Class: XII Study Material ACCOUNTANCY

80

(Ahmedabad Region) Class: XII Study Material ACCOUNTANCY (2021-22 Term-1) Kendriya Vidyalaya Sangathan

-

Upload

khangminh22 -

Category

Documents

-

view

0 -

download

0

Transcript of Class: XII Study Material ACCOUNTANCY

(Ahmedabad Region)

Class: XII Study Material

ACCOUNTANCY (2021-22 Term-1)

Kendriya Vidyalaya Sangathan

Kendriya Vidyalaya Sangathan

(Ahmedabad Region)

Class: XII Study Material ACCOUNTANCY

TERM: I (2021-22)

CHIEF PATRON: DR. JAIDEEP DAS

Deputy Commissioner, KVS RO Ahmedabad

PATRON: MS SHRUTI BHARGAVA

Assistant Commissioner, KVS RO Ahmedabad

CONVENOR: MR RAJESH TRIVEDI Principal, KV- 2 Bhuj

CO-ORDINATOR: MR ARUN SHARMA Principal, KV Naliya

CONTENT TEAM

Ms. Kirti Saini, KV – 2 Ahmedabad Cantt

Mr. Nitinkumar N. Bhetaria, KV – 1 AFS Bhuj

Ms. Meera Khalpada, KV Rajkot

Mr. Mukesh Rathod, KV – 1 Ahmedabad

Ms. Trishna Kumari KV Dwarka

COMPILATION

Dr. Mayank Srivastava KV–3 Gandhinagar Cantt

ACCOUNTANCY (055)

2021 – 22 CLASS XII CURRICULUM – TERM

WISE

TERM 1 MCQ BASED QUESTION PAPER

MM: 40 TIME: 90 MINUTES

PART – A ACCOUNTING FOR PARTNERSHIP FIRMS

FUNDAMENTALS 18 CHANGE IN PROFIT SHARING RATIO

ADMISSION OF A PARTNER COMPANY ACCOUNTS

ACCOUNTING FOR SHARES 12

PART - B ANALYSIS OF FINANCIAL STATEMENTS

Financial Statements of a Company Statement of Profit & Loss and Balance Sheet in the prescribed form with major headings and sub-headings (as per Schedule III to the Companies Act, 2013)

10 Tools of Analysis – Ratio Analysis Accounting Ratios

PROJECT PART 1 10 TOTAL 50

INDEX

UNIT NAME OF THE CHAPTER PAGE NO.

1 Fundamentals of Partnership and Change in

profit sharing ratio

1 - 11

2 Admission of a Partner

12 - 22

3 Company Accounts – Issue and Forfeiture of

Shares

23 - 31

4 Financial Statements of a Company

31 - 40

5 Analysis of Financial statement – Ratio

Analysis

41 – 53

6

CBSE Sample Question Paper and Marking

Scheme

54 - 79

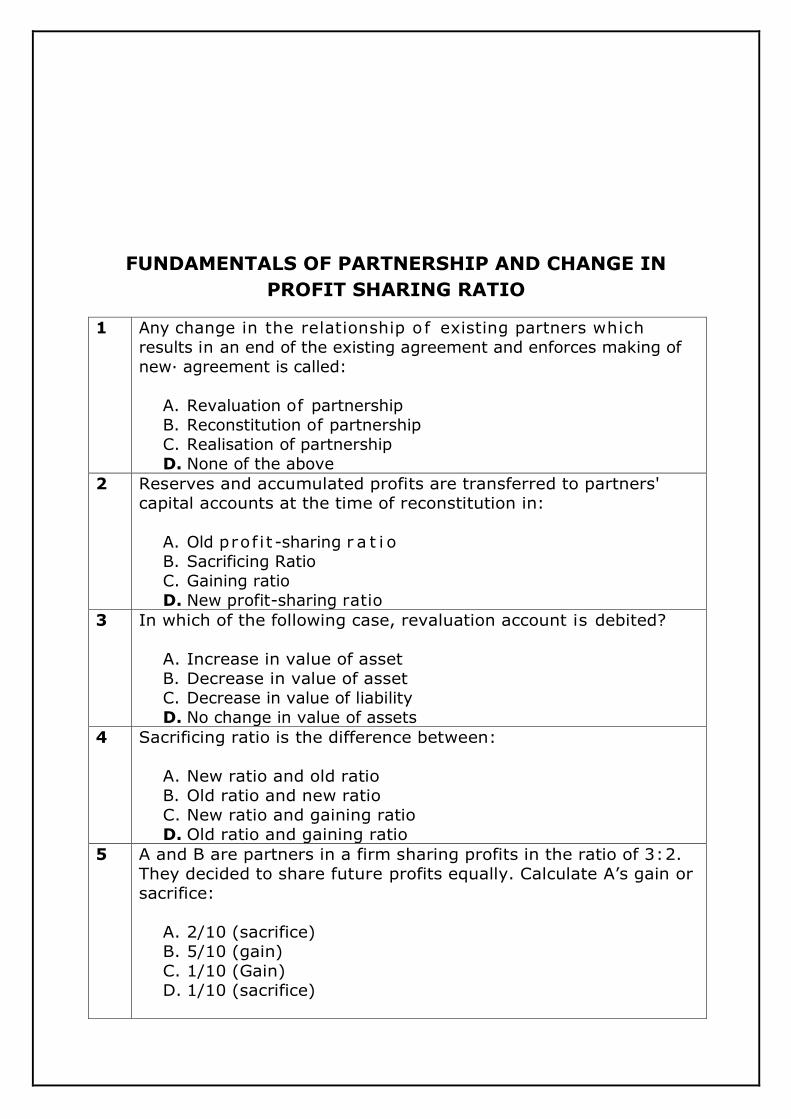

FUNDAMENTALS OF PARTNERSHIP AND CHANGE IN

PROFIT SHARING RATIO

1 Any change in the relationship o f existing partners which

results in an end of the existing agreement and enforces making of

new· agreement is called:

A. Revaluation of partnership

B. Reconstitution of partnership

C. Realisation of partnership

D. None of the above

2 Reserves and accumulated profits are transferred to partners'

capital accounts at the time of reconstitution in:

A. Old prof i t -sharing r a t i o

B. Sacrificing Ratio

C. Gaining ratio

D. New profit-sharing ratio

3 In which of the following case, revaluation account is debited?

A. Increase in value of asset

B. Decrease in value of asset

C. Decrease in value of liability

D. No change in value of assets

4 Sacrificing ratio is the difference between:

A. New ratio and old ratio

B. Old ratio and new ratio

C. New ratio and gaining ratio

D. Old ratio and gaining ratio

5 A and B are partners in a firm sharing profits in the ratio of 3:2.

They decided to share future profits equally. Calculate A’s gain or

sacrifice:

A. 2/10 (sacrifice)

B. 5/10 (gain)

C. 1/10 (Gain)

D. 1/10 (sacrifice)

6 R ; S and T sharing profits and losses in the ratio of 1:2:3,

decide to share future profit and losses equally. They also

decided to adjust the following accumulated profits, losses and

reserves without affecting their book figures, by passing a single

adjustment entry:

General Reserve 40000

Profit and Loss A/c 30000

Share Issue expenses 10000

Then necessary adjustment entry will be:

A. Dr. R and Cr. T by Rs. 10,000 B. Dr. T and Cr. R by Rs. 10,000

C. Dr. S and Cr. R by Rs. 10,000

D. Dr. R and Cr. S by Rs. 10,000

7 U V and W are partners sharing profits in the ratio of 2:3:5. They

also decide to record the effect of the following revaluations and

reassessments without affecting the book values of assets and

liabilities by passing a single adjustment entry:

Book Value

(Rs)

Revised Value

(Rs)

Land and Building 3,00,000 3,50,000

Furniture 1,50,000 1,00,000

Sundry Creditors 60,000 20,000

Outstanding Salaries 10,000 15,000

The single adjustment entry will be:

A. Dr. W and Cr. U by Rs. 10,500

B. Dr. U and Cr. W by Rs. 10,500

C. Dr. V and Cr. U by Rs. 10,500

D. Dr. W and Cr. V by Rs. 10,500

8 A and B are partners sharing profits and losses in the ratio of 3:2

having capitals of Rs.15,00,000 and Rs.10,00,000 respectively as on

31.03.2021. Drawings during the year were Rs. 30,000 and Rs.

20,000 respectively. Capital introduced during the year A Rs.

3,00,000 and B Rs. 2,00,000 which will be treated as credit

balance of their current account. If the rate of interest on capital

is 7% p.a. then the amount of interest of capital of A and B are:

A. A : Rs. 86,100 B : Rs. 57,500

B. A : Rs. 21,000 B : Rs. 14,000

C. A : Rs. 1,05,000 B : Rs.70,000

D. A : Rs. 2,100 B : Rs.1,400

9

Which section of Indian Partnership Act, 1932 defines partnership as

"Partnership is the relation between persons who have agreed to

share the profits of a business carried by all or any of them acting

for all."

A. section 4

B. section 2

C. section 40

D. section 42

10 Pick the odd one out

A. Rent to a partner

B. Manager’s commission

C. Interest to a partner’s loan

D. Interest on partner’s capital

11 A manager gets 5% commission on net profit after charging such

commission, gross profit Rs. 5,80,000 and expenses of indirect

nature other than manager's commission are Rs.1,60,000; Amount

of manager's commission is:

A. Rs.20,000

B. Rs. 21,000

C. Rs. 15,000

D. Rs 22,000

12 Feature of a partnership firm:

A. Two or more persons are carrying common business

under an agreement.

B. They are sharing profits and losses in the fixed ratio.

C. Business is carried by all or any of them acting

for all as an agent.

D. All of these

13 Maximum number of partners in a firm is specified in...

A. Partnership Deed

B. Indian partnership act, 1932

C. Companies(Miscellaneous)Rules2014

D. none of these

14 Match the following

Statement I Statement II

1. Profit and loss Appropriation a/c a. Fixed Capital

2. Current Account P & L A/c b. Extension of

3. Interest on Loan profit c. Appropriation of

4. Partner commission profit d. Charge against

A. 1-b, 2-a, 3-d, 4-c

B. 1-a, 2-b, 3-c, 4-d

C. 1-d, 2-b, 3-a, 4-c

D. 1-c, 2-d, 3-b, 4-a

15 Match the following:

Statement I Statement II

1.Assurance of profit a. Rectifying the past error

2.Manager’s commission b. Calculated on opening capital

3.Past Adjustment c. Guarantee of profit

4.Interest on capital d. Debited to profit & lossA/c

A. 1-b, 2- d, 3 – c, 4 – a

B. 1-d, 2- c , 3 – a , 4 – b

C. 1-c, 2- b , 3 – a , 4 – d

D. 1-c, 2- d , 3 – a , 4 – b

16 ___________ partner should compensate _________ partner in the

case of reconstitution of the firm.

A. Old , new

B. New , old

C. Sacrificing , gaining

D. Gaining , sacrificing

17 Goodwill may be defined as the excess amount paid for a business

over and above its _____________

A. Tangible assets

B. Current assets

C. Total assets

D. Net worth

18 Find the odd one out with reference to valuation of goodwill:

A. Super profit method, Average profit method, Capitalization of super profit method

B. Super profit method, Average profit method, Capitalization of

super profit method, Weighted average of super profit method

C. Profit for the purpose of calculation of goodwill is taken as the

profits the firm is likely to maintain in future from its business

activities.

D. All are correct.

19 Consider the following information from the books of A and B who

agree to share future profits and losses in the ratio of 3:2:

Investments 100000

Investment Fluctuation Fund 20000

Investments were valued at Rs. 75000 at the time of reconstitution

of the firm.

Which of the following treatment is correct:

A Investment DR 5000

TO Revaluation 5000

B Investment Fluctuation Fund DR 5000

TO A 2500

TO B 2500

C A DR 2500

B DR 2500

TO B 5000

D Revaluation DR 5000

To Investment 5000

20 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): A ,B and C are equal partners. Partner B gave loan

of Rs. 90,000 to the partnership firm on 1/4/2021. Net profit before

allowing Interest on loan occurred Rs. 75,000 Profit is calculated to

be credited in B’s capital account is Rs. 25,000 Reason (R): B’s capital account will be credited with Rs. 23,200

A. Both (A) and (R) are true and (R) is the correct explanation of

(A)

B. Both ( A ) and ( R ) are true and ( R ) is not correct

explanation of ( A )

C. ( A ) is true but ( R ) is false

D. ( A ) is false but ( R ) is true

21 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): The amount of interest on Mr. Anand’s drawing@

10% if he withdrew Rs. 5,00,000 during the year is Rs. 50,000

Reason (R): Anand’s capital/current account will be debited for Rs.

25,000; as in the absence of time period given, interest on drawing

is calculated on average 6 months’ time period.

A. Both (A) and ( R ) are true and ( R ) is the correct explanation

of ( A )

B. Both ( A ) and ( R ) are true and ( R ) is not correct

explanation of ( A )

C. (A ) is true but ( R ) is false

D. ( A ) is false but ( R ) is true

22 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): Aditi and Bhakti have capitals of Rs. 4,00,000 and

2,00,000 respectively. As per partnership agreement, interest on

capital will be allowed @6% p.a. Their profit-sharing ratio is 2:3. Their net profit during the year is calculated as Rs. 30,000

Reason (R): As per Profit and Loss Appropriation Account Aditi will

be allowed Rs. 20,000 and Bhakti will be allowed Rs. 10,000 as

interest on capital.

A. Both ( A ) and ( R ) are true and ( R ) is the correct

explanation of ( A )

B. Both ( A ) and ( R ) are true and ( R ) is not correct

explanation of ( A )

C. ( A ) is true but ( R ) is false

D. ( A ) is false but ( R ) is true

23 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): Partnership firm is a form of business organization where two or more persons carry on some business activity on the

basis of agreement among them.

Reason (R): In the absence of partnership agreement profit/loss

among partners will be shared equally.

A. Both ( A ) and ( R ) are true and ( R ) is the correct

explanation of ( A )

B. Both ( A ) and ( R ) are true and ( R ) is not correct

explanation of ( A )

C. ( A ) is true but ( R ) is false

D. ( A ) is false but ( R ) is true

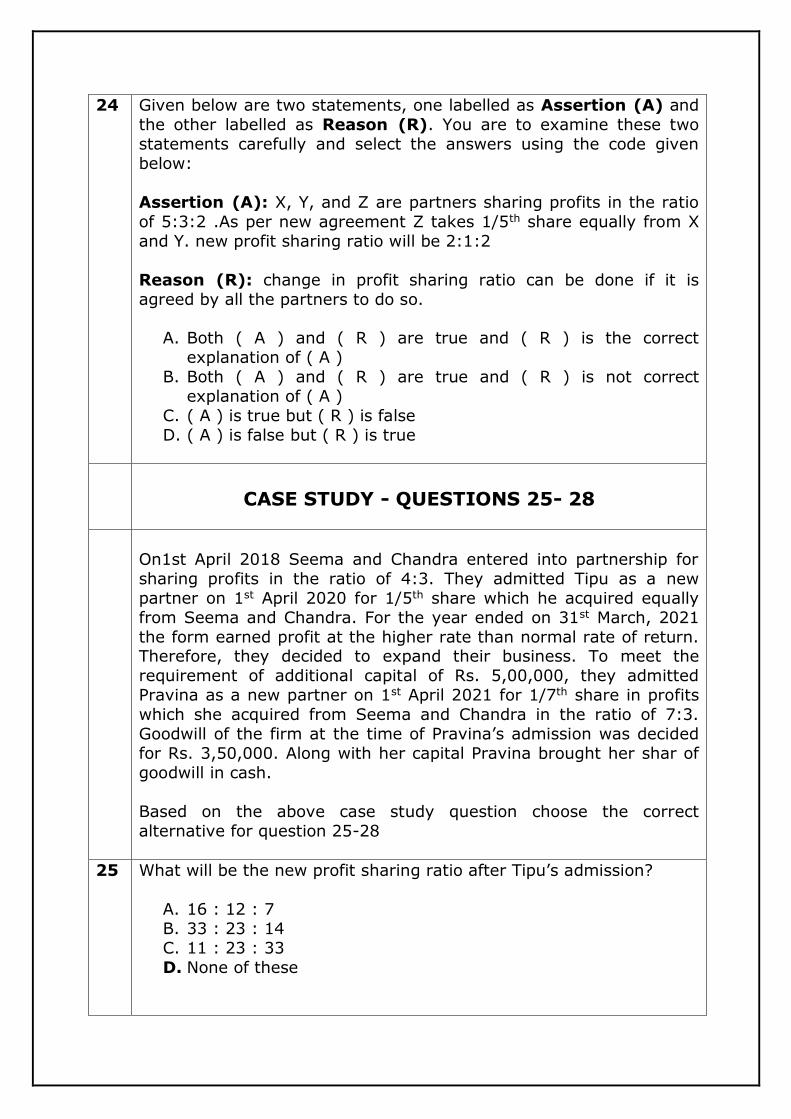

24 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): X, Y, and Z are partners sharing profits in the ratio

of 5:3:2 .As per new agreement Z takes 1/5th share equally from X

and Y. new profit sharing ratio will be 2:1:2

Reason (R): change in profit sharing ratio can be done if it is

agreed by all the partners to do so.

A. Both ( A ) and ( R ) are true and ( R ) is the correct

explanation of ( A )

B. Both ( A ) and ( R ) are true and ( R ) is not correct

explanation of ( A )

C. ( A ) is true but ( R ) is false

D. ( A ) is false but ( R ) is true

CASE STUDY - QUESTIONS 25- 28

On1st April 2018 Seema and Chandra entered into partnership for

sharing profits in the ratio of 4:3. They admitted Tipu as a new

partner on 1st April 2020 for 1/5th share which he acquired equally

from Seema and Chandra. For the year ended on 31st March, 2021

the form earned profit at the higher rate than normal rate of return. Therefore, they decided to expand their business. To meet the

requirement of additional capital of Rs. 5,00,000, they admitted

Pravina as a new partner on 1st April 2021 for 1/7th share in profits

which she acquired from Seema and Chandra in the ratio of 7:3.

Goodwill of the firm at the time of Pravina’s admission was decided

for Rs. 3,50,000. Along with her capital Pravina brought her shar of

goodwill in cash.

Based on the above case study question choose the correct

alternative for question 25-28

25 What will be the new profit sharing ratio after Tipu’s admission?

A. 16 : 12 : 7

B. 33 : 23 : 14

C. 11 : 23 : 33

D. None of these

26 What will be the new profit sharing ration among Seema, Chandra,

Tipu and Pravina

A. Equal

B. 26:10:1:5

C. 3:10:7:5

D. 13:10:7:5

27 With how much amount cash account will be debited at the time of

Pravina’s admission?

A. Rs. 1,50,000

B. Rs.8,50,000

C. Rs. 5,50,000

D. None of these

28 Which of the following journal entry is correct?

A. Seema’s A/c with Rs. 35,000 and Chandra’s A/c with Rs.

15,000

B. Seema’s A/c with Rs. 15,000 and Chandra’s A/c with Rs.

35,000

C. Seema’s A/c with Rs. 2,45,000 and Chandra’s A/c with Rs.

1,05,000

D. Seema’s A/c with Rs. 1,05,000 and Chandra’s A/c with Rs.

2,45,000

CASE STUDY - QUESTIONS 29 – 32

Radha and Sakhi are partners of 4:3. They admitted Meera for 2/9th

share in future profits from 1/4/2021 . Meera will bring Rs. 2,00,000

for her share of capital they decided to change their profit sharing

ratio. The new ratio will be 2:3:4. On the same date balance showed

the balance of Rs. 90,000

On the same date an accident occurred with one of the employees of

their firm. He claimed Rs. 99,000 for his treatment.

Based on the above case study question choose the correct

alternative for question 29-32

29 Can the claim of workman be paid from Workmen compensation

Reserve?

A. Yes

B. No

C. If the partners wish to pay

D. Only 50% of claimed amount

30 Who is gaining partner?

A. Radha

B. Sakhi

C. Meera

D. All of these

31 Who is sacrificing partner?

A. Radha

B. Sakhi

C. Meera

D. All of these

32 With how much amount revaluation account will be debited?

A. Rs.99,000

B. Rs.9,000

C. Rs. 90,000

D. None of these

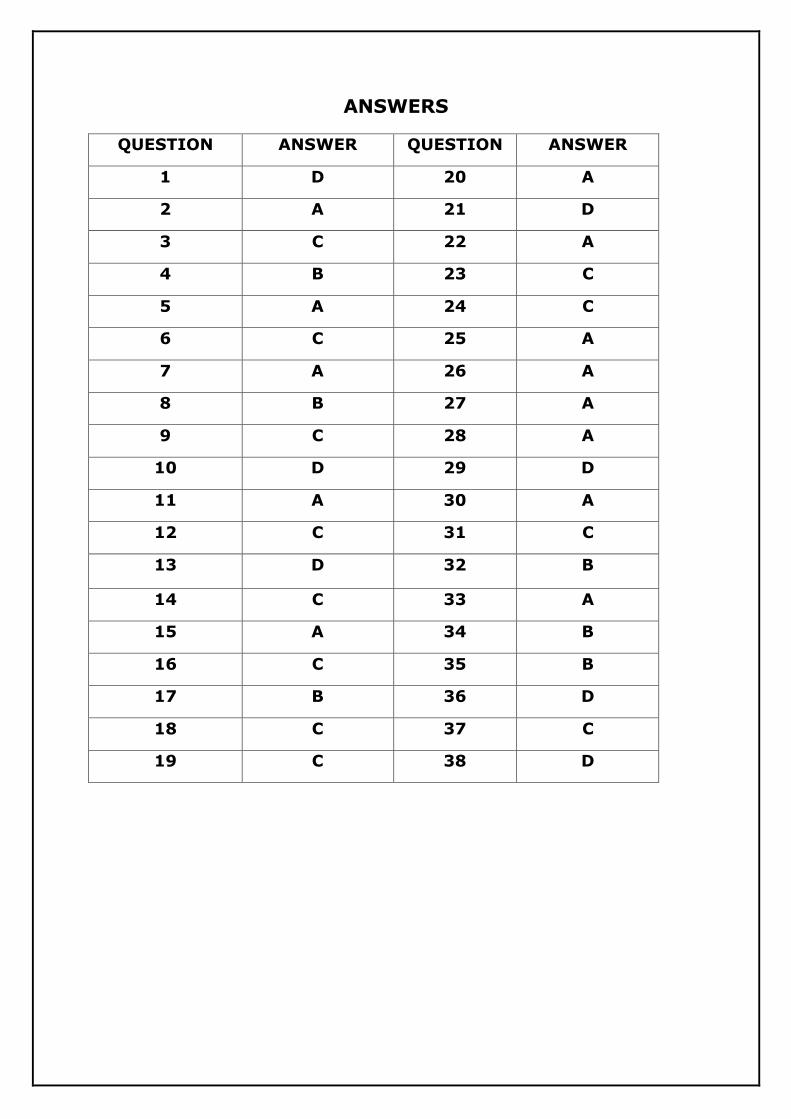

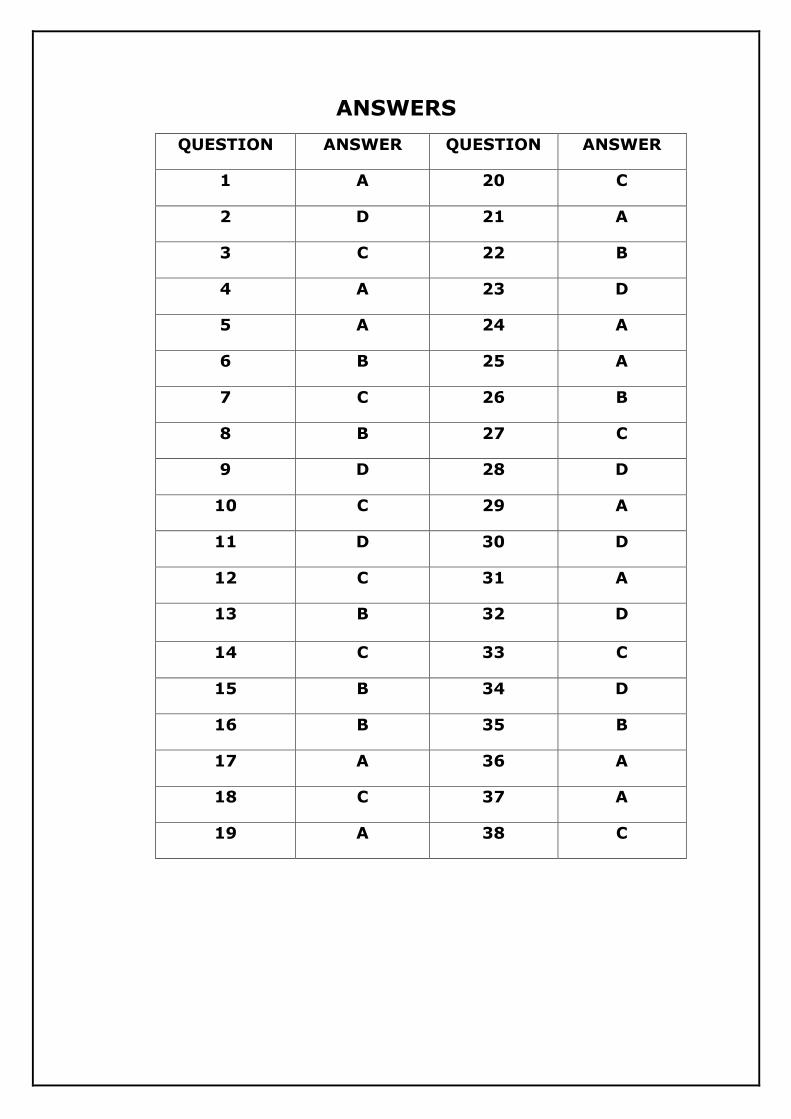

ANSWERS

QUESTION ANSWER QUESTION ANSWER

1 B 17 D

2 A 18 B

3 B 19 D

4 B 20 D

5 D 21 C

6 A 22 A

7 B 23 A

8 C 24 B

9 A 25 B

10 D 26 D

11 B 27 C

12 B 28 A

13 C 29 A

14 A 30 C

15 D 31 A

16 D 32 B

ADMISSION OF A PARTNER

1 X and Y are partners sharing profits in the ratio of 1:1. They admit Z

for 1/5th share who contributed Rs. 25,000 for his share of goodwill.

The total value of goodwill of the firm will be

A. Rs. 2,50,000

B. Rs. 50,000

C. Rs. 1,00,000

D. Rs. 1,25,000

2 Profit / Loss on Revaluation in case of admission of a new partner is

borne by:

A. Old Partners

B. New Partners

C. All Partners

D. Only Two Partners

3 Match List-I with List-II and select the correct answer using the codes

given below the lists:

List-I (Items) List-II (Distribution)

a. Future profits 1. Old Ratio

b. General Reserve 2. New ratio

c. Employee Provident Fund 3. Sacrificing Ratio d. Goodwill of Incoming Partner 4. Not distributed

A. (a)-1, (b)-2, (c)-3, (d)-4

B. (a)-1, (b)-2, (c)-4, (d)-3

C. (a)-2, (b)-1, (c)-4, (d)-3

D. (a)-2, (b)-1, (c)-3, (d)-4

4 If Capital Accounts are maintained following Fixed capital Accounts Method, balance of Revaluation Account is transferred to:

A. Partner’s Fixed Capital Account

B. Partner’s Current Account

C. Profit & Loss Account

D. Balance Sheet

5 State the ‘true’ statement:

A. Profit & Loss Adjustment A/c is prepared for revaluation of assets

and liabilities on the admission of a partner

B. The new partner is liable for the past losses of the firm

C. In case the new partner is unable to bring in cash for goodwill,

Goodwill Account may be raised in the firm’s books as per AS-26

D. When a partner is admitted, there is dissolution of firm

6 There are three partners in a firm P & Q. R is admitted in the firm for

1/3rd share of profit with the guaranteed annual profit of Rs. 18,000

p.a. The firm’s total profit for the year is Rs. 42,000. If A stood as

guarantor of guaranteed profit to R, how much profit would be given to

Q:

A. Rs. 20,000

B. Rs. 15,000

C. Rs. 10,000

D. Rs. 18,000

7 At the time of admission of a Partner, Gain (Profits) or Losses arising

on the revaluation of assets and reassessment of liabilities is

transferred to ___________ in their ___________.

A. Old partners capital a/c , old ratio

B. Sacrificing partners capital a/c, sacrificing ratio

C. Gaining partners capital a/c, gaining ratio

D. Old partners capital a/c, sacrificing ratio

8 Raj is admitted in a firm as a partner for 1/4th share in the profits for

which he brings Rs. 30,000 as goodwill. The journal entry will be:

1. Cash a/c Dr.

To Premium for goodwill a/c

2. Cash a/c Dr.

To goodwill a/c

3. Premium for goodwill a/c Dr.

To Partners capital a/c

4. Goodwill a/c Dr.

To Partners capital a/c

Which of the following statements is true:

A. Only 1

B. Both 1 and 3

C. Only 4

D. None of the above

9 A and B are sharing profits and losses in the ratio of 3 : 2. They admit

C as partner for 1/3rd share in the profits. He takes this share 3/5th

from A and 2/5th from B. New profit sharing ratio will be:

A. 5 : 6 : 3

B. 2 : 4 : 6

C. 6 : 4 : 5

D. 18 : 24 : 38

10 Investment Fluctuation Reserve is a reserve created out of profits to meet the __________ in the __________ of investments.

A. Rise, book

B. Fall, Book

C. Rise, market

D. Fall, market

11 In case the claim on account of workmen Compensation is equal to the

workmen compensation reserve, there is no treatment in revaluation

a/c.

A. True

B. False

C. Partially false

D. Can't say

12 On the admission of a new partner, old partnership continues.

A. True

B. Partially True

C. False

D. Can't say

13 Which of the following is not a right of a newly admitted partner?

A. Right to share profits of a firm

B. Right to inspect the books of accounts

C. Right to participate in the affairs of business

D. None of these

14 ___________ goodwill is the excess of desired total capital of firm over

the actual combined capital of all partners.

A. Premium

B. Share

C. Hidden

D. Old

15 Goodwill of the firm X and Y is valued at Rs.45000. It is appearing in

the books at Rs. 18000. Z is admitted in the firm. What amount is he

supposed to bring on account of goodwill?

A. Rs. 15000

B. Rs. 6000

C. Rs. 9000

D. Can't be determined

16 A and B are partners sharing profits in the ratio of 7 : 3. C is admitted

as a partner for 3/7th share in profit. If the new profit sharing ratio of

the partners is 14 : 6 : 5, sacrificing ratio will be _________.

A. 4:5

B. 3:7

C. 7:3

D. None of the above

17 The amount earlier written off as bad debt now received is credited to

___________ on admission of a partner.

A. Partners capital a/c

B. Revaluation a/c

C. Realisation a/c

D. Debtors a/c

18 X and Y are partners sharing profits in the ratio of 3 : 2, and capitals as

Rs. 100,000 and Rs. 50,000 respectively, after adjustments. Z is

admitted for 1/5th share in profits, The amount Z will contribute as

capital will be:

A. Rs.50,000

B. Rs.35,000

C. Rs.37,500 D. Rs.60,000

19 In case of admission of a partner, the entry for unrecorded investment

is:

A. Investment a/c Dr. To Old partners' capital a/c

B. Revaluation a/c Dr.

To Investment a/c

C. Investment a/c Dr.

To Revaluation a/c

D. None of the above

20 The excess of Purchase Consideration

over net assets is debited to

A. Goodwill A/c

B. Capital Reserve A/c

C. General Reserve A/c

D. Reserve Capital A/c

21 Match List-I with List-II and select the correct answer using the codes

given below the lists(at the time of admission of partner situation) :

List-I(Item/ Transaction)

List-II\(Entry) (a) Increase in liabilities 1. Credit- Revaluation a/c

(b) Bad Debts Recovered 2. Credit- Partner's Capital a/c

(c) Accumulated losses 3. Debit- Revaluation a/c

(d) Profit & Loss a/c (Cr.) 4. Debit- Partner's Capital a/c

A. (a)-3, (b)-1, (c)-2, (d)-4

B. (a)-1, (b)-3, (c)-4, (d)-2

C. (a)-1, (b)-3, (c)-2, (d)-4

D. (a)-3, (b)-1, (c)-4, (d)-2

22 If at the time of admission if there is some unrecorded liability, it will be ____________ to _______________ Account

A. Debited, Revaluation

B. Credited, Revaluation

C. Debited, Goodwill

D. Credited, Partners’ Capital

23 Sacrificing ratio is calculated because:

A. Profit shown by Revaluation Account can be credited to sacrificing

partners

B. Goodwill brought in by the incoming partner can be credited to

the new partner

C. Goodwill brought in by the incoming partner can be credited to

the sacrificing partners

D. Both a and c

24 Yash and Manan are partners sharing profits in the ratio of 2:1. They admit

Kushagra into partnership for 25% share of profit. Kushagra acquired the

share from old partners in the ratio of 3:2. The new profit sharing ratio will

be:

A. 14:31:15 B. 3:2:1 C. 31:14:15 D. 2:3:1

25 Consider the following statements:

(1) Capital Account of the partners will credited for Writing off

goodwill

(2) Capital Account of the partners will credited for distribution of

debit balance of Profit & Loss Account

(3) Capital Account of the partners will credited for Profit on

revaluation of assets and reassessment of liabilities

(4) Capital Account of the partners will credited for Loss on

revaluation of assets and reassessment of liabilities.

Which of the above statement/s is/are not true?

A. 1, 2 and 4

B. 2, 3 and 4

C. Only 2

D. None of the above

26 Given below are two statements, one labelled as Assertion (A) and the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): At the time of admission of a partner, partnership is

dissolved and not the firm

Reason (R): In case of reconstitution, existing agreement comes to an

end and a new one comes into existence.

A. Both Assertion and Reason are correct and Reason is the correct

explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

27 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): Employees provident fund is not distributed to the

partners’ capital a/c

Reason (R): Employees provident fund is a liability towards the

employees, thus, partners have no claim over it.

A. Both Assertion and Reason are correct and Reason is the correct

explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

28 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A).: It is necessary to ascertain new profit sharing ratio

for old partners when a new partner is admitted.

Reason (R): New partner acquires his share from old partners which

reduces old partner's share in profits.

A. Both Assertion and Reason are correct and Reason is the correct

explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

29 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

Assertion (A): If the amount of any liability is understated, then

revaluation account will be debited to restore the liability's amount to

its actual value.

Reason (R): Increase in amount of liability is a profit for the firm.

A. Both Assertion and Reason are correct and Reason is the correct

explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

30 Given below are two statements, one labelled as Assertion (A) and

the other labelled as Reason (R). You are to examine these two

statements carefully and select the answers using the code given

below:

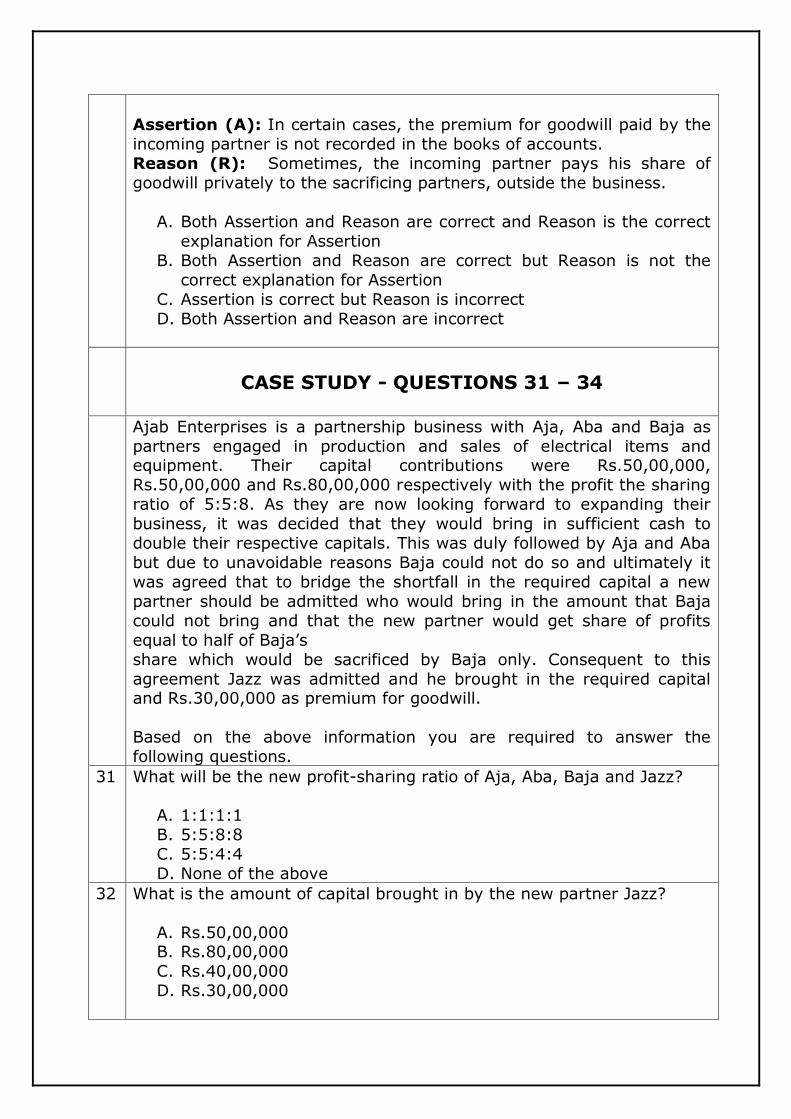

Assertion (A): In certain cases, the premium for goodwill paid by the

incoming partner is not recorded in the books of accounts.

Reason (R): Sometimes, the incoming partner pays his share of

goodwill privately to the sacrificing partners, outside the business.

A. Both Assertion and Reason are correct and Reason is the correct

explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

CASE STUDY - QUESTIONS 31 – 34

Ajab Enterprises is a partnership business with Aja, Aba and Baja as

partners engaged in production and sales of electrical items and equipment. Their capital contributions were Rs.50,00,000,

Rs.50,00,000 and Rs.80,00,000 respectively with the profit the sharing

ratio of 5:5:8. As they are now looking forward to expanding their

business, it was decided that they would bring in sufficient cash to

double their respective capitals. This was duly followed by Aja and Aba

but due to unavoidable reasons Baja could not do so and ultimately it

was agreed that to bridge the shortfall in the required capital a new

partner should be admitted who would bring in the amount that Baja

could not bring and that the new partner would get share of profits

equal to half of Baja’s

share which would be sacrificed by Baja only. Consequent to this

agreement Jazz was admitted and he brought in the required capital and Rs.30,00,000 as premium for goodwill.

Based on the above information you are required to answer the

following questions.

31 What will be the new profit-sharing ratio of Aja, Aba, Baja and Jazz?

A. 1:1:1:1

B. 5:5:8:8

C. 5:5:4:4

D. None of the above

32 What is the amount of capital brought in by the new partner Jazz?

A. Rs.50,00,000 B. Rs.80,00,000

C. Rs.40,00,000

D. Rs.30,00,000

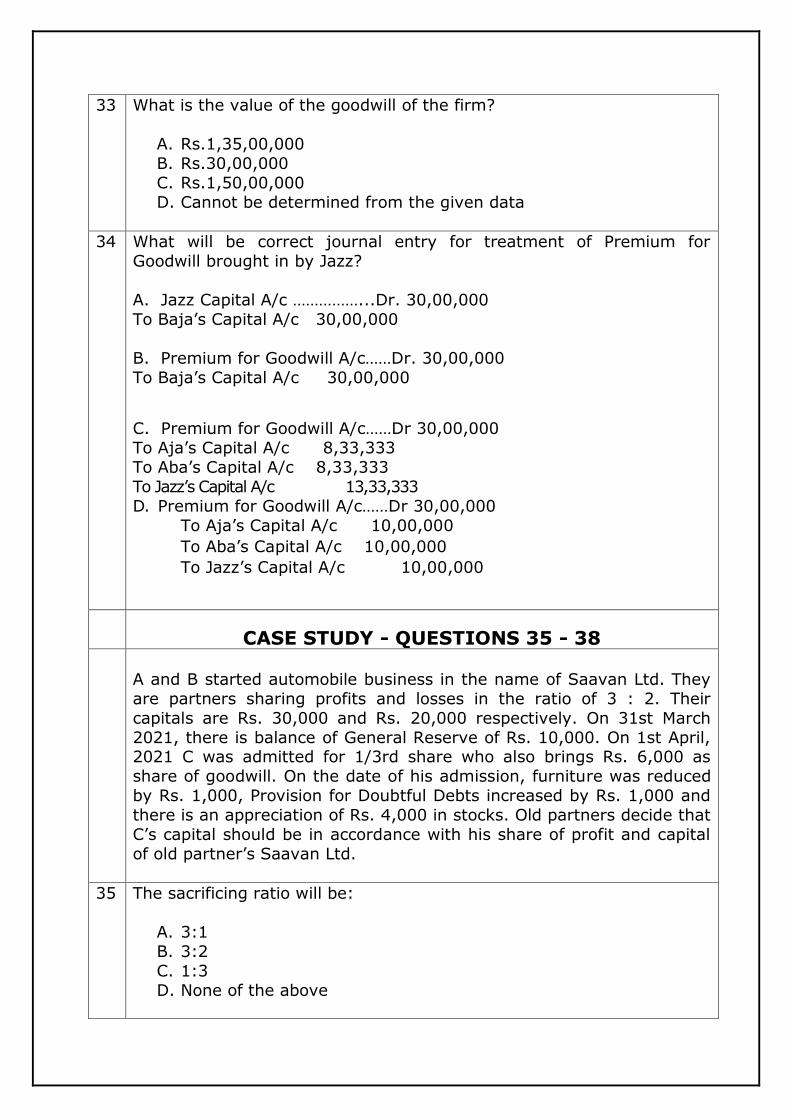

33 What is the value of the goodwill of the firm?

A. Rs.1,35,00,000

B. Rs.30,00,000

C. Rs.1,50,00,000

D. Cannot be determined from the given data

34 What will be correct journal entry for treatment of Premium for

Goodwill brought in by Jazz?

A. Jazz Capital A/c ……………...Dr. 30,00,000

To Baja’s Capital A/c 30,00,000

B. Premium for Goodwill A/c……Dr. 30,00,000

To Baja’s Capital A/c 30,00,000

C. Premium for Goodwill A/c……Dr 30,00,000

To Aja’s Capital A/c 8,33,333

To Aba’s Capital A/c 8,33,333

To Jazz’s Capital A/c 13,33,333

D. Premium for Goodwill A/c……Dr 30,00,000

To Aja’s Capital A/c 10,00,000

To Aba’s Capital A/c 10,00,000

To Jazz’s Capital A/c 10,00,000

CASE STUDY - QUESTIONS 35 - 38

A and B started automobile business in the name of Saavan Ltd. They

are partners sharing profits and losses in the ratio of 3 : 2. Their

capitals are Rs. 30,000 and Rs. 20,000 respectively. On 31st March

2021, there is balance of General Reserve of Rs. 10,000. On 1st April, 2021 C was admitted for 1/3rd share who also brings Rs. 6,000 as

share of goodwill. On the date of his admission, furniture was reduced

by Rs. 1,000, Provision for Doubtful Debts increased by Rs. 1,000 and

there is an appreciation of Rs. 4,000 in stocks. Old partners decide that

C’s capital should be in accordance with his share of profit and capital

of old partner’s Saavan Ltd.

35 The sacrificing ratio will be:

A. 3:1

B. 3:2

C. 1:3

D. None of the above

36 Capitals of A and B after all adjustments will be:

A. 50,000

B. 60,000

C. 62,000

D. 68,000

37 Profit on revaluation in the said case will be:

A. 4000

B. 3000

C. 2000

D. None of the above

38 Which of the following reconstitution of a firm?

1. Admission of a minor partner

2. Retirement of a partner

3. Dissolution of a firm

4. Merger of Firm

A. Only 1

B. Both 1 and 2

C. 1, 2 and 3

D. 1, 2 and 4

ANSWERS

QUESTION ANSWER QUESTION ANSWER

1 D 20 A

2 A 21 D

3 C 22 A

4 B 23 C

5 A 24 C

6 C 25 A

7 A 26 A

8 B 27 A

9 C 28 A

10 D 29 D

11 A 30 A

12 C 31 C

13 D 32 B

14 C 33 A

15 A 34 B

16 C 35 B

17 B 36 D

18 C 37 C

19 C 38 D

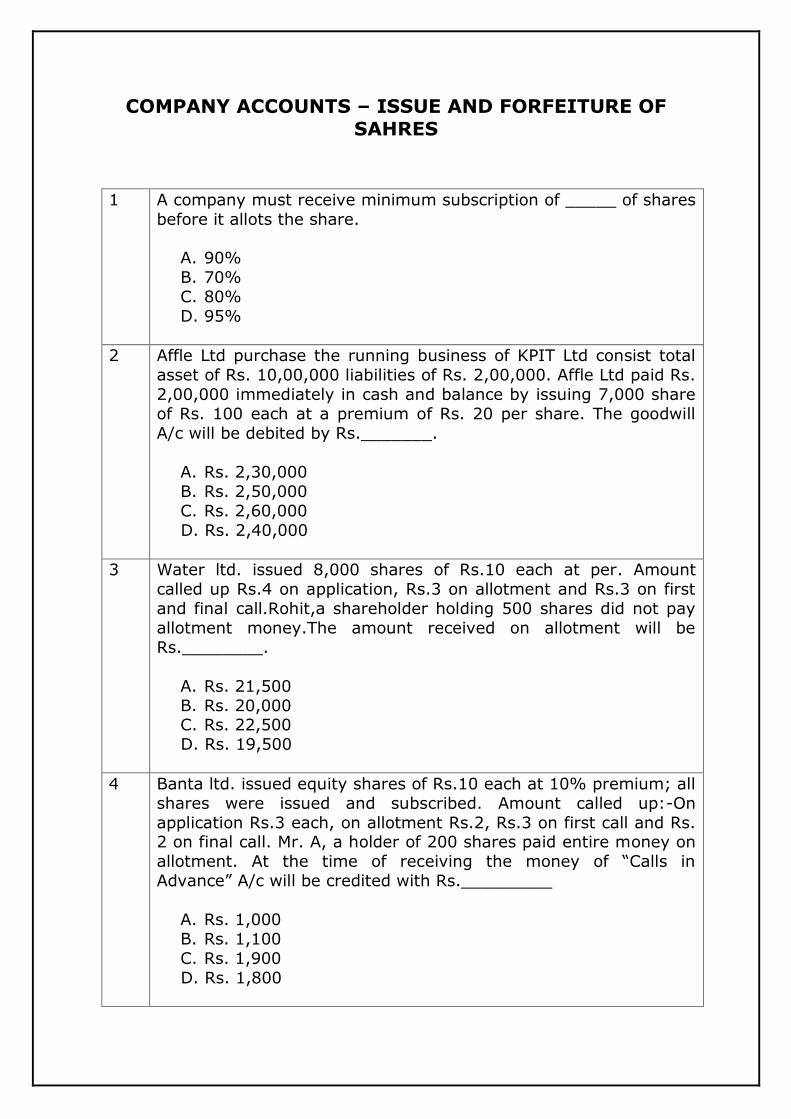

COMPANY ACCOUNTS – ISSUE AND FORFEITURE OF SAHRES

1 A company must receive minimum subscription of _____ of shares

before it allots the share.

A. 90%

B. 70%

C. 80%

D. 95%

2 Affle Ltd purchase the running business of KPIT Ltd consist total

asset of Rs. 10,00,000 liabilities of Rs. 2,00,000. Affle Ltd paid Rs.

2,00,000 immediately in cash and balance by issuing 7,000 share

of Rs. 100 each at a premium of Rs. 20 per share. The goodwill

A/c will be debited by Rs._______.

A. Rs. 2,30,000

B. Rs. 2,50,000

C. Rs. 2,60,000

D. Rs. 2,40,000

3 Water ltd. issued 8,000 shares of Rs.10 each at per. Amount

called up Rs.4 on application, Rs.3 on allotment and Rs.3 on first

and final call.Rohit,a shareholder holding 500 shares did not pay

allotment money.The amount received on allotment will be

Rs.________.

A. Rs. 21,500

B. Rs. 20,000 C. Rs. 22,500

D. Rs. 19,500

4 Banta ltd. issued equity shares of Rs.10 each at 10% premium; all

shares were issued and subscribed. Amount called up:-On

application Rs.3 each, on allotment Rs.2, Rs.3 on first call and Rs. 2 on final call. Mr. A, a holder of 200 shares paid entire money on

allotment. At the time of receiving the money of “Calls in

Advance” A/c will be credited with Rs._________

A. Rs. 1,000

B. Rs. 1,100

C. Rs. 1,900

D. Rs. 1,800

5 Alpha ltd. forfeited 200 equity shares of Rs. 10 each on which Rs.

6 was paid (including Rs. 1 premium). On reissue, the company

can allow Rs. ______as discount.

A. Rs. 5 each

B. Rs. 10 each

C. Rs. 6 each

D. Rs. 4 each

6 A company issued 10,000 shares of Rs.10 each at par for which

Application were received for 50,000 shares. Amount called up:-

On application Rs.4 each, on allotment Rs.3 and final call

remaining Amount Shares were allotted on pro-rata basis Excess

money will be refunded. After utilization for allotment and final

call. The Bank A/c will be credited with Rs. _______.

A. Rs. 4,00,000

B. Rs. 1,00,000 C. Rs. 3,00,000

D. Rs. 5,00,000

7 When the shares are reissued at a price more that face value it is

known as _______.

A. Forfeiture

B. Discount

C. Premium

D. Reserve Capital

8 Excess balance amount at Share forfeiture account will be

transferred to ______ account.

A. Forfeiture

B. Capital Reserve

C. Premium

D. Reserve Capital

9 Which of the following capital is not shown in the company’s

Balance Sheet?

A. Authorised capital

B. Issued &subscribed capital

C. Called-up & paid up-capital

D. Reserve capital

10 As per sec. of the companies Act amount. received as premium on

securities cannot be utilized for: -

A. Issuing fully paid bonus shares to the members

B. Writing off preliminary expenses

C. Purchase of fixed assets

D. Buy back of its own shares

11 The portion of authorized capital which can be called up only on the liquidation of the company: -

A. Authorised capital

B. Issued capital

C. Called-up capital

D. Reserve capital

12 When the shares are issued for consideration other than cash

which account will be debited

A. Securities Premium

B. Capital Reserve A/c

C. Vendor A/c

D. Share Capital A/c

13 X ltd. Forfeited 1,000 shares of Rs. 10 each for the non-payment

of final call of Rs. 2. The account will be debited for called up price

of a share at the time of forfeiture of shares:

A. Share Forfeiture A/c

B. Share Capital A/c

C. Share Final Call A/c

D. None of these

14 Amount of discount given at the time of reissue of shares should

be debited to:

A. Shares Capital

B. Discount on Shares

C. Share Forfeiture A/c

D. Calls-In-Areas A/c

15 A company Forfeited 2,000 shares of Rs 10 each issued at 20 %

premium to be paid at the time of allotment on which Rs 8 is called up.

company not received Rs 4 on Allotment including premium and Rs 2 in First call. What will be the amount Debited to share capital account:

A. Rs. 20,000

B. Rs. 16,000

C. Rs. 24,000

D. Rs. 18,000

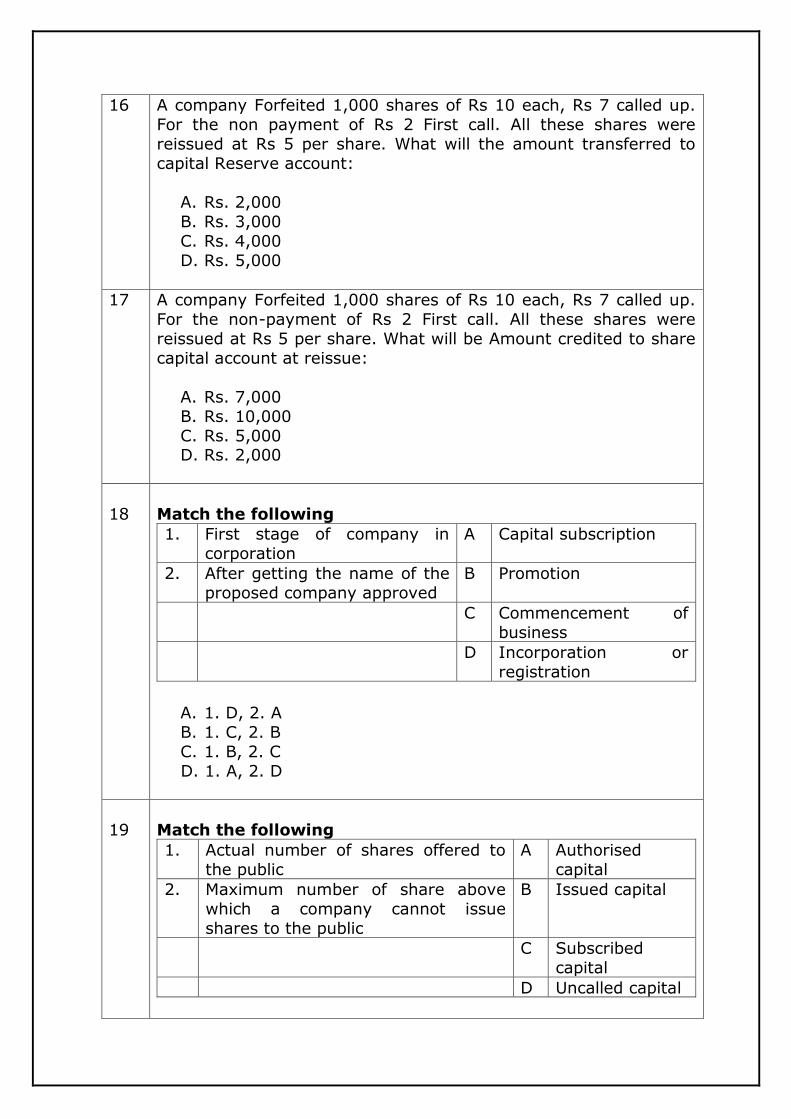

16 A company Forfeited 1,000 shares of Rs 10 each, Rs 7 called up.

For the non payment of Rs 2 First call. All these shares were

reissued at Rs 5 per share. What will the amount transferred to

capital Reserve account:

A. Rs. 2,000

B. Rs. 3,000

C. Rs. 4,000

D. Rs. 5,000

17 A company Forfeited 1,000 shares of Rs 10 each, Rs 7 called up.

For the non-payment of Rs 2 First call. All these shares were

reissued at Rs 5 per share. What will be Amount credited to share

capital account at reissue:

A. Rs. 7,000

B. Rs. 10,000

C. Rs. 5,000 D. Rs. 2,000

18

Match the following

1. First stage of company in

corporation

A Capital subscription

2. After getting the name of the

proposed company approved

B Promotion

C Commencement of

business

D Incorporation or

registration

A. 1. D, 2. A

B. 1. C, 2. B

C. 1. B, 2. C

D. 1. A, 2. D

19

Match the following

1. Actual number of shares offered to

the public

A Authorised

capital

2. Maximum number of share above

which a company cannot issue

shares to the public

B Issued capital

C Subscribed

capital

D Uncalled capital

A. 1. B, 2. A

B. 1. C, 2. B

C. 1. D, 2. C

D. 1. A, 2. D

20

Match the following

1. When the shares are issued to

promoters which account is debited

A Underwriting

commission

2. Shares issued to underwriters B Share capital

C Share Forfeiture

A/c

D Incorporation

cost

A. 1. A, 2. B

B. 1. B, 2. C

C. 1. D, 2. A

D. A. C, 2. D

21

Match the following

1. Amount of capital stated in

M.O.A

A Issued Capital

2. Entire money called up and

paid

B Authorised Capital

C Called up Capital

D Subscribed and fully

paid up

A. 1. B, 2. D

B. 1. A, 2. B

C. 1. C, 2. A D. 1. D, 2. A

22

Match the following

1. At the time of forfeiture of shares

share capital is debited with

A Amount received

2. At the time of forfeiture of shares

share Forfeiture is Credited with

B Amount not

received

C Amount

demanded

D Calls in advance

A. 1. D, 2. C

B. 1. C, 2. A C. 1. A, 2. B

D. 1. B, 2. D

23

Match the following

1. Purchase consideration is more than

net worth

A Capital

Reserve

2. Purchase consideration is less than

net worth

B Assets

C Goodwill

D vendor

A. 1. A, 2. B

B. 1. B, 2. D

C. 1. D, 2. C

D. 1. C, 2. A

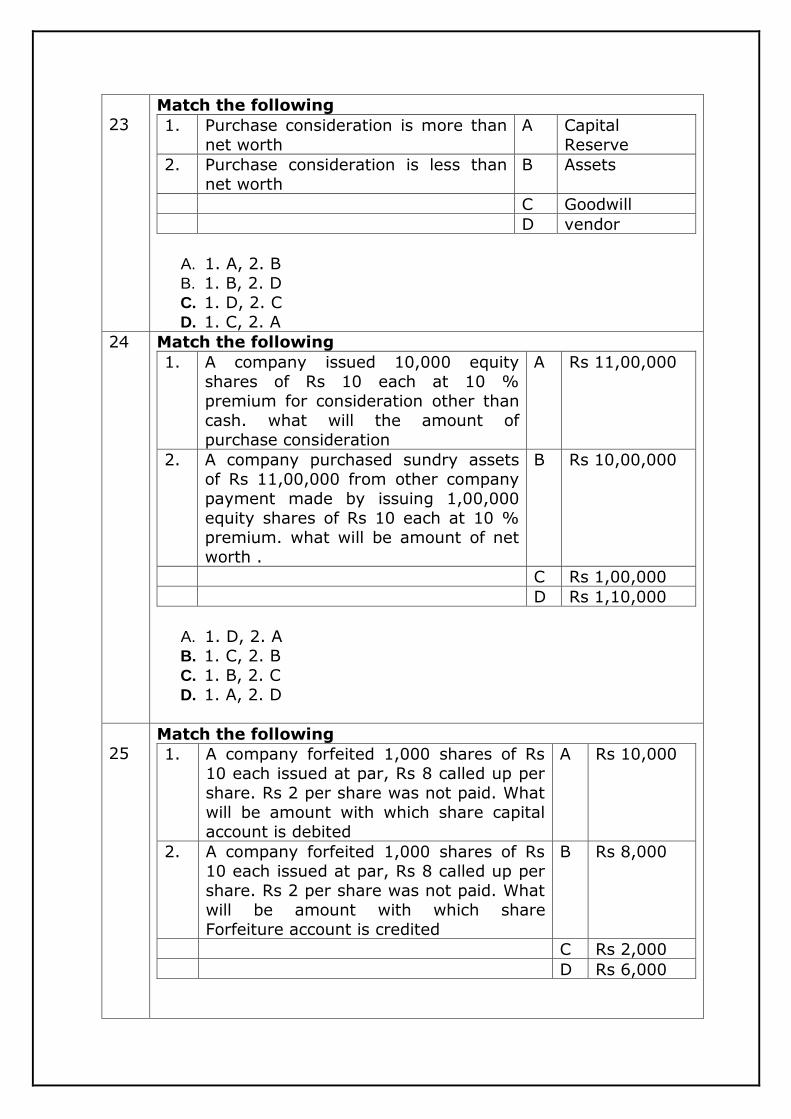

24 Match the following

1. A company issued 10,000 equity

shares of Rs 10 each at 10 %

premium for consideration other than

cash. what will the amount of

purchase consideration

A Rs 11,00,000

2. A company purchased sundry assets

of Rs 11,00,000 from other company

payment made by issuing 1,00,000

equity shares of Rs 10 each at 10 %

premium. what will be amount of net

worth .

B Rs 10,00,000

C Rs 1,00,000

D Rs 1,10,000

A. 1. D, 2. A

B. 1. C, 2. B

C. 1. B, 2. C

D. 1. A, 2. D

25

Match the following

1. A company forfeited 1,000 shares of Rs

10 each issued at par, Rs 8 called up per

share. Rs 2 per share was not paid. What

will be amount with which share capital

account is debited

A Rs 10,000

2. A company forfeited 1,000 shares of Rs

10 each issued at par, Rs 8 called up per

share. Rs 2 per share was not paid. What

will be amount with which share

Forfeiture account is credited

B Rs 8,000

C Rs 2,000

D Rs 6,000

A. 1. B, 2. D

B. 1. C, 2. A

C. 1. D, 2. C

D. 1. A, 2. B

26 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these two statements carefully and select the answers using the code

given below:

Assertion (A): Forfeiture of share refers to the cancellation or

termination of membership of a shareholder by taking away the

shares and rights of membership.

Reason (R): Forfeited shares can be reissued at a discount.

:

A. Both A and R are individually true and R is the correct

explanation of A

B. Both A and R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

27 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

:

Assertion (A): Reserve Capital is a part of ‘Uncalled capital’.

Reason (R): Reserve capital is that reserve which is created out

of capital profits.

A. Both A and R are individually true and R is the correct

explanation of A

B. Both A and R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

28 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

:

Assertion (A): ‘Securities Premium Reserve’ can be distributed

as dividend. Reason (R):Amount of securities premium reserve cannot be

distributed as dividend. It can only be used for the purposes listed

under section 52 of the Companies Act.

A. Both A and R are individually true and R is the correct

explanation of A

B. Both A and R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

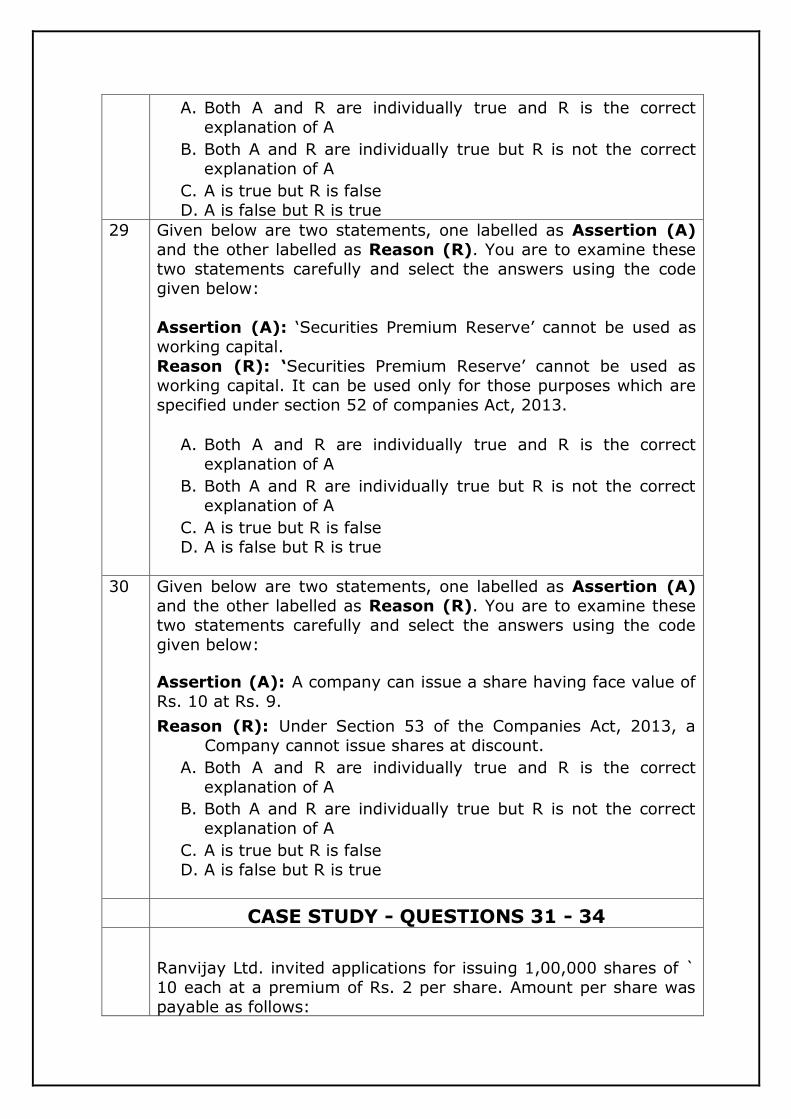

29 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A): ‘Securities Premium Reserve’ cannot be used as

working capital.

Reason (R): ‘Securities Premium Reserve’ cannot be used as

working capital. It can be used only for those purposes which are

specified under section 52 of companies Act, 2013.

A. Both A and R are individually true and R is the correct

explanation of A

B. Both A and R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

30 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A): A company can issue a share having face value of

Rs. 10 at Rs. 9.

Reason (R): Under Section 53 of the Companies Act, 2013, a

Company cannot issue shares at discount.

A. Both A and R are individually true and R is the correct

explanation of A

B. Both A and R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

CASE STUDY - QUESTIONS 31 - 34

Ranvijay Ltd. invited applications for issuing 1,00,000 shares of `

10 each at a premium of Rs. 2 per share. Amount per share was

payable as follows:

On Application — Rs. 4 (including premium Rs.1)

On Allotment — Rs. 4 (including premium Rs.1)

On First and Final Call — Balance

Applications were received for 1,50,000 shares and allotment was

made to the applicants as follows:

(i) Applicants of 80,000 shares were allotted 60,000 shares.

(ii) Applicants of 50,000 shares were allotted 40,000 shares.

(iii) No shares were allotted to the remaining applicants and their

application money was returned.

Yuraj, who belonged to category (ii) and who had applied for

5,000 shares failed to pay the allotment and call money. His

shares were forfeited. Later, half of Yuraj’s forfeited shares were reissued @ Rs. 18 per share as fully paid up.

Based on the above case study question choose the correct

alternative for question 31 - 34

31 State the amount of excess application money refunded to the

applicants.

A. Rs. 2,00,000

B. Rs. 80,000

C. Rs. 40,000

D. Rs. 1,00,000

32 State the amount of calls-in-arrears at the time of receipt of allotment money?

A. Rs. 12,000

B. Rs. 16,000

C. Rs. 18,000

D. Rs. 24,000

33 At the time of forfeiture of shares, Securities Premium Reserve Account will be debited with:

A. Rs. 4,000

B. Rs. 6,000

C. Rs. 8,000

D. Rs. 10,000

34 State the amount received at the time of reissue of forfeited

shares.

A. Rs. 20,000

B. Rs. 16,000

C. Rs. 36,000

D. Rs. 30,000

CASE STUDY - QUESTIONS 35 - 38

Wide Mart Ltd. had issued 1,00,000 Equity shares of Rs. 10 each

at a premium of Rs. 100 per share and 10,000, 10% Preference

shares of Rs. 100 each to public for subscription payable as

follows:

Equity Shares Preference Shares

On Application Rs. 55 (including Premium Rs.50)

Rs.100

On Allotment Balance Amount

Applications were received for 1.20,000 Equity shares and 15,000,

10% Preference Shares. Pro-rata allotment was made to all the

applicants. Jay to whom 1,000 Equity shares were allotted and

Veeru who had applied for 600 shares did not pay the allotment

money. Their shares were forfeited.

Based on the above case study question choose the correct

alternative for question 35 - 38

35 ____________ is the amount that the company received as

Application Money on Equity Shares.

A. Rs. 66,00,000

B. Rs. 64,00,000

C. Rs. 63,00,000

D. Rs. 67,00,000

36 ____________ is the amount that the company received as Application Money on Preference Shares.

A. Rs. 14,00,000

B. Rs. 12,00,000

C. Rs. 13,00,000

D. Rs. 15,00,000

37 ___________ is the amount transferred to Securities Premium

Reserve Account out of Equity Shares Application Account on

allotment of Equity Shares.

A. Rs. 51,00,000

B. Rs. 53,00,000

C. Rs. 55,00,000

D. Rs. 5,00,000

38 ____________ is the amount debited to Equity Share Capital

Account on forfeiture of Equity Shares.

A. Rs. 12,000

B. Rs. 17,000

C. Rs. 19,000 D. Rs. 15,000

ANSWERS

QUESTION ANSWER QUESTION ANSWER

1 A 20 C

2 D 21 A

3 C 22 B

4 A 23 D

5 A 24 A

6 B 25 A

7 C 26 B

8 B 27 C

9 D 28 D

10 C 29 A

11 D 30 D

12 C 31 A

13 B 32 D

14 C 33 C

15 B 34 D

16 B 35 B

17 A 36 A

18 C 37 A

19 A 38 C

FINANCIAL STATEMENTS OF A COMPANY

1 Which one of the following would not be included in a full set of

company financial statements?

A. The cash budget.

B. The statement of financial position.

C. The statement of changes in equity.

D. The income statements.

2 Which of the following is not a long-term borrowing of a company?

A. Debentures.

B. Term loans.

C. Loans repayable on demand from banks.

D. Long-term finance lease obligations.

3 Match List-I with List-II and select the correct answer using the

codes given below the lists:

List-I (Item of balance sheet of

company)

List-II (Heading of balance

Sheet)

a. Preliminary expenses 1. Current liabilities

b. Other liabilities 2. Current asset c. Loose Tools 3. Misc. Expenditure

d. Bill of Exchange 4. Loan & Advances

A. (a)-1, (b)-2, (c)-4, (d)-3

B. (a)-3, (b)-2, (c)-1, (d)-4

C. (a)-3, (b)-1, (c)-2, (d)-4

D. (a)-3, (b)-1, (c)-4, (d)-2

4 How the following liabilities are to be shown on the liability side of

the balance sheet in the order of permanence?

1. Current liabilities and provisions

2. Secured loans

3. Share capital

4. Unsecured loans

5. Reserves and surplus

A. 3, 5, 2 , 4 , 1

B. 3 , 2 , 1 , 4 , 5

C. 1 , 4 , 2 , 5 , 3 D. 5, 4, 3, 2, 1

5 The portion of the share capital which cannot be called up except

on the winding up is known as _______________.

A. Called up capital

B. Paid-up capital

C. Authorized capital

D. Reserve capital

6 Item to be included in reserve &surplus?

A. Capital redemption reserves

B. General reserve

C. Securities premium

D. All of the above

7 All of them are long term borrowings except _____________.

A. Cash credits

B. Public deposits

C. Debentures

D. Both A & C

8 ______ is the major head under equity and liabilities part of

company balance sheet.

A. Inventories

B. Shareholders fund

C. Non-current investment

D. Short-term loans and advances

9 Advance payment of tax is a _______.

A. Prepaid Expense

B. General Reserve

C. Interim Dividend

D. Provision for Taxation

10 Patent is shown under __________________.

A. Assets side under intangible Assets

B. Assets side under current assets

C. Liabilities side under current liability

D. None of the above

11 According to schedule VI Companies Act which of the following

items is not shown on asset side of balance sheet?

A. Investment

B. Current loan & advances

C. Provision

D. Lease holds

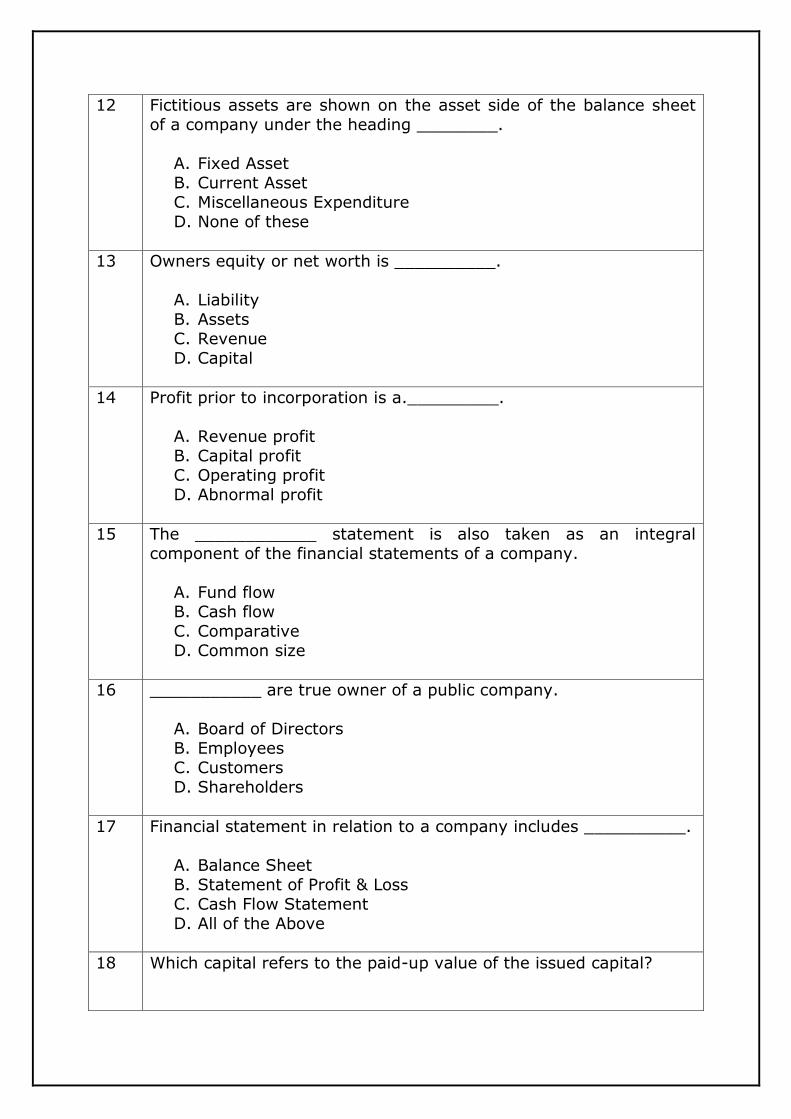

12 Fictitious assets are shown on the asset side of the balance sheet

of a company under the heading ________.

A. Fixed Asset

B. Current Asset

C. Miscellaneous Expenditure

D. None of these

13 Owners equity or net worth is __________.

A. Liability

B. Assets

C. Revenue

D. Capital

14 Profit prior to incorporation is a._________.

A. Revenue profit

B. Capital profit

C. Operating profit

D. Abnormal profit

15 The ____________ statement is also taken as an integral

component of the financial statements of a company.

A. Fund flow

B. Cash flow

C. Comparative

D. Common size

16 ___________ are true owner of a public company.

A. Board of Directors

B. Employees

C. Customers

D. Shareholders

17 Financial statement in relation to a company includes __________.

A. Balance Sheet

B. Statement of Profit & Loss

C. Cash Flow Statement

D. All of the Above

18 Which capital refers to the paid-up value of the issued capital?

A. Subscribed capital

B. Reserve capital

C. Issued capital

D. None of the above

19 Notes to Accounts are.......part of financial statement(s).

A. Integral

B. Optional

C. Auxiliary

D. Unnecessary

20 Item to be included in reserve &surplus?

A. Capital redemption reserves

B. General reserve

C. Securities premium

D. All of the above

21 Match List-I with List-II and select the correct answer using the

codes given below the lists:

List-I(Item of balance sheet of

company)

List-II\(Heading of balance

sheet)

(a) Profit prior to Incorporation 1. Provisions

(b) Proposed dividend 2. Misc. Expenditure

(c) Interest paid out of Capital 3. Current liabilities

(d) Unclaimed dividend 4. Reserve & surplus

A. (a)-4, (b)-1, (c)-3, (d)-2

B. (a)-4, (b)-1, (c)-2, (d)-3

C. (a)-1, (b)-4, (c)-2, (d)-3

D. (a)-1, (b)-4, (c)-3, (d)-2

22 Which of the following reserves cannot be distributed as dividend

to shareholders?

A. Securities premium

B. Profit on forfeiture of shares

C. Profit on sale of fixed assets D. All of the above

23 Which of the following reserve does not appear in the balance

sheet of a company?

A. Secret reserve B. General reserve

C. Capital reserve

D. Specific reserve

24 Unclaimed dividend is shown on the liability side of the balance

sheet of a company as ___________.

A. Share Capital

B. Current Liabilities

C. Reserves & Surplus

D. Non-Current Liability

25 Consider the following statements:

1. The companies Act, 2013 provides provisions related to

uniform financial year from 1st April to 31st, March.

2. The companies Act, 2013 does not provides any provision

related to 'Corporate Social Responsibility (CSR)'.

3. The companies Act, 2013 was passed by 'Rajya Sabha' on

8th August, 2013.

Which of the above statement/s is/are not true?

A. 1 and 2 B. Only 1

C. Only 2

D. 2 and 3

26 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code given below:

Assertion (A): Revenue expenditure is written off in the year in

which it occurs.

Reason

Reason (R): The benefit of revenue expenditure is consumed in

the year in which it arises.

A. Both Assertion and Reason are correct and Reason is the

correct explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

27 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A): Capital structure refers to composition of long-term funds.

Reason (R): These include equity share capital, preference share

capital, debentures, all debts and all reserves.

A. Both Assertion and Reason are correct and Reason is the

correct explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

28 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A). Accounting information refers to only events which

are concerned with business firm.

Reason (R): Accounting information is presented in financial

statements.

A. Both Assertion and Reason are correct and Reason is the

correct explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

29 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A): Many companies prepare their Balance Sheet in a

vertical form rather than in the traditional horizontal form.

Reason (R): Part IV of Schedule VI to the Companies Act 1956,

permits both the forms.

A. Both Assertion and Reason are correct and Reason is the

correct explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

30 Given below are two statements, one labelled as Assertion (A)

and the other labelled as Reason (R). You are to examine these

two statements carefully and select the answers using the code

given below:

Assertion (A): The balance sheet fails to reveal the worth of a

business.

Reason (R): Assets are merely unamortised costs.

A. Both Assertion and Reason are correct and Reason is the

correct explanation for Assertion

B. Both Assertion and Reason are correct but Reason is not the

correct explanation for Assertion

C. Assertion is correct but Reason is incorrect

D. Both Assertion and Reason are incorrect

CASE STUDY - QUESTIONS 31 - 34

M Limited is a company listed on recognized stock exchange in

India having its registered office in New Delhi. The Company is

engaged in sale, purchase, maintenance, of Auto mobile related

products and also provide consultancy services in India

M Ltd. Is in the process of preparing its Balance Sheet as per Schedule III, Part I of the Companies Act, 2013 and provides its

true and fair view of the financial position.

Based on the above case study question choose the correct

alternative for question 31 - 34

31 Under which head and sub-head will the company show ‘Stores and

Spares’ in its Balance Sheet?

A. Head: Fixed Assets Sub head ; tangible Assets

B. Head: Non-Current Assets Sub head ; other non-current

asset

C. Head: Current Assets Sub head ; Inventories

D. Head: Current Assets Sub head ; other current asset

32 What is the accounting treatment of ‘Stores and Spares’ when the

Company will calculate its Inventory Turnover Ratio?

A. While calculating Inventory Turnover Ratio it is included in

Inventories.

B. While calculating Inventory Turnover Ratio it is not included

in Inventories.

C. While calculating Inventory Turnover Ratio it is not included

in Net sales. D. While calculating Inventory Turnover Ratio it is included in

purchase.

33 The management of M Ltd. wants to analyze its Financial

Statements. The main objective of such analysis.

A. To know the financial strength

B. To make the comparative study with other firms.

C. To know the efficiency of the management.

D. All of the above.

34 Under which major headings and sub-heading will “Provision for employee benefits “shown in the Balance Sheet of a company as

per Schedule III of Companies Act, 2013?

A. Head: Non-current liability Sub head ; Deferred provision

B. Head: Non-current liability Sub head ; Long term provision

C. Head: Current liability Sub head ; Current liability

D. Head: Current liability Sub head ; Short term provision

CASE STUDY - QUESTIONS 35 – 38

ABC Ltd. Is a newly established business firm that deals in the

manufacturing of cars. It was established in the year 2019 in pre-

Covid times. Due to outbreak of pandemic, their sales went down

at first as a result of nationwide lockdown but eventually it got increased due to preference of people for use of personal vehicles

for commuting. The entity is perplexed about its performance in

the past two years and is therefore not able to provide relevant

financial information to its users. As a senior accountant of the

company, you need to provide solutions to their following

problems:

Based on the above case study question choose the correct

alternative for question 35 - 38

35 All of the following tools can be used by the company to compare

it’s performances in the past two years, except:

A. Cash flow analysis

B. Ratio analysis

C. Common size statements D. Trial balance summary

36 The document through which the company can make its users fully understand its financial statements is referred to as:

A. Audit notes

B. Notes to accounts

C. Working notes

D. Clarifications

37 The question talks about the users of accounting information.

Whom amongst the following, would you classify as an internal

user of accounting information?

A. Managers

B. Government

C. Suppliers

D. Public

38 Which of the following documents will exhibit the financial position

of ABC Ltd.?

A. Statement of Profit and Loss

B. Notes to accounts

C. Balance sheet

D. Statement of affairs

ANSWERS

QUESTION ANSWER QUESTION ANSWER

1 A 20 D

2 C 21 B

3 C 22 D

4 A 23 A

5 D 24 B

6 D 25 D

7 A 26 A

8 B 27 A

9 A 28 A

10 A 29 A

11 C 30 A

12 C 31 C

13 D 32 A

14 B 33 D

15 B 34 B

16 D 35 D

17 D 36 B

18 A 37 A

19 A 38 C

RATIO ANALYSIS

1 Afghan Ltd. has Operating profit Ratio of 20%. To maintain this ratio at

25%, management may ___________.

A. Reduce cost of revenue from operations.

B. Increase selling price of Stock-in-trade.

C. Increase selling price of Stock-in-trade & to reduce Cost of

Revenue from Operations.

D. All of the above.

2 Current Assets (at cost) Rs.24,00,000 , Credit Sales Rs. 68,00,000 ,

Cash Sales Rs.600,000 , Sales Return Rs.2,00,000. What can be Current

Assets Turnover Ratio?

A. 2 times

B. 3 times C. 4 times

D. 10 times

3 Which Ratio is not a part of Solvency Ratio?

A. Proprietary Ratio B. Current Ratio

C. Debt- Equity Ratio

D. Total Assets – Debt Ratio

4 If Revenue from Operations Rs. 3,20,000 & Gross Profit is Rs. 80,000.

Gross Profit Ratio will be________.

A. 40%

B. 25 %

C. 90%

D. 50%

5 What we can call the difference between Revenue from Operations & Operating Profit?

A. Net Profit Before Tax

B. Gross Profit Ratio

C. Proprietary Ratio

D. Operating Cost

6 For calculating Quick Assets, _____ & ______ are excluded from Current

Assets.

A. Fixed Assets & Inventory

B. Debtors & Creditors

C. Inventory & Prepaid Expenses

D. All of the above

7 Tata Ltd. made the transaction involving a decrease in Debt- Equity Ratio

by 25% & increase in Current Ratio from 2:1 to 3:1. What might be the

reason?

A. Issue of Debentures against the purchase of Fixed Assets

B. Issue of Debentures for Cash

C. Redemption of Preference shares for cash D. Issue of Equity shares for cash

8 Champion Ltd. define following data for calculating Current Ratio:

Current Assets Rs.20,00,000 ,

Inventories Rs.10,00,000 ,

Working Capital Rs.12, 00,000.

A. 3.5 : 1

B. 2.5 : 1

C. 1 : 1

D. 1 : 2

9 The data of Bemishal Ltd. given as follow : Fixed Assets Rs.12,00,000 ,

Accumulated Depreciation Rs.2,00,000 , Trade Investments Rs.1,00,000,

Current Assets Rs.4,40,000 , Current Liabilities Rs.3,40,000. Find out

Capital Employed.

A. Rs.14,00,000

B. Rs.12,00,000

C. Rs.20,00,000

D. Not any one from the above

10 Current Ratio of Bhasmang Ltd. is 2:1. On the sale of fixed asset (Book

value Rs.80, 000) for Rs.72, 000 on credit, state whether the Current

Ratio will be?

A. Decline

B. Not Change C. Improve

D. Can’t say

11 If Current Ratio of Nagin Ltd. is 2.5: 1 and its Current Liabilities are

Rs.800, 000. Working Capital will be?

A. Rs.12,00,000

B. Rs.6,00,000

C. Rs.20,00,000

D. Rs.11,11,111

12 Revenue from Operations Rs.9, 00,000, Gross Profit 25% on cost,

Operating Expenses Rs.90, 000, Operating Ratio will be?

A. 100%

B. 50%

C. 90%

D. 110%

13 If Shakuni Ltd. has a Proprietary Ratio of 30%. To maintain this ratio at

40%, management may___________.

A. Increase in Equity

B. Reduce Debt

C. Increase in Current Assets

D. Either Increase Equity or Reduce Debt

14 Narayan Ltd. shows his Non-Current Assets of Rs.52, 00,000, Current

Assets of Rs.18, 00,000, & Shareholders’ Funds are Rs.43, 00,000. Find

out Total Debts of the Narayan Ltd.

A. Rs.70,00,000

B. Rs.27,00,000

C. Rs.95,00,000 D. Rs.52,00,000

15 Current Ratio of Insan Ltd. is 4: 3. Accountant wants to maintain it at

2:1. What he/she choose from the following to maintain ideal ratio?

(i) He can repay Bills Payable (ii) He can Purchase goods on credit

(iii) He can take short –term loan

Choose the correct option:

A. Only (i) is correct

B. Only (ii) is correct

C. Only (i) and (iii) are correct

D. Only (i) and (ii) are correct

16 What can be fundamental measures of operational efficiency of a

company?

A. Liquid Ratio & Operating Ratio

B. Inventory Turnover Ratio & Working Capital Turnover Ratio

C. Liquid Ratio & Current Ratio

D. Gross Profit Margin & Net Profit Margin

17 Ideal Proprietary Ratio should be ______.

A. 90%

B. 50%

C. 25%

D. 75%

18 Average Payment Period is particularly useful for______ since it helps in

knowing the bill paying patterns of the firm.

A. Suppliers & Lenders

B. Customers

C. Shareholders

D. Debtors

19 100 – Operating Profit Ratio is equal to_______.

A. Current Ratio

B. Operating Net Profit Ratio

C. Gross Profit Ratio

D. Operating Ratio

20 Which of the following will decrease the Debt – Equity Ratio?

A. Purchase of Fixed Asset by taking a long – term loan

B. Purchase of a Fixed Asset by issuing shares for consideration

C. Sale of Fixed Assets ( Book Value Rs.90,000 ) for Rs.80,000

D. Issue of Debentures of Rs.1,50,000 in the market

21

Group X Group Y

(i) Equity (a) Current Assets – Current

Liabilities

(ii) Working Capital (b) Capital Employed – Debt

(iii) Equity (c) Revenue from Operations –

Operating Cost

Match the following

A. i-c , ii- a, iii-b

B. i-b, ii-a, iii-c

C. i-a, ii-b, iii-c

D. i-c, ii-b, iii-a

22

Group P Group M

(i) Proprietary Ratio (a) Cost Revenue from Operations

Average Inventory

(ii) Inventory Turnover Ratio (b) Proprietors’ Funds*(100)

Total Assets

(iii) Return on Investment (c)(Profit before Interest, Tax &

Dividend)*(100)

Capital Employed

Match the following

A. i-b, ii-a, iii-c

B. i-c, ii-a, iii-b

C. i-a, ii-b, iii-c

D. i-c, ii-b, iii-a

23

Group A Group B

1) Gross profit ratio will

increase

(a) Increase in revenue from

operation

2) Gross profit ratio will

decrease

(b) Increase in cost of revenue

from operation

(c) Increase in wages of

workers

(d) Increase in salary of

employees

Match the following

A. 1-a, 2-b

B. 1-b, 2-c

C. 1-c, 2-d D. 1-d, 2-a

24 Which one of the following is correct?

i. A ratio is an arithmetical relationship of one number to another

number. ii. Liquid ratio is also known as acid test ratio.

iii. Ideally accepted current ratio is 1: 1.

iv. Debt equity ratio is the relationship between outsider’s funds and

shareholders’ funds. In the context of the above two statements,

which of the following options is correct?

v.

A. All (i), (ii), (iii) and (iv) are correct.

B. Only (i), (ii) and (iv) are correct.

C. Only (ii), (iii) and (iv) are correct.

D. Only (ii) and (iv) are correct.

25 Which of the following is not an activity ratio?

A. Inventory turnover ratio

B. Interest coverage ratio

C. Working capital turnover ratio

D. Trade receivables turnover ratio

26 Given below are two statements, one labelled as Assertion (A) and the

other labelled as Reason (R)

Assertion (A): Activity Ratios are the ratios that are ratios that are

calculated for measuring the efficiency of operations of business based

on effective utilization of resources.

Reason (R): Current Ratio & Quick Ratio are liquidity ratios.

A. Both A & R are individually true & R is the correct explanation of A

B. Both A & R are individually true but R is not the correct explanation of A

C. A is true but R is false

D. A is false but R is true

27 Given below are two statements, one labelled as Assertion (A) and the

other labelled as Reason (R)

Assertion (A): Ratio Analysis is indispensable part of interpretation of

results revealed by the financial statements.

Reason (R): Ratio Analysis is a technique which involves regrouping of

data by application of arithmetical relationships, though its interpretation

is a complex matter.

A. Both A & R are individually true & R is the correct explanation of A

B. Both A & R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

28 Given below are two statements, one labelled as Assertion (A) and the

other labelled as Reason (R)

Assertion (A): The limitations of financial statements also form the

limitations of the ratio analysis.

Reason (R): Since the ratios are derived from the financial statements,

any weakness in the original financial statements will also creep in the

derived analysis in the form of Accounting Ratios.

A. Both A & R are individually true & R is the correct explanation of A

B. Both A & R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

29 Given below are two statements, one labelled as Assertion (A) and the

other labelled as Reason (R)

Assertion (A): Interest Coverage Ratio expresses the relationship

between profits available for payment of interest & the amount of

interest payable.

Reason (R): A higher ratio ensures lesser safety of interest on payable

on debts.

A. Both A & R are individually true & R is the correct explanation of A

B. Both A & R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

30 Given below are two statements, one labelled as Assertion (A) and the

other labelled as Reason (R)

Assertion (A): If debt equity ratio is 1:2, it is considered to be safe.

Reason (R): From security point of view, capital structure with less debt

& more equity is considered favorable as it reduces the chances of

bankruptcy.

A. Both A & R are individually true & R is the correct explanation of A

B. Both A & R are individually true but R is not the correct

explanation of A

C. A is true but R is false

D. A is false but R is true

CASE STUDY - QUESTIONS 31 – 34

Kohinoor Ltd. is interested to know the return on their total investment

made in their company. The company is also interested to know what

portion of total assets have been financed through Long-term Debts.

10%Long-term Debts Rs.400,000 ,Current Liabilities Rs.200,000 , Land

Rs.200,000 , Building Rs.200,000 , Fixed Assets Rs.200,000 , Debtors

Rs.200,000 , Current Assets Rs.200,000 , Net Profit After Interest & Tax

Rs.100,000 , Tax Rate 20% .

Amount of Fixed Assets & Current Assets does not include Land, Building,

& Debtors.

Based on the above case study question choose the correct alternative

for question 31 - 34

31 Define the Amount of Capital Employed.

A. Rs.12,00,000

B. Rs.600,000

C. Rs.800,000 D. Rs.16,00,000

32 Calculate Total Assets – Debt Ratio.

A. 2.4 Times

B. 4.0 Times C. 3.3 Times

D. 2.5 Times

33 The Return on Investment is_____.

A. 20.92% B. 21%

C. 19%

D. 19.62%

34 State the amount of Net Profit Before Interest & Tax.

A. Rs.1,25,000

B. Rs.2,80,000

C. Rs.2,00,000

D. Rs.1,00,000

CASE STUDY - QUESTIONS 35 – 38

Riddhish Ltd. want to analysis its liquidity position along with assessment

of Inventory position from the given information:

Inventory in the beginning was Rs.20, 000 less than Inventory at the

end; Inventory Turnover Ratio is 4 times, Gross Profit Ratio 25%,

Revenue from Operations Rs.600, 000, Current Liabilities Rs.60, 000,

Quick Ratio 75:100.

Based on the above case study question choose the correct alternative

for question 35 - 38

35 Find out the amount of Closing Inventory.

A. Rs.1,12,000

B. Rs.1,12,500

C. Rs.1,11,000

D. Rs. 80,000

36 State the amount of Cost of Revenue from the Operations.

A. Rs.4,00,000

B. Rs.4,50,000

C. Rs.4,80,000

D. Rs.4,90,000

37 State the amount of average inventory.

A. Rs.1,25,000

B. Rs.2,00,000

C. Rs.2,50,000

D. Rs.2,25,000

38 State the Current Ratio.

A. 2.4 : 1

B. 2.5 : 1

C. 2.7 : 1

D. 3.0 : 1

ANSWERS

QUESTION ANSWER QUESTIO

N

ANSWER

1 D 20 B

2 B 21 B

3 B 22 A

4 B 23 A

5 D 24 B

6 C 25 B

7 D 26 B

8 B 27 B

9 A 28 A

10 C 29 C

11 A 30 D

12 C 31 C

13 D 32 A

14 B 33 D

15 A 34 A

16 B 35 A

17 B 36 C

18 A 37 C

19 D 38 B

SAMPLE QUESTION PAPER (TERM-1) 2021-22

ACCOUNTANCY

SUBJECT CODE: 055

Time Allowed: 90 Minutes Maximum Marks: 40

General Instructions:

Read the following instructions very carefully and strictly follow them:

1. This question paper comprises three PARTS – I, II and III. There are

69 questions in the question paper.

2. Part - I -is compulsory for all candidates.

3. Part - II Analysis of Financial Statement and Part -III Computerized

Accounting. You have to attempt only one of the given OPTIONS.

4. There is an internal choice provided in each Sections.

I. Part-I, contains three Sections -A, B and C. Section A has

questions from 1 to 18 and Section B has questions from 19 to 36,

you have to attempt any 15 questions each in both the sections.

II. Part I, Section C has questions from 37 to 41. You have to

attempt any four questions.

III. Part II, contains two Sections – A and B. Section A has questions

from 42 to 48, you have to attempt any five questions and Section

B has questions from 49 to 55, you have to attempt any six

questions.

IV. Part III, contains two Sections – A and B. Section A has

questions from 49 to 62, you have to attempt any five questions

and Section B has questions from 63 to 69, you have to attempt

any six questions.

5. All questions carry equal marks. There is no negative marking.

6. Specific Instructions related to each Part and subdivisions (Section) is

mentioned clearly before the questions. Candidates should read them

thoroughly and attempt accordingly.

Part – I Section – A

Instructions:

➢ From question number 1 to 18, attempt any 15 questions.

1. Gain / loss on revaluation at the time of change in profit sharing

ratio of existing partners is shared by _(i) _ whereas in case

of admission of a partner it is shared by (ii) .

(A) (i) Remaining Partners, (ii) All Partners.

(B) (i) All Partners, (ii) Old partners.

(C) (i) New Partner, (ii) All partner.

(D) (i) Sacrificing Partner, (ii) Incoming partner.

2. Calculate the amount of second & final call when Abhijit Ltd, issues

Equity shares of ₹10 each at a premium of 40% payable on

Application ₹3, On Allotment ₹5, On First Call ₹2.

(A) Second & final call ₹3.

(B) Second & final call ₹4.

(C) Second & final call ₹1.

(D) Second & final call ₹14.

3. Anish Ltd, issued a prospectus inviting applications for 2,000

shares. Applications were received for 3,000 shares and pro- rata

allotment was made to the applicants of 2,400 shares. If Dhruv has

been allotted 40 shares, how many shares he must have applied

for?

(A) 40

(B) 44

(C) 48

(D) 52

4. Ambrish Ltd offered 2,00,000 Equity Shares of ₹10 each, of these

1,98,000 shares were subscribed. The amount was payable as ₹3

on application, ₹4 an allotment and balance on first call. If a

shareholder holding 3,000 shares has defaulted on first call, what is

the amount of money received on first call?

(A) ₹9,000.

(B) ₹5,85,000.

(C) ₹5,91,000.

(D) ₹6,09,000.

5. What will be the correct sequence of events?

(i) Forfeiture of shares. (ii) Default on Calls.

(iii) Re-issue of shares. (iv) Amount transferred to capital reserve.

Options:

(A) (i), (iv), (ii), (iii)

(B) (ii), (iv), (i), (iii)

(C) (ii), (i), (iii), (iv)

(D) (iii), (iv), (i) (ii)

6. Arun and Vijay are partners in a firm sharing profits and losses in the

ratio of 5:1.

Balance Sheet (Extract)

Liabilities ₹ Assets ₹ Machinery 40,000

If the value of machinery reflected in the balance sheet is overvalued by

33 %, find out the value of Machinery to be shown in the new Balance

Sheet:

(A) ₹ 44,000 (B)