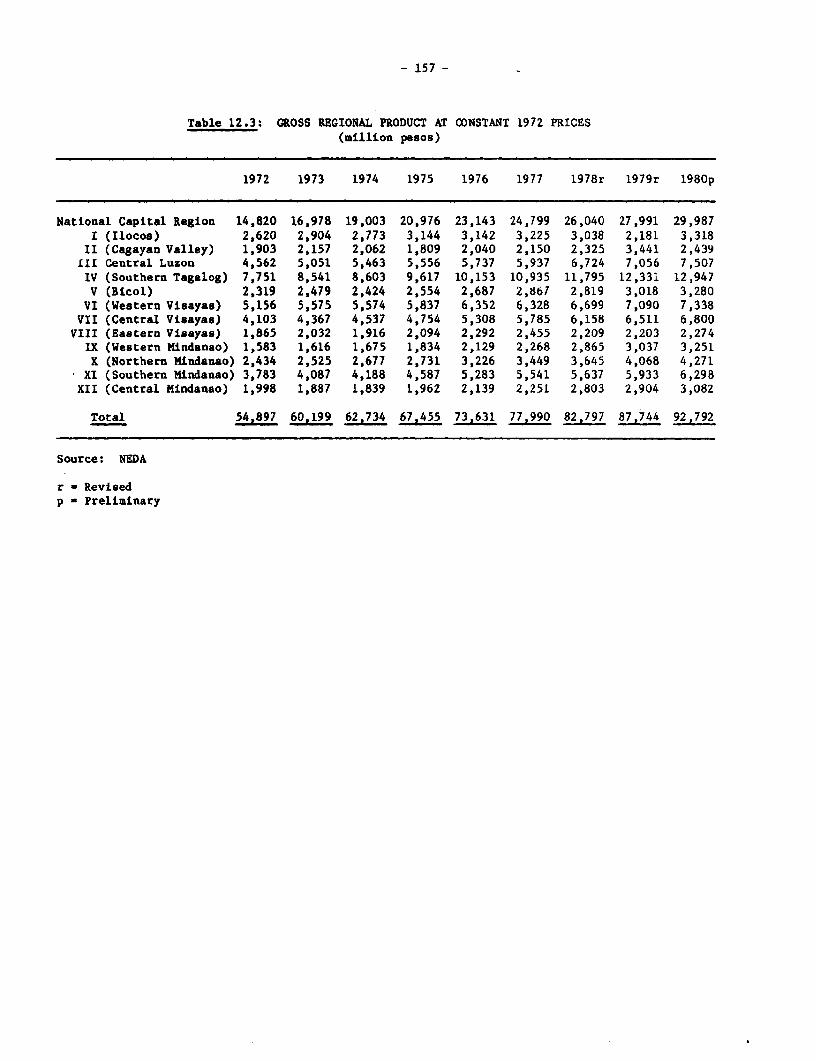

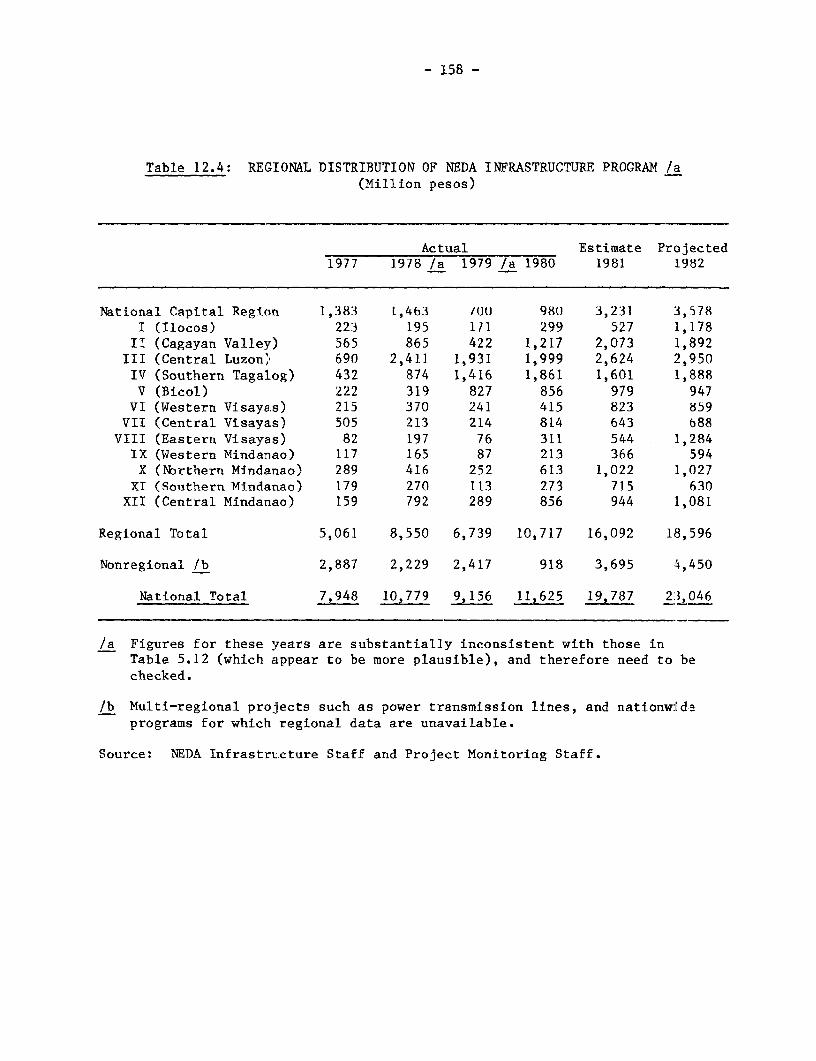

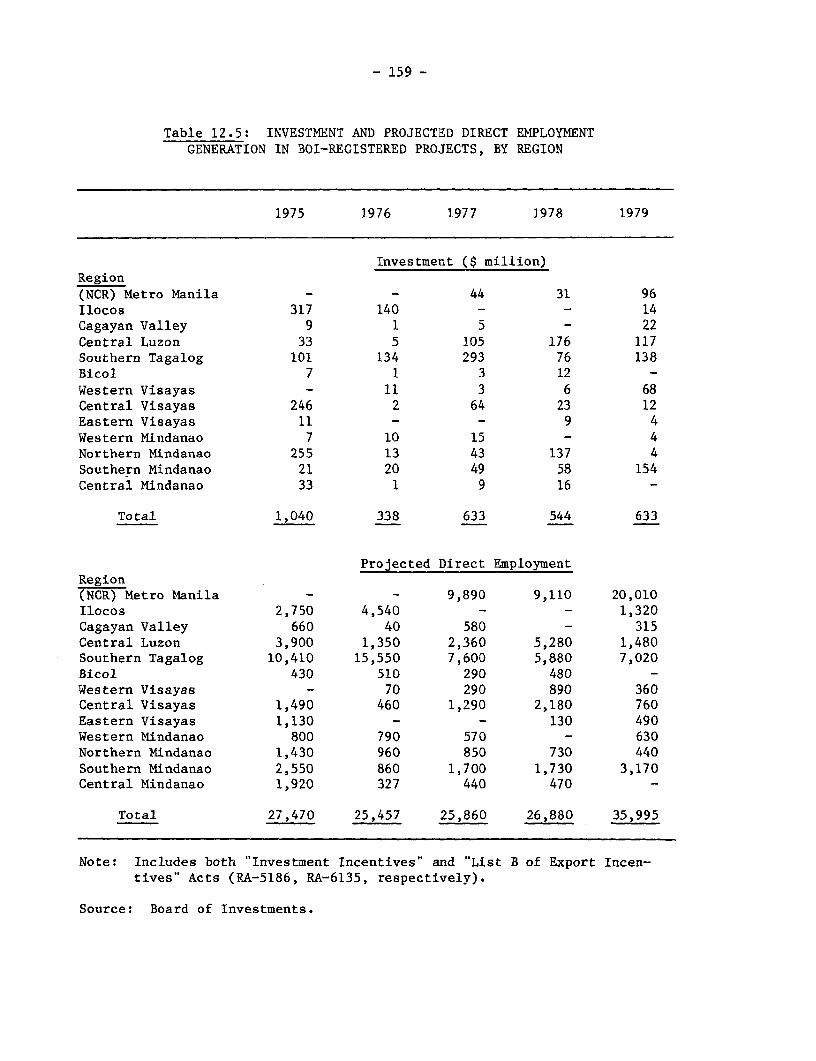

23. Historically, economic activity has been highly concentrated in theManila area; 1975, GDP per capita in Metro Manila was three times that inthe rest of the Philippines. This disparity, and the congestion and othersocial costs that can result from large-scale internal migration, argues infavor of substantial efforts to improve incomes in the poorer regions. Theprincipal aspects of the Government's regional development effort have been:

(a) better distribution of public investment among the regions;

(b) some decentralization of planning and programming functions,to promote more effective distribution of investment withinregions; and

(c) revision of industrial promotion policies to encourage a betterdistribution of industrial investment (the largest element ofprivate investment) among the regions.

There has been some progress in all of these areas but additional effortswill be needed during the 1983-87 Plan period.

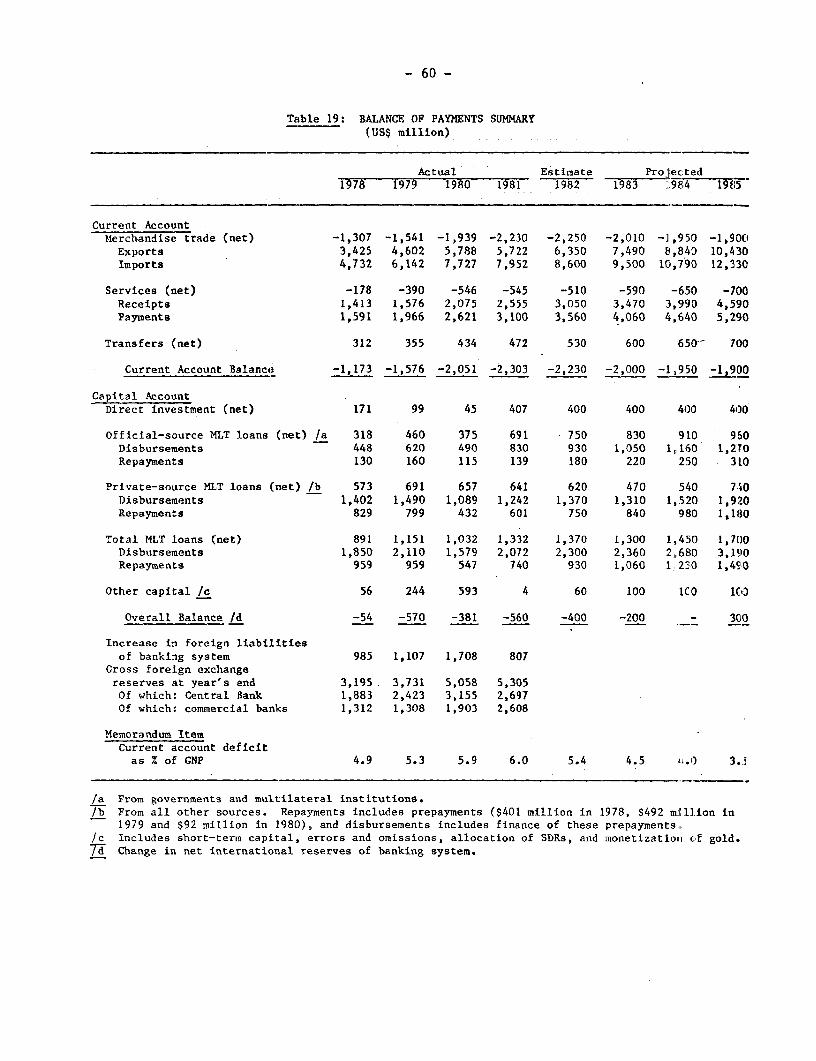

Balance of Payments Adjustment

24. Adjustment in the Current Account. During the past two years, theGovernment has undertaken substantial measures - such as strengthening ofexport incentives, trade policy reform, interest rate deregulation, and aflexible exchange rate policy to promote balance of payments adjustment.These measures will have a significant impact over the medium term.

- viii -

However, in the short term the positive impact of these measures has beenexceeded by the negative impact of the terms of trade deterioration. Tlecurrent account deficit has therefore widened from $1.2 billion (4.9% DfGNP) in 1978 to $2.3 billion (6.0% of GNP) in 1981. In 1982, the termi.s oftrade are expected to stabilize, and the current account deficit is expectedto be $2.2 billion ('5.4% of GNP).

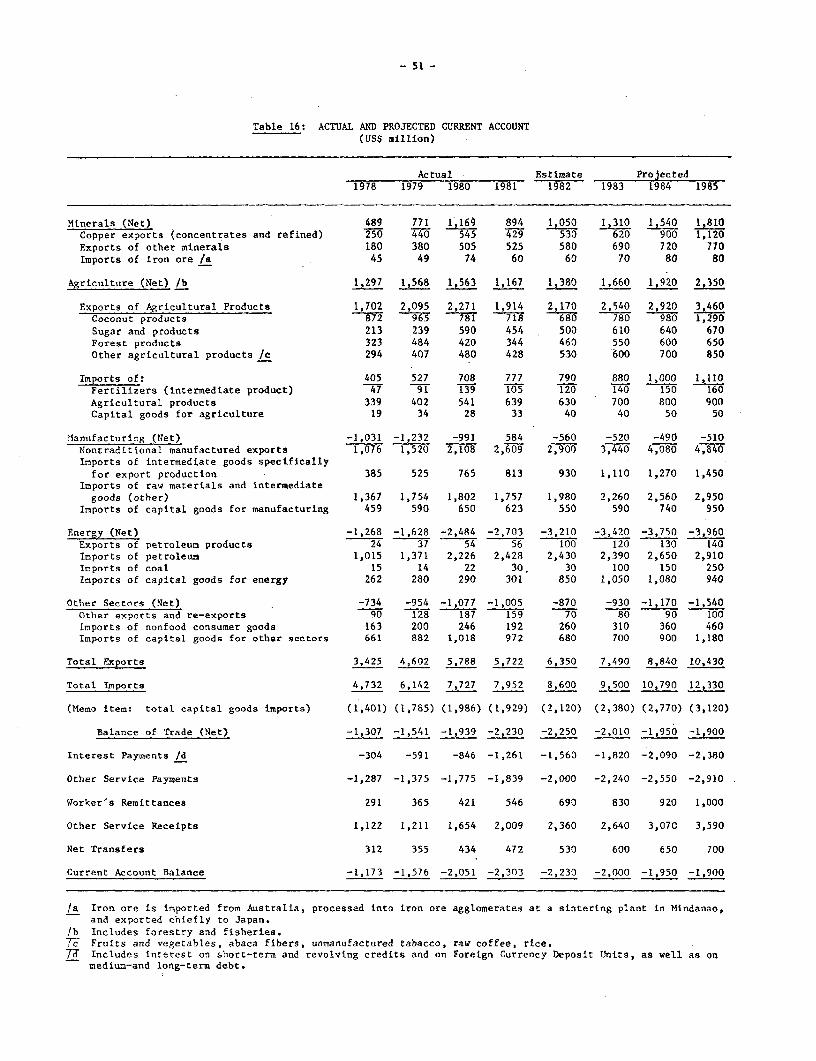

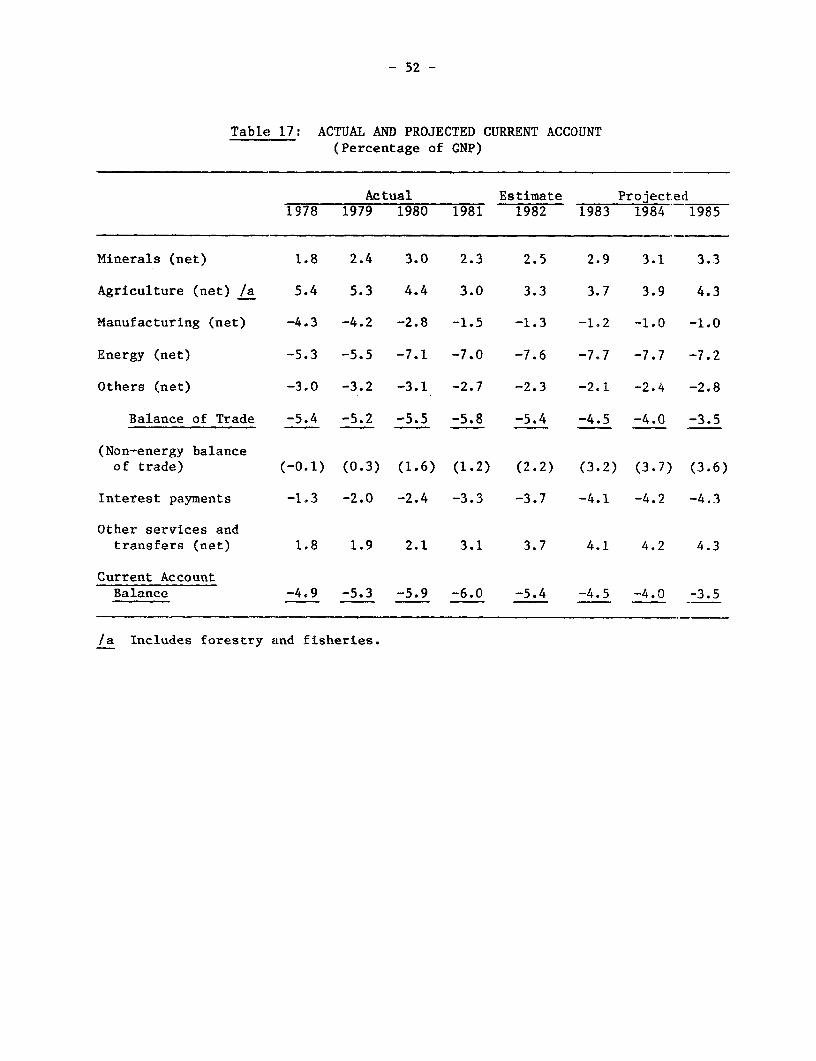

25. As the Plan recognizes, the dependence of the economy on foreignsavings must be reduiced during the Plan period, in order to maintain thIemanageability of the debt burden. This can be accomplished throughappropriate domestic resource management (fiscal and financial) policies toreduce the excess oi domestic investment over national savings; andinvestments and policies to adjust the production structure of the economyin such a way as to increase exports and efficiently replace imports.

26. The Philippines has a trade surplus in the agricultural andmineral sectors, and a trade deficit in the energy and manufacturing sectors.This is a typical pattern for a primary product-exporting, oil-importingdeveloping country. The two principal developments which have caused thewidening of the current account deficit are the growth of net energy importsare (including the e!nergy capital goods necessary for the adjustment process)from 5.3% of GNP in 1978 to 7.0% of GNP in 1981, and the growth of intesrestpayments from 1.3% of GNP in 1978 to 3.3% of GNP in 1981, reflecting both alarger volume of debt and a higher average cost. Meanwhile, the non-energybalance of trade has become positive, increasing from zero in 1978 to 1.2%of GNP in 1981. This indicates that there has been some adjustment in theeconomy generally to offset the higher energy prices and interest rates.

27. In principle, a structural adjustment program could focus onincreasing the agricultural and mineral surpluses, reducing the manufac-turing and energy deficits, or some combination of both. The Philippinestrategy is broadly to concentrate on reducing the manufacturing and eniergytrade deficits, while maintaining the agricultural and mineral surpluses.This reflects the fact that there are substantial profitable opportunitiesfor reducing the manufacturing and energy deficits through manufacturecexport growth, selective and economic import substitution in manufacturilng,and development of domestic energy production. At the same time, however,efforts are also being made to increase domestic processing of agriculturalproducts and minerals. Over the medium term, these structural adjustmeMt:efforts will reduce the vulnerability of the Philippine economy of fluc-tuations in the world prices of commodities.

28. If a substantial adjustment effort is made, and if the externalterms of trade improve as expected, then the trade deficit could be redulcedfrom $2.2 billion in 1981 to $1.9 billion by 1985. The current accountdeficit would then a:Lso be about $1.8 billion (3.5% of expected 1985 GNI').The recovery in the external terms of trade is, however, dependent on arecovery of the world economy in 1983. Because this is uncertain, the

- ix -

Philippines will have to take a cautious approach to balance of paymentsmanagement. This implies avoiding an investment program of a magnitude thatwould prevent reduction in the current account deficit, should the terms oftrade fail to recover as expected.

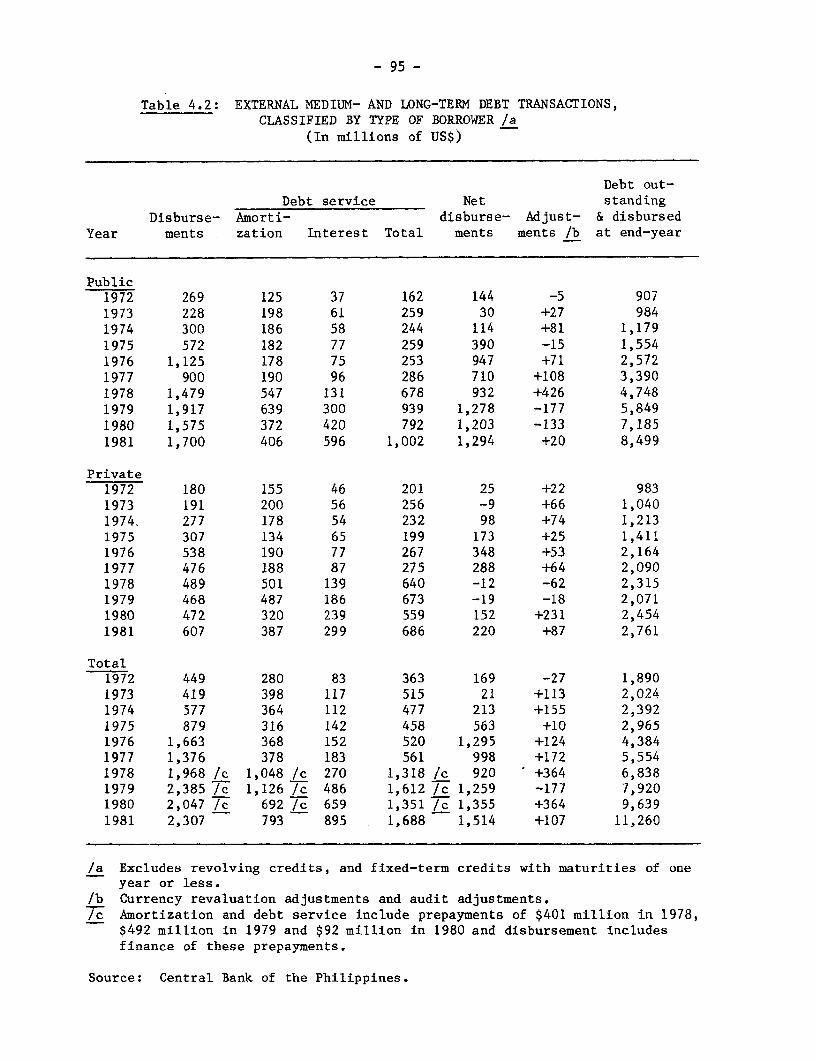

29. External Capital Requirements. Even with a strong adjustmenteffort the external capital requirements will be very considerable. TheGovernment hopes to raise more of the necessary external capital in the formof direct equity investment than it has in the past, particularly for theMIP program. Even if this effort is successful, the requirement for grossdisbursements of medium-and long-term loans would increase from $2.1 billionin 1981 to $3.2 billion by 1985. On the basis of known plans of officiallenders, disbursements of official-source loans, which were $830 million in1981, would increase by about $100 million annually. The requirement forgross disbursements from private source MLT loans would then increase from$1.2 billion in 1981 to as much as $2.0 billion annually by 1985. Thewillingness of these private sources to provide the necessary funds wouldlikely be influenced by, among other things, their perception of whether asufficient adjustment effort, to maintain the manageability of thePhilippine balance of payments over the longer term, was being made.

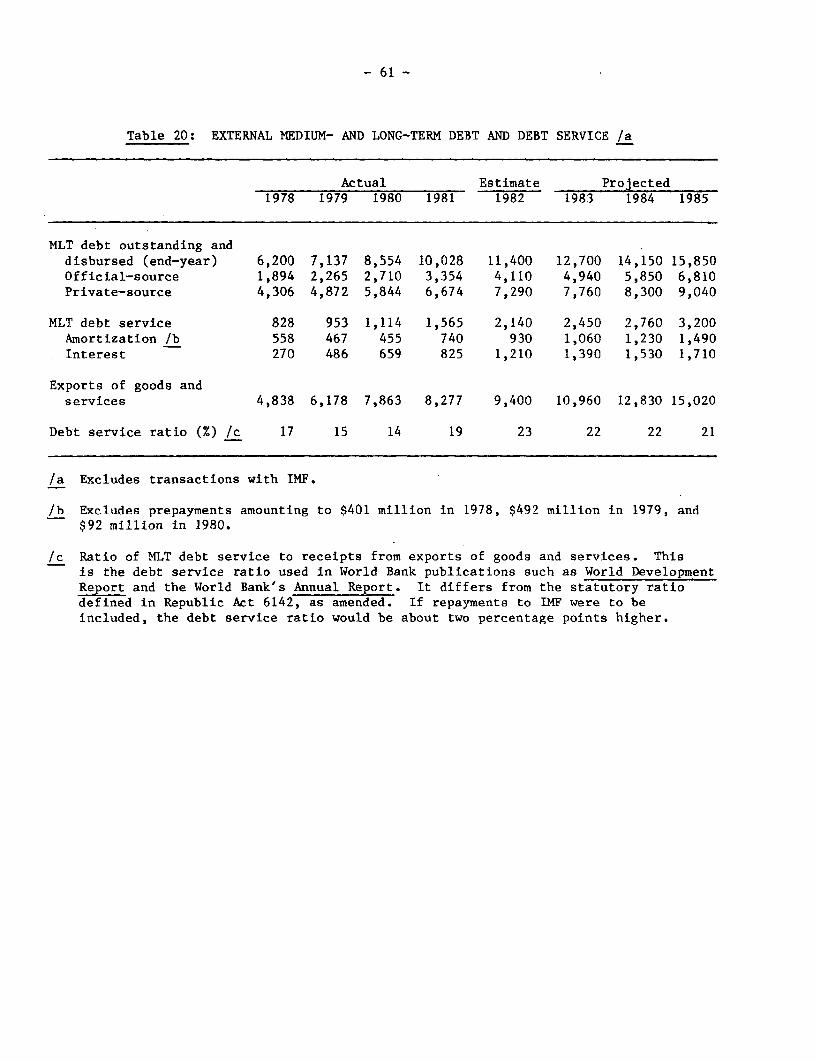

30. Assuming that export volume growth can recover to 8% p.a., and theterms of trade recover as expected, the debt service ratio, which increasedfrom 17% in 1978 to 19% in 1981 and is expected to be 23% in 1982, wouldstabilize at about 22% for the remainder of the Plan period. This would bea heavy but not an insupportable burden. The balance of payments managementissue is the need to avoid a situation in which the requirements for privateexternal capital exceed the willingness of private sources to furtherincrease their exposure in the Philippines. Should such a situationmaterialize, there would be an unplanned reduction in imports and thereby adisruption of the growth process. Such a situation can be avoided throughvigorous pursuit of the Plan strategies of increased domestic resourcemobilization and more efficient resource utilization.

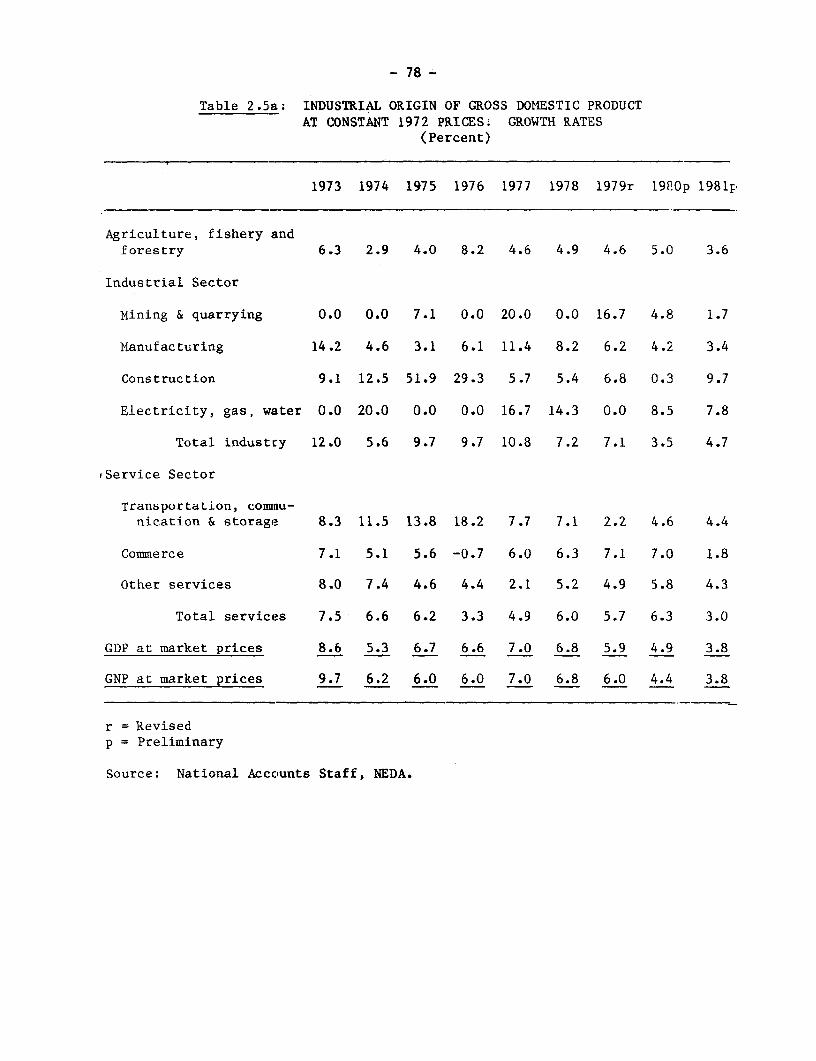

1. RECENT DEVELOPMENTS AND PROSPECTS FOR THE 1983-87 PLAN PERIOD

A. Recent Economic Developments

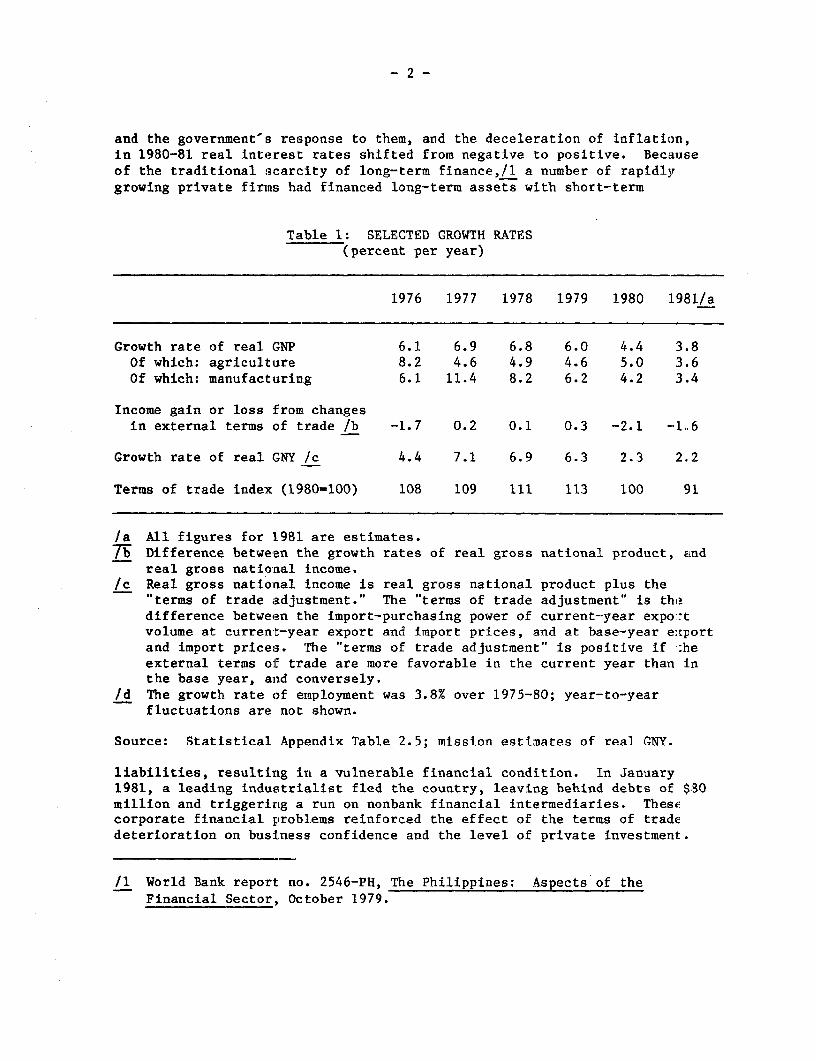

1.01 Recent Philippine economic developments have been dominated by asharp deterioration in the external terms of trade. As indicated in Table 1,the terms of trade, which had reached a depressed level in 1976-77 by long-term historical standards /1 began to recover slowly during 1977-79.However, the recovery turned out to be short-lived. In 1979 the "secondoil crisis" resulted in a major increase in the price of imported petroleum.There were also adverse price developments on the export side, some relatedto long-term trends (the growth of palm oil and soybean oil production ascompetitors to coconut oil), some related to traditionally cyclical behavior(sugar), and some related to recessionary conditions in the manufacturingand construction industries in the OECD countries (copper, lumber). Coconutprices peaked in 1979, and sugar and copper prices peaked in 1980. By 1981,the external terms of trade had fallen by 20% from the level of 1979, and by17% from the previous low in 1976-77.

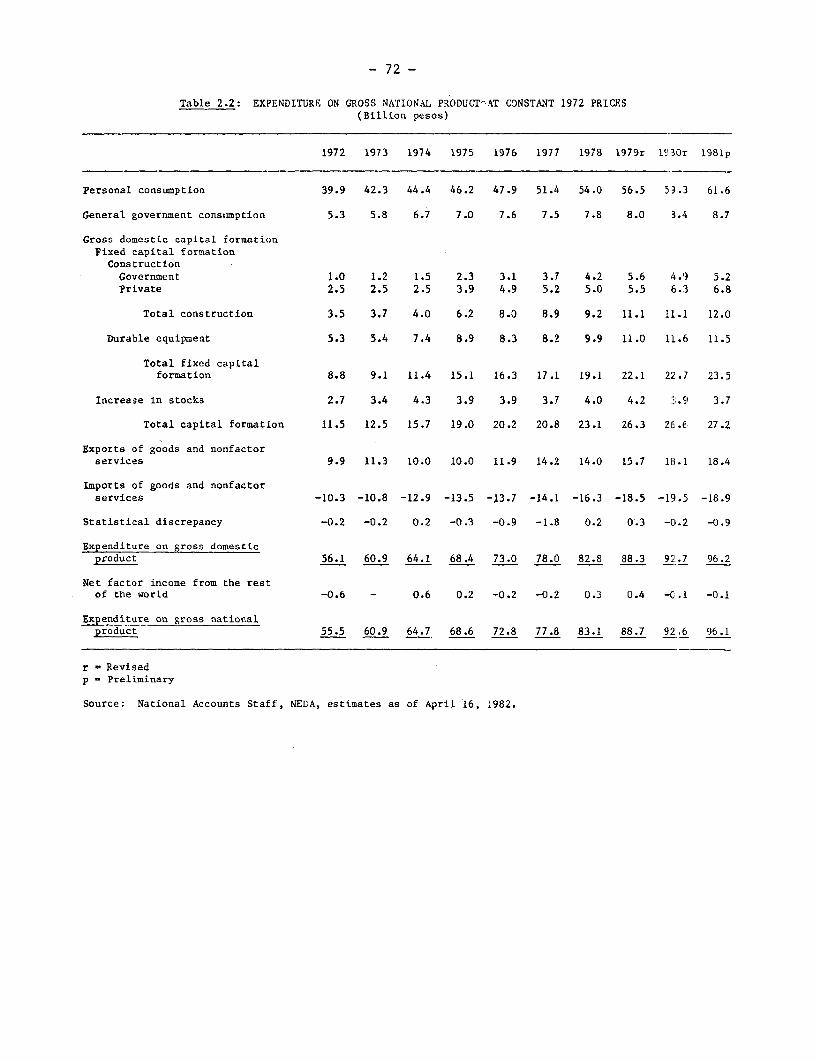

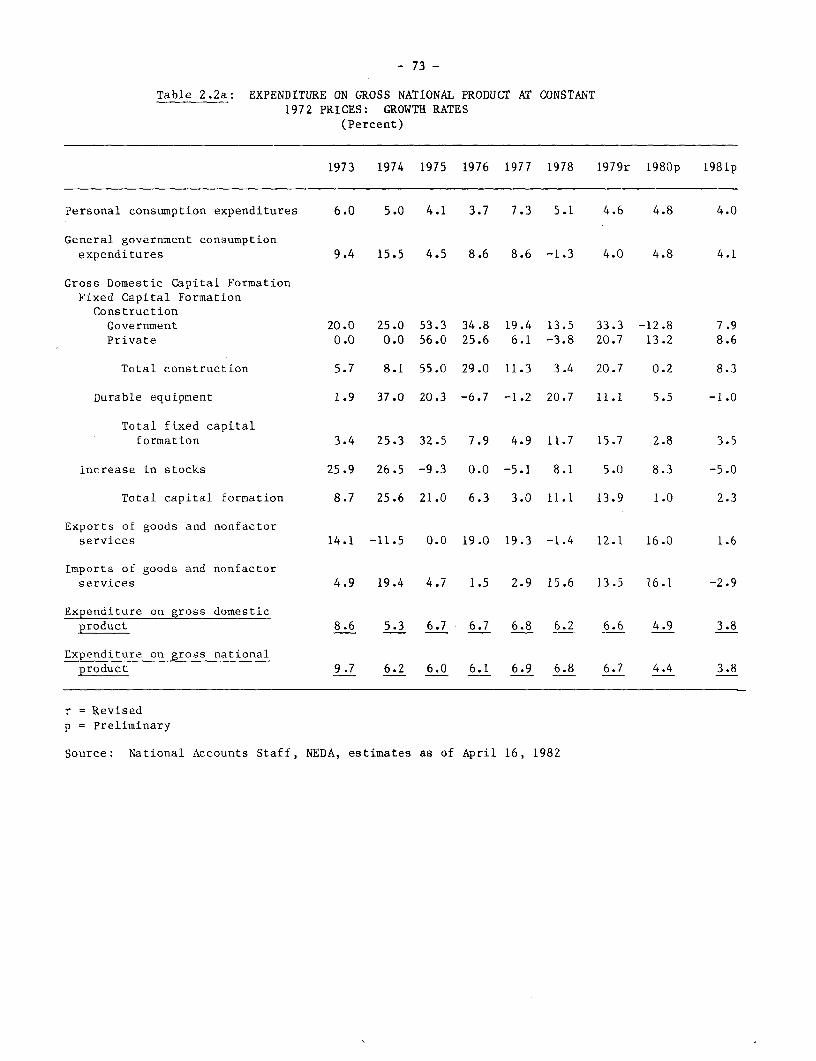

1.02 The deterioration of the terms of trade had a deflationary impacton domestic incomes and, therefore, on production for the domestic market aswell as for the export market. The growth rate of real domestic expenditure(consumption plus investment) decelerated from 6.5% in 1978 to 3.9% in 1980and 3.4% in 1981. The growth rate of real GNP decelerated from 6.8% in 1978to 4.4% in 1980 and 3.8% in 1981. Recessionary conditions have persisted inthe early part of 1982, and it is expected that real GNP growth in 1982 wouldbe about 4%.

1.03 Because of the terms of trade developments, real gross nationalincome (the purchasing power of real GNP) has been growing even more slowlythan real GNP. During 1979-81, real GNP grew by a cumulative 8.9%. However,real gross national income increased by only 4.5% during the same period.Recently population has been growing by about 2.5% annually and the laborforce (reflecting the very high fertility rates of the 1960s) has beengrowing by about 3.5% annually. It would therefore appear that real incomeshave fallen slightly since 1979. The terms of trade are expected tostabilize in 1982, and therefore real incomes should begin to recover.

1.04 The economic slowdown was one of the factors underlying atemporary crisis of confidence in the financial system in early 1981. Withthe increase in nominal interest rates arising from external developments

/1 According to the 1972-based indices published by the Central Bank,the terms of trade had reached a level in 1976-77 that was 32%below the average level prevailing in 1970-72, before the 1973/74commodty boom and the first oil crisis. The 1970-72 level was, inturn, 15% below the average level prevailing in the 1960s.

- 2 -

and the government's response to them, and the deceleration of inflation,in 1980-81 real interest rates shifted from negative to positive. Becauseof the traditional scarcity of long-term finance,/l a number of rapidlygrowing private firms had financed long-term assets with short-term

Table 1: SELECTED GROWTH RATES(percent per year)

1976 1977 1978 1979 1980 1981/a

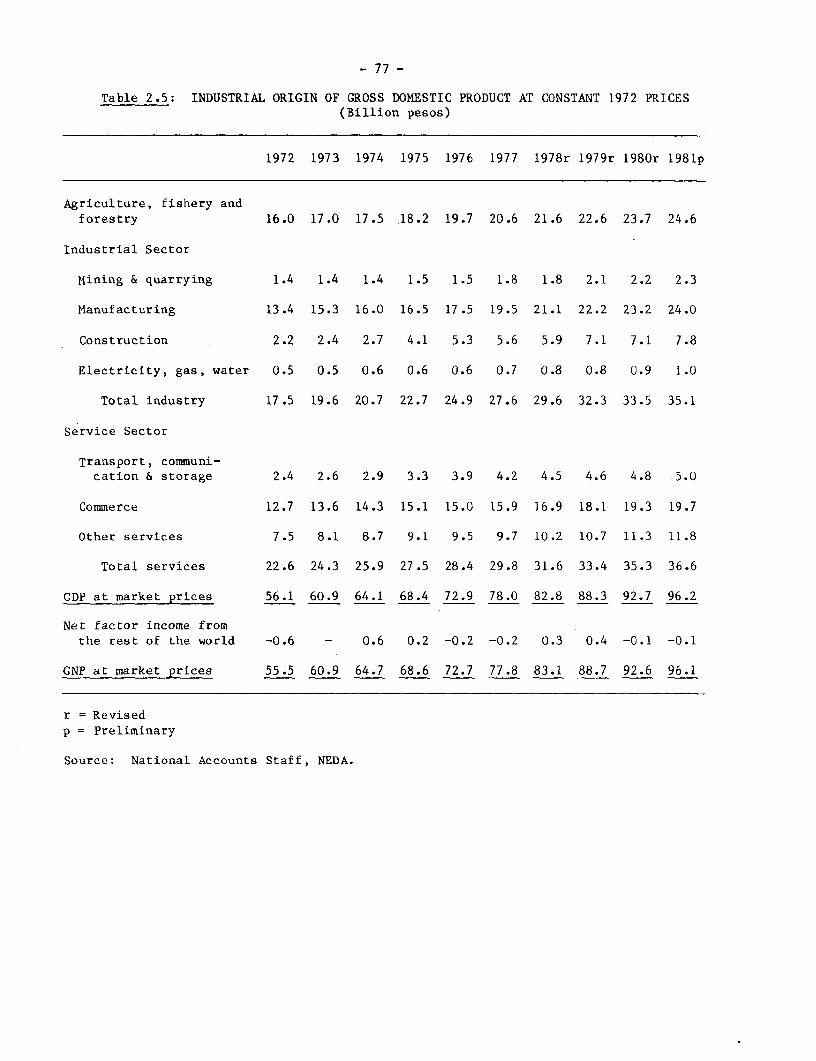

Growth rate of real GNP 6.1 6.9 6.8 6.0 4.4 3.8Of which: agriculture 8.2 4.6 4.9 4.6 5.0 3.6Of which: manufacturing 6.1 11.4 8.2 6.2 4.2 3.4

Income gain or loss from changesin external terms of trade /b -1.7 0.2 0.1 0.3 -2.1 -1.6

Growth rate of real GNY /c 4.4 7.1 6.9 6.3 2.3 2.2

Terms of trade index (1980=100) 108 109 111 113 100 91

/a All figures for 1981 are estimates.7b Difference between the growth rates of real gross national product, and

real gross national income./c Real gross national income is real gross national product plus the

"terms of trade adjustment." The "terms of trade adjustment" is thedifference betweean the import-purchasing power of current-year expo:-tvolume at currenit-year export and import prices, and at base-year e:cportand import prices. The "terms of trade adjustment" is positive if T:heexternal terms of trade are more favorable in the current year than inthe base year, and conversely.

Id The growth rate of employment was 3.8% over 1975-80; year-to-yearfluctuations are not shown.

Source: Statistical Appendix Table 2.5; mission estimates of real GNY.

liabilities, resulting in a vulnerable financial condition. In January1981, a leading industrialist fled the country, leaving behind debts of $30million and triggerirng a run on nonbank financial intermediaries. Thestcorporate financial problems reinforced the effect of the terms of tradedeterioration on business confidence and the level of private investment.

/1 World Bank report no. 2546-PH, The Philippines: Aspects of theFinancial Sector, October 1979.

-3-

1.05 The Government took a number of measures, including expansion ofpublic investment and Central Bank support to the financial institutions torestore and maintain confidence in the financial system, to counter theadverse short-term situation. At the same time, the Government has sustainedits ongoing program of longer-term structural measures and investmentsdesigned to address the fundamental problems underlying the recentdifficulties: considerable dependence of export earnings on a fewcommodities; heavy dependence of the energy sector on imported petroleum;relatively inefficient use of capital in the industrial sector, andexcessive dependence of firms on short-term finance. The Government hasalso prepared a new Development Plan setting out its strategy for addressingthese and other long-term challenges during the 1983-87 period.

B. Strategy and Prospects for the 1983-87 Plan Period

Development Challenges and Development Strategy

1.06 Most of the development challenges facing the Philippines in the1983-87 period are well described in the Plan document. These are:

(a) the need to expand productive employment in order to reduceunemployment and underemployment;

(b) the need to raise agricultural and industrial productivitythrough more effective use of land and capital;

(c) the need to redress rural and regional growth disparities, withparticular emphasis on rainfed agriculture;

(d) the need to reduce dependence on imported energy;

(e) inadequate infrastructure, particularly in the rural areas;

(f) insufficient domestic resource mobilization, leading to a highlevel of dependence on foreign borrowings; and

The need to provide for a larger population is also mentioned, but there isless recognition of the adverse implications of rapid population growth foreconomic and social development than in previous Philippine Plans. Thesevarious challenges, and Government policies and programs to meet them, arediscussed at various points later in this report.

1.07 It may be helpful to place some of the challenges facing thePhilippines in the perspective of inter-country comparisons. As indicated inTable 2, the Philippines has the highest fertility rate and the most rapidlygrowing labor force in East and Southeast Asia. The agricultural populationdensity is greater than in the Philippines' ASEAN neighbors, excluding thecity-state of Singapore, but lower than in the extremely densely populated

- 4 -

countries of Korea and China. The Philippines and Thailand currently have ahigh level of dependence on imported energy, but fortunately both countrieshave reasonably good prospects for reducing this dependence. The level ofnet external indebtedness is quite high; this indicates the need forintensified domestic resource mobilization efforts and restraint in foreignborrowing. On the positive side, the Philippines has a fairly high level ofgeneral education, and the important nonquantifiable asset of a vigorousentrepreneurial class.

Table 2: SELECTED INDICATORS: PHILIPPINES AND SOME OTHER ASIAN COUNI'RIES

Projectedlabor force Agricultural Dependence External Secondlary

Total growth population/ on imported debt/GNP schaolfertility (% p.a.) arable land energy (%)/a (%) enrollmentrate 1980-1990 (persons/ha) 1980 1980 rati (%)

Philippines 4.6 3.5 3.4 88 28 55

Indonesia 4.6 2.7 3.0 - 29/b L9

Thailand 4.3 2.7 2.0 89 20 28

Malaysia 3.8 2.9 0.7 - 22 !S8

Korea 3.3 2.7 5.9 72 29 50

/a Ratio ef net fuel imports (imports minus exports of crude petroleum,petroleu- products, and coal) to total energy consumption. For netexporters ,mport-dependence is indicated as zero.

/b Although inhionesia has a fairly high level of gross external debt, is: hasalso accumnlated very substantial foreign assets since the oil priceincreases of 1979.

Note! Data are for most recent year available unless specifically indicati,d.

Sources: World Development Report 1981; World Bank economic reports bascd onTaetional data.

1.08 The Jlan strategy flows logically from the assessment of thedevelopment challegres. The key elements of the macroeconomic strategy arethe following:

(a) ef.icient exploitation of agricultural potentials for food,agro--ei-iergy, and export crops;

- 5 -

(b) industrial development along the lines of comparative advantage,which would imply primarily labor-intensive industries, togetherwith selected capital-intensive industries based on domestic rawmaterials;

(c) expansion of necessary infrastructure to support the agriculturaland industrial growth;

(d) import-substituting investments and effective demand management inthe energy sector; and

(e) increased domestic resource mobilization, and more efficientresource utilization.

Equity aspects of development would be pursued through emphasis on employ-ment generation; a more balanced pattern of development among the regions;and increased public expenditures in sectors such as education, health,housing, and rural infrastructure. The Plan strategy is broadly appropriateto the Philippines' present situation and underlying development constraints.

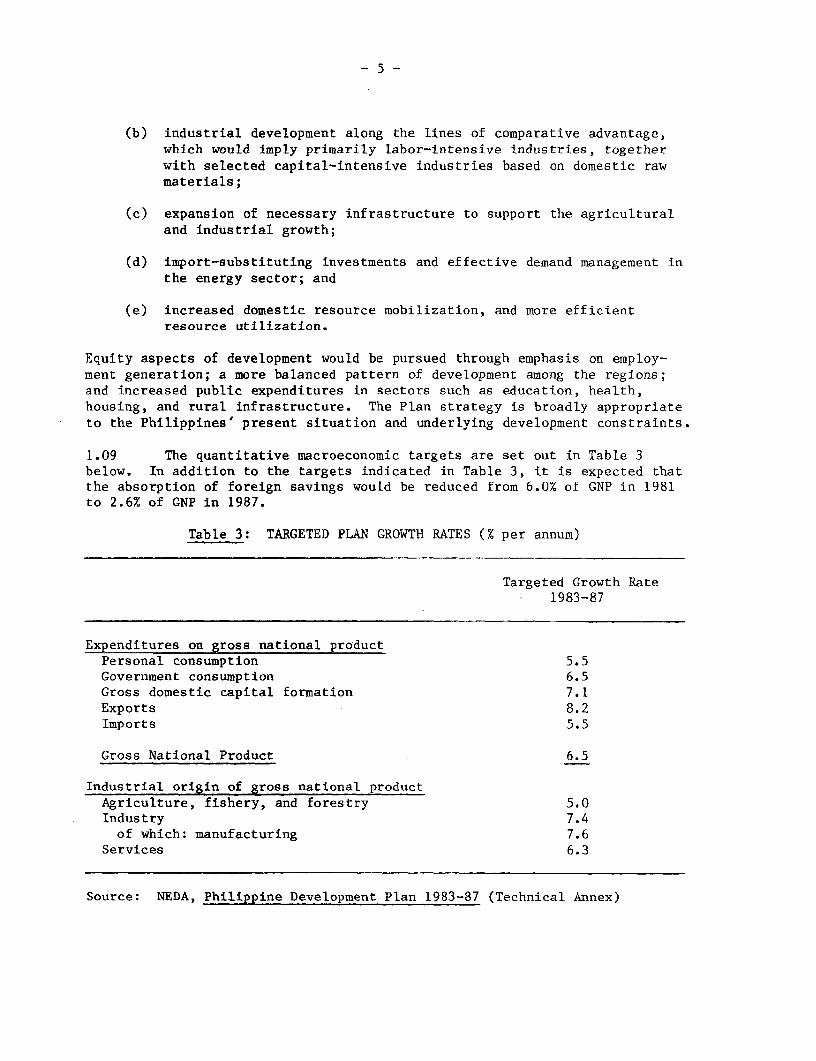

1.09 The quantitative macroeconomic targets are set out in Table 3below. In addition to the targets indicated in Table 3, it is expected thatthe absorption of foreign savings would be reduced from 6.0% of GNP in 1981to 2.6% of GNP in 1987.

Table 3: TARGETED PLAN GROWTH RATES (% per annum)

Targeted Growth Rate1983-87

Expenditures on gross national productPersonal consumption 5.5Government consumption 6.5Gross domestic capital formation 7.1Exports 8.2Imports 5.5

Gross National Product 6.5

Industrial origin of gross national productAgriculture, fishery, and forestry 5.0Industry 7.4of which: manufacturing 7.6

Services 6.3

Source: NEDA, Philippine Development Plan 1983-87 (Technical Annex)

1.10 In reviewing the targetted growth rates, it is difficult to behighly confident of quantitative projections of the Philippine economy, fortwo reasons. First, there are the usual uncertainties concerning theexternal environment. Second, the Government has initiated a structuraladjustment process, with measures in the industrial, financial, and energysectors designed to improve the structure and efficiency of the economy.While these measures can be expected to bring about a substantial improvementin economic efficiency and performance over a medium- to long-term period, thetime-path of such improvement is quite uncertain, particularly consideringthat there will be a complex interaction between the impact of these measuresand other factors such as fluctuations in the external terms of trade.

1.11 With the above caveats, some commentary on the Plan targets wouldbe appropriate. The projected export growth could be achieved by combiningcommodity export growth of 5% p.a. and manufactured export growth of 12% p.a.The volume of oil imports is expected to remain constant or possibly decreaseslightly, and therefore non-oil imports could be permitted to increase byabout 7% annually while containing overall import growth at the projecte.lrate. Thus the trade projections are broadly reasonable. The projectedgrowth of government consumption implies that the ratio of government cu-.rentexpenditures to GNP would remain constant. However, as discussed in Chapter3, there is a need for- an increase in the ratio of government currentexpenditures to GNP. The projected growth of capital formation implies t:hatthe ratio of investment to GNP would be rising. However as discussed inChapter 2, given domestic savings prospects, the necessary reduction inforeign savings probably could be achieved only with a stable or margina.lydecreasing investment ratio. It will be necessary to pursue policies whichwill improve the efficiency of investment and allocate an affordable amolant ofinvestment to the most: productive uses. In the case of private investmentthis would be done, as indicated in the Plan, largely through market-orientedinterest rates and exchange rates. In the case of public investment,difficult choices will, have to be made among competing priorities such asreducing dependence on imported petroleum, deepening the industrial stru(:tlre,and providing non-energy infrastructure in the outlying and relativelydepressed regions where most of the poorer people live.

1.12 The Plan is largely strategic rather than quantitative in nature.In order to enhance its capacity for the quantitative aspects of planning;,the Government intends to strengthen its statistical system, and itscapabilities in such areas as macroeconomic modelling and public sectorfinancial planning. A major purpose of the present report is to illustrateselected Plan period issues through suggestive quantitative analysis. Thleremainder of this chapter discusses strategy for the agricultural andindustrial sectors, which are the key engines of growth, and the populatiLnand employment prospects. Other Plan period issues, such as resourcemobilization, public eKpenditure management, regional development, and balaLnceof payments adjustment are discussed in Chapters 2 through 5.

-7-

Agricultural Strategy

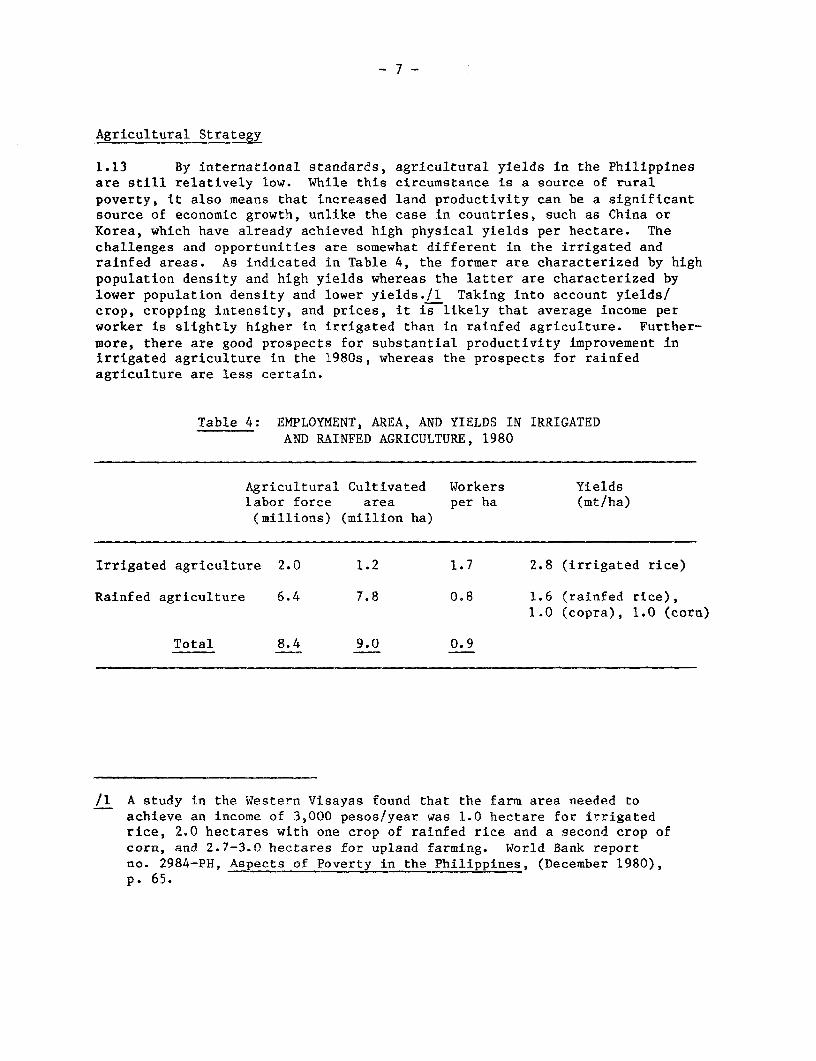

1.13 By international standards, agricultural yields in the Philippinesare still relatively low. While this circumstance is a source of ruralpoverty, it also means that increased land productivity can be a significantsource of economic growth, unlike the case in countries, such as China orKorea, which have already achieved high physical yields per hectare. Thechallenges and opportunities are somewhat different in the irrigated andrainfed areas. As indicated in Table 4, the former are characterized by highpopulation density and high yields whereas the latter are characterized bylower population density and lower yields./l Taking into account yields/crop, cropping intensity, and prices, it is likely that average income perworker is slightly higher in irrigated than in rainfed agriculture. Further-more, there are good prospects for substantial productivity improvement inirrigated agriculture in the 1980s, whereas the prospects for rainfedagriculture are less certain.

Table 4: EMPLOYMENT, AREA, AND YIELDS IN IRRIGATEDAND RAINFED AGRICULTURE, 1980

Agricultural Cultivated Workers Yieldslabor force area per ha (mt/ha)(millions) (million ha)

Irrigated agriculture 2.0 1.2 1.7 2.8 (irrigated rice)

Rainfed agriculture 6.4 7.8 0.8 1.6 (rainfed rice),1.0 (copra), 1.0 (corn)

Total 8.4 9.0 0.9

/1 A study in the Western Visayas found that the farm area needed toachieve an income of 3,000 pesos/year was 1.0 hectare for irrigatedrice, 2.0 hectares with one crop of rainfed rice and a second crop ofcorn, and 2.7-3.0 hectares for upland farming. World Bank reportno. 2984-PH, Aspects of Poverty in the Philippines, (December 1980),p. 65.

- 8 -

1.14 Irrigated Agriculture. At present, almost all of the irrigated landin the Philippines is devoted to rice cultivation and this is likely to remainthe case for the foreseeable future./l Therefore, the strategy for irrigatedagriculture is an aspect of the overall strategy for rice. In the Plan it isprojected that, due t:o ongoing and new irrigated projects, the irrigated areawould increase from an estimated 1.4 million ha in 1982 to 2.0 million ha in1987, contributing tc, a growth rate of rice production of 3.7% annually duringthe Plan period sufficient to meet the growth in domestic demand.

1.15 Alternative projections imply, however, that comparable productionincreases could be achieved with a smaller increase in the irrigated area./2It is estimated that, due to increases in yield per crop and in croppingintensity (crops/year), yields per year on irrigated area could increase by31% during the decade of the 1980s. This, together with an increase inirrigated project service area from 1.2 million ha in 1980 to 1.6 million hain 1985 from completion of ongoing projects only, is expected to result in agrowth rate of rice production of 3.4% annually during the 1980s. With thehigher yield increases and the maximum increase in irrigated area, and inthe absence of either an export program (which would require cultivation ofuniform varieties and greatly improved post-harvest handling) or a foodsubsidy program for poverty target groups, there would be surpluses on thedomestic market beginnaing in the mid-1980s, which would tend to depressprices. It would appear that raising yields, through improved extension andappropriate pricing policy, on areas which are presently irrigated or soonwill be as a consequence of ongoing projects, will be a more cost-effectivemeans of achieving necessary increases in rice production than starts on newirrigation projects.

1.16 Rainfed Agr:iculture. The bulk of the rainfed cultivated area Lnthe Philippines is devoted to rice, corn, and coconut. In contrast toirrigated agriculture which is monocultural, rainfed agriculture isdominated by mixed farming systems, thus, corn may be grown as a second (:ropafter rainfed rice, or may be grown under coconut; and livestock raisingoften accompanies cultivation of crops. The rainfed areas of thePhilippines are characterized by an enormous diversity of climatic con-ditions, slope, soil types and locational and ethnic influences. Whilethere are no clear gecgraphic lines between different rainfed areas, it isuseful to consider separately the gradually sloping lowlands, and the moresteeply sloping uplands.

/1 Sugarcane and corn are also crops which, under certain circumstances,can be grown on irrigated land. However, most of the soils underirrigation are not well suited for sugarcane or corn; irrigated corncultivation, where agronomically feasible, would be less profitable tAanirrigated rice cultivation; and sugarcane is grown principally on largeestates which, from the social point of view, are a lower priority fo:-productivity improvement than small farms.

/2 World Bank report no. 3545-PH, Irrigation Program Review.

1.17 The rainfed lowlands have relatively more economic potential. Thestrategy for these areas should consist of the promotion of mixed farmingsystems comprising a range of crops and livestock suited to particular soilsand rainfall patterns. The gains in the area and yield of irrigated rice areexpected to reduce the relative profitability of rainfed rice cultivation.The Government therefore intends to make a major effort in corn during thePlan period, including dissemination of high-yielding disease-resistantvarieties, and promotion of switching of some land from rainfed rice to corn.In the Plan, it is projected that corn production will increase by 11%annually, primarily from yield increases, a high ambitious target in relationto past growth of 5%, mostly from area increases. In some lowland areas thereare also potentials for commercial crops such as rubber, coffee, cotton, andcacao.

1.18 The more steeply sloping uplands present a more difficult develop-ment problem. In many areas, "slash and burn" agriculture (clearing the land,followed by planting of corn for a few crops until the soil becomes tooeroded) is a serious problem. The need is to combat soil erosion while simul-taneously providing a livelihood for the people living in these areas. Thiscan be accomplished by switching land away from corn toward agro-forestry(production of leafmeal, fruits and nuts, firewood, and pulpwood) and fodder-crop/livestock systems. However, such switching from annual subsistence cropsto longer-term cash crops requires credit, a substantial extension effort,land titling, and a reasonably good rural road network. All of these effortswill be difficult in these areas, which are generally more remote and lesswell-served with infrastructure and services than the lowlands.

1.19 Agricultural Prices and Terms of Trade. Farmers' incentives andincomes are strongly affected by taxes, subsidies, the exchange rate, pricecontrols, and other pricing measures on both inputs and outputs. During the1950s and 1960s, government policy discriminated against the agriculturalsector through an overvalued exchange rate, heavy protection for the domesticindustrial sector, and price controls. In the 1970s, pricing policies foragriculture were more efficient and more equitable and the farmers' terms oftrade improved. During the past couple of years, however, the farmers' termsof trade have deteriorated./1 This is probably due primarily to externalfactors such as the second oil crisis and the fall in coconut prices, butincreased agricultural productivity may also have played a role. Notwith-standing the improved policy environment for agriculture established in the1970s, a study at the Unversity of the Philippines at Los Banos has found that"As a consequence of (the net impact of) pricing policy, agricultural produc-tion is less than what it should be ...... The fact that agriculture survivesand indeed grows suggests an inherent comparative advantage to competeeffectively in the export or home market, an advantage that would be moreeffective in the absence of these policy biases."/2

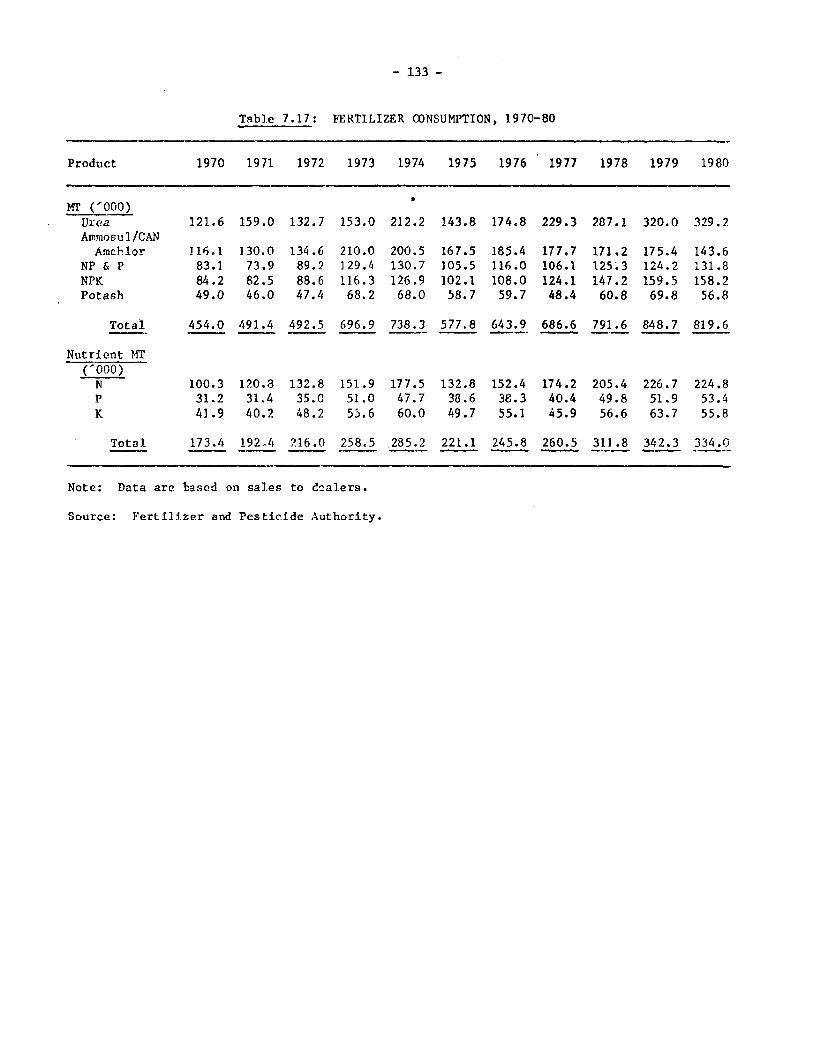

/1 Statistical Appendix Table 7.17.

/2 Christina C. David, "An Analysis of Agricultural Policies in t1lePhilippines " (1982), p. 18.

- 10 -

1.20 During the Plan period, there should be considerable increases inagricultural productivity arising from expanded irrigation, improved extensionservices, and other factors. It would be appropriate for Government policy toaim at a sharing between farmers and consumers of the benefits of improvedagricultural productivity. On the one hand, food accounts for two-thirds ofthe expenditures of low-income families, and if food prices can rise moreslowly than wages, this can be a significant element in poverty alleviation.On the other hand, raising the incomes of the farmer has been a major objec-tive of the agricultural programs, and it would be inequitable to the farmerif the impact of increased production on farm incomes were to be entirely off-set by falling prices. If the terms of trade are artificially turned againstthe agricultural sector, "premature" rural-to-urban migration (in relation toproductive job opportunities in urban areas) can result.

Industrial Strategy

1.21 Just as the agricultural strategy is centered around the moreproductive use of land, the industrial strategy is centered around the moreproductive utilization of capital. The principal elements of the Government'sindustrial strategy are:

(a) reform of overall industrial promotion policies to encourage amore efficient and competitive industrial sector, with morerapid growth of exports and employment;

(b) restructuring programs for specific subsectors;

(c) a program of eleven major industrial projects;

(d) promotion of small and medium-scale industries; and

(e) regional dispersal of industry./l

1.22 The first phase of the industrial policy reform has consisted oftrade liberalization (tariff reform and removal of quantitative importcontrols) and strengthening of export incentives. The tariff reform is i:aking^effect over a four-year period from 1981 to 1985. The maximum (nominal)tariff is being reduced to 50%; the effective rate of protection for themanufacturing sector as a whole will be reduced from 44% to 29%; and theeffective rate of protection for consumer goods manufacturing will be recucedfrom 77% to 41%. Quantitative import controls are also being removed instages over the same four-year period. Export incentives have beenstrengthened to place exporters on a free-trade basis to the maximumpracticable extent.

/1 Regional dispersal of industry is discussed in Chapter 4, RegionalAspects of Development.

- 11 -

1.23 A second phase of industrial policy reform, now under preparation,is centered around reform of fiscal incentives for investment. Under theproposed reform, the existing incentives system, which has had a capital-cheapening effect, would be replaced. The new system would compensate formarket imperfections, and would be directly related to the Government'semployment, export, and regional dispersal objectives. Economic analysiswould be more consistently employed in the selection of activities and .projects to be promoted, and the administration of the incentives would begreatly simplified to facilitate their accessibility.

1.24 Sectoral restructuring programs are designed to help specificselected industries increase competitiveness in order to adjust to the policychanges. Sector development programs are also being initiated for neglectedindustries with potential comparative advantages. Assistance includes,inter alia, the provision of fiscal incentives, financial and technicalsupport, manpower training and development, and institutional improvement.A restructuring program for the cement industry was started in 1980, and asimilar program for the textile industry will be initiated shortly. Sectordevelopment programs for the food-processing, electronics and mechanicalengineering industries are currently being formulated.

1.25 The eleven major industrial projects (MIPs) are intended to deepenthe industrial structure of the economy, through the development of selectedcapital goods and intermediate goods industries which would generate exportearnings or import savings. Two of the projects are for the production ofcapital goods, while the other nine are for the production of intermediategoods. Some of the intermediate goods projects are based on domestic rawmaterials (e.g., copper smelter, coconut-based chemicals) while others wouldbe based on imported raw materials. Intermediate goods industries aregenerally more capital-intensive and energy-intensive than either capitalgoods or consumer goods industries. Since the Philippines has a surplus oflabor and is a heavy energy importer, the comparative advantage of thePhilippines in intermediate goods projects based on imported raw materialsis not obvious, and would need to be investigated particularly carefully.The Government has displayed a flexible and pragmatic attitude towardimplementation of the MIP program, and is scrutinizing all of the projectscarefully to ensure their economic and financial viability. The need is notmerely to determine that they are export-earning or import-saving, but toensure that they are more cost-effective means of strengthening the balanceof payments than alternative investments in the economy.

1.26 Due to changes in some of the project concepts, the cost of theMIP program has been reduced from an original $6 billion to $4 billion, orabout 10% of 1981 GNP. The Government's financing strategy is to seekforeign equity investment and long-term suppliers' credits in order tominimize demands on domestic resources.

- 12 -

1.27 The importance of small- and medium-scale industries lies in theirlabor-intensity; the average capital/labor ratio in SMI is only half of thatin large-scale enterprises. During the Plan period the Government wilLexpand its program of industrial extension for SMI, which includes technicalassistance for project feasibility studies; promotion of subcontracting andother marketing assistance; and study of SMI problems and identification andtesting of solutions on an industry basis. Preferential credit programs forSMI, such as the Industrial Guarantee and Loan Fund, will be continued.

Population, Employment and Income Distribution in the Plan Period

1.28 As noted in para. 1.06, two of the major challenges facing thePhilippines are population growth arising from a high level of fertility, anda rapidly growing labor force. According to the recently published Republicof the Philippines Fertility Survey, the total fertility rate /1 fell from 5.9in 1970 to 5.0 in 1977, representing a relatively modest decline of 15% overthe seven-year period. As indicated in Table 2 this is still quite high byEast Asian standards. Most of this decline was attributable to a rise in theage of marriage; the marital fertility rate fell by only 6% during the sameperiod. The survey also found that, among married women who wished to have nomore children, only 29% were using "efficient" methods of contraception, while31% were using "inefficient" methods and 40% were not using any method at all.

1.29 In the Plan fcor 1983-87, it is projected that the crude birthrate /2 will decline by 16% from 1980 to 1987, leading to a decline in thepopulation growth rate from 2.5% in 1980 to 2.2% in 1987. However, incontrast to previous Philippine Plans, the population projection is treat:ed asa neutral projection rather than as a target. Given that the rise in the ageof marriage experienced in the 1970s will probably decelerate, the fertilityreduction implicit in the population projection could be achieved only Withmore effective family planning effort than indicated by the results of recentsurveys. Under the medium projection of the National Census and StatisticsOffice, which assumes a substantial fertility reduction, the Philippinepopulation would still increase to 70 million persons in the year 2000, ascompared with 48 million persons in 1980./3

/1 The total fertility rate is the sum of age-specific fertility rates forspecific age groups in the 15-49 years age bracket. It is therefore thenumber of children that would be born to a statistically average womnan,if she were to survive throughout the reproductive years.

/2 Unlike the total fertility rate, the crude birth rate (number of bii:thsper thousand popualation) is an indicator which is affected by theage structure of the population.

/3 Statistical Appendix Table 1.1.

- 13 -

1.30 Although the total population is presently growing by 2.5% annually,the working-age population is growing by 3.1% annually because of the veryhigh fertility rates prevailing in the 1960s before the introduction of thefamily planning program. Additionally, it is expected that there will be aslight increase in the labor force partcipation rate among women. The laborforce is therefore projected by the Plan to increase by 3.7% annually. Thisis one of the highest rates in the world; the average projected labor forcegrowth for all middle-income oil-importing developing countries is 2.3%./lBetween 1980 and 1987, the economy will have to find jobs for 5 million per-sons, or 700,000 persons annually, if an increase in unemployment is to beprevented. The industrial policy reforms are expected to promote more rapidgrowth of employment in the organized manufacturing sector. However, theorganized manufacturing sector presently accounts for only a small share oftotal employment, and the labor force will grow so rapidly that most of theincrement will have to be absorbed in the already overcrowded agricultural andservices sectors (Table 5).

1.31 The empirically observed real wages of urban workers declinedsubstantially during the 1970s. Legislated minimum wages, on the other hand,more than kept pace with inflation, but it is believed that these are notwidely observed./2 Wage statistics do not give a complete picture ofdistributional trends in the economy, since many persons are self-employed inthe agricultural sector. However, if there had been adequate income-earningopportunities in the rural areas, the observed drop in urban real wages wouldhave been prevented or at least reduced by flows between the urban and rurallabor markets (assuming well-functioning labor markets, as are believed to befound in the Philippines). Thus, there are grounds for concern over distri-butional aspects of development.

1.32 The Plan strategy for addressing distributional considerations,through emphasis on employment generation, regional development, land reformand land settlement, progressive taxation, and public expenditures on ruralinfrastructure and the social sectors, is broadly appropriate. However, theneed for fertility reduction as an element of long-term distributionalstrategy is not recognized. The implications for public sector resourcemobilization and utilization of the proposed public expenditure strategy arealso not spelled out. In order to provide a better empirical basis for thedistributional strategy, it would be desirable for the Government to updateand improve the statistics on distributional aspects of development.

/1 World Development Report 1981, p. 170.

/2 Statistical Appendix Tables 11.4 and 11.5.

- 14 -

Table 5: LABOR FORCE AND EMPLOYMENT

Actual Projected1975 1976 1977 1978 1979 1980 1983 1985 11987

Millions of personsAgriculture, fishery, forestry 7.1 7.6 7.3 8.1 8.1 9.1

Irrigated rice 2.0Rainfed agriculture /i 6.4Fishery 0.7

Manufacturing 1.5 1.6 1.6 1.8 2.6Factory /b 0.6 0.6 1.4

Nontraditional exports /c 0.1 0.5Domestic market-oriented 0.5 0.9

Unorganized (cottage) /d 1.0 1.0 1.2

Other industry /e 0.5 0.6 0.7 0.6

Services 4.3 4.7 4.9 5.3

Total Employment 13.4 14.5 14.5 15.8 16.8 17.2 19.3 20.8 22.3

Unemployed 0.6 0.8 0.8 0.8 0.7 0.8

Total Labor Force 14.0 15.2 15.3 16.6 17.5 18.1

Percent distributionAgriculture, fishery, forestry 53 53 50 52 50 53Manufacturing 11 11 11 11Other industry 4 4 4 4Services 32 32 35 33

Total employment 100 100 100 100 100 100

Unemployment rate /f 5 5 5 5 5 5

/a Including forestry./b Enterprises with five or more workers.Ic With the exception of handicrafts which are produced by the cottage sector, vi.rtually

all nontraditional maLnufactured exports are produced by the factory sector.td Enterprises with fewer than five workers.7e Mining; electricity, gas and water; and construction.If As a percentage of total labor force.

Note: Historical figures are from NCSO. Figures for manufacturing employment i.Q 1985 ateprojections from World Bank Report No. 2513-PH, Industrial Development Strategy andPolicies in the Philippines (October 1979). Figures for total employment in 1983and 1987 are from draft Plan.

- 15 -

2. RESOURCE MANAGEMENT

2.01 As the Philippine population grows toward 70 million persons in theyear 2000, the ratio of population to natural resources will becomeincreasingly unfavorable. However, global experience indicates that economicdevelopment reflects not so much the endowment of natural resources, butrather the effectiveness with which all resources are utilized, includingman-made resources (capital) and human resources as well as natural resources.In the wake of the "second oil crisis," the dependence of the Philippineeconomy on foreign resources is at a greater level than is indefinitelysustainable. The Plan's emphasis on increased domestic resource mobilizationand more effective resource utilization is therefore particularly welcome.This can be achieved through conservation of natural factors of productionsuch as soil; appropriate pricing of the relatively scarcer manmade factors(capital, energy, and foreign exchange) in order to promote fuller employmentof the more abundant factor of production (labor); and better planning.

A. Overview of Savings and Investment

Level and Sources of Savings

2.02 It was originally projected in the Development Plan for 1978-82 thatthe Philippines' savings performance would improve by 3% of GNP during thePlan period. Most of the increase was to be devoted to reducing dependence onforeign savings, which had reached a level higher than indefinitelysustainable after the "first oil crisis"; in particular, dependence on foreignsavings was to be reduced from 5% of GNP in 1978 to 3% of GNP in 1982. Thealready high investment ratio was also projected to increase slightly.However, as indicated in Table 6, the savings performance has actuallyfluctuated around 22.5% of GNP, about the average for middle-incomeoil-importing developing countries. While this is satisfactory performance bycomparative standards, the investment ratio remained sufficiently high thatthe absorption of foreign savings, instead of being reduced as planned,increased to 6% of GNP by 1981. The continued heavy absorption of foreignsavings is a reflection, of course, not only of the inability of the economyto increase domestic resource mobilization, but also of the deterioration inthe external terms of trade and recessionary conditions, which have made itmore difficult to reduce the trade gap.

2.03 In order to avoid an excessive increase in external debt service,it will pe necessary for the dependence on foreign savings to be reducedfairly rapidly during the 1983-87 Plan period - perhaps to about 3.5% of GNPby 1985. Given the historical stability of the savings ratio, and the recentslow growth of incomes, it would be unrealistic to expect a rapid increase inthe savings ratio. The reduction in the absorption of foreign savings wouldtherefore have to be achieved, as notionally indicated in Table 6, by somecombination of an increased level of national savings and a marginally lowerlevel of investment.

- 16 -

rable 6: INVESTMENT AND SAVINGS RATIOS(Percentage of GNP)

Middle-income PhilippinesOIDCs /a Actual Estimate Pro`jected

1979 1978 1979 1980 1981 1982 1985

Gross Domestic Investment 25 27.0 27.9 28.7 28.6 28.0 27.5

Fixed investment n.a. 23.9 24.7 25.7 26.0 25.0 24.5Public /b n.a. 5.5 6.5 7.8 8.2 7.6 7.0Private n.a. 18.4 18.2 17.9 17.8 17.4 17.5

Increase in stocks /c n.a. 3.1 3.2 3.0 2.6 3.0 3.0

Foreign Savings /d 3 4.9 5.3 5.9 6.0 5.4 3.5

Gross National Savings 22 22.1 22.5 22.8 22.6 22.6 24.0Public n.a. 3.7 5.0 5.1 4.4 4.1 5.0Private n.a. 18.3 17.5 17.9 18.2 18.5 [9.0

/a Middle-income oil-importing developing countries./b This is a broader definition than used in previous economic reports, as it

includes capital expenditures of non-infrastructure corporations anc .ocalgovernments, as well as the infrastructure program and non-infrastructurecapital outlays of the national government.

/c Historical figureS have been adjusted. International comparisons imp].ythat "increase in stocks" in the published Philippine national accounts areprobably overestimated.

/d Current account deficit in the balance of payments.

Sources: World Development Report 1981. Statistical Appendix Tables 2.11 and5.10; mission projections.

2.04 The private! sector has recently been saving about 17.5-18% of GNP,and the public sector has been saving about 4.5% of GNP. Although the !evelof public savings is not very low, this has been achieved by combining ,relatively low level of public sector resource mobilization with an inanequatelevel of government current expenditures. Increases in the savingsperformance of both the private and public sectors will be necessary du7iagthe Plan period. The Government has recently taken substantial steps,particularly interest rate deregulation, to promote private savings. Asdiscussed later in this chapter, public sector resource mobilization is anarea in which substantial additional effort will be needed during the Planperiod.

- 17 -

Level, Efficiency, and Planning of Investment

2.05 Recently, fixed investment in the Philippines has been about 25% ofGNP, with public investment at about 7% of GNP and private investment, about18% of GNP. These are broadly appropriate levels. In 1981, however, therewas a low level of private investment because of recessionary conditions, andthe Government therefore temporarily elevated the level of public investment.

2.06 As indicated in Table 6, the Philippines has an investment ratiothat is somewhat higher than other countries in its group. This should pro-vide the basis for a strong growth performance. However, statisticalindicators such as incremental capital/output ratios and loan recovery ratiosindicate that, in the past, not all resources have been invested efficiently.A detailed empirical investigation of this issue would require data on fixedinvestment by sector, and calculation of sectoral ICORs; unfortunately, thenecessary data are not available. The relative inefficiency of investment inthe manufacturing sector has been attributed to excessive protection, thefiscal incentives for investment and the credit allocation system./l Asdiscussed in Chapter 1, the Government has recently taken decisive steps toimprove efficiency in this sector. The efficiency of public investment couldbe strengthened by focussing resources on projects of the highest priority;devoting relatively more resources to completion of ongoing projects ascompared with starts on new projects; and consistent use of competitivebidding procedures and cost-effective design standards.

2.07 Because fixed investment determines the future capital stock, andthereby the production structure, of the economy, influencing the pattern ofboth private and public investment in desired directions is one of the mostimportant tasks of economic planning. However, at the present time thePhilippine statistical system does not generate data on fixed investment bysector or by region. Inadequate knowledge of the past pattern of investmentmakes it more difficult to formulate policies, programs, and projects toinfluence the future pattern of investment in desired directions. Addition-ally, in the case of the public sector, planning-programming-budgetinglinkages are relatively weak. It will be necessary for the Government toinfluence the level and pattern of investment in such a way as to promote amaximum contribution toward its development objectives, while simultaneouslyreducing reliance on foreign savings. In order to enhance its capacity forthis task, the Government intends to upgrade its statistical and planningsystem during the Plan period.

/1 Philippine Institute for Development Studies, Industrial PromotionPolicies in the Philippines (1979).

- 18 -

B. Mobilization and Allocation of Resources for Private Investment:The Role of the Financial Sector

2.08 The Government influences the mobilization and allocation ofresources for private investment in numerous ways: trade policy(para. 1.23); exchange rate policy (para. 5.23) fiscal incentives forinvestment (para 1.24) and other aspects of tax policy; price controls 3indsubsidies; the distribution of public investment among sectors and regiorLs(Chapters 3 and 4); and regulation of, and direct public sector involvementin, the financial sector. As referenced above, many of these influences arediscussed elsewhere in the report. Most private savings and privateinvestments are finanacially intermediated, and the present section discussesthe important role of the financial sector in the mobilization andallocation of resources for the private sectors. In particular, itdiscusses overall financial sector reform; preferential credit allocation bysector; and the role of Government financial institutions and creditprograms.

Overall Financial Sector Reform

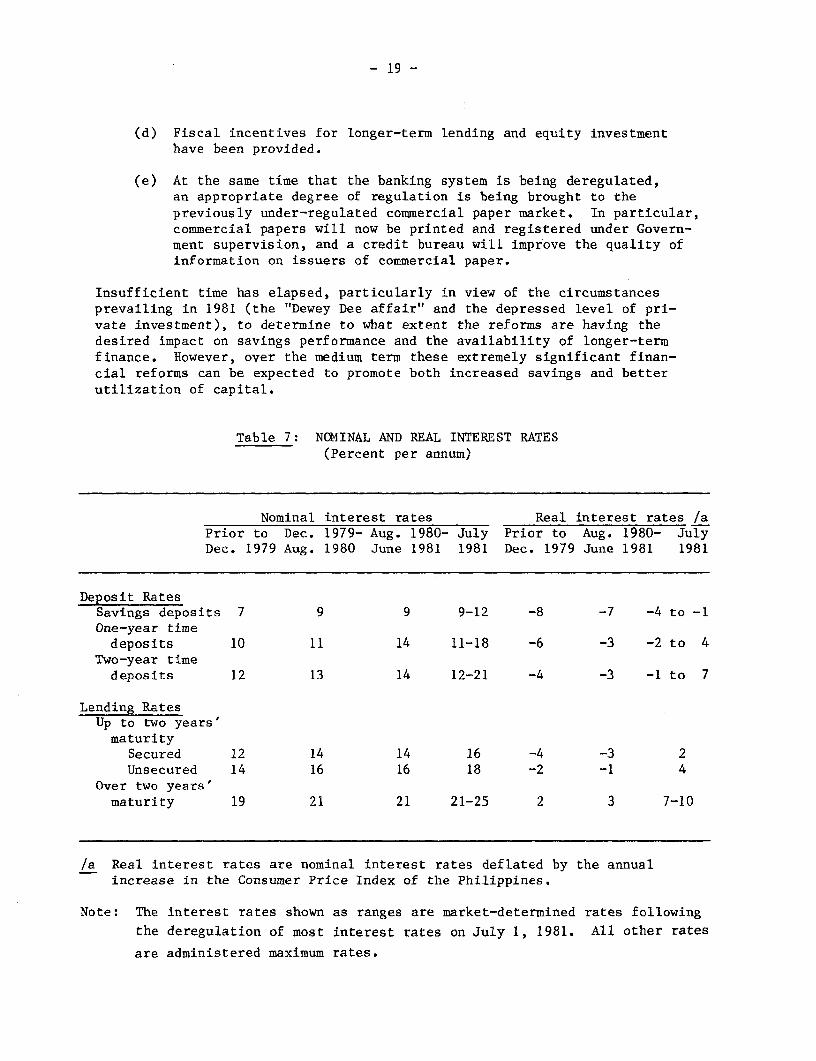

2.09 The objectives of the Government's financial sector policy are topromote savings; to :Lncrease the share of financial savings in total savings;and to increase the availability of financial savings on a longer-term basis(long-term loans or equity). In keeping with these objectives, the Govern-ment implemented a comprehensive set of regulatory reforms and relatedmonetary and fiscal measures in 1980-81:

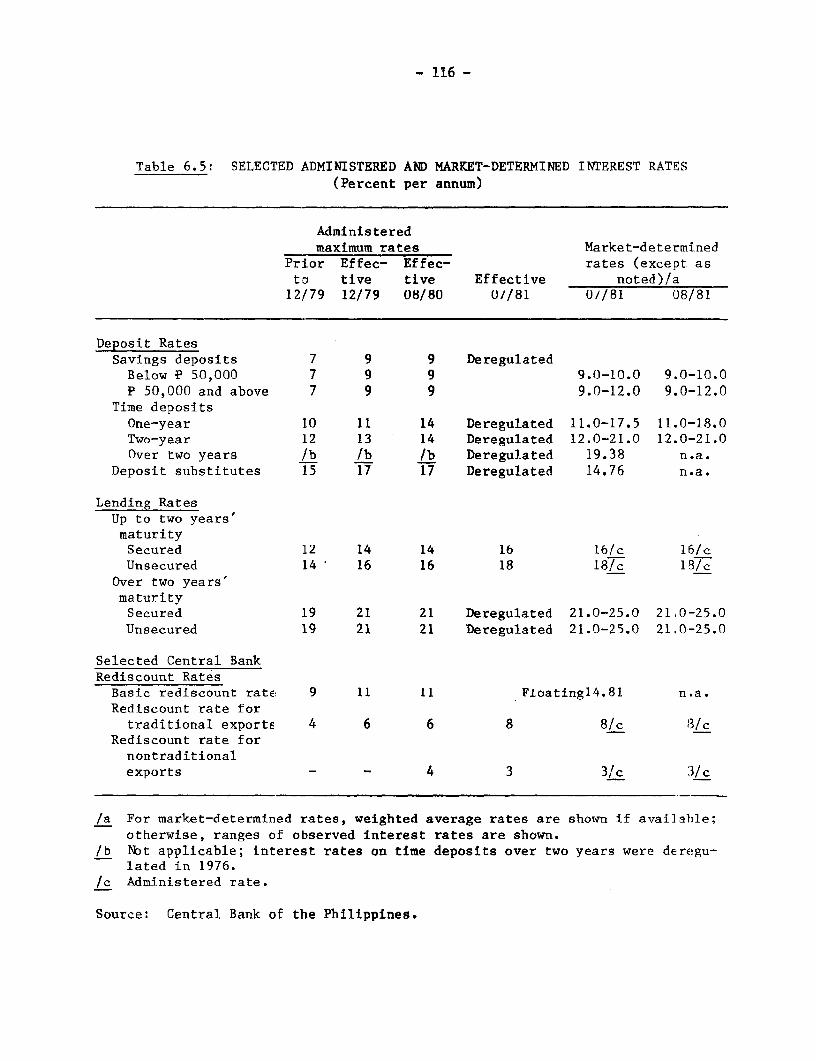

(a) Administered maximum interest rates, effectively the prevailingrates, were raised in December 1979 and again in August 1980(Table 7). Finally, in July 1981, all interest rates exceptfor lending rates of up to one year maturity were deregulatedBecause of inflation generated by the "second oil crisis", re..linterest rates were substantially negative in 1979. With thesequence of upward adjustments in administered rates followed byderegulation, positive real interest rates have now been obtalned.In order to encourage term transformation, banks are also per-mitted to nmake longer-term loans at variable interest rates(a defined margin above a variable Manila Reference Rate).

(b) Legislated specialization of financial institutions has been nub-stantially reduced. In particular, qualifying commercial ban;.s("expanded banks") may now engage in equity investment; thrift-:banks have been granted full domestic banking powers; rural banksmay engage in branch banking; and the Monetary Board has beengiven authority to move institutions into "higher", lessrestricted categories on the basis of financial resources, prc-fessional capability, and demonstrated performance.

(c) A lender-of-last-resort facility has been established by theCentral Bank.

- 19 -

(d) Fiscal incentives for longer-term lending and equity investmenthave been provided.

(e) At the same time that the banking system is being deregulated,an appropriate degree of regulation is being brought to thepreviously under-regulated commercial paper market. In particular,commercial papers will now be printed and registered under Govern-ment supervision, and a credit bureau will improve the quality ofinformation on issuers of commercial paper.

Insufficient time has elapsed, particularly in view of the circumstancesprevailing in 1981 (the "Dewey Dee affair" and the depressed level of pri-vate investment), to determine to what extent the reforms are having thedesired impact on savings performance and the availability of longer-termfinance. However, over the medium term these extremely significant finan-cial reforms can be expected to promote both increased savings and betterutilization of capital.

Table 7: NCMINAL AND REAL INTEREST RATES(Percent per annum)

Nominal interest rates Real interest rates /aPrior to Dec. 1979- Aug. 1980- July Prior to Aug. 1980- JulyDec. 1979 Aug. 1980 June 1981 1981 Dec. 1979 June 1981 1981

Deposit RatesSavings deposits 7 9 9 9-12 -8 -7 -4 to -1One-year timedeposits 10 11 14 11-18 -6 -3 -2 to 4

Two-year timedeposits 12 13 14 12-21 -4 -3 -1 to 7

Lending RatesUp to two years'maturity

Secured 12 14 14 16 -4 -3 2Unsecured 14 16 16 18 -2 -1 4

Over two years'maturity 19 21 21 21-25 2 3 7-10

/a Real interest rates are nominal interest rates deflated by the annualincrease in the Consumer Price Index of the Philippines.

Note: The interest rates shown as ranges are market-determined rates following

the deregulation of most interest rates on July 1, 1981. All other rates

are administered maximum rates.

- 20 -

Preferential Credit Policies