Interest Rates, Exchange Rates, and International Adjustment

Upload

khangminh22Category

view

6download

0

1

THE IMPACT OF INTEREST RATES ON SAVINGS AND

INVESTMENT IN NIGERIA

BEING A PROJECT PRESENTED TO THE DEPARTMENT OF

BANKING AND FINANCE, FACULTY OF BUSINESS

ADMINISTRATION, UNIVERSITY OF

NIGERIA, ENUGU CAMPUS

BY

SUNDAY, KINGSLEY UCHE

PG/MBA/08/53104

IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR

THE AWARD OF THE MASTERS IN BUSINESS

ADMINISTRATION DEGREE IN

BANKING AND FINANCE

SUPERVISOR: DR B.E. CHIKELEZE

MARCH 2012

2

CHAPTER ONE: INTRODUCTION

1.1 BACKGROUND OF THE STUDY

Interest is the reward that accrues to people who provide the fund with which capital

goods are bought (Soyibo and Adekanye, 1992). Interest can also be defined as the

payment made to a lender by a borrower for the use of a sum of money for certain

period of time. The charging of interest on loan was initially abolished during

medieval days, both was later legalized by King Henry VIII in 1545 when he

abolished the usury laws in it was condemned. These usury laws were established

during the medieval time when the payment of interest rate was strongly condemned

and termed usury. During that time it was believed that loan was an aid to an

individual or neighbour who is distressed, for such reason, they felt charging of

interest on loan was not proper (Bhatia and Khatkhate, 1973).

Interest rate deregulation was later introduced into the monetary system by Central

Bank of Nigeria, which was part of the Structural Adjustment Program (SAP), which

was introduced in July 1986 by the head of state then-Gen Ibrahim Babangida

(Osofisan, 1993). Interest can also be said to be the charge assessed for the use of

money. It can also be seen as “the payment made to owners of capital fund which

they are ready to put at the disposal of others; thus, interest rate is like a price which

bring into equilibrium the demand for resources to invest with the readiness to

establish from present consumption. Interest rate is determined by the force of

demand and supply of capital and for the condition that demand and supply of fund

are equal. Hence, interest level is arrived at by the intersection between savings and

investment (Luckett, 1984). Savings is defined as that portion of income after tax,

which is not spent on consumption goods. Savings can also be seen as that part of

income, which is not devoted to the purchase of household items and firm

3

(McKinnon, 1973). Investment on the other hand can be defined as the expenditure

of funds lending to the creation of net additions to the stock of physical capital; it is

done almost exclusively by firms. Interest rate favours the investors when the

interest rate is low. The major factor that determines investment is interest rate and

this is influenced by savings. The investors will also be favoured when the marginal

efficiency of capital is high. Marginal efficiency is defined as the expected rate of

returns from additional unit of capital asset. It refers to the expected rate of profit per

year on real investment of the most efficient type, it depends upon the entrepreneur

expectation of future return. However, there will be no investment of profit

expectation which are not very bright, this is the reason why investment falls to a low

level during a depression despite all the encouragement to stimulate private

investment (Revel, 1975).

Interest rate favours savers when the rate is high, savings were looked upon as

beneficial both for the individual and the society at large. Thus, an increase in

savings will ultimately lead to an increase in savings of the community. It was due to

this effect that the classists believed in thriftiness (Ritter and Siber, 1986). They

were of the view that an individual saving was a great private as well as social virtue.

The Keynes were at a different view, which they advocate that individual savings is a

social virtue but rather supported the view that individual savings is greatly a social

vice. Increase savings on the part of individuals will result in a general curtailment in

the expenditure. When savings increase, investment is very essential for the

economic development of an economy. With increase investment, employment is

bound to increase which will in turn increase demand, prices, profit and more

production expansion. This expansion if properly utilized will lead to economic

development of a country (Shaw, 1973).

4

Investment results as a consequence of capital accumulation, which in turn depends

upon savings (Ndulu, 1990). Savings by profit earners and their conversion into

investment was the main actor responsible for the economic development of Great

Britain in the 19th century. The realization of the role of interest rate in the attainment

of monetary policy objectives, the central bank of Nigeria decided to have a uniform

rate of interest on loan for all the commercial banks in Nigeria, as contained in its

credit guidance of 1969. The credit guidance of the Central Bank of Nigeria was later

changed in 1987. It introduced an interest rate policy based on free market forces in

view of the effort of government to deregulate the economy in the wake of the

second-tier foreign exchange market. This interest rate deregulation is a system

where the forces of demand and supply determine the prevailing interest rate. This

implies that there is no fixed rate to be charged by the bank on their loans and

advances and no given rates to be paid to depositors (Soyibo and Adekanye, 1992).

There are three main approaches in economics to the determination of interest rates.

These theories vary in their views on interest rate, although there are some

similarities among them, these theories include the following; the classical theory of

interest (loanable fund), the liquidity reference theory (Keynesian Approach), the

general equilibrium approach (modern). An overview of these theories of interest rate

reveals that interest rate can influence the growth of savings and investment in an

economy, the understanding of the nature, meaning and role of interest rate in the

same economy is crucial, in a nutshell, interest rate is a given prominent position as a

catalyst for growth in the economy and particularly a factor in determining the

growth of savings and investment (Osofisan, 1993).

5

1.2 STATEMENT OF THE PROBLEM

Many developing countries, under a crushing burden of debt and other external

disequilibria, have adopted programmes to restructure their economies. A major

cornerstone of such adjustment programmes is the liberalization of financial markets

and a greater role assigned to market forces in the allocation of financial resources,

and generally involves interest rate deregulation and relaxation or cancellation of the

policy of directed credits.

The policy of interest rate in developing countries seems to have been backed by the

McKinnon-Shaw financial intermediation hypothesis which postulates that interest

rates have a positive response to savings and economic growth (McKinnon, 1973;

Shaw, 1973). The link between interest rate responsiveness and savings, as postulated

by the McKinnon-Shaw hypothesis, is investment. However, behaviourally and

operationally, savings and investment differ (Bhatia and Khatkhate, 1975; Fry,

1978); the transfer of savings to investment being dependent on a host of factors

other than the real interest rate. Such factors include the availability of investment

opportunities at rates of return exceeding cost of funds, the existence of private and

social profitability differences, institutional constraints and the cost of administering

funds. Thus, a study of the link between real interest rates and investment cannot be

done solely via the McKinnon-Shaw hypothesis. Unfortunately, studies of financial

liberalization policies assumed the link between savings and investment as given

and/or regard specification of the effect of the real interest rate on investment as

difficult (Mwega et a!., 1990).

Also, studies of the effect of adjustment programmes on economic growth tend to

assume the existence of the Keynesian savings and investment macroeconomic

balance (Ndulu, 1990). Yet, it is known that resource gaps constrain economic

6

growth in developing countries. The successful application of financial liberalization

policies in developing countries, therefore, goes beyond demonstrating the

applicability or otherwise of the McKinnon-Shaw hypothesis. There is a need to

investigate the behavioural relationships between investment and savings (perhaps

via the real interest rate) to identify the determinants of the mechanism of

transmission of savings to investments.

In Soyibo and Adekanye (1992a), the applicability of the McKinnon-Shaw

hypothesis to Nigeria was established, though Shaw's hypothesis seems to be more

strongly supported. This suggests that the debt intermediation hypothesis holds in

Nigeria. To influence economic growth positively, the increased savings mobilized as

a result of financial system liberalization would need to be transmitted to investment.

An understanding of the savings-investment process therefore, can help inform

policy decisions aimed at promoting economic development.

At least two approaches can be adopted in this regard. First, the characteristics of the

supply side can be determined, with an analysis of the factors affecting portfolio

management decisions of suppliers of credit using their perceptions and objective

data. Second, the characteristics of the demand can be studied, establishing the

determinants of demand using perceptions as well as objective data. This paper

concerns itself with the first approach, using principally primary data to analyse the

perceptions of bankers. The limitations of this approach will be discussed later.

However, a study of banking system operators' perceptions of the impact of the

different regulatory regimes on the performance of the system has its own merits. It

can spotlight the areas of general consensus as to the effectiveness or otherwise of

government policy. Such a study can also be a type of ex post evaluation of the

7

impact of government policy on the banking system from the point of view of those

directly affected.

1.3 OBJECTIVES OF THE STUDY

The main objective of this research includes the following:

1. To determine the impact of interest rate on savings in Nigeria.

2. To determine how interest rate impact on the investment rate in Nigeria.

3. To determine the impact of savings on Investment in Nigeria

1.4 RESEARCH QUESTIONS

As a follow up to the above objectives, the following questions are asked;

1. What is the impact of interest rate on savings in Nigeria?

2. What is the impact of interest rate on investment in Nigeria?

3. Do savings have an impact on Investment in Nigeria?

1.5 HYPOTHESES

The following hypotheses have been formulated based on the objectives of study and

the research questions;

HO: There is no positive significant impact of interest rate on savings in Nigeria.

HO: There is no positive significant impact of interest rate on Investment in

Nigeria.

Ho: There is no positive significant impact of Savings on Investment in Nigeria?

8

1.6 SCOPE OF THE STUDY

In order to carry out a comprehensive and meaningful research work on the critical

effect of interest rate as a determining factor in the growth of savings and

investments in Nigeria. This work was based mainly on Central Bank of Nigeria

(CBN), which regulates the employment of interest rate, savings and investment and

on the Intercontinental Bank plc. Data used covers a period of ten years (1970 –

2008) so that the impact of interest rate on savings and investment can be compared

using the interest policies.

1.7 SIGNIFICANCE OF THE STUDY

The deterioration of the Nigeria economy calls for a scrutinization of the economic

policies. This Nigeria like all other developing countries is faced with the problem of

choosing the most appropriate policies, which will be employed to attain economic

growth. An identification of the factors, which influence the economy, becomes

necessary, the level of investment being a major influence of economic growth lead

us to the study of interest rate which is one of the factors influencing investment as

well as savings (which provides funds for investment). In order to avoid decisional

myopia there is a need for efficient and proper economic planning. The need for

undertaking this study stems from the important role the rate of interest plays in

determining the growth of savings and investment. This shall be of immense benefit

to commercial banks in general, the CBN, the general economy and to future

researchers in the field of interest rate.

9

1.8 DEFINITION OF TERMS

Marginal Efficiency of Capital is used to measure the rate of return on

investment Osofisan (1993).

Interest Rate This is the rate at which the Central Bank of

Nigeria lends to financial institution thus

supply and demand for funds Mwega, Ngola,

and Mwangi, (1990)

Interest rate policy This is the policy Central Bank uses to control

inflation in the economy. It also used to

control the money supply by the monetary

authorities, in order to achieve the stated or

desired goals Ndulu (1990).

Savings The total amount of deposit in financial

Institutions Fry (1978)

Investments investible Funds which are utilized to

expand

the growth in the economy Elliot(1984).

10

REFERENCES

Bhatia, R.J. and D.R. Khatkhate (1973) ‘‘Interest rates, Savings, and Growth in

LDCs: An assessment of recent empirical research’’, World Development,

Vol. 16, No. 5

Elliot, J.W., (1984) Money, Banking and Financial Markets, New York; West

Publishing Company

Fry, M.J., (1978) ‘‘Money and Capital or Financial deepening in Economic

Development’’, Journal of Money, Credit and Banking, Vol. 10, No. 4

Luckett, D.G., (1984), Money and Banking, New York; McGraw Hill

McKinnon, R.I., (1973) Money and Capital Market in Economic Development,

Washington, DC; The Brookings Institution,.

Mwega, F.M., S.M. Ngola, and N. Mwangi, (1990), ‘‘Real interest rates and the

Mobilization of private savings in Africa: a case study of Kenya’’, AERC

Research Paper, African Economic Research Consortium, Nairobi.

Ndulu, BJ., (1990) ‘‘Growth and adjustment in Sub-Saharan Africa’’, a paper

Presented at the World Bank Economic Issues Conference, Nairobi, Kenya,

June

Osofisan, A.O., (1993) ‘‘An asset portfolio management model for Nigerian

Commercial Banks: a case study’’, Department of Economics, University of

Ibadan, MBA Project Report.

Revel J., (1975), Solvency and Regulation in Banks, Cardiff; University of Wales

Press

Ritter, L.S. and W.L. Siber, (1986), Principles of Money, Banking and Financial

Markets, New York; Basic Books Inc

Shaw, E., (1973), Financial Deepening in Economic Development, New York;

Oxford University Press,

Soyibo, A., (1991), ‘‘Managing bank assets in a depressed economy’’, a paper

11

Presented at the Union Bank of Nigeria Area Managers' Conference, Ibadan,

17-18 May.

Soyibo, A. and F. Adekanye, (1992), ‘‘Financial System Regulation, Deregulation

and Savings Mobilization in Nigeria’’, African Economic Research

Consortium, Nairobi

12

CHAPTER TWO: REVIEW OF RELATED LITERATURES

2.1 THEORIES OF INTEREST RATE

Several theories explained why interest is paid (Elliot, 1984). The theories of interest

can be divided into two; the monetary theories and the non-monetary theories. The

monetary theories are those theories of interest that stress the liquidity aspect of

money, while the non-monetary theories of interest are those theories which give

consideration to savings and productivity aspect of money. However, for the purpose

of this study, we shall examine the three theories of interest rate; the classical or

loanable funds theory, the liquidity performance theory (The Keynesian approach),

the general equilibrium approach (Soyibo and Adekanye, 1992).

2.1.1 THE CLASSICAL THEORY OF INTEREST RATE

The classical theory postulated that interest rate is an equilibrium factor between the

demand for and the supply of investible funds. The equality between savings and

investment is brought about by the mechanism of interest rate. When saving exceeds

investment, rate of interest will fall discouraging savings on one hand and

encouraging investment on the other hand. This tendency continues operating till

equality between savings and investment get established. Similarly, if investment

exceeds savings, rate of interest rises to discourage investment and encourage savings

till equality is established between savings and investment. Thus, classical system

regards rate of interest as the equilibrium force between savings and investment.

Classical economists approach to savings – investment equality is based on the

assumption of full employment in the economy system (Mwega,Ngola, and Mwangi,

1990).

13

2.1.2 KEYNESIAN THEORY

In the Keynesian system of aggregate, the terms savings and investment refer to the

aggregate saving and aggregate investment. Investment means production that is not

currently consumed. It may take the form of machinery, equipment, building or

increased investments of consumers’ goods. Savings is the amount of the current

income, which is not spent upon consumption (Soyibo and Adekanye, 1992). The

fundamental thing in this approach is that savings and investment are always and

necessary equal. In the word of the Keynesian “provided it is agreed that income is

equal to the value of the part of current output which is not consumed and savings is

equal to the excess of income over consumption, the equality of savings and

investment necessarily follows”.

Income = value of output = consumption + investment

Savings = income – consumption.

Savings = investment.

According to Keynesian the determination of interest rate will be found in the money

market and these are basically the supply and demand for money. He identified three

motives for the desires to hold cash; transaction motive, precautionary motive and

speculative motive (McKinnon, 1973).

The first two motives are influenced by the level of income, while the speculative

motive is influenced by the level of interest rate. Keynes argues that if there were no

interest receivable, people would hold their assets in the form of cash. To get people

to hold their wealth in any other form, we must be prepared to pay them interest

because there is a cost associated with the conversion of the securities into cash.

14

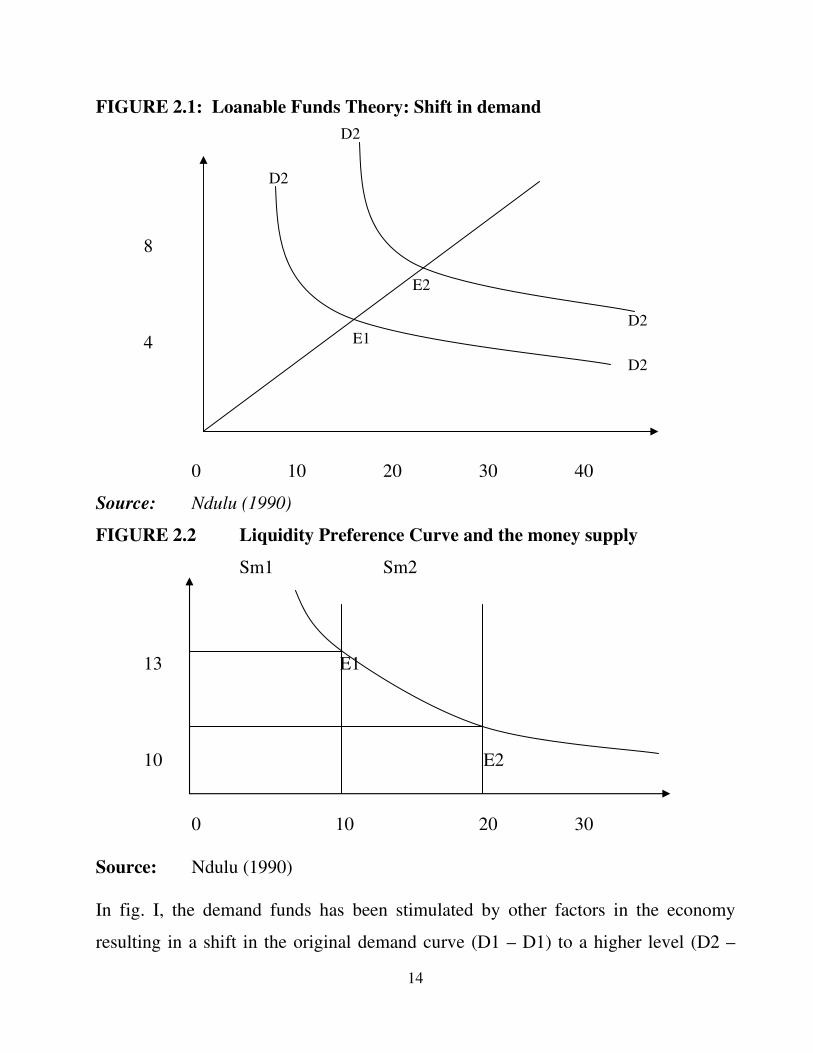

FIGURE 2.1: Loanable Funds Theory: Shift in demand

8

4

0 10 20 30 40

Source: Ndulu (1990)

FIGURE 2.2 Liquidity Preference Curve and the money supply

Sm1 Sm2

13 E1

10 E2

0 10 20 30

Source: Ndulu (1990)

In fig. I, the demand funds has been stimulated by other factors in the economy

resulting in a shift in the original demand curve (D1 – D1) to a higher level (D2 –

E1

E2

D2

D2

D2

D2

15

D2) as a result of the rise in the equilibrium rate or interest from points E1. In fig, II,

the money supply is plotted against the liquidity preference curve to demonstrate the

greater money supply, the lower the interest rates are likely to be. Liquidity

preference curve is intersected by Sm1 and Sm2, when money supply is at a lower

level (Sm1) interest rate are at 13% if supply of money increases to Sm2 this has the

effect of decreasing interest rate to 10% (Elliot, 1984).

2.1.3 THE GENERAL EQUILIBRIUM APPROACH (MODERN)

The modern theory of interest rate is superior to both the classical and the Keynesian

theories of interest rate (Osofisan, 1993). This is because it interests all the four

factors that is; savings, investment, the demand for money, and the supply of money

successfully. Modern theory of interest postulates that the equilibrium level of

money income and the equilibrium level of the rate of interest will be determined by

that particular combination of income and the rate of interest at which the double

condition of equilibrium stated below occurs given the savings, the investment, the

demand for money and the supply of money (Soyibo and Adekanye, 1992).

Thus;

I = S …………..(1)

Md = Ms ……..(2)

Where I represents investment

S represents savings

Md represents the Demand for money

Ms represents the supply of money.

According to equation one above, it them means that in the monetary sector of the

economy the demand for money is equal to the supply of money. In equation II,

investment and savings are in equilibrium in the real sector of the economy. The

16

theory claims that any other combination of income and the rate of interest either in

the monetary sector or in both sectors of the economy will be in dis-equilibrium. As

a result of this, money income and rate of interest will change until the level of

money income and that of the interest rate is re-established at which both sectors of

the economy are in equilibrium.

2.2 FACTORS WHICH CAUSES VARIATIONS IN THE INTEREST RATE

STRUCTURE

There are many factors that are responsible for the variation in the structure of

interest rate. These factors include (Adekanye, 1993).;

Rate of Inflation

Inflation can be defined as a general rise in overall price level. Criffiths, defined

inflation as a condition of generalized excess of demand of stocks of goods and flows

of real income, a rise in per capital income of stocks of flow of money income.

There is a need to distinguish between the normal interest rate and the real interest

rate in order to understand how the rate of inflation affects the level of interest rate.

Where the normal interest rate is straightforward rate, for example, 10%, the real

interest rate is the nominal rate adjusted for the expected rate of inflation. If inflation

rate is expected to exceed the level of interest during the period of the loan, the real

rate to the lender becomes negative. Therefore during the period of rapidly rising

inflation, lender expects a normal rate, which exceeds the expected inflationary rate.

The Fluctuation of the Supply of and Demand for Fund

There are different stages of the business cycle offering different columns of supply

and demand for funds. For instance, when the economy is on the peak stage (during

17

boom) the demand for fund tend to be greater than the supply of funds and thus raise

interest rates on the other hand, when the economy is declining the level of interest

rate falls as a result of slump in business activities because expected returns may not

be enough to offset the cost of capital.

Government Intervention

The government controls the rate of interest through the Central Bank. If the money

supply is reduced, interest rate will rise. The government does this by selling

securities ad in effect; controlling the rate on securities it wants to sell sufficiently so

that the public is attracted to purchase them quickly, this section government raises

interest rate.

Market Expectations

This also plays a role in causing the structure of the rate of interest to vary. When

inflation rate increases, it will raise the rate of interest and if market expectation in

that inflation rate is reduced and that a relaxed monetary control is in the pipeline, the

interest rate will fall because of the speculation.

2.3 THE CONCEPT OF SAVINGS AND INVESTMENT

This distinction between savings and investment is that they are separate acts

accomplished largely by different people and for different purpose, thus while

savings is done by households and business as well as government, investment is

done excessively by businessmen (Mwega,Ngola, and Mwangi, 1990). Savings

simple definition shows it as the act of net spending income or consumption, while

investment simply means the expenditure of funds leading to the creation of wealth

net addition to the stock of physical capital like machines, factories, other building

18

are investment. Savings then is that portion of income, which is not devoted to the

purchasing of consumer goods and services.

Macro economics defines interest in a way that it refers only to real capital goods, the

purchase of which injects a flow of money in the economy (McKinnon, 1973). Gross

private investment is divided into three distinct components thus; business fixed

investment, residential construction and net change in business inventories. Each of

these is being determined by substantially different sets of factors. There are three

types of savings on deposits kept with the bank, these are; savings, time deposits and

demand deposits. The savings and demand deposits are volatile accounts because

these accounts are easily introduced into by their owner. Time deposit is a much

more predictable account because it has a definite time dimension attached to it. In

our analysis it is important to recognize the fact that most savings are voluntary and

depends on a wide range of factors particularly the level of income. i.e., the

household, firms and government all save and that each of these three sectors uses

savings to make investment (Elliot, 1984).

In an economic sense therefore, investment is required for the following purposes;

for the business to buy new premises, machinery and to raise the fund to finance

increased manufacturing capacity, for public sector to carry out public works such as

building news or reconstruction of houses, roads, schools and hospital etc, for

individual to buy or improve existing houses, or other fixed assets and for banks,

Invest the customers’ deposits to the other projects like investing in another bank for

profit (Mwega,Ngola, and Mwangi, 1990). Thus investment increases a country’s

productive capacity and raises the standard of living. The processes of savings and

investment play central roles in the circular flow of income and in determining the

level of income (Soyibo and Adekanye, 1992). .

19

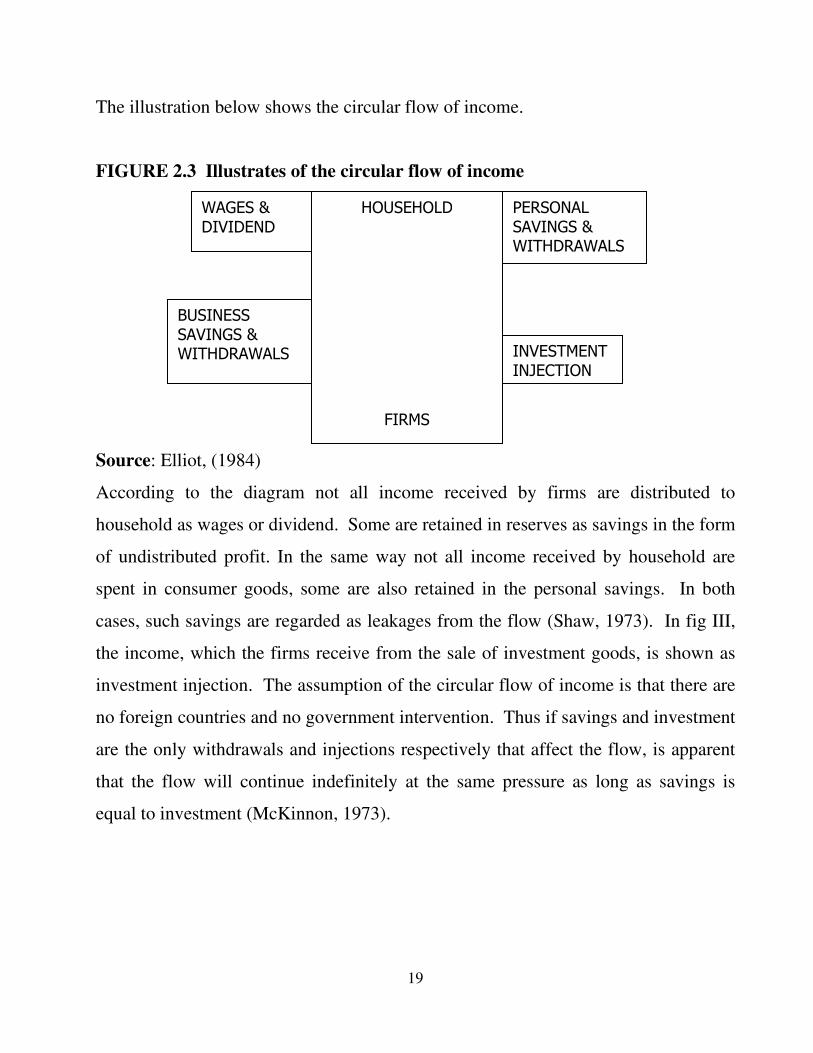

The illustration below shows the circular flow of income.

FIGURE 2.3 Illustrates of the circular flow of income

Source: Elliot, (1984)

According to the diagram not all income received by firms are distributed to

household as wages or dividend. Some are retained in reserves as savings in the form

of undistributed profit. In the same way not all income received by household are

spent in consumer goods, some are also retained in the personal savings. In both

cases, such savings are regarded as leakages from the flow (Shaw, 1973). In fig III,

the income, which the firms receive from the sale of investment goods, is shown as

investment injection. The assumption of the circular flow of income is that there are

no foreign countries and no government intervention. Thus if savings and investment

are the only withdrawals and injections respectively that affect the flow, is apparent

that the flow will continue indefinitely at the same pressure as long as savings is

equal to investment (McKinnon, 1973).

WAGES &

DIVIDEND

PERSONAL

SAVINGS &

WITHDRAWALS

HOUSEHOLD

FIRMS

INVESTMENT

INJECTION

BUSINESS

SAVINGS &

WITHDRAWALS

20

2.4 FACTORS INFLUENCING SAVINGS AND INVESTMENT

In a capitalist society, investment is undertaken mainly by firms whose objectives are

to make a profit as well as by government whose own objective is not necessarily to

make a profit but also for the welfare of its citizens. Although government

investment accounts for a lesser percentage of the total fixed investment which

includes the construction of roads, hospital, schools, etc. government however, take

decision to invest or not in the height of economic, political and social requirement.

Therefore, these are not particularly influenced by the profit motive. A business firm

is likely to invest in new capital expenditure only if the net return it expects to gain is

at least sufficient to cover the following: the cost of capital and the rate of interest on

the money involved.

Net return refers to the increase in the revenue of the firm after allowance has been

made for the maintenance and operating cost. The outstanding characteristic of

investment is its volatility as it rises sharply in boom periods and drops in

depressions. Investment depends on the expected rate of profit to be obtained from

additions to physical capital. In a nutshell investment depends on either major

factors; the level of national income, the level of the rate of interest, technological

advances and innovations, changes in size and distribution of population of expected

volume of sales, changes in government expenditure or taxes, prospects for demand

and future levels of cost and the state f business confidence and influence by other

government policies, international affairs, stock market or tangible elements in the

business environment(Adekanye, 1993)..

Savings in the complement of consumption factors which affects consumption and

savings also change with it (Osofisan, 1993). Thus, existence of a propensity to

consume implies a propensity to save. The propensity to save is the relationship

21

between savings and income. Income is the principal determinant of savings thus

when income rises, both savings and consumption rise vice versa. There are two

main reasons why people save in an economy, these are; for specific purpose and for

unspecific purpose. People may save for a specific reason or purpose. These

purposes include payment such as to pay for motor vehicle. Saving for unspecific

purpose includes savings for the rainy day or to have something to fall back on in the

event of some unexpected occurrence in the future.

2.5 INTEREST RATE LEVEL OF SAVINGS AND INVESTMENT

The analysis of savings and investment in any economy cannot be derived from an

understanding of the nature, meaning and role of interest rate in economy (Fry,

1978). Having defined the rate of interest and extensively reviewed its theories as

well as the factors that cause variations in its structure, it is pertinent to analyze

critically the nature of interest rate and how it determines the level of savings and

investment. There are basically two forms of interest rate (Luckett, 1984), which can

be allowed to depositors or charges to borrowers, they are; the fixed interest rate and

the fluctuating interest rate. When the interest rate is fixed it means that the depositor

knows in advance the amount of interest that will be allowed or charged on his/her

deposits and the borrower also know how much to be charge on his/her loan in

advance. Fluctuating rates are those that allow alternation or are liable to alteration

either upwards or downwards or with little or no notice. There are four theories that

discuss fluctuation in interest rates, these are (Osofisan, 1993);

1. The abstaince theory or classical theory of interest rate.

2. The loanable funds or neo-classical theory of interest rate.

3. The liquidity preference of Keynesian theory of interest rate.

4. The modern theory of the neo-Keynesian theory of interest rate.

22

It has been proved beyond doubts that interest rate at least has an influence on

savings and investment (Ritter and Siber, 1986). Conventional wisdom informs us

that when the interest rate is high, the level of savings will rise because depositors

will profit, as he will have more returns on his deposits. In the same view, if the

interest rate falls, the level of savings will drop, as people will not be motivated to

save. On the contrary, if the level of interest rate rises, the level of investment falls

because the cost of acquiring funds becomes expensive and when the level of interest

drops, the level of investment rises as the cost of acquiring funds for investment

purposes is reduced. In order to understand how the interest rate influences savings

and investment we shall review the following; investment demand for output, he

supply of savings, the marginal responsiveness of investment demand to interest rate

and the investment demand and the supply of savings (Luckett, 1984),.

2.6 THE SUPPLY OF SAVINGS

The supply of savings is viewed from two different perspectives; at any level of

income, it is the sum of personal savings, gross business savings and government

savings. This view emphasizes the supply of savings as potential sources of funds to

finance private investment and the total value of output minus that value of output for

personal consumption and by government. This view makes it clear that a decrease of

savings at any level of income reflects an equal increase of the demand for output at

that level of income in the form of consumption and government demand and vice

versa (Soyibo and Adekanye, 1992).

2.7 THE PROBLEMS OF BANK LENDING AND DEPOSIT IN NIGERIA

A lot of factors reduce the ability of banks to lend money to their clients. According

to Oladele (1985), the following four factors are constraints to banks lending in

Nigeria.

23

1. Personal limitation of the officer is one of the problems of banks lending in

Nigeria. Under this factor, the ability of the lending officer to interpret the

financial data of borrowing customer in order to determine the influence and

ability of the customer to service the loan facility granted is very important.

2. Limitations created by borrower are a major problem, which hinders the

chances of borrowing. In some cases proper feasibility studies are not carried

out on a project to establish its viability or resist risk before asking for loans.

In such a case, a firm has to give the lending officer false impression of the

viability of the business.

3. Limitations imposed by the institutions for instance efficiently managed banks

do prescribe priority sector for their lending and establish discretionary lending

limit for their officers and offices.

4. Banks are also constrained by specific laws and regulations, which are

intended to control them by the government such laws, include the following;

amount of capital available to savers, interest paid on the deposits, financial

markets, banking habit and record of bank performance

As savings is the excess of income of expenditure, it then means that to save one

must have an income that exceeds his/her expenditure (Bhatia and Khatkhate, 1973).

But in Nigeria where per capital income is very low, deposits are also very low.

Interest paid on capital or deposit also influences the level of savings. Interest is the

price for use of money. There is a direct relationship between interest rate on deposit

and the volume of deposit. A high rate is an inducement for people to save. A

financial market is one where securities are traded. A developed financial market has

one of its advantages, the duty of keeping investors and potential investors informed

on the economic activity in the economy (Osofisan, 1993).

24

In Nigeria, the banking habits are not developed (Soyibo, 1991). The average

Nigerian still believes the best way to save is not by keeping our money in the bank

but in communal meetings that exist in our communities and keeping ones money

under the mattress where it is easily accessible. Under this particular sector, large

blame goes to illiteracy and ignorance on the part of the public as it is deemed that

depositing money in a bank requires many formalities and bureaucracy. As a result

of this they find other means of saving their money. The final factor, which

influences the depositor in the banks, is the efficient performances of the banks. As

effective management will induce a lot of people to save; this is because there will be

confidence. Furthermore, banks should be courteous and realize the importance of

the customers.

2.8 EFFECTS OF INTEREST RATE POLICIES ON THE NIGERIAN

ECONOMY

When we analyze the interest rate policies in Nigeria, we are as a matter of fact

referring to two prominent policies, for example; the regulated policy and the

deregulated policy (Adekanye, 1993).

Under the regulated policy, the minimum and maximum interest rate for both loans

and deposits are explicitly specified. Although the regulated policy has its advantages

at least for the fact that it came into operation, it means that there is an interest

problem in the financial system, which it came to correct. However, its major defeat

was its regardless and inflexibility (thus no bank dear charges below or above the

stated interest levels). During the period when the regulated policy was in separation,

there was not significance change in the Nigerian economy. On the point of the

general policy, there was not general awareness of the role of the interest rate. Until

in 1987 when the Central Bank of Nigeria announced the deregulation of the interest

25

rate, i.e, they abolished with effect from august 1st, 1987, all control on interest rate,

hence they will now be determined by the forces of demand and supply (Osofisan,

1993). The deregulation of the interest rate in Nigeria is part of the Structural

Adjustment Program, which was designed to remove the fundamental structural

distortion prevalent in the Nigeria economy since the 1970s. Explaining the rationale

behind this measure, the Central Bank of Nigeria said that, it is recognition of the fact

that effects of interest rate control have been more adverse than favourable in

promoting the development of financial system. Hence the proper thing to do is to

allow interest rate to be determined by the forces of demand and supply in line with

the whole objectives of the Structural Adjustment Program (Adekanye, 1993).

The protagonist of the deregulation of interest rate based their judgment on the fact

that, it will encourage the inflow of capitals, which the economy requires to increase

productivity (Ritter and Siber, 1986). It is also hoping that it will stimulate savings

by making interest on deposits that are expected as a result, these policies include; It

is aimed at stimulating domestic financial savings as a result of high rates to be paid

to deposition, those who normally keep their money under the pillows or big holes

will not keep them in the banks in order to benefit from this high rate, It is aimed at

stimulating efficient resource allocation, the dynamic interest rate is also aimed at

attracting foreign investors. Given the profit maximization objectives and every

business entrepreneur there is the tendency to be attracted to where those objectives

will be achieved, deregulation of interest rate will lead to more efficient allocation of

financial market resources because interest rate will now reflect relative scarcity and

relative efficiency in different uses and the challenges of the deregulation provide the

condition for more innovations in the banking sector. It will lead to gradual

extinction of the armchair banking.

26

Deregulation of the interest rate has achieved most of its aims, but some are two sides

of a coin, the deregulation of interest rate has its good and bad effect on the economy.

Although it has brought about keen competition for customers among the banks,

customers can no negotiate for higher deposit rates and bankers now have t canvass

for customers. A higher lending rate has brought sanity into the borrowing habits of

Nigerians (Soyibo, 1991). Investors seeking loans are now more selective and

careful in the way they dispense money on projects. In the same vein, rate of deposits

have attracted enormous savings. However, the deregulation of interest rates has

been received with mixed feeling in certain circle. With the bank’s lending rate of

about 19.18% and the minimum liquidity ratio raised from 25% to 30%, the amount

of funds available to commercial banks for credit purposes has been lowered. It is

feared that this will cause greater credit squeeze in the economy (Revel 1975).

Government financing of developing projects will be adversely affected since given

the rationality of investors, people will patronize banks with high rates on deposits

than investment in government development projects. There are some fears that new

interest rate structure may create more inflation in the long run and thus, will further

compound the problem of unemployment. There is also the fear the much talked

about capital flight may not be crushed. This is because; the problem of foreign

investment is not lack of economic incentive, but that of lack of confidence in

Nigerian system as a whole. However, the empirical effect of interest rate on savings

and investment represented by deposits and loans will be determined (Fry, 1978).

27

REFERENCES

Adekanye, F.A., (1993) ‘‘Commercial bank performance in a developing economy: a

Multivariate regression analysis approach’’, PhD thesis, Department of

International Banking and Finance, Business School, City University, London

Bhatia, R.J. and D.R. Khatkhate (1973) ‘‘Interest rates, Savings, and Growth in

LDCs: An assessment of recent empirical research’’, World Development, Vol.

16, No. 5

Elliot, J.W., (1984) Money, Banking and Financial Markets, New York; West

Publishing Company

Fry, M.J., (1978) ‘‘Money and Capital or Financial deepening in Economic

Development’’, Journal of Money, Credit and Banking, Vol. 10, No. 4

Luckett, D.G., (1984), Money and Banking, New York; McGraw Hill

McKinnon, R.I., (1973) Money and Capital Market in Economic Development,

Washington, DC; The Brookings Institution.

Mwega, F.M., S.M. Ngola, and N. Mwangi, (1990), ‘‘Real interest rates and the

Mobilization of private savings in Africa: a case study of Kenya’’, AERC

Research Paper, African Economic Research Consortium, Nairobi.

Ndulu, BJ., (1990) ‘‘Growth and adjustment in Sub-Saharan Africa’’, a paper

Presented at the World Bank Economic Issues Conference, Nairobi, Kenya,

June

Nigeria Deposit Insurance Corporation (NDIC), (1989) Annual Reports and

Statement of Accounts, Lagos, December 31

Osofisan, A.O., (1993) ‘‘An asset portfolio management model for Nigerian

Commercial Banks: a case study’’, Department of Economics, University of

Ibadan, MBA Project Report.

Revel J., (1975), Solvency and Regulation in Banks, Cardiff; University of Wales

Press

Ritter, L.S. and W.L. Siber, (1986), Principles of Money, Banking and Financial

28

Markets, New York; Basic Books Inc

Shaw, E., (1973), Financial Deepening in Economic Development, New York;

Oxford University Press

Soyibo, A., (1991), ‘‘Managing bank assets in a depressed economy’’, a paper

Presented at the Union Bank of Nigeria Area Managers' Conference, Ibadan,

17-18 May.

Soyibo, A. and F. Adekanye, (1992), ‘‘Financial System Regulation, Deregulation

and Savings Mobilization in Nigeria’’, African Economic Research

Consortium, Nairobi

29

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 RESEARCH DESIGN

According to Onwumere (2005), a research design is a kind of blue print that guides

the researcher in his/her investigation and analysis. It is a format in which the

researcher employs in order to systematically apply the scientific method in the

investigation of problems.

The research design employed in this research is the ex-post facto research design.

This is because, the researcher does not aim to control any of the variables under

investigation and our pre-disposition is to observe occurrence over a period of time

(1970-2008). Another justification for the research design is the desire of the

researcher to use secondary data to test the hypothesis formulated. These are already

existing data, thus, cannot be manipulated by the researcher.

3.2 NATURE AND SOURCES OF DATA

Data refers to facts, information, ideas which can be represented in figures, charts and

graphs (Ozo, Odo, Ani and Ugwu, 2007). The nature and sources of data for this

research is secondary data sources. The secondary data source is through the Annual

Reports and Accounts of the Central Bank of Nigeria (CBN) under consideration in

the research.

Data will be collected first hand from the original source, and from data collected and

extracted from the Annual statements and accounts the Central Bank of Nigeria

(CBN).

30

3.3 SAMPLE SIZE / SAMPLING TECHNIQUES

The idea of sampling or determining sample size is to obtain a part of the population

from which some information about the entire population can be inferred. Sample in

this research refers to the portion of the universe or population which reasonable

reflects opinions, attitudes or behaviour of the entire groups.

The sampling technique adopted in this research is the non-probability sampling

method. The major non-probability sampling method adopted is the convenience

sampling method. In this case, sampling is based upon the convenience of the

researcher. Since the sample size is based on the immediate elements within his

surroundings, the elements the research can reach out and the number of elements

which we believe is convenient for this research necessitated the use of this sampling

technique. Also, the choice of the period is based on the availability of Data. Thus we

assume it will show trend on the impact of interest rate on Savings and Investment as

well as the impact of Savings on Investment.

3.4 MODEL SPECIFICATION

A model is a simplified view of reality deigned to enable a researcher describe the

essence and inter relationship within the system or phenomenon it depicts

(Onwumere, 2005). The hypotheses will be tested using the Simple Linear Regression

Model.

In writing the model equation, the following symbols were used to denote their

respective variables.

INT = Interest rate

SAV = Savings rate

31

INV = Investment rate

a = Constant of the equation

b = Coefficient of the independent variable

u = Error terms

Thus, for hypothesis one which states that Interest rate does not have positive

significant relationship Savings rate in Nigeria,

It was represented by the equation.

SAV = a + INT (b) + u …………............................................................ (i)

For hypothesis two, which states that Interest rate does not have a positive significant

impact on investment in Nigeria, it was represented by the equation

INV = a + INT (b) + u ………................................................................ (ii)

For hypothesis three, which states that Savings does not have a positive significant

impact on investment in Nigeria, it was represented by the equation

INV = a + SAV (b) + u ………................................................................ (ii)

3.5 TECHNIQUES OF ANALYSIS

As stated, data will be analyzed using our statistical tools of Simple Linear

Regression model (using the SPSS Statistical software package) because it is utilizes

for the purpose of prediction where the independent variable is used to obtain a better

32

prediction of dependent variable (Ozo, Odo, Ani and Ugwu, 2007). This was

necessitated by our use of secondary data collected from the Annual Reports and

Accounts of the Central Bank of Nigeria (CBN) for the period 1970- 2008. Thus,

given the general form of the simple linear regression model given in 3.4, the

following formulas will be used to determine the slope of the regression line and the

Y-intercept (Douglas, Willian and Mason, 2002). This will enable us determine the

impact of interest rate on savings and investment in Nigeria. Thus

b = n (∑ XY) - (∑ X) (∑ Y)

n ((∑ X2) - (∑ X

2)

a = ∑Y - b ∑ X

n n

We will analyze each microfinance bank separately within the scope under review

and also in aggregate. Thus, it is hoped that inferences will be drawn from the

analyses.

33

REFERENCES

Douglas, A. L., W. G. Willian and R. D. Mason (2002) Statistical Techniques in

Business And Economics, Boston; Mc-Graw Hill Irwin

Onwumere, J. U. J (2005), Business and Economics Research Method, Lagos; Don

Vinton Limited

Ozo, J. O. Ani and T. U, Ugwu (2007), Introduction to Project Writing for Business

And Financial Studies, Enugu; New Dimension Publishers

34

CHAPTER FOUR

PRESENTATION AND ANALYSES OF DATA

4.1 INTRODUCTION

This chapter deals with the presentation of data sourced from secondary sources

(Central Bank of Nigeria Statistical Bulletin). As stated in chapter Three, the

statistical tool to be used is the simple linear regression which was run using SPSS

software.

4.2 DATA PRESENTATION

TABLE 4.1 SAVINGS RATE, SAVINGS DEPOSIT AND LOANS AND

ADVANCES (INVESTIBLE FUNDS) (1970-2008)

YEAR WEIGHTED DEPOSIT

AND LENDING RATE

AGGREGATE SAVINGS

DEPOSIT

AGGREGATE LOANS

AND ADVANCES

(INVESTABLE FUNDS)

(%) N = MILLIONS N = MILLIONS

1970 3.00 129.70 351.50

1971 3.00 160.40 502.00

1972 3.00 200.90 619.50

1973 3.00 224.90 753.50

1974 3.00 286.70 938.10

1975 4.00 521.30 1,437.50

1976 4.00 709.20 2,123.00

1977 4.00 930.10 4,313.50

1978 5.00 1,075.70 4,114.90

1979 5.00 1,283.80 4,630.40

1980 6.00 1,589.50 6,349.10

1981 6.00 1,979.20 8,582.90

1982 7.50 2,321.20 10,275.30

1983 7.50 2,879.30 11,093.90

35

1984 9.50 3,361.30 11,503.90

1985 9.50 3,699.90 12,170.20

1986 9.80 4,270.20 15,701.60

1987 14.00 5,206.70 17,531.90

1988 14.50 7,122.70 19,561.20

1989 16.40 9,237.80 22,008.00

1990 18.80 13,013.50 26,000.00

1991 14.29 19,395.30 31,306.20

1992 16.10 26,071.10 42,736.80

1993 16.66 37,054.80 65,665.30

1994 13.50 49,601.10 66,127.60

1995 12.61 52,135.00 114,883.90

1996 11.69 68,770.90 169,437.10

1997 4.8 84,099.50 385,550.50

1998 5.49 101,373.50 272,895.50

1999 5.33 128,365.80 1,265,984.40

2000 5.29 164,624.30 1,795,768.30

2001 5.49 216,509.40 2,796,112.20

2002 4.15 244,084.10 3,606,229.10

2003 4.11 312,368.90 4,339,443.00

2004 4.19 359,311.20 5,686,669.40

2005 3.83 401,986.80 7,468,655.10

2006 3.13 592,514.80 9,542,573.80

2007 3.24 753,868.80 15,285,128.80

2008 NA 1,091,812.20 27,153,935.40

Source: CBN Statistical Bulletin, Volume 18 (2009)

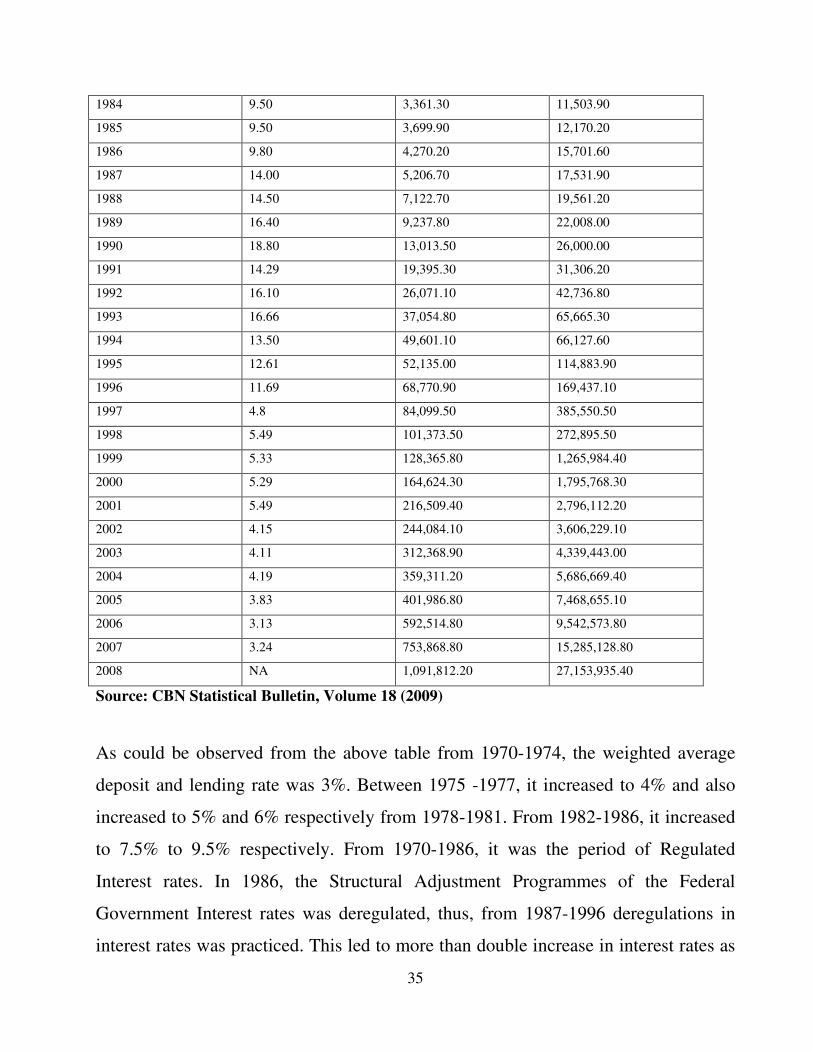

As could be observed from the above table from 1970-1974, the weighted average

deposit and lending rate was 3%. Between 1975 -1977, it increased to 4% and also

increased to 5% and 6% respectively from 1978-1981. From 1982-1986, it increased

to 7.5% to 9.5% respectively. From 1970-1986, it was the period of Regulated

Interest rates. In 1986, the Structural Adjustment Programmes of the Federal

Government Interest rates was deregulated, thus, from 1987-1996 deregulations in

interest rates was practiced. This led to more than double increase in interest rates as

36

could be observed from the table above. It peaked in 1990 when it rose to 18.8%,

however deregulation was abandon in 1996, this reflected in fall in interest rates to

4.8% in 1997 and since it has remain regulated till 2008. 2006 has witnessed the

lowest rates (3.13%) while 1998 and 2001 has had the highest from 1997-2008.

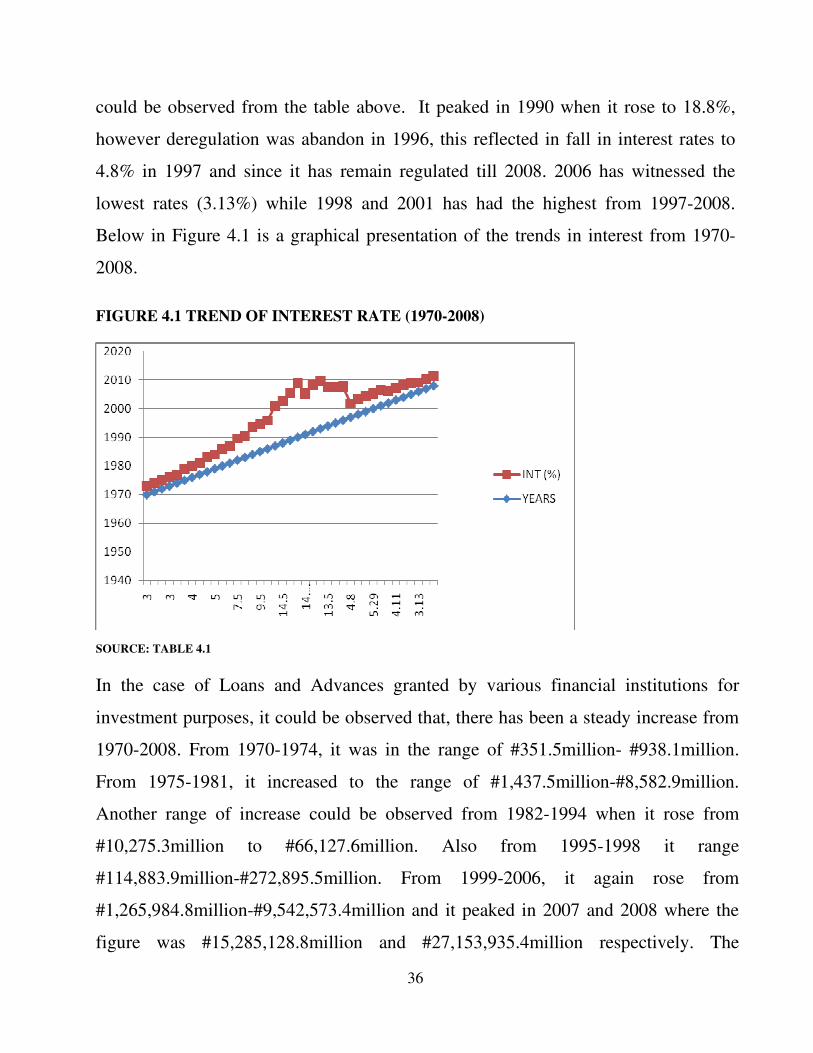

Below in Figure 4.1 is a graphical presentation of the trends in interest from 1970-

2008.

FIGURE 4.1 TREND OF INTEREST RATE (1970-2008)

SOURCE: TABLE 4.1

In the case of Loans and Advances granted by various financial institutions for

investment purposes, it could be observed that, there has been a steady increase from

1970-2008. From 1970-1974, it was in the range of #351.5million- #938.1million.

From 1975-1981, it increased to the range of #1,437.5million-#8,582.9million.

Another range of increase could be observed from 1982-1994 when it rose from

#10,275.3million to #66,127.6million. Also from 1995-1998 it range

#114,883.9million-#272,895.5million. From 1999-2006, it again rose from

#1,265,984.8million-#9,542,573.4million and it peaked in 2007 and 2008 where the

figure was #15,285,128.8million and #27,153,935.4million respectively. The

37

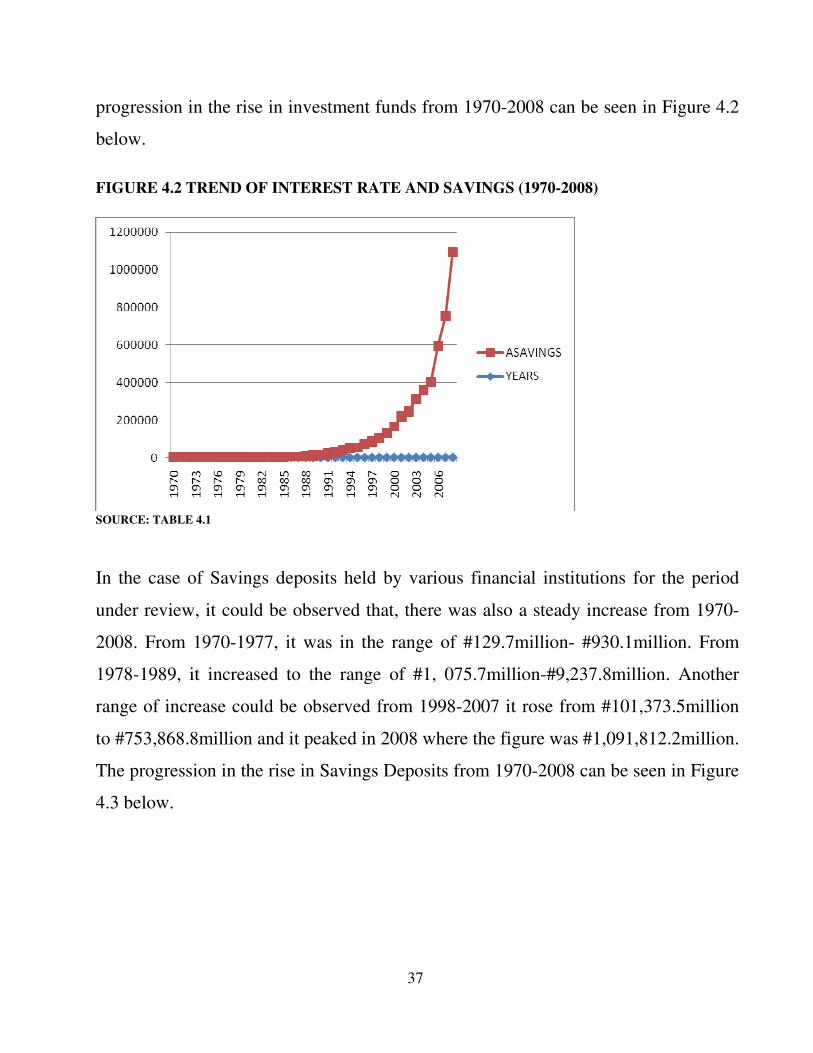

progression in the rise in investment funds from 1970-2008 can be seen in Figure 4.2

below.

FIGURE 4.2 TREND OF INTEREST RATE AND SAVINGS (1970-2008)

SOURCE: TABLE 4.1

In the case of Savings deposits held by various financial institutions for the period

under review, it could be observed that, there was also a steady increase from 1970-

2008. From 1970-1977, it was in the range of #129.7million- #930.1million. From

1978-1989, it increased to the range of #1, 075.7million-#9,237.8million. Another

range of increase could be observed from 1998-2007 it rose from #101,373.5million

to #753,868.8million and it peaked in 2008 where the figure was #1,091,812.2million.

The progression in the rise in Savings Deposits from 1970-2008 can be seen in Figure

4.3 below.

38

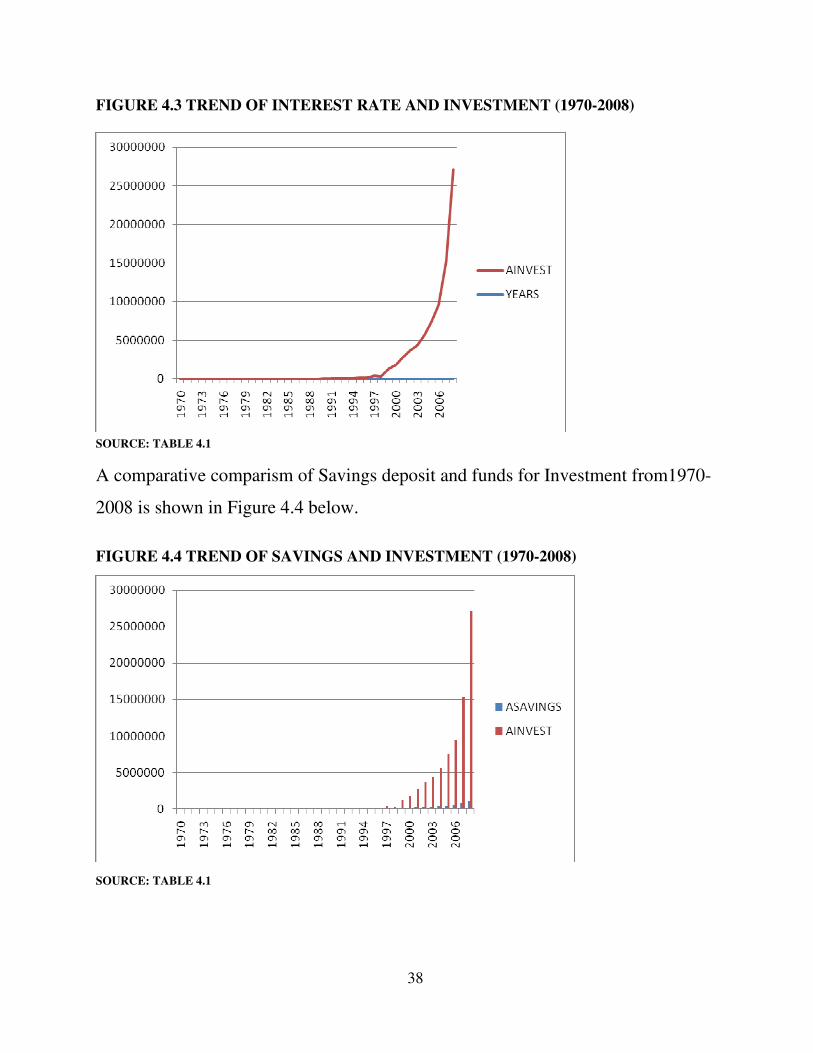

FIGURE 4.3 TREND OF INTEREST RATE AND INVESTMENT (1970-2008)

SOURCE: TABLE 4.1

A comparative comparism of Savings deposit and funds for Investment from1970-

2008 is shown in Figure 4.4 below.

FIGURE 4.4 TREND OF SAVINGS AND INVESTMENT (1970-2008)

SOURCE: TABLE 4.1

39

4.3 TEST OF HYPOTHESES

Below in a tabular form are the extract of the analysed results. The test of hypotheses

was done in three steps. These are;

Step One: Restatement of Hypothesis

Step Two: Presentation of SPSS model results

Step Three: Decision Criterion and

Step 4: Decision

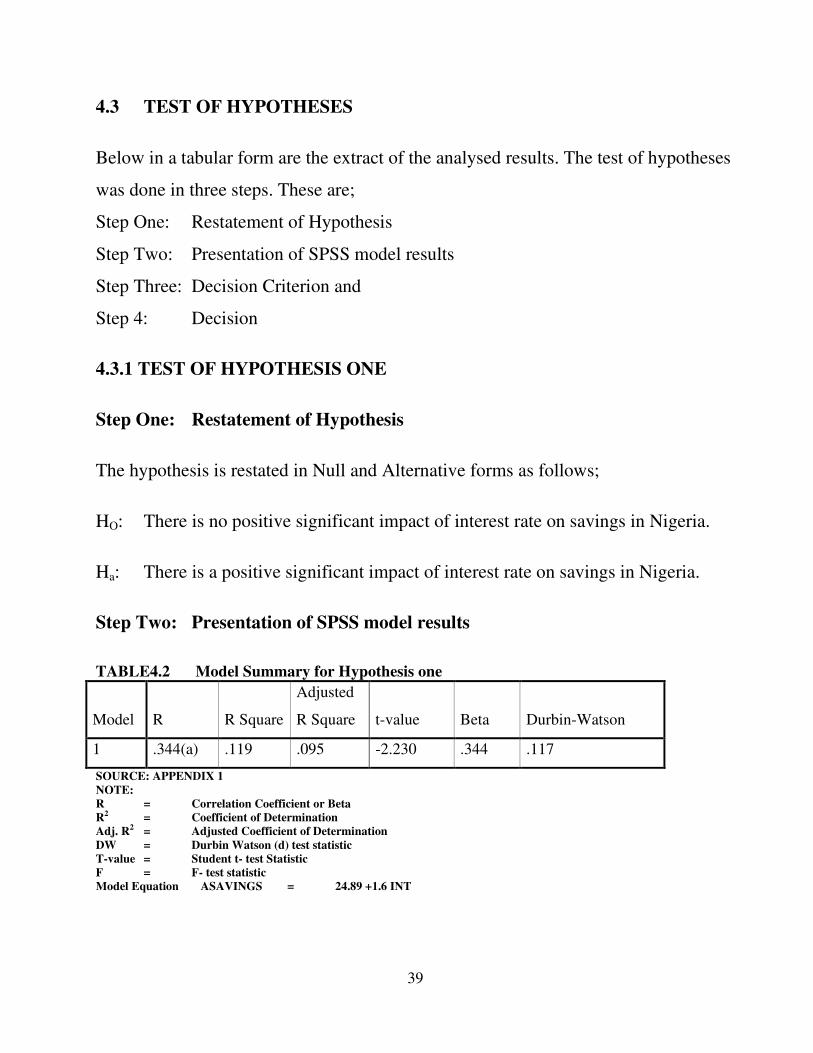

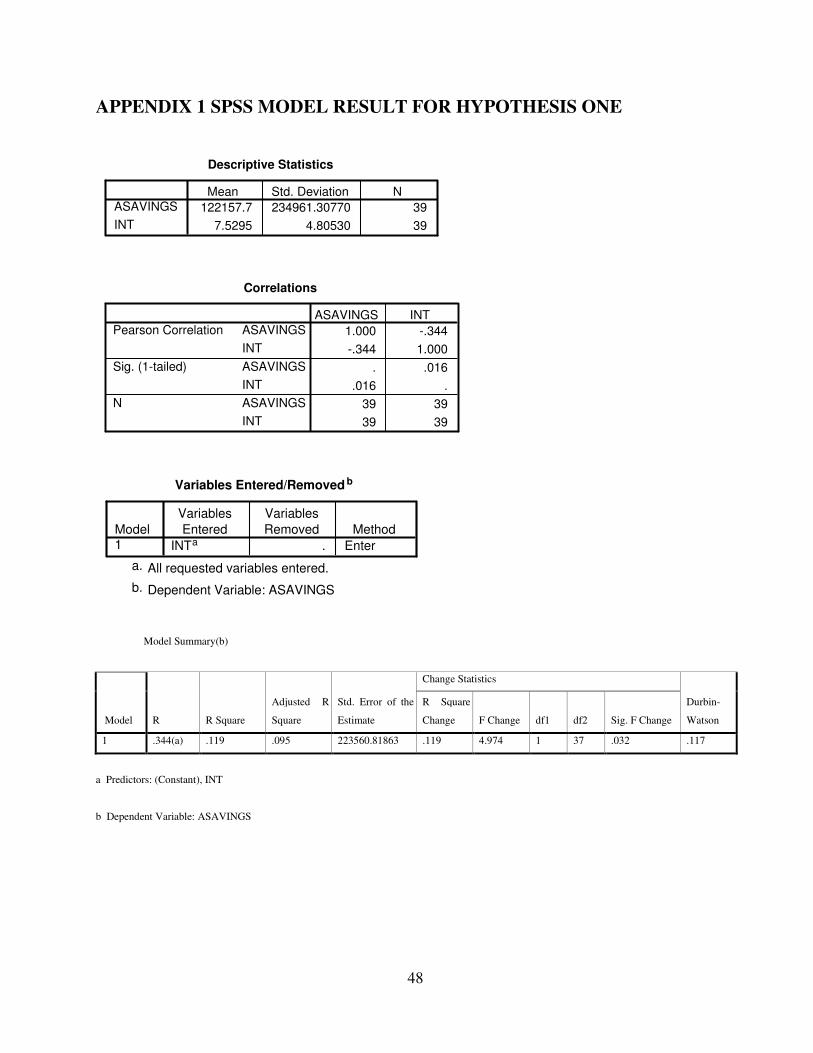

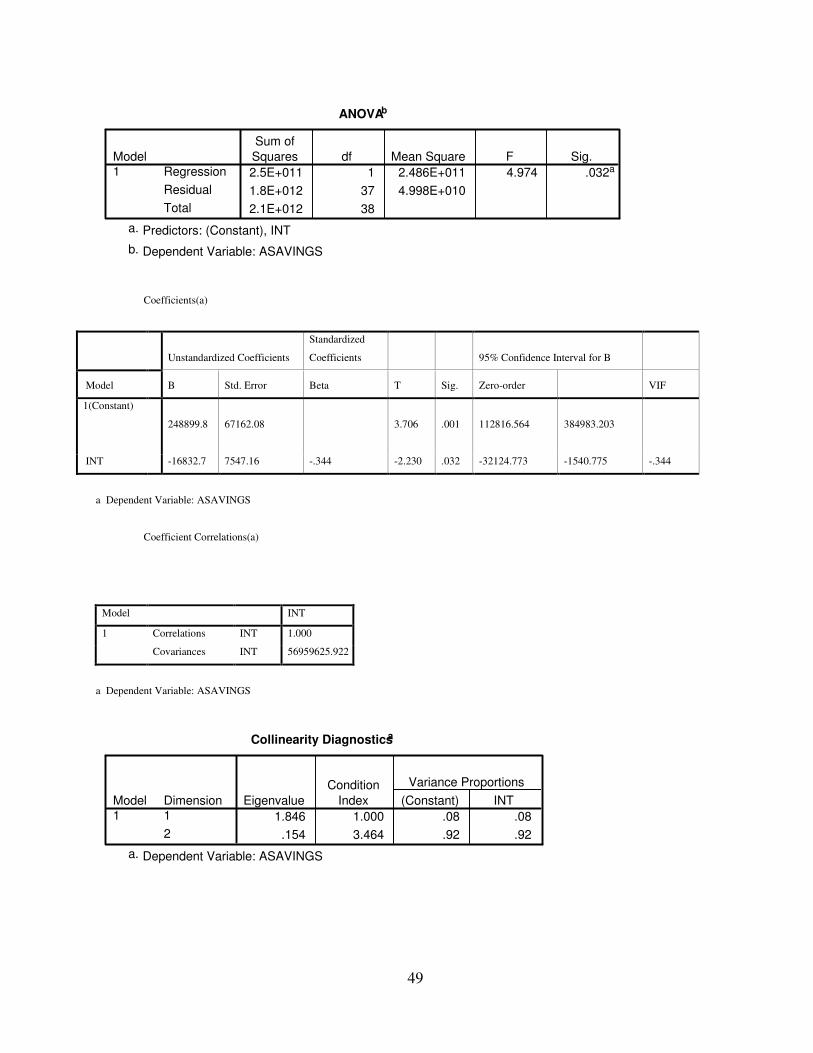

4.3.1 TEST OF HYPOTHESIS ONE

Step One: Restatement of Hypothesis

The hypothesis is restated in Null and Alternative forms as follows;

HO: There is no positive significant impact of interest rate on savings in Nigeria.

Ha: There is a positive significant impact of interest rate on savings in Nigeria.

Step Two: Presentation of SPSS model results

TABLE4.2 Model Summary for Hypothesis one

Model R R Square

Adjusted

R Square t-value Beta Durbin-Watson

1 .344(a) .119 .095 -2.230 .344 .117

SOURCE: APPENDIX 1

NOTE:

R = Correlation Coefficient or Beta

R2 = Coefficient of Determination

Adj. R2 = Adjusted Coefficient of Determination

DW = Durbin Watson (d) test statistic

T-value = Student t- test Statistic

F = F- test statistic

Model Equation ASAVINGS = 24.89 +1.6 INT

40

Step Three: Decision Criterion

The t–value is – 2.230 and from the equation the coefficient of Interest rate is 1.6,

thus there is a positive significant impact of interest rate on aggregate savings. The

correlation coefficient (R) is 0.344 but the beta indicates that it has a positive

correlation, thus, increase in interest rate leads to an increase in aggregate savings for

the periods under study. The variation that can be explained by the correlation is 12%

as indicated by the coefficient of determination. A d-test statistic value of 0.117

shows no autocorrelation.

Step 4: Decision

From the above, the Null hypothesis is rejected and the Alternative hypothesis which

states there is a positive significant impact of interest rate on savings in Nigeria is

accepted.

4.3.2 TEST OF HYPOTHESIS TWO

Step One: Restatement of Hypothesis

The hypothesis is restated in Null and Alternative forms as follows;

Ho: There is no positive significant impact of interest rate on Investment in

Nigeria.

Ha: There is positive significant impact of interest rate on Investment in

Nigeria.

41

Step Two: Presentation of SPSS model results

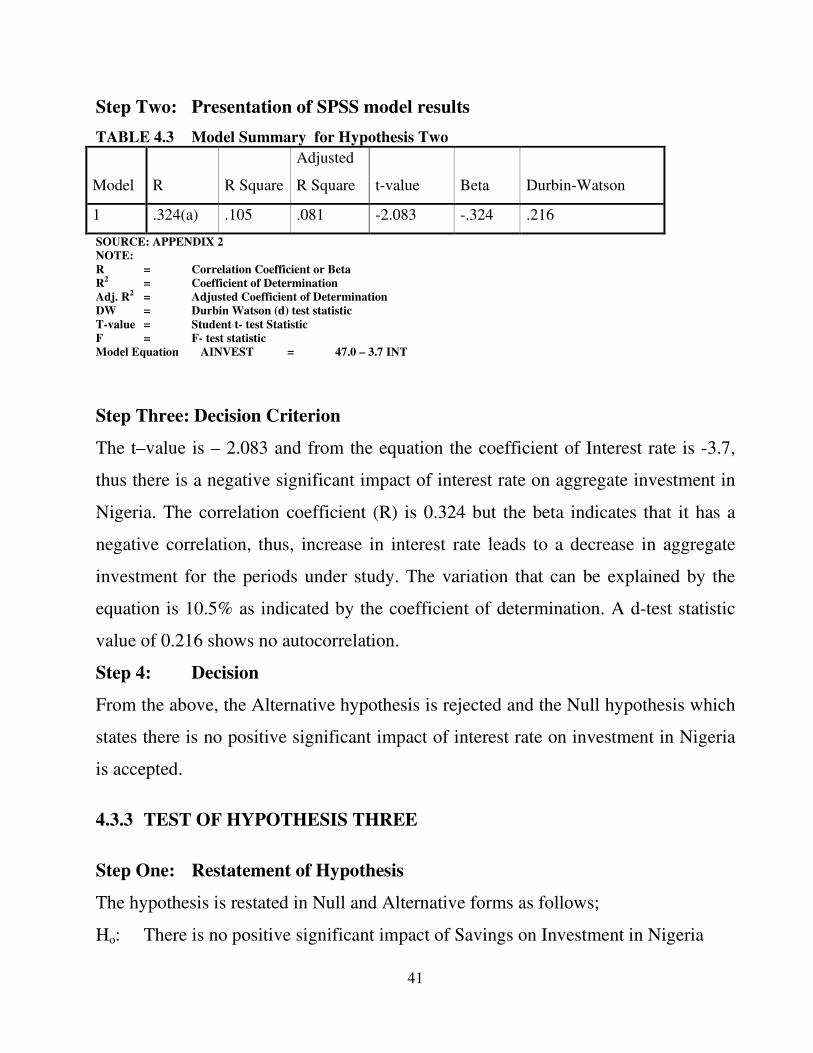

TABLE 4.3 Model Summary for Hypothesis Two

Model R R Square

Adjusted

R Square t-value Beta Durbin-Watson

1 .324(a) .105 .081 -2.083 -.324 .216

SOURCE: APPENDIX 2

NOTE:

R = Correlation Coefficient or Beta

R2 = Coefficient of Determination

Adj. R2 = Adjusted Coefficient of Determination

DW = Durbin Watson (d) test statistic

T-value = Student t- test Statistic

F = F- test statistic

Model Equation AINVEST = 47.0 – 3.7 INT

Step Three: Decision Criterion

The t–value is – 2.083 and from the equation the coefficient of Interest rate is -3.7,

thus there is a negative significant impact of interest rate on aggregate investment in

Nigeria. The correlation coefficient (R) is 0.324 but the beta indicates that it has a

negative correlation, thus, increase in interest rate leads to a decrease in aggregate

investment for the periods under study. The variation that can be explained by the

equation is 10.5% as indicated by the coefficient of determination. A d-test statistic

value of 0.216 shows no autocorrelation.

Step 4: Decision

From the above, the Alternative hypothesis is rejected and the Null hypothesis which

states there is no positive significant impact of interest rate on investment in Nigeria

is accepted.

4.3.3 TEST OF HYPOTHESIS THREE

Step One: Restatement of Hypothesis

The hypothesis is restated in Null and Alternative forms as follows;

Ho: There is no positive significant impact of Savings on Investment in Nigeria

42

Ha: There is positive significant impact of Savings on Investment in Nigeria

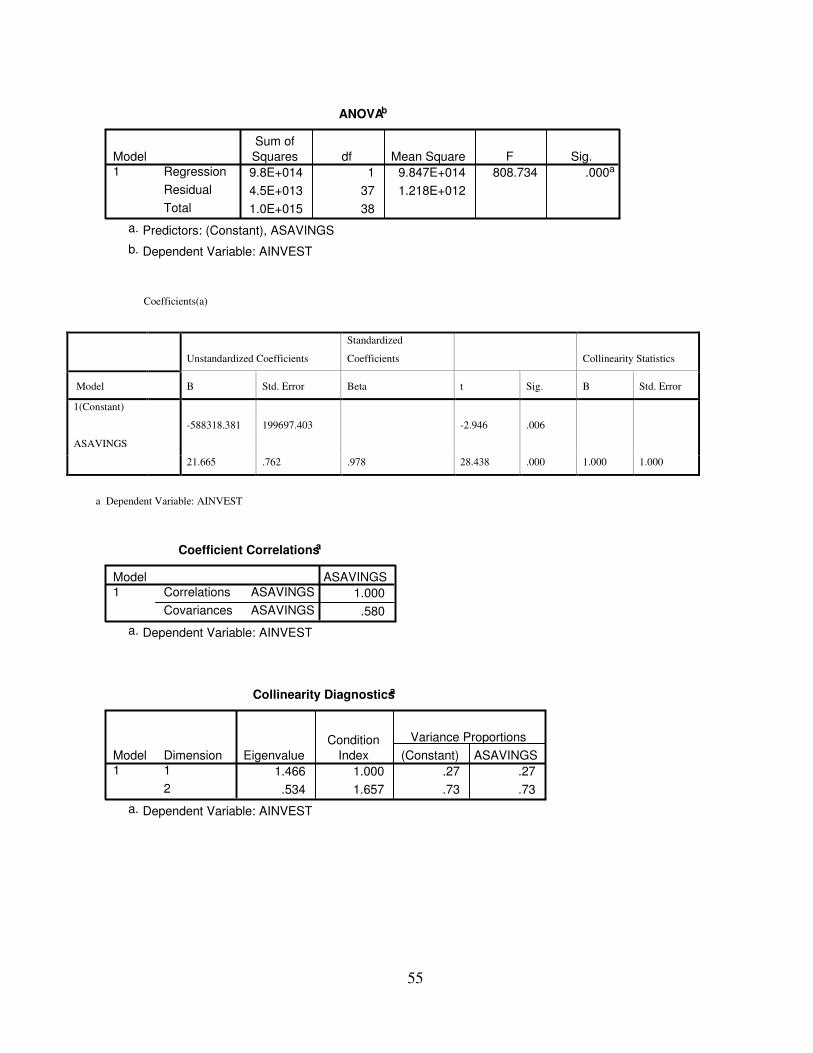

Step Two: Presentation of SPSS model results

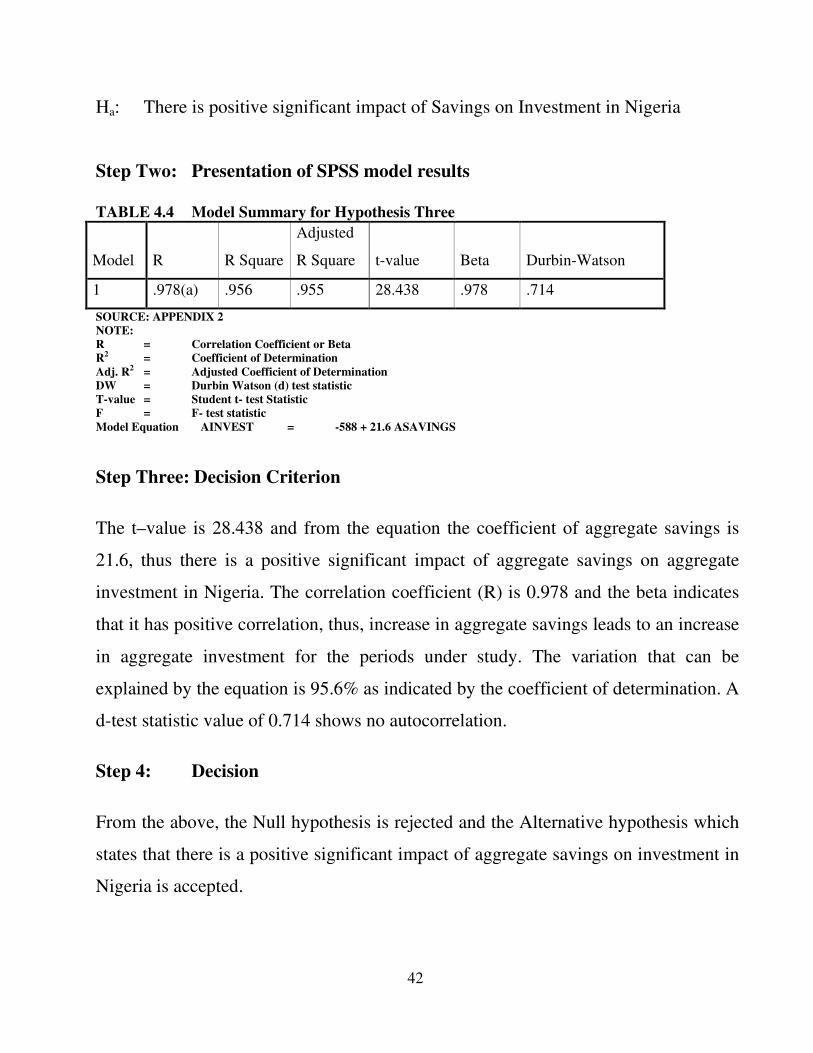

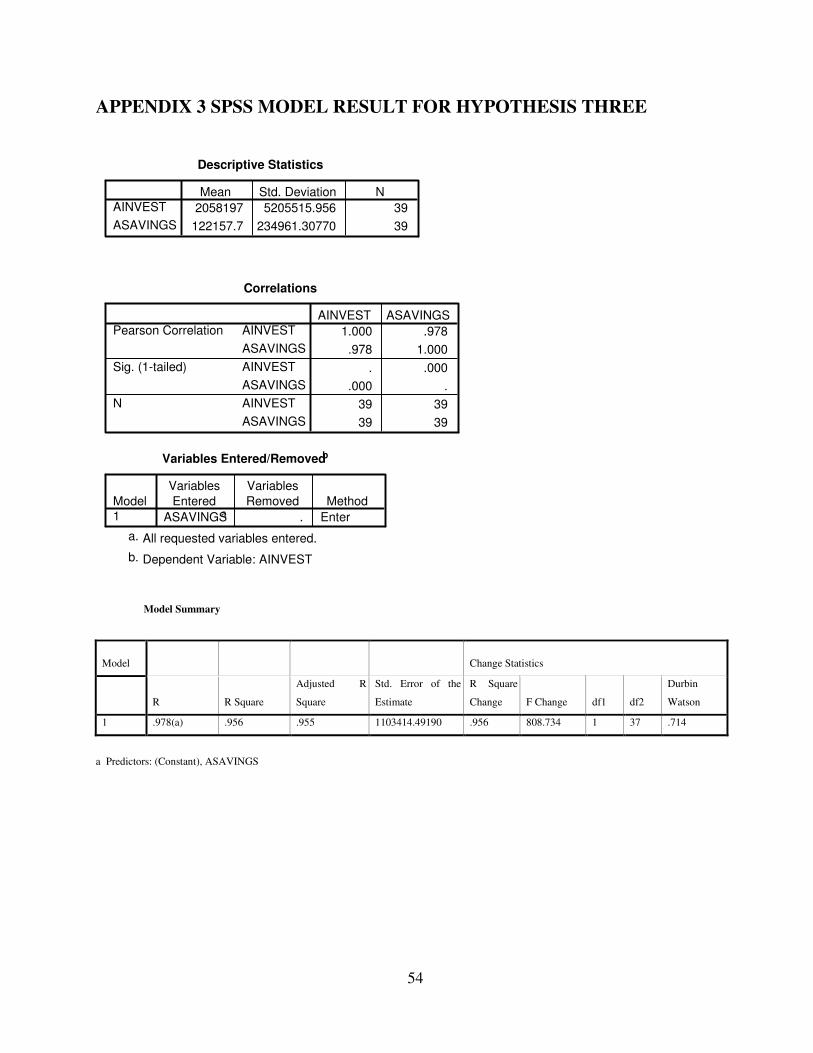

TABLE 4.4 Model Summary for Hypothesis Three

Model R R Square

Adjusted

R Square t-value Beta Durbin-Watson

1 .978(a) .956 .955 28.438 .978 .714

SOURCE: APPENDIX 2

NOTE:

R = Correlation Coefficient or Beta

R2 = Coefficient of Determination

Adj. R2 = Adjusted Coefficient of Determination

DW = Durbin Watson (d) test statistic

T-value = Student t- test Statistic

F = F- test statistic

Model Equation AINVEST = -588 + 21.6 ASAVINGS

Step Three: Decision Criterion

The t–value is 28.438 and from the equation the coefficient of aggregate savings is

21.6, thus there is a positive significant impact of aggregate savings on aggregate

investment in Nigeria. The correlation coefficient (R) is 0.978 and the beta indicates

that it has positive correlation, thus, increase in aggregate savings leads to an increase

in aggregate investment for the periods under study. The variation that can be

explained by the equation is 95.6% as indicated by the coefficient of determination. A

d-test statistic value of 0.714 shows no autocorrelation.

Step 4: Decision

From the above, the Null hypothesis is rejected and the Alternative hypothesis which

states that there is a positive significant impact of aggregate savings on investment in

Nigeria is accepted.

43

CHAPTER FIVE

SUMMARY OF FINDINGS, RECOMMENDATIONS AND CONCLUSIONS

5.1 SUMMARY OF FINDINGS

Based on the hypothesis tested in this research, we found out the following:-

1) Interest rates have a positive significant impact on Aggregate savings in

Nigeria. This was confirmed by a positive interest rate coefficient. Also there

was positive correlation between interest rate and Aggregate savings, thus an

increase in interest rate will lead to an increase in Aggregate savings in the

economy. The result can be found in the works of McKinnon (1973) and Shaw

(1973). They found out that interest rates have a positive response to savings

and economic growth thus the link between interest rate responsiveness and

savings, as postulated by the McKinnon-Shaw is positive.

2) Interest rates have a negative significant impact on Aggregate investment in

Nigeria. This was confirmed by a negative interest rate coefficient and a t-value

above the rule of thumb benchmark of two. Also, there was a negative

correlation between interest rate and Aggregate investment in Nigeria, thus an

increase in interest rate will lead to decrease in Aggregate investment in

Nigeria and vice versa.

44

3) Aggregate savings have a positive significant impact on Aggregate investment

in Nigeria. This was confirmed by a positive Aggregate savings coefficient and

a t-value greater than the rule of thumb bench mark value of two for

significance. Also there was a positive correlation between Aggregate savings

and Aggregate investment thus an increase in Aggregate savings will lead to an

increase in Aggregate investment in Nigeria.

5.2 RECOMMENDATIONS

As could be observed from the findings in this research that when the interest rate is

high, the level of savings will rise because depositors will profit, as he will have more

returns on his deposits. In the same view, if the interest rate falls, the level of savings

will drop, as people will not be motivated to save. On the contrary, if the level of

interest rate rises, the level of investment falls because the cost of acquiring funds

becomes expensive and when the level of interest drops, the level of investment rises

as the cost of acquiring funds for investment purposes is reduced. Also it was

observed that when savings increases the level of investment increases because more

funds will be available in the hands of investors to fund capital projects in the

economy. Thus the following recommendations are made;

First and foremost an understanding of the savings-investment process can help

inform policy decisions aimed at promoting economic development thus government

should ensure that interest rate payable on savings is such as to stimulate savings

rather than consumption as it has been proven from this research that interest rate

have a positive impact on savings which in turn stimulate investments.

Secondly, investment is required for the following purposes; for the business to buy

new premises, machinery and to raise the fund to finance increased manufacturing

45

capacity, for public sector to carry out public works such as building news or

reconstruction of houses, roads, schools and hospital etc, for individual to buy or

improve existing houses, or other fixed assets and for banks. Thus investment

increases a country’s productive capacity and raises the standard of living. The

processes of savings and investment play central roles in the circular flow of income

and in determining the level of income, therefore government should ensure that the

rate of interest on loans and advances are such as to stimulate investment thus leading

to increase in the gross domestic product and the living standards of the citizens.

Lastly, investors seeking loans are now more selective and careful in the way they

dispense money on projects. In the same vein, rate of deposits have attracted

enormous savings. Therefore savings culture should be cultivated by Nigerians as the

link between savings and investment is direct which means an increase in savings

leads to increase in investment.

5.3 CONCLUSIONS

As have been established in this research that interest rate favours savers when the

rate is high and not favourable when it is low. Savings is also looked upon as

beneficial both for the individual and the society at large, thus, an increase in savings

will ultimately lead to an increase in savings of the community. It was due to this

effect that the classists believed in thriftiness. They were of the view that an

individual saving was a great private as well as social virtue. The Keynes were at a

different view, which they advocate that individual savings is a social virtue but rather

supported the view that individual savings is greatly a social vice. Increase savings

on the part of individuals will result in a general curtailment in the expenditure.

When savings increase, investment also increases and investment is very essential for

the economic development of an economy. With increase investment, employment is

46

bound to increase which will in turn increase demand, prices, profit and more

production expansion. This expansion if properly utilized will lead to economic

development of a country. However in Nigeria, the banking habits are not developed.

The average Nigerian still believes the best way to save is not by keeping our money

in the bank but in communal meetings that exist in our communities and keeping ones

money under the mattress where it is easily accessible. Under this particular sector,

large blame goes to illiteracy and ignorance on the part of the public as it is deemed

that depositing money in a bank requires many formalities and bureaucracy. The

factor which influences deposit in banks is efficient performances of the banks in the

process of intermediation. Thus an effective management will induce a lot of people

to save; this is because there will be confidence. Therefore it could be said that

interest rate plays a major role on the growth of any nation.

47

REFERENCES

McKinnon, R.I., (1973) Money and Capital Market in Economic Development,

Washington, DC; The Brookings Institution

Shaw, E., (1973), Financial Deepening in Economic Development, New York;

Oxford University Press

48

APPENDIX 1 SPSS MODEL RESULT FOR HYPOTHESIS ONE

Descriptive Statistics

122157.7 234961.30770 39

7.5295 4.80530 39

ASAVINGS

INT

Mean Std. Deviation N

Correlations

1.000 -.344

-.344 1.000

. .016

.016 .

39 39

39 39

ASAVINGS

INT

ASAVINGS

INT

ASAVINGS

INT

Pearson Correlation

Sig. (1-tailed)

N

ASAVINGS INT

Variables Entered/Removed b

INTa . Enter

Model1

Variables

Entered

Variables

Removed Method

All requested variables entered.a.

Dependent Variable: ASAVINGSb.

Model Summary(b)

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

Change Statistics

Durbin-

Watson

R Square

Change F Change df1 df2 Sig. F Change

1 .344(a) .119 .095 223560.81863 .119 4.974 1 37 .032 .117

a Predictors: (Constant), INT

b Dependent Variable: ASAVINGS

49

ANOVAb

2.5E+011 1 2.486E+011 4.974 .032a

1.8E+012 37 4.998E+010

2.1E+012 38

Regression

Residual

Total

Model

1

Sum of

Squares df Mean Square F Sig.

Predictors: (Constant), INTa.

Dependent Variable: ASAVINGSb.

Coefficients(a)

Unstandardized Coefficients

Standardized

Coefficients 95% Confidence Interval for B

Model B Std. Error Beta T Sig. Zero-order VIF

1(Constant)

248899.8 67162.08 3.706 .001 112816.564 384983.203

INT -16832.7 7547.16 -.344 -2.230 .032 -32124.773 -1540.775 -.344

a Dependent Variable: ASAVINGS

Coefficient Correlations(a)

Model INT

1 Correlations INT 1.000

Covariances INT 56959625.922

a Dependent Variable: ASAVINGS

Collinearity Diagnosticsa

1.846 1.000 .08 .08

.154 3.464 .92 .92

Dimension

1

2

Model

1

Eigenvalue

Condition

Index (Constant) INT

Variance Proportions

Dependent Variable: ASAVINGSa.

50

Residuals Statisticsa

-67556.3 198401.6 122157.7 80886.49392 39

-198272 897618.8 .00000 220599.61744 39

-2.345 .943 .000 1.000 39

-.887 4.015 .000 .987 39

Predicted Value

Residual

Std. Predicted Value

Std. Residual

Minimum Maximum Mean Std. Deviation N

Dependent Variable: ASAVINGSa.

51

APPENDIX 2 SPSS MODEL RESULT FOR HYPOTHESIS TWO

Descriptive Statistics

2058197 5205515.956 39

7.5295 4.80530 39

AINVEST

INT

Mean Std. Deviation N

Correlations

1.000 -.324

-.324 1.000

. .022

.022 .

39 39

39 39

AINVEST

INT

AINVEST

INT

AINVEST

INT

Pearson Correlation

Sig. (1-tailed)

N

AINVEST INT

Variables Entered/Removedb

INTa . Enter

Model

1

Variables

Entered

Variables

Removed Method

All requested variables entered.a.

Dependent Variable: AINVESTb.

Model Summary(b)

Model R R Square

Adjusted R

Square

Std. Error of the

Estimate

Change Statistics

Durbin-

Watson

Sig. F

Change F Change df1 df2

Sig. F

Change

1 .324(a) .105 .081 4990915.97767 .105 4.338 1 37 .044 .216

a Predictors: (Constant), INT

b Dependent Variable: AINVEST

52

ANOVAb

1.1E+014 1 1.081E+014 4.338 .044a

9.2E+014 37 2.491E+013

1.0E+015 38

Regression

Residual

Total

Model

1

Sum of

Squares df Mean Square F Sig.

Predictors: (Constant), INTa.

Dependent Variable: AINVESTb.

Coefficients(a)

Model Unstandardized Coefficients Standardized Coefficients

B Std. Error Beta T Sig.

1(Constant) 4700507.554 1499369.824 3.135 .003

INT -350928.419 168487.673 -.324 -2.083 .044

a Dependent Variable: AINVEST

Coefficient Correlationsa

1.000

3E+010

INT

INT

Correlations

Covariances

Model

1

INT

Dependent Variable: AINVESTa.

Collinearity Diagnosticsa

1.846 1.000 .08 .08

.154 3.464 .92 .92

Dimension

1

2

Model

1

Eigenvalue

Condition

Index (Constant) INT

Variance Proportions

Dependent Variable: AINVESTa.

53

Residuals Statisticsa

-1896947 3647722 2058197 1686315.643 39

-3647371 2E+007 .00000 4924808.211 39

-2.345 .943 .000 1.000 39

-.731 4.727 .000 .987 39

Predicted Value

Residual

Std. Predicted Value

Std. Residual

Minimum Maximum Mean Std. Deviation N

Dependent Variable: AINVESTa.

54

APPENDIX 3 SPSS MODEL RESULT FOR HYPOTHESIS THREE

Descriptive Statistics

2058197 5205515.956 39

122157.7 234961.30770 39

AINVEST

ASAVINGS

Mean Std. Deviation N

Correlations

1.000 .978

.978 1.000

. .000

.000 .

39 39

39 39

AINVEST

ASAVINGS

AINVEST

ASAVINGS

AINVEST

ASAVINGS

Pearson Correlation

Sig. (1-tailed)

N

AINVEST ASAVINGS

Variables Entered/Removedb

ASAVINGSa . Enter

Model

1

Variables

Entered

Variables

Removed Method

All requested variables entered.a.

Dependent Variable: AINVESTb.

Model Summary

Model Change Statistics

R R Square

Adjusted R

Square

Std. Error of the

Estimate

R Square

Change F Change df1 df2

Durbin

Watson

1 .978(a) .956 .955 1103414.49190 .956 808.734 1 37 .714

a Predictors: (Constant), ASAVINGS

55

ANOVAb

9.8E+014 1 9.847E+014 808.734 .000a

4.5E+013 37 1.218E+012

1.0E+015 38

Regression

Residual

Total

Model

1

Sum of

Squares df Mean Square F Sig.

Predictors: (Constant), ASAVINGSa.

Dependent Variable: AINVESTb.

Coefficients(a)

Unstandardized Coefficients

Standardized

Coefficients Collinearity Statistics

Model B Std. Error Beta t Sig. B Std. Error

1(Constant)

ASAVINGS

-588318.381 199697.403 -2.946 .006

21.665 .762 .978 28.438 .000 1.000 1.000

a Dependent Variable: AINVEST

Coefficient Correlationsa

1.000

.580

ASAVINGS

ASAVINGS

Correlations

Covariances

Model

1

ASAVINGS

Dependent Variable: AINVESTa.

Collinearity Diagnosticsa

1.466 1.000 .27 .27

.534 1.657 .73 .73

Dimension

1

2

Model

1

Eigenvalue

Condition

Index (Constant) ASAVINGS

Variance Proportions

Dependent Variable: AINVESTa.

56

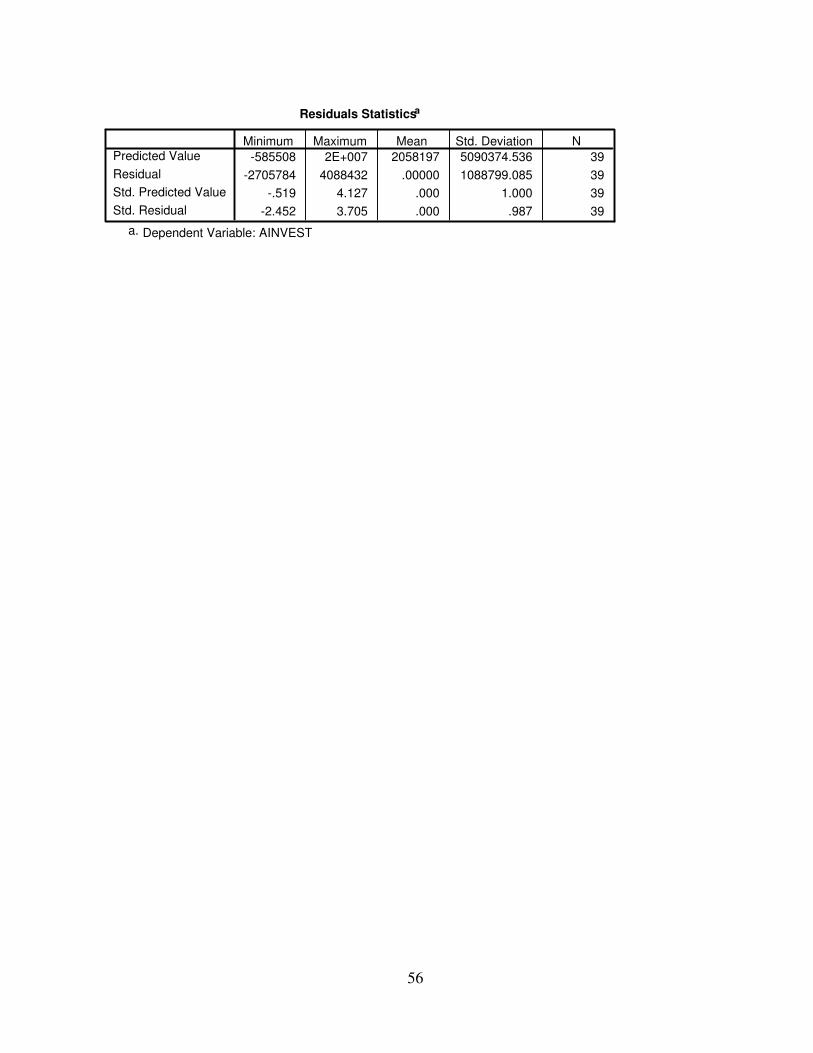

Residuals Statisticsa

-585508 2E+007 2058197 5090374.536 39

-2705784 4088432 .00000 1088799.085 39

-.519 4.127 .000 1.000 39

-2.452 3.705 .000 .987 39

Predicted Value

Residual

Std. Predicted Value

Std. Residual

Minimum Maximum Mean Std. Deviation N

Dependent Variable: AINVESTa.

57

BIBLIOGRAPHY

Adekanye, F.A., (1993) ‘‘Commercial bank performance in a developing economy: a

Multivariate regression analysis approach’’, PhD thesis, Department of

International Banking and Finance, Business School, City University, London

Bhatia, R.J. and D.R. Khatkhate (1973) ‘‘Interest rates, Savings, and Growth in

LDCs: An assessment of recent empirical research’’, World Development, Vol.

16, No. 5

CBN (2009) Central Bank of Nigeria Statistical Bulletin, Volume 18, Abuja: CBN

Publishers

Douglas, A. L., W. G. Willian and R. D. Mason (2002) Statistical Techniques in

Business And Economics, Boston; Mc-Graw Hill Irwin

Elliot, J.W., (1984) Money, Banking and Financial Markets, New York; West

Publishing Company

Fry, M.J., (1978) ‘‘Money and Capital or Financial deepening in Economic

Development’’, Journal of Money, Credit and Banking, Vol. 10, No. 4

Luckett, D.G., (1984), Money and Banking, New York; McGraw Hill

McKinnon, R.I., (1973) Money and Capital Market in Economic Development,

Washington, DC; The Brookings Institution,.

Mwega, F.M., S.M. Ngola, and N. Mwangi, (1990), ‘‘Real interest rates and the

Mobilization of private savings in Africa: a case study of Kenya’’, AERC

Research Paper, African Economic Research Consortium, Nairobi.

Ndulu, BJ., (1990) ‘‘Growth and adjustment in Sub-Saharan Africa’’, a paper

Presented at the World Bank Economic Issues Conference, Nairobi, Kenya,

June

Nigeria Deposit Insurance Corporation (NDIC), (1989) Annual Reports and

Statement of Accounts, Lagos, December 31

Onwumere, J. U. J (2005), Business and Economics Research Method, Lagos; Don

58

Vinton Limited

Osofisan, A.O., (1993) ‘‘An asset portfolio management model for Nigerian

Commercial Banks: a case study’’, Department of Economics, University of

Ibadan, MBA Project Report.

Ozo, J. O. Ani and T. U, Ugwu (2007), Introduction to Project Writing for Business

And Financial Studies, Enugu; New Dimension Publishers

Revel J., (1975), Solvency and Regulation in Banks, Cardiff; University of Wales

Press

Ritter, L.S. and W.L. Siber, (1986), Principles of Money, Banking and Financial

Markets, New York; Basic Books Inc

Shaw, E., (1973), Financial Deepening in Economic Development, New York;

Oxford University Press,

Soyibo, A., (1991), ‘‘Managing bank assets in a depressed economy’’, a paper

Presented at the Union Bank of Nigeria Area Managers' Conference, Ibadan,

17-18 May.

Soyibo, A. and F. Adekanye, (1992), ‘‘Financial System Regulation, Deregulation

and Savings Mobilization in Nigeria’’, African Economic Research

Consortium, Nairobi

Copyright © 2022 FDOKUMEN