The Determinants of the Students’ Academic Performance in Accountancy Courses: Evidence from...

43

The Determinants of the Students’ Academic Performance in Accountancy Courses: Evidence from Brazil 1. Introduction 1 The standardized large-scale tests, so-called Achievement Tests, were instituted by the Brazilian government on the second half of the 90-ies. The first test was the National Exam of Courses (ENC) so-called Provão that was accomplished over the period from 1996 to 2003 and was subsequently replaced by the National Exam of the Students’ Performance (Enade). According to the Instituto Nacional de Estudos e Pesquisas Educacionais AnísioTeixeira (INEP), the agency responsible for elaboration of the tests and promotion of the studies, research and evaluations on Brazilian Educational System, those tests were instituted as part of the evaluative policy of the courses offered by the Higher Education Institutions (IES). The main objective of both tests is to verify if the knowledge, academic skills and professional competencies of each area under evaluation were developed by students throughout the course. Those knowledge, skills and competences are previously defined by national educational guidelines. More than 470,000 students graduated in 6,5 thousand courses of 26 areas participated in the last edition of the ENC-Provão conducted in 2003 (INEP, 2004). This study focuses on the Brazilian Accountancy students, who participated in either Provão (2002 and 2003) and Enade (2006 and 2009). According to INEP, 22,694 graduating students of the Accountancy course participated in 22,694 exams in 2002, 22,976 in 2003 and 19,040 in 2006. In the Higher Education Census (CES) relative to 2009, the number of students who completed the course was 34,557. The main objective is to analyze the effect from individual and institutional characteristics on academic performance of the undergraduate students in Accountancy, by using the results of the tests accomplished in 2002, 2003 and 2006. The research question guiding this study is: how the students’ characteristics, the background your family, and Higher Education Institutions affect the accounting students’ academic performance? 1 This study was financially supported by CAPES.

Transcript of The Determinants of the Students’ Academic Performance in Accountancy Courses: Evidence from...

The Determinants of the Students’ Academic Performance in Accountancy

Courses: Evidence from Brazil

1. Introduction1

The standardized large-scale tests, so-called Achievement Tests, were instituted

by the Brazilian government on the second half of the 90-ies. The first test was the

National Exam of Courses (ENC) so-called Provão that was accomplished over the

period from 1996 to 2003 and was subsequently replaced by the National Exam of the

Students’ Performance (Enade). According to the Instituto Nacional de Estudos e

Pesquisas Educacionais AnísioTeixeira (INEP), the agency responsible for elaboration

of the tests and promotion of the studies, research and evaluations on Brazilian

Educational System, those tests were instituted as part of the evaluative policy of the

courses offered by the Higher Education Institutions (IES). The main objective of both

tests is to verify if the knowledge, academic skills and professional competencies of

each area under evaluation were developed by students throughout the course. Those

knowledge, skills and competences are previously defined by national educational

guidelines. More than 470,000 students graduated in 6,5 thousand courses of 26 areas

participated in the last edition of the ENC-Provão conducted in 2003 (INEP, 2004).

This study focuses on the Brazilian Accountancy students, who participated in

either Provão (2002 and 2003) and Enade (2006 and 2009). According to INEP, 22,694

graduating students of the Accountancy course participated in 22,694 exams in 2002,

22,976 in 2003 and 19,040 in 2006. In the Higher Education Census (CES) relative to

2009, the number of students who completed the course was 34,557. The main objective

is to analyze the effect from individual and institutional characteristics on academic

performance of the undergraduate students in Accountancy, by using the results of the

tests accomplished in 2002, 2003 and 2006. The research question guiding this study is:

how the students’ characteristics, the background your family, and Higher Education

Institutions affect the accounting students’ academic performance?

1 This study was financially supported by CAPES.

2

To answer this question, it is intended to verify the following: (1) the personal

aspects such as color, gender, age of the students are related to their academic

performance; (2) the academic performance is positively related to socioeconomic

status; (3) the characteristics of the course, such as participation in extracurricular

activities, the type of the academic material used and other inputs are related to

students’ academic performance; (4) the characteristics of the faculty in the educational

institutions, such as higher proportion of teachers with master and doctoral qualification

and the work scheme type among other aspects have a positive effect on students’

performance; and (5) how the educational institution is organized as an university or is

linked to public or private system has significant effect on students' academic

performance.

The relevance of this paper is related to low average result of the Accountancy

students at those tests, as compared to other areas evaluated in 2002, 2003 and 2006.

According to INEP (2003, 2004), the Provão editions 2002 and 2003 consisted of 40

multiple-choice objective questions with five response options, as corresponding to 60%

the exam total value, and three discursive questions corresponding to remaining 40%.

The general average of the Accountancy students was 32.0 on scale from 0 to 100, in

the Provão editions 2002 and 2003. The Enade/2006 is divided into two components.

The first component is General Training (FG) comprising eight multiple-choice

questions and two discursive questions, as corresponding to 25% the total exam. The

second part so-called Specific Component (CE), which includes 26 multiple-choice

questions and four discursive questions, corresponds to 75% the total exam value. This

exam was applied to students who were entering or graduating2 in the area. The general

average, that includes both freshmen and graduating students, was 44.1 in exam of the

General Training (FG) and 25.7 in exam of the Specific Knowledge (CE) (INEP,

2007a). In this last component, the average of the graduating students was 30.0. Among

all 15 areas3 under evaluation, the performance of the Accountancy area in FG was only

ahead Administration (42.1). Moreover, the students obtained the lowest general

average in CE, among all 15 areas3 under evaluation in 2006. This performance of the

2 Freshmen are students who attended the first year, whereas the graduating are those students who are at

the end of last year of the course. These groups of students were subjected to the same exam in

ENADE/2006

3 Administration, Archivology, Library Science, Biomedicine, Accountancy, Economics, Media, Design,

Law, Teacher Education, Music, Psychology, Executive Secretary, Tourism and Theatre.

3

area is among the worst ones, when compared to 15 areas evaluated in 2006 (INEP,

2007). In 2009, the general average achieved by graduating students in Enade was 39.9

in FG exam and 32.6 in CE exam (INEP, 2011).

Em 2009, a média geral obtida pelos estudantes concluintes da área no Enade foi

39,9, na prova de FG, e 32,6, no teste de CE (INEP, 2011). Em 2012, a média geral

obtida pelos estudantes concluintes da área no Enade foi 39,4, na prova de FG, e 32,8,

no teste de CE (INEP, 2011). Na prova de conhecimento específico da área a média dos

concluintes de 2009 foi inferior a 50,0.

However, in either Provão 2002/2003 and Enade/2006, the students indicated

difficulties to answer the exam questions4. The main options noted in Provão/2003

were: they studied the most test contents, but have already forgotten them (34.4%) since

there was a long time they studied most of them; and they studied many of those

contents during the course, but with little understanding (44.2%) (INEP, 2004). In

Enade/2006, a change occurred in the response pattern: only 4.5% graduating students

pointed out non-acquaintance of the content as factor explaining their performance. The

most frequently mentioned reasons were the different way to approach the content in

relation to what is usually used (41.1%) and lack of motivation (35.4%) (INEP, 2007a).

In Provão/2003, the percentages relative to those aspects were 50.6% and 18.8%,

respectively (INEP, 2004). These results of the students' perceptions are evidence for

possible problems in the teaching process, which may have negatively affected the

results of the evaluations.

The accountancy course has strong credencialism characteristics. The

professionals have their privileges guaranteed by legal act. For this reason, the large-

scale evaluations are so important. According to data from the Conselho Federal de

Contabilidade (CFC) relative to 2010a, (the brazilian agency that resembles the

American Institute of Certified Public Accountants - AICPA), there were 292,390 active

accountant records and 76,283 active organizations registered, as being 48,731 under

individual scheme and 27,552 as companies. It is important to emphasize the tendency

for more rigorous requirements concerning to professional accounting practice in Brazil.

The next students graduating in Accountancy will face other mechanisms that will

4 At the end of the test, there is a section in which students express their opinion on this evaluation tool.

4

restrict their entry and permanence in the labor market as Accountants, such as the

Sufficiency Exam and continuing education programs established by Law n. 12249

(2010). According to CFC, in the first edition of the Sufficiency Exam accomplished in

2011, only 30.83% participants who required the Accountant registration were

approved, a percentage considered low by CFC committee members responsible for

accomplishment of the Exam (CFC, 2010). This exam is similar to that accomplished by

AICPA for obtainment of the Certified Public Accountants (CPA).

This scenario provides evidence that professional training and qualification can

have preoccupying deficiencies. In Brazil, as pointed out by Crespo and Reis (2009), a

reduction in importance of the employee to have only a bachelor’s degree (in terms of

the remuneration differential) occurred over the period from 1982 to 2004, due to the

increased supply of qualified professionals. This fact, coupled with the increased

requirements for professional practice, emphasizes the importance of the accounting

education quality.

The main scientific works that motivated the use of the theoretical framework of

the economics of education were Hanushek (1979, 1987) and Hanushek and

Woessmann (2011). In Brazil, the studies conducted by Albernaz, Ferreira and Franco

(2002), Machado et al. (2008), Franco and Menezes-Filho (2009) particularly in

economics area have emphasized the primary education. It is possible to identify

internationally and in the case of Brazil, a pattern of results that points out a positive

and significant effect of the socioeconomic background on students` performance at all

educational levels.

There is significant international literature on education at higher level. For

example, Betts and Morell (1999), using the data from 5,000 undergraduate students at

the University of California, concluded that the personal background, the origin of high

school and the experience level of the high-school teachers significantly affect the

students’ performance in Grade Point Average (GPA). Cohn, Cohn, Balch and Bradley

Jr. (2004) evaluated the degree at which the score in the Scholastic Aptitude Test

(SAT), the average score in GPA and a categorical classification of the secondary

schools predict student performance on GPA, based on data from University of South

Carolina relative to period from 2000 to 2001. The results suggest the SAT score to be

related to academic success at graduation level. However, its requirement can reduce the

5

chances of the men and non-white students to be selected for a scholarship. Horowitz

and Spector (2005) used the GPA in order to verify the impact of the secondary school

(public x private) upon performance of 15,270 students enrolled at Ball State University

and proceeding from secondary school (public x private), during a semester in 2002.

The authors concluded that, although the effect is small, the students from religious

secondary schools achieved better performance than the students from private and

public schools. However, this effect disappears during graduation.

In Brazil, it is highlighted the scientific works carried out by Soares, Ribeiro

and Castro (2001), Gracioso (2006), Diaz (2007), Moreira (2010) and Rezende (2010),

who focused on context of other knowledge areas. Soares, Ribeiro and Castro (2001)

compared the score obtained by students in the selection test (vestibular) for higher

education at the Federal University of Minas Gerais State, with Provões of Law,

Administration and Civil Engineering courses, which were accomplished over the

period from 1996 to 1999. The evidences suggested a significant influence from the

socioeconomic conditions and previous performance of the students on their academic

performance. Gracioso (2006) focused upon effect of the school and concluded that the

use of microcomputers by students, the skills developed throughout the course and

English skills are important to explain the performance of the Administration Course’

students in Provão 2003. Moreira (2010) investigated the effect from the institutional

factors on students’ performance in areas of Biology, Civil Engineering, History and

Pedagogy in Enade 2005. The author found significant variations among the effects

from the institutional factors upon performance, as depending on the course and

administrative IES category. Diaz (2007) focused on performance of the higher

education students in the Management, Law and Civil Engineering courses, who

participated in Provão 2000. The family income has significant influence, but in a

nonlinear way. The institutional factors such as qualification and working conditions of

the faculty and the use of research activities as strategy for teaching/learning were

significant, but with reduced magnitude. Rezende (2010) analyzed the effect from

policy adoption of an accountability system in Higher Education, particularly during the

ENC period, from 1996 to 2003, upon IES performance. The evidences of this study

indicated that ENC policy had positive effect on the proportion of the teachers’

exclusive dedication, number of the vacancies offered, candidates inscribed, and

6

students registered. According to the author, this effect is differentiated according to

IES organizational structure.

In Accountancy context, the studies carried out by Andrade and Corrar (2007),

Cruz, Corrar and Slomski (2008) and Souza (2008) are distinguished. Andrade and

Corrar (2007) also used the data from Provão 2002 and, by mean tests, he concluded

that the academic (research activities, dedication to studies) and economic variables

(income, parental education level) are related to different academic performance of the

students, except for different races (majority x minorities) and frequency in using the

library. Cruz, Corrar and Slomski (2008) used the mean tests and concluded the updated

domain of the discipline contents, the teaching technique employed and the type of the

didactic resource used in classroom to be significantly associated with differences in the

educational performance achieved by students in Provão 2002. Souza (2008) used the

Course Performance Index (IDC) of Enade 2006 as proxy for educational outcome.

According to results, the following variables significantly affected the students´

academic performance: the high school from which students came, the father's

educational level, the student’s personal effort in the course, the fact the student to work

or not and family income. Another finding was the negative correlation between

maternal education and performance in the course. However, on the whole, it was

observed that parental education has positive influence on prediction of the students’

performance in the accountancy courses, in Enade. However, those studies were not

based on education economy field and their analyses were based on mean tests and

cross-section regressions.

This study aims to provide an original contribution, when basing the analyses on

more recent nationwide database and focusing on a test used as political evaluation of

the academic knowledge obtained during the undergraduate course and not on a test for

Admission of students to graduation. Furthermore, this article focus on student’s

performance in Accountancy in Brazil during the years 2002, 2003 and 2006, by using

the theoretical framework of the economics of educations. In general, our results

suggest the existence of significant association between the graduating students’

academic performance with certain characteristics, such as hours dedicated to studies, to

have attended the public high school, and some inputs from educational institutions

such as teachers who master properly the content of the courses. Those results can be

7

helpful to analyze the implications of either individual choices and educational policies

adopted by institutions concerning to students’ performance.

This article has four sections, besides this introduction. The next section

describes the Brazilian Higher Education System and the academic achievement tests.

The third section presents the hierarchical linear models of the academic performance.

The fourth section describes the data set and analyzes the results. The fifth section

presents the final comments.

2. The Higher Education System and Tests of the Brazilian Academic Performance

2.1. The Brazilian System of Higher Education

In Brazil, the courses offered by the Higher Education System (SES) are

distributed between the public and private IES. These undergraduate courses are offered

under the following modalities: presential, on-line courses (EAD) and regular courses.

The SES places are offered by different organizational structures, by

administrative category and academic organization. The classification based on

administrative categories encompasses the federal, state, municipal and private

institutions, whereas the categorization by academic organization comprises the

universities, university centers, integrated colleges, colleges, superior schools and

institutes and technical education centers. The knowledge areas offered by SES are

heterogeneous and generally refer to traditional careers in the labor market, such as

Medicine, Nursing, Administration, Civil Engineering, etc.

The Brazilian government has continuously adopted policies to increase the

supply of places and expansion of SES. According to CES consolidated data, this policy

was evident from the 70s. The actions of those policies are reflected on evolution of the

number of places offered for Superior Education (ES); in 1970, they totalized 145,000,

whereas in 1971 they reached 202,110, as increasing 39.4% and ending the decade with

402,694 places offered in 1979. Despite the slower rhythm, this growth trend continued

in the 80s, with 15.3% increase in places offered, that is 404,814 in 1980 to 466,794 in

1989. In the 90s, the increase was 92.8%. The outcomes from those policies can also be

observed in the enrollment growth rate between 1995 and 2009 in SES courses.

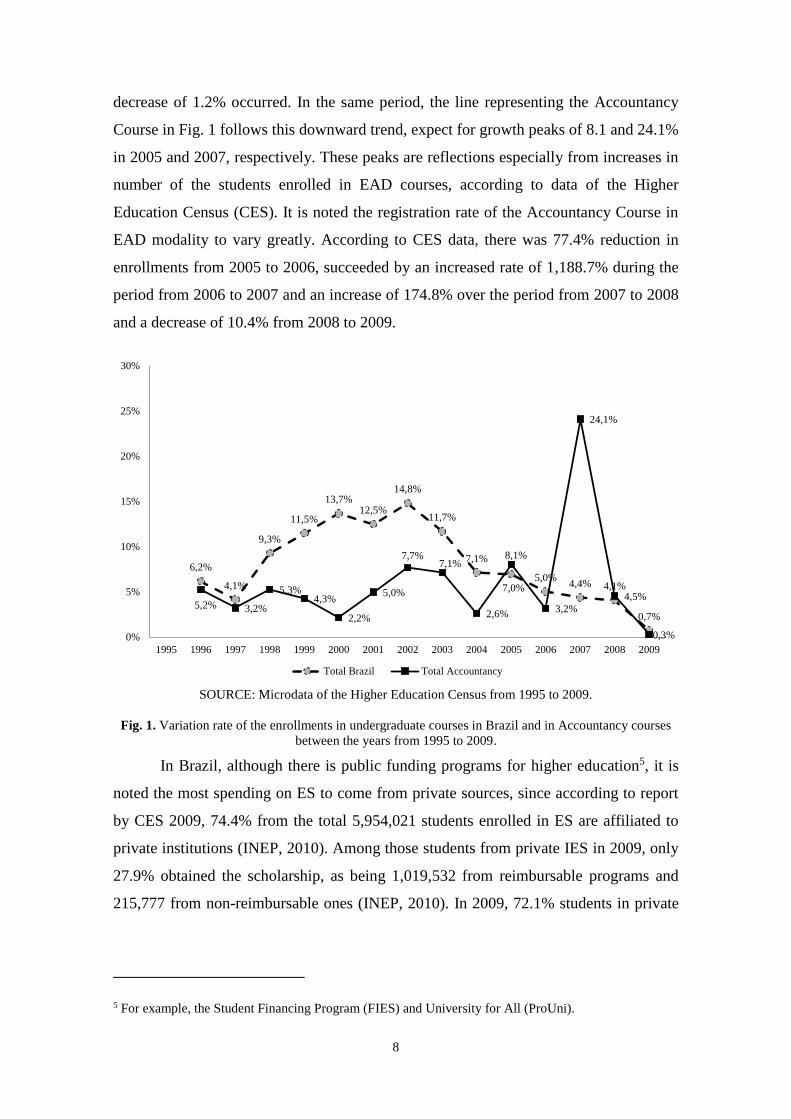

According to Fig. 1, it increased over the period from 1997 to 2002, as reaching a peak

of 14.8%. From 2003 to 2009, however, there was a downward trend and, in last year, a

8

decrease of 1.2% occurred. In the same period, the line representing the Accountancy

Course in Fig. 1 follows this downward trend, expect for growth peaks of 8.1 and 24.1%

in 2005 and 2007, respectively. These peaks are reflections especially from increases in

number of the students enrolled in EAD courses, according to data of the Higher

Education Census (CES). It is noted the registration rate of the Accountancy Course in

EAD modality to vary greatly. According to CES data, there was 77.4% reduction in

enrollments from 2005 to 2006, succeeded by an increased rate of 1,188.7% during the

period from 2006 to 2007 and an increase of 174.8% over the period from 2007 to 2008

and a decrease of 10.4% from 2008 to 2009.

SOURCE: Microdata of the Higher Education Census from 1995 to 2009.

Fig. 1. Variation rate of the enrollments in undergraduate courses in Brazil and in Accountancy courses

between the years from 1995 to 2009.

In Brazil, although there is public funding programs for higher education5, it is

noted the most spending on ES to come from private sources, since according to report

by CES 2009, 74.4% from the total 5,954,021 students enrolled in ES are affiliated to

private institutions (INEP, 2010). Among those students from private IES in 2009, only

27.9% obtained the scholarship, as being 1,019,532 from reimbursable programs and

215,777 from non-reimbursable ones (INEP, 2010). In 2009, 72.1% students in private

5 For example, the Student Financing Program (FIES) and University for All (ProUni).

6,2%

4,1%

9,3%

11,5%

13,7%12,5%

14,8%

11,7%

7,1%

7,0%5,0%

4,4% 4,1%

0,7%5,2% 3,2%

5,3%4,3%

2,2%

5,0%

7,7%7,1%

2,6%

8,1%

3,2%

24,1%

4,5%

0,3%0%

5%

10%

15%

20%

25%

30%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Total Brazil Total Accountancy

9

IES paid their studies with their own resources, with their family support or through

other sources.

According to CES 2009, the Brazilian SES offered 28,671 undergraduate

courses, from which 20,043 were linked to private IES and 8,628 to public institutions,

where the average number of students registered by course amounted 221 and 177,

respectively. The distribution of the students enrolled by IES were, on average, 2,141

students per private institution, whereas in public IES were 6,220. In case of the

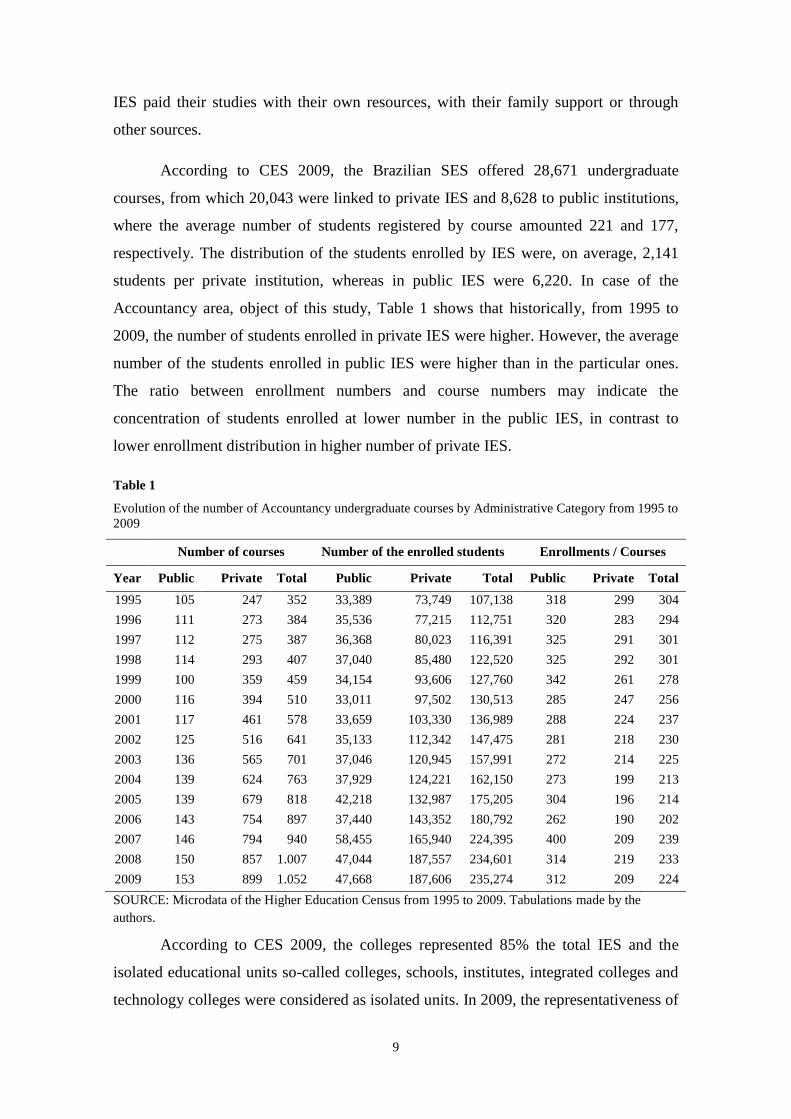

Accountancy area, object of this study, Table 1 shows that historically, from 1995 to

2009, the number of students enrolled in private IES were higher. However, the average

number of the students enrolled in public IES were higher than in the particular ones.

The ratio between enrollment numbers and course numbers may indicate the

concentration of students enrolled at lower number in the public IES, in contrast to

lower enrollment distribution in higher number of private IES.

Table 1

Evolution of the number of Accountancy undergraduate courses by Administrative Category from 1995 to

2009

Number of courses Number of the enrolled students Enrollments / Courses

Year Public Private Total Public Private Total Public Private Total

1995 105 247 352 33,389 73,749 107,138 318 299 304

1996 111 273 384 35,536 77,215 112,751 320 283 294

1997 112 275 387 36,368 80,023 116,391 325 291 301

1998 114 293 407 37,040 85,480 122,520 325 292 301

1999 100 359 459 34,154 93,606 127,760 342 261 278

2000 116 394 510 33,011 97,502 130,513 285 247 256

2001 117 461 578 33,659 103,330 136,989 288 224 237

2002 125 516 641 35,133 112,342 147,475 281 218 230

2003 136 565 701 37,046 120,945 157,991 272 214 225

2004 139 624 763 37,929 124,221 162,150 273 199 213

2005 139 679 818 42,218 132,987 175,205 304 196 214

2006 143 754 897 37,440 143,352 180,792 262 190 202

2007 146 794 940 58,455 165,940 224,395 400 209 239

2008 150 857 1.007 47,044 187,557 234,601 314 219 233

2009 153 899 1.052 47,668 187,606 235,274 312 209 224

SOURCE: Microdata of the Higher Education Census from 1995 to 2009. Tabulations made by the

authors.

According to CES 2009, the colleges represented 85% the total IES and the

isolated educational units so-called colleges, schools, institutes, integrated colleges and

technology colleges were considered as isolated units. In 2009, the representativeness of

10

the universities and university centers were 8% and 5.5%, respectively. The IES

distribution by administrative category was 89.4% private institutions and 10.6% public

institutions fractionated on 4.1% federal, 3.6% state and 2.9% municipal institutions.

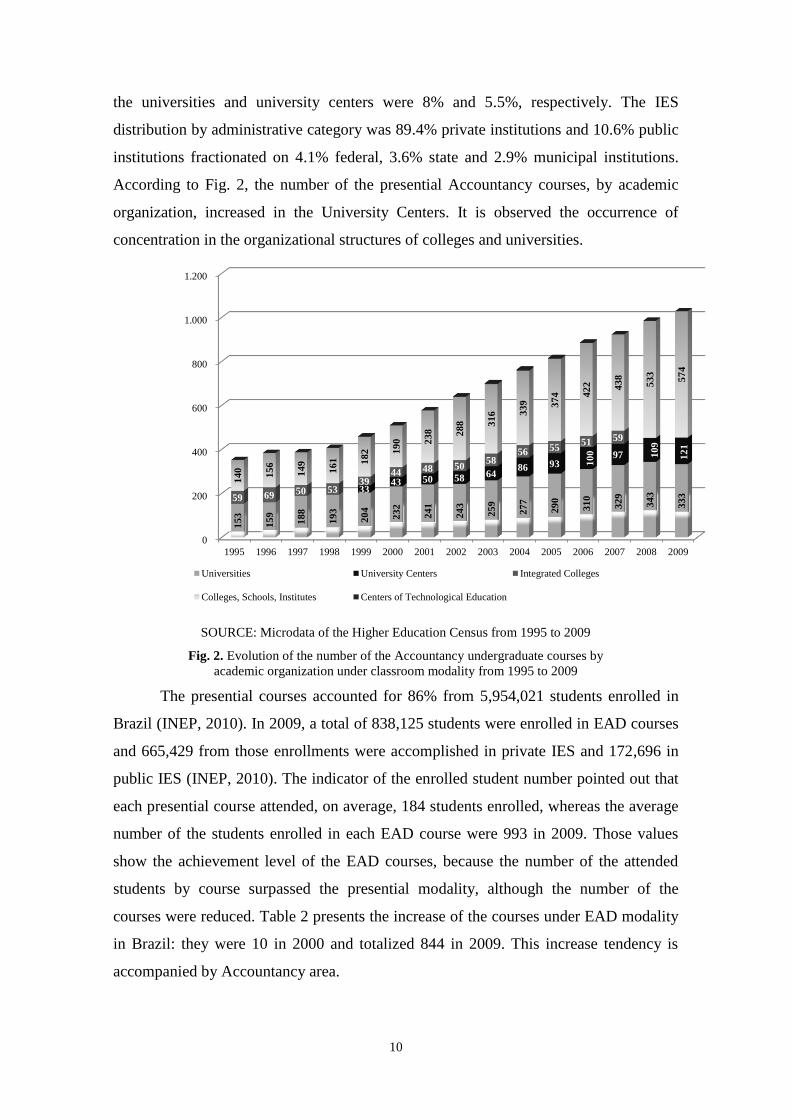

According to Fig. 2, the number of the presential Accountancy courses, by academic

organization, increased in the University Centers. It is observed the occurrence of

concentration in the organizational structures of colleges and universities.

0

200

400

600

800

1.000

1.200

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

15

3

15

9

18

8

19

3

20

4

23

2

24

1

24

3

25

9

27

7

29

0

31

0

32

9

34

3

33

3 33

43 50 58 64 86 93 1

00

97 10

9

12

1

59 69 50 53 39

44 48 50 58

56 55 51 59

14

0

15

6

14

9

16

1

18

2

19

0

23

8

28

8

31

6

33

9

37

4

42

2

43

8

53

3

57

4

Universities University Centers Integrated Colleges

Colleges, Schools, Institutes Centers of Technological Education

SOURCE: Microdata of the Higher Education Census from 1995 to 2009

Fig. 2. Evolution of the number of the Accountancy undergraduate courses by

academic organization under classroom modality from 1995 to 2009

The presential courses accounted for 86% from 5,954,021 students enrolled in

Brazil (INEP, 2010). In 2009, a total of 838,125 students were enrolled in EAD courses

and 665,429 from those enrollments were accomplished in private IES and 172,696 in

public IES (INEP, 2010). The indicator of the enrolled student number pointed out that

each presential course attended, on average, 184 students enrolled, whereas the average

number of the students enrolled in each EAD course were 993 in 2009. Those values

show the achievement level of the EAD courses, because the number of the attended

students by course surpassed the presential modality, although the number of the

courses were reduced. Table 2 presents the increase of the courses under EAD modality

in Brazil: they were 10 in 2000 and totalized 844 in 2009. This increase tendency is

accompanied by Accountancy area.

11

Table 2

Evolution of the number of undergraduate courses in Brazil and the Accountancy Course in classroom

and without the presence in classroom over the period from 1995 to 2009.

Total Accountancy Course Representativeness

Year Presential EAD Total Presential EAD Total %

Presential

%

EAD

%

Total

1995 6,252 0 6,252 352 0 352 6 0 6

1996 6,644 0 6,644 384 0 384 6 0 6

1997 6,132 0 6,132 387 0 387 6 0 6

1998 6,950 0 6,950 407 0 407 6 0 6

1999 8,878 0 8,878 459 0 459 5 0 5

2000 10,585 10 10,595 510 0 510 5 0 5

2001 12,155 14 12,169 578 0 578 5 0 5

2002 14,399 46 14,445 641 0 641 4 0 4

2003 16,453 52 16,505 701 0 701 4 0 4

2004 18,644 107 18,751 763 0 763 4 0 4

2005 20,407 189 20,596 816 2 818 4 1 4

2006 22,101 349 22,450 886 11 897 4 3 4

2007 23,488 408 23,896 923 17 940 4 4 4

2008 24,719 647 25,366 985 22 1,007 4 3 4

2009 27,827 844 28,671 1,028 24 1,052 4 3 4

SOURCE: Census microdata of the Higher Education from 1995 to 2009. Own tabs.

Along the period under study, most IES are private; there is lower concentration

of the students enrolled in public IES, who are also at lower number; and the enrollment

rate tends to decline. This reduction may be due to existence of idleness, since

occupancy rates show that over 50% places are not filled in ES. This context can

generate the SES closing and merging of institutions, possible adjustment of costs and

fees charged by private IES for their services and the loosening of the selection process

of future students.

It is emphasized that the scenario presented above refers to the period after

implementation of the SES regulatory policies, that were institutionalized especially in

the 90s. Those policies helped the implementation of either measurement tools and

evaluation of the players involved in the SES. Those tools were developed in order to

create quality of education indicators to subsidize the systematization of the evaluation

process of the quality of Higher Education and the national policies.

12

2.2. The Brazilian Academic Performance Tests

In order to evaluate the skills and academic performance in SES ambit, some

tests were institutionalized by the Brazilian government through Law no. 9131 (1995),

which created the National Course Exam (ENC). This exam so-called Provão was

conducted during the period from 1996 to 2003 and can be considered as starting point

for implementation of an evaluation system of the higher education in the country.

Besides ENC, later the Higher Education Census (CES) and the Evaluation of the

Education Conditions (ACE) were created, through visits of the external committees to

Higher Education Institutions (IES). INEP, a federal agency affiliated to Ministry of

Education and Sports, the current Ministry of Education (MEC), has the responsibility

for accomplishing periodic evaluations in institutions and higher level courses. This

process is intended to evaluate the quality and efficiency of teaching, research and

extension.

In 1996, INEP started the implementation of the Provão, by applying the first

exam for courses in Management, Law, and Civil Engineering. Until the end of the

exam in 2003, twenty six areas of knowledge participated in the test (INEP, 2004, p. 5).

The organization, elaboration and application of the exams were in charge of INEP in

partnership with other institutions. The ENC-Provão was annual and should include

minimum contents established and reported previously, for each course. The inclusion

of minimum contents aimed to assess the knowledge, skills and abilities acquired by

students at completion stage of the undergraduate courses (INEP, 2002, 2003). The

exams could be composed by multiple choice questions and discursive ones or exams

entirely consisting of discursive questions (INEP, 2003a). The adopted exam model was

under responsibility of each Course Commission (INEP, 2003a).

The Law n. 9131 (1995) defined the results from evaluation of the courses to be

broadly divulged to society by MEC. Those results were recorded on the student's report

description, concepts from A to E. The results from Exam and the reports by experts

affiliated to MEC were the basis for the Board of Higher Education (CES) to decide

about IES periodic recertification, according to Law n. 9131 (1995). This determination

allowed for decertification of courses that, according to CES, were not meeting the

educational quality standards previously established by MEC. For example, those

courses that obtained the concepts D and E in the last three exams could be closed.

13

In addition to Exam, each enrolled student received in advance, at his/her

residence, a questionnaire-survey, which should be devolved on exam day, from which

the goal was to collect the sociocultural and socioeconomic data and the student´

expectations regarding the characteristics of the courses, the resources and available

facilities, curriculum structure and teacher performance (INEP, 2003a). Students also

completed a questionnaire of impressions soon after exam, in order to generate

information that aimed at improving the next exams, particularly in relation to their "[...]

clarity and objectivity of statements, adequacy of information provided for resolution of

the questions, adequacy of the time for accomplishment of the exam and the difficulty

level and extent of the exam "(INEP, 2003a, p. 44).

In 2004, through Law no. 10861 (2004) which established the National System

of Higher Education Evaluation (SINAES), the Brazilian government made changes in

ES evaluation process and replaced the ENC by the National Exam of Student

Performance (Enade). Both exams aim to get knowledge, academic skills and

professional competencies, previously defined by educational guidelines developed by

the students along the course. Those aspects were evaluated at different stages of the

student’academic life. In the case of Provão, the exam was applied to graduating

students.

There are two important differences in Enade. The first one is that two distinct

groups of students, at different graduation times, are selected at random to participate in

exam. The first group, considered as entering students, must be coursed until the end of

the first year. The second group, the graduating students, are at the end of the last year

of the course. Both groups answer the same questions. The INEP purpose is to evaluate

the students’ performance throughout the course, with regard to knowledge, academic

abilities and professional skills.

The second difference is that Enade is divided into two components: General

Education (FG) and the Specific Component (EC). The questions of the General

Education component, common to all courses, seek to evaluate "the formation of an

ethical and competent professional who is committed to society in which he lives"

(INEP, 2007). The questions of the Specific Knowledge component seek to evaluate

whether students have developed, in the training process, the knowledge, skills and

14

competencies predefined by specialist committees, which are based on the National

Curriculum Guidelines for each course under evaluation.

For elaboration of the exam and definition of the desired objectives in relation to

attributes cited, INEP relies on specialist committees composed by teachers with

minimum Master title and yearly appointed by INEP. As FG exam is unique, only one

committee is responsible for its elaboration.

Thus, based on definition by Ryans and Frederiksen (1955), it is observed the

tests such as Provão and Enade to function as tools for measuring the educational

standards from which the objects or phenomena to be measured are the knowledge,

skills and individual achievements. In this study, the term ‘academic achievement’ will

be characterized according to Helmke and Schrader (2001), as the result from cognitive

learning produced by the process of education or cognitive knowledge that is intended

to teach in the school context. According to the authors, those cognitive results mainly

comprise the declarative knowledge of how to make and the individual ability to solve

problems and develop strategies.

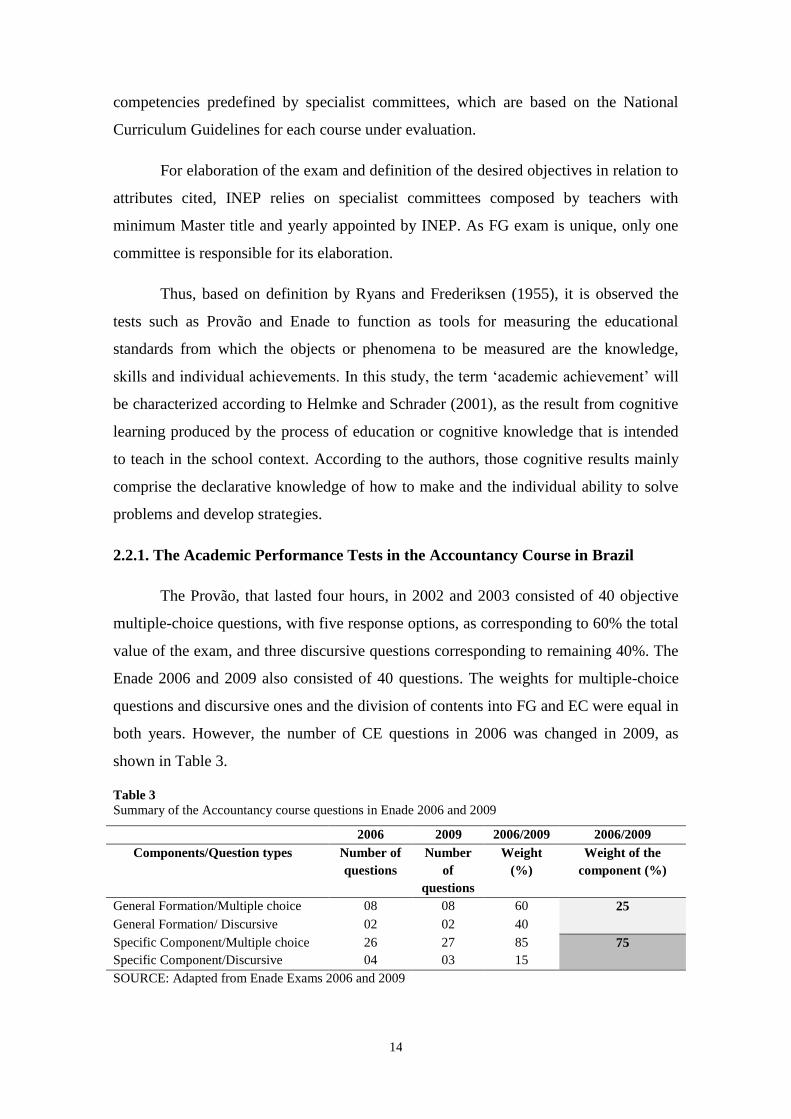

2.2.1. The Academic Performance Tests in the Accountancy Course in Brazil

The Provão, that lasted four hours, in 2002 and 2003 consisted of 40 objective

multiple-choice questions, with five response options, as corresponding to 60% the total

value of the exam, and three discursive questions corresponding to remaining 40%. The

Enade 2006 and 2009 also consisted of 40 questions. The weights for multiple-choice

questions and discursive ones and the division of contents into FG and EC were equal in

both years. However, the number of CE questions in 2006 was changed in 2009, as

shown in Table 3.

Table 3

Summary of the Accountancy course questions in Enade 2006 and 2009

2006 2009 2006/2009 2006/2009

Components/Question types Number of

questions

Number

of

questions

Weight

(%)

Weight of the

component (%)

General Formation/Multiple choice 08 08 60 25

General Formation/ Discursive 02 02 40

Specific Component/Multiple choice 26 27 85 75

Specific Component/Discursive 04 03 15

SOURCE: Adapted from Enade Exams 2006 and 2009

15

Based on Ministerial Ordinances n. 2250 (2001) and n. 3187 (2002) and INEP n.

80 (2006) and n. 83 (2009), it may be noted that all committees responsible for

elaborating the guidelines for knowledge question contents in the Accountancy area

were composed by teachers with at least Master degree, from different Brazilian regions

and different types of institutions. In addition, an INEP-conducted study analyzed the

educational projects of the courses under evaluation for the commission to establish

guidelines for elaboration of the exam (INEP, 2004).

Furthermore, by means of guidelines of the Provão 2002/2003 established by

Ministerial Decrees n. 3018 (2001a) and n. 3818 (2002a), it was verified that no great

changes occurred in their content over the period from 2002 to 2003. It is only noted a

more detailed specification of the desired profile, skills and abilities to be evaluated. In

the guidelines established by INEP Ordinances n. 121 (2006a) and n. 125 (2009) in

Enade years, the increase referring to component of the FG exam occurred. The main

changes in formats of both Provão and Enade were decided by committees, especially in

relation to specific knowledge.

Those guidelines were the basis for guiding the elaborators of the exams on how

to evaluate the contents. For example, in all tests, there was no specific question to

evaluate the student's competence to adequately express in Portuguese (language spoken

in Brazil). In the discursive questions, however, this competence was required. The

ethical behavior and the contents of Administration, Economics and Law were broached

in questions with focus on Accountancy, but with interdisciplinary nature. The

knowledge of mathematics and statistics were required to solve questions of other

topics. So, besides seeking to verify the content knowledge, each question was designed

to capture a set of interdisciplinary skills. For example, in Provão 2002, in the same

question were collected knowledge in law, professional ethics and also logical

reasoning, analysis and emission of critical judgments.

3. The Hierarchical Linear Model of Academic Performance

An econometric technique often used to estimate the educational production

function is the regression by Ordinary Least Squares (OLS) (Betts & Morell, 1999;

Cohn, Cohn, Balch, & Bradley JR., 2004; Horowitz & Spector, 2005). However, some

authors such as Hanushek and Woessmann (2011) show that although the robustness of

the method, its estimates need to be cautiously interpreted when a broad range of inputs

16

is used because it can generate estimation biases in the coefficients of variables because

endogeneity. Due to this fact, some studies have used the regression techniques with

hierarchical structure (Soares, Ribeiro, & Castro, 2001; Albernaz, Ferreira, & Franco,

2002; Diaz, 2007). According to Raudenbush and Bryk (2002), the Hierarchical Linear

Models (HLM) enable the analysis of data which structure indicates the existent of

correlation among individuals pertaining to the same group.

There are different HLM6 models. This study uses the general model with two

levels, which is composed by two sub-models so-called Level 1 and Level 2

(Raudenbush & Bryk, 2002) in order to estimate the educational production function for

each period under analysis. In this model, the data referring to each student (i) are

contained within IES representing (j) groups of students. The Level 1 model reproduces

the relationship between an explanatory variable (Xij) with a dependent variable (Tij) and

the Level 2 Model captures the influence from IES factors. Formally, there are i=1, .., n,

units of the Level 1 within j = 1, ..., J units of the Level 2. In Eq. (1) and (2) we to show

the general model equations of two levels, with the use of the notation by Raudenbush

and Bryk (2002) and the framework of the educational production function (Todd &

Wolpin, 2003; Harris, 2010; Hanushek & Woessmann, 2011):

Level 1 (students) rXRPFAT ijpijpjijjijjijjijjjij ...43210

, (1)

Level 2 (IES) uW...IRP qjhjqhj33qj22qj11q0qqj . (2)

The terms β0j, ... βpj are coefficients of the Level 1 and the terms γq0, ... yqh are

coefficients of the Level 2, which can be understood as fixed effects. The term Xij is the

exogenous variable of the Level 1, which represents the students’ individual skills (Aij),

their personal characteristics, their family background (Fij), possible effects from the

pairs (Pij) and school resources (Rij). The term Wj represents the exogenous variable of

the Level 2, which may be linked to effects of the pairs (P1j), to school resources (R2j)

and to institutional peculiarities of either school and education system (I3j). There are p

exogenous variables (Xij ) for Level 1 and h explanatory variables (Wj) for Level 2. The

equations present intercept and slope grade random (βqj) for all p exogenous variables

(X i j) Level 1, explained by h variables (Wj) Level 2. The term ri j are the random effects

of the Level 1and in the case of Level 2 it is represented by the term µq j. The terms of

6 The other models are described in: Raudenbush; Bryk (2002), Raudenbush; Bryk; Congdon (2007) and

Rabe-Hensketh; Skrondal (2008).

17

errors rij and µq j must be mutually independent with normal distribution and zero mean.

The variance (σ²) Level 1 (within groups) is represented by the term rij. The variance

and covariance (τ00, τ01) of the components Level 2, also so-called variance between

groups, refer to the term µq j referring to group level.

The substitution of the Eq. (1) in Eq. (2) results the general model given by Eq. (3):

rXuuXWWXT ij

p

1qqijqjj0

p

1qqijkjqk

h

1k

h

1kkjk0

p

1qqij0q00ij

, (3)

In Eq. (3), the term Tij is the score of the student (i) enrolled at IES (j) in the

Exam (Provão 2002/2003 and Enade 2006). The term Xqij represents the matrix of

exogenous variables to the score at Level 1. The terms µij and rij are vectors of i.i.d.

error terms, that assemble the unobservable factors affecting the score of the students in

IES (j). The intercept (γ00) refers to average of the students’ score minus the average

effects of the explanatory variables Xqij, together with the coefficient vector of the

exogenous variables WkJ, which may vary between individuals according to IES they

attended. The variance and covariance matrix of the model is represented for Level 1 by

the term σ² (variance between students) whereas for Level 2 of the IES they would be

represented by notations: var(uqj) = τ2q(q=1,..., p) e cov(uqj, ukj) = τqk(q, k= 1, ...., p).

As pointed out by Raudenbush and Bryk (2002), the terms level 1 βqj, that are the

slope degree, that is the slope parameters, can be treated at Level 2 as fixed coefficients,

nonrandom variable coefficients and random coefficients of models with random

intercepts and slope. The first option is the effect from explanatory variables (Xqij) to be

treated as constant between units of Level 2. In other words, as fixing the coefficients at

Level 1, implies that:

βqj = γq0 , (4)

where γq0 is a common effect from variables (Xqij) for each IES Level 2, that is, the

effect from coefficients (βqj) is fixed between units of Level 2. The second option would

be the slope of the term βqj in function of an average value of the term γq0 added with a

random effect of each unit from Level 2:

.u0qqj qj (5)

In this case, the term ßqj has random behavior. The third option assumes the

slope degree to depend on term Wj , and this implies that:

.uqjW0qqj j1q (6)

This third option delineates part of the variation in the slope of the term βq j to be

explained by exogenous variables (Wj) of the second level, but there is a random

18

component (uqj) that is the error term. In this case, the effect from term Wj is considered

in the model and the residual variation in term βq j which is Var (uqj) = τqj is

insignificant.

Raudenbush, Bryk and Congdon (2007) affirm that the dimension of the T

matrix depends on the number of the coefficients at Level 2, which are specified with

random variation. It is assumed that the set of the different explanatory variables of

Level 2 can be used in each equation (Q + 1) of the Model at Level 2.Although the

coefficients (γqo) Level 2 may vary according to IES attended by students, in this work

only the intercept Level 1 (β0j) presents random variation, according to IES. This means

to adopt the model that estimate different intercepts for IEs and for each explanatory

variable, either Level 1 and Level 2, for which different coefficients are separately

estimated for each IES.

Raudenbush and Bryk (2002) suggest the use of the maximum likelihood

method for unbalanced data, that is, when there are different sample sizes at Level 1 for

each organizational unit Level 2. In such cases, the integral maximum likelihood

method generates more consistent and efficient estimators. Based on this

recommendation, the maximum likelihood method, in full or integral concept, is used in

the present study in order to estimate the coefficients because unbalanced structure of

the micro data. According to Favero et al. (2009), this method estimates the variance

and covariance parameters and the fixed effect coefficients of Level 2 by maximizing

their joint probability.

Raudenbush and Bryk (2002) pointed out the need for performing some of the

tests: fixed effect coefficients, random coefficients of Level 1 and variance-covariance

for all components. The first test is carried out to verify whether there is intra-class

correlation as well as the occurrence of one more residual term. The accomplishment of

this test requires the estimation of the unconditional or null model, from which the

specification is given by Eq. (7) and (8):

ry ijj0ij , (7)

u j000j0 , (8)

This null model allows to calculate the variance of the Level 1 (σ²) or between

students and the variance of the Level 2 (τ0²). With the terms related to variances of the

Level 1 and Level 2, the intraclass correlation is calculated based on Eq. (9).

19

220

20

, (9)

In this expression, the coefficient (ρ) represents the proportion of the total

variance among groups (Level 2 units). It is expected the resulting coefficient (ρ) to be

different from zero. The intra-class correlation is called by Bryk and Raudenbush

(2002) as the cluster effect and it is applied only to models with random intercepts.

Another important assumption to be verified is whether there are significant differences

among the means of the groups (j). The null hypothesis is that no significant differences

occur among means of the groups (j). The F test is a tool to test it. To test the fixed

parameters (γ), the null hypothesis is: H0: γq j = 0.

The Wald-typed test is recommended by Raudenbush, Bryk and Congdon (2007)

to check the statistical significance of the estimated variances and covariances, from

which the structure enables to test more than one coefficient. Its null hypothesis is H0:

Cγ = 0, which considers the statistical distribution of χ². To test the hypothesis for

normality of the error terms uqj and rij, the results from Shapiro-Francia W' test, the

behavior and the parameters obtained by histogram of both residues are verified. In

addition to those tests, Bryk and Raudenbush (2002) suggest the calculation of an

auxiliary statistics so-called reduced proportion of the variance or explained variance,

which allows the comparison between the estimated variance of the null model of each

separate component with that one of another model. Thus, the specifications for

calculation of the proportion of the explained variance at Level 2 and Level 1 are given

by Eq. (10) and (11):

ˆ

ˆˆR 2

0

21

202

2

, (10)

ˆ

ˆˆR 2

0

21

202

1

, (11)

With equation 10, the proportion of the explained variation Level2 ( R22

) is

calculated. The result from equation 11 is the proportion of the variance explained at

Level 1 ( R21

). The terms ̂ 20

and ̂ 20

are estimates of the residual variance of the null

model Level 2 and Level 1, respectively, whereas the terms ̂ 21

and ̂ 21

are estimates of

the residual variance of the conditional model to be compared with the null model Level

2 and Level 1, respectively.

20

According to Todd and Wolpin (2003), the models of the educational production

function are potentially subjected to endogeneity problems, especially due to absence of

unobservable inputs or explanatory variables omitted, such as students’ innate ability. In

this context, the recommendations by Rabe-Hensketh and Skrondal (2008) were

followed. According to those authors, the Hausman test should be used in order to

check the consistency of the estimators and the possible specification problems through

hypothesis for endogeny. The null hypothesis of the test allows to verify between

estimates of two distinct models which one is efficient, consistent and more adequately

specified. This test also indicates whether the most appropriate model is the one of fixed

effects or random effects. The adoption of the fixed effect model allows to use only the

information within groups. The authors suggest more accurate estimates of the

coefficients to be obtained, when information from both models within and among

groups are used. The Hausman test is used in case of the hierarchical models, especially

for evaluating the efficiency and consistency of the parameters estimated.

Taking into account this research objectives, the information concerning to

either large-scale tests and structure of the hierarchical linear model, the data referring

to each student (i) are contained within IES (j), that represent (j) groups of students at

first level and the data of the courses and institutions (j) as second level.

4. DATA AND RESULTS

4.1. Data

The main sources of the data used in this study were the micro data from Provão

(1997 to 2003), Enade (2006) and CES (2006 to 2009), provided by INEP. The data of

either Provão and Enade not allow for identification of the students. However, it is

possible to know the undergraduate course and IES to which the students were

affiliated. CES beheld data of the courses and institutions of the higher education

system and are divided into two files. The first file consists of data from each

undergraduate course. The second file provides information on institutions to which the

courses were affiliated. This form of the data availability allowed the information to be

considered with a hierarchical structure required to make estimates using HLM.

The micro data from Provão and Enade include the students’ responses to

socioeconomic questionnaires. There are information concerning to students, such as

21

personal characteristics, socioeconomic and cultural conditions, habits of reading and

study, as well as about courses such as facilities and resources available in institutions,

curricular structure, didactic-pedagogic organization and teachers’ performance. There

were issues common to all courses involved in the evaluation process and other ones

specific to the Accountancy course. There are more than 100 questions (INEP, 2004;

2007a). On exam day, the students also express their perception in relation to exam: the

resolution difficulty, extension, time sufficiency, statement of questions, personal

problems to resolve it, and whether the content was charged during course.

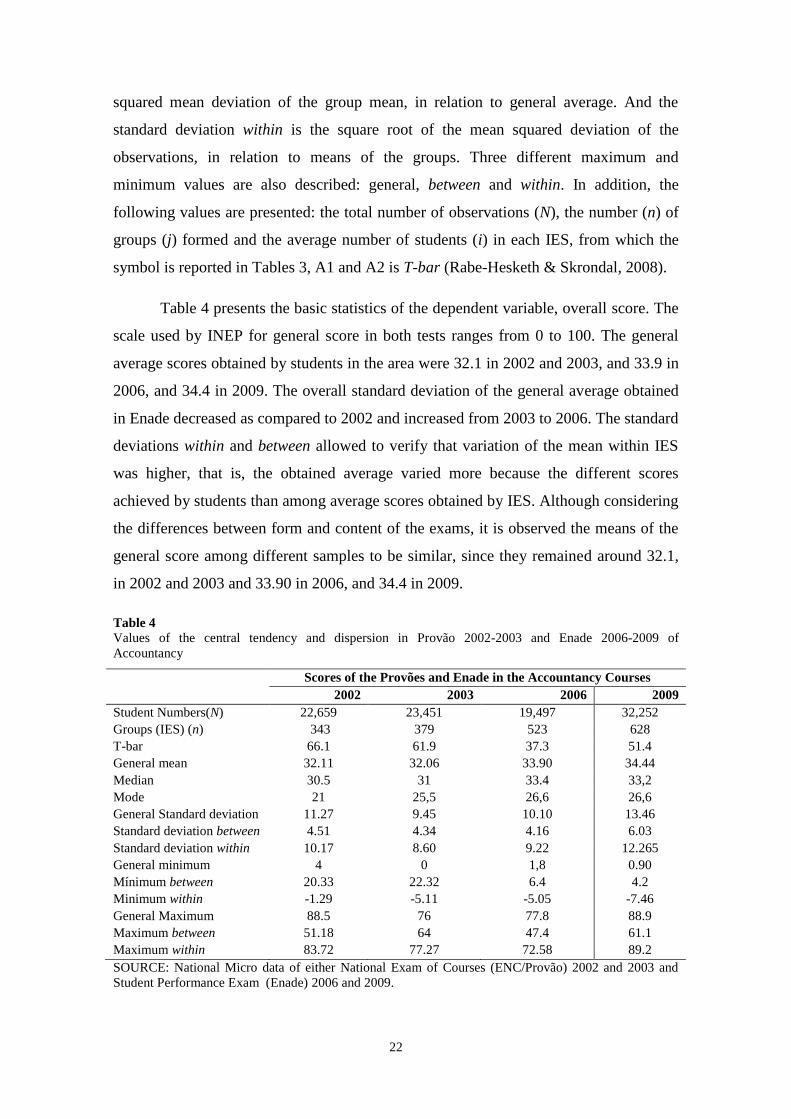

The analysis universe were the students graduating in Accountancy courses, who

attended and participated in the exams. In 2002, a total of 22,694 students were present;

in 2003, 23,495; and in 2006, 19,633. It was decided to remove from database those

students whose exam was not answered, in order to avoid the zero scores from

distorting the results, since it is possible the profile of the students who delivered the

exam in blank to be different from students who resolve the test, in terms of

commitment, dedication, etc. Then, the universe of analysis was reduced to 22,659,

23,451 and 19,497 graduating students, respectively. A total of 408 and 454 courses

participated of Provão in 2002 and 2003, respectively, as well as 811 courses in the case

of Enade/2006 (INEP, 2004; 2007a).

3.2. Descriptive analysis

In the hierarchical model, the dependent variable (Tij), which represents a proxy

of the academic performance of students graduating in Accountancy courses, always

varies at Level 1. The explanatory variables may vary among students’ observations

Level 1, among groups formed at Level 2 (of IES) and only in one of the levels (Rabe-

Hesketh & Skrondal, 2008). For example, the variable of gender varies among students,

whereas the variable indicating the type of administrative category to which the student

is affiliated (e.g., College) is constant among students and varies among IES. These

distinct variations entre among explanatory variables allow to calculate values with

central tendency and general dispersion, as considering each level.

Rabe-Hesketh and Skrondal (2008) recommend to calculate three standard

deviations for each variable. The first one is the overall or global standard deviation,

defined as the square root of the mean squared deviation of the observations, in relation

to general average. The standard deviation between groups is the square root of the

22

squared mean deviation of the group mean, in relation to general average. And the

standard deviation within is the square root of the mean squared deviation of the

observations, in relation to means of the groups. Three different maximum and

minimum values are also described: general, between and within. In addition, the

following values are presented: the total number of observations (N), the number (n) of

groups (j) formed and the average number of students (i) in each IES, from which the

symbol is reported in Tables 3, A1 and A2 is T-bar (Rabe-Hesketh & Skrondal, 2008).

Table 4 presents the basic statistics of the dependent variable, overall score. The

scale used by INEP for general score in both tests ranges from 0 to 100. The general

average scores obtained by students in the area were 32.1 in 2002 and 2003, and 33.9 in

2006, and 34.4 in 2009. The overall standard deviation of the general average obtained

in Enade decreased as compared to 2002 and increased from 2003 to 2006. The standard

deviations within and between allowed to verify that variation of the mean within IES

was higher, that is, the obtained average varied more because the different scores

achieved by students than among average scores obtained by IES. Although considering

the differences between form and content of the exams, it is observed the means of the

general score among different samples to be similar, since they remained around 32.1,

in 2002 and 2003 and 33.90 in 2006, and 34.4 in 2009.

Table 4

Values of the central tendency and dispersion in Provão 2002-2003 and Enade 2006-2009 of

Accountancy

Scores of the Provões and Enade in the Accountancy Courses

2002 2003 2006 2009

Student Numbers(N) 22,659 23,451 19,497 32,252

Groups (IES) (n) 343 379 523 628

T-bar 66.1 61.9 37.3 51.4

General mean 32.11 32.06 33.90 34.44

Median 30.5 31 33.4 33,2

Mode 21 25,5 26,6 26,6

General Standard deviation 11.27 9.45 10.10 13.46

Standard deviation between 4.51 4.34 4.16 6.03

Standard deviation within 10.17 8.60 9.22 12.265

General minimum 4 0 1,8 0.90

Mínimum between 20.33 22.32 6.4 4.2

Minimum within -1.29 -5.11 -5.05 -7.46

General Maximum 88.5 76 77.8 88.9

Maximum between 51.18 64 47.4 61.1

Maximum within 83.72 77.27 72.58 89.2

SOURCE: National Micro data of either National Exam of Courses (ENC/Provão) 2002 and 2003 and

Student Performance Exam (Enade) 2006 and 2009.

23

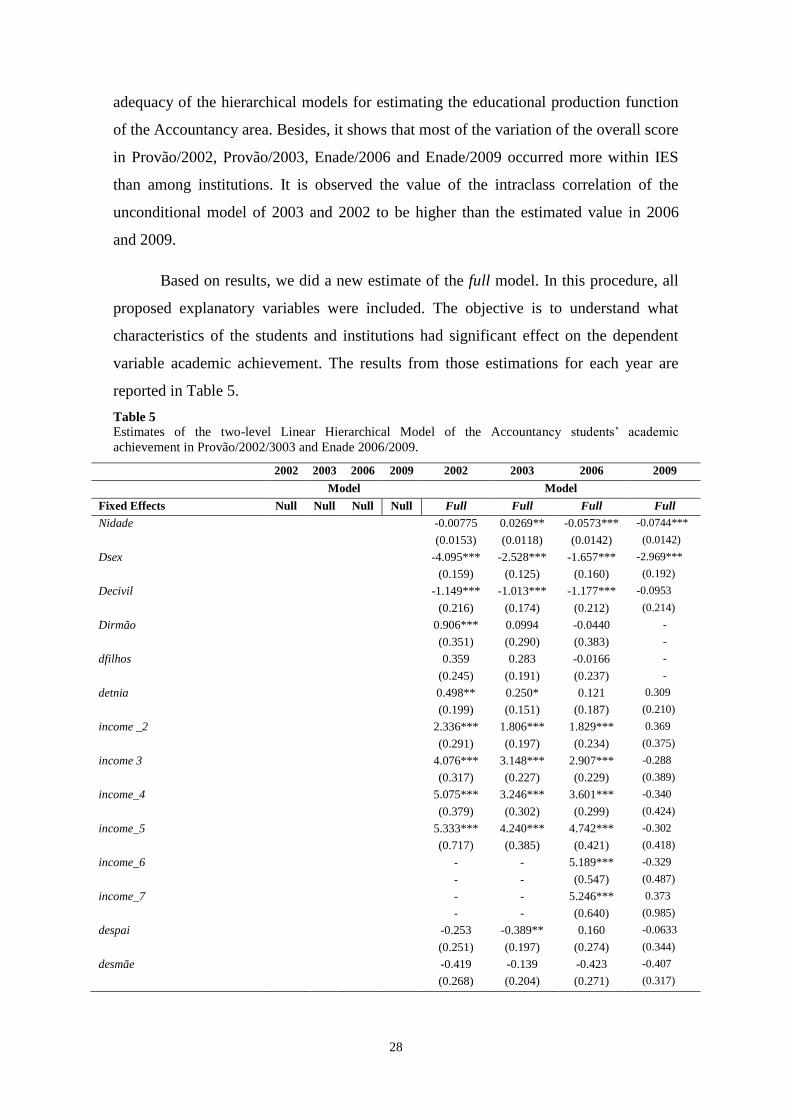

The micro data contain variables from which the level of measurement was

nominal and ordinal and at ratio scale. For cases of nominal and ordinal scale, some

procedures were adopted to represent them as numerical value. This codification of the

data in numerical measurement took into account the characteristics of the tools applied

to students by INEP. The main procedure was to construct a series of dummy variables.

It should be emphasized that some characteristics of either teachers and

educational process were collected through students, by using the variables estapr1,

dmcont1, mat1, aulexp1, csi1, pltr17. It was decided to allocate those characteristics at

level of the institutions because, although measuring the student’ perception, these

variables may be capturing choices made by managers of the institutions.

The exogenous variables used in this study were chosen with basis on the

constructs of the educational production function, the findings of the literature and the

availability of the database. For example, the choice of the variables that measure the

construct effect of the pairs was based on definition by Sacerdote (2011)8. Those

constructs or underlying attributes were used to represent a set of measurements, that

was generated by means of the variable group.

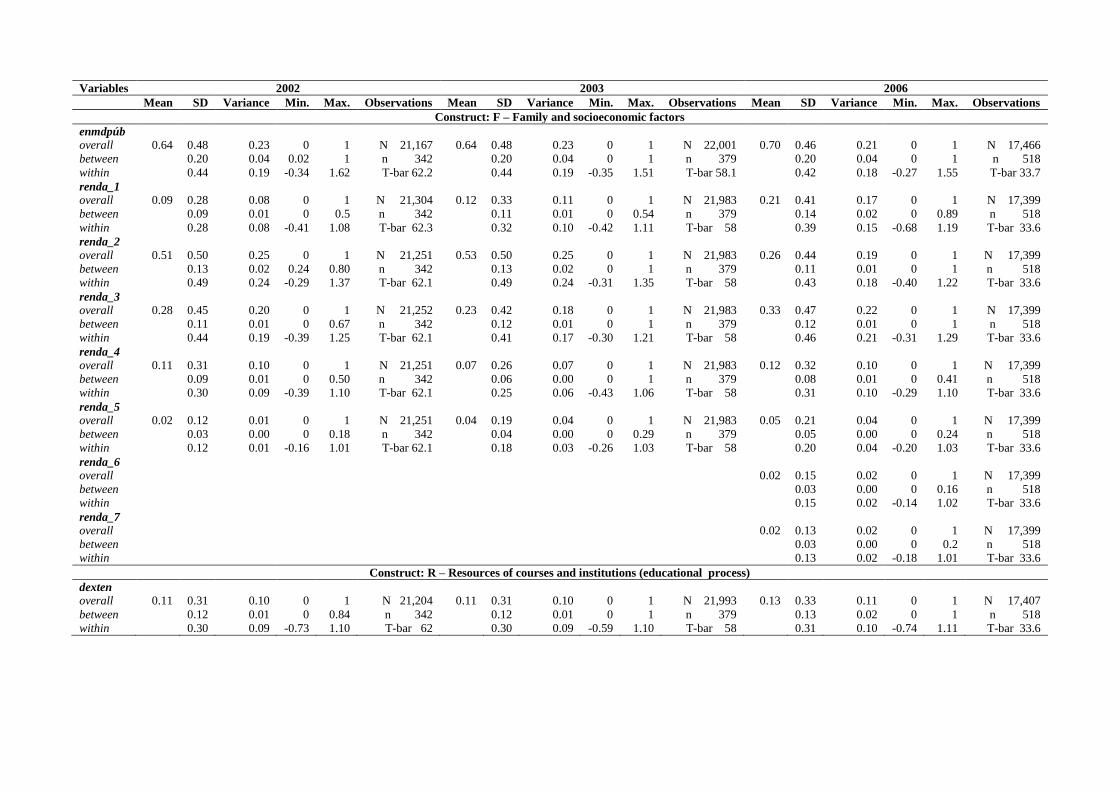

The basic statistics of the exogenous variables, as following the recommendation

by Rabe-Hesketh and Skrondal (2008), are reported in Tables A1 and A2, in Appendix.

Table A1 presents the descriptive statistics of the exogenous variables of first level. The

variables nidade, dsex, detnia and dded9 represent the construct that objectively measure

the personal characteristics of the students (Fij). In all years, the values of the means of

those variables pointed out that, among students approximately half are masculine

7 Level 2 independent variables: estapr1 = Ratio of responses given by students regarding IES to have

teachers who conducted research activities as learning strategy; mat1 = Proportion of responses given by

students regarding IES to have teachers who indicated the use of books, copies of book chapters and

handouts; aulexp1 = Proportion of responses given by students regarding IES to have the majority of

teachers whose teaching practice are predominantly lectures; csi1 = Proportion of responses given by

students in relation to IES that provided the knowledge on accounting information system; pltr1 =

Proportion of responses given by students regarding IES that the issue ‘tax planning’ was considered in

the course.

8Sacerdote (2011) defined the effect from pairs as any externality regarding the history and current

behaviors of the pairs or results that may affect its performance. The author used this ample definition,

but it limits the pair effects for externalities concerning to pairs or colleagues, family history or ongoing

actions.

9 Level 1 independent variables: nidade = Current age informed; dsex = 1 female, 0 masculine; detnia = 1

whites and yellows, 0 blacks and browns; dded = 1 spent at least one hour studying beyond classroom, 0

contrary case.

24

gender, more than half reported to be White and/or Yellow and spent at least one hour

daily to study. In each sample, the average age of students ranged from 28 to 29 years.

The standard deviations of the variables listed in Table A1 rather suggest that dispersion

around mean to have no significant changes over the years. The values of the standard

deviations within indicate the variation of those variables to be higher within than

among IES.

It is assumed the effect of the pairs (Pij) in the context of the students can be

apprehended by variables dfilhos, and dirmão decivil10. Table A1 shows that more than

half of the total students declared to be single, childless and over 90% reported to have

siblings. The dispersion of the variables reported in Table A1 was also higher within

IES than among IES.

The family and socioeconomic factors (Fij) were measured by means of the

exogenous variables despai1, desmãe, enmdpúb11 and the family income. The means of

those variables, shown in Table A1, suggest that over 80% students reported to be

children of parents who have not attained higher education, and more than half attended

the high school integrally or mostly in public school. The income ranges 6 and 7 were

reported only for 2006 in Table A1 because they were added to socioeconomic

questionnaire this year. During the periods under analysis, the mean increased in the

income ranges 1, 3 and 5. In the income range 2, the mean decreased and there was no

concentration in any income range. It was observed that the values of the means of the

income ranges 1, 3, 2 and 4 from 2003 to 2006 have changed significantly. In Table 2,

the values of the standard deviations within and between show the variations to be

greater within IES than among IES.

10 Level 1 independent variables: = dfilhos = 1 has son/daughter (s), 0 otherwise; dirmão = 1 if has sibling

(s), 0 otherwise; decivil = 1 unmarried, 0 married, separated, widowed and others.

11 Level 1 independent variables: = despai1 father with higher education, 0 otherwise; desmãe = 1 mother

with higher education, 0 otherwise; enmdpúb = 1 attended the high school in the public school, 0

otherwise. income_1 = 1 family income range up to R$ 720.00, and 0 otherwise; income _2 = 1 family

income range from R$ 721.00 to R $ 2,400.00, 0 otherwise; income_3 = 1 family income range from R$

2,401.00 to R$ 4,800.00, 0 otherwise; income_4 = 1 family income range from R$ 4,801.00 to R$

7,200.00, 0 otherwise; income 5 = 1 family income range more than R$ 7,201.00. Values of the level 1

independent variables Enade 2006: 0 otherwise. income_1 = 1 family income range up to three minimum

wages, and 0 otherwise; income _2 = 1 family income range more than 3 to 5 minimum wages; 0

otherwise; income_3 = 1 family income range more than 5 up to 10 minimum wages, 0 otherwise; income

4 = 1 family income range over 10 to 15 minimum wages, 0 otherwise; income_5 = 1 family income

range over 15 to 20 minimum wages, 0 otherwise; income_6 = 1 family income range more than 20 to 30

minimum wages, 0 otherwise; income _7 = 1 family income range more than 30 minimum wages.

25

In general, the option to participate in extension and scientific initiation

activities arises within IES and the students choose it or not. The way this choice uses

school resources (Rij) was captured through variables reported in Table A1. In this

context, it should be noted that the dispersion of those variables within IES was higher

among IES. It is emphasized that the average of the variable measuring the participation

into scientific initiation increased from 0.06 in 2002 to 0.27 in 2006. This might be a

reflection of the increase in supply of this activity by IES, which generated greater

student participation. I is noted the mean and the dispersion values referring to

extension activity were similar over the years.

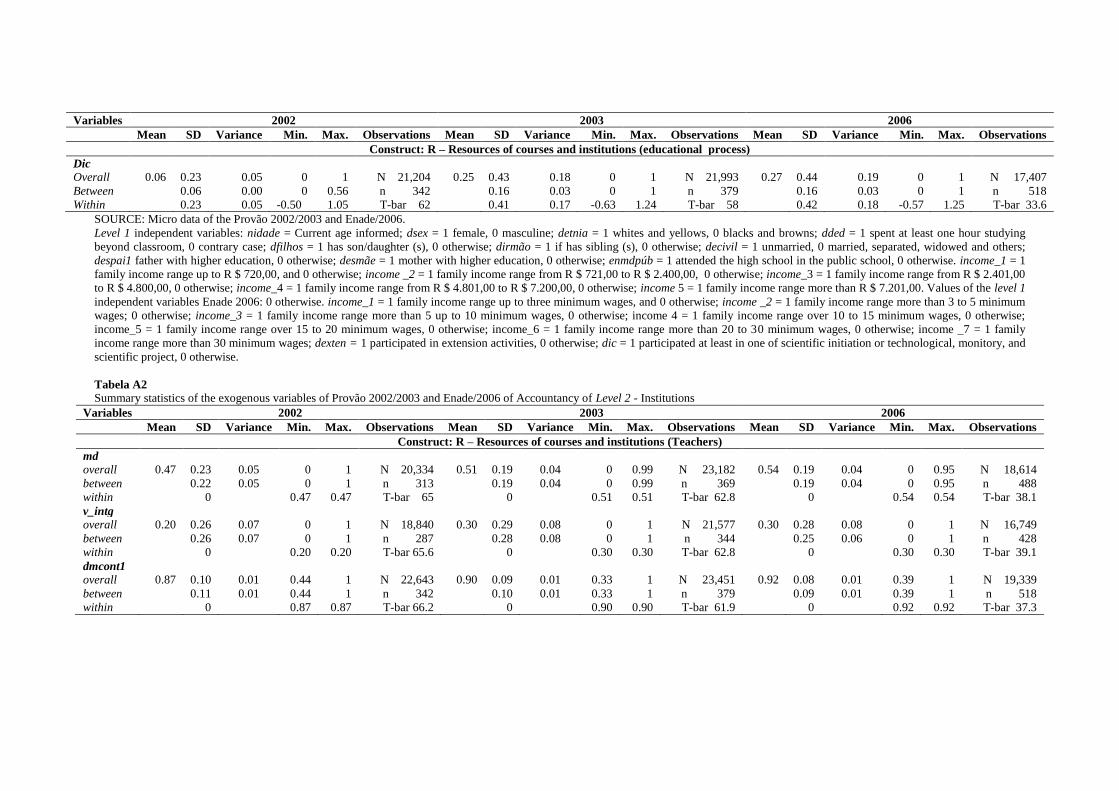

Table A2 presents the descriptive statistics of the second-leveled exogenous

variables. The within standard deviation of the variables measured at second level is

zero. Because construction, those variables vary only among IES and not among

students. Therefore, they are constant at Level 1 (Rabe-Hesketh & Skrondal, 2008).

Table A2 shows the variables referring to main characteristics of the teachers, as

considered as school resource (R2J), and the organizational form of either IES and

educational system (I3j). The mean proportions of teachers with master and doctorate

titles, full-time working hours and content domain increased over the period from 2002

to 2006. The variance of the md variable referring to proportion of the teachers with

master and doctorate degrees in the institutions decreased from 0.05 to 0.04 over the

period from 2002 to 2003. It is possible the changes in those values to be related with

the need for institutions to fulfill the percent teachers with those titles determined by

MEC. The behavior of both average ratio and standard deviation among IES of the

academic organization (dorgac) was heterogeneous. The increase in values of the

variable dorgac is related to an increased number of Universities and University centers

throughout the years. It is observed the mean and standard deviation between IES and

other variables to be similar in this period.

The statistics related to main aspects of the educational process, that were

adopted in the courses, are reported in Table A2. The values of the standard deviations

among groups of those variables were generally low. The average proportion of either

teachers who conducted research activities as teaching and learning strategy and

teachers who used lecture as teaching practice decreased over the period from 2003 to

2006. In 2006, the dispersion among IES concerning to have lecture was nonexistent

The values of the variables csi1 and pltr1 showed that the contents of the accountable

26

information system and tributary planning were included in the courses, either in 2002

and 2003. The statistics of the other variables were similar over this period.

Table A2 presents the descriptive statistics of the environmental or context

variables so-called effects of the pairs (P1j). The results of either means and standard

deviations among groups showed homogeneous character. Despite differences in

number of the observations, groups (IES) and mean number of observations within

groups (T-bar), there were little changes during the period under study.

According to data presented in Tables 3 and 4, there is high probability the most

students to compose the first generation of the family, as attending an undergraduate

course, since 80% students were sons/daughters of parents with no training in higher

education. Other uniformities were observed, such as similarity of the distribution by

gender and by frequent use of the textbooks and/or manuals and handouts as didactic

material by teachers of the course. Moreover, according to the report by INEP, the

students’ perception, certain basic contents covered on the exam were given, but the

given approach was different from the one charged (INEP, 2004). Concerning to

teachers, according to the students' perceptions of the area, the most frequent

characteristics were content domain and the use of research activity as learning strategy.

Another point was the high use of lectures or lecture with student participation, such as

technical education, with approximately 80% total responses. On average: 60% teachers

worked as hourly employees and 37% were still experts, despite the increased number

of the master and doctor teachers.

3.2. Results from estimations of the Hierarchical Linear Models

A production function of the educational course in Accounting was estimated for

each year using hierarchical linear models, with the maximum likelihood method and

based on the previously established hypotheses. The econometric procedure was done

in software Stata, version 9.1. The order for presentation of the estimates in Table 5 was

based on the literature of hierarchical models (Raudenbush & Bryk, 2002; Rabe-

Hesketh & Skrondal, 2008; Fávero et al., 2009).

The first estimate is done with the unconditional or null model without

explanatory variables. According to Fávero et al. (2009), the estimation of this model

allows to verify the following hypotheses: (1) there is significant variability in

27

performance among students of the same IES; and (2) there is significant variability in

performance among students from different IES. These assumptions allowed to evaluate

whether there were differences in performance among students and among IES.

The results from estimates of the null or unconditional model referring to Provão

2002/2003 and Enade 2006/2009 are presented in Table 5. Those estimates allowed to

calculate the IES average performance in tests (β0j) as a function of the overall average

of all IES (γ00), added with a random component (u0j). Initially, it is considered the IES

average performance did not vary from institution to institution and was treated as

constant. The results showed the expected average performance of the students, that is,

31.29 in Provão 2002, 31.67 in Provão 2003 and 33.25 in Enade/2006 and 33.94 in

Enade/2009. The residual standard deviations of Level 1 were 10.25 in Provão 2002,

8.67 in Provão 2003 and 9.35 in Enade/2006 and 12.38 in Enade/2009. The standard

deviations of the random intercepts of Level 2 were 4.26 in Provão 2002, 3.62 in Provão

2003 and 3.60 in Enade/2006 and 5.16 in Enade/2009.

The variance of the overall score in Provão/2002 among students was 104.96

(Level 1) and among institutions was 18.15 (Level 2). The sum of those variances

generated a total value of 123.11. In Provão 2003, the calculated variance for Level 1

was 75.21 whereas for Level 2 was 13.11, therefore its sum corresponds to total 88.32.

The variance of the overall score in Enade/2006 among students was 87.39 (Level 1)

and the variance among institutions was 12.97 (Level 2), and their sum equals a total

variance of 100.36. The variance of the overall score in Enade/2009 among students

was 153.44 (Level 1) and the variance among institutions was 26.67 (Level 2), and their

sum equals a total variance of 180.11. These results indicate that most variation in

overall score in each year occurred in Level 1, that is among students.

Those proportions of the level variances allowed to calculate the intraclass

variance, which indicates the proportion of the total variance due to IES groups as

defined in Level 2 (Raudenbush & Bryk, 2002; Rabe-Hesketh & Skrondal, 2008; Fávero

et al., 2009). The values of the intraclass correlation coefficients (ρ) of the null model in

Provão/2002 was 0.147, in Provão/2003 was 0.148 and in Enade/2006 was 0.129 and in

Enade/2009 was 0.148. These values suggest that part from proportion of the total

variance can be attributed to IES peculiarities. Thus, it is possible to include specific

variables of the institution level in the model, that is, at second level. This indicates

28

adequacy of the hierarchical models for estimating the educational production function

of the Accountancy area. Besides, it shows that most of the variation of the overall score

in Provão/2002, Provão/2003, Enade/2006 and Enade/2009 occurred more within IES

than among institutions. It is observed the value of the intraclass correlation of the

unconditional model of 2003 and 2002 to be higher than the estimated value in 2006

and 2009.

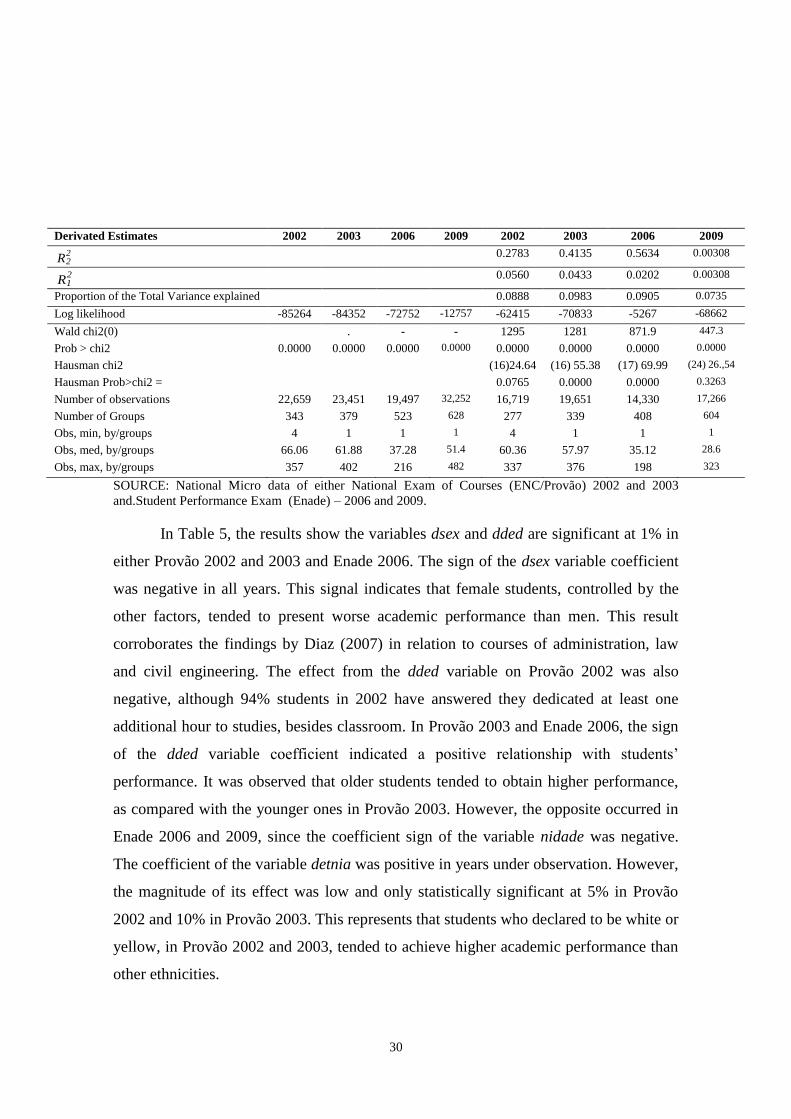

Based on results, we did a new estimate of the full model. In this procedure, all

proposed explanatory variables were included. The objective is to understand what

characteristics of the students and institutions had significant effect on the dependent

variable academic achievement. The results from those estimations for each year are

reported in Table 5.

Table 5

Estimates of the two-level Linear Hierarchical Model of the Accountancy students’ academic

achievement in Provão/2002/3003 and Enade 2006/2009.

2002 2003 2006 2009 2002 2003 2006 2009

Model Model

Fixed Effects Null Null Null Null Full Full Full Full

Nidade -0.00775 0.0269** -0.0573*** -0.0744***

(0.0153) (0.0118) (0.0142) (0.0142)

Dsex -4.095*** -2.528*** -1.657*** -2.969***

(0.159) (0.125) (0.160) (0.192)

Decivil -1.149*** -1.013*** -1.177*** -0.0953

(0.216) (0.174) (0.212) (0.214)

Dirmão 0.906*** 0.0994 -0.0440 -

(0.351) (0.290) (0.383) -

dfilhos 0.359 0.283 -0.0166 -

(0.245) (0.191) (0.237) -

detnia 0.498** 0.250* 0.121 0.309

(0.199) (0.151) (0.187) (0.210)

income _2 2.336*** 1.806*** 1.829*** 0.369

(0.291) (0.197) (0.234) (0.375)

income 3 4.076*** 3.148*** 2.907*** -0.288

(0.317) (0.227) (0.229) (0.389)

income_4 5.075*** 3.246*** 3.601*** -0.340

(0.379) (0.302) (0.299) (0.424)

income_5 5.333*** 4.240*** 4.742*** -0.302

(0.717) (0.385) (0.421) (0.418)

income_6 - - 5.189*** -0.329

- - (0.547) (0.487)

income_7 - - 5.246*** 0.373

- - (0.640) (0.985)

despai -0.253 -0.389** 0.160 -0.0633

(0.251) (0.197) (0.274) (0.344)

desmãe -0.419 -0.139 -0.423 -0.407

(0.268) (0.204) (0.271) (0.317)

29

2002 2003 2006 2009 2002 2003 2006 2009

Modelo Modelo

Null Null Null Null Full Full Full Full

Fixed Effects Coef. Coef. Coef. Coef. Coef. Coef. Coef. Coef.

enmdpúb 0.866*** 0.850*** 0.383** -0.0623

(0.180) (0.142) (0.191) (0.254)

dded -

1.687***

1.807*** 1.406*** 0.433

(0.326) (0.193) (0.246) (0.281)

dexten 0.451* -0.300 -0.199 0.145

(0.264) (0.208) (0.246) (0.254)

dic 0.193 -0.809*** -0.492** 0.150

(0.339) (0.153) (0.192) (0.223)

dorgac 0.301 0.835** 0.813** 1.992***

(0.697) (0.409) (0.363) (0.489)

dcatad -1.367 -1.783*** -1.131* -

3.367***

(0.997) (0.661) (0.585) (0.686)

Md 0.742 3.088*** 3.716*** 4.345***

(1.184) (1.185) (1.006) (0.711)

v_intg -2.258 1.683* 4.280*** -0.146

(1.401) (1.000) (0.917) (0.752)

aulexp1 12.88*** 6.698*** 741.2*** -

(2.165) (1.771) (163.2) -

estapr1 0.0362 5.835** 6.251*** -3.092

(5.216) (2.816) (1.886) (2.205)

mat1 9.605*** 3.535 -1.406 0.487

(3.370) (3.017) (2.646) (2.503)

dmcont1 5.895** 5.951*** 5.918*** 0.487

(2.792) (2.200) (2.052) (2.503)

csi1 2.675 1.657 - -

(2.043) (1.614) - -

pltr1 0.432 -1.019 - -

(2.505) (1.946) - -

espai1 5.170 5.484** 5.995*** 0.447

(3.494) (2.542) (2.281) (2.241)

esmãe1 4.222 -8.659*** -

6.569***

-2.358

(4.295) (2.793) (2.436) (2.043)

Midade 0.0339 0.00762 -0.0519 -0.165***

(0.103) (0.0734) (0.0610) (0.0713)

Constant 31.29*** 31.67*** 33.25*** 33.94*** 10.71* 11.93*** 21.68*** 42.89***

(0.247) (0.201) (0.176) (0.226) (6.368) (4.194) (3.591) (2.246)

Random Effects

sd(_cons) 4.260*** 3.621*** 3.602*** 5.164*** 3.619*** 2.773*** 2.380*** 4.219***

(0.183) (0.151) (0.135) (0.173) (0.183) (0.136) (0.127) (0.179)

sd(Residual) 10.25*** 8.672*** 9.348*** 12.38*** 9.954*** 8.482*** 9.253*** 12.253***

(0.0485) (0.0404) (0.0480) (0.492) (0.0549) (0.0432) (0.0554) (0.0554)

Derivated Estimates

R² 0.00 0.00 0.0000 0.00 0.00981 0.00810 0.00705 0.00308

Ρ 0.147 0.148 0.129 0.148 0.117 0.0966 0.0620 0.1061

Prob >= chibar2 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000 0.0000

Variance of the Level 2 18.15 13.112 12.974 26.671 13.10 7.680 5.664 17.798

variance of the Level 1 104.96 75.204 87.385 153.443 99.08 71.944 85.618 149.983

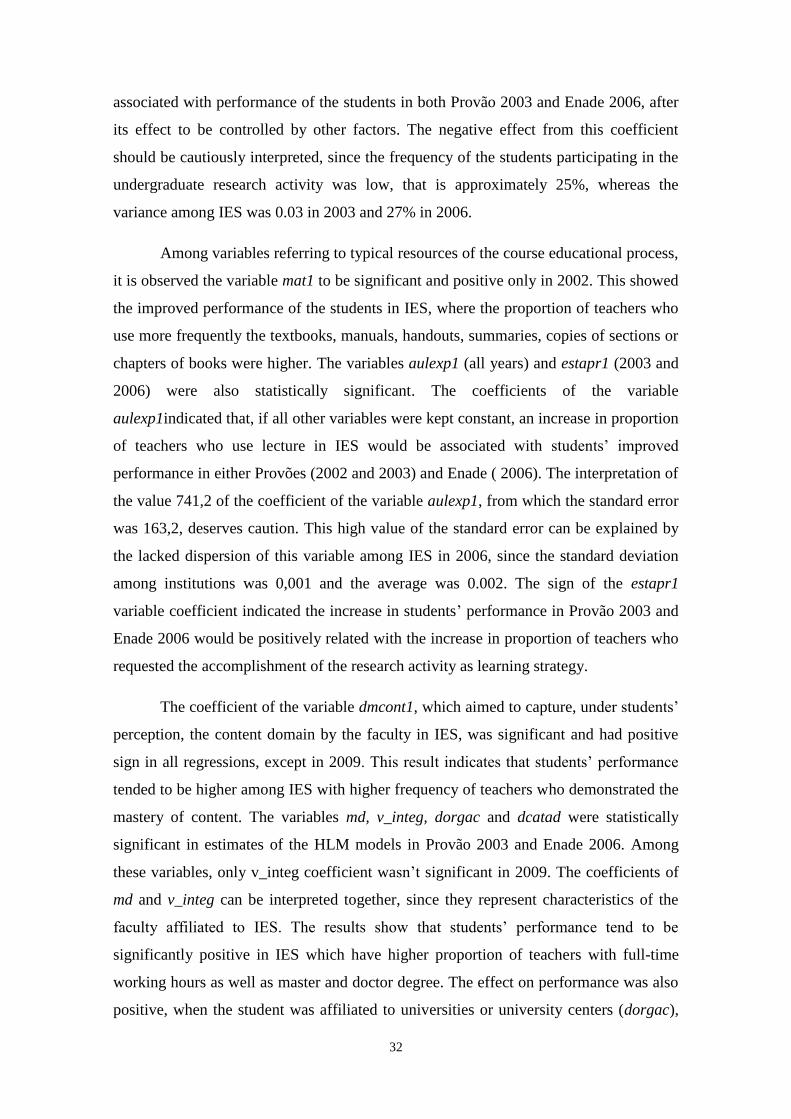

Total Variance 123.11 88.315 100.359 180.114 112.18 79.634 91.282 167.782

30