渣打國際商業銀行承銷「The Export-Import Bank of Korea US ...

247

渣打國際商業銀行承銷「The Export-Import Bank of Korea US$400,000,000 Floating Rate Notes due 2022」之美元計價普通公司債 公告 渣打國際商業銀行(以下稱承銷商)承銷「The Export-Import Bank of Korea US$400,000,000 Floating Rate Notes due 2022」之美元 計價普通公司債(以下稱本公司債),本公司債發行總金額為美金 400,000,000 元整,由承銷商洽商銷售本公司債金額為美金 400,000,000 元整,茲將銷售辦法公告於後 : 一、證券承銷商名稱、地址、總承銷數量、證券承銷商先行保留洽商銷售數量 承銷商名稱 地址 洽商銷售金額 渣打國際商業銀行股份有限公司 台北市松山區敦化北路 168 號 1 樓 美金 231,000,000 元整 群益金鼎證券股份有限公司 台北市信義區松仁路 101 號 15 樓 美金 17,000,000 元整 中國信託商業銀行股份有限公司 台北市南港區經貿二路 168 號 5 樓 美金 26,000,000 元整 凱基商業銀行股份有限公司 台北市松山區南京東路五段 125 號 美金 30,000,000 元整 凱基證券股份有限公司 台北市中山區明水路 700 號 3 樓 美金 40,000,000 元整 兆豐國際商業銀行股份有限公司 台北市中山區吉林路 100 號 美金 20,000,000 元整 統一綜合證券股份有限公司 台北市松山區東興路 8 號 美金 14,000,000 元整 上海商業儲蓄銀行股份有限公司 台北市民權東路一段 2 號 美金 14,000,000 元整 永豐金證券股份有限公司 台北市博愛路 17 號 5 樓 美金 8,000,000 元整 二、承銷總額:總計美金 400,000,000 元整。 三、承銷方式:本公司債將由承銷商包銷並以「洽商銷售」方式出售予投資人。 四、承銷期間:本公司債定價日為 2017 年 6 月 20 日,於 2017 年 7 月 4 日辦理承銷公告並於 2017 年 7 月 5 日發行。 五、承銷價格:承銷商於銷售期間內依本公司債票面金額銷售,以美金貳拾萬元整為最低銷售單位,發行價格為 100%。 六、本公司債主要發行條件 : (一) 發行日:2017 年 7 月 5 日。 (二) 到期日:2022 年 7 月 5 日。 (三) 發行人評等:Aa2 by Moody’s / AA by S&P / AA- by Fitch (四) 受償順位:無擔保主順位債券。 (五) 票面金額:美金貳拾萬元整。 (六) 票面利率:浮動利率三個月倫敦同業拆放利率 + 80 基點。 (七) 付息及還本方式:本債券為浮動利率債券。發行人將每季付息,並於債券到期日一次還本。 (八) 營業日:紐約、倫敦、台北及首爾之商業銀行對外營業之日。 (九) 準據法:英國法。 (十) 債券掛牌處所:中華民國櫃檯買賣中心及新加坡交易所。 七、銷售限制:於台灣銷售僅限財團法人中華民國證券櫃檯買賣中心外幣計價國際債券管理規則第二條之一所定義之專業投資人,另 依中華民國證券商業同業公會證券商承銷或再行銷售有價證券處理辦法第三十二條之規定,每一認購人認購數量不得超過該次承 銷總數之百分之八十,惟認購人為政府基金者不在此限。 八、通知、繳交價款及交付本公司債方式: 承銷商於發行日前通知投資人繳交價款之方式,投資人於發行日以 Euroclear 或 Clearstream(DVP)完成交割或於發行日將本公司債之認購款項匯入承銷商指定帳戶,承銷商將本公司債撥入投資人所指定之集保 帳戶。 九、公開說明書之分送、揭露及取閱方式:如經投資人同意承銷商得以電子郵件方式交付公開說明書,投資人並得至公開資訊觀測站 (http://mops.twse.com.tw )或渣打國際商業銀行網址(https://www.sc.com/tw ),群益金鼎證券股份有限公司 (https://www.capital.com.tw ),中國信託商業銀行股份有限公司(https://www.ctbcbank.com ),凱基商業銀行股份有限公司 (https://www.kgibank.com ),凱基證券股份有限公司(https://www.kgieworld.com.tw ),兆豐國際商業銀行股份有限公司 (https://www.megabank.com.tw),統一綜合證券股份有限公司(http://www.pscnet.com.tw ),上海商業儲蓄銀行股份有限公司 (http://www.scsb.com.tw),永豐金證券股份有限公司網址(http://www.sinotrade.com.tw )查詢。 十、會計師對發行人最近三年度財務資料之查核簽證意見 年度 會計師事務所 查核意見 2016 Annual Report Deloitte Fairly 2015 Annual Report Deloitte Fairly 2014 Annual Report Deloitte Fairly 十一、 其他為保護公益及投資人應補充揭露事項:無。 十二、 投資人應詳閱本公司債公開說明書。

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of 渣打國際商業銀行承銷「The Export-Import Bank of Korea US ...

渣打國際商業銀行承銷「The Export-Import Bank of Korea US$400,000,000 Floating Rate Notes due 2022」之美元計價普通公司債

公告

渣打國際商業銀行(以下稱承銷商)承銷「The Export-Import Bank of Korea US$400,000,000 Floating Rate Notes due 2022」之美元

計價普通公司債(以下稱本公司債),本公司債發行總金額為美金 400,000,000元整,由承銷商洽商銷售本公司債金額為美金

400,000,000元整,茲將銷售辦法公告於後 :

一、證券承銷商名稱、地址、總承銷數量、證券承銷商先行保留洽商銷售數量

承銷商名稱 地址 洽商銷售金額

渣打國際商業銀行股份有限公司 台北市松山區敦化北路 168號 1樓 美金 231,000,000元整

群益金鼎證券股份有限公司 台北市信義區松仁路 101號 15樓 美金 17,000,000元整

中國信託商業銀行股份有限公司 台北市南港區經貿二路 168號 5樓 美金 26,000,000元整

凱基商業銀行股份有限公司 台北市松山區南京東路五段 125號 美金 30,000,000元整

凱基證券股份有限公司 台北市中山區明水路 700號 3樓 美金 40,000,000元整

兆豐國際商業銀行股份有限公司 台北市中山區吉林路 100號 美金 20,000,000元整

統一綜合證券股份有限公司 台北市松山區東興路 8號 美金 14,000,000元整

上海商業儲蓄銀行股份有限公司 台北市民權東路一段 2號 美金 14,000,000元整

永豐金證券股份有限公司 台北市博愛路 17號 5樓 美金 8,000,000元整

二、承銷總額:總計美金 400,000,000元整。

三、承銷方式:本公司債將由承銷商包銷並以「洽商銷售」方式出售予投資人。

四、承銷期間:本公司債定價日為 2017年 6月 20日,於 2017年 7月 4日辦理承銷公告並於 2017年 7月 5日發行。

五、承銷價格:承銷商於銷售期間內依本公司債票面金額銷售,以美金貳拾萬元整為最低銷售單位,發行價格為 100%。

六、本公司債主要發行條件 :

(一) 發行日:2017年 7月 5日。

(二) 到期日:2022年 7月 5日。

(三) 發行人評等:Aa2 by Moody’s / AA by S&P / AA- by Fitch

(四) 受償順位:無擔保主順位債券。

(五) 票面金額:美金貳拾萬元整。

(六) 票面利率:浮動利率三個月倫敦同業拆放利率 + 80基點。

(七) 付息及還本方式:本債券為浮動利率債券。發行人將每季付息,並於債券到期日一次還本。

(八) 營業日:紐約、倫敦、台北及首爾之商業銀行對外營業之日。

(九) 準據法:英國法。

(十) 債券掛牌處所:中華民國櫃檯買賣中心及新加坡交易所。

七、銷售限制:於台灣銷售僅限財團法人中華民國證券櫃檯買賣中心外幣計價國際債券管理規則第二條之一所定義之專業投資人,另

依中華民國證券商業同業公會證券商承銷或再行銷售有價證券處理辦法第三十二條之規定,每一認購人認購數量不得超過該次承

銷總數之百分之八十,惟認購人為政府基金者不在此限。

八、通知、繳交價款及交付本公司債方式: 承銷商於發行日前通知投資人繳交價款之方式,投資人於發行日以 Euroclear或

Clearstream(DVP)完成交割或於發行日將本公司債之認購款項匯入承銷商指定帳戶,承銷商將本公司債撥入投資人所指定之集保

帳戶。

九、公開說明書之分送、揭露及取閱方式:如經投資人同意承銷商得以電子郵件方式交付公開說明書,投資人並得至公開資訊觀測站

(http://mops.twse.com.tw)或渣打國際商業銀行網址(https://www.sc.com/tw),群益金鼎證券股份有限公司

(https://www.capital.com.tw),中國信託商業銀行股份有限公司(https://www.ctbcbank.com),凱基商業銀行股份有限公司

(https://www.kgibank.com),凱基證券股份有限公司(https://www.kgieworld.com.tw),兆豐國際商業銀行股份有限公司

(https://www.megabank.com.tw),統一綜合證券股份有限公司(http://www.pscnet.com.tw),上海商業儲蓄銀行股份有限公司

(http://www.scsb.com.tw),永豐金證券股份有限公司網址(http://www.sinotrade.com.tw)查詢。

十、會計師對發行人最近三年度財務資料之查核簽證意見

年度 會計師事務所 查核意見

2016 Annual Report Deloitte Fairly

2015 Annual Report Deloitte Fairly

2014 Annual Report Deloitte Fairly

十一、 其他為保護公益及投資人應補充揭露事項:無。

十二、 投資人應詳閱本公司債公開說明書。

The Export-Import Bank of Korea

US$400,000,000 Floating Rate Notes due 2022

under the

US$25,000,000,000 Global Medium Term Note Programme

Issue Price: 100 per cent.

Issue Date: 5 July 2017

This information package includes the Offering Circular dated 12 May 2017 in relation to

US$25,000,000,000 Global Medium Term Note Programme (the "Offering Circular") and the Pricing Supplement dated 21 June 2017 in respect of the Notes (the "Pricing Supplement,"

together with the Offering Circular, the "Information Package").

The Notes will be issued by the Export-Import Bank of Korea (the "Issuer").

Application will be made by the Issuer for the Notes to be listed on the Taipei Exchange ("TPEx") in the Republic of China (the "ROC"). Application will also be made to list the Notes on

Singapore Exchange Securities Trading Limited.

The Notes will be traded on TPEx pursuant to the applicable rules of TPEx. Effective date of listing and trading of the Notes is on or about 5 July 2017.

TPEx is not responsible for the content of the Information Package and no representation is made by TPEx to the accuracy or completeness of the Information Package. TPEx expressly

disclaims any and all liability for any losses arising from, or as a result of the reliance on, all or

part of the contents of this Information Package. Admission to the listing and trading of the Notes on TPEx shall not be taken as an indication of the merits of the Issuer or the Notes.

The Notes have not been, and shall not be, offered, sold or re-sold, directly or indirectly to

investors other than "professional investors" as defined under Paragraph 1 of Article 2-1 of the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International

Bonds of the ROC. Purchasers of the Notes are not permitted to sell or otherwise dispose of the

Notes except by transfer to a professional investor.

Lead Manager

Standard Chartered Bank (Taiwan) Limited

Co-Managers

Capital Securities Corporation

CTBC Bank Co., Ltd.

KGI Bank

KGI Securities Co. Ltd.

Mega International Commercial Bank Co., Ltd.

President Securities Corp

Shanghai Commercial & Savings Bank, Ltd.

Sinopac Securities Corporation

Pricing Supplement

THE EXPORT-IMPORT BANK OF KOREA

Issue of US$400,000,000 Floating Rate Notes due 2022 (the “Notes”)

under the US$25,000,000,000 Global Medium Term Note Programme

THE NOTES TO WHICH THIS PRICING SUPPLEMENT RELATES HAVE NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND, UNLESS SO REGISTERED, MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE SECURITIES LAWS. ACCORDINGLY, THE NOTES WILL BE OFFERED AND SOLD ONLY OUTSIDE THE UNITED STATES TO NON-U.S. PERSONS IN RELIANCE ON REGULATION S.

Bookrunner and Lead Manager

Standard Chartered Bank (Taiwan) Limited

Co-Managers

Capital Securities Corporation CTBC Bank KGI Bank

KGI Securities Co., Ltd. Mega International Commercial Bank Co., Ltd.

President Securities

Shanghai Commercial & Savings Bank, Ltd.

Sinopac Securities Corporation

The date of this Pricing Supplement is 21 June 2017 and was deemed effective 20 June 2017

P-2

The Export-Import Bank of Korea Issue of US$400,000,000 Floating Rate Notes due 2022

under the US$25,000,000,000 Global Medium Term Note Programme

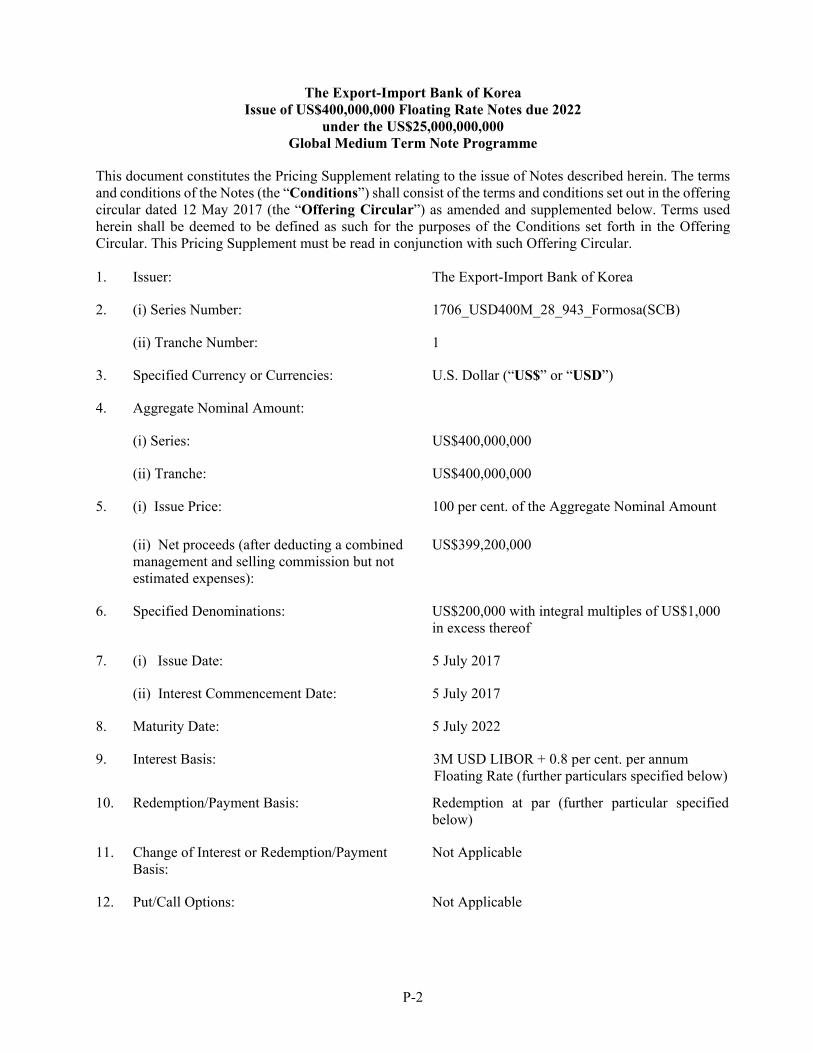

This document constitutes the Pricing Supplement relating to the issue of Notes described herein. The terms and conditions of the Notes (the “Conditions”) shall consist of the terms and conditions set out in the offering circular dated 12 May 2017 (the “Offering Circular”) as amended and supplemented below. Terms used herein shall be deemed to be defined as such for the purposes of the Conditions set forth in the Offering Circular. This Pricing Supplement must be read in conjunction with such Offering Circular. 1. Issuer: The Export-Import Bank of Korea

2. (i) Series Number: 1706_USD400M_28_943_Formosa(SCB)

(ii) Tranche Number: 1

3. Specified Currency or Currencies: U.S. Dollar (“US$” or “USD”)

4. Aggregate Nominal Amount:

(i) Series: US$400,000,000

(ii) Tranche: US$400,000,000

5. (i) Issue Price: 100 per cent. of the Aggregate Nominal Amount

(ii) Net proceeds (after deducting a combined management and selling commission but not estimated expenses):

US$399,200,000

6. Specified Denominations: US$200,000 with integral multiples of US$1,000 in excess thereof

7. (i) Issue Date: 5 July 2017

(ii) Interest Commencement Date: 5 July 2017

8. Maturity Date: 5 July 2022

9. Interest Basis: 3M USD LIBOR + 0.8 per cent. per annum Floating Rate (further particulars specified below)

10. Redemption/Payment Basis: Redemption at par (further particular specified below)

11. Change of Interest or Redemption/Payment Basis:

Not Applicable

12. Put/Call Options: Not Applicable

P-3

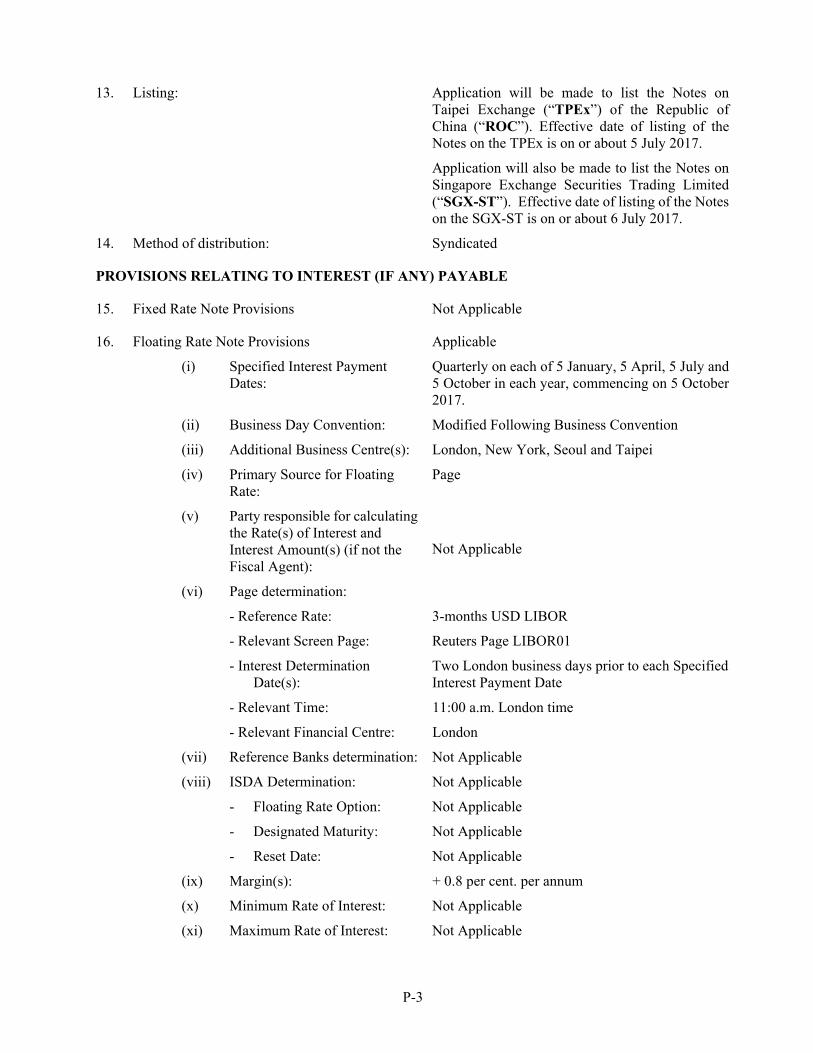

13. Listing: Application will be made to list the Notes on Taipei Exchange (“TPEx”) of the Republic of China (“ROC”). Effective date of listing of the Notes on the TPEx is on or about 5 July 2017.

Application will also be made to list the Notes on Singapore Exchange Securities Trading Limited (“SGX-ST”). Effective date of listing of the Notes on the SGX-ST is on or about 6 July 2017.

14. Method of distribution: Syndicated

PROVISIONS RELATING TO INTEREST (IF ANY) PAYABLE

15. Fixed Rate Note Provisions Not Applicable

16. Floating Rate Note Provisions Applicable

(i) Specified Interest Payment Dates:

Quarterly on each of 5 January, 5 April, 5 July and 5 October in each year, commencing on 5 October 2017.

(ii) Business Day Convention: Modified Following Business Convention

(iii) Additional Business Centre(s): London, New York, Seoul and Taipei

(iv) Primary Source for Floating Rate:

Page

(v) Party responsible for calculating the Rate(s) of Interest and Interest Amount(s) (if not the Fiscal Agent):

Not Applicable

(vi) Page determination:

- Reference Rate: 3-months USD LIBOR

- Relevant Screen Page: Reuters Page LIBOR01

- Interest Determination Date(s):

Two London business days prior to each Specified Interest Payment Date

- Relevant Time: 11:00 a.m. London time

- Relevant Financial Centre: London

(vii) Reference Banks determination: Not Applicable

(viii) ISDA Determination: Not Applicable

- Floating Rate Option: Not Applicable

- Designated Maturity: Not Applicable

- Reset Date: Not Applicable

(ix) Margin(s): + 0.8 per cent. per annum

(x) Minimum Rate of Interest: Not Applicable

(xi) Maximum Rate of Interest: Not Applicable

P-4

(xii) Day Count Fraction: Actual/360, Adjusted

(xiii) Fall back provisions, rounding provisions, denominator and any other terms relating to the method of calculating interest on Floating Rate Notes, if different from those set out in the Conditions:

As set out in the Conditions

17. Zero Coupon Note Provisions Not Applicable

18. Dual Currency Note Provisions Not Applicable

PROVISIONS RELATING TO REDEMPTION

19. Call Option Not Applicable

20. Put Option Not Applicable

21. Redemption Amount (at maturity) Redemption at par

22. Redemption for Taxation Reasons

(i) Redemption for Taxation Reasons permitted on days other than Interest Payment Dates: Yes

(ii) Redemption Amount(s) payable on redemption for taxation reasons or on event of default and/or the method of calculating the same (if required or if different from that set out in the Conditions):

Not Applicable

GENERAL PROVISIONS APPLICABLE TO THE NOTES

23. Form of Notes: Registered Notes

24. Additional Financial Centre(s) or other special provisions relating to Payment Dates:

London, New York, Seoul and Taipei

25. Talons for future Coupons or Receipts to be attached to Definitive Notes (and dates on which such Talons mature):

Not Applicable

26. Details relating to Instalment Notes: Instalment Date(s); Instalment Amount(s): Not Applicable

27. Redenomination, renominalisation and reconventioning provisions: Not Applicable

28. Consolidation provisions: Not Applicable

29. Other terms or special conditions: Not Applicable

DISTRIBUTION

30. (i) If syndicated, names of Managers: Bookrunner and Lead Manager:

Standard Chartered Bank (Taiwan) Limited

P-5

Co-Managers:

Capital Securities Corporation; CTBC Bank Co., Ltd.; KGI Bank; KGI Securities Co. Ltd.; Mega International Commercial Bank Co., Ltd.; President Securities Corp; Shanghai Commercial & Savings Bank, Ltd.; and Sinopac Securities Corporation

(ii) Stabilising Manager(s) (if any): Not Applicable

31. If non-syndicated, name of Dealer/Manager: Not Applicable

32. TEFRA: Not Applicable

33. Additional selling restrictions: The Notes have not been, and shall not be, offered, sold or resold, directly or indirectly, to investors other than “professional investors” as defined under Paragraph 1 of Article 2-1 of the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International Bonds. Purchasers of the Notes are not permitted to sell or otherwise dispose of the Notes except by transfer to a professional investor.

OPERATIONAL INFORMATION

34. ISIN Code: XS1637362507

35. Common Code: 163736250

36. CUSIP: Not Applicable

37. Any clearing system(s) other than Euroclear, Clearstream, Luxembourg and DTC and the relevant identification number(s):

Euroclear, Clearstream, Luxembourg

38. Delivery: Delivery against payment

39. Additional Paying Agent(s) (if any): Not Applicable

40. Additional Registrar (if any): Not Applicable

LISTING APPLICATION This Pricing Supplement comprises the details required to list the issue of Notes described herein pursuant to the US$25,000,000,000 Global Medium Term Note Programme of the Export-Import Bank of Korea. Application will be made to list and trade the Notes on Taipei Exchange pursuant to the applicable rules of the Taipei Exchange. Admission to the listing and trading of the Notes on the Taipei Exchange shall not to be taken as an indication of the merits of the Issuer or the Notes. Taipei Exchange is not responsible for the content of this document and the Offering Circular and any supplement or amendment thereto and no representation is made by Taipei Exchange to the accuracy or completeness of this document and the Offering Circular and any supplement or amendment thereto. Taipei Exchange expressly disclaims any and all liability

P-6

for any losses arising from, or as a result of the reliance on, all or part of the contents of this document and the Offering Circular and any supplement or amendment thereto. Application will also be made to the SGX-ST for the listing and quotation of the Notes. The SGX-ST assumes no responsibility for any of the statements made, reports contained or opinions expressed in this Pricing Supplement. Admission of the Notes to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Issuer or the Notes. NOTICES If and for so long as the Notes are listed on the Taipei Exchange and for so long as the rules of the Taipei Exchange so require, all notices regarding the Notes shall also be published on a website designated by the Taiwan Financial Supervisory Commission (currently, http://mops.twse.com.tw/T113.htm).

P-7

ROC TAXATION The following is a general description of the principal ROC tax consequences for investors receiving interest in respect of, or disposing of, the Notes and is of a general nature based on the Issuer’s understanding of current law and practice. It does not purport to be comprehensive and does not constitute legal or tax advice. This general description is based upon the law as in effect on the date hereof and that the Notes will be issued, offered, sold and re-sold to professional investors as defined under the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International Bonds only. This description is subject to change potentially with retroactive effect. Investors should appreciate that, as a result of changing law or practice, the tax consequences may be otherwise than as stated below. Investors should consult their professional advisers on the possible tax consequences of subscribing for, purchasing, holding or selling the Notes.

Interest on the Notes

As the Issuer of the Notes is not a ROC statutory tax withholder, there is no ROC withholding tax on the interest to be paid by the Issuer on the Notes.

Payments of interest under the Notes to an ROC individual holder are not subject to ROC income tax as such payments received by him/her are not considered to be ROC-sourced income. However, such holder must include the interest in calculating his/her basic income for the purpose of calculating his/her alternative minimum tax (“AMT”), unless the sum of the interest and other non- ROC-sourced income received by such holder and the person(s) who is (are) required to jointly file the tax return in a calendar year is below $1 million New Taiwan Dollars (“NT$”). If the amount of the AMT exceeds the annual income tax calculated pursuant to ROC Income Basic Tax Act (also known as the AMT Act), the excess becomes such holder’s AMT payable.

ROC corporate holders must include the interest receivable under the Notes as part of their taxable income and pay income tax at a flat rate of 17% (unless the total taxable income for a fiscal year is under NT$120,000), as they are subject to income tax on their worldwide income on an accrual basis. The AMT is not applicable.

Sale of the Notes

In general, the sale of corporate bonds or financial bonds is subject to 0.1% securities transaction tax (“STT”) on the transaction price. However, Article 2-1 of the Securities Transaction Tax Act prescribes that STT will cease to be levied on the sale of corporate bonds and financial bonds from 1 January 2010 to 31 December 2026. Therefore, the sale of the Notes will be exempt from STT if the sale is conducted on or before 31 December 2026. Starting from 1 January 2027, any sale of the Notes will be subject to STT at 0.1 % of the transaction price, unless otherwise provided by the tax laws that may be in force at that time.

Capital gains generated from the sale of bonds are exempt from income tax. Accordingly, ROC individual and corporate holders are not subject to income tax on any capital gains generated from the sale of the Notes. In addition, ROC individual holders are not subject to AMT on any capital gains generated from the sale of the Notes. However, ROC corporate holders should include the capital gains in calculating their basic income for the purpose of calculating their AMT. If the amount of the AMT exceeds the annual income tax calculated pursuant to the ROC Income Basic Tax Act (also known as the AMT Act), the excess becomes the ROC corporate holders’ AMT payable. Capital losses, if any, incurred by such holders could be carried over 5 years to offset against capital gains of same category of income for the purposes of calculating their AMT.

P-8

Non-ROC corporate holders with a fixed place of business (e.g., a branch) or a business agent in the ROC are not subject to income tax on any capital gains generated from the sale of the Notes. However, their fixed place of business or business agent should include any such capital gains in calculating their basic income for the purpose of calculating AMT.

As to non-ROC corporate holders without a fixed place of business and a business agent in the ROC, they are not subject to income tax or AMT on any capital gains generated from the sale of the Notes. ROC SETTLEMENT AND TRADING

Investors with a securities book-entry account with an ROC securities broker and a foreign currency deposit account with an ROC bank, may request the approval of the Taiwan Depositary & Clearing Corporation (“TDCC”) for the settlement of the Notes through the account of TDCC with Euroclear or Clearstream, Luxembourg and if such approval is granted by TDCC, the Notes may be so cleared and settled. In such circumstances, TDCC will allocate the respective book-entry interest of such investor in the Notes position to the securities book-entry account designated by such investor in the ROC. The Notes will be traded and settled pursuant to the applicable rules and operating procedures of TDCC and the TPEx as domestic bonds.

In addition, an investor may apply to TDCC (by filing in a prescribed form) to transfer the Notes in its own account with Euroclear or Clearstream, Luxembourg to the TDCC account with Euroclear or Clearstream, Luxembourg for trading in the domestic market or vice versa for trading in overseas markets.

For such investors who hold their interest in the Notes through an account opened and held by TDCC with Euroclear or Clearstream, Luxembourg, distributions of principal and/or interest for the Notes to such holders may be made by payment services banks whose systems are connected to TDCC to the foreign currency deposit accounts of the holders. Such payment is expected to be made on the second Taiwanese business day following TDCC’s receipt of such payment (due to time difference, the payment is expected to be received by TDCC one Taiwanese business day after the distribution date). However, when the holders will actually receive such distributions may vary depending upon the daily operations of the ROC banks with which the holder has the foreign currency deposit account.

IMPORTANT NOTICE

THIS DOCUMENT IS AVAILABLE ONLY TO INVESTORS WHO ARE NON-U.S. PERSONS WITH ADDRESSEES OUTSIDE OF THE UNITED STATES

IMPORTANT: You must read the following before continuing. If you are not the intended recipient of this message, please do not distribute or copy the information contained in this e-mail, but instead, delete and destroy all copies of this e-mail including all attachments. The following applies to the offering circular following this page, and you are therefore advised to read this carefully before reading, accessing or making any other use of the offering circular. In accessing the offering circular, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from us as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER OF SECURITIES FOR SALE IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES HAVE NOT BEEN, AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTION AND THE SECURITIES MAY NOT BE OFFERED OR SOLD WITHIN THE U.S. OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE OR LOCAL SECURITIES LAWS. THE FOLLOWING OFFERING CIRCULAR MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THIS DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. ANY INVESTMENT DECISION SHOULD BE MADE ON THE BASIS OF THE FINAL TERMS AND CONDITIONS OF THE RELEVANT SECURITIES. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORIZED AND WILL NOT BE ABLE TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN. Confirmation of your Representation: In order to be eligible to view the following offering circular or make an investment decision with respect to the securities, investors must be non-U.S. persons (within the meaning of Regulation S under the Securities Act) outside the United States. By accepting the e-mail and accessing the following offering circular, you shall be deemed to have represented to us that (1) you and any customers you represent are non-U.S. persons and that the electronic mail address that you gave us and to which this e-mail has been delivered is not located in the United States, its territories or possessions and (2) you consent to the delivery of such offering circular by electronic transmission. You are reminded that the following offering circular has been delivered to you on the basis that you are a person into whose possession the following offering circular may be lawfully delivered in accordance with the laws of jurisdiction in which you are located and you may not, nor are you authorized to, deliver or disclose the contents of the following offering circular to any other person. If this is not the case, you must return this offering circular to us immediately. The materials relating to the offering do not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that the offering be made by a licensed broker or dealer and the initial purchasers or any affiliate of the initial purchasers is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by the initial purchasers or such affiliate on behalf of the issuer in such jurisdiction. The following offering circular has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently, none of Standard Chartered Bank (Taiwan) Limited, Capital Securities Corporation, CTBC Bank Co., Ltd., KGI Bank, KGI Securities Co. Ltd., Mega International Commercial Bank Co., Ltd., President Securities Corp, Shanghai Commercial & Savings Bank, Ltd. and Sinopac Securities Corporation (the “Managers”) nor any person who controls the Manager nor any director, officer, employee nor agent of any of the Manager or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the offering circular distributed to you in electronic format and the hard copy version available to you on request from the Manager. You should not reply by e-mail to this announcement, and you may not purchase any securities by doing so. Any reply e- mail communications, including those you generate by using the “Reply” function on your e-mail software, will be ignored or rejected. You are responsible for protecting against viruses and other destructive items. Your use of this e-mail is at your own risk and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature.

Pricing Supplement

THE EXPORT-IMPORT BANK OF KOREA

Issue of US$400,000,000 Floating Rate Notes due 2022 (the “Notes”)

under the US$25,000,000,000 Global Medium Term Note Programme

THE NOTES TO WHICH THIS PRICING SUPPLEMENT RELATES HAVE NOT BEEN REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), OR WITH ANY SECURITIES REGULATORY AUTHORITY OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND, UNLESS SO REGISTERED, MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT), EXCEPT PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTION NOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT AND APPLICABLE STATE SECURITIES LAWS. ACCORDINGLY, THE NOTES WILL BE OFFERED AND SOLD ONLY OUTSIDE THE UNITED STATES TO NON-U.S. PERSONS IN RELIANCE ON REGULATION S.

Bookrunner and Lead Manager

Standard Chartered Bank (Taiwan) Limited

Co-Managers

Capital Securities Corporation CTBC Bank KGI Bank

KGI Securities Co., Ltd. Mega International Commercial Bank Co., Ltd.

President Securities

Shanghai Commercial & Savings Bank, Ltd.

Sinopac Securities Corporation

The date of this Pricing Supplement is 21 June 2017 and was deemed effective 20 June 2017

P-2

The Export-Import Bank of Korea Issue of US$400,000,000 Floating Rate Notes due 2022

under the US$25,000,000,000 Global Medium Term Note Programme

This document constitutes the Pricing Supplement relating to the issue of Notes described herein. The terms and conditions of the Notes (the “Conditions”) shall consist of the terms and conditions set out in the offering circular dated 12 May 2017 (the “Offering Circular”) as amended and supplemented below. Terms used herein shall be deemed to be defined as such for the purposes of the Conditions set forth in the Offering Circular. This Pricing Supplement must be read in conjunction with such Offering Circular. 1. Issuer: The Export-Import Bank of Korea

2. (i) Series Number: 1706_USD400M_28_943_Formosa(SCB)

(ii) Tranche Number: 1

3. Specified Currency or Currencies: U.S. Dollar (“US$” or “USD”)

4. Aggregate Nominal Amount:

(i) Series: US$400,000,000

(ii) Tranche: US$400,000,000

5. (i) Issue Price: 100 per cent. of the Aggregate Nominal Amount

(ii) Net proceeds (after deducting a combined management and selling commission but not estimated expenses):

US$399,200,000

6. Specified Denominations: US$200,000 with integral multiples of US$1,000 in excess thereof

7. (i) Issue Date: 5 July 2017

(ii) Interest Commencement Date: 5 July 2017

8. Maturity Date: 5 July 2022

9. Interest Basis: 3M USD LIBOR + 0.8 per cent. per annum Floating Rate (further particulars specified below)

10. Redemption/Payment Basis: Redemption at par (further particular specified below)

11. Change of Interest or Redemption/Payment Basis:

Not Applicable

12. Put/Call Options: Not Applicable

P-3

13. Listing: Application will be made to list the Notes on Taipei Exchange (“TPEx”) of the Republic of China (“ROC”). Effective date of listing of the Notes on the TPEx is on or about 5 July 2017.

Application will also be made to list the Notes on Singapore Exchange Securities Trading Limited (“SGX-ST”). Effective date of listing of the Notes on the SGX-ST is on or about 6 July 2017.

14. Method of distribution: Syndicated

PROVISIONS RELATING TO INTEREST (IF ANY) PAYABLE

15. Fixed Rate Note Provisions Not Applicable

16. Floating Rate Note Provisions Applicable

(i) Specified Interest Payment Dates:

Quarterly on each of 5 January, 5 April, 5 July and 5 October in each year, commencing on 5 October 2017.

(ii) Business Day Convention: Modified Following Business Convention

(iii) Additional Business Centre(s): London, New York, Seoul and Taipei

(iv) Primary Source for Floating Rate:

Page

(v) Party responsible for calculating the Rate(s) of Interest and Interest Amount(s) (if not the Fiscal Agent):

Not Applicable

(vi) Page determination:

- Reference Rate: 3-months USD LIBOR

- Relevant Screen Page: Reuters Page LIBOR01

- Interest Determination Date(s):

Two London business days prior to each Specified Interest Payment Date

- Relevant Time: 11:00 a.m. London time

- Relevant Financial Centre: London

(vii) Reference Banks determination: Not Applicable

(viii) ISDA Determination: Not Applicable

- Floating Rate Option: Not Applicable

- Designated Maturity: Not Applicable

- Reset Date: Not Applicable

(ix) Margin(s): + 0.8 per cent. per annum

(x) Minimum Rate of Interest: Not Applicable

(xi) Maximum Rate of Interest: Not Applicable

P-4

(xii) Day Count Fraction: Actual/360, Adjusted

(xiii) Fall back provisions, rounding provisions, denominator and any other terms relating to the method of calculating interest on Floating Rate Notes, if different from those set out in the Conditions:

As set out in the Conditions

17. Zero Coupon Note Provisions Not Applicable

18. Dual Currency Note Provisions Not Applicable

PROVISIONS RELATING TO REDEMPTION

19. Call Option Not Applicable

20. Put Option Not Applicable

21. Redemption Amount (at maturity) Redemption at par

22. Redemption for Taxation Reasons

(i) Redemption for Taxation Reasons permitted on days other than Interest Payment Dates: Yes

(ii) Redemption Amount(s) payable on redemption for taxation reasons or on event of default and/or the method of calculating the same (if required or if different from that set out in the Conditions):

Not Applicable

GENERAL PROVISIONS APPLICABLE TO THE NOTES

23. Form of Notes: Registered Notes

24. Additional Financial Centre(s) or other special provisions relating to Payment Dates:

London, New York, Seoul and Taipei

25. Talons for future Coupons or Receipts to be attached to Definitive Notes (and dates on which such Talons mature):

Not Applicable

26. Details relating to Instalment Notes: Instalment Date(s); Instalment Amount(s): Not Applicable

27. Redenomination, renominalisation and reconventioning provisions: Not Applicable

28. Consolidation provisions: Not Applicable

29. Other terms or special conditions: Not Applicable

DISTRIBUTION

30. (i) If syndicated, names of Managers: Bookrunner and Lead Manager:

Standard Chartered Bank (Taiwan) Limited

P-5

Co-Managers:

Capital Securities Corporation; CTBC Bank Co., Ltd.; KGI Bank; KGI Securities Co. Ltd.; Mega International Commercial Bank Co., Ltd.; President Securities Corp; Shanghai Commercial & Savings Bank, Ltd.; and Sinopac Securities Corporation

(ii) Stabilising Manager(s) (if any): Not Applicable

31. If non-syndicated, name of Dealer/Manager: Not Applicable

32. TEFRA: Not Applicable

33. Additional selling restrictions: The Notes have not been, and shall not be, offered, sold or resold, directly or indirectly, to investors other than “professional investors” as defined under Paragraph 1 of Article 2-1 of the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International Bonds. Purchasers of the Notes are not permitted to sell or otherwise dispose of the Notes except by transfer to a professional investor.

OPERATIONAL INFORMATION

34. ISIN Code: XS1637362507

35. Common Code: 163736250

36. CUSIP: Not Applicable

37. Any clearing system(s) other than Euroclear, Clearstream, Luxembourg and DTC and the relevant identification number(s):

Euroclear, Clearstream, Luxembourg

38. Delivery: Delivery against payment

39. Additional Paying Agent(s) (if any): Not Applicable

40. Additional Registrar (if any): Not Applicable

LISTING APPLICATION This Pricing Supplement comprises the details required to list the issue of Notes described herein pursuant to the US$25,000,000,000 Global Medium Term Note Programme of the Export-Import Bank of Korea. Application will be made to list and trade the Notes on Taipei Exchange pursuant to the applicable rules of the Taipei Exchange. Admission to the listing and trading of the Notes on the Taipei Exchange shall not to be taken as an indication of the merits of the Issuer or the Notes. Taipei Exchange is not responsible for the content of this document and the Offering Circular and any supplement or amendment thereto and no representation is made by Taipei Exchange to the accuracy or completeness of this document and the Offering Circular and any supplement or amendment thereto. Taipei Exchange expressly disclaims any and all liability

P-6

for any losses arising from, or as a result of the reliance on, all or part of the contents of this document and the Offering Circular and any supplement or amendment thereto. Application will also be made to the SGX-ST for the listing and quotation of the Notes. The SGX-ST assumes no responsibility for any of the statements made, reports contained or opinions expressed in this Pricing Supplement. Admission of the Notes to the Official List of the SGX-ST is not to be taken as an indication of the merits of the Issuer or the Notes. NOTICES If and for so long as the Notes are listed on the Taipei Exchange and for so long as the rules of the Taipei Exchange so require, all notices regarding the Notes shall also be published on a website designated by the Taiwan Financial Supervisory Commission (currently, http://mops.twse.com.tw/T113.htm).

P-7

ROC TAXATION The following is a general description of the principal ROC tax consequences for investors receiving interest in respect of, or disposing of, the Notes and is of a general nature based on the Issuer’s understanding of current law and practice. It does not purport to be comprehensive and does not constitute legal or tax advice. This general description is based upon the law as in effect on the date hereof and that the Notes will be issued, offered, sold and re-sold to professional investors as defined under the Taipei Exchange Rules Governing Management of Foreign Currency Denominated International Bonds only. This description is subject to change potentially with retroactive effect. Investors should appreciate that, as a result of changing law or practice, the tax consequences may be otherwise than as stated below. Investors should consult their professional advisers on the possible tax consequences of subscribing for, purchasing, holding or selling the Notes.

Interest on the Notes

As the Issuer of the Notes is not a ROC statutory tax withholder, there is no ROC withholding tax on the interest to be paid by the Issuer on the Notes.

Payments of interest under the Notes to an ROC individual holder are not subject to ROC income tax as such payments received by him/her are not considered to be ROC-sourced income. However, such holder must include the interest in calculating his/her basic income for the purpose of calculating his/her alternative minimum tax (“AMT”), unless the sum of the interest and other non- ROC-sourced income received by such holder and the person(s) who is (are) required to jointly file the tax return in a calendar year is below $1 million New Taiwan Dollars (“NT$”). If the amount of the AMT exceeds the annual income tax calculated pursuant to ROC Income Basic Tax Act (also known as the AMT Act), the excess becomes such holder’s AMT payable.

ROC corporate holders must include the interest receivable under the Notes as part of their taxable income and pay income tax at a flat rate of 17% (unless the total taxable income for a fiscal year is under NT$120,000), as they are subject to income tax on their worldwide income on an accrual basis. The AMT is not applicable.

Sale of the Notes

In general, the sale of corporate bonds or financial bonds is subject to 0.1% securities transaction tax (“STT”) on the transaction price. However, Article 2-1 of the Securities Transaction Tax Act prescribes that STT will cease to be levied on the sale of corporate bonds and financial bonds from 1 January 2010 to 31 December 2026. Therefore, the sale of the Notes will be exempt from STT if the sale is conducted on or before 31 December 2026. Starting from 1 January 2027, any sale of the Notes will be subject to STT at 0.1 % of the transaction price, unless otherwise provided by the tax laws that may be in force at that time.

Capital gains generated from the sale of bonds are exempt from income tax. Accordingly, ROC individual and corporate holders are not subject to income tax on any capital gains generated from the sale of the Notes. In addition, ROC individual holders are not subject to AMT on any capital gains generated from the sale of the Notes. However, ROC corporate holders should include the capital gains in calculating their basic income for the purpose of calculating their AMT. If the amount of the AMT exceeds the annual income tax calculated pursuant to the ROC Income Basic Tax Act (also known as the AMT Act), the excess becomes the ROC corporate holders’ AMT payable. Capital losses, if any, incurred by such holders could be carried over 5 years to offset against capital gains of same category of income for the purposes of calculating their AMT.

P-8

Non-ROC corporate holders with a fixed place of business (e.g., a branch) or a business agent in the ROC are not subject to income tax on any capital gains generated from the sale of the Notes. However, their fixed place of business or business agent should include any such capital gains in calculating their basic income for the purpose of calculating AMT.

As to non-ROC corporate holders without a fixed place of business and a business agent in the ROC, they are not subject to income tax or AMT on any capital gains generated from the sale of the Notes. ROC SETTLEMENT AND TRADING

Investors with a securities book-entry account with an ROC securities broker and a foreign currency deposit account with an ROC bank, may request the approval of the Taiwan Depositary & Clearing Corporation (“TDCC”) for the settlement of the Notes through the account of TDCC with Euroclear or Clearstream, Luxembourg and if such approval is granted by TDCC, the Notes may be so cleared and settled. In such circumstances, TDCC will allocate the respective book-entry interest of such investor in the Notes position to the securities book-entry account designated by such investor in the ROC. The Notes will be traded and settled pursuant to the applicable rules and operating procedures of TDCC and the TPEx as domestic bonds.

In addition, an investor may apply to TDCC (by filing in a prescribed form) to transfer the Notes in its own account with Euroclear or Clearstream, Luxembourg to the TDCC account with Euroclear or Clearstream, Luxembourg for trading in the domestic market or vice versa for trading in overseas markets.

For such investors who hold their interest in the Notes through an account opened and held by TDCC with Euroclear or Clearstream, Luxembourg, distributions of principal and/or interest for the Notes to such holders may be made by payment services banks whose systems are connected to TDCC to the foreign currency deposit accounts of the holders. Such payment is expected to be made on the second Taiwanese business day following TDCC’s receipt of such payment (due to time difference, the payment is expected to be received by TDCC one Taiwanese business day after the distribution date). However, when the holders will actually receive such distributions may vary depending upon the daily operations of the ROC banks with which the holder has the foreign currency deposit account.

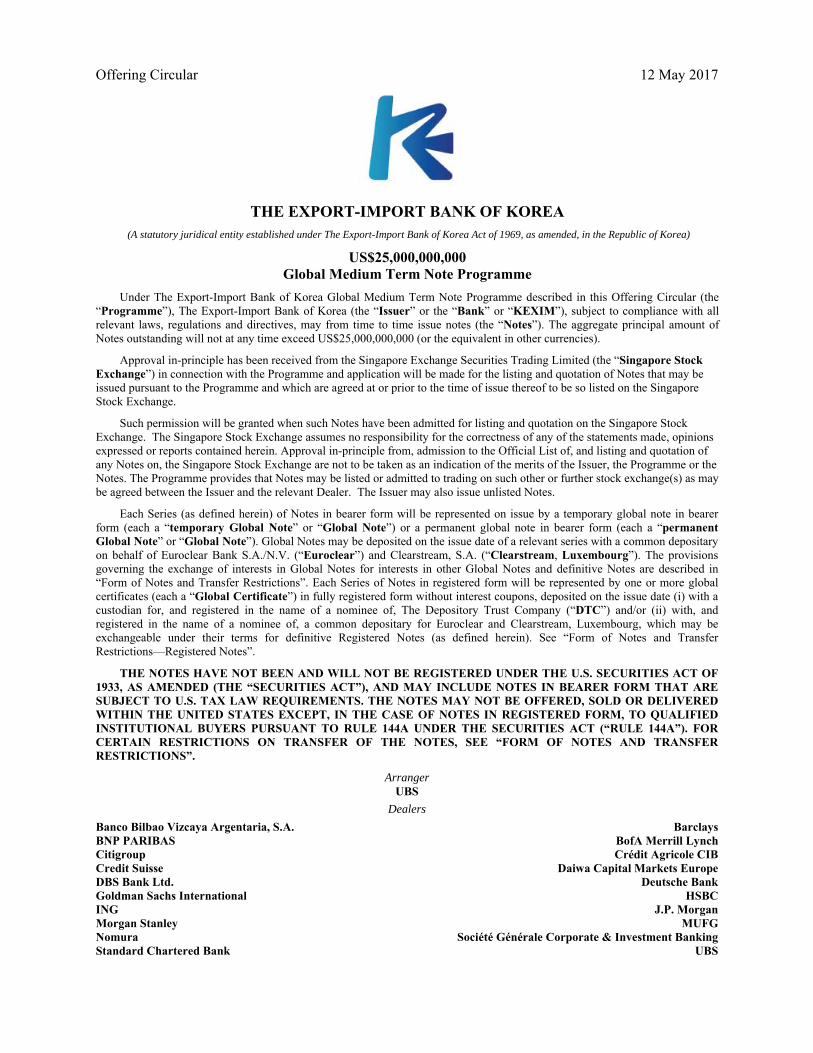

Offering Circular 12 May 2017

THE EXPORT-IMPORT BANK OF KOREA (A statutory juridical entity established under The Export-Import Bank of Korea Act of 1969, as amended, in the Republic of Korea)

US$25,000,000,000 Global Medium Term Note Programme

Under The Export-Import Bank of Korea Global Medium Term Note Programme described in this Offering Circular (the “Programme”), The Export-Import Bank of Korea (the “Issuer” or the “Bank” or “KEXIM”), subject to compliance with all relevant laws, regulations and directives, may from time to time issue notes (the “Notes”). The aggregate principal amount of Notes outstanding will not at any time exceed US$25,000,000,000 (or the equivalent in other currencies).

Approval in-principle has been received from the Singapore Exchange Securities Trading Limited (the “Singapore Stock Exchange”) in connection with the Programme and application will be made for the listing and quotation of Notes that may be issued pursuant to the Programme and which are agreed at or prior to the time of issue thereof to be so listed on the Singapore Stock Exchange.

Such permission will be granted when such Notes have been admitted for listing and quotation on the Singapore Stock Exchange. The Singapore Stock Exchange assumes no responsibility for the correctness of any of the statements made, opinions expressed or reports contained herein. Approval in-principle from, admission to the Official List of, and listing and quotation of any Notes on, the Singapore Stock Exchange are not to be taken as an indication of the merits of the Issuer, the Programme or the Notes. The Programme provides that Notes may be listed or admitted to trading on such other or further stock exchange(s) as may be agreed between the Issuer and the relevant Dealer. The Issuer may also issue unlisted Notes.

Each Series (as defined herein) of Notes in bearer form will be represented on issue by a temporary global note in bearer form (each a “temporary Global Note” or “Global Note”) or a permanent global note in bearer form (each a “permanent Global Note” or “Global Note”). Global Notes may be deposited on the issue date of a relevant series with a common depositary on behalf of Euroclear Bank S.A./N.V. (“Euroclear”) and Clearstream, S.A. (“Clearstream, Luxembourg”). The provisions governing the exchange of interests in Global Notes for interests in other Global Notes and definitive Notes are described in “Form of Notes and Transfer Restrictions”. Each Series of Notes in registered form will be represented by one or more global certificates (each a “Global Certificate”) in fully registered form without interest coupons, deposited on the issue date (i) with a custodian for, and registered in the name of a nominee of, The Depository Trust Company (“DTC”) and/or (ii) with, and registered in the name of a nominee of, a common depositary for Euroclear and Clearstream, Luxembourg, which may be exchangeable under their terms for definitive Registered Notes (as defined herein). See “Form of Notes and Transfer Restrictions—Registered Notes”.

THE NOTES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”), AND MAY INCLUDE NOTES IN BEARER FORM THAT ARE SUBJECT TO U.S. TAX LAW REQUIREMENTS. THE NOTES MAY NOT BE OFFERED, SOLD OR DELIVERED WITHIN THE UNITED STATES EXCEPT, IN THE CASE OF NOTES IN REGISTERED FORM, TO QUALIFIED INSTITUTIONAL BUYERS PURSUANT TO RULE 144A UNDER THE SECURITIES ACT (“RULE 144A”). FOR CERTAIN RESTRICTIONS ON TRANSFER OF THE NOTES, SEE “FORM OF NOTES AND TRANSFER RESTRICTIONS”.

Arranger UBS

Dealers

Banco Bilbao Vizcaya Argentaria, S.A. BNP PARIBAS Citigroup Credit Suisse DBS Bank Ltd. Goldman Sachs International ING Morgan Stanley Nomura Standard Chartered Bank

Barclays BofA Merrill Lynch Crédit Agricole CIB

Daiwa Capital Markets Europe Deutsche Bank

HSBC J.P. Morgan

MUFG Société Générale Corporate & Investment Banking

UBS

i

The Issuer accepts responsibility for the information contained in this Offering Circular. To the best of the knowledge and belief of the Issuer (which has taken all reasonable care to ensure that such is the case), the information contained in this Offering Circular is in accordance with the facts and does not omit anything likely to affect the import of such information.

The Issuer, having made all reasonable enquiries, confirms that this Offering Circular contains all information with respect to the Issuer, to the Issuer and its subsidiaries and affiliates taken as a whole (the “Group”) and to the Notes that is material in the context of the issue and offering of the Notes, the statements contained in it relating to the Issuer and to the Group are in every material particular true and accurate and not misleading, the opinions and intentions expressed in this Offering Circular with regard to the Issuer and to the Group are honestly held, have been reached after considering all relevant circumstances and are based on reasonable assumptions, there are no other facts in relation to the Issuer, the Group or the Notes the omission of which would, in the context of the issue and offering of the Notes, make any statement in this Offering Circular misleading in any material respect and all reasonable enquiries have been made by the Issuer to ascertain such facts and to verify the accuracy of all such information and statements.

To the fullest extent permitted by law, none of the Dealers, the Arranger or the Agents accept any liability in relation to the information contained or incorporated by reference in this Offering Circular, any other information provided by the Issuer in connection with the Programme or any other statement, made or purported to be made by the Arranger or any Dealer or Agent on its behalf in connection with the Issuer or the issue and offering of Notes. Each of the Arranger, Dealers and Agents accordingly disclaims all and any liability whether arising in tort or contract or otherwise (save as referred to above) which it might otherwise have in respect of this Offering Circular or any such statement.

No person has been authorised to give any information or to make any representation other than those contained in this Offering Circular in connection with the issue or sale of the Notes and, if given or made, such information or representation must not be relied upon as having been authorised by the Issuer or any of the Dealers or Arrangers (as defined in “Summary of the Programme”). Neither the delivery of this Offering Circular nor any sale made in connection herewith shall, under any circumstances, create any implication that there has been no change in the affairs of the Issuer since the date hereof or the date upon which this Offering Circular has been most recently amended or supplemented or that there has been no adverse change in the financial position of the Issuer since the date hereof or the date upon which this Offering Circular has been most recently amended or supplemented or that any other information supplied in connection with the Programme is correct as of any time subsequent to the date on which it is supplied or, if different, the date indicated in the document containing the same.

This Offering Circular does not constitute an offer to sell or the solicitation of an offer to buy any Notes in any jurisdiction to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The distribution of this Offering Circular and the offer or sale of Notes may be restricted by law in certain jurisdictions. The Issuer and the Dealers do not represent that this document may be lawfully distributed, or that any Notes may be lawfully offered, in compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by the Issuer or the Dealers which would permit a public offering of any Notes or distribution of this document in any jurisdiction where action for that purpose is required. Accordingly, no Notes may be offered or sold, directly or indirectly, and neither this Offering Circular nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Offering Circular or any Notes come must inform themselves about, and observe, any such restrictions on the distribution of this Offering Circular and the offering and sale of Notes. In particular, there are restrictions on the distribution of this Offering Circular and the offer or sale of Notes in certain jurisdictions. For a description of these and certain further restrictions on offers and sales of the Notes and distribution of this Offering Circular, see “Form of Notes and Transfer Restrictions” and “Subscription and Sale”.

This document is only being distributed to and is only directed at (i) persons who are outside the

United Kingdom or (ii) investment professionals falling within Article 19(5) of the Financial Services and

ii

Markets Act 2000 (Financial Promotion) Order 2005 (the “Order”) or (iii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (d) of the Order (all such persons together being referred to as “relevant persons”). Any Notes will only be available to, and any invitation, offer or agreement to subscribe, purchase or otherwise acquire such Notes will be engaged in only with, relevant persons. Any person who is not a relevant person should not act or rely on this document or any of its contents.

The Notes have not been and will not be registered under the Securities Act, and may include Notes in bearer form that are subject to U.S. tax law requirements. Subject to certain exceptions, the Notes may not be offered, or delivered directly or indirectly within the United States or for the account or benefit of U.S. persons as defined in Regulation S under the Securities Act. Prospective purchasers are hereby notified that a seller of the Notes may be relying on the exemption from the registration requirements of Section 5 of the Securities Act provided by Rule 144A under such act.

None of the Dealers or the Arranger has separately verified the information contained herein. None of the Dealers or the Arranger makes any representation or warranty, express or implied, or accepts any responsibility or liability, with respect to the accuracy or completeness of any of the information contained or incorporated in this Offering Circular or any other information or statement made or purported to be made in relation to the Issuer, the Programme, the Notes or the distribution of the Notes. Neither this Offering Circular nor any other financial statements are intended to provide the basis of any credit or other evaluation and should not be considered as a recommendation by any of the Issuer, the Arranger or the Dealers that any recipient of this Offering Circular or any other financial statements should purchase the Notes. Each potential purchaser of Notes should determine for itself the relevance of the information contained in this Offering Circular and its purchase of Notes should be based upon such investigation as it deems necessary. None of the Dealers or the Arranger undertakes to review the financial condition or affairs of the Issuer during the life of the arrangements contemplated by this Offering Circular nor to advise any investor or potential investor in the Notes of any information coming to the attention of any of the Dealers or the Arranger. Investors and potential investors acknowledge that they have not relied, and will not rely, on the Arranger or the Dealers in connection with their investigation of the accuracy of any information or their decision whether to invest in any Notes.

In connection with the issue of any Tranche (as defined in “Summary of the Programme”) of Notes under the Programme, the Dealer (if any) specified in the relevant Pricing Supplement as the Stabilising Managers (or any person acting on behalf of any Stabilising Manager) may over-allot or effect transactions with a view to supporting the market price of the Notes at a level higher than that which might otherwise prevail for a limited period after the issue date. However, there may be no obligation on the Stabilising Managers (or any person acting on behalf of any Stabilising Manager) to do this. Such stabilising, if commenced, may be discontinued at any time and must be brought to an end after a limited period. Such stabilising shall be in compliance with all applicable laws, regulations and rules.

THE NOTES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE U.S. SECURITIES AND EXCHANGE COMMISSION, ANY STATE SECURITIES COMMISSION IN THE UNITED STATES OR ANY OTHER U.S. REGULATORY AUTHORITY, NOR HAVE ANY OF THE FOREGOING AUTHORITIES PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OF NOTES OR THE ACCURACY OR THE ADEQUACY OF THIS OFFERING CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE IN THE UNITED STATES.

AVAILABLE INFORMATION

To permit compliance with Rule 144A under the Securities Act in connection with sales of the Notes in accordance with Rule 144A, the Bank will be required under the Terms and Conditions of the Notes to furnish, upon request, to any Noteholder and any prospective purchaser of such Notes from such Noteholder the information required to be delivered under Rule 144A(d)(4) under the Securities Act unless at the time of the request the Bank is a reporting company under Section 13 or Section 15(d) of the United States Securities Exchange Act of 1934, as amended (the “Exchange Act”), or is included in the list of foreign private issuers that claim exemption from the

iii

registration requirements of Section 12(g) of the Exchange Act (and therefore is required to furnish to the United States Securities and Exchange Commission certain information pursuant to Rule 12g3-2(b) under the Exchange Act).

ENFORCEMENT OF CIVIL LIABILITIES

The Bank is a statutory juridical entity established under The Export-Import Bank of Korea Act of 1969, as amended, in Korea. Substantially all of the officers of the Bank and certain directors and other persons named herein reside in Korea, and substantially all or a significant portion of the assets of the officers and certain directors and other persons named herein that reside in Korea and substantially all of the assets of the Bank are located in Korea. As a result, it may not be possible for investors to effect service of process outside Korea upon those persons or to enforce against them or against the Bank in any jurisdiction outside Korea judgments predicated upon the civil liability provisions of the federal securities laws of the United States. There is doubt as to the enforceability in Korea, either in original actions or in actions for enforcement of judgments of U.S. courts, of civil liabilities predicated on the U.S. federal securities laws.

FORWARD LOOKING STATEMENTS

This document includes “forward-looking statements,” as defined in Section 27A of the Securities Act and Section 21E of the Exchange Act, including statements regarding the Bank’s expectations and projections for future operating performance and business prospects. The words “believe,” “expect,” “anticipate,” “estimate,” “project,” and similar words identify forward-looking statements. In addition, all statements other than statements of historical facts included in this document are forward-looking statements. Although the Bank believes that the expectations reflected in the forward-looking statements are reasonable, it can give no assurance that such expectations will prove to be correct. This document discloses important factors that could cause actual results to differ materially from the Bank’s expectations (“Cautionary Statements”). All subsequent written and oral forward-looking statements attributable to the Bank or persons acting on behalf of the Bank are expressly qualified in their entirety by the Cautionary Statements.

Factors that could adversely affect the future performance of the Korean economy include:

• difficulties in the financial sectors in Europe and elsewhere and increased sovereign default risks in selected countries and the resulting adverse effects on the global financial markets;

• adverse conditions or uncertainty in the economies of countries and regions that are important export markets for Korea, such as the United States, Europe, Japan and China, or in emerging market economies in Asia or elsewhere, as well as increased uncertainty in the wake of a referendum in the United Kingdom in June 2016, in which the majority of voters voted in favor of an exit from the European Union (“Brexit”);

• adverse changes or volatility in foreign currency reserve levels, commodity prices (including oil prices), exchange rates (including fluctuation of the U.S. dollar, the euro or Japanese yen exchange rates or revaluation of the Chinese renminbi and the overall impact of Brexit on the value of the Korean Won), interest rates, inflation rates or stock markets;

• declines in consumer confidence and a slowdown in consumer spending;

• increasing levels of household debt;

• increasing delinquencies and credit defaults by consumer and small- and medium-sized enterprise borrowers;

• further decreases in the market prices of Korean real estate;

• the continued growth of the Chinese economy, to the extent its benefits (such as increased exports to China) are outweighed by its costs (such as competition in export markets or for foreign investment and

iv

the relocation of the manufacturing base from Korea to China), as well as a slowdown in the growth of China’s economy, which is Korea’s most important export market;

• the recent political scandal in Korea involving a confidant of the President and the resulting social unrest, as well as related investigations of Korean conglomerates and their senior management for bribery, embezzlement and other possible misconduct;

• increased sovereign default risk in select countries and the resulting adverse effects on the global financial markets;

• the economic impact of any pending or future free trade agreements;

• social and labor unrest;

• a decrease in tax revenues and a substantial increase in the Government’s expenditures for fiscal stimulus measures, unemployment compensation and other economic and social programs that, together, would lead to an increased Government budget deficit;

• financial problems or lack of progress in the restructuring of Korean conglomerates, other large troubled companies, their suppliers or the financial sector;

• loss of investor confidence arising from corporate accounting irregularities or corporate governance issues at certain Korean companies;

• increases in social expenditures to support an aging population in Korea or decreases in economic productivity due to the declining population size in Korea;

• geo-political uncertainty and risk of further attacks by terrorist groups around the world;

• the occurrence of severe health epidemics in Korea or other parts of the world, including an outbreak of severe acute respiratory syndrome, swine or avian flu, Ebola or Middle East respiratory syndrome.

• deterioration in economic or diplomatic relations between Korea and its trading partners or allies, including deterioration resulting from territorial or trade disputes or disagreements in foreign policy (such as the ongoing controversy between Korea and China regarding the decision to allow the United States to deploy the Terminal High Altitude Area Defense system in Korea);

• political uncertainty or increasing strife among or within political parties in Korea;

• natural or man-made disasters that have a significant adverse economic or other impact on Korea or its major trading partners;

• hostilities or political or social tensions involving oil producing countries in the Middle East or North Africa and any material disruption in the supply of oil or sudden increase in the price of oil; and

• an increase in the level of tensions or an outbreak of hostilities between North Korea and Korea or the United States.

CERTAIN DEFINED TERMS AND CONVENTIONS

Unless otherwise indicated, all references to “won”, “Won” or “W” contained in this Offering Circular are to the currency of Korea, references to “U.S. dollars”, “Dollars”, “USD”, “$” or “US$” are to the currency of the United States of America, references to “Canadian Dollar” or “CAD” are to the currency of Canada, references to “Euro”, “EUR” or “€” are to the currency of the European Union, references to “Japanese Yen”, “JPY” or “¥” are to the currency of Japan, references to “Chinese Renminbi” or “CNY” are to the currency of the People’s Republic of China, references to “Swiss Franc” or “CHF” are to the currency of Switzerland, references to “British Pound” or “GBP” are to the currency of the United Kingdom, references to “Deutsche Mark” are to the currency of the Federal Republic of Germany, references to “Hong Kong Dollar” or “HKD” are to the currency of Hong Kong, S.A.R., references to “Singapore dollar” or “SGD” are to the currency of Singapore, references to “Turkish Lira”

v

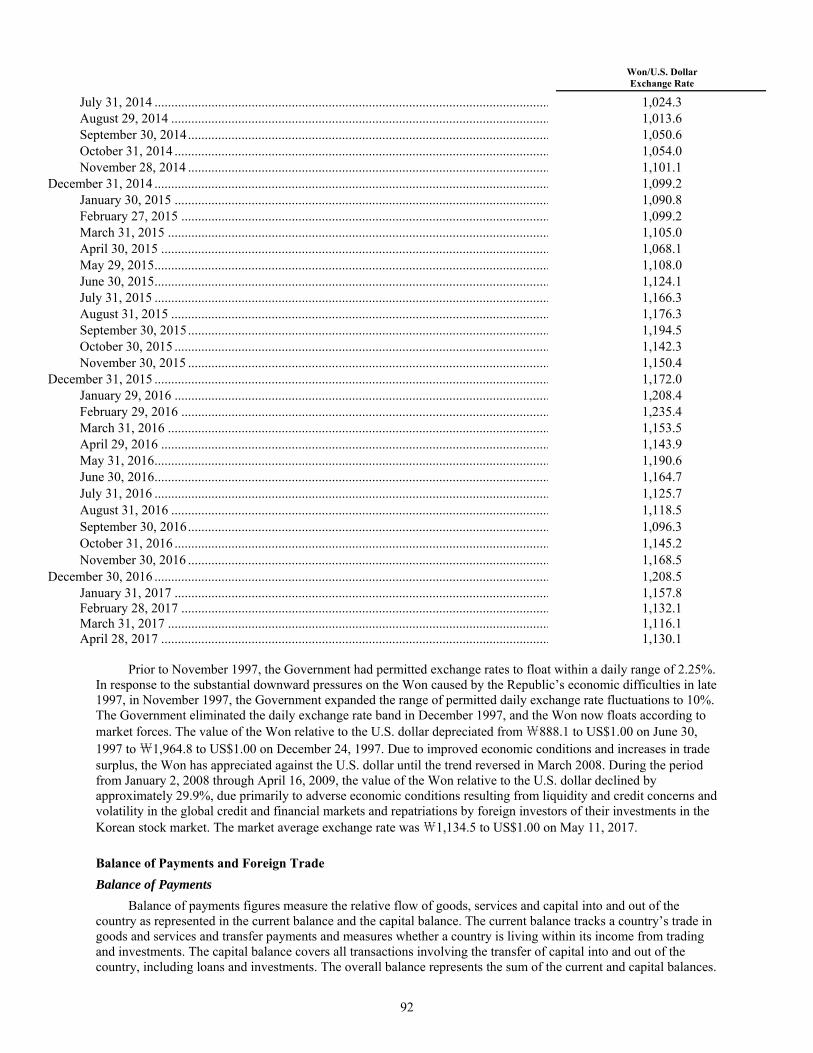

or “TRY” are to the currency of Turkey, references to “Malaysia Ringgit” or “MYR” are to the currency of Malaysia, references to “Brazilian Real” or “BRL” are to the currency of Federative Republic of Brazil, references to “Mexican Peso” or “MXN” are to the currency of the United Mexican States, references to “New Zealand Dollar” or “NZD” are to the currency of New Zealand, references to “Taiwan Dollar” or “TWD” are to the currency of Taiwan, references to “Thai Baht” or “THB” are to the currency of Thailand, references to “Australian Dollar” or “AUD” are to the currency of Australia, references to “Indian Rupee” or “INR” are to the currency of India, references to “Indonesian Rupiah” or “IDR” are to the currency of Indonesia, references to “Russian Ruble” or “RUB” are to the currency of the Russian Federation, references to “Swedish Krona” or “SEK” are to the currency of Sweden, references to “South African Rand” or “ZAR” are to the currency of South Africa, references to “Danish Krone” or “DKK” are to the currency of Denmark and references to “Peruvian Sol” or “PEN” are to the currency of Peru. Except where otherwise stated, Won amounts have been translated into Dollars at the rate of Won 1,172.0 to US$1.00, which was the market average exchange rate as announced by the Seoul Money Brokerage Services, Ltd. on 31 December 2015. No representation is made that the Won or Dollar amounts referred to herein could have been or could be converted into Dollars or Won, as the case may be, at any particular rate or at all.

References herein to “Korea” or the “Republic” are references to the Republic of Korea, and references

herein to “Government” are references to the government of the Republic of Korea. References to “we”, “us”, “our”, the “Issuer” or the “Bank” are references to The Export-Import Bank of Korea.

In this Offering Circular, where information has been presented in thousands, millions or billions of units, amounts may have been rounded up or down. Accordingly, actual numbers may differ from those contained herein due to rounding. All discrepancies in any table between totals and the sums of the amounts listed are due to rounding.

The Bank’s financial statements and separate financial information included in this Offering Circular were prepared under International Financial Reporting Standards as adopted by Korea (“Korean IFRS” or “K-IFRS”). References in this Offering Circular to “separate” financial statements and information are to financial statements and information prepared on a non-consolidated basis. Unless specified otherwise, the Bank’s financial and other information included in this Offering Circular is presented on a separate basis in accordance with Korean IFRS and does not include such information with respect to its subsidiaries.

DOCUMENTS INCORPORATED BY REFERENCE

The following documents published or issued from time to time after the date hereof shall be deemed to be incorporated in, and to form part of, this Offering Circular:

(a) the most recently published audited separate and consolidated annual financial statements and, if published later, the most recently published interim separate and consolidated financial statements (if any) of the Issuer from time to time;

(b) all supplements or amendments to this Offering Circular circulated by the Issuer from time to time; and

(c) the most recent shelf registration statement or post-effective amendment filed with the Securities and Exchange Commission by the Bank and other reports (including any prospectus supplements) filed with the Securities and Exchange Commission by the Bank since the most recent filing of the shelf registration statement or post-effective amendment, as the case may be,

save that any statement contained herein or in a document which is deemed to be incorporated by reference herein shall be deemed to be modified or superseded for the purpose of this Offering Circular to the extent that a statement contained in any such subsequent document which is deemed to be incorporated by reference herein modifies or supersedes such earlier statement (whether expressly, by implication or otherwise). Any statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this Offering Circular.

vi

The Issuer will provide, without charge, to each person to whom a copy of this Offering Circular has been delivered, upon the request of such person, a copy of any or all of the documents deemed to be incorporated herein by reference unless such documents have been modified or superseded as specified above. Requests for such documents should be directed to the Issuer at its office set out at the end of this Offering Circular. In addition, such documents will be available from the principal office in London of Deutsche Bank AG, London Branch (the “Fiscal Agent”).

The Issuer will, in connection with the listing of the Notes on the Singapore Stock Exchange, so long as the rules of such exchange so require, in the event of any material change in the information contained in this Offering Circular, prepare a supplement to this Offering Circular or publish a new Offering Circular for use in connection with any subsequent issue of the Notes to be listed on the Singapore Stock Exchange.

If the terms of the Programme are modified or amended in a manner which would make this Offering Circular, as so modified or amended, inaccurate or misleading, a new Offering Circular will be prepared.

SUPPLEMENTARY OFFERING CIRCULAR

The Issuer has given an undertaking to the Dealers that if at any time during the duration of the Programme there is a significant change affecting any matter contained in this Offering Circular whose inclusion would reasonably be required by investors and their professional advisers, and would reasonably be expected by them to be found in this Offering Circular, for the purpose of making an informed assessment of the assets and liabilities, financial position, profits and losses and prospects of the Issuer and the rights attaching to the Notes, the Issuer shall prepare an amendment or supplement to this Offering Circular or publish a replacement Offering Circular for use in connection with any subsequent offering of the Notes and shall supply to each Dealer such number of copies of such supplement hereto as such Dealer may reasonably request.

TABLE OF CONTENTS

Page

vii

Summary of the Programme ........................................................................................................................................ 1 Terms and Conditions of the Notes ............................................................................................................................. 6 Form of Pricing Supplement ...................................................................................................................................... 26 Form of Notes and Transfer Restrictions ................................................................................................................... 33 Use of Proceeds ......................................................................................................................................................... 42 The Export-Import Bank of Korea............................................................................................................................. 43

Overview .............................................................................................................................................................. 43 Capitalization ....................................................................................................................................................... 44 Business ............................................................................................................................................................... 44 Selected Financial Statement Data ....................................................................................................................... 47 Operations ............................................................................................................................................................ 49 Description of Assets and Liabilities .................................................................................................................... 53 Debt ...................................................................................................................................................................... 61 Credit Policies, Credit Approval and Risk Management ...................................................................................... 63 Capital Adequacy ................................................................................................................................................. 64 Overseas Operations ............................................................................................................................................. 65 Property ................................................................................................................................................................ 65 Management and Employees................................................................................................................................ 65 Financial Statements and the Auditors ................................................................................................................. 67

The Republic of Korea .............................................................................................................................................. 68 Land and History .................................................................................................................................................. 68 Government and Politics ...................................................................................................................................... 70 The Economy ....................................................................................................................................................... 72 Principal Sectors of the Economy ........................................................................................................................ 79 The Financial System ........................................................................................................................................... 85 Monetary Policy ................................................................................................................................................... 89 Balance of Payments and Foreign Trade .............................................................................................................. 92 Government Finance .......................................................................................................................................... 199 Debt .................................................................................................................................................................... 101

Taxation ................................................................................................................................................................... 104 Summary of Dealer Agreement ............................................................................................................................... 113 Subscription and Sale .............................................................................................................................................. 114 General Information ................................................................................................................................................ 119 Index to Financial Statements .................................................................................................................................. 121

1

SUMMARY OF THE PROGRAMME

The following summary is qualified in its entirety by the remainder of this Offering Circular. Issuer ............................................ The Export-Import Bank of Korea

Description ................................... Global Medium Term Note Programme

Size ............................................... Up to US$25,000,000,000 (or the equivalent in other currencies at the date of issue) aggregate principal amount of Notes outstanding at any one time.

Arranger ........................................ UBS AG Hong Kong Branch