NCERT Solutions for Class 11 Accountancy Financial ...

237

NCERT Solutions for Class 11 Accountancy Financial Accounting Part-1 Chapter 1 Short answers Q1 : Define accounting. Answer : Accounting is a process of identifying the events of financial nature, recording them in Journal, classifying in their respective ledgers, summarising them in Profit and Loss Account and Balance Sheet and communicating the results to the users of such information, viz. owner/s, government, creditors, investors etc. According to the American Institute of Certified Accountants, 1941, "Accounting is an art of recording, classifying and summarising in a significant manner and in terms of money transactions and events that are, in part at least, of a financial character and interpreting the results thereof." Q2 : State what is end product of financial accounting? Answer : 1. Income statements (Trading and/or Profit and Loss Account)- An income statement that includes Trading and Profit and Loss Account, ascertains the financial results of a business in terms of gross (or net) profit or loss. 2. Balance Sheet- It depicts the true financial positions of a business that provides required information like assets and liabilities of a business firm, to the users of accounting information like owners, creditors, investors, government, etc. Q3 : Enumerate main objectives of accounting. Answer : The main objectives of accounting are given below. 1. To keep a systematic record of all business transactions 2. To determine the profit earned or loss incurred during an accounting period by preparing profit and loss account 3. To ascertain the financial position of the business at the end of each accounting period by preparing balance sheet 4. To assist management for decision making, effective control, forecasting, etc. 5. To assess the progress and growth of business from year to year 6. To detect and prevent frauds and errors 7. To communicate information to various users

-

Upload

khangminh22 -

Category

Documents

-

view

1 -

download

0

Transcript of NCERT Solutions for Class 11 Accountancy Financial ...

NCERT Solutions for Class 11 Accountancy

Financial Accounting Part-1 Chapter 1 Short answers

Q1 :

Define accounting.

Answer :

Accounting is a process of identifying the events of financial nature, recording them in Journal, classifying in their respective ledgers,

summarising them in Profit and Loss Account and Balance Sheet and communicating the results to the users of such

information, viz. owner/s, government, creditors, investors etc.

According to the American Institute of Certified Accountants, 1941, "Accounting is an art of recording, classifying and summarising

in a significant manner and in terms of money transactions and events that are, in part at least, of a financial character and

interpreting the results thereof."

Q2 :

State what is end product of financial accounting?

Answer :

1. Income statements (Trading and/or Profit and Loss Account)- An income statement that includes Trading and Profit and Loss Account,

ascertains the financial results of a business in terms of gross (or net) profit or loss.

2. Balance Sheet- It depicts the true financial positions of a business that provides required information like assets and liabilities of a business

firm, to the users of accounting information like owners, creditors, investors, government, etc.

Q3 :

Enumerate main objectives of accounting.

Answer :

The main objectives of accounting are given below.

1. To keep a systematic record of all business transactions

2. To determine the profit earned or loss incurred during an accounting period by preparing profit and loss account

3. To ascertain the financial position of the business at the end of each accounting period by preparing balance sheet

4. To assist management for decision making, effective control, forecasting, etc.

5. To assess the progress and growth of business from year to year

6. To detect and prevent frauds and errors

7. To communicate information to various users

Q4 :

List any five users who have indirect interest in accounting.

Answer :

The five users who have indirect interest in accounting are given below.

1. Trade associations

2. Labour unions

3. Customers

4. Stock exchanges

5. Tax authorities

Q5 :

State the nature of accounting information required by long-term lenders.

Answer :

Accounting information required by the long term lenders are repaying capacity of the business, profitability, liquidity, operational

efficiency, potential growth of business, etc.

Q6 :

Who are the external users of information?

Answer :

External users of information are the individual or the organisations that have direct or indirect interest in the business firm; however,

are not a part of management. They do not have direct access to the internal data of the firm and uses published data or reports

like profit and loss accounts, balance sheets, annual reports, press releases, etc. Some examples of external users are government,

tax authorities, labour unions, etc.

Q7 :

Enumerate informational needs of management.

Answer :

The informational needs of management are concerned with the activities given below.

1. Assists in decision making and business planning

2. Preparing reports related to funds, costs and profits to ascertain the soundness of the business

3. Comparing current financial statements with its own historical financial statements and of other similar firms to assess the operational

efficiency of the business.

Q8 :

Give any three examples of revenues.

Answer :

Three examples of revenue are given below.

1. Sales revenue

2. Interest received

3. Dividends

Q9 :

Distinguish between debtors and creditors.

Answer :

Basis of

difference Debtors Creditors

Meaning Persons or

organisations that are

liable to pay money to

a firm are called

debtors.

Persons or organisations

to whom the firm is

liable to pay money are

called creditors.

Nature They have debit

balance to the firm.

They have credit

balance to the firm.

Payment Payments are received

from them.

Payments are made to

them.

Shown They are shown as

assets in the Balance

sheet under Current

Assets.

They are shown as

liabilities in the Balance

Sheet under Current

Liabilities.

Q10 :

'Accounting information should be comparable'. Do you agree with this statement? Give two reasons.

Answer :

Accounting information should be comparable because of the following reasons.

1. Comparable accounting information helps in inter-firm comparisons. This helps in assessing viability and advantages of various policies

adopted by different firms.

2. It also helps in intra-firm comparisons that help in determining the changes and also to ascertain the results of various policies and plans

adopted in different time periods. This also helps to figure out the errors, ascertain growth and assist in management planning.

Q11 :

If the accounting information is not clearly presented, which of the qualitative characteristic of the accounting information

is violated?

Answer :

If the accounting information is not clearly presented, then the qualitative characteristics like, comparability, reliability and

understandability, are violated. This is because if the accounting information is not clearly presented, then meaningful comparison

may not be possible, as the data is not trustworthy, which may lead to faulty conclusions.

Q12 :

The role of accounting has changed over the period of time"- Do you agree?

Explain.

Answer :

The role of accounting is ever changing. While in earlier times, accounting was merely concerned with recording the financial

events, i.e. record-keeping activity; however, now-a-days, accounting is done with the rationale of not only maintaining records, but

also providing an information system that provides important and relevant information to various accounting users. The need of this

change is brought over due to the ever-changing and dynamic business environment, which is more competitive in nature now than

it was in earlier times. Further, there are various relevant activities like decision making, forecasting, comparison, and evaluation

that make these changes in the role of accounting, inevitable.

Q13 :

Giving examples, explain each of the following accounting terms:

Fixed assets

Gain

Profit

Revenue

Expenses

Short-term liability

Capital

Answer :

Fixed assets- These are held for long term and increase the profit earning capacity of the business, over various accounting periods.

These assets are not meant for sale; for example, land, building, machinery, etc.

Revenue- It refers to the amount received from day to day activities of business, viz. amount received from sales of goods and services to

customers; rent received, commission received, dividend, royalty, interest received, etc. are items of revenue that are added to the capital.

Capital- It refers to the amount invested by the owner of a firm. It may be in form of cash or asset. It is an obligation of the business

towards the owner of the firm, since business is treated separate or distinct from the owner.

Capital = Assets - Liabilities.

Gains- Gains are incidental to the business. They arise from irregular activities or non-recurring transactions; for example, profit on sale of

fixed assets, appreciation in value of asset, profit on sale of investment, etc.

Expenses- Expenses are those costs that are incurred to maintain the profitability of business, likerent, wages, depreciation, interest,

salaries, etc. These help in the production, business operations and generating revenues.

Profit- This refers to the excess of revenue over the expense. It is normally categorised into gross profit or net profit. Net profit is added to

the capital of the owner, which increases the owner's capital. For example, goods sold above its cost

Short term liabilities- Those liabilities that are incurred with an intention to be paid or are payable within a year; for example, bank

overdraft creditors, bills payable, outstanding wages, short-term loans, etc.

Q14 :

How will you define revenues and expenses?

Answer :

Revenues- Revenues refer to the amount received from day to day activities of the business, likesale proceeds of goods and

rendering services to the customers. Rent received, commission received, royalties and interest received are considered as

revenue, as they are regular in nature and concerned with day to day activities. It is shown in the credit side of the profit and loss

account or trading account.

Expenses- Expenses refer to those costs that are incurred to earn revenue for the business. It is incurred for maintaining

profitability of the business. It indicates the amount spent to meet short-term needs of the business. It is shown in the debit side of

the profit and loss account or trading account. For example, wages, rent paid, salaries paid, outstanding wages, etc.

Q15 :

What is the primary reason for the business students and others to familiarise themselves with the accounting discipline?

Answer :

Every monetary transaction must be recorded in such a manner that various accounting users must understand and interpret these

results in the same manner without any ambiguity. The reasons for why business students and others should familiarise themselves

with the accounting discipline are given below.

1. It helps in learning the various aspects of accounting.

2. It helps in learning how to maintain books of accounts.

3. It helps in learning how to summarise accounting information.

4. It helps in learning how to interpret the accounting information with relative accuracy.

Next Chapter 2 : Theory Base of Accounting >> Long answers : Solutions of Questions on Page Number : 20

Q1 :

Explain the factors, which necessitated systematic accounting.

Answer :

The factors that necessitated systematic accounting are given below.

1. Only financial transactions are recorded- Those events that are financial in nature are only recorded in the books of accounts. For

example, salary of an employee is recorded in the books but his/her educational qualification is notrecorded.

2. Transactions are recorded in monetary terms- Only those transactions which can be expressed in monetary terms are recorded in the

books. For example, if a business has two buildings and four machines, then their monetary values is recorded in the books, i.e. two

buildings costing Rs 2,00,000, four machines costing Rs 8,00,000. Thus the total value of assets is Rs 10,00,000.

3. Art of recording- Transactions are recorded in the order of their occurrence.

4. Classification of transaction- Business transactions of similar nature are classified and posted under their respective accounts. For

example, all the transactions relating to machinery will be posted in the Machinery Account.

5. Summarising of data- All business transactions are summarised in the form of Trial Balance, Trading Account, Profit and Loss Account

and Balance Sheet that provides necessary information to various users.

6. Analysing and interpreting data- Systematic accounting records enable users to analyse and interpret the accounting data in a proper

and appropriate manner. These accounting data and information are presented in form of graphs, statements, charts that leads to easy

communication and understandability by various users. Moreover, these facilitates in decision making and future predictions.

Q2 :

Describe the brief history of accounting.

Answer :

The history of accounting can be traced long back in civilisation. Around 4000 B.C., in Babylonia and Egypt, payment of wages and

taxes were recorded on clay tablets. As history claims that Egyptians kept the record of gold and valuables deposits and withdrawal

from the treasuries. These records were reported on daily basis by the incharge of treasuries to the wazir, who used to forward the

monthly reports to the king. Babylonia and Egypt used this method to rectify and remove errors, frauds and inefficiency from the

records. Around 2000 B.C., China used sophisticated form of accounting. In Greece, accounting was used to maintain total receipts

and total payments and to balance government accounts. In Rome, around 700 B.C., receipts and payments were recorded in

daybook and were posted in the ledger at the end of the month. In India, around twenty three centuries ago, Kautilya wrote the

book Arthshastra, which describes how accounting records have to be maintained. In 1494, Luca Pacioli wrote the book Summa de

Arithmetica Geometria Proportioni et Proportionalita. In this, he explained the term debit and credit, which are used in accounting till

date.

Q3 :

Explain the development of and role of accounting.

Answer :

Development of accounting

In ancient times, around 4000 B.C., accounting was used for recording wages and salaries, deposits and withdrawals of valuable

goods (such as gold and silver) from the treasures of the king. Afterwards, it was used to record the receipts and payments and

balancing of government financial transactions. During 1500 A.D., accounting was used by business firms for recording transactions

related to business. In 1800 A.D., accounting was used to record transactions and also to provide information to various users of

financial data.

Role of accounting- While in the earlier times accounting was merely concerned with recording the financial events (i.e. record-

keeping activity); however, now-a-days, accounting is done with the rationale of not only maintaining records, but also providing an

information system that provides important and relevant information to various accounting users.

1. Substitute of memory- As, it is beyond human capabilities to remember each and every business transaction, so accounting plays an

important role in recording these transactions in the book of accounts.

2. Assistance to management- Management uses accounting information for short term and long term planning of business activities and to

control various costs and budgets.

3. Comparative study- In order to ascertain the performance of the business, accounting enables comparison of current year's profit with that

of previous years (intra-firm comparison)and also with other firms in the same business (inter-firm comparison).

4. Evidence in court- It acts as evidence that can be used or presented in the court, if any discrepancy arises in the future.

Q4 :

Define accounting and state its objectives.

Answer :

Accounting is a process of identifying the events of financial nature, recording them in the journal, classifying in their respective

accounts and summarising them in profit and loss account and balance sheet and communicating results to users of such

information, viz. owner, government, creditor, investors, etc.

According to American Institute of Certified Accountants, 1941, "Accounting is the art of recording, classifying and summarising in a

significant manner and in terms of money, transactions and events that are, in part at least, of financial character and interpreting

the results thereof."

In 1970, American Institute of Certified Public Accountants changed the definition and stated, "The function of accounting is to

provide quantitative information, primarily financial in nature, about economic entities, that is intended to be useful in making

economic decisions."

Objectives of Accounting:

1. Recording business transactions systematically- It is necessary to maintain systematic records of every business transaction, as it is

beyond human capacities to remember such large number of transactions. Skipping the record of any one of the transactions may lead to

erroneous and faulty results.

2. Determining profit earned or loss incurred- In order to determine the net result at the end of an accounting period, we need to calculate

profit or loss. For this purpose trading and profit and loss account are prepared. It gives information regarding how much of goods have

been purchased and sold, expenses incurred and amount earned during a year.

3. Ascertaining financial position of the firm- Ascertaining profit earned or loss incurred is not enough; proprietor also interested in

knowing the financial position of his/her firm, i.e. the value of the assets, amount of liabilities owed, net increase or decrease in his/her

capital. This purpose is served by preparing the balance sheet that facilitates in ascertaining the true financial position of the business.

4. Assisting management- Systematic accounting helps the management in effective decision making, efficient control on cash management

policies, preparing budget and forecasting, etc.

5. Assessing the progress of the business- Accounting helps in assessing the progress of business from year to year, as accounting

facilitates the comparison both inter-firm as well as intra-firm.

6. Detecting and preventing frauds and errors- It is necessary to detect and prevent fraud and errors, mismanagement and wastage of the

finance. Systematic recording helps in the easy detection and rectification of frauds, errors and inefficiencies, if any.

7. Communicating accounting information to various users- The important step in the accounting process is to communicate financial

and accounting information to various users including both internal and external users like owners, management, government, labour, tax

authorities, etc. This assists the users to understand and interpret the accounting data in a meaningful and appropriate manner without any

ambiguity.

Q5 :

Describe the informational needs of external users.

Answer :

There are various external users of accounting who need accounting information for decision making, investment planning and to

assess the financial position of the business. The various external users are given below.

1. Banks and other financial institutions- Banks provide finance in form of loans and advances to various businesses. Thus, they need

information regarding liquidity, creditworthiness, solvency and profitability to advance loans.

2. Creditors- These are those individuals and organisations to whom a business owes money on account of credit purchases of goods and

receiving services; hence, the creditors require information about credit worthiness of the business.

3. Investors and potential investors- They invest or plan to invest in the business. Hence, in order to assess the viability and prospectus of

their investment, creditors need information about profitability and solvency of the business.

4. Tax authorities- They need information about sales, revenues, profit and taxable income in order to determine the levy various types of tax

on the business.

5. Government- It needs information to determine national income, GDP, industrial growth, etc. The accounting information assist the

government in the formulation of various policies measures and to address various economic problems like employment, poverty etc.

6. Researcher- Various research institutes like NGOs and other independent research institutions like CRISIL, stock exchanges, etc.

undertake various research projects and the accounting information facilitates their research work.

7. Consumer- Every business tries to build up reputation in the eyes of consumers, which can be created by the supply of better quality

products and post-sale services at reasonable and affordable prices. Business that has transparent financial records, assists the customers

to know the correct cost of production and accordingly assess the degree of reasonability of the price charged by the business for its

products and thus helps in repo building of the business.

8. Public- Public is keenly interested to know the proportion of the profit that the business spends on various public welfare schemes; for

example, charitable hospitals, funding schools, etc. This information is also revealed by the profit and loss account and balance sheet of the

business.

Q6 :

What do you mean by an asset and what are different types of assets?

Answer :

Any valuable thing that has monetary value, which is owned by a business, is its asset. In other words, assets are the monetary

values of the properties or the legal rights that are owned by the business organisations.

Fixed Assets- These are those assets that are hold for the long term and increase the profit earning capacity and productive

capacity of the business. These assets are not meant for sale, for example, land, building machinery, etc.

Current Assets- Assets that can be easily converted into cash or cash equivalents are termed as current assets. These are

required to run day to day business activities; for example, cash, debtors, stock, etc.

Tangible Assets- Assets that have physical existence, i.e., which can be seen and touched, are tangible assets; for example, car,

furniture, building, etc.

Intangible Assets- Assets that cannot be seen or touched, i.e. those assets that do not have physical existence, are intangible

assets; for example, goodwill, patents, trade mark, etc.

Liquid Assets- Assets that are kept either in cash or cash equivalents are regarded as liquid assets. These can be converted into

cash in a very short period of time; for example, cash, bank, bills receivable, etc.

Fictitious Assets- These are the heavy revenue expenditures, the benefit of whose can be derived in more than one year. They

represent loss or expense that are written off over a period of time, for example, if advertisement expenditure is Rs 1,00,000 for 5

years, then each year Rs 2,00,000 will be written off.

Q7 :

Explain the meaning of gain and profit. Distinguish between these two terms.

Answer :

Profit- Excess of revenue over expense is known as profit. It is normally categorised into gross profit or net profit. It increases the

owner's capital as it is added to the capital at the end of each accounting period. For example, goods costing Rs 1, 00,000 is sold at

Rs 1,20,000, then the sale proceeds of Rs 1,20,000 is the revenue and 1,00,000 is the expense to generate this revenue. Hence,

accounting profit of Rs 20,000 (i.e. Rs 1,20,000 - Rs 1,00,000) is the difference between the revenue and expense that is earned by

the business.

Gain- It arises from irregular activities or non-recurring transactions. In other words, a gain is a result of transactions that are

incidental to the business, other than operating transactions. For example, an old machinery of book value Rs 20,000 is sold at Rs

25,000. Hence, the gain is Rs 5,000 (i.e. Rs 25,000 - Rs 20,000). Here, the sale of the old machinery is an irregular activity; so, the

difference is termed as gain

Thus, in other words the only difference between profit and gain is that profit is the excess of revenue over expense and gain arises

from other than operating transactions.

Q8 :

Explain the qualitative characteristics of accounting information.

Answer :

The following are the qualitative characteristics of accounting information:

1. Reliability- It means that the user can rely on the accounting information. All accounting information is verifiable and can be verified from

the source document (voucher), viz. cash memos, bills, etc. Hence, the available information should be free from any errors and unbiased.

2. Relevance- It means that essential and appropriate information should be easily and timely available and any irrelevant information should

be avoided. The users of accounting information need relevant information for decision making, planning and predicting the future

conditions.

3. Understandability- Accounting information should be presented in such a way that every user is able to interpret the information without

any difficulty in a meaningful and appropriate manner.

4. Comparability- It is the most important quality of accounting information. Comparability means accounting information of a current year

can be comparable with that of the previous years. Comparability enables intra-firm and inter-firm comparison. This assists in assessing the

outcomes of various policies and programmes adopted in different time horizons by the same or different businesses. Further, it helps to

ascertain the growth and progress of the business over time and in comparison to other businesses.

Q9 :

Describe the role of accounting in the modern world.

Answer :

The role of accounting has been changing over the period of time. In the modern world, the role of accounting is not only limited to

record financial transactions but also to provide a basic framework for various decision making, providing relevant information to

various users and assists in both short run and long run planning. The role of accounting in the modern world are given below.

1. Assisting management- Management uses accounting information for short term and long term planning of business activities, to predict

the future conditions, prepare budgets and various control measures.

2. Comparative study- In the modern world, accounting information helps us to know the performance of the business by comparing current

year's profit with that of the previous years and also with other firms in the same industry.

3. Substitute of memory- In the modern world, every business incurs large number of transactions and it is beyond human capability to

memorise each and every transaction. Hence, it is very necessary to record transactions in the books of accounts.

4. Information to end user- Accounting plays an important role in recording, summarising and providing relevant and reliable information to

its users, in form of financial data that helps in decision making.

NCERT Solutions for Class 11 Accountancy

Financial Accounting Part-1 Chapter 2

Theory Base of Accounting

Short answers : Solutions of Questions on Page Number : 37

Q1 :

Why is it necessary for accountants to assume that business entity will remain a going concern?

Answer :

Going Concern Concept assumes that the business entity will continue its operation for an indefinite period of time. It is necessary to

assume so, as it helps to bifurcate revenue expenditure (i.e. expenditure related to current year), and capital expenditure (i.e.

expenditure whose benefits accrue over a period of time). For example, a machinery that costs Rs 1,00,000, having an expected life

of 10 years, will be treated as a capital expenditure, as its benefit can be availed for more than one year; whereas, the per year

depreciation of the machinery, say Rs 10,000, will be regarded as a revenue expenditure.

Q2 :

When should revenue be recognised? Are there exceptions to the general rule?

Answer :

Revenue should be recognised when sales take place either in cash or credit and/or right to receive income from any source is

established. Revenue is not recognised, in case, if the income or payment is received in advance or the payment is actually

received from the debtors. In a nutshell, revenue will be recognised when the right to receive income is established. For example,

Mr. A sold goods in January and received payment in February; then revenue is considered to be recognised in the month of

January and not in February. However, if Mr A received cash in advance, i.e. in December and goods are sold in January, then the

revenue is recognised in January and not in December.

The exceptions to this rule are given below.

1) Hire purchase- When goods are sold on hire-purchase system , the amount received in instalments is treated as revenue.

2) Long term construction contract- The long term projects like construction of dams, highways, etc. have long gestation period.

Income is recognised on proportionate basis of work certified and not on the completion of contract.

Q3 :

What is the basic accounting equation?

Answer :

The basic accounting equation is,

Assets = Liabilities + Capital

It means that all the monetary value of all assets of a firm are equal to the total claims, viz. owners and outsiders.

Q4 :

The realisation concept determines when goods sent on credit to customers are to be included in the sales figure for the

purpose of computing the profit or loss for the accounting period. Which of the following tends to be used in practice to

determine when to include a transaction in the sales figure for the period. When the goods have been:

a. dispatched b. invoiced

c. delivered d. paid for

Give reasons for your answer.

Answer :

According to the realisation concept, revenue is recognised when an obligation to receive the amount arises. When the goods are

invoiced, it is treated as the transfer of ownership of goods from the seller to the buyer and hence the revenue is recognised.

Q5 :

Complete the following work sheet:

(i) If a firm believes that some of its debtors may ”²default”², it should act on this by

making sure that all possible losses are recorded in the books. This is an example of

the ___________ concept.

(ii) The fact that a business is separate and distinguishable from its owner is best

exemplified by the ___________ concept.

(iii) Everything a firm owns, it also owns out to somebody. This co-incidence is

explained by the ___________ concept.

(iv) The ___________ concept states that if straight line method of depreciation is used

in one year, then it should also be used in the next year.

(v) A firm may hold stock which is heavily in demand. Consequently, the market value

of this stock may be increased. Normal accounting procedure is to ignore this

because of the ___________.

(vi) If a firm receives an order for goods, it would not be included in the sales figure

owing to the ___________.

(vii) The management of a firm is remarkably incompetent, but the firms accountants can

not take this into account while preparing book of accounts because of ________

concept.

Answer :

(i) If a firm believes that some of its debtors may ”²default”², it should act on this by

making sure that all possible losses are recorded in the books. This is an example of

the conservatism concept.

(ii) The fact that a business is separate and distinguishable from its owner is best

exemplified by the business entity concept.

(iii) Everything a firm owns, it also owns out to somebody. This co-incidence is

explained by the dual aspect concept.

(iv) The consistency concept states that if straight line method of depreciation is used in

one year, then it should also be used in the next year.

(v) A firm may hold stock which is heavily in demand. Consequently, the market value

of this stock may be increased. Normal accounting procedure is to ignore this

because of the conservatism.

(vi) If a firm receives an order for goods, it would not be included in the sales figure

owing to the revenue recognition.

(vii) The management of a firm is remarkably incompetent, but the firm's accountants

cannot take this into account while preparing book of accounts because of money

measurement concept.

<< Previous Chapter 1 : Introduction to AccountingNext Chapter 3 : Recording of Transactions - I >> Long answers : Solutions of Questions on Page Number : 38

Q1 :

'The accounting concepts and accounting standards are generally referred to as the essence of financial accounting'.

Comment.

Answer :

Financial accounting is concerned with the preparation of the financial statements and provides financial information to various

accounting users. It is performed according to the basic accounting concepts like Business Entity, Money Measurement,

Consistency, Conservatism, etc. These concepts allow various alternatives to treat the same transaction. For example, there are a

number of methods available for calculating stock and depreciation, which can be followed by various firms. This leads to wrong

interpretation of financial results by external users due to the problem of inconsistency and incomparability of financial results

among different business entities. In order to mitigate inconsistency and incomparability and to bring uniformity in preparation of the

financial statements, accounting standards are being issued in India by the Institute of Chartered Accountant of India. Accounting

standards help in removing ambiguities and inconsistencies. Hence, accounting standards and accounting concepts are referred as

the essence of financial accounting.

Q2 :

Why is it important to adopt a consistent basis for the preparation of financial statements? Explain.

Answer :

Financial statements are drawn to provide information about growth or decline of business activities over a period of time or

comparison of the results, i.e. intra-firm (comparison within the same organisation) or inter-firm comparisons (comparison between

different firms). Comparisons can be performed only when the accounting policies are uniform and consistent.

According to the Consistency Principle, accounting practices once selected should be continued over a period of time (i.e. years

after years) and should not be changed very frequently. These help in a better understanding of the financial statements and thus

make comparisons easy. For example, if a firm is following FIFO method for recording stock, and switches over to the weighted

average method, then the results of this year cannot be compared to that of the previous years. Although consistency

does not prevent change in the accounting policies, but if change in the policies is essential for better presentation and better

understanding of the financial results, then the firm must undertake change in its accounting policies and must fully disclose all the

relevant information, reasons and effects of those changes in the financial statements.

Q3 :

Discuss the concept-based on the premise 'do not anticipate profits but provide for all losses'.

Answer :

According to the Conservatism Principle, profits should not be anticipated; however, all losses should be accounted (irrespective

whether they occurred or not). It states that profits should not be recorded until they get recognised; however, all possible losses

even though they may happen rarely, should be provided. For example, stock is valued at cost or market price, whichever is lower. If

the market price is lower than the cost price, loss should be accounted; whereas, if the former is more than the latter, then this profit

should not be recorded until unless the stock is sold. There are numerous provisions that are maintained based on the

conservatism principle like, provision for discount to debtors, provision for doubtful bad debts, etc. This principle is based on the

common sense and depicts pessimism. This also helps the business to deal uncertainty and unforeseen conditions.

Q4 :

What is matching concept? Why should a business concern follow this concept? Discuss?

Answer :

Matching Concept states that all expenses incurred during the year, whether paid or not, and all revenues earned during the year,

whether received or not, should be taken into account while determining the profit of that year. In other words, expenses incurred in

a period should be set off against its revenues earned in the same accounting period for ascertaining profit or loss. For example,

insurance premium paid for a year is Rs1200 on July 01 and if accounts are closed on March 31, every year, then the insurance

premium of the current year will be ascertained for nine months (i.e. from July to March) and will be calculated as,

Rs 1200 - Rs 900 = Rs 300

Thus, according to the matching concept, the expense of Rs 900 will be taken into account and not Rs 1200 for determining profit,

as the benefit of only Rs 900 is availed in the current accounting period.

The business entities follow this concept mainly to ascertain the true profit or loss during an accounting period. It is possible that in

the same accounting period, the business may either pay or receive payments that may or may not belong to the same accounting

period. This leads to either overcasting or undercasting of the profit or loss, which may not reveal the true efficiency of the business

and its activities in the concerned accounting period. Similarly, there may be various expenditures like, purchase of machinery,

buildings, etc. These expenditures are capital in nature and their benefits can be availed over a period of time. In such cases, only

the depreciation of such assets is treated as an expense and should be taken into account for calculating profit or loss of the

concerned year. Thus, it is very necessary for any business entity to follow the matching concept.

Q5 :

What is the money measurement concept? Which one factor can make it difficult to compare the monetary values of one

year with the monetary values of another year?

Answer :

Money Measurement Concept states that only those events that can be expressed in monetary terms are recorded in the books of

accounts. For example, 12 television sets of Rs10,000 each are purchased and this event is recorded in the books with a total

amount of Rs 1,20,000. Money acts a common denomination for all the transactions and helps in expressing different measurement

units into a common unit, for example rupees. Thus, money measurement concept enables consistency in maintaining accounting

records. But on the other hand, the adherence to the money measurement concept makes it difficult to compare the monetary

values of one period with that of another. It is because of the fact that the money measurement concept ignores the changes in the

purchasing power of the money, i.e. only the nominal value of money is concerned with and not the real value. What Rs 1 could buy

10 years back cannot buy today; hence, the nominal value of money makes comparison difficult. In fact, the real value of money

would be a more appropriate measure as it considers the price level (inflation), which depicts the changes in profits, expenses,

incomes, assets and liabilities of the business.

NCERT Solutions for Class 11 Accountancy

Financial Accounting Part-1 Chapter 3

Recording of Transactions

Short answers : Solutions of Questions on Page Number : 79

Q1 :

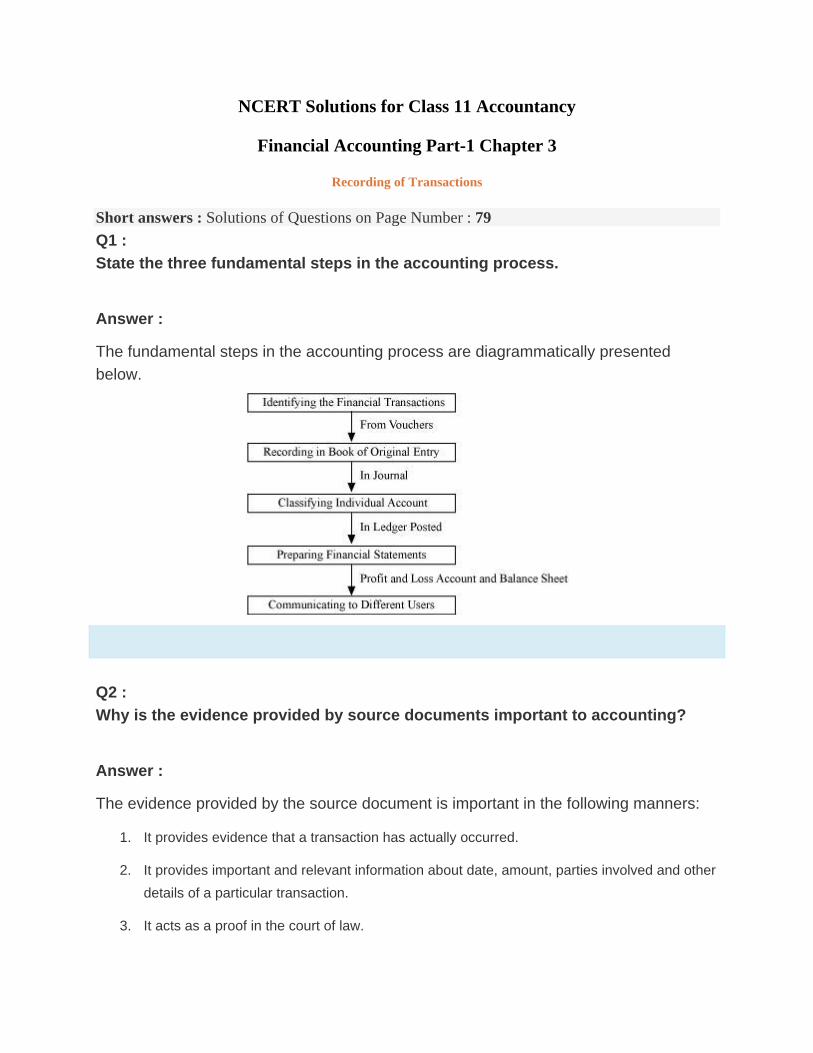

State the three fundamental steps in the accounting process.

Answer :

The fundamental steps in the accounting process are diagrammatically presented

below.

Q2 :

Why is the evidence provided by source documents important to accounting?

Answer :

The evidence provided by the source document is important in the following manners:

1. It provides evidence that a transaction has actually occurred.

2. It provides important and relevant information about date, amount, parties involved and other

details of a particular transaction.

3. It acts as a proof in the court of law.

4. It helps in verifying transactions during the auditing process.

Q3 :

Should a transaction be first recorded in a journal or ledger? Why?

Answer :

A transaction should be recorded first in a journal because journal provides complete

details of a transaction in one entry. Further, a journal forms the basis for posting the

transactions into their respective accounts into ledger. Transactions are recorded in

journal in chronological order, i.e. in the order of occurrence with the help of source

documents. Journal is also known as 'book of original entry', because with the help of

source document, transactions are originally recorded in books. The process of

recording the transactions in journal and then in ledger is presented in the below given

flow chart.

Q4 :

Are debits or credits listed first in journal entries? Are debits or credits indented?

Answer :

As per the rule of double entry system, there are two columns of 'Amount' in the journal

format namely 'Debit Amount' and 'Credit Amount'. The way of recording in a journal is

quite different from normal recording. Journal entry is recorded in journal format in

which the 'Debit Amount' column is listed before the 'Credit Amount' column.

Credits are indented. Indentation is leaving a space before writing any word. Journal

entry has its own jargon. While journalising, in the 'Particulars' column of journal format,

debited account is written first and credited account is in the next line leaving some

space, which is indentation.

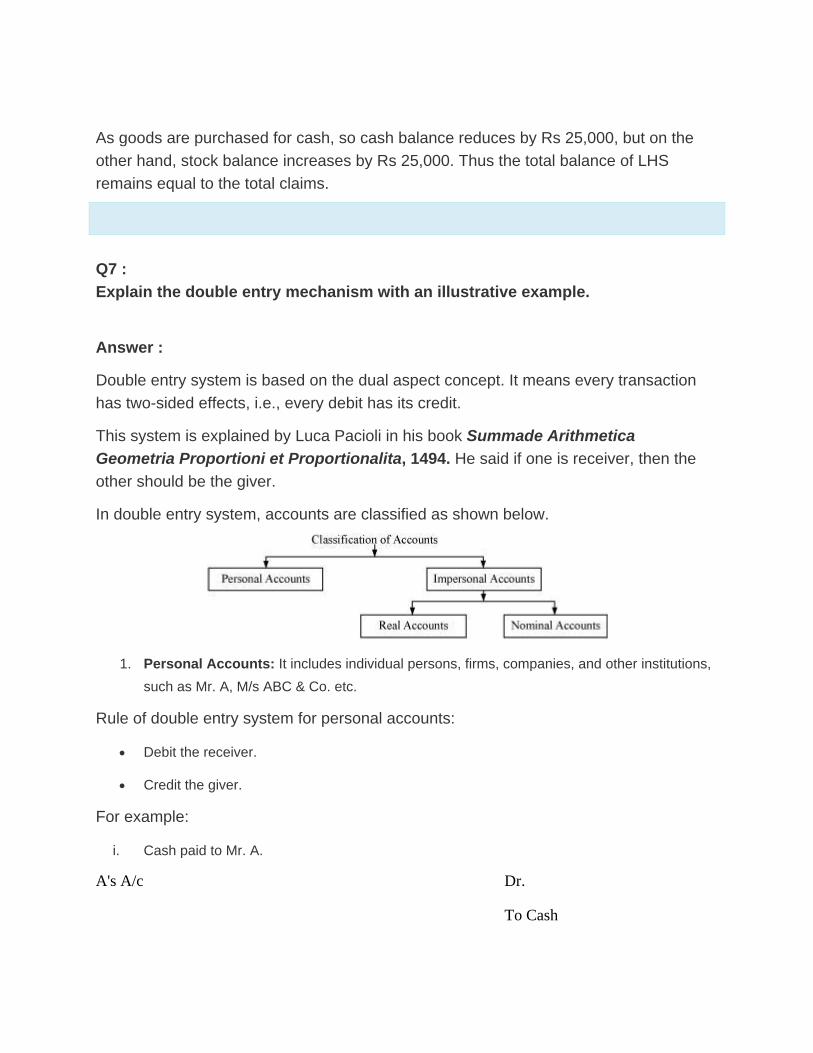

Q5 :

Why are some accounting systems called double accounting systems?

Answer :

Some accounting systems are called double accounting systems because under this

system there are two aspects of every transaction, i.e., every transaction has dual

effect. Every transaction affects two accounts simultaneously, that is represented by

debiting one account and crediting the other account. It is based on the fact that if there

is receiver, there should be a giver.

Q6 :

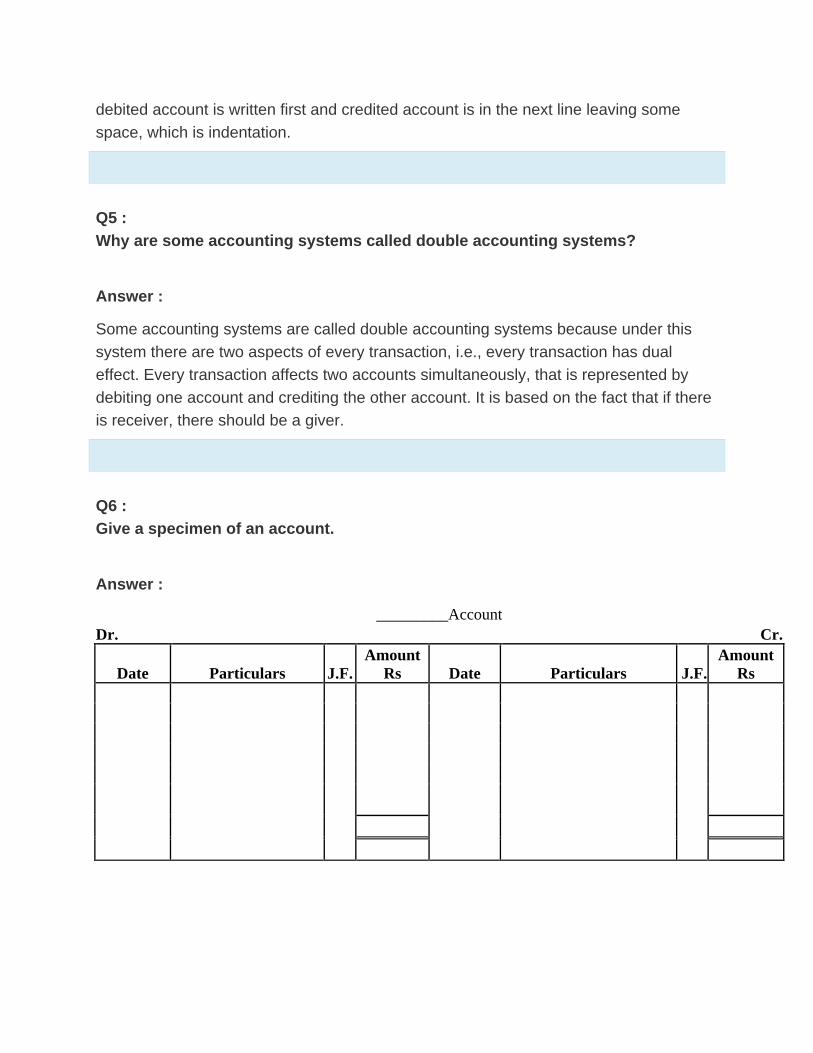

Give a specimen of an account.

Answer :

_________Account

Dr.

Cr.

Date Particulars J.F.

Amount

Rs Date Particulars J.F.

Amount

Rs

Q7 :

Why are the rules of debit and credit same for both liability and capital?

Answer :

Every business acquires funds from internal as well as from external sources. According

to the business entity concept, the amount borrowed from the external sources together

with the internal sources like, capital invested by the proprietor, is termed as liability to

the business. Business entity concept treats business and business owner separately.

Capital of the owner is treated as liability to the business because the business has to

repay the amount of capital to the owner, in case of closure of the business. As liability

incurred is credited, in the same way, fresh capital introduced and net profit increases

the owner's capital, and so, capital is credited. On the other hand, if liability is paid, it

reduces liability, and so, it is debited. Similarly, drawings from capital and net loss

reduce the capital, and so, capital is debited. Thus the rules of debit and credit are

same for both liability and capital.

Q8 :

What is the purpose of posting J.F numbers that are entered in the journal at the

time entries are posted to the accounts?

Answer :

J.F. number is the number that is entered in the ledger at the time of posting entries into

their respective accounts. It helps in determining whether all transactions are properly

posted in their accounts. It is recorded at the time of posting and notat the time of

recording the transactions.

The purpose of entering J.F. number in the ledger is because of the below given

benefits.

1. J.F. number helps in locating the entries of accounts in the journal book. In other words, J.F

number helps to locate the position of the related journal entry and subsidiary book in the

journal book.

2. J.F. number in accounts ensures that recording in the books of original entry has been

posted or not.

Q9 :

What entry (debit or credit) would you make to: (a) increase revenue (b) decrease

in expense, (c) record drawings (d) record the fresh capital introduced by the

owner.

Answer :

1. Increase in revenue

Increase in revenue is credited as it increases the capital. Capital has credit balance

and if capital increases, then it is credited.

2. Decrease in expense

Decrease in expense is credited as all expenses have debit balance. If expense

decreases, then it is credited.

3. Record drawings

Capital has credit balance; if the capital increases, then it is credited. If capital

decreases, then it is debited. Drawings are debited as they decrease the capital.

4. Record of fresh capital introduced by the owner- credit

Capital has credit balance, if capital increases, then it is credited. The introduction of

fresh capital increases the balance of capital, and so, it is credited.

Q10 :

If a transaction has the effect of decreasing an asset, is the decrease recorded as

a debit or as a credit? If the transaction has the effect of decreasing a liability, is

the decrease recorded as a debit or as a credit?

Answer :

If a transaction has a decreasing effect on an asset, then this decrease is recorded as

credit. This is because, as all assets have debit balance and if assets decrease, then it

is credited. For example, sale of furniture results in decrease in furniture (asset); so, the

sale of furniture will be credited.

If a transaction has a decreasing effect on a liability, then this decrease is recorded as

debit. This is because all liabilities have credit balance. If the liability increases, then it is

credited and if the liability decreases, then it is debited. For example, payment to the

creditors results in a decrease in the creditors (liability); so, the creditors account will be

debited.

<< Previous Chapter 2 : Theory Base of AccountingNext Chapter 4 : Recording of Transactions - II >> Numerical questions : Solutions of Questions on Page Number : 80

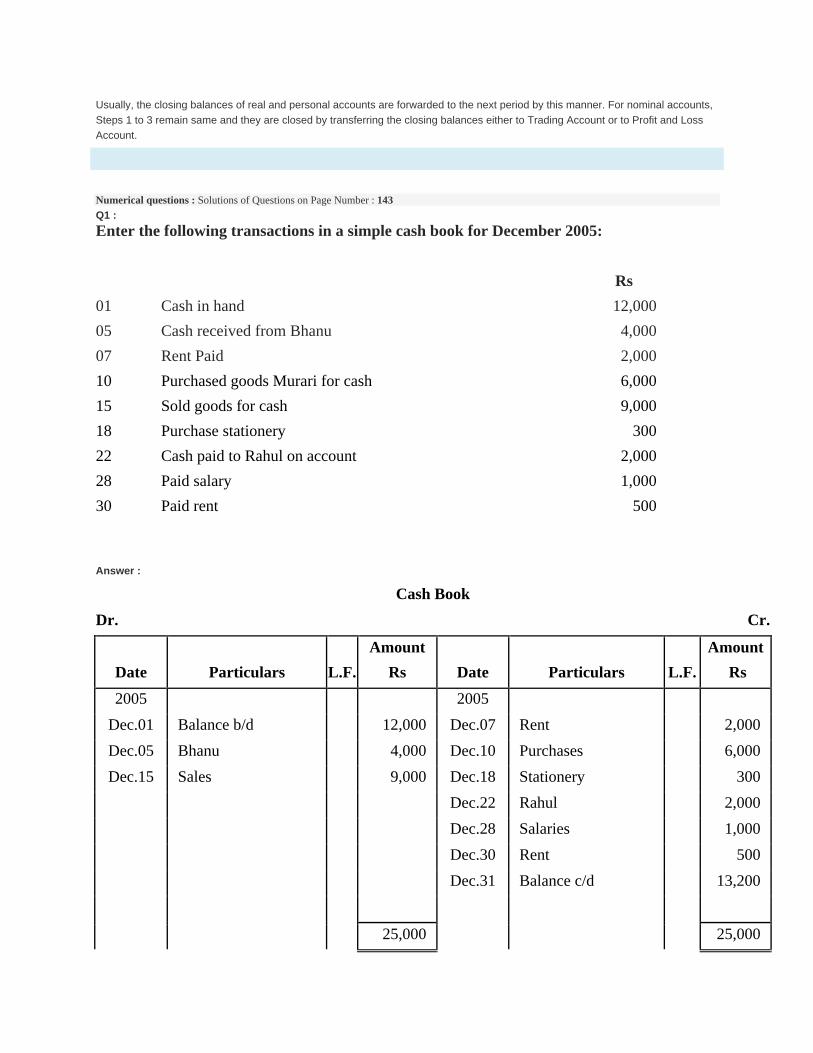

Q1 :

Prepare accounting equation on the basis of the following:

(a) Harsha started business with cash Rs 2,00,000

(b) Purchased goods from Naman for cash Rs 40,000

(c) Sold goods to Bhanu costing Rs 10,000/- Rs 12,000

(d) Bought furniture on credit Rs 7,000

Answer :

S.No. Explanation Assets

= Liabilities + Capital

Cash + Stock + Debtors + Furniture Creditors

(a) Increase in cash 2,00,000

=

Increase in capital 2,00,000

2,00,000

= NIL + 2,00,000

(b) Increase in stock

40,000

Decrease in cash (40,000)

1,60,000 + 40,000

= NIL + 2,00,000

(c) Increase in debtors

12,000

Decrease in stock

(10,000)

Profit

2,000

1,60,000 + 30,000 + 12,000

= NIL

2,02,000

(d) Increase in furniture

7,000

Increase in creditors 7,000

1,60,000 + 30,000 + 12,000 + 7,000 = 7,000 + 2,02,000

Q2 :

Prepare accounting equation from the following:

Rs

(a) Kunal started business with cash 2,50,000

(b) He purchased furniture for cash 35,000

(c) He paid commission 2,000

(d) He purchases goods on credit 40,000

(e) He sold goods (costing Rs 20,000) for cash 26,000

Answer :

S.No. Explanation Assets Liabilities + Capital

Cash + Furniture + Stock = Creditors

(a) Increase in cash 2,50,000

Increase in capital 2,50,000

2,50,000

= NIL + 2,50,000

(b) Increase in furniture

35,000

Decrease in cash (35,000)

2,15,000 + 35,000

= NIL + 2,50,000

(c) Decrease in capital (Expense)

(2,000)

Decrease in cash (2,000)

2,13,000 + 35,000

= NIL + 2,48,000

(d) Increase in stock

40,000

Increase in creditors 40,000

2,13,000 + 35,000 + 40,000

= 40,000 + 2,48,000

(e) Increase in cash 26,000

Q3 :

Mohit has the following transactions, prepare accounting equation:

Rs

(a) Business started with cash 1,75,000

(b) Purchased goods from Rohit 50,000

(c) Sales goods on credit to Manish (Costing Rs 17,500) 20,000

(d) Purchased furniture for office use 10,000

(e) Cash paid to Rohit in full settlement 48,500

(f) Cash received from Manish 20,000

(g) Rent paid 1,000

(h) Cash withdrew for personal use 3,000

Answer :

S.No. Explanation Assets Liabilities + Capital

Cash + Stock + Debtors Furniture = Creditors

(a) Increase in cash 1,75,000

Increase in capital 1,75,000

1,75,000

= NIL + 1,75,000

(b) Increase in stock

50,000

Increase in creditors (Rohit) = 50,000 + 1,75,000

1,75,000 + 50,000

= 50,000 + 1,75,000

(c) Increase in debtors (Manish)

20,000

Decrease in stock

(17,500)

Increase in capital (Profit)

2,500

1,75,000 + 32,500 + 20,000

= 50,000 + 1,77,500

(d) Increase in furniture

10,000

Decrease in cash (10,000)

Q4 :

Rohit has the following transactions:

Rs

(a) Commenced business with cash 1,50,000

(b) Purchased machinery on credit 40,000

(c) Purchased goods for cash 20,000

(d) Purchased car for personal use 80,000

(e) Paid to creditors in full settlement 38,000

(f) Sold goods for cash costing Rs 5,000 4,500

(g) Paid rent 1,000

(h) Commission received in advance 2,000

Prepare the Accounting Equation to show the effect of the above transactions on the assets,

liabilities and capital.

Answer :

S.No. Explanation Assets Liabilities + Capital

Cash + Machinery + Stock = Creditors + Unaccrued Income

(a) Increase in cash 1,50,000

Increase in capital 1,50,000

1,50,000

= NIL + 1,50,000

(b) Increase in machinery

40,000

Increase in creditors = 40,000

1,50,000 + 40,000

= 40,000 + 1,50,000

(c) Increase in stock

20,000

Decrease in cash (20,000)

1,30,000 + 40,000 + 20,000 = 40,000 + 1,50,000

(d) Decrease in cash (80,000)

Decrease in capital (Drawings) (80,000)

50,000 + 40,000 + 20,000 = 40,000 + 70,000

(e) Decrease in creditors (40,000)

Decrease in cash (38,000)

Increase in capital

(Discount received)

Q5 :

Use accounting equation to show the effect of the following transactions of M/s Royal

Traders:

Rs

(a) Started business with cash 1,20,000

(b) Purchased goods for cash 10,000

(c) Rent received 5,000

(d) Salary outstanding 2,000

(e) Prepaid Insurance 1,000

(f) Received interest 700

(g) Sold goods for cash (costing Rs 5,000) 7,000

(h) Goods destroyed by fire 500

Answer :

S.No. Explanation Assets = Liabilities + Capital

Cash + Stock + Prepaid Expenses Outstanding Expenses

(a) Increase in cash 1,20,000

Increase in capital 1,20,000

1,20,000

= NIL + 1,20,000

(b) Increase in stock

10,000

Increase in cash (10,000) =

1,10,000 + 10,000

= NIL + 1,20,000

(c) Increase in cash 5,000

Increase in capital (Profit)

5,000

1,15,000 + 10,000

= NIL + 1,25,000

(d) Increase in outstanding expenses

= 2,000

Decrease in capital (Expense) (2,000)

1,15,000 + 10,000

= 2,000 + 1,23,000

(e) Increase in prepaid expenses

1,000

Decrease in cash (1,000)

1,14,000 + 10,000 + 1,000 = 2,000 + 1,23,000

(f) Increase in cash 700

Increase in capital (Profit)

700

1,14,700 + 10,000 + 1,000 = 2,000 + 1,23,700

(g) Increase in cash 7,000

Decrease in stock

(5,000)

Increase in capital (Profit)

2,000

1,21,700 + 5,000 + 1,000 = 2,000 + 1,25,700

(h) Decrease in stock

(500)

Q6 :

Show the accounting equation on the basis of the following transaction:

(a) Udit started business with: Rs

(i) Cash 5,00,000

(ii) Goods 1,00,000

(b) Purchased building for cash 2,00,000

(c) Purchased goods from Himani 50,000

(d) Sold goods to Ashu (Cost Rs 25,000) 36,000

(e) Paid insurance premium 3,000

(f) Rent outstanding 5,000

(g) Depreciation on building 8,000

(h) Cash withdrawn for personal use 20,000

(i) Rent received in advance 5,000

(j) Cash paid to Himani on account 20,000

(k) Cash received from Ashu 30,000

Answer :

S.No. Explanation

Assets = Liabilities + Capital

Cash + Stock + Building + Debtors Creditors + Outstanding

Expenses

+ UnaccruedIncome

(a) Increase in cash 5,00,000

Increase in stock

1,00,000

Increase in capital 6,00,000

5,00,000 + 1,00,000

= NIL

+ 6,00,000

(b) Increase in building

2,00,000

Decrease in cash (2,00,000)

=

3,00,000 + 1,00,000 + 2,00,000

= NIL

+ 6,00,000

(c) Increase in stock

50,000

Increase in creditors

= 50,000

3,00,000 + 1,50,000 + 2,00,000 = 50,000

Q7 :

Show the effect of the following transactions on Assets, Liabilities and Capital through

accounting equation:

Rs

(a) Started business with cash 1,20,000

(b) Rent received 10,000

(c) Invested in shares 50,000

(d) Received dividend 5,000

(e) Purchase goods on credit from Ragani 35,000

(f) Paid cash for house hold Expenses 7,000

(g) Sold goods for cash (costing Rs 10,000) 14,000

(h)

(i)

Cash paid to Ragani

Deposited into bank

35,000

20,000

Answer :

S.No. Explanation Assets = Liabilities + Capital

Cash + Stock + Investment + Bank Creditors

(a) Increase in cash 1,20,000

Increase in capital 1,20,000

1,20,000 +

= NIL + 1,20,000

(b) Increase in cash 10,000

Increase in capital (Income) = 10,000

1,30,000

= NIL + 1,30,000

(c) Decrease in investment

50,000

Decrease in cash (50,000)

=

80,000 + 50,000 = NIL + 1,30,000

(d) Increase in cash 5,000

Increase in capital (Income)

5,000

85,000 + 50,000 = NIL + 1,35,000

(e) Increase in stock

35,000

Increase in creditor (Ragani)

35,000

85,000 + 35,000 + 50,000 = 35,000 + 1,35,000

(f) Decrease in capital

(7,000)

Decrease in cash (7,000)

78,000 + 35,000 + 50,000 = 35,000 + 1,28,000

(g) Increase in cash

Q8 :

Show the effect of following transaction on the accounting equation:

Rs

(a) Manoj started business with

(i) Cash 2,30,000

(ii) Goods 1,00,000

(iii) Building 2,00,000

(b) He purchased goods for cash 50,000

(c) He sold goods(costing Rs 20,000) 35,000

(d) He purchased goods from Rahul 55,000

(e) He sold goods to Varun (Costing Rs 52,000) 60,000

(f) He paid cash to Rahul in full settlement 53,000

(g) Salary paid by him 20,000

(h) Received cash from Varun in full settlement 59,000

(i) Rent outstanding 3,000

(j) Prepaid Insurance 2,000

(k) Commission received by him 13,000

(l) Amount withdrawn by him for personal use 20,000

(m) Depreciation charge on building 10,000

(n) Fresh capital invested 50,000

(o) Purchased goods from Rakhi 6,000

Answer :

S.No. Explanation

Assets

= Liabilities + Capital

Cash + Stock + Building + Debtors +

Prepaid

Expenses Creditors +

Outstanding

Expenses

(a) Increase in cash,

stock and building

2,30,000 + 1,00,000 + 2,00,000

Increase in capital

5,30,000

2,30,000 + 1,00,000 + 2,00,000

=

+ 5,30,000

(b) Increase in stock

50,000

Decrease in cash (50,000)

1,80,000 + 1,50,000 + 2,00,000

=

+ 5,30,000

(c) Increase in cash 35,000

Decrease in stock

(20,000)

increase in capital

(Profit)

15,000

2,15,000 + 1,30,000 + 2,00,000

Q9 :

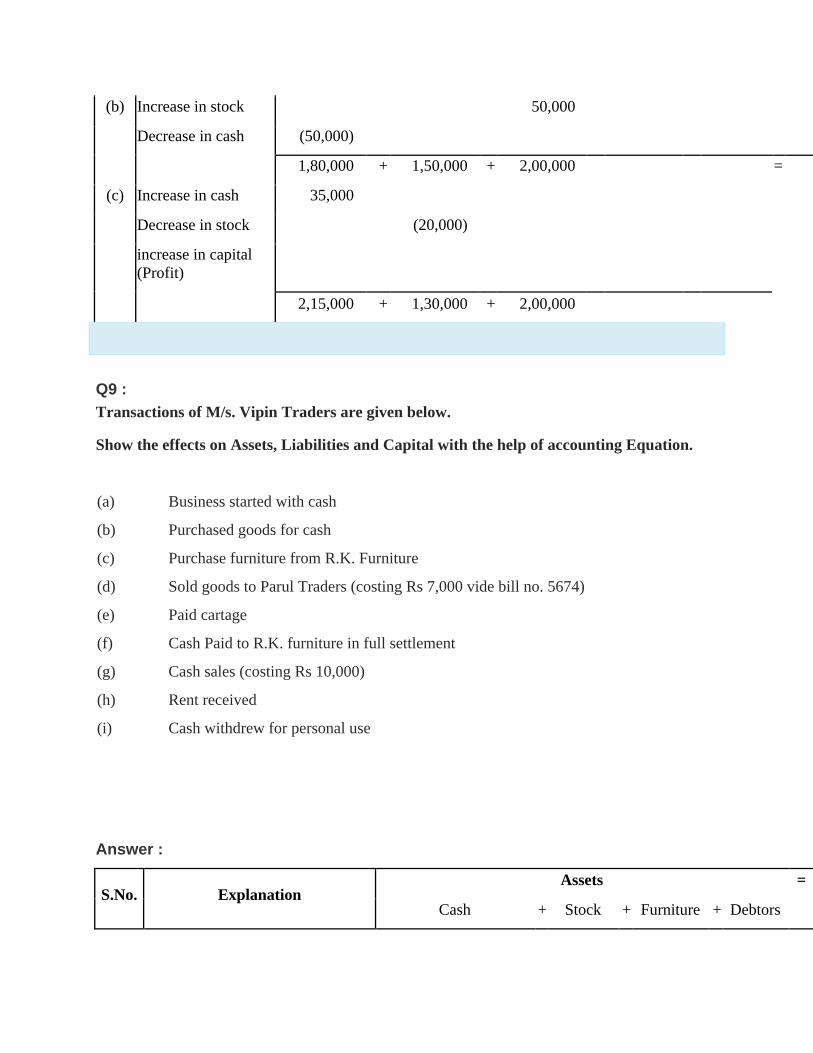

Transactions of M/s. Vipin Traders are given below.

Show the effects on Assets, Liabilities and Capital with the help of accounting Equation.

Rs

(a) Business started with cash 1,25,000

(b) Purchased goods for cash 50,000

(c) Purchase furniture from R.K. Furniture 10,000

(d) Sold goods to Parul Traders (costing Rs 7,000 vide bill no. 5674) 9,000

(e) Paid cartage 100

(f) Cash Paid to R.K. furniture in full settlement 9,700

(g) Cash sales (costing Rs 10,000) 12,000

(h) Rent received 4,000

(i) Cash withdrew for personal use 3,000

Answer :

S.No. Explanation Assets = Liabilities + Capital

Cash + Stock + Furniture + Debtors Creditors

(a) Increase in cash 1,25,000

Increase in capital 1,25,000

1,25,000 +

= NIL + 1,25,000

(b) Increase in stock

50,000

Decrease in cash (50,000) =

75,000 + 50,000

= NIL + 1,25,000

(c) Increase in furniture

10,000

=

Increase in creditors

= 10,000

75,000 + 50,000 + 10,000 = 10,000 + 1,25,000

(d) Increase in debtors

9,000

Decrease in stock

(7,000

)

Increase in capital (Profit)

2,000

75,000 + 43,000 + 10,000 + 9,000 = 10,000 + 1,27,000

(e) Decrease in capital (Cartage

Expenses)

(100)

Decrease in cash (100)

74,900 + 43,000 + 10,000 + 9,000 = 10,000 + 1,26,900

(f) Decrease in creditors

= (10,000)

Decrease in cash (9,700)

Increase in capital (Discount-

received)

300

Q10 :

Bobby opened a consulting firm and completed these transactions during November, 2005:

(a) Invested Rs 4,00,000 cash and office equipment with Rs 1,50,000 in a business called Bobbie Consulting.

(b) Purchased land and a small office building. The land was worth Rs 1,50,000 and the building worth Rs 3,50,000. The

purchase price was paid with Rs 2,00,000 cash and a long term note payable for Rs 8,00,000.

(c) Purchased office supplies on credit for Rs 12,000.

(d) Bobbie transferred title of motor car to the business. The motor car was worth Rs 90,000.

(e) Purchased for Rs 30,000 additional office equipment on credit.

(f) Paid Rs 75,00 salary to the office manager.

(g) Provided services to a client and collected Rs 30,000

(h) Paid Rs 4,000 for the month's utilities.

(i) Paid supplier created in transaction (c).

(j) Purchase new office equipment by paying Rs 93,000 cash and trading in old equipment with a recorded cost of Rs 7,000.

(k) Completed services of a client for Rs 26,000. This amount is to be paid within 30 days.

(l) Received Rs 19,000 payment from the client created in transaction (k).

(m) Bobby withdrew Rs 20,000 from the business.

Analyse the above stated transactions and open the following T-accounts:

Cash, client, office supplies, motor car, building, land, long term payables, capital,

withdrawals, salary, expense and utilities expense.

Answer :

a)

The transaction (a) increases assets by Rs 5,50,000 (cash Rs 4,00,000 and office equipment Rs

1,5,000) it will be debited and on the other hand it will increase the capital by Rs 5,50,000, so it

will be credited in capital account.

Cash Account

Office Equipment Account

Capital Account

Dr. Cr.

Dr. Cr . Dr. Cr.

(a) Rs 4,00,000

(a) Rs 1,50,000

(a) Rs 4,00,000

(a) Rs 1,50,000

b)

Purchase of land and small office building are assets. On one hand, the purchase of these items

will increase their individual accounts and this will increase the total amount of the assets in the

business; so, both the accounts will be debited. On the other hand, payment in cash on the

purchase of these assets will decrease the cash balance, so cash account will be credited to the

extent of amount paid. After payment for building in cash, the balance of building account will

be transferred to creditors for building account. This will increase the amount of the creditors,

which in turn will increase the total liabilities of the business. Long term payables are regarded

as loan to the business that will increase both cash balance (due to intake of loan) as well as

liabilities of the business.

Land Account

Building Account

Dr. Cr.

Dr. Cr.

(b) Rs 1,50,000

(b) Rs 3,50,000

Cash Account

Long Term Payable Account

Dr. Cr.

Dr. Cr.

(a) Rs 4,00,000 (b) Rs 1,50,000

(b) Rs 8,00,000

(b) Rs 8,00,000 (b) Rs 50,000

Q11 :

Journalise the following transactions in the books of Himanshu:

2005 Rs

Dec.01 Business started with cash 75,000

Dec.07 Purchased goods for cash 10,000

Dec.09 Sold goods to Swati 5,000

Dec.12 Purchased furniture 3,000

Dec.18 Cash received from Swati in full settlement 4,000

Dec.25 Paid rent 1,000

Dec.30 Paid salary 1,500

Answer :

Books of Himanshu

Journal

Date Particulars

L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Dec.01 Cash A/c Dr. 75,000

To Capital A/c

75,000

(Started business with cash)

Dec.07 Purchases A/c Dr. 10,000

To Cash A/c

10,000

(Goods purchased for cash)

Dec.09 Swati Dr. 5,000

To Sales A/c

5,000

(Goods sold on credit)

Dec.12 Furniture A/c Dr. 3,000

To Cash A/c

3,000

(Furniture purchased for cash)

Dec.18 Cash A/c Dr. 4,000

Discount Allowed A/c Dr. 1,000

To Swati

5,000

(Cash received from Swati and discount allowed)

Dec.25 Rent A/c Dr. 1,000

To Cash A/c

1,000

(Rent paid in cash)

Q12 :

Enter the following Transactions in the Journal of Mudit :

2006 Rs

Jan.01 Commenced business with cash 1,75,000

Jan.01 Building 1,00,000

Jan.02 Goods purchased for cash 75,000

Jan.03 Sold goods to Ramesh 30,000

Jan.04 Paid wages 500

Jan.06 Sold goods for cash 10,000

Jan.10 Paid for trade expenses 700

Jan.12 Cash received from Ramesh 29,500

Discount allowed 500

Jan.14 Goods purchased for Sudhir 27,000

Jan.18 Cartage paid 1,000

Jan.20 Drew cash for personal use 5,000

Jan.22 Goods use for house hold 2,000

Jan.25 Cash paid to Sudhir 26,700

Discount allowed 300

Answer :

Books of Mudit

Journal

Date Particulars

L.F.

Debit

Amount

Rs

Credit

Amount Rs

2006

Jan.0

1 Building A/c

Dr. 1,00,000

Cash A/c Dr. 1,75,000

To Capital A/c

2,75,000

(Commenced business with cash and building)

Jan.0

2 Purchases A/c Dr. 75,000

To Cash A/c

75,000

(Goods purchased for cash)

Jan.0

3 Ramesh Dr. 30,000

To Sales A/c

30,000

(Goods sold to Ramesh)

Jan.0

4 Wages A/c Dr. 500

To Cash A/c

500

(Wages paid in cash)

Jan.0

6 Cash A/c Dr. 10,000

To Sales A/c

10,000

(Goods sold for cash)

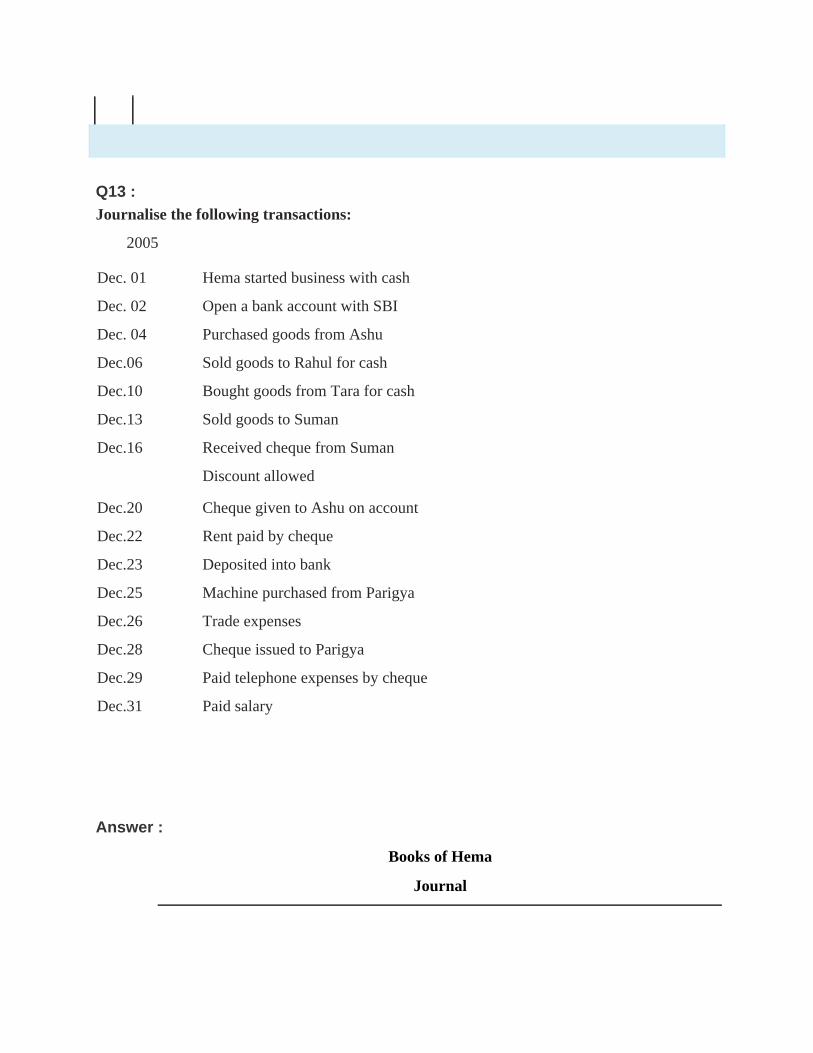

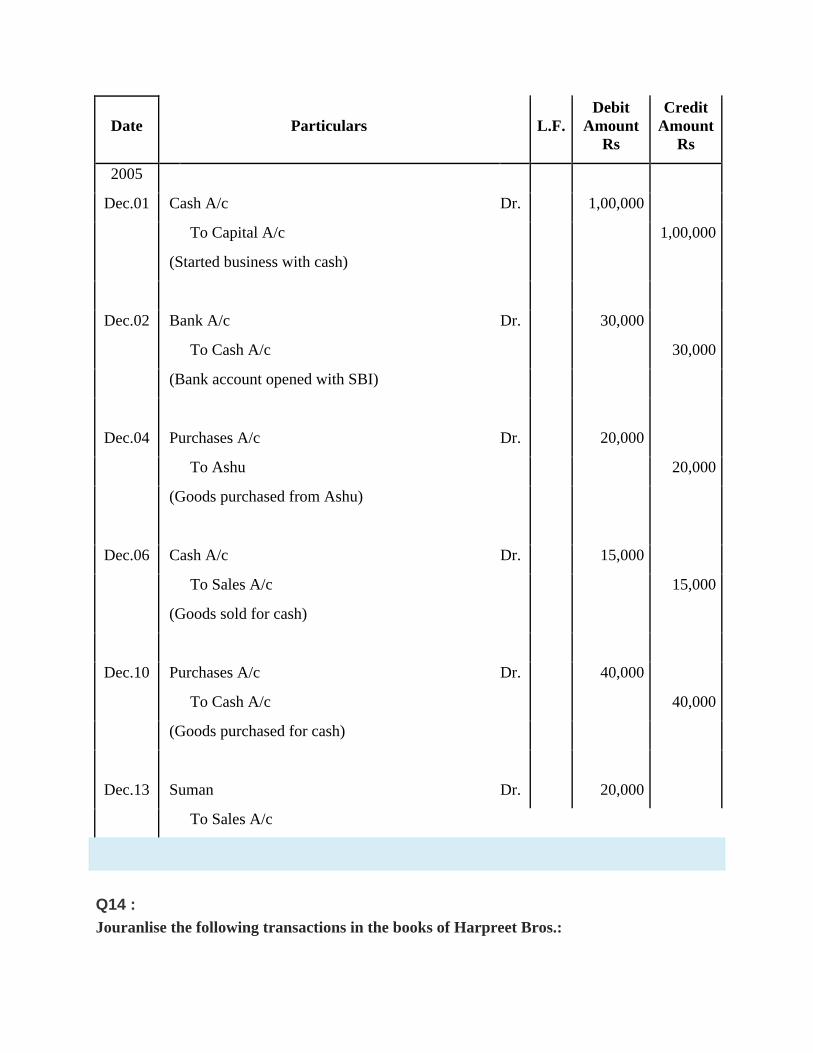

Q13 :

Journalise the following transactions:

2005 Rs

Dec. 01 Hema started business with cash 1,00,000

Dec. 02 Open a bank account with SBI 30,000

Dec. 04 Purchased goods from Ashu 20,000

Dec.06 Sold goods to Rahul for cash 15,000

Dec.10 Bought goods from Tara for cash 40,000

Dec.13 Sold goods to Suman 20,000

Dec.16 Received cheque from Suman 19,500

Discount allowed 500

Dec.20 Cheque given to Ashu on account 10,000

Dec.22 Rent paid by cheque 2,000

Dec.23 Deposited into bank 16,000

Dec.25 Machine purchased from Parigya 10,000

Dec.26 Trade expenses 2,000

Dec.28 Cheque issued to Parigya 10,000

Dec.29 Paid telephone expenses by cheque 1,200

Dec.31 Paid salary 4,500

Answer :

Books of Hema

Journal

Date Particulars

L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Dec.01 Cash A/c Dr. 1,00,000

To Capital A/c

1,00,000

(Started business with cash)

Dec.02 Bank A/c Dr. 30,000

To Cash A/c

30,000

(Bank account opened with SBI)

Dec.04 Purchases A/c Dr. 20,000

To Ashu

20,000

(Goods purchased from Ashu)

Dec.06 Cash A/c Dr. 15,000

To Sales A/c

15,000

(Goods sold for cash)

Dec.10 Purchases A/c Dr. 40,000

To Cash A/c

40,000

(Goods purchased for cash)

Dec.13 Suman Dr. 20,000

To Sales A/c

Q14 :

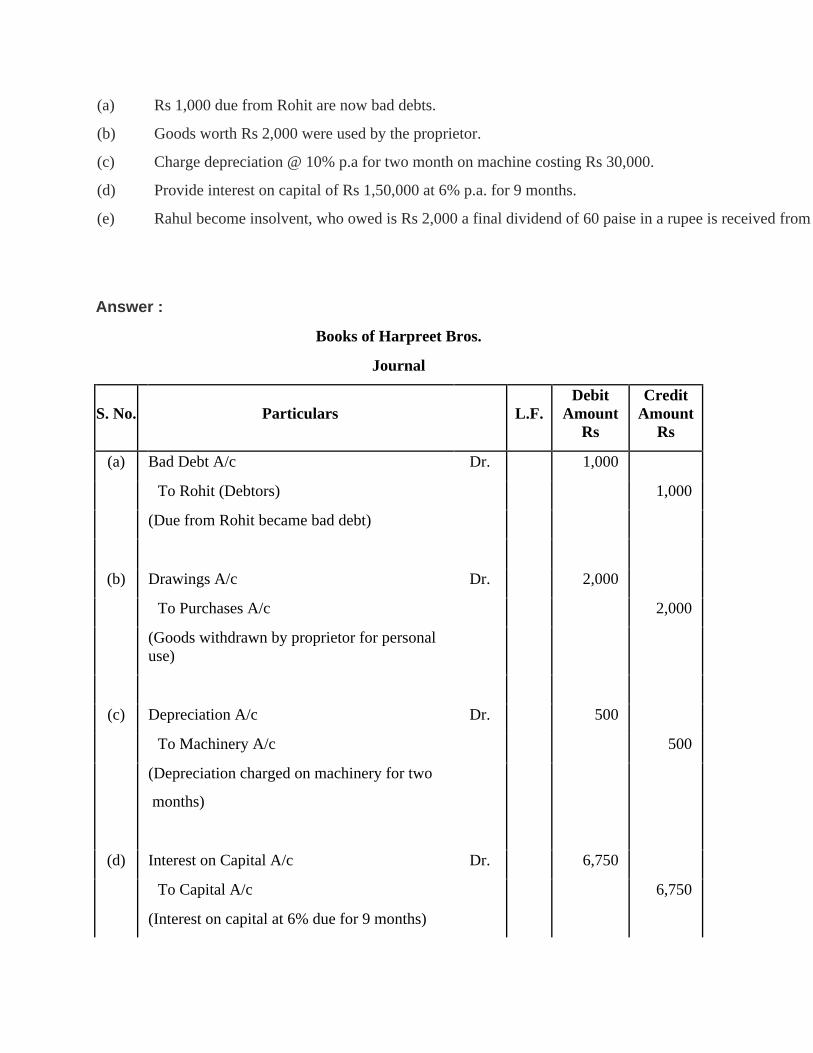

Jouranlise the following transactions in the books of Harpreet Bros.:

(a) Rs 1,000 due from Rohit are now bad debts.

(b) Goods worth Rs 2,000 were used by the proprietor.

(c) Charge depreciation @ 10% p.a for two month on machine costing Rs 30,000.

(d) Provide interest on capital of Rs 1,50,000 at 6% p.a. for 9 months.

(e) Rahul become insolvent, who owed is Rs 2,000 a final dividend of 60 paise in a rupee is received from his estate.

Answer :

Books of Harpreet Bros.

Journal

S. No.

Particulars

L.F.

Debit

Amount

Rs

Credit

Amount

Rs

(a) Bad Debt A/c Dr. 1,000

To Rohit (Debtors)

1,000

(Due from Rohit became bad debt)

(b) Drawings A/c Dr. 2,000

To Purchases A/c

2,000

(Goods withdrawn by proprietor for personal

use)

(c) Depreciation A/c Dr. 500

To Machinery A/c

500

(Depreciation charged on machinery for two

months)

(d) Interest on Capital A/c Dr. 6,750

To Capital A/c

6,750

(Interest on capital at 6% due for 9 months)

(e) Bad Debt A/c Dr. 800

Cash A/c Dr. 1,200

To Rahul (Debtor)

2,000

(Received from Rahul 60 paise in a rupee and

rest amount considered as bad debt)

Q15 :

Prepare Journal from the transactions given below :

Rs

(a) Cash paid for installation of machine 500

(b) Goods given as charity 2,000

(c) Interest charge on capital @ 7% p.a. when total capital were 70,000

(d) Received Rs 1,200 of a bad debts written-off last year.

(e) Goods destroyed by fire 2,000

(f) Rent outstanding 1,000

(g) Interest on drawings 900

(h) Sudhir Kumar who owed me Rs 3,000 has failed to pay the amount. He pays me a compensation of 45 paise

in a rupee.

(i) Commission received in advance 7,000

Answer :

Journal

S. No.

Particulars L.F.

Debit

Amount

Rs

Credit

Amount

Rs

(a) Machinery A/c Dr. 500

To Cash A/c

500

(Cash paid for installation of machinery)

(b) Charity A/c Dr. 2,000

To Purchases A/c

2,000

(Goods given as charity)

(c) Interest on Capital A/c Dr. 4,900

To Capital A/c

4,900

(Interest on capital charged @ 7% p.a.)

(d) Cash A/c Dr. 1,200

To Bad Debt Recovered A/c

1,200

(Cash received on from debtors which was

previously written off as bad)

(e) Goods Destroyed by Fire A/c Dr. 2,000

To Purchases A/c

2,000

(Goods destroyed by fire)

Q16 :

Journalise the following transactions, post to the ledger:

2005 Rs

Nov. 01 Business started with (i) Cash 1,50,000

(ii) Goods 50,000

Nov. 03 Purchased goods from Harish 30,000

Nov. 05 Sold goods for cash 12,000

Nov. 08 Purchase furniture for cash 5,000

Nov. 10 Cash paid to Harish on account 15,000

Nov. 13 Paid sundry expenses 200

Nov. 15 Cash sales 15,000

Nov. 18 Deposited into bank 5,000

Nov. 20 Drew cash for personal use 1,000

Nov. 22 Cash paid to Harish in full settlement of account 14,700

Nov. 25 Good sold to Nitesh 7,000

Nov. 26 Cartage paid 200

Nov. 27 Rent paid 1,500

Nov. 29 Received cash from Nitesh 6,800

Discount allowed 200

Nov. 30 Salary paid 3,000

Answer :

Journal

Date

Particulars

L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Nov.01 Cash A/c Dr. 1,50,000

Stock A/c Dr. 50,000

To Capital A/c

2,00,000

(Started business with cash and goods)

Nov.03 Purchases A/c Dr. 30,000

To Harish

30,000

(Goods purchased from Harish)

Nov.05 Cash A/c Dr. 12,000

To Sales A/c

12,000

Q17 :

Journalise the following transactions is the journal of M/s. Goel Brothers and post them to

the ledger.

2006 Rs

Jan. 01 Started business with cash 1,65,000

Jan. 02 Opened bank account in PNB 80,000

Jan. 04 Goods purchased from Tara 22,000

Jan.05 Goods purchased for cash 30,000

Jan.08 Goods sold to Naman 12,000

Jan.10 Cash paid to Tara 22,000

Jan.15 Cash received from Naman 11,700

Discount allowed 300

Jan. 16 Paid wages 200

Jan. 18 Furniture purchased for office use 5,000

Jan. 20 Withdrawn from bank for personal use 4,000

Jan. 22 Issued cheque for rent 3,000

Jan. 23 Goods issued for house hold purpose 2,000

Jan. 24 Drawn cash from bank for office use 6,000

Jan. 26 Commission received 1,000

Jan. 27 Bank charges 200

Jan. 28 Cheque given for insurance premium 3,000

Jan. 29 Paid salary 7,000

Jan. 30 Cash sales 10,000

Answer :

Books of M/s Goel Brothers

Journal

Date Particulars L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2006

Jan.01 Cash A/c Dr. 1,65,000

To Capital A/c

1,65,000

(Started business with cash)

Jan.02 Bank A/c

Dr. 80,000

To Cash A/c

80,000

(Bank account opened with PNB)

Jan.04 Purchases A/c

Dr. 22,000

To Tara

22,000

(Goods purchased from Tara)

Jan.05 Purchases A/c

Dr. 30,000

To Cash A/c

30,000

(Goods purchased for cash)

Jan.08 Naman

Dr. 12,000

To Sales A/c

12,000

(Sale of goods to Naman)

Q18 :

Give journal entries of M/s. Mohit traders; post them to the Ledger from the following

transactions:

August,

2005

Rs

1 Commenced business with cash 1,10,000

2 Opened bank account with H.D.F.C. 50,000

3 Purchased furniture 20,000

7 Bought goods for cash from M/s. Rupa Traders 30,000

8 Purchased good from M/s. Hema Traders 42,000

10 Sold goods for cash 30,000

14 Sold goods on credit to M/s. Gupta Traders 12,000

16 Rent paid 4,000

18 Paid trade expenses 1,000

20 Received cash from Gupta Traders 12,000

22 Goods return to Hema Traders 2,000

23 Cash paid to Hema Traders 40,000

Jan.10 Tara

Dr. 22,000

To Cash A/c

22,000

(Cash paid to Tara)

Jan.15 Cash A/c

Dr. 11,700

Discount Allowed A/c Dr. 300

To Naman

12,000

(Cash received from Naman and discount

allowed)

25 Bought postage stamps 100

30 Paid salary to Rishabh 4,000

Answer :

Books of M/s. Mohit Traders

Journal

Date Particulars L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Aug.01 Cash A/c Dr. 1,10,000

To Capital A/c

1,10,000

(Commenced business with cash)

Aug.02 Bank A/c Dr. 50,000

To Cash A/c

50,000

(Bank account opened with H.D.F.C)

Aug.03 Furniture A/c Dr. 20,000

To Cash A/c

20,000

(Furniture purchased)

Aug.07 Purchases A/c Dr. 30,000

To Cash A/c

30,000

(Goods purchased for cash)

Aug.08 Purchases A/c Dr. 42,000

To M/s. Hema Traders

42,000

(Goods purchased from M/s. Hema Traders)

Aug.10 Cash A/c Dr. 30,000

To Sales A/c

30,000

(Goods sold for cash)

Aug.14 M/s. Gupta Traders Dr. 12,000

To Sales A/c

12,000

(Goods sold to M/s. Gupta traders)

Q19 :

Journalise the following transaction in the Books of the M/s. Bhanu Traders and Post them

into the Ledger.

December, 2005 Rs

1 Started business with cash 92,000

2 Deposited into bank 60,000

4 Bought goods on credit from Himani 40,000

6 Purchased goods from cash 20,000

8 Returned goods to Himani 4,000

10 Sold goods for cash 20,000

14 Cheque given to Himani 36,000

17 Goods sold to M/s. Goyal TradeRs 3,50,000

19 Drew cash from bank for personal use 2,000

21 Goyal traders returned goods 3,500

22 Cash deposited into bank 20,000

26 Cheque received from Goyal Traders 31,500

28 Goods given as charity 2,000

29 Rent paid 3,000

30 Salary paid 7,000

31 Office machine purchased for cash 3,000

Answer :

Books of M/s. Bhanu Traders

Journal

Date

Particulars

L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Dec.01 Cash A/c Dr. 92,000

To Capital A/c

92,000

(Started business with cash)

Dec.02 Bank A/c Dr. 60,000

To Cash A/c

60,000

(Cash deposited into bank)

Dec.04 Purchases A/c Dr. 40,000

To Himani

40,000

(Goods purchased from Himani)

Q20 :

Journalise the following transaction in the Book of M/s. Beauti tradeRs Also post them in

the ledger.

Dec.

2005

Rs

1 Started business with cash 2,00,000

2 Bought office furniture 30,000

3 Paid into bank to open an current account 1,00,000

5 Purchased a computer and paid by cheque 2,50,000

6 Bought goods on credit from Ritika 60,000

8 Cash sales 30,000

9 Sold goods to Karishna on credit 25,000

12 Cash paid to Mansi on account 30,000

14 Goods returned to Ritika 2,000

15 Stationery purchased for cash 3,000

16 Paid wages 1,000

18 Goods returned by Karishna 2,000

20 Cheque given to Ritika 28,000

22 Cash received from Karishna on account 15,000

24 Insurance premium paid by cheque 4,000

26 Cheque received from Karishna 8,000

28 Rent paid by cheque 3,000

29 Purchased goods on credit from Meena Traders 20,000

30 Cash sales 14,000

Answer :

Books of Beauti Traders

Journal

Date Particulars L.F.

Debit

Amount

Rs

Credit

Amount

Rs

2005

Dec.01 Cash A/c Dr. 2,00,000

To Capital A/c

2,00,000

(Started business with cash)

Dec.02 Office Furniture A/c Dr. 30,000

To Cash A/c

30,000

(Office furniture purchased)

Dec.03 Bank A/c Dr. 1,00,000

To Cash A/c

1,00,000

(Opened a current account)

Dec.05 Computer A/c Dr.

2,50,000

Q21 :

Journalise the following transaction in the books of Sanjana and post them into the ledger:

January, 2006 Rs

1 Cash in hand 6,000

Cash at bank 55,000

Stock of goods 40,000

Due to Rohan 6,000

Due from Tarun 10,000

3 Sold goods to Karuna 15,000