THE GLOBAL CEMENT BAG RECENT MARKET DEVELOPMENTS 1M-STOCK PRICE PERFORMANCE GLOBAL HIGHLIGHT |...

27

12 th January, 2011 THE GLOBAL CEMENT BAG Kindly read last page for contact details and important disclaimer CEMENT | ISSUE NO. 09 LOCAL | DEMAND IN NEGATIVE TERRITORY For the second successive month, demand for cement recorded a – month-on-month (MoM) decline in growth rate. In November, con- sumption reached 3.9mn tons representing a 9% MoM decline whilst, for December, consumption is expected to be in the vicinity of 3mn tons. Several factors contributed to these decreases. In November, falling demand came as a result of the cooling down in construction activities due to the Greater Bairam. In December meanwhile, lower demand came about as a result of (1) the truck drivers’ strike, (2) an increase in steel prices by EGP200/ton to EGP4,000/ton led developers to slowdown their construction activi- ties (in hope that steel prices may get cheaper) and (3) the poor weather conditions. On the export front, lull quantities were ex- ported by the companies in November and December. Companies are facing real difficulties in regaining back their forgone export markets due to the lengthy ban (18 months) imposed on exports . Our coverage universe currently includes three companies: Misr Beni Suef Cement, Misr Cement (Qena), and Sinai Cement. The last of these remains our top-pick – Sinai Cement <SCEM.EY, Price EGP55, and Target Price EGP64, Strong Buy>. REGIONAL / SAUDI COMPANIES CALL FOR LIFTING THE EX- PORT BAN Since last November Saudi cement companies have been calling on their government to revoke the conditional ban imposed on cement exports. Producers see this as a crucial decision in light of the rising level of inventory in the local market coupled with the 7mn tons of new capacities expected through to 2015. This is likely to exacer- bate the industry’s stance, with some producers deciding to halt production in case the ban is not lifted. Moreover, significant export potential emerged after Qatar was chosen to host the 2022 world cup as construction activities will flourish inside the country. Re- cently, the Saudi Supreme Economic Council announced it has started to review the export regulations imposed on the cement companies. COUNTRIES’ BREAKING NEWS Egypt: Caution state on cement licenses in Egypt GCC: Not scrapping import duty on steel and cement KSA: Saudi Arabia reviews stance on cement export ban Oman: RCCI acquired Pioneer Cement of U.A.E. UAE: Has the third largest Arab cement sector France: LG announced two disposals totaling c.EUR120mn Iraq: Cement spokesman calls for protectionist measures Pakistan: Cement exports seen to rise in coming years Russia: Waives cement export duties Spain: Spanish cement consumption continues slump RECENT MARKET DEVELOPMENTS BASMA SHEBETA [email protected] GHADA REFKY [email protected] CEMENT TEAM LOCAL MARKET INDICATORS | Nov-10 * Based on 12M moving average (MA) cement production and the added effec- tive cement production capacity # Average ex-factory price including transportation costs ^ Fob price Source: CICR Database and company reports 1M-STOCK PRICE PERFORMANCE GLOBAL HIGHLIGHT | EXPANSIONS Contents Egypt: 1. ALEX looking at ready-mix concrete 2. SUCE to set a new production line KSA: 1. ARCCO’s new plant in Jordan 2. SOCCO’s Tihama plant expansion France: LG unit in Syria starts operation Germany: 1. HEI’s unit to expand at Tsela plant 2. HEI to double Indian capacity by 2012 Italy: BZU starts production at Suchoi Log in Russia Portugal: 1. CPR’s capacity increases in Brazil 2. CPR inaugurated its largest cement plant in China VALUATION AND RECOMMENDATION Gray cement Mkt indicator Unit Nov-10 MoM % YoY % Consumption k tons 3,878 -9% 6% Production k tons 4,098 2% 5% Utilization rate * 96% -20 bps -591 bps Exports k tons 12 12% NM Imports k tons 121 0% 86% Local price # EGP/ton 520 1% NA Export price ^ USD/ton 65 NM NM Section Page Local cement companies under coverage 2 Key issues 3 Key market developments in Egypt 17 Market key performance indicators 17 Companies key performance indicators 21 Companies views and outlook 22 CICR views and outlook 22 Recent financial results 24 Share performance 25 Valuation 26 Company Last Price * LCY TP (LCY) Up /Down to TP Rec. MKT Cap US$ mn PER 11e EV /EBITDA 11e Dividend Yield 10e MBSC 76.3 75.3 -1.3% S 529.7 6.0x 3.1x 4.7% MCQE 104.0 126.8 21.9% B 541.3 8.4x 6.1x 11.0% SCEM 54.5 64.1 17.6% SB 661.7 6.1x 4.2x 8.9% * As of 10-Jan-11 -6.5% -4.0% -1.3% -0.9% 6.0% 8.7% 13.9% 56.8% -9.8% -9.6% -2.6% -0.7% -0.6% 0.0% 0.0% 0.4% 0.8% 1.4% 1.8% 2.4% 3.0% 3.4% 8.1% -6.7% -5.5% -5.5% -3.7% -2.1% -1.4% -0.9% -0.7% 1.4% 1.6% 2.8% 4.4% 4.5% 4.7% -60%-40%-20% 0% 20% 40% 60% 80%100% SUCE EY TORA EY SVCE EY ALEX EY MCQE EY MBSC EY SCEM EY NCEM EY ARCCO AB RAKCC UH GCEM UH RCCI OM EACCO AB SOCCO AB TACCO AB QACCO AB OCOI OM YACCO AB SACCO AB PCEM KK KCEM KK QNCD QD YNCCO AB CPR PL IT IM SRCM IN BZU IM LG FP TITK GA HOLN VX ACPL PA ADANA TI FCCL PA HEI GR BINC IN CIMSA TI Local Regional International Source: Bloomberg ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF. Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

-

Upload

independent -

Category

Documents

-

view

2 -

download

0

Transcript of THE GLOBAL CEMENT BAG RECENT MARKET DEVELOPMENTS 1M-STOCK PRICE PERFORMANCE GLOBAL HIGHLIGHT |...

12th January, 2011

THE

GLO

BAL

CEM

ENT B

AG

Kindly read last page for contact details and important disclaimer

CEMENT | ISSUE NO. 09

LOCAL | DEMAND IN NEGATIVE TERRITORY For the second successive month, demand for cement recorded a –month-on-month (MoM) decline in growth rate. In November, con-sumption reached 3.9mn tons representing a 9% MoM decline whilst, for December, consumption is expected to be in the vicinity of 3mn tons. Several factors contributed to these decreases. In November, falling demand came as a result of the cooling down in construction activities due to the Greater Bairam. In December meanwhile, lower demand came about as a result of (1) the truck drivers’ strike, (2) an increase in steel prices by EGP200/ton to EGP4,000/ton led developers to slowdown their construction activi-ties (in hope that steel prices may get cheaper) and (3) the poor weather conditions. On the export front, lull quantities were ex-ported by the companies in November and December. Companies are facing real difficulties in regaining back their forgone export markets due to the lengthy ban (18 months) imposed on exports . Our coverage universe currently includes three companies: Misr Beni Suef Cement, Misr Cement (Qena), and Sinai Cement. The last of these remains our top-pick – Sinai Cement <SCEM.EY, Price EGP55, and Target Price EGP64, Strong Buy>.

REGIONAL / SAUDI COMPANIES CALL FOR LIFTING THE EX-PORT BAN

Since last November Saudi cement companies have been calling on their government to revoke the conditional ban imposed on cement exports. Producers see this as a crucial decision in light of the rising level of inventory in the local market coupled with the 7mn tons of new capacities expected through to 2015. This is likely to exacer-bate the industry’s stance, with some producers deciding to halt production in case the ban is not lifted. Moreover, significant export potential emerged after Qatar was chosen to host the 2022 world cup as construction activities will flourish inside the country. Re-cently, the Saudi Supreme Economic Council announced it has started to review the export regulations imposed on the cement companies.

COUNTRIES’ BREAKING NEWS Egypt: Caution state on cement licenses in Egypt GCC: Not scrapping import duty on steel and cement KSA: Saudi Arabia reviews stance on cement export ban Oman: RCCI acquired Pioneer Cement of U.A.E. UAE: Has the third largest Arab cement sector France: LG announced two disposals totaling c.EUR120mn Iraq: Cement spokesman calls for protectionist measures Pakistan: Cement exports seen to rise in coming years Russia: Waives cement export duties Spain: Spanish cement consumption continues slump

RECENT MARKET DEVELOPMENTS

BASMA SHEBETA [email protected]

GHADA REFKY [email protected]

CEMENT TEAM

LOCAL MARKET INDICATORS | Nov-10

* Based on 12M moving average (MA) cement production and the added effec-tive cement production capacity # Average ex-factory price including transportation costs ^ Fob price Source: CICR Database and company reports

1M-STOCK PRICE PERFORMANCE

GLOBAL HIGHLIGHT | EXPANSIONS

Contents

Egypt:

1. ALEX looking at ready-mix concrete 2. SUCE to set a new production line

KSA: 1. ARCCO’s new plant in Jordan 2. SOCCO’s Tihama plant expansion

France: LG unit in Syria starts operation Germany:

1. HEI’s unit to expand at Tsela plant 2. HEI to double Indian capacity by 2012

Italy: BZU starts production at Suchoi Log in Russia Portugal:

1. CPR’s capacity increases in Brazil 2. CPR inaugurated its largest cement plant

in China

VALUATION AND RECOMMENDATION

Gray cement Mkt indicator Unit Nov-10 MoM % YoY %

Consumption k tons 3,878 -9% 6%Production k tons 4,098 2% 5%Utilization rate * 96% -20 bps -591 bpsExports k tons 12 12% NMImports k tons 121 0% 86%Local price # EGP/ton 520 1% NAExport price ^ USD/ton 65 NM NM

Section Page

Local cement companies under coverage 2Key issues 3Key market developments in Egypt 17 Market key performance indicators 17 Companies key performance indicators 21 Companies views and outlook 22 CICR views and outlook 22Recent financial results 24Share performance 25Valuation 26

Com

pany Last

Price *LCY TP

(LC

Y) Up/Downto TP R

ec.

MKT Cap

US$ mn PER

11e

EV /EB

ITD

A11

e

Div

iden

dYi

eld

10e

MBSC 76.3 75.3 -1.3% S 529.7 6.0x 3.1x 4.7%MCQE 104.0 126.8 21.9% B 541.3 8.4x 6.1x 11.0%SCEM 54.5 64.1 17.6% SB 661.7 6.1x 4.2x 8.9%* As of 10-Jan-11

-6.5%-4.0%-1.3%-0.9%

6.0%8.7%13.9%

56.8%

-9.8%-9.6%

-2.6%-0.7%-0.6%

0.0%0.0%0.4%0.8%1.4%1.8%2.4%3.0%3.4%8.1%

-6.7%-5.5%-5.5%-3.7%-2.1%-1.4%-0.9%-0.7%

1.4%1.6%2.8%4.4%4.5%4.7%

-60%-40%-20% 0% 20% 40% 60% 80%100%

SUCE EYTORA EYSVCE EYALEX EY

MCQE EYMBSC EYSCEM EYNCEM EY

ARCCO ABRAKCC UHGCEM UHRCCI OM

EACCO ABSOCCO ABTACCO ABQACCO AB

OCOI OMYACCO ABSACCO AB

PCEM KKKCEM KKQNCD QD

YNCCO AB

CPR PLIT IM

SRCM INBZU IMLG FP

TITK GAHOLN VXACPL PA

ADANA TIFCCL PA

HEI GRBINC IN

CIMSA TI

Loca

lR

egio

nal

Inte

rnat

iona

l

Source: Bloomberg

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

2

THE

GLO

BAL

CEM

ENT B

AG

Local cement companies under coverage

As highlighted in the scatter graph below, local and certain regional players are rela-tively cheap. By contrast, international players—specifically the industry “titans”—are looking relatively expensive, and may begin relocating to the MENA region.

Top pick for this month maintained |SCEM| Strong Buy:

SCEM reported a YoY consolidated net profit increase of 20% to EGP175mn in 3Q10, a figure 17% below 2Q10.

SCEM reached 8%- local market share in 9M10, selling 2,723k tons, with zero ex-ports due to the export ban.

MCQE | BUY:

MCQE reported a YoY net profit increase of 31% to EGP94mn in 3Q10, a figure 10% below 2Q10.

MCQE has reached 4%-local market share in 9M10, selling 1,429k tons. Meanwhile, MCQE recorded zero exports in 9M10 due to the export ban.

MCQE approved to increase its participation to the capital of Arab National Cement Co. (ANCC) from 10% to 15% (EGP138mn for total 15%).

MCQE recently clarified that higher costs incurred in 3Q10 were due to the payment of the resource development fees. Hence, MCQE no longer expects the government waiving those fees for MCQE despite, company-specific technical condition. We have thus restated these fees to be part of MCQE’s opex rather than provisions.

MBSC | Sell:

MBSC is to introduce its second 1.5mtpa production line (if to be continued) in 2011.

MBSC reported a YoY net profit decrease of 77% to EGP21mn in 3Q10 a figure 77% 3Q10, below that seen in 2Q10.

MBSC reached 3%-local market share in 9M10, selling 945k tons. Meanwhile, MBSC recorded zero exports in 9M10 due to the export ban.

MBSC’s grinder broke down in 1Q10 and was repaired in May 2010. It broke down again in September and yet to be repaired.

MBSC approved the distribution of a 100% stock dividend on October 14th, 2010. Thus, the company’s paid-in capital increased from EGP200mn to EGP400mn, and the number of outstanding shares doubled to 40mn.

Peers’ 11e PER vs. EPS CAGR

Prices as of 10-Jan-11 Source: Bloomberg and CICR estimates

Peer

s an

alys

is

MBSC EY

MCQE EY

SCEM EY

RAKCC UH

ARCCO AB

YACCO ABSACCO AB

AKCNS TI

CIMSA TI

ADANA TI

LG FP

HOLN VX

HEI GR

IT IMBZU IM

TACCO AB

YNCCO AB

TITK GA

CPR PL

OCOI OM

RCCI OM

0.00

5.00

10.00

15.00

20.00

-50% 0% 50%

11F

PER

3-year EPS CAGR

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

3

THE

GLO

BAL

CEM

ENT B

AG

Key Issues Debt and credit facilities

■ HEI: Improved credit terms HeidelbergCement [HEI] has agreed with its core banks better terms for its EUR3bn syndicated credit facility concluded in April 2010. The amendment agreement, effec-tive immediately, includes a reduction in credit margins of up to 100 bps, depending on the ratio of net debt-to-EBITDA. The favorable credit terms reflect the recent posi-tive development of the performance of HEI. The agreement is another successful step in the company’s cost reduction program. (Company Press Release, 22-Nov-10)

■ LG: To cut debt without capital raising Lafarge [LG] revealed that it can continue to reduce the size of its debt without rais-ing fresh capital. (www.cemweeek.com, 21-Nov-10)

■ CPR: Refinanced its liabilities CIMPOR [CPR] announced a set of financial transactions refinancing its liabilities and strengthening its liquidity, thus largely overcoming the challenges of the present finan-cial markets’ situation. Overall, these transactions increased CPR’s liquidity EUR1bn and extended the average maturity of its liabilities almost two years (1.9 years, of which 0.6 years of optional nature). These transactions include a EUR320mn-syndicated alternative to the Eurobond market loan, a EUR150mn-credit facility, a EUR110mn club deal loan, a EUR100mn-committed additional three year underwrit-ing of commercial paper and the extension to USD200mn, by request of the investors, of the already announced private placement. With this US Dollar liability CIMPOR “naturally” hedges the volatility of its assets and revenues denominated in currencies highly correlated with the US Dollar. (Company Press Release, 19-Nov-10)

■ LG: Places a EUR1-bn bond Lafarge [LG] placed, under its Euro Medium-Term Note program, a EUR1-bn bond with an 8 year maturity and fixed annual coupon of 5.375% to institutional investors. The proceeds of this transaction will be used to refinance part of the Group's existing debt. The settlement and issuance of the bond are expected to occur on November 29, 2010. (Company Press Release, 18-Nov-10)

■ CPR: Private placement in North-American market CIMPOR [CPR] announced the pricing of a private placement in the North-American market of long term Notes to be issued by its wholly owned subsidiary Cimpor Finan-cial Operations B.V. This placement of USD150mn is part of a set of CPR’s liquidity enhancement and maturity extension transactions. This 10-year bullet issue will pay a 6.7% coupon, which compares favorably with the sovereign cost of risk. (Company Press Release, 16-Nov-10)

■ LG: Cutting debt with increased asset sales Lafarge [LG] may increase asset sales in the coming year in response to high debt. LG has already sold EUR350mn in assets this year. The company’s net debt was EUR15.2bn in June but had fallen to EUR14.7bn by the end of September 2010. (www.cemweeek.com, 5-Nov-10)

■ HEI: Sticks to debt target, but doubts linger Although HeidelbergCement [HEI] has failed to meet growth expectations, CEO is optimistic and ambitious. The company’s objectives for the coming year are ambitious and include debt reduction and an upswing of free cash flow. The target is to reduce net debt by the end of this 2010 from EUR9.1bn to EUR8bn. (www.cemweeek.com, 18-Oct-10)

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

4

THE

GLO

BAL

CEM

ENT B

AG

Decisions

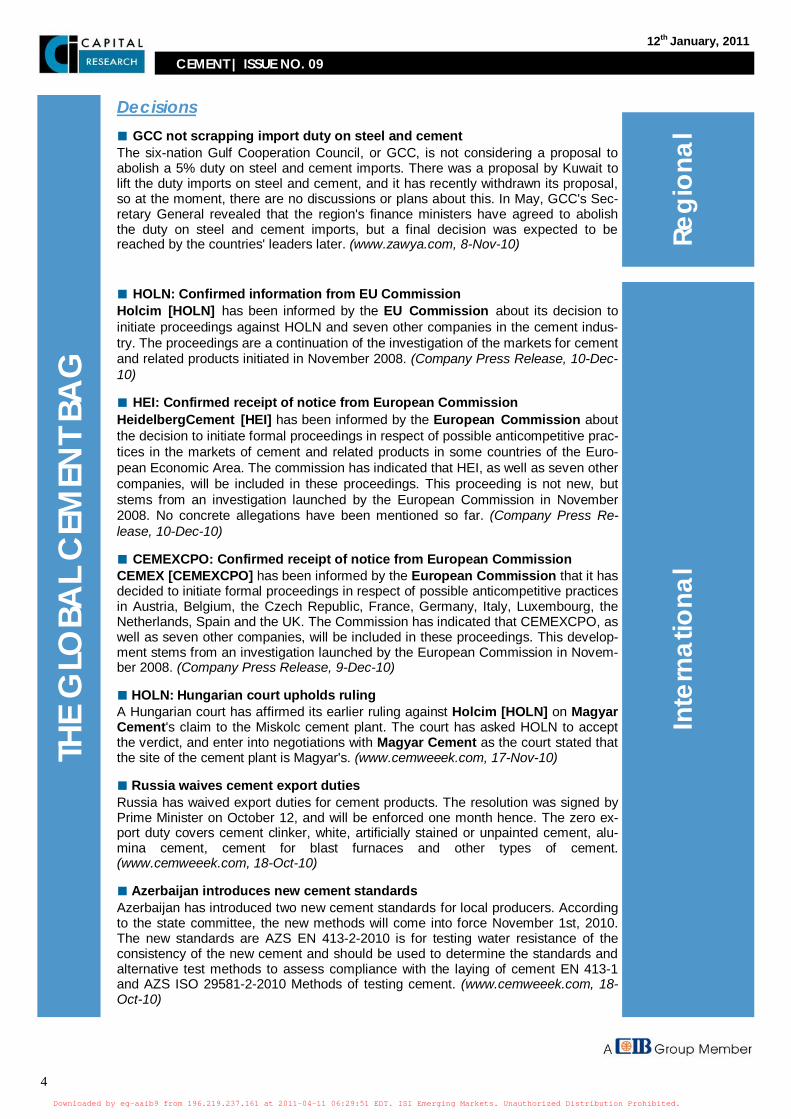

■ GCC not scrapping import duty on steel and cement The six-nation Gulf Cooperation Council, or GCC, is not considering a proposal to abolish a 5% duty on steel and cement imports. There was a proposal by Kuwait to lift the duty imports on steel and cement, and it has recently withdrawn its proposal, so at the moment, there are no discussions or plans about this. In May, GCC's Sec-retary General revealed that the region's finance ministers have agreed to abolish the duty on steel and cement imports, but a final decision was expected to be reached by the countries' leaders later. (www.zawya.com, 8-Nov-10)

■ HOLN: Confirmed information from EU Commission Holcim [HOLN] has been informed by the EU Commission about its decision to initiate proceedings against HOLN and seven other companies in the cement indus-try. The proceedings are a continuation of the investigation of the markets for cement and related products initiated in November 2008. (Company Press Release, 10-Dec-10)

■ HEI: Confirmed receipt of notice from European Commission HeidelbergCement [HEI] has been informed by the European Commission about the decision to initiate formal proceedings in respect of possible anticompetitive prac-tices in the markets of cement and related products in some countries of the Euro-pean Economic Area. The commission has indicated that HEI, as well as seven other companies, will be included in these proceedings. This proceeding is not new, but stems from an investigation launched by the European Commission in November 2008. No concrete allegations have been mentioned so far. (Company Press Re-lease, 10-Dec-10)

■ CEMEXCPO: Confirmed receipt of notice from European Commission CEMEX [CEMEXCPO] has been informed by the European Commission that it has decided to initiate formal proceedings in respect of possible anticompetitive practices in Austria, Belgium, the Czech Republic, France, Germany, Italy, Luxembourg, the Netherlands, Spain and the UK. The Commission has indicated that CEMEXCPO, as well as seven other companies, will be included in these proceedings. This develop-ment stems from an investigation launched by the European Commission in Novem-ber 2008. (Company Press Release, 9-Dec-10)

■ HOLN: Hungarian court upholds ruling A Hungarian court has affirmed its earlier ruling against Holcim [HOLN] on Magyar Cement's claim to the Miskolc cement plant. The court has asked HOLN to accept the verdict, and enter into negotiations with Magyar Cement as the court stated that the site of the cement plant is Magyar's. (www.cemweeek.com, 17-Nov-10)

■ Russia waives cement export duties Russia has waived export duties for cement products. The resolution was signed by Prime Minister on October 12, and will be enforced one month hence. The zero ex-port duty covers cement clinker, white, artificially stained or unpainted cement, alu-mina cement, cement for blast furnaces and other types of cement. (www.cemweeek.com, 18-Oct-10)

■ Azerbaijan introduces new cement standards Azerbaijan has introduced two new cement standards for local producers. According to the state committee, the new methods will come into force November 1st, 2010. The new standards are AZS EN 413-2-2010 is for testing water resistance of the consistency of the new cement and should be used to determine the standards and alternative test methods to assess compliance with the laying of cement EN 413-1 and AZS ISO 29581-2-2010 Methods of testing cement. (www.cemweeek.com, 18-Oct-10)

Regi

onal

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

5

THE

GLO

BAL

CEM

ENT B

AG

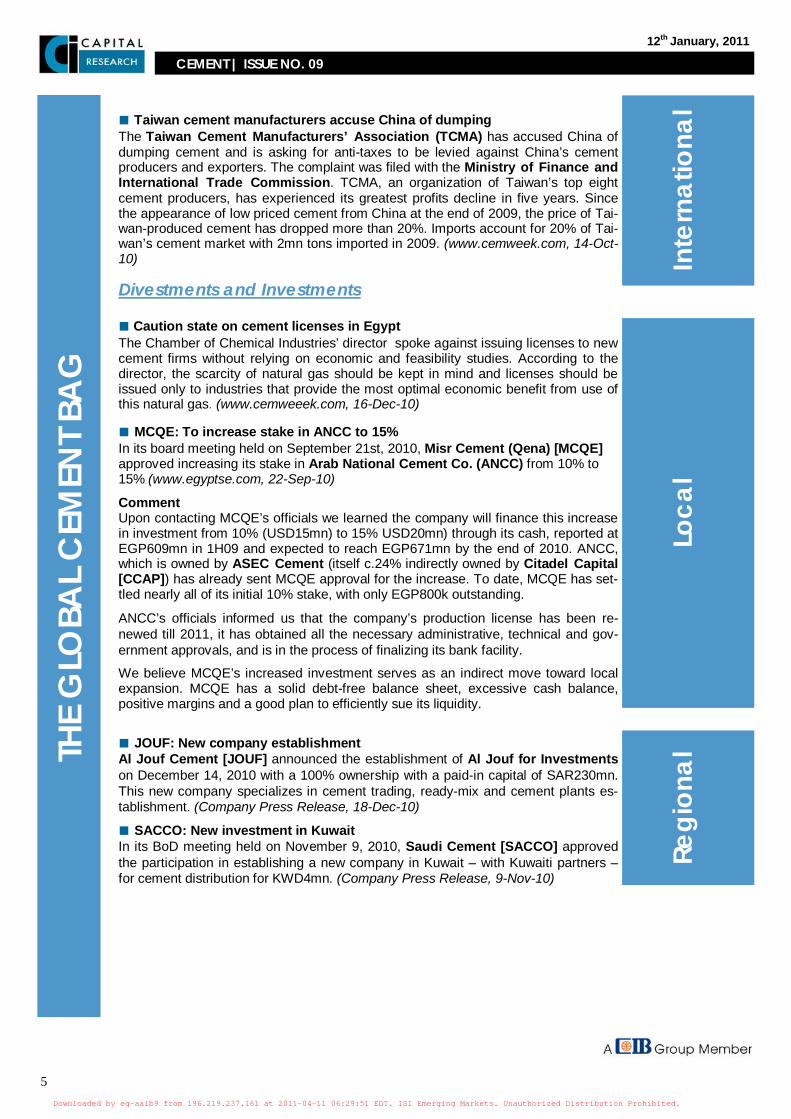

■ Taiwan cement manufacturers accuse China of dumping The Taiwan Cement Manufacturers’ Association (TCMA) has accused China of dumping cement and is asking for anti-taxes to be levied against China’s cement producers and exporters. The complaint was filed with the Ministry of Finance and International Trade Commission. TCMA, an organization of Taiwan’s top eight cement producers, has experienced its greatest profits decline in five years. Since the appearance of low priced cement from China at the end of 2009, the price of Tai-wan-produced cement has dropped more than 20%. Imports account for 20% of Tai-wan’s cement market with 2mn tons imported in 2009. (www.cemweek.com, 14-Oct-10)

Divestments and Investments ■ Caution state on cement licenses in Egypt The Chamber of Chemical Industries’ director spoke against issuing licenses to new cement firms without relying on economic and feasibility studies. According to the director, the scarcity of natural gas should be kept in mind and licenses should be issued only to industries that provide the most optimal economic benefit from use of this natural gas. (www.cemweeek.com, 16-Dec-10)

■ MCQE: To increase stake in ANCC to 15% In its board meeting held on September 21st, 2010, Misr Cement (Qena) [MCQE] approved increasing its stake in Arab National Cement Co. (ANCC) from 10% to 15%. (www.egyptse.com, 22-Sep-10)

Comment Upon contacting MCQE’s officials we learned the company will finance this increase in investment from 10% (USD15mn) to 15% USD20mn) through its cash, reported at EGP609mn in 1H09 and expected to reach EGP671mn by the end of 2010. ANCC, which is owned by ASEC Cement (itself c.24% indirectly owned by Citadel Capital [CCAP]) has already sent MCQE approval for the increase. To date, MCQE has set-tled nearly all of its initial 10% stake, with only EGP800k outstanding.

ANCC’s officials informed us that the company’s production license has been re-newed till 2011, it has obtained all the necessary administrative, technical and gov-ernment approvals, and is in the process of finalizing its bank facility.

We believe MCQE’s increased investment serves as an indirect move toward local expansion. MCQE has a solid debt-free balance sheet, excessive cash balance, positive margins and a good plan to efficiently sue its liquidity.

■ JOUF: New company establishment Al Jouf Cement [JOUF] announced the establishment of Al Jouf for Investments on December 14, 2010 with a 100% ownership with a paid-in capital of SAR230mn. This new company specializes in cement trading, ready-mix and cement plants es-tablishment. (Company Press Release, 18-Dec-10)

■ SACCO: New investment in Kuwait In its BoD meeting held on November 9, 2010, Saudi Cement [SACCO] approved the participation in establishing a new company in Kuwait – with Kuwaiti partners – for cement distribution for KWD4mn. (Company Press Release, 9-Nov-10)

Inte

rnat

iona

l

Regi

onal

Loca

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

6

THE

GLO

BAL

CEM

ENT B

AG

■ LG: Announced two disposals totaling c.EUR120mn Lafarge [LG] has disposed of the integrality of its Aggregates and Concrete busi-ness in Portugal (29 concrete plants and 4 aggregates quarries) to the Portuguese construction group Secil. This transaction is subject to approval by the Portuguese competition authorities. Moreover, LG has sold its Aggregates and Concrete busi-ness in Alsace (East of France) and Switzerland, including 8 concrete production plants (4 in Alsace and 4 in Switzerland) and 8 aggregates quarries in Alsace. The Swiss-based concrete operations have been sold to Holcim [HOLN] Switzerland and the French-based A&C activities have been sold to Eiffage Travaux Publics and HOLN France. This disposal will become effective on December 31, 2010. These transactions are part of the Group's divestment plan, exceeding the target of EUR500mn of divestments over the year. (Company Press Release, 27-Dec-10)

■ HEI: Seeking coal JVs HeidelbergCement India is currently seeking to form joint ventures with Indian com-panies, in a bid to secure more coal supplies. The company is currently seeking more coal to facilitate a planned USD265mn expansion. (www.cemweeek.com, 16-Nov-10)

■ BINC: Delisting due to low market float Binani Cement [BINC] has announced a voluntary delisting of its equity shares as Binani Industries has put in an offer to acquire the entire shareholding BINC. BINC has a capacity of c. 6.25mn in India and overseas. We feel that the 10% stake that is trading in the open markets is probably too small a size in the market. The stock’s delisting price is yet to be decided. (Bloomberg, 19-Oct-10)

■ LG: May invest EUR2bn in Russia Lafarge Cement [LG] plans to invest as much as EUR2bn in Russia over the next few years, including a plant under construction in the Kaluga region. (Bloomberg, 18-Oct-10)

■ Chinese, Indian firms eyeing expansion into Kenya Cement firms from India and China are looking to expand into Kenya, to take advan-tage of a construction boom in the East African region. Companies like Jedong De-velopment, Gleen Investments, and Aditya Birla are looking at the emerging mar-kets such as Kenya as opportunities to side step the economic cycle of a single re-gion. According to the report, bigger players are looking at buying stakes in estab-lished firms such as East Africa Portland Cement Company (EAPCC) and Athi River Mining (ARM). (www.cemweek.com, 17-Oct-10)

■ LG: Strabag deal pending anti-trust nod Lafarge Cement [LG] and Strabag’s move to combine their Central European ce-ment activities is now pending approval from the Austrian Federal Competition Authority (BWB). The two companies signed an agreement to create a new Aus-trian holding company in which LG will hold a 70% stake and Strabag 30%. The deal is expected to be operational from January 2011. The new company will have a total production capacity of 4.8mtpa, a fraction of LG's 203mtpa cement capacity. But LG revealed that the deal, which will reduce its EUR14.6bn net debt pile by just EUR77.5mn offered synergies. (www.cemweek.com, 14-Oct-10)

■ CEMEXCPO: To buy out partner Ready Mix USA In 2011 CEMEX [CEMEXCPO] declared that its joint-venture partner Ready Mix USA has decided to exercise a put option to sell its interest in the partnership to CEMEXCPO. (Bloomberg, 9-Oct-10)

■ Merchant Bridge invests in Iraq cement plant Private equity company Merchant Bridge has finalized USD220mn (Dh807mn) in-vestment in Iraq’s Karbala cement plant. Merchant Bridge assumed official control of the plant with its French building materials company partner Lafarge [LG]. The part-ners now take on full operations and management of the plant from the government

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

7

THE

GLO

BAL

CEM

ENT B

AG

of Iraq under a 15-year lease agreement. The Karbala cement plant produces less than 300ktpa of cement. Merchant Bridge and its partner LG are set to increase an-nual production to 2mn tons within 30 months. (www.uaecement.com, 5-Oct-10)

■ LG: Serbia to talk about PIM bid The Serbian government revealed that it will talk to Lafarge-Beocinska about its bid for state owned PIM. The firm offered a price of EUR16.5mn to buy the assets PIM and its exploration license, and EUR10mn for investment, which was the requirement for bid consideration. The PIM buyer will be obliged to continue the activity over the next five years and retain 442 employees for at least three years. (www.cemweek.com, 21-Sep-10)

Expansions ■ ALEX: Looking at ready-mix concrete to cement expansion Egyptian market expected to be at forefront of company's expansion push. Alexan-dria Cement [ALEX] (Titan Egypt) announced that it will consider acquisitions to boost its local capacity in ready mix and cement production. Cement for ready-mix tends to sell for more than bagged cement, making it more likely to stay profitable if energy costs rise, and building a ready-mix factory takes less capital than a full-scale cement plant (www.cemweeek.com, 15-Dec-10)

■ SUCE: To set a new production line at a cost of USD400mn Suez Cement [SUCE] is targeting to set a new production line with a capacity of 2mn tons at a cost of USD400mn as the firm plans to transfer its plants outside Hel-wan. (www.arabfinance.com, 12-Dec-10)

■ ARCCO: The new plant in Jordan In its BoD meeting on December 26, 2010, Arabian cement [ARCCO] discussed its 86%-owned Qantara plant in Jordan. It was revealed that completion of the plant was delayed and the construction costs increased by 18.6% to USD74mn. The BoD also discussed market changes in Jordan for the decreased demand and the increased production capacities that could result in financial problems in the future. Hence, ARCCO is studying the appropriate solutions for these changes. (Company Press Release, 26-Dec-10)

■ SOCCO: Tihama plant expansion to be completed by the end of 2011 Southern Province Cement Co. [SOCCO] revealed that its expansion project to add a second 5ktpd-cement clinker line at its third plant in Tihama will be completed by the end of 2011. The new line will raise the total daily production at the Tihama plant to 10k tons to meet the expected growing demand from Jizan province, border-ing Yemen. It will also increase the total daily output of SOCCO to 23k tons from 18k tons. Earlier this year, the company announced that it signed a SAR552mn(USD147mn)-contract with China's Sinoma International Engineering Co. to add the second 5ktpd cement clinker line at its third plant. (www.zawya.com, 27-Nov-10)

■ UAE has third largest Arab cement sector The UAE can pump as much as 31mtpa of cement to emerge as the third largest producer of the building material in the Arab region. Expansion at existing plants could boost that capacity to nearly 42mtpa to allow the UAE to maintain its position as the largest Arab cement producer after Saudi Arabia and Egypt. The country's present capacity accounts for nearly 17% of the total Arab cement output capacity of around 180mtpa. But the UAE's actual production is estimated at only about 17mtpa as only a tiny fraction of the output is exported and domestic demand has been smothered by the 2008 global fiscal distress. Saudi Arabia pumps close to 45mtpa but new projects will expand capacity to nearly 60mtpa in the next few years. (www.zawya.com, 22-Nov-10)

Inte

rnat

iona

l

Loca

l

Regi

onal

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

8

THE

GLO

BAL

CEM

ENT B

AG

■ HEI: A unit to expand capacity at Tsela plant Slantsy Cement, a unit of Germany's HeidelbergCement [HEI], announced it will expand the production capacity at its Tsela unit to 1.2mtpa. The firm will invest RUB4bn to fund the expansion, as it believes the Russian cement market is recover-ing. (www.cemweeek.com, 14-Dec-10)

■ HEI: To focus on emerging markets HeidelbergCement [HEI] will focus on increasing capacity in its emerging market operations and expects it to drive growth in the coming year. The company’s CEO declared that Asia and Africa may likely have a more positive demand building mate-rials in the coming years. Therefore, the firm wants to shift the proportion of cement capacity in emerging markets to increase in the long term to 70% from the current 58%. (www.cemweeek.com, 8-Dec-10)

■ Cemena Holding Company to build a cement plant in Syria Cemena Holding Company, a Middle East and North Africa (MENA) based cement company, signed an agreement with Sinoma CBMI Construction Company a sub-sidiary of Sinoma group to commence construction of a cement plant in Syria. The plant, which will be Cemena's second after (Falcon) a cement plant in the Kingdom of Bahrain; the design production capacity of the plant is 6.4ktpd with two production lines, 3.2ktpd of each production line. The construction of phase one will start in January 2011 and the initial production is to start in 18 months. The plant is strategi-cally located in Jabal Al Kahlah only 150km from the Iraqi border. The plant will bene-fit from huge demand in the fast growing Syrian market and it will also supply neighboring countries such as Iraq where state infrastructure projects, and private sector development have created substantial demand for cement. According to Ce-mena Holding Company , consumption in Syria is increasing annually by 5.2% due to the increasing number of real estate and infrastructure projects. (www.zawya.com, 1-Dec-10)

■ CPR: Capacity increases in Brazil Strengthening its presence on emerging markets, CIMPOR [CPR] announced invest-ments to increase production in Brazil to meet demand growth. As witnessed by its YoY 3Q10-18% sales growth, CPR has been increasing its participation in the Brazil-ian market, surpassing market growth (estimated at 13% for 2010) and almost reach-ing full capacity utilization. Brazil’s prospects for continuing encouraging economic dynamism and cement consumption growth outlook led CPR to approve a new EUR240mn-program of investments over the next three years (to be added to EUR10mn more of ongoing investments) to increase local cement production capac-ity by 2.3mtpa. Considering the geographic footprint of CPR in Brazil, two new inter-ventions where given priority to address the increasing cement demand in this coun-try.

The construction of a new line in the Cezarina plant and the construction of a produc-tion unit at Caxitu. The construction of a third line in Cezarina (Goiás Province, Cen-tral-West), currently producing at full capacity, will add 0.65mtpa of cement produc-tion capacity to this facility. Cezarina “Line Three” project will start in 2011 and re-quire, over the next three years to completion, an investment of up to EUR80mn. The new line specifications allow at a later stage, if required, for capacity duplication by means of a EUR40mn investment. Together with the ongoing revamping of “Line One”, “Line Three” commissioning will bring Cezarina to a total cement production capacity of 2.1mtpa by 2013.

The construction of a new cement and clinker production unit in Caxitu will enable CPR to continue to grow alongside the market in the Northeast region, complement-ing the three existing plants - João Pessoa, São Miguel dos Campos e Campo For-moso - presently at full usage of their 3mtpa-capacity.

The line to be built in Caxitu will have a cement production capacity of 1.45mtpa, re-quiring an investment of up to EUR160mn. The construction of this facility will start in 2011 and is to be finished in 2013.

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

9

THE

GLO

BAL

CEM

ENT B

AG

These two new cement production lines strengthen CPR’s presence in Brazil - its current leading contributor to both Turnover and EBITDA -, increasing the company’s local cement production capacity to c. 8.8mtpa, in 7 plants, and reinforcing its condi-tions to defend its market participation of c.10% in this country. (Company Press Re-lease, 25-Nov-10)

■ HEI: To double Indian capacity by 2012 HeidelbergCement [HEI] is to double its capacity from 3.4mn tons to 6.3mn tons by 2012. The company revealed that the increase in capacity is due to the continued growth of the Central Indian market. The capacity expansion will cost INR1,200cr., half of which will come from company coffers with the rest sourced from loans. (www.cemweeek.com, 24-Nov-10)

■ Russia to add 10mn tons of cement capacity Russia is to add an additional 10mn tons of cement capacity in the next two years. Included in these expansions is a new cement plant in the Orenburg region, which will have an installed capacity of 2.5mn tons. Also nearing completion is the cement plant of LSR in Shales of the Leningrad Region. According to the company's man-agement, the plant will be commissioned in 1H11. In the final stages of construction are the plants of Tulatsement Company, and Basel Cement capacity of 2mn and 1.5mn tons of cement each. In addition, several cement plants declare the comple-tion of the reconstruction of capacities. One of the largest cement producers in Rus-sia Mordovcement is preparing to build a new production line with a cement capac-ity of 2.35mtpa. (www.cemweeek.com, 14-Nov-10)

■ CPR: Inaugurated its largest cement plant in China CIMPOR [CPR] inaugurated in China its largest plant for cement production which will allow the company to more than double its installed capacity in the country. CPR Zaozhuang possesses a capacity for cement production, with its own clinker, of 2mtpa. This investment represents a value of c. EUR100mn. The plant is located in Zaozhuang, a city known for its construction materials companies and for the produc-tion of coal. This region is very rich in reserves of coal and limestone, the essential raw material for the production of cement. Zaozhuang is the leader in the province of Shandong’s ranking of installed cement production capacity, with around 60mn tons. CPR entered the Chinese market in May 2007 with the acquisition of 60% of the so-cial capital of the company, Shandong Liuyan, Ltd. It currently possesses two pro-duction plants for integrated cement production, in Shandong and Zaozhuang, a clinker production plant in Liyang, and two cement grinding units in Huaian and Suzhou, which together have a production capacity of cement with its own clinker of 5.3mtpa. With a presence in four continents and twelve countries, CPR is among the top ten global producers of cement, with a production capacity of 36mtpa. (Company Press Release, 3-Nov-10)

■ LG: Syria’s unit starts operation Lafarge Cement-Syria, a unit of Lafarge [LG], has started operations at its local plant--which is expected to attain its annual full capacity of 3mn tons early next year. The cost of the plant has reached nearly USD700mn.Thanks to this plant Syria will achieve self-sufficiency in cement especially since it is witnessing a growing popula-tion and a construction boom. The new plant, which will cover Syria's deficit in ce-ment production, is the largest private sector investment that has been implemented in the country so far. Syria has six state-owned cement plants, some of them going back to the fifties of the twentieth century. These plants have a combined annual ca-pacity of 5.2mn tons while the country's annual consumption is estimated at 8.4mn tons. Lafarge Cement-Syria is 80% owned by LG and 20% by Syria's MAS Eco-nomic Group. (www.zawya.com, 16-Oct-10)

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

10

THE

GLO

BAL

CEM

ENT B

AG

■ BZU: Starts production at Suchoi Log Buzzi Unicem [BZU]’s new production line in the Suchoi Log town of Russia was inaugurated on August 6th, 2010. The 1.1mtpa cement plant was developed with new machines as well as older parts salvaged from older units that have been non functional for the past ten years. The new production line also boasts of a clinker storage unit with the capacity to house around 150k tons. (www.cemweek.com, 21-Sep-10) Market volumes and pricing

Production

■ China production keep rising Chinese national cement production in November was 176.6mn tons - an increase of 3.69% relative to the previous month. For 11M10, total cement output reached 1.7bn tons. December is typically the peak season for the industry, according to the incre-mental trend of annual cement production this year is likely to exceed 1.85bn tons of cement. (www.cemweeek.com, 13-Dec-10)

■ Russian cement production to increase 15% in 2011 Russia's cement production may increase 15% next year, more than its pre-crisis levels, on the back of capacity expansions. The Union of Cement Producers of Russia (Soyuztsement) revealed that the industry is ready to produce almost twice as much cement than the current 52mn tons, but domestic real estate developers have no need for such volumes. (www.cemweeek.com, 30-Nov-10)

■ Reduction in US cement production Leading producers are trying hard to tame recession with production cut-offs and strategic cost reduction exercise. US annual demand decreased from 128mn tons in 2005 to a current of 65mn tons. The chief economist at the American Portland Ce-ment Association revealed that cement consumption increased slightly but still within the limits of 70mtpa. Meanwhile, the companies are implementing new strate-gies to bring down cost levels. Resorting to river boat cargo for transporting cement is one cost reduction technique attempted by the large facility located near the Mis-sissippi River. (www.cemweeek.com, 29-Nov-10)

■ Cement production is set to increase in China as power restrictions end China’s steel and cement industry will begin increasing production, as power supply is gradually restored to normal, following China’s decision to ease energy consump-tion restrictions. China had earlier curbed power supplies, to slash energy consump-tion by 15.6% for the period 2006 to 2010 in an attempt to meet its 20% reduction target. The power shortage had brought down cement and steel output. (www.cemweeek.com, 25-Nov-10)

■ Second cement plant to be built in Muthanna in Iraq A private-sector company is to build a cement factory, the second in southern Iraq's Al-Muthanna province, with a production capacity of 1mtpa and a total cost of USD200mn. All legal measures for contracting and handing over the land for the con-struction of a cement plant have been completed. The new plant shall witness the first steps of its construction by a Chinese company during the next few days, and will be completed within 30 months from now. (www.zawya.com, 3-Oct-10)

Inte

rnat

iona

l

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

11

THE

GLO

BAL

CEM

ENT B

AG

Demand

■ Saudi cement sales up fuelled by infrastructure spending Total sales of cement in Saudi Arabia is forecast to reach 36.5mn tons by the end of 2010, driven mainly by the aggregate expenditure on construction in the Kingdom. For 9M10 total local cement sales amounted to 34.4mn tons, an increase of 13.3% vs. 9M09. KSA’s domestic market for cement has been well supplied by the 13 local factories during the 9M10, with total production growing by 13.9% to 32.2mn tons as one more factory, Al Jouf Cement [JOUF] came on the production stream with an output of around 180k tons in September 2010. The government's budget for 2010 focuses on capital expenditure (SAR260bn) 48% of resources, being allocated to infrastructure projects. Both consumption and prices of cement have been increasing since the beginning of the year, driven by the 8% growth in construction activity by 1H10. The price of cement rose to reach SAR270/ton in September 2010. (www.zawya.com, 22-Nov and 24-Oct-10)

■ UAE listed cement companies’ 9M10 net profits declined by 54% to AED305.9mn The combined net profit of 10 cement companies listed on the Dubai and Abu Dhabi bourses plunged 54% to AED305.9mn (USD83.3mn) in 9M10 from AED665.1mn a year earlier. The cement manufacturers attributed the profit slump to the rising cost of materials used in cement production, especially oil, diesel and coal, in addition to a sharp decline in demand which led to lower cement sales prices. The decline in de-mand and cement prices was the result of an ongoing market decline and the mort-gage crisis that affected the real-estate and building materials sectors. The compa-nies' sales fell 30% to AED2.48bn in 9M10 from AED3.54bn in the corresponding period in 2009. (www.zawya.com, 18-Nov-10)

■ Cement firms struggle as demand drops in Dubai Cement makers now want to tap other markets to boost sales. Cement firms based in Duabi have been hit by sagging demand, prompting some of them to seek govern-ment permission to export their goods to help sales. Lower prices are also hitting local cement makers. Demand for cement in the emirate has dropped from more than 20mn tons in 2008 to 13mn tons today. The price of cement peaked at Dh400/ton in 2008, prompting the government to cap it at Dh360/ton. The price today is around Dh200/ton for cement ex-factory and ready mix products fetch about the same value proportionately in cubic meters. (www.cemweek.com, 12-Oct-10)

■ Russia cement consumption up 19.6% in November Russian cement consumption for its European parts has increased 19.6% year on year in November. The highest growth recorded was in the southern regions, mostly because of the Olympic preparations. In the Moscow region, cement demand also picked up because of the construction of new housing units. (www.cemweeek.com, 9-Dec-10)

■ Indian cement makers struggle in November Analysts expect supply demand mismatch to persist in the near term, as recovery will come in around mid 2011. Indian cement makers took a beating November, following a good October. The November dispatches by most cement majors remained in negative territory, except for ACC. The top five cement players have reported a 19.8% drop in combined dispatches, indicating that demand is yet to pick up suffi-ciently to support prices. (www.cemweeek.com, 6-Dec-10)

■ Low demand and high costs dampen cement sales in India November was a bleak month as far as cement makers of India is concerned with fall in sales and profits, on account of reduced construction activities. While un-seasonal rains affected cement sales in October, the festival season of November brought fur-ther bad news. Construction activities were stalled due to labour shortage during the festival period. Consequently cement prices fell to Rs 240 a bag from Rs 245 in Oc-tober. (www.cemweeek.com, 3-Dec-10)

Regi

onal

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

12

THE

GLO

BAL

CEM

ENT B

AG

■ China cement demand expected to maintain growth China's cement demand is expected to maintain its upward momentum in the coming months, as peak season approaches. Cement prices may also continue to rise, partly because the government's push to reach its annual energy saving targets, which could reduce production volumes in the cement industry. (www.cemweeek.com, 2-Dec-10)

■ Spanish cement consumption continues slump and seen dipping further in 2011 Spanish cement consumption posted a decrease of 14.8% in the first 10 months of the year. The Spanish cement plants had to adjust their production while trying to cushion the decrease of domestic demand through exports. As a result, Octo-ber showed Spanish factories selling 3.2mn tons of cement to foreign markets, representing an increase of 33.2% as compared to the corresponding period last year. Spain's cement makers expect market consumption for cement will dip to a 40 year low of 22mn tons next year. This is also 10% less than 2010 predicted consumption. It is worth mentioning that demand could hit hat 24.5mm tons in 2010 representing a 15% decline from 2009. (www.cemweeek.com, 16-Dec and 19-Nov-10)

■ BZU: Sales up 1.3% on higher cement demand Buzzi Unicem [BZU] announced that their cement and clinker sales for January to September grew 1.3% to 20mn tons. The company says this is due to a grad-ual recovery in the global economy. The company says that the stimulus pro-grams adopted by countries like the US have begun taking effect. (www.cemweeek.com, 11-Nov-10)

■ HEI: 3Q10 revenues boosted by US constriction HeidelbergCement [HEI] announced that its 3Q10 revenues came in at EUR3.4bn for the period, on stronger US construction sales. (www.cemweeek.com, 1-Nov-10)

Exports

■ Saudi Arabia reviews stance on cement export ban The Supreme Economic Council has started their review of the cement export regulations that are currently imposed on local companies. The review also in-cludes tests about the true nature of losses incurred in cement production as re-ported by the companies, including investigation into whether some companies are violating the rules and regulations. Saudi cement producers initiated a two day consultation and requisition process with the Saudi ministry of trade in a bid to persuade them to lift the export ban imposed on them, in the wake of renewed infrastructure development in neighbouring Qatar who will host the 2022 World Cup. Calling the attention of the Supreme Export Council to the rising inventory of cement stockpile, in addition to the 7mn tons of new capacity seen through 2015. Cement companies requested the Council to lift the ban on the export of cement. The General Manager of Eastern Province Cement [EACCO] threatens to halt production and lay off workers as cement inventory piles up at company premises following the continued ban on exports. According to the GM, current volumes exceed domestic demand. Surplus is expected to grow by 19% if the industry is prevented from exporting the product. Many companies are forced to work at minimal production capacity and idle capacities are estimated at total around 26mn tons. (www.cemweeek.com, 13, 9, 7-Dec and 23-Nov-10)

Inte

rnat

iona

l

Regi

onal

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

13

THE

GLO

BAL

CEM

ENT B

AG

■ Pakistan cement exports seen to rise in coming years Pakistan's cement exports are expected to grow in the coming years, as neighbour-ing countries such as Qatar and Russia ramp up their infrastructure spending. How-ever, Saudi Arabia and United Arab Emirates (UAE) would be more suitable coun-tries for Qatar to import cement for the purpose, as these two had closer ties with Qatar than Pakistan. (www.cemweeek.com, 5-Dec-10)

■ Russian cement exports seen to rise after tariff cut Government's decision to waive export duties a boon to Russian dispatches to neighboring countries. Russian cement exports are expected to surge in the coming months, after the government decided to waive customs duties on exports. The waiver also means cement products from the country will be cheaper. Prices will fall to USD68/ton from the current USD73/ton. Russian manufacturers expect export growth from 600ktpa up to 3mtpa. (www.cemweek.com, 19-Oct-10)

■ Pakistan cement exports hurt by EA tariff increase The Common External Tariff (CET) on East African cement imports is expected to increase from 25-35%, hurting Pakistan’s cement export business. Local exporters will likely react by substituting African markets for the Far East, making Sri Lanka and Myanmar the hot spots for future growth potential. (www.cemweek.com, 15-Oct-10)

Imports

■ Iraq cement spokesman calls for protectionist measures The Director of Iraq's General Cement Company indicated that annual local produc-tion reached 5mn tons as against a high imports of 20mn tons per year, bringing the government’s attention to the skewed proportion of production vs. imports. The Di-rector warned the government that high imports would be destructive to the domestic industry and will turn the country into a consumer state, he asked for tighter meas-ures to protect the local industry. (www.cemweeek.com, 23-Nov-10)

■ Votorantim keeps importing to meet demand Owing to a sudden increase in demand due to an increase in construction activities, Brazil's Votorantim has resorted to cement imports. According to the statistics, the company may rely on 400k tons of cement imports in 2010. Most of the imports are bought from Asia, owing to several factors, such as product specification, packaging of the product, which is sold in bulk in US contrary to Brazil’s measure of bagged cements and other logistics dictates. (www.cemweeek.com, 16-Nov-10)

■ East African cement makers insist on import duties Cement firms are suffering from unfair competition, because of cheaper imported products. Cement makers in East Africa continue to ask East African Community (EAC) to increase cement import duties, to help protect the local industry. Cement imported from India, China and Pakistan into the EAC member states is hurting local manufacturers since it is sold at a very cheap price than the locally manufactured products. (www.cemweek.com, 21-Sep-10)

Prices

■ Nigeria cement prices to drop as firms increase production Cement prices in Nigeria may soon drop, if massive capacity expansions by local cement makers push through. Local manufacturers are targeting to increase produc-tion to about 30mn tons by 2012, more than double the 11.5mn tons it currently pro-duces. Cement demand in the country is expected to reach 15.5mn tons in 2010. At present, a bag of cement currently sells for c. NGN1,650 in the market, though the Federal Government had targeted that it should not be more than NGN1,000/bag. About three years ago, the price had climbed to an all time high of c. NGN2,000/bag. (www.cemweeek.com, 13-Dec-10)

Inte

rnat

iona

l

Inte

rnat

iona

l

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

14

THE

GLO

BAL

CEM

ENT B

AG

■ Competition trims cement prices in Jordan Jordan's Ministry of Trade and Industry revealed that the increased competition in the market has managed to drive down cement prices. According to a study by the Kingdom's competition authorities, discounts and promos made by cement makers to distributors and traders are becoming beneficial to customers, as pass on prices have been reduced compared to a year earlier. (www.cemweek.com, 19-Oct-10)

■ Cement firms in India mull further price hikes Firms are looking to increase fees by around INR5-25/bag. Indian cement makers want to initiate another round of price hikes, barely a few weeks since they last made increases of INR10-30/bag. (www.cemweek.com, 21-Sep-10)

■ Cement prices fall in Mexico, rise in United States A survey indicated that cement retail prices in Mexico dropped 0.4% in August, al-though prices varied widely by region. The same survey indicated a small increase of 0.7% in the United States’ producer price index, despite weak construction activity. Another survey showed only a 0.2% increase. The overall outlook for the U.S. market is considered strong. This is positive for CEMEX [CEMEXCPO] in particular, given the company’s operating leverage in Mexico and the United States. (www.cemweek.com, 21-Sep-10) Mergers and Acquisitions

■ RCCI: Acquired Pioneer Cement of U.A.E. Raysut Cement Co. [RCCI], acquired Pioneer Cement Industries LLC for USD172mn. Pioneer Cement, based in Ras Al Khaimah, the UAE, has a clinker pro-duction capacity of 1.25mtpa and cement output capacity of 1.7mtpa. (Bloomberg, 3-Jan-11)

■ HOLN: Acquired several aggregates operations and ready-mix concrete plants Holcim [HOLN], together with a partner, acquired 8 aggregates pits and quarries and 4 ready-mix concrete plants in Alsace (France) and 4 ready-mix concrete plants in the Basle area (Switzerland) from Lafarge [LG] as of January 2011. This strategi-cally attractive acquisition will allow HOLN (Schweiz) AG and HOLN (France) s.a.s to supply customers even better in these markets. At the same time, the acquisition serves to secure high-quality aggregates reserves in this attractive economic area. As some gravel pits are located directly on the river Rhine, HOLN will be able to sup-ply gravel and sand by ship not only to Switzerland and South Germany but also to Luxemburg and the Netherlands. (Company Press Release, 27-Dec-10)

■ TITK: Cement plant acquisition in Kosovo Titan Group [TITK] announced the signing of a definitive agreement with the Privatization Agency of Kosovo for the purchase, through its affiliate “Sharr Beteiligungs GmbH”, of the Sharr cement plant. The acquisition is not expected to have a material impact on the Group’s results, as the plant, with a rated capacity of 600ktpa, was already under Titan management, on the basis of a lease agreement. (Company Press Release, 15-Dec-10)

■ TITK: Closing of minority stake sale in Egypt Titan Group [TITK] announced the completion of the EUR80mn-equity investment of International Finance Corporation (IFC in Alexandria Portland Cement Company [ALEX] through the purchase of a stake in TITK’s holding company Alexandria Development Limited (ADL). The transaction resulted in IFC holding through ADL a 15.2% minority stake in ALEX and subsequently in Titan’s Egyptian operations. The collaboration with an institution like the IFC is expected to add significant value to TITK’s investment in Egypt. (Company Press Release, 22-Nov-10)

Inte

rnat

iona

l

Regi

onal

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

15

THE

GLO

BAL

CEM

ENT B

AG

■ CEMEXCPO: Close to acquiring India's Murli Industries CEMEX [CEMEXCPO] is set to acquire India's Murli Industries for USD550mn. The price is still being negotiated and the final figure would depend on the outlook for ce-ment prices. Murli Industries operates a 3mn tons plant in Maharashtra’s Chandrapur, and plans to build two more, one in Rajasthan and the other in Karna-taka. The planned new units’ capacities are 3mn tons each. (www.cemweeek.com, 21-Nov-10)

■ Votorantim, BioBio purchase stakes in Peru's CIMPOR Chile's Cementos BioBio and Brazil's Votorantim have both purchased a combined 59% of Cimpor [CPR]. Biobio finance the acquisition by increasing its capital base by USD59mn. Votorantim and Biobio now have 29.5% each of CPR, while the re-maining 41% is split between CPR and Spain's IPSA. (www.cemweeek.com, 15-Nov-10)

■ CEMEXCPO: To acquire interests of its JV partner Ready Mix USA in Sep-tember 2011 CEMEX [CEMEXCPO] announced that pursuant to the exercise of a put option by Ready Mix USA it will acquire its partner's interests in the two joint ventures between CEMEXCPO and Ready Mix USA which have cement, aggregates, ready mix and block assets located in Southeastern USA. The purchase price will be determined jointly by CEMEXCPO and Ready Mix USA based on a pre-determined methodol-ogy. CEMEXCPO currently estimates the purchase price for its partner's interests will be around USD360mn. At closing, CEMEXCPO will also consolidate approximately USD17mn in net debt held by one of the joint ventures. Closing is expected to take place in September 2011. Ready Mix USA will continue to manage this joint venture until the closing of the transaction. (Company Press Release, 8-Oct-10)

■ CPR: Agrees to buy stake in Cinac of Mozambique Cimpor [CPR] agreed to buy 51% of Cinac-Cimentos de Nacala SA from Camargo Correa Cimentos SA of Brazil. Cinac, based in northern Mozambique, owns cement grinding mill and limestone quarries. (Bloomberg, 1-Oct-10)

Miscellaneous

■ Egypt looking to reduce cement plant emissions Egypt's Ministry of Trade and Industry will start the implementation of a program to use alternative fuel to power heavy industries like cement plants. The government revealed that this project will bring back economic and environmental benefits for the cement plants through the application of advanced technologies and use of alterna-tive fuels in the production of cement, and will reduce the cost of energy to the ce-ment sector at rates ranging between 20%-to-30% and the energy consumption from traditional sources by up to 30%. (www.cemweeek.com, 30-Nov-10)

■ MBSC: To increase paid-in capital by EGP200mn Misr Beni Suef Cement [MBSC] is to increase its in paid-in capital from EGP200mn to EGP400mn, via distribution of free shares at a 1:1 ratio for shareholders as of Oc-tober 13th, 2010. MBSC will finance the increase through retained earnings. (Al Ak-hbar, 28-Sep-10)

Inte

rnat

iona

l

Loca

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09

16

THE

GLO

BAL

CEM

ENT B

AG

■ LG: launches online selling platform in Brazil Lafarge [LG] has launched its new online ordering system in Brazil. The portal, www.lafarge.com.br, enables customers to access products online, making it easier for them to order and book them. Lafarge says the Customer Portal is an action that began in Brazil and will expand to the rest of the world. For the Brazilian platform the firm invested USD2.8mn. (www.cemweeek.com, 14-Dec-10)

■ CEMEXCPO: Spends USD140mn on renewable energy CEMEX [CEMEXCPO] revealed that it has invested USD140mn to fund renewable energy initiatives for its production units, which has resulted in a 20% reduction of fossil fuel use for its plants. The company’s vice president for energy and sustainabil-ity mentioned that through the use of wind energy for its cement kilns, the company is confident it can cut 25% of its CO2 emissions compared to 1990 levels. (www.cemweeek.com, 13-Dec-10)

■ IT: Moody’s changes the rating from Baa2 to Baa3 with outlook stable from negative As part of its reporting activity, Moody’s Investor Services has changed the Italce-menti [IT] rating (as well as the one of the subsidiaries Ciments Français and Ital-cementi Finance) from Baa2 to Baa3. The outlook is now stable from previous negative. (Company Press Release, 26-Nov-10)

■ US consumption outlook lowered The US Portland Cement Association explained that the economic momentum that had been gathering steam earlier in 2010 has dissipated, warranting a less optimistic outlook for cement demand. In 2010, growth will now instead be virtually unchanged at 0.3% growth, but in 2011 demand is seen rising 1.4% and the by 4% in 2012. Sus-tained growth is forecasted for 2013 and beyond, according to the PCA. (www.cemweeek.com, 7-Nov-10)

■ CEMEXCPO: Supplied ready mix concrete for one of the tallest buildings in Asia CEMEX [CEMEXCPO] announced that it is one of the main concrete suppliers for the Gaoyin 117 project in Tianjin, China, which, upon completion, will be one of the tallest buildings in Asia. So far, the company has supplied nearly 95k cu.mt. of con-crete for the underground engineering of the project. At a height of 598 mt. when completed, the Gaoyin 117 project will require over 500k cu.mt. of ready-mix con-crete in order to build its 117 stories. The project, which began construction in 2008, will take between 5-to-7 years to complete and will require a total investment of nearly USD3bn. CEMEXCPO operates four ready-mix concrete plants in China, in the northern cities of Tianjin and Qingdao, and has presence throughout Asia with operations in the Philippines, Thailand, Malaysia, and Bangladesh. (Company Press Release, 21-Oct-10)

Inte

rnat

iona

l

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09| THE GLOBAL CEMENT BAG

17

Market Key Performance Indicators

Monthly 11M10 vs. 11M09

Source: Company reports, and CICR database * Demand = Local sales + Imports

Source: Company reports, and CICR database * Demand = Local sales + Imports G

ray

cem

ent l

ocal

dem

and

*

Demand growth recorded an 6% YoY growth and a 9% MoM decline in November 2010. Cement consumption grew YoY by 4% during 11M10.

Gra

y ce

men

t Pro

duct

ion

Monthly 11M10 vs. 11M09

Source: Company reports, and CICR database Source: Company reports, and CICR database

Production registered a 5% and 2% YoY and MoM growth, respectively, in November 2010. Cement production grew YoY by 3% during 11M10.

Key market developments in Egypt 3,

671

4,20

5

4,32

0

4,11

4

4,58

0

4,11

3

4,25

2

4,34

5

4,53

0

3,77

1

3,11

6

4,28

4

3,87

8 -7%

15%

3%-5%

11%

-10%

3% 2% 4%

-17% -17%

37%

-9%

-4%

32%

11%14%

6%

1% 3%7% 9%

-14%-8%

8% 6%

-40%

-20%

0%

20%

40%

60%

-

1,000

2,000

3,000

4,000

5,000

6,000

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

000's tonsGray Cement Local Demand MoM Chg YoY Chg

RamadanLesser Bairam vacation

Greater Bairam vacation

43,589 45,302

-

10,000

20,000

30,000

40,000

50,000

60,000

11M09 11M10

000's tons

up by 4%

3,91

2

3,89

2

4,07

9

3,87

7

4,36

0

4,26

8

4,22

2

4,11

4

4,38

0

3,89

6

2,95

6

4,00

4

4,09

8

8%

0%

5%

-5%

12%

-2% -1% -3%6%

-11%-24%

35%

2%

3% 16%

3%

8%2%

6%0%

5%10%

-6%

-14%

10% 5%

-40%

-20%

0%

20%

40%

60%

-

1,000

2,000

3,000

4,000

5,000

6,000

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

000's tons Gray Cement Production MoM Chg YoY Chg

Ramadan

43,087 44,255

-

10,000

20,000

30,000

40,000

50,000

60,000

11M09 11M10

000's tons

up by 3%

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09| THE GLOBAL CEMENT BAG

18

Market Key Performance Indicators (Con’t)

Monthly

Source: Company reports, and CICR database

11M10 vs. 11M09

Gra

y ce

men

t mar

ket d

efic

it/su

rplu

s

Source: Company reports, and CICR database

As demand growth outpaced supply, deficit of 1,047k tons was recorded during 11M10, compared to a deficit of 502k tons in 11M09.

Monthly

Source: Company reports, and CICR database * Demand =Local sales + Imports

11M10 vs. 11M09

Source: Company reports and CICR database * Demand = Local sales + Imports G

ray

cem

ent d

eman

d *

vs. s

uppl

y

3%

16%

3%8%

2%

6%

0%5%

10%

-6%

-14%

10%

5%-4%

33%

13% 14%

6%

1%

3% 7%

9%

-14%

-8%8%

6%

-20%

0%

20%

40%

60%

2,000

3,000

4,000

5,000

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

000's tons Supply Demand YoY Supply Chg YoY Demand Chg

43,087 44,255 43,589 45,302

-

10,000

20,000

30,000

40,000

50,000

60,000

11M09 11M10

000's tons Supply Demand

241

(313)(241)(237)(220)

155

(30)

(231)(150)

124

(159)(279)

220

-600

-400

-200

0

200

400

600

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

000's tons

(502)

(1,047)

(1,500)

(1,000)

(500)

-

500

11M09 11M10

000's tons

up by 109%

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09| THE GLOBAL CEMENT BAG

19

Market Key Performance Indicators (Con’t)

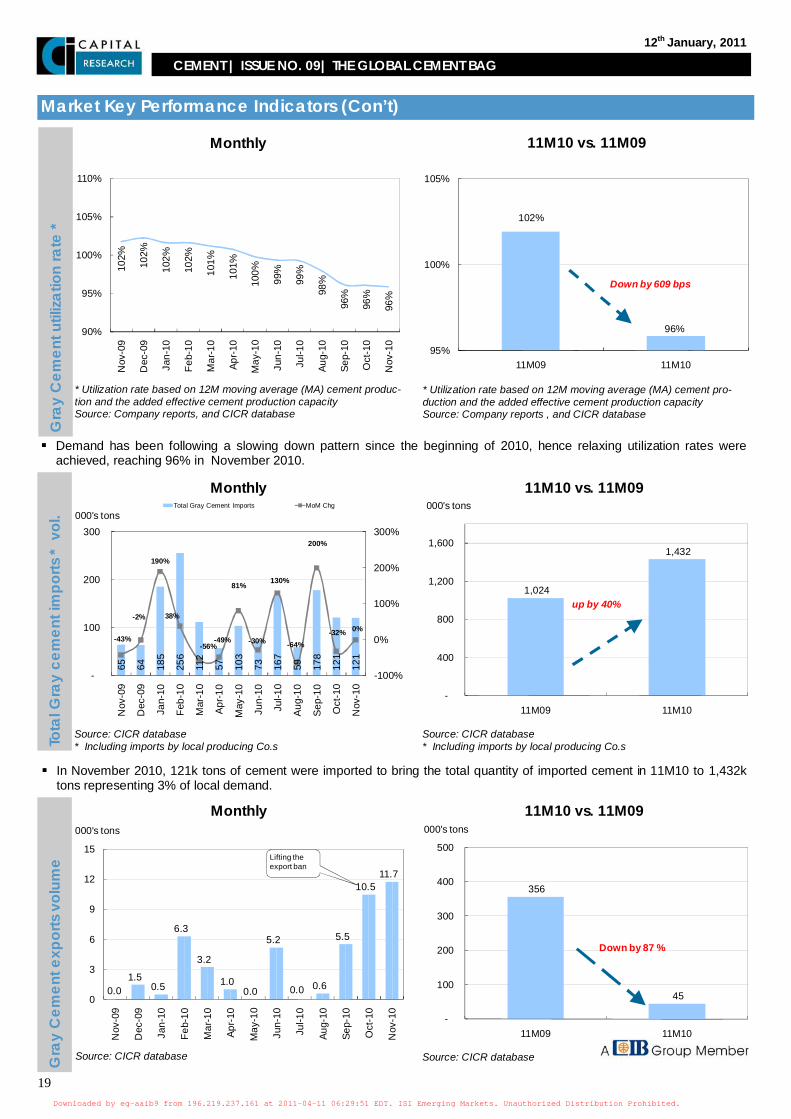

* Utilization rate based on 12M moving average (MA) cement produc-tion and the added effective cement production capacity Source: Company reports, and CICR database

Gra

y C

emen

t util

izatio

n ra

te *

* Utilization rate based on 12M moving average (MA) cement pro-duction and the added effective cement production capacity Source: Company reports , and CICR database

Monthly 11M10 vs. 11M09

Demand has been following a slowing down pattern since the beginning of 2010, hence relaxing utilization rates were achieved, reaching 96% in November 2010.

Monthly

Source: CICR database * Including imports by local producing Co.s

11M10 vs. 11M09

Source: CICR database * Including imports by local producing Co.s To

tal G

ray

cem

ent i

mpo

rts *

vol

.

In November 2010, 121k tons of cement were imported to bring the total quantity of imported cement in 11M10 to 1,432k tons representing 3% of local demand.

Gra

y C

emen

t exp

orts

vol

ume

Monthly 11M10 vs. 11M09

Source: CICR database Source: CICR database

102%

102%

102%

102%

101%

101%

100%

99%

99%

98%

96%

96%

96%

90%

95%

100%

105%

110%

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

102%

96%

95%

100%

105%

11M09 11M10

Down by 609 bps

65

64

185

256

112

57

103

73

167

59

178

121

121

-43%

-2%

190%

38%

-56%-49%

81%

-30%

130%

-64%

200%

-32% 0%

-100%

0%

100%

200%

300%

-

100

200

300

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

000's tonsTotal Gray Cement Imports MoM Chg

1,024

1,432

-

400

800

1,200

1,600

11M09 11M10

000's tons

up by 40%

0.01.5

0.5

6.3

3.2

1.00.0

5.2

0.6

5.5

10.511.7

0

3

6

9

12

15

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr-

10

May

-10

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct

-10

Nov

-10

000's tons

0.0

Lifting the export ban

356

45

-

100

200

300

400

500

11M09 11M10

000's tons

Down by 87 %

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09| THE GLOBAL CEMENT BAG

20

Market Key Performance Indicators (Cont.)

Monthly

Source: CICR database * Average ex-factory local price including transportation costs

GR

AY C

EMEN

T LO

CAL

PR

ICE

*

11M10 vs. 11M09

Source: CICR database * Average ex-factory local price including transportation costs

Local cement prices increased to reach EGP520/ton in November 2010 compared to EGP515/ton in October 2010. On a an annual perspective, prices recorded an increase of 1% in 11M10.

499

520

518

499

488

490

516

510

504

515

520

0%-4% -2%

0%5%

-1%

-1%2% 1%

0%

-8%

3%

-2% -2%

-2%-5% -7%

1%

7%

-15%

-5%

5%

15%

25%

35%

300

400

500

600

700

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

EG

P pe

r ton

Average Ex-Factory Gray Cement Local Price MoM Chg YoY Chg

NA NA

512 508

300

400

500

600

11M09 11M10

EGP per ton

Decreased by 1%

ISIEmergingMarketsPDF eg-aaib9 from 196.219.237.161 on 2011-04-11 06:29:51 EDT. DownloadPDF.

Downloaded by eg-aaib9 from 196.219.237.161 at 2011-04-11 06:29:51 EDT. ISI Emerging Markets. Unauthorized Distribution Prohibited.

12th January, 2011

CEMENT | ISSUE NO. 09| THE GLOBAL CEMENT BAG

21

Com

pani

es K

ey P

erfo

rman

ce In

dica

tors

*Inc

lude

s im

ports

by

the

prod

ucin

g co

mpa

nies

S

ourc

e: C

ompa

ny re

ports

, and

CIC

R d

atab

ase

Am

ount

Mar

ket S

hare

% o

f Pro

duct

ion

Amou

ntM

arke

t Sha

re%

of P

rodu

ctio

nA

mou

ntM

arke

t Sha

re%

of P

rodu

ctio

n

11M

105,

340

116%

5,39

312

%10

1%-

0%

0%5,

393

12%

101%

11M

095,

318

115%

5,21