The Impact of Export State Trading Enterprises Under Imperfect Competition: The Small Country Case

11

The Impact of Export State Trading Enterprises Under Imperfect Competition: The Small Country Case Murray Fultonl, Bruno Lame2 and Michele Veeman3 'Professor of Agricultural Economics and Director, Centrefor the Study of Co-operatives, University of Saskatchewan, I01 Diefenbaker Place, Saskatoon, Saskatchewan S7N SB8 2De'partement d 'e'conornierurale, Universitk Lava1 3Department of Rural Economy, University of Alberta INTRODUCTION There are two current major focal points of interest in state trading. At the broad level, there is much interest in the potential member- ship of countries like China and Russia in the World Trade Organization (WTO). However, most of the interest in state trading in agricul- tural and food products arises from a second focal point, namely the concern by some na- tions -especially the United States -over the operations of the export marketing boards of Australia, Canada and New Zealand (US- GAO, 1996). In turn, these latter nations are concerned that this targeted focus ignores the state-based institutions and practices of the United States and the European Union. The purpose of this paper is to develop a conceptual framework in which the impact of state trading enterprises (STEs) engaged in grain export can be examined. The grain in- dustry is chosen because the STEs in this in- dustry are the focus of much interest. In this paper, the impact of an STE is determined by answering the following question. What is the outcome (e.g., in terms of prices, output, ex- ports, imports, economic surplus) if an STE that operates in the international export market is removed and replaced by privately-owned traders? The assumptions used in answering this question are very important. Previous models of STEs typically assume that STE removal will result in the formation of a competitive trading sector for that commodity (Dixit and Josling). This assumption has important con- sequences for the analyses. If the alternative to the STE is a perfectly competitive trading industry, then introduction of the STE reduces the efficiency of the trading sector and the in- ternational market. However, this conclusion is not automatic if the alternative to the STE is an oligopolistic trading sector. Indeed, as the analysis in this paper shows, the introduc- tion of the STE can often improve total wel- fare. In addition, the introduction of the STE has important distributional implications, with the trading firms losing and the country intro- ducing the STE gaining. The paper is structured as follows. The next section presents empirical evidence and the- ory to show that the grain trade is oligopolistic in structure. The paper then develops a theo- retical trade model in which oligopolistic firms provide the trading function between a farm sector and a processing sector for a small country. STEs are then introduced into this model to determine their impact. The paper concludes with a section that applies the analy- sis to the case of the Australian Wheat Board (AWB) and the Canadian Wheat Board (CWB). THE OLIGOPOLISTIC GRAM TRADE - EVIDENCE AND THEORY The major actors in the world grain trading system are governments and multinationals (MNEs) (Davies). Governments play a role through domestic commodity programs, ex- Can. J. Agric. Econ. 47: 363-373 363

Transcript of The Impact of Export State Trading Enterprises Under Imperfect Competition: The Small Country Case

The Impact of Export State Trading Enterprises Under Imperfect Competition: The Small

Country Case

Murray Fu l ton l , Bruno Lame2 and Michele Veeman3

'Professor of Agricultural Economics and Director, Centre for the Study of Co-operatives, University of Saskatchewan, I01 Diefenbaker Place,

Saskatoon, Saskatchewan S7N SB8 2De'partement d 'e'conornie rurale, Universitk Lava1

3Department of Rural Economy, University of Alberta

INTRODUCTION There are two current major focal points of interest in state trading. At the broad level, there is much interest in the potential member- ship of countries like China and Russia in the World Trade Organization (WTO). However, most of the interest in state trading in agricul- tural and food products arises from a second focal point, namely the concern by some na- tions -especially the United States -over the operations of the export marketing boards of Australia, Canada and New Zealand (US- GAO, 1996). In turn, these latter nations are concerned that this targeted focus ignores the state-based institutions and practices of the United States and the European Union.

The purpose of this paper is to develop a conceptual framework in which the impact of state trading enterprises (STEs) engaged in grain export can be examined. The grain in- dustry is chosen because the STEs in this in- dustry are the focus of much interest. In this paper, the impact of an STE is determined by answering the following question. What is the outcome (e.g., in terms of prices, output, ex- ports, imports, economic surplus) if an STE that operates in the international export market is removed and replaced by privately-owned traders?

The assumptions used in answering this question are very important. Previous models of STEs typically assume that STE removal will result in the formation of a competitive trading sector for that commodity (Dixit and

Josling). This assumption has important con- sequences for the analyses. If the alternative to the STE is a perfectly competitive trading industry, then introduction of the STE reduces the efficiency of the trading sector and the in- ternational market. However, this conclusion is not automatic if the alternative to the STE is an oligopolistic trading sector. Indeed, as the analysis in this paper shows, the introduc- tion of the STE can often improve total wel- fare. In addition, the introduction of the STE has important distributional implications, with the trading firms losing and the country intro- ducing the STE gaining.

The paper is structured as follows. The next section presents empirical evidence and the- ory to show that the grain trade is oligopolistic in structure. The paper then develops a theo- retical trade model in which oligopolistic firms provide the trading function between a farm sector and a processing sector for a small country. STEs are then introduced into this model to determine their impact. The paper concludes with a section that applies the analy- sis to the case of the Australian Wheat Board (AWB) and the Canadian Wheat Board (CWB).

THE OLIGOPOLISTIC GRAM TRADE - EVIDENCE AND THEORY

The major actors in the world grain trading system are governments and multinationals (MNEs) (Davies). Governments play a role through domestic commodity programs, ex-

Can. J. Agric. Econ. 47: 363-373 363

3 64 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

port subsidies, trade barriers. They also oper- ate STEs which, along with MNEs, handle and trade grain. STEs include the AWB and the CWB, while MNEs include Cargill, Continen- tal, Bunge and Born, Louis Dreyfus, and An- dre Garnac (see Sewell for a description of these five companies).'

MNEs handle grain on their own behalf, and on behalf of other grain companies, most notably STEs and co-operatives. For instance, in the US, several large co-operatives provide grain and oilseeds for export. They arrange for delivery of the product to the port, where it is sold to one of the MNEs for sale to foreign purchasers (Cramer, Davies). MNEs also han- dle a substantial amount of grain on behalf of STEs because of the information and distribu- tion networks at their disposal. For instance, while the majority of its sales are carried out directly, the Canadian Wheat Board (CWB) also uses accredited exporters (Canadian Wheat Board, 1998).

There are strong empirical and theoretical reasons to believe the international grain trad- ing sector is oligopolistic in nature. Empiri- cally, the international grain trade is highly concentrated. Hayenga and Wisner, for in- stance, report figures that indicate that 8 1 per cent of US corn exports went through the fa- cilities of the top four firms; these same firms accounted for 65 per cent of US soybean ex- ports. For wheat, the top four firms handled 47 percent ofUS exports. Although MNEs, along with a few STEs, dominate international mar- kets, they compete in national markets with co-operatives, national trading companies, and on occasion, STEs (Hill, Davies). The re- sult is that at the country elevator level, com- petition ranges from very high to very low (Hi1 1).

On a theoretical level, the intangible and proprietary nature of important MNE assets implies that the international grain trading sec- tor is likely to be oligopolistic. All MNEs op- erate extensive information and market intel- ligence networks. They also operate vast networks of storage, handling, and transporta- tion facilities that allow them to co-ordinate various aspects of grain distribution and han- dling (Davies). Proprietary assets such as in-

formation networks and personnel with spe- cialized knowledge ofthe international market provide incumbent trading firms with econo- mies of scale and cost advantages, which in turn implies that these firms possess market power. The reasoning is as follows.

Intangible assets are different from the other assets used by firms in that they are non- rival goods that have a high degree of exclud- ability. While rival goods can only be used by one firm or person at any one time, nonrival goods can be used by different people, in dif- ferent locations, at the same time. This char- acteristic means the firm possessing intangible assets enjoys increasing returns to scale in pro- duction, since output can be increased without increasing all inputs (Romer).

With increasing returns to scale, marginal cost is less than average cost unless the nonri- val assets are obtained without cost. Firms that possess increasing returns to scale therefore cannot function as price takers in their industry unless the nonrival assets that give rise to the returns to scale can be obtained free of charge. If obtaining nonrival assets involves a cost, firms with these assets will lose money if they act as price-takers. Consequently, firms with nonrival assets must price above marginal cost if they are to remain successfid (Romer).

In summary, the international agricultural trading sector is oligopolistic in nature, with MNEs playing a dominant role. This particular market structure arises because tradin firms possess significant proprietary assets. These assets provide trading firms with significant economies of scale and scope and create cost advantages for the incumbents. The result is trading firms have oligopoly power and the

3 potential and incentive to price discriminate.

3

THE THEORETICAL MODEL Consider a small country -denoted the domes- tic country - which exports an agricultural commodity to the world market. Three sub- groups can be identified in the country - the producers of the agricultural product at the farm level, the processing firms that purchase the agricultural product, and the traders of the agricultural product. Traders purchase the ag- ricultural products from the farm production

ANNUAL MEETING PROCEEDINGS 365

$/Output 1 Domestic Country \

output y’. Y 9 %

Figure 1. Output determination by private competitive traders and an STE: Small country domestic market.

sector and sell to the processing sector. Some ofthe traders may only operate in the domestic country, while other traders will also operate internationally. Traders operating only in the domestic market are termed local traders, while those operating internationally are termed MNEs.

Figure 1 illustrates the supply curve (s) and demand curve (6) for the domestic country. The marginal costs of carrying out the trading function are assumed to be zero, as are the costs of transporting the product from the do- mestic country to ROW. The farm level price is denoted by w, while the processor price is p . The output produced by the farm sector is given by q, the output purchased by processors is labeled y, and exports are x .

The domestic country is a small country and not able to influence the terms of trade with the rest of the world (ROW). Two sce- narios are examined. The first assumes that the local and international traders are perfectly competitive, while the second assumes that the

traders have oligopoly power. In both scenar- ios, two cases are examined. The first case ex- amines the outcome in terms of prices, quan- tities and welfare when private traders handle the trading function. The second case exam- ines the outcome in terms of prices, quantities and welfare when an STE handles the trading functions.

Perfectly Competitive Private Traders Perfect competition in the trading sector means that the farm level price and the proc- essor price are equal, both in the domestic country and ROW. The price at which the ag- ricultural output can be sold on the intema- tional market is assumed to be p (see Figure 1). Thus the domestic processor price and the domestic farm price also equal p . Conse- quently, processor demand is y, domestic out- put is q, and exports are x , where x = q -y.

To examine the impact of STEs, their be- haviour must be modeled. There are many ob- jectives that STEs may pursue and many ways

366 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

in which STEs can affect trade. As a result, no one analysis can be undertaken that will cover all STEs. Rather, each STE must be modeled separately. The following analysis examines the case of an STE that maximizes producer welfare and transfers the income generated from sales to producers via pooling. The focus is on pooling schemes because this is a char- acteristic of the STEs in both Australia and Canada.

Inherent in most commercial activities in the grain industry is some form of price dis- crimination or differential pricing, and price pools run by STEs are no exception. Price dis- crimination requires the existence of at least two different markets. In the model developed here, the two markets are the domestic proc- essors and the ROW processors. While a more complete model would consider a number of different markets in the ROW, adding these additional markets would excessively compli- cate the analysis. Thus, the modeling of price discrimination in the domestic market should be viewed as a way of illustrating the effect of pooling and not as a policy that all STEs fol- low. The domestic pricing policy of a STE is often the subject of regulation by its home country.

Consider the introduction of the STE in the domestic country. Two conditions have to hold when the STE maximizes producer wel- fare and returns all revenues net of marketing costs to producers through a pooling mecha- nism. First, since the STE wishes to maximize producer welfare, it equates its marginal reve- nue in the domestic market with its marginal revenue in ROW. Second, the pricesthat emerge from the domestic and foreign markets are av- eraged (the weights are the sales to each of these respective markets) and the resulting av- erage price must equal the producer price that causes the farm sector to produce the total amount of production sold to the two markets.

The marginal revenue in ROW is given by the world selling price, p. The STE’s marginal revenue in the domestic market is shown by the curve pd in Figure 1. The position of pd depends on the degree of competition faced by the STE in the domestic market. In the case of perfect competition in the domestic market,

thepd curve corresponds to the demand curve d. If the STE must compete with a small num- ber of local traders for product to supply to the domestic processors, then pd lies between the monopolist’s marginal revenue curve and the industry demand curve. Curvepd may also lie between demand curve d and the marginal revenue curve if the STE is given a regulatory constraint under which to operate. Pricing rules such as those developed by Baumol and Bradford 1970 are one example of this type of regulatory constraint. Finally, if the STE is the only firm operating nationally in the domestic country and its monopoly power is not cur- tailed by regulation, then pd is the traditional monopoly marginal revenue curve.

Equating pd with p results in sales ofy‘ to the domestic market. The price paid by domes- tic processors is p‘. The line “pooled price schedule” shows the average price that can be returned to the farm sector as a function oftotal production. This price schedule declines with an increase in total output because any output over and above y‘ must be sold to the ROW at price p . The implicit assumption made in drawing the pooled price schedule is that any traders operating alongside the STE in the do- mestic market have to match the pooled price to be able to source product from the farm sec- tor. In effect, the situation modeled is one where a domestic dual market operates, such as is the case in Canada for feed grains and in Australia for wheat. The STE, however, is given sole authority over exports.

The equilibrium level of output produced in the domestic country is q and is determined by the intersection of the Pine “pooled price schedule” with the farm supply curve (see Al- ston and Gray for a similar derivation). The pooled price paid to the farm sector is p,. The price-output combination (pp, qp) is an equi- librium combination because p, is such that it just gives rise to output q , and q IS the output that when sold gives rise to an average price p . Since the quantities sold to the domestic ahd ROW market are chosen so that the mar- ginal revenue in each ofthese markets is equal, the solution also maximizes the total revenue generated by the STE.

P P

ANNUAL MEETING PROCEEDINGS 367

The impact ofthe STE on the domestic mar- ket can be determined by examining the out- come with and without the STE present in the market. If the alternative to an STE is a per- fectly competitive trading sector, the introduc- tion of an STE always results in a loss of wel- fare. When the STE is present, processors lose the areap’abp, while the farm sector gains the areap dfp relative to the outcome when a com- petitive trading sector is operating. Since area p’acp equals areap dep, the domestic country

P as a whole is worse off as a result of the intro- duction of the STE. The net loss to the country is the sum of the triangles abc and deJ4

P

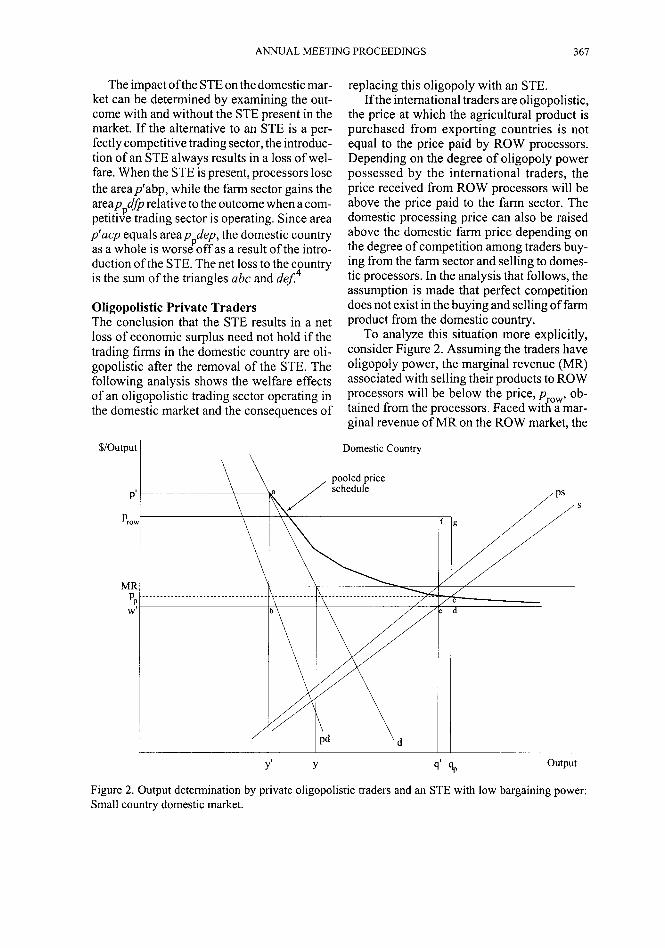

Oligopolistic Private Traders The conclusion that the STE results in a net loss of economic surplus need not hold if the trading firms in the domestic country are oli- gopolistic after the removal of the STE. The following analysis shows the welfare effects of an oligopolistic trading sector operating in the domestic market and the consequences of

$/Output j

replacing this oligopoly with an STE. If the international traders are oligopolistic,

the price at which the agricultural product is purchased from exporting countries is not equal to the price paid by ROW processors. Depending on the degree of oligopoly power possessed by the international traders, the price received from ROW processors will be above the price paid to the farm sector. The domestic processing price can also be raised above the domestic farm price depending on the degree of competition among traders buy- ing from the farm sector and selling to domes- tic processors. In the analysis that follows, the assumption is made that perfect competition does not exist in the buying and selling of farm product from the domestic country.

To analyze this situation more explicitly, consider Figure 2. Assuming the traders have oligopoly power, the marginal revenue (MR) associated with selling their products to ROW processors will be below the price, p ow, ob- tained from the processors. Faced w i d a mar- ginal revenue of MR on the ROW market, the

Domestic Country

/

pooled price / schedule ::.::::‘ d

output Y’ Y 9‘ 4p

Figure 2. Output determination by private oligopolistic traders and an STE with low bargaining power: Small country domestic market.

368 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

domestic farm price and processor price are determined by equating MR with the per- ceived demand curve (pd) and the perceived supply curve (ps) in Figure 1. The resulting processor and farm prices are p' and w', re- spectively, with corresponding quantities y' and 4'. Exports are q' - y'.

Intuitively, the pd curve represents the schedule ofprices at which the traders are will- ing to purchase given quantities of the farm product before turning around and selling the product to the processors. The ps curve repre- sents the schedule ofprices at which the traders are willing to sell any given quantity of the farm product they obtain from the farm sector. The position ofpd andps shows the oligopoly power possessed by the traders. Consider, for instance, the pd curve. If the traders act as a monopolist, then pd would be the marginal revenue curve (not shown). In contrast, if the traders are perfectly competitive, then pd would lie on the demand curve d. When the traders have a degree ofmarket power that lies between monopoly and perfect competition, curve pd lies between d and the monopolist's marginal revenue curve. A similar argument can be made for ps, where the range ofps lies between the supply curve s and the marginal outlay curve. Alston et al. provide a derivation of the perceived demand curve.6

The introduction ofan STE can be modeled in much the same way as in the previous sec- tion. To aid in the subsequent welfare com- parison, assume that the STE has the same de- gree of market power in the domestic market as did the trading firms. While this assumption may or may not be realistic, it provides a useful benchmark for the analysis that follows and it can easily be relaxed. Thus, the assumption is made that the STE sells to the domestic proc- essors at price p'. The pooled price is obtained by taking the weighted average ofthe domestic processing price and the price the STE can ob- tain on the international market. Assuming the STE does not have the wherewithal to sell di- rectly to the processors in ROW, but instead must use the international trading firms as agents, the price obtained by the STE on the international market depends on the price the

5

STE is able to negotiate with the international trading firms. Figure 2 illustrates the situation where the STE sells to the international trading firms at price w', while Figure 3 illustrates the situation where the STE sells to the interna- tional trading firms at their marginal revenue (MR).'

Figure 2 illustrates the outcome if the STE is able to negotiate a price w' with the interna- tional traders. Given an export price of w', the pooled price becomes p and the domestic country produces output q . Exports are q -

P P y' . Compared to the situation withprivatetrad- ing firms, farm welfare increases by area ppcew'. The welfare of the processing industry does not change, since the processor price is the same. Profits of the trading firms fall by an amount equal to p'abw' - efgd. The loss ofp' abw' results because the trading firms lose the domestic processor sales, while the gain of efgd results because the trading firms are able to sell an additional amount (q - 9') to ROW at price prow.

In net terms, the introduction of the STE results in an increase in total economic surplus of the area cefg. The net increase in total eco- nomic surplus hides the distributional impacts of the introduction of the STE. If the owners of the private firms live outside the domestic country, then the domestic country sees a wel- fare gain ofppcew' from introducing the STE, since the loss of profits does not enter the do- mestic calculus. However, the owners of the trading firms see a net loss from the introduc- tion of the STE.

Figure 3 illustrates the outcome if the STE is able to negotiate a price MR with the inter- national traders. Given an export price of MR, the pooled price becomespp and the domestic country produces output q . Exports are q, - y'. Compared to the situation with private trad- ing firms, farm welfare increases by area p cew'. The welfare of the processing industry &es not change, since the processor price is the same. Profits of the trading firms fall by an amount equal top'abw' + ebfg -ghij. The loss ofp'abw' results because the trading firms lose domestic processor sales, the loss ebfg results

P

P

P .

ANNUAL MEETING PROCEEDINGS 369

Domestic Country

s

Y' Y 4' 4p output

Figure 3. Output determination by private oligopolistic traders and an STE with greater bargaining power: Small country domestic market.

because the trading firms lose (MR -w') on ex- ports of (9' - y'), while the gain of ghij results because the trading firms are able to sell an additional amount (q - 9') to ROW at a net gain of 0) - MR). In net terms, the intro- duction of%e STE results in an increase in total economic surplus of the area ceji. Again, as in the example outlined in Figure 2, there are substantial distributional impacts of the in- troduction of the STE.

The models in Figure 2 and 3 assume that the STE possesses the same level of domestic market power as do the oligopolistic MNEs. Obviously, if the presence of the STE results in a lower processor price relative to where private traders handle the product, the welfare of domestic processors increases, the benefits flowing to primary producers fall, and the deadweight loss in the domestic market falls. Similarly, if the presence of the STE results in a higher processor price, processors lose, pri- mary producers gain, and the domestic dead-

P

weight loss increases. Thus, an important fac- tor in determining the impact of the STE is whether or not the degree of competition among traders selling to domestic processor falls when the STE is introduced. Other factors are also at work. As a comparison of Figures 2 and 3 indicate, the benefits of the STE are greater the higher is the export price that the STE can negotiate. In addition, the benefits of the STE are greater the larger exports are rela- tive to domestic processor demand.

While the results outlined above were de- rived under the assumption that the domestic country is a small country and where the STE is unable to trade on its own account, they carry over to the case of a large country and to the case where the STE can trade on its own ac- count. The presence of the STE in this situation can either raise or lower welfare, both domes- tically and in the other regions of the world, depending on the underlying structure of the model. To the degree that the STE raises do- mestic processor prices, global welfare is low-

370 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

ered. To the degree that the STE leads to ad- ditional competition among traders selling to the ROW, which lowers the price paid byproc- essors in the foreign country and ROW, wel- fare is increased (Veeman et al.).

In general, the presence of the STE is wel- fare improving when the STE’s ability to raise the processor price in the domestic market is low and when the processing demand is rela- tively small relative to total production (Vee- man et al.). The ability of the STE to raise the domestic processor price may be low because some competition exists even when the STE is present (i.e,, the market is reasonably con- testable) or because the STE is constrained by policy in the price it can charge. Conversely, if the STE has the ability to raise domestic processor prices (i.e., little competition exists when the STE is present because the market has low contestability) or processing demand is a large component of total output, then the introduction of the STE results in lower wel- fare.

APPLICATION OF THE MODEL The analysis above provides a framework for examining the impact of STEs on international trade. The major conclusion of the analysis is that the impact of STEs depends critically on the market structure of the industry in which they operate. As a result, blanket judgements about STEs cannot be made. Instead, a case by case analysis is required to determine if trade distortion is likely. In carrying out this analy- sis, market contestability in the domestic proc- essing market is a key element. STEs that op- erate in highly contestable domestic markets have a low potential to distort trade. In con- trast, STEs that operate in highly non-contest- able markets or which have clear adverse im- pacts on contestability in their domestic markets have the potential to distort trade. Of course, some STEs do not fall in either ofthese clear-cut cases. The remainder of this section applies the conclusions reached above to the Australian Wheat Board (AWB) and the Ca- nadian Wheat Board (CWB). The analysis is based on the broader conclusions drawn from Veeman, et al. and is not limited to the specific assumptions of the model presented above.

Clearly, for instance, both the AWB and the CWB trade on their own account, something not allowed for in the theoretical model exam- ined in this paper.

The Australian Wheat Board This statutory marketing board, a Common- wealth crown corporation run by producers, became a grower-owned private corporation in 1998; maintenance of its long-standing authority as the single-desk exporter of Aus- tralian wheat continues. Government guaran- tees ofAWB borrowings are scheduled for dis- continuance in 1999. AWB initial payments to farmers are not government-guaranteed. Importation of grain into Australia is subject to strict requirements of sanitary and phy- tosanitary standards (SPS), involving rigorous quarantine standards and procedures. For ex- ample, imported feed grains must be steam treated or cracked at the port, before they can be shipped inland. Tariffs on imports are rela- tively low and tariff rate quotas do not apply to imports.

Since 1989 the AWB has not had single desk authority over the sales of Australian wheat to the domestic market; it competes with other traders, deals in several grains, and is a relatively large trader in the domestic market, reportedly accounting for about 70 percent of grain sales in this market. The restrictive pol- icy on grain importation, based on strict SPS standards, suggests that in Australia’s domes- tic market for grain, contestability may be compromised somewhat. However, overall, the presence of the AWB appears to have changed very little the level of competition among firms selling to domestic processors. Given that Australia exports a large percent- age of its total output, the operation of the AWB is likely to have little distorting effect on world trade.

The Canadian Wheat Board The CWB, a Canadian crown corporation gov- erned by a fifteen member board (1 0 of the board members are elected by farmers), has single-desk sales authority over the sale, to ex- port markets, of Canadian wheat and barley. In addition the Board has sales authority over

ANNUAL MEETING PROCEEDINGS 37 1

wheat and barley from Western Canada that is sold for domestic human consumption (i.e., for sales of Western Canadian wheat and barley to Canadian millers, maltsters and food proc- essors). The opportunity to practice “two price systems” involving higher domestic prices than in world markets occurred in much earlier years but now no longer applies. For example, the prices at which wheat is sold to Canadian millers has for some years been constrained by policy to levels equivalent to US futures prices, plus transportation costs, and the bor- der is open to grain imports from the United States and Mexico. However, tariffrate quotas apply to imports of wheat, barley and their products from other origins.8 These arrange- ments are not administered by the CWB.

The possibility of CWB losses arising from the government-determined initial payments that are applied by the CWB is met by govern- ment guarantee of the initial payments; subsi- dies arising from specified credit guarantees of export sales are also, in effect, administered through the CWB (although it appears that these may be at less concessionary rates than those that apply for US export credit sales of wheat). These Canadian subsidies are in con- formity with the commitments of Canada re- garding the Agreement on Agriculture of the WTO.

An increase in exports of grain from Can- ada to the United States that followed the Can- ada-United States Trade Agreement (CUSTA) has stimulated opposition from US producers’ associations and politicians. These have ac- cused the CWB of subsidization and unfair trading. A numbers of inquiries have involved assessments of CWB activities and wheat ex- ports to the US. These have involved a US In- ternational Trade Commission (USITC) in- quiry on durum wheat which reported in 1990, a subsequent binational panel inquiry, con- vened under the provisions of CUSTA, and a later USITC investigation of milling wheat imports from Canada. No evidence of unfair CWB trading practices has been documented. However, there appears to be a continuing US perception that STEs are necessarily a cause of increased exports; there has been pressure to restrain exportation of grain to the US and

there seems to be a lack of understanding that Canadian grain exports to the US may well have been considerably greater in the absence of the CWB.

The specification of tariff rate quotas for wheat and barley imports and the maintenance of CWB sole-seller authority in the Canadian market, at least for wheat and barley for human consumption, could lead to the suspicion that contestability may be potentially impaired within the Canadian market. However, more careful observation indicates that this is not in fact the case, since tariff rate quotas do not apply to importation of wheat and barley from the neighbouring grain producing country of the US. Thus, the CWB is expected to have little distorting effect on domestic processor prices. Given that the Canada exports a large percentage of its total output, the operation of the CWB is likely to have little distorting effect on world trade.

CONCLUSIONS Much of the interest in state trading in agricul- tural and food products arises from the concern by countries like the United States that export marketing boards like those in Australia, Can- ada and New Zealand are distorting trade (US- GAO, 1996). While the operation of STEs can be potentially trade distorting and welfare re- ducing in a world of perfect competition among grain traders, this is not the case iftrad- ers are oligopolistic. With oligopolistic trad- ers, the presence of STEs can improve welfare. In general, the presence of the STE is welfare improving welfare when the STE’s ability to raise the processor price in the domestic mar- ket is low and when the processing demand is relatively small relative to total production. Case studies of the Australian Wheat Board and the Canadian Wheat Board indicate that both of these organizations are likely to have little distorting effect on world trade, since in both cases the presence of these STEs appears to have little effect on domestic processor prices.

NOTES ’Cargill has announced its intention to purchase Contintental’s grain merchandising business. See

372 CANADIAN JOURNAL OF AGRICULTURAL ECONOMICS

Hayenga and Wisner for a discussion of this merger. *Proprietary assets also provide the basis for the creation of MNEs in the first place. As Caves points out, attempts to make proprietary assets available to other firms through such means as licensing agreements are often prone to opportunistic behav- iour. As a consequence, firms with proprietary assets often find it advantageous to start new opera- tions themselves (i.e., to expand their operations to new locations) to obtain the benefit of their assets, rather than leasing the assets to others. In short, firms for which proprietary assets are important are likely to establish multi-plant sites within a country and to expand their operations to other countries through MNEs. The empirical evidence supports this hypothesis. Foreign investment by grain-trad- ing MNE is strongly influenced by investments in proprietary assets (Caves, Goldsmith and Spor- leder). Proprietary assets also play a similar role in decisions to vertically integrate (Caves). 3As Varian (1996) notes, firms with economies of scale - the kind of cost structure associated with proprietary assets - either have to charge a single price and restrict sales or they have to use differen- tial pricing. Differential pricing -or price discrimi- nation - is the preferred option because it leads to higher profits. Price discrimination is thus a normal commercial practice of all trading firms. The suc- cess of price discrimination depends on the degree to which the products and services provided by the trading firms are heterogeneous and the costs that customers must incur in switching from one sup- plier to another. See Veeman, et al. for hrther details on price discrimination. 4Triangle def is the loss associated with pooling relative to an ideal profit maximization price dis- criminating scheme. To optimally run a price dis- criminating scheme requires production be constrained to q through a quota system. The aver- age revenue pricing that results from pooling in- duces an increase in production (and hence exports) that results in the loss. 'Formally, the model is structured as follows. The traders in this model are MNEs and buy from and sell to a number of different countries. In doing so, they are like multi-plant manufacturers selling in several markets. They take into account the mar- ginal cost of grain from all sources in planning their sales to all locations. In equilibrium, the marginal cost from all sources used will be equated (some sources may not be used if the marginal cost of no production is greater than the marginal cost from other sources); in addition, this marginal cost will be equated with the marginal revenue in all desti-

nations. The domestic country is only one of many coun-

tries from which the traders are buying. The small country assumption implies that the domestic coun- try is small relative to all the other sources. As a result of being a small country, the traders -when determining their sales and purchases in the domes- tic country - take the marginal revenue (which equals marginal cost) as given.

More explicitly, a two-stage model is being used to model the traders' decisions. In the first stage the traders determine their sales to the import markets from all export countries except the domestic coun- try; in the second stage the traders trade in the domestic country. Solving by backward induction, the traders, in the second stage, know how much they have bought and sold in the first stage. Since the domestic country is a small country, the world price (prow) and marginal revenue (MR) from the world market are known. Thus, the decisions in period 2 are the ones modeled in the Figure 1.

6Formally, with symmetric Cournot firms, the p d curve is

and the ps curve by

where n is the number of firms, is the elasticity of processing demand, and is the elasticity of primary supply. The notion of a perceived sup- ply curve was first introduced by Just and Chern. 'By assumption, the STE in this model cannot undertake export sales on its own account since it does not have the required proprietary assets nec- essary to engage in export trade. Instead, it must use the MNEs as agents. In bargaining with the MNEs, the STE is unable to negotiate an export price of prow, since this price would leave no profits for the MNE. The model examines two different prices that the STE might be able to negotiate - w' and MR. A more complete treatment of this problem would make use a bargaining model between an MNE and the STE to make the STE's export price endogenous. 'Prior to implementation of the Canada-US Trade Agreement (superceded now by the North Ameri- can Trade Agreement), the CWB controlled impor- tation of Board-regulated grains. However, from 1991 import licensing for US grains was restricted to those grains for which US support levels ex- ceeded those for Canada; this still continues to be the case for wheat. Since 1994, Mexico has been exempted from import licensing. Consequent on the Uruguay Round outcome, in August 1995, im-

P[1 + ( l / @ l N I

w[l + ( W E > ) I ,

ANNUAL MEETING PROCEEDINGS 373

port licensing for wheat, barley and products was converted to tariff rate quotas, except for imports from the US and Mexico. 9As through the US 1994 notification to amend tariffs on imports of wheat and barley from Canada (under Article XXVIII of GATT) and the sub- sequent negotiated settlement relating to this issue.

REFERENCES Alston, J.M. and R. Gray. 1997. North American Agricultural Trade Policies: Export Subsidies and State Trading. Presented at the Conference on World Agricultural Trade: Implications for Turkey, September 18-20, Ankara Turkey. Sponsored by the Agricultural Economics Research Institute. Alston, J.M., R. J. Sexton and Mingxia Zhang. 1997. The Effects of Imperfect Competition on the Size and Distribution of Research Benefits. Ameri- can Journal of Agricultural Economics 79(4):

Canadian Wheat Board. 1998. Accredited Ex- porters. http://www.cwb.ca/markets/ae/index.htm September 18. Caves, Richard E. 1996. Multinational Enterprise and Economic Analysis. Cambridge University Press. Cambridge. Cramer, Gail. 1993. World Grain Trade. In Grain Marketing, 2nd ed. edited by Gail L. Cramer and Eric J. Wailes. Boulder: Westview Press. Davies, Susanna. 1986. The Grain Trading Com- panies. In The International Grain Trade: Prob- lems and Prospects. Nick Butler, ed. London: Croom Helm. Dixit, Praveen M. and Tim Josling. 1997. State Trading in Agriculture: An Analytical Framework. International Agricultural Trade Research Consor- tium Working Paper #97-4, July. 30 pp. Goldsmith, P.D. and T.L. Sporleder. 1998. Ana-

1252-1265.

lyzing foreign direct investment decisions by food and beverage firms: An empirical model of trans- action theory. Canadian Journal of Agricultural Economics 46(3):32946. Hayenga, M. and R. Wisner. 1999. Cargill’s Ac- quisition of Contintental Grain’ Grain Merchandis- ing Business. Staff Paper #312. Department of Economics, Iowa State University, Ames, Iowa. Hill, Lowell D. 1992. Part Five - The United States: Grain Marketing, Institutions, and Policies. In The World Grain Trade: Grain Marketing, In- stitutions and Policies, edited by Michael J. McGarry and Andrew Schmitz . Boulder: Westview Press. Just, Richard E. and Wen S. Chern. 1980. To- matoes, Technology, and Oligopsony. The Bell Journal of Economics 11: 584-602. Romer, P.M. 1990. Endogenous Technological Change. Journal of Political Economy 98(5, Part 2): 71-102. Sewell, Tom. 1992. The World Grain Trade. New York: Woodhead-Faulkner. United States General Accounting Office. 1996. Report to Congressional Requesters: Canada, Aus- tralia and New Zealand, Potential Ability of Agri- cul tural STEs to Distor t Trade. GAO/NSIAD-96-94. June. Varian, H.R. 1996. Differential Pricing and Effi- ciency. First Monday (Peer-Reviewed Journal on the Internet) Web Address - http://www.firstmon- day.dk/issues/issue2/different/index.hhnl, July 24, 1997. Veeman, M., M. Fulton and B. Larue. 1998. International Trade in Agricultural and Food Prod- ucts: The Role of State Trading Enterprises. A Report to Agriculture and Agri-Food Canada, Ottawa, November.