Perceived Organizational Support, Discretionary Treatment, and Job Satisfaction

Upload

independentCategory

view

2download

0

ABSTRACT. This study examines the relationshipsbetween a company’s emphasis on discretionary socialresponsibility, environment, and firm performance. Ittests the proposition that environmental munificenceand dynamism moderate the relationship betweendiscretionary social responsibility and financial per-formance. Social responsibility was measured with athree-item scale in a sample of 62 firms usinga questionnaire. Environmental munificence anddynamism were measured using archival sources as wasfinancial performance (return on assets and return onsales). The results of moderated regression analyses

and subgroup analyses found a significant moderatingeffect of environment on the social responsibility-firm performance relationship. Discretionary socialresponsibility contributes to firm performance inenvironments that are dynamic and munificent.

KEY WORDS: environment, firm performance,social responsibility

The issue of whether corporations have anobligation to society to behave in a sociallyresponsible way has been the subject of contin-uing controversy. In the academic literature therehave been many empirical studies that haveexamined the relationship between a firm’s socialperformance and its economic performance. Theresults of earlier studies were somewhat mixed.Some studies found a negative relationship (e.g.,Shane and Spicer, 1983), some found a positiverelationship (e.g., McGuire et al., 1988), andothers reported no relationship (e.g., Ullman,1985).

More recent advances in the understandingand measurement of corporate social responsi-bility, however, suggest a more positive relation-ship between corporate social responsibility andfirm performance (see Aupperle, 1991; Woodand Jones, 1995). Based on recent meta-analyses,researchers concluded that there is a positive orneutral relationship between corporate socialresponsibility and firm performance (e.g., Griffinand Mahon, 1997; Margolis and Walsh, 2001;Pava and Krausz, 1996; Wood and Jones, 1995).

The Moderating Effect of Environmental Munificence and Dynamism on the RelationshipBetween Discretionary Social

Irene GollResponsibility and Firm Performance Abdul A. Rasheed

Journal of Business Ethics

49: 41–54, 2004.© 2004 Kluwer Academic Publishers. Printed in the Netherlands.

Irene Goll is an Associate Professor in the Kania Schoolof Management at the University of Scranton. Shereceived her Ph.D. in Business Administration fromTemple University. Her publications include theStrategic Management Journal, OrganizationStudies, Management International Review,Industrial Relations, and Employee Responsibilitiesand Rights Journal. Her areas of research are top man-agement teams, strategy, social responsibility, decisionmaking, and firm performance.

Abdul A. Rasheed received his Ph.D. from the Universityof Pittsburgh. Currently he is a Professor of StrategicManagement and International Business at theUniversity of Texas at Arlington. His research interestsinclude strategic decision processes, corporate governance,international comparisons in strategy, and issues relatingto firm boundaries such as outsourcing and franchising.His articles have appeared in journals such as Academyof Management Review, Academy ofManagement Executive, Strategic ManagementJournal, Journal of Management, Journal ofManagement Studies, Management InternationalReview, and Journal of Business Research.

This study examines the role of environmentin moderating the relationship between corpo-rate social responsibility and firm performance.We believe that the corporate social responsibility– firm performance relationship is contextdependent and introduce environmentaldynamism and munificence as contextual vari-ables that moderate this relationship. These areimportant, yet largely unexplored factors thatmay contribute to a better understanding of thesocial performance – firm performance link. Thepresent study focuses on discretionary socialresponsibility which refers to management’svoluntary duties.

Literature review

Corporate social responsibility – firm performance link

There are two major theoretical approacheslinking corporate social responsibility to finan-cial performance. Friedman (1970) and otherneoclassical economists suggest a negative rela-tionship and argue that the social responsibilityof business is to maximize profits as firms incurcosts when acting in a socially responsiblemanner. These costs exceed any benefits thatmight result which reduce profit as well asshareholder wealth thereby contributing to acompetitive disadvantage (Waddock and Graves,1997).

Freeman’s stakeholder approach, on the otherhand, suggests a positive relationship and hasreceived a great deal of attention in the litera-ture. Stakeholder theory suggests that firms needto meet the needs of shareholders and otherstakeholders. Management’s key task is to re-concile competing stakeholder claims (Freeman,1984) and successful firms are ones wheremanagers have managed to balance these com-peting claims (Ogden and Watson, 1999).

Earlier reviews of the literature examining thesocial responsibility – firm performance linkreported mixed results (e.g., Aupperle et al.,1985; Cochran and Wood, 1984; Ullman, 1985).Several explanations have been proposed toexplain these earlier findings. Difficulties inconceptualizing and measuring corporate social

responsibility may contribute to conflictingfindings of earlier research (Aupperle, 1991).Other methodological issues such as stakeholdermismatching may also contribute to theambiguous findings of earlier studies (Wood andJones, 1995). A review of studies in whichmarket measures and market-oriented stake-holders are matched reported consistent findings(Wood and Jones, 1995).

More recent advances in the measurement ofcorporate social responsibility contribute to abetter understanding of its link to firm perfor-mance (Aupperle, 1991; Wood and Jones, 1995).The preponderance of evidence from morerecent meta-analyses suggests a neutral to positiverelationship between corporate social responsi-bility and firm performance. Pava and Krausz(1996) reviewed 21 studies that measured per-ceived corporate social responsibility and finan-cial performance and concluded that most firmsseen as acting socially responsible performedeither better than other firms or have done aswell. Griffin and Mahon (1997) extensivelyreviewed the literature and reported that thelargest number of studies showed a positiverelationship while others showed a negative orinconclusive relationship. Roman, Hayibor, andAgle (1999) reviewed the literature and con-cluded that most studies revealed a positive cor-relation between social responsibility and firmperformance. In his meta-analysis of 27 studiesexamining the relationship between sociallyirresponsible behavior and shareholder wealth,Frooman (1997) found that shareholder wealthdecreases when firms act in a socially irrespon-sible and illicit manner. A more recent andexhaustive review of 95 empirical studiesexamined the link between social performanceand financial performance (Margolis and Walsh,2001) and reported that a majority of studies inwhich corporate social performance was an inde-pendent variable, showed a positive relationship.

Discretionary social responsibility

Corporate social responsibility refers to acompany’s ability to provide benefits to society(Swanson, 1999; Wood, 1991). It includes the

42 Irene Goll and Abdul A. Rasheed

economic, legal, ethical, and discretionaryexpectations of society (Carroll, 1979). The focusof our study is on discretionary social responsi-bility which refers to management’s affirmativeand voluntary duties (Swanson, 1999). It isvoluntary and left up to individual judgment andchoice (Carroll, 1979). Discretionary socialresponsibility includes corporate philanthropyand involvement in efforts that benefit society(Swanson, 1999; Wood, 1991). While managershave latitude with respect to decisions that affecttheir economic, legal, and ethical responsibilities,we believe that they may be able to exercise thegreatest latitude with this component of socialresponsibility.

Of the four components of social responsi-bility, discretionary social responsibility isexpected to be most related to top managementbeliefs and values (Buchholtz et al., 1999). Thereis considerable support in the literature for thenotion that the beliefs and values of key managersinfluence a company’s orientation towards socialresponsibility (e.g., Aupperle et al., 1985;Epstein, 1987; Miles, 1987; Swanson, 1995,1999; Ouchi, 1981; Wartick and Cochran, 1985).A company’s social responsiveness is expected toreflect top management’s philosophy (Miles,1987). Top executives manage a company’sculture which provides a frame of reference forresponding to the environment (Schein, 1985).Their orientation is passed on in the organiza-tion by means of selection and retention of othermanagers. Empirical research found a significantrelationship between CEO values and corporatesocial performance (Agle et al., 1999) andbetween CEO values and corporate philanthropy(Lerner and Fryxell, 1994).

Managers make strategic choices based ontheir beliefs and values. According to the upperechelon perspective, managers’ backgrounds andexperiences influence decision making andorganizational outcomes (Hambrick and Mason,1984). Support for this perspective in the socialresponsibility literature comes from Wood (1991)who argues that managers can exercise choicewithin a social environment, managers have somelatitude with respect to their own behavior in thefirm, and managers are moral actors within theworkplace. In sum, managers have some latitude

as to how they will fulfill their social responsi-bilities. Finkelstein and Hambrick (1990)proposed the idea of managerial discretion whichrefers to ‘. . . the latitude of action available totop executives’ (p. 484). Discretion is low wheremanagers have little latitude. With high discre-tion, managers have greater latitude of action andtheir beliefs and values are expected to exertmore influence over organizational outcomes.Managerial discretion is expected to moderatethe relationship between top management andfirm performance. In an empirical study,Buchholtz et al. (1999) found a positive rela-tionship between firm resources and philan-thropy, a relationship mediated by managerialdiscretion and values.

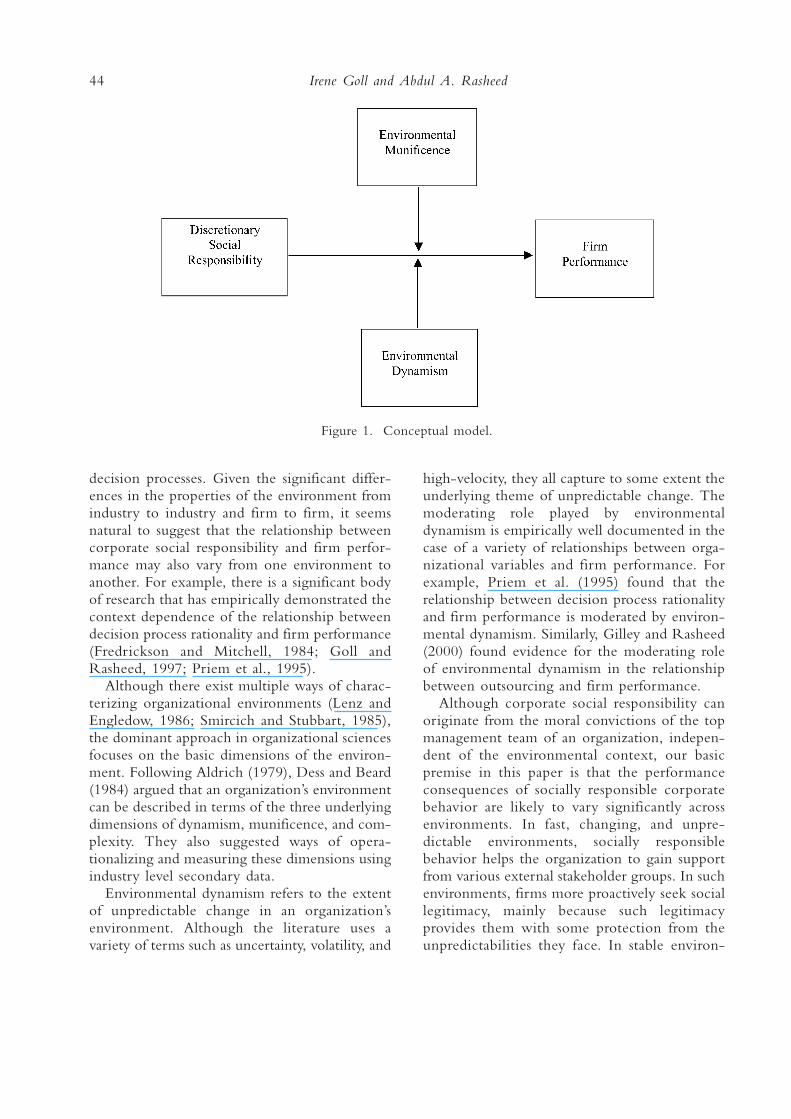

The relationship between discretionary socialresponsibility (DSR) and firm performance (FP)is expected to be moderated by the externalenvironment that managers face. In some envi-ronments, we expect the CSR – FP relationshipto be stronger. In particular, this study willexplore the role of two key dimensions of theenvironment, i.e. dynamism and munificence, inthe DSR – FP relationship. Despite calls forfurther research in the social responsibilityliterature to include additional explanatoryvariables (e.g., Margolis and Walsh, 2001), littleempirical work has examined the role of theenvironment as moderator. Figure 1 presents theconceptual model of our study. Next, we brieflyreview the literature on organizational environ-ments and develop specific hypotheses regardingthe environment’s moderating role on therelationship between discretionary social respon-sibility and firm performance.

The moderating role of the environment

Organizational environments represent one of themajor contingencies faced by a firm (Tosi andSlocum, 1984). An extensive body of research hasaccumulated in the last forty years that exploresenvironmental influences on organizationalstrategies, structures, processes, and outcomes.The decision to behave or not to behave in asocially responsible way is a conscious manage-rial choice that results from complex internal

The Moderating Effect of Environmental Munificence and Dynamism 43

decision processes. Given the significant differ-ences in the properties of the environment fromindustry to industry and firm to firm, it seemsnatural to suggest that the relationship betweencorporate social responsibility and firm perfor-mance may also vary from one environment toanother. For example, there is a significant bodyof research that has empirically demonstrated thecontext dependence of the relationship betweendecision process rationality and firm performance(Fredrickson and Mitchell, 1984; Goll andRasheed, 1997; Priem et al., 1995).

Although there exist multiple ways of charac-terizing organizational environments (Lenz andEngledow, 1986; Smircich and Stubbart, 1985),the dominant approach in organizational sciencesfocuses on the basic dimensions of the environ-ment. Following Aldrich (1979), Dess and Beard(1984) argued that an organization’s environmentcan be described in terms of the three underlyingdimensions of dynamism, munificence, and com-plexity. They also suggested ways of opera-tionalizing and measuring these dimensions usingindustry level secondary data.

Environmental dynamism refers to the extentof unpredictable change in an organization’senvironment. Although the literature uses avariety of terms such as uncertainty, volatility, and

high-velocity, they all capture to some extent theunderlying theme of unpredictable change. Themoderating role played by environmentaldynamism is empirically well documented in thecase of a variety of relationships between orga-nizational variables and firm performance. Forexample, Priem et al. (1995) found that therelationship between decision process rationalityand firm performance is moderated by environ-mental dynamism. Similarly, Gilley and Rasheed(2000) found evidence for the moderating roleof environmental dynamism in the relationshipbetween outsourcing and firm performance.

Although corporate social responsibility canoriginate from the moral convictions of the topmanagement team of an organization, indepen-dent of the environmental context, our basicpremise in this paper is that the performanceconsequences of socially responsible corporatebehavior are likely to vary significantly acrossenvironments. In fast, changing, and unpre-dictable environments, socially responsiblebehavior helps the organization to gain supportfrom various external stakeholder groups. In suchenvironments, firms more proactively seek sociallegitimacy, mainly because such legitimacyprovides them with some protection from theunpredictabilities they face. In stable environ-

44 Irene Goll and Abdul A. Rasheed

Figure 1. Conceptual model.

ments, on the other hand, organizations are in abetter position to identify and co-opt criticalexternal constituencies, thereby ensuring theirsupport.

Most of the past research on environmentsis characterized by focus on a single dimensionof the environment, namely, dynamism(Rajagopalan et al., 1993). The plea ofRajagopalan et al. (1993) for attention to otherdimensions of the environment as well as simul-taneous consideration of multiple dimensionshave been answered by recent studies such as Golland Rasheed (1997) who focused simultaneouslyon both environmental dynamism and munifi-cence.

Munificence, in general, refers to an environ-ment’s ability to support sustained growth of anorganization (Aldrich, 1979). Elaborating on theconstruct of munificence, Castrogiovanni (1991)identifies three distinct kinds of munificence:capacity, growth/decline, and opportunity/threat.Capacity refers to the level of resources availableto the firm, growth/decline refers to the changein capacity, and opportunity/threat refers to theextent of unexploited capacity. Although researchon munificence is somewhat limited comparedto the central role occupied by environmentaluncertainty in past organizational research, itsimpact on organizational strategies (McArthurand Nystrom, 1991; Koberg, 1987), structures(Yasai-Ardekani, 1989), and processes (Miller andFriesen, 1983; Goll and Rasheed, 1997) is welldocumented. In hostile or non-munificent envi-ronments, the scarcity of resources forces firmsto pay greater attention to their conservation.Staw and Swajkowski (1975) found that firms innon-munificent environments are more likely tocommit illegal acts. On the other hand, when theenvironment of an industry is munificent, firmsare likely to be more inclined to engage insocially responsible behavior as evidenced by thesurge in corporate charitable giving by hightechnology and internet related firms in themunificent environment of 1999 and early 2000.In non-munificent environments, because firmsare already short of resources, deployment of anyresources away from core product market areasis likely to have no positive effect on perfor-mance. In munificent environments, such action

further reinforces legitimacy. Thus, the well-established role of environmental munificenceand dynamism leads us to the following hypoth-esis.

H1a: Environmental dynamism moderates therelationship between discretionary socialresponsibility and firm performance.

H1b: Environmental munificence moderates therelationship between discretionary socialresponsibility and firm performance.

There is a continuing debate in both strategicmanagement and organization theory about therole of managerial choice (Astley and Van de Ven,1983). While one school of thought holds thebelief that environmental and inertial factorsrather than managerial choices determine orga-nizational outcomes (Hannan and Freeman,1977), another school takes the exact oppositeperspective (Child, 1972). The evolving dialecticbetween these two schools of thought has ledresearchers, in recent years, to attempt a synthesisbetween these two competing theories(Hrebeniak and Joyce, 1985; Zammuto, 1988).Hrebeniak and Joyce (1985) suggested thatchoice and determinism are independent char-acteristics of the environment rather thanopposite ends of a continuum. According to thisview, some environments allow managers a highdegree of choice while others do not. Similarly,Hambrick and Finkelstein’s (1987) concept ofmanagerial discretion suggests that organizationalenvironments vary in the extent of managerialdiscretion they permit. In high discretion envi-ronments, managerial decisions and actions canhave a significant impact on organizational per-formance, but in low discretion environments,managerial decisions do not make much of adifference.

In recent years, there have been a number ofempirical studies that have focused either explic-itly or implicitly on the role of managerialchoices in high discretion environments.Subsequent empirical work indicates that theextent of managerial discretion may indeed beconstrained by the environment. The relation-ship between top management team size, CEOdominance, and firm performance has been

The Moderating Effect of Environmental Munificence and Dynamism 45

found to be significant in high discretion envi-ronments but not in low discretion environments(Haleblian and Finkelstein, 1993). It has also beenfound that top management team (TMT) tenureis more strongly related to strategies and perfor-mance in high discretion industries than in lowdiscretion industries. The results of Eisenhardtand Schoonhoven’s (1990) study of organizationalgrowth in the semi conductor industry alsosuggest that in environments that are simultane-ously munificent and dynamic, managerial deci-sions and actions have the most impact. Tushmanand Anderson (1986) found that technologicalbreakthroughs are more likely to occur inenvironments characterized by high levels ofuncertainty and munificence. Goll and Rasheed(1997) found that decision process rationality isstrongly associated with performance in highdiscretion environments. Thus, environment maybe an important moderator of the relationshipbetween various organizational factors andoutcomes.

High discretion environments are character-ized by, among other factors, high demandgrowth and demand instability (Finkelstein andHambrick, 1990). As pointed out by Goll andRasheed (1997), a high demand growth ratecorresponds to a high degree of environmentalmunificence and demand instability suggestsenvironmental dynamism. They operationalizedhigh discretion environments as environmentscharacterized by high degrees of munificence anddynamism. In such environments, the perfor-mance implications of managerial decisions tendto be very pronounced. Clearly, choices aboutsocial responsibility are among the most impor-tant choices that a firm makes. This leads us tothe next hypothesis.

H2: Discretionary social responsibility is morestrongly associated with performance in envi-ronments high in munificence and high indynamism than in other types of environ-ments.

Methods

Sample

A survey was undertaken in 1985–1986 tomeasure the extent to which a company’sideology emphasizes social responsibility. Therewere 645 firms in the sample. They included thelargest manufacturing firms in the U.S. inBusiness Week’s top 1000 companies (1985). Thedata for environment, firm performance, andcontrol variables were collected from archivalsources for the period corresponding to thesurvey. A questionnaire measuring a firm’semphasis on social responsibility was mailed to akey executive in each firm (the Human ResourceVice President or CEO). This respondent wasidentified using two sources: Standard and Poor’s(1985) or Dun and Bradstreet (1985). There wasa response rate of 25% (159 firms) following twomailings. When responding and nonrespondingfirms were compared along several dimensions(industry, profitability, and size of company), wefound no significant differences.

Next, for the responding firms, we identifieda subsample of companies that were in a singleor dominant business. Our rationale for selectingthese firms is that measures of environmentalmunificence and dynamism make the most sensefor firms that are mainly in one industry.Following Rumelt (1986), Compustat was usedto identify firms whose sales in one businesssegment were 70% or more of the total sales forthe company. Compustat also identified the 4-digit SIC for each company in the subsamplewhich included 62 firms out of the original 159responding firms.

Discretionary social responsibility

The discretionary social responsibility constructwas operationalized by including three specificsurvey questions adapted from the work ofAupperle (1984). The respondents in the surveywere asked to report on the extent to which theirfirm’s philosophy explicitly emphasized each itemon a scale of one (strongly disagree) to five(strongly agree). The items included: (1) thecorporation believes in performing in a manner

46 Irene Goll and Abdul A. Rasheed

consistent with the philanthropic and charitableexpectations of society; (2) the company believesand values monitoring new opportunities whichcan enhance the company’s ability to solve socialproblems; and (3) the company’s philosophyemphasizes viewing philanthropic behavior as auseful measure of corporate performance. Thesethree items do not lend themselves to muchvariation in interpretation and have face validity.Our discretionary social responsibility scale alsodemonstrates excellent reliability as evidenced bythe high Cronbach’s alpha of 0.74. The discre-tionary social responsibility index was a mean ofthe responses to the three items. The mean dis-cretionary social responsibility score was 3.0 witha standard deviation of 0.89. The items wereadapted from the work of Aupperle (1984) whostudied the beliefs held by firms regarding itsdiscretionary social responsibility as well asethical, legal, and economic responsibilities.

Environmental munificence and dynamism

Environmental munificence and dynamism weremeasured for the ten year period (1975–1984)prior to the survey for each firm in the sub-sample. Munificence was operationalized as thegrowth rate in the value of shipments which isthe regression slope coefficient for this period.Dynamism was operationalized as the variabilityin the value of shipments which is the standarderror of the regression slope coefficient dividedby the industry mean for 1975–1984. Wefollowed Dess and Beard (1984) as well asRasheed and Prescott (1992) in operationalizingmunificence and dynamism. The data werecollected from the Census of Manufactures (U.S.Bureau of Census, 1987).

Firm performance

Financial performance was operationalized asreturn on sales (ROS) and return on assets(ROA). These figures were collected from twosources: Business Week (1986, 1987) and Standardand Poor’s (1986, 1987). A mean of two years forROA and ROS was computed for 1985 and1986.

Control variable

The study controlled for size of companymeasured as log sales for 1985 as this variable mayaffect the results (see Rowley and Berman, 2000;Buchholtz et al., 1999)

Analyses

Moderated regression analyses were undertakento test the hypotheses. Discretionary socialresponsibility was the predictor variable, envi-ronmental dynamism and munificence were themoderators, and ROA and ROS served as thecriterion variables. First, we used moderatedregression analyses to test for a moderating effectof environment on the discretionary socialresponsibility-performance link. Second, wetested to see if the environment (moderator) wasrelated to performance (criterion). Third, wewanted to test to see if discretionary socialresponsibility and environment are significantlyrelated to rule out the possibility that environ-ment is an antecedent variable to discretionarysocial responsibility. Fourth, we developed sub-groups to further explore the relationshipsbetween discretionary social responsibility andperformance in different environments (seePrescott, 1986 for how to test for moderatingeffects). We split the sample at the median onmunificence and created high versus low munif-icence subgroups. Then we split the sample atthe median on dynamism and created high versuslow dynamism subgroups. This was done to testfor the possibility that the discretionary socialresponsibility – firm performance relationshipvaries in high versus low munificence environ-ments and in high versus low dynamism envi-ronments.

Results

The means, standard deviations, and correlationsfor all the variables included in this study areshown in Table I. Next, we examined the mod-erating effect of environmental munificence anddynamism on the relationship between discre-

The Moderating Effect of Environmental Munificence and Dynamism 47

tionary social responsibility and firm performancefollowing the steps identified by Prescott (1986).

First, we used moderated regression analysis totest for the hypothesized moderating effects.Table II shows the results of regressing return onassets on munificence, dynamism, and discre-tionary social responsibility. Size of company wasincluded as a control variable. Model 1 shows themain effects whereas Model 2 includes theinteractions between discretionary social respon-sibility and munificence, discretionary socialresponsibility and dynamism, and munificenceand dynamism. The R2 for Model 1 is 0.17 andsignificant (p < 0.05). The R2 for Model 2 is 0.30and significant (p < 0.05). Following Cohen

(1968), we tested to see if this change in R2 issignificant. The increase in R2 is significant (F =8.92, df (4,48), p < 0.001). We noted that inModel 1, size of company shows a significantrelationship to ROA suggesting that larger firmsare more profitable.

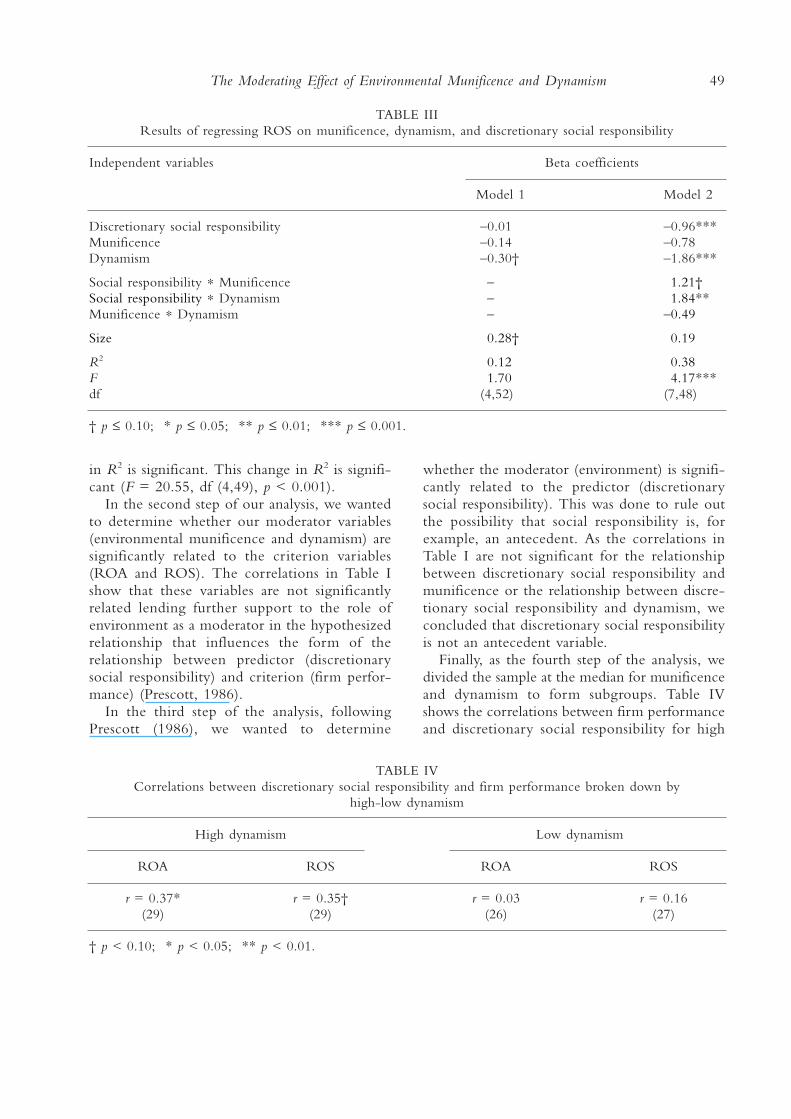

Table III shows the results of regressing returnon sales on munificence, dynamism, and discre-tionary social responsibility. Again, size ofcompany was included as a control. Model 1shows the main effects. The R2 for Model 1 was0.12 and not significant. Model 2 includes theinteraction terms. The R2 for Model 2 is 0.38and significant (p < 0.001). Again, we followedCohen (1968) and tested to see if the increase

48 Irene Goll and Abdul A. Rasheed

TABLE IIResults of regressing ROA on munificence, dynamism, and discretionary social responsibility

Independent variables Beta coefficients

Model 1 Model 2

Discretionary social responsibility 00.08 –0.43Munificence –0.30† –1.72†Dynamism –0.24 –0.94

Social responsibility

∗ Munificence 0– 01.19†Social responsibility ∗ Dynamism 0– 00.79Munificence ∗ Dynamism 0– 00.31

Size 00.35

* 00.29†

R2 00.17 00.30F 02.69* 02.87*df (4,51) (7,47)

† p ≤ 0.10; * p ≤ 0.05; ** p ≤ 0.01; *** p ≤ 0.001.

TABLE ICorrelations, means, and standard deviations of all variables

Variable Mean SD 1 2 3 4 5

1. Discretionary social responsibility 0003.00 0000.892. Munificence 2203.02 3641.25 –0.063. Dynamism 0000.01 0000.01 00.01 00.44*4. ROA 0000.03 0000.12 00.24 –0.15 –0.185. ROS 0000.02 0000.11 00.21 –0.03 –0.16 0.93*6. Size 0003.15 0000.66 00.10 00.47* 00.43* 0.10 0.09

* p < 0.05.

in R2 is significant. This change in R2 is signifi-cant (F = 20.55, df (4,49), p < 0.001).

In the second step of our analysis, we wantedto determine whether our moderator variables(environmental munificence and dynamism) aresignificantly related to the criterion variables(ROA and ROS). The correlations in Table Ishow that these variables are not significantlyrelated lending further support to the role ofenvironment as a moderator in the hypothesizedrelationship that influences the form of therelationship between predictor (discretionarysocial responsibility) and criterion (firm perfor-mance) (Prescott, 1986).

In the third step of the analysis, followingPrescott (1986), we wanted to determine

whether the moderator (environment) is signifi-cantly related to the predictor (discretionarysocial responsibility). This was done to rule outthe possibility that social responsibility is, forexample, an antecedent. As the correlations inTable I are not significant for the relationshipbetween discretionary social responsibility andmunificence or the relationship between discre-tionary social responsibility and dynamism, weconcluded that discretionary social responsibilityis not an antecedent variable.

Finally, as the fourth step of the analysis, wedivided the sample at the median for munificenceand dynamism to form subgroups. Table IVshows the correlations between firm performanceand discretionary social responsibility for high

The Moderating Effect of Environmental Munificence and Dynamism 49

TABLE IVCorrelations between discretionary social responsibility and firm performance broken down by

high-low dynamism

High dynamism Low dynamism

ROA ROS ROA ROS

r = 0.37* r = 0.35† r = 0.03 r = 0.16(29) (29) (26) (27)

† p < 0.10; * p < 0.05; ** p < 0.01.

TABLE IIIResults of regressing ROS on munificence, dynamism, and discretionary social responsibility

Independent variables Beta coefficients

Model 1 Model 2

Discretionary social responsibility –0.01 –0.96***Munificence –0.14 –0.78Dynamism –0.30† –1.86***

Social responsibility ∗ Munificence 0– 01.21†Social responsibility ∗ Dynamism 0– 01.84**Munificence ∗ Dynamism 0– –0.49

Size 00.28† 00.19

R2 00.12 00.38F 01.70 04.17***df (4,52) (7,48)

† p ≤ 0.10; * p ≤ 0.05; ** p ≤ 0.01; *** p ≤ 0.001.

versus low dynamism. In a high dynamism envi-ronment, there was a significant relationshipbetween ROA and discretionary social responsi-bility and a marginally significant relationshipbetween ROS and discretionary social responsi-bility (p ≤ 0.10). Table V shows the correlationsbetween discretionary social responsibility andfirm performance in high versus low munificenceenvironments. There was a significant correlationbetween ROA and discretionary social responsi-bility in high munificence environments. Thesame was true for ROS. These results lendfurther support for the role of environmentalmunificence and dynamism as moderators in therelationship between discretionary social respon-sibility and firm performance.

In sum, we found support for H1a, H1b, andH2.

Discussion and implications

The belief that organizational performance ispredicated upon a fit or match between theorganization and its environment is central tostrategic management and organization theory.This study has adopted the conceptualization offit as moderation (Venkatraman, 1989) and foundconsiderable empirical support for that perspec-tive. We found support for both the hypotheses,thus lending support to the basic premise of thepaper that environment is a moderator of therelationship between social responsibility andfirm performance.

The results of our study lend support toFreeman’s (1984) stakeholder theory and may

help explain some of the contradictory findingsof earlier empirical research. We found a signif-icant relationship between two measures offinancial performance (ROA and ROS) anddiscretionary social responsibility in highlymunificent but not in low munificent environ-ments. This suggests that in munificent environ-ments, firms are more likely to engage in moresocially responsible behavior whereas in envi-ronments characterized by scarce resources, firmsmay be more inclined to conserve. Our studyalso found a significant positive relationshipbetween ROA and discretionary social responsi-bility in more dynamic environments. Thissupports our expectation that one of the waysin which organizations cope with environmentaluncertainty is by enhancing social legitimacythrough socially responsible behavior. The moreinteresting result, however, is that the perfor-mance implications of socially responsiblebehavior are most pronounced in high discre-tion environments. It is precisely in these envi-ronments that managerial decisions and actionscan have the most impact on organizational per-formance (Hambrick and Finkelstein, 1987). Webelieve that by paying attention to the environ-mental and organizational contingency factorsthat affect the relationship between sociallyresponsible behavior and firm performance, wewill be able to explain many of the contradic-tions encountered in previous research.

Like all empirical research, our study hasseveral important limitations which one needsto bear in mind while interpreting its results.First, as pointed out by Waddock and Graves(1997), measurement issues are problematic in the

50 Irene Goll and Abdul A. Rasheed

TABLE VCorrelations between discretionary social responsibility and firm performance broken down by

high-low munificence

High munificence Low munificence

ROA ROS ROA ROS

r = 0.46* r = 0.50** r = –0.15 r = –0.14(27) (28) (28) (28)

* p < 0.05; ** p < 0.01.

study of corporate social responsibility. Relyingas we did on survey methodology, we do nothave an “objective” measure of a firm’s corpo-rate social performance. Instead, our measure tapsinto executive perceptions about the firm’sphilosophy and ideology. It is possible that socialdesirability bias may cause the respondents toexaggerate their firm’s commitment to socialresponsibility. Second, the sample was limited tolarge manufacturing firms, thereby potentiallylimiting its generalizability to small firms orservice businesses. Third, our study did notcontrol for potential industry effects that couldinfluence the relationships between the variables.Fourth, the study relied on single respondentsfrom each firm. Although the use of multiplerespondents could have provided greater relia-bility to our measure of social responsibility, thiswould have greatly restricted our sample size.Further, we believe that the use of single respon-dents is adequate since both environmental andperformance measures were calculated usingsecondary data sources, thereby avoiding theproblem of potential common method variance.Fifth, we are considering only two dimensions ofthe environment, namely, dynamism and munif-icence. Consideration of additional dimensionssuch as complexity would provide additionalinsights. Sixth, our operationalization of socialresponsibility focuses mostly on discretionaryaspects. A broader and more comprehensiveconceptualization and operationalization canprovide a fuller understanding of the contextspecificity of the corporate responsibility-finan-cial performance relationship. Seventh, ourresearch design is cross-sectional. The problem ofreverse causality raised by Waddock and Graves(1997), therefore, cannot be conclusively ruledout.

Finally, the survey measuring discretionarysocial responsibility took place in 1985–1986with additional archival data measuring environ-ment and performance collected later to corre-spond to the time period of the survey. As such,questions may arise as to the relevance of ourfindings to today. We believe that althoughtoday’s business environment is characterized byrapid change, the basic relationships among theconstructs of interest are not likely to change

from one decade to the next. In addition, it isimportant to have studies relating to differenttime periods. Differences in the nature of therelationships between constructs across timeperiods can lead to meaningful investigationsabout drivers of such change.

We believe that the results of this study havea number of important implications for futureresearch. First, it clearly suggests that the socialresponsibility-firm performance relationship iscontext specific. Therefore, development of boththeoretical understanding and managerial impli-cations depend very much on identifying thecontextual factors which enhance a positiverelationship between social responsibility andfirm performance. Second, by considering twohighly salient environmental dimensions simulta-neously, this study has been able to provide aricher understanding of the moderating role ofthe environment in the social responsibility-firmperformance relationship. Third, the results ofthis study reinforce the notion that managerialchoices matter more in certain types of environ-ments than in others as originally suggested byHrebeniak and Joyce (1985) and later elaboratedby Haleblian and Finkelstein (1993).

Fourth, it is important to adopt multiple con-ceptualizations of fit. As explained earlier, thisstudy has adopted the moderation perspective offit. An inherent limitation of this perspective isits inability to separate the existence of fit fromthe effects of fit (Venkatraman, 1989). Hesuggests the use of multiple perspectives, espe-cially, the mediation and matching perspectivesalong with the moderation perspective. Empiricaltesting of competing perspectives is likely toprovide a better understanding of the precise roleof environmental munificence and dynamism.

Fifth, organizational factors may play anequally important moderating role in the rela-tionship between social responsibility andorganizational outcomes. The simultaneous con-sideration of organizational and environmentalfactors is likely to provide a richer understandingof the relationship between social responsibilityand performance. Organizational factors such asa firm’s strategy and resource position could beparticularly promising internal contingencyfactors to be incorporated into future research.

The Moderating Effect of Environmental Munificence and Dynamism 51

Finally, the dependent variable of this study,namely economic performance, is influenced bya variety of firm and industry level factors.Therefore, any inference of a causal relationshipmust be done only with caution. Organizationaloutcomes more directly resulting from socialresponsibility rather than economic performancemay, therefore, be more appropriate as dependentvariables.

The results of this study also have importantimplications for practicing managers. Althoughmanagers may decide to avoid or engage insocially responsible activities based on their valuesand beliefs alone, the results of this study suggestthat such activities can also have a strongeconomic rationale in certain types of environ-ments.

In conclusion, this study points clearly to theneed for moving research on social responsibilityfrom bivariate relationships to a more contextspecific approach. The consideration of environ-mental munificence and dynamism as moderatorsis an important beginning that may provide amore comprehensive understanding of thisimportant and unresolved research issue.

References

Agle, B. R., R. K. Mitchell and J. A. Sonnenfeld:1999, ‘Who Matters to CEOs? An Investigationof Stakeholder Attributes and Salience, CorporatePerformance, and CEO Values’, Academy ofManagement Journal 42(5), 507–525.

Aldrich, H. E.: 1979, Organizations and Environments(Prentice-Hall, Englewood Cliffs, NJ).

Astley, W. G. and A. H. Van de Ven: 1983, ‘CentralPerspectives and Debates in Organization Theory’,Administrative Science Quarterly 28, 245–273.

Aupperle, K. E.: 1984, ‘An Empirical Measure ofCorporate Social Orientation’, in L. E. Preston(ed.), Research in Corporate Social Performance andPolicy, Vol. 6 ( JAI Press, Greenwich, CT), pp.27–54.

Aupperle, K. E.: 1991, ‘The Use of Forced-ChoiceSurvey Procedures in Assessing Corporate SocialOrientation’, in James E. Post (ed.), Research inCorporate Social Performance and Policy, Vol. 12 ( JAIPress, Greenwich, CT), pp. 269–279.

Aupperle, K. W., A. B. Carroll and J. D. Hatfield:1985, ‘An Empirical Examination of the Rela-

tionship Between Corporate Social Responsi-bility and Profitability’, Academy of ManagementJournal 28(2), 446–463.

Buchholtz, A. K., A. C. Amason and M. Rutherford:1999, ‘Beyond Resources: The Mediating Effect ofTop Management Discretion and Values onCorporate Philanthropy’, Business & Society 38(2),167–187.

Business Week: 1985, 1986, 1987, The Business WeekTop 1000.

Carroll, A. B.: 1979, ‘A Three-DimensionalConceptual Model of Corporate Performance’,Academy of Management Review 4(4), 497–505.

Castrogiovanni, G. J.: 1991, ‘EnvironmentalMunificence: A Theoretical Assessment’, Academyof Management Review 16, 542–565.

Child, J.: 1972, ‘Organizational Structure,Environment and Performance: The Role ofStrategic Choice’, Sociology 6, 1–22.

Cochran, P. L. and R. A. Wood: 1984, ‘CorporateSocial Responsibility and Financial Performance’,Academy of Management Journal 27(1), 42–56.

Cohen, J.: 1968, ‘Multiple Regression as a GeneralData-Analytic System’, Psychological Bulletin 70(6),426–443.

Dess, G. G. and D. W. Beard: 1984, ‘Dimensions ofOrganizational Task Environments’, AdministrativeScience Quarterly 29, 52–73.

Dun and Bradstreet: 1985, Million Dollar Directory(Dun and Bradstreet, Parsippany, NJ).

Eisenhardt, K. M. and C. B. Schoonhoven: 1990,‘Organizational Growth: Linking Founding Team,Strategy, Environment, and Growth among U.S.Semiconductor Ventures, 1978–1988’, Adminis-trative Science Quarterly 35, 504–529.

Epstein, E. M.: 1987, ‘The Corporate Social PolicyProcess: Beyond Business Ethics, Corporate SocialResponsibility, and Corporate Social Respon-siveness’, California Management Review 29(3),99–114.

Finkelstein, S. and D. C. Hambrick: 1990, TopManagement Team Tenure and OrganizationalOutcomes: The Moderating Role of ManagerialDiscretion’, Administrative Science Quarterly 35,505–538.

Fredrickson, J. W. and T. R. Mitchell: 1984, ‘StrategicDecision Processes: Comprehensiveness andPerformance in an Industry with an UnstableEnvironment’, Academy of Management Journal 27,399–423.

Freeman, R. E.: 1984, Strategic Management: AStakeholder Approach (Pitman, Boston).

Friedman, M.: 1970, ‘A Friedman Doctrine: The

52 Irene Goll and Abdul A. Rasheed

Social Responsibility of Business is to Increase itsProfits’, New York Times Magazine (September 13),33.

Frooman, J.: 1997, ‘Socially Irresponsible and IllegalBehavior and Shareholder Wealth: A Meta-Analysisof Event Studies’, Business & Society 36(3),221–249.

Gilley, K. M. and A. Rasheed: 2000, ‘Making Moreby Doing Less: An Analysis of Outsourcing andIts Effect on Firm Performance’, Journal ofManagement 26, 763–790.

Goll, I. and A. Rasheed: 1997, ‘Rational Decision-Making and Firm Performance: The ModeratingRole of Environment’, Strategic Management Journal18(7), 583–591.

Griffin, J. J. and J. F. Mahon: 1997, ‘The CorporateSocial Performance and Corporate FinancialPerformance Debate: Twenty-Five Years ofIncomparable Research’, Business & Society 36(1),5–31.

Haleblian, J. and S. Finkelstein: 1993, ‘TopManagement Team Size, CEO Dominance, andFirm Performance: The Moderating Role ofEnvironmental Turbulence and Discretion’,Academy of Management Journal 36, 844–863.

Hambrick, D. C. and S. Finkelstein: 1987,‘Managerial Discretion: A Bridge Between PolarViews of Organizations’, in L. L. Cummings andB. M. Staw (eds.), Research in OrganizationalBehavior, Vol. 9 ( JAI Press, Greenwich, CT), pp.369–406).

Hambrick, D. C. and P. Mason: 1984, ‘UpperEchelons: The Organization as a Reflection of ItsTop Managers’, Academy of Management Review 9,193–206.

Hannan, M. T. and J. H. Freeman: 1977, ‘ThePopulation Ecology of Organizations’, AmericanJournal of Sociology 82, 929–964.

Hrebeniak, L. G. and W. F. Joyce: 1985,‘Organizational Adaptation: Strategic Choice andEnvironmental Determinism’, Administrative ScienceQuarterly 30, 336–349.

Koberg, C. S.: 1987, ‘Resource Scarcity,Environmental Uncertainty, and AdaptiveOrganizational Behavior’, Academy of ManagementJournal 30, 798–807.

Lenz, R. T. and J. L. Engledow: 1986, ‘EnvironmentalAnalysis: The Applicability of Current Theory’,Strategic Management Journal 7, 329–346.

Lerner, L. D. and G. E. Fryxell: 1994, ‘CEOStakeholder Attitudes and Corporate SocialActivity in the Fortune 500’, Business & Society33(1), 58–81.

Margolis, J. D. and J. P Walsh: 2001, People and Profits?(Lawrence Erlbaum Associates, Inc., Mahwah,NJ).

McArthur, A. W. and P. C. Nystrom: 1991,‘Environmental Dynamism, Complexity, andMunificence as Moderators of Strategy-Performance Relationships’, Journal of BusinessResearch 23, 349–361.

McGuire, J. B., T. Schneeweiss and A. Sundgren:1988, ‘Corporate Social Responsibility and FirmFinancial Performance’, Academy of ManagementJournal 31(4), 854–872.

Miles, R. H.: 1987, Managing the Corporate SocialEnvironment: A Grounded Theory (Prentice-Hall,Englewood Cliffs, NJ).

Miller, D. and P. H. Friesen: 1983, ‘Strategy Makingand Environment: The Third Link’, StrategicManagement Journal 4(3), 221–235.

Ogden, S. and R. Watson: 1999, ‘CorporatePerformance and Stakeholder Management:Balancing Shareholder and Customer Interests inthe U.K. Privatized Water Industry’, Academy ofManagement Journal 42(5), 526–538.

Ouchi, W.: 1981, Theory Z: How American BusinessCan Meet the Japanese Challenge (Addison-Wesley,Reading, MA).

Pava, M. L. and J. Krausz: 1996, ‘The AssociationBetween Corporate Social-Responsibility andFinancial Performance: The Paradox of SocialCost’, Journal of Business Ethics 15(3), 321–357.

Prescott, J. E.: 1986, ‘Environments as Moderatorsof the Relationship Between Strategy andPerformance’, Academy of Management Journal 29(2),329–346.

Priem, R. L., A. Rasheed and A. G. Kotulic: 1995,‘Rationality in Strategic Decision Processes,Environmental Dynamism, and Firm Performance’,Journal of Management 21, 913–929.

Rajagopalan, N., A. Rasheed and D. K. Datta: 1993,‘Strategic Decision Processes: Critical Review andFuture Directions’, Journal of Management 19,349–384.

Rasheed, M. A. and J. E. Prescott: 1992, ‘Towardsan Objective Classification Scheme for Organ-izational Task Environments’, British Journal ofManagement 3, 197–206.

Roman, R. M., S. Hayibor and B. R. Agle: 1999,‘The Relationship Between Social and FinancialPerformance’, Business & Society 38(1), 109–125.

Rowley, T. and S. Berman: 2000, ‘A Brand NewBrand of Corporate Social Performance’, Business& Society 39(4), 397–418.

Rumelt, R. P.: 1986, Strategy, Structure, and Economic

The Moderating Effect of Environmental Munificence and Dynamism 53

Performance (Harvard Business School Press,Boston).

Schein, E. H.: 1985, Organizational Culture andLeadership ( Jossey-Bass, San Francisco).

Shane, P. B. and B. H. Spicer: 1983, ‘MarketResponse to Environmental Information ProducedOutside the Firm’, Accounting Review 58(3),521–536.

Smircich, L. and C. Stubbart: 1985, ‘StrategicManagement in an Enacted World’, Academy ofManagement Review 10, 724–736.

Standard and Poor’s: 1985, Register of Corporations,Directors, and Executives (Standard and Poor’s, NewYork).

Standard and Poor’s: 1986, 1987, Stock Reports(Standard and Poor’s, New York).

Staw, B. M. and E. Swajkowski: 1975, ‘The Scarcity-Munificence Component of OrganizationalEnvironments and the Commission of Illegal Acts’,Administrative Science Quarterly 20, 34–354.

Swanson, D. L.: 1995, ‘Addressing a TheoreticalProblem by Reorienting the Corporate SocialPerformance Model’, Academy of ManagementReview 20(1), 43–64.

Swanson, D. L.: 1999, ‘Toward an Integrative Theoryof Business and Society: A Research Strategy forCorporate Social Performance’, Academy ofManagement Review 24(3), 506–521.

Tosi, H. L. and J. W. Slocum: 1984, ‘ContingencyTheory: Some Suggested Directions’, Journal ofManagement 10, 9–26.

Tushman, M. L. and P. Anderson: 1986,Technological Discontinuities and OrganizationalEnvironments’, Administrative Science Quarterly 31,439–465.

Ullman, A. A.: 1985, ‘Data in Search of a Theory: ACritical Examination of the Relationships amongSocial Performance, Social Disclosure, andEconomic Performance of U.S. Firms’, Academy ofManagement Review 10(3), 540–557.

U.S. Bureau of Census: 1987, 1987 Census ofManufactures (U.S. Government Printing Office,Washington, DC).

Venkatraman, N.: 1989, ‘The Concept of Fit in

Strategy Research: Toward Verbal and StatisticalCorrespondence’, Academy of Management Review14, 423–444.

Waddock, S. A. and S. B. Graves: 1997, ‘TheCorporate Social Performance – FinancialPerformance Link’, Strategic Management Journal19(4), 303–319.

Wartick, S. L. and P. L. Cochran: 1985, ‘TheEvolution of the Corporate Social PerformanceModel’, Academy of Management Review 10(4),758–769.

Wood, D. J.: 1991, ‘Corporate Social PerformanceRevisited’, Academy of Management Review 16(4),691–718.

Wood, D. J. and R. E. Jones: 1995, ‘StakeholderMismatching: A Theoretical Problem in EmpiricalResearch on Corporate Social Performance’, TheInternational Journal of Organizational Analysis 3(3),229–267.

Yasai-Ardekani, M.: 1989, ‘Effects of EnvironmentalScarcity and Munificence on the Relationship ofContext to Organizational Structure’, Academy ofManagement Journal 32, 131–156.

Zammuto, R. F.: 1988, ‘Organizational Adaptation:Some Implications of Organizational Ecology forStrategic Choice’, Journal of Management Studies 25,105–119.

Irene GollKania School of Management,

University of Scranton,Scranton, PA 18510,

U.S.A.E-mail: [email protected]

Abdul A. RasheedDepartment of Management,

College of Business Administration,University of Texas at Arlington,

Arlington, TX 76019,U.S.A.

E-mail: [email protected]

54 Irene Goll and Abdul A. Rasheed

Copyright © 2022 FDOKUMEN