The Effect Of Service Quality, Customer Trust And Perceived ...

12

International Journal of Business and Management Invention (IJBMI) ISSN (Online): 2319-8028, ISSN (Print):2319-801X www.ijbmi.org || Volume 10 Issue 7 Ser. III || July 2021 || PP 05-16 DOI: 10.35629/8028-1007030516 www.ijbmi.org 5 | Page The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty With Co-Creation As Intervening Variable On Customers Using Internet Banking And Mobile Banking Bankaltimtara Sharia KCP Bontang Alfiah Mapalidara, Syarifah Hudayah, Herning Indriastuti Corresponding Author:Alfiah Mapalidara Mulawarman University, Samarinda - Indonesia ABSTRACT: This study aims to analyze the effect of service quality, customer trust and perceived value on customer loyalty with co-creation as an intervening variable. The method used is a structural equation model (SEM) with the AMOS application to analyze 192 samples of customers who use internet banking and mobile banking at Bankaltimtara Syariah KCP Bontang. The sampling technique used non-probability sampling method. The test results of the goodness of fit index show the model (fit) seen from the results of chi-square, probability, RMSEA, GFI, AGFI, CMIN/DF, TLI and CFI respectively 273.64, 0.079, 0.026, 0.901, 0.877, 1.131, 0.981 and 0.983 are all within the range of expected values so that this research model can be accepted. The results also show that co-creation variable has a positive influence as an intervening variable. Other research results are: 1). Service quality has a significant effect on co-creation. 2). Customer trust has a significant effect on co-creation. 3). Perceived value has a significant effect on co-creation 4). Service quality has a significant effect on customer loyalty. 5). Customer trust has a significant effect on customer loyalty. 6). Perceived value has a significant effect on customer loyalty. 7). Co-creation has a significant effect on customer loyalty. KEY WORD: service quality, customer trust, perceived value, customer loyalty, co-creation. --------------------------------------------------------------------------------------------------------------------------------------- Date of Submission: 12-07-2021 Date of Acceptance: 28-07-2021 --------------------------------------------------------------------------------------------------------------------------------------- I. INTRODUCTION Indonesia is a country where the majority of the population is Muslim. Based on population data in June 2020, the total population of Indonesia is 268,583,016, of which 87.2% of the population embraces Islam, so it has the potential to develop Islamic finance, one of which is in the banking sector. Based on data from OJK Indonesia in 2016, the service offices of Islamic Commercial Banks and Sharia Business Units amounted to 2,201 offices and in the latest data in January 2020, the number grew to 2,308 offices. The increasing number of businesses in the Indonesian Islamic banking industry has created increasingly competitive competition among banking companies. In order to achieve a competitive advantage in business, all banks are trying to find ways to provide quality services that are in accordance with customer perceptions so that customer trust can be achieved which is expected to make customers more loyal to the company. It can be concluded that in today's competitive banking business, customer loyalty to the bank is the main focus so that companies can gain a competitive advantage. Today many business transactions have been carried out through electronic media where this is the result of the development of information technology which has created new types and business opportunities. It is possible for everyone to make transactions easily through these technological developments, one of which is banking transactions. Banking transactions can be accelerated by technological advances that can increase the effectiveness and efficiency of customers in conducting transactions. This has become one of the competitions between banks in creating innovations and the latest outputs in the service side through the use of technology to achieve competitive advantage, one of which is internet banking and mobile banking. Bankaltimtara Sharia as one of the Islamic banks in Indonesia already has an internet banking and mobile banking application called DG Bankaltimtara. The application was only inaugurated on April 15, 2020. However, the features that have been provided still require improvement where this can be seen by the entry of complaints from customers through the call center, social media, customer feedback on the Play Store and App Store, or directly coming to the office. service to make a complaint. Thus, Bankaltimtara Syariah KCP Bontang needs to analyze in terms of service quality, customer trust and perceived value to overcome low customer loyalty and how the indirect effect of co-creation.

-

Upload

khangminh22 -

Category

Documents

-

view

4 -

download

0

Transcript of The Effect Of Service Quality, Customer Trust And Perceived ...

International Journal of Business and Management Invention (IJBMI)

ISSN (Online): 2319-8028, ISSN (Print):2319-801X www.ijbmi.org || Volume 10 Issue 7 Ser. III || July 2021 || PP 05-16

DOI: 10.35629/8028-1007030516 www.ijbmi.org 5 | Page

The Effect Of Service Quality, Customer Trust And Perceived

Value On Customer Loyalty With Co-Creation As Intervening

Variable On Customers Using Internet Banking And Mobile

Banking Bankaltimtara Sharia KCP Bontang

Alfiah Mapalidara, Syarifah Hudayah, Herning Indriastuti Corresponding Author:Alfiah Mapalidara

Mulawarman University, Samarinda - Indonesia

ABSTRACT: This study aims to analyze the effect of service quality, customer trust and perceived value on

customer loyalty with co-creation as an intervening variable. The method used is a structural equation model

(SEM) with the AMOS application to analyze 192 samples of customers who use internet banking and mobile

banking at Bankaltimtara Syariah KCP Bontang. The sampling technique used non-probability sampling

method. The test results of the goodness of fit index show the model (fit) seen from the results of chi-square,

probability, RMSEA, GFI, AGFI, CMIN/DF, TLI and CFI respectively 273.64, 0.079, 0.026, 0.901, 0.877,

1.131, 0.981 and 0.983 are all within the range of expected values so that this research model can be accepted.

The results also show that co-creation variable has a positive influence as an intervening variable. Other research results are: 1). Service quality has a significant effect on co-creation. 2). Customer trust has a

significant effect on co-creation. 3). Perceived value has a significant effect on co-creation 4). Service quality

has a significant effect on customer loyalty. 5). Customer trust has a significant effect on customer loyalty. 6).

Perceived value has a significant effect on customer loyalty. 7). Co-creation has a significant effect on customer

loyalty.

KEY WORD: service quality, customer trust, perceived value, customer loyalty, co-creation.

---------------------------------------------------------------------------------------------------------------------------------------

Date of Submission: 12-07-2021 Date of Acceptance: 28-07-2021

---------------------------------------------------------------------------------------------------------------------------------------

I. INTRODUCTION Indonesia is a country where the majority of the population is Muslim. Based on population data in

June 2020, the total population of Indonesia is 268,583,016, of which 87.2% of the population embraces Islam,

so it has the potential to develop Islamic finance, one of which is in the banking sector. Based on data from OJK

Indonesia in 2016, the service offices of Islamic Commercial Banks and Sharia Business Units amounted to

2,201 offices and in the latest data in January 2020, the number grew to 2,308 offices.

The increasing number of businesses in the Indonesian Islamic banking industry has created

increasingly competitive competition among banking companies. In order to achieve a competitive advantage in business, all banks are trying to find ways to provide quality services that are in accordance with customer

perceptions so that customer trust can be achieved which is expected to make customers more loyal to the

company. It can be concluded that in today's competitive banking business, customer loyalty to the bank is the

main focus so that companies can gain a competitive advantage.

Today many business transactions have been carried out through electronic media where this is the

result of the development of information technology which has created new types and business opportunities. It

is possible for everyone to make transactions easily through these technological developments, one of which is

banking transactions. Banking transactions can be accelerated by technological advances that can increase the

effectiveness and efficiency of customers in conducting transactions. This has become one of the competitions

between banks in creating innovations and the latest outputs in the service side through the use of technology to

achieve competitive advantage, one of which is internet banking and mobile banking.

Bankaltimtara Sharia as one of the Islamic banks in Indonesia already has an internet banking and mobile banking application called DG Bankaltimtara. The application was only inaugurated on April 15, 2020.

However, the features that have been provided still require improvement where this can be seen by the entry of

complaints from customers through the call center, social media, customer feedback on the Play Store and App

Store, or directly coming to the office. service to make a complaint. Thus, Bankaltimtara Syariah KCP Bontang

needs to analyze in terms of service quality, customer trust and perceived value to overcome low customer

loyalty and how the indirect effect of co-creation.

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 6 | Page

II. LITERATURE REVIEW Service Quality

Service quality is an important topic in marketing that has become widely available in traditional retail

settings (Arcand et al., 2017). Competition in an era where banks are struggling to maintain their market share,

the scale of measuring service quality in a certain cultural context is very important to provide practical

solutions to service companies.

Quality is an important aspect in the business world because it is able to maintain satisfaction and

loyalty as well as offer experience. Service quality in the banking sector is one of the most basic factors that

affect the level of satisfaction (Koupai et al., 2015). Several studies show that service quality affects service

through service quality.

Service quality in the context of Islamic banking according to Asnawi et al. (2019) is the company's

ability to provide products or services that meet customer expectations or even exceed customer expectations. Quality is often described as a key factor of competitive advantage and as something that can be used to build a

strong customer base (Ekaabi et al., 2020).

Customer Trust

Trust in banking services is critical to relational exchange situations and reduces the perceived risk of

service outcomes. Trust facilitates transactions with customers. Customers don't have to worry about their

personal interests, their savings in the bank, and the financial products they have purchased or plan to purchase

from the bank, including insurance and mortgage policies. With a high level of trust, customers feel confident

that their interests are well served by the bank. To some extent, a high level of trust is a buffer against negative

experiences that can arise among customers. Customers tend to "forgive" negative experiences and consider

them an exception if they trust the bank. However, with a low level of trust, negative experiences can be considered as “evidence” that the bank cannot be trusted.

The customer and the bank must rely on each other, because they cannot be certain in advance how the

other party will act. Risk in this context means that both parties perceive the risk that the other party will act in a

way that does not benefit them and therefore could potentially harm them (Frederik & Pauline, 2017). Trust is

considered as one of the most important factors that mediate the commitment between buyers and sellers. Islam

places the highest emphasis on belief as a personality trait that Muslims should possess. Ethics and adherence to

Sharia principles are highly appreciated and supported as pillars in carrying out sharia banking activities based

on trust (Nora, 2019).

Perceived Value

The concept of perceived value has become a key element used by most developed countries'

economies to determine business models in the last decades of the last century (Scridon et al., 2019). Perceived value is able to identify how much buyers want in determining their decision to buy or use services in the future

(Aini et al., 2019).

Perceived value involves an exchange between what customers get for example quality, benefits, or

utility and what they give up such as price, sacrifice and time to buy and consume a product (Mayr & Zins,

2012). Prodanova et al. (2019) states that the perceived value associated with m-banking services is a function

of the search for novelty, perceived entertainment and m-banking are ubiquitous, each explaining the epistemic

value (novelty or search for variety), hedonic (emotional ) and utilitarian values (convenience), as elements that

make up the overall perceived value.

Based on the statement above, it can be concluded that perceived value is the perception of the value of

a product or service that consumers are willing to pay. Based on Suryani's (2015) statement which explains that

the important characteristics in perceived value are divided into 2, namely: (1) Perceived value is inherent in the use of the product, which distinguishes it from personal or

organizational values.

(2) Only perceived by the customer, and cannot be determined objectively by the seller. Only customers

can see if the product or service offers value.

Co-Creation

A new paradigm in the management literature that has developed to date is co-creation, enabling

companies and customers to jointly create value through interaction (Galvagno & Dalli, 2014). This paradigm

was born from a research collaboration conducted by Vargo & Lusch (2004) which resulted in a description of

the framework which became known as Service-Dominant Logic, a new pattern in marketing management

where the role of the customer is needed in creating value and valuable experience with service provider

organizations.

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 7 | Page

S-D Logic offers opportunities for service marketing research, and highlights the role of customers as

co-creators of value throughout the service delivery process. S-D Logic presents a dynamic and sustainable

narrative about co-creation through resource integration and service exchange (Vargo & Lusch, 2017). It is important to study co-creation because co-creation encourages creativity and generates reciprocal

value for both the company and the customers themselves (Saarijärvi et al., 2013). The concept of co-creation is

becoming increasingly important in the service industry, especially in industries that are required to always be

ready to innovate such as the banking industry. The banking sector continues to experience changes in consumer

behavior with customer characteristics that demand to be adjusted to their wishes. Overall co-creation is a

product value creation process that is carried out together with customers in order to produce new, higher

quality products.

Customer Loyalty

Raza et al. (2020) explains that customer loyalty is a source of profitability and competitive advantage

for service and manufacturing companies. Customers are said to be loyal when they show dedication and loyalty to repurchase products and services in the future. Today, maintaining a loyal customer base is a challenge for

service companies and particularly for banks, as loyalty is associated with lower marketing costs and higher

profitability.

Martínez & Bosque (2013) asserts that the behavior of the customer loyalty component is related to

repeated transactions made by consumers within a certain period of time. However, repurchase behavior can be

due to satisfaction or simply because of a lack of alternatives, or as reasons of convenience or habit. Therefore

Chen & Wang (2016) say that retaining existing customers and strengthening customer loyalty is an important

task for service providers who want to achieve competitive advantage because it is very difficult to get loyal

customers on the internet.

Customer loyalty in the context of e-banking can be defined as the tendency of customers to frequently

visit bank websites, use e-banking services continuously and spread positive word of mouth about e-banking

services (Jeong & Lee, 2010; Kaur et al., 2012; Amin, 2016 in Shankar & Jebarajakirthy, 2019). Kartika et al. (2019) explains that long-term relationships with customers are economically beneficial. Loyalty is necessary

and important because selling more to old customers is easier and cheaper than new customers.

Based on the description above, the following hypothesis can be formulated:

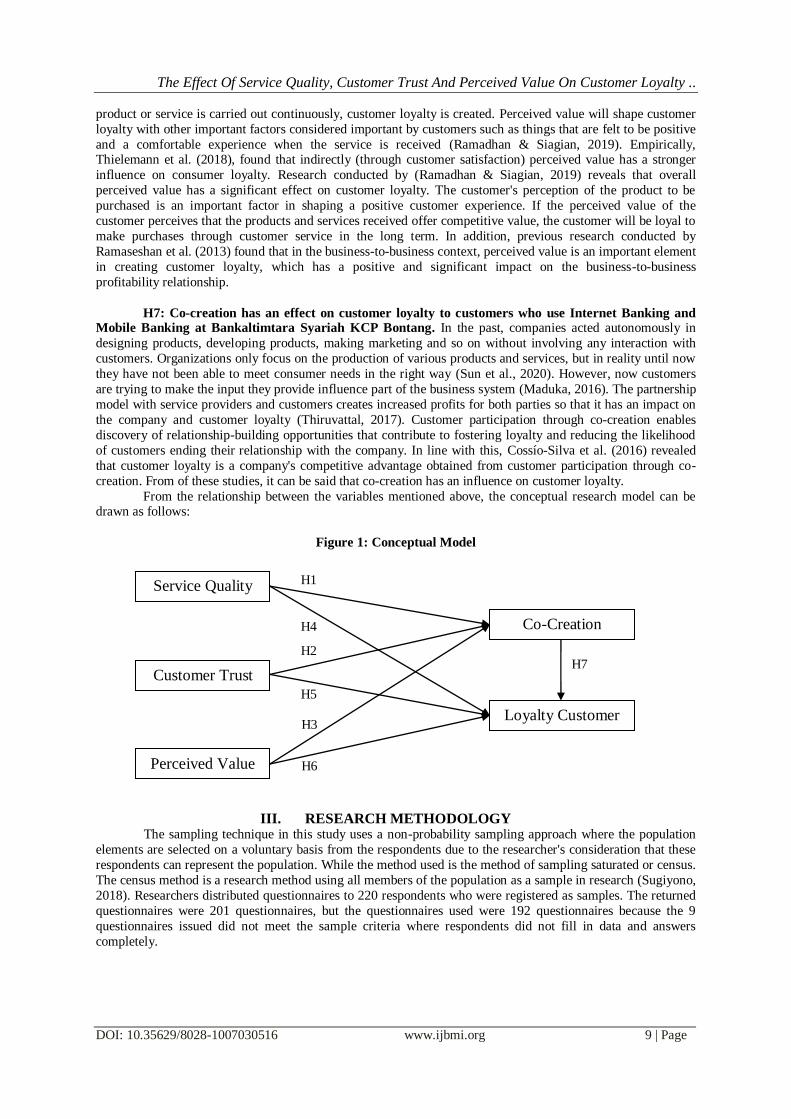

H1: Service quality affects the co-creation of Internet Banking and Mobile Banking customers at

Bankaltimtara Syariah KCP Bontang. The tight business competition requires the company to always be able

to provide the best service for its customers. To be able to achieve service quality in accordance with customer

desires, companies can improve the quality of their services through co-creation where customer involvement is

needed in developing products and services. Prayag et al. (2020), in his research revealed that the perception of

service quality can have an impact on the willingness of tourists to engage in co-creation activities with service

providers and other participants. Elsharnouby & Mahrous (2015), revealed in their research that in shaping the service experience and determining the service, the role of the customer has shifted from a passive audience to

an active player or participant. Therefore, Ramaswamy (2011) says that these changes in business and society

call for co-creation practices to develop systems, products and services through collaboration with customers,

employees and other stakeholders. In accordance with research conducted by Elsharnouby & Mahrous (2015), it

was found that four dimensions of electronic service quality significantly affect customer willingness to

participate in online co-creation experiences. Several empirical studies above prove that service quality has an

influence on co-creation.

H2: Customer trust has an effect on co-creation of Internet Banking and Mobile Banking

customers using Bankaltimtara Syariah KCP Bontang. Randall et al. (2011) in his research revealed that the

application of co-creation requires companies to be able to embrace transparency of the good and bad of the

company's products so that the trust of customers in the application of co-creation can increase. Co-creation can be used as a way to promote transparency in production and as a suggestion to improve organizational and

consumer trust which will certainly reap the benefits (Sun et al., 2020). Alves & Wagner Mainardes (2017)

explain in their research that trust can be one of the factors that influence the potential for co-creation through

exchange. A person is more willing to engage in social exchange when the relationship has a high degree of

trust. The results of research conducted by Wu et al. (2019) reveals that trust is one of the main determining

decisions of a person in co-creation in an organization. Research conducted by Fierro et al. (2018), recently

based on a sample of financial service users, it was found that the quality of the relationship which includes trust

has a positive impact on the value of co-creation with customers. Subsequent research conducted by Mostafa

(2020) also found that trust has a positive influence on co-creation. Therefore, it can be seen that the higher the

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 8 | Page

level of customer trust in the relationship with the company, the higher the possibility of co-creation of customer

value.

H3: Perceived value affects the co-creation of Internet Banking and Mobile Banking customers at

Bankaltimtara Syariah KCP Bontang. Grönroos (2011) reveals that consumers' perceived value in

consumption experiences is about value in use, because consumers are personally present in situations where co-

creation appears. Otchere et al. (2019) said that the increase in the customer's perceived value attached to the

perceived value was influenced by the successful co-creation applied. This opinion is supported by Zauner et al.

(2015) who said that a detailed understanding of consumer perceived value could contribute to a more detailed

application of empirical assessments in the future in the context of co-creation management. Kim et al. (2019)

examines the effect of customer perceptions of innovation on co-creation behavior. The study identified a

holistic concept in which customer perception of innovation is the main predictor that influences customer co-

creation behavior which ultimately leads to customer satisfaction and loyalty. Research conducted by Prebensen

& Xie (2017) has identified the perceived value and satisfaction felt by tourists are influenced by the importance of co-creation. According to Perks et al. (2012) in general creating new and innovative perceived value can be

done through co-creation as a service innovation strategy that combines consumer resources. The results of

research conducted by Otchere et al. (2019) shows that customer perceived value and performance innovation

have a positive and significant effect on co-creation. Based on previous research, it can be said that perceived

value has an effect on co-creation.

H4: Service quality affects customer loyalty to customers using Internet Banking and Mobile

Banking Bankaltimtara Syariah KCP Bontang. Service quality is a form of assessment given by consumers

for the services provided by service providers as well as one of the factors whether customer satisfaction can be

achieved which is expected to be able to get consumer loyalty. Asnawi et al. (2019) argues that in the modern

organizational paradigm, efforts to improve service quality are considered as strategic policies. This is related to

the contribution of service quality that can increase customer satisfaction and create customer loyalty within a certain period. Boonlertvanich (2019) says that to ensure customer satisfaction, trust and loyalty, banks must

focus on service quality. Kaura et al. (2015) in his research on retail banking in India stated that the quality of

service has a positive and significant influence on customers with indicators of service guarantees that can solve

customer problems and are easy to obtain. A comprehensive banking service quality model increasingly

identifies the main precursors of customer loyalty, including hierarchical models, multidimensional service

quality and other factors that influence customer loyalty. Based on the explanation above, research in various

industries (eg logistics services, supermarkets, hospitals, banking, insurance and online shopping) has proven a

positive influence between service quality and customer loyalty as research conducted by Sehrish et al. (2019);

Slack et al. (2020); Satti et al. (2020); Raza et al. (2020); Rehman et al. (2019); Khan et al. (2019).

H5: Customer trust has an effect on customer loyalty to customers using Internet Banking and Mobile Banking Bankaltimtara Syariah KCP Bontang. The trust given by customers to the bank leads to the

customer's decision to be loyal to the products and services offered by the bank. Trust eventually grows into

loyalty and is an important factor in customer service provider relationships. Trust is effective in expecting

loyalty from customers and has a deeper sentiment. Satisfied customers can become loyal customers when

customers have a high level of trust in the organization. The higher the level of trust in the bank, the more loyal

its customers are. Therefore, banks must make more efforts to gain customer trust (Haron et al., 2020). To

maintain and increase customer loyalty, banks must be trusted and committed to the services provided (Ndubisi

et al., 2007; Nomran et al., 2018; Ali & Naeem, 2019). The higher the trust in the bank and the quality of the

relationship, the more loyal the customers will be (Ndubisi et al., 2007; Ali & Naeem, 2019). Customer trust

according to Koupai et al. (2015) plays a very important role in presupposing customer loyalty. Habits and

reputation can affect customer repeat use of services and consistent relationships with the company. The results

of the study also show that customer trust has a positive and significant effect on customer loyalty to Bank Agriculture internet banking users. Osman & Sentosa (2013) also revealed that trust has an influence between

customer satisfaction and loyalty in the Malaysian tourism industry. Kassim & Abdullah (2010) argue that

loyalty will be positively affected when satisfied customers have confidence in the company. Thus, trust is seen

as a factor driving customer loyalty.

H6: Perceived value affects customer loyalty to customers using Internet Banking and Mobile

Banking Bankaltimtara Syariah KCP Bontang. Customer perceptions of the value received from a company

can influence customers to repurchase the company's products or services (Mohammed & Al-Swidi, 2019).

Customers will tend to use a company's products or services continuously when the value of the product is in

accordance with the perceived value and expectations conceptualized by the customer. When the use of a

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 9 | Page

H1

H4

H2

H5

H3

H6

product or service is carried out continuously, customer loyalty is created. Perceived value will shape customer

loyalty with other important factors considered important by customers such as things that are felt to be positive

and a comfortable experience when the service is received (Ramadhan & Siagian, 2019). Empirically, Thielemann et al. (2018), found that indirectly (through customer satisfaction) perceived value has a stronger

influence on consumer loyalty. Research conducted by (Ramadhan & Siagian, 2019) reveals that overall

perceived value has a significant effect on customer loyalty. The customer's perception of the product to be

purchased is an important factor in shaping a positive customer experience. If the perceived value of the

customer perceives that the products and services received offer competitive value, the customer will be loyal to

make purchases through customer service in the long term. In addition, previous research conducted by

Ramaseshan et al. (2013) found that in the business-to-business context, perceived value is an important element

in creating customer loyalty, which has a positive and significant impact on the business-to-business

profitability relationship.

H7: Co-creation has an effect on customer loyalty to customers who use Internet Banking and Mobile Banking at Bankaltimtara Syariah KCP Bontang. In the past, companies acted autonomously in

designing products, developing products, making marketing and so on without involving any interaction with

customers. Organizations only focus on the production of various products and services, but in reality until now

they have not been able to meet consumer needs in the right way (Sun et al., 2020). However, now customers

are trying to make the input they provide influence part of the business system (Maduka, 2016). The partnership

model with service providers and customers creates increased profits for both parties so that it has an impact on

the company and customer loyalty (Thiruvattal, 2017). Customer participation through co-creation enables

discovery of relationship-building opportunities that contribute to fostering loyalty and reducing the likelihood

of customers ending their relationship with the company. In line with this, Cossío-Silva et al. (2016) revealed

that customer loyalty is a company's competitive advantage obtained from customer participation through co-

creation. From of these studies, it can be said that co-creation has an influence on customer loyalty.

From the relationship between the variables mentioned above, the conceptual research model can be drawn as follows:

Figure 1: Conceptual Model

III. RESEARCH METHODOLOGY The sampling technique in this study uses a non-probability sampling approach where the population

elements are selected on a voluntary basis from the respondents due to the researcher's consideration that these

respondents can represent the population. While the method used is the method of sampling saturated or census.

The census method is a research method using all members of the population as a sample in research (Sugiyono,

2018). Researchers distributed questionnaires to 220 respondents who were registered as samples. The returned

questionnaires were 201 questionnaires, but the questionnaires used were 192 questionnaires because the 9

questionnaires issued did not meet the sample criteria where respondents did not fill in data and answers

completely.

Service Quality

Customer Trust

Perceived Value

Loyalty Customer

Co-Creation

H7

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 10 | Page

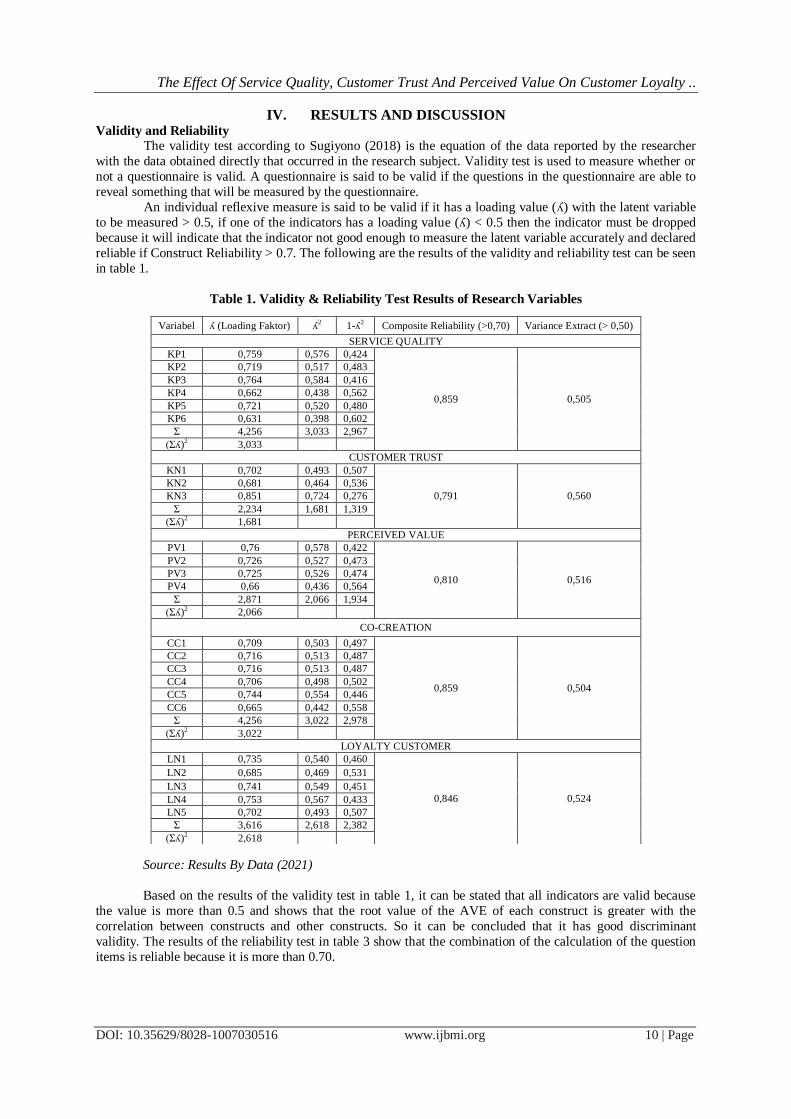

IV. RESULTS AND DISCUSSION Validity and Reliability

The validity test according to Sugiyono (2018) is the equation of the data reported by the researcher

with the data obtained directly that occurred in the research subject. Validity test is used to measure whether or

not a questionnaire is valid. A questionnaire is said to be valid if the questions in the questionnaire are able to

reveal something that will be measured by the questionnaire.

An individual reflexive measure is said to be valid if it has a loading value (ʎ) with the latent variable

to be measured > 0.5, if one of the indicators has a loading value (ʎ) < 0.5 then the indicator must be dropped

because it will indicate that the indicator not good enough to measure the latent variable accurately and declared

reliable if Construct Reliability > 0.7. The following are the results of the validity and reliability test can be seen

in table 1.

Table 1. Validity & Reliability Test Results of Research Variables

Source: Results By Data (2021)

Based on the results of the validity test in table 1, it can be stated that all indicators are valid because

the value is more than 0.5 and shows that the root value of the AVE of each construct is greater with the

correlation between constructs and other constructs. So it can be concluded that it has good discriminant

validity. The results of the reliability test in table 3 show that the combination of the calculation of the question

items is reliable because it is more than 0.70.

Variabel ʎ (Loading Faktor) ʎ2 1-ʎ

2 Composite Reliability (>0,70) Variance Extract (> 0,50)

SERVICE QUALITY

KP1 0,759 0,576 0,424

0,859 0,505

KP2 0,719 0,517 0,483

KP3 0,764 0,584 0,416

KP4 0,662 0,438 0,562

KP5 0,721 0,520 0,480

KP6 0,631 0,398 0,602

Ʃ 4,256 3,033 2,967

(Ʃʎ)2 3,033

CUSTOMER TRUST

KN1 0,702 0,493 0,507

0,791 0,560

KN2 0,681 0,464 0,536

KN3 0,851 0,724 0,276

Ʃ 2,234 1,681 1,319

(Ʃʎ)2 1,681

PERCEIVED VALUE

PV1 0,76 0,578 0,422

0,810 0,516

PV2 0,726 0,527 0,473

PV3 0,725 0,526 0,474

PV4 0,66 0,436 0,564

Ʃ 2,871 2,066 1,934

(Ʃʎ)2 2,066

CO-CREATION

CC1 0,709 0,503 0,497

0,859 0,504

CC2 0,716 0,513 0,487

CC3 0,716 0,513 0,487

CC4 0,706 0,498 0,502

CC5 0,744 0,554 0,446

CC6 0,665 0,442 0,558

Ʃ 4,256 3,022 2,978

(Ʃʎ)2 3,022

LOYALTY CUSTOMER

LN1 0,735 0,540 0,460

0,846 0,524

LN2 0,685 0,469 0,531

LN3 0,741 0,549 0,451

LN4 0,753 0,567 0,433

LN5 0,702 0,493 0,507

Ʃ 3,616 2,618 2,382

(Ʃʎ)2 2,618

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 11 | Page

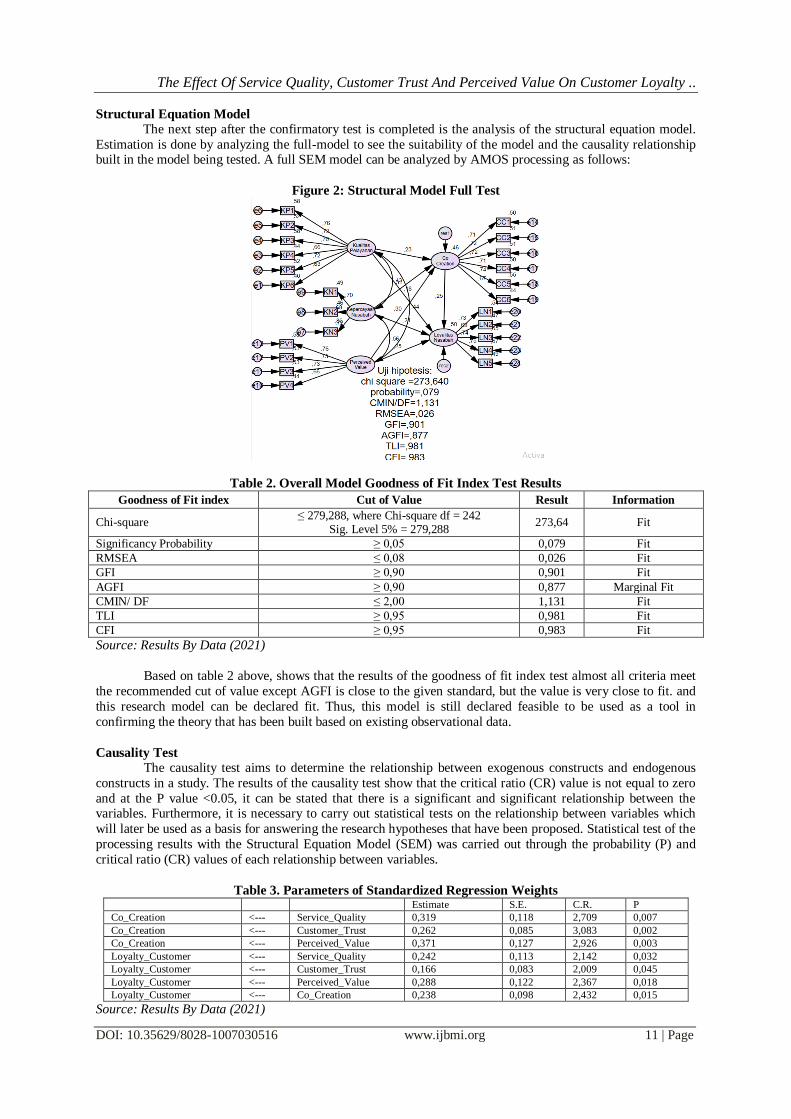

Structural Equation Model

The next step after the confirmatory test is completed is the analysis of the structural equation model.

Estimation is done by analyzing the full-model to see the suitability of the model and the causality relationship built in the model being tested. A full SEM model can be analyzed by AMOS processing as follows:

Figure 2: Structural Model Full Test

Table 2. Overall Model Goodness of Fit Index Test Results

Goodness of Fit index Cut of Value Result Information

Chi-square ≤ 279,288, where Chi-square df = 242

Sig. Level 5% = 279,288 273,64 Fit

Significancy Probability ≥ 0,05 0,079 Fit

RMSEA ≤ 0,08 0,026 Fit

GFI ≥ 0,90 0,901 Fit

AGFI ≥ 0,90 0,877 Marginal Fit

CMIN/ DF ≤ 2,00 1,131 Fit

TLI ≥ 0,95 0,981 Fit

CFI ≥ 0,95 0,983 Fit

Source: Results By Data (2021)

Based on table 2 above, shows that the results of the goodness of fit index test almost all criteria meet

the recommended cut of value except AGFI is close to the given standard, but the value is very close to fit. and

this research model can be declared fit. Thus, this model is still declared feasible to be used as a tool in

confirming the theory that has been built based on existing observational data.

Causality Test

The causality test aims to determine the relationship between exogenous constructs and endogenous

constructs in a study. The results of the causality test show that the critical ratio (CR) value is not equal to zero

and at the P value <0.05, it can be stated that there is a significant and significant relationship between the variables. Furthermore, it is necessary to carry out statistical tests on the relationship between variables which

will later be used as a basis for answering the research hypotheses that have been proposed. Statistical test of the

processing results with the Structural Equation Model (SEM) was carried out through the probability (P) and

critical ratio (CR) values of each relationship between variables.

Table 3. Parameters of Standardized Regression Weights

Estimate S.E. C.R. P

Co_Creation <--- Service_Quality 0,319 0,118 2,709 0,007

Co_Creation <--- Customer_Trust 0,262 0,085 3,083 0,002

Co_Creation <--- Perceived_Value 0,371 0,127 2,926 0,003

Loyalty_Customer <--- Service_Quality 0,242 0,113 2,142 0,032

Loyalty_Customer <--- Customer_Trust 0,166 0,083 2,009 0,045

Loyalty_Customer <--- Perceived_Value 0,288 0,122 2,367 0,018

Loyalty_Customer <--- Co_Creation 0,238 0,098 2,432 0,015

Source: Results By Data (2021)

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 12 | Page

Effect Between Variables

The analysis of the influence between variables aims to determine the strength of the influence between

one variable and another. The analysis in this research consists of direct influence analysis, indirect effect analysis and total influence analysis. The following is an explanation of each analysis:

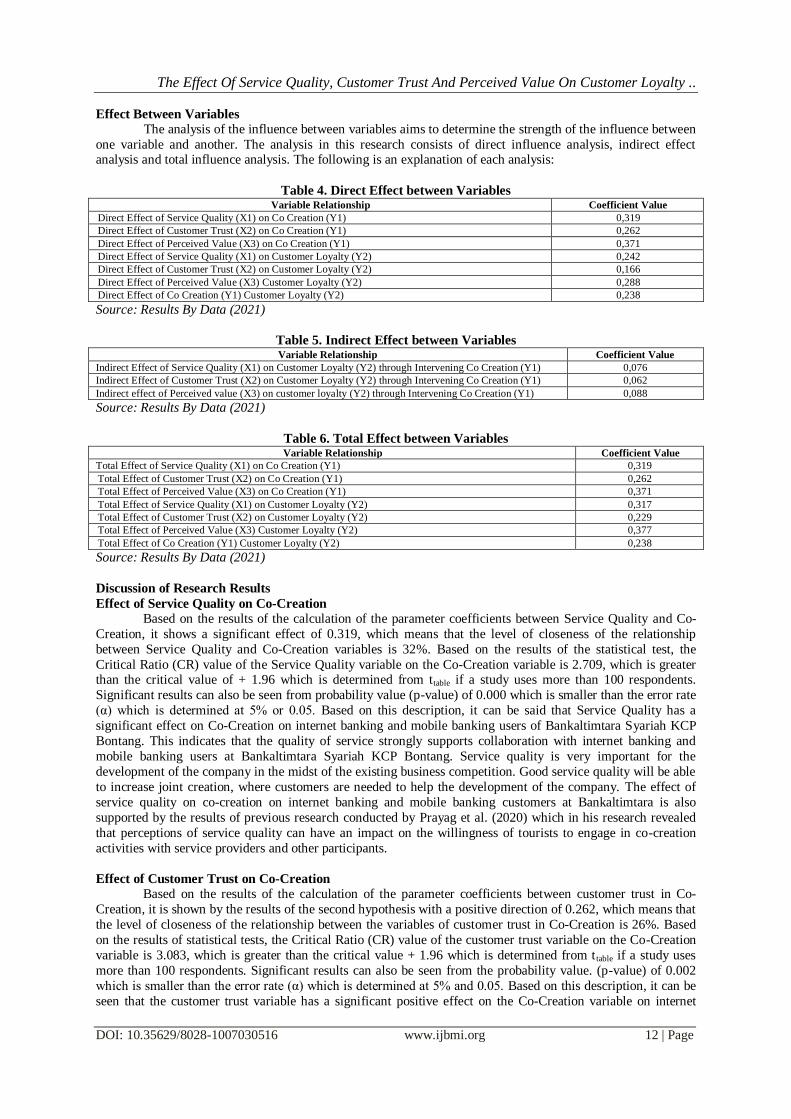

Table 4. Direct Effect between Variables Variable Relationship Coefficient Value

Direct Effect of Service Quality (X1) on Co Creation (Y1) 0,319

Direct Effect of Customer Trust (X2) on Co Creation (Y1) 0,262

Direct Effect of Perceived Value (X3) on Co Creation (Y1) 0,371

Direct Effect of Service Quality (X1) on Customer Loyalty (Y2) 0,242

Direct Effect of Customer Trust (X2) on Customer Loyalty (Y2) 0,166

Direct Effect of Perceived Value (X3) Customer Loyalty (Y2) 0,288

Direct Effect of Co Creation (Y1) Customer Loyalty (Y2) 0,238

Source: Results By Data (2021)

Table 5. Indirect Effect between Variables Variable Relationship Coefficient Value

Indirect Effect of Service Quality (X1) on Customer Loyalty (Y2) through Intervening Co Creation (Y1) 0,076

Indirect Effect of Customer Trust (X2) on Customer Loyalty (Y2) through Intervening Co Creation (Y1) 0,062

Indirect effect of Perceived value (X3) on customer loyalty (Y2) through Intervening Co Creation (Y1) 0,088

Source: Results By Data (2021)

Table 6. Total Effect between Variables Variable Relationship Coefficient Value

Total Effect of Service Quality (X1) on Co Creation (Y1) 0,319

Total Effect of Customer Trust (X2) on Co Creation (Y1) 0,262

Total Effect of Perceived Value (X3) on Co Creation (Y1) 0,371

Total Effect of Service Quality (X1) on Customer Loyalty (Y2) 0,317

Total Effect of Customer Trust (X2) on Customer Loyalty (Y2) 0,229

Total Effect of Perceived Value (X3) Customer Loyalty (Y2) 0,377

Total Effect of Co Creation (Y1) Customer Loyalty (Y2) 0,238

Source: Results By Data (2021)

Discussion of Research Results

Effect of Service Quality on Co-Creation

Based on the results of the calculation of the parameter coefficients between Service Quality and Co-

Creation, it shows a significant effect of 0.319, which means that the level of closeness of the relationship

between Service Quality and Co-Creation variables is 32%. Based on the results of the statistical test, the

Critical Ratio (CR) value of the Service Quality variable on the Co-Creation variable is 2.709, which is greater than the critical value of + 1.96 which is determined from ttable if a study uses more than 100 respondents.

Significant results can also be seen from probability value (p-value) of 0.000 which is smaller than the error rate

(α) which is determined at 5% or 0.05. Based on this description, it can be said that Service Quality has a

significant effect on Co-Creation on internet banking and mobile banking users of Bankaltimtara Syariah KCP

Bontang. This indicates that the quality of service strongly supports collaboration with internet banking and

mobile banking users at Bankaltimtara Syariah KCP Bontang. Service quality is very important for the

development of the company in the midst of the existing business competition. Good service quality will be able

to increase joint creation, where customers are needed to help the development of the company. The effect of

service quality on co-creation on internet banking and mobile banking customers at Bankaltimtara is also

supported by the results of previous research conducted by Prayag et al. (2020) which in his research revealed

that perceptions of service quality can have an impact on the willingness of tourists to engage in co-creation

activities with service providers and other participants.

Effect of Customer Trust on Co-Creation

Based on the results of the calculation of the parameter coefficients between customer trust in Co-

Creation, it is shown by the results of the second hypothesis with a positive direction of 0.262, which means that

the level of closeness of the relationship between the variables of customer trust in Co-Creation is 26%. Based

on the results of statistical tests, the Critical Ratio (CR) value of the customer trust variable on the Co-Creation

variable is 3.083, which is greater than the critical value + 1.96 which is determined from t table if a study uses

more than 100 respondents. Significant results can also be seen from the probability value. (p-value) of 0.002

which is smaller than the error rate (α) which is determined at 5% and 0.05. Based on this description, it can be

seen that the customer trust variable has a significant positive effect on the Co-Creation variable on internet

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 13 | Page

banking and mobile banking users at Bankaltimtara Syariah KCP Bontang. The higher the influence of customer

trust in using services on internet banking and mobile banking users of Bankaltimtara Syariah KCP Bontang, the

higher the involvement of customers in co-creation. The results of this study are in line with research conducted by Alves & Wagner Mainardes (2017) where in their research explains that trust can be one of the factors that

influence the potential for co-creation through exchange. A person is more willing to engage in social exchange

when the relationship has a high degree of trust.

Effect of Perceived Value on Co-Creation

The result of the calculation of the parameter coefficient between Perceived Value and Co-Creation

shows a significant effect of 0.371, which means that the level of closeness of the relationship between the

Perceived Value variable to Co-Creation is 37%. Based on the statistical test results, the Critical Ratio (CR)

value is 2,926, greater than the critical value + 1.96 determined from ttable if a study uses more than 100

respondents. Significant results can also be seen from the probability value (p-value) of 0.003 which smaller

than the error rate (α) specified at 5% or 0.05. This shows that Perceived Value has a significant effect on Co-Creation on internet banking and mobile banking users at Bankaltimtara Syariah KCP Bontang. The higher the

effect of Perceived Value, the more co-creation of internet banking and mobile banking users of Bankaltimtara

Syariah KCP Bontang will be affected. The results of this study are in line with the results of research conducted

by Otchere et al. (2019) where customer perceived value and performance innovation have a positive and

significant effect on co-creation.

Effect of Service Quality on Customer Loyalty

The calculation of the parameter coefficient between Service Quality and Customer Loyalty shows a

significant influence of 0.242, which means that the level of closeness of the relationship between the Service

Quality variable and Customer Loyalty is 24%. Based on the results of the statistical test the Critical Ratio (CR)

value of 2.142, greater than the critical value + 1.96 determined from ttable if a study uses more than 100

respondents. Significant results can also be seen from the probability value (p-value) of 0.032 which smaller than the error rate (α) specified at 5% or 0.05. Based on this description, it can be said that the Service Quality

Variable has a significant effect on the Customer Loyalty variable for internet banking and mobile banking users

of Bankaltimtara Syariah KCP Bontang. The better the quality of service received by respondents, the higher the

customer loyalty of internet banking and mobile banking users of Bankaltimtara Syariah KCP Bontang. The

results of this study are supported by previous research conducted by Sehrish et al. (2019); Slack et al. (2020);

Satti et al. (2020); Raza et al. (2020); Rehman et al. (2019); Khan et al. (2019) research in various industries (eg

logistics services, supermarkets, hospitals, banking, insurance and online shopping) which has proven a positive

influence between service quality and customer loyalty as the research conducted.

Effect of Customer Trust on Customer Loyalty

The result of the calculation of the parameter coefficient between customer trust and customer loyalty shows a significant effect with a positive direction of 0.166, which means that the level of closeness of the

relationship between the variables of customer trust and customer loyalty is 17%. Based on the results of

statistical tests, the Critical Ratio (CR) value of 2.009 is greater than the critical value + 1.96 which is

determined from ttable if a study uses more than 100 respondents. Significant results can also be seen from the

probability value (p-value) of 0.045 which is higher smaller than the specified error rate (α) of 5% or 0.05. This

shows that customer trust has a significant effect on customer loyalty to internet banking and mobile banking

users at Bankaltimtara Syariah KCP Bontang. The higher the customer trust, the higher the loyalty of internet

banking and mobile banking users of Bankaltimtara Syariah KCP Bontang will also be higher. The results of

this study are in accordance with the research conducted by Mutonyi et al. (2016), who found that trust has an

influence on buyer loyalty where trust can affect social values between producers and buyers in the supply

chain, which in turn can affect and increase producer engagement in the relationship. This will enhance mutual

benefits and strengthen long-term engagement.

Effect of Perceived Value on Customer Loyalty

The result of the calculation of the parameter coefficient between Perceived Value and Customer

Loyalty shows a significant effect of 0.288, which means that the level of closeness of the relationship between

the Perceived Value variable and Customer Loyalty is 29%. Based on the statistical test results, the Critical

Ratio (CR) value is 2,367, greater than the critical value + 1.96 determined from ttable if a study uses more than

100 respondents. Significant results can also be seen from the probability value (p-value) of 0.018 which smaller

than the error rate (α) specified at 5% or 0.05. These results indicate that the Perceived Value variable has a

significant effect on the Customer Loyalty of Internet banking and mobile banking users of Bankaltimtara

Syariah KCP Bontang, the higher the influence of Perceived Value, the loyalty of customers using internet

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 14 | Page

banking and mobile banking of Bankaltimtara Syariah KCP Bontang will also increase. The results of this study

are in line with research conducted by Ramadhan & Siagian (2019) which reveals that overall perceived value

has a significant effect on customer loyalty.

Effect of Co-Creation on Customer Loyalty

Based on the calculation of the parameter coefficients between Co-Creation on Customer Loyalty, it

shows a significant influence with a positive direction of 0.238, which means that the level of closeness of the

relationship between the Co-Creation variable on Customer Loyalty is 24%. Based on the results of the

statistical test, the Critical Ratio (CR) value between the Co-Creation variable and the Customer Loyalty

variable is 2.432, greater than the critical value + 1.96 determined from ttable if a study uses more than 100

respondents. Significant results can also be seen from probability value (p-value) is 0.015 which is smaller than

the error rate (α) which is determined at 5% or 0.05. These results indicate that the Co-Creation variable has a

significant effect on the Customer Loyalty variable for internet banking and mobile banking users of

Bankaltimtara Syariah KCP Bontang. The higher the influence of Co-Creation on internet banking and mobile banking users of Bankaltimtara Syariah KCP Bontang, the loyalty of customers using the application will also

be higher. The results of this study are also in line with the results of research conducted by Maduka (2016) that

the value of co-creation has a positive and significant influence on customer loyalty in the pension industry in

Nigeria because customers want to be an inseparable part of the services offered.

V. CONCLUSIONS AND SUGGESTIONS Conclusions

The results of data analysis and discussion that have been carried out can be concluded as follows:

(1) Service quality has a significant effect on Co-Creation on internet banking and mobile banking customers at Bankaltimtara Syariah KCP Bontang.

(2) Customer trust has a significant effect on Co-Creation on internet banking and mobile banking users of

Bankaltimtara Syariah KCP Bontang.

(3) Perceived Value has a significant effect on Co-Creation on customers who use internet banking and

mobile banking at Bankaltimtara Syariah KCP Bontang.

(4) Service Quality has a significant effect on Customer Loyalty to customers who use internet banking

and mobile banking at Bankaltimtara Syariah KCP Bontang.

(5) Customer Trust has a significant effect on Customer Loyalty to customers who use internet banking

and mobile banking at Bankaltimtara Syariah KCP Bontang.

(6) Perceive Value has a significant effect on Customer Loyalty to customers who use internet banking and

mobile banking at Bankaltimtara Syariah KCP Bontang.

(7) Co-Creation has a significant effect on Customer Loyalty on internet banking and mobile banking users of Bankaltimtara Syariah KCP Bontang.

Suggestions

Based on the results of the research that has been done and has been described in the previous chapter,

the researcher can provide the following suggestions:

(1) Regarding the service quality variable that has a significant effect on customer interest in co-creation

and has a significant effect on customer loyalty, the researcher suggests to Bankaltimtara Syariah KCP

Bontang to continue to improve its services by always issuing new service products that follow

technological developments. The new service is also expected to be adapted to the customer's wishes

which can be seen from the results of co-creation with the customer so that with the new service in

accordance with the input provided by the customer, it is hoped that customer loyalty can be maintained.

(2) The results of the study where the customer trust variable has a significant influence on customer

interest in co-creation and has a significant effect on customer loyalty, the researchers suggest that

Bankaltimtara Syariah to continue to be consistent in maintaining customer trust by providing

information that is in accordance with the facts so that customers always to be able to contribute to co-

creation with the bank. Bankaltimtara Syariah KCP Bontang can also give gifts to customers who

provide recommendations or inform others about the application as a reward for trusting Bankaltimtara

Syariah and are willing to recommend Bankaltimtara internet banking and mobile banking applications

to others where this indicates customers are increasingly loyal to Bankaltimtar Sharia KCP Bontang.

(3) While the results of the study which show that the perceived value variable has a significant effect on

customer interest in co-creation and has a significant effect on customer loyalty, the researchers suggest

that Bankaltimtara can continue to maintain the appearance of its internet banking and mobile banking applications with a simple and simple appearance. easy to use in accordance with the customer's

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 15 | Page

perceived value regarding the application so that customers become loyal and willing to do co-creation

with Bankaltimtara Syariah.

(4) Then on the results of the study which showed that the co-creation variable had a significant influence on customer loyalty, the researcher suggested that Bankaltimtara Syariah could provide a forum for

customers to carry out co-creation such as holding events to accommodate customer ideas that can be

applied to internet banking applications. and Bankaltimtara mobile banking and later the best ideas

from selected customers will be rewarded which of course can increase customer loyalty to continue

using Bankaltimtara's internet banking and mobile banking applications.

(5) For researchers who are interested in conducting similar research, it is recommended that they be able

to carry out more in-depth observations and explorations of what problems exist in Bankaltimtara

Syariah KCP Bontang in particular and other objects in general by adding other variables or using other

research methods.

BIBLIOGRAPHY [1]. Aini, Q., Rahardja, U., & Hariguna, T. (2019). The Antecedent of Perceived Value to Determine of Student Continuance Intention

and Student Participate Adoption of ilearning. Procedia Computer Science, 161, 242–249.

[2]. Ali, S. F., & Naeem, M. (2019). Does service quality increase the level of banks performance: Comparative analysis between

conventional and Islamic banks. Journal of Management Development, 38(6), 442–454.

[3]. Alves, H., & Wagner Mainardes, E. (2017). Self-efficacy, trust, and perceived benefits in the co-creation of value by consumers.

International Journal of Retail and Distribution Management, 45(11), 1159–1180. Amin, M. (2016). Internet banking service

quality and its implication on e-customer satisfaction and e-customer loyalty. International Journal of Bank Marketing, 34(3), 280–

306.

[4]. Arcand, M., PromTep, S., Brun, I., & Rajaobelina, L. (2017). Mobile banking service quality and customer relationships.

International Journal of Bank Marketing, 35(7), 1066–1087.

[5]. Asnawi, N., Sukoco, B. M., & Fanani, M. A. (2019). The role of service quality within Indonesian customers satisfaction and

loyalty and its impact on Islamic banks. Journal of Islamic Marketing, 11(1), 192–212.

[6]. Boonlertvanich, K. (2019). Service quality, satisfaction, trust, and loyalty: the moderating role of main-bank and wealth status.

International Journal of Bank Marketing, 37(1), 278–302.

[7]. Cambra-Fierro, J., Melero-Polo, I., & Sese, F. J. (2018). Customer value co-creation over the relationship life cycle. Journal of

Service Theory and Practice, 28(3), 336–355.

[8]. Chen, C. F., & Wang, J. P. (2016). Customer participation, value co-creation and customer loyalty - A case of airline online check-

in system. Computers in Human Behavior, 62, 346–352.

[9]. Cossío-Silva, F. J., Revilla-Camacho, M. Á., Vega-Vázquez, M., & Palacios-Florencio, B. (2016). Value co-creation and customer

loyalty. Journal of Business Research, 69(5), 1621–1625.

[10]. Ekaabi, M. A., Khalid, K., Davidson, R., Kamarudin, A. H., & Preece, C. (2020). Smart policing service quality: conceptualisation,

development and validation. Policing: An International Jorunal, 43(5), 707–721.

[11]. Elsharnouby, T. H., & Mahrous, A. A. (2015). Customer participation in online co-creation experience: the role of e-service quality.

Journal of Research in Interactive Marketing, 9(4), 313–336.

[12]. Frederik, R. willem, & Pauline, E. (2017). Banking System Trust, Bank Trust and Bank Loyalty. International Journal of Bank

Marketing, 35(1), 1–32.

[13]. Galvagno, M., & Dalli, D. (2014). Theory of value co-creation: A systematic literature review. Managing Service Quality, 24(6),

643–683.

[14]. Grönroos, C. (2011). Value co-creation in service logic: A critical analysis. Marketing Theory, 11(3), 279–301.

[15]. Haron, R., Subar, N. A., & Ibrahim, K. (2020). Service quality of Islamic banks: satisfaction, loyalty and the mediating role of trust.

Islamic Economic Studies, 28(1), 3–23.

[16]. Jeong, Y., & Lee, Y. (2010). A study on the customer satisfaction and customer loyalty of furniture purchaser in on‐ line shop.

Asian Journal on Quality, 11(2), 146–156.

[17]. Kartika, T., Firdaus, A., & Najib, M. (2019). Contrasting the drivers of customer loyalty; financing and depositor customer, single

and dual customer, in Indonesian Islamic bank. Journal of Islamic Marketing, 11(4), 933–959.

[18]. Kassim, N., & Abdullah, N. A. (2010). The effect of perceived service quality dimensions on customer satisfaction, trust, and

loyalty in e‐ commerce settings: A cross cultural analysis. Asia Pacific Journal of Marketing and Logistics, 22(3), 351–371.

[19]. Kaur, G., Sharma, R. D., & Mahajan, N. (2012). Exploring customer switching intentions through relationship marketing paradigm.

International Journal of Bank Marketing, 30(4), 280–302.

[20]. Kaura, V., Durga Prasad, C. S., & Sharma, S. (2015). Service quality, service convenience, price and fairness, customer loyalty, and

the mediating role of customer satisfaction. International Journal of Bank Marketing, 33(4), 404–422.

[21]. Khan, M. A., Zubair, S. S., & Malik, M. (2019). An assessment of e-service quality, e-satisfaction and e-loyalty: Case of online

shopping in Pakistan. South Asian Journal of Business Studies, 8(3), 283–302.

[22]. Kim, E., Tang, L. (Rebecca), & Bosselman, R. (2019). Customer Perceptions of Innovativeness: An Accelerator for Value Co-

Creation. Journal of Hospitality & Tourism Research, 43(6), 807–838.

[23]. Koupai, M. R., Alipourdarvish, Z., & Sardar, S. (2015). Effects of trust and perceived value on customer loyalty by mediating role

of customer satisfaction and mediating role of customer habit case study : Agricultural internet bank customers in Tehran. Advanced

Social Humanities and Management, 2(1), 102–112. www.ashm-journal.com

[24]. Maduka, O. B. (2016). Effects of Customer Value Co-Creation on Customer Loyalty in the Nigerian Service Industry. International

Journal of Business and Management, 11(12), 77.

[25]. Martínez, P., & Rodríguez del Bosque, I. (2013). CSR and customer loyalty: The roles of trust, customer identification with the

company and satisfaction. International Journal of Hospitality Management, 35, 89–99.

[26]. Mayr, T., & Zins, A. H. (2012). Extensions on the conceptualization of customer perceived value: Insights from the airline industry.

International Journal of Culture, Tourism, and Hospitality Research, 6(4), 356–376.

[27]. Mohammed, A., & Al-Swidi, A. (2019). The influence of CSR on perceived value, social media and loyalty in the hotel industry.

Spanish Journal of Marketing - ESIC, 23(3), 373–396.

[28]. Mostafa, R. B. (2020). Mobile banking service quality: a new avenue for customer value co-creation. International Journal of Bank

The Effect Of Service Quality, Customer Trust And Perceived Value On Customer Loyalty ..

DOI: 10.35629/8028-1007030516 www.ijbmi.org 16 | Page

Marketing, 38(5), 1107–1132.

[29]. Mutonyi, S., Beukel, K., Gyau, A., & Hjortsø, C. N. (2016). Price satisfaction and producer loyalty: the role of mediators in

business to business relationships in Kenyan mango supply chain. British Food Journal, 118(5).

[30]. Ndubisi, N. O., Wah, C. K., & Ndubisi, G. C. (2007). Supplier‐ customer relationship management and customer loyalty: The

banking industry perspective. Journal of Enterprise Information Management, 20(2), 222–236.

[31]. Nomran, N. M., Haron, R., & Hassan, R. (2018). Shari’ah supervisory board characteristics effects on Islamic banks’ performance:

Evidence from Malaysia. International Journal of Bank Marketing, 36(2), 290–304.

[32]. Nora, L. (2019). Trust, commitment, and customer knowledge. Management Decision, 57(11), 3134–3158.

[33]. Osman, Z., & Sentosa, I. (2013). A study of mediating effect of trust on customer satisfaction and customer loyalty relationship in

Malaysian rural tourism.

[34]. Otchere, S., Hong-Yun, T., Addy, W., & Kumaning, R. (2019). The Effect of Value Co-creation on Innovation Performance: The

Mediating Role of Customer Perceived Value. European Journal of Business and Management, 11.

[35]. Perks, H., Gruber, T., & Edvardsson, B. (2012). Co-creation in radical service innovation: A systematic analysis of microlevel

processes. Journal of Product Innovation Management, 29(6), 935–951.

[36]. Prayag, G., Gannon, M. J., Muskat, B., & Taheri, B. (2020). A serious leisure perspective of culinary tourism co-creation: the

influence of prior knowledge, physical environment and service quality. International Journal of Contemporary Hospitality

Management, 32(7), 2453–2472.

[37]. Prebensen, N. K., & Xie, J. (2017). Efficacy of co-creation and mastering on perceived value and satisfaction in tourists’

consumption. Tourism Management, 60, 166–176.

[38]. Prodanova, J., Ciunova-Shuleska, A., & Palamidovska-Sterjadovska, N. (2019). Enriching m-banking perceived value to achieve

reuse intention. Marketing Intelligence and Planning, 37(6), 617–630.

[39]. Ramadhan, L., & Siagian, Y. M. (2019). Impact of Customer Perceived Value on Loyalty: In Context Crm. Journal of Research in

Business and Management, 7(April).

[40]. Ramaseshan, B., Rabbanee, F. K., & Hui, L. T. H. (2013). Effects of customer equity drivers on customer loyalty in B2B context.

Journal of Business and Industrial Marketing, 28(4), 335–346. Ramaswamy, V. (2011). Industrial Marketing Management It ’ s

about human experiences … and beyond , to co-creation. Industrial Marketing Management, 40(2), 195–196.

[41]. Randall, W. S., Gravier, M. J., & Prybutok, V. R. (2011). Connection, trust, and commitment: Dimensions of co-creation? Journal

of Strategic Marketing, 19(1), 3–24.

[42]. Raza, S. A., Umer, A., Qureshi, M. A., & Darhi, A. S. (2020). Internet banking service quality, e-customer satisfaction and loyalty:

the modified e-SERVQUAL model. The TQM Journal, 32(6), 1443–1466.

[43]. Rehman, M. A., Osman, I., Aziz, K., Koh, H., & Awais, M. (2019). Get connected with your Takaful representatives: Revisiting

customer loyalty through relationship marketing and service quality. Journal of Islamic Marketing, 11(5), 1175–1200.

[44]. Saarijärvi, H., Kannan, P. K., & Kuusela, H. (2013). Value co-creation: theoretical approaches and practical implications. European

Business Review, 25(1), 6–19.

[45]. Satti, Z. W., Babar, S. F., Parveen, S., Abrar, K., & Shabbir, A. (2020). Innovations for potential entrepreneurs in service quality

and customer loyalty in the hospitality industry. Asia Pacific Journal of Innovation and Entrepreneurship, 14(3), 317–328.

[46]. Scridon, M. A., Achim, S. A., Pintea, M. O., & Gavriletea, M. D. (2019). Risk and perceived value: antecedents of customer

satisfaction and loyalty in a sustainable business model. Economic Research-Ekonomska Istrazivanja , 32(1), 909–924.

[47]. Sehrish, H., Waqar, A., Minhaj, I., & Ibrahim, K. M. (2019). The effect of logistics service quality on customer loyalty: case of

logistics service industry. South Asian Journal of Business Studies, 9(1), 43–61.

[48]. Shankar, A., & Jebarajakirthy, C. (2019). The influence of e-banking service quality on customer loyalty: A moderated mediation

approach. International Journal of Bank Marketing, 37(5), 1119–1142.

[49]. Slack, N., Singh, G., & Sharma, S. (2020). The effect of supermarket service quality dimensions and customer satisfaction on

customer loyalty and disloyalty dimensions. International Journal of Quality and Service Sciences, 12(3), 297–318.

[50]. Sugiyono. (2018). Metode Penelitian Kuantitatif, Kualitatif, dan R&D. Alfabeta.

[51]. Sun, H., Rabbani, M. R., Ahmad, N., Sial, M. S., Cheng, G., Zia-Ud-Din, M., & Fu, Q. (2020). CSR, Co-Creation and Green

Consumer Loyalty: Are Green Banking Initiatives Important? A Moderated Mediation Approach from an Emerging Economy. In

Sustainability (Vol. 12, Issue 24).

[52]. Suryani, S. (2015). Customers’ perceived value towards the service in Islamic banking: Confirmatory factor analysis. Journal of

Economics, Business & Accountancy Ventura, 18(2), 201.

[53]. Thielemann, V. M., Ottenbacher, M. C., & Harrington, R. J. (2018). Antecedents and consequences of perceived customer value in

the restaurant industry: A preliminary test of a holistic model. International Hospitality Review, 32(1), 26–45.

[54]. Thiruvattal, E. (2017). Impact of value co-creation on logistics customers’ loyalty. Journal of Global Operations and Strategic

Sourcing, 10(3), 334–361.

[55]. Vargo, S. L., & Lusch, R. F. (2004). Evolving to a New Dominant Logic for Marketing. Journal of Marketing, 68(1), 1–17.

[56]. Vargo, S. L., & Lusch, R. F. (2017). Service-dominant logic 2025. International Journal of Research in Marketing, 34(1), 46–67.

[57]. Wu, L. W., Wang, C. Y., & Rouyer, E. (2019). The opportunity and challenge of trust and decision-making uncertainty: Managing

co-production in value co-creation. International Journal of Bank Marketing, 38(1), 199–218.

[58]. Zauner, A., Koller, M., & Hatak, I. (2015). Customer perceived value—Conceptualization and avenues for future research. Cogent

Psychology, 2(1), 1–17.

Alfiah Mapalidara, et. al. “The Effect Of Service Quality, Customer Trust And Perceived Value On

Customer Loyalty With Co-Creation As Intervening Variable On Customers Using Internet Banking And

Mobile Banking Bankaltimtara Sharia KCP Bontang.” International Journal of Business and Management Invention (IJBMI), vol. 10(07), 2021, pp. 05-16. Journal DOI- 10.35629/8028