The ‘duty to finance’, the cost of capital and the capital structure of regulated utilities:...

14

The ‘duty to finance’, the cost of capital and the capital structure of regulated utilities: Lessons from the UK Javier Tapia * Universidad de Chile, Centre for Regulation and Competition, Pío Nono 1, Santiago, Chile WC1H 0EG, United Kingdom article info Article history: Received 28 September 2010 Accepted 5 February 2012 Keywords: Utilities Capital structure Risk Cost of capital UK abstract This work assesses the main regulatory responses to the changes in the capital structure of the utilities firms. It examines the different means of influencing the capital structure and the various concerns related to high gearing; particularly in relation to the cost of capital and risk. The paper argues that several of those concerns are unfounded and that the effectiveness of various aspects of the regulation of capital structure and the setting of the cost of capital are highly questionable. Ó 2012 Elsevier Ltd. All rights reserved. “The greater part of the public works may easily be so managed, so as to afford a particular revenue sufficient for defraying their own expense, without bringing any burden upon the general revenue of society”. 1 Adam Smith 1. Introduction This work critically assesses the main regulatory responses to the changes in the capital structure of the utilities firms occurred since privatisation, their underlying reasoning, and the criticisms that have arisen in the UK context. The aim is to provide an explanation of the interactions between the capital structure, the cost of capital and the economic incentives within regulated environments. As in other parts of the world, liberalisation and regulation of utilities in the UK were part of a major privatisation process that led to a profound change in the ownership pattern of the former state-owned monopolies and placed them in private hands. Although the process had no comprehensive list of goals, one of its principal underlying aims was the encouragement of wider employee share ownership as a means to alter the balance of political power; more shareholders would offset the power of trade unions (Vickers and Yarrow, 1988; Veljanovski, 1987). 2 Political, rather than economic concerns were the main (but not exclusive) driver of the process. 3 To expand rapid share ownership, the government explicitly promoted ‘an equity financial’ model of the firms. Shares were deliberately under priced, and bonuses were given as an incentive to small shareholders. 4 In addition, compa- nies were privatised with very low levels of debt. 5 Examples abound. In the water sector virtually all the existing debt was written-off, so firms’ balance sheets would appear ungeared before being sold to investors. 6 Likewise, gearing levels of electricity distribution companies were brought down to around 25%. Also, the allowed rate of return was generally high and the investment * Tel.: þ44 56 2 6569620. E-mail addresses: [email protected], [email protected]. 1 Smith (1991 [1776]: V.1.III.1). 2 In addition, it would lead to a bigger base of supporters of capitalism sensitive to the then conservative government. Overall, the model aimed to change ‘people’s attitudes to business and trade’ and create a ‘more entrepreneurial society’ (Veljanovski, 1987: 9). 3 Indeed, during the first phase of privatisation (1979e84) there was an economic objective: the ‘pursuit of quick cash’ to improve the public finances (Parker, 2009: 88). From 1981 onwards, privatisation became more a matter of principle and ‘entrenched as a central component of the Government’s economic strategy’ (Ibid, at 188). 4 There were even cash injections. The so-called ‘green dowry’ (equivalent to £1 billion cash) was given to water and sewerage (but not water only) companies to fulfil the new enhanced environmental requirements promulgated by the European Commission. 5 The only exception amongst utilities was the National Air Traffic Services. It was sold to a consortium that financed the purchase with 94% of debt (with a ratio of debt to regulatory capital value of 118% e see infra note 6 for an explanation of this concept). 6 Although gearing is defined as ‘debt to debt plus equity’ (D:D þ E), UK regu- lators commonly use the ratio ‘debt to Regulatory Asset Base’ (debt:RAB) as primary measure. The RAB is a regulatory concept, not a financial one. Generally speaking, it is a proxy value of the firm’s regulated operating assets, upon which investors earn a return. It is formed by investors’ stake at privatisation plus completed capital expenditures not paid out by customers. In monetary terms, it is also known as Regulatory Asset Value (RAV) or Regulatory Capital Value (RCV). The ratio ‘debt to RAB’ is known as ‘regulatory gearing’, and in general gearing measured on this basis is slightly lower than that using ‘debt to debt plus equity’. Contents lists available at SciVerse ScienceDirect Utilities Policy journal homepage: www.elsevier.com/locate/jup 0957-1787/$ e see front matter Ó 2012 Elsevier Ltd. All rights reserved. doi:10.1016/j.jup.2012.02.003 Utilities Policy 22 (2012) 8e21

-

Upload

independent -

Category

Documents

-

view

0 -

download

0

Transcript of The ‘duty to finance’, the cost of capital and the capital structure of regulated utilities:...

at SciVerse ScienceDirect

Utilities Policy 22 (2012) 8e21

Contents lists available

Utilities Policy

journal homepage: www.elsevier .com/locate/ jup

The ‘duty to finance’, the cost of capital and the capital structure of regulatedutilities: Lessons from the UK

Javier Tapia*

Universidad de Chile, Centre for Regulation and Competition, Pío Nono 1, Santiago, Chile WC1H 0EG, United Kingdom

a r t i c l e i n f o

Article history:Received 28 September 2010Accepted 5 February 2012

Keywords:UtilitiesCapital structureRiskCost of capitalUK

* Tel.: þ44 56 2 6569620.E-mail addresses: [email protected], jtap

1 Smith (1991 [1776]: V.1.III.1).2 Inaddition, itwould lead to a biggerbase of supporte

then conservative government. Overall, the model aimeto business and trade’ and create a ‘more entrepreneuria

0957-1787/$ e see front matter � 2012 Elsevier Ltd.doi:10.1016/j.jup.2012.02.003

a b s t r a c t

This work assesses the main regulatory responses to the changes in the capital structure of the utilitiesfirms. It examines the different means of influencing the capital structure and the various concernsrelated to high gearing; particularly in relation to the cost of capital and risk. The paper argues thatseveral of those concerns are unfounded and that the effectiveness of various aspects of the regulation ofcapital structure and the setting of the cost of capital are highly questionable.

� 2012 Elsevier Ltd. All rights reserved.

3 Indeed, during the first phase of privatisation (1979e84) there was aneconomic objective: the ‘pursuit of quick cash’ to improve the public finances(Parker, 2009: 88). From 1981 onwards, privatisation became more a matter ofprinciple and ‘entrenched as a central component of the Government’s economicstrategy’ (Ibid, at 188).

4 Therewere even cash injections. The so-called ‘green dowry’ (equivalent to £1 billioncash) was given to water and sewerage (but not water only) companies to fulfil the newenhanced environmental requirements promulgated by the European Commission.

5 The only exception amongst utilities was the National Air Traffic Services. It wassold toa consortiumthatfinanced thepurchasewith94%ofdebt (witha ratio ofdebt toregulatory capital value of 118% e see infra note 6 for an explanation of this concept).

6 Although gearing is defined as ‘debt to debt plus equity’ (D:D þ E), UK regu-lators commonly use the ratio ‘debt to Regulatory Asset Base’ (debt:RAB) as primary

“The greater part of the public works may easily be so managed,so as to afford a particular revenue sufficient for defraying theirown expense, without bringing any burden upon the generalrevenue of society”.1

Adam Smith

1. Introduction

Thiswork critically assesses themain regulatory responses to thechanges in the capital structure of the utilities firms occurred sinceprivatisation, their underlying reasoning, and the criticisms thathave arisen in the UK context. The aim is to provide an explanationof the interactions between the capital structure, the cost of capitaland the economic incentives within regulated environments.

As in other parts of the world, liberalisation and regulation ofutilities in the UK were part of a major privatisation process thatled to a profound change in the ownership pattern of the formerstate-owned monopolies and placed them in private hands.Although the process had no comprehensive list of goals, one of itsprincipal underlying aims was the encouragement of wideremployee share ownership as a means to alter the balance ofpolitical power; more shareholders would offset the power of tradeunions (Vickers and Yarrow, 1988; Veljanovski, 1987).2 Political,

rs of capitalismsensitive to thed to change ‘people’s attitudesl society’ (Veljanovski,1987: 9).

All rights reserved.

rather than economic concerns were the main (but not exclusive)driver of the process.3 To expand rapid share ownership, thegovernment explicitly promoted ‘an equity financial’ model of thefirms. Shares were deliberately under priced, and bonuses weregiven as an incentive to small shareholders.4 In addition, compa-nies were privatised with very low levels of debt.5 Examplesabound. In the water sector virtually all the existing debt waswritten-off, so firms’ balance sheets would appear ungeared beforebeing sold to investors.6 Likewise, gearing levels of electricitydistribution companies were brought down to around 25%. Also,the allowed rate of return was generally high and the investment

measure. The RAB is a regulatory concept, not a financial one. Generally speaking, itis a proxy value of the firm’s regulated operating assets, upon which investors earna return. It is formed by investors’ stake at privatisation plus completed capitalexpenditures not paid out by customers. In monetary terms, it is also known asRegulatory Asset Value (RAV) or Regulatory Capital Value (RCV). The ratio ‘debt toRAB’ is known as ‘regulatory gearing’, and in general gearing measured on this basisis slightly lower than that using ‘debt to debt plus equity’.

J. Tapia / Utilities Policy 22 (2012) 8e21 9

programmes involving large sums were readily approved in orderto facilitate the process and improve the level of services. Overallthe policy was deemed successful.7 Equity finance flourished andas a result a wide base of shareholders in the formerly state-ownedutilities were created.

While it is undeniably true that political considerations playedtheir part, it is also clear that the equity model was chosen (in thosecases where it was) in order to give effect to the policy objective oftransferring the firms to private ownership and control e that is tosay, in order: to expose them fully to the managerial disciplinestypically found in the private sector which were expected to driveefficiency gains; to enable them to access private sources of capitaland relieve them of public expenditure constraints; and to enableeffective competition to be introduced into contestable markets.Wider share ownership was a relevant consideration in relation tothose companies judged ‘suitable’ for retail investors (especially thepublic service utilities).8 At that time, publicly listed companies ingeneral exhibited rather low levels of gearing. Moreover, it wasrecognised that the introduction of competition, althoughprogressive, would increase business risk; that the substantialcapital investment expected to be needed to raise the capacity andservice quality in line with expected future demand (and, espe-cially, to meet environmental quality obligations) implied largeincremental financing requirements, and that, in the absence of anytrack record, regulatory and political risk would be perceived by theinvestors to be high. All these factors led Government’s advisers toadvocate that utilities be offered for sale with low (in some cases,negative) gearing, not withstanding that this was likely to reducesale proceeds. In hindsight, it is clear that this approach was undulycautious and that the consumer faced higher charges in the earlieryears following privatisation than were, strictly speaking,necessary.9

During the mid-nineties the trend reversed. Infrastructurecompanies introduced major changes in their capital structuresand there was a general trend to replace equity with debt.10 Withvariations, the trend is still witnessed across all sectors.11 Forinstance, since the last price control review, in 2004, the yearlyoverall industry weighted that an average gearing of electricitydistribution in companies has been between 45 and 50%.Recently, gearing levels are in the range of 60% as an industryaverage in the gas distribution sector.12 The situation in water isnot different, with gearing levels rising sharply above 60%. Also,

7 Under priced shares resulted in over subscriptions and immediate profits forshareholders. For that reason, as Vickers and Yarrow (1988: 160) point out, ‘Polit-ically, privatization was a winner, at least in the short term’.

8 But not all privatised entities fell in this category. E.g. Railtrack was initiallythought unsalable: when eventually privatised, it was by way of a primarily insti-tutional offering, and a number of other businesses were privatised by way ofprivate sale.

9 Some consider this as a symptom of an information deficit rather thana consequence of political choices.10 The period from mid-90s has been labelled the ‘dash for debt’, and seems tohave started in electricity distribution (see Helm, 2003: chapters 11 & 12). The trendcoincides with a worldwide increase in financial gearing across privatised utilitiesin many developing countries (Correia da Silva et al., 2004) and Europe (Bortollotiet al., 2007). See also Alexander and Chia (2003), on evidence of the increased roleof international bond-financing in utility and infrastructure companies.11 E.g. Wright et al. (2006) show ratios of debt to the market value of capital ofnine utilities for the period 1995e2005. In most cases, but not all, there wasconsiderable rise in gearing over the period. Indeed, there are variations. Forinstance, the optimal gearing ratio is likely to be higher in the water sector than intelecommunications e i.e. whilst the latter shows rapid technology change,changing market definition and -so far- growing demand, the former has bothstable technology and demand. In fact, the trend towards debt has affected mainlythe electricity, water (including both water and water and sewerage firms), gas andrailways sectors.12 See Ofgem (2009a).

even a firm 100% reliant on debt (Network Rail) currentlymanages the rail infrastructure.13 By sectors, overall, only airportsstill present relatively low levels of gearing. At the same time,however, there are considerable variations amongst firms withinan industry. For example, whilst the most geared electricitydistribution firm in 2008 had 61% of gearing (decreasing from 75%in 2005e06 and 68% in 2006e07), during the same year the leastgeared firm had only 17% (11% in 2006 and 23% in 2007). Likewise,in the water sector a study made by consultants identified fourdifferent corporate models, ranging from 100% debt to thin equitymodels and companies without ‘structured finance’ (Smith andHannan, 2003). Not withstanding the disparities, the tendencyhas been noticeable and remains fairly steady: up to now, UKutilities firms still present a relatively highly geared capitalstructures.

Regulators have reacted to the trend towards debt restricting insome form, the freedom of the firms to set their own capitalstructures with leeway. As will be shown, this approach affects thesetting of the cost of capital and its different components, and haseven given rise to concerns (somewhat overstated) about the entireregulatory regime.14

2. The regulators’ approach

In theory, mimicking competitive markets would mean thatregulated firms are free to opt for the ratio of debt and equity,they consider better suits their needs.15 UK regulators, however,have generally applied some form of ‘control’ on the capital struc-ture e however, with different degrees of intervention.16

2.1. Command and control and incentive-based approaches

The first form of control applies traditional command andcontrol (C&C) regulatory strategies. There are two differentapproaches. In the ‘strong’ form, regulators may opt for an intrusiveapproach and compulsorily instructing the adoption of certaincapital structure. With this, the firm is totally prevented fromchoosing the capital structure that it may deem optimal. Incontrast, in the ‘soft’ form regulators establish minimum levels ofequity or, conversely, prohibit gearing above a certain limit.17 Thefirm is therefore not prevented from choosing the capital structureit deems preferable, but its freedom is circumscribed to the limitsset by the regulator. This policy option is normally used in thebanking sector, where systemic effects are highly probable andhence it is likely that the general public may end up bearing some

13 Currently Network Rail’s debts are explicitly under written and funded by thegovernment. The government provides a financial guarantee through the so-calledFinancial Indemnity Mechanism (FIM). According to the regulator, the use of theFIM will be incrementally restricted and it is expected that by 2014 Network Railraises its debt on an unsupported basis (ORR, 2008).14 See e.g. NAO (2002: 18): ‘There are concerns that the standard form of pricecontrol regulation may no longer be appropriate for UK regulation’. Changes inutilities capital structures have even given rise to calls to reform the currentregulatory approach (e.g., amongst others, Barnard and Cooper, 2008; Helm, 2009;and Ofgem, 2010). To some extent, there seems to be a general feeling that Britishregulators have not completely understood or internalised the sort of ‘paradigmshift’ occurring in financing networks.15 This is the position, e.g., of Jenkinson (2006). Due to space considerations, thecriticisms to this position are beyond the scope of this work.16 In theory the control may affect all the regulated firms in a given sector or applyonly to some specific firm(s). An example of the latter would be to reduce the rateof return of high-leveraged firms to their lower cost of capital, whilst keeping thecost of capital of other firms unaffected. Generally, regulators in the UK haveadopted a generalised control.17 Having a minimum threshold is an explicit transfer of risk to the private sector(see Erhardt and Irwin, 2004: 49e50).

23 Since privatisation is a relatively recent process, information about firms isrelatively scarce. Hence the use of real debt/equity ratios (i.e. measured from thefirm’s book values) seems useless, forcing regulators to still rely heavily upon anaverage cost of capital under notional debt-equity ratios.24 The gearing data in Table 1 needs to be interpreted with care. For the period thetable covers, most of the companies to which the data relate were part of widergroups, many of which had adopted holding-company based financing structuressuch that the levels of debt dependent on the assets and cash flows of the regulatedbusinesses for continuing service were significantly higher than the borrowings of

J. Tapia / Utilities Policy 22 (2012) 8e2110

or most of the losses of financial distress.18 In utilities, the CAA(2010) has recently advocated this solution (despite recognisingits problems of implementation). The mechanism would compriseof two parts: (1) the one-year rolling average gearing level shouldbe equal to or less than the gearing assumption in the cost of capitalestimate used in the price cap determination; and (2) gearing at anytime should be less than a predetermined level (set slightly higherthan the targeted gearing assumption to provide for some flexi-bility for trading purposes).19

The use of C&Cmechanisms, however, is controversial. Arguably,C&C mechanisms seem more adequate to deal with the risk of newinfrastructure projects on an ad-hoc basis and not as a permanentregulatory regime. Aside from the familiar criticisms of inflexibilityof rules and intrusion on managerial freedoms, limiting gearing isdifficult because informational demands are severe and the appli-cable standard is likely to be highly discretionary and contentiouseindeed, raising the level of exposure to judicial review. Also, themechanisms would require close and constant monitoring ofcompliance. These criticisms apply to both the strong and the softform of C&C mechanisms. Indeed, the stronger the level of inter-vention, the more accurate the criticisms are.

Alternative methods of control that use incentive-based tech-niques are often preferred e even in presence of something akin tosystemic effects in some sectors.20 For example, there is a prom-ising but under-explored approach whereby the regulator in prin-ciple leaves the firm free to opt for the capital structure moreconvenient for its own interests, but includes in the design of theregime some mechanism that tightens the price cap in the eventthat gearing increases above the level assumed in the price deter-mination e e.g. a penalty that exceeds the amount of the benefit(tax benefit or other) arising from high gearing, or other lessintrusive means. Then the excesses would be passed through to thecustomers. This option, although already considered by someregulators, has yet to be implemented in practice.

The most widespread incentive-based option, currently appliedby most UK regulators, uses something akin to signalling.21 Regu-lators implicitly indicate their preferences for a given capitalstructure, providing incentives for companies to adopt it. This iscommonly achieved using ‘notional’ rather than ‘actual’ levels ofgearing on the calculation of the cost of capital. That is, regulatorsconsider a level of gearing deemed ‘appropriate’ for the entireindustry and then use that figure as an input in the calculation ofthe firms’ regulated returns. Underlying the method there is animplicit assumption that certain capital structures are more effi-cient than others in a given regulated environment. However, firmsare still adopting their own decisions on the capital structures attheir own convenience.22

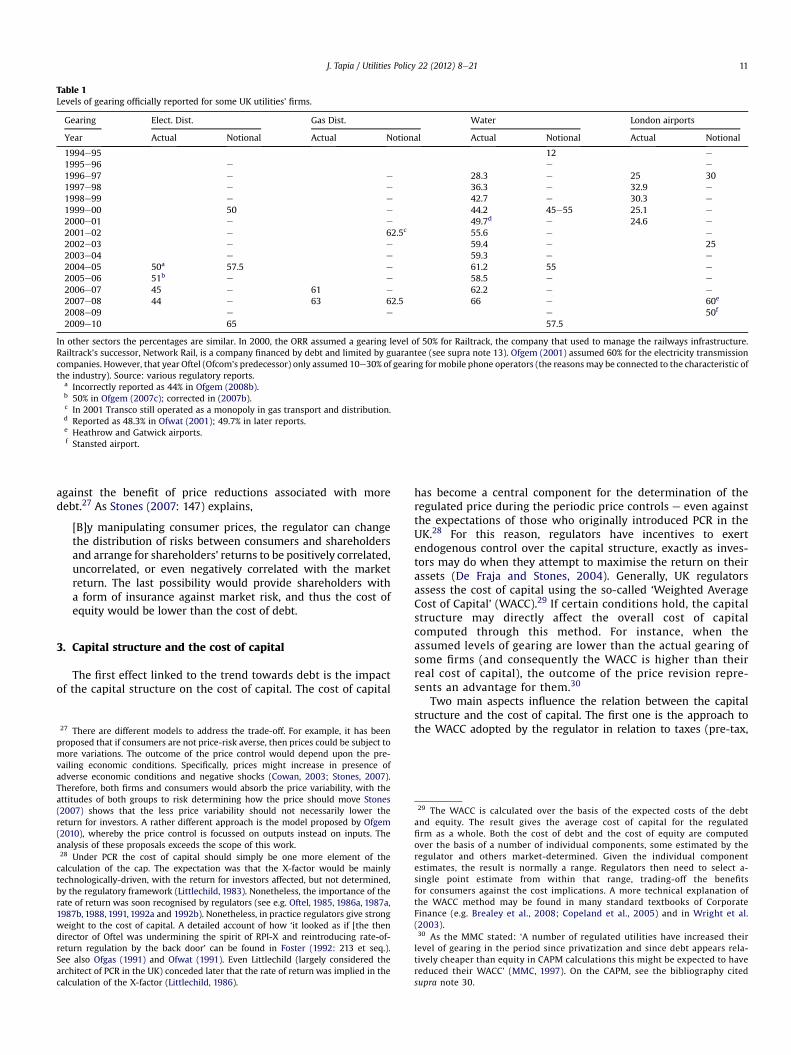

De Fraja and Stones (2004) indicate that in virtually all cases,the notional gearing has exceeded the actual level. However, it is

18 A common example is the imposition of minimum capital-adequacy ratios forbanks.19 The mechanism would be combined with a tax clawback.20 See infra note 90 and accompanying text.21 Before the last price controls, the CC (and its predecessor the MMC) used to setairports’ cost of capital over the basis of actual gearing. However, it changed itsposition and decided to use notional levels gearing for Heathrow and Gatwick (CC,2007: Annex F, F7, para. 24) and Stansted (CC, 2008: 92, paras. 11.11 et seq.). Theargument was linked to financeability (see infra section 4.1). The CC has recentlyapplied this approach in the water sector (CC, 2010a). Regulators recognise that thereason behind the use of notional gearing is the increase in levels of debt by theregulated firms. E.g. Ofgem (2009b). See also Helm (2009).22 Ofgem (2006: 54, para. 8.17) has stated that ‘[Our] gearing assumption shouldnot be interpreted as an endorsement of any particular capital structure. We believethat the companies and their financiers are best placed to decide on the mostappropriate capital structure’.

hard to make a definite assertion. Until fairly recently, not everyregulator collected data on actual gearing. Ofgem, for instance, didnot provide data before the 2004 electricity distribution pricecontrol. Also, gearing levels of gas distribution companies werepublished for the first time only in March 2009. In most sectors,the information is just recently being collected.23 What is true isthat levels of assumed gearing have been significantly increasedover the time. Estimated gearing is now much more closelyrelated to actual gearing e although it may be higher of lowerdepending on the sector-specific considerations taken intoaccount during each price control. For instance, as shown inTable 1, in 2004e05 actual gearing was lower than notionalgearing in the electricity sector, but it was higher in the watersector. Generally, however, it seems that currently regulatorsconsider efficient a level of debt of around 50e60%. This contrastsmarkedly with, for instance, the 12% estimated in the water firstprice control review in 1994.24

2.2. The regulatory concerns

Why are regulators concerned about high gearing? The increasein gearing levels has two (potentially conflicting) effects (Bucks,2005). The first one is the impact on the cost of capital. Regula-tors make a decision about the cost of debt and equity that wouldbe incurred by an efficiently financed regulated firm at the notionalgearing. Since the increase in gearing may decrease the cost ofcapital, the regulatory approach has the potential to ‘minimise’ thelatter (when notional gearing is higher than actual gearing) andhence lower the price paid by the consumers.25 However e andthis is the second effect e high gearing also introduces pricevolatility that might lead to a fragile financial position for the firmswith (allegedly) negative general consequences for the regulatoryregime. In addition, high gearing can drive the cost of capitalupwards because of the increase in price variability.26 Therefore,preventing firms to increase debt over a certain threshold (orincentivising them not to do it so) would help to ex ante preventfinancial distress and thus avoid unplanned ex post cash-injections.The regulatory task is to trade-off the costs of price uncertainty

the legal entity housing the regulated business alone. Thus the data tend tounderstate the true levels of gearing.25 Needless to say, the aim of the regulatory approach must be focused uponconsumers: if gearing is efficiency enhancing, those benefits should be capturedfor them. The CC has recently confirmed this point: ‘It might be in consumers’interest that a positive adjustment to [the regulated price] be made, for exampleif this were required to avoid an increase to [the firm]’s cost of capital’ (CC: Suttonand East Surrey Water plc: Interim Price Determination [17 June 2009], at 78, para.4.94). The protection of the interests of the consumers is a central statutory dutyestablished for all regulators. It importance has been confirmed by the case-law.E.g., Competition Appeal Tribunal: T-Mobile (UK) Limited, British Telecommunica-tions Plc, Hutchison 3G UK Limited, Cable & Wireless UK & Ors, Vodafone Limited,Orange Personal Communications Services Limited v Office of Communications[2008] CAT 12, at 98: “In any event, the lack of pass through is relevant only tothe question of whether the proposed prices had an adverse effect onend-users.”.26 Therefore, debt-only firms are not optimal, and the socially optimal capitalstructure always leaves some price uncertainty. See De Fraja and Stones(2004).

Table 1Levels of gearing officially reported for some UK utilities’ firms.

Gearing Elect. Dist. Gas Dist. Water London airports

Year Actual Notional Actual Notional Actual Notional Actual Notional

1994e95 12 e

1995e96 e e e

1996e97 e e 28.3 e 25 301997e98 e e 36.3 e 32.9 e

1998e99 e e 42.7 e 30.3 e

1999e00 50 e 44.2 45e55 25.1 e

2000e01 e e 49.7d e 24.6 e

2001e02 e 62.5c 55.6 e e

2002e03 e e 59.4 e 252003e04 e e 59.3 e e

2004e05 50a 57.5 e 61.2 55 e

2005e06 51b e e 58.5 e e

2006e07 45 e 61 e 62.2 e e

2007e08 44 e 63 62.5 66 e 60e

2008e09 e e e 50f

2009e10 65 57.5

In other sectors the percentages are similar. In 2000, the ORR assumed a gearing level of 50% for Railtrack, the company that used to manage the railways infrastructure.Railtrack’s successor, Network Rail, is a company financed by debt and limited by guarantee (see supra note 13). Ofgem (2001) assumed 60% for the electricity transmissioncompanies. However, that year Oftel (Ofcom’s predecessor) only assumed 10e30% of gearing for mobile phone operators (the reasonsmay be connected to the characteristic ofthe industry). Source: various regulatory reports.

a Incorrectly reported as 44% in Ofgem (2008b).b 50% in Ofgem (2007c); corrected in (2007b).c In 2001 Transco still operated as a monopoly in gas transport and distribution.d Reported as 48.3% in Ofwat (2001); 49.7% in later reports.e Heathrow and Gatwick airports.f Stansted airport.

J. Tapia / Utilities Policy 22 (2012) 8e21 11

against the benefit of price reductions associated with moredebt.27 As Stones (2007: 147) explains,

[B]y manipulating consumer prices, the regulator can changethe distribution of risks between consumers and shareholdersand arrange for shareholders’ returns to be positively correlated,uncorrelated, or even negatively correlated with the marketreturn. The last possibility would provide shareholders witha form of insurance against market risk, and thus the cost ofequity would be lower than the cost of debt.

3. Capital structure and the cost of capital

The first effect linked to the trend towards debt is the impactof the capital structure on the cost of capital. The cost of capital

27 There are different models to address the trade-off. For example, it has beenproposed that if consumers are not price-risk averse, then prices could be subject tomore variations. The outcome of the price control would depend upon the pre-vailing economic conditions. Specifically, prices might increase in presence ofadverse economic conditions and negative shocks (Cowan, 2003; Stones, 2007).Therefore, both firms and consumers would absorb the price variability, with theattitudes of both groups to risk determining how the price should move Stones(2007) shows that the less price variability should not necessarily lower thereturn for investors. A rather different approach is the model proposed by Ofgem(2010), whereby the price control is focussed on outputs instead on inputs. Theanalysis of these proposals exceeds the scope of this work.28 Under PCR the cost of capital should simply be one more element of thecalculation of the cap. The expectation was that the X-factor would be mainlytechnologically-driven, with the return for investors affected, but not determined,by the regulatory framework (Littlechild, 1983). Nonetheless, the importance of therate of return was soon recognised by regulators (see e.g. Oftel, 1985, 1986a, 1987a,1987b, 1988, 1991, 1992a and 1992b). Nonetheless, in practice regulators give strongweight to the cost of capital. A detailed account of how ‘it looked as if [the thendirector of Oftel was undermining the spirit of RPI-X and reintroducing rate-of-return regulation by the back door’ can be found in Foster (1992: 213 et seq.).See also Ofgas (1991) and Ofwat (1991). Even Littlechild (largely considered thearchitect of PCR in the UK) conceded later that the rate of return was implied in thecalculation of the X-factor (Littlechild, 1986).

has become a central component for the determination of theregulated price during the periodic price controls e even againstthe expectations of those who originally introduced PCR in theUK.28 For this reason, regulators have incentives to exertendogenous control over the capital structure, exactly as inves-tors may do when they attempt to maximise the return on theirassets (De Fraja and Stones, 2004). Generally, UK regulatorsassess the cost of capital using the so-called ‘Weighted AverageCost of Capital’ (WACC).29 If certain conditions hold, the capitalstructure may directly affect the overall cost of capitalcomputed through this method. For instance, when theassumed levels of gearing are lower than the actual gearing ofsome firms (and consequently the WACC is higher than theirreal cost of capital), the outcome of the price revision repre-sents an advantage for them.30

Two main aspects influence the relation between the capitalstructure and the cost of capital. The first one is the approach tothe WACC adopted by the regulator in relation to taxes (pre-tax,

29 The WACC is calculated over the basis of the expected costs of the debtand equity. The result gives the average cost of capital for the regulatedfirm as a whole. Both the cost of debt and the cost of equity are computedover the basis of a number of individual components, some estimated by theregulator and others market-determined. Given the individual componentestimates, the result is normally a range. Regulators then need to select a-single point estimate from within that range, trading-off the benefitsfor consumers against the cost implications. A more technical explanation ofthe WACC method may be found in many standard textbooks of CorporateFinance (e.g. Brealey et al., 2008; Copeland et al., 2005) and in Wright et al.(2003).30 As the MMC stated: ‘A number of regulated utilities have increased theirlevel of gearing in the period since privatization and since debt appears rela-tively cheaper than equity in CAPM calculations this might be expected to havereduced their WACC’ (MMC, 1997). On the CAPM, see the bibliography citedsupra note 30.

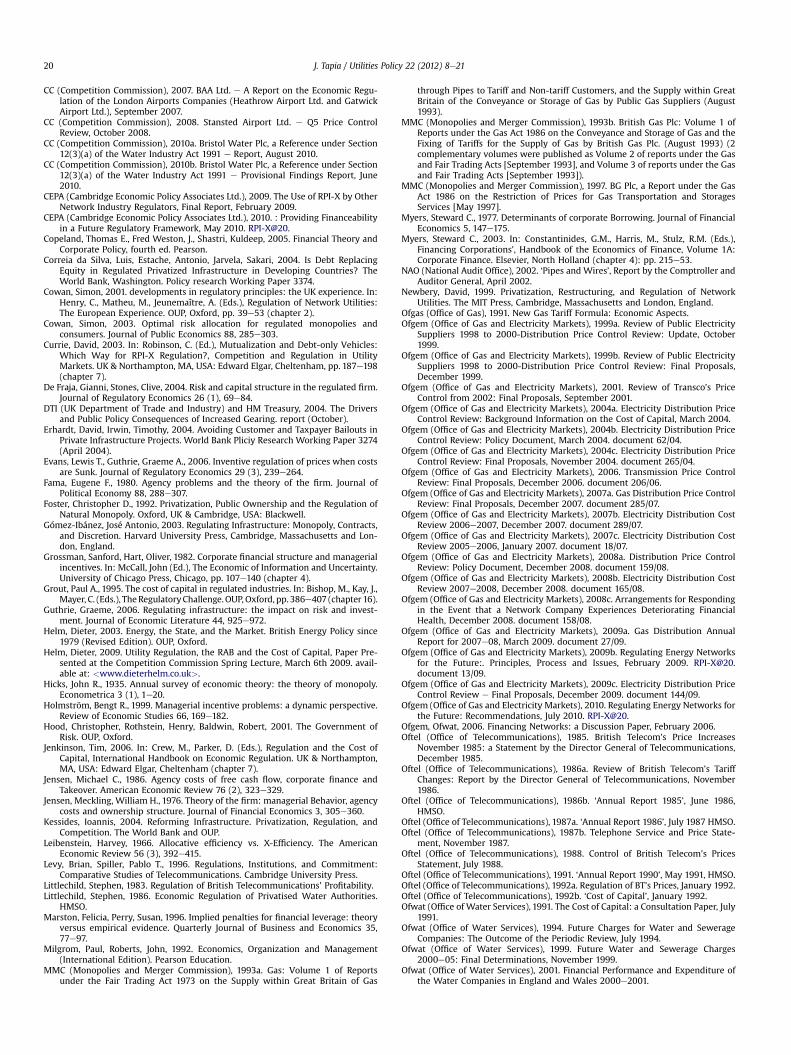

Table 2Equity Betas used by regulators in the UK.

Regulator Company Year Equity Beta

Ofwat Water companies 1994 0.67e0.751999 0.7e0.82004 1.02009 0.9

ORR Railtrack 2000 1.1e1.3a

Ofgem DPCR 1999a 1.02004 1.02009 >1.0

GDPCR 2001 1.0b

2007 1.0TPCR 2001 1.0b

2006 1.0MMC/CC London Airports 1996 0.7e0.9

2002 0.8e1.02007 0.9e1.3c

2008 1.0e1.24

a ORR (2000) argued that Railtrack’s betas reflected a ‘premium’ over otherregulated industries due to its high level of operational gearing.

b In 2001 Transco operated as a monopoly in gas transport and distribution.c The table expresses the minimum and maximum point-estimated for both

airports included in the report. The range for Heathrow was 0.9e1.15; and forGatwick 1.0e1.3. See CC (2007).

J. Tapia / Utilities Policy 22 (2012) 8e2112

post-tax or the so-called ‘vanillaWACC’), which has implications forthe tax advantages the firm might obtain from having more debt.When the WACC is calculated on a post tax basis, there is lessincentive to increase gearing because the advantage is alreadyincorporated into the model.31 The approach, however, largelydepends upon the preferences of the regulator and the character-istics of the industry, so I will not deal with this aspect in detail.32

The second aspect is related with the incorporation of riskperception (which largely depends on the capital structure) withinthe calculation of the cost of capital.

3.1. Cost of capital and risk

Risk perception is reflected in the WACC through the so-calledCAPM betas: asset, equity and debt betas.33 Whilst equity betasinclude the combined effects of both business and financial risk,asset betas reflect only the former.34 Traditionally, the relationshipbetween both the types of betas has led to the widespreadconclusion that higher gearing leads to higher equity betas, andthat the increase will be bigger the smaller the value of the corre-sponding debt beta. This should be followed by higher expectedreturns on equity and hence a higher cost of capital.35 For this tooccur, the perception of risk should be reflected in the firm’s betasas accurately as possible. Yet that has not been the regulatorypolicy. In practice, regulators have sought to ‘protect’ firms from therisk of default (section 4 below). Hence they have not only looked toinfluence the financial behaviour of firms by exerting control overgearing levels, but also ‘manipulating’ equity betas. The tendencysince the late 90s has been to set the equity betas’coefficients closeor equal to one (see Table 2), implying that the risk of the regulatedfirm is equal or very similar to an average firm in the market.36

31 E.g. Ofgem (2004c: 109, para. 8.59): one of the objectives to opt for a post-tax approach to the cost of capital was ‘reduce the incentives to increasegearing’.32 In the UK, some of the regulators have traditionally followed the pre-taxapproach. This is the case of the e.g. CC (2008 & 2007) and its predecessor(MMC, 1993a, 1993b). The same is the case for Oftel and Ofcom, Postcomm and theCAA. In contrast, others have applied a post-tax approach or the vanilla version.Ofwat has consistently applied a post-tax approach to the cost of capital. Recently,both ORR and Ofgem have been using a post-tax approach to the cost of capital inits ‘vanilla’ version. Ofgem changed its position in the electricity distribution pricecontrol review for the period 2005e2010 and has maintained it for 2010e15(compare Ofgem [2004c: para. 8.32; 2004b: para. 7.18; and 2004a] with Ofgem[1999b: para. 5.24]).33 On this concepts, see the bibliography cited supra in note 30 and Sudarsanam(2011).34 Business risk is associated with the unique circumstances of a particular firmand the overall economic environment. It arises from the operating characteristicsof an investment in real assets. Therefore, it basically represents the possibility thatthe firmwill not have the cash flow necessary to meet its operating expenses. Someelements that are included in the business risk are revenue uncertainty, labourcosts uncertainty, regulatory and political uncertainty, and risk of technologicalobsolescence, amongst others. The distinctive feature of all these elements is thatthey are independent of the means by which the assets are financed. Financial riskarises from the means by which the assets of the firm are financed. It represents thepossibility that the firm will not have the cash flow necessary to pay its equityholders when the assets are partially funded by borrowing. Amongst the elementsincluded in the financial risk are: the risk of bankruptcy, the risk of restructuring inevent of default, and the risk of suboptimal operating and inefficient investmentdecisions when the firm is in condition of financial distress. The risk of financialdistress is also known as ‘insolvency risk’.35 This is the traditional logic of the CAPM, according to the Modigliani & Millermodel. In jurisdictions such as the UK, where debt and equity are taxed differentiallyand there is a tax benefit from debt compared to equity funding, relaxation of theMeM conditions may result in the cost of capital actually falling as gearing rises, upto the point at which the incremental expected costs of failure offset the increasedvalue of the tax shield. However, this is not to undermine the substantive pointmadein the text, relating to the seemingly consistent over-estimation (in relation to thegearing assumption) of equity beta coefficients made by UK regulators.36 There are no theoretical boundaries for the value of equity betas.

UK regulators sustain their estimation of equity beta at unity fordifferent reasons. The main one is based upon inaccurate informa-tion. It is argued that there is risk inherent to large capital invest-ment programmes, whose long-termhorizonwouldmean that theyare constantly subject to uncertainties that would not be capturedby historical measures of risk. Thus, either the lack of reliableevidence or instabilities in the estimates over time is blamed for thegreater weight given to unconditional expectations, which in turnleads one to consider that utilities are of average risk. Additionally,certainty must also be taken into account. There are just a fewpublicly-quoted utilities on the London Stock Exchange withpublicly available information.37 Therefore, regulators should esti-mate a proxy of the risk faced by all of the firms based only upon theinformation available. This may be a difficult and demanding task,and the results are unlikely to be accurate. Finally, regulators maynotwant to change their estimations, looking for a sustainable long-term approach. If the long-term estimation was that firms behavelike an average firm in themarket, it may be unreasonable to reducethe estimation of betas whilst the risk is increasing for other firms.

As a result of the regulatory policy, the assumption on gearinglevels has exerted a major influence in the calculation of the costof capital because the increased level of gearing has not beenmatched with the estimated betas. However, public utilitiesshould not be ‘assumed’ to be equal to an average firm. Their riskshould be modelled according to the specific characteristics of theindustry.38 Also, the different nature of the risks should befactored into the models.39 Overall, the regulatory argument for

37 For instance, this claim has been made by Ofgem (2008a: 93, para. 5.7).Amongst the companies listed are Severn Trent, United Utilities, Northumbrian, BT,NG, Pennon and Scottish & Southern.38 For example, electricity transmission should be a lower risk activity thandistribution. Nonetheless, Ofgem (2006) has claimed that the evidence is notsufficiently robust to quantify differences between sub-sectors with accuracy.39 Armstrong et al. (1994) have convincingly argued that the correct way to modelrisk is to see it as a factor that lowers expected future cash flows, thus reducingexpected profitability without altering the cost of capital per se. They indicate thatregulatory risk is firm-specific and should be diversifiable, but recognise that ifregulators applied this model they would be recognising that there is a possibilityof future expropriation. In this line, it can also be argued that risk should beconfined only to political risk, not regulatory risk. If the cost of capital representsthe expected rate of return, then regulatory risks should not have any effect on it.

45 The evidence is presented by Wright et al. (2006). Their evidence is compatiblewith that of Marston and Perry (1996) for US firms. By the same token, the CC hasstated that does not accept the argument that higher levels of gearing producea higher cost of capital (CC, 2007: F23, para. 90).46 Similarly, Wright et al. (2006: 63): ‘Paradoxically, the attempt by the regulator

J. Tapia / Utilities Policy 22 (2012) 8e21 13

equity betas coefficients equal to one is ‘distinctly generous’(Wright et al., 2006: 14).

First, the different characteristics of the regulatory regimemust betaken into account. The evidence indicates that, in principle, betasshould be higher under PCR than under a ‘cost of service’ (CoS)ratemaking scheme e i.e. investors bear the greatest non-diversifiable risk in PCR (Alexander et al., 2000, 1999; Alexanderand Irwin, 1996), whilst CoS regulation immunises shareholdersfrom shocks to long-term cash flows (Guthrie, 2006). However, theliterature alsopoints out that inpractice CoS schemes and PCR tend tobe similar (e.g. Kessides, 2004; Grout, 1995; Baumol, 1967). The keydifferences lie mostly in the level of cost pass-through and how fastthe changes are reflected in the regulated price (which in turn isnormally a function of the length of time that elapses between pricereviews).40 In theUS, under a CoS scheme, equitybetas are very low.41

Considering the practical similarities between both regulatoryregimes, it is at least hard to justify the doubling of betasmade by theUK regulators.

In addition, there is mounting evidence that betas shoulddecrease. Old estimations made by Grout (1995) indicate that thelevel of betas should be in the bottom half of the distribution,ranging between 0 and 1, with the lowest betas appearing in thewater sector. Likewise, Alexander et al. (1999) estimated averagebetas of 0.6 for electricity, 0.84 for gas and 0.67 for water. It isunlikely that these estimations have severely changed in recenttimes. Indeed, recent evidence byWright et al. (2006) confirms thatan estimation of 0.5 is a better measure of equity betas for long-term utilities.42 Similarly, Jenkinson has argued that equity betasabove 0.4 are hard to justify (Jenkinson, 2006). Given their captivebase of customers and regulated tariffs, the revenues of utilitieshardly vary with the general state of the economy.43 In addition,most of the risk associated with large capital programmeswould bediversifiable. Jenkinson’s estimation seems to be supported byrecent calculations made by the ORR (2008) and the CC (2008).44

The latter found that utilities’ asset betas are low (0.37)compared to airports (between 0.50 and 0.61) and well below therisk an investor faces in the UK stock market (0.72).

Third, there is also strong evidence pointing in the oppositedirection to the traditional relation between the asset and equity

40 Under ‘cost of service’ regulation, investors only bear the consequences of shocksuntil the next regulatory revision of prices. In contrast, under PCR investors only bearthe consequences of shocks after the regulatory control. Hence the frequency of theprice reviews (or the possibility to pass on the costs to consumers) is crucial. Morefrequent revisions under a ‘cost of service’ scheme will led to less risk and toa decrease in the cost of capital (Brennan and Schwartz, 1982). More frequent revi-sions ormore pass-through (e.g., via ‘claw-backs’ or ‘re-openers’) under PCRwill leadto more risk and an increase in the cost of capital (Evans and Guthrie, 2006).41 Old evidence by Grout (1995) and Alexander et al. (1999) showed average betasof 0.2 in the case of electricity, gas and water utilities, and 0.5 in telecoms. Probablythe values have slightly increased recently.42 The estimation, however, present a wide confidence interval. Recently Ofwathas recognised that equity betas in the water sector are very low compare withmarket and historical trends (Ofwat, 2007: 46). See also Ofwat (2008).43 This is, indeed, a generalisation. In the case of those utilities subject to revenuecap regulation (e.g. energy networks), revenues do not vary with the level ofdemand (at least not in the short term). By contrast, in the case of those subject toprice cap regulation (e.g. water/wastewater, telecoms), revenues do vary with thelevel of demand. In the recent economic downturn, revenues of some water supplycompanies (especially those with a high proportion of industrial demand) havebeen significantly reduced. However, some effects have been moderated ex-post byregulatory protections.44 Importantly, the ORR (2008: 230, para. 14.17) has recognised that there is‘strong evidence that Network Rails’ risk profile is below that of the airports and issimilar to the energy and water sectors. We are providing Network Rail with somevery significant protections against risk, particularly related to its capital invest-ment programme. It also faces very little volatility in revenues. The majority of itsincome is fixed for the five-year control period’.

betas assumed by regulators. That is, there would be a negativerelationship between betas and gearing: in utilities, higher levels ofgearing would be associated with lower equity betas and thereforelower asset betas.45 The explanation may lie in the own regulators’behaviour: their control over the capital structure may beproducing a decrease in the underlying asset betas.46 That is,regulation itself may have reduced the volatility and uncertaintyinherent to high levels of gearing.

4. The capital structure and the financial position of the firms

Let’s focus now on insolvency risk. Allegedly, the increase ingearing might lead to a fragile financial position of the firms,generally affecting the regulatory regime. This idea is commonlydeployed through one or more of three concerns that I shall call the‘financeability concern’, the ‘under investment concern’ and the‘control concern’.

4.1. The ‘financeability concern’

According to the traditional economic view on the duty tofinance networks, which finds its roots in the classic theory of thenatural monopoly, regulators must set the price so as to allow themonopoly just to break-even. If the price is set ‘correctly’, a firmthat raises capital in the capital markets should not discriminatebetween long- and short-termwhen making investment decisions,provided that the projects generate revenues higher than the costof capital in net present value (NPV) terms. In practice, this meansthat the firm needs to earn a return at least equal to the cost ofcapital on the RAB.47

In addition, most regulators now interpret the duty to finance asa duty to maintain the so-called ‘financeability’ of the firms.48 Thisidea refers to the possibility that firm’s revenues, profits and cash

to limit the “dash for debt” may actually have sped up the process’. This factprovides an additional support for the stated view that, under regulation, changesin capital structures are influenced by regulators’ behaviour: by itself the regulatorycontrol has influenced the changes in the capital structures of regulated firms.47 Originally, it was thought the RPI-X did not require the measurement of capitaland rate of returns (Littlechild, 1983). Nonetheless, it was later recognised that ‘RPI-X and rate-of-return regulation have certain common features. Both accept theneed to secure an adequate return for the company’s shareholders in order toinduce them to continue to finance the business, without conceding unnecessarilyhigh prices at the expense of customers’ (Beesley and Littlechild, 1989: 460).Currently, financial models used to determine the X-factor already incorporatea mechanism to ensure that new investment earns the cost of capital. Regulatoryconcerns for allocative efficiency are the ones that have led regulators to considermeasurements of (and control) capital and rate of return (Armstrong et al., 1994:174). On the concept of RAB, see supra note 6.48 In this sense, e.g., CC (2007: 73, para. 5.11): ‘The CAA has no express statutoryobligation to ensure that regulated airports, including BAA, are adequately financed.The CAA is, however, required to promote the efficient, economic and profitableoperation of such airports, and also to encourage investment in new facilities atairports in a timely fashion. In this context, we consider appropriate for us toestablish whether our proposals would enable Heathrow and Gatwick to financetheir [businesses] on reasonable terms in the banking and capital markets throughsome combination of debt and equity’; Ofwat (2004: 217): ‘We have a duty tosecure that companies are able to finance the proper carrying out of their functionsas licensed undertakers (‘finance functions’). We look at this as having two strands.One is to secure that, if a company is efficiently managed and financed, it is able toearn a return at least equal to the cost of capital. The second is that its revenues,profits and cash flows must allow it to raise finance on reasonable terms in thecapital markets. We refer to this second strand as financeability’; and ORR (2008:273, para. 17.1): ‘We have a duty to act in a manner that it will not render it undulydifficult for Network Rail to finance its activities’.

54

J. Tapia / Utilities Policy 22 (2012) 8e2114

flows allow it to raise finance in the capital markets e on termsconsidered ‘reasonable’ by the regulator. Thus, the regulated priceshould provide the firm with sufficient returns to (1) keep certaincredit ratings issued by credit rating agencies (with some ‘head-room’ in the rating to avoid an immediate slip in the event ofa negative shock) and (2) meet certain ‘financeability targets’ thatunderlie the credit ratings and are linked to the firm’s achieve-ments (e.g., CC, 2007). With this aim, most regulators now applya ‘financeability test’ during price controls that goes as follow. First,a decision is made regarding the appropriate credit rating that thefirm should target (typically ‘Investment Grade’).49 Even more,benchmark provisions have been embedded into some utilities’licences compelling them to maintain minimum financial ratios.Secondly, it is decided what financial indicators and thresholds aregoing to be used. Financial indicators are mostly cash-based.50

Finally, each company is modelled and the financial indicators arecomputed and analysed. Within the financeability test, it is decidedwhat level of gearing would be consistent with the targets.

The financeability concern comes up from the mismatchbetween the calculation of the cost of capital made by regulatorsand means of financing projects by the utility (Oxera, 2006, 2010;Bucks, 2005). Whilst the regulatory model provides for a real rateof return, most firms pay out returns to creditors in nominalterms.51 The result is that, due to the difference between realinflows and nominal outflows, firms may be left with negative cashflows for a certain period of time (possibly longer than one singleprice control period). Ife and only ife a firm invests at a rate abovethe level required to replace its existing assets, this ‘cash-flow gap’increases to an extent that may lead to a deterioration of thefinancial indicators.52 In turn, this may result in a decrease in creditratings; drive the rate of return up (increasing the cost of financeprojects); and allegedly render it more difficult for the firm toaccess the financial markets.

If a firm fails the financeability test, a number of adjustmentscan be applied e typically to ‘bring revenues forward’. In the past,regulators have used NPV positive mechanisms, such as theallowance of additional revenues (‘revenue uplifts’) whilst warningthe firms not to distribute them as dividends.53 Also, ORR has

49 This means at least BBB-, Baa3 or any equivalent rating, depending on theissuer. However, at least the CC has increased the level, stating that in the currentfinancial ‘turbulence.an efficiently financed company might reasonably seek totarget an A3/Ae credit rating’ (CC, 2008: 93, para. 11.13).50 E.g. funds from operations/interest cover; net debt/RAV; and retained cashflow/net debt.51 When applying a real WACC, the effects of inflation are compensated throughindexation of the RAB. Alternatively, the cost of capital might be calculated usinga nominal WACC without RAB indexation. Both approaches are neutral in NPVterms, and the election depends on the regulator. In the UK, only Ofcom usesa nominal approach.52 That is a common situation in large infrastructure investments. Note, however,that the indexation of the RAB may reverse this effect (i.e. it may lead to positivecash balances), but only in the long-run. Note also that differing credit ratingagencies use different methods when reflecting this level of capital expenditure intheir ratings e situation that, considering the regulatory context, may be regardedas unavoidable. Some agencies reflect actual maintenance and renewal expendi-ture; others use accounting or regulatory depreciation as a proxy (data on thisbeing generally more readily available). As the two are not necessarily coincident, atleast in the short run, this could result in deteriorating financial indicators evenwhere investment is at or below the level required to renew existing assets.53 Yes, firms get extra revenues to spend on themselves! At least Ofgem and Ofwathave included vast revenue uplifts in their price controls amounting to large sumsin NPV terms. In the price control 2004 Ofgem allowed one company an extrapayment of £1.6m precisely to ‘provide a small cushion against downside risks andimprove the projected financial ratios’ and to ‘maintain a credit rating conformablywithin investment grade’ (Ofgem, 2004c: 114e5). Regulators considered that ‘themateriality of the adjustment was small’ (Ofgem and Ofwat, 2006: 46, para. 136). Inturn, Ofwat allowed payments for approximately £400m for the period 2005e10(Ofwat, 2004).

recently provided Network Rail with a ‘risk buffer’ of £1bn. over 5years, with the explicit purpose of managing risk within theregulatory settlement (ORR, 2008). The company has discretionover the use of this fund.54 The financial effect of payments ‘.is toset allowed returns at a level above the cost of capital’ (Jenkinson,2006: 13); lead to re-valuations of firms’ shares and premiums onpurchases; and make consumers pay more for services than theywould otherwise have done.55 The tendency, however, is to useNPV-neutral mechanisms. For instance, Ofgem have re-profiledrevenues to advance cash flows from future periods by acceler-ating depreciation and shortening assets lives. Likewise, the CAA(2003) and the CC (2007) have used a point estimate towards thehigher end of theWACC.56 The effect of neutral-NPVmechanisms isallegedly less detrimental for consumers: prices increase in theshort-term, but in the long run they should decrease. Whatever thesolution, though, consumers are affected.57

The solution, however, is not clear. Suitable proposals includethe conversion of non-regulated assets into cash and the renego-tiation of creditor protection arrangements. Their implementation,however, might be highly contentious and their reach out of theregulators’ means. Further, Jenkinson (2006) has proposed theadjustment of the profile on prices within a control period tomatchthe cash-flow profile and keep financial ratios at appropriate levelse in practice a solution closer to the options for risk-sharing ana-lysed in section 5 below.58 Equity injections may also be appro-priate e with the regulator providing guidance as to whether andwhen it estimates that a new equity would be needed during theprice control period.59 Nonetheless, too much reliance on thismechanismmay be imprudent. If the objective of the financeabilitytest becomes chiefly to attract equity, the test happens to betautological and to some extent whimsical e regulators boostequity because they want to avoid the ‘flight from equity’; and theway to avoid the flight from equity is by boosting equity. This isnothing more than a convenient loophole. In the end, the callshould be for a holistic approach whereby the potential actions to

ORR (2008: 235, para. 14.43) has even argued that although it increased theprotections against risk, it is ‘taking a cautious approach by not reducing the riskbuffer to take account of those further protections’.55 Fortunately, after taking stock of the weaknesses, regulators have recentlysignalled some changes. For instance, Ofwat indicated that for the price control2010e15 it would try to ease the financing constraint through several marketmechanisms, because it considered the revenue uplift is not appropriate. Shouldthis tool be adopted, it would be applied in an NPV-neutral manner (Ofwat, 2007).In the final determinations, Ofwat did not give specific uplifts for ‘known’ operatingcost increases (Ofwat, 2009: 18). On the other hand, Ofgem (2008a) has also statedthat if the cost of capital is set at the right level, revenue uplifts are unnecessary. Infact, it did not give any specific uplift in the electricity distribution price control2010e2015 (Ofgem, 2009c).56 E.g., the CC recommended two uplifts during the price control review of BAA in2002, in order to reflect the financial constraint associated with the new Terminal 5in Heathrow, along with the use of the mid-point of the WACC range (CC, 2002).Nonetheless, they were not adopted by the CAA (which has the ‘last word’ in settingthe prices for the airports) and instead a point estimate towards the higher end ofthe WACC range recommended by the CC was used (CAA, 2003). The latterapproach was also applied by the CC (2007).57 As the CC (2010b: 99, para. 10.16) has stressed, ‘It is not consistent with goodregulatory practice or the consumer objective to determine that customers shouldpay higher prices to rectify a financeability problem resulting from a company’sown decision about financial structure’. Similar statement is done in CC (2010a: 71,para. 10.24).58 Jenkinson recognises that such an approach would trade-off stability of finan-cial ratios against stability of price paths for consumers. But he argues that if cashflows cannot be stabilised, the regulator might alter the depreciation profile of thefirm and spread the effect over the years.59 In fact, Cowan (2003) notes that one of the ways whereby consumers and firmscan share risks without regulatory intervention is the buying of utilities’ shares byconsumers. However, he also points out that for this to be applicable shareholdingshould be implausibly large.

62 For instance, recently the CC did not allow an increase in prices asked by onewater company, on the grounds that it was ‘able to finance the proper carrying outof its functions with prices at their current level’ (CC: Sutton and East Surrey Waterplc: Interim Price Determination [17 June 2009], at 78, para. 4.96).63 This problem is akin to the ‘asset substitution problem’ analysed infra in note 73and accompanying text.64 Unlike non-regulated companies, regulators demand from regulated firmsquality improvements and capital investments to be made in certain periods oftime. The expectation is that they should not be reallocated across time.65 As also firms with more cash do. For a survey of the literature, see Stein (2003),who points out that the evidence does not clearly reveal why firms with more cashand less debt invest more.66 Two related effects may happen. The firm may prefer to delay improvements

J. Tapia / Utilities Policy 22 (2012) 8e21 15

address the financeability concern are ideally discussed with thefirm, consulted with consumers’ groups where possible andimplemented on an ad-hoc basis.

Notwithstanding the solution, it is clear that the financeabilitytest as it is currently appliedmust be revised. Importantly, the over-reliance on credit rating agencies (CRAs) is unjustified. First, there isan issue of circularity. Regulators rely heavily upon the informationprovided by CRAs. They even meet agencies’ representatives andlearn about the factors considered by the latter whilst gradinga firm (CC, 2008: L6, para. 25; CC, 2010a: O5, para. 21). At the sametime, however, CRAs rely heavily on regulatory measures to ascriberatings. Secondly e and related e appropriate ratings in infra-structure and utilities sectors depend largely on a good under-standing of the regulatory regime. It is at least doubtful that CRAs,more used to assess standard competitive sectors, have theexpertise and specialised knowledge to evaluate all the relevantimplications.60 Finally, some actions that CRAs may deem positivefor the purposes of achieving certain rating may in fact havenegative consequences for consumers. Considering their generaltasks, CRAs tend to prioritise actions that benefit debt-holders.Conversely, regulators need to act for the consumers’ benefit.

It does not follow from the above that CRAs should not playa part in the assessment. As CEPA (2010) has correctly stressed, thealternatives are more difficult to implement and demand expertiseon credit analysis that regulators do not (and should not) have.However, the recent financial crisis at least calls for the adoption ofa cautionary approach. High profile episodes (e.g. the collapse of bigfinancial institutions) have undermined the alleged ability of CRAsto act as ‘vehicles’ that monitor and spread information. Thefinanceability test should rely less on the fact that a firm may notachieve the targeted credit rating e its achievement should beconsidered only as minimum condition. CRAs should fulfil aninformational role and not be the central part of the assessment.

Finally, at amore fundamental level, it can bequestionedwhetherthe financeability concern exists at alle that is, whether any advanceof cash flows that goes beyond the price set during the control isnecessary. Contrary to some studies that have argued that at least insome sectors the access to equity markets is more difficult or costly(e.g. Oxera, 2006; regardingwater), it seems improbable that utilitiesreach a point where they cannot access financial markets by them-selves. Theoretically, as in any other business, an adequate rate ofreturn should be enough to provide incentives to attract capital toutilities. In fact, by definition the regulated price is set higher thanincremental cost, so the firm has incentives to invest and produce.Regulation only prevents significant departures from incrementalcost (Breyer, 1982: 18e19). This fact alone should suffice to excludeany type of expectations of advancement of cash flows (i.e., short-term cash flow gaps should be allowed for by investors); tocompensate any potential increase in the rate of return demandedbyinvestors; and certainly to avoid concerns about financeability.

Nonetheless, for this to occur it is required that the regulatedprice is set correctly by the regulator. This is not an oxymorone it isa complex, but not impossible task. If the regulator calculates theWACC using notional gearing, as they do, it is possible to base thatassumption taking into account long-term considerations e themore so if utilities are supposed to ‘mimic’ competitive markets. Inturn, this requires that investors have confidence that the regulatorwill not expropriate long-term returns. This leads to the problem of‘regulatory commitment’, revised in section 5 below. As will beshown, political risk and regulatory risk are widely seen as

60 By contrast, CEPA (2010, at 9: ‘It is difficult to conclude that on the basis of themethodology the credit agencies do not understand the industry’).61 See infra note 89 and accompanying text.

relatively low in the UK.61 To a large extent, low-risk reassures theavailability of financial resources e either from equity or debt. Infact, so far there is no evidence showing that firms are or have beenunable to raise finance.62

In sum, there are at most only weak theoretical and empiricalgrounds supporting the thinking that equity investors will not bewilling to invest in utilities when debt investors arewilling to do so.The financeability concern may well be overstated.

4.2. The ‘under investment concern’

The financeability concern is closely related with the ‘underinvestment concern’. According to this argument, stockholdersmight be willing to accept some positive NPV projects only if thefirm is financed by equity, but not if it is largely debt financed e infear that the pay-offsmight be large enough to be profitable, but notsufficient to repay the debt-holders. Therefore, some ‘good’ projectsmay be inefficiently rejected.63 The situation is aggravated if there isa possibility of financial distress, because the higher the gearing ofthe firms, the lower the possibility of absorbing financial shocks. Inutilities, it is argued, the firmwill postpone long-term investmentsdemanded by regulators in favour of short-term decisions.64 In theextreme, all of this may lead to under investment.

The under investment concern is unsound. First, it is based uponwrongmanagerial assumptions. On the one hand, it is assumed thatmanagers always act in the interest of shareholders or at least thatshareholders can control managers’ incentives and align themwiththeirs. As seen, that is a weak assumption. On the other hand, if theunder investment problem exists at all, it is erroneous to base theexplanation only on the capital structure. If in general firms withless debt invest more, as the financial evidence shows, there is noevidence showingwhy investment is positively correlated with lessdebt.65 Indeed, agency theories have shown that even if the capitalstructure is 100% reliant on equity, certain managerial attitudesmay lead to under investment.

Second, and perhapsmore essential, important incentives createdby the own regulatory regime must be taken into account. Whilstgenerally PCR leaves regulators a great margin of discretion, theregime only encourages firms tomake improvements that are repaidwithin a single review period. On the one hand, this may createincentives to cutback long-termprogrammesalreadyagreedwith theregulator.66 Sincemany types of infrastructure are durable enough tomake that under investment not result in a decline of quality ofservice or performance, the firm may be tempted to cut back on anagreed investment at thebeginningof theprice capperiod, increasingits profits.67 On the other hand, PCR does not encourage efficiencyimprovements that payback beyond the next price control

with short-term paybacks and make them after the price control, hoping to capturethe savings as profits. Also, the firm may increase its investments as the pricereview approaches, hoping to get a higher cap that allows greater future savings.67 For this reason, with PCR the regulatory burden increases, since the agencymust monitor the firm more closely to discover whether any saving is due toefficiencies rather than deviations from previous commitments.

J. Tapia / Utilities Policy 22 (2012) 8e2116

(e.g.Gómez-Ibánez, 2003:241et seq. andNewbery,1999:50e2). Thatis, PCR in itself providesfirmswith incentives to under invest in capexand quality of service.68 The reason is the lack of regulatorycommitment. Firms will make long-term investments only if theregulator commits to recognise them and incorporate them intofuture price controls. However, the essence of the system is that everyn-years period the price is reset. Intrinsically, a problem of time-inconsistency between short-term and long-term projects exists.69

In sum, the incentives to under-invest are a distinctive problemassociated with PCR regardless of the capital structure of the firm.The under investment problem is not as much associated with thefirms’ financial stability as with the regulatory regime in itself. Theproblem largely derives from the alleged inability of regulators tomake future commitments (see section 5). Therefore, it is at leastdubious that controlling the capital structure is the right way toaddress what is in essence a design problem.70

4.3. The ‘control concern’

The debt model is also disputed on the grounds of managerialcorporate control.71 It is argued that one of the key advantages ofthe equity-based model is that the structure of corporate control isfamiliar and clear. In the event of troubles, whatever the reasonmay be, shareholders have a strong incentive to replace theincumbent management. In contrast, when a company operatesunder a debt-basedmodel, incentives become less clear and heavilydepend on the deeds of covenant that are in place to protect debt-holders’ rights. The ambiguous and poor control increases the risk:weaknesses in decision-making are severely exposed and result in

68 See Armstrong et al. (1994), who formally show that by itself, PCR does nothingto encourage improvements in the quality of service.69 The under investment question might be seen as the ‘the flip side’ of theregulatory commitment problem. The latter is related to the investors’ perception ofrisk (see infra section 5).70 As Newbery (1999: 50) points out: ‘Rate-of-return regulation evolved througha series of landmark court cases in the United States . Price regulation wasdesigned in the United Kingdom to create an efficient system of regulation.’

(emphasis in the original).71 In this sense Currie (2003) and DTI and HM Treasury, 2004.72 Regarding principal-agent problems, see generally Milgrom and Roberts (1992).Note that even though the ‘control question’ is centred on the relation betweenmanagers and principals, there is also an agency problem arising between stock-holders and bondholders in firms with hybrid financial structures (i.e. structureswith presence of both debt and equity) e a problem known as the ‘asset substi-tution problem’ in the financial literature (Myers, 1977). The potential conflict arisesfrom the type of projects that will be taken on by stockholders. Once debt holdershave advanced capital to the stockholders, the latter have an incentive to undertakeprojects riskier than those the former would prefer. Recognising this incentive, debtholders will charge a higher price for debt capital (Jensen and Meckling, 1976). Theagency costs may be attenuated by the use of contracts e covenants, call provisions,conversion rights, etc. e but they can never be eliminated as long as the debtholders cannot perfectly discern if the outcome is the result of uncertainty or is dueto the actions of the manager. In turn, in a regulated environment, this agencyproblem will have an impact in the outcome of the WACC.73 For instance, the DTI and HM Treasury report (2004: 35, para. 99) states that‘Shareholders play an important role in drivingmanagers to respond to the efficiencyincentives of the RPI-X regime. The corporate governance model of shareholderownership provides a clear structure for decision making. However, these incentivescan be reduced or removed in highly geared structures, through a loss of shareholderpressure. Likewise, a consultants’ report argues that ‘The introduction of equity intothe industry at the time of privatisation is seen as the agent of the substantialimprovements in performance and efficiency in the sector. Indeed, the RPI-X regimeis seen as predicated on the active participation of equity, with the profit maximisinginterests of shareholders spurring management on continually to outperform regu-latory settlements’ (Smith andHannan, 2003: 48, para. 6.1.2).With similar reasoning,ORR (2006: 45, para. 5.1) has stated that ‘Although there are clear justifications forNetwork Rail’s current financial structure [100% reliant on debt], it does mean thatthe incentive-based regulatory framework provides weak financial incentives on thecompany to strive for continuous improvements in performance and efficiency’.

a lack of incentives for efficiency. In other words, principal-agentproblems would tend to increase with debt, and hence the overalleconomic incentives of PCR might be undermined.72

Underlying the argument is the (incorrect) assumption that theadoption of PCR in itself implies an equity financial model of thefirms e especially if its ‘high-powered’ characteristics were to bepreserved.73 Since the system works on the basis of the costreductions set by the regulator, it requires agents to be responsiveto those incentives. According to this argument, shareholderswould be the only actors capable of responding correctly. Whilstthey have incentives to outperform expected productivity of thefirm and seek managerial improvements, the only incentive fordebt holders would be not to engage in activities that mayundermine their rather secure repayments.74 Therefore, share-holders would be more suitable than debt-holders to fulfil theregulatory targets. The equity model of private ownershipbecomes not only necessary, but crucial to improve efficiencyunder PCR.

The ‘control concern’ completely misses the target e mainlybecause it pays no attention to the insights of agency theories. Firstand foremost, an equity model of the firm does not necessarilycreate managerial incentives. The ‘control concern’ implicitlyassumes that the incentives of the firm’s managers and share-holders are perfectly aligned. Moreover, it is assumed that thealignment is in favour of the latter e i.e. that managers adopt theirdecisions for the benefit of shareholders.75 This is not always true.Managers have an incentive to over-expand the size and scope ofthe firm to satisfy their own ends at the expense of the share-holders (Jensen and Meckling, 1976). Particularly, managers inprofitable companies are likely to waste money on inefficientinvestment. One of the reasons is the personal benefits associatedwith the so-called ‘empire-building’: a larger firm (allegedly)creates more opportunities for career enhancement and promo-tions, higher rewards and status. In addition, managers may bemore concerned about their own reputation and career. If that isthe case, they have incentives to take short-term actions at theexpense of the long-run shareholder value; exhibit an excessivetendency to ‘herd’ in their investment decisions ignoring their ownprivate information; or simply under-invest to not reveal theirmanagerial ability.76

Indeed, shareholders may intend to exert control overmanagers in an attempt to avoid the misalignment of incentives.On this, however, the ‘control concern’ underestimates collectiveaction problems resulting from dispersed ownership. Primarily,shareholders have an incentive to free-ride. The costs of moni-toring managers are high for an individual shareholder, who mustinvest a vast amount of time and effort to check the firm’sperformance. This problem is especially acute the smaller therelative wealth of each shareholder to the size of the firm. Henceeach shareholder would prefer that another carry out that

74 Shareholders are concerned about the upper part of the probability distributionof all the possible performance outcomes e i.e., above the outcome required to paythe debts. In contrast, claimholders receive nothing of the cash flows above theamount specified in their debt contracts. In accordance, riskier projects reduce theirexpected pay-offs.75 This ‘shareholder value maximization’, according to which shareholders arelegally entitled to demand managerial deference to their interest (even if this islimited by de facto opportunism of managers), is a traditional assumption of theAnglo-American corporate environment. It is normally understood as a sort of‘duty’ to generate (high) profits. Williamson (1984) argues in favour of thisassumption, stating that shareholders are relatively less well protected than otherparties such as workers or creditors. Since shareholders need protection the most,rules should primarily be designed to protect their interests.76 See Stein (2003) for a revision of the literature on these issues.

83 For a critique, Myers (2003: 243) (warning that the free cash flow theory doesnot provide a model for the incentives and actions of managers and does notindicates how they should arrange financing).84 This may be observed from the attempts to apply PCR to non-stockholderowned firms, most notably Network Rail, Glas Cymru (Welsh Water) andRoyal Mail. The key question is how the financial incentives inherent in PCR (e.g. to reduce unit costs) are transmitted. ‘Received wisdom’ holds that thescrutiny of financial markets in which regulated firms must compete forresources, whether debt or equity, are an important element in the transmissionof regulatory incentives. A priori, there is no particular capital structure thatperforms better in this sense than others. However, it may be argued that only

J. Tapia / Utilities Policy 22 (2012) 8e21 17

function. If free-riding is prevalent, the result is a low and ineffi-cient level of monitoring.77